GOLD: $1249.45 DOWN $5.15(COMEX TO COMEX CLOSINGS)

Silver: $16.00 DOWN 18 CENTS (COMEX TO COMEX CLOSINGS)

Closing access prices:

Gold $1248.50

silver: $16.02

ON JUNE 29 OPTIONS, FOR OTIC/LONDON GOLD EXPIRE SO EXPECT CONTINUAL WHACKING OF GOLD UNTIL TOMORROW NIGHT.

For comex gold:

JUNE/

NUMBER OF NOTICES FILED TODAY FOR JUNE CONTRACT:40 NOTICE(S) FOR 4000 OZ

TOTAL NOTICES SO FAR 6890 FOR 689000 OZ (21.430 tonnes)

For silver:

JUNE

0 NOTICE(S) FILED TODAY FOR

nil OZ/

Total number of notices filed so far this month: 1076 for 5,380,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: BID $6056/OFFER $6141: DOWN $41(morning)

Bitcoin: BID/ $6076/offer $6161: DOWN $38 (CLOSING/5 PM)

end

First Shanghai gold fix comes at 10 pm est

The second Shanghai gold fix: 2:15 pm

First Shanghai gold fix gold: 10 pm est: 1260.66

NY price at the same time: 1253.65

PREMIUM TO NY SPOT: $4.09

Second gold fix early this morning: 1253.39

USA gold at the exact same time:1253.15

PREMIUM TO NY SPOT: $0.24

AGAIN, SHANGHAI REJECTS NEW YORK PRICING.

WE WILL NOT PROVIDE LONDON FIXES AS THEY ARE NOT ACCURATE AS TO WHAT IS GOING ON AT THE SAME TIME FRAME.

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total OPEN INTEREST FELL BY A TINY 256 CONTRACTS FROM 218,492 DOWN TO 218,236 WITH YESTERDAY’S 8 CENT LOSS IN SILVER PRICING. HOWEVER AS WE ARE NOW WELL INTO THE NON ACTIVE DELIVERY MONTH OF JUNE WE CONTINUE TO WITNESS LONGS PACK THEIR BAGS AND MIGRATE OVER TO LONDON IN GREATER NUMBERS. WE WERE NOTIFIED THAT WE HAD A STRONG SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP: 2550 EFP’S FOR JULY, 827 EFP’S FOR SEPT. , 0 EFP’S FOR DECEMBER AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE: OF 3377 CONTRACTS. WITH THE TRANSFER OF 3377 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 3377 EFP CONTRACTS TRANSLATES INTO 16.805 MILLION OZ ACCOMPANYING:

1.THE 8 CENT LOSS IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES STANDING FOR JUNE COMEX DELIVERY. (5.420 MILLION OZ) DESPITE IT BEING A NON ACTIVE DELIVERY MONTH.

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF JUNE:

63,287 CONTRACTS (FOR 20 TRADING DAYS TOTAL 63,287 CONTRACTS) OR 316.44 MILLION OZ: (AVERAGE PER DAY: 3164 CONTRACTS OR 15.82 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH: 316.44* MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 39.77% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* WE HAVE ALREADY PASSED LAST MONTH AND CLOSING IN ON THE RECORD MONTH OF APRIL/2018.

ACCUMULATION IN YEAR 2018 TO DATE SILVER EFP’S: 1,632.48 MILLION OZ.

ACCUMULATION FOR JAN 2018: 236.879 MILLION OZ

ACCUMULATION FOR FEB 2018: 244.95 MILLION OZ

ACCUMULATION FOR MARCH 2018: 236.67 MILLION OZ

ACCUMULATION FOR APRIL 2018: 385.75 MILLION OZ

ACCUMULATION FOR MAY 2018: 210.05 MILLION OZ

RESULT: WE HAD A SMALL SIZED DECREASE IN COMEX OI SILVER COMEX OF 256 DESPITE THE 8 CENT LOSS IN SILVER PRICE. WE HAVE NOW ENTERED THE NEW NON ACTIVE MONTH OF JUNE AND THE CME NOTIFIED US THAT IN FACT WE HAD A STRONG SIZED EFP ISSUANCE OF 3377 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) . FROM THE CME DATA: 2550 EFP CONTRACTS FOR JULY, 827 EFP’S FOR SEPT, 0 EFP’S FOR DECEMBER AND ZERO FOR ALL OVER MONTHS FOR A DELIVERABLE FORWARD CONTRACT OVER IN LONDON WITH A FIAT BONUS (TOTAL: 3377). TODAY WE GAINED A STRONG: 3121 TOTAL OI CONTRACTS ON THE TWO EXCHANGES: i.e.3377 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH AN DECREASE OF 256 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED WITH A 8 CENT LOSS IN PRICE OF SILVER AND A CLOSING PRICE OF $16.18 WITH RESPECT TO YESTERDAY’S TRADING. YET WE STILL HAVE A GIGANTIC AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY IN THIS NON ACTIVE JUNE DELIVERY MONTH. IT SURE LOOKS LIKE A FAILED BANKER SHORT COVERING EXERCISE!!

In ounces AT THE COMEX, the OI is still represented by OVER 1 BILLION oz i.e. 1.094 MILLION OZ TO BE EXACT or 156% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT JUNE MONTH/ THEY FILED AT THE COMEX: 8 NOTICE(S) FOR 40,000 OZ OF SILVER

IN SILVER, WE HAVE NOW SET THE NEW RECORD OF OPEN INTEREST AT 243,411 AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $16.51 ON APRIL 9.2018.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ AND MAY: 36.285 MILLION OZ /AND JUNE/2018 (5.420 MILLION OZ SO FAR)

- HUGE RECORD OPEN INTEREST IN SILVER 243,411 CONTRACTS (OR 1.217 BILLION OZ/ SET APRIL 9/2018

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017

- RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ (FINAL)

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT).

In gold, the open interest ROSE BY A CONSIDERABLE 1739 CONTRACTS UP TO 470,312 DESPITE THE FALL IN THE GOLD PRICE/YESTERDAY’S TRADING (A DROP IN PRICE OF $3.60). WE ARE NOW IN THE ACTIVE DELIVERY MONTH OF JUNE. NO DOUBT THE BOYS ARE CASHING IN THEIR COMEX LONGS TO BEGIN THE PROCESS TO MOVE INTO LONDON FORWARDS. THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A GOOD SIZED 6118 CONTRACTS : JUNE SAW THE ISSUANCE OF 0 CONTRACTS , AND AUGUST SAW THE ISSUANCE OF: 6118 CONTRACTS WITH ALL OTHER MONTHS ZERO. The new OI for the gold complex rests at 470,312. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE A GOOD OI GAIN IN TOTAL CONTRACTS ON THE TWO EXCHANGES: 1739 OI CONTRACTS INCREASED AT THE COMEX AND A GOOD SIZED 6118 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN: 7857 CONTRACTS OR 785,700 OZ = 24.43 TONNES. AND STRANGELY ALL OF THIS DEMAND OCCURRED WITH A FALL IN THE PRICE OF GOLD TO THE TUNE OF $3.60.???

YESTERDAY, WE HAD 9008 EFP’S ISSUED.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF MAY : 208,103 CONTRACTS OR 20,810,300 OZ OR 647.28 TONNES (20 TRADING DAYS AND THUS AVERAGING: 10,405 EFP CONTRACTS PER TRADING DAY OR 1,040,500 OZ/ TRADING DAY),,

TO GIVE YOU AN IDEA AS TO THE HUGE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 20 TRADING DAYS IN TONNES: 647.28 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2017, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 2555 TONNES

THUS EFP TRANSFERS REPRESENTS 647.28/2550 x 100% TONNES = 25.38% OF GLOBAL ANNUAL PRODUCTION SO FAR IN JUNE ALONE.***

ACCUMULATION OF GOLD EFP’S YEAR 2018 TO DATE: 4,099.09* TONNES *SURPASSED ANNUAL PROD’N

ACCUMULATION OF GOLD EFP’S FOR JANUARY 2018: 653.22 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR FEBRUARY 2018: 649.45 TONNES (20 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR MARCH 2018: 741.89 TONNES (22 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR APRIL 2018: 713.84 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR MAY 2018: 693.80 TONNES ( 22 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR JUNE 2018 (21 TRADING DAYS)

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A CONSIDERABLE SIZED INCREASE IN OI AT THE COMEX OF 1739 DESPITE THE $3.60 DROP IN PRICING GOLD TOOK YESTERDAY // . WE ALSO HAD A GOOD SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 6118 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 6118 EFP CONTRACTS ISSUED, WE HAD AN STRONG NET GAIN OF 7857 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

6118 CONTRACTS MOVE TO LONDON AND 1739 CONTRACTS DECREASED AT THE COMEX. (in tonnes, the GAIN in total oi equates to 26.62 TONNES). ..AND BELIEVE IT OR NOT BUT ALL OF THIS DEMAND OCCURRED WITH A FALL OF $3.60 IN TRADING!!!. AT THE COMEX. THE COMEX IS AN OUTRIGHT FRAUD

we had: 11 notice(s) filed upon for 1100 oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD DOWN $5.15 TODAY: / NO CHANGES IN GOLD INVENTORY AT THE GLD

/GLD INVENTORY 821.69 TONNES

Inventory rests tonight: 821.69 tonnes.

