GOLD PRICE CLOSED: DOWN $7.00 TO $1897.80

SILVER PRICE CLOSED: DOWN $0.13 AT $22.47

Access prices: closes 4: 15 PM

Gold ACCESS CLOSE 1892.85

Silver ACCESS CLOSE: 22.41

Shanghai Gold Benchmark Price

USD oz  AM1945.83PM

AM1945.83PM

1949.88

Historical SGE Fix

New York price at the time: 1902.00

premium $43,00

xxxxxxxxxxxxxxxxxx

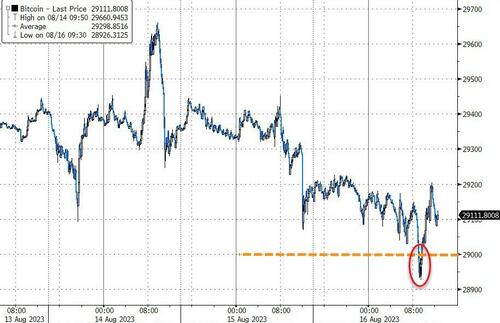

Bitcoin morning price:, $29,184 DOWN 129 Dollars

Bitcoin: afternoon price: $29,093 DOWN 220 dollars

Platinum price closing $893.10 DOWN $13.40

Palladium price; $1236,70 DOWN $29.95

END

Due to the huge rise in the dollar, we must look at gold and silver in currencies other than the dollar to understand where we are heading

I will now provide gold in Canadian dollars, British pounds and Euros/4: 15 PM ACCESS

CANADIAN GOLD: $2,560.80 DOWN 7.80 CDN dollars per oz (ALL TIME HIGH 2,775.35)

BRITISH GOLD: 1487.75 DOWN 10.20 pounds per oz//(ALL TIME HIGH//CLOSING///1630.29)

EURO GOLD: 1740.54 DOWN 4.20 euros per oz //(ALL TIME HIGH/CLOSING//1861.21)//

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

EXCHANGE: COMEX

CONTRACT: AUGUST 2023 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,902.500000000 USD

INTENT DATE: 08/15/2023 DELIVERY DATE: 08/17/2023

FIRM ORG FIRM NAME ISSUED STOPPED

190 H BMO CAPITAL 6

363 H WELLS FARGO SEC 13

657 C MORGAN STANLEY 1

709 C BARCLAYS 4

726 C CUNNINGHAM COM 1

737 C ADVANTAGE 7 3

905 C ADM 2

991 H CME 11

TOTAL: 24 24

MONTH TO DATE: 10,727

JPMorgan stopped 0 /24 contracts.

FOR AUGUST:

GOLD: NUMBER OF NOTICES FILED FOR AUGUST/2023. CONTRACT: 24 NOTICES FOR 2400 OZ or 0.0746 TONNES

total notices so far: 10,723 contracts for 1,072,300 oz (33.365 tonnes)

FOR AUGUST:

SILVER NOTICES: 9 NOTICE(S) FILED FOR 45,000 OZ/

total number of notices filed so far this month : 925 for 4,625,000 oz

XXXXXXXXXXXXXXXXXXXXXXXX

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD

WITH GOLD DOWN $7.00

INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD//HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.44 TONNES OF GOLD FROM THE GLD

INVENTORY RESTS AT 894.42 TONNES

Silver//

WITH NO SILVER AROUND AND SILVER DOWN 13 CENTS AT THE SLV// NO CHANGES IN SILVER INVENTORY AT THE SLV:

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV.

CLOSING INVENTORY: 452.290 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A TINY SIZED 97 CONTRACTS TO 138,215 AND CLOSER TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THIS FAIR SIZED GAIN IN COMEX OI WAS ACCOMPLISHED DESPITE OUR TINY $0.06 LOSS IN SILVER PRICING AT THE COMEX ON TUESDAY. TAS ISSUANCE WAS A RATHER SMALLER SIZED 650 CONTRACTS. THESE WILL BE USED FOR MANIPULATION LATER THIS MONTH/AS WELL AS TODAY. CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON TUESDAY NIGHT: 650 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS. IT THUS LOOKS LIKE THE FED (GOV’T) IS BEHIND ALL OF THESE TRADES.

WE HAVE NOW SET ANOTHER RECORD LOW AT 114,102 CONTRACTS ///JULY 3.2023// OUR BANKERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.06). BUT WERE UNSUCCESSFUL IN KNOCKING OF ANY SILVER CONTRACTS(IF ANY STILL EXIST) AS WE HAD OUR STRONG GAIN OF 608 CONTRACTS ON BOTH EXCHANGES ALONG WITH CONSIDERABLE T.A.S.LIQUIDATION THROUGHOUT THE SESSION.

WE MUST HAVE HAD:

A SMALL ISSUANCE OF EXCHANGE FOR PHYSICALS( 200 CONTRACTS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 3.105 MILLION OZ (FIRST DAY NOTICE) FOLLOWED BY TODAY’S 45,000 OZ QUEUE JUMP //NEW STANDING RISES AT 4.625 MILLION OZ + OUR NEW CRIMINAL 0 CONTRACTS OF EXCHANGE FOR RISK FOR 0.00 MILLION OZ + 1.45 MILLION OZ EX. FOR RISK/PRIOR/// NEW TOTAL STANDING FOR SILVER: 6.075 MILLION OZ/// // // FAIR SIZED COMEX OI GAIN/ SMALL SIZED EFP ISSUANCE/VI) SMALLER BUT STILL STRONG SIZED NUMBER OF T.A.S. CONTRACT ISSUANCE (650 CONTRACTS)/ZERO EXCHANGE FOR RISK ISSUED

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL -311 CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS AUGUST. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF AUGUST:

TOTAL CONTRACTS for 12 days, total 17,477 contracts: OR 87.385 MILLION OZ (1456 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 87.385 MILLION OZ

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH 2022: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 118.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 85.745 MILLION OZ (SMALLER THAN LAST MONTH)

AUGUST: 87.385 MILLION OZ (THIS MONTH IS GOING TO BE VERY STRONG

RESULT: WE HAD A TINY SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 97 CONTRACTS DESPITE OUR LOSS IN PRICE OF $0.06 IN SILVER PRICING AT THE COMEX//TUESDAY.,. THE CME NOTIFIED US THAT WE HAD A SMALL EFP ISSUANCE CONTRACTS: 200 ISSUED FOR SEPT AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS./ WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR AUGUST OF 3.105 MILLION OZ FOLLOWED BY TODAY’S 45,000 OZ QUEUE JUMP//NEW STANDING 4.625 MILLION OZ+ 1.45 MILLION OZ EXCHANGE FOR RISK NEW TOTALS 6.075 MILLION OZ//// WE HAVE A FAIR SIZED GAIN OF 297 OI CONTRACTS ON THE TWO EXCHANGES. THE TOTAL OF TAS INITIATED CONTRACTS TODAY: A SMALLER BUT STILL STRONG 650 CONTRACTS//HUGE FRONT END OF THE TAS CONTRACTS WERE LIQUIDATED DURING THE TUESDAY COMEX SESSION . THE NEW TAS ISSUANCE TUESDAY NIGHT (650) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE., .

