GOLD:$1837.60 UP $10.60 The quote is London spot price

Silver:$24.02 UP 4 CENTS London spot price ( cash market)

ACCESS MARKET

i)Gold : $1841.00 LONDON SPOT 4:30 pm

ii)SILVER: $24.08//LONDON SPOT 4:30 pm

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

2 ) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)THURSDAY MORNING/ WEDNESDAY NIGHT:

SHANGHAI CLOSED DOWN 7.24 PTS OR .21% //Hang Sang CLOSED UP 195.92 PTS OR .74% /The Nikkei closed UP 8.39 POINTS OR 0.03%//Australia’s all ordinaires CLOSED UP 0.53%

/Chinese yuan (ONSHORE) closed UP A 6.5482 /Oil UP TO 44.88 dollars per barrel for WTI and 47.97 for Brent. Stocks in Europe OPENED RED EXCEPT LONDON/ITALY// ONSHORE YUAN CLOSED UP AGAINST THE DOLLAR AT 6.5482. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.5338 TRADE TALKS STALL//YUAN LEVELS //TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED//CORONAVIRUS/PANDEMIC/TRUMP TESTS POSITIVE FOR COVID 19 : /ONSHORE YUAN TRADING BELOW LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

We had 5 kilobar transactions

ADJUSTMENTS: 4 // dealer to customer

i) JPMorgan: 675.165 oz

ii) Brinks: 160,787.156 oz (5001 kilobars)

adjustments: customer to dealer

iii) JPMorgan enhanced: 12187.100 oz

iv) Malca 642,959.245 oz

The front month of DEC registered a total of 15,718 contracts for a loss of 4492. We had 4238 notices filed upon yesterday so we lost 254 contacts or 25,400 additional oz will not stand in this very active delivery month of December as these guys morphed into London based forwards and accepted a fiat bonus for their efforts. These guys receive a hefty bonus for not taking delivery as they enter the centric merry- go- round on those London serial forwards.

January lost 123 contracts to stand at 2428 contracts. FEBRUARY GAINED a STRONG 1389 contracts UP TO 396,152.

THE BIG STORY AGAIN TODAY IS THE HIGH INITIAL OI STANDING FOR DECEMBER (93.138 tonnes).

Once our paper players are finished, then we will see the bankers queue jump longs as they attempt to put out gold fires around the world.

We had 22 notice(s) filed today for 2200 oz OR 0.0684 TONNES.

To calculate the INITIAL total number of gold ounces standing for the DEC /2020. contract month, we take the total number of notices filed so far for the month (14,191) x 100 oz , to which we add the difference between the open interest for the front month of DEC (15,718 CONTRACTS ) minus the number of notices served upon today (22 x 100 oz per contract) equals 2,994,400 OZ OR 93.138 TONNES) the number of ounces standing in this active month of DEC

thus the INITIAL standings for gold for the DEC/2020 contract month:

No of notices filed so far (14191, x 100 oz +15,718 OI) for the front month minus the number of notices served upon today (22) x 100 oz which equals 2,994,400 oz standing OR 93.138 TONNES in this active delivery month of December. This is a HUGE amount for gold standing for DEC delivery month (generally the strongest delivery month of the year). THE COMEX IS UNDER A HUGE FRONTAL ATTACK FROM EUROPEAN BANKS SEEKING PHYSICAL METAL! JUDGING FROM THE INITIAL NOTICES FILED VS THE NUMBER OF NOTICES STANDING, IT WILL BE EXTREMELY DIFFICULT FOR OUR BANKERS TO FIND THE NECESSARY GOLD TO SATISFY OUR EUROPEANS.

NEW PLEDGED GOLD: BRINKS

466,240.074, oz NOW PLEDGED SEPT 15.2020/HSBC 14.51 TONNES ( A HUGE INCREASE FROM 10.6)

60,784.803 PLEDGED APRIL 3/2020: SCOTIA: 1.3234 tonnes

deleted Int. Delaware pledge July 7 (600 tonnes)

280,010.045 oz JPM 8.70 TONNES

602,840.325 oz pledged June 12/2020 Brinks/ july 2/july 21 18.75 tonnes

88,796.123 oz Pledged August 21/regular account 1.588 tonnes jpm

98,804.139 oz Pledged Nov 27.2021 MANFRA 3.07 tonnes

total pledged gold: 1,597,479.579 oz 49.69 tonnes

total registered, pledged and eligible (customer) gold 37,229,464.770 oz 1,157.99 tonnes (INCLUDES 4 GC GOLD)

total 4 GC gold: 126.34 tonnes

total gold net of 4 GC: 1031.65 tonnes

end

I have compiled data with respect to registered (or dealer) gold taken on first day notice for each of the past 24 months

The data begins on first day notice for the May month taken on the last day of July 2018. and it continues to present day.

I then took, how many deliveries were recorded by the CME for each and every month. I also included for reference the price of gold on first day notice.

The first graph is a logarithmic graph and the second graph, linear.

You can see the huge explosion of registered gold at the comex along with deliveries.

THE GOLD COMEX SEEMS TO BE UNDER SEVERE ASSAULT FOR PHYSICAL

And now for the wild silver comex results

And now for the wild silver comex results

INITIAL STANDINGS

DEC. SILVER COMEX CONTRACT MONTH//INITIAL STANDING

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory |

117,554.456 oz

CNT

Delaware

HSBC

|

| Deposits to the Dealer Inventory |

1,199,427.840 oz

CNT

Scotia

|

| Deposits to the Customer Inventory |

nil oz

|

| No of oz served today (contracts) |

1829

CONTRACT(S)

(9,145,000 OZ)

|

| No of oz to be served (notices) |

573 contracts

2,865,000 oz)

|

| Total monthly oz silver served (contracts) | 7595 contracts

37,975,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

total dealer deposits: 1,199,427.840 oz

i) We had 0 dealer withdrawal

total dealer withdrawals: nil oz

we had 0 deposits into the customer account (ELIGIBLE ACCOUNT)

JPMorgan now has 192.834 million oz of total silver inventory or 49.66% of all official comex silver. (192.834 million/388.051 million

ii) Into everybody else: 0

total customer deposits today: 0 oz

we had 3 withdrawals:

total withdrawals 117,554.456 oz

We had 4 adjustments //all customer (eligible) to dealer (registered)

i) Out of Int. Delaware: 727,411,470 oz

ii) JPMorgan: 250,601.050 oz

iii) Out of Loomis: 575,799.300 oz

iv) Out of Scotia 1930.430 oz

Total dealer(registered) silver: 148.601million oz

total registered and eligible silver: 390.317 million oz

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

December saw a LOSS of 1021 contracts DOWN to 3337 contracts. We had 998 notices served upon yesterday so we lost 23 contracts or 115,000 additional oz will not stand in this very active delivery month of December. It seems our paper players prefer the monopoly money for circular serial forwards vs taking any metal over here/

January saw a GAIN of 50 contracts UP to 1055. FEBRUARY saw another gain of 1 contract to stand at 52. MARCH gained 121 contracts up to 127,183.

The total number of notices filed today for the DEC 2020. contract month is represented by 1829 contract(s) FOR 9,145,000 oz

To calculate the number of silver ounces that will stand for delivery in DEC we take the total number of notices filed for the month so far at 7595 x 5,000 oz = 37,975,000 oz to which we add the difference between the open interest for the front month of DEC(3337) and the number of notices served upon today 1829x (5000 oz) equals the number of ounces standing.

Thus the DEC standings for silver for the DEC/2019 contract month: 7595 (notices served so far) x 5000 oz + OI for front month of DEC(3337)- number of notices served upon today (1829) x 5000 oz of silver standing for the NOV contract month .equals 45,515,000 oz. ..VERY STRONG FOR AN ACTIVE DEC MONTH.

We lost 23 contracts or 115,000 oz will not stand as they morphed into London based forwards

TODAY’S ESTIMATED SILVER VOLUME 73,416 CONTRACTS // volume huge//

FOR YESTERDAY 81,306 ,CONFIRMED VOLUME// huge

YESTERDAY’S CONFIRMED VOLUME OF 81,306 CONTRACTS EQUATES to 0.406 billion OZ 58.0% OF ANNUAL GLOBAL PRODUCTION OF SILVER..

