GOLD: $1199.15 DOWN $4.05 (COMEX TO COMEX CLOSINGS)

Silver: $14.67 UP 0 CENTS (COMEX TO COMEX CLOSING)

Closing access prices:

Gold : 1197.40

silver: $14.64

I will try and deliver a commentary tomorrow but it will be light on stories. I will provide the essential comex data

For comex gold and silver:

OCT

NUMBER OF NOTICES FILED TODAY FOR OCT CONTRACT: 10 NOTICE(S) FOR 1000 OZ

Total number of notices filed so far for OCT: 848 for 100 OZ (2.6376 TONNES)

FOR OCTOBER

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

72 NOTICE(S) FILED TODAY FOR

360,000 OZ/

Total number of notices filed so far this month: 295 for 1,475,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: OPENING MORNING TRADE $6489: DOWN $46

Bitcoin: FINAL EVENING TRADE: $6463 DOWN $24

end

First Shanghai gold fix comes at 10 pm est

The second Shanghai gold fix: 2:15 pm

First Shanghai gold fix gold: 10 pm est: $not available

NY price at the same time:$xxx

PREMIUM TO NY SPOT: $xxx

XX

Second gold fix early this morning: $ NOT AVAILABLE

USA gold at the exact same time:$XXX

PREMIUM TO NY SPOT: $XXX

XXXX

China is controlling the gold market

WE WILL NOT PROVIDE LONDON FIXES AS THEY ARE NOT ACCURATE AS TO WHAT IS GOING ON AT THE SAME TIME FRAME.

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total OPEN INTEREST FELL BY A TINY SIZED 308 CONTRACTS FROM 200,7481UP TO 200,173 DESPITE YESTERDAY’S 20 CENT RISE IN SILVER PRICING AT THE COMEX. TODAY WE MOVED A LITTLE FURTHER FROM TO LAST MONTH’S RECORD SETTING OPEN INTEREST OF 244,196 CONTRACTS.

WE HAVE ALSO WITNESSED A LARGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY(WELL OVER 30 MILLION OZ AT THE COMEX FOR JULY , 6 MILLION OZ FOR AUGUST AND NOW JUST LESS THAN 31 MILLION OZ STANDING IN SEPTEMBER. AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A GIGANTIC SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP:

0 EFP’S FOR OCT. 4155 EFP’S FOR DECEMBER AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE: OF 4155 CONTRACTS. WITH THE TRANSFER OF 520 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 4155 EFP CONTRACTS TRANSLATES INTO 20.77 MILLION OZ ACCOMPANYING:

1.THE 20 CENT RISE IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR THE JUNE/2018 COMEX DELIVERY MONTH. (5.420 MILLION OZ); 30.370 MILLION OZ STANDING FOR DELIVERY IN JULY, FOR AUGUST: 6.065 MILLION OZ AND 39.505 MILLION OZ STANDING IN SEPT. AND 1,105,000 OZ STANDING IN OCTOBER.

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF SEPT:

7035 CONTRACTS (FOR 3 TRADING DAYS TOTAL 7035 CONTRACTS) OR 37.175 MILLION OZ: (AVERAGE PER DAY: 2345 CONTRACTS OR 11.725 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF SEPT: 37.175 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 5.31% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2018 TO DATE SILVER EFP’S: 2,250.69 MILLION OZ.

ACCUMULATION FOR JAN 2018: 236.879 MILLION OZ

ACCUMULATION FOR FEB 2018: 244.95 MILLION OZ

ACCUMULATION FOR MARCH 2018: 236.67 MILLION OZ

ACCUMULATION FOR APRIL 2018: 385.75 MILLION OZ

ACCUMULATION FOR MAY 2018: 210.05 MILLION OZ

ACCUMULATION FOR JUNE 2018: 345.43 MILLION OZ

ACCUMULATION FOR JULY 2018: 172.84 MILLION OZ

ACCUMULATION FOR AUGUST 2018: 205.23 MILLION OZ.

ACCUMULATION FOR SEPTEMBER 2018: 167,05 MILLION OZ

RESULT: WE HAD A SMALL SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 308 DESPITE THE 20 CENT RISE IN SILVER PRICING AT THE COMEX //YESTERDAY. THE CME NOTIFIED US THAT WE HAD A GIGANTIC SIZED EFP ISSUANCE OF 4155 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) .

TODAY WE GAINED A STRONG SIZED:3847TOTAL OI CONTRACTS ON THE TWO EXCHANGES:

i.e 4155 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH DECREASE OF 308 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED WITH A 20 CENT RISE IN PRICE OF SILVER AND A CLOSING PRICE OF $14.69 WITH RESPECT TO YESTERDAY’S TRADING. YET WE HAD A GIGANTIC AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY IN THE BIG JULY DELIVERY MONTH OF SLIGHTLY OVER 30 MILLION OZ, IN AUGUST ANOTHER BIG 6.065 MILLION OZ IN A NON ACTIVE MONTH AND NOW IN SEPTEMBER AN INITIAL MONSTROUS 39.505 MILLION OZ OF SILVER STANDING FOR DELIVERY… NOBODY IS PAYING ATTENTION TO THE HUGE NUMBER OF PHYSICAL OUNCES STANDING FOR SILVER THESE PAST SEVERAL MONTHS.

In ounces AT THE COMEX, the OI is still represented by OVER 1 BILLION oz i.e. 1.002 MILLION OZ TO BE EXACT or 143% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT AUGUST MONTH/ THEY FILED AT THE COMEX: 72NOTICE(S) FOR 360,000 OZ OF SILVER

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 243,411 CONTRACTS ON APRIL 9.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $16.51.

AND NOW WE RECORD FOR POSTERITY ANOTHER ALL TIME RECORD OPEN INTEREST AT THE COMEX OF 244,196CONTRACTS ON AUGUST 22/2018 AND AGAIN WHEN THIS RECORD WAS SET, THE PRICE OF SILVER WAS $14.78 AND LOWER IN PRICE THAN PREVIOUS RECORDS.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: AN INITIAL HUGE 39.505 MILLION OZ./AND NOW OCTOBER:1,105,000 oz

- HUGE RECORD OPEN INTEREST IN SILVER 243,411 CONTRACTS (OR 1.217 BILLION OZ/ SET APRIL 9/2018) AND NOW AUGUST 22/2018: 244,196 CONTRACTS, WITH A SILVER PRICE OF $14.78.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017

- RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT).

IN GOLD, THE OPEN INTEREST ROSE BY A CONSIDERABLE SIZED 5109CONTRACTS UP TO 459,776 WITh THE RISEIN THE COMEX GOLD PRICE/FRIDAY’S TRADING (A GAIN IN PRICE OF $15.80).THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED AN STRONG SIZED 13,121CONTRACTS: ALWAYS, ON THE WEEK PRIOR TO FIRST DAY NOTICE IN ANY ACTIVE MONTH WHETHER GOLD OR SILVER THE OI COLLAPSES. IT IS HERE THAT THE MIGRANTS RECEIVE THEIR FIAT BONUS FOR ENGAGING IN THIS EXERCISE. WE HAD THE FOLLOWING EFP ISSUANCE FOR TODAY:

OCTOBER HAD 0 EFP’S ISSUED AND, DECEMBER HAD AN ISSUANCE OF 13,121 CONTACTS AND ALL OTHER MONTHS ZERO. The NEW COMEX OI for the gold complex rests at 459,776. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE A GIGANTIC SIZED OI GAIN IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 18,230 CONTRACTS: 5109 OI CONTRACTS INCREASED AT THE COMEX AND 13,121 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN: 18,230 CONTRACTS OR 1,823,000 OZ = 56.70 TONNES. AND ALL OF THIS HUGE DEMAND OCCURRED WITH A RISE IN THE PRICE OF GOLD/ YESTERDAY TO THE TUNE OF $15.80

YESTERDAY, WE HAD 5966 EFP’S ISSUED.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF SEPT : 24,740CONTRACTS OR 2,474,000 OZ OR 76.95 TONNES (3 TRADING DAYS AND THUS AVERAGING: 8246 EFP CONTRACTS PER TRADING DAY OR 824,600 OZ/ TRADING DAY),,

TO GIVE YOU AN IDEA AS TO THE HUGE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 3 TRADING DAYS IN TONNES: 76.95 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2017, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 2555 TONNES