SLV/

WITH SILVER DOWN 18 CENTS TODAY / THE CROOKS ADDED 1.035 MILLION OZ OF SILVER INTO THE SLV

/INVENTORY RESTS AT 320.395 MILLION OZ/

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER FELL BY A TINY SIZED 256 CONTRACTS from 218,492 DOWN TO 218,236 (AND FURTHER FROM THE NEW COMEX RECORD SET /APRIL 9/2017 AT 243,411/SILVER PRICE AT THAT DAY: $16.53). THE PREVIOUS RECORD OTHER THAN WAS ESTABLISHED AT: 234,787, SET ON APRIL 21.2017 OVER ONE YEAR AGO. THE PRICE OF SILVER ON THAT DAY: $17.89. OUR CUSTOMARY MIGRATION OF COMEX LONGS MORPH INTO LONDON FORWARDS CONTINUES AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

2550 EFP’S FOR JULY, 827 EFP CONTRACTS FOR SEPT., 0 EFP CONTRACTS FOR DECEMBER AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 3377 CONTRACTS . EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI LOSS AT THE COMEX OF 256 CONTRACTS TO THE 3377 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A NET GAIN OF 3121 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES: 15.605 MILLION OZ!!! AND YET THIS STRONG DEMAND OCCURRED WITH A 8 CENT LOSS IN PRICE??? . THE BANKERS ORCHESTRATED THEIR CONSTANT AND NEVER ENDING RAIDS DESPERATELY TRYING TO PARE THEIR GIGANTIC OPEN INTEREST SHORT ON BOTH EXCHANGES WITH HARDLY ANY SUCCESS. HOWEVER A DRAMATIC AMOUNT OF EFP ISSUANCE IS HEADING OVER TO LONDON AND NO DOUBT WE WILL COME CLOSE TO BREAKING APRIL’S RECORD OF 385 MILLION OZ.

RESULT: A SMALL SIZED DECREASE IN SILVER OI AT THE COMEX DESPITE THE THE 8 CENT LOSS THAT SILVER TOOK IN PRICING ON YESTERDAY. BUT WE ALSO HAD ANOTHER STRONG SIZED 3377 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR JUNE, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

)THURSDAY MORNING/WEDNESDAY NIGHT: Shanghai closed DOWN 26.28 POINTS OR 0.93% /Hang Sang CLOSED UP 141.06 POINTS OR 0.50% / The Nikkei closed DOWN 1.38 POINTS OR 0.01% /Australia’s all ordinaires CLOSED UP 0.24% /Chinese yuan (ONSHORE) closed DOWN at 6.6235 AS POBC EXERCISES A HUGE DEVALUATION IN THE LAST FEW DAYS/Oil UP to 72,73 dollars per barrel for WTI and 78.14 for Brent. Stocks in Europe OPENED IN THE RED //. ONSHORE YUAN CLOSED DOWN AT 6.6235 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.6273 :HUGE DEVALUATION/PAST FEW DAYS//ONSHORE YUAN TRADING STRONGER AGAINST OFFSHORE YUAN/ONSHORE YUAN TRADING MUCH WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING MUCH WEAKER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR IS BEGINNING/

/NORTH KOREA/SOUTH KOREA

i)North Korea/South Korea/USA

b) REPORT ON JAPAN

3 c CHINA

i)China/USA

This is trouble for China. Property owners and other exotic investors have gorged themselves with USA debt at lower yields. Now dollars are scarce and the Chinese government will issue a ban on more USA denominated borrowings. Expect massive defaults in the coming few months

( zerohedge)

4. EUROPEAN AFFAIRS

The EU council cancels it’s summit press conference after Italy threatens to veto re immigration

Italy is correctly asking for help and the stupid EU refuses to help them with the influx of migrants

(courtesy zerohedge)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

i)Turkey

Even though he received 52% of the vote, he did not secure majority in the Turkish parliament and he must have a coalition with a far right anti west party

( Pepe Ecsobar/Asia Times)

ii)The Trump =Putin summit will take place next month on July 16 in Helsinki

(courtesy zerohedge)

iiiIRAN

Totally bankrupt Iran reopens a nuclear plant as Rouhani states that they will bring the USA to their knees. The problem is that they cannot find any uSA dollars to pay their external debt

(courtesy Mac Slavo/SHTPlan.com)

6 .GLOBAL ISSUES

7. OIL ISSUES

8. EMERGING MARKET

9. PHYSICAL MARKETS

i)I brought this story to you yesterday but it is worth repeating. A Chinese think tank warns of a potential financial panic

(courtesy Bloomberg/GATA)

ii)Why Russia and Turkey are such huge gold bugs now. Russia liquidated a huge percentage of its holdings of USA treasuries from 102 billion down to 49 billion

(courtesy Bershidsky/Bloomberg)

iii)Craig Hemke (and Michael Pento below) state that the flattening of the yield curve means recession

(courtesy Craig Hemke/GATA)

10. USA stories which will influence the price of gold/silver)

BEA reports final Q1 GDP at 2.0%. The two problems causing a lower figure were consumption slowing down and inflation. Remember that Q2 sees the start of the Trump stimulus..Even though initial estimates for Q2 are in the 4% range do not be surprised to see these lowered to the 2.% level

( zerohedge)

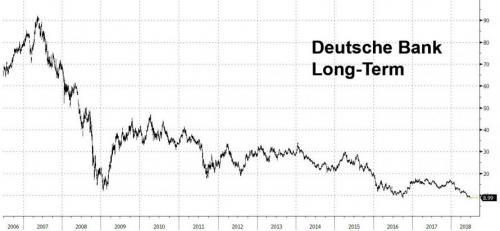

i b)This is huge!!! Deutsche bank fails the Fed test and this forces JPMorgan, Goldman and Four others to limit their payout to shareholders. This stops all funds from leaving Deutsche bank USA. Deutsche bank in Germany is now on its own and must seek help from Germany only.

iiv)SWAMP STORIES

a)Three things to note here:

- Strzok refuses to answer many questions citing many aspects are classified

- nothing is said about the DNC server as to where it is and why the DNC would not let the FBI due their due diligence on it

- and most important the DOJ refuses to release intercepted documentation which would prove Lynch’s rigging of the Clinton email scandal and quite possibly link Obama.

( zerohedge)

b)The fun begins: the House passes a measure to force the DOJ documents to be handed over by July 6. If they do not then Rosenstein will be held in contempt and maybe impeached. Rosenstein and Jordan are engaged in an extremely heated testimony

( zerohedge)

c)Rosenstein refuses to discuss whether Obama spied on the Trump campaign

d)Trey Gowdy, Jim Jordan and Gaetz slam Rosenstein over the Russian probe and other items

1/3 of voters think that a civil war is very likely soon in the USA. And 59% say that the anti Trump liberals will resort to violence

( zerohedge)

Trading Volumes on the COMEX

PRELIMINARY COMEX VOLUME FOR TODAY: 228,490 contracts

CONFIRMED COMEX VOL. FOR YESTERDAY: 171,145 contracts

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

And now for the wild silver comex results.

Total silver OI FELL BY A TINY SIZED 256 CONTRACTS FROM 218,492 UP TO 218,236 (AND A LITTLE FURTHER FROM THE THE NEW RECORD OI FOR SILVER SET APRIL 9.2018/ 243,411 CONTRACTS) DESPITE THE 8 CENT LOSS IN SILVER PRICING/ YESTERDAY. SINCE WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF JUNE, WE WERE INFORMED THAT WE HAD A STRONG SIZED 2550 EFP CONTRACT ISSUANCE FOR JULY, 827 EFP CONTRACTS FOR SEPT., 0 EFP CONTRACTS FOR DECEMBER AND ZERO FOR ALL OTHER MONTHS. THESE EFPS WERE ISSUED TO COMEX LONGS WHO RECEIVED A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. THE TOTAL EFP’S ISSUED: 3377. ON A NET BASIS WE GAINED 3121 SILVER OPEN INTEREST CONTRACTS AS WE OBTAINED A 256 CONTRACT LOSS AT THE COMEX COMBINING WITH THE ADDITION OF 3377 OI CONTRACTS NAVIGATING OVER TO LONDON.

NET GAIN ON THE TWO EXCHANGES: 3121 CONTRACTS

AMOUNT STANDING FOR SILVER AT THE COMEX

We are now in the NON active delivery month of JUNE and here the front month ROSE BY 3 contracts RISING TO 8 contracts. We had 0 notices filed upon yesterday so we gained 3 contracts or an additional 15,000 oz will stand in this non active delivery month of June AS TODAY SOMEBODY WAS IN URGENT NEED OF PHYSICAL ON THIS SIDE OF THE POND

The next big active delivery month for silver is July and here the OI LOST 20,205 contracts DOWN to 19,067. The next delivery month is August and here we GAINED 345 contracts to stand at 1156 The next active delivery month after August for silver is September and here the OI ROSE by 19,225 contracts UP to 157,143

FOR COMPARISON AT THIS TIME IN THE DELIVERY CYCLE, JUNE 29.2017, FOR SILVER, WE HAD 11,691 CONTRACTS OUTSTANDING WITH ONE DAY TO GO BEFORE FIRST DAY NOTICE. THIS COMPARES TO TODAY WITH 19,067 CONTACTS OUTSTANDING WITH ONE DAY TO GO,

WE NO DOUBT WILL HAVE A DOOZY AMOUNT OF SILVER OZ STANDING FOR THE HUGE JULY CONTRACT MONTH

FROM LAST YEARS DATA, ON FIRST DATE NOTICE FOR THE JULY 2017 COMEX DELIVERY MONTH WE HAD 12.115 MILLION OZ OF SILVER STANDING FOR DELIVERY. AT MONTH’S END WE HAD 16.435 MILLION OZ EVENTUALLY STAND AS WE ALREADY HAD QUEUE JUMPING BEGIN IN EARNEST FROM APRIL 2017 ONWARD EVEN TO TODAY.

