Gold: $1104.40 down $2.10 (comex closing time)

Silver $14.99 down 7 cents

In the access market 5:15 pm

Gold $1104.00

Silver: $15.00

Remember tomorrow is the jobs (FOMC report) and expect massive volatilty.

First, here is an outline of what will be discussed tonight:

At the gold comex today, we had a very poor delivery day, registering 0 notices for nil ounces. Silver saw 0 notices for nil oz.

Several months ago the comex had 303 tonnes of total gold. Today, the total inventory rests at 208.24 tonnes for a loss of 95 tonnes over that period.

In silver, the open interest fell by only 144 contracts despite silver being down 18 cents in Wednesday’s trading. The total silver OI now rests at 166,798 contracts In ounces, the OI is still represented by .834 billion oz or 119% of annual global silver production (ex Russia ex China).

In silver we had 0 notices served upon for nil oz.

In gold, the total comex gold OI rose by a rather large 2482 contracts to 446,382 contracts despite the fact that gold was down $7.70 yesterday. We had 0 notices filed for nil oz today.

We had a monstrous withdrawal in gold inventory at the GLD to the tune of 14.53 tonnes / thus the inventory rests tonight at 671.77 tonnes. The appetite for gold coming from China is depleting not only gold from the LBMA and GLD but also the comex is bleeding gold. It sure looks like 670 tonnes will be the rock bottom inventory in GLD gold. It looks to me that China has taken the last amounts of physical gold from the GLD. I guess the only place left for China to receive physical gold will be the FRBNY and the comex. In silver,no change in silver inventory / Inventory rests at 313.817 million oz.

We have a few important stories to bring to your attention today…

1. Today, we had the open interest in silver fell by a tiny 144 contracts down to 166,798 despite the fact that silver was down 18 cents with respect to yesterday’s trading. The total OI for gold rose by a rather large 2482 contracts to 446,382 contracts despite the fact that gold was down $7.70 yesterday.

The fact that OI continues to remain high in silver necessitates the bankers to continue raiding hoping to shake the leaves from both the gold and silver trees. Remember that December is generally a big delivery month for both gold and silver

(report Harvey)

2.Gold trading overnight, Goldcore

(/Mark OByrne)

9 USA stories/Trading of equities NY

i) Challenger Grey reports huge increase in layoffs in the energy sector/initial claims rise

(Challenger/Grey/zero hedge)

ii) unit labour costs rise less than expected/this bothers the Fed greatly

(zero hedge)

iii) Because GDP data and the unemployment rate are bogus there is another way of calculating economic output and the BLS actually reports this on a quarterly basis. It shows economic output is on the decline as well as actual jobs.

(Economic Output/BLS/zero hedge)

iv) A very important piece….the Fed is trapped. They see huge bubbles and must raise rates even though it will kill multinationals and EM nations. Now the Fed is trying to justify a rate rise by showing hidden inflation in rents.

(zero hedge)

v) Another high tech company Kura which IPO’d yesterday is crashing along with Valeant.

(zero hedge)

vii)

10. Physical stories

i) Ratio of paper gold to registered gold at the comex rises to 293 to one, the highest on record

(zero hedge)

ii) Bill Holter’s piece tonight is entitled: “A Tool? A Fool? …Or rewriting history?”

iii) Dave Kranzler on silver: the most manipulated product in the universe!

(Dave Kranzler/IRD)

Let us head over to the comex:

November contract month:

INITIAL standings for November/First day notice

Nov 5/2015

| Gold |

Ounces

|

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz nil | 2,089.75 oz

(Scotia) |

| Deposits to the Dealer Inventory in oz | nil |

| Deposits to the Customer Inventory, in oz | nil |

| No of oz served (contracts) today | 0 contracts

nil oz |

| No of oz to be served (notices) | 247 contracts

(24,700 oz) |

| Total monthly oz gold served (contracts) so far this month | 6 contracts

600 oz |

| Total accumulative withdrawals of gold from the Dealers inventory this month | nil |

| Total accumulative withdrawal of gold from the Customer inventory this month | 5361.2 oz

|

Total customer deposits nil oz

we had 0 adjustments:

November initial standings/First day notice

Nov 5/2015:

| Silver |

Ounces

|

| Withdrawals from Dealers Inventory | nil |

| Withdrawals from Customer Inventory | 681,595.600 oz

(Brinks, CNT,Scotia) |

| Deposits to the Dealer Inventory | nil |

| Deposits to the Customer Inventory | |

| No of oz served (contracts) | 0 contracts (nil oz) |

| No of oz to be served (notices) | 7 contracts

35,000 oz) |

| Total monthly oz silver served (contracts) | 5 contracts (25,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | nil oz |

| Total accumulative withdrawal of silver from the Customer inventory this month | 1,584,019.3 oz |

Today, we had 0 deposit into the dealer account:

total dealer deposit; nil oz

total customer deposits: nil oz

total withdrawals from customer: 681,595.600 oz

And now SLV

Nov 5/strange no change in silver inventory/rests tonight at 313.817 million oz/

Nov 4/2015: no change in silver inventory/rests tonight at 313.817 million oz/

Nov 3.2015; no change in silver inventory/rests tonight at 313.817 million oz/

Nov 2/a withdrawal of 716,000 oz from the SLV/Inventory rests tonight at 313.817 million oz

Oct 30.no change in silver inventory at the SLV/Inventory rests at 314.532 million oz

Oct 29/a big withdrawal of 1.001 million oz from the SLV/Inventory rests at 314.532 million oz

Oct 28.2015: no change in silver inventory at the SLV//inventory rests at 315.533 million oz.

Oct 27/no change in silver inventory at the SLV/Inventory rests at 315.533 million oz/

Oct 26/no change in silver inventory at the SLV/Inventory rests at 315.533 million oz/

Oct 23./no change in silver inventory at the SLV/Inventory rests at 315.533 million oz

Oct 22./no change in silver inventory at the SLV/Inventory rests at 315.533 million oz

Oct 21:a we had a small addition in silver ETF inventory of 381,000 oz/inventory rests tonight at 315.533 million oz

Oct 20.2015/ no change in silver ETF/Inventory rests at 315.152 million oz

Bitcoin Surges 55% In Month – Chinese Moving Capital Into Bitcoin and Gold

Bitcoin has been surging in value since mid October and gained more than 20% yesterday alone. At one point, it hit a yearly high of more than $491 (see chart).

CoinTelegraph

In August, bitcoin fell to a low for 2015 near $200 amid turmoil in the Chinese and global stock markets. But bitcoin transaction volume has been growing. Blockchain.info data shows that unique bitcoin wallet addresses—which are how users manage and trade bitcoin—are at an all-time high. Some have multiple bitcoin addresses, but such a spike suggests there are new users as well.

It’s not entirely clear what’s driven the most recent price gains. There is an assertion in an article on the front page of the FT today that the gains are due to Chinese people flocking to bitcoin in a giant pyramid scheme run on a Russian fraudsters website:

The price of the cryptocurrency bitcoin surged on Wednesday to its highest in more than a year amid a wave of Chinese testimonials for a “social financial network” called MMM, which bears the hallmarks of a pyramid scheme.

New members of MMM have to buy bitcoins to join the scheme, which is the brainchild of Sergey Mavrodi, a former Russian parliamentarian since jailed for fraud.

Although the article is unbalanced and simplistic, the truth regarding the root cause of the price movement of any market is of course much more complex – and there are many supply and demand issues to be considered.

Source: CoinDesk

Most bitcoin experts once again see Chinese demand as key. As China has been devaluing its currency, the yuan, throughout the year and the Chinese are aware of the growing risks posed to the yuan and indeed the dollar and other fiat currencies.

Also, their recent experience of the stock market crash has made bitcoin and, of course, gold more attractive again. Hence the surge in demand for gold in China again. China’s gold buying rose 7.83% year on year to 814 tons in the first three quarters, industry data from the China Gold Association (CGA) showed yesterday.

There are increasing concerns of capital controls in China and Chinese investors and companies are seeking to diversify internationally and move savings and capital out of China.

Bitcoin is an easy way for people to swap out of yuan. Goldman Sachs analysts estimated earlier this year that 80% of bitcoin volume is exchanged in and out of the Chinese yuan. Once converted to bitcoin, the owners can then swap back into other fiat currencies and indeed, physical gold.

We see value in having an allocation to bitcoin and see it as complementary to owning physical gold and silver. It is clearly more volatile than gold and even silver and is not proven as a hedging instrument and safe haven asset. Therefore, it is more speculative and merits having a lower allocation than gold and silver bullion.

DAILY PRICES

Today’s Gold Prices: USD 1107.30, EUR 1024.40 and GBP 724.75 per ounce.

Yesterday’s Gold Prices: USD 1118.00, EUR 1024.09 and GBP 724.99 per ounce.

(LBMA AM)

Gold lost $10.20 yesterday to close at $1107.50. Silver was also down by $0.20 for the day closing at $15.09. Platinum lost $8 to $953.

