GOLD PRICE CLOSED: DOWN $2.10 TO $1914.35

SILVER PRICE CLOSED: DOWN $0.06 AT $22.69

Access prices: closes 4: 15 PM

Gold ACCESS CLOSE 1913.65

Silver ACCESS CLOSE: 22.68

Shanghai Gold Benchmark Price

USD oz  AM1959.52

AM1959.52

PM1961.39

Historical SGE Fix

New York price at the time: 1915.00

premium $46.00

xxxxxxxxxxxxxxxxxx

Bitcoin morning price:, $29,417 UP 15 Dollars

Bitcoin: afternoon price: $29,372 DOWN 30 dollars

Platinum price closing $911.90 UP $17.65

Palladium price; $1293.55 UP $56.70

END

Due to the huge rise in the dollar, we must look at gold and silver in currencies other than the dollar to understand where we are heading

I will now provide gold in Canadian dollars, British pounds and Euros/4: 15 PM ACCESS

CANADIAN GOLD: $2,572.99 UP 2.99 CDN dollars per oz (ALL TIME HIGH 2,775.35)

BRITISH GOLD: 1506.86 UP 2.46 pounds per oz//(ALL TIME HIGH//CLOSING///1630.29)

EURO GOLD: 1748.42 UP 7.10 euros per oz //(ALL TIME HIGH/CLOSING//1861.21)//

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

EXCHANGE: COMEX

EXCHANGE: COMEX

CONTRACT: AUGUST 2023 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,914.400000000 USD

INTENT DATE: 08/10/2023 DELIVERY DATE: 08/14/2023

FIRM ORG FIRM NAME ISSUED STOPPED

JPMorgan stopped 2/79 contracts.

FOR AUGUST:

GOLD: NUMBER OF NOTICES FILED FOR AUGUST/2023. CONTRACT: 79 NOTICES FOR 7900 OZ or 0.2457 TONNES

total notices so far: 10,651 contracts for 1,065,100 oz (32.883 tonnes)

FOR AUGUST:

SILVER NOTICES: 0 NOTICE(S) FILED FOR nil OZ/

total number of notices filed so far this month : 896 for 4,480,000 oz

XXXXXXXXXXXXXXXXXXXXXXXX

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD

WITH GOLD DOWN $2.10

INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD//

SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .31 TONNES OF GOLD FROM THE GLD

INVENTORY RESTS AT 903.38 TONNES

Silver//

WITH NO SILVER AROUND AND SILVER DOWN 6 CENTS AT THE SLV// HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.926 MILLION OZ INTO THE SLV/

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV.

CLOSING INVENTORY: 452.452 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A TINY SIZED 87 CONTRACTS TO 137,489 AND CLOSER TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THIS TINY SIZED LOSS IN COMEX OI WAS ACCOMPLISHED DESPITE OUR $0.06 GAIN IN SILVER PRICING AT THE COMEX ON THURSDAY. TAS ISSUANCE WAS ANOTHER JUPITER SIZED 6604 CONTRACTS. THESE WILL BE USED FOR MANIPULATION LATER THIS MONTH/AS WELL AS TODAY. CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON THURSDAY NIGHT: 6604 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS. IT THUS LOOKS LIKE THE FED (GOV’T) IS BEHIND ALL OF THESE TRADES.

WE HAVE NOW SET ANOTHER RECORD LOW AT 114,102 CONTRACTS ///JULY 3.2023// OUR BANKERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.06). BUT WERE UNSUCCESSFUL IN KNOCKING OF ANY SILVER CONTRACTS(IF ANY STILL EXIST) AS WE HAD OUR STRONG GAIN OF 583 CONTRACTS ON BOTH EXCHANGES ALONG WITH CONSIDERABLE T.A.S.LIQUIDATION THROUGHOUT THE SESSION.

WE MUST HAVE HAD:

A STRONG ISSUANCE OF EXCHANGE FOR PHYSICALS( 670 CONTRACTS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 3.105 MILLION OZ (FIRST DAY NOTICE) FOLLOWED BY TODAY’S NIL OZ QUEUE JUMP //NEW STANDING RISES AT 4.480 MILLION OZ + OUR NEW CRIMINAL 0 CONTRACTS OF EXCHANGE FOR RISK FOR 0.00 MILLION OZ + 1.45 MILLION OZ EX. FOR RISK/PRIOR/// NEW TOTAL STANDING FOR SILVER: 5.930 MILLION OZ/// // // TINY SIZED COMEX OI GAIN/ STRONG SIZED EFP ISSUANCE/VI) JUPITER SIZED NUMBER OF T.A.S. CONTRACT ISSUANCE (6604 CONTRACTS)/ZERO EXCHANGE FOR RISK ISSUED

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL -268 CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS AUGUST. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF AUGUST:

TOTAL CONTRACTS for 9 days, total 15,701 contracts: OR 78.505 MILLION OZ (1744 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 78.505 MILLION OZ

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH 2022: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 118.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 85.745 MILLION OZ (SMALLER THAN LAST MONTH)

AUGUST: 78.505 MILLION OZ (THIS MONTH IS GOING TO BE GIGANTIC//WE MAY SURPASS MARCH 2022 RECORD OF 207 MILLION OZ/// )

RESULT: WE HAD A SMALL SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 87 CONTRACTS DESPITE OUR GAIN IN PRICE OF $0.06 IN SILVER PRICING AT THE COMEX//THURSDAY.,. THE CME NOTIFIED US THAT WE HAD A STRONG EFP ISSUANCE CONTRACTS: 670 ISSUED FOR SEPT AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS./ WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR AUGUST OF 3.105 MILLION OZ FOLLOWED BY TODAY’S 0 OZ QUEUE JUMP//NEW STANDING 4.480 MILLION OZ+ 1.45 MILLION OZ EXCHANGE FOR RISK NEW TOTALS 5.930 MILLION OZ//// WE HAVE A STRONG SIZED GAIN OF 583 OI CONTRACTS ON THE TWO EXCHANGES. THE TOTAL OF TAS INITIATED CONTRACTS TODAY: A MAMMOTH 6604//HUGE FRONT END OF THE TAS CONTRACTS WERE LIQUIDATED DURING THE THURSDAY COMEX SESSION . THE NEW TAS ISSUANCE THURSDAY NIGHT (6604) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE., AND MOST PROBABLY TODAY.

WE HAD 0 NOTICE(S) FILED TODAY FOR nil OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A SMALL SIZED 525 CONTRACTS TO 430,592 AND CLOSER TO TO THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: – REMOVED: 184 CONTRACTS

WE HAD A SMALL SIZED INCREASE IN COMEX OI ( 525 CONTRACTS) DESPITE OUR $1.00 LOSS IN PRICE//THURSDAY. WE ALSO HAD A RATHER SMALL INITIAL STANDING IN GOLD TONNAGE FOR AUGUST. AT 30.656 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S 2100 OZ E.F.P.JUMP TO LONDON + PRIOR ISSUANCE OF EXCHANGE FOR RISK = (.684 TONNES) //NEW STANDING 33.374 TONNES + .684 EXCHANGE FOR RISK = 34.058/ + /A FAIR (AND CRIMINAL) ISSUANCE OF 1642 T.A.S. CONTRACTS /// ALL OF..THIS HAPPENED WITH A $1.00 LOSS IN PRICE WITH RESPECT TO THURSDAY’S TRADING.WE HAD A FAIR SIZED GAIN OF 3687 OI CONTRACTS (12.037 PAPER TONNES) ON OUR TWO EXCHANGES.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 3162 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 430,408

IN ESSENCE WE HAVE A FAIR SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 3687 CONTRACTS WITH 525 CONTRACTS INCREASED AT THE COMEX// AND A FAIR 3162 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 3687 CONTRACTS OR 12.037 TONNES. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): A FAIR 1642 CONTRACTS)

