GOLD PRICE CLOSED: DOWN $12.80 TO $1886.00

SILVER PRICE CLOSED: UP $0.13 AT $22.65

Access prices: closes 4: 15 PM

Gold ACCESS CLOSE 1889.25

Silver ACCESS CLOSE: 22.67

Shanghai Gold Benchmark Price

USD oz

AM1945.83

AM1945.83

PM1949.88

Historical SGE Fi

New York price at the time: 1892.00

premium $62,00

xxxxxxxxxxxxxxxxxx

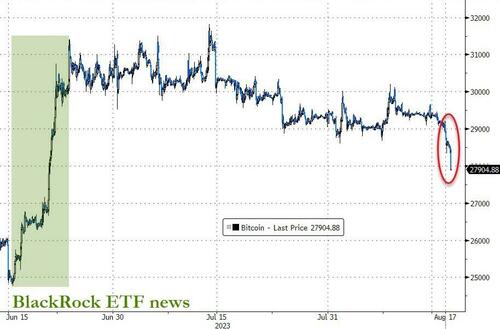

Bitcoin morning price:, $28,533 DOWN 560 Dollars

Bitcoin: afternoon price: $29,093 DOWN 220 dollars

Platinum price closing $895.10 UP $2.00

Palladium price; $1218.05 DOWN 18.65

END

Due to the huge rise in the dollar, we must look at gold and silver in currencies other than the dollar to understand where we are heading

I will now provide gold in Canadian dollars, British pounds and Euros/4: 15 PM ACCESS

CANADIAN GOLD: $2,558.59 DOWN 2.90 CDN dollars per oz (ALL TIME HIGH 2,775.35)

BRITISH GOLD: 1482.16 DOWN 5.33 pounds per oz//(ALL TIME HIGH//CLOSING///1630.29)

EURO GOLD: 1737,61 DOWN 3,42 euros per oz //(ALL TIME HIGH/CLOSING//1861.21)//

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

EXCHANGE: COMEX

EXCHANGE: COMEX

CONTRACT: AUGUST 2023 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,896.100000000 USD

INTENT DATE: 08/16/2023 DELIVERY DATE: 08/18/2023

FIRM ORG FIRM NAME ISSUED STOPPED

363 H WELLS FARGO SEC 5

657 C MORGAN STANLEY 1

690 C ABN AMRO 5

737 C ADVANTAGE 5

991 H CME 4

TOTAL: 10 10

MONTH TO DATE: 10,737

JPMorgan stopped 0 /10 contracts.

FOR AUGUST:

GOLD: NUMBER OF NOTICES FILED FOR AUGUST/2023. CONTRACT: 10 NOTICES FOR 1000 OZ or 0.03110 TONNES

total notices so far: 10,737 contracts for 1,073,700 oz (33.365 tonnes)

FOR AUGUST:

SILVER NOTICES: 5 NOTICE(S) FILED FOR 25,000 OZ/

total number of notices filed so far this month : 930 for 4,650,000 oz

XXXXXXXXXXXXXXXXXXXXXXXX

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD

WITH GOLD DOWN $12.80

INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD//NO CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.44 TONNES OF GOLD FROM THE GLD

INVENTORY RESTS AT 894.42 TONNES

Silver//

WITH NO SILVER AROUND AND SILVER UP 15 CENTS AT THE SLV// NO CHANGES IN SILVER INVENTORY AT THE SLV:

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV.

CLOSING INVENTORY: 452.290 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A GOOD SIZED 623 CONTRACTS TO 137,406 AND FURTHER FROM THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THIS GOOD SIZED LOSS IN COMEX OI WAS ACCOMPLISHED WITH OUR $0.13 LOSS IN SILVER PRICING AT THE COMEX ON WEDNESDAY. TAS ISSUANCE WAS A RATHER SMALLER SIZED 627 CONTRACTS. THESE WILL BE USED FOR MANIPULATION LATER THIS MONTH/AS WELL AS TODAY. CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON TUESDAY NIGHT: 650 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS. IT THUS LOOKS LIKE THE FED (GOV’T) IS BEHIND ALL OF THESE TRADES.

WE HAVE NOW SET ANOTHER RECORD LOW AT 114,102 CONTRACTS ///JULY 3.2023// OUR BANKERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.13). AND WERE SUCCESSFUL IN KNOCKING OF SOME SILVER CONTRACTS(IF ANY STILL EXIST) AS WE HAD OUR GOOD SIZED LOSS OF 699 CONTRACTS ON BOTH EXCHANGES ALONG WITH CONSIDERABLE T.A.S.LIQUIDATION THROUGHOUT THE COMEX SESSION.

WE MUST HAVE HAD:

A SMALL ISSUANCE OF EXCHANGE FOR PHYSICALS( 110 CONTRACTS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 3.105 MILLION OZ (FIRST DAY NOTICE) FOLLOWED BY TODAY’S 25,000 OZ QUEUE JUMP //NEW STANDING RISES AT 4.650 MILLION OZ + OUR NEW CRIMINAL 0 CONTRACTS OF EXCHANGE FOR RISK FOR 0.00 MILLION OZ + 1.45 MILLION OZ EX. FOR RISK/PRIOR/// NEW TOTAL STANDING FOR SILVER: 6.100 MILLION OZ/// // // GOOD SIZED COMEX OI LOSS/ SMALL SIZED EFP ISSUANCE/VI) SMALLER BUT STILL STRONG SIZED NUMBER OF T.A.S. CONTRACT ISSUANCE (627 CONTRACTS)/ZERO EXCHANGE FOR RISK ISSUED

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL -186 CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS AUGUST. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF AUGUST:

TOTAL CONTRACTS for 13 days, total 17,587 contracts: OR 87.935 MILLION OZ (1353 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 87.935 MILLION OZ

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH 2022: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 118.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 85.745 MILLION OZ (SMALLER THAN LAST MONTH)

AUGUST: 87.385 MILLION OZ (THIS MONTH IS GOING TO BE VERY STRONG

RESULT: WE HAD A GOOD SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 809 CONTRACTS WITH OUR LOSS IN PRICE OF $0.13 IN SILVER PRICING AT THE COMEX//WEDNESDAY.,. THE CME NOTIFIED US THAT WE HAD A SMALL EFP ISSUANCE CONTRACTS: 110 ISSUED FOR SEPT AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS./ WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR AUGUST OF 3.105 MILLION OZ FOLLOWED BY TODAY’S 25,000 OZ QUEUE JUMP//NEW STANDING 4.650 MILLION OZ+ 1.45 MILLION OZ EXCHANGE FOR RISK NEW TOTALS 6.100 MILLION OZ//// WE HAVE A FAIR SIZED LOSS OF 699 OI CONTRACTS ON THE TWO EXCHANGES. THE TOTAL OF TAS INITIATED CONTRACTS TODAY: A SMALLER BUT STILL STRONG 627 CONTRACTS//HUGE FRONT END OF THE TAS CONTRACTS WERE LIQUIDATED DURING THE WEDNESDAY COMEX SESSION . THE NEW TAS ISSUANCE WEDNESDAY NIGHT (627) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE., .

