Gold $1313.50 up $7.70

Silver 19.21 up 43 cents

In the access market 5:15 pm

Gold: 1313.45

Silver: 19.16

THE DAILY GOLD FIX REPORT FROM SHANGHAI AND LONDON

.

The Shanghai fix is at 10:15 pm est and 2:15 am est

The fix for London is at 5:30 am est (first fix) and 10 am est (second fix)

Thus Shanghai’s second fix corresponds to 195 minutes before London’s first fix.

And now the fix recordings:

Shanghai morning fix Sept 19 (10:15 pm est last night): $ 1318.17

NY ACCESS PRICE: $1316.04 (AT THE EXACT SAME TIME)

Shanghai afternoon fix: 2: 15 am est (second fix/early morning):$ 1323.24

NY ACCESS PRICE: 1316.00 (AT THE EXACT SAME TIME)

HUGE SPREAD TODAY!!

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

London Fix: Sept 19: 5:30 am est: $1315.05 (NY: same time: $1315.08: 5:30AM)

London Second fix Sept 16: 10 am est: $1314.85 (NY same time: $1314.80 , 10 AM)

It seems that Shanghai pricing is higher than the other two , (NY and London). The spread has been occurring on a regular basis and thus I expect to see arbitrage happening as investors buy the lower priced NY gold and sell to China at the higher price. This should drain the comex.

Also why would mining companies hand in their gold to the comex and receive constantly lower prices. They would be open to lawsuits if they knowingly continue to supply the comex despite the fact that they could be receiving higher prices in Shanghai.

For comex gold:The front September contract month we had 0 notices filed for nil oz

For silver: the front month of September we have a total of 27 notices filed for 135,000 oz

Last night, in my commentary to you I wrote:

I am a little worried that the bankers have called for another raid on gold/silver tomorrow. Gold/silver equity shares fell badly in the last hr against hardly any movement in the price of gold/silver. Usually that is a signal to attack. The comex OI is low and it really makes no sense to raid. Let us see what tomorrow brings.

Let us have a look at the data for today

.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total open interest FELL by 978 contracts down to 191,494. The open interest fell as the silver price was down 16 cents in Friday’s trading .In ounces, the OI is still represented by just LESS THAN 1 BILLION oz i.e. .957 BILLION TO BE EXACT or 137% of annual global silver production (ex Russia &ex China). the crooks are doing a great job fleecing unsuspecting longs

In silver we had 127 notices served upon for 135,000 oz

In gold, the total comex gold fell by 5,080 contracts as the price of gold fell BY $7.20 on Friday . The total gold OI stands at 565,539 contracts. The level of OI now is good for us as it will support a rise in gold price and it will be hardly for the boys to raid.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD

LAST NIGHT WE HAD A HUGE CHANGE out of the GLD/ 10.39 TONNES OF PAPER GOLD WERE “DEPOSITED” INTO THE GLD/

Total gold inventory rest tonight at: 942.61 tonnes of gold

SLV

we had A HUGE change with respect to inventory at the SLV/ A DEPOSIT OF 1.045 MILLION OZ

THE SLV Inventory rests at: 363.479 million oz

.

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in silver fell by 5080 contracts down to 191,496 as the price of silver fell by 16 cents with Friday’s trading.The gold open interest fell 5,080 contracts down to 565,539 as the price of gold fell $7.20 IN FRIDAY’S TRADING.

(report Harvey).

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

end

3. ASIAN AFFAIRS

i)Late SUNDAY night/MONDAY morning: Shanghai closed UP 23.20 POINTS OR .77%/ /Hang Sang closed UP 214.86 PONTS OR .92%. The Nikkei closed for holiday Australia’s all ordinaires CLOSED down 0.04% Chinese yuan (ONSHORE) closed HUGELY DOWN at 6.6720/Oil rose to 43.60 dollars per barrel for WTI and 46.31 for Brent. Stocks in Europe: ALL IN THE GREEN Offshore yuan trades 6.669 yuan to the dollar vs 6.6720 for onshore yuan.THE SPREAD BETWEEN ONSHORE AND OFFSHORE NARROWS HUGELY AGAIN TO BLOCK MORE USA DOLLARS AS IT ATTEMPTS TO LEAVE CHINA’S SHORES

REPORT ON JAPAN SOUTH KOREA NORTH KOREA AND CHINA

3a)Korea:

none

b) REPORT ON JAPAN

none today/holiday in Japan

c) REPORT ON CHINA

i)China reports that 22 billion USA has left its shores and now its holdings of USA securities is the lowest since 2013 at 3.2 trillion USA but this will be before futures transactions involving the dollar is released. Expect its real holdings of USA dollars to be around 3.1 trillion USA

( Bloomberg)

ii)Hibor rises to 23.7% as the POBC tried to:

i) punish the CNY shorts

ii) support their currency below 6.70 and thus trying to prevent dollars from leaving Chinese shores

( zero hedge)

4 EUROPEAN AFFAIRS

i)Merkel suffers a huge defeat in Berlin elections with the surge of the anti immigrant AFD party

( zero hedge)

ib)Merkel admits “mistakes were made” on the migrant crisis in explanation of her horrendous defeat in state elections (Berlin region)

( zero hedge)

ii)Deutsche bank continues to extend losses in trading and now they are close to record lows as the bank is terribly under-capitalized. Even if the fine from the D of J is reduced they will still need to raise huge amounts of capital.

( zero hedge)

iii)As Merkel lost big time in Berlin elections due to the populace wanting no more immigrant seeking asylum in their country, the doorknobs from Europe are demanding that the USA and Canada take up more refugees

iv)With high total social financing still at record highs and thus adding to the China’s shadow banking sector, we now see a massive bubble forming in their housing sectorThis will not end well

( zero hedge)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OHOH! this does not looks good! The USA admits it struck a Syrian army base killing 62 Syrian soldiers. Immediately after the hit, ISIS militants launched an offensive.Russia and of course Syria are very angry!

“Russia has repeatedly alleged that the US is failing to keep its part of the bargain. The US, on its part, has blamed Russia for not pressuring Damascus enough to facilitate humanitarian access to Syria.

Both allegations may now be moot if Russia decides to retaliate against members of the US-led coalition, or directly against US forces.”

6.GLOBAL ISSUES

none today

7.OIL ISSUES

From our resident expert of USA shale production: Steve St Angelo. He now comments that the huge BAKKEN shale oil field is down in production by 25% and EAGLE FORD at 40%. Shale production if you include costs of rigs etc has not produced a dime in profits but the losses will be immense

( St Angelo/SRSRocco report)

8.EMERGING MARKETS

none today

9.PHYSICAL STORIES

i)Alasdair Macleod explains why the EU is doomed as problems are surfacing with the huge debt of Italy:

( Alasdair Macleod..)

ii)Greyerz and Stephen Leeb comment on gold with Eric king of kingworldnews

( Stephen Leeb/Egon von Greyerz/Kingworldnews/GATA)

iii)A must listen to interview of Chris Powell

( Chris Powell/Wesleyan University Radio station/GATA)

iv)What took them so long: The BIS is flashing red lights due to the huge debt inside China at roughly 30 trillion USA or 300% of their GDP

( BIS/Ambrose Evans Pritchard/GATA)

v)Gold miners are sticking close to home in the hunt for more metal And they are seeking safer jurisdictions like Agnico Eagle’s Canada, Finland and Mexico

( Reuters/GATA))

10.USA STORIES WHICH MAY INFLUENCE THE PRICE OF GOLD/SILVER

i)Bomb explodes at New Jersey train station on Sunday after explosions occurred in New York on Saturday.

(courtesy zero hedge)

ii)Bombing suspect on the loose: identified as Ahmad Khan Rahami. And Europe is asking for more refugees?

iib)One officer shot in Elizabeth NJ with the shooter allegedly in custody. Rahami is still on the loose;

iic)Rahami arrested:

iii)Pater Tenebrarum describes a situation that is now before us whereby both ISM service and ISM manufacturing are below 52. When both of these occur at the same time, a huge recession is the resultant as indicated by the economies in 2008-2009 and 2001-2002.

a must read….

( Pater Tenebrarum/Acting-Man.com)

iv)This is a first: auto loans for cars drop for the first time since the Fed started reporting on this. And yet auto production still rises. That is going to lead to a catastrophe as more inventory is produced and nobody buying:

( zero hedge)

v)Trump odds surge as millennials are shying away from Hillary

( ICAP/zero hedge)

viii) Another great reason for Janet and Stan to raise interest rates on Wednesday: K-Mart closing 64 more stores and laying off thousand of employees

( Business Insider)

Let us head over to the comex:

The total gold comex open interest fell to an OI level of 565,539 for a loss of 5080 contracts as the price of gold FELL by $7.20 with Friday’s trading. We are now in the NON active month of SEPTEMBER/

The contract month of Sept saw it’s OI FALL by 11 contracts DOWN to 137. We had 11 notices filed yesterday so we neither gained nor lost any gold ounces that will stand for delivery. The next delivery month is October and here the OI FELL by 1994 contracts down to 37,539. This level is extremely high and no doubt many of these will wait it out and take delivery at the end of the month. The next contract month of December showed an decrease of 4,386 contracts down to 419,511 .The estimated volume today at the comex: 152,716,811 fair Confirmed volume on Friday: 152,695 which is good.

