GOLD PRICE CLOSED: DOWN $1.00 TO $1916.45

SILVER PRICE CLOSED: UP $0.06 AT $22.75

Access prices: closes 4: 15 PM

Gold ACCESS CLOSE 1914,40

Silver ACCESS CLOSE: 22.65

Shanghai Gold Benchmark Price

Shanghai Gold Benchmark Price

USD oz  AM1959.52

AM1959.52

PM1961.39

Historical SGE Fix

New York price at the time: 1915.00

premium $46.00

xxxxxxxxxxxxxxxxxx

Bitcoin morning price:, $29,501 UP 3 Dollars

Bitcoin: afternoon price: $29,402 DOWN 96 dollars

Platinum price closing $911.90 UP $17.65

Palladium price; $1293.55 UP $56.70

END

Due to the huge rise in the dollar, we must look at gold and silver in currencies other than the dollar to understand where we are heading

I will now provide gold in Canadian dollars, British pounds and Euros/4: 15 PM ACCESS

CANADIAN GOLD: $2,570.00 DOWN 18.50 CDN dollars per oz (ALL TIME HIGH 2,775.35)

BRITISH GOLD: 1505,32 DOWN5,71 pounds per oz//(ALL TIME HIGH//CLOSING///1630.29)

EURO GOLD: 1744.42 DOWN 15.37 euros per oz //(ALL TIME HIGH/CLOSING//1861.21)//

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

EXCHANGE: COMEX

EXCHANGE: COMEX

CONTRACT: AUGUST 2023 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,915.400000000 USD

INTENT DATE: 08/09/2023 DELIVERY DATE: 08/11/2023

FIRM ORG FIRM NAME ISSUED STOPPED

118 C MACQUARIE FUT 6

323 C HSBC 250

435 H SCOTIA CAPITAL 118

624 H BOFA SECURITIES 27

657 C MORGAN STANLEY 47

661 C JP MORGAN 33

690 C ABN AMRO 3

737 C ADVANTAGE 125 13

905 C ADM 42

TOTAL: 332 332

MONTH TO DATE: 10,572

JPMorgan stopped 33/332 contracts.

FOR AUGUST:

GOLD: NUMBER OF NOTICES FILED FOR AUGUST/2023. CONTRACT: 332 NOTICES FOR 33,200 OZ or 1.0326 TONNES

total notices so far: 10,572 contracts for 1,057,200 oz (32.883 tonnes)

FOR AUGUST:

SILVER NOTICES: 0 NOTICE(S) FILED FOR nil OZ/

total number of notices filed so far this month : 896 for 4,480,000 oz

XXXXXXXXXXXXXXXXXXXXXXXX

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD

WITH GOLD DOWN $1.00

INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD//

NO CHANGES IN GOLD INVENTORY AT THE GLD:

INVENTORY RESTS AT 903.69 TONNES

Silver//

WITH NO SILVER AROUND AND SILVER UP 6 CENTS AT THE SLV// HUGE CHANGES IN SILVER INVENTORY AT THE SLV: WITHDRAWAL OF 1.193 MILLION OZ FROM THE SLV/

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV.

CLOSING INVENTORY: 450.180 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A TINY SIZED 55 CONTRACTS TO 137,576 AND CLOSER TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THIS GOOD SIZED GAIN IN COMEX OI WAS ACCOMPLISHED DESPITE OUR $0.07 LOSS IN SILVER PRICING AT THE COMEX ON WEDNESDAY. TAS ISSUANCE WAS ANOTHER JUPITER SIZED 7643 CONTRACTS. THESE WILL BE USED FOR MANIPULATION LATER THIS MONTH/AS WELL AS TODAY. CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON WEDNESDAY NIGHT: 7643 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS. IT THUS LOOKS LIKE THE FED (GOV’T) IS BEHIND ALL OF THESE TRADES.

WE HAVE NOW SET ANOTHER RECORD LOW AT 114,102 CONTRACTS ///JULY 3.2023// OUR BANKERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.07). BUT WERE UNSUCCESSFUL IN KNOCKING OF ANY SILVER CONTRACTS AS WE HAD OUR HUGE GAIN OF 4420 CONTRACTS ON BOTH EXCHANGES ALONG WITH CONSIDERABLE T.A.S.LIQUIDATION.

WE MUST HAVE HAD:

AN ULTRA GIGANTIC ISSUANCE OF EXCHANGE FOR PHYSICALS( 4475 CONTRACTS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 3.105 MILLION OZ (FIRST DAY NOTICE) FOLLOWED BY TODAY’S NIL OZ QUEUE JUMP //NEW STANDING RISES AT 4.480 MILLION OZ + OUR NEW CRIMINAL 0 CONTRACTS OF EXCHANGE FOR RISK FOR 0.00 MILLION OZ + 1.45 MILLION OZ EX. FOR RISK/PRIOR/// NEW TOTAL STANDING FOR SILVER: 5.930 MILLION OZ/// // // GOOD SIZED COMEX OI GAIN/ ULTRA HUGE SIZED EFP ISSUANCE/VI) JUPITER SIZED NUMBER OF T.A.S. CONTRACT ISSUANCE (7643 CONTRACTS)/ZERO EXCHANGE FOR RISK ISSUED

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL -511 CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS AUGUST. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF AUGUST:

TOTAL CONTRACTS for 8 days, total 15,031 contracts: OR 75.156 MILLION OZ (1878 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 75.156 MILLION OZ

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH 2022: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 118.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 85.745 MILLION OZ (SMALLER THAN LAST MONTH)

AUGUST: 75.156 MILLION OZ (THIS MONTH IS GOING TO BE GIGANTIC//WE MAY SURPASS MARCH 2022 RECORD OF 207 MILLION OZ/// )

RESULT: WE HAD A SMALL SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 11 CONTRACTS WITH OUR LOSS IN PRICE OF $0.07 IN SILVER PRICING AT THE COMEX//WEDNESDAY.,. THE CME NOTIFIED US THAT WE HAD AN ULTRA HUGE EFP ISSUANCE CONTRACTS: 4475 ISSUED FOR SEPT AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS./ WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR AUGUST OF 3.105 MILLION OZ FOLLOWED BY TODAY’S 0 OZ QUEUE JUMP//NEW STANDING 4.480 MILLION OZ+ 1.45 MILLION OZ EXCHANGE FOR RISK NEW TOTALS 5.930 MILLION OZ//// WE HAVE A GIGANTIC SIZED GAIN OF 4420 OI CONTRACTS ON THE TWO EXCHANGES. THE TOTAL OF TAS INITIATED CONTRACTS TODAY: A MAMMOTH 7643//HUGE FRONT END OF THE TAS CONTRACTS WERE LIQUIDATED DURING THE WEDNESDAY COMEX SESSION . THE NEW TAS ISSUANCE WEDNESDAY NIGHT (7643) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE., PROBABLY TODAY.

WE HAD 0 NOTICE(S) FILED TODAY FOR nil OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A FAIR SIZED 2124 CONTRACTS TO 429,883 AND CLOSER TO TO THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: – REMOVED: 192 CONTRACTS

WE HAD A FAIR SIZED INCREASE IN COMEX OI ( 2124 CONTRACTS) DESPITE OUR $8.35 LOSS IN PRICE//WEDNESDAY. WE ALSO HAD A RATHER SMALL INITIAL STANDING IN GOLD TONNAGE FOR AUGUST. AT 30.656 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S 29.900 OZ QUEUE.JUMP + PRIOR ISSUANCE OF EXCHANGE FOR RISK = (.684 TONNES) //NEW STANDING 33.440 TONNES + .684 EXCHANGE FOR RISK = 34.124/ + /A FAIR (AND CRIMINAL) ISSUANCE OF 1030 T.A.S. CONTRACTS /// ALL OF..THIS HAPPENED WITH A $8.35 LOSS IN PRICE WITH RESPECT TO WEDNESDAY’S TRADING.WE HAD A STRONG SIZED GAIN OF 7174 OI CONTRACTS (22.314 PAPER TONNES) ON OUR TWO EXCHANGES.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 1030 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 429,883

IN ESSENCE WE HAVE A STRONG SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 7174 CONTRACTS WITH 2124 CONTRACTS INCREASED AT THE COMEX// AND A STRONG 5050 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 7174 CONTRACTS OR 22.314 TONNES. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): A FAIR 1030 CONTRACTS)

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A STRONG SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (5050 CONTRACTS) ACCOMPANYING THE FAIR SIZED GAIN IN COMEX OI (2124) //TOTAL GAIN FOR OUR THE TWO EXCHANGES: 7174 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR NORMAL FORMAT OF BANKERS GOING SHORT AND SPECULATORS GOING LONG ,2.) FAIR INITIAL STANDING AT THE GOLD COMEX FOR JULY AT 30.656 TONNES FOLLOWED BY TODAY’S 29,900 OZ QUEUE JUMP //NEW STANDING 33.440 TONNES + .684 TONNES (EXCHANGE FOR RISK//PRIOR) NEW TOTALS: 34.124 TONNES/// 3) ZERO LONG LIQUIDATION WITH HUGE TAS LIQUIDATION //4) FAIR SIZED COMEX OPEN INTEREST GAIN/ 5) STRONG ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER///6: FAIR T.A.S. ISSUANCE: 1030 CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023 INCLUDING TODAY

AUGUST

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF AUG :

TOTAL EFP CONTRACTS ISSUED: 24,931 CONTRACTS OR 2,493,100 OZ OR 77.546 TONNES IN 8 TRADING DAY(S) AND THUS AVERAGING: 3116 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 8 TRADING DAY(S) IN TONNES 77.546 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2022, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 77.546/3550 x 100% TONNES 2.19% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2023

