GOLD: $1267.30 DOWN $1.45(COMEX TO COMEX CLOSINGS)

Silver: $16.33 DOWN 12 CENTS (COMEX TO COMEX CLOSINGS)

Closing access prices:

Gold $1265.90

silver: $16.32

TOMORROW IS OPTIONS EXPIRY FOR COMEX/ GOLD AND SILVER AND THIS FRIDAY, FOR OTIC/LONDON GOLD SO EXPECT MORE WHACKING BY THE CROOKS.

For comex gold:

JUNE/

NUMBER OF NOTICES FILED TODAY FOR JUNE CONTRACT:19 NOTICE(S) FOR 1900 OZ

TOTAL NOTICES SO FAR 6836 FOR 683600 OZ (21.262 tonnes)

For silver:

JUNE

3 NOTICE(S) FILED TODAY FOR

15,000 OZ/

Total number of notices filed so far this month: 1076 for 5,380,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: BID $6017/OFFER $6167: DOWN $647(morning)

Bitcoin: BID/ $6117/offer $6217: UP $100 (CLOSING/5 PM)

end

First Shanghai gold fix comes at 10 pm est

The second Shanghai gold fix: 2:15 pm

First Shanghai gold fix gold: 10 pm est: 1274.11

NY price at the same time: 1270.45

PREMIUM TO NY SPOT: $4.66

Second gold fix early this morning: 1273.44

USA gold at the exact same time:1265180

PREMIUM TO NY SPOT: $8.26

AGAIN, SHANGHAI REJECTS NEW YORK PRICING.

WE WILL NOT PROVIDE LONDON FIXES AS THEY ARE NOT ACCURATE AS TO WHAT IS GOING ON AT THE SAME TIME FRAME.

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total OPEN INTEREST FELL BY A TINY 206 CONTRACTS FROM 219,254 UP TO 219,048 ACCOMPANYING FRIDAY’S GOOD 12 CENT GAIN IN SILVER PRICING. HOWEVER AS WE ARE NOW WELL INTO THE NON ACTIVE DELIVERY MONTH OF JUNE WE CONTINUE TO WITNESS LONGS PACK THEIR BAGS AND MIGRATE OVER TO LONDON IN GREATER NUMBERS. WE WERE NOTIFIED THAT WE HAD A GOOD SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP: 1202 EFP’S FOR JULY, 248 EFP’S FOR SEPT. , 0 EFP’S FOR DECEMBER AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE: OF 1450 CONTRACTS. WITH THE TRANSFER OF 1450 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 1450 EFP CONTRACTS TRANSLATES INTO 7.25 MILLION OZ ACCOMPANYING:

1.THE 12 CENT GAIN IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES STANDING FOR JUNE COMEX DELIVERY. (5.380 MILLION OZ) DESPITE IT BEING A NON ACTIVE DELIVERY MONTH.

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF JUNE:

57,140 CONTRACTS (FOR 17 TRADING DAYS TOTAL 57,140 CONTRACTS) OR 285.70 MILLION OZ: (AVERAGE PER DAY: 3361 CONTRACTS OR 16.81 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH: 285.70* MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 39.77% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* WE HAVE ALREADY PASSED LAST MONTH AND CLOSING IN ON THE RECORD MONTH OF APRIL.

ACCUMULATION IN YEAR 2018 TO DATE SILVER EFP’S: 1,601.82 MILLION OZ.

ACCUMULATION FOR JAN 2018: 236.879 MILLION OZ

ACCUMULATION FOR FEB 2018: 244.95 MILLION OZ

ACCUMULATION FOR MARCH 2018: 236.67 MILLION OZ

ACCUMULATION FOR APRIL 2018: 385.75 MILLION OZ

ACCUMULATION FOR MAY 2018: 210.05 MILLION OZ

RESULT: WE HAD A SMALL SIZED DECREASE IN COMEX OI SILVER COMEX OF 206 DESPITE THE GOOD 12 CENT GAIN IN SILVER PRICE. WE HAVE NOW ENTERED THE NEW NON ACTIVE MONTH OF JUNE AND THE CME NOTIFIED US THAT IN FACT WE HAD A GOOD SIZED EFP ISSUANCE OF 1450 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) . FROM THE CME DATA: 1202 EFP CONTRACTS FOR JULY, 248 EFP’S FOR SEPT, 0 EFP’S FOR DECEMBER AND ZERO FOR ALL OVER MONTHS FOR A DELIVERABLE FORWARD CONTRACT OVER IN LONDON WITH A FIAT BONUS (TOTAL: 1450). TODAY WE GAINED AN CONSIDERABLE: 1619 TOTAL OI CONTRACTS ON THE TWO EXCHANGES: i.e.1450 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH AN INCREASE OF 169 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED WITH A 12 CENT GAIN IN PRICE OF SILVER AND A CLOSING PRICE OF $16.45 WITH RESPECT TO YESTERDAY’S TRADING. YET WE STILL HAVE A GIGANTIC AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY IN THIS NON ACTIVE JUNE DELIVERY MONTH. IT SURE LOOKS LIKE A FAILED BANKER SHORT COVERING EXERCISE!!

In ounces AT THE COMEX, the OI is still represented by OVER 1 BILLION oz i.e. 1.097 MILLION OZ TO BE EXACT or 157% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT JUNE MONTH/ THEY FILED AT THE COMEX: 3 NOTICE(S) FOR 15,000 OZ OF SILVER

IN SILVER, WE HAVE NOW SET THE NEW RECORD OF OPEN INTEREST AT 243,411 AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $16.51 ON APRIL 9.2018.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ AND MAY: 36.285 MILLION OZ /AND JUNE/2018 (5.380 MILLION OZ SO FAR)

- HUGE RECORD OPEN INTEREST IN SILVER 243,411 CONTRACTS (OR 1.217 BILLION OZ/ SET APRIL 9/2018

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017

- RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ (FINAL)

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT).

In gold, the open interest ROSE BY A CONSIDERABLE 2976 CONTRACTS UP TO 473,193 WITH THE RISE IN THE GOLD PRICE/FRIDAY’S TRADING (A TINY RISE OF $0.25). WE ARE NOW IN THE ACTIVE DELIVERY MONTH OF JUNE. NO DOUBT THE BOYS ARE CASHING IN THEIR COMEX LONGS TO BEGIN THE PROCESS TO MOVE INTO LONDON FORWARDS. THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 4393 CONTRACTS : JUNE SAW THE ISSUANCE OF 0 CONTRACTS , AND AUGUST SAW THE ISSUANCE OF: 4393 CONTRACTS WITH ALL OTHER MONTHS ZERO. The new OI for the gold complex rests at 473,193. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE A STRONG OI GAIN IN TOTAL CONTRACTS ON THE TWO EXCHANGES: 2976 OI CONTRACTS INCREASED AT THE COMEX AND A FAIR SIZED 4393 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN: 7369 CONTRACTS OR 736,900 OZ = 22.92 TONNES. AND STRANGELY ALL OF THIS DEMAND OCCURRED WITH A TINY RISE OF $0.25.???

FRIDAY, WE HAD 12151 EFP’S ISSUED.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF MAY : 183,602 CONTRACTS OR 18,360,200 OZ OR 571.07 TONNES (17 TRADING DAYS AND THUS AVERAGING: 10,800 EFP CONTRACTS PER TRADING DAY OR 1,080,000 OZ/ TRADING DAY),,

TO GIVE YOU AN IDEA AS TO THE HUGE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 17 TRADING DAYS IN TONNES: 571.07 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2017, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 2555 TONNES

THUS EFP TRANSFERS REPRESENTS 571.07/2550 x 100% TONNES = 22.39% OF GLOBAL ANNUAL PRODUCTION SO FAR IN JUNE ALONE.***

ACCUMULATION OF GOLD EFP’S YEAR 2018 TO DATE: 4,022.90* TONNES *SURPASSED ANNUAL PROD’N

ACCUMULATION OF GOLD EFP’S FOR JANUARY 2018: 653.22 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR FEBRUARY 2018: 649.45 TONNES (20 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR MARCH 2018: 741.89 TONNES (22 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR APRIL 2018: 713.84 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR MAY 2018: 693.80 TONNES ( 22 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR JUNE 2018 (21 TRADING DAYS)

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A CONSIDERABLE SIZED INCREASE IN OI AT THE COMEX OF 2976 DESPITE THE TINY $0.25 RISE IN PRICING GOLD TOOK ON FRIDAY // ($0.25 RISE). WE ALSO HAD A FAIR SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 4393 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 4393 EFP CONTRACTS ISSUED, WE HAD A STRONG NET GAIN OF 9407 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

4393 CONTRACTS MOVE TO LONDON AND 2976 CONTRACTS INCREASED AT THE COMEX. (in tonnes, the GAIN in total oi equates to 22.92 TONNES). ..AND BELIEVE IT OR NOT BUT ALL OF THIS DEMAND OCCURRED AT THE COMEX WITH A RISE OF $0.25 IN TRADING!!!.

we had: 19 notice(s) filed upon for 1900 oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD DOWN $1.45 TODAY: / NO CHANGES IN GOLD INVENTORY AT THE GLD/

/GLD INVENTORY 824.63 TONNES

Inventory rests tonight: 824/63 tonnes.