COMMODITY LAW SUGGESTS THAT OPEN INTEREST SHOULD NOT BE MORE THAN 3% OF ANNUAL GLOBAL PRODUCTION. THE CROOKS ARE SUPPLYING MASSIVE PAPER TRYING TO KEEP SILVER IN CHECK.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price at that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

end

NPV for Sprott

1. Sprott silver fund (PSLV): NAV RISES TO- 3.84% ((DEC 3/2020)

2. Sprott gold fund (PHYS): premium to NAV FALLS TO 2.89% to NAV: (DEC 3/2020 )

Note: Sprott silver trust back into NEGATIVE territory at +%-/Sprott physical gold trust is back into NEGATIVE/3.84% (DEC 3)

(courtesy Sprott/GATA

3. SPROTT CEF .A FUND (FORMERLY CENTRAL FUND OF CANADA):

NAV 18.94 TRADING 18.19///NEGATIVE 3.95

END

And now the Gold inventory at the GLD

DEC 3/WITH GOLD UP $10.60 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS TONIGHT AT 1191.28 TONNES

DEC 2/WITH GOLD UP $12,00 TODAY: A HUGE CHANGES IN GOLD INVENTORY AT THE GLD//: A WITHDRAWAL OF 3.51 TONNES FROM THE GLD//INVENTORY RESTS AT 1191.28 TONNES

DEC 1//WITH GOLD UP $38.55 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLDE//INVENTORY RESTS AT 1194.78 TONNES

NOV 30/WITH GOLD DOWN $11.85 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1194.78 TONNES

NOV 27/WITH GOLD DOWN $18.90 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.96 TONNES OF GOLD FROM THE GLD…//INVENTORY RESTS AT 1194.78 TONNES

NOV 25//WITH GOLD UP $0.05 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A MASSIVE PAPER WITHDRAWAL OF 13.43 TONNES FROM THE GLD..IS THE GLD MAKING GOLD VAPOUR DELIVERIES FOR THE COMEX?//INVENTORY REST AT 1199.74 TONNES

NOV 24/WITH GOLD DOWN $33.00 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 7.00 TONNES FROM THE GLD//INVENTORY RESTS AT 1213.17 TONNES

NOV 23/WITH GOLD DOWN $33.95 TODAY: A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.9 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 1220.17 TONNES

NOV 20/WITH GOLD UP $11.10 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD// A WITHDRAWAL (ROBBERY) OF 1.74 TONNES FROM THE GLD//INVENTORY RESTS AT 1217.26 TONNES

NOV 19/WITH GOLD DOWN $9.80 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 7.30 TONES FROM THE GLD////INVENTORY REST AT 1219.00 TONNES

NOV 18/WITH GOLD DOWN $13.50 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 5.10 TONNES FROM THE GLD INVENTORY//INVENTORY RESTS AT 1226.30 TONNES

NOV 17/WITH GOLD DOWN 3 DOLLARS TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.92 TONNES FROM THE GLD////INVENTORY RESTS AT 1231.40 TONNES

NOV 16/WITH GOLD UP $2.20 TODAY/A HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 5.25 TONNES FROM THE GLD////INVENTORY RESTS AT 1234.32 TONNES

NOV 13/WITH GOLD UP $11.90 TODAY//A HUGE CHANGE IN GOLDINVENTORY AT THE GLD; A WITHDRAWAL OF 1.17 TONNES FROM THE GLD////INVENTORY RESTS AT 1239.57 TONNES

Nov 12/WITH GOLD UP $11.00 TODAY: A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A PAPERWITHDRAWAL OF 9.02 TONNES FROM THE GLD///INVENTORY RESTS AT 1240.74 TONNES

NOV 11/WITH GOLD DOWN $13.10 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1249.79 TONNES/

NOV 10/WITH GOLD UP $20.10 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 10.51 TONNES/INVENTORY RESTS AT 1249.79 TONNES

NOV 9/WITH GOLD DOWN $88.45 TODAY: A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIST OF 7.88 TONNES INTO THE GLD///INVENTORY RESTS AT 1260.30 TONNES

NOV 6/WITH GOLD UP $5.30 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1252.42 TONNES

NOV 5/WITH GOLD UP $51.45 TODAY: STRANGELY A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.5 TONNES FROM THE GLD////INVENTORY RESTS AT 1252.42 TONNES

NOV 4/WITH GOLD DOWN $9.35 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 1255.92 TONNES

NOV 3//WITH GOLD UP $16.85 TODAY: STRANGE!!! A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A PAPER WITHDRAWAL OF 1.75 TONNES FROM THE GLD////INVENTORY RESTS AT 1255.92 TONNES

NOV 2/WITH GOLD UP $13.60 TODAY: A SMALL CHANGE IN GOLD INVENTORY AT THE GLD:A WITHDRAWAL OF .58 TONNES AND THIS IS GENERALLY TO PAY FOR FEES (STORAGE/INSURANCE)//INVENTORY RESTS AT 1257.67 TONNES

OCT 30/WITH GOLD UP $11 TODAY: NO CHANGE IN GOLD INVENTORYAT THE GLD//INVENTORY RESTS AT 1258.25 TONNES

OCT 29/WITH GOLD DOWN $11.80 DOLLARS TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A PAPER WITHDRAWAL OF 8.47 TONNES FROM THE GLD////INVENTORY RESTS AT 1258.25 TONNES

OCT 28/STRANGE!WITH GOLD DOWN $30.50 TODAY, A HUGE CHANGE IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1266.72 TONNES

OCT 27/WITH GOLD UP $6.20 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1263.80 TONNES

OCT 26/WITH GOLD UP $1.50 TODAY; A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.77 TONNES FROM THE GLD//INVENTORY RESTS AT 1263.80 TONNES

OCT 23/WITH GOLD DOWN 80 CENTS TODAY: A HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWL OF 3.8 TONNES FROM THE GLD////INVENTORY RESTS AT 1265.55 TONNES

OCT 22/WITH GOLD DOWN $22.80 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1269.35 TONNES

OCT 21//WITH GOLD UP $17.50 DOLLARS TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 1269.93 TONNES

OCT 20/WITH GOLD UP $3.30 TODAY: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: ANOTHER PAPER WITHDRAWAL OF 2.92 TONNES//INVENTORY RESTS AT 1269.93 TONNES

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

Inventory rests tonight at

DEC 3/ GLD INVENTORY 1191.28 tonnes

LAST; 961 TRADING DAYS: +247.81 TONNES HAVE BEEN ADDED THE GLD

LAST 861 TRADING DAYS// +425.30 TONNES HAVE NOW BEEN ADDED INTO THE GLD INVENTORY

Now the SLV Inventory

DEC 3//WITH SILVER UP 4 CENTS TODAY: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV/ A WITHDRAWAL OF 236,000 OZ/INVENTORY RESTS AT 546.306 OZ

DEC 2/WITH SILVER UP ONE CENT TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.231 MILLIONOZ INTO THE SLV//INVENTORY RESTS AT 546.542 MILLION OZ//

DEC 1/WITH SILVER UP $1.46 TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 544.311 MILLION OZ/

NOV 30/WITH SILVER DOWN 15 CENTS TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 544.311 MILLION OZ.

NOV 27/WITH SILVER DOWN $0.69 TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV/: A WITHDRAWAL OF 1.813 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 544.311 MILLION OZ.

NOV 25/WITH SILVER UP $0.05 TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 4.091 MILLION PAPER OZ FROM THE SLV //// IS THE SLV MAKING SILVER VAPOUR DELIVERIES FOR THE COMEX?//INVENTORY RESTS AT 550.215 MILLION OZ..

NOV 24/WITH SILVER DOWN 33 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 10.322 MILLION OZ FROM THE SLV..//INVENTORY REST AT 550.215 MILLION OZ

AND IF ANYBODY BELIEVES THIS GARBAGE, WE HAVE A GREAT PROPERTY TO SELL YOU (FLORIDA SWAMP LANDS).

NOV 23/WITH SILVER DOWN $.70 TODAY: A HUGE CHANGE IN SILVER AT THE SLV; A WITHDRAWAL OF 2.046 MILLION OZ FROM//INVENTORY RESTS AT 562.583 MILLION OZ

NOV 20//WITH SILVER UP $0.32 TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 52.583 MILLION OZ//

NOV 19/WITH SILVER DOWN 35 CENTS TODAY; A HUGE CHANGE IN SILVER INVENTORY AT THE SLV:2 TRANSACTIONS:1) A WITHDRAWAL OF 1.396 MILLION OZ AND 2). 2.602 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 562.583 MILLION OZ

NOV 18/WITH SILVER DOWN 23 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1581 MILLION OZ FROM THE SLV…//INVENTORY RESTS AT 566.581 MILLION O

NOV 17/WITH SILVER DOWN 14 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 568.162 MILLION OZ//

NOV 16/WITH SILVER UP $.05 TODAY//A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDDRAWAL OF 1.209 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 568.162 MILLION OZ//

NOV 13/WITH SILVER UP 43 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV” A WITHDRAWAL OF 2.88 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 569.371 MILLION OZ.

NOV 12/WITH SILVER DOWN 2 CENTS TODAY: NO CHANGES IN SILVER INVENTORY FROM THE SLV//INVENTORY RESTS AT 572.254 MILLION OZ

NOV 11/WITH SILVER DOWN 8 CENTS TODAY: A HUGE 3.627 MILLION OZ WITHDRAWAL FROM THE SLV/ INVENTORY RESTS AT 572.254 MILLION OZ

NOV 10/WITH SILVER UP $.65 TODAY; A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: STRANGE ANOTHER HUGE DEPOSIT OF 4.739 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 575.881 MILLION OZ

NOV 9/WITH SILVER DOWN $1.76 TODAY: A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 10.324 MILLION OZ ADDED INTO THE SLV INVENTORY////INVENTORY RESTS AT 571.742 MILLION OZ

NOV 6/WITH SILVER UP 47 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 561.418 MILLION OZ//

NOV 5/WITH SILVER UP $1.21 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 561.418 MILLION OZ..

NOV 4/WITH SILVER DOWN 43 CENTS TODAY: TWO HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A) WITHDRAWAL OF 240,000 OZ FROM SLV//// AND THEN B) A DEPOSIT OF 1.83 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 561.418 MILLION OZ

NOV 4/WITH SILVER DOWN 43 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WIHDRAWAL OF 240,000 OZ FROM SLV////INVENTORY RESTS AT 559.558 MILLION OZ

NOV 3/WITH SILVER UP 29 CENTS TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV//INVENTORY REST AT 559.798 MILLION OZ///

NOV 2/WITH SILVER UP 40 CENTS TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 559.798 MILLION OZ//

OCT 30/WITH SILVER UP 23 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 931,000 FROM THE SLV////INVENTORY RESTS AT 559.798 MILLION OZ..

OCT 29/WITH SILVER DOWN 4 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A PAPER DEPOSIT OF 2.326 MILLION OZ//INVENTORY RESTS A 560.729 MILLION OZ..

