GOLD PRICE CLOSED: DOWN $7.45 TO $1904.80

SILVER PRICE CLOSED: DOWN $0.06 AT $22.60

Access prices: closes 4: 15 PM

Gold ACCESS CLOSE 1902.50

Silver ACCESS CLOSE: 22.53

Shanghai Gold Benchmark Price

USD oz  AM1953.30

AM1953.30

PM1957.34

Historical SGE Fix

New York price at the time: 1905.00

premium $52,00

xxxxxxxxxxxxxxxxxx

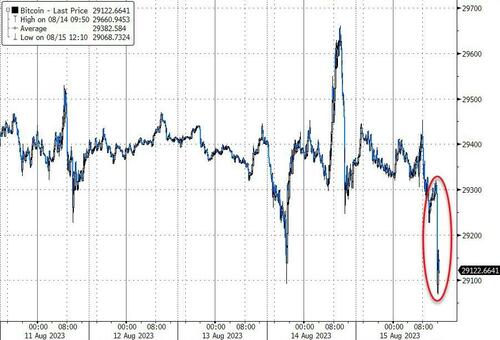

Bitcoin morning price:, $29,323 DOWN 19 Dollars

Bitcoin: afternoon price: $29,313 DOWN 29 dollars

Platinum price closing $893.10 DOWN $13.40

Palladium price; $1236,70 DOWN $29.95

END

Due to the huge rise in the dollar, we must look at gold and silver in currencies other than the dollar to understand where we are heading

I will now provide gold in Canadian dollars, British pounds and Euros/4: 15 PM ACCESS

CANADIAN GOLD: $2,568.50 UP 1.25 CDN dollars per oz (ALL TIME HIGH 2,775.35)

BRITISH GOLD: 1497.88 DOWN 5.86 pounds per oz//(ALL TIME HIGH//CLOSING///1630.29)

EURO GOLD: 1744.85 DOWN 4.93 euros per oz //(ALL TIME HIGH/CLOSING//1861.21)//

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

EXCHANGE: COMEX

CONTRACT: AUGUST 2023 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,910.600000000 USD

INTENT DATE: 08/14/2023 DELIVERY DATE: 08/16/2023

FIRM ORG FIRM NAME ISSUED STOPPED

118 C MACQUARIE FUT 16

363 H WELLS FARGO SEC 4

657 C MORGAN STANLEY 7

709 C BARCLAYS 4

737 C ADVANTAGE 30 3

905 C ADM 1

991 H CME 3

TOTAL: 34 34

MONTH TO DATE: 10,703

JPMorgan stopped 0 /34 contracts.

FOR AUGUST:

GOLD: NUMBER OF NOTICES FILED FOR AUGUST/2023. CONTRACT: 34 NOTICES FOR 3400 OZ or 0.1052 TONNES

total notices so far: 10,703 contracts for 1,070,300 oz (33.291 tonnes)

FOR AUGUST:

SILVER NOTICES: 20 NOTICE(S) FILED FOR 100,000 OZ/

total number of notices filed so far this month : 916 for 4,580,000 oz

XXXXXXXXXXXXXXXXXXXXXXXX

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD

WITH GOLD DOWN $7.45

INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD//HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.76 TONNES OF GOLD FROM THE GLD

INVENTORY RESTS AT 895.87 TONNES

Silver//

WITH NO SILVER AROUND AND SILVER DOWN 6 CENTS AT THE SLV// SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 0.275 MILLION OZ INTO THE SLV/

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV.

CLOSING INVENTORY: 452.290 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A GIGANTIC SIZED 2276 CONTRACTS TO 138,115 AND FURTHER FROM THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THIS HUGE SIZED LOSS IN COMEX OI WAS ACCOMPLISHED DESPITE OUR TINY $0.03 LOSS IN SILVER PRICING AT THE COMEX ON MONDAY. TAS ISSUANCE WAS A RATHER SMALLER SIZED 821 CONTRACTS. THESE WILL BE USED FOR MANIPULATION LATER THIS MONTH/AS WELL AS TODAY. CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON MONDAY NIGHT: 821 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS. IT THUS LOOKS LIKE THE FED (GOV’T) IS BEHIND ALL OF THESE TRADES.

WE HAVE NOW SET ANOTHER RECORD LOW AT 114,102 CONTRACTS ///JULY 3.2023// OUR BANKERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.03). AND WERE SUCCESSFUL IN KNOCKING OF SOME SILVER CONTRACTS(IF ANY STILL EXIST) AS WE HAD OUR HUGE LOSS OF 777 CONTRACTS ON BOTH EXCHANGES ALONG WITH CONSIDERABLE T.A.S.LIQUIDATION THROUGHOUT THE SESSION.

WE MUST HAVE HAD:

A STRONG ISSUANCE OF EXCHANGE FOR PHYSICALS( 976 CONTRACTS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 3.105 MILLION OZ (FIRST DAY NOTICE) FOLLOWED BY TODAY’S 100,000 OZ QUEUE JUMP //NEW STANDING RISES AT 4.580 MILLION OZ + OUR NEW CRIMINAL 0 CONTRACTS OF EXCHANGE FOR RISK FOR 0.00 MILLION OZ + 1.45 MILLION OZ EX. FOR RISK/PRIOR/// NEW TOTAL STANDING FOR SILVER: 6.030 MILLION OZ/// // // HUGE SIZED COMEX OI LOSS/ STRONG SIZED EFP ISSUANCE/VI) SMALLER BUT STILL STRONG SIZED NUMBER OF T.A.S. CONTRACT ISSUANCE (821 CONTRACTS)/ZERO EXCHANGE FOR RISK ISSUED

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL -523 CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS AUGUST. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF AUGUST:

TOTAL CONTRACTS for 11 days, total 17,277 contracts: OR 86.385 MILLION OZ (1571 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 86.385 MILLION OZ

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH 2022: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 118.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 85.745 MILLION OZ (SMALLER THAN LAST MONTH)

AUGUST: 86.385 MILLION OZ (THIS MONTH IS GOING TO BE GIGANTIC//WE WILL BE CLOSE TO MARCH 2022 RECORD OF 207 MILLION OZ/// )

RESULT: WE HAD A HUGE SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 2276 CONTRACTS DESPITE OUR TINY LOSS IN PRICE OF $0.03 IN SILVER PRICING AT THE COMEX//MONDAY.,. THE CME NOTIFIED US THAT WE HAD A STRONG EFP ISSUANCE CONTRACTS: 976 ISSUED FOR SEPT AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS./ WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR AUGUST OF 3.105 MILLION OZ FOLLOWED BY TODAY’S 100,000 OZ QUEUE JUMP//NEW STANDING 4.580 MILLION OZ+ 1.45 MILLION OZ EXCHANGE FOR RISK NEW TOTALS 6.030 MILLION OZ//// WE HAVE A HUGE SIZED LOSS OF 1300 OI CONTRACTS ON THE TWO EXCHANGES. THE TOTAL OF TAS INITIATED CONTRACTS TODAY: A SMALLER BUT STILL STRONG 821 CONTRACTS//HUGE FRONT END OF THE TAS CONTRACTS WERE LIQUIDATED DURING THE MONDAY COMEX SESSION . THE NEW TAS ISSUANCE MONDAY NIGHT (821) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE., .

WE HAD 20 NOTICE(S) FILED TODAY FOR 100,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A SMALL SIZED 197 CONTRACTS TO 431,384 AND CLOSER TO TO THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: – REMOVED: 464 CONTRACTS

WE HAD A SMALL SIZED INCREASE IN COMEX OI ( 197 CONTRACTS) DESPITE OUR $2.10 LOSS IN PRICE//MONDAY. WE ALSO HAD A RATHER SMALL INITIAL STANDING IN GOLD TONNAGE FOR AUGUST. AT 30.656 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S 3100 OZ QUEUE JUMP + PRIOR ISSUANCE OF EXCHANGE FOR RISK = (.684 TONNES) //NEW STANDING 33.502 TONNES + .684 EXCHANGE FOR RISK = 34.186/ + /A SMALL (AND CRIMINAL) ISSUANCE OF 979 T.A.S. CONTRACTS /// ALL OF..THIS HAPPENED WITH A $2.10 LOSS IN PRICE WITH RESPECT TO MONDAY’S TRADING.WE HAD A FAIR SIZED GAIN OF 2136 OI CONTRACTS (6.6407 PAPER TONNES) ON OUR TWO EXCHANGES.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 1938 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 431,848

IN ESSENCE WE HAVE A FAIR SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 2136 CONTRACTS WITH 197 CONTRACTS INCREASED AT THE COMEX// AND A FAIR 1938 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 2136 CONTRACTS OR 6,6407 TONNES. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): A STRONG 2306 CONTRACTS)

