GOLD PRICE CLOSED: DOWN $27.75 TO $2027.05

SILVER PRICE CLOSED: DOWN 8 cents AT $22.95

Access prices: closes 4: 15 PM

Gold ACCESS CLOSED 2027.50

Silver ACCESS CLOSED: 22.91

Bitcoin morning price:, 43,018 DOWN 852 DOLLARS

Bitcoin: afternoon price: $43,327 DOWN 1543 dollars

Platinum price closing $900.10 DOWN $14.10

Palladium price; $942.45 DOWN $43.65

END

Due to the huge rise in the dollar, we must look at gold and silver in currencies other than the dollar to understand where we are heading

I will now provide gold in Canadian dollars, British pounds and Euros

4: 15 PM ACCESS

*CANADIAN GOLD: $2,736.25 DOWN 23,54 CDN dollars per oz( * NEW ALL TIME HIGH 2,795.90 CDN DOLLARS PER OZ//DEC 1 272023)

*BRITISH GOLD: 1604.75 DOWN 10.51 pounds per oz// *(NEW ALL TIME HIGH//CLOSING///1655.17 BRITISH POUNDS/OZ) OCT 2/2023

*EURO GOLD: 1864.34 DOWN 13.31 euros per oz //* (ALL TIME CLOSING HIGH: 1903.75 EUROS PER OZ//DEC 1.2023)

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

EXCHANGE: COMEX

EXCHANGE: COMEX

CONTRACT: JANUARY 2024 COMEX 100 GOLD FUTURES

SETTLEMENT: 2,046.700000000 USD

INTENT DATE: 01/12/2024 DELIVERY DATE: 01/17/2024

FIRM ORG FIRM NAME ISSUED STOPPED

190 H BMO CAPITAL 9

363 H WELLS FARGO SEC 119

435 H SCOTIA CAPITAL 15

624 H BOFA SECURITIES 176

657 C MORGAN STANLEY 6

661 C JP MORGAN 16

737 C ADVANTAGE 2 9

905 C ADM 4

TOTAL: 178 178

JPMorgan stopped 40/75 contracts.

FOR JAN.:

GOLD: NUMBER OF NOTICES FILED FOR JAN/2024. CONTRACT: 178 NOTICES FOR 17,800 OZ or 0.5536 TONNES

total notices so far: 3451 contracts for 345,100 oz (10.734 tonnes)

FOR JANUARY:

SILVER NOTICES 4 NOTICE(S) FILED FOR 20,000 OZ/

total number of notices filed so far this month : 765 for 3,825,000 oz

XXXXXXXXXXXXXXXXXX

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

BOTH GLD AND SLV ARE FRAUDULENT VEHICLES

GLD

WITH GOLD DOWN $27.75

INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD/ : /NO CHANGES AT THE GLD:

INVENTORY RESTS AT 863.84 TONNES

SLV//

WITH NO SILVER AROUND AND SILVER DOWN 8 CENTS AT THE SLV//

NO CHANGES IN SILVER INVENTORY AT THE SLV

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV.

CLOSING INVENTORY: 433.500 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A MEGA HUMONGOUS SIZED 1820 CONTRACTS TO 132,268 AND FURTHER FROM THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THIS HUMONGOUS SIZED LOSS IN COMEX OI WAS ACCOMPLISHED DESPITE OUR HUGE GAIN OF $0.62 IN SILVER PRICING AT THE COMEX ON FRIDAY. WE HAD ZERO LONG LIQUIDATION, AND MASSIVE SPEC SHORT COVERING. WE HAD CONSIDERABLE T.A.S. LIQUIDATION AT THE COMEX SESSION. WE HAD A HUGE 1768 T.A.S ISSUANCE AND THESE WILL BE USED FOR MANIPULATION LATER THIS MONTH/AS WELL AS TODAY.

CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON FRIDAY NIGHT: 1768 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS. IT THUS LOOKS LIKE THE FED (GOV’T) IS BEHIND ALL OF THESE TRADES.

WE HAVE NOW SET ANOTHER RECORD LOW AT 114,102 CONTRACTS ///JULY 3.2023// OUR BANKERS WITH THE HELP OF SPECULATORS AND HIGH FREQUENCY TRADERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.62), AND WERE UNSUCCESSFUL IN KNOCKING ANY SILVER LONGS. HOWEVER WE HAD A MASSIVE SPEC SILVER SHORT COVERING AS WE HAD A MEGA GIGANTIC SIZED LOSS OF 1595 OI CONTRACTS ON OUR TWO EXCHANGES.

WE MUST HAVE HAD:

A FAIR SIZED 225 ISSUANCE OF EXCHANGE FOR PHYSICALS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 6.650 MILLION OZ (FIRST DAY NOTICE) FOLLOWED BY TODAY’S 20,000 OZ QUEUE. JUMP NEW TOTALS 6.460 MILLION OZ//

//NEW STANDING FOR SILVER IS THUS 6.460 MILLION OZ

//MEGA GIGANTIC SIZED COMEX OI LOSS/FAIR SIZED EFP ISSUANCE/ VI) HUGE SIZED NUMBER OF T.A.S. CONTRACT ISSUANCE 1768 CONTRACTS)/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL -REMOVED 280 CONTRACTS //

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS JAN ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF JAN

TOTAL CONTRACTS for 10 days, total 8165 contracts: OR 40.825 MILLION OZ (817 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 40.825 MILLION OZ

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH 2022: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 118.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 85.745 MILLION OZ (SMALLER THAN LAST MONTH)

AUGUST: 171.43 MILLION OZ (THIS MONTH IS GOING TO BE HUGE //2ND HIGHEST ON RECORD

SEPT: 72.705 MILLION OZ (SMALLER THIS MONTH)

OCT: 97.455 MILLION OZ

NOV. 50.050 MILLION OZ

DEC. 66.140 MILLION OZ//

TOTAL 2023: 1,104.10 MILLION OZ/

JAN ’24 : 40.825 MILLION OZ//WILL BE A VERY STRONG MONTH FOR ISSUANCE

RESULT: WE HAD A MEGA GIGANTIC SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 1820 CONTRACTS DESPITE OUR HUGE GAIN IN PRICE OF SILVER PRICING AT THE COMEX//FRIDAY.,. THE CME NOTIFIED US THAT WE HAD A FAIR EFP ISSUANCE CONTRACTS: 225 ISSUED FOR FEB AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS. WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR JAN. OF 6.665 MILLION OZ FOLLOWED BY TODAY’S 20,000 OZ QUEUE JUMP //NEW TOTAL 5.460 MILLION OZ TO WHICH WE ADD EX. FOR RISK ISSUANCE/PRIOR FOR 1.0 MILLION OZ //NEW TOTALS; 6.460 MILLION OZ/

NEW STANDING 6.460 million OZ /// WE HAVE A GIGANTIC SIZED LOSS OF 1595 OI CONTRACTS ON THE TWO EXCHANGES DESPITE THE HUGE GAIN IN PRICE. THE TOTAL OF TAS INITIATED CONTRACTS TODAY: A HUGE SIZED 1768 CONTRACTS//HUGE FRONT END OF THE TAS CONTRACTS WERE LIQUIDATED DURING THE FRIDAY COMEX SESSION/RAID// WITH MAMMOTH SHORT COVERINGS FROM OUR SPEC SHORTS. THE NEW TAS ISSUANCE FRIDAY NIGHT (1768) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE//PROBABLY TODAY., .