WE HAD 9 NOTICE(S) FILED TODAY FOR 45,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A FAIR SIZED 2227 CONTRACTS TO 433,611 AND CLOSER TO TO THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: – REMOVED: 1199 CONTRACTS

WE HAD A FAIR SIZED INCREASE IN COMEX OI ( 2227 CONTRACTS) DESPITE OUR $7.45 LOSS IN PRICE//TUESDAY. WE ALSO HAD A RATHER SMALL INITIAL STANDING IN GOLD TONNAGE FOR AUGUST. AT 30.656 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S 1300 OZ QUEUE JUMP + PRIOR ISSUANCE OF EXCHANGE FOR RISK = (.684 TONNES) //NEW STANDING 33.545 TONNES + .684 EXCHANGE FOR RISK = 34.229/ + /A FAIR (AND CRIMINAL) ISSUANCE OF 1371 T.A.S. CONTRACTS /// ALL OF..THIS HAPPENED WITH A $7,45 LOSS IN PRICE WITH RESPECT TO TUESDAY’S TRADING.WE HAD A STRONG SIZED GAIN OF 6096 OI CONTRACTS (18.96 PAPER TONNES) ON OUR TWO EXCHANGES.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A GOOD SIZED 3869 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 433,611

IN ESSENCE WE HAVE A STRONG SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 6096 CONTRACTS WITH 2227 CONTRACTS INCREASED AT THE COMEX// AND A GOOD 3869 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 6046 CONTRACTS OR 18.96 TONNES. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): A GOOD 3869 CONTRACTS)

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A GOOD SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (3869 CONTRACTS) ACCOMPANYING THE FAIR SIZED GAIN IN COMEX OI (2227) //TOTAL GAIN FOR OUR THE TWO EXCHANGES: 6096 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR NORMAL FORMAT OF BANKERS GOING SHORT AND SPECULATORS GOING LONG ,2.) FAIR INITIAL STANDING AT THE GOLD COMEX FOR JULY AT 30.656 TONNES FOLLOWED BY TODAY’S 3100 OZ QUEUE JUMP //NEW STANDING 33.545 TONNES + .684 TONNES (EXCHANGE FOR RISK//PRIOR) NEW TOTALS: 34.229 TONNES/// 3) ZERO LONG LIQUIDATION WITH CONSIDERABLE TAS LIQUIDATION DURING THE COMEX SESSION //4) FAIR SIZED COMEX OPEN INTEREST GAIN/ 5) GOOD ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER///6: SMALL T.A.S. ISSUANCE: 1371 CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023 INCLUDING TODAY

AUGUST

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF AUG :

TOTAL EFP CONTRACTS ISSUED: 35,502 CONTRACTS OR 3,550,200 OZ OR 110.53 TONNES IN 12TRADING DAY(S) AND THUS AVERAGING: 2958 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 12 TRADING DAY(S) IN TONNES 110.53 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2022, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 110.53/3550 x 100% TONNES 3.09% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2023

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH/2022: 409.30 TONNES //FINAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 151.69 TONNES (WEAKER THAN LAST MONTH)

AUGUST: 110.53 TONNES (A STRONGER MONTH BUT WILL NOT COME CLOSE TO MARCH 2022)

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF SEPT. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF MAY HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF JUNE., FOR BOTH GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (SEPT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER ROSE BY A TINY SIZED 97 CONTRACTS OI TO 138,215 AND CLOSER TO OUR COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE A SMALL 200 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

SEPT 200 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 200 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 97 CONTRACTS AND ADD TO THE 200 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A FAIR SIZED GAIN OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 297 CONTRACTS

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTAL 1.485 MILLION OZ

OCCURRED DESPITE OUR TINY $0.06 LOSS IN PRICE …..

END

OUTLINE FOR TODAY’S COMMENTARY

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

b, ) Gold/silver trading overnight Europe,//GOLD COMMENTARIES

(Peter Schiff)

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS//

WEDNESDAY MORNING//TUESDAY NIGHT

SHANGHAI CLOSED DOWN 26.05 PTS OR 0.82% //Hang Seng CLOSED DOWN 251.81 PTS OR 1.36% /The Nikkei CLOSED DOWN 472.07 PTS OR 1.46% //Australia’s all ordinaries CLOSED DOWN 1.44 % /Chinese yuan (ONSHORE) closed DOWN 7.2980 /OFFSHORE CHINESE YUAN DOWN TO 7.3258 /Oil UP TO 80.87 dollars per barrel for WTI and BRENT UP AT 84.91 / Stocks in Europe OPENED ALL MIXED// ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

9. USA

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A FAIR SIZED 2227 CONTRACTS UP TO 433,611 DESPITE OUR LOSS IN PRICE OF $7.45 ON TUESDAY.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE ACTIVE DELIVERY MONTH OF AUGUST… THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 3869 EFP CONTRACTS WERE ISSUED: : DEC 3869 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 3869 CONTRACTS

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A STRONG SIZED TOTAL OF 6096 CONTRACTS IN THAT 3869 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A FAIR SIZED GAIN OF 2227 COMEX CONTRACTS..AND THIS GAIN ON OUR TWO EXCHANGES HAPPENED DESPITE OUR LOSS IN PRICE OF $7.45//TUESDAY COMEX. AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS DURING MID MONTH IN THE DELIVERY CYCLE), THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR TUESDAY NIGHT WAS A FAIR 1371 CONTRACTS. THROUGHOUT THE PAST WEEKS, THE BANKERS SOLD OFF THE LONG SIDE OF THE SPREAD WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR SPREAD WHICH WILL BE LIQUIDATED TWO MONTHS HENCE)//

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: AUGUST (34.229) ( ACTIVE MONTH)

TONNES),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 34.229 TONNES (INCLUDING .6842 EXCHANGE FOR RISK)

THE SPECS/HFT WERE SUCCESSFUL IN LOWERING GOLD’S PRICE( IT LOST $7.45) //// BUT WERE UNSUCCESSFUL IN KNOCKING ANY SPECULATOR LONGS (IF ANY STILL EXIST) AS WE HAD A STRONG GAIN OF 6096 TOTAL CONTRACTS ON OUR TWO EXCHANGES. WE HAD CONSIDERABLE T.A.S. LIQUIDATION ON THE FRONT END OF YESTERDAY’S TRADING. THE T.A.S. ISSUED ON TUESDAY NIGHT WILL BE “PUT INTO THE BANK” TO BE USED AT A LATER DATE AT THE COLLUSIVE CHOOSING OF OUR BANKERS.

WE HAVE GAINED A TOTAL OI OF 18.96 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR AUGUST. (30.656 TONNES) ON FIRST DAY NOTICE FOLLOWED BY TODAY’S 1300 OZ QUEUEJUMP //NEW STANDING ADVANCES A BIT TO 33.545 TONNES + .6842 (PRIOR EXCHANGE FOR RISK) //NEW TOTAL 34.229 TONNES // ALL OF THIS WAS ACCOMPLISHED WITH OUR LOSS IN PRICE TO THE TUNE OF $7.45.

WE HAD – REMOVED 1199 CONTRACTS TO THE COMEX TRADES TO OPEN INTEREST

NET GAIN ON THE TWO EXCHANGES 6096 CONTRACTS OR 609,600 OZ OR 18.96 TONNES.

Estimated gold volume today:// 113,613 awful

final gold volumes/yesterday 173,675 poor//speculators have left the gold arena

//AUGUST 16/ FOR THE AUGUST 2023 GOLD CONTRACT

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 385.812 OZ jpm 12 KILOBARS . |

| Deposit to the Dealer Inventory in oz | nil |

| Deposits to the Customer Inventory, in oz | nil OZ |

| No of oz served (contracts) today | 24 notice(s) 2400 OZ 0.0746 TONNES |

| No of oz to be served (notices) | 58 contracts 5800 oz 0.1807 TONNES |

| Total monthly oz gold served (contracts) so far this month | 10,727 notices 1,072,700 OZ 33.365 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | x |

0 dealer deposit:

total dealer deposits: NIL oz

customer deposits: 0

total customer deposits: nil oz

we had 1 customer withdrawals

i) Out of JPMorgan: 385.812 oz

total; 385.812 oz

Adjustments; 0

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR AUGUST.

For the front month of AUGUST we have an oi of 82 contracts having LOST 21 contracts. We had 34 contracts filed

on Monday, so we gained 13 contracts or an additional 1300 oz will stand at the comex,

Sept gained 103 contracts to 2862.