OCT 28/WITH SILVER DOWN $1.09 TODAY: A HUGE WITHDRAWAL OF 2.791 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 558.403 MILLION OZ..

OCT 27/WITH SILVER UP 18 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 561.194 MILLION OZ//

OCT 26/WITH SILVER DOWN 18 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 561.194 MILLION OZ

OCT 23/WITH SILVER DOWN 9 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 561.194 MILLION OZ

OCT 22/WITH SILVER DOWN 46 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 561.194 MILLION OZ

OCT 21/WITH SILVER UP 26 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.977 MILLION OZ FROM THE SLV..//INVENTORY RESTS AT 561.194 MILLION OZ.

OCT 20/WITH SILVER UP 31 CENTS TODAY: A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 652,000 OZ INTO THE SLV////INVENTORY RESTS AT 564.171 MILLION OZ//

DEC 3.2020:

SLV INVENTORY RESTS TONIGHT AT 546.306 MILLION OZ/

PHYSICAL GOLD/SILVER STORIES

i) GOLDCORE BLOG/Mark O’Byrne

There is No Denying that Cash is Trash!

Governments are likely to continue printing money to pay their debts with devalued money. That’s the easiest and least controversial way to reduce the debt burdens and without raising taxes.

This is the only chart that matters in the world today.

Consider the following:

- Gold can only be produced at a rate of 1.6% per annum. This is a relative constant.

- Gold has returned 8% per year in Euros and 9% in USD terms over the past 20 years.

- Gold has returned 12% per year in the Euros and 10% in USD terms over the past 50 or so years.

- Global population is growing at 1.1% per year.

- USD Currency in circulation as defined by the M1 monetary base has grown by 41% in the year to November 2020.

Think about that last point. 41% in one year. All the dollars ever created have just increased by 41% in one year.

In that same period gold, which was trading at $1,190 in October 2019, has gone up by 52% to $1,812 or so.

They are very similar changes, and it is quite sobering, because the buying power of the cash in your bank account has or will soon fall by this same margin.

It will be ravaged by inflation as prices begin to rise at rates far exceeding your income and that will trigger some very dangerous economic consequences for our communities.

In the last 20 years we have seen extraordinary financial upheavals and each time the authorities reach for the same old elixir – debt!

From the Nasdaq Stock Market Bubble of 2000, to the Global Financial Crisis of 2008 through 2012, the Sovereign Debt Crisis of 2007 and 2008 and now the Covid 19 Pandemic of 2020, the cure if not the cause has been the same, load up on debt, extinguish the market fervour and wrestle the market forces into submission.

At no point have the authorities sought to examine the factors that led to these crises and address them so they would be unlikely to reoccur again.

On the horizon we have enormous risks brewing; Brexit, European cohesion, the rise of China as an economic super-power, demographic time-bombs, a burgeoning environmental crisis and the largest of all, the potential catastrophic loss of market confidence resulting from a global debt crisis.

Since 2000, global investment demand for gold has increased on average by 14% per annum and gold prices have risen 4 fold in that time.

Historically all major currencies were pegged to Gold. This changed in 1971 when Nixon closed the gold window and the US Dollar became a full fiat currency backed only by the credibility of the US treasury. Since then fiat, or currencies backed only by the governments who manage them, have drastically fallen in value.

Fiat currencies always eventually fail, as the graph so eloquently depicts. It is a matter of time and like a game of musical chairs you do not want to be caught sitting in cash when the music stops. As if on cue the powers that be are looking for alternatives. You will notice the headlines being flown like kites in the wind; announcing new innovations such as cryptographic currencies, global resets, debt forgiveness etc. They all mean the same thing, the death of money and with it the savings of many people.

The issue at the heart of the matter is not some global conspiracy as some might have us think. It is something far more benign and dangerous. It is simply called “apathy”. You see, people are generally lazy in many many ways, especially about matters they perceive to be complex and the domain of others. More often than not, they only get active when an issue occurs on their doorstep. Politicians, their officials and appointed technocrats, who are paid to manage these complex issues are also lazy. They would rather people did not ask hard questions, kick up a fuss and make a nuisance of themselves.

In many ways the cohort that is most responsible is our so-called free press and by extension our academics, who should, in the ordinary course of their day, be evaluating and testing the integrity of the systems we rely upon.

Each of these groups have generally absolved themselves of responsibility, wrapped themselves up in diversionary excuses and quietly hope that someone else will manage away the risks they all know, and fear will manifest. The only people who can drive change are the public and they need to get active before it is too late.

Gold: An Investors “Best Friend”

They say a true friend tells you what you don’t want to hear sometimes. In the same vein gold is screaming to all those that are bothered to hear, that something is very very rotten.

The reason gold is impervious to the excesses of man’s monetary shenanigans is one simple fact. It is very, very rare. In addition to this, it is heavily traded all around the world and it cannot be printed. Its values as a store of wealth transcends borders, language, culture and time. It is valuable for what it is not (a liability) and for what it is, rare and coveted.

Take a look at this next chart…

It is a measure of how loud gold will roar when the economy gets a little hairy. Over nearly 30 years, the economists at the World Gold Council studied how gold reacts when markets fall. They measure the fall in standard deviations, a fancy way of saying the degree of swings felt in a market.

The top measure states that when things are normal gold is indifferent, not doing much, like a friend who has not called you in a while, knowing you are doing just fine.

The middle measure is where gold gets interesting. Here the market is having a major fall and it is a big one in terms of its normal range. Gold is going the opposite way, its rising fast and the more the market falls the faster it rises. In this situation it is acting as a hedge, something that adjusts and protects against an adverse event. It is this behaviour that underpins gold’s credential as a great diversifier in a portfolio. This is akin to your friend looking at you late into the party, while you are on the table dancing, and pointing to their watch.

The final measure is when gold as your friend is pulling you and your finances from the flames of an inferno. The market has sold off to a massive degree and gold is going in the direction of safety and rising. For every $1 lost gold is paying you back nearly 60 cents.

You need to pay attention to these insights, when the proverbial excrement hits the fan we will not have a market for many assets out there, and people will be selling for cents on the dollar.

Buying Gold is not as good when the house is already on fire. You need to have it before the fire begins, sitting idly disinterested.

As Ray Dalio also said, “Cash is trash”.

NEWS and COMMENTARY

Gold gains as U.S. stimulus and vaccine hopes dent dollar

Treasury yields retreat as stimulus stalemate drags on

Deal on fresh U.S. coronavirus relief eluding congressional Republicans, Democrats

GOLD PRICES (USD, GBP & EUR – AM/ PM LBMA Fix)

02-Dec-20 1832.95 1822.60 1372.15 1369.14 1520.07 1508.02

01-Dec-20 1796.20 1810.75 1344.28 1356.07 1500.73 1509.80

30-Nov-20 1771.95 1762.55 1330.03 1317.51 1478.69 1469.44

27-Nov-20 1808.05 1779.30 1355.86 1333.41 1516.77 1489.63

26-Nov-20 1814.85 1807.40 1358.23 1355.73 1524.11 1518.40

25-Nov-20 1808.55 1810.20 1358.04 1354.93 1520.27 1520.57

24-Nov-20 1818.10 1799.60 1361.21 1350.60 1529.02 1517.24

23-Nov-20 1863.80 1840.20 1394.31 1378.49 1568.76 1552.02

20-Nov-20 1867.00 1875.70 1406.04 1412.21 1575.00 1580.46

19-Nov-20 1857.40 1857.35 1405.87 1404.16 1570.99 1569.46

18-Nov-20 1877.20 1876.10 1412.59 1411.20 1579.66 1580.99

17-Nov-20 1885.40 1889.05 1424.61 1425.29 1588.83 1591.52

16-Nov-20 1892.60 1885.60 1436.67 1430.98 1598.11 1594.84

Buy gold coins and bars and store them in the safest vaults in Zurich, Switzerland with GoldCore.

Learn why Switzerland remains a safe-haven jurisdiction for owning precious metals. Access Our Most Popular Guide, the Essential Guide to Storing Gold in Switzerland here

Receive Our Award Winning Market Updates In Your Inbox – Sign Up Here

ii) Important gold commentaries courtesy of GATA/Chris Powell

Craig Hemke talks about the upward turn in gold

(Craig Hemke/Sprott)

Craig Hemke at Sprott Money: Time for an upward turn in gold

7:26 ET Wednesday, December 2, 2020

Dear Friend of GATA and Gold:

The TF Metals Report’s Craig Hemke, writing tonight at Sprott Money, says gold investors should look to the new year with confidence because of these fundamental conditions:

— A falling U.S. dollar.

— A record notional amount of negative-yielding debt.

— Negative real interest rates, as adjusted for inflation.

— Pending massive new fiat-money creation programs, a.k.a “stimulus.”

— Outright debt monetization by central banks.

Hemke’s analysis is headlined “Time for a Turn” and it’s posted at Sprott Money here:

https://www.sprottmoney.com/blog/Time-for-a-Turn-Craig-Hemke-December-02…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

iii) Other physical stories:

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

Federal judge tells traders they can combine cases accusing JP Morgan of rigging metals market

- Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

- Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

A group of traders from across the U.S. who allege that J. P. Morgan Chase manipulated precious metals markets for years are one step closer to bringing a class action suit against the nation’s largest bank.

Earlier this month, a federal judge said five separate lawsuits making similar allegations against the bank could be combined, potentially including thousands of people who traded in the precious metals market from Jan. 2009 through Dec. 2015.

Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

J. P. Morgan declined to comment on this story.

Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

Vincent Briganti, a partner at the firm, filed the first suit seeking class action status in November on behalf of Dominick Cognata, a trader who alleges he suffered losses due to J.P. Morgan’s illegal trading conduct in the silver and gold futures and options markets.

