GOLD: $1206.70 UP $18.65 (COMEX TO COMEX CLOSINGS)

Silver: $14.83 UP 26 CENTS (COMEX TO COMEX CLOSINGS)

Closing access prices:

Gold $1206.20

silver: $14.82

AS PROMISED: (WRITTEN TO YOU SATURDAY MORNING)

THE PRELIMINARY COMEX OI FOR MONDAY ROSE BY ONLY 2833 CONTRACTS IN GOLD AND IN SILVER INSTEAD OF RISING CONSIDERABLY IT FELL BY 4368 CONTRACTS DOWN TO 237,,928…WE MUST HAVE HAD CONSIDERABLE BANKER AND LARGE SPECULATORS COVERING THE SHORT POSITIONS AS FAST AS THEIR LITTLE FEET COULD CARRY THEM!!

NOW BACK TO YESTERDAY’S COMMENTARY:

For comex gold:

AUGUST/

NUMBER OF NOTICES FILED TODAY FOR AUGUST CONTRACT: 4 NOTICE(S) FOR 400

TOTAL NOTICES SO FAR 2290 FOR 229000 OZ (7.1415 tonnes)

For silver:

AUGUST

0 NOTICE(S) FILED TODAY FOR

nil OZ/

Total number of notices filed so far this month: 1178 for 5,890,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: BID $6496/OFFER $6580: UP $35(morning)

Bitcoin: BID/ $6578/offer $6663: UP $117(CLOSING/5 PM)

end

First Shanghai gold fix comes at 10 pm est

The second Shanghai gold fix: 2:15 pm

First Shanghai gold fix gold: 10 pm est: $1194.33

NY price at the same time:$1186.00

PREMIUM TO NY SPOT: $8.33

XX

Second gold fix early this morning: $ 1195.09

USA gold at the exact same time:$1187.95

PREMIUM TO NY SPOT: $7.14

China is controlling the gold market

WE WILL NOT PROVIDE LONDON FIXES AS THEY ARE NOT ACCURATE AS TO WHAT IS GOING ON AT THE SAME TIME FRAME.

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total OPEN INTEREST FELL BY A VERY SMALL 899 CONTRACTS FROM 243,195 DOWN TO 242,296 DESPITE YESTERDAY’S HUGE 20 CENT FALL IN SILVER PRICING AT THE COMEX.

TODAY WE MOVED A LITTLE AWAY FROM THIS WEEK’S RECORD SETTING OPEN INTEREST OF 244,196 CONTRACTS.

WE HAVE ALSO WITNESSED A LARGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY(WELL OVER 30 MILLION OZ AT THE COMEX FOR JULY AND OVER 6 MILLION OZ FOR AUGUST) AS WELL AS CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A VERY STRONG SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP:

3633 EFP’S FOR SEPT. , 0 EFP’S FOR DECEMBER AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE: OF 3633 CONTRACTS. WITH THE TRANSFER OF 3633 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 3633 EFP CONTRACTS TRANSLATES INTO 18.165MILLION OZ AND ACCOMPANYING:

1.THE 20 CENT FALL IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR THE JUNE/2018 COMEX DELIVERY MONTH. (5.420 MILLION OZ) 30.370 MILLION OZ STANDING FOR DELIVERY IN JULY, AND NOW 6.005 MILLION OZ FOR AUGUST.

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF JULY:

26,641 CONTRACTS (FOR 18 TRADING DAYS TOTAL 26,641 CONTRACTS) OR 133.205 MILLION OZ: (AVERAGE PER DAY: 1480 CONTRACTS OR 7.400 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF JULY: 133.205 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 19.0% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2018 TO DATE SILVER EFP’S: 1,962.865 MILLION OZ.

ACCUMULATION FOR JAN 2018: 236.879 MILLION OZ

ACCUMULATION FOR FEB 2018: 244.95 MILLION OZ

ACCUMULATION FOR MARCH 2018: 236.67 MILLION OZ

ACCUMULATION FOR APRIL 2018: 385.75 MILLION OZ

ACCUMULATION FOR MAY 2018: 210.05 MILLION OZ

ACCUMULATION FOR JUNE 2018: 345.43 MILLION OZ

ACCUMULATION FOR JULY 2018: 172.84 MILLION OZ

RESULT: WE HAD A SMALL SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 899 DESPITE THE HUGE 20 CENT FALL IN SILVER PRICING AT THE COMEX YESTERDAY. THE CME NOTIFIED US THAT WE HAD A STRONG SIZED EFP ISSUANCE OF 3633 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) .

TODAY WE GAINED A STRONG SIZED: 2734 TOTAL OI CONTRACTS ON THE TWO EXCHANGES:

i.e 3633 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH A DECREASE OF 899 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED WITH A HUGE 20 CENT FALL IN PRICE OF SILVER AND A CLOSING PRICE OF $14.57 WITH RESPECT TO YESTERDAY’S TRADING. YET WE HAD A GIGANTIC AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY IN THE BIG JULY DELIVERY MONTH OF SLIGHTLY OVER 30 MILLION OZ AND NOW IN AUGUST ANOTHER BIG 6.005 MILLION OZ IN A NON ACTIVE MONTH. IT SURE LOOKS LIKE ANOTHER FAILED BANKER SHORT COVERING EXERCISE AS BANKERS ARE SCRAMBLING TO COVER THEIR HUGE SHORTFALL IN SILVER.

In ounces AT THE COMEX, the OI is still represented by OVER 1 BILLION oz i.e. 1.212 MILLION OZ TO BE EXACT or 173% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT AUGUST MONTH/ THEY FILED AT THE COMEX: 0NOTICE(S) FOR NILOZ OF SILVER

IN SILVER,PRIOR TO TODAY, WE SET THE NEW RECORD OF OPEN INTEREST AT 243,411 CONTRACTS ON APRIL 9.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $16.51.

AND NOW WE RECORD FOR POSTERITY ANOTHER ALL TIME RECORD OPEN INTEREST AT THE COMEX OF 244,196 CONTRACTS ON AUGUST 22/2018 AND AGAIN WHEN THIS RECORD WAS SET, THE PRICE OF SILVER WAS $14.78

AND LOWER IN PRICE THAN PREVIOUS RECORDS.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) AND JULY 2018 AMOUNT STANDING: 30.370 MILLION OZ ) AND NOW FOR AUGUST 6.005 MILLION OZ.

- HUGE RECORD OPEN INTEREST IN SILVER 243,411 CONTRACTS (OR 1.217 BILLION OZ/ SET APRIL 9/2018) AND NOW AUGUST 22/2018: 244,196 CONTRACTS, WITH A SILVER PRICE OF $14.78

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017

- RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT).

IN GOLD, THE OPEN INTEREST FELL BY A CONSIDERABLE SIZED 4688 CONTRACTS DOWN TO 480,516 WITH THE CONSIDERABLE LOSS IN THE COMEX GOLD PRICE/YESTERDAY’S TRADING (A FALL IN PRICE OF $9.20). THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A GOOD SIZED 5318 CONTRACTS:

AUGUST HAD AN ISSUANCE OF 0 CONTRACTS, OCTOBER HAD 0EFP’S ISSUED AND, DECEMBER HAD AN ISSUANCE OF 5318 CONTACTS AND ALL OTHER MONTHS ZERO. The NEW COMEX OI for the gold complex rests at 480,516. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE AN A SMALL OI GAIN IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 650 CONTRACTS: 4468 OI CONTRACTS DECREASED AT THE COMEX AND 5318 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN: 650 CONTRACTS OR 65,000 OZ = 2.022 TONNES. AND STRANGELY ALL OF THIS HUGE DEMAND OCCURRED WITH A GOOD SIZED LOSS IN THE PRICE OF GOLD/ YESTERDAY TO THE TUNE OF $9.20.???..

