GOLD: $1272.35 DOWN $0.65

Silver: $16.74 DOWN 5 cent(s)

Closing access prices:

Gold $1266.30

silver: $16.57

SHANGHAI GOLD FIX: FIRST FIX 10 15 PM EST (2:15 SHANGHAI LOCAL TIME)

SECOND FIX: 2:15 AM EST (6:15 SHANGHAI LOCAL TIME)

SHANGHAI FIRST GOLD FIX: $1271.99 DOLLARS PER OZ

NY PRICE OF GOLD AT EXACT SAME TIME: $12766.40

PREMIUM FIRST FIX: $5.59

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

SECOND SHANGHAI GOLD FIX: $1272,17

NY GOLD PRICE AT THE EXACT SAME TIME: $1265.30

Premium of Shanghai 2nd fix/NY:$6.87

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

LONDON FIRST GOLD FIX: 5:30 am est $1266.65

NY PRICING AT THE EXACT SAME TIME: $1266.60

LONDON SECOND GOLD FIX 10 AM: $1269.60

NY PRICING AT THE EXACT SAME TIME. $1269.55

For comex gold:

AUGUST/

NOTICES FILINGS TODAY FOR APRIL CONTRACT MONTH: 193 NOTICE(S) FOR 19,300 OZ.

TOTAL NOTICES SO FAR: 3139 FOR 313,900 OZ (9.7636 TONNES)

For silver:

AUGUST

107 NOTICES FILED TODAY FOR

535,000 OZ/

Total number of notices filed so far this month: 411 for 2,055,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Yesterday I wrote the following:

“it now looks like the boys have lost control of the gold/silver market/for sure silver with today’s attempted raid and failure. The bankers have decided to take their anger by hitting on the gold/silver equity shares.”

Again the bankers took out their frustration by whacking the gold and silver equity shares. They also whack gold and silver within seconds after the comex closes..Such crooks

end

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total open interest FELL BY A TINY 358 contracts from 207,643 DOWN TO 207,258 WITH NO GAIN IN THE PRICE THAT SILVER TOOK WITH RESPECT TO YESTERDAY’S TRADING (UP 0 CENT(S). WHEN YOU COMPARE THE HUGE GAIN IN OI FOR GOLD THEN YOU MUST ADMIT THAT IT SURE LOOKS LIKE BOTH THE SPECULATOR SHORTS AND THE BANKER SHORTS ARE HAVING SEVERE PROBLEMS TRYING TO COVER THEIR SHORTFALL WHICH CANNOT COME TO FRUITION. THE LONGS REMAIN STOIC AND NOTHING WILL BUDGE OUR SILVER LEAVES FROM DEPARTING OUR SILVER TREE. YESTERDAY’S TRADING IS EVIDENCE OF THAT

In ounces, the OI is still represented by just OVER 1 BILLION oz i.e. 1.038 BILLION TO BE EXACT or 148% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT MAY MONTH/ THEY FILED: 107 NOTICE(S) FOR 535,000 OZ OF SILVER

In gold, the open interest ROSE by A MONSTROUS 11,747 with the RISE in price of gold ($4.95 yesterday.) The new OI for the gold complex rests at 448,709. Yesterday we had the bankers supplying a major amount of short paper to newbie longs who entered the arena like gangbusters. The specs shorts covered but at a higher price.No wonder a raid was orchestrated overnight with the intention of cooling gold’s jets. It seems that the raid failed again. The bankers are losing control over the precious metal markets

we had: 193 notice(s) filed upon for 19,300 oz of gold.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD:

Today, no changes in gold inventory

Inventory rests tonight: 791.88 tonnes

IN THE LAST 14 DAYS: GLD SHEDS 45.62 TONNES YET GOLD IS HIGHER BY $48.85 . GO FIGURE!!

SLV

Today: : WE HAD NO CHANGES IN SILVER INVENTORY TONIGHT:

INVENTORY RESTS AT 341.732 MILLION OZ

end

.

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in silver FALL BY A TINY 358 contracts from 207,643 DOWN TO 207,258 (AND now A LITTLE FURTHER FROM THE NEW COMEX RECORD SET ON FRIDAY/APRIL 21/2017 AT 234,787). THE FALL IN OPEN INTEREST WAS ACCOMPANIED BY A NO GAIN IN PRICE FOR SILVER WITH RESPECT TO YESTERDAY’S TRADING (UP 0 CENTS ). WHEN WE SEE THE MASSIVE RISE IN GOLD OPEN INTEREST YESTERDAY, WE NO DOUBT WITNESSED MORE SPEC LONGS ENTER THE ARENA (with political unrest) WITH THE MAJORITY OF THE SPEC LONGS AGAIN BASICALLY REMAINING STOIC. THE SPEC LONGS SEEM TO BE TAKING ON THE BANKERS. THE SPEC SHORTS ARE DESPERATE TO COVER THEIR SHORTFALL BUT THEY ARE COMING IN CONTACT WITH A LARGE NUMBER OF NEW SPEC LONGS . THE BANKERS HAD NO CHOICE BUT TO COVER SOME OF THEIR MASSIVE SHORT PAPER DESPITE THE ZERO PRICE GAIN FROM SILVER. THE NET RESULT: A COMEX SILVER OPEN INTEREST SLIGHT DECREASE.

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)Late TUESDAY night/WEDNESDAY morning: Shanghai closed DOWN 7.58 POINTS OR 0.23% / /Hang Sang CLOSED UP 67.15 POINTS OR 0.24% The Nikkei closed UP 94.25 POINTS OR .17%/Australia’s all ordinaires CLOSED DOWN 0.45%/Chinese yuan (ONSHORE) closed DOWN at 6.7228/Oil DOWN to 49.16 dollars per barrel for WTI and 51.99 for Brent. Stocks in Europe OPENED IN THE RED , Offshore yuan trades 6.7296 yuan to the dollar vs 6.7228 for onshore yuan. NOW THE OFFSHORE IS WEAKER TO THE ONSHORE YUAN/ ONSHORE YUAN WEAKER (TO THE DOLLAR) AND THE OFFSHORE YUAN IS MUCH WEAKER TO THE DOLLAR AND THIS IS COUPLED WITH THE SLIGHTLY WEAKER DOLLAR. CHINA IS HAPPY TODAY

3a)THAILAND/SOUTH KOREA/NORTH KOREA

i)NORTH KOREA//USA

The USA launches a minuteman ICBM in a warning to North Korea

( zero hedge)

b) REPORT ON JAPAN

c) REPORT ON CHINA

Trump set to initiate section 301 of the 1974 Trade Act which calls for an investigation into the trade practices of a particular country. If it finds fault, then sanctions and cancelling of licenses etc can be called into play. The USA seems to be snubbing the WTO

( zero hedge)

4. EUROPEAN AFFAIRS

EU/ITALY

the European migrant crisis escalates again with Italy impounding a German NGO refugee ship. Italy is getting no help from the EU on the migrant issue.

( zero hedge)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

the mood is quite sombre as USA officials begin packing up reading to leave Moscow on orders from Putin

( zero hedge)

ibJust out and great reason for the crooks to hit on gold and silver

we are back to square one with respect to the original 13 demands of Qatar from the Saudi block

(courtesy Paraskova/OilPrice.com)

6 .GLOBAL ISSUES

7. OIL ISSUES

WTI slides again after another disappointing crude drawdown. Production continues to rise with all of the rigs going at full blast

( zero hedge)

8. EMERGING MARKET

VENEZUELA

We are now witnessing the beginning of hyperinflation in Venezuela. In a few short weeks-to a few months, we will see bolivar rates equal to that of Zimbabwe.

(courtesy zero hedge)

9. PHYSICAL MARKETS

wow!! this is developing to be a quite a story. Turkey imported a huge 2.8 billion USA dollars worth of gold or 68.4 tonnes in July. In June 2.1 billion dollars or 52.5 tonnes. Let’s average the two months at 60 tonnes. Then these guys will import from this day forward 720 tonnes of gold. My goodness, we have China at around 2,000 tonnes, India 1000 tonnes, Russia around 120 tonnes and the world produces 2,200 tonnes net China net Russia which do not let one oz out of the countries. Some sovereign is liquidating their official reserves!!

( zerohedge)

10. USA Stories

v)This looks ominous: Mueller just added another Obama ally to his team, Greg Andres a former Dept. of Justice attorney who served under Eric Holder.

vi)Trump signs the Russia sanction bill “with reservations” commenting that this bill encroaches on executive privilege. We now await Europe’s response

( zerohedge)

vii)Dave Kranzler of IRD talks about the crashing auto sales

viii)It looks like another 30% rise in Obamacare premiums and this is with the Fed subsidies. You can imagine what will happen if Trump cuts them off. Actually the press is now blaming Trump for all of those Obamacare increases

Let us head over to the comex:

The total gold comex open interest ROSE BY A MONSTROUS 11,747 CONTRACTS UP to an OI level of 448,709 WITH THE RISE IN THE PRICE OF GOLD ($4.95 with YESTERDAY’S trading). We had a huge number of newbie longs enter the gold area to which our crooked bankers were more than happy to comply. The specs shorts covered as fast as their feet could carry them.

We are now in the contract month of August and it is the 3rd best of the delivery months after December and June.

