GOLD: $1225.60 DOWN $5.55 (COMEX TO COMEX CLOSINGS)

Silver: $15.42 DOWN 11 CENTS (COMEX TO COMEX CLOSINGS)

Closing access prices:

Gold $1224.80

silver: $15.38

For comex gold:

JULY/

NUMBER OF NOTICES FILED TODAY FOR JULY CONTRACT:0 NOTICE(S) FOR nil oz

TOTAL NOTICES SO FAR 99 FOR 9900 OZ (0.3079 tonnes)

For silver:

JUNE

9 NOTICE(S) FILED TODAY FOR

45,000 OZ/

Total number of notices filed so far this month: 5521 for 27,605,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: BID $7653/OFFER $7738: UP $356(morning)

Bitcoin: BID/ $7688/offer $77773: UP $391 (CLOSING/5 PM)

end

First Shanghai gold fix comes at 10 pm est

The second Shanghai gold fix: 2:15 pm

First Shanghai gold fix gold: 10 pm est: 1233.67

NY price at the same time: 1232.25

PREMIUM TO NY SPOT: $1.42

XX

Second gold fix early this morning: 1233.55

USA gold at the exact same time:1221.11

PREMIUM TO NY SPOT: $2.44

China is controlling the gold market

WE WILL NOT PROVIDE LONDON FIXES AS THEY ARE NOT ACCURATE AS TO WHAT IS GOING ON AT THE SAME TIME FRAME.

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total OPEN INTEREST ROSE BY A GOOD SIZED 1394 CONTRACTS FROM 213,606 UP TO 215,000 DESPITE FRIDAY’S 10 CENT GAIN IN SILVER PRICING. WE HAVE NOW WITNESSED A SLOW COMEX ACCUMULATION THESE PAST SEVERAL DAYS. ON TOP OF THIS WE HAVE ALSO WITNESSED A LARGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY(OVER 30 MILLION OZ AT THE COMEX) AS WELL AS CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A SMALL SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP: 558 EFP’S FOR SEPT. , 0 EFP’S FOR DECEMBER AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE: OF 558 CONTRACTS. WITH THE TRANSFER OF 558 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 558 EFP CONTRACTS TRANSLATES INTO 2.79 MILLION OZ AND ACCOMPANYING:

1.THE 10 CENT GAIN IN SILVER PRICEAT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR THE JUNE/2018 COMEX DELIVERY MONTH. (5.420 MILLION OZ) AND NOW JULY/ 2018 WITH 29.685 MILLION OZ INITIALLY STANDING FOR DELIVERY(SEE DATA BELOW).

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF JUNE:

30,628 CONTRACTS (FOR 15 TRADING DAYS TOTAL 30,628 CONTRACTS) OR 153.14 MILLION OZ: (AVERAGE PER DAY: 2041 CONTRACTS OR 10.209 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF JULY: 153.14 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 21.87% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2018 TO DATE SILVER EFP’S: 1,812.86 MILLION OZ.

ACCUMULATION FOR JAN 2018: 236.879 MILLION OZ

ACCUMULATION FOR FEB 2018: 244.95 MILLION OZ

ACCUMULATION FOR MARCH 2018: 236.67 MILLION OZ

ACCUMULATION FOR APRIL 2018: 385.75 MILLION OZ

ACCUMULATION FOR MAY 2018: 210.05 MILLION OZ

ACCUMULATION FOR JUNE 2018: 345.43 MILLION OZ

RESULT: WE HAD A GOOD SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 558 WITH THE 10 CENT GAIN IN SILVER PRICING AT THE COMEX YESTERDAY. THE CME NOTIFIED US THAT WE HAD A SMALL SIZED EFP ISSUANCE OF 558 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) . FROM THE CME DATA: 558 EFP’S FOR SEPT, 0 EFP’S FOR DECEMBER AND ZERO FOR ALL OVER MONTHS FOR A DELIVERABLE FORWARD CONTRACT OVER IN LONDON WITH A FIAT BONUS (TOTAL: 558). TODAY WE GAINED A CONSIDERABLE SIZED: 1952TOTAL OI CONTRACTS ON THE TWO EXCHANGES:

i.e 558 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH AN INCREASE OF 1394 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED WITH A 10 CENT RISE IN PRICE OF SILVER AND A CLOSING PRICE OF $15.50 WITH RESPECT TO FRIDAY’S TRADING. YET WE STILL HAVE A GIGANTIC AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY IN THIS ACTIVE JULY DELIVERY MONTH OF SLIGHTLY LESS THAN 30 MILLION OZ. IT SURE LOOKS LIKE ANOTHER FAILED BANKER SHORT COVERING EXERCISE AS BANKERS ARE SCRAMBLING TO COVER THEIR HUGE SHORTFALL.

In ounces AT THE COMEX, the OI is still represented by OVER 1 BILLION oz i.e. 1.075 MILLION OZ TO BE EXACT or 154% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT JULY MONTH/ THEY FILED AT THE COMEX: 9NOTICE(S) FOR 45,000 OZ OF SILVER

IN SILVER, WE SET THE NEW RECORD OF OPEN INTEREST AT 243,411 CONTRACTS ON APRIL 9.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $16.51

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) AND NOW JULY 2018 AMOUNT INITIALLY STANDING: 29.685 MILLION OZ )

- HUGE RECORD OPEN INTEREST IN SILVER 243,411 CONTRACTS (OR 1.217 BILLION OZ/ SET APRIL 9/2018

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017

- RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT).

In gold, the open interest FELL BY A CONSIDERABLE SIZED 7786 CONTRACTS DOWN TO 515,584 DESPITE THE GAIN IN THE COMEX GOLD PRICE/FRIDAY’S TRADING (A GAIN IN PRICE OF $4.15). WE ARE NOW ENTERING THE LAST DAYS IN THIS ACTIVE DELIVERY MONTH OF JULY AND AS CUSTOMARY WE SEE THE BOYS ARE CASHING IN THEIR COMEX LONGS TO BEGIN THE PROCESS TO MOVE INTO LONDON FORWARDS. THIS PROCEDURE HAS BEEN GOING ON NOW FOR OVER 2 AND 1/2 YEARS. THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED AN ATMOSPHERIC SIZED 12,089 CONTRACTS : AUGUST SAW THE ISSUANCE OF: 12,089 CONTRACTS, DECEMBER HAD AN ISSUANCE OF 0 CONTACTS AND THEN ALL OTHER MONTHS ZERO. The new COMEX OI for the gold complex rests at 515,584. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE A SMALL OI GAIN IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 4303 CONTRACTS: 7786 OI CONTRACTS DECREASED AT THE COMEX AND 12,089 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN: 4303 CONTRACTS OR 430300 OZ = 13,38 TONNES. AND ALL OF THIS DEMAND OCCURRED WITH THE GAIN IN THE PRICE OF GOLD/ FRIDAY TO THE TUNE OF $4.15. WE MUST HAVE HAD CONSIDERABLE BANKER CAPITULATION YESTERDAY AS THEY TRIED TO SHED MUCH OF THEIR SHORTFALL IN OI CONTRACTS.

FRIDAY, WE HAD 13,868 EFP’S ISSUED.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF JUNE : 131,506 CONTRACTS OR 13,150,600 OZ OR 409.03 TONNES (15 TRADING DAYS AND THUS AVERAGING: 8767 EFP CONTRACTS PER TRADING DAY OR 876,700 OZ/ TRADING DAY),,

TO GIVE YOU AN IDEA AS TO THE HUGE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 15 TRADING DAYS IN TONNES: 409.03 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2017, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 2555 TONNES

THUS EFP TRANSFERS REPRESENTS 409.03/2550 x 100% TONNES = 16.03% OF GLOBAL ANNUAL PRODUCTION SO FAR IN JULY ALONE.***

ACCUMULATION OF GOLD EFP’S YEAR 2018 TO DATE: 4,511.88* TONNES *SURPASSED ANNUAL PROD’N

ACCUMULATION OF GOLD EFP’S FOR JANUARY 2018: 653.22 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR FEBRUARY 2018: 649.45 TONNES (20 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR MARCH 2018: 741.89 TONNES (22 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR APRIL 2018: 713.84 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR MAY 2018: 693.80 TONNES ( 22 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR JUNE 2018 650.71 TONNES (21 TRADING DAYS)

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A CONSIDERABLE SIZED DECREASE IN OI AT THE COMEX OF 7786 DESPITE THE GAIN IN PRICING (4.15 CENTS) THAT GOLD UNDERTOOK FRIDAY // . WE ALSO HAD A HUMONGOUS SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 12,089 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 12,089 EFP CONTRACTS ISSUED, WE HAD A VERY SMALL NET GAIN OF 4303 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

12,089 CONTRACTS MOVE TO LONDON AND 7786 CONTRACTS DECREASED AT THE COMEX. (in tonnes, the GAIN in total oi equates to 13.38 TONNES). ..AND THIS DEMAND OCCURRED WITH THE GAIN OF $4.15 IN FRIDAY’S TRADING AT THE COMEX!!!.

we had: 0 notice(s) filed upon for NIL oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD DOWN $5.55 TODAY: /

NO CHANGES IN GOLD INVENTORY AT THE GLD:

/GLD INVENTORY 798.13 TONNES

Inventory rests tonight: 798.13 tonnes.

