by harveyorgan · in Uncategorized · Leave a comment·Edit

by harveyorgan · in Uncategorized · Leave a comment·Edit

GOLD PRICE CLOSED: DOWN $9.90 TO $1909.95

SILVER PRICE CLOSED: DOWN $0.50 AT $22.69

Access prices: closes 4: 15 PM

Gold ACCESS CLOSE 1916.45

Silver ACCESS CLOSE: 23.14

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

Bitcoin morning price:, $31,193 UP 693 Dollars

Bitcoin: afternoon price: $30,500 DOWN 485 dollars

Platinum price closing $907.00 DOWN $14.55

Palladium price; $1245.40 DOWN $17.70

END

Due to the huge rise in the dollar, we must look at gold and silver in currencies other than the dollar to understand where we are heading

I will now provide gold in Canadian dollars, British pounds and Euros/4: 15 PM ACCESS

CANADIAN GOLD: $2,553.00 UP 8.20 CDN dollars per oz (ALL TIME HIGH 2,775.35)

BRITISH GOLD: 1499.71 DOWN 9.08 pounds per oz//(ALL TIME HIGH//CLOSING///1630.29)

EURO GOLD: 1754,32 DOWN 11.48 euros per oz //(ALL TIME HIGH/CLOSING//1861.21)//

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

EXCHANGE: COMEX

EXCHANGE: COMEX

CONTRACT: JULY 2023 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,919.600000000 USD

INTENT DATE: 07/05/2023 DELIVERY DATE: 07/07/2023

FIRM ORG FIRM NAME ISSUED STOPPED

118 C MACQUARIE FUT 90

323 C HSBC 320

363 H WELLS FARGO SEC 22

435 H SCOTIA CAPITAL 97

624 H BOFA SECURITIES 75

657 C MORGAN STANLEY 14

661 C JP MORGAN 64

690 C ABN AMRO 14

726 C CUNNINGHAM COM 2

737 C ADVANTAGE 30 27

905 C ADM 27

TOTAL: 391 391

MONTH TO DATE: 1,760

JPMorgan stopped 64/391 contracts.

FOR JULY:

GOLD: NUMBER OF NOTICES FILED FOR JULY/2023. CONTRACT: 391 NOTICES FOR 39,100 OZ or 1.2162 TONNES

total notices so far: 1760 contracts for 176,000 oz (5.474 tonnes)

FOR JULY:

SILVER NOTICES: 96 NOTICE(S) FILED FOR 480,000 OZ/

total number of notices filed so far this month : 3337 for 16,685,000 oz

XXXXXXXXXXXXXXXXXXXXXXXX

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD

WITH GOLD DOWN $9.90

INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD//

HUGE CHANGES IN GOLD INVENTORY AT THE GLD A HUGE WITHDRAWAL OF 4.04 TONNES OF GOLD FROM THE GLD:////

INVENTORY RESTS AT 917.86 TONNES

Silver//

WITH NO SILVER AROUND AND SILVER DOWN 50 CENTS AT THE SLV// HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.667 MILLIONOZ OF SILVER FROM THE SLV//

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV.

CLOSING INVENTORY: 466.474 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY AN HUGE SIZED 2965 CONTRACTS TO 117,386, MOVING ABOVE THE NEW RECORD LOW SET ON FRIDAY AND CLOSER TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THIS HUGE SIZED GAIN IN COMEX OI WAS ACCOMPLISHED WITH OUR $0.30 GAIN IN SILVER PRICING AT THE COMEX ON WEDNESDAY. TAS ISSUANCE WAS A GOOD SIZED 510 CONTRACTS. THESE WILL BE USED FOR MANIPULATION LATER THIS MONTH . CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON WEDNESDAY NIGHT: 510 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS. IT THUS LOOKS LIKE THE FED (GOV’T) IS BEHIND ALL OF THESE TRADES.

WE HAVE NOW SET ANOTHER RECORD LOW AT 114,102 CONTRACTS ///JULY 3.2023// OUR BANKERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.30). AND WERE UNSUCCESSFUL IN KNOCKING ANY SPEC LONGS AS WE HAD A HUGE GAIN ON OUR TWO EXCHANGES OF 17,210 CONTRACTS. WE HAD 0 CRIMINAL NOTICES FILED IN THE CATEGORY OF EXCHANGE FOR RISK TRANSFER FOR 0 MILLION OZ// ( THE TOTAL ISSUED IN THIS CATEGORY SO FAR THIS MONTH TOTAL 0 MILLION OZ.). WE HAVE NOW RETURNED TO OUR USUAL AND CUSTOMARY SCENARIO: BANKERS SHORT AND SPECS LONG WITH MANIPULATION NOW MID MONTH AND BEYOND, DUE TO (TAS) MANIPULATION.

WE MUST HAVE HAD:

A GOOD ISSUANCE OF EXCHANGE FOR PHYSICALS( 477 CONTRACTS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 16.110 MILLION OZ (FIRST DAY NOTICE) FOLLOWED BY TODAY’S HUGE 325,000 OZ QUEUE JUMP.//NEW STANDING: 17.830 MILLION OZ/ // HUGE SIZED COMEX OI GAIN/ GOOD SIZED EFP ISSUANCE/VI) GOOD NUMBER OF T.A.S. CONTRACT ISSUANCE (510 CONTRACTS)/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL –444 CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS JULY. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF JUNE:

TOTAL CONTRACTS for 2 days, total 581 contracts: OR 2.905 MILLION OZ (291 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 0.520 MILLION OZ

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 118.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 2.905 MILLION OZ

RESULT: WE HAD A HUGE SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 2965 CONTRACTS WITH OUR GAIN IN PRICE OF $0.30 IN SILVER PRICING AT THE COMEX//WEDNESDAY.,. THE CME NOTIFIED US THAT WE HAD A GOOD EFP ISSUANCE CONTRACTS: 477 ISSUED FOR JULY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS./ WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR JULY OF 16.110 MILLION OZ FOLLOWED BY TODAY’S 325,000 OZ QUEUE JUMP: TOTAL NOW STANDING 17.830 MILLION OZ///// .. WE HAVE A HUGE SIZED GAIN OF 3442 OI CONTRACTS ON THE TWO EXCHANGES. THE TOTAL OF TAS INITIATED CONTRACTS TODAY: A GOOD 510//ZERO FRONT END OF THE TAS CONTRACTS WERE LIQUIDATED DURING THE WEDNESDAY COMEX SESSION. THE NEW TAS ISSUANCE TODAY (510) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE.

WE HAD 96 NOTICE(S) FILED TODAY FOR 480,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A STRONG SIZED 4591 CONTRACTS TO 452,654 AND FURTHER FROM THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED –1852 CONTRACTS

WE HAD A STRONG SIZED INCREASE IN COMEX OI ( 4591 CONTRACTS) DESPITE OUR $2.20 LOSS IN PRICE. WE ALSO HAD A STRONG INITIAL STANDING IN GOLD TONNAGE FOR JULY. AT 5.1975 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S 0.2301 TONNE QUEUE JUMP: NEW TOTAL OF GOLD STANDING FOR JULY: 6.5069 TONNES// + /A HUGE ISSUANCE OF 1707 T.A.S. CONTRACTS /// ALL OF..THIS HAPPENED WITH A $2.20 LOSS IN PRICE WITH RESPECT TO WEDNESDAY’S TRADING.WE HAD A STRONG SIZED GAIN OF 5709 OI CONTRACTS (23.517 PAPER TONNES) ON OUR TWO EXCHANGES.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 1118 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 452,654

IN ESSENCE WE HAVE A VERY STRONG SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 5709 CONTRACTS WITH 4591 CONTRACTS INCREASED AT THE COMEX// AND A FAIR 1118 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 5709 CONTRACTS OR 17.76 TONNES. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): A HUGE 1707 CONTRACTS)

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (1118 CONTRACTS) ACCOMPANYING THE STRONG SIZED GAIN IN COMEX OI (4591) //TOTAL GAIN FOR OUR THE TWO EXCHANGES: 5709 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR NORMAL FORMAT OF BANKERS GOING SHORT AND SPECULATORS GOING LONG ,2.) GOOD INITIAL STANDING AT THE GOLD COMEX FOR JULY AT 5.1975 TONNES FOLLOWED BY TODAY’S 0.2301 TONNE QUEUE JUMP//NEW TOTAL 6.5069 TONNES ///// /3) ZERO LONG LIQUIDATION//4) STRONG SIZED COMEX OPEN INTEREST GAIN/ 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER///6: HUGE T.A.S. ISSUANCE: 1707 CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023 INCLUDING TODAY

JULY

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF JULY :

TOTAL EFP CONTRACTS ISSUED: 2233 CONTRACTS OR 223,300 OZ OR 6.94556 TONNES IN 2 TRADING DAY(S) AND THUS AVERAGING: 1115 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 2 TRADING DAY(S) IN TONNES 6.94556 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2022, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 6.94556/3550 x 100% TONNES 0.1831% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2023

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 6.94556 TONNES

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF JUNE. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF MAY HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF JUNE., FOR BOTH GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (JUNE), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER ROSE BY A HUGE SIZED 2965 CONTRACTS OI TO 117,386 AND CLOSER TO OUR COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 477 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

SEPT 50 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 477 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 2965 CONTRACTS AND ADD TO THE 477 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A STRONG SIZED GAIN OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 3442 CONTRACTS

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTAL 17.210 MILLION OZ

OCCURRED WITH OUR $0.30 GAIN IN PRICE …..