The active August contract LOST 1290 contract(s) to stand at 2972 contracts. We had 1,309 notices filed upon yesterday so we SURPRISINGLY GAINED 19 contracts or an additional 1900 oz will stand at the comex and 0 EFP’s were issued which entitles the long holder to a fiat bonus plus a futures contract and most probably that would be a London based forward. That is a first for gold: the longs refusing an EFP!!!!

The non active September contract month saw it’s OI fall by 22 contracts up to 1867.

The next active contract month is Oct and here we saw a rise of 5233 contracts up to 48,330.

The very big active December contract month saw it’s OI rise by 7744 contracts up to 344,426.

We had 193 notice(s) filed upon today for 19,300 oz

For those keeping score: in the upcoming front delivery month of August:

LAST YEAR WE HAD A MONSTROUS 44.7 TONNES OF GOLD INITIALLY. BY THE CONCLUSION OF THE AUGUST CONTRACT MONTH 44.358 TONNES STOOD FOR DELIVERY.

We are now in the next big non active silver contract month of August and here the OI SURPRISINGLY FELL BY ONLY 53 contracts. We had 71 notices filed yesterday. Thus we gained a huge 18 contracts or an additional 90,000 oz will stand. We are proceeding again where we left off last month (July) and the month before that (June), and finally the month before that(May), where the amount standing increases as the month proceeds and it begins right on day 2.

The next active contract month is September (and the last active month until December) saw it’s OI fall by 1493 contacts down to 138,414. The next non active contract month for silver after September is October and here the OI 20 contacts. After October, the big active contract month is December and here the OI rose by 1033 contracts up to 59,254 contracts.

We had 107 notice(s) filed for 535,000 oz for the AUGUST 2017 contract

VOLUMES: for the gold comex

Today the estimated volume was 109,249 contracts which is POOR/

Yesterday’s confirmed volume was 231,323 contracts which is GOOD

volumes on gold are STILL HIGHER THAN NORMAL!

August 2/2017.

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz |

nil oz

|

| Deposits to the Dealer Inventory in oz | oz |

| Deposits to the Customer Inventory, in oz |

32,150.000 oz

Scotia

1000 kilobars

|

| No of oz served (contracts) today |

193 notice(s)

19,300 OZ

|

| No of oz to be served (notices) |

2779 contracts

(277,900 oz)

|

| Total monthly oz gold served (contracts) so far this month |

3139 notices

313,900 oz

9.7636 tonnes

|

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | nil oz |

Today, 0 notice(s) were issued from JPMorgan dealer account and 3 notices were issued from their client or customer account. The total of all issuance by all participants equates to 193 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 10 notice(s) was (were) stopped/ Received) by j.P.Morgan customer account.

| Silver | Ounces |

| Withdrawals from Dealers Inventory | nil |

| Withdrawals from Customer Inventory |

190,814.170 oz

Scotia

|

| Deposits to the Dealer Inventory |

nil oz

|

| Deposits to the Customer Inventory |

599451.890

oz

Scotia

|

| No of oz served today (contracts) |

107 CONTRACT(S)

(535,000 OZ)

|

| No of oz to be served (notices) |

209 contracts

( 1,045,000 oz)

|

| Total monthly oz silver served (contracts) | 411 contracts (2,055,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month | 190,814.170 oz |

NPV for Sprott and Central Fund of Canada

Sprott’s hostile 3.1 billion bid to take over Central Fund of Canada

(courtesy Sprott/GATA)

Sprott makes hostile $3.1 billion bid for Central Fund of Canada

Submitted by cpowell on Thu, 2017-03-09 01:19. Section: Daily Dispatches

From the Canadian Press

via Canadian Broadcasting Corp. News, Toronto

Wednesday, March 8, 2017

http://www.cbc.ca/news/canada/calgary/sprott-takeover-bid-central-fund-c…

Toronto-based Sprott Inc. said Wednesday it’s making an all-share hostile takeover bid worth $3.1 billion US for rival bullion holder Central Fund of Canada Ltd.

The money-management firm has filed an application with the Court of Queen’s Bench of Alberta seeking to allow shareholders of Calgary-based Central Fund to swap their shares for ones in a newly-formed trust that would be substantially similar to Sprott’s existing precious metal holding entities.

The company is going through the courts after its efforts to strike a friendly deal were rebuffed by the Spicer family that controls Central Fund, said Sprott spokesman Glen Williams.

“They weren’t interested in having those discussions,” Williams said.

Sprott is using the courts to try to give holders of the 252 million non-voting class A shares a say in takeover bids, which Central Fund explicitly states they have no right to participate in. That voting right is reserved for the 40,000 common shares outstanding, which the family of J.C. Stefan Spicer, chairman and CEO of Central Fund, control.

If successful through the courts, Sprott would then need the support of two-thirds of shareholder votes to close the takeover deal, but there’s no guarantee they will make it that far.

“It is unusual to go this route,” said Williams. “There’s no specific precedent where this has worked.”

Sprott did have success last year in taking over Central GoldTrust, a similar fund that was controlled by the Spicer family, after securing support from more than 96 percent of shareholder votes cast.

The firm says Central Fund’s shares are trading at a discount to net asset value and a takeover by Sprott could unlock US$304 million in shareholder value.

Central Fund did not have any immediate comment on the unsolicited offer. Williams said Sprott had not yet heard from Central Fund on the proposal but that some shareholders had already contacted them to voice their support.

Sprott’s existing precious metal holding companies are designed to allow investors to own gold and other metals without having to worry about taking care of the physical bullion.

end

And now the Gold inventory at the GLD

August 2/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 791.88 TONNES

Aug 1/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 791.88 TONNES

July 31/NO CHANGES AT THE GLD/INVENTORY RESTS AT 791.88 TONNES

July 28/ANOTHER MASSIVE WITHDRAWAL OF 3.54 TONNES OF GOLD WITH GOLD UP $9.15/INVENTORY RESTS AT 791.88 TONNES

July 27/LATE LAST NIGHT, A HUGE WITHDRAWAL OF 5.03 TONNES WITH GOLD UP $10.45 ON THE DAY/INVENTORY RESTS AT 795.42 TONNES

July 26/NO CHANGE IN GLD INVENTORY WITH GOLD DOWN $2.55/INVENTORY RESTS AT 800.45 TONNES

July 25/A MASSIVE 9.17 TONNES OF GOLD WITHDRAWN FROM THE GLD/INVENTORY RESTS AT 800.45 TONNES

July 24/A massive 9.62 tonnes withdrawal and yet the price remains constant (down only 25 cents)..inventory drops to 809.62 tonnes

July 21/with gold up $8.75 again, we had no changes in gold inventory at the GLD/inventory rests at 816.13 tonnes

July 20/WITH GOLD UP AGAIN TODAY ($3.50) WE HAD NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 816.13 TONNES

jULY 19/STRANGE!! AGAIN WITH GOLD UP $0.50 WE HAD ANOTHER HUGE 5.32 TONNES WITHDRAWAL FROM THE GLD/INVENTORY RESTS AT 816.13 TONNES THIS GOLD IS HEADING TO SHANGHAI

July 18/STRANGE AGAIN/WITH GOLD UP $7.50 WE HAD ANOTHER HUGE 5.62 TONNES WITHDRAWAL FROM THE GLD/INVENTORY RESTS AT 821.45 TONNES

July 17/strange again! with gold up $4.20 we had another huge withdrawal of 1.77 tonnes/inventory rests at 827.07 tonnes

July 14/strange@!!with gold up $12.00 today, we had a huge withdrawal of 3.55 tonnes/inventory rests at 828.84 tonnes

July 13/no change in gold inventory at the GLD/inventory rests at 832.39 tonnes

JULY 12/no change in gold inventory at the GLD/inventory rests at 832.39 tonnes

July 11/strange!@! we had a big withdrawal of 2.96 tonnes despite gold’s advance today/inventory rests tonight at 832.39 tonnes

July 10/no changes in gold inventory at the GLD/inventory rests at 835.35 tonnes

July 7/a massive withdrawal of 5.32 tonnes of paper gold were removed and this was used in the attack today/inventory rests at 835.35 tonnes

July 6/no changes in tonnage at the GLD/Inventory rests at 840.67 tonnes

July 5/A MASSIVE 5.62 TONNES OF GOLD LEFT THE GLD AND NO DOUBT WAS USED IN THE RAID THIS MORNING/INVENTORY REST

July 3/ A MASSIVE 7.37 TONNES OF GOLD LEAVE THE GLD/INVENTORY RESTS AT 846.29 TONNES

end

Now the SLV Inventory

August 2/NO CHANGES IN SILVER INVENTORY AT THE SLV

INVENTORY RESTS AT 341.732 MILLION OZ/

August 1/A HUGE WITHDRAWAL OF 945,000 OZ/INVENTORY RESTS AT 341.732 MILLION OZ/

July 31/no change in silver inventory at the SLV/inventory rests at 342.677 million oz

July 28/ A HUGE WITHDRAWAL OF 1.15 MILLION OZ OF SILVER LEAVES THE SLV DESPITE SILVER BEING UP 11 CENTS TODAY/INVENTORY RESTS AT 342.677 MILLION OZ

July 27/NO CHANGE IN SILVER INVENTORY/INVENTORY RESTS AT 343.812 MILLION OZ WITH SILVER UP 13 CENTS TODAY.