Download Essential Guide To Storing Gold In Switzerland

end

There Are Now 293 Ounces Of Paper Gold For Every Ounce Of Physical As Comex Registered Gold Hits New Low

Unlike Bitcoin, which has doubled in the past few weeks (as the predicted Chinese buying onslaught indeedmaterialized), it hasn’t been a good week for spot gold prices which have tumbled from $1,180 to just over $1,100. While the reason for the selling is unknown, with recurring speculation that an imminent Fed rate hike will make holding gold even more unwelcome in real terms (if not in India where gold now pays interest on par with inflation), what we do know is that as of yesterday the total registered gold at the Comex had dropped to a fresh record low following another transfer of “registered” gold into “eligible.”

This reduced overnight the total amount of registered gold by a third to just over 151,000 ounces, or under 5 tons as the zoomed in chart below shows.

And since the gold open interest continues to rise modestly…

… this means that as of today, the gold “coverage” ratio, or the amount of paper claims for every ounce of physical, has just hit a new all time high of 293 ounces of paper per ounce of registered physical.

Curiously, the last time we observed a comparable surge in the Comex dilution ratio took place just two months agowhen a comparable “adjustment” reduced JPM’s “Registered” inventory by 122,124 ounces. Back then many said the adjustment would be promptly reversed.

Two months later not only has that not happened, but JPM is now down to just 10,777 ounces of Registered while many other vaults continue to see either outright withdrawals or comparable adjustments.

How much longer can this exponential surge in the dilution ratio continue? We don’t know, although with less than 5 tons of registered gold left in the Comex vault system, we hope that the mystery of what is really going on at the Comex will finally be unveiled.

end

Dave Kranzler on Silver fundamentals:

(courtesy Dave Kranzler IRD)

Silver Is The Most Manipulated Market In History

The price of paper silver has been mauled since Janet Yellen and her band of FOMC merry clowns released their policy statement last Wednesday which made the claim that there was strong possibility that the Fed would hike its Fed Funds rate in December. Silver is now down 8.5% since that statement hit the tape (click images to enlarge):

But as you can see, silver is still in an nice uptrend, up over 7% from the bottom it hit in late August. Of course, in testament to just how manipulated the markets are, the S&P 500 – which should have experienced the same type of sell-off as silver and gold on the threat of higher rates – is up 1.3%.

Part of the reason silver may be getting hit is the news of a report from the investment conference in New Orleans last week that some company had invented an aluminum-based replacement for silver used in solar panels. Obviously, if this were true, it would impact the amount of silver going into India (see this report in which the U.S. exporting 100’s of tons of silver India). And it would impact the amount silver China is using in the development of its massive solar program.

However, if you investigate the “beneath the surface headlines” of this claim being made, the Company has not proved its technology works or is practical in commercial applications. I’ve seen at least two claims by companies over the last 10 years that they’ve developed a pill to cure alcoholism. Still haven’t seen that cure hit the market. And for how many centuries has the world had to endure claims from “scientists” who state they had figured out how to convert lead into gold? As for this company’s claim? I’ll believe it when I see it in action. Until then, it’s nothing but hot air.

Feel free to read the source story here: Natcore swaps silver for aluminum in solar cells.

Until proven otherwise with real life, profit-making applications, I believe that this story will fall into history’s dust-bin of false-flags. Seems a bit coincidental that this story emerges just as the Fed/bullion banks are in the process of raiding the paper precious metals markets…again. The only thing missing from this story is Jordan Belfort (the Wolf of Wall Street) resurrecting his old Stratton Oakmont penny stock brokerage and taking this company public.

The anti-gold/silver propaganda is reaching epic levels again. It also happens to coincide with another multiple-day run on the gold in GLD and a record-breaking run up in the paper/gold ratio on the Comex. The paper to gold ratio at close to 300 is nothing more than a reflection of how desperate the banks are becoming to keep a lid on the price gold/silver.

This paper to underlying deliverable physical commodity ratio is many multiples beyond the ratio that the CFTC and CME allow in ANY other commodity market. It completely destroys the purpose of futures markets. It’s crystal clear that gold futures were introduced in 1974, one year after the U.S. devalued the dollar vs. the yen and Paul Volker admitted over 20 years ex post facto that the Fed made a mistake not preventing the price of gold from moving higher when the dollar was devalued. They couldn’t manipulate the price of gold in 1973 because gold futures didn’t exist.

When history looks back on this period, one of the biggest official frauds will be the Fed’s empty threat of raising interest rates and the world will understand how and why it was used to help keep a lid on the precious metals.  But most of us who have been involved in this market already know the reason…Et tu, Janet?

But most of us who have been involved in this market already know the reason…Et tu, Janet?

This commment from “Martin” is most apropo with respect the aluminum for silver claim:

I remember the year 2011 whcen the German company Schott AG made the announcement that they had developed a solar cell completely void of silver. They said they successfully replaced the precious metal by copper. I could not find their press release, but found some news about it in the Internet: LINK So now 4 years have passed. I have not heard since then that silver in solar cells has been replaced by copper. So I do not put to much confidence in any such news in regard to solar technique that silver may replaced by some other metal. At least not on a big scale.

end

A Tool? A Fool? …Or rewriting history?

1 Chinese yuan vs USA dollar/yuan remains constant , this time at 6.3355 Shanghai bourse: in the green, hang sang:red

2 Nikkei closed up 243.67 or 1.30%

3. Europe stocks mostly in the green /USA dollar index up to 98.05/Euro up to 1.0865

3b Japan 10 year bond yield: falls slightly to .318% !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 121.98

3c Nikkei now just above 18,000

3d USA/Yen rate now well above the important 120 barrier this morning

3e WTI: 46.37 and Brent: 48.69

3f Gold up /Yen down

3gJapan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa.

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil up for WTI and up for Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10 yr bund rises to .600 per cent. German bunds in negative yields from 5 years out

Greece sees its 2 year rate rise to 8.04%/: still expect continual bank runs on Greek banks

3j Greek 10 year bond yield falls to : 7.73% (yield curve inverted)

3k Gold at $1110.90 /silver $15.07 (8:00 am est)

3l USA vs Russian rouble; (Russian rouble down 1/100 in roubles/dollar) 63.21

3m oil into the 46 dollar handle for WTI and 48 handle for Brent/ China purchases huge supplies from Saudi Arabia

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation (already upon us). This can spell financial disaster for the rest of the world/China forced to do QE!! as it lowers its yuan value to the dollar.

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning .9962 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.0828 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p Britain’s serious fraud squad investigating the Bank of England on criminal charges/

3r the 5 year German bund now in negative territory with the 10 year rises to +.600%/German 5 year rate negative%!!!

3s The ELA lowers to 82.4 billion euros,

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.23% early this morning. Thirty year rate below 3% at 2.99% / yield curve flatten/foreshadowing recession.

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

(courtesy Jim Reid/Bloomberg/Deutsche bank/zero hedge)

S&P Futures Spike Back Over 2100 On Central Banks, Yen Carry Levitation, China Bull Market

For those eager to cut to the chase and curious if overnight we have had another standard USDJPY ramp levitating US equity futures on low volume, the answer is yes. And since the USDJPY carry was patient enough, it managed to trigger the 2100 ES stops and as of this moment the futures were comfortably on the politically-correct side of 2100.

The levitation is across the board:

- S&P 500 futures up 0.3% to 2102

- Stoxx 600 up 0.1% to 381

- MSCI Asia Pacific down 0.2% to 135

- US 10-yr yield up less than 1bp to 2.23%

- Dollar Index up 0.09% to 98.04

- WTI Crude futures up less than 0.1% to $46.35

- Brent Futures up 0.3% to $48.73

- Gold spot up less than 0.1% to $1,108

- Silver spot down 0.4% to $15.03

With the summary out of the way, let’s look at the key overnight event in an otherwise sleepy tape which for the second day in a row came out of China, where starting with yesterday’s purposefully “leaked” old news by the PBOC that led to a limit-up surge in brokers, today we saw a continuation of this with euphoric sentiment and the SHCOMP soared in early trading, jumping over 20% from its August lows and entering a fresh bull market. This is the 3rd time since the crash in June that Chinese stocks have staged a substantial rise.

