GOLD PRICE CLOSED: UP $7.25 TO $1940.85

SILVER PRICE CLOSED:UP $0.01 AT $23.62

Access prices: closes 4: 15 PM

Gold ACCESS CLOSE 1941.80

Silver ACCESS CLOSE: 23.61

Shanghai Gold Benchmark Price

USD oz gram kilo tola

AM1973.83

PM1975.07

New York price at the time: 1933.00

premium $40.00

Shanghai again never saw the raid .

xxxxxxxxxxxxxxxxxx

Bitcoin morning price:, $29174 DOWN 39 Dollars

Bitcoin: afternoon price: $29,094 DOWN 119 dollars

Platinum price closing $925.45 UP $7.25

Palladium price; $1268,45 UP $8.40

END

Due to the huge rise in the dollar, we must look at gold and silver in currencies other than the dollar to understand where we are heading

I will now provide gold in Canadian dollars, British pounds and Euros/4: 15 PM ACCESS

CANADIAN GOLD: $2,598.30 UP 15.10 CDN dollars per oz (ALL TIME HIGH 2,775.35)

BRITISH GOLD: 1523.44 UP 1.00 pounds per oz//(ALL TIME HIGH//CLOSING///1630.29)

EURO GOLD: 1764.18 DOWN 3.38 euros per oz //(ALL TIME HIGH/CLOSING//1861.21)//

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

EXCHANGE: COMEX

EXCHANGE: COMEX

CONTRACT: AUGUST 2023 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,932.000000000 USD

INTENT DATE: 08/03/2023 DELIVERY DATE: 08/07/2023

FIRM ORG FIRM NAME ISSUED STOPPED

072 C GOLDMAN 299

104 C MIZUHO 557

118 H MACQUARIE FUT 1

152 C DORMAN TRADING 1

190 H BMO CAPITAL 162

323 C HSBC 12

323 H HSBC 100

363 H WELLS FARGO SEC 66

435 H SCOTIA CAPITAL 112

523 C INTERACTIVE BRO 10

624 H BOFA SECURITIES 189

661 C JP MORGAN 29 408

690 C ABN AMRO 4

709 C BARCLAYS 29

737 C ADVANTAGE 13

TOTAL: 996 996

JPMorgan stopped 468/7746 contracts.

FOR AUGUST:

GOLD: NUMBER OF NOTICES FILED FOR AUGUST/2023. CONTRACT: 996 NOTICES FOR 99,600 OZ or 3.0773 TONNES

total notices so far: 7746 contracts for 774,600 oz (20.995 tonnes)

FOR AUGUST:

SILVER NOTICES: 34 NOTICE(S) FILED FOR 170,000 OZ/

total number of notices filed so far this month : 788 for 3,940,000 oz

XXXXXXXXXXXXXXXXXXXXXXXX

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD

WITH GOLD UP $7,25

INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD//

HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.18 TONNES FROM THE GLD///

INVENTORY RESTS AT 909.18 TONNES

Silver//

WITH NO SILVER AROUND AND SILVER UP 1 CENT AT THE SLV// HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF2.294 MILLION OZ FROM THE SLV..

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV.

CLOSING INVENTORY: 448.987 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A HUGE SIZED 3578 CONTRACTS TO 137,515 AND FURTHER FROM THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THIS HUGE SIZED LOSS IN COMEX OI WAS ACCOMPLISHED WITH OUR $0.16 LOSS IN SILVER PRICING AT THE COMEX ON THURSDAY. TAS ISSUANCE WAS A HUMONGOUS SIZED 1847 CONTRACTS. THESE WILL BE USED FOR MANIPULATION LATER THIS MONTH. CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON THURSDAY NIGHT: 1847 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS. IT THUS LOOKS LIKE THE FED (GOV’T) IS BEHIND ALL OF THESE TRADES.

WE HAVE NOW SET ANOTHER RECORD LOW AT 114,102 CONTRACTS ///JULY 3.2023// OUR BANKERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.16). BUT WERE UNSUCCESSFUL IN KNOCKING OF ANY SILVER CONTRACTS AS DESPITE THE HUGE LOSS IN COMEX CONTRACTS, THE ENTIRE LOSS WAS THE USE OF T.A.S. TO LOWER THE SILVER PRICE.

WE MUST HAVE HAD:

A HUMONGOUS ISSUANCE OF EXCHANGE FOR PHYSICALS( 2760 CONTRACTS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 3.105 MILLION OZ (FIRST DAY NOTICE) FOLLOWED BY TODAY’S 180,000 OZ QUEUE JUMP //NEW STANDING RISES AT 3.950 MILLION OZ + OUR NEW CRIMINAL 1,250 CONTRACTS OF EXCHANGE FOR RISK FOR 1.25 MILLION OZ/ NEW TOTAL STANDING FOR SILVER: 5.20 MILLION OZ/// // // HUGE SIZED COMEX OI LOSS/ HUMONGOUS SIZED EFP ISSUANCE/VI) HUMONGOUS NUMBER OF T.A.S. CONTRACT ISSUANCE (1847 CONTRACTS)/HUGE EXCHANGE FOR RISK ISSUED (1.25 MILLION OZ OR 250 CONTRACTS)/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL –10 CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS AUGUST. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF JULY:

TOTAL CONTRACTS for 4 days, total 3947 contracts: OR 19.735 MILLION OZ (986 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 19.735 MILLION OZ

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 118.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 85.745 MILLION OZ (SMALLER THAN LAST MONTH)

AUGUST: 19.735 MILLION OZ

RESULT: WE HAD A HUGE SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 3578 CONTRACTS WITH OUR STRONG LOSS IN PRICE OF $0.16 IN SILVER PRICING AT THE COMEX//THURSDAY.,. THE CME NOTIFIED US THAT WE HAD A HUMONGOUS EFP ISSUANCE CONTRACTS: 2760 ISSUED FOR SEPT AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS./ WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR AUGUST OF 3.105 MILLION OZ FOLLOWED BY TODAY’S 180,000 OZ QUEUE JUMP//NEW STANDING 3.95 MILLION OZ+ 1.25 MILLION OZ EXCHANGE FOR RISK NEW TOTALS 5.20 MILLION OZ//// .. WE HAVE A HUGE SIZED LOSS OF 818 OI CONTRACTS ON THE TWO EXCHANGES. THE TOTAL OF TAS INITIATED CONTRACTS TODAY: A HUGE 1847//HUGE FRONT END OF THE TAS CONTRACTS WERE LIQUIDATED DURING THE THURSDAY COMEX SESSION//RAID . THE NEW TAS ISSUANCE TODAY (1847) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE./

WE HAD 34 NOTICE(S) FILED TODAY FOR 170,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A FAIR SIZED 4017 CONTRACTS TO 435,395 AND CLOSER TO TO THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED: 296 CONTRACTS

WE HAD A FAIR SIZED DECREASE IN COMEX OI ( 4017 CONTRACTS) WITH OUR $5.25 LOSS IN PRICE//THURSDAY. WE ALSO HAD A RATHER SMALL INITIAL STANDING IN GOLD TONNAGE FOR AUGUST. AT 30.656 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S 12,800 OZ QUEUE. JUMP + PRIOR ISSUANCE OF EXCHANGE FOR RISK = (.684 TONNES) //NEW STANDING 31.150 TONNES + .684 EXCHANGE FOR RISK = 31.8342/ + /A FAIR (AND CRIMINAL) ISSUANCE OF 1528 T.A.S. CONTRACTS /// ALL OF..THIS HAPPENED WITH A $5.25 LOSS IN PRICE WITH RESPECT TO THURSDAY’S TRADING.WE HAD A SMALL SIZED LOSS OF 853 OI CONTRACTS (2.684 PAPER TONNES) ON OUR TWO EXCHANGES.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 3154 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 435,395