July 26/NO CHANGE IN SILVER INVENTORY/INVENTORY RESTS AT 343.812 MILLION OZ

July 25/A MASSIVE 3.309 MILLION OZ OF INVENTORY WITHDRAWN FROM THE SLV DESPITE SILVER’S 10 CENT RISE TODAY.

July 24/no change in silver inventory despite its 4 cent drop/inventory remains at 347.121 million oz

July 21/STRANGE! WITH SILVER UP AGAIN TODAY (11 CENTS), NO CHANGE IN SILVER INVENTORY AT THE SLV/inventory 347.121 million oz/

July 20/STRANGE! WITH SILVER UP AGAIN TODAY, THE SLV INVENTORY LOWERS BY 945,000 OZ/INVENTORY RESTS AT 347.121 MILLION OZ/

July 19/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 348.066 MILLION OZ

July 18/a huge 946,000 oz withdrawal from the SLV despite silver’s 16 cent gain!

Inventory rests at 348.066 million oz

July 17/no change in silver inventory at the SLV/Inventory rests at 349.012 million oz

July 14/no change in silver inventory/inventory rests at 349.012 million oz/

July 13/no change in silver inventory/inventory at the SLV rests at 349.012 million oz/

JULY 12/another massive 1.986 million oz of silver added into the SLV/inventory rests at 349.012 million oz/the last 3 days saw 7.281 million oz added into the SV

July 11/ANOTHER MASSIVE INCREASE OF 2.364 MILLION OZ into the SLV inventory/inventory rests at 347.026 million oz

July 10/ A HUGE INCREASE OF 2.931 MILLION OZ OF SILVER DESPITE THE EARLY HIT ON SILVER THIS MORNING/INVENTORY RESTS AT 344.662 MILLION OZ.

July 7/Strange: no change in inventory (compare that with gold) Inventory rests at 341.731 million oz

July 6/ANOTHER MASSIVE DEPOSIT OF 2.126 MILLION OZ INTO THE SLV INVENTORY/INVENTORY RESTS AT 341.731 MILLION OZ.

July 5/STRANGE! NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 339.605 MILLION OZ

July 3/strange! with the huge whacking of silver we got an increase of 379,000 oz into inventory.

August 2.2017:

-

Indicative gold forward offer rate for a 6 month duration+ 1.27%

Indicative gold forward offer rate for a 6 month duration+ 1.27% -

+ 1.44%

end

END

Major gold/silver trading/commentaries for WEDNESDAY

GOLDCORE/BLOG/MARK O’BYRNE.

GOLD/SILVER

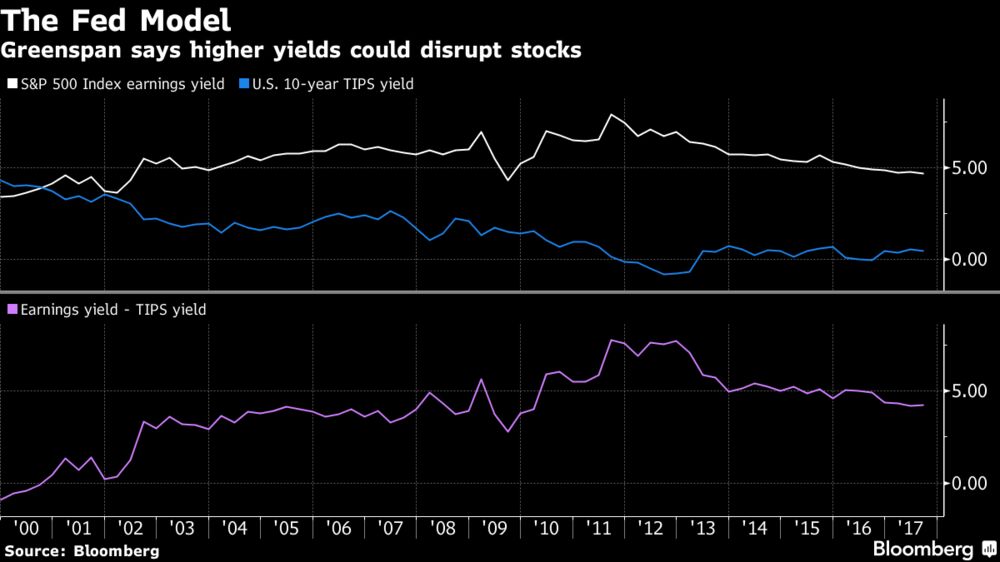

Greenspan Warns Stagflation Like 1970s “Not Good For Asset Prices”

– Former Fed Chairman warns of bond bubble, stagflation

– “Moving into a … stagflation not seen since the 1970s”

– This will not be “good for asset prices”

– 10 Yr Gov bond yields fell from 15.8% in 1981 to 2.3%

– Interest rates will not stay low, will rise ‘reasonably fast’

– “Normal” interest rates in 4%-5% range

– Inflation will not stay at historically low levels

– Gold “protects savings” and is “store of value”

– Gold is the “ultimate insurance policy” says Greenspan

Editor: Mark O’Byrne

Greenspan warns of Bond Bubble

‘We are experiencing a bubble, not in stock prices but in bond prices. This is not discounted in the marketplace.’

There are a lot of warnings on Bloomberg, CNBC and other financial media these days about a bubble in the stock market, particularly in FANG stocks and the tech sector.

But former Fed Chair Alan Greenspan is not in agreement. He is continuing his message of the last two years, that there is a bond bubble and which is more dangerous than what is going on in the stock market.

He is not the only one, in recent months there has been a growing number of those who are concerned that real bond yields in the U.S., UK, EU and elsewhere are well below where growth and inflation rates seem to suggest they should be.

They correctly warn that it is only a matter of time before the inflationary pressures (that we are feeling) hit the bond market.

Stagflation on the horizon

Greenspan’s warning this week comes a little over a year after he last warned us that we were currently in the worst period he has seen since he began public service, including the financial crisis.

Things are so bad, he said that he wished he could “find something positive to say.”

At the time he pointed towards the problem of ‘entitlements’ (welfare / warfare spending of the ‘welfare warfare state’). Something, he argued, is uneconomic and unsustainable. The main reason for its lack of sustainability is the low growth rates developed countries around the world are experiencing (around 2%).

Now, this lack of growth is prompting calls of concern from Greenspan regarding stagflation:

“We’ve been in a period of stagnation since 2008 as a consequence of the sharp decline of capital investment and productivity growth… We are moving into a different phase of the economy — to a stagflation not seen since the 1970s. That is not good for asset prices.”

Felder Report via ZeroHedge

Asset prices obviously include the bond market, and this is where Mr Greenspan believes we should focus our concerns. Thanks to the unsustainable levels of low interest rates. Something which he has expressed concern about before.

Worried about interest rates

“By any measure, real long-term interest rates are much too low and therefore unsustainable,” the former Federal Reserve chairman, 91, said in this latest interview.

“When they move higher they are likely to move reasonably fast. We are experiencing a bubble, not in stock prices but in bond prices. This is not discounted in the marketplace.”

Two years ago Greenspan told Bloomberg that the bond market price-to-earnings ratio was in an ‘extraordinary position’ and that interest rates sitting below 4% was not normal.

“We have pressed the interest rates well below normal for a protracted period of time and the danger is they will come up to back up to where they have always been…There are two possibilities. Either we move slowly back to normal, or we do it in a fairly aggressive manner. History tells us it’s the latter which tends to be more prevalent than the former,” Greenspan said, the market impact, therefore, will be “not good.”

Yields on the US 10-year Treasury note have been below 4% since the summer of 2008 (see chart below).

No more air for the bubble

Currently around $1.5 trillion a year is created by central banks through money printing schemes. The major central banks (US Federal Reserve, the European Central Bank and the Bank of Japan) have collectively gathered around $13 trillion of government bonds on their balance sheets.

All of them, including others such as the Bank of England, are signalling that times are changing. For as long as money is being printed then bond prices have been going up. Great news for investors and pension owners, but those same investors would like to be able get out quickly.

This has been possible in recent years, thanks to what is basically a globally co-ordinated scheme of massive currency creation and bond buying.

However, we now appear to be heading into a period of co-ordinated global rate-hiking. This means that as interest rates start to climb then liquidity conditions will not work in investors’ favours.

There is little reason why we will not see a domino effect of increased interest rates, heightened volatility, falling bond prices and then perhaps even a crash in the stock and bond markets.

According to the 207 investment professionals surveyed by BAML last month, this would be disastrous for the market. They warned that a crash in the global bond market is the biggest tail risk for markets.

But so far these warning cries are little heeded in the mutual fund and wider market. According to Morningstar retail and high net worth investors alike are still ploughing cash into bonds.

Fixed-income products attracted $355bn in net new money between January to May 2017. Consider that next to the $375bn of net inflows for all of 2016. The figure also surpasses the entire year’s figures for 2013, 2014 and 2015.

Some of those who are buying believe that as inflation rates are low then it is unlikely to be a cause for concern to central banks, who are then less likely to raise rates rapidly. However, as we have covered here, the real rates of inflation really are a growing concern and are now on the radar of concerned central bankers.