To be sure, the rally is not based on fundamentals, with China’s GDP continuing to slide, its commodity sector under grueling stress, and as moments ago China’s Mofcom reported:

- CHINA MOFCOM: MAJOR COMMODITY PRICES TO STAY LOW INTO NEXT YR

- CHINA MOFCOM: EXPECTS SHARP DROP IN IMPORTS THIS YEAR

- CHINA MOFCOM: DIFFICULT TO SEE FAST EXPORT GROWTH IN Q4

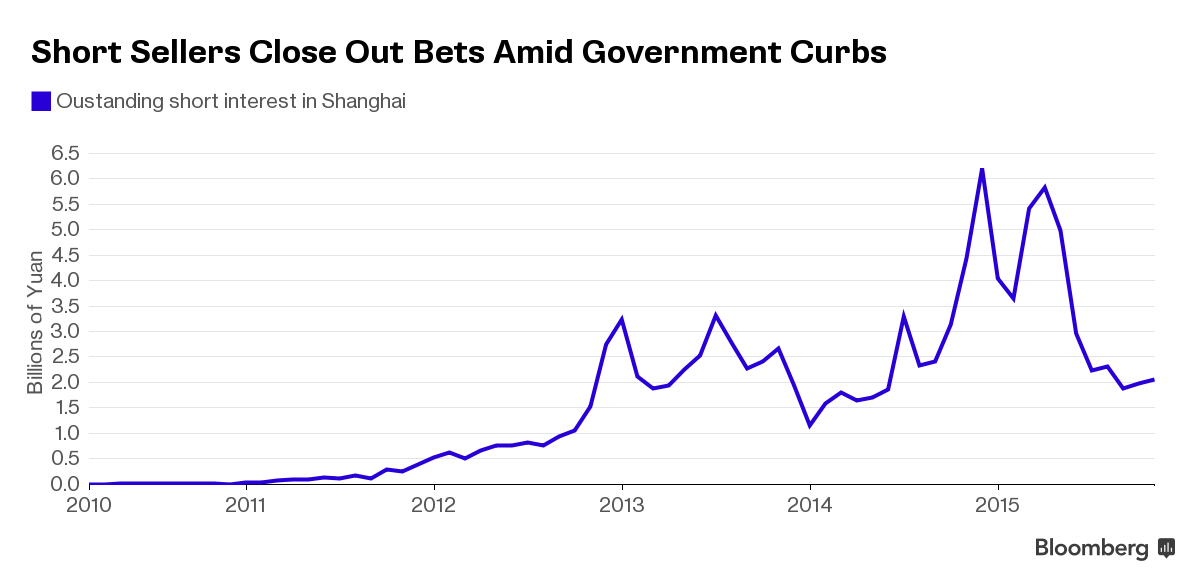

So what is going on? The following three charts from Bloomberg explain it.

First, short sellers are now officially gone (and unofficially arrested). Per BBG, “Short sellers have largely been shut out of China’s market after curbs by both the government and brokers made it more difficult to bet on falling share prices.”

Then, just like with Bitcoin, there has been a recent surge in volume: “Trading has picked up in Shanghai as shares rallied, an indication that ordinary investors are starting to take over from the government-run funds that propped up prices during the depths of the rout.”

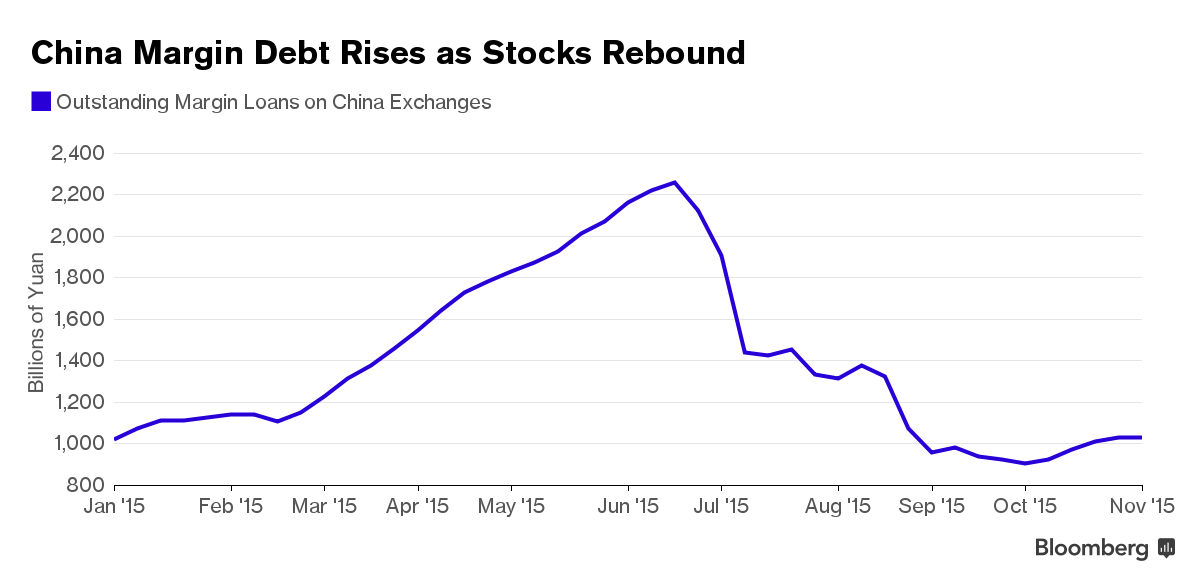

Most importantly, margin debt is once again coming back: “Investors are slowly rebuilding positions using borrowed money. Margin financing surged to more than 2.2 trillion yuan at the height of the stock boom, before falling by more than half in the bust. It’s now back above 1 trillion yuan, adding fuel to the rally but also raising the odds of bigger price swings.”

End result: Chinese markets closed higher with the Shanghai Comp. (+2.2%) in bull-market territory. Even with this latest surge, it remains around 30% lower than their June highs, which were the highest levels seen in the index for 7 years.

Elsewhere in Asia equity markets traded mixed following the weak close on Wall St.

where commodity weakness and prospects for a December rate hike weighed

on sentiment. This saw pressure in the ASX 200 (-0.9%) with financials

among the underperformers, after earnings from CBA. Nikkei 225 (+1.0%)

was lifted as JPY remains weak, following strong results from Japan

Tobacco and Fast Retailing’s Uniqlo.

Asian wrap:

- MSCI Asia Pacific down 0.2% to 135

- Nikkei 225 up 1% to 19116

- Hang Seng down less than 0.1% to 23051

- Shanghai Composite up 1.8% to 3523

- S&P/ASX 200 down 0.9% to 5193

Key Asian news from BBG:

- Australia Halts RMBS Auctions After Volumes Less Than Expected: No bids were accepted by govt at last RMBS auction

- Draghi Beating Kuroda in Easing Drives Europeans to Japan Debt: Foreign buying of JGBs reaches record for Jan.- Sept. period

- JPMorgan India Fund Woes Spurs Tighter Redemption Regulations: Sebi demands greater disclosures from credit rating agencies

- China Regulator Probes Accusations Alibaba Pressured Merchants: Agency accepts request to examine Singles’ Day tactics: JD

* * *

On to Europe where stocks are likewise solidly in the green after the latest disappointing news out of Germany where German industrial orders dropped “unexpectedly” in September due mainly to weaker foreign demand, in a sign that Europe’s biggest economy may loose steam at the end of this year.

According to Reuters, contracts for ‘Made in Germany’ goods were down by 1.7% on the month, the economy ministry said on Thursday. It is the first time since the summer of 2011 that orders have dropped for three consecutive months and compares with a Reuters consensus forecast for a rise of 1.0 percent.

If that wasn’t enough to push the Stoxx50 higher, we also got a miss in EU Retail Sales, which declined -0.1% in October, down from 0.0% in September and below the 0.2% increase expected.

Ironically, at the same time, the EU released its latest forecast for 2015 which saw an increase for 2015. TheWSJ reports that “low oil prices and easy money will boost European growth this year more than previously expected, the European Union said Thursday, but it cautioned that a slowdown in emerging economies and increased global uncertainty could damp the economy’s positive momentum.”

Economists at the commission forecast that gross domestic product in the 19-nation eurozone would grow 1.6% this year, up from their previous estimate in May of 1.5%. They predicted growth of 1.9% in the 28-nation EU, up from 1.8% in May. However, the commission slightly trimmed its forecasts for next year, seeing eurozone growth at 1.8%, down from the 1.9% it forecast in May and EU growth at 2%, down from the previously forecast 2.1%.

It is not clear why this is not bad news for markets since an increase in growth expectations makes more Q€ less likely, although the answer is simple: nobody believes the forecast.

As a result of this negative current data coupled with clueless optimistic forecasts, stocks in Europe are broadly up, with the Euro Stoxx: 0.5%, with defensive sectors outperforming ahead of key risk events later today in the form of the BoE’s Super Thursday and US NFP tomorrow, while Bunds trade marginally lower in line with today’s supply, which equates to around 109k Bund futures and the Short-Sterling curve trades a touch steeper as market participants position for the upcoming BoE events. In terms of stock specific news, Adecco (-8.8%) and Credit Agricole (-6.0%) are among the worst performers after reporting their earnings pre market.

Europe Wrap:

- Stoxx 600 up 0.1% to 381

- FTSE 100 down 0.4% to 6385

- DAX up 0.6% to 10905

- German 10Yr yield down 1bp to 0.59%

- Italian 10Yr yield down less than 1bp to 1.67%

- Spanish 10Yr yield up less than 1bp to 1.76%

- S&P GSCI Index down 0.2% to 359.5

Key European news from BBG:

- German Factory Orders Unexpectedly Decline for Third Month: Indicator unexpectedly extended a series of declines in September amid a slump in demand for investment goods in the euro area.

- SocGen Net Rises on Consumer Bank Before Branch Closures: Co. reported 28% increase in 3Q profit on improved consumer- banking results that outweighed a slump in trading revenue.

