GOLD: $1254.60 DOWN $3.60(COMEX TO COMEX CLOSINGS)

Silver: $16.18 DOWN 8 CENTS (COMEX TO COMEX CLOSINGS)

Closing access prices:

Gold $1252.05

silver: $16.07

ON JUNE 29 OPTIONS, FOR OTIC/LONDON GOLD EXPIRE SO EXPECT CONTINUAL WHACKING OF GOLD UNTIL FRIDAY NIGHT.

For comex gold:

JUNE/

NUMBER OF NOTICES FILED TODAY FOR JUNE CONTRACT:40 NOTICE(S) FOR 4000 OZ

TOTAL NOTICES SO FAR 6890 FOR 689000 OZ (21.430 tonnes)

For silver:

JUNE

0 NOTICE(S) FILED TODAY FOR

nil OZ/

Total number of notices filed so far this month: 1076 for 5,380,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: BID $6059/OFFER $6145: DOWN $54(morning)

Bitcoin: BID/ $6076/offer $6161: DOWN $38 (CLOSING/5 PM)

end

First Shanghai gold fix comes at 10 pm est

The second Shanghai gold fix: 2:15 pm

First Shanghai gold fix gold: 10 pm est: 1259.14

NY price at the same time: 1255.05

PREMIUM TO NY SPOT: $4.09

Second gold fix early this morning: 1258.45

USA gold at the exact same time:1256.45

PREMIUM TO NY SPOT: $2.00

AGAIN, SHANGHAI REJECTS NEW YORK PRICING.

WE WILL NOT PROVIDE LONDON FIXES AS THEY ARE NOT ACCURATE AS TO WHAT IS GOING ON AT THE SAME TIME FRAME.

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total OPEN INTEREST FELL BY A CONSIDERABLE 2488 CONTRACTS FROM 220,905 DOWN TO 218,492 WITH YESTERDAY’S 8 CENT LOSS IN SILVER PRICING. HOWEVER AS WE ARE NOW WELL INTO THE NON ACTIVE DELIVERY MONTH OF JUNE WE CONTINUE TO WITNESS LONGS PACK THEIR BAGS AND MIGRATE OVER TO LONDON IN GREATER NUMBERS. WE WERE NOTIFIED THAT WE HAD A GOOD SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP: 802 EFP’S FOR JULY, 544 EFP’S FOR SEPT. , 0 EFP’S FOR DECEMBER AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE: OF 1346 CONTRACTS. WITH THE TRANSFER OF 1346 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 1346 EFP CONTRACTS TRANSLATES INTO 6.73 MILLION OZ ACCOMPANYING:

1.THE 8 CENT LOSS IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES STANDING FOR JUNE COMEX DELIVERY. (5.405 MILLION OZ) DESPITE IT BEING A NON ACTIVE DELIVERY MONTH.

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF JUNE:

59,910 CONTRACTS (FOR 19 TRADING DAYS TOTAL 59,910 CONTRACTS) OR 299.55 MILLION OZ: (AVERAGE PER DAY: 3153 CONTRACTS OR 15.76 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH: 299.55* MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 39.77% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* WE HAVE ALREADY PASSED LAST MONTH AND CLOSING IN ON THE RECORD MONTH OF APRIL/2018.

ACCUMULATION IN YEAR 2018 TO DATE SILVER EFP’S: 1,615.67 MILLION OZ.

ACCUMULATION FOR JAN 2018: 236.879 MILLION OZ

ACCUMULATION FOR FEB 2018: 244.95 MILLION OZ

ACCUMULATION FOR MARCH 2018: 236.67 MILLION OZ

ACCUMULATION FOR APRIL 2018: 385.75 MILLION OZ

ACCUMULATION FOR MAY 2018: 210.05 MILLION OZ

RESULT: WE HAD A CONSIDERABLE SIZED DECREASE IN COMEX OI SILVER COMEX OF 2488 DESPITE THE 8 CENT LOSS IN SILVER PRICE. WE HAVE NOW ENTERED THE NEW NON ACTIVE MONTH OF JUNE AND THE CME NOTIFIED US THAT IN FACT WE HAD A GOOD SIZED EFP ISSUANCE OF 1346 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) . FROM THE CME DATA: 802 EFP CONTRACTS FOR JULY, 544 EFP’S FOR SEPT, 0 EFP’S FOR DECEMBER AND ZERO FOR ALL OVER MONTHS FOR A DELIVERABLE FORWARD CONTRACT OVER IN LONDON WITH A FIAT BONUS (TOTAL: 1346). TODAY WE LOST AN GOOD: 1142 TOTAL OI CONTRACTS ON THE TWO EXCHANGES: i.e.1346 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH AN DECREASE OF 2488 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED WITH A 8 CENT LOSS IN PRICE OF SILVER AND A CLOSING PRICE OF $16.25 WITH RESPECT TO YESTERDAY’S TRADING. YET WE STILL HAVE A GIGANTIC AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY IN THIS NON ACTIVE JUNE DELIVERY MONTH. IT SURE LOOKS LIKE A FAILED BANKER SHORT COVERING EXERCISE!!

In ounces AT THE COMEX, the OI is still represented by OVER 1 BILLION oz i.e. 1.110 MILLION OZ TO BE EXACT or 158% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT JUNE MONTH/ THEY FILED AT THE COMEX: 0 NOTICE(S) FOR NIL OZ OF SILVER

IN SILVER, WE HAVE NOW SET THE NEW RECORD OF OPEN INTEREST AT 243,411 AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $16.51 ON APRIL 9.2018.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ AND MAY: 36.285 MILLION OZ /AND JUNE/2018 (5.405 MILLION OZ SO FAR)

- HUGE RECORD OPEN INTEREST IN SILVER 243,411 CONTRACTS (OR 1.217 BILLION OZ/ SET APRIL 9/2018

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017

- RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ (FINAL)

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT).

In gold, the open interest FELL BY A LARGE 6325 CONTRACTS DOWN TO 468,573 WITH THE FALL IN THE GOLD PRICE/YESTERDAY’S TRADING (A DROP IN PRICE OF $9.10). WE ARE NOW IN THE ACTIVE DELIVERY MONTH OF JUNE. NO DOUBT THE BOYS ARE CASHING IN THEIR COMEX LONGS TO BEGIN THE PROCESS TO MOVE INTO LONDON FORWARDS. THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 9008 CONTRACTS : JUNE SAW THE ISSUANCE OF 0 CONTRACTS , AND AUGUST SAW THE ISSUANCE OF: 9008 CONTRACTS WITH ALL OTHER MONTHS ZERO. The new OI for the gold complex rests at 468,573. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE A GIGANTIC OI GAIN IN TOTAL CONTRACTS ON THE TWO EXCHANGES: 6325 OI CONTRACTS DECREASED AT THE COMEX AND A STRONG SIZED 9008 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN: 2683 CONTRACTS OR 268300 OZ = 8.34 TONNES. AND STRANGELY ALL OF THIS DEMAND OCCURRED WITH A FALL IN THE PRICE OF GOLD TO THE TUNE OF $9.10.???

YESTERDAY, WE HAD 9375 EFP’S ISSUED.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF MAY : 201,985 CONTRACTS OR 20,198,500 OZ OR 628.258 TONNES (19 TRADING DAYS AND THUS AVERAGING: 10,630 EFP CONTRACTS PER TRADING DAY OR 1,063,000 OZ/ TRADING DAY),,

TO GIVE YOU AN IDEA AS TO THE HUGE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 19 TRADING DAYS IN TONNES: 628.26 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2017, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 2555 TONNES

THUS EFP TRANSFERS REPRESENTS 628,26/2550 x 100% TONNES = 24.63% OF GLOBAL ANNUAL PRODUCTION SO FAR IN JUNE ALONE.***

ACCUMULATION OF GOLD EFP’S YEAR 2018 TO DATE: 4,080.07* TONNES *SURPASSED ANNUAL PROD’N

ACCUMULATION OF GOLD EFP’S FOR JANUARY 2018: 653.22 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR FEBRUARY 2018: 649.45 TONNES (20 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR MARCH 2018: 741.89 TONNES (22 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR APRIL 2018: 713.84 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR MAY 2018: 693.80 TONNES ( 22 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR JUNE 2018 (21 TRADING DAYS)

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A CONSIDERABLE SIZED DECREASE IN OI AT THE COMEX OF 6325 WITH THE $9.10 DROP IN PRICING GOLD TOOK YESTERDAY // . WE ALSO HAD A STRONG SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 9008 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 9008 EFP CONTRACTS ISSUED, WE HAD AN ATMOSPHERIC NET GAIN OF 2683 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

9008 CONTRACTS MOVE TO LONDON AND 6325 CONTRACTS DECREASED AT THE COMEX. (in tonnes, the GAIN in total oi equates to 8.34 TONNES). ..AND BELIEVE IT OR NOT BUT ALL OF THIS DEMAND OCCURRED WITH A FALL OF $9.10 IN TRADING!!!. AT THE COMEX. THE COMEX IS AN OUTRIGHT FRAUD

we had: 40 notice(s) filed upon for 4000 oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD DOWN $3.60 TODAY: / TWO HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4.42 TONNES FROM THE GLD INVENTORY/ AND THEN A WITHDRAWAL OF 2.94 TONNES

/GLD INVENTORY 821.69 TONNES

Inventory rests tonight: 821.69 tonnes.