At this point it is worth recalling another nugget of wisdom from Greenspan. He said back in 2014, ‘When bubbles emerge, they take on a life of their own. It is very difficult to stop them, short of a debilitating crunch in the marketplace.’

What does this mean for gold?

Mr Greenspan is a well-known gold-bug. Just earlier this year he said in an interview that investors were diversifying into gold and silver due to the deepening lack of trust in the financial system and currency markets.

Whilst interest rates are likely to rise, so is inflation which as Greenspan has previously argued, is good for gold:

“Significant increases in inflation will ultimately increase the price of gold. Investment in gold now is insurance.”

Gold is not only insurance against inflationary pressures but it is insurance against the unknown whether that be the outlook for the dollar or for the survival of the euro itself which Greenspan warned about earlier this year.

Earlier interviews with Greenspan have provided insight into how often bodies such as the Federal Reserve misjudge economic situations which then results in poor policy making. Of course, no one knows how the financial future will evolve, especially as each crisis comes with new financial strategies, technology and human behaviour.

Greenspan is unable to predict when the bond bubble will burst, and many disagree that it will happen, instead pointing to a stock market problem.

The bottom line is no one has a crystal ball. We simply don’t know now how this will pan out.

But we do know that the current situation is unsustainable. Most asset markets look overvalued and the value of major currencies are slowly being eroded.

Gold will hedge and insure against these real risks.

Related

Greenspan Says Gold “Ultimate Insurance Policy” as has “Grave Concerns About Euro”

News and Commentary

Irish gold bullion broker GoldCore tops sales of $1bn (IrishTimes.com)

Gold edges away from 7-week high as dollar steadies (Reuters.com)

Gold settles at nearly 8-week high (MarketWatch.com)

Greenspan stresses ‘ominous’ worries about bond bubble (MarketWatch.com)

Fears rise on £200bn debt pile as Moody’s warns Britons may be borrowing too much (CityAM.com)

Source Bank of England via CityAm

Greenspan Sees No Stock Excess, Warns of Bond Market Bubble (Bloomberg.com)

Independent German Central Bank Responsible For Two Monetary Disasters (HandelsBlatt.com)

Importance of Rebalancing Portfolio – Now Good Time To Rebalance (StansBerryChurcHouse.com)

This Chart Might Make You Rethink the Adage “Stocks Always Come Back” (TheDailyCoin.org)

Popularity Rises For Precious Metals’ Initial Coin Offerings (ICOs) (Gold-Eagle.com)

Rickards: Scaramucci’s Chinese Operation May Have Pushed Him Out (DailyReckoning.com)

Gold Prices (LBMA AM)

02 Aug: USD 1,266.65, GBP 956.83 & EUR 1,069.56 per ounce

01 Aug: USD 1,267.05, GBP 957.76 & EUR 1,072.30 per ounce

31 Jul: USD 1,266.35, GBP 965.59 & EUR 1,079.06 per ounce

28 Jul: USD 1,259.60, GBP 961.96 & EUR 1,075.45 per ounce

27 Jul: USD 1,262.05, GBP 960.29 & EUR 1,076.53 per ounce

26 Jul: USD 1,245.40, GBP 956.72 & EUR 1,071.29 per ounce

25 Jul: USD 1,252.00, GBP 960.78 & EUR 1,074.59 per ounce

Silver Prices (LBMA)

02 Aug: USD 16.67, GBP 12.60 & EUR 14.09 per ounce

01 Aug: USD 16.74, GBP 12.67 & EUR 14.17 per ounce

31 Jul: USD 16.76, GBP 12.77 & EUR 14.29 per ounce

28 Jul: USD 16.56, GBP 12.66 & EUR 14.15 per ounce

27 Jul: USD 16.79, GBP 12.77 & EUR 14.34 per ounce

26 Jul: USD 16.37, GBP 12.54 & EUR 14.06 per ounce

25 Jul: USD 16.31, GBP 12.52 & EUR 14.00 per ounce

Recent Market Updates

– What Investors Can Learn From the Japanese Art of Kintsukuroi

– Bitcoin, ICO Risk Versus Immutable Gold and Silver

– This Is Why Shrinkflation Is Making You Poor

– Gold A Good Store Of Value – Protect From $217 Trillion Global Debt Bubble

– Why Surging UK Household Debt Will Cause The Next Crisis

– Gold Seasonal Sweet Spot – August and September – Coming

– Commercial Property Market In Dublin Is Inflated and May Burst Again

– Gold Hedges Against Currency Devaluation and Cost Of Fuel, Food, Beer and Housing

– Millennials Can Punt On Bitcoin, Own Gold and Silver For Long Term

– “Time To Position In Gold Is Right Now” says Jim Rickards

– Bloomberg Silver Price Survey – Median 12 Month Forecast Of $20

– “Bigger Systemic Risk” Now Than 2008 – Bank of England

– “Financial Crisis” Coming By End Of 2018 – Prepare Urgently

end

wow!! this is developing to be a quite a story. Turkey imported a huge 2.8 billion USA dollars worth of gold or 68.4 tonnes in July. In June 2.1 billion dollars or 52.5 tonnes. Let’s average the two months at 60 tonnes. Then these guys will import from this day forward 720 tonnes of gold. My goodness, we have China at around 2,000 tonnes, India 1000 tonnes, Russia around 120 tonnes and the world produces 2,200 tonnes net China net Russia which do not let one oz out of the countries. Some sovereign is liquidating their official reserves!!

I

(courtesy zerohedge)

Turks Panic-Buy The Most Gold Ever In July

A funny thing has happened in Turkey since President Recep Tayyip Erdogan installed himself as ‘Sultan for life’…

The Lira collapsed...

And Turks have been importing gold at an unprecedented rate…

As Bloomberg reports, preliminary trade data from Turkey’s Ministry of Customs and Trade showed the deficit widening to $8.8 billion in July.

An eight-fold increase in gold imports to $2.8 billion from $354 million in the same month last year made the precious metal the second-most imported product and one of the main contributors to the trade gap.

June gold imports were also up by 216 percent year-on-year to $2.1 billion, according to final figures reported by Turkstat, the state statistics agency.

The question is – just like in India – how long before Erdogan ‘dictates’ an end to gold imports, imposes tariffs, or confiscates the precious metal?

end

Your early WEDNESDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight

1 Chinese yuan vs USA dollar/yuan WEAKER 6.7228(DEVALUATION SOUTHBOUND /OFFSHORE YUAN MOVES WEAKER TO ONSHORE AT 6.7296/ Shanghai bourse CLOSED DOWN 7.58 POINTS OR 0.23% / HANG SANG CLOSED UP 67.15 POINTS OR 0.24%

2. Nikkei closed UP 94.25 POINTS OR .17% /USA: YEN RISES TO 110.75

3. Europe stocks OPENED IN THE RED ( /USA dollar index FALLS TO 92.96/Euro UP to 1.1827

3b Japan 10 year bond yield: FALLS TO +.078%/ GOVERNMENT INTERVENTION !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 114.34/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD FINALLY IN THE POSITIVE/BANK OF JAPAN LOSING CONTROL OF THEIR YIELD CURVE AS THEY PURCHASE ALL BONDS TO GET TO ZERO RATE!!

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 49.16 and Brent: 51.99

3f Gold DOWN/Yen DOWN

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil DOWN for WTI and DOWN for Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund FALLS TO +.494%/Italian 10 yr bond yield DOWN to 2.021%

3j Greek 10 year bond yield RISES to : 5.493???

3k Gold at $1266.80 silver at:16.65 (8:15 am est) SILVER BELOW RESISTANCE AT $18.50

3l USA vs Russian rouble; (Russian rouble DOWN 30/100 in roubles/dollar) 60.65-

3m oil into the 49 dollar handle for WTI and 51 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation (already upon us). This can spell financial disaster for the rest of the world/China forced to do QE!! as it lowers its yuan value to the dollar/GOT A SMALL SIZED DEVALUATION SOUTHBOUND

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 110.75 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 0.9691 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1462 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now POSITIVE territory with the 10 year FALLING to +0.494%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.2745% early this morning. Thirty year rate at 2.8798% /POLICY ERROR)GETTING DANGEROUSLY HIGH

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

(courtesy Jim Reid/Bloomberg/Deutsche bank/zero hedge)

Dow To Rise Above 22,000 On Apple Earnings; Europe Pressured By Surging Euro

Nasdaq 100 futures jumped 0.8% after Apple surged to record highs following a strong beat and optimistic projections ahead of the launch of the company’s new batch of iPhones. Eminis are little changed, up 0.1% to 2,475, trailing Asian markets, while European stocks and crude oil fall.

Apple surged 6% after-hours to a new record highm taking its market capitalization above $830 billion. That should help carry the Dow through the 22,000 mark when the market opens. Among Asia’s Apple suppliers, LG Innnotek jumped 10 percent and SK Hynix, the world’s second-biggest memory chip maker, rose 3.8 percent. Murata Manufacturing firmed 4.9 percent and Taiyo Yuden 4.4 percent, helping the Nikkei up 0.47 percent.

“It is all about Apple,” said Naeem Aslam chief market analyst at Think Markets. “The firm comfortably topped its forecast and produced stellar numbers for its revenue and profit.”

