GOLD: $1193.85 DOWN $18.00 (COMEX TO COMEX CLOSINGS)

Silver: $15.00 DOWN 31 CENTS (COMEX TO COMEX CLOSINGS)

Closing access prices:

Gold $1193.65

silver: $15.00

For comex gold:

AUGUST/

NUMBER OF NOTICES FILED TODAY FOR AUGUST CONTRACT: 3 NOTICE(S) FOR 300

TOTAL NOTICES SO FAR 1709 FOR 170900 OZ (5.316 tonnes)

For silver:

AUGUST

10 NOTICE(S) FILED TODAY FOR

50,000 OZ/

Total number of notices filed so far this month: 774 for 3,870,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: BID $6410/OFFER $6495: UP $54(morning)

Bitcoin: BID/ $6228/offer $6313: DOWN $27 (CLOSING/5 PM)

end

First Shanghai gold fix comes at 10 pm est

The second Shanghai gold fix: 2:15 pm

First Shanghai gold fix gold: 10 pm est: $1209.51

NY price at the same time:$1209.20

PREMIUM TO NY SPOT: $0.31

XX

Second gold fix early this morning: $ 1209.51

USA gold at the exact same time:$1209.20

PREMIUM TO NY SPOT: $0.31

China is controlling the gold market

WE WILL NOT PROVIDE LONDON FIXES AS THEY ARE NOT ACCURATE AS TO WHAT IS GOING ON AT THE SAME TIME FRAME.

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total OPEN INTEREST ROSE BY A TINY SIZED 246 CONTRACTS FROM 239,464 UP TO 239,710 DESPITE FRIDAY’S CONSIDERABLE 15 CENT FALL IN SILVER PRICING AT THE COMEX. WE HAVE NOW WITNESSED A SLOW COMEX ACCUMULATION THESE PAST SEVERAL DAYS. ON TOP OF THIS WE HAVE ALSO WITNESSED A LARGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY(WELL OVER 30 MILLION OZ AT THE COMEX FOR JULY AND OVER 4 MILLION OZ FOR AUGUST) AS WELL AS CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A VERY GOOD SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP:

1618 EFP’S FOR SEPT. , 0 EFP’S FOR DECEMBER AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE: OF 1618 CONTRACTS. WITH THE TRANSFER OF 1618 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 1618 EFP CONTRACTS TRANSLATES INTO 8.09 MILLION OZ AND ACCOMPANYING:

1.THE 15 CENT FALL IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR THE JUNE/2018 COMEX DELIVERY MONTH. (5.420 MILLION OZ) 30.370 MILLION OZ STANDING FOR DELIVERY IN JULY, AND NOW 4.585 MILLION OZ FOR AUGUST.

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF JULY:

8487 CONTRACTS (FOR 9 TRADING DAYS TOTAL 8487 CONTRACTS) OR 42.435 MILLION OZ: (AVERAGE PER DAY: 943 CONTRACTS OR 4.715 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF JULY: 42.435 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 6.06% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2018 TO DATE SILVER EFP’S: 1,871.33 MILLION OZ.

ACCUMULATION FOR JAN 2018: 236.879 MILLION OZ

ACCUMULATION FOR FEB 2018: 244.95 MILLION OZ

ACCUMULATION FOR MARCH 2018: 236.67 MILLION OZ

ACCUMULATION FOR APRIL 2018: 385.75 MILLION OZ

ACCUMULATION FOR MAY 2018: 210.05 MILLION OZ

ACCUMULATION FOR JUNE 2018: 345.43 MILLION OZ

ACCUMULATION FOR JULY 2018: 172.84 MILLION OZ

RESULT: WE HAD A TINY SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 246 DESPITE THE 15 CENT LOSS IN SILVER PRICING AT THE COMEX FRIDAY. THE CME NOTIFIED US THAT WE HAD A VERY GOOD SIZED EFP ISSUANCE OF 1618 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) .

TODAY WE GAINED A GOOD SIZED: 1864 TOTAL OI CONTRACTS ON THE TWO EXCHANGES:

i.e 1618 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH A INCREASE OF 246 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED DESPITE A 15 CENT FALL IN PRICE OF SILVER AND A CLOSING PRICE OF $15.30 WITH RESPECT TO YESTERDAY’S TRADING. YET WE HAD A GIGANTIC AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY IN THE BIG JULY DELIVERY MONTH OF SLIGHTLY OVER 30 MILLION OZ AND NOW IN AUGUST ANOTHER BIG 4.525 MILLION OZ IN A NON ACTIVE MONTH. IT SURE LOOKS LIKE ANOTHER FAILED BANKER SHORT COVERING EXERCISE AS BANKERS ARE SCRAMBLING TO COVER THEIR HUGE SHORTFALL IN SILVER.

In ounces AT THE COMEX, the OI is still represented by OVER 1 BILLION oz i.e. 1.168 MILLION OZ TO BE EXACT or 167% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT AUGUST MONTH/ THEY FILED AT THE COMEX: 10 NOTICE(S) FOR =50,000 OZ OF SILVER

IN SILVER, WE SET THE NEW RECORD OF OPEN INTEREST AT 243,411 CONTRACTS ON APRIL 9.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $16.51

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) AND JULY 2018 AMOUNT STANDING: 30.370 MILLION OZ ) AND NOW FOR AUGUST 4.585 MILLION OZ.

- HUGE RECORD OPEN INTEREST IN SILVER 243,411 CONTRACTS (OR 1.217 BILLION OZ/ SET APRIL 9/2018

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017

- RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT).

IN GOLD, THE OPEN INTEREST ROSE BY A CONSIDERABLE SIZED 3242 CONTRACTS UP TO 466,612 DESPITE THE FALL IN THE COMEX GOLD PRICE/FRIDAY’S TRADING (A DROP IN PRICE OF $0.55). THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A VERY GOOD SIZED 7675 CONTRACTS:

AUGUST HAD AN ISSUANCE OF 0 CONTRACTS, OCTOBER HAD 0 EFP’S ISSUED AND, DECEMBER HAD AN ISSUANCE OF 7675 CONTACTS AND ALL OTHER MONTHS ZERO. The NEW COMEX OI for the gold complex rests at 466,612. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE A VERY STRONG OI GAIN IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 10,917 CONTRACTS: 3242 OI CONTRACTS INCREASED AT THE COMEX AND 7675 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN: 10917 CONTRACTS OR 1,091,700 OZ = 33.96 TONNES. AND ALL OF THIS VERY STRONG DEMAND OCCURRED WITH A LOSS IN THE PRICE OF GOLD/ FRIDAY TO THE TUNE OF $0.55.???

YESTERDAY, WE HAD 4029 EFP’S ISSUED.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF JUNE : 61,065 CONTRACTS OR 6,106,500 OZ OR 189.94 TONNES (9 TRADING DAYS AND THUS AVERAGING: 6785 EFP CONTRACTS PER TRADING DAY OR 678,500 OZ/ TRADING DAY),,

TO GIVE YOU AN IDEA AS TO THE HUGE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 9 TRADING DAYS IN TONNES: 189.94 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2017, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 2555 TONNES

THUS EFP TRANSFERS REPRESENTS 189.94/2550 x 100% TONNES = 7.44% OF GLOBAL ANNUAL PRODUCTION SO FAR IN JULY ALONE.***

ACCUMULATION OF GOLD EFP’S YEAR 2018 TO DATE: 4,900.48* TONNES *SURPASSED ANNUAL PROD’N

ACCUMULATION OF GOLD EFP’S FOR JANUARY 2018: 653.22 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR FEBRUARY 2018: 649.45 TONNES (20 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR MARCH 2018: 741.89 TONNES (22 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR APRIL 2018: 713.84 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR MAY 2018: 693.80 TONNES ( 22 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR JUNE 2018 650.71 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR JULY 2018 605.5 TONNES (21 TRADING DAYS)

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A CONSIDERABLE SIZED INCREASE IN OI AT THE COMEX OF 3242 DESPITE THE LOSS IN PRICING ($0.55 THAT GOLD UNDERTOOK FRIDAY) // . WE ALSO HAD A VERY GOOD SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 7675 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 7675 EFP CONTRACTS ISSUED, WE HAD A STRONG NET GAIN OF 10,917 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

7675 CONTRACTS MOVE TO LONDON AND 3242 CONTRACTS INCREASED AT THE COMEX. (in tonnes, the GAIN in total oi equates to 33.96 TONNES). ..AND THIS HUGE DEMAND OCCURRED WITH A LOSS OF $0.55 IN FRIDAY’S TRADING AT THE COMEX!!!.

we had: 3 notice(s) filed upon for 300 oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD DOWN $18.00 TODAY: /

NO CHANGES IN GOLD INVENTORY AT THE GLD/

.

