GOLD: $1318,20 DOWN $ 2,35 (COMEX TO COMEX CLOSINGS)

Silver: $16.62 DOWN 10 CENTS (COMEX TO COMEX CLOSINGS)

Closing access prices:

Gold $1313.50

silver: $16.52

For comex gold:

MAY/

NUMBER OF NOTICES FILED TODAY FOR MAY CONTRACT:3 NOTICE(S) FOR 300 OZ.

TOTAL NOTICES SO FAR 621 FOR 62100 OZ (1.9315 tonnes)

For silver:

MAY

72 NOTICE(S) FILED TODAY FOR

360,000 OZ/

Total number of notices filed so far this month: 5909 for 29,545,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: BID $8361/OFFER $8461: DOWN $17(morning)

Bitcoin: BID/ $8777/offer $8877: UP $398 (CLOSING/5 PM)

end

First Shanghai gold fix comes at 10 pm est

The second Shanghai gold fix: 2:15 pm

First Shanghai gold fix gold: 10 pm est: 1327.92

NY price at the same time: 1320.25

PREMIUM TO NY SPOT: $7,67

ss

Second gold fix early this morning: 1328.02

USA gold at the exact same time: 1321.00

PREMIUM TO NY SPOT: $7.02

AGAIN, SHANGHAI REJECTS NEW YORK PRICING.

WE WILL NOT PROVIDE LONDON FIXES AS THEY ARE NOT ACCURATE AS TO WHAT IS GOING ON AT THE SAME TIME FRAME.

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total OPEN INTEREST FELL BY A TINY 347 CONTRACTS FROM 198,275 FALLING TO 197,928 WITH FRIDAY’S 2 CENT LOSS IN SILVER PRICING. WE ARE NOW WITNESSING OUR USUAL AND CUSTOMARY COMEX LONG LIQUIDATION AS WE ENTERED INTO THE ACTIVE DELIVERY MONTH OF MAY AS LONGS PACK THEIR BAGS AND MIGRATE OVER TO LONDON. WE WERE NOTIFIED THAT WE HAD A STRONG SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP : 2799 EFP’S FOR JULY AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE OF 2799 CONTRACTS. WITH THE TRANSFER OF 2799 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 2799 EFP CONTRACTS TRANSLATES INTO 16.31 MILLION OZ ACCOMPANYING:

1.THE TINY 2 CENT FALL IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES STANDING FOR MAY COMEX DELIVERY. (30.04 MILLION OZ)

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF APRIL: (FINAL)

18,995 CONTRACTS (FOR 10 TRADING DAYS TOTAL 18,995 CONTRACTS) OR 94.975 MILLION OZ: AVERAGE PER DAY: 1900 CONTRACTS OR 9.500 MILLION OZ/DAY

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH: 94.975 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 13.567% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)

ACCUMULATION IN YEAR 2018 TO DATE SILVER EFP’S: 1,240.3 MILLION OZ.

ACCUMULATION FOR JAN 2018: 236.879 MILLION OZ

ACCUMULATION FOR FEB 2018: 244.95 MILLION OZ

ACCUMULATION FOR MARCH 2018: 236.67 MILLION OZ

ACCUMULATION FOR APRIL 2018: 385.75 MILLION OZ

RESULT: WE HAD A TINY SIZED DECREASE IN COMEX OI SILVER COMEX OF 347 WITH THE 2 CENT LOSS IN SILVER PRICE. WE HAVE NOW ENTERED THE NEW ACTIVE MONTH OF MAY. THE CME NOTIFIED US THAT IN FACT WE HAD AN STRONG SIZED EFP ISSUANCE OF 2799 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) . FROM THE CME DATA: 2799 EFP CONTRACTS FOR JULY, AND ZERO FOR ALL OVER MONTHS FOR A DELIVERABLE FORWARD CONTRACT OVER IN LONDON WITH A FIAT BONUS (TOTAL: 2799). TODAY WE GAINED 2452 TOTAL OI CONTRACTS ON THE TWO EXCHANGES: i.e. 2799 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH AN DECREASE OF 347 OI COMEX CONTRACTS. AND ALL OF THIS HAPPENED WITH THE FALL IN PRICE OF SILVER OF 2 CENTS AND A CLOSING PRICE OF $16.71 WITH RESPECT TO YESTERDAY’S TRADING. YET WE STILL HAVE A STRONG AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY IN THIS ACTIVE MAY DELIVERY MONTH. IT SURE SEEMS THAT WE MUST HAVE HAD SOME BANKER SHORT COVERING ON BOTH EXCHANGES.

In ounces AT THE COMEX, the OI is still represented by UNDER 1 BILLION oz i.e. .990 MILLION OZ TO BE EXACT or 142% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT MAY MONTH/ THEY FILED AT THE COMEX: 72 NOTICE(S) FOR 360,000 OZ OF SILVER

IN SILVER, WE HAVE NOW SET THE NEW RECORD OF OPEN INTEREST AT 243,411 AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $16.51 ON APRIL 9.2018.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH: 27 MILLION OZ , APRIL: 2.485 MILLION OZ AND MAY: 30.04 MILLION OZ )

- HUGE RECORD OPEN INTEREST IN SILVER 243,411 CONTRACTS (OR 1.217 BILLION OZ/ SET APRIL 9/2018

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017

- RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ (FINAL)

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT). IT ALSO LOOKS LIKE BANKER CAPITULATION IN SILVER AS THEY STRUGGLE TO REMOVE SOME OF THEIR HUGE OBLIGATIONS.

In gold, the open interest FELL BY A CONSIDERABLE 4138 CONTRACTS DOWN TO 502,178 WITH THE LOSS IN THE GOLD PRICE/FRIDAY’S TRADING (LOSS OF $1.75). WE ARE NOW IN THE NON ACTIVE DELIVERY MONTH OF MAY. THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A SMALL SIZED 2819 CONTRACTS : JUNE SAW THE ISSUANCE OF 2819 CONTRACTS , MAY SAW THE ISSUANCE OF 0 CONTRACTS AND AUGUST SAW THE ISSUANCE OF: 0 CONTRACTS WITH ALL OTHER MONTHS ZERO. The new OI for the gold complex rests at 502,732. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE A SMALL SIZED OI LOSS IN TOTAL CONTRACTS ON THE TWO EXCHANGES: 4138 OI CONTRACTS DECREASED AT THE COMEX AND AN SMALL SIZED 2819 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON.THUS TOTAL OI LOSS: 1319 CONTRACTS OR 131,900 OZ = 4.10 TONNES. AND ALL OF THIS OCCURRED WITH A LOSS OF $1.75

FRIDAY, WE HAD 8945 EFP’S ISSUED.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF MAY : 88,950 CONTRACTS OR 8,895,000 OZ OR 276.67 TONNES (10 TRADING DAYS AND THUS AVERAGING: 8,895 EFP CONTRACTS PER TRADING DAY OR 889,500 OZ/ TRADING DAY),,

TO GIVE YOU AN IDEA AS TO THE HUGE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 10 TRADING DAYS IN TONNES: 276.67 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2017, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 2555 TONNES

THUS EFP TRANSFERS REPRESENTS 276.67/2550 x 100% TONNES = 10.84% OF GLOBAL ANNUAL PRODUCTION SO FAR IN APRIL ALONE.*** THE ACCUMULATION OF EFP CONTRACTS IS RISING PER MONTH.

ACCUMULATION OF GOLD EFP’S YEAR 2018 TO DATE: 3,034.61* TONNES *SURPASSED ANNUAL PROD’N

ACCUMULATION OF GOLD EFP’S FOR JANUARY 2018: 653.22 TONNES

ACCUMULATION OF GOLD EFP’S FOR FEBRUARY 2018: 649.45 TONNES

ACCUMULATION OF GOLD EFP’S FOR MARCH 2018: 741.89 TONNES (22 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR APRIL 2018: 713.84 TONNES (21 TRADING DAYS)

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A CONSIDERABLE SIZED DECREASE IN OI AT THE COMEX OF 4138 WITH THE $1.75 FALL IN PRICE // GOLD TRADING FRIDAY ($1.75 LOSS). WE ALSO HAD A SMALL SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 2819 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 2819 EFP CONTRACTS ISSUED, WE HAD A SMALL SIZED NET LOSS OF 1319 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

2819 CONTRACTS MOVE TO LONDON AND 4138 CONTRACTS DECREASED AT THE COMEX. (in tonnes, the LOSS in total oi equates to 4.10 TONNES). ..AND ALL OF THESE OCCURRED AT THE COMEX WITH A LOSS OF $1.75 IN TRADING.

we had: 3 notice(s) filed upon for 300 oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD…

WITH GOLD DOWN $2.35 /TWO HUGE CHANGES IN GOLD INVENTORY AT THE GLD/a) A DEPOSIT OF 4.68 TONNES (ARRIVED LAST FRIDAY NIGHT)

b) a withdrawal of 1.48 tonnes: net transaction: a gain of 3.2 tonnes

Inventory rests tonight: 866.17 tonnes.