END

OUTLINE FOR TODAY’S COMMENTARY

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

b, ) Gold/silver trading overnight Europe,//GOLD COMMENTARIES

(Peter Schiff)

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS//

THURSDAY MORNING//WEDNESDAY NIGHT

SHANGHAI CLOSED DOWN 17.37 PTS OR 0.54% //Hang Seng CLOSED DOWN 577.33 PTS OR 3.02% /The Nikkei closed DOWN 565.68 OR 1.70% //Australia’s all ordinaries CLOSED DOWN 1.18 % /Chinese yuan (ONSHORE) closed UP 7.2332 /OFFSHORE CHINESE YUAN UP TO 7.2439 /Oil UP TO 72.10 dollars per barrel for WTI and BRENT UP AT 76.77 / Stocks in Europe OPENED ALL RED// ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE STRONGER

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

9. USA

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A STRONG SIZED 4591 CONTRACTS UP TO 452,654 DESPITE OUR SMALL LOSS IN PRICE OF $2.20 ON TUESDAY,

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE NON ACTIVE DELIVERY MONTH OF JULY… THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 1118 EFP CONTRACTS WERE ISSUED: : AUGUST 1118 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 1118 CONTRACTS

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A STRONG SIZED TOTAL OF 5709 CONTRACTS IN THAT 1118 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A STRONG SIZED GAIN OF 4591 COMEX CONTRACTS..AND THIS STRONG SIZED GAIN ON OUR TWO EXCHANGES HAPPENED WITH OUR LOSS IN PRICE OF $2.20//WEDNESDAY COMEX. AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS DURING MID MONTH IN THE DELIVERY CYCLE), THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR WEDNESDAY NIGHT WAS A HUGE 1707 CONTRACTS. THROUGHOUT LAST WEEK, THE BANKERS SOLD OFF THE LONG SIDE OF THE SPREAD WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR SPREAD WHICH WILL BE LIQUIDATED TWO MONTHS HENCE)//THE HUGE NUMBER OF T.A.S. CONTRACTS INITIATED OVER THE PAST SEVERAL WEEKS SPELLS TROUBLE FOR THE GOLD/SILVER MARKET AS RAIDS WILL SURELY BE UPON US.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: JULY (6.5059) (NON ACTIVE MONTH)

TONNES),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 6.5069 TONNES

THE SPECS/HFT WERE SUCCESSFUL IN LOWERING GOLD’S PRICE( IT FELL $2.20) //// BUT WERE UNSUCCESSFUL IN KNOCKING ANY SPECULATOR LONGS AS WE HAD OUR STRONG SIZED GAIN OF 5709 CONTRACTS ON OUR TWO EXCHANGES. WE HAD ZERO TAS LIQUIDATION THROUGHOUT THE WEDNESDAY COMEX SESSION . THE TAS ISSUED WEDNESDAY NIGHT, WILL BE “PUT INTO THE BANK” TO BE USED AT A LATER DATE AT THE COLLUSIVE CHOOSING OF OUR BANKERS.

WE HAVE GAINED A TOTAL OI OF 17.76 PAPER TONNES OF TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR JULY. (5.11974 TONNES) ON FIRST DAY NOTICE FOLLOWED BY TODAY’S QUEUE JUMP OF 0.2301 TONNES//TOTAL STANDING FOR JULY GOLD: 6.5069 TONNES // ALL OF THIS WAS ACCOMPLISHED WITH OUR LOSS IN PRICE TO THE TUNE OF $2.20.

WE HAD –REMOVED 1852 CONTRACTS TO THE COMEX TRADES TO OPEN INTEREST AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 5709 CONTRACTS OR 570900 OZ OR 17.76 TONNES.

Estimated gold volume today:// 233,343 FAIR

final gold volumes/yesterday 262,852 FAIR

//JULY 6/ FOR THE JULY 2023 CONTRACT

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 96.453 OZ Brinks 3 kilobars . |

| Deposit to the Dealer Inventory in oz | 32,013.521 oz Brinks |

| Deposits to the Customer Inventory, in oz | nil OZ |

| No of oz served (contracts) today | 391 notice(s) 39,100 OZ 1.2162 TONNES |

| No of oz to be served (notices) | 332 contracts 33200 oz 1.0326 TONNES |

| Total monthly oz gold served (contracts) so far this month | 1760 notices 176,000 OZ 5.474 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | x |

0ne dealer deposit:

i)Into Brinks: 32,013.521 oz

Customer deposits: 0

total customer deposits: nil oz

total dealer deposits: 32,013.521 oz Brinks

we had 1 customer withdrawal:

i) Out of Brinks 96.453 oz

total withdrawals: 96.453 oz

Adjustments; 1 JPMorgan dealer to customer

1) 6,462.351 oz

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR JULY.

For the front month of JULY we have an oi of 723 contracts having LOST 583 contracts. We had 657 contracts served on Wednesday. Thus we gained 74 contracts or an additional 7400 oz of gold will stand at the comex.

AUGUST LOST 577 contracts DOWN to 350,695 contracts

SEPT gained 32 contracts to stand at 93

We had 391 contracts filed for today representing 39,100 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 391 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 64 notice(s) was (were) stopped received by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the JULY /2023. contract month,

we take the total number of notices filed so far for the month (1760 x 100 oz ), to which we add the difference between the open interest for the front month of JULY (723 CONTRACT) minus the number of notices served upon today 391 x 100 oz per contract equals 209,200 OZ OR 6.5069 TONNES the number of TONNES standing in this NON active month of July.

thus the INITIAL standings for gold for the JULY contract month: No of notices filed so far (1760) x 100 oz + (723) {OI for the front month} minus the number of notices served upon today (391) x 100 oz) which equals 209,200 oz standing OR 6.5069 TONNES

TOTAL COMEX GOLD STANDING: 6.5069 TONNES WHICH IS STRONG FOR A NON ACTIVE DELIVERY MONTH.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 2,063,541.609 OZ 64.18 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 22,426,482.155 OZ

TOTAL REGISTERED GOLD: 11,833,589.245 (368.07 tonnes)..

TOTAL OF ALL ELIGIBLE GOLD: 10,592,892.910 O Z

REGISTERED GOLD THAT CAN BE SERVED UPON: 9,770,048 OZ (REG GOLD- PLEDGED GOLD) 303.88 tonnes//

END

SILVER/COMEX

JULY 6//2023// THE JULY 2023 SILVER CONTRACT

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 506,849.300 oz LOOMIS . |

| Deposits to the Dealer Inventory | nil oz |

| Deposits to the Customer Inventory | 1,200,601.270 oz Brinks cnt |

| No of oz served today (contracts) | 96 CONTRACT(S) (480,000 OZ) |

| No of oz to be served (notices) | 229 contracts (1,145,000 oz) |

| Total monthly oz silver served (contracts) | 3337 Contracts (16,685,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

i) 0 dealer deposits

total dealer deposit: nil oz

total dealer deposits: 0

i) We had 0 dealer withdrawal

total dealer withdrawals: oz

We had 1 deposits customer account:

i) Into Brinks: 1,200,601.270 oz

total customer deposits: 1,200,601.270 oz

JPMorgan has a total silver weight: 140.580 million oz/279.029 million =50.53% of comex .//dropping fast

Comex withdrawals 1

i) Out of lOOMIS: 506,849.359 OZ

total withdrawals: 506,849.359 oz

adjustments: 1

BRINKS/DEALER TO CUSTOMER:

607,874.500 OZ

TOTAL REGISTERED SILVER: 38.996 MILLION OZ//.TOTAL REG + ELIGIBLE. 278.335 million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR JULY:

silver open interest data:

FRONT MONTH OF JULY /2023 OI: 325 CONTRACTS HAVING LOST 276 CONTRACT(S). WE HAD 341 NOTICES FILED ON WEDNESDAY SO WE GAINED A STRONG 65 CONTRACTS OR AN ADDITIONAL 325,000 OZ WILL STAND AT THE COMEX FOR DELIVERY IN JULY.