/GLD INVENTORY 786.08 TONNES

Inventory rests tonight: 786.08 tonnes.

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

SLV/

WITH SILVER DOWN 31 CENTS TODAY

NO CHANGES IN SILVER INVENTORY AT THE SLV:

/INVENTORY REMAINS AT 327.223 MILLION OZ.

NOTE THE DIFFERENCE BETWEEN THE GLD AND SLV: THE CROOKS CAN RAID GOLD BECAUSE THEY DO HAVE SOME PHYSICAL. THEY DO NOT RAID SILVER PROBABLY BECAUSE THERE IS NO REAL SILVER INVENTORIES BEHIND THEM

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER ROSE BY A TINY SIZED 246CONTRACTS from 239,534 UP TO 239,710 (AND A LITTLE CLOSER TO A NEW COMEX RECORD. THE LAST RECORD WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). THE PREVIOUS RECORD TO THAT WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 1 1/4 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89. AS YOU CAN SEE, WE HAVE RECORD HIGH OPEN INTERESTS IN SILVER ACCOMPANIED BY A CONTINUAL LOWER PRICE WHEN THAT RECORD WAS SET…..VERY STRANGE INDEED

.

OUR CUSTOMARY MIGRATION OF COMEX LONGS MORPH INTO LONDON FORWARDS CONTINUES AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

0 EFP CONTRACTS FOR AUGUST., 1618 EFP CONTRACTS FOR SEPTEMBER, 0 CONTRACTS FOR DECEMBER AND AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 1618 CONTRACTS . EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI GAIN AT THE COMEX OF 246 CONTRACTS TO THE 1618 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A NET GAIN OF 1864 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES: 9.320 MILLION OZ!!! AND YET WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESSED A FINAL STANDING OF GREATER THAN 30 MILLION OZ FOR JULY AND NOW ANOTHER STRONG 4.585 MILLION OZ FOR AUGUST... AND YET ALL OF THIS HUGE DEMAND OCCURRED DESPITE A 15 CENT PRICING FALL AT THE SILVER COMEX.

RESULT: A SMALL SIZED INCREASE IN SILVER OI AT THE COMEX DESPITE THE 15 CENT PRICING GAIN THAT SILVER UNDERTOOK IN PRICING YESTERDAY.BUT WE ALSO HAD A VERY GOOD SIZED 1618 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR AUGUST, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)MONDAY MORNING/SUNDAY NIGHT: Shanghai closed DOWN 9.44 POINTS OR 0.34% /Hang Sang CLOSED DOWN 430.05 POINTS OR 1.52%/ / The Nikkei closed DOWN 440.65 POINTS OR 1.98%/Australia’s all ordinaires CLOSED DOWN 0.40% /Chinese yuan (ONSHORE) closed DOWN at 6.8839 AS POBC RESUMES ITS HUGE DEVALUATION /Oil UP to 67.31 dollars per barrel for WTI and 72.63 for Brent. Stocks in Europe OPENED DEEPLY IN THE RED //. ONSHORE YUAN CLOSED WELL DOWN AT 6.8839 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.8925: HUGE DEVALUATION/PAST SEVERAL DAYS RESUMES FULL BLAST : /ONSHORE YUAN TRADING STRONGER AGAINST OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

/NORTH KOREA/SOUTH KOREA

i)North Korea/South Korea/USA/Russia

b) REPORT ON JAPAN

3 c CHINA

i)China/Iran/France’s Total

China, in total defiance of Trump, will now take over Total’s share in the giant South Pars natural gas find

( zerohedge)

ii)Petro China the sovereign wealth company of China announces that it will halt all USA LNG purchases

(courtesy zerohedge)

iii)Panic breaks out in China after a panic bank run on Peer to Peer lenders. This was an accident waiting to happen

( zerohedge)

4. EUROPEAN AFFAIRS

i)Germany:

Economic Minister calls on Europe to defy Trump’s Iranian sanctions

( zerohedge)

ii)Meet your probable next leader of the ruling British conservative party: Boris Johnson

( Kern/Gatestone)

iii)Markets have yet to react to Italy’s latest ultimatum to the ECB something that the central bank cannot do:

guarantee bond spreads due to the ever widening of the bond yields

( zerohedge)

iv)ITALY, MALTA SPAIN

Looks like Malta and Spain has had enough. Italy blocks a migrant ship after both Malta and Spain refuse to take them in

( zerohedge)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

6 .GLOBAL ISSUES

7. OIL ISSUES

8. EMERGING MARKET

i)last night: South Africa/south African rand

The rand crashes 10% as contagion spreads to this nation

( zerohedge)

Argentina et al

9. PHYSICAL MARKETS

I)David Brady: Gold will find no bottom until the trade war ends

( David Brady/Sprott Money)

ii)Russia will ditch its remaining USA securities amid sanctions

(courtesy Reuters,GATA)

10. USA stories which will influence the price of gold/silver)

i)Market trading /GOLD/MARKET MOVERS:

MARKET TRADING

iv)SWAMP STORIES

Let us head over to the comex:

FOR THOSE THAT WISH TO FOLLOW TODAY’S SILVER OI VS LAST YR

AUGUST 14.2017: 103,727 OPEN INTEREST CONTACTS STILL OPEN FOR THE UPCOMING SEPT ACTIVE CONTRACT MONTH VS TODAY AUG 13.2018: 147,957 CONTRACTS.

Major gold/silver trading /commentaries for MONDAY

GOLDCORE/BLOG/MARK O’BYRNE.

This Wee

Andrew Maguire’s Kinesis money which is a “bitcoin” but backed 100% by allocated gold and silver is set to go.

it think it would be a great idea to look at this!

please read at: https://kinesis.money/#/

(Andrew Maguire)

|

|

Dear Harvey Organ,

Thank you for your participation in our webinar on June 7th with our host and CEO of Kinesis, Thomas Coughlin.

The response we received has been incredible, we appreciate you taking the time to join us and hope you found it to be beneficial.

Due to such a high influx of questions we received we were unable to have them all answered. Nevertheless, if there was anything which requires more clarification, or you have a query which needs to be rectified, we invite you to join our telegram group:

We apologize for the technical issues we incurred during the webinar which resulted in it running a little over schedule, we hope that the next one we host will run seamlessly.

A video has been put together and uploaded onto our YouTube channel which can be found here:

Please share and subscribe to our YouTube channel to be notified of all the latest videos as they become available.

The rapid growth that we are currently experiencing has been incredible and with your support, is only going to get better.

We are working behind the scenes very hard to create a better experience for everyone involved! Stay tuned in as we have many more announcements to be released in the upcoming days.

Kind Regards,

|

Kinesis Money

a:C/O ILS Fiduciaries (IOM) Limited, First Floor,Millennium House, Victoria Road, Douglas, Isle of Man IM2 4RW

|

The following is self explanatory

(courtesy GATA/Chris Powell and Harvey Organ)

GATA asks bank regulator to check risks of gold

futures maneuver

Submitted by cpowell on Sun, 2018-06-10 16:17. Section: Daily Dispatches

12:21p ET Sunday, June 10, 2018

Dear Friend of GATA and Gold:

GATA has appealed to the U.S. comptroller of the currency, who has regulatory authority over banks, to review financial risks certain banks may have incurred through derivatives in the monetary metals markets, particularly through the recent heavy use of the “exchange for physicals” mechanism of settling gold and silver futures contracts on the New York Commodities Exchange.

The appeal was made in a letter sent May 5 to the comptroller, Joseph M. Otting, whose office is part of the U.S. Treasury Department, by your secretary/treasurer and GATA futures market consultant Harvey Organ.

“Exchange for physical” settlements of futures contracts long were considered emergency procedures when a seller was not able to deliver metal from an exchange-approved warehouse and wanted to settle with delivery elsewhere. But now such settlements appear to constitute most gold and silver futures settlements on the Comex. It is a strange development that appears to have been necessitated by the increasing difficulties of central banking’s gold and silver price suppression policy.

