GOLD: $1288.50 DOWN $1.45 (COMEX TO COMEX CLOSINGS)

Silver: $15.60 DOWN 4 CENTS (COMEX TO COMEX CLOSING)

Closing access prices:

Gold : 1289.40

silver: $15.60

For comex gold and silver:

JANUARY

NUMBER OF NOTICES FILED TODAY FOR JAN CONTRACT: 5 NOTICE(S) FOR 500 OZ (0.0155 tonnes)

TOTAL NUMBER OF NOTICES FILED SO FAR: 538 NOTICES FOR 53800 OZ (1.6734 TONNES)

SILVER

FOR JANUARY

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

22 NOTICE(S) FILED TODAY FOR 110,000 OZ/

total number of notices filed so far this month: 637 for 3,185,000

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: OPENING MORNING TRADE $3612: DOWN 13

Bitcoin: FINAL EVENING TRADE: $3534 DOWN $90

end

XXXX

JPMorgan or Goldman Sachs are taking a huge issuance (stopping) of gold at the comex.

today 4/5

DLV615-T CME CLEARING

BUSINESS DATE: 01/14/2019 DAILY DELIVERY NOTICES RUN DATE: 01/14/2019

PRODUCT GROUP: METALS RUN TIME: 20:14:08

EXCHANGE: COMEX

CONTRACT: JANUARY 2019 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,289.100000000 USD

INTENT DATE: 01/14/2019 DELIVERY DATE: 01/16/2019

FIRM ORG FIRM NAME ISSUED STOPPED

____________________________________________________________________________________________

661 C JP MORGAN 4

737 C ADVANTAGE 5 1

____________________________________________________________________________________________

TOTAL: 5 5

MONTH TO DATE: 538

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total OPEN INTEREST ROSE BY AN GOOD SIZED 1433 CONTRACTS FROM 189,936 UP TO 191,369 WITH YESTERDAY’S 1 CENT RISE IN SILVER PRICING AT THE COMEX. TODAY WE ARRIVED SLIGHTLY CLOSER TO AUGUST’S RECORD SETTING OPEN INTEREST OF 244,196 CONTRACTS.

WE HAVE ALSO WITNESSED A LARGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY AS WE NOW HAVE JUST LESS THAN 22 MILLION OZ STANDING IN DECEMBER. AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A TINY SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP:

31 EFP’S FOR MARCH, 0 FOR APRIL AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE: OF 31 CONTRACTS. WITH THE TRANSFER OF 31 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 31 EFP CONTRACTS TRANSLATES INTO 0.155 MILLION OZ ACCOMPANYING:

1.THE 1 CENT RISE IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST SIX MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING FOR NOVEMBER AND

21.925 MILLION OZ FINALLY STAND FOR DECEMBER.

AND NOW: INITIALLY 5.565 MILLION OZ STAND IN JANUARY.

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF JANUARY: 26,157 CONTRACTS (FOR 10 TRADING DAYS TOTAL 26,157 CONTRACTS) OR 130.785 MILLION OZ: (AVERAGE PER DAY: 2616 CONTRACTS OR 13.080 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF JAN: 130.78 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 18.65% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2019 TO DATE SILVER EFP’S: 130.78 MILLION OZ.

RESULT: WE HAD A GOOD SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 1466 WITH THE TINY 1 CENT RISE IN SILVER PRICING AT THE COMEX //YESTERDAY..THE CME NOTIFIED US THAT WE HAD A STRONG SIZED EFP ISSUANCE OF 31 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) .

TODAY WE GAINED A CONSIDERABLE SIZED: 1487 TOTAL OI CONTRACTS ON THE TWO EXCHANGES:

i.e 31 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH INCREASE OF 1466 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED WITH A 1 CENT RISE IN PRICE OF SILVER AND A CLOSING PRICE OF $15.64 WITH RESPECT TO YESTERDAY’S TRADING. YET WE HAD A GIGANTIC AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY

In ounces AT THE COMEX, the OI is still represented by JUST UNDER 1 BILLION oz i.e. .896 BILLION OZ TO BE EXACT or 128% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT JANUARY MONTH/ THEY FILED AT THE COMEX: 22 NOTICE(S) FOR 110,000 OZ OF SILVER

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 243,411 CONTRACTS ON APRIL 9.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $16.51.

AND NOW WE RECORD FOR POSTERITY ANOTHER ALL TIME RECORD OPEN INTEREST AT THE COMEX OF 244,196 CONTRACTS ON AUGUST 22/2018 AND AGAIN WHEN THIS RECORD WAS SET, THE PRICE OF SILVER WAS $14.78 AND LOWER IN PRICE THAN PREVIOUS RECORDS.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./ DEC. AT 21.925 MILLION OZ AND NOW JANUARY AT 5.565 MILLION OZ.

- HUGE RECORD OPEN INTEREST IN SILVER 243,411 CONTRACTS (OR 1.217 BILLION OZ/ SET APRIL 9/2018) AND NOW AUGUST 22/2018: 244,196 CONTRACTS, WITH A SILVER PRICE OF $14.78.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017

- RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT).

IN GOLD, THE OPEN INTEREST ROSE BY A HUMONGOUS SIZED 15,044 CONTRACTS UP TO 494,828 WITH THE SMALL GAIN IN THE COMEX GOLD PRICE/(A RISE IN PRICE OF $1.65//YESTERDAY’S TRADING)

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 6045 CONTRACTS:

FEBRUARY HAD AN ISSUANCE OF 6045 CONTACTS AND ALL OTHER MONTHS ZERO. The NEW COMEX OI for the gold complex rests at 494,828. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE A HUGELY ATMOSPHERIC SIZED GAIN IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 21,089 CONTRACTS: 15,044 OI CONTRACTS INCREASED AT THE COMEX AND 6045 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN: 21,089 CONTRACTS OR 2,108,900 OZ = 65.59 TONNES. AND ALL OF THIS HUMONGOUS DEMAND OCCURRED WITH A RISE IN THE PRICE OF GOLD/ YESTERDAY TO THE TUNE OF A TINY $1.65??????????

YESTERDAY, WE HAD 5979 EFP’S ISSUED.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF JANUARY : 79,429 CONTRACTS OR 7,942,900 OZ OR 247.05 TONNES (10 TRADING DAYS AND THUS AVERAGING: 7943 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE HUGE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 10 TRADING DAYS IN TONNES: 247.05 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2017, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 2555 TONNES

THUS EFP TRANSFERS REPRESENTS 247.05/2550 x 100% TONNES = 9.68% OF GLOBAL ANNUAL PRODUCTION SO FAR IN DECEMBER ALONE.***

ACCUMULATION OF GOLD EFP’S YEAR 2019 TO DATE: 247.05 TONNES

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A GIGANTIC SIZED INCREASE IN OI AT THE COMEX OF 15,044 WITH THE TINY GAIN IN PRICING ($1.65) THAT GOLD UNDERTOOK YESTERDAY) //.WE ALSO HAD A VERY HUGE SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 6045 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 6045 EFP CONTRACTS ISSUED, WE HAD AN UNBELIEVABLE GAIN OF 21,089 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

6045 CONTRACTS MOVE TO LONDON AND 15,089 CONTRACTS INCREASED AT THE COMEX. (IN TONNES, THE GAIN IN TOTAL OI EQUATES TO 65.59 TONNES). ..AND ALL OF THIS DEMAND OCCURRED WITH THE TINY GAIN OF $1.65 IN YESTERDAY’S TRADING AT THE COMEX??????????

we had: 5 notice(s) filed upon for 500 oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD DOWN $1.45 TODAY

NO CHANGES IN GOLD INVENTORY AT THE GLD

/GLD INVENTORY 797.71 TONNES

Inventory rests tonight: 797.71 tonnes.

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

SLV/

WITH SILVER DOWN 4 CENTS TODAY:

A SMALL CHANGE IN SILVER INVENTORY/

A WITHDRAWAL OF 469,000 OZ FROM ITS INVENTORY

/INVENTORY RESTS AT 313.163 MILLION OZ.

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER ROSE BY A GOOD SIZED 1433 CONTRACTS from 189,936 UP TO 191,309 AND MOVING CLOSER TO THE NEW COMEX RECORD SET LAST IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 1 1/3 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89. AS YOU CAN SEE, WE HAVE RECORD HIGH OPEN INTERESTS IN SILVER ACCOMPANIED BY A CONTINUAL LOWER PRICE WHEN THAT RECORD WAS SET…..

.

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

31 CONTRACTS FOR MARCH. 0 CONTRACTS FOR APRIL AND AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 31 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI GAIN AT THE COMEX OF 1433 CONTRACTS TO THE 31 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A CONSIDERABLE GAIN OF 1464 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES: 7.32 MILLION OZ!!! AND YET WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESSED A FINAL STANDING OF GREATER THAN 30 MILLION OZ FOR JULY, A STRONG 6.065 MILLION OZ FOR AUGUST.. A HUGE 39.505 MILLION OZ STANDING FOR SILVER IN SEPTEMBER… OVER 2 million OZ STANDING FOR THE NON ACTIVE MONTH OF OCTOBER., 7.440 MILLION OZ FINALLY STANDING IN NOVEMBER. 21.925 MILLION OZ STANDING IN DECEMBER AND 5.655 MILLION OZ STANDING IN JANUARY..