SLV/

WITH SILVER DOWN 10 CENTS A SMALL CHANGES IN THE SILVER INVENTORY AT THE SLV INVENTORY/ A WITHDRAWAL OF 848,000 OZ FROM THE SLV

/INVENTORY RESTS AT 319.591 MILLION OZ/

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER FELL BY A TINY SIZED 347 CONTRACTS from 198,275 UP TO 197,928 (AND, FURTHER FROM THE NEW COMEX RECORD SET /APRIL 9/2017 AT 243,411/SILVER PRICE AT THAT DAY: $16.53). THE PREVIOUS RECORD OTHER THAN WAS ESTABLISHED AT: 234,787, SET ON APRIL 21.2017 OVER ONE YEAR AGO. THE PRICE OF SILVER ON THAT DAY: $17.89. OUR CUSTOMARY MIGRATION OF COMEX LONGS MORPH INTO LONDON FORWARDS CONTINUES AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE: 0 EFP CONTRACTS FOR APRIL, 0 EFP CONTRACTS FOR MAY (WE DO NOT GET A LOOK AT THESE CONTRACTS AS IT IS PRIVATE BUT THE CFTC DOES AUDIT THEM), AND 2799 EFP’S FOR JULY AND ALL OTHER MONTHS ZERO. TOTAL EFP ISSUANCE: 2799 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI LOSS AT THE COMEX OF 347 CONTRACTS TO THE 2799 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A GAIN OF 2452 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES: 12.26 MILLION OZ!!! AND THIS OCCURRED WITH A 2 CENT LOSS IN PRICE . THE BANKERS ORCHESTRATED THEIR RAID THROUGHOUT LAST WEEK DESPERATELY TRYING TO PARE THEIR GIGANTIC OPEN INTEREST SHORT ON BOTH EXCHANGES BUT TO NO AVAIL. JUDGING BY THE RECORD NUMBER OF EFP ISSUANCE DURING LAST MONTH OF APRIL AT 385.75 MILLION OZ AND THE TOTAL OI GAIN ON THE TWO EXCHANGES, I DO NOT THINK THAT OUR BANKERS HAVE BEEN TOO SUCCESSFUL. THE CONSTANT RAIDS ARE NOW BEING CALLED UPON BY OUR BANKER FRIENDS ARE DONE IN AN ATTEMPT TO SHAKE AS MANY SILVER LEAVES FROM THE SILVER TREE AS POSSIBLE.

RESULT: A TINY SIZED DECREASE IN SILVER OI AT THE COMEX WITH THE 2 CENT FALL IN SILVER PRICING FRIDAY. BUT WE ALSO HAD ANOTHER STRONG SIZED 2799 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR APRIL, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)MONDAY MORNING/SUNDAY NIGHT: Shanghai closed UP 10.77 points or 0 .34% /Hang Sang CLOSED UP 419,02 points or 1.35% / The Nikkei closed UP 107.18 POINTS OR 0.47% /Australia’s all ordinaires CLOSED UP .30% /Chinese yuan (ONSHORE) closed DOWN at 6.3379/Oil DOWN to 70.77 dollars per barrel for WTI and 77.34 for Brent. Stocks in Europe OPENED RED. ONSHORE YUAN CLOSED UP AT 6.3379 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.3303/ONSHORE YUAN TRADING WEAKER AGAINST OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW LOOKS LIKE A FULL TRADE WAR IS BEGINNING/

/NORTH KOREA/SOUTH KOREA

i)North Korea/South Korea/USA

b) REPORT ON JAPAN

3 c CHINA

Is this why Trump folded on Chinese telecom ZTE?

( zerohedge)

4. EUROPEAN AFFAIRS

ITALY

i)Saturday: The Italian coalition takes shape and the platform includes a parallel currency something that the EU will certainly frown upon

( Mish Shedlock/Mishtalk)

ii)An extremely important commentary from Tom Luongo re the merger or the two Euroskeptic parties to form a government. In essence, Luongo correctly states that the two parties will pinpoint immigration immediately and not target leaving the euro immediately. The new government’s new platform consists of a flat tax of 15% which will surely win over the populace. The new government intends on introducing a parallel currency which will help stimulate their moribund economy. In short order, Italy’s deficit will increase dramatically, setting the stage for the government to eventually leave the Euro

( Tom Luongo)

iii)The 5 tar and League have now reached a deal clearing way for the first European” anti establishment government”. The key question: Who will buy Italian bonds once the ECB stops its QE. The ECB is the only buyer of Italian bonds!!

( zerohedge)

iv)ECB

The ECB has been constant with their rhetoric that QE will end by September. How on earth investors are spooked on is beyond me

( zerohedge)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

ii)ISRAEL

Sunday: Israeli Air Force strikes the Gaza strip as more than 20 missiles have been fired

( zerohedge)

( zerohedge)

iv)ISRAEL/GAZA STRIP

( zerohedge)

v)IRAN/CHINA

A fallout from the Iran sanctions: China is now set to replace the huge oil company Total with its own sovereign wealth company: CNPC

Beijing also launches a new Iranian train route from Beijing to Tehran

( zerohedge)

6 .GLOBAL ISSUES

7. OIL ISSUES

Even though Europe continues to buy Iranian oil, it is the financing of these purchases through banks that may be thwarted.

( Paraskova/OilPrice.com)

8. EMERGING MARKET

i)ARGENTINA

Sunday

Argentina has been suffering with high inflation as the government cuts off subsidies. Now the higher dollar is creating massive problems for this nation which has massive external debt denominated in dollars

( zero hedge)

Monday

The Argentine government has spent on Friday 1 billion defending its currency at 24 to the dollar. Today, it is offering 5 billion dollars in the peso market at 25 to the dollar and that is 10% of its entire reserves

( zero hedge)

9. PHYSICAL MARKETS

10. USA stories which will influence the price of gold/silver

c)In our Friday commentary we noted that there is an FBI mole who became part of the Trump team. The hunt for him (her) intensifies. We now have information that Brennan Strzok and Kerry set “spy traps” for the Trump team.( zerohedge)

d)Another biggy!!

Steven Calabresi who clerked for Antonin Scalia writes a scathing attack on Mueller in the Wall Street Journal claiming that his appointment was unconstitutional. His reasoning is straight forward.

a must read…

(zerohedge)

e)funny!!

Trading Volumes on the COMEX

PRELIMINARY COMEX VOLUME FOR TODAY: 236,657 contracts

CONFIRMED COMEX VOL. FOR YESTERDAY: 295,690 contracts

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

And now for the wild silver comex results.

Total silver OI FELL BY A TINY SIZED 347 CONTRACTS FROM 198,275 DOWN TO 197,928 (AND CLOSER TO THE NEW RECORD OI FOR SILVER SET APRIL 9.2018/ 243,411 CONTRACTS) WITH THE 2 CENT FALL IN SILVER PRICING ON FRIDAY. SINCE WE ARE NOW INTO THE ACTIVE DELIVERY MONTH OF MAY. WE WERE INFORMED THAT WE HAD A STRONG SIZED 2799 EFP CONTRACT ISSUANCE FOR JULY AND ZERO FOR ALL OTHER MONTHS. THESE EFPS WERE ISSUED TO COMEX LONGS WHO RECEIVED A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. THE TOTAL EFP’S ISSUED: 2799. ON A NET BASIS WE GAINED 2640 SILVER OPEN INTEREST CONTRACTS AS WE OBTAINED A 347 CONTRACT LOSS AT THE COMEX COMBINING WITH THE ADDITION OF 2799 OI CONTRACTS NAVIGATING OVER TO LONDON.

NET GAIN ON THE TWO EXCHANGES: 2452 CONTRACTS

AMOUNT STANDING FOR SILVER AT THE COMEX

We are now in the active delivery month of MAY and here the front month LOST 156 contracts FALLING TO 170 contracts. We had 173 notices filed upon yesterday so we SURPRISINGLY AGAIN GAINED 17 contracts or 85,000 additional ounces will stand for delivery in this active delivery month of May AS SOMEBODY AGAIN WAS DESPERATE FOR PHYSICAL SILVER ON THIS SIDE OF THE POND..

June saw a GAIN of 37 contracts to stand at 784 The next big delivery month for silver is July and here the OI FELL by 1655 contracts DOWN to 139,242. The next active delivery month after July for silver is September and here the OI ROSE by 917 contracts UP to 25,061

We had 72 notice(s) filed for 360,000 OZ for the MAY 2018 contract for silver

INITIAL standings for MAY/GOLD

MAY 14/2018.

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz |

nil OZ

|

| Deposits to the Dealer Inventory in oz | NIL oz |

| Deposits to the Customer Inventory, in oz | nil OZ |

| No of oz served (contracts) today |

3 notice(s)

300 OZ

|

| No of oz to be served (notices) |

101 contracts

(10100 oz)

|

| Total monthly oz gold served (contracts) so far this month |

621 notices

62100 OZ

1.9315 TONNES

|

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

For MAY:

Today, 0 notice(s) were issued from JPMorgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equates to 3 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 3 notice(s) was (were) stopped/ Received) by j.P.Morgan customer account.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

To calculate the INITIAL total number of gold ounces standing for the MAY. contract month, we take the total number of notices filed so far for the month (621) x 100 oz or 62100 oz, to which we add the difference between the open interest for the front month of MAY. (104 contracts) minus the number of notices served upon today (3 x 100 oz per contract) equals 72,200 oz, the number of ounces standing in this active month of APRIL (2.227 tonnes)

Thus the INITIAL standings for gold for the MAY contract month:

No of notices served (621 x 100 oz) + {(104)OI for the front month minus the number of notices served upon today (3 x 100 oz )which equals 72,200 oz standing in this active delivery month of MAY . THERE ARE 9.0356 TONNES OF REGISTERED GOLD AVAILABLE FOR DELIVERY SO FAR.

