GOLD PRICE CLOSED: DOWN $14.70 TO $1967.05

SILVER PRICE CLOSED: DOWN 59 CENTS AT $22.53

Access prices: closes 4: 15 PM

Gold ACCESS CLOSE 1968.69

Silver ACCESS CLOSE: 22.61

NOV 3

Shanghai Gold Benchmark Price

Shanghai Gold Benchmark Price

USD oz

AM2022.97

PM2026.08

Investor Information

PREMIUM SHANGHAI OVER NY: $46

xxxxxxxxxxxxxxxxxx

Bitcoin morning price:, 34,719 DOWN 332 DOLLARS

Bitcoin: afternoon price: $35,596 UP 545. dollars

Platinum price closing $894.75 DOWN $16.75

Palladium price; $1063,60 DOWN $42,75

END

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

Due to the huge rise in the dollar, we must look at gold and silver in currencies other than the dollar to understand where we are heading

I will now provide gold in Canadian dollars, British pounds and Euros/4: 15 PM ACCESS

*CANADIAN GOLD: $2,709.80 UP $1.94 CDN dollars per oz( * NEW ALL TIME HIGH 2,782.61//OCT 272023)

*BRITISH GOLD: 1601.12 DOWN 1.13 pounds per oz// *(NEW ALL TIME HIGH//CLOSING///1655.17) OCT 2/2023

*EURO GOLD: 1840.52 DOWN 5.34 euros per oz //* (NEW *ALL TIME HIGH/CLOSING//1898.24)//high.* OCT 27.2023

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

EXCHANGE: COMEX

EXCHANGE: COMEX

CONTRACT: NOVEMBER 2023 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,981.600000000 USD

INTENT DATE: 11/06/2023 DELIVERY DATE: 11/08/2023

FIRM ORG FIRM NAME ISSUED STOPPED

072 H GOLDMAN 1

159 C MAREX CAPITAL M 1

435 H SCOTIA CAPITAL 109

624 H BOFA SECURITIES 7

661 C JP MORGAN 95

732 C RBC CAP MARKETS 3

737 C ADVANTAGE 9 19

TOTAL: 122 122

MONTH TO DATE: 1,559

JPMorgan stopped 95/122 contracts.

FOR NOV.:

GOLD: NUMBER OF NOTICES FILED FOR NOV/2023. CONTRACT: 155 NOTICES FOR 15,500 OZ or 0.4821 TONNES

total notices so far: 1559 contracts for 155,900 oz (4.8491 tonnes)

FOR NOV:

SILVER NOTICES:0 NOTICE(S) FILED FOR NIL OZ/

total number of notices filed so far this month : 306 for 1,530,000 oz

XXXXXXXXXXXXXXXXXXXXXXXX

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

BOTH GLD AND SLV ARE FRAUDULENT VEHICLES

GLD

WITH GOLD DOWN $14.70//

INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD/ : / HUGE CHANGES IN GOLD INVENTORY AT THE GLD: THE GLD/ A DEPOSIT OF 4,33 TONNES OF GOLD INTO THE GLD

INVENTORY RESTS AT 867.57 TONNES

SLV//

WITH NO SILVER AROUND AND SILVER DOWN 59 CENTS AT THE SLV// NO CHANGES IN SILVER INVENTORY AT THE SLV:

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV.

CLOSING INVENTORY: 440.631 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A STRONG SIZED 802 CONTRACTS TO 129,499 AND FURTHER FROM THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THIS STRONG SIZED LOSS IN COMEX OI WAS ACCOMPLISHED DESPITE OUR TINY $0.06 LOSS IN SILVER PRICING AT THE COMEX ON MONDAY. WE HAD CONSIDERABLE SPEC SHORT COVERING EPISODE IN MONDAY’S COMEX TRADING.. TAS ISSUANCE WAS A HUMONGOUS SIZED 2246 CONTRACTS. THESE WILL BE USED FOR MANIPULATION LATER THIS MONTH/AS WELL AS TODAY. CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON MONDAY NIGHT: 2246 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS. IT THUS LOOKS LIKE THE FED (GOV’T) IS BEHIND ALL OF THESE TRADES.

WE HAVE NOW SET ANOTHER RECORD LOW AT 114,102 CONTRACTS ///JULY 3.2023// OUR BANKERS WITH THE HELP OF SPECULATORS AND HIGH FREQUENCY TRADERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.06). AND WERE SUCCESSFUL IN KNOCKING SOME SILVER LONGS AS WE HAD A STRONG SIZED LOSS OF 802 OI CONTRACTS ON OUR TWO EXCHANGES AS THE SPEC SHORTS TRIED AGAIN DESPERATELY TO COVER THEIR SHORTFALLS WITH LITTLE SUCCESS.

WE MUST HAVE HAD:

A STRANGE 0 ISSUANCE OF EXCHANGE FOR PHYSICALS( 0 CONTRACTS FOR NIL OZ) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 1.430 MILLION OZ (FIRST DAY NOTICE) FOLLOWED BY TODAY’S 10,000 OZ QUEUE JUMP +

//NEW STANDING IS THUS 1.990 MILLION OZ

//STRONG SIZED COMEX OI LOSS/ 0 SIZED EFP ISSUANCE/VI) HUMONGOUS SIZED NUMBER OF T.A.S. CONTRACT ISSUANCE 2246 CONTRACTS)/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL – REMOVED 265 CONTRACTS (the cme will no longer provide preliminary no to be except through a paywall)

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS OCT ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF NOV:

TOTAL CONTRACTS for 5 days, total 1017 contracts: OR 5.085 MILLION OZ (170 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 5.085 MILLION OZ

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH 2022: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 118.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 85.745 MILLION OZ (SMALLER THAN LAST MONTH)

AUGUST: 171.43 MILLION OZ (THIS MONTH IS GOING TO BE HUGE //2ND HIGHEST ON RECORD

SEPT: 72.705 MILLION OZ (SMALLER THIS MONTH)

OCT: 97.455 MILLION OZ

NOV. 5.085 MILLION OZ (GOING TO BE QUITE SMALL THIS MONTH)

RESULT: WE HAD A STRONG SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 802 CONTRACTS WITH OUR LOSS IN PRICE OF $0.06 IN SILVER PRICING AT THE COMEX//MONDAY.,. THE CME NOTIFIED US THAT WE HAD A ZERO 0 EFP ISSUANCE CONTRACTS: 0 ISSUED FOR DEC AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS. . WE HAVE A SMALL INITIAL SILVER OZ STANDING FOR SEPT OF 1.432 MILLION OZ FOLLOWED BY TODAY’S 10,000 OZ QUEUE JUMP

NEW STANDING 1,990,000 OZ/// /// WE HAVE A STRONG SIZED LOSS OF 802 OI CONTRACTS ON THE TWO EXCHANGES. THE TOTAL OF TAS INITIATED CONTRACTS TODAY: A HUMONGOUS SIZED 2246 CONTRACTS//SOME FRONT END OF THE TAS CONTRACTS WERE LIQUIDATED DURING THE MONDAY COMEX SESSION. THE NEW TAS ISSUANCE FRIDAY NIGHT A HUGE (2246) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE., .

WE HAD 0 NOTICE(S) FILED TODAY FOR NIL OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A FAIR SIZED 1567 CONTRACTS TO 487,483 AND CLOSER TO THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: – REMOVED 1344 CONTRACTS

WE HAD A FAIR SIZED INCREASE IN COMEX OI ( 1597 CONTRACTS) DESPITE OUR $9.90 LOSS IN PRICE//MONDAY. WE ALSO HAD A RATHER STRONG INITIAL STANDING IN GOLD TONNAGE FOR NOV. AT 4.3514 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S 11,800 OZ QUEUE JUMP + TODAY’S 750 CONTRACT ISSUANCE OF EXCHANGE FOR RISK FOR 2.3325 TONNES (3RD DAY IN A ROW FOR ISSUANCE OF EXCHANGE FOR RISK) // ALL OF..THIS HAPPENED WITH OUR $9.90 LOSS IN PRICE WITH RESPECT TO MONDAY’S TRADING.WE HAD A FAIR SIZED GAIN OF 3187 OI CONTRACTS (9.912 PAPER TONNES) ON OUR TWO EXCHANGES.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 1620 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 487,483

IN ESSENCE WE HAVE A GOOD SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 4531 CONTRACTS WITH 2911 CONTRACTS INCREASED AT THE COMEX// AND A FAIR SIZED 1620 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 3189 CONTRACTS OR 9.912 TONNES. WE HAD ANOTHER OF THOSE STRANGE EXCHANGE FOR RISK = 750 CONTRACTS OR 2.3332 TONNES. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): A STRONG 2,350 CONTRACTS)

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (1620 CONTRACTS) ACCOMPANYING THE FAIR SIZED GAIN IN COMEX OI (1567) //TOTAL GAIN FOR OUR THE TWO EXCHANGES: 3,187 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR FORMER FORMAT OF BANKERS GOING LONG AND SPECULATORS GOING SHORT ,2.) FAIR INITIAL STANDING AT THE GOLD COMEX FOR NOV. AT 4.3514 TONNES FOLLOWED BY TODAY’S 11800 OZ QUEUE JUMP: NEW STANDING 4.8771 TONNES + 2.332 TONNES EXCHANGE FOR RISK TODAY + .8585 TONNES EX. FOR RISK PRIOR: TOTAL EXCHANGE FOR RISK 3.1905 TONNES //THUS NEW TOTAL FOR GOLD STANDING: 8.0676 TONNES // /// 3) ZERO LONG LIQUIDATION AND SOME TAS LIQUIDATION BUT WE HAD SOME SPEC SHORT COVERINGS DURING THE COMEX SESSION //4) FAIR SIZED COMEX OPEN INTEREST GAIN/ 5) STRONG ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER///6: HUGE T.A.S. ISSUANCE: 2350 CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023 INCLUDING TODAY

NOV

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF NOV. :

TOTAL EFP CONTRACTS ISSUED: 18,543 CONTRACTS OR 1,854,300 OZ OR 57.67 TONNES IN 5 TRADING DAY(S) AND THUS AVERAGING: 3708 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 5 TRADING DAY(S) IN TONNES 57,67 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2022, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 57,67/3550 x 100% TONNES 1.63% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2023

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH/2022: 409.30 TONNES //FINAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 151.69 TONNES (WEAKER THAN LAST MONTH)

AUGUST: 195.28 TONNES (A STRONGER MONTH)//FINAL

SEPT: 254.709 TONNES (WILL BE LARGER THAN LAST MONTH AND A STRONG MONTH)

OCT. 248.09 TONNES. LIKE SILVER, THIS MONTH IS GOING TO BE A STRONG E.F.P. ISSUANCE.