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH/2022: 409.30 TONNES //FINAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 151.69 TONNES (WEAKER THAN LAST MONTH)

AUGUST: 77.546 TONNES (A HUGE MONTH BUT WILL NOT EQUAL MARCH 2022)

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF SEPT. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF MAY HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF JUNE., FOR BOTH GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (SEPT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

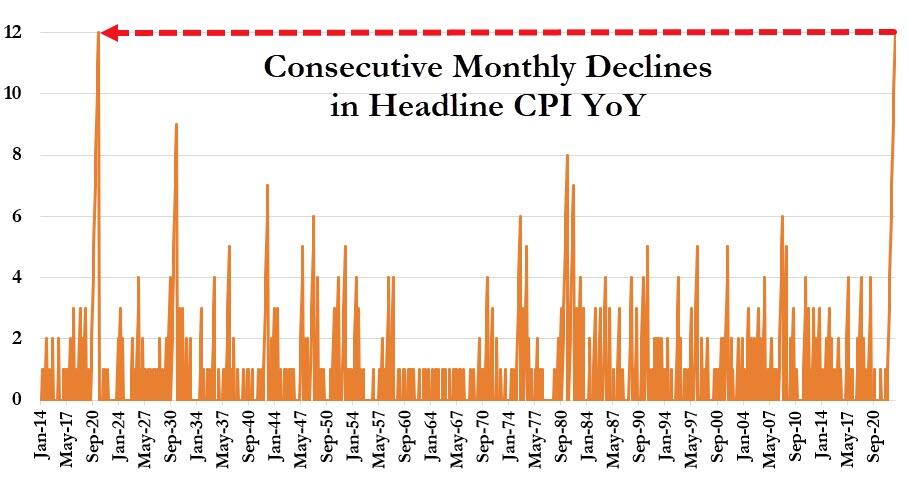

1.Today, we had the open interest at the comex, in SILVER FELL BY A TINY SIZED 55 CONTRACTS OI TO 137,576 AND CLOSER TO OUR COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE AN ULTRA HUGE 4475 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

SEPT 2062 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 4475 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 55 CONTRACTS AND ADD TO THE 4475 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A HUGE SIZED GAIN OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 4420 CONTRACTS

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTAL 22.100 MILLION OZ

OCCURRED DESPITE OUR $0.07 LOSS IN PRICE …..

END

OUTLINE FOR TODAY’S COMMENTARY

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

b, ) Gold/silver trading overnight Europe,//GOLD COMMENTARIES

(Peter Schiff)

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS//

THURSDAY MORNING//WEDNESDAY NIGHT

SHANGHAI CLOSED UP 10.07 PTS OR 0.31% //Hang Seng CLOSED UP 2.23 PTS OR 0.01% /The Nikkei CLOSED UP 269.32 PTS OR 0.84% //Australia’s all ordinaries CLOSED UP 0.32 % /Chinese yuan (ONSHORE) closed UP 7.2084 /OFFSHORE CHINESE YUAN UP TO 7.2195 /Oil UP TO 83.97 dollars per barrel for WTI and BRENT UP AT 87.26 / Stocks in Europe OPENED ALL GREEN// ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE STRONGER

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

9. USA

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A FAIR SIZED 2124 CONTRACTS UP TO 429,883 DESPITE OUR LOSS IN PRICE OF $8.35 ON WEDNESDAY.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE ACTIVE DELIVERY MONTH OF AUGUST… THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 5050 EFP CONTRACTS WERE ISSUED: : DEC 5050 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 5050 CONTRACTS

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A STRONG SIZED TOTAL OF 7174 CONTRACTS IN THAT 5050 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A FAIR SIZED GAIN OF 2316 COMEX CONTRACTS..AND THIS GAIN ON OUR TWO EXCHANGES HAPPENED DESPITE OUR LOSS IN PRICE OF $8.35//WEDNESDAY COMEX. AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS DURING MID MONTH IN THE DELIVERY CYCLE), THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR WEDNESDAY NIGHT WAS A FAIR 1030 CONTRACTS. THROUGHOUT THE PAST WEEKS, THE BANKERS SOLD OFF THE LONG SIDE OF THE SPREAD WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR SPREAD WHICH WILL BE LIQUIDATED TWO MONTHS HENCE)//THE HUGE NUMBER OF T.A.S. CONTRACTS INITIATED OVER THE PAST SEVERAL WEEKS SPELLS TROUBLE FOR THE GOLD/SILVER MARKET AS RAIDS WILL SURELY BE UPON US TRYING TO CONTAIN OUR PRECIOUS METALS RISE IN PRICE.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: AUGUST (34.124) ( ACTIVE MONTH)

TONNES),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 34.124 TONNES (INCLUDING .6842 EXCHANGE FOR RISK)

THE SPECS/HFT WERE SUCCESSFUL IN LOWERING GOLD’S PRICE( IT LOST $8.35) //// BUT WERE UNSUCCESSFUL IN KNOCKING ANY SPECULATOR LONGS AS WE HAD A STRONG GAIN OF 7174 TOTAL CONTRACTS ON OUR TWO EXCHANGES. WE HAD CONSIDERABLE T.A.S. LIQUIDATION. THE T.A.S. ISSUED ON WEDNESDAY NIGHT WILL BE “PUT INTO THE BANK” TO BE USED AT A LATER DATE AT THE COLLUSIVE CHOOSING OF OUR BANKERS.

WE HAVE GAINED A TOTAL OI OF 22.314 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR AUGUST. (30.656 TONNES) ON FIRST DAY NOTICE FOLLOWED BY TODAY’S 29,900 OZ QUEUE JUMP//NEW STANDING ADVANCES TO 33.440 TONNES + .6842 (PRIOR EXCHANGE FOR RISK) //NEW TOTAL 34.124 TONNES // ALL OF THIS WAS ACCOMPLISHED WITH OUR LOSS IN PRICE TO THE TUNE OF $8.35.

WE HAD – REMOVED 192 CONTRACTS TO THE COMEX TRADES TO OPEN INTEREST

NET GAIN ON THE TWO EXCHANGES 7174 CONTRACTS OR 717,400 OZ OR 22.314 TONNES.

Estimated gold volume today:// 167,193 poor

final gold volumes/yesterday 149,055 awful

//AUGUST 10/ FOR THE AUGUST 2023 GOLD CONTRACT

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 32.151 BRINKS 1 kilobar . |

| Deposit to the Dealer Inventory in oz | nil |

| Deposits to the Customer Inventory, in oz | 57,488.988 OZ HSBC |

| No of oz served (contracts) today | 332 notice(s) 33,200 OZ 1.0326TONNES |

| No of oz to be served (notices) | 179 contracts 17,900 oz 0.5567 TONNES |

| Total monthly oz gold served (contracts) so far this month | 10,572 notices 1,057,200 OZ 32.883 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | x |

0 dealer deposit:

total dealer deposits: NIL oz

customer deposits: 0

total customer deposits: nil oz

we had 1 customer withdrawals

i) Out of Brinks oz 32.151 oz 1 kilobar)

Adjustments; 5//dealer to customer

i) Asahi 43,699.630 oz

ii) Brinks 18,298.580 oz

iii) Int. Delaware 23,148.720 oz

iv) JPMorgan 134,250.649 oz

v) Manfra 21,165.884 oz

total movement to eligible from reg: 240,593.263 oz or 7.48 tonnes

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR AUGUST.

For the front month of AUGUST we have an oi of 511 contracts having GAINED 19 contracts. We had 280 contracts filed

on Wednesday, so we gained 299 contracts or an additional 29,900 oz will stand at the comex

Sept lost 39 contracts to 2687.

Oct gained 756 contracts to 33,739 contracts.

We had 332 contracts filed for today representing 33,200 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 332 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 33 notice(s) was (were) stopped received by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the AUGUST /2023. contract month,

we take the total number of notices filed so far for the month (10,572 x 100 oz ), to which we add the difference between the open interest for the front month of AUGUST (511 CONTRACT) minus the number of notices served upon today 320 x 100 oz per contract equals 1,075,100 OZ OR 33.440 TONNES the number of TONNES standing in this active month of AUGUST. + .684 TONNES EXCHANGE FOR RISK/prior = 34.126 tonnes

thus the INITIAL standings for gold for the AUGUST contract month: No of notices filed so far (10,572) x 100 oz + (xxx) {OI for the front month} minus the number of notices served upon today (320) x 100 oz) which equals 1,075,100 oz standing OR 32.510 TONNES + .684 TONNES OF EXCHANGE FOR RISK/prior = 34.126 TONNES

TOTAL COMEX GOLD STANDING: 34.126 TONNES WHICH IS SMALL FOR AN ACTIVE DELIVERY MONTH.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 2,088,571,380 OZ 64.96 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 22,207,629,516 OZ

TOTAL REGISTERED GOLD: 11,796,956.901 (366,93 tonnes)..

