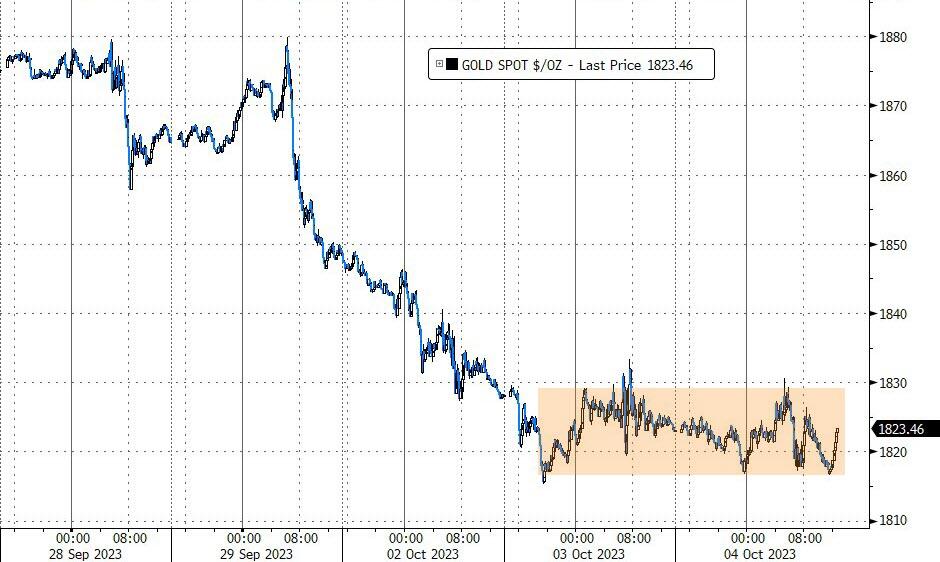

GOLD PRICE CLOSED: DOWN $7.40 TO $1819.70

SILVER PRICE CLOSED: DOWN $0.34 AT $20.96

Access prices: closes 4: 15 PM

Gold ACCESS CLOSE 1821.75.

Silver ACCESS CLOSE: 21.02

SEPT 27//SHANGHAI GOLD

Shanghai Gold Benchmark Price

USD oz  AM2014.57

AM2014.57

PM1985.03

Historical SGE Fix

premium $122,00

xxxxxxxxxxxxxxxxxx

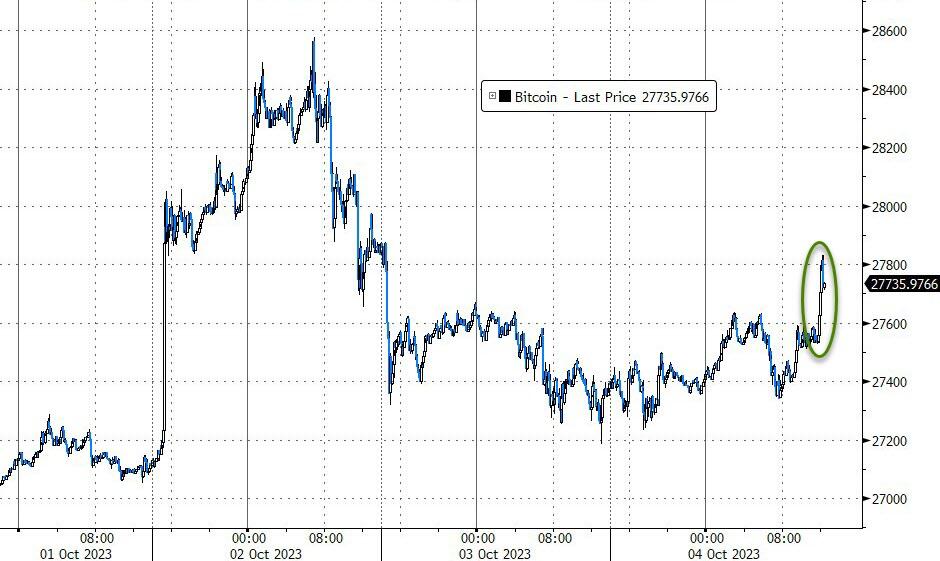

Bitcoin morning price:, $27,560 UP 303 Dollars

Bitcoin: afternoon price: $27,817 UP 46 dollars

Platinum price closing $870.35 DOWN $4.65

Palladium price; $1170.75 DOWN $17.15

END

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

Due to the huge rise in the dollar, we must look at gold and silver in currencies other than the dollar to understand where we are heading

I will now provide gold in Canadian dollars, British pounds and Euros/4: 15 PM ACCESS

CANADIAN GOLD: $2,504.09 UP 3.40 CDN dollars per oz (ALL TIME HIGH 2,775.35)

BRITISH GOLD: 1499.98 DOWN 9.72 pounds per oz//(ALL TIME HIGH//CLOSING///1630.29)

EURO GOLD: 1733.36 DOWN 9.80 euros per oz //(ALL TIME HIGH/CLOSING//1861.21)//

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

EXCHANGE: COMEX

EXCHANGE: COMEX

CONTRACT: OCTOBER 2023 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,824.600000000 USD

INTENT DATE: 10/03/2023 DELIVERY DATE: 10/05/2023

FIRM ORG FIRM NAME ISSUED STOPPED

323 H HSBC 103

357 C WEDBUSH 4

624 H BOFA SECURITIES 50

657 H MORGAN STANLEY 110

661 C JP MORGAN 39

686 C STONEX FINANCIA 1

726 C CUNNINGHAM COM 1 1

737 C ADVANTAGE 26 21

972 C IRONBEAM INC 2

TOTAL: 179 179

MONTH TO DATE: 8,587

JPMorgan stopped 0/179 contracts.

FOR OCT.:

GOLD: NUMBER OF NOTICES FILED FOR OCT/2023. CONTRACT: 179 NOTICES FOR 17,900 OZ or .5567 TONNES

total notices so far: 8597 contracts for 859700 oz (26.709 tonnes)

FOR OCT:

SILVER NOTICES:34 NOTICE(S) FILED FOR 170,000 OZ/

total number of notices filed so far this month : 317 for 1,585,000 oz

XXXXXXXXXXXXXXXXXXXXXXXX

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD

WITH GOLD DOWN $7,40

INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD/ : / HUGE CHANGES IN GOLD INVENTORY AT THE GLD// A WITHDRAWAL OF 1.73 TONNES OF GOLD OUT OF THE GLD.

INVENTORY RESTS AT 873,35 TONNES

Silver//

WITH NO SILVER AROUND AND SILVER DOWN 34 CENTS AT THE SLV// HUGE CHANGES IN SILVER INVENTORY AT THE SLV: :A WHOPPING DEPOSIT OF 6.311 MILLION OZ INTO THE SLV//

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV.

CLOSING INVENTORY: 448.194 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY GIGANTIC SIZED 2885 CONTRACTS TO 125,847 AND FURTHER FROM THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THIS HUGE SIZED LOSS IN COMEX OI WAS ACCOMPLISHED DESPITE OUR TINY $0.02 LOSS IN SILVER PRICING AT THE COMEX ON TUESDAY. TAS ISSUANCE WAS A GIGANTIC SIZED 952 CONTRACTS. THESE WILL BE USED FOR MANIPULATION LATER THIS MONTH/AS WELL AS TODAY. CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON TUESDAY NIGHT: 952 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS. IT THUS LOOKS LIKE THE FED (GOV’T) IS BEHIND ALL OF THESE TRADES

WE HAVE NOW SET ANOTHER RECORD LOW AT 114,102 CONTRACTS ///JULY 3.2023// OUR BANKERS WITH THE HELP OF SPECULATORS AND HIGH FREQUENCY TRADERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.02). BUT WERE UNSUCCESSFUL IN KNOCKING ANY SILVER LONGS AS WE HAD A GOOD SIZED GAIN OF 441 OI CONTRACTS ON OUR TWO EXCHANGES.

WE MUST HAVE HAD:

A MEGA HUMONGOUS ISSUANCE OF EXCHANGE FOR PHYSICALS( 3326 CONTRACTS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 1.530 MILLION OZ (FIRST DAY NOTICE) FOLLOWED BY TODAY’S 90,000 OZ QUEUE JUMP//NEW STANDING 1.665 MILLION O///HUGE SIZED COMEX OI LOSS/ HUGE SIZED EFP ISSUANCE/VI) HUGE SIZED NUMBER OF T.A.S. CONTRACT ISSUANCE 952 CONTRACTS)/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL -352 CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS OCT ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF OCT:

TOTAL CONTRACTS for 3 days, total 6926 contracts: OR 34.630 MILLION OZ (1154 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 34.630 MILLION OZ

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH 2022: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 118.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 85.745 MILLION OZ (SMALLER THAN LAST MONTH)

AUGUST: 171.43 MILLION OZ (THIS MONTH IS GOING TO BE HUGE //2ND HIGHEST ON RECORD

SEPT: 72.705 MILLION OZ (SMALLER THIS MONTH)

OCT: 34.630 MILLION OZ (THIS IS GOING TO BE A HUGE MONTH FOR EFP ISSUANCE)

RESULT: WE HAD A HUGE SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 2885 CONTRACTS DESPITE OUR TINY LOSS IN PRICE OF $0.02 IN SILVER PRICING AT THE COMEX//TUESDAY.,. THE CME NOTIFIED US THAT WE HAD A MEGA HUMONGOUS EFP ISSUANCE CONTRACTS: 3326 ISSUED FOR OCT AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS./ WE HAVE A SMALL INITIAL SILVER OZ STANDING FOR SEPT OF 1.532 MILLION OZ FOLLOWED BY TODAY’S 90,000 OZ QUEUE JUMP:NEW TOTAL STANDING 1.665 MILLION OZ /// WE HAVE A GOOD SIZED GAIN OF 441 OI CONTRACTS ON THE TWO EXCHANGES. THE TOTAL OF TAS INITIATED CONTRACTS TODAY: A GIGANTIC SIZED 952 CONTRACTS//HUGE FRONT END OF THE TAS CONTRACTS WERE LIQUIDATED DURING THE TUESDAY COMEX SESSION. THE NEW TAS ISSUANCE TUESDAY NIGHT (952) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE., .