Oil came under pressure again as higher than expected US inventories and reports of rising OPEC output helped drive prices below back below $48/bbl (WTI crude). In FX markets, the USD dollar gave up some gains late in the session with DXY edging down by 0.1% and the euro rising to $1.1827. Treasury yields are 0.5-2bps higher across the curve with the 10y at 2.273%.

The MSCI tech index for Asia climbed 0.9 percent to ground not trod since early 2000, bringing its gains for the year to a heady 40 percent. Asian markets rose, supported by tech shares after Apple’s surprising beat guidance boost as well as stronger Chinese manufacturing PMIs (the Caixin/Markit survey of private Chinese manufacturing rose to 51.1 in July, its highest level in four months). Japan’s Nikkei gained after the strong Apple sales outlook helped boost tech shares; Korea’s Kospi and the Hang Seng were also firmer while the ASX 200 slipped on commodities pullback. The NZ kiwi dropped sharply after New Zealand’s employment unexpectedly fell. Australian government bonds trimmed early gains after monthly building approvals surged; WTI crude futures drift lower toward $48.50; Dalian iron ore January futures 1.6% weaker

In Europe, the Stoxx Europe 600 Index declined 0.2%, the U.K.’s FTSE 100 Index decreased 0.3 % while Germany’s DAX Index dropped 0.1%. Mining and oil shares weighed on Europe’s benchmark equity index as crude fell for a second day and most industrial metals traded lower. Meanwhile, following its best month since March 2016 the Euro’s gains continued, reached a new two-and-a-half-year high against the ailing dollar, and leading to a stop-loss triggered spike around 4:30am ET, which sent the EURUSD as high as 1.1870, pressuring the Eurostoxx 600 lower, as traders ktrimmed long-dollar positions ahead of U.S. payrolls data on Friday. Rio Tinto Plc led the decline among basic resources shares after first-half profit missed estimates. Banks dropped after Standard Chartered Plc said it can’t resume dividends amid an uncertain recovery, while Societe Generale SA slumped as litigation costs increased. Oil extended a retreat from its brief rise above $50 a barrel as U.S. crude stockpiles expanded, while copper dropped a second day.

“The ECB is going to be the central bank to watch for the rest of the year,” said JP Morgan Asset Management global market strategist Alex Dryden. “We think they are going to take 9-12 months to get out of the market but that is a big question … it could even be six months,” he added.

With the dollar index near a two-year low, the options market shows that traders are gearing up for more euro strength with demand growing for calls, according to Bloomberg. The currency’s strength has pushed European earnings revisions into negative territory, according to Credit Suisse Group AG.

The pound retains bullish trading ahead of the Bank of England policy decision on Thursday, rising as high as 1.3240. European government bonds slipped before Germany’s sale of 10-year bunds, which priced at an average yield of 0.49%, down from 0.59% previously (Bid to cover 1.52, retention of 19.5%).

The key overnight FX move included a tumble in the New Zealand dollar, which fell more than half a percent after second-quarter employment unexpectedly declined. Most emerging Asian currencies fell initially as the dollar recovered after capping a fifth straight month of declines in July. The MSCI EM Asia Index of shares is up for a third day, with bonds in the region mostly higher. However, as the night progressed, dollar gains fizzled and the Bloomberg Dollar Index was down less than 0.1% after bing up 0.1% earlier, following Tuesday’s 0.2% advance, which came after a sharp 2.6% slide in July.

China’s money-market squeeze returned, with sovereign bonds beginning to feel the heat as the central bank keeps liquidity on a tight leash, without adding any net new reverse repo liquidity for another day, and concerns grow about a wall of fund maturities this month. 10-year bond yield little changed at 3.64%, hovering near the highest level in 8 weeks as PBOC refrains from boosting liquidity for third day. Onshore, offshore yuan both drop; Shanghai Composite Index down 0.2%. In a statement on its microblog, SAFE said it didn’t target specific companies as in a media report that it checked their collaterals for loans overseas.

Expect data on MBA mortgage applications later, along with earnings reports from Tesla, MetLife and Time Warner among others.

Market Snapshot

- Dow futures +53

- Dow cash closed +72.80 to 21,963.92

- S&P 500 futures +3.5, up 0.1% to 2,474.75

- S&P 500 cash closed +0.24% to 2,476.35

- 10Y UST yield +2bps to 2.273%

- STOXX Europe 600 down 0.2% to 379.33

- MSCI Asia Pacific down 0.02% to 161.30

- MSAPJ up 0.05% to 531.62

- Nikkei up 0.5% to 20,080.04

- Topix up 0.4% to 1,634.38

- Hang Seng Index up 0.2% to 27,607.38

- Shanghai Composite down 0.2% to 3,285.06

- Sensex down 0.08% to 32,549.91

- Australia S&P/ASX 200 down 0.5% to 5,744.20

- Kospi up 0.2% to 2,427.63

- German 10Y yield rose 0.4 bps to 0.495%

- Euro up 0.5% to 1.1866 per US$

- Italian 10Y yield fell 7.4 bps to 1.727%

- Spanish 10Y yield rose 3.9 bps to 1.477%

- Brent Futures down 0.5% to $51.53/bbl

- old spot down 0.1% to $1,267.36

- U.S. Dollar Index down 0.3% to 92.80

Top Overnight News from BBG

- Apple Results Push Global Tech Higher; White House Considers China Trade Action; Oil Slips on Surprise Jump in Stockpiles

- Apple Inc. gave a revenue forecast that highlighted resilient demand for the iPhone ahead of the launch of its new models and the growing significance of the company’s supporting businesses

- Deutsche Bank AG envisions shifting almost half its U.K. positions to the European continent over coming years as the lender’s Brexit plans take shape

- Auto sales fell the most since August 2010, a year after the federal government’s “Cash for Clunkers” program to stimulate demand came to an end

- Central banks around the globe are stocking up on Treasuries again, giving bond traders one more reason to wager on a steeper U.S. yield curve in the months ahead

- Clients said to have pulled 15% of their assets from Paul Tudor Jones main fund in 2Q

- Trump’s Russia Ties Get No Scrutiny as House Panel Eyes Clinton

- Trump’s CEO Brain Trust Comes Up Short on Big Ideas for Policies

- Democrats Say They Had ‘Bizarre’ Meeting With Trump’s Ex-Im Pick

- Wal-Mart Puts New Scrutiny on Suppliers With Chemicals Project

- Apple FY4Q Rev. View Midpoint Tops Est; Gross Margin View Trails

- Fleetcor Raised $3.975b of Pro-Rata Loans Alongside $350m TLB

- Global Smartphone Sales Rise 5.5% as Xiaomi Re-Joins Top Five

- Teck Says BC Hydro Exercised Right on Interest in Waneta Dam

- Methode to Buy All Pacific Insight Shares for About C$144m Cash

- CVS Sees Removing 17 Products From Standard Control Formulary

- Match Group Names Mandy Ginsberg to Succeed Greg Blatt as CEO

- Amazon Cloud Users Told Not to Bypass China Internet Rules: WSJ

Asian stocks traded mostly higher taking the impetus from Wall Street’s gains where the DJIA homed in on the 22,000 level and NASDAQ futures surged after-market following Apple’s (+5% after-market) strong Q3 earnings. This supported the Apple supply chain and resulted to outperformance of the TAIEX (+0.7%), while Nikkei 225 (+0.6%) was underpinned by a weaker currency. Conversely, losses in the commodities complex and financials weighed on ASX200 (-0.4%), while Shanghai Comp (+0.1%) was indecisive and traded choppy due to a lack of drivers and a reduced liquidity operation by the PBoC. Finally, 10Y JGBs were relatively flat amid the positive risk tone in Japan with only mild gains seen following a respectable Rinban announcement in which the BoJ are in the market for over JPY ltln JGBs ranging from ly to 10Y maturities.

The Kiwi tumbled after ugly jobs data:

- New Zealand Employment Change (Q2) Q/Q -0.2% vs. Exp. 0.7% (Prey. 1.2%)

- New Zealand Employment Change (Q2) Y/Y 3.1% vs. Exp. 4.1% (Prey. 5.7%)

- New Zealand Unemployment Rate (Q2) 4.8% vs. Exp. 4.8% (Prey. 4.9%)

Top Asian News

- GIC Is Said to Invest $100 Million in Japan Activist Fund Misaki

- China Billionaire Triples Wealth and Shorts See a Fat Target

- Hongqiao to Shut and Replace More Than 2 Mln Tons Alu Capacity

- Sleepy Japan Stocks Set for Rude Awakening, Strategists Say

- Noble Group May Challenge Yancoal Equity Raising for Rio Deal

- BNP Paribas Is Said to Expand Japan Operations With 30 Hires

European bourses traded with modest losses with energy and material names underperforming, the latter weighed by Rio Tinto post their soft earnings report. Apple suppliers performing well this morning with the likes of Dialog Semiconductors trading with modest gains after Apple profits rose ahead of analyst estimates. Standard Chartered and SocGen lower this morning following soft financial results. EGB yields ticking higher this morning, while firmer Eurozone PPI figures have also led to the upside. Notable outperformance observed in the German 5Y with the yield falling 0.2bps.

