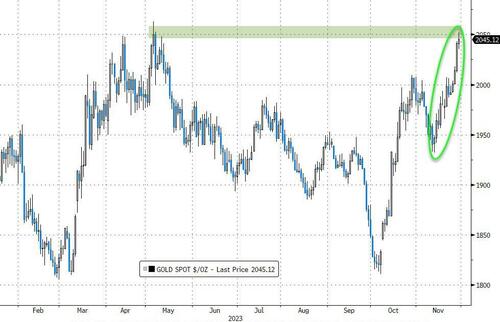

GOLD PRICE CLOSED: UP $7.20 TO $2045.95

SILVER PRICE CLOSED: UP 15 CENTS AT $25.06

Access prices: closes 4: 15 PM

Gold ACCESS CLOSE 2044.35

Silver ACCESS CLOSE: 25.00

NOV 27

Shanghai Gold Benchmark Price

USD oz  AM2038.21

AM2038.21

PM2039.46

Historical SGE Fix

SHANGHAI GOLD PREMIUM OVER NY: 27 DOLLARS

Bitcoin morning price:, 38,251 UP 36 DOLLARS

Bitcoin: afternoon price: $37,719 DOWN 496. dollars

Platinum price closing $944.70 UP $24.95

Palladium price; $1057.75 DOWN $2.25

END

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

Due to the huge rise in the dollar, we must look at gold and silver in currencies other than the dollar to understand where we are heading

I will now provide gold in Canadian dollars, British pounds and Euros

4: 15 PM ACCESS

*CANADIAN GOLD: $2,778.59 UP $5.23 CDN dollars per oz( * NEW ALL TIME HIGH 2,782.61//OCT 272023)

*BRITISH GOLD: 1610.11 UP 2.03 pounds per oz// *(NEW ALL TIME HIGH//CLOSING///1655.17) OCT 2/2023

*EURO GOLD: 1862,93 UP 5.06 euros per oz //* (NEW *ALL TIME HIGH/CLOSING//1898.24)//high.* OCT 27.2023

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

EXCHANGE: COMEX

EXCHANGE: COMEX

CONTRACT: NOVEMBER 2023 COMEX 100 GOLD FUTURES

SETTLEMENT: 2,039.700000000 USD

INTENT DATE: 11/28/2023 DELIVERY DATE: 11/30/2023

FIRM ORG FIRM NAME ISSUED STOPPED

624 H BOFA SECURITIES 120

657 C MORGAN STANLEY 26

661 C JP MORGAN 86

737 C ADVANTAGE 3

905 C ADM 5

TOTAL: 120 120

MONTH TO DATE: 6,016

JPMorgan stopped 0/120 contracts.

FOR NOV.:

GOLD: NUMBER OF NOTICES FILED FOR NOV/2023. CONTRACT: 120 NOTICES FOR 12000 OZ or 0.37325 TONNES

total notices so far: 6016 contracts for 601,600 oz (18.7122 tonnes)

FOR NOV:

SILVER NOTICES 0 NOTICE(S) FILED FOR 0 OZ/

total number of notices filed so far this month : 904 for 4,520,000 oz

XXXXXXXXXXXXXXXXXX

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

BOTH GLD AND SLV ARE FRAUDULENT VEHICLES

GLD

WITH GOLD UP $7.20//

INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD/ : / HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.73 TONNES OF GOLD FROM THE GLD

INVENTORY RESTS AT 880.55 TONNES

SLV//

WITH NO SILVER AROUND AND SILVER UP 15 CENTS AT THE SLV// HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A SHOCKER: A WITHDRAWAL OF 4.122 MILLION OZ OF SILVER

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV.

CLOSING INVENTORY: 436.051 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A GOOD SIZED 607 CONTRACTS TO 138,164 AND CLOSER TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THIS GOOD SIZED GAIN IN COMEX OI WAS ACCOMPLISHED WITH OUR STRONG $0.64 GAIN IN SILVER PRICING AT THE COMEX ON TUESDAY. WE HAD A MAJOR SPEC SHORT COVERING EPISODE IN TUESDAY’S COMEX TRADING BUT AT MUCH HIGHER PRICES.. TAS ISSUANCE WAS A HUGE SIZED 859 CONTRACTS. THESE WILL BE USED FOR MANIPULATION LATER THIS MONTH/AS WELL AS TODAY.

CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON TUESDAY NIGHT: 859 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS. IT THUS LOOKS LIKE THE FED (GOV’T) IS BEHIND ALL OF THESE TRADES.

WE HAVE NOW SET ANOTHER RECORD LOW AT 114,102 CONTRACTS ///JULY 3.2023// OUR BANKERS WITH THE HELP OF SPECULATORS AND HIGH FREQUENCY TRADERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.64). AND WERE UNSUCCESSFUL IN KNOCKING ANY SILVER LONGS AS WE HAD A TINY SIZED LOSS OF 46 OI CONTRACTS ON OUR TWO EXCHANGES AS THE SPEC SHORTS TRIED AGAIN DESPERATELY TO COVER THEIR SHORTFALLS BUT AT MUCH HIGHER PRICES AS THEY ARE CONTINUALLY BEING SENT TO THE SLAUGHTERHOUSE

WE MUST HAVE HAD:

A STRONG SIZED 561 ISSUANCE OF EXCHANGE FOR PHYSICALS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 1.430 MILLION OZ (FIRST DAY NOTICE) FOLLOWED BY TODAY’S 0 OZ QUEUE JUMP +0 EXCHANGE FOR RISK ISSUANCE FOR 0 MILLION OZ//NEW EXCHANGE FOR RISK 1.245 MILLION

//NEW STANDING FOR SILVER IS THUS 4.525 MILLION OZ + 1.245 (EX. FOR RISK) = 5.770 MILLION OZ.

//GOOD SIZED COMEX OI LOSS/ GOOD SIZED EFP ISSUANCE/VI) HUGE GIGANTIC SIZED NUMBER OF T.A.S. CONTRACT ISSUANCE 859 CONTRACTS)/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL – REMOVED A HUGE 1047 CONTRACTS (the cme will no longer provide preliminary no to be except through a paywall)

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS NOV. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF NOV:

TOTAL CONTRACTS for 20 days, total 9130 contracts: OR 45.650 MILLION OZ (457 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 45.650 MILLION OZ

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH 2022: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 118.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 85.745 MILLION OZ (SMALLER THAN LAST MONTH)

AUGUST: 171.43 MILLION OZ (THIS MONTH IS GOING TO BE HUGE //2ND HIGHEST ON RECORD

SEPT: 72.705 MILLION OZ (SMALLER THIS MONTH)

OCT: 97.455 MILLION OZ

NOV. 45.650 MILLION OZ (GOING TO BE QUITE SMALL THIS MONTH)

RESULT: WE HAD A GOOD SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 607 CONTRACTS DESPITE OUR GAIN IN PRICE OF $0.64 IN SILVER PRICING AT THE COMEX//TUESDAY.,. THE CME NOTIFIED US THAT WE HAD A GOOD EFP ISSUANCE CONTRACTS: 561 ISSUED FOR DEC AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS. WE HAVE A SMALL INITIAL SILVER OZ STANDING FOR NOV. OF 1.432 MILLION OZ FOLLOWED BY TODAY’S 10,000 OZ E.F.P. JUMP TO LONDON

NEW STANDING 4.525 OZ + 1.245 MILLION OZ EXCHANGE FOR RISK: NEW TOTAL 5.770 MILLION OZ/// /// WE HAVE A TINY SIZED LOSS OF 46 OI CONTRACTS ON THE TWO EXCHANGES. THE TOTAL OF TAS INITIATED CONTRACTS TODAY: A HUGE SIZED 859 CONTRACTS//SOME FRONT END OF THE TAS CONTRACTS WERE LIQUIDATED DURING THE TUESDAY COMEX SESSION. THE NEW TAS ISSUANCE TUESDAY NIGHT A HUGE (859) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE., .

