JULY 21//GOLD CLOSED DOWN $3.80 TO $1964.75//SILVER CLOSED DOWN 14 CENTS TO $14 CENTS//PLATINUM CLOSED UP $7.80 TO $966.70//PALLADIUM CLSOED UP $10.35 TO $1295.00//IMPORTANT READS FOR TODAY: ALASDAIR MACLEOD//USA SENDS THOUSANDS OF MARINES TO WARD OFF IRANIAN ATTACKS ON GULF CARRIERS//COVID UPDATES/VACCINE UPDATES//DR PAUL ALEXANDER//SLAY NEWS/EVOLV NEWS//NEWS ADDICTS//UPDATES ON THE YELLOW CARRIER STRIKE/STARWOOD’S CEO CLAIMS THAT CRE IS IN A CATEGORY 5 HURRICANE AND HE SHOULD KNOW//HUGE SWAMP STORIES FOR YOU TONIGHT ESPECIALLY ON THE SENATOR GRASSIE FBI DOCUMENT RELEASE//

132 C SG AMERICAS 14 190 H BMO CAPITAL 3 363 H WELLS FARGO SEC 600 435 H SCOTIA CAPITAL 19 624 H BOFA SECURITIES 616 690 C ABN AMRO 12 726 C CUNNINGHAM COM 1 737 C ADVANTAGE 1 905 C ADM 6

TOTAL: 636 636

MONTH TO DATE: 3,270

JPMorgan stopped 0/636 contracts.

FOR JULY:

GOLD: NUMBER OF NOTICES FILED FOR JULY/2023. CONTRACT: 636 NOTICES FOR 63,600 OZ or 1.9782 TONNES

total notices so far: 3270 contracts for 327000 oz (10.1710 tonnes)

FOR JULY:

SILVER NOTICES: 234 NOTICE(S) FILED FOR 1,170,000 OZ/

total number of notices filed so far this month : 5055 for 25,295,000 oz

XXXXXXXXXXXXXXXXXXXXXXXX

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD

WITH GOLD DOWN $3.80

INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD//

NO CHANGES IN GOLD INVENTORY AT THE GLD//

INVENTORY RESTS AT 913.80 TONNES

Silver//

WITH NO SILVER AROUND AND SILVER DOWN $0.14 AT THE SLV// HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.101 MILLION OZ OF SILVER FROM THE SLV//

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV.

CLOSING INVENTORY: 453.306 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A SMALL SIZED 209 CONTRACTS TO 149,599 AND FURTHER FROM THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THIS HUGE SIZED GAIN IN COMEX OI WAS ACCOMPLISHED DESPITE OUR STRONG $0.38 LOSS IN SILVER PRICING AT THE COMEX ON THURSDAY. TAS ISSUANCE WAS A STRONG SIZED 1498 CONTRACTS. THESE WILL BE USED FOR MANIPULATION LATER THIS MONTH . CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON THURSDAY NIGHT: 1498 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS. IT THUS LOOKS LIKE THE FED (GOV’T) IS BEHIND ALL OF THESE TRADES.

WE HAVE NOW SET ANOTHER RECORD LOW AT 114,102 CONTRACTS ///JULY 3.2023// OUR BANKERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.38). BUT WERE UNSUCCESSFUL IN KNOCKING ANY SPEC LONGS AS WE HAD A HUGE GAIN ON OUR TWO EXCHANGES OF 1178CONTRACTS. WE HAD A HUGE 0 CRIMINAL NOTICES FILED IN THE CATEGORY OF EXCHANGE FOR RISK TRANSFER FOR 0 MILLION OZ// ( THE TOTAL ISSUED IN THIS CATEGORY SO FAR THIS MONTH TOTAL 5.25MILLION OZ.). WE HAVE NOW RETURNED TO OUR USUAL AND CUSTOMARY SCENARIO: BANKERS SHORT AND SPECS LONG WITH MANIPULATION NOW MID MONTH AND BEYOND, DUE TO (TAS) MANIPULATION.

WE MUST HAVE HAD:

A HUGE ISSUANCE OF EXCHANGE FOR PHYSICALS( 1387 CONTRACTS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 16.110 MILLION OZ (FIRST DAY NOTICE) FOLLOWED BY TODAY’S HUGE 1.975 MILLION OZ QUEUE JUMP+ 0 MILLION OZ EXCHANGE FOR RISK FOR TODAY//NEW STANDING: 25.415 MILLION OZ + 5.25 MILLION OZ EXCHANGE FOR RISK/PRIOR: NEW TOTAL 30.665 MILLION OZ// // SMALL SIZED COMEX OI GAIN/ HUGE SIZED EFP ISSUANCE/VI) HUGE NUMBER OF T.A.S. CONTRACT ISSUANCE (1498CONTRACTS)/ZERO EXCHANGE FOR RISK ISSUED/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL –385 CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS JULY. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF JULY:

TOTAL CONTRACTS for 13 days, total 15,341 contracts: OR 76.705 MILLION OZ (1180 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 76.705 MILLION OZ

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 118.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 76.705 MILLION OZ (LARGER THAN LAST MONTH)

RESULT: WE HAD A SMALL SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 209 CONTRACTS DESPITE OUR STRONG LOSS IN PRICE OF $0.38 IN SILVER PRICING AT THE COMEX//THURSDAY.,. THE CME NOTIFIED US THAT WE HAD A HUGE EFP ISSUANCE CONTRACTS: 1387 ISSUED FOR JULY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS./ WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR JULY OF 16.110 MILLION OZ FOLLOWED BY TODAY’S MASSIVE 1.972 OZ QUEUE JUMP + 0 MILLION OZ EXCHANGE FOR RISK TODAY + (PRIOR EXCHANGE FOR RISK : 5.25 MILLION OZ): TOTAL NOW STANDING 25.415 MILLION OZ NORMAL STANDING + 5.25 MILLION EXCHANGE FOR RISK = 30.665 MILLION OZ.///// .. WE HAVE A HUGE SIZED GAIN OF1553 OI CONTRACTS ON THE TWO EXCHANGES. THE TOTAL OF TAS INITIATED CONTRACTS TODAY: A HUGE 1387//CONSIDERABLE FRONT END OF THE TAS CONTRACTS WERE LIQUIDATED DURING THE THURSDAY COMEX SESSION TO CONTAIN SILVER PRICE’S RISE. THE NEW TAS ISSUANCE TODAY (1498) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE./

WE HAD 234 NOTICE(S) FILED TODAY FOR 1,170,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A SMALL SIZED 701 CONTRACTS TO 483,396 AND CLOSER TO THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED: 863 CONTRACTS

WE HAD A SMALL SIZED DECREASE IN COMEX OI ( 701CONTRACTS) DESPITE OUR STRONG $8.70 LOSS IN PRICE. WE ALSO HAD A STRONG INITIAL STANDING IN GOLD TONNAGE FOR JULY. AT 5.1975 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S 1.972 TONNE QUEUE JUMP: NEW TOTAL OF GOLD STANDING FOR JULY: 10.267 TONNES// + /A FAIR (AND CRIMINAL) ISSUANCE OF 1130 T.A.S. CONTRACTS /// ALL OF..THIS HAPPENED WITH A $8.70 LOSS IN PRICEWITH RESPECT TO THURSDAY’S TRADING.WE HAD A FAIR SIZED GAIN OF 1100 OI CONTRACTS (3.421 PAPER TONNES) ON OUR TWO EXCHANGES.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 1801CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 483,396

IN ESSENCE WE HAVE A FAIR SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 1100 CONTRACTS WITH 701 CONTRACTS DECREASED AT THE COMEX// AND A FAIR 1801 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 1100CONTRACTS OR 3.421 TONNES. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): A FAIR 1130 CONTRACTS)

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (1130 CONTRACTS) ACCOMPANYING THE SMALL SIZED LOSS IN COMEX OI (701) //TOTAL GAIN FOR OUR THE TWO EXCHANGES: 1100 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR NORMAL FORMAT OF BANKERS GOING SHORT AND SPECULATORS GOING LONG ,2.) GOOD INITIAL STANDING AT THE GOLD COMEX FOR JULY AT 5.1975 TONNES FOLLOWED BY TODAY’S 1.9720TONNE QUEUE JUMP//NEW TOTAL 10.267 TONNES ///// /3) ZERO LONG LIQUIDATION BUT CONSIDERABLE TAS LIQUIDATION TO CONTAIN GOLD’S PRICE//4) SMALL SIZED COMEX OPEN INTEREST LOSS/ 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER///6: FAIR T.A.S. ISSUANCE: 1130 CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023 INCLUDING TODAY

JULY

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF JULY :