THUS EFP TRANSFERS REPRESENTS 76.95/2550 x 100% TONNES = 3.01% OF GLOBAL ANNUAL PRODUCTION SO FAR IN JULY ALONE.***

ACCUMULATION OF GOLD EFP’S YEAR 2018 TO DATE: 5,744.52* TONNES *SURPASSED ANNUAL PROD’N

ACCUMULATION OF GOLD EFP’S FOR JANUARY 2018: 653.22 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR FEBRUARY 2018: 649.45 TONNES (20 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR MARCH 2018: 741.89 TONNES (22 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR APRIL 2018: 713.84 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR MAY 2018: 693.80 TONNES ( 22 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR JUNE 2018 650.71 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR JULY 2018 605.5 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR AUG. 2018 488.54 TONNES (23 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR SEPT 2018 470.64 TONNES (19 TRADING DAYS)

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A CONSIDERABLE SIZED INCREASE IN OI AT THE COMEX OF 5109 WITH THE GAIN IN PRICING ($15,80 THAT GOLD UNDERTOOK YESTERDAY) //. WE ALSO HAD AN GOOD SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 13121 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 13121 EFP CONTRACTS ISSUED, WE HAD A HUMONGOUS GAIN OF 18230CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

13121` CONTRACTS MOVE TO LONDON AND 5109 CONTRACTS INCREASED AT THE COMEX. (in tonnes, the GAIN in total oi equates to 56.70 TONNES). ..AND ALL OF GOOD DEMAND OCCURRED WITH A GAIN OF $15.80 IN YESTERDAY’S TRADING AT THE COMEX.???

we had: 10 notice(s) filed upon for 1000 oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD DOWN $4.05 TODAY: /

A HUGE CHANGE IN GOLD INVENTORY AT THE GLD:

A LARGE WITHDRAWAL OF 6.18 TONNES

OBVIOUSLY THIS GOLD WAS USED TO THE RAID TODAY

/GLD INVENTORY 731.64 TONNES

Inventory rests tonight: 731.64 tonnes.

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

SLV/

WITH SILVER FLAT TODAY

STRANGE. WE HAD A MONSTROUS DEPOSIT FOR SILVER :

A HUGE 1.879 MILLION OZ AND THIS WAS DONE ON A ZERO PRICE GAIN???

/INVENTORY RESTS AT 334.791 MILLION OZ.

NOTE THE DIFFERENCE BETWEEN THE GLD AND SLV: THE CROOKS CAN RAID GOLD BECAUSE THEY DO HAVE SOME PHYSICAL. THEY DO NOT RAID SILVER PROBABLY BECAUSE THERE IS NO REAL SILVER INVENTORIES BEHIND THEM

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER FELL BY A TIN SIZED 308 CONTRACTS from 200,481 DOWN TO 200,173 AND MOVING A LITTLE FURTHER NEW COMEX RECORD SET LAST MONTH AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 1 1/3 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89. AS YOU CAN SEE, WE HAVE RECORD HIGH OPEN INTERESTS IN SILVER ACCOMPANIED BY A CONTINUAL LOWER PRICE WHEN THAT RECORD WAS SET…..

.

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

4155 CONTRACTS FOR DECEMBER AND AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 4155 CONTRACTS . EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI LOSS AT THE COMEX OF308CONTRACTS TO THE 4155 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A STRONG NET GAIN OF 3847 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES: 19.43 MILLION OZ!!! AND YET WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESSED A FINAL STANDING OF GREATER THAN 30 MILLION OZ FOR JULY, A STRONG 6.065 MILLION OZ FOR AUGUST.. A HUGE 39.505 MILLION OZ STANDING FOR SILVER IN SEPTEMBER…AND NOW 1.105 million OZ STANDING FOR THE NON ACTIVE MONTH OF OCTOBER.

RESULT: A SMALL SIZED DECREASE IN SILVER OI AT THE COMEX DESPITE THE 20 CENT PRICING GAIN THAT SILVER UNDERTOOK IN PRICING YESTERDAY.BUT WE ALSO HAD A STRONG SIZED 4155 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR SEPTEMBER, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

SHANGHAI CLOSED FOR A HOLIDAY

/Hang Sang CLOSED DOWN 35.12 POINTS OR 0.13% //The Nikkei closed DOWN 159.66 POINTS OR 0.66%/ Australia’s all ordinaires CLOSED UP 0.31% /Chinese yuan (ONSHORE) closed UP at 6.8689 AS POBC STOPS ITS HUGE DEVALUATION /DELEGATION COMING TO THE USA TO SEE TRUMP IN NOVEMBER CANCELLED/Oil UP to 75.23dollars per barrel for WTI and 84.7 for Brent. Stocks in Europe OPENED GREEN//. ONSHORE YUAN CLOSED DOWN AT 6.8686 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.8689: HUGE DEVALUATION/PAST SEVERAL DAYS STOPS// TRADE TALKS STOPPED : /ONSHORE YUAN TRADING STRONGER AGAINST OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

3A/NORTH KOREA/SOUTH KOREA

i)North Korea/South Korea/USA/

b) REPORT ON JAPAN

3 C/ CHINA

4/EUROPEAN AFFAIRS

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

6. GLOBAL ISSUES

7. OIL ISSUES

8 EMERGING MARKET ISSUES

i)ARGENTINA

9. PHYSICAL MARKETS

10. USA stories which will influence the price of gold/silver)

MARKET TRADING

iv)SWAMP STORIES

i

Let us head over to the comex:

We are now in the non active delivery month of October and here we had surprisingly gain of 3 contracts to stand at 82 contracts. We had 48 notices filed YESTERDAY so we gained 51 contracts or 255,000 oz will stand for delivery at the comex as these guys refused to accept a London based forward plus as well as a fiat bonus

After October, is the non active delivery month of November and here we lost 11 contracts down to 445 contracts. After November, we have a December contract and here we lost 542 contracts down to 168,703.

AND NOW COMPARISON FOR OCTOBER:

Major gold/silver trading /commentaries for WEDNESDAY

GOLDCORE/BLOG/MARK O’BYRNE.

Perth Mint’s Gold and Silver Bullion Coin Sales Soar In September

3, October

Perth Mint’s Gold and Silver Bullion Coin Sales Soar In September

via Reuters

Sales of gold products by the Perth Mint surged in September to their highest since January 2017, while silver sales more than doubled from August to mark an over two-year peak, boosted by lower bullion prices, the mint said on Wednesday.

Sales of gold coins and minted bars surged 61 percent from August to 62,552 ounces last month, the mint said in a blog post.

Gold sales in September rose about 35 percent from a year-ago period. Gold prices dropped 0.8 percent in September, declining for

a sixth consecutive month in their longest losing streak in two decades.

“We have experienced added interest in our bullion coins since the drop in price of both gold and silver during August. Some of this is down to the previously dormant U.S. market, which at last is showing signs of reawakening,” said Neil Vance, Group Manager, minted products, at Perth Mint.

Silver sales soared 151 percent from August to 1,305,600 ounces, their highest since March 2016. From a year earlier, sales advanced about 87 percent. Silver prices inched up 0.7 percent in September, after falling for three straight months, and marking an over 9 percent decline in the quarter ended September.

The Perth Mint refines more than 90 percent of newly mined gold in Australia, the world’s second-largest gold producer after China.

Gold prices edged up on Wednesday after gaining over 1 percent in the previous session, buoyed by safe-haven demand as Italy’s budget plan sets it on course for a potential clash with the European Union.

Period Gold (oz) Silver (oz)

(year-month)

2018-September 62,552 1,305,600

2018-August 38,904 520,245

2018-July 29,921 486,821

2018-June 16,847 229,280

2018-May 14,800 557,120

2018-April 15,161 458,655

2018-March 29,883 975,921

2018-Feb 26,473 992,954

2018-Jan 37,174 1,067,361

2017-Dec 27,009 874,437

2017-Nov 23,901 544,436

2017-Oct 44,618 999,425

2017-Sept 46,415 697,849

2017-Aug 23,130 392,091

2017-July 23,675 1,167,963

2017-June 19,259 1,215,071

2017-May 29,679 826,656

2017-April 10,490 468,977

2017-March 22,232 716,283

2017-Feb 25,257 502,353

2017-Jan 72,745 1,230,867

2016-Dec 63,420 430,009

2016-Nov 54,747 984,622

2016-Oct 79,048 1,084,213

2016-Sept 58,811 1,031,858

2016-Aug 14,684 376,461

2016-July 16,870 693,447

2016-June 31,368 1,220,817

2016-May 21,035 974,865

2016-April 47,542 1,161,766

2016-March 47,948 1,756,238

2016-Feb 37,063 1,049,062

2016-Jan 47,759 1,473,408

Listen on iTunes, SoundCloud & Blubrry. Watch on YouTube above

News and Commentary

Gold settles at nearly 2-week high amid Italy budget jitters, even as dollar gains (MarketWatch.com)

