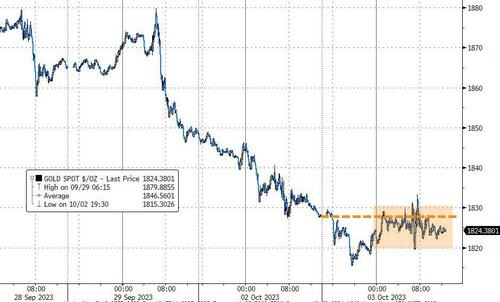

GOLD PRICE CLOSED: DOWN $6.90 TO $1825.10

SILVER PRICE CLOSED: DOWN $0.02 AT $21.20

Access prices: closes 4: 15 PM

Gold ACCESS CLOSE 1824.00.

Silver ACCESS CLOSE: 21.20

SEPT 27//SHANGHAI GOLD

Shanghai Gold Benchmark Price

USD oz  AM2014.57

AM2014.57

PM1985.03

Historical SGE Fix

premium $122,00

xxxxxxxxxxxxxxxxxx

Bitcoin morning price:, $27,505 DOWN 299 Dollars

Bitcoin: afternoon price: $27,257 DOWN 547 dollars

Platinum price closing $875.00 DOWN $7.20

Palladium price; $1187.90 DOWN $20.25

END

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

Due to the huge rise in the dollar, we must look at gold and silver in currencies other than the dollar to understand where we are heading

I will now provide gold in Canadian dollars, British pounds and Euros/4: 15 PM ACCESS

CANADIAN GOLD: $2,501.42 UP 1.40 CDN dollars per oz (ALL TIME HIGH 2,775.35)

BRITISH GOLD: 1509.98 DOWN 3.02 pounds per oz//(ALL TIME HIGH//CLOSING///1630.29)

EURO GOLD: 1742.36 DOWN 2.80 euros per oz //(ALL TIME HIGH/CLOSING//1861.21)//

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

EXCHANGE: COMEX

JPMorgan stopped 399/2499 contracts.

FOR OCT.:

GOLD: NUMBER OF NOTICES FILED FOR OCT/2023. CONTRACT: 2572 NOTICES FOR 257,200 OZ or 8.0000 TONNES

total notices so far: 8408 contracts for 840,800 oz (26.152 tonnes)

FOR OCT:

SILVER NOTICES:133 NOTICE(S) FILED FOR 665,000 OZ/

total number of notices filed so far this month : 283 for 1,415,000 oz

XXXXXXXXXXXXXXXXXXXXXXXX

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD

WITH GOLD DOWN $6.90

INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD/ : / HUGE CHANGES IN GOLD INVENTORY AT THE GLD// A DEPOSIT OF 1.44 TONNES OF GOLD INTO THE GLD.

INVENTORY RESTS AT 875.08 TONNES

Silver//

WITH NO SILVER AROUND AND SILVER DOWN 2 CENTS AT THE SLV// NO CHANGES IN SILVER INVENTORY AT THE SLV: :

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV.

CLOSING INVENTORY: 441.883 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY STRONG SIZED 850 CONTRACTS TO 128,732 AND CLOSER TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THIS HUGE SIZED GAIN IN COMEX OI WAS ACCOMPLISHED DESPITE OUR $0.98 LOSS IN SILVER PRICING AT THE COMEX ON MONDAY. TAS ISSUANCE WAS A GIGANTIC SIZED 1399 CONTRACTS. THESE WILL BE USED FOR MANIPULATION LATER THIS MONTH/AS WELL AS TODAY. CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON MONDAY NIGHT: 1399 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS. IT THUS LOOKS LIKE THE FED (GOV’T) IS BEHIND ALL OF THESE TRADES

WE HAVE NOW SET ANOTHER RECORD LOW AT 114,102 CONTRACTS ///JULY 3.2023// OUR BANKERS WITH THE HELP OF SPECULATORS AND HIGH FREQUENCY TRADERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.98). BUT WERE UNSUCCESSFUL IN KNOCKING ANY SILVER LONGS AS WE HAD A GIGANTIC SIZED GAIN OF 3972 OI CONTRACTS ON OUR TWO EXCHANGES.

WE MUST HAVE HAD:

A HUGE ISSUANCE OF EXCHANGE FOR PHYSICALS( 2825 CONTRACTS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 1.530 MILLION OZ (FIRST DAY NOTICE) FOLLOWED BY TODAY’S 35,000 OZ QUEUE JUMP//NEW STANDING 1.575 MILLION O///HUGE SIZED COMEX OI GAIN/ HUGE SIZED EFP ISSUANCE/VI) HUGE SIZED NUMBER OF T.A.S. CONTRACT ISSUANCE 1399 CONTRACTS)/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL 297 CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS OCT ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF OCT:

TOTAL CONTRACTS for 2 days, total 3600 contracts: OR 18.000 MILLION OZ (1800 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 18.000 MILLION OZ

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH 2022: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 118.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 85.745 MILLION OZ (SMALLER THAN LAST MONTH)

AUGUST: 171.43 MILLION OZ (THIS MONTH IS GOING TO BE HUGE //2ND HIGHEST ON RECORD

SEPT: 72.705 MILLION OZ (SMALLER THIS MONTH)

OCT: 18.00 MILLION OZ

RESULT: WE HAD A HUGE SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 850 CONTRACTS DESPITE OUR HUGE LOSS IN PRICE OF $0.98 IN SILVER PRICING AT THE COMEX//MONDAY.,. THE CME NOTIFIED US THAT WE HAD A HUGE EFP ISSUANCE CONTRACTS: 2825 ISSUED FOR OCT AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS./ WE HAVE A SMALL INITIAL SILVER OZ STANDING FOR SEPT OF 1.532 MILLION OZ FOLLOWED BY TODAY’S 35,000 OZ QUEUE JUMP:NEW TOTAL STANDING 1.575 MILLION OZ /// WE HAVE A GIGANTIC SIZED GAIN OF 3675 OI CONTRACTS ON THE TWO EXCHANGES. THE TOTAL OF TAS INITIATED CONTRACTS TODAY: A GIGANTIC SIZED 1399 CONTRACTS//HUGE FRONT END OF THE TAS CONTRACTS WERE LIQUIDATED DURING THE MONDAY COMEX SESSION. THE NEW TAS ISSUANCE MONDAY NIGHT (1399) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE., .

WE HAD 133 NOTICE(S) FILED TODAY FOR 665,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A FAIR SIZED 513 CONTRACTS TO 433,033 AND CLOSER TO THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: – REMOVED: –780 CONTRACTS

WE HAD A GOOD SIZED INCREASE IN COMEX OI ( 5521 CONTRACTS) DESPITE OUR $19.35 LOSS IN PRICE//MONDAY. WE ALSO HAD A RATHER STRONG INITIAL STANDING IN GOLD TONNAGE FOR SEPT. AT 16.562 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S HUGE 200200 OZ QUEUE JUMP/NEW STANDING 26.452 TONNES/ + /A STRONG (AND CRIMINAL) ISSUANCE OF 3220 T.A.S. CONTRACTS /// ALL OF..THIS HAPPENED WITH OUR $19.35 LOSS IN PRICE WITH RESPECT TO MONDAY’S TRADING.WE HAD A STRONG SIZED GAIN OF 5521 OI CONTRACTS (17.17 PAPER TONNES) ON OUR TWO EXCHANGES.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 5008 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 433,003

IN ESSENCE WE HAVE A STRONG SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 5521 CONTRACTS WITH 513 CONTRACTS INCREASED AT THE COMEX// AND A STRONG SIZED 5008 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 5521 CONTRACTS OR 17.17 TONNES. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): A STRONG 3220 CONTRACTS)

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A STRONG SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (5008 CONTRACTS) ACCOMPANYING THE SMALL SIZED GAIN IN COMEX OI (513) //TOTAL GAIN FOR OUR THE TWO EXCHANGES: 5521 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR FORMER FORMAT OF BANKERS GOING LONG AND SPECULATORS GOING SHORT ,2.) FAIR INITIAL STANDING AT THE GOLD COMEX FOR OCT. AT 16.562 TONNES FOLLOWED BY TODAY’S 200,200 OZ QUEUE JUMP//NEW STANDING 26.452 TONNES// /// 3) ZERO LONG LIQUIDATION BUT CONSIDERABLE TAS LIQUIDATION AND HUGE SPEC SHORT ADDITIONS DURING THE COMEX SESSION //4) FAIR SIZED COMEX OPEN INTEREST GAIN/ 5) STRONG ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER///6: STRONG T.A.S. ISSUANCE: 3220 CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023 INCLUDING TODAY