TOTAL OF ALL ELIGIBLE GOLD: 10,410,672.615 O Z

REGISTERED GOLD THAT CAN BE SERVED UPON: 9,708,385 OZ (REG GOLD- PLEDGED GOLD) 301.97 tonnes//

END

SILVER/COMEX

AUGUST 10

//2023// THE AUGUST 2023 SILVER CONTRACT

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 639,532.969 oz CNT Delaware Loomis . |

| Deposits to the Dealer Inventory | nil oz |

| Deposits to the Customer Inventory | 505,602.860 oz Brinks |

| No of oz served today (contracts) | 0 CONTRACT(S) (0 OZ) |

| No of oz to be served (notices) | 0 contracts (nil oz) |

| Total monthly oz silver served (contracts) | 896 Contracts (4,480,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

i) 0 dealer deposit

total dealer deposit: 0 oz

i) We had 0 dealer withdrawal

total dealer withdrawals: 0 oz

We had 1 deposits customer account:

i)Into Brinks: 505,602.860 oz

total customer deposits: 505,602.860 oz

JPMorgan has a total silver weight: 140.871 million oz/281.172 million =50.16% of comex .//

Comex withdrawals 3

i) Out of Loomis 17,050.316 oz

ii) Out of Delaware 17,050.316 oz

iii) out of CNT 311,182.800 oz

adjustments: 0

TOTAL REGISTERED SILVER: 31.066 MILLION OZ//.TOTAL REG + ELIGIBLE. 281.172 million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR JULY:

silver open interest data:

FRONT MONTH OF AUGUST /2023 OI: 0 CONTRACTS HAVING LOST 4 CONTRACT(S). WE HAD

4 NOTICES FILED ON WEDNESDAY SO WE GAINED 0 CONTRACTS OR AN ADDITIONAL NIL OZ WILL STAND IN THIS NON ACTIVE DELIVERY MONTH OF AUGUST.

SEPT HAS A LOSS OF 6265 CONTRACTS DOWN TO 77,187

OCT GAINED 21 CONTRACTS TO STAND AT 230.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 0 for NIL oz

Comex volumes// est. volume today 86,690 strong/t.a.s.induced /

Comex volume: confirmed yesterday: 93.699 strong/t.a.s induced

To calculate the number of silver ounces that will stand for delivery in AUGUST. we take the total number of notices filed for the month so far at 896 x 5,000 oz = 4,480,000 oz

to which we add the difference between the open interest for the front month of AUGUST (0) and the number of notices served upon today 0 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the AUGUST/2023 contract month: 896 (notices served so far) x 5000 oz + OI for the front month of AUGUST (0) – number of notices served upon today (0 )x 500 oz of silver standing for the AUGUST contract month equates to 4.480 million oz.+ 0.0 MILLION OZ EXCHANGE FOR RISK ISSUED TODAY+ 1.45 MILLION OZ EXCHANGE FOR RISK PRIOR//NEW TOTALS: 5.930 MILLION oz.

There are 31.066 million oz of registered silver.

Thus if we take today’s standing at 5.930 and add last month’s 30.9 million oz we have 36.830 million oz against only 31.066 million registered silver.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS

AUGUST 10/WITH GOLD DOWN $1.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD: /// //INVENTORY RESTS AT 903.69 TONNES

AUGUST 9/WITH GOLD DOWN $8.75 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD: /// //INVENTORY RESTS AT 903.69 TONNES

AUGUST 8/WITH GOLD DOWN $9.60 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.31 TONNES FORM THE GLD /// //INVENTORY RESTS AT 903.69 TONNES

AUGUST 7/WITH GOLD DOWN $5.45 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD: /// //INVENTORY RESTS AT 906.00 TONNES

AUGUST 4/WITH GOLD UP $7.25 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.18 TONNES OF GOLD FROM THE GLD/// .///INVENTORY RESTS AT 906.00 TONNES

AUGUST 3/WITH GOLD DOWN $5.25 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD //: //: / .////INVENTORY RESTS AT 909.18 TONNES

AUGUST 2/WITH GOLD DOWN $3.45 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 3.75 TONNES OF GOLD FROM THE GLD//: //: / .////INVENTORY RESTS AT 909.18 TONNES

AUGUST 1/WITH GOLD DOWN $28.45 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 2.89 TONNES OF GOLD FROM THE GLD//: //: / .////INVENTORY RESTS AT 912.93 TONNES

JULY 31/WITH GOLD UP $9.50 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 2.89 TONNES OF GOLD FROM THE GLD//: //: / .////INVENTORY RESTS AT 912.93 TONNES

JULY 28/WITH GOLD UP $14.15 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 1.44 TONNES OF GOLD FROM THE GLD//: //: / .////INVENTORY RESTS AT 915,82 TONNES

JULY 27/WITH GOLD DOWN $21.80 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 1.74 TONNES OF GOLD FROM THE GLD//: //: / .////INVENTORY RESTS AT 917.26 TONNES

JULY 26/WITH GOLD UP $6.35 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD: //: / .////INVENTORY RESTS AT 919.00 TONNES

JULY 25/WITH GOLD UP $2.45 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD: //: / .////INVENTORY RESTS AT 919.00 TONNES

JULY 24/WITH GOLD DOWN $4.65 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 5.20 TONNES OF GOLD INTO THE GLD//: / .////INVENTORY RESTS AT 919.00 TONNES

JULY 21/WITH GOLD DOWN $3.80 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD: / .////INVENTORY RESTS AT 913.80 TONNES

JULY 20/WITH GOLD DOWN $8.70 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.73 TONNES FROM THE GLD/ .////INVENTORY RESTS AT 913.80 TONNES

JULY 19/WITH GOLD UP $0.65 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .86 TONNES FROM THE GLD/ .////INVENTORY RESTS AT 912.07 TONNES

JULY 18/WITH GOLD UP $23.45 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD: .////INVENTORY RESTS AT 912.93 TONNES

JULY 17/WITH GOLD DOWN $6.60 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.73 TONNES OF GOLD FROM THE GLD.////INVENTORY RESTS AT 912.93 TONNES

JULY 14/WITH GOLD UP $0.75 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD: ////INVENTORY RESTS AT 914.66 TONNES

JULY 13/WITH GOLD UP $3.30 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 0.29 TONNES OF GOLD OUT OF THE GLD////INVENTORY RESTS AT 914.66 TONNES

JULY 12/WITH GOLD UP $24.50 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 0.31 TONNES OF GOLD OUT OF THE GLD////INVENTORY RESTS AT 914.95 TONNES

JULY 11/WITH GOLD UP $6.15 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.0 TONNES OF GOLD OUT OF THE GLD////INVENTORY RESTS AT 915.26 TONNES

JULY 10 WITH GOLD DOWN $1.35 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.60 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 916.26 TONNES.

JULY 7 WITH GOLD UP $16.80 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 917.86 TONNES.

JULY 6/WITH GOLD DOWN $9.90 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.04 TONNES OF GOLD FROM THE GLD//INVENTORY RESTS AT 917.86 TONNES

JULY 5/WITH GOLD DOWN $2.20 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD; A WITHDRAWAL OF 2.6 TONNES FROM THE GLD///INVENTORY RESTS AT 921.90 TONNES

JULY 3/WITH GOLD UP $1.90 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 924.50 TONNES//

JUNE 30/WITH GOLD UP $10.00 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.31 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 924.50 TONNES

JUNE 29/WITH GOLD DOWN $3.20 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.26 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 926.81 TONNES

GLD INVENTORY: 903.69 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

AUGUST 10/WITH SILVER UP 6 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 8,807 MILLION OZ OUT OF THE SLV/: // OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 450.180 MILLION OZ

AUGUST 9/WITH SILVER DOWN 7 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 8,807 MILLION OZ OUT OF THE SLV/: // OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 450.180 MILLION OZ

AUGUST 8/WITH SILVER DOWN 40 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: // OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 458.987 MILLION OZ

AUGUST 7/WITH SILVER DOWN 46 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: // OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 458.987 MILLION OZ

AUGUST 4/WITH SILVER UP 1 CENT TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.294 MILLION OZ FROM THE SLV// OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 458.987 MILLION OZ

AUGUST 3/WITH SILVER DOWN 16 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 189,000 OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 451.281 MILLION OZ

AUGUST 2/WITH SILVER DOWN 43 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 275,000 OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 451.471 MILLION OZ

AUGUST 1/WITH SILVER DOWN 61 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 184,000 OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 451.746 MILLION OZ

JULY 31/WITH SILVER UP 45 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 184,000 OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 451.746 MILLION OZ

JULY 28/WITH SILVER UP 15 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 550,000 OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 451.930 MILLION OZ

JULY 27/WITH SILVER DOWN 59 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: .////INVENTORY RESTS AT 452.480 MILLION OZ

JULY 26/WITH SILVER UP 15 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: .////INVENTORY RESTS AT 452.480 MILLION OZ/

JULY 25/WITH SILVER UP 24 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A SMALL WITHDRAWAL OF 826,000 OZ FROM THE SLV..////INVENTORY RESTS AT 452.480 MILLION OZ/

JULY 24/WITH SILVER DOWN 23 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: ////INVENTORY RESTS AT 453.306 MILLION OZ/

JULY 21/WITH SILVER DOWN 14 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 1.101 MILLION OZ OF SILVER FROM THE SLV ////INVENTORY RESTS AT 453.306 MILLION OZ/

JULY 20/WITH SILVER DOWN 38 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 1.468 MILLION OZ OF SILVER FROM THE SLV ////INVENTORY RESTS AT 454.107 MILLION OZ/

JULY 19/WITH SILVER UP 11 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV:A ////INVENTORY RESTS AT 455.875 MILLION OZ/

JULY 18/WITH SILVER DOWN 19 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV:A ////INVENTORY RESTS AT 455.875 MILLION OZ/

JULY 17/WITH SILVER UP 25 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 4.856 MILLION OZ OF SILVER FROM THE SLV////////INVENTORY RESTS AT 455.875 MILLION OZ/

JULY 14/WITH SILVER UP 27 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 2.21 MILLION OZ OF SILVER FROM THE SLV////////INVENTORY RESTS AT 455.875 MILLION OZ/