And now for the wild silver comex results. Total silver OI fell by 978 contracts from 192,474 down to 191,496 with the FALL in price of silver to the tune of 16 cents on Friday. We are moving away from the all time record high for silver open interest set on Wednesday August 3: (224,540). We are now into the next active month of September and here the OI fell by 91 contracts down to 711. We had 149 notices filed on FRIDAY so we GAINED BACK ANOTHER 58 contracts or 290,000 additional oz will stand for delivery in this active month of September. The next non active delivery movement of October hardly moved as it ROSE by 15 contracts UP to 291 contracts. The next big delivery month is December and here it FELL by 1098 contracts DOWN to 166,269. The volume on the comex today (just comex) came in at 55,503 which is excellent The confirmed volume on Friday (comex and globex) was very good at 44,812 . Silver is not in backwardation. London is in backwardation for several months.

today we had 27 notices filed for silver: 135,000 oz

| Gold |

Ounces

|

| Withdrawals from Dealers Inventory in oz |

NIL |

| Withdrawals from Customer Inventory in oz nil |

100.219 oz

Scotia

|

| Deposits to the Dealer Inventory in oz | NIL oz |

| Deposits to the Customer Inventory, in oz |

63,437.219 oz

Scotia

|

| No of oz served (contracts) today |

0 notices

nil oz

|

| No of oz to be served (notices) |

137 contracts

(13,700 oz)

|

| Total monthly oz gold served (contracts) so far this month |

2427 contracts

242,700 oz

7.5489 tonnes

|

| Total accumulative withdrawals of gold from the Dealers inventory this month | 192.90 oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | 170,109.9 oz |

Today, 0 notices were issued from JPMorgan dealer account and 0 notices were issued form their client or customer account. The total of all issuance by all participants equates to 0 contract of which 0 notices were stopped (received) by jPMorgan dealer and 0 notice(s) was (were) stopped (received) by jPMorgan customer account.

| Silver |

Ounces

|

| Withdrawals from Dealers Inventory | NIL |

| Withdrawals from Customer Inventory |

1,323,951.843 oz

HSBC

Scotia

|

| Deposits to the Dealer Inventory |

nil OZ

|

| Deposits to the Customer Inventory |

2,477,518.610 oz

CNT

HSBC

Scotia

|

| No of oz served today (contracts) |

27 CONTRACTS

(135,000 OZ)

|

| No of oz to be served (notices) |

653 contracts

(3,420,000 oz)

|

| Total monthly oz silver served (contracts) | 2486 contracts (12,430,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month | 5,345,623.9 oz |

SEPT 9/ we had a big changes tonight out of the GLD/ there were two major withdrawals

i) first early morning: 1.19 tonnes

ii) second: 10.68 tonnes of gold

total: 11.87 tonnes

Total gold inventory rest tonight at: 939.94 tonnes of gold

end

NPV for Sprott and Central Fund of Canada

end

‘Hard’ Brexit Looms For Ireland

O’Brien outlines the risks on the horizon in the article in the Sunday Independent is well worth a read as it highlights the risks posed by Brexit to the Irish economy.

“A hard Brexit is now the most probable of the possible outcomes, with all the negative consequences for this island that such a rupture would entail.”

‘Things go from bad to worse for Ireland as a ‘hard’ Brexit looms over the horizon’ can be read here

Gold and Silver Bullion – News and Commentary

Gold Climbs as Investors Count Down to Fed Meeting, Dollar Sags (Bloomberg)

Gold prices gain in Asia on rebound as investors eye central bank meets (Investing)

Gold steady on uncertainty ahead of central bank meetings (Reuters)

Funds Dump Gold at Fastest Pace Since May as Fed Outlook Shifts (Bloomberg)

World’s gold miners stick close to home in hunt for more metal (Reuters)

Things go from bad to worse for Ireland as a ‘hard’ Brexit looms (Independent)

Ireland, Apple and Leprechaun Economics – Keiser Report (MaxKeiser)

Why Has Gold Stalled? (GoldSeek)

War is Peace, Ignorance Is Strength, Silver is Plentiful … (SilverSeek)

BIS flashes red alert for a banking crisis in China (Telegraph)

Gold Prices (LBMA AM)

19 Sep: USD 1,315.05, GBP 1,007.99 & EUR 1,177.36 per ounce

16 Sep: USD 1,314.25, GBP 999.56 & EUR 1,170.08 per ounce

15 Sep: USD 1,320.10, GBP 998.26 & EUR 1,174.23 per ounce

14 Sep: USD 1,323.20, GBP 1,001.40 & EUR 1,177.91 per ounce

13 Sep: USD 1,328.50, GBP 1,000.36 & EUR 1,183.69 per ounce

12 Sep: USD 1,327.50, GBP 1,000.80 & EUR 1,182.54 per ounce

09 Sep: USD 1,335.65, GBP 1,004.68 & EUR 1,184.86 per ounce

08 Sep: USD 1,348.00, GBP 1,009.11 & EUR 1,195.81 per ounce

Silver Prices (LBMA)

19Sep: USD 19.12, GBP 14.65 & EUR 17.13 per ounce

16 Sep: USD 18.91, GBP 14.36 & EUR 16.85 per ounce

15 Sep: USD 18.96, GBP 14.32 & EUR 16.87 per ounce

14 Sep: USD 19.04, GBP 14.42 & EUR 16.96 per ounce

13 Sep: USD 19.16, GBP 14.44 & EUR 17.06 per ounce

12 Sep: USD 18.72, GBP 14.11 & EUR 16.68 per ounce

09 Sep: USD 19.41, GBP 14.58 & EUR 17.23 per ounce

08 Sep: USD 19.93, GBP 14.90 & EUR 17.65 per ounce

Recent Market Updates

– EU Bail In Rules Ignored By Italy – Mother Of All Systemic Threats and World War?– Buy Gold – Bonds Are ‘Biggest Bubble In World’ – Billionaire Singer Warns

– Silver Bullion Market – “Most Bullish Story Ever Told?”

– “Sorry, You Can’t Have Your Gold Bullion”

– Global Stocks, Bonds Fall Sharply – Gold Consolidates After Two Weeks Of Gains

– Gold, Silver, Blockchain and Fintech – Solutions To Negative Rates, Bail-ins, Cash Confiscations and Cashless Society

– Jan Skoyles Appointed Research Executive At GoldCore

– Silver Bullion Surges 3.5% To Over $20/oz

– Ireland “Especially Exposed” To “International Shocks” Warns Central Bank

– Deutsche Bank Tries To Explain Failure To Deliver Physical Gold

– Physical Gold Delivery Failure By German Banks

– Avoid Paper Gold – “Gold Delivery” Refused By Gold Exchange Traded Commodity

– Debt Bubble in Ireland and Globally Sees Wealthy Diversify Into Gold

– “Why Case Against Gold Is Wrong” – James Rickards

end

Alasdair Macleod explains why the EU is doomed as problems are surfacing with the huge debt of Italy:

(courtesy Alasdair Macleod..)

Why The EU Is Doomed

Submitted by Alasdair Macleod via The Mises Institute,

We are accustomed to looking at Europe’s woes in a purely financial context. This is a mistake, because it misses the real reasons why the EU will fail and not survive the next financial crisis. We normally survive financial crises, thanks to the successful actions of central banks as lenders of last resort. However, the origins and construction of both the the euro and the EU itself could ensure the next financial crisis commences in the coming months, and will exceed the capabilities of the ECB to save the system.

It should be remembered that the European Union was originally a creation of US post-war foreign policy. The priority was to ensure there was a buffer against the march of Soviet communism, and to that end three elements of the policy towards Europe were established. First, there was the Marshall Plan, which from 1948 provided funds to help rebuild Europe’s infrastructure. This was followed by the establishment of NATO in 1949, which ensured American and British troops had permanent bases in Germany. And lastly, a CIA sponsored organisation, the American Committee on United Europe was established to covertly promote European political union.

It was therefore in no way a natural European development. But in the post-war years the concept of political union, initially the European Coal and Steel Community, became fact in the Treaty of Paris in 1951 with six founding members: France, West Germany, Belgium, Luxembourg and Italy. The ECSC evolved into the EU of today, with an additional twenty-one member states, not including the UK which has now decided to leave.

With the original founders retaining their national characteristics, the EU resembles a political portmanteau, a piece of assembled furniture, each component retaining its original characteristics.After sixty-five years, a Frenchman is still a staunch French nationalist. Germans are characteristically German, and the Italians remain delightfully Italian. Belgium is often referred to as a non-country, and is still riven between Walloons and the Flemish. As an organisation, the EU lacks national identity and therefore political cohesion.