WE HAD 4 NOTICE(S) FILED TODAY FOR 20,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A MEGA GIGANTIC SIZED 20,090 CONTRACTS TO 498,334 AND CLOSER TO THE RECORD (SET JAN 24/2020) AT 799,733 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: – removed 580 CONTRACTS

WE HAD AN ATMOSPHERIC SIZED INCREASE IN COMEX OI ( 10,495 CONTRACTS) WITH OUR $31.65 GAIN IN PRICE//FRIDAY. WE ALSO HAD A RATHER STRONG INITIAL STANDING IN GOLD TONNAGE FOR JAN. AT 8.214 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S 37200 OZ QUEUE JUMP//NEW STANDING: 11.5169 TONNES // ALL OF THIS HAPPENED WITH OUR $31.65 GAIN IN PRICE WITH RESPECT TO FRIDAY’S TRADING. WE HAD AN ATMOSPHERIC SIZED GAIN OF 21,604 OI CONTRACTS (67.19) PAPER TONNES) ON OUR TWO EXCHANGES.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 2109 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 497.739

IN ESSENCE WE HAVE A HUMONGOUS SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 19,495 CONTRACTS WITH 20,090 CONTRACTS INCREASED AT THE COMEX// AND A FAIR SIZED 2109 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 21,604 CONTRACTS.. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): A MEGA MEGA MEGA HUMONGOUS SIZED 34,364 CONTRACTS. ( THE 5TH CONSECUTIVE MEGA ISSUANCE FOR T.A.S. //. GREATER THAN 30,000 ISSUANCE)

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (2109 CONTRACTS) ACCOMPANYING THE HUMONGOUS SIZED GAIN IN COMEX OI (19,495) //TOTAL GAIN FOR OUR THE TWO EXCHANGES: 21,604 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR FORMER FORMAT OF BANKERS GOING LONG AND SPECULATORS GOING SHORT ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR JAN AT 8.214 TONNES FOLLOWED BY TODAY’S 37,200 OZ QUEUE JUMP//NEW STANDING 11.5769 TONNES. / 3) ZERO LONG LIQUIDATION AND HUGE TAS LIQUIDATION WITH MAJOR SHORT COVERINGS// 4) HUGE SIZED COMEX OPEN INTEREST GAIN/ 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER///6: HUMONGOUS T.A.S. ISSUANCE: 34,364 CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023-2024 INCLUDING TODAY

JAN.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF JAN. :

TOTAL EFP CONTRACTS ISSUED: 34,440 CONTRACTS OR 3,444,000 OZ OR 107.12 TONNES IN 10 TRADING DAY(S) AND THUS AVERAGING: 3440 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 10 TRADING DAY(S) IN TONNES 107.12 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2022, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 107.12/3550 x 100% TONNES 3.01% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2023

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH/2022: 409.30 TONNES //FINAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 151.69 TONNES (WEAKER THAN LAST MONTH)

AUGUST: 195.28 TONNES (A STRONGER MONTH)//FINAL

SEPT: 254.709 TONNES (WILL BE LARGER THAN LAST MONTH AND A STRONG MONTH)

OCT. 248.09 TONNES. LIKE SILVER, THIS MONTH IS GOING TO BE A STRONG E.F.P. ISSUANCE.

NOV. 239.16 TONNES//WILL BE STRONG THIS MONTH,

DEC. 213.704 TONNES. A STRONG MONTH//

TOTAL FOR YEAR 2023: 2,569.57 TONNES VS 2578 TONNES LAST YEAR

JAN ’24: 107.12 TONNES (WILL EQUAL LAST MONTH’S ISSUANCE OR A LITTLE GREATER)

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF FEB. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (FEB), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER FELL BY A GIGANTIC SIZED 1820 CONTRACTS OI TO 132,268 AND CLOSER TO THE COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 225 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MARCH 225 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 225 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 1540 CONTRACTS AND ADD TO THE 225 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A HUGE SIZED LOSS OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 1595 CONTRACTS

THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES TOTAL 7.97 MILLION OZ

OCCURRED DESPITE OUR $.62 GAIN IN PRICE …..

END

OUTLINE FOR TODAY’S COMMENTARY

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

b, ) Gold/silver trading overnight Europe,//GOLD COMMENTARIES

(Peter Schiff)

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS//

TUESDAY MORNING/MONDAY NIGHT

SHANGHAI CLOSED UP 7.70 PTS OR 0.27% //Hang Seng CLOSED DOWN 350.41 PTS OR 2.16% /The Nikkei CLOSED DOWN 282.61 OR 0.79% //Australia’s all ordinaries CLOSED DOWN 1.07% /Chinese yuan (ONSHORE) closed DOWN AT 7.1895 /OFFSHORE CHINESE YUAN CLOSED DOWN TO 7.2137 /Oil DOWN TO 73.08 dollars per barrel for WTI and BRENT UP AT 7.24/ Stocks in Europe OPENED ALL RED// ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER

A)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

9. USA

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A HUMONGOUS SIZED 19,494 CONTRACTS TO 498,334 WITH OUR GAIN IN PRICE OF $31.65 WITH RESPECT TO FRIDAY TRADING. WE MUST HAVE HAD ZERO LONG SPEC LIQUIDATIONS IN THE COMEX SESSION WITH MAJOR SPEC SHORT COVERINGS.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE NON ACTIVE DELIVERY MONTH OF JAN..… THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 2109 EFP CONTRACTS WERE ISSUED: : FEB 2109 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 2109 CONTRACTS

ON A NET BASIS IN OPEN INTEREST WE LOST THE FOLLOWING TODAY ON OUR TWO EXCHANGES: AN ATMOSPHERIC SIZED TOTAL OF 21,604 CONTRACTS IN THAT 2109 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A HUMONGOUS SIZED 19,495 COMEX CONTRACTS..AND THIS HUGE GAIN ON OUR TWO EXCHANGES HAPPENED WITH OUR GAIN IN PRICE OF $31.65 FRIDAY COMEX. AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS DURING MID MONTH IN THE DELIVERY CYCLE), THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR FRIDAY NIGHT WAS A MEGA MEGA GIGANTIC SIZED 34,364 CONTRACTS. (SO MUCH FOR LAW AND ORDER AT THE COMEX). THROUGHOUT THE PAST SEVERAL WEEKS, THE BANKERS SOLD OFF THE LONG SIDE OF THE SPREAD WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR/T.A.S. SPREAD WHICH WILL BE LIQUIDATED IN DAYS HENCE//.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: JAN (11.5769 TONNES) ( NON ACTIVE MONTH)

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

NOV: 18.7122 TONNES + 16.2505 EX. FOR RISK = 34.9627 TONNES

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707TONNES

TOTAL 2023 YEAR : 436.546 TONNES

JAN ’24. 11.5769 TONNES

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT GAINED $31.65) //// AND WERE UNSUCCESSFUL IN KNOCKING ANY SPECULATOR LONGS AS WE HAD A HUGE SIZED GAIN OF 21,604 TOTAL CONTRACTS ON OUR TWO EXCHANGES. WE HAD A HUGE T.A.S. LIQUIDATION ON THE FRONT END OF FRIDAY’S TRADING . THE T.A.S. ISSUED ON FRIDAY NIGHT, WILL BE “PUT INTO THE BANK” TO BE USED AT A LATER DATE AT THE COLLUSIVE CHOOSING OF OUR BANKERS. WE ALSO EXPERIENCED CONSIDERABLE SPECULATOR SHORT COVERING

WE HAVE GAINED A TOTAL OI OF 69.048 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR JAN. (8,214 TONNES) ON FIRST DAY NOTICE FOLLOWED BY TODAY’S 37,200 OZ QUEUE JUMP (1.157 TONNES): NEW TOTAL STANDING 11.5769 TONNES/ ALL OF THIS WAS ACCOMPLISHED WITH OUR GAIN IN PRICE TO THE TUNE OF $31.65

WE HAD – REMOVED 514 CONTRACTS TO THE COMEX TRADES TO OPEN INTEREST (CROOKS)

NET GAIN ON THE TWO EXCHANGES 21,604 CONTRACTS OR 2,160,400 OZ OR 67.19 TONNES.

Estimated gold volume today:// 299,804 good //t.a.s. induced.

final gold volumes/yesterday 344,938/ strong t.a.s. induced

//speculators have left the gold arena

JAN 16 INITIAL

/ /// THE JAN 2024 GOLD CONTRACT

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 482.265 OZ JPMorgan 15 kilobars . |

| Deposit to the Dealer Inventory in oz | nil oz |

| Deposits to the Customer Inventory, in oz | nil oz |

| No of oz served (contracts) today | 178 notice(s) 17800 OZ 0.5538 TONNES |

| No of oz to be served (notices) | 271 contracts 27100 oz 0.8429 TONNES |

| Total monthly oz gold served (contracts) so far this month | 3451 notices 345,100 oz 10.734 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | x |

0 dealer deposit:

total dealer deposits: nil oz

total customer withdrawals: 1

i)JPMorgan: 482.265 oz

(15 kilobars)

total withdrawals 482.265 oz

we had 0 deposits

total deposits NIL oz

Adjustments; 0

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR JAN.

For the front month of JANUARY we have an oi of 449 contracts having GAINED 297 contracts. We had 75 notices served on Friday, so we gained 372 contracts or an additional 37,200 oz will stand for delivery at the comex

FEB LOST ONLY 11,215 CONTRACTS FALLING TO 241,986

March GAINED 2 contracts to stand at 335.

APRIL GAINED 26,280 CONTRACTS RISING TO 190,677.

