DEC 5//GOLD CLOSED DOWN $5.85 TO $2618.30//SILVER CLOSED DOWN 34 CENTS TO $24.17//PLATINUM CLOSED DOWN $17.15 TO $921.55 WHILE PALLADIUM CLOSED DOWN $33.55 TO $942.95//UPDATES ON HUGE PROBLEMS FACING DUBLIN WITH THEIR MASSIVE INTAKE OF MIGRANTS//UPDATES ON ISRAEL VS HAMAS: ISRAEL CONTEMPLATING USING SEA WATER TO FLOOD THE TUNNELS//ISRAEL IS NOW SURROUNDING THE SOUTHERN CITY OF KHAN YOUNIS//ISRAEL IS FINISHING UP ITS NORTHERN GAZA ATTACK SURROUNDING JABILYA//COVID UPDATES/VACCINE UPDATES// VACCINE INJURIES/DR PAUL ALEXANDER//SLAY NEWS//USA REPORTS THAT LABOUR DATA RE JOLTS JUST IMPLODED// SWAMP STORIES FOR YOU TONIGHT//

190 H BMO CAPITAL 246 323 C HSBC 250 363 H WELLS FARGO SEC 131 624 H BOFA SECURITIES 53 657 C MORGAN STANLEY 19 661 C JP MORGAN 30 271 686 C STONEX FINANCIA 2 690 C ABN AMRO 4 4 700 C UBS 14 732 C RBC CAP MARKETS 5 26 737 C ADVANTAGE 5 14 905 C ADM 6

TOTAL: 540 540 MONTH TO DATE: 11,993

JPMorgan stopped 271/540 contracts.

FOR DEC.:

GOLD: NUMBER OF NOTICES FILED FOR DEC/2023. CONTRACT: 540 NOTICES FOR 54,000 OZ or 1.6796 TONNES

total notices so far: 11,973 contracts for 1,197,300 oz (37.303 tonnes)

FOR DEC:

SILVER NOTICES 205 NOTICE(S) FILED FOR 1,015,000 OZ/

total number of notices filed so far this month : 2274 for 11,370,000 oz

XXXXXXXXXXXXXXXXXX Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

BOTH GLD AND SLV ARE FRAUDULENT VEHICLES

GLD

WITH GOLD DOWN $5.85//

INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD/ : / HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.30 TONNES OF GOLD FROM THE GLD

SOMEBODY RAIDED THE COOKIE JAR!

INVENTORY RESTS AT 881.12 TONNES

SLV//

WITH NO SILVER AROUND AND SILVER DOWN 34 CENTS AT THE SLV// SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A 0.305 MILLION OZ WITHDRAWAL.

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV.

CLOSING INVENTORY: 433.090 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A MEGA GIGANTIC SIZED 2740 CONTRACTS TO 142,826 AND FURTHER FROM THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THIS HUGE SIZED LOSS IN COMEX OI WAS ACCOMPLISHED WITH OUR HUGE $0.90 LOSS IN SILVER PRICING AT THE COMEX ON MONDAY. WE HAD A MAJOR SPEC SHORT COVERING EPISODE EARLY IN SUNDAY’S COMEX GLOBEX TRADING BUT AT HIGHER PRICES AND THEN WE HAD HUGE SPEC LIQUIDATION AS THE FED INDUCED RAID COMMENCED. WE HAD A GIGANTIC 700 T.A.S ISSUANCE AND THESE WILL BE USED FOR MANIPULATION LATER THIS MONTH/AS WELL AS TODAY.

CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON MONDAY NIGHT: 1614 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS. IT THUS LOOKS LIKE THE FED (GOV’T) IS BEHIND ALL OF THESE TRADES.

WE HAVE NOW SET ANOTHER RECORD LOW AT 114,102 CONTRACTS ///JULY 3.2023// OUR BANKERS WITH THE HELP OF SPECULATORS AND HIGH FREQUENCY TRADERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.90), AND WERE SUCCESSFUL IN KNOCKING SOME SILVER LONGS AS WE HAD A HUGE SIZED LOSS OF 1859 OI CONTRACTS ON OUR TWO EXCHANGES. HOWEVER WE DID HAVE SOME SPEC COVERINGS EARLY IN THE COMEX GLOBEX SESSION.

WE MUST HAVE HAD:

A HUGE SIZED 1614 ISSUANCE OF EXCHANGE FOR PHYSICALS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 18.755 MILLION OZ (FIRST DAY NOTICE) FOLLOWED BY TODAY’S STRONG 315,000 OZ E.F.P. JUMP TO LONDON//NEW TOTAL STANDING 18.115 MILLION OZ.+ 3.5 MILLION EX. FOR RISK= NEW TOTAL OF 21.615 MILLION OZ

//NEW STANDING FOR SILVER IS THUS 21.615 MILLION OZ

//HUGE SIZED COMEX OI LOSS/ HUGE SIZED EFP ISSUANCE/VI) HUGE SIZED NUMBER OF T.A.S. CONTRACT ISSUANCE 1614 CONTRACTS)/

HUGE SIZED EX.FOR RISK =700 CONTRACTS OR 3.5 MILLION OZ/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL – REMOVED 1040 CONTRACTS (the cme will no longer provide preliminary no to be except through a paywall)

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS DEC. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF DEC:

TOTAL CONTRACTS for 3 days, total 2236 contracts: OR 11.180 MILLION OZ (745 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 11.180 MILLION OZ

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH 2022: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 118.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 85.745 MILLION OZ (SMALLER THAN LAST MONTH)

AUGUST: 171.43 MILLION OZ (THIS MONTH IS GOING TO BE HUGE //2ND HIGHEST ON RECORD

SEPT: 72.705 MILLION OZ (SMALLER THIS MONTH)

OCT: 97.455 MILLION OZ

NOV. 50.050 MILLION OZ

DEC. 11.180 MILLION OZ

RESULT: WE HAD A HUGE SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 2740CONTRACTS WITH OUR HUGE LOSS IN PRICE OF $0.90 IN SILVER PRICING AT THE COMEX//MONDAY.,. THE CME NOTIFIED US THAT WE HAD A HUGE EFP ISSUANCE CONTRACTS: 700 ISSUED FOR FEB AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS. WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR DEC. OF 18.755 MILLION OZ FOLLOWED BY TODAY’S 315,000 OZ E.F.P. JUMP TO LONDON//NEW TOTAL STANDING 18.115 MILLION OZ//+ 3.5 MILLION EX. FOR RISK//NEW TOTAL 21.615 MILLION OZ.

NEW STANDING 21.615 OZ /// WE HAVE A HUGE SIZED LOSS OF 1859OI CONTRACTS ON THE TWO EXCHANGES. THE TOTAL OF TAS INITIATED CONTRACTS TODAY: A HUGE SIZED 1614CONTRACTS//HUGE FRONT END OF THE TAS CONTRACTS WERE LIQUIDATED DURING THE MONDAY COMEX SESSION. THE NEW TAS ISSUANCE MONDAY NIGHT (1614) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE., .

WE HAD 205 NOTICE(S) FILED TODAY FOR 1,015,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A VERY STRONG SIZED 14,810 CONTRACTS TO 494,948 AND CLOSER TO THE RECORD (SET JAN 24/2020) AT 799733 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: – REMOVED 895 CONTRACTS

WE HAD A VERY STRONG SIZED DECREASE IN COMEX OI ( 14,810 CONTRACTS) WITH OUR $43.15 LOSS IN PRICE//MONDAY. WE ALSO HAD A RATHER LIGHT INITIAL STANDING IN GOLD TONNAGE FOR DEC.. AT 44.914 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S 12,200 OZ QUEUE JUMP+ ANOTHER UNUSUAL ISSUANCE OF 1,490 EX. FOR RISK CONTRACTS FOR 149;000 OZ OR 4.634 TONNES/ // TOTAL GOLD STANDING FOR DEC SO FAR INCREASES TO 47.125 TONNES // ALL OF..THIS HAPPENED WITH OUR $43.15 LOSS IN PRICE WITH RESPECT TO MONDAY’S TRADING. WE HAD A STRONG SIZED LOSS OF 7667OI CONTRACTS (23.847)PAPER TONNES) ON OUR TWO EXCHANGES.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 7143CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 494,948

IN ESSENCE WE HAVE A STRONG SIZED DECREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 7,667 CONTRACTS WITH 14,810 CONTRACTS INCREASED AT THE COMEX// AND A STRONG SIZED 7143EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI LOSS ON THE TWO EXCHANGES OF 7667 CONTRACTS OR 23.847 TONNES. WE HAD 1490 CONTRACTS EXCHANGE FOR RISK FOR 4.634 TONNES//NEW TOTAL STANDING 21.615 TONNES.. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): A HUGE 2434 CONTRACTS.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A STRONG SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (7143 CONTRACTS) ACCOMPANYING THE VERY STRONG SIZED LOSS IN COMEX OI (14,810) //TOTAL LOSS FOR OUR THE TWO EXCHANGES: 7667 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR FORMER FORMAT OF BANKERS GOING LONG AND SPECULATORS GOING SHORT ,2.) FAIR INITIAL STANDING AT THE GOLD COMEX FOR DEC. AT 44.914 TONNES FOLLOWED BY TODAY’S 12,200 OZ QUEUE + 4.634 TONNES EX. FOR RISK//NEW STANDING 47.125 TONNES / / 3) CONSIDERABLE LONG LIQUIDATION AND HUGE TAS LIQUIDATION BUT ALSO MASSIVE SHORT LIQUIDATION AT HIGHER PRICES EARLY IN THE COMEX-GLOBEX SESSION 4) STRONG SIZED COMEX OPEN INTEREST LOSS/ 5) STRONG ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER///6: HUGE T.A.S. ISSUANCE: 2434 CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023 INCLUDING TODAY