IN ESSENCE WE HAVE A SMALL SIZED DECREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 853 CONTRACTS WITH 4017 CONTRACTS DECREASED AT THE COMEX// AND A FAIR 3154 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI LOSS ON THE TWO EXCHANGES OF 853 CONTRACTS OR 2.684 TONNES. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): A FAIR 1541 CONTRACTS)

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (3154 CONTRACTS) ACCOMPANYING THE FAIR SIZED LOSS IN COMEX OI (4017) //TOTAL LOSS FOR OUR THE TWO EXCHANGES: 853 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR NORMAL FORMAT OF BANKERS GOING SHORT AND SPECULATORS GOING LONG ,2.) FAIR INITIAL STANDING AT THE GOLD COMEX FOR JULY AT 30.656 TONNES FOLLOWED BY TODAY’S 12,800 OZ QUEUE JUMP //NEW STANDING 31.150 TONNES + .684 TONNES (EXCHANGE FOR RISK//PRIOR) NEW TOTALS: 31.8342 TONNES/// 3) ZERO LONG LIQUIDATION WITH CONSIDERABLE TAS LIQUIDATION //4) FAIR SIZED COMEX OPEN INTEREST LOSS/ 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER///6: FAIR T.A.S. ISSUANCE: 1541 CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023 INCLUDING TODAY

AUGUST

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF AUG :

TOTAL EFP CONTRACTS ISSUED: 13,782 CONTRACTS OR 1,379,200 OZ OR 42.898 TONNES IN 4 TRADING DAY(S) AND THUS AVERAGING: 3448 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 4 TRADING DAY(S) IN TONNES 42.898 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2022, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 42.898/3550 x 100% TONNES 1.21% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2023

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 151.69 TONNES (WEAKER THAN LAST MONTH)

AUGUST: 42.898 TONNES

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF JUNE. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF MAY HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF JUNE., FOR BOTH GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (JUNE), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER FELL BY A HUGE SIZED 3578 CONTRACTS OI TO 137,515 AND FURTHER FROM OUR COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE A HUMONGOUS 2760 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

SEPT 2260 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 2760 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 3578 CONTRACTS AND ADD TO THE 2760 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A HUGE SIZED LOSS OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 818 CONTRACTS

THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES TOTAL 4.090 MILLION OZ

OCCURRED WITH OUR $0.16 LOSS IN PRICE …..

END

OUTLINE FOR TODAY’S COMMENTARY

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

b, ) Gold/silver trading overnight Europe,//GOLD COMMENTARIES

(Peter Schiff)

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS//

FRIDAY MORNING//THURSDAY NIGHT

SHANGHAI CLOSED UP 7,62 PTS OR 0.23% //Hang Seng CLOSED UP 118.59 PTS OR 0.61% /The Nikkei CLOSED UP 33.47 PTS OR 0.10% //Australia’s all ordinaries CLOSED UP 0.18 % /Chinese yuan (ONSHORE) closed UP 7.1862 /OFFSHORE CHINESE YUAN UP TO 7.1936 /Oil UP TO 81.07 dollars per barrel for WTI and BRENT UP AT 85.38 / Stocks in Europe OPENED ALL RED// ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

9. USA

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A FAIR SIZED 4017 CONTRACTS DOWN TO 435,395 WITH OUR LOSS IN PRICE OF $5.25 ON THURSDAY.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE NON ACTIVE DELIVERY MONTH OF JULY… THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 3154 EFP CONTRACTS WERE ISSUED: : DEC 3154 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 3154 CONTRACTS

ON A NET BASIS IN OPEN INTEREST WE LOST THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A SMALL SIZED TOTAL OF 853 CONTRACTS IN THAT 3154 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A FAIR SIZED LOSS OF 4017 COMEX CONTRACTS..AND THIS LOSS ON OUR TWO EXCHANGES HAPPENED WITH OUR LOSS IN PRICE OF $5.25//THURSDAY COMEX. AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS DURING MID MONTH IN THE DELIVERY CYCLE), THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR THURSDAY NIGHT WAS A FAIR 1541 CONTRACTS. THROUGHOUT THE PAST WEEKS, THE BANKERS SOLD OFF THE LONG SIDE OF THE SPREAD WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR SPREAD WHICH WILL BE LIQUIDATED TWO MONTHS HENCE)//THE HUGE NUMBER OF T.A.S. CONTRACTS INITIATED OVER THE PAST SEVERAL WEEKS SPELLS TROUBLE FOR THE GOLD/SILVER MARKET AS RAIDS WILL SURELY BE UPON US TRYING TO CONTAIN OUR PRECIOUS METALS RISE IN PRICE.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: AUGUST (31.436) (NON ACTIVE MONTH)

TONNES),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 31.436 TONNES (INCLUDING .6842 EXCHANGE FOR RISK)

THE SPECS/HFT WERE SUCCESSFUL IN LOWERING GOLD’S PRICE( IT LOST $5.25) //// BUT WERE UNSUCCESSFUL IN KNOCKING ANY SPECULATOR LONGS AS WE HAD A SMALL LOSS OF 853 TOTAL CONTRACTS ON OUR TWO EXCHANGES ALL OF WHICH CAME FROM T.A.S. LIQUIDATION. THE T.A.S. ISSUED ON THURSDAY NIGHT WILL BE “PUT INTO THE BANK” TO BE USED AT A LATER DATE AT THE COLLUSIVE CHOOSING OF OUR BANKERS.

WE HAVE LOST A TOTAL OI OF 2.684 PAPER TONNES OF TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR AUST. (30.656 TONNES) ON FIRST DAY NOTICE FOLLOWED BY TODAY’S 12,800 OZ QUEUE JUMP //NEW STANDING ADVANCES TO 31.150 TONNES + .6842 (PRIOR EXCHANGE FOR RISK) //NEW TOTAL 31.8352 TONNES // ALL OF THIS WAS ACCOMPLISHED WITH OUR LOSS IN PRICE TO THE TUNE OF $5.25.

WE HAD – REMOVED 296 CONTRACTS TO THE COMEX TRADES TO OPEN INTEREST

NET LOSS ON THE TWO EXCHANGES 853 CONTRACTS OR 85300 OZ OR 2.684 TONNES.

Estimated gold volume today:// 140,607 poor

final gold volumes/yesterday 181,519 poor

//AUGUST 4/ FOR THE AUGUST 2023 GOLD CONTRACT

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | NIL . |

| Deposit to the Dealer Inventory in oz | nil |

| Deposits to the Customer Inventory, in oz | nil OZ |

| No of oz served (contracts) today | 996 notice(s) 99,600 OZ 3.0773 TONNES |

| No of oz to be served (notices) | 2269 contracts 226,900 oz 7.0575 TONNES |

| Total monthly oz gold served (contracts) so far this month | 7746 notices 774,600 OZ 24.0933 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | x |

0 dealer deposit:

total dealer deposits: NIL oz

total customer deposits: NIL oz

we had NIL customer withdrawals

Adjustments; 0 /

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR AUGUST.

For the front month of AUGUST we have an oi of 3265 contracts having GAINED 84 contracts. We had 44 contracts filed

on Thursday, so we gained 128 contracts or an additional 12,800 oz will stand at the comex

Sept gained 52 contracts to 2472.

Oct lost 428 contracts to 33,584 contracts.