AUGUST GAINED 29 CONTRACTS TO STAND AT 491

SEPT HAS A GAIN OF 2871 CONTRACTS DOWN TO 102,649

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 96 for 430,000 oz

Comex volumes// est. volume today 61,739 GOOD /

Comex volume: confirmed yesterday:84,631 STRONG

To calculate the number of silver ounces that will stand for delivery in JULY. we take the total number of notices filed for the month so far at 3337 x 5,000 oz = 16,685,000 oz

to which we add the difference between the open interest for the front month of JULY(325) and the number of notices served upon today 96 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the JULY/2023 contract month: 3337 (notices served so far) x 5000 oz + OI for the front month of JULY (325) – number of notices served upon today (96 )x 500 oz of silver standing for the JULY contract month equates to 17.830 million oz +

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS

JULY 6/WITH GOLD DOWN $9.90 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.04 TONNES OF GOLD FROM THE GLD//INVENTORY RESTS AT 917.86 TONNES

JULY 5/WITH GOLD DOWN $2.20 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD; A WITHDRAWAL OF 2.6 TONNES FROM THE GLD///INVENTORY RESTS AT 921.90 TONNES

JULY 3/WITH GOLD UP $1.90 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 924.50 TONNES//

JUNE 30/WITH GOLD UP $10.00 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.31 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 924.50 TONNES

JUNE 29/WITH GOLD DOWN $3.20 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.26 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 926.81 TONNES

JUNE 28/WITH GOLD DOWN $1.15 NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 925.65 TONNES

JUNE 27/WITH GOLD DOWN $9.15 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.45 TONNES OF GOLD FROM THE GLD./INVENTORY RESTS AT 925.65 TONNES

JUNE 26/WITH GOLD UP $4.65 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.6 TONNES OF GOLD FROM THE GLD/////INVENTORY RESTS AT 927.10 TONNES

JUNE 23/WITH GOLD UP $5.15 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: WITHDRAWALS OF 4.33 TONNES OF GOLD OVER THE PAST TWO DAYS. /INVENTORY RESTS AT 929.70 TONNES

JUNE 21/WITH GOLD DOWN $2.45 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY REST AT 934.03 TONNES

JUNE 20/WITH GOLD DOWN $22.40 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 934.03 TONNES

JUNE 16/WITH GOLD UP $0.70 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4.33 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 934.03 TONNES

JUNE 15/WITH GOLD UP $2.80 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES OF GOLD FROM THE GLD//INVENTORY RESTS AT 929.70 TONNES

JUNE 14/WITH GOLD UP $10.30 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 931.44 TONNES

JUNE 13/WITH GOLD DOWN $10.30 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.01 TONNES FORM THE GLD///INVENTORY RESTS AT 931.44

JUNE 12/WITH GOLD DOWN $7.10 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 934.65 TONNES

JUNE 9/WITH GOLD DOWN $1.00: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 934.65 TONNES

JUNE 8/WITH GOLD UP $20.45 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.46 TONNES FROM THE GLD///INVENTORY RESTS AT 934.65 TONNES

JUNE 7 WITH GOLD DOWN $22.15 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.45 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 938.11 TONNES

JUNE 6/WITH GOLD UP $6.90 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.45 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 939.56 TONNES

JUNE 5/WITH GOLD UP $5.00 TODAY : NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 938.11 TONNES

JUNE 2/WITH GOLD DOWN $24.40 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.45 TONNES FROM THE GLD///INVENTORY RESTS AT 938.11 TONNES

JUNE 1/WITH GOLD UP $14.10 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 939.56 TONNES

MAY 31/WITH GOLD UP $5.70 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.73 TONNES OF GOLD FROM THE GLD///INVENTORY RESTS AT 939.56 TONNES

MAY 30/WITH GOLD UP $14.55 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 941.29 TONNES

MAY 26/WITH GOLD UP $.90 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY REST AT 941.29 TONNES

MAY 25/WITH GOLD DOWN $19.70 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 941.29 TONNES

MAY 24/WITH GOLD DOWN $9.50 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.45 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 941.29 TONNES

MAY 23/WITH GOLD $2.25 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 942.74 TONNES

MAY 22/WITH GOLD DOWN $4.70 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 5.83 TONES OF GOLD INTO THE GLD DESPITE THE L0SS IN PRICE//INVENTORY RESTS AT 942.74 TONNES

MAY 19/WITH GOLD UP $22.20 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 936.96 TONNES

MAY 18/WITH GOLD DOWN $23.80 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.02 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 936.96 TONNES

GLD INVENTORY: 917.86 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

JULY 6/WITH SILVER DOWN 50 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.667 MILLION OZ FORM THE SLV///INVENTORY RESTS AT 466.474 MILLION OZ//

JULY5/WITH SILVER UP 30 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 468.141 MILLION OZ//

JULY 3/WITH SILVER UP 7 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 468.141 MILLION OZ//

JUNE 30/WITH SILVER UP 19 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.377 MILLION OZ INTO THE SLV/////INVENTORY RESTS AT468.141 MILLION OZ//

JUNE 29/WITH SILVER DOWN 23 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.763 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 466.764 MILLION OZ//

JUNE 28/WITH SILVER DOWN 2 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 470.527 MILLION OZ//

JUNE 27/WILVER SILVER UP 7 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 734,000 OZ INTO THE SLV////INVENTORY RESTS AT 470.527 MILLION OZ

JUNE 26/WITH SILVER UP 44 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY REST AT 469.793 MILLION OZ.

JUNE 23/WITH SILVER DOWN 9 CENTS TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A NET DEPOSIT OF 6.61 MILLION OZ INTO THE SLV OVER THESE PAST TWO DAYS//INVENTORY RESTS AT 469.793 MILLION OZ//

JUNE 21/WITH SILVER DOWN $.40 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 5.784 MILLION OZ OF SILVER INTO THE SLV////INVENTORY RESTS AT 463.183 MILLION OZ//

JUNE 20/WITH SILVER DOWN 89 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 463.183 MILLION OZ//

JUNE 16/WITH SILVER UP 23 CENTS TODAY :SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 459,000 OZ FROM THE SLV///INVENTORY RESTS AT 463.183 MILLION OZ

JUNE 15/WITH SILVER DOWN 17 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.377 MILLION OZ OF SILVER FROM THE SLV////INVENTORY RESTS AT 463.642 MILLION OZ//

JUNE 14/WITH SILVER UP 29 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 735,000 OZ FROM THE SLV///INVENTORY RESTS AT 465.019 MILLION OZ//

JUNE 13/WITH SILVER DOWN 25 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.515 MILLION OZ OF SILVER FROM THE SLV///INVENTORY RESTS AT 465.754 MILLION OZ//

JUNE 12/WITH SILVER DOWN 26 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 467.269 MILLION OZ//

JUNE 9/WITH SILVER UP 7 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF SILVER TO THE TUNE OF 550,000 OZ//INVENTORY RESTS AT 467.269 MILLION OZ

JUNE 8/WITH SILVER UP $0.63 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 467.819 MILLION OZ/

JUNE 7/WITH SILVER DOWN 17 CENTS TODAY:HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.01 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 467.819 MILLION OZ/

JUNE 6/WITH SILVER UP 7 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 466.809 MILLION OZ//

JUNE 5/WITH SILVER DOWN $.13 TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 266,000 OZ FROM THE SLV////INVENTORY RESTS AT 466.809 MILLION OZ/

JUNE 2/WITH SILVER DOWN 23 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 918,000 OZ FROM THE SLV./INVENTORY RESTS AT 467.015 MILLION OZ/

JUNE 1/WITH SILVER UP 49 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 467.933 MILLION OZ

MAY 31/WITH SILVER UP 37 CENTS TODAY:SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 367,000 OZ FROM THE SLV////INVENTORY RESTS AT 467.933 MILLION OZ//

MAY 30/WITH SILVER DOWN 9 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 468.300 MILLION OZ//

MAY 26/WITH SILVER UP $0.44 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.306 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 468.300 MILLION OZ//

MAY 25.WITH SILVER DOWN $0.32 TODAY; SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 276,000 OZ INTO THE SLV////INVENTORY RESTS AT 471.606 MILLION OZ//

MAY 24/WITH SILVER DOWN $.35 TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 471.330 MILLION OZ//

MAY 23/WITH SILVER DOWN 22 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.801 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 471.330 MILLION OZ//

MAY 22/WITH SILVER DOWN 19 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 468.529 MILLION OZ//

MAY 19/WITH SILVER UP 38 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 468.529 MILLION OZ

MAY 18/WITH SILVER DOWN 23 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 919,000 OZ FROM THE SLV////INVENTORY RESTS AT 468.529 MILLION OZ/

MAY 17/WITH SILVER DOWN 2 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 469.448 MILLION OZ//

CLOSING INVENTORY 466.474 MILLION OZ//

PHYSICAL GOLD/SILVER COMMENTARIES

1:Peter Schiff/Mike Maharrey

Many central banks increased their gold holdings in May. Turkey sold 63 tons but that sale was to local buyers as Turkey has a huge gold consuming nation

(Schiff.gold)

Eight Central Banks Increased Gold Holdings In May

THURSDAY, JUL 06, 2023 – 07:20 AM

Excluding another big sale by Turkey, central banks were net buyers of gold in May, according to the latest data compiled by the World Gold Council.

Eight central banks added gold to their reserves in May with net purchases totaling 50 tons.

But with Turkey dumping another 63 tons of gold in May, global net central bank gold holding fell by 27 tons.

Turkey has sold nearly 160 tons of gold since March. According to the World Gold Council, this is a response to local market dynamics and doesn’t likely reflect a change in the Turkish central bank’s long-term gold strategy.

According to the WGC, “Gold was sold into Turkey’s domestic market to satisfy very strong bar, coin and jewelry demand following a temporary partial ban on gold bullion imports.”

According to a Reuters report, the Turkish government suspended some gold imports in February in an effort to soften the economic impact of significant earthquakes.

Poland was the biggest buyer in May, adding 19 tons of gold to its reserves. This follows on the heels of a 15-ton increase in April when the National Bank of Poland resumed buying gold. May’s purchase was the largest increase in the country’s reserves since June 2019 when the bank boosted gold holdings by almost 100 tons.

