work in progress!!/i have to leave so i am publishing everything. I will update the data when I come home later this evening.

GOLD: $1272.55 DOWN $3.55(COMEX TO COMEX CLOSINGS)

Silver: $16.32 DOWN 1 CENT (COMEX TO COMEX CLOSINGS)

Closing access prices:

Gold $1269.80

silver: $16.30

For comex gold:

JUNE/

NUMBER OF NOTICES FILED TODAY FOR JUNE CONTRACT:18 NOTICE(S) FOR 1800 OZ

TOTAL NOTICES SO FAR 6792 FOR 679200 OZ (21.125 tonnes)

For silver:

JUNE

33 NOTICE(S) FILED TODAY FOR

165,000 OZ/

Total number of notices filed so far this month: 1073 for 5,365,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: BID $6574/OFFER $6573: DOWN $110(morning)

Bitcoin: BID/ $6702/offer $6802: UP $16 (CLOSING/5 PM)

end

First Shanghai gold fix comes at 10 pm est

The second Shanghai gold fix: 2:15 pm

First Shanghai gold fix gold: 10 pm est: 1281.07

NY price at the same time: 1275.25

PREMIUM TO NY SPOT: $5.82

Second gold fix early this morning: 1279.04

USA gold at the exact same time:1274.30

PREMIUM TO NY SPOT: $4.74

AGAIN, SHANGHAI REJECTS NEW YORK PRICING.

WE WILL NOT PROVIDE LONDON FIXES AS THEY ARE NOT ACCURATE AS TO WHAT IS GOING ON AT THE SAME TIME FRAME.

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total OPEN INTEREST FELL BY A FAIR 1481 CONTRACTS FROM 220,295 DOWN TO 219,142 ACCOMPANYING YESTERDAY’S 11 CENT LOSS IN SILVER PRICING. HOWEVER AS WE ARE NOW WELL INTO THE NON ACTIVE DELIVERY MONTH OF JUNE WE CONTINUE TO WITNESS LONGS PACK THEIR BAGS AND MIGRATE OVER TO LONDON IN GREATER NUMBERS. WE WERE NOTIFIED THAT WE HAD A HUMONGOUS SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP: 8574 EFP’S FOR JULY, 319 EFP’S FOR SEPT. , 0 EFP’S FOR DECEMBER AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE: OF 8893 CONTRACTS. WITH THE TRANSFER OF 8893 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 8893 EFP CONTRACTS TRANSLATES INTO 44.465 MILLION OZ ACCOMPANYING:

1.THE 11 CENT LOSS IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES STANDING FOR JUNE COMEX DELIVERY. (5.370 MILLION OZ) DESPITE IT BEING A NON ACTIVE DELIVERY MONTH.

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF JUNE:

51,193 CONTRACTS (FOR 14 TRADING DAYS TOTAL 51,193 CONTRACTS) OR 255.96 MILLION OZ: (AVERAGE PER DAY: 3656 CONTRACTS OR 18.28 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH: 255.96* MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 36.56% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* WE HAVE ALREADY PASSED LAST MONTH AND CLOSING IN ON THE RECORD MONTH OF APRIL.

ACCUMULATION IN YEAR 2018 TO DATE SILVER EFP’S: 1,572.08 MILLION OZ.

ACCUMULATION FOR JAN 2018: 236.879 MILLION OZ

ACCUMULATION FOR FEB 2018: 244.95 MILLION OZ

ACCUMULATION FOR MARCH 2018: 236.67 MILLION OZ

ACCUMULATION FOR APRIL 2018: 385.75 MILLION OZ

ACCUMULATION FOR MAY 2018: 210.05 MILLION OZ

RESULT: WE HAD A FAIR SIZED DECREASE IN COMEX OI SILVER COMEX OF 1481 WITH THE 11 CENT FALL IN SILVER PRICE. WE HAVE NOW ENTERED THE NEW NON ACTIVE MONTH OF JUNE AND THE CME NOTIFIED US THAT IN FACT WE HAD A HUMONGOUS SIZED EFP ISSUANCE OF 8893 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) . FROM THE CME DATA: 8574 EFP CONTRACTS FOR JULY, 319 EFP’S FOR SEPT, 0 EFP’S FOR DECEMBER AND ZERO FOR ALL OVER MONTHS FOR A DELIVERABLE FORWARD CONTRACT OVER IN LONDON WITH A FIAT BONUS (TOTAL: 8893). TODAY WE GAINED AN ATMOSPHERIC: 7712 TOTAL OI CONTRACTS ON THE TWO EXCHANGES: i.e.8893 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH AN DECREASE OF 1481 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED WITH A 11 CENT FALL IN PRICE OF SILVER AND A CLOSING PRICE OF $16.33 WITH RESPECT TO YESTERDAY’S TRADING. YET WE STILL HAVE A GIGANTIC AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY IN THIS NON ACTIVE JUNE DELIVERY MONTH. IT SURE LOOKS LIKE A FAILED BANKER SHORT COVERING EXERCISE!!

In ounces AT THE COMEX, the OI is still represented by OVER 1 BILLION oz i.e. 1.094 MILLION OZ TO BE EXACT or 157% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT JUNE MONTH/ THEY FILED AT THE COMEX: 33 NOTICE(S) FOR 165,000 OZ OF SILVER

IN SILVER, WE HAVE NOW SET THE NEW RECORD OF OPEN INTEREST AT 243,411 AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $16.51 ON APRIL 9.2018.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ AND MAY: 36.285 MILLION OZ /AND JUNE/2018 (5.370 MILLION OZ SO FAR)

- HUGE RECORD OPEN INTEREST IN SILVER 243,411 CONTRACTS (OR 1.217 BILLION OZ/ SET APRIL 9/2018

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017

- RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ (FINAL)

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT).

In gold, the open interest ROSE BY A SMALL 226 CONTRACTS UP TO 468,345 DESPITE THE FALL IN THE GOLD PRICE/YESTERDAY’S TRADING (A FALL OF $1.50). WE ARE NOW IN THE ACTIVE DELIVERY MONTH OF JUNE. NO DOUBT THE BOYS ARE CASHING IN THEIR COMEX LONGS TO BEGIN THE PROCESS TO MOVE INTO LONDON FORWARDS. THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 13,559 CONTRACTS : JUNE SAW THE ISSUANCE OF 0 CONTRACTS , AND AUGUST SAW THE ISSUANCE OF: 13,559 CONTRACTS WITH ALL OTHER MONTHS ZERO. The new OI for the gold complex rests at 468,345. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE A STRONG OI GAIN IN TOTAL CONTRACTS ON THE TWO EXCHANGES: 226 OI CONTRACTS INCREASED AT THE COMEX AND A STRONG SIZED 13,559 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN: 13,785 CONTRACTS OR 1,378,500 OZ = 42.88 TONNES. AND STRANGELY ALL OF THIS DEMAND OCCURRED WITH A FALL OF $1.50.???

YESTERDAY, WE HAD 12,781 EFP’S ISSUED.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF MAY : 159,070 CONTRACTS OR 15,907,000 OZ OR 494.77 TONNES (14 TRADING DAYS AND THUS AVERAGING: 11,362 EFP CONTRACTS PER TRADING DAY OR 1,136,200 OZ/ TRADING DAY),,

TO GIVE YOU AN IDEA AS TO THE HUGE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 14 TRADING DAYS IN TONNES: 494.77 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2017, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 2555 TONNES

THUS EFP TRANSFERS REPRESENTS 494.77/2550 x 100% TONNES = 19.40% OF GLOBAL ANNUAL PRODUCTION SO FAR IN APRIL ALONE.***

ACCUMULATION OF GOLD EFP’S YEAR 2018 TO DATE: 3,946.6* TONNES *SURPASSED ANNUAL PROD’N

ACCUMULATION OF GOLD EFP’S FOR JANUARY 2018: 653.22 TONNES

ACCUMULATION OF GOLD EFP’S FOR FEBRUARY 2018: 649.45 TONNES

ACCUMULATION OF GOLD EFP’S FOR MARCH 2018: 741.89 TONNES (22 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR APRIL 2018: 713.84 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR MAY 2018: 693.80 TONNES ( 22 TRADING DAYS)

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A SMALL SIZED INCREASE IN OI AT THE COMEX OF 226 DESPITE THE $1.50 FALL IN PRICING GOLD TOOK ON YESTERDAY // GOLD TRADING YESTERDAY ($1.50 DROP). WE ALSO HAD A STRONG SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 13,559 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 13,559 EFP CONTRACTS ISSUED, WE HAD A STRONG NET GAIN OF 13,785 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

13559 CONTRACTS MOVE TO LONDON AND 226 CONTRACTS INCREASED AT THE COMEX. (in tonnes, the GAIN in total oi equates to 42.88 TONNES). ..AND BELIEVE IT OR NOT BUT ALL OF THIS DEMAND OCCURRED AT THE COMEX WITH A FALL OF $1.50 IN TRADING!!!.

we had: 18 notice(s) filed upon for 1800 oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD DOWN $3.55 TODAY: / NO CHANGES IN GOLD INVENTORY AT THE GLD/ /GLD INVENTORY 828.76 TONNES

Inventory rests tonight: 828.76 tonnes.