We had 996 contracts filed for today representing 99,600 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 29 notices were issued from their client or customer account. The total of all issuance by all participants equate to 996 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 458 notice(s) was (were) stopped received by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the AUGUST /2023. contract month,

we take the total number of notices filed so far for the month (7746 x 100 oz ), to which we add the difference between the open interest for the front month of AUGUST (3265 CONTRACT) minus the number of notices served upon today 996 x 100 oz per contract equals 1,001,500 OZ OR 31.8342 TONNES the number of TONNES standing in this active month of AUGUST. + .684 TONNES EXCHANGE FOR RISK/prior = 31.8342 tonnes

thus the INITIAL standings for gold for the AUGUST contract month: No of notices filed so far (7746) x 100 oz + (3265) {OI for the front month} minus the number of notices served upon today (996) x 100 oz) which equals 1,001,500 oz standing OR 30.752 TONNES + .684 TONNES OF EXCHANGE FOR RISK = 31.8342 TONNES

TOTAL COMEX GOLD STANDING: 31.8342 TONNES WHICH IS SMALL FOR AN ACTIVE DELIVERY MONTH.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 2,058,278.651 OZ 64.02 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 22,202,871.168 OZ

TOTAL REGISTERED GOLD: 12,102,270.124 (376,43 tonnes)..

TOTAL OF ALL ELIGIBLE GOLD: 10,100,601.044 O Z

REGISTERED GOLD THAT CAN BE SERVED UPON: 10,050,880 OZ (REG GOLD- PLEDGED GOLD) 313.62 tonnes//

END

SILVER/COMEX

AUGUST4

//2023// THE AUGUST 2023 SILVER CONTRACT

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | NIL . |

| Deposits to the Dealer Inventory | N/A oz |

| Deposits to the Customer Inventory | 302,302.770 oz DELAWARE LOOOMIS |

| No of oz served today (contracts) | 34 CONTRACT(S) (170,000 OZ) |

| No of oz to be served (notices) | 2 contracts (10,000 oz) |

| Total monthly oz silver served (contracts) | 788 Contracts (3,940,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

i) 0 dealer deposit

total dealer deposit: 0 oz

i) We had 0 dealer withdrawal

total dealer withdrawals: 0 oz

We had 2 deposits customer account:

i) Into Delaware: 1979.970 oz

ii) Into Loomis: 300,322.800 oz

total customer deposits: 302,302.770 oz

JPMorgan has a total silver weight: 139.910 million oz/281.947 million =49.64% of comex .//

Comex withdrawals 0

adjustments: 0

TOTAL REGISTERED SILVER: 31.692 MILLION OZ//.TOTAL REG + ELIGIBLE. 281.947 million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR JULY:

silver open interest data:

FRONT MONTH OF AUGUST /2023 OI: 36 CONTRACTS HAVING GAINED 29 CONTRACT(S). WE HAD

7 NOTICES FILED ON THURSDAY SO WE GAINED 36 CONTRACTS OR AN ADDITIONAL 180,000 OZ WILL STAND IN THIS NON ACTIVE DELIVERY MONTH OF AUGUST.

SEPT HAS A LOSS OF 7492 CONTRACTS DOWN TO 98,652

OCT GAINED 16 CONTRACTS TO STAND AT 86.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 34 for 170,000 oz

Comex volumes// est. volume today 64,929 fair /

Comex volume: confirmed yesterday: 83,729 strong

To calculate the number of silver ounces that will stand for delivery in AUGUST. we take the total number of notices filed for the month so far at 788 x 5,000 oz = 3,940,000 oz

to which we add the difference between the open interest for the front month of AUGUST (36) and the number of notices served upon today 34 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the AUGUST/2023 contract month: 788 (notices served so far) x 5000 oz + OI for the front month of AUGUST (36) – number of notices served upon today (34 )x 500 oz of silver standing for the AUGUST contract month equates to 3.950 million oz.+ 1.25 MILLION OZ EXCHANGE FOR RISK ISSUED TODAY//NEW TOTALS: 5.200 MILLION

There are 31.54 million oz of registered silver.

thus if we take today’s standing at 5.20 and add last month’s 30.9 million oz we have 36.100 million oz against only 31.5 million registered silver.

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS

AUGUST 4/WITH GOLD UP $7.25 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.18 TONNES OF GOLD FROM THE GLD/// .///VENTORY RESTS AT 906.00 TONNES

AUGUST 3/WITH GOLD DOWN $5.25 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD //: //: / .////INVENTORY RESTS AT 909.18 TONNES

AUGUST 2/WITH GOLD DOWN $3.45 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 3.75 TONNES OF GOLD FROM THE GLD//: //: / .////INVENTORY RESTS AT 909.18 TONNES

AUGUST 1/WITH GOLD DOWN $28.45 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 2.89 TONNES OF GOLD FROM THE GLD//: //: / .////INVENTORY RESTS AT 912.93 TONNES

JULY 31/WITH GOLD UP $9.50 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 2.89 TONNES OF GOLD FROM THE GLD//: //: / .////INVENTORY RESTS AT 912.93 TONNES

JULY 28/WITH GOLD UP $14.15 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 1.44 TONNES OF GOLD FROM THE GLD//: //: / .////INVENTORY RESTS AT 915,82 TONNES

JULY 27/WITH GOLD DOWN $21.80 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 1.74 TONNES OF GOLD FROM THE GLD//: //: / .////INVENTORY RESTS AT 917.26 TONNES

JULY 26/WITH GOLD UP $6.35 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD: //: / .////INVENTORY RESTS AT 919.00 TONNES

JULY 25/WITH GOLD UP $2.45 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD: //: / .////INVENTORY RESTS AT 919.00 TONNES

JULY 24/WITH GOLD DOWN $4.65 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 5.20 TONNES OF GOLD INTO THE GLD//: / .////INVENTORY RESTS AT 919.00 TONNES

JULY 21/WITH GOLD DOWN $3.80 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD: / .////INVENTORY RESTS AT 913.80 TONNES

JULY 20/WITH GOLD DOWN $8.70 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.73 TONNES FROM THE GLD/ .////INVENTORY RESTS AT 913.80 TONNES

JULY 19/WITH GOLD UP $0.65 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .86 TONNES FROM THE GLD/ .////INVENTORY RESTS AT 912.07 TONNES

JULY 18/WITH GOLD UP $23.45 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD: .////INVENTORY RESTS AT 912.93 TONNES

JULY 17/WITH GOLD DOWN $6.60 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.73 TONNES OF GOLD FROM THE GLD.////INVENTORY RESTS AT 912.93 TONNES

JULY 14/WITH GOLD UP $0.75 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD: ////INVENTORY RESTS AT 914.66 TONNES

JULY 13/WITH GOLD UP $3.30 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 0.29 TONNES OF GOLD OUT OF THE GLD////INVENTORY RESTS AT 914.66 TONNES

JULY 12/WITH GOLD UP $24.50 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 0.31 TONNES OF GOLD OUT OF THE GLD////INVENTORY RESTS AT 914.95 TONNES

JULY 11/WITH GOLD UP $6.15 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.0 TONNES OF GOLD OUT OF THE GLD////INVENTORY RESTS AT 915.26 TONNES

JULY 10 WITH GOLD DOWN $1.35 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.60 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 916.26 TONNES.

JULY 7 WITH GOLD UP $16.80 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 917.86 TONNES.

