DEC 1/2023//LIKE CLOCKWORK GOLD GOES UP POST FIRST DAY NOTICE: GOLD RISES BY A HUGE $32.05 TO $2069.30 //SILVER ROSE BY $.15 TO $25.41/PLATINUM WAS DOWN $ 3.00 TO $X933.00 WHILE PALLADIUM WAS DOWN $14.00 TO $1002.65//TODAY’S IMPORTANT PODCAST FROM ANDREW MAGUIRE AND IT IS A MUST SEE//ISRAEL VS HAMAS: HAMAS REFUSES TO GIVE THE NEXT LIST OF 10 ABDUCTEES AND THUS ISRAEL RE STARTED THE WAR//ISRAEL TAKES OUT TERROR CELL IN LEBANON//NO MORE AID WILL BE ALLOWED TO COME IN THROUGH EGYPT//CHINESE STOCKS TUMBLE AND THIS FORCES CHINESE AUTHORITIES TO BUY EFT’S TO STIMULATE THEIR ECONOMY//COVID//VACCINE INJURIES REPORT//BIG STORY PFIZER SUED BY TEXAS AS THE STORY IS NOW OUT AS TO THE HUGE DAMAGE THE VACCINE IS CAUSING//DR PAUL ALEXANDER//SLAY NEWS/NEWS ADDICTS//USA ECONOMIC DATA:MFG DATA RELEASED SUGGESTS STAGLATION//GOOD COMMENTARY FROM VICTOR DAVIS HANSON//SWAMP STORIES FOR YOU TONIGHT//

118 C MACQUARIE FUT 45 159 C MAREX CAPITAL M 18 167 C MAREX 8 190 H BMO CAPITAL 104 357 C WEDBUSH 1 363 H WELLS FARGO SEC 91 365 C MAREX CAPITAL M 1 435 H SCOTIA CAPITAL 13 624 C BOFA SECURITIES 256 624 H BOFA SECURITIES 133 661 C JP MORGAN 264 879 686 C STONEX FINANCIA 12 1 690 C ABN AMRO 2 700 C UBS 36 732 C RBC CAP MARKETS 66 737 C ADVANTAGE 39 9 880 C CITIGROUP 764 905 C ADM 4 1 972 C IRONBEAM INC 1

TOTAL: 1,374 1,374 MONTH TO DATE: 11,220

JPMorgan stopped 879/1374 contracts.

FOR DEC.:

GOLD: NUMBER OF NOTICES FILED FOR DEC/2023. CONTRACT: 1374 NOTICES FOR 137,400 OZ or 4.2737 TONNES

total notices so far: 11,220 contracts for 1,122,000 oz (34.898 tonnes)

FOR DEC:

SILVER NOTICES 159 NOTICE(S) FILED FOR 795,000 OZ/

total number of notices filed so far this month : 1668 for 8,340,000 oz

XXXXXXXXXXXXXXXXXX Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

BOTH GLD AND SLV ARE FRAUDULENT VEHICLES

GLD

WITH GOLD UP $32.05//

INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD/ : / HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.02 TONNES OF GOLD FROM THE GLD

SOMEBODY RAIDED THE COOKIE JAR!

INVENTORY RESTS AT 876.51 TONNES

SLV//

WITH NO SILVER AROUND AND SILVER UP 15 CENTS AT THE SLV// HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A SHOCKER:A MASSIVE 1.923 MILLION OZ WITHDRAWAL DESPITE THE HUGE RUNNUP IN PRICES.

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV.

CLOSING INVENTORY: 434.128 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A GIGANTIC SIZED 1485 CONTRACTS TO 142,849 AND FURTHER FROM THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THIS HUGE SIZED LOSS IN COMEX OI WAS ACCOMPLISHED DESPITE OUR $0.20 GAIN IN SILVER PRICING AT THE COMEX ON THURSDAY. WE HAD A SOME SPEC SHORT COVERING EPISODE IN THURSDAY’S COMEX TRADING BUT THE BULK OF THE LOSS IN OI WAS DUE TO SPREADER AND T.A.S.LIQUIDATION . TAS ISSUANCE WAS A MONSTROUS SIZED 1720 CONTRACTS. THESE WILL BE USED FOR MANIPULATION LATER THIS MONTH/AS WELL AS TODAY.

CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON THURSDAY NIGHT: 1720 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS. IT THUS LOOKS LIKE THE FED (GOV’T) IS BEHIND ALL OF THESE TRADES.

WE HAVE NOW SET ANOTHER RECORD LOW AT 114,102 CONTRACTS ///JULY 3.2023// OUR BANKERS WITH THE HELP OF SPECULATORS AND HIGH FREQUENCY TRADERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.20), AND WERE UNSUCCESSFUL IN KNOCKING ANY SILVER LONGS AS WE HAD A HUGE SIZED LOSS OF 1035 OI CONTRACTS ON OUR TWO EXCHANGES WITH ALL OF THAT LOSS IN OI DUE TO SPREADER FINALIZATION AND T.A.S LIQUIDATION

WE MUST HAVE HAD:

A GOOD SIZED 450 ISSUANCE OF EXCHANGE FOR PHYSICALS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 18.755 MILLION OZ (FIRST DAY NOTICE) FOLLOWED BY TODAY’S STRONG 250,000 OZ QUEUE JUMP//NEW TOTAL STANDING 19.110 MILLION OZ.

//NEW STANDING FOR SILVER IS THUS 19.110 MILLION OZ

//HUGE SIZED COMEX OI LOSS/ GOOD SIZED EFP ISSUANCE/VI) HUMONGOUS SIZED NUMBER OF T.A.S. CONTRACT ISSUANCE 1720 CONTRACTS)/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL – REMOVED 155 CONTRACTS (the cme will no longer provide preliminary no to be except through a paywall)

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS DEC. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF DEC:

TOTAL CONTRACTS for 1 days, total 450 contracts: OR 2.250 MILLION OZ (450 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 2.250 MILLION OZ

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH 2022: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 118.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 85.745 MILLION OZ (SMALLER THAN LAST MONTH)

AUGUST: 171.43 MILLION OZ (THIS MONTH IS GOING TO BE HUGE //2ND HIGHEST ON RECORD

SEPT: 72.705 MILLION OZ (SMALLER THIS MONTH)

OCT: 97.455 MILLION OZ

NOV. 50.050 MILLION OZ

DEC. 2.25 MILLION OZ

RESULT: WE HAD A HUGE SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 1485CONTRACTS DESPITE OUR GAIN IN PRICE OF $0.20 IN SILVER PRICING AT THE COMEX//THURSDAY.,. THE CME NOTIFIED US THAT WE HAD A GOOD EFP ISSUANCE CONTRACTS: 450 ISSUED FOR FEB AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS. WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR DEC. OF 18.755 MILLION OZ FOLLOWED BY TODAY’S 250,000 OZ QUEUE JUMP//NEW TOTAL STANDING 19.110 MILLION OZ//

NEW STANDING 19.110 OZ /// WE HAVE A HUGE SIZED LOSS OF 1035OI CONTRACTS ON THE TWO EXCHANGES. THE TOTAL OF TAS INITIATED CONTRACTS TODAY: A HUMONGOUS SIZED 1720CONTRACTS//HUGE FRONT END OF THE TAS CONTRACTS WERE LIQUIDATED ALONG WITH SPREADERS DURING THE THURSDAY COMEX SESSION. THE NEW TAS ISSUANCE THURSDAY NIGHT (1720) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE., .

WE HAD 159 NOTICE(S) FILED TODAY FOR 795,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A STRONG SIZED 9600 CONTRACTS TO 499,616 AND CLOSER TO THE RECORD (SET JAN 24/2020) AT 799733 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: – REMOVED 931 CONTRACTS

WE HAD A STRONG SIZED DECREASE IN COMEX OI ( 9600 CONTRACTS) WITH OUR $8.70 LOSS IN PRICE//THURSDAY. WE ALSO HAD A RATHER LIGHT INITIAL STANDING IN GOLD TONNAGE FOR DEC.. AT 44.914 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S 76500 OZ E.F.P. JUMP TO LONDON/ // TOTAL GOLD STANDING FOR DEC SO FAR LOWERS TO 42.5972 TONNES // ALL OF..THIS HAPPENED WITH OUR $8.70 LOSS IN PRICE WITH RESPECT TO THURSDAY’S TRADING. WE HAD A GOOD SIZED LOSS OF 5607OI CONTRACTS (17.44)PAPER TONNES) ON OUR TWO EXCHANGES.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 3993CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 499,616

IN ESSENCE WE HAVE A GOOD SIZED DECREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 4676 CONTRACTS WITH 8669 CONTRACTS DECREASED AT THE COMEX// AND A STRONG SIZED 3993EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI LOSS ON THE TWO EXCHANGES OF 5607 CONTRACTS OR 17,446 TONNES. WE HAD 0 CONTRACT EXCHANGE FOR RISK FOR 0 TONNES. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): A HUGE 4188 CONTRACTS.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A STRONG SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (3993 CONTRACTS) ACCOMPANYING THE STRONG SIZED LOSS IN COMEX OI (8669) //TOTAL LOSS FOR OUR THE TWO EXCHANGES: 5607 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR FORMER FORMAT OF BANKERS GOING LONG AND SPECULATORS GOING SHORT ,2.) FAIR INITIAL STANDING AT THE GOLD COMEX FOR DEC. AT 44.914 TONNES FOLLOWED BY TODAY’S 76,500 OZ E.F.P TO LONDON//NEW STANDING 42.5972 TONNES / / 3) ZERO LONG LIQUIDATION AND HUGE TAS LIQUIDATION AND SPREADER LIQUIDATION 4) STRONG SIZED COMEX OPEN INTEREST LOSS/ 5) STRONG ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER///6: HUGE T.A.S. ISSUANCE: 4676 CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023 INCLUDING TODAY

DEC

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF DEC. :

TOTAL EFP CONTRACTS ISSUED: 3993 CONTRACTS OR 399,300 OZ OR 12.419 TONNES IN 1 TRADING DAY(S) AND THUS AVERAGING: 3993 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 1 TRADING DAY(S) IN TONNES 12.419 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2022, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 12.419/3550 x 100% TONNES 6.73% OF GLOBAL ANNUAL PRODUCTION

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH/2022: 409.30 TONNES //FINAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 151.69 TONNES (WEAKER THAN LAST MONTH)

AUGUST: 195.28 TONNES (A STRONGER MONTH)//FINAL

SEPT: 254.709 TONNES (WILL BE LARGER THAN LAST MONTH AND A STRONG MONTH)

OCT. 248.09 TONNES. LIKE SILVER, THIS MONTH IS GOING TO BE A STRONG E.F.P. ISSUANCE.