WE HAD 34 NOTICE(S) FILED TODAY FOR 170,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A FAIR SIZED 1857 CONTRACTS TO 431,226 AND FURTHER FROM THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: – REMOVED: –432 CONTRACTS

WE HAD A FAIR SIZED DECREASE IN COMEX OI ( 1857 CONTRACTS) WITH OUR $6.90 LOSS IN PRICE//TUESDAY. WE ALSO HAD A RATHER STRONG INITIAL STANDING IN GOLD TONNAGE FOR SEPT. AT 16.562 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S STRONG 18,600 OZ QUEUE JUMP/NEW STANDING 27.039 TONNES/ + /A STRONG (AND CRIMINAL) ISSUANCE OF 2041 T.A.S. CONTRACTS /// ALL OF..THIS HAPPENED WITH OUR $6.90 LOSS IN PRICE WITH RESPECT TO TUESDAY’S TRADING.WE HAD A FAIR SIZED GAIN OF 2228 OI CONTRACTS (6.930 PAPER TONNES) ON OUR TWO EXCHANGES.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A GOOD SIZED 4085 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 431,226

IN ESSENCE WE HAVE A FAIR SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 2228 CONTRACTS WITH 1857 CONTRACTS DECREASED AT THE COMEX// AND A GOOD SIZED 4085 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 2228 CONTRACTS OR 6.930 TONNES. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): A STRONG 2041 CONTRACTS)

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A GOOD SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (4085 CONTRACTS) ACCOMPANYING THE FAIR SIZED LOSS IN COMEX OI (1857) //TOTAL GAIN FOR OUR THE TWO EXCHANGES: 2228 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR FORMER FORMAT OF BANKERS GOING LONG AND SPECULATORS GOING SHORT ,2.) FAIR INITIAL STANDING AT THE GOLD COMEX FOR OCT. AT 16.562 TONNES FOLLOWED BY TODAY’S 18,600 OZ QUEUE JUMP//NEW STANDING 27.039 TONNES// /// 3) ZERO LONG LIQUIDATION BUT CONSIDERABLE TAS LIQUIDATION AND SOME SPEC SHORT COVERINGS DURING THE COMEX SESSION //4) FAIR SIZED COMEX OPEN INTEREST LOSS/ 5) GOOD ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER///6: STRONG T.A.S. ISSUANCE: 2041 CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023 INCLUDING TODAY

OCT

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF OCT :

TOTAL EFP CONTRACTS ISSUED: 14,257 CONTRACTS OR 1,425,700 OZ OR 44.345 TONNES IN 3TRADING DAY(S) AND THUS AVERAGING: 4752 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 3 TRADING DAY(S) IN TONNES 44.345 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2022, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 44.345/3550 x 100% TONNES 1.23% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2023

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH/2022: 409.30 TONNES //FINAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 151.69 TONNES (WEAKER THAN LAST MONTH)

AUGUST: 195.28 TONNES (A STRONGER MONTH)//FINAL

SEPT: 254.709 TONNES (WILL BE LARGER THAN LAST MONTH AND A STRONG MONTH)

OCT. 44.345 TONNES

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF SEPT. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF MAY HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF JUNE., FOR BOTH GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (SEPT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER FELL BY A HUGE SIZED 2885 CONTRACTS OI TO 125,847 AND CLOSER TO OUR COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE A MEGA GIGANTIC 3326 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

DEC 3326 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 3326 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 2885 CONTRACTS AND ADD TO THE 3326 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A GOOD SIZED GAIN OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 441 CONTRACTS

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTAL 3.965 MILLION OZ

OCCURRED DESPITE OUR HUGE $0.02 LOSS IN PRICE …..

END

OUTLINE FOR TODAY’S COMMENTARY

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

b, ) Gold/silver trading overnight Europe,//GOLD COMMENTARIES

(Peter Schiff)

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS//

WEDNESDAY MORNING//TUESDAY NIGHT

SHANGHAI CLOSED UP 3.16 PTS OR .10% //Hang Seng CLOSED DOWN 135.33 PTS OR 0.78% /The Nikkei CLOSED DOWN 711.06 PTS OR 2.28% //Australia’s all ordinaries CLOSED DOWN 0.82 % /Chinese yuan (ONSHORE) closed UP AT 7.3015 /OFFSHORE CHINESE YUAN CLOSED UP TO 7.3171 /Oil DOWN TO 87.52 dollars per barrel for WTI and BRENT DOWN AT 89.40 / Stocks in Europe OPENED ALL MIXED// ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE STRONGER

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

9. USA

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A FAIR SIZED 1857 CONTRACTS TO 431,226 WITH OUR STRONG LOSS IN PRICE OF $6.90 ON TUESDAY.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE NON ACTIVE DELIVERY MONTH OF OCT..… THE CME REPORTS THAT THE BANKERS ISSUED A STRONG SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 4085 EFP CONTRACTS WERE ISSUED: : DEC 4085 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 4085 CONTRACTS

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A FAIR SIZED TOTAL OF 2228 CONTRACTS IN THAT 4085 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A FAIR SIZED LOSS OF 1425 COMEX CONTRACTS..AND THIS GAIN ON OUR TWO EXCHANGES HAPPENED DESPITE OUR LOSS IN PRICE OF $6.90//TUESDAY COMEX. AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS DURING MID MONTH IN THE DELIVERY CYCLE), THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR TUESDAY NIGHT WAS A FAIR 2041 CONTRACTS. THROUGHOUT THE PAST WEEKS, THE BANKERS SOLD OFF THE LONG SIDE OF THE SPREAD WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR SPREAD WHICH WILL BE LIQUIDATED TWO MONTHS HENCE)//

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: OCT (27.039) ( ACTIVE MONTH)

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 27.039 TONNES

THE SPECS/HFT WERE SUCCESSFUL IN LOWERING GOLD’S PRICE( IT LOST $6.90) //// BUT WERE UNSUCCESSFUL IN KNOCKING ANY SPECULATOR LONGS AS WE HAD A FAIR GAIN OF 2228 TOTAL CONTRACTS ON OUR TWO EXCHANGES. WE HAD A CONSIDERABLE T.A.S. LIQUIDATION ON THE FRONT END OF TUESDAY’S TRADING. THE T.A.S. ISSUED ON TUESDAY NIGHT WILL BE “PUT INTO THE BANK” TO BE USED AT A LATER DATE AT THE COLLUSIVE CHOOSING OF OUR BANKERS.

WE HAVE GAINED A TOTAL OI OF 6.930 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR OCT. (16.562 TONNES) ON FIRST DAY NOTICE FOLLOWED BY TODAY’S 18,600 OZ QUEUE JUMP//NEW TOTALS STANDING:27.039 TONNES ALL OF THIS WAS ACCOMPLISHED WITH OUR LOSS IN PRICE TO THE TUNE OF $6.90. FOR THE PAST WEEK, THE SPECULATORS HAVE GONE MASSIVELY SHORT WITH OUR BANKERS NET LONG. THE BIG QUESTION IS WHEN WILL THE BANKERS PULL THE PLUG ON OUR SPECS.

WE HAD – REMOVED 432 CONTRACTS TO THE COMEX TRADES TO OPEN INTEREST

NET GAIN ON THE TWO EXCHANGES 2228 CONTRACTS OR 222800 OZ OR 6.93 TONNES.

Estimated gold volume today:// 194,681 fair

final gold volumes/yesterday 228,148 fair/

//speculators have left the gold arena

//OCT 4/ /// THE OCT. 2023 GOLD CONTRACT

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 94,556.091 oz OZ Brinks Malca 4 kilobars Brinks 2957 kilobars Malca . |

| Deposit to the Dealer Inventory in oz | nil |

| Deposits to the Customer Inventory, in oz | nil oz |

| No of oz served (contracts) today | 179 notice(s) 17,900 OZ .5567 TONNES |

| No of oz to be served (notices) | 96 contracts 9600 oz 0.2985 TONNES |

| Total monthly oz gold served (contracts) so far this month | 8597 notices 859,700 OZ 26.709 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | x |

0 dealer deposit:

total dealer deposits: 0 oz

customer deposits: 0

total customer deposits: 0 oz

we had 2 customer withdrawals

i) Out of Brinks: 128.604 oz (4 kilobars)

ii) Out of Malca: 94,427.487 oz (2937 kilobars)

total withdrawals 94,556.091. oz (2941 kilobars)

Adjustments; 3 dealer to customer

i)Ashai: 15,620.374 oz

ii) Brinks: 78,061.499 oz

iii) JPMorgan 633.758 oz

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR OCT.