In the fall of 2021, Bank of Poland President Adam Glapiński said the central bank planned to add 100 tons of gold to its reserves in 2022. It’s unclear why the bank didn’t follow through. This recent purchase could signal the beginning of another round of buying to reach that 100-ton goal.

Poland currently holds 263 tons of gold.

The People’s Bank of China extended its gold buying spree for a seventh-straight month with a 16-ton addition to its official reserves.

Since recommencing reports of purchases in November 2022, the Peoples Bank of China has added 144 tons to its official gold holdings. Officially, Chinese gold holdings stand at 2,092 tons.

The Chinese central bank accumulated 1,448 tons of gold between 2002 and 2019, and then suddenly went silent until it resumed reporting in November 2022. Many speculate that the Chinese continued to add gold to its holdings off the books during those silent years.

There has always been speculation that China holds far more gold than it officially reveals. As Jim Rickards pointed out on Mises Daily back in 2015, many people speculate that China keeps several thousand tons of gold “off the books” in a separate entity called the State Administration for Foreign Exchange (SAFE).

Last year, there were large unreported increases in central bank gold holdings. Central banks that often fail to report purchases include China and Russia. Many analysts believe China is the mystery buyer stockpiling gold to minimize exposure to the dollar.

The central banks of Singapore (4 tons), Russia (3 tons), India (2 tons), the Czech Republic (2 tons), Iraq (2 tons), and the Kyrgyz Republic (2 tons) were the other notable buyers.

A statement by the Iraqi central bank said, “The purchase came with the aim of increasing its holdings of gold in light of the economic and political conditions that the world is witnessing.”

Along with Turkey, the Central Bank of Uzbekistan and the National Bank of Kazakhstan were both sellers, reducing their holdings by 11 tons and 2 tons respectively. These two banks were the biggest sellers of gold during the first quarter of this year. It is not uncommon for banks that buy from domestic production – such as Uzbekistan and Kazakhstan – to switch between buying and selling.

Despite the dip in overall global reserves in April and May due to Turkish selling, it doesn’t appear central banks have lost their appetite for gold. After a record-setting 2022, central banks continued to buy gold in the first quarter of 2023, setting a new Q1 record.

Overall, global central bank gold reserves increased by 228 tons through the first three months of 2023. This was 38% higher than the previous first-quarter record set in 2013.

Total central bank gold buying in 2022 came in at 1,136 tons. It was the highest level of net purchases on record dating back to 1950, including since the suspension of dollar convertibility into gold in 1971. It was the 13th straight year of net central bank gold purchases.

According to the 2023 Central Bank Gold Reserve Survey recently released by the World Gold Council, 24% of central banks plan to add more gold to their reserves in the next 12 months. Seventy-one percent of central banks surveyed believe the overall level of global reserves will increase in the next 12 months. That was a 10-point increase over last year.

end

2 Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens//JAMES RICKARDS//JOHN RUBINO

Jim Rickards….

Rickards: Globalist Elites Fear You

WEDNESDAY, JUL 05, 2023 – 05:00 PM

Authored by James Rickards via DailyReckoning.com,

Globalist elites like to talk about democracy. But in reality, they don’t believe in democracy.

When the U.K. voted for Brexit in June 2016, the globalists were stunned.

They couldn’t believe it. They then did everything they could to delay and fight Brexit.

Then when Donald Trump won the election as president in November 2016, the globalists were even more stunned.

They went into complete denial and put their heads in the sand.

They comforted themselves with the convenient myth that Russian interference lost them the election, not a popular rejection of their ideology.

Yet it kept getting worse for globalists. Both China and Russia have become more nationalistic and completely turned their backs on globalism. The war in Ukraine has only intensified that trend.

The pandemic only strengthened the trend away from globalism, and the ongoing supply chain issues we’ve been seeing expose globalism’s fragile underbelly.

These chains may be efficient and economical, but when they break down, it has a rippling effect on the global economy. It’s like pulling on one strand on a carpet. The entire thing is affected.

“Tariffs Are as American as Apple Pie”

Globalists worship at the altar of free trade. But free trade is a myth. It doesn’t exist outside classrooms. France subsidizes agriculture. The U.S. subsidizes electric vehicles. China subsidizes a long list of national champions with government contracts, cheap loans and currency manipulation.

Every major economy subsidizes one or more sectors using fiscal and monetary tools and tariffs and nontariff barriers to trade.

America grew rich and powerful from 1787–1962, a period of 175 years, using tariffs, subsidies and other barriers to trade to nurture domestic industry and protect high-paying manufacturing jobs.

In fact, tariffs are as American as apple pie.

Beginning in 1962, the U.S. turned its back on a successful legacy of protecting its jobs and industry and embraced the free trade theory. This was done first through the General Agreement on Tariffs and Trade, or GATT, one of the original Bretton Woods institutions in addition to the World Bank and IMF.

Against the mercantilist system was a theory of free trade based on comparative advantage as advocated by British economist David Ricardo in the early 19th century. Ricardo’s theory said that trading nations are endowed with attributes that gave them a relative advantage in producing certain goods versus others.

These attributes could consist of natural resources, climate, population, river systems, education, ports, financial capacity or any other factor of production. Nations should produce those goods as to which they have a natural advantage and trade with other nations for goods where the advantage was not so great.

Countries should specialize in what they do best, and let others also specialize in what they do best. Then countries could simply trade the goods they make for the goods made by others. All sides would be better off because prices would be lower as a result of specialization in those goods where you have a natural advantage.

Works in Theory, Not in Fact

It’s a nice theory often summed up in the idea that Tom Brady should not mow his own lawn because it makes more sense to pay a landscaper while he practices football.

For example, if the U.K. had an advantage in textile production and Portugal had an advantage in wine production, then the U.K. and Portugal should trade wool for wine. But if the theory of comparative advantage were true, Japan would still be exporting tuna fish instead of cars, computers, TVs, steel and much more.

The problem with the theory of comparative advantage is that the factors of production are not permanent and they are not immobile.

If labor moves from the countryside to the city in China, then suddenly China has a comparative advantage in cheap labor. If finance capital moves from New York banks to direct foreign investment in Chinese factories, then China has the comparative advantage in capital also.

Before long, China has the advantage in labor and capital and is running huge trade surpluses with the U.S., putting Americans out of work and shutting down U.S. factories in the process.

Worse yet, countries such as China can pull comparative advantage out of thin air with government subsidies.

We’ve been living in a world where the U.S. has been a free trade sucker and everyone else breaks the rules. In a world where a few parties are free traders but most are mercantilists, the mercantilists win every time. They are like parasites sucking the free traders dry.

Globalization at All Costs

But to globalists, the moral arc of the universe bends in one direction, and that’s toward increasing globalization. Populism and protectionism are therefore moral evils that must be condemned.

But globalists have slowly realized that the nationalist trend is not an anomaly but a powerful force that is reversing globalist policies that have been ascendant since 1989, or even since the end of World War II, when institutions like the IMF and World Bank were established to promote globalist goals.

But right now, free trade is on the ropes, currency wars are rampant, there’s an actual war in Eastern Europe and geopolitical hotspots like Taiwan are becoming more dangerous.

What happened to globalism?

The globalist-in-chief is Columbia University academic Jeffrey D. Sachs. He led the charge for “market” solutions in Russia in the 1990s, which backfired into a takeover by oligarchs and the rise of Putin.

He also led the charge for “opening” China in the early 2000s, which led to the rise of Xi Jinping and the strongest form of Communism since the death of Mao Zedong.

Is Sachs willing to admit any mistakes? No. Like most globalists who are too arrogant to question their own worldviews and assumptions, Sachs instead says the problem is democracy itself.

Essentially, Sachs wants to abandon traditional voting in the U.S. and U.K. to create a system more favorable to globalists. Sure, you can let voters choose center-right candidate x or center-left candidate y, who might be 10% apart on many issues. Neither of them will really rock the boat and have no fundamental disagreement with globalism in general.

Globalists Don’t Trust You

As far as globalists are concerned, voters cannot be trusted to vote on fundamental issues like Brexit. They also can’t be trusted to vote against presidential candidates like Trump. Such decisions should be beyond democratic control, globalists believe.

In fact, Time magazine ran an article gloating about how corporate and media elites essentially conspired to prevent Trump from winning the 2020 election.

Media refusal to cover the Hunter Biden laptop scandal was just one example. Former intelligence officials joined in by claiming it bore all the trademarks of “Russian disinformation.” Of course, we all know the laptop was real. But they wouldn’t allow it to influence the election.

Meanwhile, recent disclosures by Twitter revealed the extent to which the company worked with the federal government to censor viewpoints they didn’t like.

The bottom line is, when elites don’t like the potential outcome, just change the rules.

The Climate Change Trojan Horse

Another issue that unites globalists is climate change. Globalists argue that climate change is too important to trust to voters in individual countries. Climate change is the perfect cover for globalism because combating it requires an internationally coordinated policy run by elites.

Their real agenda is to define a “global problem” so they can advance “global solutions” such as world governance, world taxation and world rule by elites. It doesn’t matter that the actual science behind hysterical climate alarmism is extremely weak.

Unfortunately, the media, corporations, governments and international organizations are run mostly by globalists.

