by harveyorgan · in Uncategorized · Leave a comment·Edit

GOLD PRICE CLOSED: UP $10.00 TO $1920.15

SILVER PRICE CLOSED: UP $0.19 AT $22.81

Access prices: closes 4: 15 PM

Gold ACCESS CLOSE 1918.25

Silver ACCESS CLOSE: 22,75

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

Bitcoin morning price:, $30,871 UP 296 Dollars

Bitcoin: afternoon price: $30,451 DOWN 124 dollars

Platinum price closing $906.10 UP $4/65

Palladium price; $1232/5- UP $1.80

END

Due to the huge rise in the dollar, we must look at gold and silver in currencies other than the dollar to understand where we are heading

I will now provide gold in Canadian dollars, British pounds and Euros/4: 15 PM ACCESS

CANADIAN GOLD: $2,541.28 UP 14 10 CDN dollars per oz (ALL TIME HIGH 2,775.35)

BRITISH GOLD: 1510,70 DOWN 2.56 pounds per oz//(ALL TIME HIGH//CLOSING///1630.29)

EURO GOLD: 1758.53 UP 2.18 euros per oz //(ALL TIME HIGH/CLOSING//1861.21)//

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

EXCHANGE: COMEX

EXCHANGE: COMEX

CONTRACT: JULY 2023 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,909.200000000 USD

INTENT DATE: 06/29/2023 DELIVERY DATE: 07/03/2023

FIRM ORG FIRM NAME ISSUED STOPPED

118 C MACQUARIE FUT 199

190 H BMO CAPITAL 200

363 H WELLS FARGO SEC 4

435 H SCOTIA CAPITAL 19

624 H BOFA SECURITIES 91

657 C MORGAN STANLEY 9

661 C JP MORGAN 15 27

661 H JP MORGAN 108

690 C ABN AMRO 21

726 C CUNNINGHAM COM 2

737 C ADVANTAGE 17

905 C ADM 48

TOTAL: 380 380

MONTH TO DATE: 38

JPMorgan stopped 27/380 contracts.

FOR JULY:

GOLD: NUMBER OF NOTICES FILED FOR JULY/2023. CONTRACT: 380 NOTICES FOR 38,000 OZ or 1.1819 TONNES

total notices so far: 380 contracts for 38,000 oz (1.1819 tonnes)

FOR JULY:

SILVER NOTICES: 2710 NOTICE(S) FILED FOR 13,550,000 OZ/

total number of notices filed so far this month : 2710 for 13,550,000 oz

XXXXXXXXXXXXXXXXXXXXXXXX

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD

WITH GOLD UP $10.00

INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD//

HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 2.31 TONNES OF GOLD FROM THE GLD:////

INVENTORY RESTS AT 924.50 TONNES

Silver//

WITH NO SILVER AROUND AND SILVER UP 19 CENTS AT THE SLV// HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.377 MILLION OZ FROM THE SLV//

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV.

CLOSING INVENTORY: 468.141 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A HUGE SIZED 1380 CONTRACTS TO 117,327 AND FURTHER FROM THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THIS HUGE SIZED LOSS IN COMEX OI WAS ACCOMPLISHED WITH OUR $0.23 LOSS IN SILVER PRICING AT THE COMEX ON THURSDAY. TAS ISSUANCE WAS A GOOD SIZED 439 CONTRACTS. THESE WILL BE USED FOR MANIPULATION LATER THIS MONTH . CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON THURSDAY NIGHT: 439 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS. IT THUS LOOKS LIKE THE FED (GOV’T) IS BEHIND ALL OF THESE TRADES.

WE HAVE NOW SET ANOTHER RECORD LOW AT 117,327 CONTRACTS ///JUNE 30.2023// OUR BANKERS WERE BASICALLY SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.23). BUT WERE SUCCESSFUL IN KNOCKING SOME SPEC LONGS AS WE HAD A STRONG LOSS ON OUR TWO EXCHANGES OF 1031 CONTRACTS. WE HAD 0 CRIMINAL NOTICES FILED IN THE CATEGORY OF EXCHANGE FOR RISK TRANSFER FOR 0 MILLION OZ// ( THE TOTAL ISSUED IN THIS CATEGORY SO FAR THIS MONTH TOTAL 0 MILLION OZ.). WE HAVE NOW RETURNED TO OUR USUAL AND CUSTOMARY SCENARIO: BANKERS SHORT AND SPECS LONG WITH MANIPULATION NOW MID MONTH AND BEYOND, DUE TO (TAS) MANIPULATION. TODAY WE WITNESSED FOR THE FOURTH STRAIGHT DAY: HUGE SPREADER LIQUIDATION ON THE COMEX

WE MUST HAVE HAD:

A STRONG ISSUANCE OF EXCHANGE FOR PHYSICALS( 541 CONTRACTS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 16.110 MILLION OZ (FIRST DAY NOTICE) // HUGE SIZED COMEX OI LOSS/ STRONG SIZED EFP ISSUANCE/VI) GOOD NUMBER OF T.A.S. CONTRACT ISSUANCE (439 CONTRACTS)//HUGE COMEX SPREADER LIQUIDATION//

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL –192 CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS JUNE. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF JUNE:

TOTAL CONTRACTS for 19 days, total 22,029 contracts: OR 110.145 MILLION OZ (1159 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 110.145 MILLION OZ

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 118.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.145 MILLION OZ//MUCH LARGER THAN LAST MONTH

RESULT: WE HAD A HUMONGOUS SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 1572 CONTRACTS WITH OUR LOSS IN PRICE OF $0.23 IN SILVER PRICING AT THE COMEX//THURSDAY.,. THE CME NOTIFIED US THAT WE HAD A STRONG EFP ISSUANCE CONTRACTS: 439 ISSUED FOR JULY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS./ WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR JULY OF 16.110 MILLION OZ///// .. WE HAVE A HUGE SIZED LOSS OF 1031 OI CONTRACTS ON THE TWO EXCHANGES. THE TOTAL OF TAS INITIATED CONTRACTS TODAY: A GOOD 439//SOME FRONT END OF THE TAS CONTRACTS WERE LIQUIDATED DURING THE THURSDAY COMEX SESSION BUT THE REAL LIQUIDATION TODAY WAS THAT OF COMEX SPREADERS (CONCLUSION) . THE NEW TAS ISSUANCE TODAY (439) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE.

WE HAD 2710 NOTICE(S) FILED TODAY FOR 13,550,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A STRONG SIZED 7369 CONTRACTS TO 436,825 AND FURTHER FROM THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED –594 CONTRACTS

WE HAD A STRONG SIZED INCREASE IN COMEX OI ( 7369 CONTRACTS) DESPITE OUR $3.20 LOSS IN PRICE. WE ALSO HAD A STRONG INITIAL STANDING IN GOLD TONNAGE FOR JULY. AT 5.1975 TONNES ON FIRST DAY NOTICE + /A GOOD ISSUANCE OF 690 T.A.S. CONTRACTS /// ALL OF..THIS HAPPENED WITH A $3.20 LOSS IN PRICE WITH RESPECT TO THURSDAY’S TRADING.WE HAD A VERY STRONG SIZED GAIN OF 11,265 OI CONTRACTS (35.03 PAPER TONNES) ON OUR TWO EXCHANGES.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A GOOD SIZED 3896 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 436,825

IN ESSENCE WE HAVE A VERY STRONG SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 11,265 CONTRACTS WITH 7369 CONTRACTS INCREASED AT THE COMEX//TAS CONTRACTS INITIATED (ISSUED): A GOOD 690 CONTRACTS) AND A GOOD 3896 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 11,265 CONTRACTS OR 35.03 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A GOOD SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (3896 CONTRACTS) ACCOMPANYING THE STRONG SIZED GAIN IN COMEX OI (7369) //TOTAL GAIN FOR OUR THE TWO EXCHANGES: 11,265 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR NORMAL FORMAT OF BANKERS GOING SHORT AND SPECULATORS GOING LONG ,2.) GOOD INITIAL STANDING AT THE GOLD COMEX FOR JULY AT 5.1975 TONNES ///// /3) ZERO LONG LIQUIDATION//4) STRONG SIZED COMEX OPEN INTEREST GAIN/ 5) GOOD ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER///6: GOOD T.A.S. ISSUANCE: 690 CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023 INCLUDING TODAY

JULY

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF JUNE :

TOTAL EFP CONTRACTS ISSUED: 53,036 CONTRACTS OR 5,303,600 OZ OR 164.96 TONNES IN 19 TRADING DAY(S) AND THUS AVERAGING: 2791 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 19 TRADING DAY(S) IN TONNES 164.96 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2022, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 164.96/3550 x 100% TONNES 4.64% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2023

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 164.96 TONNES (WEAKER ISSUANCE THIS MONTH)

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF JUNE. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF MAY HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF JUNE., FOR BOTH GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (JUNE), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER FELL BY A HUGE SIZED 1572 CONTRACTS OI TO 117,327 AND FURTHER FROM OUR COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO. HOWEVER WE HAVE SET A NEW RECORD LOW OF 117,327 CONTRACTS JUNE 30.2023

EFP ISSUANCE 439 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

JULY 439 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 439 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 1527 CONTRACTS AND ADD TO THE 439 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A HUGE SIZED LOSS OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 1031 CONTRACTS

THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES TOTAL 5.155 MILLION OZ

OCCURRED DESPITE OUR TINY $0.23 LOSS IN PRICE …..