NOV. 239.16 TONNES//WILL BE STRONG THIS MONTH,

DEC. 12.419 TONNES

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF SEPT. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF DEC., FOR BOTH GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (SEPT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER FELL BY A HUGE SIZED 1485CONTRACTS OI TO 142,847 AND FURTHER FROM OUR COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 450 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

DEC 450 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 450 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 1487 CONTRACTS AND ADD TO THE 450 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A HUGE SIZED LOSS OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 1035 CONTRACTS

THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES TOTAL 5.175 MILLION OZ

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS//

FRIDAY MORNING/THURSDAY NIGHT

SHANGHAI CLOSED UP 1.96 PTS OR 0.06% //Hang Seng CLOSED UP 212.56 PTS OR 1.25% /The Nikkei CLOSED DOWN 55.36 PTS OR 0.17% //Australia’s all ordinaries CLOSED DOWN 0.17 % /Chinese yuan (ONSHORE) closed DOWN AT 7.1430 /OFFSHORE CHINESE YUAN CLOSED DOWN TO 7.1549 /Oil DOWN TO 75.78 dollars per barrel for WTI and BRENT DOWN AT 80.65/ Stocks in Europe OPENED ALL GREEN// ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A STRONG SIZED 9600 CONTRACTS TO 498,685 WITH OUR LOSS IN PRICE OF $8.70 WITH RESPECT TO THURSDAY TRADING. WE MUST HAVE SOME SPEC SHORT COVERINGS BUT MOST OF THE LOSS IN OI WAS DUE TO SPREADER LIQUIDATION AND T.A.S. LIQUIDATION.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE ACTIVE DELIVERY MONTH OF DEC..… THE CME REPORTS THAT THE BANKERS ISSUED A STRONG SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 3993 EFP CONTRACTS WERE ISSUED: : FEB 3993 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 3993CONTRACTS

ON A NET BASIS IN OPEN INTEREST WE LOST THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A STRONG SIZED TOTAL OF 5607 CONTRACTS IN THAT 3993LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A STRONG SIZED LOSS OF 9,600 COMEX CONTRACTS..AND THIS LOSS ON OUR TWO EXCHANGES HAPPENED WITH OUR LOSS IN PRICE OF $8.70//THURSDAY COMEX. AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS DURING MID MONTH IN THE DELIVERY CYCLE), THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR THURSDAY NIGHT WAS A HUGE SIZED 4188 CONTRACTS. THROUGHOUT THE PAST SEVERAL WEEKS, THE BANKERS SOLD OFF THE LONG SIDE OF THE SPREAD WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR SPREAD WHICH WILL BE LIQUIDATED TWO MONTHS HENCE)//. THE HUGE LOSS IN COMEX OI TONIGHT WAS DUE TO FINALIZATION OF SPREADER AND ALSO T.A.S. LIQUIDATION!

// WE HAVE A LIGHT AMOUNT OF GOLD TONNAGE STANDING: DEC (42.5972 TONNES ( ACTIVE MONTH)

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

THE SPECS/HFT WERE SUCCESSFUL IN LOWERING GOLD’S PRICE( IT LOST $8.70) //// BUT WERE UNSUCCESSFUL IN KNOCKING ANY SPECULATOR LONGS AS WE HAD A STRONG SIZED LOSS OF5607 TOTAL CONTRACTS ON OUR TWO EXCHANGES. WE HAD A HUGE T.A.S. LIQUIDATION ON THE FRONT END OF THURSDAY’S TRADING ALONG WITH SPREADER LIQUIDATION. THE T.A.S. ISSUED ON THURSDAY NIGHT, WILL BE “PUT INTO THE BANK” TO BE USED AT A LATER DATE AT THE COLLUSIVE CHOOSING OF OUR BANKERS. WE ALSO EXPERIENCED SOME SPECULATOR SHORT COVERING

WE HAVE LOST A TOTAL OI OF 17,446 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR DEC. (44.914 TONNES) ON FIRST DAY NOTICE, FOLLOWED BY TODAY’S HUGE 765 CONTRACT E.F.P TO LONDON FOR 76,500 OZ//NEW TOTAL STANDING FALLS TO 42.5972 TONNES../ ALL OF THIS WAS ACCOMPLISHED WITH OUR LOSS IN PRICE TO THE TUNE OF $8.70.

WE HAD REMOVED –931 CONTRACTS TO THE COMEX TRADES TO OPEN INTEREST (CROOKS)

NET LOSS ON THE TWO EXCHANGES 5607 CONTRACTS OR 560,700 OZ OR 17.446 TONNES.

Total monthly oz gold served (contracts) so far this month

11,220 notices 1,122,000 oz 34.898 TONNES

Total accumulative withdrawals of gold from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of gold from the Customer inventory this month

x

0 dealer deposit:

total dealer deposits: nil oz

customer deposits: 0

total customer deposits: nil oz

we had 0 customer withdrawals

total withdrawals 0 oz

Adjustments; 0

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR DEC.

For the front month of DECEMBER we have an oi of 3849 contracts having LOST 10,611 contracts. .We had 9846

contracts served upon Thursday, so we lost 765 or an additional 76,500 oz (2.37 tonnes) as is there customer, they were

immediately E.F.P’d to London where they could take delivery on a T + 2 basis instead of waiting for metal over here.

JAN. lost 113 contracts FALLING TO 3366 contracts.

FEB GAINED 797 CONTRACTS RISING TO 411,440.

We had 1374 contracts filed for today representing 137,400 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 264 notices were issued from their client or customer account. The total of all issuance by all participants equate to 1374 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 879 notice(s) was (were) stopped ( received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the DEC. /2023. contract month, we take the total number of notices filed so far for the month (11,220 x 100 oz ), to which we add the difference between the open interest for the front month of DEC. (3849 CONTRACTS) minus the number of notices served upon today 1374 x 100 oz per contract equals 1,369,500 OZ OR 42.5972 TONNES

thus the INITIAL standings for gold for the DEC.contract month: No of notices filed so far (11,220) x 100 oz + (3849) {OI for the front month} minus the number of notices served upon today (1374) x 100 oz) which equals 1,369,500 oz standing OR 42.5972 TONNES

TOTAL COMEX GOLD STANDING FOR DEC: 42.5972 TONNES WHICH IS LIGHT FOR THE BIGGEST ACTIVE DELIVERY MONTH IN THE CALENDAR. THEY PROBABLY KNOW THAT NO REAL GOLD IS PRESENT AT THE COMEX.

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD: 19,937,493.603 OZ

TOTAL REGISTERED GOLD 10,163,133.467 (316,11 tonnes).

TOTAL OF ALL ELIGIBLE GOLD: 9,834,360.136 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 8,603,784 (REG GOLD- PLEDGED GOLD) 267,61

END

SILVER/COMEX

DEC 1

//2023// THE DEC 2023 SILVER CONTRACT

Silver

Ounces

Withdrawals from Dealers Inventory

NIL oz

Withdrawals from Customer Inventory

795,303.130 oz

Brinks Delaware

.

Deposits to the Dealer Inventory

603,134.04 oz ASAHI

Deposits to the Customer Inventory

1,081,409.300 oz CNT

No of oz served today (contracts)

159 CONTRACT(S) (795,000 OZ)

No of oz to be served (notices)

2154 contracts (10,770,000 oz)

Total monthly oz silver served (contracts)

1668 Contracts (8,340,000 oz)

Total accumulative withdrawal of silver from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of silver from the Customer inventory this month

i) 1 dealer deposit

i)Into ASAHI 603,134.04 oz

total dealer deposit: 603,134.04 oz

i) We had 0 dealer withdrawal

total dealer withdrawals: 0 oz

We had 1 deposits customer account:

i) Into CNT: 1,081,409.380 oz

total customer deposit 1,081,409.380 oz

JPMorgan has a total silver weight: 134.441 million oz/267,080 million or 50.33%

Comex withdrawals 1

we had 1 customer withdrawals

i) Out of Brinks 791,298.400 oz

ii) Out of Delaware: 4004.77

total withdrawals 795.308.13 oz

adjustments: 1

Delaware dealer to customer; 4963.280 oz

TOTAL REGISTERED SILVER: 42.888 MILLION OZ//.TOTAL REG + ELIGIBLE. 267,080 million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR DECEMBER:

silver open interest data:

FRONT MONTH OF DEC /2023 OI: 2313 CONTRACTS HAVING LOST 1459 CONTRACT(S).

WE HAD 1509 CONTRACTS SERVED ON THURSDAY, SO WE GAINED 50 CONTRACTS OR 250,000 OZ WERE

QUEUE JUMPED IN ORDER TO RECEIVE SILVER OVER HERE.

JAN GAINED 37 CONTRACTS UP TO 1854 CONTRACTS

FEB GAINED ITS INITIAL 14 CONTRACTS TO STAND AT 14

MARCH LOST 314 CONTRACTS TO 123,500 .

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 159 for 795,000 oz

Comex volumes// est. volume today 69,171,// poor

Comex volume: confirmed yesterday 54,952 poor

To calculate the number of silver ounces that will stand for delivery in DEC. we take the total number of notices filed for the month so far at 1668 x 5,000 oz = 8,340,000 oz

to which we add the difference between the open interest for the front month of DEC. (3849) and the number of notices served upon today 159 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the DEC/2023 contract month: 1668 (notices served so far) x 5000 oz + OI for the front month of DEC. (3849) – number of notices served upon today (159 )x 500 oz of silver standing for the DEC contract month equates to 19.110 MILLION OZ

There are 42.290 million oz of registered silver.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS//

BOTH GLD AND SLV ARE MASSIVE FRAUDS!

DEC 1/WITH GOLD UP $32.05 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.02 TONNES OF GOLD FROM THE GLD. // / / // // INVENTORY RESTS AT 876.51 TONNES

NOV 30/WITH GOLD DOWN $8.70 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.02 TONNES OF GOLD FROM THE GLD. // / / // // INVENTORY RESTS AT 878.53 TONNES

NOV 29/WITH GOLD UP $7.20 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.73 TONNES OF GOLD FROM THE GLD. // / / // // INVENTORY RESTS AT 880.55 TONNES

NOV 28/WITH GOLD UP $26.45 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD: // / / // // INVENTORY RESTS AT 882.28 TONNE

NOV 27/WITH GOLD UP $9,85 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD: // / / // // INVENTORY RESTS AT 882.28 TONNES

NOV 24/WITH GOLD UP $11.20 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.15 TONNES OF GOLD FROM THE GLD// / / // // INVENTORY RESTS AT 882.28 TONNES

NOV 22/WITH GOLD DOWN $8.45 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD / / // // INVENTORY RESTS AT 883.43 TONNES

NOV 21/WITH GOLD UP $21.65 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD / / // // INVENTORY RESTS AT 883.43 TONNES

NOV 20/WITH GOLD DOWN $4.15 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD A MAMMOTH DEPOSIT OF 12.98 TONNES INTO THE GLD:/ / // // INVENTORY RESTS AT 883.43 TONNES

NOV 17/WITH GOLD DOWN $1.85 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD:/ / // // INVENTORY RESTS AT 870.45 TONNES

NOV 16/WITH GOLD UP $22.70 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD:/ / // // INVENTORY RESTS AT 870.45 TONNES

NOV 15/WITH GOLD DOWN $1.00 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD:/ / // // INVENTORY RESTS AT 870.45 TONNES

NOV 14/WITH GOLD UP $16.35 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD:/ / // //A DEPOSIT OF 2.3 TONNES OF GOLD INTO THE GLD// INVENTORY RESTS AT 870.45 TONNES

NOV 13/WITH GOLD UP $12.00 TODAY:SMALL CHANGES IN GOLD INVENTORY AT THE GLD:/ / // //A DEPOSIT OF .87 TONNES OF GOLD INTO THE GLD// INVENTORY RESTS AT 868.15 TONNES