YESTERDAY, WE HAD 5246 EFP’S ISSUED.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF JUNE : 123,988 CONTRACTS OR 12,398,800 OZ OR 385.65 TONNES (18 TRADING DAYS AND THUS AVERAGING: 6888 EFP CONTRACTS PER TRADING DAY OR 688,800 OZ/ TRADING DAY),,

TO GIVE YOU AN IDEA AS TO THE HUGE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 18 TRADING DAYS IN TONNES: 385.65 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2017, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 2555 TONNES

THUS EFP TRANSFERS REPRESENTS 385.65/2550 x 100% TONNES = 15.12% OF GLOBAL ANNUAL PRODUCTION SO FAR IN JULY ALONE.***

ACCUMULATION OF GOLD EFP’S YEAR 2018 TO DATE: 5,104.36* TONNES *SURPASSED ANNUAL PROD’N

ACCUMULATION OF GOLD EFP’S FOR JANUARY 2018: 653.22 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR FEBRUARY 2018: 649.45 TONNES (20 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR MARCH 2018: 741.89 TONNES (22 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR APRIL 2018: 713.84 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR MAY 2018: 693.80 TONNES ( 22 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR JUNE 2018 650.71 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR JULY 2018 605.5 TONNES (21 TRADING DAYS)

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A CONSIDERABLE SIZED DECREASE IN OI AT THE COMEX OF 4668 WITH THE GOOD SIZED LOSS IN PRICING ($9.20 THAT GOLD UNDERTOOK YESTERDAY) // . WE ALSO HAD A GOOD SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 5318 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 5318 EFP CONTRACTS ISSUED, WE HAD A SMALL GAIN OF 650 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

5318 CONTRACTS MOVE TO LONDON AND 4668 CONTRACTS DECREASED AT THE COMEX. (in tonnes, the GAIN in total oi equates to 2.02 TONNES). ..AND STRANGELY THIS DEMAND OCCURRED WITH THE LOSS OF $9.20 IN YESTERDAY’S TRADING AT THE COMEX!!!. ????(RAID)

we had: 4 notice(s) filed upon for 400 oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD UP $18.65 TODAY: /

A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.53 TONNES

/GLD INVENTORY 7687.23 TONNES

Inventory rests tonight: 767.23 tonnes.

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

SLV/

WITH SILVER UP 26 CENTS TODAY

NO CHANGE IN SILVER INVENTORY AT THE SLV

/INVENTORY RESTS AT 329.104 MILLION OZ.

NOTE THE DIFFERENCE BETWEEN THE GLD AND SLV: THE CROOKS CAN RAID GOLD BECAUSE THEY DO HAVE SOME PHYSICAL. THEY DO NOT RAID SILVER PROBABLY BECAUSE THERE IS NO REAL SILVER INVENTORIES BEHIND THEM

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER FELL BY A SMALL SIZED 899 CONTRACTS from 243,195 DOWN TO 242,296 AND MOVING A LITTLE AWAY FROM THE NEW COMEX RECORD SET THIS WEEK AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018).. THE PREVIOUS RECORD WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 1 1/4 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89. AS YOU CAN SEE, WE HAVE RECORD HIGH OPEN INTERESTS IN SILVER ACCOMPANIED BY A CONTINUAL LOWER PRICE WHEN THAT RECORD WAS SET…..

.

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

0 EFP CONTRACTS FOR AUGUST., 3633 EFP CONTRACTS FOR SEPTEMBER, 0 CONTRACTS FOR DECEMBER AND AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 3633 CONTRACTS . EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI LOSS AT THE COMEX OF 899 CONTRACTS TO THE 3633 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A NET GAIN OF 3018 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES: 13.67 MILLION OZ!!! AND YET WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESSED A FINAL STANDING OF GREATER THAN 30 MILLION OZ FOR JULY AND NOW ANOTHER STRONG 6.005 MILLION OZ FOR AUGUST... AND YET ALL OF THIS HUGE PHYSICAL DEMAND OCCURRED DESPITE A 20 CENT PRICING LOSS AT THE SILVER COMEX!!!!????.

RESULT: A SMALL SIZED DECREASE IN SILVER OI AT THE COMEX DESPITE THE 20 CENT PRICING LOSS THAT SILVER UNDERTOOK IN PRICING YESTERDAY. BUT WE ALSO HAD A STRONG SIZED 3633 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR AUGUST, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i) FRIDAY MORNING/ THURSDAY NIGHT: Shanghai closed UP 4.81 POINTS OR 0.18% /Hang Sang CLOSED DOWN 118.59 POINTS OR 0.43%/ / The Nikkei closed UP 190.95 POINTS OR 0.85%/Australia’s all ordinaires CLOSED DOWN 0.04% /Chinese yuan (ONSHORE) closed UP at 6.8483 AS POBC HALTS ITS HUGE DEVALUATION /DELEGATION COMING TO THE USA TO SEE TRUMP IN NOVEMBER/Oil UP to 68.72 dollars per barrel for WTI and 75.61 for Brent. Stocks in Europe OPENED IN THE GREEN //. ONSHORE YUAN CLOSED UP AT 6.8483 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.8395: HUGE DEVALUATION/PAST SEVERAL DAYS STOPS// TRADE TALKS NOT DOING TOO GOOD : /ONSHORE YUAN TRADING STRONGER AGAINST OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING MUCH STRONGER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

/NORTH KOREA/SOUTH KOREA

i)North Korea/South Korea/USA/

In a surprise move, Trump tells Pompeo not to go to North Korea as the North Koreans have not made sufficient progress with respect to the denuclearization of the Korean penisula

( zerohedge)

b) REPORT ON JAPAN

3 c CHINA

i)No further talks are scheduled: the China/USA trade negotiations over the past two days are a complete failure

( zerohedge)

ii)The POBC introduce counter-cyclicator factors in determining the value of the yuan. In other words they wanted to show support for the yuan even though their was no USA-China trade deal.. The shorts were killed and that caused gold to rise..

( zerohedge)

iii)A good one by Danielle Lacalle. He states that the devaluation of the yuan is hurting China because of their huge debt. He emphasizes that the devaluation hurts the debt in Chinese yuan because some of their costs are in dollar related terms like energy and USA interest costs plus commodities. A devaluation makes them less profitable

a must read..

(courtesy Danielle Lacalle)

4. EUROPEAN AFFAIRS

i)Italy

This is a big story! Italy now threatens to stop EU funding unless other European countries accept refugees

( zerohedge)

i b)

A very angry Salvini has there is no deal on the migrant redistribution. Also the 177 migrants are still stranded on a ship that is docked in an Italian port. Italy has threatened to block all distribution moneys owed to the EU

( zerohedge)

ii)Another important commentary: it seems that we now have had two consecutive months of foreigners correctly dumping huge numbers of Italian bonds. The buyer of last resort: Italian banks as the “doom loop” exodus continues unabated. This will be disastrous for Italy as the ECB has already announced that it will cease purchasing all European bonds by Sept 2018 with a taper until Dec 2018.

( zerohedge)

an excellent paper by Tom Luongo as he writes that Trump is trying to put a wedge between Russia and Germany but in actual fact, he may be pushing them together. The key is NATO that behemoth that is too costly for the uSA. They must spend much bucks with military bases and personnel to protect Europe. Germany needs cheap Iranian oil to power Europe over the USA

an excellent piece..

(courtesy Tom Luongo)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

6 .GLOBAL ISSUES

7. OIL ISSUES

Why a price war between Iran and Saudi Arabia could break up OPEC

( Irina Slav/OilPrice.com)

8. EMERGING MARKET

9. PHYSICAL MARKETS

Chris Powell correctly criticizes John Hathaway for not telling investors that governments are suppressing the gold market

(courtesy Chris Powell/GATA/Tocqueville./Hathaway)

10. USA stories which will influence the price of gold/silver)

i)Market trading /GOLD/MARKET MOVERS:

MARKET TRADING

Very important; the yield curve is collapsing with the 2 over 10 yield differential in the “teens” and for the first time, the USA rate differential is below Japan something that the mavens at Jackson hole should pay attention to.

( zerohedge)

Hard data, durable goods orders drop the most in 6 months indicating that the USA slowdown is accelerating

( zerohedge)

b)It seems that the ECB bank governors are boycotting the Jackson Hole symposium. Do not know why Kuroda of Japan will not appear

c)Powell’s speech at Jackson Hole causes the dollar to drop and a corresponding rise in risk assets as he states that inflation is under control. Gold rises on the drop of the dollar

( zerohedge)

d)Our good friends at Wells Fargo are not doing so good:

e)Subprime is now beginning to haunt credit card balances.

iv)SWAMP STORIES

a)It seems that Mueller wants what is inside the National Inquirer’s safe. It will probably contain documents of the affair that Trump had with McDougal and the $130,000 hush money payment.

( zerohedge)

b)The Manhattan DA may file criminal charges against the Trump Organization for faulty accounting in the payment by Cohen of $130,000 in the Stormy Daniels case

( zerohedge)

d)Today, Allen Weisselberg, the CFO of the Trump Organization has been granted immunity by USA prosecutors in the payment of the $130,000 hush money. Trust me…there is no illegality here.

