FINALIZED DRAFT

GOLD: $1195.20 DOWN $3.75 (COMEX TO COMEX CLOSINGS)

Silver: $14.14 DOWN 2 CENTS (COMEX TO COMEX CLOSING)

Closing access prices:

Gold $1196.60

silver: $14.16

H

For comex gold:

AUGUST/

And now Sept:

NUMBER OF NOTICES FILED TODAY FOR SEPT CONTRACT: 63 NOTICE(S) FOR 6300 oz

Total number of notices filed so far for Sept: 498 for 49,800 (1.5489 tonnes)

For silver:

Sept

295 NOTICE(S) FILED TODAY FOR

1,475,000 OZ/

Total number of notices filed so far this month: 4959 for 24,795,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: BID $6324/OFFER $6409: DOWN $92(morning)

Bitcoin: BID/ $6377/offer $6467: DOWN $39(CLOSING/5 PM)

end

First Shanghai gold fix comes at 10 pm est

The second Shanghai gold fix: 2:15 pm

First Shanghai gold fix gold: 10 pm est: $1206.75

NY price at the same time:$1202.25

PREMIUM TO NY SPOT: $4.50

XX

Second gold fix early this morning: $ 1206.26

USA gold at the exact same time:$1201.50

PREMIUM TO NY SPOT: $4.76

XXXX

China is controlling the gold market

WE WILL NOT PROVIDE LONDON FIXES AS THEY ARE NOT ACCURATE AS TO WHAT IS GOING ON AT THE SAME TIME FRAME.

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total OPEN INTEREST ROSE BY A SMALL 420 CONTRACTS FROM 210,042 UP TO 210,462 DESPITE YESTERDAY’S SMALL 4 CENT FALL IN SILVER PRICING AT THE COMEX. TODAY WE MOVED CONSIDERABLY FURTHER AWAY FROM LAST MONTH’S RECORD SETTING OPEN INTEREST OF 244,196 CONTRACTS.

WE HAVE ALSO WITNESSED A LARGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY(WELL OVER 30 MILLION OZ AT THE COMEX FOR JULY , 6 MILLION OZ FOR AUGUST AND NOW OVER 31 MILLION OZ STANDING IN SEPTEMBER. AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD HUMONGOUS SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP:

0 EFP’S FOR SEPT. 1230 EFP’S FOR DECEMBER AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE: OF 1230 CONTRACTS. WITH THE TRANSFER OF 1230 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 1230 EFP CONTRACTS TRANSLATES INTO 6.15MILLION OZ ACCOMPANYING:

1.THE 4 CENT FALL IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR THE JUNE/2018 COMEX DELIVERY MONTH. (5.420 MILLION OZ); 30.370 MILLION OZ STANDING FOR DELIVERY IN JULY, FOR AUGUST: 6.065 MILLION OZ AND NOW 30.345 MILLION OZ STANDING SO FAR IN SEPT.

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF SEPT:

12,026 CONTRACTS (FOR 4 TRADING DAYS TOTAL 12,026 CONTRACTS) OR 60.130 MILLION OZ: (AVERAGE PER DAY: 3006 CONTRACTS OR 15.03 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF SEPT: 60.130 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 8.59% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2018 TO DATE SILVER EFP’S: 2,097.96 MILLION OZ.

ACCUMULATION FOR JAN 2018: 236.879 MILLION OZ

ACCUMULATION FOR FEB 2018: 244.95 MILLION OZ

ACCUMULATION FOR MARCH 2018: 236.67 MILLION OZ

ACCUMULATION FOR APRIL 2018: 385.75 MILLION OZ

ACCUMULATION FOR MAY 2018: 210.05 MILLION OZ

ACCUMULATION FOR JUNE 2018: 345.43 MILLION OZ

ACCUMULATION FOR JULY 2018: 172.84 MILLION OZ

ACCUMULATION FOR AUGUST 2018: 205.23 MILLION OZ.

RESULT: WE HAD A SMALL SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 420 DESPITE THE 4 CENT FALL IN SILVER PRICING AT THE COMEX YESTERDAY. THE CME NOTIFIED US THAT WE HAD A GOOD SIZED EFP ISSUANCE OF 1230 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) .

TODAY WE GAINED A GOOD SIZED: 1650 TOTAL OI CONTRACTS ON THE TWO EXCHANGES:

i.e 1230 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH A INCREASE OF 420 OI COMEX CONTRACTS. AND ALL OF THIS GAIN IN DEMAND HAPPENED WITH A SMALL 4 CENT LOSS IN PRICE OF SILVER AND A CLOSING PRICE OF $14.16 WITH RESPECT TO YESTERDAY’S TRADING. YET WE HAD A GIGANTIC AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY IN THE BIG JULY DELIVERY MONTH OF SLIGHTLY OVER 30 MILLION OZ, IN AUGUST ANOTHER BIG 6.065 MILLION OZ IN A NON ACTIVE MONTH AND NOW IN SEPTEMBER AN INITIAL MONSTROUS 30.345 MILLION OZ OF SILVER STANDING FOR DELIVERY… NOBODY IS PAYING ATTENTION TO THE HUGE NUMBER OF PHYSICAL OUNCES STANDING FOR SILVER THESE PAST SEVERAL MONTHS.

In ounces AT THE COMEX, the OI is still represented by OVER 1 BILLION oz i.e. 1.054 MILLION OZ TO BE EXACT or 150% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT AUGUST MONTH/ THEY FILED AT THE COMEX: 291 NOTICE(S) FOR 1,455,000 OZ OF SILVER

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 243,411 CONTRACTS ON APRIL 9.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $16.51.

AND NOW WE RECORD FOR POSTERITY ANOTHER ALL TIME RECORD OPEN INTEREST AT THE COMEX OF 244.,196 CONTRACTS ON AUGUST 22/2018 AND AGAIN WHEN THIS RECORD WAS SET, THE PRICE OF SILVER WAS $14.78 AND LOWER IN PRICE THAN PREVIOUS RECORDS.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. AND NOW SEPT: AN INITIAL HUGE 30.345 MILLION OZ.

- HUGE RECORD OPEN INTEREST IN SILVER 243,411 CONTRACTS (OR 1.217 BILLION OZ/ SET APRIL 9/2018) AND NOW AUGUST 22/2018: 244,196 CONTRACTS, WITH A SILVER PRICE OF $14.78.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017

- RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT).

IN GOLD, THE OPEN INTEREST ROSE BY A good SIZED 3634 CONTRACTS UP TO 469,843 WITH THE GAIN IN THE COMEX GOLD PRICE/YESTERDAY’S TRADING (A RISE IN PRICE OF $3.05). THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A GOOD SIZED 4749 CONTRACTS:

OCTOBER HAD 0 EFP’S ISSUED AND, DECEMBER HAD AN ISSUANCE OF 4749 CONTACTS AND ALL OTHER MONTHS ZERO. The NEW COMEX OI for the gold complex rests at 469,843. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE AN STRONG SIZED OI GAIN IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 8,383 CONTRACTS: 3634 OI CONTRACTS INCREASED AT THE COMEX AND 4749 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN: 8,383 CONTRACTS OR 838,300 OZ = 26.07 TONNES. AND ALL OF THIS HUGE DEMAND OCCURRED WITH A TINY GAIN IN THE PRICE OF GOLD/ YESTERDAY TO THE TUNE OF $3.05

YESTERDAY, WE HAD 5303 EFP’S ISSUED.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF SEPT : 30,034 CONTRACTS OR 3,003,400 OZ OR 93.41 TONNES (4 TRADING DAYS AND THUS AVERAGING: 7509 EFP CONTRACTS PER TRADING DAY OR 750,900 OZ/ TRADING DAY),,

TO GIVE YOU AN IDEA AS TO THE HUGE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 12 TRADING DAYS IN TONNES: 93.41 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2017, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 2555 TONNES

THUS EFP TRANSFERS REPRESENTS 93.41/2550 x 100% TONNES = 3.66% OF GLOBAL ANNUAL PRODUCTION SO FAR IN JULY ALONE.***

ACCUMULATION OF GOLD EFP’S YEAR 2018 TO DATE: 5,290.36* TONNES *SURPASSED ANNUAL PROD’N

ACCUMULATION OF GOLD EFP’S FOR JANUARY 2018: 653.22 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR FEBRUARY 2018: 649.45 TONNES (20 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR MARCH 2018: 741.89 TONNES (22 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR APRIL 2018: 713.84 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR MAY 2018: 693.80 TONNES ( 22 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR JUNE 2018 650.71 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR JULY 2018 605.5 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR AUG. 2018 488.54 TONNES (23 TRADING DAYS)

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A VERY STRONG SIZED INCREASE IN OI AT THE COMEX OF 3634 WITH THE GAIN IN PRICING ($3.05 THAT GOLD UNDERTOOK YESTERDAY) // . WE ALSO HAD A STRONG NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 4749 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 4749 EFP CONTRACTS ISSUED, WE HAD A GAIN OF 8383 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

4749 CONTRACTS MOVE TO LONDON AND 3634 CONTRACTS INCREASED AT THE COMEX. (in tonnes, the GAIN in total oi equates to 26.07 TONNES). ..AND THIS HUGE DEMAND OCCURRED WITH A TINY GAIN OF $3.05 IN YESTERDAY’S TRADING AT THE COMEX.

we had: 63 notice(s) filed upon for 6300 oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD DOWN $3.75 TODAY: /

A CHANGE IN GOLD INVENTORY AT THE GLD/ ANOTHER WITHDRAWAL OF 1.48 TONES

/GLD INVENTORY 745.44 TONNES

Inventory rests tonight: 745.44 tonnes.