JULY 6/WITH GOLD DOWN $9.90 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.04 TONNES OF GOLD FROM THE GLD//INVENTORY RESTS AT 917.86 TONNES

JULY 5/WITH GOLD DOWN $2.20 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD; A WITHDRAWAL OF 2.6 TONNES FROM THE GLD///INVENTORY RESTS AT 921.90 TONNES

JULY 3/WITH GOLD UP $1.90 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 924.50 TONNES//

JUNE 30/WITH GOLD UP $10.00 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.31 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 924.50 TONNES

JUNE 29/WITH GOLD DOWN $3.20 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.26 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 926.81 TONNES

GLD INVENTORY: 906.00 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

AUGUST 4/WITH SILVER UP 1 CENT TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.294 MILLION OZ FROM THE SLV// OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 458.987 MILLION OZ

AUGUST 3/WITH SILVER DOWN 16 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 189,000 OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 451.281 MILLION OZ

AUGUST 2/WITH SILVER DOWN 43 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 275,000 OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 451.471 MILLION OZ

AUGUST 1/WITH SILVER DOWN 61 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 184,000 OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 451.746 MILLION OZ

JULY 31/WITH SILVER UP 45 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 184,000 OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 451.746 MILLION OZ

JULY 28/WITH SILVER UP 15 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 550,000 OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 451.930 MILLION OZ

JULY 27/WITH SILVER DOWN 59 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: .////INVENTORY RESTS AT 452.480 MILLION OZ

JULY 26/WITH SILVER UP 15 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: .////INVENTORY RESTS AT 452.480 MILLION OZ/

JULY 25/WITH SILVER UP 24 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A SMALL WITHDRAWAL OF 826,000 OZ FROM THE SLV..////INVENTORY RESTS AT 452.480 MILLION OZ/

JULY 24/WITH SILVER DOWN 23 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: ////INVENTORY RESTS AT 453.306 MILLION OZ/

JULY 21/WITH SILVER DOWN 14 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 1.101 MILLION OZ OF SILVER FROM THE SLV ////INVENTORY RESTS AT 453.306 MILLION OZ/

JULY 20/WITH SILVER DOWN 38 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 1.468 MILLION OZ OF SILVER FROM THE SLV ////INVENTORY RESTS AT 454.107 MILLION OZ/

JULY 19/WITH SILVER UP 11 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV:A ////INVENTORY RESTS AT 455.875 MILLION OZ/

JULY 18/WITH SILVER DOWN 19 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV:A ////INVENTORY RESTS AT 455.875 MILLION OZ/

JULY 17/WITH SILVER UP 25 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 4.856 MILLION OZ OF SILVER FROM THE SLV////////INVENTORY RESTS AT 455.875 MILLION OZ/

JULY 14/WITH SILVER UP 27 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 2.21 MILLION OZ OF SILVER FROM THE SLV////////INVENTORY RESTS AT 455.875 MILLION OZ/

JULY 13/WITH SILVER UP 64 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//////INVENTORY RESTS AT 462.941 MILLION OZ/

JULY 12/WITH SILVER UP $1.00 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.881 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 462.941 MILLION OZ/

JULY 11/WITH SILVER DOWN 5 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF .020 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 464.822 MILLION OZ/

JULY 10/WITH SILVER UP 2 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.672 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 464.802 MILLION OZ

JULY 7/WITH SILVER UP 42 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 466.474 MILLION OZ

JULY 6/WITH SILVER DOWN 50 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.667 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 466.474 MILLION OZ//

JULY5/WITH SILVER UP 30 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 468.141 MILLION OZ//

JULY 3/WITH SILVER UP 7 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 468.141 MILLION OZ//

CLOSING INVENTORY 448.987 MILLION OZ//

PHYSICAL GOLD/SILVER COMMENTARIES

1:Peter Schiff/Mike Maharrey

end

2 Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens//JAMES RICKARDS//JOHN RUBINO

END

3,Chris Powell of GATA provides to us very important physical commentaries

They finally admit: by revaluing gold they can regain their solvency. Question: what about those huge derivatives the bankers placed on gold and silver?

(Jan Nieuwenhuijs)

Jan Nieuwenhuijs: Central banks admit they can regain solvency with gold revaluation

Submitted by admin on Thu, 2023-08-03 20:55Section: Daily Dispatches

9p ET Thursday, August 3, 2023

Dear Friend of GATA and Gold:

Gold market researcher Jan Nieuwenhuijs notes today that some European central banks, particularly the Geman Bundesbank, openly acknowledge that national gold reserves, as registered in central bank gold revaluation accounts, are capable of restoring a central bank’s solvency against any and all losses from their holdings of government bonds.

That is, for central banks with gold reserves, revaluing gold upward is a powerful mechanism of money creation — and of currency and debt devaluation (call it repudiation if you’d like) — and central banks with balance sheets showing losses may eventually be on the same side of the market as gold investors, and indeed already may be surreptitiously, as they are surreptitious in most important things they do.

This is essentially what the U.S. economists Paul Brodsky and Lee Quaintance wrote in a study brought to your attention by GATA 11 years ago —

https://www.gata.org/node/11373

— and what the Scottish economist Peter Millar wrote in a study brought to your attention by GATA 16 years ago:

https://www.gata.org/node/4843

Nieuwenhuijs’ analysis is headlined “German Central Bank:Gold Revaluation Account Underlies Soundness of Balance Sheet” and it’s posted at the Gainesville Coins internet site here:

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

Russia to resume currency and gold to support the Rouble.

(Bloomberg)

Russia to resume buying currency and gold as energy income revives

Submitted by admin on Thu, 2023-08-03 19:15Section: Daily Dispatches

From Bloomberg News

Thursday, August 3, 2023

Russia will start buying foreign currency and gold as a recovery in energy revenue brought it above the target set in the budget.

The Finance Ministry said today it will purchase 40.5 billion rubles ($433 million) during the Aug. 7-Sept. 6 period under a budgetary mechanism designed to insulate the economy from the volatility of commodity markets.

Since purchases were halted in late January 2022, followed by the program’s suspension after the invasion of Ukraine the following month, the Finance Ministry has only sold foreign currency this year as part of the revamped fiscal mechanism. …

… For the remainder of the report:

END

Your weekend reading material

(Alasdair Macleod)

Alasdair Macleod: Gold is replacing the dollar

Submitted by admin on Thu, 2023-08-03 12:06Section: Daily Dispatches

By Alasdair Macleod

GoldMoney, Toronto

Thursday, August 3, 2023

Financial developments in the Russian and Chinese axis are being generally ignored. The confirmation by Russia that a trade settlement currency for an expanded BRICS group is on the agenda at the Johannesburg summit this month has barely been reported, and even sound money advocates are highly sceptical.

But all will be revealed in three weeks. Meanwhile this article looks at how gold standards could return in the wake of a new gold-backed trade-settlement currency, if that is what emerges, using the currency board model as a template.

This is followed by an explanation of why gold reserves must cover the bank note issue.

I assess the cover afforded to both the rouble and the renminbi, incorporating assumed levels of non-reserve gold bullion held by both Russia and China. The conclusion is that both nations have ample cover to implement proper gold standards — and that gives the opportunity for other allied nations to implement currency boards with the renminbi.

The availability of above-ground gold stocks to support a global retreat from fiat currencies back to the stability of legal money — gold — is then addressed.

The conclusion is that with bullion having migrated in vast quantities from the West to the East in recent decades, there is a deficit for the fiat-committed Western alliance and nations in its sphere of influence to back their own currencies. …

… For the remainder of the analysis:

https://www.goldmoney.com/research/gold-is-replacing-the-dollar?gmrefcode=gata

* * *

END

4, OTHER IMPORTANT GOLD/SILVER COMMENTARIES/SILVER

Good reasons why gold will replace treasuries as the ultimate store of value

(Nick Giamburno/International Man)

9 Reasons Why Gold Will Soon Replace Treasuries As The Ultimate Store-Of-Value Asset

FRIDAY, AUG 04, 2023 – 07:20 AM

Authored by Nick Giambruno via InternationalMan.com,

In the age of fiat currency, the distinct concepts of saving and investing have become conflated and confused.

Saving is producing more than you consume and then setting it the difference aside.

Investing is allocating capital to a productive business to create more wealth. Investing has more risk—and potential reward—than saving.

Today, however, what most people think of as saving is actually investing.

That’s because most people take the excess of their production over consumption and put it into the stock or bond market.

Most people understand that it’s not optimal to simply hold fiat currency, which the central banks continuously debase. So they put their money into other assets, primarily bonds and stocks.

In other words, fiat currency and inflation have ruined saving for most people. It has forced them further down the risk curve into stocks, bonds, and other investments in a struggle to maintain their purchasing power.

However, there is no guarantee those investments will even keep up with inflation. But suppose they do. They will then be subject to a capital gains tax, even if it’s only a nominal gain, not a real one.