RESULT: A GOOD SIZED INCREASE IN SILVER OI AT THE COMEX WITH THE 1 CENT PRICING GAIN THAT SILVER UNDERTOOK IN PRICING// YESTERDAY.BUT WE ALSO HAD A TINY SIZED 31 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR SEPTEMBER, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)TUESDAY MORNING/ MONDAY NIGHT:

SHANGHAI CLOSED UP 34.58 PTS OR 1.56% //Hang Sang CLOSED UP 531.96 POINTS OR 2.02% /The Nikkei closed UP 195.59 PTS OR .96%/ Australia’s all ordinaires CLOSED UP 0.66%

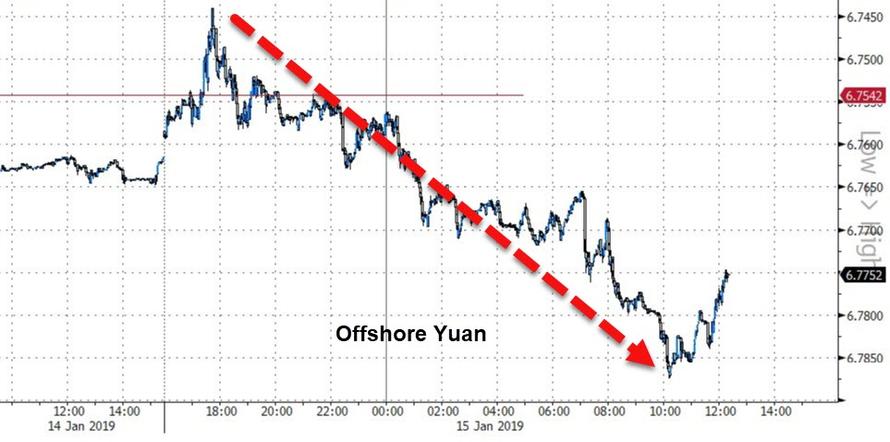

/Chinese yuan (ONSHORE) closed UP at 6.7614 AS TRUCE DECLARED FOR 3 MONTHS /Oil DOWN to 51.10 dollars per barrel for WTI and 59.91 for Brent. Stocks in Europe OPENED /RED

//. ONSHORE YUAN CLOSED UP AT 6.7614 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.7695: HUGE DEVALUATION/PAST SEVERAL DAYS RESUMES// TRADE TALKS NOW ON/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

3A/NORTH KOREA/SOUTH KOREA

i)North Korea/South Korea/USA/CHINA

b) REPORT ON JAPAN

3 C/ CHINA

i)CHINA/USA

4/EUROPEAN AFFAIRS

i)ITALY/EUROPE/

According to Italy’s PMi Salvini, Europe could collapse over the migration issue.

( zerohedge)

ii)Italy now wants to build an anti EU axis on the populist program. They are teaming up with Hungary on this issue. The central them is that they are anti immigrate

( Kern/Gatestone)

iii)France

Riots continue in France where the police are now using semi automatic weapons trying to quell the yellow vests. Macron is losing grip on his country.

(courtesy zerohedge)

iv)UK/the historical vote:

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

IRAN

Iran launches a satellite and it fails to reach its third stage and thus did not go into orbit. A lot of money down the drain for this bankrupt nation

( zerohedge)

6. GLOBAL ISSUES

i)The following is a good bellwether for global growth: Goodyear tire slashes guidance and blames China and Europe

( zerohedge)

ii)the global slowdown is much more advanced that originally thought.

7. OIL ISSUES

8 EMERGING MARKET ISSUES

ii)INDIAThis will hurt India’s GDP: India just staged the largest strike in its history as 200 million workers took to the street; This lasted for two days.

( zerohedge)

9. PHYSICAL MARKETS

( Ahval/GATA)

10. USA stories which will influence the price of gold/silver)

MARKET TRADING

After being up in the early morning, Chuck Grassley admitted that there was little progress in the latest Chinese trade talks. I have been telling you that there will be no deal struck between China and the uSA

( zero hedge)

ii)Market data/

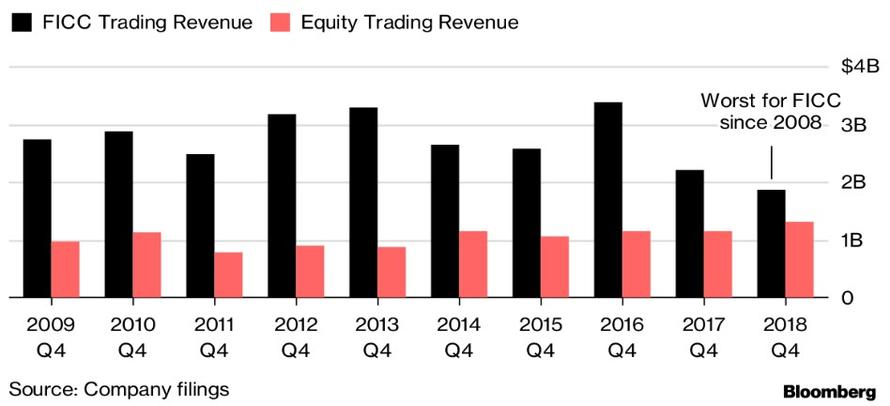

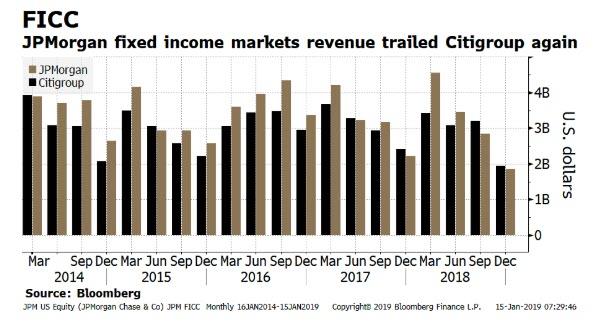

a)This is a major surprise: our crooked friends over at JPMorgan miss on the earnings and revenue . It seems that the entire globe is having trouble

( zerohedge)

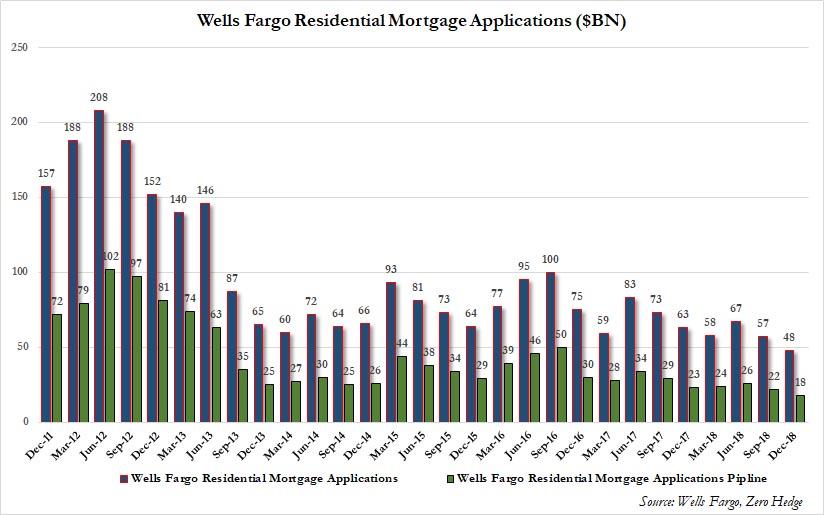

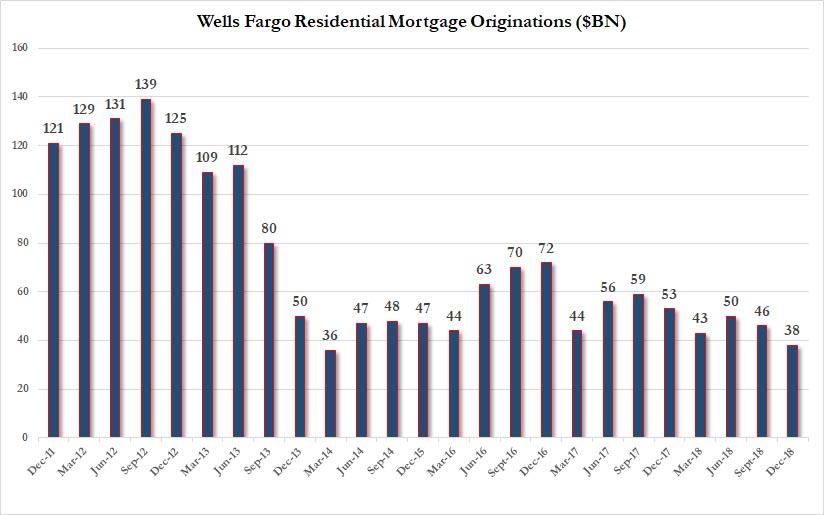

b)Wells Fargo the leader in the USA mortgage field, just reported its worst number since the financial crisis began in 2008. Another indicator that the USA economy is faltering.

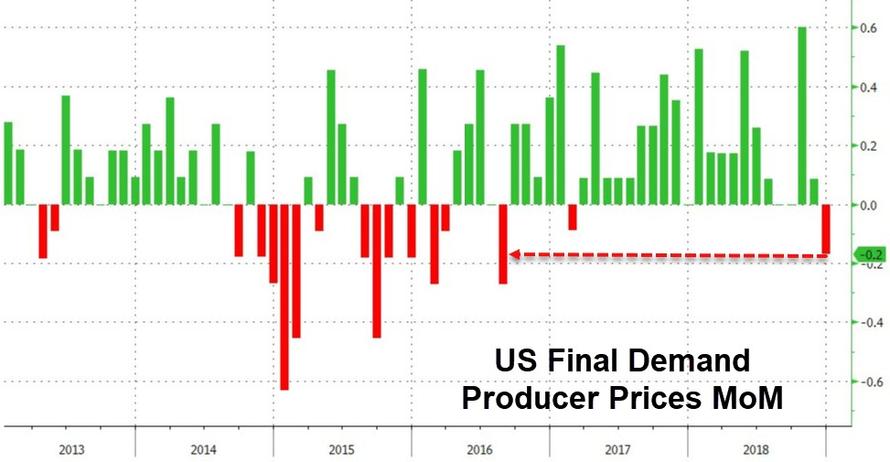

c)Another good indicator that the economy is coming to a screeching halt: USA producer prices disappoint again, dropping .2% month/month

( zerohedge

a) Los Angeles sees it’s first teacher strike in 30 years as 30,000 teachers were not in their classrooms and instead were picketing, It will impact 480,000 students.

( zerohedge

(courtesy Michael Snyder)

c)Quite an op ed. Usually they do not allow anonymous op eds However this one is from a senior Trump official and he hopes for a long shutdown to smoke out the resistance.