We had 8 notice(s) filed for 40,000 OZ for the JUNE 2018 COMEX contract for silver

INITIAL standings for JUNE/GOLD

JUNE 28/2018.

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz |

227,691.255 OZ

JPMorgan

7.08 tonnes

|

| Deposits to the Dealer Inventory in oz | NIL oz |

| Deposits to the Customer Inventory, in oz | nil

oz |

| No of oz served (contracts) today |

11 notice(s)

1100 OZ

|

| No of oz to be served (notices) |

31 contracts

(3100 oz)

|

| Total monthly oz gold served (contracts) so far this month |

6901 notices

690,100 OZ

21.465TONNES

|

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

For JUNE:

Today, 0 notice(s) were issued from JPMorgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equates to 11 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped/ Received) by j.P.Morgan customer account.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

To calculate the INITIAL total number of gold ounces standing for the JUNE. contract month, we take the total number of notices filed so far for the month (6901) x 100 oz or 690,100 oz, to which we add the difference between the open interest for the front month of JUNE. (42 contracts) minus the number of notices served upon today (11 x 100 oz per contract) equals 693,200 oz, the number of ounces standing in this active month of JUNE (21.561 tonnes)

Thus the INITIAL standings for gold for the JUNE contract month:

No of notices served (6901 x 100 oz) + {(42)OI for the front month minus the number of notices served upon today (11 x 100 oz )which equals 693,200 oz standing in this active delivery month of JUNE .

WE LOST A SMALL 0 CONTRACTS OR AN ADDITIONAL NIL OZ WILL STAND FOR DELIVERY AS THESE GUYS REFUSED TO MORPH INTO LONDON BASED FORWARDS AND RECEIVE AN ADDITIONAL SWEETENER FOR THEIR EFFORT..

THERE ARE ONLY 7.4177 TONNES OF REGISTERED GOLD AVAILABLE FOR DELIVERY AGAINST 21.561 TONNES STANDING WHICH IS MAKING THIS JUNE CONTRACT MONTH AN EXTREMELY INTERESTING ONE TO WATCH.

WE HAVE HAD 3 ADJUSTMENTS FROM DEALER TO THE CUSTOMER ACCOUNT SO FAR THIS MONTH AND THAT USUALLY MEANS A SETTLEMENT:

I) 5.90 TONNES (TWO WEEKS AGO)

II) 7.9 TONNES (3 DAYS AGO)

III) .56 TONNES (TWO DAYS AGO)

IV) ZERO (FRIDAY/JUNE 22)

v) ZERO (jUNE 25)

vi) zero (June 26)

vii) zero (June 27)

viii) june 28 huge withdrawal from JPMorgan and a probable settlement: 7.09 tonnes

TOTAL: 21.45TONNES HAVE BEEN SETTLED AGAINST THE 21.561TONNES STANDING.

IN THE LAST 18 MONTHS 88 NET TONNES HAS LEFT THE COMEX.

end

And now for silver

AND NOW THE APRIL DELIVERY MONTH

JUNE INITIAL standings/SILVER

| Silver | Ounces |

| Withdrawals from Dealers Inventory | nil oz |

| Withdrawals from Customer Inventory |

533,088.58 oz

Brinks

HSBC

I-D

|

| Deposits to the Dealer Inventory |

nil;

oz

|

| Deposits to the Customer Inventory |

610,640,100

oz

CNT

|

| No of oz served today (contracts) |

8

CONTRACT(S)

(40,000 OZ)

|

| No of oz to be served (notices) |

0 contracts

(NIL oz)

|

| Total monthly oz silver served (contracts) | 1084 contracts

(5,420,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

we had 0 inventory movement at the dealer side of things

total dealer deposits: nil oz

we had 1 deposits into the customer account

i) Into JPMorgan: NIL oz

*** JPMorgan for most of 2017 and in 2018 has adding to its inventory almost every single day.

JPMorgan now has 141 million oz of total silver inventory or 52.0% of all official comex silver. (141 million/270 million)

ii) Into CNT: 610,640.100 oz

total customer deposits today: 610,640.100 oz

we had 3 withdrawals from the customer account;

i) Out of Brinks: 21,124,200.oz

ii) Out of HSBC: 505,007.45 oz

iii) Out of I-Delaware: 6956.93

total withdrawals: 533,088.58 oz

we had 0 adjustment/

total dealer silver: 69.384 million

total dealer + customer silver: 275.367 million oz

The total number of notices filed today for the JUNE. contract month is represented by 8 contract(s) FOR 40,000 oz. To calculate the number of silver ounces that will stand for delivery in JUNE., we take the total number of notices filed for the month so far at 1084 x 5,000 oz = 5,420,000 oz to which we add the difference between the open interest for the front month of JUNE. (8) and the number of notices served upon today (8 x 5000 oz) equals the number of ounces standing.

.

Thus the INITIAL standings for silver for the JUNE/2018 contract month: 1084(notices served so far)x 5000 oz + OI for front month of JUNE(8) -number of notices served upon today (8)x 5000 oz equals 5,420,000 oz of silver standing for the JUNE contract month

PLEASE NOTE THE FOLLOWING FOR COMPARISON PURPOSES:

WITH THE JUNE 29/2017 READING HAD 11,691 CONTRACTS STANDING SO FAR FOR THE JULY 2017 DELIVERY MONTH VS.19,270 OUTSTANDING TODAY/WITH EXACTLY ONE DAY TO GO BEFORE FDN FOR BOTH YEARS..

AT THE CONCLUSION OF JUNE 2017: 4.92 MILLION OZ FINALLY STOOD (INITIALLY 1.98 MILLION OZ STOOD FOR DELIVERY/ JUNE 1) AS QUEUE JUMPING STARTED IN EARNEST AND THROUGHOUT THE ENSUING YEAR IT CONTINUED WITH RECKLESS ABANDON INCLUDING WHAT YOU ARE WITNESSING TODAY.THIS IS COMPARED TO TODAY’S AMOUNT STANDING: 5.420 MILLION OZ.(INITIAL STANDING JUNE 1/2018 WAS 1.780 MILLION OZ)

FOR THE JUNE 2018 CONTRACT MONTH:

We gained 3 contracts or an additional 15,000 oz will stand in this non active delivery month of June as nobody was in urgent need of silver today. IN SILVER QUEUE JUMPING HAS BEEN THE NORM FOR OVER A YEAR. IT LOOKS LIKE GOLD IS TAKING A HOLIDAY FROM THIS SAME PHENOMENON…

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

ESTIMATED VOLUME FOR TODAY: 130,686 CONTRACTS

CONFIRMED VOLUME FOR YESTERDAY: 171,145 CONTRACTS absolutely criminal

YESTERDAY’S CONFIRMED VOLUME OF 171,145 CONTRACTS EQUATES TO 855 million OZ OR 122,1% OF ANNUAL GLOBAL PRODUCTION OF SILVER

COMMODITY LAW SUGGESTS THAT OPEN INTEREST SHOULD NOT BE MORE THAN 3% OF ANNUAL GLOBAL PRODUCTION. THE CROOKS ARE SUPPLYING MASSIVE PAPER TRYING TO KEEP SILVER IN CHECK.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price at that day at $18.42

The previous record was 224,540 contracts with the price at that time of $20.44

end

NPV for Sprott

1. Sprott silver fund (PSLV): NAV FALLS TO -4.11% (JUNE 28/2018)

2. Sprott gold fund (PHYS): premium to NAV FALLS TO -0.57% to NAV (JUNE 28/2018 )

Note: Sprott silver trust back into NEGATIVE territory at -4.11%-/Sprott physical gold trust is back into NEGATIVE/

(courtesy Sprott/GATA)

3.SPROTT CEF.A FUND (FORMERLY CENTRAL FUND OF CANADA): NAV FALLS TO -3.53%: NAV 13.21/TRADING 12.80//DISCOUNT 3.53.