WE HAD 5 NOTICE(S) FILED TODAY FOR 25,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A FAIR SIZED 1137 CONTRACTS TO 434,748 AND CLOSER TO TO THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: – REMOVED: 586 CONTRACTS

WE HAD A GOOD SIZED INCREASE IN COMEX OI ( 1137 CONTRACTS) DESPITE OUR $7.00 LOSS IN PRICE//WEDNESDAY. WE ALSO HAD A RATHER SMALL INITIAL STANDING IN GOLD TONNAGE FOR AUGUST. AT 30.656 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S 600 OZ QUEUE JUMP + PRIOR ISSUANCE OF EXCHANGE FOR RISK = (.684 TONNES) //NEW STANDING 33.564 TONNES + .684 EXCHANGE FOR RISK = 34.248/ + /A SMALL (AND CRIMINAL) ISSUANCE OF 831 T.A.S. CONTRACTS /// ALL OF..THIS HAPPENED WITH A $7,00 LOSS IN PRICE WITH RESPECT TO WEDNESDAY’S TRADING.WE HAD A GOOD SIZED GAIN OF 3996 OI CONTRACTS (12.336 PAPER TONNES) ON OUR TWO EXCHANGES.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 2829 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 434,748

IN ESSENCE WE HAVE A GOOD SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 3996 CONTRACTS WITH 1137 CONTRACTS INCREASED AT THE COMEX// AND A FAIR 2829 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 3996 CONTRACTS OR 12.336 TONNES. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): A SMALL 831 CONTRACTS)

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (2829 CONTRACTS) ACCOMPANYING THE FAIR SIZED GAIN IN COMEX OI (1137) //TOTAL GAIN FOR OUR THE TWO EXCHANGES: 3966 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR NORMAL FORMAT OF BANKERS GOING SHORT AND SPECULATORS GOING LONG ,2.) FAIR INITIAL STANDING AT THE GOLD COMEX FOR JULY AT 30.656 TONNES FOLLOWED BY TODAY’S 600 OZ QUEUE JUMP //NEW STANDING 33.564 TONNES + .684 TONNES (EXCHANGE FOR RISK//PRIOR) NEW TOTALS: 34.248 TONNES/// 3) ZERO LONG LIQUIDATION WITH CONSIDERABLE TAS LIQUIDATION DURING THE COMEX SESSION //4) FAIR SIZED COMEX OPEN INTEREST GAIN/ 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER///6: SMALL T.A.S. ISSUANCE: 1831 CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023 INCLUDING TODAY

AUGUST

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF AUG :

TOTAL EFP CONTRACTS ISSUED: 36,333 CONTRACTS OR 3,633,300 OZ OR 113.01 TONNES IN 13TRADING DAY(S) AND THUS AVERAGING: 2794 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 13 TRADING DAY(S) IN TONNES 113.01 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2022, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 113.01/3550 x 100% TONNES 3.18% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2023

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH/2022: 409.30 TONNES //FINAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 151.69 TONNES (WEAKER THAN LAST MONTH)

AUGUST: 113.01 TONNES (A STRONGER MONTH)

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF SEPT. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF MAY HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF JUNE., FOR BOTH GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (SEPT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER FELL BY A GOOD SIZED 809 CONTRACTS OI TO 137,406 AND CLOSER TO OUR COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE A SMALL 110 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

SEPT 110 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 110 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 809 CONTRACTS AND ADD TO THE 110 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A FAIR SIZED LOSS OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 699 CONTRACTS

THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES TOTAL 3.495 MILLION OZ

OCCURRED DESPITE OUR TINY $0.13 LOSS IN PRICE …..

END

OUTLINE FOR TODAY’S COMMENTARY

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

b, ) Gold/silver trading overnight Europe,//GOLD COMMENTARIES

(Peter Schiff)

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS//

THURSDAY MORNING//WEDNESDAY NIGHT

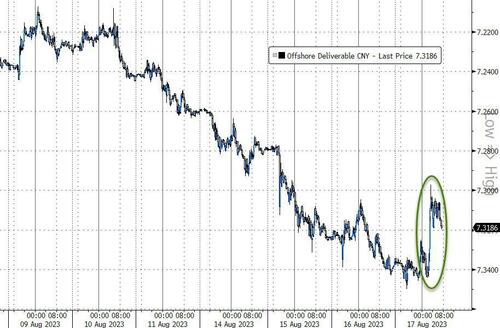

SHANGHAI CLOSED UP 13.61 PTS OR 0.43% //Hang Seng CLOSED DOWN 2.67 PTS OR 0.01% /The Nikkei CLOSED DOWN 140.82 PTS OR 0.44% //Australia’s all ordinaries CLOSED DOWN 0.54 % /Chinese yuan (ONSHORE) closed UP 7.2439 /OFFSHORE CHINESE YUAN UP TO 7.3113 /Oil UP TO 80.18 dollars per barrel for WTI and BRENT UP AT 84.25 / Stocks in Europe OPENED ALL RED// ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE STRONGER

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

9. USA

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A FAIR SIZED 1137 CONTRACTS UP TO 434,748 DESPITE OUR LOSS IN PRICE OF $7.00 ON WEDNESDAY.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE ACTIVE DELIVERY MONTH OF AUGUST… THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 2829 EFP CONTRACTS WERE ISSUED: : DEC 2829 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 2829 CONTRACTS

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A GOOD SIZED TOTAL OF 3996 CONTRACTS IN THAT 2829 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A FAIR SIZED GAIN OF 1137 COMEX CONTRACTS..AND THIS GAIN ON OUR TWO EXCHANGES HAPPENED DESPITE OUR LOSS IN PRICE OF $7.00//WEDNESDAY COMEX. AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS DURING MID MONTH IN THE DELIVERY CYCLE), THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR WEDNESDAY NIGHT WAS A SMALL 831 CONTRACTS. THROUGHOUT THE PAST WEEKS, THE BANKERS SOLD OFF THE LONG SIDE OF THE SPREAD WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR SPREAD WHICH WILL BE LIQUIDATED TWO MONTHS HENCE)//

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: AUGUST (34.248) ( ACTIVE MONTH)

TONNES),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 34.248 TONNES (INCLUDING .6842 EXCHANGE FOR RISK)

THE SPECS/HFT WERE SUCCESSFUL IN LOWERING GOLD’S PRICE( IT LOST $7.00) //// BUT WERE UNSUCCESSFUL IN KNOCKING ANY SPECULATOR LONGS (IF ANY STILL EXIST) AS WE HAD A GOOD GAIN OF 4552 TOTAL CONTRACTS ON OUR TWO EXCHANGES. WE HAD CONSIDERABLE T.A.S. LIQUIDATION ON THE FRONT END OF YESTERDAY’S TRADING. THE T.A.S. ISSUED ON WEDNESDAY NIGHT WILL BE “PUT INTO THE BANK” TO BE USED AT A LATER DATE AT THE COLLUSIVE CHOOSING OF OUR BANKERS.

WE HAVE GAINED A TOTAL OI OF 12.336 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR AUGUST. (30.656 TONNES) ON FIRST DAY NOTICE FOLLOWED BY TODAY’S 600 OZ QUEUEJUMP //NEW STANDING ADVANCES A BIT TO 33.564 TONNES + .6842 (PRIOR EXCHANGE FOR RISK) //NEW TOTAL 34.248 TONNES // ALL OF THIS WAS ACCOMPLISHED WITH OUR LOSS IN PRICE TO THE TUNE OF $7.00.

WE HAD – REMOVED 586 CONTRACTS TO THE COMEX TRADES TO OPEN INTEREST

NET GAIN ON THE TWO EXCHANGES 3996 CONTRACTS OR 396,600 OZ OR 12.336 TONNES.

Estimated gold volume today:// 144,882 awful

final gold volumes/yesterday 135,545 awful//speculators have left the gold arena

//AUGUST 17/ FOR THE AUGUST 2023 GOLD CONTRACT

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 171,215.199 OZ jpm, BRINKS Hsbc, Manfra 5 KILOBARS (Brinks) rest real gold leaving . |

| Deposit to the Dealer Inventory in oz | nil |

| Deposits to the Customer Inventory, in oz | nil OZ |

| No of oz served (contracts) today | 10 notice(s) 1000 OZ 0.03110 TONNES |

| No of oz to be served (notices) | 54 contracts 5400 oz 0.1678 TONNES |

| Total monthly oz gold served (contracts) so far this month | 10,737 notices 1,073,700 OZ 33.396 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | x |

0 dealer deposit:

total dealer deposits: NIL oz

customer deposits: 0

total customer deposits: nil oz

we had 4 customer withdrawals

i) Out of JPMorgan: 134,780.449 oz

ii) Out of Brinks 160.75 oz (5 kilobares)

iii) Out of HSBC; 15,251.245 oz

iv) Out of Manfra 21,522.755 oz

total; 171,215.199 oz and most of this is real gold leaving

Adjustments; 0

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR AUGUST.