Let us head over to the comex:

FOR THOSE THAT WISH TO FOLLOW TODAY’S SILVER OI VS LAST YR

AUGUST 24.2017: 69,434 OPEN INTEREST CONTACTS STILL OPEN FOR THE UPCOMING SEPT ACTIVE CONTRACT MONTH VS TODAY AUG 24.2018: 75,270 CONTRACTS.(DEMAND REMAINS EXTREMELY STRONG DESPITE THE LOWER PRICE)

our large speculators,

those large specs who have been long in gold added 1721 contracts to their long side

those large specs who have been short in gold added 6743 contracts to their short side and for the first time in quite some time, the short specs are greater than the long specs. ..very unusual

our commercials,

those commercials who have been long in gold added 2334 contracts to their long side

those commercials who have been short in gild covered (transferred) 3331 contracts from their short side

the commercials short position and long position are basically neck and neck..also very rare

our small speculators

those small specs who have been long in gold pitched (transferred) 1478 contracts from their long side

those small specs that have been short in gold covered (transferred) 835 contracts from their short side.

Conclusion:

from the comex side of things, this has to be bullish as the commercials never lose. also remember that the bankers initiated another raid on Wed and Thur which the speculators dutifully followed in earnest.

and now our silver COT

| Silver COT Report: Futures | |||||

| Large Speculators | Commercial | ||||

| Long | Short | Spreading | Long | Short | |

| 91,428 | 98,586 | 28,647 | 91,362 | 98,780 | |

| -1,918 | 2,404 | 135 | 6,705 | 1,747 | |

| Traders | |||||

| 114 | 69 | 60 | 40 | 39 | |

| Small Speculators | Open Interest | Total | |||

| Long | Short | 244,196 | Long | Short | |

| 32,759 | 18,183 | 211,437 | 226,013 | ||

| -764 | -128 | 4,158 | 4,922 | 4,286 | |

| non reportable positions | Positions as of: | 184 | 145 | ||

| Tuesday, August 21, 2018 | © SilverSee | ||||

our large speculators,

those large specs that have been long in silver pitched (transferred) 1918 contracts from their long side

those large specs that have been short in silver added 2404 contracts to their short side

in the large spec category the shorts are greater than the longs by about 7,000 contracts.

our commercials,

those commercials that have been long in silver added 6705 contracts to its long side

those commercials that have been short in silver added 1747 contracts to its short side

commercials have never been this long, as the short side of things is coming closer to the long side numbers

our small speculators

those smalls specs who have been long in silver pitched (transferred) 764 contracts from its long side

those small specs who have been short in silver covered (transferred) 128 contracts from its short side.

end

Major gold/silver trading /commentaries for FRIDAY

GOLDCORE/BLOG/MARK O’BYRNE.

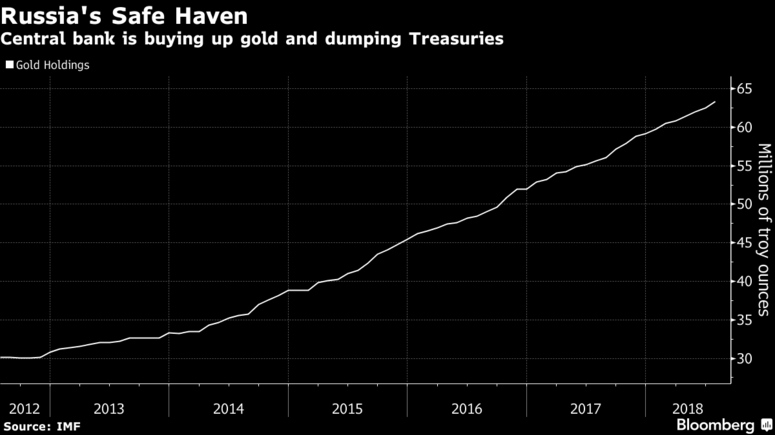

This is huge: Russia buys 24 tonnes of gold in July. They mine about 20 tonnes so they took in 4 tonnes from the west

News, Market Updates and Videos You May Have Missed

News, Market Updates and Videos You May Have Missed

Here is our weekly digest of the key news, market updates, charts and videos.

This week we brought you a series of short videos from an interview between Stephen Flood, CEO of GoldCore.com, and commodities trading expert Carley Garner.

We also broke the news regarding the Russian central bank’s accelerated diversification out of the U.S. dollar and into gold.

The “scoop” quickly went mini-viral on Zerohedge and on many investment and gold websites and consequently on social media. Bloomberg and other mainstream media covered the important story the following day.

We have been getting some great feedback on our recently released Jim Rogers interview, which now has over 26,000 views, so why not check out some of our recent interviews this weekend.

Videos This Week

Market Updates and News This Week

Russia Buys 800,000 Ounces Of Gold In July

Bears Pile Into Gold – Exactly The Wrong Time?

Banks Now Long Gold, Short Dollar. What Do They Know?

Chinese, Asian and European ETF Investors Buy Gold As US Sells

Gold Gains on Bargain Hunting; U.S.-China Trade Talks In Focus

It’s Time for Contrarians to Get Bullish on Gold

Charts This Week

Source: Bloomberg

Source: Bloomberg

Source: ZeroHedge

Source: ZeroHedge

Source: Bloomberg

Source: Bloomberg

News and Commentary

Gold steady, but rate hike views could dampen appeal (Reuters.com)

U.S., Asia stocks fall after U.S.-China trade talks end without progress (Reuters.com)

U.S. New-Home Sales Fall to Nine-Month Low While Supply Rises (Bloomberg.com)

Mortgage rates hit a four-month low as housing market stagnates (MarketWatch.com)

IHS Markit indexes signal softer growth in August in potential hint (MarketWatch.com)

Mortgage rates hit a four-month low as housing market stagnates (MarketWatch.com)

Source: SrsRoccoReport

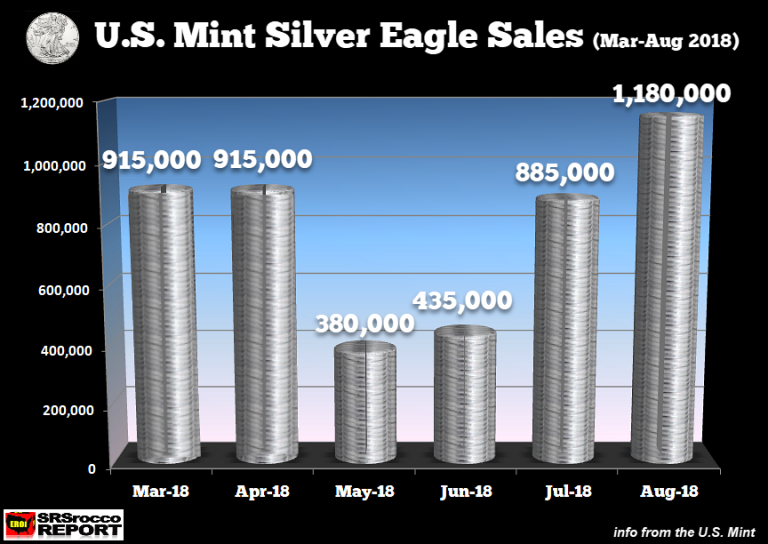

U.S. Mint Silver Eagle Sales Jump In August On Lower Prices (SrsRoccoReport.com)

Here’s who owns a record $21.21 trillion of U.S. debt (MarketWatch.com)

Stock Market’s Latest Sell Signal Has Happened Only 5 Previous Times Since 1895 (MarketWatch.com)

Services Rendered by Jeff Thomas (InternationalMan.com)

5 ways Trump could upend the strong dollar trend, say ING strategists (MarketWatch.com)

What’s a portfolio, and how do you build one? (MoneyWeek.com)

Listen on SoundCloud , Blubrry & iTunes. Watch on YouTube below

Gold Prices (LBMA AM)

23 Aug: USD 1,187.30, GBP 923.24 & EUR 1,027.61 per ounce

22 Aug: USD 1,196.85, GBP 928.25 & EUR 1,032.88 per ounce

21 Aug: USD 1,194.10, GBP 931.28 & EUR 1,036.12 per ounce

20 Aug: USD 1,188.75, GBP 933.29 & EUR 1,042.41 per ounce

17 Aug: USD 1,176.70, GBP 925.59 & EUR 1,032.79 per ounce

16 Aug: USD 1,179.65, GBP 928.38 & EUR 1,037.74 per ounce

15 Aug: USD 1,186.70, GBP 933.10 & EUR 1,047.74 per ounce

Silver Prices (LBMA)

23 Aug: USD 14.63, GBP 11.34 & EUR 12.62 per ounce

22 Aug: USD 14.81, GBP 11.49 & EUR 12.77 per ounce

21 Aug: USD 14.78, GBP 11.52 & EUR 12.83 per ounce

20 Aug: USD 14.76, GBP 11.57 & EUR 12.93 per ounce

17 Aug: USD 14.66, GBP 11.54 & EUR 12.87 per ounce

16 Aug: USD 14.61, GBP 11.51 & EUR 12.85 per ounce

15 Aug: USD 14.83, GBP 11.66 & EUR 13.10 per ounce

Recent Market Updates

– This Week’s Golden Nuggets

– Video: Is Silver Set for a Massive Breakout?

