GOLD: $1282.85 UP $4.00

Silver: $17.08 UP 3 cents

Closing access prices:

Gold $1280.50

silver: $17.02

SHANGHAI GOLD FIX: FIRST FIX 10 15 PM EST (2:15 SHANGHAI LOCAL TIME)

SECOND FIX: 2:15 AM EST (6:15 SHANGHAI LOCAL TIME)

SHANGHAI FIRST GOLD FIX: $1285.54 DOLLARS PER OZ

NY PRICE OF GOLD AT EXACT SAME TIME: $1276.15

PREMIUM FIRST FIX: $9.39

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

SECOND SHANGHAI GOLD FIX: $1286.85

NY GOLD PRICE AT THE EXACT SAME TIME: $1277.10

Premium of Shanghai 2nd fix/NY:$9.75

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

LONDON FIRST GOLD FIX: 5:30 am est $1273.50

NY PRICING AT THE EXACT SAME TIME: $1273.20

LONDON SECOND GOLD FIX 10 AM: $1274.60

NY PRICING AT THE EXACT SAME TIME. 1273.86

For comex gold:

NOVEMBER/

NOTICES FILINGS TODAY FOR OCT CONTRACT MONTH: 0 NOTICE(S) FOR nil OZ.

TOTAL NOTICES SO FAR: 991 FOR 99,100 OZ (3.082TONNES)

For silver:

NOVEMBER

2 NOTICE(S) FILED TODAY FOR

10,000 OZ/

Total number of notices filed so far this month: 874 for 4,370,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: BID $6545 OFFER /$6570 up $26.00 (MORNING)

BITCOIN CLOSING; BID $6609 OFFER: $6637 // UP $91.00

end

Quote of the day:

*Dennis Gartman…

“We have not been of the school of thought over the years that gold is and has been manipulated by powerful forces intent upon keeping gold weak, but we shall admit that things do indeed look very, very strange in recent weeks and the “conspiratorialists” are sounding more and more plausible with each passing day.”

Just one question: what planet is he on?

h

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total open interest FELL BY A SMALL 236 contracts from 199,358 DOWN TO 199,122 DESPITE YESTERDAY’S TRADING IN WHICH SILVER ROSE NICELY BY 16 CENTS. AS I WAS PREPARING FOR TODAY’S REPORT I WROTE THE FOLLOWING: “JUDGING FROM THE MASSIVE VOLUME, IT LOOKS LIKE WE DID NOT GET ANY LONG LIQUIDATION BUT AGAIN IT LOOKS LIKE WE GOT A FEW MORE COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP ROUTE.” I WAS EXACTLY CORRECT AS WE HAD A HUGE 702 DECEMBER EFP’S ISSUED ALONG WITH 84 EFP’S FOR MARCH FOR A TOTAL ISSUANCE OF 786 CONTRACTS. THE ISSUANCE FOR MARCH BOTHERS ME A LOT AS THIS IS SUPPOSE TO BE FOR EMERGENCY IN THE UPCOMING DELIVERY MONTH. I GUESS WHAT THE CME IS STATING IS THAT THERE IS NO SILVER TO BE DELIVERED UPON AT THE COMEX AND THEY MUST EXPORT THEIR OBLIGATION TO LONDON.

RESULT: A SMALL SIZED DROP IN OI COMEX WITH THE 16 CENT PRICE RISE. COMEX LONGS EXITED OUT OF THE COMEX AND FROM THE CME DATA 786 EFP’S WERE ISSUED FOR A DELIVERABLE CONTRACT OVER IN LONDON WITH A FIAT BONUS WHICH DEFINITELY EXPLAINS THE FALL IN OI. IN ESSENCE WE DID NOT GET A FALL IN DEMAND IN OPEN INTEREST ONLY A TRANSFER TO OTHER JURISDICTIONS.

In ounces, the OI is still represented by just OVER 1 BILLION oz i.e. 0.995 BILLION TO BE EXACT or 142% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT OCT MONTH/ THEY FILED: 2 NOTICE(S) FOR 10,000 OZ OF SILVER

In gold, the open interest ROSE BY A SMALLER THAN EXPECTED 1,996 CONTRACTS DESPITE THE GOOD RISE IN PRICE OF GOLD ($4.85) WITH YESTERDAY’S TRADING . YESTERDAY’S TRADING SAW NO GOLD LEAVES FALL FROM THE GOLD TREE. THE TOTAL NUMBER OF GOLD EFP’S ISSUED YESTERDAY TOTAL: 6577 CONTRACTS WHICH IS HUGE. THE MONTH OF DECEMBER SAW 5077 CONTRACTS AND FEB SAW THE ISSUANCE OF 1500 CONTRACTS. The new OI for the gold complex rests at 532,781.

Result: A SMALLER SIZED INCREASE IN OI DESPITE THE RISE IN PRICE IN GOLD ON YESTERDAY ($4.85). WE HAD A HUGE NUMBER OF COMEX LONG TRANSFERS TO LONDON THROUGH THE EFP ROUTE AS (6577 EFP’S). THERE DOES NOT SEEM TO BE MUCH PHYSICAL AT THE COMEX AND WE ARE APPROACHING THE HUGE DELIVERY MONTH OF DECEMBER. WE ALSO HAD NO GOLD COMEX OI LEAVE THE COMEX GOLD ARENA.

we had: 0 notice(s) filed upon for NIL oz of gold.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD:

A small change in gold inventory at the GLD/ a deposit of .300 tonnes

Inventory rests tonight: 843.39 tonnes.

SLV

TODAY WE HAD NO CHANGE IN SILVER INVENTORY AT THE SLV

INVENTORY RESTS AT 318.074 MILLION OZ

end

.

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in silver FELL BY 236 contracts from 199,358 DOWN TO 199,122 (AND now A LITTLE FURTHER FROM THE NEW COMEX RECORD SET ON FRIDAY/APRIL 21/2017 AT 234,787) DESPITE THE RISE IN SILVER PRICE (A GAIN OF 16 CENTS). OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE 702 PRIVATE EFP’S FOR DECEMBER(WE DO NOT GET A LOOK AT THESE CONTRACTS) AND 84 EFP’S FOR MARCH, WHICH GIVES OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. THIS IS QUITE EARLY FOR THESE EFP ISSUANCE..USUALLY WE WITNESS THIS ONE WEEK PRIOR TO FIRST DAY NOTICE AND THIS CONTINUES RIGHT UP UNTIL FDN. WE ALSO HAD MINIMAL SILVER COMEX LIQUIDATION. TOTAL EFP’S ISSUED YESTERDAY BY THE CME IN SILVER TOTAL 786 CONTRACTS.

RESULT: A SMALL SIZED DECREASE IN SILVER OI AT THE COMEX DESPITE THE 16 CENT RISE IN PRICE (WITH RESPECT TO YESTERDAY’S TRADING). WE HAD ANOTHER 786 EFP’S ISSUED TRANSFERRING OUR COMEX LONGS OVER TO LONDON TOGETHER WITH NO SILVER COMEX LIQUIDATION.

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

)Late MONDAY night/TUESDAY morning: Shanghai closed DOWN 18.29 points or .53% /Hang Sang CLOSED DOWN 30.06 pts or 0.10% / The Nikkei closed UP 0.98 POINTS OR 0.00%/Australia’s all ordinaires CLOSED DOWN 0.80%/Chinese yuan (ONSHORE) closed UP at 6.6378/Oil DOWN to 56.52 dollars per barrel for WTI and 62.85 for Brent. Stocks in Europe OPENED RED EXCEPT LONDON . ONSHORE YUAN CLOSED UP AGAINST THE DOLLAR AT 6.6378. OFFSHORE YUAN CLOSED WEAKER TO THE ONSHORE YUAN AT 6.6431 //ONSHORE YUAN STRONGER AGAINST THE DOLLAR/OFF SHORE STRONGER TO THE DOLLAR/. THE DOLLAR (INDEX) IS WEAKER AGAINST ALL MAJOR CURRENCIES. CHINA IS VERY HAPPY TODAY

i

3a)THAILAND/SOUTH KOREA/NORTH KOREA

i)North Korea//South Korea

b) REPORT ON JAPAN

c) REPORT ON CHINA

4. EUROPEAN AFFAIRS

i)GERMANY

The lower value of the Euro is a catalyst to Germany for growth as this exporting behemoth is certainly taking advantage due to weaker partners in the Euro zone. Its GDP rose at a 0.8% quarter over quarter. Yearly growth is reported at 2.3% and underlying growth at 2.8%,.

( zerohedge)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

i)YEMEN

Very sad: the blockade in Yemen is having a devastating effect on citizens and their economy.

( Mike Krieger/Liberty BlitzkriegBlog)

Saudi Arabia

( Pat Buchanan/Buchanan.org)

6 .GLOBAL ISSUES

Zimbabwe

There is a military coup in Zimbabwe as it looks like 93 yr old Mugabe is out:

( zerohedge)

7. OIL ISSUES

i)The IEA throws cold water on OPEC optimism for global demand for crude oil. They state that global oil demand is shrinking and this is after huge stockpiling by China.

( zerohedge)

ii)We have been bringing you terrific articles on the rapid demise of the welfare state of Saudi Arabia

(David Stockman and R Meijer). Now Charles Hugh Smith comments also on how these guys are in serious trouble.

( Charles Hugh Smith/TwoMinds Blog)

8. EMERGING MARKET

9. PHYSICAL MARKETS

i)Gold trading today:

the crooks try and break the 200 day average for gold and fail: this caused gold to rise to 1280

( zerohedge)

ii)Interesting: Gartman hardly acknowledges GATA and yet he discloses in his latest letter the BIS involvement of gold swaps which is critical to the manipulation of gold

( GATA/Chris Powell./Gartman)

iii)Lawrie Williams found religion. We now have another gold writer who is now compelled to admit that the gold market is rigged

( GATA/Chris Powell/Lawrie Williams)

iv)Seems that Turkish citizens are not too enthralled with Erdogan and his economic and governing policies. They have bought the most gold ever as the Lira tumbles. So far in this 2017 year citizens have thought 47 tonnes. Also the Turkish government has also increased its reserves dramatically as in the 3rd quarter they bought over 30 tonnes of gold.

