GOLD: $1334.70 UP $0.30

Silver: $16.70 down 7 cents

Closing access prices:

Gold $1339.60

silver: $16.72

SHANGHAI GOLD FIX: FIRST FIX 10 15 PM EST (2:15 SHANGHAI LOCAL TIME)

SECOND FIX: 2:15 AM EST (6:15 SHANGHAI LOCAL TIME)

SHANGHAI FIRST GOLD FIX: $1339.75 DOLLARS PER OZ

NY PRICE OF GOLD AT EXACT SAME TIME: $1330.00

PREMIUM FIRST FIX: $9.75

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

SECOND SHANGHAI GOLD FIX: $1344.47

NY GOLD PRICE AT THE EXACT SAME TIME: $1332.70

Premium of Shanghai 2nd fix/NY:$11.77

SHANGHAI REJECTS NY /LONDON PRICING OF GOLD

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

LONDON FIRST GOLD FIX: 5:30 am est $1337.10

NY PRICING AT THE EXACT SAME TIME: $1336.00

LONDON SECOND GOLD FIX 10 AM: $1333.60

NY PRICING AT THE EXACT SAME TIME. $1333.95

For comex gold:

FEBRUARY/

NUMBER OF NOTICES FILED TODAY FOR FEBRUARY CONTRACT: 431 NOTICE(S) FOR 43100 OZ.

TOTAL NOTICES SO FAR:1302 FOR 130200 OZ (4.049 TONNES),

For silver:

jANUARY

0 NOTICE(S) FILED TODAY FOR

nil OZ/

Total number of notices filed so far this month: 124 for 620,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: BID $7,518/OFFER $7,582: DOWN $1014(morning)

Bitcoin: BID/ $7167/offer $7237: down $1360 (CLOSING/5 PM)

end

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total open interest ROSE BY GIGANTIC 6702 contracts from 202,554 (CME CORRECTED) RISING TO 209,256 DESPITE FRIDAY’S HUGE 43 CENT FALL IN SILVER PRICING. WE OBVIOUSLY (SHOCKINGLY) HAD NO COMEX LIQUIDATION. HOWEVER, WE WERE AGAIN NOTIFIED THAT WE HAD ANOTHER HUGE SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP ROUTE: 4782 EFP’S FOR MARCH AND AND 14 EFP’S FOR MAY AND ZERO FOR ALL OTHER MONTHS AND THUS TOTAL ISSUANCE OF 4796 CONTRACTS. HOWEVER THE MOVEMENT ACROSS TO LONDON IS NOT AS SEVERE AS IN GOLD AS THERE SEEMS TO BE MAJOR PLAYERS WILLING TO TAKE ON THE BANKS AT THE COMEX. STILL, WITH THE TRANSFER OF 4796 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24 HRS IN THE ISSUING OF EFP’S. THE 4796 CONTRACTS TRANSLATES INTO 23.98 MILLION OZ

ACCUMULATION FOR EFP’S/SILVER/ STARTING FROM FIRST DAY NOTICE/FOR MONTH OF FEBRUARY:

11,342 CONTRACTS (FOR 4 TRADING DAYS TOTAL 11,342 CONTRACTS OR 56.710 MILLION OZ: AVERAGE PER DAY: 2835 CONTRACTS OR 14.175 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH: 56.71 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 8.10% OF ANNUAL GLOBAL PRODUCTION

ACCUMULATION IN YEAR 2018 TO DATE SILVER EFP’S: 291.68 MILLION OZ.

ACCUMULATION FOR JAN 2018: 236.879 MILLION OZ

RESULT: A HUGE SIZED GAIN IN OI SILVER COMEX DESPITE THE GIGANTIC 43 CENT FALL IN SILVER PRICE. WE HOWEVER HAD A HUGE SIZED EFP ISSUANCE OF 4796 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER . FROM THE CME DATA 4796 EFP’S FOR MONTHS MARCH AND MAY WERE ISSUED FOR MONDAY FOR A DELIVERABLE FORWARD CONTRACT OVER IN LONDON WITH A FIAT BONUS. WE REALLY GAINED 11,498 OI CONTRACTS i.e. 4796 open interest contracts headed for London (EFP’s) TOGETHER WITH A INCREASE OF 6702 OI COMEX CONTRACTS. AND ALL OF THIS HAPPENED WITH THE FALL IN PRICE OF SILVER OF 43 CENTS AND A CLOSING PRICE OF $16.77 WITH RESPECT TO FRIDAY’S TRADING. YET WE STILL HAVE A FAIR AMOUNT OF SILVER STANDING AT THE COMEX.

In ounces AT THE COMEX, the OI is still represented by just OVER 1 BILLION oz i.e. 1.046 BILLION TO BE EXACT or 149% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT FEBRUARY MONTH/ THEY FILED: 0 NOTICE(S) FOR NIL OZ OF SILVER

In gold, the open interest FELL BY A TINY 704 CONTRACTS DOWN TO 548,278 (CME CORRECTED) DESPITE THE GOOD SIZED FALL IN PRICE OF GOLD WITH FRIDAY’S TRADING ($10.50). IN ANOTHER DEVELOPMENT, WE RECEIVED THE TOTAL NUMBER OF GOLD EFP’S ISSUED FOR MONDAY AND IT TOTALED A GIGANTIC SIZED 14,200 CONTRACTS OF WHICH APRIL SAW THE ISSUANCE OF 13500 CONTRACTS AND JUNE SAW THE ISSUANCE OF 700 CONTRACTS AND THEN ALL OTHER MONTHS ZERO. The new OI for the gold complex rests at 548,278. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. DEMAND FOR GOLD INTENSIFIES GREATLY AS WE CONTINUE TO WITNESS A HUGE NUMBER OF EFP TRANSFERS TOGETHER WITH THE MASSIVE INCREASE IN GOLD COMEX OI TOGETHER WITH THE TOTAL AMOUNT OF GOLD OUNCES STANDING FOR FEBRUARY COMEX. EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER (BIG RISE IN BOTH GOFO AND SIFO) AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES. IN ESSENCE TODAY WE HAVE A GAIN OF 13,496 CONTRACTS: 704 OI CONTRACTS DECREASED AT THE COMEX AND A STRONG SIZED 14,200 OI CONTRACTS WHICH NAVIGATED OVER TO LONDON.(14,200 CONTRACTS EQUATES TO 41.97 TONNES)

YESTERDAY, WE HAD 6579 EFP’S ISSUED.

ACCUMULATION OF EFP’S/ GOLD(EXCHANGE FOR PHYSICAL) FOR THE MONTH OF FEBRUARY STARTING WITH FIRST DAY NOTICE: 43,412 CONTRACTS OR 4,341,200 OZ OR 135.02 TONNES (4 TRADING DAYS AND THUS AVERAGING: 10,853 EFP CONTRACTS PER TRADING DAY OR 1,085,300 OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SIZE OF THESE EFP TRANSFERS : SO FAR THIS MONTH IN 4 TRADING DAYS: IN TONNES: 135.02 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2017, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 2200 TONNES

THUS EFP TRANSFERS REPRESENTS 135.02/2200 x 100% TONNES = 6.13% OF GLOBAL ANNUAL PRODUCTION SO FAR IN FEBRUARY ALONE.

ACCUMULATION OF GOLD EFP’S YEAR 2018 TO DATE: 787.33 TONNES

ACCUMULATION OF GOLD EFP’S FOR JANUARY 2018: 653.22 TONNES

Result: A SURPRISING TINY SIZED DECREASE IN OI AT THE COMEX DESPITE THE CONSIDERABLE FALL IN PRICE IN GOLD TRADING FRIDAY ($10.50). IT IS WITHOUT A DOUBT THAT MANY OF THE DEPARTED COMEX LONGS RECEIVED THEIR PRIVATE EFP CONTRACT FOR EITHER APRIL OR JUNE. WE HAD ANOTHER GOOD SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 14200 AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX AND YET WE ALSO OBSERVED A HUGE DELIVERY MONTH FOR THE MONTH OF DECEMBER. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 14,200 EFP CONTRACTS ISSUED, WE HAD A NET GAIN IN OPEN INTEREST OF 13,496 contracts ON THE TWO EXCHANGES:

14,200 CONTRACTS MOVE TO LONDON AND 704 CONTRACTS DECREASED AT THE COMEX. (in tonnes, the GAIN in total oi equates to 41.97 TONNES).

we had: 431 notice(s) filed upon for 43100 oz of gold.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD

STRANGE, WITH ALL OF TODAY’S TURMOIL: No change in gold inventory at the GLD/

Inventory rests tonight: 841.35 tonnes.

SLV/

HUGE CHANGES IN SILVER INVENTORY AT THE SLV/ A DEPOSIT OF 1.31 MILLION OZ INTO THE SLV

/INVENTORY RESTS AT 314.045 MILLION OZ/

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in silver ROSE BY A HUGE 6702 contracts from 202,554 (CME CORRECTED) UP TO 209,256 (AND now A LITTLE CLOSER TO THE NEW COMEX RECORD SET ON FRIDAY/APRIL 21/2017 AT 234,787) DESPITE THE FALL IN PRICE OF SILVER (43 CENTS WITH RESPECT TO FRIDAY’S TRADING). OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE ANOTHER GOOD 4782 PRIVATE EFP’S FOR MARCH AND 14 EFP CONTRACTS OR MAY (WE DO NOT GET A LOOK AT THESE CONTRACTS AS IT IS PRIVATE BUT THE CFTC DOES AUDIT THEM) AND 0 EFP’S FOR ALL OTHER MONTHS . EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. WE HAD ZERO COMEX SILVER COMEX LIQUIDATION. IF WE TAKE THE OI GAIN AT THE COMEX OF 6702 CONTRACTS TO THE 4796 OI TRANSFERRED TO LONDON THROUGH EFP’S WE OBTAIN A GAIN OF 11,498 OPEN INTEREST CONTRACTS. WE STILL HAVE A GOOD AMOUNT OF SILVER OUNCES THAT ARE STANDING FOR METAL IN JANUARY (SEE BELOW). THE NET GAIN TODAY IN OZ ON THE TWO EXCHANGES: 57.490 MILLION OZ!!!