SLV/

WITH SILVER DOWN 12 CENTS TODAY /NO CHANGES IN THE SILVER: ANOTHER DEPOSIT OF 941,000 OZ/

/INVENTORY RESTS AT 320.301 MILLION OZ/

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER FELL BY A TINY SIZED 209 CONTRACTS from 219,254 DOWN TO 219,048 (AND, FURTHER FROM THE NEW COMEX RECORD SET /APRIL 9/2017 AT 243,411/SILVER PRICE AT THAT DAY: $16.53). THE PREVIOUS RECORD OTHER THAN WAS ESTABLISHED AT: 234,787, SET ON APRIL 21.2017 OVER ONE YEAR AGO. THE PRICE OF SILVER ON THAT DAY: $17.89. OUR CUSTOMARY MIGRATION OF COMEX LONGS MORPH INTO LONDON FORWARDS CONTINUES AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

1202 EFP’S FOR JULY, 248 EFP CONTRACTS FOR SEPT., 0 EFP CONTRACTS FOR DECEMBER AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 1450 CONTRACTS . EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI GAIN AT THE COMEX OF 169 CONTRACTS TO THE 1450 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A GOOD GAIN OF 1244 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES: 6.220 MILLION OZ!!! AND THIS OCCURRED WITH A GOOD 12 CENT GAIN IN PRICE . THE BANKERS ORCHESTRATED THEIR CONSTANT AND NEVER ENDING RAIDS DESPERATELY TRYING TO PARE THEIR GIGANTIC OPEN INTEREST SHORT ON BOTH EXCHANGES WITH HARDLY ANY SUCCESS. HOWEVER A DRAMATIC AMOUNT OF EFP ISSUANCE IS HEADING OVER TO LONDON AND NO DOUBT WE WILL COME CLOSE TO BREAKING APRIL’S RECORD OF 385 MILLION OZ.

RESULT: A TINY SIZED DECREASE IN SILVER OI AT THE COMEX DESPITE THE GOOD THE 12 CENT GAIN THAT SILVER TOOK IN PRICING ON YESTERDAY. BUT WE ALSO HAD ANOTHER STRONG SIZED 1450 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR JUNE, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)MONDAY MORNING/SUNDAY NIGHT: Shanghai closed DOWN 30.42 POINTS OR 1.05% /Hang Sang CLOSED DOWN 277.31 POINTS OR 1.29% / The Nikkei closed DOWN 178.68 POINTS OR 0.79% /Australia’s all ordinaires CLOSED DOWN 0.21% /Chinese yuan (ONSHORE) closed DOWN at 6.5402 AS POBC EXERCISED A HUGE DEVALUATION/Oil UP to 68.80 dollars per barrel for WTI and 74.33 for Brent. Stocks in Europe OPENED DEEPLY IN THE RED//. ONSHORE YUAN CLOSED DOWN AT 6.5402 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.5472 HUGH DEVALUATION/ONSHORE YUAN TRADING STRONGER AGAINST OFFSHORE YUAN/ONSHORE YUAN TRADING MUCH WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING MUCH WEAKER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR IS BEGINNING/

/NORTH KOREA/SOUTH KOREA

i)North Korea/South Korea/USA

b) REPORT ON JAPAN

3 c CHINA

i)China/USA

China tries to compensate for the trade wars by unlocking 700 billion yuan in the Reverse Ratios as it is experiencing massive defaults and margin calls

(courtesy zerohedge)

ii)There is no question that global growth has been occurring due to credit creation inside China and that has been the lightening rod for good economic growth for the world. Now we are witnessing a huge slowdown in Chinese liquidity and credit impulse and that is sending shockwaves to the rest of the world

( zerohedge/Nomura/McElligott)

4. EUROPEAN AFFAIRS

i)Germany/EU/USA/SYRIA/ITALY

Our resident expert on European affairs gives a terrific commentary on how Europe et al got into the mess they are now facing

( TomLuongo)

ii)GREECE

The Troika kicked the can down the road again. Greece’s debt to GDP is still a staggering 180 but debt servicing does not begin for another 20 years or so. Greece is enslaved to Brussels for eternity unless the return to the drachma

( Mish Shedlock/Mishtalk)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

i)JORDAN/SYRIA/IRAN/ISRAEL/USA/RUSSIA

We have been highlighting to you the area of south west Syria which is of extreme importance to Israel. It is now being inhabited by ISIS and rebels who are against Assad. For the last few years, Israel has been helping both parties. Assad has been warned by the USA to stay away from this area but I guess he is not listening as he is sending Syrian troops along with Hezbehollah fighters to liberate that last part of Syria not under his control. Israel will never have any Iranian forces next to her in the Golan. There is going to be a fierce battle over this region and just about everybody will be involved

( zerohedge)

ii)Italy/Migrants/EU

The Turkish lira initially surges after the no surprise Erdogan re-election. Early this morning the Lira tumbled to 4.70 to the dollar

( zerohedge)

6 .GLOBAL ISSUES

7. OIL ISSUES

The supposed deal on Friday has now ended with output confusion. The deal is unraveling:

(courtesy zerohedge)

8. EMERGING MARKET

9. PHYSICAL MARKETS

i)Sprott praises our letter to the OCC concerning EFP’s

(courtesy GATA/Eric Sprott/Craig Hemke)

ii)Ron Paul continues to correctly harp on the theme of constantly manipulation of markets and the most important the rigging of gold

(courtesy Paul /Mises Alabama)

iii)The rial has plummeted from 80,000 to a record 90,000 per dollar as gold rises above a 300% rise in just 3 months

(courtesy Radio/Farda)

10. USA stories which will influence the price of gold/silver)

i)Monday morning trading

Chaos, this morning as Trump initiates restricting investments from China into the USA and China continues to weaponize the yuan by devaluing.

( zerohedge)

b)Strange!! Mnuchin calls all 3: Bloomberg, Wall Street Journal and the London’s Financial times as issuing fake news on the USA restricting Chinese investment into the uSA

d)Who is running USA trade policy? Now Navarro says that “there is no plan for investment restrictions”. Trump will not allow any Chinese company to buy USA tech companies and steal their technology(courtesy zerohedge)

ii)Market data

iib)Somebody at the Dallas fed exclaims that the trade wars have now caused stagflation to enter into the uSA as input costs have increased dramatically.( zerohedge)

iv)Trump will not like this at all: Harley Davidson will move some of its production of motor bicycles outside of the uSA due to the rise of Eu tariffs( zerohedge)

v)SWAMP STORIES

a)Meet our two new love birds: Agent 5 Moyer and Agent 1 who have since got married. Also agent no 2 has been identified as: Clinesmith

( zerohedge)

b)Strzok has been subpoenaed and must appear before Congress in 5 days. The date set is June 27/2018.

( zerohedge)

c)We now have proof from Ben Rhodes advisor to Obama that the USA under Obama’s leadership supported ISIS/rebels in Syria

( zerohedge)

d)This is getting real bad as the left attacks two important employees of the Government in eating establishments as attack them while trying to eat out

e)What a farce: Mueller now snags Blackwater founder Erik Prince, phones and computer. He is the brother of Education Minister Betsy de Voes

Trading Volumes on the COMEX

PRELIMINARY COMEX VOLUME FOR TODAY: 188,721 contracts

CONFIRMED COMEX VOL. FOR YESTERDAY: 197,819 contracts

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

And now for the wild silver comex results.

Total silver OI FELL BY A TINY SIZED 206 CONTRACTS FROM 217,254 UP TO 219,048 (AND A LITTLE FURTHER FROM THE THE NEW RECORD OI FOR SILVER SET APRIL 9.2018/ 243,411 CONTRACTS) ACCOMPANYING THE 12 CENT GAIN IN SILVER PRICING/ YESTERDAY. SINCE WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF JUNE, WE WERE INFORMED THAT WE HAD A GOOD SIZED 1202 EFP CONTRACT ISSUANCE FOR JULY, 248 EFP CONTRACTS FOR SEPT., 0 EFP CONTRACTS FOR DECEMBER AND ZERO FOR ALL OTHER MONTHS. THESE EFPS WERE ISSUED TO COMEX LONGS WHO RECEIVED A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. THE TOTAL EFP’S ISSUED: 1450. ON A NET BASIS WE GAINED 1244 SILVER OPEN INTEREST CONTRACTS AS WE OBTAINED A 206 CONTRACT GAIN AT THE COMEX COMBINING WITH THE ADDITION OF 1450 OI CONTRACTS NAVIGATING OVER TO LONDON.