For the front month of OCTOBER we have an oi of 275 contracts having LOST 2387 contracts. We had 2572 contracts filed on Tuesday, so we gained 186 contracts or an additional 18,600 oz will stand for delivery in this active delivery month of October. Somebody, for the third day in a row, was in urgent need of a huge supply of physical gold over here.

NOV LOST 38 CONTRACTS to stand at 1202

December LOST 3139 contracts down to 371,914 contracts.

We had 179 contracts filed for today representing 17,900 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 39 notices were issued from their client or customer account. The total of all issuance by all participants equate to 170 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped received by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the OCT. /2023. contract month, we take the total number of notices filed so far for the month (8587 x 100 oz ), to which we add the difference between the open interest for the front month of OCT. (275 CONTRACTS) minus the number of notices served upon today 179 x 100 oz per contract equals 869,300 OZ OR 27.039 TONNES the number of TONNES standing in this active month of OCT.

thus the INITIAL standings for gold for the OCT. contract month: No of notices filed so far (8587) x 100 oz + (275) {OI for the front month} minus the number of notices served upon today (179) x 100 oz) which equals 869,300 oz standing OR 27.039 TONNES

TOTAL COMEX GOLD STANDING: 27.039 TONNES WHICH IS HUGE FOR AN ACTIVE BUT GENERALLY WEAK DELIVERY MONTH. (OCT). Somebody is after a considerable amount of gold from the comex.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 2,023,223.140 OZ 62.93 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 20,817,366.795 OZ

TOTAL REGISTERED GOLD 10,216,290.252 (317.76 tonnes)..

TOTAL OF ALL ELIGIBLE GOLD: 10,601,076.543 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 8,193,067 OZ (REG GOLD- PLEDGED GOLD) 254.83 tonnes//dropping like a stone

END

SILVER/COMEX

OCT 4

//2023// THE OCT 2023 SILVER CONTRACT

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 0 oz nil . |

| Deposits to the Dealer Inventory | nil oz |

| Deposits to the Customer Inventory | 615,134.170 oz CNT Delaware |

| No of oz served today (contracts) | 34 CONTRACT(S) (170,000 OZ) |

| No of oz to be served (notices) | 16 contracts (80,000 oz) |

| Total monthly oz silver served (contracts) | 317 Contracts (1,585,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

i) 0 dealer deposit

total dealer deposit: 0

total: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: 0 oz

We had 2 deposit customer account:

i) Into CNT: 600,040.061 oz

ii) Into Delaware: 15,094.170 oz

total customer deposit 615,134.231oz

JPMorgan has a total silver weight: 136.236 million oz/272.755 million or 48.38%

Comex withdrawals 0

total: nil oz

adjustments: 0

TOTAL REGISTERED SILVER: 37.638 MILLION OZ//.TOTAL REG + ELIGIBLE. 272.755 million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR August:

silver open interest data:

FRONT MONTH OF OCT /2023 OI: 50 CONTRACTS HAVING LOST 115 CONTRACT(S). WE HAD 133 NOTICES FILED

ON MONDAY, SO WE GAINED 18 CONTRACTS AS WE HAD A QUEUE JUMP OF 90,000 OZ

NOVEMBER LOST 27 CONTRACTS TO STAND AT 522

DEC. LOST 3379 CONTRACTS TO STAND AT 109.729 .

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 34 for 170,000 oz

Comex volumes// est. volume today 67,796 //good

Comex volume: confirmed yesterday 87,400 strong//

To calculate the number of silver ounces that will stand for delivery in OCT. we take the total number of notices filed for the month so far at 317 x 5,000 oz = 1,585,000 oz

to which we add the difference between the open interest for the front month of OCT (50) and the number of notices served upon today 34 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the OCT/2023 contract month: 317 (notices served so far) x 5000 oz + OI for the front month of OCT (50) – number of notices served upon today (34 )x 500 oz of silver standing for the OCT contract month equates to 1.665 million oz.

There are 37.638 million oz of registered silver.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS

OCT 4/WITH GOLD DOWN $7.40 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.73 TONNES OF GOLD INTO THE GLD/// : // //INVENTORY RESTS AT 873.35 TONNES

OCT 3/WITH GOLD DOWN $6.90 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.44 TONNES OF GOLD INTO THE GLD/// : // //INVENTORY RESTS AT 875.08 TONNES

OCT 2/WITH GOLD DOWN $19.35 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD: LD/ : // //INVENTORY RESTS AT 873,64 TONNES

SEPT 29/WITH GOLD DOWN $11.15 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD: LD/ : // //INVENTORY RESTS AT 873,64 TONNES

SEPT 28/WITH GOLD DOWN $13.45 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A HUGE WITHDRAWAL OF 4.88 TONNES OF GOLD OUT OF THE GLD/ : // //INVENTORY RESTS AT 873,64 TONNES

SEPT 26/WITH GOLD DOWN $XXX TODAY:SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 0.31 TONNES OF GOLD OUT 05 THE GLD/ : // //INVENTORY RESTS AT 878.52 TONNES

SEPT 26/WITH GOLD DOWN $13.40 TODAY:SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 0.31 TONNES OF GOLD OUT 05 THE GLD/ : // //INVENTORY RESTS AT 878.52 TONNES

SEPT 22/WITH GOLD UP $5.70 TODAY:SMALL CHANGES IN GOLD INVENTORY AT THE GLD DEPOSIT OF 0.58 TONNES OF GOLD INTO THE GLD/ : // //INVENTORY RESTS AT 878.83 TONNES

SEPT 21/WITH GOLD DOWN $25.60 TODAY:SMALL CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 0.58 TONNES OF GOLD FROM THE GLD/ : // //INVENTORY RESTS AT 878.25 TONNES

SEPT 19/WITH GOLD UP $0.60 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD : // //INVENTORY RESTS AT 880.217 TONNES

SEPT 18/WITH GOLD UP $8.40 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD : A DEPOSIT OF 0.57 TONNES OF GOLD INTO THE GLD// //INVENTORY RESTS AT 880.217 TONNES

SEPT 15/WITH GOLD UP $13.20 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD : A WITHDRAWAL OF 1.055 TONNES OF GOLD FROM THE GLD// //INVENTORY RESTS AT 879.70 TONNES

SEPT 14/WITH GOLD UP $1.00 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD : A WITHDRAWAL OF 4.63 TONNES OF GOLD FROM THE GLD// //INVENTORY RESTS AT 882.01 TONNES

SEPT 13/WITH GOLD DOWN $2.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD : / //INVENTORY RESTS AT 886.64 TONNES

SEPT 12/WITH GOLD DOWN $11.20 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD : / //INVENTORY RESTS AT 886.64 TONNES

SEPT 11/WITH GOLD UP $4.45 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD : / //INVENTORY RESTS AT 886.64 TONNES

SEPT 8/WITH GOLD UP $0.35 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD : / //INVENTORY RESTS AT 886.64 TONNES

SEPT 7/WITH GOLD DOWN $0.20 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 3.22 TONNES OF GOLD INTO THE GLD.: / //INVENTORY RESTS AT 886.69 TONNES

SEPT 6/WITH GOLD DOWN $8.80 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 1.16 TONNES OF GOLD INTO THE GLD.: / //INVENTORY RESTS AT 889.81 TONNES

SEPT 5/WITH GOLD DOWN $13.50 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF 0.87 TONNES OF GOLD INTO THE GLD.: / //INVENTORY RESTS AT 890.97 TONNES

SEPT 1/WITH GOLD UP $1.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF 0.87 TONNES OF GOLD INTO THE GLD.: / //INVENTORY RESTS AT 890.10 TONNES

AUGUST 31/WITH GOLD DOWN $1.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF 0.87 TONNES OF GOLD INTO THE GLD.: / //INVENTORY RESTS AT 890.10 TONNES

AUGUST 30/WITH GOLD UP $8.15 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF 2.59 TONNES OF GOLD INTO THE GLD.: / //INVENTORY RESTS AT 889.23 TONNES

AUGUST 29/WITH GOLD UP 17.05 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF 2.6 TONNES OF GOLD INTO THE GLD.: / //INVENTORY RESTS AT 886.64 TONNES

AUGUST 28/WITH GOLD UP $6.90 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD: / //INVENTORY RESTS AT 884.04 TONNES

AUGUST 25/WITH GOLD DOWN $6.05 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .87 TONNES OF GOLD FROM THE GLD// //INVENTORY RESTS AT 884.04 TONNES