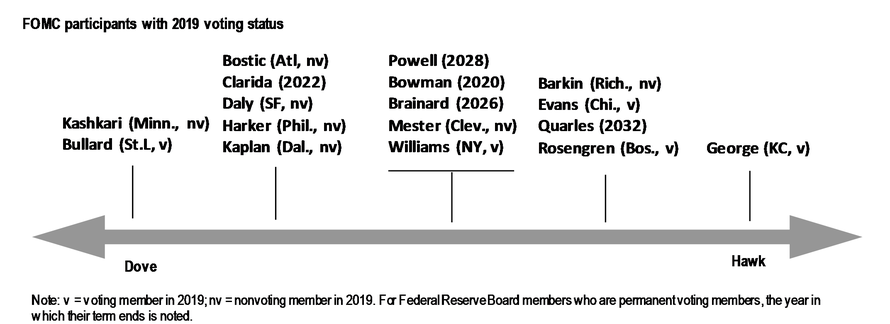

d)this is huge!! The biggest hawk of the them all: Esther George, just threw in the towel and states that it is a good time to pause hikes in rates. It indicates that all Fed govs and presidents now believe that the economy is sinking. I still think that Powell will blow up the system and continue to raise rates.( zerohedge)

iv)SWAMP STORIES

Today, we have the hearings for the new AG. Barr states that there is no “witch hunt” against Trump but he is shocked by the texts of FBI agents. I think this is grandstanding..he will make his move once he is confirmed.

( zerohedge)

Let us head over to the comex:

THE NEXT NON ACTIVE DELIVERY MONTH IS FEBRUARY AND HERE THE OI ROSE BY 5 CONTRACTS DOWN TO 457. AFTER FEBRUARY IS THE VERY BIG AND ACTIVE DELIVERY MONTH OF MARCH AND HERE THE OI ROSE BY 331 CONTRACTS UP TO 143,323 CONTRACTS.

FOR COMPARISON TO THE COMEX 2017 CONTRACT MONTH AND JANUARY 2018 CONTRACT MONTH

ON FIRST DAY NOTICE JAN 1/2018 CONTRACT MONTH WE HAD A GOOD 2.695 MILLION OZ STAND FOR DELIVERY’

AT THE CONCLUSION OF JAN/2018 WE HAD 3.650 MILLION OZ STAND AS QUEUE JUMPING WAS THE NORM FOR SILVER

.

i) Out of Delaware;: 1217.18 oz

ii) Out of HSBC: 8587.106 oz

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

end

–

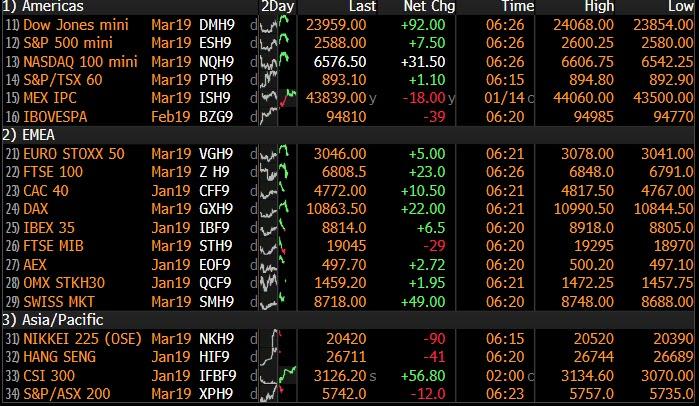

Your early TUESDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED UP TO 6.7614/HUGE DEVALUATION FOR THE PAST FOUR WEEKS STOPS ON TRUCE/

//OFFSHORE YUAN: 6.7695 /shanghai bourse CLOSED UP 24.58 PTS OR 1.56%

HANG SANG CLOSED UP 531.96POINTS OR 2.02%

2. Nikkei closed UP 195.59 POINTS OR .96%

3. Europe stocks OPENED ALL RED

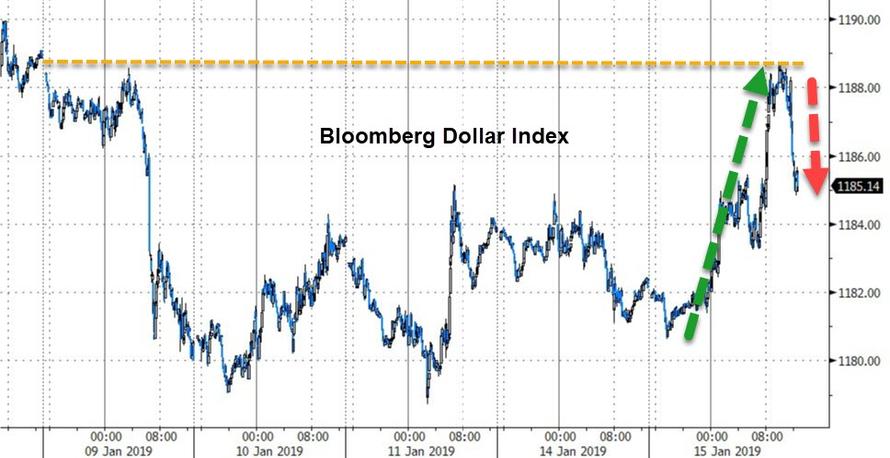

/USA dollar index RISES TO 95.91/Euro FALLS TO 1.1422

3b Japan 10 year bond yield: FALLS TO. +.01/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 108.11/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD IS NOW TARGETED AT .11%/JAPAN LOSING CONTROL OF THEIR BOND MARKET

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 50.97 and Brent: 59.61

3f Gold DOWN/JAPANESE Yen DOWN CHINESE YUAN: ON -SHORE UP/OFF- SHORE: DOWN

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil DOWN for WTI and DOWN FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund FALLS TO +.21%/Italian 10 yr bond yield UP to 2.85% /SPAIN 10 YR BOND YIELD DOWN TO 1.39%…ITALIAN 10 YR BOND YIELD/GERMAN BUND: 2.64: DANGEROUS FOR THE ITALIAN BANKING SYSTEM

3j Greek 10 year bond yield FALLS TO : 4.27

3k Gold at $1290.90 silver at:15.59 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble DOWN 7/100 in roubles/dollar) 67.08

3m oil into the 50 dollar handle for WTI and 59 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 108.36 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 0.9869 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1269 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now POSITIVE territory with the 10 year FALLING to +0.21%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.69% early this morning. Thirty year rate at 3.04%

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

6. TURKISH LIRA: UP TO 5.4466

Global Rally Fizzles As Traders Look Beyond Latest Chinese Stimulus

One week after unveiling its latest monetary easing in the form of an RRR cut, China unveiled yet more stimulus, this time fiscal, announcing it will cut taxes “on a larger scale,” increasingly relying on tax cuts as the first line of defense against a slowing economy, in a departure from the infrastructure binges of the past. And while this was sufficient to boost global equities overnight, and helped push most global markets into the green…

… much of the rally fizzled as US equity futures trimmed half of their overnight gains…

… while European stocks were almost unchanged after starting off sharply higher.

Earlier, Asian stocks rose on Tuesday, supported by a bounce in Chinese shares amid hopes for government stimulus following the latest dismal Chinese trade data. MSCI’s index of Asia-Pacific shares ex-Japan recovered from early losses and advanced 1.3%. South Korea’s Kospi hit a one-month high and Japan’s Nikkei added 1 percent as the USDJPY rebounded in early trading.

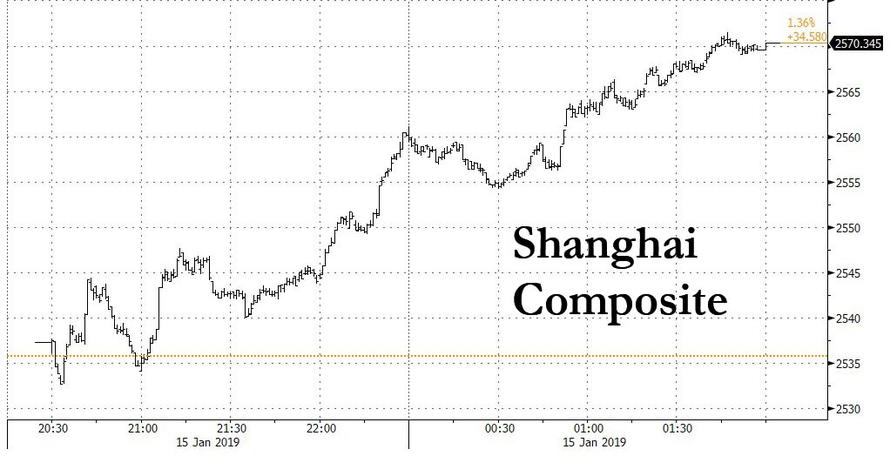

In China, the CSI300 index of Shanghai and Shenzhen shares was up 1.7% amid expectations of more government policy measures to prop-up a slowing economy while lending data from the country beat estimates in December. The Shanghai Composite closed at session highs, up 1.4%.

China’s state planning agency said on Tuesday it will aim to achieve “a good start” in the first quarter for the economy in a signal of more growth-boosting steps. State television also quoted Chinese Premier Li Keqiang as saying the government is seeking to establish conditions helpful to meeting this year’s economic goals.

As Bloomberg notes, the potential stimulus in China and warm welcome it received from markets reflects the delicate balance underpinning 2019’s risk-asset rebound: The same weak macro data that prompted a sell-off at the end of last year has the potential to spur looser monetary policies and therefore ignite a rally.

Cyclical shares led the gains in Asia-Pacific, with Australian financial shares at their highest since early December while Japanese electronics and machinery makers shares rose to their best levels in six weeks. “It is interesting that cyclicals are leading the gains today. It appears some contrarian investors are starting to buy cyclicals, looking beyond the last economic slowdown,” said Nobuhiko Kuramochi, chief strategist at Mizuho Securities. “But I would suspect there will be heavy selling if we go up further, to around 2,650 in the S&P500 and 21,500 in the Nikkei,” Kuramochi added.

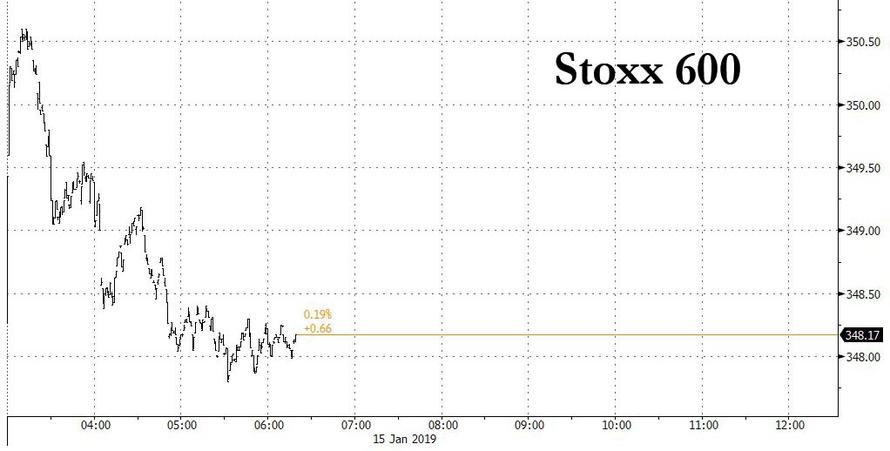

The rally carried over to Europe with the Stoxx Europe 600 Index still higher for the fifth day in six, though the rally fizzled as the session progressed as traders discounted China’s latest promise stimulus.