NET GAIN ON THE TWO EXCHANGES: 1244 CONTRACTS

AMOUNT STANDING FOR SILVER AT THE COMEX

We are now in the NON active delivery month of JUNE and here the front month ROSE BY 2 contracts RISING TO 3 contracts. We had 0 notices filed upon yesterday so we gained 2 contracts or an additional 10,000 oz will stand in this non active delivery month of June AS TODAY SOMEBODY WAS IN URGENT NEED OF PHYSICAL ON THIS SIDE OF THE POND

The next big active delivery month for silver is July and here the OI LOST 111,133 contracts DOWN to 62,578. The next delivery month is August and here we GAINED 21 contracts to stand at 554 The next active delivery month after August for silver is September and here the OI ROSE by 10,227 contracts UP to 116,763

FOR COMPARISON AT THIS TIME IN THE DELIVERY CYCLE, JUNE 26.2017, FOR SILVER, WE HAD 48,785 OPEN INTEREST CONTACTS STILL STANDING.VS 62,578 TODAY. LAST YEAR AT THIS TIME WE HAD 4 MORE TRADING DAYS LEFT BEFORE FIRST DAY NOTICE (JUNE 27-JUNE 30), THIS YEAR WE HAVE 4 MORE TRADING DAYS BEFORE FDN (JUNE 26-29). WE NO DOUBT WILL HAVE A DOOZY AMOUNT OF SILVER OZ STANDING FOR THE HUGE JULY CONTRACT MONTH.

FROM LAST YEARS DATA, ON FIRST DATE NOTICE FOR THE JULY 2017 COMEX DELIVERY MONTH WE HAD 12.115 MILLION OZ OF SILVER STANDING FOR DELIVERY. AT MONTH’S END WE HAD 16.435 MILLION OZ EVENTUALLY STAND AS WE ALREADY HAD QUEUE JUMPING BEGIN IN EARNEST FROM APRIL 2017 ONWARD EVEN TO TODAY.

We had 3 notice(s) filed for 15,000 OZ for the JUNE 2018 COMEX contract for silver

INITIAL standings for JUNE/GOLD

JUNE 25/2018.

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz |

99.85 OZ

Delaware

|

| Deposits to the Dealer Inventory in oz | NIL oz |

| Deposits to the Customer Inventory, in oz | nil

oz |

| No of oz served (contracts) today |

19 notice(s)

1900 OZ

|

| No of oz to be served (notices) |

115 contracts

(11,500 oz)

|

| Total monthly oz gold served (contracts) so far this month |

6836 notices

683,600 OZ

21.262 TONNES

|

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

For JUNE:

Today, 0 notice(s) were issued from JPMorgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equates to 19 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped/ Received) by j.P.Morgan customer account.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

To calculate the INITIAL total number of gold ounces standing for the JUNE. contract month, we take the total number of notices filed so far for the month (6836) x 100 oz or 683600 oz, to which we add the difference between the open interest for the front month of JUNE. (134 contracts) minus the number of notices served upon today (19 x 100 oz per contract) equals 695,100 oz, the number of ounces standing in this active month of JUNE (21.620 tonnes)

Thus the INITIAL standings for gold for the JUNE contract month:

No of notices served (6836 x 100 oz) + {(134)OI for the front month minus the number of notices served upon today (19 x 100 oz )which equals 695,100 oz standing in this active delivery month of JUNE .

WE LOST A SMALL 36 CONTRACTS OR AN ADDITIONAL 3600 OZ WILL NOT STAND FOR DELIVERY AS THESE GUYS MORPHED INTO LONDON BASED FORWARDS AND RECEIVED AN ADDITIONAL SWEETENER FOR THEIR EFFORT..

THERE ARE ONLY 7.334 TONNES OF REGISTERED GOLD AVAILABLE FOR DELIVERY AGAINST 21.620 TONNES STANDING WHICH IS MAKING THIS JUNE CONTRACT MONTH AN EXTREMELY INTERESTING ONE TO WATCH.

WE HAVE HAD 3 ADJUSTMENTS FROM DEALER TO THE CUSTOMER ACCOUNT THIS MONTH AND THAT USUALLY MEANS A SETTLEMENT:

I) 5.90 TONNES (TWO WEEKS AGO)

II) 7.9 TONNES (3 DAYS AGO)

III) .56 TONNES (TWO DAYS AGO)

IV) ZERO (FRIDAY/JUNE 22)

v) ZERO jUNE 25

TOTAL: 14.36 TONNES HAVE BEEN SETTLED AGAINST THE 21.620TONNES STANDING.

IN THE LAST 18 MONTHS 80 NET TONNES HAS LEFT THE COMEX.

end

And now for silver

AND NOW THE APRIL DELIVERY MONTH

JUNE INITIAL standings/SILVER

| Silver | Ounces |

| Withdrawals from Dealers Inventory | nil oz |

| Withdrawals from Customer Inventory |

NIL oz

|

| Deposits to the Dealer Inventory |

nil;

oz

|

| Deposits to the Customer Inventory |

1,122,508.55

oz

Brinks

CNT

|

| No of oz served today (contracts) |

3

CONTRACT(S)

(15,000 OZ)

|

| No of oz to be served (notices) |

0 contracts

(5,000 oz)

|

| Total monthly oz silver served (contracts) | 1076 contracts

(5,380,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

we had 0 inventory movement at the dealer side of things

total dealer deposits: nil oz

we had 2 deposits into the customer account

i) Into JPMorgan: NIL oz

*** JPMorgan for most of 2017 and in 2018 has adding to its inventory almost every single day.

JPMorgan now has 141 million oz of total silver inventory or 52.0% of all official comex silver. (141 million/270 million)

ii) Into Brinks: 508,097.450 oz

iii) into CNT: 614,411.100 oz

total customer deposits today: 1,122,508.55 oz

we had 0 withdrawals from the customer account;

we had 0 adjustment/

total dealer silver: 69.668 million

total dealer + customer silver: 273.920 million oz

The total number of notices filed today for the JUNE. contract month is represented by 3 contract(s) FOR NIL oz. To calculate the number of silver ounces that will stand for delivery in JUNE., we take the total number of notices filed for the month so far at 1076 x 5,000 oz = 5,380,000 oz to which we add the difference between the open interest for the front month of JUNE. (3) and the number of notices served upon today (3 x 5000 oz) equals the number of ounces standing.

.

Thus the INITIAL standings for silver for the JUNE/2018 contract month: 1076(notices served so far)x 5000 oz + OI for front month of JUNE(3) -number of notices served upon today (3)x 5000 oz equals 5,380,000 oz of silver standing for the JUNE contract month

PLEASE NOTE THE FOLLOWING FOR COMPARISON PURPOSES:

WITH THE JUNE 26/2017 READING HAD 48,785 CONTRACTS STANDING SO FAR FOR THE JULY 2017 DELIVERY MONTH (WHICH WILL ALWAYS BE A VERY VERY ACTIVE MONTH) VS.62,953 OUTSTANDING TODAY/JUNE 25.2018.

AT THE CONCLUSION OF JUNE 2017: 4.92 MILLION OZ FINALLY STOOD (INITIALLY 1.98 MILLION OZ STOOD FOR DELIVERY/ JUNE 1) AS QUEUE JUMPING STARTED IN EARNEST AND THROUGHOUT THE ENSUING YEAR IT CONTINUED WITH RECKLESS ABANDON INCLUDING WHAT YOU ARE WITNESSING TODAY.THIS IS COMPARED TO TODAY’S AMOUNT STANDING: 5.380 MILLION OZ.(INITIAL STANDING JUNE 1/2018 WAS 1.780 MILLION OZ)

FOR THE JUNE 2018 CONTRACT MONTH:

We gained 2 contracts or an additional 10,000 oz will stand in this non active delivery month of June as nobody was in urgent need of silver today. IN SILVER QUEUE JUMPING HAS BEEN THE NORM FOR OVER A YEAR. IT LOOKS LIKE GOLD IS TAKING A HOLIDAY FROM THIS SAME PHENOMENON…

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

ESTIMATED VOLUME FOR TODAY: 96,275 CONTRACTS

CONFIRMED VOLUME FOR YESTERDAY: 103,801 CONTRACTS absolutely criminal

YESTERDAY’S CONFIRMED VOLUME OF 103,801 CONTRACTS EQUATES TO 519 million OZ OR 74.14% OF ANNUAL GLOBAL PRODUCTION OF SILVER

COMMODITY LAW SUGGESTS THAT OPEN INTEREST SHOULD NOT BE MORE THAN 3% OF ANNUAL GLOBAL PRODUCTION. THE CROOKS ARE SUPPLYING MASSIVE PAPER TRYING TO KEEP SILVER IN CHECK.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price at that day at $18.42

The previous record was 224,540 contracts with the price at that time of $20.44

end

NPV for Sprott

1. Sprott silver fund (PSLV): NAV FALLS TO -4.11% (JUNE 25/2018)

2. Sprott gold fund (PHYS): premium to NAV FALLS TO -0.57% to NAV (JUNE 25/2018 )

Note: Sprott silver trust back into NEGATIVE territory at -4.11%-/Sprott physical gold trust is back into NEGATIVE/

(courtesy Sprott/GATA)

3.SPROTT CEF.A FUND (FORMERLY CENTRAL FUND OF CANADA): NAV FALLS TO -3.42%: NAV 13.21/TRADING 12.80//DISCOUNT 3.53.