We had 178 contracts filed for today representing 17800 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 178 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 16 notice(s) was (were) stopped ( received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the JAN. /2023. contract month, we take the total number of notices filed so far for the month (3451 x 100 oz ), to which we add the difference between the open interest for the front month of JAN. (449 CONTRACTS) minus the number of notices served upon today 178 x 100 oz per contract equals 372,200 OZ OR 11.5769 TONNES

thus the INITIAL standings for gold for the JAN. contract month: No of notices filed so far (3451) x 100 oz + (449) {OI for the front month} minus the number of notices served upon today (178) x 100 oz) which equals 372,200 oz standing OR 11.5769 TONNES

TOTAL COMEX GOLD STANDING FOR JAN: 11.5769 TONNES WHICH IS GREAT FOR AN INACTIVE DELIVERY MONTH IN THE CALENDAR.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 1,474,682.951 45.86 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD: 20,025,132,045 OZ

TOTAL REGISTERED GOLD 9,237,397.739 (287,32 tonnes).

TOTAL OF ALL ELIGIBLE GOLD: 10,787,734,306 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 7,762,715 oz (REG GOLD- PLEDGED GOLD) 241.45 tonnes

END

SILVER/COMEX

JAN 16/INITIAL

//2024// THE JAN 2023 SILVER CONTRACT//INITIAL

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 78,596.550 oz Delaware CNT . |

| Deposits to the Dealer Inventory | nil OZ |

| Deposits to the Customer Inventory | 599,332.020 oz CNT |

| No of oz served today (contracts) | 4 CONTRACT(S) (20,000 OZ) |

| No of oz to be served (notices) | 327 contracts (1,635,000 oz) |

| Total monthly oz silver served (contracts) | 765 Contracts (3,825,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

i) 0 dealer deposit

total dealer deposit: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: 0 oz

We had 1 deposits customer account:

i) Into CNT 599,337.020 oz

total customer deposits 599,337.020 oz

JPMorgan has a total silver weight: 132.534 million oz/280.977 million or 46.97%

Comex withdrawals: 2

i0 Out of Delaware 998.400 oz

ii) Out of CNT: 77,579.150 oz

total deposit: 78,596.550 oz

TOTAL REGISTERED SILVER: 42.810 MILLION OZ//.TOTAL REG + ELIGIBLE. 280.977 million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR DECEMBER:

silver open interest data:

FRONT MONTH OF JAN. /2023 OI: 331 CONTRACTS HAVING LOST 62 CONTRACT(S). WE HAD 67 NOTICES SERVED ON FRIDAY, SO WE GAINED 5 CONTRACTS OR AN ADDITIONAL 25,000 OZ WILL STAND FOR DELIVERY AT THE COMEX

FEB GAINED 97 CONTRACTS TO STAND AT 807

MARCH LOST 2480 CONTRACTS TO 102,534

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 4 for 20,000 oz

Comex volumes// est. volume today 62,045//fair

Comex volume: confirmed yesterday 76,975excellent//t.a.s.induced

To calculate the number of silver ounces that will stand for delivery in JAN. we take the total number of notices filed for the month so far at 765 x 5,000 oz = 3,825,000 oz

to which we add the difference between the open interest for the front month of JAN. (331) and the number of notices served upon today 4 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the DEC/2023 contract month: 765 (notices served so far) x 5000 oz + OI for the front month of JAN. (331) – number of notices served upon today (4 )x 500 oz of silver standing for the JAN contract month equates to 5.460 MILLION OZ. to which we add our exchange for RISK of 1.0 million oz//new total 6.460 million oz/

New total standing: 6.460 million oz.

There are 42,810 million oz of registered silver.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS//

BOTH GLD AND SLV ARE MASSIVE FRAUDS!

JAN 15/WITH GOLD DOWN $27.75 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD;//://INVENTORY RESTS AT 864.99 TONNES

JAN 12/WITH GOLD UP $31.65 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD; A MASSIVE WITHDRAWAL OF 4.61 TONNES OF GOLD FROM THE GLD//://INVENTORY RESTS AT 864.99 TONNES

JAN 11/WITH GOLD DOWN $7.40 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD; A MASSIVE WITHDRAWAL OF 4.61 TONNES OF GOLD FROM THE GLD//://INVENTORY RESTS AT 864.99 TONNES

JAN 10/WITH GOLD DOWN $4.80 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD://INVENTORY RESTS AT 869.60 TONNES

JAN 9/WITH GOLD UP $0.95 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD://INVENTORY RESTS AT 869.60 TONNES

JAN 8/WITH GOLD DOWN $16.85 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD:A WITHDRAWAL OF 4.61 TONNES FROM THE GLD. INVENTORY RESTS AT 869.60 TONNES

JAN 5/WITH GOLD UP $0.80 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD:///. // INVENTORY RESTS AT 874.21 TONNES

JAN 4/WITH GOLD UP $7.60 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD:///. // INVENTORY RESTS AT 874.21 TONNES

JAN 3/WITH GOLD DOWN $29.40 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.90 TONNES OF GOLD INTO THE GLD///. // INVENTORY RESTS AT 874.21 TONNES

JAN 2/WITH GOLD UP $1.50 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.44 TONNES OF GOLD INTO THE GLD///. // INVENTORY RESTS AT 879.11 TONNES

DEC 29/WITH GOLD DOWN $10.25 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.16 TONNES OF GOLD INTO THE GLD///. // INVENTORY RESTS AT 880.55 TONNES

DEC 28/WITH GOLD DOWN $8.35 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.45 TONNES OF GOLD INTO THE GLD///. // INVENTORY RESTS AT 881.71 TONNES

DEC 27/WITH GOLD UP $23.25 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.01 TONNES OF GOLD INTO THE GLD///. // INVENTORY RESTS AT 880.26 TONNES

DEC 26/WITH GOLD UP $1.25 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD:/. // INVENTORY RESTS AT 878.25 TONNES

DEC 22/WITH GOLD UP $17,85 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD:/. // INVENTORY RESTS AT 878.25 TONNES

DEC 21/WITH GOLD UP $5.10 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD:A DEPOSIT .58 TONNES OF 2.02 TONNES OF GOLD INTO THE GLD//. // INVENTORY RESTS AT 878.25 TONNES

DEC 20/WITH GOLD DOWN $3.60 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD:A WITHDRAWAL OF 2.02 TONNES OF GOLD FROM THE GLD//. // INVENTORY RESTS AT 877.67 TONNES

DEC19/WITH GOLD UP $12.15 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD:. // INVENTORY RESTS AT 879.69 TONNES

DEC18/WITH GOLD UP $5.50 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD:. /A DEPOSIT OF 173 TONNES INTO THE GLD// INVENTORY RESTS AT 879.69 TONNES

DEC14/WITH GOLD UP $47.35 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD:. /A DEPOSIT OF 2.42 TONNES FROM THE GLD// INVENTORY RESTS AT 877.96 TONNES

DEC13/WITH GOLD UP $3.90 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD:. /A WITHDRAWAL OF 2.89 TONNES FROM THE GLD// INVENTORY RESTS AT 875,65 TONNES

DEC12/WITH GOLD DOWN $0.60 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD:. /A WITHDRAWAL OF 2.01 TONNES FROM THE GLD// INVENTORY RESTS AT 878.54 TONNES

GLD INVENTORY: 864.99 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

JAN 16/WITH SILVER DOWN $0.08 TODAY NO CHANGES IN SILVER INVENTORY AT THE SLV: // //INVENTORY RESTS AT 433.500 MILLION OZ

JAN 12/WITH SILVER UP $0.62 TODAY NO CHANGES IN SILVER INVENTORY AT THE SLV: // //INVENTORY RESTS AT 433.500 MILLION OZ

JAN 11/WITH SILVER DOWN 34 CENTS TODAY NO CHANGES IN SILVER INVENTORY AT THE SLV: // //INVENTORY RESTS AT 433.912 MILLION OZ

JAN 10/WITH SILVER DOWN 3 CENTS TODAY SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 450,000 OZ FROM THE SLV// //INVENTORY RESTS AT 433.912 MILLION OZ

JAN 9/WITH SILVER DOWN 20 CENTS TODAY NO CHANGES IN SILVER INVENTORY AT THE SLV //INVENTORY RESTS AT 434.370 MILLION OZ

JAN 8/WITH SILVER DOWN 8 CENTS TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 1,602,000 OZ INTO THE SLV//:././/////INVENTORY RESTS AT 434.370 MILLION OZ

JAN 5/WITH SILVER UP 20 CENTS TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV A DEPOSIT OF 916,000 OZ INTO THE SLV//:././/////INVENTORY RESTS AT 435.972 MILLION OZ