TOTAL EFP CONTRACTS ISSUED: 29,799 CONTRACTS OR 2,979,900 OZ OR 95,803 TONNES IN 13 TRADING DAY(S) AND THUS AVERAGING: 2292 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 13 TRADING DAY(S) IN TONNES 95.803 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2022, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 95.803/3550 x 100% TONNES 2.70% OF GLOBAL ANNUAL PRODUCTION

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 95.803 TONNES

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF JUNE. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF MAY HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF JUNE., FOR BOTH GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (JUNE), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER ROSE BY A SMALL SIZED GAIN OF 166 CONTRACTS OI TO 149,974 AND CLOSER TO OUR COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 1387 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

SEPT 1387and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 1387 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 2945 CONTRACTS AND ADD TO THE 1387 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A HUGE SIZED GAIN OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 1178 CONTRACTS

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTAL 5.890 MILLION OZ

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS//

FRIDAY MORNING//THURSDAY NIGHT

SHANGHAI CLOSED DOWN 1.78 PTS OR 0.06% //Hang Seng CLOSED UP 147.24 PTS OR 0.78% /The Nikkei CLOSED DOWN 185.27 PTS OR 0.57% //Australia’s all ordinaries CLOSED DOWN 0.20 % /Chinese yuan (ONSHORE) closed DOWN 7.1795 /OFFSHORE CHINESE YUAN DOWN TO 7.1838 /Oil UP TO 75.53 dollars per barrel for WTI and BRENT UP AT 80.46 / Stocks in Europe OPENED ALL MIXED// ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A SMALL SIZED 701CONTRACTS DOWN TO 483,396 DESPITE OUR STRONG LOSS IN PRICE OF $8.70 ON THURSDAY.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE NON ACTIVE DELIVERY MONTH OF JULY… THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 1801 EFP CONTRACTS WERE ISSUED: : AUGUST 1801 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 1801 CONTRACTS

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A FAIR SIZED TOTAL OF 1963 CONTRACTS IN THAT 1801LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A SMALL SIZED LOSS OF 701 COMEX CONTRACTS..AND THIS FAIR SIZED GAIN ON OUR TWO EXCHANGES HAPPENED DESPITE OUR LOSS IN PRICE OF $8.70//THURSDAY COMEX. AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS DURING MID MONTH IN THE DELIVERY CYCLE), THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR THURSDAY NIGHT WAS A FAIR 1130 CONTRACTS. THROUGHOUT THE PAST WEEKS, THE BANKERS SOLD OFF THE LONG SIDE OF THE SPREAD WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR SPREAD WHICH WILL BE LIQUIDATED TWO MONTHS HENCE)//THE HUGE NUMBER OF T.A.S. CONTRACTS INITIATED OVER THE PAST SEVERAL WEEKS SPELLS TROUBLE FOR THE GOLD/SILVER MARKET AS RAIDS WILL SURELY BE UPON US TRYING TO CONTAIN OUR PRECIOUS METALS RISE IN PRICE. IT MAY BE TO NO AVAIL!!

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: JULY (10.267) (NON ACTIVE MONTH)

TONNES),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.267 TONNES

THE SPECS/HFT WERE SUCCESSFUL IN LOWERING GOLD’S PRICE( IT LOST $8.70) //// AND WERE UNSUCCESSFUL IN KNOCKING ANY SPECULATOR LONGS AS WE HAD A FAIR SIZED GAIN OF 1100 CONTRACTS ON OUR TWO EXCHANGES. WE HAD CONSIDERABLE TAS LIQUIDATION THROUGHOUT THE THURSDAY COMEX SESSION TRYING DESPERATELY TO CONTAIN GOLD’S RISE. THE TAS ISSUED THURSDAY NIGHT, WILL BE “PUT INTO THE BANK” TO BE USED AT A LATER DATE AT THE COLLUSIVE CHOOSING OF OUR BANKERS. THE MASSIVE T.A.S. ISSUED ON MONDAY WAS USED THROUGHOUT THE WEEK CONTAINING GOLD’S RISE.

WE HAVE GAINED A TOTAL OI OF 3.421 PAPER TONNES OF TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR JULY. (5.11974 TONNES) ON FIRST DAY NOTICE FOLLOWED BY TODAY’S MASSIVE QUEUE JUMP OF 1.972 TONNES//TOTAL STANDING FOR JULY GOLD: 10.267 TONNES // ALL OF THIS WAS ACCOMPLISHED WITH OUR STRONG LOSS IN PRICE TO THE TUNE OF $8.70.

WE HAD – REMOVED 863 CONTRACTS TO THE COMEX TRADES TO OPEN INTEREST AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 1100 CONTRACTS OR 110,000 OZ OR 3.421 TONNES.

Total monthly oz gold served (contracts) so far this month

3270 notices 327,000 OZ 10.1710 TONNES

Total accumulative withdrawals of gold from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of gold from the Customer inventory this month

x

0 dealer deposit:

total dealer deposits: nil oz

total customer deposits: 0 oz

we had 1 customer withdrawals:

i)out of Brinks 203.400 oz

total withdrawals: 203.400 oz

Adjustments; 2// dealer to customer

i) Brinks 183,453.006 oz

ii) Out of JPMorgan 7916.198 oz

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR JULY.

For the front month of JULY we have an oi of 667 contracts having GAINED 607 contracts. We had 27 contracts served on Thursday. Thus we gained 634 contracts or an additional 63,400 oz of gold will stand at the comex.

AUGUST LOST 17,096 contracts DOWN to 179,016 contracts

SEPT gained 207 contracts to stand at 732

We had 636 contracts filed for today representing 63,600 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 636 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped received by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the JULY /2023. contract month,

we take the total number of notices filed so far for the month (3270 x 100 oz ), to which we add the difference between the open interest for the front month of JULY (667 CONTRACT) minus the number of notices served upon today 636 x 100 oz per contract equals 330,100 OZ OR 10.267 TONNES the number of TONNES standing in this NON active month of July.

thus the INITIAL standings for gold for the JULYcontract month: No of notices filed so far (3270) x 100 oz + (667) {OI for the front month} minus the number of notices served upon today (636) x 100 oz) which equals 330,100oz standing OR 10.267 TONNES

TOTAL COMEX GOLD STANDING: 10.267 TONNES WHICH IS STRONG FOR A NON ACTIVE DELIVERY MONTH.

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 22,242,511.168 OZ

TOTAL REGISTERED GOLD: 11,641,351.245 (362.10 tonnes)..

TOTAL OF ALL ELIGIBLE GOLD: 10,601,159.920 O Z

REGISTERED GOLD THAT CAN BE SERVED UPON: 9,769,793 OZ (REG GOLD- PLEDGED GOLD) 303.88 tonnes//

END

SILVER/COMEX

JULY 21

//2023// THE JULY 2023 SILVER CONTRACT

Silver

Ounces

Withdrawals from Dealers Inventory

NIL oz

Withdrawals from Customer Inventory

nil

.

Deposits to the Dealer Inventory

nil oz

Deposits to the Customer Inventory

600,739.378 oz CNT

No of oz served today (contracts)

234 CONTRACT(S) (1,170,000 OZ)

No of oz to be served (notices)

28 contracts (140,000 oz)

Total monthly oz silver served (contracts)

5055 Contracts (25.275,000 oz)

Total accumulative withdrawal of silver from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of silver from the Customer inventory this month

i) 0 dealer deposit

total dealer deposit: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: 0 oz

We had 1 deposits customer account:

i) Into CNT: 600,739.378 oz

total customer deposits: 600,739.378 oz

JPMorgan has a total silver weight: 139.936 million oz/276.718 million =50.59% of comex .//

Comex withdrawals 0

total: nil oz

adjustments: 0

TOTAL REGISTERED SILVER: 35.379 MILLION OZ//.TOTAL REG + ELIGIBLE. 276.718 million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR JULY:

silver open interest data:

FRONT MONTH OF JULY /2023 OI: 262 CONTRACTS HAVING GAINED 207 CONTRACT(S). WE HAD 2 NOTICES FILED ON THURSDAY SO WE GAINED 209 CONTRACTS OR AN ADDITIONAL 1,045,000 OZ WILL STAND AT THE COMEX FOR DELIVERY IN JULY,

AUGUST LOST 13 CONTRACTS TO STAND AT 830

SEPT HAS A LOSS OF 1366 CONTRACTS UP TO 126,069

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 234 for 1,170,000 oz

Comex volumes// est. volume today 36,962 poor /

Comex volume: confirmed yesterday: 61,615 good

To calculate the number of silver ounces that will stand for delivery in JULY. we take the total number of notices filed for the month so far at 5055 x 5,000 oz = 25,275,000 oz

to which we add the difference between the open interest for the front month of JULY(262) and the number of notices served upon today 234 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the JULY/2023 contract month: 5055 (notices served so far) x 5000 oz + OI for the front month of JULY (262) – number of notices served upon today (234 )x 500 oz of silver standing for the JULY contract month equates to 25.415 million oz + 0.0 MILLION OZ EXCHANGE FOR RISK TODAY//PRIOR EXCHANGE FOR RISK TOTALS 5.25 MILLION OZ /NEW TOTAL STANDING FOR DELIVERY: 30.665 MILLION OZ..WE HAVE 35 MILLION OZ OF REGISTERED SILVER AT THE COMEX//