Gauges in Hong Kong and Shanghai were among the biggest gainers after senior Chinese officials vowed tax cuts to boost growth,

Contracts on the S&P 500, Nasdaq and Dow Jones indexes all rose, with the EMini briefly breaching the 2,600 resistance level before heading lower.

The dollar strengthened and the yen fell. The euro dropped after German data confirmed the weakest year for growth since 2013 although after German GDP dipped 0.2%, the Federal Statistics Office said the country had narrowly avoided a recession.

Treasuries edged higher as most European bonds gained. The sterling braced for the vote in parliament over the British government’s plan to exit the European Union.

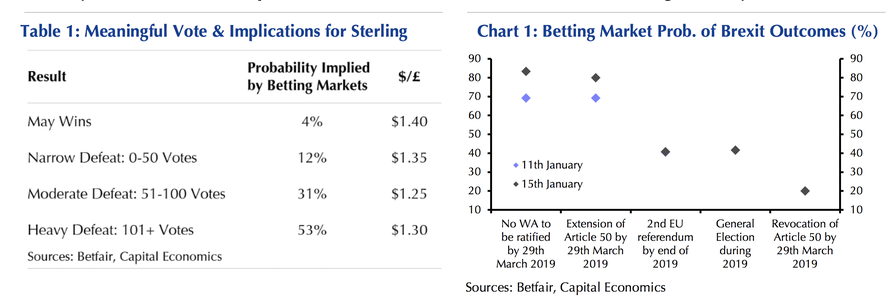

However, despite a barrage of bank earnings, the British pound is expected to steal the limelight later in the day as the Britain’s parliament votes on the proposed Brexit deal. On Monday, May urged lawmakers to take a “second look” at her deal, which lawmakers are expected to reject. Such a result could produce a wide range of outcomes, from a disorderly exit from the union to a reversal of Brexit.

“Markets have priced in a rejection of May’s plan and there are many scenarios after that. Still I’d think the most likely outcome is to extend the (March 29) deadline of Brexit,” said Masahiro Ichikawa, senior strategist at Sumitomo Mitsui Asset Management.

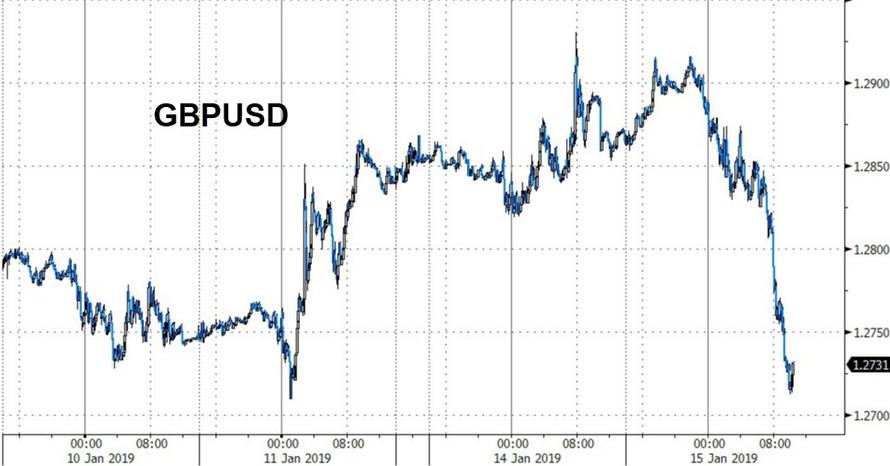

Indeed, currency option markets are barely pricing in the chances of sharp moves in sterling. The pound’s one-month implied volatility stood at 12.625 percent, above the average for the past year of around 8.8 percent well off 20-percent plus levels seen in the days just before the UK referendum on June 23, 2016.

The pound dropped below $1.29, having hit a two-month high of $1.2930 on Monday after a report, subsequently denied, that a pro-Brexit faction of lawmakers could support May’s deal. Additionally, Germany denied reports that German Chancellor Merket offered concessions to UK PM May; following reports that German Chancellor Merkel has offered PM May certain last-minute assistance, while reports also noted that PM May is considering a 2nd vote on Brexit deal if first one is rejected. German Foreign Minister Maas later said that if the current deal is rejected by UK parliament there could be new talks with the EU. UK cabinet ministers suggested that PM May will be expected to stand down if she is heavily defeated in the Brexit vote, according to source report.

UK Labour MP Benn has confirmed he has pulled amendment this morning as part of an effort by Labour party to table vote of no confidence this evening. The amendment, if passed, would reject the withdrawal agreement, convey a lack of support for no deal and pave the way for MPs to put forward alternative plans for Brexit. Opposition for the amendment comes from Labour leadership believing that it’s passage would offer PM May the opportunity to pull her deal, therefore sparing her a crushing defeat. Furthermore, Sky analysis believes that the UK Government are to lose the meaningful vote by 226 votes.

In geopolitical news President Trump is said to have sent a letter to North Korea leader Kim and reports also noted North Korean official Kim Yong Chol may visit Washington D.C. this week regarding a 2nd Trump-Kim summit. Furthermore, it was also reported that US Secretary of State Pompeo may conduct talks this week with North Korea. Additionally, US President Trump tweeted that he spoke with Turkish President Erdogan in which topics discussed included economic development between US and Turkey, while he also suggested that there is great potential for a significant expansion.

China’s Foreign Ministry says facts show China is safe and Canada has arbitrarily detained foreign citizen; adding that the Canadian side can abandon prejudices and quit making irresponsible remarks. Adding that it is clear the Huawei Executive Meng’s case is not normal and is an abuse of legal procedures

Elsewhere in commodities, oil prices also rebounded on supply cuts by producer club OPEC and Russia. International Brent crude oil futures were at $59.80 per barrel, or 1.37 percent from their last close.

Market Snapshot

- S&P 500 futures up 0.3% to 2,588.75

- STOXX Europe 600 up 0.4% to 349.02

- MXAP up 1.1% to 152.24

- MXAPJ up 1.4% to 492.62

- Nikkei up 1% to 20,555.29

- Topix up 0.9% to 1,542.72

- Hang Seng Index up 2% to 26,830.29

- Shanghai Composite up 1.4% to 2,570.34

- Sensex up 1.2% to 36,281.60

- Australia S&P/ASX 200 up 0.7% to 5,814.56

- Kospi up 1.6% to 2,097.18

- German 10Y yield fell 2.6 bps to 0.205%

- Euro down 0.3% to $1.1432

- Italian 10Y yield fell 1.1 bps to 2.483%

- Spanish 10Y yield fell 3.5 bps to 1.384%

- Brent futures up 0.9% to $59.52/bbl

- Gold spot down 0.3% to $1,288.12

- U.S. Dollar Index up 0.2% to 95.84

Top Overnight News

- British and European Union diplomats are now working on the assumption that the U.K. will leave the bloc later than the planned exit date of March 29 if Prime Minister Theresa May loses Tuesday’s Brexit deal vote in Parliament

- China’s government is turning increasingly to tax cuts as the first line of defense against a slowing economy, in a departure from the infrastructure binges of the past

- China’s credit growth exceeded expectations in December, with the second acceleration in a row indicating the government and central bank’s efforts to spur lending are having an effect

- Germany’s economy narrowly avoided a recession at the end of 2018 after a slump in industry raised concerns over Europe’s growth engine

- Swedish Social Democrat leader Stefan Lofven has one day to form consensus for a new government

- Donald Trump and Turkish President Recep Tayyip Erdogan spoke by phone and tamped down their public rhetoric Monday after the U.S. president warned the country risked economic ruin if it defies him. Wild lira ride awaits if the central bank cut rates

- OPEC and its allies plan to hold a meeting in March to assess their oil-production accord in Azerbaijan, and then ministers will gather to set policy in April, according to the organization’s top official

- Kim Jong Un told the world this month that North Korea took steps to stop making nuclear weapons in 2018, a shift from his earlier public statements. The evidence shows production has continued, and possibly expanded

Asian equity markets were mostly higher as sentiment in the region recovered from the recent China-triggered weakness that had been due to disappointing trade data which dragged the US major indices to their first consecutive loss of the year. Nonetheless, risk appetite improved overnight with both ASX 200 (+0.7%) and Nikkei 225 (+0.9%) positive, in which the latter recovered from early selling pressure as it initially tracked the prior day’s losses on return from its long weekend. Elsewhere, Shanghai Comp. (+1.4%) and Hang Seng (+2.0%) were underpinned amid a deluge of comments from Chinese agencies including the Finance Ministry which stated that China will implement larger tax and fee cuts, while the NDRC said China will continue implementing proactive fiscal policies. In addition, the PBoC conducted a respectable liquidity injection of CNY 180bln but expects a rapid decline of banking liquidity in the approaching days, while there were also hopes for an improvement in the trade environment after reports that super tankers carrying 6mln bbls of crude left the Texas coast and are likely heading to China. Finally, 10yr JGBs were subdued as the gains in stocks sapped demand for safe-havens and following the recent similar pressure in T-notes, but with losses stemmed amid the BoJ’s presence for JPY 1tln of JGBs with maturities spread across the curve.

Top Asian News

- China’s Yuan Defies Dismal Economy to Head for Six-Month High

- China Is Making Tax Cuts the Key Weapon Against the Slowdown

- China Adding Stimulus Emboldens Asia Stock Traders to Hit ‘Buy’

- UBS Asset Turns Bullish on Junk China Property Dollar Bonds

Major European indices are relatively flat [Euro Stoxx 50 +0.1%] as equity markets gave up initial gains post German FY GDP of +1.5%. Marginal underperformance is seen in the FTSE MIB (-0.2%) where banking names such as UBI Banca (-5.7%), Bper Banca (-4.3%) and Banco BPM (-3.8 %) are at the bottom of the index following the ECB asking Italian banks to set aside additional money to fully cover impaired loans by 2026. Sectors are similarly all in the green, with outperformance in materials and industrials. Other notable movers include gambling names after the US Justice Department stated that all online gambling is now illegal; as such William Hill (-1.6%) and Paddy Power (-1.8%) are in the red. At the bottom of the Stoxx 600 are Provident Financial (-18.0%) following the Co stating that they expect 2018 profits to report towards the lower end of market expectations.