That means savers face the daunting task of not only keeping up with inflation but also outpacing the capital gains tax on the nominal gain just to maintain their purchasing power.

That’s made saving an impossible task for most.

Before the era of easy-to-produce fiat currency, people could simply save in money, which was either gold or a derivation of it.

There was no need for a dentist, construction worker, or taxi driver also to become a hedge fund manager to try to keep their head above water.

That’s how the fiat era monetized stocks, bonds, real estate, and other assets that wouldn’t have otherwise been.

For example, 50 years ago, the market cap of all the gold in the world was roughly equal to the market cap of all the stocks in the world. Today, the market cap of gold is about 10% of the world’s equities.

It’s an indication of how capital that used to be allocated to saving in gold became allocated to the stock market instead.

That doesn’t mean there isn’t a legitimate place for stocks, bonds, and real estate—there certainly is. It’s just that people would use them for investing—or, in the case of real estate, its utility value—and not as savings vehicles.

Bonds in general and Treasuries in particular, became the “go-to” savings vehicles to store wealth in the fiat era.

However, I think that will change soon as bonds will be incapable of storing value in the face of financial repression.

With 2022 being the worst year for Treasuries in American history, the shift away from bonds has probably already begun.

That means a lot of the capital parked in bonds will be looking for a new home that functions as a better store of value.

Gold: Make Saving Great Again

Gold has been mankind’s most enduring store-of-value asset because of its unique characteristics.

Gold is durable, divisible, consistent, convenient, scarce, and most importantly, the “hardest” of all physical commodities.

In other words, gold is the one physical commodity that is the “hardest to produce” (relative to existing stockpiles) and, therefore, the most resistant to debasement.

Gold is indestructible, and its stockpiles have built up over thousands of years. That’s a big reason why the new annual gold supply growth—typically 1-2% per year—is insignificant.

In other words, nobody can arbitrarily inflate the supply. That makes gold an excellent store of value and gives the yellow metal its superior monetary properties.

People in every country of the world value gold. Its worth doesn’t depend on any government or any counterparty at all. Gold has always been an inherently international and politically neutral asset. This is why different civilizations worldwide have used gold to store value for millennia.

From a historical point of view, using government bonds as a savings vehicle is a relatively new concept. As it fades, I expect people will rediscover the world’s premier store-of-value asset: gold.

It’s already starting to happen in a big way…

Last year, central banks bought roughly 37 million ounces of gold—a multi-decade record.

It’s no coincidence that the worst year ever for US Treasuries also saw the highest central bank gold buying spree in over 55 years.

As Treasuries’ political and debasement risks rise, nobody should be surprised that demand for gold is skyrocketing. I expect this trend to accelerate.

Instead of parking their savings in Treasuries, people, companies, and countries will increasingly park their savings in gold.

We are already seeing that with central banks.

So far this year, central banks have bought about 25% of worldwide gold production.

China is one of the biggest gold buyers.

China has dumped over 25% of its massive stash of Treasuries since 2021. At the same time, China has bought vast amounts of gold—five million ounces since last November, or nearly $10 billion.

Observation #9: Gold is the top store-of-value alternative to Treasuries. As demand for Treasuries falls, demand for gold will soar.

Central banks and governments are the largest individual holders of gold in the world.

Together they own over 1.1 billion troy ounces of gold out of the 6.8 billion ounces humans have mined over thousands of years.

And those are just the official numbers that governments report. The actual gold holdings could be much higher because governments are often opaque about their gold, which they consider a crucial part of their economic security.

Russia and China—the US’ top geopolitical rivals—have been the biggest gold buyers over the last two decades.

It’s no secret that China has been stashing away as much gold as possible for many years.

China is the world’s largest producer and buyer of gold. Russia is number two. Most of that gold finds its way into the Chinese and Russian government’s coffers.

As the trend of financial repression unfolds, I expect central banks to accelerate their Treasury sales and gold purchases.

Conclusion

Here is the investment thesis for gold:

Observation #1: The US government can’t repay its debt. Default is inevitable.

Observation #2: It will not be an explicit default.

Observation #3: The debt will continue to grow at an accelerating pace.

Observation #4: Foreigners are not buying as many Treasuries.

Observation #5: The US government cannot allow interest rates to rise much further.

Observation #6: The Federal Reserve is the only big buyer of Treasuries stepping up, which means currency debasement.

Observation #7: The US government will use financial repression to debase the currency in a controlled fashion, though it could spiral into out-of-control inflation.

Observation #8: Treasuries will no longer be the “go-to” store-of-value asset as people look for alternatives.

Observation #9: Gold is the top store-of-value alternative to Treasuries. As demand for Treasuries falls, demand for gold will soar.

In short, we are on the verge of a paradigm shift in international finance as gold replaces Treasuries as the world’s premier store-of-value asset.

The last time the international monetary system experienced a paradigm shift of this magnitude was in 1971.

Then, gold skyrocketed from $35 per ounce to $850 in 1980—a gain of over 2,300% or more than 24x.

I expect the percentage rise in the price of gold to be at least as significant as it was during the last paradigm shift.

That’s because this coming gold bull market could be fundamentally different than other cyclical bull markets. It will be riding the wave of a powerful trend: the re-monetization of gold as the king store-of-value asset. It could lead to the biggest gold bull market ever.

While this megatrend is already well underway, I believe the most significant gains are still ahead.

That’s precisely why I just released an urgent report on where this is all headed and what you can do about it… including three strategies everyone needs today. Click here to download the PDF now.

end

Dr Daniel Lacalle interviewed by Andrew Maguire:

“The mo

5 a. IMPORTANT COMMENTARIES ON COMMODITIES: LUXURY GOODS

Luxury goods//diamonds crashing to pre covid levels

Luxury Turmoil: Diamond Prices Crash To Pre-COVID Levels; Used Rolex Prices Hit New Six-Month Low

FRIDAY, AUG 04, 2023 – 06:55 AM

We asked in May Did Europe’s Luxury Bubble Just Burst?

By June, we pointed out Luxury Recession: Diamond Prices Crash, Rolex Downturn Persists.

And there were signs in July that Richemont, the owner of Cartier and Van Cleef & Arpels jewelry, reported a surprise drop in revenue in the second quarter. As we noted then, “Faltering demand in one of its biggest markets is an ominous sign of a weakening consumer.”

Besides Richemont, LVMH faces troubles as the US luxury market sours in the second quarter. The so-called ‘strong consumer’ narrative is cracking. This comes as consumers have been battered by two years of negative real wage growth, forcing some to draw down on personal savings while racking up insurmountable credit card debt to make ends meet. On top of this, interest rates are at 22-year highs, and the latest Senior Loan Officers Opinion Survey on Bank Lending Practices shows even tighter bank lending standards that suggest a less favorable economic outlook for the US in the coming quarters.

Considering all these factors, it makes sense why diamond prices have collapsed to pre-Covid levels. The latest data from the Diamond Index via International Diamond Exchange shows the index was at 116.12 on Aug. 1, breaching the floor of 116.26 set on Mar. 24, 2020.

Also, the secondhand luxury watch market has yet to find a bottom.

The Bloomberg Subdial Watch Index, which tracks prices for the 50 most-traded watches by value on the secondary market, continues to slide, breaching a six-month support level of around $35,762, now printing about $35,271. The index has slumped 41% since peaking around $60,600 in March 2022.

Burberry and Prada have also reported weakening demand in the US market. Without stimulus checks, the luxury goods boom is no more. Just wait until student debt payments restart in under a month..

end

5 B GLOBAL COMMODITY ISSUES/FOOD IN GENERAL//FREIGHT

Interesting: global container rates are jumping the most in two years

(zerohedge)

Global Container Rates Jump The Most In Two Years

FRIDAY, AUG 04, 2023 – 05:45 AM

Spot rates for shipping containers have been rising for four weeks. The latest data from the Drewry World Container Index composite shows the most significant weekly gain in the index in more than two years. The 23-month slump in ocean-freight costs appears to be ending.