AUGUST 24/WITH GOLD UP $0.65 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD //INVENTORY RESTS AT 884.91 TONNES

AUGUST 23/WITH GOLD UP $21.35 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 4.32 TONNES OF GOLD FROM THE GLD//: //: /// //INVENTORY RESTS AT 884.91 TONNES

AUGUST 22/WITH GOLD UP $2.95 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 0.87 TONNES OF GOLD FROM THE GLD//: //: /// //INVENTORY RESTS AT 889.23 TONNES

AUGUST 21/WITH GOLD UP $7.15 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF 2.60 TONNES OF GOLD FROM THE GLD//: //: /// //INVENTORY RESTS AT 890.10 TONNES

AUGUST 18/WITH GOLD UP $1.15 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 6.92 TONNES OF GOLD FROM THE GLD//: //: /// //INVENTORY RESTS AT 887.50 TONNES

AUGUST 17/WITH GOLD DOWN $12.80 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD: //: /// //INVENTORY RESTS AT 894.42 TONNES

GLD INVENTORY: 875.08 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

OCT 4/WITH SILVER DOWN 34 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV:. A MASSIVE DEPOSIT OF 6.311 MILLION OZ INTO THE SLV/// /.////INVENTORY RESTS AT 48.194 MILLION OZ

OCT 3/WITH SILVER DOWN 2 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV:. : // /.////INVENTORY RESTS AT 441.883 MILLION OZ

OCT 2/WITH SILVER DOWN 98 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV:. : // /.////INVENTORY RESTS AT 441.883 MILLION OZ

SEPT 29/WITH SILVER DOWN 28 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV:. A WITHDRAWAL OF 0.183 MILLION OZ FROM THE SLV: // /.////INVENTORY RESTS AT 441.883 MILLION OZ

SEPT 28/WITH SILVER DOWN 8 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV:. A WITHDRAWAL OF 4.88 MILLION OZ FROM THE SLV: // /.////INVENTORY RESTS AT 442.066 MILLION OZ

SEPT 27/WITH SILVER DOWN 20 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV:. A WITHDRAWAL OF .641 MILLION OZ FROM THE SLV: // /.////INVENTORY RESTS AT 448.392 MILLION OZ

SEPT 26/WITH SILVER DOWN 20 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV:. A WITHDRAWAL OF .641 MILLION OZ FROM THE SLV: // /.////INVENTORY RESTS AT 448.392 MILLION OZ

SEPT 22/WITH SILVER UP 13 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV:. : // /.////INVENTORY RESTS AT 449.492 MILLION OZ

SEPT 21/WITH SILVER DOWN 13 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV:. : // /.////INVENTORY RESTS AT 449,033 MILLION OZ

SEPT 19/WITH SILVER UP 0 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 1.1 MILLION OZ INTO THE SLV. : // /.////INVENTORY RESTS AT 449.033 MILLION OZ

SEPT 18/WITH SILVER UP 11 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A DEPOSIT OF 1.651 MILLION OZ INTO THE SLV. : // /.////INVENTORY RESTS AT 441.332 MILLION OZ

SEPT 15/WITH SILVER UP 37 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 2.31 MILLION OZ FROM THE SLV. : // /.////INVENTORY RESTS AT 439.681 MILLION OZ

SEPT 14/WITH SILVER DOWN 16 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: : // /.////INVENTORY RESTS AT 440.736 MILLION OZ

SEPT 13/WITH SILVER DOWN 23 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1,009 MILLION OZ INTO THE SLV//: // /.////INVENTORY RESTS AT 440.736 MILLION OZ

SEPT 12/WITH SILVER UP 1 CENT TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 3.209 MILLION OZ INTO TEH SLV//: // /.////INVENTORY RESTS AT 439.727 MILLION OZ

SEPT 11/WITH SILVER UP 19 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 3.209 MILLION OZ INTO TEH SLV//: // /.////INVENTORY RESTS AT 439.727 MILLION OZ

SEPT 8/WITH SILVER DOWN 8 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: // /.////INVENTORY RESTS AT 436.518 MILLION OZ

SEPT 7/WITH SILVER DOWN 21 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: // /.////INVENTORY RESTS AT 436.518 MILLION OZ

SEPT 6/WITH SILVER DOWN 36 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.373 OZ OF SILVER OUT OF THE THE SLV// /.////INVENTORY RESTS AT 436.518 MILLION OZ

SEPT 5/WITH SILVER DOWN 69 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 734,000 OZ OF SILVER OUT OF THE THE SLV// /.////INVENTORY RESTS AT 437.891 MILLION OZ

SEPT 1/WITH SILVER DOWN 20 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.375 MILLION OZ OF SILVER OUT OF THE THE SLV// /.////INVENTORY RESTS AT 440.00 MILLION OZ

AUGUST 31/WITH SILVER DOWN 20 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.375 MILLION OZ OF SILVER OUT OF THE THE SLV// /.////INVENTORY RESTS AT 438.625 MILLION OZ

AUGUST 30/WITH SILVER DOWN 2 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.834 MILLION OZ OF SILVER OUT OF THE THE SLV// /.////INVENTORY RESTS AT 443.210 MILLION OZ

AUGUST 29/WITH SILVER UP 49 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 183,000 OF SILVER INTO THE THE SLV// /.////INVENTORY RESTS AT 445.044 MILLION OZ

AUGUST 28/WITH SILVER UP 3 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.281 MILLION OZ OZ FROM THE SLV// /.////INVENTORY RESTS AT 444.861 MILLION OZ

AUGUST 25/WITH SILVER UP ONE CENT TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.751 MILLION OZ OZ FROM THE SLV// /.////INVENTORY RESTS AT 446.145 MILLION OZ

AUGUST 24/WITH SILVER DOWN 16 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.651 MILLION OZ OZ FROM THE SLV// /.////INVENTORY RESTS AT 448.896 MILLION OZ

AUGUST 23/WITH SILVER UP 94 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 826,000 OZ FROM THE SLV// /.////INVENTORY RESTS AT 450.547 MILLION OZ

AUGUST 22/WITH SILVER UP 12 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: /.////INVENTORY RESTS AT 451.373 MILLION OZ

AUGUST 21/WITH SILVER UP 59 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 917,0000 OZ FROM THE SLV//.////INVENTORY RESTS AT 451.373 MILLION OZ

AUGUST 18/WITH SILVER UP 4 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//.////INVENTORY RESTS AT 452.290 MILLION OZ

AUGUST 17/WITH SILVER UP 15 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//.////INVENTORY RESTS AT 452.290 MILLION OZ

CLOSING INVENTORY 448.194 MILLION OZ//

PHYSICAL GOLD/SILVER COMMENTARIES

1:Peter Schiff/Mike Maharrey

end

2 Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens//JAMES RICKARDS//JOHN RUBINO

James Rickards..

Something “Big & Stupid” Is Coming…

WEDNESDAY, OCT 04, 2023 – 09:45 AM

Authored by James Rickards via DailyReckoning.com,

With debt levels reaching all-time highs in major developed and developing economies, and with debt-to-GDP ratios also in record territory (not including contingent liabilities such as Social Security, health care and other entitlements, which make matters worse), it seems time to consider just how nations will deal with this problem.

The debt crisis may not be imminent, but it is unavoidable. When it happens, it may present the greatest financial disaster of all time. It’s never too soon for investors to consider the fallout.

When you issue debt in a currency you print, there’s no need for default in the sense of non-payment.

You can just have the central bank buy the debt (by printing money). This is the situation today in the U.S., Japan, the U.K. and the European Monetary Union (the countries that use the euro). They all have huge debt burdens, but they all have central banks that can simply buy the debt by printing money to avoid default.

Non-Payment Is Not the Issue

There are many bad consequences to printing money and storing up debt on central bank balance sheets, but non-payment of debt is not one of them. This is the mantra of the Modern Monetary Theorists (MMT) and their thought leader Stephanie Kelton.

In my view, MMT is garbage as economic policy, but the no-default tenet is valid. George Soros says the same thing.

That said, we are well past the point where the debt can be managed with real growth. That threshold is about a 90% debt-to-GDP ratio. A 60% debt-to-GDP ratio is even more comfortable and can be managed.

Unfortunately, the major reserve currency economies are all well past the 90% ratio as are those of many smaller countries. The U.S. ratio is 134%, an all-time high. The U.K. ratio is 102%. France is 111%. Spain is 112%. Italy is 145%.

China reports a figure of 77% but this is highly misleading because it ignores provincial debt for which Beijing is ultimately responsible. China’s actual figure is over 200% when provisional debt is included.

The champion debtor is Japan at 261%. The only major economy with a halfway respectable ratio is Germany at 67%. It’s Germany’s misfortune that they are probably responsible for the rest of Europe through the ECB Target2 system.

All these countries are headed for default. But we must consider the different ways to conduct a default.

There are three basic ways to default: non-payment, inflation and debt restructuring. You can take non-payment off the table for the reason mentioned above — you can always just print the money.

The same goes for restructuring. Inflation is clearly the best way to default. You pay back the money in nominal terms, but it’s worth very little in real terms. The creditor loses and the debtor countries win.