NOV 10/WITH GOLD DOWN $30.70 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD:/ / // // INVENTORY RESTS AT 867.28 TONNES

NOV 9/WITH GOLD UP $12.50 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD:/ / // // INVENTORY RESTS AT 867.28 TONNES

NOV 8/WITH GOLD DOWN $14.95 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD:A MASSIVE DEPOSIT OF 4.04 TONNES OF GOLD INTO THE GLD/ / // // INVENTORY RESTS AT 867.28 TONNES

NOV 7/WITH GOLD DOWN $14.70 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD:A DEPOSIT OF 4.33 TONNES OF GOLD INTO THE GLD/ / // // INVENTORY RESTS AT 863.24 TONNES

NOV 6/WITH GOLD DOWN $9.90 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD:A DEPOSIT OF 1.73 TONNES OF GOLD INTO THE GLD/ / // // INVENTORY RESTS AT 863.24 TONNES

NOV 3/WITH GOLD UP $5.75 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD: / // // INVENTORY RESTS AT 861.51 TONNES

NOV 2/WITH GOLD UP $6.55 TODAY:BIG CHANGES IN GOLD INVENTORY AT THE GLD: A HUGE DEPOSIT OF 2.02 TONNES OF GOLD INTO THE GLD/ // // INVENTORY RESTS AT 861.51 TONNES

NOV 1/WITH GOLD DOWN $6.15 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD // // INVENTORY RESTS AT 859.49 TONNES

OCT 31/859.49 TONNES//

OCT 30/WITH GOLD UP $7.80 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD // // INVENTORY RESTS AT 861.80 TONNES

OCT 27/WITH GOLD UP $1.20 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD // // INVENTORY RESTS AT 861.80 TONNES

OCT 26/WITH GOLD UP $2.90 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF 1.73 TONNES OF GOLD INTO THE GLD// // INVENTORY RESTS AT 861.80 TONNES

OCT 25/WITH GOLD UP $9.00 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD:/: //: // INVENTORY RESTS AT 860.07 TONNES

GLD INVENTORY: 876.51 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

DEC 1/WITH SILVER UP 15 CENTS TODAY:HUGE CHANGES IN SILVER INVENTORY AT THE SLV/: A WITHDRAWAL OF 1.923 MILLION OZ FROM THE SLV// //://// //INVENTORY RESTS AT 434.128 MILLION OZ

NOV 30/WITH SILVER UP 20 CENTS TODAY:NO CHANGES IN SILVER INVENTORY AT THE SLV/ //://// //INVENTORY RESTS AT 436.051 MILLION OZ

NOV 29/WITH SILVER UP 15 CENTS TODAY:HUGE CHANGES IN SILVER INVENTORY AT THE SLV” A MASSIVE WITHDRAWAL OF 4.122 MILLION OZ FROM THE SLV// //://// //INVENTORY RESTS AT 436.051 MILLION OZ

NOV 28/WITH SILVER UP 64 CENTS TODAY:NO CHANGES IN SILVER INVENTORY AT THE SLV //://// //INVENTORY RESTS AT 440.173 MILLION OZ

NOV 27/WITH SILVER UP 32 CENTS TODAY:HUGE CHANGES IN SILVER INVENTORY AT THE SLV //:////A WITHDRAWAL OF 1,008,000 OZ FROM THE SLV. //INVENTORY RESTS AT 440.173 MILLION OZ

NOV 24/WITH SILVER UP 70 CENTS TODAY:HUGE CHANGES IN SILVER INVENTORY AT THE SLV //:////A WITHDRAWAL OF 549,000 OZ FROM THE SLV. //INVENTORY RESTS AT 441.181 MILLION OZ

NOV 22/WITH SILVER DOWN 21 CENTS TODAY:NO CHANGES IN SILVER INVENTORY AT THE SLV //://// //INVENTORY RESTS AT 441.730 MILLION OZ

NOV 21/WITH SILVER UP 32 CENTS TODAY:HUGE CHANGES IN SILVER INVENTORY AT THE SLV A DEPOSIT OF 2.794 OZ FROM THE SLV//://// //INVENTORY RESTS AT 441.730 MILLION OZ

NOV 20/WITH SILVER DOWN 26 CENTS TODAY:HUGE CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 1,824,000 OZ FROM THE SLV//://// //INVENTORY RESTS AT 438.936 MILLION OZ

NOV 17/WITH SILVER DOWN 6 CENTS TODAY:HUGE CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 1,832,000 OZ FROM THE SLV//://// //INVENTORY RESTS AT 437,104 MILLION OZ

NOV 16/WITH SILVER UP 38 CENTS TODAY:SMALL CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 778,000 OZ FROM THE SLV//://// //INVENTORY RESTS AT 440.768 MILLION OZ

NOV 15/WITH SILVER UP 39 CENTS TODAY:NO CHANGES IN SILVER INVENTORY AT THE SLV://// //INVENTORY RESTS AT 441.587 MILLION OZ

NOV 14/WITH SILVER UP 78 CENTS TODAY:SMALL CHANGES IN SILVER INVENTORY AT THE SLV:A DEPOSIT OF 183,000 OZ INTO THE SLV ////// //INVENTORY RESTS AT 441.587 MILLION OZ

NOV 13/WITH SILVER UP 5 CENTS TODAY:NO CHANGES IN SILVER INVENTORY AT THE SLV: ////// //INVENTORY RESTS AT 441.364 MILLION OZ

NOV 10/WITH SILVER DOWN 59 CENTS TODAY:HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF .733 MILLION OZ INTO THE SLV////// //INVENTORY RESTS AT 441.364 MILLION OZ

NOV 9/WITH SILVER UP 17 CENTS TODAY:NO CHANGES IN SILVER INVENTORY AT THE SLV: //// //INVENTORY RESTS AT 440.631 MILLION OZ

NOV 8/WITH SILVER UP 13 CENTS TODAY:NO CHANGES IN SILVER INVENTORY AT THE SLV: //// //INVENTORY RESTS AT 440.631 MILLION OZ

NOV 7/WITH SILVER DOWN 59 CENTS TODAY:NO CHANGES IN SILVER INVENTORY AT THE SLV: //// //INVENTORY RESTS AT 440.631 MILLION OZ

NOV 6/WITH SILVER DOWN 6 CENTS TODAY:NO CHANGES IN SILVER INVENTORY AT THE SLV: //// //INVENTORY RESTS AT 440.631 MILLION OZ

NOV 3/WITH SILVER UP 41 CENTS TODAY:BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.638 MILLION OZ OF SILVER FROM THE SLV///// /// /INVENTORY RESTS AT 440.631 MILLION OZ

NOV 2/WITH SILVER UP 11 CENTS TODAY:BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.924 OZ OF SILVER FROM THE SLV///// /// /INVENTORY RESTS AT 439.993 MILLION OZ

NOV 1/WITH SILVER DOWN 11 CENTS TODAY:BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 916,000 OZ OF SILVER FROM THE SLV///// /// /INVENTORY RESTS AT 441.917 MILLION OZ

OCT 31/442.833 MILLION OZ///INVENTORY

OCT 30/WITH SILVER UP 46 CENTS TODAY:NO CHANGES IN SILVER INVENTORY AT THE SLV: /// /// /INVENTORY RESTS AT 443.750 MILLION OZ

OCT 27/WITH SILVER UP 3 CENTS TODAY:BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 641,000 OZ FROM THE SLV/// /// /INVENTORY RESTS AT 443.750 MILLION OZ

OCT 26/WITH SILVER DOWN 14 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/ /// /INVENTORY RESTS AT 444.391 MILLION OZ

OCT 25/WITH SILVER DOWN 6 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/ /// /INVENTORY RESTS AT 444.391 MILLION OZ

CLOSING INVENTORY 434.128 MILLION OZ//

PHYSICAL GOLD/SILVER COMMENTARIES

1:Peter Schiff/Mike Maharrey

end

2,c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens, John Rubino

3. CHRIS POWELL//GATA GOLD COMMENTARIES:

very poor ruling.

(Courtesy Reuters/GATA)

LME vindicated for cancelling nickel trades; Comex must feel relief

Submitted by admin on Thu, 2023-11-30 12:47Section: Daily Dispatches

LME Triumphs in Lawsuit Over Cancelled Nickel Trades

By Sam Tobin and Pratima Desai Reuters Wednesday, November 29, 2023

LONDON — The London Metal Exchange won Wednesday a legal battle with U.S. financial firms that brought a case demanding $472 million in compensation after the exchange cancelled billions of dollars in nickel trades last year following a surge in prices.

Hedge fund Elliott Associates and market maker Jane Street Global Trading brought the case after the world’s largest metals marketplace cancelled $12 billion in trades when prices shot to records above $100,000 a metric ton in a few hours of chaotic trade in March 2022.

In its written ruling, London’s High Court said the LME could cancel trades in exceptional circumstances and was not obligated to consult market players prior to its decision.

“This judgment recognises the LME’s obligation to maintain orderly markets and its powers to intervene to this end, including by cancelling trades,” the LME said.

Other exchanges were closely watching the case because it could have wider ramifications on their ability to react to crisis situations. …

In this week’s episode of Live from the Vault, Andrew Maguire prepares us for 2024 with a new-look studio and shares some explosive predictions for next year and a recap of 2023’s stairsteps.

Looking back at the very first episode of LFTV, when Andrew first predicted a gold price reset, it is now time to reveal what the economic effects of this might be. The precious metals expert explains how the coming shock might even be weaponized.