The Drewry World Container Index jumped 11.79% to $1,761 for a 40-foot container, the largest weekly gain since June 24, 2021 — or the period when shipping costs worldwide were sky-high because of snarled supply chains.

All major shipping lines have experienced a multi-year decline.

Some of the largest gains in the last four weeks have been on the Shanghai to Los Angeles and Shanghai to New York routes.

Senior editor Greg Miller of logistics firm FreightWaves wrote a note last week explaining:

Spot rates have been on the rise for three straight weeks, rebounding to levels last seen in early 2023 and late 2022, according to several index providers. U.S. import bookings remain above pre-COVID levels, and multiple analysts are now highlighting positive rate effects from reduced vessel capacity.

While managing vessel capacity appears to be working, French shipper CMA CGM SA warned East-West trade lanes are under more pressure and dropping faster than the North-South trade, which remains pretty dynamic.”

In early May, A.P. Moller-Maersk A/S, a bellwether for global trade, expected weaker results for the rest of 2023 after a slump in the first quarter. Maersk is slated to report on Friday.

Goldman updated clients on its Supply Chain Congestion Scale registers a “2,” which means the weekly bottleneck metrics for global supply chains appear to have normalized after the snarls during Covid.

Economists and analysts have been optimistic in recent weeks that the Federal Reserve can engineer a soft landing and avoid a recession (remember, there’s stealth QE).

“We believe the Fed is on track for a soft landing … and the data this week has been consistently good. It adds to my conviction,” Jan Hatzius, chief economist at Goldman Sachs, recently said.

In the world’s second-largest economy, signs of slowing growth and weakness in China persists. Perhaps the surge in container rates is more or less a function of reduced capacity instead of a rise in demand.

END

6.CRYPTOCURRENCY//DIGITAL CURRENCY// COMMENTARIES/

END

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS FRIDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED DOWN TO 7.1862

OFFSHORE YUAN: DOWN TO 7.1936

SHANGHAI CLOSED UP 7.62 PTS OR 0.23%

HANG SENG CLOSED UP 111.59 PTS OR 0.61%

2. Nikkei closed UP 33.47 PTS OR 0.10%

3. Europe stocks SO FAR: ALL RED

USA dollar INDEX DOWN TO 102.73 EURO FALLS TO 1.0946 DOWN 4 BASIS PTS

3b Japan 10 YR bond yield: RISES TO. +.632 Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 142.62/JAPANESE YEN FALLING AS WELL AS LONG TERM 10 YR. YIELDS RISING //EVENTUALLY THIS WILL BREAK THE JAPANESE CENTRAL BANK

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen DOWN CHINESE ON SHORE YUAN: DOWN// OFF- SHORE: DOWN

3f Japan is to buy INFINITE TRILLION YEN’S worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and UP FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund UP TO +2.6115***/Italian 10 Yr bond yield RISES to 4.315*** /SPAIN 10 YR BOND YIELD RISES TO 3.669…**

3i Greek 10 year bond yield RISES TO 3.9117

3j Gold at $1940.00 silver at: 23.50 1 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble DOWN 0 AND 17 /100 roubles/dollar; ROUBLE AT 95.16//

3m oil into the 81 dollar handle for WTI and 85 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 142.62// 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 0.632% STILL ON CENTRAL BANK (JAPAN) INTERVENTION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.8770 as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9600 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.192 UP 0 BASIS PTS…

USA 30 YR BOND YIELD: 4.298 UP 0 BASIS PTS/

USA 2 YR BOND YIELD: 4.934 UP 4 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 26.99…(TURKEY SET TO BLOW UP FINANCIALLY)

GREAT BRITAIN/10 YEAR YIELD: UP 4 BASIS PTS AT 4.5365

end

2.a Overnight: Newsquawk and Zero hedge:

Futures Rally Fizzles As Apple Slides, Payrolls Loom

FRIDAY, AUG 04, 2023 – 08:16 AM

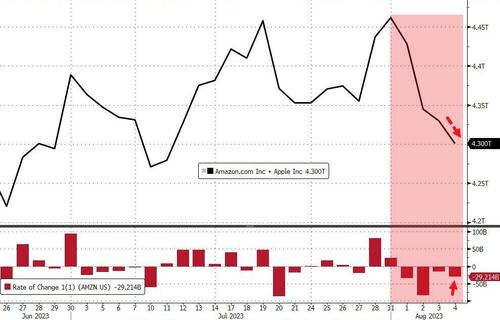

An earlier rally in US equity futures fizzled and Treasuries steadied after days of sharp losses as Apple sunk to session lows, while traders awaited employment data for clues on the path for Federal Reserve interest rates. As of 7:45am ET S&P futures were fractionally in the red at 4,520 erasing a earlier gain of 0.3% and set to extend their biggest weekly decline since March; meanwhile Nasdaq futures were still in the green, up 0.2% thanks to Amazon.com surging 9% in premarket trading after revenue at the world’s largest e-commerce and cloud services company beat estimates. Europe’s Stoxx 600 index turned lower while Asian stocks rose, trimming their weekly decline, on pockets of good news in China and shreds of optimism that the spike in bond yields won’t last. The Bloomberg dollar index rose 0.1% while 10Y TSY yields added one basis point to trade at 4.19%.

In premarket trading, Apple’s market value dropped 2%, sliding below the historic $3 trillion level after the world’s biggest company posted a third straight quarter of declining sales, sparking worries over tepid demand for its handsets and other gadgets

On the other end, Amazon.com shares jumped as much as 9.1% as analysts hiked their price targets for the stock en masse after the e-commerce and cloud computing company reported second-quarter results that beat expectations and gave a positive forecast. Here are the other notable premarket movers:

- Airbnb shares dip 0.2% after the company reported a lower-than-expected number of nights and experiences booked in the second quarter. Analysts saw the results as solid overall, though Citi said the miss could weigh on shares. .

- Amgen’s second-quarter earnings assuage investor concerns over the biotech’s performance after its weak first-quarter report, analysts say, noting inventory and volume both recovered and EPS slightly beat expectations.

- Assertio Holdings shares plummet 42% after the pharmaceutical company withdrew its full-year 2023 financial outlook to assess the impact of an FDA-approved generic indomethacin, an arthritis drug.

- Atlassian shares soar 23% after the team- collaboration software maker beat estimates on cloud revenue and operating margin. Outlook for margins to hit a bottom in fiscal 2024 was highlighted as a positive by analysts, even though the cloud growth guidance was viewed as conservative and the company struggled to sign up new customers amid slower corporate spending.

- Block Inc shares slide 4.1% in premarket trading Friday after its July gross profit growth forecast fell short for investors. The company also boosted its adjusted operating income guidance for the full year; the outlook beat the average analyst estimate.

- Coinbase rises 1.2%, after the cryptocurrency company reported revenue for the second quarter that beat the average analyst estimate, driven by higher retail transaction fee rates, analysts say.

- DraftKings shares soar 14% after the online sportsbook reported second- quarter revenue that beat consensus expectations and raised its forecast for the year. Analysts had a positive reaction to the print, with Goodbody saying it was an “excellent” update overall.

- Tupperware Brands shares soar 52% after the food-storage container company reached an agreement with its lenders to restructure its existing debt obligations, as it continues its turnaround efforts.

The market has been largely frozen ahead of today’s non-farm payrolls number (due at 830am) which is forecast to show the US added 200,000 jobs in July with crowd-soured whisper number higher at 222,000 (full preview here). While that would be the weakest print since the end of 2020, it’s still strong historically and a number exceeding that may fuel bets on more Fed hikes. A report Thursday underscored resilient US demand for workers and the mood in markets remains cautious. Here is a breakdown of payrolls forecasts by bank

- 290,000 – Citigroup

- 250,000 – Barclays

- 250,000 – Goldman

- 240,000 – HSBC

- 210,000 – Wells

- 200,000 – Credit Suisse

- 190,000 – Morgan Stanley

- 190,000 – SocGen

- 175,000 – Deutsche Bank

- 175,000 – JP Morgan Chase

- 150,000 – UBS

“With NFP still to come, I shouldn’t think investors are too willing to jump in with both feet just yet,” said James Athey, investment director at Abrdn.