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (3162 CONTRACTS) ACCOMPANYING THE SMALL SIZED GAIN IN COMEX OI (525) //TOTAL GAIN FOR OUR THE TWO EXCHANGES: 3687 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR NORMAL FORMAT OF BANKERS GOING SHORT AND SPECULATORS GOING LONG ,2.) FAIR INITIAL STANDING AT THE GOLD COMEX FOR JULY AT 30.656 TONNES FOLLOWED BY TODAY’S 2100 OZ E.F.P. JUMP TO LONDON //NEW STANDING 33.374 TONNES + .684 TONNES (EXCHANGE FOR RISK//PRIOR) NEW TOTALS: 34.058 TONNES/// 3) ZERO LONG LIQUIDATION WITH CONSIDERABLE TAS LIQUIDATION //4) SMALL SIZED COMEX OPEN INTEREST GAIN/ 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER///6: FAIR T.A.S. ISSUANCE: 1642 CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023 INCLUDING TODAY

AUGUST

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF AUG :

TOTAL EFP CONTRACTS ISSUED: 28,093 CONTRACTS OR 2,809,300 OZ OR 87.380 TONNES IN 9 TRADING DAY(S) AND THUS AVERAGING: 3121 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 9 TRADING DAY(S) IN TONNES 87.380 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2022, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 87.380/3550 x 100% TONNES 2.45% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2023

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH/2022: 409.30 TONNES //FINAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 151.69 TONNES (WEAKER THAN LAST MONTH)

AUGUST: 87.350 TONNES (A STRONG MONTH BUT WILL NOT EQUAL MARCH 2022)

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF SEPT. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF MAY HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF JUNE., FOR BOTH GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (SEPT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER FELL BY A TINY SIZED 87 CONTRACTS OI TO 137,489 AND FURTHER FROM OUR COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE A STRONG 670 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

SEPT 670 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 670 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 87 CONTRACTS AND ADD TO THE 670 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A STRONG SIZED GAIN OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 583 CONTRACTS

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTAL 2.915MILLION OZ

OCCURRED DESPITE OUR $0.06 GAIN IN PRICE …..

END

OUTLINE FOR TODAY’S COMMENTARY

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

b, ) Gold/silver trading overnight Europe,//GOLD COMMENTARIES

(Peter Schiff)

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS//

FRIDAY MORNING//THURSDAY NIGHT

SHANGHAI CLOSED DOWN 65.31 PTS OR 2.01% //Hang Seng CLOSED DOWN 173.07 PTS OR 0.90% /The Nikkei CLOSED //Australia’s all ordinaries CLOSED DOWN 0.19 % /Chinese yuan (ONSHORE) closed DOWN 7.2323 /OFFSHORE CHINESE YUAN DOWN TO 7.2511 /Oil UP TO 83.22 dollars per barrel for WTI and BRENT UP AT 86.93 / Stocks in Europe OPENED ALL RED// ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

9. USA

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A SMALL SIZED 525 CONTRACTS UP TO 430,408 DESPITE OUR SMALL LOSS IN PRICE OF $1.00 ON THURSDAY.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE ACTIVE DELIVERY MONTH OF AUGUST… THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 3162 EFP CONTRACTS WERE ISSUED: : DEC 3162 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 3162 CONTRACTS

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A FAIR SIZED TOTAL OF 3687 CONTRACTS IN THAT 3162 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A SMALL SIZED GAIN OF 525 COMEX CONTRACTS..AND THIS GAIN ON OUR TWO EXCHANGES HAPPENED DESPITE OUR LOSS IN PRICE OF $1.00//THURSDAY COMEX. AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS DURING MID MONTH IN THE DELIVERY CYCLE), THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR THURSDAY NIGHT WAS A FAIR 1642 CONTRACTS. THROUGHOUT THE PAST WEEKS, THE BANKERS SOLD OFF THE LONG SIDE OF THE SPREAD WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR SPREAD WHICH WILL BE LIQUIDATED TWO MONTHS HENCE)//THE HUGE NUMBER OF T.A.S. CONTRACTS INITIATED OVER THE PAST SEVERAL WEEKS SPELLS TROUBLE FOR THE GOLD/SILVER MARKET AS RAIDS WILL SURELY BE UPON US TRYING TO CONTAIN OUR PRECIOUS METALS RISE IN PRICE.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: AUGUST (34.058) ( ACTIVE MONTH)

TONNES),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 34.058 TONNES (INCLUDING .6842 EXCHANGE FOR RISK)

THE SPECS/HFT WERE SUCCESSFUL IN LOWERING GOLD’S PRICE( IT LOST $1.00) //// BUT WERE UNSUCCESSFUL IN KNOCKING ANY SPECULATOR LONGS (IF ANY STILL EXIST) AS WE HAD A FAIR GAIN OF 3687 TOTAL CONTRACTS ON OUR TWO EXCHANGES. WE HAD CONSIDERABLE T.A.S. LIQUIDATION ON THE FRONT END. THE T.A.S. ISSUED ON THURSDAY NIGHT WILL BE “PUT INTO THE BANK” TO BE USED AT A LATER DATE AT THE COLLUSIVE CHOOSING OF OUR BANKERS.

WE HAVE GAINED A TOTAL OI OF 12.037 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR AUGUST. (30.656 TONNES) ON FIRST DAY NOTICE FOLLOWED BY TODAY’S 2100 OZ E.F.P JUMP TO LONDON//NEW STANDING LOWERS A BIT TO 33.374 TONNES + .6842 (PRIOR EXCHANGE FOR RISK) //NEW TOTAL 34.058 TONNES // ALL OF THIS WAS ACCOMPLISHED WITH OUR LOSS IN PRICE TO THE TUNE OF $1.00.

WE HAD – REMOVED 184 CONTRACTS TO THE COMEX TRADES TO OPEN INTEREST

NET GAIN ON THE TWO EXCHANGES 3687 CONTRACTS OR 368,700 OZ OR 12.037 TONNES.

Estimated gold volume today:// 139,877 awful

final gold volumes/yesterday 179,336 awful

//AUGUST 11/ FOR THE AUGUST 2023 GOLD CONTRACT

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 96,753.000 Brinks 3000 kilobars . |

| Deposit to the Dealer Inventory in oz | nil |

| Deposits to the Customer Inventory, in oz | 643.02 OZ Brinks 20 kilobars |

| No of oz served (contracts) today | 79 notice(s) 7,900 OZ 0.2457TONNES |

| No of oz to be served (notices) | 79 contracts 7900 oz 0.2457 TONNES |

| Total monthly oz gold served (contracts) so far this month | 10,651 notices 1,065,100 OZ 33.129 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | x |

0 dealer deposit:

total dealer deposits: NIL oz

customer deposits: 1

i) Into Brinks 643.02 oz (20 kilobars)

total customer deposits: 643.02 oz

we had 1 customer withdrawals

i) Out of Brinks oz 96,453.000 oz (3000 kilobars)

Adjustments; 4 of which 3 are dealer to customer

i) Brinks 3894.78 oz

ii) HSBC 594.69 oz

iii) manfra 8383.867 oz

and one customer to dealer JPMorgan

a) 4963.63 oz

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR AUGUST.

For the front month of AUGUST we have an oi of 158 contracts having LOST 353 contracts. We had 332 contracts filed

on Thursday, so we lost 21 contracts or an additional 2100 oz will not stand at the comex, as these guys took a ferry over to London to take delivery over there.

Sept lost 80 contracts to 2607.

Oct lost 446 contracts to 33,293 contracts.

We had 79 contracts filed for today representing 7900 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 79 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 33 notice(s) was (were) stopped received by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the AUGUST /2023. contract month,

we take the total number of notices filed so far for the month (10,572 x 100 oz ), to which we add the difference between the open interest for the front month of AUGUST (158 CONTRACT) minus the number of notices served upon today 320 x 100 oz per contract equals 1,073,000 OZ OR 33.374 TONNES the number of TONNES standing in this active month of AUGUST. + .684 TONNES EXCHANGE FOR RISK/prior = 34.058 tonnes

thus the INITIAL standings for gold for the AUGUST contract month: No of notices filed so far (10,572) x 100 oz + (158) {OI for the front month} minus the number of notices served upon today (320) x 100 oz) which equals 1,073,000 oz standing OR 33.374 TONNES + .684 TONNES OF EXCHANGE FOR RISK/prior = 34.058 TONNES

TOTAL COMEX GOLD STANDING: 34.058 TONNES WHICH IS SMALL FOR AN ACTIVE DELIVERY MONTH.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 2,101,333.235 OZ 65.36 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 22,111,819.566 OZ

TOTAL REGISTERED GOLD: 11,797,047.194 (366,93 tonnes)..