Oct lost 287 contracts to 32,865 contracts.

We had 24 contracts filed for today representing 2400 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 24 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped received by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the AUGUST /2023. contract month,

we take the total number of notices filed so far for the month (10,727 x 100 oz ), to which we add the difference between the open interest for the front month of AUGUST (82 CONTRACT) minus the number of notices served upon today 24 x 100 oz per contract equals 1,078,500 OZ OR 33.545 TONNES the number of TONNES standing in this active month of AUGUST. + .684 TONNES EXCHANGE FOR RISK/prior = 34.229 tonnes

thus the INITIAL standings for gold for the AUGUST contract month: No of notices filed so far (10,727) x 100 oz + (82) {OI for the front month} minus the number of notices served upon today (24) x 100 oz) which equals 1,078,500 oz standing OR 33.545 TONNES + .684 TONNES OF EXCHANGE FOR RISK/prior = 34.229 TONNES

TOTAL COMEX GOLD STANDING: 34.229 TONNES WHICH IS SMALL FOR AN ACTIVE DELIVERY MONTH.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 2,101,333.235 OZ 65.36 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 22,003,399.946 OZ

TOTAL REGISTERED GOLD: 11,680,181.113 (363.30 tonnes)..

TOTAL OF ALL ELIGIBLE GOLD: 10,323,218.833 O Z

REGISTERED GOLD THAT CAN BE SERVED UPON: 9,578,848 OZ (REG GOLD- PLEDGED GOLD) 297.942 tonnes//

END

SILVER/COMEX

AUGUST 16

//2023// THE AUGUST 2023 SILVER CONTRACT

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 606,991.000 oz Brinks CNT Delaware . |

| Deposits to the Dealer Inventory | nil oz |

| Deposits to the Customer Inventory | 582,290.332 oz Manfra |

| No of oz served today (contracts) | 9 CONTRACT(S) (45,000 OZ) |

| No of oz to be served (notices) | 0 contracts (nil oz) |

| Total monthly oz silver served (contracts) | 925 Contracts (4,625,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

i) 0 dealer deposit

total dealer deposit: 0 oz

i) We had 0 dealer withdrawal

total dealer withdrawals: 0 oz

We had 1 deposits customer account:

i)Into Manfra: 582,290.352 oz

total customer deposits: 582,290,352 oz

JPMorgan has a total silver weight: 139.276 million oz/279.167 million =49.82% of comex .//

Comex withdrawals 3

i) Out of Brinks 908.860 oz

ii) Out of CNT: 600,003.420 oz

iii) Out of Delaware 5988.720 oz

total: 606,991.000 oz

adjustments: 0

TOTAL REGISTERED SILVER: 30.828 MILLION OZ//.TOTAL REG + ELIGIBLE. 279.167 million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR JULY:

silver open interest data:

FRONT MONTH OF AUGUST /2023 OI: 9 CONTRACTS HAVING LOST 11 CONTRACT(S). WE HAD

20 NOTICES FILED ON TUESDAY SO WE GAINED 9 CONTRACTS OR AN ADDITIONAL 45,000 OZ WILL STAND IN THIS NON ACTIVE DELIVERY MONTH OF AUGUST.

SEPT HAS A LOSS OF 1933 CONTRACTS DOWN TO 60,283

OCT LOST 1 CONTRACT TO STAND AT 479.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 9 for 45,000 oz

Comex volumes// est. volume today 53,432 fair

Comex volume: confirmed yesterday: 77,977 good

To calculate the number of silver ounces that will stand for delivery in AUGUST. we take the total number of notices filed for the month so far at 925 x 5,000 oz = 4,625,000 oz

to which we add the difference between the open interest for the front month of AUGUST (9) and the number of notices served upon today 9 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the AUGUST/2023 contract month: 916 (notices served so far) x 5000 oz + OI for the front month of AUGUST (9) – number of notices served upon today (9 )x 500 oz of silver standing for the AUGUST contract month equates to 4.625 million oz.+ 0.0 MILLION OZ EXCHANGE FOR RISK ISSUED TODAY+ 1.45 MILLION OZ EXCHANGE FOR RISK PRIOR//NEW TOTALS: 6.075 MILLION oz.

There are 30.828 million oz of registered silver.

Thus if we take today’s standing at 6.075 and add last month’s 30.9 million oz we have 36.975 million oz against only 30.828 million registered silver.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS

AUGUST 16/WITH GOLD DOWN $7.00 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.44 TONNES FORM THE GLD//: /// //INVENTORY RESTS AT 894.42 TONNES

AUGUST 15/WITH GOLD DOWN $7,45 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.76 TONNES FORM THE GLD//: /// //INVENTORY RESTS AT 895.87 TONNES

AUGUST 14/WITH GOLD DOWN $2.10 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.75 TONNES FORM THE GLD//: /// //INVENTORY RESTS AT 899.63 TONNES

AUGUST 11/WITH GOLD DOWN $2.10 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .31 TONNES FORM THE GLD//: /// //INVENTORY RESTS AT 903.31 TONNES

AUGUST 10/WITH GOLD DOWN $1.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD: /// //INVENTORY RESTS AT 903.69 TONNES

AUGUST 9/WITH GOLD DOWN $8.75 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD: /// //INVENTORY RESTS AT 903.69 TONNES

AUGUST 8/WITH GOLD DOWN $9.60 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.31 TONNES FORM THE GLD /// //INVENTORY RESTS AT 903.69 TONNES

AUGUST 7/WITH GOLD DOWN $5.45 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD: /// //INVENTORY RESTS AT 906.00 TONNES

AUGUST 4/WITH GOLD UP $7.25 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.18 TONNES OF GOLD FROM THE GLD/// .///INVENTORY RESTS AT 906.00 TONNES

AUGUST 3/WITH GOLD DOWN $5.25 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD //: //: / .////INVENTORY RESTS AT 909.18 TONNES

AUGUST 2/WITH GOLD DOWN $3.45 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 3.75 TONNES OF GOLD FROM THE GLD//: //: / .////INVENTORY RESTS AT 909.18 TONNES

AUGUST 1/WITH GOLD DOWN $28.45 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 2.89 TONNES OF GOLD FROM THE GLD//: //: / .////INVENTORY RESTS AT 912.93 TONNES

JULY 31/WITH GOLD UP $9.50 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 2.89 TONNES OF GOLD FROM THE GLD//: //: / .////INVENTORY RESTS AT 912.93 TONNES

JULY 28/WITH GOLD UP $14.15 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 1.44 TONNES OF GOLD FROM THE GLD//: //: / .////INVENTORY RESTS AT 915,82 TONNES

JULY 27/WITH GOLD DOWN $21.80 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 1.74 TONNES OF GOLD FROM THE GLD//: //: / .////INVENTORY RESTS AT 917.26 TONNES

JULY 26/WITH GOLD UP $6.35 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD: //: / .////INVENTORY RESTS AT 919.00 TONNES

JULY 25/WITH GOLD UP $2.45 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD: //: / .////INVENTORY RESTS AT 919.00 TONNES

JULY 24/WITH GOLD DOWN $4.65 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 5.20 TONNES OF GOLD INTO THE GLD//: / .////INVENTORY RESTS AT 919.00 TONNES

JULY 21/WITH GOLD DOWN $3.80 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD: / .////INVENTORY RESTS AT 913.80 TONNES

JULY 20/WITH GOLD DOWN $8.70 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.73 TONNES FROM THE GLD/ .////INVENTORY RESTS AT 913.80 TONNES

JULY 19/WITH GOLD UP $0.65 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .86 TONNES FROM THE GLD/ .////INVENTORY RESTS AT 912.07 TONNES

JULY 18/WITH GOLD UP $23.45 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD: .////INVENTORY RESTS AT 912.93 TONNES

JULY 17/WITH GOLD DOWN $6.60 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.73 TONNES OF GOLD FROM THE GLD.////INVENTORY RESTS AT 912.93 TONNES

JULY 14/WITH GOLD UP $0.75 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD: ////INVENTORY RESTS AT 914.66 TONNES

JULY 13/WITH GOLD UP $3.30 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 0.29 TONNES OF GOLD OUT OF THE GLD////INVENTORY RESTS AT 914.66 TONNES

JULY 12/WITH GOLD UP $24.50 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 0.31 TONNES OF GOLD OUT OF THE GLD////INVENTORY RESTS AT 914.95 TONNES

JULY 11/WITH GOLD UP $6.15 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.0 TONNES OF GOLD OUT OF THE GLD////INVENTORY RESTS AT 915.26 TONNES

JULY 10 WITH GOLD DOWN $1.35 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.60 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 916.26 TONNES.