DEC

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF DEC. :

TOTAL EFP CONTRACTS ISSUED: 18,419 CONTRACTS OR 1,841,900 OZ OR 57.290 TONNES IN 3 TRADING DAY(S) AND THUS AVERAGING: 6139 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 3 TRADING DAY(S) IN TONNES 57.290 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2022, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 57.290/3550 x 100% TONNES 1.61% OF GLOBAL ANNUAL PRODUCTION

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH/2022: 409.30 TONNES //FINAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 151.69 TONNES (WEAKER THAN LAST MONTH)

AUGUST: 195.28 TONNES (A STRONGER MONTH)//FINAL

SEPT: 254.709 TONNES (WILL BE LARGER THAN LAST MONTH AND A STRONG MONTH)

OCT. 248.09 TONNES. LIKE SILVER, THIS MONTH IS GOING TO BE A STRONG E.F.P. ISSUANCE.

NOV. 239.16 TONNES//WILL BE STRONG THIS MONTH,

DEC. 57.290 TONNES. THIS MONTH MAY TURN INTO A WHOPPER OF E.F.P. ISSUANCE

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF DEC. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (SEPT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER FELL BY A MEGA GIGANTIC SIZED 2740CONTRACTS OI TO 142,826 AND FURTHER FROM OUR COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 700 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

DEC 700 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 700 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 1700 CONTRACTS AND ADD TO THE 700 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A HUGE LOSS OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 1859CONTRACTS

THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES TOTAL 4.095 MILLION OZ

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS//

TUESDAY MORNING/MONDAY NIGHT

SHANGHAI CLOSED DOWN 50.42 PTS OR 1.67% //Hang Seng CLOSED DOWN 318.19 PTS OR 1.91% /The Nikkei CLOSED DOWN 455.45 PTS OR 1.37% //Australia’s all ordinaries CLOSED DOWN 0.90 % /Chinese yuan (ONSHORE) closed DOWN AT 7.1437 /OFFSHORE CHINESE YUAN CLOSED DOWN TO 7.1562 /Oil DOWN TO 72.75 dollars per barrel for WTI and BRENT DOWN AT 77.92/ Stocks in Europe OPENED MOSTLY GREEN// ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A VERY STRONG SIZED 14,810 CONTRACTS TO 494,948 WITH OUR HUGE LOSS IN PRICE OF $43.15 WITH RESPECT TO MONDAY TRADING. WE MUST HAVE CONSIDERABLE SPEC LIQUIDATIONS LATER IN THE SESSION (AT LOWER PRICES) AND SPEC CONVERINGS EARLY IN THE EVENING AT MUCH HIGHER PRICES.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE ACTIVE DELIVERY MONTH OF DEC..… THE CME REPORTS THAT THE BANKERS ISSUED A STRONG SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 7143 EFP CONTRACTS WERE ISSUED: : FEB 7143 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 7143CONTRACTS

ON A NET BASIS IN OPEN INTEREST WE LOST THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A STRONG SIZED TOTAL OF 7,667 CONTRACTS IN THAT 7143 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A VERY STRONG SIZED LOSS OF 14,810 COMEX CONTRACTS..AND THIS LOSS ON OUR TWO EXCHANGES HAPPENED WITH OUR HUGE LOSS IN PRICE OF $43.15//MONDAY COMEX. AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS DURING MID MONTH IN THE DELIVERY CYCLE), THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR MONDAY NIGHT WAS A STRONG SIZED 2434 CONTRACTS. THROUGHOUT THE PAST SEVERAL WEEKS, THE BANKERS SOLD OFF THE LONG SIDE OF THE SPREAD WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR SPREAD WHICH WILL BE LIQUIDATED TWO MONTHS HENCE)//. HOWEVER WE DID HAVE A RATHER STRANGE 1,490 CONTRACT EXCHANGE FOR RISK ISSUED FOR 4.634 TONNES. IT IS HERE THAT THE BUYER TAKES THE RISK THAT HE CAN TAKE DELIVERY OF PHYSICAL GOLD FORM THE BUYER. USUALLY EXCHANGE FOR RISK OCCURS LATE IN THE DELIVERY CYCLE AND RARELY ON DAY 3.

// WE HAVE A LIGHT AMOUNT OF GOLD TONNAGE STANDING: DEC (47.175 TONNES ( ACTIVE MONTH)

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

DEC. 42.471 + 4.634 TONNES OF EXCHANGE FOR RISK = 47.175 TONNES

THE SPECS/HFT WERE SUCCESSFUL IN LOWERING GOLD’S PRICE( IT LOST $43.15) //// AND WERE SUCCESSFUL IN KNOCKING SOME SPECULATOR LONGS AS WE HAD A STRONG SIZED LOSS OF7,667TOTAL CONTRACTS ON OUR TWO EXCHANGES. WE HAD A STRONG T.A.S. LIQUIDATION ON THE FRONT END OF MONDAY’S TRADING . THE T.A.S. ISSUED ON MONDAY NIGHT, WILL BE “PUT INTO THE BANK” TO BE USED AT A LATER DATE AT THE COLLUSIVE CHOOSING OF OUR BANKERS. WE ALSO EXPERIENCED SOME SPECULATOR SHORT COVERING

WE HAVE LOST A TOTAL OI OF 23.847 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR DEC. (44.914 TONNES) ON FIRST DAY NOTICE, FOLLOWED BY TODAY’S 12200 OZ QUEUE JUMP TO LONDON FOR 0,379 TONNES//NEW TOTAL STANDING FALLS TO 42.491 + 4.634 TONNES EXCHANGE FOR RISK : NEW TOTAL 47.175 TONNES../ ALL OF THIS WAS ACCOMPLISHED WITH OUR LOSS IN PRICE TO THE TUNE OF $43.15

WE HAD REMOVED –XXX CONTRACTS TO THE COMEX TRADES TO OPEN INTEREST (CROOKS)

NET LOSS ON THE TWO EXCHANGES 7667 CONTRACTS OR 766,700 OZ OR 23.847 TONNES.

Total monthly oz gold served (contracts) so far this month

11,973 notices 1,197300 oz 37.303 TONNES

Total accumulative withdrawals of gold from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of gold from the Customer inventory this month

x

0 dealer deposit:

total dealer deposits: nil oz

customer deposits: 0

total customer deposits: nil oz

we had 1 customer withdrawals

i) Out of JPMorgan: 385.812 oz

(12 kilobars)

total withdrawals 385.812 oz

Adjustments; 1

JPMorgan/customer to dealer: 24,113.250 oz (750 kilobars) or 3/4 tonne

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR DEC.

For the front month of DECEMBER we have an oi of 2228 contracts having LOST 111 contracts. .We had 233

contracts served upon MONDAY, so we GAINED or an additional 122 CONTRACTS OR 12,200 OZ (0.3794 tonnes) will stand for delivery at the comex

in this very active delivery month of December.

JAN. gained 120 contracts RISING TO 3666 contracts.

FEB LOST A WHOPPING 20,467 CONTRACTS FALLING TO 400,682.

We had 540 contracts filed for today representing 54000 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 30 notices were issued from their client or customer account. The total of all issuance by all participants equate to 540 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 1271 notice(s) was (were) stopped ( received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the DEC. /2023. contract month, we take the total number of notices filed so far for the month (11,973 x 100 oz ), to which we add the difference between the open interest for the front month of DEC. (2228 CONTRACTS) minus the number of notices served upon today 540 x 100 oz per contract equals 1,366,100 OZ OR 42.491 TONNES + 4.634 TONNES EX. FOR RISK ISSUED (FOR DELIVERY HERE) = 47.125 TONNES.

thus the INITIAL standings for gold for the DEC.contract month: No of notices filed so far (11,973) x 100 oz + (2228) {OI for the front month} minus the number of notices served upon today (540) x 100 oz) which equals 1,366,100 oz standing OR 42.491 TONNES = 47.125 TONNES

TOTAL COMEX GOLD STANDING FOR DEC: 47.125 TONNES WHICH IS LIGHT FOR THE BIGGEST ACTIVE DELIVERY MONTH IN THE CALENDAR. THEY PROBABLY KNOW THAT NO REAL GOLD IS PRESENT AT THE COMEX.

To calculate the number of silver ounces that will stand for delivery in DEC. we take the total number of notices filed for the month so far at 2274 x 5,000 oz = 10,345,000 oz

to which we add the difference between the open interest for the front month of DEC. (1554) and the number of notices served upon today 205 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the DEC/2023 contract month: 2274 (notices served so far) x 5000 oz + OI for the front month of DEC. (1554) – number of notices served upon today (205 )x 500 oz of silver standing for the DEC contract month equates to 18.115 MILLION OZ. However we had another strange transaction as silver also experienced a very early issuance of 700 exchange for risk contracts or 3.5 million oz. The buyer assumes the risk that he is going to be delivered upon. Thus total silver standing at the comex advances to 21,615 million oz.