SLV/

WITH SILVER DOWN 1 CENT TODAY /A HUGE CHANGE IN THE SILVER/A DEPOSIT OF 2.35 MILLION OZ

/INVENTORY RESTS AT 316.442 MILLION OZ/

THIS IS A GOOD SIGN..THE RAIDS WILL NOW STOP

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER FELL BY A FAIR SIZED 1481CONTRACTS from 220,295 DOWN TO 218,814 (AND, FURTHER FROM THE NEW COMEX RECORD SET /APRIL 9/2017 AT 243,411/SILVER PRICE AT THAT DAY: $16.53). THE PREVIOUS RECORD OTHER THAN WAS ESTABLISHED AT: 234,787, SET ON APRIL 21.2017 OVER ONE YEAR AGO. THE PRICE OF SILVER ON THAT DAY: $17.89. OUR CUSTOMARY MIGRATION OF COMEX LONGS MORPH INTO LONDON FORWARDS CONTINUES AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

8574 EFP’S FOR JULY, 319 EFP CONTRACTS FOR SEPT., 0 EFP CONTRACTS FOR DECEMBER AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 8893 CONTRACTS . EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI LOSS AT THE COMEX OF 1481 CONTRACTS TO THE 8893 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A GAIN OF 7412 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES: 37.06 MILLION OZ!!! AND THIS OCCURRED DESPITE A 11 CENT FALL IN PRICE . THE BANKERS ORCHESTRATED THEIR RAID YESTERDAY DESPERATELY TRYING TO PARE THEIR GIGANTIC OPEN INTEREST SHORT ON BOTH EXCHANGES WITH HARDLY ANY SUCCESS. HOWEVER A DRAMATIC AMOUNT OF EFP ISSUANCE IS HEADING OVER TO LONDON AND NO DOUBT WE WILL COME CLOSE TO BREAKING APRIL’S RECORD OF 385 MILLION OZ.

RESULT: A FAIR SIZED DECREASE IN SILVER OI AT THE COMEX WITH THE 11 CENT FALL THAT SILVER TOOK IN PRICING ON FRIDAY. BUT WE ALSO HAD ANOTHER HUMONGOUS SIZED 8893 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR JUNE, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

)WEDNESDAY MORNING/TUESDAY NIGHT: Shanghai closed UP 7.91 POINTS OR 0.27% /Hang Sang CLOSED UP 228.02 POINTS OR 0.77% / The Nikkei closed UP 276.95 POINTS OR 1.24% /Australia’s all ordinaires CLOSED UP 1.06% /Chinese yuan (ONSHORE) closed UP at 6.4738/Oil UP to 65.10 dollars per barrel for WTI and 75.10 for Brent. Stocks in Europe OPENED DEEPLY IN THE GREEN//. ONSHORE YUAN CLOSED UP AT 6.4738 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.4777/ONSHORE YUAN TRADING STRONGER AGAINST OFFSHORE YUAN/ONSHORE YUAN TRADING MUCH STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING MUCH WEAKER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW LOOKS LIKE A FULL TRADE WAR IS BEGINNING/

/NORTH KOREA/SOUTH KOREA

i)North Korea/South Korea/USA

b) REPORT ON JAPAN

3 c CHINA

i)China/USA

4. EUROPEAN AFFAIRS

i)DEUTSCHE BANK/GERMANY/EURO ZONE

As always, a terrific commentary from the Mises Institute (Polleit). Here the author describes the problems at Deutsche bank as they are already deleveraging. This creates a deflationary cycle and is opposite to what the central bank (ECB ) wants. Central banks must inflate their debt and will always supply the necessary fiat money cheap to the banks. The guys at the top of the pyramid benefit and everybody else suffers.

this is where we are heading..

a must read.

(courtesy Polleit/Mises Institute_

(courtesy zerohedge)

iii)Spain

You will recall the Migrant ship that was refused entry into Italy..but was rescued by Italians who then put all of those migrants onto Spanish soil. I stated that the Spanish will not be happy. It seems that the Migrants are heading for dormitories form which students pay 750 euros per month. Spanish students must give up their rooms to these migrants and I can assure you this will go over quite well!! (sorry for the pun)

( zerohedge)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

Another important paper..The author discusses how Russia has sold off greater than 50% of their holdings in dollars. No doubt the sanctions and trade wars were a large integral part of that decision. This is coming at a bad time for the USA who are counting on foreign central banks buying these debt instruments. You will recall that David Stockman believes that by the mid 2019, the USA will issue 1.8 trillion dollars in paper debt. (the author below states 1.4 trillion dollars)

( Savitsky/Strategic Culture Foundation)

6 .GLOBAL ISSUES

7. OIL ISSUES

Oil expert Paraskova claims that global oil demand will remain strong in the second half of this year

( Paraskova/OilPrice.com)_

8. EMERGING MARKET

9. PHYSICAL MARKETS

10. USA stories which will influence the price of gold/silver)

I)Market data

Yesterday I reported to you the huge slump in permits despite a surge in starts. Now wehave the third release and it backs the permits as we see a huge slump in existing home sales. The reason of course is affordability

( zerohedge)

ii)The truth behind the latest illegal immigrant problems facing the USA

a must read for you to understand what is going on…

( Benny Johnson/DailyCaller)

iv)TRUMP signs the executive order keeping migrant families together at the border but zero tolerance will continue( zerohedge)

v)SWAMP STORIES

a)Strzok was escorted out of the FBI building last Friday night but is still on their payroll

( zerohedge)

b)Bombshells galore yesterday on day 2 on Horowitz testimony:

c)Comey snaps back at Hillary for not knowing what her case was all about. Comey was using his personal computer sending non classified stuff out. Hillary sent out classified stuff.

(courtesy zerohedge)

d)Giuliani is just stalling. Trump will never ever go before Mueller as this is nothing but a witch hunt

(courtesy zerohedge)

Trading Volumes on the COMEX

PRELIMINARY COMEX VOLUME FOR TODAY: 130,997 contracts

CONFIRMED COMEX VOL. FOR YESTERDAY: 302,482 contracts

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

And now for the wild silver comex results.

Total silver OI FELL BY A FAIR SIZED 1153 CONTRACTS FROM 220,295 DOWN TO 218,814 (AND A LITTLE FURTHER FROM THE NEW RECORD OI FOR SILVER SET APRIL 9.2018/ 243,411 CONTRACTS) ACCOMPANYING THE 11 CENT LOSS IN SILVER PRICING/ YESTERDAY. SINCE WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF JUNE, WE WERE INFORMED THAT WE HAD A HUMONGOUS SIZED 8574 EFP CONTRACT ISSUANCE FOR JULY, 319 EFP CONTRACTS FOR SEPT., 0 EFP CONTRACTS FOR DECEMBER AND ZERO FOR ALL OTHER MONTHS. THESE EFPS WERE ISSUED TO COMEX LONGS WHO RECEIVED A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. THE TOTAL EFP’S ISSUED: 8893. ON A NET BASIS WE GAINED 7740 SILVER OPEN INTEREST CONTRACTS AS WE OBTAINED A 1481 CONTRACT LOSS AT THE COMEX COMBINING WITH THE ADDITION OF 8893 OI CONTRACTS NAVIGATING OVER TO LONDON.

NET GAIN ON THE TWO EXCHANGES: 7412 CONTRACTS

AMOUNT STANDING FOR SILVER AT THE COMEX

We are now in the NON active delivery month of JUNE and here the front month ROSE BY 18 contracts RISING TO 34 contracts. We had 15 notices filed upon yesterday so we gained 33 contracts or an additional 165,000 oz will stand in this non active delivery month of June TODAY SOMEBODY WAS IN URGENT NEED OF PHYSICAL ON THIS SIDE OF THE POND AS A DEALER JUMPED QUEUE AHEAD OF THOSE INITIALLY STANDING

The next big active delivery month for silver is July and here the OI LOST 9048 contracts DOWN to 93,657. The next delivery month is August and here we GAINED 90 contracts to stand at 349. The next active delivery month after August for silver is September and here the OI ROSE by 7340 contracts UP to 87,283

FOR COMPARISON AT THIS TIME IN THE DELIVERY CYCLE, JUNE 19.2017, FOR SILVER, WE HAD 82,061 OPEN INTEREST CONTACTS STILL STANDING.VS 93,657 TODAY. LAST YEAR AT THIS TIME WE HAD 9 MORE TRADING DAYS LEFT BEFORE FIRST DAY NOTICE, THIS YEAR WE HAVE 8 MORE TRADING DAYS BEFORE FDN.

We had 33 notice(s) filed for 165,000 OZ for the JUNE 2018 COMEX contract for silver

INITIAL standings for JUNE/GOLD

JUNE 20/2018.

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz |

nil OZ

|

| Deposits to the Dealer Inventory in oz | NIL oz |

| Deposits to the Customer Inventory, in oz | nil

oz |

| No of oz served (contracts) today |

18 notice(s)

1800 OZ

|

| No of oz to be served (notices) |

199 contracts

(19900 oz)

|

| Total monthly oz gold served (contracts) so far this month |

6792 notices

679200 OZ

21.125 TONNES

|

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

For JUNE:

Today, 0 notice(s) were issued from JPMorgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equates to 18 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped/ Received) by j.P.Morgan customer account.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

To calculate the INITIAL total number of gold ounces standing for the JUNE. contract month, we take the total number of notices filed so far for the month (6792) x 100 oz or 679200 oz, to which we add the difference between the open interest for the front month of JUNE. (217 contracts) minus the number of notices served upon today (18 x 100 oz per contract) equals 699,100 oz, the number of ounces standing in this active month of JUNE (21.744 tonnes)

Thus the INITIAL standings for gold for the JUNE contract month:

No of notices served (6792 x 100 oz) + {(217)OI for the front month minus the number of notices served upon today (18 x 100 oz )which equals 699,100 oz standing in this active delivery month of JUNE .