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

SLV/

WITH SILVER DOWN 11 CENTS TODAY :

NO CHANGES IN SILVER INVENTORY AT THE SLV

/INVENTORY RESTS AT 328.962 MILLION OZ/

NOTE THE DIFFERENCE BETWEEN THE GLD AND SLV: THE CROOKS CAN RAID GOLD BECAUSE THEY DO HAVE SOME PHYSICAL. THEY DO NOT RAID SILVER PROBABLY BECAUSE THERE IS NO REAL SILVER INVENTORIES BEHIND THEM

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER ROSE BY A GOOD SIZED 1394 CONTRACTS from 212,996 UP TO 215,000 (AND CLOSER TO THE NEW COMEX RECORD SET /APRIL 9/2017 AT 243,411/SILVER PRICE AT THAT DAY: $16.53). THE PREVIOUS RECORD OTHER THAN WAS ESTABLISHED AT: 234,787, SET ON APRIL 21.2017 OVER ONE YEAR AGO. THE PRICE OF SILVER ON THAT DAY: $17.89. OUR CUSTOMARY MIGRATION OF COMEX LONGS MORPH INTO LONDON FORWARDS CONTINUES AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

558 EFP CONTRACTS FOR SEPT., 0 EFP CONTRACTS FOR DECEMBER AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 558 CONTRACTS . EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI GAIN AT THE COMEX OF 1394 CONTRACTS TO THE 558 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A FAIR NET GAIN OF 1952 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES: 9.76 MILLION OZ!!! AND YET WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESS AN INITIAL STANDING OF SLIGHTLY LESS THAN 30 MILLION OZ AND YET ALL OF THIS DEMAND OCCURRED DESPITE A SMALL 10 CENT GAIN IN PRICE???. WE DEFINITELY HAD BANKER CAPITULATION ON FRIDAY AS THEY TRIED DESPERATELY TO SHED SOME OF THEIR HUGE SILVER SHORTFALL. THE CABAL DID NOT LIKE WHAT THEY HEARD FROM TRUMP THAT HE IS ANGRY WITH THE FED AND WANTS LOWER INTEREST RATES. THAT WILL PROPEL BOTH GOLD AND SILVER.

IT SURE LOOKS LIKE WE ARE GETTING SOME COVERING FROM THE BANKERS SIDE ESPECIALLY WHEN YOU SEE A GOOD GAIN IN PRICE AND THEN A FALL IN COMEX OI AND A SMALLER THAN EXPECTED EFP ISSUANCE.

RESULT: A GOOD SIZED INCREASE IN SILVER OI AT THE COMEX DESPITE THE SMALL 10 CENT GAIN THAT SILVER UNDERTOOK IN PRICING ON FRIDAY. BUT WE ALSO HAD A SMALL SIZED 558 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR JULY, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON AS WELL AS THE STRONG AMOUNT OF PHYSICAL STANDING FOR METAL AT THE COMEX. BANKER CAPITULATION ON FRIDAY

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

)MONDAY MORNING/SUNDAY NIGHT: Shanghai closed UP 30.27 POINTS OR 1.07% /Hang Sang CLOSED UP 31.64 POINTS OR 0.11%/ / The Nikkei closed DOWN 300.89 POINTS OR 1.33%/Australia’s all ordinaires CLOSED DOWN 0.90% /Chinese yuan (ONSHORE) closed DOWN at 6.7899 AS POBC CONTINUES ITS HUGE DEVALUATION /Oil UP to 69.08 dollars per barrel for WTI and 74.05 for Brent. Stocks in Europe OPENED RED//. ONSHORE YUAN CLOSED DOWN AT 6.7899 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.8008: HUGE DEVALUATION/PAST SEVERAL DAYS RESUMES : TARIFF WARS INTENSIFIES UNABATED AND AT FULL TILT//ONSHORE YUAN TRADING STRONGER AGAINST OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

/NORTH KOREA/SOUTH KOREA

i)North Korea/South Korea/USA/Russia

b) REPORT ON JAPAN

Big news last night: The Bank of Japan, even though they are tapering, offers to buy unlimited supplies of Japanese bonds at the .11% rate after rates around the world started to rise. Bank earnings, especially in Eurpe have been awful and central authorities are trying to create a steepening but it will have no real effect because investors are too scared of a huge downfall in pricing of bonds.

(courtesy zerohedge)

3 c CHINA

i)The USA are monitoring China’s currency war very close. On Oct 15 2018, is forum to address this formally. If Trump decides to counter, the trade/currency war could evolve into something worse

( zero hedge)

ii)wow!! this is something to behold!! Officials from the Central Bank of China has choice words with the Ministry of Finance as there is much fingerpointing at who is responsible for China’s economic mess.

( zerohedge)

iii)The worse case scenario deepens as the Chinese are overwhelmingly ready to boycott all USA goods in a trade war morphing into a currency war

( zerohedge)

4. EUROPEAN AFFAIRS

UK

In a poll, most Brits overwhelmingly reject May’s new soft Brexit plan. They are turning to Boris Johnson and Nigel Farage to lead them out of the wilderness

( zerohedge)

ii)UK/EU

Mish blasts Theresa May and here soft Brexit plan. He is correct in everything he says: The EU will be in far worse shape than the UK

( zerohedge)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

i)Russia/USA

Putin is furious with this; A mole inside the Russian hypersonic weapons labs smuggles top secret files on their development to the West

and the USA is still furious that Russia “influenced” USA elections;

( zerohedge)

ii)Trump continues to show the Russians his strength against them as they slams Putin’s offer for a referendum on Eastern Ukraine

Turkey’s Erdogan is dictator for life: any dissenters to his rule will be fired

( zerohedge)

iv)ISRAEL/SYRIA

This is a good one: Israel late Saturday night rescued 800 White Helmet members from Syria and delivered them through Israel to Jordan. These members are anti Assad and they fared for their lives because Assad has entered the North west part of Syria where they were located. Israel has been supporting them in a very clandestine manner

( zerohedge)

v)ISRAEL/SYRIA

( zerohedge)

vi)IRAN/USA

( zerohedge)

Now that the Syrian civil war is wearing down, Trump is now going after a regime change in Iran

(courtesy zerohedge)

6 .GLOBAL ISSUES

It is even happening here: In Greektown, two people are dead, and a third, the killer, along with 15 wounded after a terrorist attack in Toronto.

( zerohedge)

7. OIL ISSUES

8. EMERGING MARKET

9. PHYSICAL MARKETS

i)There is a lot more to this story. It seems that depositors allocated gold ended up being unallocated and then this gold disappeared. This story is developing…

( Kingworldnews/Andrew Maguire)

ii)Do you blame them?: Turkey refuses to hand back refined gold belonging to Venezuela.

( Reuters/GATA)

iii)Bill Murphy explains that even though the dollar is falling: the only reason for the flal is manipulation to the highest degree

( GATA)

iv)A good article on Don Trump’s feud with the Fed. The question of course is interest rates and Trump now does not like rates rising against a currency war. Trump will win out…

( New York Sun/GATA)

v)The Russians are well aware of gold suppression and they are using it to buy massive amount of physical gold. I believe that the last 47 billion dollars worth of gold wiped out all of the physical gold in the west.

( Russia Today/Gata)

vii) Lawrie Williams/two commentaries

a)Russia announces that it added 15.6 tonnes to officially hold 1,944 tonnes of gold. The June number is before Russia sold off its entire USA treasuries and bought with the proceeds, gold, in early July

b)Although high for the first half at 400 tonnes, we are witnessing a little slowdown in refining from Switzerland but a pickup in refining capacity in other jurisdictions.

Demand for gold in the first half is 1,000 tonnes so they have a demand for the year at 2000 tonnes. The world produces around 2550 tonnes ex China ex Russia who refuse to sell any gold (and silver) out of their country

( Lawrie Williams/Sharp’s Pixley)

10. USA stories which will influence the price of gold/silver)

i)Market trading /GOLD/MARKET MOVERS:

11 am est

10 yr treasury yields spike to one month highs with the yuan testing new lows:

USA 10 yr bond yield: 2.9467

USA 30 yr : 3.0790

USA:CNY (onshore) 6.7986

USA/CNH: (offshore) 6.8174

a)Do not read anything into this.. Barclay’s is predicting that the first estimate of Q2 GDP will come in at 5.3%. They state that this is late stage in the economic cycle. However even they admit that eventually it will come in when final numbers come in 3 months later will be at the 2% level

( zerohedge)

iv)SWAMP STORIES

a)Supposedly Trump waives Attorney Client privilege on a secret Cohen tape recording. It makes no sense that he did!