For the front month of AUGUST we have an oi of 64 contracts having LOST 18 contracts. We had 24 contracts filed

on Wednesday, so we gained 6 contracts or an additional 600 oz will stand at the comex,

Sept gained 52 contracts to 2919.

Oct lost 350 contracts to 33,215 contracts.

We had 10 contracts filed for today representing 1000 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 10 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped received by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the AUGUST /2023. contract month,

we take the total number of notices filed so far for the month (10,737 x 100 oz ), to which we add the difference between the open interest for the front month of AUGUST (64 CONTRACT) minus the number of notices served upon today 10 x 100 oz per contract equals 1,079,100 OZ OR 33.564 TONNES the number of TONNES standing in this active month of AUGUST. + .684 TONNES EXCHANGE FOR RISK/prior = 34.248 tonnes

thus the INITIAL standings for gold for the AUGUST contract month: No of notices filed so far (10,737) x 100 oz + (64) {OI for the front month} minus the number of notices served upon today (10) x 100 oz) which equals 1,079,100 oz standing OR 33.564 TONNES + .684 TONNES OF EXCHANGE FOR RISK/prior = 34.248 TONNES

TOTAL COMEX GOLD STANDING: 34.248 TONNES WHICH IS SMALL FOR AN ACTIVE DELIVERY MONTH.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 2,101,333.235 OZ 65.36 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 21,832,184.747 OZ

TOTAL REGISTERED GOLD: 11,680,181.113 (363.30 tonnes)..

TOTAL OF ALL ELIGIBLE GOLD: 10,182,003.634 O Z

REGISTERED GOLD THAT CAN BE SERVED UPON: 9,578,848 OZ (REG GOLD- PLEDGED GOLD) 297.942 tonnes//

END

SILVER/COMEX

AUGUST 17

//2023// THE AUGUST 2023 SILVER CONTRACT

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 44,778.445 oz Delaware . |

| Deposits to the Dealer Inventory | nil oz |

| Deposits to the Customer Inventory | 584,333.390 oz Delaware Loomis |

| No of oz served today (contracts) | 5 CONTRACT(S) (25,000 OZ) |

| No of oz to be served (notices) | 0 contracts (nil oz) |

| Total monthly oz silver served (contracts) | 930 Contracts (4,650,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

i) 0 dealer deposit

total dealer deposit: 0 oz

i) We had 0 dealer withdrawal

total dealer withdrawals: 0 oz

We had 2 deposits customer account:

i)Into Delaware: 1001.000 oz

ii) Into Loomis 583,333.390

total customer deposits: 584,333.390 oz

JPMorgan has a total silver weight: 139.276 million oz/279.707 million =49.69% of comex .//

Comex withdrawals 1

i) Out of Delaware 44,778.445 oz

total: 44,778.445 oz

adjustments: 1 and it was a dandy: 3,223,848.270 oz adjusted out of the dealer Brinks into the customer account

TOTAL REGISTERED SILVER: 27.604 MILLION OZ//.TOTAL REG + ELIGIBLE. 279.707 million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR JULY:

silver open interest data:

FRONT MONTH OF AUGUST /2023 OI: 5 CONTRACTS HAVING LOST 4 CONTRACT(S). WE HAD

9 NOTICES FILED ON WEDNESDAY SO WE GAINED 5 CONTRACTS OR AN ADDITIONAL 25,000 OZ WILL STAND IN THIS NON ACTIVE DELIVERY MONTH OF AUGUST.

SEPT HAS A LOSS OF 2176 CONTRACTS DOWN TO 58,109

OCT GAINED 9 CONTRACT TO STAND AT 488.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 5 for 25,000 oz

Comex volumes// est. volume today 74,416 good

Comex volume: confirmed yesterday: 58,800 fair

To calculate the number of silver ounces that will stand for delivery in AUGUST. we take the total number of notices filed for the month so far at 9230 x 5,000 oz = 4,650,000 oz

to which we add the difference between the open interest for the front month of AUGUST (5) and the number of notices served upon today 5 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the AUGUST/2023 contract month: 930 (notices served so far) x 5000 oz + OI for the front month of AUGUST (5) – number of notices served upon today (5 )x 500 oz of silver standing for the AUGUST contract month equates to 4.625 million oz.+ 0.0 MILLION OZ EXCHANGE FOR RISK ISSUED TODAY+ 1.45 MILLION OZ EXCHANGE FOR RISK PRIOR//NEW TOTALS: 6.075 MILLION oz.

There are 27.604 million oz of registered silver.

Thus if we take today’s standing at 6.075 and add last month’s 30.9 million oz we have 36.975 million oz against only 27.604 million registered silver.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS

AUGUST 17/WITH GOLD DOWN $12.80 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD: //: /// //INVENTORY RESTS AT 894.42 TONNES

AUGUST 16/WITH GOLD DOWN $7.00 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.44 TONNES FORM THE GLD//: /// //INVENTORY RESTS AT 894.42 TONNES

AUGUST 15/WITH GOLD DOWN $7,45 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.76 TONNES FORM THE GLD//: /// //INVENTORY RESTS AT 895.87 TONNES

AUGUST 14/WITH GOLD DOWN $2.10 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.75 TONNES FORM THE GLD//: /// //INVENTORY RESTS AT 899.63 TONNES

AUGUST 11/WITH GOLD DOWN $2.10 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .31 TONNES FORM THE GLD//: /// //INVENTORY RESTS AT 903.31 TONNES

AUGUST 10/WITH GOLD DOWN $1.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD: /// //INVENTORY RESTS AT 903.69 TONNES

AUGUST 9/WITH GOLD DOWN $8.75 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD: /// //INVENTORY RESTS AT 903.69 TONNES

AUGUST 8/WITH GOLD DOWN $9.60 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.31 TONNES FORM THE GLD /// //INVENTORY RESTS AT 903.69 TONNES

AUGUST 7/WITH GOLD DOWN $5.45 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD: /// //INVENTORY RESTS AT 906.00 TONNES

AUGUST 4/WITH GOLD UP $7.25 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.18 TONNES OF GOLD FROM THE GLD/// .///INVENTORY RESTS AT 906.00 TONNES

AUGUST 3/WITH GOLD DOWN $5.25 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD //: //: / .////INVENTORY RESTS AT 909.18 TONNES

AUGUST 2/WITH GOLD DOWN $3.45 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 3.75 TONNES OF GOLD FROM THE GLD//: //: / .////INVENTORY RESTS AT 909.18 TONNES

AUGUST 1/WITH GOLD DOWN $28.45 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 2.89 TONNES OF GOLD FROM THE GLD//: //: / .////INVENTORY RESTS AT 912.93 TONNES

JULY 31/WITH GOLD UP $9.50 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 2.89 TONNES OF GOLD FROM THE GLD//: //: / .////INVENTORY RESTS AT 912.93 TONNES

JULY 28/WITH GOLD UP $14.15 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 1.44 TONNES OF GOLD FROM THE GLD//: //: / .////INVENTORY RESTS AT 915,82 TONNES

JULY 27/WITH GOLD DOWN $21.80 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 1.74 TONNES OF GOLD FROM THE GLD//: //: / .////INVENTORY RESTS AT 917.26 TONNES

JULY 26/WITH GOLD UP $6.35 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD: //: / .////INVENTORY RESTS AT 919.00 TONNES

JULY 25/WITH GOLD UP $2.45 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD: //: / .////INVENTORY RESTS AT 919.00 TONNES

JULY 24/WITH GOLD DOWN $4.65 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 5.20 TONNES OF GOLD INTO THE GLD//: / .////INVENTORY RESTS AT 919.00 TONNES

JULY 21/WITH GOLD DOWN $3.80 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD: / .////INVENTORY RESTS AT 913.80 TONNES

