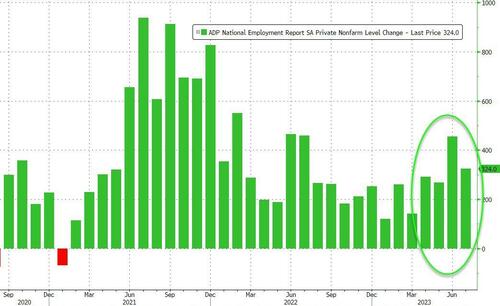

AUGUST 2//AS TELEGRAPHED YESTERDAY WITH THE HUGE T.A.S. ISSUANCE: GOLD FELL $3.45 TO $1938.85 WHILE SILVER FELL BY 43 CENTS TO $23.77//PLATINUM CLOSED DOWN $26.50 TO $926.60 WITH PALLADIUM CLOSING DOWN $40.65 TO $1245.50//EXCELLENT COMMENTARY TODAY FROM EGON VON GREYERZ//BIG NEWS OF THE DAY: THE MASSIVE AMOUNT OF USA DEBT THAT NEEDS TO BE ISSUED IN THE NEXT 5 MONTHS//UKRAINE VS RUSSIA: RUSSIA STRIKES A DEFENSELESS PORT OF DANUBE//POLAND REINFORCES ITS BORDER WITH BELARUS//COVID UPDATES//VACCINE UPDATES/SLAY NEWS/EVOL NEWS//NEWS ADDICTS//ADP REPORTS FAIR JOBS GAINS BUT MANUFACTURING JOBS ARE SUFFERING//TRUMP INDICTED FOR THE THIRD TIME//MORE SWAMP STORIES FOR YOU TONIGHT//

118 H MACQUARIE FUT 1 190 H BMO CAPITAL 84 323 C HSBC 73 363 H WELLS FARGO SEC 40 435 H SCOTIA CAPITAL 30 555 C BNP PARIBAS SEC 2 624 H BOFA SECURITIES 59 661 C JP MORGAN 173 110 690 C ABN AMRO 2 709 C BARCLAYS 9 737 C ADVANTAGE 10 3

TOTAL: 298 298 MONTH TO DATE: 6,706

JPMorgan stopped 110/298 contracts.

FOR AUGUST:

GOLD: NUMBER OF NOTICES FILED FOR AUGUST/2023. CONTRACT: 298 NOTICES FOR 29,800 OZ or 0.9269 TONNES

total notices so far: 6706 contracts for 670,600 oz (20.858 tonnes)

FOR AUGUST:

SILVER NOTICES: 31 NOTICE(S) FILED FOR 155,000 OZ/

total number of notices filed so far this month : 747 for 3,735,000 oz

XXXXXXXXXXXXXXXXXXXXXXXX

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD

WITH GOLD DOWN $3.45

INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD//

HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.75 TONNES OF GOLD FROM THE GLD//

INVENTORY RESTS AT 909.18 TONNES

Silver//

WITH NO SILVER AROUND AND SILVER DOWN 43 CENTS AT THE SLV// small CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 275,000 OZ FROM THE SLV..

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV.

CLOSING INVENTORY: 451.471 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A FAIR SIZED 670 CONTRACTS TO 144,138 AND FURTHER FROM THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THIS FAIR SIZED LOSS IN COMEX OI WAS ACCOMPLISHED WITH OUR STRONG $0.45 LOSS IN SILVER PRICING AT THE COMEX ON TUESDAY. TAS ISSUANCE WAS A HUMONGOUS SIZED 1233 CONTRACTS. THESE WILL BE USED FOR MANIPULATION LATER THIS MONTH. CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON TUESDAY NIGHT: 1235 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS. IT THUS LOOKS LIKE THE FED (GOV’T) IS BEHIND ALL OF THESE TRADES.

WE HAVE NOW SET ANOTHER RECORD LOW AT 114,102 CONTRACTS ///JULY 3.2023// OUR BANKERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.45). AND WERE UNSUCCESSFUL IN KNOCKING OF ANY SILVER CONTRACTS AS WE HAD JUST A TINY LOSS OF 235 CONTRACTS.

WE MUST HAVE HAD:

A FAIR ISSUANCE OF EXCHANGE FOR PHYSICALS( 435 CONTRACTS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 3.105 MILLION OZ (FIRST DAY NOTICE) FOLLOWED BY TODAY’S HUGE QUEUE JUMP OF 10,000 OZ//NEW STANDING 3.770 MILLION OZ// // // FAIR SIZED COMEX OI LOSS/ FAIR SIZED EFP ISSUANCE/VI) HUMONGOUS NUMBER OF T.A.S. CONTRACT ISSUANCE (1434CONTRACTS)/ZERO EXCHANGE FOR RISK ISSUED/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL –218 CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS AUGUST. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF JULY:

TOTAL CONTRACTS for 2 days, total 887 contracts: OR 4.435 MILLION OZ (444 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 4.435 MILLION OZ

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 118.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 85.745 MILLION OZ (SMALLER THAN LAST MONTH)

AUGUST: 4.435 MILLION OZ

RESULT: WE HAD A FAIR SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 670 CONTRACTS WITH OUR LOSS IN PRICE OF $0.45 IN SILVER PRICING AT THE COMEX//TUESDAY.,. THE CME NOTIFIED US THAT WE HAD A FAIR EFP ISSUANCE CONTRACTS: 435 ISSUED FOR SEPT AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS./ WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR AUGUST OF 3.105 MILLION OZ FOLLOWED BY TODAY’S 10,000 QUEUE JUMP//NEW STANDING 3.770 MILLION OZ// .. WE HAVE A TINY SIZED LOSS OF235 OI CONTRACTS ON THE TWO EXCHANGES. THE TOTAL OF TAS INITIATED CONTRACTS TODAY: A HUGE 1233//HUGE FRONT END OF THE TAS CONTRACTS WERE LIQUIDATED DURING THE TUESDAY COMEX SESSION . THE NEW TAS ISSUANCE TODAY (1233) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE./

WE HAD 31 NOTICE(S) FILED TODAY FOR 155,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A STRONG SIZED 5203 CONTRACTS TO 439,383 AND FURTHER FROM TO THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED: 616 CONTRACTS

WE HAD A STRONG SIZED DECREASE IN COMEX OI ( 4587CONTRACTS) WITH OUR STRONG $9.50 LOSS IN PRICE//TUESDAY. WE ALSO HAD A RATHER SMALL INITIAL STANDING IN GOLD TONNAGE FOR AUGUST. AT 30.656 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S 155,000 OZ QUEUE JUMP//NEW STANDING 30.793 TONNES/ + /A FAIR (AND CRIMINAL) ISSUANCE OF 1430 T.A.S. CONTRACTS /// ALL OF..THIS HAPPENED WITH A $9.50 LOSS IN PRICEWITH RESPECT TO TUESDAY’S TRADING.WE HAD A FAIR SIZED LOSS OF 2078 OI CONTRACTS (6.463 PAPER TONNES) ON OUR TWO EXCHANGES.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 3125CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 439,383.

IN ESSENCE WE HAVE A FAIR SIZED DECREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 2078 CONTRACTS WITH 5203 CONTRACTS DECREASED AT THE COMEX// AND A FAIR 3125 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI LOSS ON THE TWO EXCHANGES OF 2078CONTRACTS OR 6,463 TONNES. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): A FAIR 1402 CONTRACTS)

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (3125 CONTRACTS) ACCOMPANYING THE GOOD SIZED LOSS IN COMEX OI (5203) //TOTAL LOSS FOR OUR THE TWO EXCHANGES: 2078 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR NORMAL FORMAT OF BANKERS GOING SHORT AND SPECULATORS GOING LONG ,2.) FAIR INITIAL STANDING AT THE GOLD COMEX FOR JULY AT 30.656 TONNES FOLLOWED BY TODAY’S 155,000 OZ QUEUE JUMP //NEW STANDING 30.793 TONNES/// 3) SOME LONG LIQUIDATION WITH CONSIDERABLE TAS LIQUIDATION //4) FAIR SIZED COMEX OPEN INTEREST LOSS/ 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER///6: FAIR T.A.S. ISSUANCE: 1430 CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023 INCLUDING TODAY

AUGUST

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF AUG :

TOTAL EFP CONTRACTS ISSUED: 5493 CONTRACTS OR 549,300 OZ OR 17.085 TONNES IN 2 TRADING DAY(S) AND THUS AVERAGING: 2746 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 2 TRADING DAY(S) IN TONNES 17,085 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2022, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 17.085/3550 x 100% TONNES 0.778% OF GLOBAL ANNUAL PRODUCTION

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 151.69 TONNES (WEAKER THAN LAST MONTH)

AUGUST: 17.085 TONNES

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF JUNE. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF MAY HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF JUNE., FOR BOTH GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (JUNE), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER FELL BY A FAIR SIZED 670 CONTRACTS OI TO 144,138 AND CLOSER TO OUR COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 435 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

SEPT 435and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 435 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 670 CONTRACTS AND ADD TO THE 435 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A TINY SIZED LOSS OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 235 CONTRACTS

THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES TOTAL 1.175 MILLION OZ

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS//

WEDNESDAY MORNING//TUESDAY NIGHT

SHANGHAI CLOSED DOWN 29.26 PTS OR 0.89% //Hang Seng CLOSED DOWN 493.74 PTS OR 2.47% /The Nikkei CLOSED DOWN 768.89 PTS OR 2.30% //Australia’s all ordinaries CLOSED DOWN 1.24 % /Chinese yuan (ONSHORE) closed DOWN 7.1759 /OFFSHORE CHINESE YUAN DOWN TO 7.1876 /Oil UP TO 81.99 dollars per barrel for WTI and BRENT UP AT 85.42 / Stocks in Europe OPENED ALL RED// ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A GOOD SIZED 5203CONTRACTS DOWN TO 439,383 DESPITE OUR STRONG LOSS IN PRICE OF $9.50 ON TUESDAY. ALL OF THE LOSS WAS DUE TO T.A.S. LIQUIDATION.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE NON ACTIVE DELIVERY MONTH OF JULY… THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 3125 EFP CONTRACTS WERE ISSUED: : DEC 3125 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 3125 CONTRACTS

ON A NET BASIS IN OPEN INTEREST WE LOST THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A FAIR SIZED TOTAL OF 2078 CONTRACTS IN THAT 3125LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A GOOD SIZED LOSS OF 5203 COMEX CONTRACTS..AND THIS LOSS ON OUR TWO EXCHANGES HAPPENED WITH OUR STRONG LOSS IN PRICE OF $9.50//TUESDAY COMEX. AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS DURING MID MONTH IN THE DELIVERY CYCLE), THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR TUESDAY NIGHT WAS A FAIR 1430 CONTRACTS. THROUGHOUT THE PAST WEEKS, THE BANKERS SOLD OFF THE LONG SIDE OF THE SPREAD WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR SPREAD WHICH WILL BE LIQUIDATED TWO MONTHS HENCE)//THE HUGE NUMBER OF T.A.S. CONTRACTS INITIATED OVER THE PAST SEVERAL WEEKS SPELLS TROUBLE FOR THE GOLD/SILVER MARKET AS RAIDS WILL SURELY BE UPON US TRYING TO CONTAIN OUR PRECIOUS METALS RISE IN PRICE.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: AUGUST (30.793) (NON ACTIVE MONTH)

TONNES),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 30.793 TONNES

THE SPECS/HFT WERE SUCCESSFUL IN LOWERING GOLD’S PRICE( IT LOST $9.50) //// AND WERE UNSUCCESSFUL IN KNOCKING ANY SPECULATOR LONGS AS, ALL THE LOSS WAS DUE TO T.A.S. LIQUIDATION THROUGHOUT THE TUESDAY COMEX SESSION WHICH BASICALLY TOOK CARE OF THE ENTIRE LOSS IN OPEN INTEREST. THE T.A.S. ISSUED ON TUESDAY NIGHT WILL BE “PUT INTO THE BANK” TO BE USED AT A LATER DATE AT THE COLLUSIVE CHOOSING OF OUR BANKERS.

WE HAVE LOST A TOTAL OI OF 6.463 PAPER TONNES OF TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR AUST. (30.656 TONNES) ON FIRST DAY NOTICE FOLLOWED BY TODAY’S 155,000 OZ QUEUE JUMP //NEW STANDING 30.793 TONNES // ALL OF THIS WAS ACCOMPLISHED WITH OUR STRONG LOSS IN PRICE TO THE TUNE OF $9.50.

WE HAD – REMOVED 616 CONTRACTS TO THE COMEX TRADES TO OPEN INTEREST

NET LOSS ON THE TWO EXCHANGES 2078 CONTRACTS OR 207,800 OZ OR 6.463 TONNES.

Total monthly oz gold served (contracts) so far this month

6706 notices 670,600 OZ 20.858 TONNES

Total accumulative withdrawals of gold from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of gold from the Customer inventory this month

x

0 dealer deposit:

total dealer deposits: nil oz

total customer deposits: 0 oz

we had 2 customer withdrawals:

i) Out of Brinks: 289.36 oz (9 kilobars)

ii) Out of JPMorgan: 6430.200 oz (200 kilobars)

total withdrawals: 6719.56 oz

Adjustments; 0 /

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR AUGUST.

For the front month of AUGUST we have an oi of 3492 contracts having LOST 851 contracts. We had 1006 contracts filed

on Tuesday, so we gained 155 contracts or an additional 15,500 oz will stand at the comex.

Sept lost 85 contracts to 2367.

Oct gained 881 contracts to 32,510 contracts.

We had 298 contracts filed for today representing 29,800 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 173 notices were issued from their client or customer account. The total of all issuance by all participants equate to 298 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 298 notice(s) was (were) stopped received by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the AUGUST /2023. contract month,

we take the total number of notices filed so far for the month (6706 x 100 oz ), to which we add the difference between the open interest for the front month of AUGUST (3492 CONTRACT) minus the number of notices served upon today 298 x 100 oz per contract equals 990,000 OZ OR 30.793 TONNES the number of TONNES standing in this active month of AUGUST.

thus the INITIAL standings for gold for the AUGUSTcontract month: No of notices filed so far (6706) x 100 oz + (3492) {OI for the front month} minus the number of notices served upon today (298) x 100 oz) which equals 990,000 oz standing OR 30.793 TONNES

TOTAL COMEX GOLD STANDING: 30.793 TONNES WHICH IS SMALL FOR AN ACTIVE DELIVERY MONTH.

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 22,202,871.168 OZ

TOTAL REGISTERED GOLD: 12,102,270.124 (376,43 tonnes)..

TOTAL OF ALL ELIGIBLE GOLD: 10,100,601.044 O Z

REGISTERED GOLD THAT CAN BE SERVED UPON: 10,050,880 OZ (REG GOLD- PLEDGED GOLD) 313.62 tonnes//

END

SILVER/COMEX

AUGUST 2

//2023// THE AUGUST 2023 SILVER CONTRACT

Silver

Ounces

Withdrawals from Dealers Inventory

NIL oz

Withdrawals from Customer Inventory

493,526.702 oz CNT

.

Deposits to the Dealer Inventory

149,457.960 oz ASAHI

Deposits to the Customer Inventory

300,867.100 oz Loomis

No of oz served today (contracts)

31 CONTRACT(S) (155,000 OZ)

No of oz to be served (notices)

7 contracts (35,000 oz)

Total monthly oz silver served (contracts)

747 Contracts (3,735,000 oz)

Total accumulative withdrawal of silver from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of silver from the Customer inventory this month

i) 1 dealer deposit

i) Into ASAHI: 149,457.960 oz

total dealer deposit: 149,457.960 oz oz

i) We had 0 dealer withdrawal

total dealer withdrawals: 0 oz

We had 1 deposits customer account:

i)Into Loomis: 300,867.100 oz

total customer deposits: 300,867.100 oz

JPMorgan has a total silver weight: 139.910 million oz/281.652 million =49.71% of comex .//

Comex withdrawals 1

i)Out of CNT 493,526.702 oz

total: 493,526.702 oz

adjustments: 0

TOTAL REGISTERED SILVER: 31.692 MILLION OZ//.TOTAL REG + ELIGIBLE. 281.652 million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR JULY:

silver open interest data:

FRONT MONTH OF AUGUST /2023 OI: 38 CONTRACTS HAVING LOST 232 CONTRACT(S). WE HAD

234 NOTICES FILED ON TUESDAY SO WE GAINED TWO CONTRACTS OR AN ADDITIONAL 10,000 OZ WILL STAND IN THIS NON ACTIVE DELIVERY MONTH OF AUGUST.

SEPT HAS A LOSS OF 1796 CONTRACTS UP TO 112,212

OCT GAINED 21 CONTRACTS TO STAND AT 74.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 31 for 155,000 oz

Comex volumes// est. volume today 76,418 good/raid /

Comex volume: confirmed yesterday: 57,976 poor

To calculate the number of silver ounces that will stand for delivery in AUGUST. we take the total number of notices filed for the month so far at 747 x 5,000 oz = 3,735,000 oz

to which we add the difference between the open interest for the front month of AUGUST (38) and the number of notices served upon today 31 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the AUGUST/2023 contract month: 747 (notices served so far) x 5000 oz + OI for the front month of AUGUST (38) – number of notices served upon today (31 )x 500 oz of silver standing for the AUGUST contract month equates to 3.770 million oz.

There are 31.54 million oz of registered silver.

thus if we take today’s standing at 3.73 and add last month’s 30.9 million oz we have 34,63 million oz against only 31.5 million registered silver.

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS

AUGUST 2/WITH GOLD DOWN $3.45 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 3.75 TONNES OF GOLD FROM THE GLD//: //: / .////INVENTORY RESTS AT 909.18 TONNES

AUGUST 1/WITH GOLD DOWN $28.45 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 2.89 TONNES OF GOLD FROM THE GLD//: //: / .////INVENTORY RESTS AT 912.93 TONNES

JULY 31/WITH GOLD UP $9.50 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 2.89 TONNES OF GOLD FROM THE GLD//: //: / .////INVENTORY RESTS AT 912.93 TONNES

JULY 28/WITH GOLD UP $14.15 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 1.44 TONNES OF GOLD FROM THE GLD//: //: / .////INVENTORY RESTS AT 915,82 TONNES

JULY 27/WITH GOLD DOWN $21.80 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 1.74 TONNES OF GOLD FROM THE GLD//: //: / .////INVENTORY RESTS AT 917.26 TONNES

JULY 26/WITH GOLD UP $6.35 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD: //: / .////INVENTORY RESTS AT 919.00 TONNES

JULY 25/WITH GOLD UP $2.45 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD: //: / .////INVENTORY RESTS AT 919.00 TONNES

JULY 24/WITH GOLD DOWN $4.65 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 5.20 TONNES OF GOLD INTO THE GLD//: / .////INVENTORY RESTS AT 919.00 TONNES

JULY 21/WITH GOLD DOWN $3.80 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD: / .////INVENTORY RESTS AT 913.80 TONNES

JULY 20/WITH GOLD DOWN $8.70 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.73 TONNES FROM THE GLD/ .////INVENTORY RESTS AT 913.80 TONNES

JULY 19/WITH GOLD UP $0.65 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .86 TONNES FROM THE GLD/ .////INVENTORY RESTS AT 912.07 TONNES

JULY 18/WITH GOLD UP $23.45 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD: .////INVENTORY RESTS AT 912.93 TONNES

JULY 17/WITH GOLD DOWN $6.60 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.73 TONNES OF GOLD FROM THE GLD.////INVENTORY RESTS AT 912.93 TONNES

JULY 14/WITH GOLD UP $0.75 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD: ////INVENTORY RESTS AT 914.66 TONNES

JULY 13/WITH GOLD UP $3.30 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 0.29 TONNES OF GOLD OUT OF THE GLD////INVENTORY RESTS AT 914.66 TONNES

JULY 12/WITH GOLD UP $24.50 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 0.31 TONNES OF GOLD OUT OF THE GLD////INVENTORY RESTS AT 914.95 TONNES

JULY 11/WITH GOLD UP $6.15 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.0 TONNES OF GOLD OUT OF THE GLD////INVENTORY RESTS AT 915.26 TONNES

JULY 10 WITH GOLD DOWN $1.35 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.60 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 916.26 TONNES.