TOTAL OF ALL ELIGIBLE GOLD: 10,410,672.615 O Z

REGISTERED GOLD THAT CAN BE SERVED UPON: 9,695,714 OZ (REG GOLD- PLEDGED GOLD) 301.57 tonnes//

END

SILVER/COMEX

AUGUST 11

//2023// THE AUGUST 2023 SILVER CONTRACT

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 614,436.845 oz CNT Delaware JPM . |

| Deposits to the Dealer Inventory | nil oz |

| Deposits to the Customer Inventory | 39,422.792 oz Delaware |

| No of oz served today (contracts) | 0 CONTRACT(S) (0 OZ) |

| No of oz to be served (notices) | 0 contracts (nil oz) |

| Total monthly oz silver served (contracts) | 896 Contracts (4,480,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

i) 0 dealer deposit

total dealer deposit: 0 oz

i) We had 0 dealer withdrawal

total dealer withdrawals: 0 oz

We had 1 deposits customer account:

i)Into Delaware: 39,422.792 oz

total customer deposits: 39,422.792 oz

JPMorgan has a total silver weight: 139.877 million oz/280.597 million =50.00% of comex .//

Comex withdrawals 3

i) Out of JPM 15,246.590 oz

ii) Out of Delaware 5891.495 oz

iii) out of CNT 15,246.590 oz

adjustments: 1/dealer to customer

i) Brinks 237,678.040 oz

TOTAL REGISTERED SILVER: 30.828 MILLION OZ//.TOTAL REG + ELIGIBLE. 280.829 million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR JULY:

silver open interest data:

FRONT MONTH OF AUGUST /2023 OI: 0 CONTRACTS HAVING LOST 0 CONTRACT(S). WE HAD

0 NOTICES FILED ON THURSDAY SO WE GAINED 0 CONTRACTS OR AN ADDITIONAL NIL OZ WILL STAND IN THIS NON ACTIVE DELIVERY MONTH OF AUGUST.

SEPT HAS A LOSS OF 5854 CONTRACTS DOWN TO 71,333

OCT GAINED 128 CONTRACTS TO STAND AT 358.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 0 for NIL oz

Comex volumes// est. volume today 60,678 fair

Comex volume: confirmed yesterday: 97,428 strong/t.a.s induced

To calculate the number of silver ounces that will stand for delivery in AUGUST. we take the total number of notices filed for the month so far at 896 x 5,000 oz = 4,480,000 oz

to which we add the difference between the open interest for the front month of AUGUST (0) and the number of notices served upon today 0 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the AUGUST/2023 contract month: 896 (notices served so far) x 5000 oz + OI for the front month of AUGUST (0) – number of notices served upon today (0 )x 500 oz of silver standing for the AUGUST contract month equates to 4.480 million oz.+ 0.0 MILLION OZ EXCHANGE FOR RISK ISSUED TODAY+ 1.45 MILLION OZ EXCHANGE FOR RISK PRIOR//NEW TOTALS: 5.930 MILLION oz.

There are 31.066 million oz of registered silver.

Thus if we take today’s standing at 5.930 and add last month’s 30.9 million oz we have 36.830 million oz against only 31.066 million registered silver.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS

AUGUST 11/WITH GOLD DOWN $2.10 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .31 TONNES FORM THE GLD//: /// //INVENTORY RESTS AT 903.31 TONNES

AUGUST 10/WITH GOLD DOWN $1.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD: /// //INVENTORY RESTS AT 903.69 TONNES

AUGUST 9/WITH GOLD DOWN $8.75 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD: /// //INVENTORY RESTS AT 903.69 TONNES

AUGUST 8/WITH GOLD DOWN $9.60 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.31 TONNES FORM THE GLD /// //INVENTORY RESTS AT 903.69 TONNES

AUGUST 7/WITH GOLD DOWN $5.45 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD: /// //INVENTORY RESTS AT 906.00 TONNES

AUGUST 4/WITH GOLD UP $7.25 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.18 TONNES OF GOLD FROM THE GLD/// .///INVENTORY RESTS AT 906.00 TONNES

AUGUST 3/WITH GOLD DOWN $5.25 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD //: //: / .////INVENTORY RESTS AT 909.18 TONNES

AUGUST 2/WITH GOLD DOWN $3.45 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 3.75 TONNES OF GOLD FROM THE GLD//: //: / .////INVENTORY RESTS AT 909.18 TONNES

AUGUST 1/WITH GOLD DOWN $28.45 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 2.89 TONNES OF GOLD FROM THE GLD//: //: / .////INVENTORY RESTS AT 912.93 TONNES

JULY 31/WITH GOLD UP $9.50 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 2.89 TONNES OF GOLD FROM THE GLD//: //: / .////INVENTORY RESTS AT 912.93 TONNES

JULY 28/WITH GOLD UP $14.15 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 1.44 TONNES OF GOLD FROM THE GLD//: //: / .////INVENTORY RESTS AT 915,82 TONNES

JULY 27/WITH GOLD DOWN $21.80 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 1.74 TONNES OF GOLD FROM THE GLD//: //: / .////INVENTORY RESTS AT 917.26 TONNES

JULY 26/WITH GOLD UP $6.35 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD: //: / .////INVENTORY RESTS AT 919.00 TONNES

JULY 25/WITH GOLD UP $2.45 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD: //: / .////INVENTORY RESTS AT 919.00 TONNES

JULY 24/WITH GOLD DOWN $4.65 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 5.20 TONNES OF GOLD INTO THE GLD//: / .////INVENTORY RESTS AT 919.00 TONNES

JULY 21/WITH GOLD DOWN $3.80 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD: / .////INVENTORY RESTS AT 913.80 TONNES

JULY 20/WITH GOLD DOWN $8.70 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.73 TONNES FROM THE GLD/ .////INVENTORY RESTS AT 913.80 TONNES

JULY 19/WITH GOLD UP $0.65 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .86 TONNES FROM THE GLD/ .////INVENTORY RESTS AT 912.07 TONNES

JULY 18/WITH GOLD UP $23.45 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD: .////INVENTORY RESTS AT 912.93 TONNES

JULY 17/WITH GOLD DOWN $6.60 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.73 TONNES OF GOLD FROM THE GLD.////INVENTORY RESTS AT 912.93 TONNES

JULY 14/WITH GOLD UP $0.75 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD: ////INVENTORY RESTS AT 914.66 TONNES

JULY 13/WITH GOLD UP $3.30 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 0.29 TONNES OF GOLD OUT OF THE GLD////INVENTORY RESTS AT 914.66 TONNES

JULY 12/WITH GOLD UP $24.50 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 0.31 TONNES OF GOLD OUT OF THE GLD////INVENTORY RESTS AT 914.95 TONNES

JULY 11/WITH GOLD UP $6.15 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.0 TONNES OF GOLD OUT OF THE GLD////INVENTORY RESTS AT 915.26 TONNES

JULY 10 WITH GOLD DOWN $1.35 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.60 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 916.26 TONNES.