WE GAINED A SMALL 1 CONTRACT OR AN ADDITIONAL 100 OZ WILL STAND FOR DELIVERY AS THESE GUYS REFUSED TO MORPH INTO LONDON BASED FORWARDS AND RECEIVE AN ADDITIONAL SWEETENER FOR THEIR EFFORT..

“THERE ARE ONLY 7.878 TONNES OF REGISTERED GOLD AVAILABLE FOR DELIVERY AGAINST 21.744 TONNES STANDING WHICH IS MAKING THIS JUNE CONTRACT MONTH AN EXTREMELY INTERESTING ONE TO WATCH. iF YOU RECALL, 5.9 TONNES OF GOLD WAS ADJUSTED OUT OF THE DEALER TWO WEEKS AGO AND THAT HAS BEEN THE ONLY TRANSACTION INDICATING A SETTLEMENT. SINCE 21.744 TONNES IS STANDING THEY NEXT 8 TONNES OF WHICH THEY ONLY HAVE 7.87 TONNES.

IN THE LAST 18 MONTHS 74 NET TONNES HAS LEFT THE COMEX.

end

And now for silver

AND NOW THE APRIL DELIVERY MONTH

JUNE INITIAL standings/SILVER

| Silver | Ounces |

| Withdrawals from Dealers Inventory | nil oz |

| Withdrawals from Customer Inventory |

9959.09 oz

CNT

|

| Deposits to the Dealer Inventory |

nil;

oz

|

| Deposits to the Customer Inventory |

632,043.680

oz

DELAWARE

SCOTIA

|

| No of oz served today (contracts) |

33

CONTRACT(S)

(165,000 OZ)

|

| No of oz to be served (notices) |

1 contracts

(5,000 oz)

|

| Total monthly oz silver served (contracts) | 1073 contracts

(5,365,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

we had 0 inventory movement at the dealer side of things

total dealer deposits: nil oz

we had 2 deposits into the customer account

i) Into JPMorgan: NIL oz

*** JPMorgan for most of 2017 and in 2018 has adding to its inventory almost every single day.

JPMorgan now has 141 million oz of total silver inventory or 52.0% of all official comex silver. (141 million/270 million)

ii) Into Delaware: 2068.35 oz

iii) Into Scotia: 629,975.300

total customer deposits today: 632,043.680 oz

we had 1 withdrawals from the customer account;

i) Out of CNT: 9959.09

total withdrawals; 9959.09 oz

we had 1 adjustment/

i) Out of Scotia, 503,237.810 oz was adjusted out of the customer and this landed into the dealer account of Scotia oz

total dealer silver: 69.028 million

total dealer + customer silver: 272.794 million oz

The total number of notices filed today for the JUNE. contract month is represented by 33 contract(s) FOR 165,000 oz. To calculate the number of silver ounces that will stand for delivery in JUNE., we take the total number of notices filed for the month so far at 1073 x 5,000 oz = 5,365,000 oz to which we add the difference between the open interest for the front month of JUNE. (34) and the number of notices served upon today (33 x 5000 oz) equals the number of ounces standing.

.

Thus the INITIAL standings for silver for the JUNE contract month: 1073(notices served so far)x 5000 oz + OI for front month of JUNE(34) -number of notices served upon today (33)x 5000 oz equals 5,370,000 oz of silver standing for the JUNE contract month

PLEASE NOTE THE FOLLOWING FOR COMPARISON PURPOSES:

ON MAY 31.2017 WE INITIALLY HAD 396 OPEN INTEREST STAND OR A LARGE 1.98 MILLION OZ

STOOD FOR METAL.

THE JUNE 20/2017 READING HAD 82,061 CONTRACTS STANDING SO FAR FOR THE JULY DELIVERY MONTH WHICH IS A VERY VERY ACTIVE MONTH VS.93,969 OUTSTANDING TODAY.

AT THE CONCLUSION OF JUNE 2017: 4.92 MILLION OZ FINALLY STOOD AS QUEUE JUMPING STARTED IN EARNEST AND IN THE ENSUING YEAR, IT CONTINUED WITH RECKLESS ABANDON INCLUDING WHAT YOU ARE WITNESSING TODAY.THIS IS COMPARED TO TODAY’S AMOUNT STANDING: 5.370 MILLION OZ.

We gained 33 contracts or an additional 165,000 oz will stand in this non active delivery month of June as somebody was in urgent need of silver today. IN SILVER QUEUE JUMPING HAS BEEN THE NORM FOR OVER A YEAR. IT LOOKS LIKE GOLD IS TAKING A HOLIDAY FROM THIS SAME PHENOMENON…

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

ESTIMATED VOLUME FOR TODAY: 44,432 CONTRACTS

CONFIRMED VOLUME FOR YESTERDAY: 145,205 CONTRACTS absolutely criminal

YESTERDAY’S CONFIRMED VOLUME OF 145,205 CONTRACTS EQUATES TO 726 million OZ OR 103.8% OF ANNUAL GLOBAL PRODUCTION OF SILVER

COMMODITY LAW SUGGESTS THAT OPEN INTEREST SHOULD NOT BE MORE THAN 3% OF ANNUAL GLOBAL PRODUCTION. THE CROOKS ARE SUPPLYING MASSIVE PAPER TRYING TO KEEP SILVER IN CHECK.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price at that day at $18.42

The previous record was 224,540 contracts with the price at that time of $20.44

end

NPV for Sprott

1. Sprott silver fund (PSLV): NAV FALLS TO -2.72% (JUNE 20/2018)

2. Sprott gold fund (PHYS): premium to NAV RISES TO -0.46% to NAV (JUNE 20/2018 )

Note: Sprott silver trust back into NEGATIVE territory at -2.72%-/Sprott physical gold trust is back into NEGATIVE/ territory at -0.46%/Central fund of Canada’s is still in jail but being rescued by Sprott.

Sprott WINS hostile 3.1 billion bid to take over Central Fund of Canada

(courtesy Sprott/GATA)

3.SPROTT CEF.A FUND (FORMERLY CENTRAL FUND OF CANADA): NAV FALLS TO -2.87%: NAV 13.21/TRADING 12.84//DISCOUNT 2.87.

END

And now the Gold inventory at the GLD/

JUNE 20/WITH GOLD DOWN $3.55/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 828.76 TONNES

JUNE 19/WITH GOLD DOWN $1.50/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 828.76 TONES

JUNE 18/WITH GOLD UP $1.90/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 828.76 TONNES

JUNE 15/WITH GOLD DOWN $28.90/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 828.76 TONNES

JUNE 14/WITH GOLD UP $7.10/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 828.76 TONNES/

JUNE 13/WITH GOLD UP $2.20/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 828.76 TONNES

JUNE 12/WITH GOLD DOWN $4.75:NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 828.76 TONNES

JUNE 11/WITH GOLD UP 65 CENTS/THE CROOKS RAIDED THE COOKIE JAR FOR 3.83 TONNES/INVENTORY RESTS AT 828.76 TONNES

JUNE 8/WITH GOLD DOWN 10 CENTS/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY REMAINS AT 832.59 TONNES./

JUNE 7/WITH GOLD UP $1.45, THE CROOKS DECIDED TO RAID AGAIN THE GLD GOLD COOKIE JAR TO THE TUNE OF 3.54 TONNES/GOLD INVENTORY LOWERS TO 832.59 TONNES

JUNE 6/WITH GOLD UP $1.30 TODAY, WE HAD NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 836.13 TONNES

JUNE 5/WITH GOLD UP $5.30 TODAY, WE HAD A TINY WITHDRAWAL OF .29 TONNES AND THAT NO DOUBT WAS TO PAY FOR FEES/836.13 TONNES

JUNE 4/WITH GOLD DOWN ONLY $2.50, THE CROOKS UNLEASHED A MASSIVE WITHDRAWAL OF 10.61 TONNES OF GOLD FROM THE GLD/INVENTORY RESTS AT 836.42 TONNES

JUNE 1/WITH GOLD DOWN $5.10 TODAY, A HUGE 4.42 TONNES OF GOLD WAS WITHDRAWN FROM THE GLD AND THIS WAS USED IN THE RAID TODAY/INVENTORY RESTS AT 847.03 TONNES

MAY 31/WITH GOLD DOWN 1.60/NO CHANGE IN GOLD INVENTORY/INVENTORY REMAINS AT 851.45 TONNES

MAY 30/WITH GOLD UP $2.70: A HUGE DEPOSIT OF 2.95 TONNES INTO THE GLD/INVENTORY REMAINS AT 851.45 TONNES

MAY 29/2018/WITH GOLD DOWN $4.50/ NO CHANGES IN GLD INVENTORY/INVENTORY REMAINS AT 848.50 TONNES

May 25/WITH GOLD UP ON THE WEEK BUT DOWN 80 CENTS TODAY: WE HAD A HUGE 3.54 TONNES OF GOLD WITHDRAWAL FROM THE CROOKED GLD/

MAY 24/WITH GOLD UP $12.40/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 852.04