JAN 4/WITH SILVER UP 5 CENTS TODAY NO CHANGES IN SILVER INVENTORY AT THE SLV/:././/////INVENTORY RESTS AT 435.056 MILLION OZ

JAN 3/WITH SILVER DOWN 78 CENTS TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV/: A WITHDRAWALOF 2.294 MILLION OZ OZ FROM THE SLV././/////INVENTORY RESTS AT 435.056 MILLION OZ

JAN 2/WITH SILVER DOWN 9 CENTS TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV/: A WITHDRAWALOF 915,000 OZ FORM THE SLV././/////INVENTORY RESTS AT 437.35 MILLION OZ

DEC 29/WITH SILVER DOWN 29 CENTS TODAY NO CHANGES IN SILVER INVENTORY AT THE SLV/: //////INVENTORY RESTS AT 438.265 MILLION OZ

DEC 28/WITH SILVER DOWN 25 CENTS TODAY NO CHANGES IN SILVER INVENTORY AT THE SLV/: //////INVENTORY RESTS AT 438.265 MILLION OZ

DEC 27/WITH SILVER UP 20 CENTS TODAY:HUGE CHANGES IN SILVER INVENTORY AT THE SLV/: A WITHDRAWAL OF 1.374 MILLION OZ FROM THE SLV//////INVENTORY RESTS AT 438.265 MILLION OZ

THIS IS THE 3RD STRAIGHT DAY THAT THE SLV HAS ENGAGED IN WITHDRAWALS

DEC 26/WITH SILVER DOWN 14 CENTS TODAY:HUGE CHANGES IN SILVER INVENTORY AT THE SLV/: A WITHDRAWAL OF 1.465 MILLION OZ FROM THE SLV//////INVENTORY RESTS AT 439.639 MILLION OZ

DEC 22/WITH SILVER UP 0 CENTS TODAY:HUGE CHANGES IN SILVER INVENTORY AT THE SLV/: A WITHDRAWAL OF 2.289 MILLION OZ FROM THE SLV//////INVENTORY RESTS AT 441.104 MILLION OZ

DEC 21/WITH SILVER DOWN 2 CENTS TODAY:NO CHANGES IN SILVER INVENTORY AT THE SLV/: NO CHANGES IN SILVER INVENTORY AT THE SLV//////INVENTORY RESTS AT 443.393 MILLION OZ

DEC 20/WITH SILVER UP 28 CENTS TODAY:NO CHANGES IN SILVER INVENTORY AT THE SLV/: NO CHANGES IN SILVER INVENTORY AT THE SLV//////INVENTORY RESTS AT 443.393 MILLION OZ

DEC 19/WITH SILVER UP 27 CENTS TODAY:BIG CHANGES IN SILVER INVENTORY AT THE SLV/: A MASSIVE DEPOSIT OF 2.747 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 443.393 MILLION OZ

DEC 18/WITH SILVER DOWN 9 CENTS TODAY:BIG CHANGES IN SILVER INVENTORY AT THE SLV/: A WITHDRAWAL OF 0.794 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 440.646 MILLION OZ

DEC 14/WITH SILVER DOWN 8 CENTS TODAY:BIG CHANGES IN SILVER INVENTORY AT THE SLV/: A MASSIVE WITHDRAWAL OF 3.00000 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 441.470 MILLION OZ

DEC 13/WITH SILVER DOWN 8 CENTS TODAY:BIG CHANGES IN SILVER INVENTORY AT THE SLV/: A DEPOSIT OF 10.326 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 444.470 MILLION OZ

DEC 12/WITH SILVER DOWN 5 CENTS TODAY:BIG CHANGES IN SILVER INVENTORY AT THE SLV/: A WITHDRAWAL OF 594,000 OZ FROM THE SLV////INVENTORY RESTS AT 434.144 MILLION OZ

CLOSING INVENTORY 433.500 MILLION OZ//

PHYSICAL GOLD/SILVER COMMENTARIES

1:Peter Schiff/Mike Maharrey

END

2,c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens, John Rubino

Mathew Piepenburg…

END

3. CHRIS POWELL//GATA GOLD COMMENTARIES:

END

3. CHRIS POWELL//GATA GOLD COMMENTARIES:

Sprott’s John Hathaway: Why gold and gold mining shares should be soaring

Submitted by admin on Fri, 2024-01-12 22:32Section: Daily Dispatches

11:07p ET Friday, January 12, 2024

Dear Friend of GATA and Gold:

Sprott Asset Management portfolio manager John Hathaway this week issued another one of those painstakingly researched and detailed reports showing why the gold price and the prices of gold mining company shares should be soaring but without explaining why they are not already keeping up with what would seem to be the traditional fundamentals for the monetary metal.

How can the gold price and the prices of gold mining shares be analyzed without reference to the great force of government policy long applied to keep those prices down?

Hathaway is expert at it. Even so, as always something is missing.

Hathaway’s report is headlined “Gold Mining Stocks, A Clear and Compelling Investment Case,” and it’s posted at the Sprott internet site here:

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

Alasdair Macleod….

Alasdair Macleod carries the sound-money message to Substack

Submitted by admin on Sun, 2024-01-14 20:38Section: Daily Dispatches

By Alasdair Macleod

Saturday, January 13, 2024

It is clear to me that as head of research for Goldmoney, most of the time I am preaching to the converted — those of us who understand the difference between gold and fiat currencies. We are all broadly aware that the price of gold is rising because governments are debasing their currencies.

Over the decades, GATA has done a magnificent job of exposing the manipulation and government propaganda side-lining gold, which we know is real money. We all owe Chris Powell and Bill Murphy our gratitude for their tireless and mostly thankless dedication to the sound-money cause over the last 25 years.

I believe it now behoves us to redouble our efforts to build on GATA’s work and spread our knowledge to the widest possible audience. The timing couldn’t be better, for the following reasons.

Gold is now establishing the $2,000 level as a base, and if it continues to rise through $2,100, we can be certain that public interest in gold will grow. Those wholly unfamiliar with why gold is rising will want to know why and whether they should buy gold and related investments. This includes investment managers who have lost sight of the commodity space generally.

Global investment portfolios are estimated to be worth $150 trillion and are less than 1% invested in gold and gold exchange-traded funds. With increasing credit and geopolitical risks, including those faced by fiat currencies themselves, we can be certain that this anomaly will lead to substantial demand for gold and related investments. To put this in context, a 1% increase in global portfolio exposure to gold would be the equivalent of a purchase of more than 23,000 tonnes at current values.

Despite above-ground stocks estimated at about 200,000 tonnes, physical liquidity in bullion markets is severely limited now that central banks are buying in record quantities. When a bull market in gold becomes more widely recognized, severe underweighting in portfolios and lack of liquidity are bound to have a dramatic impact on prices.

The reasons for these potential developments are and will continue to be poorly understood. I believe that there is important work to be done educating and explaining to a wider audience why gold appears to be rising when in fact it is the value of currencies falling. For this reason, I have established an internet site —

— to reach the widest possible audience, exploiting social media channels to spread the word.

I continue to write and act for Goldmoney, but from next month my more detailed analyses will be available only to paying subscribers on my Substack channel.

I would ask regular readers of GATA’s dispatches to similarly educate their families and friends, or if that proves too difficult or inappropriate, to encourage them to subscribe to my Substack channel.

—–

END

In case you missed this important podcast, I am repeating it for you

(Andrew Maguire/Live from the vault)

Physical pricing replaces derivative pricing of gold and oil this year, Maguire says

Submitted by admin on Fri, 2024-01-12 21:41Section: Daily Dispatches

9:42p ET Friday, January 12, 2024

Dear Friend of GATA and Gold:

This will be the year when the derivatives system of pricing gold and oil is replaced by physical pricing, London metals trader Andrew Maguire tells Shane Morand on this week’s edition of Kinesis Money’s “Live from the Vault” program.

Indeed, Maguire says one central bank may begin repricing gold as soon as this month.