Gold prices rise as Italy uncertainty boosts safe-haven demand (Reuters.com)

Gold Prices Surge More Than 1%, Rise Above $1200 Level (Investing.com)

Gold jumps amid mild risk-off trade as dollar eases off highs (FXStreet.com)

Perth Mint’s Sept gold, silver sales soar (Reuters.com)

Source: ZeroHedge

“Gold Is Very Oversold And Due A Bounce” said GoldCore (MarketWatch.com)

Markets are cyclical – but how can you tell where we are in the cycle? (MoneyWeek.com)

Merkel’s End Could Spark EU Breakdown (ZeroHedge.com)

It Will End In Tears: World Stocks, Euro Slide As Italian Contagion Spreads (ZeroHedge.com)

Key metals player Bank of Nova Scotia admits rigging gold and silver futures (Gata.org)

Listen on SoundCloud , Blubrry & iTunes. Watch on YouTube below

Gold Prices (LBMA AM)

02 Oct: USD 1,192.65, GBP 919.77 & EUR 1,035.46 per ounce

01 Oct: USD 1,185.30, GBP 907.94 & EUR 1,021.02 per ounce

28 Sep: USD 1,183.50, GBP 906.44 & EUR 1,020.41 per ounce

27 Sep: USD 1,196.00, GBP 911.59 & EUR 1,020.91 per ounce

26 Sep: USD 1,198.80, GBP 910.49 & EUR 1,018.86 per ounce

25 Sep: USD 1,199.45, GBP 912.30 & EUR 1,019.77 per ounce

Silver Prices (LBMA)

02 Oct: USD 14.51, GBP 11.20 & EUR 12.59 per ounce

01 Oct: USD 14.55, GBP 11.16 & EUR 12.53 per ounce

28 Sep: USD 14.31, GBP 10.97 & EUR 12.35 per ounce

27 Sep: USD 14.42, GBP 10.98 & EUR 12.31 per ounce

26 Sep: USD 14.48, GBP 11.01 & EUR 12.32 per ounce

25 Sep: USD 14.29, GBP 10.86 & EUR 12.15 per ounce

Recent Market Updates

– “I’m Favouring Equities and Gold Over Bonds” – Stepek

– Poland Buys Gold For First Time In 20 years

– This Week’s Golden Nuggets – Central Banks, Goldman, Bank of America Positive On Undervalued Gold

– Central Banks Positivity Towards Gold Will Provide Long Term “Support To Gold Prices”

– Europe Unveils “Special Purpose Vehicle” With Russia and China To Bypass SWIFT, Jeopardizing Dollar’s Reserve Status

– Gold Set to Soar Above $1,300 – Goldman and Bank of America

– Goldnomics Podcast: Silver Guru – David Morgan – Silver and Gold Will Protect in the Coming Currency Collapse

– This Week’s Golden Nuggets – Dalio’s Dollar Crisis, Fitt’s U.S. Government “Missing” $21 Trillion and Silver Guru’s End of Empire

– Dalio Warns Of Dollar Crisis – “History Is Doomed To Repeat Itself”

– Silver Guru Video: “The End of Empire and End of Fiat Currencies”

– Silver Is ‘Undervalued’ Relative to Stocks, Bonds, Gold – GoldCore

– We Are In “Never Never Land” Accounting As U.S. Government Is “Missing” $21 Trillion

Andrew Maguire’s Kinesis money which is a “bitcoin” but backed 100% by allocated gold and silver is set to go.

it think it would be a great idea to look at this!

please read at: https://kinesis.money/#/

(Andrew Maguire)

|

|

Dear Harvey Organ,

Thank you for your participation in our webinar on June 7th with our host and CEO of Kinesis, Thomas Coughlin.

The response we received has been incredible, we appreciate you taking the time to join us and hope you found it to be beneficial.

Due to such a high influx of questions we received we were unable to have them all answered. Nevertheless, if there was anything which requires more clarification, or you have a query which needs to be rectified, we invite you to join our telegram group:

We apologize for the technical issues we incurred during the webinar which resulted in it running a little over schedule, we hope that the next one we host will run seamlessly.

A video has been put together and uploaded onto our YouTube channel which can be found here:

Please share and subscribe to our YouTube channel to be notified of all the latest videos as they become available.

The rapid growth that we are currently experiencing has been incredible and with your support, is only going to get better.

We are working behind the scenes very hard to create a better experience for everyone involved! Stay tuned in as we have many more announcements to be released in the upcoming days.

Kind Regards,

|

Kinesis Money

a:C/O ILS Fiduciaries (IOM) Limited, First Floor,Millennium House, Victoria Road, Douglas, Isle of Man IM2 4RW

|

The following is self explanatory

(courtesy GATA/Chris Powell and Harvey Organ)

GATA asks bank regulator to check risks of gold futures maneuver

Submitted by cpowell on Sun, 2018-06-10 16:17. Section: Daily Dispatches

12:21p ET Sunday, June 10, 2018

Dear Friend of GATA and Gold:

GATA has appealed to the U.S. comptroller of the currency, who has regulatory authority over banks, to review financial risks certain banks may have incurred through derivatives in the monetary metals markets, particularly through the recent heavy use of the “exchange for physicals” mechanism of settling gold and silver futures contracts on the New York Commodities Exchange.

The appeal was made in a letter sent May 5 to the comptroller, Joseph M. Otting, whose office is part of the U.S. Treasury Department, by your secretary/treasurer and GATA futures market consultant Harvey Organ.

“Exchange for physical” settlements of futures contracts long were considered emergency procedures when a seller was not able to deliver metal from an exchange-approved warehouse and wanted to settle with delivery elsewhere. But now such settlements appear to constitute most gold and silver futures settlements on the Comex. It is a strange development that appears to have been necessitated by the increasing difficulties of central banking’s gold and silver price suppression policy.

GATA has received no acknowledgment of the letter. Its text is below and a PDF copy of it is here:

http://www.gata.org/files/ComptrollerOfCurrencyLetter.pdf

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

* * *

May 5, 2018

Joseph M. Otting, Comptroller of the Currency

U.S. Treasury Department

400 7th Street, SW

Washington DC 20219

Dear Comptroller Otting:

Please let us bring to your attention financial risks to major banks involving their possibly unreported exposure to derivatives in the monetary metals markets.

In recent months gold and silver future contracts issued by U.S. banks on the New York Commodities Exchange have been moved off-exchange for delivery through a mechanism known as “exchange for physical” (EFP) contracts. Until recently use of this mechanism was considered an emergency procedure when a seller did not have access to metal for delivery through Comex warehouses. Now the mechanism seems to be in use for a large share of front-month contracts for which delivery is sought.

Here is an example that is happening at the Comex in the front active month of April for gold and the inactive delivery month of April for silver.

In gold, there were 229,436 EFP contracts for 713.64 tonnes, an average of 10,925 contracts and 1,092,500 ounces per trading day.

In silver, there were 77,150 EFP contracts for 385,750,000 ounces, an average of 3,673 contracts and 18,369,000 ounces per trading day.

London Bullion Market Association rules suggest that these contracts may not be reported to regulators. The LBMA’s bylaws say:

“Figures above exclude any contracts not subject to risk-based capital requirements, such as FX contracts with an original maturity of 14 days or less, futures contracts, written options, and basis swaps. Therefore, the total notional amount of derivatives by maturity will not add to the total derivatives figure in this table.”

We are told that these EFP contracts are transferred from the Comex to London as what are called “serial forwards” and their duration is always less than 14 days, which exempts them from being reported.

It is our understanding that in each quarter your office prepares a report detailing risk undertaken by the banks under the comptroller’s supervision.

These risks include derivatives undertaken by U.S. banks and other obligations that may cause a bank to fail. Our concern is that your office may not be aware of large unreported derivative exposure by banks.

Could you review this matter and let us know your conclusions?

Sincerely,

CHRIS POWELL

Secretary/Treasurer

HARVEY ORGAN

Consultant

Gold Anti-Trust Action Committee Inc.

7 Villa Louisa Road

Manchester, Connecticut 06043-7541

end

Finally, they replied and it was a complete brush off

(courtesy zerohedge)

Currency comptroller brushes off GATA’s inquiry on gold, silver EFPs

Submitted by cpowell on Fri, 2018-08-10 15:37. Section: Daily Dispatches

11:35a ET Friday, August 10, 2018

Dear Friend of GATA and Gold:

The U.S. comptroller of the currency, a bank regulator, has declined GATA’s request to inquire into the strange explosion of the use of the emergency procedure of “exchange for physicals” in the settlement by banks of the gold and silver futures contracts they have sold on the New York Commodities Exchange.