Top European News

- Draghi Readies for First New Year Speech as Economy Falter

- Brexit Donor Hargreaves Says U.K. May’s Deal Should Be Rejected

- Hungary Faces Price Dilemma as Core Inflation Quickens Again

- Russia Has Room to Cut Dollar Reserves by Another $35b, ING Says

In FX, EUR largely on the backfoot amid a strengthening Dollar and following the release of German annual GDP which printed in-line with forecasts at 1.50% Y/Y, the weakest performance in five years with market participants noting that a German technical recession could have been narrowly missed (with the Q4 release scheduled on 14th Feb). EUR/USD sits around the bottom of a 1.1423-91 band ahead of a double-Draghi day, his first speech however provided little in way of monetary policy commentary. Back to the dollar, DXY received a wave of demand shortly after the German numbers with DXY spiking to highs of around 95.900 from overnight lows of 95.450 with State-side news flow on the light side.

JPY, CHF – Conforming more to the bout of dollar strength rather than an unwind in safe-haven positions with both USD/JPY and USD/CHF higher by around 0.4% on the day ahead of the Brexit meaningful vote. USD/JPY advances further above 108.00 after having reclaimed the handle during overnight trade and currently resides nearer to the top of a 108.15-75 range ahead of a Fib a 109.16 with little to report on the options expiry front. Similar action with the Franc as USD/CHF breached 0.9850 to the upside ahead of its 100 and 200 DMAs at 0.9878 and 0.9889 respectively.

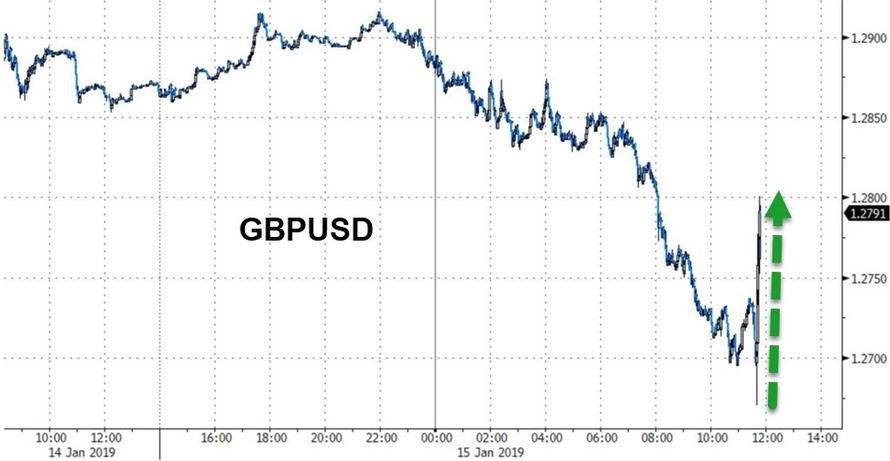

- GBP – Choppy session for the Pound thus far as traders eye the long-awaited House of Commons meaningful vote scheduled for later today (full schedule available on the headline feed), as PM May attempts to accumulate MP backing to pass her deal. According to the Sun’s Political Editor, Senior Tories believe the Premier is poised for a 150-160 vote defeat tonight, though a list of amendments will be released at the start of the Parliamentary session around 12.45GMT with special focus on Murrison amendment (setting an expiry date of 31st December 2021 to the NI backstop) as a way of snatching a narrow defeat. Tory Brexiteers and the DUPs are known to not support a deal which includes a timeless backstop or a unilateral exit clause, Murrison’s amendment seeks to readdress this and if passed, may shore up some support from the rebels, DUP are said to have rejected this amendment in belief the EU will not be bound by the expiry date. Earlier in the day Hilary Benn’s amendment was pulled out amid the opposition leaders’ desire for PM May to suffer a crushing defeat (the amendment, if it was to be passed, would have rejected the withdrawal agreement, convey a lack of support for no deal and pave the way for MPs to put forward alternative plans for Brexit). As such, Cable pared back overnight gains and gave up the 1.2900 handle to test the psychological (and 50 HMA) at 1.2850 to the downside and currently resides at the bottom of a 1.2831-1.2915 intraday range. Meanwhile, Morgan Stanley assumes that Cable at current levels is pricing in a lot of uncertainty and assumes GBP/USD to reach 1.30 in around 6-month and 1.50 by year-end as Cable’s PPP fair value estimate stands at 1.40.

In commodities, Brent (+1.7%) and WTI (+1.6%) are higher as the risk tone improves from the Chinese-trade sparked downturn seen in yesterday’s session, with prices just under the USD 60/bbl and USD 51/bbl respectively. Focus is on the API weekly release later in the day, where crude oil inventories are expected to have declined by 2.5mln/bbl; separately, the EIA are to release their Short-Term Energy Outlook today which contains their expanded forecast discussion. Saudi Energy Minister Al Falih says he sees oil demand growth for the foreseeable future, and that the 1.2mln BPD OPEC+ cut will have a strong impact which will take some time to be reflected within the market. Gold (-0.1%) prices are down as the demand for safe havens has declined with the improvement in risk sentiment; with the yellow metal trading towards the bottom of its USD 5/oz range. Elsewhere, the US Senate are to begin voting today on a resolution which criticises the Trump administration’s decision to reduce sanctions on companies which are connected to Russian oligarch Deripaska; which includes aluminium company Rusal.

US Event Calendar

- 8:30am: Empire Manufacturing, est. 10, prior 10.9

- 8:30am: PPI Final Demand MoM, est. -0.1%, prior 0.1%; PPI Ex Food and Energy MoM, est. 0.2%, prior 0.3%

- 8:30am: PPI Ex Food, Energy, Trade MoM, est. 0.2%, prior 0.3%;PPI Ex Food and Energy YoY, est. 2.95%, prior 2.7%

DB’s Jim Reid concludes the overnight wrap

If you want to depress yourself this morning read the guidance from the British Nutrition Foundation released yesterday which suggested that for optimum health food portion sizes should be measured by hands, thumbs and fists. After reading it I indeed wanted to use my fists but not for the reason intended by the author.

As examples, if you’re having jacket potatoes the correct portion size is a clenched fist (I might try to use Mike Tyson’s). For cheese it should be the size of two thumbs (I note that the largest thumb ever recorded was a Chinese man who had one measuring 10.2 inches), for pasta or rice two handfuls is the recommended amount (I shall resort to wearing wicket keeping or baseball gloves while cooking). All rather depressing. Maybe instead you should join me in “Dry January”. Yes this month I shall only be indulging in dry white wine, dry champagnes, dry martinis, dry sherry and dry gins and tonics.

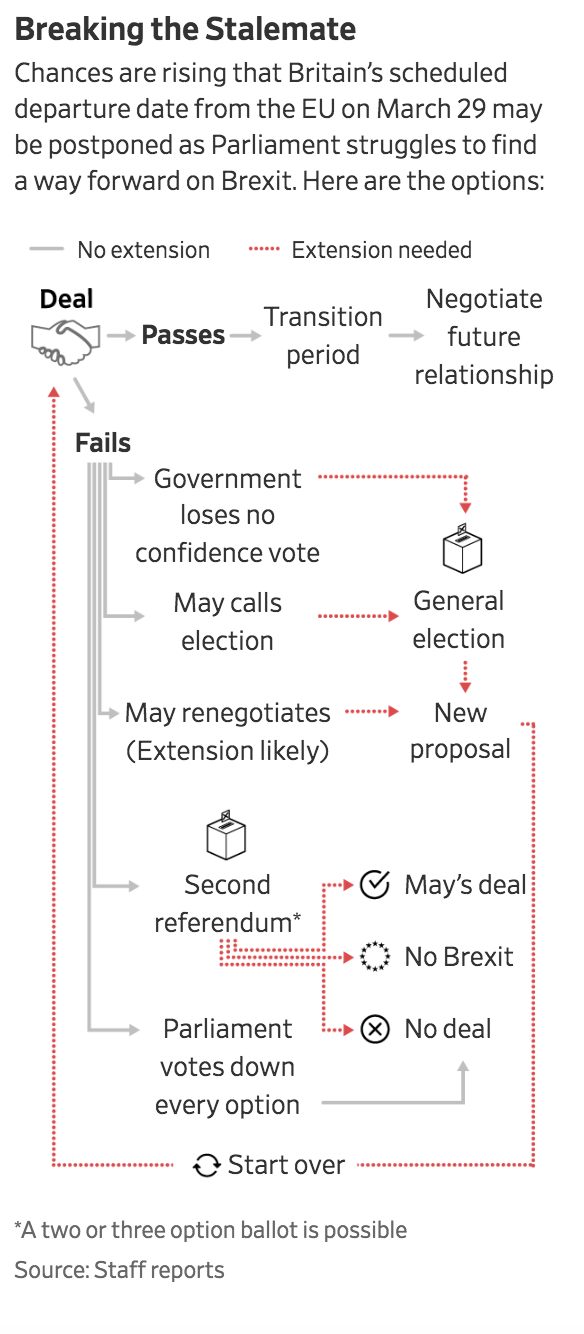

You may need a stiff drink to work out what happens next after tonight’s Brexit vote in the House of Commons. On timings the vote is due to take place after the debate finishes at 7pm GMT with votes on amendments coming first. In all likelihood the vote looks set to fail given that PM May has failed to secure the necessary support from MPs in recent weeks. DB’s Oliver Harvey estimates a 20% probability of May resigning post the vote (or cabinet collectively withdrawing support) and an 80% chance of her staying on as leader. In the case of the latter, the government will have to provide an updated strategy by Monday after last week’s surprise amendment that voted to shorten it from over three weeks to three days.