( zerohedge)

v)Koos Jansen provides a great commentary on the 777 tonnes of gold supplied to the citizens of China for the previous 3 quarters. Annualized it looks like China will import over 1,036 tonnes. This gold is not official gold whereby China always buys with USA dollars. All gold produced in China becomes official gold and at last look they mined 430 tonnes of gold.

( Koos Jansen/Bullionstar)

10. USA stories which will influence the price of gold/silver

i)Trading today: The long end of the yield curve crashes especially the 10 and 30 yr. The 10 yr is now at yearly lows. The flatter the yield curve, the more indication of a recession will be forthcoming

( zerohedge)

ii)This will not be good for the markets as CALPERS, California’s largest pension fund has just dumped 50 billion dollars worth of stocks as they have just called the top

( zerohedge)

iii)My goodness! what kept him so long: Sessions is now considering appointing a special council to investigate the Clintons

( zerohedge)

iv)Trump will make a major statement when he gets back onto USA soil

( zerohedge)

v a)The House tax reform bill will likely pass this Thursday, but the Senate version is now being marked up. To mee it seems hopeless that we will get a tax reform bill passed.

( zerohedge)

v b)As promised to you on several occasions, the SALT DEDUCTIONS will stay in the House bill and will never be removed

( zerohedge)

v c)Now the senate is proposing to strip the individual mandate from Health care in order to pass the tax bill. It would free up 300 to 400 billion Moderate Republicans will have difficulty in supporting this. No Democrat would vote for this.

( zerohedge)

vi)The IRS is perplexed? Out of 500,000 exchange Coinbase users only 900 reported gains or losses??

( zerohedge)

Let us head over to the comex:

The total gold comex open interest SURPRISINGLY ROSE BY ONLY 1996 CONTRACTS UP to an OI level of 532,400 DESPITE THE FAIR SIZED RISE IN THE PRICE OF GOLD ($4.85 RISE WITH RESPECT TO YESTERDAY’S TRADING). OBVIOUSLY WE DID NOT HAVE ANY GOLD COMEX LIQUIDATION. WE HAD 6577 COMEX LONGS EXIT THE COMEX ARENA THROUGH THE EFP ROUTE AS THEY RECEIVE A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS. THE CME REPORTS THAT 5077 EFPS WERE ISSUED FOR DECEMBER AND 1500 WERE ISSUED FOR MARCH. THE OBLIGATION STILL RESTS WITH THE BANKERS ON THESE TRANSFERS.

Result: a SURPRISE SMALL INCREASE IN OPEN INTEREST DESPITE THE FAIR SIZED RISE IN THE PRICE OF GOLD ($4.85.)

.

We have now entered the NON active contract month of NOVEMBER.HERE WE HAD A LOSS OF 0 CONTRACT(S) REMAINING AT 71. We had 2 notices filed YESTERDAY so GAINED 2 contracts or 200 additional oz will stand for delivery in this non active month of November. TO SEE BOTH GOLD AND SILVER RISE IN AMOUNT STANDING (QUEUE JUMPING) IS A GOOD INDICATOR OF PHYSICAL SHORTNESS FOR BOTH OF OUR PRECIOUS METALS.

The very big active December contract month saw it’s OI LOSE 9,219 contracts DOWN to 291,870 (OF WHICH 5077 WERE EFP TRANSFERS). January saw its open interest rise by 60 contracts up to 864. FEBRUARY saw a gain of 10,239 contacts up to 167,245.

.

We had 0 notice(s) filed upon today for NIL oz

VOLUME FOR TODAY : 176,626 (PRELIMINARY)

CONFIRMED VOLUME YESTERDAY: 248,933

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

And now for the wild silver comex results.

Total silver OI SURPRISINGLY FELL BY 236 CONTRACTS FROM 199,358 DOWN TO 199,122 DESPITE YESTERDAY’S 16 CENT GAIN IN PRICE . WE HAD 702 PRIVATE EFP’S ISSUED FOR DECEMBER AND 84 EFP’S FOR MARCH BY OUR BANKERS TO COMEX LONGS WHO RECEIVED A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. THIS IS QUITE EARLY FOR THE ISSUANCE. USUALLY WE WITNESS THIS EVENT ONE WEEK PRIOR TO FIRST DAY NOTICE AND IT CONTINUES RIGHT UP TO FDN. WE HAD NO LONG SILVER COMEX LIQUIDATION. THUS THE TOTAL EFP’S ISSUED YESTERDAY TO OUR COMEX LONGS TOTAL 786 AND THUS DEMAND FOR SILVER OPEN INTEREST CONTINUES TO RISE TAKING INTO ACCOUNT THE INCREASE EFP’S ISSUED.

The new front month of November saw its OI FALL by 0 contract(s) and thus it stands at 3. We had 1 notice(s) served YESTERDAY so we gained 1 contracts or an additional 5,000 oz will stand in this non active month of November. After November we have the big active delivery month of December and here the OI FALL by 4,284 contracts DOWN to 110,412. January saw A GAIN OF 21 contracts RISING TO 1052.

We had 2 notice(s) filed for 10,000 oz for the OCT. 2017 contract

INITIAL standings for NOVEMBER

Nov 14/2017.

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz |

21,364.844

oz

Scotia

144 kilobars

&

JPMorgan

|

| Deposits to the Dealer Inventory in oz | nil oz |

| Deposits to the Customer Inventory, in oz |

nil oz

|

| No of oz served (contracts) today |

0 notice(s)

NIL OZ

|

| No of oz to be served (notices) |

71 contracts

(7100 oz)

|

| Total monthly oz gold served (contracts) so far this month |

991 notices

99,100 oz

3.082 tonnes

|

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

WE HAD nil DEALER DEPOSIT:

total dealer deposits: nil oz

We had nil dealer withdrawals:

total dealer withdrawals: nil oz

we had 0 customer deposit(s):

total customer deposits nil oz

We had 2 customer withdrawal(s)

i) out of Scotia: 4,629.600 OZ (144 kilobars)

ii) Out of JPMorgan: 16,735.244

total customer withdrawals; 21,364.844 oz

we had 0 adjustment(s)

For NOVEMBER:

Today, 0 notice(s) were issued from JPMorgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equates to 0 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped/ Received) by j.P.Morgan customer account.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

To calculate the INITIAL total number of gold ounces standing for the NOVEMBER. contract month, we take the total number of notices filed so far for the month (991) x 100 oz or 99100 oz, to which we add the difference between the open interest for the front month of NOV. (71 contracts) minus the number of notices served upon today (0 x 100 oz per contract equals 106,100 oz, the number of ounces standing in this NON active month of NOV

Thus the INITIAL standings for gold for the NOVEMBER contract month:

No of notices served (991) x 100 oz or ounces + {(71)OI for the front month minus the number of notices served upon today (0) x 100 oz which equals 106,200 oz standing in this active delivery month of NOVEMBER (3.303 tonnes)

WE GAINED 1 ADDITIONAL CONTRACTS OR 100 OZ OF ADDITIONAL GOLD STANDING FOR METAL AT THE COMEX

THIS IS THE FIRST TIME EVER THAT WE HAVE WITNESSED CONSIDERABLE QUEUE JUMPING IN GOLD AT THE COMEX. SILVER’S QUEUE JUMPING STARTED IN MAY 2017 AND HAS NOT LET UP ONCE COMMENCED.

.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

Total dealer inventory 527,069.052 or 16.394 tonnes (dealer gold continues to disappear)

Total gold inventory (dealer and customer) = 8,676,238.163 or 269,74 tonnes

I have a sneaky feeling that these withdrawals of gold in kilobars are being used in the hypothecating process and are being used in the raiding of gold!

The gold comex is an absolute fraud. The use of kilobars and exact weights makes the data totally absurd and fraudulent! To me, the only thing that makes sense is the fact that “kilobars: are entries of hypothecated gold sent to other jurisdictions so that they will not be short with their underwritten derivatives in that jurisdiction. This would be similar to the rehypothecated gold used by Jon Corzine at MF Global.

IN THE LAST 14 MONTHS 85 NET TONNES HAS LEFT THE COMEX.

end

And now for silver

AND NOW THE NOVEMBER DELIVERY MONTH

NOVEMBER INITIAL standings

| Silver | Ounces |

| Withdrawals from Dealers Inventory | nil |

| Withdrawals from Customer Inventory |

585,448.02 oz

SCOTIA

Brinks

Delaware

|

| Deposits to the Dealer Inventory |

nil oz

|

| Deposits to the Customer Inventory |

900,930.966

oz

CNT

Delaware

|

| No of oz served today (contracts) |

2 CONTRACT(S)

(10,000,OZ)

|

| No of oz to be served (notices) |

1 contract

(5,000 oz)

|

| Total monthly oz silver served (contracts) | 874 contracts(4,370,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

Nov 13/ 2017

today, we had 0 deposit(s) into the dealer account:

total dealer deposit: nil oz

we had nil dealer withdrawals:

total dealer withdrawals: nil oz

we had 3 customer withdrawal(s):

i) Out of SCOTIA: 563,275.100 oz

ii) Out of Delaware: 927.300 oz

iii) Out of Scotia: 563,275.100 oz

TOTAL CUSTOMER WITHDRAWAL 585,448.02 oz

We had 2 Customer deposit(s):

i) Into Delaware: 301,653.366 oz

ii) Into CNT: 599,277.600 oz

***deposits into JPMorgan have stopped again

In the month of March and February, JPMorgan stopped (received) almost all of the comex silver contracts.

why is JPMorgan bringing in so much silver??? why is this not criminal in that they are also the massive short in silver

total customer deposits: 900,930.966 oz

we had 0 adjustment(s)

The total number of notices filed today for the NOVEMBER. contract month is represented by 2 contracts FOR 10,000 oz. To calculate the number of silver ounces that will stand for delivery in NOVEMBER., we take the total number of notices filed for the month so far at 874 x 5,000 oz = 4,370,0000 oz to which we add the difference between the open interest for the front month of NOV. (3) and the number of notices served upon today (2 x 5000 oz) equals the number of ounces standing.