Investors indeed are biding their time until after the jobs report is out: the jolt from Fitch Ratings stripping the US of its triple-A credit ranking was compounded by news Wednesday that the government will boost quarterly debt sales to $103 billion, more than expected. Yields soared to the highest since November as traders fretted over the increased supply, wiping out the Treasury market’s gains for 2023.

Meanwhile, the recent tumult in markets is making investors wary. Bank of America’s clients are moving out of equities as the risk of an economic contraction remains high, strategist Michael Hartnett said. “Private clients are shifting back to ‘risk-off’ mode,” he wrote in a note, adding that a hard landing was still a risk for the second half amid the higher bond yields and tighter financial conditions.

Europe’s Stoxx 600 index rose 0.3% as it looks to snap a three-day losing streak as travel and leisure shares outperformed. European natural gas headed for the biggest weekly gain since June. Here are the most notable European movers:

- Credit Agricole shares rise as much as 6.1% after the French lender reported a surge in profit for the second quarter and beat consensus expectations, analysts said

- Bpost gains as much as 7.8% after the postal company had second-quarter results which analysts say were overall positive, with a decent performance in Belgium offsetting a softer US market

- Commerzbank dropped as much as 3.8%, the worst performer on the Stoxx 600 Banks Index, as a lack of detail in the German lender’s 2H share buyback plan, overshadowed a 2Q beat on net interest income and an improved full-year outlook for lending

- Carl Zeiss Meditec falls as much as 6.9%, the most since May, after the German medical optics firm reported a “disappointing” set of 3Q figures, according to Oddo analysts, who flag lower mid-term guidance as another key negative

- WPP shares fall as much as 8%, the most in a year, after the advertising agency reduced its full-year organic growth forecast, citing lower revenue from US technology clients and a weaker-than-expected sales rebound in China

- IMCD shares dropped as much as 8.3%, the biggest drop since May last year, after the chemicals distributor reported revenue in the first half of the year that missed analyst estimates

- Genmab fell as much as 3.6% after the Danish biotech reported its latest earnings, which analysts said highlighted a pipeline that’s mostly unexciting until 2024

- Freenet shares fall as much as 2.3% to the lowest level since January, erasing an earlier 1.9% gain, after the telecom and media firm’s core mobile communications segment missed 2Q revenue estimates

- Lanxess shares slide as much as 4.9%, with Morgan Stanley highlighting weak free cash flow in the chemicals company’s 2Q result as a key negative, caused by a fall in adjusted Ebitda

- Sika shares drop as much as 3.9% after the Swiss construction-materials company reported 1H results that were below expectations, partially due to costs related to its recent

Asian stocks rose, trimming their weekly decline, on pockets of good news in China and shreds of optimism that the spike in bond yields won’t last. The MSCI Asia Pacific Index advanced as much as 0.5%, before fading most of the gains with benchmarks in Hong Kong, China and Vietnam among the biggest gainers. The MSCI regional gauge is still headed for a more than 2% drop this week, its worst since late June, as the dollar strengthened and bond yields spiked globally as traders assess the outlook for the US economy.

The macro backdrop has become more favorable for Asian equities, according to Goldman Sachs. Investors should “use the potential soft late-summer seasonality to position for the typically strong 4Q,” as US economic data support soft-landing prospects and China’s Politburo meeting positively surprised, strategist Timothy Moe wrote in a note.

- Chinese stocks got a boost Friday on expectations of more funding for the property sector and a jump in brokerage shares due to a cut in a reserve payment ratio. The People’s Bank of China said it will step up its monetary support for the economy and help banks control liability costs.

- Stocks dipped in Australia, Taiwan and Singapore, with benchmarks in the latter two poised to cap their worst week since October.

- Australia’s ASX 200 was rangebound as gains in the commodity-related sectors and financials were counterbalanced by weakness in defensives, while the RBA’s quarterly Statement of Monetary Policy provided little to shift the dial and reiterated that some further tightening may be required.

- The Nikkei 225 swung between gains and losses as an early retreat beneath the 32,000 level was met with dip buying which then petered out.

- Indian stocks ended their three-day long losing streak on Friday boosted by gains in technology and pharmaceutical companies. The S&P BSE Sensex rose 0.7% to 65,721.25 in Mumbai, while the NSE Nifty 50 Index advanced by the same magnitude. For the week, both indexes closed with 0.7% losses but fell less than the 2.4% decline in the MSCI Asia Pacific Index.

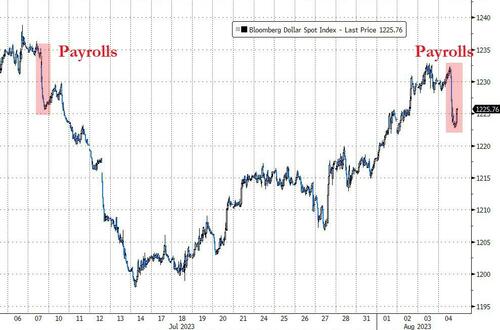

In FX, the Bloomberg Dollar Spot Index is up 0.1% amid position unwinds ahead of the US nonfarm payroll data. However, the measure is still set for a third weekly advance. The Aussie added as much as 0.6%, extending an exporter-driven gain after the central bank implied that rates may have to remain at elevated levels for longer. The Swiss franc is the worst performer among the G-10’s, falling 0.4% versus the greenback.

“Solid ADP likely raised market expectations for NFP already, which means that the USD is vulnerable to a sell-on- rally reaction tonight,” said Fiona Lim, senior currency analyst at Malayan Banking Berhad in Singapore. “We had seen a bout of strong US data for much of the past week that lifted the USD,” she added

In rates, 30-year bonds edged higher with yields down 2bps while two-year borrowing costs rise 4bps. 10Y Yields were flat at 4.18%. The treasury curve was flatter into early US session, paring a four-day steepening move for 2s10s and 5s30s spreads. 5s30s returns to negative after flipping positive for the first time since June 13 on Thursday. Front-end-led weakness follows similar bear-flattening in bunds and gilts during London morning. Bunds are lower, having extended declines after German factory orders saw their largest rise in three-years.

In commodities, crude futures advance with WTI rising 0.5% to trade near $82. Spot gold is little changed around $1,934.

Bitcoin is under marked pressure in relatively narrow ranges which remain above the USD 29k mark given overall price action is somewhat tentative pre-NFP.

Looking ahead to today, we have the US July jobs report, the UK July construction PMI, new car registrations, Italian June industrial production, German construction PMI for July as well as factory orders, French Q2 wages and June industrial production, the Eurozone June retail sales and the Canadian jobs report for July. We will hear from the BoE’s Pill, and earnings releases from Dominion Energy and LyondellBasell.