JULY 7 WITH GOLD UP $16.80 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 917.86 TONNES.

JULY 6/WITH GOLD DOWN $9.90 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.04 TONNES OF GOLD FROM THE GLD//INVENTORY RESTS AT 917.86 TONNES

JULY 5/WITH GOLD DOWN $2.20 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD; A WITHDRAWAL OF 2.6 TONNES FROM THE GLD///INVENTORY RESTS AT 921.90 TONNES

JULY 3/WITH GOLD UP $1.90 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 924.50 TONNES//

JUNE 30/WITH GOLD UP $10.00 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.31 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 924.50 TONNES

JUNE 29/WITH GOLD DOWN $3.20 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.26 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 926.81 TONNES

JUNE 28/W

GLD INVENTORY: 909.18 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

AUGUST 2/WITH SILVER DOWN 43 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 275,000 OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 451.471 MILLION OZ

AUGUST 1/WITH SILVER DOWN 61 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 184,000 OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 451.746 MILLION OZ

JULY 31/WITH SILVER UP 45 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 184,000 OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 451.746 MILLION OZ

JULY 28/WITH SILVER UP 15 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 550,000 OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 451.930 MILLION OZ

JULY 27/WITH SILVER DOWN 59 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: .////INVENTORY RESTS AT 452.480 MILLION OZ

JULY 26/WITH SILVER UP 15 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: .////INVENTORY RESTS AT 452.480 MILLION OZ/

JULY 25/WITH SILVER UP 24 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A SMALL WITHDRAWAL OF 826,000 OZ FROM THE SLV..////INVENTORY RESTS AT 452.480 MILLION OZ/

JULY 24/WITH SILVER DOWN 23 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: ////INVENTORY RESTS AT 453.306 MILLION OZ/

JULY 21/WITH SILVER DOWN 14 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 1.101 MILLION OZ OF SILVER FROM THE SLV ////INVENTORY RESTS AT 453.306 MILLION OZ/

JULY 20/WITH SILVER DOWN 38 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 1.468 MILLION OZ OF SILVER FROM THE SLV ////INVENTORY RESTS AT 454.107 MILLION OZ/

JULY 19/WITH SILVER UP 11 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV:A ////INVENTORY RESTS AT 455.875 MILLION OZ/

JULY 18/WITH SILVER DOWN 19 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV:A ////INVENTORY RESTS AT 455.875 MILLION OZ/

JULY 17/WITH SILVER UP 25 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 4.856 MILLION OZ OF SILVER FROM THE SLV////////INVENTORY RESTS AT 455.875 MILLION OZ/

JULY 14/WITH SILVER UP 27 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 2.21 MILLION OZ OF SILVER FROM THE SLV////////INVENTORY RESTS AT 455.875 MILLION OZ/

JULY 13/WITH SILVER UP 64 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//////INVENTORY RESTS AT 462.941 MILLION OZ/

JULY 12/WITH SILVER UP $1.00 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.881 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 462.941 MILLION OZ/

JULY 11/WITH SILVER DOWN 5 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF .020 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 464.822 MILLION OZ/

JULY 10/WITH SILVER UP 2 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.672 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 464.802 MILLION OZ

JULY 7/WITH SILVER UP 42 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 466.474 MILLION OZ

JULY 6/WITH SILVER DOWN 50 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.667 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 466.474 MILLION OZ//

JULY5/WITH SILVER UP 30 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 468.141 MILLION OZ//

JULY 3/WITH SILVER UP 7 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 468.141 MILLION OZ//

The Everything Bubble is about to turn to the Everything Collapse!

This is the inescapable outcome for the Western world.

The world economy should have collapsed in 2008 were it not for a massive Hocus Pocus exercise by Western central banks. At that time, global debt was $125 trillion plus derivatives. Today debt is $325 trillion plus quasi-debt or derivatives of probably $2+ quadrillion.

The US is today running bigger deficits than ever at a time when:

The interest rate cycle is strongly up

There is only one buyer of US debt – the Fed

Dedollarisation will lead to a rapid decline of the dollar.

The financial system should have been allowed to collapse 15 years ago when the problem was 1/3 of today. But governments and central bankers prefer to postpone the inevitable and thus passing the batten to their successors thereby exacerbating the problem.

FALSEHOOD IS THE MOTTO

The world is now desperately clinging on to a false prosperity, based on false money, false moral values, false financial values, false politics and politicians, false media, false reporting of reality whether vaccines, climate, genders or history etc.

Let’s look at some synonyms to false or falsehood according to Thesaurus:

Cover-up, deceit, deception, dishonesty,

fabrication, fakery, perjury, sham etc.

Yes, all of the above fits today’s West and especially the US. But as I often point out, history repeats itself so this is nothing new. But since most major cycles can take 100 years from boom to bust and back again, very few people experience a severe depression in their lifetime.

In the West, the last major depression was in the 1930s followed by WWII.

Yes, I have repeated a similar message for quite a while. My purpose with this repetition is obvious. The world and in particular the Western economies are facing a wealth destruction never before seen in history and very few people are prepared for it.

As the Romans said: “Repetition is the mother of learning”.

Let’s just look at a couple of quotes from the Greek philosopher Plato 2,500 years ago.

DEBT IS THE CONSEQUENCE NOT THE CAUSE

So nothing has changed but just as we have climate cycles, there are also well defined economic cycles of boom and bust.

Major economic cycles normally have a similar ending as von Mises said:

“a final and total catastrophe of the currency system involved.”

Or as Voltaire expressed it: “Paper money eventually returns to its intrinsic value – ZERO.”

Debt is not the reason for the problems which the world is now facing. Instead debt is a consequence of the falsehood culture that that is toxifying the world.

Unacceptable increases in sovereign debt arises when governments can no longer tell the truth, if they ever could!

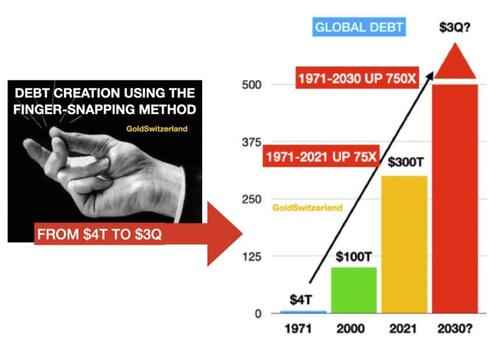

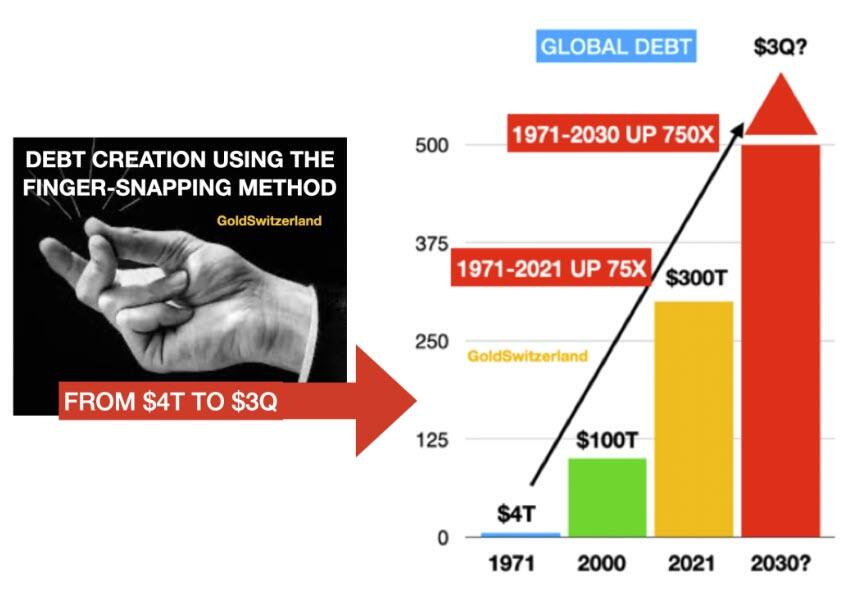

So the end of the current economic cycle started when Nixon closed the gold window on August 15,1971. At that point, he realised that the US could no longer continue to run budget deficits as they had done since the early 1930s. To get rid of the disciplinary shackles of gold allowed the US government and most central banks to create “finger-snapping” money. This is what a Swedish Riksbank official called creating money out of thin air.