END

OUTLINE FOR TODAY’S COMMENTARY

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

b, ) Gold/silver trading overnight Europe,//GOLD COMMENTARIES

(Peter Schiff)

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS//

FRIDAY MORNING//THURSDAY NIGHT

SHANGHAI CLOSED DOWN 16.68 PTS OR 0.62% //Hang Seng CLOSED DOWN 17.93 PTS OR 0.09% /The Nikkei closed DOWN 45.10 OR 0.14% //Australia’s all ordinaries CLOSED UP 0.16 % /Chinese yuan (ONSHORE) closed DOWN 7.2689 /OFFSHORE CHINESE YUAN DOWN TO 7.2820 /Oil UP TO 69.96 dollars per barrel for WTI and BRENT UP AT 74.59 / Stocks in Europe OPENED ALL GREEN// ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

9. USA

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A STRONG SIZED 7369 CONTRACTS DOWN TO 436,825 DESPITE OUR LOSS IN PRICE OF $3.20 ON THURSDAY,

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE NON ACTIVE DELIVERY MONTH OF JULY… THE CME REPORTS THAT THE BANKERS ISSUED A GOOD SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 3896 EFP CONTRACTS WERE ISSUED: : AUGUST 3896 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 3896 CONTRACTS

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A VERY STRONG SIZED TOTAL OF 11,265 CONTRACTS IN THAT 3896 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A STRONG SIZED GAIN OF 7369 COMEX CONTRACTS..AND THIS VERY STRONG SIZED GAIN ON OUR TWO EXCHANGES HAPPENED DESPITE OUR LOSS IN PRICE OF $3.20//THURSDAY COMEX. AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS DURING MID MONTH IN THE DELIVERY CYCLE), THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR THURSDAY NIGHT WAS A GOOD 690 CONTRACTS. THROUGHOUT LAST WEEK, THE BANKERS SOLD OFF THE LONG SIDE OF THE SPREAD WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR SPREAD WHICH WILL BE LIQUIDATED TWO MONTHS HENCE)//THE HUGE NUMBER OF T.A.S. CONTRACTS INITIATED OVER THE PAST SEVERAL WEEKS SPELLS TROUBLE FOR THE GOLD/SILVER MARKET AS RAIDS WILL SURELY BE UPON US.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: JULY (5.1975) (NON ACTIVE MONTH)

TONNES),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 5.1975 TONNES

THE SPECS/HFT WERE SUCCESSFUL IN LOWERING GOLD’S PRICE( IT FELL $3.20) //// BUT WERE UNSUCCESSFUL IN KNOCKING ANY SPECULATOR LONGS AS WE HAD OUR VERY STRONG SIZED GAIN OF 11,265 CONTRACTS ON OUR TWO EXCHANGES. WE HAD CONSIDERABLE TAS LIQUIDATION THROUGHOUT THE THURSDAY COMEX SESSION . THE TAS ISSUED THURSDAY NIGHT, WILL BE “PUT INTO THE BANK” TO BE USED AT A LATER DATE AT THE COLLUSIVE CHOOSING OF OUR BANKERS.

WE HAVE GAINED A TOTAL OI OF 35.03 PAPER TONNES OF TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR JULY. (5.1975 TONNES) // ALL OF THIS WAS ACCOMPLISHED WITH OUR LOSS IN PRICE TO THE TUNE OF $3.20.

WE HAD –REMOVED 594 CONTRACTS TO THE COMEX TRADES TO OPEN INTEREST AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 11,265 CONTRACTS OR 1,126,500 OZ OR 35.03 TONNES.

Estimated gold volume today:// 174,859 POOR

final gold volumes/yesterday 220,784 FAIR

//JUNE 30/ FOR THE JULY 2023 CONTRACT

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 225,057 OZ Brinks 7 kilobars . |

| Deposit to the Dealer Inventory in oz | 0 oz |

| Deposits to the Customer Inventory, in oz | 15,673.410 OZ |

| No of oz served (contracts) today | 380 notice(s) 38,000 OZ 1.1819 TONNES |

| No of oz to be served (notices) | 1291 contracts 129,100 oz 4.0155 TONNES |

| Total monthly oz gold served (contracts) so far this month | 380 notices 38,000 OZ 1.1819 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | x |

No dealer withdrawals

Customer deposits: 1

i) Into HSBC: 15,673.410 oz

total deposits: 15,673.410 oz

total dealer deposits: nil oz

we had 1 customer deposit:

i) Into HSBC: 15,673.410 oz

total deposits: 15,673.410 oz

Adjustments; 1 JPMorgan dealer to customer

i)482.265 oz

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR JULY.

For the front month of JULY we have an oi of 1671 contracts having LOST 68 contracts.

Thus by definition, the initial amount of gold standing in this non active delivery month of July is as follows:

1671 notices x 100 oz per notice = 167,100 oz or 5.1975 tonnes

AUGUST GAINED 4846 contracts UP to 346,530 contracts

SEPT lost 56 contracts down to 13,420.

We had 380 contracts filed for today representing 38,000 oz

Today, 8 notice(s) were issued from J.P.Morgan dealer account and 125 notices were issued from their client or customer account. The total of all issuance by all participants equate to 380 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 27 notice(s) was (were) stopped received by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the JULY /2023. contract month,

we take the total number of notices filed so far for the month (380 x 100 oz ), to which we add the difference between the open interest for the front month of JULY (1671 CONTRACT) minus the number of notices served upon today 380 x 100 oz per contract equals 167,100 OZ OR 5.1975 TONNES the number of TONNES standing in this NON active month of July.

thus the INITIAL standings for gold for the JULY contract month: No of notices filed so far (380) x 100 oz + (1671) {OI for the front month} minus the number of notices served upon today (380) x 100 oz) which equals 167,100 oz standing OR 5.1975 TONNES

TOTAL COMEX GOLD STANDING: 5.1975 TONNES WHICH IS STRONG FOR A NON ACTIVE DELIVERY MONTH.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 2,063,541.609 OZ 64.18 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 22,404,531.897 OZ

TOTAL REGISTERED GOLD: 11,808,038.075 (367,27 tonnes)..

TOTAL OF ALL ELIGIBLE GOLD: 10,596.493.822 O Z

REGISTERED GOLD THAT CAN BE SERVED UPON: 9,744,979.00 OZ (REG GOLD- PLEDGED GOLD) 303.109 tonnes//

END

SILVER/COMEX

JUNE 30//2023// THE JULY 2023 SILVER CONTRACT

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 152,182.899 oz CNT Delaware . |

| Deposits to the Dealer Inventory | nil oz |

| Deposits to the Customer Inventory | 2,950,873.420 oz Brinks Delaware |

| No of oz served today (contracts) | 2710 CONTRACT(S) (13,550,000 OZ) |

| No of oz to be served (notices) | 512 contracts (2,560,000 oz) |

| Total monthly oz silver served (contracts) | 2710 Contracts (13,550,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

i) 0 dealer deposits

total dealer deposit: nil oz

total dealer deposits: 0

i) We had 0 dealer withdrawal

total dealer withdrawals: oz

We had 2 deposits customer account:

i) Into Brinks: 1,800,557.143 oz

ii) Into Delaware 1,150,316.340 oz

total customer deposits: 2,950,873.483 oz

JPMorgan has a total silver weight: 141.315 million oz/276.512 million =51.03% of comex .//dropping fast

Comex withdrawals 2

i) Out of CNT 145,172.850 oz

ii) Out of Delaware: 7010.049 oz

total withdrawals: 152,182.899 oz

adjustments: 1

a whopper: 6,825,153.420 oz adjusted customer to dealer account: Brinks

TOTAL REGISTERED SILVER: 38.996 MILLION OZ//.TOTAL REG + ELIGIBLE. 276.512 million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR JULY:

silver open interest data:

FRONT MONTH OF JULY /2023 OI: 3222 CONTRACTS HAVING LOST 4053 CONTRACT(S).