GLD INVENTORY: 903.31 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

AUGUST 11/WITH SILVER DOWN 6 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A DEPOSIT OF 1.926 MILLION OZ INTOTHE SLV/: // OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 452.106 MILLION OZ

AUGUST 10/WITH SILVER UP 6 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 8,807 MILLION OZ OUT OF THE SLV/: // OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 450.180 MILLION OZ

AUGUST 9/WITH SILVER DOWN 7 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 8,807 MILLION OZ OUT OF THE SLV/: // OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 450.180 MILLION OZ

AUGUST 8/WITH SILVER DOWN 40 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: // OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 458.987 MILLION OZ

AUGUST 7/WITH SILVER DOWN 46 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: // OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 458.987 MILLION OZ

AUGUST 4/WITH SILVER UP 1 CENT TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.294 MILLION OZ FROM THE SLV// OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 458.987 MILLION OZ

AUGUST 3/WITH SILVER DOWN 16 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 189,000 OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 451.281 MILLION OZ

AUGUST 2/WITH SILVER DOWN 43 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 275,000 OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 451.471 MILLION OZ

AUGUST 1/WITH SILVER DOWN 61 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 184,000 OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 451.746 MILLION OZ

JULY 31/WITH SILVER UP 45 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 184,000 OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 451.746 MILLION OZ

JULY 28/WITH SILVER UP 15 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 550,000 OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 451.930 MILLION OZ

JULY 27/WITH SILVER DOWN 59 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: .////INVENTORY RESTS AT 452.480 MILLION OZ

JULY 26/WITH SILVER UP 15 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: .////INVENTORY RESTS AT 452.480 MILLION OZ/

JULY 25/WITH SILVER UP 24 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A SMALL WITHDRAWAL OF 826,000 OZ FROM THE SLV..////INVENTORY RESTS AT 452.480 MILLION OZ/

JULY 24/WITH SILVER DOWN 23 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: ////INVENTORY RESTS AT 453.306 MILLION OZ/

JULY 21/WITH SILVER DOWN 14 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 1.101 MILLION OZ OF SILVER FROM THE SLV ////INVENTORY RESTS AT 453.306 MILLION OZ/

JULY 20/WITH SILVER DOWN 38 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 1.468 MILLION OZ OF SILVER FROM THE SLV ////INVENTORY RESTS AT 454.107 MILLION OZ/

JULY 19/WITH SILVER UP 11 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV:A ////INVENTORY RESTS AT 455.875 MILLION OZ/

JULY 18/WITH SILVER DOWN 19 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV:A ////INVENTORY RESTS AT 455.875 MILLION OZ/

JULY 17/WITH SILVER UP 25 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 4.856 MILLION OZ OF SILVER FROM THE SLV////////INVENTORY RESTS AT 455.875 MILLION OZ/

JULY 14/WITH SILVER UP 27 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 2.21 MILLION OZ OF SILVER FROM THE SLV////////INVENTORY RESTS AT 455.875 MILLION OZ/

JULY 13/WITH SILVER UP 64 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//////INVENTORY RESTS AT 462.941 MILLION OZ/

JULY 12/WITH SILVER UP $1.00 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.881 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 462.941 MILLION OZ/

JULY 11/WITH SILVER DOWN 5 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF .020 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 464.822 MILLION OZ/

JULY 10/WITH SILVER UP 2 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.672 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 464.802 MILLION OZ

//

CLOSING INVENTORY 42.106 MILLION OZ//

PHYSICAL GOLD/SILVER COMMENTARIES

1:Peter Schiff/Mike Maharrey

end

2 Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens//JAMES RICKARDS//JOHN RUBINO

end

3,Chris Powell of GATA provides to us very important physical commentaries

A must read…your weekend reading material

(Alasdair Macleod)

Alasdair Macleod: Beware the great unwind

Submitted by admin on Thu, 2023-08-10 12:10Section: Daily Dispatches

By Alasdair Macleod

GoldMoney, Toronto

Thursday, August 10, 2023

The chart published with this essay strongly suggests that U.S. Treasury bond yields, widely regarded as the risk-free yardstick against which all other credit is measured, are going significantly higher, not stabilising close to current levels before going lower as commonly believed.

I conclude that U.S. Treasury bond yields could easily double, and the political class will be powerless to stop them going even higher. The implications for interest rates globally are that they will be forced considerably higher as well.

This article concludes that reasoned analysis takes us to this inevitable conclusion. It is consistent with the end of the post-Bretton Woods fiat currency era, and the return to credit backed by real values.

The collapse of unbacked credit’s value was only a matter of time, which is now rapidly approaching. The Great Unwind is under way. It is the consequence of monetary and currency distortions that have accumulated since the end of Bretton Woods 52 years ago. It will not be a trivial matter.

The trigger will be capital flows leaving the dollar, creating a funding crisis for the U.S. government. Foreigners, who have accumulated $32 trillion in deposits and other dollar-denominated financial assets, will no longer need to maintain dollar balances to the same extent, perhaps even paring them back to a minimum.

Furthermore, economic factors are turning sharply negative with energy prices rising ahead of the Northern Hemisphere winter, springing debt traps on Western alliance governments.

So how could bond yields possibly decline materially in the coming months? …

… For the remainder of the analysis:

https://www.goldmoney.com/research/beware-the-great-unwind?gmrefcode=gata

END

Two interviews for you; Bill Murphy of GATA and Peter Grandich

(GATA)

GoldSeek Radio’s Waltzek interviews Bill Murphy and Peter Grandich

Submitted by admin on Thu, 2023-08-10 21:07Section: Daily Dispatches

9:12p ET Thursday, August 10, 2023

Dear Friend of GATA and Gold (and Silver):

GoldSeek Radio’s Chris Waltzek interviewes GATA Chairman Bill Murphy about whether the monetary metals will ever reverse upward as the U.S. government’s debt becomes ever-more stratospheric.

The interview is 10 minutes long and can be heard at GoldSeek here:

Waltzek also interviews market analyst Peter Grandich, who sees great opportunity in monetary metals mining stocks despite the worst sentiment he has ever seen in the sector. The interview is 18 minutes long and can be heard at GoldSeek here:

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@ATA.org

end

4, OTHER IMPORTANT GOLD/SILVER COMMENTARIES

The BRICS gold-backed commodity structure revealed

Andrew Maguire breaks down the structure behind the new “sanction-proof” BRICS gold-backed wo.

The BRICS gold-backed commodity structure revealed

In this week’s episode of Live from the Vault, Andrew Maguire breaks down the structure behind the new “sanction-proof” BRICS gold-backed world settlement currency, and provides a teaser ahead of the upcoming BRICS Plus summit.

The whistleblower digs deeper into gold’s potential as a first-tier asset class alternative to high counterparty-risk US treasuries, and shares his thoughts on how the Federal Reserve has been so wrong-footed by gold in recent months.

https://kinesis.money/live-from-the-vault

END

From the beginning of 2023, Poland sovereign has bough 2.3 million oz (71 tonnes of gold) of which 2.23 tonnes were added in July.

At this rate, the country will have added 84 tonnes for the year which is huge for them. Their official reserves now stand at around 300 tonnes. This is real gold and this will cause nightmares for our bankers who have huge amount of paper (non backed) gold

(ReMix)

Poland Continues To Aggressively Buy Gold

FRIDAY, AUG 11, 2023 – 03:30 AM

Poland’s national bank has increased its gold holdings by 2.3 million ounces since the start of the year…

The National Bank of Poland (NBP) increased its gold reserves for the fourth consecutive month in July as the country continues to aggressively stockpile the precious metal.

According to calculations by the DGP newspaper, 720,000 ounces of gold were bought last month, valued at about $1.4 billion. This is more than in any of the previous three months. The paper estimated that the total gold reserves held by the Polish central bank have increased to 9.6 million ounces, or nearly 300 tons.

Since the beginning of the year, the NBP has increased its gold supply by 2.3 million ounces.

Before starting his second term as the president of the NBP, Adam Glapiński announced that he would increase gold reserves by 100 tons. With this year’s purchases, he has already fulfilled over two-thirds of that promise.

Monetary gold held by the NBP was valued at $18.8 billion at the end of July.

It accounted for 10.4 percent of the central bank’s official reserve assets. In the local currency, the gold held by the central bank was valued at 75.3 billion złotys.

Foreign currency reserves are primarily meant to ensure the financial stability of the economy. That’s why the money is invested in safe and liquid assets, meaning those that can be quickly sold. However, they should also generate income.