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

SLV/

WITH SILVER DOWN 2 CENTS TODAY

A REAL SHOCKER:

WE HAD A HUGE DEPOSIT OF: 3.008 MILLION OZ INTO THE SLV

/INVENTORY RESTS AT 332.717 MILLION OZ.

NOTE THE DIFFERENCE BETWEEN THE GLD AND SLV: THE CROOKS CAN RAID GOLD BECAUSE THEY DO HAVE SOME PHYSICAL. THEY DO NOT RAID SILVER PROBABLY BECAUSE THERE IS NO REAL SILVER INVENTORIES BEHIND THEM

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER ROSE BY A SMALL SIZED 420 CONTRACTS from 210,042 UP TO 210,462 AND MOVING A LITTLE CLOSER TO THE NEW COMEX RECORD SET LAST MONTH AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 1 1/3 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89. AS YOU CAN SEE, WE HAVE RECORD HIGH OPEN INTERESTS IN SILVER ACCOMPANIED BY A CONTINUAL LOWER PRICE WHEN THAT RECORD WAS SET…..

.

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

0 EFP CONTRACTS FOR SEPTEMBER, 1230 CONTRACTS FOR DECEMBER AND AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 1230 CONTRACTS . EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI GAIN AT THE COMEX OF 420 CONTRACTS TO THE 1230 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A NET GAIN OF 1650 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES: 8.250 MILLION OZ!!! AND YET WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESSED A FINAL STANDING OF GREATER THAN 30 MILLION OZ FOR JULY, A STRONG 6.065 MILLION OZ FOR AUGUST.. AND NOW A HUGE 30.345 MILLION OZ INITIALLY STAND FOR SILVER IN SEPTEMBER….

RESULT: A SMALL SIZED INCREASE IN SILVER OI AT THE COMEX DESPITE THE 4 CENT PRICING LOSS THAT SILVER UNDERTOOK IN PRICING YESTERDAY. BUT WE ALSO HAD A GOOD SIZED 1230 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR SEPTEMBER, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i) FRIDAY MORNING/ THURSDAY NIGHT: Shanghai closed UP 10.71 POINTS OR 0.40% /Hang Sang CLOSED DOWN 1.35 POINTS OR 0.01%/ / The Nikkei closed DOWN 180.88 POINTS OR 0.80%/Australia’s all ordinaires CLOSED DOWN 0.25% /Chinese yuan (ONSHORE) closed DOWN at 6.8425 AS POBC RESUMES SLIGHTLY ITS HUGE DEVALUATION /DELEGATION COMING TO THE USA TO SEE TRUMP IN NOVEMBER/Oil DOWN to 67.86 dollars per barrel for WTI and 76.67 for Brent. Stocks in Europe OPENED RED //. ONSHORE YUAN CLOSED DOWN AT 6.8425 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.8480: HUGE DEVALUATION/PAST SEVERAL DAYS RESUMES// TRADE TALKS NOT DOING TOO GOOD : /ONSHORE YUAN TRADING STRONGER AGAINST OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

3A/NORTH KOREA/SOUTH KOREA

i)North Korea/South Korea/USA/

b) REPORT ON JAPAN

3 C/ CHINA

i)China intercepts a British warship in the Parcel Islands, in international waters as they claim expanded territorial rights. The uSA is not amused

( zerohedge)

(courtesy zerohedge)

4/EUROPEAN AFFAIRS

i)Mainland China orders NHA to sell its entire stake in Deutsche bank and that sends its stock southbound.

( zerohedge)

ii)This could present many problems. Danish owned Danske bank in Estonia laundered an astonishing 150 billion dollars as a criminal investigation has been launched. This comes 6 months after neighbour Latvian bank ABLV was also caught dealing in bribery and money laundering

( zerohedge)

iii)An excellent paper from Michael Harnett of Bank of America. In 1998 we had contagion but the stimulus to that contagion was the piercing of the bubble in Japan. That set of Japan into a two decade period of deflation. The contagion of 2018 is missing one ingredient…what will be the big piercing of a bubble. His answer: Europe with it’s huge debt and now the ECB willing to stop the purchase of sovereign bonds from which those in the southern half of Europe will certainly fell the pain

( zerohedge)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

i)Iraq/USA

Last night the Green zone was under attack when at least 3 mortars struck near the USA embassy gate in the heart of the Iraqi capital.

( zerohedge)

ib )The Sunni denominated Basra witnesses the storming of the Iranian embassy in the oil rich area. This follows shia forces shelling the Green zone inside the capital of Baghdad

( zerohedge)

ii)SYRIA/USA

Trump does another 180 degree shift and now calls on a regime change in Syria

( zerohedge)

iv)Iran

The economy in Iran is tanking faster than a speeding bullet as the Riyal reaches 150,000 to one and many staple goods disappear like diapers

(courtesy zerohedge)

6. GLOBAL ISSUES

7. OIL ISSUES

8 EMERGING MARKET ISSUES

9. PHYSICAL MARKETS

i)The gold market intervention in June by the BIS translates into a loss of 100 dollars per oz

( Robert Lambourne/GATA)

ii)The next stage for gold as there will be a realignment of monetary systems and that system will be backed by gold. This is why China and Russia have been massively buying gold

(courtesy Alasdair Macleod/GATA)

iii)My goodness: demand for gold in China is again on the rise with SGE withdrawals = demand coming in at 191 tonnes. If they continue on this pace, they will exceed 2200 tonnes of gold. To get the customer demand you must remove the sovereign gold addition. China now produces around 420 tonnes per year. We should also subtract around 100 tonnes for scrap gold. Thus demand from the Chinese citizens: 1680 tonnes per year and this gold will all come from the west.

( Lawrie Williams/Sharp’s Pixley)

iv)Good reason for the crooks to bash silver; silver demand surges enough to empty the Mint of their 2018 American eagles.

( Adrian Ash)

10. USA stories which will influence the price of gold/silver)

i)Market trading /GOLD/MARKET MOVERS:

MARKET TRADING

Dollar rises, yields rise on a red hot wage gain plus gain in hourly earnings

(courtesy zerohedge)

a)Supposedly the wage growth comes in red hot as they add 201,000 jobs above the 191,000 consensus. The key hourly earnings also game in red hot rising to .4% much higher than the expected .2%. The dollar rises, gold falls, and yields spike (see above)

( zerohedge)

iv)SWAMP STORIES

a)The FBI hid the fact that on wiretaps, Russia thought Carter Page was an “idiot” and unworthy of recruiting. These facts were left out of the FISA applications

( zerohedge)

b)Guiliani states (and he is correct to do so) that Trump will not answer any questions about obstruction

c)Trump on the warpath as he demands Sessions to investigate that anonymous Op-Ed. He is also looking at legal action. I personally do not think it is anybody at the senior level. I agree with Craig Roberts that it was written by a deep stater like Brennan or Rosenstein(courtesy zerohedge)

Let us head over to the comex:

The next active delivery month after August for silver is September and here the OI FELL by 332 contracts DOWN to 1110.

We had 291 notices filed on yesterday so we lost 41 number of contracts or 205,000 oz will not stand at the comex as these guys accepted a fiat bonus on top of a London based forwards. For the past 17 months starting in April 2017, we have been witnessing on a constant basis queue jumping as the commercials seek physical silver immediately after first day notice. Today after a one day hiatus, queue jumping took a little holiday.