There are 43.825 million oz of registered silver.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS//

BOTH GLD AND SLV ARE MASSIVE FRAUDS!

DEC 5/WITH GOLD DOWN $5.85 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.30 TONNES OF GOLD FROM THE GLD. // / / // // INVENTORY RESTS AT 881.12 TONNES

DEC 4/WITH GOLD DOWN $43.15 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.31 TONNES OF GOLD FROM THE GLD. // / / // // INVENTORY RESTS AT 878.82 TONNES

DEC 1/WITH GOLD UP $32.05 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.02 TONNES OF GOLD FROM THE GLD. // / / // // INVENTORY RESTS AT 876.51 TONNES

NOV 30/WITH GOLD DOWN $8.70 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.02 TONNES OF GOLD FROM THE GLD. // / / // // INVENTORY RESTS AT 878.53 TONNES

NOV 29/WITH GOLD UP $7.20 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.73 TONNES OF GOLD FROM THE GLD. // / / // // INVENTORY RESTS AT 880.55 TONNES

NOV 28/WITH GOLD UP $26.45 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD: // / / // // INVENTORY RESTS AT 882.28 TONNE

NOV 27/WITH GOLD UP $9,85 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD: // / / // // INVENTORY RESTS AT 882.28 TONNES

NOV 24/WITH GOLD UP $11.20 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.15 TONNES OF GOLD FROM THE GLD// / / // // INVENTORY RESTS AT 882.28 TONNES

NOV 22/WITH GOLD DOWN $8.45 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD / / // // INVENTORY RESTS AT 883.43 TONNES

NOV 21/WITH GOLD UP $21.65 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD / / // // INVENTORY RESTS AT 883.43 TONNES

NOV 20/WITH GOLD DOWN $4.15 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD A MAMMOTH DEPOSIT OF 12.98 TONNES INTO THE GLD:/ / // // INVENTORY RESTS AT 883.43 TONNES

NOV 17/WITH GOLD DOWN $1.85 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD:/ / // // INVENTORY RESTS AT 870.45 TONNES

NOV 16/WITH GOLD UP $22.70 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD:/ / // // INVENTORY RESTS AT 870.45 TONNES

NOV 15/WITH GOLD DOWN $1.00 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD:/ / // // INVENTORY RESTS AT 870.45 TONNES

NOV 14/WITH GOLD UP $16.35 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD:/ / // //A DEPOSIT OF 2.3 TONNES OF GOLD INTO THE GLD// INVENTORY RESTS AT 870.45 TONNES

NOV 13/WITH GOLD UP $12.00 TODAY:SMALL CHANGES IN GOLD INVENTORY AT THE GLD:/ / // //A DEPOSIT OF .87 TONNES OF GOLD INTO THE GLD// INVENTORY RESTS AT 868.15 TONNES

NOV 10/WITH GOLD DOWN $30.70 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD:/ / // // INVENTORY RESTS AT 867.28 TONNES

NOV 9/WITH GOLD UP $12.50 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD:/ / // // INVENTORY RESTS AT 867.28 TONNES

NOV 8/WITH GOLD DOWN $14.95 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD:A MASSIVE DEPOSIT OF 4.04 TONNES OF GOLD INTO THE GLD/ / // // INVENTORY RESTS AT 867.28 TONNES

NOV 7/WITH GOLD DOWN $14.70 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD:A DEPOSIT OF 4.33 TONNES OF GOLD INTO THE GLD/ / // // INVENTORY RESTS AT 863.24 TONNES

NOV 6/WITH GOLD DOWN $9.90 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD:A DEPOSIT OF 1.73 TONNES OF GOLD INTO THE GLD/ / // // INVENTORY RESTS AT 863.24 TONNES

NOV 3/WITH GOLD UP $5.75 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD: / // // INVENTORY RESTS AT 861.51 TONNES

NOV 2/WITH GOLD UP $6.55 TODAY:BIG CHANGES IN GOLD INVENTORY AT THE GLD: A HUGE DEPOSIT OF 2.02 TONNES OF GOLD INTO THE GLD/ // // INVENTORY RESTS AT 861.51 TONNES

NOV 1/WITH GOLD DOWN $6.15 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD // // INVENTORY RESTS AT 859.49 TONNES

OCT 31/859.49 TONNES//

OCT 30/WITH GOLD UP $7.80 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD // // INVENTORY RESTS AT 861.80 TONNES

OCT 27/WITH GOLD UP $1.20 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD // // INVENTORY RESTS AT 861.80 TONNES

OCT 26/WITH GOLD UP $2.90 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF 1.73 TONNES OF GOLD INTO THE GLD// // INVENTORY RESTS AT 861.80 TONNES

OCT 25/WITH GOLD UP $9.00 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD:/: //: // INVENTORY RESTS AT 860.07 TONNES

GLD INVENTORY: 891.12 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

DEC 5/WITH SILVER DOWN 34 CENTS TODAY:SMALL CHANGES IN SILVER INVENTORY AT THE SLV/: A WITHDRAWAL OF 0.305 MILLION OZ FROM THE SLV// //://// //INVENTORY RESTS AT 433.090 MILLION OZ

DEC 4/WITH SILVER DOWN 90 CENTS TODAY:HUGE CHANGES IN SILVER INVENTORY AT THE SLV/: A WITHDRAWAL OF 0.7333 MILLION OZ FROM THE SLV// //://// //INVENTORY RESTS AT 433.395 MILLION OZ

DEC 1/WITH SILVER UP 15 CENTS TODAY:HUGE CHANGES IN SILVER INVENTORY AT THE SLV/: A WITHDRAWAL OF 1.923 MILLION OZ FROM THE SLV// //://// //INVENTORY RESTS AT 434.128 MILLION OZ

NOV 30/WITH SILVER UP 20 CENTS TODAY:NO CHANGES IN SILVER INVENTORY AT THE SLV/ //://// //INVENTORY RESTS AT 436.051 MILLION OZ

NOV 29/WITH SILVER UP 15 CENTS TODAY:HUGE CHANGES IN SILVER INVENTORY AT THE SLV” A MASSIVE WITHDRAWAL OF 4.122 MILLION OZ FROM THE SLV// //://// //INVENTORY RESTS AT 436.051 MILLION OZ

NOV 28/WITH SILVER UP 64 CENTS TODAY:NO CHANGES IN SILVER INVENTORY AT THE SLV //://// //INVENTORY RESTS AT 440.173 MILLION OZ

NOV 27/WITH SILVER UP 32 CENTS TODAY:HUGE CHANGES IN SILVER INVENTORY AT THE SLV //:////A WITHDRAWAL OF 1,008,000 OZ FROM THE SLV. //INVENTORY RESTS AT 440.173 MILLION OZ

NOV 24/WITH SILVER UP 70 CENTS TODAY:HUGE CHANGES IN SILVER INVENTORY AT THE SLV //:////A WITHDRAWAL OF 549,000 OZ FROM THE SLV. //INVENTORY RESTS AT 441.181 MILLION OZ

NOV 22/WITH SILVER DOWN 21 CENTS TODAY:NO CHANGES IN SILVER INVENTORY AT THE SLV //://// //INVENTORY RESTS AT 441.730 MILLION OZ

NOV 21/WITH SILVER UP 32 CENTS TODAY:HUGE CHANGES IN SILVER INVENTORY AT THE SLV A DEPOSIT OF 2.794 OZ FROM THE SLV//://// //INVENTORY RESTS AT 441.730 MILLION OZ

NOV 20/WITH SILVER DOWN 26 CENTS TODAY:HUGE CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 1,824,000 OZ FROM THE SLV//://// //INVENTORY RESTS AT 438.936 MILLION OZ

NOV 17/WITH SILVER DOWN 6 CENTS TODAY:HUGE CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 1,832,000 OZ FROM THE SLV//://// //INVENTORY RESTS AT 437,104 MILLION OZ

NOV 16/WITH SILVER UP 38 CENTS TODAY:SMALL CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 778,000 OZ FROM THE SLV//://// //INVENTORY RESTS AT 440.768 MILLION OZ

NOV 15/WITH SILVER UP 39 CENTS TODAY:NO CHANGES IN SILVER INVENTORY AT THE SLV://// //INVENTORY RESTS AT 441.587 MILLION OZ

NOV 14/WITH SILVER UP 78 CENTS TODAY:SMALL CHANGES IN SILVER INVENTORY AT THE SLV:A DEPOSIT OF 183,000 OZ INTO THE SLV ////// //INVENTORY RESTS AT 441.587 MILLION OZ

NOV 13/WITH SILVER UP 5 CENTS TODAY:NO CHANGES IN SILVER INVENTORY AT THE SLV: ////// //INVENTORY RESTS AT 441.364 MILLION OZ

NOV 10/WITH SILVER DOWN 59 CENTS TODAY:HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF .733 MILLION OZ INTO THE SLV////// //INVENTORY RESTS AT 441.364 MILLION OZ

NOV 9/WITH SILVER UP 17 CENTS TODAY:NO CHANGES IN SILVER INVENTORY AT THE SLV: //// //INVENTORY RESTS AT 440.631 MILLION OZ