THUS BY DEFINITION, THE INITIAL AMOUNT OF SILVER OZ STANDING IN THIS VERY ACTIVE DELIVERY MONTH OF JULY IS AS FOLLOWS:

3222 NOTICES X 5000 OZ PER NOTICE = 16,110,000 OZ

AUGUST GAINED 60 CONTRACTS TO STAND AT 433

SEPT HAS A GAIN OF 2334 CONTRACTS UP TO 100,609

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 2710 for 13,550,000 oz

Comex volumes// est. volume today 43,382 POOR /

Comex volume: confirmed yesterday:63,792 GOOD

To calculate the number of silver ounces that will stand for delivery in JULY. we take the total number of notices filed for the month so far at 2710 x 5,000 oz = 13,550,000 oz

to which we add the difference between the open interest for the front month of JULY(3222) and the number of notices served upon today 2710 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the JULY/2023 contract month: 2710 (notices served so far) x 5000 oz + OI for the front month of JULY (3222) – number of notices served upon today (2710 )x 500 oz of silver standing for the JULY contract month equates to 16.110 million oz +

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS

JUNE 30/WITH GOLD UP $10.00 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.31 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 924.50 TONNES

JUNE 29/WITH GOLD DOWN $3.20 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.26 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 926.81 TONNES

JUNE 28/WITH GOLD DOWN $1.15 NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 925.65 TONNES

JUNE 27/WITH GOLD DOWN $9.15 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.45 TONNES OF GOLD FROM THE GLD./INVENTORY RESTS AT 925.65 TONNES

JUNE 26/WITH GOLD UP $4.65 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.6 TONNES OF GOLD FROM THE GLD/////INVENTORY RESTS AT 927.10 TONNES

JUNE 23/WITH GOLD UP $5.15 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: WITHDRAWALS OF 4.33 TONNES OF GOLD OVER THE PAST TWO DAYS. /INVENTORY RESTS AT 929.70 TONNES

JUNE 21/WITH GOLD DOWN $2.45 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY REST AT 934.03 TONNES

JUNE 20/WITH GOLD DOWN $22.40 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 934.03 TONNES

JUNE 16/WITH GOLD UP $0.70 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4.33 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 934.03 TONNES

JUNE 15/WITH GOLD UP $2.80 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES OF GOLD FROM THE GLD//INVENTORY RESTS AT 929.70 TONNES

JUNE 14/WITH GOLD UP $10.30 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 931.44 TONNES

JUNE 13/WITH GOLD DOWN $10.30 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.01 TONNES FORM THE GLD///INVENTORY RESTS AT 931.44

JUNE 12/WITH GOLD DOWN $7.10 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 934.65 TONNES

JUNE 9/WITH GOLD DOWN $1.00: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 934.65 TONNES

JUNE 8/WITH GOLD UP $20.45 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.46 TONNES FROM THE GLD///INVENTORY RESTS AT 934.65 TONNES

JUNE 7 WITH GOLD DOWN $22.15 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.45 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 938.11 TONNES

JUNE 6/WITH GOLD UP $6.90 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.45 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 939.56 TONNES

JUNE 5/WITH GOLD UP $5.00 TODAY : NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 938.11 TONNES

JUNE 2/WITH GOLD DOWN $24.40 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.45 TONNES FROM THE GLD///INVENTORY RESTS AT 938.11 TONNES

JUNE 1/WITH GOLD UP $14.10 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 939.56 TONNES

MAY 31/WITH GOLD UP $5.70 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.73 TONNES OF GOLD FROM THE GLD///INVENTORY RESTS AT 939.56 TONNES

MAY 30/WITH GOLD UP $14.55 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 941.29 TONNES

MAY 26/WITH GOLD UP $.90 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY REST AT 941.29 TONNES

MAY 25/WITH GOLD DOWN $19.70 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 941.29 TONNES

MAY 24/WITH GOLD DOWN $9.50 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.45 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 941.29 TONNES

MAY 23/WITH GOLD $2.25 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 942.74 TONNES

MAY 22/WITH GOLD DOWN $4.70 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 5.83 TONES OF GOLD INTO THE GLD DESPITE THE L0SS IN PRICE//INVENTORY RESTS AT 942.74 TONNES

MAY 19/WITH GOLD UP $22.20 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 936.96 TONNES

MAY 18/WITH GOLD DOWN $23.80 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.02 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 936.96 TONNES

GLD INVENTORY: 924.50 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

JUNE 30/WITH SILVER UP 19 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.377 MILLION OZ INTO THE SLV/////INVENTORY RESTS AT468.141 MILLION OZ//

JUNE 29/WITH SILVER DOWN 23 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.763 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 466.764 MILLION OZ//

JUNE 28/WITH SILVER DOWN 2 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 470.527 MILLION OZ//

JUNE 27/WILVER SILVER UP 7 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 734,000 OZ INTO THE SLV////INVENTORY RESTS AT 470.527 MILLION OZ

JUNE 26/WITH SILVER UP 44 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY REST AT 469.793 MILLION OZ.

JUNE 23/WITH SILVER DOWN 9 CENTS TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A NET DEPOSIT OF 6.61 MILLION OZ INTO THE SLV OVER THESE PAST TWO DAYS//INVENTORY RESTS AT 469.793 MILLION OZ//

JUNE 21/WITH SILVER DOWN $.40 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 5.784 MILLION OZ OF SILVER INTO THE SLV////INVENTORY RESTS AT 463.183 MILLION OZ//

JUNE 20/WITH SILVER DOWN 89 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 463.183 MILLION OZ//

JUNE 16/WITH SILVER UP 23 CENTS TODAY :SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 459,000 OZ FROM THE SLV///INVENTORY RESTS AT 463.183 MILLION OZ

JUNE 15/WITH SILVER DOWN 17 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.377 MILLION OZ OF SILVER FROM THE SLV////INVENTORY RESTS AT 463.642 MILLION OZ//

JUNE 14/WITH SILVER UP 29 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 735,000 OZ FROM THE SLV///INVENTORY RESTS AT 465.019 MILLION OZ//

JUNE 13/WITH SILVER DOWN 25 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.515 MILLION OZ OF SILVER FROM THE SLV///INVENTORY RESTS AT 465.754 MILLION OZ//

JUNE 12/WITH SILVER DOWN 26 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 467.269 MILLION OZ//

JUNE 9/WITH SILVER UP 7 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF SILVER TO THE TUNE OF 550,000 OZ//INVENTORY RESTS AT 467.269 MILLION OZ

JUNE 8/WITH SILVER UP $0.63 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 467.819 MILLION OZ/

JUNE 7/WITH SILVER DOWN 17 CENTS TODAY:HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.01 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 467.819 MILLION OZ/

JUNE 6/WITH SILVER UP 7 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 466.809 MILLION OZ//

JUNE 5/WITH SILVER DOWN $.13 TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 266,000 OZ FROM THE SLV////INVENTORY RESTS AT 466.809 MILLION OZ/

JUNE 2/WITH SILVER DOWN 23 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 918,000 OZ FROM THE SLV./INVENTORY RESTS AT 467.015 MILLION OZ/

JUNE 1/WITH SILVER UP 49 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 467.933 MILLION OZ

MAY 31/WITH SILVER UP 37 CENTS TODAY:SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 367,000 OZ FROM THE SLV////INVENTORY RESTS AT 467.933 MILLION OZ//

MAY 30/WITH SILVER DOWN 9 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 468.300 MILLION OZ//

MAY 26/WITH SILVER UP $0.44 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.306 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 468.300 MILLION OZ//

MAY 25.WITH SILVER DOWN $0.32 TODAY; SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 276,000 OZ INTO THE SLV////INVENTORY RESTS AT 471.606 MILLION OZ//

MAY 24/WITH SILVER DOWN $.35 TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 471.330 MILLION OZ//

MAY 23/WITH SILVER DOWN 22 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.801 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 471.330 MILLION OZ//

MAY 22/WITH SILVER DOWN 19 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 468.529 MILLION OZ//

MAY 19/WITH SILVER UP 38 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 468.529 MILLION OZ

MAY 18/WITH SILVER DOWN 23 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 919,000 OZ FROM THE SLV////INVENTORY RESTS AT 468.529 MILLION OZ/

MAY 17/WITH SILVER DOWN 2 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 469.448 MILLION OZ//

CLOSING INVENTORY 4668.141 MILLION OZ//

PHYSICAL GOLD/SILVER COMMENTARIES

1:Peter Schiff/Mike Maharrey

end

2 Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens//JAMES RICKARDS//JOHN RUBINO

END

3,Chris Powell of GATA provides to us very important physical commentaries

This new Moscow gold exchange will be part of the gold-Brics currency format to be rolled out AUG 22

Moscow Exchange launches quarterly gold futures, plans perpetual futures soon

Submitted by admin on Fri, 2023-06-30 00:05Section: Daily Dispatches

Moscow Exchange to Launch Perpetual Gold Futures in July

From Interfax, Moscow

Thursday, June 29, 2023

https://interfax.com/newsroom/top-stories/91995/

MOSCOW — The Moscow Exchange plans to start trading in perpetual gold futures in the near future, Maria Patrikeyeva, head of the exchange’s derivatives market, said.