Top European News

- Deutsche Bank Brexit Base Case Said to See 4,000 Jobs Move

- Standard Chartered First Half Adjusted Operating Income $7.2 Bln

- U.K. July Construction PMI 51.9 vs 54.8 in June; Est. 54

- Glencore Asks Australia to Focus on Economy Before Climate Deal

- Brexit Angst Is So 2016 as These Indicators Show: Markets Live

- UniCredit, Mediobanca, Generali to Cut Crossholdings: Repubblica

- Thyssenkrupp Said to Consider Break-Up as Plan B to Tata

In currencies, NZD underperformed last night post the release of soft jobs figures which took NZD back towards 0.74. Consequently, the jobs data alongside the relatively tepid Fonterra GDT auction reinforces the RBNZ’s current neutral stance on interest rates, in the wake of the data, AUD/NZD broke back above 1.07. CAD noticeably weaker this morning, largely on the back of softer crude prices following last night’s surprise API build. The recent bearish trend looks to have broken down with USDCAD now hovering around last week’s high of 1.2577 and looking to make a move above 1.26. JPY weaker across the board, USD/JPY eying 111.00 to the upside after offers just above 110.50 failed to cap strength. EURJPY holding 131.00 for now as gains have been led by rise in EUR/USD which tripped through 118.00. GBP relatively choppy this morning following a sizeable miss on the Construction PMI reading (51.9 vs. Exp. 54.5), GBPUSD ticking off some 20 pips before trading back to pre-announced levels

In commodities, WTI crude futures were drilled below USD 49/bbl following a surprise build in API inventories and a survey which suggested OPEC supply rose in July. Elsewhere, gold (-0.3%) retreated from near 8-week highs amid profit taking and with the safe-haven also dampened by the increased risk appetite, while copper prices were also lower alongside the broad-based weakness across the commodities complex. WTI and Brent crude futures tracking lower following last night’s API report. Iron ore futures also saw a slight pullback from its recent advances, declining over 1% in Asian trade.

Taking a look now at the day ahead, we will get the ADP employment number for July due (190k expected; 158k previous). At present the three month trailing average of ADP private employment gains (179k) is tracking close to that of BLS private payrolls (180k). So our US economist believes it would take a material miss relative to expectations for us to change our payroll forecast. Major US companies due to report earnings include: American International Group (AIG), Metlife, Mondelez International and Time Warner.

US Event Calendar

- 7am: MBA Mortgage Applications, prior 0.4%

- 8:15am: ADP Employment Change, est. 190,000, prior 158,000

- 11am: Fed’s Mester Speaks to Community Banking Conference

- 3:30pm: Fed’s Williams Speaks in Las Vegas on Monetary Policy

DB’s Jim Reid concludes the overnight wrap

Many in the market continue to talk about it being a carry trade until at least Jackson Hole in 3 and a half weeks’ time. The chatter on the US debt ceiling that we’ve discussed before also continues in the background with some saying the Trump administration will struggle to build a consensus around the smooth raising of it as we approach it around October time. The thing that worries investors most from an immediate event risk point of view is an escalation of tensions between the US and North Korea. Could we wake up one morning to find the US has used force in some way in the peninsula? Clearly its impossible to predict but that doesn’t prevent some from using it to handicap their view. We also have the Fed and the ECB likely to stop reinvestment and announce a fresh taper in September and October respectively. So plenty to think about after the holidays are over but for now most investors are riding carry trades. In the days leading up Jackson Hole it’ll be interesting to see if that changes but markets probably have two weeks before it comes into view enough to focus on.

Ahead of the likely August lull, government bond yields fell across all regions and maturities yesterday, with the German Bunds down to the lowest level since early July (2Y: -2bp; 10Y: -5bps). For other sovereigns, the Italian BTPs (2Y: -3bps; 10Y: -8bps) fell the most, followed by the OATs (2Y: -6bps; 10Y: -6bps) and Gilts (2Y: -1bps; 10Y: -2bps). The bund yield started higher in the morning, but fell ~5bp in the afternoon to 0.49%. The change was similar to intraday falls in the UST 10Y, partly driven by the mixed US macro data and lower auto sales by US car markers (sales at GM -15% yoy). To be fair, as we type, UST 10Y yields have bounced back from the lows and is now ~1.5bp higher this morning.

In commodities, WTI oil fell 2 %, marking the first decline after 6 consecutive days of gain. The softness was partly associated with an industry report (American Petroleum Institute) showing rising US inventories and a Reuters survey indicating higher OPEC production in July, led by a further recovery in supply from Libya. Iron ore softened 0.2%, after a 7% rise the day before on positive Chinese steel PMI data. Elsewhere, precious metals were slightly lower (Gold -0.1%; Silver -0.2%) and industrial metals also softened (Copper -0.4%; Aluminium -0.1%).

Onto equities, US bourses continue to edge ahead, following supportive results. The S&P and the Nasdaq were both up 0.2%. The Dow was up 0.3% to another record close – the fifth record high and closer to the 22,000 mark. Within the S&P, modest gains in the financials (+0.8%) and IT sector (+0.5%) were partly offset by losses in health care and industrials. After the bell, Apple was up ~4% on a solid quarterly result and upgraded revenue forecast.

European markets also strengthened, aided by the lower Euro and sound results from BP and Rolls-Royce. The Stoxx 600 was up 0.6%, with most sectors increasing on the day. Utilities and the energy sector was up 1%, while health care was the only sector down (-0.2%). The DAX was up 1.1%, with similar increases across the region: FTSE 100 (+0.7%), CAC (+0.7%) and Italian FTSE MIB (+0.6%). Turning to currency, the US dollar index gained 0.2% on the back of mixed but slightly supportive data. The Euro/USD and Sterling/USD both softened marginally, falling 0.3% and 0.1% respectively.

Turning to Tuesday’s data, the key focus was on the Markit PMI and ISM data out of Europe and the US respectively. Before we take a detailed look at these numbers, we quickly recap some of the other economic data releases out yesterday. Away from the PMIs in Europe we saw the advance Q2 GDP estimate for the Eurozone that came in line with expectations at +2.1% YoY (+0.6% mom), up from +1.9% YoY in Q1. After factoring this in and the clear lift in momentum seen in other indicators, our European team now expects full year growth in 2017 to be 2.2% up (vs. 1.9% previous) and 2018 growth to be 2.0% (vs. 1.6% previous). Meanwhile over in the US personal income growth was flat in June (vs. +0.4% expected) while personal spending also slowed in line with expectations at +0.1% mom (+0.2% previous). Real personal spending was however flat on the month against expectations of an increase of +0.1%.

Turning to the manufacturing PMI data now. In Europe we saw manufacturing PMIs for Germany (58.1 vs. 58.3 flash), France (54.9 vs. 55.4 flash) and the Eurozone (56.6 vs. 56.8 flash) all revised slightly lower. Elsewhere we also got the first look at the Spanish PMI (54.0 vs. 54.5 expected) that disappointed while Italy (55.1 vs. 55.0 expected) and the UK (55.1 vs. 54.5 expected) beat expectations. The UK number had fallen for the last three months and the rise was on the back of the strongest rise in export orders since April 2010. Has the devaluation finally had an impact?

Across the pond the ISM reading dipped to 56.3 (vs. 56.4 expected; 57.8 previous), but was largely in line with expectations. The production index fell to 60.6 (vs. 62.4 previous) while new orders slipped to 60.4 (vs. 63.5 previous). New export orders also fell to 57.5 (vs. 59.5 expected). One interesting dynamic to take note of is the prices paid index that climbed significantly more than expected to 62.0 (vs. 55.8 expected; 55.0 previous). Of the 18 manufacturing industries surveyed, 14 reported an increase in the prices paid for raw materials in July. While part of the climb could be attributed to the fact that the index was quite low in June (lowest level since November 2016), the US dollar weakness in July likely played an important role in driving up raw material costs for US manufacturers.

Away from the markets, the WSJ reported that US senate democratic leader Schumer wrote to President Trump and urged him to put all Chinese M&A activity in the US on hold until China takes more aggressive actions to address the evolving North Korean situation.

This morning, Asian markets have followed the lead from US, with the Nikkei (+0.4%), the Kospi (+0.2%) and Hang Seng (+0.3%) all higher but with Chinese bourses broadly flat.

Taking a look now at the day ahead, today’s calendar appears to be fairly quiet. In Europe the Eurozone PPI for June (-0.1% mom expected; -0.4% previous) is the only data of note, while the US has the ADP employment number for July due (190k expected; 158k previous). At present the three month trailing average of ADP private employment gains (179k) is tracking close to that of BLS private payrolls (180k). So our US economist believes it would take a material miss relative to expectations for us to change our payroll forecast. Major US companies due to report earnings include: American International Group (AIG), Metlife, Mondelez International and Time Warner.