WE GAINED 300 OZ OF GOLD (3 CONTRACTS) STANDING IN THIS NON ACTIVE DELIVERY MONTH OF MAY AS SOMEBODY BADLY NEEDED PHYSICAL GOLD AT THIS SIDE OF THE POND..

IN THE LAST 18 MONTHS 73 NET TONNES HAS LEFT THE COMEX.

end

And now for silver

AND NOW THE APRIL DELIVERY MONTH

MAY INITIAL standings/SILVER

| Silver | Ounces |

| Withdrawals from Dealers Inventory | nil oz |

| Withdrawals from Customer Inventory |

15,010.580 oz

Delaware

|

| Deposits to the Dealer Inventory |

nil

oz

|

| Deposits to the Customer Inventory |

nil oz

|

| No of oz served today (contracts) |

72

CONTRACT(S)

(360,000 OZ)

|

| No of oz to be served (notices) |

98 contracts

(490,000 oz)

|

| Total monthly oz silver served (contracts) | 5909 contracts

(29,545,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

we had 0 inventory movement at the dealer side of things

i

total dealer deposits: nil oz

we had 0 deposits into the customer account

i) Into JPMorgan: nil oz

*** JPMorgan for most of 2017 and in 2018 has adding to its inventory almost every single day.

JPMorgan now has 140 million oz of total silver inventory or 53.4% of all official comex silver. (140 million/263 million)

JPMorgan did not deposit into its warehouses (official) today.

ii) Into everybody else: 0

total customer deposits today: 0 oz

we had 1 withdrawals from the customer account;

i) out of Delaware:

total withdrawals; 15,010.580 oz

we had 0 adjustments

i

total dealer silver: 69.161 million

total dealer + customer silver: 268,521 million oz

The total number of notices filed today for the MAY. contract month is represented by 72 contract(s) FOR 360,000 oz. To calculate the number of silver ounces that will stand for delivery in MAY., we take the total number of notices filed for the month so far at 5909 x 5,000 oz = 29,545,000 oz to which we add the difference between the open interest for the front month of MAY. (170) and the number of notices served upon today (72 x 5000 oz) equals the number of ounces standing.

.

Thus the INITIAL standings for silver for the MAY contract month: 5909(notices served so far)x 5000 oz + OI for front month of MAY(170) -number of notices served upon today (72)x 5000 oz equals 30,035,000 oz of silver standing for the MAY contract month

WE GAINED 17 CONTRACTS OR AN ADDITIONAL 85,000 OZ WILL STAND AT THE COMEX AS SOMEBODY WAS IN URGENT NEED OF PHYSICAL SILVER ON THIS SIDE OF THE POND.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

ESTIMATED VOLUME FOR TODAY: 63,081 CONTRACTS

CONFIRMED VOLUME FOR YESTERDAY: 91,311 CONTRACTS

YESTERDAY’S CONFIRMED VOLUME OF 91311 CONTRACTS EQUATES TO 456 MILLION OZ OR 65.22% OF ANNUAL GLOBAL PRODUCTION OF SILVER

COMMODITY LAW SUGGESTS THAT OPEN INTEREST SHOULD NOT BE MORE THAN 3% OF ANNUAL GLOBAL PRODUCTION. THE CROOKS ARE SUPPLYING MASSIVE PAPER TRYING TO KEEP SILVER IN CHECK.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price at that day at $18.42

The previous record was 224,540 contracts with the price at that time of $20.44

end

NPV for Sprott

1. Sprott silver fund (PSLV): NAV FALLS TO -1.59% (MAY14/2018)

2. Sprott gold fund (PHYS): premium to NAV FALLS TO -0.42% to NAV (MAY 14/2018 )

Note: Sprott silver trust back into NEGATIVE territory at -1.59%-/Sprott physical gold trust is back into NEGATIVE/ territory at -0.42%/Central fund of Canada’s is still in jail but being rescued by Sprott.

Sprott WINS hostile 3.1 billion bid to take over Central Fund of Canada

(courtesy Sprott/GATA)

3.SPROTT CEF.A FUND (FORMERLY CENTRAL FUND OF CANADA): NAV FALLS TO -2.29%: NAV 13.60/TRADING 13.37//DISCOUNT 2.29.

END

And now the Gold inventory at the GLD/

MAY 14/ WITH GOLD DOWN $2.35: A HUGE DEPOSIT OF 4.68 TONNES OF GOLD INTO THE GLD and then a withdrawal of 1.48 tonnes /INVENTORY RESTS AT 866.17

A net gain of 3.2 tonnes of gold.

MAY 11/WITH GOLD DOWN $1.75/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 862.96 TONNES/

MAY 10/WITH GOLD UP $9.60/A WITHDRAWAL OF 1.17 TONNES FROM THE GLD/INVENTORY RESTS AT 862.96 TONNES/SUCH CROOKS

MAY 9/WITH GOLD DOWN $0.55/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 864.13 TONNES

MAY 8/WITH GOLD DOWN $0.10/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 864.13 TONNES

MAY 7/WITH GOLD DOWN $0.55/ANOTHER WITHDRAWAL OF 1.47 TONNES OF GOLD FROM THE GLD/INVENTORY RESTS AT 864.13 TONNES

MAY 4/WITH GOLD UP $2.05/A WITHDRAWAL OF 1.13 TONNES OF GOLD FROM THE GLD/INVENTORY RESTS AT 865.60 TONNES

MAY 3/WITH GOLD UP $7.05/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 866.77 TONNES

MAY 2/WITH GOLD DOWN $1.15/ A HUGE WITHDRAWAL OF 4.43 TONNES FROM THE GLD/INVENTORY RESTS AT 866.77 TONNES

MAY 1/WITH GOLD DOWN $12.15/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 871.20 TONNES

APRIL 30/WITH GOLD DOWN $4.05/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 871.20 TONNES.

APRIL 27./WITH GOLD UP $5.90/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 871.20 TONNES/

APRIL 26/WITH GOLD DOWN $4.90/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 871.20 TONNES

APRIL 25/AFTER 9 CONSECUTIVE DAYS OF NO MOVEMENT OF GOLD INTO OUT OF THE GLD, WE HAD A HUGE DEPOSIT OF 5.31 TONNES OF GOLD INTO THE GLD/INVENTORY RESTS AT 871.20 TONNES.

APRIL 24./WITH GOLD UP $9.90, WE HAD NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 865.89 TONNES/

APRIL 23.2018/WITH GOLD DOWN $14.00/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 865.89 TONNES.

APRIL 20/WITH GOLD DOWN $10.20: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 865.89 TONNES

APRIL 19/WITH GOLD DOWN $4.25: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 865.89 TONNES/

APRIL 18/WITH GOLD UP $3.65: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 865.89 TONNES

APRIL 17/WITH GOLD DOWN $1.00 NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 865.89 TONNES/

April 16/WITH GOLD UP$2.80/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 865.89 TONNES/

April 13/WITH GOLD UP $6.15, A HUGE DEPOSIT OF 5.90 TONNES INTO THE GLD INVENTORY/INVENTORY RESTS AT 865.89 TONNES

April 12/WITH GOLD DOWN $17.40/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 859.99 TONNES

April 11/WITH GOLD UP $13.85/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 859,99 TONNES

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

MAY 14/2018/ Inventory rests tonight at 866.17 tonnes

*IN LAST 381 TRADING DAYS: 74.84 NET TONNES HAVE BEEN REMOVED FROM THE GLD

*LAST 331 TRADING DAYS: A NET 81.46TONNES HAVE NOW BEEN ADDED INTO GLD INVENTORY.

end

Now the SLV Inventory/

MAY 14/WITH SILVER DOWN 10 CENTS/A SMALL CHANGES IN SILVER INVENTORY AT THE SLV/ A WITHDRAWAL OF 858,000 FROM THE SLV/INVENTORY RESTS AT 319.591 MILLION OZ/

MAY 11/WITH SILVER DOWN 2 CENTS/THE CROOKS WITHDREW A MONSTROUS 2.824 MILLION OZ FROM THE SLV INVENTORY/INVENTORY RESTS AT 320.439 MILLION OZ/

MAY 10/WITH SILVER UP 22 CENTS/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 323.263 MILLION OZ/

MAY 9/WITH SILVER UP 6 CENTS/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 323.263 MILLION OZ/

MAY 8/WITH SILVER DOWN 2 CENTS:NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 323.263 MILLION OZ.

MAY 7/WITH SILVER FLAT: A BIG CHANGE IN SILVER INVENTORY AT THE SLV// A WITHDRAWAL OF 942,000 OZ OF SILVER FROM THE SLV INVENTORY/INVENTORY RESTS AT 323.263 MILLION OZ/

MAY4/WITH SILVER UP 5 CENTS/A BIG CHANGES IN SILVER INVENTORY AT THE SLV/ A DEPOSIT OF 1.224 MILLION OZ/INVENTORY RESTS AT 324.205 MILLION OZ/

MAY 2/WITH SILVER UP 24 CENTS/A HUGE CHANGE IN SILVER INVENTORY AT THE SLV// A DEPOSIT OF 6.082 MILLION OZ INTO THE SLV/INVENTORY RESTS AT 322.981 MILLION OZ/

MAY 1/WITH SILVER DOWN 24 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316.899 MILLION OZ/

APRIL 30/WITH SILVER DOWN 11 CENTS/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316.899 MILLION OZ/

APRIL 27/WITH SILVER DOWN 5 CENTS/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316.899 MILLION OZ/

APRIL 26/WITH SILVER DOWN 2 CENT/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316,899 MILLION OZ/

APRIL 25./WITH SILVER DOWN 18 CENTS/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316.899 MILLION OZ/

APRIL 24./WITH SILVER UP 8 CENTS/SOMETHING SPOOKED OUR CROOKS TO ADD SOME PAPER SILVER: A DEPOSIT OF 1.601 MILLION OZ/INVENTORY RESTS AT 316.899 MILLION OZ/

APRIL 23.2018/WITH SILVER DOWN 50 CENTS, ANOTHER HUGE WITHDRAWAL FROM THE SLV INVENTORY: A WITHDRAWAL OF 1.413 MILLION OZ/INVENTORY RESTS AT 315.298 MILLION OZ.