Nice and Easy Does It

The key to inflating away the real value of debt is to go slowly. It’s like stealing money from your mother’s purse. If she has $50 and you take $40, she’ll notice. If you take one dollar, she won’t notice. But a dollar stolen every day adds up over time.

This is what the U.S. did from 1945–1980. At the end of World War II, the U.S. debt-to-GDP ratio was 120% (about where it is now). By 1980, the ratio was 30%, which is entirely manageable.

Of course, nominal debt and GDP soared, but nominal GDP went up faster than nominal debt, so the ratio fell. If you can keep inflation around 3% and interest rates around 2% and exert fiscal discipline (which we did under Eisenhower, Kennedy, Nixon and Ford), the nominal GDP will grow faster than nominal debt (due to the Fed capping rates).

If you improve the ratio by, say, 2% per year and keep it up for 35 years (1945–1980), you can cut the ratio by 70%. That’s what we did.

The key was to do it slowly (like stealing from your mom’s purse). Almost no one noticed the decline in the real value of money until we got to the blow-off stage (1978–1981). But by then it was mission accomplished.

So there are two ways to deal with excessive debt: fiscal discipline and inflation. From 1945–1980, the U.S. did just that. If you run inflation at 3% and interest rates are 2%, you melt the real value of debt. If you exert fiscal discipline relative to GDP, you decrease the nominal debt-to-GDP ratio.

We did both.

The reason the debt-to-GDP ratio is back up to 134% is that Bush 45, Obama, Trump and Biden ignored the formula. Since 2000, fiscal policy has been reckless so the formula doesn’t work. The problem isn’t really “money printing” (most of the money the Fed prints just comes back to the Fed as excess reserves, so it doesn’t do anything in the real economy).

The problem is that nominal debt is going up faster than nominal GDP, so the debt-to-GDP ratio goes up. This dynamic will be made much worse by the huge increase in interest rates over the past 18 months.

You can’t borrow your way out of a debt crisis. We have also been unable to generate much inflation. Inflation ran below 2% for almost all of the 2009–2019 recovery.

Japan Writ Large

Looking at the global picture, it’s important to understand that Japan is just a bigger version of the U.S. They don’t have fiscal discipline and they can’t get inflation to save their lives. The only way out for Japan is hyperinflation, which will come but not yet.

Japan can probably keep the debt game going for a while. The crash will come when the currency collapses. When I started in banking, USD/JPY was 400. Those were the days!

A debt crisis is on the way. Something big and stupid (in the words of the brilliant analyst Stephanie Pomboy) is coming from policymakers to address the issue. But the solution won’t be a policy and it won’t be a plan. A crisis will just happen almost overnight and seem to come from nowhere.

But it will come.

3,Chris Powell of GATA provides to us very important physical commentaries

Gold did hold up well in September against rising real rates

(Jan Nieuwenhuijs)

Jan Nieuwenhuijs: Gold held up well in September against rising real rates

Submitted by admin on Tue, 2023-10-03 16:23Section: Daily Dispatches

By Jan Nieuwenhuijs

Gainesville Coins, Lutz, Florida

Tuesday, October 3, 2023

Despite the gold price declining for several months, its performance is extremely strong considering sharply rising real interest rates. To measure gold’s performance against real rates (TIPS yield) I’m introducing the “Gold Price–TIPS Model Tracker” to improve our understanding of how the gold price is set and its future potential.

As we have discussed repeatedly on these pages, the gold price has been set by Western institutional money for nearly a century, and from 2006 through February 2022 there was a tight inverse correlation between the price of gold and the yield of 10-year Treasury Inflation Protected Securities (TIPS), which reflect real interest rates.

Then, early 2022, things started to change. …

… For the remainder of the analysis:

end

end

4, OTHER IMPORTANT GOLD/SILVER COMMENTARIES//

END

5 a. IMPORTANT COMMENTARIES ON COMMODITIES:ORANGE JUICE

END

5 B GLOBAL COMMODITY ISSUES/FOOD IN GENERAL//FREIGHT

END

6.CRYPTOCURRENCY//DIGITAL CURRENCY// COMMENTARIES/

END

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS TUESDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED UP AT 7.3015

OFFSHORE YUAN: UP TO 7.3171

SHANGHAI CLOSED UP 3.16 PTS OR .10%

HANG SENG CLOSED DOWN 135.33 PTS OR 0.78%

2. Nikkei closed DOWN 711.06 PTS OR 2.28 %

3. Europe stocks SO FAR: ALL MIXED

USA dollar INDEX DOWN TO 106.52 EURO RISES TO 1.0501 UP 33 BASIS PTS

3b Japan 10 YR bond yield: RISES TO. +.794 Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 148.96/JAPANESE YEN FALLING AS WELL AS LONG TERM 10 YR. YIELDS RISING //EVENTUALLY THIS WILL BREAK THE JAPANESE CENTRAL BANK

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen UP CHINESE ONSHORE YUAN: UP// OFFSHORE: UP

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil DOWN for WTI and DOWN FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund DOWN TO +2.9415***/Italian 10 Yr bond yield UP to 4.915*** /SPAIN 10 YR BOND YIELD UP TO 4.048…**

3i Greek 10 year bond yield RISES TO 4.401

3j Gold at $1829.60 silver at: 21.40 1 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble UP 0 AND 13 /100 roubles/dollar; ROUBLE AT 99.48//

3m oil into the 87 dollar handle for WTI and 89 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 148.97// 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 0.794% STILL ON CENTRAL BANK (JAPAN) INTERVENTION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.9178 as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9636 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.774 DOWN 3 BASIS PTS…

USA 30 YR BOND YIELD: 4.888 DOWN 5 BASIS PTS/

USA 2 YR BOND YIELD: 5.138 DOWN 1 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 27.57…(TURKEY SET TO BLOW UP FINANCIALLY)

GREAT BRITAIN/10 YEAR YIELD: UP 4 BASIS PTS AT 4.638

end

2.a Overnight: Newsquawk and Zero hedge:

USA EARLY MORNING REPORT

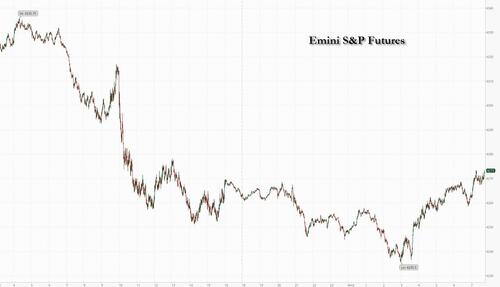

Global Stock Rout Reverses As Yields Dip After 30Y Treasury Tags 5%

WEDNESDAY, OCT 04, 2023 – 08:14 AM

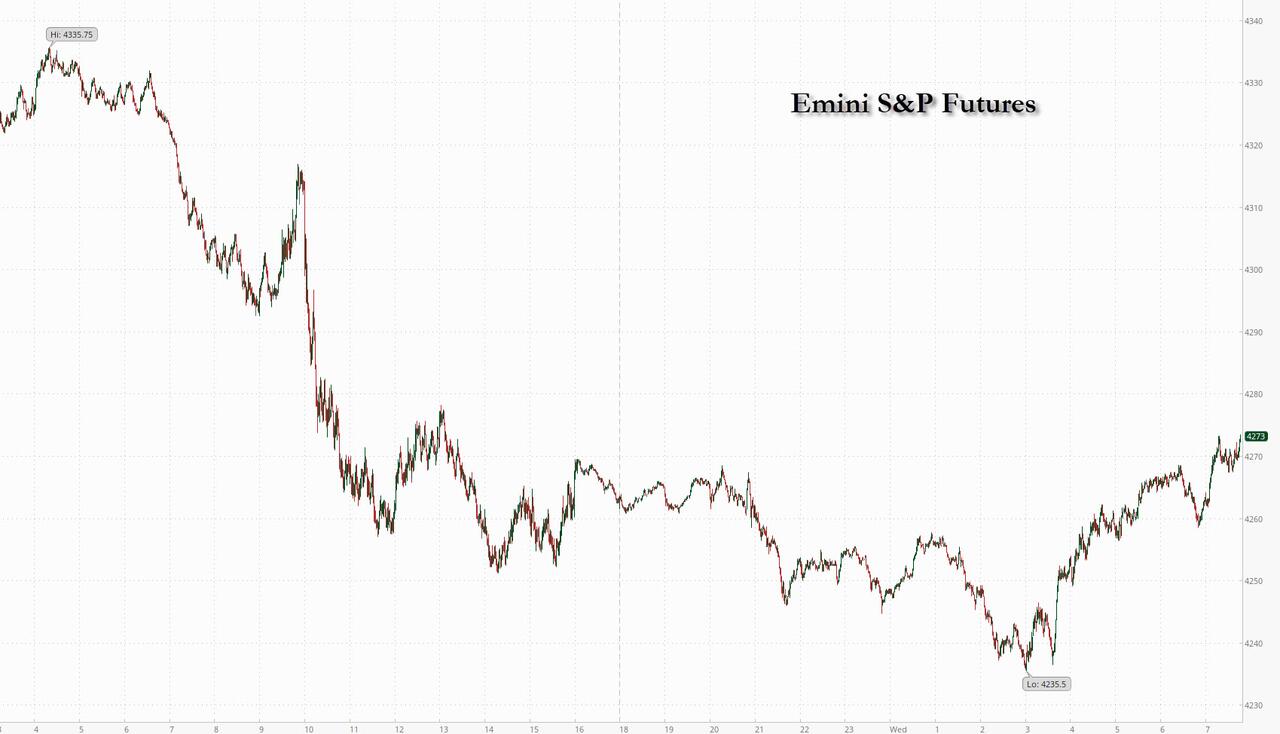

Global stocks and US futures were in freefall earlier this session, with spoos tumbling to a four month low of 4,235 and tracking the relentless drop in Treasuries tick for tick which briefly sent 30Y yields above 5.00% – the highest since Sept 2007 – around the time Europe opened…

… before a bout of buying kicked in and yields dropped sharply while futures reversed all losses and as of 7:45am, S&P futures were up 0.2% to 4,273 while Nasdaq futures were up 0.1% after slumping sharply earlier.