WE HAD 0 NOTICE(S) FILED TODAY FOR 0 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A VERY STRONG SIZED 9188 CONTRACTS TO 505,658 AND CLOSER TO THE RECORD (SET JAN 24/2020) AT 799733 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: – REMOVED 940 CONTRACTS

WE HAD A VERY STRONG SIZED INCREASE IN COMEX OI ( 9,188 CONTRACTS) WITH OUR $26.45 GAIN IN PRICE//TUESDAY. WE ALSO HAD A RATHER STRONG INITIAL STANDING IN GOLD TONNAGE FOR NOV. AT 4.3514 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S 12,000 OZ QUEUE JUMP + TODAY’S 0 CONTRACT ISSUANCE OF EXCHANGE FOR RISK// TOTAL EX. FOR RISK: 16.2505 TONNES/ // TOTAL GOLD STANDING FOR NOV: 18.7122 TONNES + 16.2505 TONNES (EX. FOR RISK) = 34.9627 TONNES // ALL OF..THIS HAPPENED WITH OUR $26.45 GAIN IN PRICE WITH RESPECT TO TUESDAY’S TRADING.WE HAD A GIGANTIC SIZED GAIN OF 16,193 OI CONTRACTS (50.36) PAPER TONNES) ON OUR TWO EXCHANGES.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 7005 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 506,598

IN ESSENCE WE HAVE A GIGANTIC SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 16,193 CONTRACTS WITH 9188 CONTRACTS INCREASED AT THE COMEX// AND A STRONG SIZED 7005 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 16,193 CONTRACTS OR 50.36TONNES. WE HAD 0 CONTRACT EXCHANGE FOR RISK FOR 0 TONNES. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): A STRONG 2628 CONTRACTS.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A STRONG SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (7005 CONTRACTS) ACCOMPANYING THE VERY STRONG SIZED GAIN IN COMEX OI (10,128) //TOTAL GAIN FOR OUR THE TWO EXCHANGES: 16,193 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR FORMER FORMAT OF BANKERS GOING LONG AND SPECULATORS GOING SHORT ,2.) FAIR INITIAL STANDING AT THE GOLD COMEX FOR NOV. AT 4.3514 TONNES FOLLOWED BY TODAY’S 12,00 OZ QUEUE JUMP : NEW STANDING 18.7122 TONNES + 16.2505 TONNES EXCHANGE /THUS NEW TOTAL FOR GOLD STANDING: 34.9627 TONNES // /// 3) ZERO LONG LIQUIDATION AND HUGE TAS LIQUIDATION HELPING THE PRICE GAIN, AND WE HAD ATTEMPTED SPEC SHORT COVERINGS DURING THE COMEX SESSION BUT AT MUCH HIGHER PRICES AS THE SPECS ARE CONTINUALLY USHERED INTO THE SLAUGHTERHOUSE //4) VERY STRONG SIZED COMEX OPEN INTEREST GAIN/ 5) STRONG ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER///6: STRONG T.A.S. ISSUANCE: 2828 CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023 INCLUDING TODAY

NOV

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF NOV. :

TOTAL EFP CONTRACTS ISSUED: 71,722 CONTRACTS OR 7,172,200 OZ OR 223.085 TONNES IN 20 TRADING DAY(S) AND THUS AVERAGING: 3586 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 20 TRADING DAY(S) IN TONNES 223.085 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2022, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 223.085/3550 x 100% TONNES 5.66% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2023

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH/2022: 409.30 TONNES //FINAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 151.69 TONNES (WEAKER THAN LAST MONTH)

AUGUST: 195.28 TONNES (A STRONGER MONTH)//FINAL

SEPT: 254.709 TONNES (WILL BE LARGER THAN LAST MONTH AND A STRONG MONTH)

OCT. 248.09 TONNES. LIKE SILVER, THIS MONTH IS GOING TO BE A STRONG E.F.P. ISSUANCE.

NOV. 223.085 TONNES//WILL BE STRONG THIS MONTH,

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF SEPT. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF MAY HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF JUNE., FOR BOTH GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (SEPT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER FELL BY A GOOD SIZED 607 CONTRACTS OI TO 139,144 AND FURTHER FROM OUR COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 561 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

DEC 561 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 561 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 607 CONTRACTS AND ADD TO THE 561 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A TINY SIZED GAIN OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 46 CONTRACTS

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTAL 0.23 MILLION OZ

OCCURRED WITH OUR $0.64 GAIN IN PRICE …..

END

OUTLINE FOR TODAY’S COMMENTARY

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

b, ) Gold/silver trading overnight Europe,//GOLD COMMENTARIES

(Peter Schiff)

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS//

WEDNESDAY MORNING/TUESDAY NIGHT

SHANGHAI CLOSED DOWN 16.87 PTS OR 0.56% //Hang Seng CLOSED DOWN 360.70 PTS OR 2,08% /The Nikkei CLOSED DOWN 87,17 PTS OR 0.26% //Australia’s all ordinaries CLOSED UP .31 % /Chinese yuan (ONSHORE) closed UP AT 7.1277 /OFFSHORE CHINESE YUAN CLOSED UP TO 7.1373 /Oil UP TO 77.75 dollars per barrel for WTI and BRENT DOWN AT 82.89/ Stocks in Europe OPENED ALL GREEN// ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE STRONGER

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

9. USA

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A VERY STRONG SIZED 9,188 CONTRACTS TO 506,598 WITH OUR STRONG GAIN IN PRICE OF $26.45 WITH RESPECT TO TUESDAY TRADING. WE MUST HAVE HAD SOME SPEC SHORT COVERING.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE NON ACTIVE DELIVERY MONTH OF NOV..… THE CME REPORTS THAT THE BANKERS ISSUED A STRONG SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 7005 EFP CONTRACTS WERE ISSUED: : DEC 7005 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 7005 CONTRACTS

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A HUMONGOUS SIZED TOTAL OF 16,193 CONTRACTS IN THAT 7005 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A VERY STRONG SIZED GAIN OF 9,188 COMEX CONTRACTS..AND THIS GAIN ON OUR TWO EXCHANGES HAPPENED WITH OUR GAIN IN PRICE OF $26.45//TUESDAY COMEX. AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS DURING MID MONTH IN THE DELIVERY CYCLE), THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR TUESDAY NIGHT WAS A FAIR SIZED 2628 CONTRACTS. THROUGHOUT THE PAST SEVERAL WEEKS, THE BANKERS SOLD OFF THE LONG SIDE OF THE SPREAD WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR SPREAD WHICH WILL BE LIQUIDATED TWO MONTHS HENCE)//.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: NOV (34.7627 TONNES ( NON ACTIVE MONTH)

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

NOV: 18.7122 TONNES + 16.2505 EX. FOR RISK = 34.9627 TONNES

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT GAINED $26.45) //// AND WERE UNSUCCESSFUL IN KNOCKING ANY SPECULATOR LONGS AS WE HAD A HUMONGOUS SIZED GAIN OF 16,193 TOTAL CONTRACTS ON OUR TWO EXCHANGES. WE HAD CONSIDERABLE T.A.S. LIQUIDATION ON THE FRONT END OF TUESDAY’S TRADING TO THE GOOD SIDE OF THE TRADE. THE T.A.S. ISSUED ON TUESDAY NIGHT, WILL BE “PUT INTO THE BANK” TO BE USED AT A LATER DATE AT THE COLLUSIVE CHOOSING OF OUR BANKERS. WE ALSO EXPERIENCED MASSIVE SPECULATOR SHORT COVERING BUT AT MUCH HIGHER PRICES

WE HAVE GAINED A TOTAL OI OF 50.36 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR NOV. (4.3514 TONNES) ON FIRST DAY NOTICE FOLLOWED BY TODAY’S HUGE 12,000 OZ QUEUE JUMP //NEW TOTALS STANDING:18.7122 TONNES + 0 TONNES exchange for risk today + TOTAL EX. FOR RISK/PRIOR : 16.2505 TONNES/// NEW TOTAL STANDING: 34.9627 TONNES ALL OF THIS WAS ACCOMPLISHED WITH OUR GAIN IN PRICE TO THE TUNE OF $26.45. FOR THE PAST SEVERAL WEEKS, THE SPECULATORS HAVE GONE MASSIVELY SHORT WITH OUR BANKERS NET LONG. THE BIG QUESTION IS NOW HOW MUCH GOLD WILL THE BANKERS PULL FROM OUR SHORT SPECULATORS.

WE HAD REMOVED – 940 CONTRACTS TO THE COMEX TRADES TO OPEN INTEREST (CROOKS)

NET GAINED ON THE TWO EXCHANGES 16,193 CONTRACTS OR 1,619,300 OZ OR 50.36 TONNES.

Estimated gold volume today:// 207,868 fair//

final gold volumes/yesterday 382,965 very good//roll

//speculators have left the gold arena

NOV 29

/ /// THE NOV. 2023 GOLD CONTRACT

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 32.151 oz Brinks 1 kilobar . |

| Deposit to the Dealer Inventory in oz | nil |

| Deposits to the Customer Inventory, in oz | nil |

| No of oz served (contracts) today | 120 notice(s) 12000 OZ 0.37325 TONNES |

| No of oz to be served (notices) | 0 contracts 000 oz 0.000 TONNES |

| Total monthly oz gold served (contracts) so far this month | 6016 notices 601600 oz 18.7122 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | x |

0 dealer deposit:

total dealer deposits: 0 oz

customer deposits: 0

total customer deposits: nil oz

we had 1 customer withdrawals

i) Out of Brinks 32.151 oz (one kilobar)

total withdrawals 32.151 oz

Adjustments; 2

a) customer to dealer ASAHI 64,009.031 oz

b) dealer to customer/Brinks 3375.855 oz (105 kilobars)

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR NOV.

For the front month of NOVEMBER we have an oi of 120 contracts having LOST 34 contracts. We had 154 contracts filed on TUESDAY, so we GAINED 120 contracts or an additional 12,000 oz will stand for delivery at the comex in this NON active delivery month of NOVEMBER Our short speculators have been met with physical delivery demands by the bank. The only way they can obtain gold is through these EFP’s where delivery is taken in London on a T + 2 basis.

December LOST 35,256 contracts DOWN to 24,208 contracts. We have just 1 more trading day left before FDN.