October gained 28 contracts to stand at 675. November saw a gain of 0 contracts to stand at 14.

ON FIRST DAY NOTICE FOR THE SEPT/2017 SILVER CONTRACT MONTH: 20.515 MILLION OZ STOOD FOR DELIVERY AND BY MONTH’S END: A HUGE 32.875 MILLION OZ WAS THE FINAL STANDING AS WE WERE WELL INTO THE PHENOMENON OF QUEUE JUMPING IN SILVER. THUS WE ARE WAY AHEAD OF LAST YEAR AS ALREADY WE HAVE 30.345 MILLION OZ OF SILVER INITIALLY STAND. WE WILL NO DOUBT PASS LAST YEAR’S TOTAL OF 32.875 MILLION OZ ONCE SEPTEMBER ENDS AS THE BANKS SCRAMBLE FOR PHYSICAL SILVER.

| Gold COT Report – Futures | ||||||

| Large Speculators | Commercial | Total | ||||

| Long | Short | Spreading | Long | Short | Long | Short |

| 199,762 | 213,259 | 55,455 | 168,732 | 162,207 | 423,949 | 430,921 |

| Change from Prior Reporting Period | ||||||

| -7,608 | 2,826 | -5,369 | 3,151 | -11,636 | -9,826 | -14,179 |

| Traders | ||||||

| 163 | 107 | 81 | 54 | 47 | 255 | 199 |

| Small Speculators | © GoldSeek.com | |||||

| Long | Short | Open Interest | ||||

| 49,169 | 42,197 | 473,118 | ||||

| 3,661 | 8,014 | -6,165 | ||||

| non reportable positions | Change from the previous reporting period | |||||

| COT Gold Report – Positions as of | Tuesday, September 4, 2018 | |||||

our large speculators

those large specs who have been long in gold pitched (transferred) a huge 7608 contracts from their long side

those large specs who have been short in gold added 2826 contracts to their short side.

specs go net short by 10,400 contracts.

our commercials

those commercials who have been long in gold added 3151 contracts to their long side

those commercials who have been short in gold covered a huge 11,635 contracts

commercials go net long by 14,500 contacts

our small speculators.

those small specs who have been long in gold added 3661 contracts to their long side

those small specs who have been short in gold added 8014 contracts to their short side

Conclusions: the specs have never been this net short and commercials have never been this net long at the comex

however we do not know what happened to all of those EFP issuance.

silver COT

| Silver COT Report: Futures | |||||

| Large Speculators | Commercial | ||||

| Long | Short | Spreading | Long | Short | |

| 83,061 | 112,035 | 16,989 | 81,421 | 66,808 | |

| -3,479 | 8,897 | -4,065 | -6,117 | -19,313 | |

| Traders | |||||

| 107 | 80 | 42 | 46 | 33 | |

| Small Speculators | Open Interest | Total | |||

| Long | Short | 212,391 | Long | Short | |

| 30,920 | 16,559 | 181,471 | 195,832 | ||

| -1,277 | -457 | -14,938 | -13,661 | -14,481 | |

| non reportable positions | Positions as of: | 172 | |||

our large speculators

those large specs who have been long in silver pitched (transferred) 3479 contracts from their long side

those large specs who have been short in silver added a huge 8897 contracts to their short side

our commercials

those commercials who have been long in silver pitched (transferred) 6117 contracts from their long side

those commercials who have been short in silver covered (transferred) a huge 19313 contracts from their short side.

our small speculators.

those small specs who have been long in silver pitched (transferred) 1277 contracts from their long side

those small specs who have been short in silver covered (transferred) 457 contracts from their short side.

wow!! this is unbelievable

the speculators are now at record levels of net short

and the commercials are now at record levels of net long

Major gold/silver trading /commentaries for FRIDAY

GOLDCORE/BLOG/MARK O’BYRNE.

Gold Remains An “Excellent Way to Hedge” for Longer Term – BNP Interview

– “Why hedge because everything is going straight up”?

– Now “is exactly the time when should hedge” as volatility in U.S. markets is low

– “September is the most dangerous month of the year for equities”

– Gold is an “excellent way to hedge for the longer term against the possibility that both equities and bonds go down together at some point and that is quite likely in the next 12 months…

– “Hedging is a form of insurance. You want to buy it when it is cheap and you hope never to use it”

– “The best time to hedge is when prices are low”

Watch Bloomberg Video of BNP Paribas’ global head of equity derivative strategy Edmund Shing on hedging the U.S. markets and gold as a long term hedge and insurance

News and Commentary

Gold rises on dollar weakness, physical demand (Reuters.com)

Asian Stocks Head for One-Year Low, Yen Advances (Bloomberg.com)

Nasdaq falls as U.S. lawmakers grill Facebook, Twitter executives (Reuters.com)

US Mint Gold Coins sales sink in August (ScrapRegister.com)

U.S. Trade Gap Widens Most Since 2015; China Deficit Hits Record (Bloomberg.com)

Source: Bloomberg.com

ASIA’s super rich advised to add more gold to their portfolios (SCMP.com)

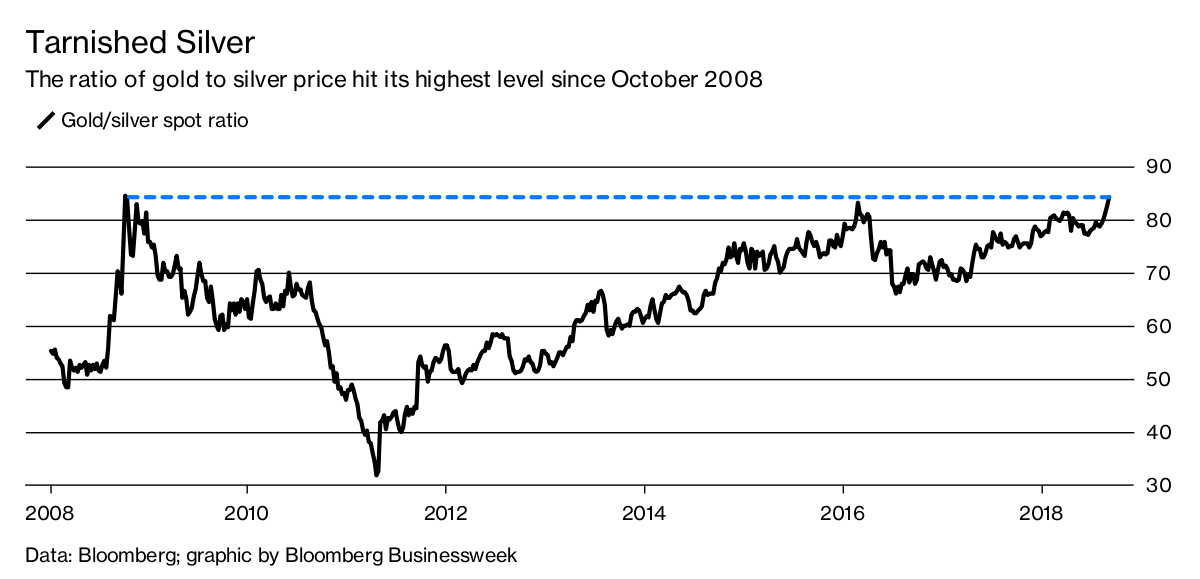

Gold And Silver Are Acting Like It’s 2008. They May Be Right (DollarCollapse.com)

Gold’s Ratio to Silver Hits Its Highest Level Since 2008 (Bloomberg.com)

Emerging-Market Contagion Fear Sparks Deepening Rout: Inside EM (Bloomberg.com)

Why Pain in Argentina And Turkey Is Hurting Indonesia (Bloomberg.com)

America’s Finances Seem Fishy (BonnerAndPartners.com)

Listen on SoundCloud , Blubrry & iTunes. Watch on YouTube below

Gold Prices (LBMA AM)

05 Sep: USD 1,194.70, GBP 932.46 & EUR 1,031.74 per ounce

04 Sep: USD 1,195.75, GBP 932.57 & EUR 1,034.20 per ounce

03 Sep: USD 1,201.70, GBP 933.00 & EUR 1,035.75 per ounce

31 Aug: USD 1,206.85, GBP 927.58 & EUR 1,034.03 per ounce

30 Aug: USD 1,202.35, GBP 924.25 & EUR 1,028.49 per ounce

29 Aug: USD 1,204.30, GBP 935.14 & EUR 1,032.33 per ounce

Silver Prices (LBMA)

05 Sep: USD 14.17, GBP 11.05 & EUR 12.22 per ounce

04 Sep: USD 14.25, GBP 11.11 & EUR 12.33 per ounce

03 Sep: USD 14.53, GBP 11.27 & EUR 12.50 per ounce

31 Aug: USD 14.66, GBP 11.27 & EUR 12.56 per ounce

30 Aug: USD 14.67, GBP 11.27 & EUR 12.54 per ounce

29 Aug: USD 14.69, GBP 11.40 & EUR 12.60 per ounce

Recent Market Updates

– Video: Gold Surges To Record Highs In Emerging Market Currencies – New Highs In USD, EUR, GBP In the Coming Months?