The uSA is becoming lawless

( zerohedge)

b)the Carter Page FISA application exposes the garbage that the FBI provided to the court in their witch hunt..just awful

( zerohedge)

c)This is a good one:

Trading Volumes on the COMEX

PRELIMINARY COMEX VOLUME FOR TODAY: 382,296 contracts

CONFIRMED COMEX VOL. FOR YESTERDAY: 426,170 CONTRACT,

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

And now for the wild silver comex results.

Total silver OI ROSE BY A GOOD SIZED 1205 CONTRACTS FROM 213,606 UP TO 215,000 (AND A LITTLE CLOSER TO THE THE NEW RECORD OI FOR SILVER SET APRIL 9.2018/ 243,411 CONTRACTS) DESPITE THE SMALL 10 CENT RISE IN SILVER PRICING/ FRIDAY. SINCE WE ARE NOW INTO THE ACTIVE DELIVERY MONTH OF JULY, WE WERE INFORMED THAT WE VERY SMALL SIZED 558 EFP CONTRACTS FOR SEPT., 0 EFP CONTRACTS FOR DECEMBER AND ZERO FOR ALL OTHER MONTHS. THESE EFPS WERE ISSUED TO COMEX LONGS WHO RECEIVED A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. THE TOTAL EFP’S ISSUED: 558. ON A NET BASIS WE GAINED 1952 SILVER OPEN INTEREST CONTRACTS AS WE OBTAINED A 1394 CONTRACT GAIN AT THE COMEX COMBINING WITH THE ADDITION OF 558 OI CONTRACTS NAVIGATING OVER TO LONDON.

NET GAIN ON THE TWO EXCHANGES: 1952 CONTRACTS

AMOUNT STANDING FOR SILVER AT THE COMEX

We are now in the active delivery month of JULY and here the front month FELL by 139 contacts to stand at 425 contracts. We had 32 notices filed yesterday so we LOST 107 contracts or an additional 535,000 oz decided to morph into London based forwards and they received a fiat bonus for their efforts. I guess there was no silver around on this side of the pond for these last transfers and so they are trying their luck in England. Silver and gold are terribly backward over there meaning huge scarcity.

The next delivery month, after July is the non active delivery month of August and here we gained 13 contracts to stand at 1165. The next active delivery month after August for silver is September and here the OI rose by 1102 contracts down to 154,037

We had 9 notice(s) filed for 45,000 OZ for the JULY 2018 COMEX contract for silver

FROM LAST YEARS DATA, ON FIRST DATE NOTICE FOR THE JULY 2017 SILVER COMEX DELIVERY MONTH WE HAD 12.115 MILLION OZ OF SILVER STANDING FOR DELIVERY. AT MONTH’S END WE HAD 16.435 MILLION OZ EVENTUALLY STAND AS WE ALREADY HAD QUEUE JUMPING BEGIN IN EARNEST FROM APRIL 2017 ONWARD EVEN TO TODAY. SO WITH TODAY’S NUMBERS WE SURPASSED LAST YEAR’S LEVEL BY A WIDE MARGIN.

AND NOW COMPARISON VS AUGUST LAST YR:

ON FIRST DAY NOTICE JULY 31/2017: 1,965,000 OZ STOOD FOR DELIVERY

THE FINAL AMOUNT OF SILVER STANDING: AUGUST 30.2017: 6,245,000 OZ AS WE HAD CONSIDERABLE QUEUE JUMPING.

FOR THE AUGUST CONTRACT MONTH:

LAST YEAR AT THIS TIME JULY 20.2017 WE HAD 468 SILVER COMEX OI OUTSTANDING VS TODAY: 1165

SO, AS IN GOLD, WE ARE GOING TO HAVE A CONSIDERABLY LARGER AMOUNT OF SILVER STANDING FOR THE NON ACTIVE CONTRACT MONTH OF AUGUST THAN LAST YEAR.

INITIAL standings for JULY/GOLD

JULY 23/2018.

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz |

nil OZ

|

| Deposits to the Dealer Inventory in oz | NIL oz |

| Deposits to the Customer Inventory, in oz |

nil oz

|

| No of oz served (contracts) today |

0 notice(s)

NIL OZ

|

| No of oz to be served (notices) |

136 contracts

(13,600 oz)

|

| Total monthly oz gold served (contracts) so far this month |

99 notices

9900 OZ

.3079TONNES

|

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

For JULY:

Today, 0 notice(s) were issued from JPMorgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equates to 0 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped/ Received) by j.P.Morgan customer account.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

To calculate the INITIAL total number of gold ounces standing for the JULY. contract month, we take the total number of notices filed so far for the month (99) x 100 oz or 9900 oz, to which we add the difference between the open interest for the front month of JULY. (137 contracts) minus the number of notices served upon today (0 x 100 oz per contract) equals 23,600 oz,(.7340 tonnes) the number of ounces standing in this non active month of JULY

Thus the INITIAL standings for gold for the JULY contract month:

No of notices served (99 x 100 oz) + {(137)OI for the front month minus the number of notices served upon today (0 x 100 oz )which equals 23,600 oz standing in this NON – active delivery month of JULY .

We lost 0 contracts or an additional nil oz will stand for comex delivery and these guys refused to morph into London based forwards..

THERE ARE ONLY 7.6588 TONNES OF REGISTERED COMEX GOLD AVAILABLE FOR DELIVERY AGAINST 0.7433 TONNES STANDING FOR JULY

IN THE LAST 24 MONTHS 85 NET TONNES HAS LEFT THE COMEX.

end

And now for silver

AND NOW THE APRIL DELIVERY MONTH

JULY INITIAL standings/SILVER

| Silver | Ounces |

| Withdrawals from Dealers Inventory | nil oz |

| Withdrawals from Customer Inventory |

982.460oz

jpmorgan

|

| Deposits to the Dealer Inventory |

nil

oz

|

| Deposits to the Customer Inventory |

3069.701

jpm

oz

|

| No of oz served today (contracts) |

9

CONTRACT(S)

(45,000 OZ)

|

| No of oz to be served (notices) |

416 contracts

(2,080,000 oz)

|

| Total monthly oz silver served (contracts) | 5521 contracts

(27,605,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

we had 0 inventory movement at the dealer side of things

total dealer deposits: nil oz

total dealer withdrawals: nil oz

we had 1 deposit into the customer account

i) Into JPMorgan: 3069.710 oz

*** JPMorgan for most of 2017 and in 2018 has adding to its inventory almost every single day.

JPMorgan now has 141 million oz of total silver inventory or 52.0% of all official comex silver. (141 million/270 million)

ii) into everybody else: nil oz

total customer deposits today: 3069.710 oz

we had1 withdrawals from the customer account;

i) Out of jpmorgan” 982.460 oz

total withdrawals: 982.460 oz

we had 0 adjustments/

total dealer silver: 78.908 million

total dealer + customer silver: 280.532 million oz

The total number of notices filed today for the JULY. contract month is represented by 9 contract(s) FOR 45,000 oz. To calculate the number of silver ounces that will stand for delivery in JULY., we take the total number of notices filed for the month so far at 5521 x 5,000 oz = 27,605,000 oz to which we add the difference between the open interest for the front month of JULY. (425) and the number of notices served upon today (9 x 5000 oz) equals the number of ounces standing.

.

Thus the INITIAL standings for silver for the JULY/2018 contract month: 5521(notices served so far)x 5000 oz + OI for front month of JULY(425) -number of notices served upon today (9)x 5000 oz equals 29,685,000 oz of silver standing for the JULY contract month

WE LOST 107 CONTRACTS OR AN ADDITIONAL 535,000 OZ WILL NOT STAND AS THESE GUYS

MORPHED INTO LONDON BASED FORWARDS AND RECEIVED A FIAT SWEETENER FOR THEIR EFFORTS.

PLEASE NOTE THE FOLLOWING FOR COMPARISON PURPOSES:

THE INITIAL STANDING FOR SILVER AT THE COMEX JULY 2017: 12.115 MILLION OZ ALTHOUGH AT MONTH’S END: 16.435 MILLION OZ STOOD FOR DELIVERY. THIS COMPARES WITH TODAY’S INITIAL STANDING FOR SILVER OF 29.685 MILLION OZ.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

ESTIMATED VOLUME FOR TODAY:61,306 CONTRACTS

CONFIRMED VOLUME FOR YESTERDAY: 85,716 CONTRACTS absolutely criminal

YESTERDAY’S CONFIRMED VOLUME OF 85,716 CONTRACTS EQUATES TO 428 million OZ OR 61.2% OF ANNUAL GLOBAL PRODUCTION OF SILVER

COMMODITY LAW SUGGESTS THAT OPEN INTEREST SHOULD NOT BE MORE THAN 3% OF ANNUAL GLOBAL PRODUCTION. THE CROOKS ARE SUPPLYING MASSIVE PAPER TRYING TO KEEP SILVER IN CHECK.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price at that day at $18.42

The previous record was 224,540 contracts with the price at that time of $20.44

end

NPV for Sprott

1. Sprott silver fund (PSLV): NAV RISES TO -3.34% (JULY 23/2018)

2. Sprott gold fund (PHYS): premium to NAV RISES TO -1.00% to NAV (JULY 23/2018 )

Note: Sprott silver trust back into NEGATIVE territory at -3.34%-/Sprott physical gold trust is back into NEGATIVE/

(courtesy Sprott/GATA)

3.SPROTT CEF.A FUND (FORMERLY CENTRAL FUND OF CANADA):

NAV 12.65/TRADING 12.19//DISCOUNT 3.44.