WE WILL PROBABLY HAVE AROUND 40 to 50 TONNES OF GOLD STANDING FOR DELIVERY IN DECEMBER.

JAN. GAINED 151 contracts RISING TO 3376 contracts.

We had 120 contracts filed for today representing 12000 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 86 notices were issued from their client or customer account. The total of all issuance by all participants equate to 154 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped received by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the NOV. /2023. contract month, we take the total number of notices filed so far for the month (6016 x 100 oz ), to which we add the difference between the open interest for the front month of NOV. (120 CONTRACTS) minus the number of notices served upon today 120 x 100 oz per contract equals 601,600 OZ OR 18.7122 TONNES + total ex. for risk = 16.2505//THUS TOTAL STANDING: 34.9627 TONNES

thus the INITIAL standings for gold for the NOV. contract month: No of notices filed so far (6016) x 100 oz + (120) {OI for the front month} minus the number of notices served upon today (120) x 100 oz) which equals 601,600 oz standing OR 18.7122 TONNES + 16.2505 EX FOR RISK FOR MONTH = 34.9627 TONNES

TOTAL COMEX GOLD STANDING: 34.9627 TONNES WHICH IS HUGE FOR AN ACTIVE BUT GENERALLY WEAK DELIVERY MONTH. (OCT). Somebody is after a considerable amount of gold from the comex.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 1,570,924.315 OZ 48.86 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD: 19,934,659.007 OZ

TOTAL REGISTERED GOLD 10,111,873.231 (314.52 tonnes).

TOTAL OF ALL ELIGIBLE GOLD: 9,822,785.776 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 8,540,949 (REG GOLD- PLEDGED GOLD) 265.66 tonnes//dropping like a stone

END

SILVER/COMEX

NOV 29

//2023// THE NOV 2023 SILVER CONTRACT

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 587,653.122 oz DELAWARE Brinks . |

| Deposits to the Dealer Inventory | nil oz |

| Deposits to the Customer Inventory | 598,834.290 oz Loomis |

| No of oz served today (contracts) | 0 CONTRACT(S) (0,000 OZ) |

| No of oz to be served (notices) | 0 contracts (0 oz) |

| Total monthly oz silver served (contracts) | 904 Contracts (4,520,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

i) 0 dealer deposit

total dealer deposit: 0

total: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: 0 oz

We had 1 deposits customer account:

customer deposits: 1

i) Into Loomis: 598,834.290 oz

total customer deposit 598,834.290 oz

JPMorgan has a total silver weight: 134.441 million oz/266,393 million or 50.31%

Comex withdrawals 2

we had 2 customer withdrawals

i) out of Delaware 585,694.602

ii) Out of Brinks 1958.20 oz

total withdrawals 598,834.290 oz

adjustments: 2 and it is huge

ASAHI customer to dealer 2948,495.600 oz

Delaware: customer to dealer 622,267.299 oz

TOTAL REGISTERED SILVER: 37.377 MILLION OZ//.TOTAL REG + ELIGIBLE. 266,314 million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR August:

silver open interest data:

FRONT MONTH OF NOV /2023 OI: 0 CONTRACTS HAVING LOST 10 CONTRACT(S). WE HAD 10 NOTICES FILED ON TUESDAY, SO WE LOST 0 CONTRACTS OR AN ADDITIONAL NIL OZ WILL STAND FOR SILVER IN NOVEMBER AT THE COMEX

DEC. LOST 13,638 CONTRACTS TO STAND AT 7119. WE WILL PROBABLY HAVE 20 TO 25 MILLION OZ OF SILVER STAND FOR DELIVERY.

JANUARY GAINED 394 CONTRACTS TO STAND AT 1909

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 0 for NIL oz

Comex volumes// est. volume today 73,165,// very good

Comex volume: confirmed yesterday 123,733 mega huge/roll

To calculate the number of silver ounces that will stand for delivery in NOV. we take the total number of notices filed for the month so far at 904 x 5,000 oz = 4,520,000 oz

to which we add the difference between the open interest for the front month of NOV. (0) and the number of notices served upon today 0 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the NOV/2023 contract month: 904 (notices served so far) x 5000 oz + OI for the front month of NOV (0) – number of notices served upon today (0 )x 500 oz of silver standing for the NOV contract month equates to 4.525 MILLION OZ +0 MILLION OZ EXCHANGE FOR RISK TODAY + 1.245 MILLION OZ (EXCHANGE FOR RISK/PRIOR) =5.77MILLION OZ

There are 37.377 million oz of registered silver.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS//

BOTH GLD AND SLV ARE MASSIVE FRAUDS!

NOV 29/WITH GOLD UP $7.20 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.73 TONNES OF GOLD FROM THE GLD. // / / // // INVENTORY RESTS AT 880.55 TONNES

NOV 28/WITH GOLD UP $26.45 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD: // / / // // INVENTORY RESTS AT 882.28 TONNE

NOV 27/WITH GOLD UP $9,85 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD: // / / // // INVENTORY RESTS AT 882.28 TONNES

NOV 24/WITH GOLD UP $11.20 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.15 TONNES OF GOLD FROM THE GLD// / / // // INVENTORY RESTS AT 882.28 TONNES

NOV 22/WITH GOLD DOWN $8.45 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD / / // // INVENTORY RESTS AT 883.43 TONNES

NOV 21/WITH GOLD UP $21.65 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD / / // // INVENTORY RESTS AT 883.43 TONNES

NOV 20/WITH GOLD DOWN $4.15 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD A MAMMOTH DEPOSIT OF 12.98 TONNES INTO THE GLD:/ / // // INVENTORY RESTS AT 883.43 TONNES

NOV 17/WITH GOLD DOWN $1.85 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD:/ / // // INVENTORY RESTS AT 870.45 TONNES

NOV 16/WITH GOLD UP $22.70 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD:/ / // // INVENTORY RESTS AT 870.45 TONNES

NOV 15/WITH GOLD DOWN $1.00 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD:/ / // // INVENTORY RESTS AT 870.45 TONNES

NOV 14/WITH GOLD UP $16.35 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD:/ / // //A DEPOSIT OF 2.3 TONNES OF GOLD INTO THE GLD// INVENTORY RESTS AT 870.45 TONNES

NOV 13/WITH GOLD UP $12.00 TODAY:SMALL CHANGES IN GOLD INVENTORY AT THE GLD:/ / // //A DEPOSIT OF .87 TONNES OF GOLD INTO THE GLD// INVENTORY RESTS AT 868.15 TONNES

NOV 10/WITH GOLD DOWN $30.70 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD:/ / // // INVENTORY RESTS AT 867.28 TONNES

NOV 9/WITH GOLD UP $12.50 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD:/ / // // INVENTORY RESTS AT 867.28 TONNES

NOV 8/WITH GOLD DOWN $14.95 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD:A MASSIVE DEPOSIT OF 4.04 TONNES OF GOLD INTO THE GLD/ / // // INVENTORY RESTS AT 867.28 TONNES

NOV 7/WITH GOLD DOWN $14.70 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD:A DEPOSIT OF 4.33 TONNES OF GOLD INTO THE GLD/ / // // INVENTORY RESTS AT 863.24 TONNES

NOV 6/WITH GOLD DOWN $9.90 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD:A DEPOSIT OF 1.73 TONNES OF GOLD INTO THE GLD/ / // // INVENTORY RESTS AT 863.24 TONNES

NOV 3/WITH GOLD UP $5.75 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD: / // // INVENTORY RESTS AT 861.51 TONNES

NOV 2/WITH GOLD UP $6.55 TODAY:BIG CHANGES IN GOLD INVENTORY AT THE GLD: A HUGE DEPOSIT OF 2.02 TONNES OF GOLD INTO THE GLD/ // // INVENTORY RESTS AT 861.51 TONNES

NOV 1/WITH GOLD DOWN $6.15 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD // // INVENTORY RESTS AT 859.49 TONNES

OCT 31/859.49 TONNES//

OCT 30/WITH GOLD UP $7.80 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD // // INVENTORY RESTS AT 861.80 TONNES

OCT 27/WITH GOLD UP $1.20 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD // // INVENTORY RESTS AT 861.80 TONNES

OCT 26/WITH GOLD UP $2.90 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF 1.73 TONNES OF GOLD INTO THE GLD// // INVENTORY RESTS AT 861.80 TONNES

OCT 25/WITH GOLD UP $9.00 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD:/: //: // INVENTORY RESTS AT 860.07 TONNES

GLD INVENTORY: 880.55 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

NOV 29/WITH SILVER UP 15 CENTS TODAY:HUGE CHANGES IN SILVER INVENTORY AT THE SLV” A MASSIVE WITHDRAWAL OF 4.122 MILLION OZ FROM THE SLV// //://// //INVENTORY RESTS AT 436.051 MILLION OZ

NOV 28/WITH SILVER UP 64 CENTS TODAY:NO CHANGES IN SILVER INVENTORY AT THE SLV //://// //INVENTORY RESTS AT 440.173 MILLION OZ

NOV 27/WITH SILVER UP 32 CENTS TODAY:HUGE CHANGES IN SILVER INVENTORY AT THE SLV //:////A WITHDRAWAL OF 1,008,000 OZ FROM THE SLV. //INVENTORY RESTS AT 440.173 MILLION OZ