– September Is The Best Month For Gold and Worst Month For Stocks

– Pound Investors Face Months of Volatility Into Brexit Endgame

– This Week’s Golden Nuggets

– Video: “Financial War” Deepens as Russia Buys Gold and Dollar Hegemony At Risk – Rickards on CNN

– Will Indebted Nations Globally Follow Venezuela Into Hyperinflation?

– End Of Dollar Hegemony May Happen Soon and Badly Impact Indebted America

– 10 Incredible Photos From Venezuela Show The Disastrous Risks Of Currency Devaluation

– This Week’s Golden Nuggets

– Video: Is Silver Set for a Massive Breakout?

– Banks Now Long Gold, Short Dollar. What Do They Know?

– Russia Buys 800,000 Ounces Of Gold In July

– Gold Season – Is This It?

Andrew Maguire’s Kinesis money which is a “bitcoin” but backed 100% by allocated gold and silver is set to go.

it think it would be a great idea to look at this!

please read at: https://kinesis.money/#/

(Andrew Maguire)

|

|

Dear Harvey Organ,

Thank you for your participation in our webinar on June 7th with our host and CEO of Kinesis, Thomas Coughlin.

The response we received has been incredible, we appreciate you taking the time to join us and hope you found it to be beneficial.

Due to such a high influx of questions we received we were unable to have them all answered. Nevertheless, if there was anything which requires more clarification, or you have a query which needs to be rectified, we invite you to join our telegram group:

We apologize for the technical issues we incurred during the webinar which resulted in it running a little over schedule, we hope that the next one we host will run seamlessly.

A video has been put together and uploaded onto our YouTube channel which can be found here:

Please share and subscribe to our YouTube channel to be notified of all the latest videos as they become available.

The rapid growth that we are currently experiencing has been incredible and with your support, is only going to get better.

We are working behind the scenes very hard to create a better experience for everyone involved! Stay tuned in as we have many more announcements to be released in the upcoming days.

Kind Regards,

|

Kinesis Money

a:C/O ILS Fiduciaries (IOM) Limited, First Floor,Millennium House, Victoria Road, Douglas, Isle of Man IM2 4RW

|

The following is self explanatory

(courtesy GATA/Chris Powell and Harvey Organ)

GATA asks bank regulator to check risks of gold

futures maneuver

Submitted by cpowell on Sun, 2018-06-10 16:17. Section: Daily Dispatches

12:21p ET Sunday, June 10, 2018

Dear Friend of GATA and Gold:

GATA has appealed to the U.S. comptroller of the currency, who has regulatory authority over banks, to review financial risks certain banks may have incurred through derivatives in the monetary metals markets, particularly through the recent heavy use of the “exchange for physicals” mechanism of settling gold and silver futures contracts on the New York Commodities Exchange.

The appeal was made in a letter sent May 5 to the comptroller, Joseph M. Otting, whose office is part of the U.S. Treasury Department, by your secretary/treasurer and GATA futures market consultant Harvey Organ.

“Exchange for physical” settlements of futures contracts long were considered emergency procedures when a seller was not able to deliver metal from an exchange-approved warehouse and wanted to settle with delivery elsewhere. But now such settlements appear to constitute most gold and silver futures settlements on the Comex. It is a strange development that appears to have been necessitated by the increasing difficulties of central banking’s gold and silver price suppression policy.

GATA has received no acknowledgment of the letter. Its text is below and a PDF copy of it is here:

http://www.gata.org/files/ComptrollerOfCurrencyLetter.pdf

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

* * *

May 5, 2018

Joseph M. Otting, Comptroller of the Currency

U.S. Treasury Department

400 7th Street, SW

Washington DC 20219

Dear Comptroller Otting:

Please let us bring to your attention financial risks to major banks involving their possibly unreported exposure to derivatives in the monetary metals markets.

In recent months gold and silver future contracts issued by U.S. banks on the New York Commodities Exchange have been moved off-exchange for delivery through a mechanism known as “exchange for physical” (EFP) contracts. Until recently use of this mechanism was considered an emergency procedure when a seller did not have access to metal for delivery through Comex warehouses. Now the mechanism seems to be in use for a large share of front-month contracts for which delivery is sought.

Here is an example that is happening at the Comex in the front active month of April for gold and the inactive delivery month of April for silver.

In gold, there were 229,436 EFP contracts for 713.64 tonnes, an average of 10,925 contracts and 1,092,500 ounces per trading day.

In silver, there were 77,150 EFP contracts for 385,750,000 ounces, an average of 3,673 contracts and 18,369,000 ounces per trading day.

London Bullion Market Association rules suggest that these contracts may not be reported to regulators. The LBMA’s bylaws say:

“Figures above exclude any contracts not subject to risk-based capital requirements, such as FX contracts with an original maturity of 14 days or less, futures contracts, written options, and basis swaps. Therefore, the total notional amount of derivatives by maturity will not add to the total derivatives figure in this table.”

We are told that these EFP contracts are transferred from the Comex to London as what are called “serial forwards” and their duration is always less than 14 days, which exempts them from being reported.

It is our understanding that in each quarter your office prepares a report detailing risk undertaken by the banks under the comptroller’s supervision.

These risks include derivatives undertaken by U.S. banks and other obligations that may cause a bank to fail. Our concern is that your office may not be aware of large unreported derivative exposure by banks.

Could you review this matter and let us know your conclusions?

Sincerely,

CHRIS POWELL

Secretary/Treasurer

HARVEY ORGAN

Consultant

Gold Anti-Trust Action Committee Inc.

7 Villa Louisa Road

Manchester, Connecticut 06043-7541

end

Finally, they replied and it was a complete brush off

(courtesy zerohedge)

Currency comptroller brushes off GATA’s inquiry on

gold, silver EFPs

Submitted by cpowell on Fri, 2018-08-10 15:37. Section: Daily Dispatches

11:35a ET Friday, August 10, 2018

Dear Friend of GATA and Gold:

The U.S. comptroller of the currency, a bank regulator, has declined GATA’s request to inquire into the strange explosion of the use of the emergency procedure of “exchange for physicals” in the settlement by banks of the gold and silver futures contracts they have sold on the New York Commodities Exchange.

Your secretary/treasurer and GATA’s consultant about the Comex, Harvey Organ, wrote to the comptroller, James M. Otting, on May 5, calling attention to the recent enormous use of EFPs, which implies derivatives risks being undertaken by U.S. banks that could cause the banks to fail:

http://www.gata.org/node/18303

“Our concern is that your office may not be aware of large unreported derivative exposure by banks,” GATA wrote.

As months passed without any acknowledgment from the comptroller’s office, your secretary/treasurer appealed to his U.S. representative, John B. Larson, D-Connecticut, to ask the comptroller’s office to reply. The congressman’s office made a second inquiry on Monday this week and today the comptroller’s office provided Larson with a copy of a reply written and mailed Wednesday.

The comptroller’s reply, signed by the deputy comptroller for public affairs, Bryan Hubbard, said only that the comptroller’s office has “dedicated examiners” at the largest banks who “continuously evaluate the credit, market, operational, reputation, and compliance risks of bank trading and derivative activities.”

The reply did not say anything about the use of the “exchange for physicals” procedure for settling futures contracts. That is, the reply was a begrudged brushoff and GATA’s letter would have been ignored completely if not for Representative Larson’s repeated intervention.

Of course GATA hardly expected a conscientious reply to its letter, the comptroller’s office being not an independent regulator but part of the Treasury Department, whose mandate includes administration of the Gold Reserve Act of 1934, which, as amended in the 1970s, authorizes the department’s Exchange Stabilization Fund to secretly intervene in and rig any market in the world, directly or through intermediaries:

https://www.treasury.gov/resource-center/international/ESF/Pages/esf-ind…

But there’s always value in demonstrating government’s lack of candor about what it is doing, especially in regard to the monetary metals.