END

And now the Gold inventory at the GLD/

JULY 23/WITH GOLD DOWN $5.55: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 798.13 TONNES

JULY 20/WITH GOLD UP $4.15 A HUGE DEPOSIT OF 4.12 TONNES OF GOLD INTO THE GLD.INVENTORY RESTS AT 798.13 TONNES

JULY 19./WITH GOLD DOWN $1.00: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 794.01 TONNES

JULY 18/WITH GOLD UP 0.40: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 794.01 TONNES

JULY 17/WITH GOLD DOWN $12.40, WE HAD A BIG WITHDRAWAL OF 1.18 TONNES FROM THE GLD/INVENTORY RESTS AT 794.01 TONNES

JULY 16/WITH GOLD DOWN $1.55/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 795.19 TONNES

JULY 13/WITH GOLD DOWN $5.35 THE CROOKS RAID THE COOKIE JAR AGAIN TO THE TUNE OF 3.83 TONNES/INVENTORY RESTS AT 795.19 TONNES

JULY 12/WITH GOLD UP $2.30: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 799.02 TONNES

JULY 11/WITH GOLD DOWN $10.75 THE CROOKS RAIDED THE COOKIE JAR AGAIN TO THE TUNE OF 1.75 TONNES/INVENTORY RESTS AT 799.02 TONNES

JULY 10/WITH GOLD DOWN $3.85: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 800.77 TONNES

july 9/WITH GOLD UP $4.00/ANOTHER RAID ON THE GOLD COOKIE JAR: TWO WITHDRAWALS OF 1.18 TONNES THIS MORNING AND 1.47 TONNES THIS AFTERNOON/INVENTORY RESTS AT 800.77 TONNES

JULY 6/WITH GOLD DOWN $2.45: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 803.42 TONNES

JULY 5/WITH GOLD UP ANOTHER $5.15, THE CROOKS RAIDED THE COOKIE JAR AGAIN TO THE TUNE OF 5.89 TONNES/INVENTORY RESTS AT 803.42 TONNES IN THE LAST 10 TRADING DAYS GLD HAS LOST A HUGE 25.34 TONNES WITH A LOSS OF ONLY $15.25 IN PRICE

July 3/WITH GOLD UP $11.15/THE CROOKS RAIDED THE GLD INVENTORY AGAIN TO THE TUNE OF 9.73 TONNES/INVENTORY RESTS AT 809.31 TONNES

JULY 2/WITH GOLD DOWN $12.15, THE CROOKS RAIDED THE GLD INVENTORY AGAIN BY 1.47 TONNES DOWN./INVENTORY RESTS AT 819.04 TONNES

JUNE 29/WITH GOLD UP $3.70/A WITHDRAWAL OF 1.18 TONNES OF GOLD FROM THE GLD/INVENTORY RESTS AT 820.51 TONNES

JUNE 28/WITH GOLD DOWN $5.15/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 821.69 TONNES

June 27/WITH GOLD DOWN $3.60// TWO ENTRIES:/STRANGELY THE CROOKS RETURNED THE WITHDRAWAL OF 4.42 TONNES LAST NIGHT (THUS WE HAD A DEPOSIT OF 4.42 TONNES/INVENTORY RESTS AT 824.63 TONNES. /THEN LATE THIS AFTERNOON A WITHDRAWAL OF 2.94 TONNES

INVENTORY RESTS AT 821.69 TONNES/THIS VEHICLE IS AN OUTRIGHT FRAUD.

june 26/LATE LAST NIGHT, WITH GOLD DOWN $9.10 WE HAD A HUGE WITHDRAWAL OF 4.42 TONNES OF GOLD/INVENTORY RESTS AT 820.21 TONES

JUNE 25/WITH GOLD DOWN $1.45/NO CHANGE IN GOLD INVENTORY AT THE GLD.INVENTORY RESTS AT 824.63 TONNES

JUNE 22/WITH GOLD UP 25 CENTS TODAY, THE CROOKS WITHDREW A MASSIVE 4.13 TONNES OF GOLD/INVENTORY RESTS AT 824.63 TONNES

JUNE 21/WITH GOLD DOWN $4.00/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 828.76 TONNES

JUNE 20/WITH GOLD DOWN $3.55/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 828.76 TONNES

JUNE 19/WITH GOLD DOWN $1.50/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 828.76 TONES

JUNE 18/WITH GOLD UP $1.90/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 828.76 TONNES

JUNE 15/WITH GOLD DOWN $28.90/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 828.76 TONNES

JUNE 14/WITH GOLD UP $7.10/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 828.76 TONNES/

JUNE 13/WITH GOLD UP $2.20/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 828.76 TONNES

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

JULY 23/2018/ Inventory rests tonight at 798.13 tonnes

*IN LAST 415 TRADING DAYS: 132.80 NET TONNES HAVE BEEN REMOVED FROM THE GLD

*LAST 365 TRADING DAYS: A NET 23,74 TONNES HAVE NOW BEEN ADDED INTO GLD INVENTORY.

end

Now the SLV Inventory/

JULY 23/WITH SILVER DOWN 11 CENTS/NO CHANGES IN SILVER INVENTORY INTO THE SLV/INVENTORY RESTS AT 328.962 MILLION OZ/

JULY 20/WITH SILVER UP 10 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.411 MILLION OZ INTO THE SLV INVENTORY

INVENTORY RESTS AT 328.962 MILLION OZ

JULY 19/WITH SILVER DOWN 17 CENTS TODAY; A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 752,000 OZ INTO THE SLV INVENTORY/INVENTORY RESTS AT 327.551 MILLION OZ/

JULY 18/WITH SILVER DOWN 3 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 326.799 MILLION OZ/

JULY 17/WITH SILVER DOWN 20 CENTS TODAY: A CHANGE IN SILVER INVENTORY A WITHDRAWAL OF 1.001 MILLION OZ FROM THE SLV: INVENTORY RESTS AT 326.799 MILLION OZ/

JULY 16/WITH SILVER FLAT TODAY, A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.128 MILLION OZ//INVENTORY RESTS AT 327.880 MILLION OZ

JULY 13/WITH SILVER DOWN 16 CENTS TODAY/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 326.752 MILLION OZ.

JULY 12/WITH SILVER UP 12 CENTS TODAY: ANOTHER BIG CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.035 MILLION OZ/INVENTORY RESTS AT 326.752 MILLION OZ/

JULY 11/WITH SILVER DOWN 22 CENTS TODAY: ANOTHER HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 565,000/INVENTORY RESTS AT 325.717 MILLION OZ

JULY 10/WITH SILVER DOWN 3 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 325.151 MILLION OZ

july 9/WITH SILVER UP 5 CENTS: ANOTHER BIG CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 847,000 OZ ADDED TO INVENTORY/INVENTORY RESTS AT 825.151 MILLION OZ/

JULY 6/WITH SILVER DOWN 2 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 324.305 MILLION OZ/

JULY 5/WITH SILVER UP 6 CENTS, A GOOD CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 470,000 OZ/INVENTORY RESTS AT 324.305 MILLION OZ/ FOR THE PAST 10 TRADING DAYS, SILVER INVENTORY HAS ADVANCED BY 4.945 MILLION OZ WITH A LOSS OF 33 CENTS/PLEASE COMPARE THIS WITH THE GLD.

JULY 3/WITH SILVER UP 17 CENTS, A HUGE DEPOSIT OF 1.37 MILLION OZ ADDED TO THE SLV/INVENTORY RESTS AT 323.835 MILLION OZ.

JULY 2/WITH SILVER DOWN 31 CENTS/A HUGE 2.070 MILLION OZ DEPOSIT AT THE SLV/INVENTORY RESTS AT 322.465 MILLION OZ/

JUNE 29/WITH SILVER UP 14 CENTS TODAY, NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS THIS WEEKEND AT 320.395 MILLION OZ/

JUNE 28/WITH SILVER DOWN 18 CENTS, THE CROOKS ADDED 1.035 MILLION OZ OF SILVER INTO THE SLV/INVENTORY RESTS AT 320.395 MILLION OZ

JUNE 27.2018/WITH SILVER DOWN 8 CENTS/NO CHANGE IN SILVER INVENTORY/INVENTORY RESTS AT 819.360 MILLION OZ/

june 26./2018/WITH SILVER DOWN 8 CENTS, THE CROOKS WITHDREW THE DEPOSIT OF TWO DAYS AGO; 941,000 OZ OUT OF INVENTORY/INVENTORY RESTS AT 819.360 OZ

JUNE 25/WITH SILVER DOWN 12 CENTS/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 320.301 MILLION OZ/

JUNE 22/WITH SILVER UP 12 CENTS TODAY,ANOTHER BIG CHANGE IN SILVER INVENTORY AT THE SLV” A DEPOSIT OF 941,000 OZ INTO INVENTORY/INVENTORY RESTS THIS WEEKEND AT 320.301 MILLION OZ/

JUNE 21/WITH SILVER UP ONE CENT/ANOTHER CHANGE IN SILVER INVENTORY AT THE SLV/: A DEPOSIT OF 2.918 MILLION OZ/INVENTORY RESTS AT 319.360 MILLION OZ/ THUS FOR TWO STRAIGHT DAYS A TOTAL OF 5.26 MILLION OZ OF SILVER HAS BEEN ADDED WITH NO CHANGE IN PRICE.