That was after the federal court in Connecticut unsealed a criminal plea agreement by John Edmonds, a former J.P. Morgan metals trader. In his guilty plea, Edmonds, who is 36-years old, admitted that he and other “unnamed co-conspirators” fraudulently manipulated the precious metals markets while they were employed at J. P. Morgan from 2009 to 2015.

Edmonds said he had learned the illegal trading tactics from senior traders, and then used them hundreds of times with the knowledge of and consent of his immediate supervisors.

Briganti’s lawsuit also names John Edmonds and a group of yet-to-be-identified precious metals traders and the bank as defendants.

On Wednesday, the lawyers sent a letter to Judge Koeltl saying they were having difficulty locating Edmonds to serve him legal papers and requested a 30-day extension to do so, which the judge granted on Thursday. Briganti noted that they have been in contact with Edmonds’ attorney in the criminal case. Edmonds’ attorney and Briganti could not be reached for comment.

“We are hopeful that this extension will result in completing service on Mr. Edmonds without formal motion practice and a request for alternative means of service,” Briganti said in the letter.

The next step in the civil case is for the plaintiffs to file an amended class action complaint and set a schedule for defendants to respond.

In addition to the proposed class action, J. P. Morgan also faces a separate civil suit which also accuses the bank of rigging precious metals markets.

end

March 4.2019

Parker City News

JP Morgan faces potential class action lawsuit after guilty pleas by a former metals trader

Traders from across the U.S. are banding together to accuse J. P. Morgan Chase of manipulating precious metals markets for years.

At least six lawsuits, all making similar allegations against the nation‘s largest bank, have been filed in New York federal court in the past month, since federal prosecutors in Connecticut with a former J. P. Morgan Chase metals trader.

The cases could potentially include thousands of people who traded in the precious metals market. The White Plains, N.Y., law firm Lowey Dannenberg is asking the court to combine the cases and name it as the lead.

The law firm‘s commodities group is led by Vincent Briganti, the attorney who filed the first lawsuit on behalf of Dominick Cognata, a New York resident who alleges he suffered losses due to J. P. Morgan‘s trading conduct in the silver and gold futures and options markets.

A combined case, seeking class action status, would include anyone who purchased or sold futures contracts or an option on NYMEX platinum or palladium or COMEX silver or gold between at least Jan. 1, 2009, and Dec. 31, 2015. The lawyers believe that “at least hundreds, if not thousands” of traders would be eligible to join the case.

Named as defendants in all of the lawsuits are John Edmonds, a 36-year old former metals trader at J. P. Morgan, a group of yet-to-be-identified precious metals traders and the bank.

Edmonds, a New York resident, pleaded guilty in October to one count of conspiracy to defraud the market and manipulate prices of precious metals futures contracts and one count of commodities fraud. In the criminal plea, Edmonds admitted that he and other “unnamed co- conspirators” at J. P. Morgan, fraudulently manipulated precious metals markets from 2009 to 2015, the same time frame covered in the class action suits.

Briganti filed the initial class action on Nov. 7, just one day after the Justice Department unsealed Edmonds‘ plea in the U.S. District Court of Connecticut.

Edmonds admitted in his guilty plea that he deployed the illegal trading scheme hundreds of times with the direct knowledge and consent of his immediate supervisors. Plaintiffs say they have suffered economic injury, including monetary losses, as a direct result of actions by Edmonds and the other unnamed J. P. Morgan metals traders in the futures and options contracts.

One of the suits alleges that “the number of unlawful trades that JP Morgan traders executed in precious metals futures markets is at least in the thousands.”

J. P. Morgan declined to comment. Lowey Dannenberg did not respond to a request for comment by CNBC.

The Justice Department‘s criminal investigation is still ongoing and recently caused a separate related civil case to be put on hold for at least six months while the government continues its investigation. That civil lawsuit, which also accuses J. P. Morgan of rigging the precious metals market, was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders.

After reviewing the details of the plea agreement, David Kovel, the attorney for Shak‘s suit, sought to re- interview Edmonds, along with two other current and former senior traders at the bank. However, the government argued that reopening questioning would be detrimental to the ongoing criminal investigation. The federal judge overseeing the proceedings ordered a six-month stay in the civil case.

Kovel declined to comment.

Edmonds was originally scheduled to be sentenced in Hartford, Conn., on Wednesday, Dec. 19, but a court filing on Nov. 27 shows the sentencing has been postponed until June. A spokesman for the U.S. Attorney for Connecticut could not elaborate on why the sentencing was postponed since the court filing is under seal.

-END-

Futures Stuck At All Time High As Dollar Slide Continues

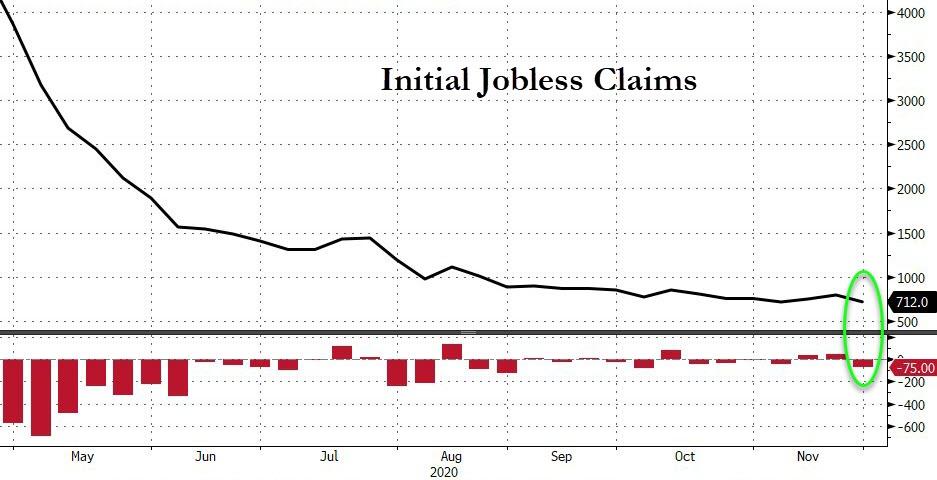

That “gamma gravity” at 3,650 we have been discussing for the past three days continued to make its presence known overnight as futures tried another break above all time highs and failed, eventually fading back to unchanged and last trading at 3,665, two points the Wednesday close as European stocks erased an earlier loss, while the dollar selloff continued and 10Y yields were fractionally lower ahead of initial jobless claims data which are expected to show another 775K workers were laid off in the latest week.

S&P 500 futures stalled after the cash index closed at another record high. In notable moves, Splunk tumbled 21% in the pre-market after the data-software company’s revenue forecast missed estimates, while Micron gained after the chipmaker raised its guidance. Waddell & Reed jumped 46% after Australia’s Macquarie Group announced a deal to buy the wealth manager for $1.7 billion. Finally, Nasdaq 100 futures were up 19.5 points, or 0.16% as Tesla rose about 3% premarket after Goldman Sachs raised its rating to “buy” from “neutral” in the run up to the electric-car maker’s addition to the S&P 500.

Risk assets remain buoyed by fiscal stimulus hopes with House Majority Leader Steny Hoyer expressing hope that a fiscal stimulus deal could be reached “in the next few days”, and any legislation would likely need to be supplemented with further aid next year, although even as Democrats scale down their stimulus demands, Mitch McConnell has yet to show any interest in a compromise deal. Democrats backed a bipartisan proposal for a scaled-back $908 billion stimulus package, with Nancy Pelosi and Chuck Schumer saying that should be the baseline for negotiations with Congressional Republicans and the White House as they walked back from pre-election demands. The compromise deal “would be more about stabilizing than stimulating the economy, but increasing the unemployment benefit reduces the fear of people in work and encourages them to spend the savings accumulated during lockdowns,” UBS chief economist Paul Donovan wrote.