This is why the European Commission in Brussels has to go to great lengths to assert itself. But it has an insurmountable problem, and that is it has no democratic authority. The EU parliament was set up to be toothless, which is why it fools only the ignorant. With power still residing in a small cabal of nation states, national powerbrokers pay little more than lip-service to the Brussels bureaucracy.

The relationship between national leaders and the European Commission has been deliberately long-term, in the sense that loss of sovereignty is used to gradually subordinate other EU members into the Franco-German line. The driving logic has been to make the European region a protected trade area in Franco-German joint interests, and to protect them from free markets.

It was not easy to find the necessary compromise. Since the Second World War, France has been strongly protectionist over her own culture, insisting that the French only buy French goods. Germany’s success was rooted in savings, which encouraged industrial investment, leading to strong exports. These two nations with a common border had, and still have, very different values, but they managed to conceive and set up the European Central Bank and the euro.

In Germany, the sound-money men in the Bundesbank lost out to industrial interests, which sought to profit from a weaker currency. This was actually in line with her political preferences, and it was the political class that controlled the relationship with France. In France the integrationists, politicians again, defeated the industrialists, who sought to insulate their home markets from German competition.

When a common currency was first mooted, two future problems were ignored. The first was how would the other states joining the euro adapt to the loss of their national currencies, and the second was how would the UK, with her Anglo-Saxon market-based culture adapt to a more European model. It wasn’t long before the latter issue was met head-on, with the withdrawal of sterling from the Exchange Rate Mechanism, the forerunner of the euro, in September 1992.

The euro was eventually born at the turn of the century. The Franco-German compromise led to the appointment of a Frenchman, Jean-Claude Trichet, as the ECB’s second president. All was well, because the abandonment of national currencies and the gradual acceptance of the euro meant that states in the Eurozone were able to borrow more cheaply in euros than they ever could in their own national currencies.

Bond risk was measured against German bunds, traditionally the lowest yielding bonds in Europe. It was not long before the spread between bunds and other Eurozone debt was commonly seen as a profitable opportunity, instead of a reflection of relative risk. European banks, insurance companies and pension funds all benefited from the substantial rise in the prices of bonds issued by peripheral EU members, and invested accordingly. In turn, these borrowers were only too willing to supply this demand by issuing enormous quantities of debt, in contravention of the Maastricht Treaty. Bank credit expanded as well, leaving the banking system highly geared.

The control mechanism for this explosion in borrowing was meant to be the Exchange Stability and Growth Pact, agreed in Maastricht in 1993. This laid down five rules, of which two concern us. Member states were bound to keep their national budget deficits to a maximum of 3% of GDP, and national government debt was limited to 60% of GDP. Neither Germany nor France qualified on the debt criteria, without rigging their national accounts, and the only reason that deficits came within the Pact was a mixture of dodgy accounting and fortuitous timing of the economic cycle. The control mechanism was never enforced.

So from the outset, no nation had any sense of responsibility towards the new currency. The rules were ignored and the euro became a gravy-chain for all member governments, spectacularly brought to public attention by the failure of Greece.

The Eurozone’s banking system, incorporating the national central banks and the ECB, bound together in a bizarre settlement system called TARGET, became the means for member nations to buy German goods on credit. Very good for Germany, you may say, but the problem was that the credit was supplied by Germany herself. It is the same as lending money to the buyer of your business in a rigged transaction. This flaw in the system’s construction is now a rumbling volcano ready to blow at any moment.

The Germans want their money back, or at least don’t want to write it off. The debtors cannot pay, and need to borrow more money just to survive. Neither side wishes to face reality. It started with Ireland, then Cyprus, followed by Greece and Portugal. These are the smaller creditors, which Germany, led by its Finance Minister Wolfgang Schäuble, managed to crush into debtor submission and are now economic zombies. The real problem comes with Italy, which is also failing and has a debt-to-GDP ratio estimated to be over 133% and rising. If Italy goes, it will be followed by Spain and France. Herr Schäuble cannot force these major creditors into line so easily, because at this stage the whole Eurozone banking system will be in deep trouble, as will the German government itself. German savers are also becoming acutely aware that they will pick up the bill.

The first line of defense, as always, will be for the ECB as lender of last resort to keep the banks afloat. The only way it can do this is to accelerate the printing of euros and to monopolise Eurozone debt markets. Whether or not the ECB can hold the currency with all these liabilities on board its own balance sheet, and for how long, remains to be seen.

For the moment, the euro stands there like a Goliath, seemingly invincible. It represents the anti-free-market European establishment, which no one has dared to challenge. This surely is the underlying reason the ECB can impose negative interest rates and get away with it. But serious cracks are appearing. First we had Brexit, likely to be followed by other small states wanting out. The Italian banking crisis is almost certain to come to a head soon, and an Italian referendum on the constitution next month is also an important hurdle to be overcome. The politicians are in panic mode, reassuring everyone there is nothing wrong more integration and a new army won’t cure.

Meanwhile, the overbearing attitude of the European Commission and the refugee crisis are undermining public support for the status quo. Angela Merkel, hitherto regarded as invincible, has lost her public support in Germany. Marine Le Pen, leader of the Front National and who wants France to leave the EU, led the opinion polls recently for France’s next President, due to be elected next year. The strongmen of Europe are on the back foot.

All the elements for a mighty political and economic smash are now there. Whether or not it will be the trigger for, or itself be triggered by external events remains to be seen. Either way, the Eurozone’s crisis time-line now appears to be measured in months.

The market effect, besides being a severe shock to all markets, is likely to be two-fold. Firstly, international flows will sell down the euro in favour of the dollar. Given the euro’s weighting in the dollar index, this will be a major disruption for all currency markets. Secondly, Eurozone residents with bank deposits are likely to increasingly seek refuge in physical gold, as signs of their currency’s impending collapse emerge, because there is nowhere else for them to go.

Whichever way one looks at it, it is increasingly difficult to accept any other outcome than a complete collapse of this ill-found political construction, originally promoted in US interests by a CIA-sponsored organisation. The euro, being dependent on political cohesion instead of original market demand, will simply cease to be money, somewhat rapidly.

END

Greyerz and Stephen Leeb comment on gold with Eric king of kingworldnews

(courtesy Stephen Leeb/Egon von Greyerz/Kingworldnews)

Greyerz and Leeb comment on gold at King World News

Submitted by cpowell on Sun, 2016-09-18 23:02. Section: Daily Dispatches

7p ET Sunday, September 18, 2016

Dear Friend of GATA and Gold:

At King World News, gold fund manager Egon von Greyerz predicts that the euro won’t survive, driving Europeans into gold:

http://kingworldnews.com/greyerz-the-roadmap-to-a-staggering-10000-gold-…

And fund manager Stephen Leeb argues that China wants an orderly transition to a new world monetary system, which for the time being requires controlling the gold price:

http://kingworldnews.com/chinas-stunning-plan-for-gold-a-new-monetary-sy…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

A must listen to interview of Chris Powell

(courtesy Chris Powell/Wesleyan University Radio station)

GATA secretary interviewed on Wesleyan University radio station

Submitted by cpowell on Sun, 2016-09-18 13:42. Section: Daily Dispatches

9:41a ET Sunday, September 18, 2016

Dear Friend of GATA and Gold:

Your secretary/treasurer was interviewed about gold market rigging by central banks for about an hour yesterday, with occasional musical relief, on John Way’s “The Blue Cafe” program on WESU-FM88.1, the radio station of Wesleyan University in Middletown, Connecticut. The program has been archived at Soundcloud.com here:

https://soundcloud.com/johnlway/tbc017_chris-powell-gold-the-value-of-mo…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

What took them so long: The BIS is flashing red lights due to the huge debt inside China at roughly 30 trillion USA or 300% of their GDP

(courtesy BIS/Ambrose Evans Pritchard)

BIS flashes red alert for a banking crisis in China

Submitted by cpowell on Sun, 2016-09-18 14:00. Section: Daily Dispatches

By Ambrose Evans-Pritchard

The Telegraph, London

Sunday, September 18, 2016

China has failed to curb excesses in its credit system and faces mounting risks of a full-blown banking crisis, according to early warning indicators released by the world’s top financial watchdog.

A key gauge of credit vulnerability is now three times over the danger threshold and has continued to deteriorate, despite pledges by Chinese premier Li Keqiang to wean the economy off debt-driven growth before it is too late.