END

And now the Gold inventory at the GLD/

JUNE 28/WITH GOLD DOWN $5.15/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 821.69 TONNES

June 27/WITH GOLD DOWN $3.60// TWO ENTRIES:/STRANGELY THE CROOKS RETURNED THE WITHDRAWAL OF 4.42 TONNES LAST NIGHT (THUS WE HAD A DEPOSIT OF 4.42 TONNES/INVENTORY RESTS AT 824.63 TONNES. /THEN LATE THIS AFTERNOON A WITHDRAWAL OF 2.94 TONNES

INVENTORY RESTS AT 821.69 TONNES/THIS VEHICLE IS AN OUTRIGHT FRAUD.

june 26/LATE LAST NIGHT, WITH GOLD DOWN $9.10 WE HAD A HUGE WITHDRAWAL OF 4.42 TONNES OF GOLD/INVENTORY RESTS AT 820.21 TONES

JUNE 25/WITH GOLD DOWN $1.45/NO CHANGE IN GOLD INVENTORY AT THE GLD.INVENTORY RESTS AT 824.63 TONNES

JUNE 22/WITH GOLD UP 25 CENTS TODAY, THE CROOKS WITHDREW A MASSIVE 4.13 TONNES OF GOLD/INVENTORY RESTS AT 824.63 TONNES

JUNE 21/WITH GOLD DOWN $4.00/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 828.76 TONNES

JUNE 20/WITH GOLD DOWN $3.55/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 828.76 TONNES

JUNE 19/WITH GOLD DOWN $1.50/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 828.76 TONES

JUNE 18/WITH GOLD UP $1.90/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 828.76 TONNES

JUNE 15/WITH GOLD DOWN $28.90/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 828.76 TONNES

JUNE 14/WITH GOLD UP $7.10/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 828.76 TONNES/

JUNE 13/WITH GOLD UP $2.20/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 828.76 TONNES

JUNE 12/WITH GOLD DOWN $4.75:NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 828.76 TONNES

JUNE 11/WITH GOLD UP 65 CENTS/THE CROOKS RAIDED THE COOKIE JAR FOR 3.83 TONNES/INVENTORY RESTS AT 828.76 TONNES

JUNE 8/WITH GOLD DOWN 10 CENTS/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY REMAINS AT 832.59 TONNES./

JUNE 7/WITH GOLD UP $1.45, THE CROOKS DECIDED TO RAID AGAIN THE GLD GOLD COOKIE JAR TO THE TUNE OF 3.54 TONNES/GOLD INVENTORY LOWERS TO 832.59 TONNES

JUNE 6/WITH GOLD UP $1.30 TODAY, WE HAD NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 836.13 TONNES

JUNE 5/WITH GOLD UP $5.30 TODAY, WE HAD A TINY WITHDRAWAL OF .29 TONNES AND THAT NO DOUBT WAS TO PAY FOR FEES/836.13 TONNES

JUNE 4/WITH GOLD DOWN ONLY $2.50, THE CROOKS UNLEASHED A MASSIVE WITHDRAWAL OF 10.61 TONNES OF GOLD FROM THE GLD/INVENTORY RESTS AT 836.42 TONNES

JUNE 1/WITH GOLD DOWN $5.10 TODAY, A HUGE 4.42 TONNES OF GOLD WAS WITHDRAWN FROM THE GLD AND THIS WAS USED IN THE RAID TODAY/INVENTORY RESTS AT 847.03 TONNES

MAY 31/WITH GOLD DOWN 1.60/NO CHANGE IN GOLD INVENTORY/INVENTORY REMAINS AT 851.45 TONNES

MAY 30/WITH GOLD UP $2.70: A HUGE DEPOSIT OF 2.95 TONNES INTO THE GLD/INVENTORY REMAINS AT 851.45 TONNES

MAY 29/2018/WITH GOLD DOWN $4.50/ NO CHANGES IN GLD INVENTORY/INVENTORY REMAINS AT 848.50 TONNES

May 25/WITH GOLD UP ON THE WEEK BUT DOWN 80 CENTS TODAY: WE HAD A HUGE 3.54 TONNES OF GOLD WITHDRAWAL FROM THE CROOKED GLD/

MAY 24/WITH GOLD UP $12.40/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 852.04

MAY 22/WITH GOLD UP $1.05/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 852.04 TONNES

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

JUNE 28/2018/ Inventory rests tonight at 821,69 tonnes

*IN LAST 405 TRADING DAYS: 104,90 NET TONNES HAVE BEEN REMOVED FROM THE GLD

*LAST 355 TRADING DAYS: A NET 51.40 TONNES HAVE NOW BEEN ADDED INTO GLD INVENTORY.

end

Now the SLV Inventory/

JUNE 28/WITH SILVER DOWN 18 CENTS, THE CROOKS ADDED 1.035 MILLION OZ OF SILVER INTO THE SLV/INVENTORY RESTS AT 320.395 MILLION OZ

JUNE 27.2018/WITH SILVER DOWN 8 CENTS/NO CHANGE IN SILVER INVENTORY/INVENTORY RESTS AT 819.360 MILLION OZ/

june 26./2018/WITH SILVER DOWN 8 CENTS, THE CROOKS WITHDREW THE DEPOSIT OF TWO DAYS AGO; 941,000 OZ OUT OF INVENTORY/INVENTORY RESTS AT 819.360 OZ

JUNE 25/WITH SILVER DOWN 12 CENTS/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 320.301 MILLION OZ/

JUNE 22/WITH SILVER UP 12 CENTS TODAY,ANOTHER BIG CHANGE IN SILVER INVENTORY AT THE SLV” A DEPOSIT OF 941,000 OZ INTO INVENTORY/INVENTORY RESTS THIS WEEKEND AT 320.301 MILLION OZ/

JUNE 21/WITH SILVER UP ONE CENT/ANOTHER CHANGE IN SILVER INVENTORY AT THE SLV/: A DEPOSIT OF 2.918 MILLION OZ/INVENTORY RESTS AT 319.360 MILLION OZ/ THUS FOR TWO STRAIGHT DAYS A TOTAL OF 5.26 MILLION OZ OF SILVER HAS BEEN ADDED WITH NO CHANGE IN PRICE.

JUNE 20/WITH SILVER DOWN ONE CENT/A HUGE CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY / A DEPOSIT OF 2.35 MILLION OZ/INVENTORY RESTS AT 316.442 MILLION OZ/

JUNE 19/2018/WITH SILVER DOWN 11 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 314.090 MILLION OZ/

JUNE 18/WITH SILVER DOWN 6 CENTS TODAY/NO CHANGE IN SILVER INVENTORY/INVENTORY RESTS AT 314.090 MILLION OZ/

JUNE 15/WITH SILVER DOWN 75 CENTS/A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.788 MILLION OZ//INVENTORY RESTS AT 314.090 MILLION OZ

JUNE 14/WITH SILVER UP 30 CENTS, THE CROOKS DECIDED THAT THEY NEEDED SILVER INVENTORY BADLY SO THEY RAID THE SLV OF 1.412 MILLION OZ/INVENTORY RESTS AT 315.878 MILLION OZ/

JUNE 13/WITH SILVER UP 11 CENTS TODAY/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 317.290 MILLION OZ/

JUNE 12/WITH SILVER DOWN 5 CENTS/A HUGE CHANGES IN SILVER INVENTORY AT THE SLV/ THE CROOKS RAID THE SILVER COOKIE JAR BY 1.976 MILLION OZ/INVENTORY LOWERS TO 317.290 MILLION OZ/

jUNE 11/NO CHANGE IN SILVER INVENTORY/319.266 MILLION OZ

JUNE 8/WITH SILVER DOWN 5 CENTS/A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.412 MILLION OZ//INVENTORY LOWERS TO 319.266 MILLION OZ/

JUNE 7/WITH SILVER UP ANOTHER 12 CENTS/A HUGE CHANGE IN SILVER INVENTORY AT THE SL: A WITHDRAWAL OF 1.883 MILLION OZ WITH ALL OF THAT SILVER DEMAND//INVENTORY RESTS AT 320.678 MILLION OZ/

JUNE 6/WITH SILVER UP 14 CENTS TODAY/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 322.561 MILLION OZ/

JUNE 5/WITH SILVER UP 10 CENTS NO CHANGE IN SILVER INVENTORY/INVENTORY RESTS AT 322.561 MILLION OZ

JUNE 4/WITH SILVER DOWN 1 CENTA SMALL CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 522,000 OZ INTO THE SLV/.INVENTORY RISES AT 322.561 MILLION OZ/

JUNE 1/WITH SILVER DOWN 3 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY REMAINS AT 322.039 MILLION OZ/

MAY 31/WITH SILVER DOWN 7 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY REMAINS AT 322.039 MILLION OZ/

MAY 30/WITH SILVER UP 16 CENTS: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV/ A DEPOSIT OF 2.071 MILLION OZ/INVENTORY RESTS AT 322.039 MILLION OZ/

MAY 29.2018/ NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.968 OZ

May 25/INVENTORY LOWERS TO 319.968 AS WE HAD A WITHDRAWAL OF 1.035 MILLION OZ

MAY 24/WITH SILVER UP 27 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 321.003 MILLION OZ/

MAY 22/WITH SILVER UP 6 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 321.003 MILLION OZ/

JUNE 28/2018:

Inventory 320.395 MILLION OZ

6 Month MM GOFO 2.15/ and libor 6 month duration 2.50

Indicative gold forward offer rate for a 6 month duration/calculation:

G0FO+ 2.15%

libor 2.50 FOR 6 MONTHS/

GOLD LENDING RATE: .35%

XXXXXXXX

12 Month MM GOFO

+ 2.76%

LIBOR FOR 12 MONTH DURATION: 2.57

GOFO = LIBOR – GOLD LENDING RATE

GOLD LENDING RATE = +.19

end

Major gold/silver trading /commentaries for THURSDAY

GOLDCORE/BLOG/MARK O’BYRNE.

Why Russia and Turkey Diversifying Into Gold May Signal A Bigger Global Shift

Russia and Turkey’s moves out of U.S. debt and into the precious metal could be precursors of a bigger global shift.

by Leonid Bershidsky of Bloomberg

U.S. government debt and the world’s foreign exchange and gold reserves. Source: Bloomberg

Since December 2017, Russia has cut its holdings of U.S. foreign debt by more than half.