END

And now the Gold inventory at the GLD/

JUNE 25/WITH GOLD DOWN $1.45/NO CHANGE IN GOLD INVENTORY AT THE GLD.INVENTORY RESTS AT 824.63 TONNES

JUNE 22/WITH GOLD UP 25 CENTS TODAY, THE CROOKS WITHDREW A MASSIVE 4.13 TONNES OF GOLD/INVENTORY RESTS AT 824.63 TONNES

JUNE 21/WITH GOLD DOWN $4.00/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 828.76 TONNES

JUNE 20/WITH GOLD DOWN $3.55/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 828.76 TONNES

JUNE 19/WITH GOLD DOWN $1.50/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 828.76 TONES

JUNE 18/WITH GOLD UP $1.90/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 828.76 TONNES

JUNE 15/WITH GOLD DOWN $28.90/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 828.76 TONNES

JUNE 14/WITH GOLD UP $7.10/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 828.76 TONNES/

JUNE 13/WITH GOLD UP $2.20/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 828.76 TONNES

JUNE 12/WITH GOLD DOWN $4.75:NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 828.76 TONNES

JUNE 11/WITH GOLD UP 65 CENTS/THE CROOKS RAIDED THE COOKIE JAR FOR 3.83 TONNES/INVENTORY RESTS AT 828.76 TONNES

JUNE 8/WITH GOLD DOWN 10 CENTS/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY REMAINS AT 832.59 TONNES./

JUNE 7/WITH GOLD UP $1.45, THE CROOKS DECIDED TO RAID AGAIN THE GLD GOLD COOKIE JAR TO THE TUNE OF 3.54 TONNES/GOLD INVENTORY LOWERS TO 832.59 TONNES

JUNE 6/WITH GOLD UP $1.30 TODAY, WE HAD NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 836.13 TONNES

JUNE 5/WITH GOLD UP $5.30 TODAY, WE HAD A TINY WITHDRAWAL OF .29 TONNES AND THAT NO DOUBT WAS TO PAY FOR FEES/836.13 TONNES

JUNE 4/WITH GOLD DOWN ONLY $2.50, THE CROOKS UNLEASHED A MASSIVE WITHDRAWAL OF 10.61 TONNES OF GOLD FROM THE GLD/INVENTORY RESTS AT 836.42 TONNES

JUNE 1/WITH GOLD DOWN $5.10 TODAY, A HUGE 4.42 TONNES OF GOLD WAS WITHDRAWN FROM THE GLD AND THIS WAS USED IN THE RAID TODAY/INVENTORY RESTS AT 847.03 TONNES

MAY 31/WITH GOLD DOWN 1.60/NO CHANGE IN GOLD INVENTORY/INVENTORY REMAINS AT 851.45 TONNES

MAY 30/WITH GOLD UP $2.70: A HUGE DEPOSIT OF 2.95 TONNES INTO THE GLD/INVENTORY REMAINS AT 851.45 TONNES

MAY 29/2018/WITH GOLD DOWN $4.50/ NO CHANGES IN GLD INVENTORY/INVENTORY REMAINS AT 848.50 TONNES

May 25/WITH GOLD UP ON THE WEEK BUT DOWN 80 CENTS TODAY: WE HAD A HUGE 3.54 TONNES OF GOLD WITHDRAWAL FROM THE CROOKED GLD/

MAY 24/WITH GOLD UP $12.40/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 852.04

MAY 22/WITH GOLD UP $1.05/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 852.04 TONNES

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

JUNE 25/2018/ Inventory rests tonight at 824,63 tonnes

*IN LAST 404 TRADING DAYS: 101,96 NET TONNES HAVE BEEN REMOVED FROM THE GLD

*LAST 354 TRADING DAYS: A NET 54.34 TONNES HAVE NOW BEEN ADDED INTO GLD INVENTORY.

end

Now the SLV Inventory/

JUNE 25/WITH SILVER DOWN 12 CENTS/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 320.301 MILLION OZ/

JUNE 22/WITH SILVER UP 12 CENTS TODAY,ANOTHER BIG CHANGE IN SILVER INVENTORY AT THE SLV” A DEPOSIT OF 941,000 OZ INTO INVENTORT/INVENTORY RESTS THIS WEEKEND AT 320.301 MILLION OZ/

JUNE 21/WITH SILVER UP ONE CENT/ANOTHER CHANGE IN SILVER INVENTORY AT THE SLV/: A DEPOSIT OF 2.918 MILLION OZ/INVENTORY RESTS AT 319.360 MILLION OZ/ THUS FOR TWO STRAIGHT DAYS A TOTAL OF 5.26 MILLION OZ OF SILVER HAS BEEN ADDED WITH NO CHANGE IN PRICE.

JUNE 20/WITH SILVER DOWN ONE CENT/A HUGE CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY / A DEPOSIT OF 2.35 MILLION OZ/INVENTORY RESTS AT 316.442 MILLION OZ/

JUNE 19/2018/WITH SILVER DOWN 11 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 314.090 MILLION OZ/

JUNE 18/WITH SILVER DOWN 6 CENTS TODAY/NO CHANGE IN SILVER INVENTORY/INVENTORY RESTS AT 314.090 MILLION OZ/

JUNE 15/WITH SILVER DOWN 75 CENTS/A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.788 MILLION OZ//INVENTORY RESTS AT 314.090 MILLION OZ

JUNE 14/WITH SILVER UP 30 CENTS, THE CROOKS DECIDED THAT THEY NEEDED SILVER INVENTORY BADLY SO THEY RAID THE SLV OF 1.412 MILLION OZ/INVENTORY RESTS AT 315.878 MILLION OZ/

JUNE 13/WITH SILVER UP 11 CENTS TODAY/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 317.290 MILLION OZ/

JUNE 12/WITH SILVER DOWN 5 CENTS/A HUGE CHANGES IN SILVER INVENTORY AT THE SLV/ THE CROOKS RAID THE SILVER COOKIE JAR BY 1.976 MILLION OZ/INVENTORY LOWERS TO 317.290 MILLION OZ/

jUNE 11/NO CHANGE IN SILVER INVENTORY/319.266 MILLION OZ

JUNE 8/WITH SILVER DOWN 5 CENTS/A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.412 MILLION OZ//INVENTORY LOWERS TO 319.266 MILLION OZ/

JUNE 7/WITH SILVER UP ANOTHER 12 CENTS/A HUGE CHANGE IN SILVER INVENTORY AT THE SL: A WITHDRAWAL OF 1.883 MILLION OZ WITH ALL OF THAT SILVER DEMAND//INVENTORY RESTS AT 320.678 MILLION OZ/

JUNE 6/WITH SILVER UP 14 CENTS TODAY/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 322.561 MILLION OZ/

JUNE 5/WITH SILVER UP 10 CENTS NO CHANGE IN SILVER INVENTORY/INVENTORY RESTS AT 322.561 MILLION OZ

JUNE 4/WITH SILVER DOWN 1 CENTA SMALL CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 522,000 OZ INTO THE SLV/.INVENTORY RISES AT 322.561 MILLION OZ/

JUNE 1/WITH SILVER DOWN 3 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY REMAINS AT 322.039 MILLION OZ/

MAY 31/WITH SILVER DOWN 7 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY REMAINS AT 322.039 MILLION OZ/

MAY 30/WITH SILVER UP 16 CENTS: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV/ A DEPOSIT OF 2.071 MILLION OZ/INVENTORY RESTS AT 322.039 MILLION OZ/

MAY 29.2018/ NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.968 OZ

May 25/INVENTORY LOWERS TO 319.968 AS WE HAD A WITHDRAWAL OF 1.035 MILLION OZ

MAY 24/WITH SILVER UP 27 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 321.003 MILLION OZ/

MAY 22/WITH SILVER UP 6 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 321.003 MILLION OZ/

JUNE 25/2018:

Inventory 320.301 MILLION OZ

6 Month MM GOFO 2.04/ and libor 6 month duration 2.51

Indicative gold forward offer rate for a 6 month duration/calculation:

G0FO+ 2.04%

libor 2.51 FOR 6 MONTHS/

GOLD LENDING RATE: .47%

XXXXXXXX

12 Month MM GOFO

+ 2.78%

LIBOR FOR 12 MONTH DURATION: 2.52

GOFO = LIBOR – GOLD LENDING RATE

GOLD LENDING RATE = +.26

end

Major gold/silver trading /commentaries for MONDAY

GOLDCORE/BLOG/MARK O’BYRNE.

GOLD/SILVER

Manipulation of Gold and Silver Is “Undeniable”

Manipulation of Gold and Silver by Bullion Banks Is “Undeniable”

by David Brady via ZeroHedge

– Manipulation in precious metals is undeniable

– Now so chronic that it is obvious and therefore predictable

– Central banks around the world are repatriating their gold from the U.S. in preparation for some major event to come

– I want to be long … “when that event occurs”

As a former spot currency trader for a major international bank, I have had first-hand experience of central banks directly intervening in currency markets in massive size, repeatedly.

You’ll hear a lot of people say market manipulation is a conspiracy theory, despite the fact that it has been proven in court several times in various assets classes and especially in precious metals.

Books have been written about gold and silver manipulation for decades. Central bankers have admitted it publicly. Now it has become so obvious that it’s predictable.