Europe was mixed as German 10-year yields reached the highest level since 2011 too as the Treasury moves rippled across markets. Investors are now focuing on term-premium and demanding greater compensation to hold onto long-dated debt with rates set to remain higher for longer, while concerns about the ridiculous pace of Treasury issuance – US debt rose by a whopping $275 billion on the first day of October – to address rising budget deficits are also weighing. Elsewhere, the dollar also dropped, as did oil, with WTI slipping further below the $90-per-barrel mark as an OPEC+ meeting is set to announce no changes to its policy.

In premarket trading, Apple fell 1%, after the stock was downgraded at KeyBanc Capital Markets, which said shares of the iPhone maker are trading near all-time high valuation levels, though its sales growth is likely to slow, while CEO Tim Cook sold $41 million in stock after taxes, his biggest sale in more than two years. Brooge Energy rose 21% after the company confirmed receipt of an acquisition offer from Gulf Navigation Holdings in a filing. Palantir gained 2% as the data analysis firm has emerges as the top pick for a contract to overhaul the UK’s National Health Service.

The latest leg of the bond selloff was fueled by Tuesday’s grotesquely manipulated and better-than-expected US job data, one which even Goldman mocked as being ridiculously adjusted, as well as a slew of hawkish comments from Federal Reserve officials. Data on U.S. private payrolls due later from the ADP Research Institute could fan more volatility, coming on the heels of Tuesday’s JOLTS survey.

“It’s fair to say there’s going to be a volatile environment until we have more clarity” on the direction of rates, Virginie Maisonneuve, global chief investment officer for equites at Allianz Global Investors, said in an interview with Bloomberg Television. “If you have a long-term time horizon find those stocks that have very strong structural backing for growth and have quality balance sheets.”

Meanwhile, there are signs that buyers are already emerging to take advantage of the stock swoon. The S&P 500 is officially in oversold territory based on its relative strength index of below 30. Francisco Simón, European head of strategy at Santander AM, is among those eyeing cheapened assets.

“The current weakness of equities would be an opportunity to enter those sectors and companies with high sensitivity to rates,” he said. “We hope they will do a catch-up again once rates stabilize. Current yields are already at very high levels for the expected inflation and growth in the medium and long term.”

European stocks managed to squeeze out marginal gains with the Stoxx 600 adding 0.2%. In individual stock moves Wednesday, airline SAS AB fell as much as 96% after the bankrupt Scandinavian flag carrier announced plans to be taken private. Tesco shares gain as much as 3.2%, the most since March 29, after the UK grocer increased its guidance for retail adjusted operating profit for the year. Here are the most notable European movers:

- Sanofi shares rise as much as 0.9%, outperforming the Stoxx 600 Health Care Index, after the company agreed to pay Teva Pharmaceutical as much as $1.5 billion to help develop and sell a medicine for inflammatory bowel disease

- Orange rose as much as 2.5%, outperforming declining European markets, after BofA upgraded its rating by two notches and said the investment case for the French group ticked all the boxes

- Fresenius Medical falls as much as 5.4%, the most since mid-August, after attorneys general in New York, New Jersey and Georgia filed a complaint against Fresenius Vascular Care, Inc. alleging unnecessary kidney disease surgeries

- Cellnex drops as much as 3.9%, to the lowest in almost a year, after Barclays downgrades the tower operator to equal-weight, flagging overhang risks from sector M&A and some tailwinds turning into headwinds

- BW LPG shares fall as much as 14% in Oslo, the most intraday since August 2022, after an offering of 8.4m shares by holders via DNB Markets

- Spirent shares plummeted 40%, most since 2002, after the UK network testing firm said a slow summer and disappointing September meant it fell short of expectations for the third quarter

- Airline SAS falls as much as 96% after announcing plans to be taken private late on Tuesday as part of a restructuring process as it emerges from Chapter 11 bankruptcy proceeding in the US.

Earlier in the session, Asian stocks tumbled, with several local benchmarks tracking the key regional gauge toward a correction, as the risk-off mood intensified after strong US jobs data amplified concerns of higher-for-longer interest rates. The MSCI Asia Pacific Index fell 1.7%, pushing it down more than 10% from a July high. Tech stocks were the biggest drag as the 10-year Treasury yield climbed to a fresh 16-year high. South Korea’s Kospi and Japan’s Nikkei 225 were among the region’s worst performers Wednesday, also flirting with technical-correction territory. Markets had become complacent about macro concerns in recent months as excitement over artificial intelligence helped drive stocks higher globally. That rally has now all but faded in the wake of strong economic data that’s backed the case for the Federal Reserve to keep interest rates elevated.

- Hang Seng conformed to the downbeat mood amid the continued absence of mainland participants and with pressure on tech, energy and casino stocks.

- ASX 200 was dragged lower by underperformance in tech, real estate and the top-weighted financial sector with headwinds amid the continued upside in yields.

- Nikkei 225 extended on losses beneath the 31,000 level amid wide speculation of FX intervention and with Japanese officials out in force but refusing to confirm or deny whether they intervened.

- KOSPI underperformed on return from the extended holiday despite encouraging Industrial Production data which showed a surprise expansion.

- India stocks declined for a second consecutive session, tracking losses in regional peers as investors shun riskier assets on worries over interest rates staying higher for longer. The S&P BSE Sensex fell 0.4% to 65,226.04 as of 03:45 p.m. in Mumbai, the lowest since Aug. 31. The NSE Nifty 50 Index declined 0.5% to 19,436.10, the lowest since Sept. 1. BSE’s small- and mid-cap gauges also fell by more than 1% each. Foreign investors have turned sellers of Indian shares, taking out $2.3b in September, their first selloff after six straight months of purchases.

In FX, the Bloomberg Dollar Spot Index falls 0.1%. The kiwi underperforms after the RBNZ left rates on hold, falling 0.2% versus the greenback. USDJPY is down to 148.88 after Japanese officials declined to comment on speculation they intervened in the currency market on Tuesday when the pair briefly rose above 150.

In rates, Treasury yields reversed an earlier spike which extended Tuesday’s bond market rout during London trading. 10-year reached 4.76% and keeping pace with bunds, gilts in the sector,while 30-year yields briefly exceeded 5% but were down to 4.88% last. As conviction grew that US interest rates could rise further from current 22-year highs, 30-year yields touched 5% for the first time since 2007. Markets are pricing a one-in-three chance of a November. US yields from belly to long-end are little changed with front-end yields marginally richer on the day; 2s5s10s fly cheaper by ~3bp on the day as belly underperforms. Recent activity in Treasury options sees traders positioning for 10-year yield above 5%. The Dollar IG issuance slate includes Kommuninvest 2Y; all companies considering deals Tuesday stood down Tuesday

In commodities, crude futures decline, with WTI falling almost 2% to trade around $88, at the lowest level in three weeks.

Looking to the day ahead now, the US session has heavy economic data slate, starting with ADP employment change at 8:15am New York time; it will also include the ISM services index along with factory orders for August. Elsewhere, there’s the final services and composite PMIs for September from around the world, and in the Euro Area there’s retail sales and PPI for August. Central bank speakers include ECB President Lagarde, Vice President de Guindos, and the ECB’s Centeno and Panetta, along with the Fed’s Bowman and Goolsbee.