GLD INVENTORY: 894.42 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

AUGUST 16/WITH SILVER DOWN 13 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 0.275 MILLION OZ INTOTHE SLV/: / .////INVENTORY RESTS AT 452.290 MILLION OZ

AUGUST 15/WITH SILVER DOWN 6 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 0.275 MILLION OZ INTOTHE SLV/: / .////INVENTORY RESTS AT 452.290 MILLION OZ

AUGUST 14/WITH SILVER DOWN 3 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV A DEPOSIT OF 0.459 MILLION OZ INTOTHE SLV/: //////INVENTORY RESTS AT 452.565 MILLION OZ

AUGUST 11/WITH SILVER DOWN 6 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A DEPOSIT OF 1.926 MILLION OZ INTOTHE SLV/: // OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 452.106 MILLION OZ

AUGUST 10/WITH SILVER UP 6 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 8,807 MILLION OZ OUT OF THE SLV/: // OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 450.180 MILLION OZ

AUGUST 9/WITH SILVER DOWN 7 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 8,807 MILLION OZ OUT OF THE SLV/: // OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 450.180 MILLION OZ

AUGUST 8/WITH SILVER DOWN 40 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: // OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 458.987 MILLION OZ

AUGUST 7/WITH SILVER DOWN 46 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: // OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 458.987 MILLION OZ

AUGUST 4/WITH SILVER UP 1 CENT TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.294 MILLION OZ FROM THE SLV// OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 458.987 MILLION OZ

AUGUST 3/WITH SILVER DOWN 16 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 189,000 OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 451.281 MILLION OZ

AUGUST 2/WITH SILVER DOWN 43 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 275,000 OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 451.471 MILLION OZ

AUGUST 1/WITH SILVER DOWN 61 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 184,000 OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 451.746 MILLION OZ

JULY 31/WITH SILVER UP 45 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 184,000 OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 451.746 MILLION OZ

JULY 28/WITH SILVER UP 15 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 550,000 OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 451.930 MILLION OZ

JULY 27/WITH SILVER DOWN 59 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: .////INVENTORY RESTS AT 452.480 MILLION OZ

JULY 26/WITH SILVER UP 15 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: .////INVENTORY RESTS AT 452.480 MILLION OZ/

JULY 25/WITH SILVER UP 24 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A SMALL WITHDRAWAL OF 826,000 OZ FROM THE SLV..////INVENTORY RESTS AT 452.480 MILLION OZ/

JULY 24/WITH SILVER DOWN 23 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: ////INVENTORY RESTS AT 453.306 MILLION OZ/

JULY 21/WITH SILVER DOWN 14 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 1.101 MILLION OZ OF SILVER FROM THE SLV ////INVENTORY RESTS AT 453.306 MILLION OZ/

JULY 20/WITH SILVER DOWN 38 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 1.468 MILLION OZ OF SILVER FROM THE SLV ////INVENTORY RESTS AT 454.107 MILLION OZ/

JULY 19/WITH SILVER UP 11 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV:A ////INVENTORY RESTS AT 455.875 MILLION OZ/

JULY 18/WITH SILVER DOWN 19 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV:A ////INVENTORY RESTS AT 455.875 MILLION OZ/

JULY 17/WITH SILVER UP 25 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 4.856 MILLION OZ OF SILVER FROM THE SLV////////INVENTORY RESTS AT 455.875 MILLION OZ/

JULY 14/WITH SILVER UP 27 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 2.21 MILLION OZ OF SILVER FROM THE SLV////////INVENTORY RESTS AT 455.875 MILLION OZ/

JULY 13/WITH SILVER UP 64 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//////INVENTORY RESTS AT 462.941 MILLION OZ/

JULY 12/WITH SILVER UP $1.00 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.881 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 462.941 MILLION OZ/

JULY 11/WITH SILVER DOWN 5 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF .020 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 464.822 MILLION OZ/

JULY 10/WITH SILVER UP 2 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.672 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 464.802 MILLION OZ

//

CLOSING INVENTORY 452.290 MILLION OZ//

PHYSICAL GOLD/SILVER COMMENTARIES

1:Peter Schiff/Mike Maharrey

A must read: For 10 months, the total budget deficit for 2023 is 1.61 trillion heading for a total deficit of around 1.8 trillion. Total debt is 32.66 trillion. Thisis unsustainable. Total interest costs will rise will above 1 trillion dollars for fiscal 2024.

(Mike Maharrey)

Biden Budget Deficits Look Like Those Normally Seen In Recessions

WEDNESDAY, AUG 16, 2023 – 07:20 AM

Authored by Michael Maharrey via SchiffGold.com,

To hear President Joe Biden tell it, the US economy is booming. Meanwhile, the Biden administration is running monthly budget deficits that you would normally see during a deep recession.

With two months left to go, the deficit for fiscal 2023 now stands at $1.61 trillion, after the federal government charted another massive shortfall in July.

And Biden wants to spend even more.

To put the $1.61 trillion deficit in perspective, prior to the pandemic, the US government had only run deficits over $1 trillion four times — all in the aftermath of the 2008 financial crisis. Trump almost hit the $1 trillion mark in 2019 and was on pace to run a trillion-dollar deficit prior to the pandemic. The economic catastrophe caused by the government’s response to COVID-19 gave policymakers an excuse to spend with no questions asked. Now the Biden administration has settled into the new status quo – running ’08 financial crisis-like deficits every single year.

The July budget deficit came in at $220.78 billion, according to the latest Month Treasury Statement. The shortfall was due to a double whammy of big spending and falling government tax receipts.

The Treasury collected $276.16 billion in July, a big drop from June’s $418 billion in revenue. That was slightly above July 2022 receipts, but the revenue trend in 2023 has generally been downward.

The federal government enjoyed a revenue windfall in fiscal 2022. According to a Tax Foundation analysis of Congressional Budget Office data, federal tax collections were up 21%. Tax collections also came in at a multi-decade high of 19.6% as a share of GDP. But CBO analysts warned it won’t last. And government tax revenue will decline even faster as the economy spins into a recession.

The bigger problem is on the spending side of the ledger.

The Biden administration blew through another $496.94 billion in July. That was a 3.4% increase over July 2022 spending.

Now, you might be thinking that with the spending cuts in the Fiscal Responsibility Act, Congress fixed this problem. But we live in an upside-down world where spending cuts mean spending keeps going up.

In other words, the spending cuts will not put a dent in current spending levels. That means we can expect these massive deficits to continue month after month.

And the Biden administration already wants more money. Just last week, the president asked Congress to appropriate $40 billion in additional spending, including $24 billion for Ukraine and other international needs, $4 billion related to border security and $12 billion for disaster relief.

Keep in mind, the feds now have a credit card with no limit.

The fundamental issue wasn’t that the US government couldn’t borrow enough money. The fundamental problem was, and still is, that the US government spends too much money. Despite the pretend spending cuts, the debt ceiling deal didn’t address that problem. Even with the new plan in place, spending will go up. And it’s already historically high. That means big budget deficits will continue and the national debt will mount.