GATA has received no acknowledgment of the letter. Its text is below and a PDF copy of it is here:

http://www.gata.org/files/ComptrollerOfCurrencyLetter.pdf

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

* * *

May 5, 2018

Joseph M. Otting, Comptroller of the Currency

U.S. Treasury Department

400 7th Street, SW

Washington DC 20219

Dear Comptroller Otting:

Please let us bring to your attention financial risks to major banks involving their possibly unreported exposure to derivatives in the monetary metals markets.

In recent months gold and silver future contracts issued by U.S. banks on the New York Commodities Exchange have been moved off-exchange for delivery through a mechanism known as “exchange for physical” (EFP) contracts. Until recently use of this mechanism was considered an emergency procedure when a seller did not have access to metal for delivery through Comex warehouses. Now the mechanism seems to be in use for a large share of front-month contracts for which delivery is sought.

Here is an example that is happening at the Comex in the front active month of April for gold and the inactive delivery month of April for silver.

In gold, there were 229,436 EFP contracts for 713.64 tonnes, an average of 10,925 contracts and 1,092,500 ounces per trading day.

In silver, there were 77,150 EFP contracts for 385,750,000 ounces, an average of 3,673 contracts and 18,369,000 ounces per trading day.

London Bullion Market Association rules suggest that these contracts may not be reported to regulators. The LBMA’s bylaws say:

“Figures above exclude any contracts not subject to risk-based capital requirements, such as FX contracts with an original maturity of 14 days or less, futures contracts, written options, and basis swaps. Therefore, the total notional amount of derivatives by maturity will not add to the total derivatives figure in this table.”

We are told that these EFP contracts are transferred from the Comex to London as what are called “serial forwards” and their duration is always less than 14 days, which exempts them from being reported.

It is our understanding that in each quarter your office prepares a report detailing risk undertaken by the banks under the comptroller’s supervision.

These risks include derivatives undertaken by U.S. banks and other obligations that may cause a bank to fail. Our concern is that your office may not be aware of large unreported derivative exposure by banks.

Could you review this matter and let us know your conclusions?

Sincerely,

CHRIS POWELL

Secretary/Treasurer

HARVEY ORGAN

Consultant

Gold Anti-Trust Action Committee Inc.

7 Villa Louisa Road

Manchester, Connecticut 06043-7541

end

Finally, they replied and it was a complete brush off

(courtesy zerohedge)

Currency comptroller brushes off GATA’s inquiry on

gold, silver EFPs

Submitted by cpowell on Fri, 2018-08-10 15:37. Section: Daily Dispatches

11:35a ET Friday, August 10, 2018

Dear Friend of GATA and Gold:

The U.S. comptroller of the currency, a bank regulator, has declined GATA’s request to inquire into the strange explosion of the use of the emergency procedure of “exchange for physicals” in the settlement by banks of the gold and silver futures contracts they have sold on the New York Commodities Exchange.

Your secretary/treasurer and GATA’s consultant about the Comex, Harvey Organ, wrote to the comptroller, James M. Otting, on May 5, calling attention to the recent enormous use of EFPs, which implies derivatives risks being undertaken by U.S. banks that could cause the banks to fail:

http://www.gata.org/node/18303

“Our concern is that your office may not be aware of large unreported derivative exposure by banks,” GATA wrote.

As months passed without any acknowledgment from the comptroller’s office, your secretary/treasurer appealed to his U.S. representative, John B. Larson, D-Connecticut, to ask the comptroller’s office to reply. The congressman’s office made a second inquiry on Monday this week and today the comptroller’s office provided Larson with a copy of a reply written and mailed Wednesday.

The comptroller’s reply, signed by the deputy comptroller for public affairs, Bryan Hubbard, said only that the comptroller’s office has “dedicated examiners” at the largest banks who “continuously evaluate the credit, market, operational, reputation, and compliance risks of bank trading and derivative activities.”

The reply did not say anything about the use of the “exchange for physicals” procedure for settling futures contracts. That is, the reply was a begrudged brushoff and GATA’s letter would have been ignored completely if not for Representative Larson’s repeated intervention.

Of course GATA hardly expected a conscientious reply to its letter, the comptroller’s office being not an independent regulator but part of the Treasury Department, whose mandate includes administration of the Gold Reserve Act of 1934, which, as amended in the 1970s, authorizes the department’s Exchange Stabilization Fund to secretly intervene in and rig any market in the world, directly or through intermediaries:

https://www.treasury.gov/resource-center/international/ESF/Pages/esf-ind…

But there’s always value in demonstrating government’s lack of candor about what it is doing, especially in regard to the monetary metals.

A PDF copy of the reply from the comptroller’s office is posted at GATA’s internet site here:

http://www.gata.org/files/ComptrollerOfCurrencyReply-08-08-2018.pdf

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

David Brady: Gold will find no bottom until the trade war ends

(courtesy David Brady/Sprott Money)

David Brady at Sprott Money: No bottom in gold until trade war ends

Submitted by cpowell on Fri, 2018-08-10 18:06. Section: Daily Dispatches

2:08p ET Friday, August 10, 2018

Dear Friend of GATA and Gold:

Fund manager and market analyst David Brady, writing for Sprott Money, today predicts that gold will keep declining with the Chinese yuan as long as China’s trade war with the United States continues but that the war may lead in a few months to a stock market crash in the United States, which will prompt the Federal Reserve to return to massive money creation, sending gold way up.

Brady’s commentary is headlined “No Bottom in Gold Until Trade War Ends” and it’s posted at Sprott Money here:

https://www.sprottmoney.com/Blog/no-bottom-in-gold-until-trade-war-ends….

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

Russia will ditch its remaining USA securities amid sanctions

(courtesy Reuters,GATA)

Russia says it will ditch U.S. securities amid sanctions

Submitted by cpowell on Sun, 2018-08-12 13:32. Section: Daily Dispatches

By Andrey Ostroukh

Reuters

Sunday, August 12, 2018

MOSCOW — Russia will further decrease its holdings of U.S. securities in response to new sanctions against Moscow but has no plans to shut down U.S. companies in Russia, Finance Minister Anton Siluanov said on state TV today, RIA news agency reported.

On Friday, Prime Minister Dmitry Medvedev said Russia would regard any U.S. move to curb the activities of its banks as a “declaration of economic war” and would take retaliatory action. …

… For the remainder of the report:

https://www.reuters.com/article/us-usa-russia-sanctions-response/russia

END

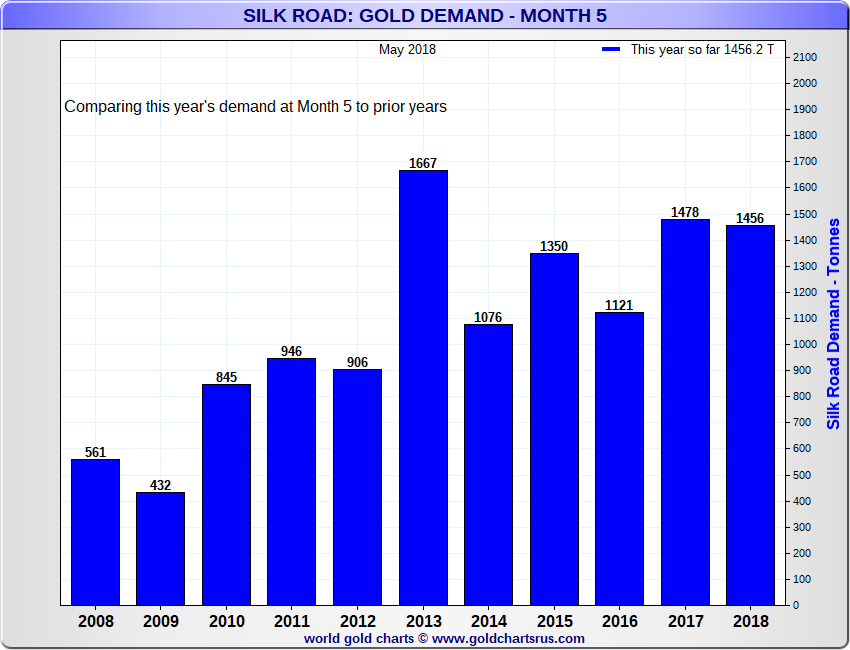

Here is a good look at Shanghai gold withdrawals (equals gold demand)

(courtesy Jessie’s Americain cafe)

10 AUGUST 2018

Shanghai Gold Withdrawals Remain Brisk – Silk Road Demand

Shanghai gold withdrawals remain brisk.On its own, Shanghai is taking a big chunk of total world gold production by itself as shown in the third chart.