Since the beginning of this year, gold prices in global markets have increased by over 6 percent. It currently costs just over $1,900 per ounce. In terms of return rate since the beginning of the year, gold has performed the best among the main metals.

Silver has depreciated by 2.2 percent and platinum by 15 percent. The rise in gold prices has in part been due to buying it as a way to hedge against inflation.

And it’s not just Poland.

Despite significant selling by Turkey that slowed net central bank gold buying in the second quarter, central banks added a record amount of gold to their reserves through the first half of 2023.

Net central bank gold purchases totaled 387 tons through the first half of the year, according to data compiled by the World Gold Council. That was the highest first-half total since the organization started compiling quarterly data in 2000.

end

5 a. IMPORTANT COMMENTARIES ON COMMODITIES:

end

5 B GLOBAL COMMODITY ISSUES/FOOD IN GENERAL//FREIGHT

END

6.CRYPTOCURRENCY//DIGITAL CURRENCY// COMMENTARIES/

Sam Bankman-Fried Heads Back To Jail After Bail Revoked

FRIDAY, AUG 11, 2023 – 03:30 PM

FTX Founder Sam Bankman-Fried is headed back to jail after the judge in the case revoked his bail over alleged witness intimidation, after he showed a journalist from the NY Times private writings from his ex-girlfriend and business partner, Caroline Ellison, and used a VPN in violation of a previous order not to.

Late last month the DOJ sought to have SBF’s bail revoked over the leaked diary, and allegedly used the Signal app to obstruct the investigation, as the app auto-deletes content after a period of time.

John Reed Stark, former US SEC’s Office of Internet Enforcement Chief, suggested that Judge Lewis Kaplan could view SBF’s actions as an effort to improperly influence witnesses and choose to either make further modifications to his bail conditions or revoke his bail entirely. Obviously, Kaplan chose the latter.

“The documents are in part personal and intimate. They are personally oriented, not business oriented. There’s something that someone who has been in a relationship would be unlikely to share with anyone except to hurt and frighten the subject,” said Judge Kaplan, adding “In view of the evidence, my conclusion is that there is probable cause to believe that the defendant has attempted to tamper with witnesses at least twice under Section 1512(b).”

Click into this Twitter thread from Inner City Press for the blow-by-blow:

END

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS FRIDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED DOWN TO 7.2323

OFFSHORE YUAN: DOWN TO 7.2511

SHANGHAI CLOSED DOWN 65.31 PTS OR 2.01%

HANG SENG CLOSED DOWN 173.07 PTS OR 0.90%

2. Nikkei closed

3. Europe stocks SO FAR: ALL RED

USA dollar INDEX DOWN TO 102.32 EURO RISES TO 1.0995 UP 14 BASIS PTS

3b Japan 10 YR bond yield: FALLS TO. +.580 Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 144.53/JAPANESE YEN FALLING AS WELL AS LONG TERM 10 YR. YIELDS RISING //EVENTUALLY THIS WILL BREAK THE JAPANESE CENTRAL BANK

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen DOWN CHINESE ON SHORE YUAN: DOWN// OFF- SHORE: DOWN

3f Japan is to buy INFINITE TRILLION YEN’S worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and UP FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund UP TO +2.5875***/Italian 10 Yr bond yield RISES to 4.215*** /SPAIN 10 YR BOND YIELD RISES TO 3.594…**

3i Greek 10 year bond yield RISES TO 3.849

3j Gold at $1919.00 silver at: 22.72 1 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble DOWN 0 AND 97 /100 roubles/dollar; ROUBLE AT 98.43//

3m oil into the 83 dollar handle for WTI and 86 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 144.53// 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 0.580% STILL ON CENTRAL BANK (JAPAN) INTERVENTION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.8757 as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9627 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.100 UP 2 BASIS PTS…

USA 30 YR BOND YIELD: 4.258 UP 2 BASIS PTS/

USA 2 YR BOND YIELD: 4.829 UP 1 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 27.05…(TURKEY SET TO BLOW UP FINANCIALLY)

GREAT BRITAIN/10 YEAR YIELD: UP 11 BASIS PTS AT 4.5205

end

2.a Overnight: Newsquawk and Zero hedge:

Futures Flat, Global Markets Slide As Attention Turns To China’s “Ticking Time Bomb”

FRIDAY, AUG 11, 2023 – 08:18 AM

US futures are flat, with European and Asian stocks red, as concern about local government debt in China and hawkish language from a US central banker put traders in a risk-off mood. Meanwhile, in the latest diplomatic fiasco from Joe Biden, the US president blasted China’s economic problems as a “ticking time bomb” and referred to Communist Party leaders as “bad folks,” his latest barb against President Xi Jinping’s government even as his administration seeks to improve overall ties with Beijing. As of 7:45am ET, S&P futures were flat while Nasdaq 100 futs were down 0.1%. Treasurys yields are 1-4bps lower led by the front-end with 10Ys at 4.10%; the USD reversed an earlier gain and was last trading near session lows. Commodities are mixed with oil reversing earlier losses and following gold higher. Today, the macro focus will be PPI and U of Mich survey: the Street expects PPI to print 0.2% MoM vs. 0.1% prior, while U of Mich Consumer Sentiment is expected to drop to 71.3 consensus from 71.6 prior.

In premarket trading, mega cap tech are mostly lower. UBS rose as much as 5.9% after the Swiss bank said it would end an agreement with the Swiss government to cover Credit-Suisse- related losses, a move which analysts said was very reassuring. Virgin Galactic shares rose as much as 3.7% in premarket trading on Friday, after the company, founded by billionaire businessman Richard Branson, said it aims to launch its next space tourist mission in early September. Cano Health shares plummet as much as 53% in US premarket trading, after the healthcare provider issued a going concern warning and said it is exploring a sale. Citi downgrades Cano’s rating on the stock to hold, while TD Cowen describes the fall in 2Q Ebitda as “stunning.” Here are some other notable premarket movers:

- IonQ rises as much as 8.2% in premarket trading on Friday, after the computing hardware and software company boosted its bookings forecast for the full year.

- Maxeon Solar Technologies shares slump 27% in premarket trading after the renewable energy equipment maker issued weaker-than-expected revenue forecast for the third quarter.

- Medical Properties shares fall as much as 5.7% in premarket trading after both Raymond James and BofA downgraded the healthcare REIT to underperform, citing its exposure to top tenant Steward Health Care.

- Rigetti Computing shares are up 18% in premarket trading after the quantum-computers company reported second-quarter results that spurred an upgrade.

- Sealed Air shares drop 1.6% in premarket trading after the packaging company was downgraded to neutral from buy at UBS, which sees a return to growth taking longer to play out.

- Semler Scientific jumps 18% in premarket trading Friday after reporting revenue and net income for the second quarter that topped Wall Street’s estimates.

Markets were on edge after SF Fed President Mary Daly said the Fed still has “more work to do” to combat rising prices, damping the impact of broadly positive inflation data on Thursday. Meanwhile, as noted earlier, China moved to bailout as much as 1 trillion yuan in local government debt, LGFV, a key threat to the nation’s financial stability, while property developer Country Garden Holdings predicted a multibillion-dollar loss for the first half of this year. The MSCI Asia Pacific Index dropped to the lowest level in a month.

“There may be other accidents waiting to happen as a result of sharply higher rates that we just haven’t seen come through yet,” said Richard Flax, chief investment officer at European digital wealth manager Moneyfarm. “Policymakers seem to be trying to signal to investors that they may be too optimistic to be looking for early rate cuts.”

Perhaps anticipating the next market drop, this week has seen a marked move into haven assets and out of stocks, according to Bank of America Corp. strategists. Cash funds attracted $20.5 billion of inflows, while investors poured $6.9 billion into bonds in the week through August 9, according to Bank of America, citing data from EPFR Global. In the meantime, US stocks had their first outflow in three weeks at $1.6 billion.