SLV/

WITH SILVER DOWN 8 CENTS TODAY /ANOTHER HUGE CHANGE IN THE SILVER: A WITHDRAWAL OF 941,000 OZ/ STRANGE!! YESTERDAY THEY ADDED THE EXACT SAME 941,000 OZ!!! WHAT CROOKS

/INVENTORY RESTS AT 319.360 MILLION OZ/

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER FELL BY A CONSIDERABLE SIZED 2488 CONTRACTS from 221,411 DOWN TO 218,492 (AND CLOSER TO THE NEW COMEX RECORD SET /APRIL 9/2017 AT 243,411/SILVER PRICE AT THAT DAY: $16.53). THE PREVIOUS RECORD OTHER THAN WAS ESTABLISHED AT: 234,787, SET ON APRIL 21.2017 OVER ONE YEAR AGO. THE PRICE OF SILVER ON THAT DAY: $17.89. OUR CUSTOMARY MIGRATION OF COMEX LONGS MORPH INTO LONDON FORWARDS CONTINUES AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

802 EFP’S FOR JULY, 544 EFP CONTRACTS FOR SEPT., 0 EFP CONTRACTS FOR DECEMBER AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 1346 CONTRACTS . EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI GAIN AT THE COMEX OF 925 CONTRACTS TO THE 1346 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A NET LOSS OF 1142 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES: 5.71 MILLION OZ!!! AND YET THIS STRONG DEMAND OCCURRED WITH A 8 CENT LOSS IN PRICE??? . THE BANKERS ORCHESTRATED THEIR CONSTANT AND NEVER ENDING RAIDS DESPERATELY TRYING TO PARE THEIR GIGANTIC OPEN INTEREST SHORT ON BOTH EXCHANGES WITH HARDLY ANY SUCCESS. HOWEVER A DRAMATIC AMOUNT OF EFP ISSUANCE IS HEADING OVER TO LONDON AND NO DOUBT WE WILL COME CLOSE TO BREAKING APRIL’S RECORD OF 385 MILLION OZ.

RESULT: A SMALL SIZED INCREASE IN SILVER OI AT THE COMEX DESPITE THE THE 8 CENT LOSS THAT SILVER TOOK IN PRICING ON YESTERDAY. BUT WE ALSO HAD ANOTHER STRONG SIZED 1346 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR JUNE, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)WEDNESDAY MORNING/TUESDAY NIGHT: Shanghai closed DOWN 31.33 POINTS OR 1.10% /Hang Sang CLOSED DOWN 525.14 POINTS OR 1.82% / The Nikkei closed DOWN 70.23 POINTS OR 0.31% /Australia’s all ordinaires CLOSED DOWN 0.03% /Chinese yuan (ONSHORE) closed DOWN at 6.6075 AS POBC EXERCISES A HUGE DEVALUATION IN THE LAST FEW DAYS/Oil UP to 71.06 dollars per barrel for WTI and 76.89 for Brent. Stocks in Europe OPENED IN THE GREEN EXCEPT SPAIN//. ONSHORE YUAN CLOSED DOWN AT 6.6075 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.5990 :HUGE DEVALUATION/PAST FEW DAYS//ONSHORE YUAN TRADING WEAKER AGAINST OFFSHORE YUAN/ONSHORE YUAN TRADING MUCH WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING MUCH WEAKER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR IS BEGINNING/

/NORTH KOREA/SOUTH KOREA

i)North Korea/South Korea/USA

b) REPORT ON JAPAN

3 c CHINA

i)China/USA

Last night, the yuan tumbles to a 6 month low at 6.61 to th dollar. News out of China suggests that they will reduce their purchases of USA treasuries something that the uSA desperately needs

( zerohedge)

ii)Then this morning, Trump blinks and decides against the harshest measures on Chinese investment

( zerohedge)

iii) This Chinese think tank is worried that markets are going to collaps

(courtesy zerohedge)

4. EUROPEAN AFFAIRS

Germany/Deutsche Bank

No reason given but Deutsche bank[‘s stock fell below 9 euros. Deutsche bank is the world’s largest derivative player and owner of one of the largest portfolio of junk bonds

( zerohedge)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

6 .GLOBAL ISSUES

A town in rural Mexico Ocampo has seen its entire police force arrested on suspicion of murder after a mayoral candidate for the town was assassinated

( zerohedge)

7. OIL ISSUES

8. EMERGING MARKET

9. PHYSICAL MARKETS

Turkey in one year has doubled its official gold reserves from 116 tonnes up to 239 tonnes

( Lawrie Williams/Sharp’s Pixley)

10. USA stories which will influence the price of gold/silver)

i)Wednesday morning trading

Crude jumps to 72 dollars on fears that Trump may be winning in his battle with Iran

( zerohedge)

ib)LATE MORNING

(courtesy zerohedge)

ic)Afternoon:

Dow gives up all of its morning gains and breaks below critical support

(courtesy zerohedge)_

a)Seems that the USA economy has turned on a dime: today core durable goods slump with the main culprit capital spending

( zerohedge)

b)Another indicator that the economy has stalled: Pending home sales slumped again

(courtesy zerohedge)

iii)New Jersey is on the brink of a shutdown as they still have not passed a budget. The governors party wants to raise corporate income tax to the highest level in the country. New Jersey is second to Illinois in the basket case category

( zerohedge)

iv)the left is going nuts as they surround Trump employees and politicians demanding better immigration policy

(courtesy zerohedge)

v)After Trump blinked, Mnuchin states it is “unfortunate” that the markets got mixed messages. CFIUS will not target China specifically

(courtesy zerohedge)

vi)As expected, the House rejects the second immigration bill after the hardline measure failed earlier in the week.

(courtesy zerohedge)

vii)SWAMP STORIES

a)The house approves a resolution demanding the DOJ/FBI documents that Rosenstein has restricted the oversight boys from seeing. If Rosenstein does not comply they will initiate impeachment

( Sara Carter)

Trading Volumes on the COMEX

PRELIMINARY COMEX VOLUME FOR TODAY: 240,145 contracts

CONFIRMED COMEX VOL. FOR YESTERDAY: 262,236 contracts

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

And now for the wild silver comex results.

Total silver OI FELL BY A CONSIDERABLE SIZED 2488 CONTRACTS FROM 220,980 DOWN TO 218,492 (AND A LITTLE FURTHER FROM THE THE NEW RECORD OI FOR SILVER SET APRIL 9.2018/ 243,411 CONTRACTS) DESPITE THE 8 CENT LOSS IN SILVER PRICING/ YESTERDAY. SINCE WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF JUNE, WE WERE INFORMED THAT WE HAD A GOOD SIZED 802 EFP CONTRACT ISSUANCE FOR JULY, 544 EFP CONTRACTS FOR SEPT., 0 EFP CONTRACTS FOR DECEMBER AND ZERO FOR ALL OTHER MONTHS. THESE EFPS WERE ISSUED TO COMEX LONGS WHO RECEIVED A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. THE TOTAL EFP’S ISSUED: 1346. ON A NET BASIS WE LOST 1142 SILVER OPEN INTEREST CONTRACTS AS WE OBTAINED A 2488 CONTRACT LOSS AT THE COMEX COMBINING WITH THE ADDITION OF 1346 OI CONTRACTS NAVIGATING OVER TO LONDON.

NET LOSS ON THE TWO EXCHANGES: 1142 CONTRACTS

AMOUNT STANDING FOR SILVER AT THE COMEX

We are now in the NON active delivery month of JUNE and here the front month ROSE BY 4 contracts RISING TO 5 contracts. We had 0 notices filed upon yesterday so we gained 4 contracts or an additional 20,000 oz will stand in this non active delivery month of June AS TODAY SOMEBODY WAS IN URGENT NEED OF PHYSICAL ON THIS SIDE OF THE POND

The next big active delivery month for silver is July and here the OI LOST 14,911 contracts DOWN to 39,272. The next delivery month is August and here we GAINED 123 contracts to stand at 811 The next active delivery month after August for silver is September and here the OI ROSE by 11,053 contracts UP to 137,918

FOR COMPARISON AT THIS TIME IN THE DELIVERY CYCLE, JUNE 27.2017, FOR SILVER, WE HAD 40,677 OPEN INTEREST CONTACTS STILL STANDING.VS 39,272 TODAY. LAST YEAR AT THIS TIME WE HAD 3 MORE TRADING DAYS LEFT BEFORE FIRST DAY NOTICE (JUNE 27-JUNE 30), THIS YEAR WE HAVE 2 MORE TRADING DAYS BEFORE FDN (JUNE 26-29).

ON JUNE 28/2017 WE HAD 25,397 CONTRACTS OUTSTANDING VS 39,272 WITH THE EXACT NUMBER OF DAYS LEFT BEFORE FDN I.E. TWO TRADING DAYS.WE NO DOUBT WILL HAVE A DOOZY AMOUNT OF SILVER OZ STANDING FOR THE HUGE JULY CONTRACT MONTH

FROM LAST YEARS DATA, ON FIRST DATE NOTICE FOR THE JULY 2017 COMEX DELIVERY MONTH WE HAD 12.115 MILLION OZ OF SILVER STANDING FOR DELIVERY. AT MONTH’S END WE HAD 16.435 MILLION OZ EVENTUALLY STAND AS WE ALREADY HAD QUEUE JUMPING BEGIN IN EARNEST FROM APRIL 2017 ONWARD EVEN TO TODAY.