The program is 46 minutes long and can be viewed at YouTube here:

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

4. OTHER GOLD/SILVER //COMMENTARIES//PODCASTS

END

4. OTHER GOLD/SILVER //COMMENTARIES//PODCASTS

end

5 a. IMPORTANT COMMENTARIES ON COMMODITIES /lithium

5 B GLOBAL COMMODITY ISSUES/FOOD IN GENERAL//FREIGHT

END

6.CRYPTOCURRENCY//DIGITAL CURRENCY// COMMENTARIES/

end

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS TUESDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED DOWN AT 7.1895

OFFSHORE YUAN: DOWN TO 7.2137

SHANGHAI CLOSED UP 7.70 PTS OR 0.27%

HANG SENG CLOSED DOWN 350.91 PTS OR 2.16%

2. Nikkei closed DOWN 282.61 PTS OR 0.79%

3. Europe stocks SO FAR: ALL RED

USA dollar INDEX UP TO 102.93 EURO FALLS TO 1.0885 DOWN 59 BASIS PTS

3b Japan 10 YR bond yield:RISES TO. +.590 Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 146.70/JAPANESE YEN NOW RISING AS WELL AS LONG TERM 10 YR. YIELDS RISING //EVENTUALLY THIS WILL BREAK THE JAPANESE CENTRAL BANK

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen DOWN CHINESE ONSHORE YUAN: DOWN// OFFSHORE: DOWN

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil DOWN for WTI and DOWN FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund UP TO +2.2040***/Italian 10 Yr bond yield UP to 3.795** /SPAIN 10 YR BOND YIELD UP TO 3.148…**

3i Greek 10 year bond yield UP TO 3.287

3j Gold at $2038.50 silver at: 23.05 1 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble DOWN 0 AND 24 /100 roubles/dollar; ROUBLE AT 87.83//

3m oil into the 73 dollar handle for WTI and 78 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 145,48// 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 0.590% STILL ON CENTRAL BANK (JAPAN) INTERVENTION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.8603 as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.9366 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.005 UP 6 BASIS PTS…

USA 30 YR BOND YIELD: 4.224 UP 4 BASIS PTS/

USA 2 YR BOND YIELD: 4.213 UP 8 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 30.11…(TURKEY SET TO BLOW UP FINANCIALLY)

GREAT BRITAIN/10 YEAR YIELD: UP 8 BASIS PTS AT 3.824

end

2.a Overnight: Newsquawk and Zero hedge.

Futures Slide As Dollar Surges, 10Y Yields Rise Above 4%

TUESDAY, JAN 16, 2024 – 08:02 AM

US equity futures fell for a second day as the dollar rose to a one-month high and as 10Y yield pushed back over 4.00% after various central banks pushed back against bets on aggressive interest rate cuts. As of 7:30am, S&P futures were down 0.4%, well off session lows, while Nasdaq futures lost about 0.5%. Meanwhile, Brent rose to around $79 a barrel as Houthi attacks on ships in the Red Sea keep tensions high. In other news, Iowa voters delivered Donald Trump a victory in Monday’s caucuses, moving him one step closer to a White House return. Among corporate highlights, Morgan Stanley and Goldman Sachs Group report earnings before the markets open.

In premarket trading, Boeing slumped again after Wells Fargo downgrades the planemaker to equal-weight from overweight, seeing a higher risk of production and/or delivery impacts with the US Federal Aviation Administration taking a closer look into Boeing’s operations. Elon Musk leaned on Tesla’s board to arrange another massive performance award for him after he sold a significant chunk of his stake in the company to acquire Twitter. Tesla shares slip 2.3% in US premarket trading after Elon Musk said he would rather build AI products outside of the the electric vehicle maker if he doesn’t have 25% voting control, suggesting the billionaire may prefer a bigger stake in the company.

Stocks pared losses after the ECB’s monthly survey showed consumer expectations for euro-zone inflation fell to the lowest in more than 1 1/2 years in November. Money markets held interest-rate cut wagers broadly steady after the ECB data, pricing the first quarter-point reduction by April followed by almost five more by year-end. Economic data in the UK, meanwhile, also supported the case for Bank of England rate cuts in the coming months, with wage growth cooling at one of the fastest paces on record. The pound weakened as much as 0.8% against the dollar and gilt yields edged lower.

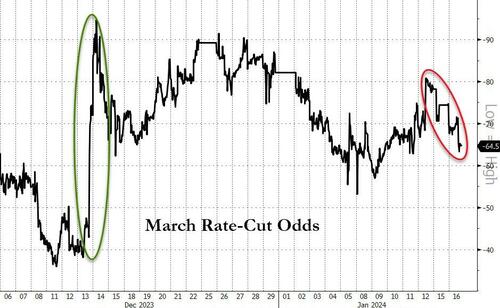

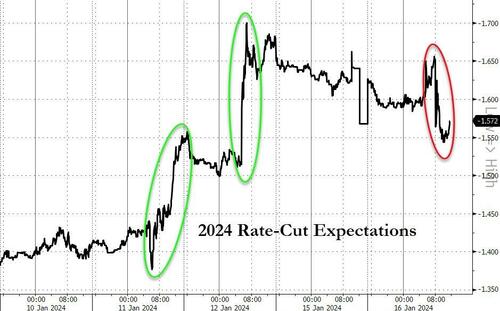

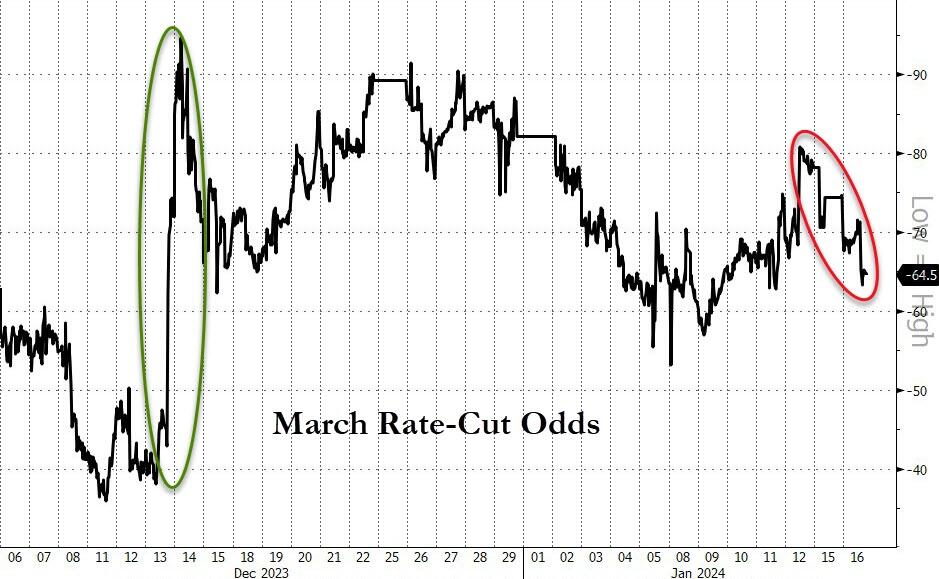

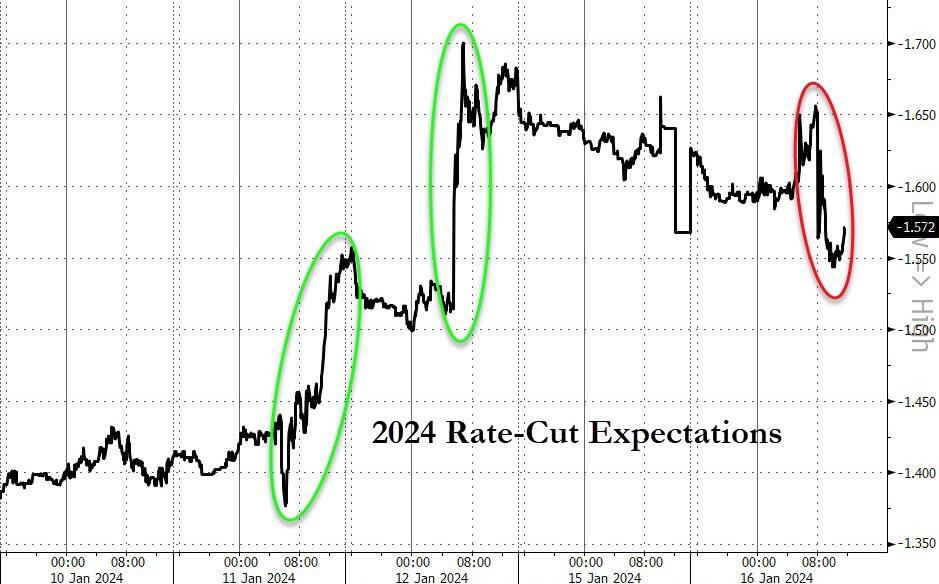

Still, sentiment was dented after hawkish comments from the ECB’s Nagel on Monday who said that it was too early to discuss rate cuts. A similar comment was made by ECB Governing Council member Robert Holzmann on Monday who indicated that cuts this year were not assured given lingering inflation and geopolitical risks. Their sentiments echoed prior comments from ECB President Christine Lagarde warning that it’s too early to talk about trimming borrowing costs. All were subsequently echoed on Tuesday in Davos, when ECB Governing Council member Francois Villeroy de Galhau said that it’s too early to declare victory on inflation. Traders are now awaiting Federal Reserve Governor Christopher Waller’s speech later Tuesday for cues on the timing of a Fed rate cut, with money markets seeing a two-in-three chance of a reduction in March.