JUNE 20/WITH SILVER DOWN ONE CENT/A HUGE CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY / A DEPOSIT OF 2.35 MILLION OZ/INVENTORY RESTS AT 316.442 MILLION OZ/

JUNE 19/2018/WITH SILVER DOWN 11 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 314.090 MILLION OZ/

JUNE 18/WITH SILVER DOWN 6 CENTS TODAY/NO CHANGE IN SILVER INVENTORY/INVENTORY RESTS AT 314.090 MILLION OZ/

JUNE 15/WITH SILVER DOWN 75 CENTS/A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.788 MILLION OZ//INVENTORY RESTS AT 314.090 MILLION OZ

JUNE 14/WITH SILVER UP 30 CENTS, THE CROOKS DECIDED THAT THEY NEEDED SILVER INVENTORY BADLY SO THEY RAID THE SLV OF 1.412 MILLION OZ/INVENTORY RESTS AT 315.878 MILLION OZ/

JUNE 13/WITH SILVER UP 11 CENTS TODAY/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 317.290 MILLION OZ/

JULY 23/2018:

Inventory 328.962 MILLION OZ

6 Month MM GOFO 1.92/ and libor 6 month duration 2.52

Indicative gold forward offer rate for a 6 month duration/calculation:

G0FO+ 1.92%

libor 2.52 FOR 6 MONTHS/

GOLD LENDING RATE: .60%

XXXXXXXX

12 Month MM GOFO

+ 2.80%

LIBOR FOR 12 MONTH DURATION: 2.42

GOFO = LIBOR – GOLD LENDING RATE

GOLD LENDING RATE = +.38

end

Major gold/silver trading /commentaries for FRIDAY

GOLDCORE/BLOG/MARK O’BYRNE.

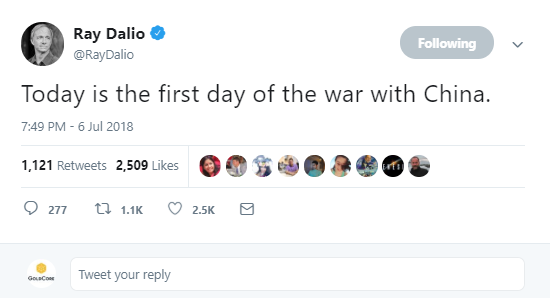

Trump and War With China? Goldnomics Podcast

Research Director of GoldCore and respected precious metals commentator Mark O’Byrne and GoldCore CEO Stephen Flood in discussion with Dave Russell in Episode 6 of the Goldnomics Podcast.

We discuss the “Tweet” of Ray Dalio, the founder of hedge fund Bridgewater Associates,: “Today is the first day of war with China.”

The tweet from the founder of the world’s largest hedge fund, which manages some $160 billion, comes after the U.S. slapped levies on some of China’s exports to the U.S., and President Donald Trump threatened further action.

Is he suggesting that there is something more than just a Trade War brewing between the U.S and China?

Is he warmongering, is he suggesting that Donald Trump is warmongering, or is he just alluding to what the unintended consequence of a trade war could be, as we have seen throughout history?

Is this part of Trump’s goal to Make America Great Again? We look at the serious unintended consequences of these actions. We look at the backdrop to these trade wars and how Globalization can be a double edged sword and how Ray Dalio is “right to be concerned.”

Listen to the full episode or skip directly to one of the following discussion points:

2:52: Why a trade war, why now?

4:22: The effects of a mass migration of Chinese from agriculture to trade and industry.

4:27 What effect does globalization have on the work-force

5:04: How China leverage their cheap labour force as a international competitive advantage.

5:22: Imported Chinese Goods are cheaper than the goods that are being domestically produced in America, how is this effecting peoples’ jobs in America.

5:40: Are Chinese workers now competing with the Vietnamese workers?

6:04: How Trump’s intention to safeguard American manufacturers and workers may cause the American consumers to pay more for domestically produced goods instead of buying cheaper imported goods

8:06 The U.S. has a Deficit with 140 countries around the world, why this can’t be fixed with a trade war.

8:30: History suggests that trade war initiates currency wars which eventually result in actual wars.

9.00: Hawks versus Doves: Hawks are increasingly in the ascendant in Trump’s America

12:45: Nationalism on the rise in America: “USA, USA, USA!”

13:30: “To jaw-jaw is always better than to war-war” Winston Churchill

14.27: Unforeseeable consequences warned of by Churchill: “The Statesman who yields to war fever must realize that once the signal is given, he is no longer the master of policy, but the slave of unforeseeable and uncontrollable events. Let us learn our lessons.”

15:10: What is the response of China?

15:11 How Trump’s action to protect the domestic industries and workers is not just targeting China but also involving Europe and Canada as well

16:14: Why Trump’s supporters continue to back his actions and decisions

17:36 How the European Union is responding

17:50 Harley Davidson and the unintended consequence playing out.

18:00 How Trump’s actions to protect domestic jobs are resulting in the contrary

18:41 How Trade War will add an extra premium to the cost of doing business all over the world

19:05 Why China is putting more and more money in Infrastructure & Power Systems so they can easily get their goods to the market

20:52 Behind the scenes of trade war, is a currency war actually going on?

21:52 Why are the Chinese continuing to quietly invest in Gold

22:22 The Chinese government are planning for the long term, unlike the U. S. government

23:26: How the personal prosperity of Americans is diminishing while certain corporations continue to do better

23:44: Trump’s actions to protect jobs are reflected in his suggested policies

24:34 Why globalization is not delivering security to individuals and their families

24:41: Historically trade wars were the portent of an actual war

27:00 Why the media’s mocking actions are encouraging the trade war

29:10 How Europe’s massive global economy has an important role to play in this trade war

29:38: What action might the investors and savers take in this situation?

32:08 Trump’s actions until now only focusing on the short term protection of the U.S. economy

32:47: Why investors need to diversify their investments and re-balance portfolios

33:07: Why diversification needs to be geographical and not just asset based

33:54 How gold can be used to protect wealth in trade wars or actual wars

35:17 Ray Dalio’s Tweet doesn’t necessarily signify the first day of war with China but there’s definitely a trade war going on between U.S. & China and as the gloves come off, we could see unintended consequences…

People mentioned in this episode:

Ray Dalio: https://twitter.com/RayDalio

Harald Malmgren: https://twitter.com/Halsrethink

Pippa Malmgren: https://twitter.com/DrPippaM

Gerald Celente: https://twitter.com/geraldcelente

News and Commentary

PRECIOUS-Gold rises further as U.S. dollar eases (Reuters.com)

Doubts raised over Russian treasure ship with $190 billion in gold (News.com)

Trump warns Iran’s President Rouhani: ‘NEVER, EVER THREATEN THE UNITED STATES AGAIN’ (CNBC.com)

EU warns of Brexit crash (Reuters.com)

Italian Markets Rattled After Tria’s Future Is Thrown Into Doubt (Bloomberg.com)

Currency War Erupts, Threatening to Ripple Across Global Markets (Bloomberg.com)

London’s luxury new-build property is in big trouble (MoneyWeek.com)

Almost 70% of millennials regret buying their homes. Here’s why (CNBC.com)

Global Economy Lives on the Edge as Crisis Veterans Sound Alarms (Bloomberg.com)

The Case For Gold Is Not About Price (ZeroHedge.com)

Listen on SoundCloud , Blubrry & iTunes. Watch on YouTube below

Gold Prices (LBMA AM)

20 Jul: USD 1,224.85, GBP 940.56 & EUR 1,050.80 per ounce

19 Jul: USD 1,217.40, GBP 936.06 & EUR 1,048.79 per ounce

18 Jul: USD 1,223.45, GBP 938.02 & EUR 1,052.29 per ounce

17 Jul: USD 1,243.65, GBP 938.46 & EUR 1,059.96 per ounce

16 Jul: USD 1,244.90, GBP 938.41 & EUR 1,063.52 per ounce

13 Jul: USD 1,240.50, GBP 945.14 & EUR 1,066.83 per ounce

Silver Prices (LBMA)

20 Jul: USD 15.37, GBP 11.79 & EUR 13.19 per ounce

19 Jul: USD 15.26, GBP 11.75 & EUR 13.16 per ounce

18 Jul: USD 15.44, GBP 11.85 & EUR 13.29 per ounce

17 Jul: USD 15.77, GBP 11.91 & EUR 13.46 per ounce

16 Jul: USD 15.81, GBP 11.90 & EUR 13.49 per ounce

13 Jul: USD 15.81, GBP 12.04 & EUR 13.60 per ounce

Recent Market Updates

– Weekly Digest – News, Market Updates and Videos You May Have Missed

– Financial Terrorism In The UK – Collusion between Government, Regulators & Two Bailed-Out UK Banks

– “Biggest Bubble in the History of Mankind” Is “Going To Burst” – Ron Paul

– Global Debt Time Bomb Surges To Nearly $250,000,000,000,000 – GoldCore Video

– Trump, Russia, Brexit and the Demand For Gold and Silver – GoldCore Video Interview

– Trump Is Serious About A Global Trade War

– Ponzi Economy Will Lead To Next Global Financial Crisis

– World Cup Is 200 Ounces Of Gold Worth £140,000 – 30% Less Than Harry Kane’s Weekly Wage

– Chaotic BREXIT More Likely: Risk To London, While Frankfurt, Luxembourg, Paris and Dublin Benefit

– VIDEO: Italy €2.4 Trillion Debt To Create Eurozone Contagion and Global Debt Crisis?