Your secretary/treasurer and GATA’s consultant about the Comex, Harvey Organ, wrote to the comptroller, James M. Otting, on May 5, calling attention to the recent enormous use of EFPs, which implies derivatives risks being undertaken by U.S. banks that could cause the banks to fail:

http://www.gata.org/node/18303

“Our concern is that your office may not be aware of large unreported derivative exposure by banks,” GATA wrote.

As months passed without any acknowledgment from the comptroller’s office, your secretary/treasurer appealed to his U.S. representative, John B. Larson, D-Connecticut, to ask the comptroller’s office to reply. The congressman’s office made a second inquiry on Monday this week and today the comptroller’s office provided Larson with a copy of a reply written and mailed Wednesday.

The comptroller’s reply, signed by the deputy comptroller for public affairs, Bryan Hubbard, said only that the comptroller’s office has “dedicated examiners” at the largest banks who “continuously evaluate the credit, market, operational, reputation, and compliance risks of bank trading and derivative activities.”

The reply did not say anything about the use of the “exchange for physicals” procedure for settling futures contracts. That is, the reply was a begrudged brushoff and GATA’s letter would have been ignored completely if not for Representative Larson’s repeated intervention.

Of course GATA hardly expected a conscientious reply to its letter, the comptroller’s office being not an independent regulator but part of the Treasury Department, whose mandate includes administration of the Gold Reserve Act of 1934, which, as amended in the 1970s, authorizes the department’s Exchange Stabilization Fund to secretly intervene in and rig any market in the world, directly or through intermediaries:

https://www.treasury.gov/resource-center/international/ESF/Pages/esf-ind…

But there’s always value in demonstrating government’s lack of candor about what it is doing, especially in regard to the monetary metals.

A PDF copy of the reply from the comptroller’s office is posted at GATA’s internet site here:

http://www.gata.org/files/ComptrollerOfCurrencyReply-08-08-2018.pdf

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

t

end______________________________________________________________________________________________________________________________________________________

Your early WEDNESDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED UP TO 6.8689/HUGE DEVALUATION FOR THE PAST FOUR WEEKS STOPS/CHINESE COMING TO USA FOR TRADE TALKS IN NOVEMBER CANCELLED //OFFSHORE YUAN: 6.8841 /shanghai bourse CLOSED HOLIDAY

. HANG SANG CLOSED DOWN 35.12 POINTS OR 0.13%

2. Nikkei closed DOWN 159.66 POINTS OR 0.66%/USA: YEN RISES TO 113.86/

3. Europe stocks OPENED IN THE GREEN EXCEPT GERMAN DAX

/USA dollar index RISES TO 95.58/Euro FALLS TO 1.1535

3b Japan 10 year bond yield: RISES TO. +.14/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 113.86/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD IS NOW TARGETED AT .11%/JAPAN LOSING CONTROL OF THEIR BOND MARKET

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 75.09 and Brent: 84.56

3f Gold DOWN/JAPANESE Yen DOWN/ CHINESE YUAN: ON SHORE UP/OFF- SHORE: UP

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil DOWN for WTI and DOWN FOR Brent this morning

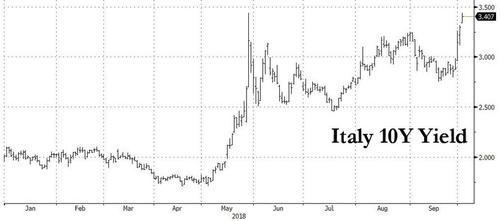

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund RISES TO +.40%/Italian 10 yr bond yield DOWN to 3.31% /SPAIN 10 YR BOND YIELD DOWN TO 1.53%

3j Greek 10 year bond yield RISES TO : 4.42

3k Gold at $1204.15 silver at:14.73 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble DOWN 20/100 in roubles/dollar) 65.71

3m oil into the 75 dollar handle for WTI and 84 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 113.86DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 0.9881 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1397 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now POSITIVE territory with the 10 year RISING to +0.46%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 3.08% early this morning. Thirty year rate at 3.24%

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

6. TURKISH LIRA: UP TO 6.0282

Market Rebound Fades As Italian Budget

Details Emerge

The euphoria following the late report that Italy’s government had bowed to pressure from the European Union to trim its budget-deficit target, when Corriere della Sera reported that Rome would seek to contain its budget deficit at 2% in 2021, down from 2.4% (with 2019 remaining at 2.4% and 2020 shrinking to 2.2%), has faded across key asset classes and the EURUSD is now barely changed, dropping to 1.1560 after rising as high as 1.1590…

… Italian 10Y bonds have resumed their selloff…

… and the Italian stock market, the FTSE MIB retraced almost of its initial move higher.

Excitement quickly faded after details from the proposed budget proposal said a “minimum” of €10bln is to be set aside for citizens income and that there are no plans to alter the deficit if GDP growth disappoints. This led to investors repeating concerns over fiscal irresponsibility and the possibility of debt/GDP rising over 3% should GDP growth forecasts not come in line. It also hit market sentiment, with equities now flat after having been in positive territory in the early morning. Note, that the DAX is closed for trading on this session for German Unity day.

Enthusiasm was also dented after Deputy Premier Luigi Di Maio said that for his Five Star Movement, “either this is the people’s budget or it’s not worth it,” in remarks to reporters at Rome parliament. Di Maio says budget deficit target at 2.4% confirmed for 2019 and clarified the government position saying that “the discussion in Europe on the budget law is very long. They are not going to say no tomorrow morning.” He also made it clear that Italy’s words of hope are just that, as the government had no plans to insert in its budget an automatic mechanism to lower the deficit if growth fails to live up to targets.

While over the weekend, economy Minister Giovanni Tria said over the weekend that there would be an automatic stabiliser in the budget that would cut spending should growth be lower than forecasts, Di Maio refuted this and said that “we don’t currently have plans for an automatic stabilizer” and simply said that spending could be cut later should growth turn out to be lower than expected.

Italy’s other deputy Premier, Matteo Salvini, also dented enthusiasm when he said that he is certain that starting next year debt will fall “because more people will go back to work,” in interview with Canale 5 television. Asked whether govt has gone into reverse on budget, replies: “We have always said that this year we want to maintain at least part of the commitments with Italians” but added that “I don’t give a damn about threats from European Union, France” as “I answer only to Italians.”

Even assuming the concession stays, the EU’s response to the revised targets remains a key hurdle for investors as Brussels may still balk at the proposed 2.4% budget busting which then assumes that the Italian economy grows just shy of 2% to reduce the deficit, a very aggressive assumption. As a reminder, the original plan for a deficit target of 2.4% over three years had prompted a stern push-back, with the European Commission Vice President Valdis Dombrovskis saying that it went “substantially beyond” what is allowed.

So for now, all eyes on Europe and the official and final contents of the final budget proposal. Meanwhile, even as Italian and European risk assets faded the initial euphoria, with the Stoxx 50 sliding from opening highs…

… US equity futures traded near session highs, with much of the world in a sea of green.

Meanwhile, the excitement over Italy’s potential relent wasn’t enough for Asia, where the MSCI Asia Pacific index fell for a third day, with Japanese and South Korean equities leading declines. The rupiah and the rupee remained under pressure on surging oil prices. The rupiah fell to 15,090 to a dollar, its weakest level since the 1998 Asian financial crisis. The rupee slumped past 73 per dollar to reach a fresh all-time low as traders returned from Tuesday’s holiday.

In India, the focus was also back on the country’s financial sector after Prime Minister Narendra Modi’s government took control of IL&FS (Infrastructure Leasing & Financial Services), promising to end the group’s string of defaults.

Investors have been on edge this week with the market impact of European politics and emerging-market strains still high on the agenda. A very close encounter between a U.S. and a Chinese warship in the disputed South China Sea added to tensions between two countries already embroiled in an escalating trade war. Meanwhile, Treasury yields remain near the top of the recent range after Fed Chair Powell welcomed wage growth but expressed confidence that low unemployment won’t spur a takeoff in prices that forces more aggressive tightening.

Elsewhere Aston Martin shares tumbled on their trading debut after an initial public offering valued the company on a par with competitor Ferrari. The Turkish lira also fell after the country’s inflation surged. The pound climbed ahead of a major speech from U.K. Prime Minister Theresa May.

After hitting fresh 4 year highs, Brent dipped back under $85 a barrel after a Reuters report that Saudi Arabia and Russia had agreed to boost output through December.