“Central banks pushing back on rate cuts is not helping risky assets,” said Mohit Kumar, chief European economist at Jefferies International. “The market has gone a bit ahead of itself.”

And then there are earnings: Morgan Stanley and Goldman Sachs are among the companies reporting results Tuesday, and are expected to reveal the continued lull in investment banking activity as high borrowing costs, geopolitical tensions and recessionary risks dampen deal-making.

European markets were red across the board, extending Monday’s losses. The Stoxx 600 is down 0.6%, with food beverage and media shares are the biggest outperformers, while banking shares leading the decline as JPMorgan analysts said lending revenue will be capped by the peak in interest rates. Here are the biggest movers Tuesday:

- Experian gains as much as 3.2%, the most in a month, after the credit-data agency narrowed its expectations for full-year organic revenue growth to the 5%-6% area, compared to the previous 4%-6% forecast and the Bloomberg consensus of 5.16%

- Lindt & Spruengli shares jump as much as 6.8%, most since July 2022, after the Swiss chocolate maker reported 2023 organic sales growth that beat the highest analyst estimate, according to Vontobel

- Dassault Systemes shares gain as much as 1.8%, outperforming a falling tech sector, after Deutsche Bank raises the stock to buy from hold. Industry checks suggest that the adoption of the software firm’s cloud-based design platform 3DExperience is increasing in the automotive industry

- Ocado rallies as much as 7.8%, rebounding from the one-month low hit yesterday, after its grocery business delivered faster sales growth in the fourth quarter than expected

- Publicis rises as much as 1.4%, to its highest intraday level on record after Goldman Sachs raised the stock to buy, and rated media peers including Relx, Wolters Kluwer, Informa and UMG as buy, saying the most compelling stocks within Europe’s internet and media sector are those that benefit from structural tailwinds

- QinetiQ Group shares rise as much as 7.9% to touch a two-month high, after the defense company announced a £100 million share buyback program and issued a trading update detailing a rise in full-year revenue

- DocMorris shares rise as much as 5.7% after full-year 2023 revenue at the Swiss online pharmacy achieved the upper end of its guidance range. The company also reported an increase in active customer numbers for the first time since 2021

- THG rises as much as 9.4%, rebounding after hitting its lowest level since late October on Monday, after the e-commerce retail company’s guidance for FY23 adjusted Ebitda came in ahead of forecasts, and several of its divisions returned to revenue growth in the latest quarter

- Hugo Boss shares dropped as much as 11% in Frankfurt, their worst day in nearly four years, with analysts flagging that the German high-end clothing maker’s Ebit disappointed, even as its fourth-quarter sales performance was robust

- Air France-KLM slips as much as 3.2% to the lowest in six weeks after announcing it would scrap a year-old cargo alliance with container shipping giant CMA CGM, citing a “tight regulatory environment”

- Wise shares fall as much as 3.4% after the money-transfer firm’s results showed that per-user transaction volume fell among both personal and business accounts. The decline was seen by analysts as a headwind to medium-term growth

Earlier in the session, Asian stocks declined, set to snap three days of gains, as risk sentiment took a breather ahead of key economic data from China and after the ECB tamped down rapid rate cut expectations. The MSCI Asia Pacific Index slid as much as 1.2%, with Tencent, Samsung and BHP among the biggest drags. Equity benchmarks in Hong Kong and Australia posted the biggest declines, while Japanese equities fell amid signs that the market may be overbought after eight-straight days of gains for the Topix. China remains in focus ahead of gross domestic product, industrial production and retail sales data due Wednesday. Numbers are projected to show improvement in the economy in a rebound from periods of pandemic restrictions, and some investors have been turning bullish on the country’s beaten-down stock market.

- Hang Seng and Shanghai Comp conformed to the downbeat mood but with the losses in the mainland initially cushioned after a substantial PBoC liquidity operation, while Beijing reportedly told some institutional investors in recent days not to sell stocks.

- Nikkei 225 extended beneath the 36,000 level owing to slightly higher yields and firmer-than-expected PPI data.

- ASX 200 retreated with miners among the worst hit after lower iron ore output and shipments by Rio Tinto.

- Stocks in India posted their first retreat in six sessions on Tuesday, dragged by profit taking in index heavyweight Reliance Industries and information technology firms, which had rallied recently. The S&P BSE SENSEX Index fell 0.3% to 73,128.77 in Mumbai, while the NSE Nifty 50 Index declined by a similar measure. BSE’s measure of real estate companies, which was the best performer among its sectoral gauges in 2023, slipped 1.6% — its biggest single-day drop since Dec. 20.

There have been “a few recent economic data points challenging the consensus view of rapid and deep rate cuts,” said Matthew Haupt, a portfolio manager at Wilson Asset Management. “It’s been enough for equity investors to pause and sell into the recent strength.”

In FX, the Bloomberg dollar index climbed to a one-month high and Treasury yields rose, as trading re-opened after MLK Jr. Day. The risk sensitive Scandinavian currencies and Australian dollar led Group-of-10 losses, as central bankers pushed back on market rate cut bets. The Japanese yen sunk to a one-month low, while the British pound dropped on cooling UK wage growth.

- The Bloomberg Dollar Index rose to its highest level since Dec. 13 as the dollar gained against all Group-of-10 peers, the Australian dollar, Swedish krona and Norwegian krone led losses as risk-off sentiment swept through markets

- USD/JPY climbed as much as 0.6% to 146.65, a one-month high; One-week implied volatility between the currency pair implied traders don’t expected fireworks out of next week’s BOJ meeting but are positioning for the possibility of surprisingly hawkish forward guidance

- GBP/USD dropped as much as 0.7% to 1.2635, the lowest level since Jan. 5; UK wage growth data cooled at one of the fastest paces on record

- EUR/USD fell as much as 0.6% to 1.0883 as the euro fell for a fourth day; Consumer expectations for euro-zone inflation dropped to the lowest in more than one and a half years, ECB’s Villeroy said rate cuts were probable but pushed back on the timing priced by markets

In rates, Treasury yields cheaper by 6bp to 7bp across the curve as cash market reopens following Monday’s close, during which futures were led lower by bunds. Treasury 10-year yields around 4.01%, cheaper by around 7bp vs Friday’s close with higher yields helping the greenback, with the Bloomberg Dollar Spot Index rising 0.6% ahead of a speech by Fed Governor Waller. Curve spreads are broadly within 1bp of Friday levels. Fed-dated OIS have around 17bp of rate cuts priced in for the March policy meeting vs 19bp on Friday. In Europe, the slide in bunds occurred after ECB policymaker Holzmann warned against rate cuts this year. Fed’s Waller is slated to speak at 11am New York time, heavy corporate issuance is expected this week and a 20-year bond auction is ahead Wednesday.