JULY 20/WITH GOLD DOWN $8.70 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.73 TONNES FROM THE GLD/ .////INVENTORY RESTS AT 913.80 TONNES

JULY 19/WITH GOLD UP $0.65 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .86 TONNES FROM THE GLD/ .////INVENTORY RESTS AT 912.07 TONNES

JULY 18/WITH GOLD UP $23.45 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD: .////INVENTORY RESTS AT 912.93 TONNES

JULY 17/WITH GOLD DOWN $6.60 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.73 TONNES OF GOLD FROM THE GLD.////INVENTORY RESTS AT 912.93 TONNES

JULY 14/WITH GOLD UP $0.75 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD: ////INVENTORY RESTS AT 914.66 TONNES

JULY 13/WITH GOLD UP $3.30 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 0.29 TONNES OF GOLD OUT OF THE GLD////INVENTORY RESTS AT 914.66 TONNES

JULY 12/WITH GOLD UP $24.50 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 0.31 TONNES OF GOLD OUT OF THE GLD////INVENTORY RESTS AT 914.95 TONNES

JULY 11/WITH GOLD UP $6.15 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.0 TONNES OF GOLD OUT OF THE GLD////INVENTORY RESTS AT 915.26 TONNES

JULY 10 WITH GOLD DOWN $1.35 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.60 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 916.26 TONNES.

GLD INVENTORY: 894.42 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

AUGUST 17/WITH SILVER UP 15 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//.////INVENTORY RESTS AT 452.290 MILLION OZ

AUGUST 16/WITH SILVER DOWN 13 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 0.275 MILLION OZ INTOTHE SLV/: / .////INVENTORY RESTS AT 452.290 MILLION OZ

AUGUST 15/WITH SILVER DOWN 6 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 0.275 MILLION OZ INTOTHE SLV/: / .////INVENTORY RESTS AT 452.290 MILLION OZ

AUGUST 14/WITH SILVER DOWN 3 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV A DEPOSIT OF 0.459 MILLION OZ INTOTHE SLV/: //////INVENTORY RESTS AT 452.565 MILLION OZ

AUGUST 11/WITH SILVER DOWN 6 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A DEPOSIT OF 1.926 MILLION OZ INTOTHE SLV/: // OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 452.106 MILLION OZ

AUGUST 10/WITH SILVER UP 6 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 8,807 MILLION OZ OUT OF THE SLV/: // OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 450.180 MILLION OZ

AUGUST 9/WITH SILVER DOWN 7 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 8,807 MILLION OZ OUT OF THE SLV/: // OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 450.180 MILLION OZ

AUGUST 8/WITH SILVER DOWN 40 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: // OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 458.987 MILLION OZ

AUGUST 7/WITH SILVER DOWN 46 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: // OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 458.987 MILLION OZ

AUGUST 4/WITH SILVER UP 1 CENT TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.294 MILLION OZ FROM THE SLV// OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 458.987 MILLION OZ

AUGUST 3/WITH SILVER DOWN 16 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 189,000 OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 451.281 MILLION OZ

AUGUST 2/WITH SILVER DOWN 43 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 275,000 OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 451.471 MILLION OZ

AUGUST 1/WITH SILVER DOWN 61 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 184,000 OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 451.746 MILLION OZ

JULY 31/WITH SILVER UP 45 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 184,000 OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 451.746 MILLION OZ

JULY 28/WITH SILVER UP 15 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 550,000 OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 451.930 MILLION OZ

JULY 27/WITH SILVER DOWN 59 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: .////INVENTORY RESTS AT 452.480 MILLION OZ

JULY 26/WITH SILVER UP 15 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: .////INVENTORY RESTS AT 452.480 MILLION OZ/

JULY 25/WITH SILVER UP 24 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A SMALL WITHDRAWAL OF 826,000 OZ FROM THE SLV..////INVENTORY RESTS AT 452.480 MILLION OZ/

JULY 24/WITH SILVER DOWN 23 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: ////INVENTORY RESTS AT 453.306 MILLION OZ/

JULY 21/WITH SILVER DOWN 14 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 1.101 MILLION OZ OF SILVER FROM THE SLV ////INVENTORY RESTS AT 453.306 MILLION OZ/

JULY 20/WITH SILVER DOWN 38 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 1.468 MILLION OZ OF SILVER FROM THE SLV ////INVENTORY RESTS AT 454.107 MILLION OZ/

JULY 19/WITH SILVER UP 11 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV:A ////INVENTORY RESTS AT 455.875 MILLION OZ/

JULY 18/WITH SILVER DOWN 19 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV:A ////INVENTORY RESTS AT 455.875 MILLION OZ/

JULY 17/WITH SILVER UP 25 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 4.856 MILLION OZ OF SILVER FROM THE SLV////////INVENTORY RESTS AT 455.875 MILLION OZ/

JULY 14/WITH SILVER UP 27 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 2.21 MILLION OZ OF SILVER FROM THE SLV////////INVENTORY RESTS AT 455.875 MILLION OZ/

JULY 13/WITH SILVER UP 64 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//////INVENTORY RESTS AT 462.941 MILLION OZ/

JULY 12/WITH SILVER UP $1.00 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.881 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 462.941 MILLION OZ/

JULY 11/WITH SILVER DOWN 5 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF .020 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 464.822 MILLION OZ/

JULY 10/WITH SILVER UP 2 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.672 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 464.802 MILLION OZ

//

CLOSING INVENTORY 452.290 MILLION OZ//

PHYSICAL GOLD/SILVER COMMENTARIES

1:Peter Schiff/Mike Maharrey

2 Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens//JAMES RICKARDS//JOHN RUBINO

end

3,Chris Powell of GATA provides to us very important physical commentaries

end

4, OTHER IMPORTANT GOLD/SILVER COMMENTARIES

Simon Black is always a great read….

(Simon Black)

I’m rooting for gold to go to zero. Too bad it won’t

![]()

BY SOVEREIGN MAN

WEDNESDAY, AUG 16, 2023 – 15:23

by Simon Black via Sovereign Man

By the time Wang Mang seized the imperial throne of China’s Han dynasty in the year 9 AD, he had already been a long-standing politician and government bureaucrat with decades of experience.

Not that Wang’s experience was especially helpful to the people of China.

As a seasoned politician, Wang’s biggest skills were setting up his opponents, cheating his way to the throne, and coming up with terrible ideas to destroy prosperity.

China’s Han dynasty had once been the pinnacle of civilization, most likely even surpassing the grandeur and wealth of the Roman Republic and ancient Greece. But Wang was one of the key figures who helped tear it down.

As emperor he was a total disaster. Wang had a thing for social and economic justice… so he imposed a bunch of idiotic land reforms to reduce inequality and form a more egalitarian society.

Instead of the ‘justice’ that he had envisioned, agricultural production plummeted and a lot of people went hungry.

Failing to see his error in judgment, Wang Mang doubled down by nationalizing entire industries, which only stifled investment and entrepreneurship.

Soon the Chinese economy was in the dumps. Prices soared. So the Emperor then (naturally) hatched the genius idea of imposing severe price controls… resulting in even more shortages and economic hardship.

He then tried to fix the shortages by taking over the labor market and essentially try to control what everyone did and where they worked.

But Emperor Wang wasn’t quite finished with his crusade for justice. He tried to pay for his mistakes by severely debasing the currency… which caused even more inflation and social unrest.

Wang Mang’s story is one of how complete and total incompetence results in disastrous consequences for an entire nation. History has witnessed countless other examples… and we’re seeing it play out again in our own time.

Today’s incompetent leadership is just as bad as Wang Mang; as I spelled out in yesterday’s missive, the US government has lost all ability to live within its means. They have spent trillions of dollars on their perverted ‘justice’ programs and environmental crusades.

Spending has gotten so bad that a $2 trillion yearly deficit is NOTHING anymore. Yet the continued accumulation of these deficits has created a gargantuan national debt.

As I mentioned yesterday, MOST of US national debt will mature over the next several years. Since the Treasury Department clearly does not have the money to pay back $25+ trillion in debt, their only option will be to issue NEW debt to pay off the old debt.