The Bank for International Settlements warned in its quarterly report that China’s “credit to GDP gap” has reached 30.1, the highest to date and in a different league altogether from any other major country tracked by the institution. It is also significantly higher than the scores in East Asia’s speculative boom on 1997 or in the US subprime bubble before the Lehman crisis. …

… For the remainder of the report:

http://www.telegraph.co.uk/business/2016/09/18/bis-flashes-red-alert-for…

end

Gold miners are sticking close to home in the hunt for more metal And they are seeking safer jurisdictions like Agnico Eagle’s Canada, Finland and Mexico

(courtesy Reuters)

Gold miners stick close to home in hunt for more metal

Submitted by cpowell on Sun, 2016-09-18 14:21. Section: Daily Dispatches

By Susan Taylor and Nicole Mordant

Reuters

Sunday, September 18, 2016

The world’s biggest gold miners are taking a cautious approach in their hunt for bullion, spending more money to explore around existing mines rather than new territory in a strategy that may have short-term gains but risks future production growth.

Top producers are relying more than ever on small companies to do the heavy lifting of searching for new deposits and increasingly taking 10 to 20 percent equity stakes in the junior miners.

Exploring close to home is more cost efficient and improves the odds of discoveries. But the chances of making major new finds are limited, diminishing global gold output, which is expected to decline by nearly 9 percent in the next three years. …

… For the remainder of the report:

http://www.reuters.com/article/us-mining-gold-idUSKCN11O0F8

end

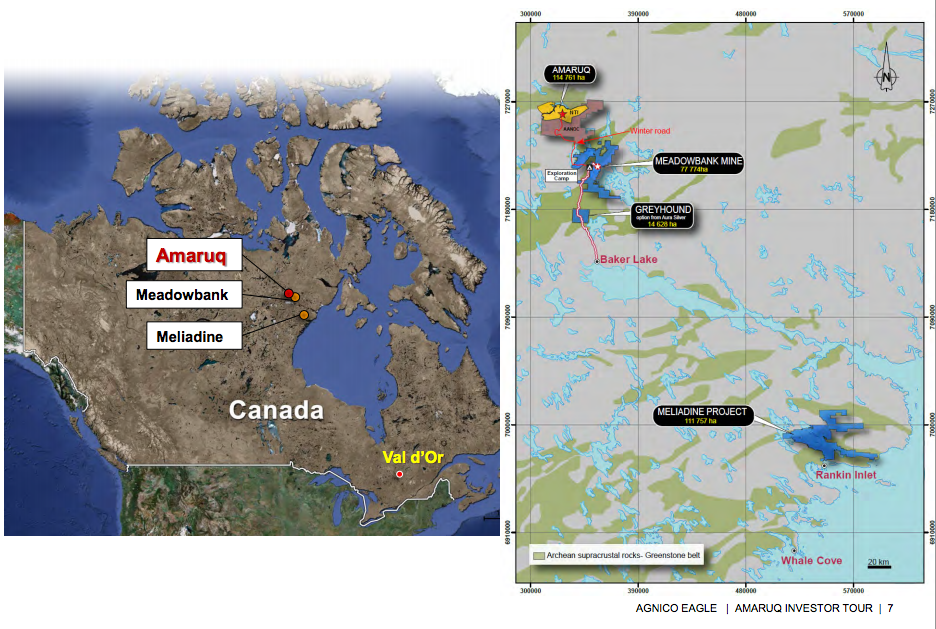

For those of you who are following Agnico Eagle: their new Amaruq project near Meadowbank is going to be a dandy

(courtesy seeking alpha)

Agnico Eagle – Production Update On Amaruq Project In The Kivalliq- Nunavut, Northern Canada

Sep. 19, 2016 12:14 AM ET

Summary

AEM released an Update on exploration drilling results at its Amaruq gold project in Nunavut, northern Canada.

Overall mineral resources increased by 13% in the Amaruq project. 3.714 million Oz from 3.283 million Oz in December 31, 2015.

AEM is one of my main long-term gold miners with a solid balance sheet and constant production stream. I recommend the stock as a hold on valuation.

On September 15, 2016, Agnico Eagle announced the following:

Update on exploration drilling results at its Amaruq gold project in Nunavut, northern Canada. This deposit continues to grow and remains a focus for the Company given its potential and its proximity to Agnico Eagle’s Meadowbank mine and mill. This update includes an expanded mineral resource estimate for the project based on drilling through June 30, 2016.

- Overall mineral resources increased by 13% at the Amaruq project.3.71 million ounces of gold (19.4 million tonnes grading 5.97 grams per tonne (“g/t”) gold) as of June 30, 2016.

- Open pit mineral resources increase by 33%. 598,000-ounce increase (on a contained gold basis) in open pit inferred mineral resources to 2.42 million ounces gold (13.6 million tonnes grading 5.53 g/t).

- 319% expansion in the IVR deposit mineral resources; V Zone confirmed as potential second source of open pit ore

The Amaruq gold project in Nunavut, Northern Canada, is located 50 kms (31.25 miles) northwest of Agnico Eagle’s Meadowbank mine. The project hosts the Whale Tail gold deposit as well as the I, R, V, and Mammoth 1 and 2 zones, and several other targets. The company acquired the original property in 2013.

M. Sean Boyd, Agnico Eagle’s Vice-Chairman and Chief Executive Officer said:

The 2016 exploration program at Amaruq has resulted in an increase in gold resources and the delineation of a potential second source of open pit ore at the V Zone. In just a short period of time, we have seen Amaruq advance from a grassroots discovery to a significant development project with 3.7 million ounces of gold resources.

We anticipate an updated mineral resource estimate in February 2017, and Amaruq is expected to provide a new source of ore for the Meadowbank mill starting in 2019.

Amaruq is a satellite of the Meadowbank mine, as we can see in the plan above. AEM indicated at the 2Q’16 results.

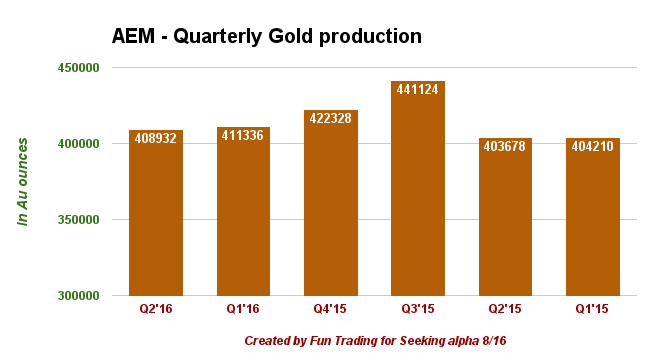

Meadowbank – Good Cost Performance Despite Lower Production Volumes in the Second Quarter of 2016

The 100% owned Meadowbank mine in Nunavut, northern Canada, achieved commercial production in March 2010.

The Meadowbank mill processed an average of 10,918 tpd in the second quarter of 2016, compared to the 11,199 tpd achieved in the second quarter of 2015. Year-over-year, mill throughput levels were lower primarily due to harder ore being processed from the Vault pit. Minesite costs per tonne were approximately C$73 in the second quarter of 2016. These costs were lower than the C$74 per tonne in the second quarter of 2015. The lower costs per tonne in the 2016 period were primarily due to lower production costs (for drilling, blasting and fuel consumption) and an increase in deferred stripping compared to the 2015 period.

Studies are ongoing to investigate additional opportunities to extend production at Meadowbank through year-end 2018. Potential opportunities include the development of the Phaser pit, which is located to the southwest of the Vault pit, and an additional pushback to access additional ore in the E3 pit at the Portage deposit.

It is not a secret, AEM is interested in the development of this segment, even if Meadowbank mine is slowly reaching the end of the road. Just as a reminder, the company took a big loss of $1 billion on Meadowbank, in early 2015. The mine was slated to close in 3Q’2017, but recently the company indicated that it may extend the production at Meadowbank through year-end 2018. Probably to be prepared for the Amaruq mine in 2019.

AEM has now two encouraging prospects near the Meadowbank mine. The Amaruq deposit, just 50 kilometers north of Meadowbank, and the Meliadine project near Rankin Inlet.

M. Sean Boyd indicated in the 2Q’16 conference call that Meliadine is now fully permitted. The company will look at Meliadine in the context of

the overall entire Nunavut strategy, so the focus remains on looking at ways that we can optimize construction capital as well as work some of the large resources into the mine plant. So those efforts continue and we will have an update on that early in 2017.

As we can see with this news update, the Kivalliq sector of the Nunavut region will be a significant part of the gold production by 2019. Agnico Eagle is facing a production gap at Meadowbank/Amaruq. In an interview last year, M. Boyd, explained it well:

Meadowbank has done a really good job getting their costs down. There’s a really good skillset there. We clearly want to continue to utilize that skillset in Nunavut. The best opportunity to do that is Amaruq. It’s a satellite deposit. The only way that it can work, based on what we know now, is to truck the material to Meadowbank. It’s still early, but it has the potential to continue our business at Meadowbank, to preserve all those jobs, to continue to use all those skills and allow us to use a lot of that Meadowbank equipment because it fits the type of mine that would begin potentially at Amaruq, a larger open pit. We couldn’t use any of the things at Meadowbank for Meliadine, because Meliadine is going to start as an underground mine.