NOV 8/WITH SILVER UP 13 CENTS TODAY:NO CHANGES IN SILVER INVENTORY AT THE SLV: //// //INVENTORY RESTS AT 440.631 MILLION OZ

NOV 7/WITH SILVER DOWN 59 CENTS TODAY:NO CHANGES IN SILVER INVENTORY AT THE SLV: //// //INVENTORY RESTS AT 440.631 MILLION OZ

NOV 6/WITH SILVER DOWN 6 CENTS TODAY:NO CHANGES IN SILVER INVENTORY AT THE SLV: //// //INVENTORY RESTS AT 440.631 MILLION OZ

NOV 3/WITH SILVER UP 41 CENTS TODAY:BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.638 MILLION OZ OF SILVER FROM THE SLV///// /// /INVENTORY RESTS AT 440.631 MILLION OZ

NOV 2/WITH SILVER UP 11 CENTS TODAY:BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.924 OZ OF SILVER FROM THE SLV///// /// /INVENTORY RESTS AT 439.993 MILLION OZ

NOV 1/WITH SILVER DOWN 11 CENTS TODAY:BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 916,000 OZ OF SILVER FROM THE SLV///// /// /INVENTORY RESTS AT 441.917 MILLION OZ

OCT 31/442.833 MILLION OZ///INVENTORY

OCT 30/WITH SILVER UP 46 CENTS TODAY:NO CHANGES IN SILVER INVENTORY AT THE SLV: /// /// /INVENTORY RESTS AT 443.750 MILLION OZ

OCT 27/WITH SILVER UP 3 CENTS TODAY:BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 641,000 OZ FROM THE SLV/// /// /INVENTORY RESTS AT 443.750 MILLION OZ

OCT 26/WITH SILVER DOWN 14 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/ /// /INVENTORY RESTS AT 444.391 MILLION OZ

OCT 25/WITH SILVER DOWN 6 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/ /// /INVENTORY RESTS AT 444.391 MILLION OZ

CLOSING INVENTORY 433.090 MILLION OZ//

PHYSICAL GOLD/SILVER COMMENTARIES

1:Peter Schiff/Mike Maharrey

2,c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens, John Rubino

3. CHRIS POWELL//GATA GOLD COMMENTARIES:

END

4, OTHER IMPORTANT GOLD/SILVER COMMENTARIES/ l

all central banks are buying physical gold except the Fed

.

Russians bought record number of gold bars in 2022, data shows

Reuters

February 3, 20236:40 AM ESTUpdated 10 months ago

[1/2]Ingots of 99.99 percent pure gold are placed in a workroom at Krastsvetmet precious metals plant in the Siberian city of Krasnoyarsk, Russia, January 31, 2023. REUTERS/Alexander Manzyuk Acquire Licensing Rights

Summary

Companies

This content was produced in Russia, where the law restricts coverage of Russian military operations in Ukraine.

MOSCOW, Feb 3 (Reuters) – Russians bought an all-time record number of gold bars in 2022, finance ministry data showed on Friday, as tax cuts on precious metals encouraged people to stock up on bullion as a safe asset.

Moscow scrapped its 20% VAT on physical gold trades for individuals last March in a bid to draw people away from using the U.S. dollar as a safe haven.

It also exempted people from paying income tax on profits gained from selling gold bars, further boosting

END

5 a. IMPORTANT COMMENTARIES ON COMMODITIES CORN

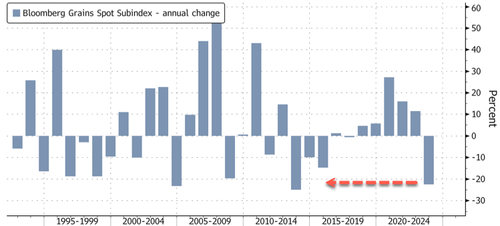

Sliding Corn Prices Sends Grain Index To Decade-Low

TUESDAY, DEC 05, 2023 – 04:15 AM

Corn prices tumbled to a three-year low as mounting supplies from the US and Brazil collided with sliding demand. This downturn helped push down the Bloomberg Grain Spot Subindex, which tracks near-term futures contracts for soybeans, corn, and wheat, leading to its largest annual decline in a decade.

Bloomberg Grain Spot Subindex records the worst yearly slump since 2013.

Bloomberg Grain Spot Subindex records the worst yearly slump since 2013.

Ag traders are waiting for a US Department of Agriculture’s monthly WASDE report on Friday to gauge the status of foreign and domestic harvests.

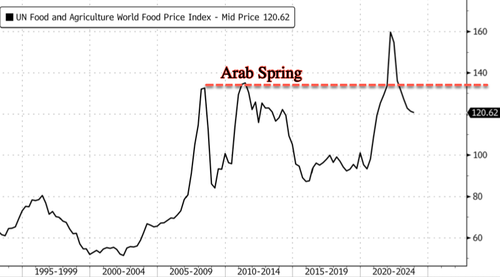

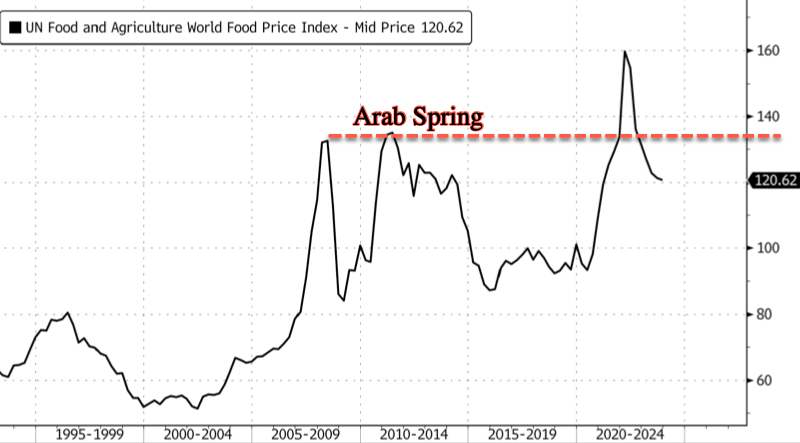

Despite the large decline in grain prices, the Food and Agriculture Organization’s global food price index, which tracks the most globally traded food commodities, is still at highs responsible for the Arab Spring food riots across the Middle East in 2010-11.

Last month, Sara Menker, founder and CEO of Gro Intelligence, warned the current global food crisis has surpassed that of the Arab Spring because crop prices remain high while local currencies around the world have plunged against the dollar.

end

END

5 B GLOBAL COMMODITY ISSUES/FOOD IN GENERAL//FREIGHT

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS TUESDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED DOWN AT 7.1434

OFFSHORE YUAN: DOWN TO 7.1562

SHANGHAI CLOSED DOWN 50.42PTS OR 1.67%

HANG SENG CLOSED DOWN 318.19 PTS OR 1.91%

2. Nikkei closed DOWN 455.45 PTS OR 1.3%

3. Europe stocks SO FAR: MOSTLY GREEN

USA dollar INDEX UP TO 103.73 EURO FALLS TO 1.0814 DOWN 23 BASIS PTS

3b Japan 10 YR bond yield: FALLS TO. +.661 Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 147.06/JAPANESE YEN FALLING AS WELL AS LONG TERM 10 YR. YIELDS RISING //EVENTUALLY THIS WILL BREAK THE JAPANESE CENTRAL BANK

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen UP CHINESE ONSHORE YUAN: DOWN// OFFSHORE: DOWN

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil DOWN for WTI and DOWN FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund DOWN TO +2.2895***/Italian 10 Yr bond yield DOWN to 4.043** /SPAIN 10 YR BOND YIELD DOWN TO 3.288…**

3i Greek 10 year bond yield DOWN TO 3.428

3j Gold at $2028.00 silver at: 24.33 1 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble DOWN 1 AND 24 /100 roubles/dollar; ROUBLE AT 92.16//

3m oil into the 72 dollar handle for WTI and 77 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 147,06// 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 0.661% STILL ON CENTRAL BANK (JAPAN) INTERVENTION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.8738 as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.9451 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.226 DOWN 6 BASIS PTS…

USA 30 YR BOND YIELD: 4.387 DOWN 5 BASIS PTS/

USA 2 YR BOND YIELD: 4.627 DOWN 3 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 28.94…(TURKEY SET TO BLOW UP FINANCIALLY)

GREAT BRITAIN/10 YEAR YIELD: DOWN 4 BASIS PTS AT 4.1560

end

2.a Overnight: Newsquawk and Zero hedge

Stocks, Futures Slide For Second Day As Rally Fizzles Ahead Of Jobs Data Deluge

TUESDAY, DEC 05, 2023 – 08:16 AM

US stocks were set to extend Monday’s drop into a second day after hitting 20-month highs, as the recent rally looks increasingly stretched and traders scale back rate-cut bets while Chinese stocks tumbled to fresh five year lows after Moody’s downgraded China’s credit outlook to negative on soaring debt. As of 7:40am ET, S&P 500 futures slid 0.4%, trading at session lows, after the benchmark rose last week to its highest since March 2022 on bets the Fed would soon pivot to monetary easing; Nasdaq 100 futures dropped 0.5%. Bond yields eased as did the USD; 10Y TSY yield dropped 2bps to 4.22%. Commodities were seeing a bid within Ags and Energy while metals underperformed on China weakness despite better than expected PMIs. Bitcoin held near a 19-month high, just below the $42,000 mark.Today’s macro data focus is on JOLTS job openings and ISM Services (52.3 consensus vs. 51.8 prior).