We had 0 notice(s) filed for NIL OZ for the JUNE 2018 COMEX contract for silver

INITIAL standings for JUNE/GOLD

JUNE 27/2018.

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz |

1,480.152 OZ

Scotia

|

| Deposits to the Dealer Inventory in oz | NIL oz |

| Deposits to the Customer Inventory, in oz | nil

oz |

| No of oz served (contracts) today |

40 notice(s)

4000 OZ

|

| No of oz to be served (notices) |

42 contracts

(4200 oz)

|

| Total monthly oz gold served (contracts) so far this month |

6890 notices

689,000 OZ

21.430TONNES

|

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

For JUNE:

Today, 0 notice(s) were issued from JPMorgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equates to 40 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped/ Received) by j.P.Morgan customer account.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

To calculate the INITIAL total number of gold ounces standing for the JUNE. contract month, we take the total number of notices filed so far for the month (6890) x 100 oz or 689,000 oz, to which we add the difference between the open interest for the front month of JUNE. (82 contracts) minus the number of notices served upon today (40 x 100 oz per contract) equals 693,200 oz, the number of ounces standing in this active month of JUNE (21.561 tonnes)

Thus the INITIAL standings for gold for the JUNE contract month:

No of notices served (6890 x 100 oz) + {(182)OI for the front month minus the number of notices served upon today (40 x 100 oz )which equals 693,200 oz standing in this active delivery month of JUNE .

WE LOST A SMALL 12 CONTRACTS OR AN ADDITIONAL 1200 OZ WILL NOT STAND FOR DELIVERY AS THESE GUYS MORPHED INTO LONDON BASED FORWARDS AND RECEIVED AN ADDITIONAL SWEETENER FOR THEIR EFFORT..

THERE ARE ONLY 7.4177 TONNES OF REGISTERED GOLD AVAILABLE FOR DELIVERY AGAINST 21.561 TONNES STANDING WHICH IS MAKING THIS JUNE CONTRACT MONTH AN EXTREMELY INTERESTING ONE TO WATCH.

WE HAVE HAD 3 ADJUSTMENTS FROM DEALER TO THE CUSTOMER ACCOUNT SO FAR THIS MONTH AND THAT USUALLY MEANS A SETTLEMENT:

I) 5.90 TONNES (TWO WEEKS AGO)

II) 7.9 TONNES (3 DAYS AGO)

III) .56 TONNES (TWO DAYS AGO)

IV) ZERO (FRIDAY/JUNE 22)

v) ZERO (jUNE 25)

vi) zero (June 26)

vii) zero (June 27)

TOTAL: 14.36 TONNES HAVE BEEN SETTLED AGAINST THE 21.561TONNES STANDING.

IN THE LAST 18 MONTHS 81 NET TONNES HAS LEFT THE COMEX.

end

And now for silver

AND NOW THE APRIL DELIVERY MONTH

JUNE INITIAL standings/SILVER

| Silver | Ounces |

| Withdrawals from Dealers Inventory | nil oz |

| Withdrawals from Customer Inventory |

106,913.17 oz

Scotia

|

| Deposits to the Dealer Inventory |

nil;

oz

|

| Deposits to the Customer Inventory |

nil

oz

|

| No of oz served today (contracts) |

0

CONTRACT(S)

(NIL OZ)

|

| No of oz to be served (notices) |

5 contract

(25,000 oz)

|

| Total monthly oz silver served (contracts) | 1076 contracts

(5,380,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

we had 0 inventory movement at the dealer side of things

total dealer deposits: nil oz

we had 0 deposits into the customer account

i) Into JPMorgan: NIL oz

*** JPMorgan for most of 2017 and in 2018 has adding to its inventory almost every single day.

JPMorgan now has 141 million oz of total silver inventory or 52.0% of all official comex silver. (141 million/270 million)

ii) Into everybody else: 0

total customer deposits today: nil oz

we had 1 withdrawals from the customer account;

i) Out of Scotia: 106,913.17.oz

total withdrawals: 106,913.17 oz

we had 0 adjustment/

total dealer silver: 69.384 million

total dealer + customer silver: 275.290 million oz

The total number of notices filed today for the JUNE. contract month is represented by 0 contract(s) FOR NIL oz. To calculate the number of silver ounces that will stand for delivery in JUNE., we take the total number of notices filed for the month so far at 1076 x 5,000 oz = 5,380,000 oz to which we add the difference between the open interest for the front month of JUNE. (5) and the number of notices served upon today (0 x 5000 oz) equals the number of ounces standing.

.

Thus the INITIAL standings for silver for the JUNE/2018 contract month: 1076(notices served so far)x 5000 oz + OI for front month of JUNE(5) -number of notices served upon today (0)x 5000 oz equals 5,405,000 oz of silver standing for the JUNE contract month

PLEASE NOTE THE FOLLOWING FOR COMPARISON PURPOSES:

WITH THE JUNE 27/2017 READING HAD 40,677 CONTRACTS STANDING SO FAR FOR THE JULY 2017 DELIVERY MONTH (WHICH WILL ALWAYS BE A VERY VERY ACTIVE MONTH/3 DAYS LEFT BEFORE FDN) VS.39,272 OUTSTANDING TODAY/JUNE 27.2018 (2 DAYS LEFT BEFORE FDN).

AT THE CONCLUSION OF JUNE 2017: 4.92 MILLION OZ FINALLY STOOD (INITIALLY 1.98 MILLION OZ STOOD FOR DELIVERY/ JUNE 1) AS QUEUE JUMPING STARTED IN EARNEST AND THROUGHOUT THE ENSUING YEAR IT CONTINUED WITH RECKLESS ABANDON INCLUDING WHAT YOU ARE WITNESSING TODAY.THIS IS COMPARED TO TODAY’S AMOUNT STANDING: 5.405 MILLION OZ.(INITIAL STANDING JUNE 1/2018 WAS 1.780 MILLION OZ)

FOR THE JUNE 2018 CONTRACT MONTH:

We gained 5 contracts or an additional 25,000 oz will stand in this non active delivery month of June as nobody was in urgent need of silver today. IN SILVER QUEUE JUMPING HAS BEEN THE NORM FOR OVER A YEAR. IT LOOKS LIKE GOLD IS TAKING A HOLIDAY FROM THIS SAME PHENOMENON…

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

ESTIMATED VOLUME FOR TODAY: 150,612 CONTRACTS

CONFIRMED VOLUME FOR YESTERDAY: 139,685 CONTRACTS absolutely criminal

YESTERDAY’S CONFIRMED VOLUME OF 139,685 CONTRACTS EQUATES TO 698 million OZ OR 99.7% OF ANNUAL GLOBAL PRODUCTION OF SILVER

COMMODITY LAW SUGGESTS THAT OPEN INTEREST SHOULD NOT BE MORE THAN 3% OF ANNUAL GLOBAL PRODUCTION. THE CROOKS ARE SUPPLYING MASSIVE PAPER TRYING TO KEEP SILVER IN CHECK.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price at that day at $18.42

The previous record was 224,540 contracts with the price at that time of $20.44

end

NPV for Sprott

1. Sprott silver fund (PSLV): NAV FALLS TO -4.11% (JUNE 27/2018)

2. Sprott gold fund (PHYS): premium to NAV FALLS TO -0.57% to NAV (JUNE 27/2018 )

Note: Sprott silver trust back into NEGATIVE territory at -4.11%-/Sprott physical gold trust is back into NEGATIVE/

(courtesy Sprott/GATA)

3.SPROTT CEF.A FUND (FORMERLY CENTRAL FUND OF CANADA): NAV FALLS TO -3.53%: NAV 13.21/TRADING 12.80//DISCOUNT 3.53.

END

And now the Gold inventory at the GLD/

June 27/WITH GOLD DOWN $3.60// TWO ENTRIES:/STRANGELY THE CROOKS RETURNED THE WITHDRAWAL OF 4.42 TONNES LAST NIGHT (THUS WE HAD A DEPOSIT OF 4.42 TONNES/INVENTORY RESTS AT 824.63 TONNES. /THEN LATE THIS AFTERNOON A WITHDRAWAL OF 2.94 TONNES

INVENTORY RESTS AT 821.69 TONNES/THIS VEHICLE IS AN OUTRIGHT FRAUD.

june 26/LATE LAST NIGHT, WITH GOLD DOWN $9.10 WE HAD A HUGE WITHDRAWAL OF 4.42 TONNES OF GOLD/INVENTORY RESTS AT 820.21 TONES

JUNE 25/WITH GOLD DOWN $1.45/NO CHANGE IN GOLD INVENTORY AT THE GLD.INVENTORY RESTS AT 824.63 TONNES

JUNE 22/WITH GOLD UP 25 CENTS TODAY, THE CROOKS WITHDREW A MASSIVE 4.13 TONNES OF GOLD/INVENTORY RESTS AT 824.63 TONNES

JUNE 21/WITH GOLD DOWN $4.00/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 828.76 TONNES

JUNE 20/WITH GOLD DOWN $3.55/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 828.76 TONNES

JUNE 19/WITH GOLD DOWN $1.50/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 828.76 TONES

JUNE 18/WITH GOLD UP $1.90/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 828.76 TONNES

JUNE 15/WITH GOLD DOWN $28.90/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 828.76 TONNES

JUNE 14/WITH GOLD UP $7.10/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 828.76 TONNES/

JUNE 13/WITH GOLD UP $2.20/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 828.76 TONNES