JULY 13/WITH SILVER UP 64 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//////INVENTORY RESTS AT 462.941 MILLION OZ/

JULY 12/WITH SILVER UP $1.00 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.881 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 462.941 MILLION OZ/

JULY 11/WITH SILVER DOWN 5 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF .020 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 464.822 MILLION OZ/

JULY 10/WITH SILVER UP 2 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.672 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 464.802 MILLION OZ

JULY 7/WITH SILVER UP 42 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 466.474 MILLION OZ

JULY 6/WITH SILVER DOWN 50 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.667 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 466.474 MILLION OZ//

JULY5/WITH SILVER UP 30 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 468.141 MILLION OZ//

JULY 3/WITH SILVER UP 7 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 468.141 MILLION OZ//

CLOSING INVENTORY 450.180 MILLION OZ//

PHYSICAL GOLD/SILVER COMMENTARIES

1:Peter Schiff/Mike Maharrey

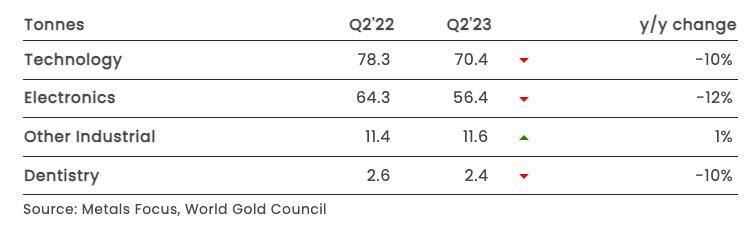

Another Recession Signal: Plunge In Demand For Gold In The Electronics Sector

THURSDAY, AUG 10, 2023 – 12:20 PM

With much stronger-than-expected second-quarter GDP growth and continued labor market strength, a growing number of people in the mainstream now think the US has escaped the clutches of a recession despite the Fed driving interest rates to the highest level in 16 years. But there are plenty of signs that a recession is looming. For instance, a big plunge in the sale of cardboard boxes indicates a slowdown in economic activity.

There’s another off-the-beaten-path indicator that flashes recession — a big drop in the demand for gold in the technology sector.

The demand for gold in tech fell by 10% year-on-year in the second quarter to 70 tons.

The big second quarter drop continued a trend we’ve seen since the beginning of the year. Tech demand for gold through the first half of 2023 came in at 140 tons, the weakest H1 since the World Gold Council has tracked the data. This includes the first half of 2020 as governments shut down their economies due to COVID-19.

According to the World Gold Council, the big drop in demand for gold in tech was driven by weak consumer spending on electronics.

The weakness in gold demand in industrial applications carried into Q2 as surging inflation rates continued to severely impact the entire electronics supply chain, from chip manufacturers to end-users.”

Electronics production used 56 tons of gold in Q2, a 12% decline.

According to the World Gold Council, this is “a direct consequence of weak end-user demand for consumer electronics – the major demand area for gold in electronics applications.”

This has led to negative shipment forecasts for most major device categories in 2023, including smartphones, PCs and laptops. And the weakness is reflected in chip manufacturer financial reports.”

For example, Samsung recently reported a 96% fall in second-quarter operating profit.

Breaking down various categories within the electronics sector we find the amount of old used to produce light emitting diodes (LEDs), circuit boards, and memory chips all dropped in Q2 in response to constrained consumer buying.

The drop in demand for gold in the tech sector reveals a global slowdown in consumer spending. Price inflation and rising interest rates have squeezed consumers around the world. The drop in demand for electronics reflects real consumer behavior. It’s a much better indication of the condition of the global economy than government-produced numbers.

Despite the drop in demand for gold in technology, overall demand for physical gold was strong in the second quarter, driven by investment and central bank gold buying.

Industrial demand pales in comparison to the demand for gold in jewelry-making and investment purposes. Nevertheless, gold is one of the most useful metals on the planet and would probably have even more practical applications if it wasn’t so rare and expensive. The truth is gold did not become money because it wasn’t useful for anything else. Its role as money evolved because it is so valuable and has so many uses.

For instance, gold was an integral component in the mirrors on the James Webb Space Telescope (JWST).

Gold has also enjoyed a growing role in healthcare. The yellow metal is used in a large number of diagnostic tools and is of increasing interest to companies developing innovative new ways to treat disease.

Some uses for gold in medicine sound like something right out of a science fiction film. A team of Chinese researchers announced they were able to partially restore the sight of blind mice by replacing their deteriorated photoreceptors – sensory structures inside the eye that respond to light – with nano-wires made of gold and titanium.

Ultimately, gold is money, but it serves many other useful purposes and that’s part of what gives it enduring value.

end

2 Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens//JAMES RICKARDS//JOHN RUBINO

Rickards: The Greater Financial Crisis Of 2024

THURSDAY, AUG 10, 2023 – 09:55 AM

Authored by James Rickards via DailyReckoning.com,

You’re probably aware that Fitch has downgraded the credit rating of the United States from AAA to AA+. It was big news last week.

That’s nothing to cheer about, though it’s not likely to have much impact on the markets in the short run. It’s more of a long-term problem.

But it’s certainly another straw in the wind showing that the U.S. is on a non-sustainable fiscal course that can only end in default, hyperinflation or protracted depression-level growth.

Meanwhile, another major credit ratings agency, Moody’s, has just issued its own downgrades that may foretell a much more immediate threat.

And they don’t involve the government.

Downgraded!

On Monday, Moody’s cut the credit ratings of 10 small and midsize U.S. banks, while placing six large banks on watch for potential downgrades.

The six large banks include Bank of New York Mellon, U.S. Bancorp, State Street and Truist Financial.

Moody’s has also lowered its outlook to negative for 11 major banks, including Capital One, Citizens Financial and Fifth Third Bancorp.

Here’s what Moody’s said yesterday:

Many banks’ second-quarter results showed growing profitability pressures that will reduce their ability to generate internal capital.

This comes as a mild U.S. recession is on the horizon for early 2024 and asset quality looks set to decline, with particular risks in some banks’ commercial real estate (CRE) portfolios.

It Won’t Be Subprime Mortgages Next Time

We all remember the Global Financial Crisis of 2007–08, which was allegedly caused by subprime mortgages in the residential real estate sector.

In reality, subprime loans played a role in the crisis, but they were more a symptom than a cause. The real cause was excessive monetary tightening by Ben Bernanke in 2006–07. With that as background, pundits are again looking at residential mortgages and inflated home values as a potential source of crisis.

But they’re looking in the wrong place.

Since 2009, conditions for mortgage loans have tightened considerably. A down payment of 20% or more is routinely required. Full documentation (tax returns, W-2s, employment verifications, title insurance, etc.) is necessary and co-signers are often required.

This does not guarantee loans don’t default, but there will certainly be far fewer defaults and larger owner equity cushions to absorb any losses. For warning signs this time, investors might do well to look at commercial real estate, as Moody’s downgrades indicate.

The Looming CRE Crisis

CRE is crashing on several levels. In the first place, valuations are falling and vacancies are rising, partly in response to the post-pandemic work-from-home movement and the general urban flight due to high crime and vagrancy.

At some point, owners are underwater on rents and just drop off the keys with the lender and walk away.

The other problem is that new building construction is not financed with long-term mortgage, but with short-term construction loans. I don’t want to get too deep in the weeds here, but it’s important to understand the basic dynamics.

These short-term loans have two- or three-year maturities. When the building is finished, the developer gets a long-term mortgage and pays off the construction loan in full. The difficulty arises when credit conditions charge materially between the time the project is started and when it is completed.

That’s exactly what happened in 2021 during the post-pandemic boom, and what will happen in 2024 when a lot of the construction loans are due.

If developers can’t get the long-term financing on favorable terms, that becomes another reason to walk away. Then you’re looking at a cascading crisis as the losses pile up.

“I Want My Money Back!”

Each financial crisis begins with distress in a particular distressed sector and then spreads from sector to sector until the whole world is screaming, “I want my money back!”

First, one asset class has a surprise drop. The leveraged investors sell the sinking asset, but soon the asset is unwanted by anyone. Margin calls roll in. Investors then sell good assets to raise cash to meet the margin calls. This spreads the panic to banks and dealers who were not originally involved with the weak asset.

Soon the contagion spreads to all banks and assets, as everyone wants their money back all at once. Banks begin to fail, panic spreads and finally central banks step in to separate winners and losers and reliquefy the system for the benefit of the winners.

Typically, small investors (and some bankrupt banks) get hurt the worst while the big banks get bailed out and live to fight another day.

That much panics have in common.

Fighting the Last War

What varies in financial panics is not how they end but how they begin. The 1987 crash started with computerized trading. The 1994 panic began in Mexico.

The 1997–98 panic started in Asian emerging markets but soon spread to Russia and the big banks. The 2000 crash began with dot-coms. The 2008 panic was triggered by defaults in subprime mortgages.

And the next panic might well be triggered by defaults in commercial real estate. Risk hasn’t gone away, it’s simply shifted.

But today the regulators are like generals who are fighting the last war. They’re too focused on the last war to know where the next one will begin or how to fight it.

They’ll be blindsided, along with most investors.

There’s Time to Prepare

Does that mean we’re going to see a crisis tomorrow? No, not necessarily. Both the panics of 1998 and 2008 began over a year before they reached the level of an acute global liquidity crisis.

Investors had ample time to reduce risky positions, increase cash and gold allocations and move to the sidelines until the crisis abated. At that point there were bargains galore for those with cash.

An investor with cash in 2008 could have preserved wealth during the crisis and nearly made six times his money since then by buying the Dow Jones index at 6,550 (it’s trading over 35,300 today).