OCT

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF OCT :

TOTAL EFP CONTRACTS ISSUED: 10,172 CONTRACTS OR 1,017,200 OZ OR 31.639 TONNES IN 2TRADING DAY(S) AND THUS AVERAGING: 5086 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 2 TRADING DAY(S) IN TONNES 31.639 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2022, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 31.639/3550 x 100% TONNES 0.902% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2023

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH/2022: 409.30 TONNES //FINAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 151.69 TONNES (WEAKER THAN LAST MONTH)

AUGUST: 195.28 TONNES (A STRONGER MONTH)//FINAL

SEPT: 254.709 TONNES (WILL BE LARGER THAN LAST MONTH AND A STRONG MONTH)

OCT. 32.639 TONNES

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF SEPT. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF MAY HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF JUNE., FOR BOTH GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (SEPT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER ROSE BY A HUGE SIZED 850 CONTRACTS OI TO 128,732 AND CLOSER TO OUR COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE A HUGE 3825 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

DEC 2825 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 2825 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 850 CONTRACTS AND ADD TO THE 2825 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A GIGANTIC SIZED GAIN OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 3675 CONTRACTS

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTAL 17.17 MILLION OZ

OCCURRED DESPITE OUR HUGE $0.98 LOSS IN PRICE …..

END

OUTLINE FOR TODAY’S COMMENTARY

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

b, ) Gold/silver trading overnight Europe,//GOLD COMMENTARIES

(Peter Schiff)

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS//

TUESDAY MORNING//MONDAY NIGHT

SHANGHAI CLOSED //Hang Seng CLOSED DOWN 478.44 PTS OR 2.69% /The Nikkei CLOSED DOWN 521.94 PTS OR 1.64% //Australia’s all ordinaries CLOSED DOWN 1.31 % /Chinese yuan (ONSHORE) closed /OFFSHORE CHINESE YUAN CLOSED DOWN TO 7.3280 /Oil DOWN TO 88,36 dollars per barrel for WTI and BRENT DOWN AT 90.04 / Stocks in Europe OPENED ALL RED// ONSHORE YUAN TRADING XXX LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING XXX AGAINST US DOLLAR/OFFSHORE WEAKER

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

9. USA

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A FAIR SIZED 1293 CONTRACTS TO 433,863 DESPITE OUR STRONG LOSS IN PRICE OF $19.35 ON MONDAY.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE NON ACTIVE DELIVERY MONTH OF OCT..… THE CME REPORTS THAT THE BANKERS ISSUED A STRONG SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 5008 EFP CONTRACTS WERE ISSUED: : DEC 5008 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 5008 CONTRACTS

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A STRONG SIZED TOTAL OF 5,521 CONTRACTS IN THAT 5008 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A SMALL SIZED GAIN OF 513 COMEX CONTRACTS..AND THIS GAIN ON OUR TWO EXCHANGES HAPPENED DESPITE OUR LOSS IN PRICE OF $19.35//MONDAY COMEX. AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS DURING MID MONTH IN THE DELIVERY CYCLE), THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR MONDAY NIGHT WAS A STRONG 3220 CONTRACTS. THROUGHOUT THE PAST WEEKS, THE BANKERS SOLD OFF THE LONG SIDE OF THE SPREAD WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR SPREAD WHICH WILL BE LIQUIDATED TWO MONTHS HENCE)//

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: OCT (26.432) ( ACTIVE MONTH)

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT.26.452 TONNES

THE SPECS/HFT WERE SUCCESSFUL IN LOWERING GOLD’S PRICE( IT LOST $19.35) //// BUT WERE UNSUCCESSFUL IN KNOCKING ANY SPECULATOR LONGS AS STRANGELY WE HAD A STRONG GAIN OF 6301 TOTAL CONTRACTS ON OUR TWO EXCHANGES. WE HAD A CONSIDERABLE T.A.S. LIQUIDATION ON THE FRONT END OF MONDAY’S TRADING. THE T.A.S. ISSUED ON MONDAY NIGHT WILL BE “PUT INTO THE BANK” TO BE USED AT A LATER DATE AT THE COLLUSIVE CHOOSING OF OUR BANKERS.

WE HAVE GAINED A TOTAL OI OF 17.17 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR OCT. (16.562 TONNES) ON FIRST DAY NOTICE FOLLOWED BY TODAY’S 200,200 OZ QUEUE JUMP//NEW TOTALS STANDING:26.452 TONNES ALL OF THIS WAS ACCOMPLISHED WITH OUR LOSS IN PRICE TO THE TUNE OF $19.35. FOR THE PAST WEEK, THE SPECULATORS HAVE GONE MASSIVELY SHORT WITH OUR BANKERS NET LONG. THE BIG QUESTION IS WHEN WILL THE BANKERS PULL THE PLUG ON OUR SPECS.

WE HAD – REMOVED 780 CONTRACTS TO THE COMEX TRADES TO OPEN INTEREST

NET GAIN ON THE TWO EXCHANGES 5521 CONTRACTS OR 552,100 OZ OR 17.17 TONNES.

Estimated gold volume today:// 210,536 fair

final gold volumes/yesterday 213,821 fair/raid

//speculators have left the gold arena

//OCT 3/ /// THE OCT. 2023 GOLD CONTRACT

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 160.755. OZ Brinks 5 kilobars . |

| Deposit to the Dealer Inventory in oz | nil |

| Deposits to the Customer Inventory, in oz | nil oz |

| No of oz served (contracts) today | 2572 notice(s) 257200 OZ 8.0000 TONNES |

| No of oz to be served (notices) | 90 contracts 9000 oz 0.2799 TONNES |

| Total monthly oz gold served (contracts) so far this month | 8408 notices 840800 OZ 26.152 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | x |

0 dealer deposit:

total dealer deposits: 0 oz

customer deposits: 0

total customer deposits: 0 oz

we had 1 customer withdrawal

i) Out of Brinks: 160.755 oz (5 kilobars)

total withdrawals 160.755. oz

Adjustments; 0

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR OCT.

For the front month of OCTOBER we have an oi of 2662 contracts having LOST 447 contracts. We had 2449 contracts filed on Monday, so we gained a whopping 2002 contracts or an additional 200,200 oz will stand for delivery in this active delivery month of October. Somebody, for the second day in a row, was in urgent need of a huge supply of physical gold over here.

NOV GAINED 179 CONTRACTS to stand at 1240

December LOST 751 contracts down to 375,053 contracts.

We had 2572 contracts filed for today representing 257,200 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 100 notices were issued from their client or customer account. The total of all issuance by all participants equate to 2572 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 29 notice(s) was (were) stopped received by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the OCT. /2023. contract month, we take the total number of notices filed so far for the month (8408 x 100 oz ), to which we add the difference between the open interest for the front month of OCT. (2662 CONTRACTS) minus the number of notices served upon today 2572 x 100 oz per contract equals 849,800 OZ OR 26.432 TONNES the number of TONNES standing in this active month of OCT.

thus the INITIAL standings for gold for the OCT. contract month: No of notices filed so far (8408) x 100 oz + (2662) {OI for the front month} minus the number of notices served upon today (2572) x 100 oz) which equals 849,800 oz standing OR 26.432 TONNES

TOTAL COMEX GOLD STANDING: 26.432 TONNES WHICH IS HUGE FOR AN ACTIVE BUT GENERALLY WEAK DELIVERY MONTH. (OCT). Somebody is after a considerable amount of gold from the comex.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 2,009,719.720 OZ 62.51 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 20,911,922.886 OZ

TOTAL REGISTERED GOLD 10,310,605.883 (320.0703 tonnes)..