The US Treasury blew up the national debt by $850 billion in June alone as it scrambled to make up the ground it lost while the government was up against its borrowing limit. The national debt now stands at $32.66 trillion.

Meanwhile, according to the National Debt Clock, the debt-to-GDP ratio stands at 119.1%. Despite the lack of concern in the mainstream, debt has consequences. More government debt means less economic growth. Studies have shown that a debt-to-GDP ratio of over 90% retards economic growth by about 30%. This throws cold water on the conventional “spend now, worry about the debt later” mantra, along with the frequent claim that “we can grow ourselves out of the debt” now popular on both sides of the aisle in DC.

To put the debt into perspective, every American citizen would have to write a check for $97,547 in order to pay off the national debt.

This is an unsustainable trajectory, especially in a high-interest rate environment.

And if you believe the rhetoric coming out of the Federal Reserve, rates aren’t going down any time soon.

Meanwhile, the federal government has paid more than half a trillion dollars ($561 billion) on interest payments alone in fiscal 2023. In July, Uncle Sam forked out $67 billion in interest payments. The only spending categories that were larger were Social Security and Medicare. Last month, the US government spent more on interest expenses than it did on national defense.

According to an analysis by the New York Times, net interest costs rose by 41% last year. The Peterson Foundation said the jump in interest expense was larger than the biggest increase in interest costs in any single fiscal year, dating back to 1962.

The cost of financing the debt will almost certainly rise even more now that Congress has done away with the debt ceiling for two years.

As the Treasury floods the market with new debt, bond prices will likely fall in order to create enough demand for all of those Treasuries. Bond yields are inversely correlated with bond prices, and as prices fall, interest rates rise.

We’re already seeing extreme weakness in the bond market. Financial analyst Jim Grant recently said we could be heading toward a generational bear market in bonds. This would mean rising interest rates for the US government even if the Fed stepped in and tried to push rates down. This is an unsustainable trajectory for the US government. It simply cannot continue to borrow at this pace in a high-interest rate environment.

In fact, if interest rates remain elevated or continue to rise, interest expenses could climb rapidly into the top three federal expenses. (You can read a more in-depth analysis of the national debt HERE.)

It’s easy to blame the Federal Reserve’s rate hikes for this problem, but the real problem started with more than a decade of artificially low interest rates and easy money. This incentivized borrowing. The federal government’s rising interest expense is just one example of the debt chickens coming home to roost. And it’s one of the reasons Peter Schiff says the Fed will never get price inflation back to its 2% target.

end

This is a big story: India and the UAE complete the first oil sale of 1 million barrels of oil. India pays in rupees. However initially gold is purchased by India through an UAE exporter and then no doubt that gold is funneled back to UAE.

(Mike Maharrey)

Another Blow To The Petrodollar: India & The UAE Complete First Oil Sale In Rupees

WEDNESDAY, AUG 16, 2023 – 08:20 AM

Authored by Michael Maharrey via SchiffGold.com,

In another blow to dollar dominance, India and the United Arab Emirates settled an oil trade without converting local currencies to dollars for the first time on Monday, as India’s top refiner made a payment for oil in rupees.

Indian Oil Corp. bought a million barrels of oil from Abu Dhabi National Oil Company in a dollar-free transaction.

The oil sale was the first after the two countries entered a Memorandum of Understanding (MoU) in July. The deal established the Local Currency Settlement (LCS) system, facilitated by the Reserve Bank of India and the Central Bank of the United Arab Emirates. The system allows the two countries to engage in bilateral trade using the rupee and dirham. According to a statement by the Reserve Bank of India, the agreement will facilitate “seamless cross-border transactions and payments, and foster greater economic cooperation.”

The first test of the LCS involved the sale of 25 kg of gold from a UAE gold exporter to a buyer in India at about 128.4 million rupees ($1.54 million).

According to WIONews in India, the LCS system will reduce costs and speed up transactions between the two countries.

Additionally, reliance on national currencies is anticipated to bolster economic resilience and strengthen bilateral relations. Moreover, any surplus balances in the local currencies can be invested in various local assets, including corporate bonds, government securities, and equity markets.”

India has also purchased oil from Russia using non-dollar currencies.

India ranks as the third-largest oil importer in the world.

If the trend of dollarless transactions expands to other countries, the minimization of the dollar in the global oil trade would be bad news for the United States.

As it stands, the majority of global oil sales are priced in dollars. This ensures a constant demand for the greenback since every country needs dollars to buy oil. This helps support the US government’s “borrow and spend” policies, along with its massive deficits. As long as the world needs dollars for oil, it guarantees demand for greenbacks. That means the Federal Reserve can keep printing dollars to monetize the debt.

ZeroHedge explained how the process works.

One of the core staples of the past 40 years, and an anchor propping up the dollar’s reserve status, was a global financial system based on the petrodollar – this was a world in which oil producers would sell their product to the US (and the rest of the world) for dollars, which they would then recycle the proceeds in dollar-denominated assets and while investing in dollar-denominated markets, explicitly prop up the USD as the world reserve currency, and in the process backstop the standing of the US as the world’s undisputed financial superpower.”

Simply put, de-dollarization would drastically diminish US economic power and wreck the country’s economy.

And India isn’t the only country drifting away from the dollar.

In January, Saudi Arabia Finance Minister Mohammed Al-Jadaan said the country is open to discussing trade in currencies other than the US dollar.

“There are no issues with discussing how we settle our trade arrangements, whether it is in the US dollar, whether it is the euro, whether it is the Saudi riyal,” Al-Jadaan said in an interview with Bloomberg TV.

Al-Jadaan went on to say, “I don’t think we are waving away or ruling out any discussion that will help improve the trade around the world.”

Saudi Arabia has sold oil exclusively for dollars since 1974 under a deal with the Nixon administration. If the Saudis shift away from the dollar and sell oil in other currencies, other countries would likely follow suit due to the country’s influence on the global oil market.

While the current de-dollarization trend doesn’t directly threaten the dollar’s role as the world reserve currency — yet — it could foreshadow bigger problems down the road, especially if the trend continues to accelerate. After the Russian invasion of Ukraine, IMF Managing Director Gita Gopinath warned that sanctions on Russia could erode the dollar’s dominance by encouraging smaller trading blocs using other currencies. That’s exactly what we’re seeing.

If the demand for dollars were to plunge significantly, interest rates on US Treasury bonds would soar. This would be an untenable situation for a government servicing more than $32 trillion in debt.

While the world isn’t on the verge of jettisoning the dollar, there does seem to be an increasing likelihood the petrodollar could face competition from other currencies. This is yet another sign that the dollar may eventually lose its status as the sole reserve currency. Americans should be wary of counting on long-term dollar dominance to prop up its house of cards economy.

end

How Turkey’s Love Affair With Gold Impacted The Global Market

WEDNESDAY, AUG 16, 2023 – 03:30 AM

Turkey’s love affair with gold has had a major impact on global gold flows, especially through the first half of 2023.

Turks have historically held a lot of gold, both in jewelry and investment form. The country ranks as the fifth-largest gold market in the world. But with recent economic turmoil in the country demand for gold has exploded.

According to the World Gold Council, Turkish demand for gold bars and gold coins increased five-fold during the second quarter of this year, pushing total demand to a record 98 tons through the first half of 2023.

Gold jewelry demand has also surged in Turkey this year, posting a fourth consecutive double-digit percentage increase in Q2, H1 demand came in at 20 tons. That was up 25% year-on-year and marked a five-year high.

Since the start of 2020 Turkish bar and coin demand has made up, on average, 9% of the global total. That’s more than double the country’s 4% share between 2010 and 2020. Turkey’s surging investment demand accounted for 17% of global bar and coin demand in Q2’23.