JUNE 12/WITH GOLD DOWN $4.75:NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 828.76 TONNES

JUNE 11/WITH GOLD UP 65 CENTS/THE CROOKS RAIDED THE COOKIE JAR FOR 3.83 TONNES/INVENTORY RESTS AT 828.76 TONNES

JUNE 8/WITH GOLD DOWN 10 CENTS/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY REMAINS AT 832.59 TONNES./

JUNE 7/WITH GOLD UP $1.45, THE CROOKS DECIDED TO RAID AGAIN THE GLD GOLD COOKIE JAR TO THE TUNE OF 3.54 TONNES/GOLD INVENTORY LOWERS TO 832.59 TONNES

JUNE 6/WITH GOLD UP $1.30 TODAY, WE HAD NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 836.13 TONNES

JUNE 5/WITH GOLD UP $5.30 TODAY, WE HAD A TINY WITHDRAWAL OF .29 TONNES AND THAT NO DOUBT WAS TO PAY FOR FEES/836.13 TONNES

JUNE 4/WITH GOLD DOWN ONLY $2.50, THE CROOKS UNLEASHED A MASSIVE WITHDRAWAL OF 10.61 TONNES OF GOLD FROM THE GLD/INVENTORY RESTS AT 836.42 TONNES

JUNE 1/WITH GOLD DOWN $5.10 TODAY, A HUGE 4.42 TONNES OF GOLD WAS WITHDRAWN FROM THE GLD AND THIS WAS USED IN THE RAID TODAY/INVENTORY RESTS AT 847.03 TONNES

MAY 31/WITH GOLD DOWN 1.60/NO CHANGE IN GOLD INVENTORY/INVENTORY REMAINS AT 851.45 TONNES

MAY 30/WITH GOLD UP $2.70: A HUGE DEPOSIT OF 2.95 TONNES INTO THE GLD/INVENTORY REMAINS AT 851.45 TONNES

MAY 29/2018/WITH GOLD DOWN $4.50/ NO CHANGES IN GLD INVENTORY/INVENTORY REMAINS AT 848.50 TONNES

May 25/WITH GOLD UP ON THE WEEK BUT DOWN 80 CENTS TODAY: WE HAD A HUGE 3.54 TONNES OF GOLD WITHDRAWAL FROM THE CROOKED GLD/

MAY 24/WITH GOLD UP $12.40/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 852.04

MAY 22/WITH GOLD UP $1.05/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 852.04 TONNES

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

JUNE 27/2018/ Inventory rests tonight at 821,69 tonnes

*IN LAST 404 TRADING DAYS: 104,90 NET TONNES HAVE BEEN REMOVED FROM THE GLD

*LAST 354 TRADING DAYS: A NET 51.40 TONNES HAVE NOW BEEN ADDED INTO GLD INVENTORY.

end

Now the SLV Inventory/

JUNE 27.2018/WITH SILVER DOWN 8 CENTS/NO CHANGE IN SILVER INVENTORY/INVENTORY RESTS AT 819.360 MILLION OZ/

june 26./2018/WITH SILVER DOWN 8 CENTS, THE CROOKS WITHDREW THE DEPOSIT OF TWO DAYS AGO; 941,000 OZ OUT OF INVENTORY/INVENTORY RESTS AT 819.360 OZ

JUNE 25/WITH SILVER DOWN 12 CENTS/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 320.301 MILLION OZ/

JUNE 22/WITH SILVER UP 12 CENTS TODAY,ANOTHER BIG CHANGE IN SILVER INVENTORY AT THE SLV” A DEPOSIT OF 941,000 OZ INTO INVENTORY/INVENTORY RESTS THIS WEEKEND AT 320.301 MILLION OZ/

JUNE 21/WITH SILVER UP ONE CENT/ANOTHER CHANGE IN SILVER INVENTORY AT THE SLV/: A DEPOSIT OF 2.918 MILLION OZ/INVENTORY RESTS AT 319.360 MILLION OZ/ THUS FOR TWO STRAIGHT DAYS A TOTAL OF 5.26 MILLION OZ OF SILVER HAS BEEN ADDED WITH NO CHANGE IN PRICE.

JUNE 20/WITH SILVER DOWN ONE CENT/A HUGE CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY / A DEPOSIT OF 2.35 MILLION OZ/INVENTORY RESTS AT 316.442 MILLION OZ/

JUNE 19/2018/WITH SILVER DOWN 11 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 314.090 MILLION OZ/

JUNE 18/WITH SILVER DOWN 6 CENTS TODAY/NO CHANGE IN SILVER INVENTORY/INVENTORY RESTS AT 314.090 MILLION OZ/

JUNE 15/WITH SILVER DOWN 75 CENTS/A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.788 MILLION OZ//INVENTORY RESTS AT 314.090 MILLION OZ

JUNE 14/WITH SILVER UP 30 CENTS, THE CROOKS DECIDED THAT THEY NEEDED SILVER INVENTORY BADLY SO THEY RAID THE SLV OF 1.412 MILLION OZ/INVENTORY RESTS AT 315.878 MILLION OZ/

JUNE 13/WITH SILVER UP 11 CENTS TODAY/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 317.290 MILLION OZ/

JUNE 12/WITH SILVER DOWN 5 CENTS/A HUGE CHANGES IN SILVER INVENTORY AT THE SLV/ THE CROOKS RAID THE SILVER COOKIE JAR BY 1.976 MILLION OZ/INVENTORY LOWERS TO 317.290 MILLION OZ/

jUNE 11/NO CHANGE IN SILVER INVENTORY/319.266 MILLION OZ

JUNE 8/WITH SILVER DOWN 5 CENTS/A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.412 MILLION OZ//INVENTORY LOWERS TO 319.266 MILLION OZ/

JUNE 7/WITH SILVER UP ANOTHER 12 CENTS/A HUGE CHANGE IN SILVER INVENTORY AT THE SL: A WITHDRAWAL OF 1.883 MILLION OZ WITH ALL OF THAT SILVER DEMAND//INVENTORY RESTS AT 320.678 MILLION OZ/

JUNE 6/WITH SILVER UP 14 CENTS TODAY/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 322.561 MILLION OZ/

JUNE 5/WITH SILVER UP 10 CENTS NO CHANGE IN SILVER INVENTORY/INVENTORY RESTS AT 322.561 MILLION OZ

JUNE 4/WITH SILVER DOWN 1 CENTA SMALL CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 522,000 OZ INTO THE SLV/.INVENTORY RISES AT 322.561 MILLION OZ/

JUNE 1/WITH SILVER DOWN 3 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY REMAINS AT 322.039 MILLION OZ/

MAY 31/WITH SILVER DOWN 7 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY REMAINS AT 322.039 MILLION OZ/

MAY 30/WITH SILVER UP 16 CENTS: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV/ A DEPOSIT OF 2.071 MILLION OZ/INVENTORY RESTS AT 322.039 MILLION OZ/

MAY 29.2018/ NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.968 OZ

May 25/INVENTORY LOWERS TO 319.968 AS WE HAD A WITHDRAWAL OF 1.035 MILLION OZ

MAY 24/WITH SILVER UP 27 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 321.003 MILLION OZ/

MAY 22/WITH SILVER UP 6 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 321.003 MILLION OZ/

JUNE 27/2018:

Inventory 319.360 MILLION OZ

6 Month MM GOFO 2.12/ and libor 6 month duration 2.50

Indicative gold forward offer rate for a 6 month duration/calculation:

G0FO+ 2.12%

libor 2.50 FOR 6 MONTHS/

GOLD LENDING RATE: .38%

XXXXXXXX

12 Month MM GOFO

+ 2.77%

LIBOR FOR 12 MONTH DURATION: 2.50

GOFO = LIBOR – GOLD LENDING RATE

GOLD LENDING RATE = +.27

end

Major gold/silver trading /commentaries for WEDNESDAY

GOLDCORE/BLOG/MARK O’BYRNE.

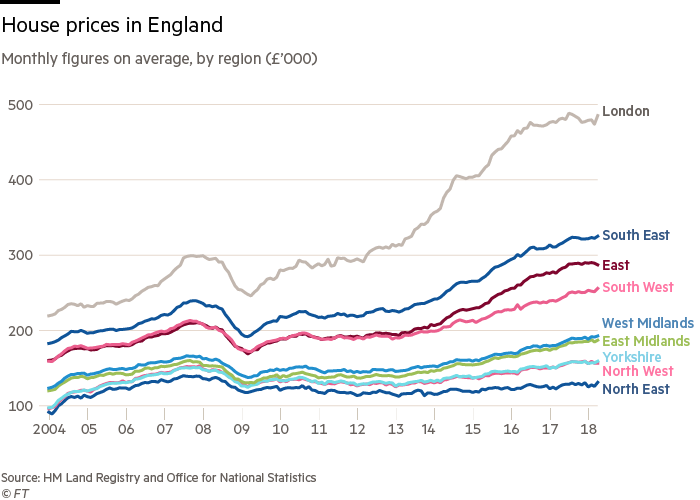

London House Prices Fall 1.9% In Quarter – Bubble Bursting?

– London house prices down 1.9 per cent in Q2 (yoy)

– London house prices still 50% above 2007 bubble peak (see chart)

– Brexit and weak consumer confidence to blame say experts

– Little sign that U.K. property “weakness” is likely to change

– London property bubble appears to be bursting

From Bloomberg:

U.K. house-price growth has slowed to the weakest pace in five years, while London values are falling, according to Nationwide Building Society.