The Stoxx 600 index dropped 0.8%, snapping two days of gains and trimming its fourth weekly advance in five. Mining and energy stocks are leading declines although all 20 sectors are in the red except for telecommunications. The British pound led gains among G-10 currencies against the dollar after the strongest quarterly growth in more than a year. Here are the most notable European movers:

- UBS rises as much as 5.9% after the Swiss bank said it would end an agreement with the Swiss government to cover Credit-Suisse- related losses. Analysts say the move is very reassuring

- Bechtle rises as much as 5.9% after the German computer and office supplies firm reported 2Q pretax profit margin that beat estimates, driven by strength in the managed services unit

- Lotus Bakeries shares rise as much as 5.7% after the Belgian cookie- and cake-maker reported first-half earnings that beat estimates. KBC hails a “very nice set” of results from the firm

- Saipem rises as much as 4.7%. The company was awarded two new contracts for a total value of about $700 million, while Berenberg raised the price target to a Street high

- EMIS jumps as much as 25% after Britain’s competition watchdog provisionally cleared the British health technology firm’s acquisition by US health-care group UnitedHealth

- Telecom Italia shares rise as much as 5.6% after KKR signed a memorandum of understanding with Italy to include the government in its €23 billion bid for the carrier’s network

- EFG International shares fall as much as 5% after the Swiss private bank was downgraded to neutral from buy at Citi. The broker says it struggles to justify EFG’s premium to peers

Earlier in the session, Asian equities dropped, on course for a second weekly loss, as concerns about the property sector spurred a broader selloff in China. The MSCI Asia Pacific excluding Japan Index declined as much as 0.8%, with Country Garden Holdings among the biggest decliners on the gauge after saying it expects to post net losses for the first half of the year.

- Hang Seng and Shanghai Comp declined with developers pressured including Country Garden after it flagged a loss of up to CNY 55BN for H1 and hired CICC for debt restructuring. Furthermore, shares in Fantasia Holdings dropped more than 50% on resumption of trade after being halted since March last year, while participants await details from the securities regulator’s emergency meeting with developers and financial institutions. Conversely, Alibaba, China Mobile and Li Ning were among the best performers in Hong Kong following their results including the beat on top and bottom lines by China’s e-commerce giant.

- ASX 200 was lackluster with the upside in consumer stocks negated by the losses in the commodity-related sectors, while RBA Governor Lowe’s testimony provided very little in the way of fresh insight in which he reiterated that further tightening may be required.

- Stocks in India declined on Friday to post their third consecutive weekly drop as rally in local shares tapers amid rising worries over inflation and global economic growth. The S&P BSE Sensex fell 0.6% to 65,322.65 in Mumbai, while the NSE Nifty 50 Index declined by a similar measure. For the week, the gauges fell more than 0.5% each, taking their losses since July peak levels to more than 3%. Foreigners, who turned buyers of Indian equities since start of March, have eased their purchases in recent weeks. For this month through Aug. 9, global funds have bought $241 million worth of shares versus net purchases of $4.1 billion in July

- Japan was closed for a public holiday

“A lot of the moves in China this week are Country Garden credit-driven” and CSRC needs to come out with a more forceful response or framework to rescue the company and thereby minimize fallout, said Aninda Mitra, head of Asia macro and investment strategy at BNY Mellon Investment Management. Investors remain concerned over China’s flagging economy following weak data earlier in the week and with the potential worsening of its property sector. Still, strong earnings from Alibaba may be a positive sign of a pick-up in the broader consumption space. Gains in the nation’s online shopping leader helped offset some of the losses in its peers including Tencent and Meituan.

Chipmakers continued to slide after some firms reported earnings. Brokers downgraded Hua Hong Semiconductor, China’s second largest chip foundry, following weak guidance for future sales. A Bloomberg gauge of semiconductor stocks in Asia slumped to its lowest level since May 25.

In FX, the Bloomberg Dollar Spot traded around flat, on track for its fourth week of gains, the longest streak since February. The pound, Australian dollar and yen rose, offsetting a drop in the Norwegian krone and Swedish krona. GBP/USD rose 0.4% to $1.27 after stronger-than-anticipated second quarter GDP data boosted gilt yields. USD/JPY slipped 0.1% to 144.58 as the persistently wide interest-rate gap kept the yen close to the psychological 145 level.

In rates, Treasuries curve were steeper with long-end yields cheaper on the day while front-end and belly of the curve outperform. US 10-year yields around 4.10%, slightly richer on the day with gilts lagging by 11bp in the sector following UK GDP data and bunds cheaper by around 7bp vs Treasuries. Treasury long-end yields were cheaper by around 2bp on the day with front-end and belly richer by 2bp, steepening 2s10s and 5s30s spreads by 1.5bp and 3bp vs Thursday closing levels. Gilts lag sharply in an aggressive bear-steepening move after the UK economy unexpectedly grew 0.2% in the second quarter. US session includes July PPI and University of Michigan sentiment gauge.

In commodities, crude futures decline with WTI falling 0.6% to trade near $82.30. Spot gold adds 0.3%.

Looking ahead to today, in the US we will get the PPI print for July, which will be monitored in part for components that feed into core PCE (such as airfares and medical), and also the August University of Michigan consumer survey. In the UK, we will get the Q2 GDP print– our UK economist expects a 0.0% qoq print, in line with consensus – and accompanying monthly activity data. In the euro area, we get final July inflation prints in France and Spain, Germany June current account balance and France Q2 unemployment.

Market Snapshot

- S&P 500 futures down 0.1% to 4,479.75

- MXAP down 0.7% to 163.83

- MXAPJ down 1.0% to 516.48

- Nikkei up 0.8% to 32,473.65

- Topix up 0.9% to 2,303.51

- Hang Seng Index down 0.9% to 19,075.19

- Shanghai Composite down 2.0% to 3,189.25

- Sensex down 0.3% to 65,506.75

- Australia S&P/ASX 200 down 0.2% to 7,340.13

- Kospi down 0.4% to 2,591.26

- STOXX Europe 600 down 0.8% to 460.29

- German 10Y yield little changed at 2.57%

- Euro up 0.1% to $1.0993

- Brent Futures little changed at $86.38/bbl

- Gold spot up 0.3% to $1,917.61

- U.S. Dollar Index little changed at 102.55

Top Overnight News

- The JPY is at a key level (145) and if it weakens through it, the BOJ could be forced to make further hawkish adjustments to the YCC policy (the BOJ isn’t so much looking to fight inflation but instead bolster the yen). BBG

- China’s M2 money supply growth fell to +10.7% in July (down from +11.3% in June and below the Street’s +11% forecast) while new yuan loans were just CNY346B (a huge miss vs. the Street’s CNY780B forecast). BBG

- President Biden blasted China’s economic problems as a “ticking time bomb” and referred to Communist Party leaders as “bad folks,” his latest barb against President Xi Jinping’s government even as his administration seeks to improve overall ties with Beijing. BBG

- China will allow provincial-level governments to raise about 1 trillion yuan ($139 billion) via bond sales to repay the debt of local-government financing vehicles and other off-balance sheet issuers, a small step toward addressing one of the biggest threats to the nation’s economy and financial stability. BBG

- Beijing is making one of its biggest top-down efforts in years to tackle the debts racked up by local governments in a sign of authorities’ mounting concern over the risk to financial stability as the Chinese economy falters. China’s State Council, the country’s cabinet, is sending teams of officials to more than 10 of the financially weakest provinces to scrutinize their books — including the liabilities of opaque off-balance sheet entities — and find ways to cut their debts. FT

- UBS says it no longer needs the SFR19B Swiss gov’t backstop or SFR100B liquidity facility implemented as part of the Credit Suisse deal, a statement of confidence welcomed by markets. FT

- The UK economy surprised with its strongest quarterly growth in more than a year. GDP rose 0.2% last quarter, defying expectations it would stagnate. Output in June jumped 0.5%, more than double the pace expected, adding to speculation the BOE will feel emboldened to further raise rates. The pound strengthened. BBG

- Iran and the United States appear to be observing an informal agreement under which Iran has limited its nuclear program and restrained proxy militias. NYT

- World oil demand is approaching record levels while supply plunges, raising the risk of tighter markets and higher prices (“Deepening OPEC+ supply cuts have collided with improved macroeconomic sentiment and all-time high world oil demand”). IEA

A more detailed look at global markets courtesy of Newsquawk

APAC stocks traded mostly lower after the post-CPI dovish unwinding seen stateside and amid Chinese developer concerns, with trade also hampered by thinned conditions with Japanese participants away for Mountain Day. ASX 200 was lackluster with the upside in consumer stocks negated by the losses in the commodity-related sectors, while RBA Governor Lowe’s testimony provided very little in the way of fresh insight in which he reiterated that further tightening may be required. Hang Seng and Shanghai Comp declined with developers pressured including Country Garden after it flagged a loss of up to CNY 55bln for H1 and hired CICC for debt restructuring. Furthermore, shares in Fantasia Holdings dropped more than 50% on resumption of trade after being halted since March last year, while participants await details from the securities regulator’s emergency meeting with developers and financial institutions. Conversely, Alibaba, China Mobile and Li Ning were among the best performers in Hong Kong following their results including the beat on top and bottom lines by China’s e-commerce giant.