I know because I made 500% in less than 24 hours on Friday last on a 1-week SLV 15.50 strike put option I bought on Thursday at 2 pm. I bought that put expecting the Bullion banks to come in and hammer the metals, given the typical signals I was seeing ahead of each time they slam Gold and/or Silver lower. Moreover, I began warning people on Twitter a week ahead of time that this could happen (note the dates posted):

I’ll provide those typical signals later, but let’s take a look at what happened to Gold…

Since May 24th, Gold has been capped at its 200 day moving average despite being oversold, extreme overbearish per the DSI and Funds positioning being at levels that has consistently led to strong rallies over the past 3 years. Yet, on this occasion the price went down?

So why did the price go down? Below is the daily changes in Gold open interest (“OI”) on the COMEX up to and including Friday last.

Notice how OI rose significantly around May 10, and the price of Gold fell hard. Then OI fell consistently but the price did not rise, instead it remained capped under its 200-day MA. Then, beginning Tuesday, June 12 and for the next two days, open interest rose a total of 18k contracts. Given that the price only appears to go down when open interest rises and sideways when it falls, it seemed safe to assume that the price would fall on Friday as it did around May 10, and that is exactly what happened. In fact, open interest rose again on Friday for a cumulative 26k contracts in just four days.

Looking at a cumulative chart, you can see how open interest fell steadily since mid-May. This is normally bullish. In fact, open interest fell below 450k which, as the chart below shows, is very bullish for Gold. Yet Gold didn’t rise. Then note how cumulative open interest suddenly rose in the days up to and including Friday. Something was brewing. And based on multiple similar experiences in the past, I expected the worst, and we got it Friday.

But we didn’t have to rely on open interest alone to figure out what was happening. The COT data for June 5 already told us in advance. The Banks had previously been extremely long, which is rare for them and almost always leads to higher Gold (and Silver) prices—they are the so-called “smart money” after all—but it did not in this case. Gold remained below its 200-day moving average. On June 5, the COT report showed that the Banks had raced to get short in just one week, so fast that it was at a record pace. Now why would Banks be racing to get short unless they believed or knew that the price was going down? And down it went, on schedule, the following week.

The chart below shows the one week change in Banks (“Swaps”) positioning on June 5:

The chart below shows the change in the Banks’ absolute position from net long to net short on June 5 and increased further on Friday, June 12, just as open interest rose. Note how the price did not rise when they were long, and yet it did in every other instance. Instead, it fell this time around.

This was even clearer in Silver. When the Banks significantly cut their short position or go long, the price of Silver rises. Yet the price did not rise when they were extreme long recently, whereas it did every time they were less long in the past. Yet, it fell the moment they went short!

This is just a sample of the Bullion Banks’ ability to manipulate Gold (and Silver) prices by capping them and forcing them lower. Why? To make a profit. Then why don’t they buy it and make a profit on the upside? Because as several central bankers have admitted, a rising Gold price reflects an increasing lack of confidence in the system and specifically in the dollar. The Big Banks own and work with the Federal Reserve in maintaining confidence in the dollar and the system at large by suppressing the price of Gold. Manipulation is always to the downside for this reason. Easy money for the banks, which can create and sell naked futures contracts at will, but it comes at the expense of everyone else. Markets are a zero-sum game, and the banks don’t lose money in Gold and Silver. At least, JP Morgan does not, ever.

The signals of pending manipulation in Silver are similar to those in Gold . While Platinum tends to follow its two bigger siblings. I saw several of these signals in Silver last week, telling me that it was about to dump on Friday and based on multiple similar situations, I have come up with the following list which I use to predict when the Banks are about to slam Silver. Not all of these factors are required, but usually it’s a combination of several when manipulation occurs:

- Following a Large Rally (almost always the case)

- Silver price > 200D MA – push price below the 200D MA to trigger “algo” selling for maximum effect

- Overbought: RSI >65 and sometimes negatively divergent

- Sentiment is extremely bullish (DSI)

- MACD Histogram (and sometimes with MACD Line) is overextended to the upside or negatively divergent or both – yes, banks watch charts too.

- At key resistance (trendline resistance, prior high, or key Fibonacci resistance)

- Large increase in open interest ahead of time

- Funds load up long – either (1) Massive or record net long position or (2) huge increase in longs over two or more previous weeks

- Time it on or shortly after a special event: Fed rate hike, Presidential election, Non-Farm Payrolls, announcement of QT

- Time it during illiquid periods for maximum effect: holidays (e.g. Chinese week-long holiday, “Golden Week”—note the irony—Chinese New Year, July 3rd or 5th, Thanksgiving week, Christmas holidays), Fridays or Mondays.

- Time it post Futures / Options expirations also – e.g. triple /quad witching

Watch for these factors to expect the risk of another sell-off, triggered by short-selling on the part of the Bullion Banks using naked futures.

Why is this important? Because despite what everyone tells you to the contrary, markets are controlled, and Gold and Silver in particular. Technicals, sentiment, and positioning are important tools, but you need to be aware of the risk of manipulation undermining the message these tools are telling you.

So why bother with such tools at all? Why buy Gold or Silver? The banks use the same tools we do to determine when to force prices lower, which is why their behavior is predictable. Second, manipulation has an expiration date, as demonstrated in the 2000s and 1970s in particular. They cannot stop metal prices going up forever, and you want to be around for when Gold and Silver soar next. They are the most undervalued assets out there today. Plus, I follow the smart money. And China, Russia, and JP Morgan have been loading up on physical metals for years now.

Central banks around the world are also repatriating their Gold from the U.S. in preparation for some major event to come. I want to be long, too, when that event occurs.

In summary, manipulation in metals is undeniable. It has become so chronic that it is now obvious and therefore predictable.

Unfortunately, it can temporarily undermine or render traditional analytical tools as useless. You need to be aware of this to protect yourself when it is about to happen again, because it will.

by David Brady, Sprott Money News via ZeroHedge

Never miss an episode of The Goldnomics Podcast – Listen and subscribe on YouTube, ITunes, Soundcloud or Blubrry

News and Commentary

Gold prices climb as dollar weakens on EU-U.S. trade woes (Reuters.com)

Protests Erupt In Tehran As Iranian Currency Takes A Nose-Dive (RadioFarda.com)

Trump is reportedly planning new restrictions against China (CNBC.com)

Asian Stocks Drop With U.S. Futures (Bloomberg.com)

Silver Speculators Cut Back On Bullish Net Positions For 1st Time In 7 Weeks (Investing.com)

Iran Central Bank Agree to Control Gold Coin Bull Run (FinancialTribune.com)

Gold rises 300% in three months against Iranian rial (Gata.org)

Central bankers constantly rig the gold price – Ron Paul (Mises.org)

Gold and silver market rigging is so obvious that you can trade it – Brady (Gata.org)

Parabolic Global Debt Will Collapse Bullion Bank System – Hemke – (Youtube.com)

Just How Low Are Today’s Interest Rates? (DailyReckoning.com)

Listen on SoundCloud , Blubrry & iTunes. Watch on YouTube below

Gold Prices (LBMA AM)

22 Jun: USD 1,269.70, GBP 954.05 & EUR 1,088.26 per ounce

21 Jun: USD 1,263.70, GBP 963.32 & EUR 1,096.51 per ounce

20 Jun: USD 1,273.25, GBP 967.29 & EUR 1,100.60 per ounce

19 Jun: USD 1,279.00, GBP 971.14 & EUR 1,108.89 per ounce

18 Jun: USD 1,281.25, GBP 966.96 & EUR 1,103.93 per ounce

15 Jun: USD 1,300.10, GBP 978.98 & EUR 1,120.04 per ounce

14 Jun: USD 1,305.30, GBP 971.27 & EUR 1,103.89 per ounce

Silver Prices (LBMA)

22 Jun: USD 16.43, GBP 12.35 & EUR 14.11 per ounce

21 Jun: USD 16.25, GBP 12.33 & EUR 14.07 per ounce

20 Jun: USD 16.29, GBP 12.38 & EUR 14.09 per ounce

19 Jun: USD 16.36, GBP 12.42 & EUR 14.16 per ounce

18 Jun: USD 16.61, GBP 12.53 & EUR 14.29 per ounce

15 Jun: USD 17.23, GBP 12.96 & EUR 14.86 per ounce

14 Jun: USD 17.12, GBP 12.75 & EUR 14.48 per ounce

Recent Market Updates

– Manipulation of Gold & Silver by Bullion Banks Is “Undeniable”

– “Perfect Environment For Gold” As Fed Will Weaken Dollar and Create Inflation – Rickards

– Russia Buys 600,000 oz Of Gold In May After Dumping Half Of US Treasuries In April

– In Gold, Silver and Bitcoin We Trust? Goldnomics Podcast with Ronald-Peter Stoeferle

– Own A “Bit Of Gold” As We Are Moving Ever Closer To A Trade War

– Bitcoin Price To $0 Or $1 Million In One Year? MoneyConf 2018 Poll

– Cashless Society – Good or Bad? MoneyConf 2018 Video

– Do We Still Need Banks In The Age Of Fintech?