What drove this big spike in demand?

In a nutshell: currency depreciation.

According to the World Gold Council, “A combination of high inflation and regular currency depreciation over the past few decades has fueled healthy growth in retail gold demand in recent years.”

The Turkish economy has long been subject to bouts of price inflation, but moves by the government and the central bank over the last two years put price inflation on steroids.

At the assistance of President Tayyip Erdoğan, Turkey’s central bank began cutting interest rates in September 2021. According to a CNN report at the time, the Turkish president holds the unorthodox view that interest rate cuts can rein in price inflation.

Predictably, the lira crashed. It lost 15% against the dollar in a single day in November 2021.

When the Central Bank of Turkey began cutting rates, price inflation was already running at 19%. As the central bank slashed rates, the official Turkish CPI climbed to 85% on an annual basis by October 2022. Independent economists measured the country’s price inflation at 185%.

As price inflation soared, Turks piled into hard assets, including real estate and gold in an attempt to protect their wealth from the country’s rapidly depreciating currency.

Moves by the Turkish government earlier this year only served to increase the demand for gold.

After a catastrophic earthquake in February 2023, the country’s treasury imposed an additional 20% fee on gold imports from countries outside the EU that did not have a free trade agreement with Turkey. According to Reuters, the move was intended to shrink the country’s rapidly growing trade deficit.

The government later banned some gold imports.

Predictably, these import restrictions caused a big drop in gold supply within the country even as demand was surging.

In order to meet local demand, the Central Bank of Turkey sold 165 tons of gold into the domestic gold market over a three-month period.

Prior to March, the central bank ranked as the world’s biggest gold buyer. With the Turkish bank significantly reducing its gold holdings, net central bank gold reserves fell for several months.

The Central Bank of Turkey returned to gold buying in June.

As the government put the squeeze on the gold supply, premiums soared, hitting levels between $100 and $150 per ounce. But even those high premiums couldn’t dent the Turkish appetite for gold.

The country normalized gold import regulations in July. Premiums dropped back to normal levels, but according to the World Gold Council, there was little selling by the public, despite record-high gold prices in lira terms.

And this month, the Turkish government has reinstated gold import quotas in order to lower the country’s current account deficit and replenish central bank reserves. It also slapped additional taxes back on some gold imports.

The Central Bank of Turkey got a new governor in June. He reportedly holds more conventional views on monetary policy.

According to the World Gold Council, “Against this backdrop, it seems likely that Turkish investment demand will remain strong.”

The government is strictly controlling gold imports for now, but whether that continues – and whether the TCMB is again forced to sell gold domestically to satisfy unmet needs – depends upon the performance of the broader Turkish economy and the nation’s foreign exchange position. Needless to say, these issues will attract attention from global gold market followers.”

end

2 Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens//JAMES RICKARDS//JOHN RUBINO

The Great American Blunder

WEDNESDAY, AUG 16, 2023 – 01:45 PM

Authored by James Rickards via DailyReckoning.com,

From a geopolitical perspective, the U.S. today has never been weaker than since the post-Vietnam era.

Remember the images of U.S. helicopters taking off from its South Vietnamese embassy in 1975, loaded with refugees trying to escape the country?

It was a national humiliation.

So was the disastrous U.S. withdrawal from Afghanistan in 2022. Desperate Afghans, eager to escape Taliban rule, clung to American transports leaving Kabul.

It might represent an even greater national humiliation.

In both cases, U.S. weakness was on full display for the world to see. Its defeat in Vietnam led to Soviet geopolitical gains throughout the world.

U.S. credibility around the world was restored during the 1980s as Reagan rebuilt the U.S. military into a powerful force.

U.S. geopolitical power peaked after its dramatic victory in the First Gulf War in 1991. But the U.S. proceeded to squander that power in the wake of 9/11, with strategic failures in Iraq and Afghanistan.

Meanwhile, for the past 20 years, the U.S. focused on fighting terrorists that have limited combat capability, not serious rivals like Russia with significant conventional forces.

Wonder Weapons?

Many U.S. weapons systems supplied to Ukraine have proven to be inadequate or in some cases, total failures.

Patriot missile batteries cannot shoot down Russian hypersonic missiles. The Patriot batteries are being blown up one-by-one at a cost of $1 billion each.

U.S. Bradley fighting vehicles have been left in flames and ruins on the battlefields of Ukraine due to Russian mines.

The M-777 howitzers the U.S. and its allies have sent to Ukraine have proved too fragile to withstand the high rates of fire required on the Ukrainian battlefields.

And U.S. HIMARS precision artillery doesn’t always work because the Russians have learned to jam the guidance systems with electronic warfare techniques.

Don’t think that the rest of the world hasn’t taken note of all this.

Meanwhile, the U.S. industrial capacity to provide the weapons and ammunition to fight this type of attritional war is highly inadequate.

The U.S. produces about 14,000 artillery shells per month, which it hopes to double over the next few years. That might seem like a lot. But 14,000 shells is only enough to supply Ukraine for about a week at current firing rates.

On the other hand, it’s estimated that the Russians are producing anywhere from 250,000-400,000 shells per month.

You do the math.

The Weakest Link in the Chain

But the weakest link in the chain isn’t inadequate ammunition or substandard equipment. The weakest link in the chain is U.S. senior leadership, particularly Joe Biden. The Russians and the Chinese have taken note.

They just conducted joint naval operations off the coast of Alaska and well within sight of U.S. territory in the Aleutian Islands.

Few Americans may realize or recall that, during World War II, the Japanese Imperial Navy actually did invade and occupy parts of Alaska close to where the Russians and Chinese are conducting surveillance today.

Weakness breeds weakness and eventually war. The weak leadership in the U.S. is inviting unprecedented challenges from our main rivals. Expect more of this until someday two ships collide or two planes collide in mid-air, potentially leading to a shooting war.

This wasn’t inevitable. For years, the U.S. has driven Russia into the arms of China through a combination of hubris and strategic shortsightedness. That was a massive mistake.

Worse Than a Crime, It Was a Blunder

Russia, China and the U.S. are the only true superpowers and the only three countries that ultimately matter in geopolitics. That’s not a slight against any other power. But all others are secondary powers (the UK, France, Germany, Japan, Israel, etc) or tertiary powers (Iran, Turkey, India, Pakistan, Saudi Arabia, etc).

One of the keys to U.S. foreign policy in the last 50 or 60 years has been to make sure that Russia and China never form an alliance. Keeping them separated was key.

Specifically, the U.S. has strived to ensure that no power, or combination of powers, could dominate the Eurasian landmass.

This meant that the ideal posture for the U.S. is to ally with Russia (to marginalize China) or ally with China (to marginalize Russia), depending on overall geopolitical conditions.

The U.S. conducted this kind of triangulation successfully from the 1970s until the early 2000s.

In 1972, Nixon pivoted to China to put pressure on Russia. In 1991, the U.S. pivoted to Russia to put pressure on China after the Tiananmen Square massacre.

Unfortunately, the U.S. lost sight of this basic rule of international relations. It is now Russia and China that have formed a strong alliance, to the disadvantage of the United States.

The war in Ukraine has intensified this dynamic.

Historians Will Scratch Their Heads

One leg of the China-Russia relationship is their joint desire to see the U.S. dollar lose its status as the world’s dominant reserve currency. They’ve chafed against the ways in which the U.S. has used the dollar as a financial weapon.

Again, the unprecedented sanctions against Russia have accelerated this process. We’ll see it come to fruition next week, when the BRICS nations are expected to launch a new gold-backed currency.

Ultimately, this two-against-one strategic alignment of China and Russia against the U.S. is a strategic blunder by Washington.

The fact is, Washington has squandered a major opportunity to shape the geopolitical world in America’s favor.