Throwing all the balls into the air, DB’s Oli Harvey believes there are five corresponding scenarios. The most likely scenario (at a 30% probability) is May pivots towards a cross party consensus on a new mandate which would instruct the government to renegotiate the Political Declaration on the Future Relationship towards a softer relationship. For this to be reached, it might be necessary for the Labour Party to call, and lose, a vote of no confidence in the government first. A small extension on Article 50 is probably necessary for this scenario as well as another round of EU negotiations. The other four scenarios are; a 10% chance of May using multiple votes to force through the existing deal in the face of a crash Brexit, a 15% chance of a second referendum, a 15% chance of a new election and a 10% chance of no deal/crash Brexit. Regarding the worst case latter scenario, the news that the EU appears prepared to extend Article 50 to July or beyond does appear to be a material positive to lowering the odds of no deal at all. Anyway more in Oli’s note from yesterday here .

Ahead of vote today on PM May’s deal, the Commons Speaker, John Bercow will select amendments from those suggested by MPs. The amendments to be considered range from Labour’s, which rejects the current deal while also repudiating a no-deal Brexit and calling for the Government to examine all available options, to the Lib-Dem’s, which calls for a second referendum. A vast majority of others are related to the Northern Ireland backstop arrangement with the Conservative MP Andrew Murrison calling for an amendment that would put a time limit on the Northern Ireland backstop, aimed at reducing the scale of the expected government defeat. Meanwhile, Labour MP Hilary Benn is withdrawing his amendment, which had cross-party support and rejected both the current deal and a no-deal outcome (similar to Labour’s proposal). Mrs May is reportedly considering amendments which would put time limits on the Northern Ireland backstop, in an effort to regain support from the DUP. Such a framework has already been rejected by the EU, so it’s not clear how useful a winning vote on this would be. Sterling is up +0.26% in early trade this morning ahead of today’s vote.

Onto markets and for only the third time this year US equities closed lower across the board yesterday as that soft trade data out of China in the morning, in addition to a bit of general fatigue for risk assets following the recent strong run, appeared to be enough of an excuse for investors to pull back a little. The S&P 500, NASADQ and DOW closed -0.53%, -0.94% and -0.36% respectively although at one stage it looked like it might have been worse firstly with PG&E (-53.36%) taking the wider utilities sector (-2.23%) down after announcing plans to file for Chapter 11 and then Citigroup reporting lower than expected Q4 revenues. However, the latter never really fed its way through to the wider banks sector with Citi’s shares, actually closing up +3.95% after the CEO said that conditions have improved so far in January. Plus, digging into the results, credit quality improved for both corporate and consumer loans, and expenses declined. The wider S&P Banks sector ending +1.36% in what was a rare bright spot for the broader index. JP Morgan and Wells Fargo, two of the three largest US banks by market cap, are due to report earnings later today.

Meanwhile, US HY cash spreads edged +4bps wider, while 10-year Treasury yields traded flat. Two-year yields rallied -0.6bps, helping the 2s10s curve to steepen slightly at 16.5bps and more or less in the middle of the range since the start of December. The USD was a touch weaker, as Fed Vice Chair Clarida reiterated his recent guidance in an interview. He said the Fed can afford to be patient and assess policy “meeting by meeting”, so continuing to signal no immediate urgency to raise rates. WTI oil ticked down -1.61% to mark the first two-day decline for oil this year.

A quick refresh of our screens this morning indicates that risk-on is back in Asia with the Nikkei (+0.80%), Hang Seng (+1.54%), Shanghai Comp (+0.96%) and Kospi (+1.31%) all up as China indicated that it will cut taxes “on a larger scale” to help support its slowing economy, according to agreements reached by top leadership at the economic work conference last month. China’s onshore yuan is up +0.23% alongside most Asian currencies. Elsewhere, futures on the S&P 500 are up +0.58% while crude oil prices (WTI +1.15% and Brent +1.12%) are also trading higher.

Aside from the China data yesterday, the only other major release of note came in Europe with the November industrial production reading for the Euro Area. The data was worse than feared at -1.7% mom (vs. -1.5% expected) and means the year-on-year reading is now down to -3.3% and the lowest since 2012. In Germany, wholesale prices fell -1.2% mom, the sharpest drop since 2014 and the second sharpest since 2009. There is increasing chatter about a technical recession being possible in Germany for Q4 and Q1 so data like this isn’t helping rule that out.

To the day ahead now, where the early data releases in Europe this morning include the final December CPI revisions in France and the final 2018 GDP reading for Germany. For the latter the consensus is expecting a 1.5% increase in real GDP after 2.2% in 2017 (our economists forecast 1.6%). Also out this morning is the November trade balance for the Euro Area, while this afternoon in the US, we’ve got the January empire manufacturing print and December PPI report. The latter is expected to show a -0.1% mom decline in the headline and +0.2% mom increase for the core. Away from the data, we’re due to hear from ECB President Draghi this afternoon, followed by Fed officials Kashkari, George and Kaplan later on. Needless to say the aforementioned Brexit vote this evening will be a big focus while the key companies reporting earnings include JP Morgan, Wells Fargo, Delta Airlines and UnitedHealth.

3. ASIAN AFFAIRS

i)TUESDAY MORNING/ MONDAY NIGHT:

SHANGHAI CLOSED UP 34.58 PTS OR 1.56% //Hang Sang CLOSED UP 531.96 POINTS OR 2.02% /The Nikkei closed UP 195.59 PTS OR .96%/ Australia’s all ordinaires CLOSED UP 0.66%

/Chinese yuan (ONSHORE) closed UP at 6.7614 AS TRUCE DECLARED FOR 3 MONTHS /Oil DOWN to 51.10 dollars per barrel for WTI and 59.91 for Brent. Stocks in Europe OPENED /RED

//. ONSHORE YUAN CLOSED UP AT 6.7614 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.7695: HUGE DEVALUATION/PAST SEVERAL DAYS RESUMES// TRADE TALKS NOW ON/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

3 a NORTH KOREA/USA

3 b JAPAN AFFAIRS

3 C CHINA

4.EUROPEAN AFFAIRS

ITALY/EUROPE/

According to Italy’s PMi Salvini, Europe could collapse over the migration issue.

(courtesy zerohedge)

Europe Could “Collapse” Over Migration Says Italy PM; Salvini Insists “Paris-Berlin Axis” Must Change

Italy’s Prime Minister, Giuseppe Conte, said on Monday that the European Union risks collapsing unless it is able to find common ground on mass migration.

Italian Prime Minister Giuseppe Conte“If we continue to stall without a shared path, we risk bringing down the European building,” Conte remarked at a press conference discussing a recent meeting in Rome with European Home Affairs Commissioner Dimitris Avramopoulos.

Italian Prime Minister Giuseppe Conte“If we continue to stall without a shared path, we risk bringing down the European building,” Conte remarked at a press conference discussing a recent meeting in Rome with European Home Affairs Commissioner Dimitris Avramopoulos.

“We presented what Italy has done up to now to Avramopoulos,” said Conte, adding “We are bringing in a change of direction that is bearing fruit.”

While discussing Italian efforts to curb mass migration, Conte said: Italy had been left alone and now are are coping alone. We didn’t talk about a naval blockade with Avramopoulos but we discussed instruments to defend the borders, which is a very important issue for managing (migrant) flows.”

Avramopoulos also met with Italy’s Deputy Prime Minister and Interior Minister Matteo Salvini, who has led the country’s tough stance against NGO-operated migrant transport ships across the mediterranean to Italian ports.

Salvini, speaking with RAI’s Tg2 bulletin, Salvini knocked France and Germany for “dictating legislature” over the past decade, adding that he and his allies in other EU countries “want to change Europe, not destroy it,” reports Bloomberg.

French President Emmanuel Macron, Italian Interior Minister Matteo Salvini“For many years France and Germany have been laying down the law in Europe,” said Salvini, adding “Everything has been done based on the Paris-Berlin axis.”

French President Emmanuel Macron, Italian Interior Minister Matteo Salvini“For many years France and Germany have been laying down the law in Europe,” said Salvini, adding “Everything has been done based on the Paris-Berlin axis.”

“I am trying to put together an alliance focusing on jobs and families,” Salvini stated. “In Italy we have done better than the governments of Mario Monti and Matteo Renzi, in Europe we’ll do better than Juncker and Schulz.”

END

Italy now wants to build an anti EU axis on the populist program. They are teaming up with Hungary on this issue. The central them is that they are anti immigrate

(courtesy Kern/Gatestone)

Italy Building Anti-EU Axis

France

Riots continue in France where the police are now using semi automatic weapons trying to quell the yellow vests. Macron is losing grip on his country.

(courtesy zerohedge)

French Riot Police Deploy Semi-Automatic Weapons Against Yellow Vests As Macron Loses Grip On Country

French riot police were pictured brandishing Heckler & Koch G36 semi-automatic rifles with 30-round magazines near the Arc de Triomphe in Paris on Saturday afternoon, reports the Daily Mail.

The deployment of rifles with presumably live ammunition visible through the magazine is an intimidating escalation as President Emmanuel Macron continues to lose his grip over France following nine weeks of country-wide protests by the Gilet Jaunes (Yellow Vest) movement.

The Gilet Jaunes began as a demonstration against a climate change-linked fuel tax, which quickly morphed into a general anti-government protest against the Macron administration and the world’s highest taxes. We’re sure France’s plege to send 1 billion euros to rebuild Iraq will help calm them down.

Drew Ludwig@drew_ludwig93Riot police in France now armed with G36 assault rifles against unarmed civilians. WHERE IS THE NEWS COVERAGE?https://streamable.com/wh802

Yellow Vest demonstrator Gilles Caron told the Mail “The CRS with the guns were wearing riot control helmets and body armour – they were not a specialised firearms unit,” adding “Their job was simply to threaten us with lethal weapons in a manner which is very troubling. We deserve some explanations.”

A French National Police spokesman confirmed that the CRS were equipped with H&K G36s on Saturday, but would not discuss their operational use ‘for security reasons’.

A G36 was stolen from inside a police van during a similar Yellow Vest demonstration by the Arc de Triomphe on December 1.

A number of vehicles belonging to the 21stIntervention Company of the Paris Prefecture were stormed, suggesting that the theft was an opportunistic one during a day of intense violence, when the Arc de Triomphe itself was vandalised. –Daily Mail

Former French conservative minister Luc Ferry called for live rounds to be used against the Yellow Vest “thugs” who “beat up police,” such as this former pro heavyweight boxer, 37-year-old Christophe Dettinger who was arrested after squaring off with several French police officers.