Relatively few investors did this. Instead they suffered from “fear of missing out” as markets rose until the panic began. They persisted in the mistaken belief that they could “get out in time” if markets reversed, not realizing that reversals happen much faster than rallies. They held onto losing positions hoping they would “come back” (they did after 10 years) and so on.

Investors don’t need to worry about subprime home loans this time around. But they would do well to pay attention to the CRE space. That’s one canary in the coal mine of the next global financial crisis.

I advise you to plan accordingly.

end

3,Chris Powell of GATA provides to us very important physical commentaries

END

4, OTHER IMPORTANT GOLD/SILVER COMMENTARIES/SILVER

5 a. IMPORTANT COMMENTARIES ON COMMODITIES:

end

5 B GLOBAL COMMODITY ISSUES/FOOD IN GENERAL//FREIGHT

END

6.CRYPTOCURRENCY//DIGITAL CURRENCY// COMMENTARIES/

END

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS THURSDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED UP TO 7.2084

OFFSHORE YUAN: UP TO 7.2195

SHANGHAI CLOSED UP 10.07 PTS OR 0.31%

HANG SENG CLOSED UP 2.23 PTS OR 0.01%

2. Nikkei closed UP 269.32 PTS OR 0.84%

3. Europe stocks SO FAR: ALL GREEN

USA dollar INDEX DOWN TO 101.98 EURO RISES TO 1.1027 UP 50 BASIS PTS

3b Japan 10 YR bond yield: RISES TO. +.583 Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 143.78/JAPANESE YEN FALLING AS WELL AS LONG TERM 10 YR. YIELDS RISING //EVENTUALLY THIS WILL BREAK THE JAPANESE CENTRAL BANK

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen DOWN CHINESE ON SHORE YUAN: UP// OFF- SHORE: UP

3f Japan is to buy INFINITE TRILLION YEN’S worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and UP FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund UP TO +2.4965***/Italian 10 Yr bond yield RISES to 4.158*** /SPAIN 10 YR BOND YIELD RISES TO 3.548…**

3i Greek 10 year bond yield RISES TO 3.779

3j Gold at $1921.25 silver at: 22.78 1 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble DOWN 1 AND 16 /100 roubles/dollar; ROUBLE AT 97.36//

3m oil into the 83 dollar handle for WTI and 87 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 143.78// 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 0.583% STILL ON CENTRAL BANK (JAPAN) INTERVENTION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.8732 as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9628 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.009 UP 0 BASIS PTS…

USA 30 YR BOND YIELD: 4.165 UP 0 BASIS PTS/

USA 2 YR BOND YIELD: 4.798 UP 0 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 27.04…(TURKEY SET TO BLOW UP FINANCIALLY)

GREAT BRITAIN/10 YEAR YIELD: DOWN 2 BASIS PTS AT 4.4135

end

2.a Overnight: Newsquawk and Zero hedge:

Futures Rise, Dollar Slides Ahead Of “Dovish” CPI Report

THURSDAY, AUG 10, 2023 – 08:10 AM

US equity futures and European bourses rebounded from yesterday’s slump and are higher into CPI, which may provide clues on the Federal Reserve’s next steps, with slight outperformance from MegaCap Tech. As of 7:45am ET, both S&P and Nasdaq 100 futures were up 0.5%. The Stoxx 600 was up 0.4%, with travel and luxury companies among the biggest gainers on speculation that companies will benefit an increase in Chinese tourism spending after Beijing lifted travel curbs. The dollar dropped against all majors except the yen; bond yields are flat and oil slipped while metals and ags prices are higher. Today’s focus is on the CPI print at 8.30am; there are two Fed speakers this afternoon.

In premarket trading, Disney shares rose 1.6% in premarket trading after saying capital spending and outlays for movies and TV shows are coming in lower than projected; the stock earlier slumped after the company reported only the second ever drop in Disney+ streaming subs: it appears that Disney plans to make up in price what it loses in volume, always a winning strategy. Elsewhere, Capri soared as much as 34% after it was acquired by Tapestry, the parent company of Michael Kors and Versace among others, for $57. Here are some other notable premarket movers:

- Plug Power slides 11% after the green- hydrogen company reported results that included a revenue beat but weaker-than-expected margins.

- Galera Therapeutics falls as much as 83% after the biopharmaceutical company said it received a complete response letter from the US FDA regarding the company’s new drug application for avasopasem manganese.

- Penn Entertainment dips 1.1% after the sports-entertainment company was downgraded to hold from buy at Truist Securities, which said it sees sizable execution risks in its exclusive partnership with Disney’s (DIS US) ESPN.

- TaskUS falls as much as 12% after the business process outsourcing services provider cut its revenue guidance for the full year. RBC Capital Markets downgraded the stock to sector perform from outperform.

- Trade Desk (TTD US) falls as much as 4.5% after results as analysts said the advertising technology company may not have lived up to high investor expectations.

- Sonos jumps 7.4% after the wireless-speaker manufacturer reported third-quarter revenue and adj. Ebitda that Morgan Stanley said “handily beat” their expectations.

- Roblox rises as much as 3.1% as Morgan Stanley raised its rating to equal-weight from underweight, noting that the shares now fairly reflect the near- term headwinds.

- AppLovin surges as much as 25% in premarket trading on Thursday, after the company reported second-quarter results that beat expectations and gave an outlook seen as strong by analysts.

As previewed earlier, all eyes will be trained on today’s CPI which according to JPM’s trading desk will be “more dovish than hawkish”, and which is set to show a second consecutive reading on core inflation in line with the Federal Reserve’s target, but the first increase in annual CPI since June 2022. Bloomberg Economics expects CPI, excluding food and energy, to rise by 0.2% for the month, similar to June. “July’s CPI report will show a wave of disinflation hitting the US economy,’’ the team, led by Anna Wong, said. The report will be critical for investors trying to determine whether the Fed will stop raising interest rates.

“A higher-than-expected number would produce some short-term equity and bond volatility,” said Andrew Bell, chief executive officer at Witan Investment Trust. “But I doubt it would change expectations for the peak in Fed rates as there is a weight of evidence pointing to the economy disinflating.” Indeed, historical data shows that CPI days have been largely a snoozer so far in 2023.

One potential pressure point could be commodities, which are rising after a year of falling. Oil traded near the highest level in almost nine months, with West Texas Intermediate futures above $84 a barrel after climbing 3% over the previous two sessions.

In Europe, the Stoxx 600 was up 0.4%, boosted by gains in luxury and travel stocks after China announced plans to relax travel curbs. LVMH and Hermes International added at least 2% after China’s Ministry of Culture and Tourism said it would lift a group travel ban to countries including the US, UK, Australia, South Korea and Japan. Buyers from China account for about 25% of European luxury-goods sales, including purchases made by tourists, according to latest estimates from Goldman Sachs Group Inc. Here are the most notable European movers:

- LVMH lead luxury stocks higher in Europe on Thursday, as China lifted a ban on group tours, boosting the case for travelers spending money on high-end watches and fashion

- Persimmon rises as much as 5.2% on relief that the UK housebuilder maintained its profit guidance despite weaker sales

- Allianz rises as much as 3.9% after the German insurer reported second-quarter results that beat expectations. The results show “underlying quality,” analysts say

- Thyssenkrupp shares gain 4.2% after the German industrial company forecasted full-year adjusted Ebit would reach the upper end of its prior profit guidance

- Knorr-Bremse shares jump as much as 7.4% after the German braking-systems manufacturer reported a beat for orders and boosted its full- year revenue forecast

- H&M gains as much as 2.3% after its founding family’s investment vehicle, Ramsbury Invest, bought about 1.9 million shares in the retailer from August 7-9, according to a filing

- Deliveroo gains as much as 4.5% after the food delivery firm raised its FY Ebitda forecast and beat analyst estimates, showing cost cuts and price hikes are bearing fruit

- Siemens shares fall as much as 6.1% after its 3Q industrial business profit missed consensus estimates. Jefferies sees investors focusing on digital industries

- Novo Nordisk slides as much as 2.3%, dropping for a second day since hitting a record high on Tuesday. Analysts highlighted new guidance is already reflected in current consensus

- Spirax drops as much as 7.6% with analysts expecting cuts to consensus Ebit expectations following a weak first half for the UK steam management and pumps manufacturer

- Rheinmetall falls as much as 4% after the German defense contractor’s second-quarter earnings missed expectations, weighed down by its non-defense automotive business

- Orsted shares fall as much as 2.5% after the Danish power generator’s earnings for the second quarter fell from a year earlier, missing analyst expectations

Earlier in the session, Asian equities traded mixed as strength in energy and industrial shares help limit the impact of a selloff in the technology sector as investors exercised caution ahead of critical US inflation data. The MSCI Asia Pacific Index fell as much as 0.4% before paring the gain. Chipmakers and Chinese internet shares were among the biggest drags as higher US Treasury bond yields and skepticism over the AI-led rally prompted profit-taking. Gains in oil lifted commodities-related stocks. Investors in Asia have been cautious this week as rising yields and China’s economic woes sap risk appetite. The regional benchmark is down 3.6% so far in August after gaining nearly 8% in the previous two months. All eyes are on US monthly inflation data due later Thursday for clues on the Federal Reserve’s next policy move.

“The upcoming US CPI data could dictate the trend over coming weeks, largely seen as key in determining if a September rate hike is needed,” Jun Rong Yeap, market strategist at IG Asia wrote in a note. Meanwhile, China investors are “keeping a lookout for any worst-is-over” scenario, he added.