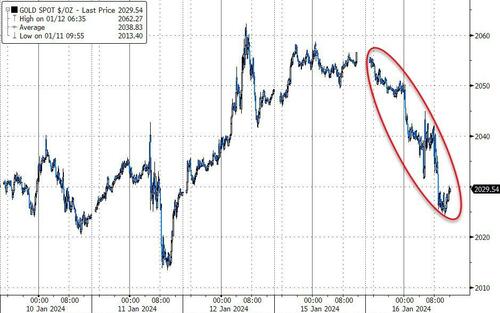

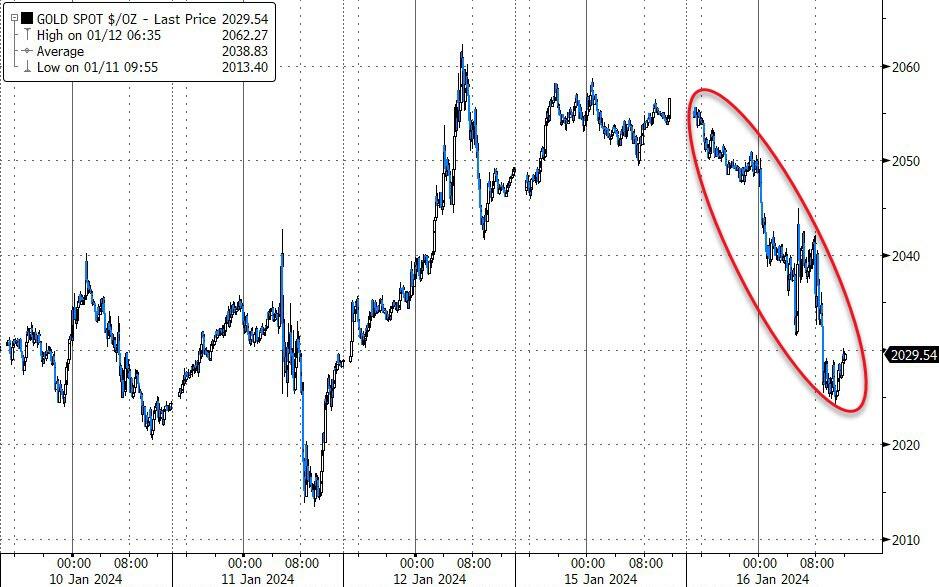

In commodities, oil prices were steady as continued Houthi attacks on ships in the Red Sea that are keeping tensions high in the Middle East were offset by a shaky global economic outlook and gains in the dollar. Global benchmark Brent held above $78 a barrel, while West Texas Intermediate traded around $73. Spot gold fell 0.9% below $2040.

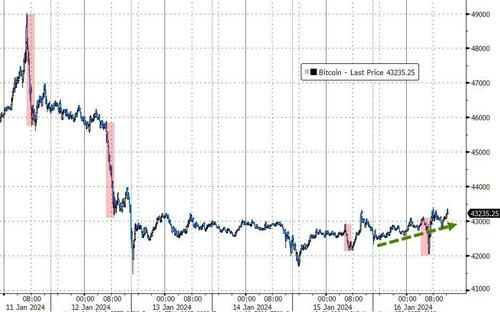

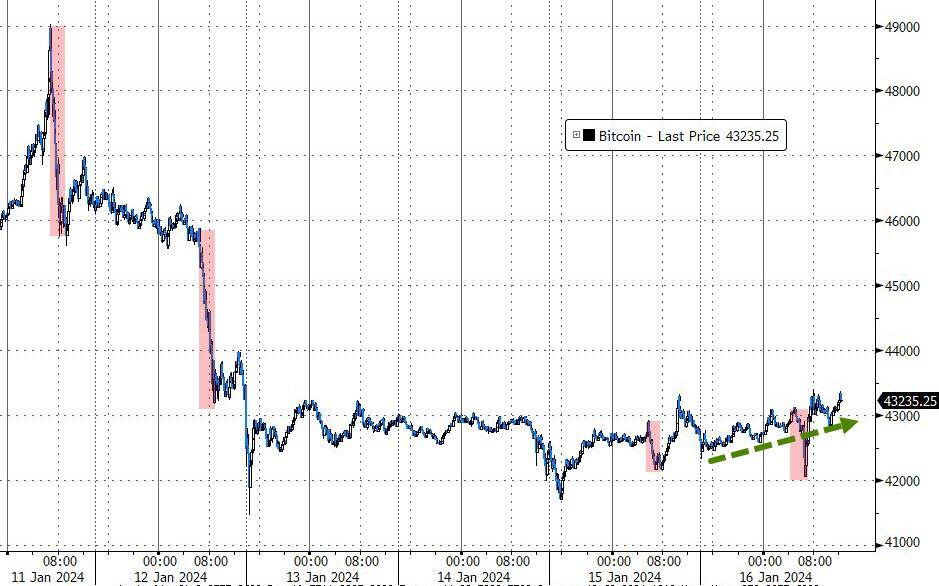

Bitcoin rose +0.4%, holding just below the $43k level with Ethereum also posting modest gains.

Looking to the day ahead now, data releases include UK labor market data, Germany’s ZEW survey for January, Canada’s CPI for December, and in the US, we get the Empire State manufacturing survey for January. From central banks, we’ll hear from BoE Governor Bailey, Fed Governor Waller and the ECB’s Villeroy. Lastly, earnings releases include Goldman Sachs and Morgan Stanley.

Market Snapshot

- S&P 500 futures down 0.5% to 4,793.25

- MXAP down 1.4% to 165.28

- MXAPJ down 1.5% to 503.27

- Nikkei down 0.8% to 35,619.18

- Topix down 0.8% to 2,503.98

- Hang Seng Index down 2.2% to 15,865.92

- Shanghai Composite up 0.3% to 2,893.99

- Sensex down 0.2% to 73,170.25

- Australia S&P/ASX 200 down 1.1% to 7,414.79

- Kospi down 1.1% to 2,497.59

- STOXX Europe 600 down 0.4% to 472.12

- German 10Y yield little changed at 2.22%

- Euro down 0.5% to $1.0894

- Brent Futures up 0.6% to $78.62/bbl

- Gold spot down 0.8% to $2,041.01

- U.S. Dollar Index up 0.70% to 103.12

Top Overnight News from Bloomberg

- China is weighing 1 trillion yuan ($139 billion) of new debt issuance under a so-called special sovereign bond plan, only the fourth such sale in the past 26 years. The sale of ultra-long bonds would fund projects in areas including food and energy, people familiar said. BBG

- William Lai Ching-te won the Taiwan presidential election on Saturday, as expected, securing a 3rd term in power for the Democratic Progressive Party (DPP). Lai took 40% of the vote followed by Hou Yu-I from the Kuomintang (KMT) at 33.5% (the KMT is considered more conciliatory toward China) and Ko Wen-je from Taiwan People’s Party (TPP) at 26.5%. RTRS

- AAPL is offering rare discounts on its iPhones in China, cutting retail prices by as much as 500 yuan ($70) amid growing competitive pressure in the world’s biggest smartphone market. RTRS

- ECB’s Holzmann warns markets not to expect the first rate cut in April and says there may not be any decreases this year. CNBC

- Houthi militants hit a US-owned container vessel with a missile in the Gulf of Aden. Gibraltar Eagle, carrying steel products, suffered limited damage. Washington warned its merchant ships to avoid the area. PM Rishi Sunak told Parliament that the UK wants to reduce tensions and its air strikes are “self-defense.” BBG

- Though the Federal Reserve stopped raising interest rates last summer, it is quietly tightening monetary policy through another channel: shrinking its $7.7 trillion holdings of bonds and other assets by around $80 billion a month. Now that, too, may change. Fed officials are to start deliberations on slowing, though not ending, that so-called quantitative tightening as soon as their policy meeting this month. WSJ

- Biden’s campaign raises $97MM in Q4 and has $117MM of cash on hand, formidable numbers that provide an important monetary tailwind for the president heading into November. BBG

- Trump dominates Iowa (as expected) at 51% followed by DeSantis at 21.2% and Haley at 19.1% while Ramaswamy exits the race w/a 7.7% showing. WaPo

- Global core inflation picked up modestly in December on a 1-month basis, but the 3-month annualized rate has slowed further to 2.0%. We still expect the Fed to start easing in March, with a total of 5 cuts in 2024 (slightly less than market pricing). The ECB should follow in April and the BoE in May, and our views on both central banks are somewhat dovish relative to market pricing. By contrast, we expect only modest macro policy easing in China, despite sluggish growth and very low inflation. The combination of falling inflation, easier monetary policy, and solid growth should provide a friendly backdrop for risk asset markets. GIR

A more detailed look at global markets courtesy of Newsquawk

APAC stocks were pressured in the absence of a lead from Wall Street and amid the upside in yields. ASX 200 retreated with miners among the worst hit after lower iron ore output and shipments by Rio Tinto. Nikkei 225 extended beneath the 36,000 level owing to slightly higher yields and firmer-than-expected PPI data. Hang Seng and Shanghai Comp conformed to the downbeat mood but with the losses in the mainland initially cushioned after a substantial PBoC liquidity operation, while Beijing reportedly told some institutional investors in recent days not to sell stocks.

Top Asian News

- PBoC injected CNY 760bln via 7-day reverse repos with the rate at 1.80% for a CNY 695bln net injection.

- Chinese authorities reportedly told some institutional investors in recent days not to sell stocks as the Chinese stock rout resumes, according to FT.

- Chinese President Xi stresses boosting high-quality development of the country’s financial sector, according to Reuters citing state media.

- Microsoft (MSFT) CEO says China is not a large business for the Co.

- China is said to be mulling more stimulus with USD 139bln of special bonds, according to Bloomberg sources; proposals include the sale of ultra-long sovereign bonds to fund projects. Projects are related to projects related to food, energy, supply chains and urbanisation, sources added.