A PDF copy of the reply from the comptroller’s office is posted at GATA’s internet site here:

http://www.gata.org/files/ComptrollerOfCurrencyReply-08-08-2018.pdf

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

The gold market intervention in June by the BIS translates into a loss of 100 dollars per oz

(courtesy Robert Lambourne/GATA)

Gold market intervention by BIS declines after $100 price plunge

Submitted by cpowell on Thu, 2018-09-06 14:59. Section: Documentation

By Robert Lambourne

Thursday, September 6, 2018

Gold swaps and gold derivatives undertaken by the Bank for International Settlements appear to have declined by about 24 percent in August, according to the bank’s statements of account for that month and July:

https://www.bis.org/banking/balsheet/statofacc180831.pdf

https://www.bis.org/banking/balsheet/statofacc180731.pdf

The information provided in the BIS’ monthly statements is not sufficient to calculate a precise amount of gold-related derivatives, including swaps, but the bank’s total estimated exposure as of August 31 was about 370 tonnes of gold, down 115 tonnes from the approximately 485 tonnes as of July 31.

The bank’s gold swaps and derivatives had increased by 17 percent from June through July. During this period the gold price fell by about $100 per ounce.

The BIS provides little information on what it is doing in the gold market, why, and for whom and refuses to answer questions about its activity in the market:

http://www.gata.org/node/17793

But it is evident that the bank continues to trade constantly in gold, and its secrecy engenders suspicion that the bank seeks to control the monetary metal’s price on behalf of its member central banks.

—–

Robert Lambourne is a retired business executive in the United Kingdom who consults with GATA about the involvement of the Bank for International Settlements in the gold market.

END

The next stage for gold as there will be a realignment of monetary systems and that system will be backed by gold. This is why China and Russia have been massively buying gold

(courtesy Alasdair Macleod)

Alasdair Macleod: Apocalypse, or not?

Submitted by cpowell on Thu, 2018-09-06 17:29. Section: Daily Dispatches

1:33p ET Thursday, September 6, 2018

Dear Friend of GATA and Gold:

Civilization is not heading for the apocalypse, GoldMoney research director Alasdair Macleod writes today, but rather toward a realignment of empires and monetary systems, away from domination by the United States and its dollar toward Asian power and the return of sound money — currencies backed by and convertible into gold.

But Macleod acknowledges that the transition won’t be smooth.

His analysis is headlined “Apocalypse, or Not?” and it’s posted at GoldMoney here:

https://www.goldmoney.com/research/goldmoney-insights/apocalypse-or-not-…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

Alasdair Macleod….

Apocalypse, Or Not?

Members of the American libertarian movement, particularly extremist preppers, are often associated with a belief that a complete breakdown in society is the only outcome from government economic policies and will lead to complete social disintegration. At the centre of their concerns is monetary destruction, with other issues, such as the erosion of personal freedom and the right to bear arms, important but peripheral. They cite history, particularly the hyperinflationary collapses, from Rome to Zimbabwe, and now Venezuela. They draw on Austrian economic theory, which fans their dislike of government and their expectation of total chaos.

Properly reasoned economic theory certainly reduces the science to one of black and white conclusions, which suits conclusion-jumpers. But the whole point of it is to explain society’s errors, so that they may be corrected. It is only by understanding the errors of state intervention and socialism, both communistic and fascist, that solutions can be found. Solutions then need to be applied, not taken into a mountain or forest retreat never to be implemented.

The real world does not work on black and white economic theories. It progresses along a muddled course, torn between statist mistakes and society’s unending patience with government intervention. Governments are the source of all wars and wealth destruction, but societies tolerate them. Philosophers have argued over this from Plato versus Aristotle onwards, and we are still here, two and a half millennia later, chewing over the same bones.

History records our philosophical chewing, and Man’s continuing conflict with and tolerances of the state. It records the rise and fall of kings, emperors, dictators and governments. Hermits and other preppers come and go, either unrecorded or, like Saint Simeon Stylites, noted as little more than historical footnotes. To future generations, prepping will almost certainly be a bygone curiosity, and humanity will continue despite government suppression.

This article is an attempt to rationalise an apparently apocalyptic future into how it is likely to evolve over the coming years. In the absence of a nuclear Armageddon, what we fear, more than anything else, is actually uncertainty and change.

Out with the old

Uncertainty and change are with us all the time. In a truly free market economy we embrace it because they are driven by our personal economic interests, and it is a continual process. But the desire for change is driven by us only in our role as consumers; as workers or businessmen facing competition for our existing labour and skills we tend to resist it. It is that side of us that a government taps into.

Modern governments, except where they are overtly mercantilist, don’t do change. Their support, indeed their reason for being, is based on anti-progressive lobbying from both establishment businesses and socialistic pressure groups. Government economists do not recognise progress, living in a stagnant world of historical statistics. Progressive change interferes with their certainties and is therefore never properly considered.

This is what the welfare states in the West have become, societies managed by anti-progressive governments, nominally responsible to their electorates, but in fact with a life of their own. The interests of governments have long since departed from those of consumers and increasingly conflict with their needs and wants. It is a process that has evolved to the current position over the last hundred years, when governments had understood their role should be strictly limited to identifiable national interests, when government employees deferred to the general public as their civil servants, and importantly, when the national currency was based on money chosen collectively by individuals.

It is therefore a much larger issue than just money. It is about the direction of political travel. For individuals it has become a prolonged road to serfdom, where power and personal freedom have been sequestered by the government from the consumer. The consumer has lost the right to keep his own income, and his preferences are now regarded by the state as subject to its control, to plan and dispose of as it sees fit.

The so-called free world was first ruled by the British and then by the Americans. The roots of both regimes were trade, protected by a government enforcing the rules of property ownership, the certainties of contract law and laws that protected individuals in their interpersonal relationships. As law-makers, governments now legislate to extend control over their peoples. And now the American government, in the name of American business, is even directing its own citizens not to buy from foreigners and is taxing them if they do so.

It is not the first time the state has interfered with our preferences in this way. The lurch into protectionism that led to the Smoot-Hawley Tariff Act of 1930 was one example, and the nationalisation policies of Britain’s post-war government another. These were errors from which a retreat proved possible. Today, the West’s democratic system has reached a point from which no ordered retreat back to free markets, to personal freedom and to governments which serve the people and not themselves, seems possible. Change will only come from the ultimate collapse of a system that promotes interests over freedom.

Transiting to the new

Western doomsters, seeing the contradictions around them and armed with little more than libertarian ideals, believe the world is coming to an impasse. They know it will end badly, and America’s resistance to decline by retreating into yet greater suppression of freedom confirms this view. The mistake is to assume nothing will replace the disintegration of the American state.

Money is the talisman for the doomsters’ vision. The destruction of paper currencies is inevitable, they say. Given these dissenters are very much American-based, their approbation is reserved for the dollar. But we should all take notice because the dollar is the reserve currency. That is to say, we measure our own currencies primarily against the dollar, and we use the dollar to settle our international trade. Our central banks tend to the view that they should generally manage their currencies in dollar terms. Therefore, if the dollar falls, we should all fall with it.

After a temporary bout of strength, concerns that the dollar will enter a terminal decline are spreading in some quarters. There are those who point to the seemingly limitless accumulation of unproductive debt, and the fact that the lessons from succeeding credit crises are always ignored. Today, the chatter is of a global monetary reset, with proposed solutions incorporating debt write-offs, the mobilisation of super-monies such as SDRs, and monetary applications of blockchain technology. The libertarians talk of total monetary failure and of gold, somehow rising from the ashes of the dollar’s immolation. All these solutions ignore wider issues. For the fact of the matter is we face the end of an empire. The American global empire is being superseded by an Asian phoenix.

The loss of influence to rivals is always painful. America’s geopolitical strategists feel acutely threatened by the Russian-Chinese partnership. America’s backing for Georgia in 2008, stimulating colour revolutions in Ukraine, and a proxy war over Syria have all failed to destabilise Russia. Afghanistan and Iran are works in progress, or rather non-progress. In the past, America could rely on unwavering support from her NATO allies. One of them, Turkey, has now all but defected, and the Europeans are breaking ranks on sanctions over Iran and Russian energy imports.