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS

JULY 21/WITH GOLD DOWN $3.80 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD: / .////INVENTORY RESTS AT 913.80 TONNES

JULY 20/WITH GOLD DOWN $8.70 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.73 TONNES FROM THE GLD/ .////INVENTORY RESTS AT 913.80 TONNES

JULY 19/WITH GOLD UP $0.65 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .86 TONNES FROM THE GLD/ .////INVENTORY RESTS AT 912.07 TONNES

JULY 18/WITH GOLD UP $23.45 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD: .////INVENTORY RESTS AT 912.93 TONNES

JULY 17/WITH GOLD DOWN $6.60 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.73 TONNES OF GOLD FROM THE GLD.////INVENTORY RESTS AT 912.93 TONNES

JULY 14/WITH GOLD UP $0.75 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD: ////INVENTORY RESTS AT 914.66 TONNES

JULY 13/WITH GOLD UP $3.30 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 0.29 TONNES OF GOLD OUT OF THE GLD////INVENTORY RESTS AT 914.66 TONNES

JULY 12/WITH GOLD UP $24.50 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 0.31 TONNES OF GOLD OUT OF THE GLD////INVENTORY RESTS AT 914.95 TONNES

JULY 11/WITH GOLD UP $6.15 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.0 TONNES OF GOLD OUT OF THE GLD////INVENTORY RESTS AT 915.26 TONNES

JULY 10 WITH GOLD DOWN $1.35 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.60 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 916.26 TONNES.

JULY 7 WITH GOLD UP $16.80 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 917.86 TONNES.

JULY 6/WITH GOLD DOWN $9.90 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.04 TONNES OF GOLD FROM THE GLD//INVENTORY RESTS AT 917.86 TONNES

JULY 5/WITH GOLD DOWN $2.20 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD; A WITHDRAWAL OF 2.6 TONNES FROM THE GLD///INVENTORY RESTS AT 921.90 TONNES

JULY 3/WITH GOLD UP $1.90 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 924.50 TONNES//

JUNE 30/WITH GOLD UP $10.00 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.31 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 924.50 TONNES

JUNE 29/WITH GOLD DOWN $3.20 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.26 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 926.81 TONNES

JUNE 28/WITH GOLD DOWN $1.15 NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 925.65 TONNES

JUNE 27/WITH GOLD DOWN $9.15 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.45 TONNES OF GOLD FROM THE GLD./INVENTORY RESTS AT 925.65 TONNES

JUNE 26/WITH GOLD UP $4.65 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.6 TONNES OF GOLD FROM THE GLD/////INVENTORY RESTS AT 927.10 TONNES

JUNE 23/WITH GOLD UP $5.15 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: WITHDRAWALS OF 4.33 TONNES OF GOLD OVER THE PAST TWO DAYS. /INVENTORY RESTS AT 929.70 TONNES

JUNE 21/WITH GOLD DOWN $2.45 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY REST AT 934.03 TONNES

JUNE 20/WITH GOLD DOWN $22.40 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 934.03 TONNES

JUNE 16/WITH GOLD UP $0.70 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4.33 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 934.03 TONNES

JUNE 15/WITH GOLD UP $2.80 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES OF GOLD FROM THE GLD//INVENTORY RESTS AT 929.70 TONNES

JUNE 14/WITH GOLD UP $10.30 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 931.44 TONNES

JUNE 13/WITH GOLD DOWN $10.30 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.01 TONNES FORM THE GLD///INVENTORY RESTS AT 931.44

GLD INVENTORY: 913.80 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

JULY 21/WITH SILVER DOWN 14 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 1.101 MILLION OZ OF SILVER FROM THE SLV ////INVENTORY RESTS AT 453.306 MILLION OZ/

JULY 20/WITH SILVER DOWN 38 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 1.468 MILLION OZ OF SILVER FROM THE SLV ////INVENTORY RESTS AT 454.107 MILLION OZ/

JULY 19/WITH SILVER UP 11 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV:A ////INVENTORY RESTS AT 455.875 MILLION OZ/

JULY 18/WITH SILVER DOWN 19 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV:A ////INVENTORY RESTS AT 455.875 MILLION OZ/

JULY 17/WITH SILVER UP 25 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 4.856 MILLION OZ OF SILVER FROM THE SLV////////INVENTORY RESTS AT 455.875 MILLION OZ/

JULY 14/WITH SILVER UP 27 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 2.21 MILLION OZ OF SILVER FROM THE SLV////////INVENTORY RESTS AT 455.875 MILLION OZ/

JULY 13/WITH SILVER UP 64 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//////INVENTORY RESTS AT 462.941 MILLION OZ/

JULY 12/WITH SILVER UP $1.00 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.881 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 462.941 MILLION OZ/

JULY 11/WITH SILVER DOWN 5 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF .020 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 464.822 MILLION OZ/

JULY 10/WITH SILVER UP 2 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.672 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 464.802 MILLION OZ

JULY 7/WITH SILVER UP 42 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 466.474 MILLION OZ

JULY 6/WITH SILVER DOWN 50 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.667 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 466.474 MILLION OZ//

JULY5/WITH SILVER UP 30 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 468.141 MILLION OZ//

JULY 3/WITH SILVER UP 7 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 468.141 MILLION OZ//

JUNE 30/WITH SILVER UP 19 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.377 MILLION OZ INTO THE SLV/////INVENTORY RESTS AT468.141 MILLION OZ//

JUNE 29/WITH SILVER DOWN 23 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.763 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 466.764 MILLION OZ//

JUNE 28/WITH SILVER DOWN 2 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 470.527 MILLION OZ//

JUNE 27/WILVER SILVER UP 7 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 734,000 OZ INTO THE SLV////INVENTORY RESTS AT 470.527 MILLION OZ

JUNE 26/WITH SILVER UP 44 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY REST AT 469.793 MILLION OZ.

JUNE 23/WITH SILVER DOWN 9 CENTS TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A NET DEPOSIT OF 6.61 MILLION OZ INTO THE SLV OVER THESE PAST TWO DAYS//INVENTORY RESTS AT 469.793 MILLION OZ//

JUNE 21/WITH SILVER DOWN $.40 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 5.784 MILLION OZ OF SILVER INTO THE SLV////INVENTORY RESTS AT 463.183 MILLION OZ//

JUNE 20/WITH SILVER DOWN 89 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 463.183 MILLION OZ//

JUNE 16/WITH SILVER UP 23 CENTS TODAY :SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 459,000 OZ FROM THE SLV///INVENTORY RESTS AT 463.183 MILLION OZ

JUNE 15/WITH SILVER DOWN 17 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.377 MILLION OZ OF SILVER FROM THE SLV////INVENTORY RESTS AT 463.642 MILLION OZ//

JUNE 14/WITH SILVER UP 29 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 735,000 OZ FROM THE SLV///INVENTORY RESTS AT 465.019 MILLION OZ//

JUNE 13/WITH SILVER DOWN 25 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.515 MILLION OZ OF SILVER FROM THE SLV///INVENTORY RESTS AT 465.754 MILLION OZ//

JUNE 12/WITH SILVER DOWN 26 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 467.269 MILLION OZ//

3,Chris Powell of GATA provides to us very important physical commentaries

the new BRICS currency backed by gold is not on summit agenda?

(Reuters)

BRICS currency not on summit agenda, S. African official says

Submitted by admin on Thu, 2023-07-20 19:24Section: Daily Dispatches

By Rachel Savage and Carien du Plessis Reuters Thursday, July 20, 2023

JOHANNESBURG, South Africa — A BRICS currency will not be on the agenda of the bloc’s summit in South Africa next month, but Brazil, Russia, India, China, and South Africa will continue to switch away from the U.S. dollar, South Africa’s senior BRICS diplomat said today.

“There’s never been talk of a BRICS currency. It’s not on the agenda,” Anil Sooklal, South Africa’s ambassador at large for Asia and BRICS, told a media briefing. “What we have said and we continue to deepen is trading in local currencies and settlement in local currencies.”

Brazil’s President Luiz Inacio Lula da Silva and Russian foreign minister Sergei Lavrov are among BRICS leaders who touted the idea of a common currency as the bloc aims to challenge the Western dominance of global finance amid Russia’s sanctions-imposed exile after it invaded Ukraine last year.