TOTAL OF ALL ELIGIBLE GOLD: 10,601,317.003 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 8,300,886 OZ (REG GOLD- PLEDGED GOLD) 258,192 tonnes//dropping like a stone

END

SILVER/COMEX

OCT 3

//2023// THE OCT 2023 SILVER CONTRACT

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 36,964.689 oz Brinks Delaware . |

| Deposits to the Dealer Inventory | 594,581.604 oz ASAHI |

| Deposits to the Customer Inventory | 1,250,468.500 oz CNT Loomis |

| No of oz served today (contracts) | 2133 CONTRACT(S) (665,000 OZ) |

| No of oz to be served (notices) | 32 contracts (160,000 oz) |

| Total monthly oz silver served (contracts) | 283 Contracts (1,415,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

i) 0 dealer deposit

total dealer deposit: 1

i) Into ASAHI: 594,581.604 oz

total: 593,581.604 o

i) We had 0 dealer withdrawal

total dealer withdrawals: 0 oz

We had 2 deposit customer account:

i) Into CNT: 607,423.160 oz

ii) Into Loomis 643,045.340 o

total customer deposit 1,250,468.500 oz

JPMorgan has a total silver weight: 136.236 million oz/272.134 million or 50.00%

Comex withdrawals 2

i) Out of Brinks 7919.650 o

ii) Out of Delaware: 29,045.039 oz

total: 36,964.688 oz

adjustments: 0

TOTAL REGISTERED SILVER: 37.638 MILLION OZ//.TOTAL REG + ELIGIBLE. 272.134 million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR August:

silver open interest data:

FRONT MONTH OF OCT /2023 OI: 165 CONTRACTS HAVING LOST 19 CONTRACT(S). WE HAD 26 NOTICES FILED

ON MONDAY, SO WE GAINED 7 CONTRACTS AS WE HAD A QUEUE JUMP OF 35,000 OZ

NOVEMBER GAINED 19 CONTRACTS TO STAND AT 549

DEC.GAINED 47 CONTRACTS TO STAND AT 113,108 .

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 133 for 665,000 oz

Comex volumes// est. volume today 79,977 //strong

Comex volume: confirmed yesterday 104,305 huge raid//

To calculate the number of silver ounces that will stand for delivery in OCT. we take the total number of notices filed for the month so far at 283 x 5,000 oz = 1,415,000 oz

to which we add the difference between the open interest for the front month of OCT (165) and the number of notices served upon today 133 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the OCT/2023 contract month: 283 (notices served so far) x 5000 oz + OI for the front month of OCT (165) – number of notices served upon today (133 )x 500 oz of silver standing for the OCT contract month equates to 1.575 million oz.

There are 37.638 million oz of registered silver.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS

OCT 3/WITH GOLD DOWN $6.90 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.44 TONNES OF GOLDINTO THE GLD/// : // //INVENTORY RESTS AT 875.08 TONNES

OCT 2/WITH GOLD DOWN $19.35 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD: LD/ : // //INVENTORY RESTS AT 873,64 TONNES

SEPT 29/WITH GOLD DOWN $11.15 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD: LD/ : // //INVENTORY RESTS AT 873,64 TONNES

SEPT 28/WITH GOLD DOWN $13.45 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A HUGE WITHDRAWAL OF 4.88 TONNES OF GOLD OUT OF THE GLD/ : // //INVENTORY RESTS AT 873,64 TONNES

SEPT 26/WITH GOLD DOWN $XXX TODAY:SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 0.31 TONNES OF GOLD OUT 05 THE GLD/ : // //INVENTORY RESTS AT 878.52 TONNES

SEPT 26/WITH GOLD DOWN $13.40 TODAY:SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 0.31 TONNES OF GOLD OUT 05 THE GLD/ : // //INVENTORY RESTS AT 878.52 TONNES

SEPT 22/WITH GOLD UP $5.70 TODAY:SMALL CHANGES IN GOLD INVENTORY AT THE GLD DEPOSIT OF 0.58 TONNES OF GOLD INTO THE GLD/ : // //INVENTORY RESTS AT 878.83 TONNES

SEPT 21/WITH GOLD DOWN $25.60 TODAY:SMALL CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 0.58 TONNES OF GOLD FROM THE GLD/ : // //INVENTORY RESTS AT 878.25 TONNES

SEPT 19/WITH GOLD UP $0.60 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD : // //INVENTORY RESTS AT 880.217 TONNES

SEPT 18/WITH GOLD UP $8.40 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD : A DEPOSIT OF 0.57 TONNES OF GOLD INTO THE GLD// //INVENTORY RESTS AT 880.217 TONNES

SEPT 15/WITH GOLD UP $13.20 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD : A WITHDRAWAL OF 1.055 TONNES OF GOLD FROM THE GLD// //INVENTORY RESTS AT 879.70 TONNES

SEPT 14/WITH GOLD UP $1.00 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD : A WITHDRAWAL OF 4.63 TONNES OF GOLD FROM THE GLD// //INVENTORY RESTS AT 882.01 TONNES

SEPT 13/WITH GOLD DOWN $2.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD : / //INVENTORY RESTS AT 886.64 TONNES

SEPT 12/WITH GOLD DOWN $11.20 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD : / //INVENTORY RESTS AT 886.64 TONNES

SEPT 11/WITH GOLD UP $4.45 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD : / //INVENTORY RESTS AT 886.64 TONNES

SEPT 8/WITH GOLD UP $0.35 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD : / //INVENTORY RESTS AT 886.64 TONNES

SEPT 7/WITH GOLD DOWN $0.20 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 3.22 TONNES OF GOLD INTO THE GLD.: / //INVENTORY RESTS AT 886.69 TONNES

SEPT 6/WITH GOLD DOWN $8.80 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 1.16 TONNES OF GOLD INTO THE GLD.: / //INVENTORY RESTS AT 889.81 TONNES

SEPT 5/WITH GOLD DOWN $13.50 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF 0.87 TONNES OF GOLD INTO THE GLD.: / //INVENTORY RESTS AT 890.97 TONNES

SEPT 1/WITH GOLD UP $1.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF 0.87 TONNES OF GOLD INTO THE GLD.: / //INVENTORY RESTS AT 890.10 TONNES

AUGUST 31/WITH GOLD DOWN $1.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF 0.87 TONNES OF GOLD INTO THE GLD.: / //INVENTORY RESTS AT 890.10 TONNES

AUGUST 30/WITH GOLD UP $8.15 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF 2.59 TONNES OF GOLD INTO THE GLD.: / //INVENTORY RESTS AT 889.23 TONNES

AUGUST 29/WITH GOLD UP 17.05 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF 2.6 TONNES OF GOLD INTO THE GLD.: / //INVENTORY RESTS AT 886.64 TONNES

AUGUST 28/WITH GOLD UP $6.90 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD: / //INVENTORY RESTS AT 884.04 TONNES

AUGUST 25/WITH GOLD DOWN $6.05 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .87 TONNES OF GOLD FROM THE GLD// //INVENTORY RESTS AT 884.04 TONNES

AUGUST 24/WITH GOLD UP $0.65 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD //INVENTORY RESTS AT 884.91 TONNES

AUGUST 23/WITH GOLD UP $21.35 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 4.32 TONNES OF GOLD FROM THE GLD//: //: /// //INVENTORY RESTS AT 884.91 TONNES

AUGUST 22/WITH GOLD UP $2.95 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 0.87 TONNES OF GOLD FROM THE GLD//: //: /// //INVENTORY RESTS AT 889.23 TONNES

AUGUST 21/WITH GOLD UP $7.15 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF 2.60 TONNES OF GOLD FROM THE GLD//: //: /// //INVENTORY RESTS AT 890.10 TONNES

AUGUST 18/WITH GOLD UP $1.15 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 6.92 TONNES OF GOLD FROM THE GLD//: //: /// //INVENTORY RESTS AT 887.50 TONNES

AUGUST 17/WITH GOLD DOWN $12.80 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD: //: /// //INVENTORY RESTS AT 894.42 TONNES

GLD INVENTORY: 875.08 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

OCT 2/WITH SILVER DOWN 2 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV:. : // /.////INVENTORY RESTS AT 441.883 MILLION OZ

OCT 2/WITH SILVER DOWN 98 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV:. : // /.////INVENTORY RESTS AT 441.883 MILLION OZ

SEPT 29/WITH SILVER DOWN 28 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV:. A WITHDRAWAL OF 0.183 MILLION OZ FROM THE SLV: // /.////INVENTORY RESTS AT 441.883 MILLION OZ