– U.S. China Trade War Escalates as Russia and China Accumulate Gold

– Irish Gold Money Rings Found – Mystery Surrounds What May Be Ancient, Pre-Historic Currency

– Gold $10,000 In Currency Reset? Russia, China Gold Demand To Overwhelm Gold Futures Manipulation (GOLDCORE VIDEO)

ANDREW MAGUIRE’S KINESIS WHICH IS A”BITCOIN’ BACKED 100% BY ALLOCATED GOLD AND SILVER

Andrew Maguire’s Kinesis money which is a “bitcoin” but backed 100% by allocated gold and silver is set to go.

it think it would be a great idea to look at this!

please read at: https://kinesis.money/#/

(Andrew Maguire)

|

|

Dear Harvey Organ,

Thank you for your participation in our webinar on June 7th with our host and CEO of Kinesis, Thomas Coughlin.

The response we received has been incredible, we appreciate you taking the time to join us and hope you found it to be beneficial.

Due to such a high influx of questions we received we were unable to have them all answered. Nevertheless, if there was anything which requires more clarification, or you have a query which needs to be rectified, we invite you to join our telegram group:

We apologize for the technical issues we incurred during the webinar which resulted in it running a little over schedule, we hope that the next one we host will run seamlessly.

A video has been put together and uploaded onto our YouTube channel which can be found here:

Please share and subscribe to our YouTube channel to be notified of all the latest videos as they become available.

The rapid growth that we are currently experiencing has been incredible and with your support, is only going to get better.

We are working behind the scenes very hard to create a better experience for everyone involved! Stay tuned in as we have many more announcements to be released in the upcoming days.

Kind Regards,

|

Kinesis Money

a:C/O ILS Fiduciaries (IOM) Limited, First Floor,Millennium House, Victoria Road, Douglas, Isle of Man IM2 4RW

|

The following is self explanatory

(courtesy GATA/Chris Powell and Harvey Organ)

GATA asks bank regulator to check risks of gold

futures maneuver

Submitted by cpowell on Sun, 2018-06-10 16:17. Section: Daily Dispatches

12:21p ET Sunday, June 10, 2018

Dear Friend of GATA and Gold:

GATA has appealed to the U.S. comptroller of the currency, who has regulatory authority over banks, to review financial risks certain banks may have incurred through derivatives in the monetary metals markets, particularly through the recent heavy use of the “exchange for physicals” mechanism of settling gold and silver futures contracts on the New York Commodities Exchange.

The appeal was made in a letter sent May 5 to the comptroller, Joseph M. Otting, whose office is part of the U.S. Treasury Department, by your secretary/treasurer and GATA futures market consultant Harvey Organ.

“Exchange for physical” settlements of futures contracts long were considered emergency procedures when a seller was not able to deliver metal from an exchange-approved warehouse and wanted to settle with delivery elsewhere. But now such settlements appear to constitute most gold and silver futures settlements on the Comex. It is a strange development that appears to have been necessitated by the increasing difficulties of central banking’s gold and silver price suppression policy.

GATA has received no acknowledgment of the letter. Its text is below and a PDF copy of it is here:

http://www.gata.org/files/ComptrollerOfCurrencyLetter.pdf

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

* * *

May 5, 2018

Joseph M. Otting, Comptroller of the Currency

U.S. Treasury Department

400 7th Street, SW

Washington DC 20219

Dear Comptroller Otting:

Please let us bring to your attention financial risks to major banks involving their possibly unreported exposure to derivatives in the monetary metals markets.

In recent months gold and silver future contracts issued by U.S. banks on the New York Commodities Exchange have been moved off-exchange for delivery through a mechanism known as “exchange for physical” (EFP) contracts. Until recently use of this mechanism was considered an emergency procedure when a seller did not have access to metal for delivery through Comex warehouses. Now the mechanism seems to be in use for a large share of front-month contracts for which delivery is sought.

Here is an example that is happening at the Comex in the front active month of April for gold and the inactive delivery month of April for silver.

In gold, there were 229,436 EFP contracts for 713.64 tonnes, an average of 10,925 contracts and 1,092,500 ounces per trading day.

In silver, there were 77,150 EFP contracts for 385,750,000 ounces, an average of 3,673 contracts and 18,369,000 ounces per trading day.

London Bullion Market Association rules suggest that these contracts may not be reported to regulators. The LBMA’s bylaws say:

“Figures above exclude any contracts not subject to risk-based capital requirements, such as FX contracts with an original maturity of 14 days or less, futures contracts, written options, and basis swaps. Therefore, the total notional amount of derivatives by maturity will not add to the total derivatives figure in this table.”

We are told that these EFP contracts are transferred from the Comex to London as what are called “serial forwards” and their duration is always less than 14 days, which exempts them from being reported.

It is our understanding that in each quarter your office prepares a report detailing risk undertaken by the banks under the comptroller’s supervision.

These risks include derivatives undertaken by U.S. banks and other obligations that may cause a bank to fail. Our concern is that your office may not be aware of large unreported derivative exposure by banks.

Could you review this matter and let us know your conclusions?

Sincerely,

CHRIS POWELL

Secretary/Treasurer

HARVEY ORGAN

Consultant

Gold Anti-Trust Action Committee Inc.

7 Villa Louisa Road

Manchester, Connecticut 06043-7541

end

There is a lot more to this story. It seems that depositors allocated gold ended up being unallocated and then this gold disappeared. This story is developing…

(courtesy Kingworldnews/Andrew Maguire)

Swiss banks won’t let depositors withdraw gold,

Maguire tells KWN

Submitted by cpowell on Fri, 2018-07-20 19:35. Section: Daily Dispatches

3:35p ET Friday, July 20, 2018

Dear Friend of GATA and Gold:

London metals trader Andrew Maguire today tells King World News he is hearing more complaints from gold owners that they lately have been refused withdrawal of their gold by Swiss banks, even though the gold supposedly was being held on an allocated basis.

These reports probably won’t be taken seriously outside the gold bug community until the expropriated depositors identify themselves and their banks and complain in public. But then the advice to gold investors from Jim Sinclair, James Turk, and others long has been not to store gold in the banking system. Maybe people need a reminder.

Maguire’s interview is summarized at KWN here:

https://kingworldnews.com/wtf-is-going-on-andrew-maguire-now-says-a-swis…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

Do you blame them?: Turkey refuses to hand back refined gold belonging to Venezuela.

(courtesy Reuters/GATA)

Venezuelan gold doesn’t seem to be returning from

Turkey

Submitted by cpowell on Sat, 2018-07-21 03:55. Section: Daily Dispatches

Venezuela Exported $779 Million in Gold to Turkey in 2018, Data Says

By Humeyra Pamuk and Corina Pons

Reuters

Thursday, July 19, 2018

Venezuela exported $779 million of gold to Turkey in 2018, according to Turkish government statistics, further evidence that the South American country is shifting its pattern of trade following a wave of sanctions that began last year.

Venezuela’s Mining Minister Victor Cano on Wednesday said the central bank was exporting gold to Turkey rather than Switzerland due to concerns about sanctions, without specifying the amount that was being sent.

…

.

The latest data on Turkey’s Statistical Institute website show that between January and May, Venezuela exported 20.15 tonnes of gold to Turkey, compared with none in 2017. Turkey did not send an equivalent amount of gold back to Venezuela, the data showed.

Cano on Wednesday said the gold exported to Turkey would ultimately return to Venezuela to become part of the central bank’s portfolio of assets.