“We launched settled quarterly gold futures yesterday, and in the near future, in July, we will launch new perpetual gold futures,” Patrikeyeva said at the press lunch “Options Market on the Moscow Exchange: New Opportunities.”

The Moscow Exchange began trading in settled futures contracts for gold in Russian rubles on June 28.

The underlying asset is the GLDRUB_TOM instrument from the exchange’s precious metals market. A lot is 1 gram, the tick size is 0.1 rubles, and tick value is also 0.1 rubles.

The strike price is the RUGOLD index price, calculated by the Moscow Exchange on the basis of transactions with the underlying asset in the precious metals market on the day the contract is settled.

Contracts with settlement in September and December 2023 as well as in March and June 2024 are admitted to trading.

The Moscow Exchange also trades settled futures for gold denominated in U.S. dollars, as well as a spot instrument for gold on the precious metals market.

* * *

END

Your weekend reading material

Alasdair Macleod…

Alasdair Macleod: Geopolitical evolution

Submitted by admin on Thu, 2023-06-29 10:38Section: Daily Dispatches

By Alasdair Macleod

GoldMoney, Toronto

Thursday, June 29, 2023

The increasing number of nations seeking to join the BRICS brings geopolitics into the spotlight. At the time of this writing, existing members, those who have applied to join, and those expressing an interest total 36 nations, with over 60% of the world’s population and a third of global GDP.

Plans for a new trade currency backed by gold appear to be on the agenda for the BRICS meeting in Johannesburg in August. In this article the geopolitical aspects of its introduction are considered, and the indications that how it will involve gold are discussed. The mechanics of this project are then suggested.

But first we look at the situation in Ukraine, attempting to put the recent Wagner rebellion into context.

Furthermore, Russia’s deteriorating trade surplus, weakness of the rouble, and rising bond yields suggest that it is time for President Putin to put an end to Ukraine’s misery. He is likely to do this by attacking Kiev, which is only 60 miles from Belarus, while the bulk of Ukraine’s army is distracted by operations over 400 miles to the south and east. …

… For the remainder of the analysis:

https://www.goldmoney.com/research/geopolitical-evolution-2023?gmrefcode=gata

end

4, OTHER IMPORTANT GOLD/SILVER COMMENTARIES/

The apocalyptic 8000-tonne gold miscalculation

5 a. IMPORTANT COMMENTARIES ON COMMODITIES:

end

5 B GLOBAL COMMODITY ISSUES/FOOD IN GENERAL

6.CRYPTOCURRENCY//DIGITAL CURRENCY// COMMENTARIES/

END

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS/FRIDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED DOWN TO 7.2689

OFFSHORE YUAN: DOWN TO 7.2820

SHANGHAI CLOSED DOWN 16.68 PTS OR 0.62%

HANG SENG CLOSED DOWN 17.93 PTS OR 0.09%

2. Nikkei closed DOWN 45.10 PTS OR 0.14%

3. Europe stocks SO FAR: ALL GREEN

USA dollar INDEX DOWN TO 103.07 EURO FALLS TO 1.0852 DOWN 11 BASIS PTS

3b Japan 10 YR bond yield: RISES TO. +.397 Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 144.71/JAPANESE YEN FALLING AS WELL AS LONG TERM 10 YR. YIELDS RISING //EVENTUALLY THIS WILL BREAK THE JAPANESE CENTRAL BANK

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen UP CHINESE ON SHORE YUAN: DOWN// OFF- SHORE: DOWN

3f Japan is to buy INFINITE TRILLION YEN’S worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and UP FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund UP TO +2.4275***/Italian 10 Yr bond yield RISES to 4.101*** /SPAIN 10 YR BOND YIELD RISES TO 3.415…** DANGEROUS//

3i Greek 10 year bond yield RISES TO 3.675

3j Gold at $1907.20 silver at: 22.44 1 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble DOWN 1 AND 83 /100 roubles/dollar; ROUBLE AT 89.12//

3m oil into the 69 dollar handle for WTI and 74 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 144.71// 10 YEAR YIELD AFTER BREAKING .54%, RISES TO .397% STILL ON CENTRAL BANK (JAPAN) INTERVENTION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.9008 as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9779 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 3.876 UP 2 BASIS PTS…

USA 30 YR BOND YIELD: 3.926 UP 2 BASIS PTS/

USA 2 YR BOND YIELD: 4.918 UP 4 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 26.05…(TURKEY SET TO BLOW UP FINANCIALLY)

GREAT BRITAIN/10 YEAR YIELD: UP 0 BASIS PTS AT 4.488 UP 14 PTS

end

2. Overnight: Newsquawk and Zero hedge:

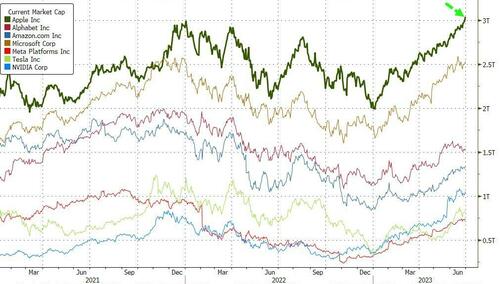

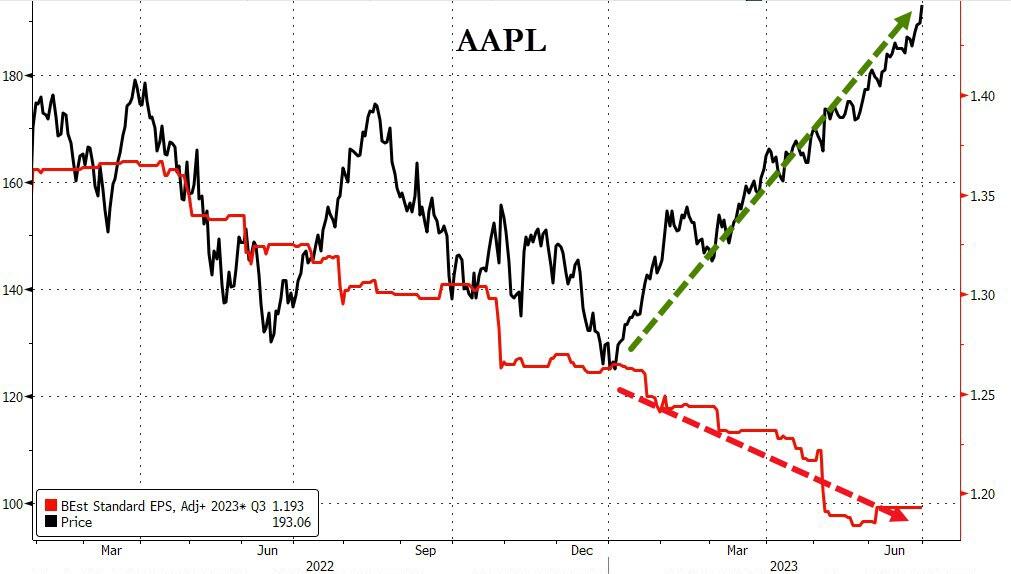

Futures Rise As Apple Market Cap Tops $3 Trillion

FRIDAY, JUN 30, 2023 – 08:20 AM

The second quarter – and first half – of 2023 is coming to a close on an upbeat note, as US equity futures are higher, led by megacap tech, and especially Apple, which is set to open with a market cap over $3 trillion following a bizarre initiation report from Citi yesterday late, which set a $240 price target on the world’s biggest company, just in time to catch its all time high. As of 7:45am ET, S&P futures were 0.4% higher, set to close out a third straight quarterly gain…

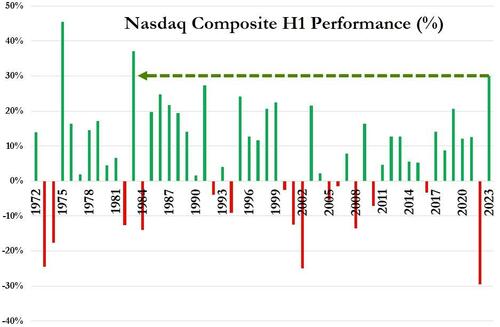

… while Nasdaq futures rose 0.5%, indicating the index is set to extend its 37% surge since the start of the year, its best start to the year since 1982.