SEPT 28/WITH SILVER DOWN 8 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV:. A WITHDRAWAL OF 4.88 MILLION OZ FROM THE SLV: // /.////INVENTORY RESTS AT 442.066 MILLION OZ

SEPT 27/WITH SILVER DOWN 20 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV:. A WITHDRAWAL OF .641 MILLION OZ FROM THE SLV: // /.////INVENTORY RESTS AT 448.392 MILLION OZ

SEPT 26/WITH SILVER DOWN 20 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV:. A WITHDRAWAL OF .641 MILLION OZ FROM THE SLV: // /.////INVENTORY RESTS AT 448.392 MILLION OZ

SEPT 22/WITH SILVER UP 13 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV:. : // /.////INVENTORY RESTS AT 449.492 MILLION OZ

SEPT 21/WITH SILVER DOWN 13 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV:. : // /.////INVENTORY RESTS AT 449,033 MILLION OZ

SEPT 19/WITH SILVER UP 0 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 1.1 MILLION OZ INTO THE SLV. : // /.////INVENTORY RESTS AT 449.033 MILLION OZ

SEPT 18/WITH SILVER UP 11 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A DEPOSIT OF 1.651 MILLION OZ INTO THE SLV. : // /.////INVENTORY RESTS AT 441.332 MILLION OZ

SEPT 15/WITH SILVER UP 37 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 2.31 MILLION OZ FROM THE SLV. : // /.////INVENTORY RESTS AT 439.681 MILLION OZ

SEPT 14/WITH SILVER DOWN 16 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: : // /.////INVENTORY RESTS AT 440.736 MILLION OZ

SEPT 13/WITH SILVER DOWN 23 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1,009 MILLION OZ INTO THE SLV//: // /.////INVENTORY RESTS AT 440.736 MILLION OZ

SEPT 12/WITH SILVER UP 1 CENT TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 3.209 MILLION OZ INTO TEH SLV//: // /.////INVENTORY RESTS AT 439.727 MILLION OZ

SEPT 11/WITH SILVER UP 19 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 3.209 MILLION OZ INTO TEH SLV//: // /.////INVENTORY RESTS AT 439.727 MILLION OZ

SEPT 8/WITH SILVER DOWN 8 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: // /.////INVENTORY RESTS AT 436.518 MILLION OZ

SEPT 7/WITH SILVER DOWN 21 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: // /.////INVENTORY RESTS AT 436.518 MILLION OZ

SEPT 6/WITH SILVER DOWN 36 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.373 OZ OF SILVER OUT OF THE THE SLV// /.////INVENTORY RESTS AT 436.518 MILLION OZ

SEPT 5/WITH SILVER DOWN 69 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 734,000 OZ OF SILVER OUT OF THE THE SLV// /.////INVENTORY RESTS AT 437.891 MILLION OZ

SEPT 1/WITH SILVER DOWN 20 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.375 MILLION OZ OF SILVER OUT OF THE THE SLV// /.////INVENTORY RESTS AT 440.00 MILLION OZ

AUGUST 31/WITH SILVER DOWN 20 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.375 MILLION OZ OF SILVER OUT OF THE THE SLV// /.////INVENTORY RESTS AT 438.625 MILLION OZ

AUGUST 30/WITH SILVER DOWN 2 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.834 MILLION OZ OF SILVER OUT OF THE THE SLV// /.////INVENTORY RESTS AT 443.210 MILLION OZ

AUGUST 29/WITH SILVER UP 49 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 183,000 OF SILVER INTO THE THE SLV// /.////INVENTORY RESTS AT 445.044 MILLION OZ

AUGUST 28/WITH SILVER UP 3 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.281 MILLION OZ OZ FROM THE SLV// /.////INVENTORY RESTS AT 444.861 MILLION OZ

AUGUST 25/WITH SILVER UP ONE CENT TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.751 MILLION OZ OZ FROM THE SLV// /.////INVENTORY RESTS AT 446.145 MILLION OZ

AUGUST 24/WITH SILVER DOWN 16 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.651 MILLION OZ OZ FROM THE SLV// /.////INVENTORY RESTS AT 448.896 MILLION OZ

AUGUST 23/WITH SILVER UP 94 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 826,000 OZ FROM THE SLV// /.////INVENTORY RESTS AT 450.547 MILLION OZ

AUGUST 22/WITH SILVER UP 12 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: /.////INVENTORY RESTS AT 451.373 MILLION OZ

AUGUST 21/WITH SILVER UP 59 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 917,0000 OZ FROM THE SLV//.////INVENTORY RESTS AT 451.373 MILLION OZ

AUGUST 18/WITH SILVER UP 4 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//.////INVENTORY RESTS AT 452.290 MILLION OZ

AUGUST 17/WITH SILVER UP 15 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//.////INVENTORY RESTS AT 452.290 MILLION OZ

CLOSING INVENTORY 441.883 MILLION OZ//

PHYSICAL GOLD/SILVER COMMENTARIES

1:Peter Schiff/Mike Maharrey

Peter Schiff: Banks Have A Bigger Real Estate Problem Today Than They Did in 2007

TUESDAY, OCT 03, 2023 – 07:20 AM

Banks are more vulnerable to the housing market now than they were in 2007.

Most people in the mainstream will scoff at that statement. They’ll tell you that the situation is very different today. After all, we don’t have a big problem in the subprime mortgage market. We’re not seeing a big spike in defaults. That’s true. The problem is different this time. And it’s actually worse.

Most people will acknowledge that there are problems in the real estate market. Home sales continue to decline as mortgage rates climb. Pending home sales fell more than expected in August, with the National Association of Realtors’ Pending Home Sales Index falling to the lowest level since September 2022.

Meanwhile, home prices have fallen off the peak we saw in 2021, but they haven’t declined as much as you might expect because housing inventory remains tight.

So, what’s the problem?

As Peter Schiff explained in a recent podcast, the problem this time is the mortgages themselves.

The banks are in worse shape and more vulnerable to the housing market now than they were in 2007 when everything collapsed and we had the financial crisis.”

The problem in 2007 and 2008 was defaults. As interest rates rose, people couldn’t afford to pay their mortgages. That forced banks to foreclose. With the real estate bubble deflating, banks couldn’t recoup their loans by selling the houses.

The problem was the banks had loaned out a lot of money with zero down or negative AM, and then housing prices went down, and then people started defaulting. Because of the defaults, the banks lost money. But the vast majority of mortgages didn’t default. It was just a large enough percentage that it caused insolvency at these banks.”

Because we have a fractional reserve system, banks don’t have nearly enough reserves to cover even a small number of their loans.

Today we have a much different scenario. Peter says it’s worse.

It’s not about default now. In fact, defaults would actually help. The banks would actually be better off if people defaulted on the mortgages. The problem is the mortgage itself. The banks are losing money on the mortgage.”

Banks wrote these mortgages when interest rates were extremely low. A 3% mortgage wasn’t uncommon a few years ago. Now mortgage rates are above 7%.

The banks are losing money on every mortgage that’s outstanding. So, even though people are still paying their mortgages, the bank is still losing.”

In 2009, the Fed slashed interest rates. That meant all the mortgages the banks owned that didn’t default went up in value. Those mortgages appreciated because the Fed slashed interest rates.

So, even though some mortgages that went bad, the mortgages that didn’t go bad, which were the vast majority, appreciated in value. Even with that, we still had the financial crisis.”

Today, there aren’t a lot of defaults. People aren’t struggling to pay a 3% mortgage. And while home prices have declined, most homeowners aren’t currently underwater. Even if they are, people aren’t selling. They don’t want to give up a 3% mortgage for a 7%-plus mortgage. That’s why inventory remains tight and that is holding prices up.

As Peter points out, a 3% mortgage is a huge asset for the borrower. But it’s a huge liability for the lender. So, defaults would benefit the banks. They could theoretically repossess the home and resell it to somebody else and write a mortgage at a much higher rate.

So, this is a very different crisis. But it’s worse because they’re losing money on every single mortgage they have whether or not they go into default. … So, this is bigger. It is a bigger problem for the banks. They’re losing more money, and they will lose more money now than they did in 2008. That means we’ll need an even bigger bailout. All these ‘too big to fail’ banks have an even bigger problem now than they did then, and it’s going to take an even bigger round of QE to bail them out. The problem is how’s the Fed going to do that when inflation is as high as it is and going higher?”