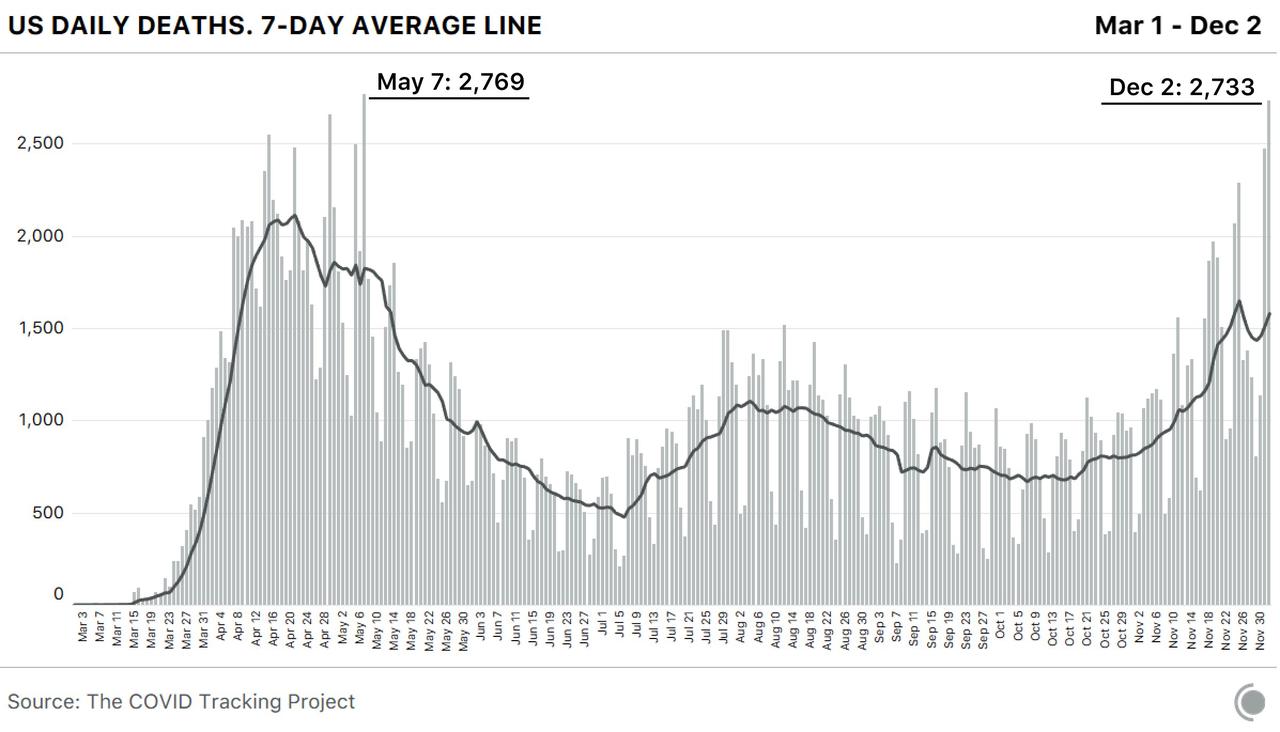

On the opposite end, the pandemic’s spread has tempered the buoyant mood that propelled global stocks to a record monthly gain in November on vaccine breakthroughs. The U.S. saw the deadliest day for Covid-19 fatalities, while Los Angeles ordered residents to stay home.

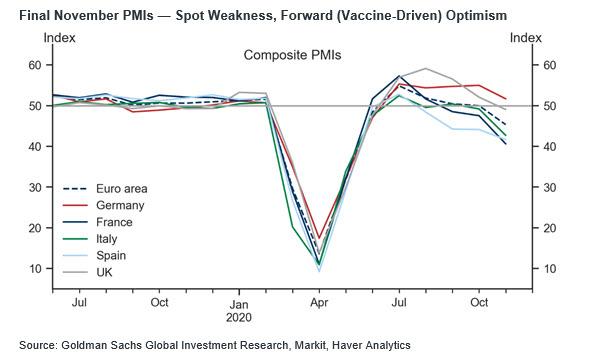

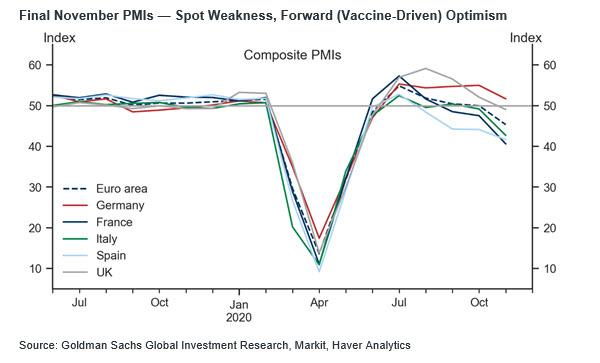

European shares initially edged lower, with chemicals, energy sectors down more than 1% while travel & leisure, consumer products, basic resources are main gainers. However, the Stoxx recovered all losses by 7am ET and was trading flat. The latest PMI data showed U.K. output shrank for the first time since June amid virus restrictions; at the same time the Euro area composite PMI was revised up by 0.2pt from its flash estimate of 45.1 for November to 45.3, as the Service PMI printed at 41.7, above the 41.3 expected. This reflected upward revisions in both France and the periphery, which were partly offset by a modest downward revision in Germany. The Spanish composite PMI declined less than expected, whereas the Italian composite PMI surprised expectations to the downside. The UK composite PMI was revised up significantly on the back of stronger services momentum towards month-end. According to Goldman, “the November PMI readings across the Euro area and the UK indicate a significant near-term contraction in services activity amid continued relative resilience in manufacturing”; the bank looks for a renewed contraction in GDP in Q4 across Western Europe, albeit a much shallower one than in the spring.

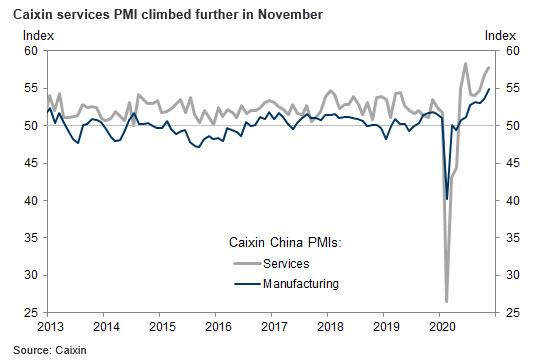

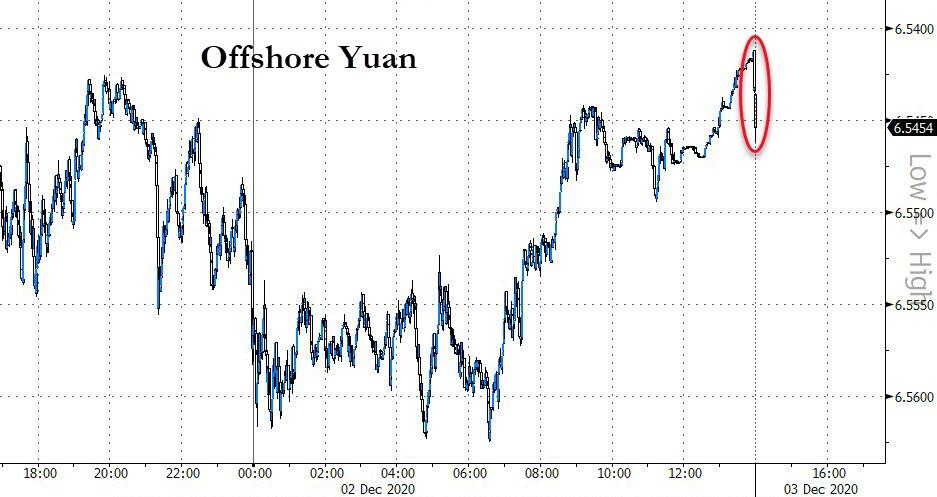

Earlier in the session, markets edged up in Asia with the MSCI Asia Pacific Index adding 0.6%. Japan’s Nikkei 225 swung between gains and losses amid an indecisive currency and with participants digesting reports the government will extend the Go To Travel subsidy campaign. Hang Seng (+0.7%) and Shanghai Comp. (-0.2%) traded mixed despite encouraging Caixin Services PMI which printed at its second highest in a decade and added to the recent streak of solid Chinese PMI data, with sentiment in the mainland clouded after the PBoC drained liquidity again and following the US House approval of the China delisting bill which requires foreign companies to comply with US auditing rules or risk being delisted from US exchanges.

The ASX 200 (+0.4%) was positive with broad strength in the commodity sectors led by iron ore miners including Fortescue Metals which rose to an all-time high and Rio Tinto shares also printed their best levels in 12 years amid record Dalian iron ore prices and after Vale recently lowered its 2020 iron ore output guidance.

In rates, treasuries trade near session highs as U.S. trading gets underway, holding small gains after erasing declines. Yields remain within about 1bp of Wednesday’s closing levels, with 10-year’s daily range less than 2bp. Yields are lower across the curve, by as much as 1bp at long end, 10-year by 0.8bp at 0.93% vs Wednesday’s high 0.964%; Treasuries trail bunds after German Markit PMIs were slightly weaker than expected. Still, strong demand failed to emerge during Asia session despite long-end selloff over past two days. The recent spike in Treasury yields should meet resistance as the Federal Reserve puts aside inflation concerns for now, economist Ed Yardeni said. That will contain the recent selloff in Treasuries and keep 10-year yields anchored below 1%, he said.

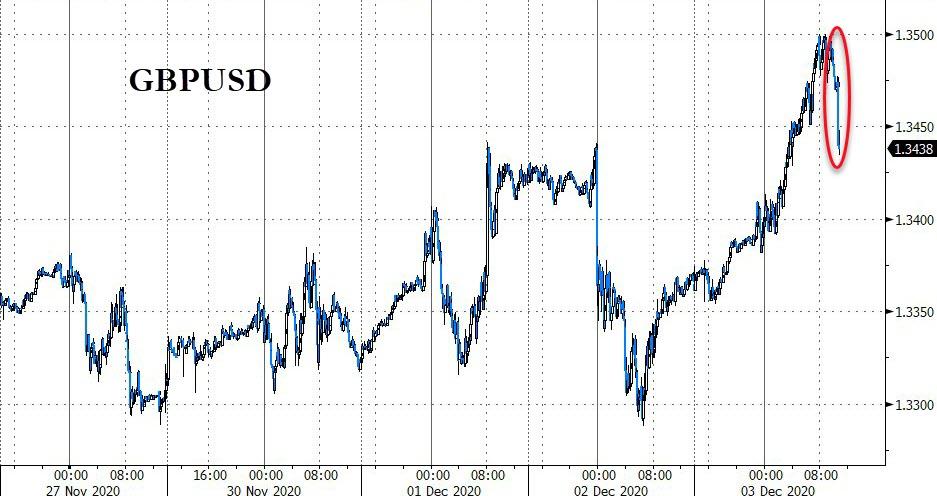

In FX, the Bloomberg Dollar Spot Index tumbled for a third day to the lowest level since April 2018 ahead of U.S. jobs data due Friday. The pound was the biggest gainer in G10, recouping Wednesday’s drop as traders took in stride France’s threat to veto a Brexit deal; cable was last seen at 1.3448 the highest since May 2018. The dollar plunge sent the Australian dollar and the Korean won to their highest levels versus the greenback in more than two years, and the Swiss franc to its strongest since 2015.