Gold continues to move from West to East.

I could not happen to notice this evening when someone mentioned the US’ current issues with Russia, Turkey, and China, that all of these countries have been major accumulators of physical gold.

The other big major is India, the government of which has been engaging in all sorts of gimmicks to attempt to dampen the private gold demand driven by the people who use gold jewelry as a means of savings.

Got to serve and protect that petrodollar, right?

Central bank Gold purchases advance 8% during the first half of 2018

NEW YORK (Scrap Register): Central banks added 89.4 tons (on a net basis) to global gold reserves in Q2, down 7% year-on-year. While the pace of purchasing lags that of recent years, volumes remain healthy. Looking at H1, net purchases totalled 193.3t, 8% higher than the same period last year, according to the World Gold Council.

Purchases in Q2 and H1 were dominated by the familiar trio of Russia, Kazakhstan and Turkey. Russia again led the way, accumulating a net 53.2t in Q2, 49% up on Q2 2017. This brought H1 net purchases to 105.3t (5% y-o-y), and gold reserves to 1,944t at the end of June (17% of total reserves). Russia’s voracious appetite for gold is strategic – amidst geopolitical tensions it looks to diversify away from the US dollar.

Kazakhstan continued its lengthy buying run. The central bank continued its monthly buying, with the result that gold reserves grew by 11.6t during Q2 to 20.7t (3% y- o-y). The country’s gold reserves have now grown for 68 consecutive months.

At the end of the quarter there were calls in Kazakhstan’s lower house of Parliament for the bank to further increase gold reserves in the face of geopolitical and economic risks, and uncertainty arising from the global shift towards a multicurrency system.

Turkey’s central bank further increased gold reserves, albeit at a slightly slower pace. H1 net purchases totalled 38.1t (+82% y?o?y) after net purchases of 8.3t (-60% y?o?y) in Q2. Despite the lower level of purchases in recent months, Turkey retains its strategic commitment to gold. Gold reserves totalled 240.2t at the end of June, 107% higher than when net purchases began in May 2017.

The Reserve Bank of India (RBI) bought 2.5t of gold in March, following a fractional 0.3t addition in December. These increases in gold reserves are the first since November 2009, when the RBI purchased 200t from the IMF. Currently, there is little to suggest this is indicative of a strategic move, but it is noteworthy given how long the level of gold reserves has been unchanged.

During H1, the State Oil Fund of the Republic of Azerbaijan (SOFAZ) added around 2.8t of gold to its portfolio. This is the sovereign wealth fund’s first purchase of gold since Q4 2013, with gold reserves now standing at 33t.

Once again, net reductions remained trivial in relation to increases. Among the handful of central banks that reduced their gold reserves in H1, Venezuela was the most significant. Gold reserves have declined 11.9t in H1 2018 (accounted for solely in January) in response to the perilous economic situation facing the country.

However, it was later reported that Venezuela sought to recover some gold lost through the lapsed swap at the end of 2017. Gold reserves in Australia (4.1t), Qatar (Xt), Germany (3.8t), Sri Lanka (2.4t) and the Ukraine (1.2t) have also declined in H1.

end

Your early MONDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED DOWN TO 6.8825/HUGE DEVALUATION FOR THE PAST FOUR WEEKS RESUMES //OFFSHORE YUAN: 6.8925 /shanghai bourse CLOSED DOWN 9.44 POINTS OR 0.34% /HANG SANG CLOSED DOWN 430.05 POINTS OR 1.52%

2. Nikkei closed DOWN 440.65 POINTS OR 1.98%/USA: YEN FALLS TO 110.39/

3. Europe stocks OPENED DEEPLY IN THE RED //USA dollar index RISES TO 96.46/Euro FALLS TO 1.1376

3b Japan 10 year bond yield: FALLS TO . +.10/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 110.39/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD IS NOW TARGETED AT .11%/JAPAN LOSING CONTROL OF THEIR BOND MARKET

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 67.31 and Brent: 72.63

3f Gold DOWN/JAPANESE Yen DOWN/ CHINESE YUAN DOWN

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil DOWN for WTI and DOWN FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund FALLS TO +.310%/Italian 10 yr bond yield UP to 3.06% /SPAIN 10 YR BOND YIELD UP TO 1.49%

3j Greek 10 year bond yield RISES TO : 4.26

3k Gold at $1199.00 silver at:15.15 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble DOWN 45 /100 in roubles/dollar) 68.15

3m oil into the 67 dollar handle for WTI and 72 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 110.39 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 0.9944 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1311 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now POSITIVE territory with the 10 year FALLING to +0.31%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.86% early this morning (THIS IS DEADLY TO ALL MARKETS). Thirty year rate at 3.03%

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

(courtesy Jim Reid/Bloomberg/Deutsche bank/zero hedge)

Global Stocks Tumble Amid Growing Contagion

From Turkish Crisis

Global stocks and US equity futures were a sea of red on Monday morning as the Turkish economic crisis accelerated, and the Lira plunge continued even as measures by both the Turkish banking regulator and the central bank failed to stem the collapse in the TRY.

The lira plunged together with the country’s equity index after President Recep Tayyip Erdogan maintained his defiance toward the U.S. and refused to change financial track in speeches on Sunday.

Erdogan stated the economy is not in a crisis and that weakness in TRY is a currency plot, while he added that “Turkey will win this economic war” and are undergoing preparations to use national currencies for trade with nations such as China and Russia. There were also comments from Turkish Finance Minister Albayrak that the government has an action plan regarding the currency and will take necessary measures on Monday to ease market concerns, while he stated they will not convert nor seize FX deposits and that the currency is being directly targeted by the US President. In related news, Turkish Presidency Communication Chief Altun stated Erdogan’s comments were a warning against FX flight, while the banking regulator also announced to limit swap transactions in which banks’ total swap transactions has been capped at 50% of banks’ equity.

As Bloomberg notes, the lira’s plunge and subsequent sell-off in Turkey is giving investors a flashback to past crises in emerging markets, especially the Asian currency crisis of 1997, and was rattling nerves worldwide and leaving traders speculating on how bad contagion can get.

Commenting on the Turkish contagion, Kerry Craig, global market strategist at JPMorgan Asset Management, said that the rout in the lira “may fuel volatility in emerging-market assets and dampen investor sentiment in the near term, as markets are already skittish. But the drivers of the lira’s decline are very specific to Turkey – therefore it should not derail the positive fundamentals in other emerging markets over a longer-term.”

So far traders disagree, and Emerging Markets were on the verge of a full blown crisis amid fears that potential capital controls by Turkey could prompt accelerated capital outflows from other risky nations…

… and the JPM Emerging Market FX index continued its plunge on Monday.

That said, Emerging Asian currencies pared some losses as central banks stepped in to calm markets. Indonesia and India intervened in the market, while Philippines said it had enough buffers to defend the peso.

“While Asia is still largely insulated from the Turkey turmoil in some ways, what is apparent is that the deficit currencies such as the peso, rupee and the rupiah have generally come under pressure, and are more vulnerable in an environment where risk- aversion picks up and capital flows start taking a hit,” said Mitul Kotecha, senior EM strategist at TD Securities in Singapore

The pressure across EMs spread quickly and the South African rand hit the lowest since June 2016, flash crashing in Asian trading with some noting carry-related selling from Japan, although USDZAR eventually unwound nearly all the move higher.

European equity markets open lower, with sentiment in the region soured by contagion concerns as the Turkish Lira extending last week’s slump. As such, Turkey-exposed banks plumb the depths again with BNP Paribas (-1.0%), BBVA (-3.7%) and Unicredit (-3.2%) all near the foot of their respective bourses, even as the early selloff failed to pick up speed and saw little follow through.

Elsewhere, Germany’s DAX 30 was dragged lower by its third largest constituent, Bayer (-11.2%), whose shares plunged by the most in almost seven years on concern about the potential costs of a legal battle over Roundup weed killer after recently acquired Monsanto was ordered to pay $289MM in fines as a court ruled the company’s weedkiller caused cancer.

Meanwhile, Italian bonds led losses among European sovereign debt markets as the Turkish currency turmoil fueled fears of a contagion effect across riskier assets. Yields on two-year securities climbed to the highest levels in more than a week.