APRIL 20/WITH SILVER DOWN 11 CENTS: ANOTHER HUGE CHANGE IN SILVER INVENTORY: A WITHDRAWAL OF 1.13 MILLION OZ//SLV RESTS TONIGHT AT 316.711 MILLION OZ/

APRIL 19/WITH SILVER UP 3 CENTS TODAY: WE HAD A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.355 MILLION OZ/ MAKES ABSOLUTELY NO SENSE!!/INVENTORY RESTS AT 317.841 MILLION OZ

APRIL 18/WITH SILVER UP 44 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 320.196 MILLION OZ

APRIL 17/WITH SILVER UP 10 CENTS TODAY/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 320.196 MILLION OZ

April 16/WITH SILVER UP 7 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 320.196 MILLION OZ/

April 13/WITH SILVER UP 17 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 320.196 MILLION OZ.

April 12/WITH SILVER DOWN 27 CENTS/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 320.196 MILLION OZ/

April 11/2018/WITH SILVER UP 16 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 320.196 MILLION OZ/

MAY 14/2018:

Inventory 319.591 million oz

end

6 Month MM GOFO 2.11/ and libor 6 month duration 2.54

Indicative gold forward offer rate for a 6 month duration/calculation:

G0FO+ 2.09%

libor 2.54 FOR 6 MONTHS/

GOLD LENDING RATE: .43%

XXXXXXXX

12 Month MM GOFO

+ 2.77%

LIBOR FOR 12 MONTH DURATION: 2.54

GOFO = LIBOR – GOLD LENDING RATE

GOLD LENDING RATE = +.23

end

Major gold/silver trading /commentaries for MONDAY

GOLDCORE/BLOG/MARK O’BYRNE.

GOLD/SILVER

“Oil price highest in 3 years, gold ready to follow”, by Daniel March

“Oil price highest in 3 years, goldready to follow”, by Daniel March

- U.S. withdraws from Iran nuclear deal

- Oil jumps past $70

- Argentina hikes interest rates to 40%

- S. 10 year disparity

- Western buying returns to gold

Gold and silver both ended slightly up in a week dominated by heightening geopolitical news, weakening inflation data, and emerging market concerns.With gold closing the week at $1,318 (up 0.28%), €1,104 (0.37%), and £973 (0.2%).

In sterling, gold was up strongly on Thursday following the BOE’s decision not to raise rates, and from the weaker than expected industrial production data.

Listen on SoundCloud , Blubrry & iTunes. Watch on YouTube below

On Tuesday the U.S. pulled out a nuclear deal with Iran with oil jumping on the news, pushing past $70 for the first time since November 2014. In other markets, the move was less pronounced, prompting suggestions the move in oil was more over concerns of losing production (at a time of already falling crude inventory), rather than from the geopolitical event itself.

However, with middle east tensions rising by the day, the geopolitical risk remains extremely high. With the main question remaining, will gold soon follow oil’s move higher as investors seek protection in the world’s premium safe haven asset?

Economic data this week came in worse than expected, with inflation readings of 0.1% vs consensus of 0.2%. The market was initially unmoved following the PPI release on Tuesday, but once CPI confirmed the prospect of weakening inflationary pressures on Thursday, both gold and silver reacted along with the rest of the commodities sector, including platinum, palladium and copper, all ending the day notably higher.

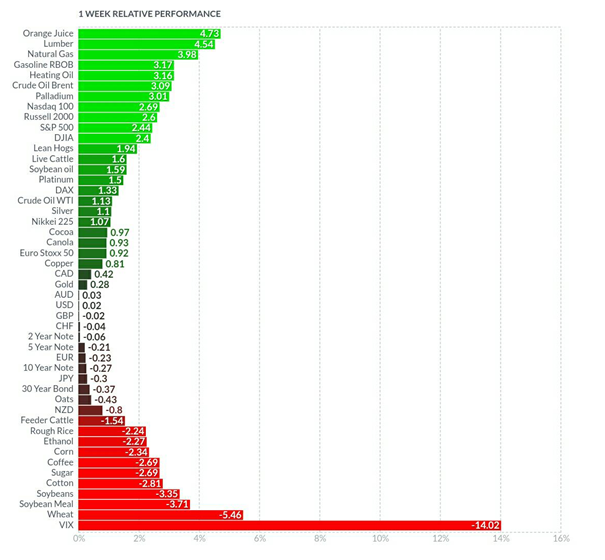

Stocks were one of the best performing assets this week, with U.S. indices up between 2-3%, with investors in the short-term moving back into risk assets. The U.S. dollar ended the week flat (up 0.02%), giving back early weak gains from the miss in inflation, and talk of ‘profit taking’. Yields, like the dollar, started the week strong but ended the week down 0.27%. Full weekly performance, courtesy of Finviz.com. (https://finviz.com/futures_performance.ashx?v=12)

Emerging markets continued to deteriorate this week, with Argentina and Turkey notably effected. Argentina has recently hiked interest rates to 40% in an attempt to stabilise a free falling peso,and is currently seeking assistance from the IMF to avoid outright default.Turkey are taking similar measures, albeit not so aggressive, but still in attempt to fight soaring inflation at 11%

A strong U.S. dollar, and bond yield (when compared to global peers), is the main catalyst behind the deteriorating situation. During the expansionary period, following the 2008 financial crisis, low interest rates and an abundant supply of fresh Central Bank liquidity allowed easy money to flow into the emerging markets.But as U.S. yields went up, so too did the funding costs, making emerging market investments a less attractive prospect, causing capital to flow out of these markets and back into the ‘perceived’ safety of a 3% return in the U.S.

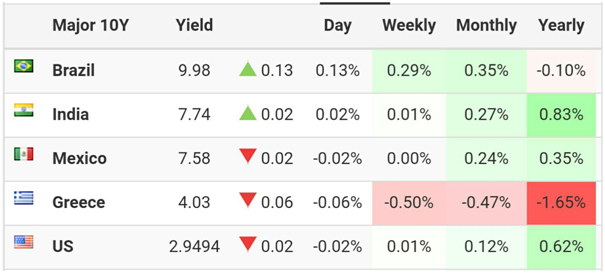

Highlighting the disparity in global yields,only Greece, Mexico, India and Brazil currently pay more than the U.S. to service their 10 year debt – quite a startling statistic for the world’s reserve currency.

https://tradingeconomics.com/bonds

While Fed members have indicated they are staying put on their current ‘dot plot’ rate hike trajectory, at some point they will need to take note of the growing yield disparity.It’s this writer’s view that if the spread continues to widen, and the effects start to begin to spill over into the wider economy, the Fed will be forced to take action and realign to a more accomodative global policy – all of which is a bullish prospect for the precious metals complex.

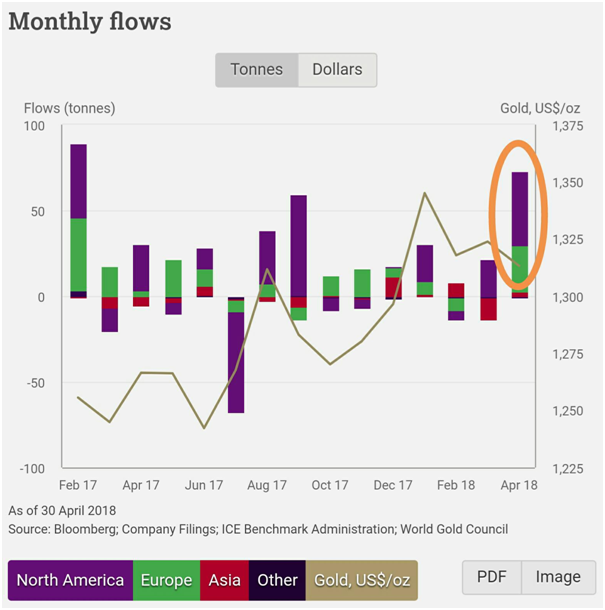

Taking a look at the latest fundamental developments, the WGC have released their ETF inflow/outflow data this week, with the report showing strong growth in April.

“Global gold-backed ETFs holdings added 72.2 tonnes (t) to 2,481t in April. This is the strongest month of net inflows in more than a year. Growth in global holdings was les by significant North American and European inflows and supported by a small increase in Asia” (https://www.gold.org/data/gold-etf-holdings)

While the latest data represents the largest monthly inflow since February 2017, more importantly it shows North American and European buyers coming back into the market. Western demand has long been regarded as the key to higher gold pricing, and while this is first significant inflow from the west this year, should this trend continue it has bullish implications moving forward.

From a technical perspective, we can see gold has found significant support at 200 day moving average ($1307), while building positive momentum that looks poised to breakout to the upside.