.

Thus the INITIAL standings for silver for the NOVEMBER contract month: 874 (notices served so far)x 5000 oz + OI for front month of NOVEMBER(3) -number of notices served upon today (2)x 5000 oz equals 4,375,000 oz of silver standing for the NOVEMBER contract month. This is EXCELLENT for this NON active delivery month of November.

We gained 1 contract(s) or an additional 5,000 oz will stand for metal in the non active delivery month of November.

AS I MENTIONED ABOVE, WE HAVE BEEN WITNESSING QUEUE JUMPING IN SILVER FROM MAY 1 2017 ONWARD. IT IS NOW COMFORTING TO SEE CONSIDERABLE QUEUE JUMPING OCCURRING CONTINUALLY IN GOLD FOR THE FIRST TIME SINCE RECORDED TIME AT THE GOLD COMEX!!(1974). QUEUE JUMPING CAN ONLY OCCUR ON PHYSICAL METAL SHORTAGE.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

ESTIMATED VOLUME FOR TODAY: 32,820

CONFIRMED VOLUME FOR YESTERDAY: 86,794 CONTRACTS

YESTERDAY’S CONFIRMED VOLUME OF 86,794 CONTRACTS EQUATES TO 443 MILLION OZ OR 63.4% OF ANNUAL GLOBAL PRODUCTION OF SILVER

Total dealer silver: 43.218 million

Total number of dealer and customer silver: 230.473 million oz

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price at that day at $18.42

The previous record was 224,540 contracts with the price at that time of $20.44

end

NPV for Sprott and Central Fund of Canada

1. Central Fund of Canada: traded at Negative 1.8 percent to NAV usa funds and Negative 1,5% to NAV for Cdn funds!!!!

Percentage of fund in gold 62.3%

Percentage of fund in silver:37.4%

cash .+.3%( Nov 14/2017)

2. Sprott silver fund (PSLV): STOCK RISES TO -0.77% (Nov 14 /2017)

3. Sprott gold fund (PHYS): premium to NAV RISES TO -0.70% to NAV (Nov 14/2017 )

Note: Sprott silver trust back into NEGATIVE territory at -0.77%-/Sprott physical gold trust is back into NEGATIVE/ territory at -0.70%/Central fund of Canada’s is still in jail but being rescued by Sprott.

Sprott WINS hostile 3.1 billion bid to take over Central Fund of Canada

(courtesy Sprott/GATA)

END

And now the Gold inventory at the GLD

NOV 14/a small deposit of .300 tonnes into the GLD inventory/Inventory rests at 843.39 tonnes

Nov 13/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 843.09 TONNES

Nov 10/no change in gold inventory at the GLD/Inventory rests at 843.09 tonnes

Nov 9/no changes in inventory at the GLD/Inventory rests at 843.09 tonnes

NOV 8/ANOTHER HUGE WITHDRAWAL OF 1.18 TONNES OF GOLD FROM THE GLD DESPITE GOLD’S RISE TODAY. INVENTORY RESTS AT 843.09

Nov 7/a huge withdrawal of 1.48 tonnes of gold from the GLD/Inventory rests at 844.27 tonnes

NOV 6/ a tiny withdrawal of .29 tonnes to pay for fees etc/inventory rests at 845.75 tonnes

Nov 3/no change in gold inventory at the GLD/Inventory rests at 846.04 tonnes

NOV 2/STRANGE!!! WE HAD ANOTHER WITHDRAWAL OF 3.55 TONNES FROM THE GLD DESPITE GOLD’S RISE OF $6.60 YESTERDAY AND $1.55 TODAY/INVENTORY RESTS AT 846.04 TONNES

Nov 1/a withdrawal of 1.18 tonnes of gold from the GLD/Inventory rests at 849.59 tonnes

OCT 31/no change in gold inventory at the GLD/Inventory rests at 850.77 tonnes

Oct 30/STRANGE WITH GOLD UP THESE PAST TWO TRADING DAYS, THE GLD HAS A WITHDRAWAL OF 1.18 TONNES FROM ITS INVENTORY/INVENTORY RESTS AT 850.77 TONES

Oct 27/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 851.95 TONNES

Oct 26./A WITHDRAWAL OF 1.18 TONNES OF GOLD FROM THE GLD/INVENTORY RESTS AT 851.95 TONNES

Oct 25/NO CHANGE (SO FAR) IN GOLD INVENTORY/INVENTORY RESTS AT 853.13 TONNES

Oct 24./no change in gold inventory at the GLD/inventory rests at 853.13 tonnes

OCT 23./NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY REMAINS AT 853.13 TONNES

OCT 20/NO CHANGE IN GOLD INVENTORY AT THE GLD/ INVENTORY REMAINS AT 853.13 TONNES

oCT 19/NO CHANGE/853.13 TONNES

Oct 18 /no change in gold inventory at the GLD/ inventory rests at 853.13 tonnes

Oct 17./no change in gold inventory at the GLD/inventory rests at 853.13 tonnes

Oct 16/A HUGE WITHDRAWAL OF 5.32 TONNES FROM THE GLD/INVENTORY RESTS AT 853.13 TONNES

0CT 13/ NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 858.45 TONNES

Oct 12/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 858.45 TONNES

Oct 10/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 858.45 TONNES

Oct 9/ANOTHER DEPOSIT OF 4.43 TONNES INTO GLD/INVENTORY RESTS AT 858.45 TONNES

Oct 6/A DEPOSIT OF 2.96 TONNES OF GOLD INVENTORY INTO THE GLD/TONIGHT IT RESTS AT 854.02 TONNES

Oct 5/A LOSS OF 3.24 TONNES OF GOLD INVENTORY FROM THE GLD/INVENTORY RESTS AT 851.06 TONNES

Oct 4/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 854.30 TONNES

oCT 3/ A HUGE WITHDRAWAL OF 10.35 TONNES FROM THE GLD/INVENTORY RESTS AT 854.30 TONNES

Oct 2/STRANGE/WITH GOLD’S CONTINUAL WHACKING WE GOT A BIG FAT ZERO OZ LEAVING THE GLD/INVENTORY RESTS AT 864.65 TONNES

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

Nov 14/2017/ Inventory rests tonight at 843.39 tonnes

*IN LAST 271 TRADING DAYS: 97.56 NET TONNES HAVE BEEN REMOVED FROM THE GLD

*LAST 206 TRADING DAYS: A NET 59,72 TONNES HAVE NOW BEEN ADDED INTO GLD INVENTORY.

*FROM FEB 1/2017: A NET 28.61 TONNES HAVE BEEN ADDED.

end

Now the SLV Inventory

NOV 14/no change in silver inventory at the SLV/Inventory rests at 318.074 tonnes

Nov 13/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.074 MILLION OZ

Nov 10/no change in silver inventory at the SLV/Inventory rests at 318.074 million oz/

Nov 9/no change in silver inventory at the SLV/inventory rests at 318.074 million oz.

NOV 8/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.074 MILLION OZ

Nov 7/a huge withdrawal of 944,000 oz from the SLV/inventory rests at 318.074 million oz/

NOV 6/no change in silver inventory at the SLV/Inventory rests at 319.018 million oz/

Nov 3/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS TONIGHT AT 319.018 MILLION OZ.

NOV 2/A TINY LOSS OF 137,000 OZ BUT THAT WAS TO PAY FOR FEES LIKE INSURANCE AND STORAGE/INVENTORY RESTS AT 319.018 MILLION OZ/

Nov 1/STRANGE! WITH SILVER’S HUGE 48 CENT GAIN WE HAD NO GAIN IN INVENTORY AT THE SLV/INVENTORY RESTS AT 319.155 MILLION OZ/

Oct 31/no change in silver inventory at the SLV/Inventory rests at 319.155 million oz

Oct 30/STRANGE!WITH SILVER UP THESE PAST TWO TRADING DAYS, WE HAD A HUGE WITHDRAWAL OF 1.133 MILLION OZ FROM THE SLV/INVENTORY RESTS AT 319.155 MILLION OZ/

Oct 27/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 320.288 MILLION OZ

Oct 26/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 320.288 MILLION OZ/

Oct 25/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 320.288 MILLION OZ

Oct 24/no change in inventory at the SLV/inventory rests at 320.288 million oz/

oCT 23./STRANGE!!WITH SILVER RISING TODAY WE HAD A HUGE WITHDRAWAL OF 1.039 MILLION OZ/inventory rests at 320.288 million oz/

OCT 20NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 321.327 MILLION OZ

oCT 19/INVENTORY LOWERS TO 321.327 MILLION OZ

Oct 18 no change in silver inventory at the SLV/inventory rest at 322.271 million oz

Oct 17/ A MONSTROUS WITHDRAWAL OF 3.494 MILLION OZ FROM THE SLV/INVENTORY RESTS AT 322.271 MILLION OZ

Oct 16/ NO CHANGES IN SILVER INVENTORY AT THE SLV.INVENTORY RESTS AT 325.765 MILLION OZ

oCT 13/ NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 325.765 MILLION OZ

Oct 12/THE LAST TWO DAYS WE LOST 1.113 MILLION OZ FROM THE SLV/INVENTORY RESTS AT 325.765 MILLION OZ

Oct 10/NO CHANGE IN INVENTORY AT THE SLV/INVENTORY RESTS AT 326.898 MILLION OZ/

Oct 9/A HUGE DEPOSIT OF 1.227 MILLION OZ INTO THE INVENTORY OF THE SLV/INVENTORY RESTS AT 326.898 MILLION OZ

Oct 6/NO CHANGE IN SILVER INVENTORY/ INVENTORY RESTS AT 325.671 MILLON OZ

Oct 5/ANOTHER WITHDRAWAL OF 944,000 OZ FROM THE SLV/INVENTORY RESTS AT 325.671 MILLION OZ

OCT 4/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 326.615 MILLION Z

Oct 3/A TINY WITHDRAWAL OF 143,000 FROM THE SLV FOR FEES/INVENTORY RESTS AT 326.615 MILLION OZ

Oct 2/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 326,757 MILLION OZ

Nov 14/2017:

Inventory 318.074 million oz

end

6 Month MM GOFO

Indicative gold forward offer rate for a 6 month duration

+ 1.50%

12 Month MM GOFO

+ 1.73%

30 day trend

end

Major gold/silver trading/commentaries for TUESDAY

GOLDCORE/BLOG/MARK O’BYRNE.