- Adidas Raises 2015 Forecasts, Plans to Cut Jobs at Golf Unit: Co. raised FY forecasts, said it’s cutting jobs at its languishing golf-gear division as it tries to appease investors pushing for faster change.

In FX markets, EUR saw initial softness after the unexpected fall in German factory orders (M/M -1.70% vs. Exp. 1.00%), however EUR/GBP has since recovered and trades little changed , with EUR/USD also initially moved higher on touted profit taking following the recent slide, while EUR/USD 1-month vol which captures Dec ECB policy meeting remains elevated and trades at 12.4 (vs.9.6 on Monday) and despite the negative outlook for the pair, touted corporate buying and option hedging flow saw the pair recover off overnight lows. Elsewhere, USD/JPY earlier saw strength after tripping stops on the break of yesterday’s high, however further upside by USD/JPY has been capped by touted double-no-touch (DNT) expiry at 122.00 (118.00 and 122.00 structure).

RBA Governor Stevens said that accommodative policy would be appropriate for some time and if policy were to change, it would be easing rather than tightening . Stevens also commented that he doesn’t see a significant effect of the bank mortgage increases which so far is equal to around a half of a 25bps rate reduction.

In commodities, oil trades relatively flat in what has been a choppy session for commodities after yesterday saw DoE crude oil inventories (W/W 2847K vs. Exp. 2500K, Prey. 3376K) showed a greater than expected build causing WTI and Brent prices to fall. NatGas has trended lower with the EIA natural gas storage change later today expected to show a build (Exp. 53bcf, Prey. 63 bcf). The metals complex has seen gold trade relatively flat to remain near their lowest levels in a month following comments from Fed Chair Yellen that a December Fed hike remains a live possibility.

On today’s calendar, the main focus in the European session today will be the UK’s BoE meeting which will see the latest inflation report released, the meeting minutes and also comments from the BoE’s Carney shortly after. Datawise, Euro area retail sales and German factory orders are the main releases of note this morning.

In the US we get Q3 nonfarm productivity and unit labour costs due along with the latest initial jobless claims. It’s a big day for Fedspeak also with Dudley and Fischer set to speak at 1.30pm GMT (along with the IMF’s Lagarde), followed by Lockhart at 6.30pm GMT. Former Fed Chair Bernanke is also scheduled to give the keynote speech at an IMF conference at 9pm GMT tonight. In terms of earnings, we’ve got 24 S&P 500 companies set to report their latest quarterly numbers including Kraft Heinz and Walt Disney. In the Stoxx 600 we’ve got 32 companies scheduled to report including Astra Zeneca and Deutsche Telekom.

Top News:

- Fed’s Most Powerful Trio Keep Dec. Rate Rise on the Table: Speaking in New York hours after Yellen’s House testimony, Dudley said he agreed with the chair, but “let’s see what the data shows.”

- Whole Foods Plunges as Flagging Sales Renew Growth Concerns: Same-store sales fell 0.2% in 4Q, representing worst performance in more than 5 years.

- Facebook Sales Top Estimates, Fueled by Mobile Advertising: Social network now has 1.01b daily visitors; monthly users jumped 14% percent to 1.55b.

- Autodesk CEO Blasts Activist Investors After Sachem Head’s Move: Comments about focus only on short-term results come after activist reveals 5.7% stake.

- Credit Agricole Plunges on Lower Trading, Consumer Bank Sales: Shares down most since Aug. after lender reported decline in profit at its investment bank, also decline in consumer-banking revenue at the French LCL branch network.

- Jet.com Said to Near Funds Valuing Amazon Rival at $1.5b: Co. close to raising $500m-$550m in funding round led by Fidelity Investments, according to person familiar.

- Jana Partners Exits Valeant, Takes Microsoft, Baxter Stakes: Jana established position in Valeant in 4Q 2014 and owned 1.3m shares at end of June.

- Tech, Banking, Farming Among U.S. Winners in Pacific Trade Deal: U.S. Releases text of Trans-Pacific Partnership accord

- Bomb-Plot Suspicion Becomes Top Theory in Crash of Egypt Jet: Preliminary evidence suggested Islamic State involvement, investigators examining prospect that someone was bribed to get bomb on board.

- Musk’s SpaceX Finds Crowd for $3.5 Billion NASA Contract: Co. in four-way derby with Boeing, Orbital ATK, Sierra Nevada, each of which relies to some extent on rockets with Russian engines.

- China Stocks Enter Bull Market as State Stimulus Reverses Rout: Shanghai Composite climbed 1.8% to 3,522.82 at close, taking its advance from its Aug. 26 low to >20%. China Signals Reserve Ratios May Be Used to Discipline Banks: Officials want to control competition after freeing up rates.

Bulletin Headline Summary from Bloomberg and RanSquawk

- Stocks in Europe have been fairly mixed with defensive sectors outperforming ahead of key risk events later today, while Shanghai Composite has now gained over 20% from August lows

- EUR saw initial softness after the unexpected fall in German factory orders (M/M -1.70% vs. Exp. 1.00%), however EUR has since recovered and trades little changed against both GBP and USD

- Today’s highlights include BoE’s ‘Super Thursday, US challenger job cuts, weekly jobs data and EIA Natgas storage change, as well as comments from ECB’s Draghi, Fed’s Harker, Dudley, Evans, Tarullo and Lockhart

- Treasuries little changed, 2Y yields highest since 2011 as markets prepare for October payrolls report tomorrow; Yellen yesterday said a rate hike next month was a “live possibility.”

- Also yesterday: NY Fed’s William Dudley both said the Fed could boost interest rates as soon as next month, while Vice Chairman Stanley Fischer voiced confidence that inflation isn’t too far below the central bank’s goal

- The European Commission cut its euro-area growth and inflation outlook for next year, citing more challenging global conditions and fading impetus from lower oil prices and a weaker euro

- Germany’s expanding refugee population should lift the nation’s economy by boosting spending in the short term and expanding the labor market in the years ahead, the EC said

- EC President Jean-Claude Juncker, whose appointment Great Britain’s David Cameron sought to block, has handed the U.K. PM ammunition to use against his opponents as the British government prepares to submit its wish-list of EU reforms as early as next week

- China’s stocks rose, with the benchmark index entering a bull market, after an unprecedented state rescue effort halted a $5t crash and ordinary investors returned to the market

- $5.6b IG priced yesterday, $1.2b HY priced yesterday. BofAML Corporate Master Index OAS narrows 1bp to +163, YTD range 180/129. High Yield Master II OAS narrows 4bp to +573, YTD range 683/438

- Sovereign 10Y bond yields mostly lower. Asian stocks mostly lower, European stocks gain; U.S. equity-index futures rise. Crude oil and gold little changed, copper falls

Key US Events

- 7:30am: Challenger Job Cuts y/y, Oct. (prior 93.2%)

- 8:30am: Initial Jobless Claims, Oct. 31, est. 262k (prior 260k)

- Continuing Claims, Oct. 24, est. 2.140m (prior 2.144m)

- 8:30am: Non-farm Productivity, 3Q P, est. -0.3% (prior 3.3%)

- Unit Labor Costs, 3Q P, est. 2.5% (prior -1.4%)

- 9:45am: Bloomberg Consumer Comfort, Nov. 1 (prior 42.8)

Speakers:

- 7:00am: Bank of England bank rate, est. 0.50% (prior 0.50%)

- 7:45am: BOE’s Carney holds news conference

- 8:30am: Fed’s Harker speaks in Philadelphia

- 8:30am: Fed’s Dudley and Fischer and IMF’s Lagarde speak in New York

- 12:45pm: Fed’s Tarullo speaks in Chicago

- 1:30pm: Fed’s Lockhart speaks in Bern, Switzerland

- 7:30pm: Reserve Bank of Australia issues monetary policy statement

- 11:00pm: Bank of Japan’s Kuroda speaks in Tokyo

DB’s Jim Reid completes the overnight wrap

Central bankers continue to shake and stir markets at the moment. Yesterday it was Yellen’s turn again after her hawkish remarks sent 2-year US yields to their highest since April 2011, the Dollar up +0.82%, commodities lower (WTI -3.30%) and the probability of a rate hike next month to 58% from 50% the day before. It’s clear that the committee want to give themselves every chance of being able to hike in December which means they have to try to get the probability of such an event higher. Obviously if this has a detrimental impact on global assets the probabilities will drop again and the Fed are less likely to go. So the dance starts again.

Some strong-ish data reinforced those themes yesterday. The ADP employment change report for October came in pretty much as expected at 182k (vs. 180k) firming expectations for a similar number at Friday’s payrolls. The ISM non-manufacturing print for last month rose 2.2pts to a solid 59.1 (vs. 56.5 expected), with the employment subcomponent in particular (59.2 vs. 58.3) up again and back near its July post-recession high. Interestingly the spread between the employment components in the two ISM’s (manufacturing and non-manufacturing) is now at the second largest on record. Meanwhile the final October services PMI was revised up 0.4pts to 54.8 leaving it just shy of the September reading, while the composite nudged up half a point to 55 which matches September. Finally the September trade deficit reading of $40.8bn more or less matched expectations, reaching a seven-month low on lower fuel imports. Yesterday’s data saw the Atlanta Fed revise their Q4 GDP forecast once again, upgrading it back up to 2.3% from 1.9% on Tuesday.