The problem, of course, is that the new debt comes with MUCH higher interest rates… and I explained that simply paying interest on the debt could exceed $2 trillion within the next five years.

On top of that, mandatory entitlement spending like Social Security and Medicare will hit $3 trillion. This means that just paying for Social Security/Medicare, and interest on the debt, could exceed 100% of tax revenue.

This scenario is potentially just five years away. At that point, it will be almost impossible for investors to have confidence in US government bonds.

US government bonds have long been considered the safest asset in the world. But if the Treasury Department has to blow $2 trillion just to pay interest, investors will quickly start looking for other safe havens. And one of those will be gold.

Think about it: there’s (currently) $32+ trillion in total US government bonds. This is MUCH larger than the gold market. So if even a small fraction of that US debt were to flow into gold instead, the gold price would go through the roof.

But there’s another scenario to consider, which frankly I think is more likely: the Fed steps in to save the US government.

One of the key reasons why the US government is in trouble (aside from their horrific spending habits) is that interest rates are so much higher than they used to be.

So the Fed can help the government out by slashing interest rates back down to 0%, which will make it affordable for the US government to finance its debt.

But this would come at a consequence; if the Fed slashes rates back down to zero, this would almost certainly result in another nasty bout of inflation… which would also mean higher gold prices.

So either scenario is bullish for gold.

Of course these two scenarios don’t even scratch the surface of all the political, financial, and economic problems in the US.

For example, there are still major risks lurking in the US banking system, including the fact that the Federal Reserve itself is hopelessly insolvent.

Social Security has less than a decade until it needs a bailout to the tune of tens of trillions of dollars.

And there’s also the likely possibility of the US dollar losing its dominance as the global reserve currency, likely this decade.

Gold should perform extremely well in any of these scenarios.

So in what scenario does gold NOT do well?

Well, gold does poorly in the “everything is just fine” scenario.

The war ends. Sensible politicians reign in spending. China plays nice and stops threatening to invade Taiwan. Economic growth goes through the roof. Inflation falls due to high levels of productivity and relative peace. Global trade booms.

As I’ve written before, this scenario is completely achievable, presuming competent leaders were in charge. And I’m really rooting for it.

In this scenario, gold would become a pointless relic… but I would happily welcome that outcome because everything else would be fantastic.

Unfortunately that scenario is unlikely… because the world is being run by a bunch of morons like Wang Mang.

If you feel like the trend in the world is more stupidity, more war, more socialism, more bad leadership, then you really ought to consider owning gold. In my view, a $5,000+ gold price is a pretty conservative estimate of where things go from here.

Want more articles like this? Sign up here to receive Sovereign Man letters to your email.

Contributor posts published on Zero Hedge do not necessarily represent the views and opinions of Zero Hedge, and are not selected, edited or screened by Zero Hedge editors.

end

5 a. IMPORTANT COMMENTARIES ON COMMODITIES:

end

5 B GLOBAL COMMODITY ISSUES/FOOD IN GENERAL//FREIGHT

END

6.CRYPTOCURRENCY//DIGITAL CURRENCY// COMMENTARIES/

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS THURSDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED UP TO 7.2438

OFFSHORE YUAN: UP TO 7.3113

SHANGHAI CLOSED UP 13.61 PTS OR 0.43%

HANG SENG CLOSED DOWN 2.67 PTS OR 0.01%

2. Nikkei closed DOWN 140.82 OR 0.44%

3. Europe stocks SO FAR: ALL RED

USA dollar INDEX DOWN TO 103.17 EURO RISES TO 1.0891 UP 17 BASIS PTS

3b Japan 10 YR bond yield: FALLS TO. +.642 Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 145.83/JAPANESE YEN FALLING AS WELL AS LONG TERM 10 YR. YIELDS RISING //EVENTUALLY THIS WILL BREAK THE JAPANESE CENTRAL BANK

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen UP CHINESE ON SHORE YUAN: UP// OFF- SHORE: UP

3f Japan is to buy INFINITE TRILLION YEN’S worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and UP FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund UP TO +2.6795***/Italian 10 Yr bond yield RISES to 4.384*** /SPAIN 10 YR BOND YIELD RISES TO 3.728…**

3i Greek 10 year bond yield RISES TO 3.953

3j Gold at $1898.90 silver at: 22.77 1 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble UP 1 AND 17 /100 roubles/dollar; ROUBLE AT 93.50//

3m oil into the 80 dollar handle for WTI and 84 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 145.83// 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 0.642% STILL ON CENTRAL BANK (JAPAN) INTERVENTION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.8775 as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9537well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.307 UP 4 BASIS PTS…

USA 30 YR BOND YIELD: 4.413 UP 6 BASIS PTS/

USA 2 YR BOND YIELD: 4.961 DOWN 2 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 27.10…(TURKEY SET TO BLOW UP FINANCIALLY)

GREAT BRITAIN/10 YEAR YIELD: UP 11 BASIS PTS AT 4.7560

end

2.a Overnight: Newsquawk and Zero hedge:

Markets On Edge As Global Yields Hit 15 Year High, China Woes Mount

THURSDAY, AUG 17, 2023 – 08:05 AM

S&P futures reversed earlier losses that brought them perilously close to the 4400 support level, as global govt bond yields extended their recent surge to the highest levels since the financial crisis after Fed minutes showed the central bank remains worried about persistent inflation and signaled the possibility of further rate hikes while stubbornly resilient US economic data – one might say purposefully manipulated for political purposes and boosted by massive deficit spending – challenges the view that central banks rates are peaking.

As of 7:30am ET, S&P futures were up 0.2%, reversing a similar drop earlier in the session. Nasdaq 100 futures also rose 0.2% The USD reversed an earlier gain and trade near session lows, helping commodities catch a bid. Sentiment was hammered around the globe: European stocks slumped for a third day with Spain outperforming on the move lower (UKX -0.3%, SX5E -0.5%, SXXP -0.4%, DAX -0.2%.) while Asian stocks dropped to their lowest level since March amid further signs of weakness in China and mounting concerns over elevated interest rates in the US. Today’s macro/micro focus is on jobless claims, the Leading Index, and AMAT/WMT earnings.

In premarket trading, BAE Systems Plc fell as much as 4.8% in London, its biggest drop in nine months, after it agreed to buy the aerospace division of soda-can giant Ball Corp. for $5.6 billion. Ball climbed as much as 5.5% in US premarket trading. Cisco Systems rose as much as 2.9% in the US premarket, after the maker of networking equipment gave a forecast that helped ease concerns about a sales slowdown. Here are some other notable premarket movers:

- Adobe rose 1.7% in premarket trading on Thursday after BofA Global Research raised the recommendation on the software company’s stock to buy from neutral, saying the company is “emerging as an AI leader.”

- Hawaiian Electric Industries fell as much as 26%, putting shares on track to decline for an eighth straight session amid Wall Street concern over the company’s potential liabilities following the Maui wildfires.

- Walmart gains 1.0% in premarket trading after boosting its net sales and adjusted earnings per share projections for the fiscal year. The retailer also posted stronger-than-expected second-quarter US comparable sales and profit.

In early trading on Thursday, the 30-year Treasury yield rose as much as seven basis points to 4.42%, slightly exceeding last year’s high, and the highest level since 2011. It was below 4% as recently as July 31. The US 10-year yield approached 4.31%; if it closes here it would be the highest since 2008. The equivalent UK yield jumped to a 15-year high, while its German counterpart approached the highest since 2011.

Bond market woes were precipitated after a surprisingly weak 20-year bond sale in Japan priced with the longest yield tail since 1987, reflecting mounting bets the Bank of Japan’s YCC will soon be loosened. It’s also a significant warning sign for global government debt at a time when yields are already at 15-year highs. Soaring JGB yields would put further upward pressure on the rest of the world, and also mean tougher fiscal budget challenges.