American trade tariffs against China must also be regarded in this light. Recent moves to retain influence in key African nations as well are too late. China is already the largest infrastructure provider to sub-Saharan Africa by far, and she is not making the mistake of just giving money to African politicians. The politicians get their money from extended aid and new donations dressed up as trade deals from America and Britain, as they always have. The West cannot even buy respect, let alone influence, because the Chinese are doing the real work.

America never had very much influence in sub-Saharan Africa anyway. Instead, she focused on North Africa and the Middle East. Regimes from Iraq to Libya have been changed at America’s behest.

It was the agreement with Saudi Arabia in 1974 that oil would be sold exclusively for dollars that legitimised the dollar as the global trade and pricing currency. When Iraq proposed to sell oil for euros, it was invaded, and Saddam Hussein deposed and executed. When Libya proposed a new central African currency based on gold, civil war suddenly broke out and Ghadaffy was hounded and shot by a mob. The message was simple: don’t mess with America and the dollar.

This has now changed. China is buying oil for yuan, and there’s nothing America can do about it. America has tried to destabilise Russia with dollar sanctions, unsuccessfully. President Trump has leant on Angela Merkle not to do business with Russia and Iran. He has also threatened this NATO ally with trade tariffs. The message to Germany is clear, the alliance with America no longer applies. Consequently, Germany is quietly turning her back on America and continuing to trade with Russia. The old threats just don’t work anymore.

China and Russia have long planned to jointly lead Asia and Eastern Europe into a new economic bloc. The Shanghai Cooperation Organisation was set up firstly to coordinate security and anti-terrorist activities, but this morphed into unifying Asian trade. China is building the infrastructure to make the Asian continent the most powerful economic unit ever seen. No doubt she will rebuild Syria when the Americans have left. No wonder America’s strategic planners are worried.

Post-apocalypse currencies

In 1983, China enacted the Regulations of the PRC on the Control of Gold and Silver, giving the People’s Bank of China the responsibility for all the nation’s gold and silver resources under Article 4 of those regulations. In 2002, the Shanghai Gold Exchange was launched by the PBOC and private individuals were permitted to own gold. It is clear that the PBOC over two decades had accumulated sufficient gold to then allow ordinary citizens to do the same. China even advertised the merits of gold ownership, encouraging individuals to accumulate gold. We have no knowing how much gold the Chinese state had accumulated, but given contemporary gold prices, inward dollar flows in the 1980s and trade surpluses thereafter, China could easily have accumulated a strategic reserve of 20,000 tonnes before the public was authorised to acquire gold. We may never know the true figure. We do know that in addition to the state’s accumulation, some 17,000 tonnes have been withdrawn from SGE vaults by the general public.

The Russian government has belatedly begun to accumulate gold reserves, and has now declared reserves of 2,170 tonnes, and importantly, has reduced its dollar reserves substantially to do so. Even India, a staunchly Keynesian state, has finally started accumulating additional gold reserves, having repeatedly tried and failed to encourage its own people to transfer gold to the government. Its nationals have probably accumulated over 10,000 tonnes since the Gold Control Act was repealed in 1990. Other Asian states from Turkey to Mongolia have all been building official gold reserves as well.

There can be no doubt that Asians and their governments not only hold the traditional view that gold is the ultimate money, but their coordinated physical accumulation is strong circumstantial evidence that gold will have an official monetary role in future. In this context, even Germany’s gold policy is interesting. We know the Bundesbank traditionally retains a strong anti-inflation bias and is unlikely to view the ECB’s management of the euro with favour. Furthermore, Germany decided to repatriate some of her gold reserves held at the New York Fed. After an embarrassing row with the US authorities, the gold sought was eventually returned. Various motives were ascribed to this move by Germany, but perhaps the most interesting possibility – which was never reported – is that Germany’s deep state was looking to the East.

Other European nations, particularly France and Italy, retain substantial gold reserves, which places them in a good position to adapt to a Eurasian world without the dollar. We can see that a future without it, and without other fiat currencies backed by nothing other than dollar reserves is certainly possible. It will involve enormous challenges, not least for governments relying on inflationary financing. To secure sound money, governments will be forced to discard socialism and embrace freer markets to bring their own financial demands under control. Those that don’t could rapidly descend into an Argentinian or even a Venezuelan monetary hell.

The US, which still records the largest official reserves, can also stabilise the dollar by offering gold backing and convertibility. To do so would require a significantly higher gold price, as indeed would be the situation for China’s yuan. But it also requires an enormous leap in official imagination, not only concerning gold’s reintroduction as backing for the dollar, but over America’s imperial role. It requires an acceptance that America can never win the geopolitical war with China and Russia, and must accept a diminished global status, just as Britain did when she rapidly shed her colonies in the 1960s.

It is hard to see America giving up her hegemony willingly, and therefore it will be down to events. America and other welfare states also face a transition into more free-market oriented economies with considerably less state intervention. That will not be easy either. Furthermore, there is no guarantee Russia and China will take on the mantle of world domination successfully, but we can be reasonably certain they have planned for this eventuality for a long time.

In the absence of a transformation towards sound money, the loss of purchasing power for pure fiat money will not be a smooth process. The next credit crisis, itself an event of which we can be sure, will almost certainly be met with lower interest rates and more quantitative easing, designed to support the banks with new money and to finance rocketing government deficits. State-issued currencies are bound to accelerate in their decline following this renewed inflation of supply, but for currencies to really collapse requires the public to change its preferences in favour of goods and totally against fiat money. In practice, the public tends to hold onto their belief in state money longer than might seem reasonable, in the hope that its purchasing power will stabilise.

It will be at the next credit crisis, if not before, that China and Russia will reveal their plans to protect their currencies from a financial and currency collapse in the West.

Conclusion

The prospects for fiat currencies and welfare states are not good, but it is a mistake to think homo economicus will sink with them. The views of the super-bears appear to be fundamentally parochial, particularly among the preppers in America. Instead of society’s destruction, we face a period of seismic change, notably the rise of Asia as the centre for global economic power.

Asia’s two major currencies, the yuan and the rouble, will not survive in their current form. They will have to be backed by gold, but fortunately for the world this has long been China’s backstop plan, and Russia is now belatedly acquiring the gold necessary to back the rouble as well. Depending how China and Russia go about it, this could easily be achieved with current levels of gold backing and a somewhat higher gold price.[i]

America could save the dollar by following suit. She probably has sufficient gold reserves, but to do so requires her to abandon almost everything the government and the Fed currently believe in and is therefore only likely to happen under duress.

But our central conclusion is that we will survive, and to retreat into mountain and jungle hideaways to escape an apocalypse is a mistake. We do not face a new Dark Age. What we do face are some home truths about unsound money, bringing with them considerable uncertainty and change.

[i] I wrote about this here: https://www.goldmoney.com/research/goldmoney-insights/gold-s-monetary-rehabilitation

_

Fed rejects bank for being too safe

Submitted by cpowell on Thu, 2018-09-06 17:40. Section: Daily Dispatches

1:49p ET Thursday, September 6, 2018

Dear Friend of GATA and Gold:

Bloomberg News opinion columnist Matt Levine today reports that the Federal Reserve is blocking the bid of a bank recently formed in Connecticut to give ordinary bank depositors access to the much higher rate of interest paid by the Fed to regular banks.

The availability to ordinary depositors of such a mechanism, Levine writes, might overthrow the banking business as currently constituted, since ordinary depositors then might flee regular banks to enjoy the risk-free higher interest now reserved for those banks by the Fed.

The Fed’s obstruction of the new bank’s concept seems to confirm longstanding suspicions that the central bank’s primary objective is to serve the banking industry rather than the people.

Levine’s commentary is headlined “Fed Rejects Bank for Being Too Safe” and it’s posted at Bloomberg News here:

https://www.bloomberg.com/view/articles/2018-09-06/fed-rejects-bank-for-…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

My goodness: demand for gold in China is again on the rise with SGE withdrawals = demand coming in at 191 tonnes. If they continue on this pace, they will exceed 2200 tonnes of gold. To get the customer demand you must remove the sovereign gold addition. China now produces around 420 tonnes per year. We should also subtract around 100 tonnes for scrap gold. Thus demand from the Chinese citizens: 1680 tonnes per year and this gold will all come from the west.