Should gold push higher from here, key resistance will be at the $1360/$1370 level, an area gold continues to test. (Charts courtesy of Stockchart.com)

In silver we can see the 200 day moving average ($16.81)acting as resistance. However, just like gold, positive momentum is building.

Key resistance for silver will be at $17.30, and then $17.70, with further resistance at the psychological $18 level. Given the bullish technical picture in both gold and silver, and improving COT positioning, means we a likely building a base here, for a more substantial move higher.

The U.S. is meeting with North Korea this weekend, in an attempt to forge a long standing agreement. With the U.S. withdrawing from the Iran nuclear deal this week, it will interesting to see if this impacts the North Korean’s willingness to enter into such a deal. As always the key will be in the detail

In Europe, Italian bond yields continue to climb on the prospect of an anti-establishment coalition coming to power, with the League and 5-star movement party making significant steps towards forming government. Their final policies are an unknown factor for the markets, but with Italy the 3rd largest economy in Eurozone, investors should take note of the Italian yield, and more importantly yields in the rest of the Eurozone, for signs on how the situation is developing.

On economic data next week, investors should pay close attention to ‘Retail Sales’and the ‘Philadelphia Fed Manufacturing Index’ for further signs of weakness, April ‘CPI’ from Europe for the latest on inflationary pressures, and April ‘Industrial Production’ from China for an update on global growth.

These events, plus developments in the middle east, will help shape the near term direction in the dollar, bonds, stocks, and more importantly the next direction for gold and silver.

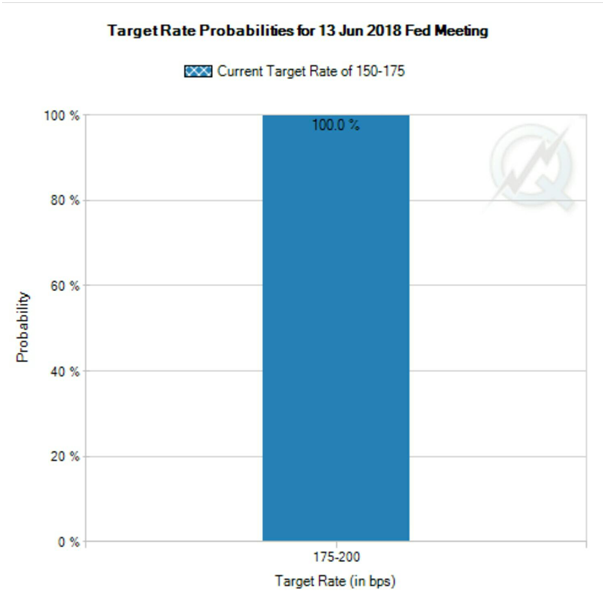

And finally, a quick look to the key FOMC meeting next month, and the latest Fed Futures pricing (a tool from the CME to indicates future rate hike probabilities). Where, as of the 12th May, the market is pricing a 100% chance of a rate hike June

(http://www.cmegroup.com/trading/interest-rates/countdown-to-fomc.html)

Given the market is pricing the event as a certainty means there’s a good chance we could be setting up for disappointment,where gold sells off in the run up the meeting only to rally on the news. A play gold has followed many times on recent rate hike announcements.

All of which means the prospect for the seasonal ‘summer doldrums’ (a seasonal phenomenon discussed last week 5th May) may be short lived, and the buying opportunity in gold may come a lot sooner than many people expect.

News and Commentary

PRECIOUS-Gold eases on firmer dollar; but eyes first weekly gain in four (Reuters.com)

Gold steady as dollar hovers below 2018 peak (Reuters.com)

Bottom in place? Gold jumped to 10-day high (FXStreet.com)

U.K. House-Price Gauge Drops to 5 1/2-Year Low as London Slumps (Bloomberg.com)

London house prices predicted to keep falling (CityAM.com)

Source: US Funds

Gold Love Trade Looks Promising in India and China (USFunds.com)

The Wealthy Are Hoarding $10 Billion of Bitcoin in Bunkers (Bloomberg.com)

Gold Gets a Lifeline From a Surprising Source: Cheap Flights and Cars (Bloomberg.com)

Putin Wants to `Break’ With the Dollar But Dumps Euros Instead (Bloomberg.com)

The 1970s All Over Again? Part 1: The Middle East Explodes (GoldSeek.com)

Central Banks: The Great Experiment Has Failed (DailyReckoning.com)

Listen on SoundCloud , Blubrry & iTunes. Watch on YouTube below

Gold Prices (LBMA AM)

10 May: USD 1,314.80, GBP 969.27 & EUR 1,106.80 per ounce

09 May: USD 1,306.85, GBP 965.11 & EUR 1,102.07 per ounce

08 May: USD 1,310.05, GBP 969.44 & EUR 1,101.88 per ounce

04 May: USD 1,309.35, GBP 965.78 & EUR 1,094.09 per ounce

03 May: USD 1,313.30, GBP 966.19 & EUR 1,094.64 per ounce

02 May: USD 1,310.75, GBP 960.52 & EUR 1,091.99 per ounce

Silver Prices (LBMA)

10 May: USD 16.60, GBP 12.24 & EUR 13.97 per ounce

09 May: USD 16.44, GBP 12.12 & EUR 13.84 per ounce

08 May: USD 16.45, GBP 12.17 & EUR 13.85 per ounce

04 May: USD 16.42, GBP 12.10 & EUR 13.72 per ounce

03 May: USD 16.47, GBP 12.12 & EUR 13.74 per ounce

02 May: USD 16.35, GBP 11.98 & EUR 13.62 per ounce

Recent Market Updates

– Gold Mining Supply Globally Looks Set To Decline

– Gold Bullion Demand In Iran May Surge On Trump Sanctions

– “Money Is Gold — and Nothing Else”

– U.K. Home Prices Plunge 3.1% In April – Largest Monthly Drop Since Financial Crisis In 2011

– Weekly Gold Update – Gold In Dollars Lower Despite Poor US Jobs and Other Data

– Own Some Gold and Avoid Overvalued Assets

– Gold Demand Falls In Q1 Despite Robust Central Bank and Investment Demand and Surging Demand In Turkey and Iran

– Smart Money Diversifying Into Gold – One Billionaire Invests Half His Net Worth

– “Blood In The Streets” Of U.S. Gold Bullion Market As Sale Of Gold Coins Collapse

– Most Important Chart Of The Century For Investors?

– Gold Mining Shares Are Speculative Making Gold Bullion A Better Investment

– Gold Price Increasingly Influenced By Declining Dollar Rather Than Interest Rates

– Cash “Vanishes” From Bank Accounts In Ireland

END

Andrew Maguire’s Kinesis money which is a “bitcoin” but backed 100% by allocated gold and silver is set to go.

it think it would be a great idea to look at this!

please read at: https://kinesis.money/#/

(Andrew Maguire)

|

2:57 PM (1 hour ago) | ||

|

|||

Harvey

Here It is my friend! https://kinesis.money/#/ Please let everyone know.

Let catch up on Monday if you have time. We have billions in the hopper ready to be allocated on the 1st day of trading. The paper market days are over.

Warm regards

Andy

U.S. retreat from trade deals poses new threat to the dollar

Submitted by cpowell on Sun, 2018-05-13 13:49. Section: Daily Dispatches

By Chelsey Dulaney and Joshua Zumbrun

The Wall Street Journal

Sunday, May 13, 2018

Trade friction is emerging as the latest threat to the U.S. dollar’s position at the heart of the global financial system.

For decades, central banks have held the bulk of their foreign-exchange reserves in the dollar, reflecting the dominant role the U.S. and its currency have played in global trade. As the U.S. pulls back from partnerships while countries like Mexico and Japan strike their own trade deals, the dollar’s dominance could be undermined, investors and analysts said. That dominance has been referred to as an “exorbitant privilege,” allowing the U.S. to borrow cheaply and run persistent deficits.

Though a less U.S.-centric trade system would take years to fully evolve, it would have significant implications for global central bankers charged with allocating some $11 trillion in reserves. Many are now ramping up investment in such currencies as the euro and Chinese yuan, reflecting the effects of such moves as the U.S. retreat from the North American Free Trade Agreement and Trans-Pacific Partnership.

While the U.S. and Mexico remain in negotiations over Nafta, which could come to a head in the coming days as House Speaker Paul Ryan has set a Thursday deadline to receive paperwork, Mexico has struck major trade deals in recent months with the European Union and the group of Pacific Rim nations that make up the TPP.

Alejandro Díaz de León, governor of Mexico’s central bank, said that while the U.S. remains Mexico’s most important trade partner, he expects the euro to play a bigger role in the country’s foreign-exchange holdings in coming years as the balance of the nation’s bilateral trade shifts in that direction. …

Jens Nordvig, chief executive of analytics firm Exante Data, estimates global central banks could shift $200 billion to $300 billion in reserves into the yuan, euro and a handful of other foreign currencies this year as a result of trade changes. His estimate is based on central banks’ increased buying of Chinese bonds in the first few months this year.

While he cautions that central bankers tend to adjust reserves slowly, “the flows that potentially come out of this are really big.”

Few are calling for an immediate end to the dollar’s reign as the world’s primary reserve currency.

Central banks held about 63% of their reserves in U.S. dollars at the end of last year, the lowest level in four years, according to data from the International Monetary Fund. Meanwhile, allocations to the euro rose to 20% and reserves held in the Japanese yen rose to 4.9%.