– Total US Government Debt Is $200 Trillion – Debt Clock Ticking To Next Crisis

– All Gold is Not Equal – Goldnomics Podcast (Episode 4)

– “Without Gold I Would Have Starved To Death” – ECB Governor

– Swiss Government Pension Fund To Buy Gold Bars Worth Some €600 Million

– Turkey Uses Gold Bullion To Stabilise Its Currency And Economy

– Case for Gold in a Diversified Investment Portfolio

– Get “Positioned In Gold” Now As “You Will Not Have Time To Get Positioned” Later

ANDREW MAGUIRE’S KINESIS WHICH IS A”BITCOIN’ BACKED 100% BY ALLOCATED GOLD AND SILVER

Andrew Maguire’s Kinesis money which is a “bitcoin” but backed 100% by allocated gold and silver is set to go.

it think it would be a great idea to look at this!

please read at: https://kinesis.money/#/

(Andrew Maguire)

|

|

Dear Harvey Organ,

Thank you for your participation in our webinar on June 7th with our host and CEO of Kinesis, Thomas Coughlin.

The response we received has been incredible, we appreciate you taking the time to join us and hope you found it to be beneficial.

Due to such a high influx of questions we received we were unable to have them all answered. Nevertheless, if there was anything which requires more clarification, or you have a query which needs to be rectified, we invite you to join our telegram group:

We apologize for the technical issues we incurred during the webinar which resulted in it running a little over schedule, we hope that the next one we host will run seamlessly.

A video has been put together and uploaded onto our YouTube channel which can be found here:

Please share and subscribe to our YouTube channel to be notified of all the latest videos as they become available.

The rapid growth that we are currently experiencing has been incredible and with your support, is only going to get better.

We are working behind the scenes very hard to create a better experience for everyone involved! Stay tuned in as we have many more announcements to be released in the upcoming days.

Kind Regards,

|

Kinesis Money

a:C/O ILS Fiduciaries (IOM) Limited, First Floor,Millennium House, Victoria Road, Douglas, Isle of Man IM2 4RW

|

The following is self explanatory

(courtesy GATA/Chris Powell and Harvey Organ)

GATA asks bank regulator to check risks of gold

futures maneuver

Submitted by cpowell on Sun, 2018-06-10 16:17. Section: Daily Dispatches

12:21p ET Sunday, June 10, 2018

Dear Friend of GATA and Gold:

GATA has appealed to the U.S. comptroller of the currency, who has regulatory authority over banks, to review financial risks certain banks may have incurred through derivatives in the monetary metals markets, particularly through the recent heavy use of the “exchange for physicals” mechanism of settling gold and silver futures contracts on the New York Commodities Exchange.

The appeal was made in a letter sent May 5 to the comptroller, Joseph M. Otting, whose office is part of the U.S. Treasury Department, by your secretary/treasurer and GATA futures market consultant Harvey Organ.

“Exchange for physical” settlements of futures contracts long were considered emergency procedures when a seller was not able to deliver metal from an exchange-approved warehouse and wanted to settle with delivery elsewhere. But now such settlements appear to constitute most gold and silver futures settlements on the Comex. It is a strange development that appears to have been necessitated by the increasing difficulties of central banking’s gold and silver price suppression policy.

GATA has received no acknowledgment of the letter. Its text is below and a PDF copy of it is here:

http://www.gata.org/files/ComptrollerOfCurrencyLetter.pdf

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

* * *

May 5, 2018

Joseph M. Otting, Comptroller of the Currency

U.S. Treasury Department

400 7th Street, SW

Washington DC 20219

Dear Comptroller Otting:

Please let us bring to your attention financial risks to major banks involving their possibly unreported exposure to derivatives in the monetary metals markets.

In recent months gold and silver future contracts issued by U.S. banks on the New York Commodities Exchange have been moved off-exchange for delivery through a mechanism known as “exchange for physical” (EFP) contracts. Until recently use of this mechanism was considered an emergency procedure when a seller did not have access to metal for delivery through Comex warehouses. Now the mechanism seems to be in use for a large share of front-month contracts for which delivery is sought.

Here is an example that is happening at the Comex in the front active month of April for gold and the inactive delivery month of April for silver.

In gold, there were 229,436 EFP contracts for 713.64 tonnes, an average of 10,925 contracts and 1,092,500 ounces per trading day.

In silver, there were 77,150 EFP contracts for 385,750,000 ounces, an average of 3,673 contracts and 18,369,000 ounces per trading day.

London Bullion Market Association rules suggest that these contracts may not be reported to regulators. The LBMA’s bylaws say:

“Figures above exclude any contracts not subject to risk-based capital requirements, such as FX contracts with an original maturity of 14 days or less, futures contracts, written options, and basis swaps. Therefore, the total notional amount of derivatives by maturity will not add to the total derivatives figure in this table.”

We are told that these EFP contracts are transferred from the Comex to London as what are called “serial forwards” and their duration is always less than 14 days, which exempts them from being reported.

It is our understanding that in each quarter your office prepares a report detailing risk undertaken by the banks under the comptroller’s supervision.

These risks include derivatives undertaken by U.S. banks and other obligations that may cause a bank to fail. Our concern is that your office may not be aware of large unreported derivative exposure by banks.

Could you review this matter and let us know your conclusions?

Sincerely,

CHRIS POWELL

Secretary/Treasurer

HARVEY ORGAN

Consultant

Gold Anti-Trust Action Committee Inc.

7 Villa Louisa Road

Manchester, Connecticut 06043-7541

END

* * *

Sprott praises our letter to the OCC concerning EFP’s

(courtesy GATA/Eric Sprott/Craig Hemke)

Sprott applauds GATA for pressing currency comptroller about EFPs

Submitted by cpowell on Sat, 2018-06-23 14:35. Section: Daily Dispatches

10:40a ET Saturday, June 29, 2018

Dear Friend of GATA and Gold:

Mining entrepreneur Eric Sprott, in his weekly interview with the TF Metals Report’s Craig Hemke for Sprott Money News, praises GATA for pressing the U.S. Treasury Department’s comptroller of the currency for an explanation of the explosive use by bullion banks of the emergency “exchange for physicals” procedure for settling Comex gold and silver futures contracts.

(See: http://www.gata.org/node/18303.)

Sprott also:

— Condemns the bullion banks for manipulating the gold and silver futures markets to destroy the value of the options they had sold to their own customers.

Says it seems unlikely that the Comex has much if any gold available for delivery.

— Notes that governments increasingly are exchanging currencies for physical gold, considering the monetary metal a better store of value.

— And muses on the monetary metals mining industry’s failure to complain about market manipulation.

The interview is 11 minutes long and can be heard at Sprott Money here:

https://www.sprottmoney.com/Blog/eric-sprott-on-global-demand-for-physic…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

Ron Paul continues to correctly harp on the theme of constantly manipulation of markets and the most important the rigging of gold

(courtesy Paul /Mises Alabama)

Their policies strive to convince the unknowing that the dollar is strong and its status as the world’s reserve currency is secure, no matter how many new dollars they create of out of thin air. It is claimed that our foreign debt is always someone else’s fault and never related to our own monetary and economic mismanagement.Official government reports inevitably claim inflation is low and we must work harder to increase it, claiming price increases somehow mystically indicate economic growth.

The Consumer Price Index is the statistic manipulated to try to prove this point just as they use misleading GDP numbers to do the same. Many people now recognizing these reports are nothing more than propaganda. Anybody who pays the bills to maintain a household knows the truth about inflation.

Ever since the Great Depression, controlling the dollar price of gold and deciding who gets to hold gold was official policy. This advanced the Federal Reserve’s original goal of demonetizing precious metals, which was fully achieved in August 1971. Today, even though the official position of all central banks is that gold is not money, central bankers constantly rig the dollar price of gold, pretending the dollar is stronger than it really is. Just as the market overrode the artificial price of $35 per ounce in the 1970s, today’s price will soar when the dollar is dethroned as the king of the world’s currencies. …

… For the remainder of the report:

END

The rial has plummeted from 80,000 to a record 90,000 per dollar as gold rises above a 300% rise in just 3 months

(courtesy Radio/Farda)

Gold rises 300% in three months against Iranian rial

Submitted by cpowell on Sun, 2018-06-24 18:53. Section: Daily Dispatches

Protests Erupt in Tehran As Iranian Currency Takes a Nosedive

From Radio Farda

(Radio Free Europe / Radio Liberty)

Prague, Czech Republic

Sunday, June 24, 2018

Tehran’s cell phone market went on strike today, with store owners and people marching in protest in Jomhouri (Republic) Avenue as the city’s forex market, just a stone’s throw away, recorded the highest value for the U.S. dollar against the Iranian currency, the rial.

Cell phone sellers decided it was impossible to sell any handset considering the exchange rate of more than 90,000 rials per dollar. They said the rising exchange rate has brought about an uncertainty in the market that made cell phones extremely expensive for buyers.

User-generated videos received by Radio Farda show buyers urging store owners to shut down and protest and the crowd pours into the street, with others joining them.

Meanwhile, traders stopped buying and selling dollars at the unofficial forex market — the black market — the Iranian Students News Agency reported.

The U.S. dollar rose from 80,000 rials to 90,000 in just one day.

The forex market also experienced a record high for other foreign currencies. The British pound was traded for over 120,000 rials and euros for 106,000 just before the market decided to close, the report said.