The yield on a Bloomberg index for total returns on global sovereign debt rose to 3.3% Wednesday, the highest since August 2008 as sovereign bonds worldwide have handed investors a loss of 1.2% this year, making the asset class the worst performer across Bloomberg’s major debt indexes. Treasuries have been a key driver of the global debt selloff as resilience in the US economy defies expectations that more than five percentage points of Federal Reserve interest-rate hikes would bring on a recession. Officials at the last policy meeting remained concerned that inflation would fail to recede and that further rate increases would be needed, minutes of the meeting showed.

“Recent data has been firmer, fueling expectations that central banks have a little more work to do,” said Prashant Newnaha, a macro strategist at TD Securities Inc. in Singapore. “The current selloff is being led by the longer end, underscoring concerns about supply and liquidity.”

Indeed, while many investors had believed that the Federal Reserve was done raising interest rates, that’s no longer a sure thing after minutes from last meeting suggested officials are considering tighter policy.

As a result, moves across bond markets have been sharp and swift this week. The 10-year Treasury yield rose four basis points to 4.29% on Thursday, approaching the highest level since 2007. In the UK, equivalent maturity gilts touched 4.71%, the highest since the financial crisis of 2008. Japan’s 20-year bond yield surged after a debt auction drew tepid investor demand.

“Markets are taking the prospect of another hike from the Fed increasingly seriously, with futures now pricing in a 45% chance of a further hike by the November meeting,” Deutsche Bank AG strategist Jim Reid wrote. “Investors are adjusting to the fact that rates could remain at a higher level for some time.”

Meanwhile, China also continued to weigh on sentiment. According to Bloomberg, the picture emerging from property agents and private data providers suggest the slump in the real estate market may be worse than official reports show. These figures show existing-home prices falling at least 15% in prime neighborhoods of major metropolitan areas like Shanghai and Shenzhen. China also ramped up its efforts to stem losses in its currency on Thursday by offering the most forceful guidance since October through its daily reference rate for the managed currency. The offshore yuan slipped against the greenback.

“Equity markets are currently faced with two headwinds — first, real rates are surging again, as the US economy is showing numbers consistent with an economic recovery,” said Florian Ielpo, head of macro research at Lombard Odier Asset Management. “Second, China is starting to emit dire signals that must remind investors of the awful summer 2015, with a troubled housing market and shadow banking system.”

European stocks were set to fall for the third straight session: the Stoxx 600 is down 0.4% with the industrial, construction and travel sectors leading declines while banks and energy were the bright spots. Here are the biggest European movers Thursday:

- Adyen plunges a record 27% after the payment firm’s processing volume, revenue growth and profitability all came in lower than estimates. The misses fueled analyst concerns over competition

- BAE Systems declines as much as 4.9% after the London-based defense giant agreed to buy Ball Corp.’s aerospace division for $5.6 billion. Analysts said the deal is strategic but expensive

- Nibe falls as much as 12% after the Swedish heat-pump manufacturer said demand for its products is faltering in Europe as governments discuss subsidies for the energy-efficient heating solution

- Coloplast declines as much as 6.9% after the Danish wound and continence care firm reported a disappointing 3Q earnings, with analysts attributing the miss to inflationary effects in its Wound care division

- GN Store Nord shares drop as much as 14% and erasing YTD gains after cutting guidance for its Audio division. The new outlook will lead to high single-digit downgrades to consensus estimates

- Geberit drops as much as 5.4% after the building materials firm reported Ebitda and sales below estimates. The results represent a “sizeable” miss and there’ll be “heavy scrutiny,” Jefferies says

- Aegon falls as much as 5.2% on the back of earnings. First half-year headline group solvency ratio missed consensus expectations, even as the Dutch insurer posted better operating capital generation

- Tremor International falls as much as 34% in their biggest one-day drop in more than four years after the advertising technology firm reported lower-than-expected 2Q Ebitda and cut its full-year revenue

- Calliditas Therapeutics falls as much as 14%, the most since May, after the Swedish pharmaceutical firm published 1H earnings, which included a trimmed outlook for net sales for its key drug Tarpeyo

- Philips gains as much as 5.1% in Amsterdam after Dutch financial daily Het Financieele Dagblad reports details of Goldman Sachs’ involvement in a stake purchase by Exor

- FLSmidth gains as much as 7.6% after investment firm Altor announced it would be increasing its stake in the Danish cement-and-mining services firm to 14.9% by buying 2.21m at an 11% premium

- ITM Power rises as much as 5.8% after the clean-fuel company reported FY results and said it’s making good strategic progress. Its simplified electrolyser product offering is encouraging, Morgan Stanley said

Asian stocks dropped to their lowest level since March amid further signs of weakness in China and mounting concerns over elevated interest rates in the US. The MSCI Asia Pacific Index fell as much as 1.6% on Thursday, set for a fifth day of declines, led by health-care and industrial shares. Pessimism is deepening as investors see no easy fix to the Chinese economy’s ailments given a drumbeat of dour corporate and macro news. Meanwhile, steps taken by policymakers so far have failed to boost sentiment as traders call for more forceful measures.

Most regional markets were down, led by Japan, while Chinese and Hong Kong shares pared earlier losses on dip buying.

- Hang Seng and Shanghai Comp were pressured at the open which saw the Hong Kong benchmark enter bear market territory after declining more than 20% from its January high amid earnings-related disappointment following results from Tencent and JD.com, although Chinese markets then recovered most of the earlier losses following another firm liquidity injection by the central bank and recent economic pledges by Premier Li.

- Nikkei 225 declined after soft data releases including the miss on machinery orders and although the declines in exports and imports weren’t as bad as feared, exports printed in contraction territory for the first time in 29 months.

- ASX 200 retreated as participants digested a slew of earnings releases and disappointing jobs data which showed a surprise contraction in the headline employment change and a larger-than-expected uptick in the unemployment rate.

In FX, the Bloomberg Dollar Index was up 0.1%. The Aussie is the weakest of the G-10 currencies, falling 0.4% versus the greenback after unemployment rose more than expected. The krone rose briefly before fading after the Norges Bank raised rates and pointed to another increase in September.

As noted above, Treasuries are lower, with US 10-year yields rising another 4bps to 4.30% as yields across the long-end of the curve continue to cheapen, with the 30-year rising through 4.42% and onto highest since 2011. Subsequently the curve continues to steepen with 5s30s spread back to re-testing positive. US yields cheaper by 3bp to 7bp from belly out to long-end of the curve with front-end outperforming and marginally richer on the day; spreads steeper with 2s10s, 5s30s widening 5.7bp and 4.5bp on the day with 2s10s steepest since May 25. Similar bear steepening moves seen across core European rates. Bunds and gilts are also in the red with 10-year borrowing costs in Germany and the UK rising by 4bps and 3bps respectively.

In commodities, crude futures advance, with WTI rising 0.2%. Spot gold adds 0.1%.

To the day ahead now, and data releases from the US include the weekly initial jobless claims, the Philadelphia Fed’s business outlook for August, and the Conference Board’s Leading Index for July. Otherwise, earnings releases include Walmart and Applied Materials.

Market Snapshot

- S&P 500 futures up 0.2% to 4,427.75

- MXAP down 0.4% to 158.71

- MXAPJ down 0.4% to 501.02

- Nikkei down 0.4% to 31,626.00

- Topix down 0.3% to 2,253.06

- Hang Seng Index little changed at 18,326.63

- Shanghai Composite up 0.4% to 3,163.74

- Sensex down 0.6% to 65,156.28

- Australia S&P/ASX 200 down 0.7% to 7,146.00

- Kospi down 0.2% to 2,519.85

- STOXX Europe 600 down 0.3% to 453.96

- German 10Y yield little changed at 2.68%

- Euro little changed at $1.0876

- Brent Futures up 0.3% to $83.74/bbl

- Brent Futures up 0.3% to $83.74/bbl

- Gold spot up 0.2% to $1,895.65

- U.S. Dollar Index little changed at 103.44

Top Overnight News from Bloomberg

- Global yields for government bonds extended their climb to the highest levels since 2008 as resilient economic data dashed investor optimism that central banks will soon halt or start reversing interest-rate hikes.