– Banks Now Long Gold, Short Dollar. What Do They Know?

– Russia Buys 800,000 Ounces Of Gold In July

– Gold Season – Is This It?

– This Week’s Golden Nuggets

– Gold And Silver Prices Fall 1.6% and 4.3% To Near 2 Year Lows

– London House Prices Fall At Fastest Annual Rate Since Height Of Financial Crisis

– Jim Rogers on Gold, Silver, Bitcoin and Blockchain’s “Spectacular Future”

– This Week’s Golden Nuggets

– The Stock Market is Stretched to Double Tech-Bubble Extremes

– Jim Rogers and the World’s New Reserve Currency

– Gold—Even at its Lowest Levels in 2018—is Behaving Just as Prescribed

Andrew Maguire’s Kinesis money which is a “bitcoin” but backed 100% by allocated gold and silver is set to go.

it think it would be a great idea to look at this!

please read at: https://kinesis.money/#/

(Andrew Maguire)

|

|

Dear Harvey Organ,

Thank you for your participation in our webinar on June 7th with our host and CEO of Kinesis, Thomas Coughlin.

The response we received has been incredible, we appreciate you taking the time to join us and hope you found it to be beneficial.

Due to such a high influx of questions we received we were unable to have them all answered. Nevertheless, if there was anything which requires more clarification, or you have a query which needs to be rectified, we invite you to join our telegram group:

We apologize for the technical issues we incurred during the webinar which resulted in it running a little over schedule, we hope that the next one we host will run seamlessly.

A video has been put together and uploaded onto our YouTube channel which can be found here:

Please share and subscribe to our YouTube channel to be notified of all the latest videos as they become available.

The rapid growth that we are currently experiencing has been incredible and with your support, is only going to get better.

We are working behind the scenes very hard to create a better experience for everyone involved! Stay tuned in as we have many more announcements to be released in the upcoming days.

Kind Regards,

|

Kinesis Money

a:C/O ILS Fiduciaries (IOM) Limited, First Floor,Millennium House, Victoria Road, Douglas, Isle of Man IM2 4RW

|

The following is self explanatory

(courtesy GATA/Chris Powell and Harvey Organ)

GATA asks bank regulator to check risks of gold

futures maneuver

Submitted by cpowell on Sun, 2018-06-10 16:17. Section: Daily Dispatches

12:21p ET Sunday, June 10, 2018

Dear Friend of GATA and Gold:

GATA has appealed to the U.S. comptroller of the currency, who has regulatory authority over banks, to review financial risks certain banks may have incurred through derivatives in the monetary metals markets, particularly through the recent heavy use of the “exchange for physicals” mechanism of settling gold and silver futures contracts on the New York Commodities Exchange.

The appeal was made in a letter sent May 5 to the comptroller, Joseph M. Otting, whose office is part of the U.S. Treasury Department, by your secretary/treasurer and GATA futures market consultant Harvey Organ.

“Exchange for physical” settlements of futures contracts long were considered emergency procedures when a seller was not able to deliver metal from an exchange-approved warehouse and wanted to settle with delivery elsewhere. But now such settlements appear to constitute most gold and silver futures settlements on the Comex. It is a strange development that appears to have been necessitated by the increasing difficulties of central banking’s gold and silver price suppression policy.

GATA has received no acknowledgment of the letter. Its text is below and a PDF copy of it is here:

http://www.gata.org/files/ComptrollerOfCurrencyLetter.pdf

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

* * *

May 5, 2018

Joseph M. Otting, Comptroller of the Currency

U.S. Treasury Department

400 7th Street, SW

Washington DC 20219

Dear Comptroller Otting:

Please let us bring to your attention financial risks to major banks involving their possibly unreported exposure to derivatives in the monetary metals markets.

In recent months gold and silver future contracts issued by U.S. banks on the New York Commodities Exchange have been moved off-exchange for delivery through a mechanism known as “exchange for physical” (EFP) contracts. Until recently use of this mechanism was considered an emergency procedure when a seller did not have access to metal for delivery through Comex warehouses. Now the mechanism seems to be in use for a large share of front-month contracts for which delivery is sought.

Here is an example that is happening at the Comex in the front active month of April for gold and the inactive delivery month of April for silver.

In gold, there were 229,436 EFP contracts for 713.64 tonnes, an average of 10,925 contracts and 1,092,500 ounces per trading day.

In silver, there were 77,150 EFP contracts for 385,750,000 ounces, an average of 3,673 contracts and 18,369,000 ounces per trading day.

London Bullion Market Association rules suggest that these contracts may not be reported to regulators. The LBMA’s bylaws say:

“Figures above exclude any contracts not subject to risk-based capital requirements, such as FX contracts with an original maturity of 14 days or less, futures contracts, written options, and basis swaps. Therefore, the total notional amount of derivatives by maturity will not add to the total derivatives figure in this table.”

We are told that these EFP contracts are transferred from the Comex to London as what are called “serial forwards” and their duration is always less than 14 days, which exempts them from being reported.

It is our understanding that in each quarter your office prepares a report detailing risk undertaken by the banks under the comptroller’s supervision.

These risks include derivatives undertaken by U.S. banks and other obligations that may cause a bank to fail. Our concern is that your office may not be aware of large unreported derivative exposure by banks.

Could you review this matter and let us know your conclusions?

Sincerely,

CHRIS POWELL

Secretary/Treasurer

HARVEY ORGAN

Consultant

Gold Anti-Trust Action Committee Inc.

7 Villa Louisa Road

Manchester, Connecticut 06043-7541

end

Finally, they replied and it was a complete brush off

(courtesy zerohedge)

Currency comptroller brushes off GATA’s inquiry on

gold, silver EFPs

Submitted by cpowell on Fri, 2018-08-10 15:37. Section: Daily Dispatches

11:35a ET Friday, August 10, 2018

Dear Friend of GATA and Gold:

The U.S. comptroller of the currency, a bank regulator, has declined GATA’s request to inquire into the strange explosion of the use of the emergency procedure of “exchange for physicals” in the settlement by banks of the gold and silver futures contracts they have sold on the New York Commodities Exchange.

Your secretary/treasurer and GATA’s consultant about the Comex, Harvey Organ, wrote to the comptroller, James M. Otting, on May 5, calling attention to the recent enormous use of EFPs, which implies derivatives risks being undertaken by U.S. banks that could cause the banks to fail:

http://www.gata.org/node/18303

“Our concern is that your office may not be aware of large unreported derivative exposure by banks,” GATA wrote.

As months passed without any acknowledgment from the comptroller’s office, your secretary/treasurer appealed to his U.S. representative, John B. Larson, D-Connecticut, to ask the comptroller’s office to reply. The congressman’s office made a second inquiry on Monday this week and today the comptroller’s office provided Larson with a copy of a reply written and mailed Wednesday.

The comptroller’s reply, signed by the deputy comptroller for public affairs, Bryan Hubbard, said only that the comptroller’s office has “dedicated examiners” at the largest banks who “continuously evaluate the credit, market, operational, reputation, and compliance risks of bank trading and derivative activities.”

The reply did not say anything about the use of the “exchange for physicals” procedure for settling futures contracts. That is, the reply was a begrudged brushoff and GATA’s letter would have been ignored completely if not for Representative Larson’s repeated intervention.

Of course GATA hardly expected a conscientious reply to its letter, the comptroller’s office being not an independent regulator but part of the Treasury Department, whose mandate includes administration of the Gold Reserve Act of 1934, which, as amended in the 1970s, authorizes the department’s Exchange Stabilization Fund to secretly intervene in and rig any market in the world, directly or through intermediaries:

https://www.treasury.gov/resource-center/international/ESF/Pages/esf-ind…

But there’s always value in demonstrating government’s lack of candor about what it is doing, especially in regard to the monetary metals.

A PDF copy of the reply from the comptroller’s office is posted at GATA’s internet site here:

http://www.gata.org/files/ComptrollerOfCurrencyReply-08-08-2018.pdf

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

Chris Powell correctly criticizes John Hathaway for not telling investors that governments are suppressing the gold market

(courtesy Chris Powell/GATA/Tocqueville./Hathaway)

Tocqueville’s Hathaway marvels at gold’s depression but declines to explain it

Submitted by cpowell on Thu, 2018-08-23 15:04. Section: Daily Dispatches

11:14a ET Thursday, August 23, 2018

Dear Friend of GATA and Gold:

In his latest market letter, John Hathaway of the Tocqueville Gold Fund notes what seems like the record bearishness in the monetary metals sector, what with huge short positions by speculators, a washout in metals shares, and huge long positions by speculators in the U.S. dollar. He also notes that this bearishness contradicts what seem like the fundamentals for the sector.