And many of them are working hard to silence dissent. We’re in a Brave New World.

end

PAM AND RUSS MARTENS

A HUGE STORY

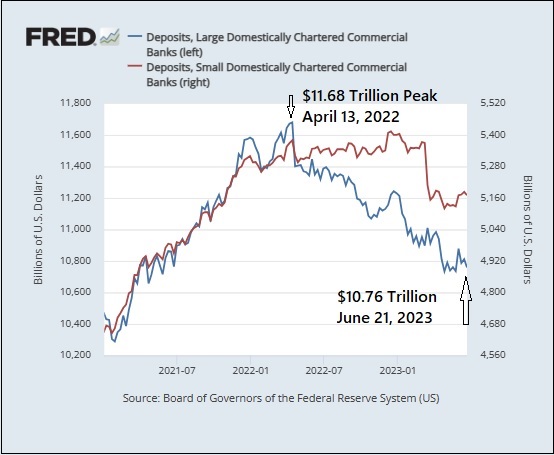

Large Banks Have Bled $921 Billion in Deposits Since April 2022 — the Fastest Pace in 40 Years — and a Much Larger Decline than Small Banks

By Pam Martens and Russ Martens: July 6, 2023

You may recall reading a burst of headlines during the banking crisis in March of this year about depositors fleeing small banks for the perceived comfort of the largest banks. Unfortunately, those headlines were never put in context or updated to reflect a broader picture.

In fact, using deposit data that is updated weekly from the Federal Reserve’s own H.8 releases, it becomes crystal clear that the large banks are bleeding deposits at the fastest pace in 40 years.

As the Federal Reserve data in the chart above indicates, deposits at the largest 25 commercial banks in the U.S. peaked at $11,679,758,700,000 on April 13, 2022. The most recent H.8 release shows that the deposits of the 25 largest banks as of June 21 stood at $10,758,977,000,000. That’s a percentage decline of 7.88 percent or $920,781,700.

The Fed’s H.8 data defines small domestically- chartered banks as all other commercial banks outside of the 25 largest. As of March 31, that would be 4,071 “small” banks, although more than two dozen of those had between $40 billion to $150 billion in consolidated assets as of March 31.

Deposits at the smaller banks didn’t peak until December 14, 2022, reaching $5,413,667,700,000. The most current reading on June 21 was $5,170,296,000,000, a decline of 4.5 percent from the peak versus the 7.88 percent decline at the 25 largest banks. In actual dollar terms, those 4,071 banks shed just $243.37 billion versus the $920.78 billion at the 25 largest banks.

It should be noted that the Fed’s initial H.8 weekly releases are static. That data is not updated at the H.8 web page, whereas the St. Louis Fed’s FRED H.8 data is updated for charting purposes. We used non- seasonally adjusted numbers, which we feel are more reliable given the unprecedented nature of this year’s banking crisis where three of the four largest banking failures in U.S. history have occurred.

To make your own charts, you will find the Fed’s updated large commercial bank deposit data her e and the small commercial bank deposit data her e. (Place your cursor on the various points of the chart for a date and dollar level reading.)

One of the most striking examples of distorted reporting on deposits by the financial press came on April 28 when a Bloomberg column by John Authers was syndicated to the Washington Post. Authers included this misleading narrative about the four largest U.S. banks: JPMorgan Chase, Bank of America, Wells Fargo and Citigroup’s Citibank.

“This summary from the Canadian firm Palos Management explains neatly why the bigger banks are still OK:

“The first quarter’s performance of the big four was consistent with a broad consensus that the big banks have capitalized on massive depositor inflows, clearly related to the well- documented liquidity stresses facing their smaller, regionally based brethren. This should come as no surprise. The panic-fueled depositor exodus from the smaller banks to the larger ‘too big to fail’ banks is simply a rational decision. Protection of capital rules.”

As we reported on May 8, the actual reality is this: Deposits at JPMorgan Chase, Bank of America and Wells Fargo Shrank by $465 Billion Y-O-Y; More than Twice the Total of 4,000 Small Banks. Using deposit data from the banks’ own regulatory filings, we reported as follows:

“The deposit losses at JPMorgan Chase, Bank of America and Wells Fargo are more than twice what the 4,000 small banks lost in total during the same period. Their combined loss in deposits was just $210 billion…

“Bank of America and Wells Fargo not only lost those large deposit sums on a year-over-year basis, but both banks saw deposits fall during the past five quarters, including the quarter ending March 31, 2023 when headlines were declaring that they were seeing big inflows of deposits as a result of the banking crisis. JPMorgan Chase lost deposits in each of the quarters in 2022 and then saw a small increase in deposits in the first quarter of this year – likely from all of those misleading headlines. (This information is easily obtained from the financial statements the firms file publicly with the SEC.)”

On May 21, the Wall Street Journal ran a big article (paywall) on how the banking crisis has “only made JPMorgan stronger.” Reporter David Benoit writes as follows about JPMorgan Chase’s purchase of the collapsed bank, First Republic:

“Yet JPMorgan’s show of strength, for many, exposed a weakness in the U.S. financial system. The bank and its largest rivals have become so big, their reach so extensive, that the government would almost surely step in to prevent their failure. That implicit guarantee encourages people and businesses to move their money to them in times of stress creating a feedback loop that makes big banks bigger at the expense of their smaller peers.”

JPMorgan Chase’s purchase of the failed First Republic was not a “show of strength,” but a revolting demonstration of regulatory capture at its worst. Despite JPMorgan Chase having admitted to five felony counts brought by the U.S. Department of Justice since 2014; despite it signing a non-prosecution agreement and three deferred prosecution agreements over the same time span with the Justice Department; and despite it being currently scandalized around the globe for functioning as the cash conduit for Jeffrey Epstein’s sex-trafficking of school-age girls for more than a decade, this is the sweetheart deal the bank got from the FDIC to take over First Republic: the FDIC would eat 80 percent of any losses on single-family residential mortgages for 7 years and 80 percent of any losses on commercial loans, including commercial real estate, for five years. The FDIC also provided JPMorgan Chase with a $50 billion, five-year fixed- rate loan at an undisclosed interest rate.

END

3,Chris Powell of GATA provides to us very important physical commentaries

END

4, OTHER IMPORTANT GOLD/SILVER COMMENTARIES/

Bix Weir posted this on silver demand from Ted Butler

Here are 3 big one’s that Ted Butler posted today…

The World’s Appetite for Solar Panels is Squeezing Silver Supply

Silver News: Could a Composite of Minerals Including Silver Replace Lithium in Batteries?

SILVER: A Highly Undervalued Golden Opportunity

end

5 a. IMPORTANT COMMENTARIES ON COMMODITIES:

end

5 B GLOBAL COMMODITY ISSUES/FOOD IN GENERAL

6.CRYPTOCURRENCY//DIGITAL CURRENCY// COMMENTARIES/

END

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS/THURSDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED UP TO 7.2320

OFFSHORE YUAN: UP TO 7.2439

SHANGHAI CLOSED DOWN 17.37 PTS OR 0.34%

HANG SENG CLOSED DOWN 577.33 PTS OR 3.02%

2. Nikkei closed DOWN 565.68 PTS OR 1.70%

3. Europe stocks SO FAR: ALL RED

USA dollar INDEX DOWN TO 102.64 EURO RISES TO 1.0895 UP 40 BASIS PTS

3b Japan 10 YR bond yield: RISES TO. +.412 Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 143.72/JAPANESE YEN FALLING AS WELL AS LONG TERM 10 YR. YIELDS RISING //EVENTUALLY THIS WILL BREAK THE JAPANESE CENTRAL BANK

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen UP CHINESE ON SHORE YUAN: UP// OFF- SHORE: UP

3f Japan is to buy INFINITE TRILLION YEN’S worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and UP FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund UP TO +2.5405***/Italian 10 Yr bond yield RISES to 4.242*** /SPAIN 10 YR BOND YIELD RISES TO 3.595…** DANGEROUS//

3i Greek 10 year bond yield RISES TO 3.843

3j Gold at $1927.00 silver at: 23.23 1 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble DOWN 0 AND 48 /100 roubles/dollar; ROUBLE AT 91,48//

3m oil into the 72 dollar handle for WTI and 76 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 143.72// 10 YEAR YIELD AFTER BREAKING .54%, RISES TO 0.412% STILL ON CENTRAL BANK (JAPAN) INTERVENTION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.8954 as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9755 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

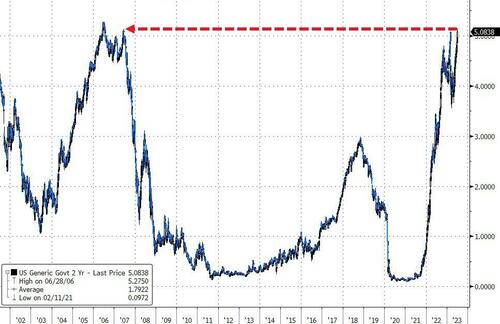

USA 10 YR BOND YIELD: 3.973 UP 3 BASIS PTS…

USA 30 YR BOND YIELD: 3.950 UP 1 BASIS PTS/

USA 2 YR BOND YIELD: 4.970 UP 2 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 26.03…(TURKEY SET TO BLOW UP FINANCIALLY)