Top Asian News

- China is to shift USD 139bln of troubled local government financing vehicle debt to provinces under a new program that aims to support financial stability and named 12 cities and provinces as high-risk, according to Bloomberg.

- US President Biden said China is a “ticking time bomb” because of its economic challenges and that the country is in trouble because of weak growth, according to Reuters.

- China is to pause plans to build a new embassy in London, according to a Reuters source.

- New Zealand national intelligence agency said competition between countries is becoming more acute and some countries are seeking advantage through subversive and dishonest means such as espionage and foreign interference against New Zealand. Furthermore, it is aware of ongoing activity against New Zealand and near regions linked to China’s intelligence services and said this is a complex intelligence concern.

- RBA Governor Lowe said things are moving in the right direction but it is too early to declare victory on inflation and the board remains resolute in its determination to return inflation to the 2%-3% target range. Lowe added it is possible that some further tightening of monetary policy will be required to ensure that inflation returns to target within a reasonable timeframe and whether or not this is the case will depend upon the data and the Board’s evolving assessment of the outlook and risks. Furthermore, Lowe said rates are restrictive so they are in a calibration stage with policy, while the worst is over for inflation and they are in a reasonable place to return it to the target.

European bourses are under modest pressure as benchmarks gradually dip in catalyst thin trade, Euro Stoxx 50 -0.7% Sectors are mainly in the red with Telecoms and Financial Services slightly firmer, the former aided by a source report re. Telecom Italia. Stateside, futures are near the unchanged mark with drivers limited pre-PPI/UoM; ES +0.1%.

Top European News

- ECB’s Lane says that interest rates will likely settle at low levels, but not super-low when the current inflation shock is over. Part of a podcast recorded in July

FX

- DXY trades modestly softer intraday but has reclaimed the 102.50 mark in 102.44-102.66 boundaries.

- Sterling is the standout G10 outperformer following an upward surprise to UK GDP, Cable above 1.27 at best while EUR/GBP slipped beneath 0.8650.

- EUR unreactive to incremental revisions to regional data with the single currency failing to benefit from modest USD pressure as GBP strength works to offset this.

- JPY and CHF diverge slightly but remain in very close proximity to the unchanged mark, USD/JPY at 144.50 and EUR/CHF near 0.9630.

- PBoC set USD/CNY mid-point at 7.1587 vs exp. 7.2193 (prev. 7.1576)

Fixed Income

- Currently, fixed benchmarks are under modest pressure with the price action a continuation of the downside seen over the last few sessions and has EGBs on track to end the week at the midpoint of its range

- Gilts are in-fitting but today’s magnitude is more pronounced while USTs buck the trend and are little changed ahead of PPI.

- Post-GDP market pricing for the BoE saw a modest hawkish adjustment and now ascribes around a 70% chance to a 25bp hike in September, pricing which remains more-dovish than the SONIA strip; currently, the September contract has a 25bp hike fully priced

Commodities

- WTI Sep and Brent Oct futures are flat in early European trade with news flow also on the quiet side this morning, after settling lower yesterday by USD 1.58/bbl and USD 1.15/bbl respectively.

- WTI trades on either side of USD 83/bbl and Brent on either side of 86.50/bbl, with the contracts looking for clear direction amidst summer conditions.

- Dutch TTF prices have receded from highs on the front-month contract, which trades with losses of around 1% at the time of writing, but looking further ahead, the Nov and Dec contracts remain firm.

- Spot gold trades with a positive bias as the DXY remains subdued, with the yellow metal around the USD 1,915/oz mark in a narrow USD 10/oz range; base metals subdued.

- IEA maintains 2023 demand growth forecast and lowers its 2024 forecast by 150k BPD; says global oil demand hit record and prices may climb

Geopolitic

- US Secretary of State Blinken said the release of Americans in Iran from prison is a positive step but this is just the beginning of the process and more work is to be done to bring the Americans in Iran home. Blinken added that Iran will not receive any sanctions relief and that the US will continue to enforce all of its Iran sanctions.

- China took measures against a Chinese national accused of spying for the CIA, according to state TV.

- Airspace over Moscow’s Vnukovo airport closed, according to Tass; Al Arabiya writes airspace closed “after monitoring a march heading towards the capital”. Airspace has since reopened, with Russia confirming a drone was shotdown.

- China Maritime Authority says China to conduct military exercise around the waters in East China Sea between Aug 12-14th.

US Event Calendar

- 08:30: July PPI Final Demand MoM, est. 0.2%, prior 0.1%

- July PPI Final Demand YoY, est. 0.7%, prior 0.1%

- July PPI Ex Food and Energy MoM, est. 0.2%, prior 0.1%

- July PPI Ex Food and Energy YoY, est. 2.3%, prior 2.4%

- 10:00: Aug. U. of Mich. Sentiment, est. 71.3, prior 71.6

- Aug. U. of Mich. 1 Yr Inflation, est. 3.5%, prior 3.4%

- Aug. U. of Mich. 5-10 Yr Inflation, est. 3.0%, prior 3.0%

- Aug. U. of Mich. Current Conditions, est. 76.9, prior 76.6

- Aug. U. of Mich. Expectations, est. 67.3, prior 68.3

DB’s Jim Reid concludes the overnight wrap

I’m off on holiday today, driving to the French Alps with iPads fully charged across the back seat and with Brontë very grumpy for 14 hours further back in the car. Long-term readers will remember this journey from around 7 years ago when as my wife was feeding 6 month old Maisie I took Brontë for a walk around a motorway service station. I let her off lead in what I thought was an enclosed pen, only for her to escape under the fence and run wild across and around the motorway for 2 hours. It was petrifying. My wife and I celebrate 10 years of marriage next week while we’re away and this event 7 years ago was the only time she’s asked for a divorce. I probably would have taken that low hit rate back in August 2013 and hopefully we can laugh about it over dinner on our anniversary, although it might be too soon for her. So I’ll see you towards the end of the month. Henry will be in the hot seat for the next couple of weeks but with Peter Sidorov stepping in on Monday. Be gentle on him as he has twins younger than mine, no doubt running rings round him.