NOV 24/WITH SILVER UP 70 CENTS TODAY:HUGE CHANGES IN SILVER INVENTORY AT THE SLV //:////A WITHDRAWAL OF 549,000 OZ FROM THE SLV. //INVENTORY RESTS AT 441.181 MILLION OZ

NOV 22/WITH SILVER DOWN 21 CENTS TODAY:NO CHANGES IN SILVER INVENTORY AT THE SLV //://// //INVENTORY RESTS AT 441.730 MILLION OZ

NOV 21/WITH SILVER UP 32 CENTS TODAY:HUGE CHANGES IN SILVER INVENTORY AT THE SLV A DEPOSIT OF 2.794 OZ FROM THE SLV//://// //INVENTORY RESTS AT 441.730 MILLION OZ

NOV 20/WITH SILVER DOWN 26 CENTS TODAY:HUGE CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 1,824,000 OZ FROM THE SLV//://// //INVENTORY RESTS AT 438.936 MILLION OZ

NOV 17/WITH SILVER DOWN 6 CENTS TODAY:HUGE CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 1,832,000 OZ FROM THE SLV//://// //INVENTORY RESTS AT 437,104 MILLION OZ

NOV 16/WITH SILVER UP 38 CENTS TODAY:SMALL CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 778,000 OZ FROM THE SLV//://// //INVENTORY RESTS AT 440.768 MILLION OZ

NOV 15/WITH SILVER UP 39 CENTS TODAY:NO CHANGES IN SILVER INVENTORY AT THE SLV://// //INVENTORY RESTS AT 441.587 MILLION OZ

NOV 14/WITH SILVER UP 78 CENTS TODAY:SMALL CHANGES IN SILVER INVENTORY AT THE SLV:A DEPOSIT OF 183,000 OZ INTO THE SLV ////// //INVENTORY RESTS AT 441.587 MILLION OZ

NOV 13/WITH SILVER UP 5 CENTS TODAY:NO CHANGES IN SILVER INVENTORY AT THE SLV: ////// //INVENTORY RESTS AT 441.364 MILLION OZ

NOV 10/WITH SILVER DOWN 59 CENTS TODAY:HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF .733 MILLION OZ INTO THE SLV////// //INVENTORY RESTS AT 441.364 MILLION OZ

NOV 9/WITH SILVER UP 17 CENTS TODAY:NO CHANGES IN SILVER INVENTORY AT THE SLV: //// //INVENTORY RESTS AT 440.631 MILLION OZ

NOV 8/WITH SILVER UP 13 CENTS TODAY:NO CHANGES IN SILVER INVENTORY AT THE SLV: //// //INVENTORY RESTS AT 440.631 MILLION OZ

NOV 7/WITH SILVER DOWN 59 CENTS TODAY:NO CHANGES IN SILVER INVENTORY AT THE SLV: //// //INVENTORY RESTS AT 440.631 MILLION OZ

NOV 6/WITH SILVER DOWN 6 CENTS TODAY:NO CHANGES IN SILVER INVENTORY AT THE SLV: //// //INVENTORY RESTS AT 440.631 MILLION OZ

NOV 3/WITH SILVER UP 41 CENTS TODAY:BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.638 MILLION OZ OF SILVER FROM THE SLV///// /// /INVENTORY RESTS AT 440.631 MILLION OZ

NOV 2/WITH SILVER UP 11 CENTS TODAY:BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.924 OZ OF SILVER FROM THE SLV///// /// /INVENTORY RESTS AT 439.993 MILLION OZ

NOV 1/WITH SILVER DOWN 11 CENTS TODAY:BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 916,000 OZ OF SILVER FROM THE SLV///// /// /INVENTORY RESTS AT 441.917 MILLION OZ

OCT 31/442.833 MILLION OZ///INVENTORY

OCT 30/WITH SILVER UP 46 CENTS TODAY:NO CHANGES IN SILVER INVENTORY AT THE SLV: /// /// /INVENTORY RESTS AT 443.750 MILLION OZ

OCT 27/WITH SILVER UP 3 CENTS TODAY:BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 641,000 OZ FROM THE SLV/// /// /INVENTORY RESTS AT 443.750 MILLION OZ

OCT 26/WITH SILVER DOWN 14 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/ /// /INVENTORY RESTS AT 444.391 MILLION OZ

OCT 25/WITH SILVER DOWN 6 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/ /// /INVENTORY RESTS AT 444.391 MILLION OZ

CLOSING INVENTORY 436.041 MILLION OZ//

PHYSICAL GOLD/SILVER COMMENTARIES

1:Peter Schiff/Mike Maharrey

Did Deutsche Bank Economists Just Imply The Fed Will Create More Inflation In 2024?

WEDNESDAY, NOV 29, 2023 – 07:20 AM

Authored by Michael Maharrey via SchiffGold.com,

Deutsche Bank economists say the Federal Reserve will create more inflation in 2024.

OK, that’s not exactly what they said. But that is the implication of their latest forecast.

The Deutsche Bank analyst forecast that the Fed will cut rates by 175 basis points in 2024 in response to a “mild” recession. That would drive the Federal Reserve funds rate down to between 3.5% and 3.75%.

This loosening monetary policy, by definition, would create more inflation.

The Fed currently has interest rates set at between 5.25% and 5.5%.

Most mainstream analysts now think the central bank will cut rates next year, but not as steeply as Deutsche Bank economists.

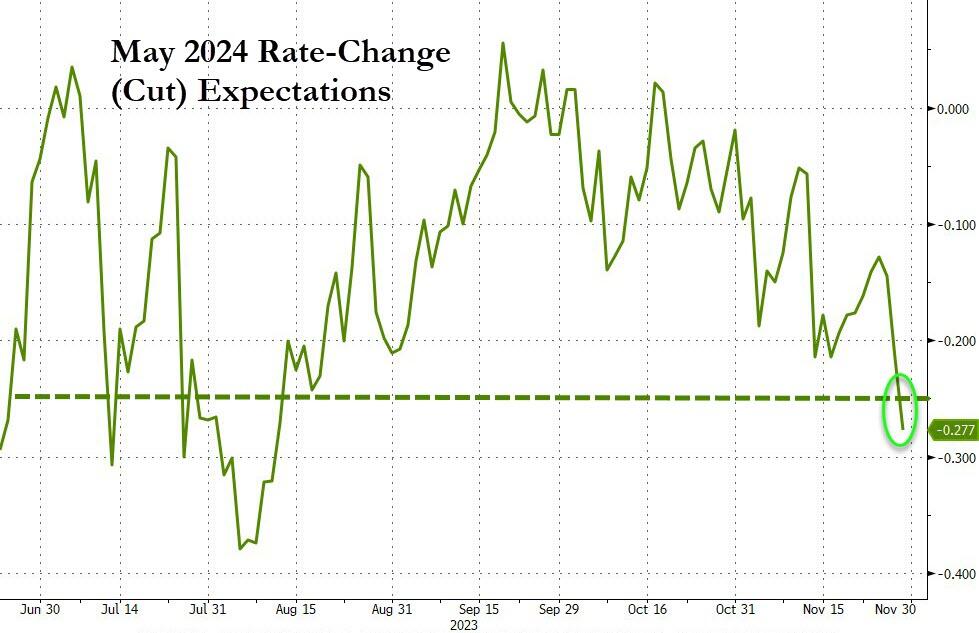

The dominant narrative today is that the Fed has successfully beaten down price inflation. A cooler-than-expected CPI report for October reinforced this notion. With inflation on the run, mainstream analysts think that the Fed has initiated its last hike and will pivot to rate cuts next year to guide the economy to a “soft landing.” Even before the CPI data release markets were pricing in 75 basis points of rate decreases in 2024.

[ZH: The market is pricing in 110bps of cuts next year after yesterday’s comments from Fed Gov. Waller]

Many mainstream analysts and financial news network pundits have taken a recession completely off the table. But Deutsche Bank senior US economist Brett Ryan told Reuters he expects the US economy to hit a “soft patch” that will lead to a “more aggressive cutting profile.”

Ryan said he expects this economic weakness to further ease inflationary pressure.

The Problems With the Forecast

There are several problems with the Deutsche Bank projections, and the entire mainstream narrative more generally.

In the first place, the death of inflation is greatly exaggerated. No matter how you slice and dice the data, none of the numbers come close to the Fed’s 2% target. Core CPI is still double that number.

Ryan says the “mild” recession will put additional downward pressure on price inflation, but the monetary policy he expects the Fed to follow is inflation.

Rate cuts will ease financial conditions and allow for more money creation and credit expansion.

Rising prices are a symptom of monetary inflation.

And monetary inflation is exactly what we will get when the central bank reverts to a looser monetary policy.

In other words, as soon as the Fed declares victory and starts cutting rates, inflation wins. The Fed goes right back to the inflationary policy that got us into this mess to begin with.