Market Snapshot

- S&P 500 futures up 0.4% to 4,538.25

- MXAP little changed at 166.06

- MXAPJ little changed at 526.16

- Nikkei up 0.1% to 32,192.75

- Topix up 0.3% to 2,274.63

- Hang Seng Index up 0.6% to 19,539.46

- Shanghai Composite up 0.2% to 3,288.08

- Sensex up 0.4% to 65,513.20

- Australia S&P/ASX 200 up 0.2% to 7,325.34

- Kospi little changed at 2,602.80

- STOXX Europe 600 up 0.1% to 458.55

- German 10Y yield little changed at 2.63%

- Euro little changed at $1.0943

- Brent Futures up 0.3% to $85.43/bbl

- Gold spot down 0.0% to $1,933.24

- U.S. Dollar Index little changed at 102.56

Top Overnight News

- China continues to speak forcefully about providing stimulus to the economy and bolstering growth – the PBOC on Thurs pledged to channel more financial resources into the private economy. RTRS

- China will relax a range of social control policies as the gov’t scrambles to pull various stimulus levels to bolster the economy. SCMP

- Japan’s state pension fund — the world’s largest — posted a record 9.5% gain of ¥18.98 trillion ($133 billion) in the three months through June. Domestic stocks were the top performers, gaining 14.4% as stable inflation and bigger stakes from investors including Warren Buffett reinvigorated local markets. Overseas bonds gained 8.1%. BBG

- Maersk cuts its outlook for global container volume growth in 2023 (given the weak start of the year and the continued destocking, Maersk now sees the global container volume growth in the range of -4% to -1% compared to -2.5% to +0.5% previously). BBG

- Ukraine attacked the oil export infrastructure that helps fund Moscow’s invasion for the first time on Friday, using a drone strike to damage a Russian naval vessel outside the port of Novorossiysk. FT

- Chase Coleman’s Tiger Global has built a big stake in private equity group Apollo Global as the hedge fund looks outside of the technology investments that have been its mainstay in recent years in a hunt for better returns. FT

- GIR’s BOTTOM LINE on NFP: Estimate nonfarm payrolls rose 250k in July, above consensus of +200k and roughly in line with the +244k average pace of the last three months. Estimate private payrolls rose 225k. Estimate the unemployment rate edged down by 0.1pp to 3.5% reflecting a rise in household employment and unchanged labor force participation at 62.6%. 0.3% increase in average hourly earnings that lowers the year-on-year rate to 4.2%, reflecting waning upward wage pressures and positive calendar effect. GIR

A more detailed look at global markets courtesy of Newsquawk

APAC stocks traded mixed as most bourses in the region lacked firm direction after a lackluster handover from the US, while participants reflected on tech giant earnings and the latest PBoC support pledges. ASX 200 was rangebound as gains in the commodity-related sectors and financials were counterbalanced by weakness in defensives, while the RBA’s quarterly Statement of Monetary Policy provided little to shift the dial and reiterated that some further tightening may be required. Nikkei 225 swung between gains and losses as an early retreat beneath the 32,000 level was met with dip buying which then petered out. Hang Seng and Shanghai Comp were positive with gains led by the property sector after the latest policy support pledges by the PBoC which announced it is to rollout guidelines to support private firms and will expand debt financing tools, as well as implement differentiated housing credit policies.

Top Asian News

- PBoC official said RRR cuts, open market operations, MLF and all structural policy tools need to be flexibly used to maintain reasonably ample liquidity in the banking system and they will guide banks to effectively adjust mortgage interest rates and support banks to reasonably control the cost of liabilities. Furthermore, the official said monetary policy room is ample and they will step up counter-cyclical adjustment, as well as reasonably handle the interest rate level to prevent capital arbitrage, according to Reuters.

- China NDRC official said China’s economy is to keep stable, improving momentum in H2 and they will strengthen policy reserves to release huge market potential, while they will study a batch of policy reserves with greater intensity, according to Reuters.

- China’s Global Times tweeted that Shanghai’s securities regulator will conduct on-site inspections of securities companies such as Morgan Stanley Securities and Changjiang Financing Services as it targets employee management and anti-money laundering.

- US President Biden is being urged to limit further US investment in Chinese stocks and bonds ahead of an expected new order next week, according to FT citing US House China Committee Chair Mike Gallagher. It was also reported that the House China Committee Chair held out the possibility of a subpoena in the Blackrock (BLK) and MSCI (MSCI) probe if they do not provide “fulsome” answers about investments in blacklisted Chinese companies.

- China’s MOFCOM lifted anti-dumping and anti-subsidy tariffs on Australian barley from August 5th.

- RBA Statement on Monetary Policy said some further tightening may be required and the board considered hiking rates at the August meeting but decided the stronger case was to hold steady. RBA also stated that risks around inflation are broadly balanced but much depends on inflation expectations and inflation is moving in the right direction which is consistent with reaching the target by late 2025, while it added that tightening could provide some further insurance against upside inflation risks.

European bourses are modestly firmer, Euro Stoxx 50 +0.4%, in largely contained trade ahead of the US NFP report. Sectors are mixed with outperformance in Travel & Leisure amid strength in airliners and some gambling names, elsewhere Banking and Energy names are supported by yields and benchmarks respectively. Stateside, futures are a touch firmer and largely in-fitting with European peers, ES +0.3%; aside from NDP, participants are digesting the numerous after-hours results on Thursday including Amazon +8.8% and Apple -1.8%.

Top European News

- BoE Governor Bailey said rates will have to remain restrictive and it is “too early” to see victory on inflation, while he noted the last mile of the inflation fight is to take some time, according to a Bloomberg TV interview.

- UK PM Sunak is considering skipping the annual gathering of world leaders at the UN, according to the Telegraph.

- UK Chancellor Hunt asked the FCA to carry out an urgent review on concerns around “debanking” and the government will determine whether further action is necessary based on the findings. FCA is to ask the biggest banks and building societies for data on account terminations and the reasons for them, while it will provide an initial assessment of account terminations by mid-September.

- ECB says median and mean underlying inflation measures suggest that underlying inflation likely peaked in the first half of 2023. Although most measures are showing signs of easing, underlying inflation remains high overall. *Persistent and common components of inflation appear to have started to decline for service.

- A.P. Moeller-Maersk (MAERSK DC) Q2 (USD): EBIT 1.6bln (exp. 0.89bln), EBITDA 2.9bln (exp. 2.4bln). Forecast global container volume growth in a -4% to -1% range (prev. -2.5% to +0.5%), based on the continued destocking. “Overall, the environment for container trade and logistics services remains challenging. Currently, there is no sign of a substantial rebound in volumes in the second half of the year.”.

FX

- The broader Dollar and index trades on either side of 102.50 but closer towards the upper end of a tight intraday parameter thus far, underpinned by the upside in yields as US bonds remain under pressure.

- The antipodeans narrowly outperform in the G10 space, trading flat/firmer, after consecutive sessions of hefty underperformance amid a combination of the RBA pause, risk aversion, and softer data from the region. AUD could also be feeling some relief from reports that China’s MOFCOM lifts anti-dumping and anti-subsidy tariffs on Australian barley.

- Traditional havens give up some recent risk-induced gains in the run-up to the US jobs report, with little in terms of fresh newsflow to drive price action in recent trade.

- EUR and GBP are relatively flat against the USD and each other amid a light European calendar and quiet newsflow in the region. EUR/USD was unreactive to mixed EZ retail sales and the surprise and substantial growth in German Industrial Orders.

- PBoC set USD/CNY mid-point at 7.1418 vs exp. 7.1808 (prev. 7.1495)

Fixed Income

- Overall, comparably contained trade but bearish drivers continue to dictate action given an absence of fresh catalysts pre-NFP.

- As it stands, EGBs and USTs are pressured and at incremental lows for the week as the majority of price action remains driven by supply-side dynamics from the US.

Commodities

- WTI and Brent front-month futures exhibit a slightly firmer bias as markets gear up for the OPEC+ JMMC and thereafter the US jobs report.

- Spot gold is trading sideways in the run-up to the US jobs report with the yellow metal contained within yesterday’s range (USD 1,929.19-1,937.79/oz).

- Base metals remain mostly subdued amid the indecisive mood but hold onto a bulk of recent gains as all eyes turn to NFP. 3M LME copper holds above USD 8,500/t but declined from a USD 8,686/t overnight high.

- OPEC+ JMMC meeting to start at 12:30 BST/07:30EDT, according to EnergyIntel’s Bakr (previously guided for 13:00BSt/08:00EDT)

- White House’s Kirby said the US is to continue working with producers and consumers to ensure the energy market promotes growth after the Saudi decision on oil production.