“What’s sure is that over the long term, if trade relations change, it will have an implication on the currency makeup of the reserves,” said Christian Deseglise, global head of central banks for HSBC . “As trade becomes more denominated in euros [and yuan], they’ll need to have currencies to match.” …

… For the remainder of the report:

https://www.wsj.com/articles/u-s-retreat-from-trade-deals-poses-a-new-th…

end

Your early MONDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED DOWN 6.3379 /shanghai bourse CLOSED UP 10.77 POINTS OR 0 .34% / HANG SANG CLOSED UP 419.02 POINTS OR 1.35%

2. Nikkei closed UP 107.18 POINTS OR 0.47% / /USA: YEN FALLS TO 109.51/

3. Europe stocks OPENED RED /USA dollar index FALLS TO 92.33/Euro RISES TO 1.1987

3b Japan 10 year bond yield: RISES TO . +.05/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 109.51/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD FINALLY IN THE POSITIVE/BANK OF JAPAN LOSING CONTROL OF THEIR YIELD CURVE AS THEY PURCHASE ALL BONDS TO GET TO ZERO RATE!!

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 70.77 and Brent: 77.34

3f Gold DOWN/Yen DOWN

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil DOWN for WTI and UP FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund RISES TO +.60%/Italian 10 yr bond yield UP to 1.92% /SPAIN 10 YR BOND YIELD UP TO 1.31%

3j Greek 10 year bond yield FALLS TO : 4.04?????????????????

3k Gold at $1319.40 silver at:16.63 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble UP 28/100 in roubles/dollar) 61.64

3m oil into the 71 dollar handle for WTI and 77 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 109.51 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 0.9980 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1957 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now POSITIVE territory with the 10 year RISING to +0.60%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.98% early this morning (THIS IS DEADLY TO ALL MARKETS). Thirty year rate at 3.11%

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

(courtesy Jim Reid/Bloomberg/Deutsche bank/zero hedge)

S&P Futures Jump After Trump’s ZTE U-Turn As Nervous Traders Eye Italy; EMs Boosted By Weaker Dollar

S&P futures are higher, maintaining overnight gains as most Asian markets advance with the MSCI Asia Pacific index 0.5% higher, as sentiment was boosted by President Trump unexpected reversal on China telecom giant ZTE over the weekend when in a Sunday morning tweet, Trump vowed to get the Chinese telco back to business in a surprising policy U-turn after the company announced a halt to major operating activities following a US 7-year supply ban order.

Europe was broadly, if modestly, in the red as a result of the EUR rising to session highs just shy of 1.20, the highest in over a week, after the ECB’s Villeroy said the first rate hike could come quarters, not years after the end of asset purchases, while political strains in Italy outweighed optimism over waning global trade tensions. Thanks to the weaker dollar, emerging-market stocks built on their first weekly advance in four weeks.

Elsewhere in Asia, Malaysia’s markets showed only short-lived post-election panic, with the ringgit rebounding from 1% drop while stocks in Kuala Lumpur recover opening losses to gain 0.5% as trade returns after a historic election loss by the ruling Razal-led coalition, its first in over 60 years.

Also in Asia, the PBOC conducted a 156BN yuan MLF operation to boost liquidity helping H shares rally 1.5%. And speaking of China, the onshore yuan surged the most in almost three weeks against the trade-weighted basket of currencies, as the central bank boosted its daily reference rate for a second day, pushing up the yuan fixing by 0.28% to 6.3345 per dollar, extending the two-day increase to 0.66%. The Bloomberg replica of the CFETS RMB Index, which tracks the yuan against 24 exchange rates, jumped 0.18%, the most since April 24, to 97.77; According to Bloomberg that was the highest level since China adjusted the basket in Jan. 2017.

Emerging markets currencies were stronger as the Bloomberg dollar index softened marginally, with the euro and pound rising to the top of G-10 scoreboard. The Bloomberg Dollar Spot Index fell 0.2% to hover near Friday’s one-week low. The euro gained 0.4% to touch $1.1990, the strongest in more than a week, while sterling gained as much as 0.4% to $1.3597 after advancing 0.2% on Friday. The Swiss franc climbed 0.1% to $0.9992, staying close to Friday’s one- week high.

Treasuries are weaker, with the firmer with 10-year yield rising from 2.96% at the European open to a session high of 2.985%, while Australian and Japanese government bonds grind sideways. European bonds edge higher after ECB’s Villeroy says the first rate hike could come “some quarters, but not years,” after policy makers end their bond-buying program.

While the EUR strengthened, there was some modest selling for Italian government bonds following late Sunday’s news that the 5-Star and League have reached an agreement on forming the first anti-establishment government, although so far the move remains largely contained and is far less troubling than the capitulation some had expected with Italy faced with a populist coalition.

In a curious rate arb move, Bloomberg reports that the U.K.’s biggest bond-mutual fund is shifting money to the other side of the Atlantic as the interest-rate gap between Europe and the U.S. widens to record levels. M&G Ltd. has boosted U.S. holdings in its 23.4 billion-pound ($32 billion) Optimal Income Fund this year to more than a third. To cushion inflation risks and the impact of rising U.S. rates, it’s gorging on short-term Treasury bills and paring credit risk.

Oil prices are modestly lower, subdued on continued profit taking with WTI crude below the USD 71.00/bbl level, while some reports also noting increased efforts by European nations to salvage the Iranian nuclear deal and will be meeting with Iranian Foreign Minister Zarif tomorrow. Dalian iron ore strengthens for second day. Elsewhere, gold trades flat with marginal gains observed on the back of a subdued USD, while copper (-0.5%) is lower amid reports Japanese miners plan to boost Chilean copper output this year. Aluminium prices eased for a third session as markets continue to correct following the rally last month supported by US sanctions against Rusal. Meanwhile, Chinese iron ore prices extended gains, supported by a firm demand outlook and a decline in the metal’s inventories at ports

In geopolitical updates, Iranian foreign minister Zarif said he had good meetings with China and Russian counterparts, adding they will soon determine how nations can guarantee Iran’s benefit under the nuclear deal. As reported over the weekend, North Korea is planning to take apart its nuclear test site during a ceremony to be held between May 23rd-25th, while there were also comments from US Secretary of State Pompeo that North Korea sanctions will be lifted if the nation proceeds with total denuclearizarion of the Korean peninsula.

In central bank news, Fed’s Mester (Voter, Hawk) said she doesn’t expect inflation to pick up sharply and she supports gradual rise in US interest rates and adds she does not expect to hike rates beyond 3% in the near future.

Earlier, ECB’s Villeroy (Dovish) said the end of net asset purchases is nearing, but whether this is in September of December is not an existential question, adding that communication will be adjusted given current rate guidance is conditioned on the end of net asset purchases, could give additional guidance on timing of rate hike – “well past” seeming some quarters rather than years. He believes underlying inflation is set to strengthen irrespective of short-run fluctuations in energy inflation, sees the current slowdown in inflation as temporary and expects it to resume its progress in the coming months.

Also overnight, Norges bank Governor Olsen reiterates outlook shows it will be the right time to hike key interest rates soon; adding that their latest analyses presented in March 2018 suggest that the key interest rate will likely be raised after summer 2018.

It’s a quiet day, with the only expected data including mortgage delinquencies and foreclosures. Agilent, Invitation Homes, and Vipshop are among companies reporting earnings. ECB Executive Board member Sabine Lautenschlaeger, chief economist Peter Praet, Executive Board member Benoit Coeure speak.

Bulletin Headline Summary from RanSquawk

- The biggest DXY currency components are leading broad gains vs the Dollar

- Italian President Mattarella to hold government formation talks with 5 Star at 16:30 (15:30 BST), with League at 18:00 (17:00 BST)

- Looking ahead, highlights include the OPEC Monthly Report (05:40 CDT/11:40 BST), Fed’s, Bullard, ECB’s Praet, Lautenschlaeger, Coeure

Market Snapshot

- S&P 500 futures up 0.2% to 2,736.25

- STOXX Europe 600 down 0.06% to 392.16

- MSCI Asia Pacific up 0.5% to 176.48

- MSCI Asia Pacific ex Japan up 0.5% to 576.26

- Nikkei up 0.5% to 22,865.86

- Topix up 0.6% to 1,805.92

- Hang Seng Index up 1.4% to 31,541.08

- Shanghai Composite up 0.3% to 3,174.03

- Sensex down 0.1% to 35,488.55

- Australia S&P/ASX 200 up 0.3% to 6,135.30

- Kospi down 0.06% to 2,476.11

- German 10Y yield rose 2.3 bps to 0.582%

- Euro up 0.3% to $1.1974

- Italian 10Y yield fell 6.2 bps to 1.616%

- Spanish 10Y yield rose 3.0 bps to 1.303%

- Brent futures down 0.1% at $77.04/bbl

- Gold spot up 0.1% at $1,320.94

- U.S. Dollar Index down 0.2% to 92.34

Top Overnight News

- In a sign that the U.S. may be open to easing trade tensions ahead of a meeting in Washington with Chinese officials this week, President Trump made a major reversal on an earlier move to block telecom equipment maker ZTE Corp. from its American suppliers

- Chinese regulators have restarted their review of Qualcomm Inc.’s application to acquire NXP Semiconductors NV after having shelved the work earlier in reaction to the growing trade tensions with the U.S., according to people familiar with the matter

- Italy’s populist duo has all but completed a governing plan that includes a flat tax as low as 15%, a guaranteed income for the poor and a lower retirement age as they prepare to seek a green light to form an administration from the president on Monday