- China ramped up its efforts to stem losses in the yuan by offering the most forceful guidance since October through its daily reference rate for the managed currency.

- China’s top leaders pledged to expand domestic consumption and support the private sector without detailing any new stimulus measures, the latest in a series of rhetorical attempts to boost confidence in the economy as markets sink and growth disappoints.

- Norway’s central bank raised borrowing costs to the highest level since the 2008 financial crisis and signaled it still plans another quarter-point hike in the current tightening cycle.

- UK government bonds slid to send benchmark yields to the highest since the financial crisis, on concerns major central banks will continue to raise interest rates to quell inflation.

- Australia’s unemployment rate rose more than expected in July as the economy surprisingly shed jobs, signaling the labor market may be approaching a turning point and sending the currency lower.

A more detailed look at global markets courtesy of Newsquawk

APAC stocks mostly suffered another day of selling and followed suit to the losses on Wall St as yields continued to edge higher after the FOMC Minutes noted most officials saw significant upside risks to inflation which could require further tightening, while participants also reflected on several weak data releases from the region. ASX 200 retreated as participants digested a slew of earnings releases and disappointing jobs data which showed a surprise contraction in the headline employment change and a larger-than-expected uptick in the unemployment rate. Nikkei 225 declined after soft data releases including the miss on machinery orders and although the declines in exports and imports weren’t as bad as feared, exports printed in contraction territory for the first time in 29 months. Hang Seng and Shanghai Comp were pressured at the open which saw the Hong Kong benchmark enter bear market territory after declining more than 20% from its January high amid earnings-related disappointment following results from Tencent and JD.com, although Chinese markets then recovered most of the earlier losses following another firm liquidity injection by the central bank and recent economic pledges by Premier Li.

Top Asian News

- China reportedly told state banks to escalate Yuan intervention this week, according to Bloomberg sources.

- PBoC said it will keep the Yuan rate basically stable, will keep liquidity reasonably ample, prudent policy will be precise and forceful, and will resolutely prevent over-adjustment risks of CNY exchange rate.

- China shadow banking Co. Zhongzhi plans a debt restructuring and hired KPMG, while it is seeking strategic investors, according to sources cited by Reuters.

European bourses trade on the backfoot after succumbing to the selling pressure seen Stateside and during APAC trade, while macro newsflow has been light. Sectors are mostly lower with Industrial Goods & Services names bottom of the pile amid losses in BAE Systems (BA/ LN) after the Co. confirmed the acquisition of the Ball Aerospace business from Ball Corporation (BALL) for USD 5.55bln in cash. Elsewhere, other laggards include Travel & Leisure and Construction & Materials, whilst to the upside. Stateside, equity futures are flat/modestly firmer following risk-off trade seen at yesterday’s close with the FOMC Minutes unable to cap the negativity.

Top European News

- Norges Bank hiked its Key Policy Rate by 25bps as expected to 4.00%, and sees another hike in September. The future policy rate path will depend on economic developments. If the economy evolves as currently anticipated, the policy rate will be raised further in September. Activity in the Norwegian economy remains high, and the labour market is tight. Consumer price inflation has edged down but remains high and markedly above the target. Underlying inflation has remained elevated. If the NOK proves to be weaker than previously projected or pressures in the economy persist, a higher policy rate than signalled in June may be needed to bring down inflation. If there is a more pronounced slowdown in the Norwegian economy or inflation declines more rapidly, the policy rate may be lower than envisaged in June.

- ECB’s Kazaks said it is good news that inflation is coming down, needs to see the new ECB forecasts before deciding on hikes; any additional hikes would be small, according to Bloomberg.

- Spain’s Socialist Party reaches agreement in principle with Catalan Separatist party Junts to elect lower House Speaker, via ABC Newspaper.

FX

- DXY faded from best levels after extending gains on the back of broad risk aversion and further weakness in EM currencies rather than independent factors.

- AUD and NOK are at opposite ends of the G10 spectrum, the Aussie suffered a double whammy as the labour market report revealed an unexpected fall in employment and firmer than forecast unemployment rate. Conversely, the Norwegian Krona saw enough in the Norges Bank’s accompanying statement to test bids/support around 11.5000 vs the Euro.

- PBoC set USD/CNY mid-point at 7.2076 vs exp. 7.3047 (prev. 7.1986)

- China’s major state-owned banks’ branches were seen selling dollars to buy yuan in the offshore FX market during London and New York trading hours this week and were also seen selling dollars to buy yuan in the onshore FX market, according to sources cited by Reuters.

- RBI was likely selling dollars via state-run banks, according to traders cited by Reuters.

Fixed Income

- Debt futures have been choppy in the aftermath of a risk-off APAC session and with some follow-through from the FOMC minutes that featured a hawkish line, but in the context of recent sessions price action has been somewhat restrained.

- Bunds, Gilts and the T-note all remain in negative territory between 130.89-40, 92.00-91.61 and 109.20+/109-05+ respective bounds, though inside current w-t-d ranges awaiting the next major market-mover or catalyst.

- France sold EUR 8.44bln vs. Exp. EUR 7.5-8.5bln 2.50% 2026, 2.75% 2029, 1.50% 2031 OAT.

Commodities

- WTI and Brent front-month futures tilted higher this morning following APAC consolidation, with little in the way of fresh newsflow to drive price action.

- Spot gold is flat intraday under the USD 1,900/oz mark after relinquishing the level amid the recent Dollar strength, with the yellow metal pulling further away from its 200 DMA (1,905.86/oz).

- Base metals are holding modest gains with some impetus seen from the aforementioned revivals of Chinese sentiment towards the end of their trading day.

- Woodside Energy (WDS AT) workers will reportedly vote tonight on industrial action at LNG platforms, according to CNBC TV citing sources.

- US reportedly plans to escalate its dispute with Mexico over genetically modified corn, according to Bloomberg sources.

- NHC said Hilary forecast to rapidly intensify and become a Hurricane very soon, according to Reuters.

Geopolitics

- US plan new tariffs on food-can metal from China, Germany and Canada, according to WSJ; Levies announced in response to dumping allegations could raise canned food prices, industry group saysChinese products would be subject to the highest tariffs of the three countries, a levy of 122.52% o their import value.

- Russian Ambassador to the US said issues of prisoner swaps are being solved by relevant bodies of Russia and the US, while he added that this channel has proved to be effective, according to Reuter.

- South Korean lawmaker said there is a possibility for another spy satellite launch in North Korea between the end of August and early September, while there are signs that North Korea is preparing an ICBM launch, citing the spy agency.

- North Korea and Russia agreed to military cooperation during a recent meeting between North Korean leader Kim and Russia’s Defence Minister, according to Yonhap.

US Event Calendar

- 08:30: Aug. Initial Jobless Claims, est. 240,000, prior 248,000

- 08:30: Aug. Continuing Claims, est. 1.7m, prior 1.68m

- 08:30: Aug. Philadelphia Fed Business Outl, est. -10.2, prior -13.5

- 10:00: July Leading Index, est. -0.4%, prior -0.7%

DB’s Jim Reid concludes the overnight wrap

Markets have witnessed some big milestones over the last 24 hours, as robust US data and fresh signs of inflationary pressures sent global yields up to new highs. Most notably, yesterday saw the 10yr US Treasury yield rise another +3.9bps to 4.25%, which is its highest closing level since 2008, and this morning it’s up a further +3.6bps to 4.29%. That comes as markets are taking the prospect of another hike from the Fed increasingly seriously, with futures now pricing in a 45% chance of a further hike by the November meeting. But as well as the upcoming decisions, it’s clear that investors are adjusting to the fact that rates could remain at a higher level for some time. Indeed, futures for the rate at the Fed’s December 2024 meeting are now at their highest level so far this cycle, at 4.34%.