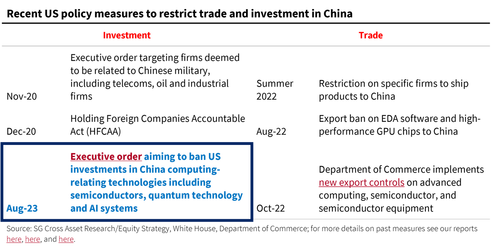

- Hang Seng and Shanghai Comp were pressured after US President Biden’s executive order to ban some new investments in ‘narrow subsets’ of Chinese sensitive technologies such as semiconductors and microelectronics, quantum information technologies and certain AI systems, which drew criticism from China.

- Nikkei 225 benefited from yen weakness but was initially choppy after mixed PPI data and with newsflow in Japan dominated by earnings releases which provided the catalysts for the biggest individual stock movers.

- ASX 200 was rangebound with notable outperformance in the energy sector with oil prices at a 9-month high and following the recent surge in gas prices amid disruption concerns with strike action planned for Australian LNG, although Woodside Energy has since provided some optimism on the bargaining process in which it noted that positive progress is being made and an in-principle agreement was reached on a number of issues.

- Stocks in India declined after the central bank kept borrowing costs unchanged but raised outlook for inflation while announcing a surprise move for curbing excess liquidity. The S&P BSE Sensex fell 0.5% to 65,688.18 in Mumbai, while the NSE Nifty 50 Index declined by a similar magnitude. MSCI Asia Pacific Index climbed 0.3% for the day. The central bank kept the policy rate unchanged at 6.50% for a third straight meeting, in line with a Bloomberg survey of economists. The RBI ordered banks to set aside more cash to mop up excess liquidity as it raised its inflation forecast to 5.4% for the year ending March, from 5.1% in its last review. Banks and consumer staples firms were among key drags in India.

In FX, the Bloomberg Dollar Spot Index is down 0.2%, falling against all its G-10 rivals except the yen which is down 0.1%; the Swiss Franc led group-of-10 gains rising as much as 0.5%

- AUD/USD climbed 0.4%, while NOK/USD rose 0.2%, as potential strikes at major LNG facilities in Australia sent shock-waves through energy markets

- MXN/USD steadied ahead of the Mexican Central Bank’s decision where policy is expected to remain unchanged; attention turns to the outlook for rate cuts and longevity of Peso-based carry trades

In rates, Treasuries are slightly lower with the US 10-year yield unchanged at 4.01%. The treasuries curve is marginally steeper with short-end and belly slightly outperforming ahead of July CPI data and $23 billion bond auction. Treasuries price action is rangebound with core European rates underperforming, as July CPI readings are expected to support a pause to the Fed’s hiking cycle for September. The Treasury 2-year yields richer by around 1.5bp on the day with 2s10s and 5s30s spreads steeper by 1bp and 1.5bp vs Wednesday close; 10-year yields around 4% are near flat on the day, with bunds and gilts lagging by 3.5bp and 1.5bp in the sector. Treasury auction cycle concludes with $23b 30-year bond sale at 1pm New York time; demand was robust for 3- and 10-year auctions earlier this week. WI 30-year yield at ~4.165% is around 25.5bp cheaper than July’s stop-out, which tailed by 2bp, and higher than 30-year stops since 2011

In commodities, Crude futures are little changed with WTI trading near $84.40. European natural gas futures fall 5%. Spot gold adds 0.3%.

Looking at today’s calendar, we have the all-important CPI print in the US. Aside from this, we will get the latest weekly claims data and monthly budget statement in US. With 90% of S&P 500 companies having now published their Q2 results, upcoming earnings releases are weighted towards Europe with today’s results including Novo Nordisk, Alibaba, Siemens, Deutsche Telekom, Allianz, Tokyo Electron, Orsted, RWE, Rheinmetall and HelloFresh.

Market Snapshot

- S&P 500 futures up 0.5% to 4,510.25

- MXAP up 0.2% to 165.21

- MXAPJ little changed at 521.62

- Nikkei up 0.8% to 32,473.65

- Topix up 0.9% to 2,303.51

- Hang Seng Index little changed at 19,248.26

- Shanghai Composite up 0.3% to 3,254.56

- Sensex down 0.6% to 65,595.37

- Australia S&P/ASX 200 up 0.3% to 7,357.39

- Kospi down 0.1% to 2,601.56

- STOXX Europe 600 up 0.6% to 463.18

- German 10Y yield little changed at 2.53%

- Euro up 0.4% to $1.1022

- Brent Futures up 0.4% to $87.89/bbl

- Gold spot up 0.3% to $1,919.63

- U.S. Dollar Index down 0.32% to 102.16

Top Overnight News from Bloomberg

- The White House unveiled its long-anticipated order restricting US investment in some Chinese firms, although the measure isn’t as harsh as feared. BBG

- China has lifted pandemic-era restrictions on group tours for more countries, including key markets such as the US, Japan, South Korea and Australia in a potential boon for their tourism industries. The decision was announced by China’s culture and tourism ministry on Thursday, effective immediately. European luxury stocks climbing higher as a result. RTRS

- BABA +3% after reporting strong FQ1/June results. Overall revenue climbed 14% Y/Y to RMB234.1B (solidly ahead of the Street’s RMB223.7B forecast) while EPS surged 48% to RMB17.37/shr (above the Street’s RMB14.14 forecast). RTRS

- China’s securities watchdog is meeting real estate developers and banks tomorrow, according to people familiar, underscoring growing urgency among regulators to deal with a worsening property crisis. Country Garden was not among those invited. BBG

- India’s RBI left rates unchanged, as expected, but took steps to drain liquidity and raised its inflation forecast while expressing concern about a jump in food prices. RTRS

- Potential strikes at three major LNG facilities in Australia may disrupt about 10% of global exports and deliver a new energy price shock across Asia and Europe. Yesterday, EUROPEAN GAS FUTURES JUMPED 40%, BIGGEST GAIN SINCE MARCH 2022. Positioning very much exacerbated that move. Reverting lower a bit today. GS GBM

- Ecuador declared a state of emergency after a presidential candidate was assassinated less than two weeks before the country’s election. Fernando Villavicencio, a journalist known for his crusade against corruption, was polling second to replace President Guillermo Lasso. One suspect also died in a shootout while six others were arrested. BBG

- The average U.S. 30-year mortgage rate jumped to a nine-month peak yesterday and hit the second-highest rate since 2001, as interest rates reacted sharply to a downgrading of U.S. government debt. The average 30-year mortgage rate shot up to 7.09% for the week ending Aug. 4, a 16 basis point increase from the previous week’s 6.93% rate, according to a weekly report released by the Mortgage Bankers Association. RTRS

- Manhattan apartment rents hit fresh all-time highs, up 2.3% M/M to a median of $4,400 (although the number of lease signings fell M/M and Y/Y, signaling a softening in demand). BBG