This has pushed countries to find alternatives to the dollar, especially among non-U.S. allies. …

China’s central bank manipulates Shanghai gold price

(Jan Nieuwenjuijs)

Jan Nieuwenhuijs: China’s central bank manipulates Shanghai gold price

Submitted by admin on Thu, 2023-07-20 16:06Section: Daily Dispatches

By Jan Nieuwenhuijs Gainsville Coins, Lutz, Florida Thursday, July 20, 2023

By obstructing gold imports and exports, the People’s Bank of China greatly amplifies the gold premiums or discounts on the Shanghai Gold Exchange relative to metal traded in London.

In the past 12 months the PBoC has restricted gold imports to curb capital flight and defend the renminbi, resulting in exaggerated Shanghai Gold Exchange premiums. With these interventions the Chinese central bank risks preventing the gold market it supervises from functioning properly, and stagnates internationalization

The core responsibilities of the PBoC are to “maintain financial stability … and to maintain the stability of the value of the currency and thereby promote economic growth.”

To this end it wants to strengthen China’s economic security by letting the population accumulate gold. Additionally, the Chinese central bank uses capital controls to manage the renminbi’s exchange rate.

A dilemma arises, for example, when Chinese people rush to buy gold as a form of capital flight, which undesirably weakens the renminbi.

Since 2016 there have been several periods in which the PBoC restricted gold imports into the Chinese domestic market to stem capital flight, lifting Shanghai premiums over the international benchmark (London spot).

Remarkably, when there is no capital flight and China is a net gold importer, the PBoC seems to aim at a 0.5% floor for Shanghai premiums. …

Submitted by admin on Thu, 2023-07-20 13:06Section: Daily Dispatches

By Alasdair Macleod GoldMoney, Toronto Thursday, July 20, 2023

Last week in my Goldmoney Insight I analysed the rationale for a new gold-backed trade settlement currency on the agenda of the BRICS summit in Johannesburg on August 22-24. This article is about the consequences for the dollar-based fiat currency regime.

There is strong evidence that planning for this new trade settlement currency has been in the works for some time and has been properly considered

That being so, we are witnessing the initial step away from fiat to gold-backed currencies. Without the burden of expensive welfare commitments, all the attendees in Johannesburg can back or tie their currency values to gold with less difficulty than our welfare-dependent nations. And it is now in their commercial interests to do so.

We have been brainwashed with Keynesian misconceptions and the state theory of money for so long that our statist establishments and market participants fail to see the logic of sound money, and the threat it presents to our own currencies and economies. But there is a precedent for this foolishness from John Law, the proto-Keynesian who bankrupted France in 1720. I explain the similarities.

That experience, and why it led to the destruction of Law’s livre currency, illustrates our own dilemma and its likely outcome.

It’s not just a comparison between fiat currency and gold. America’s financial position is dire, more so than is generally realised. The euro is additionally threatened with extinction because of flaws in the euro system, and the UK is already in a deeper credit crisis than most commentators understand. …

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS FRIDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED DOWN TO 7.1795

OFFSHORE YUAN: DOWN TO 7.1838

SHANGHAI CLOSED DOWN 1.78 PTS OR 0.06%

HANG SENG CLOSED UP 147,24 PTS OR 0.78%

2. Nikkei closed DOWN 185.27 PTS OR 0.57%

3. Europe stocks SO FAR: ALL MIXED

USA dollar INDEX DOWN TO 100.84 EURO FALLS TO 1.1118 DOWN 15 BASIS PTS

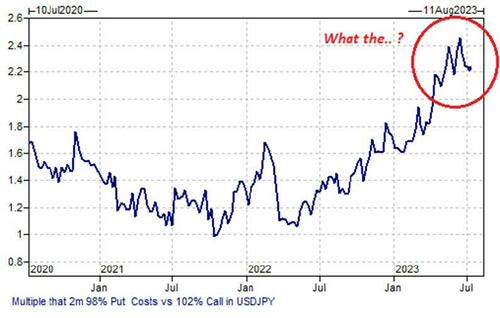

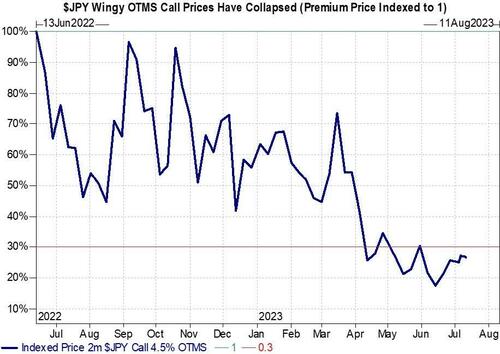

3b Japan 10 YR bond yield: FALLS TO. +.421 Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 141.77/JAPANESE YEN FALLING AS WELL AS LONG TERM 10 YR. YIELDS RISING //EVENTUALLY THIS WILL BREAK THE JAPANESE CENTRAL BANK

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen DOWN CHINESE ON SHORE YUAN: DOWN// OFF- SHORE: DOWN

3f Japan is to buy INFINITE TRILLION YEN’S worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and UP FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund UP TO +2.4510***/Italian 10 Yr bond yield RISES to 4.095*** /SPAIN 10 YR BOND YIELD RISES TO 3.479…**

3i Greek 10 year bond yield RISES TO 3.761

3j Gold at $1966.90 silver at: 24.85 1 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble UP 0 AND 14 /100 roubles/dollar; ROUBLE AT 90.37//

3m oil into the 76 dollar handle for WTI and 80 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 141.77// 10 YEAR YIELD AFTER BREAKING .54%, FALLS TO 0.421% STILL ON CENTRAL BANK (JAPAN) INTERVENTION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.8663 as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9632 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 3.850 DOWN 1 BASIS PTS…

USA 30 YR BOND YIELD: 3.901 DOWN 1 BASIS PTS/

USA 2 YR BOND YIELD: 4.801 UP 2 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 26.93…(TURKEY SET TO BLOW UP FINANCIALLY)

GREAT BRITAIN/10 YEAR YIELD: UP 10 BASIS PTS AT 4.3405

end

2. Overnight: Newsquawk and Zero hedge:

Futures Rebound After Thursday’s Tech Rout As Record July OpEx Looms

FRIDAY, JUL 21, 2023 – 08:19 AM

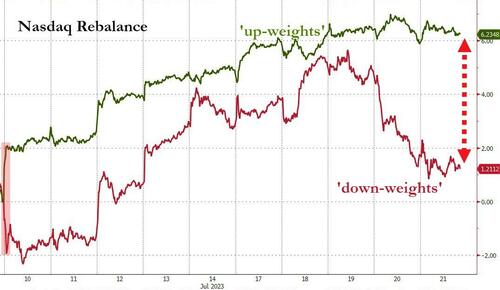

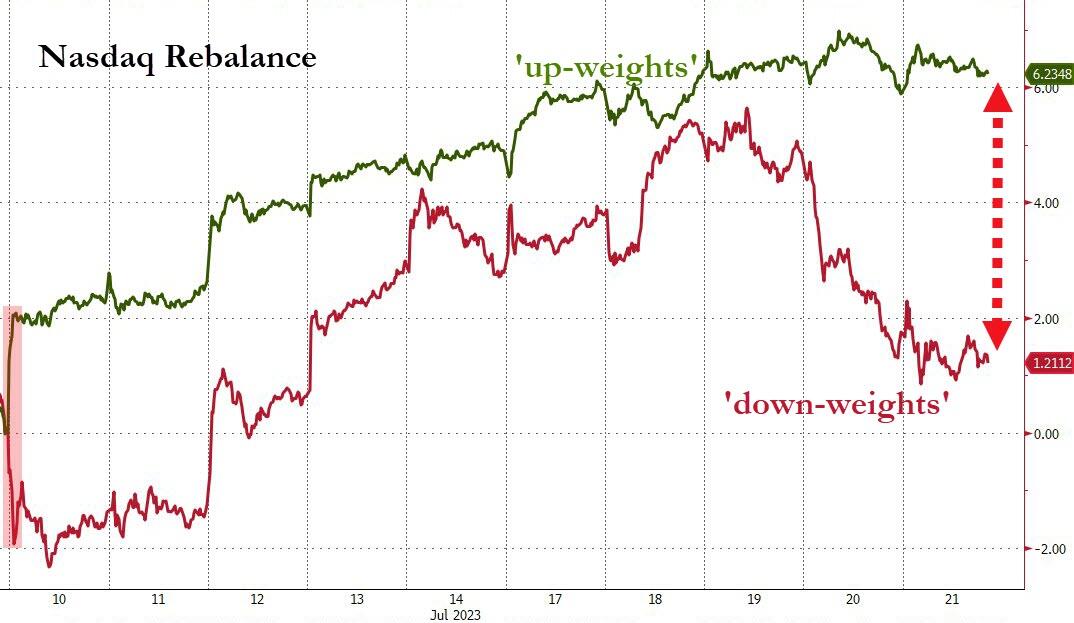

US equity futures are higher as futures pointed to a rebound from yesterday’s selloff, while the yen weakened on a BBG report that the the Bank of Japan won’t make any changes to its yield curve control program. As of 7:45am ET, S&P futures were 0.2% higher while Nasdaq futures rebounded 0.4% from yesterday’s 2.3% rout. Netflix and Tesla climbed in pre-market trading after leading the Nasdaq to sharp losses on Thursday on the back of disappointing results. The Bloomberg Dollar Spot Index traded near the day’s highs, pressuring most Group-of-10 currencies, with the yen suffering the biggest declines after Bloomberg reported that Bank of Japan officials see little urgent need to address the side effects of its yield curve control program. Treasury yields were little changed, mirroring lackluster trading in European and UK bond markets. Brent crude rose more than 1%, while gold fell and Bitcoin gained 0.2%. The Nasdaq rebalance will take effect after close today. Headlines remain quiet this morning; next week, we will receive key MegaCap Tech earnings, starting with GOOGL and MSFT on Tuesday (7/25), and the July FOMC on Wednesday.