There were several catalysts behind the latest moves, but an important one was some further upside surprises in US data that led to growing optimism about the state of the economy. In particular, July’s industrial production grew by +1.0% (vs. +0.3% expected), and there was a very strong monthly growth rate of +5.2% for motor vehicles and parts. As a result, the Atlanta Fed’s GDPNow model moved to forecast that Q3 growth would come in at an annualised pace of +5.8%, and our own US economists have upgraded their Q3 growth forecast to an annualised +3.1% (link here). But all the good news on the economy wasn’t entirely positive for markets, as it helped cement investors’ conviction that tight monetary policy was likely to persist for some time.

That view was then given added support by the latest Fed minutes from the July meeting, which confirmed that the FOMC still had a tightening bias. For instance, it said that most participants “continued to see significant upside risks to inflation, which could require further tightening of monetary policy”. The minutes also echoed Chair Powell’s focus on growth and labour markets, and whether “product and labour markets were reaching a better balance between demand and supply”. So while inflation has been more encouraging of late, activity data that’s still strong ought to keep the Fed’s hawkish bias as we move towards the September meeting. According to the minutes, a “couple” of members favoured keeping rates unchanged in July, which is effectively in line with the June dot plot that had two dots for no further hikes in 2023.

The Fed minutes added some impetus to the Treasury sell-off, with several new milestones across the curve. As mentioned at the top, the 10yr Treasury yield (+3.9bps) moved higher for a 5th consecutive session to close at 4.25%, its highest level since 2008. And it was real yields that led the increase, with the 10yr real yield (+4.9bps) closing at a post-2009 high of 1.93%, whilst the 2yr real yield (+5.5bps) hit its own post-2009 high of 3.15%. There were also growing signs that higher yields were filtering through to the real economy, as MBA data showed that the average 30yr fixed rate mortgage reached 7.16% last week, in line with its previous peak last October.

With the prospect of higher rates for longer continuing to loom ahead of Jackson Hole next week, equities put in another downbeat performance. The S&P 500 shed another -0.76% to hit a 5-week low, and the NASDAQ (-1.15x%) saw an even larger decline as it hit a 7-week low. The megacap tech stocks were among the worst performers yesterday, with the FANG+ index (-1.69%) posting a sizeable decline. Over in Europe, the equity decline was more modest, with the STOXX 600 down -0.06% to its own 5-week low.

That tone has continued overnight as well, with the major equity indices in Asia posting modest losses for the most part. That includes the KOSPI (-0.39%), the Nikkei (-0.32%), the Hang Seng (-0.12%) and the CSI 300 (-0.05%), although the Shanghai Comp is up +0.01%. Indeed at one point earlier in the session this morning, the Hang Seng was on track for bear market territory, having shed more than 20% since its recent peak in January, although it’s since pared back those losses. The offshore Yuan has also continued to weaken overnight, and now stands at 7.340 per US dollar, which is almost at its recent low from early November when it closed at 7.343.

Elsewhere in markets yesterday, UK gilts were the biggest underperformer after the latest CPI print for July pointed to resilient price pressures. It’s true that the headline CPI print fell to +6.8%, but it was still a tenth above expectations and the core CPI rate also remained at +6.9% (vs. +6.8% expected). In addition, even as the headline measure has been coming down, the latest print still leaves the UK with the highest inflation rate in the G7, whilst the closely-watched services CPI rate actually moved up two-tenths to +7.4%.

That UK release follows some very strong wage growth data earlier in the week, and meant that investors continued to price in a more aggressive path of rate hikes from the BoE over the months ahead. For instance, overnight index swaps are now pricing in a 30% likelihood of a larger 50bps move at the next meeting, as well as a terminal policy rate above 6%. Gilt yields also moved higher across the curve, with the 10yr yield up +5.7bps to 4.64%, whilst the 10yr real yield (+3.9bps) hit its highest level since last year’s mini-budget turmoil at 0.86%. However, there was a stronger performance elsewhere in Europe, with yields on 10yr bunds (-2.5bps), OATs (-2.3bps) and BTPs (-0.4bps) all moving lower.

Yesterday’s risk-off tone was also evident among commodities. For instance, oil prices fell by more than 1% for the second day in a row, with Brent down -1.70% to $83.45/bl and WTI down -1.99% to $79.38/bl. Meanwhile, Bloomberg’s industrials metals index fell to its lowest since February 2021, having declined by -8.59% since the end of July.

Lastly, we had a few other data releases yesterday, including on US housing. That showed housing starts up to an annualised pace of 1.452m in July (vs. 1.450m expected), and building permits up to an annualised 1.442m (vs. 1.463m expected). Meanwhile in the Euro Area, industrial production grew by +0.5% in June (vs. unch expected), though our economists note that this outperformance versus expectations came due to the distorted data from Ireland.

To the day ahead now, and data releases from the US include the weekly initial jobless claims, the Philadelphia Fed’s business outlook for August, and the Conference Board’s Leading Index for July. Otherwise, earnings releases include Walmart and Applied Materials.

2 b) NOW NEWSQUAWK (EUROPE/REPORT)/ASIA REPORT

EUROPE/ASIA

European bourses lower, US equities bid, AUD underperforms; US IJC & WMT earning due – Newsquawk US Market Open

THURSDAY, AUG 17, 2023 – 06:14 AM

- European bourses trade on the backfoot after succumbing to the selling pressure seen Stateside and during APAC trade, while macro newsflow has been light.

- DXY faded from best levels after extending gains on the back of broad risk aversion, EUR sees several large option expiries, AUD underperforms after the Aussie jobs report.

- WTI and Brent front-month futures tilted higher this morning following APAC consolidation, with little in the way of fresh newsflow to drive price action.

- Norges Bank hiked its Key Policy Rate by 25bps as expected to 4.00%, and sees another hike in September.

- Looking ahead, highlights include highlights include US IJC, Philadelphia Fed Business Index, Norges Policy Announcement, Earnings from Walmart & Applied Materials.

More Newsquawk in 3 steps:

1. Subscribe to the free premarket movers reports

2. Listen to this report in the market open podcast (available on Apple and Spotify)

3. Trial Newsquawk’s premium real-time audio news squawk box for 7 days

EUROPEAN TRADE

EQUITIES

- European bourses trade on the backfoot after succumbing to the selling pressure seen Stateside and during APAC trade, while macro newsflow has been light.

- Sectors are mostly lower with Industrial Goods & Services names bottom of the pile amid losses in BAE Systems (BA/ LN) after the Co. confirmed the acquisition of the Ball Aerospace business from Ball Corporation (BALL) for USD 5.55bln in cash. Elsewhere, other laggards include Travel & Leisure and Construction & Materials, whilst to the upside.

- Stateside, equity futures are flat/modestly firmer following risk-off trade seen at yesterday’s close with the FOMC Minutes unable to cap the negativity.

- Click here for more detail.

- Click here and here for a recap of the main European equity updates.

FX

- DXY faded from best levels after extending gains on the back of broad risk aversion and further weakness in EM currencies rather than independent factors.

- AUD and NOK are at opposite ends of the G10 spectrum, the Aussie suffered a double whammy as the labour market report revealed an unexpected fall in employment and firmer than forecast unemployment rate. Conversely, the Norwegian Krona saw enough in the Norges Bank’s accompanying statement to test bids/support around 11.5000 vs the Euro.

- PBoC set USD/CNY mid-point at 7.2076 vs exp. 7.3047 (prev. 7.1986)

- China’s major state-owned banks’ branches were seen selling dollars to buy yuan in the offshore FX market during London and New York trading hours this week and were also seen selling dollars to buy yuan in the onshore FX market, according to sources cited by Reuters.

- RBI was likely selling dollars via state-run banks, according to traders cited by Reuters.

- Click here for more detail.

- Click here for the Option Expires for the NY Cut.

FIXED INCOME

- Debt futures have been choppy in the aftermath of a risk-off APAC session and with some follow-through from the FOMC minutes that featured a hawkish line, but in the context of recent sessions price action has been somewhat restrained.