When future historians look back on the 2010s they will be baffled by the lost opportunity for the U.S. to mend fences with Russia, develop economic relations and create a win-win relationship between the world’s greatest technology innovator and the world’s greatest natural resources provider.

It will seem a great loss for the world.

Russia is the nation that the U.S. should have tried to court and should still be courting. That’s because China is the greatest geopolitical threat to the U.S. because of its economic and technological advances and its ambition to push the U.S. out of the Western Pacific sphere of influence.

Russia may be a threat to some of its neighbors (ask Ukraine), but it is far less of a threat to U.S. strategic interests. It’s not the Soviet Union anymore. Therefore, a logical balance of power in the world would be for the U.S. and Russia to find common ground in the containment of China and to jointly pursue the reduction of Chinese power.

Of course, that hasn’t happened. And we could be paying the price for years to come. Who’s to blame for this U.S. strategic failure? You can start with the globalist elites…

It’s All About Trump

The elites’ efforts to derail Trump gave rise to the “Russia collusion” hoax. While no one disputes that Russia sought to sow confusion in the U.S. election in 2016, that’s something the Russians and their Soviet predecessors had been doing since 1917. By itself, little harm was done.

Yet the elites seized on this to concoct a story of collusion between Russia and the Trump campaign. The real collusion was among Democrats, Ukrainians and Russians to discredit Trump.

It took the Robert Mueller investigation two years finally to conclude there was no collusion between Trump and the Russians. By then, the damage was done.

It was politically toxic for Trump to reach out to the Russians. That would be spun by the media as more evidence of “collusion.”

Whatever you think of Trump personally, the collusion story was always bogus.

Now, just a few short years later, Russia and China are successfully spearheading efforts to break away from the dollar and are conducting joint naval exercises within sight of American territory.

The U.S. has no one to blame but itself.

end

3,Chris Powell of GATA provides to us very important physical commentaries

Fitch warns it may have to downgrade dozens of banks, including JPM

Submitted by admin on Tue, 2023-08-15 13:57Section: Daily Dispatches

By Hugh Son

CNBC, New York

Tuesday, August 15, 2023

A Fitch Ratings analyst warned that the U.S. banking industry has inched closer to another source of turbulence — the risk of sweeping rating downgrades on dozens of U.S. banks that could even include the likes of JPMorgan Chase.

The ratings agency cut its assessment of the industry’s health in June, a move that analyst Chris Wolfe said went largely unnoticed because it didn’t trigger downgrades on banks.

But another one-notch downgrade of the industry’s score, to A+ from AA-, would force Fitch to reevaluate ratings on each of the more than 70 U.S. banks it covers, Wolfe told CNBC in an exclusive interview at the firm’s New York headquarters.

… For the remainder of the report:

https://www.cnbc.com/2023/08/15/fitch-warns-it-may-be-forced-to-downgrade-dozens-of-banks.html

end

Ed Steer: A much better than expected COT report

Submitted by admin on Tue, 2023-08-15 21:00Section: Daily Dispatches

9p ET Tuesday, August 15, 2023

Dear Friend of GATA and Gold (and Silver):

The weekend edition of Ed Steer’s Gold and Silver Digest, published by GATA board member Ed Steer, is headlined “A Much Better Than Expected COT Report” and it’s posted in the clear at SilverSeek here:

https://silverseek.com/article/much-better-expected-cot-report

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

4, OTHER IMPORTANT GOLD/SILVER COMMENTARIES

end

5 a. IMPORTANT COMMENTARIES ON COMMODITIES:

end

5 B GLOBAL COMMODITY ISSUES/FOOD IN GENERAL//FREIGHT

END

6.CRYPTOCURRENCY//DIGITAL CURRENCY// COMMENTARIES/

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS WEDNESDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED DOWN TO 7.2980

OFFSHORE YUAN: DOWN TO 7.3258

SHANGHAI CLOSED DOWN 26.05 PTS OR 0.82%

HANG SENG CLOSED DOWN 251.81 PTS OR 1.36%

2. Nikkei closed DOWN 472.07 OR 1.46%

3. Europe stocks SO FAR: ALL MIXED

USA dollar INDEX DOWN TO 102.99 EURO RISES TO 1.0917 UP 13 BASIS PTS

3b Japan 10 YR bond yield: FALLS TO. +.618 Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 145.73/JAPANESE YEN FALLING AS WELL AS LONG TERM 10 YR. YIELDS RISING //EVENTUALLY THIS WILL BREAK THE JAPANESE CENTRAL BANK

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen DOWN CHINESE ON SHORE YUAN: DOWN// OFF- SHORE: DOWN

3f Japan is to buy INFINITE TRILLION YEN’S worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil DOWN for WTI and DOWN FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund DOWN TO +2.6505***/Italian 10 Yr bond yield FALLS to 4.340*** /SPAIN 10 YR BOND YIELD FALLS TO 3.691…**

3i Greek 10 year bond yield FALLS TO 3.921

3j Gold at $1903.95 silver at: 22.67 1 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble UP 0 AND 83 /100 roubles/dollar; ROUBLE AT 96.14//

3m oil into the 80 dollar handle for WTI and 84 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 145.73// 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 0.619% STILL ON CENTRAL BANK (JAPAN) INTERVENTION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.8803 as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9616well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.195 DOWN 3 BASIS PTS…

USA 30 YR BOND YIELD: 4.307 DOWN 2 BASIS PTS/

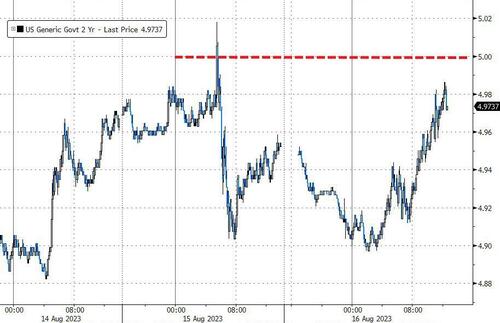

USA 2 YR BOND YIELD: 4.920 DOWN 1 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 27.06…(TURKEY SET TO BLOW UP FINANCIALLY)

GREAT BRITAIN/10 YEAR YIELD: DOWN 4 BASIS PTS AT 4.6590

end

2.a Overnight: Newsquawk and Zero hedge:

Futures Flat Ahead Of Fed Minutes As China Turmoil Grows

WEDNESDAY, AUG 16, 2023 – 08:05 AM

US equity futures and European stocks are little changed, having swung between gains and losses, following a broadly negative session in Asia where concerns surrounding the Chinese economy (home prices fell for the first time this year, fueling recession concerns despite increasing expectations for more stimulus) and the implosion of shadow banking giant Zhongrong (China’s Blackstone) continued to weigh on sentiment with focus remaining on earnings.

As of 7:30am, S&P 500 and Nasdaq 100 futures were unchanged, with JPM’s trading desk wondering if “there is enough momentum to stage a relief rally today” (full note available to pro subs). Commodities are rebounding across all three complexes with USD weaker. Government bonds in the US and Europe were broadly stronger, with US 10-year yields falling 3bps to 4.18%, halting a run of losses that was fueled by concern interest rates will be kept at high levels for longer than expected. The dollar rebounded from an early selloff while the pound strengthened as UK inflation topped expectations. Today’s macro focus is the Fed Minutes, housing data, Industrial Production, and Consumer-sector earnings.

In premarket trading, shares of Target jumped on a strong profit rebound at the retailer even as the company slashed its guidance, while electric-vehicle makers are lower again after Tesla cut its prices in China for the second time in three days, further fueling concerns of renewing a price war that had showed some signs of abating (Tesla -1.5%, Rivian -1.7% and Nikola -2.1%). Keep an eye on banks, which got hit on news of a potential sector-wide ratings downgrade; XLF and KRE are indicated flat pre-mkt. Here are some other notable premarket movers:

- Cava rises 12% after the fast-casual Mediterranean restaurant chain said it expects higher profits this year.