Hathaway doesn’t attempt to explain what has brought the metals to this low estate, but then he also makes no inquiry into the metals market positioning of governments and central banks, a largely prohibited subject in the monetary metals business though it might offer some insight.

Inquiry in that respect is left to GATA, whose board members long have been resigned to doing without invitations to the lovely Christmas parties sponsored by financial houses and indeed without invitations to speak at financial conferences whose primary objective is to unload more mining stock on investors who still think there are markets rather than interventions.

But the most recent monthly report of the Bank for International Settlements, as parsed by GATA consultant Robert Lambourne, might contain a clue to the situation in the monetary metals that Hathaway is only marveling at. That is, in July the BIS’ surreptitious intervention in the gold market on behalf of its member central banks increased by 17 percent:

http://www.gata.org/node/18419

Hathaway warns gold shorts and dollar longs that they better run for the hills and encourages those still invested in the monetary metals to hang on. Of course GATA hopes he’s right, insofar as restoration of free markets in the monetary metals is a prerequisite of individual liberty and the defeat of imperialism. GATA also understands that greater awareness of central bank intervention against gold will not necessarily help Hathaway and mining company executives sell shares in the short term.

But the longstanding policy of Western governments and central banks to suppress the gold price, a policy painstakingly summarized and documented by GATA here ––

http://www.gata.org/node/14839

— is the proverbial elephant in the room wherever metals prices are discussed, and not mentioning the elephant has not prevented it from stomping metals investors, including Hathaway’s own. If he thinks, as his long avoidance of the subject suggests, that governments and central banks are not manipulating the monetary metals markets, he’d do his investors a favor by telling them so. If he suspects that governments and central banks are manipulating those markets, he would seem to have an obligation to tell them.

Hathaway’s letter is headlined “Gold: A Case of Extremes” and it’s posted at the Tocqueville internet site here:

http://tocqueville.com/gold-a-case-of-extremes/

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

* * *

Very important..and I will bring you the interview for you to see on Monday

(courtesy Bill Holter/JSMineset)

_

As you might know by now, Jim and I will be interviewing with Greg Hunter tomorrow for early Sunday release. We plan on talking about the current “technical” dollar short created by all the emerging market dollar loans currently on the books. Richards Russell first spoke of this and called it the “synthetic” dollar short. You see, when a borrower from a nation with a currency of their own, borrows dollars, the loan must be paid back in dollars. This creates artificial/short term yet very real demand for dollars when the loan is paid back.

What I want to talk about today is “MOPE”, management of perspective economics and give you a little background as to what to listen for when Jim and I talk. I’m doing this in the hope it will make listening to the interview more fruitful rather than listening to it

cold.

So, Jim coined the phrase many years back to describe a situation where lying about the current fundamentals could be supported or confirmed by pricing in markets. In other words, “the economy is great, just look at the Dow Jones”! Of course, markets were taken over by machines that used the fuel provided by the central bank(s) and lowered interest rates. It became one glorious and they hoped, self sustaining circle (bubble). The thought was, if markets are up then people will feel good and then borrow and spend more. They were right, but the problem is the game has “no ending” because after markets close for the day, they must reopen again the next day. What I mean here is, no matter what levels the markets got to …there is always tomorrow to deal with.

Our talk will basically be that “tomorrow” is in fact here as evidenced by the emerging market credit bubble being popped and trade wars commencing. These events show two things that do not fit into the MOPE scenario. First, Mother Nature’s law that there is a limit as to what can be borrowed and serviced has been reached by the emerging (and developed) markets. Second, trade wars and tariffs have begun because the economic “pie” has not grown fast enough to keep up with the debt many players have taken on. In other words, since the pie is not expanding, everyone wants a bigger slice of it.

The emerging market problems we are told will not be “contagious”. Do you remember hearing the same thing regarding real estate debt back in 2008? Speaking of real estate, we are already seeing 2008 2.0 begin to play out all over the world as sales volume has turned decidedly negative and is being naturally followed by softer pricing. Don’t ever forget, real estate (as have nearly ALL assets) has been pushed higher by the use of easy credit, credit is now beginning to tighten. The world is totally financially interconnected where nearly everyone trades with everyone else, and everyone owns everyone else’s debts (and these debts are considered assets). Because of this structural cross ownership and trade, contagion is guaranteed.

And this folks is the GIANT RUB and what you need to be thinking about when you listen to our interview. MOPE is running head first directly into reality! The reality is that rates could not really go below zero percent even though it was tried. We reached global debt saturation levels for all intents and purposes. It is the emerging markets that are first showing stress. This will spread to Asian emerging markets, then to China/EU/Japan and of course finally to the U.S..

“They” (central banks) will never let it happen you say? Well, maybe you are correct and I can guarantee the central banks will certainly try to prevent a credit meltdown. But you do understand the only tool they have to prevent such an event, right? Central banks can ONLY reverse present course and immediately crank up QE all over again …except in much larger quantities because the debt (and derivatives) outstanding are so much larger than they were just a few short years ago. Global debt is now $247 trillion (derivatives maybe 5 times that), even a 5% interest rate means that debt service is $12 trillion or so. Do you see the problem? The problem is that $12 trillion (or $18-20 trillion if rates were fully normalized) is FAR TOO MUCH FOR A $75 trillion global economy to support!

OK, enough of the “why” as we forecast it and have beaten it worse than any dead horse. Rather, listen for “why now”. It is now because the official story is coming apart at the seams. Emerging market debt cannot be hidden with derivatives. The debt is either serviced, not serviced, or …central banks must begin QE again which means printing money and lowering rates to zero again. The same can be said for the softening and very heavy global real estate markets, derivatives which have been used in all paper markets have no effect of support whatsoever. Remember, “debt” is not only a liability on one side, it is also and asset on the other side. Please read this to better understand www.zerohedge.com And in case you have not been paying attention, the only equity market that is up so far this year is the US, and ALL global debt (bond) markets are down as rates have moved higher. Markets have and are turning down all over the world, the US will not stand alone. Don’t fool yourself that the U.S.is the cleanest dirty shirt of the batch, the entire load will be cleaned in a re set.

To finish, listen closely to our interview because market participants worldwide are all huddled on the same side of the bubble boat …at a time when years of MOPE is being disproven. The vast majority who are offside also have debt carrying assets and have made moves to “chase yield”. The only assets without credit supporting price are basically gold and silver. There is great credit in those markets but that credit has been employed to keep prices from rising. The canaries in the coal mine (gold and silver) have been silenced but that hasn’t stopped participants from beginning to keel over. In the words of Sir Richard Russell, “inflate or die”. It is here and now …this is exactly the crossroads we will speak of with Greg Hunter.

Standing watch,

Bill Holter

Holter-Sinclair collaboration

_______________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________

Your early FRIDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED UP TO 6.8483/HUGE DEVALUATION FOR THE PAST FOUR WEEKS STOPS/CHINESE COMING TO USA FOR TRADE TALKS //OFFSHORE YUAN: 6.8395 /shanghai bourse CLOSED UP 4.81 POINTS OR 0.18% /HANG SANG CLOSED DOWN 118.59 POINTS OR 0.43%

2. Nikkei closed UP 190.95 POINTS OR 0.85%/USA: YEN RISES TO 110.37/

3. Europe stocks OPENED ALL GREEN

/USA dollar index FALLS TO 95.39/Euro RISES TO 1.1583

3b Japan 10 year bond yield: REMAINS AT . +.10/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 111.37/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD IS NOW TARGETED AT .11%/JAPAN LOSING CONTROL OF THEIR BOND MARKET

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 68.72 and Brent: 75.61

3f Gold UP/JAPANESE Yen FLAT/ CHINESE YUAN WELL UP

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil UP for WTI and UP FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund FALLS TO +.340%/Italian 10 yr bond yield UP to 3.13% /SPAIN 10 YR BOND YIELD UP TO 1.38%

3j Greek 10 year bond yield RISES TO : 4.20

3k Gold at $1192.35silver at:14.64 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble UP 44 /100 in roubles/dollar) 67.79

3m oil into the 68 dollar handle for WTI and 75 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 111.37 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 0.9836 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1394 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now POSITIVE territory with the 10 year FALLING to +0.34%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.84% early this morning (THIS IS DEADLY TO ALL MARKETS). Thirty year rate at 2.99%

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

Relief rally in the Turkish lira…no developments at all…

(courtesy Jim Reid/Bloomberg/Deutsche bank/zero hedge)

Dollar Slides Ahead Of Powell Speech, Stocks Rise After

China Market Intervention

In a generally quiet session ahead of today’s main event, the dollar dropped on Friday, set for its biggest weekly decline since March as traders prepared for a keynote speech by Fed chair Jerome Powell in Wyoming looking for hints on the direction of monetary policy, while global stocks were fractionally higher.