Emerging-market currencies and equities pushed higher to their best levels since the early days of the trade war as investors pinned their hopes on coronavirus vaccines and prospects for U.S. stimulus. MSCI Inc.’s index for developing-nation stocks rose to the strongest level since February 2018, with India’s benchmark trading near a record high. Turkey’s lira led gained in currencies, having initially weakened after a government report showed inflation accelerated in November by more than the highest economist forecast.

In commodities, the front-month Brent crude oil contract fell 0.70% as OPEC and non-OPEC producers edged towards an agreement that would see production cuts gradually phased out in H1 2021. Discussions are now focused on a proposal to gradually roll back output cuts over several months and do month-to-month assessments, instead of a 3 or 6 month extension. Russia is inclined toward easing curbs within the first quarter, a person familiar said. The Kremlin said it was too soon to comment on a pact. It’s not clear yet whether the proposals would return that same volume of production over a longer period, or a different amount. The recent gold surge continued with the yellow metal last trading at $1840.

Looking at the day ahead, To the day ahead now, the global services and composite PMIs for November will be the main data highlight. Otherwise from the US, there’s also the November ISM services index and the weekly initial jobless claims, and from the Euro Area we’ll get October’s retail sales.

Market Snapshot

- S&P 500 futures flat at 3,667.00

- STOXX Europe 600 down 0.3% to 390.47

- German 10Y yield fell 1.9 bps to -0.538%

- Euro down 0.1% to $1.2103

- Italian 10Y yield fell 4.2 bps to 0.521%

- Spanish 10Y yield fell 1.7 bps to 0.086%

- MXAP up 0.5% to 192.58

- MXAPJ up 0.7% to 635.41

- Nikkei up 0.03% to 26,809.37

- Topix up 0.07% to 1,775.25

- Hang Seng Index up 0.7% to 26,728.50

- Shanghai Composite down 0.2% to 3,442.14

- Sensex up 0.03% to 44,629.24

- Australia S&P/ASX 200 up 0.4% to 6,615.27

- Kospi up 0.8% to 2,696.22

- Brent futures down 0.3% to $48.13/bbl

- Gold spot up 0.2% to $1,835.53

- U.S. Dollar Index down 0.1% to 91.01

Top Overnight News from Bloomberg

- One by one, the dollar is dropping to multi-year lows against its peers in December.

- European Union officials are resisting calls from derivatives traders — and even one regulator — to allow access to London’s dominant markets after the Brexit transition ends this month, saying upheaval in the market does not pose a risk to financial stability

- The U.S. House of Representatives approved legislation that could ultimately lead to Chinese companies getting kicked off American exchanges if regulators aren’t allowed to review their financial audits

- The U.S. had its deadliest day ever, with Covid-19 fatalities topping 2,700, according to Johns Hopkins University. Hospitalizations in the country surpassed 100,000 for the first time. Germany extends partial lockdown until Jan. 10 to curb virus

- Oil was steady before an OPEC+ meeting as key powerbrokers in the alliance haggle over output policy after failed talks earlier in the week.

- France warned it could veto a trade deal between the U.K. and the European Union if it doesn’t like the terms, piling pressure on the EU negotiating team not to make further concessions as talks build to a climax.

- U.S. stocks registered a record high for a second consecutive day amid renewed optimism over U.S. stimulus talks and a rebound in crude oil. Treasury yields rose, while the dollar touched a more than two-year low.

A quick look at global markets courtesy of NewsSquawk

In Asia, a tentative mood was seen in Asia-Pac bourses following the flat performance on Wall St where recent vaccine developments and stimulus hopes were offset by weak jobs data in which ADP Employment disappointed ahead of Friday’s NFPs and amid lingering US-China tensions. ASX 200 (+0.4%) was positive with broad strength in the commodity sectors led by iron ore miners including Fortescue Metals which rose to an all-time high and Rio Tinto shares also printed their best levels in 12 years amid record Dalian iron ore prices and after Vale recently lowered its 2020 iron ore output guidance. However, upside for the index was capped by losses in financials, tech and defensives, as well as ongoing tensions with China whereby Australian Treasurer Frydenberg stated they will not give ground on 14 China grievances. Nikkei 225 (Unch) swung between gains and losses amid an indecisive currency and with participants digesting reports the government will extend the Go To Travel subsidy campaign. Hang Seng (+0.7%) and Shanghai Comp. (-0.2%) traded mixed despite encouraging Caixin Services PMI which printed at its second highest in a decade and added to the recent streak of solid Chinese PMI data, with sentiment in the mainland clouded after the PBoC drained liquidity again and following the US House approval of the China delisting bill which requires foreign companies to comply with US auditing rules or risk being delisted from US exchanges. Finally, 10yr JGBs were choppy and oscillated around the 152.00 focal point amid the indecision in stocks and following mostly weaker results at the 30yr JGB auction.

Top Asian News

- Saudi Wealth Fund Seeks Up to $7 Billion Loan for New Deals

- WeChat Deletes Australian PM’s Appeal to Chinese Community

- Turk Inflation Soars, Raising Pressure on New Central Banker

In Europe, major European bourses are choppy (Euro Stoxx 50 -0.1%) following a relatively uninspiring cash open as the region initially took its cue from a mixed APAC handover, whilst US equity futures see little action. That said, the breadth of losses still remain somewhat shallow amid a lack of fresh fundamental drivers, although with a number of risk events developing in the background including Brexit and OPEC heading into tomorrow’s US jobs report. Sector in Europe maintain the mixed picture seen at the open with no clear risk profile to be derived, whilst the sectoral breakdown sees Travel & Leisure topping the charts on the ongoing vaccine optimism following UK’s approval of the Pfzier/BioNTech candidate coupled with some looser lockdown measures for the holiday periods, with Deutsche Lufthansa (+0.4%) also recording a sharp rise in intercontinental and intra-European bookings for the upcoming New Year and Christmas travel season. Elsewhere, Oil & Gas does not fare well given the recent developments in the crude complex on the back of OPEC, whilst Basic Resources piggyback on the surge in iron ore prices (see the Commodities section). Banks meanwhile fail to derive much traction from source reports that the ECB is reportedly mulling allowing banks 15-25% dividends as one of its options. In terms of individual movers, Rolls Royce (+5.7%) stands as the Stoxx 600 leader as it attempts to capitalise on the slower travel market, stating that it is an opportunity to return to narrow-body jets. Meanwhile, Orange (-2.5%) trades lower amid reports that the Co. is mulling a public takeover bid for Orange Belgium (+35%). State-side, WSJ reports that the EU is completing rules on content, competition that are likely to apply to Google, Facebook and Amazon, whereby the Commission plans sanctions for violators that include fines and possible separation of asses – although shares are unreactive pre-market.

Top European News

- Germany Extends Restrictions to Fight Stubborn Virus Spread

- EU ‘Plan B’ Can Cut Poland and Hungary Out of Coronavirus Fund

- U.K. Output Shrinks as Companies Pin Hopes on Recovery Next Year

- Rolls-Royce Sees Chance to Return to Narrow-Body Jet Market

In FX, no new negative catalysts or factors behind the latest bout of almost all round Dollar selling against major counterparts, but the technical backdrop is increasingly bearish and momentum is building to the detriment of the Buck in contrast to its G10 peers. Hence, the index has now extended its decline to 90.834 from 92.000+ at the start of the week after yet another brief bounce and fade below a prior recovery high, albeit trying to keep tabs on the 91.000 handle amidst a downturn in broad risk sentiment ahead of a busy US agenda, including Challenger lay-offs, initial weekly and continuing claims, the final Markit services and composite PMIs and non-manufacturing ISM.

- GBP – Sterling’s Brexit vigil continues, and hopes of a deal have been revived or remain alive into what has been dubbed as the crucial last 48 hours of trade discussions amidst reports that more progress has been made towards resolving at least one of the 3 last bones of contention (level playing field said to be in the final stages of resolving differences between the UK and EU, leaving ‘just’ fishing and state aid to be sorted out). Cable is back up around the 1.3400 handle and Eur/Gbp has retreated through 0.9050, with perhaps some assistance from an unexpected upward revision to the final UK services PMI that pushed the composite closer to the 50.0 threshold.

- JPY – The Yen has recouped some losses vs the Greenback to trade back over 104.50, but faces even stiffer resistance at 104.00 via massive option expiry interest at the strike (3.4 bn) assuming it is not dragged back by expiries between 104.45-50 (1.5 bn) in the meantime. Conversely, the less buoyant risk tone and some retracement in extreme bear-steepening along the US Treasury curve may keep Usd/Jpy capped.

- CHF/AUD/EUR/NZD – All narrowly mixed against their US rival, with the Franc forging more gains beyond 0.8950, Aussie topping 0.7400 in wake of somewhat mixed trade data (surplus wider than forecast and exports encouraging, but imports only just recovering after a sharp slide) and Euro continuing its march to test offers into 1.2150 having breached and closed above a key Fib retracement level. However, the Kiwi has lost a bit more impetus following attempts to reach 0.7100 and more so vs its Antipodean neighbour as the Aud/Nzd cross rebounds further from recent lows to straddle 1.0500 ahead of Aussie retail sales data.

- CAD/NOK/SEK – The Loonie has pulled up within single digits of 1.2900 amidst ongoing pre-OPEC+ uncertainty that is playing out via choppy crude prices and the Norwegian Krona also on the defensive circa 10.7000 vs the Euro awaiting the outcome following latest reports suggesting a 500k bpd increase in output from January 2020. Elsewhere, some traction for the Swedish Crown and protection from 10.3000 via an acceleration in the services PMI.