MAY 22/WITH GOLD UP $1.05/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 852.04 TONNES

MAY 21/WITH GOLD DOWN 50 CENTS/A HUGE CHANGE IN GOLD INVENTORY/A WITHDRAWAL OF 3.24 TONNES FORM GLD INVENTORY/INVENTORY RESTS AT 852.04 TONNES

MAY 18/WITH GOLD UP $1.80/A HUGE CHANGE IN GOLD INVENTORY AT THE GLD/ A DEPOSIT OF 9.11 TONNES INTO GLD INVENTORY/INVENTORY RESTS AT 865.28 TONNES/

GLD WAS ONE MASSIVE FRAUD

May 17/WITH GOLD DOWN $1.75/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 856.17 TONNES

MAY 16./WITH GOLD UP $1.05: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 856.17 TONNES

MAY 15/WITH GOLD DOWN $27.35, THE CROOKS WITHDREW 10 TONNES OF GOLD FROM THE GLD WHICH WAS USED IN THE RAID TODAY/INVENTORY RESTS AT 856.17 TONNES

MAY 14/ WITH GOLD DOWN $2.35: A HUGE DEPOSIT OF 4.68 TONNES OF GOLD INTO THE GLD and then a withdrawal of 1.48 tonnes /INVENTORY RESTS AT 866.17

A net gain of 3.2 tonnes of gold.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

JUNE 20/2018/ Inventory rests tonight at 828,76 tonnes

*IN LAST 401 TRADING DAYS: 97.83 NET TONNES HAVE BEEN REMOVED FROM THE GLD

*LAST 351 TRADING DAYS: A NET 58.47 TONNES HAVE NOW BEEN ADDED INTO GLD INVENTORY.

end

Now the SLV Inventory/

JUNE 20/WITH SILVER DOWN ONE CENT/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 314.090 MILLION OZ/

JUNE 19/2018/WITH SILVER DOWN 11 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 314.090 MILLION OZ/

JUNE 18/WITH SILVER DOWN 6 CENTS TODAY/NO CHANGE IN SILVER INVENTORY/INVENTORY RESTS AT 314.090 MILLION OZ/

JUNE 15/WITH SILVER DOWN 75 CENTS/A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.788 MILLION OZ//INVENTORY RESTS AT 314.090 MILLION OZ

JUNE 14/WITH SILVER UP 30 CENTS, THE CROOKS DECIDED THAT THEY NEEDED SILVER INVENTORY BADLY SO THEY RAID THE SLV OF 1.412 MILLION OZ/INVENTORY RESTS AT 315.878 MILLION OZ/

JUNE 13/WITH SILVER UP 11 CENTS TODAY/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 317.290 MILLION OZ/

JUNE 12/WITH SILVER DOWN 5 CENTS/A HUGE CHANGES IN SILVER INVENTORY AT THE SLV/ THE CROOKS RAID THE SILVER COOKIE JAR BY 1.976 MILLION OZ/INVENTORY LOWERS TO 317.290 MILLION OZ/

jUNE 11/NO CHANGE IN SILVER INVENTORY/319.266 MILLION OZ

JUNE 8/WITH SILVER DOWN 5 CENTS/A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.412 MILLION OZ//INVENTORY LOWERS TO 319.266 MILLION OZ/

JUNE 7/WITH SILVER UP ANOTHER 12 CENTS/A HUGE CHANGE IN SILVER INVENTORY AT THE SL: A WITHDRAWAL OF 1.883 MILLION OZ WITH ALL OF THAT SILVER DEMAND//INVENTORY RESTS AT 320.678 MILLION OZ/

JUNE 6/WITH SILVER UP 14 CENTS TODAY/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 322.561 MILLION OZ/

JUNE 5/WITH SILVER UP 10 CENTS NO CHANGE IN SILVER INVENTORY/INVENTORY RESTS AT 322.561 MILLION OZ

JUNE 4/WITH SILVER DOWN 1 CENTA SMALL CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 522,000 OZ INTO THE SLV/.INVENTORY RISES AT 322.561 MILLION OZ/

JUNE 1/WITH SILVER DOWN 3 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY REMAINS AT 322.039 MILLION OZ/

MAY 31/WITH SILVER DOWN 7 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY REMAINS AT 322.039 MILLION OZ/

MAY 30/WITH SILVER UP 16 CENTS: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV/ A DEPOSIT OF 2.071 MILLION OZ/INVENTORY RESTS AT 322.039 MILLION OZ/

MAY 29.2018/ NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.968 OZ

May 25/INVENTORY LOWERS TO 319.968 AS WE HAD A WITHDRAWAL OF 1.035 MILLION OZ

MAY 24/WITH SILVER UP 27 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 321.003 MILLION OZ/

MAY 22/WITH SILVER UP 6 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 321.003 MILLION OZ/

MAY 21/ WITH SILVER UP 5 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 321.003 MILLION OZ/

MAY 18/WITH SILVER DOWN 5 CENTS A SMALL CHANGE IN SILVER INVENTORY AT THE SLV/ A WITHDRAWAL OF 942,000 OZ/INVENTORY RESTS AT 321.003 MILLION OZ/

May 17/WITH GOLD UP 6 CENTS/A SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 471,000 OZ//INVENTORY RESTS AT 321.945 MILLION OZ/

MAY 16./WITH SILVER UP 10 CENTS/A HUGE DEPOSIT OF 1.883 MILLION OZ OF SILVER INTO THE SLV/INVENTORY RESTS AT 321.474 MILLION OZ

MAY 15/WITH SILVER DOWN 33 CENTS, NO CHANGES AT THE SLV; THE CROOKS COULD NOT BORROW ANY SILVER BECAUSE THERE IS NONE: INVENTORY RESTS AT 319.591 MILLION OZ

MAY 14/WITH SILVER DOWN 10 CENTS/A SMALL CHANGES IN SILVER INVENTORY AT THE SLV/ A WITHDRAWAL OF 858,000 FROM THE SLV/INVENTORY RESTS AT 319.591 MILLION OZ/

JUNE 20/2018:

Inventory 314.090 million oz

end

6 Month MM GOFO 2.12/ and libor 6 month duration 2.50

Indicative gold forward offer rate for a 6 month duration/calculation:

G0FO+ 2.12%

libor 2.50 FOR 6 MONTHS/

GOLD LENDING RATE: .38%

XXXXXXXX

12 Month MM GOFO

+ 2.76%

LIBOR FOR 12 MONTH DURATION: 2.55

GOFO = LIBOR – GOLD LENDING RATE

GOLD LENDING RATE = +.21

end

Major gold/silver trading /commentaries for WEDNESDAY

GOLDCORE/BLOG/MARK O’BYRNE.

GOLD/SILVER

In Gold, Silver and Bitcoin We Trust? Goldnomics Podcast with Ronald-Peter Stoeferle

In Gold, Silver and Bitcoin We Trust? Goldnomics Podcast (Episode 5) interview with Ronald-Peter Stoferle

We interview our friend Ronald-Peter Stoeferle, partner in Incrementum in Liechtenstein and author of the must read, annual gold report ‘In Gold We Trust’ in this the fifth episode of the Goldnomics Podcast.

There are 3 key “tides of change” that Ronni has analysed and he warns that the “liquidity party” of the last 10 years is coming to an end and this will impact stocks, bonds, property, bitcoin and gold in the coming years.

Never miss an episode of The Goldnomics Podcast – Subscribe on YouTube, ITunes, Soundcloud or Blubrry

Topics covered in this episode of The Goldnomics Podcast are

– Have we expected too much of gold over the past few years?

– What will be the catalyst which changes sentiment towards gold?

– While it is relatively cheap – Is this the perfect time to buy gold?

– Why is Bitcoin stealing gold’s lustre?

– What is the best way to own and hold gold to hedge and protect your portfolio?

– What is the best allocation to gold for your portfolio?

– Why will 99% of crypto-currencies fail over the next few years?

– What effect will China have on the dollar and on the gold price?

Listen to the full episode or skip directly to one of the following discussion points

1:11 Introducing our special guest Ronald Peter Stoferle of Incrementum and author of the respected “In Gold We Trust” report

2:26 The 3 tides of change that we are seeing in financial markets

3:07 The Monetary Policy Tide – The end of the party

3:58 The deflationary effect of the monetary policy changes

4:40 Why quantitive tightening will have negative effects for asset values

4.59 The second tide – The De-Dollarization the financial markets

6:08 The Crypto-currency Tide

9:02 The monetary policy versus the monetary order and the elephant in the room

9:50 The flip side of “The Everything Bubble”

10:45 The monetary order

11:30 The only way to get ourselves out of our current economic and financial problem

11:50 The “Pandora’s Box” of liquidity

12:35 Some people are not seeing the benefit of “The Everything Bubble”

13:25 Gold will protect the investor from what is to come

14:55 How the monetary tide will affect the gold price

15:45 Are we expecting too much from gold at the moment?

17:25 When the headwind from asset markets become a tailwind, gold benefits

18:00 Why the current correlation between equities and bonds could be positive for gold when the tides turn

20:20 What allocation to gold is recommended in these markets?

22:20 “Nobody cares about gold at the moment…… that’s why you should have a close look at gold”

23:15 The collapse in Google searches for “Buy gold” versus “Buy Bitcoin”, shows the sentiment is negative towards gold

24:30 No strong opinion from analysts on gold versus 2008, and why this is a positive indicator for gold

26:30 Is currency competition a good thing for the market?