We have our best people focused on trying to find opportunities in the North. Amaruq looks good because my experience tells me if that team and the leaders of that group-Alain Blackburn and Guy Gosselin-are excited, then we should be excited. Our biggest dilemma now is, if we follow the general timeline of getting things moving in Nunavut, we’re going to have a production gap. That’s no good. What we’re trying to do is work at it from the Meadowbank end and see if we can extend the life maybe a year.

Conclusion:

In my preceding article my technical analysis was quite clear and accurate. I said,

Technically, I estimate that the resistance should be around $60, and the downside from here, could be around $51.50 (first support).

If the first support does not hold, then we will have to look for the low-$40s eventually. Personally, I started to take profit off the table at $56, and will continue on any upside. My goal is to bring down my long-term AEM position by about 40%.

I was able to add my first small lot after selling about 42% of my holding as I have indicated above at around $56-$59. I do not suggest an active trading with AEM, but the situation was quite exceptional and it was time to take a large profit off the table due to an atypical overbought situation. The stock has corrected a little, but is still pricey with a Price earnings to growth — PEG — at over 9 and price to Free cash flow — P/FCF — at over 100.

AEM confirmed again, with this update, that it is a company that should be considered as a long-term investment grade. However, I still believe that the stock is overvalued, especially with the uncertainty hovering around the gold price situation and what will be the move of the FED this month. I recommend now a hold.

Important note: Do not forget to follow me on AEM and the gold sector. Thank you

Disclosure: I am/we are long AEM.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

end

Motley fool has just come out with their rare buy signal of a gold mining company: and they agree with me that the new Amaruq deposit is going to be a dandy!

(courtesy Motley Fool)

Agnico Eagle Mines Ltd. Will Grow Gold Production Like a Weed

By Ryan Vanzo – September 19, 2016 More on: AEM AEM

With gold prices up 26% this year, most gold miners have seen their stocks explode higher. Agnico Eagle Mines Ltd. (TSX:AEM)(NYSE:AEM), for example, is up 88% since January.

This week, the company released some data showing that gold reserves are ramping up. This growth is expected to continue for some time and, in a short time, result in production gains. Plus, the CEO has made some rosy comments about his expectations for the future price of gold.

Continued resource growth at its biggest project

Amaruq, a mega project located in Nunavut, which was acquired in 2013, is seeing big strides in both production and reserves.

Drilling in the first half of 2016 resulted in an updated inferred mineral resource estimate of 3.71 million ounces of gold. This represents an increase of 432,000 ounces compared to the company’s previous estimate. Additionally, the company discovered a new resource vein that may hold over 500,000 ounces of gold.

“The 2016 exploration program at Amaruq has resulted in an increase in gold resources and the delineation of a potential second source of open pit ore at the V Zone. In just a short period of time, we have seen Amaruq advance from a grassroots discovery to a significant development project with 3.7 million ounces of gold resources,” said Sean Boyd, Agnico’s CEO.

Exploration efforts are expected to wrap up in October with new results to be released in February.

Is growth ready to roar?

Thanks to its successful exploration attempts, Agnico has quickly built a portfolio of high-quality assets that will likely produce 30-40% more gold by 2020. Costs are also low and falling. This year they should come in at $840-880 per ounce (previously $850-890).

Even if you missed gold’s climb to a two-year high in early July, CEO Sean Boyd recently said that the rally in gold miners is just getting started.

“I think in this cycle, they will ultimately set an all-time high,” Boyd commented, adding that Agnico is “one of the very few companies that can see its output 30-40% higher in five years from now from stuff we already own.”

There are some major macroeconomic tailwinds ready to drive the gold market to new heights.

“There’s still a tremendous amount of debt in the system,” he said. “There’s an inability to create conditions for growth. You’ve got a negative-interest-rate environment, which is a great environment for gold from an opportunity-cost standpoint. And you’ve still got very strong demand coming out of China and India. So all the factors are there that can steadily move gold up.”

Next year the average Wall Street analyst is expecting the company to grow earnings by about 80%.

Is the valuation too high?

This summer Agnico was downgraded three times by Wall Street analysts due to an overstretched valuation. It appears as if the market has caught on to the company’s record of success.

Still, according to an analysis done by Royal Bank of Canada, Agnico’s stock is only pricing in gold prices of $1,315 an ounce–slightly below the current price of $1,319. The valuation looks fully priced, but if you’re a believer in higher gold prices (like Agnico’s CEO), shares surely have further upside to go.

The exclusive buy “signal” you can’t ignore

Over the course of The Motley Fool U.S.’s 23-year history, this rare buy “signal” has generated massive wealth for those that have been smart enough to pay attention to it. It’s so rare, that it’s happened less than two dozen times… but when it does, it’s made investors undoubtedly rich. If you’re interested in knowing the stock behind this rare buy “signal”–and you’re excited to take advantage of this golden opportunity, then you’re going to want to read this. Click here to unlock all the details behind this new recommendation from Stock Advisor Canada.

end

Your early MONDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight

:

1 Chinese yuan vs USA dollar/yuan DOWN to 6.6720( REVALUATION NORTHBOUND /CHINA UNHAPPY TODAY CONCERNING USA DOLLAR RISE/MORE $ USA DOLLARS LEAVE CHINA/OFFSHORE YUAN NARROWS HUGELY TO 6.6691) / Shanghai bourse CLOSED UP 23.20 POINTS OR .77% / HANG SANG CLOSED UP 214.86 POINTS OR 0.92%

2 Nikkei closed /USA: YEN FALLS TO 101.84

3. Europe stocks opened ALL IN THE GREEN ( /USA dollar index DOWN to 95.89/Euro UP to 1.1164

3b Japan 10 year bond yield: REMAINS CONSTANT AT -.039% !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 101.87/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY.

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 43.60 and Brent: 46.31

3f Gold UP /Yen UP

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” ON THE TABLE

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil DOWN for WTI and DOWN for Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10 yr bund RISES to +.010%

3j Greek 10 year bond yield RISE to : 8.645%

3k Gold at $1314.60/silver $19.12(7:45 am est) SILVER FINAL RESISTANCE AT $18.50 WILL BE DEFENDED

3l USA vs Russian rouble; (Russian rouble UP 48/100 in roubles/dollar) 64.80-

3m oil into the 43 dollar handle for WTI and 46 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation (already upon us). This can spell financial disaster for the rest of the world/China forced to do QE!! as it lowers its yuan value to the dollar/GOT a DEVALUATION DOWNWARD from POBC.

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 101.84 DESTROYING WHATEVER IS LEFT OF OUR YEN CARRY TRADERS

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning .9806 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.0947 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT

3r the 10 Year German bund now POSITIVE territory with the 10 year RISES to +.010%

/German 10+ year rate BASICALLY negative%!!!

3s The Greece ELA NOW at 71.4 billion euros,AND NOW THE ECB WILL ACCEPT GREEK BONDS (WHAT A DISASTER)

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 1.689% early this morning. Thirty year rate at 2.438% /POLICY ERROR)

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

(courtesy Jim Reid/Bloomberg/Deutsche bank/zero hedge)

Global Stocks, US Futures Rebound As Oil Rises, Dollar Drops

Stocks across the board, and US equity futures are broadly in the green this morning as markets shrug off the terror-related events in the NYC area over the weekend. There wasn’t a single positive “reason” for the green price action but the bond “tantrum” that caught the attention of stocks beginning back on 9/8 is increasingly fading and investors are hopeful this week’s central bank decisions (BOJ and FOMC both on Wed 9/21) will further ease yield anxieties.

One of the catalysts for the rebound in stocks was today’s rise in oil, which rebounded from Friday’s lows as renewed clashes halted what would be the first crude shipment from one of Libya’s largest export terminals since 2014. The tanker Seadelta suspended loading after fighting started Sunday between local Petroleum Facilities Guard units and forces loyal to eastern-based military commander Khalifa Haftar. Brent added 1.3 percent to $46.36. OPEC may call an extraordinary meeting if ministers reach consensus at an informal gathering next week, Secretary General Mohammed Barkindo said, according to Algerian Press Service.

“Sentiment is being boosted by a rebound in oil,” Vasu Menon, VP at Oversea-Chinese Banking Corp. in Singapore told Bloomberg. “Investors are also hoping the BOJ will do something more dramatic though I don’t think that’s going to make a lot of difference. With inflation numbers picking up a little bit in the U.S., the market will start worrying about the Fed again at some stage down the road.”

Major oil producers will meet next week in Algiers to discuss cooperating to shore up prices amid a global oversupply that has hurt state budgets. Before that, the Bank of Japan will undertake a review of its monetary policy and the Federal Reserve will meet to determine whether to raise rates. Volatility has picked up in financial markets over the past two weeks amid concern central banks are becoming reluctant to loosen monetary policy, while at least three bombs discovered in New York and New Jersey over the weekend may increase political turmoil.