The Venezuelan Central Bank did not respond to a request for comment. …

Data from Turkey’s Statistics Institute does not show any gold exports back to Venezuela in 2018, so it is possible the refined gold is being sold there or in other markets. …

… For the remainder of the report:

https://www.reuters.com/article/venezuela-gold-turkey/corrected-venezuel…

* * *

END

Bill Murphy explains that even though the dollar is falling: the only reason for the flal is manipulation to the highest degree

(courtesy GATA)

Dollar isn’t rising, isn’t causing gold’s fall,

Murphy tells GoldSeek Radio

Submitted by cpowell on Sat, 2018-07-21 14:32. Section: Daily Dispatches

10:33a ET Saturday, July 21, 2018

Dear Friend of GATA and Gold:

GATA Chairman Bill Murphy, interviewed this week by GoldSeek Radio’s Chris Waltzek, says that contrary to the general impression in the markets, the U.S. dollar has not been rising lately and has not been the cause of the sharp declines in gold and silver. Rather, Murphy says, gold and silver have been knocked down by market manipulation. Despite the raids on the monetary metals, Murphy adds, gold and silver mining shares have not been knocked down much.

The interview is 16 minutes long and can be heard at GoldSeek Radio here:

http://radio.goldseek.com/nuggets/murphy.07.19.18.mp3

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

A good article on Don Trump’s feud with the Fed. The question of course is interest rates and Trump now does not like rates rising against a currency war. Trump will win out…

(courtesy New York Sun/GATA)

New York Sun: Will Trump take on the Fed?

Submitted by cpowell on Sat, 2018-07-21 14:41. Section: Daily Dispatches

From the New York Sun

Saturday, July 21, 2018

… What, though, are we to make of the fact that two years after lacing into the Fed for keeping interest rates low, Mr. Trump, now president, is jawboning the Fed for letting interest rates start to rise? Two years ago he tweeted a prediction that rates would have to rise. Now that he is proven right, he complains: “I don’t like all of this work that we’re putting into the economy and then I see rates going up

Our own view is that this is an opportunity for Mr. Trump take on the problem of fiat money. That means dollars lacking a definition in law, currency not backed by gold or any other specie. We plunged into the era of fiat money in 1971, when America defaulted on its undertakings at Bretton Woods. By the end of the 1970s, we’d inked an IMF amendment that forbade countries from defining their money in gold. …

Far better to open this issue up now, which, the president comes so close to doing in, say, his interview with CNBC’s Joe Kernan. Mr. Trump acceded to the presidency at a time when Congress was primed to start work on monetary reform. Were Mr. Trump to take on the leadership of monetary reform, he could, in addition to all else, get some respite from the scandals of the day and secure his achievement on the economy.

… For the remainder of the commentary:

https://www.nysun.com/editorials/will-trump-take-on-the-fed/90336/

END

The Russians are well aware of gold suppression and they are using it to buy massive amount of physical gold. I believe that the last 47 billion dollars worth of gold wiped out all of the physical gold in the west.

(courtesy Russia Today/gata)

Russian financial analyst expects gold price suppression

Submitted by cpowell on Sun, 2018-07-22 18:50. Section: Daily Dispatches

Russia Ditching U.S. Treasuries for Gold to Protect Economy and Diversify, Analysts Tell RT

From Russia Today, Moscow

Sunday, July 22, 2018

Russia ditching U.S. Treasuries for gold in bid to protect economy and diversify, analysts tell RT

Russia has left the top-30 list of top lenders to the United States by radically slashing US Treasury bills ownership. RT-polled analysts have shared their opinion on the move.

Both political and economic reasons could be found here. The central bank may have thought that Russian-owned Treasuries could be frozen because of geopolitical tensions. The regulator announced in the spring that it plans to diversify its reserves,” said Zhanna Kulakova, financial consultant at TeleTrade.

The analyst thinks the Russian central bank could re-invest the money from the sale into Chinese bonds and gold. “Gold is a tangible asset that cannot be completely depreciated under any circumstances. In periods of global financial or political crises, gold will be much more useful than securities or cash,” Kulakova said, noting that gold is also prone to price fluctuations from time to time. …

Vladimir Rojankovski, an expert at the International Financial Center in Moscow, gives another reason for Russia withdrawing its assets from the United States. “They could be frozen by foreign courts based on the results of biased/politicized legal proceedings,” he said. …

Rojankovski praises the move by the Russian central bank to diversify, but warns that gold prices could be manipulated on the market like oil. “In the event of a global decline in the interest of large sovereign investors in U.S. Treasury bonds, I expect an increase in speculative activity in precious metals in order to artificially lower their market valuation,” he said.

… For the remainder of the report:

https://www.rt.com/business/433950-russia-us-treasury-dumping/

end

Russia announces that it added 15.6 tonnes to officially hold 1,944 tonnes of gold. The June number is before Russia sold off its entire USA treasuries and bought with the proceeds, gold, in early July

(courtesy Lawrie Williams)

LAWRIE WILLIAMS: Russia continues to add to its gold reserves

In June Russia added a further 500,000 ounces (15.6 tonnes) of gold into its forex reserves bringing them to a total of 62.5 million ounces (1,944 tonnes) so heading for a year-end total of over 2,000 tonnes.

This will keep it comfortably in fifth place – after the USA, Germany, Italy and France in the global table of national gold holdings as reported to the IMF. China, which remains in sixth place, though has reported zero gold reserve increases for 20 successive months though and we believe that in reality its true level of gold holdings is considerably higher with a large proportion being held in accounts it feels no need to report to the IMF. (See: China’s gold reserves – fact or fiction?)

So far this year Russia has added a total of 106 tonnes of gold to its reserves, while at the same time running down its holdings of U.S. Treasuries to near zero from $100 billion at the beginning of the year. This year to date build-up in reserves is similar to the kinds of figures added for the previous three years – the country has been maintaining a 200 tonne plus annual increase over this period – and is seen as a defensive position against any financial action that might be taken against the state by the West – and by the USA in particular.

President Trump’s meeting with Russia’s President Putin in Helsinki has gone down far from well amongst both the U.S. Democrat opposition and even some of his own supporters. Anti-Russian feeling runs deep in the USA! Perestroika from the Reagan/Gorbachev era , which led to the break-up of the Soviet Union as was, seems long forgotten. But from a neutral observer’s point of view dialogue between the two superpowers has to be a positive move be they competitors, as President Trump appears to call them, or deadly adversaries as seems to be the position taken by many in the USA. One would expect the Democrats to try and blacken Trump’s name – they are still sore from the loss of the Presidency, and Congress control, to the hated Republicans – while the U.S. right wing, as represented by the various elements in the Republican party is probably at heart anti-Russian – but then President Trump is probably not a true Republican in political terms and ploughs his own furrow. Some of his statements and policies seem crass and reprehensible but to brand him a traitor for sitting down with Putin and seemingly siding with him on some of the anti-Russian views being expressed by hostile elements in the U.S. state seems enormously over the top. Trump does not fit the bill of a traitor at all, quite the opposite – at least in this writer’s opinion. But then I don’t live in the USA and am not exposed day-in-day-out to the opinions of the U.S. media and intelligentsia which from here seems to be largely anti-Trump – as is our own media in the U.K.

Russia though obviously still feels the need to protect itself from U.S. financial actions as much of global trade relies on the U.S. dollar to smooth its path. Sanctions have been imposed, primarily over the annexation of Crimea and the ongoing military action in east Ukraine – and one suspects Russian support for Syria’s President Assad will not have helped here nor its potential support for what the USA has branded rogue states like Iran and North Korea.

Trade sanctions against Russia are having only a limited effect though – the Russian economy after a minor negative period, appears to be growing again with China replacing the West in many trade areas so sanctions are being survived. In some cases the sanctions will be more damaging to some of those countries being forced to impose them – particularly if the U.S. takes retaliatory action against those accused of sanctions breaking.

end

21 Jul 2018

Although high for the first half at 400 tonnes, we are witnessing a little slowdown in refining from Switzerland but a pickup in refining capacity in other jurisdictions.

Demand for gold in the first half is 1,000 tonnes so they have a demand for the year at 2000 tonnes. The world produces around 2550 tonnes ex China ex Russia who refuse to sell any gold (and silver) out of their country

(courtesy Lawrie Williams/Sharp’s Pixley)

LAWRIE WILLIAMS: China imports 400 tonnes of Swiss gold in H1

Gold flows from West to East seem to be holding up well, at least as far as imports into Greater China from Switzerland are concerned. The small European nation, which has a number of specialist gold refineries, has exported so far this year some 400 tonnes of gold to China and to its special administrative region of Hong Kong in the ratio of around 69% direct to the Chinese mainland and 31% to Hong Kong – with most of the latter ultimately destined for mainland China too.

The actual Swiss gold export figures for the first six months of the year are Mainland China 274 tonnes, Hong Kong 126 tonnes. Overall this Swiss export figure alone is equivalent to almost 30% of global new mined gold output over the period excluding that from China itself. All the Chinese gold output remains within the country as gold exports are prohibited. With China also importing gold directly from countries like the UK, USA, Australia and no doubt others this one country probably absorbs the best part of half the global new mined output of gold and with the country’s middle class continuing to grow, and the country’s own output beginning to fall, gold imports are likely to increase in the years ahead putting additional pressure on the global supply/demand balance.