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (1938 CONTRACTS) ACCOMPANYING THE SMALL SIZED GAIN IN COMEX OI (197) //TOTAL GAIN FOR OUR THE TWO EXCHANGES: 2136 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR NORMAL FORMAT OF BANKERS GOING SHORT AND SPECULATORS GOING LONG ,2.) FAIR INITIAL STANDING AT THE GOLD COMEX FOR JULY AT 30.656 TONNES FOLLOWED BY TODAY’S 3100 OZ QUEUE JUMP //NEW STANDING 33.502 TONNES + .684 TONNES (EXCHANGE FOR RISK//PRIOR) NEW TOTALS: 34.186 TONNES/// 3) ZERO LONG LIQUIDATION WITH CONSIDERABLE TAS LIQUIDATION DURING THE COMEX SESSION //4) SMALL SIZED COMEX OPEN INTEREST GAIN/ 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER///6: SMALL T.A.S. ISSUANCE: 979 CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023 INCLUDING TODAY

AUGUST

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF AUG :

TOTAL EFP CONTRACTS ISSUED: 31,633 CONTRACTS OR 3,163,300 OZ OR 98.39 TONNES IN 11TRADING DAY(S) AND THUS AVERAGING: 2875 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 11 TRADING DAY(S) IN TONNES 98.39 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2022, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 98.39/3550 x 100% TONNES 2.76% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2023

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH/2022: 409.30 TONNES //FINAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 151.69 TONNES (WEAKER THAN LAST MONTH)

AUGUST: 98.39 TONNES (A STRONGER MONTH BUT WILL NOT COME CLOSE TO MARCH 2022)

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF SEPT. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF MAY HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF JUNE., FOR BOTH GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (SEPT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER FELL BY A HUGE SIZED 2276 CONTRACTS OI TO 138,115 AND CLOSER TO OUR COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE A STRONG 976 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

SEPT 976 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 976 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 2276 CONTRACTS AND ADD TO THE 976 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A HUGE SIZED LOSS OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 1300 CONTRACTS

THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES TOTAL 6.500 MILLION OZ

OCCURRED DESPITE OUR TINY $0.03 LOSS IN PRICE …..

END

OUTLINE FOR TODAY’S COMMENTARY

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

b, ) Gold/silver trading overnight Europe,//GOLD COMMENTARIES

(Peter Schiff)

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS//

TUESDAY MORNING//MONDAY NIGHT

SHANGHAI CLOSED DOWN 2.25 PTS OR 0.07% //Hang Seng CLOSED DOWN 192.44 PTS OR 1.03% /The Nikkei CLOSED UP 178.98 PTS OR 0.56% //Australia’s all ordinaries CLOSED UP 0.34 % /Chinese yuan (ONSHORE) closed DOWN 7.2871 /OFFSHORE CHINESE YUAN DOWN TO 7.3221 /Oil UP TO 81.34 dollars per barrel for WTI and BRENT UP AT 85.38 / Stocks in Europe OPENED ALL RED// ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

9. USA

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A SMALL SIZED 197 CONTRACTS UP TO 431,384 DESPITE OUR SMALL LOSS IN PRICE OF $2.10 ON MONDAY.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE ACTIVE DELIVERY MONTH OF AUGUST… THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 1938 EFP CONTRACTS WERE ISSUED: : DEC 1938 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 1938 CONTRACTS

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A FAIR SIZED TOTAL OF 2136 CONTRACTS IN THAT 1938 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A SMALL SIZED GAIN OF 197COMEX CONTRACTS..AND THIS GAIN ON OUR TWO EXCHANGES HAPPENED DESPITE OUR LOSS IN PRICE OF $2.10//MONDAY COMEX. AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS DURING MID MONTH IN THE DELIVERY CYCLE), THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR MONDAY NIGHT WAS A SMALL 979 CONTRACTS. THROUGHOUT THE PAST WEEKS, THE BANKERS SOLD OFF THE LONG SIDE OF THE SPREAD WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR SPREAD WHICH WILL BE LIQUIDATED TWO MONTHS HENCE)//THE HUGE NUMBER OF T.A.S. CONTRACTS INITIATED OVER THE PAST SEVERAL WEEKS SPELLS TROUBLE FOR THE GOLD/SILVER MARKET AS RAIDS WILL SURELY BE UPON US TRYING TO CONTAIN OUR PRECIOUS METALS RISE IN PRICE.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: AUGUST (34.186) ( ACTIVE MONTH)

TONNES),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 34.186 TONNES (INCLUDING .6842 EXCHANGE FOR RISK)

THE SPECS/HFT WERE SUCCESSFUL IN LOWERING GOLD’S PRICE( IT LOST $2.10) //// BUT WERE UNSUCCESSFUL IN KNOCKING ANY SPECULATOR LONGS (IF ANY STILL EXIST) AS WE HAD A FAIR GAIN OF 2136 TOTAL CONTRACTS ON OUR TWO EXCHANGES. WE HAD CONSIDERABLE T.A.S. LIQUIDATION ON THE FRONT END OF YESTERDAY’S TRADING. THE T.A.S. ISSUED ON MONDAY NIGHT WILL BE “PUT INTO THE BANK” TO BE USED AT A LATER DATE AT THE COLLUSIVE CHOOSING OF OUR BANKERS.

WE HAVE GAINED A TOTAL OI OF 6.6407 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR AUGUST. (30.656 TONNES) ON FIRST DAY NOTICE FOLLOWED BY TODAY’S 3100 OZ QUEUEJUMP //NEW STANDING ADVANCES A BIT TO 33.502 TONNES + .6842 (PRIOR EXCHANGE FOR RISK) //NEW TOTAL 34.186 TONNES // ALL OF THIS WAS ACCOMPLISHED WITH OUR LOSS IN PRICE TO THE TUNE OF $2.10.

WE HAD – REMOVED 464 CONTRACTS TO THE COMEX TRADES TO OPEN INTEREST

NET GAIN ON THE TWO EXCHANGES 2136 CONTRACTS OR 213600 OZ OR 6.6407 TONNES.

Estimated gold volume today:// 155,571 awful

final gold volumes/yesterday 128,833 awful//speculators have left the gold arena

//AUGUST 15/ FOR THE AUGUST 2023 GOLD CONTRACT

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 43,699.630 OZ ASAHI REAL GOLD LEAVING . |

| Deposit to the Dealer Inventory in oz | nil |

| Deposits to the Customer Inventory, in oz | nil OZ |

| No of oz served (contracts) today | 34 notice(s) 3400 OZ 0.1057TONNES |

| No of oz to be served (notices) | 68 contracts 6800 oz 0.2115 TONNES |

| Total monthly oz gold served (contracts) so far this month | 10,703 notices 1,070,300 OZ 33.291 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | x |

0 dealer deposit:

total dealer deposits: NIL oz

customer deposits: 0

total customer deposits: nil oz

we had 1 customer withdrawals

i) Out of ASAHI: 43,699.630 oz (real gold leaving)

Adjustments; 0

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR AUGUST.

For the front month of AUGUST we have an oi of 103 contracts having GAINED 13 contracts. We had 18 contracts filed

on Monday, so we gained 31 contracts or an additional 3100 oz will stand at the comex,

Sept gained 102 contracts to 2759.

Oct lost 289 contracts to 33,152 contracts.

We had 34 contracts filed for today representing 3400 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 34 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped received by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the AUGUST /2023. contract month,

we take the total number of notices filed so far for the month (10,703 x 100 oz ), to which we add the difference between the open interest for the front month of AUGUST (103 CONTRACT) minus the number of notices served upon today 34 x 100 oz per contract equals 1,077,100 OZ OR 33.502 TONNES the number of TONNES standing in this active month of AUGUST. + .684 TONNES EXCHANGE FOR RISK/prior = 34.186 tonnes

thus the INITIAL standings for gold for the AUGUST contract month: No of notices filed so far (10,703) x 100 oz + (103) {OI for the front month} minus the number of notices served upon today (34) x 100 oz) which equals 1,077,100 oz standing OR 33.409 TONNES + .684 TONNES OF EXCHANGE FOR RISK/prior = 34.186 TONNES

TOTAL COMEX GOLD STANDING: 34.186 TONNES WHICH IS SMALL FOR AN ACTIVE DELIVERY MONTH.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 2,101,333.235 OZ 65.36 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 22,003,785.758 OZ

TOTAL REGISTERED GOLD: 11,714,518.831 (364,37 tonnes)..

TOTAL OF ALL ELIGIBLE GOLD: 10,289,267,377 O Z

REGISTERED GOLD THAT CAN BE SERVED UPON: 9,613,185 OZ (REG GOLD- PLEDGED GOLD) 299.01 tonnes//

END

SILVER/COMEX

AUGUST 15

//2023// THE AUGUST 2023 SILVER CONTRACT

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 995,463.387 oz HSBC Manfra . |

| Deposits to the Dealer Inventory | nil oz |

| Deposits to the Customer Inventory | 601,200.800 oz CNT |

| No of oz served today (contracts) | 20 CONTRACT(S) (100,000 OZ) |

| No of oz to be served (notices) | 0 contracts (nil oz) |

| Total monthly oz silver served (contracts) | 916 Contracts (4,580,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

i) 0 dealer deposit

total dealer deposit: 0 oz

i) We had 0 dealer withdrawal

total dealer withdrawals: 0 oz

We had 1 deposits customer account:

i)Into CNT 601,200.800 oz

total customer deposits: 601,200.800 oz

JPMorgan has a total silver weight: 139.276 million oz/279.192 million =49.87% of comex .//

Comex withdrawals 2

i) Out of HSBC: 506,595.250 oz

ii) Out of Manfra: 488,868.637 oz

total: 955,463.887 oz

adjustments: 0

TOTAL REGISTERED SILVER: 30.828 MILLION OZ//.TOTAL REG + ELIGIBLE. 279.192 million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR JULY:

silver open interest data:

FRONT MONTH OF AUGUST /2023 OI: 20 CONTRACTS HAVING GAINED 20 CONTRACT(S). WE HAD

0 NOTICES FILED ON THURSDAY SO WE GAINED 20 CONTRACTS OR AN ADDITIONAL 100,000 OZ WILL STAND IN THIS NON ACTIVE DELIVERY MONTH OF AUGUST.