The MSCI All-Country World index was barely in the black, as markets in Europe edged higher led by banks followed a new report that UniCredit has retained Rothschild to purchase SocGen, while U.S. index futures were also higher after a mixed session in Asia as trade negotiations with China drew a blank.

In early Asia trading, stocks fell after U.S.-China trade talks ended without any progress and with “no further talk scheduled”. MSCI’s broadest index of Asia-Pacific shares outside Japan shed 0.2 percent; it was still up about 1 percent on the week. Hong Kong’s Hang Seng fell 0.4%, Australian stocks rose 0.05% after the country’s prime minister Malcolm Turnbull was kicked out, and South Korea’s KOSPI advanced half a percent. Japan’s Nikkei climbed 0.85 percent, helped by a weaker yen.

But the big story was again out of China, where after sliding in early trading, A-shares stocks jumped on Friday afternoon, erasing a morning drop, as financial shares led the advance. Analysts told Bloomberg the gains could be the result of purchases by the “national team,” i.e. state funds controlled by Beijing.

“Banks and financial stocks rising could be the result of national team buying,” said Wang Mingli, analyst at Guoyuan Securities in Shanghai. “We don’t see clear logic or a catalyst behind the inflow of cash today, so exterior ’stability’ considerations may be present,” added Wang Jun, analyst at Huachuang Securities in Beijing. And this is what the latest Chinese “stability” intervention in markets looked like:

China was also supported by the PBOC’s decision inject CNY 149bln through a 1yr Medium-term Lending Facility, a move meant to help with upcoming maturities of Local Government bonds.

Raw-materials suppliers led gains in the Stoxx Europe 600 Index as commodities prices rallied, particularly oil. The Europe STOXX 600 index rose 0.2%, boosted by banking names as a result of reports suggesting Unicredit (+0.7%) had hired Rothschild for a deal with SocGen (+1.2%). The gains in banking names are broad based, with the sector outperforming (Stoxx Europe 600 Banking Index +0.4%) and co.’s in the sector leading bourses.

Investors who were hoping for good news on global trade were disappointed after U.S. talks with China ended with no progress, increasing the likelihood that tit-for-tat tariffs will escalate and casting a shadow over the global-growth outlook. For now, however, the focus shifts back to Fed policy and Jerome Powell’s speech in a few hours at Jackson Hole. Where Powell stands on the pace of interest rate hikes will be scrutinized after minutes from the Fed’s most recent policy meeting indicated the central bank would tighten monetary policy soon.

“Global risk sentiment remains somewhat jittery ahead of Fed Chair Powell’s speech with U.S.-Sino trade talks failing to yield any immediate progress,” strategists at OCBC Bank wrote.

The Fed should raise rates further this year and probably next year as well, despite Trump’s opposition to tighter policy, Kansas City Fed President Esther George said in interviews aired on Thursday. Dallas Fed President Robert Kaplan said he sees 3-4 hikes in the next 9-12 months and stated he is comfortable with 4 hikes this year, while he also commented that officials will ignore political pressure or attacks and that he hopes Fed can get to the neutral rate without seeing a yield curve inversion.

“Any comments on current Fed policy will draw even more than the usual attention given recent and unprecedented criticism of the Fed by President Trump,” GAM chief economist Larry Hatheway told Bloomberg. “While Powell prefers to speak plainly and in non-technical terms, he may find reason to take a more guarded approach in order to avoid the appearance of open conflict with the Administration.”

Meanwhile bond traders continue to clink to bets for two rate hikes by year-end as they brave turmoil in emerging markets, trade tensions and a U.S. president who openly pushed policy ideas on the central bank days before Powell speaks. While most question focus on what the Fed will do in 2019, it is unlikely that the “data-dependent” Powell will provide any detail that far in advance, especially with the FOMC Minutes making it clear that trade tensions pose a substantial threat to the pace of future rate hikes.

In the main political news overnight, Australia’s dollar climbed against all its G-10 peers, paring some of Thursday’s losses, after Treasurer Scott Morrison won a leadership ballot to become party leader and prime minister replacing Malcolm Turnbull, and ending a week of political turmoil; Morrison won 45 votes to 40 over right-wing populist Peter Dutton in a closed-door meeting of ruling Liberal party lawmakers.

The greenback fell sharply, giving up all gains from the past 24 hours, while the euro found support from German growth data; the solid performance in the three months through June has helped alleviate concerns that a slowdown in the first quarter would persist.

Elsewhere in FX, the Japanese yen held overnight weakness after weaker-than-expected domestic CPI showed that Kuroda’s 2.0% inflation target remains as elusive as ever:

- Japanese National CPI (Jul) 0.9% vs. Exp. 1.0% (Prev. 0.7%).

- Japanese National CPI Ex. Fresh Food (Jul) 0.8% vs. Exp. 0.9% (Prev. 0.8%)

- Japanese National CPI Ex. Fresh Food & Energy (Jul) 0.3% vs. Exp. 0.3% (Prev. 0.2%)

The Swedish krona erased an earlier decline after Riksbank Deputy Governor Kerstin af Jochnick said that the central bank’s rate path points to a hike toward year-end. New Zealand’s dollar recovered after sliding following comments by New Zealand Central Bank Governor Adrian Orr that the bank hasn’t ruled out cutting interest rates if needed to achieve its inflation target.

Attention as usual focused on any sharp moves in the yuan, and one emerged in mid-morning, when the USDCNH turned sharply lower amid little news, which in turn pushed the dollar down across rest of G-10.

In rates, US Treasuries were initially steady as investors awaited Powell’s scheduled comments at the Jackson Hole retreat later Friday; Treasuries later extended declines to new intra-day lows as the dollar came under pressure led by CNH strength, supporting equity gains. Italian BTP futures gapped higher at the open in reaction to Italian press report that Trump offered Italy PM Conte to help with buying BTPs at meeting 3 weeks ago, however the gains were quickly faded as there were no details on the plan and given the lack of executive power to enforce such an idea.

In commodities, oil was poised for its first weekly gain in 2 months after testing the 200-day moving average. WTI advanced amid prospect of tightening supplies from the U.S. to Iran. Both WTI and Brent up ~1.0% and extending gains above USD 68.00/BBL and USD 75.00/BBL respectively. This comes amid reports of continued strike action at Total’s North Sea oil and gas fields alongside a softer USD. In the metals scope gold is benefitting from a softer USD and is up 0.4% on the day, with the yellow metal set for a 0.3% gain for the week. Copper has pared early losses and is set for its first positive session in three, alongside the best week in four, as the construction material has shed-off trade concerns. Steel prices have seen a recovery (0.5%) as a fall in Chinese steel stocks has been noted, but is still set for it’s worst week in eight (-1.2%)

Expected data include durable goods orders. Foot Locker and Ubiquiti Networks are among companies reporting earnings

Market Snapshot

- S&P 500 futures up 0.2% to 2,863.25

- STOXX Europe 600 up 0.2% to 383.98

- MXAP up 0.06% to 163.27

- MXAPJ down 0.2% to 528.65

- Nikkei up 0.9% to 22,601.77

- Topix up 0.7% to 1,709.20

- Hang Seng Index down 0.4% to 27,671.87

- Shanghai Composite up 0.2% to 2,729.43

- Sensex down 0.2% to 38,266.64

- Australia S&P/ASX 200 up 0.05% to 6,247.33

- Kospi up 0.5% to 2,293.21

- German 10Y yield rose 0.2 bps to 0.341%

- Euro up 0.2% to $1.1566

- Brent Futures up 0.7% to $75.26/bbl

- Italian 10Y yield rose 2.7 bps to 2.816%

- Spanish 10Y yield unchanged at 1.372%

- Brent futures up 0.7% to $75.26/bbl

- Gold spot up 0.4% to $1,190.17

- U.S. Dollar Index down 0.2% to 95.49

Top Overnight News

- U.S. and China fail to make progress in trade talks; Chinese officials note possibility that no further negotiations can happen until after November mid-term elections

- New York State prosecutors have taken preliminary steps to open criminal investigations into President Donald Trump’s former lawyer, Michael Cohen, and possibly the president’s business, according to people familiar with the matter

- Candidates to become Europe’s next top banking watchdog could find that for all their competence, experience and political support, the trump card might be gender

- President Donald Trump told Italian Prime Minister Giuseppe Conte the U.S. is willing to help the country by buying government bonds next year as Italy seeks to refinance its debt, Corriere della Sera reported, citing three high-level Italian officials

- A government-appointed commission recommended against a proposal by Norway’s $1 trillion sovereign wealth fund to dump more than $40 billion in oil and gas stocks

- China removed limits on foreign holdings in domestic banks and asset management companies, formalizing a previously announced step toward opening its $40 trillion financial sector

- China Finance Minister Liu Kun says counter-strikes at the U.S. over trade will remain as targeted as possible to avoid harming businesses in China – whether Chinese or foreign, Reuters reports, citing interview.