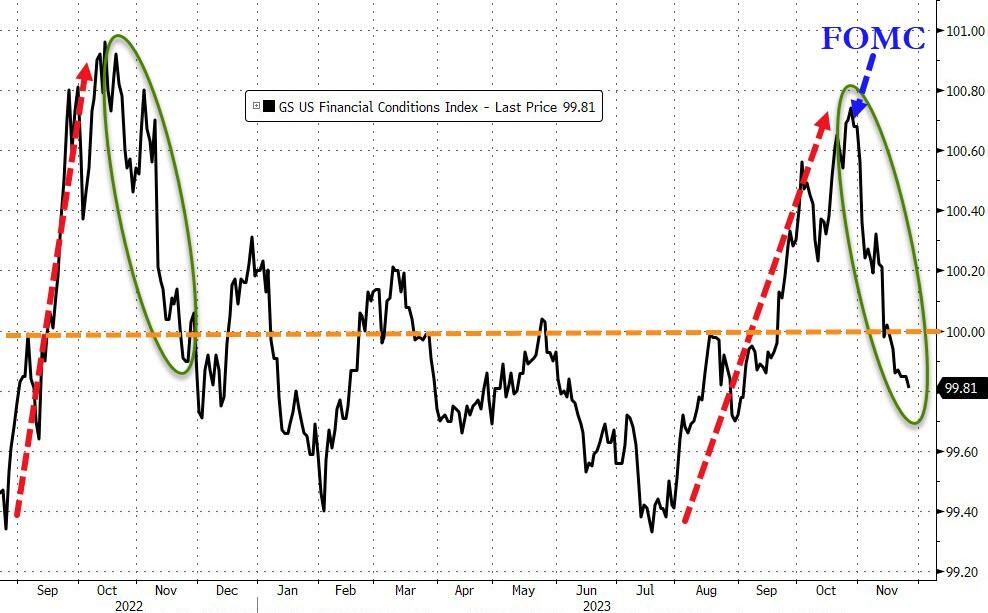

It’s also important to note that even with interest rates at 5.5%, monetary conditions aren’t tight. The Chicago Fed’s Financial Conditions Index confirms this. As of the end of Nov. 17, the index stood at -0.47. Any negative number indicates loose financial conditions. So, despite all of the tightening, the Fed is still running a slightly inflationary monetary policy.

Deutsche Bank projects the Fed will loosen policy even more next year, and yet we’re supposed to believe inflationary pressures will ease.

Second, while an economic downturn can dampen demand and cause some prices to drop, recessions come with their own inflationary pressures, especially when the Fed cuts rates. Those inflationary pressures come in the form of a weaker dollar.

Peter Schiff has pointed out that dollar strength helped do the Fed’s inflation-fighting work over the last year or so. As the dollar rose, commodity prices dropped, driving the CPI lower.

The gains that have been made with respect to measuring inflation have been because of the strong dollar. But here’s the problem; the minute the Fed claims victory, or even the markets think that the Fed is winning, even before the Fed actually declares ‘mission accomplished,’ the markets start trading down the dollar. The dollar starts to fall. As long as the markets think the Fed is winning, the dollar will keep falling. It was when they thought the Fed was losing that they wanted to buy dollars because that meant the Fed was going to fight harder and have to raise rates. But if the fight is over and the Fed has won, well, then there are no more rate hikes.”

Finally, the looming recession isn’t going to be “mild.” In fact, the much anticipated “soft landing” is impossible.

Schiff raises a key question: why do people think the Fed can raise rates from 0 to over 5% and get away without plunging the economy into a recession?

Why would that be if you look at the recent experiences with the Fed having rates too low and then raising them? Go back to the late 1990s and the decline we had in the economy, the recession, the stock market in 2000-2001. Look at the experience in 2008. And look at what happened even before COVID in 2018 when the Fed tried to raise rates from a low level and had to abort it very quickly when the wheels started falling off the bus in the fourth quarter of that year.”

History makes it clear that the Federal Reserve has a hard time normalizing rates. In fact, the attempt to bring rates from around 1% to just over 5% in 2007 led to the greatest recession since the Great Depression.

So, why would anyone believe that the Fed can normalize rates now and not have a similar consequence? Because, after all, the rate hikes expose all of the malinvestments and the misallocation of resources that take place when rates are artificially low.”

The Deutsche Bank forecast is less optimistic than most mainstream projections. Its economists at least recognize the looming recession on the horizon. And they are likely correct that the Fed will cut rates next year — or at whatever point this bubble economy pops. But they are wrong to think that the economic downturn will be short and mild, and that it will be deflationary. It will be the exact opposite. When the economy crashes, the Fed will cut interest rates – likely back to zero. And it will almost certainly go back to quantitative easing.

That’s inflation.

So, when you boil it all down, without realizing it, Deutsche Bank economists are projecting more inflation — not less.

In fact, they’re reading the recipe for stagflation.

end

end

2,c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens, John Rubino

3. CHRIS POWELL//GATA GOLD COMMENTARIES:

CHRIS POWELL…..

Chris is perfectly correct on this issue!

No, gold market manipulation didn’t end in 2008

Submitted by admin on Tue, 2023-11-28 16:40Section: Daily Dispatches

5:11p ET Tuesday, November 28, 2023

Dear Friend of GATA and Gold:

Gold advocate John Rubino writes this month that the gold market used to be manipulated by Wall Street traders “spoofing” the futures market, by commercial fabricators trying to trick hedge funds and other speculators in the futures market, and by Western central banks lending gold to bullion banks so they would sell it into the market to depress the price and thereby defend government currencies against competition from the monetary metal.

Only the latter manipulation has long-term impact, Rubino writes, and it ended in 2008 when other central banks turned from net sellers of gold to net buyers. If there is any manipulation left in the gold market, Rubino contends, it is now manipulation up:

https://rubino.substack.com/p/is-gold-a-manipulated-market

Rubino’s assertions leave much room for argument.

First, while particular “spoof” trades indeed may have impact for only a day or two, repeated “spoof” trades over a long period may largely set the entire tone of a market, demoralizing traders on the wrong side of the “spoofs.” The U.S. Justice Department would not have managed to fine JPMorganChase $920 million in 2020 for “spoofing” the gold and silver futures markets if that “spoofing” had only momentary impact.

The same with any trickery attempted by commercial fabricators in the gold market. One day’s trickery may work only for that day or the next, but the trickery of day after day for six months well might work much longer.

Second, while gold does seem to have regained adherents in central banking during the last decade and a half, even central banks may prefer to buy low and sell high. If, as suggested by some observers, like the U.S. economists Paul Brodsky and Lee Quaintance, for some years now central bank policy has been to acquire and redistribute gold among themselves in anticipation of devaluation of government currencies and debt and upward revaluation of the monetary metal —

https://www.gata.org/node/11373

— central banks wouldn’t want to overpay. They would want to control the timing of the revaluation, not share it with mere citizens of Planet Earth, and central banks often justify themselves as being necessary to maintain order in the foreign exchange markets, where gold can be a most inconvenient participant.

Since there is no comprehensive public record of all central bank trades in the gold market in recent decades, Rubino’s conclusion that market manipulation by the official sector ended in 2008 is just speculation.

What is fact is that surreptitious intervention in the gold market by central banks has continued from 2008 to the present day, as documented by GATA consultant Robert Lambourne’s calculation of the monthly volumes of gold swaps undertaken by the Bank for International Settlements, the central bank of all the major central banks and their gold broker.

Using the monthly statements of account from the BIS, Lambourne has shown that while the BIS’ gold swaps have trended largely down since 2020, reaching zero in December 2022, since then they have trended up again. The monthly levels of swaps are charted on the fourth page of the PDF illustration here:

Insofar as it is generally acknowledged that “paper gold,” unbacked gold derivatives being traded in the gold market, vastly outweighs the actual metal available in the market by as much as 100 to 1, the likelihood of a downward manipulation in gold would seem far greater than the likelihood of an upward manipulation.

So how does the gradually rising gold price of the last quarter century square with the price suppression policy of Western central banks? It’s really not so hard to understand. With a paper-to-real ratio of 92 to 1, a huge naked short position in the market, gold probably would have risen much faster if central banks were not striving to restrain it.

The economist, author, and Defense Department adviser James G. Rickards has explained it many times. He says Western central banks don’t mind a rising gold price so much; they just don’t want gold to rise so fast that it attracts much notice and starts making problems for their own currencies.

That’s why the biggest offense in central bank policy here isn’t gold price suppression but the general destruction of free markets and the cheating of market participants.

Yes, GATA’s purpose has been to press the issue of gold price suppression until markets are free and transparent. But we wouldn’t mind winning that struggle and turning to easier work — like proving the existence of UFOs, Bigfoot, or the Loch Ness Monster. Then our adversaries would be weaker and we’d get far more notice and respect from mainstream news organizations.

But even if UFOs, Bigfoot, and the Loch Ness Monster were proven to be as real as gold market manipulation, what difference would it make if the world remained subject to the tyranny of modern central banking?