The MSCI All-Country World Index climbed 0.4 percent at 11:16 a.m. in London as U.S. crude added 1.6 percent to $43.73 a barrel. The Bloomberg Dollar Spot Index declined 0.3 percent.

The Stoxx Europe 600 Index climbed 0.9% after its biggest weekly slide in three months. Rio Tinto Group and BHP Billiton Ltd. rose at least 2.8 percent, contributing the most to gains among miners. Total SA and BP Plc were among those that led oil-related stocks higher. Weir Group Plc added 3.1 percent after JPMorgan Chase & Co. recommended buying shares of the maker of fracking pumps for oil companies, citing improving prospects. U.K. builders gained, with Barratt Development Plc and Berkeley Group Holdings Plc adding 1.2 percent or more, as a report showed London house prices rebounded from their post-Brexit drop in September. HSBC Holdings Plc was among banks that gained the most. Deutsche Bank AG, which sparked a selloff on Friday after rebuffing a U.S. Justice Department claim to settle a probe tied to mortgage-backed securities, bucked the trend on Monday, with a 0.3 percent drop.

Emerging-market shares and currencies rallied with developed markets, led by a 2.8 percent gain in Taiwan’s Taiex Index and a 0.8 percent advance in Taiwan’s dollar. HTC surged 10 percent in Taiwan, the biggest gain since May 25, on reports the company will unveil a new mobile-phone handset.

S&P 500 Index futures added 0.5%, indicating U.S. equities will recover from Friday’s 0.4 percent retreat.

The yield on Treasuries due in a decade was little changed at 1.69 percent. It erased a three basis point decline on Friday following the release of the American inflation data, which boosted the probability of an interest-rate hike this year by five percentage points in the futures market to 55 percent. Spanish and Italian securities led gains in Europe. The yield on 10-year Spanish bonds slipped three basis points to 1.05 percent, while that on similar-maturity Italian debt fell two basis points to 1.32 percent, after adding nine basis points last week. Portugal’s 10-year bond yield was steady at 3.39 percent, after surging 26 basis points last week. The nation’s debt rating was affirmed on Friday by S&P, which forecast the economy will lose momentum this year.

Market Wrap

- S&P 500 futures up 0.5% to 2142

- Stoxx 600 up 1% to 341

- FTSE 100 up 1.5% to 6810

- DAX up 0.8% to 10357

- German 10Yr yield up less than 1bp to 0.01%

- Italian 10Yr yield down 1bp to 1.33%

- Spanish 10Yr yield down 2bps to 1.06%

- S&P GSCI Index up 0.8% to 350.7

- MSCI Asia Pacific up 0.9% to 138

- Hang Seng up 0.9% to 23550

- Shanghai Composite up 0.8% to 3026

- S&P/ASX 200 down less than 0.1% to 5295

- US 10-yr yield up less than 1bp to 1.69%

- Dollar Index down 0.27% to 95.85

- WTI Crude futures up 1.5% to $43.69

- Brent Futures up 1.2% to $46.33

- Gold spot up 0.4% to $1,316

- Silver spot up 1.7% to $19.13

Global Headline News

- More Guns to Greet New York as Another Suspicious Package Found: 1,000 more police blanket NYC, videos of Chelsea street sought

- Stiglitz Grades Trump F on Economics, Cites China Trade Risk: Nobelist says more American jobs would be lost than created

- Market Resilience Post-Brexit Masks Underlying Risks, BIS Says: Rally in stocks as bond yields plunged signals ‘dissonance’

- EU’s Vestager Signals Apple Just the Start of U.S. Tax Probes: Competition chief will meet in Washington with Lew, lawmakers

- Merkel Dealt Berlin Defeat With Worst Result Since World War II: Voters punish two biggest German parties in capital city vote

- U.K. Business Confidence Drops to Four-Year Low, Lloyds Says: Economic uncertainty, U.K. demand seen as biggest threats, according to Lloyds’ Business in Britain report

- Global Investors Bet $7.3b on Australia’s No. 1 Port: Port of Melbourne handles 2.6m containers a year

- Saudi Telecom Said to Mull Options for Stake in Malaysia’s Maxis: Gulf carrier owns indirect holding valued at $1.8b

- Noble Group Eyes Investor as Profit Seen Up to 2 Years Away: Strategic partner ‘still very possible,’ founder Elman says

- Oracle’s Ellison Takes Shot at Amazon With New Cloud Services: co. unveiled new services that help customers take advantage of cloud computing

- Oracle Buys Palerra to Boost ‘Security Stack’: TechCrunch: Terms weren’t disclosed, TechCrunch reports

Looking at regional markets, we start in Asia, where stock markets began the week relatively quiet with Japan away for public holiday, while a glitch in ASX interrupted trade in Australia. Nonetheless, the region’s bourses were mostly higher amid a rebound across the commodities complex, with Shanghai Comp (+0.8%) and Hang Seng (+0.9%) also lifted following a firm injection by the PBoC and continued strength in the property sector. Elsewhere, TAIEX (+2.8%) outperformed following recent advances in tech names with Apple suppliers boosted by record breaking demand for the iPhone 7. Chinese House Prices soared (Aug) Y/Y 9.2% (Prey. 7.9%). House prices rose M/M in 64 out of 70 cities (Prey. 51) and Y/Y in 62 cities (Prey. 58). The monthly jump was the biggest increase in more than six years. PBoC set mid-point at 6.6786 (Prey. 6.6895) and injected CNY 180bIn via 7-day reverse repo and CNY 70bIn via 28-day reverse repos. As noted earlier, Hong Kong overnight funding rates soared to over 23%, the second highest on record as the PBOC continued its onslaught against Yuan shorts.

Top Asian News

- Yuan Interbank Rate Surges in Hong Kong in Sign of Intervention: Overnight Hibor increases 15.7 ppts on Monday

- Warning Indicator for China Banking Stress Climbs to Record: Credit-to-GDP “gap” exceeds all other nations in BIS study

- China’s Home Prices Rise Most in Six Years as Sales Gain: New-home prices gained in 64 cities in August vs 51 in July

- Hanjin Reduces Fleet by Returning Chartered Carriers to Owners: Returned 4 box movers, 3 bulk carriers to charterers

- Samsung Exploding Battery Crisis Began With Rush to Beat IPhone: Korean company recalls 2.5m phones weeks after launch

- ASX Closes Stock Market for Rest of Monday on Technical Problem: No closing price auction that normally takes place at end of trading day

In Europe, stocks trade higher as the much anticipated Fed/BoJ week begins, with Eurostoxx 50 trading higher by 1.1% and the Energy/Materials heavy FTSE 100 (+1.3%) outperforming. It is worth noting that Japanese Silver Week has kept some participants away from market for the European morning, as such volumes have been marginally lighter than usual. Fixed income markets have been uneventful so far with German 10y hovering around 0% yield with Portuguese paper reversing Friday’s S&P inspired caution and the periphery generally benefiting from the modest return of risk to the market with Spanish and Italian yields tighter to the German benchmark.

Top European News:

- Permira Said Near Deal to Buy German Payroll Provider P&I: Owner HgCapital said to fetch more than $900m for firm

- EDF Cashes In on U.K. Heatwave That Made Power Prices Jump: Aurora Energy estimates EDF plants made $152m early September

- Deutsche Bank Needs $14b Even Without an RMBS Fine, SocGen Says: Lender is “significantly undercapitalized” by about EU12.5b, Societe Generale says in note

- London Asking Prices Picked Up in September as Lull Ended: Prices rose 1.9% from the previous month, Rightmove says

- Siemens CEO Says Geopolitical Upheaval Could Crimp Orders: Kaeser speaks in interview with Bloomberg TV in Singapore

- Rolls-Royce Cuts 200 Managers to Extend Savings Push: Restructuring adds to earlier plans to trim 400 senior roles

In FX, the Bloomberg Dollar Spot Index fell back after a 0.7 percent advance on Friday, when data showed the U.S. consumer-price index climbed 0.2 percent after being little changed in July. Economists predicted a 0.1 percent increase, a Bloomberg survey showed. The Japanese yen gained 0.4 percent and the British pound rose 0.4 percent. Australia’s dollar strengthened 0.8 percent versus the greenback, buoyed by the pickup in oil prices and the A$9.7 billion ($7.3 billion) sale of a 50-year lease in Australia’s busiest port to a group of global investors. Among the currencies of other crude-exporting nations, the Mexican peso and the Canadian dollar rose at least 0.4 percent, while the Norwegian krone was up 0.3 percent. The offshore yuan was one of the few currencies to lose ground against the dollar, weakening 0.3 percent to 6.6702 per dollar. Its overnight borrowing costs in Hong Kong almost tripled to 23.7 percent on Monday, spurring speculation China was mopping up liquidity to deter bets on depreciation before the yuan joins the International Monetary Fund’s basket of reserve currencies next month. “The result is to support the currency at a time when 6.70 suddenly seems a very important line in the sand,” said Michael Every, Hong Kong-based head of financial markets research for Asia-Pacific at Rabobank Group. “You’d almost think it was a pegged currency.”