When In 1971, global debt was a “mere” $4 trillion. In 2023 global debt is $325T excluding derivatives. This is clearly a major timebomb as I wrote about recently.

By 2030, debt could be as high as $3 quadrillion. This assumes that the quasi debt of global derivatives of $2 – $2.5 quadrillion has been “rescued” by central banks in order to stop the financial system from imploding.

First we will obviously see major pressures in the on balance sheet credit market. Corporate bankruptcy filings are increasing in most countries. In the US it is on a 13 year high for example, up 53% from 2022. Moody expects global corporate defaults to keep surging as financial conditions tighten.

The US banks are grappling with deposit flight, higher rates and major risks in the property sector.

The pressures in the commercial property market and in housing will lead to a wave of defaults necessitating further money printing. S&P reports that 576 banks are at risk of overexposure to commercial property loans and surpassing regulatory guidelines.

BORROWERS WILL DEFAULT AND BANKS GO BANKRUPT

The bank failures in mid-March starting with Silicon Valley Bank were just a warning shot.

Banks need high rates and a reduction in the loan portfolio to survive.

But borrowers, both commercial and private, need lower rates and more credit to survive.

This is a dilemma without solution. It will end up with both sides losing. Borrowers will default and banks will go bankrupt.

Before that there will be the biggest debt feast in the history of the world.

Luckily it requires no skill, no assets, no security to create the quadrillions of dollars which will temporarily defer the problem.

All that is needed is a bit more finger-snapping.

It will all happen first gradually and then suddenly as Hemingway described the process of going bankrupt. I have described this gradual/sudden process in previous articles, the first time I believe in 2017 when I talk about “Exponential moves as terminal”

Imagine a football stadium which is filled with water. Every minute one drop is added. The number of drops doubles every minute. Thus it goes from 1 to 2, 4, 8 16 etc. So how long would it take to fill the entire stadium? One day, one month or a year? No it would be a lot quicker and only take 50 minutes! That in itself is hard to understand but even more interestingly, how full is the stadium after 45 minutes? Most people would guess 75-90%. Totally wrong. After 45 minutes the stadium is only 7% full! In the final 5 minutes the stadium goes from 7% full to 100% full.

So if we take 1971 as the beginning of the debt explosion we can see that the real exponential phase happens in the final 5 minutes which are still to come.

And this is how global debt can explode in the final phase of a credit boom.

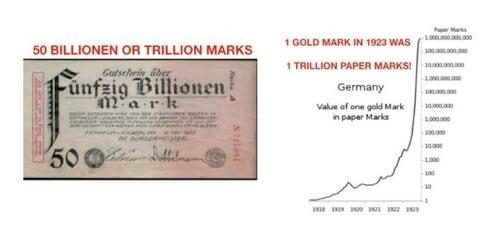

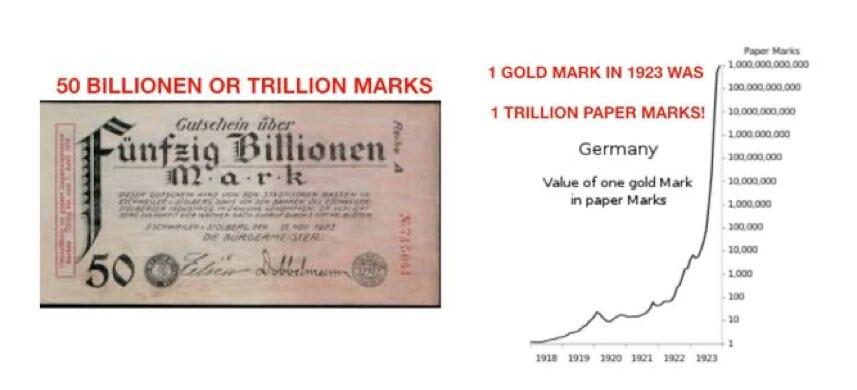

The hyperinflation in Weimar Germany in the early 1920s show a similar pattern:

As the graph above of the gold price in marks shows, the price of an ounce of gold went from below 10,000 marks at the beginning of 1923 to over 1 trillion by the end of the year.

No one should expect gold to go to $1 trillion but everyone should expect the dollar and most currencies to fall precipitously.

THE PERFECT WEALTH DESTRUCTION SCENARIO

So we now have a perfect setup for the coming wealth destruction scenario:

Global debt has gone up 80X between $4T in 1971 to $325 trillion in 2023

Bursting of the derivatives bubble could push debt to $3+ quadrillion

High interest rates and high inflation lead to sovereign and private defaults

Bubble assets like stocks, bonds and property will fall dramatically in real terms

Major debasement of USD and most currencies

Real assets – commodities, metals, oil, gas, uranium etc will rise strongly

Higher taxes, bail-ins, failure of pension and social security system

Central banks will fail to save the system leading to debt implosion and defaults

A deflationary depression will hit the West worst in a long term decline

The East and South (BRICS, SCO etc) will also suffer but emerge much stronger

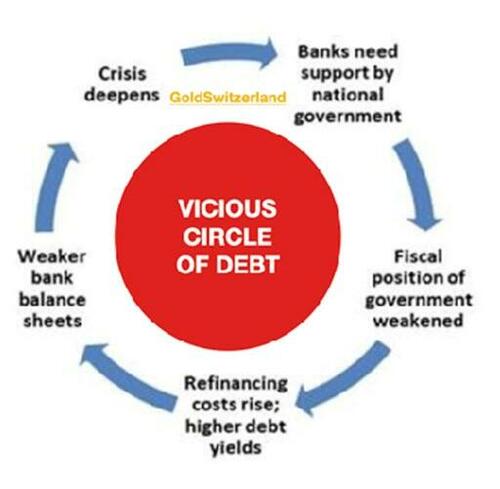

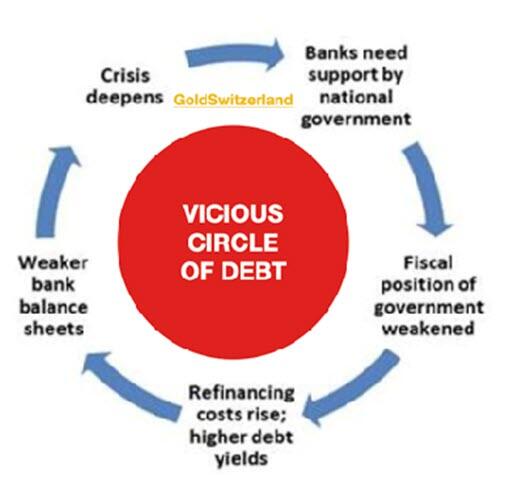

So we now have a perfect vicious circle of debt eventual leading to default:

DESPERATE GOVERNMENTS TAKE DESPERATE ACTIONS

Yes, the West led by a bankrupt USA will try all tricks in the books. That will include CBDCs (Central Bank Digital Currencies), much higher taxes especially for the wealthy, bank bail-ins (forcing depositors to buy 10-30 year government bonds), martial law and many more measures to restrict people’s everyday lives.

These government bonds will have zero value since there will be no buyers.

CBDCs will also soon become worthless as they are just another form of unlimited paper or finger-snapping money.

I doubt ordinary people will accept these draconian measures. Thus there will be civil unrest which governments will be unable to control. Neither police nor the military will accept to turn against suffering fellow citizens.

PROTECTING RISK IS ESSENTIAL – TIMING IS NOT

I am obviously aware that the consequences I have outlined above of the biggest global debt bubble in history can be wrong.

I have not specified the timing of these events. I have learnt that forecasting timing is a mug’s game.

Interestingly mug comes from the Swedish MUGG which is a drinking cup with the alcohol turning you to a mug or fool.

Personally I believed that the system was ready to collapse after the 2006-9 subprime crisis but today 14 years later, the system is still standing but only JUST!

But since we are most probably in the final 5 minutes as I explained above, timing becomes irrelevant. We need to take all the measures we can before events start to unravel.

We are now talking about financial survival and for many also physical survival.

In a world with financial and economic misery, high unemployment, a collapsing support system whether social security or pensions, a failing health system, social unrest and possibly war, we are all going to suffer.

HOW TO PROTECT YOUR WEALTH

Since we can’t forecast when the greatest wealth destruction in history will start, we need to prepare today. As I often repeat, you can’t buy fire insurance after the fire has started.

So now is the time to put your house in order.

Forget about gluttony or greed. Forget about trying to get out of stocks at the top. Forget about the old axioms that stocks and property always go up. Forget about the notion that sovereign debt is always safe.

Just remember one thing the next however many years is all about economic survival.

If you haven’t made your money from ordinary investments in the last 20+ years, you are very unlikely to make it now.

And if you hang on to your portfolio of conventional investments like stocks, bonds and investment properties, you are standing the risk of a severe decline of 50-90% of your portfolio for a very, very long period.