(courtesy Lawrie Williams/Sharp’s Pixley)

LAWRIE WILLIAMS: Chinese gold demand on the rise

Contrary to media reports suggesting weak Chinese gold demand based primarily on a big fall in gold imports from Hong Kong, the latest gold withdrawal figures out of the Shanghai Gold Exchange paint a very different picture. August gold withdrawals came to just short of 191 tonnes compared with 161 tonnes for the same month a year earlier and 144 tonnes in August 2016. Year to date SGE gold withdrawals at 1,366 tonnes are around 6% up on the first 8 months of 2017 and over 10% up on the corresponding 2016 figure. If this advantage is maintained for the remainder of the year the full year figure could well be in excess of 2,150 tonnes – and bring the full year total close to the second best year for SGE gold withdrawals ever.

| Month | 2018 | 2017 | 2016 | % change 2017-2018 | % change 2016- 2018 |

| January | 223.58 | 184.41 | 225.08 | +21.2% | -0.7% |

| February* | 118.42 | 148.24 | 107.60 | -20.1% | +10.7% |

| March | 192.61 | 192.25 | 183.24 | +0.2% | +5.1% |

| April | 212.64 | 165.78 | 171.40 | +28.3% | +24.1% |

| May | 150.58 | 138.08 | 147.28 | +9.1% | +2.2% |

| June | 140.59 | 155.51 | 138.51 | -9.6% | +1.5% |

| July | 137.41 | 144.71 | 117.58 | -5.0% | +16.9% |

| August | 190.59 | 161.41 | 144.44 | +18.1% | +32.0% |

| September | 214.24 | 170.90 | |||

| October* | 151.54 | 153.25 | |||

| November | 189.10 | 214.72 | |||

| December | 185.21 | 196.37 | |||

| Year to date | 1,366.43 | 1290.46 | 1235.13 | + 5.9% | +10.6% |

| Full Year | 2,030.48 | 1,970.37 |

Source: Shanghai Gold Exchange. Lawrieongold.com

* These months include week long New Year and Golden Week holiday periods

But back to the Hong Kong figures. The media made great play of the fact that July gold exports from Hong Kong to Mainland China were substantially down on the previous month – China’s July net gold imports via Hong Kong plunge 45 pct m/mwas the Reuters headline – and the article went on to make the very out-of-date comment that the Hong Kong figures serve as a proxy for total Chinese gold imports, which they have not done for some years now. Judging by known gold export figuresfrom countries which report these it is doubtful whether even half mainland China’s gold imports are routed through Hong Kong nowadays. The greater part now comes in via Beijing and Shanghai and perhaps other ports of entry.

It is true, though, that perhaps July was a weakish month for Chinese gold demand – but not significantly so as shown in the SGE withdrawal figures above. And, of course, August figures are likely to be much stronger with SGE gold withdrawals that month the highest for 3 years, although still well short of the record 2015 figure when withdrawals from the SGE totalled over 260 tonnes. In August.

Gold imports into China can be somewhat obscure, particularly where they involve the import of gold bearing concentrates for refining from Chinese-owned and other properties which have implemented deals direct with Chinese refiners. The latest of these is probably Polymetals’s big new Kyzyl gold mine in Kazakhstan which has just started up and is shipping its goldconcentrate directly into the Chinese mainland for refining. This is a world class operation and will, on its own, produce around 10 tonnes of gold a year from 2019. While 10 tonnes is not a hugely significant amount of gold in the context of annual Chinese gold imports, it will not show up in easily monitored statistics like those from Switzerland, Hong Kong, the UK, the U.S. and Australia all of which break down their gold exports on a country-by country basis. It is the sum of known gold imports, plus China’s own production (China is comfortably the world’s largest producer of gold) plus an allowance for scrap and imports from unknown sources as being close to the SGE annual withdrawals total which leads us to equate SGE gold withdrawals to Chinese total annual demand which should yet again total over 2,000 tonnes this year.

With the low gold price also seen as boosting demand in India, the world’s second largest gold consumer which, according to GFMS, has just recorded particularly strong gold imports in August – apparently a 15-month high, gold is perhaps performing more strongly than its COMEX- manipulated price might suggest. Hang in there. There should be better times ahead.

https://www.sharpspixley.com/articles/lawrie-williams- chinese-gold-demand-on-the-rise-_282915.html

06 Sep 2018

end

Good reason for the crooks to bash silver; silver demand surges enough to empty the Mint of their 2018 American eagles.

(courtesy Adrian Ash)

Silver Demand Surge empties Mint of 2018 American Eagle Silver Coins

September 7, 2018 |

Silver Demand Surge empties Mint of 2018 American Eagle Silver Coins

The U.S. Mint has temporarily sold out of its 2018 American Eagle Silver Coins and is currently in the process of producing more.

“This is to inform you that due to recent increased demand, the United States Mint has temporarily sold out of its inventories of 2018 American Eagle Silver Bullion Coins,” U.S. Mint said in a press release published on Thursday.

The announcement comes amidst the strongest silver sales from the U.S. Mint since the start of last year. In August, the U.S. Mint sold 1.53 million one-ounce American Eagle Silver coins, up 72% from the previous month.

In contrast, sales of American Eagle Gold coins fell to a four-month low in August, mirroring a decrease in sales from the same period last year.

While silver coins have done much better than gold coins, physical silver continues to lag in price performance. The gold-silver ratio has expanded to 84.75, while silver has fallen to two-year lows.

Peter Hug, director of Global Trading at Kitco, said that the wholesalers responded by raising premiums by as much as 25%.

“We think that the increase is temporary and may mitigate in about two weeks. We mention it for the investors that have grown weary of the silver market. For those that have thrown in the towel and want to exit their silver positions, the upside is that bid premiums have also gone higher,” he said in a commentary Thursday. – David Lin

Silver Demand Surge empties Mint of 2018 American Eagle Silver Coins

The United States Mint notified its authorized purchasers Sept. 6 that the bureau’s inventory of American Eagle silver coins is temporarily exhausted.

Mint spokesman Michael White released the notification memo that was sent to the authorized purchasers:

“This is to inform you that due to recent increased demand, the United States Mint has temporarily sold out of its inventories of 2018 American Eagle Silver Bullion Coins,” the memo reads. “All orders received prior to this communication shall be honored.

“The United States Mint is in the process of producing additional 2018 American Eagle Silver Coins. We will make these coins available for sale shortly.”

-END-

____________________________________________________________________________________________________________________________________________________________________________________

Your early FRIDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED DOWN TO 6.8425/HUGE DEVALUATION FOR THE PAST FOUR WEEKS RESUMES/CHINESE COMING TO USA FOR TRADE TALKS IN NOVEMBER //OFFSHORE YUAN: 6.8480 /shanghai bourse CLOSED UP 10.71 POINTS OR 0.40% /HANG SANG CLOSED DOWN 1.35 POINTS OR 0.01%

2. Nikkei closed DOWN 180.88 POINTS OR 0.80%/USA: YEN RISES TO 110.84/

3. Europe stocks OPENED DEEPLY IN THE RED

/USA dollar index FALLS TO 94.93/Euro FALLS TO 1.1619

3b Japan 10 year bond yield: REMAINS AT. +.11/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 110.84/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD IS NOW TARGETED AT .11%/JAPAN LOSING CONTROL OF THEIR BOND MARKET

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 67.86 and Brent: 76.67

3f Gold UP/JAPANESE Yen DOWN/ CHINESE YUAN: ON SHORE DOWN/OFF- SHORE: DOWN

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil DOWN for WTI and DOWN FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund RISES TO +.370%/Italian 10 yr bond yield DOWN to 2.99% /SPAIN 10 YR BOND YIELD DOWN TO 1.44%

3j Greek 10 year bond yield FALLS TO : 4.25

3k Gold at $1201.50 silver at:14.19 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble DOWN 14 /100 in roubles/dollar) 69.37

3m oil into the 67 dollar handle for WTI and 76 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 110.84DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 0.9659 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1223 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now POSITIVE territory with the 10 year RISING to +0.37%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.88% early this morning (THIS IS DEADLY TO ALL MARKETS). Thirty year rate at 3.06%

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

6. TURKISH LIRA: UP TO 6.4643

Global Stocks Slide On Tariff, Payrolls Suspense; Dollar

Drops

Global markets slumped in suspense over today’s main events, with S&P 500 futures falling along with European and Asian shares as investors awaited the latest move in the U.S.-China trade war after the comment period deadline passed overnight, even as August payrolls data loomed later on Friday. A weaker dollar helped emerging-market equities snap seven days of declines while EM currencies also rose.