LINE PRESS@LinePress#GiletsJaune très forte mobilisation à #Paris le peuple en colère force les barrages de police #Acte8 #ActeVIII #05janvier #05janvier2019

Ferry – a full time philosopher now, said: “What I don’t understand is that we don’t give the means to the police to put an end to this violence.” When challenged with the suggestion that the guns might lead to bloodshed, Ferry said: “So what? Listen, frankly, when you see guys beating up an unfortunate policeman on the floor, that’s when they should use their weapons once and for all! That’s enough.”

What the H&K G36 looks like in action:

UK/the historical vote:

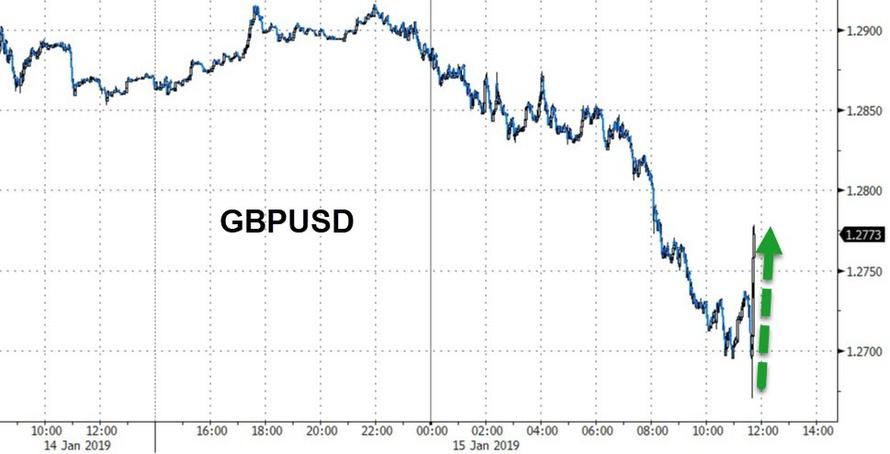

In Humiliating Defeat For May, Brexit Deal Rejected By Overwhelming 230-Vote Margin

Update 9: The House has adjourned for the day, and cable has continued its ascent toward the $1.2850 level.

* * *

Update 8: Steve Baker, director of the Brexiteer faction in the European Research Group, has met with May to lay out what is presumably their preferred alternative to May’s Brexit plan.

A temporary free-trade agreement only about the movement of goods, which wouldn’t need the ratification of the EU’s 27 members A temporary zero tariff on some imports from the EU in order to keep food prices down The U.K. could withhold some or all of its 39 billion-pound annual contribution, as it is not in an implementation period May’s government could force the measure through by secondary legislation to an existing act of Parliament or amend future legislation

Meanwhile, amid the chaos in the aftermath of Tuesday’s vote, this quote reportedly used by Winston Churchill to mock Americans is once again being thrown around to mock the fractiousness in May’s conservative party.

“You can always count on them to do the right thing – after they have tried everything else.”

A reporter for one German newspaper, citing several EU27 sources, said they would support delaying Brexit Day until the end of June (though a recent ECJ decision granted the EU unilateral authority to do so).

* * *

Update 7: In a silver lining for May, the DUP has said it will back May in Wednesday’s no confidence vote, meaning that the only way for the opposition to topple the government would be for a number of Tory rebels to side with Labour which is…unlikely.

* * *

Update 6: Comment from European leaders are starting to break on twitter, with the Austrian PM insisting that, though the defeat of the deal is unfortunate, there won’t be a renegotiation of the deal.

In one of the more aggressive comments, Donald Tusk seemed to imply that, if the deal is so unpopular, maybe the UK should reconsider this whole Brexit thing.

Donald Tusk

✔@eucopresident

If a deal is impossible, and no one wants no deal, then who will finally have the courage to say what the only positive solution is?

The pound has broken above $1.28.

* * *

Update 5: The pound kneejerked lower, but swiftly recovered as traders realized that the overwhelming defeat means the EU may now reconsider its decision not to reopen negotiations.

It’s now up on the day.

May said in a speech that “we must focus on ideas that are genuinely negotiable.” She also denied that the government’s strategy is to run down the clock.

Before officially tabling his motion of no confidence, Jeremy Corbyn called for a permanent customs union, saying a permanent customs union must be secured, after gloating over the worst defeat for a government since the 1920s. No deal must be taken off the table and people’s rights and protections must be secured.

“I inform you Mr. Speaker I have now tabled a motion of no confidence in this government and I’m pleased that motion will be debated tomorrow so this House can give its verdict on the sheer incompetence of this government.”

* * *

Update 4: May has lost by a 230 vote margin. As the results were read out, the Commons erupted in commotion.

The final results: 432-202

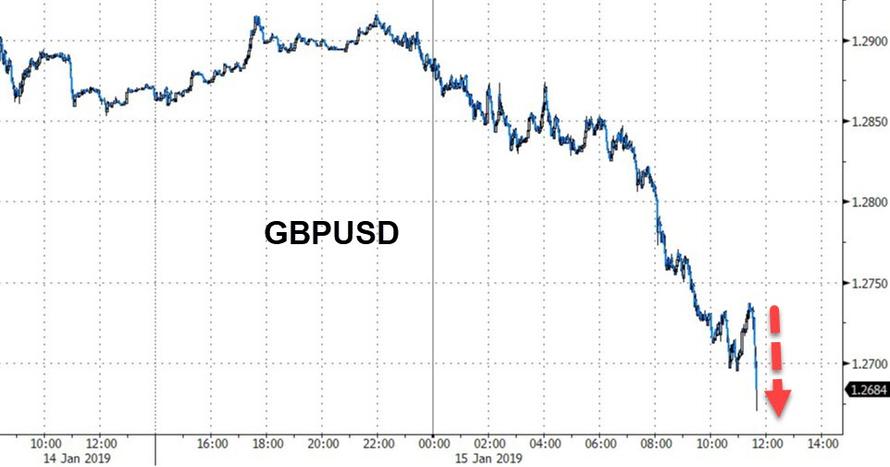

The pound is puking.

* * *

Update 3: Minutes before the final results are due, reporters have noted that the ‘no’ lobby is mobbed. “It’s safe to say May’s deal is sunk”, one commented.

Word is the government only has 202 votes – which would mean a sizable defeat. That would be 475 against, an overwhelming rejection that would bring her ability to schedule another vote into question.

Though that’s nothing we didn’t already know.

* * *

Update 2: The Baron amendment has been rejected by a vote of 24-600. The amendment would have called for the UK to have the ability to unilaterally leave the backstop.

The Bent Nebulouser #WTOBrexit@RealityCheckout

The rejection of the amendment, which May opposed, is a resounding win for the prime minister. Cable has caught a slight bid on the news.

Stocks legged lower after the Brexit headline hit, which could be a sign that algos read “reject” in the headline and reflexively dumped.

* * *

Update: The voting has just begun but there’s already been a handful of surprises. Three of the four accepted amendments have been dropped, so voting will proceed on the final amendment (the Baron amendment, backed by a cross-party group of legislators) before proceeding directly to the motion to pass.

BBC Politics

✔@BBCPolitics

MPs begin their #BrexitVote, starting with amendment by Conservative MP John Baron

Live updates: http://bbc.in/2DaADGH

317 is the magic number needed for the motion to pass.

Bloomberg now expects the final tally to arrive by 2:30 pm ET. Cable is flat as voting begins.

* * *

After months of fractious negotiations during which Theresa May has repeatedly tried – and failed – to win over intransigent Tories and members of the small Northern Irish party upon which she depends for her tenuous Parliamentary majority, May’s supremely unpopular Brexit withdrawal deal is finally coming up for a vote in the House of Commons.

Almost nobody, including May herself, expects it to pass. In fact, most analysts expect the deal to be defeated by a wide margin of at least 150 votes, which would be tantamount to the worst defeat for a British government in 95 years, according to Bloomberg.

At least 70 members of May’s party have publicly pledged to oppose the deal, and members of the Brexiteer European Research Group have also vowed to vote down each of the four proposed amendments that MPs will be decided before the deal comes up for a vote.

The debate and the votes will be broadcast live from Westminster following a speech from May. Readers can watch the action below:

May has just over two months to secure a withdrawal agreement palatable to both Parliament and the EU27 leaders, or risk a delay of Article 50 – which would push back the Brexit deadline – or possibly a chaotic ‘no deal’ outcome (though Parliament has recently taken steps to ensure that a ‘no deal’ exit would require the explicit approval of Parliament). UK diplomats are reportedly already working under the assumption that the March 29 “Brexit Day” will likely be delayed.

Per the Wall Street Journal, four amendments to the motion to pass the deal have been selected by John Bercow, the Speaker of the House of Commons, including one that would exclude a no-deal Brexit and another that would put a time limit on the UK’s transition out of the EU. Another amendment, which May has said isn’t palatable to Brexiteers (or the EU) is the Leigh amendment, which would put a time limit on the backstop.

Steven Swinford

✔@Steven_Swinford

BREAKING

Bad news for Downing Street

John Bercow has selected FOUR amendments:

Corbyn amendment, SNP amendment, Edward Leigh amendment and John Baron amendment.

NOT Murrison or Swire

In theory, the amendments would give May, Parliament and the EU a better idea of what Parliament would accept. May is expected to return to Brussels within 48 hours of Tuesday’s vote to meet with EU leaders, who have recently signaled that they might be open to making some minor changes to the deal. But a stunning defeat in Parliament is seen as an essential step before this can happen.

Shortly before the vote was scheduled to begin, headlines crossed the wires reporting that May would return with an even better Brexit deal next week (an amendment passed last week requires May to return with a ‘Plan B’ within a few days of the deal’s defeat).

The latest reports suggest that May’s efforts to convince some Tories to abstain instead of voting against the deal have been ineffective, which suggests the deal likely will lose by a sizable margin. Labour has confirmed that it will be voting against the deal. Party leader Jeremy Corbyn has also threatened to table a motion of no-confidence in May’s government if she loses the vote, saying that Labour would seek another general election.

As analysts try to suss out what the vote could mean for the pound, a team from Capital Economics said that an inconclusive moderate defeat could be the worst outcome because it would increase uncertainty by taking away some incentives for May and the EU to compromise. A narrow defeat of only 50 votes could send sterling higher, perhaps above $1.30, while a miracle victory for May could send the pound all the way to $1.40.

Meanwhile, cable slipped under $1.27 as traders waited for the votes to begin (currency traders have weighed in with various takes on what they believe could happen to the pound).