As an indicator of potential Chinese domestic purchasing capacity, sales on ‘Singles Day’ – the 11thof November annual promotion launched by Chinese internet shopping phenomenon, Alibaba, dwarfs anything in the U.S. In a 24 hour period, Singles Day accounted last year for around double the turnover achieved in the USA over the whole Thanksgiving holiday, which includes the Black Friday and Cyber Monday mega shopping days! And the Singles Day sales volume seems to grow exponentially every year. Some purchasing power.

The latest Swiss Gold Export figures for June on a country-by-country basis are set out in the below chart from Nick Laird’s http://www.goldchartsrus service.

As can be seen from the country-by-country totals, Asia and the Middle East again accounted for over 89% of all the Swiss gold exports in June with mainland China and Hong Kong between them accounting for nearly 60% of the total.

Overall Swiss gold exports though are running lower this year than last at 718 tonnes as against 805 tonnes in the same period of 2017, while imports came in at 682 tonnes in H1this year, compared with 877 tonnes in H1 2017. The decline in both imports and exports is probably due to the growth in gold refining capacity elsewhere, notably in the main destination areas with some of these new refineries being set up by the Swiss refiners themselves.

But the Swiss figures, even at the lower level this year, serve to emphasise the two points of a continuing flow of gold from the world’s gold mines and the West to what are seen as stronger hands in Asia, and also demonstrates the declining importance of Hong Kong as a conduit for Chinese gold imports. As we pointed out earlier (See: China H1 gold demand exceeds 1,000 tonnes) Chinese demand as represented by gold withdrawals from the Shanghai Gold Exchange (SGE) is back on the growth path again. This is by far the most important demand source for gold globally and with China’s own gold output apparently slipping – although it still remains by far the world’s largest gold producer – the potential for ever- rising imports continues to grow with the purchasing class becoming bigger and wealthier and domestic supplies slipping.

-END-

Your early MONDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED DOWN TO 6.7899/HUGE DEVALUATION FOR THE PAST TWO WEEKS CONTINUES /shanghai bourse CLOSED UP 30.27 POINTS OR 1,07% /HANG SANG CLOSED UP 31,64 POINTS OR 0.11%

2. Nikkei closed DOWN 300.89 POINTS OR 1.33%/USA: YEN FALLS TO 111.09/

3. Europe stocks OPENED RED /

USA dollar index FALLS TO 94.42/Euro FALLS TO 1.1715

3b Japan 10 year bond yield: RISES TO . +.09/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 111.09/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD IS NOW TARGETED AT .11%/JAPAN LOSING CONTROL OF THEIR BOND MARKET

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 69.08 and Brent: 74.05

3f Gold DOWN/Yen UP

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil UP for WTI and UP FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund RISES TO +.380%/Italian 10 yr bond yield UP to 2.57% /SPAIN 10 YR BOND YIELD UP TO 1.36%

3j Greek 10 year bond yield FALLS TO : 3.85

3k Gold at $1231.50 silver at:15.52 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble UP 44/100 in roubles/dollar) 63.07

3m oil into the 69 dollar handle for WTI and 74 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 111.09 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 0.9913 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1614 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now POSITIVE territory with the 10 year RISING to +0.38%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.88% early this morning (THIS IS DEADLY TO ALL MARKETS). Thirty year rate at 3.02%

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

(courtesy Jim Reid/Bloomberg/Deutsche bank/zero hedge)

Yuan Resumes Slide As Dollar Rebounds; JGB

Yields Surge As Global Stocks Stall

One day after Steven Mnuchin engaged in damage control in Buenos Aires, saying there was “no chance” that a currency war would break out in the aftermath of Trump’s comments from last week, and which saw a turbulent start to the week with both the BOJ and PBOC stepping up to stabilize markets, European stocks opened lower as traders reacted to warnings from the G-20 about the adverse impact of protectionism on growth before gradually edging back with the auto sector underperforming while US equity futures pointed towards a muted open with ES trading just below the unchanged line.

The big overnight news came early in the session, when Japanese 10-year government bonds plunged as cash markets caught up with Friday’s drop in futures on a media report of possible changes to the BOJ’s ultra-loose monetary policy, sending the yield up the most in almost two years…

… while the yen surged to a 2-week high, sending the USDJPY briefly below 111 below rebounding modestly.

“It’s all that concern investors have about the move from global quantitative easing to global quantitative tightening. That fear gets stoked when you have reports such as this,” said Psigma Investment Management’s Rory McPherson. “The ECB meeting this week will be more in focus now that we’ve had this concern about Japan.”

The sharp drop in JGBs spurred the central bank to offer to buy an unlimited amount of bonds in a fixed-rate operation at a rate of 0.11% (which was left unused), reinforcing Kuroda’s Yield Curve Control policy. Yet while the BOJ denied the report of an imminent change to its YCC framework, JGBs slumped throughout the session seemingly uncomforted by the BOJ’s actions.

Looking at the dollar, it initially slumped in continuation from Friday’s Trump-induced jawboning which saw the president warn that a strong dollar hurts the economy, but has since rebounded as US traders started coming in; they may be taking Treasury Secretary Steven Mnuchin’s comments at face value, after he gave assurances of the U.S. commitment to a strong greenback at the weekend G-20 summit. The Bloomberg Dollar Spot Index turned positive, recouping all losses and sending the euro, pound and yuan lower in tandem.

“The current U.S. administration has a clear preference for lower U.S. dollar rates and a weaker currency,” said Australia & New Zealand Banking Group’s Daniel Been in a note to clients Monday. “This will keep markets wary of further strength in the U.S. dollar; especially given the scale of the recent rally and the large long position already held by the market.”

Dollar strength also led to a reversal in China’s yuan, which erased a gain of as much as 0.66% to trade little changed at 6.7863 per dollar as of 4:41pm in Shanghai, while the offshore yuan slumped as low as 6.8165 after trading as low as 6.77.

The PBOC was also active, halting reverse-repurchase operations and draining net 170b yuan via open- market operations, but at the same time it provided 502BN yuan in one-year Medium-term Lending Facility and keeps interest rate unchanged at 3.30%. Today’s MLF operation adds to 188.5BN yuan of such loans provided on July 13 that matched the maturities on the day with the monthly net MLF injections the highest since December 2016 as China continues to gradually ease financial conditions.

Going back to equities, Europe’s Stoxx 600 fell 0.2% in early morning trade as investors braced for a packed earnings week and a meeting between European Commission President Jean-Claude Juncker and Trump to discuss threatened auto tariffs which could damage carmakers. “The pattern of Trump’s meetings has generally been more conciliatory when he meets in person. It could actually be good for autos,” Psigma’s McPherson said.

Europe’s autos sector fell 0.6 percent, hitting a 2-1/2 week low, led by Fiat Chrysler (-2.1%) which announced the sudden departure of long-time CEO Sergio Marchionne. The index is down 9% this year and is among the worst performing European sectors. Goldman analysts said auto tariffs, if they came to pass, were likely to cause weakness in the Canadian dollar and Mexican peso, possibly also affecting the euro, pound, yen, and Korean won as investors priced in a hit to the economy.

“The global economy is still okay, but the risk is now very high, and if trade policies don’t make a U-turn very soon, we’ll see a measurable impact on growth already next year,” UniCredit chief economist Erik Nielsen said.

Earlier in the session MSCI’s index of Asia-Pacific shares outside Japan fell 0.2 percent. In Japan the Nikkei closed 1.3% to 22,396.99, while the Topix was only 0.4% lower to 1,738.70. The reason behind the divergence of Japan’s two benchmark equity indexes: the price action of one stock, Fast Retailing. The shares of the $48 billion Uniqlo owner – which was down as much as 5.2% on Monday – have a material 8.3% weighting in Nikkei 225, but a tiny 0.3% weighting in Topix.

Emerging market equities traded down 0.1% as the dollar recovered. Dollar strength has driven selling in EM stocks this year as the currency puts pressure on emerging economies with large dollar-denominated debt piles.

Europe’s bond yields climbed after a Reuters report that the BoJ was discussing modifying its huge easing program sent Japan’s 10-year bond yield to a six-month high. The report rekindled anxieties about monetary stimulus easing around the world and piled further pressure on investors already struggling to navigate rising protectionism.

The yield on Europe’s benchmark bond, the German 10-year Bund hit a one-month high of 0.39% and U.S. 10-year Treasury yields also hit their highest in a month at 2.90% before retracing all gains as the dollar rose, and were trading at 2.88% last.

In other overnight news, G20 officials reaffirmed FX commitments made in March and will subsequently pledge to not engage in competitive devaluations. They said global growth remains robust and many emerging-market countries are better prepared to face crises, but risks to the world economy have increased.

US President Trump warned Iranian President Rouhani to never threaten the US again or they will suffer consequences the likes of which few throughout history have ever suffered before. Trump added that US will no longer stand for Iran’s demented words of violence & death, while he warned the Iranian President to be cautious. This was after comments from Rouhani that the US cannot prevent Iran from exporting oil and who warned a confrontation would be the ‘mother of all wars’. US President Trump was also said to be asking for daily updates on how North Korean negotiations are proceeding and is said to have shown frustration regarding the pace despite tweeting about how well it is going.