GOLD/SILVER

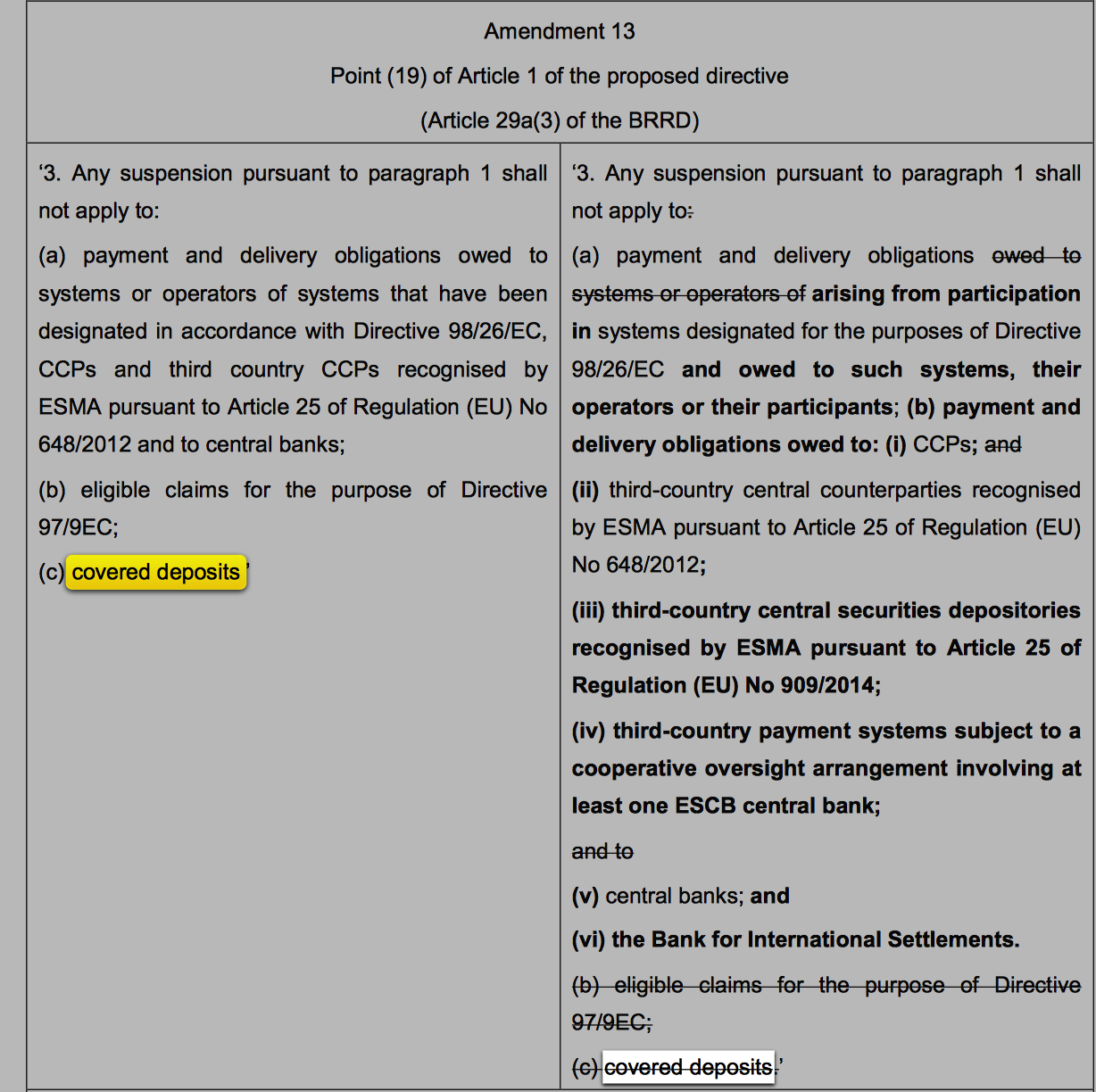

Preemptive Strike on Euro Savings. Protect Your Savings With Gold: ECB Propose End To Deposit Protection

Protect Your Savings With Gold: ECB Propose End To Deposit Protection

– New ECB paper proposes ‘covered deposits’ should be replaced to allow for more flexibility

– Fear covered deposits may lead to a run on the banks

– Savers should be reminded that a bank’s word is never its bond and to reduce counterparty exposure

– Physical gold enable savers to stay out of banking system and reduce exposure to bail-ins

It is the ‘opinion of the European Central Bank’ that the deposit protection scheme is no longer necessary:

‘covered deposits and claims under investor compensation schemes should be replaced by limited discretionary exemptions to be granted by the competent authority in order to retain a degree of flexibility.’

To translate the legalese jargon of the ECB bureaucrats this could mean that the current €100,000 (£85,000) deposit level currently protected in the event of a bail-in may soon be no more.

But worry not fellow savers as the ECB is fully aware of the uproar this may cause so they have been kind enough to propose that:

“…during a transitional period, depositors should have access to an appropriate amount of their covered deposits to cover the cost of living within five working days of a request.”

So that’s a relief, you’ll only need to wait five days for some ‘competent authority’ to deem what is an ‘appropriate amount’ of your own money for you to have access to in order eat, pay bills and get to work.

The above has been taken from an ECB paper published on 8 November 2017 entitled ‘on revisions to the Union crisis management framework’.

It’s 58 pages long, the majority of which are proposed amendments to the Union crisis management framework and the current text of the Capital Requirements Directive (CRD).

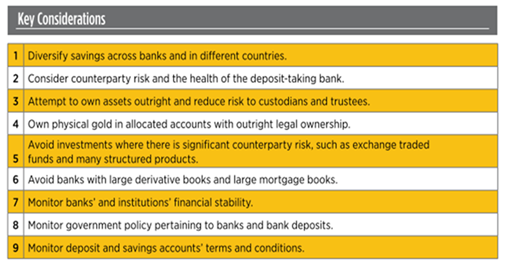

It’s pretty boring reading but there are some key snippets which should be raising a few alarms. It is evidence that once again a central bank can keep manipulating situations well beyond the likes of monetary policy. It is also a lesson for savers to diversify their assets in order to reduce their exposure to counterparty risks.

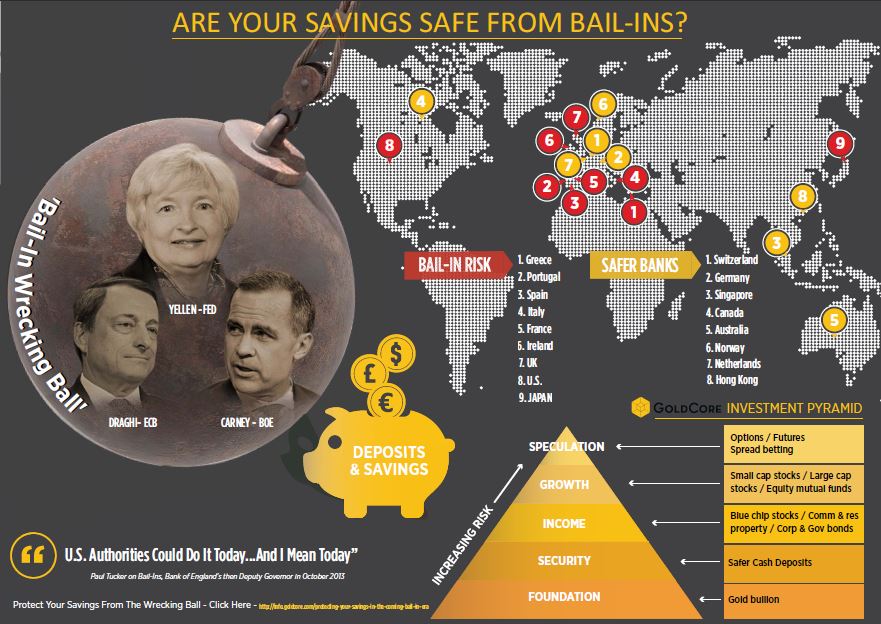

Bail-ins, who are they for?

According to the May 2016 Financial Stability Review, the EU bail-in tool is ‘welcome’ as it:

…contributes to reducing the burden on taxpayers when resolving large, systemic financial institutions and mitigates some of the moral hazard incentives associated with too-big-to-fail institutions.

As we have discussed in the past, we’re confused by the apparent separation between ‘taxpayer’ and those who have put their hard-earned cash into the bank. After all, are they not taxpayers?

This doesn’t matter, believes Matthew C.Klein in the FT who recently argued:

Bail-ins are theoretically preferable because they preserve market discipline without causing undue harm to innocent people.

Ultimately bail-ins are so central banks can keep their merry game of easy money and irresponsibility going. They have been sanctioned because rather than fix and learn from the mess of the bailouts nearly a decade ago, they have just decided to find an even bigger band-aid to patch up the system.