Back to Yellen quickly and her comments yesterday in front of Congress. Of significance, the Fed Chair said that ‘at the moment what we see is a domestic economy that is pretty strong and growing at a solid pace, offset by some weakening spilling over to us from the global economy’. She went on to say that ‘what the committee has been expecting is that the economy will continue to grow at a pace that is sufficient to generate further improvements in the labour market and to return inflation to our 2% target over the medium term’. Reinforcing the hawkish tone from the FOMC, this led Yellen to suggest that ‘if the incoming information supports that expectation then our statement indicates that December would be a live possibility’.

Those comments were then backed up at the end of the US session by NY Fed President Dudley who said that he fully agrees with the view of Yellen that December is a live possibility, but also wanted to ‘see what the data shows’ and that he would ‘probably want to see a little bit more in terms of wage inflation’. Earlier in the day Fed Governor Brainard had said that the domestic outlook is encouraging, while on inflation noted that survey measures of expectations have been reassuring for the most part but that some market-based measures have dipped lower.

Yellen’s comments saw risk assets end their strong start to the week yesterday. The S&P 500 retreated -0.35% as energy stocks were hit hard (Oil also under pressure following the latest US inventory numbers) while the Dow was -0.28%. US credit indices widened with CDX IG out a couple of basis points by the end of the session although it didn’t stop nearly $6bn of new issues pricing.

Despite that weaker showing for risk assets last night, the news this morning is of a strong session for Chinese equities with the Shanghai Comp (+2.81%) technically entering a bull market having now risen over 20% from the August 26th lows. The CSI 300 is up over 3% despite there appearing to be little in the way of new news out. Markets in Japan have seen reasonable gains also with the Nikkei and Topix +1.01% and +0.95% respectively, while the Hang Seng is +0.10%. Elsewhere in Asia, markets are generally following the US lead with bourses in Taiwan, Korea, Australia and Indonesia all moderately lower as we go to print. US equity futures are more or less unchanged while credit indices in Asia are generally a basis point wider.

It was a bit more of a mixed session in Europe yesterday. The Stoxx 600 closed +0.51% along with modest gains for the CAC (+0.25%) and IBEX (+0.08%) although it was a much weaker day for German equities as the DAX tumbled -0.97% having being dragged down by a 10% fall for VW following the latest fallout in the scandal regarding the internal probe and CO2 emissions in petrol vehicles which we touched upon yesterday.

There was better news in yesterday’s October PMI numbers out of Europe however. The final Euro area services reading was revised down a modest 0.1pts to 54.1, which saw the composite PMI at 53.9 (flash 54.0, September 53.6) remaining resilient. Germany saw a slight negative surprise in its final composite reading (-0.3pts to 54.2) although was still up relative to September. Moderate gains were seen for France (+0.3pts to 52.6), Italy (+0.5pts to 53.9) and Spain (+0.4pts to 55.0). Our colleagues in Europe noted that the solid October survey data point to resilient Euro area growth and that the PMI’s are in line with +0.4% qoq Euro area growth. They also point out that if we see no change for the rest of 2015, then this represents a slight upside to their +0.3% qoq Q4 call, which is down to their more cautious view on Germany.

Meanwhile, there was some chatter out of the ECB yesterday too with Governing Council member Smets saying that inflation is too low following an interview with German press Handelsblatt. Smets said that ‘even if this low inflation is related mainly to falling oil prices, there is a danger that it will have a negative impact on inflation expectations and they could lose their anchoring’. Echoing Draghi’s comments, Smets went on to say that ‘as central bankers, it is our job to be concerned’ and that ‘we will re-evaluate the situation at our next council meeting’.

Yesterday saw 25 S&P 500 report their latest quarterly numbers, the highlight being a better than expected Q3 report from Facebook (beating revenue and earnings expectations) which sent shares up into the close. Time Warner was also out with their latest Q3 report which, while coming in ahead of expectations, saw management downgrade 2016 guidance which resulted in the share price collapsing nearly 7%. All told 18 (72%) companies beat earnings expectations yesterday and 15 (60%) notched a beat at the sales line. The latter was much better than the overall trend so far and helped to lift revenue beats now to 45% from 44% this time yesterday, while earnings beats have held steady at 73%. Meanwhile in Europe we’ve seen 257 Stoxx 600 companies report and the trend continues to remain weak with just 49% beating earnings expectations and 46% beating sales expectations.

Moving onto the day ahead, the main focus in the European session today will be the UK’s BoE meeting which will see the latest inflation report released, the meeting minutes and also comments from the BoE’s Carney shortly after. Datawise, Euro area retail sales and German factory orders are the main releases of note this morning. Across the pond this afternoon we’ve got the Q3 nonfarm productivity and unit labour costs due along with the latest initial jobless claims. It’s a big day for Fedspeak also with Dudley and Fischer set to speak at 1.30pm GMT (along with the IMF’s Lagarde), followed by Lockhart at 6.30pm GMT. Former Fed Chair Bernanke is also scheduled to give the keynote speech at an IMF conference at 9pm GMT tonight. In terms of earnings, we’ve got 24 S&P 500 companies set to report their latest quarterly numbers including Kraft Heinz and Walt Disney. In the Stoxx 600 we’ve got 32 companies scheduled to report including Astra Zeneca and Deutsche Telekom.

end

Mission Accomplished? Chinese Stocks Re-Enter “Bull Market” – Up 24% From August Lows

For the 3rd time since the crash in June, Chinese stocks have staged a magnificent recovery. Amid the selling bans, arrests, deaths, manipulation, massive direct government buying, and general happy-talk propoganda, Chinese stocks are now up 24% from the August lows… Of course, we are sure every one of the grandmas and farmers – fully levered – clung on through the dips.. and are now still 32% down from the June highs…

Where next?

Charts: Bloomberg

2.1 Million Greeks Face Blackout As Public Power Company Unpaid Bills Soars

Greece’s Public Power Company is angry. The amount of unpaid bills by its customers has reached the astronomic EUR 2.5 billion. The PPC is so angry that it plans to cut the power to those without outstanding debts as soon as possible – a whopping 2.1 million Greeks face darkness.

As KeepTakingGreece reports, many Greeks cannot afford to pay the bi-monthly bill mostly because the amount to be paid doubles due to added extra fees like emissions, green-whatever, municipality fees, state tv fees, etc.

For example bi-monthly electricity consumption is estimated by DEH to be €52 but i am asked to pay €100 because of the extra charges. The bill includes 13% Value Added Tax but also “interest” of €0.44 although I pay per monthly bank order and I am never late. Every 4 months I receive a bill based on my real consumption – and not just an ‘estimation’ – and then I find my self in a state of passing out. Summer months are more expensive due to the use of A/C, winter months are also expensive due to the use of electric devices like A/C to heat the apartment. Bills explode to several hundred euros.

I am not alone in my struggle to pay the bill. But many cannot even afford it.

According to Greek media reports, 2.1 million consumers have outstanding debts to the Greek PPC. They are private households, businessmen of small and medium enterprises, merchants, craftsmen.

Now the PPC plans to “turn the power off” and leave them in the dark. Not without previous notice, though. It will send consumers a warning and if they won’t comply, they will desperately seek to turn on the lights in the evening, cook for their kids, keep the cheese in the fridge, use their wireless phone, watch tv, heat their homes opr complain about their situations on the internet.

The business debts are reportedly 1.8 billion euro.

Exempted from the planned power outages will be consumers in the program of “social price policy”, even though the PPC plans also to screen anew this customers’ category, as some apparently have misused this provision aimed solely for the poor households and people with disabilities.

Some consumers rush to make settlements for their debts but then the monthly payments to PPC are higher than the payments they can afford. Furthermore, the real life has showed that once in PPC debt, one is always in PPC debt unless one pays once for all the debt. There is not even 0.001% reduction in cases the consumer has paid 1,000 euro at once – just to name an example.

Households and businesses started to sink in PPC debts after the government incorporated the Special Property Tax in the PPC bills in 2011. Debts to PPC increased rapidly because consumers were simply unable to pay the bi-monthly bills that skyrocketed from let’s say 100 euro to more than 250 and thus amid the economic crisis of recession, unemployment and income decreases.

Meanwhile the Property Tax comes separately and directly from the tax office, but that incredibly bad practice imposed on 2011 and 2012 and the outstanding debts keep holding households and businesses as hostages for the rest of their lives.

Two months ago, I had posted about a jobless neighbor who was victim of PPC’s power outage since last March. Her bill was 700 euro. She will not be affected by the new power outages. She still lives in the dark and has no means to heat her home.

* * *

On a final note, KTG wonders aloud…

I wonder what the PPC will win if it cuts the power. It will not receive any money by those who do not have any anyway.

US Spec Ops Already On The Ground In Syria Sources Say, As Russian Troop Presence Grows To 4,000

On Tuesday evening, we notedthat the US is set to send F-15C Eagle twin-engine fighters to Incirlik. This suggests that the Pentagon is preparing for air-to-air combat with the Russians.