27:45 Why 99% of cryptocurrencies are bogus and will be wiped out in the next few years

28:45 The need for efficient payment technology and how we’ve lost faith in government money

29:45 How central bankers are acting like taxmen and abused their position

31:30 The Gold/Crypto cross-over and what that might mean for the future of money

31:50 The best way to own and hold gold – a gold ETF in a big Wall Street bank – REALLY??

32:30 The only way to hold gold for insurance and hedging purposes

33:10 The important considerations when choosing how you own and hold gold

34:30 Crypto bullion and asset backed cryptos will do well in the future

34:45 Why the notion that Bitcoin is a store of value has yet to be proven

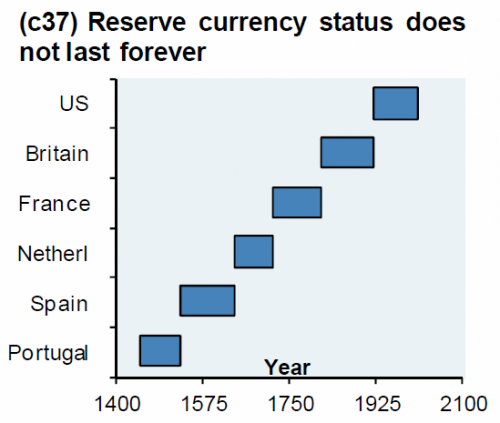

37:15 Remimbi backed oil contracts what effect will this have on for the future? Are they moving in to reserve currency status?

38:30 The dying petro-dollar versus a rising Remimbi all part of the de-dollarization of world markets.

40:00 The flow of gold from East to West, what does this mean?

41:05 Are the rising geopolitical tensions a result of the fundamental flaws of our currency system?

41:45 Can we trace the route of our currency problems back to 1971 and the actions of Richard Nixon?

You can download the “In Gold We Trust” report here:

In Gold we Trust: 3 Important Factors Leading to the “Turning of the Monetary Tides”

Or you can follow them on Twitter here: https://twitter.com/IGWTreport

People mentioned in this podcast

Ronald-Peter Stoeferle – https://twitter.com/RonStoeferle

Mark Valek – Co-Author of “In Gold We Trust” – https://twitter.com/MarkValek

Adrian Day – www.adriandayassetmanagement.com/

Friedrich von Hayek – https://twitter.com/FriedrichHayek

Website Mentioned in this video: www.goldcore.com

Make sure you don’t miss a single episode……

Subscribe to the Goldnomics Podcasts on iTunes, Soundcloud, or YouTube:

https://YouTube.com/user/GoldCoreLimited

https://itunes.apple.com/ie/podcast/goldnomics/id1328292057

Follow us on social media:

GoldCore on Twitter: https://twitter.com/goldcore

GoldCore on Facebook: https://www.facebook.com/GoldCore/

GoldCore on Linkedin: https://ie.linkedin.com/company/goldcore

News and Commentary

Russian central bank diversifies holdings amid geopolitical risks (Reuters.com)

Asian markets rebound on bargain-hunting, shrug off trade war threats (Reuters.com)

Trump determined to hit China as tit-for-tat tariff war erupts (Reuters.com)

South Korea lobbies India to relax gold import restrictions (MiningWeekly.com)

Gold Glitters on Inflation Fears and U.S. Budget Imbalance (GoldSeek.com)

Gold Street Is Where South Africa’s Mining History Goes to Die (Bloomberg.com)

Fiat Currency Always Ends In Collapse (ZeroHedge.com)

Ike Was Right About the MI Complex (BonnerAndPartners.com)

Failed States: Hopeless European Millennials And The Populist Takeover (DollarCollapse.com)

World Cup Kaliningrad mines ‘Baltic gold’… and ‘digital gold’ (FT.com)

Gold Prices (LBMA AM)

19 Jun: USD 1,279.00, GBP 971.14 & EUR 1,108.89 per ounce

18 Jun: USD 1,281.25, GBP 966.96 & EUR 1,103.93 per ounce

15 Jun: USD 1,300.10, GBP 978.98 & EUR 1,120.04 per ounce

14 Jun: USD 1,305.30, GBP 971.27 & EUR 1,103.89 per ounce

13 Jun: USD 1,294.40, GBP 971.58 & EUR 1,101.92 per ounce

12 Jun: USD 1,298.30, GBP 968.27 & EUR 1,100.44 per ounce

11 Jun: USD 1,296.05, GBP 969.32 & EUR 1,099.57 per ounce

Silver Prices (LBMA)

19 Jun: USD 16.36, GBP 12.42 & EUR 14.16 per ounce

18 Jun: USD 16.61, GBP 12.53 & EUR 14.29 per ounce

15 Jun: USD 17.23, GBP 12.96 & EUR 14.86 per ounce

14 Jun: USD 17.12, GBP 12.75 & EUR 14.48 per ounce

13 Jun: USD 16.91, GBP 12.68 & EUR 14.37 per ounce

12 Jun: USD 16.85, GBP 12.58 & EUR 14.30 per ounce

11 Jun: USD 16.76, GBP 12.55 & EUR 14.23 per ounce

Recent Market Updates

– Own A “Bit Of Gold” As We Are Moving Ever Closer To A Trade War

– Bitcoin Price To $0 Or $1 Million In One Year? MoneyConf 2018 Poll

– Cashless Society – Good or Bad? MoneyConf 2018 Video

– Do We Still Need Banks In The Age Of Fintech?

– Total US Government Debt Is $200 Trillion – Debt Clock Ticking To Next Crisis

– All Gold is Not Equal – Goldnomics Podcast (Episode 4)

– “Without Gold I Would Have Starved To Death” – ECB Governor

– Swiss Government Pension Fund To Buy Gold Bars Worth Some €600 Million

– Turkey Uses Gold Bullion To Stabilise Its Currency And Economy

– Case for Gold in a Diversified Investment Portfolio

– Get “Positioned In Gold” Now As “You Will Not Have Time To Get Positioned” Later

– Consequences of Ignoring Economic Reality Are Dangerous

– Are Gold And Silver Bullion Obsolete In The Crypto Age?

– In Gold we Trust: 3 Important Factors Leading to the “Turning of the Monetary Tides”

– Silver Trading in Tight $1 Range As Pressure Builds For A Breakout

Never miss an episode of The Goldnomics Podcast

– On SoundCloud , Blubrry & iTunes. Watch on YouTube below

ANDREW MAGUIRE’S KINESIS WHICH IS A”BITCOIN’ BACKED 100% BY ALLOCATED GOLD AND SILVER

Andrew Maguire’s Kinesis money which is a “bitcoin” but backed 100% by allocated gold and silver is set to go.

it think it would be a great idea to look at this!

please read at: https://kinesis.money/#/

(Andrew Maguire)

|

|

Dear Harvey Organ,

Thank you for your participation in our webinar on June 7th with our host and CEO of Kinesis, Thomas Coughlin.

The response we received has been incredible, we appreciate you taking the time to join us and hope you found it to be beneficial.

Due to such a high influx of questions we received we were unable to have them all answered. Nevertheless, if there was anything which requires more clarification, or you have a query which needs to be rectified, we invite you to join our telegram group:

We apologize for the technical issues we incurred during the webinar which resulted in it running a little over schedule, we hope that the next one we host will run seamlessly.

A video has been put together and uploaded onto our YouTube channel which can be found here:

Please share and subscribe to our YouTube channel to be notified of all the latest videos as they become available.

The rapid growth that we are currently experiencing has been incredible and with your support, is only going to get better.

We are working behind the scenes very hard to create a better experience for everyone involved! Stay tuned in as we have many more announcements to be released in the upcoming days.

Kind Regards,

|

Kinesis Money

a:C/O ILS Fiduciaries (IOM) Limited, First Floor,Millennium House, Victoria Road, Douglas, Isle of Man IM2 4RW

|

The following is self explanatory

(courtesy GATA/Chris Powell and Harvey Organ)

GATA asks bank regulator to check risks of gold

futures maneuver

Submitted by cpowell on Sun, 2018-06-10 16:17. Section: Daily Dispatches

12:21p ET Sunday, June 10, 2018

Dear Friend of GATA and Gold:

GATA has appealed to the U.S. comptroller of the currency, who has regulatory authority over banks, to review financial risks certain banks may have incurred through derivatives in the monetary metals markets, particularly through the recent heavy use of the “exchange for physicals” mechanism of settling gold and silver futures contracts on the New York Commodities Exchange.

The appeal was made in a letter sent May 5 to the comptroller, Joseph M. Otting, whose office is part of the U.S. Treasury Department, by your secretary/treasurer and GATA futures market consultant Harvey Organ.

“Exchange for physical” settlements of futures contracts long were considered emergency procedures when a seller was not able to deliver metal from an exchange-approved warehouse and wanted to settle with delivery elsewhere. But now such settlements appear to constitute most gold and silver futures settlements on the Comex. It is a strange development that appears to have been necessitated by the increasing difficulties of central banking’s gold and silver price suppression policy.

GATA has received no acknowledgment of the letter. Its text is below and a PDF copy of it is here:

http://www.gata.org/files/ComptrollerOfCurrencyLetter.pdf

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

* * *

May 5, 2018

Joseph M. Otting, Comptroller of the Currency

U.S. Treasury Department

400 7th Street, SW

Washington DC 20219

Dear Comptroller Otting:

Please let us bring to your attention financial risks to major banks involving their possibly unreported exposure to derivatives in the monetary metals markets.