SEPT HAS A LOSS OF 5273 CONTRACTS DOWN TO 62,214

OCT GAINED 93 CONTRACTS TO STAND AT 480.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 20 for 100,000 oz

Comex volumes// est. volume today 68,475 fair

Comex volume: confirmed yesterday: 73,501 good

To calculate the number of silver ounces that will stand for delivery in AUGUST. we take the total number of notices filed for the month so far at 916 x 5,000 oz = 4,580,000 oz

to which we add the difference between the open interest for the front month of AUGUST (20) and the number of notices served upon today 20 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the AUGUST/2023 contract month: 916 (notices served so far) x 5000 oz + OI for the front month of AUGUST (20) – number of notices served upon today (20 )x 500 oz of silver standing for the AUGUST contract month equates to 4.580 million oz.+ 0.0 MILLION OZ EXCHANGE FOR RISK ISSUED TODAY+ 1.45 MILLION OZ EXCHANGE FOR RISK PRIOR//NEW TOTALS: 6.030 MILLION oz.

There are 30.828 million oz of registered silver.

Thus if we take today’s standing at 6.030 and add last month’s 30.9 million oz we have 36.930 million oz against only 30.828 million registered silver.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS

AUGUST 15/WITH GOLD DOWN $7,45 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.76 TONNES FORM THE GLD//: /// //INVENTORY RESTS AT 895.87 TONNES

AUGUST 14/WITH GOLD DOWN $2.10 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.75 TONNES FORM THE GLD//: /// //INVENTORY RESTS AT 899.63 TONNES

AUGUST 11/WITH GOLD DOWN $2.10 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .31 TONNES FORM THE GLD//: /// //INVENTORY RESTS AT 903.31 TONNES

AUGUST 10/WITH GOLD DOWN $1.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD: /// //INVENTORY RESTS AT 903.69 TONNES

AUGUST 9/WITH GOLD DOWN $8.75 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD: /// //INVENTORY RESTS AT 903.69 TONNES

AUGUST 8/WITH GOLD DOWN $9.60 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.31 TONNES FORM THE GLD /// //INVENTORY RESTS AT 903.69 TONNES

AUGUST 7/WITH GOLD DOWN $5.45 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD: /// //INVENTORY RESTS AT 906.00 TONNES

AUGUST 4/WITH GOLD UP $7.25 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.18 TONNES OF GOLD FROM THE GLD/// .///INVENTORY RESTS AT 906.00 TONNES

AUGUST 3/WITH GOLD DOWN $5.25 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD //: //: / .////INVENTORY RESTS AT 909.18 TONNES

AUGUST 2/WITH GOLD DOWN $3.45 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 3.75 TONNES OF GOLD FROM THE GLD//: //: / .////INVENTORY RESTS AT 909.18 TONNES

AUGUST 1/WITH GOLD DOWN $28.45 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 2.89 TONNES OF GOLD FROM THE GLD//: //: / .////INVENTORY RESTS AT 912.93 TONNES

JULY 31/WITH GOLD UP $9.50 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 2.89 TONNES OF GOLD FROM THE GLD//: //: / .////INVENTORY RESTS AT 912.93 TONNES

JULY 28/WITH GOLD UP $14.15 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 1.44 TONNES OF GOLD FROM THE GLD//: //: / .////INVENTORY RESTS AT 915,82 TONNES

JULY 27/WITH GOLD DOWN $21.80 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 1.74 TONNES OF GOLD FROM THE GLD//: //: / .////INVENTORY RESTS AT 917.26 TONNES

JULY 26/WITH GOLD UP $6.35 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD: //: / .////INVENTORY RESTS AT 919.00 TONNES

JULY 25/WITH GOLD UP $2.45 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD: //: / .////INVENTORY RESTS AT 919.00 TONNES

JULY 24/WITH GOLD DOWN $4.65 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 5.20 TONNES OF GOLD INTO THE GLD//: / .////INVENTORY RESTS AT 919.00 TONNES

JULY 21/WITH GOLD DOWN $3.80 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD: / .////INVENTORY RESTS AT 913.80 TONNES

JULY 20/WITH GOLD DOWN $8.70 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.73 TONNES FROM THE GLD/ .////INVENTORY RESTS AT 913.80 TONNES

JULY 19/WITH GOLD UP $0.65 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .86 TONNES FROM THE GLD/ .////INVENTORY RESTS AT 912.07 TONNES

JULY 18/WITH GOLD UP $23.45 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD: .////INVENTORY RESTS AT 912.93 TONNES

JULY 17/WITH GOLD DOWN $6.60 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.73 TONNES OF GOLD FROM THE GLD.////INVENTORY RESTS AT 912.93 TONNES

JULY 14/WITH GOLD UP $0.75 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD: ////INVENTORY RESTS AT 914.66 TONNES

JULY 13/WITH GOLD UP $3.30 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 0.29 TONNES OF GOLD OUT OF THE GLD////INVENTORY RESTS AT 914.66 TONNES

JULY 12/WITH GOLD UP $24.50 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 0.31 TONNES OF GOLD OUT OF THE GLD////INVENTORY RESTS AT 914.95 TONNES

JULY 11/WITH GOLD UP $6.15 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.0 TONNES OF GOLD OUT OF THE GLD////INVENTORY RESTS AT 915.26 TONNES

JULY 10 WITH GOLD DOWN $1.35 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.60 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 916.26 TONNES.

GLD INVENTORY: 895.87 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

AUGUST 15/WITH SILVER DOWN 6 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 0.275 MILLION OZ INTOTHE SLV/: / .////INVENTORY RESTS AT 452.290 MILLION OZ

AUGUST 14/WITH SILVER DOWN 3 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV A DEPOSIT OF 0.459 MILLION OZ INTOTHE SLV/: //////INVENTORY RESTS AT 452.565 MILLION OZ

AUGUST 11/WITH SILVER DOWN 6 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A DEPOSIT OF 1.926 MILLION OZ INTOTHE SLV/: // OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 452.106 MILLION OZ

AUGUST 10/WITH SILVER UP 6 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 8,807 MILLION OZ OUT OF THE SLV/: // OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 450.180 MILLION OZ

AUGUST 9/WITH SILVER DOWN 7 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 8,807 MILLION OZ OUT OF THE SLV/: // OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 450.180 MILLION OZ

AUGUST 8/WITH SILVER DOWN 40 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: // OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 458.987 MILLION OZ

AUGUST 7/WITH SILVER DOWN 46 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: // OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 458.987 MILLION OZ

AUGUST 4/WITH SILVER UP 1 CENT TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.294 MILLION OZ FROM THE SLV// OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 458.987 MILLION OZ

AUGUST 3/WITH SILVER DOWN 16 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 189,000 OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 451.281 MILLION OZ

AUGUST 2/WITH SILVER DOWN 43 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 275,000 OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 451.471 MILLION OZ

AUGUST 1/WITH SILVER DOWN 61 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 184,000 OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 451.746 MILLION OZ

JULY 31/WITH SILVER UP 45 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 184,000 OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 451.746 MILLION OZ

JULY 28/WITH SILVER UP 15 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 550,000 OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 451.930 MILLION OZ

JULY 27/WITH SILVER DOWN 59 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: .////INVENTORY RESTS AT 452.480 MILLION OZ

JULY 26/WITH SILVER UP 15 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: .////INVENTORY RESTS AT 452.480 MILLION OZ/

JULY 25/WITH SILVER UP 24 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A SMALL WITHDRAWAL OF 826,000 OZ FROM THE SLV..////INVENTORY RESTS AT 452.480 MILLION OZ/

JULY 24/WITH SILVER DOWN 23 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: ////INVENTORY RESTS AT 453.306 MILLION OZ/

JULY 21/WITH SILVER DOWN 14 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 1.101 MILLION OZ OF SILVER FROM THE SLV ////INVENTORY RESTS AT 453.306 MILLION OZ/

JULY 20/WITH SILVER DOWN 38 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 1.468 MILLION OZ OF SILVER FROM THE SLV ////INVENTORY RESTS AT 454.107 MILLION OZ/

JULY 19/WITH SILVER UP 11 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV:A ////INVENTORY RESTS AT 455.875 MILLION OZ/

JULY 18/WITH SILVER DOWN 19 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV:A ////INVENTORY RESTS AT 455.875 MILLION OZ/

JULY 17/WITH SILVER UP 25 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 4.856 MILLION OZ OF SILVER FROM THE SLV////////INVENTORY RESTS AT 455.875 MILLION OZ/

JULY 14/WITH SILVER UP 27 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 2.21 MILLION OZ OF SILVER FROM THE SLV////////INVENTORY RESTS AT 455.875 MILLION OZ/

JULY 13/WITH SILVER UP 64 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//////INVENTORY RESTS AT 462.941 MILLION OZ/

JULY 12/WITH SILVER UP $1.00 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.881 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 462.941 MILLION OZ/

JULY 11/WITH SILVER DOWN 5 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF .020 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 464.822 MILLION OZ/

JULY 10/WITH SILVER UP 2 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.672 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 464.802 MILLION OZ

//

CLOSING INVENTORY 452.290 MILLION OZ//

PHYSICAL GOLD/SILVER COMMENTARIES

1:Peter Schiff/Mike Maharrey

Silver Price Inexcusably Low Given The Market Dynamics

TUESDAY, AUG 15, 2023 – 03:20 PM

Authored by Michael Maharrey via SchiffGold.com,

Silver is significantly undervalued right now. One analyst called the current price in the $22 an ounce range “inexcusably low.”