Banks face another problem in this high interest rate environment. They’re losing depositors. Investors want yield. They can pull their money out of the bank and put it in money markets with a 5.5% yield. Peter said this is “the ultimate in crowding out.”

Everybody wants to take their money out of the banks, and the banks in theory could loan that money to the private sector, but they want to take that money out of the banks and put it in a money market that’s loaning the money to the government. … So, private businesses can’t get credit because all the credit is going to the government to finance these massive deficits.”

The fact that banks continue to borrow money from the Fed’s bailout program reveals the problems bubbling below the surface.

As Peter put it, the crisis is easy to see. But most people in the mainstream don’t see it.

end

2 Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens//JAMES RICKARDS//JOHN RUBINO

3,Chris Powell of GATA provides to us very important physical commentaries

a total joke!

(Pam and Russ Martens)

Pam and Russ Martens: JPMorgan Chase gets another fine, for 40 million derivative violations

Submitted by admin on Mon, 2023-10-02 11:58Section: Daily Dispatches

By Pam and Russ Martens

Wall Street on Parade

Monday, October 2, 2023

In the eyes of Wall Street veterans who are paying close attention to what’s going down at the mega banks on Wall Street, federal regulators are making the crime wave at these banks worse, not better. The federal fines for egregious behavior at these banks are getting smaller and more meaningless by the day.

Take what happened on Friday. The Commodity Futures Trading Commission fined three of the largest trading houses on Wall Street a combined $53 million for derivative reporting violations. Those trading houses were units of Goldman Sachs, Bank of America, and JPMorgan Chase.

But what was particularly tone-deaf about the CFTC’s settlement with JPMorgan Chase was the tiny amount of the monetary fine and the praise heaped on the five-count felon bank for its “cooperation” with the federal regulator.

According to the CFTC, over a period of five years, spanning 2017 to 2022, JPMorgan Chase Bank and two of its units “failed to report, or failed to correctly report, more than 40 million swap transactions.” The fine was a pathetic $15 million in total for the three JPMorgan units, meaning it cost this global behemoth just 37½ cents per violation.

Last year JPMorgan Chase reported $37.7 billion in net income. A fine of $15 million for 40 million violations of law is something that traders will make jokes about around the water cooler. …

… For the remainder of the commentary:

end

4, OTHER IMPORTANT GOLD/SILVER COMMENTARIES//

END

5 a. IMPORTANT COMMENTARIES ON COMMODITIES:ORANGE JUICE

END

5 B GLOBAL COMMODITY ISSUES/FOOD IN GENERAL//FREIGHT

END

6.CRYPTOCURRENCY//DIGITAL CURRENCY// COMMENTARIES/

END

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS TUESDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED

OFFSHORE YUAN: DOWN TO 7.3280

SHANGHAI CLOSED

HANG SENG CLOSED DOWN 478.44 PTS OR 2.69%

2. Nikkei closed DOWN 521.94 PTS OR 1.64 %

3. Europe stocks SO FAR: ALL RED

USA dollar INDEX UP TO 106.85 EURO FALLS TO 1.0473 DOWN 7 BASIS PTS

3b Japan 10 YR bond yield: FALLS TO. +.750 Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 149.97/JAPANESE YEN FALLING AS WELL AS LONG TERM 10 YR. YIELDS RISING //EVENTUALLY THIS WILL BREAK THE JAPANESE CENTRAL BANK

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen UP CHINESE ONSHORE YUAN: XX// OFFSHORE: DOWN

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil DOWN for WTI and DOWN FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund UP TO +2.9535***/Italian 10 Yr bond yield UP to 4.890*** /SPAIN 10 YR BOND YIELD UP TO 4.044…**

3i Greek 10 year bond yield RISES TO 4.366

3j Gold at $1826.00 silver at: 21.10 1 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble UP 0 AND 58 /100 roubles/dollar; ROUBLE AT 99.18//

3m oil into the 88 dollar handle for WTI and 90 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 149.97// 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 0.750% STILL ON CENTRAL BANK (JAPAN) INTERVENTION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.9231 as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9667 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.741 UP 5 BASIS PTS…

USA 30 YR BOND YIELD: 4.862 UP 7 BASIS PTS/

USA 2 YR BOND YIELD: 5.127 UP 2 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 27.50…(TURKEY SET TO BLOW UP FINANCIALLY)

GREAT BRITAIN/10 YEAR YIELD: UP 11 BASIS PTS AT 4.6250

end

2.a Overnight: Newsquawk and Zero hedge:

USA EARLY MORNING REPORT.

It’s Deja Vu All Over Again: Futures Tumble As Yields Surge

TUESDAY, OCT 03, 2023 – 08:14 AM

In a deja vu repeat of Monday’s open, and really a carbon copy of most mornings in the past month, what was a modest attempt to push futures higher has crashed and burned with US equity futures sliding to session lows as yields resumed their surge once again, the 10Y rising up to a new 16 year high of 4.74%, with 30Ys also rising to the highest since 2007, hitting 4.856%.

As a result what was a modest 0.3% gain in spoos turned into a 0.4% loss as S&P futures dropped to session lows of 4,307 as of 7:35am with Nasdaq futures dragged 0.5% lower. The Bloomberg Dollar Spot Index followed yields tick for tick and rose to an 10-month high, pressuring most Group-of-10 currencies. The selloff rippled across equity and commodity markets, with Europe’s Stoxx 600 sliding to a six-month low as WTI traded near $89 a barrel and gold and Bitcoin fell.

In US premarket trading, HP gained after BofA double upgraded its rating on the PC maker to buy from underperform, with positive commentary expected at next week’s analyst day. MSP Recovery rose as much as 26% in premarket trading on Tuesday as its Chief Legal Officer Frank Carlos Quesada reported a purchase of stock to the US Securities and Exchange Commission. Here are some other notable premarket movers:

- ALX Oncology surges as much as 149% in premarket trading Tuesday, erasing an earlier drop, after reporting interim mid-stage data from a trial of its drug evorpacept for the treatment of advanced gastric cancer.

- McCormick slides 3% in premarket trading, after the spice maker reported net sales that trailed the average analyst estimate and a larger-than-expected decline in product volume. Sales in the consumer segment in the Asia-Pacific region were particularly weak, which the company attributed to a slower-than-expected economic recovery in China.

- Oddity Tech Ltd. rallied 18% in premarket trading after Truist Securities analyst Youssef Squali raised the recommendation to buy from hold based on the firm’s preliminary third quarter results and its “compelling” valuation.

- Point Biopharma surges 85% in premarket trading Tuesday after Eli Lilly & Co. agreed to buy the biotech firm for $12.50 per share in cash in a bid to expand its oncology capabilities into radioligand therapies.

Wall Street strategists are warning about the impact that elevated interest rates on equities, with Goldman Sachs, Morgan Stanley and JPMorgan all saying there’s a risk of further stock-market declines. Currently, traders are pricing roughly a one-in-three chance of a rate hike in November.

“We had not anticipated such an increase in rates,” said Vincent Juvyns, global market strategist at JPMorgan Asset Management. “This is something which will at least slow down, or even reverse the progress of equity markets.”

And indeed all eyes are on rates this morning, as Treasury yields extend to fresh cycle highs in 5-year out to long-end of the curve, as the selloff gathers pace in early US session. Futures volumes pick up as 10-year tenor breaks through earlier session lows and through the 107-00 level. In the long-end of the curve 30-year yields breach 4.855% and onto highest levels since 2007.

- In Treasury options demand seen for bearish plays targeting higher yields, matching the early price action.

- US yields cheaper by up to 6.5bp on the day across long-end of the curve; breaking through 4.856% in 30-year tenor and onto highest yield to highest since 2007

- Selloff extended as 10-year futures breached 107-00 level to the downside reaching as low as 106-30+; into the move around 22,000 Dec23 contracts traded over a one-minute period, highest volumes of the session

- In Treasury options early demand seen for downside protection as yields continue to climb higher; flows have included TY Nov23 107.00/106.00 put spread bought in 3,500 at 24 ticks says London trader

- Some information comes from rates traders familiar with the transactions, who asked not to be identified because they are not authorized to speak publicly

This week’s Treasury selloff came after US lawmakers managed to avert a government shutdown, prompting traders to increase bets that the Fed could raise rates in November. Comments from two Fed policymakers reinforced that view, with Cleveland Fed president Loretta Mester saying on Monday that one more rate hike was likely needed and Governor Michelle Bowman urging multiple increases.