The Italian 10-year spread over German bunds hit the highest since May even as Deputy Prime Minister Luigi Di Maio was reported as saying in an interview Monday that his country won’t be subject to an attack by speculators.”“It’s just a flight to safety move, with peripherals and in particular short-term BTPs hit relatively hard,” said Martin van Vliet, senior interest-rate strategist at ING Groep NV. “Di Maio’s comment on speculative attacks is also not taken positively, as this sort of echoes the economic warfare rhetoric from the Turkey leadership.”

As EM currencies tumbled, the yen advanced for second day, approaching the 110 level, as investors shunned risk and turned to safe assets on concern about a spillover from the financial turmoil in Turkey. Japanese government bonds gained along with U.S. sovereign debt.

Asian equity markets began the week lower across the board with sentiment similarly spooked on Turkey contagion concerns. The ASX 200 (-0.4%) was dragged down by mining names, while Nikkei 225 (-2.0%) underperformed on safe-haven flows into JPY and with Mitsui Mining & Smelting down 15% post-earnings. Elsewhere, Shanghai Comp. (-0.3%) and Hang Seng (-1.5%) were also heavily weighed alongside the broad EM-triggered mayhem and continued liquidity inaction by the PBoC. The offshore Yuan was trading near session lows for much of the session.

South Korea wasn’t spared either, with the Kospi index falling 1.9% to the lowest level since May 2017 as foreign investors sold a net 155BN won worth of shares; Samsung Electronics dropped -1.5%, and was the biggest drag on Kospi. Small-cap Kosdaq -3.5% while the MSCI Asia Pacific Index -1.7%.

Across the Pacific, futures on the Dow, S&P 500 and Nasdaq were all all lower spooked by big declines across Asian and European markets. In addition to the strong yen, traders rushed into that other safe haven, the US Dollar, which traded at the strongest in a year as the euro dipped below 1.14.

As the dollar surged, gold tested lows near $1,200 an ounce while 10Y TSY yields were slightly lower.

In geopolitical news, North Korea reportedly rejected several denuclearization proposals made by the US, while South Korea and North Korea are said to hold a summit in September. Russian Finance Minister Siluanov stated that Russia will further reduce holdings of US securities in response to sanctions, but is not planning to shut down US firms. Additionally, Russian Finance Minister said Russia is to halt FX purchases for reserve, as speculated. Meanwhile, Russia’s Kremlin said President Putin has not yet given any orders on drawing up retaliatory sanctions against the US as the scope of planned US measures is unclear.

Elsewhere, commodities dropped, with West Texas crude trading below $68 a barrel and base metals retreating. WTI and Brent were in close proximity their 50 DMA to the downside at USD 67.14/bbl and USD 72.43/bbl respectively. Spot gold fell to the lowest since March 15th 2017, weighed by the greenback as the yellow metal detaches itself from safe-haven properties. London copper is subdued on USD action and the risk-off sentiment. India’s Oil Corporation says Iran is giving insurance cover for oil shipments, having enough term oil shipments to cushion any Iranian shortfall.

There are no economic releases scheduled today; scheduled earnings include Sysco and Stars Group.

Market Snapshot

- S&P 500 futures down 0.2% to 2,829.75

- STOXX Europe 600 down 0.4% to 384.49

- MXAP down 1.6% to 162.80

- MXAPJ down 1.6% to 528.58

- Nikkei down 2% to 21,857.43

- Topix down 2.1% to 1,683.50

- Hang Seng Index down 1.5% to 27,936.57

- Shanghai Composite down 0.3% to 2,785.87

- Sensex down 0.4% to 37,712.05

- Australia S&P/ASX 200 down 0.4% to 6,252.17

- Kospi down 1.5% to 2,248.45

- German 10Y yield unchanged at 0.318%

- Euro down 0.3% to $1.1380

- Italian 10Y yield rose 9.4 bps to 2.722%

- Spanish 10Y yield rose 2.9 bps to 1.436%

- Brent Futures up 0.2% to $72.93/bbl

- Gold spot down 0.6% to $1,203.77

- U.S. Dollar Index up 0.1% to 96.46

Top Overnight News from Bloomberg

- South Africa’s rand plunged the most in almost a decade and Mexico’s peso slumped as financial turmoil in Turkey sapped demand for emerging-market assets

- Turkey’s President Recep Tayyip Erdogan maintained his defiance toward the U.S. and financial-market orthodoxy in speeches on Sunday even after the nation’s currency slumped at the end of last week to record lows

- Turkey signaled a clampdown on news and social media, with officials including the public prosecutor warning that criticism may be viewed as “economic attacks” on the country

- China’s commercial banks sharply cut their holdings of corporate bonds last month in response to a heavy supply of local government paper, even as recent easing measures announced by the central bank encourage lenders to buy more company notes

- South Africa is planning a 59 billion- rand ($4.2 billion) bailout for state-owned companies including the post office, arms manufacturer Denel SOC Ltd. and South African Airways, the Johannesburg-based Sunday Times reported, citing unidentified government officials

- U.K. Prime Minister Theresa May is drawing up a plan to keep key European Union rules for longer after Brexit in order to break the deadlock in negotiations, a move that risks angering euroskeptics in her party

- CBRT: domestic banks to be allowed to borrow 1-month FX deposits (prev. only 1 week); lowers RRR for all TRY liabilities by 250bps; FX RRR lower by 400bps on 1-3y maturities; steps taken will provide liquidity of TRY 10b, USD 6b and equivalent USD 3b in gold

- Italian govt. reportedly had talks with the ECB regarding possibilities and consequences of speculator attacks against Italy; Salvini says law raising retirement age will be dismantled whether the EU likes it or not

- PBOC: will not use the yuan as a tool to cope with trade tensions and it will not conduct any “strong” economic stimulus

- Russia Finance Minster confirms stoppage of FX buying for reserves, in order to help support RUB; USD is becoming a risky payment instrument, does not rule out switching to national currencies in its oil supply deals

- Oil traded near $68 a barrel after Iran ruling out talks with the U.S. heightened concerns over global supply, offsetting signs of a potential increase in American output

Asian equity markets began the week lower across the board with sentiment in the region spooked on spill-over concerns as the Turkish lira extended on last week’s slump following a defiant tone from Turkish President Erdogan, which triggered capital control concerns and who labelled the weakness in TRY as a ‘currency plot’. This pressured the major indices from the getgo with ASX 200 (-0.4%) dragged by mining names, while Nikkei 225 (-2.0%) underperformed on safe-haven flows into JPY and with Mitsui Mining & Smelting down 15% post-earnings. Elsewhere, Shanghai Comp. (-0.3%) and Hang Seng (-1.5%) were also heavily weighed alongside the broad EM-triggered mayhem and continued liquidity inaction by the PBoC. Finally, 10yr JGBs were higher with prices underpinned by safe-haven demand, although upside was also capped amid a lack of Rinban announcement with the BoJ only in the market for Treasury discount bills.

Top Asian News

- China Faces Problem in Getting Its Banks to Lend More Money

- Chinese Education Stocks Take a Tumble on Draft Rule Uncertainty

- India FinMin Is Said to Favor More RBI OMO Bond Purchases

European equities kick-start the week lower across the board (Eurostoxx 50 -0.6%) with sentiment in the region soured by contagion concerns as the Turkish Lira extends on last week’s slump. As such, Turkey-exposed banks plumb the depths again with BNP Paribas (-1.0%), BBVA (-3.7%) and Unicredit (-3.2%) all near the foot of their respective bourses. Elsewhere, Germany’s DAX 30 is dragged lower by its third largest constituent, Bayer (-11.2%), after recently acquired Monsanto was ordered to pay USD 289mln in fines as a court ruled the company’s weedkiller caused cancer

Top European News

- Turkey Central Bank Takes Steps to Support Banks as Lira Slides

- May Is Said to Weigh Brexit Fix that Keeps EU Rules for Longer

- Erdogan Effectively Rules Out a Quick End to Turkish Crisis

In FX, the Lira remains front and centre of attention after more rousing attempts by Turkish President Erdogan to shore up the currency and coral support from the international investor community largely fell on deaf ears, with Usd/Try soaring through 7.0000 to a new record peak around 7.2150, and prompting the CBRT into action. However, still unable to intervene via conventional means (ie rate hikes) the Bank resorted to cutting Reserve Requirement Ratios for non-core FX liabilities by 400 bp alongside the Lira Required Reserve by 250 bp for all maturities, and the relief has been relatively limited as a result. EM – Lira contagion has spread further across the region, with the Rand hit especially hard (Usd/Zar 15.4700+ at one stage , but the Idr, Twn and other Asian units also weakening to intervention tolerance levels, while the Mxn has unwound more NAFTA-related gains to trade back below 19.0000 vs the Usd. DXY – Riding high amidst all the turmoil in high-beta/risk/yield currency counterparts, with the index just off fresh 2018 highs at 96.530, and now looking at chart targets ahead of 97.000 with fair resistance seen around 96.841. JPY – Still bucking overall trends and outperforming due to its ultra safe-haven allure, with Usd/Jpy pulling back further from 111.00 and through 110.50 to test the water ahead of 110.00 where decent expiry option interest resides (1.3 bn up to 110.05 to be precise).