END

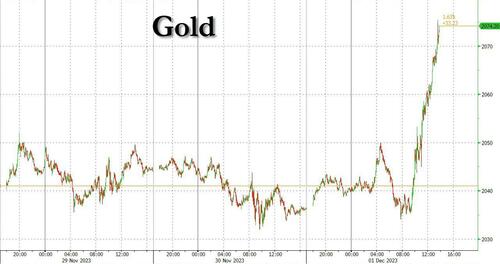

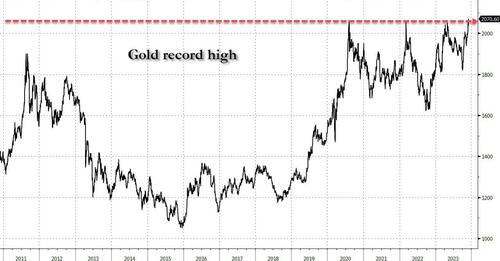

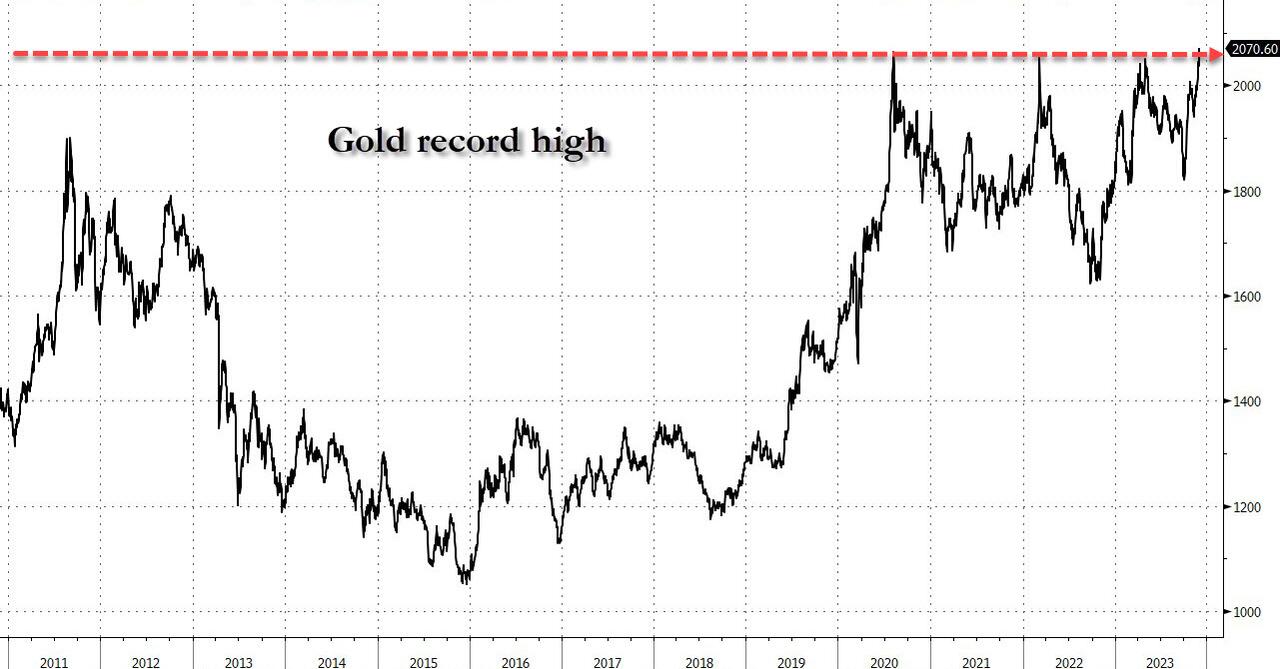

Gold rises to its all time high at 2075.00 surpassing previous high of 2070.

h

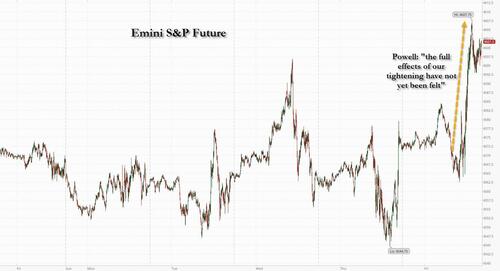

Powell, You Have A Problem: Gold Hits All Time High As Markets Price In Rate Cuts As Soon As March

FRIDAY, DEC 01, 2023 – 02:07 PM

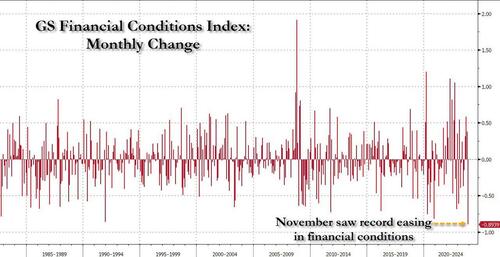

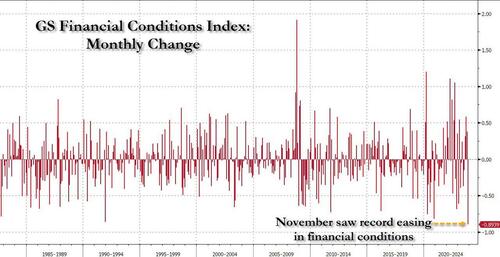

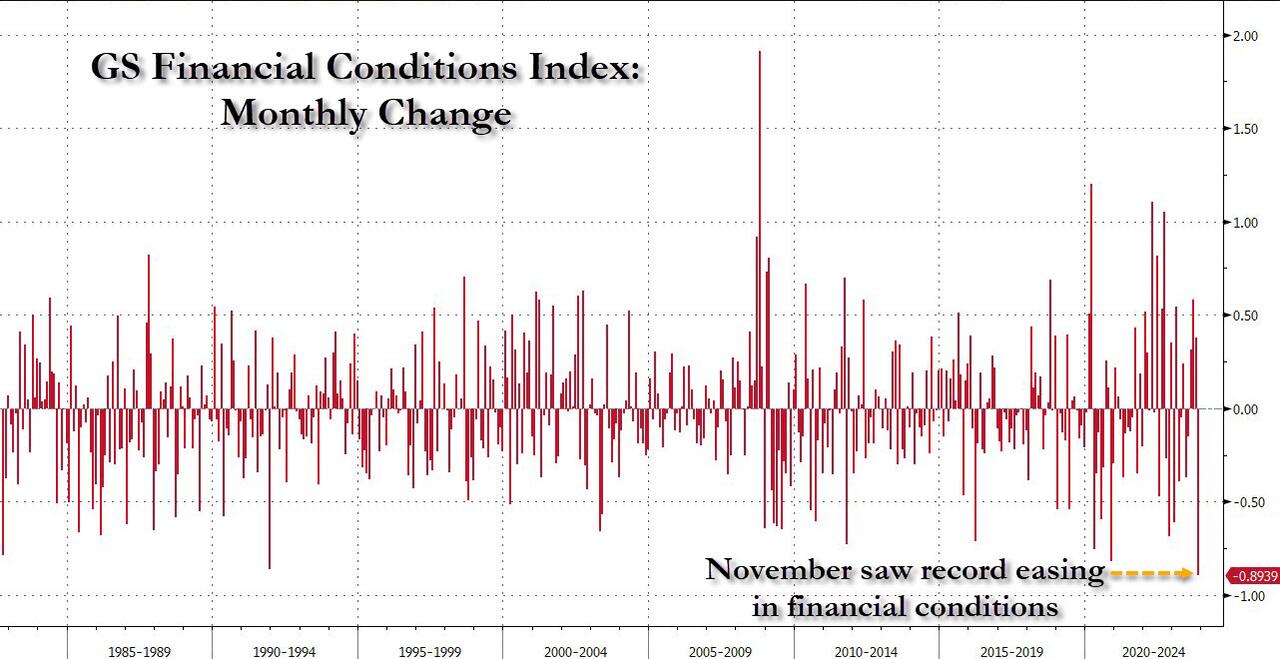

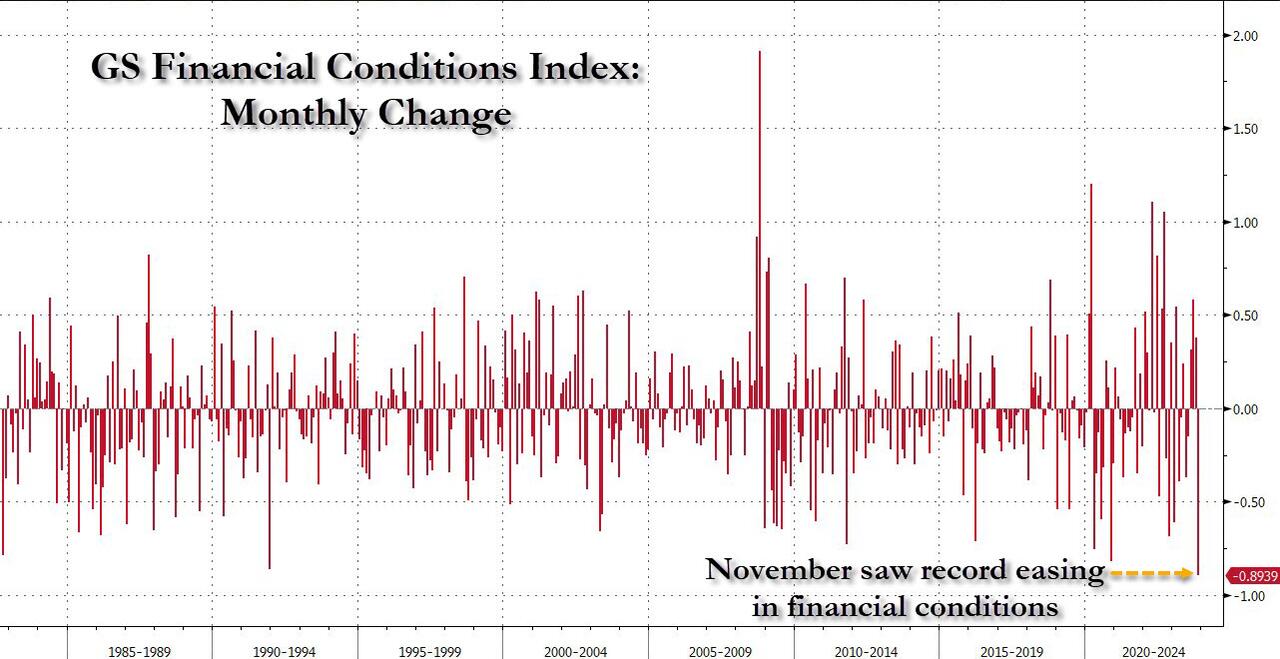

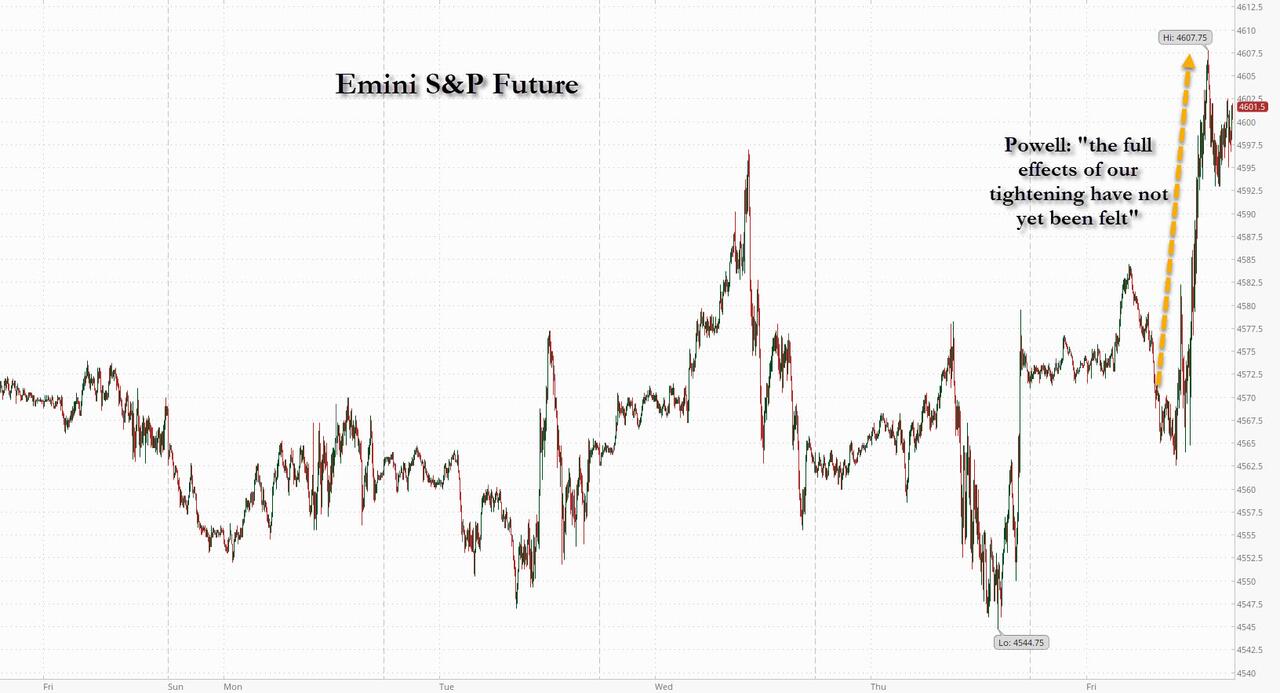

Ahead of the looming Fed blackout period – which lasts until the Dec 13 FOMC meeting – Powell had once last chance to tame euphoric markets after the best November in the past 40 years… and he blew it. Instead of pushing forcefully against the meltup in risk assets after the biggest easing in financial conditions on record during November…