NOV. 57.67 TONNES//

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF SEPT. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF MAY HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF JUNE., FOR BOTH GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (SEPT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER FELL BY A STRONG SIZED 802 CONTRACTS OI TO 129,764 AND CLOSER TO OUR COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE ZER0 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

DEC 0 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 0 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 802 CONTRACTS AND ADD TO THE 0 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A STRONG SIZED LOSS OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 802 CONTRACTS

THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES TOTAL 2.65 MILLION OZ

OCCURRED WITH OUR $0.06 LOSS IN PRICE …..

END

OUTLINE FOR TODAY’S COMMENTARY

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

b, ) Gold/silver trading overnight Europe,//GOLD COMMENTARIES

(Peter Schiff)

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS//

TUESDAY MORNING//MONDAY NIGHT

SHANGHAI CLOSED DOWN 1.14 PTS OR 0.04% //Hang Seng CLOSED DOWN 296.43 PTS OR 1.65% /The Nikkei CLOSED DOWN 296.43 PTS OR 1.65% //Australia’s all ordinaries CLOSED DOWN 0.22 % /Chinese yuan (ONSHORE) closed DOWN AT 7.2843 /OFFSHORE CHINESE YUAN CLOSED DOWN TO 7.2897 /Oil DOWN TO 79.43 dollars per barrel for WTI and BRENT UP AT 83.61/ Stocks in Europe OPENED ALL RED// ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

9. USA

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A FAIR SIZED 1597 CONTRACTS TO 487,483 DESPITE OUR LOSS IN PRICE OF $9.90 ON MONDAY TRADING.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE NON ACTIVE DELIVERY MONTH OF NOV..… THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 1620 EFP CONTRACTS WERE ISSUED: : DEC 1620 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 1620 CONTRACTS

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A FAIR SIZED TOTAL OF 3187 CONTRACTS IN THAT 1620 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A FAIR SIZED GAIN OF 1567 COMEX CONTRACTS..AND THIS GAIN ON OUR TWO EXCHANGES HAPPENED DESPITE OUR LOSS IN PRICE OF $9.90//MONDAY COMEX. AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS DURING MID MONTH IN THE DELIVERY CYCLE), THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR MONDAY NIGHT WAS A STRONG 2350 CONTRACTS. THROUGHOUT THE PAST WEEKS, THE BANKERS SOLD OFF THE LONG SIDE OF THE SPREAD WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR SPREAD WHICH WILL BE LIQUIDATED TWO MONTHS HENCE)//

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: NOV (8,0676 TONNES (ACTIVE MONTH)

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

NOV: 4.8771 TONNES + 3.1905 (EX. FOR RIS) = 8.0676 TONNES

THE SPECS/HFT WERE SUCCESSFUL IN LOWERING GOLD’S PRICE( IT LOST $9.90) //// BUT WERE UNSUCCESSFUL IN KNOCKING ANY SPECULATOR LONGS AS WE HAD A GOOD GAIN OF 3,187 TOTAL CONTRACTS ON OUR TWO EXCHANGES. WE HAD A SOME T.A.S. LIQUIDATION ON THE FRONT END OF MONDAY’S TRADING. THE T.A.S. ISSUED ON MONDAY NIGHT WILL BE “PUT INTO THE BANK” TO BE USED AT A LATER DATE AT THE COLLUSIVE CHOOSING OF OUR BANKERS. IT DID HAVE SOME SPECULATOR SHORT COVERING WITH THE MASSIVE PRICE INCREASE.

WE HAVE GAINED A TOTAL OI OF 9.912 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR OCT. (4.3514 TONNES) ON FIRST DAY NOTICE FOLLOWED BY TODAY’S 11,800 OZ QUEUE JUMP //NEW TOTALS STANDING:4.8771 TONNES +750 CONTRACTS EX. FOR RISK FOR 2.332 TONNES + EXCHANGE RISK TOTALS PRIOR= .8585 EXCHANGE FOR RISK//TOTAL FOR EXCHANGE FOR RISK3.1905 : NEW TOTAL FOR GOLD STANDING: 8.0676 TONNES + ALL OF THIS WAS ACCOMPLISHED WITH OUR LOSS IN PRICE TO THE TUNE OF $9.90. FOR THE PAST SEVERAL WEEKS, THE SPECULATORS HAVE GONE MASSIVELY SHORT WITH OUR BANKERS NET LONG. THE BIG QUESTION IS NOW HOW MUCH GOLD WILL THE BANKERS PULL FROM OUR SHORT SPECULATORS. SPECULATORS YESTERDAY ADDED TO THEIR HUGE SHORTS.

WE HAD REMOVED 1344 CONTRACTS TO THE COMEX TRADES TO OPEN INTEREST

NET GAIN ON THE TWO EXCHANGES 3187 CONTRACTS OR 318,700 OZ OR 9.912 TONNES.

Estimated gold volume today:// 250,897 fair

final gold volumes/yesterday 168,799 poor

//speculators have left the gold arena

//NOV 7

/ /// THE NOV. 2023 GOLD CONTRACT

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | NIL . |

| Deposit to the Dealer Inventory in oz | nil |

| Deposits to the Customer Inventory, in oz | nil oz |

| No of oz served (contracts) today | 155 notice(s) 15500 OZ 0.4821 TONNES |

| No of oz to be served (notices) | 9 contracts 900 oz 0.0279 TONNES |

| Total monthly oz gold served (contracts) so far this month | 1559 notices 155,900 OZ 4.8491 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | x |

0 dealer deposit:

total dealer deposits: 0 oz

customer deposits: 0

total customer deposits: nil oz

we had 0 customer withdrawals

total withdrawals NIL oz

Adjustments; 1//DEALER TO CUSTOMER HSBC

96.45 OZ (3 KILOBARS)

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR NOV.

For the front month of NOVEMBER we have an oi of 146 contracts having GAINED 108 contracts. We had 10 contracts filed on MONDAY, so we gained 118 contracts or an additional 11800 oz will stand for delivery at the comex in this NON active delivery month of NOVEMBER. Our short speculators have been met with physical delivery demands by the bank. The only way they can obtain gold is through these EFP’s where delivery is taken in London on a T + 2 basis.

December LOST 5198 contracts DOWN to 360,639 contracts.

JAN. gained 472 contracts RISING TO 508 contracts.

We had 155 contracts filed for today representing 15500 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 155 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 95 notice(s) was (were) stopped received by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the NOV. /2023. contract month, we take the total number of notices filed so far for the month (1559x 100 oz ), to which we add the difference between the open interest for the front month of NOV. (146 CONTRACTS) minus the number of notices served upon today 155 x 100 oz per contract equals 156,800 OZ OR 4.8771 TONNES + 2.332 TONNES EX FOR RISK TODAY/.8585 EX. FOR RISK/PRIOR//THUS TOTAL STANDING: 8,0676 TONNES

thus the INITIAL standings for gold for the NOV. contract month: No of notices filed so far (1559) x 100 oz + (XXX) {OI for the front month} minus the number of notices served upon today (155) x 100 oz) which equals 156,800 oz standing OR 4.8771 TONNES + 3.1905 EX FOR RISK FOR MONTH = 8.0676 TONNES

TOTAL COMEX GOLD STANDING: 8.0676 TONNES WHICH IS HUGE FOR AN ACTIVE BUT GENERALLY WEAK DELIVERY MONTH. (OCT). Somebody is after a considerable amount of gold from the comex.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 1,880,539.272 OZ 58,49 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 19,887,388.319 OZ

TOTAL REGISTERED GOLD 10,059,260.534 (312.882 tonnes)..