Looking at the day ahead, it’s a very quiet start to the week on Monday with the only data of note being the final July CPI revisions for Italy. Looking further out, there are a slew of data releases to monitor. Final July CPI data will print in Germany, France, Spain, the euro area aggregate, and the UK. Euro area core inflation is expected to be confirmed at 1.1%, below the ECB’s target but sufficient for the central bank to maintain its current policy path. Several major US retailers report earnings throughout the week, and July retail sales will print on Wednesday.

US Event Calendar

- Aug. 13-Aug. 17: Mortgage Delinquencies, prior 4.63%

- Aug. 13-Aug. 17: MBA Mortgage Foreclosures, prior 1.16%

DB’s Jim Reid concludes the overnight wrap

What is it about August? Without necessarily fact checking, my memory is that August is always a popular month for an EM crisis. Turkey has been negatively bubbling up for a while but Friday’s moves were extraordinary and they are carrying on in the Asian session overnight. Turkey’s problems are quite idiosyncratic and should be relatively well-contained outside of the obvious short-term risk-off unless there’s a major investor retrenchment from EM generally. However, the situation may be emblematic of potential risks going forward as major central banks withdraw their extraordinary policy accommodation of recent years. Financial crises are always likely to happen somewhere in a Fed tightening cycle, especially when a lot of money chased high yielding assets in the easing stage of the cycle.

Back to Friday, the Turkish lira fell -13.71% (-19.2% at the lows for the day and now -43.7% YTD) – the third most severe move for the currency since 1990. Five years ago a dollar bought 2.0 Turkish lira, now it buys around 6.74 as we type (-4.6%). Notably the currency dropped to as low as 7.236 this morning, before recovering to 6.58 but then resumed its decline later on. The modest recovery from session lows was in part due to Turkey’s banking regulator stepping in to limit swap transactions on the Lira and the Finance Minister Albayrak telling the Hurriyet newspaper on Sunday that the country has plans to ease investors’ concerns and “from Monday onwards our institutions will take the necessary steps….” without elaborating more (per Reuters ).

The two more severe daily moves for the Lira than Friday were in April 1994 and February 2001, which came amid conventional EM crises. In both previous cases, the exchange rate was fundamentally misaligned, twin deficits had risen, and the central bank was overly accommodative. Both crises were eventually resolved through a combination of 1) central bank tightening to discourage capital outflows and reduce domestic demand and 2) IMF assistance to provide firepower and credibility. The currency remained at depreciated levels in both cases. Some combination of these solutions will surely be required again although Turkey could possibly buy itself some limited breathing space by releasing US pastor Brunson.

Over the weekend President Erdogan hasn’t exactly indicated that reconciliation is imminent though as he said on Saturday “I call out to those in the United States. It is a shame. You are trading a strategic NATO ally for a pastor,” and going on to say “You cannot tame our people with threats”. Then on Sunday when talking about the crisis said “There is no economic reason… It’s an operation against Turkey.” (per Bloomberg & Reuters )

This morning in Asia, markets are trading in a sea of red with the Nikkei (-1.90%), Kospi (-1.80%), Hang Seng (-1.83%) and Shanghai Comp. (-1.73%) all down while risk aversion seems to be benefiting 10y treasuries (yields -2bp) and the Yen (+0.6%). Meanwhile the Chinese Yuan (-0.5%) and Euro have declined (-0.3%) while futures on the S&P are also pointing to a softer start. Elsewhere Bloomberg has cited unnamed sources which noted that Saudi Arabia’s sovereign wealth fund which has built up a c5% stake in Tesla, is exploring how it can be involved in a potential privatisation deal, although no firm decision has been made.

Back to Turkey and for those who don’t track the country closely we thought we’d lay out a simple top level explanation of how we go here. The straw that has broken the camel’s back is the diplomatic row over Turkey’s continued detention of the American pastor Brunson, who was arrested and put behind bars back in October 2016 in the aftermath of the attempted coup attempt. Ahead of the US mid-terms this issue seems to have resurfaced and the recent sanctions have further focused the market’s attention on how small, open, indebted, and reliant on overseas capital the Turkish economy seems to be. This year’s Turkish presidential and parliamentary elections were also a big factor in the recent malaise. Spending promises to enhance support at the polls damaged fiscal credibility and encouraged inflation which, with a falling currency, became ever more self-fulfilling. President Erdogan’s speech in London in May where he suggested that high interest rates were “the mother and father of all evil” started to frighten more global investors as did his pledges to take more control over the central bank if he was returned to power in the June elections (per Reuters ). He has repeatedly said that he believes high interest rates cause high inflation which has mystified global investors.

Following on from this credibility loss, the Turkish Central bank kept interest rates unchanged in July, despite: consensus market expectations for a 100 basis point hike, inflation rising to almost 16% yoy, downgrades in credit rating by all three major agencies this year, and further deterioration in market sentiment against Turkey.

Prior to the last couple of years Turkey has been a darling of international investors as growth outside of the GFC has averaged around 7% under Erdogan’s 15 year watch. Pro-business policies and a youthful entrepreneurial population enhanced the attraction for overseas investors at a time of loose global monetary policy and low returns elsewhere. FDI increased from hundreds of millions of dollars per year prior to Erdogan’s rule to an average of $13 billion a year over his tenure. More recently, headwinds have materialised: global QE is coming to an end, the Fed is tightening policy and the dollar has strengthened. Turkey, like most of the EM universe benefitted from large inflows during the Fed’s large scale asset purchases, as developed market investors were pushed into foreign assets in he search for yield. With the Fed unwinding this stimulus, raising rates and shrinking the balance sheet, associated demand for Turkish assets has declined at a time of erratic domestic policy economically and politically. Historically, financial stress tends to flare when the Fed tightens policy (indeed, the Fed rate hikes in 1994 partially contributed to a prior currency crisis in Turkey). The latest developments are therefore familiar to global investors even if there is always a hope that this time is different.

In addition, with Mr Trump signalling a retreat on globalisation and embarking on various trade wars, Turkey started to become exposed to a reversal of proglobalisation flows. So Turkey is in the eye of a potential storm of being a small open economy with large external financing requirements at a time when economic imbalances have built up due to internal politics and a secular shift in global financing conditions from very loose to increasingly tight (especially in the US). So that’s a potted history of the crisis.

Back to the fall out, European banks were a major victim on Friday with the Euro banks index -3.23% – the second worst day over the last two years. However as our European bank’s team point out there are ‘only’ five European banks (BBVA, Unicredit, ING, BNP, and HSBC) in their coverage universe with a notable presence in and/or exposure to Turkey. Depending on how the situation proceeds, there may be somewhat significant capital and earnings implications for the most-exposed banks, but they do not expect systemic implications and believe the impact should be broadly manageable for European banks. See their note here for details.

Elsewhere on Friday the S&P fell -0.71% and the Stoxx 600 closed down -1.07% with core bonds rallying hard with 10yr Bunds and USTs -5.8bp and -5.3bp respectively. However Italian 2 and 10yr yields rose +16.1 and +9.2bps, weighed down by contagion concerns. Other emerging market currencies sold off in unison with the Lira, with the Argentine peso, South African rand, and Hungarian forint losing -3.84%, -2.62%, and -1.72% against the dollar, respectively. The VIX edged up 1.89 points to 13.16 with the European equivalent (V2X) +2.62 points to 15.11.

Following on with Italy, over the weekend the Deputy PM Salvini told the Corriere della Sera that “we’ll dismantle the Fornero Law (part of prior austerity measures to raise the pension age), whether the EU likes it or not”, meanwhile he also added that “the government will do its best to respect EU pacts, but rights of Italian people come first”. Elsewhere, the Deputy President of the Forza Italia Party Mr Tajani noted that “for Italy exceeding the deficit over EU’s limit of 3% of GDP isn’t a taboo”, in part as “we need to exceed it, for example, to pay previous debts that public administration has with enterprises”.