In premarket trading, Take-Two Interactive shares declined after the company’s Rockstar Games unit released the first trailer for the highly-anticipated Grand Theft Auto VI video game. With the title planned for 2025, analysts were disappointed by the lack of an exact release date. Robinhood gained after the online brokerage said November crypto notional trading volumes were about 75% above October levels. Here are some other notable premarket movers:

Recommended Videos

Stock market rally is sustainable: asset manager

32K

5

Ad

Skip Ad

Albemarle and Livent fell after Piper Sandler cut its rating on both stocks to underweight from neutral. The broker said the downgrades reflect a significant deterioration of global lithium markets.

Gitlab jumped 16% as after the application software company reported third-quarter results that beat expectations and raised its full-year forecast.

JOANN shares slumped 18% after the fabric and crafts retailer reported third-quarter net sales that missed estimates and a wider-than-expected adjusted loss per share.

Nio ADRs gained 3.1% after the Chinese EV maker reported profitability that beats estimates, including better-than-expected adjusted earnings and vehicle gross margin. Revenue outlook for current quarter is well below estimates.

Take-Two Interactive shares declined 6.1% after the company’s Rockstar Games unit released the first trailer for the highly-anticipated Grand Theft Auto VI video game, which will be released in 2025. While analysts saw the trailer as positive, they note the game being released in 2025 and the lack of an exact release date as a source of disappointment.

As November’s epic 12% rally on hopes that global central bankers were ready to shift to easy policy fizzles, investors are starting to doubt if it will extend in December especially after Goldman’s flows guru Scott Rubner warned that the rally has “Absolutely Run Out Of Gas.” As such, what had become the prevailing wisdom last month — that a “Goldilocks” scenario can be fulfilled by US central bankers in early, rapid rate cuts in 2024 — is now grounds for debate. US jobs data later in the week is seen as a key piece of the puzzle to understanding the economy and the risk that wage growth fans inflation, leading to higher borrowing costs for longer. A salvo of US job numbers are expected every day for the rest of week, including JOLTS, ADP, jobless claims, non-farm payrolls and the unemployment rate.

“Even though US PMI and JOLTs data may increase market volatility in the afternoon, the “wait and see” stance will likely continue as investors brace for the crucial US jobs data due tomorrow and Friday,” said Pierre Veyret, a technical analyst at ActivTrades. “Meanwhile, a particular focus should be maintained towards central bankers’ speeches, as traders need to check whether their dovish expectations will be confirmed.”

Meanwhile, market breadth on the S&P 500 now looks extremely extended with the benchmark now firmly overbought for more than two weeks, while Goldman pointing out that the proportion of index members in overbought territory reached 33%, the highest reading since June 2020.

“It’s remarkable how quickly we’ve swung from different market narratives this year,” Hugh Gimber, global market strategist for JPMorgan Asset Management in London, said in an interview on Bloomberg Television. “Now it feels like we’ve gone full circle again.”

European stocks were mixed and US equity futures are down after Moody’s downgraded China’s sovereign debt outlook to negative. Euro Stoxx 50 rises 0.3%. IBEX outperforms peers, adding 0.5%, FTSE 100 lags, dropping 0.4%, after LSE faced issues earlier. Real estate, utilities and construction are the strongest-performing sectors in Europe. German markets got a boost from comments from European Central Bank policymaker Isabel Schnabel that further interest rate hikes are unlikely. The DAX Index added 0.2%, closing in on a record high and outperforming the broader Stoxx 600. Here are the biggest movers Tuesday:

Ericsson rises as much as 9.9%, among the top performers on the Stoxx 600, after winning a contract with AT&T that could amount to almost $14 billion over five years. Nokia, which lost out on the contract, fell as much as 10%

SSP Group gains as much as 4.9% after the food services company boosted its 2024 revenue guidance. The guidance should be “reassuring” for the outlook of travel retail, RBC said

Pirelli shares rise as much as 6%, the most intraday in a year, after UBS upgraded the Italian tiremaker to buy, citing earnings upside risk, deleveraging potential and an attractive valuation

Alm Brand gains as much as 5.9% after the Danish financial services firm announced a DKK250 million share buyback program due to its “very strong solvency coverage”

Moonpig shares advance as much as 3.5% after the onling gifting company reported first-half underlying Ebitda and adjusted earnings per share that beat estimates

Hapag-Lloyd and Maersk decline as Barclays says the global shipping market faces “the dawn of a new annus horribilis” due to industry oversupply and muted demand

Ashtead falls as much as 5.4% after the UK-based industrial and construction equipment rental firm reported 2Q earnings. While the results were solid, they may not reassure fully, RBC says

Carl Zeiss Meditec drops as much as 4.9% after JPMorgan initiated coverage on the German medical optics firm with an underweight rating

Auction Technology drops as much as 6.2% after Barclays downgraded its rating on the online auction technology provider to equal-weight, citing a more cautious view in the near term

Earlier in the session, Asian stocks tumbled and were on pace for their worst day since Nov. 20 as sharp selling in Chinese and Hong Kong shares hurt sentiment. The MSCI Asia Pacific Index slid as much as 1.1%, with Tencent, Samsung Electronics and AIA Group leading losses. Mainland China and Hong Kong stocks slumped in the wake of a move by Moody’s Investors Service to cut its outlook on the nation’s sovereign debt to negative. The MSCI China Index slid as much as 2.3% toward its lowest close since November 2022. On the mainland, the benchmark CSI 300 Index finished 1.9% lower as foreigners sold the largest amount of shares since mid-October. Sentiment was also dragged by a selloff in technology stocks across the region, tracking similar losses for US tech giants Monday. The MSCI Asia Information Technology Index fell the most since October.

“The accumulation of news over last few weeks would be raising questions on China’s economy into 2024,” said Xin-Yao Ng, an investment director for Asian equities at abrdn. “Macro data has been soft. The big concern over the property slump remains as sales volume are still very weak.”

Hang Seng and Shanghai Comp retreated which saw the latter breach the psychological 3,000 level to the downside amid lingering frictions after China criticised the US for seeing it as a threat following calls by Commerce Secretary Raimondo for more funds to back chip curbs, while encouraging Caixin Services PMI data which printed a 3-month high at 51.5 (exp. 50.7) only provided a brief tailwind.

Nikkei 225 continued to weaken and slipped below the 33,000 level despite softer-than-expected Tokyo inflation data.

ASX 200 was led lower by the commodity-related industries with underperformance in gold miners after the precious metal faded the recent surge, while sentiment was also not helped by weak data and after the unsurprising RBA rate decision in which the central bank kept rates unchanged and reiterated its forward guidance.

In FX, the Bloomberg dollar spot index was steady. JPY and GBP were the strongest performers in G-10 FX, AUD and NZD underperformed.

EUR/USD pared a loss of 0.3% to trade flat at 1.0839, after the ECB’s Schnabel said that the moderation in inflation has made another rate hike unlikely; euro-area bonds rallied

AUD/USD sank as much as 0.8% to 0.6569, a one-week low, after the Reserve Bank left its policy rate unchanged and said inflation is continuing to slow

USD/CNH and USD/CNY steadied following Moody’s cut to its Chinese debt outlook to negative

In rates, treasuries held small gains amid steeper rally in bunds after ECB’s Schnabel said she sees further rate hikes as unlikely, citing a “remarkable” fall in inflation, according to Reuters. US yields are richer by 1bp-2bp across the curve with spreads flatter but still within 1bp of Monday close; 10-year yields around 4.23% with bunds and gilts outperforming by 3bp in the sector as core European rates drive gains. German bonds rose, with the front end outperforming comparable USTs and gilts, and money markets up their ECB easing bets after ECB’s Isabel Schnabel said that further interest rate hikes are unlikely. Peripheral spreads tighten to Germany. Dollar IG issuance slate includes JPMorgan 3Y and IADB 3Y; seven names priced almost $9b Monday and at least one stood down. Treasury coupon issuance is on hiatus until next week’s 3-, 10- and 30-year sales. US session includes ISM services index and JOLTS job openings data.

In commodities, oil steadied after three days of losses. Saudi Arabia said recent cuts by OPEC+ would be honored in full and could be extended. Most base metals trade in the red. Spot gold falls roughly $3 to trade near $2,027/oz.

Bitcoin held near a 19-month high, just below the $42,000 mark.

To the day ahead now, and data releases from the US include the ISM services index for November, and the JOLTS job openings for October. Elsewhere, there’s the global services and composite PMIs for November and Euro Area PPI for October. From central banks, we’ll get the ECB’s Consumer Expectations Survey for October.