RESULT: A HUGE SIZED INCREASE IN SILVER OI AT THE COMEX DESPITE THE HUGE SIZED FALL OF 43 CENTS IN PRICE (WITH RESPECT TO FRIDAY’S TRADING). BUT WE ALSO HAD ANOTHER GOOD 4796 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE GOOD SIZED AMOUNT OF SILVER OUNCES STANDING FOR FEBRUARY, DEMAND FOR PHYSICAL SILVER INTENSIFIES AS WE WITNESS MAJOR BANK SHORT COVERING ACCOMPANIED BY INCREASES IN GOFO AND SIFO RATES INDICATING SCARCITY.

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)Late SUNDAY night/MONDAY morning: Shanghai closed UP 25.41 points or 0.73% /Hang Sang CLOSED DOWN 356.56 or 1.09% / The Nikkei closed DOWN 592.45 POINTS OR 2.55%/Australia’s all ordinaires CLOSED DOWN 1.63%/Chinese yuan (ONSHORE) closed DOWN at 6.2915/Oil DOWN to 64.89 dollars per barrel for WTI and 67.64 for Brent. Stocks in Europe OPENED RED . ONSHORE YUAN CLOSED DOWN AGAINST THE DOLLAR AT 6.2915. OFFSHORE YUAN CLOSED DOWN AGAINST THE ONSHORE YUAN AT 6.2928//ONSHORE YUAN A LITTLE WEAKER AGAINST THE DOLLAR/OFF SHORE A LITTLE WEAKER TO THE DOLLAR/. THE DOLLAR (INDEX) IS MUCH STRONGER AGAINST ALL MAJOR CURRENCIES. CHINA IS NOT TOO HAPPY TODAY.(WEAKER CURRENCY AND WEAK MARKETS THROUGHOUT THE GLOBE )

3a)THAILAND/SOUTH KOREA/NORTH KOREA

i)North Korea

b) REPORT ON JAPAN

3 c CHINA

4. EUROPEAN AFFAIRS

GERMANY

Support for the 2nd largest party in Germany, the SPD under Martin Schulz dives and puts the German coalition in doubt. Maybe this coalition lasts a year to which another election is called and both Schulz and Merkel step down.

( Mish Shedlock)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

Hamas leader in the Gaza Strip warns that war with Israel will erupt within days. There have been rockets fired into Israel from Gaza to which Israel responded by blowing up a military weapons depot in the south of GAZA

( zero hedge)

6 .GLOBAL ISSUES

7. OIL ISSUES

This should save Suncor tonnes of money: They are replacing 400 truck drivers with self driving trucks

(courtesy zerohedge)

8. EMERGING MARKET

9. PHYSICAL MARKETS

i)Gold expert Robert Lambourne reports that BIS gold derivatives fell by quite a bit in December but the sight swaps still remain relatively high. This is the major source of gold used by the bankers to whack gold

( Robert Lambourne/GATA)

ii)This should hurt the price of Bitcoin: USA banks are set to ban to use of credit cards to purchase bitcoin

( zerohedge)

iii)Bitcoin tumbles to below $8,000.00 as China launches another new crypto crackdown

( zerohedge)

10. USA stories which will influence the price of gold/silver

( David Stockman/ContraCorner)

iv b)With three days to go before another shutdown both sides are not any closer. They also seem to forget about the big debt ceiling which will come on or about March 5

v)Take your pick: either the uSA service spikes to a 13 year high or slumps to a 9 month low

After the release of the memo, GOP reps are now seeking criminal prosecution of certain FBI and Dept of Justice officials for illegal misconduct and “treason”

( zerohedge)

vii)In Hannity on Friday night, Nunes remarks that the release of the memo is just phase one. They are now targeting the State Dept and the likes of Clapper

viii)Here we see certain CIA and FBI agents responding to the Nunes memo. Take particular interest in CIA agent Ray McGovern’s commentary including the excellent summary of events by Publicus Tacitus( zerohedge)

ix)It sure looks like his days are numbered: Rod Rosenstein apparently threatened Nunes with a subpoena trying to stop the release of the 4 page memo and on obtaining all of their texts and messages between them

( zerohedge)

xi)The FISA memo is just the beginning in the fight to drain the swamp

xii)Here is the Democrats version and it is total garbage: read Byron York of the Washington Examiner who puts the issue in total perspective

xiii)It looks like the House Intel Committee wil take up the Democratic memo on Monday and will likely allow its release to the public( zerohedge)

xiv)Seems that the FBI are accused of blocking key details on the Trump Dossier’s author, Glen Simpson

( zerohedge)

xv)The war between the FBI and the Dept of Justice just went nuclear..and it should

Trump attorneys approve a second special counsel to probe the FBI and the Dept of Justice with respect to the election of Nov 8 2016

( zerohedge)

Let us head over to the comex:

The total gold comex open interest SURPRISINGLY FELL BY ONLY 704 CONTRACTS DOWN to an OI level 548,278 (CME CORRECTED) DESPITE THE GOOD SIZED FALL IN THE PRICE OF GOLD ($10.5 LOSS WITH RESPECT TO FRIDAY’S TRADING). WE HAD NO COMEX GOLD LIQUIDATION. HOWEVER THE CME REPORTS THAT THE BANKERS ISSUED ANOTHER STRONG COMEX TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS. WE HAD A GOOD SIZED 13,500 EFP’S ISSUED FOR APRIL AND 700 EFP’s FOR JUNE AND ZERO FOR ALL OTHER MONTHS: TOTAL 14,200 CONTRACTS. THE OBLIGATION STILL RESTS WITH THE BANKERS ON THESE TRANSFERS. ALSO REMEMBER THAT THERE IS NO DOUBT A HUGE DELAY IN THE ISSUANCE OF EFP’S AND IT PROBABLY TAKES AT LEAST 48 HRS AFTER LONGS GIVE UP THEIR COMEX CONTRACTS FOR THEM TO RECEIVE THEIR EFP’S AS THEY ARE NEGOTIATING THIS CONTRACT WITH THE BANKS FOR A FIAT BONUS PLUS THEIR TRANSFER TO A LONDON FORWARD… THE COMEX IS NOW AN ABSOLUTE FRAUD!!

ON A NET BASIS IN OPEN INTEREST WE GAINED TODAY: 15,876 OI CONTRACTS IN THAT 14200 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE GAINED 1676 COMEX CONTRACTS.

NET GAIN ON THE TWO EXCHANGES: 15,876 contracts OR 1,587,600 OZ OR 49.38 TONNES,

Result: A GOOD SIZED INCREASE IN COMEX OPEN INTEREST DESPITE THE LOSS IN YESTERDAY’S GOLD TRADING ($10.50.) WE HAD ZERO COMEX GOLD LIQUIDATION. TOTAL OPEN INTEREST GAIN ON THE TWO EXCHANGES: 13,496 OI CONTRACTS..

We have now entered the active contract month of FEBRUARY where we lost 689 contracts to 2239 contracts. We had 196 notices filed upon yesterday, so we lost 490 contracts or 49,000 oz will not stand in this active contract month of February AND THESE WERE MORPHED INTO LONDON BASED FORWARDS.

March saw a GAIN of 35 contracts UP to 2110. April saw a LOSS of 1358 contracts DOWN to 394,477.

We had 431 notice(s) filed upon today for 19600 oz

PRELIMINARY COMEX VOLUME FOR TODAY: 250,485 contracts

CONFIRMED COMEX VOLUME FOR YESTERDAY: 446,668

comex gold volumes are RISING AGAIN

Here is a summary of the latest gold trading volumes at the Comex per year

certainly the introduction of EFP’s has certainly had an effect:

Trading Volumes on the COMEX

Meanwhile, gold-trading volumes on the COMEX have never been higher:

end

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

And now for the wild silver comex results.