Market Snapshot

- S&P 500 futures down 0.1% to 4,259.25

- STOXX Europe 600 little changed at 440.75

- MXAP down 1.6% to 152.35

- MXAPJ down 1.1% to 479.26

- Nikkei down 2.3% to 30,526.88

- Topix down 2.5% to 2,218.89

- Hang Seng Index down 0.8% to 17,195.84

- Shanghai Composite up 0.1% to 3,110.48

- Sensex down 0.8% to 64,971.11

- Australia S&P/ASX 200 down 0.8% to 6,890.25

- Kospi down 2.4% to 2,405.69

- Brent Futures down 0.7% to $90.32/bbl

- Gold spot down 0.1% to $1,821.18

- U.S. Dollar Index little changed at 106.93

- German 10Y yield little changed at 2.98%

- Euro up 0.2% to $1.0484

Top Overnight News

- 1) Japan’s central bank made unscheduled purchases of government debt on Wednesday as yields on benchmark bonds hit their highest mark in a decade, while a global market sell-off also continued to drive US Treasury yields to 16-year highs. FT

- 2) Softbank’s Son says AI will surpass human intelligence within the next decade as he spent an hour at the annual Softbank World event extolling the benefits of the technology. WSJ

- 3) Oil edged lower ahead of an OPEC+ market review. The group may not suggest any change in its policy, with Saudi Arabia reaffirming plans to stick with its current curbs. In the US, crude inventories fell 4.21 million barrels last week, API data is said to show. That would lower total stockpiles to the least since March 2022 if confirmed by the EIA. BBG

- 4) ECB’s Lagarde reiterates that policy rates have likely hit their peak for the cycle (but will stay elevated for an extended period). ECB

- 5) US companies probably added 150,000 jobs in September, ADP data is expected to show. That’s the lowest since March, adding to signs of moderating labor demand before Friday’s payrolls data. Jeffrey Gundlach warned that even a small tick up in unemployment should put markets on “recession alert.” BBG

- 6) The House has voted to remove Rep. McCarthy as speaker. This has no immediate policy consequence, nor does it impact government funding, which was recently extended to Nov. 17. That said, a leadership vacuum in the House raises the odds of a government shutdown when the current funding extension expires. We continue to view a shutdown in Q4 as the base case, likely when funding expires Nov. 17. GIR

- 7) Bond slump threatens to undercut the potential for an economic soft landing while the velocity of the move could stoke disruptions in financial markets. WSJ

- 8) More than 75,000 workers are preparing for the largest health care strike in US history today after talks between Kaiser Permanente and a coalition of unions so far failed to produce a resolution. The three-day walkout may interrupt services for almost 13 million people, primarily in western states as well as the Mid-Atlantic and Washington, D.C., area. BBG

- 9) Ford offered striking workers a more than 20% wage increase and said it would halve the time it takes new employees to reach top pay. BBG

- 10) Large landlords bought 0.4% of U.S. homes in the second quarter, down from a peak of 2.4% at the end of 2021, as higher debt costs and moderating rent growth ate into investment returns…

A more detailed look at global markets courtesy of Newsquawk

APAC stocks declined following the losses on Wall Street where stocks and bonds resumed their slide. ASX 200 was dragged lower by underperformance in tech, real estate and the top-weighted financial sector with headwinds amid the continued upside in yields. Nikkei 225 extended on losses beneath the 31,000 level amid wide speculation of FX intervention and with Japanese officials out in force but refusing to confirm or deny whether they intervened. KOSPI underperformed on return from the extended holiday despite encouraging Industrial Production data which showed a surprise expansion. Hang Seng conformed to the downbeat mood amid the continued absence of mainland participants and with pressure on tech, energy and casino stocks.

Top Asian News

- Japan’s top currency diplomat Kanda reiterated ‘no comment’ on FX intervention and wouldn’t comment on whether he discussed a weak yen with PM Kishida, while he said it is normal for authorities not to comment on whether they intervened or not.

- Japanese Finance Minister Suzuki said currency rates should be set by the market and rapid FX moves are undesirable. Suzuki added that FX stability is important and won’t rule out any options against excessive moves, while he responded ‘no comment’ when asked if Japan intervened.

- Japanese Chief Cabinet Secretary Matsuno said ‘no comment’ on whether Japan intervened in the FX market and said it is important for currencies to move stably reflecting fundamentals. Matsuno also reiterated that they will continue to take appropriate steps on FX.

- BoJ Governor Ueda said “no comment” when asked about FX, according to Reuters.

- BoJ to conduct funds-supplying operations against pooled collateral on October 6th 2023; duration of loans will be from October 10, 2023 through October 10, 2028; amount of loans to be notified when conducting the operations.

- BoJ data suggest that there was likely no forex intervention on Tuesday, as the current account balance that was projected to be within market estimates, according to Reuters.

- RBNZ kept the OCR unchanged at 5.50% as expected, while it noted that the Committee agreed the OCR needs to remain at a restrictive level and that interest rates are constraining economic activity and reducing inflationary pressure as required. RBNZ said demand growth in the economy continues to ease and that GDP growth in the June quarter was stronger than anticipated but the growth outlook remains subdued. Furthermore, it stated that with monetary conditions remaining restrictive, spending growth is expected to decline further.

European bourses are now mostly but modestly firmer after trimming the losses seen at the cash open. Futures were initially pressured alongside yet another pick-up in yields which saw the German 10yr hit 3% for the first time since 2011, however, equities were able to claw back some lost ground as moves in the fixed income space began to stabilise. Sectors in Europe are now mostly firmer with Utilities, Optimised Personal Care Drug & Groceries, Real Estate, and Media as the current top performers, while Energy, Travel & Leisure, Autos & Parts, and Retail sit as the laggards at time of writing. US futures scaled back earlier losses to hover around neutral levels, with the ES back above 4,250.

Top European News

- Germany is seeking a “grand bargain” with France to resolve the stalemate regarding nuclear power and help pave the way for a sweeping reform of the bloc’s electricity market, according to FT.

- Italy risks garnering “near zero” proceeds from a one-off bank tax, according to Reuters sources. Italian banks would find it hard to justify shareholders paying the tax. The opt-out option in the latest version of the tax would have no impact on distribution policies.

- ECB’s President Lagarde reiterated her stance that rates are sufficiently restrictive, according to Reuters.

- BoE Governor Bailey said the labour market explains part of UK inflation, in an interview with Prospect Magazine. He added the job is not done on fighting inflation, and is likely to fall this year, in an interview with Orcadian.

FX

- DXY gravitates as Treasury yields slip, risk sentiment improves and various institutions step up intervention – with the index retreating from 107.240 to 106.760 awaiting US ADP, ISM and more Fed speakers

- Yen straddles 149.00 vs Dollar after jolt through 150.00 irrespective of no confirmed Japanese buying.

- Euro probes 1.0500 against Buck and Sterling regains 1.2100+ status post-decent UK PMI upgrades.

- Kiwi lags after a less hawkish than anticipated RBNZ hold as NZD/USD hovers just under 0.5900.

Fixed Income

- Debt complex feels reprieve following a deeper downturn in futures and an extension in yields.

- Bunds bounce within the 126.62-127.23 range as the 10-year benchmark probed 3% and pared back.

- Gilts recovered from 91.50 to 92.02 after a solid 2025 DMO auction.

- T-note nearer 106-22+ top than 106-03+ bottom ahead of ADP, services ISM and more Fed speakers.

- UK sold GBP 4.25bln vs exp. GBP 4.25bln 3.50% 2025 Gilt: b/c 2.61x (prev. 2.67x), average yield 4.964% (prev. 5.272%) & tail 1.1bps (prev. 0.9bps).

- Germany sells EUR 2.392bln vs exp. EUR 3bln 2.40% 2030 Bund: b/c 2.67x (prev. 2.40x), average yield 2.89% (prev. 2.53%) & retention 20.27% (prev. 18.97%).

- Total orders for the new 5yr BTP Valore have now reached EUR 10bln since the beginning of the offering, according to Reuters.

Commodities

- Crude is softer intraday and fails to benefit from the improvement in risk tone as the OPEC+ JMMC is expected to recommend no change to current policy while Russia and Saudi are to maintain voluntary curbs at current levels.

- Spot gold is flat and confined to a narrow USD 1,816.90-1,824.89/oz range but remains within yesterday’s parameters awaiting the next catalyst.

- Base metals are now flat after trimming deeper APAC losses, with the broader market move more constructive than it was overnight.

- Saudi Energy Ministry reaffirmed it will continue its voluntary cut of 1mln BPD starting in November until the end of December 2023, as expected, via Reuters.

- Russia’s PM Novak said Russia is to continue additional voluntary supply cut of oil exports by 300k BPD until the end of December 2023; the decision will be reviewed next month to consider deepening the cut or increasing oil production, according to Reuters.

- OPEC+ unlikely to tweak policy as Saudi and Russia keep voluntary oil cuts, according to Reuters citing sources.

- Russian government is ready to partially lift its ban on diesel exports in the coming days, via Kommersant citing sources. The ban would only be lifted only on pipeline exports of diesel and volumes may be subject to quotas to avoid surges in wholesale prices. The ban on gasoline exports will remain in force for now. Russia’s Energy Minister said partial permission for fuel export is under discussion at all levels, via Tass – further decisions on regulating the fuel market will be published soon.

- UAE’s ADNOC sets October Murban Crude OSP at USD 93.92/bbl (prev. USD 87.28/bbl in October), according to Reuters.

Geopolitics

- North Korea criticised the US for describing China and Russia as a threat in a new WMD strategy, while North Korea will counter US provocations with a massive response, according to KCNA.

- European Commission has formally started the probe into Chinese EV subsidies (as expected), according to Bloomberg. China said European Commission requested China to hold consultations within a very short period of time for EV subsidy probe and did not provide effective material; this severely damaged China’s rights, according to Reuters.