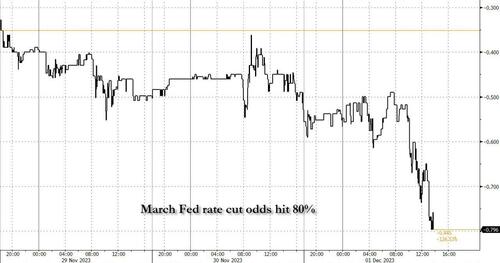

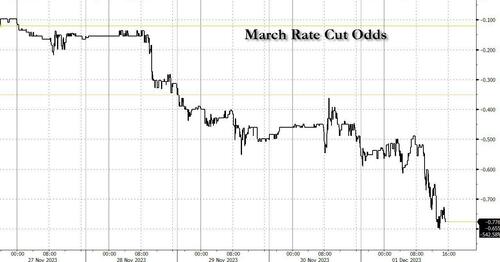

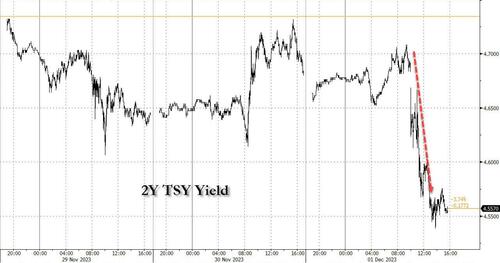

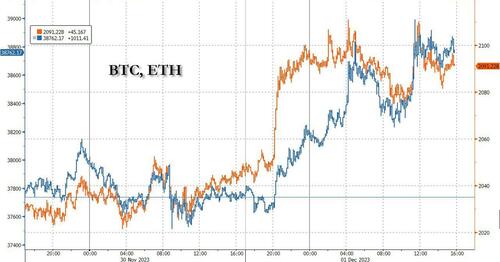

… the Fed chair appeared largely nonchallant, and in his fireside chat earlier today, what the market focused on was Powell’s comment that rates are “well into restrictive territory” which not only assured there would be no more rate hikes, but steamrolled Powell’s other, hawkish warning, that it is premature to speculate when the Fed might ease. The result was a collapse in yields, a surge in stocks, bitcoin spiking to new 2023 highs above $38,000, all driven by renewed bets that the Fed will cut rates as soon as March where the market now assigns odds of a rate cut as high as 80%, roughly double from yesterday.

And while it is unclear if it was Powell’s intention to give markets the green light to keep rallying into year-end, a problem has emerged, the same problem that emerges every time the market views the Fed as willing to sacrifice the dollar to prop up risk assets: gold.

After surging from a ytd low of $1820 in early October, to a high of $2,040 last week, largely thanks to a relentless gold buying spree out of China as we reported previously, gold has finally realized which way the wind is blowing and as shown below, it exploded higher amid a frenzy of institutional, ETF and retail buying (and perhaps continued Chinese buying), all of which managed to finally push the yellow metal to hit new all time highs of $2,075.41, the highest on record.

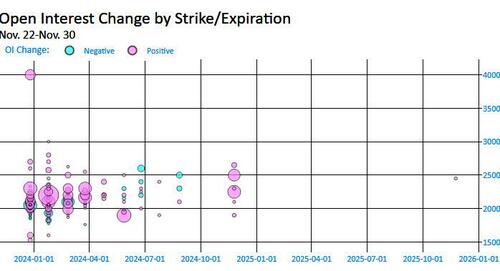

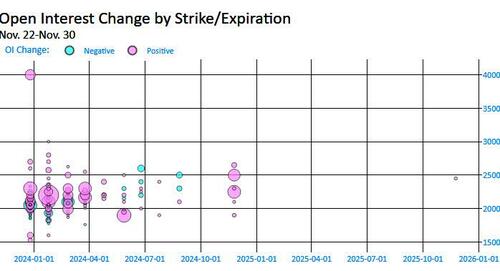

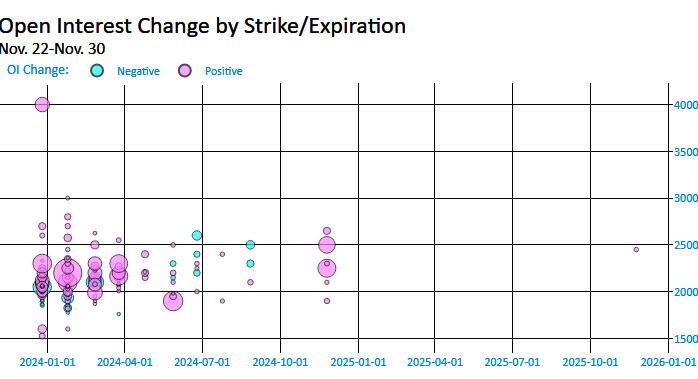

That’s just the start. As Bloomberg notes, gold calls were also in strong demand, both for futures and the biggest ETF tied to the metal, as bullion marched closer to a record high Friday. As shown in the chart below, the buildup of open interest between $2,000 and $2,500 has been relentless over the past week on growing optimism that rates are primed to decline:

That, alongside continued Chinese buying, and perhaps a reversal in ETF selling now that gold is clearly breaking out to new all time highs, means that the Fed has a new “old” problem on its hands: wholesale flight from fiat and into the safety of hard currencies, such as gold. No wonder “digital gold”, aka bitcoin, is also surging… although that one still has a ways to go to reach its previous all time high.

Then again, if the Fed is indeed set to cut rates as soon as March, and then proceed with more QE which will be inevitable to monetize the soaring US budget deficit and exploding interest payments, then we are set for new all time highs in everything – gold, bitcoin, stocks… oh and oil; because after the current bout of CTA selling is finally over, oil and commodities will be the next asset class to hit record highs at which point Powell’s mutation into Arthur Burns will be complete, confidence in the Fed will be crushed as the next – and far sharper inflation cycle kicks in – and the countdown to the end of the Dollar reserve currency system can finally begin.

5 a. IMPORTANT COMMENTARIES ON COMMODITIES

END

5 B GLOBAL COMMODITY ISSUES/FOOD IN GENERAL//FREIGHT

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS FRIDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED DOWN AT 7.1430

OFFSHORE YUAN: DOWN TO 7.1549

SHANGHAI CLOSED UP 1.96 PTS OR 0.06%

HANG SENG CLOSED UP 212.56 PTS OR 1.25%

2. Nikkei closed UP 212.56 PTS OR 1.25%

3. Europe stocks SO FAR: ALL GREEN

USA dollar INDEX UP TO 103.45 EURO FALLS TO 1.0883 DOWN 9 BASIS PTS

3b Japan 10 YR bond yield: RISES TO. +.705 Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 148.30/JAPANESE YEN FALLING AS WELL AS LONG TERM 10 YR. YIELDS RISING //EVENTUALLY THIS WILL BREAK THE JAPANESE CENTRAL BANK

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen DOWN CHINESE ONSHORE YUAN: DOWN// OFFSHORE: DOWN

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil DOWN for WTI and DOWN FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund UP TO +2.4430***/Italian 10 Yr bond yield UP to 4.1840** /SPAIN 10 YR BOND YIELD UP TO 3.447…**

3i Greek 10 year bond yield UP TO 3.638

3j Gold at $2036.20 silver at: 25.12 1 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble DOWN 0 AND 75 /100 roubles/dollar; ROUBLE AT 90.20//

3m oil into the 75 dollar handle for WTI and 80 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 148,30// 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 0.703% STILL ON CENTRAL BANK (JAPAN) INTERVENTION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.8761 as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.9534 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.346 DOWN 1 BASIS PTS…

USA 30 YR BOND YIELD: 4.513 UP 1 BASIS PTS/

USA 2 YR BOND YIELD: 4.706 DOWN 1 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 28.87…(TURKEY SET TO BLOW UP FINANCIALLY)

GREAT BRITAIN/10 YEAR YIELD: UP 6 BASIS PTS AT 4.2405

end

2.a Overnight: Newsquawk and Zero hedge:

Futures Drop In First Trading Day Of Last Month As Powell “Fireside Chat” Looms

FRIDAY, DEC 01, 2023 – 08:20 AM

US futures reversed some of Thursday’s gains to start the final month of the year after a blowout performance in November, as European stocks gained, and Asia stuttered. US Treasuries and the dollar posted small moves before comments from Fed Chair Jerome Powell at 11am ET that may offer clues on the path of interest rates. Oil rebounded after OPEC+ promised further output cuts but was hazy on details. Israel resumed fighting against Hamas in the Gaza Strip after a weeklong truce ended: Israel’s army said Hamas violated the cease-fire terms by firing toward its territory. Bitcoin soared to its highest price so far this year. Base metals are rallying after the strong China Caixin Mfg. PMI results (50.7 s. 49.6 survey vs. 49.5 prior). Today, we get the November ISM-Mfg. at 10am ET (exp. 47.9, last 46.7) and hear from Powell at a “fireside chat” at Spelman College in Atlanta on Friday at 11am ET ahead of Fed’s blackout period. Focus for Powell events is whether he’ll back dovish comments earlier this week by Fed Governor Waller, which spurred a rally across front-end of the Treasuries curve.

In premarket trading, Pfizer dropped 3.5% after dropping development of its experimental weight-loss pill. Tesla slipped 2.1% as the electric-vehicle maker kicked off deliveries of its Cybertruck. RBC said the vehicle is priced at the higher end of expectations. Here are some other notable premarket movers:

Marvell Technology slipped 5% after the chipmaker’s fourth-quarter revenue forecast fell short of expectations.

PagerDuty rose 5% after the company reported third-quarter results that beat expectations and raised its full-year forecast.

Dell Technologies drops 5.4% after reporting revenue that declined more than expected, buffeted by continued sluggish corporate demand for personal computers.

Lemonade falls 3.2% after Oppenheimer downgraded the insurance company, noting the outlook for weather patterns to return to normal in 2024 after a relatively quiet 2023.

Samsara, a provider of GPS fleet tracking, gains 13% after boosting its profit and revenue guidance for the full year.

UiPath jumps 14% as analysts hike their targets after third-quarter results beat expectations at the robotic process automation software company.

Ulta Beauty gains 12% after the cosmetics retailer reported forecast-beating comparable sales growth in the third quarter.