The lender said the “subdued economic activity” and squeezed household budgets are keeping a lid on demand, and the national market is unlikely to see any change to the recent trend in the near term.

From City AM:

London weakness

The capital was the weakest performing region across the board for the second quarter of the year, with Nationwide reporting London house prices were down 1.9 per cent year-on-year, down from the one per cent fall posted in the first quarter.

“But despite the recent underperformance, prices in the capital are still more than 50 per cent above their 2007 peak, while prices in the UK overall are only 15 per cent higher,” Gardner pointed out.

“There are few signs of an imminent change. Surveyors continue to report subdued levels of new buyer enquiries, while the supply of properties on the market remains more of a trickle than a torrent.

Looking further ahead, much will depend on how broader economic conditions evolve, especially in the labour market, but also with respect to interest rates.”

Editors Note: The London property bubble appears to be in the early stages of bursting. House prices are falling with reports of falls of as much as 15% in some London markets.

The question not being asked is how far prices will fall and will this be a relatively mild correction, a sharp correction or indeed another property crash?

We have long contended that London house prices would crash. The mantra that London is “unique” and “this time is different” is faulty given the massive over valuation in the London property market. This massive over valuation in conjunction with the fragile nature of the massively indebted UK consumers, corporates, banks and government and the many geo-political risks looming over the London and the UK including Brexit makes a crash more and more likely.

A crash in London property prices has obvious ramifications for the rest of the UK property market and other property markets. Psychology is a powerful thing and a crash in leading financial capital London will likely curb property investors enthusiasm for other over valued and frothy property markets including Toronto, Vancouver, Sydney, Melbourne, Perth, San Francisco, Los Angeles, Amsterdam, Frankfurt, Paris and Dublin.

Property investors should consider diversifying into safe haven gold which will again hedge and protect investors in a crash.

Related Content

London Property Bubble Bursting?

Is London’s Property Bubble Set To Burst?

London Property Market Vulnerable To Crash

Never miss an episode of The Goldnomics Podcast – Listen and subscribe on YouTube, ITunes, Soundcloud or Blubrry

News and Commentary

Gold prices hover near six-month low as dollar firms (Reuters.com)

Asian Stocks Fall on Trade; Crude Extends Rally (Bloomberg.com)

Consumer confidence falls in June despite expectations for gains (CNBC.com)

Markets gipped by trade war fears; London house prices fall (TheGuardian.com)

London house prices down 1.9% in last quarter (CityAM.com)

Source: FT

Russia And China Are Stockpiling Gold (ZeroHedge.com)

Where The Rich Park Their Money (ZeroHedge.com)

Expect global trade tensions to get worse before they get better (MoneyWeek.com)

Once a Trump Favorite, Harley Now Feels the Pinch From Trade War (Bloomberg.com)

Crypto Collapse Spreads With Hundreds of Coins Plunging in Value (Bloomberg.com)

Gold’s Haven Luster Fades … For Now (Bloomberg.com)

Listen on SoundCloud , Blubrry & iTunes. Watch on YouTube below

Gold Prices (LBMA AM)

26 Jun: USD 1,257.15, GBP 949.15 & EUR 1,077.63 per ounce

25 Jun: USD 1,269.80, GBP 959.46 & EUR 1,090.25 per ounce

22 Jun: USD 1,269.70, GBP 954.05 & EUR 1,088.26 per ounce

21 Jun: USD 1,263.70, GBP 963.32 & EUR 1,096.51 per ounce

20 Jun: USD 1,273.25, GBP 967.29 & EUR 1,100.60 per ounce

19 Jun: USD 1,279.00, GBP 971.14 & EUR 1,108.89 per ounce

18 Jun: USD 1,281.25, GBP 966.96 & EUR 1,103.93 per ounce

Silver Prices (LBMA)

26 Jun: USD 16.23, GBP 12.25 & EUR 13.90 per ounce

25 Jun: USD 16.38, GBP 12.35 & EUR 14.05 per ounce

22 Jun: USD 16.43, GBP 12.35 & EUR 14.11 per ounce

21 Jun: USD 16.25, GBP 12.33 & EUR 14.07 per ounce

20 Jun: USD 16.29, GBP 12.38 & EUR 14.09 per ounce

19 Jun: USD 16.36, GBP 12.42 & EUR 14.16 per ounce

18 Jun: USD 16.61, GBP 12.53 & EUR 14.29 per ounce

Recent Market Updates

– London House Prices Fall 1.9% In Quarter – Bubble Bursting?

– Gold Exports To London From U.S. Surge 152% In 2018

– Manipulation of Gold & Silver by Bullion Banks Is “Undeniable”

– “Perfect Environment For Gold” As Fed Will Weaken Dollar and Create Inflation – Rickards

– Russia Buys 600,000 oz Of Gold In May After Dumping Half Of US Treasuries In April

– In Gold, Silver and Bitcoin We Trust? Goldnomics Podcast with Ronald-Peter Stoeferle

– Own A “Bit Of Gold” As We Are Moving Ever Closer To A Trade War

– Bitcoin Price To $0 Or $1 Million In One Year? MoneyConf 2018 Poll

– Cashless Society – Good or Bad? MoneyConf 2018 Video

– Do We Still Need Banks In The Age Of Fintech?

– Total US Government Debt Is $200 Trillion – Debt Clock Ticking To Next Crisis

– All Gold is Not Equal – Goldnomics Podcast (Episode 4)

– “Without Gold I Would Have Starved To Death” – ECB Governor

– Swiss Government Pension Fund To Buy Gold Bars Worth Some €600 Million

ANDREW MAGUIRE’S KINESIS WHICH IS A”BITCOIN’ BACKED 100% BY ALLOCATED GOLD AND SILVER

Andrew Maguire’s Kinesis money which is a “bitcoin” but backed 100% by allocated gold and silver is set to go.

it think it would be a great idea to look at this!

please read at: https://kinesis.money/#/

(Andrew Maguire)

|

|

Dear Harvey Organ,

Thank you for your participation in our webinar on June 7th with our host and CEO of Kinesis, Thomas Coughlin.

The response we received has been incredible, we appreciate you taking the time to join us and hope you found it to be beneficial.

Due to such a high influx of questions we received we were unable to have them all answered. Nevertheless, if there was anything which requires more clarification, or you have a query which needs to be rectified, we invite you to join our telegram group:

We apologize for the technical issues we incurred during the webinar which resulted in it running a little over schedule, we hope that the next one we host will run seamlessly.

A video has been put together and uploaded onto our YouTube channel which can be found here:

Please share and subscribe to our YouTube channel to be notified of all the latest videos as they become available.

The rapid growth that we are currently experiencing has been incredible and with your support, is only going to get better.

We are working behind the scenes very hard to create a better experience for everyone involved! Stay tuned in as we have many more announcements to be released in the upcoming days.

Kind Regards,

|

Kinesis Money

a:C/O ILS Fiduciaries (IOM) Limited, First Floor,Millennium House, Victoria Road, Douglas, Isle of Man IM2 4RW

|

The following is self explanatory

(courtesy GATA/Chris Powell and Harvey Organ)

GATA asks bank regulator to check risks of gold

futures maneuver

Submitted by cpowell on Sun, 2018-06-10 16:17. Section: Daily Dispatches

12:21p ET Sunday, June 10, 2018

Dear Friend of GATA and Gold:

GATA has appealed to the U.S. comptroller of the currency, who has regulatory authority over banks, to review financial risks certain banks may have incurred through derivatives in the monetary metals markets, particularly through the recent heavy use of the “exchange for physicals” mechanism of settling gold and silver futures contracts on the New York Commodities Exchange.

The appeal was made in a letter sent May 5 to the comptroller, Joseph M. Otting, whose office is part of the U.S. Treasury Department, by your secretary/treasurer and GATA futures market consultant Harvey Organ.

“Exchange for physical” settlements of futures contracts long were considered emergency procedures when a seller was not able to deliver metal from an exchange-approved warehouse and wanted to settle with delivery elsewhere. But now such settlements appear to constitute most gold and silver futures settlements on the Comex. It is a strange development that appears to have been necessitated by the increasing difficulties of central banking’s gold and silver price suppression policy.

GATA has received no acknowledgment of the letter. Its text is below and a PDF copy of it is here:

http://www.gata.org/files/ComptrollerOfCurrencyLetter.pdf

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

* * *

May 5, 2018

Joseph M. Otting, Comptroller of the Currency

U.S. Treasury Department

400 7th Street, SW

Washington DC 20219

Dear Comptroller Otting:

Please let us bring to your attention financial risks to major banks involving their possibly unreported exposure to derivatives in the monetary metals markets.

In recent months gold and silver future contracts issued by U.S. banks on the New York Commodities Exchange have been moved off-exchange for delivery through a mechanism known as “exchange for physical” (EFP) contracts. Until recently use of this mechanism was considered an emergency procedure when a seller did not have access to metal for delivery through Comex warehouses. Now the mechanism seems to be in use for a large share of front-month contracts for which delivery is sought.

Here is an example that is happening at the Comex in the front active month of April for gold and the inactive delivery month of April for silver.

In gold, there were 229,436 EFP contracts for 713.64 tonnes, an average of 10,925 contracts and 1,092,500 ounces per trading day.

In silver, there were 77,150 EFP contracts for 385,750,000 ounces, an average of 3,673 contracts and 18,369,000 ounces per trading day.