- U.K. Prime Minister Theresa May faces a crunch week for her leadership and Brexit plan, with ministers and backbenchers in her Conservative Party feuding over Britain’s future ties to the European Union. May issued a plea for unity in an opinion piece in the Sunday Times newspaper, calling on Brexiters to “trust me to deliver.” “I will not let you down,” she wrote

- One of Trump’s most contentious foreign policy projects, the inauguration of a U.S. embassy in Jerusalem, will be carried out Monday with the president addressing the ceremony via video. His daughter and son-in-law, Ivanka Trump and Jared Kushner, Treasury Secretary Steven Mnuchin, and deputy Secretary of State John Sullivan are among the U.S. delegation

- Fed’s Mester (voter): recent move higher in PCE inflation may not last due to base effects; Fed may eventually need to raise federal funds above its longer-run neutral rate

- ECB’s Villeroy: ECB could give additional guidance on timing of first hike; current “well past” language means at least some quarters, but not years

- German Construction sector agrees wage hike of roughly 6% for over 800,000 workers; strongest wage deal sealed so far this year: Reuters

- U.S. sells three-, six-month bills; St. Louis Fed President James Bullard speaks at a blockchain technology conference

Asian equity markets began the week mostly positive but with trade relatively rangebound following Friday’s mixed performance on Wall St, where stocks saw an indecisive finish to their best week since March. In addition, US equity futures also received a modest uplift after US President Trump provided a lifeline for ZTE over the weekend as he vowed to get the Chinese telco back to business in a surprising policy U-turn after the Co. had announced a halt to major operating activities following a US 7-year supply ban order. ASX 200 (+0.3%) was positive with M&A activity underpinning Healthscope, while Nikkei 225 (+0.5%) was also in the green as

earnings remained in focus with Shiseido among the index leaders on record Q1 sales. Shanghai Comp. (+0.3%) and Hang Seng (+1.4%) conformed to the broad risk appetite as trade concerns eased following the ZTE policy reversal by Trump and as participants also reacted to better than expected lending data. Elsewhere, KLCI (+0.4%) saw an early slump with losses of over 2% on reopen from the surprise election result, but then pared all the weakness as the fears of a new government gradually subsided. Finally, 10yr JGBs were flat amid similar price action in T-notes and with demand sapped amid gains in stocks, while downside was also counterbalanced by the BoJ’s presence in the market for a respectable JPY 1.03tln of JGBs in 1yr-10yr maturities. US President Trump said he instructed the US Commerce Department to assist Chinese telecoms firm ZTE to get back into business which is seen as a U-turn on the firm which was previously placed under a 7-year supply ban by the US.

Top Asian News

- ZTE China Suppliers Jump After Trump Provides Lifeline to Firm

- Nissan Forecast Misses Estimates on Yen, Slower U.S. Demand

- Hong Kong’s Most Popular ETF Is Short the Whole Stock Market

- Sumitomo Mitsui Sees Lower Profit as Negative Rates Persist

European equities are currently trading with no firm directions (Euro Stoxx 50 -0.1%) with the SMI the outperforming bourse (+0.3%) aided by Novartis (+0.8%) and Roche (+1.2%) both receiving positive news from the FDA pertaining to drug expansions. The modestly underperforming bourse is currently the FTSE MIB (-0.5%) with traders mindful of upcoming developments on the Italian Government formation. The automotive sector is being weighed on following the US proposition of 20% tariffs of foreign cars imported to the US. Further effects in European equities from US actions has seen the healthcare sector showing positivity in the wake of the Trump administration releasing a (vague) blueprint for drug pricing; and Ericsson and Nokia down on Trump’s tweet that he will help the penalized ZTE. In stock specifics, strength is being seen for IWG (+21.2%) on the news that the co. has received separate takeover proposals from private equity groups Starwood, Lone Star and TDR Capital, raising prospects of a bidding war.

Top European News

- Norway’s Olsen Says Outlook Indicates Soon Right to Raise Rates

- TPG Is Said to Mull Sale of U.K.’s Poundworld: Sky News

- Germany Seeks Out Russia, Ukraine to Ease Nord Stream 2 Rift

- Nordea Says EUR/SEK Above 10 ‘Is Here to Stay’ Due to Riksbank

- Airbus CFO Wilhelm to Leave in 2019 Along With CEO Enders

In FX, the biggest DXY currency components are leading broad gains vs the Dollar on a combination of supportive fundamentals (relatively hawkish rhetoric from ECB’s Villeroy and further progress towards an Italian coalition Government in the case of the single currency), and a more positive technical landscape after recent sharp declines. It appears that Eur/Usd and Cable have both formed fairly solid bases circa 1.1820 and 1.3460 respectively, and dip-buyers/fresh longs are looking for extended recoveries towards 1.2000 and 1.3600 with stops said to be poised around 1.1980 and 1.3610. Market contacts also note that chart resistance in Eur/Jpy has been breached at 130.86, with bulls eyeing a 50% Fib next (131.86 vs 131.20 top so far). CAD/AUD/CHF: All mildly firmer vs the aforementioned depressed Greenback overall (index still sub-92.500), with the Loonie still benefiting from latest NAFTA reports suggesting a deal could be forthcoming by Thursday and Usd/Cad retesting bids/support ahead of 1.2750. Aud/Usd is maintaining recovery momentum around 0.7550 amidst less against on the global trade front after US President Trump’s volte-face on China’s ZTE, and with cross Aud/Nzd also a prop (over 1.0850 and edging towards the 200 DMA at 108.81). Usd/Chf is holding just below parity, prompting more pledges from the SNB to keep rates negative and active in terms of direct FX intervention to curb Franc demand/appreciation. NZD/JPY: The G10/major laggards and bucking the overall trend with losses vs the Usd, albeit modest, as the Kiwi hovers near 0.6950 and Usd/Jpy rebounds from the low 109.00 area to 109.50.

Top Asian News

- ZTE China Suppliers Jump After Trump Provides Lifeline to Firm

- Nissan Forecast Misses Estimates on Yen, Slower U.S. Demand

- Hong Kong’s Most Popular ETF Is Short the Whole Stock Market

- Sumitomo Mitsui Sees Lower Profit as Negative Rates Persist

In commdities, oil prices are lower, subdued on continued profit taking with WTI crude below the USD 71.00/bbl level, while some reports also noting increased efforts by European nations to salvage the Iranian nuclear deal and will be meeting with Iranian Foreign Minister Zarif tomorrow. Elsewhere, gold trades flat with marginal gains observed on the back of a subdued USD, while copper (-0.5%) is lower amid reports Japanese miners plan to boost Chilean copper output this year. Aluminium prices eased for a third session as markets continue to correct following the rally last month supported by US sanctions against Rusal. Meanwhile, Chinese iron ore prices extended gains, supported by a firm demand outlook and a decline in the metal’s inventories at ports.

US Event Calendar

- May 14-May 18: Mortgage Delinquencies, prior 5.17%

- May 14-May 18: MBA Mortgage Foreclosures, prior 1.19%

- 2:45am: Fed’s Mester Speaks at Bank of France Conference

- 9:40am: Fed’s Bullard Speaks at Crypto Conference in New York

DB’s Jim Reid concludes the overnight wrap

At first glance the week looks a bit less hectic than my weekend with the US retail sales number and the monthly China data dump tomorrow being the data highlights. We do have a busy Fedspeak calendar though and expect a lot of focus on the recent slightly weaker-than-expected inflation numbers. Meanwhile trade talks might come back to the fore with China’s Vice Premier traveling to Washington to continue talks with Treasury Secretary Steven Mnuchin. There’s also a few Brexit meetings to flag and Iran, North Korea and the Oil price will no doubt stay on the radar. The full week ahead preview is at the end today.

We start this morning with Italy, where we seem to be inching closer to a new government. The leaders from the two largest parties are expected to meet the head of state later today and “report back on everything” they had negotiated over the weekend. Earlier, La Repubblica reported that the Leaders of the 5SM (Luigi Di Maio) and League party (Matteo Salvini) have decided that neither should be Premier of the new government, but did not elaborate on a potential candidate.

According to Bloomberg and newspaper Repubblica, measures agreed in a draft government program include: a citizen’s income for the poor, a flat tax at 15% (20% for higher earners), renegotiating EU accords and complying with EU limits on public spending. However, there are no details on how they will fund these proposals but at first glance this seems like a lot of potential spending promises.

Now turning to other headlines over the weekend. On trade, President Trump seemed to partly reverse the sanctions on China’s number 2 telco company (ZTE) as he and China’s President Xi are working together to give ZTE “a way to get back into business, fast”. He added that the “(US) Commerce Department has been instructed to get it done”. In geopolitics, North Korea said it will dismantle its nuclear test sites within two weeks and invited international journalists to watch. On the other side, the US National Security adviser Bolton said “we’re prepared to open the trade and investment with North Korea as soon as we can” while the Secretary of State Pompeo noted that NK will have access to US capital if “complete, verifiable, irreversible denuclearisation” occurs. Then finally on Iran, Security adviser Mr Bolton warned that US sanctions on European companies that continue to maintain business dealings with Iran were “possible”, while Mr Pompeo was hopeful that the US and its allies can strike a new nuclear deal with Iran.

This morning in Asia, markets are broadly higher, with the Hang Seng (+1.28%), Nikkei (+0.40%) and Shanghai Comp. (+0.55%) all up while the Kospi is slightly lower. Elsewhere, the Malaysian ringgit pared back losses to be broadly flat vs. the USD as markets resumed trading following Mahathir’s historic election victory last week. Datawise, Japan’s April PPI eased 0.1ppt mom to an in line print of 2.0% yoy.