- Japanese inflation failed to deliver an expected uptick in July, underscoring the persistent weakness in consumer prices that has forced the Bank of Japan to take an increasingly longer-term view of its mission to achieve 2% inflation

Asian equity markets traded mixed as the region digested the weak lead from Wall St, a lack of progress during US-China trade discussions and change of leadership in Australia. ASX 200 (+0.1%) traded choppy amid the tumultuous political climate, although sentiment later improved after Treasurer Morrison beat former Home Affairs Minister Dutton to become the PM. Elsewhere, Nikkei 225 (+0.8%) was underpinned by a weaker JPY, while Hang Seng (-0.4%) and Shanghai Comp. (+0.2%) were initially the worst performers following the stalemate at US-China trade talks and with the biggest movers amongst Hong Kong’s large caps also dictated by earnings, but the Shanghai Comp. reversed course close to end of trade, and ended the day up. Finally, 10yr JGBs were uneventful with demand subdued amid strength in Tokyo stocks, although downside was also stemmed by the BoJ’s presence in the market for JPY 950bln in 1yr-10yr JGBs and following softer than expected CPI data. PBoC refrained from reverse repos but later injected CNY 149bln through 1yr Medium-term Lending Facility. PBoC set CNY mid-point at 6.8710 (Prev. 6.8367)

Top Asian News

- Uber, Airbus Enlisted to Help Japan Develop Flying Cars

- China Ex- Billionaire Goes Missing, Sparking Rout in Casino Stock

European equites started the flat, with the FTSE MIB the outperforming bourse. This is being driven by banking names, and comes as a result of reports suggesting Unicredit (+0.7%) have hired Rothschild for a deal with SocGen (+1.2%). The gains in banking names are broad based, with the sector outperforming (Stoxx Europe 600 Banking Index +0.4%) and co.’s in the sector leading bourses such as: CAC (SocGen +1.2% & BNP Paribas +1.0%); FTSE MIB (Unicredit +0.7%); DAX (Commerzbank +0.9%); SMI (UBS +1.5%, Credit Suisse +0.9%); Shire (+2.4%) are leading the gains in the FTSE 100 as they received approval for a ground-breaking hereditary angioedema treatment.

Top European News

- Norway Wealth Fund Should Keep Oil Stocks, Commission Recommends

- UniCredit Working With Rothschild’s Bouton on SocGen Deal: MF

- Ceconomy Buyout of Fnac Darty Is Said to Be Stalled by Dispute

- ECB Is Said to Prefer Woman to Head Powerful Banking Watchdog

In FX, we start with AUD where there was some calm after the political storm, and a positive market response (so far) to the prospect of former Treasurer Morrison taking over from Turnbull as leader of the Liberal Party and PM. Indeed, Aud/Usd has bounced firmly from circa 0.7235-40 lows to around 0.7290 and eyeing hefty option expiry interest just above at 0.7305 (1.4 bn), while the Aud/NZD cross is back up near 1.0950 having only just held above 1.0900 amidst the unfolding drama overnight. However, the Kiwi has also caught a bid on the more stable situation down under to retest 0.6650 vs its US peer. The SEK was another major outperformer and gainer, but largely due to Riksbank commentary via Af Jochnick noting inflation rising and nearing target, above forecast Q2 growth and the rate path indicating an October hike. She also acknowledged that recent Krona weakness should underpin price pressures ahead, and on the note Swedish PPI data for July picked up pace from the previous month. Eur/Sek down to 10.5260 from 10.5815 at one stage, with 10.5000 the obvious objective. EM – The Rub and Zar continue to rebound and are on course to end a turbulent week in better shape than other regional currencies (such as the Try and Brl) still suffering from multiple bearish/negative factors, like sanctions, diplomatic tensions, tariffs, on top of domestic political, economic and fiscal issues. Meanwhile, after no material progress in US-China trade talks, the Yuan is back on the wane and the PBoC has resumed its rising mid-point fixing trend. EUR/GBP – Also firmer vs the Greenback, but within recent ranges as the DXY pivots around 95.500 awaiting Fed chair Powell and a raft of other FOMC members all attending the Jackson Hole Symposium. However, the single currency remains capped ahead of 1.1600 and within proximity of decent expiries from 1.1545-55 (1.2 bn), while Cable is back within 1.2800-50 parameters amidst no Brexit progress on the 20% outstanding and make or break sticking points between the UK and EU. Hence, the Eur/Gbp cross remains above 0.9000, albeit not breaching major technical resistance in the 0.9030-35 area.

In commodities, WTI crude advanced, heading for the first weekly gain in two months, amid prospect of tightening supplies from the U.S. to Iran. Both WTI and Brent up ~1.0% and extending gains above USD 68.00/BBL and USD 75.00/BBL respectively. This comes amid reports of continued strike action at Total’s (FP FP) North Sea oil and gas fields alongside a softer USD. In the metals scope gold is benefitting from a softer USD and is up 0.4% on the day, with the yellow metal set for a 0.3% gain for the week. Copper has pared early losses and is set for its first positive session in three, alongside the best week in four, as the construction material has shed-off trade concerns. Steel prices have seen a recovery (0.5%) as a fall in Chinese steel stocks has been noted, but is still set for it’s worst week in eight (-1.2%)

US Event Calendar

- 8:30am: Durable Goods Orders, est. -1.0%, prior 0.8%; Durables Ex Transportation, est. 0.5%, prior 0.2%

- 8:30am: Cap Goods Orders Nondef Ex Air, est. 0.5%, prior 0.2%; Cap Goods Ship Nondef Ex Air, est. 0.3%, prior 0.7%

Looking ahead to today, apart from Chair Powell’s speech, there are other scheduled speakers including BOE’s Haldane as well as various professors from US universities. On the data front, the final reading of second quarter German GDP will print at 7:00am London, followed by US durable and capital goods orders for July due at 13:30 London. The July PPI for Spain and July finance loans for housing in the UK are also due.

DB’s Jim Reid concludes the overnight wrap

The last 36 hours or so feels like a microcosm of how markets have gone about their business this year. A flurry of political drama related headlines, stress over tit-for-tat tariffs, solid but unspectacular PMIs, and markets which continue to trudge along. Yesterday was clearly impacted by well below average volumes, with the S&P 500 (-0.17%), DOW (-0.30%) and NASDAQ (-0.13%) all finishing on the softer side. It wasn’t much more exciting in Europe where the Stoxx 600 closed -0.17%. Bunds and Treasuries also ended with moves of less than 0.5bps although the 2s10s Treasury curve hit a fresh cyclical low of 20.9bps which is lower than Japan for the first time since November 2007. Quite a landmark moment.

Meanwhile the USD (+0.55%) finally rose for the first time in seven sessions which didn’t seem to help EM currencies with the added distraction of Mr Trump tweeting that he had instructed Secretary of State Mike Pompeo to “closely study the South Africa land and farm seizures and expropriations and the large scale killing of farmers.” In response the Rand fell -1.71%, though Wednesday’s inflation print at 5.1% did not help sentiment either. Elsewhere, the Brazilian Real (-1.74%) continued to lead losses in EM as investors positioned ahead of this autumn’s election. The Real is now within 1.5% of its weakest-ever level. The Hungarian Forint and Turkish Lira also weakened -1.02% and -1.19% versus the dollar, respectively.

While politics may have preoccupied the market for most of this week, the focus for the next couple of days may well turn back to monetary policy with the Fed’s annual Jackson Hole symposium due to kick off today and continue into the weekend. As a reminder, the topic of this year’s conference is the rather vague “Changing Market Structure and Implications for Monetary Policy” and Fed Chair Powell is due to speak this afternoon at 15.00pm London time on the even more vague “Monetary Policy in a Changing Economy”. While the title of Powell’s speech gives few clues away, our US economists believe that he is unlikely to move market expectations in either a more hawkish or dovish direction. That said, he could discuss some market relevant topics, including: uncertainty around estimates of the natural rate of unemployment; the potentially flatter Philips curve; the outlook for inflation; the ongoing balance sheet runoff process; changes to how monetary policy is implemented by the Open Markets Desk (i.e. floor versus corridor system); macroprudential regulatory adjustments (e.g. countercyclical capital buffer, or CCyB); or changes to the Fed’s monetary policy framework (e.g. price level targeting). So worth keeping an eye on.