London Bullion Market Association rules suggest that these contracts may not be reported to regulators. The LBMA’s bylaws say:

“Figures above exclude any contracts not subject to risk-based capital requirements, such as FX contracts with an original maturity of 14 days or less, futures contracts, written options, and basis swaps. Therefore, the total notional amount of derivatives by maturity will not add to the total derivatives figure in this table.”

We are told that these EFP contracts are transferred from the Comex to London as what are called “serial forwards” and their duration is always less than 14 days, which exempts them from being reported.

It is our understanding that in each quarter your office prepares a report detailing risk undertaken by the banks under the comptroller’s supervision.

These risks include derivatives undertaken by U.S. banks and other obligations that may cause a bank to fail. Our concern is that your office may not be aware of large unreported derivative exposure by banks.

Could you review this matter and let us know your conclusions?

Sincerely,

CHRIS POWELL

Secretary/Treasurer

HARVEY ORGAN

Consultant

Gold Anti-Trust Action Committee Inc.

7 Villa Louisa Road

Manchester, Connecticut 06043-7541

END

Turkey in one year has doubled its official gold reserves from 116 tonnes up to 239 tonnes

(courtesy Lawrie Williams/Sharp’s Pixley)

* * *

Your early WEDNESDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED DOWN TO 6.6075/HUGE DEVALUATION /shanghai bourse CLOSED DOWN 31.33 POINTS OR 1.10%// HANG SANG CLOSED DOWN 525.14 PTS OR 1.82%

2. Nikkei closed DOWN 70.23 POINTS OR 0.31% / /USA: YEN RISES TO 109.98/

3. Europe stocks OPENED DEEPLY IN THE GREEN EXCEPT SPAIN / /USA dollar index RISES TO 94.89/Euro FALLS TO 1.1612

3b Japan 10 year bond yield: RISES TO . +.04/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 109987/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD FINALLY IN THE POSITIVE/BANK OF JAPAN LOSING CONTROL OF THEIR YIELD CURVE AS THEY PURCHASE ALL BONDS TO GET TO ZERO RATE!!

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 71.06 and Brent: 76.89

3f Gold DOWN/Yen DOWN

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil UP for WTI and UP FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund FALLS TO +.33%/Italian 10 yr bond yield DOWN to 2.83% /SPAIN 10 YR BOND YIELD DOWN TO 1.34%

3j Greek 10 year bond yield FALLS TO : 4.09

3k Gold at $1258.30 silver at:16.26 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble DOWN 4/100 in roubles/dollar) 62.97

3m oil into the 71 dollar handle for WTI and 76 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 109.98 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 0.9928 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1531 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now POSITIVE territory with the 10 year FALLING to +0.33%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.85% early this morning (THIS IS DEADLY TO ALL MARKETS). Thirty year rate at 3.00%

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

(courtesy Jim Reid/Bloomberg/Deutsche bank/zero hedge)

Global Markets Slide As Trade Fears Return:

China Bear Market Deepens, Deutsche Hits

Record Low

Trade fears have returned with a twist, as global market weakness has spread to European banks while safe havens including the yen and sovereign bonds are broadly higher amid renewed risk-off sentiment.

Once again, it started in China where the Shanghai Composite slumped for another session, dropping 1.1%, and falling deeper into a bear market.

The weakness was prompted by a renewed decline in the “weaponized” Yuan, which fell for a 10th consecutive day, matching a record losing stretch, and prompting questions whether Beijing is seeking to retaliate to Trump’s protectionism with another round of devaluation.

As we noted last night, last time the yuan devalued this fast, it unleashed hell on the world’s financial markets

The continued slump in the yuan has stoked concerns that Chinese policy makers are less willing to temper its decline, which may remove an anchor of stability for emerging-market currencies. Still, it may not be all Beijing’s doing as policymakers set the fixing at a level that was stronger than analysts expected on Wednesday, while the decline could have been far worse when at least one major Chinese bank sold the dollar in the onshore market to keep the yuan stronger than 6.6, according to two traders, prompting speculation of intervention.

A foreign-exchange trader in Asia told Bloomberg the offshore yuan ran into a large dollar-seller – possibly an agent bank working for Chinese authorities – after weakening beyond 6.61 per dollar. Tommy Ong, managing director for treasury and markets at DBS Hong Kong Ltd., said he wouldn’t be surprised if the People’s Bank of China intervened if speculative bets against the yuan grew. “The PBOC may think that fundamentally the yuan should weaken, but the move is too fast in the past week and that could ignite capital outflows,” Ong said. “Any intervention should aim only to smooth out such market moves

Whatever Beijing’s intentions, the Chinese drop pressured the MSCI Asia Pacific index lower for third day, while the yuan led to a decline in Asian currencies, as developing-market stocks also tumbled, with the MSCI Emerging Markets Index hitting the lowest in 10 months.

In Europe, the Stoxx 600 reversed initial gains and fell with beaten-down autos sector index resuming its sell-off, down 0.8% and hitting its lowest level since September 2017 amid worries over trade tensions.

The banking sector did not help, as Deutsche Bank suffered a sharp selloff shortly after the start of trading, sending the stock to new all time lows, and dragging the European banking sector to the lowest level since 2016, and down 14% YTD.

U.S. equity-index futures also slid amid a rush for safety, which sent the dollar higher and the yield on 10Y Treasurys as low as 2.84%, briefly sending the 2s10s below 33 bps.

In FX, the dollar was headed for a second day of gains in early trading, only surpassed by the yen, which was boosted by demand for haven assets. The pound slipped while Brexit tensions kept demand for pound puts strong across tenors, though BOE policy maker Ian McCafferty’s stance that officials shouldn’t wait any longer to increase interest rates eases pressure on the medium term. The kiwi led declines among Group- of-10 peers, dropping to its lowest since November and also dragging down the Aussie, before the RBNZ’s interest-rate decision on Thursday,

Continued mixed signals on global trade have complicated the investment picture, after President Donald Trump signaled he may take a less confrontational path toward curbing Chinese investments, only for his trade representative Robert Lighthizer to once again pour fuel on the showdown with countries including the EU, blasting the various retaliatory tariffs the U.S.’ trading partners have advanced in reaction to the Trump administration’s trade policies, calling the tariffs proof of the “complete hypocrisy” of the global trade system.

“[T]he European Union has concocted a groundless legal theory to justify immediate tariffs on U.S. exports. Other WTO Members, including China, have adopted a similar approach. These retaliatory tariffs underscore the complete hypocrisy that governs so much of the global trading system,” Lighthizer said in a statement Tuesday evening.

Also overnight, the US House voted 400 vs. 2 in favor of passing bill to tighten oversight of US foreign investment due to concern over China. In related news, US President Trump suggested he would back down from his demand for new tight restrictions on Chinese investments into technology and instead rely on other channels already in place such as CFIUS.

And speaking of trade, the Fed’s Bostic who is a FOMC voter this year noted overnight that “the more (trade tensions) progresses in this more contentious way, the more it pulls me to feel like the risks are on the downside for the broader economy”. He added that “there is some likelihood I’ll be moving away from four (rate hikes) as a real possibility”. Elsewhere, the Fed’s Kaplan spoke on the yield curve as being a signal of recession. He said based on past experience “I’m loathe to say this time will be different. It’s significant to watch the yield curve”. For now, he noted the flattening yield curve is telling you that the short term US growth is strong while medium and long term growth is “sluggish”. Meanwhile the Fed’s Barkin noted the “aggregate effects of corporate tax cuts are especially hard to predict…and given these many uncertainties, the FOMC has been cautious when assessing the future impacts of the recent tax legislation”. That said, he added it’s reasonable to expect “at least a moderate boost” for the economy from recent tax cuts.

In commodities, oil was up ~0.8% on the day and around the month-long high levels seen post Tuesday afternoon’s rally after reports the US was pressing its allies to halt all oil imports from the nation by November. Further, API inventory report showed the largest drawdown to crude stockpiles since September 2016, although the impact was relatively contained on slight fatigue considering WTI had already rallied over 3% prior to the release. In the metals scope, gold is uneventful at its lowest levels since December 2017 as the overnight weakening has abated slightly. Copper has hit 12 week lows as trade concerns have hit the building material at USD 6,679/tonne, alongside ongoing supply concerns from Chile.

Expected data include MBA mortgage applications, wholesale inventories, and durable-goods orders. Canopy Growth, General Mills, Paychex, Bed Bath & Beyond and Rite Aid are among companies reporting earnings

Market Snapshot

- S&P 500 futures down 0.6% to 2,713.00

- STOXX Europe 600 down 0.8% to 374.43

- German 10Y yield fell 2.9 bps to 0.311%

- Euro down 0.2% to $1.1631

- Italian 10Y yield rose 6.2 bps to 2.619%

- Spanish 10Y yield fell 2.9 bps to 1.364%

- Brent futures up 0.1% to $76.41/bbl

- Gold spot down 0.2% to $1,256.19

- U.S. Dollar Index up 0.1% to 94.78

- MXAP down 0.7% to 165.81

- MXAPJ down 1.1% to 535.03

- Nikkei down 0.3% to 22,271.77

- Topix up 0.02% to 1,731.45

- Hang Seng Index down 1.8% to 28,356.26

- Shanghai Composite down 1.1% to 2,813.18

- Sensex down 0.7% to 35,244.36

- Australia S&P/ASX 200 down 0.03% to 6,195.86

- Kospi down 0.4% to 2,342.03

Top Overnight News from Bloomberg

- U.S. President Donald Trump signaled he may take a less confrontational path toward curbing Chinese investments in sensitive American technologies, potentially relying on a U.S. committee that scrutinizes foreign acquisitions for national security risks

- An accelerating slump in China’s yuan is stoking fear that policy makers are less willing to temper the currency’s decline as the economy slows and a trade battle with the U.S. worsens

- The Canadian government is preparing new measures to prevent a potential flood of steel imports from global producers seeking to avoid U.S. tariffs, according to people familiar with the plans

- S&P Global Ratings affirmed the U.S.’s sovereign credit score at AA+, the assessor’s second- highest grade, citing the country’s “diversified and resilient economy” while noting the impact of ongoing political wrangling on public finances

- Oil held gains above $70 a barrel as the U.S. pressed allies to end Iranian imports by a November deadline and after industry data showed American inventories declined

- U.K. house-price growth slowed in June, dropping to its weakest pace in five years, according to Nationwide Building Society.