Treasuries extended a selloff, with yields rising 4-6 bps across the curve as two-year yields rose about five basis points to 4.92%, adding to Thursday’s 16-point jump. The 10-year yield increased three points to its highest level since mid-March. Swap markets now indicate a nearly 50% chance of a second US hike by year-end sparked by robust US economic growth and jobs data that fueled bets on more interest rate hikes. The USD is higher, and commodities are mixed with the energy complex higher and base metals lower. Today, focus will be on the latest PCE report where consensus expects core PCE to print 4.7% vs. 4.7% prior and headline PCE to drop to 3.8% vs. 4.4% prior. In addition, keep an eye on Personal Income/ Spending, MNI Chicago PMI and the revision of UMich. data. Also, the supreme Court will decide on Biden’s student loan forgiveness today.

In premarket trading, it was a less positive picture for sportswear giant Nike, whose shares fell 3.7% after the retailer’s outlook for the full year failed to impress. While sales beat forecasts, however, and analysts highlighted Nike’s better-than-anticipated performance in China as a bright spot. The results also showed Nike is still working to sell off its high stockpiles of merchandise that have eroded profitability. “Nike is a solid brand,” said Neil Saunders, an analyst at GlobalData Retail. But “it isn’t on the front foot either, and has to accept that the year ahead will be one of resetting, retrenching, and reformulating the way it does business.” Here are some other notable premarket movers:

- Apple shares rise 0.8% in premarket trading Friday, with the iPhone maker’s market value set to exceed the historic $3 trillion threshold.

- Aurinia Pharmaceuticals shares jump as much as 19% in US premarket trading after the drug developer said that it is exploring options, including a sale. Analysts say the announcement is positive for the shares and could see the company being an attractive target for a bigger pharma firm in the rheumatology space, touting a possible takeout price in the high teens.

- XPeng shares jump over 7% in US premarket trading after the Chinese company unveiled its new G6 electric SUV. Analysts say the product has a competitive price and could stock sales.

- Smart Global shares rose 5.2% in post-market trading after the company forecast adjusted earnings per share for the fourth quarter that exceeded the average analyst estimate at the midpoint.

Thursday’s readings on US jobless claims and the gross domestic product showed the world’s biggest economy was in better shape than many had envisioned at the start of 2023. After the data came out, the US yield-curve inversion intensified — with longer-dated yields rising less than shorter-maturity ones. That means the economy may look stronger now, but investors expect the Fed’s rate increases to curb future growth, which could boost the risk of a recession down the road.

Bets on further Fed tightening will be will be tested by US price measures due Friday, including figures on personal income and spending as well as the PCE deflator, the Federal Reserve’s preferred gauge of underlying inflation pressures. The numbers are expected to show some softening while still indicating inflation remains sticky.

“Markets are still really caught up in the ‘strong data’ narrative,” said James Rossiter, head of global macro strategy at TD Securities. “But ultimately the Fed’s going to be focused on where inflation is right now. It’s going to be a more difficult decision for them in July, especially given how much tightening they’ve already put in the system that still has to play out.”

The Stoxx Europe 600 index climbed more than 1% led by energy, real estate and banks, with all sectors rising barring tech. Euro Stoxx 50 rises 0.6%. FTSE MIB outperforms peers, adding 0.9%, FTSE 100 lags, adding 0.6%. Among individual movers, Engie SA rose after the French utility raised its full-year earnings forecast. ASML Holding NV dropped after the Dutch chipmaker was slapped with more restrictions on exports to China. The European benchmark is on track to end the quarter flat after failing to build on its 7.8% first-quarter gain amid outflows from European stocks totaling $27 billion this year. A gauge of global equities, meanwhile, headed for a quarterly rise of 4.5%, defying rising interest rates and the risk of recessions in major economies. Here are today’s most notable movers:

- Kion shares rise as much as 7.6%, the most since November, with Warburg expecting the German warehouse equipment firm to present solid second-quarter figures on 27 July

- LEG Immobilien jumped 7.5% after the German real estate company boosted its guidance for adjusted funds from operations and EBITDA margin for the full year, boosting the whole real estate sector

- Steico rises as much as 11% after Morgan Stanley raised its recommendation to overweight, saying the manufacturer of insulation materials is close to the bottom of the downgrade cycle

- Societe Generale rises as much as 2.3% to a one-month high after Deutsche Bank raised its recommendation to buy from hold, noting tailwinds for 2024 such as a recovery in NII

- Engie rises as much as 2.7% after the French utility raised its FY earnings forecast. Morgan Stanley attributes the guide upgrade stems to the company’s global energy management and sales

- Drax shares climb as much as 3.9% after Credit Suisse raised its recommendation on the British utility to outperform saying the valuation looks attractive on most cashflow-based metrics

- Nordex rises as much as 4.5% after Deutsche Bank initiated coverage of the German wind turbine maker with buy, saying it’s well-positioned in most key regions with impressive recent share gain

- ASML falls as much as 3.8%, its biggest intraday decline since April, after a Reuters report said the US plans to force the company to ship fewer of its deep ultraviolet lithography machines to China

- Bawag shares fell the most in more than three months, tumbling as much as 14% in Vienna, after activist investor Petrus Advisers Ltd. published a report that identified potential red flags

- Aperam slides as much as 7.1% after the steelmaker was downgraded by two brokerage firms. Degroof Petercam cuts the stock to hold, citing a lack of short-term visibility on earnings recovery

- Fevertree shares drop as much as 7.4%, the most intraday since April 27, after Bank of America cut its recommendation on the high-end tonic maker to underperform, citing an “unjustified” valuation

Earlier in the session, Asian stocks traded with cautious gains amid the higher yield environment and as participants digested a slew of data releases at quarter-end including the latest Chinese official PMIs.

- Hang Seng and Shanghai Comp were initially choppy but ultimately gained after the latest Chinese PMI data in which headline Manufacturing PMI matched estimates and Non-Manufacturing PMI was slightly softer-than-expected although remained at a firm expansion.

- ASX 200 lacked direction as gains in the commodity-related sectors and utilities offset losses in real estate and tech.

- Nikkei 225 was subdued after mixed data releases including disappointing Industrial Production and softer-than-expected Tokyo CPI although the losses were cushioned as USD/JPY briefly climbed above 145.00.

In FX, the Bloomberg Dollar Spot Index remains little changed; NOK/USD leads G-10 gains climbing 0.5%, while EURUSD slumps 0.2% after data showed euro-area core inflation re-accelerating. The yen briefly weakened past 145 for the first time since November, putting markets on watch for possible Japanese intervention. It since retraced to around 144.70 after Finance Minister Shunichi Suzuki told reporters the government would respond appropriately to any excessive moves in the currency market. The offshore yuan remained in the spotlight after the recent slide to its lowest level in seven months. It appreciated Friday, for the first time in three days, after the People’s Bank of China again set the daily reference rate for currency at a level stronger than the average estimate in a Bloomberg survey. The currency is down almost 5% against the dollar this year, prompting extra scrutiny from Chinese regulators, according to people familiar with the matter. Purchasing managers’ index data from China on Friday underscored concern that the economy is losing steam, bolstering calls for more policy support.

In rates, treasuries extended a weekly slide gilts fall sharply following a bundle of UK economic data. Treasury losses continued to be led by front-end and belly of the curve, deepening inversion of 2s10s, 5s30s spreads. Yields on the two- year climbing six basis points to 4.92% and yields on the 10- year rising 4 basis points to 3.88%; euro bonds see broad-based selling. 2s10s, 5s30s spreads flatter by 1.3bp and 2bp on the day; 10-year yields around 3.87%, cheaper by 3bp vs Thursday close. Yields except 30-year are at highest levels since March as expectations have mounted for two more Fed rate increases this year, and the Bloomberg Treasury Index is headed for a second straight monthly loss. Month-end index rebalancing at 4pm is estimated to extend its duration by 0.07 year. US session includes May personal income and spending report that embeds PCE deflators.

Yields on European bonds retreated from session highs and the euro pared a decline after data showed inflation in the common-currency area slowed more than economists’ expectations in June. Core prices re-accelerated, though, in a setback for the European Central Bank that may reinforce its determination to raise interest rates next month.

“An extra interest rate hike at the next monetary policy meeting is nearly a done deal,” said Daniele Antonucci, chief economist and macro strategist at Quintet Private Bank. “Further out, the picture is less clear. How far the ECB will have to go remains an open question and depends on how much it’s willing to sacrifice in terms of job losses.”