But many analysts are bullish on silver in the medium term with projections of prices climbing to $50 to $100 an ounce over the next two to five years.

The question is when will we finally start to see this correction?

Silver has languished in 2023. While gold is up over 4% on the year, the price of silver has declined by over 5%.

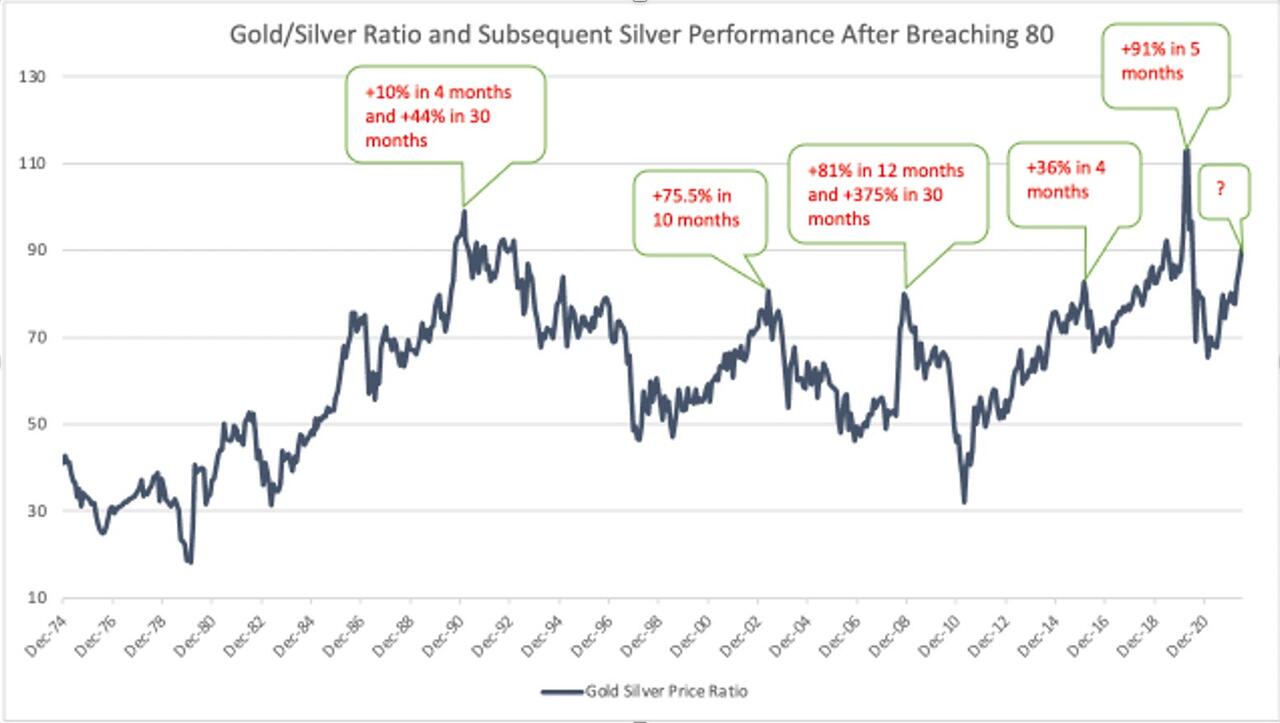

We can see the growing spread between silver and gold in the silver-gold ratio, currently running at over 84-1. That means it takes over 84 ounces of silver to buy one ounce of gold. To put the current ratio into perspective, the average in the modern era has been between 40:1 and 50:1.

Historically, the ratio has always returned to that mean. And when it does, it does it with a vengeance. The ratio fell to 30-1 in 2011 and below 20-1 in 1979.

When the spread gets this wide, silver doesn’t just outperform gold, it goes on a massive run in a short period of time. Since January 2000, this has happened four times. As this chart shows, the snapback is swift and strong.

Current Dynamics

Silver has faced the same headwinds as gold with the Federal Reserve pushing interest rates higher to battle price inflation. Fed monetary policy has strengthened the dollar and sticky price inflation has kept investors on edge with expectations of more rate hikes. This has pressured the price of both gold and silver lower.

Silver has faced additional bearish sentiment due to a slowing economy. Sagging demand for consumer electronics has impacted industrial demand for both silver and gold. BMO Capital Markets commodities analyst Colin Hamilton noted that while the global economy has held up better than expected in the face of monetary tightening, “This is almost solely down to resiliency in the services economy while the manufacturing side is clearly feeling the strain.”

This disproportionately impacts silver because industrial demand makes up over 50% of total silver demand, as compared to only ~7% of gold.”

But looking at the longer term, the supply and demand dynamics are bullish for silver. In fact, there is a looming supply shortage.

Analysts believe that the growing demand for silver in the solar power industry will likely put a significant squeeze on supply in the coming years, and the current price of silver does not reflect the likely shortages.

We’re already seeing a tightening silver supply. While silver demand set records in every category in 2022, supply was flat with mine output falling by 0.6%. This resulted in a 237.7 million ounce market deficit in 2022.

It was the second consecutive annual deficit in a row. The Silver Institute called it “possibly the most significant deficit on record.” It also noted that “the combined shortfalls of the previous two years comfortably offset the cumulative surpluses of the last 11 years.”

This trend is not expected to reverse. Silver Bullion Pte Ltd. CEO Gregor Gregersen recently noted that silver mine production has fallen due to a lack of investment.

Production cannot be materially increased over the short term as it can take over 10 years to commence new mining operations. Therefore, increased silver prices will not lead to increased mine production for a long time.”

Meanwhile, we are likely about to see a huge increase in demand for the white metal thanks to the push for green energy.

Due to its outstanding electrical conductivity, silver is an important element in the production of solar panels. It is used to conduct electrical charges out of the solar cell and into the system. Each solar panel only uses a small amount of silver, but with the demand for solar panels growing exponentially every year, those small amounts of silver add up.

According to a research paper by scientists at the University of New South Wales, solar manufacturers will likely require over 20% of the current annual silver supply by 2027. And by 2050, solar panel production will use approximately 85–98% of the current global silver reserves.

Recession worries would typically dampen industrial demand for silver, but the photovoltaic industry and the “green energy” sector more generally are essentially recession-proof due to support from governments around the world. With battling climate change a priority, it is highly unlikely investment in solar power and other green energy technologies will fall, even in the midst of an economic downturn.

And it’s important to keep in mind that while silver is an industrial metal, more fundamentally, it is money. Despite being more volatile in the short term, silver tends to track with gold over time. If you are inclined to think the Federal Reserve will lose the inflation fight, you should be bullish on both gold and silver.

At some point, investors will have to reckon with the shrinking supply of silver coupled with rising demand, along with the Fed’s inability to bring inflation back to its 2% target. When that happens, the price of silver will likely take off.

Given the supply and demand dynamics, the skewed silver-gold ratio and the likelihood that the Fed will not beat price inflation, $22 silver looks like a great buying opportunity.

end

2 Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens//JAMES RICKARDS//JOHN RUBINO

Rickards: Where’s The Darn Recession?

BY TYLER DURDEN

TUESDAY, AUG 15, 2023 – 04:20 PM

Authored by James Rickards via DailyReckoning.com,

Analyzing today’s economic conditions is a challenge.

If the world is in good economic health, you can describe the policy reasons behind that condition and identify specific stocks and sectors that will outperform the market.

You’d point to trends such as low inflation, positive real interest rates (a sign of strong growth resulting from a healthy competition for funds) and stable exchange rates (indicating that investment decisions are made on the basis of fundamentals rather than speculation).

If the world is in poor economic health, the analytic process is much the same but with very different inputs and forecasts.

You’d expect to see widespread inflation (or deflation), high unemployment, declining GDP growth (or negative growth), declining world trade and a host of poor public policy choices including high tax rates, tariffs, export subsidies, overregulation and counterproductive policies based on climate alarmism.

In either the good scenario or the bad scenario, the analyst knows how to approach policy recommendations or investment allocations.

Without being glib, if you’re in a good place, keep it going. If you’re heading in the wrong direction, turn around.

Well, what if we had both dynamics at once?

That’s a pretty good description of where the world is today. The U.S. is a good place to draw the contrast between good and bad news.