GREAT BRITAIN/10 YEAR YIELD: UP 0 BASIS PTS AT 4.639 UP 14 PTS

end

2. Overnight: Newsquawk and Zero hedge:

Futures Slide As Rising Yields Spook Markets

THURSDAY, JUL 06, 2023 – 08:29 AM

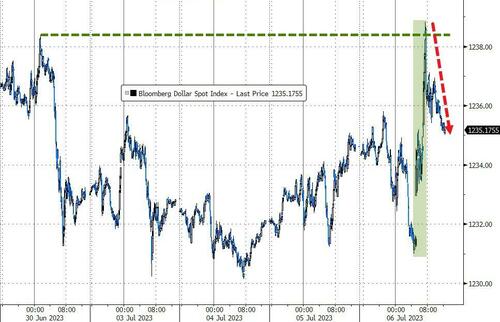

US futures extended losses as markets finally noticed the recent surge in Treasury yields across the globe, sparking fears of stagflation and following recent remarks from the Federal Reserve that were more hawkish than anticipated. Sentiment was also cautious ahead of fresh employment data. Stocks have struggled as a result, with the Stoxx 600 down 1.2% and on course for its largest fall in six weeks. As of 8:00am, ET, S&P 500 and Nasdaq 100 futures lose 0.6%. Treasury yields rose across the curve, adding to gains on Wednesday spurred by the Fed minutes. The policy sensitive two-year rate inched up to 4.96%. The dollar initially dropped but then spiked after a blow out ADP report.

Exxon Mobil fell in premarket trading after forecasting a $4 billion hit to earnings, while Meta Platforms Inc. rose after Instagram officially launched an app designed as a rival to Twitter. Freight transportation companies are likely to see “challenging” results in the second quarter, according to Morgan Stanley, though companies may be more upbeat about the outlook for future periods. Here are some other notable premarket movers:

- Genius Sports Limited rises 13% after the sports data provider and the National Football League (NFL) agreed to a multi-year extension of their strategic partnership.

- Microsoft’s artificial intelligence-driven gains can propel it to join Apple Inc. in the elite category of stocks with a market capitalization of more than $3 trillion, according to Morgan Stanley analysts. Shares are up 0.8%.

- Sweetgreen Inc. climbs 5.1% after BofA raises the salad chain to buy from neutral, citing increasing foot traffic, the prospect that same-store sales growth will see continued momentum, and plans to automate operations.

- Affirm Holdings Inc. shares declined 4.8% in premarket trading Thursday after Piper Sandler cut its recommendation on the buy-now-pay- later firm to underweight from neutral as higher rates and competition put pressure on margins.

- Perion shares gain 9.4% in US premarket trading after the digital media company reported preliminary second-quarter revenue that beat estimates.

- Nkarta rose 2.3% in after-hours trading Wednesday after the biotechnology company announces Alyssa Levin will be its new chief financial and business officer.

- JetBlue shares fell 0.5% in postmarket trading after the company said it’s decided not to appeal a court ruling against the carrier’s Northeast Alliance (NEA) with American Airlines, and that it has initiated the termination of the alliance.

In other news, Treasury Secretary Janet Yellen lands in Beijing in a visit aimed at repairing ties between the world’s two largest economies. That’s as Tesla and Chinese rivals signaled truce in a brutal price war that rattled the EV industry this year. And Elon Musk’s Twitter now faces a direct threat from Instagram’s text app Threads, which lured more than 10 million sign-ups in its first seven hours.