In commodities, WTI drifts 1% higher to trade near $70.54. Brent crude oil is on track for the worst run of quarterly losses in three decades as persistent concerns over the demand outlook and robust supplies weigh on prices. Spot gold falls roughly $5 to trade near $1,903/oz.

Bitcoin is on a firmer footing intraday but remains under the USD 31k level. RBNZ is to ramp up monitoring of stablecoins and crypto assets but noted that regulation of crypto assets is not currently required.

Looking at today’s data, releases include the Euro Area flash CPI reading for June. In Germany, we’ll also get retail sales for May and unemployment for June. And in the US, there’s the PCE reading for May, and personal income and personal spending data.

Market Snapshot

- S&P 500 futures up 0.1% to 4,442.00

- MXAP down 0.2% to 162.88

- MXAPJ little changed at 512.81

- Nikkei down 0.1% to 33,189.04

- Topix down 0.3% to 2,288.60

- Hang Seng Index little changed at 18,916.43

- Shanghai Composite up 0.6% to 3,202.06

- Sensex up 1.0% to 64,562.15

- Australia S&P/ASX 200 up 0.1% to 7,203.30

- Kospi up 0.6% to 2,564.28

- STOXX Europe 600 up 0.7% to 459.63

- German 10Y yield little changed at 2.45%

- Euro down 0.2% to $1.0839

- Brent Futures up 0.9% to $75.02/bbl

- Gold spot down 0.4% to $1,900.84

- U.S. Dollar Index up 0.18% to 103.53

Top Overnight News from Bloomberg

- China’s June NBS PMIs better than feared, with manufacturing ticking up to 49 (vs. 48.8 in May and inline w/the Street) while services cool to 53.2 (down from 54.5 in May and a tiny bit below the Street’s 53.5 forecast). RTRS

- U.S. counterintelligence officials are amping up warnings to American executives about fresh dangers to doing business in China under an amended Chinese law to combat espionage. WSJ

- Japan’s Tokyo CPI for June undershoots the Street, coming in at +3.1% headline (vs. the Street’s +3.4% and down from +3.2% in May) and +3.8% core (vs. the Street’s +4% and down from +3.9% in May. BBG

- ECB’s hawkishness in part a function of events in the UK where inflation continues to surprise to the upside (ECB officials don’t want to take their foot off the tightening gas until they are absolutely certain core inflation is on a sustainable downward trajectory). FT

- Eurozone CPI for June undershoots the Street, with headline coming in at +5.5% (vs. the Street +5.6% and down from +6.1% in May) and core +5.4% (vs. the Street +5.5% and up from +5.3% in May). BBG

- “Shaky” flows into Pimco are prompting Allianz to push deeper into alternative asset classes such as real estate, where manager’s fees tend to be higher and client assets are stickier. While the bond manager attracted €14 billion in the first quarter after a €75 billion streak of outflows, investors are still skittish, Allianz CEO Oliver Baete said. BBG

- PCE: Based on details in the PPI, CPI, and import price reports, we forecast that the core PCE price index rose by 0.32% month-over-month in May, corresponding to a 4.64% increase from a year earlier. Additionally, we expect that the headline PCE price index increased by 0.13% in May, corresponding to a 3.87% increase from a year earlier. We expect that personal income increased by 0.5% and personal spending increased by 0.2% in May. GIR

- NKE delivered a solid F4Q23 revenue result, with stronger DTC growth and momentum in Greater China driving the outperformance. However, we note that this was offset by weaker than expected F4Q margins and a below-consensus F1Q guide. We step away from the quarter with our constructive view intact. While near-term growth and margins are more challenged than our expectations on wholesale shipment timing / liquidation sales / transitory cost headwinds / SG&A investments, we believe this quarter continued to deliver several key proofpoints of the bull case. GIR

- META is planning to allow people in the EU download apps through Facebook ads, a move that will eventually put it in direct competition w/the app stores from Google and Apple. The Verge

- Nasdaq 100 GREEN in July 15 consecutive years with an avg return of +4.64%…

A more detailed look at global markets courtesy of Newsquawk

APAC stocks mostly traded with cautious gains amid the higher yield environment and as participants digested a slew of data releases at quarter-end including the latest Chinese official PMIs. ASX 200 lacked direction as gains in the commodity-related sectors and utilities offset losses in real estate and tech. Nikkei 225 was subdued after mixed data releases including disappointing Industrial Production and softer-than-expected Tokyo CPI although the losses were cushioned as USD/JPY briefly climbed above 145.00. Hang Seng and Shanghai Comp were initially choppy but ultimately gained after the latest Chinese PMI data in which headline Manufacturing PMI matched estimates and Non-Manufacturing PMI was slightly softer-than-expected although remained at a firm expansion.

Top Asian News

- China may announce more property market support measures although measures might be incremental, while China is expected to revise certain home purchase restrictions and has room to lower the down payment ratio, according to China Securities Journal.

- PBoC set USD/CNY mid-point at 7.2258 vs exp. 7.2525 (prev. 7.2208).

- PBoC surveyed some foreign banks about USD deposit rates, according to Reuters sources.

- Japan Chief Cabinet Secretary Matsuno said sharp, one-sided currency moves are seen recently, and they are closely watching FX moves with a high sense of urgency. Matsuno said they are to take appropriate steps on excess FX moves, according to Reuters.

- Japan MOF says FX intervention amounted to JPY 0.00 in the period from May 30th to June 28th, according to Reuters.

European bourses trade on the front-foot with the Stoxx 600 on track to close the week out with gains, with little action seen on the EZ Flash CPI metrics. US equity futures are around flat/tilting higher ahead of today’s key PCE data for May, before traders head out for the long Independence Day holiday weekend. Equity sectors in Europe are higher across the board with the exception of technology which is being weighed on by ASML which is also acting as a drag on the AEX following news that the Dutch Foreign Ministry has issued new computer chip equipment export rules whereby an export license will be required for certain technologies.

Top European News

- ASML Hit With New Dutch Limits on Chip Gear Exports to China

- Fevertree Drops After Bank of America Cuts to Underperform

- Polish Inflation Eases for Fourth Month, Fueling Rate Cut Bets

- ASML Says Dutch Measures Won’t Have ‘Material Impact’ on Outlook

- Germany June Adj. Unemployment Rate Rises to 5.7%; Est. 5.6%

- Swiss Chalets Become Target Amid Eastern Europe’s Property Woes

FX

- DXY remains relatively resilient and firmly underpinned, with the index forming a solid base above 103.000 between 103.23-54 parameters.

- EUR was unreactive to a batch of mixed EZ data, whilst headline inflation printed cooler than expected, although the core metrics marginally topped expectations.

- Cyclical currencies are held up fairly well on the back of buoyant risk appetite.

- Kiwi got another confidence boost from an improvement in ANZ consumer sentiment.

- Yen is flat despite more verbal intervention from Japanese officials.

- Brazil’s Finance Minister said the National Monetary Council decided to set the 2026 inflation target at 3%, while the government expects rates to fall from August, according to Reuters.

Fixed Income

- Debt futures appear destined for a bleak finish and further losses heading into month, quarter, HY-end.

- Bunds, Gilts and the T-note hover precariously over deeper intraday lows, at 133.09, 94.71 and 111-25+ respectively.

Geopolitics

- The US is expected to curb exports of some Dutch chip equipment to specific facilities in China, according to a source cited by Reuters. ASML (ASML NA) does not expect the Dutch government’s chip export measures to have a material impact on its financial outlook, according to the press release.

- Russian Foreign Minister Lavrov said he sees no argument for a Black Sea Grain Deal extension, according to a press conference.

- US State Department approved the potential sale of logistics supply support to Taiwan for an estimated cost of USD 108mln, while it approved the possible sale of 30mm ammunition and related equipment to Taiwan for an estimated USD 332mln, according to Reuters.

- Australian and EU trade ministers spoke as hopes of a free trade deal rise, according to Reuters citing sources; there is optimism a deal could be struck by mid-year. Another meeting could be held next fortnight.

Commodities

- WTI and Brent front-month futures are on a firmer footing intraday despite the firmer Dollar but as equities see cautious gains.

- Spot gold remains heavy as the Dollar extends gains, with the yellow metal threatening another breach of USD 1,900/oz to the downside this morning

- Base metals are mostly but copper bucks the trend and outperforms, with the LME 3M contract back above USD 8,250/t at the time of writing. Reports last night noted an electrical accident at Codelco’s largest copper mine – the El Teniente mine.

- HSBC lowered Brent oil price assumptions to USD 80/bl in H2’23, USD 80/bl in FY23, USD 75/b in FY24 and long-term, according to Reuters.