The U.S. has some of the lowest unemployment rate readings since the 1960s. Real wages have finally begun to grow slightly after years of negative readings.

Inflation is still too high (and the damage from past inflation will be with us permanently), but the dip has been undeniable. From 9.1% in June 2022 to 3.0% in June 2023, inflation (measured as CPI, year-over-year) has come far toward the Federal Reserve’s goal of 2.0%.

Of course, the stock market has been on a tear and some major indexes are inching toward new all-time highs or already there. No wonder that Joe Biden has decided to base his campaign on “Bidenomics.”

Still, the negative side of the picture is in plain sight.

U.S. industrial production has been declining for over a year. Some economists claim that manufacturing is a shrinking part of U.S. GDP and that services dominate economic growth.

That’s true as a first approximation, but it ignores the fact that much demand for services comes from those who work in factories, mines and assembly lines.

If the factory is closed, no one laid off will be buying tickets to the Taylor Swift concert.

Also, bank lending is contracting, and credit conditions are being tightened. This doesn’t mean a full-scale credit crunch is upon us or that the economy is falling off a cliff.

It does mean that a trend toward reduced liquidity is in place and will likely grow worse until it leads to business failures and bad debts.

What about the world beyond U.S. shores?

The EU is already in recession and Japan and the U.K. are close to zero growth and heading toward recession fast. Within the EU, individual recessions have hit in Germany and Ireland, with Italy and France showing growth barely above zero.

The idea of a real recession in China may seem incomprehensible, but we may be witnessing one.

The “reopening” narrative following the end of the ridiculous Zero COVID policy was always a myth (and I said so last year) but Wall Street bought into it until the data made its failure undeniable.

Today, China is not only underperforming the narrative, it’s slipping close to contraction.

The point is with the EU, China, Japan, the U.K. and others in recession or close to it, how can the U.S. expect to remain afloat?

Globalization may be on the decline, but it’s still the dominant path to global production. Aggregate world trade may be shrinking, but it’s still a large part of global GDP on a country-by-country basis.

How can the world shrink while the U.S. grows?

That won’t happen unless U.S. growth is so strong it pulls the world out of a collective rut. There’s no evidence for that. So there’s the dilemma.

Ample signs of growth are surrounded by large and growing signs of an economic stall. The U.S. is showing relatively strong growth, while the rest of the world coasts to a halt.

How do we reconcile the data? Where do we go from here?

Read on for the answers…

Time Will Catch up to the U.S.

Why does the U.S. economy look so strong in comparison with the rest of the world? The answer is timing.

The economy does not go from growth to recession like throwing a switch. It takes time.

The positive signs are real but they’re fading. The negative signs are real and they’re growing. Some data lead the economy; other data follow with a lag. It’s the analyst’s job to know which is which, and to focus on trends, not snapshots.

First off, low unemployment may not be a source of comfort because employment trends tend to lag the economy. The latest unemployment report (July’s) showed an unemployment rate of 3.5%, among the lowest since the 1960s.

That’s a healthy report on its face but there are two serious characteristics that need to be taken into account. The first involves what’s known as the labor force participation rate (LFPR).

This counts all of the working-age population of the U.S. who do not have jobs as a percentage of the total working-age population. That’s different from the unemployment rate because to be counted as “unemployed” you must be looking for a job.

There are tens of millions of working-age Americans who do not have jobs but are not looking for one. They are not counted as unemployed, but they do show up in the LFPR calculations.

Right now, the LFPR is 62.6%. That’s the same level the U.S. first reached in November 1977 when women were entering the workforce in large numbers. It’s significantly below the 67.2% level reached in January 2001, when baby boomers were in the prime of their careers. Essentially, 6.7 million workers have simply dropped out of seeking work relative to 2001.

If those 6.7 million workers were added to the number of unemployed today, the national unemployment rate would be 7.6%, a rate more closely associated with a recession. In effect, the low participation rate is hiding a large unemployed cohort not being counted by the government in the official employment report.

The second and even more critical defect in using employment statistics in economic forecasting is that employment reports are lagging indicators, not leading indicators. When the economy begins to slow down, businesses will do everything except lay off workers to keep the doors open.

They’ll cut inventories, lower prices, seek rent reductions, cut administrative costs and a lot else before they fire valuable workers. All of those strategies are clear signs of a failing economy, but they don’t show up in the employment reports.

By the time employers get around to firing workers, it’s too late for the economy. So you can’t rely on low unemployment rates to conclude all is well. The opposite could easily be true.

Still, there are powerful indicators suggesting the U.S. economy is in or near a severe recession in addition to better-known measures such as the unemployment rate. The first of these is an inverted yield curve.

I’m not going to get too technical here, but it’s important to understand the basics and their implications. A yield curve shows interest rates on securities of different maturities from one issuer or it can show interest rates on a single instrument at different points in the future.

In either case, the curve is normally upward sloping (longer maturities or later settlement dates have higher interest rates). That makes sense. If you’re lending money for longer or betting on rates further into the future, you want a higher interest rate to compensate you for the added risk from such events as inflation, credit downgrades, bankruptcy and more.

Yield curves in U.S. Treasury securities are steeply inverted today. So are yield curves in SOFR (formerly Eurodollar) futures contracts. Again, don’t worry about the technical details. Just understand that these are important warning signals. The last time both yield curves were this steeply inverted was prior to the global financial crisis of 2008.

If you’re not factoring this signal into your forecast, you’re missing a five-alarm fire. The system is flashing red.

There are many other such warning signs such as negative swap spreads. Without getting into the technical details, it’s enough to understand that negative swap spreads mean that bank balance sheets are contracting. Balance sheet capacity is strained. That’s another early warning of a credit crunch that presages a recession.

There are other warning signs and, again, I’m not going to get into the technical details here. It’s enough to say that all of the technical signs are unusual and all point in the direction of a recession. They all have good track records of predicting recessions going back to the 1970s and earlier depending on the time series.

So in the U.S., the fundamentals (industrial output, global trade, inventory accumulation, credit, commercial real estate) are negative. The technicals (yield curves, swap spreads, bank equity) are negative. The only positives are unemployment (a lagging indicator) and the stock market (a cap-weighted bubble). Unfortunately for investors, stocks and jobs are the only things the financial TV talking heads talk about. Don’t fall for it.

Investors who look abroad for rescue by former highfliers such as China, Japan and Germany will also be disappointed. China is slowing dramatically; the reopening narrative was always a myth.

Meanwhile, Japan is hanging by a thread partly because of its close economic alignment with China. Germany is already in recession and that will get worse as the Ukraine war drags on and one whom the Russians call General Winter appears by November.

It’s becoming increasingly apparent that we’re looking at a global recession, if not a global financial crisis. These are highly unusual. It’s often the case that one or more major economies are in recession while others display growth and help pull the weak performers out of the ditch.

But today, we’re facing a case where, one after the other, all of the major economies are falling into the ditch. Now, that doesn’t mean investors should just throw their hands up in the air and run for the hills.

But they should lighten up on equities, increase allocations to cash (paying good 5% yields these days), allocate about 10% of investable assets to gold and silver and take a close look at sectors such as energy, agriculture, mining and natural resources that will stand the test of time.

You don’t have to follow everyone else off a cliff.

end

3,Chris Powell of GATA provides to us very important physical commentaries

China’s authorities are using import curbs on gold. That has caused the premium to London of over 40 dollars. The higher prices are stifling demand from citizens

(YahooNews)

China’s gold prices believed to exceed rest of world’s because of import curbs

Submitted by admin on Tue, 2023-08-15 09:15Section: Daily Dispatches

From Bloomberg News

via Yahoo News

Tuesday, August 15, 2023

China’s gold price is rising against levels in London, a trend that local traders say is due to government curbs on imports of the precious metal.

The Shanghai spot price was more than $40 an ounce higher than that in London on Aug. 14, according to Bloomberg calculations based on exchange data. That’s the biggest premium in more than five months, with the gap steadily widening from late June even as consumer demand in China remained sluggish.

Authorities moving to limit gold imports appear to be a major driver behind the growing gap, according to traders and importers.

The government has reduced or stopped issuing import quotas to some local banks, according to people familiar with the matter, who asked not to be identified as the information is private.

That has resulted in a drop in flows over the last few months, two of the people said, and there’s no immediate prospect of the affected quotas being issued again. The reason for the curbs isn’t clear. …

… For the remainder of the report:

https://finance.yahoo.com/news/chinas-gold-prices-rising-higher-220000714.html

end

Brien Lundin: You may not know them but you need to listen to them

Submitted by admin on Mon, 2023-08-14 16:33Section: Daily Dispatches

GATA’s Bill Murphy and Chris Powell will be among the speakers at the New Orleans Investment Conference.

* * *

By Brien Lundin

Publisher, Gold Newsletter

CEO, New Orleans Investment Conference

Monday, August 14, 2023

I’m excited.

Not by the metals and mining markets, mind you. They’re still stuck in the mud.

In fact, gold is testing key support around the $1,900 level once again … and in the process testing my theory that the metals bottomed in early July

If I’m proven wrong, however, it’s very likely just a temporary setback for gold, silver and mining stocks. That’s because this interest-rate hiking cycle is essentially ended. The 10-year Treasury yield has leaped above 4%, challenging the highest levels in 15 years. The last time yields were this high, the federal debt was just one-third as large as it is today.