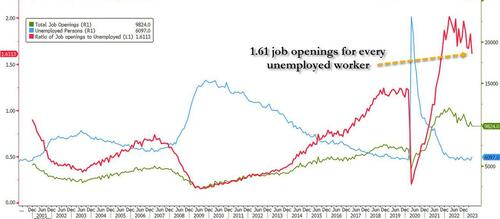

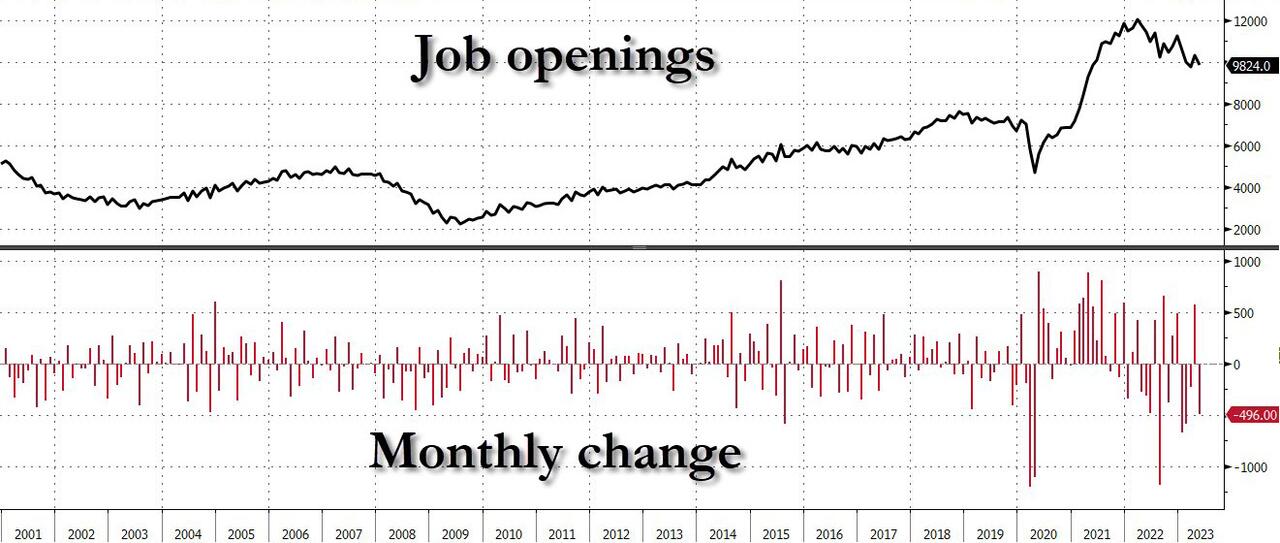

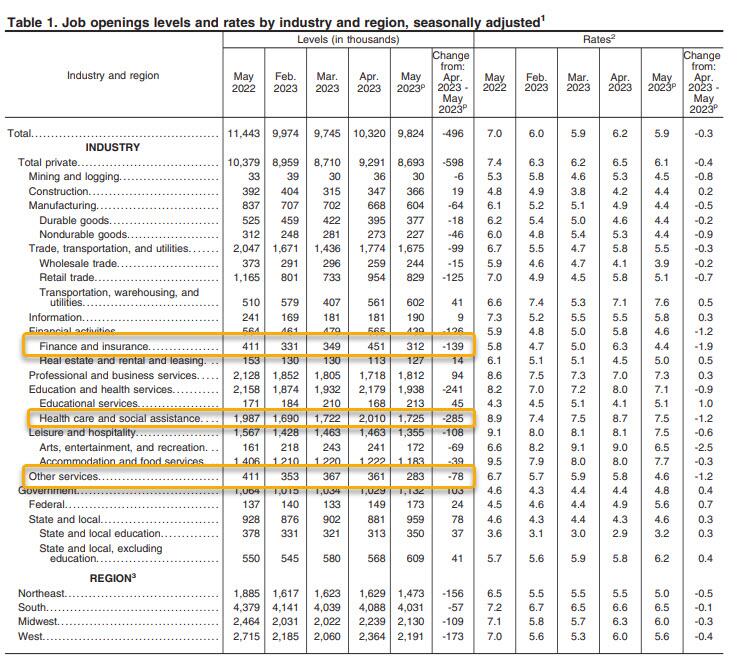

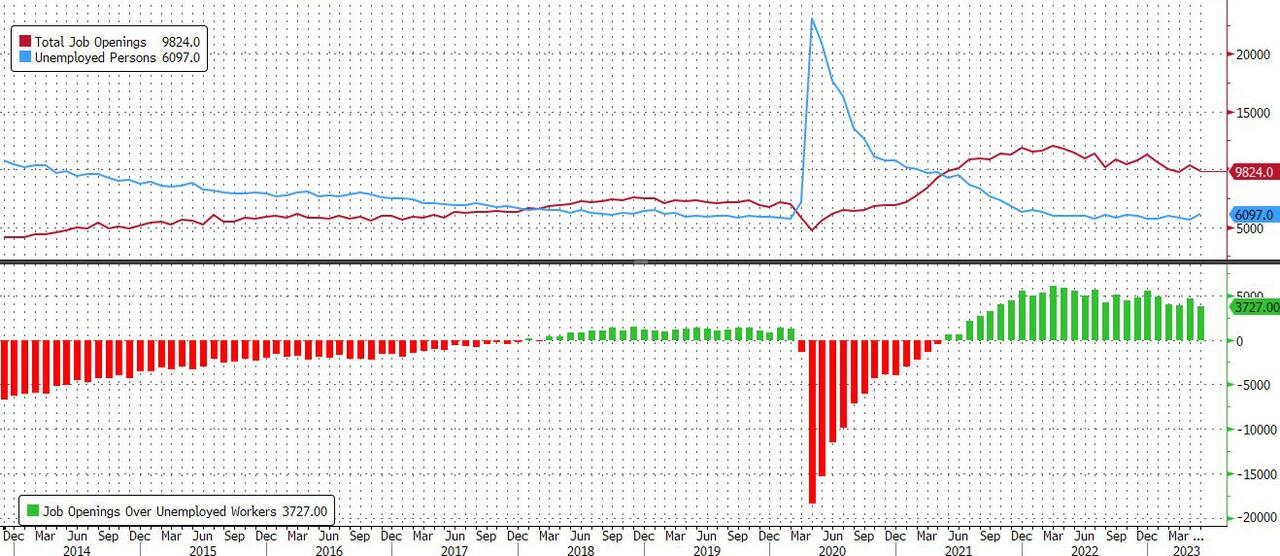

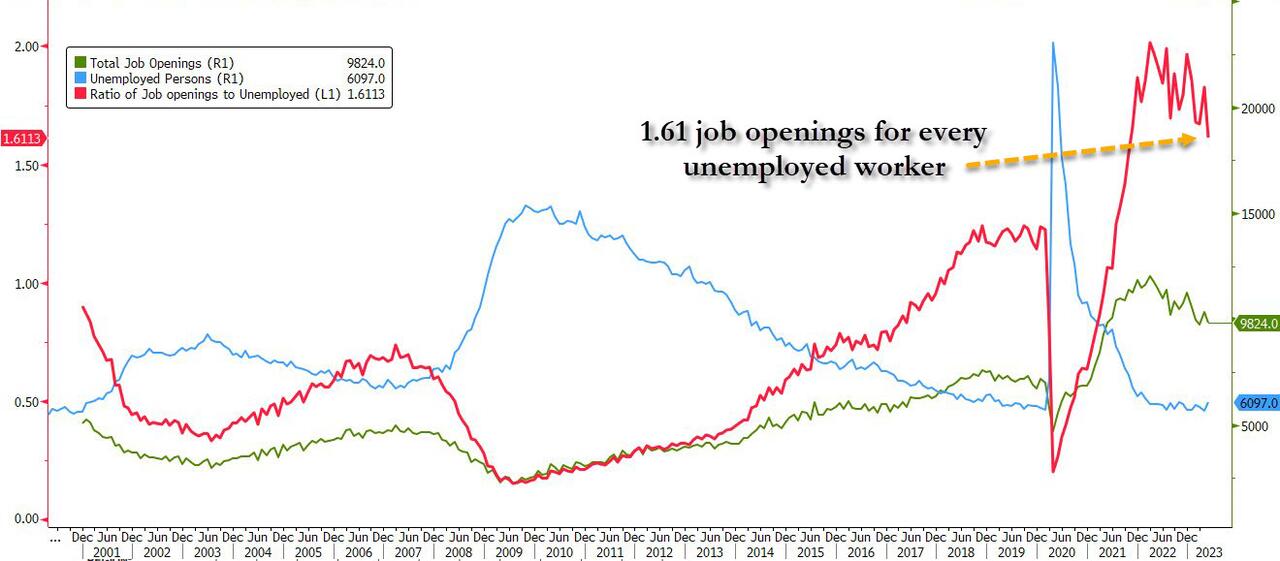

US employment reports this week may provide clues on the path for policy. Ahead of the closely watched nonfarm payrolls release on Friday, the so-called JOLTS report of job openings is expected to show a tapering of available positions, and a separate measure of jobless claims is anticipated to tick higher.

Stocks have lost some ground after a strong first half of the year as continued hawkishness from central banks damps hopes of a soft landing for the global economy. Minutes from the Fed’s June meeting showed division among policymakers over the decision to pause rate hikes, with the voting members on track to take rates higher this month.

“The fact that the FOMC has now officially adopted the staff forecasts for a recession in the US is bad for risk assets,” said James Athey, investment director at Abrdn. “What we get now is that the Fed expects to cause a recession but that won’t stop them hiking at least twice more this year. If that’s not bad for risk assets priced at 20 times earnings, I don’t know what is.”

European stocks retreated following hawkish minutes from the Federal Reserve’s last policy meeting, with investors also weighing early corporate earnings reports. Stoxx 600 dropped down 1.2% and on course for its largest fall in six weeks. United Utilities shares rise as much as 3.2% after Morgan Stanley upgraded the stock to overweight saying it sees a long- term, “unprecedented growth opportunity” for UK water companies, that isn’t factored into current prices. Here are some other notable European movers:

- U-blox gains as much as 4.1%, most since May 30, after Baader raised its recommendation on the Swiss semiconductor company to buy from add.

- Hunting shares surge as much as 19% after the energy services provider said it has performed ahead of expectations in the first half. Guidance is increased again for 2023, and Hunting added that the outlook for 2024 is improving.

- Suedzucker shares rise as much as 5% following its results, with Warburg describing the German food ingredients firm’s start to the year as “stellar.”

- Edmond de Rothschild Private Banking cut its exposure to luxury stocks in May given their expensive valuation, its chief investment officer said. LVMH shares fall as much as 2% Hermes as much as 2.7%.

- Currys shares sink as much as 15% after the UK electronics- and-appliances retailer noted an uncertain economic outlook in its main markets and said it isn’t paying a final dividend.

- Embracer shares fall as much as 14% after an offering of 80m class B shares priced at SEK25 apiece, representing 9.2% discount to last close.

- Ocado shares drop as much as 3.6% after Morgan Stanley lowered its price target and estimates ahead of the UK online grocer’s first-half results. The broker said that recent share-price strength has been surprising.

Earlier in the session, Asian stocks were mostly lower following the post-Independence Day hangover in the US owing to recent weak global data releases, a rising yield environment and after the FOMC Minutes provided little to deviate from the current view of future rate increases.Chinese stocks in Hong Kong fell by the most since Jan. 30 with banks among the biggest drags, amid broad weakness in the Asia Pacific region. Hang Seng China Enterprises Index falls as much as 3.7%. Banks were among the biggest drags: China Construction Bank down as much as 3.3%; Industrial and Commercial Bank -3%; Bank of China -1.8%. The selling was acute after China’s largest lenders cut rates for corporate US dollar deposits amid efforts to support the yuan and with banks said to have stopped buying bonds issued in the Shanghai free trade zone after heightened regulatory scrutiny, while losses in the mainland were stemmed ahead of US Treasury Secretary Yellen’s arrival in Beijing for meetings with senior officials. Nikkei 225 was pressured at the open with selling exacerbated after slipping beneath the 33,000 level. Australia’s ASX 200 traded lower as underperformance in the mining and materials-related industries spearheaded the declines seen in nearly all sectors and with risk appetite also sapped by a rise in Aussie yields.

In FX, the Bloomberg Dollar Spot Index slipped 0.1% as the yen led gains against Group-of-10 peers as regional stock markets racked up losses, boosting haven demand. A gauge of the dollar consolidated after Wednesday’s gain. USD/JPY drops 0.8% to 143.56 while EUR/JPY weakens 0.8% to 155.85. In China, the central bank extended support for the yuan via a stronger daily reference rate. Chinese investors don’t expect policymakers to unveil aggressive stimulus or big economic reforms at a key meeting expected later this month, according to Goldman Sachs Group Inc.

In rates, Treasury yields rose as much as 5bps across the curve, adding to gains on Wednesday spurred by the Fed minutes. The policy sensitive two-year rate was 3bps higher at 4.97% after the Fed minutes signaled they are on track to raise rates again this month. In the UK, yields on 10-year government bonds climbed as much as 10bps to 4.59%, highest since October when then Prime Minister Liz Truss’s fiscal plan unnerved markets. Traders are now fully pricing a terminal Bank of England rate of 6.5% by February, sending two-year yields rise 8bps to 5.46% .

In commodities, crude futures advance, with WTI rising 0.7% to trade near $72.30. Spot gold adds 0.2% to around $1,919. Bitcoin adds 3%

Notable upside has been seen throughout the morning in key crypto’s including Bitcoin and ETH, up over 2% thus far with Bitcoin surpassing and climbing further above the USD 31k mark.

Looking to the day ahead, and there’s several US data releases including the ISM services index for June, the weekly initial jobless claims, the ADP’s report of private payrolls for June, the JOLTS job openings for May and the trade balance for May. Meanwhile in Europe, there’s German factory orders and Euro Area retail sales for May, along with the German and UK construction PMIs for June.

Market Snapshot

- S&P 500 futures down 0.5% to 4,463.25

- MXAP down 1.4% to 162.61

- MXAPJ down 1.6% to 511.35

- Nikkei down 1.7% to 32,773.02

- Topix down 1.3% to 2,277.08

- Hang Seng Index down 3.0% to 18,533.05

- Shanghai Composite down 0.5% to 3,205.58

- Sensex up 0.3% to 65,615.34

- Australia S&P/ASX 200 down 1.2% to 7,163.45

- Kospi down 0.9% to 2,556.29

- STOXX Europe 600 down 1.2% to 452.54

- German 10Y yield little changed at 2.51%

- Euro little changed at $1.0849

- Brent Futures up 0.3% to $76.90/bbl

- Gold spot up 0.1% to $1,916.85

- U.S. Dollar Index little changed at 103.35

Top Overnight News from Bloomberg

- Bets on the trajectory of the Bank of England’s key interest rate surged to the highest level in a quarter century as traders questioned officials’ ability to tame inflation without hobbling the UK economy.