After we predicted one month ago to brace for a face-ripping rally in November…

… that’s precisely what happened, as US stocks posted their best month in close to a year-and-a-half and had their second-best November since 1980s, defying the skeptical calls and fueling hopes that more gains are to come, while the MSCI All Country World Index saw its third-largest monthly gain in the past decade. The Bloomberg Dollar Spot Index dropped by the most in a year, while US Treasury yields tumbled about 60 basis points in the month. This was mostly down to plunging bond yields amid mounting signs that the Federal Reserve is managing to tame inflation without breaking the economy. Money-market fund assets surged to a fresh all-time high and Cathie Wood got in on the action too, with her ARKK Innovation ETF racking up a 31% gain for the month.

“Almost everyone was offsides coming into November,” said Ryan Detrick, chief market strategist at Carson Group. Everyone except for our raders that is. “There’s still a big opportunity for traders to chase gains in December, too.”

This morning, investors were trying to assess if November’s scorching gains across asset classes can go further. Yesterday’s core PCE data showed that the Fed’s favorite measure of inflation eased in October, adding to the case for an end to the Fed’s tightening and bolstering the narrative that lifted markets globally last month. Some suggest optimistic market wagers on the timing of interest-rate cuts next year read too much into recent comments by Fed officials. Powell is set to speak at Spelman College in Atlanta on Friday.

“The market is wondering whether it has gone ahead of itself in expecting US rate cuts next year,” said Sébastien Barbé, head of emerging-market research and strategy at Credit Agricole. “From Powell’s point of view, it may be tempting to warn the market against excess optimism about possible rate cuts in order to keep monetary conditions tight enough to make sure disinflation is sustainable.”

Meanwhile, oil prices steadied after the drop suffered yesterday following an OPEC+ meeting which sewed confusion among traders. The cartel promised further cuts to output but was hazy on the details, with the lack of a concluding press conference and final communiques leaving the market puzzled. Notably, the cuts agreed are voluntary, so whether the additional supply cuts that were announced will be delivered remains to be seen. Part of the rebound was driven by news Israel resumed fighting against Hamas in the Gaza Strip after a weeklong truce ended. Israel’s army said Hamas violated the cease-fire terms by firing toward its territory. Jets started striking Gaza soon after the deadline passed. Israel dropped leaflets telling people to leave some parts of southern Gaza. Qatar said truce negotiations continue

European stocks gain in early Friday trading, with the advance led by the Stoxx 600 Basic Resources index, as mining stocks outperform after broker upgrades, with the Automotive and Food, Beverage & Tobacco sectors the worst performing. Anglo American and Rio Tinto led gains in the Stoxx 600 Index after China’s manufacturing data beat estimates. The Euro Stoxx 50 rose 0.7% with the FTSE 100 outperforming regional peers. Here are the biggest movers Friday:

Mining shares outperform in Europe on Friday as Anglo American and Rio Tinto are upgraded to buy at UBS and Liberum, respectively, with Anglo American gaining as much as 7.6%, the most since September

Signify shares rise as much as 6.6% after the lighting maker announced a new divisional structure and said it will implement measures to reduce non-manufacturing costs by more than €200 million

Jenoptik rises as much as 5.8% after the optical systems technology firm upgraded its Ebitda margin target for 2025, citing better-than-expected organic development in its semiconductors and electronics businesses

Technogym gains as much as 11% after NIF Holding bought about 8.8 million ordinary shares of the fitness-equipment maker at €9.20 apiece in a reverse accelerated bookbuilding

Leonteq shares tumble as much as 18% to the lowest level since 2020 after the Swiss technology and service provider revised down its FY2023 forecast. ZKB flags that the dividend could be reduced

LVMH shares fall as much as 1.9% after the luxury goods maker is downgraded to equal-weight at Morgan Stanley given the likelihood of a further deterioration in demand for the industry in the fourth quarter

Viaplay shares plunge as much as 83%, the most on record, in early Friday trading. Analysts said shareholders can expect to see their holdings reduced to almost nothing under a new recapitalization plan

Ceres Power shares plunge as much as 27%, the most since 2012, after the UK-based energy generator and distributor said it hasn’t been able to conclude a new license partnership in this financial year

ITV shares fall as much as 2.9% after Deutsche Bank downgraded rating on the broadcaster to hold from buy, citing headwinds from a continued slump in advertising revenue

Swiss Re shares fall as much as 2% as investors focus on its new reserving allowance, which is expected to have a “negative impact” of approximately $500 million on profit after tax

Earlier in the session, Asian stocks fell as concerns about China’s economy persisted, with sentiment cautious ahead of comments from Federal Reserve Chair Jerome Powell later on Friday. The MSCI Asia Pacific Index dropped as much as 0.4%, led by technology shares, as some Fed officials remained wary of interest rate cuts next year. Tech-heavy markets such as South Korea and Taiwan also fell. Stocks in Japan gained as a stall in yen strength boosted exporters. Chinese shares declined, extending their recent underperformance versus global peers, with the CSI 300 Index set for its lowest close since 2019. Investors remained concerned about the weak economic recovery even as a private survey of China’s manufacturing activity unexpectedly expanded. The decline in home sales also accelerated in November despite more funding support for developers. Chinese’s losses were almost erased, however, after the China Securities Journal reported that the “National Team” was back as an unidentified Chinese state institution bought exchange-traded funds whose underlying assets are A-shares issued by central state-owned enterprises in the domestic stock market Friday.

Hang Seng and Shanghai Comp were gradually pressured following the PBoC’s substantial net liquidity drain, whilst the latter eventually moved into the green amid reports China state-owned capital operating Co. reportedly bought ETFs on Friday, whilst the session also saw a surprise return to expansion territory for the Chinese Caixin Manufacturing PMI.

Japan’s Nikkei 225 traded indecisively as encouraging data releases offset the headwinds from early currency strength.

Australia’s ASX 200 was dragged lower by underperformance in tech and consumer-related sectors amid higher yields.

In FX, US equity futures are steady, while the dollar was slightly down ahead of speeches by the Fed’s Powell and Goolsbee. US ISM manufacturing data is also due. DKK and EUR are the weakest performers in G-10 FX, NOK and SEK outperform.

In rates, Treasuries were slightly cheaper across the curve with losses led by long-end, moving inverted 2s10s spread back toward top of Thursday’s range. TSY yields are cheaper by up to 2bp across long-end of the curve with 2s10s spread wider by 0.5bp on the day; 10-year yields around 4.345% with bunds outperforming by 3.5bp in the sector, Italian 10-year by 5bp. Focus for Powell events is whether he’ll back dovish comments earlier this week by Fed Governor Waller, which spurred a rally across front-end of the Treasuries curve. Fed-dated OIS currently price in a 25bp rate cut in May and a total of 112bp cuts by the December FOMC meeting. US economic data includes November S&P Global manufacturing PMI (9:45am New York time), October construction spending and November ISM manufacturing (10am). In Europe, Italian bonds outperform following surprise drop in Italy’s manufacturing PMI for November; bund 10-year yields are down some 2 bps, outperforming comparable USTs and gilts. US session includes manufacturing data and two scheduled appearances by Fed Chair Powell.

In commodities, oil pared some post-OPEC+ losses. WTI trades within Thursday’s range, adding 0.3% to trade near $76.20. Spot gold was on track for a third weekly gain, rising roughly $8 to trade near $2,045/oz as it inches toward its all-time high after Israel resumed its war against Hamas; it was then summarily smacked down by some central bank amid fears a new all time high will lead to a surge in gold to $2500 and higher and destabilize the fiat system. Most base metals trade in the green after China’s Caixin Mfg PMI unexpectedly entered expansion, rising to 50.7 from 49.5, and beating estimates of 49.8; LME tin rose 1.3%, outperforming peers.

To the day ahead now, and central bank speakers include Fed Chair Powell, the Fed’s Barr, Goolsbee and Cook, ECB President Lagarde, and the ECB’s Elderson and De Cos. Data releases include the global manufacturing PMIs, along with the ISM manufacturing reading from the US.

Market Snapshot

S&P 500 futures up 0.2% to 4,583.75

MXAP down 0.3% to 161.81

MXAPJ down 0.6% to 503.36

Nikkei down 0.2% to 33,431.51

Topix up 0.3% to 2,382.52

Hang Seng Index down 1.2% to 16,830.30

Shanghai Composite little changed at 3,031.64

Sensex up 0.7% to 67,464.96

Australia S&P/ASX 200 down 0.2% to 7,073.18

Kospi down 1.2% to 2,505.01

STOXX Europe 600 up 0.7% to 464.87

German 10Y yield little changed at 2.42%

Euro little changed at $1.0898

Brent Futures down 0.4% to $80.51/bbl

Gold spot up 0.6% to $2,048.93

U.S. Dollar Index down 0.17% to 103.32

Top overnight news

China’s Caixin manufacturing PMI for Nov came in ahead of plan at 50.7, up from 49.5 in Oct and above the Street’s 49.6 forecast (this follows the NBS PMIs Wed night falling short of expectations). RTRS

Europe’s final manufacturing PMI for Nov came in at 44.2, up from the flash reading of 43.8. BBG

Ukraine president Volodymyr Zelenskyy has pushed to “accelerate” the construction of military fortifications at key points along the frontline in the east of the country where Russian forces have stepped up attacks in recent weeks. FT

Israel resumed fighting against Hamas in the Gaza Strip after a weeklong truce ended. Israel’s army said Hamas violated the cease-fire terms by firing toward its territory. Jets started striking Gaza soon after the deadline passed. Israel dropped leaflets telling people to leave some parts of southern Gaza. Qatar said truce negotiations continue. BBG

Washington aims to slash Russia’s oil and gas revenue by 50% by the end of the decade to ensure Putin doesn’t have the funds to attack his neighbors. FT

Caracas has for over 200 years claimed rights over Essequibo, a vast swath of the territory of neighbouring Guyana. But only now has it opted to hold a referendum among Venezuelans on taking over the 160,000 sq km of land. FT

PFE announces a setback in its GLP1 anti-obesity ambitions. Its twice-daily danuglipron formulation will NOT advance into P3 studies. The drug achieved weight reductions of 8-13% over 32 weeks and 5-9.5% at 26 weeks, less than the 14-15% many thought would be needed to compete in the market. More significantly (and negatively), there were high rates of adverse side effects (up to 73% nausea; up to 47% vomiting; up to 25% diarrhea) and high discontinuation rates (greater than 50%). RTRS

Apple and Paramount Global have discussed bundling their streaming services at a discount, the latest attempt by rival entertainment giants to team up as they look to make their offerings more affordable and attractive. WSJ

BPCE is exploring options for its $1.2 trillion Natixis asset management business, including selling a majority stake, people familiar said. BBG

A more detailed look at global markets courtesy of Newsquawk

APAC stocks began the new month with price action rangebound as markets paused following the November rally amid another busy day of economic releases, while the conflict in Gaza also resumed. ASX 200 was dragged lower by underperformance in tech and consumer-related sectors amid higher yields. Nikkei 225 traded indecisively as encouraging data releases offset the headwinds from early currency strength. Hang Seng and Shanghai Comp were gradually pressured following the PBoC’s substantial net liquidity drain, whilst the latter eventually moved into the green amid reports China state-owned capital operating Co. reportedly bought ETFs on Friday, whilst the session also saw a surprise return to expansion territory for the Chinese Caixin Manufacturing PMI.

Top Asian news

China state-owned capital operating Co. reportedly bought ETFs on Friday, according to Bloomberg.