TOTAL OF ALL ELIGIBLE GOLD: 9,828,127.685 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 8,178,525(REG GOLD- PLEDGED GOLD) 254.386 tonnes//dropping like a stone

END

SILVER/COMEX

NOV 7

//2023// THE NOV 2023 SILVER CONTRACT

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 80,381.43 oz HSBC . |

| Deposits to the Dealer Inventory | nil oz |

| Deposits to the Customer Inventory | 594,193.900 oz ASAHI |

| No of oz served today (contracts) | 0 CONTRACT(S) (NIL OZ) |

| No of oz to be served (notices) | 92 contracts (460,000 oz) |

| Total monthly oz silver served (contracts) | 306 Contracts (1,530,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

i) 0 dealer deposit

total dealer deposit: 0

total: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: 0 oz

We had 1 deposits customer account:

i0 Into ASAHI 594,193.900 oz

total customer deposit 594,193.900 oz

JPMorgan has a total silver weight: 134.441 million oz/267.526 million or 50.08%

Comex withdrawals 1

i) Out of HSBC: 80,381.430 oz

total: 80,381.430 oz

adjustments: 0

TOTAL REGISTERED SILVER: 38.327 MILLION OZ//.TOTAL REG + ELIGIBLE. 267.526 million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR August:

silver open interest data:

FRONT MONTH OF NOV /2023 OI: 92 CONTRACTS HAVING LOST 0 CONTRACT(S). WE HAD 2 NOTICES FILED ON MONDAY, SO WE GAINED 2 CONTRACTS OR AN ADDITIONAL 10,000 OZ WILL STAND FOR SILVER IN NOVEMBER

DEC. LOST 3159 CONTRACTS TO STAND AT 90,921

JANUARY LOST 7 CONTRACTS TO STAND AT 670

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 0 for NIL oz

Comex volumes// est. volume today 83.865// good

Comex volume: confirmed yesterday 50,820 poor

To calculate the number of silver ounces that will stand for delivery in NOV. we take the total number of notices filed for the month so far at 306 x 5,000 oz = 1,530,000 oz

to which we add the difference between the open interest for the front month of NOV. (92) and the number of notices served upon today 0 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the NOV/2023 contract month: 306 (notices served so far) x 5000 oz + OI for the front month of NOV (92) – number of notices served upon today (0 )x 500 oz of silver standing for the NOV contract month equates to 1.990 MILLION OZ

There are 38.327 million oz of registered silver.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS//

BOTH GLD AND SLV ARE MASSIVE FRAUDS!

NOV 7/WITH GOLD DOWN $14.70 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD:A DEPOSIT OF 4.33 TONNES OF GOLD INTO THE GLD/ / // // INVENTORY RESTS AT 863.24 TONNES

NOV 6/WITH GOLD DOWN $9.90 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD:A DEPOSIT OF 1.73 TONNES OF GOLD INTO THE GLD/ / // // INVENTORY RESTS AT 863.24 TONNES

NOV 3/WITH GOLD UP $5.75 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD: / // // INVENTORY RESTS AT 861.51 TONNES

NOV 2/WITH GOLD UP $6.55 TODAY:BIG CHANGES IN GOLD INVENTORY AT THE GLD: A HUGE DEPOSIT OF 2.02 TONNES OF GOLD INTO THE GLD/ // // INVENTORY RESTS AT 861.51 TONNES

NOV 1/WITH GOLD DOWN $6.15 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD // // INVENTORY RESTS AT 859.49 TONNES

OCT 31/859.49 TONNES//

OCT 30/WITH GOLD UP $7.80 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD // // INVENTORY RESTS AT 861.80 TONNES

OCT 27/WITH GOLD UP $1.20 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD // // INVENTORY RESTS AT 861.80 TONNES

OCT 26/WITH GOLD UP $2.90 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF 1.73 TONNES OF GOLD INTO THE GLD// // INVENTORY RESTS AT 861.80 TONNES

OCT 25/WITH GOLD UP $9.00 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD:/: //: // INVENTORY RESTS AT 860.07 TONNES

OCT 24/WITH GOLD DOWN $1.30 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A MASSIVE WITHDRAWAL OF 3.17 TONNES OF GOLD OUT OF THE GLD//WHAT A MASSIVE FRAUD! //: //: // INVENTORY RESTS AT 860.07 TONNES

OCT 23/WITH GOLD DOWN $6.80 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A MASSIVE 15.00 TONNES OF GOLD INTO THE GLD//WHAT A MASSIVE FRAUD! //: //: // INVENTORY RESTS AT 863.24 TONNES

OCT 20/WITH GOLD UP $14.50 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD //: //: // INVENTORY RESTS AT 848.24 TONNES

OCT 19/WITH GOLD UP $12.90 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 5.19 TONNES OF GOLD FROM THE GLD//: //: // INVENTORY RESTS AT 848.24 TONNES

OCT 18/WITH GOLD UP $32.55 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 2.02 TONNES OF GOLD FROM THE GLD//: //: // INVENTORY RESTS AT 853.43 TONNES

OCT 17/WITH GOLD UP $1.50 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD: //: // INVENTORY RESTS AT 855.45 TONNES

OCT 16/WITH GOLD DOWN $6.45 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 6.92 TONNES OF GOLD FROM THE GLD //: // INVENTORY RESTS AT 855.45 TONNES

OCT 13/WITH GOLD UP $57.60 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD: //: / /// // INVENTORY RESTS AT 862.37 TONNES

OCT 12/WITH GOLD DOWN $3.00 TODAY:BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF .86 TONNES OF GOLD INTO THE GLD//: / /// // INVENTORY RESTS AT 862.37 TONNES

OCT 11/WITH GOLD UP $11.20 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD:HUGE CHANGES: / /// // INVENTORY RESTS AT 861.51 TONNES

OCT 10/WITH GOLD UP $30.60 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD:HUGE CHANGES: A WITHDRAWAL OF 5.77 TONNES OF GOLD FROM THE GLD// /// // INVENTORY RESTS AT 861.81 TONNES

OCT 6/WITH GOLD UP $13.05 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD:HUGE CHANGES: A WITHDRAWAL OF 1.73 TONNES OF GOLD FROM THE GLD// /// // INVENTORY RESTS AT 867.58 TONNES

OCT 5/WITH GOLD DOWN $1.35 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD:HUGE CHANGES: A MASSIVE WITHDRAWAL OF 5.77 TONNES OF GOLD FROM THE GLD// /// // INVENTORY RESTS AT 869.31 TONNES

OCT 4/WITH GOLD DOWN $7.40 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.44 TONNES OF GOLD INTO THE GLD/// : // //INVENTORY RESTS AT 875.08 TONNES

OCT 3/WITH GOLD DOWN $6.90 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.44 TONNES OF GOLD INTO THE GLD/// : // //INVENTORY RESTS AT 875.08 TONNES

OCT 2/WITH GOLD DOWN $19.35 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD: LD/ : // //INVENTORY RESTS AT 873,64 TONNES

SEPT 29/WITH GOLD DOWN $11.15 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD: LD/ : // //INVENTORY RESTS AT 873,64 TONNES

SEPT 28/WITH GOLD DOWN $13.45 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A HUGE WITHDRAWAL OF 4.88 TONNES OF GOLD OUT OF THE GLD/ : // //INVENTORY RESTS AT 873,64 TONNES

SEPT 26/WITH GOLD DOWN $XXX TODAY:SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 0.31 TONNES OF GOLD OUT 05 THE GLD/ : // //INVENTORY RESTS AT 878.52 TONNES

GLD INVENTORY: 863.24 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

NOV 7/WITH SILVER DOWN 59 CENTS TODAY:NO CHANGES IN SILVER INVENTORY AT THE SLV: //// //INVENTORY RESTS AT 440.631 MILLION OZ

NOV 6/WITH SILVER DOWN 6 CENTS TODAY:NO CHANGES IN SILVER INVENTORY AT THE SLV: //// //INVENTORY RESTS AT 440.631 MILLION OZ

NOV 3/WITH SILVER UP 41 CENTS TODAY:BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.638 MILLION OZ OF SILVER FROM THE SLV///// /// /INVENTORY RESTS AT 440.631 MILLION OZ

NOV 2/WITH SILVER UP 11 CENTS TODAY:BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.924 OZ OF SILVER FROM THE SLV///// /// /INVENTORY RESTS AT 439.993 MILLION OZ

NOV 1/WITH SILVER DOWN 11 CENTS TODAY:BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 916,000 OZ OF SILVER FROM THE SLV///// /// /INVENTORY RESTS AT 441.917 MILLION OZ

OCT 31/442.833 MILLION OZ///INVENTORY

OCT 30/WITH SILVER UP 46 CENTS TODAY:NO CHANGES IN SILVER INVENTORY AT THE SLV: /// /// /INVENTORY RESTS AT 443.750 MILLION OZ

OCT 27/WITH SILVER UP 3 CENTS TODAY:BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 641,000 OZ FROM THE SLV/// /// /INVENTORY RESTS AT 443.750 MILLION OZ

OCT 26/WITH SILVER DOWN 14 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/ /// /INVENTORY RESTS AT 444.391 MILLION OZ

OCT 25/WITH SILVER DOWN 6 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/ /// /INVENTORY RESTS AT 444.391 MILLION OZ

OCT 24/WITH SILVER DOWN 8 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A MASSIVE DEPOSIT OF 2.52 MILLION OZ INTO THE SLV/// /// /INVENTORY RESTS AT 444.391 MILLION OZ

OCT 23/WITH SILVER DOWN 23 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV:/ /// /INVENTORY RESTS AT 441.871 MILLION OZ

OCT 20/WITH SILVER UP 50 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV:.A WITHDRAWAL OF 2.658 MILLION OZ FROM THE SLV/ /// /INVENTORY RESTS AT 441.871 MILLION OZ

OCT 19/WITH SILVER UP XXX CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV:. A /// /INVENTORY RESTS AT 444.529 MILLION OZ

OCT 18/WITH SILVER UP 11 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV:. A WITHDRAWAL OF 3.207 MILLLION OZ FROM THE SLV///// /.////INVENTORY RESTS AT 444.529 MILLION OZ

OCT 17/WITH SILVER UP 23 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV:. : // /.////INVENTORY RESTS AT 447.736 MILLION OZ

OCT 16/WITH SILVER DOWN 9 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV:. : //A WITHDRAWAL OF 2.664 MILLION OZ OUT OF THE SLV// /.////INVENTORY RESTS AT 447.730 MILLION OZ

OCT 13/WITH SILVER UP 90 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV:. : //A WITHDRAWAL OF 1.375 MILLION OZ OUT OF THE SLV// /.////INVENTORY RESTS AT 450.394 MILLION OZ

OCT 12/WITH SILVER DOWN 19 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV:. : //A WITHDRAWAL OF 0.825 MILLION OZ OUT OF THE SLV// /.////INVENTORY RESTS AT 451.769 MILLION OZ