As hyperbolic as that might sound, there’s really no alternative explanation for why Washington would send the fighters to Syria unless of course ISIS and/or the mishmash of rebels and militants fighting for control of the country have air forces no one has ever heard about.

Indeed, Russia made a similar move by sending Sukhoi Su-30s to Latakia and according to several sources, those planes had a run-in with Israeli jets over Lebanon last month.

The interesting thing, from our perspective anyway, is that Lebanese sources were out on Wednesday claiming that US spec ops are already on the ground – and they’re operating in the west. Here’s Sputnik:

US military advisors are alleged to have started training so-called moderate rebels near the city of Salma in the Latakia province in what amounts to breaking a pledge not to put US boots on the ground in Syria, Lebanon’s satellite television channel al-Mayadeen reported, citing an unnamed military source.

And here’s Salma:

Now bear in mind, this is Russian media citing an unnamed Lebanese source, so that would be a bit like American media citing an unnamed Saudi correspondent, but still, even the suggestion that Washington has placed “advisers” in Salma is alarming. That is, the going assumption was that these spec ops forces would be placed with the YPG or somewhere near Raqqa to avoid even the appearance that The Pentagon is set to place troops with soldiers that are in direct contact with Iranian ground forces and as such could potentially get hit with Russian airstrikes.

Of course we won’t get much in the way of clarity from Washington. US Assistant Secretary for Near Eastern Affairs Anne Patterson told the House Foreign Affairs Committee on Wednesday that the “the activities and location of the special forces are classified.” Patterson also said that “Russia’s military intervention has dangerously exacerbated an already complex environment,” on the way to claiming that “the opposition puts up a very strong fight.”

Obviously, it’s difficult to know where even to start in terms of analyzing that bit of nonsense. First, the situation is indeed “already complex” thanks to Washington, Riyadh, Ankara, and Doha who collectiively decided that “start civil war via the funding of terrorists” was the proper “strategy” for bringing about regime change in Damascus. Second, it’s not clear that the “opposition” is putting up a “very strong fight,” and even if it were, that’s at least partly attributable to the Pentagon handing rebels things like anti-tank weapons. If Patterson thinks that’s constructive, well, maybe she needs to find a new occupation.

Meanwhile, Western media reports indicate that there are as many as 4,000 Russian troops in Syria (so, i) just “slightly” more than the 50 Obama is sending, ii) far less than the number of militants the US and its regional allies have trained, and iii) far less than the Iranian contingent, which, between Shiite militas from Iraq, Hezbollah, and the Quds, probably number more than 10 or 15,000). Here’s Reuters:

Moscow’s military force in Syria has grown to about 4,000 personnel, but this and more than a month of Russian air strikes have not led to pro-government forces making significant territorial gains, U.S. security officials and independent experts said.

Moscow, which has maintained a military presence in Syria for decades as an ally of the ruling Assad family, had an estimated 2,000 personnel in the country when it began air strikes on Sept. 30. The Russian force has since roughly doubled and the number of bases it is using has grown, U.S. security officials said.

The Russians have suffered combat casualties, including deaths, said three U.S. security officials familiar with U.S. intelligence reporting, adding that they did not know the exact numbers.

Russia’s foreign ministry declined to comment on the size of the Russian contingent in Syria or any casualties it has suffered. It referred questions to the Russian Defense Ministry, which did not respond to written questions submitted by Reuters.

The Kremlin has said there are no Russian troops in combat roles in Syria, though it has said there are trainers and advisers working alongside the Syrian military and also forces guarding Russia’s bases in western Syria.

A U.S. defense official said Russian aircraft are now operating out of four bases, but multiple rocket launcher crews and long-range artillery batteries are deployed outside the facilities.

“They have a lot of people outside the wire,” he said.

The main Russian base is at the Bassel al-Assad International Airport near the port city of Latakia. All of Moscow’s fixed wing aircraft are flying from there in support of ground offensives by the Syrian army and foreign Shiite militias, the defense official said.

Three other bases – Hama, Sharyat and Tiyas – are being used for helicopter gunships, he said. The Russians began operating from Tiyas only this week, the official said.

Russia’s air fleet in Syria comprises 34 fixed-wing aircraft and 16 helicopters, the U.S. officials said.

In a testament to what we said above, Reuters goes on to note that the rebels’ ability to fight off pro-regime forces stems largely from the delivery of U.S.-made TOW anti-tank missiles. Saudi Arabia is supplying them to forces battling Iran near Aleppo:

Despite the Russian air strikes, the offensives have failed to make significant advances, the U.S. officials and independent experts said. A key factor appears to be significant losses by pro-government forces of tanks and other armored vehicles to U.S.-made TOW anti-tank missiles that Saudi Arabia has been supplying to the anti-Assad rebels.

Once again, this is just about the silliest damn thing imaginable. Here’s Riyadh giving US-made anti-tank missiles to anti-Assad forces who are using them to target the very same Iran-backed militias who are driving Abrams tanks in Iraq and helping the US-trained Iraqi regulars battle ISIS. Clearly, Washington has gotten itself so intertwined in the Sunni-Shiite battle between Iran and Saudi Arabia that the Pentagon no longer knows what to do, leading to a schizophrenic strategy that varies by country.

In any event, the takeaway here is that reports now suggest US troops are operating near Latakia and that means they’ll be in contact with Iranian ground troops, Russian fighter jets, and quite possibly with some of the 4,000 Russian troops stationed in the country. Perhaps now we know why The Pentagon sent the F-15C Eagles. Maybe US spec ops will indeed be engaging the Russians and Iranians on the ground and will need the air force to shoot down Moscow’s warplanes in the event they try to hit US positions.

end

I give up!!

(courtesy zero hedge)

CIA, Saudis To Give “Select” Syrian Militants Weapons Capable Of Downing Commercial Airliners

Wednesday brought a veritable smorgasbord of “new” information about the Russian passenger jet which fell out of the sky above the Sinai Peninsula last weekend.

First there was an audio recording from ISIS’ Egyptian affiliate reiterating that they did indeed “down” the plane. Next, the ISIS home office in Raqqa (or Langley or Hollywood) released a video of five guys sitting in the front yard congratulating their Egyptian “brothers” on the accomplishment.

Then the UK grounded air traffic from Sharm el-Sheikh noting that the plane “may well” have had an “explosive device” on board.

Finally, US media lit up with reports that according toAmerican “intelligence” sources, ISIS was probably responsible for the crash.

Over the course of the investigation, one question that’s continually come up is whether militants could have shot the plane down. Generally speaking, the contention that ISIS (or at least IS Sinai) has the technology and/or the expertise to shoot down a passenger jet flying at 31,000 feet has been discredited by “experts” and infrared satellite imagery.

But that’s nothing the CIA can’t fix.

With the Pentagon now set to deploy US ground troops to Syria (and indeed they may already be there, operating near Latakia no less), Washington is reportedly bolstering the supply lines to “moderate” anti-regime forces at the urging of (guess who) the Saudis and Erdogan.

Incredibly, some of the weapons being passed out may be shoulder-fire man-portable air-defense systems, or Manpads, capable of hitting civilian aircraft.

But don’t worry, those will only be given to “select rebels.” Here’s more from WSJ:

The U.S. and its regional allies agreed to increase shipments of weapons and other supplies to help moderate Syrian rebels hold their ground and challenge the intervention of Russia and Iran on behalf of Syrian President Bashar al-Assad, U.S. officials and their counterparts in the region said.

The deliveries from the Central Intelligence Agency, Saudi Arabia and other allied spy services deepen the fight between the forces battling in Syria, despite President Barack Obama’s public pledge to not let the conflict become a U.S.-Russia proxy war.

Saudi officials not only pushed for the White House to keep the arms pipeline open, but also warned the administration against backing away from a longstanding demand that Mr. Assad must leave office.

In the past month of intensifying Russian airstrikes, the CIA and its partners have increased the flow of military supplies to rebels in northern Syria, including of U.S.-made TOW antitank missiles, these officials said. Those supplies will continue to increase in coming weeks, replenishing stocks depleted by the regime’s expanded military offensive.

An Obama administration official said the military pressure is needed to push Mr. Assad from power.

“Assad is not going to feel any pressure to make concessions if there is no viable opposition that has the capacity, through the support of its partners, to put pressure on his regime,” the official said.

In addition to the arms the U.S. has agreed to provide, Saudi and Turkish officials have renewed talks with their American counterparts about allowing limited supplies of shoulder-fire man-portable air-defense systems, or Manpads, to select rebels. Those weapons could help target regime aircraft, in particular those responsible for dropping barrel bombs, and could also help keep Russian air power at bay, the officials said.

Mr. Obama has long rebuffed such proposals, citing the risk to civilian aircraft and fears they could end up in the hands of terrorists. To reduce those dangers, U.S. allies have proposed retrofitting the equipment to add so-called kill switches and specialized software that would prevent the operator from using the weapon outside a designated area, said officials in the region briefed on the option.

U.S. intelligence agencies are concerned that a few older Manpads may already have been smuggled into Syria through supply channels the CIA doesn’t control.