US Event Calendar

- 07:00: Sept. MBA Mortgage Applications -6.0%, prior -1.3%

- 08:15: Sept. ADP Employment Change, est. 150,000, prior 177,000

- 09:45: Sept. S&P Global US Services PMI, est. 50.2, prior 50.2

- 09:45: Sept. S&P Global US Composite PMI, est. 50.1, prior 50.1

- 10:00: Aug. Durable Goods Orders, est. 0.2%, prior 0.2%

- Durables Less Transportation, est. 0.4%, prior 0.4%

- Cap Goods Ship Nondef Ex Air, prior 0.7%

- Cap Goods Orders Nondef Ex Air, est. 0.9%, prior 0.9%

- 10:00: Aug. Factory Orders, est. 0.3%, prior -2.1%

- Factory Orders Ex Trans, est. 0.2%, prior 0.8%

- 10:00: Sept. ISM Services Index, est. 53.5, prior 54.5

Central Bank speakers

- 10:25: Fed’s Bowman Speaks at Community Banking Research Conference

- 10:30: Fed’s Goolsbee Speaks at Chicago Payments Symposium

- 15:00: Fed’s Goolsbee Moderates Discussion With Raghuram Rajan

DB’s Jim Reid concludes the overnight wrap

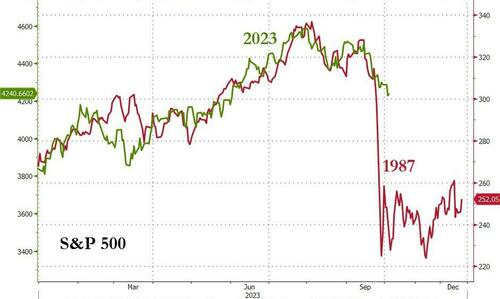

We’re at risk of repeating ourselves on a daily basis now, but the last 24 hours saw the relentless bond sell-off continue, with yields rising to fresh multi-year highs on both sides of the Atlantic.That included the 10yr Treasury yield (+11.7bps), which closed at a post-2007 high of 4.80% (4.838% this morning), whilst the 10yr real yield (+10.9bps) also hit a post-GFC high of 2.44%. But unlike some previous days, the sell-off was evident across several asset classes, with sizeable losses across equities and credit as well. In fact, the S&P 500 (-1.37%) closed at a 4-month low, and the index has now lost nearly 8% since its recent peak in late-July. That makes this now the biggest sell-off so far this year, having now surpassed the scale of the losses in February and March at the time of SVB’s collapse. Meanwhile, the Stoxx 600 is back to levels it first breached in 2023 on January 6th. US CDX HY widened +20bps to the widest since May and now wider than where we started 2023. So this is starting to be a significant correction. I struggle to see how the recent yield moves don’t increase the risk of an accident somewhere in the financial system given the relatively abrupt end over recent quarters of a near decade and a half where the authorities did everything they could to control yields. So risky times. If all that wasn’t enough, the US House speaker Kevin McCarthy was ousted late last night leaving a leadership vacuum with large uncertainty as to how this will be filled ahead of the next government shutdown deadline of November 17th .

We dig deeper into some of these issues below but first the main factor behind yesterday’s declines was the JOLTS report of job openings for August, which showed the US labour market was proving more resilient than expected. The big headline was that job openings unexpectedly rose to 9.610m (vs. 8.815m expected), taking them up from their two-year low in July. So that made a big change from the narrative in the last report, when job openings hit a two-year low and there was a growing sense that the tight labour market was beginning to ease. And it comes on top of some strong readings in other data recently, including the ISM manufacturing print on Monday, as well as the last couple of weekly jobless claims. There were maybe parts of the JOLTS report that weren’t as buoyant as the headline number (e.g., a stable quits rate and the hiring rate at its lowest since the first Covid wave) but that was not a nuance that was relevant yesterday.

For markets, it meant another rate hike from the Fed was kept firmly on the table. Indeed, futures suggested that the likelihood of another hike by December was up to 52%, having reached 57%, its highest since August, intra-day. And in turn, yields on 6-month T-bills hit a post-2001 high of 5.58%. Moreover, the sense that rates would remain higher for longer was cemented by Atlanta Fed President Bostic, who said the Fed should “hold for a long time ”. Later on, Cleveland Fed President Mester then said she would support a November hike if the economy “looks the way it did at the next meeting similar to the way it looked at our recent meeting”.

All that meant the bond sell-off continued apace, with lots of new milestones around the world. As discussed at the top, for the 10yr Treasury yield, there was another +11.7bps jump up to 4.80%. Furthermore, the 30yr yield (+13.5bps) moved above its intraday peak from 2010, reaching levels last seen in 2007. From a financial conditions perspective, it was notable how real yields led the sell-off once again, with the 10yr real yield (+10.9bps) up to a post-2008 high of 2.44%. This dramatic rise in long-dated borrowing costs has also led to a major curve steepening in recent weeks, with the 2s10s curve steepening another +6.9bps yesterday to -35.9bps (-31.9bps overnight). Given its role as a leading indicator of recessions, there has been some excitement about a soft landing because of those moves. But as Henry pointed out yesterday (here) most cycles normally see a curve steepening in the months just before the recession begins. So we’re some way from sounding the all clear just yet.

Over in Europe, there was also a sharp sell-off for sovereign bonds. Among others, we saw yields on 10yr bunds (+4.5bps) hit a post-2011 high of 2.96%, yields on 10yr OATs (+5.6bps) at a post-2011 high of 3.53%, and yields on 10yr BTPs (+13.3bps) at a post-2012 high of 4.93%. The 10yr BTP-Bund spread thus reached its highest level since March at +197bps. As in the US, there was a sharp rise in European real yields, with the German 10yr real yield up +4.9bps to 0.62%. And here in the UK, the 30yr gilt yield (+3.8bps) reached its highest closing level since 2002, at 5.05%.

With nominal and real rates rising around the world, it was a very bad day for risk assets, with the S&P 500 slumping -1.37% to a 4-month low. That leaves its YTD advance at just +10.16%, and on an equal-weighted basis the index is now -2.06% lower since the start of the year. Indeed, 273 of its constituents are now down YTD, with only 230 stocks higher. In a reversal of the past few days, tech stocks underperformed with the Nasdaq down -1.87% and the Magnificent Seven mega caps down -2.12%. The VIX volatility index traded above 20 for the first time since May, before closing up +2.17pts at 19.78. Over in Europe, the STOXX 600 (-1.10%) fell to a 6-month low, having now shed -6.58% since its peak in late-July. It’s true that the index is still up +3.72% YTD, but that’s mainly because the index had such a strong January, and we actually passed these current levels as soon as January 6th. So we’ve effectively gone sideways since.

Overnight in Asia, the sell-off continues. As I type, the Nikkei is down -2.03%, the Hang Seng -1.04% and the Kospi -2.30% after returning from 2 days of holidays. Markets in China are closed all week. Taking a quick look at Japan, the global fixed income sell-off saw yields on Japan’s five-year government bonds rise to their highest level since 2013. The yen weakened to 149.21 against the dollar after speculation that price action in Tuesday’s session was driven by official intervention. Officials remained quiet this morning, as the top currency official Masato Kanda declined to comment whether any intervention had been conducted but did state that they “will respond as always to excessive FX moves”. In other news, the Reserve Bank of New Zealand decided to keep rates on hold at 5.5%. We continue to think the central bank has now reached its terminal rate. See our economist’s reaction here.

In US political news, after the US closed, the House of Representatives voted to remove Speaker Kevin McCarthy, the first time in US history the Speaker has been ousted from their post. The move was led by a small group of conservative Republicans with Democrats joining in on a 216-210 vote. Votes on a new Speaker might begin on October 11th, according to reports, but uncertainty may linger (it took 15 rounds of voting for McCarthy to get the job back in January). From a market perspective, this brings extra uncertainty on the ability of Congress to pass a new spending bill after the latest stopgap measure expires on November 17th. With conservative Republicans having opposed McCarthy’s deal last weekend, his ouster may raise the risk that we will get a government shutdown in November, or that the Senate is forced to accept spending cuts demanded by House Republicans to avoid a shutdown. So a fiscal risk to keep in mind for later in Q4. Taking the temperature of the day ahead, S&P 500 and NASDAQ futures are slightly lower this morning (both around -0.2%) but off their overnight lows.

To the day ahead now, and data releases from the US will include the ISM services index and the ADP’s report of private payrolls for September, along with factory orders for August. Elsewhere, there’s the final services and composite PMIs for September from around the world, and in the Euro Area there’s retail sales and PPI for August. Central bank speakers include ECB President Lagarde, Vice President de Guindos, and the ECB’s Centeno and Panetta, along with the Fed’s Bowman and Goolsbee.

2 B) NOW NEWSQUAWK (EUROPE/REPORT)

Equities trim losses, DXY lower as yields slip; US ADP, ISM & Durable Goods due – Newsquawk US Market Open

WEDNESDAY, OCT 04, 2023 – 05:56 AM

- European bourses are now mostly but modestly firmer after trimming the losses seen at the cash open; US futures scaled back earlier losses to hover around neutral levels.

- DXY gravitates as Treasury yields slip, risk sentiment improves and various institutions step up intervention – with the index retreating from 107.240.