OCT 11/WITH SILVER UP 17 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV:. : //A WITHDRAWAL OF .366 MILLION OZ OUT OF THE SLV// /.////INVENTORY RESTS AT 452.594 MILLION OZ

OCT 10/WITH SILVER UP 25 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV:. : //A DEPOSIT OF 1.833 MILLION OZ INTO THE SLV// /.////INVENTORY RESTS AT 452.960 MILLION OZ

OCT 6/WITH SILVER UP 69 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV:. : //A DEPOSIT OF 0.916 MILLION OZ INTO THE SLV// /.////INVENTORY RESTS AT 451.127 MILLION OZ

OCT 5/WITH SILVER DOWN 8 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV:. : //A MASSIVE DEPOSIT OF 8.328 MILLION OZ INTO THE SLV// /.////INVENTORY RESTS AT 450.211 MILLION OZ

OCT 4/WITH SILVER DOWN 34 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV:. : // /.////INVENTORY RESTS AT 441.883 MILLION OZ

OCT 3/WITH SILVER DOWN 2 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV:. : // /.////INVENTORY RESTS AT 441.883 MILLION OZ

OCT 2/WITH SILVER DOWN 98 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV:. : // /.////INVENTORY RESTS AT 441.883 MILLION OZ

SEPT 29/WITH SILVER DOWN 28 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV:. A WITHDRAWAL OF 0.183 MILLION OZ FROM THE SLV: // /.////INVENTORY RESTS AT 441.883 MILLION OZ

SEPT 28/WITH SILVER DOWN 8 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV:. A WITHDRAWAL OF 4.88 MILLION OZ FROM THE SLV: // /.////INVENTORY RESTS AT 442.066 MILLION OZ

SEPT 27/WITH SILVER DOWN 20 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV:. A WITHDRAWAL OF .641 MILLION OZ FROM THE SLV: // /.////INVENTORY RESTS AT 448.392 MILLION OZ

SEPT 26/WITH SILVER DOWN 20 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV:. A WITHDRAWAL OF .641 MILLION OZ FROM THE SLV: // /.////INVENTORY RESTS AT 448.392 MILLION OZ

CLOSING INVENTORY 440.631 MILLION OZ//

PHYSICAL GOLD/SILVER COMMENTARIES

1:Peter Schiff/Mike Maharrey

.

end

2 Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens//JAMES RICKARDS//JOHN RUBINO

3. CHRIS POWELL//GATA GOLD COMMENTARIES:

For your interest…

Colombia accelerates plan to recover up to $20 billion in sunken treasure

Submitted by admin on Mon, 2023-11-06 08:41Section: Daily Dispatches

By Jim Wysss

Bloomberg News

Friday, November 3, 2023

Colombia is accelerating its effort to recover as much as $20 billion in gold, silver and gems from a three-century-old shipwreck, even as U.S. treasure hunters sue for half the value.

President Gustavo Petro told officials to set up a public-private partnership, or do a deal with a private firm, to get the San Jose galleon off the Caribbean Sea floor as soon as possible, according to the minister of culture.

This is one of the priorities for the Petro administration,” Minister of Culture Juan David Correa said Wednesday in a phone interview. “The president has told us to pick up the pace.”

Petro wants to recover the wreck before his term ends in 2026, though its unclear whether that will be possible, Correa said.

When the 62-gun Spanish galleon was sunk in battle by the British in 1708, it was gorged with six years’ worth of accumulated treasure: silver and gold from mines in Peru, chests full of Colombian emeralds, and millions of pesos in gold and silver coins, according to “The Treasure of the San Jose” by historian Carla Rahn Phillips.

No one knows how much the treasure might be worth, but in decades of court cases, its value has been estimated at $4 billion to $20 billion. …

… For the remainder of the report:

* * *

end

Four men charged in theft of the still missing golden toilet

(AP)

Four charged in theft of still-missing satirical golden toilet at Churchill’s birthplace

Submitted by admin on Mon, 2023-11-06 19:07Section: Daily Dispatches

Have they searched the seventh floor at 62 Threadneedle St. in London? There’s a lot of stuff there that belongs in a golden toilet.

* * *

By Sulvia Hui

Associated Press

Monday, November 6, 2023

LONDON — Four men were charged today over the theft of an 18-carat gold toilet from Blenheim Palace, the sprawling English country mansion where British wartime leader Winston Churchill was born.

The toilet, valued at 4.8 million pounds ($5.95 million), was an artwork titled “America” and intended as a pointed satire about excessive wealth by Italian conceptual artist Maurizio Cattelan. It was part of an art installation at Blenheim Palace, near the city of Oxford, a few days before it vanished overnight in September 2019.

The Crown Prosecution Service said it has authorized criminal charges against four men, ages 35-39, over the theft. They are accused of burglary and conspiracy to transfer criminal property.

Seven people had been arrested over the heist, but no charges have been brought until today, four years after the toilet was stolen. The artwork has never been found. …

… For the remainder of the report:

https://apnews.com/article/blenheim-palace-golden-toilet-theft-f0cd428df82be5343a799479a168f4be

END

4, OTHER IMPORTANT GOLD/SILVER COMMENTARIES/

end

5 a. IMPORTANT COMMENTARIES ON COMMODITIES: ORANGE JUICE

END

END

5 B GLOBAL COMMODITY ISSUES/FOOD IN GENERAL//FREIGHT

END

6.CRYPTOCURRENCY//DIGITAL CURRENCY// COMMENTARIES/

end

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS TUESDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED DOWN AT 7.2842

OFFSHORE YUAN: DOWN TO 7.2897

SHANGHAI CLOSED DOWN 1.14 PTS OR 0.04%

HANG SENG CLOSED DOWN 436.66 PTS OR 1.34%

2. Nikkei closed DOWN 436.66 PTS OR 1.34%

3. Europe stocks SO FAR: ALL RED

USA dollar INDEX UP TO 105.45 EURO FALLS TO 1.0683 DOWN 36 BASIS PTS

3b Japan 10 YR bond yield: RISES TO. +.872 Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 150.47/JAPANESE YEN FALLING AS WELL AS LONG TERM 10 YR. YIELDS RISING //EVENTUALLY THIS WILL BREAK THE JAPANESE CENTRAL BANK

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen DOWN CHINESE ONSHORE YUAN: DOWN// OFFSHORE: DOWN

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil DOWN for WTI and DOWN FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund UP TO +2.7035***/Italian 10 Yr bond yield UP to 4.537*** /SPAIN 10 YR BOND YIELD UP TO 3.759…**

3i Greek 10 year bond yield RISES TO 3.959

3j Gold at $1958.80 silver at: 22.51 1 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble DOWN 0 AND 9 /100 roubles/dollar; ROUBLE AT 92.48//

3m oil into the 79 dollar handle for WTI and 83 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 150.47// 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 0.872% STILL ON CENTRAL BANK (JAPAN) INTERVENTION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.9009 as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9625 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.634 DOWN 3 BASIS PTS…

USA 30 YR BOND YIELD: 4.806 DOWN 3 BASIS PTS/

USA 2 YR BOND YIELD: 4.953 UP 1 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 28.50…(TURKEY SET TO BLOW UP FINANCIALLY)

GREAT BRITAIN/10 YEAR YIELD: DOWN 2 BASIS PTS AT 4.3583

end

2.a Overnight: Newsquawk and Zero hedge:

US Futures End Six-Day Winning Streak As Fed Speakers Dampen Hopes Of Rate Cuts

TUESDAY, NOV 07, 2023 – 08:13 AM

US stocks were set to snap a six-day rally on Tuesday as traders reassessed expectations of Fed interest-rate policy after hawkish comments Monday by Minneapolis Fed President Neel Kashkari dampened hopes of speedy interest rate cuts from the US central bank. Kashkari is back today for round two; Indeed, traders appear to be awaiting more from Fed officials on the rate path outlook following Kashkari’s comments, with Fed Chair Jerome Powell also set to speak later in the week, but first we have to get through today’s calendar:

- 07:30: Kashkari

- 08:00: Goolsbee

- 09:15: Barr

- 09:50: Schmid

- 10:00: Waller

- 12:00: Williams

- 13:25: Logan

As of 7:50am, S&P 500 futures are down 0.3% to 4372 with Nasdaq futures dropping by the same amount, while Europe’s Stoxx 600 index posted a similar loss.

Commodities ex-base metals/natgas are weaker while WTI slides under $80 for the first time in 2 months despite a war raging in the middle east. Today’s Macro data is primarily focused on consumer credit, the 7 Fed speakers, and the 3Y auction at 1pm. MegaCap Tech names are weaker premarket; here are some of the most notable premarket movers:

- Alteryx shares rise 17% after the software company reported better-than-expected results, providing relief following last quarter’s disappointing revenue forecast. Analysts said that the firm’s execution improved, showing some resilience against a tough backdrop and prompting some price target hikes.

- Coherus Bio shares tumble 18% as the biotech company cut its net product revenue and combined R&D and SG&A expenses forecast for the full year.

- DigitalOcean Holdings shares gain 8.2% as Goldman Sachs double-upgrades its rating on the cloud computing firm to buy, saying in note that cyclical risks appear to be priced in.

- Hims & Hers Health shares jump 7.0% after reporting third-quarter revenue that beat estimates and boosting its adjusted Ebitda guidance for the full year ahead of expectations. Analysts saw the results as strong, highlighting the execution of management.

- RingCentral shares rise 9.7% after the communications software provider narrowed its software subscription revenue guidance for the full year and reported what analysts said was a strong set of results, boosting hopes of further growth.

- TransMedics Group shares climb 37% after the organ transplant company boosted its sales forecast for the full year. The health-care firm also reported third-quarter revenue that exceeded the average analyst estimates.