Total silver OI ROSE BY A HUGE 6702 CONTRACTS FROM 202,554(CME CORRECTED UP TO 209,256 DESPITE FRIDAY’S 43 CENT LOSS. WE WERE ALSO INFORMED THAT WE HAD ANOTHER HUGE SIZED 4782 EMERGENCY EFP’S FOR MARCH ISSUED BY OUR BANKERS (WITH 14 EFP CONTRACTS FOR MAY AND ZERO FOR ALL OTHER MONTHS) TO COMEX LONGS WHO RECEIVED A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON: THE TOTAL EFP’S ISSUED: 4796. THE SILVER BOYS HAVE STARTED TO MIGRATE TO LONDON FROM THE START OF DELIVERY MONTH AND CONTINUING RIGHT THROUGH UNTIL FIRST DAY NOTICE JUST LIKE WE ARE WITNESSING TODAY. USUALLY WE NOTED THAT CONTRACTION IN OI OCCURRED ONLY DURING THE LAST WEEK OF AN UPCOMING ACTIVE DELIVERY MONTH AS WE HAVE JUST SEEN IN GOLD TODAY. THIS PROCESS HAS JUST BEGUN IN EARNEST IN SILVER STARTING IN SEPTEMBER 2017. HOWEVER, IN GOLD, WE HAVE BEEN WITNESSING THIS FOR THE PAST 2 YEARS. NICK LAIRD WAS KIND ENOUGH TO SUPPLY US THE TOTAL FOR 2017 GOLD EFP’S AND IT WAS 6600 TONNES FOR THE ENTIRE YEAR. WE OBVIOUSLY HAD ZERO LONG COMEX SILVER LIQUIDATION AND A HUGE SIZED GAIN IN TOTAL SILVER OI. WE ARE ALSO WITNESSING A FAIR AMOUNT OF SILVER OUNCES STANDING FOR COMEX METAL IN THIS NON ACTIVE JANUARY AS WELL AS THAT CONTINUAL MIGRATION OF EFPS OVER TO LONDON. ON A PERCENTAGE BASIS THERE ARE MORE EFP’S ISSUED FOR GOLD THAN SILVER. ON A NET BASIS WE GAINED 11,498 SILVER OPEN INTEREST CONTRACTS:

6702 CONTRACT GAIN AT THE COMEX COMBINING WITH THE ADDITION OF 4796 OI CONTRACTS NAVIGATING OVER TO LONDON.

NET GAIN TWO EXCHANGES: 11,498 CONTRACTS

We are now in the poor non active delivery month of FEBRUARY and here the front month lost 2 contracts DOWN TO 1 contracts. We had 0 notices filed upon yesterday so we LOST 1 contracts or 5,000 ADDITIONAL oz will NOT stand for delivery AND THIS CONTACT MORPHED INTO A LONDON BASED FORWARD.

The March contract GAINED 1027 contracts UP to 127,259

April gained 9 contracts up to 11.

.

We had 0 notice(s) filed for NIL NIL for the FEBRUARY 2018 contract for silver

INITIAL standings for FEBRUARY

Feb5/2018.

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz |

31,950.851 oz

DELAWARE

SCOTIA

|

| Deposits to the Dealer Inventory in oz | nil oz |

| Deposits to the Customer Inventory, in oz |

128,128.425

oz HSBC

|

| No of oz served (contracts) today |

431 notice(s)

43,100 OZ

|

| No of oz to be served (notices) |

1808 contracts

(180,800 oz)

|

| Total monthly oz gold served (contracts) so far this month |

1302 notices

130,200 oz

4.049 tonnes

|

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

For FEBRUARY:

Today, 0 notice(s) were issued from JPMorgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equates to 431 contract(s) of which 392 notices were stopped (received) by j.P. Morgan dealer and 24 notice(s) was (were) stopped/ Received) by j.P.Morgan customer account.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

To calculate the INITIAL total number of gold ounces standing for the FEBRUARY. contract month, we take the total number of notices filed so far for the month (1302) x 100 oz or 130,200 oz, to which we add the difference between the open interest for the front month of FEB. (2239 contracts) minus the number of notices served upon today (431 x 100 oz per contract) equals 321,000 oz, the number of ounces standing in this active month of FEBRUARY

Thus the INITIAL standings for gold for the FEBRUARY contract month:

No of notices served (1302 x 100 oz or ounces + {(2239)OI for the front month minus the number of notices served upon today (431 x 100 oz )which equals 321,000 oz standing in this active delivery month of February (9.9944 tonnes). THERE IS 12.68 TONNES OF REGISTERED GOLD AVAILABLE FOR DELIVERY SO FAR.

WE LOST 490 CONTRACTS OR AN ADDITIONAL 49,000 OZ WILL NOT STAND BUT THEY WILL JOIN OTHER LONGS AS THEY HAVE BEEN TRANSFERRED TO A LONDON BASED FORWARD THROUGH THE EFP ROUTE.

THE COMEX IS NOW UNDER STRESS AS THE REGISTERED GOLD FALLS BELOW 13 TONNES.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

IN THE LAST 17 MONTHS 63 NET TONNES HAS LEFT THE COMEX.

end

And now for silver

AND NOW THE DECEMBER DELIVERY MONTH

FEBRUARY FINAL standings

| Silver | Ounces |

| Withdrawals from Dealers Inventory | nil oz |

| Withdrawals from Customer Inventory |

983.81 oz

DELAWARE

|

| Deposits to the Dealer Inventory |

nil

oz

|

| Deposits to the Customer Inventory |

1,553,271.050 OZ

JP.MORGAN

MALCA

|

| No of oz served today (contracts) |

0

CONTRACT(S)

(NIL OZ)

|

| No of oz to be served (notices) |

1 contracts

(5,000 oz)

|

| Total monthly oz silver served (contracts) | 124 contracts

(620,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

we had no inventory movement at the dealer side of things

total inventory movement dealer: nil oz

we had 1 inventory deposits into the customer account

i) into JPMORGAN: 952,899.140 oz

ii) into Malca: 600,371.910 oz

total inventory deposits: 1,553,271.050 oz

JPMORGAN CONTINUES TO ADD TO ITS INVENTORY DESPITE BEING THE BIGGEST SHORT AT THE COMEX. ACCORDING TO BUTLER JPMORGAN HAS AMASSED IN 2 YRS: 700 MILLION OZ PHYSICAL SILVER. THIS COULD EASILY BE PROVEN. THIS BEHAVIOUR IS TOTALLY CRIMINAL

we had 2 withdrawals from the customer account;

i) out of DELAWARE: 1527.480 oz

ii) out of Scotia: 30,423.371 oz

total withdrawals; 31,950.851 oz

we had 1 adjustment

i) from international Delaware vault:

50,619.981 oz was removed from I-D dealer into the customer account of ID

total dealer silver: 43.080 million

total dealer + customer silver: 248.051 million oz

The total number of notices filed today for the FEBRUARY. contract month is represented by 0 contract(s) FOR NIL oz. To calculate the number of silver ounces that will stand for delivery in FEBRUARY., we take the total number of notices filed for the month so far at 124 x 5,000 oz = 620,000 oz to which we add the difference between the open interest for the front month of FEB. (1) and the number of notices served upon today (0 x 5000 oz) equals the number of ounces standing.

.

Thus the INITIAL standings for silver for the FEB contract month: 124(notices served so far)x 5000 oz + OI for front month of FEBRUARY(1) -number of notices served upon today (0)x 5000 oz equals 625,000 oz of silver standing for the FEBRUARY contract month.

WE LOST 1 CONTRACTS OR AN ADDITIONAL 5,000 OZ WILL NOT STAND AT THE COMEX

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

ESTIMATED VOLUME FOR TODAY: 85.186

CONFIRMED VOLUME FOR YESTERDAY: 152,793 CONTRACTS

YESTERDAY’S CONFIRMED VOLUME OF 152,793 CONTRACTS EQUATES TO 763 MILLION OZ OR 109.1% OF ANNUAL GLOBAL PRODUCTION OF SILVER

COMMODITY LAW SUGGESTS THAT OPEN INTEREST SHOULD NOT BE MORE THAN 3% OF ANNUAL GLOBAL PRODUCTION. THE CROOKS ARE SUPPLYING MASSIVE PAPER TRYING TO KEEP SILVER IN CHECK.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price at that day at $18.42

The previous record was 224,540 contracts with the price at that time of $20.44

end

NPV for Sprott

1. Sprott silver fund (PSLV): NAV RISES TO -2.24% (FEB 5/2018)

2. Sprott gold fund (PHYS): premium to NAV FALLS TO -0.65% to NAV (FEB 5/2018 )

Note: Sprott silver trust back into NEGATIVE territory at -2.24%-/Sprott physical gold trust is back into NEGATIVE/ territory at -0.65%/Central fund of Canada’s is still in jail but being rescued by Sprott.

Sprott WINS hostile 3.1 billion bid to take over Central Fund of Canada

(courtesy Sprott/GATA)

3.SPROTT CEF.A FUND (FORMERLY CENTRAL FUND OF CANADA): NAV FALLS TO -3.49%: NAV 13.77/TRADING 13.30//DISCOUNT 3.49%

END

And now the Gold inventory at the GLD/

Feb 5 Strange,with all of today’s turmoil, the crooks at the GLD decided to add zero ounces into GLD inventory/inventory rests at 841.35 tonnes

Feb 2/no change in gold inventory at the GLD/Inventory rests at 841.35 tonnes

Feb 1/with gold up by $8.00/the crooks decided not to add any new physical gold metal into the GLD./inventory rests at 841.35 tonnes

Jan 31/with gold up $3.15 today, GLD shed another 5.32 tonnes of gold from its inventory/inventory rests at 841.35 tonnes

jan 30/with gold down by $4.85/GLD shed another 1.47 tonnes of gold from its inventory/inventory rests at 846.67 tonnes

JAN 29/with gold down $11.25, the GLD shed 1.18 tonnes of gold/inventory rests at 848.14 tonnes

jan 26/2018/no changes in gold inventory at the GLD/inventory rests at 849.32 tonnes

jan 25/no changes in gold inventory at the GLD/inventory rests at 849.32 tonnes

Jan 24/A HUGE DEPOSIT OF 2.65 TONNES OF GOLD INTO GLD/INVENTORY RESTS AT 849.32 TONNES

Jan 23/NO CHANGE IN GOLD INVENTORY DESPITE GOLD’S RISE/INVENTORY RESTS AT 846.67 TONNES

Jan 22/a huge deposit of 5.71 tonnes of gold despite a drop in price/inventory rests at 846.67 tonnes. In 3 trading days, the GLD has added 17.71 tonnes/the bankers are now in trouble!!