In commodities, WTI and Brent futures have trimmed some of the losses seen in wake of source reports that OPEC+ is closing in on an agreement to modestly boost their collective oil output by 500k barrels a day starting Jan 2021. Market expectations were leaning towards the second tranche (7.7mln BPD cuts) being extended through Q1 2021, with desks suggesting anything less would be a disappointment. EnergyIntel’s Bakr provided a preliminary breakdown of one of the options considers which would see Jan cuts at 7.2mln BPD (in-line with the WSJ report), Feb at 6.7mln BPD, March at 6.2mln BPD and April at 5.7mln BPD for an average cut across the four months at 6.7mln BPD (vs. Exp. 7.7mln BPD for three months). Meanwhile, Kremlin’s spokesperson noted that it is too soon to comment on OPEC+. In terms of today’s event, the official confab is slated for 13:00GMT/08:00EST (subject to delays) with source reports likely to trickle throughout the day. (REMINDER: the exclusive Newsquawk Twitter Dashboard for the event is available here. The rolling headline feed can be accessed here). The other touted options reported earlier in the week include 1) Extend the current cuts by three months, 2) Raise output from January, but gradually and by less than the 2mln BPD under the current plan, and 3) Raise output as planned from January. WTI Jan hovers around USD 45/bbl (vs. low USD 44.70/bbl), whilst Brent Feb sees itself ~USD 48/bbl (vs. low USD 47.67/bbl). Elsewhere, precious metals have been moving in tandem with the Dollar throughout the European morning, but spot gold holds into USD +1800/oz status (1826-1843 range) and spot silver resides in the low USD 24/oz levels (23.80-24.26 range). Turning to base metals, iron ore prices notched a seven-year high following an output guidance cut by one of its largest producers Vale. Finally, LME copper sees contained price action amid the lackluster tone in the market and caged Dollar.

OPEC and its allies are closing in on an agreement to modestly boost their collective oil output by as much as 500,000 barrels a day starting next month, people familiar with the matter said cited by WSJ. (WSJ) One OPEC+ option being mulled: Jan: 7.7- 0.5=7.2 cut Feb: 6.7 cut March: 6.2 cut April: 5.7 cut Average cut for 3 months will be 6.7 instead of 7.7, according to EnergyIntel.

US Event Calendar

- 7:30am: Challenger Job Cuts YoY, prior 60.4%

- 8:30am: Initial Jobless Claims, est. 775,000, prior 778,000

- 8:30am: Continuing Claims, est. 5.8m, prior 6.07m

- 9:45am: Bloomberg Consumer Comfort, prior 49.6

- 9:45am: Markit US Services PMI, est. 57.5, prior 57.7; Markit US Composite PMI, prior 57.9

- 10am: ISM Services Index, est. 55.8, prior 56.6

DB’s Jim Reid concludes the overnight wrap

I got the most amount of incoming emails yesterday to one of my CoTD’s since it was launched back in early July. It showed that the S&P 500 CAPE ratio (or the cyclically adjusted price-to-earnings ratio) has this week moved above its levels on the eve of the 1929 stock market crash ( link here). The only time higher over the last 140 years being the 1998-2001 period. There are reasons why the CAPE may have structurally shifted higher, with an often-used one being the four-decade decline in yields to what are now close to all-time multi-century lows. That said, the fact that we’re beyond the September 1929 levels is obviously an important milestone, and will only add to concerns that current US equity valuations have become disconnected from real economic performance. As we said in the piece this ratio is heavily skewed towards the mega-cap growth stocks and as the world normalises post pandemic they’ll be the key to valuations over the next few months and quarters. Can they maintain their value even as cyclicals rebound? If you want to get the CoTD daily direct please email jim-reid.thematicresearch@db.com.

Staying on the theme, global equity markets remained near their all-time or recent highs yesterday, as hopes over the likelihood of a fresh US stimulus package edged out concerns over the economic recovery and rising Covid-19 cases. By the close the S&P 500 had eked out a +0.18% gain to a new record high, while tech stocks lagged as the NASDAQ saw a slight dip (-0.05%). Cyclicals once again led the market higher with Energy (+3.34%) and Bank (+1.91%) stocks the best-performing industries, while pandemic outperformers such as software (-1.03%) pulled back.

The moves came as US stimulus talks took a promising turn with Speaker Pelosi and Senate Minority leader Schumer indicating support for a $908 billion bipartisan stimulus proposal,which will set off a fresh round of negotiations with the White House. It is down from their original position of $2.4 trillion, but still significantly above the Majority Leader McConnell’s $500 billion plan. For more on the machinations of any lame-duck stimulus and the transition to the Biden administration, listen to a new podcast with Matthew Luzzetti, Chief US Economist and Frank Kelly, Head of DB Government and Public Affairs where they discuss US political developments and implications for the economic outlook. Listen to it here.

As the S&P 500 reached yet another record yesterday, Fed Chair Powell and Treasury Secretary Mnuchin spoke before the House Financial Services panel. For the second straight day Chair Powell denied any rift between himself and Secretary Mnuchin over the closing of some of the emergency lending programs, saying that committee was “concerned that the public would interpret this as the Fed stepping back — and that’s not the case.” To that end, Mr. Powell also indicated that the Fed was not rushing to taper its sizeable bond buying program. However, he did not give any indication that he and the other central bankers would be looking to increase the rate of purchases when the FOMC meets on December 15-16.

Amidst Mr. Powell’s remarks, there was a further sell-off in sovereign bond markets yesterday, with yields on 10yr US Treasuries up another +1.0bps to 0.936%, raising questions over whether yields will manage to break the 1% barrier for the first time since March. Inflation expectations also rose further, with US 10yr breakevens up a further +4.1bps to 1.87%, their highest in over 18 months. Meanwhile, the dollar index weakened a further -0.21% to a fresh 2-year low, helping the euro to break through the $1.21 mark at one point in trading for the first time since April 2018.

This morning we have seen China’s November Caixin services PMI printing at 57.8 (vs. 56.4 expected) bringing the composite read to 57.5 (vs. 55.7 last month). Similarly, Japan’s services PMI also printed 1.1pts stronger than the flash at 47.8 bringing the composite reading to 48.1 (vs. 47.0 in flash). European data will come out this morning. Despite stronger PMIs, Asian markets are struggling to find clear momentum with the Hang Seng (+0.44%) and Kospi (+0.32%) up while the Nikkei (-0.13%) and Shanghai Comp (-0.20%) are lower. Chinese bourses are likely weighed down by the passage of a bill in the US House of Representatives that could ultimately lead to Chinese companies – such as Alibaba Group and Baidu Inc. – getting delisted from American exchanges if regulators aren’t allowed to review their financial audits. The legislation has now moved to President Trump’s desk, who is expected to sign it. Futures on the S&P 500 are down -0.13%, with a similar picture for their European equivalents.

In other overnight news, Bloomberg reported that OPEC+ is making headway in negotiations with discussions now focusing on proposals for the gradual easing of output cuts over several months while adding that it is unclear whether the tapering would start in January, or would be delayed to later in the first quarter. We should get more clarity after today’s meeting of the group.

Turning to the coronavirus, the main news yesterday was that UK regulators have approved the 95% effective Pfizer/BioNTech vaccine, making the UK the first country to do so. 800,000 doses are expected to arrive this week from Belgium, with care home residents, frontline health and social care workers, and those with underlying health conditions being prioritised. Given the required -70C to store the vaccine, the first vaccinations will probably take place in facilities which already have the necessary infrastructure, such as hospitals. Furthermore, the UK has ordered only enough doses to vaccinate about 30% of British adults, and it remains unclear how long it will take for the remaining vaccines to be delivered, with the country’s Chief Medical Officer reminding us that ‘we can’t lower our guard yet’.

Given that the vaccine rollout in the coming weeks was already priced in, there hasn’t been much market reaction, though along with sterling’s depreciation (more on which below), the moves may have supported the FTSE 100 (+1.23%) to be one of the top-performing indices yesterday, since the UK has been much quicker out of the starting block than other regions. The FDA in the US isn’t expected to make a decision until a meeting on December 10th, while Europe’s EMA has stated that it may give emergency approval on December 29th, since it needs more time to review evidence. Overnight, Germany’s Health Minister Jens Spahn has said that the country is conducting direct negotiations with domestic Covid-19 vaccine developers including BioNTech to obtain more doses than would be allocated through the shared EU plan. Elsewhere, New York Governor Cuomo has said that he expects the state to receive 170,000 doses of Pfizer’s vaccine on December 15 and added that health-care workers in the most high-risk jobs, such as emergency rooms, as well as nursing-home residents and staffers will receive the vaccine first.

In terms of the numbers, sadly the US reported over 2,836 Covid-19 deaths over the past 24 hours marking the deadliest day of the pandemic yet, though record-keeping likely caught up somewhat from the holiday weekend. Weekly deaths have been over 10,000 for two straight weeks, after falling below that threshold back in mid-May. Hospitalisations in the US have been increasing by over 1,000 a day and now Covid-19 accounts for over a fifth of all hospitalised patients in North Dakota and South Dakota, Rhode Island, New Mexico, Indiana, Illinois, Minnesota and Michigan. Overnight, Los Angeles has ordered residents to stay home and businesses that require in-person work to cease operations. While case numbers are declining in Europe there were still two pieces of new news on restrictions. First, German Chancellor Merkel said the country will extend its partial lockdown three more weeks meaning that bars, gyms and cinemas will remain closed until January 10 and the government will discuss all restrictions with regional leaders on January 4. Second, Spain announced that families will be allowed to meet in groups of up to 10 for the Christmas and New Year holidays. Travel will also be restricted between mainland Spanish regions from Dec. 23 to Jan. 6, unless the travel is for family gatherings. Elsewhere, Japan’s Osaka Prefecture will likely issue a red alert today, signaling that the region is in a state of emergency, due to the rising number of seriously ill patients.