- TripAdvisor shares jump 11% after the online travel company reported third-quarter adjusted earnings per share and revenue that came ahead of estimates. Analysts said the results were better than expected, highlighting the performance of TripAdvisor Core and Viator.

- Ventyx Biosciences shares drop 73%, set for a record fall, after the biotech said it’s terminating its Phase 2 trial of VTX958 in plaque psoriasis and psoriatic arthritis as efficacy results did not meet the internal target to support further development. The update prompted a downgrade from Wells Fargo, with the broker saying that its thesis on the stock is “busted.”

- Vimeo shares rise as much as 14% in premarket trading after the video software company reported better-than-expected 3Q revenue and boosted its adjusted Ebitda guidance for the full year

- Clover Health shares fall as much as 19% in premarket trading on Tuesday after reporting third quarter revenue that missed the average analyst estimate.

Kashkari, speaking in an interview on Fox News on Monday, said it’s too soon to declare victory over inflation. He added that while there have been three months of promising data on inflation, it isn’t enough.

“The Kashkari comment has injected a sense of reality back into the market, which had got carried away thinking that policy easing was just around the corner,” said Stuart Cole, head macro economist at brokerage Equiti Capital.

Meanwhile, bond markets rallied, led by the UK, as Bank of England Chief Economist Huw Pill hinted rate cuts may be on the table by the middle of 2024 and German industrial output figures suggested that recession isn’t far off. Two-year gilt yields fell 10 basis points to 4.6% and the rate on 10-year Treasuries slid five basis points to 4.59%.

European stocks are lower, with the Stoxx 600 falling 0.2%. Among individual stock movers, oil producers dragged down European equity benchmarks, with Shell Plc and BP Plc sliding more than 1%. UBS gained as much as 5%, most in two months, as the Swiss bank’s third-quarter results were “messy” yet better than expected as expenses were lower, according to analysts. Here are some of the other notable European movers:

- Engie shares gain as much as 2.4% after the French utility company raised its full-year guidance and reaffirmed its dividend policy. Morgan Stanley sees 7% upside to current consensus estimates for 2023 net income

- Associated British Foods shares rise as much as 7%, reaching the highest since July 2021, after reporting full-year adjusted operating profit that beat estimates and announcing an additional £500 million buyback

- NatWest Group rises as much as 2.3% and is among the biggest gainers on the Stoxx 600 banks index on Tuesday after BNP Paribas Exane double-upgrades its rating on the UK lender to outperform from underperform

- Nexi shares jump as much as 4.4% on Tuesday after newspaper MF reported the Canada Pension Plan and Francisco Partners are among firms that may be interested in the payments company. It didn’t say where it obtained the information

- Watches of Switzerland shares jump as much as 15%, the biggest intraday gain since Sept. 25, after the luxury watch retailer reported second-quarter results that analysts said showed resilience in a tough macroeconomic environment

- Poste Italiane shares gain as much as 2.3%, the most intraday since Oct. 10, after the company boosted its full-year Ebit guidance and released what Morgan Stanley called a strong set of third-quarter results

- Daimler Truck shares fall as much as 4.8% to their lowest intraday since June after the German commercial vehicle maker’s third-quarter Ebit showed the impact of supply-chain bottlenecks and missed estimates, says Citi

- Demant shares drop as much as 8.7%, the most in a year and dragging peer GN Store Nord lower, after the Danish hearing-aid maker reported third-quarter sales that missed expectations and narrowed its organic revenue forecast for the year

- RS Group shares fall as much as 19% after a tough first half as weakness in electronics weighs on the industrial and electronic products distributor sales, according to analysts

- OCI slumps as much as 5.8% after the Dutch fertilizer maker’s third-quarter results saw a big miss on adjusted Ebitda. There could be double-digit downgrades to full-year Ebitda numbers, Morgan Stanley says

- The Restaurant Group shares fall as much as 3.3% after Wheel Topco, the owner of Pizza Express, said it won’t make an offer for the owner of Wagamama due to “market conditions”

Earlier in the session, Asian equities declined, halting their best four-day advance since November 2022, with Chinese and Korean stocks leading the selloff in the region: South Korea’s Kospi Index lost 2.3% after Monday’s rally that was triggered by a short-selling ban, while Australia resumed policy tightening and raised its inflation forecast, a sign that central banks are not necessarily done hiking interest rates.

The MSCI Asia Pacific Index fell as much as 1.3%, its biggest drop since Oct. 26, with POSCO, Alibaba and AIA Group among the top laggards. Korean stocks were headed for their worst day in more than a year on profit-taking after a ban on short-selling triggered their biggest rally since March 2020 on Monday. Chinese shares also declined after data showed that exports unexpectedly deepened in October, underscoring the country’s fragile economic recovery. A gauge of technology stocks in Hong Kong fell the most in a week.

- Hang Seng and Shanghai Comp opened lower amid the broader market mood. Muted price action was seen after the narrower-than-expected October Chinese Trade Balance, although imports saw surprise growth, while China Vanke’s shares firmed after state shareholders showed signs of providing liquidity support.

- Australia’s ASX 200 saw its downside led by Financials, Energy, and Materials, although the index clambered off worst levels following the RBA’s dovish hike.

- Japan’s Nikkei 225 fell back under 32,500 as the index conforms to the losses across the region.

- Indian stocks ended a three-day rally to end flat amid declines in Asia and European markets. The S&P BSE Sensex settled at 64,942.40, erasing an intraday loss off 0.5%. The NSE Nifty 50 Index also ended flat at 19,406.70. The MSCI Asia Pacific Index slid as much as 1.4%, ending a four-day winning run that was the longest since October 12.

Asian equities started November with gains after three successive months of decline over hopes that the higher-for-longer interest rates narrative may be fading. Still, sentiment has slightly soured amid fresh doubts over the Fed’s policy path and as Australia resumed its interest rate hikes after stronger than expected inflation data. “Following the stellar rallies across the region yesterday, indexes are giving back some of their gains, with a recovery in bond yields and a firmer US dollar to start the week,” said Jun Rong Yeap, market analyst at IG Asia Pte.

In FX the Bloomberg Dollar Spot Index is up 0.2%. The Aussie is the weakest of the G-10 currencies, falling 1% versus the greenback after the RBA signaled a higher hurdle to further policy tightening.

In rates, Treasuries rose along with the dollar, ahead of a flurry of Fed speakers later on Tuesday and following wider gains across European rates. 10Y TSY are trading at 4.625% down 2bps from yesterday’s close. Gilts in particular underwent a sharp bull-steepening after Bank of England chief economist Huw Pill said there will be a “sharp further fall” in inflation for October and hinted that interest rates could be cut by the middle of next year. Adding to the upward pressure on UK bonds, market research firm Kantar reported UK grocery price inflation slowed to single digits for the first time in 16 months. UK two-year yields fall 10bps to 4.62%.

The US session includes at least seven Fed officials scheduled to speak and $48b 3-year note sale at 1pm New York time. US are yields richer by less than 2bp across the curve with gains led by belly, steepening 5s30s spread by around 1bp on the day; gilts lead gains across core European rates with 2-year sector richer by 10bp on the day into early US session, while in 10-year sector gilts outperform Treasuries by 4.5bp.

In commodities, West Texas Intermediate crude dropped below $80 a barrel for the first time in more than two months. WTI fell 2% to trade near $79.20. Spot gold falls 0.5%.

Looking to the day ahead now, data releases include German industrial production, Euro Area PPI, and the US trade balance for September. From central banks, we’ll hear from the Fed’s Barr, Schmid, Waller, Williams and Logan, along with the ECB’s Nagel. Finally in the political sphere, the King’s speech is taking place in the UK, where the government outlines its legislative agenda for the next parliamentary session. In the US, there are also 2 gubernatorial elections taking place today in Kentucky and Mississippi.

Market Snapshot

- S&P 500 futures down 0.3% to 4,373.00

- MXAP down 1.3% to 157.64

- MXAPJ down 1.2% to 493.63

- Nikkei down 1.3% to 32,271.82

- Topix down 1.2% to 2,332.91

- Hang Seng Index down 1.6% to 17,670.16

- Shanghai Composite little changed at 3,057.27

- Sensex little changed at 64,907.46

- Australia S&P/ASX 200 down 0.3% to 6,977.07

- Kospi down 2.3% to 2,443.96

- STOXX Europe 600 down 0.2% to 442.82

- German 10Y yield little changed at 2.71%

- Euro down 0.2% to $1.0694

- Brent Futures down 2.1% to $83.38/bbl

- Gold spot down 0.5% to $1,967.78

- U.S. Dollar Index up 0.29% to 105.52

Top Overnight News

- RBA hiked rates by 25bp to 4.35% (market expectations were close to 50/50 about whether they would move at this meeting) although the accompanying language evolved in a dovish fashion. RTRS

- China’s exports fall short of expectations in Oct, coming in -6.4% Y/Y (vs. the Street estimate of -3.5%), although imports were a bit better (+3% vs. the Street -5%). RTRS

- Tumbling pork prices could push China back into deflation this week, as the largest listed hog farmers flood the domestic market and complicate Beijing’s efforts to bolster confidence in the world’s second-largest economy. FT

- China steps in to provide support to stressed developer Vanke, with Shenzhen Metro, a state-owned enterprise, vowing to provide full support to the company. WSJ

- German industrial production for Sept comes in cooler than anticipated (-1.4% M/M vs. the Street’s -0.1% forecast). BBG

- The BOE might wait until the middle of next year before cutting interest rates from their current 15-year high, the BoE’s Chief Economist Huw Pill said on Monday. Pill said pricing in financial markets – that currently points to a first rate cut to Bank Rate in August 2024 – “doesn’t seem totally unreasonable, at least to me.” RTRS

- UBS shares climbed as stronger-than-expected client inflows and progress in cost savings overshadowed its first quarterly loss in six years. Sergio Ermotti said Credit Suisse has stabilized though remains structurally unprofitable, while demand for UBS debt is strong. BBG

- The UN reported the reopening of the crossing between Gaza and Egypt. Benjamin Netanyahu said he sees his country having security control over Gaza for an “indefinite period.” BBG

- James Gorman signaled he plans to step down as Morgan Stanley’s chairman by the end of 2024 as he prepares to vacate his CEO post this year. He pushed back on the notion of entering politics, saying, “I don’t like sharks.” BBG

A more detailed look at global markets courtesy of Newsquawk

Asia-Pac stocks were softer across the board following the prior day’s gains and the choppy/mixed lead from Wall Street. South Korea’s KOSPI is the notable underperformer – slumping over 2.8% – after surging yesterday on the back of the stock short-selling ban. ASX 200 saw its downside led by Financials, Energy, and Materials, although the index clambered off worst levels following the RBA’s dovish hike. Nikkei 225 fell back under 32,500 as the index conforms to the losses across the region. Hang Seng and Shanghai Comp opened lower amid the broader market mood. Muted price action was seen after the narrower-than-expected October Chinese Trade Balance, although imports saw surprise growth, while China Vanke’s shares firmed after state shareholders showed signs of providing liquidity support.