In premarket trading, American Express fell almost 3% after the company reported discount revenue for the second quarter that missed the average analyst estimate. Tesla led electric-vehicle stocks higher in US premarket trading after weighing on the sector on Thursday. The stock had slumped after the world’s most valuable carmaker warned of more hits to its already-shrinking profitability. Digital World Acquisition Corp, the SPAC working to bring Donald Trump’s media venture public, soared 21% in premarket trading on Friday after the SEC said it settled fraud charges against the SPAC. Here are some other notable premarket movers:

Intuitive Surgical shares drop 4.9% in premarket trading. The medtech’s second- quarter earnings beat was overshadowed by a continued decline in growth rates for bariatric surgery in the US amid patient interest in the new class of weight-loss drugs as an alternative. The weakness in this area was the only “nitpick” in performance across the company’s procedures, Truist Securities said.

Emergent BioSolutions rises as much as 20% in premarket trading on Friday after the company said it got FDA approval for its anthrax vaccine. Cowen analyst notes that the approval is an incremental positive as it was largely expected.

Sirius XM falls 10% in premarket trading on Friday after Evercore ISI cut its rating on the satellite radio company’s stock to underperform from in line. The downgrade comes after a 42% rally on Thursday that was powered by a short squeeze rather than any fundamental change in the business, the analyst notes.

Rayonier Advanced Materials obtains $250m term loan financing from Oaktree Capital Management funds. The stock jumped 9% in postmarket trading.

Scholastic climbed 9% in postmarket trading as the distributor of children’s educational books reported adjusted earnings per share for the fourth quarter that rose over 30% from the same quarter a year earlier.

Trading on Friday will be affected by a flood of expiring options before an out-of-cycle rebalancing in the Nasdaq 100. The index shuffle, which takes effect on Monday, is designed to reduce the dominance of megacaps and boost the presence of smaller members. The tech-heavy index’s rejig coincides with the monthly options expiration – which at $2.4 trillion is a record for the month of July (see our preview here)- at a time when traders are anxiously waiting for corporate earnings and next week’s Federal Reserve policy meeting for clues on the market’s outlook.

Stocks slipped Thursday for the first time this week as fresh signs of labor-market resiliency bolstered the case for at least another Fed hike this year. Underscoring the risk-off mood, investors withdrew $2.1 billion from equity funds in the week to July 19, while adding $7.5 billion to money markets and $1.4 billion to bond funds, according to BofA’s Michael Hartnett.

The main focus continues to be whether the rally in a handful of megacap stocks and hype over artificial intelligence has staying power. The S&P 500 has already surpassed most estimates for where it would end the year, confounding strategists convinced that 2023 would be another bad year for markets heading into recession.

“So where we are right now, we are resting after the massive move over the course of many weeks,” Ken Mahoney, CEO of Mahoney Asset Management, wrote in a note. “A lot of stocks were creating and still are creating bases to break out higher from. No one could believe their eyes after being so conditioned to 2022’s nasty selling conditions when this market gained steam again.”

European stocks were mixed, trading between gains and losses with the German DAX underperforming as SAP shares slump after cloud sales missed estimates. Here are the most notable European stock moves:

Schindler shares climb as much as 6.9% to highest since March, after the Swiss elevator maker surprised analysts with a full- year net income guidance that beat estimates, thanks to an uptick in orders

Wartsila gains as much as 15%, the most since April 2021, after the Finnish power and marine propulsion products maker positively surprised the market with better-than- expected margins and reassuring order intake

Recordati gains as much as 3.6%, the most intraday since June 1, after the Italian drugmaker made an agreement with GSK to commercialize Avodart and Combodart/Duodart products across 21 countries

Volvo Cars gained as much as 7.3% after being double-upgraded to outperform at BNP Paribas Exane, which shifts its focus in autos manufacturers to now favor “affordable premium”

Babcock shares gain as much as 6.5%, as Citi analyst Samuel Burgess raised his recommendation on the stock to buy from hold, a day after the defense outsourcing company released strong full-year results. He also increased the PT by 35%

Truecaller shares surge as much as 34%, the most since Oct. 2021, as the Swedish caller-ID platform delivered results which DNB expects will trigger a rise in 2024 Ebitda consensus by up to 10%

Viaplay gains as much as 31% after France’s Canal+ Group said it has built a stake in the Swedish streaming entertainment group. The jump trims some of Thursday’s 49% drop

SAP drops as much as 5.6%, the biggest intraday decline since 2022, after the software company reported second-quarter sales in its cloud unit that missed estimates. Jefferies says the miss is a surprise

Lonza shares drop as much as 10% as the Swiss pharmaceutical company cut its core Ebitda margin forecast for the full year after posting “weak” 1H, Citi says. ZKB was also critical of communication toward investors

Thales falls as much as 4.9%, after the French defense group posted results slightly above expectations but produced a revised assumption on the impact of currency swings

SSAB shares plunge as much as 16% after the Swedish steelmaker reported weaker-than-expected second-quarter earnings and gave an outlook that pointed to a worsening environment

Stora Enso shares dropped as much as 7.7%, the most in four months, after the Finnish paper & packaging company’s operating Ebit for the second quarter missed estimates

Norsk Hydro shares fall as much as 3.9% after the aluminum miner reported 2Q results. Analysts say the firm’s decision to hike its capital expenditure guidance outweighs the earnings beat

Earlier in the session, Asian stocks dropped, as tech stocks led losses following TSMC’s guidance cut while benchmarks in Hong Kong climbed. The MSCI Asia Pacific Index slumped 1.5% mainly because of the sharp drop in Indian stocks. TSMC, Tokyo Electron and other chip stocks were the biggest drags on the gauge after TSMC cut its annual outlook for revenue and delayed production at a planned facility in Arizona. The Hang Seng China Enterprises Index advanced as much as 1.4%, while other other Hang Seng gauges were also among the region’s notable outperformers. Their gains come after losses in the past several sessions amid disappointments over the second-quarter growth figures and underwhelming support pledges from Beijing. Investors said the valuations of Chinese equities remained cheap even as it may take time to see a comeback in investor confidence.

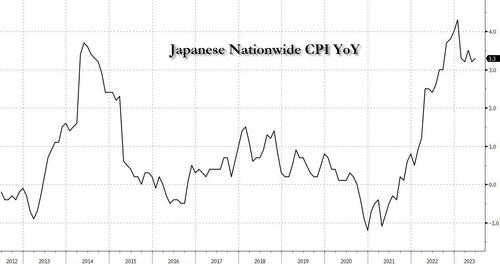

Japan’s Nikkei 225 slumped at the open but was well off its lows amid currency swings and somewhat ambiguous CPI data which printed mostly in line with expectations but showed a slight acceleration for the headline and core inflation.

Key stock gauges in India snapped a six-day winning run to end as the worst performing market in the region on Friday due to a sell off in technology stocks. The S&P BSE Sensex fell 1.3% to 66,684.26 in Mumbai, while the NSE Nifty 50 Index declined 1.2% to 19,745.00. For the week, Sensex and Nifty climbed about 0.9% on continued net buying from foreign institutional investors amid optimism for earnings growth. Global funds net buying of India stocks have climbed to more than $15 billion since February. The MSCI India index ended with a 9.2% drop after a sudden decline in the index around 1:20 pm with index provider MSCI saying it is looking into the movement.