- Europe’s junk-debt investors are gaining ground after years of borrowers chipping away at the safeguards enshrined in the small print of bond documents

- Bank of Japan’s Deputy Governor Masayoshi Amamiya sees the central bank as “very far off from the exit”, underpinning monetary policy divergence that could keep the pair in bullish trajectory as long as trade concerns ease

Asian equity markets were negative with the region cautious as trade concerns lingered, albeit with a slight moderation after US President Trump suggested he would ease off on demands for new tight restrictions regarding Chinese investments and instead go through channels already in place such as the Committee on Foreign Investment in the United States. ASX 200 (flat) was choppy as the initial gains led by the energy sector were briefly eclipsed by weakness in telecoms and financials, while Nikkei 225 (-0.3%) exporter names were dampened by currency strength. Elsewhere, Hang Seng (-1.8%) and Shanghai Comp. (-1.1%) were also subdued amid the current backdrop of trade concerns and after a net liquidity drain by the PBoC which saw the mainland index extend on its descent through bear market territory. Finally, 10yr JGBs were relatively flat with only minimal support seen from the risk-averse tone in Japan and the BoJ’s presence for JPY 810bln of JGBs across the curve. Chinese President Xi is said to have warned leaders to be prepared in the event of a full-scale trade war with US during a 2-day meeting, according to a note from SGH Macro Advisors that also suggested the PBoC will refrain from buying US Treasuries and seek to lower them.

Top Asian News

- BreadTalk Soars to Record High as It Presents at Citi Roadshow

- Bank Rakyat Is Said to Revive Sale of Stake in Life Insurer

- China H Shares, Once World’s Hottest, Tumble Into Bear Market

- Yuan’s Rapid Selloff Puts China’s Market-Anchor Role in Danger

European equity bourses were initially negative across the board as trade concerns hit European markets following US congressional approval of increased US-Chinese investment scrutinization. There was a turnaround, however, into positive territory with the DAX currently the outperforming bourse, after hitting 2 month lows, on the back of US Defence Secretary Mattis striking a positive tone after talks with Chinese President Xi. Most bourses are still below their 100DMA, however, and have not been able to eliminate the losses seen throughout the week, with the DAX at 12,210 vs. its 50DMA of 12,761, the FTSE 100 at 7,534 vs its 50DMA of 7,616 and the CAC at 5,268 vs. its 50DMA of 5,473. The financial sector (-0.4%) is currently underperforming as falling treasury yields are weighing on the sector.

Top European News

- European Banks Decline as Deutsche Bank Hits Fresh Low

- Banks in Denmark Are Facing a Capital Hit as Early as This Year

- Norway Sells Out of SAS in Move That May Ease Consolidation

- Bulgaria Blames ‘Constantly Changing’ Demands for Euro Delay

In FX, it was a cagey start to European trade in FX markets with most majors sticking to their recent ranges. Subsequently, the USD trades relatively unchanged thus far with the DXY sitting just above 94.50 as markets pause for breath after US President Trump took a slightly more conciliatory tone yesterday by suggesting he would ease off on demands for new tight restrictions regarding Chinese investments. That said, despite these comments from Trump, they are unlikely to signal a U-turn in US trade policy and the threat of an escalation in trade tensions remains at the forefront of investor sentiment. From a Chinese perspective, preparations are said to be made by leaders of the communist regime to help protect the nation’s economy in the event of a trade war with the US. It’s worth noting that the PBoC set the CNY mid-point fix at its softest level since 25th December last year with USD/CNY back below 6.6000 as the recent move to the downside continues to gather momentum; scepticism remains as to whether this is actually a targeted policy measure by China and how fair they would be willing to tolerate the move given the risk of capital outflows. Elsewhere, not too much to report for EUR as focus on the most recent ECB policy announcements and communications somewhat abates Subsequently, in the absence of any major USD traction at this stage of the session, option activity could dictate performance for the pair with 1.6bln in expiries at 1.1650, 3.3bln at 1.1625 and 2.4bln at 1.1600.

In commodities, oil is up ~0.8% on the day and around the month-long high levels seen post Tuesday afternoon’s rally after reports the US was pressing its allies to halt all oil imports from the nation by November. Further, API inventory report showed the largest drawdown to crude stockpiles since September 2016, although the impact was relatively contained on slight fatigue considering WTI had already rallied over 3% prior to the release. In the metals scope, gold is uneventful at its lowest levels since December 2017 as the overnight weakening has abated slightly. Copper has hit 12 week lows as trade concerns have hit the building material at USD 6,679/tonne, alongside ongoing supply concerns from Chile.

Looking at the day ahead, the main focus will likely be on the preliminary May durable and capital goods orders data, while the May advance goods trade balance is also due along with May pending home sales. Central bank speak continues with the BoE’s Carney speaking in the morning about the BoE’s Financial Stability Report, followed later by the ECB’s Praet and Fed’s Rosengren.

US Event Calendar

- 7am: MBA Mortgage Applications, prior 5.1%

- 8:30am: Advance Goods Trade Balance, est. $69.0b deficit, prior $68.2b deficit, revised $67.3b deficit

- 8:30am: Wholesale Inventories MoM, est. 0.2%, prior 0.1%; Retail Inventories MoM, prior 0.6%, revised 0.5%

- 8:30am: Durable Goods Orders, est. -1.0%, prior -1.6%; Durables Ex Transportation, est. 0.5%, prior 0.9%

- 8:30am: Cap Goods Orders Nondef Ex Air, est. 0.45%, prior 1.0%; Cap Goods Ship Nondef Ex Air, est. 0.3%, prior 0.9%

- 10am: Pending Home Sales MoM, est. 0.5%, prior -1.3%; Pending Home Sales NSA YoY, prior 0.4%

DB’s Jim Reid concludes the overnight wrap

Unlike London’s rail network during a heatwave, the fallout from the weekend trade related headlines proved to be fairly short-lived in the end with the last 24 hours making for a much calmer affair in markets. Last night the S&P 500 closed +0.22% with energy names leading the way after WTI Oil surged +3.60% while the Dow (+0.12%) rose for only the second time in the last eleven sessions. The Nasdaq closed +0.39% while prior to that in Europe the Stoxx 600 closed out an uneventful session +0.02% with volumes well below average. The VIX edged back below 16 and is now back to its YTD average again more or less while moves for bond markets were similarly muted outside of the periphery with Bunds just 1.3bp higher while Treasuries nudged down -0.3bps. The US dollar index (+0.41%) was stronger also.

As for the newsflow, well Peter Navarro’s soothing words on Monday night appeared to do its job although to be honest yesterday felt more like a no news is good news sort of day. President Trump did tweet his disdain at Harley Davidson’s pledge to move production out of the US, saying that “it will be the beginning of the end” and that “they will be taxed like never before”. Harley Davidson’s shares fell as much as -2.70% before ending -0.60% lower. Trump also tweeted that his administration is finishing its study of tariffs on cars from the EU, while House Speaker Paul Ryan also weighed in with some comments of his own yesterday afternoon. Speaking to reporters in response to the Harley-Davidson situation, Ryan said that “there are better tools than tariff increases” and that “tariffs aren’t the right way to go”. All in all then, nothing that really got the market too excited. Later in the session though Trump then spoke at the White House and indicated that he might be favouring Treasury Secretary Steven Mnuchin’s softer approach towards protecting US intellectual property from China, specifically by using the Committee on Foreign Investments in the US (CFIUS).

Despite that, this morning, after China’s Shanghai Comp won the race to be the first major equity index to hit correction territory this year, the index is extending on losses (-0.45%) while the rest of Asia is also trading modestly lower with the Nikkei (-0.27%), Kospi (-0.13%) and Hang Seng (-0.58%) all down. In the US, rating agency S&P has affirmed the US’s sovereign credit rating of AA+ with stable outlook and noted “we expect that debates over funding the government and raising the debt ceiling will continue to be resolved at the last minute”. Meanwhile Reuters cited unnamed sources saying that Canada may be preparing higher tariffs on steel to prevent a flood of steel imports as producers divert their output away from the US. Back in Asia, BOJ’s Deputy Governor Amamiya sees the BOJ as “very far off from exit” in terms of stimulus policies, in part as he does not think “the side effects exceed the benefits at this point”, although “the effects are cumulative and we’re watching this carefully”. As for data this morning, China’s May industrial profits moderated 0.8ppt mom to a still solid level of 21.1% yoy.