Market Snapshot

S&P 500 futures down 0.2% to 4,566.50

STOXX Europe 600 up 0.1% to 466.33

MXAP down 1.0% to 159.84

MXAPJ down 1.1% to 497.42

Nikkei down 1.4% to 32,775.82

Topix down 0.8% to 2,342.69

Hang Seng Index down 1.9% to 16,327.86

Shanghai Composite down 1.7% to 2,972.30

Sensex up 0.6% to 69,290.91

Australia S&P/ASX 200 down 0.9% to 7,061.55

Kospi down 0.8% to 2,494.28

German 10Y yield little changed at 2.30%

Euro little changed at $1.0840

Brent Futures up 1.1% to $78.85/bbl

Gold spot up 0.1% to $2,030.89

U.S. Dollar Index down 0.10% to 103.60

Top Overnight News

Moody’s lowered China’s credit outlook to negative from stable while retaining a long-term rating of A1 on the nation’s sovereign bonds, according to a statement. China’s usage of fiscal stimulus to support local governments and its spiraling property downturn is posing risks to the nation’s economy, the grader said. BBG

China’s Caixin services PMI for Nov comes in ahead of plan at 51.5, up from 50.4 in Oct and above the Street’s 50.5 expectation. RTRS

Japan’s Tokyo CPI undershoots the Street in Nov, w/the core (ex-food/energy) number coming in at +3.6% (down from +3.8% in Oct and below the Street’s +3.7% forecast). BBG

South Korea’s CPI undershoots the Street in Nov, with the core number coming in at +3% (down from +3.2% and below the Street’s +3.1% forecast). BBG

The ECB can take further interest rate hikes off the table given a “remarkable” fall in inflation and policymakers should not guide for rates to remain steady through mid-2024, ECB board member Isabel Schnabel told Reuters. RTRS

Qatar Holding, a subsidiary of the Qatar Investment Authority that helped bail out Barclays during the global financial crisis, launched the sale on Monday of almost 362mn shares of Barclays, worth about £510mn. The QIA is Barclays’ second-biggest shareholder, according to Bloomberg data, and the stock sale is expected to reduce its stake from 5.3% to 2.9%. FT

The head of Airbus has said the group “might need some support” from European governments for a new, multibillion-dollar commercial aircraft program as it gears up for a successor to its best-selling A320 family of jets. FT

Israeli forces closed in on the city of Khan Younis in the Gaza Strip on Tuesday, engaging in close combat with Hamas fighters in what could be the decisive battle of the two-month-old war, while residents fled from the fighting amid a worsening humanitarian plight. WSJ

CVS Health will overhaul how drugs are paid for, adopting a “cost plus” model whereby it will charge a simple markup and a flat fee on top of what it pays for pharmaceuticals. WSJ

A more detailed look at global markets courtesy of Newsquawk

APAC stocks declined following the mostly negative lead from Wall St where the major indices were choppy and ultimately weighed amid a rebound in yields ahead of key data releases. ASX 200 was led lower by the commodity-related industries with underperformance in gold miners after the precious metal faded the recent surge, while sentiment was also not helped by weak data and after the unsurprising RBA rate decision in which the central bank kept rates unchanged and reiterated its forward guidance. Nikkei 225 continued to weaken and slipped below the 33,000 level despite softer-than-expected Tokyo inflation data. Hang Seng and Shanghai Comp retreated which saw the latter breach the psychological 3,000 level to the downside amid lingering frictions after China criticised the US for seeing it as a threat following calls by Commerce Secretary Raimondo for more funds to back chip curbs, while encouraging Caixin Services PMI data which printed a 3-month high at 51.5 (exp. 50.7) only provided a brief tailwind.

Top Asian News

RBA kept the Cash Rate Target unchanged at 4.35%, as expected, while it reiterated its forward guidance that whether further tightening is required to ensure inflation returns to the target in a reasonable timeframe will depend upon data and evolving assessment of risks. RBA also repeated that the Board remains resolute in its determination to return inflation to target and will do what is necessary to achieve that outcome, as well as noted there are still significant uncertainties around the outlook and that the limited information received on the domestic economy since the November meeting has been broadly in line with expectations.

Moody’s affirms China’s A1 rating; changes outlook to Negative from Stable. Reflects risks relating to persistently lower medium-term economic growth and ongoing downsizing of the property sector.

Chinese Finance Ministry says Chinese economy will maintain its rebound and positive trend; we expect the Q4 economy to keep the positive trend

Foxconn (2317 TW) November Sales +17.95% Y/Y (October -4.56% Y/Y); outlook for Q4 should be better than the original guidance for “significant growth”; revenue performance in the first two months of Q4 has been slightly higher than expected

European equities, Eurostoxx50 +0.3%, are mixed, with the FTSE100, -0.2%, once again the relative underperformer, largely hampered by ongoing losses in Basic Resources which is the worst performing sector. European sectors are mixed with a slight positive tilt; Real Estate outperforms following broker upgrades at British Land, +1.3%, and Land Securities, +0.8%. US equity futures are trading on the backfoot, continuing the losses seen in the prior days’ session as the year’s final few key events/releases begin with JOLTS.

Top European News

ECB’s Schnabel says current level of restriction is sufficient, has increased confidence that 2% target will be met in 2025; must not declare victory prematurely; further hikes “rather unlikely” after November inflation data. Must be more cautious with rate cuts than markets pricing; further hikes “rather unlikely” after November inflation data. Inflation developments are encouraging, fall in core prices is remarkable

YouGov/Citi survey showed the British public’s expectation for inflation in 5yr-10yr’s time rose to 3.5% from a prior 3.3% view in September.

German Ifo: Retailers Expect Little Help from Christmas Sales; Business Situation -8.8 (prev. -13.5).

Kantar UK Supermarket update (Nov): grocery price inflation 9.71% in the four weeks to Nov 26th; UK grocery sales +6.3% Y/Y.

ECB Survey of Consumer Expectations (October 2023): median consumer inflation expectations for the next 12 months and for three years ahead remained unchanged.

The London Stock Exchange (LSEG LN) is currently investigating an issue impacting its trading/information system. We are now resuming trading on impacted instruments. Instruments will go into auction at 09:55GMT with uncrossing beginning at 10:15GMT. All live orders remain on the system. LSE: Impacted securities are now in regular trading.

FX

DXY extended on the upper end of its overnight range towards 103.84 ahead of the European equity cash open and now resides within the middle of today’s range of 103.84-53.

EUR/USD is trading around flat having bounced off lows on revisions higher to Services & Composite PMI data.

The Japanese Yen is the G10 outperformer at the time of writing amid a combination of a pullback in US yields coupled with the broader risk aversion overnight.

AUD, NZD, CAD are all softer to varying degrees amid the initial broader risk tone, but the Aussie is the marked G10 laggard in the aftermath of the RBA policy decision which lacked hawkish undertones.

PBoC set USD/CNY mid-point at 7.1127 vs exp. 7.1476 (prev. 7.1011).

China’s major state-owned banks were seen acquiring dollars via onshore swaps and selling them in the spot FX market, while it was also reported that the RBI was likely selling dollars near the 83.38-83.39 rupee level, according to sources and traders cited by Reuters.

Fixed Income

ECB’s Schnabel (Hawk) says that further hikes are now “rather unlikely” following the November inflation data.

Commentary which drove Bunds to a 134.17 peak; though, upward revisions to PMIs have prompted a pullback, but one that is limited by the reports internal commentary.

Similar action has been seen in Gilts which perhaps derived initial support from the latest YouGov findings as well.

Finally, USTs are directionally in-fitting but with magnitudes more contained at the mid-point of 110.10 to 110.18 parameters ahead of JOLTS & PMIs/ISM.

UK sells GBP 1.5bln 0.75% 2033 I/L Gilt: b/c 2.68x (prev. 2.94x) and real yield 0.724% (prev. 0.831%)

Germany to sell EUR 3.66bln vs exp. EUR 4.5bln 3.10% 2025 Schatz: b/c 2.48x (prev. 1.7x), average yield 2.64% (prev. 3.06%), retention 18.67% (prev. 17.82%)

Commodities

WTI and Brent, +0.7%, front-month futures are on firmer footings after choppy trade on Monday amid continued fallout from OPEC+ in the backdrop of cooling economic data and volatile Middle East tensions.

Metals are mixed with precious metals moving horizontally as the DXY trades flat intraday spot gold and spot silver taking a breather following yesterday’s hefty losses.

Libya’s NOC Chair says current production is 1.3mln BPD (vs 1.218mln on 6th Nov), planning a bidding round for offshore/onshore blocks for end-2024. In the early stage to identify blocks. Says seeing a lot of interest for upcoming bid round from US, European and Asian firms. On track to increase production capacity to 2mln BPD in the next three-five years. Says hopefully oil production will increase by 100k BPD by end-2024.

Russia’s Kremlin, when asked if Russian President Putin will discuss coordinated actions on oil market, says such discussions are held in OPEC+ format but the issue is always on the agenda; Kremlin confirms Putin will visit Saudi and UAE on Wednesday. Russian President Putin is to discuss oil market issues in the UAE and Saudi Arabia, according to Tass

Brazilian miner Vale expects iron ore market to remain tight in the coming years, says China cannot control the price of iron ore and there is no supply coming

China’s NDRC will cut retail gasoline and diesel prices by CNY 55/ton and CNY 50/ton, respectively, commending Dec 6th; NDRC sees weaker oil prices in the short term

Geopolitics

Israel is reportedly mulling a plan to flood Gaza tunnels with seawater, according to WSJ.