“We need to see evidence of economic data recovering,” Abhilash Narayan, senior investment strategist at Standard Chartered Wealth Management, said in an interview with Bloomberg TV. “But from a valuation perspective, Chinese equities are extremely cheap,” he said adding that there is “a fairly good likelihood” that they will outperform global peers over the next 12 months. The main Asian equity benchmark is set for about a 1% decline this week, its worst weekly performance this month. Investors are monitoring corporate earnings reports with many heavyweights in Asia scheduled to report their quarterly results next week.

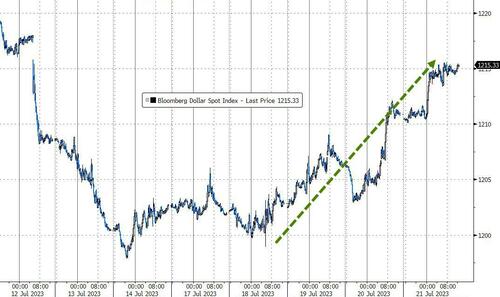

In FX, the Bloomberg dollar index extended gains to a fourth day, its longest winning streak since May. The yen tumbled as much as 1.4% and led losses among Group-of-10 currencies after traders confirmed what we have been saying all along – that there is little chance for a hawkish surprise at the BOJ’s policy decision next week as Bloomberg reported that officials see little urgent need to address the side effects of its yield curve control at this point.

The currency traded at 141.81 against the dollar, its weakest level in almost three weeks, amid reduced odds for a hawkish surprise at the BOJ’s policy decision next Friday.

In rates, treasury yields edged lower as US trading day begins, led by longer-dated tenors. Narrow ranges during Asia session and European morning include 2.4bp for 10-year yield. On the week, yields are likewise mixed with the curve flatter, after swaps fully priced in a Fed rate hike on July 26 while auctions of 20-year bonds and 10-year TIPS drew strong demand. Yields remain within about 2bp of Thursday’s closing levels, 10- year around 3.84%, holding above 50-day average level breached this week for the first time since May; most other sovereign debt markets also little changed. Inverted 2s10s curve slightly flatter on the day at around -100bp; Thursday’s low -105bp was deepest inversion since July 6. Fed swaps continue to fully price in a 25bp rate hike on July 26 and about a third of an additional quarter-point hike this year.

The pound also jumped after UK retail sales topped estimates, although gains proved short lived with cable now negative. The Bloomberg Dollar Spot Index is up 0.3%. European stocks are little changed with the Stoxx 600 flat after a three-day rally.

Wall Street looks set for a higher open with S&P futures up 0.2% and Nasdaq 100 futures adding 0.4%. Gilts are in the red while bunds and Treasuries trade close to unchanged. Crude futures advance, with WTI rising 1.2% to trade near $76.60

In bitcoin, US House Republicans introduced a new digital assets oversight bill that aims to establish a regulatory framework to protect crypto investors, according to CoinDesk. FTX sues Sam Bankman-Fried and other former executives to recoup hundreds of millions of dollars of alleged fraudulent transfers, according to Reuters.

In commodities,

Wheat fell about 3% as Ukraine made preparations to continue a grain-export deal, which Russia exited this week. The grain is still poised for a weekly gain of 7%, after prices surged on threats to ships arriving at Black Sea ports. The rise in prices could again stoke food costs and feed inflation.

Looking to the day ahead, it’s a fairly quiet one on the calendar with nothing on the US docket. Global data releases include UK retail sales for June, which came in handily above expectations, while earnings releases include American Express which missed expectations.

Market Snapshot

S&P 500 futures up 0.2% to 4,574.75

STOXX Europe 600 little changed at 463.76

German 10Y yield little changed at 2.48%

Euro little changed at $1.1136

MXAP down 1.5% to 164.63

MXAPJ down 1.7% to 519.09

Nikkei down 0.6% to 32,304.25

Topix little changed at 2,262.20

Hang Seng Index up 0.8% to 19,075.26

Shanghai Composite little changed at 3,167.75

Sensex down 1.1% to 66,806.37

Australia S&P/ASX 200 down 0.2% to 7,313.89

Kospi up 0.4% to 2,609.76

Brent Futures up 0.7% to $80.22/bbl

Gold spot down 0.3% to $1,964.31

U.S. Dollar Index up 0.10% to 100.98

Top Overnight News from Bloomberg

Japan’s BOJ is “leaning towards” keeping the YCC policy unchanged at next week’s meeting as policymakers want to see further data before making adjustments. RTRS

Japan’s national CPI for June overshoots the Street at +3.3% on the headline (vs. the Street’s +3.2% and up from +3.2% in May) while ex-energy and ex-energy/food are inline at +3.3% and +4.2%, respectively (the ex-energy/food number of +4.2% ticked down from +4.3% in May, leading some to think inflation may have peaked in Japan). RTRS

Chinese authorities announced measures on Friday intended to help boost sales of automobiles and electronics with the goal of shoring up a sluggish economy, but the steps failed to impress investors who have been clamoring for stronger stimulus. RTRS

The Asian Infrastructure Investment Bank, Beijing’s answer to the World Bank, has approved one of its highest-profile international partnerships, just weeks after it was accused of being infiltrated by China’s Communist party. FT

In the most detailed public account yet given by a U.S. official, the director of the C.I.A. offered a biting assessment on Thursday of the damage done to President Vladimir V. Putin of Russia by the mutiny of the Wagner mercenary group, saying the rebellion had revived questions about Mr. Putin’s judgment and his detachment from events. NYT

Russia’s navy conducted a live fire exercise at a training range in the Black Sea, escalating the war’s risk to global food markets. Wheat headed for a weekly gain of more than 10% as the tensions added to concern about extreme weather. BBG

Fed Vice Chair for Supervision Michael Barr has laid out a plan to increase capital requirements for the nation’s largest banks in the wake of recent bank failures and is expected to unveil the broad proposal to implement new risk-based capital requirements on July 27, according to three industry officials. RTRS

The potential strike by 340,000 UPS workers threatens to revive two of the US economy’s biggest hurdles: inflation and supply-chain disruptions. A walkout would snarl the 19 million US packages UPS moves daily and enable competitors to raise prices. But meeting the Teamsters’ wage demands may also spur inflation pressures. BBG

FTX sued Sam Bankman-Fried and his top lieutenants over $1 billion in bad deals as it tries to recover cash for creditors. BBG

A more detailed look at global markets courtesy of newsqquawk

APAC stocks were mixed as further support efforts from China partially offset the headwinds from Wall St where the Nasdaq 100 suffered its second-worst day of the year on tech disappointment and amid a rising yield environment. ASX 200 was subdued amid losses in tech, financials and the mining-related sectors, albeit with downside limited amid the lack of catalysts from Australia. Nikkei 225 slumped at the open but was well off its lows amid currency swings and somewhat ambiguous CPI data which printed mostly in line with expectations but showed a slight acceleration for the headline and core inflation. Hang Seng and Shanghai Comp were underpinned by further supportive efforts from China in which the NDRC released policies to boost electronics products consumption and measures to promote automobile consumption.

Top Asian News

China’s NDRC released policies to boost electronic product consumption and encourages scientific research institutes and market entities to apply domestic AI technology to improve the intelligence level of electronic products.

NDRC also issued measures to promote automobile consumption and are to encourage regions with purchase restrictions to issue annual purchase targets as soon as possible, according to Reuters.

China is to explain anti-espionage law and mineral export restrictions to Japanese, US, South Korean and EU company executives on Friday, according to Jiji.

China’s state planner NDRC is to hold a press conference on Monday at 10am local time (03:00BST) on private investments.

European bourses are relatively steady after mixed APAC performance as Chinese support offset the subdued handover, Euro Stoxx 50 -0.1%; in Europe, Tech lags with SAP -3.9%. Sectors are somewhat mixed with Energy seeing upside on benchmark pricing, though off best as the USD picks up, while Tech and the DAX 40 -0.5% lag after SAP missed on top & bottom. Stateside, futures are little changed amid a sparse US-specific docket ahead, ES +0.1%; NQ +0.3% is the incremental outperformer after Thursday’s marked pressure and as the dovish-BoJ reports lend support via lower yields.

Top European News

UK PM Sunak’s ruling Conservative party won Boris Johnson’s former parliamentary seat of Uxbridge and South Ruislip but lost the seat of Somerton and Frome, as well as the Selby and Ainsty seat in the by-elections, while the Selby loss broke the record for the largest Tory majority overturned at a byelection by Labour since 1945, according to The Guardian’s Pippa Crerar.

UK-India trade talks have gained momentum in the latest rounds, though there is still a long way to go, according to Reuters citing sources.

VCI, German Chemical Industry Association’s H1 update: Production -10.5% YY; Revenue -11.5% YY; Producer Prices +5% YY. 2023 guidance: Production -8% (prev. -5%); Revenue -14% (prev. -7%).

FX

Yen slides as UST/JGB spreads blow out amidst BoJ sources saying no inclination to tweak YCC next week.