Jan 19/no change in gold inventory at the GLD/Inventory rests at 840.76 tonnes

Jan 18/SHOCKINGLY A HUGE DEPOSIT OF 11.80 TONNES WITH GOLD DOWN ALMOST $12.00/INVENTORY RESTS AT 840.76

Jan 17/no changes in gold inventory at the GLD/inventory rests at 828.96 tonnes

Jan 16/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 828.96 TONNES

Jan 12/no changes in inventory at the GLD despite the rise in gold price/inventory rests at 828.96 tonnes

Jan 11/ANOTHER IDENTICAL WITHDRAWAL OF 2.95 TONNES FROM THE GLD INVENTORY/INVENTORY RESTS AT 828.96 TONNES

Jan 10/with gold up today, a strange withdrawal of 2.95 tonnes/inventory rests at 831.91 tonnes

Jan 9/no changes in gold inventory at the GLD/Inventory rests at 834.88 tonnes

Jan 8/with gold falling by a tiny $1.40 and this being after 12 consecutive gains, today they announce another 1.44 tonnes of gold withdrawal from the GLD/

Jan 5/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 836.32 TONNES

Jan 4/2018/no change in gold inventory at the GLD/Inventory rests at 836.32 tonnes

Jan 3/a huge withdrawal of 1.18 tonnes of gold from the GLD/Inventory rests at 836.32 tonnes

Jan 2/2018/no changes in gold inventory at the GLD/inventory rests at 837.50 tonnes

Dec 29/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 837.50 TONNES

Dec 28/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 837.50 TONNES

Dec 27/NO CHANGES IN GOLD INVENTORY AT THE GLD/ INVENTORY RESTS AT 837.50 TONNES

Dec 26/no change in gold inventory at the GLD

Dec 22/ A DEPOSIT OF 1.48 TONNES OF GOLD INTO GLD INVENTORY/INVENTORY RESTS AT 837.50 TONNES

Dec 21′ NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 836.02 TONNES

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

Feb 5/2018/ Inventory rests tonight at 841.35 tonnes

*IN LAST 319 TRADING DAYS: 99.80 NET TONNES HAVE BEEN REMOVED FROM THE GLD

*LAST 253 TRADING DAYS: A NET 57.51 TONNES HAVE NOW BEEN ADDED INTO GLD INVENTORY.

end

Now the SLV Inventory

Feb 5/ we had HUGE change in silver inventory at the SLV/ A DEPOSIT OF 1.131 MILLION OZ INTO THE SLV/Inventory rests at 314.045 million oz/

Feb 2/we lost 982,000 oz from the SLV inventory /inventory rests at 312.914 million oz/

Feb 1/no change in silver inventory at the SLV/Inventory rests at 313.896 million oz/

Jan 31/ no change in inventory at the slv in total contrast to gold/inventory rests at 313.896 million oz/

Jan 30/no change in inventory/SLV inventory rests at 313.896 million oz/

Jan 29/no change in inventory/SLV inventory rests at 313.896 million oz/

Jan 26.2018/inventory rests at 313.896 million oz

Jan 25/with silver up today and yesterday, the SLV could only muster a gain of 848,000 oz

Inventory rests at 313.896 oz

jan 24/NO CHANGE IN SILVER INVENTORY DESPITE THE GOOD ADVANCE IN PRICE/INVENTORY RESTS AT 313.048 MILLION OZ/

Jan 23/ANOTHER HUGE WITHDRAWAL OF 1.131 MILLION OZ OF SILVER DESPITE THE TINY LOSS/THE CROOKS ARE USING THE INVENTORY TO RAID ON SILVER.

JAN 22.2018/with silver down by 5 cents/ the crooks at the SLV liquidate 1.321 million oz of silver/inventory rests at 314.179 million oz/

Jan 19/ no changes in silver inventory at the SLV/inventory rests at 315.500 million oz/

jan 18/A WITHDRAWAL OF 848,000 OZ OF SILVER FROM THE SLV/INVENTORY RESTS AT 315.500 MILLION OZ/

Jan 17/no changes in silver inventory at the SLV/inventory rests at 316.348 million oz/

Jan 16/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316.348 MILLION OZ

Jan 12/no changes in silver inventory at the SLV/inventory rests at 316.348 million oz/

Jan 11/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316.348 MILLION OZ/

Jan 10/with silver up again, we had a huge withdrawal of 1.227 million oz from the SLV/inventory rests at 316.348 million oz

Jan 9/a withdrawal of 848,000 oz from the SLV/Inventory rests at 317.575 million oz/

jan 8/no change in silver inventory at the SLV/Inventory rests at 318.423 million oz/

Jan 5/DESPITE NO CHANGE IN SILVER PRICING, WE HAD A HUGE WITHDRAWAL OF 2.026 MILLION OZ/INVENTORY RESTS AT 318.423 MILLION OZ.

Jan 4.2018/a slight withdrawal of 180,000 oz and this would be to pay for fees/inventory rests at 320.449 million oz/

Jan 3/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 320.629 MILLION OZ.

Jan 2/WITH SILVER UP DRAMATICALLY THESE PAST 4 TRADING DAYS, THE FOLLOWING MAKES NO SENSE: WE HAD A WITHDRAWAL OF 2.83 MILLION OZ FROM THE SLV

INVENTORY RESTS AT 320.629 MILLION OZ/

Dec 29/no changes in silver inventory at the SLV/inventory rests at 323.459 million oz/

Dec 28/DESPITE THE RISE IN SILVER AGAIN BY 13 CENTS, WE LOST ANOTHER 1,251,000 OZ OF SILVER FROM THE SILVER.

Dec 27/WITH SILVER UP AGAIN BY 17 CENTS, WE LOST ANOTHER 802,000 OZ OF SILVER INVENTORY/WHAT CROOKS/INVENTORY RESTS AT 324.780 MILLION OZ/

Dec 26/no change in silver inventory at the SLV./Inventory rests at 325.582

Dec 21/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 326.227 MILLION OZ/

.

Feb 5/2017:

Inventory 314.045 million oz

end

6 Month MM GOFO

Indicative gold forward offer rate for a 6 month duration

+ 1.68%

12 Month MM GOFO

+ 2.10%

end

Major gold/silver trading /commentaries for MONDAY

GOLDCORE/BLOG/MARK O’BYRNE.

GOLD/SILVER

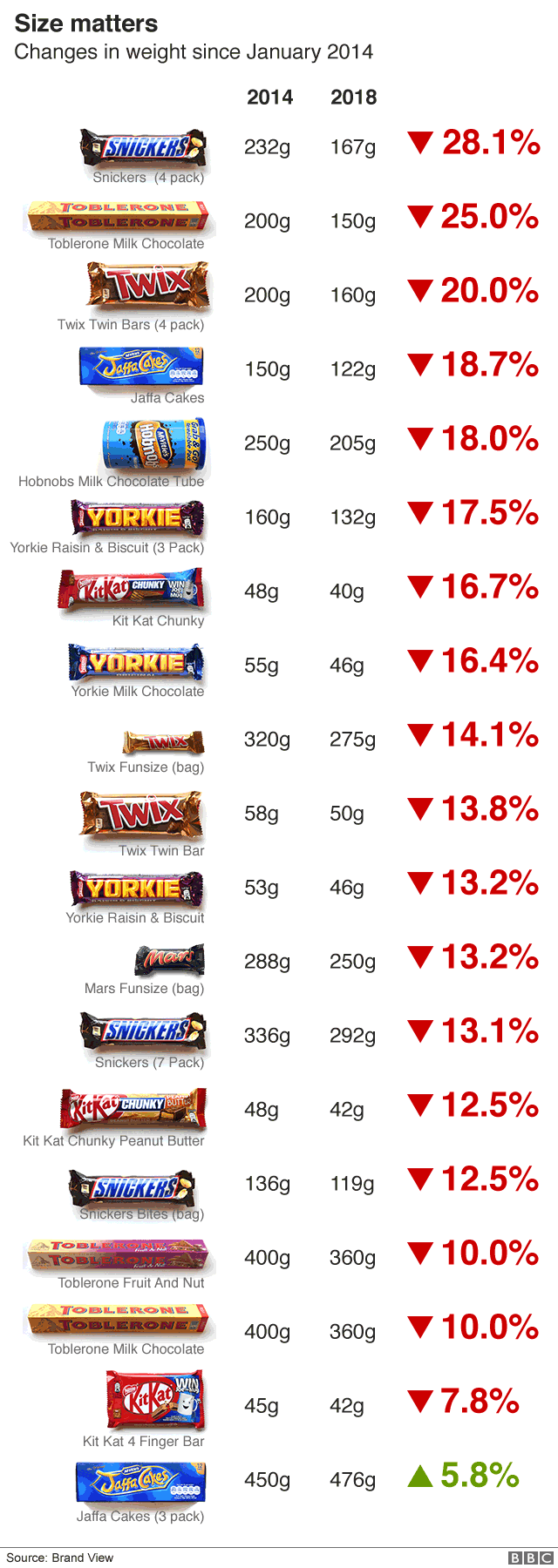

Shrinkflation Intensifies – Stealth Inflation As Thousands of Food Products Shrink In Size, Not Price

– Shrinkflation continues to take hold across UK, Ireland and US for sixth year running

– Shrinkflation sees consumers gets less product, but at the same or increased price

– 2,500 products have shrunk according to Office of National Statistics in UK

– Reported inflation is between 1.7% and 3% but actually much higher

– Shrinkflation is financial fraud, unreported inflation in stealth mode

– Gold is hedging inflation and shrinkflation

Editor: Mark O’Byrne

Two bars of the Toblerone Swiss chocolate. New style 150 gram bar showing the reduction in triangular pieces (front) and older style 360 gram bar at back. Credit: Alastair Grant via The Telegraph

Two bars of the Toblerone Swiss chocolate. New style 150 gram bar showing the reduction in triangular pieces (front) and older style 360 gram bar at back. Credit: Alastair Grant via The Telegraph

Your wallet might still be feeling the pinch after Christmas. Shrinkflation means this is likely to continue. Now in its sixth (official) year the phenomenon that sees you get less product for the same price is beginning to be covered more frequently.