Top Asian News

- RBA hikes its Cash Rate by 25bps as expected to 4.35% from 4.10%, and tweaked its forward guidance to say “Whether further tightening of monetary policy is required…will depend upon the data” (prev. “Some further tightening of monetary policy may be required”). The RBA also noted inflation in Australia has passed its peak but is still too high and is proving more persistent than expected a few months ago.

- China’s Commerce Ministry has issued new rules to strengthen management of rare earth exports, effective Oct 31 2023 to Oct 31, 2025; issued new rules to strengthen import management of crude oil, iron ore, copper concentrate, potash, according to Reuters.

- PBoC Deputy Governor said he is not too worried about the Chinese economy, and added the overall debt level of the Chinese government is in the mid to lower range by international standards, according to Reuters.

- PBoC injected CNY 353bln via 7-day reverse repos with the rate at 1.80% for a CNY 259bln net daily drain.

- Japan ruling ally Kometo tax chief says should not pre-decide to limit income tax cuts to just a year, according to Reuters.

- South Korean Vice Finance Minister says FX authorities will continue to monitor currency markets as done now even after rule changes in licenses, according to Reuters.

- IMF upgrades China’s GDP Growth forecasts: 2023 5.4% (prev. 5%), 2024 4.6% (prev. 4.2%); follows strong Q3 and growth policies.

European bourses are in the red, Euro Stoxx 50 -0.2%, but have been fairly contained throughout the morning with specific catalysts light and the tone thus far largely emanating from APAC pressure. Sectors are mixed with outperformance in Retail names post-AB Foods while Banks derive support from UBS despite yield pressure; in M&A Telefonica’s offer to purchase the remainder of Telefonica Deutschland has led to gains of circa. 40% for the German telecom name. Stateside, futures are in the red printing broad-based losses in a continuation of Monday’s/APAC risk tone, ES -0.2%, docket today features notable data incl. Manheim and numerous Fed speakers before a handful of earnings.

Top European News

- ECB’s de Guindos says low growth or economic standstill is expected to carry on into Q4 for the Eurozone.

- Telefonica Seeks 28% in German Unit for About €2 Billion

- UBS Seeks to Get Rid of $5 Billion in Rich Clients’ Assets

- Sunak Aims to Trap Labour With Election-Geared King’s Speech

- Aldi and Lidl Are Now Just as Middle Class as Other UK Grocers

FX

- Aussie retreats as risk aversion and less hawkish RBA guidance outweigh the widely anticipated 25bp hike, AUD/USD closer to 0.6400 than 0.6500, AUD/NZD cross sub-1.0850 from just under 1.0900.

- Buck maintains recovery momentum almost across the board as DXY climbs to 105.63 from a 105.25 low awaiting US trade data and a slew of Fed speakers.

- Euro losing grip of 1.0700 handle, Pound probes 1.2300 and Yen back below 150.00 all over again.

- Loonie undermined by a slide in oil ahead of Canadian trade with USD/CAD closer towards the top of 1.3755-1.3691 range.

- PBoC set USD/CNY mid-point at 7.1776 vs exp. 7.2854 (prev. 7.1780)

- BCB Minutes: It was decided to maintain the recent communication, which already includes the appropriate conditionality in an uncertain environment; rate cuts of 50bps are appropriate to keep the necessary contractionary monetary policy for the disinflationary process.

Fixed Income

- Debt futures resurgent after further retracement and curves revert to a flatter trajectory ahead of US refunding.

- Bunds bounce from 129.35 to 130.20 and Gilts from 94.47 to 95.42 in the wake of solid demand for 2034 UK issuance.

- T-note back on 108-00 handle within 107-19+/108-03+ range.

Commodities

- Crude benchmarks remain under pressure after slipping during APAC trade in-fitting with the broader risk tone and have been unable to stage any form of recovery this morning, despite equity performance being much more contained in comparison.

- WTI Dec’23 and Brent Jan’23 lose the USD 80/bbl and USD 84/bbl handles respectively, an action which pushes the benchmarks to multi-month lows with support seen around USD 78/bbl mark in WTI from late-August.

- Metals feature marked pressure in spot gold with the stronger USD offsetting any potential haven demand that may typically have been expected from the current tone, a tone which is weighing on base metal peers.

- US DoE announced a supplemental solicitation for up to 3mln barrels of oil for delivery in January 2024 for US Strategic Reserve.

- OPEC Secretary General says oil demand continues to rise significantly; Oil demand to grow more than 2mln BPD in 2024.

Geopolitics

- Israeli PM Netanyahu says Israel is open to “short pauses” in Gaza, but ruled out a ceasefire, according to Bloomberg.

- The Biden administration is reportedly planning a USD 320mln transfer of precision bombs for Israel, according to WSJ.

- Russian Defence Ministry says Russia destroyed 17 Ukraine-launched drones over Russian territory, according to RIA.