USD/JPY close to 142.00 after breach of Fib and psych levels on the way up from sub-140.00 low; subsequent remarks from Kanda pressured it back to 141.40 briefly.

DXY boosted by Yen collapse as index tops 101.00 within 100.710-101.080 range.

Kiwi and Aussie undermined by a downturn in risk sentiment and Greenback gains, with NZD/USD and AUD/USD under 0.6200 and 0.6750 respectively, while AUD/NZD cross eyes expiry at 1.0900.

Sterling unable to appreciate better than forecast UK retail sales as Cable retreats from just over 1.2900 towards 21 DMA not far below 1.2850 in face of broad Buck strength.

Euro clings to 1.1100 handle and Loonie underpinned by decent expiry interest around 1.3150 ahead of Canadian retail sales.

PBoC set USD/CNY mid-point at 7.1456 vs exp. 7.1965 (prev. 7.1466)

China’s FX regulator said yuan flexibility is increasing and market understanding of two-way fluctuation and risk-neutral also increased. China will prevent sharp volatility in the exchange rate and will keep the yuan basically stable at balanced levels in a forceful manner, as well as comprehensively use policy measures to stabilise expectations.

Turkey introduced a 15% reserve requirement for FX-protected Lira deposits and is to withdraw TRY 450bln-500bln liquidity from the market through the change in reserves, according to Reuters.

Fixed Income

Bonds see-saw in aimless fashion, beyond Gilts and JGBs that have a clearer sense of direction.

Bunds volatile either side of 133.00 and T-note pivoting parity within 112-02/08+ confines.

Gilts retrace more post-UK CPU upside between 96.70-11 parameters and JGBs rebound firmly from 147.73 to 148.74 at best on the back of dovish BoJ sources

Commodities

WTI and Brent September futures are firmer in the early European hours of Friday and hold onto the APAC gains which emanated from further Chinese economic support measures.

Spot gold is pressured by the Yen-induced Dollar strength and dips from its intraday peak of USD 1,973.40/oz closer to its 100 DMA which resides around USD 1,960.55/oz today.

Base metals meanwhile are broadly underpinned by the aforementioned Chinese stimulus measures.

Russian Deputy PM Novak says Russia is not ruling out introducing oil export products quotas; says some domestic refineries postponed maintenance to a later date, via IFX.

Asian refiners have booked near-record volumes of August crude for August shipping, replacing Middle Eastern oil, via Reuters citing sources; amid competitive prices and large supplies attracting substantial purchases. Source adds that recently US crude is being aggressively pushed to Asia.

Russian missiles have hit the grain terminal of an agricultural enterprise in Ukraine’s Odessa region, with two people injured, according to the Governor of the region cited by Reuters.

Geopolitics

US Central Command said the US is to deploy a marine unit following Iran’s recent attempts to seize ships.

Poland is to move military formations from the west to the east of the nation due to possible threats from Russia’s Wagner group, according to PAP.

Russian navy carried out live fire ‘exercise’ in Black Sea: defence ministry, according to AFP.

Russia’s Black Sea Fleet practices firing rockets at surface targets following a warning to Ukraine on ships, via the Defence Ministry. Warships and planes practised sealing off areas temporarily closed to shipping and seizing ships.

US Event Calendar

07:00: Bloomberg July United States Economic Survey

DB’s Jim Reid concludes the overnight wrap

After a pretty strong last couple of weeks for bonds and equities, both sold off yesterday in the US, with tech having one of the worst days of the year. Ironically, outside of disappointing tech earnings, the main catalyst was actually some positive US data, which shifted the debate back towards next week not necessarily being the last Fed hike in the cycle.

Indeed, more hawkish expectations meant that the 2yr real yield hit a post-GFC high intra-day, though it was breakevens that drove the rates sell off at the end of the day. The rates environment was a setback for equities, while weak tech earnings releases weighed even more, with the NASDAQ falling -2.05% in its biggest post-SVB decline and the 3rd worst day of the year.

In terms of the specific data releases, the most important were the weekly US initial jobless claims, which fell to 228k (vs. 240k expected) over the week ending July 15. That’s the lowest claims number we’ve had in a couple of months, and there are growing signs that this is a trend, with the 4-week moving average down for a third week running to 237.5k. It’s true that the continuing claims were above expectations at 1.754m (vs. 1.722m expected), but that was for the previous week ending July 8, and the broader trend downwards is also still evident from the chart. As well as the jobless claims, the Philadelphia Fed released their manufacturing business outlook survey, with the headline index up slightly to -13.5 (vs. -10.0 expected). But the much better news was on the expectations side, with the headline index for 6 months from now up to a 23-month high of 29.1.

With those more positive releases in hand, investors moved to price in a growing chance of further hikes over the months ahead. For instance, futures raised the chances of a second further hike from the Fed after next week to 35%, having been at 30% the previous day. They also dialled back the chances of rate cuts in 2024, with the rate priced in for December up +10.4bps on the day to 4.03%. In Europe it was much the same story, albeit to a lesser extent, with pricing for a second ECB hike after next week up from 87% to 94%.

All that led to a significant selloff among sovereign bonds, with yields on 10yr Treasuries up +10.3bps on the day to 3.85%. That’s their biggest increase in three weeks, and this was echoed across the curve, with the 2yr yield up +7.4bps to 4.84%. As mentioned at the top, there was a shift in the drivers of higher rates through the course of the day. The 2yr real yield hit a post-GFC high intra-day, but breakevens drove most of increase by the close with 10yr breakevens (+8.6bps) seeing their sharpest daily rise since January.

Europe got some positive, albeit backward looking, economic news as well yesterday, as the latest data revisions showed that the Euro Area avoided a technical recession over the winter. That’s because growth in Q1 was revised up to 0.0% (vs. -0.1% previously), so the latest data now only shows one quarterly contraction in Q4, rather than the two consecutive contractions that are often used to define a recession. Alongside the US data, that supported a fresh rise in yields there too, with those on 10yr bunds (+4.6bps), OATs (+5.0bps) and BTPs (+2.9bps) all moving higher.

This put a dent in US equities, with the S&P 500 (-0.68%) seeing its biggest decline in two weeks. That said, more than 50% of the S&P 500 actually posted gains on the day with the decline driven by tech stocks. Tesla (-9.74%) and Netflix (-8.41%) both lost significant ground following their earnings after the previous day’s close. This weakness among tech stocks meant that the NASDAQ (-2.05%) suffered its worst day in four months, whilst the FANG+ index (-4.60%) of megacap tech stocks had its worst day of 2023 so far. In other negative news on the tech front, leading chipmaker TSMC cut its 2023 outlook and signaled a delay on a new planned production facility in Arizona. TSMC shares are trading more than -3% lower in Asia this morning. Finally, the underperformance of tech megacaps may have been exacerbated by a special rebalancing of the NASDAQ 100 index, which will be effective as of next Monday (24 July) and will see a decline in the index weights of the tech megacaps.

On the other hand, with utilities, energy and industrials outperforming, the Dow Jones (+0.47%) advanced for a 9th consecutive session for the first time since 2017. The European bourses also fared much better, with the STOXX 600 up +0.42% to a one-month high.

In the geopolitical sphere, Ukraine said that ships heading to Russian ports may be military targets following the collapse of the Black Sea grain deal, which comes in response to Russia announcing a similar move regarding ships heading to Ukraine. Wheat prices initially spiked higher following the news, but they pared back their gains and ended the session -0.10% lower after a run of 5 consecutive gains. They are +17% up from their recent lows on 12 July.

Asian equity markets are mixed this morning with the Hang Seng (+0.80%) leading gains while the CSI (+0.24%) and the Shanghai Composite (+0.08%) edging higher after the Chinese government announced detailed measures to support the private sector. Elsewhere, the Nikkei (-0.22%) is lower with the KOSPI (-0.08%) swinging between gains and losses. S&P 500 (+0.12%) and NASDAQ 100 (+0.11%) futures have seen a small rebound.

Early morning data showed that Japan’s consumer inflation climbed by +3.3% y/y in June (v/s +3.2% expected), and slightly higher than May’s +3.2% increase while the core consumer prices rose +3.3% y/y in June, in line with market expectations and against the prior month’s gain of +3.2%. Core core was in-line at +4.2% y/y, down a tenth from last month, the first decrease in the y/y rate since January and likely marks the start of a trend lower. The pace of the decline will determine the BoJ’s policy over that period though. Remember we have an important BoJ meeting next week with some whispers of policy change although the market will be once bitten twice shy on this.

In UK by-elections, the Conservative government suffered a double by-election defeat after Selby and Ainsty (considered as a safe seat) voted against the government giving the Labour its largest swing since 1997 and its biggest ever reversal of a numeric majority in a by-election in history. The Government surprisingly held ex-PM Boris Johnson’s seat in Uxbridge London, as an unpopular scheme by the Labour London mayor on expanding the ultra low emissions zone in the capital, put off voters.