Instead, it’s been increasing the share of gold in its international reserves. That’s understandable behavior for a country that has to deal with an unpredictable U.S. sanctions policy, but it’s also part of a trend.

Foreign governments and international organizations account for a decreasing share of outstanding U.S. debt, and some economies have in recent years aggressively upped the share of gold in their reserves instead.

The Russian reduction of Treasury holdings, to $48.7 billion in April 2018 from $102.2 billion in December 2017, has been nothing short of dramatic, though it wasn’t a huge blow to the U.S. Russia’s holdings of American government bonds have long been dwarfed by those of China and Japan, as well as Brazil and some European countries. The U.S., with a debt of almost $21.2 trillion, can afford not to notice fluctuations in the tens of billions of dollars by an authoritarian state’s damage-control efforts and attempts to get away from the dollar.

U.S. Borrowing Faster Than the World Saves

The U.S. can lull itself into a certain sense of security as it watches the foreign-owned stock of its debt securities increase in absolute terms and as the dollar slips only slowly as a share of official foreign exchange reserves. The U.S. currency, according to the International Monetary Fund, made up 62.7 percent of these reserves in the fourth quarter of 2017, down from 64.59 percent in 2014 — but then the share of the next biggest reserve currency, the euro, has also dropped to 20.15 percent from 21.57 percent. This is hardly a tectonic shift.

And yet the U.S. does have a few things to worry about when it comes to its dominance of other countries’ official international reserves. In relative terms, governments and central banks are less and less interested in the ballooning U.S. debt.

Wary of U.S. Debt

U.S. debt, of course, is growing faster than global international reserves, and that partly explains the declining role of foreign countries in keeping the U.S. government solvent.

On the other hand, there’s plenty of U.S. debt to buy, but countries aren’t keen to increase its share in their reserves.

Instead, the share of U.S. Treasury securities has gone down to 25.4 percent currently from 28.1 percent in 2008, while the share of gold has held steady at about 11 percent over the same period, according to the World Gold Council.

That’s in part thanks to the efforts of a few eccentric gold bug authoritarians. Apart from Russia, they include Belarus, Kazakhstan and, recently, Turkey, where President Recep Tayyip Erdogan believes the West is out to punish Turkey for his sovereignty-enhancing policies.

Excerpt Above and Full Article From Bloomberg View – Access Here

Never miss an episode of The Goldnomics Podcast – Listen and subscribe on YouTube, ITunes, Soundcloud or Blubrry

News and Commentary

Gold Seen Fighting Back as Dollar Rebound Is Poised to Reverse (Bloomberg.com)

Gold edges higher, but lingers near 6-month trough (Reuters.com)

Asian Stocks Drop, Yen Gains on Trade Skepticism (Bloomberg.com)

Wall Street rally fizzles as tech stocks drag (Reuters.com)

U.S. Stocks Slide as Trade Angst Grows; Oil Climbs: Markets Wrap (Bloomberg.com)

Source: ZeroHedge

Why Russia and Turkey Diversifying Into Gold May Signal A Bigger Global Shift (Bloomberg.com)

Hedge Fund Managers See Echo of Past Crashes in Markets (Bloomberg.com)

China Think Tank Warns of Potential ‘Financial Panic’ in Leaked Note (Bloomberg.com)

Deutsche Bank Tumbles To New Record Low, Drags European Banks (ZeroHedge.com)

Listen on SoundCloud , Blubrry & iTunes. Watch on YouTube below

Gold Prices (LBMA AM)

27 Jun: USD 1,256.80, GBP 951.40 & EUR 1,079.97 per ounce

26 Jun: USD 1,257.15, GBP 949.15 & EUR 1,077.63 per ounce

25 Jun: USD 1,269.80, GBP 959.46 & EUR 1,090.25 per ounce

22 Jun: USD 1,269.70, GBP 954.05 & EUR 1,088.26 per ounce

21 Jun: USD 1,263.70, GBP 963.32 & EUR 1,096.51 per ounce

20 Jun: USD 1,273.25, GBP 967.29 & EUR 1,100.60 per ounce

19 Jun: USD 1,279.00, GBP 971.14 & EUR 1,108.89 per ounce

Silver Prices (LBMA)

27 Jun: USD 16.21, GBP 12.27 & EUR 13.93 per ounce

26 Jun: USD 16.23, GBP 12.25 & EUR 13.90 per ounce

25 Jun: USD 16.38, GBP 12.35 & EUR 14.05 per ounce

22 Jun: USD 16.43, GBP 12.35 & EUR 14.11 per ounce

21 Jun: USD 16.25, GBP 12.33 & EUR 14.07 per ounce

20 Jun: USD 16.29, GBP 12.38 & EUR 14.09 per ounce

19 Jun: USD 16.36, GBP 12.42 & EUR 14.16 per ounce

Recent Market Updates

– London House Prices Fall 1.9% In Quarter – Bubble Bursting?

– Gold Exports To London From U.S. Surge 152% In 2018

– Manipulation of Gold & Silver by Bullion Banks Is “Undeniable”

– “Perfect Environment For Gold” As Fed Will Weaken Dollar and Create Inflation – Rickards

– Russia Buys 600,000 oz Of Gold In May After Dumping Half Of US Treasuries In April

– In Gold, Silver and Bitcoin We Trust? Goldnomics Podcast with Ronald-Peter Stoeferle

– Own A “Bit Of Gold” As We Are Moving Ever Closer To A Trade War

– Bitcoin Price To $0 Or $1 Million In One Year? MoneyConf 2018 Poll

– Cashless Society – Good or Bad? MoneyConf 2018 Video

– Do We Still Need Banks In The Age Of Fintech?

– Total US Government Debt Is $200 Trillion – Debt Clock Ticking To Next Crisis

– All Gold is Not Equal – Goldnomics Podcast (Episode 4)

– “Without Gold I Would Have Starved To Death” – ECB Governor

– Swiss Government Pension Fund To Buy Gold Bars Worth Some €600 Million

ANDREW MAGUIRE’S KINESIS WHICH IS A”BITCOIN’ BACKED 100% BY ALLOCATED GOLD AND SILVER

Andrew Maguire’s Kinesis money which is a “bitcoin” but backed 100% by allocated gold and silver is set to go.

it think it would be a great idea to look at this!

please read at: https://kinesis.money/#/

(Andrew Maguire)

|

|

Dear Harvey Organ,

Thank you for your participation in our webinar on June 7th with our host and CEO of Kinesis, Thomas Coughlin.

The response we received has been incredible, we appreciate you taking the time to join us and hope you found it to be beneficial.

Due to such a high influx of questions we received we were unable to have them all answered. Nevertheless, if there was anything which requires more clarification, or you have a query which needs to be rectified, we invite you to join our telegram group:

We apologize for the technical issues we incurred during the webinar which resulted in it running a little over schedule, we hope that the next one we host will run seamlessly.

A video has been put together and uploaded onto our YouTube channel which can be found here:

Please share and subscribe to our YouTube channel to be notified of all the latest videos as they become available.

The rapid growth that we are currently experiencing has been incredible and with your support, is only going to get better.

We are working behind the scenes very hard to create a better experience for everyone involved! Stay tuned in as we have many more announcements to be released in the upcoming days.

Kind Regards,

|

Kinesis Money

a:C/O ILS Fiduciaries (IOM) Limited, First Floor,Millennium House, Victoria Road, Douglas, Isle of Man IM2 4RW

|

The following is self explanatory

(courtesy GATA/Chris Powell and Harvey Organ)

GATA asks bank regulator to check risks of gold

futures maneuver

Submitted by cpowell on Sun, 2018-06-10 16:17. Section: Daily Dispatches

12:21p ET Sunday, June 10, 2018

Dear Friend of GATA and Gold:

GATA has appealed to the U.S. comptroller of the currency, who has regulatory authority over banks, to review financial risks certain banks may have incurred through derivatives in the monetary metals markets, particularly through the recent heavy use of the “exchange for physicals” mechanism of settling gold and silver futures contracts on the New York Commodities Exchange.

The appeal was made in a letter sent May 5 to the comptroller, Joseph M. Otting, whose office is part of the U.S. Treasury Department, by your secretary/treasurer and GATA futures market consultant Harvey Organ.

“Exchange for physical” settlements of futures contracts long were considered emergency procedures when a seller was not able to deliver metal from an exchange-approved warehouse and wanted to settle with delivery elsewhere. But now such settlements appear to constitute most gold and silver futures settlements on the Comex. It is a strange development that appears to have been necessitated by the increasing difficulties of central banking’s gold and silver price suppression policy.

GATA has received no acknowledgment of the letter. Its text is below and a PDF copy of it is here:

http://www.gata.org/files/ComptrollerOfCurrencyLetter.pdf

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

* * *

May 5, 2018

Joseph M. Otting, Comptroller of the Currency

U.S. Treasury Department

400 7th Street, SW

Washington DC 20219

Dear Comptroller Otting:

Please let us bring to your attention financial risks to major banks involving their possibly unreported exposure to derivatives in the monetary metals markets.

In recent months gold and silver future contracts issued by U.S. banks on the New York Commodities Exchange have been moved off-exchange for delivery through a mechanism known as “exchange for physical” (EFP) contracts. Until recently use of this mechanism was considered an emergency procedure when a seller did not have access to metal for delivery through Comex warehouses. Now the mechanism seems to be in use for a large share of front-month contracts for which delivery is sought.