In commodities, oil rose as renewed clashes halted what would be the first crude shipment from one of Libya’s largest export terminals since 2014. The tanker Seadelta suspended loading after fighting started Sunday between local Petroleum Facilities Guard units and forces loyal to eastern-based military commander Khalifa Haftar. Brent added 1.3 percent to $46.36. OPEC may call an extraordinary meeting if ministers reach consensus at an informal gathering next week, Secretary General Mohammed Barkindo said, according to Algerian Press Service. Nickel rebounded from the biggest weekly slump in ten months after the Philippines said more mine closures were possible. The metal used in stainless steel gained 1.9 percent to $9,910 a metric ton. Copper dropped 0.7 percent, declining from a four-week high as Anglo American Plc restarted operations after a strike at its Los Bronces mine in central Chile, bolstering supply from the world’s largest producer. Gold climbed 0.3 percent to $1,314.35 an ounce and silver jumped 1.7 percent.

It’s a fairly quiet start datawise today with nothing particularly interesting in Europe this morning and just the NAHB housing market index reading in the US to highlight.

US Event Calendar

- 10am: NAHB Housing Market Index, Sept., est. 60 (prior 60)

Bulletin Headline Summary From RanSquawk and Bloomberg

- European equities start the week off on the front-foot with the FTSE 100 outperforming alongside gains in energy and mining names

- Early FX trade on Monday pretty thin, with 2-way flow seeing some moderation in the USD against most of its counterparts

- Looking ahead, highlights include the US NAHB Housing Market Index

- Treasuries little changed in overnight trading with global equities and commodities higher, U.S. dollar lower, FOMC rate decision on Wednesday afternoon followed by BOJ in the evening. Japan closed for holiday today.

- Time and again, Fed officials have tried to jawbone investors into believing they were finally ready to raise interest rates. Yet time and again, whether it was because of Brexit, a slowing Chinese economy or just lackluster growth at home, they lost their nerve

- If the BOJ wants to increase price pressure in a sustainable manner and weaken the yen the central bank will have to come up with something new, Commerzbank strategist Thu Lan Nguyen writes in a client note

- Norway’s central bank is predicted to leave its key policy rate unchanged at a record low 0.5% as the economy of western Europe’s biggest oil producer fights off the biggest slump in crude prices in a generation

- Chancellor Angela Merkel’s party was dealt another blow in a regional election, posting its worst result in Berlin since the end of World War II as the anti-immigration Alternative for Germany extended its challenge to the political establishment by siphoning off voters

- Deutsche Bank AG extended losses as analysts signaled that the German lender’s capital position will be eroded by mounting legal costs such as charges for a U.S. penalty tied to faulty securities

- A warning indicator for banking stress rose to a record in China in the first quarter, underscoring risks to the nation and the world from a rapid build-up of Chinese corporate debt

- Hitting forecasts for next year would require S&P 500 Index companies to increase profits by 13%, something that hasn’t happened since 2011. Failing to do so would risk inflating equity valuations that at 20 times annual income are already the highest since the financial crisis

- Homeland security and terror threats are back on the front burner for the presidential campaign after an explosive device blew up in New York City on Saturday night, injuring 29 people, following incidents in New Jersey and Minnesota earlier in the day

* * *

DB’s Jim Reid concludes the overnight wrap

Perhaps the more interesting and market moving event will now be the BoJ meeting which concludes earlier that morning with BoJ Governor Kuroda due to speak after 7.30am BST. To say I’ve no idea what they are going to do is an understatement. Last week’s press speculation hasn’t helped as it’s suggested a split in the committee. Do they really have time to build a consensus if these reports are true? However a lot is up for discussion. Will we see a small rate cut, will we see an adjustment of long-end purchases, will policy be skewed towards steepening the curve? Difficult to tell. Overall our economists expect them to keep powder dry at this meeting. Indeed they maintain their view that the BoJ is unlikely to cut rates further (or deepen NIRP) and will do little more than indicate its intent to base its policy implementation on the yield curve. A strengthening of forward guidance would theoretically encourage a downward shift in intermediate yields, thus realizing a steepening effect in the long sector, so the adoption of this measure is therefore a possibility. That said they also highlight that the effect is likely to be minimal since few market participants consider the 2% price stability target achievable. As it stands the wider market is also leaning towards the BoJ holding the current -0.10% policy rate as is, albeit by a narrow margin.

In terms of the interesting snippets from the weekend, the latest round of regional elections took place in Germany yesterday, this time in Berlin. Wires are dominated by the news that the populist Alternative for Germany (AfD) party has secured a foothold in the city having taking 12% of the votes, although it’s worth highlighting that this is less than what the pre-election opinion polls had suggested (15% according to the FT) and also the party’s lofty 20% target. Merkel’s Christian Democratic Party secured 18% which is the party’s lowest ever tally in Berlin and down 5% from the 2011 elections and means that the party will possibly lose its position as junior partner in the coalition in Berlin. The governing Social Democrats’ share also tumbled 5% to 23%.

Elsewhere, the rest of the headlines are dominated by the news of the bomb blast in New York which has put the city on high alert. Despite the news risk appetite appears to be fairly decent this morning with US equity index futures currently up +0.30% and emerging market currencies also off to a decent start. Bourses in Asia are also trading with a relatively positive tone with the Hang Seng (+0.51%), Shanghai Comp (+0.54%) and Kospi (+0.55%) all up, with bourses in China reopening following a public holiday. Markets in Japan are closed today for the same reason. The August home prices data has also been released in China this morning. Prices were reported as gaining in 64 of the 70 cities tracked by the government, compared with 51 in July. Prices fell in only 4 cities as opposed to 16 in July.

Also of significance in markets this morning is the huge spike in the overnight offshore yuan interbank rate. The CNH-HIBOR has jumped 15.7ppts to 23.7% and so putting it at the highest level since January. This follows a number of similar moves in the last week or so with speculation mounting that the PBoC has been intervening to make it more expensive to short the yuan.

A quick run through Friday’s session now. Markets concluded a fairly volatile and choppy week with a pretty soft day on Friday. The S&P 500 finished -0.38% and in the process pared its weekly gain to just +0.53%. Energy and financials were most under pressure and it was the same in Europe where the Stoxx 600 closed -0.74%, and down -2.23% over the five days. WTI finished a shade above $43/bbl following a -2% decline on Friday as expectations rose that the supply glut would be back in focus with the resumption of exports from the Ras Lanuf port in Libya following the country’s civil strife. However the news this morning that the country has been forced to halt loading from the port following further fighting has seen WTI rally back +1.60% in early trading. With the OPEC meeting just 8 days away now and an expected informal sideline meeting of major producers’, it wouldn’t be a surprise to see plenty of jawboning on the topic this week.

Meanwhile, Friday’s slightly higher than expected inflation numbers in the US helped to support the Greenback (Dollar index +0.86%) and also send 2y Treasury yields up nearly 4bps. Headline CPI printed at +0.2% mom last month, ahead of the +0.1% expected and helped to send the YoY rate up three-tenths to +1.1%. The core (+0.3% mom vs. +0.2% expected) was also ahead of the market although it’s worth noting that the unrounded number was +0.252%. That also helped lift the annual rate up to +2.3% from +2.2%. Prices did however benefit from a massive surge in medical costs (+0.9% mom) which was in fact the largest since 1990 so it’ll be interesting to see if there is any payback next month. Interestingly that inflation data was in contrast to the preliminary University of Michigan September survey where 1y inflation expectations declined two-tenths to 2.3% from August. 5-10y inflation expectations did stay put at 2.5%. The headline sentiment reading was unchanged at 89.8 (vs. 90.6 expected) while the current conditions index slumped to 103.5 from 107.0 which puts it at the lowest reading since October last year. There was better news in the expectations component which rose 2.4pts to 81.1 and a three month high.

The other big mover on Friday came in currency markets where Sterling (-1.79%) had its worst day since June 27th. The move appeared to come as a result of comments from Chancellor Hammond who said that the UK is ready to accept that it will have to give up membership of the EU’s single market in order to achieve immigration restrictions. Reports suggest that Treasury staff are drawing up plans which they hope will allow Britain’s financial services firms to retain similar levels of access to the continent.

Turning now to what looks set to be a pivotal week ahead in markets. It’s actually a fairly quiet start datawise today with nothing particularly interesting in Europe this morning and just the NAHB housing market index reading in the US tonight to highlight. Tomorrow we have PPI data for Germany in the morning, before we get the August housing starts and building permits data in the US in the afternoon. The key day is of course Wednesday. During Asia time we’ll have the all important BoJ meeting, while the latest Japan trade data for August will also be released. In the UK we then get the latest public sector net borrowing data. That’s before we turn focus over to the Fed in the evening when we’ll get the outcome of the two-day FOMC meeting and also the latest economic projections from the committee members. Kicking things off on Thursday will be France with September confidence indicators, while in the UK the CBI trends data for this month is released. In the US on Thursday there’s a bunch of second tier data including initial jobless claims, Chicago Fed national activity index, existing home sales, leading index and Kansas City Fed’s manufacturing survey. The Euro area consumer confidence reading (for September) also gets released on Thursday afternoon. Friday is all about the PMI’s where we’ll firstly get the flash September manufacturing print in Japan, followed by the flash services, manufacturing and composite readings for the Euro area, Germany and France. The US will also release the flash manufacturing print. Away from that we get the final Q2 GDP revisions in France.