Back to Friday but somewhat overshadowed by the Turkey news, July US CPI printed in line with our and consensus expectations, rising 0.2% mom and 2.9% yoy. Core inflation rose 2.4% yoy, its fastest pace since 2008. This pace of price increases is consistent with the Fed’s price stability target. Coupled with unemployment far below their estimate of the natural rate, the latest data will likely support the Fed’s plans to continue hiking interest rates at a quarterly pace. In the UK, the preliminary 2Q GDP was in line with expectations at 0.4% qoq and 1.3% yoy, with household expenditure up +0.3% qoq and business investment +0.5% qoq. Meanwhile the June industrial expectations was slightly above market at 0.4% mom (vs. 0.3% expected).

Looking at the day ahead, it’s a very quiet start to the week on Monday with the only data of note being the final July CPI revisions for Italy. Looking further out, there are a slew of data releases to monitor. Final July CPI data will print in Germany, France, Spain, the euro area aggregate, and the UK. Euro area core inflation is expected to be confirmed at 1.1%, below the ECB’s target but sufficient for the central bank to maintain its current policy path. Several major US retailers report earnings throughout the week, and July retail sales will print on Wednesday.

3. ASIAN AFFAIRS

i)MONDAY MORNING/SUNDAY NIGHT: Shanghai closed DOWN 9.44 POINTS OR 0.34% /Hang Sang CLOSED DOWN 430.05 POINTS OR 1.52%/ / The Nikkei closed DOWN 440.65 POINTS OR 1.98%/Australia’s all ordinaires CLOSED DOWN 0.40% /Chinese yuan (ONSHORE) closed DOWN at 6.8839 AS POBC RESUMES ITS HUGE DEVALUATION /Oil UP to 67.31 dollars per barrel for WTI and 72.63 for Brent. Stocks in Europe OPENED DEEPLY IN THE RED //. ONSHORE YUAN CLOSED WELL DOWN AT 6.8839 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.8925: HUGE DEVALUATION/PAST SEVERAL DAYS RESUMES FULL BLAST : /ONSHORE YUAN TRADING STRONGER AGAINST OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

3 a NORTH KOREA/USA

North Korea/South Korea/USA/China

3 b JAPAN AFFAIRS

c) REPORT ON CHINA/HONG KONG

China/Iran/France’s Total

China, in total defiance of Trump, will now take over Total’s share in the giant South Pars natural gas find

(courtesy zerohedge)

Iran Sanctions Fallout: China Takes Over French Share In Giant Iran Gas Project

When it comes to the Middle East, China has not been shy about its recent ambitions to expand its geopolitical influence in the Gulf region: Just last week we reported that the Chinese Ambassador to Syria, Qi Qianjin, shocked Middle East pundits and observers by indicating the Chinese military may fill the void left in the wake of the collapse of ISIS – and most regional armies – and directly assist the Syrian Army in an upcoming major offensive on jihadist-held Idlib province.

The “[Chinese] military is willing to participate in some way alongside the Syrian army that is fighting the terrorists in Idlib and in any other part of Syria,” the ambassador said in an interview with the pro-government daily newspaper Al-Watan, subsequently translated by The Middle East Media Research Institute (MEMRI).

And having staked a military claim in Syria, China was next set to expand its national interest in that other key regional nation which has been the source of so much consternation to its neighbors and world powers in recent months and which has emerged as a key source of crude oil exports to Beijing: Iran.

It did so today when China’s state-owned energy giant, CNPC – the world’s third largest oil and gas company by revenue behind Saudi Aramco and the National Iranian Oil Company – finally took over the share in Iran’s multi-billion dollar South Pars gas project held by France’s Total, Iran’s official news agency Shana reported on Saturday.

To many the move had been expected, with only the details set to be ironed out. Recall that back in May we wrote that CNPC – the world’s third largest oil and gas company by revenue behind Saudi Aramco and the National Iranian Oil Company – was set to take over a leading role held by Total in a huge gas project in Iran should the French energy giant decide to quit amid US sanctions against the Islamic Republic.

That finally happened when the Chinese energy giant took advantage of Trump’s sanctions to step in the void left by the French major. As a reminder, Total signed a contract in 2017 to develop Phase II of South Pars field with an initial investment of $1 billion, marking the first major Western energy investment in the country after sanctions were lifted in 2016. South Pars has the world’s biggest natural gas reserves ever found in one place.

And after hen the French company said it would pull out unless it secured a U.S. sanctions waiver – which it was unable to do – in June, the deputy head of the National Iranian Oil Company, Gholamreza Manouchehri, said that CNPC would take over if Total were to walk away.

“China National Petroleum Corp (CNPC) has replaced Total of France with an 80.1 percent stake in the phase 11 of the South Pars (gas field),” IRNA quoted Mohammad Mostafavi, director of investment of Iran’s state oil firm NIOC, as saying, although there was no immediate confirmation of the IRNA report by CNPC.

Following the transaction, CNPC – which earlier held a 30% stake in the project – will now hold an 80.1% stake in the prokject, having taken over Total’s 50.1% share. The remainder is held by Iran’s Petropars.

Total has not yet said what it would do with its stake following the pull out, and it has until Nov. 4 to wind down its Iran operations. Total had spent €40 million on the project by May when it said it would have to withdraw from Iran if it couldn’t secure sanctions waivers from the U.S. Treasury.

So is China willing to risk Trump’s wrath and suffer economic sanctions for taking over where Total left off? It certainly looks like it: back in May we wrote that CNPC will use its banking unit, Bank of Kunlun, as a funding and clearing vehicle if it takes over operation of South Pars. The bank was used to settle tens of billions of dollars worth of oil imports during the UN sanctions against Tehran between 2012 and 2015, and is thus well-equipped to skirt US sanctions.

Sure enough, the US Treasury sanctioned Kunlun in 2012 for conducting business with Iran, however since most of the bank’s settlements during that time were in euros and Chinese renminbi, there was little it could do in terms of credible punishment.

If CNPC goes ahead, it would also likely have to develop crucial equipment, such as large-powered compressors needed for developing gas deposits on this scale, on its own. And since leading manufacturers like U.S. firm GE and Germany’s Siemens could be barred from supplying to Iran under US sanctions, it means even more Chinese companies will find willing demand for their services in Iran.

end

PetroChina To Impose Temporary Halt On US LNG Purchases

Energy traders were on alert when Reuters reported last week that Chinese energy giant, PetroChina – the world’s first company to hit (and lose) a $1 trillion market cap long before Apple – was in advanced discussions with Qatar to purchase liquefied natural gas (LNG) under short- and long-term agreements. The superficial explanation was that China needed to secure generous amount of LNG to supply its push to replace coal with cleaner burning natural gas to reduce air pollution. And sure enough, after Beijing started the program last year, China had overtaken South Korea as the world’s second-biggest buyer of LNG.

The deal also made sense from the perspective of the “blockaded” Qatar, the world’s biggest LNG producer, as the isolated Middle Eastern country sought buyers for a planned output expansion.

As it turns out there was another reason for the PetroChina supply diversification: PetroChina may temporarily halt purchases of spot U.S. liquefied natural gas spot cargoes through the winter to avoid potential tariffs as a result of the trade war between the U.S. and China, Bloomberg reported on Sunday according to sources with knowledge of the strategy.

Under the plan, PetroChina would boost buying of spot cargoes from other countries or swap U.S. shipments with other nations in East Asia to avoid paying additional tariffs, said the people, who asked not to be identified because the information isn’t public. PetroChina, a unit of the state-owned China National Petroleum Corp., couldn’t immediately comment when contacted by Bloomberg.

In retaliation to the latest round of tariffs imposed on China by the US, Beijing responded that it was considering a 25% tariff on U.S. LNG, which had been missing from previously targeted goods, direct hitting American gas exporters.

The move comes ahead of the winter heating season when demand and prices typically peak and shows two things: i) that Xi Jinping may be willing to suffer some pain to avoid backing down from U.S. President Donald Trump’s trade dispute, and ii) China is planning on lasting out the trade war for the long haul, suggesting that a near-term solution looks unlikely.