This means that not only is federal debt out of control (it’ll probably grow by $3 trillion this fiscal year alone) … but the interest expense on the debt will continue to soar.

It’s all going to come to a head in the weeks just in front of us. That’s because this rate-hike cycle has peaked, and the big money is already positioning for the downside of the cycle.

That’s one reason why I’m excited. The other is the amazing speakers we’ve locked in for this year’s New Orleans Investment Conference, to be held from Wednesday through Saturday, November 1-4.

… You Need To Hear These Superstars …

I was recently perusing our line-up for New Orleans ’23 and realized that the list could be divided into two groups: Widely recognized names and others that many of our attendees might not be aware of.

I mean that every serious investor knows about James Rickards, Danielle DiMartino Booth, Peter Boockvar, George Gammon, Rick Rule, and the dozens of other big names and newsletter editors who have graced our stage in the past and are coming again this year.

But there are some more that are new to our event or are emerging superstars on the investment scene that you may not know very well.

So let me fix that by introducing some of these experts to you now.

Lyn Alden — OK, it might be a bit insulting to insinuate that you don’t know who Lyn is. After all, she’s widely regarded as perhaps today’s most cogent and insightful macro-economic analyst.

And Lyn has participated in past New Orleans Conferences on a virtual basis. But she rarely speaks in person at investment events, which makes it even more special that she’s chosen to travel to New Orleans this year to clearly outline the remarkable forces at work in the markets today, put them into historical perspective, and provide her trademark deadly accurate forecasts.

Let me put it this way: I’ve read and heard from thousands of top macro experts over the nearly 40 years I’ve been in this business. So believe me when I tell you that Lyn Alden is the best I’ve seen — and you absolutely must hear what she has to tell you this year.

Matt Taibbi — Again, lots of people know who Matt Taibbi is, from his investigative reporting over many years in Rolling Stone to his more recent exposés of the “Twitter Files,” showing how government and other entities conspired to censor the truth about Covid.

But I’ve found that many investors don’t realize just how important Matt is, and his ongoing discoveries on how government and media continue to hide the truth and work against your interests.

In my opinion, Matt is the single most important journalist of this generation. Even more important, he will soon provide New Orleans attendees with an exclusive briefing on the latest assaults on your liberties.

Konstantin Kisin — One of my great joys in recent months has been exposing Konstantin Kisin to many of my friends and subscribers I’ve talked with at conferences.

He is at once one of the most entertaining and thought-provoking speakers I’ve ever seen. If I had to compare him to anyone, it would be my late, great friend Charles Krauthammer, who was beloved by our New Orleans Conference attendees.

To get a brief taste of Konstantin’s viewpoints and talent, watch this video recording of his speech earlier this year at an annual Oxford Union debate. You’ll see why he has hundreds of thousands of Twitter followers, and why his speech at New Orleans ’23 (and his appearance on our Geopolitical Panel with Matt Taibbi, George Gammon, and Dominic Frisby) are not to be missed.

James Lavish — You haven’t heard of James being added to our roster because we were just able to lock him in a few days ago. I’m very excited about this because he is not only among the most astute macro analysts I’ve run across but, perhaps more importantly, has the ability to clearly and cogently explain even the most complex topics.

In New Orleans, James will describe the developing U.S. debt spiral step by step and reveal how the end game will play out. This presentation alone will be worth the price of attending, and added on top of it will be James’ contributions to our “Future of Money” panel, along with James Rickards and Danielle DiMartino Booth.

James Stack — Another speaker that should be familiar to many, Jim is actually an old friend of mine and the conference, having made regular appearances for many years in the 1980s and 1990s. Because of the demands of his renowned investment letter and money management firm, however, he hadn’t appeared in person for quite some time, before his participation last year.

I wanted to highlight his appearance this year because Jim has been, in my view, simply the most accurate market analyst and timer, not just for today but for decades.

He is known as the man who has predicted every bursting bubble of recent times, which obviously makes it crucial for you to hear him this year. Get ready, because Jim’s bringing his crystal ball, backed by reams of proprietary technical analysis, to show us what lies ahead.

… Plus Dozens More Leading Experts …

The speakers I’ve highlighted above just scratch the surface of our New Orleans ’23 roster.

I think this is, from top to bottom, the finest array of experts ever gathered for not only a New Orleans Conference, but any investment event.

That’s not hyperbole. I’ve seen it all over the years, and this faculty is simply unsurpassed. If you’re a serious investor, you need to be at New Orleans ’23.

Don’t just take my word for it. I urge you to discover why you can’t afford to miss this event. Just visit here:

end

end

4, OTHER IMPORTANT GOLD/SILVER COMMENTARIES

end

5 a. IMPORTANT COMMENTARIES ON COMMODITIES:

end

5 B GLOBAL COMMODITY ISSUES/FOOD IN GENERAL//FREIGHT

END

6.CRYPTOCURRENCY//DIGITAL CURRENCY// COMMENTARIES/

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS TUESDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED DOWN TO 7.2871

OFFSHORE YUAN: DOWN TO 7.3221

SHANGHAI CLOSED DOWN 2.25 PTS OR 0.07%

HANG SENG CLOSED DOWN 192.44 PTS OR 1.03%

2. Nikkei closed UP 178.98 OR 0.56%

3. Europe stocks SO FAR: ALL RED

USA dollar INDEX DOWN TO 103.04 EURO RISES TO 1.0914 UP 6 BASIS PTS

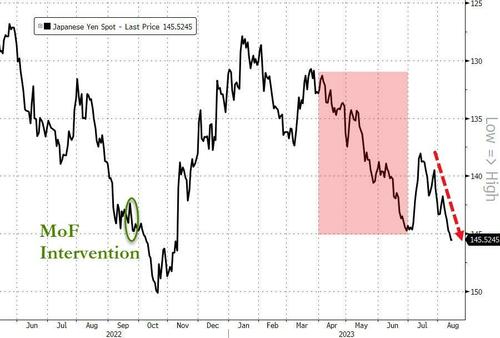

3b Japan 10 YR bond yield: RISES TO. +.627 Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 145.66/JAPANESE YEN FALLING AS WELL AS LONG TERM 10 YR. YIELDS RISING //EVENTUALLY THIS WILL BREAK THE JAPANESE CENTRAL BANK

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen DOWN CHINESE ON SHORE YUAN: DOWN// OFF- SHORE: DOWN

3f Japan is to buy INFINITE TRILLION YEN’S worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and UP FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund UP TO +2.7215***/Italian 10 Yr bond yield RISES to 4.396*** /SPAIN 10 YR BOND YIELD RISES TO 3.750…**

3i Greek 10 year bond yield RISES TO 3.985

3j Gold at $1904.00 silver at: 22.46 1 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble UP 0 AND 83 /100 roubles/dollar; ROUBLE AT 98.48//

3m oil into the 81 dollar handle for WTI and 85 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 145.66// 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 0.627% STILL ON CENTRAL BANK (JAPAN) INTERVENTION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.8781 as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9585 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.2521 UP 7 BASIS PTS…

USA 30 YR BOND YIELD: 4.337 UP 6 BASIS PTS/

USA 2 YR BOND YIELD: 5.003 UP 4 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 27.06…(TURKEY SET TO BLOW UP FINANCIALLY)

GREAT BRITAIN/10 YEAR YIELD: UP 4 BASIS PTS AT 4.6930

end

2.a Overnight: Newsquawk and Zero hedge:

Futures, World Markets Tumble After China Surprise Rate Cut Sparks Growth Fears

TUESDAY, AUG 15, 2023 – 08:18 AM

US futures and global markets are weaker and bond yields resume their ascent, amid growing concerns that China’s economic slowdown and debt problems – which prompted Beijing to unexpectedly cut rates the most since 2020 amid mounting economic gloom …

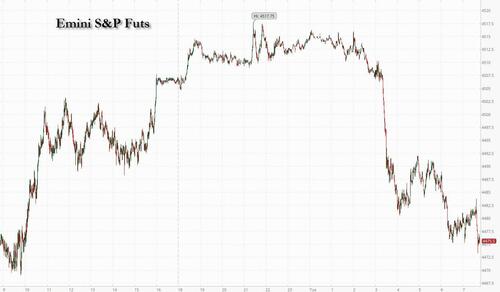

… will spread to the global economy. As of 7:45am ET, S&P futures were at session lows, down 0.7% while Nasdaq futures dropped 0.6%, with Tech outperforming on the move lower.