US Event Calendar

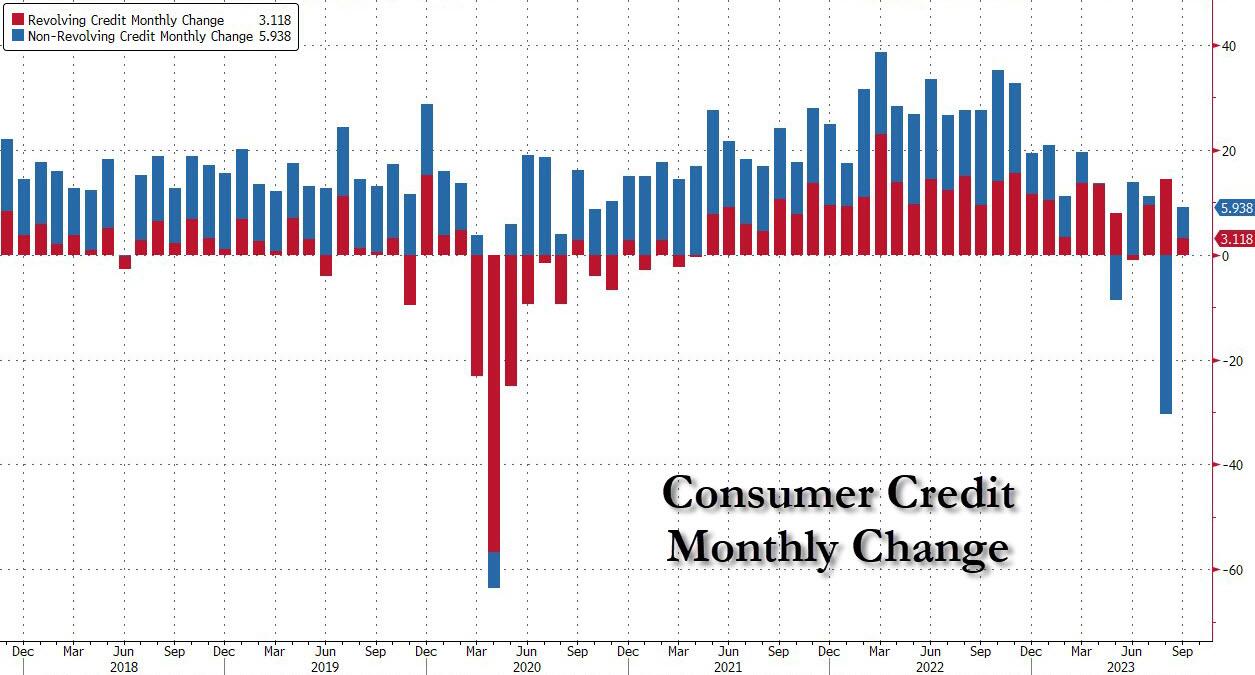

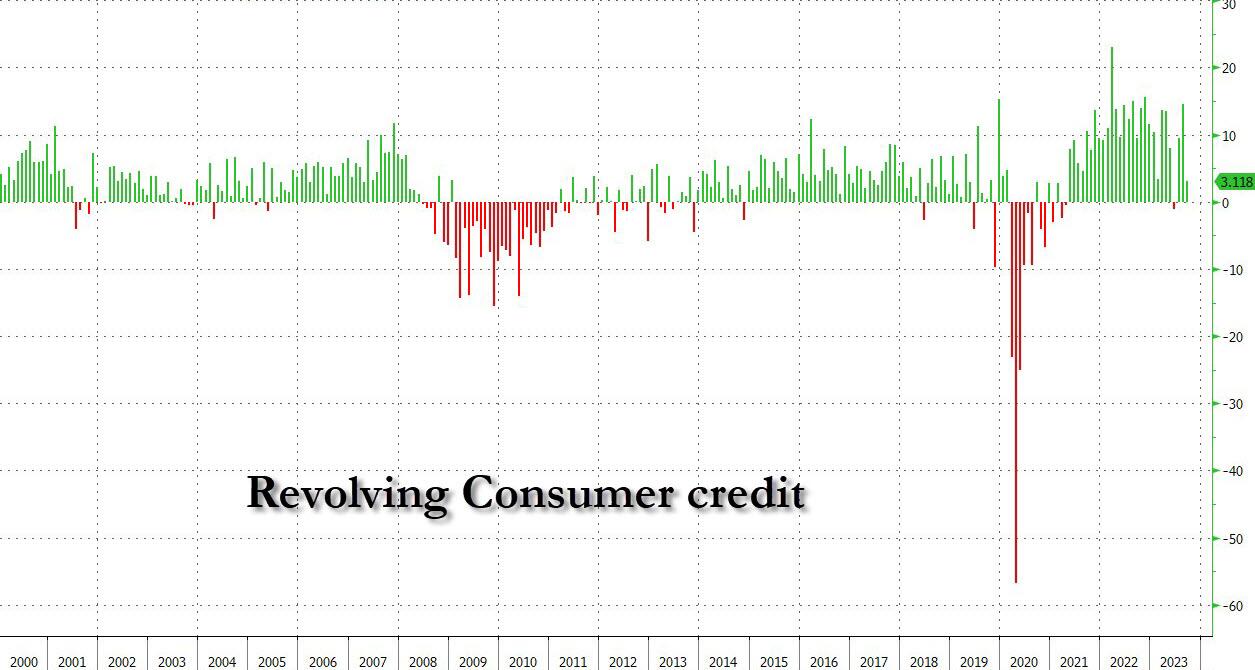

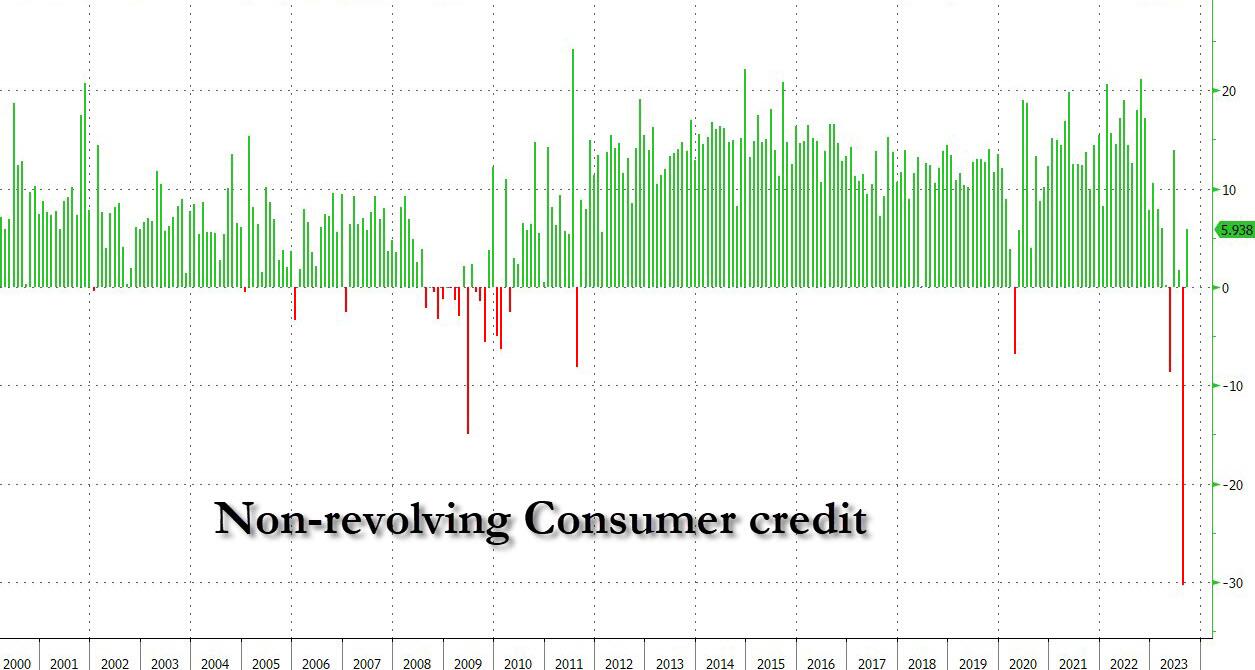

- 08:30: Sept. Trade Balance, est. -$59.8b, prior -$58.3b

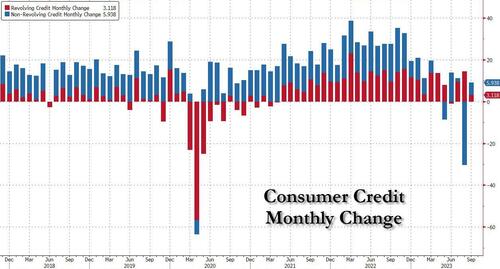

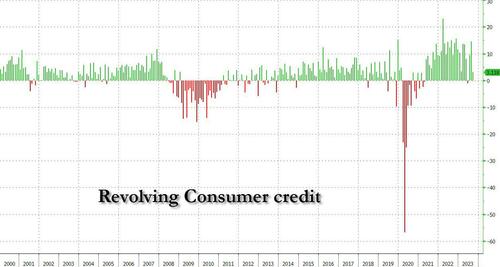

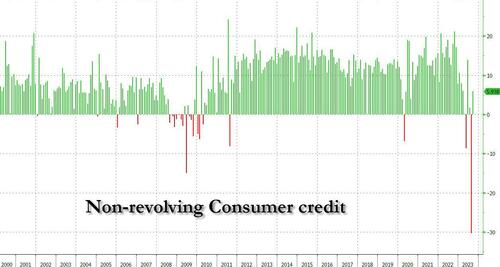

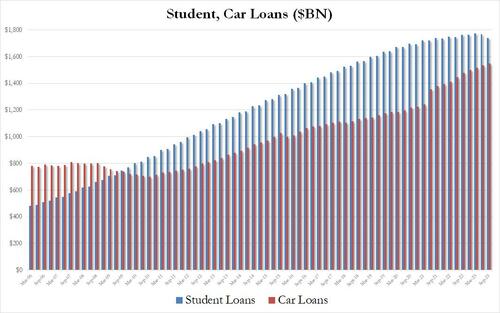

- 15:00: Sept. Consumer Credit, est. $9.5b, prior -$15.6b

Central Banks

- 07:30: Fed’s Kashkari Speaks on Bloomberg Television

- 08:00: Fed’s Goolsbee Speaks on CNBC

- 09:15: Fed’s Barr Speaks on Financial Technology

- 09:50: Fed’s Schmid Speaks at Dallas/Kansas City Energy Conference

- 10:00: Fed’s Waller Speaks at St. Louis Fed Conference

- 12:00: Fed’s Williams Moderates Discussion in New York

- 13:25: Fed’s Logan Participates in Moderated Discussion

DB’s Jim Reid concludes the overnight wrap

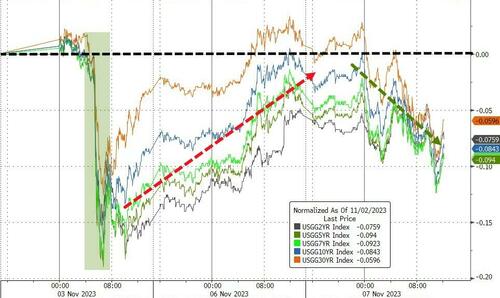

Just when you thought it was safe to go back into the water and hoover up every bond in sight, yesterday saw yields do yet another 180 degree turn, something we’ve been used to seeing in recent weeks, even if last three days of last week was one way traffic. 2yr US yields led the way (+9.6bps). T he S&P 500 managed to eke out a narrow gain (+0.18%) but US small caps (Russell 2000 -1.29%) suffered again with higher rates.

Diving in, the bond selloff perhaps came as investors began to wonder if last week’s narrative about rate cuts was overdone. For instance, market pricing for the Fed now implies a 16% chance of another rate hike, up from 11% on Friday. Moreover, the rate priced in by the December 2024 meeting was up +12.4bps to 4.47%. So there was a clear, albeit partial unwinding of last week’s moves. After the market close, we heard from Minneapolis Fed Kashkari, one of the more hawkish FOMC voices, who said that “we need to let the data keep coming to us to see if we really have got the inflation genie back in the bottle”. So some pushback against declaring victory over inflation.

For markets, this is hardly the first time we’ve seen expectations of a dovish pivot, and Henry pointed out yesterday (link here) that this is at least the 7th time this cycle where markets have reacted notably in response to dovish speculation. Clearly rates aren’t going to keep going up forever, but on the previous 6 occasions we saw hopes for near-term rate cuts dashed every time. Note that we’ve still got above-target inflation in every G7 country. With that in mind, next week’s US CPI release will be an important factor on that front, and our US economists expect core CPI to remain at +0.3% for a third consecutive month .

In the latter half of the US session, we got the latest Senior Loan Officer Opinion Survey (SLOOS) from the Fed, which looks at bank lending standards and has traditionally been a strong leading indicator for the economy more broadly. This showed some improvement in banks’ willingness to lend compared to the previous quarter’s lows, with the net balance of banks reporting tighter lending standards falling from 50.8 to 33.9 for commercial & industrial loans and from 71.7 to 64.9 for CRE loans. However, more banks reported tightening standards for mortgages, up from 13.8 to 16.0. So the general SLOOS improvement is welcome but most measures are still at levels usually associated with recessions. Can the SLOOS improve quickly enough over the next 2-3 quarters before the current tight lending standards cause an accident or a serious growth slowdown. We likely have a race against time.