“The market is probably evenly split on whether central banks will need to continue raising rates or not so the bond marker is testing investors,” said Brian O’Reilly, head of market strategy at Mediolanum International Funds. “With 10-year yields around 4.6%, the asset allocation decision for equities is getting quite difficult.”

European stocks were also lower, spooked by the surge in rates. The Stoxx 600 is down 0.7% at session lows, led by declines in the utility sector; retail stocks were dragged down on a warning from online retailer Boohoo Group Plc, which fell 10%. Here are the biggest European movers:

- AstraZeneca shares rise as much as 1.1% after the drugmaker agreed to pay $425 million to settle US product liability lawsuits related to heartburn and stomach acid treatments Nexium and Prilosec

- Novo Nordisk shares rise as much as 2.8% after the drugmaker won denial of a challenge to two US patents backing semaglutide

- Sika shares gain as much as 1.1% after Swiss chemicals company raised its annual sales growth and Ebitda margin targets for medium term

- Burberry falls as much as 4.7% in London to hit the lowest level since Nov. 2022, after the luxury stock was cut to sell from neutral at UBS

- Greggs shares slip as much as 3.2% after Tuesday’s third-quarter trading statement, with analysts taking an overall positive view but noting the lack of any guidance upgrade

- Eramet lost as much as 4.5% in early Paris trading on Tuesday after AlphaValue/Baader cut its rating for the French mining group, arguing there is further downward potential for the stock

- Boohoo shares tumble as much as 11%, to the lowest since August 2015, after the online fast fashion retailer cut its revenue forecast for the year

- Aker Carbon Capture drops as much as 7%, to lowest in almost five months, after Citi cuts to neutral due to perceived risks

Earlier in the session, Asian stocks declined as hawkish signals from the Federal Reserve spurred risk-off sentiment, while losses in Hong Kong intensified as traders returned from a holiday. The MSCI Asia Pacific Index fell as much as 1.6% to reach its lowest since late December. The Hang Seng China Enterprises Index fell more than 3% in the region’s worst performance among major gauges, dragged lower by tech stocks Meituan and Alibaba. Mainland China remains shut for Golden Week holiday, while South Korean markets are also closed. The broad selloff came as the latest commentary from Fed officials stirred concerns that the central bank will continue to raise interest rates. Traders boosted bets on a November rate hike to a roughly one-in-three chance, up from the 25% likelihood priced on Friday. Positive Chinese travel data did little to lift sentiment as investors focus on uncertainties lingering in the world’s second-largest economy.

- Hang Seng was the worst hit on return from holiday amid losses in property, tech and energy with developers suffering despite an early spike in Evergrande shares by around 35% on resumption of trade.

- Nikkei 225 weakened with all industries pressured and energy firms leading the broad declines.

- ASX 200 was dragged lower by underperformance in the mining-related sectors due to the recent declines in commodity prices and with headwinds from the rising yields after Australia’s 10yr yield rose to its highest since 2011, while the RBA decision to keep rates steady provided no major fireworks.

- In India, key stock gauges in India slid, tracking weakness in regional peers, with lenders and energy sector companies leading the selloff. The S&P BSE Sensex fell 0.5% to 65,512.10 in Mumbai, while the NSE Nifty 50 Index declined 0.6% to 19,528.75. The MSCI Asia Pacific Index was down 1.5%. Banks, energy and automakers were among the worst sectoral performers during the session. HDFC Bank contributed the most to the Sensex’s decline, decreasing 1.2%. Out of 30 shares in the Sensex index, 11 climbed, while 19 fell.

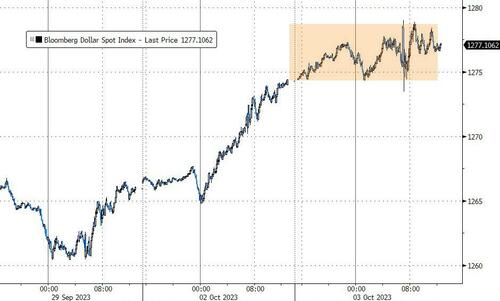

In FX, the Bloomberg Dollar Spot Index rises 0.1%, hitting a fresh 10-month high and the euro falling to its lowest against the dollar since last December at 1.049.

- The Australian dollar extended declines after the Reserve Bank of Australia held its cash rate; AUD/USD dropped as much as 0.9% to 0.6306, weakest since November

- The euro and the pound were also little changed after erasing earlier losses against the greenback

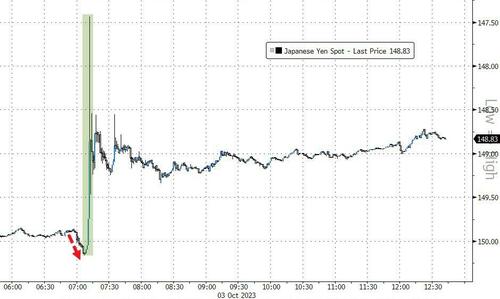

- The yen swung between gains and losses, staying near cycle lows amid intervention speculation

- USD/JPY is hovering just below 150.

In rates, Treasuries are trading at the lows of the day, with 10-year yields rising 6bps to 4.74%, while gilts outperform their German counterparts after data showed UK shop price-inflation fell to a one-year low in September. UK two-year yields fall 3bps to 4.95%. Treasury yields once again rose to session highs across the curve with futures under or near Monday’s lows; 10- to 30-year yields reached fresh multiyear highs. Gilts outperform Treasuries on the back of supportive food inflation data. US 10-year yields around 4.75%, cheaper by ~5bps on the day near session high; gilts outperform by nearly 5bp in the sector as they unwind a portion of Monday’s losses. US 2s10s curve steeper by 4bp on the day with front-end slightly outperforming; spread breached -41bp, least inverted since May 5. Fed-dated OIS continues to price around 35% odds of a 25bp rate hike for the November policy meeting; Cleveland Fed President Loretta Mester said late Monday that one more rate hike may be needed this year. Dollar IG issuance slate empty so far after five names priced $5b Monday; a slow week is expected with many companies entering earnings blackout periods. US session highlights include August JOLTS job openings data and comments from Fed’s Bostic.

In commodities, crude futures are little changed with WTI trading near $88.90. Spot gold falls 0.1%.

Bitcoin is under pressure after experiencing a marked upside in recent sessions, which took BTC to near USD 29k. Currently, residing around the USD 27.5k mark but well within recent ranges.

Looking to the day ahead now, and the main data highlight will be the US JOLTS release of job openings for August. Otherwise, central bank speakers include the ECB’s Simkus, Lane and Villeroy, along with the Fed’s Bostic.

Market Snapshot

- S&P 500 futures up 0.2% to 4,332.75

- MXAP down 1.4% to 154.63

- MXAPJ down 1.3% to 485.09

- Nikkei down 1.6% to 31,237.94

- Topix down 1.7% to 2,275.47

- Hang Seng Index down 2.7% to 17,331.22

- Shanghai Composite up 0.1% to 3,110.48

- Sensex down 0.4% to 65,585.91

- Australia S&P/ASX 200 down 1.3% to 6,943.42

- Kospi little changed at 2,465.07

- STOXX Europe 600 up 0.1% to 446.12

- German 10Y yield little changed at 2.90%

- Euro little changed at $1.0485

- Brent Futures down 0.3% to $90.45/bbl

- Gold spot up 0.0% to $1,828.42

- U.S. Dollar Index little changed at 106.99

Top Overnight News

- Several Taiwanese companies are helping Huawei build infrastructure for a secret network of chip plants across southern China, a Bloomberg investigation found. At a time when China regularly threatens Taiwan with military action, the island’s tech firms risk spurring a backlash by potentially helping US-sanctioned Huawei effectively break an American blockade. BBG

- India has told Canada to withdraw dozens of diplomats from the country, in an escalation of the crisis that erupted when Prime Minister Justin Trudeau said New Delhi may have been linked to the murder of a Canadian Sikh. FT

- ECB’s Chief Economist Philip Lane warned that there is still work needed to be done to fully tackle the EU’s inflation problem. BBG