Here is an example that is happening at the Comex in the front active month of April for gold and the inactive delivery month of April for silver.

In gold, there were 229,436 EFP contracts for 713.64 tonnes, an average of 10,925 contracts and 1,092,500 ounces per trading day.

In silver, there were 77,150 EFP contracts for 385,750,000 ounces, an average of 3,673 contracts and 18,369,000 ounces per trading day.

London Bullion Market Association rules suggest that these contracts may not be reported to regulators. The LBMA’s bylaws say:

“Figures above exclude any contracts not subject to risk-based capital requirements, such as FX contracts with an original maturity of 14 days or less, futures contracts, written options, and basis swaps. Therefore, the total notional amount of derivatives by maturity will not add to the total derivatives figure in this table.”

We are told that these EFP contracts are transferred from the Comex to London as what are called “serial forwards” and their duration is always less than 14 days, which exempts them from being reported.

It is our understanding that in each quarter your office prepares a report detailing risk undertaken by the banks under the comptroller’s supervision.

These risks include derivatives undertaken by U.S. banks and other obligations that may cause a bank to fail. Our concern is that your office may not be aware of large unreported derivative exposure by banks.

Could you review this matter and let us know your conclusions?

Sincerely,

CHRIS POWELL

Secretary/Treasurer

HARVEY ORGAN

Consultant

Gold Anti-Trust Action Committee Inc.

7 Villa Louisa Road

Manchester, Connecticut 06043-7541

END

I brought this story to you yesterday but it is worth repeating. A Chinese think tank warns of a potential financial panic

(courtesy Bloomberg/GATA)

China think tank warns of potential ‘financial panic’

Submitted by cpowell on Wed, 2018-06-27 14:02. Section: Daily Dispatches

From Bloomberg News

Wednesday, June 27, 2018

A leaked report from a Chinese government-backed think tank has warned of a potential “financial panic” in the world’s second-largest economy, a sign that some members of the nation’s policy elite are growing concerned as market turbulence and trade tensions increase.

Bond defaults, liquidity shortages, and the recent plunge in financial markets pose particular dangers at a time of rising U.S. interest rates and a trade spat with Washington, according to a study by the National Institution for Finance & Development that was seen by Bloomberg News and confirmed by a NIFD official. The think tank warned that leveraged purchases of shares have reached levels last seen in 2015 — when a market crash erased $5 trillion of value.

.

“We think China is currently very likely to see a financial panic,” NIFD said in the study, which appeared briefly on the Internet on Monday, before being removed. “Preventing its occurrence and spread should be the top priority for our financial and macroeconomic regulators over the next few years.” …

… For the remainder of the report:

https://www.bloomberg.com/news/articles/2018-06-27/china-think-tank-warn…

END

Why Russia and Turkey are such huge gold bugs now. Russia liquidated a huge percentage of its holdings of USA treasuries from 102 billion down to 49 billion

(courtesy Bershidsky/Bloomberg)

Why Russia and Turkey are such gold bugs

Submitted by cpowell on Thu, 2018-06-28 00:37. Section: Daily Dispatches

By Leonid Bershidsky

Bloomberg News

Wednesday, June 17, 2018

Since December 2017 Russia has cut its holdings of U.S. foreign debt by more than half. Instead, it’s been increasing the share of gold in its international reserves.

That’s understandable behavior for a country that has to deal with an unpredictable U.S. sanctions policy, but it’s also part of a trend. Foreign governments and international organizations account for a decreasing share of outstanding U.S. debt, and some economies have in recent years aggressively upped the share of gold in their reserves instead.

The Russian reduction of Treasury holdings, to $48.7 billion in April 2018 from $102.2 billion in December 2017, has been nothing short of dramatic, though it wasn’t a huge blow to the U.S. Russia’s holdings of American government bonds have long been dwarfed by those of China and Japan, as well as Brazil and some European countries. The U.S., with a debt of almost $21.2 trillion, can afford not to notice fluctuations in the tens of billions of dollars by an authoritarian state’s damage-control efforts and attempts to get away from the dollar.

The U.S. can lull itself into a certain sense of security as it watches the foreign-owned stock of its debt securities increase in absolute terms and as the dollar slips only slowly as a share of official foreign exchange reserves.

… For the remainder of the report:

https://www.bloomberg.com/view/articles/2018-06-27/why-russia-and-turkey…

END

Craig Hemke (and Michael Pento below) state that the flattening of the yield curve means recession

(courtesy Craig Hemke/GATA)

Craig Hemke at TF Metals Report: As the yield curve

flattens

Submitted by cpowell on Thu, 2018-06-28 03:11. Section: Daily Dispatches

11:12p ET Wednesday, June 27, 2018

Dear Friend of GATA and Gold:

With the interest rate curve flattening, the TF Metals Report’s Craig Hemke writes today, a recession is looming along with an end to interest rate hikes, leading to higher monetary metals prices. Hemke’s analysis is headlined “As the Yield Curve Flattens” and it’s posted at the TF Metals Report here:

https://www.sprottmoney.com/Blog/as-the-yield-curve-flattens.html

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

Your early THURSDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED DOWN TO 6.6235/HUGE DEVALUATION /shanghai bourse CLOSED DOWN 26.28 POINTS OR 0.93%// HANG SANG CLOSED UP 141.06 PTS OR 0.50%

2. Nikkei closed DOWN 1.38 POINTS OR 0.01% / /USA: YEN RISES TO 110.24/

3. Europe stocks OPENED DEEPLY IN THE RED / /USA dollar index RISES TO 95.17/Euro FALLS TO 1.15850

3b Japan 10 year bond yield: RISES TO . +.04/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 110.24/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD FINALLY IN THE POSITIVE/BANK OF JAPAN LOSING CONTROL OF THEIR YIELD CURVE AS THEY PURCHASE ALL BONDS TO GET TO ZERO RATE!!

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 72.73 and Brent: 78.14

3f Gold DOWN/Yen DOWN

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil UP for WTI and UP FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund FALLS TO +.30%/Italian 10 yr bond yield DOWN to 2.83% /SPAIN 10 YR BOND YIELD UP TO 1.35%

3j Greek 10 year bond yield FALLS TO : 4.07

3k Gold at $1251.65 silver at:16.05 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble DOWN 10/100 in roubles/dollar) 63.06

3m oil into the 72 dollar handle for WTI and 78 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 110.24 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 0.9974 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1554 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now POSITIVE territory with the 10 year FALLING to +0.30%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.83% early this morning (THIS IS DEADLY TO ALL MARKETS). Thirty year rate at 2.97%

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

(courtesy Jim Reid/Bloomberg/Deutsche bank/zero hedge)

US Futures Rebound Amid Emerging Markets

Rout; China Drops To 2 Year Low

Bulletin Headline summary from RanSquawk

- European equities are lower across the board (Eurostoxx 50 -0.6%) as trade tensions continue to weigh on sentiment

- DXY remains above 95.00 in European trade after an early bout of strength (now off best-levels)

- Looking ahead, highlights include German national CPI, US GDP (F), weekly jobs, EU summit, BoE’s Haldane, US 7yr note auction

US equity markets are looking to undo yesterday’s bearish reversal, with index futures higher this morning, reversing the trend from earlier markets where Asian stocks flirted with a 9 month low and Europe was mixed.

The MSCI Asia Pacific index started off the overnight session by declining for a fourth day, helping drag a gauge of developing-market stocks to the lowest level in almost a year, although at a slower pace as Chinese stocks sank deeper into a bear market, if at a more modest pace …

… helped by a modest stabilization in the recent Yuan rout. In the end, however, the Shanghai Composite Index fell 0.9%, dropping below 2800 for the first time since March 2016 and erasing an earlier gain of 0.5%, as sentiment remained subdued amid trade concerns.

Meanwhile, the Chinese yuan remained weak but the selloff was more controlled than in recent days, with the onshore yuan declining for the sixth session, its longest losing streak since June 2017, while the offshore yuan, or CNH, dropping for a record 11th day…

… rose as high as 6.64, the highest since November 2017, before reversing some losses. Property developers and airlines have been among the hardest hit by the yuan’s decline due to their large amounts of dollar debt. Like the offshore yuan, Air China has fallen for 11 straight days in Hong Kong, its longest ever losing streak. China Southern Airlines has plunged 35% in 10 days, while developer Country Garden Holdings is the worst performer on the Hang Seng Index this week.

“The news that China will crack down on property speculation in 30 cities hurt sentiment and put pressure on shares,” said Dai Ming, Shanghai-based fund manager with Hengsheng Asset Management Co. “It makes investors agitated whenever China tightens regulation over the property sector.”

The woes of real estate companies were further compounded Thursday after the government said it was starting a six-month campaign to root out violations in the housing market. That followed a tightening this week of loan approvals for redeveloping shanty-town projects and regulators urging companies to use proceeds from overseas bond sales to repay debt.

European stocks followed the decline across Asia as investors remained confused by America’s strategy toward Chinese trade and investment. Technology companies and carmakers were the biggest losers as the Stoxx Europe 600 Index dropped.

Futures on the S&P 500 pointed to a firmer open in the wake of Wednesday’s slump. West Texas Intermediate crude extended gains and China’s yuan headed for another drop. The British pound weakened, and Italian bonds slipped after a disappointing auction.