US judge blocked the Montana state ban on Tiktok from taking effect, according to a court order.

US lawmakers seek a Biden administration investigation into Chinese drone maker Autel Robotics due to national security concerns.

Japan’s largest trade union RENGO said it formally agreed on a 2024 pay hike demand of 5% or more, according to Reuters.

European equities, Eurostoxx50, +0.5%, are extending gains; FTSE100, +0.8%, which has been lifted by mining-related stocks. European sectors are mostly in the green, with significant outperformance in Basic Resources, being propped up by mining stocks following broker upgrades at Anglo American, +6.4%, and Antofagasta, +4.7%; Optimised Personal Care & Grocery is marginally hampered by a Tesco, -1.3%, downgrade. US Futures are trading on the front foot, albeit to a lesser extent in comparison to their European counterparts ahead of ISM & Powell; RTY, +0.3%, slightly outperforms.

Top European news

ECB’s Nagel said recent inflation developments are encouraging but the ECB cannot be satisfied yet and inflation risks are still on the upside so a further rate hike cannot be ruled out. Nagel also stated that longer-term inflation expectations are still some way from 2% and that a leaner ECB balance sheet is desirable and the reduction can accelerate, while he added it is far too early to discuss rate cuts.

EU weighs concessions in the US steel feud amid concerns over a Trump return, according to Bloomberg sources.

German government spokesperson, re. budget talks, says they are aware of the urgency and there is a lot of momentum to solve this as soon as possible

FX

Dollar drifts after month-end revival awaiting US manufacturing ISM for interim impetus before guidance from Fed Chair Powell; DXY dithering within 103.45-26 range.

Kiwi back in sight of 0.6200 vs Greenback after hawkish RBNZ rhetoric from Hawkesby.

Aussie encouraged by China’s Caixin manufacturing PMI rebound to 50.0+ level as AUD/USD hold above 0.6600.

Loonie underpinned ahead of Canadian LFS with USD/CAD sub-1.3550.

Cable firm on 1.2600 handle after upward revision to final UK manufacturing PMI.

Euro tethered to 1.0900 vs Dollar amidst nearby option expiries and post-mostly better than flash or forecast Eurozone manufacturing PMIs.

PBoC set USD/CNY mid-point at 7.1104 vs exp. 7.1458 (prev. 7.1018).

Fixed Income

Debt futures back on a firmer footing, on balance, after steep month end retracement.

Bunds bounce further from sub-132.00 towards 133.00 again.

Gilts towards top of 96.80-25 range, but still lagging in run up to Fitch UK rating review.

T-note hovering around 110-00 within 110-04/109-27+ confines awaiting US manufacturing ISM and Fed speakers headlined by Chair Powell twice.

Commodities

WTI and Brent are modestly firmer intraday in the aftermath of the OPEC+ confab on Thursday which ultimately underwhelmed the market given that output cuts are voluntary; as it stands, benchmarks are holding incrementally above the unchanged mark in narrow ranges around the prior session’s trough.

Spot gold holds an upward bias as the Dollar remains subdued; Base metals are firmer across the board amid upbeat Chinese data overnight, and upward bias in risk sentiment in Europe.

OPEC Secretariat announced several OPEC+ countries will conduct additional voluntary cuts to the total of 2.2mln BPD (exp. 2.0mln). It was confirmed that Brazil will join OPEC+ from January 2024.

Saudi Arabia will extend its voluntary cut of 1mln BPD to the end of Q1 2024 with its production to be approx. 9mln BPD and Russia is also to extend its voluntary cut in oil supplies until the end of Q1 2024 with its voluntary supply cut to reach 500k BPD. Kuwait is to make a further 135k BPD OPEC+ oil output cut, while the UAE is to make an additional 160k BPD OPEC+ output cut and Iraq is said to cut its production by 220k BPD in Q1. Conversely, Angola rejected its OPEC quota for 1.11mln BPD and said it will produce 1.18mln BPD, according to Bloomberg. Click here for the detailed headline.

US is purchasing 2.73mln bbls of oil for the strategic reserve, according to a document cited by Reuters.

US aims to halve Russia’s energy revenue by 2030, while Assistant Secretary of State for Energy Resources Pyatt said Western sanctions will continue for years to come to curb Moscow’s war machine, according to FT.

US President Biden and Angola’s President welcomed the launch of a US-Angola energy security dialogue in 2024 during a meeting on Thursday, according to the White House

US State Department said the US reiterated its pledge to ‘reconsider’ the steps it took to ease sanctions on Venezuela if the latter fails to comply with certain commitments by the end-November deadline, while it added that Venezuela must define steps for lifting bans on opposition candidates and begin the release of Venezuelan political prisoners and wrongfully detained Americans. It was later reported that banned Venezuelan candidates would be allowed to take their cases to a tribunal.

Morgan Stanley says commitment to new OPEC+ cuts appears to be uncertain, expect compliance to only be partial, Foresees Saudi Arabia ultimately extending the cuts to Q2-2024. Maintain Brent forecast at USD 85/bb and flat throughout 2024. Lowered OPEC+ production forecast for Q1-2024 by 0.6mln BPD, still see the oil market turning into a small surplus again in Q2 & Q3.

Russia’s Kremlin says OPEC+ contributes to stabilisation of energy markets and creation of conditions for supporting energy prices at a balanced level; Russia is interested in continuing working with OPEC+.

First Quantum is suspending production guidance for Cobre Panama for the current year

Geopolitics

Israel’s military said that Hamas violated the truce and fired towards Israeli territory, while it has resumed combat against Hamas in Gaza

Initial reports suggested Israel and Hamas agreed to extend the truce for an eighth day, according to Egyptian officials cited by WSJ. However, there was no official statement made by Israel, Hamas or mediator Qatar.

Rocket sirens sounded in Israeli areas near the Gaza border and the Israeli military said one launch was detected from Gaza which was intercepted, while Hamas-affiliated media reported that explosions and gunfire were heard in the northern Gaza Strip. Furthermore, Israeli planes were reportedly flying over Gaza and Israeli army vehicles are firing in the northwest of the Gaza Strip, according to a correspondent cited by Al Jazeera.

The Israeli army raises the alert on the border with Lebanon, according to Al Arabiya

Qatari and Egyptian mediators have been in contact with Hamas and Israel since fighting resumed in Gaza on Friday, according to Reuters citing sources; negotiations between both sides is continuing

Senior Hezbollah member says Lebanon remain ready to confront any danger from Israel, adds Gaza developments can still affect the Lebanon situation

US Treasury Department issued new North Korean sanctions targeting 8 individuals and the hacking group Kimsuky, while South Korea imposed sanctions on 11 North Korean individuals, according to the Foreign Ministry.

US Event Calendar

09:45: Nov. S&P Global US Manufacturing PM, est. 49.5, prior 49.4

10:00: Oct. Construction Spending MoM, est. 0.3%, prior 0.4%

10:00: Nov. ISM Employment, est. 47.2, prior 46.8

10:00: Nov. ISM New Orders, est. 46.7, prior 45.5

10:00: Nov. ISM Prices Paid, est. 45.9, prior 45.1

10:00: Nov. ISM Manufacturing, est. 47.8, prior 46.7

Central Banks

03:00: Fed’s Barr Speaks on Bank Supervision and Regulation

10:00: Fed’s Goolsbee Participates in Moderated Discussion

11:00: Fed’s Powell Speaks in Fireside Chat

14:00: Fed’s Powell, Cook Participate in Roundtable Discussion

DB’s Jim Reid concludes the overnight wrap

Happy December. My wife is organizing Santa’s Grotto at the kids’ school tomorrow and until yesterday was missing one key thing. A Santa! A call over the last few weeks for a volunteer amongst all parents and grandparents had fallen upon deaf ears so my wife rung a couple of agencies and found the cheapest Santa was £600 for 90mins work. So that’s a great business to get into, although I accept the work might have a seasonal bias!

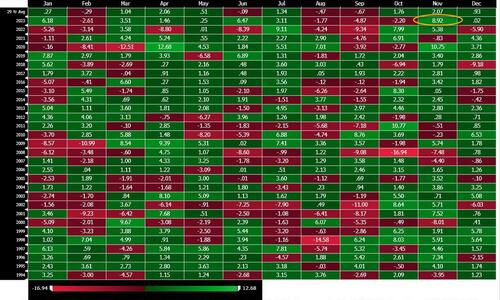

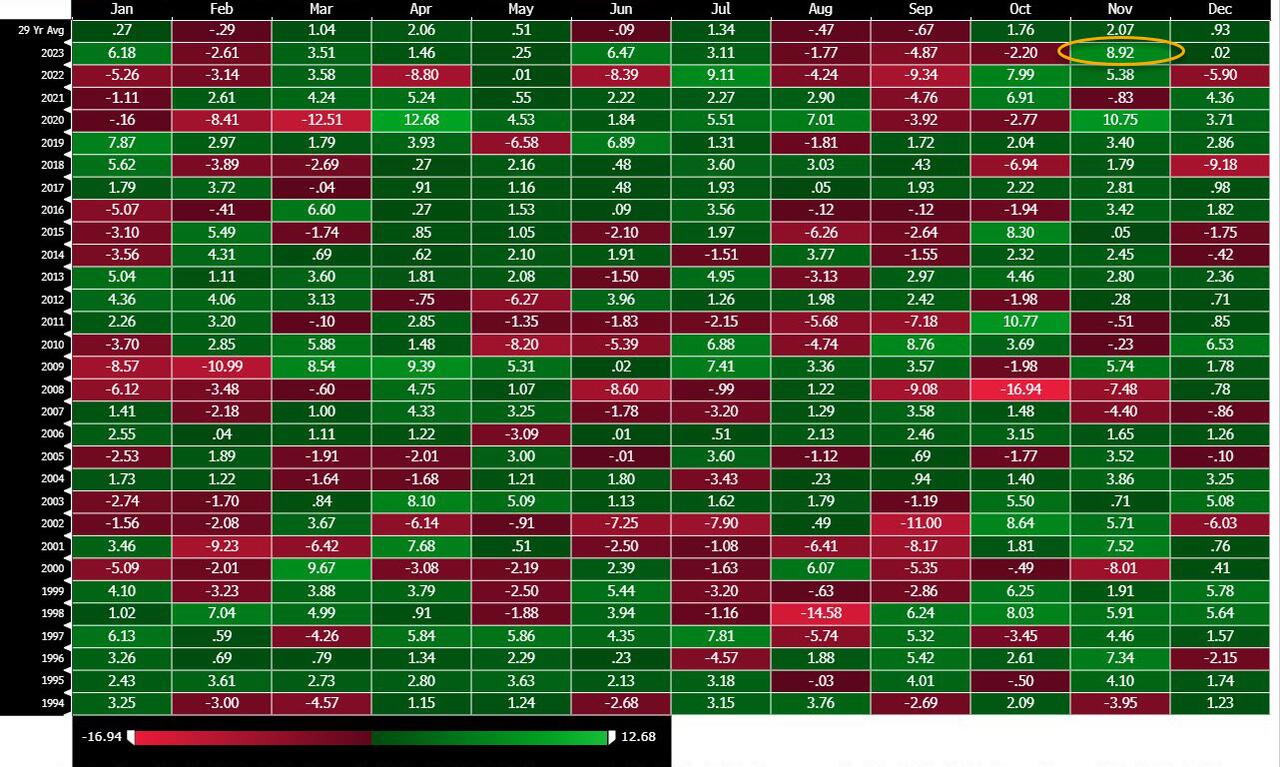

Since it’s the start of December this morning, we’ll shortly be releasing our monthly performance review for November. Overall, it was a great month for markets after a run of three fairly weak ones, which has led to a big turnaround in some of the YTD numbers for 2023. In fact, it was the best month for global bonds since December 2008, the best month for US bonds since May 1985, as well as the strongest month for the S&P 500 this year. The full report will be in your inboxes shortly.