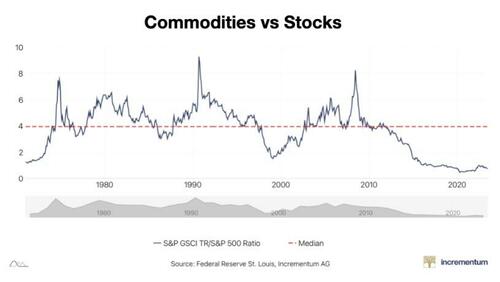

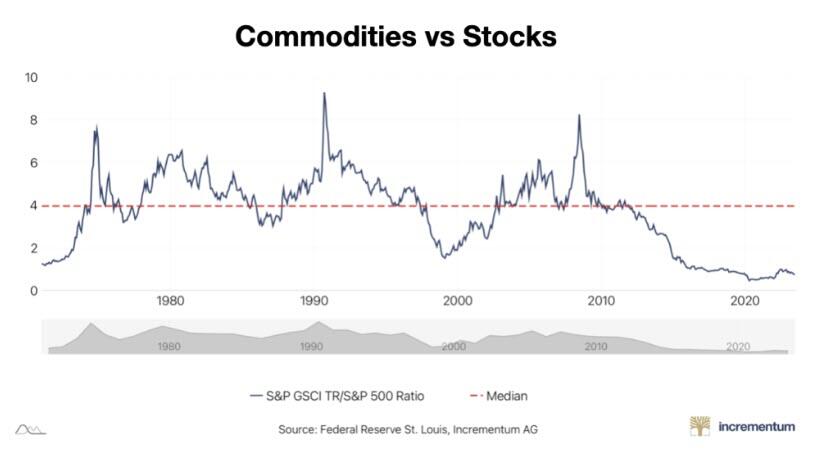

More safe investments in the current climate are commodities.

Look at the chart below showing Commodities versus Stocks (S&P) years. We are looking at a 50+ year low.

Best stocks to hold would be in precious metals, oil, and uranium.

The king of wealth preservation is gold. Silver is very undervalued and thus has more upside potential than gold but is much more volatile.

For the best protection, gold and silver should be held in physical form directly by the investor and stored in the safest private vaults in the safest jurisdictions.

After having organised our financial affairs, we must think about the people that need our help in whatever form.

Then enjoy life with family, friends as well as nature, books, music etc which are all free pleasures.

END

3,Chris Powell of GATA provides to us very important physical commentaries

USAGold’s ‘News & Views’ letter for August has July’s top 10 commentaries

Submitted by admin on Tue, 2023-08-01 15:17Section: Daily Dispatches

3:15p ET Tuesday, August 1, 2023

Dear Friend of GATA and Gold:

USAGold’s “News & Views” letter for August with its top 10 gold-related reports and commentaries for the past month is pretty encouraging for the monetary metal and it’s posted here:

CHRIS POWELL, Secretary/Treasurer Gold Anti-Trust Action Committee Inc. CPowell@GATA.org

end

4, OTHER IMPORTANT GOLD/SILVER COMMENTARIES/SILVER

5 a. IMPORTANT COMMENTARIES ON COMMODITIES: RARE EARTHS

A very important commentary on rare earths

(Senergy Capital)

China Threatens to Weaponize Rare Earth Materials; Establishing Additional Sources of North American REE Production is Now Even More Important

BY SENERGY CAPITAL

On July 3, China announced it will impose export restrictions on eight gallium and six germanium products beginning on August 1 for national security reasons. These exotic metals, which are byproducts from refining aluminum and zinc, are used in numerous cutting-edge technologies, particularly in silicon chips for the semiconductor sector. China’s move is widely viewed as retaliation for U.S. curbs on the sale of technologies to China. China’s gallium and germanium export controls could lay the groundwork for an even broader action, the curtailment of exports of rare earth elements (REEs), crucial materials used in a wide variety of technology devices such as smartphones, digital cameras, flat screen televisions, and electronic displays. The clean energy and defense contracting industries are also heavy users of REEs. Not surprisingly, the demand for rare earths is soaring: the independent research firm Adamas Intelligence projects the global demand for rare earth oxides (REOs) will more than triple by 2035 to US$46 billion from US$15 billion in 2022.

China has restricted the exports of rare earths before — an action which caused prices of some REOs to rise almost exponentially for several years. In 2010, China severely restricted sales to Japan following a territorial dispute regarding the Japan-administered Senkaku Islands. China also claims those islands and calls them Diaoyu. In turn, Japan scrambled to find alternative sources, forcing prices higher.

What are Rare Earth Elements?

REEs are relatively plentiful in the earth’s crust but are typically widely dispersed, rendering their mining in a single location quite expensive (unless the site is determined to have enormous resources). The molecular structure of REEs is such that they frequently occur together in minerals, perhaps even in multiple mineral structures. Not surprisingly, these characteristics generally make their separation and extraction difficult.

The 17 rare earth elements are generally categorized as light or heavy elements. Each source of rare earth material will generally contain the entire spectrum of REEs, but in varying percent ages. The heavy REEs (HREEs) are rarer and generally sell for significantly higher prices, as they are less common and more costly to separate. In contrast, light rare earth elements (LREEs) are produced in larger quantities because they occur naturally in greater quantities. Producers strive to meet the high demand for Neodymium (Nd) and Praseodymium (Pr), which necessitates the over-production of all associated LREEs like lower-priced cerium and lanthanum. For example, a typical rare earth concentrate from a mining operation may contain 75% of lower priced lanthanum (La) and cerium (Ce), perhaps 15% of higher-priced Nd and Pr, and about 10% other HREEs like dysprosium (Dy) and terbium (Tb).

China’s Dominant Rare Earth Position

According to the U.S. Geological Survey, China produced 70% of all rare earths mined globally in 2022. Even more important, Adamas Intelligence estimates that China controls at least 85% of the world’s rare earth refining capacity – the ability to transform mined rare earth ores into extremely valuable rare earth oxides (REOs).

In recent years, the U.S. has managed to reduce its dependence on China for rare earth supply, but only slightly. According to Reuters, America sourced 74% of its rare earths from China between 2018 and 2021.

North American REE Industry

MP Materials Corp. (NYSE: $MP) owns and operates the Mountain Pass facility in southern California, the only integrated rare earth mining and processing site in North America. The bastnaesite ore body at Mountain Pass has been mined as a principal source of REEs for more than 60 years. In 2022, Mountain Pass produced about 42,500 tonnes of REOs. Today, MP’s stock market capitalization is around US$4.4 billion.

Defense Metals Corp. (TSXV: $DEFN; OTC: $DFMTF) is a much lower-priced (C$67 million stock market cap) rare earth play. The company owns 100% of the advanced-stage Wicheeda project in central British Columbia, Canada, which has the potential to be the next North American rare earth mine. The Wicheeda deposit has favorable geology and mineralogy; it hosts bastnaesite and monazite; rare earth minerals that are found at Mountain Pass and at Mount Weld, the major Australian rare earth mine. Rare earth deposits comprised of bastnaesite, and monazite have been the only rare earth minerals that have been exploited as sources of profitable commercial rare earth production. See Figure 1.

Figure 1: Defense Metals Wicheeda Mineralogy and Metallurgy Compares Favorably with the World’s Primary Producing Rare Earth Facilities

Source: Defense Metals Corp. Independent Preliminary Economic Assessment for the Wicheeda Rare Earth Element Project, British Columbia, Canada, dated January 6, 2022, with an effective date of November 7, 2021, and prepared by SRK Consulting (Canada) Inc. is filed under Defense Metals Corp.’s Issuer Profile on SEDAR (“PEA”).

The 6,759-hectare (~16,702-acre) Wicheeda Project contains five million tonnes of indicated resources at a total REO grade of 2.95%, and 29.5 million tonnes of inferred resources at a 1.83% grade, reported at a cut-off grade of 0.5% total REO within a conceptual (LG) pit shell (see PEA). In addition, the project is ideally situated both for mining and production. It is just 80 kilometers (km) northeast of Prince George, a mining center with a skilled labor force, and sits along a major forestry road that connects to a paved highway. A hydroelectric power line, nat ural gas pipeline, and a Canadian National Railway line are also nearby. The busy port of Prince Rupert is just 500 km to the west. See Figure 2.

In addition to completing significant exploration drilling to define the Wicheeda REE deposit, Defense Metals has completed extensive metallurgical testing that showing the ability to produce a > 40% REO flotation concentrate that is amenable to hydrometallurgical processing to produce a rare earth oxide product for sale to end users. See Figure 1. All of this work is being incorporated into a pre-feasibility study that is expected to be released in the first half of 2024.

If Wicheeda begins to produce REOs it could be one of the biggest REO production facilities in the world. More specifically, the project should produce about 25,000 tonnes of REO annually, or about 10% of global REO manufactured in the world. See Figure 3.

Figure 3: Wicheeda Could Supply ~10% of Current Global Production

Source: Defense Metals Corp. PEA

Defense Metals last traded at C$0.235 on the TSX Venture Exchange and USD$0.183 on the OTC Markets, as of July 28th 2023.

Qualified Person

The scientific and technical information contained herein as it relates to the Wicheeda REE Project has been reviewed and approved by Kristopher J. Raffle, P.Geo. (B.C.), Principal and Consultant of APEX Geo science Ltd. of Edmonton, Alberta, who is a director of Defense Metals and a “Qualified Person” (“QP”) as defined in NI 43-101.