- Boliden’s (BOL SS) Ronnskar production partially resumed; several of production lines may have to operate at limited capacity; all other production lines at Ronnskar are expected to ready for production during July.

- Shanghai INE adjusts trading limit and margin requirements for international copper and crude oil futures, effective from settlement on July 4, according to Reuters.

US Event Calendar

- 08:30: May Personal Income, est. 0.3%, prior 0.4%

- May Personal Spending, est. 0.2%, prior 0.8%

- May Real Personal Spending, est. 0.1%, prior 0.5%

- May PCE Deflator MoM, est. 0.1%, prior 0.4%

- May PCE Deflator YoY, est. 3.8%, prior 4.4%

- May PCE Core Deflator YoY, est. 4.7%, prior 4.7%

- May PCE Core Deflator MoM, est. 0.3%, prior 0.4%

- 09:45: June MNI Chicago PMI, est. 43.8, prior 40.4

- 10:00: June U. of Mich. Sentiment, est. 63.9, prior 63.9

- June U. of Mich. Expectations, est. 61.3, prior 61.3

- June U. of Mich. Current Conditions, est. 68.0, prior 68.0

- June U. of Mich. 1 Yr Inflation, est. 3.3%, prior 3.3%

- June U. of Mich. 5-10 Yr Inflation, est. 3.0%, prior 3.0%

DB’s Jim Reid concludes the overnight wrap

Welcome to the last day of H1. We’ll have our full review on Monday but with a day left to go here is a quick and selected spot check of where we are in 2023 so far. The S&P 500 is +14.5%, the Nasdaq +29.9%, FANG+ +70.9%, EU Stoxx 600 +7.5%, 2 and 10yr USTs +43.4bps and -3.7bps, 2 and 10yr Gilts +170bps and +71bps, EU Crossover -68.7bps, CDX HY +1.4bps and with Crude Oil -13.47%. So in general a good half year for risk, with yield curves steepening and long-term bond yields going mostly sideways unless of course you’re in the UK. H1 has mostly been a risk rebound from stressed levels in 2022 so the performance should be put in some perspective but with AI giving things an added kicker. Let’s see what H2 brings. Much will depend on whether the US recession starts. We still think it does in Q4 with risks that it gets delayed to Q1 rather than doesn’t happen. There’s a long long way before you can be sure you’re out of the gravitational pull of the lag of aggressively tighter monetary policy over the last year or so. Remember that this time last year the ECB was only about to end QE on July 1st and hike rates at the end of that month.

The recession call was something we asked in our summer survey this week. We’ve now released the results in a slidepack (link here). It’s evident that a lot of people are pushing back their timing of the next US recession, but mostly that’s just a shift from 2023 into 2024, rather than thinking we’ll avoid one altogether. We’ve also seen more bearishness since our last survey, with a majority now expecting the next 10% move in the S&P to be down rather than up (the opposite to the last survey), whilst it’s pretty much 50/50 as to whether 10yr Treasury yields hit 4.5% or 2.5% first. For other opinions on central banks, ChatGPT and the chance of Donald Trump being President again, click on the full chartbook for more.

The big story of the last 24 hours was another strong round of US data, which triggered a massive bond selloff that sent Treasury yields to their highest levels since SVB collapsed. In particular, the latest weekly US jobless claims dropped back to 239k (vs. 265k expected), marking their biggest single-week decline since October 2021, and importantly ending a run of 5 consecutive weekly gains. Alongside that, the continuing claims fell to their lowest level since February, and the latest Q1 GDP data saw a big upward revision to a +2.0% annualised pace, having previously been estimated at +1.3%.

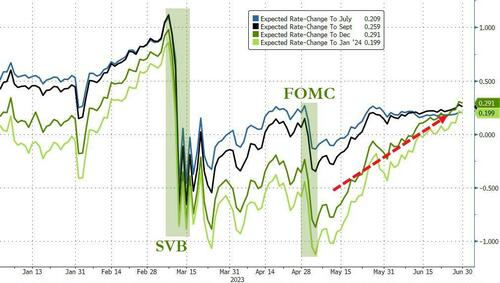

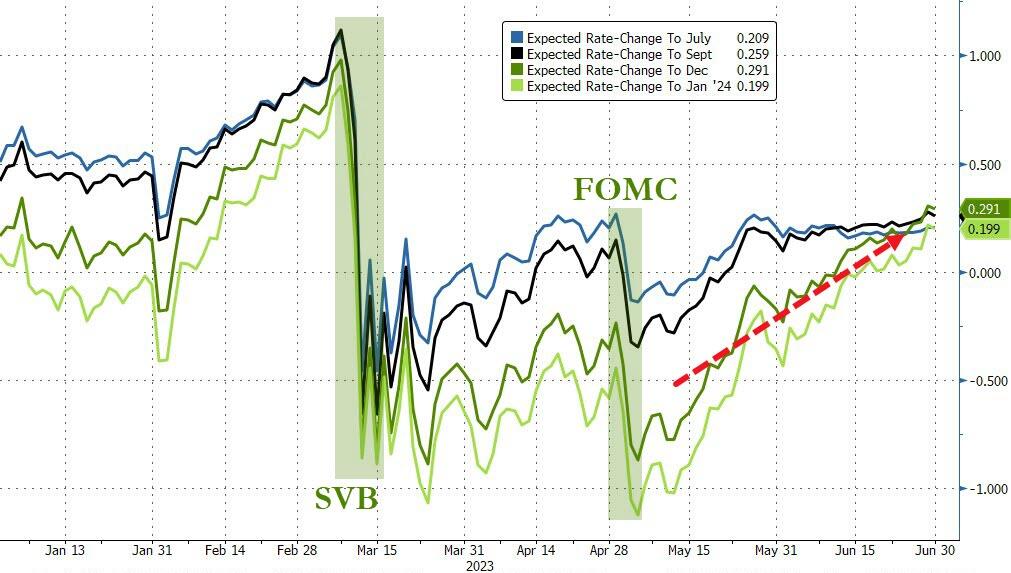

All this positive data played into the recent market narrative, which is that strong growth and sticky inflation will see central banks hold rates at restrictive levels for much longer than previously expected. In fact, if you look at market pricing for deep into 2024, it was clear how investors were adjusting to a much more prolonged period of high rates. For instance, expectations for the Fed’s policy rate by December 2024 moved back above 4% again to their highest level since SVB’s collapse (the low was 2.70% after peaking at 4.22% before SVB). Now admittedly, that’s still beneath the 4.6% level in the Fed’s latest dot plot, but it shows how markets are increasingly coming round to the Fed’s view of the world.

This shift was evident for the very near-term as well, with futures now pricing in a 83% chance of a July hike, the highest to date. They even see a 38% chance that by November the Fed will now deliver the second additional hike they signalled for 2023. So that’s still some way from 100%, but it goes to show how the previous scepticism towards two more Fed hikes is increasingly fading. US Core PCE will be a big event on this front today.

This re-appraisal of the outlook was very bad news for Treasuries across the board. It saw the 10yr yield surge by +13.1bps on the day to 3.84%, marking its highest level since SVB’s collapse in March. At the same time, the 2yr yield (+15.4bps) hit a post-SVB high of its own at 4.86%, and thus inverting the 2s10s curve further to -102.1bps. Meanwhile the 6m T-bill (+1.0bps) rose to its highest level since 2001, at 5.46%. It was real yields that led the gains as well, with the 2yr real yield (+12.6bps) hitting a post-2008 high of 2.79%, and another milestone was reached after the 5yr real yield crossed the 2% mark on an intraday basis for the first time since 2008 (ending the day at 1.99%).

With all eyes on central banks and the rates path, markets will now focus on today’s Euro Area flash CPI print for June, with particular attention on the core reading. Ahead of that, we got some more of the country releases yesterday, including from Germany, the largest European economy. That showed a rebound in inflation to +6.8% on the EU-harmonised measure as expected, up from +6.3% in May. In part, the rebound occurred because last year saw an offer of cheap rail tickets that dropped outside the annual comparison. But there was also an upside in Spain as well, since even as headline inflation dropped beneath the ECB’s 2% target, core inflation (on the national definition) still came in at +5.9% (vs. +5.5% expected). With the country releases so far, our Euro Area economists see slight upside risks to the +5.6% yoy headline (+5.5% core) consensus expectation for today.

We’ll have to see what today’s numbers show, but the movements in European rates very much followed what happened in the US yesterday. That included rises in yields on 10yr bunds (+10.3bps), OATs (+10.9bps) and BTPs (+12.1bps), along with a more moderate rise for gilts (+6.3bps). Similarly, investors also grew in confidence that the ECB would keep taking rates higher, and now see a 58% chance that we’ll have had two hikes by the time of the meeting-after-next in September.