Whether the trends of November continue into Xmas might in part depend on Powell’s speech later today (4pm GMT), just before the FOMC blackout. Market moves have been so great since he suggested that tight financial conditions were doing some of the Fed’s job for them (November 1st) that you have to think he will address the subsequent moves and either push back or endorse. On balance I think he may take a similar tone to Williams yesterday and push back a little while acknowledging the progress that has seemingly been made .

On that theme, NY Fed President Williams’ remarks yesterday helped the month end on a soggier tone, especially for bonds. He said he expects “it will be appropriate to maintain a restrictive stance for quite some time to fully restore balance and to bring inflation back to our 2% longer-run goal on a sustained basis .” Separately, San Francisco President Daly said that “I’m not thinking about rate cuts at all right now”.

Those developments had a notable impact on sovereign bonds, which pared back some of their recent gains on both sides of the Atlantic. For instance, the 10yr Treasury yield bounced back +7.1bps to 4.33%. Over in Europe there were slightly smaller moves for 10yr bunds (+1.5bps), OATs (+2.3bps) and BTPs (+5.5bps), while Gilts underperformed (+8.0bps) .

This came even as the data generally pointed in a dovish direction. In particular, we had the latest PCE inflation data for October yesterday, which is the measure the Fed officially targets. That showed headline PCE at a monthly 0.0% (vs. +0.1% expected), which brought the year-on-year number down to +3.0%, and the lowest since March 2021. It also brings us closer to the sort of numbers where the Fed has historically pivoted towards rate cuts in the past. Core PCE was still a bit higher at +3.5%, but to be fair, the more recent figures have been better, and if you just look at the last 6 months alone, core PCE is now down to an annualised +2.5% .

Over in the Euro Area, there was similarly good news from the flash CPI reading for November. It showed headline annual inflation was down to +2.4% (vs +2.7% expected) , the lowest since July 2021, and almost back at the ECB’s 2% target. This was partly down to a big negative impetus from energy prices, which are currently down -11.5% year-on-year. Core inflation remained more elevated at +3.6% but this also surprised clearly on the downside (+3.9% exp) with a marked slowdown in the past three months, down from +5.3% as recently as August.

Amidst the better news on inflation, the bigger concern came from the labour market, where the latest data showed things were continuing to soften. For example, US continuing jobless claims were up to their highest level in almost two years, at 1.927m (vs. 1.865m expected). Seasonals seem to be a little all over the place this year so some caution is required. Meanwhile in Germany, the r egistered unemployment rate climbed to a two-and-a-half year high of 5.9%, so this wasn’t just a US theme. As it happens, we’re now just a week away from the final US jobs report of the year, and it was last month that the unemployment rate hit its highest since January 2022. So if it does show any further softening, that’ll only ramp up the H1 2024 rate cut speculation as we get closer to the Fed’s December meeting just a few days later .

With the data softening, US equities continued their pretty flat performance this week. But a sizeable rally in the final 30 minutes of US trading, probably reflecting month-end flows, left the S&P 500 posting a decent rise (+0.38%). Bank stocks outperformed for the second day in a row (+1.03%), while a strong day for industrials led the Dow Jones index to a +1.47% gain. Tech stocks underperformed, with the NASDAQ (-0.23%) and the FANG+ index (-0.27%) dipping. Meanwhile in Europe, the STOXX 600 (+0.55%) continued its recent outperformance, closing at a two-month high .

This morning Asian equity markets are drifting lower at the start of the last month of the year despite the late-day rebound on Wall Street overnight. As I check my screens, the KOSPI (-1.03%) is the biggest underperformer across the region with the CSI (-0.91%), the Hang Seng (-0.69%) and the Shanghai Composite (-0.32%) also trading in the red amid mixed economic signals from China (more on this below). Elsewhere, the Nikkei (+0.03%) is flickering between gains and losses this morning. In overnight trading, US stock futures are indicating a negative start with those on the S&P 500 (-0.06%) just below flat while those on the NASDAQ 100 (-0.19%) inching lower.

Coming back to China, the Caixin PMI measure of the manufacturing sector unexpectedly expanded in November, hitting 50.7 (v/s 49.6 expected). That was the fastest expansion in three months and up from 49.5 in October. Of course, the Caixin PMI stands in contrast to the latest official PMI which dropped to 49.4, highlighting that mores stimulus will likely be required to reinvigorate growth in the world’s second biggest economy.

Elsewhere, Japan’s unemployment rate edged down to 2.5% in October (v/s 2.6% expected) while the job-to-application ratio slightly went up to 1.30 after having stayed at 1.29 in the preceding three months. In a separate report, capital spending in 3Q23 advanced +3.4% y/y as expected after a +4.5% gain in the previous quarter.

Elsewhere yesterday, oil prices gave up their earlier gains following the conclusion of the OPEC+ meeting. T he group agreed additional supply cuts totalling about 900kb/d on top of an existing reduction of 1,300kb/d by Saudi Arabia and Russia . However, the move was in the form of “voluntary cuts” by several OPEC+ countries rather than a more typical agreement on reduced production quotas, leaving questions over how disciplined the implementation of the supply curbs will be. WTI crude had been trading c. 2% higher on the day prior to the news but fell by more than 5% intra-day and was down -2.44% by the close at $75.96/bbl. Brent crude saw more modest swings, and was down -0.32% to $82.83/bbl yesterday. Overnight, Brent crude prices are under pressure, trading -2.61% lower to trade at $80.67/bbl on softer output cuts .

To the day ahead now, and central bank speakers include Fed Chair Powell, the Fed’s Barr, Goolsbee and Cook, ECB President Lagarde, and the ECB’s Elderson and De Cos. Data releases include the global manufacturing PMIs, along with the ISM manufacturing reading from the US.

END

2 B) NOW NEWSQUAWK (EUROPE/REPORT)

European bourses bid whilst US Futures contained ahead of Fed’s Powell & US ISM – Newsquawk US Market Open

FRIDAY, DEC 01, 2023 – 06:22 AM

European equities extend gains; FTSE100 propped up by mining names; US futures contained pre-Powell

DXY is marginally weaker, with mild outperformance in the Kiwi post-hawkish commentary from Hawkesby

Bonds bounce and back on a firmer footing, after steep month-end retracement

Crude contained post-OPEC; base metals boosted by the softer Dollar & firmer Chinese data

Israel’s military said that Hamas violated the truce and fired towards Israeli territory, while it has resumed combat against Hamas in Gaza

Looking ahead, US and Canadian Manufacturing PMI (Final), Canadian Unemployment Rate, Speeches from Fed’s Powell, Goolsbee & Cook, ECB’s Lagarde

2. Listen to this report in the market open podcast (available on Apple and Spotify)

3. Trial Newsquawk’s premium real-time audio news squawk box for 7 days

EUROPEAN TRADE

EQUITIES

European equities, Eurostoxx50, +0.5%, are extending gains; FTSE100, +0.8%, which has been lifted by mining-related stocks.

European sectors are mostly in the green, with significant outperformance in Basic Resources, being propped up by mining stocks following broker upgrades at Anglo American, +6.4%, and Antofagasta, +4.7%; Optimised Personal Care & Grocery is marginally hampered by a Tesco, -1.3%, downgrade.

US Futures are trading on the front foot, albeit to a lesser extent in comparison to their European counterparts ahead of ISM & Powell; RTY, +0.3%, slightly outperforms.

Click here and here for the sessions European pre-market equity newsflow, including earnings.

Dollar drifts after month-end revival awaiting US manufacturing ISM for interim impetus before guidance from Fed Chair Powell; DXY dithering within 103.45-26 range.

Kiwi back in sight of 0.6200 vs Greenback after hawkish RBNZ rhetoric from Hawkesby.

Aussie encouraged by China’s Caixin manufacturing PMI rebound to 50.0+ level as AUD/USD hold above 0.6600.

Loonie underpinned ahead of Canadian LFS with USD/CAD sub-1.3550.

Cable firm on 1.2600 handle after upward revision to final UK manufacturing PMI.

Euro tethered to 1.0900 vs Dollar amidst nearby option expiries and post-mostly better than flash or forecast Eurozone manufacturing PMIs.

PBoC set USD/CNY mid-point at 7.1104 vs exp. 7.1458 (prev. 7.1018).

WTI and Brent are modestly firmer intraday in the aftermath of the OPEC+ confab on Thursday which ultimately underwhelmed the market given that output cuts are voluntary; as it stands, benchmarks are holding incrementally above the unchanged mark in narrow ranges around the prior session’s trough.

Spot gold holds an upward bias as the Dollar remains subdued; Base metals are firmer across the board amid upbeat Chinese data overnight, and upward bias in risk sentiment in Europe.

OPEC Secretariat announced several OPEC+ countries will conduct additional voluntary cuts to the total of 2.2mln BPD (exp. 2.0mln). It was confirmed that Brazil will join OPEC+ from January 2024.

Saudi Arabia will extend its voluntary cut of 1mln BPD to the end of Q1 2024 with its production to be approx. 9mln BPD and Russia is also to extend its voluntary cut in oil supplies until the end of Q1 2024 with its voluntary supply cut to reach 500k BPD. Kuwait is to make a further 135k BPD OPEC+ oil output cut, while the UAE is to make an additional 160k BPD OPEC+ output cut and Iraq is said to cut its production by 220k BPD in Q1. Conversely, Angola rejected its OPEC quota for 1.11mln BPD and said it will produce 1.18mln BPD, according to Bloomberg. Click here for the detailed headline.

US is purchasing 2.73mln bbls of oil for the strategic reserve, according to a document cited by Reuters.

US aims to halve Russia’s energy revenue by 2030, while Assistant Secretary of State for Energy Resources Pyatt said Western sanctions will continue for years to come to curb Moscow’s war machine, according to FT.

US President Biden and Angola’s President welcomed the launch of a US-Angola energy security dialogue in 2024 during a meeting on Thursday, according to the White House

US State Department said the US reiterated its pledge to ‘reconsider’ the steps it took to ease sanctions on Venezuela if the latter fails to comply with certain commitments by the end-November deadline, while it added that Venezuela must define steps for lifting bans on opposition candidates and begin the release of Venezuelan political prisoners and wrongfully detained Americans. It was later reported that banned Venezuelan candidates would be allowed to take their cases to a tribunal.

Morgan Stanley says commitment to new OPEC+ cuts appears to be uncertain, expect compliance to only be partial, Foresees Saudi Arabia ultimately extending the cuts to Q2-2024. Maintain Brent forecast at USD 85/bb and flat throughout 2024. Lowered OPEC+ production forecast for Q1-2024 by 0.6mln BPD, still see the oil market turning into a small surplus again in Q2 & Q3.