Israel’s army said its fighter jets attacked Hezbollah positions, infrastructure and military in response to a recent shooting, according to AJA Breaking via social media platform X.

Investors with prior knowledge of the October 7th attack on Israel by Hamas made at least tens of millions of pounds shorting Israeli stocks, according to The Telegraph.

US National Security Advisor Sullivan said attacks on vessels in the Red Sea are a threat to international peace and stability, while they have every reason to believe these attacks were fully enabled by Iran. Sullivan also said the US is engaging with allies on the next steps after the Red Sea attacks and weapons used by the Houthis in the attacks are being supplied by Iran.

White House warned that a failure to approve additional aid for Ukraine would ‘kneecap’ Kyiv, according to FT.

US Event Calendar

09:45: Nov. S&P Global US Services PMI, est. 50.8, prior 50.8

10:00: Oct. JOLTs Job Openings, est. 9.3m, prior 9.55m

10:00: Nov. ISM Services Index, est. 52.3, prior 51.8

Nov. ISM Services New Orders, est. 54.9, prior 55.5

Nov. ISM Services Employment, est. 51.4, prior 50.2

Nov. ISM Services Prices Paid, est. 58.0, prior 58.6

DB’s Jim Reid concludes the overnight wrap

Markets have lost a little of their recent poise over the last 24 hours, with the S&P 500 (-0.54%) coming off its YTD high from Friday, just as yields on 2yr Treasury yields (+9.6bps) moved back up to 4.64%. There hasn’t been a specific catalyst for the softness, but the astonishing rally in November and long positioning has led to some scepticism about how much further it’s able to run, at least until we get some more data that’s soft-landing friendly. After all, even though markets are fully pricing in a Fed rate cut by the May meeting in just 5 months’ time, this isn’t the first time this year that rate cut speculation has built up. In fact, at the height of the SVB turmoil in March, futures were fully pricing in a rate cut by the July meeting, which was just 4 months away. So it’ll be fascinating to see the extent to which the FOMC’s dot plot next week validates or pushes back on current market pricing, which is now looking for 124bps of cuts in 2024 .

When it comes to the Fed’s next meeting, today kicks off a run of important data releases that will help shape the 2024 outlook. That includes the ISM services index, which will be in particular focus after the manufacturing number underwhelmed on Friday. Indeed, the Atlanta Fed’s GDPNow forecast for Q4 stands at just 1.2%, which if realised would be the weakest quarterly growth since Q2 2022. Alongside that, we’ll get the JOLTS report for October, which have shown job openings actually ticking back up over the last couple of months, suggesting that the labour market was still pretty tight. For instance, there were still 1.5 job vacancies per unemployed individual in September, which is still clearly above its pre-pandemic level around 1.2. We’ll see if that’s changed today.

Ahead of those releases, the S&P 500 (-0.54%) was unable to sustain its recent gains, suffering its worst start to a week since February. To be fair, it’s worth noting that the decline was fairly concentrated among big tech stocks, with the equal-weighted S&P 500 up a marginal +0.03%. And the small cap Russell 2000 index (+1.04%) actually rose for the fourth session in a row. But even so, it wasn’t much consolation for those segments that did lose ground, with both the NASDAQ (-0.84%) and the Magnificent 7 (-1.61%) seeing a notable underperformance .

Meanwhile on the rates side, there was a fairly sharp bounceback in Treasury yields following last week’s declines. The 10yr yield rose +5.8bps to 4.21%, though it rallied in the latter part of the US session having been up as much as +10bps intra-day. There were larger moves at the front-end as the 2yr yield (+9.6bps) saw its biggest daily increase in four weeks, moving back up to 4.63%. That came as investors took out some of the cuts priced in for 2024, with the total amount falling by -10.2bps to 124bps. And in turn, with investors expecting slightly fewer rate cuts, real yields also bounced back, with the 10yr real yield (+7.2bps) moving back above 2% again .

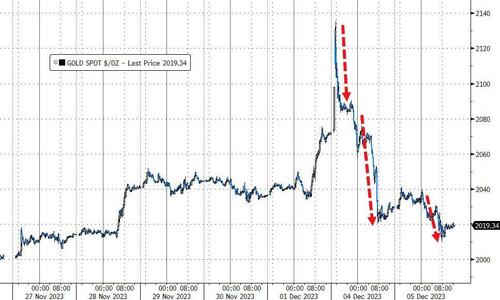

That advance in real yields put a pause to the gold rally over recent days. At the open, gold prices did manage to hit an all-time intraday high of $2135/oz, but by the close they were down a full -2.23% to $2026/oz. So a 5.56pp range on the day, which is a huge intra-day swing for Gold. Although we hit fresh all-time highs during the session, it’s worth noting that this is still only a nominal high point, since if you adjust for inflation then prices were higher in the early 1980s, in 2011, and even at the recent peak in 2020. Elsewhere in the commodities space, Brent Crude oil prices (-1.08%) were down again to $78.03/bbl, building on their run of 6 consecutive weekly declines .

Over in Europe, the market moves were much less aggressive yesterday, with the STOXX 600 only falling -0.09%. Similarly for sovereign bonds, yields on 10yr bunds (-0.8bps) actually fell back to a 5-month low of 2.35%, and others including 10yr OATs (+0.2bps) and BTPs (+2.5bps) only saw a modest increase. Gilts were the main exception to that pattern, with the 10yr yield up +5.5bps, as the 10yr real yield (+9.6bps) even hit a one-month high.

Asian equity markets are slipping this morning with the Hang Seng (-1.76%) emerging as the biggest underperformer followed by the Nikkei (-1.15%), the CSI (-0.80%), the Shanghai Composite (-0.69%) and the KOSPI (-0.38%). S&P 500 (-0.21%) and NASDAQ 100 (-0.24%) futures are edging lower.

Early morning data showed that Tokyo’s inflation rate rose by +2.6% y/y in November (v/s +3.0% expected), its slowest rise since July 2022 and compared with a downwardly revised increase of +3.2% in the previous month. Core CPI rose +2.3% in November (v/s +2.4% expected) from a year earlier down from a +2.7% gain in October thus clouding the BOJ’s exit path a touch. The BOJ next meet on Dec. 18-19 with our view that they will remove YCC in January. Elsewhere, China’s Caixin services PMI for November advanced to a three-month high of 51.5 (v/s 50.5 expected and 50.4 in October), thus diverging from the nation’s official PMI data that showed a contraction .

In monetary policy action, the Reserve Bank of Australia (RBA) decided to keep its official cash rate (OCR) unchanged at a 12-year high of 4.35% as consensus expected at its final board meeting of 2023. With the RBA’s statement viewed as being on the dovish side, the Aussie currency has come under renewed selling pressure, dropping -0.54% to trade at 0.6584 versus the dollar .

Looking back at yesterday’s data, October factory orders were the one notable release in the US. These saw a -3.6% monthly decline (vs -3.0% exp) and with September revised down to +2.3% from +2.8%. The less volatile non-defense capital goods series was revised down to -0.2% from 0.0% in the advance reading. So adding to a sense of weakening US growth momentum in Q4.

To the day ahead now, and data releases from the US include the ISM services index for November, and the JOLTS job openings for October. Elsewhere, there’s the global services and composite PMIs for November and Euro Area PPI for October. From central banks, we’ll get the ECB’s Consumer Expectations Survey for October.

END

2 B) NOW NEWSQUAWK (EUROPE/REPORT)

European equities firmer whilst US Futures are in the red; DXY flat & AUD underperforms post RBA; US JOLTS due – Newsquawk US Market Open

TUESDAY, DEC 05, 2023 – 05:59 AM

European equities trade on the front foot though the FTSE100 is once again hampered by losses in Basic Resources; US Futures are in the red

DXY trades around the unchanged mark, with the Aussie underperforming post RBA hold

Fixed was initially driven higher by ECB Schnabel’s comments; though now off best levels after EZ PMI revisions

ECB’s Schnabel (Hawk) says that further hikes are now “rather unlikely” following the November inflation data.

Crude is on a modestly firmer footing whilst spot Gold takes a breather following yesterday’s hefty losses

Looking ahead US Composite & Services Final PMIs, ISM Services PMI, JOLTS & Australian AIG Manufacturing Index

2. Listen to this report in the market open podcast (available on Apple and Spotify)

3. Trial Newsquawk’s premium real-time audio news squawk box for 7 days

EUROPEAN TRADE

EQUITIES

European equities, Eurostoxx50 +0.3%, are mixed, with the FTSE100, -0.2%, once again the relative underperformer, largely hampered by ongoing losses in Basic Resources which is the worst performing sector.

European sectors are mixed with a slight positive tilt; Real Estate outperforms following broker upgrades at British Land, +1.3%, and Land Securities, +0.8%.

US equity futures are trading on the backfoot, continuing the losses seen in the prior days’ session as the year’s final few key events/releases begin with JOLTS.

Click here and here for the sessions European pre-market equity newsflow, including earnings.

DXY extended on the upper end of its overnight range towards 103.84 ahead of the European equity cash open and now resides within the middle of today’s range of 103.84-53.

EUR/USD is trading around flat having bounced off lows on revisions higher to Services & Composite PMI data.

The Japanese Yen is the G10 outperformer at the time of writing amid a combination of a pullback in US yields coupled with the broader risk aversion overnight.