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

4, OTHER IMPORTANT GOLD/SILVER COMMENTARIES/

5 a. IMPORTANT COMMENTARIES ON COMMODITIES:

END

5 B GLOBAL COMMODITY ISSUES/FOOD IN GENERAL//FREIGHT

END

6.CRYPTOCURRENCY//DIGITAL CURRENCY// COMMENTARIES/

end

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS WEDNESDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED UP AT 7.1277

OFFSHORE YUAN: UP TO 7.1373

SHANGHAI CLOSED DOWN 16.87 PTS OR 0.56%

HANG SENG CLOSED DOWN 360.70 PTS OR 2.08%

2. Nikkei closed DOWN 87,17PTS OR 0.26%

3. Europe stocks SO FAR: ALL GREEN

USA dollar INDEX UP TO 102.73 EURO FALLS TO 1.0984 DOWN 20 BASIS PTS

3b Japan 10 YR bond yield: FALLS TO. +.673 Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 147,66/JAPANESE YEN FALLING AS WELL AS LONG TERM 10 YR. YIELDS RISING //EVENTUALLY THIS WILL BREAK THE JAPANESE CENTRAL BANK

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen UP CHINESE ONSHORE YUAN: UP// OFFSHORE: UP

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and UP FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund DOWN TO +2.4455***/Italian 10 Yr bond yield DOWN to 4.189** /SPAIN 10 YR BOND YIELD DOWN TO 3.443…**

3i Greek 10 year bond yield DOWN TO 3.616

3j Gold at $2041.35 silver at: 24.96 1 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble UP 0 AND 93 /100 roubles/dollar; ROUBLE AT 88.50//

3m oil into the 77 dollar handle for WTI and 82 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 147,66// 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 0.673% STILL ON CENTRAL BANK (JAPAN) INTERVENTION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.8763 as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.9628 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.250 DOWN 4 BASIS PTS…

USA 30 YR BOND YIELD: 4.474 DOWN 5 BASIS PTS/

USA 2 YR BOND YIELD: 4.689 DOWN 5 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 28.92…(TURKEY SET TO BLOW UP FINANCIALLY)

GREAT BRITAIN/10 YEAR YIELD: DOWN 10 BASIS PTS AT 4.1595

end

2.a Overnight: Newsquawk and Zero hedge:

Futures, Treasuries Gain As Attention Turns To Timing Of Fed Rate Cuts

WEDNESDAY, NOV 29, 2023 – 08:23 AM

US equity futures, global markets and Treasuries extended their recent rallyall boosted by expectations that the Federal Reserve is not only done with hjking but will soon pivot and start cut rates early next year; in fact, according to Bill Ackman who has again flipflopped, the Fed will cut as soon as March (i.e., he is now long the same bonds he was so passionately shorting just a few months ago). This occurs as consumer confidence moved higher with holiday, retail sales numbers that illustrate a still strong consumer. As of 7:45am, US equity futures are up 0.4%, rising to the highest since Sept 1 and just shy of 2023 highs, while Nasdaq futures gained 0.6%; gold traded near record high, the dollar slide halted but is certainly not over, WTI oil futures rose 1.7% on the day, adding to Tuesday’s advance, while bitcoin traded just above $38K. The big question now is whether this rally can extend into December; the answer may be predicated on fundamentals rather than positioning/technicals. BBG reporting an uptick in corporate insider buying alongside stronger buyback activity. Today’s macro data focus includes 23Q3 GDP/Consumption/PCE, Beige Book, inventories, trade balance, and mtge applications.

In premarket trading, tech and small-caps are outperforming; megacap teach names are higher having added almost 14% MTD. General Motors jumped almost 6% in US premarket trading after announcing it will boost its dividend by 33% and implement a $10 billion share buyback program. Las Vegas Sands shares fell 5.6% as Miriam Adelson is selling $2 billion of stock in the casino company so the family can acquire a majority stake in the Dallas Mavericks NBA franchise from Mark Cuban. GameStop shares jump 12%, putting the stock on track to extend gains for a second consecutive session, ahead of its third-quarter results next week. Here are some other notable premarket movers:

- Airbnb shares slip 0.8% after Jefferies cut its recommendation on the short-term rental platform’s stock to hold from buy, citing a recent slowdown in bookings.

- CrowdStrike Holdings shares edged higher, rising 3.0%, after the security software company reported third-quarter results that beat expectations and raised its full-year revenue forecast.

- Fluence Energy shares jump 19% after the energy storage company’s results beat expectations, with analysts positive on its orders and prospects for 2024, especially against investors’ more sombre view on the renewables sector.

- NetApp shares jump 12% after the data storage company boosted its full-year adjusted earnings per share forecast above analyst expectations. Additionally, the company also reported second-quarter revenue that beat estimates. Analysts highlighted the traction in new products as well as strength in all-flash solutions.

- Okta shares fell 6.2% after the applications software company said it has found that hackers who had breached its network stole information on all users of its customer support system.

- Workday shares rise 8.92% after the application software company reported third-quarter results that beat expectations and raised its full-year forecast for subscription revenue.

- Foot Locker Inc surged as much as 13% after comparable sales beat the average analyst estimate.

The November stock party continues and the MSCI All Country World Index of stocks has gained 8.7% so far this month, the most since November 2020 amid a collapsing dollar (which however today paused a four-day retreat). It’s not just stocks that are soaring: in the latest rerun of the QE trade, bonds are climbing at the fastest monthly pace since 2008 as inflation continues to slow and Fed officials strike a dovish tone.

The latest leg higher for stocks and bonds came after the otherwise hawkish Fed Governor Christopher Waller suggested the central bank is well positioned to push inflation to a 2% target. And then overnight, Bill Ackman said he’s betting Fed cuts could come as soon as the first quarter, something we first said two weeks ago.

“The market is hanging on to everything Fed speakers say,” said Justin Onuekwusi, chief investment officer at UK wealth manager St James Place. “It was only the end of October when we were talking of 5% yields on US Treasuries. It does feel like the market is being a bit complacent.”

Now, traders are looking ahead to data on Thursday that include the Fed’s preferred measure of underlying inflation, the core PCE, as well as a speech by Fed Chair Jerome Powell at the end of the week that could offer clues on potential policy easing. “I would expect some pushback on market rate expectations,” said Marc Ostwald, chief economist & global strategist at ADM Investor Services Int. Ltd. “Inflation will have to drop sharply in the coming months, and the labor market will need to loosen a lot more to justify a rate cut in the first half of 2024.”

European stocks are in the green after posting back-to-back losses for the first time in three weeks. The Stoxx 600 is up 0.6%, led by gains in real estate, auto and technology shares. The autos and real estate sectors are the best performers, with many property shares getting a boost from a renewed decline in yields. The energy and insurance sectors are the worst performers. Philips slumps on a new apnea machine safety issue. Here are some of the biggest movers on Wednesday:

- Vestas shares rise as much as 4% after Berenberg lifts recommendation on Danish wind turbine producer to buy from hold, citing rising momentum in margins over the last two quarters.

- BMW shares rise as much as 3.6%, with JPMorgan lauding a well balanced growth strategy at the German automaker and upgrading it to overweight from neutral.

- Musti shares gain as much as 29%, the most since the pet care firm went public in 2020, after the company’s board recommended a voluntary public cash tender offer from a group of investors that values the outstanding equity at €868m.

- Harbour Energy shares rise as much as 5.1% and is among leading gainers on the Stoxx 600 energy index on Wednesday, after delivering a nine-month update that analysts describe as solid.

- Ferrovial shares gain as much as 3.2% after Spanish construction firm agreed to sell its stake in the parent company of Heathrow Airport to Ardian and Saudi Arabia’s Public Investment Fund for a total of $3 billion.

- Saipem shares gain as much as 3% after the engineering company got two offshore contracts in Guyana and Brazil worth approximately $1.9b.

- Philips falls as much as 7.7% after the Food and Drug Administration warned about a new safety issue involving the company’s DreamStation 2 machines used to treat obstructive sleep apnea.

- Halfords shares slide as much as 23%, the biggest intraday decline since Jan. 12, after the motoring and cycling products retailer reported interim results. RBC Capital Markets said pretax profit was below their expectations due to a softer showing in the company’s retail business, while Peel Hunt noted that the wider market was “not playing ball.”

- Aroundtown shares slump as much as 11%, its second slump this month, after third quarter results showed deleveraging remains a major issue at the German real estate firm, according to Morgan Stanley.

- Kindred shares fall as much as 9.7%, the most since January, after the Stockholm-listed online gambling operator reported third-quarter earnings weighed down by poor margins in its sports betting segment. The outcome of a strategic review is, however, seen as positive due to cost savings.

The MSCI Asia Pacific gauge fell 0.3% erasing earlier gains, even as the US 10-year yield dropped below the closely watched 100-day average, as gains in Australia were tempered by heavy losses in Chinese technology shares. Meituan was the biggest drag on the regional gauge after the Chinese firm warned that growth in its main meal delivery business would slow this quarter. A measure of technology stocks in Hong Kong also dropped to its lowest level in two weeks.

- Hang Seng and Shanghai Comp declined with underperformance in Hong Kong after the recent rises in domestic money market rates and with the PBoC’s open market operations resulting in a net daily drain.

- Nikkei 225 swung between gains and losses with early pressure from a firmer currency before the index rebounded off lows, while there were also comments from BoJ Adachi who stuck to the dovish script as he noted it is appropriate to patiently maintain easy policy and if needed, the BoJ will take additional easing steps.