CE published a table of odds for various outcomes, putting a heavy defeat at the highest likelihood with 53%>

Given the confusion around the arcane Commons rules being invoked to push through the amendments, the House of Commons twitter account has published a handy guide to how the voting will proceed.

UK House of Commons

✔@HouseofCommons

How will voting on amendments work this evening?

After announcing his provisional selection of amendments, the Speaker explained the process and we’ve turned it into a diagram to make it easier to understand.Watch the Speaker’s explanation: https://parliamentlive.tv/event/index/27d512b5-9b1d-43a4-80dd-371b0c5c1a5e?in=12:56:53 … #BrexitVote

Looking beyond Tuesday’s vote, Deutsche Bank tabulated the odds for various Brexit outcomes. Ultimately, a loss of 150 votes or more could increase the chances that May resigns or is pushed out following the vote (text courtesy of Deutsche Bank).

A) May resignation/withdrawal of cabinet support: 20% probability. While we think this unlikely, there is a chance Prime Minister May resigns following the vote, particularly should the government’s loss be toward the top end of the scale mentioned above. Another possibility is the cabinet collectively withdraw support, making her position untenable. The main reason why we see this as unlikely is that under Conservative Party rules, unless MPs can agree on a single candidate to replace the Prime Minister, a leadership contest would follow. As Conservative MPs will find it difficult to agree on a single replacement candidate, unless Prime Minister May chooses to resign, we think the cabinet will seek to avoid a de-stabilising leadership contest. Should May resign and a leadership contest materialise, we would anticipate a pro Brexit candidate to be successful. 1While this would increase the likelihood of a no deal Brexit, our base case would be that new elections result, particularly if government policy pivots towards no deal.

B) May remains as leader: 80% probability. The government will then have to provide an updated Brexit strategy to parliament by Monday 21st January. In these circumstances, we see five corresponding scenarios, in order of least to most disruptive.

1) A cross party consensus: 30% probability. Having lost the vote, Prime Minister May pivots towards a cross party approach to EU negotiations or parliament agrees an alternative negotiating mandate and instructs the government to follow it at the next vote on the 21st January or subsequently. For a cross party compromise to be reached, we think it may be necessary for the Labour Party to call, and lose, a vote of no confidence in the government first. We envisage a new mandate would instruct the government to renegotiate the Political Declaration on the Future Relationship towards a softer future relationship. 2 In conjunct with firmer EU commitments linking the Withdrawal Agreement and Political Declaration on the Future Relationship, such a deal should probably carry majority support in parliament. A small (two to four weeks) extension of Article 50 becomes necessary, as well as another round of EU negotiations. We envisage the EU27 would be flexible on both extending Article 50 and reopening talks on the future relationship. This is the most positive scenario, with markets being able to forecast an orderly outcome with a relatively high degree of confidence.

2) A lack of alternatives: 10% probability. Parliamentary consensus does not emerge on the next steps by the vote on the 21st January, or subsequently. Prime Minister May then uses multiple votes to force the existing deal through parliament in the face of a crash Brexit, perhaps after some cosmetic changes to the existing Withdrawal Agreement, and likely with market pressure. Again an extension of Article 50 from the EU27 becomes necessary. This is a more bearish scenario in that it may require market pressure or downside economic risks materialising for MPs to agree.

3) A second referendum: 15% probability. The government’s policy switches to seeking a second Brexit referendum, or (more likely) MPs direct the government to call one at the vote on the 21st January or subsequently. Article 50 is extended to July, or perhaps beyond. We have slightly increased the probability of a second referendum following reports over the last few days the EU27 could envisage an extension of Article 50 beyond the EU Parliament elections in late May, and perhaps well beyond when MEPs take their seats in July. We still believe a bigger sticking point to a second Brexit vote is that while parliamentary consensus could emerge to hold one, consensus on the question asked of the electorate will be more difficult.

4) A new election: 15% probability. May loses the vote and the Labour Party calls a successful confidence motion in the government. After two weeks, assuming a new government cannot be formed, a new election would follow under the Fixed Term Parliament Act. In this scenario, again an extension of Article 50 would be required. We do not see this as a positive scenario in that polls indicate both major parties are close to tied, leading to the risk of an election leading to similar parliamentary gridlock as at present. For a no confidence motion to be successful, the government will have to formally lose the support of the DUP, or a similar number of Conservative MPs from either the extreme pro Brexit or soft Brexit wings of the party.

5) A no deal/crash Brexit: 10% probability. Political deadlock leads to no deal Brexit. This could materialise if a parliamentary consensus does not emerge on an alternative deal, or Prime Minister May fails to get the current Withdrawal Agreement through parliament after multiple times of asking, and a motion of no confidence in the government is unsuccessful.

Scenarios not discussed:

May winning tomorrow’s vote. While we had attached a probability of 40% to May securing political support for the Withdrawal Agreement last week, this was contingent on May pivoting towards a cross party approach in the meantime, which has not materialised. We now do not think there is a realistic probability of the government winning tomorrow’s vote.

Revocation of A50. Following a ruling from the ECJ, it is now technically possible for the UK to unilaterally revoke the Article 50 process (the UK’s exit from the EU). Revoking Article 50 would carry an enormously high political price, however, and we do not see it as likely at this stage.

* * *

Amid all of the chaos ahead of the vote, there are really only two outcomes that most analysts agree on. May will almost certainly lose on Tuesday, and Brexit Day will almost certainly be delayed as May and the EU finally begin work on a modified deal that might have a chance of passing Parliament.

5.RUSSIAN AND MIDDLE EASTERN AFFAIRS

IRAN

Iran launches a satellite and it fails to reach its third stage and thus did not go into orbit. A lot of money down the drain for this bankrupt nation

(courtesy zerohedge)

Iran Satellite Launch Fails After Defying US Warnings

Iran on Tuesday conducted at least one of two planned satellite launches despite warnings from the United States, however the satellite failed to reach the “necessary speed” in its third stage and did not enter orbit, according to an official.

The rocket carrying the Payam satellite failed to reach the “necessary speed” in the third stage of its launch, Telecommunications Minister Mohammad Javad Azari Jahromi said.

Jahromi said the rocket had successfully passed its first and second stages before developing problems in the third. He didn’t elaborate on what caused the rocket failure but promised that Iranian scientists would continue their work. –CBS News

The launch took place at Imam Khomeini Space Center in the province of Semnan, and was overseen by the country’s Defense Ministry according to Jahromi. Images published last week by CNN show activity at the launch site.

Tuesday’s launch follows warnings by Secretary of State Mike Pompeo, who said that the launches would violate a 2015 United Nations Security Resolution by incorporating ballistic missile technology, passed in order to endorse the Iran nuclear deal which Trump withdrew from last May.

“The United States will not stand by and watch the Iranian regime’s destructive policies place international stability and security at risk,” said Pompeo in a Jan. 3 statement. “We advise the regime to reconsider these provocative launches and cease all activities related to ballistic missiles in order to avoid deeper economic and diplomatic isolation.”

That said, the Security Council resolution says Iran “is called upon” not to conduct any activity related to ballistic missiles, but does not ban the activity.

Next up is the Doosti satellite, which may or may not be delayed according to Jahromi, who just tweeted that: “Doosti is waiting for orbit,” adding “We should not come up short or stop. It’s exactly in these circumstances that we Iranians are different than other people in spirit and bravery.”

The Payam satellite was meant for use in communications and imaging and had four cameras, Reuters reports.

Iranian state television had aired footage of its reporter narrating the launch of the Simorgh rocket, shouting over its roar that it sent “a message of the pride, self-confidence and willpower of Iranian youth to the world!”

The TV footage shows the rocket becoming just a pinpoint of light in the darkened sky, but not the moment of its failure. Jahromi’s comments that the problem developed in the launch’s third stage suggest something went wrong after the rocket pushed the satellite out of the Earth’s atmosphere. –CBS News

Israeli Prime Minister Benjamin Netanyahu slammed Iran over the launch, accusing Tehran of lying about the “innocent satellite” which was actually “the first stage of an intercontinental missile.”

6. GLOBAL ISSUES

The following is a good bellwether for global growth: Goodyear tire slashes guidance and blames China and Europe

(courtesy zerohedge)

Goodyear Tire Slashes Guidance, Blames China, Europe

First Fedex, then Apple, then Delta, then Barnes and Noble, Macys, then American Airlines, then Alibaba, and now Goodyear Tire has just slashed guidance.

In an 8-K filed moments after the tire giant made negative comments at the Detroit auto show, Goodyear warned that full year operating income is now expected to come below the Company’s previous guidance of approximately $1.3 billion, and cautioned that Q4 2018 tire unit volumes declined by approximately 3%. The company blamed the usual suspects, namely the slowing economies in China and Europe as well as supply constraint in the US, to wit:

- continued weakening of the OE environment in China and India,

- declines in the winter tire market in Europe late in the quarter,

- supply constraints on volume for high-value-added consumer and commercial truck tires in the United States.

The company also noted that while price/mix was positive during the fourth quarter of 2018, it was “less than anticipated due to weaker mix, partially as a result of the supply constraints referred to above.”

In addition, GT added that earnings fell in other tire-related businesses, including with respect to the Company’s U.S. chemical operations.

As a result, Goodyear now expected 2018 net income to be “adversely affected” and the Company’s total segment operating income is expected to be “slightly below” the Company’s previous guidance of approximately $1.3 billion.

The stock promptly tumbled after the warning, and has dragged down peers such as Cooper Tire.

The company’s 8-K (found here) is below:

On January 15 and 16, 2019, representatives of The Goodyear Tire & Rubber Company (the “Company”) will present at conferences hosted in conjunction with the Detroit Auto Show and will provide an update on the Company’s preliminary 2018 performance.

As part of those presentations, the Company will announce that fourth quarter of 2018 tire unit volumes declined by approximately 3% due to (1) continued weakening of the OE environment in China and India, (2) declines in the winter tire market in Europe late in the quarter, and (3) supply constraints on volume for high-value-added consumer and commercial truck tires in the United States. Price/mix was positive during the fourth quarter of 2018 but was less than anticipated due to weaker mix, partially as a result of the supply constraints referred to above. In addition, earnings fell in other tire-related businesses, including with respect to the Company’s U.S. chemical operations.

As a result of these factors, for the full year of 2018, Goodyear net income is expected to be adversely affected and the Company’s total segment operating income is expected to be slightly below the Company’s previous guidance of approximately $1.3 billion.