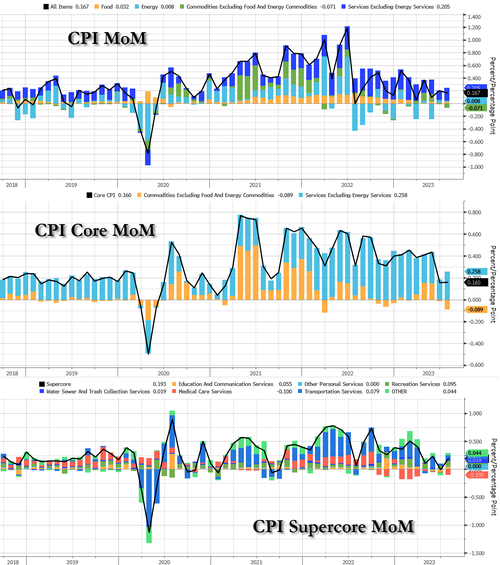

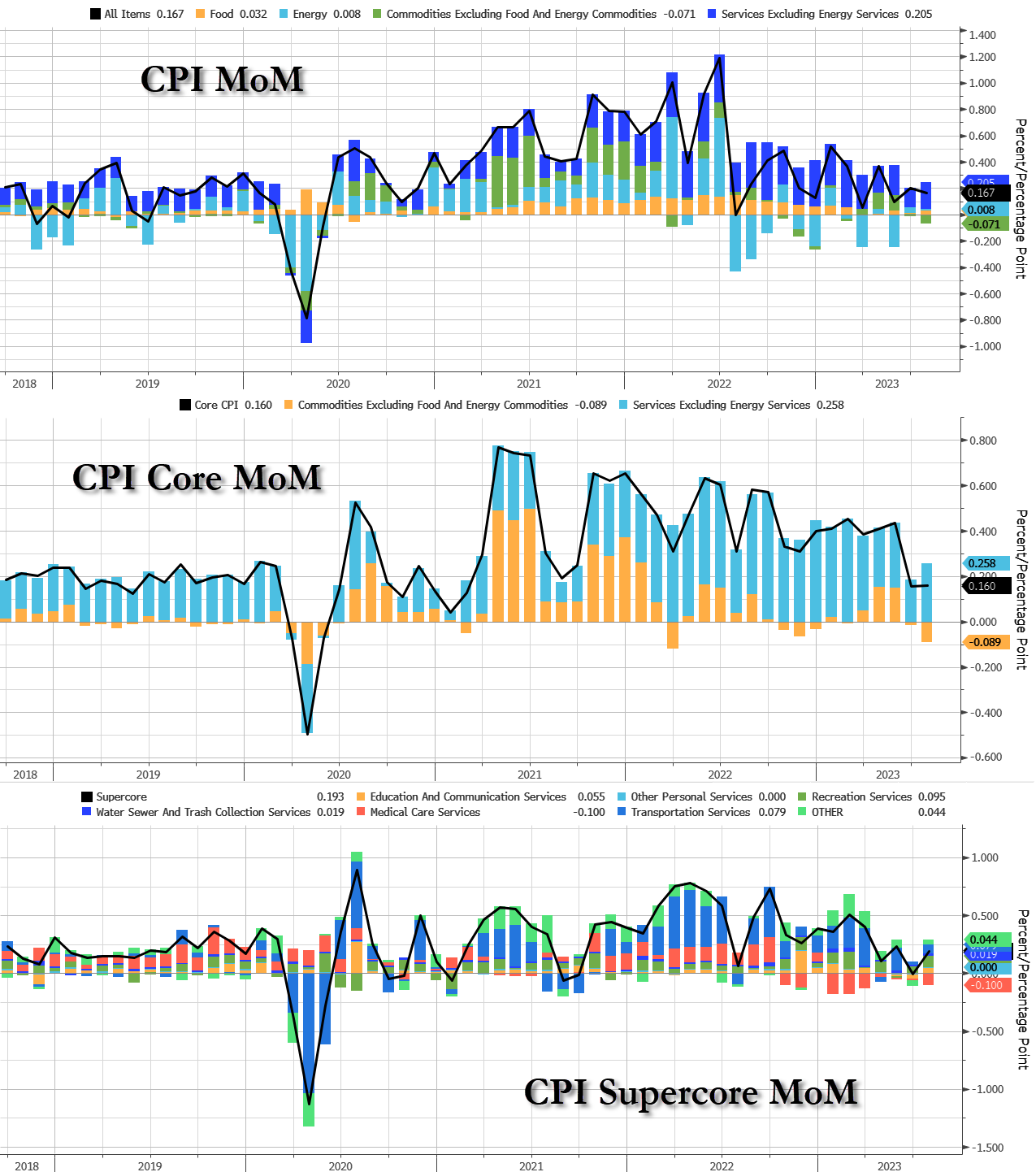

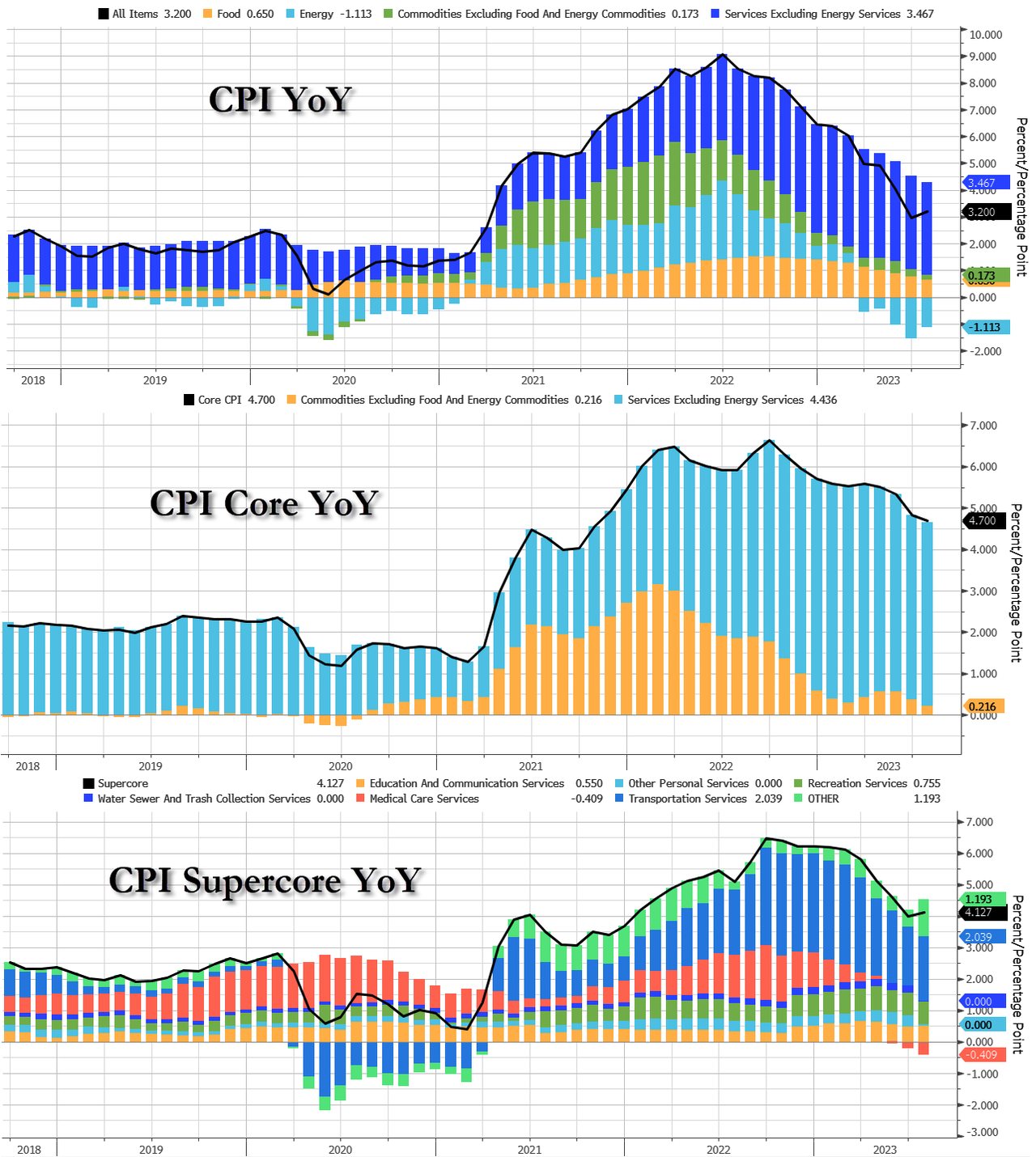

- We expect a 0.15% increase in July core CPI (vs. 0.2% consensus), corresponding to a year-over-year rate of 4.66% (vs. 4.8% consensus). We expect a 0.16% increase in July headline CPI (vs. 0.2% consensus), which corresponds to a year-over-year rate of 3.17% (vs. 3.3% consensus). Going forward, we expect monthly core CPI inflation to remain in the 0.2-0.3% range in the next few months, reflecting continued moderation in shelter inflation, lower used car prices, and slower nonhousing services inflation as labor demand continues to moderate

A more detailed look at global markets courtesy of Newsquawk

- APAC stocks were mixed with the regional bourses mostly rangebound amid a slew of earnings releases and with the mood tentative ahead of incoming US inflation data, while participants also reflected on US efforts to restrict investment in some Chinese tech.

- ASX 200 was rangebound with notable outperformance in the energy sector with oil prices at a 9-month high and following the recent surge in gas prices amid disruption concerns with strike action planned for Australian LNG, although Woodside Energy has since provided some optimism on the bargaining process in which it noted that positive progress is being made and an in-principle agreement was reached on a number of issues.

- Nikkei 225 benefitted from yen weakness but was initially choppy after mixed PPI data and with newsflow in Japan dominated by earnings releases which provided the catalysts for the biggest individual stock movers.

- Hang Seng and Shanghai Comp were pressured after US President Biden’s executive order to ban some new investments in ‘narrow subsets’ of Chinese sensitive technologies such as semiconductors and microelectronics, quantum information technologies and certain AI systems, which drew criticism from China.

Top Asian News

- US President Biden signed an executive order to regulate future US investments in a narrow set of technologies in China, Hong Kong and Macau, while the order is a ‘narrow and targeted action’ to complement existing export controls and inbound investment screening. Furthermore, US actions will focus on protecting the most critical technologies for military advancement, including semiconductors, quantum computing and certain artificial intelligence, according to Reuters.

- There were earlier reports that the White House will detail plans restricting some US investments in China in which the regulations will only affect future investments, not current ones, according to a person briefed on the executive order. Restrictions are expected to be implemented next year after multiple rounds of public comment including an initial 45-day comment period on the proposed rulemaking.

- China’s MOFCOM said China is gravely concerned about the US order on foreign investment reviews and reserves the right to take measures, while it hopes the US will respect the law of the market economy and the principle of fair competition, according to Reuters.

- China’s Ministry of Foreign Affairs said China filed a diplomatic complaint against the US regarding the investment curbs, according to Bloomberg.

- Chinese Embassy in the US said China is very disappointed the US went ahead with new investment restrictions and it opposes the US overuse of national security on trade, while it added that China will firmly safeguard its rights and interests, according to Reuters.

- China’s internet giants rush to order USD 5bln of Nvidia (NVDA) chips to power AI ambitions amid concerns over impending US export controls, according to FT sources.

- China Culture and Tourism Bureau released a third list of destination countries for Chinese group tourism including Japan, Australia, Germany, UK and US, while China also permitted group tours to South Korea.

European bourses are in the green, Euro Stoxx 50 +0.7%, as sentiment inches higher with macro drivers thin; FTSE 100 lags given a large amount of ex-dividend trade. Sectors are primarily bid with only Health Care in the red as Novo Nordisk trims recent gains post-earnings; Insurance outperforms following Allianz and Zurich Insurance with Luxury also bolstered as China continues to reopen. Stateside, futures are in the green as they take impetus from European action and attempt to recover some of the losses felt on Wednesday, ES +0.6%. Action has been relatively contained for US futures after they staged a recovery in APAC hours with drivers since light and the clock counting down to CPI, Fed speak and supply.