In overnight central banks news, Fed Chair Powell said a downward yield curve could signal that Fed policy is tight and policy is not that tight at the moment. He said trade tariffs could increase prices but US is not yet seeing effects from trade policy. Powell added gradual rates are meant to balance risks and there is a “remarkably positive outlook” on inflation and employment. Fed’s Kaplan said he is happy with one more rate hike this year in December, base case is two next year. He is hopeful the Fed can raise rates to neutral without inverting the yield curve and the US economy is at or past full employment, while he said his view that US GDP will grow at 3% this year, 2.5% next year as fiscal stimulus fades. In regards to oil, he sees more upside risk to prices.

On today’s calendar, Lennar and RPM International are among companies reporting earnings; Expected data include mortgage applications and employment change.

Market Snapshot

- S&P 500 futures up 0.2% to 2,934.50

- MXAP down 0.6% to 162.72

- MXAPJ down 0.1% to 515.24

- Nikkei down 0.7% to 24,110.96

- Topix down 1.2% to 1,802.73

- Hang Seng Index down 0.1% to 27,091.26

- Shanghai Composite up 1.1% to 2,821.35

- Sensex down 0.6% to 36,311.30

- Australia S&P/ASX 200 up 0.3% to 6,146.07

- Kospi down 1.3% to 2,309.57

- STOXX Europe 600 up 0.3% to 383.03

- German 10Y yield rose 2.6 bps to 0.448%

- Euro up 0.2% to $1.1573

- Italian 10Y yield rose 15.0 bps to 3.08%

- Spanish 10Y yield fell 1.2 bps to 1.527%

- Brent futures up 0.2% to $85.00/bbl

- Gold spot little changed at $1,203.40

- U.S. Dollar Index down 0.1% to 95.37

Top Overnight News from Bloomberg

- Italy’s populist government will bow to European Union pressure to reduce its budget deficit to 2 percent of gross domestic product in 2021, reversing plans to maintain a bigger shortfall for the next three years, Corriere della Sera reported, citing a Cabinet meeting

- Italian bonds may recover from four days of selling after the government signaled it’s bowing to pressure from the European Union to trim a budget deficit target

- New York state tax authorities have opened an investigation into allegations reported in the New York Times that President Donald Trump and his family created their real estate empire through “instances of outright fraud,” evading taxes on hundreds of millions of dollars

- Federal Reserve Chairman Jerome Powell welcomed recent increases in Americans’ wages while expressing confidence that low unemployment won’t spur a takeoff in prices that would force him to hike interest rates aggressively

- Finland’s Olli Rehn joined key European Central Bank decision-makers including Benoit Coeure in stressing the need for flexibility in preparing investors for eventual increases in borrowing costs

- Britain and the European Union will begin a frantic week of diplomacy on Wednesday aimed at thrashing out the final shape of the Brexit deal. Brexit Secretary Dominic Raab is planning to visit Brussels next week and expects progress on the thorny issue of the Irish border, according to a senior official who declined to be named. Diplomats in Brussels said they expect the contours of the exit agreement to emerge by the middle of next week

- President Trump participated in dubious tax schemes during the 1990s, including instances of outright fraud, that greatly increased the fortune he received from his parents, an investigation by The New York Times has found

- Turkey’s consumer inflation climbed near the highest levels since President Recep Tayyip Erdogan came to power 15 years ago, spurring calls for higher interest rates to rein in prices

Asian stocks traded choppy following a mixed lead from the US where the Dow hit all-time highs aided by gains in Intel shares, while Nasdaq was pressured by large-cap tech names tumbling over a percent. ASX 200 (+0.3%) outperformed as miners boosted the index, while Nikkei 225 (-0.7%) was weighed on by auto names with Honda and Toyota falling 3% and 2% respectively, while the index was also mirroring currency fluctuations throughout the session. Elsewhere, Hang Seng (-0.6%) traded lower amid weakness in financial names and as the tech sector failed to support the index following Tencent’s plans to IPO it’s music arm in the US, in what could be one the biggest IPOs to date. Meanwhile, mainland China and South Korea were shut due to public holidays. NEC Director Kudlow said US and China keep talking about trade, while the White House Advisory said China has not made a serious enough effort at appeasing the US.

Top Asian News

- Dubai Bank Said to Weigh Paying Sberbank Less in Turkey Deal

- Indonesia Rocked by Volcanic Eruption After Deadly Quake

- Peer-to-Peer Lending Crash in China Leads to Suicide and Protest

- Indonesia Central Bank Expects Currency Pressure to Ease in 2019

European equities started the day on the front foot after the early morning risk tone benefited from Italy confirming the debt/GDP target from 2020 at 2.2% vs. the originally quoted 2.4%. This, however, reversed course after the details from their budget proposal said a “minimum” of EUR 10bln is to be set aside for citizens income and that there are no plans to alter the deficit if GDP growth disappoints. This has led to investors repeating concerns over fiscal irresponsibility and the possibility of debt/GDP rising over 3% should GDP growth forecasts not come in line. This hit market sentiment, with equities now flat after having been in positive territory in the early morning. Note, that the DAX is closed for trading on this session for German Unity day. Norsk Hydro and Tesco are leading the losses in Wednesday’s session. The Scandinavian company is being hit by the ceasing of operations at their Alunorte site in Brazil. Tesco is struggling after reporting earnings wherein profit missed expectations.

Top European News

- U.K. Set for Solid Third Quarter Even as Services Growth Ebbs

- Japan Waves Goodbye to U.K. as ‘Gateway to Europe’ Post- Brexit

- Tesco Falls as Overseas Weakness Gives CEO a New Headache

- Record-Breaking Italian 5G Sale Dents Telecom Carrier Finances

In FX, markets reacted quickly to reports that Italy was seeking a cut to their 2021 deficit/GDP ratio to 2.0% from 2.4%. EUR immediately caught a bid as the reports signal a potential compromise from Italy. The EUR strength weighed more on the Japanese currency than the USD with EUR/JPY and EUR/USD spiking higher by 82 pips and 53 pips respectively. DXY fell to session lows while USD/JPY rose just over 20 pips. Elsewhere, AUD experienced weakness earlier in the session amid a substantial miss in the Australian building approvals with NZD/USD moving lower in sympathy.

In commodities, the source report story suggesting Russia and Saudi Arabia are to boost oil output in December hit the oil market, which started in the green off the back of yesterday’s smaller than expected build in API crude stocks. The crude complex is now flat as suggestions of increased supply halted Brent’s advance over the USD 85/BBL with the benchmark now hovering just below the big figure. The Iraqi Energy Minister said that they will assess increased OPEC output in November. In the metals scope, gold is unchanged after having risen by over 1% in the previous session. The biggest mover in the commodities scope can be found in aluminium, which has rallied to over 5 week highs after Norsk Hydro announced the cessation of operations at their Alunorte site in Brazil, stoking the flames of supply concerns for the industrial metal.

Looking at the day ahead, the US we’ve got the September ADP reading followed closely by those September PMIs and September ISM non-manufacturing

US Event Calendar:

- 7am: MBA Mortgage Applications, prior 2.9%

- 8:15am: ADP Employment Change, est. 184,000, prior 163,000

- 9:45am: Markit US Services PMI, est. 53, prior 52.9

- 9:45am: Markit US Composite PMI, prior 53.4

- 10am: ISM Non-Manufacturing Index, est. 58, prior 58.5

Central Banks:

- 6:30am: Fed’s Evans Speaks in London

- 8:05am: Fed’s Barkin Speaks at Economic Conference in West Virginia

- 2pm: Fed’s Brainard Speaks in Chicago about Payment System

- 2:15pm: Fed’s Mester Speaks at Community Banking Conference

- 4pm: Fed’s Powell Speaks in Washington

DB’s Jim Reid concludes the overnight wrap

Like the weather it continues to be a year of conflicts. The global economy is fine but the weakest links are being punished in a way they weren’t in recent years (e.g. EM and Italy) as global policy tightens. Inflation is edging higher but without a killer blow yet. Shocks keep happening but vol doesn’t stay elevated for long. US equities are around record highs but yields keep on staying in check just as they look to be breaking out on the upside of their ranges. The thing we’ve struggled to come to terms with this year is that we did think we’d get more shocks but we also thought we’d get higher yields. Can we get both? The answer is that we probably can but we need more evidence of inflation. The ambiguity about where inflation is heading is undoubtedly the glue holding markets together at the moment.