‘Bailouts, by contrast, are unfair and inefficient. Governments tend to do them, however, out of misplaced concern about “preserving the system”. This stokes (justified) resentment that elites care about protecting their friends more than they care about helping regular people.’ Matthew C. Klein

But what about the regular people who have placed their money in the bank, believing they’re safe from another financial crisis? Are they not ‘innocent’ and deserving of protection?

When Klein wrote his latest on bail-ins, it was just over a week before the release of this latest ECB paper. With fairness to Klein at the time of his writing depositors with less than €100,000 in the bank were protected under the terms of the ECB covered deposit rules.

This still seemed absurd to us who thought it questionable that anyone’s money in the bank could suddenly be sanctioned for use to prop up an ailing institution. We have regularly pointed out that just because there is currently a protected level at which deposits will not be pilfered, this could change at any minute.

The latest proposed amendments suggest this is about to happen.

Why change the bail-in rules?

The ECB’s 58-page amendment proposal is tough going but it is about halfway through when you come across the suggestion that ‘covered deposits’ no longer need to be protected. This is determined because the ECB is concerned about a run on the failing bank:

If the failure of a bank appears to be imminent, a substantial number of covered depositors might still withdraw their funds immediately in order to ensure uninterrupted access or because they have no faith in the guarantee scheme.

This could be particularly damning for big banks and cause a further crisis of confidence in the system:

Such a scenario is particularly likely for large banks, where the sheer amount of covered deposits might erode confidence in the capacity of the deposit guarantee scheme. In such a scenario, if the scope of the moratorium power does not include covered deposits, the moratorium might alert covered depositors of the strong possibility that the institution has a failing or likely to fail assessment.

Therefore, argue the ECB the current moratorium that protects deposits could be ‘counterproductive’. (For the banks, obviously, not for the people whose money it really is:

The moratorium would therefore be counterproductive, causing a bank run instead of preventing it. Such an outcome could be detrimental to the bank’s orderly resolution, which could ultimately cause severe harm to creditors and significantly strain the deposit guarantee scheme. In addition, such an exemption could lead to a worse treatment for depositor funded banks, as the exemption needs to be factored in when determining the seriousness of the liquidity situation of the bank. Finally, any potential technical impediments may require further assessment.

The ECB instead proposes that ‘certain safeguards’ be put in place to allow restricted access to deposits…for no more than five working days. But let’s see how long that lasts for.

Therefore, an exception for covered depositors from the application of the moratorium would cast serious doubts on the overall usefulness of the tool. Instead of mandating a general exemption, the BRRD should instead include certain safeguards to protect the rights of depositors, such as clear communication on when access will be regained and a restriction of the suspension to a maximum of five working days by avoiding a cumulative use by the competent authority and the resolution authority.

Even after a year of studying and reading bail-ins I am still horrified that something like this is deemed to be preferable and fairer to other solutions, namely fixing the banking system. The bureaucrats running the EU and ECB are still blind to the pain such proposals can cause and have caused.

Look to Italy for damage prevention

At the beginning of the month, we explained how the banking meltdown in Veneto Italy destroyed 200,000 savers and 40,000 businesses.

In that same article, we outlined how exposed Italians were to the banking system. Over €31 billion of sub-retail bonds have been sold to everyday savers, investors, and pensioners. It is these bonds that will be sucked into the sinkhole each time a bank goes under.

A 2015 IMF study found that the majority of Italy’s 15 largest banks a bank rescue would ‘imply bail-in of retail investors of subordinated debt’. Only two-thirds of potential bail-ins would affect senior bond-holders, i.e. those who are most likely to be institutional investors rather than pensioners with limited funds.

Why is this the case? As we have previously explained:

Bondholders are seen as creditors. The same type of creditor that EU rules state must take responsibility for a bank’s financial failure, rather than the taxpayer. This is a bail-in scenario.

In a bail-in scenario the type of junior bonds held by the retail investors in the street is the first to take the hit. When the world’s oldest bank Monte dei Paschi di Siena collapsed ordinary people (who also happen to be taxpayers) owned €5 billion ($5.5 billion) of subordinated debt. It vanished.

Despite the biggest bail-in in history occurring within the EU, few people have paid attention and protested against such measures. A bail-in is not unique to Italy, it is possible for all those living and banking within the EU.

Yet, so few protests. We’re not talking about protesting on the streets, we’re talking about protesting where it hurts – with your money.

Read well, protest loudly and trust what you know and not just what you are told.

As we have seen from the EU’s response to Brexit and Catalonia, officials could not give two hoots about the grievances of its citizens. So when it comes to banking there is little point in expressing disgust in the same way.

Instead, investors must take stock and assess the best way for them to protect their savings from the tyranny of central bank policy.

To refresh your memory, the ECB is proposing that in the event of a bail-in it will give you an allowance from your own savings. An allowance it will control:

“…during a transitional period, depositors should have access to an appropriate amount of their covered deposits to cover the cost of living within five working days of a request.”

Savers should be looking for means in which they can keep their money within instant reach and their reach only. At this point physical, allocated and segregated gold and silver comes to mind.

This gives you outright legal ownership. There are no counterparties who can claim it is legally theirs (unlike with cash in the bank) or legislation that rules they get first dibs on it.

Gold and silver are the financial insurance against bail-ins, political mismanagement, and overreaching government bodies. As each year goes by it becomes more pertinent than ever to protect yourself from such risks.

Related content

Invest In Gold To Defend Against Bail-ins

Precious Metals Are “Best Defence” Against Bail-ins In Economic Crisis

Bail-Ins Coming To Italy? World’s Oldest Bank “Survival Rests On Savers”

News and Commentary

Pound ‘pounded’ by political uncertainty, Gold steady (FX Street)

Gold prices steady as dollar holds up on higher U.S. bond yields (Reuters)

Dalio’s Bridgewater Boosts Gold Holdings in SPDR, iShares (Bloomberg)

Nothing to See Here as Gold Held in Tightest Range in Four Years (Bloomberg)

U.S. runs $63 billion budget deficit in October (Reuters)

Junk-bond investors are getting jittery – do they know something we don’t? (Moneyweek)

Global Gold Investment Demand To Overwhelm Supply During Next Market Crash (Gold Eagle)

“Banks Are Rigging All Markets” (US Watchdog)

Here’s how to tell if property prices are crazy – or not (SCH)

Gold Prices (LBMA AM)

14 Nov: USD 1,273.70, GBP 972.47 & EUR 1,086.59 per ounce

13 Nov: USD 1,278.40, GBP 977.59 & EUR 1,097.89 per ounce

10 Nov: USD 1,284.45, GBP 976.44 & EUR 1,102.19 per ounce

09 Nov: USD 1,284.00, GBP 980.98 & EUR 1,106.29 per ounce

08 Nov: USD 1,282.25, GBP 976.82 & EUR 1,105.43 per ounce

07 Nov: USD 1,276.35, GBP 970.92 & EUR 1,103.28 per ounce

06 Nov: USD 1,271.60, GBP 969.72 & EUR 1,095.61 per ounce

Silver Prices (LBMA)

14 Nov: USD 16.94, GBP 12.92 & EUR 14.45 per ounce

13 Nov: USD 16.93, GBP 12.93 & EUR 14.53 per ounce

10 Nov: USD 17.00, GBP 12.92 & EUR 14.60 per ounce

09 Nov: USD 17.10, GBP 13.03 & EUR 14.69 per ounce

08 Nov: USD 17.00, GBP 12.96 & EUR 14.65 per ounce

07 Nov: USD 17.01, GBP 12.95 & EUR 14.70 per ounce

06 Nov: USD 16.92, GBP 12.90 & EUR 14.59 per ounce

Recent Market Updates

– Internet Shutdowns Show Physical Gold Is Ultimate Protection

– Gold Coins and Bars Saw Demand Rise 17% to 222T in Q3

– Prepare For Interest Rate Rises And Global Debt Bubble Collapse

– Platinum Bullion ‘May Be One Of The Only Cheap Assets Out There’

– World’s Largest Gold Producer China Sees Production Fall 10%

– German Investors Now World’s Largest Gold Buyers

– Gold Price Reacts as Central Banks Start Major Change

– Why Switzerland Could Save the World and Protect Your Gold

– Invest In Gold To Defend Against Bail-ins

– Stumbling UK Economy Shows Importance of Gold

– Wozniak and Thiel Fuel Bitcoin-Gold Debate: Gold Comes Out On Top

– Russia Buys 34 Tonnes Of Gold In September

– Gold Will Be Safe Haven Again In Looming EU Crisis

END

Gold trading today:

the crooks try and break the 200 day average for gold and fail: this caused gold to rise to 1280

(courtesy zerohedge)

Gold Bounces Off Key Technical Support On Massive Volume

The last 48 hours has been quite a chaotic one in precious metals markets with massive volumes of ‘paper’ gold flushed in and out of the futures markets. This morning – shortly after the US open failed to spark a panic-bid in stocks – gold futures bounced off their 200-day moving average on huge volume (around $4.5 billion notional) breaking above the 100DMA…

The last day or so has seen a plunge below the 100DMA (on 33,000 contracts – around $4.2 billion notional), then another flush to the 200DMA as Europe opened overnight (on 22,000 contracts – around $2.8 billion notional) and then shortly after the US equity open, a 35,000 contract ($4.5 billion notional) rip higher off the critical moving average…

Once again the moves in gold appear to mirror manipulation in USDJPY…

Silver is echoing Gold’s moves today but yesterday’s standalone move remains…

end

Interesting: Gartman hardly acknowledges GATA and yet he discloses in his latest letter the BIS involvement of gold swaps which is critical to the manipulation of gold

(courtesy GATA/Chris Powell./Gartman)

Gartman Letter relies on GATA’s disclosure of BIS’ latest intervention in gold

Submitted by cpowell on Mon, 2017-11-13 18:45. Section: Daily Dispatches

1:51p ET Monday, November 13, 2017

Dear Friend of GATA and Gold:

What is the world coming to when commodity market analyst and newsletter writer Dennis Gartman of The Gartman Letter (https://www.thegartmanletter.com/) starts relying on GATA for research?