Another example of this came last week when McVitie’s biscuits, some of the most popular digestive biscuits in the UK and Ireland, saw a 20% cut in volume, but not in price.

Officially, inflation is pretty low across the developed world. In the US, it is so low (1.8%) that it is proving to be a cause for concern for policy wonks. It is 1.7% in the EU and in the UK it is at 3%. None of those readings are a true reflection of where prices really are and how much the cost of living has increased.

One of the best measures of inflation is shrinkflation. We’ve written about it before in reference to Toblerones and toilet rolls. This time, its all about the Brits’ and Irish precious McVitie’s Digestive biscuits.

Last month the manufacturer announced they were shrinking the packet a 500g packet of 34 biscuits down to 400g. The price will be 10p less, but this is nowhere near the 20% cut in product amount.

McVitie’s insists the quality is the same. The reduction in biscuits is thanks to rising raw ingredient and manufacturing costs. Rather than increase the price onto customers they have decided to maintain quality, but with fewer biscuits.

When the UK’s rate of inflation fell from 3.1% to 3% last month, many economists and financial commentators were quick to point out that this was evidence that the era of low inflation had not yet come to an end.

The problem is inflation measures as published by central banks and campaigned upon by governments, do not give markets a real portrayal of how much living really does cost.

Shrinkflation is a real indicator of inflation

Just a simple glance at a packet of biscuits gives you more information than any RPI or CPI reading can. For example, in the case of the digestive biscuits, under the RRP of £1.25 for the 500g packet, each biscuit cost roughly 0.037 pence. Now, the price is under the RRP of £1.15 for the 400g packet, which means each biscuit costs roughly 0.043 pence.

McVitie’s is just one in a long line (2,500 to be exact) of food and other household items that have fallen victim to the invisible inflation ray that has so far eluded the sights of so many economists.

In the last four years Snickers, Toblerone and KitKat have each shrunk by at least 20% in size, not always accompanied by a matching price change. A bag of Snickers Bites rocketed from 74p per 100g to £1.26, up 70.9 per cent, whilst a four-finger KitKat bar lost just 3g in weight, dropping from 45g to 42g, a difference of 7.8 per cent, yet 100g of the snack soared by 62.7 per cent, from 89p to £1.45.

The two main culprits of rising prices, according to the manufacturers is the cost of raw materials and the weak pound, which makes imports more expensive. Obviously the pound has gained in strength recently and the European import price of sugar has been falling since the middle of 2014, and reached a record low in March 2017, but consumers shouldn’t expect these to make much difference.

Source: BBC

A lack of innovation?

Food manufactures do not want to be seen bowing down to rising costs and passing them onto consumers. It’s obviously bad for business as most food items have straight forward substitutes to which consumers have few qualms when it comes to switching to. Yet there is also a growing view amongst the consumers that ‘rich’ manufacturers should not pass on rising costs to the poor consumer. It is bad PR basically.

But the manufacturer does still have to run a profitable business. Hence why shrinkflation is such a common phenomenon. They have been accused of lacking innovative ideas by Clive Black, head of research at Shore Capital.

Speaking at the Food Manufacturer’s Business Forum Black told leaders shrinkflation should be the last resort. He asked whether shrinkflation is “an admittance of a lack of innovation, a lack of capability to add value to a product and keep it relevant in consumers’ minds?”

It seems to me that manufacturers are perhaps showing little innovation but more likely they have little choice. Margins are being squeezed, uncertainty is rife when it comes to which manufacturers the Brexit deal will leave you able to work with and costs are rising despite statistics telling you otherwise.

The BBC has recently tried to argue that a decrease in product size sometimes means sees a bigger fall in price. However when looking at their analysis it is clear to see that products which did not increase in price were mainly those in ‘bulk buy’ or large pack products. This just shows that economies of scale makes margins less stringent.

This is perhaps the only place where ‘innovation’ can currently be seen.

Ultimately a smaller pack size does mean a higher price.

How to protect yourself from the rising of living

This is a bit like the Emperor’s New Clothes scenario. We can all see inflation is happening in front of our very eyes, yet economists and central banks are telling us the opposite.

Shrinkflation is happening and real inflation is much higher than is being reported.

Your purchasing power and your wealth can be preserved from the ravages of shrinkflation. Investments such as gold and silver by their very nature are immune to the shrinkflation effect and are an important hedge against it.

Gold prices in GBP (10 Years) via GoldCore

Next time you’re considering that packet of biscuits at the supermarket checkout, just imagine how much is missing compared to when you would have bought it say 10 years ago, or anytime before the financial crisis.

Then consider how much a bar of gold would have changed since then. The fact is that it hasn’t. You would still have the same sized gold bars (1 oz), with the same gold content or purity and they are worth a lot more now than they were 10, 15 or 20 years ago.

Related reading

This Is Why Shrinkflation Is Impacting Your Financial Wellbeing

Shrinkflation in UK & Ireland – Real Inflation Much Higher Than Reported

Gold Hedges Devaluation, Rise in Oil, Food and Cost of Living Since 1971 – Must See Charts

News and Commentary

PRECIOUS-Gold rises on declining equities amid rate hike views (Reuters.com)

Gold edges up on global cues, jewellers’ buying (AsianAge.com)

Stocks Extend Selloff as Dollar Drops; Gold Rises: Markets Wrap (Bloomberg.com)

Yellen Says Prices `High’ for Stocks, Commercial Real Estate (Bloomberg.com)

Source: Bloomberg

Crypto Isn’t Like Gold During a Stock Rout (Bloomberg.com)

Stockmarkets have finally noticed the widening cracks in the bond market (MoneyWeek.com)

History says we’re nearing the end of the U.S. bull market (StansBerryChurcHouse.com)

Gold-Backed Cryptocurrencies: Icing On An Already Tasty Cake (GoldSeek.com)

Forget bitcoin and give unloved gold a chance (Independent.ie)

Gold Prices (LBMA AM)

05 Feb: USD 1,337.10, GBP 947.20 & EUR 1,072.49 per ounce

02 Feb: USD 1,345.00, GBP 946.48 & EUR 1,077.61 per ounce

01 Feb: USD 1,341.10, GBP 941.99 & EUR 1,077.98 per ounce

31 Jan: USD 1,343.35, GBP 950.29 & EUR 1,078.98 per ounce

30 Jan: USD 1,345.70, GBP 954.37 & EUR 1,083.56 per ounce

29 Jan: USD 1,348.40, GBP 955.07 & EUR 1,085.46 per ounce

Silver Prices (LBMA)

05 Feb: USD 16.88, GBP 12.01 & EUR 13.56 per ounce

02 Feb: USD 17.14, GBP 12.05 & EUR 13.72 per ounce

01 Feb: USD 17.19, GBP 12.09 & EUR 13.82 per ounce

31 Jan: USD 17.23, GBP 12.17 & EUR 13.84 per ounce

30 Jan: USD 17.30, GBP 12.24 & EUR 13.91 per ounce

29 Jan: USD 17.34, GBP 12.33 & EUR 13.99 per ounce

Recent Market Updates

– U.S. Debt Is “Extraordinarily High” and Are Stock And Bond Bubbles – Greenspan

– Gold Bullion Price Suppression To End? Bullion Bank Traders Arrested For Manipulating Market

– ATMs Hit By Malware “Jackpotting” Attacks That Dispense All Cash In Minutes

– London Property Market Tumbles As Glut of Luxury Apartments Grows To 3,000

– Silver Bullion: Once and Future Money

– Greatest Stock Bubble In History? GoldNomics Podcast Transcript

– Davos – My Personal Experience of the $100,000 Event, $60 Burgers, Massive Inequality and the Blockchain Revolution

– Is This The Greatest Stock Market Bubble In History? Goldnomics Podcast

– Cyber War Coming In 2018?

– Government Shutdown Ends – Markets Ignore Looming Debt and Bond Market Threat

– Global Pension Ponzi – Carillion Collapse One Of Many To Come

– The Next Great Bull Market in Gold Has Begun – Rickards

– Gold Bullion May Have Room to Run As Chinese New Year Looms

end

Gold expert Robert Lambourne reports that BIS gold derivatives fell by quite a bit in December but the sight swaps still remain relatively high. This is the major source of gold used by the bankers to whack gold

(courtesy Robert Lambourne/GATA)

Robert Lambourne: BIS gold derivatives fall in December but remain hefty

Submitted by cpowell on Sat, 2018-02-03 21:27. Section: Documentation

The bank still fails to explain its activity in the gold market.

* * *

By Robert Lambourne

Disclosures in the December 2017 statement of account published by the Bank for International Settlements —

https://www.bis.org/banking/balsheet/statofacc171231.pdf

— indicate that during December the bank reduced substantially its use of gold swaps and other gold-related derivatives. The information provided in the BIS monthly statement of account is not sufficient to calculate a precise amount of gold-related derivatives, including swaps, but it appears that the total exposure as of December 31, 2017, was around 450 tonnes of gold. This compares to estimates of 570 tonnes and 600 tonnes respectively at the October and November month ends and an audited swaps figure of 438 tonnes as of March 31, 2017.

Despite the substantial reduction made in December, the BIS is still party to a substantial volume of gold swaps and the amount held is still higher than any of the year-end gold swap levels quoted in the eight-year table below. It is evident that the BIS remains an active participant in the gold swaps market with seemingly high volumes of trade taking place regularly.