In recent months gold and silver future contracts issued by U.S. banks on the New York Commodities Exchange have been moved off-exchange for delivery through a mechanism known as “exchange for physical” (EFP) contracts. Until recently use of this mechanism was considered an emergency procedure when a seller did not have access to metal for delivery through Comex warehouses. Now the mechanism seems to be in use for a large share of front-month contracts for which delivery is sought.

Here is an example that is happening at the Comex in the front active month of April for gold and the inactive delivery month of April for silver.

In gold, there were 229,436 EFP contracts for 713.64 tonnes, an average of 10,925 contracts and 1,092,500 ounces per trading day.

In silver, there were 77,150 EFP contracts for 385,750,000 ounces, an average of 3,673 contracts and 18,369,000 ounces per trading day.

London Bullion Market Association rules suggest that these contracts may not be reported to regulators. The LBMA’s bylaws say:

“Figures above exclude any contracts not subject to risk-based capital requirements, such as FX contracts with an original maturity of 14 days or less, futures contracts, written options, and basis swaps. Therefore, the total notional amount of derivatives by maturity will not add to the total derivatives figure in this table.”

We are told that these EFP contracts are transferred from the Comex to London as what are called “serial forwards” and their duration is always less than 14 days, which exempts them from being reported.

It is our understanding that in each quarter your office prepares a report detailing risk undertaken by the banks under the comptroller’s supervision.

These risks include derivatives undertaken by U.S. banks and other obligations that may cause a bank to fail. Our concern is that your office may not be aware of large unreported derivative exposure by banks.

Could you review this matter and let us know your conclusions?

Sincerely,

CHRIS POWELL

Secretary/Treasurer

HARVEY ORGAN

Consultant

Gold Anti-Trust Action Committee Inc.

7 Villa Louisa Road

Manchester, Connecticut 06043-7541

END

Your early WEDNESDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED UP TO 6.4738 /shanghai bourse CLOSED UP 7.91 POINTS OR 0.27%// HANG SANG CLOSED UP 228.02 PTS OR 0.77%

2. Nikkei closed UP 276,95 POINTS OR 1.24% / /USA: YEN RISES TO 110.06/

3. Europe stocks OPENED DEEPLY IN THE GREEN / /USA dollar index RISES TO 95.13/Euro FALLS TO 1.1565

3b Japan 10 year bond yield: RISES TO . +.04/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 110.06/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD FINALLY IN THE POSITIVE/BANK OF JAPAN LOSING CONTROL OF THEIR YIELD CURVE AS THEY PURCHASE ALL BONDS TO GET TO ZERO RATE!!

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 65.10 and Brent: 75.20

3f Gold DOWN/Yen DOWN

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil UP for WTI and UP FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund RISES TO +.37%/Italian 10 yr bond yield DOWN to 2.55% /SPAIN 10 YR BOND YIELD UP TO 1.24%

3j Greek 10 year bond yield FALLS TO : 4.36

3k Gold at $1273.80 silver at:16.29 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble UP 29/100 in roubles/dollar) 63.59

3m oil into the 64 dollar handle for WTI and 74 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 110.06 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 0.9969 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1530 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now POSITIVE territory with the 10 year RISING to +0.37%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.90% early this morning (THIS IS DEADLY TO ALL MARKETS). Thirty year rate at 3.03%

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

(courtesy Jim Reid/Bloomberg/Deutsche bank/zero hedge)

Global Markets, US Futures Rebound As Trade

War Panic Fades

After 6 consecutive declines in the Dow Jones, the longest stretch since March 2017, and erasing all of 2018’s gains, the cash index is finally set for a rebound, trading some 130 points higher in the premarket, as trade war panic fades for now (even if the list of what can go wrong next is long). As a result, the market snapshot this morning is a sea of green…

… with S&P futures trading near session highs.

“There has yet to be any positive developments on trade tensions, but the rebound of the U.S. stock market from an intra-day low helped,” said ANZ FX strategist Irene Cheung. “China’s stronger-than-expected yuan fixing should help to calm the market and the visit of the North Korean leader to China suggests that perhaps there is room for trade negotiations” she added.

More Dow strength was assured after yesterday’s decision to replace Dow Jones stalwart General Electric with Walgreens, even if the expulsion of the “last true industrial” stock was not that surprising in light of its collapsing performance…

… and 51% drop in EPS over the past year.

With lack of new trade war rumblings, traders were quick to add to risk around the globe, and European stocks also rose adding to momentum from Asia, as the panic surrounding a potential global trade war showed signs of easing. The European rally was broad-based with every sector advancing in the Stoxx Europe 600 Index, which jumped following three days of losses.

Earlier in Asia, shares in Japan and China both reversed declines, even though the Shanghai Composite Index was unable to rebound above the 3,000 level it fell through on Tuesday. The Shanghai Composite gained 0.5%, the most since June 12, after falling as much as 1.2% in morning; Shenzhen Composite Index likewise advanced 1.4% higher, while Hong Kong’s Hang Seng Index added 1.4%, and the Hang Seng China Enterprises Index +0.9%. Consumer staples and health-care stocks lead gains in both markets; firms’ reliance on domestic market makes them largely immune to a China-U.S. trade war.

China’s 10-year treasury futures dived near 0.5%, the biggest drop this month, due to profit-taking amid improving risk sentiment. It surged 0.4% on Tuesday as China’s stock market crashed.

There were some fireworks in FX trading, where the euro whipsawed as the market’s knee-jerk reaction to comments by ECB policymakers came amid otherwise muted flows. Ahead of the ECB’s Sintra conference conclusion later today, the EUR briefly erased an early loss after Bank of France Governor Francois Villeroy de Galhau said in a letter released Wednesday that the first ECB interest-rate rise “could come as of the summer of 2019.” Villeroy later specified that his comments were in line with the Governing Council’s rate guidance issued after its June 14 meeting.

The Euro then sharply tumbled to a 1.1537 day low after Governing Council member Ewald Nowotny highlighted that monetary policy divergence is helping to weaken the currency against the dollar, and that the ECB’s slow policy normalization is fueling the common currency’s weakness against the dollar, suggesting that it was the ECB’s purpose to weaken the EUR. This is what Nowotny said:

“What we also see, is that we have a development of the exchange rate that’s leading to a significant weakening of the exchange rate against the dollar. That’s surely primarily a development of the interest-rate policy, where the ECB wants to keep its rates on hold at least until summer of next year, while the U.S. has announced rate hikes, so that the difference between European and U.S. rates becomes stronger.”

The EURUSD then subsequently steadied near 1.1560 as options-related bids above 1.1500 kept absorbing selling pressure while offers according to three traders quoted by Bloomberg.

Elsewhere, the onshore yuan jumped after the People’s Bank of China set its daily reference rate at a stronger level than all analyst and trader projections.

Separately, the Bloomberg Dollar Index reversed earlier Asian-session losses following buying after the London open, and was fractionally higher on Wednesday. Part of the dollar strength came from a weakening pound ahead of a second vote on whether the U.K. Parliament should get a say on what happens if there’s no deal at the end of the Brexit talks with the EU. Sterling dropped 0.2% to touch 1.3148, a fresh seven-month low. As Bloomberg explains, if the House of Commons decides in favor of Parliament having a “meaningful vote” it could have an impact on Prime Minister Theresa May’s political future and the path Brexit negotiations take.

The relative calm spread to emerging markets, which had been hit hard in recent weeks, but developing-nation risk assets rose on Wednesday, paring their plunge a day earlier. And while there were no major outliers in the FX space, Turkey’s lira fell again, before an election this weekend.

US Treasury yields were unchanged at 2.896%. Germany’s 10Y yield rose less than 1bp to 0.38%, the first advance in more than a week, while Britain’s 10Y Gilt yield also gained 1 bp to 1.283%, also its first advance in a week. Meanwhile, Italian 10-year yields dropped 2 bps to 2.535%, the lowest in almost four weeks.

Commodities are trading mixed with oil extending gains as energy ministers emerge ahead of the key OPEC+ meeting later this week. WTI reclaimed the USD 65/bbl overnight, and is now eyeing USD 65.50/bbl while Brent trades north of USD 75.50/bbl. Yesterday’s API inventories printed a larger than expected draw, in which energy prices gradually edged higher in the aftermath. In terms of comments, the Russian Deputy Energy Minister expressed the country is ready to talk about all OPEC+ proposals and they expect to reach an agreement in terms of an ease in output cuts by June 23rd, while the Nigerian Energy Minister stated all options are on the table, however it is too early to tell if they will support a hike in production. An Iranian official said Iran will only accept production increases to push compliance to 100% on the condition that producers stick to their quotas. Elsewhere, oil output in Libya dropped to 700k BPD from just over 1mln BPD amid conflict in the region.

Moving onto the metals complex, gold (-0.3%) trades lower on the day, subdued by a firmer dollar. London copper futures bounced off 3-week lows following a near-2% loss during Tuesday’s session although escalating trade tensions cap any recovery in risk appetite. Elsewhere, iron ore futures trimmed losses amid a 5% drop in Chinese iron ore outputs for May while Shanghai steel rebounds after slumping nearly 3% in yesterday’s session.