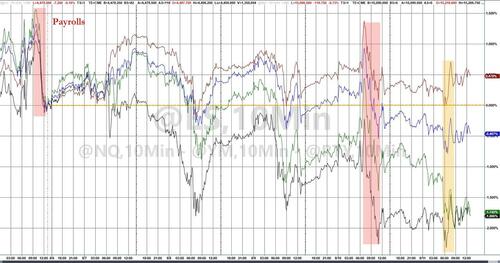

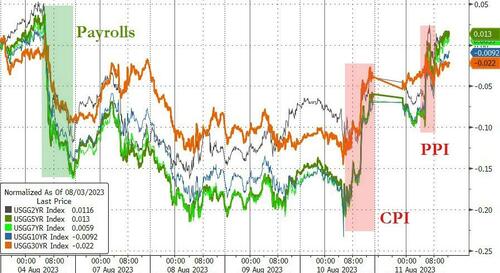

Before my hols, yesterday we saw the second of the four big prints we needed to get through before September’s FOMC. We had the payrolls report last Friday and a US CPI print yesterday. They have generally been supportive of the view that the Fed has hiked for the last time in this cycle. Neither were complete slam dunks though but haven’t changed anyone’s opinions with terminal rate pricing still in a remarkably tight 7bps range for the last six weeks versus the 93bps range it was in the pre- and post-SVB period. Risk immediately liked the CPI report but soon fell below levels seen immediately before the report and struggled for direction for the rest of the day (S&P 500 +0.03%). With commodity prices rising of late and yields and breakevens remaining elevated there is no certainty that a last hike in the cycle would mean easier policy anytime soon. On the yield front, late in the session a tough 30-year auction undid some of the positivity from the decent 3 and 10yr auctions earlier in this first week of the new larger refunding wave. That led to 10yr US yields +9.5bps on the day and after the auction, but 16.7bps higher than the lows shortly after the CPI print. So another volatile but ultimately negative day for US bonds.

In more detail now, the July US CPI print saw monthly headline inflation come in at +0.17% (+0.18% prev.) and core inflation at +0.16% (+0.16% prev). So in line with the 0.2% mom consensus for both but with unrounded numbers on the lower side. As a result, annual headline inflation came in +3.2%, a touch below consensus of +3.3%, while core was in line at +4.7%. The CPI print marked the third month in a row for headline, and the second month in a row for core, that monthly inflation has been near a 2% annualised pace.

In terms of details, goods prices were helped lower by used cars (-1.3%) as well as other products, such as a record -2.9% mom decline in prices of toys (I need to move to the US). Meanwhile, airfares (-8.1%) have now seen the sharpest 2-month decline (-15%) outside the initial Covid lockdown period which seems a little strange. Nevertheless, this will add some more attention to the US PPI print today, as it is the PPI airfares measure that is used for core PCE (also relevant for medical services which were low in the CPI print). So if one wanted to search for a more alarmist take, core services excluding airfares and medical remained elevated, a reminder of inflation persistence risks. We do see drivers of structurally higher inflation as something to be a wary of (see Henry’s note on the topic last month here), but it could be a mistake to ignore the volatile downward components now, much as it proved wrong to treat sharp spikes in specific goods in 2021 as transitory. Our US economics team reviewed the release here and suggest that overall this report was necessary but not yet fully sufficient to cement a September pause.

Indeed, we heard a cautious take on the CPI print from San Francisco Fed President Daly, who said that the “CPI data came in largely as expected but not a data point that says victory is ours” and that “if core services ex housing stalls out, that would be concerning”. Overall, she struck a clearly data dependent tone without giving any view on the September meeting. She added that the conversation about cuts will be had next year, leaning against any prospects of an imminent Fed pivot.

Bonds initially rallied on the CPI print, with 10yr treasuries down more than -6bps at one point. However, this reversed into a bear steepening over the course of the day, with 10yr yields closing +9.5bps higher and 2yr yields up +3.4bps. Much of the sell-off came after a soft 30yr auction that saw $23bn of bonds issued at 4.189% with the highest primary dealer take up since February. 30yr yields closed at 4.25% (+8.2bps). So refunding questions resurfacing after strong 3yr and 10yr auctions the previous two days. With markets continuing to price a low probability of a September hike (from 12% to 10% yesterday), it was 2024 pricing that saw intra-day volatility, with December 2024 futures trading -10bps lower in the morning but closing +6.4bps higher at 4.11%.

In Europe, bonds saw a modest sell-off, with 10yr bunds up +3.1bps. OATs (+3.0bps) saw a similar move in France, while BTPs outperformed (-0.1bps). There was little change in ECB pricing, with a 40% likelihood of a 25bp hike priced for September, while Jun-24 pricing was up +3.5bps on the day.

Equities took a strongly positive initial view of the CPI print, with the S&P 500 trading over +1.3% higher in morning trading, before paring back this gain to close near flat (+0.03%) with only one of the 24 industry groups seeing a move of more than 0.5%. Small cap stocks underperformed with the Russell 2000 (-0.42% yesterday) now down -4.02% since the start of August.

Over in Europe, the STOXX 600 rose by +0.79%, closing before the full US reversal. France’s CAC outperformed (+1.52%) as news that China would end its ban on outbound international group tours supported travel and luxury stocks (LVMH and Hermes each rose by over 3%). The DAX (+0.91%) and FSTE MIB (+0.94%) also posted solid gains. The FTSE 100 underperformed in the UK (+0.41%) though this was in part due to ex-div effects on the index. European banks continued to recover (+1.69%) from their sharp fall on Tuesday, while industrials (-0.11%) underperformed amid disappointing results from Vestas (-4.05%) and Siemens (-3.11%).

In the commodities space, oil prices retreated from their multi-month highs, with Brent Crude down -1.31% to $86.40 and WTI -1.87% to $82.82.

Asian equity markets are mostly trading lower this morning after the rally on Wall Street last night fizzled out towards the end of the session. Sentiment has also been hurt by fresh concerns amongst some large Chinese housebuilders. In terms of specific moves, China’s CSI 300 is lower (-1.40%) followed by the Shanghai Composite (-1.19%) and the Hang Seng (-0.62%). That comes even as stock in Alibaba (e-commerce titan) has rallied after it posted its strongest quarterly revenue growth in almost two years. Elsewhere, the KOSPI (+0.12%) is bucking the regional trend while the markets in Japan are closed for a public holiday. Signs of an economic slowdown are growing in Singapore as the island state’s GDP grew just +0.5% yoy in Q2 – lower than the +0.7% estimate. The official growth forecasts for the full year in 2023 were also lowered to between +0.5% and +1.5% from the prior range of +0.5% to +2.5%. Outside of Asia, US equity futures are seesawing between gains and losses with those on the S&P 500 (-0.06%) just below flat while those tied to the NASDAQ 100 (+0.07%) trading marginally higher.

In central bank news, the Reserve Bank of Australia (RBA) outgoing Governor Philip Lowe in his speech indicated that the worst was over for inflation while reiterating “it is possible that some further tightening of monetary policy will be required”, depending on incoming data and evolving risks. Early morning data showed that factory activity in New Zealand contracted at its fastest pace for the year in July, as the manufacturing PMI came in at 46.3 deteriorating further from a revised level of 47.4 while marking the sector’s fifth consecutive contraction this year.

In other data yesterday, we received slightly less encouraging news on the US labour market, as initial weekly jobless claims jumped to +248k (+230k exp, +227k prev), their highest since late June. However, continuing claims eased to 1684k (1707k exp.) and the jump in initial claims was driven by only a few states. Over in Europe, it was quiet day for data, with Italy’s July inflation print revised a touch lower, from 6.4% to 6.3% yoy.

Looking ahead to today, in the US we will get the PPI print for July, which will be monitored in part for components that feed into core PCE (such as airfares and medical), and also the August University of Michigan consumer survey. In the UK, we will get the Q2 GDP print– our UK economist expects a 0.0% qoq print, in line with consensus – and accompanying monthly activity data. In the euro area, we get final July inflation prints in France and Spain, Germany June current account balance and France Q2 unemployment.

2 b) NOW NEWSQUAWK (EUROPE/REPORT)/ASIA REPORT

EUROPE

Equities slip, GBP bid & Gilts lag on hotter GDP; PPI and UoM due – Newsquawk US Market Open

FRIDAY, AUG 11, 2023 – 05:58 AM

- European bourses are under modest pressure as benchmarks gradually dip in catalyst thin trade; US futures near unchanged

- DXY is incrementally softer with GBP the standout outperformer post UK GDP

- Given the above, Gilts lag though EGBs are also lower while USTs remain afloat pre-data

- Crude benchmarks are near unchanged after Thursday’s subdued settlement, XAU bid

- Looking ahead, highlights include US PPI & UoM (Prelim).

More Newsquawk in 3 steps:

1. Subscribe to the free premarket movers reports

2. Listen to this report in the market open podcast (available on Apple and Spotify)