- Australian stocks climbed after inflation cooled more-than-expected in October, bolstering the case for the Reserve Bank to resume pausing interest rates next week. New Zealand stocks also rose after its central bank kept rates unchanged.

- Indian stocks rallied, with the NSE Nifty 50 Index reclaiming the psychological 20,000 mark for the first time since dropping below it in September. The S&P BSE Sensex rose 1.1% to 66,901.91 at the 3:30 p.m. close in Mumbai, while the Nifty finished 1% higher at 20,096.60. The Nifty has logged similar or greater gains eight times in the past year. The gauge rose further the next day on six occasions, posting an average 0.4% gain, according to data compiled by Bloomberg. Wednesday’s gains were driven by automobiles and banks, which rose over 1.5% each. The laggards were media and realty, which ended in the red.

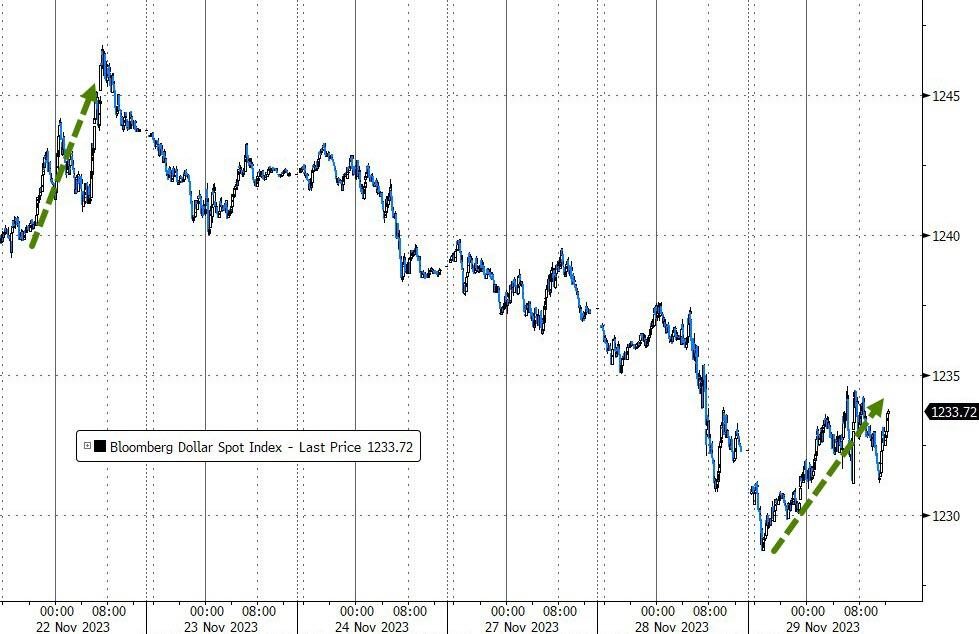

In FX, the Bloomberg Dollar Spot Index is unchanged after falling as much 0.2% to 1228,70, its lowest since early August amid growing bets that the Federal Reserve may start cutting interest rates next year, after two hawkish Fed officials signaled they could be comfortable holding rates steady for now. The kiwi is the best performer among the G-10’s, rising 0.2% versus the greenback after a hawkish hold from the RBNZ. The Aussie lags after CPI slowed in October. Oil prices advance, with WTI rising 1.4% to trade near $77.40. Spot gold falls 0.2%.

In rates, treasuries were richer by 4bps-5bps across the curve amid bigger gains in core European rates following bullish German state CPI readings ahead of the national print at 8am New York time. Two-year Treasury yields dropped four basis points to 4.69% after shedding 15 basis points Tuesday. Fed swaps are anticipating over 100 basis points of rate cuts by the end of 2024. Meanwhile, 10-year TSY yields are around 4.28%, richer by 4bp vs Tuesday close while trailing bunds and gilts in the sector by 1.5bp and 1bp on the day; new 2-year note auctioned Monday traded as rich as 4.664%, lowest for a current issue since mid-July and approaching 200-day moving average. Swaps market looks for deeper rate cuts next year, with May contracts priced for 23bp of cuts, or 92% chance of a 25bp move. German bonds rallied for a third day, the longest stretch in a month, after regional and state inflation data showed that inflation continued to slow. German 10-year yields fall 4bps to 2.45%.

“Attention will now move to Chair Powell’s speech on Friday to see if the tone points to a clear pivot towards easing,” Daragh Maher, head of FX strategy for the US at HSBC, wrote in a research note. “If it materializes, this would clearly be a challenge to our bullish US dollar view”

In commodities, oil climbed for a second day as traders awaited a high-stakes OPEC+ meeting on supply. WTI rose 1.4% to trade near $77.40. Gold extended gains to its highest level since May, also buoyed by hopes of a Fed policy shift.

To the day ahead now, and data releases include the preliminary German CPI reading for November, UK mortgage approvals for October, and in the US there’s the second estimate of Q3’s GDP (median est. 5% vs 4.9% initial). From central banks, we’ll hear from BoE Governor Bailey, Cleveland Fed President Mester, and the Fed will be releasing their Beige Book.

Market Snapshot

- S&P 500 futures up 0.3% to 4,576.75

- STOXX Europe 600 up 0.5% to 459.11

- MXAP down 0.3% to 161.59

- MXAPJ down 0.3% to 504.05

- Nikkei down 0.3% to 33,321.22

- Topix down 0.5% to 2,364.50

- Hang Seng Index down 2.1% to 16,993.44

- Shanghai Composite down 0.6% to 3,021.69

- Sensex up 1.1% to 66,881.45

- Australia S&P/ASX 200 up 0.3% to 7,035.35

- Kospi little changed at 2,519.81

- German 10Y yield little changed at 2.47%

- Euro down 0.1% to $1.0979

- Brent Futures up 0.4% to $82.01/bbl

- Gold spot down 0.3% to $2,035.68

- U.S. Dollar Index up 0.11% to 102.86

Top Overnight News

- Jack Ma has urged Alibaba to “change and reform” as the ecommerce giant he founded tries to find a new path after abandoning parts of its ambitious restructuring plan and its main Chinese rival gains ground. FT

- Australia’s inflation cools, with the CPI rising 4.9% in Oct (down from +5.6% in Sept and below the Street’s +5.2% forecast). BBG

- Spanish inflation unexpectedly eased, retreating for the first time since June thanks to drops in the costs of fuel and tourism. Consumer prices rose 3.2% from a year earlier in November, data Wednesday showed. That compares with 3.5% the previous month and defied the median estimate in a Bloomberg survey of economists for an acceleration to 3.7%. BBG

- German regional inflation cools in Nov, including Baden Wuerttemberg +3.4% (down from +4.4% in Oct), Bavaria +2.8% (down from +3.7% in Oct), Brandenburg +4.1% (down from +4.6% in Oct), Hesse +2.9% (down from +3.6% in Oct), North Rhine Westphalia +3% (down from +3.1% in Oct), and Saxony +3.9% (down from +4.5% in Oct). BBG

- Russian President Vladimir Putin will not make peace in Ukraine before he knows the results of the November 2024 U.S. election, a senior U.S. State Department official said on Tuesday, amid concerns that a potential victory for former President Donald Trump could upend Western support for Kyiv. RTRS

- Bill Ackman is betting the Federal Reserve will begin cutting interest rates sooner than markets are predicting. The Pershing Square Capital Management founder said such a move could happen as soon as the first quarter. Traders are fully pricing in a rate cut in June, with the chance of a cut happening in May priced at about 80%, according to swaps market data. BBG

- WDAY shares rose more than 8% premarket after the cloud enterprise company raised its outlook for the year and reported higher-than-expected revenue in the third quarter. WSJ

- OpenAI’s revamped board of directors doesn’t plan to include representatives from outside investors, according to a person familiar with the situation. It’s a sign that the board will prioritize safety practices ahead of investor returns. The Information

- The head of Amazon’s cloud division has used recent turmoil at OpenAI to launch a thinly veiled attack on Microsoft, the artificial intelligence company’s biggest investor. “Things are moving so fast [in AI] and in that type of environment the ability to adapt is the most valuable capability that you can have,” Selipsky, AWS chief executive, said at its annual developer conference in Las Vegas on Tuesday. “You don’t want a cloud provider that’s beholden primarily to one model provider, you need a real choice . . . The events of the past 10 days have made that very clear.” FT

A more detailed look at global markets courtesy of Newsquawk

APAC stocks were mixed after the choppy performance on Wall St where stocks wavered, Treasuries rallied and the Dollar dipped on dovish Fed rhetoric, while the region also digested the RBNZ’s hawkish hold where it kept rates unchanged but signalled risks of a hike. ASX 200 was positive with the index helped by encouraging data including better-than-expected Construction Work Done which feeds into next week’s GDP release and after softer monthly CPI all but guaranteed a pause at the December RBA meeting. Nikkei 225 swung between gains and losses with early pressure from a firmer currency before the index rebounded off lows, while there were also comments from BoJ Adachi who stuck to the dovish script as he noted it is appropriate to patiently maintain easy policy and if needed, the BoJ will take additional easing steps. Hang Seng and Shanghai Comp declined with underperformance in Hong Kong after the recent rises in domestic money market rates and with the PBoC’s open market operations resulting in a net daily drain.