When it comes to its activities in the gold market, the BIS is like a duck seeming to glide smoothly over the surface of the water, but underneath the surface it is paddling furiously to reach its destination. The bank’s lack of transparency fuels the suspicion that all this underwater activity is not being properly explained.

The use of gold swaps reported by the BIS in recent years is summarized here:

— March 2010: 346 tonnes.

— March 2011: 409 tonnes.

— March 2012: 355 tonnes.

— March 2013: 404 tonnes.

— March 2014: 236 tonnes.

— March 2015: 47 tonnes.

— March 2016: 0 tonnes.

— March 2017: 438 tonnes.

As this table shows, the use of gold swaps by the BIS fell considerably from 2013 to zero in March 2016. In the financial year ending in March 2017 a new year-end peak of 438 tonnes was reported.

In addition, while 2017 saw record use of gold derivatives by the BIS, this has been happening when the bank’s traditional gold banking business has been in decline with far less gold being deposited by central banks in BIS-controlled gold sight accounts.

In March 2010 gold swaps represented just 20 percent of the gold that the BIS had placed in gold sight accounts with central banks. By March 2017 59 percent of the gold the BIS had placed in gold sight accounts with central banks had come from gold swaps and other gold derivatives.

From the BIS statement of account for October 2017 it appears that gold swaps and other gold-related derivatives accounted for 66 percent of the gold the BIS had placed in gold sight accounts at central banks.

Hence gold derivatives have become the dominant source of gold used in the BIS banking business. The BIS itself has elected not to highlight or explain this change.

Indeed, the BIS has offered no explanation for its renewed use of gold swaps since March 2016. By contrast, back in 2010 the BIS discussed its gold swaps with the Financial Times in an article published July 29 that year. BIS General Manager Jaime Caruana said the gold swaps were “regular commercial activities” for the bank:

http://www.ft.com/cms/s/0/3e659ed0-9b39-11df-baaf-00144feab49a.html

Here are excerpts from the article:

“Some analysts speculated that the swap deals were a surreptitious bailout of the European banking system ahead of last week’s publication of stress tests. But bankers and officials have described the transactions as ‘mutually beneficial.’ …

“‘The client approached us with the idea of buying some gold with the option to sell it back,’ said one European banker, referring to the BIS.

“Another banker said: ‘From time to time central banks or the BIS want to optimize the return on their currency holdings.'”

None of these comments in the FT article focused on the gold market itself but implicitly accepted that gold was being used as collateral to support dollar loans to commercial banks.

An alternative explanation — that the swap transactions were initiated by the BIS to place more unallocated gold in the hands of certain central banks — seemed plausible, since the gold market was tight at the time.

Perhaps not coincidentally, the BIS has renewed its use of gold swaps since March 2016 just when many commentators consider gold market conditions to be tightening again, as they were in 2010 and 2011.

—–

Robert Lambourne is a retired business executive in the United Kingdom who consults with GATA about the involvement of the Bank for International Settlements in the gold market.

end

This should hurt the price of Bitcoin: USA banks are set to ban to use of credit cards to purchase bitcoin

(courtesy zerohedge)

Bitcoin ban expands across credit cards as big U.S. banks recoil

Submitted by cpowell on Sat, 2018-02-03 22:03. Section: Daily Dispatches

By Jennifer Surane and Laura J. Keller

Bloomberg News

Friday, February 2, 2018

A growing number of big U.S. credit-card issuers are deciding they don’t want to finance a falling knife.

JPMorgan Chase & Co., Bank of America Corp., and Citigroup Inc. said they’re halting purchases of bitcoin and other cryptocurrencies on their credit cards. JPMorgan, enacting the ban today, doesn’t want the credit risk associated with the transactions, company spokeswoman Mary Jane Rogers said.

Bank of America started declining credit card transactions with known crypto exchanges on Friday. The policy applies to all personal and business credit cards, according to a memo. It doesn’t affect debit cards, said company spokeswoman Betty Riess.

And late Friday Citigroup said it too will halt purchases of cryptocurrencies on its credit cards. “We will continue to review our policy as this market evolves,” company spokeswoman Jennifer Bombardier said. …

… For the remainder of the report:

https://www.bloomberg.com/news/articles/2018-02-02/bofa-to-decline-all-c…

end

Sudan devalues its pound to 28.85 to 31.5 pounds per dollar

(courtesy Reuters/gata)

Sudanese pound is on the way to becoming an ounce

Submitted by cpowell on Sun, 2018-02-04 21:40. Section: Daily Dispatches

Sudan Central Bank Weakens Bank Trading Exchange Rate to 31.5 Pounds to Dollar

From Reuters

Sunday, February 4, 2018

KHARTOUM, Sudan — Sudan’s central bank said today it had decided to weaken the exchange rate at which banks can trade their scarce supply of dollars to an upper limit of 31.5 Sudanese pounds per U.S. dollar.

The Sudanese pound has plummeted to record lows on the black market this year after it was devalued to 18 per dollar from 6.7 following a call by the International Monetary Fund to let the currency float freely.

That band will weaken to 28.8-31.5 pounds per dollar, effective Monday, Central Bank Governor Hazem Abdelqader told Reuters. The black market exchange rate on Sunday was 38 pounds per dollar, according to traders. …

… For the remainder of the report:

https://www.reuters.com/article/us-sudan-economy-exclusive/exclusive-sud..

end

Eric Sprott in his latest remarks states that the jobs number on Friday were really not very good. He also states that the fines against the bullion banks for market rigging vindicates GATA who for years have stated that the bullion banks have been rigging the precious metals markets.

(courtesy Eric Sprott/GATA)

Fines against bullion banks for market rigging vindicate GATA, Sprott says

Submitted by cpowell on Mon, 2018-02-05 01:46. Section: Daily Dispatches

8:47p ET Sunday, February 4, 2018

Dear Friend of GATA and Gold:

Reviewing last week’s market action in an interview with Craig Hemke for Sprott Money News, mining entrepreneur Eric Sprott remarks that the details of Friday’s U.S. jobs report were actually not very good. Sprott adds that the U.S. Commodity Futures Trading Commission’s fining last week of three European bullion banks for gold and silver market manipulation since 2008 vindicates GATA and others who have complained about such manipulation.

The interview with Sprott is 16 minutes long and can be heard here:

https://soundcloud.com/sprottmoney/sprott-money-news-weekly-wrap-up-2218

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

Bitcoin tumbles to below $8,000.00 as China launches another new crypto crackdown

(courtesy zerohedge)

Bitcoin Tumbles Below $8,000 As China Launches New Crypto-Crackdown

After surging to $20,000 less than three weeks ago, Bitcoin tumbled below $8,000 again overnight following a report from Chinese media that China will block all websites related to cryptocurrency trading and initial coin offerings (ICOs) – including foreign platforms – in a bid to finally quash the market completely, according to Sina.

On February 4, 2018, according to the Financial Times newspaper run by the People’s Bank of China, a series of regulatory measures will be taken against ICO and virtual currency transactions at home and abroad, including banning the existence of relevant businesses and banning and disposing of domestic and foreign virtual currency exchange websites. –Sina (translated)

As SCMP adds, quoting an article published on Sunday night by Financial News, a publication affiliated to the People’s Bank of China (PBOC), “To prevent financial risks, China will step up measures to remove any onshore or offshore platforms related to virtual currency trading or ICOs.”

Meanwhile, reports are rolling in that crypto-related content are being actively blocked by Chinese search engines.

The rest of the major cryptocurrencies are taking hits as well:

The cryptoheatmap is, in a word, red.

In September of last year, Bitcoin plunged around 20% after seven Chinese ministries banned ICOs and shuttered local Bitcoin exchanges in their “Notice on Preventing the Financing Risk of Token Issuance.”

Fast forward to today, when China appears to have unleashed its latest crackdown on cryptos. In the Financial News article, it acknowledged that recent attempts to stamp out digital currencies by shutting down domestic exchanges had failed to completely eradicate trading.

“ICOs and virtual currency trading did not completely withdraw from China following the official ban … after the closure of the domestic virtual currency exchanges, many people turned to overseas platforms to continue participating in virtual currency transactions.

Chinese authorities pointed to Bitcoin’s ability to facilitate “illegal fund-raising and other types of illegal financial activities,” pointing to “pyramid schemes, fraud and other issues.”

In response, some of those business have simply sidestepped the September regulations by relocating their business off of mainland China to Hong Kong. Sunday’s announcement is designed to mitigate that by banning domestic and foreign “virtual currency exchange websites” from web searches.

“Overseas transactions and regulatory evasion have resumed … risks are still there, fuelled by illegal issuance, and even fraud and pyramid selling,” the article said.

China’s official Xinhua news agency quoted the PBOC on Monday afternoon as saying it would tighten regulations on domestic investors’ participation in overseas transactions of ICOs and virtual currencies, as risks are still high in the sector.

To that end, Chinese search engines Baidu and microblog Weibo have begun blocking crypto-conent.

the South China Morning Post news site reported that when the terms, in Chinese, bitcoin, cryptocurrency, and ICO were searched on Chinese search-engine Baidu and microblog Weibo, no obvious paid sponsored content came up alongside the expected organic results.

While Baidu had stopped advertising cryptocurrency-related searches back in August 2016, it is unclear when they started allowing them again, and they have not confirmed any new crypto-based advertising block. Weibo has confirmed that they have banned cryptocurrency-related advertising. –Cointelegraph.com

“It is common for people to use VPNs [virtual private networks] to trade cryptocurrencies, as many exchange platforms relocated to Japan or Singapore,” said Donald Zhao, an individual bitcoin trader who relocated to Tokyo from Beijing late last year, following the ban.

“I think the new move literally means it would be even harder to circumvent the ban in China … people promoting related business programmes may be arrested,” Zhao said.