- Switzerland’s core CPI for Sept dips to +1.3%, down from +1.5% in Aug and below the Street’s +1.5% forecast (headline inflation ticked up to +2% from +1.9% in Aug. BBG

- British shoppers enjoyed the first monthly drop in food prices in more than two years as retailers cut the cost of dairy products, fish and vegetables amid “fierce competition” between stores, a survey found. BBG

- Federal Reserve Bank of Cleveland President Loretta Mester said the US central bank will likely need to raise rates once more this year and then hold them at higher levels for some time to get inflation back to its 2% target. BBG

- Rep. Matt Gaetz (R-Fla.) on Monday night filed a formal motion to eject the speaker Kevin McCarthy, a maneuver last attempted in 1910 and never successfully completed. The House must act by Wednesday on the matter — and while McCarthy may yet survive depending on how Democrats vote, even a failed challenge to his speakership weakens him going forward. Politico

- The slide in Treasuries has been excessive given recent economic data and Federal Reserve policy, suggesting it’s instead being driven by fears over the swelling US deficit. BBG

- America’s shale pioneers have vowed to keep a lid on drilling even if oil hits $100 a barrel, citing a need to maintain capital discipline and what they claim is a “war” on fossil fuels waged by the Joe Biden administration. FT

- In the new ‘higher for longer’ rates environment, the key risk for S&P 500 ROE will be higher interest expenses and lower leverage. Our rates strategists recently raised their forecast for the nominal 10Y UST and now expect rates to end 2023 at 4.3% and then rise to 4.6% in 1H 2024 before receding back to 4.3% at the end of 2024. Although the long-maturity, fixed-rate debt structures of S&P 500 companies generally insulate them from higher rates, borrow costs for S&P 500 companies have ticked up on a year/year basis by the largest amount in nearly two decades. GIR

A more detailed look at global markets courtesy of Newsquawk

APAC stocks declined amid the rising global yield environment and the continued absence of some key markets, while the focus turned to central bank announcements beginning with the RBA. ASX 200 was dragged lower by underperformance in the mining-related sectors due to the recent declines in commodity prices and with headwinds from the rising yields after Australia’s 10yr yield rose to its highest since 2011, while the RBA decision to keep rates steady provided no major fireworks. Nikkei 225 weakened with all industries pressured and energy firms leading the broad declines. Hang Seng was the worst hit on return from holiday amid losses in property, tech and energy with developers suffering despite an early spike in Evergrande shares by around 35% on resumption of trade.

Top Asian News

- RBA kept the Cash Rate Target unchanged at 4.10%, as expected, while it reiterated that some further tightening of monetary policy may be required and that the Board remains resolute in its determination to return inflation to the target. Furthermore, it stated that returning inflation to the target within a reasonable timeframe remains the Board’s priority and recent data are consistent with inflation returning to the 2–3% target range over the forecast period but also noted significant uncertainties around the outlook..

- “(China) has seen a recovery in consumer spending in terms of trips and transportation, with market confidence and vitality both on the continuous rise” following the first four days of the Chinese holiday, according to Global Times.

European bourses have been mixed but are currently a touch softer, Euro Stoxx 50 -0.2%; newsflow is relatively light and markets remain focused on yields. Sectors are similarly mixed, featuring outperformance in Banks and Insurance names while Utilities and Basic Resources are the relative laggards. Stateside, futures are modestly firmer, ES +0.2%, with recent pressure being attributed to yields but action comparably more contained thus far in today’s session ahead of JOLTS and Fed’s Bostic & Mester. For reference, APAC trade remains limited given mass holiday closures though the return of the Hang Seng saw it experience marked pressure and close with downside of circa. 3.0%, with the move similarly attributed to recent yield action.

Top European News

- EU is to assess risks of four critical technologies being used by third countries such as semiconductors, AI, quantum technologies and biotechnologies, while the EU aims to take measures next year to mitigate risks to these technologies, according to an EU official cited by Reuters.

- Brussels will unfreeze about EUR 13bln in EU funding to Hungary as it seeks help for Ukraine, according to FT.

- ECB’s Lane says they have reached the interest rate level that will help tame inflation; the key is to maintain this rate level for as long as needed; seeing wage data coming in lower is very important. Would not focus on December as a critical decision; December is not the end of the inflation challenge. Says he welcomes September inflation data, but we need to see further progress.

- ECB’s Valimaki (sitting in for ECB’s Rehn) says further rate hikes cannot be ruled out, appears as if a wage-price spiral can be avoided.

- ECB’s Simkus says rates need to stay restrictive to tame prices; prompt response of monetary policy was effective; inflation still faces many lines of resistance; inflation shock is not over.

FX

- Dollar resumes bull run before running into chart and round number resistance, DXY probes Fib at 107.170 and fades within 107.210-106.930 range.

- Yen continues to defend 150.00 vs. Buck, but barely and with 1.1bln option expiries helping, Euro eyes expiry interest at 1.0495 against Greenback after a bounce from 1.0461 and Sterling pivots Fib retracement between 1.2062-96 parameters.

- Aussie lags post-on hold RBA and Kiwi down in sympathy awaiting RBNZ to follow suit, AUSD/USD and NZD/USD cling to 0.6300 and 0.5900 handles respectively.

- Franc deflated after softer than forecast Swiss CPI, USD/CHF hovers above 0.9200.

- Japanese Finance Minister Suzuki said it is important for currencies to move in a stable manner reflecting fundamentals and they will take appropriate steps on FX moves with a sense of urgency, while he added that they will stand ready to respond while closely watching FX moves. Furthermore, he said currency interventions are not targeting FX levels and whether to carry out FX intervention is determined by volatility, according to Reuters.

Fixed Income

- EGB underperformance gradually spills over as Bunds retreat from 127.95 to 127.45 and BTPs reverse through 109.00 within a 109.49-108.86 range.

- Gilts and T-note suffer contagion between 93.18-92.68 and 107-14/06 respective parameters ahead of Fed’s Bostic and JOLTS US job openings.

- Orders for the new 5-year BTP Valore have reached EUR 5bln since the beginning of the offer, via Reuters citing Bourse data.

Commodities

- Crude benchmarks are little changed overall having lifted incrementally off initial lows as the USD moves below the 107.00 mark while crude specifics have been light as attention turns to this week’s JMMC.

- Currently, WTI and Brent are trading in USD 87.76-88.71/bbl and USD 89.50-90.46/bbl respective ranges.

- Spot gold is essentially flat intraday with the yellow metal holding around USD 1825/oz while spot silver is a touch firmer after Monday’s pronounced pressure, finally base metals have seen similar directional action to crude with the metals off lows as the USD eases a touch.

- Spain’s Energy Minister showed support for the Dutch call to phase out fossil fuel subsidies.

- India’s petroleum minister says an oil price above USD 100/bbl is not going to be in anyone’s interest.

- Poland and Ukraine announced a breakthrough on Ukrainian grain transit, according to AFP.

Geopolitics

- Israel carried out an air attack on Syrian armed forces positions in the vicinity of Deir al Zor, according to Syrian state media.

- India told Canada to withdraw dozens of diplomatic staff whereby it must repatriate around 40 diplomats by October 10th, according to FT.

US Event Calendar

- Sept. Wards Total Vehicle Sales, est. 15.4m, prior 15m

- 10:00: Aug. JOLTs Job Openings, est. 8.82m, prior 8.83m

Central bank speakers

- 08:00: Fed’s Bostic Speaks on Economic Outlook, Inflation

DB’s Jim Reid concludes the overnight wrap

It might have been a brand new quarter, but yesterday was another challenging day for markets, especially with the bond sell-off showing no sign of letting up. In fact, the 10yr Treasury yield (+10.8bps) closed at a post-2007 high of 4.68%, whilst the 10yr real yield (+9.7bps) closed at a post-GFC high of 2.33%. And despite some better-than-expected data, risk assets came under pressure alongside WTI crude (-2.17%) falling back beneath $90/bbl. Equities were weak in Europe and down for much of the day in the US but a late rally left the S&P 500 (+0.01%) flat by the close. Europe’s STOXX 600 (-1.03%) fell to a 6-month low, and the German 10yr real yield (+12.1bps) hit a post-2011 high of 0.58%. The main event today is the US JOLTS data as we see how tight the labour market still is under the surface.