With equity markets relatively calm, it was all about the dollar, which remained above 95.00 in European trade after an early bout of strength, which has since reversed and the BBG dollar index dipped to session lows, with trade posturing remained a key focus for investor sentiment.

As a result of the stronger dollar and rising oil price, it was generally a bloodbath across EM FX, with the Indian rupee slumping to record low, while the Indonesian rupiah weakened to lowest since 2015. Kiwi slides to two-year low after dovish RBNZ statement.

Separately, the rout across the broader Emerging Markets FX space sent the MSCI EM FX index to the lowest level since November 2017.

USD strength has however somewhat abated as the session progresses with some commentators highlighting month-end rebalancing flows set to come into-play. Models suggest the USD could be sold amid equity re-balancing and thus provide some support for EURUSD which has thus far been able to maintain at 1.1500 handle. The Euro initially dipped then edged toward session highs against the dollar following Italian inflation data that modestly beat expectations, and may presage euro-zone CPI figures on Friday; the European summit is also later today. The USDJPY edged lower after gaining 0.2% Wednesday when White House adviser Larry Kudlow said the president wasn’t retreating on China and China growth was “not doing well.”

In terms of the latest state-of-play, trade uncertainties remain in focus after White House economic adviser Kudlow rejected the perception that Trump was softening his stance on China. Markets continued to weigh counter-measures from China with CNY devaluation increasingly becoming part of the narrative in the spat between the two nations with China also announcing adjustments of tariffs on some imports from other Asia-Pac nations.

In overnight central bank news, the RBNZ maintained the Official Cash Rate at 1.75% as unanimously expected, while it reiterated that it expects to keep rates at current expansionary level for considerable period and that the next direction is equally balanced between up and down. RBNZ added that global economic growth is likely to underpin demand for New Zealand products and services, but also stated that recent weaker GDP implies marginally more spare capacity in economy than anticipated and that CPI remains below target. Furthermore, the RBNZ later announced from 2019 onwards rate decisions will be announced after 1400 local time on a Wednesday and implemented the following day.

Ahead of today’s EU summit, German Interior Minister Seehofer said the CSU party is not seeking a break-up of the coalition government nor oust Chancellor Merkel, while there were also comments from German Finance Minister Scholz said he does not rule out possibility coalition can reach solution to migration issue. German Chancellor Merkel said on migration, “we are not where we want to be yet”; adding “we won’t be able to reach a common migration agreement at the June Summit”. She went on to say Germany must consider coalition of the willing on migrant policy if an agreement is not reached by the 28 EU members and the migrant policy may make or break the EU.

In geopolitics, South Korean and US Defence Chiefs agree UN Sanctions against North Korea will be in place until North Korea takes solid, irreversible measures towards denuclearisation.

10-year Treasury yields remained immune to any risk on sentiment, with the yield barely rising 1bp to 2.83%. The yield curve flattened in U.S. on Wednesday as Treasuries rallied following Kudlow’s comments.

West Texas Intermediate crude extended gains and China’s yuan headed for another drop. The British pound weakened, and Italian bonds slipped after a disappointing auction

Expected data include jobless claims and GDP. Accenture, McCormick, Shaw Communications, Walgreens Boots and Nike are among those reporting earnings.

Top Overnight News from Bloomberg

- The European Central Bank warned in its Economic Bulletin that global growth — already forecast to slow as many advanced economies approach capacity constraints — might take an additional hit from recent threats to trade

- Chancellor Angela Merkel said German-French proposals for the euro area won’t lead to a “debt union” and rejected unilateral measures to curb migration as she headed to a summit with other European Union leaders

- China is slowing approvals for offshore bonds and considering whether to ban short-dated issuance in dollars, according to people familiar with the matter, moves that would reduce financing options for the developers that have led record sales of such debt

- China’s expansion looks to have slowed further this month, underscoring the fragility of its economy as the next wave of tariffs in the trade dispute with the U.S. approaches

- The Indian rupee slumped to an all-time low as a resurgence in crude prices and the emerging-market selloff took a toll on the currency of the world’s third-biggest oil consumer

- United Co. Rusal is doing everything it can to avoid punitive U.S. restrictions due for full enforcement in October, according to the Russian aluminum giant’s acting Chief Executive Officer Evgeny Nikitin

- Treasury Secretary Steven Mnuchin won a battle inside the Trump administration over trade policy this week after a series of setbacks as he tries to ease economic tensions with China

- Russia’s Finance Ministry is on track for its biggest bond-issuance miss in 3 years as investors demand a premium to hold the nation’s debt after the toughest U.S. sanctions to date and a selloff in emerging markets

- U.K. Treasury said it was won over by Jonathan Haskel’s expertise in productivity and innovation when choosing the only man among the five candidates to join the Bank of England’s Monetary Policy Committee

- Hungarian forint tumbled to a record against the euro as the central bank maintained a dovish monetary policy seen as out of line with the rest of Europe

Market Snapshot

- S&P 500 futures little changed at 2,706.25

- STOXX Europe 600 down 0.2% to 379.38

- MXAP down 0.4% to 164.48

- MXAPJ down 0.6% to 530.47

- Nikkei down 0.01% to 22,270.39

- Topix down 0.3% to 1,727.00

- Hang Seng Index up 0.5% to 28,497.32

- Shanghai Composite down 0.9% to 2,786.90

- Sensex down 0.4% to 35,085.11

- Australia S&P/ASX 200 up 0.3% to 6,215.39

- Kospi down 1.2% to 2,314.24

- German 10Y yield fell 0.3 bps to 0.318%

- Euro down 0.1% to $1.1539

- Italian 10Y yield fell 7.8 bps to 2.541%

- Spanish 10Y yield unchanged at 1.356%

- Brent futures up 0.1% to $77.73/bbl

- Gold spot down 0.2% to $1,249.37

- U.S. Dollar Index little changed at 95.33

Asia equity markets traded somewhat indecisive following the headwinds from Wall St where all major indices wiped out intraday gains, as trade uncertainties remained in focus after White House economic adviser Kudlow rejected the perception that Trump was softening his stance on China. ASX 200 (+0.2%) and Nikkei 225 (Unch) were mixed with Australia kept afloat by commodity names as the energy sector outperformed on further gains in crude and with Santos underpinned after the board approved a new dividend policy which targets paying 10%-30% of free cash flow, while a firmer currency and disappointing Retail Sales data weighed on sentiment in Tokyo. Hang Seng (+0.4%) and Shanghai Comp. (+0.2%) were choppy on the trade uncertainties and following another net liquidity drain by the PBoC, although Chinese stocks later recovered amid pre-emptive measures in the face of a looming trade war including a further devaluation of the currency and adjustments of tariffs on some imports from other Asia-Pac nations. Finally, 10yr JGBs traded flat amid the indecisive risk tone and amid weaker demand at today’s 2yr auction later, in which accepted prices also declined from prior.

Top Asian News

- Vietnam Forces Facebook and Google to Pick Privacy or Growth

- Rupee Hits Record Low as India Pays for Insatiable Oil Demand

- China Turmoil Batters Last Emerging-Market Haven as Rout Deepens

- China Digs In on Trade as Tariffs Near, Economy Deepens Slowdown

European equities are lower across the board (Eurostoxx 50 -0.6%) in recent trade with all major bourses in the red as trade tensions continue to weigh on sentiment. Consumer staples outperform while IT names lag behind (Europe’s tech sector -1.7%) amid NEC Director Kudlow rejecting the notion that US President Trump has softened his stance in regards to China on foreign investment, adding that the approach is aimed at “protecting our technological family jewels”. In terms of stocks specifics, Shire (+2.1%) shares are higher after Takeda shareholders rejected a proposal which opposed a deal with Shire.

Top European News

- ECB Publishes Methodology for New Euro Short-Term Interest Rate

- Takeda’s Shareholder Vote Signals Support for Shire Takeover

- BP to Buy U.K.’s Largest Electric Vehicle Charging Company

- Merkel Says Stronger Europe Is in Germany’s National Interest

In FX, the DXY remains above 95.00 in European trade after an early bout of strength (now off best-levels) with trade posturing remaining a key focus for investor sentiment. In terms of the latest state-of-play, trade uncertainties remain in focus after White House economic adviser Kudlow rejected the perception that Trump was softening his stance on China. Markets continue to weigh countermeasures from China with CNY devaluation increasingly becoming part of the narrative in the spat between the two nations with China also announcing adjustments of tariffs on some imports from other Asia-Pac nations. GBP has managed to recoup some of it’s initial losses against the USD (albeit still on a 1.3000 handle) after taking out stops to the downside at 1.3100 early doors in Europe before then running into support around 7-month lows at 1.3068. From a fundamental perspective, BoE’s Cunliffe did little to reveal his voting intentions at the August QIR and instead focused on household debt with a more medium-term focus. Narrative for the GBP could now shift towards Brexit ahead of the EU leaders summit; albeit expectations for any progress are particularly low with PM May set to get a slap on the wrist from her peers. USD/CAD is continuing to return to pre-Poloz levels amid USD softening after the BoC head took time to note the uncertainties facing the Canadian economy which saw pricing for a rate hike decline to beneath 50%. Large option expiries could come into play for CAD with 1.3bln in USD/CAD at 1.3345-50.