On today’s calendar, expected data include MBA mortgage applications, current account, and existing home sales. Micron and Actuant are among companies reporting earnings. ECB President Draghi, Fed Chair Jerome Powell, RBA Governor Philip Lowe take part in a policy panel in Sintra, Portugal.

Market Snapshot

- S&P 500 futures up 0.3% to 2,775.50

- STOXX Europe 600 up 0.7% to 385.78

- MXAP up 0.6% to 169.70

- MXAPJ up 0.7% to 552.15

- Nikkei up 1.2% to 22,555.43

- Topix up 0.5% to 1,752.75

- Hang Seng Index up 0.8% to 29,696.17

- Shanghai Composite up 0.3% to 2,915.73

- Sensex up 0.5% to 35,476.49

- Australia S&P/ASX 200 up 1.2% to 6,172.58

- Kospi up 1% to 2,363.91

- German 10Y yield rose 0.9 bps to 0.382%

- Euro down 0.3% to $1.1560

- Italian 10Y yield rose 0.3 bps to 2.292%

- Spanish 10Y yield fell 1.2 bps to 1.229%

- Brent futures up 0.4% to $75.41/bbl

- Gold spot down 0.1% to $1,273.00

- U.S. Dollar Index up 0.2% to 95.20

Top Overnight News from Bloomberg

- The U.S. economy is booming this quarter as tax cuts power consumers and businesses. Yet risks are mounting that the high will be short-lived

- China’s direct investment in the U.S. slumped in the first half of this year, amid deteriorating economic relations between the two nations, according to research firm Rhodium Group LLC

- The European Union is on course to hand dozens of U.K.-based companies a pre-Brexit tax bombshell, according to people familiar with a state-aid probe that could lead to bills exceeding 1 billion pounds ($1.3 billion)

- The gap between real barrels and those that exist only on paper means that the impact on the market of any agreement between the OPEC and its allies to increase supply is likely to be about one-third smaller than the headline announcement, according to Bloomberg calculations

- Iran put itself on a collision course with Saudi Arabia at this week’s OPEC meeting, rejecting a potential compromise that would allow a small oil-production increase to appease energy consumers

Asia stocks traded mixed as the region attempted to compose itself from the prior day’s sell-off and after some late reprieve on Wall St. where the majors still finished negative but well off worst levels, aside from the DJIA which underperformed as industrials and materials suffered the brunt of the heightened trade tensions. ASX 200 (+1.0%) was the biggest gainer and reached its highest intraday level in a decade with upside led by its largest weighted financials sector, while Nikkei 225 (+0.6%) traded indecisive and at the whim of a choppy currency. Hang Seng (+0.3%) swung between gains and losses, while Shanghai Comp. (-0.6%) remained downbeat on the tariff-threat overhang. Finally, 10yr JGBs are marginally lower with demand sapped by the improved picture in the region, although downside was also limited amid the indecision throughout most of the session in Japan and with the BoJ present in the market for JPY 690bln of JGBs in the belly to super-long end.

Top Asian News

- Thailand Bucks Southeast Asia Trend by Keeping Rates on Hold

- Ackman-Backed Platform Is Said to Discuss Unit Sale With UPL

- Goldman Sachs Hires Veteran Dealmaker for China Investment Bank

- China’s Investment in the U.S. Is Collapsing as Trade War Flares

- China Stocks Bear Market to Last Next 12 Months: Morgan Stanley

European equities are recovering some of the losses seen yesterday as trade war news flow slows. The FTSE 100 is the outperforming bourse, coming off of month lows hit in Tuesday’s trade, as the GBPUSD extends losses at 6 month lows. The DAX is currently underperforming, with automotive names hit (Continental (-0.6%), Daimler (-0.5%)).Volkswagen (+0.8%) is bucking the trend, however, following an announcement of a possible alliance with Ford to develop and make transporter vans as according to sources. Imperial Brand’s (+3.0%) naming as a top pick at Liberum has pushed the co. to the top of the FTSE 100. Dialog Semiconductor (+2.2%) confirmed it is in discussions on a potential acquisition of Synaptics and is to proceed with due diligence.

Top European News

- U.K. Companies Said to Face Pre-Brexit Tax Bombshell From EU

- Nowotny Says Euro Weakening on Fed-ECB Policy Path Differences

- The Macron-Merkel Euro Plan Is Released. Here’s How It Stacks Up; Franco-German Plan Adds to Pressure on Banks to Tackle Bad Debt

- Ferragamo Plunges After Controlling Family Sells Shares

Commodities are trading mixed with oil extending gains as energy ministers emerge ahead of the key OPEC+ meeting later this week. WTI reclaimed the USD 65/bbl overnight, and is now eyeing USD 65.50/bbl while Brent trades north of USD 75.50/bbl. Yesterday’s API inventories printed a larger than expected draw, in which energy prices gradually edged higher in the aftermath. In terms of comments, the Russian Deputy Energy Minister expressed the country is ready to talk about all OPEC+ proposals and they expect to reach an agreement in terms of an ease in output cuts by June 23rd, while the Nigerian Energy Minister stated all options are on the table, however it is too early to tell if they will support a hike in production. An Iranian official said Iran will only accept production increases to push compliance to 100% on the condition that producers stick to their quotas. Elsewhere, oil output in Libya dropped to 700k BPD from just over 1mln BPD amid conflict in the region. Moving onto the metals complex, gold (-0.3%) trades lower on the day, subdued by a firmer dollar. London copper futures bounced off 3-week lows following a near-2% loss during Tuesday’s session although escalating trade tensions cap any recovery in risk appetite. Elsewhere, iron ore futures trimmed losses amid a 5% drop in Chinese iron ore outputs for May while Shanghai steel rebounds after slumping nearly 3% in yesterday’s session.

In currency markets, it was all eyes on the EUR which in contrast to broadly still waters elsewhere, some choppy price action on early ECB commentary from the Sintra symposium as the single currency rebounded further from Tuesday’s lows and towards 1.1600 vs the Usd on an apparent less dovish nuance from Villeroy vis-à-vis rate guidance (subsequently corrected to conform with consensus), but then retreated to sub-1.1540 when Nowotny noted Eur depreciation vs the Dollar on divergent interest rate policy. Technically, 1.1510 is still nearest support vs circa 1.1600 resistance and the 20DMA at 1.1686. CHF/JPY: Both on the back foot vs a firm Greenback, as the DXY holds above 95.000 and risk sentiment overall stabilises, but with the Franc also increasingly wary about SNB intervention via Thursday’s policy meeting in the shape of NIRP and direct FX action should the Chf strengthen too much. Usd/Chf hovering above 0.9950 and Eur/Chf over 1.1500. Meanwhile, after largely irrelevant and rather dated BoJ minutes Usd/Jpy has bounced off yesterday’s base into a firmer range around 110.00, but perhaps capped by decent option expiry interest at and north of the big figure (around 2 bn from 110.00-05 and then between 110-40-50). GBP/CAD: Still hampered by Brexit and NAFTA uncertainty, with Cable struggling around a chart pivot at 1.3165, while the Loonie has extended losses vs its US counterpart to 1.3300+ and appears vulnerable or primed for a test of 12 month lows at 1.3348.

Looking at the day ahead, the ECB’s Villeroy, Knot, Lautenschlager and Coeure will speak at separate events while at Sintra there is a policy panel featuring President Draghi, Fed Chair Powell and BoJ Governor Kuroda. So expect lots of headlines. Away from that, Germany’s PPI for May, UK CBI selling prices data for June and May existing home sales in the US will be released. Elsewhere, the OPEC International Seminar is due to begin in Vienna.

US Event Calendar

- 7am: MBA Mortgage Applications, prior -1.5%

- 8:30am: Current Account Balance, est. $129.0b deficit, prior $128.2b deficit

- 9:30am: Draghi, Powell, Kuroda and Lowe speak in Sintra, Portugal

- 10am: Existing Home Sales, est. 5.52m, prior 5.46m; MoM, est. 1.1%, prior -2.5%

DB’s Jim Reid concludes the overnight wrap

A quieter day at the World Cup yesterday but glancing at Russia vs Egypt last night reminded me of one of my favourite jokes. What do you call a young river in Egypt? Punchline at the end after the day ahead.

Not even an ancient Egyptian prophet could be expected to predict the exact path of this escalating trade war at the moment. The war of words are clearly worsening though and markets are starting to move towards pricing in this not being a short-term spat. It’s fair to say they have a long way further to fall if a compromise isn’t found, but we also have to try to work out what Mr Trump’s agenda and goal is. Is this a genuine crusade to get huge concessions from the Chinese or is he making a calculated gamble ahead of the mid-terms and will be happy to get relatively small last minute concessions that he can grandstand to voters? The problem with the latter outcome is that we have 4 and half months until voters go to the polls and thus plenty of potential uncertainty. Maybe Mr Trump is a master tactician as the tax cut does give the US economy and equity markets enough strength for him to be able to avoid blinking for now. For someone that focuses on equity markets like Mr Trump, the S&P 500 is still up +3.33% in 2018 (DOW went negative YTD again yesterday though) and outperforming virtually every other main global equity market. With Chinese equities down -3.5% to -5.8% yesterday and down c0.5% this morning, his actions are creating more issues for others than himself on a relative basis at the moment. Until the pain in US markets is higher, then he may carry on with his current tactics.