World shares limped toward their worst week in almost six months on Friday, with Asia carving out a 14-month trough as investors braced for a new salvo of Sino-U.S. tariffs. A Thursday slump in U.S. chip stocks and reports that President Trump had also weighed a trade feud with Japan dragged on tech-heavy Asia overnight, while Europe’s main bourses faded after an initial attempt push higher, with the Stoxx 600 index falling to session low, down 0.3% reversing gains of 0.2%, driven lower by banks and as travel stocks declined. The Europe STOXX 600 was set to end the week with a 2.3% loss, its worst weekly performance since the end of March. Emerging market stocks have lost even more, some 3%, while U.S. equity futures pointed to a softer open following a negative session in Asia as equities fell in Japan, South Korea and Australia, while those in China posted gains.

European banks dropped 1% after Dow Jones reported that China asked HNA Group to exit Deutsche Bank, and ING said its license to operate could be threatened because of information technology and working system problems. As a result, the European Bank Index dropped lowest since November 2016.

Core European bonds fell, while Italian bonds gained on optimism the government will stick to European Union budget-deficit rules. In fact, Italian bonds headed for the biggest weekly gain in almost three months after the country’s finance chief reassured investors that this month’s budget won’t breach European Union rules.

Chinese blue chips had managed their 0.5 percent bounce as beaten-down health care stocks found buyers after taking a savaging in recent months amid vaccine scandals. MSCI’s broadest index of Asia-Pacific shares outside Japan had still lost 0.3% though, having earlier reached its lowest since mid-July last year. The Nikkei shed 0.8 percent, undermined by a rising yen and reports U.S. President Donald Trump could be contemplating taking on Japan over trade.

Trader nerves have been frayed further after the public comment period for proposed tariffs on an additional $200 billion worth of Chinese imports passed. The tariffs could now go into effect at any moment, although there was no clear timetable. China has warned of retaliation if Washington launches any new measures. Australia’s dollar, often used in as play on China’s fortunes due to its huge metals exports there, hit a 2-1/2 year low early on it Europe.

“It is all linked to the trade comment period expiring and now we are wondering what the implementation plan is going to be and how China is going to respond,” Saxo Bank’s head of FX strategy John Hardy said. “The Aussie dollar of course is a proxy within G10 for that,” he added, also pointing to shares in mining giants such as BHP trading down near key technical levels.

There was a silver lining after the MSCI Emerging Market Index jumped 0.4%, on course to snap a 7-day losing streak after falling into a bear market earlier in the week. China had closed higher overnight despite the tariff feud and Turkey’s lira and South Africa’s rand and Argentina’s peso all looked relatively calm early on.

Other emerging markets were trying to steady after a punishing week, with Indonesia and the Philippines still badly scarred by fears of capital flight following crises in Argentina and Turkey and the rumbling U.S.-China trade strains.

“It seems unlikely the tariffs are not implemented as the U.S. administration believes that they are winning the trade war and will be in a stronger position to negotiate if they put more pressure on China,” JPMorgan analysts wrote in a note. “The tech sector was also very weak overnight, with a slide in Micron of almost 10 percent and further weakness in the Chinese Internet ADRs.”

Elsewhere in EM, Brazil’s stocks and currency jumped after presidential candidate Jair Bolsonaro was stabbed during a street rally as traders bet that the attack will wind up creating sympathy for the candidate and help propel him into the second round of voting.

The Turkish lira advanced for a third day and Turkish bonds rallied as an emerging-market currency rout showed signs of easing.

With the EM rout fading for now, traders returned to more familiar themes: trade tensions and central banks. The Thursday deadline for public comment on proposed U.S. tariff hikes on an additional $200 billion of Chinese imports came and went without any fresh announcement from Washington. Eyes now turn to the U.S. payrolls report for August which is expected to show a robust rise of 191,000 – in part as July was temporarily depressed by the closure of the Toys R Us chain that month – which investors will watch with particular attention following dovish comments by New York Fed President John Williams on Thursday.

Still, as we noted previously, Goldman analysts cautioned that: “Despite employment indicators pointing to another strong report, it is worth noting that there is a tendency for August payrolls to initially disappoint and then be revised up noticeably later.”

Just as important will be figures on U.S. wages where a rise above the 0.2 percent forecasted would likely boost the dollar and pressure Treasury prices.

The dollar could do with the lift, having lost out to the safe-haven yen and Swiss franc. It was changing hands at 110.70 yen after falling 0.7 percent on Thursday, the sharpest one-day loss in seven weeks. Part of the decline came after a Wall Street Journal columnist reported Trump had mused about starting a trade fight with Japan. The dollar also hit a four-month low on the franc around $0.9645. Against a basket of currencies, the dollar index nudged lower to 94.939 and was heading for a fourth weekly drop.

Elsewhere in G-10 FX, the pound was little changed on the day and headed for its first weekly loss since mid-August. The euro was a shade higher at $1.1645, while sterling idled at $1.2939 amid ongoing uncertainty over Brexit negotiations. The dollar dipped and Treasuries moved lower before the U.S. payroll report on Friday, which will offer clues on the labor market’s health, the state of wage inflation and the pace of future Fed rate hikes.

In commodities, WTI and Brent futures were marginally higher in early European trade thus far with the former hovering around the USD 68/bbl level. According to Reuters trade flow data, US imports of crude oil from Saudi Arabia in August and September are set to reach the highest 2-month level early of 2017, citing the relatively cheap prices as advantageous for US refiners. News flow remains light for the complex, however, next week will see the release of the EIA short-term energy outlook, OPEC’s monthly report and IEA’s oil market report. Elsewhere, spot gold trades flat as the yellow metal flirts with the USD 1200/oz level ahead of the release of key US jobs data later, while copper underperforms amid ongoing trade-related concerns.

Market Snapshot

- S&P 500 futures down 0.08% to 2,876.75

- STOXX Europe 600 down 0.1% to 373.05

- MXAP down 0.2% to 160.23

- MXAPJ down 0.2% to 515.81

- Nikkei down 0.8% to 22,307.06

- Topix down 0.5% to 1,684.31

- Hang Seng Index down 0.01% to 26,973.47

- Shanghai Composite up 0.4% to 2,702.30

- Sensex up 0.2% to 38,302.99

- Australia S&P/ASX 200 down 0.3% to 6,143.81

- Kospi down 0.3% to 2,281.58

- Brent Futures up 0.2% to $76.68/bbl

- Gold spot up 0.1% to $1,201.26

- U.S. Dollar Index down 0.1% to 94.91

- German 10Y yield rose 0.8 bps to 0.363%

- Euro up 0.2% to $1.1645

- Brent Futures up 0.2% to $76.68/bbl

- Italian 10Y yield rose 2.9 bps to 2.694%

- Spanish 10Y yield fell 0.7 bps to 1.442%

Top Headline News from Bloomberg

- President Trump described his good relations with Japanese leadership in a Thursday phone call but added “of course that will end as soon as I tell them how much they have to pay,” according to an opinion piece from Wall Street Journal’s James Freeman, who added that it seems that Trump is still bothered by the terms of U.S. trade with Japan

- Some of America’s most prominent technology companies and retailers made a last-minute push to convince President Donald Trump to reverse course on a plan to impose tariffs on $200 billion in Chinese imports

- The Federal Reserve shouldn’t hesitate to invert the yield curve if raising short-term interest rates above long-term yields becomes necessary to achieve the U.S. central bank’s targets, New York Fed President John Williams said

- President Donald Trump said he’d like to shut down the U.S. government to try to force congressional Democrats to fund a wall along the Mexican border, but likely won’t do it before the midterm elections

- Mario Draghi will only just manage to raise the European Central Bank’s interest rates before his term as president ends in October 2019 amid continued risks from U.S. tariffs and Italian politics, according to a Bloomberg survey of economists

- Nafta talks between the U.S. and Canada have seemed upbeat, but are not expected to lead to a deal this week, a Canadian government official said, speaking on condition of anonymity

- Germany’s industry is experiencing further signs of strain amid trade tensions between the U.S. and the European Union, with production unexpectedly declining for a second consecutive month

- Euro-area GDP increased 0.4 percent in the second quarter, matching an earlier estimate

- Sweden’s two traditional political blocs are running neck-and-neck ahead of Sunday’s election, with neither close to a majority amid growing support for the nationalist Sweden Democrats

- French President Emmanuel Macron is preparing for a showdown between supporters of liberal values and proponents of nationalism as he bids to rally support ahead of European elections in May