This morning in Asia, markets are trading mixed with the Nikkei (+0.69%) and Kospi (+0.15%) both up while the Hang Seng (-0.69%) and Shanghai Comp. (-0.35%) are down as we type. Elsewhere on trade, the latest talks between the US and China seems to have yielded little material progress, although China’s Commerce ministry indicated the two countries had “constructive, honest” talks on trade issues and both parties will keep dialogue open. Meanwhile China has removed the foreign ownership limits in its banks and asset managers, consistent with prior commitments by President Xi. Datawise, Japan’s July CPI was slightly softer than expectations and remains well below the BoJ’s target. The core CPI (ex-fresh food) was flat mom at 0.8% yoy (vs. 0.9% expected) while the stricter CPI measure (ex-fresh food and energy) rose one-tenth mom to an in line print of 0.3% yoy.

Back to the PMIs. In Europe the composite reading of 54.4 was a shade lower than expected (54.5) mainly due to a half point fall in the manufacturing print to 54.6 (vs. 55.2 expected). That’s the lowest reading for the manufacturing component since November 2016 but the broader composite continues to be supported by the services sector where the PMI rose 0.2pts to an in-line 54.4 reading. As far as pricing pressure was concerned, the survey revealed that “although input cost and selling price inflation rates remained among the highest seen over the past seven years, both cooled to three-month lows”. Output prices were also reported as easing in both manufacturing and services, and signs of capacity constraints (delivery times, backlogs of work) also declined.

At a country level the composite reading for France rose a solid 0.7pts to 55.1 (vs. 54.6 expected) while Germany also surprised to the upside, jumping an identical 0.7pts to 55.7 (vs. 55.1 expected). The latter was driven by the services sector with the manufacturing actually sliding more than expected, albeit at still robust levels. What yesterday’s data did imply is bit of softer read through for the periphery to the tune of about 0.8pts in the view of our economists. That being said, the broad level data still points to a solid +0.5% qoq growth in Q3 for the Euro area. As for the US, the PMIs yesterday largely continued the trend of some moderately weaker readings from recent survey data. The composite fell 0.7pts to 55.0 with both the manufacturing (-0.8pts to 54.5; 55.0 expected) and services (-0.8pts to 55.2; 55.8 expected) down more than expected. Interestingly the survey did reveal that “inflationary pressures moderated in August, reflecting the least marked rise in average cost burden since the start of 2018”. As far as the other data was concerned yesterday, last week’s initial jobless claims declined by 2,000 to 210,000 and continuing claims printed at 1,727,000. Both series remain near their recent cyclical lows and not far away from their all-time lows. The FHFA House Price Index for June rose 0.2% versus 0.3% expected, and new home sales declined slightly in July. We continue to expect the housing sector to weigh slightly on growth for the next few quarters, but the risks are skewed to the downside so this trend bears watching.

Away from the data, there appeared to be some recycling of headlines yesterday suggesting that German Chancellor Merkel was not going to push for a German ECB President. That would seemingly take Bundesbank President Weidmann out of the race which also implies that there is no obvious favourite for Draghi’s successor. The European Commission President job also needs to be addressed with the Juncker’s current term ending in October next year – the same as Draghi’s – with Handelsblatt reporting that Merkel favoured a German for the Commission President role.

Speaking of the ECB, the minutes yesterday from the latest policy meeting didn’t appear to throw up any real curveballs and indeed they confirmed that “members widely expressed satisfaction that the communication of the June seems to ratify current market pricing which does not include a rate hike until autumn 2019. The minutes did cite the “risk of persistent heightened financial market volatility,” which could be a veiled reference to the situation in Italy.

In other European political news, the UK released its plans in the event that no Brexit deal is reached, causing some negative sentiment around the pound which depreciated -0.74% versus the dollar yesterday. However, there was nothing particularly new in the releases and we continue to expect the Withdrawal Agreement for the UK’s exit from the EU to be resolved by the end of the year, even if it requires a “fudge” around certain details of the future relationship. Separately, Italian Deputy Prime Minister Di Maio from Five Star said that Italy would suspend EU funding next year if leaders could not reach an agreement to divvy up migrants and ease the burden on Italy. Di Maio is known as a more combative voice in the government, but the rhetoric marginally raises the chances of confrontation with the EU over the budget over the next few weeks.

Finally there were more Fed speak on rates and yield curve yesterday. The Fed’s George told Bloomberg TV that “based on what I see today, I think two more rate hikes (this year) could be appropriate” along with several more next year was the Fed move rates back to a neutral setting of around 3%. Conversely the more dovish Fed’s Kaplan noted that “…to get to a neutral level (on rates), I think that means we need to be raising rates 3 or 4 times over the next 9 to 12 months” and then reassess based on incoming data. Meanwhile he noted the flattening yield curve “…it’s something that I’ll be watching. So I’m hopeful we can get to neutral without creating an inverted yield curve”. Elsewhere the Fed’s Bostic noted “the yield curve gives us important and useful information….but it is only one signal among many that we use…” whilst adding that “correlation does not imply causality. This is a particularly important point to keep in mind when

discussing the yield curve”.

Looking ahead to today, apart from Chair Powell’s speech, there are other scheduled speakers including BOE’s Haldane as well as various professors from US universities. On the data front, the final reading of second quarter German GDP will print at 7:00am London, followed by US durable and capital goods orders for July due at 13:30 London. The July PPI for Spain and July finance loans for housing in the UK are also due.

3. ASIAN AFFAIRS

i) FRIDAY MORNING/ THURSDAY NIGHT: Shanghai closed UP 4.81 POINTS OR 0.18% /Hang Sang CLOSED DOWN 118.59 POINTS OR 0.43%/ / The Nikkei closed UP 190.95 POINTS OR 0.85%/Australia’s all ordinaires CLOSED DOWN 0.04% /Chinese yuan (ONSHORE) closed UP at 6.8483 AS POBC HALTS ITS HUGE DEVALUATION /DELEGATION COMING TO THE USA TO SEE TRUMP IN NOVEMBER/Oil UP to 68.72 dollars per barrel for WTI and 75.61 for Brent. Stocks in Europe OPENED IN THE GREEN //. ONSHORE YUAN CLOSED UP AT 6.8483 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.8395: HUGE DEVALUATION/PAST SEVERAL DAYS STOPS// TRADE TALKS NOT DOING TOO GOOD : /ONSHORE YUAN TRADING STRONGER AGAINST OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING MUCH STRONGER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

3 a NORTH KOREA/USA

North Korea/South Korea/USA/China

In a surprise move, Trump tells Pompeo not to go to North Korea as the North Koreans have not made sufficient progress with respect to the denuclearization of the Korean penisula

(courtesy zerohedge)

3 b JAPAN AFFAIRS

c) REPORT ON CHINA/HONG KONG

No further talks are scheduled: the China/USA trade negotiations over the past two days are a complete failure

(courtesy zerohedge)

“No Further Talks Scheduled”: China-U.S. Trade

Negotiations A Complete Bust

When reports emerged last week of a low-level Chinese delegation coming to meet with members of the Treasury department ahead of what the WSJ described would be a November trade summit in the US, stocks spiked and yields ran up (they have since tumbled with the 2s10s yield curve collapsing to just 20 basis points) on hopes that the long-running trade feud between the US and China may finally be coming to an end.

Skeptics laughed and said that after three rounds of failed trade talks, the fourth one would be no different.

The skeptics were right because after the conclusion on Thursday of the second day of the closely watched trade talks between the U.S. and China, there was “no major progress” according to Bloomberg, with the stage once again set for further escalation of the trade war between the US and China.

Worse, according to the Bloomberg source, not only are no further talks scheduled at this point but the Chinese officials have reportedly raised the possibility that no further negotiations could happen until after November’s mid-term elections in the U.S.

The White House issued a statement which said the countries “exchanged views on how to achieve fairness, balance, and reciprocity in the economic relationship, including by addressing structural issues in China” identified by the U.S. in an investigation into Chinese intellectual-property practices. The Chinese commerce ministry was even more terse, stating that two nations had “constructive, candid” communication, and will keep in touch about the next steps.

Translation: nobody was willing to compromise by even an inch.

Here’s what happened according to the Bloomberg source: the U.S. Treasury presented a revised version of the “provocative” list of demands presented by the Trump administration when the two sides had their first high-level meetings in May. The Chinese delegation, meanwhile, showed no signs of bringing any significant compromises to the table this week