On that front, it was interesting yesterday to see that Amazon is to raise the minimum wage for employees in the US to $15 an hour and to £9.50 for staff in the UK with a higher rate for those in London. Amazon’s CEO Jeff Bezos said that the company had “listened to our critics” and “decided we want to lead” while encouraging others to join. To put that rate in perspective the US federal minimum wage is $7.25 however 29 US states do have requirements above that level. As we know ‘Amazonification’ has been commonly referred to as being disinflationary so signs of wage growth inflation is an interesting contrast. In the grand scheme of things this move is unlikely to move the dial much but the precedent that it sets is perhaps more important. Speaking with DB’s Matt Luzzetti yesterday he suggested that this move may only add a few bps to AHE over time but that it demonstrated how tight the labour market is. Earlier this year Walmart raised its minimum hourly wage in the US to $11, while Target has indicated that it intends to raise its own minimum wage to $15 by 2020. So it’s an interesting topic of debate ahead of Friday’s average hourly earnings report.

In markets, Amazon’s share price bounced between gains and losses yesterday but ultimately closed -1.65% post that news. Broader US equity markets were once again characterised by small cap underperformance however. Indeed, the Russell 2000 closed -1.01% compared to +0.46% gains for the DOW, which closed at a new all-time high. That means the Russell 2000 has now lost -2.39% in the last 2 sessions compared to a +1.19% gain for the DOW. That differential over two consecutive sessions is the most since August 2011. The S&P 500 came within 10pts of a new all-time high, but pared its gains to close -0.04% after Fed Chair Powell gave a bullish speech on the economic outlook (more below).

Prior to this in Europe the STOXX 600 had ended -0.52%. It had looked like Italian equities might be in for another day of sharp under-performance following the price action in the first hour of the session yesterday but in the end they largely closed off the lows. The FTSE MIB (-0.23%) actually outperformed most European bourses while Italian Banks (-1.17%) pared back losses of as much as -4.09% at one stage, though they remain -13.2% lower over the last week after 5 straight sessions of losses.

The same stabilisation couldn’t be said for BTPs however with 2y (+16.4bps) and 10y (+15.4bps) yields selling off and the latter at the highs for the session and the highest level since early 2014. The 10y BTP-Bund spread also widened another 20.2bps yesterday (Bunds finished -5.0bps) which takes the three-day move to a fairly eye watering 67bps. At 302bps it’s also now eclipsed the May and August closing wides and so putting it at levels last seen in June 2013. The saving grace for now is that 2yr yields at 1.454% (+71bps over 3 days) remain comfortably below May’s peak of 2.766%. It’s hard to remember now that they were -0.33% in early May.

Driving the early price action yesterday was Head of the Lower House Budget Committee Claudio Borghi saying in the morning that Italy would have solved its fiscal problems if it had its own currency and that the government would have declared a 3.1% budget deficit for next year if it had wanted to confront the EU. He later softened his tone by confirming that there is no plan for Italy to leave the euro, regardless of his personal conviction. Deputy PM Luigi Di Maio also added to the early headlines by saying that the government would not retreat from the 2019 budget by even a “millimetre”. It’s worth noting however that overnight Corriere della Sera has reported that Italy’s draft budget plan will pledge to cut the deficit to 2% in 2021, after initially suggesting the deficit would be 2.4% for the three years up to and including then. As you’ll see shortly that’s helped to lift the euro overnight. Meanwhile on the European side yesterday, European Commission VP Valdis Dombrovskis reiterated similar comments made by his counterparts by saying that Italy’s deficit plans go “substantially beyond” the rules, while the ECB’s Olli Rehn said that the plan poses a “serious concern”. The ECB’s Francois Villeroy de Galhau also confirmed that the ECB would resist fiscal dominance and not alter course to accommodate highly indebted nations. This wasn’t a great surprise. As you’ll see in the day ahead Italy Finance Minister Tria is due to speak this morning so worth keeping an eye on the headlines.

Elsewhere, 10y Treasuries rallied another -2.0bps yesterday but what continues to stand out is the incredibly low volatility for Treasuries in the face of bigger moves for rates here in Europe. After falling to a YTD low on Monday the MOVE index is still only hovering above that level. Fed Chair Powell did speak late last night and largely reiterated his existing views, stressing the need for ongoing gradual rate hikes and emphasizing the importance of stable inflation expectations. However, equities retreated from their intraday highs as Powell described the economic outlook as “remarkably positive” and said that asset prices are high by historical standards. Rates and FX were little changed as Powell spoke.

Overnight sentiment in Asia has remained fairly sanguine.The Nikkei, which has been the star of the show in the region of late, is down -0.82% joining the Hang Seng (-0.52%) with markets in China and South Korea closed. The euro (+0.26%) has received a small lift from that Italy story we referenced above and is currently snapping a five-day losing streak while US equity futures are broadly flat. EM currency markets have gotten more focus overnight with the Indian Rupee (-0.65%) falling to a all-time low and the Indonesian Rupiah (-0.21%) has extended its decline to fresh 20-year lows with both under pressure from the Oil move.

Elsewhere sterling fell as much as +0.78% yesterday and is now over 2% lower from its Sep 20 peak as the newsflow continued to undermine Prime Minister May’s Brexit plan, which includes regulatory checks between Northern Ireland and the UK mainland. Two key members of May’s governing coalition partner spoke out against the proposal, with the DUP’s leader Arlene Foster saying she opposes “any form” of border in the Irish sea. The DUP’s longest-serving MP Jeffrey Donaldson said that the border issue is a “red line.” Later in the day, Boris Johnson spoke at the Conservative Party conference and attacked May’s Chequers proposal, though he stopped short of openly challenging her leadership. So overall, though our base case remains for a “soft” Brexit, we continue to question the ability of the government to produce a parliamentary majority in favour of such an outcome and we place the odds of a successful vote this year at 50%.

Looking at today’s calendar, this morning expect the early focus to be in emerging markets and specifically Turkey where we get the September CPI report. The consensus is for a +3.4% mom (yes mom not yoy) print however economists’ forecasts range anywhere from +1.7% to +4.1%. A reading in-line with the consensus would however push the annual rate up from +17.9% yoy to +21.1% yoy and the highest since 2003. Also due out this morning are the remaining September PMIs in Europe (services and composite readings) before we get August retail sales data for the euro area. This afternoon in the US we’ve got the September ADP reading followed closely by those September PMIs and September ISM non-manufacturing. Away from that it’s another busy day for central bank speak. The ECB’s Mersch is due to speak this morning before we hear from the Fed’s Evans, Barkin, Brainard, Mester and Powell over the course of the day. The latter is due to moderate a discussion at an Aspen Institute event. As mentioned at the top, keep an eye on those scheduled comments from Italian Finance Minister Tria this morning. Finally, UK PM Theresa May is due to deliver the closing speech at the Conservative Party conference today.

‘.

3. ASIAN AFFAIRS

i) WEDNESDAY MORNING/ TUESDAY NIGHT:

SHANGHAI CLOSED FOR A HOLIDAY

/Hang Sang CLOSED DOWN 35.12 POINTS OR 0.13% //The Nikkei closed DOWN 159.66 POINTS OR 0.66%/ Australia’s all ordinaires CLOSED UP 0.31% /Chinese yuan (ONSHORE) closed UP at 6.8689 AS POBC STOPS ITS HUGE DEVALUATION /DELEGATION COMING TO THE USA TO SEE TRUMP IN NOVEMBER CANCELLED/Oil UP to 75.23dollars per barrel for WTI and 84.7 for Brent. Stocks in Europe OPENED GREEN//. ONSHORE YUAN CLOSED DOWN AT 6.8686 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.8689: HUGE DEVALUATION/PAST SEVERAL DAYS STOPS// TRADE TALKS STOPPED : /ONSHORE YUAN TRADING STRONGER AGAINST OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

3 a NORTH KOREA/USA

North Korea/South Korea/USA/China

3 b JAPAN AFFAIRS

3C CHINA

4.EUROPEAN AFFAIRS

ITALY

IT seems that Italy has folded. They are going to reduce their deficit to 2.0% b 2022 but they will still have a 2.0% deficit. Still not sure but Brussels will say with this new proposal from Rome

(courtesy zerohedge)

Italy Folds To Europe, Pledges To Shrink

Budget Deficit To 2.0%; Euro Surges

After two days of brutal punishment by the markets which sent Italian bond yields to 4 years highs and slammed the euro, the Italian government appears to have folded to pressure from Brussels (and the one place in the world where the bond vigilantes still operate, just ask Sylvio Berlusconi), and according to Corriere della Sera, Italy’s draft budget plan will pledge to cut the deficit to 2% in 2021, after Rome reversed a proposal to maintain a 2.4% shortfall in the face of pressure from the EU. As a result, while the 2019 deficit will still rise to 2.4% of GDP in 2019, it will decline by 0.2% to 2.2% in 2020, and another 0.2% the year after.