The market for gold coins also came to a standstill as the price of a standard coin reached 32 million rials, almost three times its price in March. …

… For the remainder of the report:

https://en.radiofarda.com/a/breaking-news-protest-in-tehran-over-/293166…

END

Russia’s gold reserves now top 1909 tonnes, from which in late April they added another 18.662 tonnes

we are now waiting for May’s addition

(courtesy Smaulgld)

Russian Central Bank Gold Reserves Rise to 1909.75 Tons in April.

Russian gold reserves are the fifth largest in the world.

Russia added 600,000 ounces of gold (18.6620861 tons) to reserves in April.

Russia added a record 224 tons of gold to reserves in 2017.

Since June 2015, the Central Bank of Russia has added over 628 tons of gold to reserves.

Overall Russian reserves rose from $457.995 billion in March to $459.883 billion in April.

Russian holdings of U.S. Treasuries were at $96.1 in March 2018.

Gold reserves worth $81.146 billion constitute 17.64% of overall Russian reserves.

Watch the video companion to “Russian Gold Reserves Top 1900 Tons”:

https://www.bitchute.com/embed/oRv5J5PiARJy/

or watch on Bitchute

You can buy Bitcoin, Ethereum and Litecoin through Coinbase.

Click HERE to open a coin base account and get $10 of free Bitcoin.*

Check out all the Smaulgld podcasts here.

Not a Smaulgld subscriber? Sign up here.

Donate To Smaulgld.com via paypal

Russian Gold Reserves

After adding 6,700,000 ounces (208 tonnes) of gold to her reserves in 2015, the Russian Central Bank added 6,400,000 ounces (199 tonnes) in 2016 and another 224 tons (7,202,000 ounces) in 2017.

The Central Bank of Russia ended 2016 with 1838.21 tonnes of gold on their balance sheet.

Central Bank of Russia added 7.2 Million ounces (approximately 223.945 tonnes) in 2017.

Through April 2018, the Central Bank of Russia has added 2.3 million ounces or approximately 71.54 tons of gold.

The chart below shows the Central Bank of Russia’s Gold Reserves by month with tonnage rounded to the nearest metric ton.

The Central bank of Russia has added about 628 tons of gold to her reserves from June 2015 – to March 2018.

You can compare pricing a

Rather than write on a planned topic, I received at least 20 e-mails yesterday on the same subject so had to switch gears. The e-mails were all panicky because an analyst who works in the precious metals industry suggested that silver will not perform as gold will in the coming reset. I feel the need to address this because I believe it is faulty analysis and may have motivation behind it. I will not name the analyst but can be easily discerned.

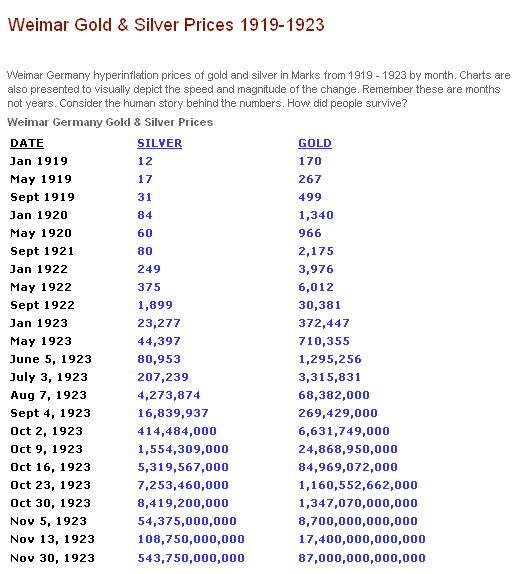

In an interview it was said that during the Weimar experience, gold performed extremely well but silver lagged. It is for this reason they suggested not to pay attention to the current out of whack silver to gold ratio north of 80-1 and it will not narrow. This is just wrong for so many reasons. First, the ratio of silver to gold worldwide at the time was roughly 15-1. Silver was priced at $1.385 per ounce while gold was at $20.67 per ounce in dollar terms. This 15-1 ratio was much closer to the ratio of silver versus gold in the Earth’s crust and extracted via mining. Silver actually exists at a ratio of slightly less than 10-1 versus gold, this is what I call “God’s ratio”.

Back in 1923, most of the world held at this ratio, if it was true that gold vastly outperformed silver in reichmarks, this would mean the ratio of value for gold versus silver was moving higher. If this were to have occurred, there would have immediately been arbitrage where gold would have flooded in to Germany while it would have been emptied of all silver over the 15-1 ratio. Yes it would have been clunky and slower than in today’s world but it would have occurred nonetheless. As a side note, the analyst claimed a 160-1 silver to gold ratio prior to the German hyperinflation and the same ratio afterwards which would mean silver and gold moved in lockstep. At that time with a 15-1 ratio worldwide, ALL silver would have been drained via arbitrage from Germany! To suggest this happened and silver that would have been undervalued versus gold and was not arbitraged out of Germany is simply false. Think of it this way, you could swap one gold ounce for 160 silver ounces in Germany, ship the silver out to America or elsewhere and then re swap for 10 times more gold than you started with …this most assuredly did not happen.

This has been added since the article went out to subscribers.

An article discussing this in 2006 can be found here. The article concludes “we decided an extra zero was not mistakenly added to gold, rather the price of gold exploded because of fear a repeat of the Russian revolution took place and gold was 16 times easier to transport due to weight”. As I originally wrote, NOTHING back in 1923 happened at the speed of light. Are we to believe gold jumped 10 fold in one week back in a day when ALL transactions were cash rather than derivative in nature? If true, forget about arbitraging gold and silver from outside of German borders, why not arbitrage from the cities where knowledge was fresh and rip off farmers on the countryside where there was no knowledge of the “magical” 10 fold jump in the price of gold? And why does the data end just 30 days after this supposed anomaly? Yes the currency failed and was replaced but if gold truly shot up 10 fold versus silver, wouldn’t this be lore that would not only be common knowledge by now … but burned into the brains of precious metals investors? Rather, it seems far more plausible there is one too many zeroes in the gold price …)

Looking past the current man made ratio of 80-1, there are no large stockpiles of silver held by central banks currently. It is reported that JP Morgan has amassed more than 600 million ounces and long been rumored that China may hold 2 billion ounces. Silver for the most part is used once it is mined. It is used for industrial, technology, armaments, solar, medicinal and many other uses …which year after year have been increasing. My point is this, silver is mostly used and little in the way of large stockpiles exist to be actually be dumped on to the market which has always been the fear in gold.

As for this fear, real physical gold and silver have not hit the markets to cause prices to drop. The supply has been that of paper contracts where the real metal does not exist. The “supply” has been grossly diluted and distorted. To illustrate just how bad the paper scheme has gotten, so far in less than 6 months this year, COMEX has sent EFP contracts to London representing 1.6 billion silver ounces and 4,000 tons of gold. The world only produces less than 800 million ounces of silver and roughly 2,400 tons of gold (ex Chinese and Russian production) per year. At these rates of so called delivery, we are being led to believe London will deliver three times the amount of gold mined and 4 times the amount of silver mined this year. This is clearly fraudulent!

As to this analyst scaring people away from silver and toward gold, I believe is extremely disingenuous. The fundamentals do not support the case at all, in fact they support being far more heavily weighted in silver rather than gold. Checking for possible other motivation I called their firm to query purchasing a specific coin. I asked their pricing on a MS63 $20 St. Gaudens which should be priced slightly under $1,400. The price quoted was $1,653. In this case, gold is better “for the dealer” but not the customer? Folks, as my partner Jim Sinclair says, “silver will be gold on steroids when this plays out” …and he is widely known as “Mr. Gold” but suggesting silver will massively outperform gold!

Do not allow yourself to be fooled. Follow logic and the fundamentals only. The fact is, sovereign central banks and treasuries are widely on the precipice of collapse due to over indebtedness of the state and financial systems. They are the ones who “print” the money which you should consider as nothing more than IOU’s. If you are smart and do not want to accept and hold IOU’s from an insolvent issuer, you then turn to gold and silver which are purely asset money with no liability attached. With history as a guide, silver is extremely undervalued versus gold. In fact, the argument that silver is the cheapest asset on the planet is correct in my opinion.

(This article was posted for subscribers over the weekend and released to the public on Monday). http://www.jsmineset.com

Standing watch and shaking my head,

Bill Holter,

Holter-Sinclair collaboration

Your early MONDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED DOWN TO 6.5402/HUGE DEVALUATION /shanghai bourse CLOSED DOWN 30.42 POINTS OR 1.05%// HANG SANG CLOSED DOWN 377.31 PTS OR 1.29%

2. Nikkei closed DOWN 178.68 POINTS OR 0.79% / /USA: YEN FALLS TO 109.57/

3. Europe stocks OPENED DEEPLY IN THE RED / /USA dollar index FALLS TO 94.49/Euro RISES TO 1.1677

3b Japan 10 year bond yield: RISES TO . +.04/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 110.15/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD FINALLY IN THE POSITIVE/BANK OF JAPAN LOSING CONTROL OF THEIR YIELD CURVE AS THEY PURCHASE ALL BONDS TO GET TO ZERO RATE!!