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS WEDNESDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED DOWN TO 7.1759

OFFSHORE YUAN: DOWN TO 7.1876

SHANGHAI CLOSED DOWN 29.26 PTS OR 0.89%

HANG SENG CLOSED DOWN 493.74 PTS OR 2.47%

2. Nikkei closed DOWN 768.89 PTS OR 2.30%

3. Europe stocks SO FAR: ALL RED

USA dollar INDEX UP TO 102.05 EURO FALLS TO 1.0976 DOWN 31 BASIS PTS

3b Japan 10 YR bond yield: RISES TO. +.620 Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 142.74/JAPANESE YEN FALLING AS WELL AS LONG TERM 10 YR. YIELDS RISING //EVENTUALLY THIS WILL BREAK THE JAPANESE CENTRAL BANK

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen UP CHINESE ON SHORE YUAN: DOWN// OFF- SHORE: DOWN

3f Japan is to buy INFINITE TRILLION YEN’S worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and UP FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund UP TO +2.4665***/Italian 10 Yr bond yield RISES to 4.122*** /SPAIN 10 YR BOND YIELD RISES TO 3.521…**

3i Greek 10 year bond yield RISES TO 3.749

3j Gold at $1951.00 silver at: 24.41 1 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble DOWN 0 AND 70 /100 roubles/dollar; ROUBLE AT 93.03//

3m oil into the 81 dollar handle for WTI and 85 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 142.74// 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 0.620% STILL ON CENTRAL BANK (JAPAN) INTERVENTION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.8634 as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9642 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.018 DOWN 3 BASIS PTS…

USA 30 YR BOND YIELD: 4.094 DOWN 1 BASIS PTS/

USA 2 YR BOND YIELD: 4.866 DOWN 5 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 26.97…(TURKEY SET TO BLOW UP FINANCIALLY)

GREAT BRITAIN/10 YEAR YIELD: UP 0 BASIS PTS AT 4.424

end

2.a Overnight: Newsquawk and Zero hedge:

“The Market Is Looking For Excuses To Take Profits”: Futures Slide As US Downgrade Shakes Sentiment

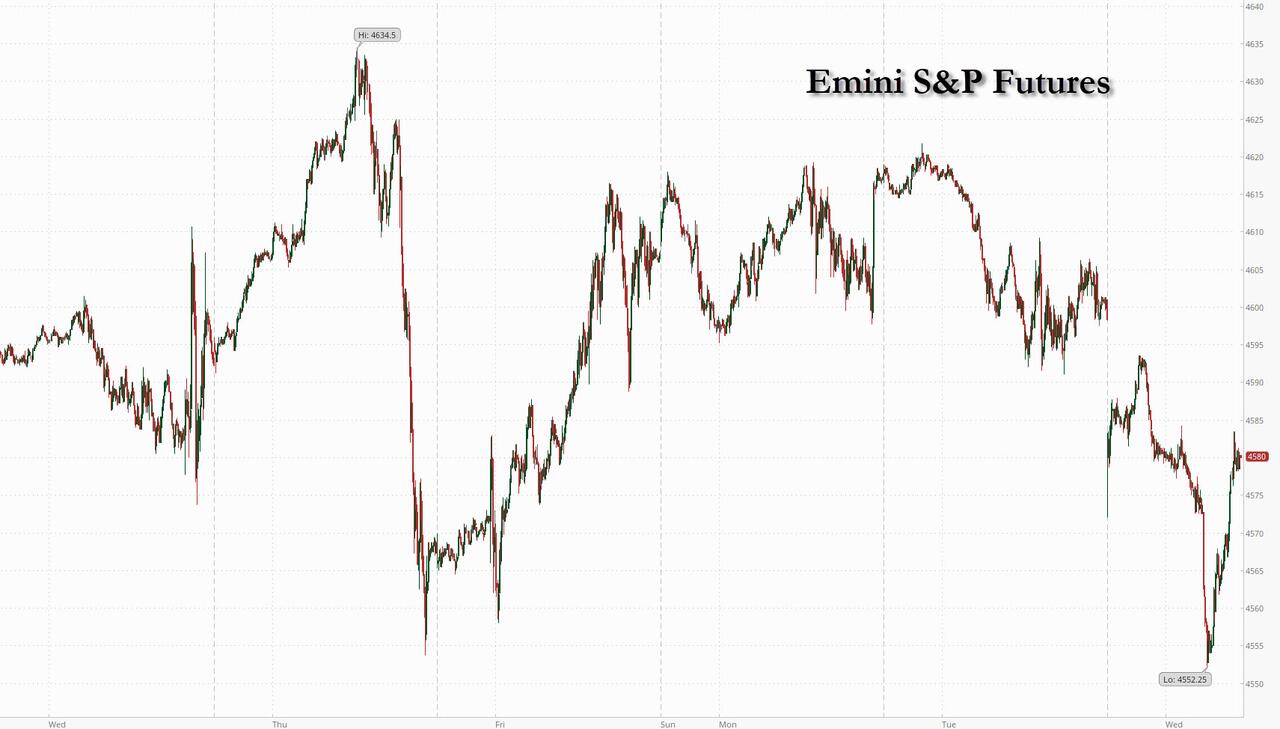

WEDNESDAY, AUG 02, 2023 – 08:08 AM

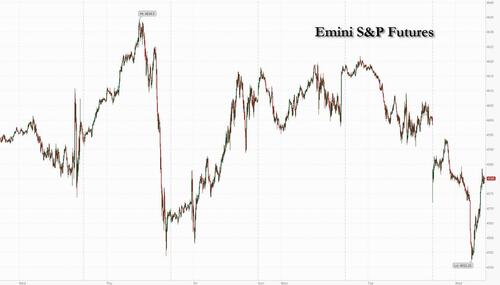

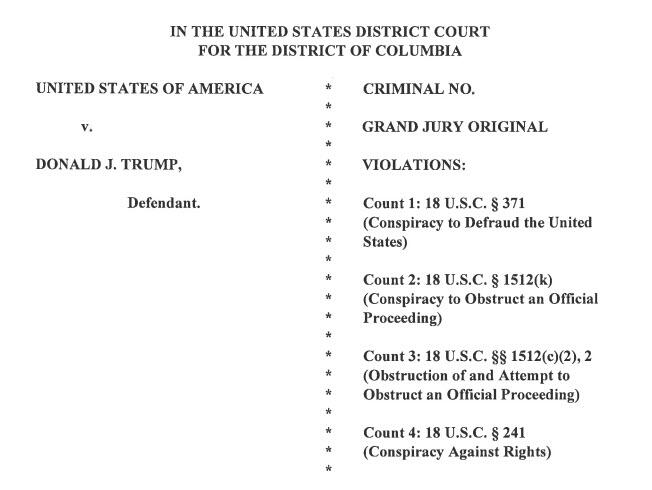

US futures slumped as part of a global risk-off tone (but were well off their lows, which were down as much as 1%), after the US was stripped of its AAA top-tier credit rating by Fitch (which joined S&P in doing so back in 2011), due to growing fiscal deficits and an “erosion of governance” even as Treasuries yields and the Dollar were steady. And in a complete coincidence, at the exact same time, Donald Trump was indicted for a record third time on federal charges over his efforts to overturn the 2020 presidential election, and has a court date set for Thursday.

As of 7:45am, emini S&P futures were down 0.5%, while Nasdaq 100 futures slid 0.8%, signaling a pullback later Wednesday for a market that has surged 44% in 2023. Broad losses in Europe dragged all industry groups in the benchmark regional index into the red. Asian and European stocks slumped, while the Treasury curve steepened with two-year TSY yields falling 4bps to 4.86%; the Bloomberg Dollar Spot Index was barely changed, up 0.1%.

In premarket trading, AMD rose as much as 1.2% in premarket trading on Wednesday, after the chipmaker reported better-than-expected second-quarter results and said it was making further inroads in artificial-intelligence computing. Analysts noted that there are indications that the PC business was recovering and they were also optimistic about the company’s AI potential. Starbucks dropped as its quarterly sales fell short of analysts’ estimates, a sign that momentum may be slowing for the coffee giant amid higher prices and tighter pocketbooks. Pinterest slid after the social networking company failed to meet heightened expectations. Apple and Amazon.com are among companies scheduled to report this week, with investors on the lookout for clues on how high interest rates are affecting the economy. Here are some other notable premarket movers:

Cardlytics shares jumped as much as 19% and are set to reach their highest level since last Sept., after the company, which makes software to analyze customer purchases, reported results that beat expectations, helping to ease worries over a tough backdrop for the advertising industry. JPMorgan raised its price target on the stock, positive on the progress seen with new products and initiatives.

KeyCorp upgraded to neutral at JPMorgan, with analysts noting that the risks of a dividend cut at the financial services company had waned after US regulators gave it more time to comply with new capital rules. Shares fell as much as 1.8%, however, after Fitch’s downgrade of the US sovereign credit grade hit sentiment across risky assets.

Lumen Technologies shares fall 8.4% in US premarket after the wireline telecommunications company posted what analysts saw as a mixed set of 2Q results with free cash flow weaker than expected.

Oatly Group fell 2.0% after JPMorgan downgraded the oat-milk producer to neutral from overweight due to the “increasingly opaque” growth story.

Pinterest shares fall as much as 5% in premarket trading on Wednesday, after the social networking company reported its second-quarter results and provided an outlook. Citi said the report failed to meet heightened expectations.

Rover Group rises as much as 27% in premarket trading after the online pet care platform boosted its year revenue and adjusted Ebitda forecast. International growth remains solid, with strong lifetime value metrics and product improvements driving tailwinds for top and bottom-line results, says William Blair.

SolarEdge Technologies shares slid as much as 14% in US premarket trading after the solar-equipment maker’s third-quarter revenue forecast disappointed as elevated levels of inventory among its customers weighed on demand. Other solar stocks fell in US premarket trading after the report.

Starbucks shares fall 1.3% after the coffee- chain operator’s third-quarter comparable sales missed estimates. Overall, analysts were disappointed in the print, flagging lower-than-expected comparable sales in North America as well as the weaker-than-anticipated outlook for the metric in China.

Virgin Galactic fell as much as 8.9% after the company’s revenue fell short of analysts’ expectations, even as the space-tourism company gears up for monthly commercial flights. Analysts note that while the firm will continue to burn cash, it does have enough on its balance sheet to fund near-term investments.