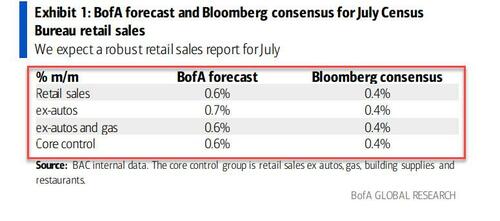

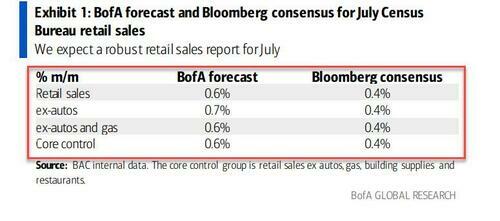

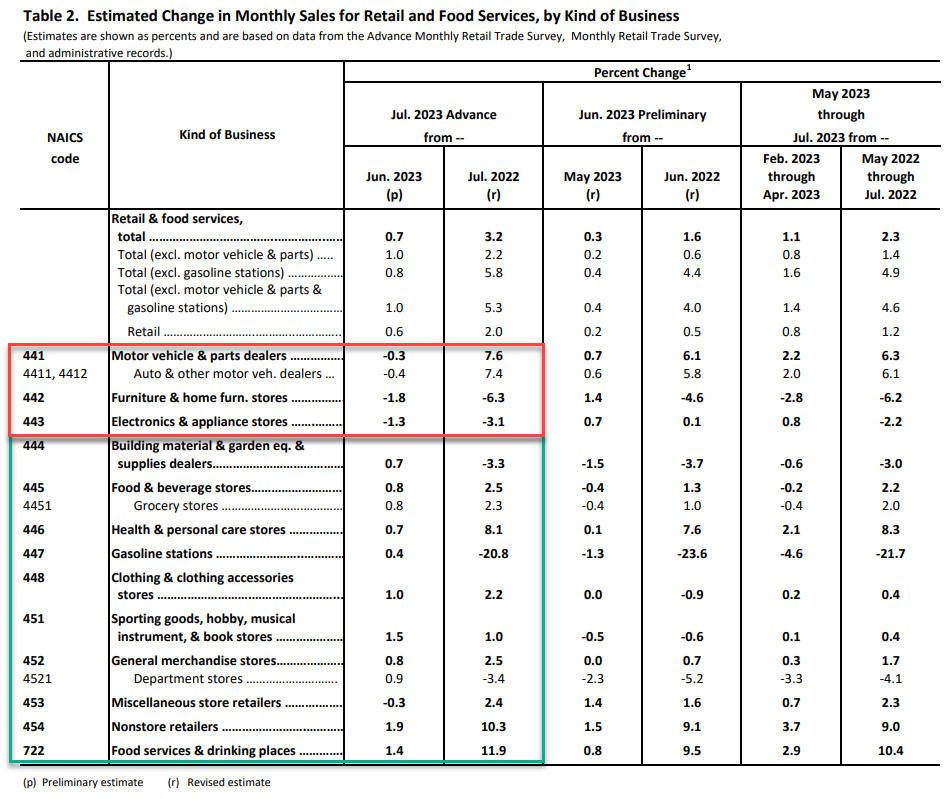

Global bonds fell. Treasury yields extended their climb, with the 10-year rate trading at 4.23%, the highest since October. UK gilts slid and the pound climbed after wage growth accelerated to the strongest pace on record. Commodities are weaker: oil fell and gold held near its lowest close since March as traders pared expectations for Fed rate cuts next year and beyond; the USD erased earlier losses after the latest NY Fed consumer survey showed 1Y inflation expectations dropped to 3.5%, down from 3.8%, and the lowest since Apr 2021. On today’s calendar, Retail Sales is today’s key macro data where BofA card data suggests the July print will come well ahead of consensus estimates.

Away from the US, major markets are all lower ex-Italy; UK the biggest laggard as macro data shows increased wage growth despite increased unemployment. Regional bond yields are higher on the data as the market prices in more rate hikes. Japan GDP surprised to the upside as China macro data disappoints leading to surprise rate cut. In factors, Momentum is leading, Vol is lagging; Growth over Value; Defensives over Cyclicals. UKX -1.2%, SX5E -0.8%, SXXP -0.8%, DAX -0.8%. In the tail end of earnings season, consumer-sector earnings remain in focus.

In premarket trading, NVDA is up 1.6% following an FT reports that China, Saudi Arabia, and UAE are ramping purchases from NVDA to fuel growth in AI, while UBS raised its price target on the semiconductor company’s stock, and follows Morgan Stanley boosting its PT ahead of the technology giant’s earnings report next week. The big banks are all lower premarket as CNBC reports that Fitch may be forced to downgrade multiple banks including JPM. Here are the other notable premarket movers:

- The Arena Group jumps 12% as the publisher of media brands including Sports Illustrated signed a letter of intent with 5-hour Energy drink founder Manoj Bhargava and his firm Simplify Inventions.

- Navitas Semiconductor gains about 7% after projecting revenue for the third quarter that topped the average analyst estimate.

- CareDx Inc. gains 4.4% as Raymond James analyst Andrew Cooper upgraded the firm to outperform from market perform, citing a risk-reward “that skews positive.”

- F45 Training tumbles 65% in premarket trading, after the fitness company backed by actor Mark Wahlberg said it plans to voluntarily delist from the New York Stock Exchange and deregister its common stock.

- Freedom Holding fell 7.1% after Hindenburg disclosed a short position on the financial services holding company’s stock.

- Getty Images shares drop 16% after the photo-services company cut its full-year revenue outlook. Analysts highlighted the impact of the writers’ and actors’ strike in Hollywood, with Citigroup noting that Getty’s guidance assumes these will last through the second half of the year.

- Navitas Semiconductor shares are up 6.7% after the semiconductor device company reported second-quarter results that beat expectations and gave an outlook.

- Redfin Corp. shares are up 0.6% after Oppenheimer upgraded the online real estate company to market perform from underperform.

Attention is increasingly turning to China whose emergence from pandemic lockdowns has been disappointing, fanning concern the world’s economic engine is sputtering. The nation is struggling to contain a potential default at developer Country Garden Holdings Co. after it missed payments on its debt. In a striking development, Beijing announced that it would stop reporting Chinese youth unemployment data after it hit a record high above 21% last month.

“China property worries and today China unexpectedly cutting two key rates are sending a clear signal that growth may not reach its GDP guidance of 5% by year-end,” said Stephane Ekolo, a strategist at TFS Derivatives. “Hence global growth is likely to suffer and the probability of a real slowdown or recession is growing.”

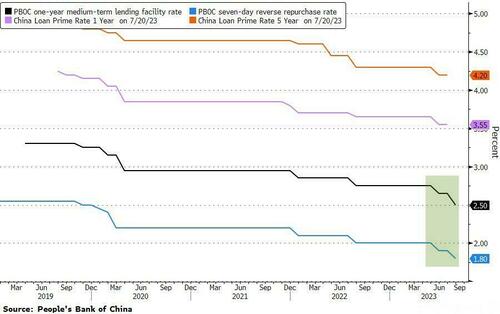

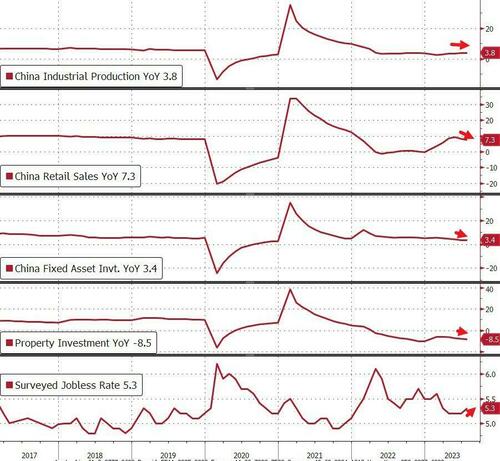

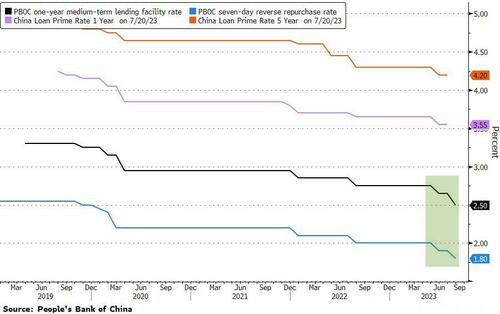

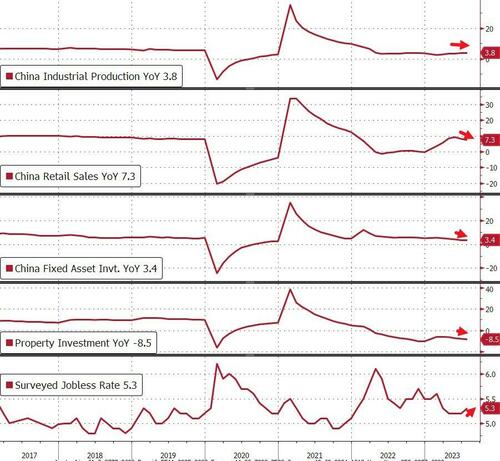

China’s yuan slipped as much as 0.5% after policymakers lowered the rate on one-year loans — known as the medium-term lending facility — by 15 basis points to 2.5%. Data for July underscored the economic slide, showing growth in consumer spending, industrial output and investment dropping across the board and unemployment picking up.

Instead of reassuring investors, China’s surprise rate cut only deepened anxiety about policy steps to revive growth, driving Europe’s Stoxx 600 index down as much as 1.2% to the lowest in a month. China’s rate cut came amid a raft of news depressing risk appetite, from a devaluation in Argentina to an attempt by Russia on Tuesday to stem the ruble’s slide with an emergency rate hike.