From today’s edition:

“Turning to gold, Friday was again a disaster as Fridays have been for the gold market all too often in the course of the past several years. Indeed, the best that gold can do at this point is hold its lows forged very late on Friday. The Bank for International Settlements reports that its ‘swaps’ position has gone to its highest level in history and that may have been the reason for the assault upon gold on Friday.”

The disclosure about the BIS’ latest gold swaps was made Sunday by GATA consultant Robert Lambourne here:

http://www.gata.org/node/17790

Of course a little attribution to GATA would have been courteous, but if The Gartman Letter can acknowledge the surreptitious involvement in the gold market by the BIS and its likely suppressive influence on the price of the monetary metal, the word is probably getting around pretty well these days, even if no financial journalist dares yet question the BIS about what it’s doing and on whose behalf.

While this does not necessarily foretell a return to free markets, truth, justice, and the American way as it used to be, it does suggest at least that the totalitarians are slowly being dragged into the open, which is the first step. So Arthur Hugh Clough may have been right. At least Churchill thought so.

Say not the struggle nought availeth,

The labor and the wounds are vain,

The enemy faints not, nor faileth,

And as things have been they remain.

If hopes were dupes, fears may be liars;

It may be, in yon smoke concealed,

Your comrades chase e’en now the fliers,

And, but for you, possess the field.

For while the tired waves, vainly breaking

Seem here no painful inch to gain,

Far back through creeks and inlets making,

Comes silent, flooding in, the main.

And not by eastern windows only,

When daylight comes, comes in the light.

In front the sun climbs slow, how slowly,

But westward, look, the land is bright.

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

Lawrie Williams found religion. We now have another gold writer who is now compelled to admit that the gold market is rigged

(courtesy GATA/Chris Powell/Lawrie Williams)

Another insider feels compelled to admit the gold market is rigged

Submitted by cpowell on Tue, 2017-11-14 00:54. Section: Daily Dispatches

8:02p ET Monday, November 13, 2017

Dear Friend of GATA and Gold:

Writing over the weekend for the Sharps Pixley bullion dealership in London, market analyst Lawrie Williams confided that he increasingly believes that the gold market is being rigged. Williams wrote that he has been pushed to such a conclusion by the growing number of smashes to the market out of the blue.

Williams wrote: “We have just seen yet another instance of a totally insane volume of notional gold hitting the futures markets, surely designed to stop any positive momentum for gold in its tracks. I say ‘insane’ because in a true fair market no one in their right minds would put so much on the market in such a short space of time even if it involves only paper gold rather than actual bullion.

These ‘flash crashes’ in the precious metals prices seem to be happening every time we start to see positive moves in the gold price. That cannot be coincidental. [GATA board member] Ed Steer, who publishes a daily newsletter to subscribers, called it ‘a picture-postcard waterfall decline’ — an apt description . …

“Ed places the latest ‘flash crash’ firmly at the hands of JP Morgan and the other bullion banks that hold large short positions in the precious metals — particularly in gold and silver — and thus have a vested interest in keeping the price suppressed. Ed’s views are well-known on market manipulation and are not seen as reality by some precious metals market mainstream observers, but these ‘coincidental’ flash crashes do seem increasingly to support his viewpoint as a counter-argument to what might be considered the mainstream financial establishment, which is very much in denial — probably because such manipulation appears to be an integral part of doing business in the sector.”

Bingo, Lawrie. Yes, the gold industry is the market-rigging industry, a giant real-life episode of “The Emperor’s New Clothes,” where everybody can see what is going on but no one dares say it except a few naive little kids who happened to pass by the parade, were not let in on the scheme, and only gradually deduced its evil and world-encompassing intent.

But things are changing if even some respected insiders like Williams and Dennis Gartman can question the scheme in public within a few hours of each other. Indeed, it has started to seem as if the central banks and governments masterminding the scheme are now in such stress that they can’t worry about being caught — that they know they have been caught and increasingly must resort to smashing the gold market in the open to try to warn off and intimidate investors, telling them in a crude way what Federal Reserve Chairman Alan Greenspan told them in testimony to Congress in 1998: “Central banks stand ready to lease gold in increasing quantities should the price rise”:

https://www.federalreserve.gov/boarddocs/testimony/1998/19980724.htm

But if they are not scared of being caught anymore, that doesn’t mean that central banks are not still scared — scared of losing control of what used to be markets.

Don’t believe us? Then try putting to central banks and anyone in the gold industry the four crucial and for the moment essentially prohibited questions about gold:

1) Are governments and central banks active in the monetary metals markets or not?

2) Are the documents compiled by GATA from government archives and other official sources asserting such activity genuine or forgeries?

3) If governments and central banks are active in the monetary metals markets, is it just for fun or is it for policy purposes?

4) If such activity by governments and central banks is for policy purposes, do those purposes involve the traditional objectives of defeating an independent world currency that competes with government currencies and interferes with government control of interest rates and, indeed, interferes with control of the entire economy and society itself?

If you get any answers, please forward them to your secretary/treasurer, whose e-mail address is below.

Williams might try putting these questions to Sharps Pixley’s own proprietor, Ross Norman, another gold market participant who has a respectable reputation to lose.

Williams’ commentary is headlined “Europe Pushes Gold higher — USA Slams It Down Yet Again!” and it’s posted at Sharps Pixley here:

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

Seems that Turkish citizens are not too enthralled with Erdogan and his economic and governing policies. They have bought the most gold ever as the Lira tumbles. So far in this 2017 year citizens have thought 47 tonnes. Also the Turkish government has also increased its reserves dramatically as in the 3rd quarter they bought over 30 tonnes of gold.

(courtesy zerohedge)

Turks Just Bought The Most Gold Ever As Lira Tumbles

Since President Recep Tayyip Erdogan installed himself as ‘Sultan for life’, the Turks appear to have had a dramatic change of heart towards the barbarous relic…

The Turks have never imported a greater value of gold than in the last 12 months…

Additionally, as Bloomberg reports, Bar and coin purchases, a measure of investment demand, were 47 metric tons so far in 2017, compared with 14.8 tons in the same period a year ago, according to a report from the World Gold Council published Thursday.

The weak lira and “President Erdogan’s pro-gold comments in November last year continued to lend support to the market,” the gold council said.

But it’s not just the average Turk who is buying gold, Turkey’s central bank is also buying gold, increasing purchases by 30.4 tons during the third quarter.

While the central bank has cited a good old-fashioned diversification policy, some analysts speculated that the country could be shoring up reserves amid rising tensions between Turkey and its traditional Western allies.

A year ago, President Recep Tayyip Erdogan urged Turks to prefer gold to the U.S. dollar as a savings vehicle, and asked the central bank to support that policy.

And gold is doing exactly what it should do as faith in fiat falters.

The question is – just like in India – how long before Erdogan ‘dictates’ an end to gold imports, imposes tariffs, or confiscates the precious metal?

end

Koos Jansen provides a great commentary on the 777 tonnes of gold supplied to the citizens of China for the previous 3 quarters. Annualized it looks like China will import over 1,036 tonnes. This gold is not official gold whereby China always buys with USA dollars. All gold produced in China becomes official gold and at last look they mined 430 tonnes of gold.

(courtesy Koos Jansen/Bullionstar)

China Gold Import Jan-Sep 777 tonnes. Who’s Supplying?

China Gold Import Jan-Sep 777 tonnes. Who’s Supplying?

While the gold price is slowly crawling upward in the shadow of the current cryptocurrency boom, China continues to import huge tonnages of yellow metal. As usual, Chinese investors bought on the price dips in the past quarters, steadfastly accumulating for a rainy day. The Chinese appear to be price sensitive regarding gold, as was mentioned in the most recent World Gold Council Demand Trends report, and can also be observed by Shanghai Gold Exchange (SGE) premiums – going up when the gold price goes down – and by withdrawals from the vaults of the SGE which are often increasing when the price declines. Net inflow into China accounted for an estimated 777 tonnes in the first three quarters of 2017, annualized that’s 1,036 tonnes.

Demonstrated in the chart above Chinese gold imports and known gold demand by the Rest Of the World (ROW) add up to thousands of tonnes more than what the ROW produces from its mines. One might wonder where Chinese gold imports come from, which is why I thought it would be interesting to analyse as detailed as possible who’s supplying China. Is one country, or only the West, supplying China? Although absolute facts are difficult to cement, my conclusion is that China is supplied by a wide variety of countries on several continents this year.

China doesn’t publish its gold import figures so we have to measure exports from other countries to the Middle Kingdom for this exercise. This year the primary hubs that exported to China have been Switzerland and Hong Kong.

The Swiss net exported 18 tonnes to China in September, which brings the year to date total to 221 tonnes, down 4 percent year on year. Because Switzerland is the global refining centre, a storage centre and trading hub I’ve plotted a chart showing its gross imports and exports per region.

In the above chart we can see that Switzerland was a net exporter to China in all months, but in most months Switzerland in total was a net importer, displayed by the red line; for each of those months Switzerland itself was not the supplier to China.

Combined with data from Eurostat (on the UK’s total net flow) and USGS (on the US’ total net flow) the Swiss data tells me that gold moving from Switzerland to China had several sources this year. In January, for example, it was the UK that was supplying – being a net exporter in total and a large exporter to Switzerland. I must add that in theory little gold from the UK arrived in China via Switzerland, as the numbers don’t say which bar from whom was sent to who. But we can say “the UK made it possible China bought an X amount of gold in the open market at the prevailing price that month”. The same approach suggests that in June it was the US and Switzerland (Switzerland being a net exporter that month), and in September it was Asia (including the Middle-East) supplying gold to customers of Swiss refineries at the prevailing prices. There was not one source of above ground stock that exported to China (via Switzerland) as far as I can see.