The tighter regulation from the PBOC will “definitely weigh on the cryptocurrency universe,” said Wayne Cao, who runs a company that recently offered 10 billion tokens in an ICO. “Most of the Chinese ICO projects are invested in by Chinese investors. So if they are blocked, the whole cryptocurrency market will be dragged down.”

* * *

As we reported on Friday, NYU economist Nouriel “Dr. Doom” Roubini, after taking a very, very long sabbatical from the media scene – told Bloomberg TV that Bitcoin is “the biggest bubble in human history” and that this “mother of all bubbles” is finally crashing.

Given that the skyrocketing price of Bitcoin and other cryptocurrencies has driven the price of video cards (used to mine cryptocurrency) through the roof – robbing eager PC gamers of their cutting edge rigs, it will be interesting to see if a protracted drop in the price of Bitcoin and other cryptocurrencies will result in a flood of cheap GPUs hitting the market. Shares of AMD and Nvidia – the primary manufacturers of cards used for crypto mining, should also be interesting to watch.

end

Late this afternoon, with the only thing entity up was gold/silver, suddenly cryptos rose mimicking the proper behaviour of what gold/silver should have done if they were not manipulated:

(courtesy zerohedge)

Cryptos Are Suddenly Soaring

Just as the S&P plummeted into the abyss, tumbling to a low of 24,022 or over 1,500 points…

… cryptos found a bid, and after plunging all day in what until this afternoon was one of the worst days for bitcoin and the crypto space in history, cryptos suddenly blasted off and soared at precisely 3pm just as stocks were crashing, in the process undoing much of today’s staggering losses.

The move prompted some to ask if the new “great rotation” is out of crashing equities and into post-crash cryptos?

The good news: the 3pm is still here. The bad news, if only for stocks, is that it now appears to target cryptocurrencies.

end

Basically most of Swiss exports land into China and India

(courtesy Lawrie Williams/Lawrie on Gold)

Swiss Gold Exports in 2017 – Down but far from out

February 3, 2018lawrieongold

Another of my articles published on the Sharps Pixley website looks at total gold exports from Switzerland last year – the lowest level for 11 years, but still substantial at 1,600 tonnes. As has been apparent throughout the year over 80% of the gold routed through Switzerland has been headed for relatively strong hands in Asia and the Middle East, and taken together with gold production in Asia in particular – mostly China, but also in countries like Indonesia which is a significant producer in its own right (No. 9 in the world in 2016) [see:World Top 20 Gold: Countries, Companies and Mines]– these areas probably account for the accumulation of more than 80% of all the world’s newly mined gold. China in particular absorbs goldlike a sponge and doesn’t release it back into the global market place.

With Asian populations growing, gold demand will continue to rise there given the propensity for the citizenry to own gold, while peak newly mined gold is almost certainly already with us we are going to see supplies squeezed in the years ahead with a consequent positive effect on the price regardless of the powers that be trying to suppress it. Switzerland’s re-refining and expoirt business thus remains an excellent pointer to current and future gold flows.

The Sharps Pixley article follows:

SWISS GOLD EXPORTS IN 2017 LOWER BUT STILL 80% PLUS FLOWING EAST

The continued accumulation of physical gold in Asia and the Middle East goes on regardless as shown by gold exports from Switzerland – the leading national conduit for gold bullion. Switzerland has achieved this position through its refineries specialising in taking gold in unmarketable forms and importing dore bullion from mines and refining, or re-refining it into the sizes and purities in demand in the eastern market place. This is combined with the great reputation of Switzerland in the gold marketplace and as a conduit for such activities.

Although Swiss gold exports in 2017 were the lowest in 11 years they were still substantial at over 1,600 tonnes. That is equivalent to half the world’s annual new mined gold output, and with China the world’s largest gold miner already, and a known non-exporter, the Asian and Middle Eastern regions will have accumulated at least 65% of global gold output adding up the imports from Switzerland plus Chinese domestic production alone. But other countries also export gold directly to Asian and Middle Eastern refineries and we would guesstimate that perhaps 80% of all the gold bullion moving around the world may be ending up in these regions – a huge proportion of what remains the world’s No.1 monetary asset (in our opinion at least). With bitcoin continuing to crash – it has lost almost 60% of its value from its peak in December and could well crash much further as scared investors offload on the way down – gold may be again coming into its own as a key investment asset class in the minds of investors seeking to preserve their wealth.

In December, Swiss gold exports followed the pattern established over the year with India the no. 1 individual destination with 32.3 tonnes – or around 21.5% of the total – closely followed by China (25.7 tonnes) and Hong Kong (21.1 tonnes). Assuming that most, if not all, the Hong Kong exports are also bound for the Chinese mainland, greater China was thus the biggest recipient of the Swiss gold. Overall around 86% of Switzerland’s December gold exports (totalling 150.4 tonnes) was destined for Asian and Middle Eastern nations.

If we look at the full year 20i7 figures for Swiss gold exports – neatly laid out in the bar chart below from Nick laird’s http://www.goldchartsrus service – we see that these proportions pretty well mimic the full annual picture:

This chart shows that over the full year around 81.6% of the Swiss gold was headed for Asia and the Middle East with India the biggest individual national importer with 26.2%, but with China and Hong Kong combined taking 35.8%.

The other point which is apparent from the Swiss gold export figures is something we have stressed continually over the past year – that Hong Kong gold exports to mainland China can no longer be seen as a proxy for Chinese gold imports – or even a rough guide. Mainstream media, and some analysts who should know better, still seem to equate the regularly published Hong Kong gold export figures as such, but as the Swiss figures show the greater part of mainland China’s gold imports now comes in direct – avoiding Hong Kong altogether. This percentage of direct imports appears to be growing.

The figures also show that there has been a major recovery in Indian gold imports last year after a very low 2016 figure, but still Greater China remains comfortably the biggest importer – and if you add China’s own gold production of perhaps 450 tonnes last year into the mix, as well as direct imports from a number of other countries, China remains easily the world’s No. 1 accumulator of gold – although the breakdown of where this gold actually goes internally is rather less certain – hence the seeming anomalies in the nation’s estimated consumption figures from the big precious metals consultancies like Metals Focus and GFMS.

https://lawrieongold.com/2018/02/03/swiss-gold-exports- in-2017-down-but-far-from-out/

-END-

The following is a huge story. China produces around 445 tonnes per year, so it needs to import to satisfy its citizens. In all of 2017, total conduction in China hit almost 1090 tonnes.

China tops gold consumption table for fifth consecutive year

by Weida Li Feb 05, 2018 08:43 INVESTMENT MARKETS

The consumption of gold in China hit 1089.07 tonnes in 2017 – the highest in the world for the fifth consecutive year. China News Service

China is among 25 countries where capital punishment is still not only written in the criminal code, but also regularly enforced.

The consumption of gold in China hit 1089.1 tonnes in 2017, making the country the world’s largest gold consumer for the fifth consecutive year, according to statistics released by the China Gold Association (CGA) on February 1.

China consumed 696.5 tonnes of gold jewellery and 276.39 tonnes of bullion last year – an increase of 10.35 and 7.28 percent respectively compared to 2016. However, the 26 tonnes of gold coin procured marks a decrease of 16.64 percent, reports Chinese news outlet Xinhua.

The main reasons behind the increase in gold investment are the recovery of high-end consumption in 2017, especially in second- and third-tier cities, and the fluctuations experienced in the real estate and securities markets, said the CGA.

China’s total domestic gold production stood at 426.14 tonnes in 2017, down 6.35 percent year on year, which represents the first fall since 2000.

Despite production being the highest in the world for the 11th straight year, the implementation of environmental and resource taxes, plus the closure of gold mines in nature reserves, has played a key part in this decline.

https://gbtimes.com/china-tops-gold-consumption-table- for-fifth-consecutive-year

–END-

Your early MONDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED DOWN AT 6.2915 /shanghai bourse CLOSED UP AT 25.41 POINTS 0.73% / HANG SANG CLOSED DOWN 356.56 POINTS OR 1.09%

2. Nikkei closed DOWN 592.45 POINTS OR 2.55% /USA: YEN RISES TO 109.81

3. Europe stocks OPENED RED /USA dollar index RISES TO 89.81/Euro FALLS TO 1.2443

3b Japan 10 year bond yield: FALLS TO . +.084/ (CENTRAL BANK INTERVENTION THIS MORNING) GOVERNMENT INTERVENTION !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 109.88/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD FINALLY IN THE POSITIVE/BANK OF JAPAN LOSING CONTROL OF THEIR YIELD CURVE AS THEY PURCHASE ALL BONDS TO GET TO ZERO RATE!!

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 64.89 and Brent: 67.64

3f Gold UP/Yen UP

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil DOWN for WTI and DOWN FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund FALLS TO +.728%/Italian 10 yr bond yield UP to 2.017% /SPAIN 10 YR BOND YIELD UP TO 1.452%

3j Greek 10 year bond yield RISES TO : 3.722?????????????????

3k Gold at $1335.40 silver at:16.81: 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble DOWN 16/100 in roubles/dollar) 56.70

3m oil into the 64 dollar handle for WTI and 67 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 109.81 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 0.9322 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1598 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now POSITIVE territory with the 10 year FALLING to +0.728%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.8356% early this morning (THIS IS DEADLY TO ALL MARKETS). Thirty year rate at 3.0970% /

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

(courtesy Jim Reid/Bloomberg/Deutsche bank/zero hedge)

Global Market Rout Resumes: Asian Bloodbath Spills Over Into Europe, US Sharply Lower

Global markets were routed for the second day in a row on Monday, with Asian and European indexes opening lower and bond yields rising as resurgent U.S. inflation raised the possibility central banks would tighten policy more aggressively than had been expected.