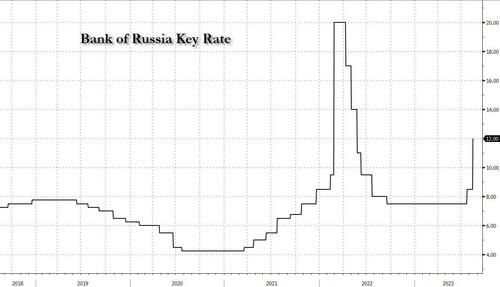

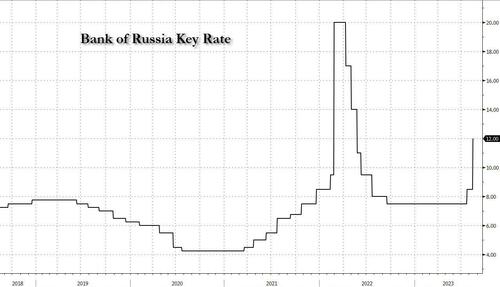

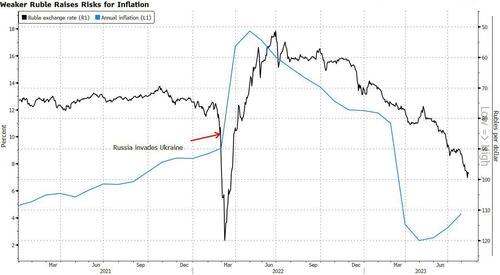

As reported earlier, the ruble erased earlier gains and resumed its drop after Russia unexpectedly raised its key rate to 12% from 8.5% and said another increase is possible.

Meanwhile, Argentina’s already-distressed debt slumped after a populist who vowed to burn down the central bank won surprisingly strong support in a primary vote. Its under-siege government submitted to a 18% currency devaluation.

European stocks extended a drop to a session low as investors worried about higher-for-longer interest rates as well as the impact from a gloomy economic outlook in China. The Stoxx 600 dropped 1.1% as US bond yields jump, driven by a slide in real estate and mining stocks lead while energy outperformed. Here are the biggest European movers:

- Tecan rallies as much as 11%, the most in a year, after the Swiss laboratory equipment maker reported first-half earnings and reiterated its guidance, which analysts said was a key positive

- Marks & Spencer jumps as much as 9.7%, to the highest since January 2022, after the UK retailer provided an unscheduled sales update and increased its profit outlook for the year

- Pandora gains as much as 3.8% after the Danish jewelry chain reported 2Q Ebit that beat estimates and boosted its full-year organic revenue outlook. Analysts said the results were better than expected

- Embracer falls as much as 11% after Axios reported that Saudi-funded Savvy Games was the partner behind a $2 billion deal which fell through in May, sending shares plunging as much as 45%

- Straumann shares drop as much as 6.1%, the most since December, after the Swiss dental equipment company’s decision to keep guidance unchanged overshadowed better-than-expected 1H earnings

- 888 shares drop as much as 8.7%, before paring the decline, after the online betting firm toned down expectations for full-year sales amid suspension of VIP accounts in the Middle East

- Alfen plunges as much as 11% after cutting its revenue forecast for the full year citing destocking challenges in its EV charging sales channels. The guidance missed the average analyst estimate

- Hexatronic declines as much as 16% after the Swedish fiber-optic cable manufacturer reported a weak growth outlook in several key markets in its latest earnings report, Redeye notes

- TKH falls as much as 11% after the telecommunications firm warned that challenging market conditions might dampen growth for its Smart Visions unit in the second half of the year

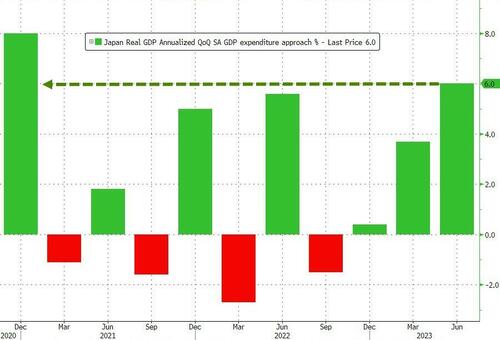

Earlier in the session, Asian stocks traded mixed amid gains in Japan after its economy expanded more than expected, while Chinese stocks extended recent declines on disappointing economic data. The MSCI Asia Pacific dropped 0.2%. Japan’s Toyota and Sony were among the biggest boosts while Chinese tech stocks including Alibaba dragged on the benchmark. Key indexes in Australia and Taiwan also advanced, while markets in South Korea and India were closed for holidays. Japan’s gross domestic product increased 6% in the second quarter, more than double economists’ forecasts, showing resilience in the face of global recession fears. That stands in marked contrast to China, where the latest retail sales and factory output data missed estimates. An unexpected rate cut by the People’s Bank of China provided little market cheer Tuesday. Pressure is building across Chinese financial markets amid spiraling crises in the non-bank lending industry as well as ongoing real estate woes. The CSI 300 Index is on track to erase all of its gains since a key political meeting in July provided some hope for efforts to boost the economy.

“Investors are now worried about credit events, not just from the ailing property sector, but also on the shadow banking system which the authorities are unlikely to bail out,” said Redmond Wong, market strategist at Saxo Capital Markets. Cutting rates can help margins, but it may not be “very effective in boosting loan demand when confidence is still weak in the corporate and household sectors.”

- Nikkei 225 benefitted from a strong GDP report which showed Japan’s economy expanded by the fastest annualised pace since Q4 2020 but was led by exports as private consumption contracted for the first time in 3 quarters.

- ASX 200 was firmer with most sectors in the green including the top-weighted financials after earnings from big 4 bank NAB which also announced a share buyback, while the RBA minutes provided little in the way of new information and kept the door open for further rate hikes although the latest Wage Price Index printed softer-than-expected.

In FX, the Bloomberg Dollar Spot Index steadied after three days of gains. The pound rallied as much as 0.3% against the dollar to $1.2721 before paring some of those gains, while gilts fell, led by the front end of the curve after data showed April to June wages excluding bonuses rose 7.8% from the prior year, beating analyst estimates of 7.4%. The market has now fully priced in a 25-basis-point hike in September, as well as an additional 50 basis points of tightening through March. Focus turns to the UK’s July CPI data due Wednesday. The Swiss franc tops the intraday G-10 rankings, rising 0.3% versus the greenback.

“The US dollar and US yields are still the pre-eminent driver of global financial conditions, and volatility could pick up as US rates inch higher,” Michael Wan, senior currency analyst at MUFG Bank, wrote in a note

In rates, treasuries remain under pressure after declining during Asia session and European morning, led by core euro-zone bonds. Yields across the curve reached highest levels in at least several weeks, with 10- to 30-year yields attaining new YTD highs: the 10-year yield 3 basis points higher at 4.23%. Treasury yields cheaper by 3bp-4bp across intermediate and long-end sectors, steepening 2s10s by ~3bp, 5s30s by less than 1bp; 10-year yields around 4.23%, with bunds and gilts cheaper by additional 4bp and 2bp in the sector. French 10-year yields reached highest level since 2011 as money markets price in the European Central Bank raising interest rates as high as 4%. Gilts have led a sell off in the bond markets after record wage growth in the UK prompted traders to raise bets on the BOE terminal rate to around 6%. UK two-year yields are up 9bps while the German equivalent add 6bps. During Asia session, Treasury futures traded heavy also, following losses in Aussie bonds even as RBA minutes signaled a greater bar to further rate hikes and China data disappointed. The US session has packed economic data slate including retail sales.

In commodities, crude futures decline with WTI falling 0.2% to around $82.40. Spot gold drops 0.2%

Looking at the day ahead now, and US data releases include retail sales for July, the Empire State manufacturing survey for August, and the NAHB’s housing market index for August. Elsewhere, we’ll get UK employment for June, the German ZEW survey for August, and Canada’s CPI for July. Otherwise, central bank speakers include the Fed’s Kashkari, and earnings releases include Home Depot.

Market Snapshot

- S&P 500 futures down 0.5% to 4,482.75

- MXAP down 0.2% to 161.15

- MXAPJ down 0.5% to 507.38

- Nikkei up 0.6% to 32,238.89

- Topix up 0.4% to 2,290.31

- Hang Seng Index down 1.0% to 18,581.11

- Shanghai Composite little changed at 3,176.18

- Sensex up 0.1% to 65,401.92

- Australia S&P/ASX 200 up 0.4% to 7,304.96

- Kospi down 0.8% to 2,570.87

- STOXX Europe 600 down 0.8% to 456.05

- German 10Y yield little changed at 2.69%

- Euro up 0.1% to $1.0920

- Brent Futures little changed at $86.20/bbl

- Gold spot down 0.1% to $1,904.43

- U.S. Dollar Index little changed at 103.12

Top Overnight News from Bloomberg

- UK wage growth accelerated at the strongest pace on record, underscoring the Bank of England’s concerns that it hasn’t yet broken the wage-price spiral feeding inflation across the economy.

- China’s central bank unexpectedly reduced a key interest rate by the most since 2020 to bolster an economy that’s facing fresh risks from a worsening property slump and weak consumer spending.