The Hong Kong Census And Statistics Department (HKCSD) has recently published data indicating China absorbed 30 tonnes from the Special Administrative Region in September, down 8 percent relative to August and down 44 percent compared to September last year. A decline was expected because China has stimulated direct gold imports circumventing Hong Kong since 2014. Nevertheless, Hong Kong net exported 515 tonnes to the mainland through the first three quarters of 2017 (down 15 percent year on year).

Hong Kong is a gold trading hub too, though. If Hong Kong is a net exporter to China, the actual source can be any country. Have a look at the next chart that shows the net flows through Hong Kong per region: the West, East and ROW (1). I’ve also added the net flow with China.

First observe the red line, “Hong Kong total net flow”. We can see that in 2013 Hong Kong became a massive net importer until about half way through 2015. The major suppliers to Hong Kong during this period were Switzerland and the UK, next to the ROW. I’m not aware of what type of entities were accumulating in Hong Kong at the time. The largest net importer from Hong Kong was China (included in the East).

After 2015 supply from the West (through Hong Kong) has slowly dried up while demand by China continued, shown by the blue line coming to zero and the yellow bars remaining to trend sub-zero. And thus Hong Kong commenced net exporting gold itself as we can see the red line in the chart falling far below zero. Apparently, since 2015 Hong Kong is a net exporter.

How much gold is left in Hong Kong? Unfortunately, online data from the HKCSD goes back only to 2002. The HKCSD does keep physical records from its international merchandise trade statistics from before 2002 but strangely “gold export” from 1972 until 1998 is omitted in these books (2).

As you can see in this last chart Hong Kong has suffered net exports from 2002 until 2008 and after 2015. It’s possible there is still bullion in Hong Kong if it had been accumulated before 1998, but since 1998 Hong Kong already “net lost” 727 tonnes. Another possibility is that refineries in Hong Kong import a lot of scrap gold, which is nearly impossible to track in customs reports and is not included in any of my data, that is being refined into bullion and exported. In this case Hong Kong is not a net exporter, or less of a net exporter. We’ll see in coming months or years if Hong Kong can continue net exporting bullion.

In exhibit 4 we can see a vague correlation between “Hong Kong net export to the China” and “Hong Kong’s total net export” for 2016 and 2017. It looks like Hong Kong is feeding its big brother. Or is it?

There is a gold kilobar futures contract listed on the COMEX that is physically deliverable in Hong Kong. The trading volume of this contract is neglectable, and so is physical delivery, but remarkably the designated vault (Brinks) throughput is sky-high. When looking at a chart of kilobars received and withdrawn at the Brinks vault in Hong Kong, supplemented by cross-border gold trade, there is a pattern revealed: the amount of kilobars received and withdrawn, and Hong Kong’s gold total import and re-export to China are correlated.

The chart suggests that Hong Kong is mainly supplying China from its imports (and any gold supplying other countries than China was stored in Hong Kong in previous years or was sourced from scrap). As the imports are correlated to kilobars received in the Brinks vault and kilobars withdrawn are correlated to re- exports to China, both flows seem to be one and the same trade. I don’t know for sure, but I think this is largely true.

The next question is from what countries does Hong Kong import bullion to dispatch to China? From countries all over the world. Have a look.

The composition is quite diverse. From the first until the the third quarter of this year gold came in from Switzerland, South-Africa, the US, Australia and the Philippines, inter alia.

Next to gold flowing through Switzerland and Hong Kong to China, countries that supplied gold directlyto China this year have been Australia at 20 tonnes (3), the US at 14 tonnes, Japan at 3 tonnes and Canada at 4 tonnes. The UK has practically exported zero gold directly to China this year.

In total Hong Kong (515 tonnes), Switzerland (221 tonnes), Australia (20 tonnes), the US (14 tonnes), Japan (3 tonnes) and Canada (4 tonnes) net exported 777 tonnes to China mainland in the first three quarters of 2017 (4).

Conclusion

It must be mentioned that in theory gold import by China arrives in the Shanghai Free Trade Zone (which is not the domestic market) where the Shanghai International Gold Exchange (SGEI) operates. As most of you know the SGEI can serve foreign customers that can import gold traded on the SGEI, for example into India. Hence, it’s possible not all gold imported into China mainland arrives in the domestic market but ends up in the Shanghai Free Trade Zone or abroad. Global cross-border trade statistics by COMTRADE, however, show that barely any country is importing from China.

Until new evidence shows up my best guess is that China net imported 777 tonnes in the first nine months of 2017, sourced from all corners of the world: the UK, South- Africa, Australia, Switzerland, the US, Middle-East and Philippines. It seems Chinese banks are active all over the world looking to buy gold on the dips. Snapping up physical metal when the time is right.

Chinese imports add to China’s domestic mining output. The China Gold Association disclosed on November 1 that mine production accounted for 313 tonnes, down 10 % compared to last year. Nearly all this gold (313 + 777) is sold through the SGE. Withdrawals from the vaults of the SGE accounted for 1,505 tonnes over this period, implying 415 tonnes (1,505 – 313 – 777) was supplied by scrap and disinvestment (or partially recycled through the SGE system).

Since all non-monetary gold imported and mine production ends up in the private sector, my estimate for total gold owned by the Chinese people now stands at 16,575 tonnes. Added by a more speculative estimate of 4,000 tonnes held by the PBOC makes 20,575 tonnes.

If you like to learn more about the Chinese gold market please read The Chinese Gold Market Essentials or visit the BullionStar University.

-END-

(GATA) BIS refuses to answer questions about its activity in the gold market

Submitted by cpowell on 02:06PM ET Tuesday, November 14, 2017.

Section: Daily Dispatches

9:15a ET Tuesday, November 14, 2017

Dear Friend of GATA and Gold:

The Bank for International Settlements today refused to answer questions from the Gold Anti-Trust Anti-Trust Action Committee about the bank’s activity in the gold market.

On Monday your secretary/treasurer wrote to the bank’s public information office calling attention to GATA consultant Robert Lambourne’s latest analysis of the bank’s October statement of account involving gold, which Lambourne construed to show a substantial increase in the bank’s use of gold swaps.

Your secretary/treasurer wrote:

“Dear BIS Press Office:

“On November 12 the Gold Anti-Trust Action Committee Inc. published an analysis by its consultant, Robert Lambourne, of the recent increase in gold swaps undertaken by the Bank for International Settlements:

http://www.gata.org/node/17790

“Could you please tell me whether this analysis is correct or, if it is in error in any way, how so?

“Could you also please tell me the BIS’ purpose and objectives with these gold swaps and with the bank’s involvement in the gold and gold derivatives markets generally?

“Thanks for your help.”

GATA received this unsigned response from the BIS today:

“Dear Sir,

“Many thanks for your e-mail enquiry.

“We do not comment on specific accounts / holdings of central banks or of the BIS. Please see our latest annual report for details on gold. Further information can be gleaned from central banks directly.

“With kind regards

“BIS

Communications

4002 Basel, Switzerland

Telephone: +41 61 280 81 88

E-mail: press@bis.org

http://www.bis.org”

But the bank does comment on its gold business when the inquiry comes from a source that is important enough.

For as Lambourne noted in his analysis November 12, in a report published in the Financial Times on July 29, 2010, the bank’s general manager himself, Jaime Caruana, discussed the bank’s gold swaps and said they were “regular commercial activities” for the bank:

http://www.ft.com/cms/s/0/3e659ed0-9b39-11df-baaf- 00144feab49a.html

As for the assertion by the BIS press office that “further information can be gleaned from central banks directly,” the last few seconds of this video shows what happened when, at the end of a presentation at Virginia Military Institute on March 31, 2016, a GATA supporter asked the president of the Federal Reserve Bank of New York, William Dudley, about the Fed’s involvement in gold swaps:

https://www.youtube.com/watch? v=p0JYoJ_rKxQ&t=14s

No information at all was available from Dudley.

For as was explained by the secret March 1999 report of the staff of the International Monetary Fund, central banks conceal their gold swaps and leases to facilitate their surreptitious interventions in the gold and currency markets:

http://www.gata.org/node/12016

The BIS’ refusal to respond to GATA and to validate or reject Lambourne’s analysis of the bank’s latest statement of account in regard to gold confirms GATA’s belief that bringing central banks to account and restoring democracy and free markets require financial journalists to find the courage to do their job and the monetary metals mining industry to stand up for itself and its investors.

If you know any financial journalists or if you’re invested in any monetary metals mining companies, please forward this to them.

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

Your early TUESDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED UP AT 6.6378/shanghai bourse CLOSED DOWN AT 18.29 POINTS .53% / HANG SANG CLOSED DOWN 30.06 POINTS OR 0.10%

2. Nikkei closed DOWN 0.98 POINTS OR 0.00% /USA: YEN FALLS TO 113.66

3. Europe stocks OPENED RED EXCEPT LONDON /USA dollar index FALLS TO 94.24/Euro RISES TO 1.1725

3b Japan 10 year bond yield: RISES TO . +.050/ GOVERNMENT INTERVENTION !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 114.07/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD FINALLY IN THE POSITIVE/BANK OF JAPAN LOSING CONTROL OF THEIR YIELD CURVE AS THEY PURCHASE ALL BONDS TO GET TO ZERO RATE!!

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 56.52 and Brent: 62.85

3f Gold DOWN/Yen DOWN

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil DOWN for WTI and DOWN FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund RISES TO +.411%/Italian 10 yr bond yield DOWN to 1.813% /SPAIN 10 YR BOND YIELD DOWN TO 1.509%

3j Greek 10 year bond yield RISES TO : 5.097???