On Brexit, sterling weakened by -0.41% against the US dollar and was the weakest performing G10 currency, with the moves following chief EU negotiator Michel Barnier’s reported comments to EU ambassadors that a trade deal is ‘in the balance’. As ever, it was the main sticking points of the level playing field, governance and fisheries that are still unresolved, though we did hear yesterday from a Guardian report that the UK has reduced its demand for fish caught by EU fleets in UK waters from 80% to 60%, though this is still a long way from the EU’s offer of 15-18% of catches. Later in the session, we also got reports from RTE’s Tony Connelly, who said that Mr. Barnier had told EU ambassadors that if the UK government’s Finance Bill contained clauses that breached international law (as happened with the Internal Market Bill), then that would put the talks “in crisis”. So definitely one to watch as this might be released in the coming days. Overnight, Bloomberg is reporting that at yesterday’s EU 27 ambassadors meeting, France warned that it could veto the trade deal if it doesn’t like the terms and the French envoy warned Mr. Barnier against making too many concessions simply because time was running out. The French position was backed by Belgium, the Netherlands and Denmark, and several ambassadors pressed to see draft text so that they could have enough time to scrutinise it properly. A request which Mr. Barnier swerved. Despite the negative headlines, Sterling is up +0.17% this morning mainly due to weakness in the broad US dollar index which is down -0.13%.

Wrapping up with yesterday’s data, the ADP’s report of private payrolls showed only a +307k increase in November (vs. 440k expected), which is the weakest monthly increase since July and doesn’t bode well for Friday’s payrolls. Over in Europe meanwhile, German retail sales rose by a stronger-than-expected 2.6% in October (vs. +1.2% expected), while the Euro Area unemployment rate fell by a tenth to 8.4%.

To the day ahead now, the global services and composite PMIs for November will be the main data highlight. Otherwise from the US, there’s also the November ISM services index and the weekly initial jobless claims, and from the Euro Area we’ll get October’s retail sales.

3A/ASIAN AFFAIRS

i)THURSDAY MORNING/ WEDNESDAY NIGHT:

SHANGHAI CLOSED DOWN 7.24 PTS OR .21% //Hang Sang CLOSED UP 195.92 PTS OR .74% /The Nikkei closed UP 8.39 POINTS OR 0.03%//Australia’s all ordinaires CLOSED UP 0.53%

/Chinese yuan (ONSHORE) closed UP A 6.5482 /Oil UP TO 44.88 dollars per barrel for WTI and 47.97 for Brent. Stocks in Europe OPENED RED EXCEPT LONDON/ITALY// ONSHORE YUAN CLOSED UP AGAINST THE DOLLAR AT 6.5482. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.5338 TRADE TALKS STALL//YUAN LEVELS //TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED//CORONAVIRUS/PANDEMIC/TRUMP TESTS POSITIVE FOR COVID 19 : /ONSHORE YUAN TRADING BELOW LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

3 a./NORTH KOREA/ SOUTH KOREA

South Korea

b) REPORT ON JAPAN

3 C CHINA

CHINA/USA

The House passes the bill forcing Chinese companies to agree to audit oversight or else they will be delisted from the USA

(zerohedge)

House Passes Bill Forcing Chinese Companies To Agree To Audit Oversight Or Delist From US

Not long after a top US intelligence official unveiled the existence of a Chinese intelligence operation, the House passed a bill that, should it become law, would force Chinese companies listed in the US to either adhere to strict American accounting standards, or delist and go elsewhere.

We’ve reported on the push to pass the bill several times. Trump made the issue a high priority this fall as election day neared. The bill targets a loophole that allows Chinese companies to essentially write their own rules when it comes to auditing, something that has led to literally dozens of corporate frauds that have cost American and international investors billions of dollars.

The collapse of Luckin Coffee and the CCP’s bailout of Evergrande helped to underscore the fact that Chinese companies essentially play by their own rules, and if foreign investors get screwed, so be it.

But the Trump team made it a centerpiece of its late game push against China, and now the legislation has finally passed the Democrat-controlled House. It’s in Trump’s hands now, as GOP Sen John Kennedy, one of its authors, pointed out in a tweet. Though we suppose it’s possible the US could strike some kind of deal with Beijing in the mean time.

The news has hit the offshore yuan; it has perhaps also stoked fears that the US might somehow miss out in the economic resurgence reportedly taking place in Asia, which has done a much better job of stamping out the virus than the rest of the world.

The surfeit of fraud-ridden Chinese firms created an atmosphere where short sellers like Citron Research and Muddy Waters Research minted reputations (and billions of dollars for themselves and their backers) as they rooted out evidence of fraud like a kind of hedfe fund blood sport.

These firms have collectively worked, along with others, to help expose innumerable frauds and misstatements from companies based in China. A movie, “The China Hustle”, was even made about this very topic.

The Public Company Accounting Oversight Board, an entity created by Sarbannes-Oxley to oversee accounting standards at US-listed companies, has been repeatedly unsucessful in its attempts to secure cooperation from China on a broad scale. The PCAOB has often had to sue Chinese audit firms and negotiate with Chinese regulators for more information. Now, new regulations could put the responsibility on the listing exchanges, like NASDAQ and NYSE, who choose to give credibility to China-based entities by accepting their listing fees and putting them on their well known exchanges.

It has been reported that the administration is trying to pass the new rules before outgoing SEC head Jay Clayton leaves at the end of the year. The Biden administration can then presumably “tweak” them to a degree.

Ma is now getting his comeuppance after publicly griping about some obscure regulatory feature in China, apparently angering China’s leaders to such a degree that they cancelled the spinoff of Alibaba’s Ant Financial.

end

Hong Kong opposition leader, already in Denmark seeks asylum in the UK. Dissident publisher Jimmy Lai has been denied bail. How on earth can any country trade with China now?

(zerohedge)

Hong Kong Opposition Leader Seeks Asylum In UK As Dissident Publisher Jimmy Lai Denied Bail

The CCP’s destruction of the pro-democracy movement is nearly complete.

And that crackdown on Hong Kong’s democratic freedoms – well, former democratic freedoms – continued Thursday as publisher Jimmy Lai was denied bail on fraud charges and so will be imprisoned until his trial, while a former opposition lawmaker moves to seek asylum in Britain.

While the news about Lai being remanded broke Thursday morning in Hong Kong, reports that former LegCo lawmaker Ted Hui Chi-fung is seeking exile in Britain hit Thursday morning in the US.

Confirmation of Hui’s whereabouts and his decision to seek asylum ends days of speculation about whether or not Hui had managed to escape Hong Kong, where he is facing nine charges tied to his role in the pro-democracy movement – charges that carry a high chance of jail time.

Britain has insisted that it will grant asylum to any Hong Kongers who are being persecuted for their activism, eliciting furious rebukes from Beijing, though there’s not much they can do about it.

Jimmy Lai

Lai was initially arrested for charges related to the new Hong Kong NatSec bill.

Both men are extremely high-profile – Lai’s company, Next Digital, publishes one of the largest newspapers in the territory, called “Apple Daily”. And Hui was formerly a key player in the opposition, which has been de facto disbanded by Beijing.

With youthful activists Agnes Chow and Joshua Wong also facing jail time, Beijing is making an example of some of the highest-profile individuals involved with a protest movement that is officially leaderless.

Hui has already fled to Denmark, where he announced Thursday his plans to seek asylum. He admitted in an interview he likely won’t return to Hong Kong for fear of being jailed.

“There is no word to explain my pain and it’s hard to hold back tears,” Hui said on Thursday evening. “Since the national security law, we have fallen into the darkness of tyranny and it breaks my heart to hear the fate of many of my friends.”

Revealing that Britain would be his next stop, Hui said he would make it his “life mission to widen Hong Kong’s international battle front” with activists living there, including Nathan Law Kwun-chung, who earlier fled to London.

Hui also claimed that his family members were being harassed by the authorities, one of the CCP’s favorite tactics for exerting pressure on exiles.

Fortunately, Hui believes that so long as he stays out of Hong Kong, his family should be safe.

“My whole family feels threatened…If I come back to Hong Kong, there will be very, very serious consequences – maybe at the airport immediately,” he told the B.T. newspaper. “It’s too early to say where I should go and where I will go.”

Hui urged Copenhagen to offer “safe haven” plans for Hong Kong protesters and take a more active role in speaking out against Beijing’s human rights abuses.

Ted Hui

According to the SCMP, Hui, a former Democratic Party lawmaker, met the president and vice-president of the Danish Parliament’s Foreign Policy Committee on Wednesday, where he called on the EU to push forward a law that would punish human rights abusers in China, in a style similar to the Magnitsky Act in the US.

“The response was positive,” one SCMP source said.

Under the Hong Kong national security law, imposed by Beijing back in June, it’s illegal for a Hong Konger to ask a foreign power to impose sanctions on Beijing, so by openly advocating for Denmark to speak out against China’s behavior, Hui is in effect sealing his fate – at least as far as Beijing is concerned.

With Hong Kong’s protest movement on its knees, and the leaders of the former pro-democracy movement scrambling to flee or possibly face arrest and imprisonment, Hui likely won’t be the last high-profile figure to seek asylum.