Away from the data the key speakers will of course come after the two Central Bank meetings on Wednesday with BoJ Governor Kuroda and Fed Chair Yellen both due to speak. Also of note is the scheduled speech from ECB President Draghi on Thursday at a conference in Frankfurt, with the BoE’s Cunliffe also scheduled to speak. The Fed’s Harker, Mester and Lockhart are also due to take part in a conference on Friday evening.

end

3.REPORT ON JAPAN SOUTH KOREA NORTH KOREA AND CHINA

i)Late SUNDAY night/MONDAY morning: Shanghai closed UP 23.20 POINTS OR .77%/ /Hang Sang closed UP 214.86 PONTS OR .92%. The Nikkei closed for holiday Australia’s all ordinaires CLOSED down 0.04% Chinese yuan (ONSHORE) closed HUGELY DOWN at 6.6720/Oil rose to 43.60 dollars per barrel for WTI and 46.31 for Brent. Stocks in Europe: ALL IN THE GREEN Offshore yuan trades 6.669 yuan to the dollar vs 6.6720 for onshore yuan.THE SPREAD BETWEEN ONSHORE AND OFFSHORE NARROWS HUGELY AGAIN TO BLOCK MORE USA DOLLARS AS IT ATTEMPTS TO LEAVE CHINA’S SHORES

3a)NORTH KOREA:

none today

b) REPORT ON JAPAN

c) Report on CHINA

(courtesy Bloomberg)

China reports that 22 billion USA has left its shores and now its holdings of USA securities is the lowest since 2013 at 3.2 trillion USA but this will be before futures transactions involving the dollar is released. Expect its real holdings of USA dollars to be around 3.1 trillion USA

( Bloomberg)

China’s Holdings of U.S. Treasuries Fall to Lowest Since ’13

end

Hibor rises to 23.7% as the POBC tried to:

i) punish the CNY shorts

ii) support their currency below 6.70 and thus trying to prevent dollars from leaving Chinese shores

(courtesy zero hedge)

Overnight Hibor Soars To 23.7%, Second Highest On Record, As PBOC War With Yuan Shorts Turns Ugly

When last week Hong Kong’s overnight CNH funding rates exploded to the highest since January, many ascribed it to the liquidity scarcity ahead of Chinese holidays on Thursday and Friday. However, we claimed that as the PBOC continues its struggles to prevent USDCNH from rising above 6.70, pushing funding costs to stratospheric levels was precisely one of the tools it was using.

As we explained last Wednesday, “one reason for the latest surge in funding costs is that with Chinese and Hong Kong holidays on deck, liquidity is scarce. The Hong Kong market will be closed on Friday for the mid-autumn festival and the China markets will be closed on Thursday and Friday. China has traditionally intervened in currency markets just before holidays: last October using illiquidity just before its long National Day celebrations to intervene in Hong Kong and reduce an embarrassingly wide gap between the offshore and onshore rates. Of course, next week we will have the Fed and BOJ meetings as well, where uncertainty is leading to even more illiquidty.”

However, the most likely explanation is that in order to force Yuan shorts to capitulate as 6.70 remains just barely within reach, the PBOC is simply continuing to squeeze the yuan shorts and raising the cost of shorting yuan, as explained last week. Ultimately, the PBoC weakened its yuan fix by 169 pips to 6.6895 versus yesterday’s 6.6726, even as many were expecting the USDCNY to finally breach the the 6.70 resistance level, the defense of which may have explained today’s aggressive spike in HIBOR tightening.

This theory was validated overnight when the overnight interbank yuan rate surged the most since January in Hong Kong amid what Bloomberg said was “speculation China’s central bank is intervening to fend off bearish bets on the currency.” The offshore yuan funding cost, known as Hibor, jumped 15.7% points in its second-biggest gain on record to 23.7% according to a fixing from the Treasury Markets Association. That’s the highest since January, when the People’s Bank of China was also suspected to be mopping up liquidity to boost the exchange rate. Funding conditions tightened on Monday even after the Hong Kong Monetary Authority said Thursday banks in the city had tapped its liquidity facilities. The three-month yuan interbank rate climbed 81 basis points in Hong Kong to 5.86%, the highest since February, while the one-month rate increased to an eight-month high.

As we explained previously, amid expectations that the Yuan would fall following the end of last week’s G-20 meeting in China, the yuan instead stabilized as offshore funding costs climbed ahead of last week’s holidays and amid speculation the PBOC was engineering a squeeze. Such a crunch would help discourage short positions on the currency before the Federal Reserve’s review of monetary policy this week and the yuan’s entry into the International Monetary Fund’s basket of reserve currencies next month.

A jump in yuan Hibor hurts bears in two ways: by increasing the cost to borrow the currency and sell it, and also by prompting lenders that want to avoid paying the higher rates to buy the yuan they need in the spot market instead, bolstering the exchange rate. The rate surged to a record 66.8 percent in January, prompting turmoil in local and global financial markets.

“The result is to support the currency at a time when 6.70 suddenly seems a very important line in the sand,” said Michael Every, Hong Kong-based head of financial markets research for Asia-Pacific at Rabobank Group. “You’d almost think it was a pegged currency.”

Sure enough, the USDCNH has remained under 6.70 however at a price: namely the PBOC tipping its hands that it has to actively punish Yuan shorts by making shorting effectively impossible.

Additionally, despite last week’s dollar gains, the PBOC strengthened the yuan’s fixing by 0.16 percent Monday, in another sign stability is preferred before the U.S. and Japan both deliberate monetary policy this week.

There is another reason why rates have soared: according to Sue Trinh, Royal Bank of Canada’s Hong Kong-based head of Asian foreign-exchange strategy, the recent crunch was partly caused by the PBOC not rolling over its forward positions from last year . Chinese banks were suspected to have sold dollar-yuan forwards last year at the PBOC’s behest, and now that these positions aren’t being extended, the lenders have to settle the contracts by delivering yuan.

“It is reasonable to say that the Chinese authorities are increasingly ‘de-sensitizing’ the yuan from external uncertainties and potential shocks from the Bank of Japan and Fed this week,” said Christy Tan, head of markets strategy in Hong Kong at National Australia Bank Ltd. Tight liquidity before Mid-Autumn Festival holidays last week and the weeklong break in October “provides an additional avenue for the Chinese authorities to maintain the squeeze and ward off speculative selling in the offshore yuan,” she added.

Some more sellside observations on the ongoing liquidity squeeze in the Hong Kong overnight market:

Rabobank Group (Michael Every, head of financial markets research for Asia Pacific)

- Hibor isn’t as high as in January but same message is being sent

- CNH liquidity is tight either by design or by error; result is to support the currency at a time when 6.70 suddenly seems a very important line in the sand. See more

RBC (Sue Trinh, head of Asian FX strategy)

- If China doesn’t roll over positions built during the intervention last yr as they come to maturity it removes CNH liquidity from the market

- As intervention was heaviest in Sept. 2015, funding squeeze related to 1-yr fwd intervention last year maturing will abate

Societe Generale (Frances Cheung, head of Asia ex-Japan rates strategy)

- CNH Hibor rates are probably boosted by temporary demand on offshore yuan as China might choose not to rollover previous positions in forward market

- Liquidity is tightening as previous forward/swap positions that China probably built since last August mature. See more

Mizuho Bank (Ken Cheung, FX strategist)

- CNH liquidity remains tight despite HKMA yuan injection, suggesting market participants are cautious in offering CNH in the interbank market

- Soaring carry costs for short positions appear to reverse bearish sentiment on the yuan

- Cash supply will remain relatively tight as HKMA’s liquidity injection looks to have failed to smooth over concerns

NAB (Christy Tan, head of markets strategy)

- Chinese authorities are increasingly “desensitizing” yuan from external uncertainties from BOJ and Fed meetings this week; Preference is for currency stability ahead of the October 1 SDR entry

- Thin liquidity ahead of the Mid-Autumn holiday and then the Golden Week holidays provides an additional avenue for China to maintain the squeeze and ward off speculative selling in CNH

Commerzbank (Zhou Hao, economist)

- Betting against yuan won’t be profitable now

- PBOC is trying to squeeze out bears by pushing the costs to short the currency very high

It remains to be seen how long the PBOC can maintain this charade of stability and lack of outflows at the expense of crushing shorts and anyone else who dares to take on the Chinese central bank.

end