3k Gold at $1273.60 silver at:16.95: 6 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble DOWN 34/100 in roubles/dollar) 59.73

3m oil into the 56 dollar handle for WTI and 62 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation (already upon us). This can spell financial disaster for the rest of the world/China forced to do QE!! as it lowers its yuan value to the dollar/GOT A GOOD SIZED REVALUATION NORTHBOUND

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 113.66 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 0.9947 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1663 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now POSITIVE territory with the 10 year RISING to +0.411%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.391% early this morning. Thirty year rate at 2.849% /

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

(courtesy Jim Reid/Bloomberg/Deutsche bank/zero hedge)

US Futures, Global Stocks Extend Decline After Disappointing Chinese Data, Dollar Slides

U.S. index futures declined for the second day in a row, dipping 0.1% to the lowest in more than a week following declines in Asian and European shares. European stocks tried and failed to shrug off the negative sentiment that spurred broad-based declines in Asia following another month of disappointing Chinese macro data…

… eventually reversing gains as the euro strengthened on German growth data. The euro was up a fifth day, rising above 1.1700 for the first time in nearly three weeks after data showed that German GDP was on track for its best year since 2011, forcing Europe’s Stoxx 600 Index to retreat. The U.K.’s FTSE 100 Index jumped 0.1 percent, while Germany’s DAX Index gained less than 0.05%.

Mining companies led the drop, with many commodity prices also falling in the wake of data showing China’s economy moderating. That also weighed on Asian equity gauges, though the Nikkei closed little changed after dropping for four days. The yield on China’s 10-year debt briefly breached 4 percent for the first time in more than three years. China’s CSI300 Index slid as much as 1%, its biggest intraday drop this month, as tech shares lead decline. Sanan Optoelectronics Co. slumps 7% to pace declines on the CSI300 Index; Unigroup Guoxin Co. -5.2% as second-worst performer.

Earlier, Asian stocks dropped headed for a third day of declines, as data showed China’s economy is moderating. The MSCI Asia Pacific Index retreated 0.4 percent to 169.44, with telcos and energy producers leading losses. Despite earlyer gains, the Nikkei closed fractionally in the red again as foreigners resumed selling after a record month of buying in October. The Yen pared losses against the dollar, as traders wait on U.S. inflation data from Tuesday and look for progress on the tax reforms. Japan’s Topix dropped 0.3% while South Korea’s Kospi lost 0.2%. Australia’s benchmark index slumped 0.9% after Royal Dutch Shell Plc sold its entire stake in Woodside Petroleum Ltd., sending the latter’s shares down the most in more than a year.

According to Bloomberg, Asian equities were taking a pause from a world-leading 2017 rally as traders tuned in to China’s economic data. Numbers released Tuesday show the country’s expansion dialed back a notch as factory output, investment and retail sales all decelerated.

“Investors have concerns about a possible fourth-quarter slowdown in China,” said Ronald Wan, chief executive at Partners Capital International in Hong Kong. MSCI Inc. announced the results of its November 2017 semi-annual index review which included the deletion of Qantas Airways Ltd. and the addition of Japan’s Sumco Corp.

Markets have been under pressure for the past few days after a global rally took U.S. stocks to records and Japan’s to the highest in a quarter century. This morning market participants were monitoring an ECB conference featuring appearances by Mario Draghi, Janet Yellen, Mark Carney and Haruhiko Kuroda. Meanwhile, U.S. inflation and retail sales numbers that could influence Federal Reserve interest-rate hike odds are on the docket tomorrow, and U.S. tax discussions are ongoing. Fed’s Kaplan stated that the Fed are actively discussing lifting rates next month

Elsewhere, and as reported earlier, Venezuela was declared in default by S&P Global Ratings after missing two interest payments on its debt. Indian sovereign bonds fell for a third day, with the benchmark 10-year yield reaching the highest since September 2016, on accelerating consumer inflation data. Bitcoin edged higher after three days falling.

The common currency heads for a bullish reversal of its trend since the 2 1/2 year high of 1.2092 hit on Sept. 8 as the short- squeeze started on Thursday gained momentum. Investors that are short the euro see their trailing stops being filled, while short-term accounts were stopped out on Tuesday’s run up to 1.1720 high, traders in London and Europe told Bloomberg.

“It is not the dollar that is weak, it is the euro that is strong,” said John Hardy, Saxo Bank’s head of FX strategy. Combined with signs of a move up again in European bond yields, that suggested some traders were back to pricing in an end to the ECB’s stimulus, he said.

In geopolitical developments, overnight President Trump tweets: “After my tour of Asia, all Countries dealing with us on TRADE know that the rules have changed. The United States has to be treated fairly and in a reciprocal fashion. The massive TRADE deficits must go down quickly!” Russian PM Medvedev says Russia has stake in peace on Korean Peninsula, as South Korean President Moon calls for enhanced ‘strategic’ dialogue between South Korea & Russia. US House Ways & Means chair Brady says that the GOP leadership is confident that it has votes for passage of tax bill, major changes to house tax bill are unlikely at committee stage.

In macro, German growth data pressured investors with short-euro exposure as the common currency hit its strongest level in almost three weeks. The dollar was broadly lower within tight ranges during Asia hours before the weakness grew in the London session. The British pound was tipped lower as inflation missed forecasts, and the dollar broke out of a tight range to weaken as traders continue to weigh the chances of a meaningful tax overhaul. Data from the CFTC released on Monday showed the net short position in the Japanese yen to be the largest since January 2014 and in the Swiss franc to the biggest since December 2016.

In rates, yields on 2Y Treasurys hit a fresh nine-year high of 1.6910% on Monday, shrinking the 2s-10s spread to near its smallest since 2007. The trend reflects market bets the Fed’s plans to raise rates in December and two or three times next year will slow the economy. On Tuesday, European bonds turned positive. Aussie bonds were hurt after business conditions printed at highest on record, while China’s sovereign bond selloff reached a fresh milestone, with 10-year yields breaching 4% for the first time in more than three years, before retracing losses and closing back under 4%.

Tom Porcelli, chief U.S. economist at RBC Capital Markets, said history suggested a flatter, and particularly an inverted, yield curve was “compelling as an early warning sign” of recession. But with the average amount of time it has taken the curve to go from flat to inverted being 18 months and another 18 months to go from inverted to recession, it suggests the expansion still has multiple years in it, said Porcelli.

In commodity markets, gold inched down to $1,272.50 an ounce. The metal has stayed broadly within $15 an ounce of its 100-day moving average, currently at $1,277 an ounce, for most of the last month. Oil prices held in a tight range as support from Middle East tensions and record long bets by fund managers balanced rising U.S. production. U.S. crude was off 19 cents at $56.57, while Brent crude futures eased 23 cents to $62.92 a barrel.

Mining shares lead the drop amid weakness in commodity prices. Economic data include small business optimism index and PPI readings, while Home Depot and TJX are set to report earnings.

Bulletin Headline Summary from RanSquawk

- Lower than expected UK CPI weighs on GBP

- EUR bid following German GDP

- Looking ahead, Draghi, Yellen, Carney, Kuroda all currently speak, with US PPI and APIs due later

Market Snapshot

- S&P 500 futures down 0.1% to 2,579

- STOXX Europe 600 down 0.08% to 385.82

- MSCI Asia down 0.4% to 169.53

- MSCI Asia ex Japan down 0.3% to 556.72

- Nikkei unchanged at 22,380.01

- Topix down 0.3% to 1,778.87

- Hang Seng Index down 0.1% to 29,152.12

- Shanghai Composite down 0.5% to 3,429.55

- Sensex down 0.2% to 32,964.82

- Australia S&P/ASX 200 down 0.9% to 5,968.75

- Kospi down 0.2% to 2,526.64

- German 10Y yield fell 0.2 bps to 0.415%

- Euro up 0.3% to $1.1706

- Italian 10Y yield fell 1.2 bps to 1.568%

- Spanish 10Y yield fell 2.7 bps to 1.505%

- Brent Futures down 0.3% to $63.00/bbl

- Gold spot down 0.4% to $1,273.54

- U.S. Dollar Index down 0.1% to 94.39

Top Headline News

- Brexit Secretary David Davis reckons it’s as close as 50-50 whether he gets a breakthrough in divorce talks by December, according to European business leaders he briefed at a meeting Monday. His spokesman later said this news was “categorically untrue” and that Davis had not made such a comment

- Trump is seeking a qualified candidate to serve as Federal Reserve chairman nominee Jerome Powell’s vice-chair; candidate doesn’t necessarily have to be Ph.D. economist

- Trump said he will be making a major statement once back in Washington

- U.K. inflation came in less than forecast as cheaper auto fuel offset the rising cost of fuel, but the measure still held close to a 5 1/2-year high

- German growth steamed ahead in the third quarter, keeping Europe’s largest economy on track for its best year since 2011. That expansion is bolstering the euro area’s upturn and supporting the global outlook. Similar data from Italy showed the economy expanded at a faster pace last quarter

- Traders are increasing bets on the divergence of the world’s three major central banks, ramping up long future positions on German bunds and Japanese debt while shorting Treasuries, if open interest is any guide

- China’s economic expansion dialed back a notch in October, as a campaign to manage credit risks took hold and the Communist Party signaled a less stringent approach to hitting growth targets

- Fed’s Kaplan: Actively considering a December rate hike; there’s a mounting case for moving ahead of signs of price increases: FT

- Brady says confident House Republicans have votes to pass tax bill

- German 3Q GDP q/q: 0.8% vs 0.6% est; y/y 2.8% vs 2.3% est.

- U.K. Oct. CPI y/y: 3.0% vs 3.1% est; food inflation largest upside contributor +4.2% y/y, most in 4 years

- German Nov. ZEW expectations: 18.7 vs 19.5 est; current situation 88.8 vs 88.0 est.