In kneejerk reaction, futures lept to fresh session highs, Treasury yields jumped by 2bps to 3.07% and the EURUSD spiked 50 pips higher to 1.1590.

Italy is not out of the woods yet though: according to Mizuho, the sustainability of the euro’s rebound will depend on whether the EU sees Italy’s latest budget plan as appropriate. It could be that Italy has already made compromise with the EU, but hard to predict whether the euro’s rebound has more legs until we see a reaction from the EU: “It all boils down to the EU’s response”, and if the ongoing war of words is any indication, merely promising to trim the deficit in the next three years will hardly be smiled upon.

Others were even more skeptical. According to bond fund manager Daintree Capital, “The euro’s definitely reacting to the headlines on Italian budget plans, and it will continue to do so for future headlines.” However, “anyone who believes a populist government is all of a sudden going to be particularly responsible in a fiscal sense, has a misguided view.”

As a result, Daintree’s Justin Tyler said that “I do see the euro as potentially being a bit of a weak point in G-10. There’s lots of political risks coming out of Italy.”

Finally, there is Bloomberg’s Mark Cudmore who writes that the “euro reaction is excessive and won’t sustain” because the proposed budget deficit target is still too late “and it’s two years too late anyways. There’s justification for some positivity in that the Italian government are trying to address market concerns. But that’s largely eroded by the fact that this is little more than a token gesture and insufficient to ease Italy’s debt burden. And that suggests that the government still don’t register the severity of the situation.”

Finally, even if the deficit were to shrink modestly, that only impacts one of the three triggers listed by Goldman earlier today why volatility in Italian bonds won’t sustain. The other two – the phasing out of the ECB’s QE and the collapse in Italian bond volatility – are here to stay, and merely await the next catalyst out of Italy’s populist government to send yields soaring even higher.

Finally, don’t be surprised if a member of government comes out in the next few hours and denies the whole thing

Italy’s Dragging Europe Into The Fiscal-

Spending Party

Authored by Kevin Muir via The Macro Tourist blog,

Today’s post will poke a lot of fun at the EU Commission President Jean-Claude Juncker, so I warn you now – if you are a fan, click next. To a large degree, it’s not really sporting going after JC as he offers such a treasure trove of opportunities.

We’ll start with his most infamous slip. “When it becomes serious, you have to lie.”

Yeah, I get it. He just said out loud what everyone knows. But it was still a dumb thing to say. Do you think Bill Clinton looks forward to going to church Sunday morning after a rough Saturday night chatting up inappropriately young women? Not a chance. But he keeps quiet and heads off. Which is what JC should have done. Kept his mouth shut.

Speaking of keeping your mouth shut…

Why I am picking on good ‘ole JC so much today? Well, it’s his comments about Italy.

From Bloomberg:

“One crisis was enough,” Commission President Jean-Claude Juncker said in televised remarks at an event in Freiburg, Germany. “After the toughest management of the Greece crisis, we have to do everything to avoid a new Greece – this time an Italy – crisis.”

You see, Jean-Claude is upset that the Italians are not adhering to EU rules about the size of their deficit. He wants them to get into line and balance their budget. The Italian coalition government has tabled a budget with a 2.4% deficit as a percentage of GDP – much higher than allowed under EU rules. Given the EU’s staunch opposition to deficits of this size, they have increased rhetoric in attempt to force the Italians to back down.

This has spooked markets and sent the Italian bond market tumbling.

The German bund market has equally been affected by the bad news with a big flight-to-safety-bid.

Yet let’s take a moment to consider this “monstrous Italian transgression.” The Italian government is proposing running a deficit of 2.4% of GDP. But what does that look like compared to other nations? Like for example, the United States…

Wow. Sure looks like 2.4% would be a welcome level for the United States.

For all my hard-money pals, I am sure they are gleefully rubbing their hands together at JC’s tough stance. Yeah, regardless of whether that is the correct course to take, it doesn’t matter one iota because the world is headed the other way. Fiscal deficits are what all the new cool kids are doing. Juncker should just realize his view is antiquated and no one wants to hang out with him.

I have said it in the past, and I will repeat it again. Italy is far more in control of this situation than anyone at the EU commission will admit. What’s that saying about banks and owing $1 million dollars? It should be changed to:

Italy is far too large for the EU to even consider kicking out. It’s not going to happen and Italy knows it.

This budget deficit is simply Italy calling the EU’s bluff. What are they going to do? The largest country in the world, the reserve currency issuer, is running an almost 4% of GDP fiscal deficit with unemployment at record lows. If the United States is doing it, why shouldn’t Italy?

The world is changing. Deficits are the new normal and Italy’s latest salvo is just one of many changes that will happen in the coming months and years.

The days of the EU being able to throttle back fiscal expansion are behind us.

What does this mean for the markets?

Although many market participants are clearly anxious about the budget showdown, I expect it to be resolved with the EU backing down and monetizing the Italian debt. So even though I would never bet on the Italian/German spread tightening, neither would I be inclined to put on positions assuming it will get worse.

The spread between the Italian and the German 10-year bond yield has spiked over the past week, but it has simply rallied back near the highs of the summer.

I think 2.63% which was the previous topping level will hold again as the situation resolves itself.

But what does this mean on a longer term basis? More fiscal spending will mean more inflation. For Europe, that’s lower bond prices and higher stocks. Italy’s foray into the fiscal spending onslaught will finally bring Europe to where the United States has been since Trump’s election.

And then once Italy breaks the seal, it’s only a matter of time until the rest of Europe follows.

Juncker marks last-generation thinking, and given his behaviour (gotta give this tool’s antics a watch) – it’s none too soon

end

Euro Tumbles In Late Trading As Hawkish

Powell Sends Dollar, Yields Soaring

Just when dollar bears and Treasury bulls thought the pain was finally over, the previously discussed hawkish Powell comments hit the tape.

In a remarkable sequence of comments, Powell basically said that not only is the Fed not worried about stifling growth by tightening too much, the he took the opportunity to underscore why he remains so complacent about the US economy, saying “it’s a remarkably positive set of economic circumstances,” and “there’s no reason to think it can’t continue for quite some time.”

Powell also praised the recent wage increases, saying some gains are welcome and noting that “the Phillips curve is not dead, just resting” and repeated what he said after the last week’s FOMC announcement, saying that “interest rates are still accommodative” because “rates have just now, in real terms, moved above zero.”

And here is the reason for dollar bear pain after hours: Powell said that not only are rates far away from the neutral rate of interest – or the interest rate that neither stimulates nor holds back the economy – suggesting that the Fed will keep hiking for a long time, but that the Fed may also go past “neutral” as the tightening process continues:

“interest rates are still accommodative, but we’re gradually moving to a place where they’ll be neutral – – not that they’ll be restraining the economy. We may go past neutral. But we’re a long way from neutral at this point, probably.”

And whether it was after-hours momentum, or Powell’s unexpected hawkishness that the Fed is a “long way from neutral”, today’s dramatic surge in yields and the dollar, and the plunge in the Euro, accelerated after hours. And, as shown below, once EURUSD took out the 1.15 stops, the pair tumbled as low as 1.147, the lowest level since late August…

… while the 10Y Yield continued its relentless levitation to the highest level in 7 years…

… a move which during the cash session finally sent stock reeling amid concerns that rate had risen too far, too fast.

As for the dollar, it surged above 96 and is now putting enough pressure on financial conditions to hit S&P futures.

Which is ironic, because during his speech, Powell said that “we don’t detect financial instability as elevated now.” Well, a few more such comments, and he will.

And with the dollar now in blast off mode, we hope the emerging markets enjoyed their brief respite and got their affairs in order, because overnight it’s about to get ugly again.

5.RUSSIAN AND MIDDLE EASTERN AFFAIRS

end

TURKEY

big trouble for Turkey today as inflation is skyrocketing past 24% which means higher rates are coming.

(courtesy zerohedge)

“Shocking” Turkish Inflation Hits 15 Year

High, Unleashing Stagflationary Shockwave;

Lira Plunges

A few days ago we discussed how soaring oil prices have been a stagflationary double whammy to emerging markets, which have been hit not only by a surging dollar, resulting in a collapse in local currencies and spiking import costs, but a spike in local currency oil and gasoline prices resulting in a surge in inflation and a slowdown in the economy as local infrastructure grinds to a halt.

This morning, this dynamic was revealed clearly – and painfully for Turkish residents – when Ankara reported that consumer inflation climbed to one of the highest levels since President Recep Erdogan came to power 15 years ago, spurring more calls for higher interest rates to rein in prices or at least for Erdogan to normalize relations with the US.