Top European News

- UK PM Sunak is reportedly facing increasing calls from the Cabinet to put leaving the European Convention on Human Rights at the centre of the Tory election campaign if migrant deportation flights to Rwanda are blocked, according to The Telegraph.

- Lloyds of London underwriters are leading insurers in raising rates and cutting cover over Taiwan risks, via Reuters citing sources; some insurers are imposing exclusions on Taiwan in political risk or political violence policies.

- ECB Economic Bulletin: Inflation continues to decline but is still expected to remain too high for too long. The Governing Council is determined to ensure that inflation returns to its 2% medium-term target in a timely manner.

- Norges Bank survey of bank lending: Broadly unchanged credit demand and credit standards.

FX

- A soft morning thus far for the broader Dollar and index despite the firming in bond yields seen after the European cash close yesterday.

- A clear divergence is seen between the traditional havens, with the CHF taking advantage of the receding Dollar whilst the JPY is hampered by recent yield dynamics.

- JPY remains on the back foot and on course for a fourth consecutive session of losses. The pair briefly topped 144.00 overnight to a 144.11 high before trimming upside, with an intraday low print at 143.64.

- Antipodeans are taking advantage of the softer Dollar alongside the constructive risk mood, albeit they are still some way off WTD bests. The Loonie lags with no obvious fresh fundamental driver this morning.

- The Single Currency currently stands as the second-best G10 performer as the Dollar resides around session lows in the run-up to CPI, with fresh newsflow also quiet in summer trading. On that note, amid the quieter condition, it’s worth being aware of large EUR/USD option expiries.

- PBoC set USD/CNY mid-point at 7.1576 vs exp. 7.2023 (prev. 7.1588)

Fixed Income

- Core benchmarks are in the red, a deterioration that has been very steady in nature and largely a function of the improved but still somewhat tentative risk tone pre-CPI.

- Bunds are the incremental laggards trading lower to the tune of 40 ticks but just off of the 132.36 trough. A low below Wednesday’s 132.57 base but someway shy of the WTD 131.33 base that was printed on Monday.

- As mentioned, newsflow for the UK/Gilts has been equally dearth aside from the RICS survey that shows continued pressure for the housing market on the back of the ongoing tightening cycle.

- USTs are in the red with yields bid across the curve but overall action is very limited in summer conditions and ahead of US CPI. Currently, USTs are at the mid-point of 111.06+ to 111.12+ parameters.

Commodities

- WTI and Brent front-month futures hold a positive bias amid the softer Dollar and constructive risk tone in the run-up to US CPI.

- There hasn’t been much by way of crude-specific news, but some sectoral support may be felt with the recent rise in LNG prices.

- Spot gold is modestly firmer amid the softer Dollar but price action is limited ahead of the US CPI report, with the current intraday range between 1,9414.91-21.31/oz.

- Unions representing workers at Woodside and Chevron LNG sites have applied for “protected ballot orders”; FT citing a source reports that a move to vote on action will likely occur early next week unless a resolution is agreed. Elsewhere, Eneos exec. says they are not aware of any significant impact from possible strikes at Australian LNG facilities.

Geopolitics

- Russian Defence Ministry said 11 Ukrainian drones were downed near Sevastopol, according to RIA. It was separately reported that Russian air defence systems shot down two military drones heading towards Moscow.

- North Korean leader Kim convened a military meeting and vowed to step up preparation for war, while he called for war drills to be conducted to efficiently operate new weapons, according to Yonhap.

- Belarusian Security Council says they will take measures to respond to the militarization of Poland and the Baltic states, according to Al Arabiya.

US Event Calendar

- 08:30: Aug. Initial Jobless Claims, est. 230,000, prior 227,000

- July Continuing Claims, est. 1.71m, prior 1.7m

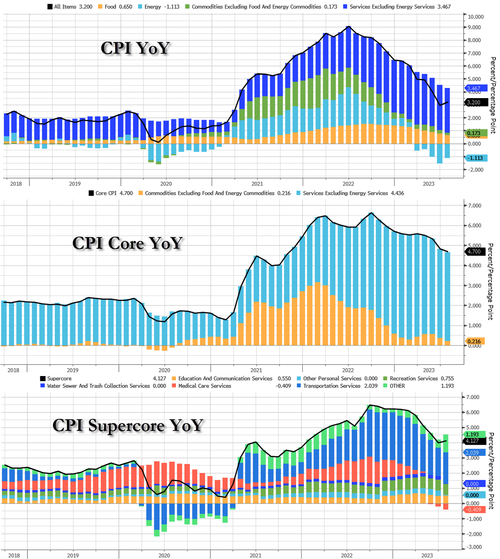

- 08:30: July CPI MoM, est. 0.2%, prior 0.2%

- July CPI YoY, est. 3.3%, prior 3.0%

- July CPI Ex Food and Energy MoM, est. 0.2%, prior 0.2%

- July CPI Ex Food and Energy YoY, est. 4.7%, prior 4.8%

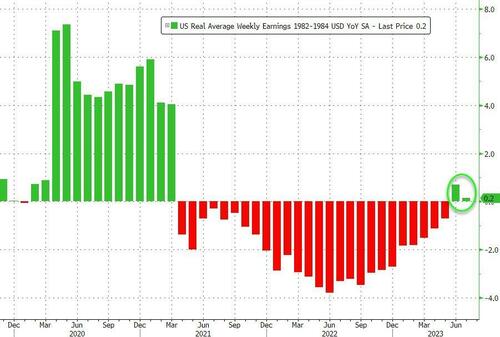

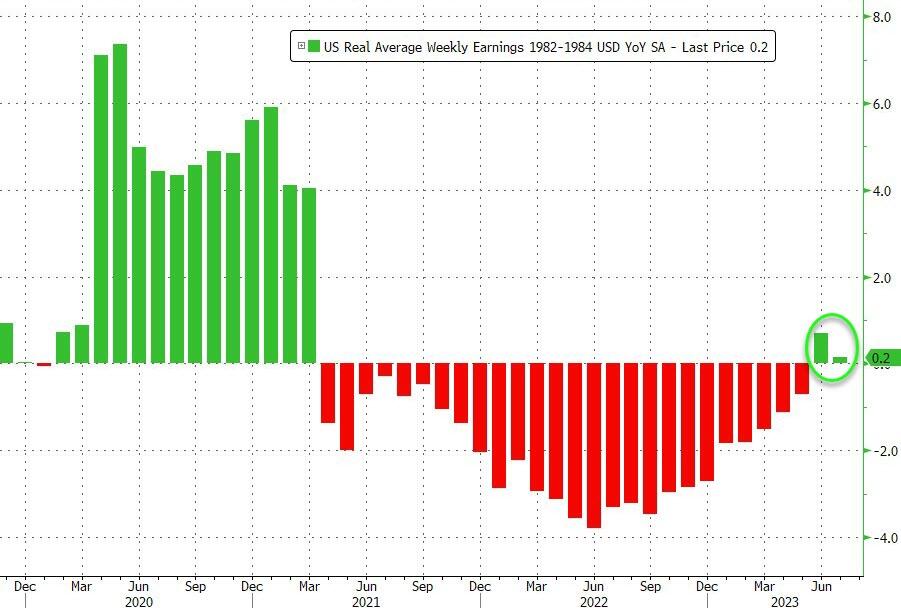

- July Real Avg Hourly Earning YoY, prior 1.2%, revised 1.3%

- July Real Avg Weekly Earnings YoY, prior 0.6%, revised 0.7%

- 14:00: July Monthly Budget Statement, est. -$135b, prior – $211.1b

DB’s Jim Reid concludes the overnight wrap

While it would be hard to say this has been a bad August for markets so far, it seems to be hard to get through a day at the moment without a negative shock of some description. I’ll need my holiday from tomorrow to have a lie down. Yesterday’s negativity was from a +27% spike in European natural gas prices (with a +40% intra-day high), the largest percentage increase since early March 2022, albeit still -87% below the peaks back in late August 2022. Oil also edged up above its April highs to the highest levels since last November.

These inflationary moves ironically come ahead of a big US CPI today which has of late been the print to give most encouragement to the soft landing argument. It’s likely too early for any recent commodity increases to show up in the data but we’ll all be watching oil, gas and food prices over the next few weeks and months. As it stands they should help to push up headline inflation shortly before the September FOMC which will be a bit uncomfortable even if core will be the main focus.

In terms of today, consensus expects a +0.2% monthly print for both headline and core inflation. Should this materialise, it would be the second consecutive MoM print close to the 2% annualised target, especially if the decimal roundings are favourable. Our US economists expect a marginally weaker headline reading (+0.17% vs. +0.18% prev.), with core inching up from its 28-month low seen in June (+0.21% vs. +0.16% prev). In terms of the drivers, they ironically see gas prices helping headline inflation lower with core goods also falling but services inflation remaining elevated. In annual terms, they see headline CPI in line with consensus at +3.3% (+3.0% prev.) and core inflation just about staying at +4.8% (consensus +4.7%). You can see our US economists’ full preview of the print here, as well as register for their post-CPI webinar at 9am EST today.

Ahead of today’s data, a risk-off tone dominated US equities, with the S&P 500 down -0.70% after selling off around -0.5% in the final half an hour of trading and closer to the earlier session lows. Banks (-1.57%) posted a second sizeable decline in a row, while tech also underperformed. The NASDAQ closed -1.17% lower with the FANG+ mega cap index down -2.11%, led by chip maker Nividia which saw a -4.72% fall. Energy stocks (+1.22%) rose alongside a strong day for oil prices. S&P and Nasdaq futures are back up +0.36% and +0.39% respectively overnight continuing the down/up nature of the month so far.