Despite the rates move, equities were remarkably resilient, with the S&P 500 posting a +0.45% gain. Banks (+2.62%) led the advance amidst the prospect of higher rates, and positive US stress test results the night before, but other cyclical sectors also put in a decent performance. Indeed, the small-cap Russell 2000 advanced for a 4th consecutive day, finishing +1.23% by the close. By contrast, the NASDAQ index was unchanged (-0.00%), with the tech megacap FANG+ index underperforming (-0.75%). Back in Europe there were also modest advances, with the STOXX 600 posting a modest +0.13% gain.

Asian equity markets are mixed on the final trading day of the first half of the year. As I type, the Nikkei (-0.53%) is struggling with the Hang Seng (-0.05%) swinging between gains and losses. Otherwise, the Shanghai Composite (+0.73%), the CSI (+0.54%) and the KOSPI (+0.28%) are gaining ground this morning. In overnight trading, US stock futures are slightly higher with those on the S&P 500 (+0.07%) and NASDAQ 100 (+0.18%) printing mild gains.

Early morning data showed that China’s factory activity remained in contraction territory in June as the official manufacturing PMI came in at 49.0, barely improving from prior month’s reading of 48.8, thus adding pressure on the administration to deliver more stimulus. Additionally, the services sector also recorded its weakest reading since China abandoned its stringent COVID curbs late last year. The official non-manufacturing PMI eased to 53.2 from 54.5 in May, highlighting that the recovery in the world’s second biggest economy has lost some traction.

Elsewhere, consumer prices in Tokyo rose +3.1% y/y in June (+3.4% expected, down from the +3.2% recorded in the preceding month). Ex-food and energy came in at 3.8% vs. 4% expected. Separately, Japan’s labour market remained tight as the jobless rate remained unchanged at 2.6% in May while industrial output contracted -1.6% m/m in May, its first fall since January (v/s -1.0% decline expected) after increasing +0.7% previously.

In FX, the Japanese yen went past the 145 mark versus the US dollar in early Asia trade, touching its lowest in over seven months, prompting more intervention calls. They intervened at around 146 last year. Meanwhile, slightly hawkish comments on desired FX stability from Japan’s Finance Minister Shunichi Suzuki did trigger the pair’s retreat from 145.07 earlier to 144.71 as we go to print.

When it came to yesterday’s other data, UK mortgage approvals saw a larger-than-expected increase in May to 50.5k (vs. 49.7k expected). Furthermore, the M4 money supply came in unchanged on a year-on-year basis, which is the lowest it’s been since September 2015. Elsewhere, the European Commission’s economic sentiment indicator for the Euro Area continued to decline, with a move to a 7-month low of 95.3 in June (vs. 95.7 expected), adding to the negative trend in Euro Area data surprises over the past two months.

To the day ahead now, and data releases include the Euro Area flash CPI reading for June. In Germany, we’ll also get retail sales for May and unemployment for June. And in the US, there’s the PCE reading for May, and personal income and personal spending data.

2 b) NOW NEWSQUAWK (EUROPE/REPORT)/ASIA REPORT

Equities are firmer while bonds dip and Dollar’s bid ahead of US PCE – Newsquawk US Market Open

FRIDAY, JUN 30, 2023 – 05:58 AM

- European bourses trade on the front-foot with the Stoxx 600 on track to close the week out with gains, with little action seen on the EZ Flash CPI metrics.

- US equity futures are around flat/tilting higher ahead of today’s key PCE data for May, before traders head out for the long Independence Day holiday weekend.

- ASML does not expect the Dutch government’s chip export measures to have a material impact on its financial outlook.

- China may announce more property market support measures although measures might be incremental, according to China Securities Journal.

- Looking ahead, highlights include US PCE, EU leaders’ meeting

More Newsquawk in 3 steps:

1. Subscribe to the free premarket movers reports

2. Listen to this report in the market open podcast (available on Apple and Spotify)

3. Trial Newsquawk’s premium real-time audio news squawk box for 7 days

EUROPEAN TRADE

EQUITIES

- European bourses trade on the front-foot with the Stoxx 600 on track to close the week out with gains, with little action seen on the EZ Flash CPI metrics.

- US equity futures are around flat/tilting higher ahead of today’s key PCE data for May, before traders head out for the long Independence Day holiday weekend.

- Equity sectors in Europe are higher across the board with the exception of technology which is being weighed on by ASML which is also acting as a drag on the AEX following news that the Dutch Foreign Ministry has issued new computer chip equipment export rules whereby an export license will be required for certain technologies.

- Click here for more detail.

- Click here and here for a recap of the main European updates.

FX

- DXY remains relatively resilient and firmly underpinned, with the index forming a solid base above 103.000 between 103.23-54 parameters.

- EUR was unreactive to a batch of mixed EZ data, whilst headline inflation printed cooler than expected, although the core metrics marginally topped expectations.

- Cyclical currencies are held up fairly well on the back of buoyant risk appetite.

- Kiwi got another confidence boost from an improvement in ANZ consumer sentiment.

- Yen is flat despite more verbal intervention from Japanese officials.

- Brazil’s Finance Minister said the National Monetary Council decided to set the 2026 inflation target at 3%, while the government expects rates to fall from August, according to Reuters.

- Click here for more detail.

- Click here for the notable option expiries.

FIXED INCOME

- Debt futures appear destined for a bleak finish and further losses heading into month, quarter, HY-end.

- Bunds, Gilts and the T-note hover precariously over deeper intraday lows, at 133.09, 94.71 and 111-25+ respectively.

- Click here for more detail.

COMMODITIES

- WTI and Brent front-month futures are on a firmer footing intraday despite the firmer Dollar but as equities see cautious gains.

- Spot gold remains heavy as the Dollar extends gains, with the yellow metal threatening another breach of USD 1,900/oz to the downside this morning

- Base metals are mostly but copper bucks the trend and outperforms, with the LME 3M contract back above USD 8,250/t at the time of writing. Reports last night noted an electrical accident at Codelco’s largest copper mine – the El Teniente mine.

- HSBC lowered Brent oil price assumptions to USD 80/bl in H2’23, USD 80/bl in FY23, USD 75/b in FY24 and long-term, according to Reuters.

- Boliden’s (BOL SS) Ronnskar production partially resumed; several of production lines may have to operate at limited capacity; all other production lines at Ronnskar are expected to ready for production during July.

- Shanghai INE adjusts trading limit and margin requirements for international copper and crude oil futures, effective from settlement on July 4, according to Reuters.

- Click here for more detail.

NOTABLE US HEADLINES

- Fed Discount Window loans at USD 3.21bln in June 28th week (prev. USD 3.21bln W/W), while BTFP lending was USD 103.1bln (prev. USD 102.7bln W/W) and ‘Other credit’ was USD 168.3bln (prev. USD 172.3bln W/W).

- Nike (NKE) – Q4 2023 (USD): EPS 0.66 (exp. 0.67), Revenue 12.83bln (exp. 12.59bln). North America revenue USD 5.36bln (exp. 5.28bln). EMEA revenue USD 3.35bln (exp. 3.29bln). Greater China rev. USD 1.81bln (exp. 1.64bln). Asia Pacific & Latin America rev. USD 1.70bln (exp. 1.72bln). Inventory USD 8.45bln (exp. 8.88bln). Guides FY24 rev. growth of mid-single digits and gross margin growth of 140bps-160bps, according to earnings call. (Newswires) NKE shares -4.3% after-market.

EUROPEAN DATA RECAP

- German Retail Sales YY Real* (May) -3.6% vs. Exp. -4.3% (Prev. -4.3%)

- German Retail Sales MM Real* (May) 0.4% (Prev. 0.8%)

- UK Nationwide house price mm* (Jun) 0.1% vs. Exp. -0.3% (Prev. -0.1%)

- UK Nationwide house price yy* (Jun) -3.5% vs. Exp. -4.0% (Prev. -3.4%)

- German Import Prices YY* (May) -9.1% vs. Exp. -9.1% (Prev. -7.0%)

- German Import Prices MM* (May) -1.4% vs. Exp. -1.4% (Prev. -1.7%)

- UK GDP YY * (Q1) 0.2% vs. Exp. 0.2% (Prev. 0.2%)

- UK GDP QQ * (Q1) 0.1% vs. Exp. 0.1% (Prev. 0.1%)

- German Unemployment Change SA (Jun) 28.0k vs. Exp. 13.0k (Prev. 9.0k)

- German Unemployment Rate SA (Jun) 5.7% vs. Exp. 5.6% (Prev. 5.6%)