Before we look at the day ahead a quick wrap of yesterday’s other data. US existing home sales for June fell to an annualised rate of 4.16m (vs. 4.20m expected), which is their lowest level in 5 months. Separately, the Conference Board’s leading index for June posted a -0.7% decline (vs. -0.6% expected), marking its 15th consecutive monthly decline. Finally in Europe, German PPI inflation fell to just +0.1% in June, which is its lowest level since November 2020.

To the day ahead now, and it’s a fairly quiet one on the calendar. Data releases include UK and Canadian retail sales for June, whilst earnings releases include American Express.

2 b) NOW NEWSQUAWK (EUROPE/REPORT)/ASIA REPORT

EUROPE

BoJ sources spark dovish reaction in JPY & JGBs, effects seen in broader assets – Newsquawk US Market Open

FRIDAY, JUL 21, 2023 – 05:45 AM

BoJ sources around YCC spark marked dovish reaction in JPY and JGBs, which has filtered through to broader assets

DXY back above 101.00 with USD/JPY testing 142.00; action which eroded GBP’s retail-driven upside

European/US equity benchmarks relatively contained, Tech hit by SAP while NQ benefits from yield action

JGB upside briefly lifts peers with EGBs/USTs struggling for direction while Gilts slip on data

Crude largely resilient to the USD’s upside with base metals underpinned on Chinese stimulus, XAU pressured

Looking ahead, highlights include Canadian Retail Sales. Earnings from American Express & Schlumberger

2. Listen to this report in the market open podcast (available on Apple and Spotify)

3. Trial Newsquawk’s premium real-time audio news squawk box for 7 days

BOJ

BoJ is reportedly leaning towards keeping its yield control policy unchanged at the upcoming meeting, via Reuters citing sources. No consensus within the BoJ on how soon it should begin phasing out stimulus; many policymakers see no imminent need for fresh steps given the 10yr yield is trading stably within the 0.50% cap. Adding, BoJ can wait until there is more clarity on whether a hard landing can be avoided and allow for further wage increases next year. Sources add, YCC needs to end at some point. Though, the timing is not now. Another source said even if tweaks were made, likely be a minor fine-tuning to make YCC sustainable. Expected to revise up core inflation forecasts for FY23, via source; though, FY23 & FY25 expected to be largely in-line with current projections.

Subsequently, BoJ reportedly sees little need to act on YCC for now, via Bloomberg.

Reports which sparked a marked dovish reaction in the JPY and BoJ, click here for details and analysis. A reaction that has also had an influence on the USD, lifting the DXY above 101.00 to the detriment of FX peers and the commodity space across the European morning.

Most recently, Japanese Top Currency Diplomat Kanda says excessive FX moves are undesirable and watching FX markets with a sense of urgency, according to JiJi; Considering all options from the standpoint that excessive moves are undesirable. Will not comment on the current situation.

An update which sparked a brief pullback in USD/JPY, to circa. 141.40 before the move largely reversed.

Japanese Top Currency Diplomat Kanda says he is not in a position to comment on monetary policy; says expectations are spreading in the market of possible monetary policy changes. Expects the BoJ to make appropriate judgement taking account of price conditions and its outlook at every meeting. Signs of changes in corporate price-setting behaviours are emerging.

EUROPEAN TRADE

EQUITIES

European bourses are relatively steady after mixed APAC performance as Chinese support offset the subdued handover, Euro Stoxx 50 -0.1%; in Europe, Tech lags with SAP -3.9%.

Sectors are somewhat mixed with Energy seeing upside on benchmark pricing, though off best as the USD picks up, while Tech and the DAX 40 -0.5% lag after SAP missed on top & bottom.

Stateside, futures are little changed amid a sparse US-specific docket ahead, ES +0.1%; NQ +0.3% is the incremental outperformer after Thursday’s marked pressure and as the dovish-BoJ reports lend support via lower yields.

Click here and here for a recap of the main European equity updates.

FX

Yen slides as UST/JGB spreads blow out amidst BoJ sources saying no inclination to tweak YCC next week.

USD/JPY close to 142.00 after breach of Fib and psych levels on the way up from sub-140.00 low; subsequent remarks from Kanda pressured it back to 141.40 briefly.

DXY boosted by Yen collapse as index tops 101.00 within 100.710-101.080 range.

Kiwi and Aussie undermined by a downturn in risk sentiment and Greenback gains, with NZD/USD and AUD/USD under 0.6200 and 0.6750 respectively, while AUD/NZD cross eyes expiry at 1.0900.

Sterling unable to appreciate better than forecast UK retail sales as Cable retreats from just over 1.2900 towards 21 DMA not far below 1.2850 in face of broad Buck strength.

Euro clings to 1.1100 handle and Loonie underpinned by decent expiry interest around 1.3150 ahead of Canadian retail sales.

PBoC set USD/CNY mid-point at 7.1456 vs exp. 7.1965 (prev. 7.1466)

China’s FX regulator said yuan flexibility is increasing and market understanding of two-way fluctuation and risk-neutral also increased. China will prevent sharp volatility in the exchange rate and will keep the yuan basically stable at balanced levels in a forceful manner, as well as comprehensively use policy measures to stabilise expectations.

Turkey introduced a 15% reserve requirement for FX-protected Lira deposits and is to withdraw TRY 450bln-500bln liquidity from the market through the change in reserves, according to Reuters.

Click here for the notable option expiries, NY cut.

FIXED INCOME

Bonds see-saw in aimless fashion, beyond Gilts and JGBs that have a clearer sense of direction.

Bunds volatile either side of 133.00 and T-note pivoting parity within 112-02/08+ confines.

Gilts retrace more post-UK CPU upside between 96.70-11 parameters and JGBs rebound firmly from 147.73 to 148.74 at best on the back of dovish BoJ sources

WTI and Brent September futures are firmer in the early European hours of Friday and hold onto the APAC gains which emanated from further Chinese economic support measures.

Spot gold is pressured by the Yen-induced Dollar strength and dips from its intraday peak of USD 1,973.40/oz closer to its 100 DMA which resides around USD 1,960.55/oz today.

Base metals meanwhile are broadly underpinned by the aforementioned Chinese stimulus measures.

Russian Deputy PM Novak says Russia is not ruling out introducing oil export products quotas; says some domestic refineries postponed maintenance to a later date, via IFX.

Asian refiners have booked near-record volumes of August crude for August shipping, replacing Middle Eastern oil, via Reuters citing sources; amid competitive prices and large supplies attracting substantial purchases. Source adds that recently US crude is being aggressively pushed to Asia.

Russian missiles have hit the grain terminal of an agricultural enterprise in Ukraine’s Odessa region, with two people injured, according to the Governor of the region cited by Reuters.

US President Biden launched a working group aimed at ending debt-limit standoffs and the White House will explore all legal and policy options to prevent a future debt-ceiling standoff, while it will examine potential actions Congress could take to make default risk a thing of the past, according to a White House official.

US President Biden’s admin. says it has come to a deal with large tech names to place more safeguards around AI, via WSJ; reminder, Biden will meet with the CEO’s of the Cos on Friday at the White House. Cos include Amazon (AMZN), Alphabet’s (GOOGL) Google, Meta (META) and Microsoft (MSFT).

NOTABLE EUROPEAN HEADLINES

UK PM Sunak’s ruling Conservative party won Boris Johnson’s former parliamentary seat of Uxbridge and South Ruislip but lost the seat of Somerton and Frome, as well as the Selby and Ainsty seat in the by-elections, while the Selby loss broke the record for the largest Tory majority overturned at a byelection by Labour since 1945, according to The Guardian’s Pippa Crerar.

UK-India trade talks have gained momentum in the latest rounds, though there is still a long way to go, according to Reuters citing sources.

VCI, German Chemical Industry Association’s H1 update: Production -10.5% YY; Revenue -11.5% YY; Producer Prices +5% YY. 2023 guidance: Production -8% (prev. -5%); Revenue -14% (prev. -7%).

DATA RECAP

UK Retail Sales MM (Jun) 0.7% vs. Exp. 0.2% (Prev. 0.3%); YY (Jun) -1.0% vs. Exp. -1.5% (Prev. -2.1%)

UK Retail Sales Ex-Fuel MM (Jun) 0.8% vs. Exp. 0.2% (Prev. 0.1%); YY (Jun) -1.0% vs. Exp. -1.5% (Prev. -2.1%)

UK GfK Consumer Confidence (Jul) -30.0 vs. Exp. -26.0 (Prev. -24.0)

GEOPOLITICS

US Central Command said the US is to deploy a marine unit following Iran’s recent attempts to seize ships.