Top Asian News

- China’s Vice Foreign Minister recently met with the EU’s external action service deputy secretary and said that China is ready to strengthen communication and coordination with the EU side and make preparations for a China-EU summit before the end of the year. Furthermore, it was stated that the two sides need to grasp the general direction of China-EU relations, uphold mutually beneficial and win-win cooperation, as well as fully respect each other’s core interests, according to Reuters.

- Japan’s Finance Ministry will raise the assumed interest rate paid on bonds in the government’s annual budget proposal for the first time in 17 years in fiscal 2024, reflecting policy shifts by the BoJ that have allowed yields to rise, according to Nikkei.

- BoJ Board Member Adachi said Japan is yet to see a positive wage-inflation cycle become embedded enough and it is appropriate to patiently maintain easy policy. Adachi also stated that if needed, the BoJ will take additional easing steps, while he added that the steps the BoJ took in October to make YCC more flexible are not aimed at laying the groundwork for policy normalisation.

- RBNZ kept the OCR unchanged at 5.50% as expected, while it reiterated that interest rates will need to remain at a restrictive level for a sustained period of time and interest rates are restricting spending in the economy with consumer price inflation declining as is necessary to meet the committee’s remit. RBNZ said inflation remains too high and the committee remains wary of ongoing inflationary pressures, as well as noted that demand growth has eased but by less than anticipated and if inflationary pressures were to be stronger than anticipated, the OCR would likely need to increase further. Furthermore, the committee is confident the current OCR level is restricting demand but slightly raised OCR and CPI forecasts with the OCR seen at 5.63% in March 2024 (prev. 5.58%), 5.66% in December 2024 (prev. 5.50%), and 5.56% (prev. 5.36%) in March 2025, while annual CPI is seen at 2.5% by December 2024 (prev. 2.4%).

- RBNZ Governor Orr said in the press conference that they’ve been adamant on holding rates through next year and noted that the projection shows upward bias to rates but it is not a done deal. Orr also stated the risk to inflation is still more to the upside, while he is nervous that inflation has been outside the band for so long and concerned that longer-term inflation expectations are creeping up.

- REUTERS POLL: Chinese New Home Prices Growth expects at +3.0% Y/Y 2023 (vs 0% in August poll); 1.1% Y/Y in 2024 (1.0% in August poll)

European equities, Euro Stoxx 50 +0.6% are extending gains, but with clear underperformance in the FTSE100 -0.2%, albeit the UK index is off lows. European sectors have a strong positive tilt; featuring strength in Autos & Parts whilst Energy lags but with both sectors underpinned by broker moves. US Futures are trading on the front foot, NQ & ES +0.4%, with clear outperformance in the RTY +0.8% as it pares back yesterday’s losses.

Top European News

- The number of businesses set up in the UK in 2022 fell by 7% to 337k as UK business creation was hit by high borrowing costs and weaker demand, according to analysis by FT citing data released last week by the Office of National Statistics.

- Several ECB regulators are reportedly planning to push to ease bank payout stance, according to Bloomberg

- ECB’s Stournaras says ECB April cut bets seem a bit optimistic, via Politico; says the first rate cut could come in the middle of 2024. Early PEPP winddown risks hurting ECB credibility

- OECD raises 2023 US growth forecast to 2.4% (prev. 2.2%), 1.5% in 2024 (prev. 1.3%), sees 1.7% 2025; Sees Chinese growth 5.2% (prev. 5.1%), 4.7% (prev. 4.6%), 4.2% in 2025; Raises UK growth forecast to 0.5% (prev. 0.3%), trims 2024 0.7% (prev. 0.8%), 1.2% in 2025.

FX

- DXY finds underlying bids just shy of 102.50 and aims for 103.00

- Kiwi outperforms after hawkish RBNZ hold and Aussie caught in AUD/NZD cross-fire with added downside pressure from soft inflation data

- NZD/USD elevated within 0.6208-0.6134 range, AUD/USD depressed between 0.6676-20 parameters

- Euro undermined by weaker than forecast German state and Spanish CPI metrics. EUR/USD sub-1.1000, but holding near decent option expiry interest and former Fib resistance/breakout area

- Yen retreats towards 148.00 from circa 146.68 after dovish guidance from BoJ’s Adachi

- PBoC set USD/CNY mid-point at 7.1031 vs exp. 7.1340 (prev. 7.1132).

Fixed Income

- Bonds still well bid, but off new m-t-d highs

- Bunds hold comfortably above 132.00 within 132.72-131.95 range

- Gilts midway between 97.31-96.91 bounds and T-note a tad closer to 109-29 trough vs 110-14+ peak ahead of revised US Q3 GDP, Fed’s Mester and Beige Book

- UK and German issuance less well covered after lack of concession

- UK sells GBP 4.25bln 3.5% 2025 Gilt: b/c 2.36x (prev. 2.61x), average yield 4.554% (prev. 4.964%) & tail 2.0bps (prev. 1.1bps)

- Italy sells EUR 6.5bln vs exp. EUR 5.5-6.5bln 4.10% 2029, 4.20% 2034 BTP & 0.75-1bln 2026 CCTeu: 4.10% 2029: b/c 1.45x (prev. 1.45x) & gross yield 3.61% (prev. 4.12%). 4.20% 2034: b/c 1.45x (prev. 1.33x) & gross yield 4.17% (prev. 4.76%). 2026 CCTeu: b/c 1.99x (prev. 2.0x) & gross yield 4.43% (prev. 4.12%)

- Germany sells EUR 2.82bln vs exp. EUR 3.5bln 2.60% 2033: b/c 1.74x (prev. 2.55x), average yield 2.45% (prev. 2.64%) & retention 19.4% (prev. 17.40%)

Commodities

- WTI and Brent, +1.3%, extend gains with the complex initially boosted by the recent weaker Dollar, and as the clock ticks down to the OPEC+ meeting tomorrow; though, the USD has since bounced but crude remains underpinned nonetheless.

- Spot gold briefly topped USD 2050/oz overnight to levels last seen in May, whilst base metals are flat/mixed taking a breather from yesterday’s Dollar-induced gains as the index lifts back towards 103.00.

- Strike at Las Bambas copper mine in Peru is limited to 48 hours after the labour authority declared the protest inappropriate.

- First Quantum (FM CA) said the Cobre Panama Mine suspended commercial production and is applying a programme of preservation and safe maintenance after the recent court ruling that its contract was unconstitutional.

- OPEC+ talks are ongoing continuing no fresh delays currently expected to tomorrow’s meeting, according to Reuters sources

Geopolitics: Israel-Hamas

- Israeli negotiators are offering Hamas a further three days of ceasefire through to Sunday morning if the group releases all the remaining women and children they believe it is holding, according to sources close to talks in Qatar cited by The Times.

- G7 Foreign Ministers’ joint statement on Israel and Gaza stated that they welcome the release of hostages and the pause in hostilities, while they support a further extension of the pause and future pauses as needed.

- White House’s Kirby said they hope to see more Americans released by Hamas and will work to see if they can extend the pause.

- US paused drone flights over Gaza as part of the truce between Israel and Hamas, according to a Pentagon spokesperson.

- Source close to Hamas says group willing to extend truce by four more days, according to AFP.

- “Israeli vehicles fire their weapons at different areas northwest of Gaza City”, according to Al Arabiya.

Geopolitics: NATO

- US State Department senior official said Turkey’s Foreign Minister told NATO he is working on the ratification of Sweden and gave the likely timeline of a ‘few weeks’.

- Swedish Foreign Minister says Turkey’s Foreign Minister said that ratification for Sweden’s accession to NATO could occur within weeks

US Event Calendar

- 07:00: Nov. MBA Mortgage Applications, prior 3.0%

- 08:30: 3Q Core PCE Price Index QoQ, est. 2.4%, prior 2.4%

- 08:30: 3Q GDP Price Index, est. 3.5%, prior 3.5%

- 08:30: 3Q Personal Consumption, est. 4.0%, prior 4.0%

- 08:30: Oct. Retail Inventories MoM, est. 0.6%, prior 0.9%

- 08:30: Oct. Advance Goods Trade Balance, est. -$86.5b, prior -$85.8b, revised -$86.8b

- 08:30: Oct. Wholesale Inventories MoM, est. 0.2%, prior 0.2%

- 08:30: 3Q GDP Annualized QoQ, est. 5.0%, prior 4.9%

- 14:00: Federal Reserve Releases Beige Book

Central Bank speakers

- 13:45: Fed’s Mester Speaks on Financial Stability

DB’s Jim Reid concludes the overnight wrap

As I fly over what are snowy Alpine peaks at the moment, the main highlight over the last 24 hours has been a further dovish pivot for rates with central bank speakers really impacting the market with 2yr Treasury yields leading the charge and down -11.8bps to a 4 month low and down another -4bps overnight. The next hurdles for markets are today’s German CPI and the second reading of US Q3 GDP.