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 68.80 and Brent: 74.33

3f Gold UP/Yen UP

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil UP for WTI and UP FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund FALLS TO +.33%/Italian 10 yr bond yield DOWN to 2.79% /SPAIN 10 YR BOND YIELD UP TO 1.37%

3j Greek 10 year bond yield FALLS TO : 4.14

3k Gold at $1269.90 silver at:16.44 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble UP 16/100 in roubles/dollar) 62.82

3m oil into the 68 dollar handle for WTI and 74 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 109.57 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 0.9876 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1534 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now POSITIVE territory with the 10 year FALLING to +0.33%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.89% early this morning (THIS IS DEADLY TO ALL MARKETS). Thirty year rate at 3.03%

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

(courtesy Jim Reid/Bloomberg/Deutsche bank/zero hedge)

Global Stocks Dive On Fears Of “Irreversible”

Trade War; Italian Bonds, Turkish Lira Tumble

Bulletin Headline Summary from RanSquawk:

- Trump is said to be planning new restrictions on tech exports to China

- PBoC says they are to cut the re-lending rate for SME loans by 50bps, following the RRR cut over the weekend

- Looking ahead, highlights include, US New Home Sales and BoJ’s Sakurai speaking

Global stocks are diving in what has been a generally quiet session, amid renewed trade war fears following reports that the Treasury Department is planning to heighten scrutiny of Chinese investments in sensitive U.S. industries under an emergency law, putting Washington’s trade war with Beijing on what Bloomberg dubbed a “potentially irreversible course”, while at the same time Trump threatened “more than reciprocity” to trade barriers.

According to overnight news reports, the US Treasury is devising rules to block firms with 25% Chinese ownership from acquiring companies involved in industrially significant technologies and that it plans using International Emergency Economic Powers Act 1977 to impose investment restrictions. “This one could well result in an escalating trade war,” Lee Ferridge, a macro strategist at State Street Corp., told Bloomberg TV in Hong Kong. “Volatility is going to continue to rise from here.”

Adding to the trade war jitters, an EU internal memo says trade crisis “set to deepen in coming months” and warns of the breakdown of rules-based trading. The EU Commission has also warned of a direct response to any new taxes on EU cars imported into the US.

The result has been a sea of red with European equities following Asia lower from the open, with the mining and auto sectors underperforming, resulting in a sea of red across global stock markets.

Europe’s Stoxx 600 Index declined as every industry sector fell. Earlier, equities in Shanghai and Hong Kong led a retreat in Asia in the wake of various reports the Trump administration is preparing new curbs on Chinese investments. Nasdaq and S&P futures are also near session lows, while the 10Y Tsy has been bid, its yield sliding as low as 2.865%.

A solid German IFO came and went with little impact on the market:

- German Ifo Expectations New (Jun) 98.6 vs. Exp. 98.1 (Prev. 98.5, Rev. 98.6)

- German Ifo Current Conditions New (Jun) 105.1 vs. Exp. 105.7 (Prev. 106.0, Rev. 106.1)

- German Ifo Business Climate New (Jun) 101.8 vs. Exp. 101.8 (Prev. 102.2, Rev. 102.3)

As Holger Zschaepitz notes, Germany’s Ifo business climate at 101.8 still at elevated levels, and points to GDP YoY growth of 2%.

Italian concerns added to the volatile mix, with bonds slumping after the League party continued its post-election bounce in a second round of municipal voting coupled with an EU emergency meeting on refugees which suggested that Italy now has the upper hand over Germany, putting Merkel’s political future in doubt. As Italian bonds slumped, yields on the 2Y BTP have blown out on Monday, rising back over 1%.

European banks followed suit with the Stoxx 600 Banks Index dropping 1.4%, the worst performing group in the broader market, led by Commerzbank and Italian banks.

China’s shares and currency fell after Sunday’s announcement the PBOC would cut China’s Required Reserve Ratio, freeing up more than $100 billion in the banking system to help cushion a slowing economy, a move that was anticipated, and which however has been seen as insufficient to offset the potential economic slowdown that may be inflicted on China as Trump escalates protectionist measures. Chinese Property developer shares were among the worst performers in Hong Kong, as China’s planned reserve requirement cut isn’t seen boosting housing market, but rather channel funding to debt-equity swaps and SMEs; unlikely to benefit developers or homebuyers looking for mortgages. Hang Seng Property Index drops as much as 1.5% to two-month low.

Following the RRR cut, the onshore Yuan dropped to its lowest since early January while the offshore CNH tumbled to levels last seen in 2017, as the Shanghai composite failed to rebound on China’s easing and dropped more than 1%.

Despite the latest major liquidity injection, markets failed to respond positively because not only was the RRR cut telegraphed well in advance, it reflects officials’ concern over the economy, leverage and trade outlook. As Bloomberg reminds us, the move comes into effect one day before the first round of U.S. tariffs on Chinese goods begin, fueling trade tensions between the world’s two-largest economies, even as stress increases between the U.S. and its European trade partners.

Elsewhere in Asia, the Singapore Straits Times Index fell as much as 1.1% Monday, poised to enter technical correction, as rising key interest rates and mounting trade concerns put regional economies under the spotlight and affect the outlook of a key Asian trading hub.

The 10Y Treasury climbed and emerging-market equities slid, in another sign of a risk-off impulse. Recep Tayyip Erdogan’s double victory in Turkey’s presidential and parliamentary elections triggered a lira rally, however, as we previewed the “optimism” was short lived, and the Turkish lira has since tumbled back to unchanged.

As we noted last night, and as sellside commentary published in the aftermath of Erdogan’s re-election confirmed, while Turkey’s lira drew support from Erdogan’s victory, any gains will probably be short-lived amid concerns about the independence of the nation’s central bank and its monetary policy, according to investors and analysts. Not everyone agrees: Ark Capital, a Dubai- based hedge fund, which made money from the lira’s slump in recent months, is now seeking to profit from the currency’s advance after Erdogan’s election win.

Elsewhere in FX, the dollar was range-bound, giving up some overnight gains, as London came into the market, although it has since seen a bid return and was trading near session highs; the yen gained against all Group- of-10 peers, while the euro stabilized in European morning hours, drawing some support from the trimming of long-dollar positions while Scandinavian currencies slid along with commodity currencies in reflection of the worsening risk sentiment. The big story, however, was once again in Emerging Markets which after enjoying a brief respite at the end of last week, have once again been hammered.

In overnight central bank news, ECB’s Vasiliauskas states the ECB could start to discuss lifting short-term interest rates from autumn 2019. Also overnight, the ECB’s Praet (Dovish) said prolonging the purchase of assets for 2019 is an option. In the BoJ’s Summary of Opinions from June 14th-15th meeting stated it is appropriate to pursue powerful monetary easing with persistence under the current guideline as inflation is a long way from target but added the momentum towards achieving 2% is maintained. Furthermore, Summary of Opinions stated that although Japan’s GDP for the March quarter of 2018 contracted for the first time in nine quarters, this largely reflects temporary factors such as irregular weather.

In the latest Brexit news, at least 50 UK Conservative MPs are willing to rebel against the government if PM May fails to inject more money into defence, an ally of Gavin Williamson, the defence secretary, said last night. The FT added that over 50 Conservative MPs are prepared to block any attempt to remove Britain from the EU without a deal — including some sitting ministers — according to senior Conservative politicians. UK Trade Secretary Fox told Sky he would accept an extended Brexit transition period given it was for technical reasons.

Commodities trade mixed with WTI (+USD 0.21/bbl) now in the green, if below Friday’s highs after the conclusion of the latest OPEC+Russia summit in which member states vaguely agreed to boost production. Brent (-USD 1.01/bbl) on the other hand is lower as the global benchmark reacts to the OPEC and OPEC+ meetings at the back-end of last week. The oil producers agreed on an output hike, though no specific numbers were confirmed. The output increase is yet to be distributed amongst the members. Saudi Energy Minister Al-Falih said on Saturday that the increase is to be closer to 1mln BPD than to 600K BPD. The metal complex looks relatively mixed, gold and copper trades flat, synchronised with the uneventful dollar moves. Elsewhere, Shanghai steel rebar prices dropped for a second consecutive session following a rise in steel product inventories raising concerns about oversupply and weakening demand in the market.

Looking at the day ahead, we get new home sales data and the Chicago Fed national activity index, while earnings are expected from Carnival.

Market Snapshot

- S&P 500 futures down 0.6% to 2,743.75

- STOXX Europe 600 down 0.8% to 381.82

- MXAP down 0.8% to 167.93

- MXAPJ down 1% to 545.35

- Nikkei down 0.8% to 22,338.15

- Topix down 1% to 1,728.27

- Hang Seng Index down 1.3% to 28,961.39

- Shanghai Composite down 1.1% to 2,859.34

- Sensex down 0.3% to 35,584.89

- Australia S&P/ASX 200 down 0.2% to 6,210.41

- Kospi up 0.03% to 2,357.88

- German 10Y yield fell 1.7 bps to 0.32%

- Euro up 0.09% to $1.1662

- Brent Futures down 0.7% to $75.02/bbl

- Italian 10Y yield fell 3.7 bps to 2.427%

- Spanish 10Y yield rose 0.8 bps to 1.361%

- Brent Futures down 0.7% to $75.02/bbl

- Gold spot down 0.02% to $1,270.32

- U.S. Dollar Index down 0.03% to 94.50

Top Overnight News from Bloomberg