3. ASIAN AFFAIRS

i)Late TUESDAY night/WEDNESDAY morning: Shanghai closed DOWN 7.58 POINTS OR 0.23% / /Hang Sang CLOSED UP 67.15 POINTS OR 0.24% The Nikkei closed UP 94.25 POINTS OR .17%/Australia’s all ordinaires CLOSED DOWN 0.45%/Chinese yuan (ONSHORE) closed DOWN at 6.7228/Oil DOWN to 49.16 dollars per barrel for WTI and 51.99 for Brent. Stocks in Europe OPENED IN THE RED , Offshore yuan trades 6.7296 yuan to the dollar vs 6.7228 for onshore yuan. NOW THE OFFSHORE IS WEAKER TO THE ONSHORE YUAN/ ONSHORE YUAN WEAKER (TO THE DOLLAR) AND THE OFFSHORE YUAN IS MUCH WEAKER TO THE DOLLAR AND THIS IS COUPLED WITH THE SLIGHTLY WEAKER DOLLAR. CHINA IS HAPPY TODAY

3a)THAILAND/SOUTH KOREA/NORTH KOREA

NORTH KOREA/USA

The USA launches a minuteman ICBM in a warning to North Korea

(courtesy zero hedge)

In Warning To North Korea, US Releases Video Of Overnight Minuteman ICBM Launch

As previewed last night, at 2:10am PT, the U.S. military successfully test-launched an unarmed Intercontinental Ballistic Missile from Vandenberg Air Force Base in California, about 130 miles northwest of Los Angeles, and just days after North Korea’s second test of an ICBM. An Air Force statement said that the test was not a response to recent North Korean actions, but shows that America’s nuclear enterprise is “safe, secure, effective and ready to be able to deter, detect and defend against attacks on the United States and its allies.”

The launch is said to “validate and verify the effectiveness, readiness, and accuracy of the weapon system,” according to Colonel Michael Hough, commander of Air Force Global Strike Command’s 30th Air Wing.

“Team V is postured to work with Air Force Global Strike Command to test launch the Minuteman III missile,” Hough said in a statement. “Our long history in partnering with the men and women of the 576th Flight Test Squadron shows that the Western Range stands ready and able to create a safe launch environment.”

The ICBM was equipped with a test reentry vehicle – just like the previous three launches in 2017 – which officials said showed it traveled about 4,200 miles to the Kwajalein Atoll in the Marshall Islands. The operation was conducted by a team of Air Force Global Strike Command Airmen from the 90th Missile Wing, along with the 576th Flight Test Squadron and the 30th Space Wing stationed at Vandenberg.

This is the fourth Minuteman ICBM launched from the Vandenberg base this year. The first 2017 test took place in February, involving a Minuteman III that traveled to the Marshall Islands, carrying a non-explosive warhead. Another test was conducted by the Air Force on April 26. Days later, a third test missile launched from Vandenberg base.

Air Force Global Strike Command has tested 299 Minuteman III ICBMs over the program’s history. The Minuteman IIIs are the U.S. military’s only land-based ICBMs. And while some have suggested that the launches are in direct retaliation to the recent NKorea ICBM launch, the U.S. military schedules four test-launches each fiscal year, with the actual schedule plotted out several years in advance, so it’s unrelated to recent events, Air Force Capt. Michele Rollins, a spokesperson for the strike command, told NBC.

Last week, North Korea tested an ICBM for the second time. The missile flew for 45 minutes and traveled more than 1,000 kilometers laterally, defense officials and analysts said. U.S. officials believe the missile broke up upon re-entering the atmosphere.

The Minuteman III ICBM launches during an operational test at 2:10 a.m. PT

on Aug. 2, 2017, at Vandenberg Air Force Base in California

Analysts said that the North’s test Friday demonstrated that a broader part of the mainland United States, including Los Angeles and Chicago, is now in range of Pyongyang’s weapons. Asked about possible U.S. military action against North Korea, White House Press Secretary Sarah Huckabee Sanders reiterated on Tuesday that “all options are on the table” but the administration would not “broadcast what we’re going to do.”

The focus for the administration remains on stopping North Korea’s nuclear program and halting their aggression, Sanders said.

As we reported yesterday, Sen. Lindsey Graham said Tuesday that President Donald Trump has told him he’s willing to go to war over North Korea’s missile program if the rogue nation continues to aim ICBMs at America.

Meanwhile, Japanese Foreign Ministry spokesman Norio Maruyama said he was unaware of the remarks, but that his country was in favor of the Trump administration’s posture “using both words and action to show that all choices are on the table.”

Separately, another longstanding ally in the region, the Philippines, is set to host an international regional security meeting on Monday, when leaders could pressure Pyongyang to halt its intermediate-range missile tests. Secretary of State Rex Tillerson is expected to attend the meeting in Manila. On Wednesday, Philippine President Rodrigo Duterte went on the attack against North Korean leader Kim Jong Un, whom he referred to in a speech as a “fool” and a “son of a bitch” according to Reuters.

“That chubby face that looks kind … If he commits a mistake, the Far East will become an arid land,” Duterte said. “It must be stopped, this nuclear war.”

“A limited confrontation and it blows up here, I will tell you, the fallout can deplete the soil, the resources and I don’t know what will happen to us,” he added. Duterte has previously called for the U.S. to show restraint in dealing with Kim’s totalitarian regime.

b) REPORT ON JAPAN

end

c) REPORT ON CHINA

Trump set to initiate section 301 of the 1974 Trade Act which calls for an investigation into the trade practices of a particular country. If it finds fault, then sanctions and cancelling of licenses etc can be called into play. The USA seems to be snubbing the WTO

(courtesy zero hedge)

Trump Set To Retaliate To China’s “Unfair Trade Practices”

President Trump has given China six months to prove that it is committed to preventing a nuclear-armed North Korea, and it seems his tolerance for China’s dithering has finally reached its limit. Now that President Xi Jinping has established that his government is unwilling to engage in a meaningful crackdown on its neighbor, the era of using carrots like improving trade relations to coax China into helping solve the “North Korea problem” has ended. It is now time for the stick.

According to reports in the New York Times, Wall Street Journal and Associated Press, the Trump administration is planning to use an obscure 1970s law to launch a “broad-based” investigation into whether China’s trade-related intellectual property policies constitute “unfair trade practices.

The US inquiry could become an obstacle for one of the Communist Party’s top economic priorities: the Made in China 2025 initiative, which calls for China to become a “global leader” in ten industries with the help of huge infusions of state money.

In the coming days, the US trade rep will launch a “Section 301” investigation, named after a portion of the 1974 Trade Act. Here’s a breakdown of the likely timeline for the investigation, as well as possible outcomes, courtesy of the NYT:

“Under the process that the Trump administration plans to set in motion, the Office of the United States Trade Representative will start an investigation into China’s trade practices. Following the investigation, which could be completed in as little as a few months, the United States could impose steep tariffs on Chinese imports, rescind licenses for Chinese companies to do business in the United States, or take other measures. The process is known as a Section 301 investigation, after the relevant portions of the 1974 Trade Act.”

Another option being considered by the Trump administration would involve invoking the International Emergency Economic Powers Act, another 1970s law that gives the president broad powers to regulate commerce after declaring a “national emergency,” according to WSJ.

A Section 301 investigation could “pave the way for the U.S. to impose sanctions on Chinese exporters or to further restrict the transfer of advanced technology to Chinese firms or to U.S.-China joint ventures.”

This latest – and, to date, most aggressive – change of heart follows an unsuccessful meeting on July 21 between US and Chinese trade officials where the two sides failed to agree to anything beyond an Obama-era trade deal. Bilateral trade talks had earlier shown some progress when the two sides agreed to an expansion of the Obama trade deal back in May.

It’s also the latest vacillation in the administration’s China stance since Trump initially decided to soften his China-bashing campaign rhetoric following a meeting with President Xi at Mar-a-Lago back in April.

In the past, Trump has hammered China for its massive trade surplus and widespread government intervention in its corporate sector. But by instead focusing the investigation on intellectual property, the administration is going to bat for business groups that have long griped about China’s penchant for stealing trade secrets, according to WSJ.

“American business frustration with Chinese trade and market-access practices has mounted in recent years, with U.S. business groups urging the government to take a tougher trade line with China. Many organizations have complained that the Trump administration hasn’t pushed hard enough in areas like intellectual property, as it has focused more on Chinese manufacturing and China’s $347 billion trade surplus with the U.S. last year.

That discontent has intensified as China’s economy continued to expand and its computer and software sectors became bigger competitors internationally. Western firms fear China will use the regulations to bar foreign investments in areas that Beijing targets for investment, including semiconductors, advanced-machine tools and artificial intelligence.”

Many questions remain, but one of the biggest is the role that the WTO will play in resolving a trade dispute between the world’s two largest economies. Trump administration officials have in the past favored a unilateral approach that circumvents the WTO, according to WSJ.

“One big question hanging over the White House review is whether the administration pursues any complaint through the World Trade Organization, or whether it chooses to impose penalties on its own without first seeking permission from the international body, which some Trump advisers have argued is incapable of dealing with China’s trade practices. Trump aides have regularly vowed to pursue a more unilateral approach to trade but have so far done little along those lines.”

Just invoking Section 301 would be an implicit snub to the WTO, which was created to prevent unilateral actions in trade disputes, WSJ continues.

“Widely used in the 1970s and 1980s, Section 301 cases have largely disappeared since the 1995 creation of the WTO, which has its own dispute-settlement process. A main goal of the Geneva-based institution was to curb such unilateral trade actions and to have them handled by a more neutral international arbiter. U.S. administrations over the past two decades have decided to steer nearly all trade complaints through the WTO and have rarely touched Section 301.”