Commodities are mixed with choppy trade in gold (unch) after initially hitting 6-month lows as the yellow metal tracks the change in the dollar. WTI (+0.3%) and Brent (+0.1%) are back in positive territory, printing fresh highs for the day at USD 72.87/bbl and USD 77.93/bbl respectively. During the week, API and EIA crude inventories printed the largest drawdown since September 2016 with oil stocks dropping by nearly 10mln barrels. Traders will be mindful of halted oil exports in Libya following the country’s Eastern NOC’s instructions. Meanwhile, India’s oil ministry requested that refiners prepare for a ‘drastic reduction or zero’ imports from Iran from November, (according to sources) following US President Trump asking allies to quit importing Iranian oil. Libya’s Eastern NOC have instructed companies in the East of the nation to halt oil exports. Tankers attempting to enter East Libyan ports will be deemed illegal, a tanker due at Libya’s Zueitina port is said to have been turned away. (Newswires)

Looking at the day ahead, the big focus will likely be the EU Summit in Brussels where leaders are due to discuss migration policy, the EU budget, Brexit, security and reforming the economic and monetary union. In the US the third and final reading for Q1 GDP and Core PCE is due, as well as the June Kansas City Fed manufacturing activity index and latest weekly initial jobless claims data. The Fed’s Bullard and Bostic and the BOE’s Haldane and Bailey are due to speak. The Fed will also release part two of its annual bank stress test results.

US Event Calendar

- 8:30am: Initial Jobless Claims, est. 220,000, prior 218,000; Continuing Claims, est. 1.72m, prior 1.72m

- 8:30am: GDP Annualized QoQ, est. 2.2%, prior 2.2%;

- Personal Consumption, est. 1.0%, prior 1.0%

- Core PCE QoQ, prior 2.3%

- 9:45am: Bloomberg Consumer Comfort, prior 56.5

- 11am: Kansas City Fed Manf. Activity, est. 26, prior 29

DB’s Jim Reid concludes the overnight wrap

The flip-flopping (mostly flopping) of trade related headlines is enough to be driving markets crazy at the moment with sentiment swinging from more positive early on yesterday to negative by the close. By the end of play the S&P 500 ended -0.86% and was down -1.69% from intraday highs, while the Dow closed -0.68% and Nasdaq -1.54%. Within the S&P, financials (-1.26%) continued a run of now 13 consecutive losing days – the longest streak on record and are now off -12.6% since the late January highs and -5.9% down from c3 weeks ago. The Energy sector was a bright spot (+1.34%) once again with Oil more than doing its part after WTI and Brent rose +3.16% and +1.72%, respectively, following supply outages in Libya and data which showed the biggest fall in US stockpiles since 2016. WTI hit YTD intraday highs yesterday in trading above $73.

In bonds, US 10y yields fell 5.1bps to 2.826% – the lowest since late May, while Bunds (-2bp) and Gilts (-5.8bp) also firmed amidst the risk off tone. The relentless flattening of the Treasury curve did continue however with 2s10s down another 2.2bps and to a new fresh post 2007 low of 32.1bps. Before the late US selloff, Europe indices were actually quick to wipe out early losses with the Stoxx 600 (+0.72%) and DAX (+0.93%) finishing higher on the back of a solid rally in European energy stocks (+2.63%).

With Oil back to the highest since December 2014 (+22% in YTD 2018) and bond yields generally heading towards the lower end of their recent ranges we’re set up for interesting European inflation numbers over the next two days. Certainly something to watch. Also watch for headlines from the important EU summit over the next couple of days. There a fuller preview below.

This morning in Asia, markets are trading mixed but have improved from a weaker opening with the Hang Seng (+0.58%) and Shanghai Comp. (+0.19%) rebounding while the Nikkei (-0.09%) and Kospi (-0.82%) are both down as

we type. The Chinese Yuan is weakening further (-0.1%) while the Yen is up marginally. Meanwhile after a 14 hour marathon session, the budget committee of the German Parliament has approved a €344bn budget plan for 2018 that will boost spending by 4% yoy without incurring any new debt. The budget will boost investments by €2.8bn to €39.8bn with additional funding for jobs in police / security forces. As for data, Japan’s May retail sales fell the most in c2 years and was below market at -1.7% mom (vs. -0.8%), which has led to annual growth of 0.6% yoy.

Back to yesterday and to detail the Trump trade turnaround seen. Initially markets were stronger following the news that President Trump intends to use the CFIUS as opposed to emergency law for passing legislation concerning the violation of intellectual property rights on US companies – the latest development in this seemingly never-ending story. Significantly, this is seen as a softening stance of sorts for the President and one which puts him more in line with Treasury Secretary Steven Mnuchin. The Treasury Secretary also added yesterday that moves to strengthen CFIUS “is not intended to target China” and that it was “unfortunate” that the market got mixed messages. Late in the European afternoon though Trump’s top economic advisor Larry Kudlow told Fox Business News that Trump is not softening his stance on China and that China’s reaction to trade demands from the US has not been satisfactory.

So as we look ahead to today, expect trade to be one of or if not, the big talking point at today’s EU summit which kicks off in Brussels and continues into Friday. There’s a laundry list of agenda points to get through for EU leaders with the not so insignificant talking points like Brexit, migration policy, the EU budget, security and the economic and monetary union amongst the big topics. The summit will be of particular significance for Merkel given domestic political tensions of late however yesterday the CDU and Social Democrats confirmed that no headway was made on migration talks in a meeting in Berlin which will only heighten the pressure on Merkel. Notably, the CSU Party leader Seehofer did reaffirm on ARD TV that “I know of nobody in my party who either wants to endanger the government….or bring down the Chancellor”. Meanwhile Italy PM Conte also confirmed that the EU draft on migration was dropped which should not be a great surprise given the limited headway made from Sunday’s mini summit.

As discussed above, it’s worth also keeping an eye on some of the regional flash European CPI reports today. Data for Italy will be out this morning with the consensus at +0.2% mom for June. Germany will be out later this afternoon with +0.2% mom also expected however base effects are expected to push the annual rate down to +2.1%.

Staying with data, US Q2 GDP prospects were given a boost yesterday after the May advance goods trade balance revealed a smaller than expected deficit of $64.8bn (vs. $69.0bn expected). That also compares to $67.3bn in April and it means that the trade balance has now narrowed for three consecutive months to a 9 month high. The durable and capital goods orders data was a little more disappointing (durable ex transport -0.3% vs. +0.5% expected, core capex orders -0.1% mom vs. +0.3% expected) but upward revisions to prior months made that more of a wash. Pending home sales (-0.5% mom vs. +0.5% expected) were notably softer however. It’s worth noting that our US economists are forecasting Q2 GDP growth of 3.8%.

In Europe, the Euro area’s May M3 money supply was stronger than expected at 4% yoy (vs. 3.8%). After adjusting for sales and securitizations, growth in household loans was steady at 2.9% yoy for a sixth consecutive month but growth in non-financial corporate loans increased to a new cyclical high of 3.6% yoy. Meanwhile, France’s June consumer confidence index fell 2pt mom to a 21- month low of 97 (vs. 100 expected) while Italy’s overall June economic sentiment index rose 0.8pts to a three-month high of 105.4. Over in the UK, the June Nationwide house price index slowed less than expected with annual growth at 2% yoy (vs. 1.7% expected; 2.4% previous). Elsewhere, the CBI’s distributive trades survey indicated that retailers were continuing to see better conditions in Q2, with a net 32% of retailers reporting annual sales growth in June – the best result since last September.

Looking at the day ahead, the big focus will likely be the EU Summit in Brussels where leaders are due to discuss migration policy, the EU budget, Brexit, security and reforming the economic and monetary union. Datawise, it is looking like a busy day for inflation releases in Europe with preliminary June CPI reports due in Spain, Italy and Germany (2.1% yoy expected). We’ll also get June confidence indicators for the Euro area and the ECB’s economic bulletin, while in the US the third and final reading for Q1 GDP and Core PCE is due, as well as the June Kansas City Fed manufacturing activity index and latest weekly initial jobless claims data. The Fed’s Bullard and Bostic and the BOE’s Haldane and Bailey are due to speak. The Fed will also release part two of its annual bank stress test results.

3. ASIAN AFFAIRS

i)THURSDAY MORNING/WEDNESDAY NIGHT: Shanghai closed DOWN 26.28 POINTS OR 0.93% /Hang Sang CLOSED UP 141.06 POINTS OR 0.50% / The Nikkei closed DOWN 1.38 POINTS OR 0.01% /Australia’s all ordinaires CLOSED UP 0.24% /Chinese yuan (ONSHORE) closed DOWN at 6.6235 AS POBC EXERCISES A HUGE DEVALUATION IN THE LAST FEW DAYS/Oil UP to 72,73 dollars per barrel for WTI and 78.14 for Brent. Stocks in Europe OPENED IN THE RED //. ONSHORE YUAN CLOSED DOWN AT 6.6235 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.6273 :HUGE DEVALUATION/PAST FEW DAYS//ONSHORE YUAN TRADING STRONGER AGAINST OFFSHORE YUAN/ONSHORE YUAN TRADING MUCH WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING MUCH WEAKER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR IS BEGINNING/

3 a NORTH KOREA/USA

North Korea/South Korea/usa

3 b JAPAN AFFAIRS

c) REPORT ON CHINA/HONG KONG