Turkish inflation soared to 24.5% in September from a year earlier (up 6.3% on the month, the highest since April 2001), rising for the 6th consecutive month driven by an across-the-board spike provoked by the lira’s meltdown; it was also the highest since June 2003 and rising above all Wall Street expectations where the median estimate was 21.1%. Worse, the CPI print was higher than the central bank’s policy rate of 24% suggesting more rate hikes are now imminent… but will Erdogan agree?

Medley Global analyst Nigel Rendell said the inflation figure was “a shocker” but said he was cautiously optimistic that weak consumption might offset inflationary pressures at some point.

“Interest rates of 24 percent provide some protection, and there is a sense that the weakness of domestic demand will be the dominating disinflationary force in a few months’ time once the foreign exchange pass-through has fed its way through the system.”

As the following key highlights from the Turkstat report show, the price increases was broad based across virtually all categories (via Bloomberg):

- Food prices, which make up nearly a quarter of the inflation basket, rose an annual 27.7 percent, from 19.8 percent in August

- Energy inflation accelerated to 27.03 percent from 21.3 percent

- Producer prices rose 46.15 percent from 32.13 percent

- Core inflation, a gauge that excludes volatile items such as food, energy and gold, climbed to 24.05 percent from 17.2 percent; median estimate in a Bloomberg survey called for an acceleration to 19.3 percent

- Apparel prices rose 17.16 percent from 13.6 percent and the cost of housing rose 21.84 percent from 16.3 percent

Commenting on the soaring prices, Turkey’s Treasury and Finance Minister Berat Albayrak blamed hoarders and speculators, and predicted inflation would stop quickening in October. Whether that is the case remains to be seen, but the latest inflation report put the central bank – already frowned upon by Erdogan – in a bind, as its recent interest rate hike to the highest level in nearly two decades, has failed to halt price increases which have exploded in 2018.

“An inflation print so bad that it truly feels like old Turkey,” said Inan Demir, an economist at Nomura International in London. “But this is simply too bad to ignore. Note that annual headline inflation is now above the bank’s policy rate at 24 percent, which calls for another rate hike.”

Not only is CPI now higher than Turkey’s official interest rate, but it is almost five times the central bank’s target of 5 percent and almost double its 2018 forecast. Meanwhile, given Erdogan’s distaste for higher rates and the sudden slowdown in the economy, the central bank now finds itself trapped with little room to hike rates further.

And with the lira losing 40% of its value against the dollar since the beginning of the year, the worst may be yet to come, especially since today’s inflation report sent the lira sharply lower, reversing gains achieved in recent days.

As noted above, speaking after the data release, finmin Albayrak attributed much of the increase to “hoarding and speculative pricing by businesses taking advantage of volatility.” Yesterday, Erdogan urged citizens to report any businesses that were seen as gouging consumers; it was not clear what the punishment would be for enterprises who had the temerity of trying to pass through prices, the result of the lira’s collapse, to consumers.

Turkish officials will soon be meeting representatives of various sectors of the economy for a new framework to curb prices that the government will likely announce next week, he said.

“The current trend will be broken in October,” Albayrak promised, although judging by the Turkish lira, the market is not so confident.

Another problem is the speed with which CPI is catching up with producers’ rising costs, said BlueBay Asset Management LLC strategist Tim Ash. Producer prices exploded in September, rising 10% from the previous month, and over 46% from a year ago.

So what can Turkey do to end this toxic spiral into economic collapse? According to Ash, given the sudden economic slowdown, there is little justification to raise rates at this point, but the strategist said that the government should end its spat with the U.S. over the detained U.S. pastor to relieve market turmoil and pressure on the central bank. In light of Erdogan’s continued war of words with the US, this will not happen until Turkey is in a deep depression… and even that is not certain.

6. GLOBAL ISSUES

7 OIL ISSUES

8. EMERGING MARKETS

Your early morning currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings WEDNESDAY morning 7:00 am

Euro/USA 1.1535 DOWN .0016 REACTING TO MERKEL’S FAILED COALITION/ REACTING TO +GERMAN ELECTION WHERE ALT RIGHT PARTY ENTERS THE BUNDESTAG/ huge Deutsche bank problems + USA election:///ITALIAN CHAOS /AND NOW ECB TAPERING BOND PURCHASES/JAPAN TAPERING BOND PURCHASES /USA RISING INTEREST RATES /FLOODING/EUROPE BOURSES IN THE GREEN EXCEPT GERMANY

USA/JAPAN YEN 113.86 UP 0.291 (Abe’s new negative interest rate (NIRP), a total DISASTER/NOW TARGETS INTEREST RATE AT .11% AS IT WILL BUY UNLIMITED BONDS TO GETS TO THAT LEVEL

GBP/USA 1.30005 UP 0.0022 (Brexit March 29/ 2017/ARTICLE 50 SIGNED/BREXIT FEES WILL BE CAPPED

USA/CAN 1.2839 UP .00138CANADA WORRIED ABOUT TRADE WITH THE USA WITH TRUMP ELECTION/ITALIAN EXIT AND GREXIT FROM EU/(TRUMP INITIATES LUMBER TARIFFS ON CANADA/CANADA HAS A HUGE HOUSEHOLD DEBT/GDP PROBLEM)

Early THIS WEDNESDAY morning in Europe, the Euro FELL by 16 basis point, trading now ABOVE the important 1.08 level FALLING to 1.1535; / Last night Shanghai composite CLOSED FOR A HOLIDAY

//Hang Sang CLOSED DOWN 35.12 POINTS OR 0.13%

/AUSTRALIA CLOSED UP 0.31% / EUROPEAN BOURSES ALL GREEN EXCEPT GERMAN DAX

The NIKKEI: this WEDNESDAY morning CLOSED DOWN 159.66 POINTS OR 0.66%

Trading from Europe and Asia

1/EUROPE OPENED ALL GREEN EXCEPT GERMAN DAX

2/ CHINESE BOURSES / :Hang Sang CLOSED DOWN 35.12 POINTS OR 0.13%

/SHANGHAI CLOSED HOLIDAY

Australia BOURSE CLOSED UP 0.31%

Nikkei (Japan) CLOSED DOWN 159.66 POINTS OR 0.66%

INDIA’S SENSEX IN THE RED

Gold very early morning trading: 1204.15

silver:$14.73

Early WEDNESDAY morning USA 10 year bond yield: 3.08% !!! UP 2 IN POINTS from TUESDAY night in basis points and it is trading WELL ABOVE resistance at 2.27-2.32%. (POLICY FED ERROR)/

The 30 yr bond yield 3.24 UP 2 IN BASIS POINTS from TUESDAY night. (POLICY FED ERROR)/

USA dollar index early WEDNESDAY morning: 95.58 up 7 CENT(S) from TUESDAY’s close.

This ends early morning numbers WEDNESDAY MORNING

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

And now your closing WEDNESDAY NUMBERS \1: 00 PM

Portuguese 10 year bond yield: 1.89% DOWN 1 in basis point(s) yield from TUESDAY/

JAPANESE BOND YIELD: +.14% UP 1 BASIS POINTS from TUESDAY/JAPAN losing control of its yield curve/EXTREMELY VOLATILE YESTERDAY

SPANISH 10 YR BOND YIELD: 1.53% DOWN 1 IN basis point yield from TUESDAY/

ITALIAN 10 YR BOND YIELD: 3.31 DOWN 14 POINTS in basis point yield from TUESDAY/

the Italian 10 yr bond yield is trading 178 points HIGHER than Spain.

GERMAN 10 YR BOND YIELD: RISES UP TO +.47% IN BASIS POINTS ON THE DAY//

END

IMPORTANT CURRENCY CLOSES FOR WEDNESDAY

Closing currency crosses for WEDNESDAY night/USA DOLLAR INDEX/USA 10 YR BOND YIELD/1:00 PM

Euro/USA XXXX

USA/Japan: XXXX down XXX basis points/

Great Britain/USA XXX DOWN .XXX( POUND DOWN XX BASIS POINTS)

USA/Canada XXX Canadian dollarXXXBasis points AS OILXXX

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

This afternoon, the Euro was FELL BY XXX BASIS POINTS to trade at XXX

The Yen rose to XXX for a gain of XX Basis points as NIRP is STILL a big failure for the Japanese central bank/HELICOPTER MONEY IS NOW DELAYED/BANK OF JAPAN NOW WORRIED AS AS THEY ARE RUNNING OUT OF BONDS TO BUY AS BOND YIELDS RISE

The POUND LOST XXXbasis points, trading at XXX/