Asian stocks suffered broad losses, with the MSCI Asia-Pacific index ex-Japan plunging as much as 2%, its largest daily drop since late 2016, while S&P futures extended Friday’s decline; the Nikkei dropped 2.6% while Hang Seng plunged as much as 2.7% before rebounding. The selling fed through into Europe, however without heavy continuing momentum.

Meanwhile, U.S. equity futures are above initial lows printed straight from Globex electronic re-open, helped in part by reports that China’s regulator would act to “mitigate” the equity selloff, which helped Chinese indices to rally into close, and close green.

Friday’s payrolls report showed wages growing at their fastest pace in more than eight years, fuelling expectations for both inflation and interest rates would rise more than previously forecast. That sparked a global sell-off that continued on Monday. Futures markets priced in the risk of three, or even more, rate rises by the Federal Reserve this year.

“This added fuel to a bond market sell-off, pushing US 10 year Treasury bond yields closer to the magic 3 percent level, which will only increase borrowing costs for corporates following years of cheap financing, thus ushering equities further from recent highs,” said Mike van Dulken, head of research at Accendo Markets.

As a result, all eyes remain on the 10Y US Treasury for indication if last week’s rout would continue, and while treasuries remain under pressure, with the yield briefly touching 2.885%, the selloff appears to have since moderated. Elsewhere, Aussie bonds were sharply lower aided by soft 15-year auction, while the 10Y JGB was trading comfortably below the BOJ’s 0.11% redline, at 0.084%. German 10-year yields rose to 0.774%, their highest since September 2015. German 30-year yields rose to two-year highs at 1.429%.

The Bloomberg Dollar Index was little changed, modestly lower from the Friday close; yen marginally firmer. The Norwegian crown, a key commodity currency, was one of the biggest losers in Europe on Monday, down 0.3 percent against the U.S. dollar. In emerging markets, the South African rand fell 0.7 percent and the Chinese yuan and Polish zloty 0.2 percent.

The yen gained against all its major peers as shares slumped across Asia following a rout in U.S. equities and Treasuries on Friday. Japan’s currency gained for the first time in four days against the dollar as the Nikkei 225 Stock Average headed for its biggest slide since November 2016.

““Higher U.S. yields are weighing on risk assets, exerting upward pressure on the yen from risk aversion,” said Minori Uchida, Tokyo head of global market research at Bank of Tokyo- Mitsubishi UFJ Ltd.

“Nikkei’s big drop is behind the yen’s strength today,” says Masakazu Satou, currency adviser in Tokyo at Gaitame Online, retail FX brokerage. “While U.S. stocks are likely undergoing a temporary adjustment, today’s performance is important. If U.S. stocks fall further significantly, they will likely enter a full-blown correction phase.”

In China, the PBOC weakened the daily CNY fixing and drained a net 40b yuan of liquidity after the 8th consecutive day of no open market reverse-repo operations; Shanghai Composite pares early losses after Caixin services PMI beats estimates and following reports of possible regulatory intervention to prop up stocks. Dalian iron 1.2% stronger.

Europe’s benchmark Stoxx 600 index fell 0.9%, its sixth consecutive day of losses totaling 4.1%, the biggest decline since Brexit and the longest rout since November; more importantly, the Stoxx 600 dipped below its 200-DMA for first time since early December and is now at two-month lows. As a reminder, European stocks suffered their biggest weekly selloff since November 2016 last week amid rising bond yields. The Stoxx 600 is now down 1.3% in 2018.

All major indexes in Europe fell: the UK’s FTSE 100 dropped 1 percent, France’s CAC 40 0.8 percent and Germany’s DAX 0.6 percent. In terms of sector specifics, losses have been relatively broad-based thus far with all ten sectors in the red. Airline names have been suffering this morning with RyanAir (-3%) softer in the wake of a disappointing earnings update, subsequently dragging easyJet (-2.3%) lower. Deutsche Lufthansa (-1.6%) were seen lower at the open amid reports that German coalition negotiators could drop proposal to abolish air transport tax. Elsewhere, markets will be looking out for any follow up to Friday’s reports that US regulators are seeking major fines for Fiat Chrysler as part of its motor settlement.

As we reported on Friday night, the Federal Reserve sanctioned Wells Frago after the fake accounts scandal. Wells Fargo said it could reduce profits by as much as USD 400mln this year, and the stock was down over 9% in the premarket.

Meanwhile, according to Bloomberg, investors are watching closely for clues on the direction of the rout that started in U.S. Treasuries and spread across global markets last week, with some pointing to synchronized economic growth as a reason to remain optimistic. European Central Bank President Mario Draghi could help stem further losses when he delivers an annual report to the European Parliament on Monday.

In the commodities complex, WTI and Brent crude futures pared earlier losses after hitting a one-month low in early European trade. Friday’s rig count saw oil drillers add rigs for the second consecutive week, a sign that US oil production could soon exceed 10mln bpd. The Iranian Oil Minister Zanganeh stated that OPEC’s step to push up oil prices is short-lived and that any country that builds oil output capacity will ultimately win, while he also suggested to wait until the June meeting for a decision regarding an extension of cuts. In metals markets, spot gold trades higher, benefiting from its safe-haven status, albeit gains are relatively modest thus far with reports suggesting that Indian gold imports fell to a 17-month low in Jan. Elsewhere, Chinese steel futures were seen lower in quiet trading conditions while nickel prices in London have recovered from recent losses.

In other news, UK PM May will face a coup that would install Boris Johnson, Jacob Rees-Mogg and Michael Gove if she persists with plans to keep Britain in a customs union with the European Union, Tory MPs warned according to the Sunday Times. Downing Street has since ruled out joining a customs union with the EU, while EU and UK said to seek quick Brexit agreement on defence and security.

The Bank of England is expected to raise interest rates twice this year after a surprisingly strong showing from the economy at the end of last year and a brightening outlook in 2018, leading economists say.

Germany’s CDU, CSU, and SPD want to present a coalition agreement by Tuesday.

Reports stated that Italian election polls could be downplaying possibility that centre-right coalition backed by Berlusconi could be closer to a majority victory at election next month.

Outgoing Fed Chair Yellen stated that asset valuations are generally elevated but added that she doesn’t want to call it a bubble.

Economic data include Markit PMIs. Bristol-Myers Squibb, Sysco, Skyworks are among companies reporting earnings.

Bulletin Headline Summary from RanSquawk

- European equities join the global sell-off as markets reassess their Fed outlook for 2018

- UK PM May rules out staying in the Customs Union post-Brexit amid reports that she faces a coup from pro-

- Brexit MPs

- Looking ahead, highlights today include: US Markit Services PMI, ISM Non-Manufacturing and ECB’s Draghi

- speaks

Top Overnight News from BBG:

- Chancellor Angela Merkel and party leaders of SPD, CSU want to present a final grand coalition agreement on Tuesday, Rheinische Post reports, citing an internal SPD planning paper

- U.K. Prime Minister Theresa May has ruled out staying in the EU’s customs union after Brexit, a government official said, adding it isn’t government policy to stay in “a” customs union either

- Tory MPs earlier said May would face a coup to install three pro-Brexit leaders if she continues with plans to keep Britain in a customs union with the EU

- Investors have ramped up bets that the follow- up to BOE’s November’s tightening — the first in a decade — will come as soon as May

- Maintaining QE and 2% inflation target are still important, BOJ Governor Haruhiko Kuroda says in Japan’s parliament on Monday; PM Abe says that while Japan hasn’t escaped from deflation yet, momentum toward 2% inflation is still maintained

- China composite PMI rose to 53.7 in January, up from 53 in December and to the highest reading since January 2011

- ellen: Wages are beginning to rise at a faster pace; asset values are high but would not say they are too high; a drop in asset values would not unduly damage core financial system

- Fed’s Williams: no need to change path of gradual hikes; not too bothered by inflation overshooting target for a time

- European Jan. Service PMIs: Spain 56.9 vs 55.0 est; Italy 57.7 vs 55.9 est; France 59.2 vs 59.3 est; Germany 57.3 vs 57.0 est; Eurozone 58.0 vs 57.6 est; Markit note first concurrent rise in selling prices across survey nations since July 2008

- U.K. Jan. Services PMI: 53.0 vs 54.1 est; slowest upturn in services output for 16 months

- German Coalition: parties want to present final grand coalition agreement on Tuesday: Rheinische Post

- China regulator (CSRC) is urging domestic brokerages to ask investors to add to their collateral when share prices drop instead of closing out the positions according to people familiar

Market Snapshot

- S&P 500 futures down 0.1% at 2,752.90

- STOXX Europe 600 down 0.9% to 384.54

- MSCI Asia Pacific down 1.4% to 179.82

- MSCI Asia Pacific ex Japan down 1.3% to 590.34

- Nikkei down 2.6% to 22,682.08

- Topix down 2.2% to 1,823.74

- Hang Seng Index down 1.1% to 32,245.22

- Shanghai Composite up 0.7% to 3,487.50

- Sensex down 1.1% to 34,692.40

- Australia S&P/ASX 200 down 1.6% to 6,026.23

- Kospi down 1.3% to 2,491.75

- German 10Y yield fell 2.9 bps to 0.738%

- Euro up 0.09% to $1.2474

- Brent Futures down 0.6% to $68.16/bbl

- Italian 10Y yield rose 8.4 bps to 1.781%

- Spanish 10Y yield fell 3.9 bps to 1.433%

- Brent Futures down 0.5% to $68.25/bbl

- Gold spot up 0.2% to $1,335.43

- U.S. Dollar Index down 0.2% to 89.06