If that sounds insane to you, that’s because it is.Even as US intelligence (which we can only assume emanates from the CIA) indicates that IS Sinai likely brought down a Russian passenger jet with 224 people on board, the same CIA is working with the Saudis to supply “select rebels” with weapons capable of shooting down commercial airliners.

In order to make sure no one ends up blowing a 747 out of the sky, Washington will “retrofit” the weapons with “special” software that makes sure they can only be used in certain areas.

Make no mistake, this has gone beyond absurd and is now bordering on the bizarre. It’s apparently not enough that the US is supplying anti-tank missiles to rebels shooting at the very same Iran-backed militias that the US implicitly supports across the border in Iraq so now, the CIA and Saudi Arabia will give these rebels the firepower to shoot down planes, meaning that in the “best” case scenario they’ll be firing at Russian fighter jets, and in the worst case scenario these weapons will end up in the “wrong” hands and be used to down commercial flights.

It’s difficult to see how John Kerry can attend “peace” talks in Vienna and keep a straight face while chatting with Sergei Lavrov. That’s not to say that Russia bears no responsibility for its role in the conflict (sure, Moscow is supporting a “legitimate” government in Syria but they’re still dropping bombs on populated areas), but the US and the Saudis are arming Sunni extremist groups and encouraging them to shoot at Russian and Iranian forces. For Obama to suggest this isn’t a proxy war is absurd.

Putting this all together, it now appears possible that the US is, i) sending anti-tank weapons to rebels who are shooting at Iranian soldiers, ii) embedding ground troops near Latakia which means they’ll almost certainly be engaging Hezbollah directly, and iii) passing weapons capable of downing a commercial airliner to “select” militants days after a Russian passenger jet exploded in the skies above the Sinai Peninsula.

This is all in conjunction with the Saudis and Erodgan, who just rigged an election in Turkey on the way to rewriting his country’s constitution.

And the Western media reports this with a straight face as though it all makes some measure of sense…

US Officials: ISIS “Likely” Had Bomb On Russian Plane

On Wednesday, IS Sinai released a statementreiterating the contention that the Russian passenger jet which fell out of the sky over the Sinai Peninsula last weekend was “downed” by an act of terrorism. The ISIS “home office” (so to speak) in Raqqa aired a video congratulating their Egyptian “brothers” on the “achievement.”

In the immediate aftermath of the crash, officials attempted to discredit the ISIS video which purported to show the plane exploding in mid-air. While we were quick to note that it’s virtually impossible to verify the video’s authenticity, we also pointed out that if the footage was indeed genuine, someone on the ground knew exactly when to start filming which would certainly seem to suggest that whatever happened to the Russian jet was premeditated.

Whatever one chooses to believe, evidence continues to pile up to support the contention that the plane broke apart in the sky – i.e. that the plane exploded.

For instance, an Egyptian forensics expert noted that the scattering of body parts over an eight kilometer radius seems to prove that there was an explosion of board. Meanwhile the UK on Wednesday suspended flights from Sharm el-Sheikh in Egypt after saying that the Russian jet “may well” have been destroyed by an “explosive device.”

That seemed to indicate that Western governments were set to “confirm” ISIS’ contention that a bomb is to blame for the crash.

Now, Western media are reporting that according to US “intelligence”, an ISIS bomb was indeed the cause of the catastrophe that claimed the lives of 224 people last Saturday. Here’s Reuters:

Evidence now suggests that a bomb planted by the Islamic State militant group is the likely cause of last weekend’s crash of a Russian airliner over Egypt’s Sinai peninsula, U.S. and European security sources said on Wednesday.

Islamic State, which controls swathes of Iraq and Syria and is battling the Egyptian army in the Sinai Peninsula, said again on Wednesday it brought down the airplane, adding it would eventually tell the world how it carried out the attack.

The Airbus A321M crashed on Saturday in the Sinai Peninsula shortly after taking off from the resort of Sharm el-Sheikh on its way to the Russian city of St Petersburg, killing all 224 people on board.

The U.S. and European security sources stressed they had reached no final conclusions about the crash.

And here’s more from NBC:

There’s significant evidence that a bomb brought down Russia’s Metrojet Flight 9268 over the Sinai Peninsula last weekend, U.S. officials told NBC News on Wednesday, saying U.S. investigators are focusing on ISIS operatives or sympathizers as the likely bombers.

Questions have swirled over whether foul play or terrorism may have downed the Metrojet-operated Airbus A321 since it crashed in Egypt on Saturday, killing all 224 people aboard. ISIS’s media office in Sinai released an audio message Wednesday reiterating its claim of responsibility. Neither Wednesday’s claim nor an earlier one immediately after the crash said how ISIS is supposed to have brought down the plane.

U.S. officials stressed that while they believe it’s “likely” that a bomb was on the plane, it’s still too early to conclude that for certain. They told NBC News that mechanical failure remains a possibility.

A U.S. official said investigators are looking at the possibility that an explosive device was planted aboard the plane by ground crews, baggage handlers or other ground staff at the Sharm el-Sheikh airport before takeoff.Passengers and the flight crew weren’t significantly suspected after intelligence scrub of the passenger manifest and the crew showed no one with suspected ties to any terrorist group, officials said.

Three top officials at the airport, including the head of security, were fired Wednesday after investigators uncovered numerous lax security procedures, officials told NBC News.

So apparently, US officials have more evidence about what happened to this plane than either the Russians or the Egyptians do and Washington is now confident enough to say that ISIS is “likely” responsible.

Needless to say, there are any number of questions that should be asked here, but at least NBC gets one thing right:

A U.S. official told NBC News he expects Russia to retaliate “heavily and militarily” if the theory is borne out.

end

ALARMING!!!

(courtesy yournewswire and the times of Israel/and special thanks to Robert for sending this to us.

Robert comments:

“Now ask yourself if the call on this event as a ” political event ” may not be justified ?”

http://yournewswire.com/us-israel-conducted-war-games-in-russian-plane-crash-location/

US & Israel Conducted ‘War Games’ Near Russian Plane Crash Location

Israeli and the US took part in operation ‘Blue Flag’, an air-force combat drill taking place in the Arava desert at the same time Metrojet Flight 9268 went down.

Startling new revelations show that both the US and Israel were conducting war games in the Arava desert when Flight 9268 dropped off the radar, shortly before breaking up in mid-air and crashing in the Sinai, Egypt.

The Russian plane crash has been blamed on ISIS fighters shooting it down, but now evidence has emerged, via Israeli state media, that an operation named “Blue Skies” or “Blue Flag” was taking place at the exact location and at the exact time as the crash.

As reported by The Times Of Israel, in their headline, Blue Skies: Israeli, American, Greek, and Polish air personnel square off against a fictional enemy state in two-week drill (Oct. 30, 2015):

“Air forces from around the world have gathered deep in the Arava desert in the south of Israel for the past week and a half to take part in the largest aerial exercise in the history of the Israeli Air Force.

The “Blue Flag” exercise, which is continuing through November 3, pits the Israeli Air Force, the United States Air Force, Greece’s Hellenic Air Force and the Polish Air Force against a fictional enemy state, the captain in charge of all IAF exercises told The Times of Israel Thursday night.”

American Everyman reports:

Why is this significant? Well, just take a look at two maps.

Are you kidding me? The Israelis and US running an air-force combat drill in the same general area of the downed Russian passenger plane?

end

(courtesy zero hedge)

Meanwhile In Kenya, “Investors” Are Rushing Into Treasury Bills

You know it’s bad when…

Complacency has returned with a vengeance as investors rushed into 3-month T-Bills when Kenyan Treasury issued them this week…

The weighted average yield on Kenya’s 91-day Treasury bill plummeted to 13.763 percent at a heavily oversubscribed auction on Thursday, compared to 19.471 percent at last week’s sale, the central bank said.

As the auction’s bid-to-cover spiked to a massively unprecedented record high.

It offered bills worth 4.0 billion shillings ($39.20 million) and received bids worth 44.6 billion shillings. It accepted bids worth 7.3 billion shillings ($71.53 million).

* * *

After all – what could go wrong in 3 months, right?

Charts: Bloomberg

none

Euro/USA 1.0865 up .0002

USA/JAPAN YEN 121.98 up .456

GBP/USA 1.5288 down .0096

USA/CAN 1.3154 down .0002

Early this morning in Europe, the Euro rose by a minuscule 2 basis points, trading now well below the 1.09 level rising to 1.0865; Europe is still reacting to deflation, announcements of massive stimulation (QE), a proxy middle east war, and the ramifications of a default at the Austrian Hypo bank, an imminent default of Greece, Glencore,and now Nysmark and the Ukraine, along with rising peripheral bond yield. Last night the Chinese yuan flat in value (onshore). The USA/CNY rate at closing last night: 6.3355 / (yuan flat)

In Japan Abe went all in with Abenomics with another round of QE purchasing 80 trillion yen from 70 trillion on Oct 31/2014. The yen now trades in a slight southbound trajectory as settled down again in Japan by 46 basis points and trading now well above the all important 120 level to 121.98 yen to the dollar.