AUD, NZD, CAD are all softer to varying degrees amid the initial broader risk tone, but the Aussie is the marked G10 laggard in the aftermath of the RBA policy decision which lacked hawkish undertones.

PBoC set USD/CNY mid-point at 7.1127 vs exp. 7.1476 (prev. 7.1011).

China’s major state-owned banks were seen acquiring dollars via onshore swaps and selling them in the spot FX market, while it was also reported that the RBI was likely selling dollars near the 83.38-83.39 rupee level, according to sources and traders cited by Reuters.

ECB’s Schnabel (Hawk) says that further hikes are now “rather unlikely” following the November inflation data.

Commentary which drove Bunds to a 134.17 peak; though, upward revisions to PMIs have prompted a pullback, but one that is limited by the reports internal commentary.

Similar action has been seen in Gilts which perhaps derived initial support from the latest YouGov findings as well.

Finally, USTs are directionally in-fitting but with magnitudes more contained at the mid-point of 110.10 to 110.18 parameters ahead of JOLTS & PMIs/ISM.

UK sells GBP 1.5bln 0.75% 2033 I/L Gilt: b/c 2.68x (prev. 2.94x) and real yield 0.724% (prev. 0.831%)

Germany to sell EUR 3.66bln vs exp. EUR 4.5bln 3.10% 2025 Schatz: b/c 2.48x (prev. 1.7x), average yield 2.64% (prev. 3.06%), retention 18.67% (prev. 17.82%)

WTI and Brent, +0.7%, front-month futures are on firmer footings after choppy trade on Monday amid continued fallout from OPEC+ in the backdrop of cooling economic data and volatile Middle East tensions.

Metals are mixed with precious metals moving horizontally as the DXY trades flat intraday spot gold and spot silver taking a breather following yesterday’s hefty losses.

Libya’s NOC Chair says current production is 1.3mln BPD (vs 1.218mln on 6th Nov), planning a bidding round for offshore/onshore blocks for end-2024. In the early stage to identify blocks. Says seeing a lot of interest for upcoming bid round from US, European and Asian firms. On track to increase production capacity to 2mln BPD in the next three-five years. Says hopefully oil production will increase by 100k BPD by end-2024.

Russia’s Kremlin, when asked if Russian President Putin will discuss coordinated actions on oil market, says such discussions are held in OPEC+ format but the issue is always on the agenda; Kremlin confirms Putin will visit Saudi and UAE on Wednesday. Russian President Putin is to discuss oil market issues in the UAE and Saudi Arabia, according to Tass

Brazilian miner Vale expects iron ore market to remain tight in the coming years, says China cannot control the price of iron ore and there is no supply coming

China’s NDRC will cut retail gasoline and diesel prices by CNY 55/ton and CNY 50/ton, respectively, commending Dec 6th; NDRC sees weaker oil prices in the short term

ECB’s Schnabel says current level of restriction is sufficient, has increased confidence that 2% target will be met in 2025; must not declare victory prematurely; further hikes “rather unlikely” after November inflation data. Must be more cautious with rate cuts than markets pricing; further hikes “rather unlikely” after November inflation data. Inflation developments are encouraging, fall in core prices is remarkable

YouGov/Citi survey showed the British public’s expectation for inflation in 5yr-10yr’s time rose to 3.5% from a prior 3.3% view in September.

German Ifo: Retailers Expect Little Help from Christmas Sales; Business Situation -8.8 (prev. -13.5).

Kantar UK Supermarket update (Nov): grocery price inflation 9.71% in the four weeks to Nov 26th; UK grocery sales +6.3% Y/Y.

ECB Survey of Consumer Expectations (October 2023): median consumer inflation expectations for the next 12 months and for three years ahead remained unchanged.

The London Stock Exchange (LSEG LN) is currently investigating an issue impacting its trading/information system. We are now resuming trading on impacted instruments. Instruments will go into auction at 09:55GMT with uncrossing beginning at 10:15GMT. All live orders remain on the system. LSE: Impacted securities are now in regular trading.

DATA RECAP

EZ PMI data across the board (bar Spain) showed a mild upward revision, though remained comfortably within contractionary territory; internal commentary was bleak on the growth outlook with potential technical recessions in the EZ & Germany while price/inflationary pressures remain.

UK S&P Global/CIPS Services PMI Final (Nov) 50.9 vs. Exp. 50.5 (Prev. 50.5); Composite PMI Final 50.7 vs. Exp. 50.1 (Prev. 50.1)

German HCOB Services PMI (Nov) 49.6 vs. Exp. 48.7 (Prev. 48.7); Composite Final PMI 47.8 vs. Exp. 47.1 (Prev. 47.1)

EU HCOB Services Final PMI (Nov) 48.7 vs. Exp. 48.2 (Prev. 48.2); Composite Final PMI 47.6 vs. Exp. 47.1 (Prev. 47.1)

Spanish Services PMI (Nov) 51.0 vs. Exp. 51.5 (Prev. 51.1)

Italian HCOB Composite PMI (Nov) 48.1 (Prev. 47.0); Services PMI 49.5 vs. Exp. 48.2 (Prev. 47.7)

French S&P Global Services PMI (Nov) 45.4 vs. Exp. 45.3 (Prev. 45.3); Composite PMI 44.6 vs. Exp. 44.5 (Prev. 44.5)

UK BRC Retail Sales YY (Nov) 2.6% vs. Exp. 2.5% (Prev. 2.6%)

EU Producer Prices MM (Oct) 0.2% vs. Exp. 0.2% (Prev. 0.5%); YY -9.4% vs. Exp. -9.5% (Prev. -12.4%)

NOTABLE US HEADLINES

NIO Inc (NIO/9866 HK) Q3 2023 (USD): EPS -0.31 (exp. -0.30), Revenue 2.39bln (exp. 2.66bln). Q3 deliveries +75.4% Y/Y at 55,432; expects Q4 deliveries between 47,000-49,000. Shares -3.4% in the pre-market.

Israel is reportedly mulling a plan to flood Gaza tunnels with seawater, according to WSJ.

Israel’s army said its fighter jets attacked Hezbollah positions, infrastructure and military in response to a recent shooting, according to AJA Breaking via social media platform X.

Investors with prior knowledge of the October 7th attack on Israel by Hamas made at least tens of millions of pounds shorting Israeli stocks, according to The Telegraph.

US National Security Advisor Sullivan said attacks on vessels in the Red Sea are a threat to international peace and stability, while they have every reason to believe these attacks were fully enabled by Iran. Sullivan also said the US is engaging with allies on the next steps after the Red Sea attacks and weapons used by the Houthis in the attacks are being supplied by Iran.

White House warned that a failure to approve additional aid for Ukraine would ‘kneecap’ Kyiv, according to FT.

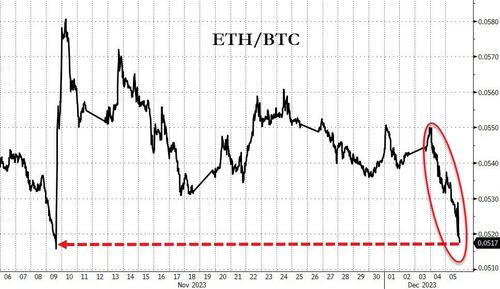

CRYPTO

Bitcoin, -0.7%, takes a breather after yesterday’s spike, whilst Ethereum, -1.7%, posts losses of a slightly larger magnitude.

APAC TRADE

APAC stocks declined following the mostly negative lead from Wall St where the major indices were choppy and ultimately weighed amid a rebound in yields ahead of key data releases.

ASX 200 was led lower by the commodity-related industries with underperformance in gold miners after the precious metal faded the recent surge, while sentiment was also not helped by weak data and after the unsurprising RBA rate decision in which the central bank kept rates unchanged and reiterated its forward guidance.

Nikkei 225 continued to weaken and slipped below the 33,000 level despite softer-than-expected Tokyo inflation data.

Hang Seng and Shanghai Comp retreated which saw the latter breach the psychological 3,000 level to the downside amid lingering frictions after China criticised the US for seeing it as a threat following calls by Commerce Secretary Raimondo for more funds to back chip curbs, while encouraging Caixin Services PMI data which printed a 3-month high at 51.5 (exp. 50.7) only provided a brief tailwind.

NOTABLE HEADLINES

RBA kept the Cash Rate Target unchanged at 4.35%, as expected, while it reiterated its forward guidance that whether further tightening is required to ensure inflation returns to the target in a reasonable timeframe will depend upon data and evolving assessment of risks. RBA also repeated that the Board remains resolute in its determination to return inflation to target and will do what is necessary to achieve that outcome, as well as noted there are still significant uncertainties around the outlook and that the limited information received on the domestic economy since the November meeting has been broadly in line with expectations.

Moody’s affirms China’s A1 rating; changes outlook to Negative from Stable. Reflects risks relating to persistently lower medium-term economic growth and ongoing downsizing of the property sector.

Chinese Finance Ministry says Chinese economy will maintain its rebound and positive trend; we expect the Q4 economy to keep the positive trend

Foxconn (2317 TW) November Sales +17.95% Y/Y (October -4.56% Y/Y); outlook for Q4 should be better than the original guidance for “significant growth”; revenue performance in the first two months of Q4 has been slightly higher than expected

DATA RECAP