Starting with markets and there were several factors driving the latest sell-off. First up, the lack of a US government shutdown over the weekend was seen in a more bearish light as the day progressed, as it removed a tangible risk for the economy and was seen as raising the likelihood of more rate hikes. For instance, futures raised the likelihood of a hike at the next meeting in November from 19% on Friday to 28% yesterday. And looking at the prospect of a hike by December, the likelihood rose from 39% last Friday to 51% by yesterday’s close.

Second, the sell-off then got added fuel from the latest ISM manufacturing print for September, which was notably better than expected. The headline print came in at 49.0 (vs. 47.6 expected), which was the highest since November 2022. And there was lots of good news at the component level as well, with new orders (49.2) at a 13-month high and employment (51.2) back in expansionary territory. That was echoed by the final manufacturing PMI as well, where the final reading was revised up to 49.8 (vs. flash 48.9). So there were several signs that the economy was proving more resilient than expected.

Third, comments from numerous Fed speakers reiterated the higher-for-longer narrative. Governor Bowman, one of the more hawkish FOMC members, suggested that multiple further rate hikes may be needed while Cleveland Fed President Mester saw another hike this year as likely. Comments from Vice Chair of Supervision Barr erred on the more cautious side, saying that the more important question was “how long we will need to hold rates at a sufficiently restrictive level”. Overall, despite the more encouraging recent inflation data, the latest Fed commentary shows no signs of a downshift from the September median dot plot view of another rate hike by year-end.

Speaking of US economic resilience, our own US economists have just released an updated set of forecasts overnight. Their baseline still sees a recession taking place, but they now see that starting a bit later in Q1 2024, and only lasting two quarters. Their view is that the soft landing case has strengthened over recent months, but there are still plenty of headwinds, including depleted savings, tightening credit conditions, and a return of student debt payments. For the Fed, they continue to see the tightening cycle as over now, albeit with the risk of another hike. And they now expect the Fed to start cutting rates from June 2024, with 175bps of cuts next year. See their full update here.

With some more positivity about the economy, bonds continued to sell off throughout the day, with yields on 10yr Treasuries up +10.8bps to a post-2007 high of 4.68%. The 30yr yield (+8.9bps) also pushed higher to close at 4.79%. It was real yields that drove the increase in rates, with the 2yr real yield (+7.3bps) at a new post-GFC high of 3.07%, and the 10yr real yield (+9.7bps) at 2.33%. At the same time, the 2s10s curve continued to steepen, with a +4.9bps increase to -42.8bps. On one level, that might be seen as a positive sign given the 2s10s is a classic recessionary indicator, but then again, the last 4 cycles saw it move out of inversion territory just before the recession began.

Over in Europe, there was a similarly strong bond sell-off, with yields on 10yr bunds (+8.2bps), OATs (+7.8bps) and BTPs (+2.6bps) all moving higher. But it was gilts that led the moves, with the 10yr yield up +12.7bps to 4.56%, whilst the 30yr gilt yield (+11.4bps) surpassed its mini-budget peak yesterday to close above 5% for the first time since 2002. Similarly to the US, it was real yields that led those moves, and the German 10yr real yield (+12.1bps) hit a post-2011 high of 0.58%.

The bond sell-off created a tough backdrop for equities. The S&P 500 traded around half a percent lower for most of the day, but a rally in the last hour of the US session left it flat on the day (+0.01%). Tech stocks were a big winner though, with the FANG+ Index (+1.38%) going against the broader trend to advance for a 4th consecutive session. The breadth of losses outside of tech was highlighted by the equal weight index declining -1.11% with only 22% of the S&P 500 constituents up on the day despite its flat headline performance. Small caps also underperformed with the Russell 2000 index down -1.58%. Back in Europe there were larger losses, leaving the STOXX 600 (-1.03%), the DAX (-0.91%), the CAC 40 (-0.94%) and FTSE 100 (-1.28%) lower on the day.

Across other asset classes, the dollar was a key beneficiary, with the broad index (+0.69%) rising to a 10-month high and the euro falling to its lowest against the dollar since last December at 1.049. Meanwhile, oil declined for third day in a row, with WTI crude falling back below $90/bl (-2.17% to $88.82/bl). Both WTI (-5%) and Brent (-6%) have seen their sharpest 3-day decline since the oil price rally started in June. So some evidence that uncertainty over the demand outlook is weighing on the strong recent oil rally.

Overnight in Asia, regional equities are also selling off with the Nikkei 225 down -1.43%. The Hang Seng is down -2.98% after reopening post Monday’s holiday. Many other markets remain closed in this holiday week. There was also an RBA decision overnight, with the central bank keeping rates at 4.10% with much of the statement identical to the last one. S&P 500 futures are almost unchanged (-0.06%), with Treasury yields up less than a basis point across the curve.

Elsewhere yesterday, the main data highlight came from the final manufacturing PMIs, although they mostly echoed the initial impressions from the flash reading. Indeed, the Euro Area PMI was exactly in line with the flash print at 43.4, and Germany’s was revised down slightly to 39.6 (vs. flash 39.8). Otherwise, the Euro Area unemployment rate was back at its recent low of 6.4% in August, which is its joint-lowest level since the formation of the single currency.

To the day ahead now, and the main data highlight will be the US JOLTS release of job openings for August. Otherwise, central bank speakers include the ECB’s Simkus, Lane and Villeroy, along with the Fed’s Bostic.

2 B) NOW NEWSQUAWK (EUROPE/REPORT)

European bourses weaker & US equities tentative ahead of US JOLTS; Fed’s Bostic due – Newsquawk US Market Open

TUESDAY, OCT 03, 2023 – 06:04 AM

- European bourses are a touch softer with yields in focus, US futures slightly firmer ahead of data & Fed speak

- DXY ran into resistance and has faded from a 107.21 best, but does remain incrementally firmer; Antipodeans lag post on-hold RBA

- EGBs pressured with BTPs seemingly leading and pulling Gilts and USTs lower in sympathy

- Crude benchmarks and precious metals little changed overall with the USD dictating

- Looking ahead, highlights include US IBD/TIPP & JOLTS, Australian PMI (Final), Fed’s Bostic. Earnings from McCormick & Company

More Newsquawk in 3 steps:

1. Subscribe to the free premarket movers reports

2. Listen to this report in the market open podcast (available on Apple and Spotify)

3. Trial Newsquawk’s premium real-time audio news squawk box for 7 days

EUROPEAN TRADE

EQUITIES

- European bourses have been mixed but are currently a touch softer, Euro Stoxx 50 -0.2%; newsflow is relatively light and markets remain focused on yields.

- Sectors are similarly mixed, featuring outperformance in Banks and Insurance names while Utilities and Basic Resources are the relative laggards.

- Stateside, futures are modestly firmer, ES +0.2%, with recent pressure being attributed to yields but action comparably more contained thus far in today’s session ahead of JOLTS and Fed’s Bostic & Mester.

- For reference, APAC trade remains limited given mass holiday closures though the return of the Hang Seng saw it experience marked pressure and close with downside of circa. 3.0%, with the move similarly attributed to recent yield action.

- Click here for more details.

FX

- Dollar resumes bull run before running into chart and round number resistance, DXY probes Fib at 107.170 and fades within 107.210-106.930 range.

- Yen continues to defend 150.00 vs. Buck, but barely and with 1.1bln option expiries helping, Euro eyes expiry interest at 1.0495 against Greenback after a bounce from 1.0461 and Sterling pivots Fib retracement between 1.2062-96 parameters.

- Aussie lags post-on hold RBA and Kiwi down in sympathy awaiting RBNZ to follow suit, AUSD/USD and NZD/USD cling to 0.6300 and 0.5900 handles respectively.

- Franc deflated after softer than forecast Swiss CPI, USD/CHF hovers above 0.9200.

- Japanese Finance Minister Suzuki said it is important for currencies to move in a stable manner reflecting fundamentals and they will take appropriate steps on FX moves with a sense of urgency, while he added that they will stand ready to respond while closely watching FX moves. Furthermore, he said currency interventions are not targeting FX levels and whether to carry out FX intervention is determined by volatility, according to Reuters.

- Click here for more details.

- Click here for the Option Expires for the NY Cut.

FIXED INCOME

- EGB underperformance gradually spills over as Bunds retreat from 127.95 to 127.45 and BTPs reverse through 109.00 within a 109.49-108.86 range.