There was disagreement over the consequences of the Fitch downgrade: some said it serves up an extra dose of jeopardy for equity investors already concerned over the risks of recession and whether this year’s run-up in stocks is sustainable; others looked at the complete lack of reaction in Treasuries and claims it is a complete non-event, and that it will be forgotten by the market in a few hours. And indeed, Treasuries were steady, in keeping with Janet Yellen’s assertion that they remain “the world’s preeminent safe and liquid asset” for now.

“One can have the feeling that the market is looking for excuses to take some profits,” said Alexandre Baradez, chief market analyst at IG Markets in Paris. “But rather than the Fitch downgrade, I suspect that what’s currently being priced is the growing risk of an economic slowdown. The downward trend started to emerge yesterday on the back of disappointing Chinese and US data, which suggests it’s not really about the rating downgrade, but rather the risk of a slowdown.”

Indeed, the consequences of the latest downgrade seem positively tame by comparison: the last time the US sovereign credit rating was downgraded, the S&P plunged 6.7% with all stocks in the red for the first time since at least 1996, and briefly dropped into a bear market (the benchmark eventually erased those losses five trading days later and is up 282% since). Also, yields tumbled, gold exploded and the SNB was forced to devalue the franc.

European stocks also slumped with the Stoxx 600 down 1.3% and on course for its largest fall in almost four-weeks. Ferrari slumped more than 4% after the Italian supercar maker issued disappointing guidance. Siemens Healthineers AG fell after the German medical technology company missed estimates. Hugo Boss AG dropped after the fashion retailer’s margin fell short of expectations and inventories rose. Here are the biggest European movers:

BAE Systems shares rose as much as 6.6% after the defense and aerospace company upgraded its 2023 guidance and approved a further buyback of as much as £1.5 billion

Taylor Wimpey shares rose as much as 4.7% after the residential housing developer’s results for the first-half exceeded expectations. Analysts said that the company raising the bottom end of its guidance range for UK completions for the year was a positive sign in a tough market

Melexis shares rise as much as 6.5% after the chipmaker raised margin guidance and boosted revenue outlook to top end of its prior range, a sign that strong demand for automotive chips continues to benefit the Belgian company

Virgin Money gains as much as 3.3%, outperforming a broader market decline, after the UK lender announced a share buyback. It also reported steady net interest margins

ConvaTec shares gain as much as 7.8%, the biggest intraday gain since November 2022, after the wound care and ostomy products provider reported first-half revenue that beat estimates and boosted its full-year organic revenue forecast. Citi said it was particularly impressed by growth in wound care as well as the strong gross margin

Iveco shares advance as much as 5.5%, the most since mid-March, after the truckmaker delivered another boost to full-year guidance that analysts say will prompt a significant increase in consensus expectations

Siemens Healthineers falls as much as 8%, the most since May, after the German medical technology firm’s Varian unit weighed on its latest quarterly earnings, with margins a particular concern, analysts say

JDE Peet’s falls as much as 4.4%, after the Dutch coffee company cut its adjusted Ebit guidance on uncertainty over the transition from international brands to local brands in Russia

Hugo Boss shares declined as much as 5% at the open on Wednesday but then pared losses to 0.7% by 9:36 am in Frankfurt. While the German fashion group raised its guidance for 2023 and second-quarter earnings beat most expectations

Schaeffler drops as much as 5.2% as Citi writes that the German automotive and industrial supplier’s second- quarter results were overshadowed by “concerning” organic growth underperformance in auto-tech

Man Group shares drop as much as 3.7%, adding to Tuesday’s 5.5% decline, following results which reflected a lower-margin long-only shift from clients. The recent stock price weakness is an “over-reaction,” according to UBS

Auto1 shares fall as much as 14%, the most since January, after the used-car trading platform reported second-quarter revenue and units sold below estimates

Earlier in the session, Asian stocks posted the biggest decline in more than four months as technology names dropped. Japanese stocks slumped the most this year as gains in the yen dented the outlook for corporate profit; the Nikkei 225 underperformed and dipped below the 33,000 level as the focus shifted to corporate earnings and despite comments from BoJ’s Deputy Governor Uchida who stuck to a dovish tone.

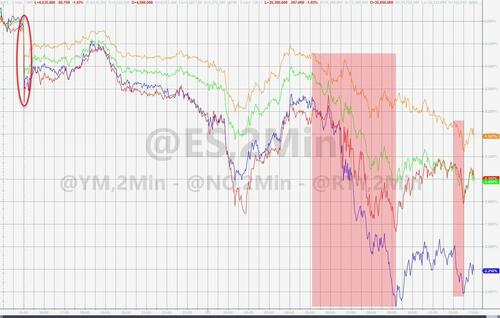

The MSCI Asia Pacific Index fell 1.5%, with all sectors and major markets in the red. Benchmarks dropped more than 1% in Japan, South Korea and Taiwan, and about 2% in Hong Kong, as investors booked profits on chip and electric-vehicle stocks that have surged on artificial intelligence and net-zero emissions trades. “It’s buyers’ fatigue,” said Derek Tay, head of investments at Kamet Capital Partners. US stock futures declined after Fitch stripped the US of its top-tier credit grade, though few market participants saw that as having a major impact on Asian equities. Some investors rather appeared to be taking bets off the table ahead of US employment data later this week, which may influence the Federal Reserve’s next policy decision. “We’ve had an extraordinary run in risk markets and we are starting to get some steepening in the yield curve,” said Matthew Haupt, portfolio manager at Wilson Asset Management in Sydney. “We might get some squeeze on that big rate-cut trade,” he added. The MSCI Asian benchmark earlier this week flirted with its highest close since last April after a rally fueled by hopes for Chinese efforts to boost its economic recovery and a peak-out in US interest rates. The gauge is still up about 6% since the start of June. Australia’s ASX 200 declined with utilities, real estate and financials leading the broad-based retreat and with weaker AIG Manufacturing and Construction data adding to the glum mood.

In FX, the Bloomberg dollar index erased losses as investors bought into the dip that followed Fitch Ratings’ US sovereign credit-rating downgrade. Leveraged short covering of the yen and Australian dollar was short-lived with the latter breaching support below 0.6600 as an Asia Pacific equity gauge headed for the biggest decline in almost a month. New Zealand’s dollar was sold for the greenback and Aussie as a jump in the nation’s jobless rate fueled bets that rates had peaked.

In rates, the front-end of the Treasury curve led gains, extending Tuesday’s steepening move and leaving 2-year notes richer by around 4bp in early US trading. Longer Treasuries broadly shrugged off the US downgrade news. US 10-year yields are little changed on the day, sitting around 4.02% and offering muted reaction to the Fitch downgrade; bunds outperform by around 4bp in the sector while gilts trade slightly cheaper. Front-end gains on the day steepen 2s10s, 5s30s spreads by 3.8bp and 3bp, with both remaining near session highs. For the first time since November 2020, the quarterly unveiling of auction amounts is expected to feature across-the- board increases to the Treasury’s seven main offerings of notes and bonds. German two-year yields fall 6bps to a two-week low of 3.01%. Dollar IG issuance slate empty so far; Tuesday session was inactive for new deals, while August volume projection is around $85 billion. A focus of the day is the quarterly refunding announcement at 8:30am New York time.

“US Treasuries are the world’s largest and most liquid sovereign bond market,” said Alvin Tan, head of Asia FX strategy at RBC Capital Markets in Singapore. “It’s unthinkable large global bond investors will decide to entirely exclude US Treasuries from their holdings. If they do, what USD-denominated bonds will they hold?”

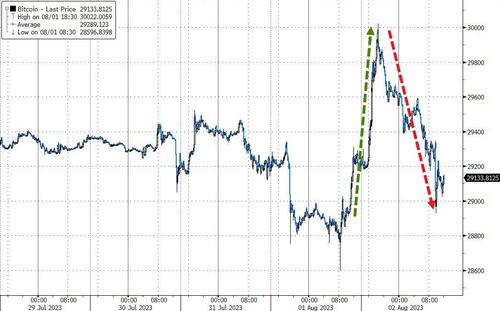

In commodities, oil extended its rally with Brent crude up 0.8%, after API pointed to a huge, in fact a record 15 million drawdown in US inventories, adding to signals the market is tightening. Spot gold adds 0.3%. Bitcoin gains 0.9%

After a data heavy day yesterday, we have only the US July ADP report as the major data release to look forward to today. But watch out for the refunding announcement. Key company earnings include semiconductor firm Qualcomm, as well as Teva, Shopify, PayPal, Occidental Petroleum, Equinix, Kraft Heinz, DoorDash, Albemarle, MGM Resorts, Zillow, and Etsy.