“If the tariff is implemented before winter, it would potentially increase the competition for non U.S. supply to the Asian market and hence drive up spot prices in Asia this winter,” Maggie Kuang, an analyst with Bloomberg NEF in Singapore said in an email. “Australia, Qatar, and Southeast Asia will most likely benefit.”

Meanwhile, US LNG exporters such as Cheniere would be hit hardest as a result of the import halt. PetroChina in February signed a 25-year deal to buy LNG from Cheniere Energy with a portion of that supply expected to start this year. That said, while China is currently the third-largest buyer of LNG, American cargoes only made up about 5.7% of its imports over the last year, according to Sanford C. Bernstein.

China may may have a more strategic view: yesterday Iran announced that another state-owned Chinese giant, China National Petroleum Corp (CNPC) had taken over the share of France major Total in the development of the giant South Pars oil field, giving the Chinese company an 80.1% stake in the project.

Clearly unconcerned about the threat of US sanctions, and taking advantage of the ongoing chaos in the middle east, China – which recently launched its own petroleum futures contract which many say is the first step toward internationalizing the PetroYuan – is aggressively ramping up its influence in the Gulf with the intention of becoming a dominant force in the regional energy market.

Meanwhile, Russia is making no secret of its intention to dedollarize its oil industry, with the unstated purpose of shifting toward the Petroyuan axis.

As we reported earlier today, speaking in an interview for the Rossiya 1 TV channel, Russia’s Finance Minister Anton Siluanov said that Russia “aims to keep reducing its investments in American securities” following new U.S. sanctions and said that the “US dollar is becoming an unreliable tool for payments in international trade.” The minister also hinted at the possibility of using national currencies instead of the dollar in oil trade.

“I do not rule it out. We have significantly reduced our investment in US assets. In fact, the dollar, which is considered to be the international currency, becomes a risky tool for payments,” Siluanov noted.

And with Russia hinting that it is close to giving up on the dollar entirely in oil trade and shifting to a petroyuan-based regime, how long before other nations follow suit, especially as China no longer shows any qualsm when it comes to severing existing US energy ties – whether in retaliation to trade war or otherwise – and pursuing alternative sources of production?

end

Panic breaks out in China after a panic bank run on Peer to Peer lenders. This was an accident waiting to happen

(courtesy zerohedge)

Social Unrest Breaks Out In China After “Panic” Bank Run On Peer-2-Peer Lenders

One week ago, when discussing the “source of China’s next debt crisis“, namely the recent explosion in Chinese household debt which over the past year has soared by over 40% even as credit growth across other debt categories remained relatively stable…

… and which was on the verge of surpassing the nation’s corporations as the biggest source of credit demand, we highlighted the one financial sector that has recently emerged as most at risk in China’s economy: online peer-to-peer lenders who collect money from retail investors and dispense small loans to consumers, usually without collateral, putting the loans at risk of a default with zero recovery.

We pointed out that outstanding loans on P2P platforms rose 50% just last year to total Rmb1.49 trillion ($215 billion) – making the size of China’s P2P industry far bigger than in the rest of the world combined – and due to their lack of collateral, interest rates often are as high as 37%, with additional charges for late payment.

P2P, in which platforms gather funds from retail investors and loan the money to small corporate and individual borrowers, promising high returns, started to flourish nearly unregulated in China in 2011. At its peak in 2015, there were about 3,500 such businesses.

But after Beijing launched a campaign several years ago to defuse debt bubbles and reduce risks in the economy (a campaign which recently reversed once the Trump trade war started getting hot), including the country’s enormous non-bank lending sector, cracks began to appear as investors pulled their funds.

As a result, the peer-to-peer lending channel not only got clogged up, but went in reverse. In a recent article, the WSJ reported that a string of Chinese internet lenders have already shut their doors in recent weeks, stranding investors as the economy slows and regulators tighten controls over an unruly side of the fintech sector.

Across China, more than 200 internet-based fund managers since late June have either shut down, closed parts of their operations or are reeling from cash crunches, missing executives and other problems, according to industry tracker Wangdaizhijia.

The tide began to turn even more forcefully against the sector ahead of a late June deadline for new stringent registration regulations. With a slowing economy making it difficult for some companies to pay back loans, many lenders decided to simply shut down. Meanwhile, investors, already souring on the sector, began pulling out funds, further pinching the lending platforms, and as Reuters reports, since June, 243 online lending platforms have gone bust, according to wdzj.com, a P2P industry data provider. In that period, the industry saw its first monthly net fund outflows since at least 2014.

And, as we noted last week, it was only a matter of time before social unrest spread as Chinese investors who had funded these usually small, unregulated P2P operations, found they had lost all their money demanding a bail out.

That’s precisely what happened… except for one thing: Beijing was already one step ahead of the protesters.

Take the case of Peter Wang: as Reuters reports, Wang was asleep at his home in Beijing last Monday when police officers arrived before dawn to detain him, saying he had helped organize a protest planned for later that day. Peter wasn’t alone, and across Beijing, others who had lost money investing in China’s online peer-to-peer (P2P) lending platforms – including some who had traveled from half way across the country – got similar visits from police.

Why the crackdown?

Because by the time they were released, the demonstration they had planned using social media chat groups had fizzled amid a massive security response around the China Banking and Insurance Regulatory Commission (CBIRC) headquarters in the heart of Beijing’s financial district. Those protesters who did show up were in for a surprise: instead of demanding that the government bail out the hundreds of collapsed P2P companies, they were forced onto buses and carted away to Jiujingzhuang, a holding center for petitioners on the outskirts of Beijing, according to two Reuters sources.

“Once the police checked your ID cards and saw your petition materials, they knew you are here looking to protect your rights. Then they put you on a bus directly,” said Wang, who works at an auto repair shop, and who is a perfect representative of China’s prevailing ideology that a government bailout of any investment is a fundamental “right.”

Wang did not give up and after his detention he joined a separate, smaller protest in a different part of Beijing. “There was no channel to solve any problems. All they care about was preventing any disturbance.”

* * *

The latest burst of anger, which led to the planned protests, flared up ahead of a June 30 deadline for companies to comply with new business practice standards, which are still being finalised, and as noted above, many P2Ps shut down rather than face tougher regulations, Zane Wang, chief executive of online micro-loan provider China Rapid Finance told Reuters.

That caused panic in the broader market. Investors tried to pull funds from P2P companies, causing liquidity problems for many smaller operators, Wang said, although larger ones are faring better. “Some platforms might become a winner out of this, and some platforms, probably a large portion of the platforms, might not be able to make it,” he said.

Naturally, to avoid an even bigger panic, no mainland Chinese media – official mainstream papers or more independent-leaning publications – reported the attempts to protest in China’s capital. The media blackout took place as China’s propaganda machine swung into action as Beijing sought “to reassure people that the Chinese economy and financial markets are healthy” despite a trade war with the United States and steep declines in the value of stock prices and the yuan.

As part of the government’s crackdown, many would-be protesters “were forced to give fingerprints and blood samples and prevented from traveling to Beijing. Some were even removed from Beijing-bound trains ahead of the protests, said a Shanghai-based P2P investor who lost 1.3 million yuan.” She declined to be named out of fear for her safety.

What is surprising, is just how worried about the prospect of widespread social unrest Beijing was: even after the demonstrations were effectively snuffed out, hundreds of security personnel patrolled around CBIRC’s office, “highlighting authorities’ sensitivity to any form of social instability” according to Reuters.

It has reason to be worried: on Sunday, Xinhua reported that the government has proposed 10 measures to reduce risk in the P2P sector, including a strict ban on new P2P companies and online finance platforms, and a blacklist under China’s social credit rating system for those who don’t repay their loans. This means that P2P investors will soon suffer tens of billions in more losses (although it may well end up being good news for those who borrowed money from the insolvent P2Ps as there will be nobody left to collect).

* * *

This is not the first time China was burned on P2P platforms, which traditionally lend to customers that might be deemed too risky for a commercial bank, which has resulted in liquidity crises when too many investors demand their funds at once if loans appear to be going south.

The most famous case of P2P fraud is Ezubao – a $7.6 billion Ponzi scam involving more than 900,000 investors – which we described in early 2016, and which led to a similar forceful government crackdown after the public demanded a full bailout. While none has come close to the scale of Ezubao’s collapse, there are currently more than 100 publicly listed Chinese companies that are involved in P2P, and 32 of those own more than 30% of a P2P company, according to a July research report by CITIC Securities.