Notably, the last Section 301 case was brought by a union, and was largely ineffective, as the NYT notes.

“The last Section 301 case was in 2010 and was initiated by a labor union, the United Steel Workers, instead of by the government, as the Trump administration is preparing to do. The case focused on Chinese business practices in the solar panel and wind turbine industries, and the Chinese government later promised to limit some of these practices.

But China’s solar and wind turbine industries have gone on to dominate their global industries, after receiving multibillion-dollar loans from China’s state-controlled banking system despite major defaults on earlier loans.”

Trade Representative Robert Lighthizer worked on many Section 301 investigations during his stint as a deputy trade rep in the Reagan administration. As the NYT notes, the US “energetically” invoked Section 301 to resolve trade disputes during the 1980s (notably before the birth of the WTO).

Of course, other WTO members could be reluctant to chastise the US for confronting China over its intellectual-property policies, which in many cases are tantamount to extortion, as China demands companies essentially hand over their trade secrets in exchange for access to the Chinese market. According to the AP, “foreign companies have long complained over rampant piracy and technology theft by Chinese companies.” It’s a testament to the Communist Party’s power that China has been allowed to steal technology from other companies and countries with impunity.

A confrontation is overdue.

4. EUROPEAN AFFAIRS

EU/ITALY

the European migrant crisis escalates again with Italy impounding a German NGO refugee ship. Italy is getting no help from the EU on the migrant issue.

(courtesy zero hedge)

European Migrant Crisis Escalates: Italy Impounds German NGO Refugee Ship

In the latest shot across the bow by Italy in Europe’s latest refugee crisis, BBC and AP report that the Italian Coast Guard has impounded a German NGO migrant rescue boat and is questioning its crew on the isle of Lampedusa, amid a growing dispute over Italy’s code of conduct for handling migrants at sea. Lampedusa is a tiny Italian island near North Africa which has struggled to house boatloads of migrants in recent years.

The Iuventa, which is operated by the German NGO Jugend Rettet previously discussed in “NGO Fleet Bussing Migrants Into The EU Has Ties To George Soros, Hillary Clinton Donors“, called the Italian check “a standard procedure”.

The reason for the escalation is that Jugend Rettet, Doctors Without Borders (MSF) and various other aid NGOs have rejected a new Italian “code of conduct” when it comes to dealing with refugees, according to which Italy plans to send warships close to the Libyan coast to pick up migrants, bypassing Europe’s NGO fleet altogether. According to BBC, the Italian parliament is debating the plan, which has already been agreed upon by the government, and aims to stopping the flow of unstable, overcrowded migrant boats across the Mediterranean to Italy.

A tweet from Jugend Rettet (Youth Rescues) said the Iuventa “was not confiscated. Our crew is not arrested. What happened is a standard procedure,” it said.

The IUVENTA was not confiscated. Our Crew is not arrested. What happened is a standard procedure. We wait for more Infos.

Two Syrian migrants were taken ashore from the vessel, Italian media reported.

One week ago, Libya asked for Italian naval support in its battle against human smugglers operating in its territorial waters, a move that Rome has long considered vital to stemming the wave of migration from north Africa to Europe. After meeting Fayez al-Serraj, head of Libya’s UN-backed government, Paolo Gentiloni, Italy’s prime minister, said the request was being weighed by the Italian defence ministry. Most of the migrants arriving in Italy set off from a stretch of coastline west of Tripoli, the Libyan capital.

“It is very relevant news in the fight against human trafficking in Libya, if we respond positively. I believe this is necessary,” said Mr Gentiloni.

Italy has already offered the Libyan coast guard aid and training to intercept migrants before they reach international waters. Even so, the Libyan coast guard’s ability to monitor its coastline is limited by a lack of resources and the weakness of Mr Serraj’s government, which has struggled to exert its influence beyond Tripoli.

As the FT reported last week, the breakthrough on the joint Libyian-Italian naval missions came a day after Serraj met General Khalifa Haftar, a renegade military officer whose forces control much of eastern Libya, to try to forge a peace deal and move to elections next year. Serraj and Gen Haftar met in Paris, shepherded by Emmanuel Macron, the French president, in a diplomatic move which as discussed previously infuriated Rome as Italy is at the centre of diplomatic activity in Libya.

On Monday three out of nine aid NGOs nine operating in the central Mediterranean, accepted the Italian code of conduct. But MSF and Jugend Rettet object to the requirement for armed police to board their ships and for rescuers to stop transferring migrants from one ship to another. They want to minimise their trips back to port, because those trips cost them precious time and money.

As a reminder, Médicins Sans Frontiéres also operates several ships in the migrant fleet – the Dignity 1, the Bourbon Argos and the Aquarius. As reported previously, MSF has received funding from George Soros’ Open Society Foundation.

Meanwhile, Italy which has expressed growing frustration and recently anger with Europe’s unwillingness to assist it with its growing refugee problem which has resulted in nearly 100,000 migrants landing in Italy with an uncertain future, says its naval deployment is being negotiated with the UN-recognised Libyan government in Tripoli, led by Prime Minister Fayez Sarraj. Sarraj said his administration had agreed to receive only training and arms from Italy. “Libya’s national sovereignty is a red line that nobody must cross,” he said.

The Libyan foreign ministry later said preventing the illegal flow of migrants – a lucrative business for people smugglers – “may require the presence of some Italian naval vessels to work from Tripoli’s maritime port, for this purpose only“. But Italy’s role would have to be coordinated with the Libyan authorities, the statement said.

As reported previously, more than 94,000 migrants have crossed the Mediterranean to Italy so far this year, – a record number. More than 2,370 have died trying to reach Italy.

Migrants picked up in Libyan coastal waters – and not international waters – can be legally returned to Libya, but aid workers say conditions in migrant reception camps there are dire, in large part because nobody else in Europe wants to grant the refugees currently in Italy access. Since 2015 as many as a dozen NGO aid ships have been patrolling off Libya to pick up migrants in distress. So far this year they have handled 35% of the rescues, Italy’s Coast Guard says.

end

5. RUSSIA AND MIDDLE EASTERN AFFAIRS

Russia/USA

the mood is quite sombre as USA officials begin packing up reading to leave Moscow on orders from Putin

(courtesy zero hedge)

“The Mood Is Very Pessimistic”: US Begins “Removing Furniture And Equipment” From Seized Compound In Russia

Two days after Russian President Vladimir Putin formally expelled 755 American diplomats and announced plans to seize two compounds used by US State Department employees, US officials have started “removing furniture and equipment from the compounds”, according to Reuters.

The early start suggests that the US is making every effort to comply with Putin’s demand that the US reduce its 1,200 diplomatic personnel by 60% before Sept. 1, made in retaliation to a bill authorizing fresh sanctions against Russia that President Donald Trump is expected to sign. Late last year, the Obama administration expelled 35 Russian diplomats and seized two Russian diplomatic compounds near Washington, D.C. Putin refrained from responding at the time.

According to Reuters, the movers at the US compounds arrived at around 7 a.m. (0400 GMT) and were seen packing furniture, including beds and lamps, into three white vans over the course of three hours.

Ironically, the US is allowed to choose who stays and who leaves. Because of this, it’s expected that many of those who will be let go will be Russian citizens, Reuters noted. Putin’s decision has severely impacted morale among State Department employees, many of whom have given up on working and are instead updating their resumes and looking for new jobs online, Reuters reports.

“One person at the embassy, who spoke on condition of anonymity because they are not authorized to talk to the media, said staff there were feeling depressed and despondent as they came to terms with the Kremlin’s order.

‘The mood in the office is very pessimistic,’ the person said. ‘Everyone is just loitering, or sitting on job websites looking for a new job.’”

Reuters also noted that Putin’s ultimatum was carefully calibrated to preserve his relationship with Trump after the two world leaders purportedly hit it off over the course of several meetings at a G-20 summit in Hamburg last month.

“The ultimatum issued by the Russian leader is a display to voters at home that he is prepared to stand up to Washington – but is also carefully calibrated to avoid directly affecting the U.S. investment he needs, or burning his bridges with Trump.”

Congress’s sanctions bill risks derailing already tense US-Russia relations, despite Trump’s expressed desire to work more closely with Russia on areas of mutual benefit like containing ISIS in Syria. Vetoing the bill would be seen as a waste of political capital by Trump, who is fighting off allegations that his campaign colluded with the Russian government to tilt the election in his favor, because Congress, which passed the bill with overwhelming majorities in both the House and Senate, would likely be able to override it with a 2/3rds majority.

Despite Trump’s calls for closer ties, the Pentagon may be already contemplating its next steps in the escalating conflict with Russia, which as the WSJ reported will likely involve supplying Ukraine with antitank missiles and other weaponry – a red line for the Kremlin not even the Obama administration dared to cross.

By escalating tensions with Russia, the US also risks straining its relationship with Europe. On Monday, the Germany economy minister said that new penalties against Moscow proposed by US lawmakers violate international law, and that officials in Brussels should consider countermeasures.

Speaking to Funke Mediengruppe newspaper, Brigitte Zypries said that “we consider this as being against international law, plain and simple.” She added that “of course we don’t want a trade war. But it is important the European Commission now looks into countermeasures.”