Market Snapshot

S&P 500 futures down 1.0% to 4,554.25

MXAP down 1.7% to 167.30

MXAPJ down 2.1% to 528.37

Nikkei down 2.3% to 32,707.69

Topix down 1.5% to 2,301.76

Hang Seng Index down 2.5% to 19,517.38

Shanghai Composite down 0.9% to 3,261.69

Sensex down 1.4% to 65,517.16

Australia S&P/ASX 200 down 1.3% to 7,354.60

Kospi down 1.9% to 2,616.47

STOXX Europe 600 down 1.8% to 458.96

German 10Y yield little changed at 2.52%

Euro little changed at $1.0986

Brent Futures up 0.4% to $85.25/bbl

Gold spot up 0.4% to $1,951.76

U.S. Dollar Index down 0.16% to 102.14

Top Overnight News

BOJ deputy governor pushes back on speculation the central bank is planning an early exit from a policy of extreme accommodation (the recent YCC tweak was aimed at making it more sustainable). RTRS

South Korea’s CPI undershoots the Street (+2.3% vs. the Street +2.4% and down from +2.7% in June) and falls to a 25-month low. RTRS

SoftBank’s Arm is targeting an IPO at a valuation of between $60 billion and $70 billion as soon as September, people familiar said. Arm execs may still be gunning for $80 billion, but the odds of achieving that are uncertain. BBG

China will curb the amount of time kids can spend on their smartphones, dealing a potential blow to Tencent, ByteDance and other social media leaders. Minors will be banned from accessing the internet from 10:00 pm to 6:00 am and mobile usage will be cut to two hours for those aged 16 to 18. BBG

Binance, the world’s largest crypto exchange, was supposed to leave China behind when the country made cryptocurrency trading illegal in 2021. Almost two years later, users traded $90 billion of cryptocurrency-related assets in China in a single month, according to internal figures viewed by The Wall Street Journal and current and former employees. The transactions made China Binance’s biggest market by far, accounting for 20% of volume worldwide, excluding trades made by a subset of very large traders. WSJ

Fitch cut the US credit rating from AAA to AA (it warned back in May that a downgrade was possible). Fitch’s move follows a similar cut by S&P about 12 years ago. Moody’s continues to rate the US AAA. Fitch says its downgrade “reflects the expected fiscal deterioration over the next three years, a high and growing general government debt burden, and the erosion of governance relative to ‘AA’ and ‘AAA’ rated peers over the last two decades that has manifested in repeated debt limit standoffs and last-minute resolutions”. Fitch

The major entertainment studios and thousands of striking writers have agreed to meet to restart talks after a three-month standoff, according to the writers guild. NYT

US prosecutors have charged Donald Trump in connection with his attempts to overturn the results of the 2020 election, the second federal indictment brought against the former president in as many months. Trump was charged with four criminal counts including conspiracy to defraud the US, to obstruct an official proceeding and to threaten individual rights, according to an indictment filed in federal court in Washington on Tuesday. FT

US crude stockpiles saw a jumbo drawdown last week as inventories plunged 15.4 million barrels, the API is said to have reported. That would be the biggest in data going back to 1982 if confirmed by the EIA. BBG

Foreign buying of U.S. homes fell for a sixth straight year, sinking to the lowest level on record, though some signs of turnaround are starting to emerge. WSJ

A more detailed look at global markets courtesy of Newsquawk

APAC stocks traded lower following the mostly negative lead from Wall St where sentiment was dampened by higher yields and weak data, while participants also digested Fitch’s credit rating downgrade for the US from AAA to AA+. ASX 200 declined with utilities, real estate and financials leading the broad-based retreat and with weaker AIG Manufacturing and Construction data adding to the glum mood. Nikkei 225 underperformed and dipped below the 33,000 level as the focus shifted to corporate earnings and despite comments from BoJ’s Deputy Governor Uchida who stuck to a dovish tone. Hang Seng and Shanghai Comp conformed to the risk aversion albeit with the downside in the mainland initially cushioned by further policy support and jawboning by Chinese agencies.

Top Asian News

China’s Finance Ministry said it cut value-added tax for small taxpayers, according to Reuters.

China’s cyberspace regulator drafts guidelines to strengthen the limit around minors’ use of apps, smart terminals and app stores, according to Reuters.

China said reports that it obstructed G20 discussions in reducing fossil fuels use are inconsistent with facts, while China regrets a failure to reach an agreement and blames geopolitical issues brought up by other countries, according to Reuters.

BoJ Deputy Governor Uchida said at present, the risk of losing the chance to hit the price target with a premature shift from easy policy is bigger than the risk of being too late in tightening and Japan is now at a phase where it is important to patiently maintain easy policy. Furthermore, Uchida said last week’s decision was a pre-emptive step at continuing monetary easing without disruptions and the BoJ must fine-tune YCC at times and make the policy more flexible. Adds, depending on the speed of the moves, BoJ will step in before the 10yr yield hits 1%.

BoJ minutes from the June 15th-16th meeting noted members agreed BoJ must maintain current monetary easing to stably and sustainably achieve the price target, while many members said it was appropriate to sustain monetary easing to support changes seen in corporate wages and price-setting behaviour. Furthermore, a few members said a premature policy shift could mean the BoJ will lose the opportunity to achieve the price target.

Australian Trade Minister says they are hopeful that in the next few days, there will be a positive decision from China re. barley tariffs, if not will restart the WTO process.

European bourses are in the red, Euro Stoxx 50 -1.4%, as sentiment continues to deteriorate from a downbeat Wall St./APAC handover. Sectors are similarly in the red with earnings dominating stock specifics while the Energy sector is the relative outperformer, but still lower, given benchmark action. Stateside, futures are lower as the risk-off trade continues with sizeable attention on Fitch’s action, ES -0.8%; ADP and Quarterly Refunding dominate the calendar ahead intersected by numerous earnings.

Top European News

The Times’ Shadow MPC voted 8-1 in favour of a 25bps rate hike this month. All members agreed that the Bank should not provide financial markets with guidance about the future path of interest rates due to economic uncertainty.

ECB’s de Guindos says “Policymakers should focus on preserving bank resilience to strengthen macroprudential stability at a time of economic uncertainty. This would ensure that sufficient capital buffers are available should widespread losses arise”. Overall, the stress test confirms European banks could withstand a severe economic downturn.

FX

The broader Dollar and index are firmer in the European morning, propped up by the risk aversion seen across the market after Fitch downgraded US, upside levels include the 100 DMA (102.35), yesterday’s high (102.43), then the 50 DMA (102.45).

The JPY is the current G10 outperformer following three consecutive sessions of losses in the aftermath of the BoJ’s decision last Friday, with potential tailwinds seen from the broader risk-off sentiment across markets.

Antipodeans are once again the marked laggards amid the broader risk tone, hangover from the RBA hold, and overall bearish Kiwi jobs data overnight, while EUR and GBP are resilient to the Dollar’s strength despite a lack of headlines, data, and broader risk aversion.

PBoC set USD/CNY mid-point at 7.1368 vs exp. 7.1664 (prev. 7.1283)

Fixed Income

EGBs are firmer and currently benefiting from traditional haven allure as the broader risk tone continues to deteriorate despite an absence of fresh catalysts.

Gilts are the sole core benchmark in the red as we near Thursday’s BoE announcement where another 25bp hike is expected though there is around a 35% chance of 50bp priced and 75bp of total tightening implied by February 2023.

USTs are faring relatively well and giving up some of the marked concession which was built in on Tuesday’s session both before and after the afternoon’s data docket, concession which comes ahead of today’s quarterly refunding announcement; Though, we are above Tuesday’s 110.26+ low by circa. 10 ticks as it stands.

Commodities

WTI and Brent futures are off best levels but remain modestly firmer intraday, with the downside from risk aversion (after US’ rating downgrade by Fitch) cushioned by the mammoth drawdown in Private Inventories yesterday.

Over to metals, the risk-off picture is clear. Spot gold and silver are firmer amid heaven flow and despite the stronger Dollar as the former initially battled overnight resistance at USD 1,950/oz but meanders around the level in European hours.

Base metals are softer across the board as risk aversion and the Greenback hit the industrial metals, 3M LME copper declined from a USD 8,669/t high but maintains status above USD 8,500/t.

Operations suspended at Ukraine’s Izmail port on Danube, according to Reuters citing sources.

US Energy Inventory Data (bbls): Crude -15.4mln (exp. -1.4mln), Gasoline -1.7mln (exp. -1.3mln), Distillate -0.5mln (exp. +0.1mln), Cushing -1.8mln

US Energy Department spokesperson announced the US pulled its offer to buy 6mln bbls of oil for the SPR due to market conditions, while a Bloomberg reporter noted that the Biden administration delayed the replenishment of the SPR after deciding the offers it received were too expensive.

OPEC+ is unlikely to tweak its current output policy when it meets on Friday, according to multiple OPEC sources cited by Reuters.

UK Government suspends anti-dumping duty on hot-rolled flat iron, non-alloy or other alloy steel with goods originating in Iran or Russia in some cases.

Geopolitics

Explosions were reported in Ukraine’s capital of Kyiv and anti-aircraft units were in operation, according to Reuters citing Mayor Klitschko and military officials.

Russian drones reportedly attacked port and grain storage facilities in Ukraine’s Odesa region which set some of them on fire, according to the regional governor.

Poland’s Defence Ministry said it is deploying additional troops along the border with Belarus after 2 helicopters violated airspace, according to BNO News.

Taiwan’s Presidential Office said Vice President Lai will transit in New York and San Francisco, while it noted reports that VP Lai is planning to transit through Washington DC are false. Furthermore, it stated the transit arrangement is based on comfort and safety and should not be an excuse for conflict.

US and Mongolia reportedly prepare to sign an “open skies” deal which would grant airlines from both countries the right to operate in each other’s countries, according to Reuters sources.

Russian Kremlin says a call between President Putin and Turkish President Erdogan is taking place now.

Russia’s Defence Ministry says Russian forces start navy drills in the Baltic sea, according to Ria.

Crypto

Binance Japan launched crypto services with 34 virtual currencies, according to Nikkei.

Binance CEO Zhao attempted to shut down the crypto exchange’s US offshoot earlier this year to protect the much larger global exchange amid mounting regulatory scrutiny, according to sources cited by The Information.

US Event Calendar

07:00: July MBA Mortgage Applications, prior -1.8%

08:15: July ADP Employment Change, est. 190,000, prior 497,000

DB’s Jim Reid concludes the overnight wrap