- Coherent falls 20% after the semiconductor device company forecast revenue for the first quarter that came in below analysts’ estimates.

- Dlocal shares soared 30% after the Uruguayan financial technology firm reported second-quarter net income that beat estimates and named e-commerce veteran Pedro Arnt as co-CEO. Analysts said the results were strong and applauded Arnt’s appointment.

- Occidental edges up 0.4% after the oil producer said it agreed to acquire Canadian startup Carbon Engineering Ltd. for $1.1 billion in cash.

- Target (TGT) climbs 7.7% after reporting fiscal second-quarter adjusted earnings per share and gross margin that topped the average analyst estimates. Adjusted EPS $1.80 vs. 39c y/y, estimate $1.40. Still, the retailer lowered its full-year sales and profit expectations.

- VinFast Auto falls 12% after the Vietnamese automaker’s shares surged 255% on Tuesday when it debuted on the Nasdaq Global Select Market, becoming the latest beneficiary of frenzy around SPAC deals.

- AngioDynamics (ANGO) gains 8.4% after the company said the FDA has granted breakthrough device designation for AngioVac System “for use to include the non-surgical removal of vegetation from the right heart.”.

- Coherent falls 24% after the semiconductor device company gave a forecast that was weaker than expected.

- Nubank (NU) shares advance 3.4% after the digital bank reported second-quarter net income that beat estimates. Morgan Stanley said the results were solid, while Numis noted that the company had achieved the objectives that were core to its business model.

Market sentiment was dented by a renewed concerns about China’s economic woes despite a slew of stimulus steps by authorities, with the onshore yuan sinking toward its weakest in 16 years against the dollar and the MSCI China Index of stocks set to erase gains seen since a key policy meeting in late July.

China’s central bank moved again on Wednesday to boost fragile sentiment with a stronger-than-expected reference rate for the yuan and the largest injection of short term cash to the financial system since February. So far the steps have failed to restore optimism and market moves suggest traders are looking for more aggressive supportive measures. “Market participants are watching the developments on the real estate markets in China and the US with growing concern,” said Andreas Lipkow, a strategist at Comdirect Bank. Realizing the futility of China’s piecemeal interventions which do nothing, a PBOC central banker has now called for at least 3 trillion yuan in helicopter money to stimulate flagging consumer demand.

Meanwhile, money-market wagers for the Bank of England’s peak interest rate held steady at 6% after the UK inflation print came in hotter than expected as the cost of travel and holidays climbed. The numbers added to hot wage figures and US retail statistics that rattled markets on Tuesday, spurring bets tight central bank policy will be in place for longer. inneapolis Fed President Neel Kashkari warned that inflation was “still too high.”

European equities moved between modest gains and losses as growing pessimism around China’s economic outlook prompted caution among investors. Higher-than-expected UK inflation data also weighed on sentiment. The Stoxx Europe 600 was little changed after falling to the lowest level in a month on Tuesday. Retailers led gains while energy and travel and leisure stocks were the biggest laggards. Among individual stocks, Admiral Group Plc rallied after reporting results that Jefferies said showed that its UK car business had recovered well. Elsewhere, nutrition firm Glanbia Plc advanced after boosting its full-year adjusted earnings guidance. Here are the biggest European movers:

- Aviva rises as much as 3% after the UK insurer and asset manager said 2023 earnings should exceed medium-term targets. Morgan Stanley notes improving property and casual insurance

- Sectra gains as much as 9.9%, the most since June, after the medical imaging firm announced it has won an enterprise imaging contract with “one of the larger multi-region healthcare systems in the US”

- Demant gains as much as 5.3% after the Danish hearing-aid maker raised its sales and earnings outlook for the year. Still, the guidance upgrade was “widely anticipated,” according to Citi analysts

- B&M European Value Retail rises as much as 3.2% in a third day of gains amid speculation that the company could bid for collapsed British discounter Wilko

- Glanbia shares climb as much as 5.7% to the highest since September 2021 after the Irish food and nutrition company increased its outlook for the year and named Hugh McGuire as its new CEO

- Balfour Beatty falls as much as 4.8%, the most intraday since February, after the UK construction and infrastructure group’s 1H EPS came below expectations and its net cash position fell, Liberum writes

- Prosus shares drop as much as 3.9% in Amsterdam trading after Tencent’s second-quarter revenue missed expectations, held back by lower-than-expected sales from games both at home and abroad

- Antofagasta falls as much as 2.4% after RBC Capital downgrades to underperform, citing growing capital expenditure and a risk to the premium valuation the miner has built year-to-date

- Storskogen falls as much as 26% after the Swedish acquisition group’s second-quarter Ebit dropped 11% y/y and fell 19% short of consensus expectations, also guiding for continued challenges

Asian equities retreat for fourth day as risk appetite remained low in the wake of growing economic concerns in China and prospects of the Federal Reserve keeping rates higher for longer. The MSCI Asia Pacific Index fell as much as 1.4%, set for its lowest close since May 31. Chinese equities weighed on the regional benchmark as disappointing economic data worsened the recent selloff, while South Korean gauges were the worst performers regionally as foreign investors sold shares amid a stronger dollar. Hang Seng falls 1.2% and mainland indexes lose ground. Japanese, South Korean and Australian stock indexes all decline.

“A recent set of disappointing economic data out of China has not been encouraging for the region,” Jun Rong Yeap, Market Analyst at IG Asia Pte. said in a note. The aggressive 15 bps cut by Chinese central bank to its one-year policy interest reflects the severity of the economic weakness that authorities foresee to drag on for longer, Yeap said.

- The Hang Seng and Shanghai Comp remained pressured amid China growth concerns as recent poor data releases have prompted several banks to cut their growth forecasts for the world’s second-largest economy including JPMorgan which now anticipates 4.8% GDP growth for China this year, while the latest House Price data also showed a contraction Y/Y to add to the ongoing developer woes. The MSCI China Index is on course to erase all its gains made since last month’s Politburo meeting, reflecting growing anxiety among investors that Asia’s largest economy needs major economic stimulus to boost its consumption and property sector.

- Japanese stocks fell on Wednesday amid concerns that interest rates will stay higher for longer in the US and as the outlook for the Chinese economy remained downbeat. The Topix Index fell 1.3% to 2,260.84 while the Nikkei declined 1.5% to 31,766.82. Materials-related stocks such as steel and non-ferrous metals declined, as did trading company stocks.

- In Australia, the ASX 200 was led lower by the large industries, while participants also digested earnings and a softer leading index.

- Stocks in India erased initial losses to end higher as utilities and automakers gained. Local shares were among major gainers in Asia as most regional peers fell amid concerns over slowing growth in China. The S&P BSE Sensex rose 0.2% to 65,539.42 in Mumbai. The NSE Nifty 50 Index advanced by a similar measure before recovering from a drop of as much as 0.6%. Trading in India was closed on Tuesday for a local holiday.

In FX, the Bloomberg Dollar Spot Index edged lower, falling as much as 0.2% after four-straight days of increases. The dollar was lower against all G10 peers.

- The pound rose as much as 0.5% to $1.2766, set for a second day of gains versus the dollar after inflation data came in slightly stronger than expected. It’s the best performer among the G-10’s with the kiwi, which rose after the RBNZ left the door open to further rate hikes.

- EUR/USD snapped three days of declines against the US dollar, rising about 0.3% to 1.0934

- The New Zealand dollar reversed an intraday decline after the Reserve Bank left its key rate unchanged at 5.5% but signaled a small chance of another rate hike. Yields on 2-year swaps also reversed its 2.5-basis point slidethanks earlier in the day

- A selloff in Chinese assets deepened on Wednesday, with a key equity gauge set to erase all gains seen since last month’s Politburo meeting and the yuan falling toward a 16-year low.