Moving on. There was a bit of macro data out yesterday in the US with the June consumer confidence print coming in at a weaker than expected 126.4 (vs. 128.0 expected). It also fell 2.4pts from May although the absolute level is still indicative of an upbeat US consumer (130.0 is the post-recession high made back in February). In the details the present conditions gauge was actually more or less unchanged at 161.1 although the expectations gauge did slip 4pts to 103.2. Meanwhile the Richmond Fed manufacturing index rose 4pts to 20 (vs. 15 expected) with new orders rising to the highest since February and prices paid the highest since 2012.

Meanwhile, Sterling was kept busy yesterday with a couple of BoE speakers doing the rounds in the morning. Incoming MPC member Jonathan Haskel said that “given current conditions and economic data, I agree with the broad direction of travel” but also that “the first risk involved in raising interest rates would be if this is done too quickly, disturbing investment and borrowing plans by more than would have been expected”. Haskel’s testimony leant slightly dovish at the margin which was in contrast to outgoing MPC member and well-known hawk Ian McCafferty who said that the BOE “should not dally” in raising rates.

Unsurprisingly there was greater weight placed on Haskel’s comments with Sterling falling as much as -0.55%, before paring some of that move into the close to finish -0.42%. Gilts were also the relative outperformer yesterday in bond markets (2y closing +0.4bps higher and 10y +1.0bps higher) while the probability of a hike at the August meeting continues to hover just north of a coin flip (currently 58%).

Over in the US, the Fed’s Bostic who is a FOMC voter this year noted “the more (trade tensions) progresses in this more contentious way, the more it pulls me to feel like the risks are on the downside for the broader economy”. He added that “there is some likelihood I’ll be moving away from four (rate hikes) as a real possibility”. Elsewhere, the Fed’s Kaplan spoke on the yield curve as being a signal of recession. He said based on past experience “I’m loathe to say this time will be different. It’s significant to watch the yield curve”. For now, he noted the flattening yield curve is telling you that the short term US growth is strong while medium and long term growth is “sluggish”. Meanwhile the Fed’s Barkin noted the “aggregate effects of corporate tax cuts are especially hard to predict…and given these many uncertainties, the FOMC has been cautious when assessing the future impacts of the recent tax legislation”. That said, he added it’s reasonable to expect “at least a moderate boost” for the economy from recent tax cuts.

Coming back to Oil, the complex rallied around 3% (WTI +3.60%; Brent +2.11%) yesterday on the prospect of reduced oil supply after Bloomberg reported the US has pressed its allies to stop importing oil from Iran by the November 4 deadline as part of its sanction efforts. Notably, an unnamed State Department official said the US administration would not rule out waivers or extensions to the November deadline, but it is not discussing those options either. Meanwhile, the US energy secretary Perry also noted the recent OPEC plans for higher crude output “may be a little short” of what’s required to prevent an oil price spike.

As for other news, there was some positive headlines in Germany yesterday with two CSU leaders (Seehofer and Dobrindt) stressing that they do not want to break up the coalition. Merkel also added that the CDU sees scope for broad agreement with the CSU on migration however she also added that it’s unlikely that this week’s EU summit will make for an overall deal on all aspects of migrant policy. So expect this to drag on a little longer. Elsewhere, it was interesting to note a Bloomberg story yesterday suggesting that Special Counsel Robert Mueller is intending to accelerate his investigation into the Russia-US election probe. The story suggested that Mueller and his team have a view to present conclusions by Autumn, conveniently timed with the US mid-terms.

Before we wrap up, a quick mention that yesterday our House View team published a note focusing on the latest trade war developments. The report has a special focus on (1) Trade tensions – different measures, potential macro impact and the scope for policy response in the US and China, and (2) Policy divergence between the Fed and ECB. It also covers the upcoming EU council summit later this week. The document as usual also summarises our economists’ macro and monetary policy outlook and forecasts, as well as the key strategy views across rates, FX and Credit. You can find a link to the report here.

Looking at the day ahead, it looks set to be a relatively quiet session in Europe with the only data due being June consumer confidence data in France and May M3 money supply data for the Euro area are due. In the US the main focus will likely be on the preliminary May durable and capital goods orders data, while the May advance goods trade balance is also due along with May pending home sales. Central bank speak continues with the BoE’s Carney speaking in the morning about the BoE’s Financial Stability Report, followed later by the ECB’s Praet and Fed’s Rosengren.

3. ASIAN AFFAIRS

i)WEDNESDAY MORNING/TUESDAY NIGHT: Shanghai closed DOWN 31.33 POINTS OR 1.10% /Hang Sang CLOSED DOWN 525.14 POINTS OR 1.82% / The Nikkei closed DOWN 70.23 POINTS OR 0.31% /Australia’s all ordinaires CLOSED DOWN 0.03% /Chinese yuan (ONSHORE) closed DOWN at 6.6075 AS POBC EXERCISES A HUGE DEVALUATION IN THE LAST FEW DAYS/Oil UP to 71.06 dollars per barrel for WTI and 76.89 for Brent. Stocks in Europe OPENED IN THE GREEN EXCEPT SPAIN//. ONSHORE YUAN CLOSED DOWN AT 6.6075 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.5990 :HUGE DEVALUATION/PAST FEW DAYS//ONSHORE YUAN TRADING WEAKER AGAINST OFFSHORE YUAN/ONSHORE YUAN TRADING MUCH WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING MUCH WEAKER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR IS BEGINNING/

3 a NORTH KOREA/USA

North Korea/South Korea/usa

3 b JAPAN AFFAIRS

c) REPORT ON CHINA/HONG KONG

Last night, the yuan tumbles to a 6 month low at 6.61 to th dollar. News out of China suggests that they will reduce their purchases of USA treasuries something that the uSA desperately needs

(courtesy zerohedge)

4. EUROPEAN AFFAIRS

Germany/Deutsche Bank

No reason given but Deutsche bank[‘s stock fell below 9 euros. Deutsche bank is the world’s largest derivative player and owner of one of the largest portfolio of junk bonds. What is really scaring the market is a BREXIT as huge amounts of underwriting have been done in England with various counterparties. The big question: what happens when Great Britain leaves?

(courtesy zerohedge)

Deutsche Bank Tumbles To New Record Low, Drags European Banks

Global systemic fears re-emerged this morning, when in addition to ongoing concerns about trade wars which dragged Chinese stocks deeper into a bear market as the Yuan fell for a 10th consecutive day, now there are European banks to also worry about.

Having been relatively stable for much of the recent slide, on Wednesday morning, Deutsche Bank came under heavy selling pressure, tumbling 5% shortly after the start of trading, and dropping to a new all time low of €8.76, and bringing its market cap to just $21BN. By comparison, JPMorgan’s market cap is $357BN.

The stock has since rebounded modestly, and was down 2.3% last, after breaking below €9 for the first time since 2016, when Germany’s largest bank was seen to be on the verge of collapse…

… however the dead cat bounce appears to be nothing more than a temporary respite: “Falling bellow the €9 level adds more pressure to the stock as that was seen as a technical low bottom,” Ignacio Cantos, investment director at ATL Capital in Madrid, told Bloomberg.

The drop in Deutsche Bank sent the The Stoxx Banks Index down 1.8%, to the lowest level since 2016. European Banks Index is now 14% down YTD, of which Deutsche Bank is the worst performer, down 44% YTD.

And sent the index of the global systemically important banks to a 14-month low.

What caused the slump? As Bloomberg’s Paul Dobson writes, there is plenty to worry about besides the usual worries about trade wars, emerging markets, and Italy, including hedge funds warning of a crisis, talk of higher counter-cyclical buffers, as well as sliding bond yields, the deflationary bogeyman for European banks, which in turn is sending European credit risk higher this morning.

Whatever the reason, it appears that whatever risks were latent and starting to emerge as a result of trade war concerns as starting to spread as contagion now hits Europe’s arguably most sensitive sector.

end.

Who Will Call The First Bluff? US Threatens Turkey With Sanctions Over Russian S-400 Purchase

Despite an ostentatious “roll out” ceremony by Lockheed Martin last week in Fort Worth to mark the handover of the first F-35-A Lightning II jet bound for Turkey, the advanced stealth multi-role fighter isn’t going anywhere anytime soon as we previously explained after the Senate passed a draft defense bill for FY 2019 that would halt the transfer until the secretary of state certifies that Turkey will not accept deliveries of Russian S-400 ‘Triumf’ air-defense systems.

Following upon previous warnings, the US State Department has again threatened that Turkey will be targeted by sanctions if it receives the S-400 from Russia under a contract finalized between Ankara and Moscow at the end of 2017, said to be worth $2.5 billion.

The State Department recalled that this decision is a result of the bill President Donald Trump signed into law last summer, which seeks to punish companies that do business with the Russian defense industry.

On Tuesday a top State Department official — Assistant Secretary of State for European and Eurasian Affairs Wess Mitchell — stated the following at a hearing of the Senate Foreign Relations Committee:

“We made it clear that if Turkey buys S-400s… there will be consequences. We will introduce sanctions within Countering America’s Adversaries Through Sanctions Act (CAATSA).”

“We believe that we have existing legal authorities that would allow us to withhold transfer under certain circumstances, including national security concerns,” he said. “We believe that we continue to have the time and ability to ensure Turkey does not move forward on S-400 before having to take a decision on – on F-35. We’re being very clear in our messaging to the Turks that there will be consequences.”