The negative trade rhetoric continued after we went to print yesterday. President Trump told the National Federation of Independent business that “we’ve got to do something about it….we’re going to make it fair”. Meanwhile, White House adviser Navarro said “China does have much more to lose than we do” and that “China may have underestimated the strong resolve of President Trump”. On the other side, China’s PBOC sought to calm market sentiment as it indicated the central bank was prepared for outside shocks and “we’ll be forward-looking, prepare relevant policies and comprehensively use all kinds of monetary policy tools”. Meanwhile, Governor Yi also said China “has room to face all sorts of trade friction”.

This morning in Asia, markets are broadly higher with the Kospi (+1.03%), Nikkei (+0.56%) and Hang Seng (+0.41%) modestly up while Chinese bourses are down 0.1% to 0.6% as we type. Meanwhile China’s Yuan is slightly stronger vs. the dollar for the first time in three days (+0.10%) while futures on the S&P are marginally up. Elsewhere onto the latest BOJ minutes, most members said it was appropriate to stop providing the projected timing on when the 2% inflation target will be achieved. Members also agreed that even if the projected timing was reviewed in the latest meeting, the Bank’s monetary policy stance would not change at all.

Turning back to trade tensions and its potential impacts, DB’s Zhiwei Zhang and team have updated their analysis and estimate that if the trade war escalates to include US$200bn of Chinese exports at a tariff rate of 10%, it would have a meaningful impact on both sides, with the cumulative impact on China’s GDP growth at 0.2-0.3ppt (this includes the 25% tariff on the first $50bn of exports). The products affected would likely include consumer goods, which the US government has so far been carefully trying to avoid hitting. Notably, the big question on our economists’ mind is whether China will move beyond trade and target US business interests in China. The team estimate that US firms sold US$448bn worth of goods and services to China in 2017, with c37% through trade and c63% ($280bn) through local operations by US subsidiaries in China. Overall, China has not threatened officially to target US firms in China, but it’s one to watch and a risk that our economists see as rising as trade tensions build.

Our US economists’ base case remains that the trade conflict with China will be settled before it progresses significantly beyond the initial imposition of tariffs on $50bn of imports in both directions. However, recent events have clearly increased the risks that the conflict will begin to have measurable negative economic effects. If things deteriorate further, there is the possibility of a stock market correction in the -5% to -10% range, although if a settlement is then negotiated quickly, equities could recover and the risks to GDP mitigated. However, if a trade war gathers further momentum, it could well induce the next recession.

As for markets yesterday, risk assets sold off while core bonds and the Yen firmed as the US / China trade tensions intensified. China’s Shanghai. Comp. dropped -3.78% to a two year low, while European bourses also weakened, with the export biased DAX (-1.22%) leading the decline. That said, the Stoxx 600 (-0.70%) and S&P (-0.40%) was relatively resilient, as the latter staged a steady recovery throughout the day while the domestically focused small- cap Russell 2000 index edged up +0.06%. Within the S&P, materials and industrials stocks that are more exposed to a potential trade war with China underperformed (GM -3.9%; Boeing -3.8%; Caterpillar -3.6%), while telco, health care and utilities stocks all advanced. Meanwhile the VIX rose for the second straight day (+8.5% to 13.35).

Government bonds firmed on the back of flight to safety and continued dovish commentaries from the ECB. 10y yields on US treasuries fell as much as 6.6bp intraday before closing -2bp lower at 2.897%, while Bunds (-2.6bp), OATs (-2.1bp) and Gilts (-4.1bp) were also in demand. The US 2s10s spread has nudged 1.5bp lower yesterday to a fresh post GFC low of 35.2bp. In Europe, Mr Draghi seemed to reinforce the ECB’s dovish stance as he noted “we’ll remain patient in determining the timing of the first rate rise and will take a gradual approach to adjusting policy thereafter”. He added that “the path of very short-term interest rates that is implicit in the term structure of today’s money-market interest rates broadly reflects these principles”. Meanwhile, the ECB’s Liikanen took a step further and added that the ECB can hold rates steady even after summer 2019 “if necessary”.

In commodities, soybeans fell to a fresh c2 year low (-2.20%) while wheat (-2.39%) and base metals (Copper -1.07%; Zinc -0.89%; Aluminium -1.12%) retreated on higher trade tensions. WTI oil also traded lower ahead of this Friday’s OPEC meeting (-1.18%). Over in FX, the US dollar index firmed for the first time in three days (+0.27%) while the Euro and Sterling fell -0.28% and -0.54% respectively.

Away from the markets and onto “a new chapter” for the EU as termed by Germany’s Merkel. After her meeting with French President Macron, Chancellor Merkel said Germany and France has agreed to cooperate to reform the EU’s asylum system as we both “understand the topic of migration is a joint task” and “our goal remains a European answer to the challenge”. Elsewhere, the two leaders agreed to an in principle plan to strengthen the Euro area, including setting up a euro-area budget and a crisis backstop under the ESM (European stability mechanism). Overall, Ms Merkel summed it up as “an important step for Europe….we can say we’ve taken a small step along the road”. Meanwhile Mr Macron suggested the proposal will be presented to other countries, with specifics to be worked out later this year and the plans to take effect from 2021. Staying with Europe, today sees a key Brexit vote in the U.K. House of Commons and again covers how much say parliament should have on the final deal or if negotiations break down. If the Government loses it could have major implications for PM May so one to watch.

Before we take a look at today’s calendar, we wrap up with other data releases from yesterday. In the US, the May housing starts rebounded more than expected, up 5% mom to 1.35m (vs. 1.31m expected). Conversely, housing permits fell more than expected at -4.6% mom to 1.30m (vs. 1.35m), but annual growth is still up 8% yoy and broadly in line with growth in recent months. In Europe, the ECB’s April current account surplus was narrower than last month at €28.4bn (vs. €32.8bn previous), but still lifted the 12-month running surplus to a new high of €410bn.

Looking at the day ahead, the ECB’s Villeroy, Knot, Lautenschlager and Coeure will speak at separate events while at Sintra there is a policy panel featuring President Draghi, Fed Chair Powell and BoJ Governor Kuroda. So expect lots of headlines. Away from that, Germany’s PPI for May, UK CBI selling prices data for June and May existing home sales in the US will be released. Elsewhere, the OPEC International Seminar is due to begin in Vienna.

………..Juvenile.

3. ASIAN AFFAIRS

i)WEDNESDAY MORNING/TUESDAY NIGHT: Shanghai closed UP 7.91 POINTS OR 0.27% /Hang Sang CLOSED UP 228.02 POINTS OR 0.77% / The Nikkei closed UP 276.95 POINTS OR 1.24% /Australia’s all ordinaires CLOSED UP 1.06% /Chinese yuan (ONSHORE) closed UP at 6.4738/Oil UP to 65.10 dollars per barrel for WTI and 75.10 for Brent. Stocks in Europe OPENED DEEPLY IN THE GREEN//. ONSHORE YUAN CLOSED UP AT 6.4738 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.4777/ONSHORE YUAN TRADING STRONGER AGAINST OFFSHORE YUAN/ONSHORE YUAN TRADING MUCH STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING MUCH WEAKER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW LOOKS LIKE A FULL TRADE WAR IS BEGINNING/

3 a NORTH KOREA/USA

North Korea/South Korea/usa

3 b JAPAN AFFAIRS

c) REPORT ON CHINA/HONG KONG

China/USA

4. EUROPEAN AFFAIRS

DEUTSCHE BANK/GERMANY/EURO ZONE

As always, a terrific commentary from the Mises Institute (Polleit). Here the author describes the problems at Deutsche bank as they are already deleveraging. This creates a deflationary cycle and is opposite to what the central bank (ECB ) wants. Central banks must inflate their debt and will always supply the necessary fiat money cheap to the banks. The guys at the top of the pyramid benefit and everybody else suffers.

this is where we are heading..

a must read.

THIS MORNING

(courtesy Polleit/Mises Institute_

Deutsche Bank’s Troubles Raise Worries About

The Future Of The Euro Zone

Authored by Thorstein Polleit via The Mises Institute,

The euro banking sector is huge: In April 2018, its total balance sheet amounted to 30.9 trillion euro, accounting for 268 per cent of gross domestic product (GDP) in the euro area. Unfortunately, however, many euro banks are in lousy shape. They suffer from low profitability and carry an estimated total bad loan exposure of around 759 billion euro, which accounts for roughly 30 per cent of their equity capital.

Share price developments suggest that investors have lost quite some confidence in the viability of euro banks’ businesses: While US bank stocks are up 24 per cent since the beginning of 2006, the index for euro-area bank stocks is still down by around 70 per cent. Perhaps most notably, ’Germany’s two largest banks, Deutsche Bank and Commerzbank, have lost 85 and 94 per cent, respectively, of their market capitalization.

With a balance sheet of close to 1.5 trillion euro in March 2018, Deutsche Bank accounted for around 45 per cent of German GDP. In international comparison, this an enormous, downright frightening dimension. It is mostly the result of the bank still having an extensive (though not profitable) footprint in the international investment banking business. The bank has already started reducing its balance sheet, though.

Beware of big banks — this is what we could learn from the latest financial and economic crises 2008/2009. Big banks have the potential to take an entire economy hostage: When they get into trouble, they can drag everything down with them, especially the innocent bystanders – taxpayers and, if and when the central banks decide to bail them out, those holding fiat money and fixed income securities denominated in fiat money.

Banking Risks