The pound was down this morning by 96 basis points as it now trades just below the 1.53 level at 1.5288.

The Canadian dollar is now trading up 2 basis points to 1.3154 to the dollar.

We are seeing that the 3 major global carry trades are being unwound. The BIGGY is the first one;

1. the total dollar global short is 9 trillion USA and as such we are now witnessing a sea of red blood on the streets as derivatives blow up with the massive rise in the rise in the dollar against all paper currencies and especially with the fall of the yuan carry trade. The emerging market which house close to 50% of the 9 trillion dollar short is feeling the massive pain as their debt is quite unmanageable.

2, the Nikkei average vs gold carry trade (blowing up)

3. Short Swiss franc/long assets (European housing/Nikkei etc. This has partly blown up (see Hypo bank failure).(blew up)

These massive carry trades are terribly offside as they are being unwound. It is causing global deflation ( we are at debt saturation already) as the world reacts to lack of demand and a scarcity of debt collateral. Bourses around the globe are reacting in kind to these events as well as the potential for a GREXIT>

The NIKKEI: this THURSDAY morning:closed up 189.50 or 1.00%

Trading from Europe and Asia:

1. Europe stocks mostly mostly in the green except Germany

2/ Asian bourses mostly in the red … Chinese bourses: Hang Sang red (massive bubble forming) ,Shanghai in the green (massive bubble ready to burst), Australia in the red: /Nikkei (Japan) in the green/India’s Sensex in the red/

Gold very early morning trading: $1108.25

silver:$15.02

Early Thursday morning USA 10 year bond yield: 2.23% !!! up 2 in basis points from Wednesday night and it is trading well below resistance at 2.27-2.32%. The 30 yr bond yield falls to 2.99 down 1 in basis point.

USA dollar index early Thursday morning: 98.05 cents up 16 cents from Wednesday’s close. (Resistance will be at a DXY of 100)

This ends early morning numbers Thursday morning

WTI Crude Tumbles To $45 Handle – Erases Post-FOMC Euphoria

Having pushed up towards $49 in its exuberant “a hawkish fed must mean everything in the world is awesome” way, yesterday’s reality check on inventories (rising), production (rising), and The Fed (we are going to hike no matter what) which means the dollar too is surging and is pushing down on commodity prices, has dumped WTI Crude back below $46 and erased all of the gains post-FOMC.

WTI gives it all back:

Shifting WTI red post-FOMC, joining gold and bonds:

How long before stocks catch on?

Saudis Bring Oil War To Europe With Largest Price Discount Since 2009

With oil exports to Europe having slipped from 13% of Saudi’s total to just 10% in the last six months, The FT reports, the de facto leader of OPEC has slashed its Official Selling Price (OSP) to Europe in an effort to regain market share. Saudi lowered its OSP for its Arab light crude grade in Europe by $1.30 a barrel for December, taking its discount to the weighted average of the North Sea Brent benchmark to $4.75 a barrel – the largest discount since February 2009.

The move, as we detailed previously, is basically going after Russia’s customer base, has raised heckles in Moscow, with Rosneft CEO Igor Sechin complaining last month about Saudi “dumping” after he revealed the kingdom was selling oil to refineries in Poland.

Chart: Bloomberg

As The FT reports, the de facto leader of Opec, which produces more than one in every ten barrels of oil in the world, has been squeezed in Europe over the past year as rival producers have sent more oil to the region.

Rising shipments from Iraqi Kurdistanthat are delivered into the Mediterranean via the Turkish port of Ceyhan have displaced some Saudi shipments this year, traders and analysts said, while more crude from west Africa is also flowing to Europe.

Saudi Arabia has responded by trying to find new customers, including targeting refineries that have traditionally taken the majority of their supplies from Russia and the North Sea.

The global oil market remains oversupplied by at least 1m barrels a day, a move exacerbated by both Saudi Arabia and Iraq raising production since Opec decided last year to focus on squeezing out higher cost producers rather than defending price.

“If Saudi Arabia and Iraq went back to producing what they were before last November’s Opec meeting, the market would now be in a deficit,” said Paul Horsnell, head of commodities research at Standard Chartered: “The policy can’t be characterised solely as a market share battle. Anything coming into the Mediterranean competes first with Russian and Iraqi crude.”

Russia’s oil output has also risen to post-Soviet era highs in 2015, despite crude prices more than halving to less than $50 a barrel since summer 2014. Russia is also sending more crude into Asia via its Eastern Siberia Pacific Ocean pipeline, increasing competition in those markets.

“ESPO has taken a fair share of Saudi’s market share as well,” one trader said.

* * *

USA/Chinese Yuan: 6.3458 up .103 on the day (yuan down)

New York equity performances for today:

FedSpeak & Fireworks Day Leave Crude Crushed, Copper Clubbed, Stocks Soft, & Bonds Bruised

With The Fed now on 24 hours a day jawboning expectations up for a rate-hike in December (which has suddenly spooked assets) and Fireworks Day (Guy Fawkes may have been on to something after all) across the pond, stocks, bonds, and commodities all leaked lower ahead of tomorrow’s “most important ever” payrolls…

Stocks started the day off with the usual pre-eopn ramp

With Trannies somehow outperforming today…

In spite of the collapse in crude…

S&P 2100 was once again all important… driven sending VXX to the low of the day…

Stocks were glued to USDJPY all day – especially after crude decoupled…

But there are 3 stocks worth noting before we leave the casino…

Valeant collapsed…

Herbalife ripped..

And Straight Path Communications…

Stocks started to catch down to credit…

And catching down to VIX (hedgers ahead of payrolls)…

Treasury yields continued to rise today (with the short-end underperforming)…the buy-sell-buy pattern continues

Leaving 2Y Yields at their highest since May 2010…

The US Dollar was almost perfectly unchanged today against the majors (with modest strength in EUR offset by weakness in Cable)…

Commodities contonued to slide despite the lack of movement in the dollar…

With crude giving up all the post-FOMC gains…

Charts: Bloomberg

Bonus Chart: A Gentle Reminder from earlier of the rollover in payrolls ahead of tomorrow…

The data is very interesting today. Challenger Grey reports a huge increase in energy related layoffs and are now back to 6 month highs!

(courtesy zero hedge/Challenger/Gray)

Initial Jobless Claims Jump Most In 8 Months As Energy Sector Layoffs Spike Back To 6-Month Highs

Just when you thought (for the 10th time this year) that the worst was over in the US energy space, Challenger Grey reports a massive spike in Energy sector layoffs – to six-month highs. For context,energy sector layoffs are 9 times higher in 2015 than 2014 and Texas – with 103,422 layoffs – is the worst state for job cuts (despite Dallas Fed Fisher’s previous insistence that the state is ‘diversified’). Despite the ongoing side in initial jobless claims, employers have announced 543,935 job cuts in 2015 so far, 31% higher than 2014.

Claims surged 16k in the last week – a 6.15% rise which is the most since February…

Is this the catch up?

It’s not over…

Led by a surge in Texas…

As Challenger concludes, it could be about to get a lot worse…

“Now, we are heading into what has historically been a period of heavy job cutting, even in the strongest economy. The fourth quarter is when many companies make adjustments to operations and payrolls in order to hit year-end earnings goals.”

US weekly jobless claims total 276,000 vs 262,000 estimateReuters

New U.S. applications for unemployment benefits last week recorded their largest increase in eight months, but remained at levels consistent with a fairly healthy labor market.

Initial claims for state unemployment benefits rose 16,000 to a seasonally adjusted 276,000 for the week ended Oct. 24, the Labor Department said on Thursday. It was the largest weekly gain since late February.

Claims had hovered near 42-year lows for much of October.

The prior week’s claims were unrevised. It was the 35th straight week that claims were below the 300,000 threshold, which is normally associated with a strong jobs market.

Economists polled by Reuters had forecast claims rising to 262,000 last week. A Labor Department analyst said there were no special factors influencing the data.

The four-week moving average of claims, considered a better measure of labor market trends as it strips out week-to-week volatility, rose 3,500 to 262,750 last week.

Last week’s claims report has no bearing on the October employment report due for release on Friday. New applications for jobless benefits were low last month relative to September.

According to a Reuters survey of economists, nonfarm payrolls increased 180,000 in October, well above the average gain of 139,000 jobs for August and September. The unemployment rate is forecast at 5.1 percent.

The claims report showed the number of people still receiving benefits after an initial week of aid increased 17,000 to 2.16 million in the week ended Oct. 24. The four-week moving average of continuing claims fell 11,500 to 2.16 million, the lowest level since November 2000.

The trend in continuing claims suggests more long-term unemployed are finding work.

-END-

Unit Labor Costs Miss For 3rd Quarter In A Row (For The First Time In 12 Years)

A modest 1.4% rise in unit labor costs in Q3 was dramatically below the expected (and hope-strewn) 2.5% growth and means unit labor costs have missed expectations for the 3rd quarter in a row for the first time since 2003. Perhaps just as bad, historical (weak) data was revised notably lower but of course, as Yellen and Fisher have made clear – none of this matters for the data-un-dependent Fed’s December decision.