Now briefly recapping markets from Friday. The Stoxx 600 edged up +0.11% while the S&P rose +0.17%, supported by the telco sector as Verizon jumped 3.0% after announcing a buyback of its debt securities. In government bonds, core 10y bond yields were slightly higher (UST +0.8bp; Bunds +0.2bp; Gilts +1.2bp) while peripherals outperformed. The yield on 10y Italian BTPs fell -6.3bp, reversing its prior losses on Thursday. In FX, the US dollar index was marginally higher (+0.02%), while the Euro and Sterling rose 0.23% and 0.17% respectively. Lastly, WTI oil fell for the first time in three days (-0.92% to $70.70/bbl) and precious metals softened slightly (Gold -0.17%; Silver -0.31%) while other base metals were little changed.

Now turning to the Fed Bullard’s views on the yield curve. He noted that “…the yield curve inversion is getting close to crunch time” and that we “could be talking about it in September”, although he does not think it’s likely to happen that fast, but it will be an issue next year. On inflation, he said “we’re not in any danger of any breakout in inflation any time over the forecast horizon” and he basically has “no problem with some overshooting of the (2%) target”. On rates, he believes the Fed does not need to raise rates further, in part as rates have reached its neutral setting and “it’s not necessary to change the policy rate to keep inflation at target”.

Ahead of more Brexit talks this week, the UK’s PM May wrote in the Sunday Times newspaper to reiterate her calls for unity over Brexit, she noted that “you can trust me to deliver….the path I’m setting out is the path to deliver the Brexit people voted for”. So lots bubbling along until we get more clarity on the issue.

Before we take a look at this week’s calendar, we wrap up with other data releases from Friday. In the US, the May University of Michigan consumer sentiment index was steady mom and slightly above consensus at 98.8 (vs. 98.3 expected). In the details, the current conditions index edged down 1.6pts mom to 113.3, while the expectations index firmed 1.1pts mom to 89.5. The 1y inflation expectation edged up 0.1ppt mom to 2.8% while the 5-10y inflation expectation was steady mom at 2.5%. Elsewhere, import prices rose 0.3% mom in April while exports grew 0.6% mom. Following the above, the NY Fed’s Nowcast measure of Q2 GDP growth ended the week unchanged at 3.0% saar, while the Atlanta Fed estimate is 4.0% saar. In Europe, the final reading of Spain’s April inflation was unrevised at 1.1% yoy.

On Monday’s Calendar, central bank speak will be the focus of today with the Fed’s Mester and ECB’s Villeroy both speaking in the morning in Paris, followed by the ECB’s Lautenschlaeger, Praet and Coeure later in the day. Brexit developments could also come back to the forefront with the EU’s Barnier due to brief European affairs ministers on the status of talks. Datawise the only release of note is the Bank of France industry sentiment print for April. Senior officials from Euro area finance ministries are also due to meet to discuss the latest Greek bailout review.

3. ASIAN AFFAIRS

i)MONDAY MORNING/SUNDAY NIGHT: Shanghai closed UP 10.77 points or 0 .34% /Hang Sang CLOSED UP 419,02 points or 1.35% / The Nikkei closed UP 107.18 POINTS OR 0.47% /Australia’s all ordinaires CLOSED UP .30% /Chinese yuan (ONSHORE) closed DOWN at 6.3379/Oil DOWN to 70.77 dollars per barrel for WTI and 77.34 for Brent. Stocks in Europe OPENED RED. ONSHORE YUAN CLOSED UP AT 6.3379 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.3303/ONSHORE YUAN TRADING WEAKER AGAINST OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW LOOKS LIKE A FULL TRADE WAR IS BEGINNING/

3 a NORTH KOREA/USA

North Korea/South Korea/usa

END.

3 b JAPAN AFFAIRS

end

c) REPORT ON CHINA/HONG KONG

Is this why Trump folded on Chinese telecom ZTE?

(courtesy zerohedge)

Is This Why Trump Folded: China Holds Up U.S. Pork,

Auto Imports

President Trump surprised pundits and assorted watchers of the ongoing simmering trade war between China and the US on Sunday, when he pledged to help China’s telecom giant ZTE Corp “get back into business, fast” after a U.S. ban crippled the technology company, offering a job-saving concession to Beijing ahead of high-stakes trade talks this week.

Donald J. Trump

✔@realDonaldTrump

President Xi of China, and I, are working together to give massive Chinese phone company, ZTE, a way to get back into business, fast. Too many jobs in China lost. Commerce Department has been instructed to get it done!

What surprised most, however, is that Trump appears to make this concession out of the blue, without any obvious pressure out of China which has been patiently biding its time until the US implements sanctions under Section 301.

Maybe not: according to Reuters, on Monday China’s customs said it had ramped up inspections of U.S. pork and had taken unspecified regulatory steps on high-risk waste imports. In a move that could potentially cripple another group of exporting US farmer, China’s General Administration of Customs said it has increased inspections of U.S. pork imports “after finding problems recently”, according to a fax it sent to Reuters.

Today’s news confirms a report from Reuters which last week, according to which Beijing had stepped up inspections of pork imported from the United States, a move that many saw as a warning by Beijing in response to sweeping U.S. trade demands made on China.

And while China’s customs administration denied that it was targeting the US, saying it had not taken extra steps to check imports of U.S. agricultural products, instead giving equal treatment to inspections of agricultural products from all countries and districts, the U.S. had become the largest exporter of waste that failed checks, the customs said. Surely this was purely a coincidence.

The pork halt was merely the latest quiet escalation in China’s response arsenal: the North American unit of a Chinese customs inspection firm said on May 4 it would suspend checks on cargoes of scrap metal from the United States for a month, effectively halting all imports of U.S. scrap.

Last week, Reuters also reported that imported Ford vehicles are being held up at Chinese ports, underscoring how U.S. goods are facing increased customs scrutiny in China amid a tense trade stand-off.

Three people said Ford cars and those of its premium Lincoln brand were facing unusual delays at customs, with officials asking for extra technical checks. Two of the people said U.S.-made models of some German carmakers, mainly SUVs, being brought into China, were also affected.

Ford was being asked to do extra checks on emission components, said a China-based Ford executive familiar with the matter, asking not be named because of the sensitivity of the issue.

The world’s two largest economies have been dragged into a trade spat in recent months, which has spread to the agricultural sector, fuelling worries that Beijing and Washington may plunge into full-scale trade war.

The United States has proposed tariffs on $50 billion of Chinese goods under its “Section 301” probe. Those could go into effect in June following the completion of a 60-day consultation period, but activation plans have been kept vague. China has said its own retaliatory tariffs on U.S. goods, including soybeans and aircraft, will go into effect if the U.S. duties are imposed.

However, all that may soon be moot if Trump has indeed folded on the crackdown against Chinese telecom such as ZTE, which more than anything is just a signal to Xi that Beijing may have won the war without firing a single shot.

4. EUROPEAN AFFAIRS

Saturday: The Italian coalition takes shape and the platform includes a parallel currency something that the EU will certainly frown upon

(courtesy Mish Shedlock/Mishtalk)

Italian Coalition Takes Shape: Platform Includes Parallel Currency

Authored by Mike Shedlock via MishTalk,

Five Star and Lega want another three days to conclude talks. Neither Di Maio nor Salvini would be Prime Minister.

A reader informed me yesterday that Five Star was pro-Europe and not Eurosceptic.

Compared to what?

Certainly Five Star leader Luigi Di Maio is a far cry from former Five Star leader, Beppe Grillo. But some of that change in positioning was little more than political expediency to win votes.

The platform now in the works includes a parallel currency, reduced immigration, and flat taxes.

Eurointelligence Comments

This is what real coalition negotiations look like. The leaders meet and set the agenda for sub-committees to talk about specific policy issues. That process will start in Italy tomorrow, when the deputy leaders of the two parties come together, but some of the outlines have already been drawn up by the leaders themselves.

What do we know so far? Five Star and Lega are very different political parties, but they have enough in common for a radical legislative agenda. The two sides seem to be inching towards a neutral prime minister, in other words neither Di Maio nor Salvini. The name mentioned by Italian newspapers this morning is that of Giampiero Massolo, a career diplomat who seems to be acceptable to both parties. Massolo will clearly only be the frontman. Power will rest with Di Maio and Salvini.

It will be interesting to see how the two sides will legislate together on issues that might affect Silvio Berlusconi personally. We don’t think he accepted to step aside and let Salvini run the show himself without any clandestine conditions. Any undertaking Salvini might have given him would be difficult for Five Star politically, though.

Corriere della Sera lists the following as the main legislative priorities. If implemented it would be the biggest shake-up of the Italian economic system in modern times.

Platform Provisions

- The end of the pension reforms under Mario Monti; Five Star is softer on this point than Lega, but together the two parties can be expected to agree fundamental changes.

- A flat tax on companies and people – in other words a massive tax reduction.

- A study on the so-called minibot. This is a parallel currency based on future tax receipts, similar to the plans proposed by Yanis Varoufakis in Greece. The minibot was in the Lega’s election manifesto. Five Star is far less radical on the eurozone, having dropped the idea of a referendum, but also seeks changes that are incompatible with the the EU fiscal rules. A parallel currency stands a much greater chance of success in Italy, and it would go some way to solving the government’s fiscal dilemmas. The open question is whether it would constitute a slippery slope towards euro exit.