- German factory orders rebounded in May, a sign the manufacturing slump may be easing as Europe’s biggest economy shakes off a recession.

- Federal Reserve officials were less united at their June meeting than their unanimous decision suggested, as some favored interest-rate increases but went along with the move to leave policy unchanged.

- After months of central banks dominating foreign-exchange markets, commodities may be starting to bear more influence over currencies.

- China’s central bank extended support for the yuan via a stronger daily reference rate, a day after its flagship newspaper reassured investors that authorities have sufficient ammunition to stabilize the weakening currency.

A more detailed look at global markets courtesy of Newsquawk

APAC stocks were mostly lower following the post-Independence Day hangover in the US owing to recent weak global data releases, a rising yield environment and after the FOMC Minutes provided little to deviate from the current view of future rate increases. ASX 200 traded lower as underperformance in the mining and materials-related industries spearheaded the declines seen in nearly all sectors and with risk appetite also sapped by a rise in Aussie yields.Nikkei 225 was pressured at the open with selling exacerbated after slipping beneath the 33,000 level. Hang Seng and Shanghai Comp declined with acute selling in Hong Kong-listed Chinese banks after China’s largest lenders cut rates for corporate US dollar deposits amid efforts to support the yuan and with banks said to have stopped buying bonds issued in the Shanghai free trade zone after heightened regulatory scrutiny, while losses in the mainland were stemmed ahead of US Treasury Secretary Yellen’s arrival in Beijing for meetings with senior officials.

Top Asian News

- Chinese banks stopped buying bonds issued in the Shanghai free trade zone after heightened regulatory scrutiny.

- US Commerce Department firmly opposes export controls announced by China on gallium and germanium, while the US will engage with allies and partners to address the export controls announced by China.

- China Stocks Sink in Hong Kong on Growth Woes, Fed Concerns

- China Sees Suicide Rise Among Young People

- Mining Sector Raised to Hold at Liberum on Balanced Price Risks

- Malaysia Keeps Key Rate Steady to Support Slowing Economy

- Dalian Wanda Commercial Rating Cut to B1 From Ba2 at Moody’s

- ETFs Dominate Emerging-Market Flows as Money Managers Lose Share

- US Warned Hong Kong Banks on Tech Exports to Russia, Nikkei Says

- SoftBank Takes Advantage of BOJ’s Dovish Stance to Sell Bond

- Tesla and Chinese Rivals Signal Truce in Brutal EV Price War

- Japan in Talks to Buy Gas From Qatar Amid Diversification Shift

European bourses are in the red with cyclicals in particular lagging on ongoing growth concerns, Euro Stoxx 50 -1.5%. Sectors are all in the red with the negative price action extending shortly after the cash open given Construction PMIs, Cyclicals lag while Defensive names are the relative outperformers but remain firmly negative. Stateside, futures slip ahead of a busy data docket with the RTY -0.7% lagging given the above while the NQ -0.4% fares slightly better given META +1.7% pre-market action as Threads launches. Meta (META) CEO Zuckerberg says Threads passed 10mln signups in seven hours. ASML “told the Global Times on Thursday that it did not roll out a special-edition lithography machine for the Chinese market, responding to the market rumour of a special ASML DUV system for Chinese market.”

Top European News

- SNB’s Maechler said the SNB still sees inflation as being very high and doesn’t rule out further rate increases, according to Le Temps.

- BoE’s Bailey says moves by regulators on retail prices, particularly in the fuel market, will help to lower inflation, via BBC; evidence that some retailers are overcharging customers. Expects quite a marked fall in inflation but it will be hard for borrowers, cannot provide a date for when interest rates will begin to come down.

- BoE Decision Maker Panel: One-year ahead CPI inflation expectations decreased to 5.7% in June, down from 5.9% in May. Expected year-ahead wage growth slightly increased to 5.3% on the month in June (up from 5.2% in May) although the three-month moving average decreased by 0.1 percentage points to 5.3%.

- UK PM Sunak has reportedly tapped German Chancellor Scholz to help delay the EU EV tariff, according to Bloomberg News.

FX

- Yen turns the tide in choppy risk waters, with USD/JPY reversing through 144.00 where hefty option expiries reside and JPY crosses also retracing a chunk of their recent upside.

- DXY slips from post-FOMC minutes peak within 103.460-100 range as focus shifts to ADP, IJC, ISM services and JOLTS.

- Aussie and Kiwi resist aversion with the former underpinned by encouraging trade data and both relieved to see Yuan propped by PBoC; AUD/USD and NZD/USD towards upper end of 0.6686-34 and 0.6214-0.6164 bands.

- Euro is losing sight of 1.0900, but holding above key support and Pound propped around 1.2700 as BoE rate expectations continue to rocket.

- PBoC set USD/CNY mid-point at 7.2098 vs exp. 7.2510 (prev. 7.1968)

Fixed Income

- No respite for debt and hawkish Central Bank vibes compound bearish technical impulses.

- Bunds probe support zone between 132.09-65 bounds, Gilts towards base of 93.14-94.03 range and T-note nearer 11-01+ than 111-15 overnight high.

- OATs and Bonos weak after lacklustre demand for French and Spanish supply irrespective of marked concessions.

Commodities

- WTI and Brent are firmer by around USD 0.30/bbl a piece with specific drivers limited and despite broader growth concerns impacting elsewhere.

- Reminder, the OPEC summit has entered its second day though remarks thus far have been less impactful than Saudi’s commentary on Wednesday.

- Spot gold is benefitting from the softer USD and downbeat sentiment with the yellow metal attempting to move above USD 1920/oz.

- Base metals are, in contrast, lower and in-fitting with broader sentiment with LME Copper slipping below USD 8250/T, despite Codelco warning its copper production will end 2023 at the low-end of its forecast range.

- US Energy Inventory Data (bbls): Crude -4.4mln (exp. -1.8mln), Cushing +0.3mln, Gasoline +1.6mln (exp. -1.1mln), Distillate +0.6mln (exp. +0.5mln)

- Caspian Pipeline Consortium says all pumping stations are working as usual.

Geopolitics

- Ukrainian President Zelensky said he wanted the counteroffensive to happen much earlier and he told US and European leaders that Ukraine needed the weapons for that, while he also noted that difficulties on the battlefield slowed the pace of the counteroffensive, according to a CNN interview.

- US Air Force said 3 Russian fighter jets harassed drones during a mission against ISIS which forced the US to perform evasive manoeuvres, according to AJA Breaking.

- Swedish PM Kristersson said after meeting with US President Biden that Biden expressed very strong support for Sweden’s NATO accession and they both agreed the NATO Summit in Vilnius is a natural time for Swedish NATO accession, according to Reuters.

- US Secretary of State Blinken stressed the importance of NATO unity in a call with the Turkish Foreign Minister and encouraged Turkey’s support for Sweden to join the NATO alliance now.

- Two shells fired by Israel towards southern Lebanon fell after a missile was fired from Kafr Shuba, according to Al Arabiya. Additionally, at least one rocket has been fired from Southern Lebanon towards Israel, via Reuters citing three security sources. Subsequently, “There was no rocket from Lebanon into Israel this morning, there is controlled mine explosions being conducted along the border.”, according to AuroraIntel. Most recently, Israel’s Kan Radio saying Israeli forces shelling Lebanon is in response to rocket launch.

- Belarusian President Lukashenko says Russia will consult with Belarus in case nuclear weapons are used, according to Tass; says we are not going to attack anyone with nuclear weapons, but if aggression is shown, the response will be immediate. Adding that targets have been determined.

- Belarusian President Lukashenko says talks on Ukraine hit dead end; nuclear weapons will not be used during special military operation, it’s only possible in case of NATO aggression, according to Tass.

US Event Calendar

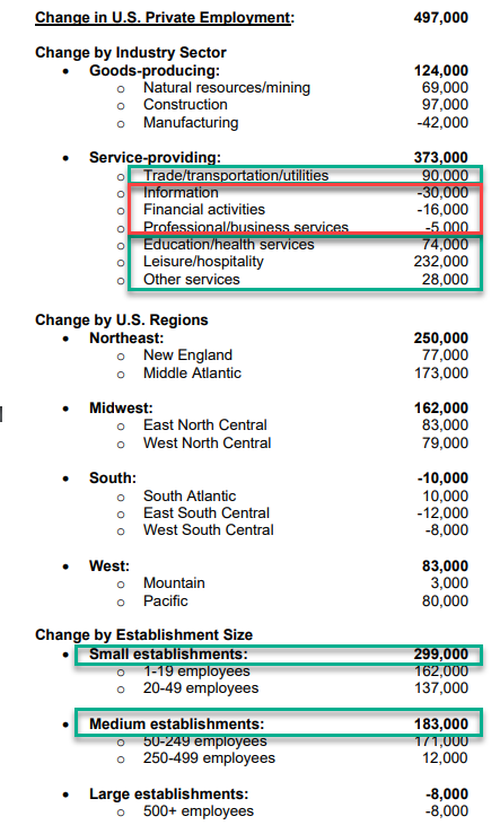

- 08:15: June ADP Employment Change 497,000, est. 225,000, prior 278,000

- 08:30: July Initial Jobless Claims, est. 245,000, prior 239,000