In terms of the actual moves for bonds, 10yr Treasury yields ended the day up +7.1bps to 4.64%. Real yields drove the increase, with the 10yr real yield up +5.2bps to 2.23%, following its biggest weekly decline of 2023 so far last week. The sell-off was stronger at the front-end, with 2yr yields up +9.6bps to 4.94%. $24bn worth of corporate bond deals getting priced on Monday may have added upward pressure on yields. It’s worth highlighting that although the QRA was more positive last week, supply and QT is a regular part of life now and today kicks off a 3-day Treasury auction schedule with 3yr notes today, 10yr tomorrow and 30yr bonds on Thursday. So markets will still have to price these to sell over the coming months.

Meanwhile in Europe, the rises in yields were also significant, with those on 10yr bunds (+9.3bps), OATs (+10.2bps) and BTPs (+13.3bps) all moving higher. Indeed, for BTPs it was the joint largest daily rise in yields since July 6. However the front end rise was more contained with German, French and Italian 2yr yields up +3.9 bps, +3.2bps and +9.1bps respectively .

The bond moves were an obvious headwind to equities, but the S&P 500 (+0.18%) still managed to build on last week’s advance, with a 6th consecutive gain for the first time since June. However, this advance was a narrow one with only 31% of the S&P constituents up on the day. The biggest driver were tech mega caps, with the Magnificent Seven index up +0.87%, and the NASDAQ (+0.30%) rising for a 7th consecutive session for the first time since January. On the other hand, small-caps put in a very weak performance, with the Russell 2000 (-1.29%) losing ground after recording its strongest week since February 2021. As with bonds, the picture was a bit weaker in Europe, with losses for the STOXX 600 (-0.16%), the DAX (-0.35%) and the CAC 40 (-0.48%).

Asian equity markets have turned negative this morning following the softer markets yesterday. As I check my screens, the KOSPI (-3.07%) is sliding hard after posting its best session yesterday (+6.43%) since late March 2020 following the renewed ban on short selling over the weekend. Elsewhere, the Hang Seng (-1.50%), the Nikkei (-1.12%), the CSI (-0.68%) and the Shanghai Composite (-0.35%) are also retreating. Meanwhile, the S&P/ASX 200 (-0.15%) is also trading lower after the RBA increased its key interest rate by 25bps as expected (more on this below). S&P 500 (-0.21%) and NASDAQ 100 (-0.15%) futures are ticking lower. Treasury yields have fallen 0 to -1.5bps across the curve, led by the front end.

The latest trade data from China showed that exports declined for a 6th consecutive month, dropping -6.4% y/y, worse than Bloomberg’s estimate of a -3.5% drop and against a -6.2% drop in September. Imports surprisingly rebounded +3.0% y/y in October (v/s -5.0% expected) after a revised -6.3% drop the previous month. The resulting trade surplus amounted to $56.53 billion (v/s $82.0 billion expected).

Elsewhere, the RBA lifted its cash rate for the first time in five months (+25bps) to a 12-year high of 4.35% citing a slower-than-expected decline in inflation while still indicating that inflation would return to its target range of 2% to 3% in a reasonable timeframe. The Aussie dollar (-0.79%) dropped against the US dollar in response to the rate hike as the central bank’s statement failed to confirm the possibility of another hike in this cycle. Policy sensitive 3yr government bond yields fell -3.1 bps to 4.24% before slightly recovering, standing at 4.25% as I type.

Looking at yesterday’s data, there wasn’t too much but we did get some of the final PMI readings from Europe, where the main headlines were in line with the flash prints from a couple of weeks ago. For instance, the final Euro Area composite PMI was exactly in line with the flash reading at 47.8, and in Germany it was revised by only -0.1pts to 45.8. One source of concern was Italy, where the composite PMI fell -2.0pts to 47.0, its lowest in 12 months. Otherwise, the latest reading on German factory orders for September showed a +0.2% expansion (vs. -1.5% expected), but with this upside offset by a major downward revision to the previous month (+1.9% vs +3.9% previously). This still leaves German factory orders down -4.3% year-on-year.

To the day ahead now, and data releases include German industrial production, Euro Area PPI, and the US trade balance for September. From central banks, we’ll hear from the Fed’s Barr, Schmid, Waller, Williams and Logan, along with the ECB’s Nagel. Finally in the political sphere, the King’s speech is taking place in the UK, where the government outlines its legislative agenda for the next parliamentary session. In the US, there are also 2 gubernatorial elections taking place today in Kentucky and Mississippi.

2 B) NOW NEWSQUAWK (EUROPE/REPORT)

Equities in the red, DXY bid & Antipodeans sink post-RBA hike; slew of Fed speak due – Newsquawk US Market Open

TUESDAY, NOV 07, 2023 – 06:23 AM

- European equities/US futures in the red with sentiment sour ahead of a busy day of Fed speak

- Fixed benchmarks are back in bull-flattening mode, lifting from yesterday’s lows pre-supply

- DXY firmly above 105.50, whilst Antipodeans sink on weaker sentiment and post-RBA hike

- As expected, the RBA announced a 25bps hike, ensuing initial upside in the AUD before slipping on weaker forward guidance

- Crude benchmarks pare back yesterday’s gains, with base metals also in the red owing to the firmer Dollar and general market sentiment

- Looking ahead, highlights include US International Trade, IBD/TIPP, Manheim Index, NY Fed Q3 Household Debt & Credit Report, Speeches from Fed’s Goolsbee, Schmid, Williams, Logan, Barr, Waller, UK King’s Speech and Earnings from CNH Industrial, Uber, eBay & Occidental Petroleum Corp

More Newsquawk in 3 steps:

1. Subscribe to the free premarket movers reports

2. Listen to this report in the market open podcast (available on Apple and Spotify)

3. Trial Newsquawk’s premium real-time audio news squawk box for 7 days

EUROPEAN TRADE

EQUITIES

- European bourses are in the red, Euro Stoxx 50 -0.2%, but have been fairly contained throughout the morning with specific catalysts light and the tone thus far largely emanating from APAC pressure.

- Sectors are mixed with outperformance in Retail names post-AB Foods while Banks derive support from UBS despite yield pressure; in M&A Telefonica’s offer to purchase the remainder of Telefonica Deutschland has led to gains of circa. 40% for the German telecom name.

- Stateside, futures are in the red printing broad-based losses in a continuation of Monday’s/APAC risk tone, ES -0.2%, docket today features notable data incl. Manheim and numerous Fed speakers before a handful of earnings.

- Click here and here for the sessions European pre-market equity newsflow, including earnings.

- Click here for more details.

FX

- Aussie retreats as risk aversion and less hawkish RBA guidance outweigh the widely anticipated 25bp hike, AUD/USD closer to 0.6400 than 0.6500, AUD/NZD cross sub-1.0850 from just under 1.0900.

- Buck maintains recovery momentum almost across the board as DXY climbs to 105.63 from a 105.25 low awaiting US trade data and a slew of Fed speakers.

- Euro losing grip of 1.0700 handle, Pound probes 1.2300 and Yen back below 150.00 all over again.

- Loonie undermined by a slide in oil ahead of Canadian trade with USD/CAD closer towards the top of 1.3755-1.3691 range.

- PBoC set USD/CNY mid-point at 7.1776 vs exp. 7.2854 (prev. 7.1780)

- BCB Minutes: It was decided to maintain the recent communication, which already includes the appropriate conditionality in an uncertain environment; rate cuts of 50bps are appropriate to keep the necessary contractionary monetary policy for the disinflationary process.

- Click here for more details.

- Click here for the Option Expires for the NY Cut.

FIXED INCOME

- Debt futures resurgent after further retracement and curves revert to a flatter trajectory ahead of US refunding.

- Bunds bounce from 129.35 to 130.20 and Gilts from 94.47 to 95.42 in the wake of solid demand for 2034 UK issuance.

- T-note back on 108-00 handle within 107-19+/108-03+ range.

- Click here for more details.

COMMODITIES

- Crude benchmarks remain under pressure after slipping during APAC trade in-fitting with the broader risk tone and have been unable to stage any form of recovery this morning, despite equity performance being much more contained in comparison.

- WTI Dec’23 and Brent Jan’23 lose the USD 80/bbl and USD 84/bbl handles respectively, an action which pushes the benchmarks to multi-month lows with support seen around USD 78/bbl mark in WTI from late-August.

- Metals feature marked pressure in spot gold with the stronger USD offsetting any potential haven demand that may typically have been expected from the current tone, a tone which is weighing on base metal peers.

- US DoE announced a supplemental solicitation for up to 3mln barrels of oil for delivery in January 2024 for US Strategic Reserve.

- OPEC Secretary General says oil demand continues to rise significantly; Oil demand to grow more than 2mln BPD in 2024.

- Click here for more details.

NOTABLE EUROPEAN HEADLINES

- ECB’s de Guindos says low growth or economic standstill is expected to carry on into Q4 for the Eurozone.

EUROPEAN DATA

- UK BRC Retail Sales YY (Oct) 2.6% vs Exp. 2.4% (Prev. 2.8%)

- UK Halifax House Prices MM (Oct) 1.1% (Prev. -0.4%, Rev. -0.3%)

- German Industrial Output MM (Sep) -1.4% vs. Exp. -0.1% (Prev. -0.2%)

- EU HCOB Construction PMI (Oct) 42.7 (Prev. 43.6); German HCOB Construction PMI (Oct) 38.3 (Prev. 39.3)

- EU Producer Prices MM (Sep) 0.5% vs. Exp. 0.5% (Prev. 0.6%, Rev. 0.7%); YY (Sep) -12.4% vs. Exp. -12.5% (Prev. -11.5%)

NOTABLE US HEADLINES