- Japanese government is to increase new bond issuance by USD 3.43bln to fund extra budget reserves (following recent earthquakes); there will be no change to JGB issuance sold to market

- Chinese Premier Li says China’s economy is making steady progress; Chinese economy rebounded in 2023 and had an estimated growth of 5.2%, higher than the 5% target; says in promoting development, China did not resort to massive stimulus. Comes ahead of the Chinese GDP and activity data on Wednesday.

European equities, Stoxx 600 (-0.5%), are trading on the back-foot having sunk at the open, following a negative handover from APAC trade overnight, in the absence of a lead from Wall Street. European sectors have a strong negative tilt; Media is marginally firmer after a broker upgrade at Publicis (+1.2%). Banks are lower following a slew of downgrades at JPM and a cut in EPS estimates for Commerzbank (-4.5%). US equity futures are lower across the board, in tandem with European counterparts, though with losses slightly more pronounced; the Russell 2000 (-0.9%) underperforms. Earnings from Goldman Sachs and Morgan Stanley due, among others, in the pre-market.

Top European News

- British pension funds are preparing to “flood the market” with billions of GBP’s of private assets, according to Bloomberg. As much as GBP 200bln in assets could be offloaded as rising interest rates provide funds with an opportunity to offload the part of the risk of meeting future liabilities.

- BofA January Fund Manager Survey: cash levels up, more investors expect short term rates to be lower in the next 12 months, more expect a weaker Chinese economy than a stronger one.

- Ocado (OCDO LN) Retail CEO is not expecting much impact on business from the Red Sea/Suez Canal disruptions

- German economy is expected to grow 0.3% in 2024, according to German BDI Industry Association; German economy is at a standstill and there is no change of a rapid recovery

- ECB Consumer Inflation Expectations survey (Nov) – 12-months ahead 3.2% (prev. 4.0%); 3-year ahead 2.2% (prev. 2.5%). Economic growth expectations for the next 12 months -1.2% (prev. -1.3%)

FX

- Dollar is firmer alongside the risk averse mood and as US yields rise after cash closure for MLK day; DXY took out 103.00 and surpassed the post-NFP high of 103.10, with the 200DMA at 103.41 now in sight. Fed’s Waller at 16:00GMT/11:00EST will be in focus for the Dollar.

- EUR/USD has lost its 1.09 status amid the strength in the USD, less hawkish ECB speak and softer consumer inflation expectations. Today’s trough at 1.0881 with yesterday’s low at 1.0876 just below.

- Cable is swept up by Dollar buying, with lower UK wage data also not helping the Pound. On release, Cable sank lower before then entirely paring the move.

- Antipodeans are the G10 underperformers, in tandem with the cautious risk tone; support at 0.66 for the AUD/USD has broken in recent trade.

- USD/CNH bid and continuing to lift; focus on earlier sources around potential special bond stimulus and thereafter Premier Li on GDP, ahead of Wednesday’s figures.

- PBoC set USD/CNY mid-point at 7.1134 vs exp. 7.1783 (prev. 7.1084).

Fixed Income

- Treasuries pressured to a 112-05 trough, yields bear-flattening as cash reacts to Monday’s ECB speak.

- Bunds are struggling for direction & drawn to the mid-point of 134.94-135.42 parameters after Monday’s hawkish move on numerous ECB officials. Remarks thus far from Villeroy, Centeno & Valimaki at Davos stress data-dependency.

- Despite the dovish wage figures, Gilts opened 16 ticks lower at 99.91 as the bias from US yields dominates. Since, Gilts have lifted to a 100.33 peak, shy of last week’s 100.47-69 highs.

- UK sells GBP 1.5bln 2033 I/L Gilt: b/c 3.04x (prev. 2.68x) and real yield 0.423% (prev. 0.724%)

- Germany sells EUR 3.2bln vs exp. EUR 4.0bln 2.10% 2029 Bobl; b/c 2.1x (prev. 2.07x), average yield 2.12% (prev. 2.56%), and retention 20.0% (prev. 19.2%)

- France is seeing in excess of EUR 74bln in demand for its new green bond, according to lead managers; spread set at 8bps over outstanding June 2044 (initial guidance +10bp)

Commodities

- An upward bias is seen in crude prices this morning, with the complex resilient to the surging Dollar and broader risk aversion as the downside is countered by escalating geopolitics coupled with reports of further Chinese stimulus and Premier Li on GDP; Brent at highs of USD 79.18/bbl.

- Precious metals feel the pressure from the surge in the Dollar and yields stateside; XAU fell from a USD 2,055.22/oz intraday peak to levels under its 21 DMA (USD 2,044.44/oz).

- Base metals are mostly lower but were lifted off worst levels amid reports that China is mulling further stimulus.

- First Quantum is to reduce operating activities at its Ravensthorpe nickel operation and will cut workforce at the site by 30% after a significant downturn in nickel prices during 2023, combined with higher operating costs in Western Australia.

- India’s Oil Minister says India has opened up to every possible supplier; Indian demand for energy will not peter off for a while

Central Bank speak

- ECB’s Villeroy says it is too early to declare victory over inflation, most monetary policy transmission is more or less over. Will not remark on the season for the next ECB move; but the next move should be a cut this year. Can see a soft landing in both Europe and the US. Estimates R to be around zero within the Euro-area.

- ECB’s Centeno says ECB needs to be prepared for all topics, including rate cuts; says recent data confirmed Dec projections, but inflation was slightly below forecast. Inflation is coming down sustainably, should not be worried about resurgence of real wages. Q1 growth could remain around zero. Expects contained wage demand. Inflation trajectory is very positive at this point.

- ECB’s Valimaki says inflation is on the right track but job is not done so restrictive monetary policy is still called for; must not jump the gun on rate cuts and best to wait a bit longer than exit prematurely. Soft landing for economy still the baseline but risks tilted towards downside. Wage data so far consistent with ECB’s December projections.

- ECB’s Nagel (hawk) says it’s too early to discuss rate cuts as inflation remains too high, maybe the ECB can wait until after the summer break; markets are sometimes over optimistic – Bloomberg TV interview.

- ECB’s Holzmann (hawk) says rate cut expectations are optimistic; shouldn’t count on rate cuts at all in 2024 – CNBC interview.

- ECB’s Herodotou says it is too soon to contemplate policy easing or the pace of easing – Econostream Media interview

- ECB’s Lane, weekend remarks: will have key data by June to decide on rates and that changing rates too fast can be harmful, while he added that once the ECB begins lowering rates, this would not be by a single decision of a rate cut and there would likely be a sequence of rate cuts – Corriere Della Serra.

Geopolitics: Middle East

- Explosions were reported in different areas in Erbil, northern Iraq and in Syria, according to Al Arabiya IRGC said it attacked and destroyed the espionage headquarters of Israel’s Mossad in Iraq’s Kurdistan and it targeted Islamic State in Syria in response to the group’s recent terrorist attacks in Iran, according to Reuters.

- US State Department said the US strongly condemned Iran’s attacks in Erbil on Monday, while US officials said no US facilities were impacted by missile strikes in Erbil, Iraq and there were no US casualties, according to Reuters.

- UK PM Sunak signalled the UK could participate in further strikes against Houthi rebels and told MPs that Britain will not hesitate to protect its interests where required, according to FT.

- Houthi military spokesman said they consider all American and British vessels and warships participating in aggression against them as hostile targets, according to Reuters.

- Iran’s Islamic Revolutionary Guard Corps commanders and advisors are on the ground in Yemen and playing a direct role in Houthi rebel attacks on commercial traffic in the Red Sea, according to SEMAFOR.

Geopolitics: Other

- Ukraine President Zelenskiy asked Switzerland to organise a high-level peace conference, while teams will start on plans today.

- North Korea decided to shut down organisations dealing with unification and inter-Korean tourism, while North Korean leader Kim said they do not want war but have no intention to avoid it. Furthermore, Kim said war will destroy South Korea and deal an unimaginable defeat to the US, according to KCNA.

- South Korean President Yoon said North Korea’s recent missile launch and artillery firing are political acts to divide South Koreans and its provocations will be met with response on a multiplied scale, according to Reuters.

US Event Calendar

- 08:30: Jan. Empire Manufacturing, est. -5.0, prior -14.5

Central Bank Speakers

- 11:00: Fed’s Waller Speaks on Economic Outlook and Monetary Policy

DB’s Jim Reid concludes the overnight wrap

As we go to print, we have 95% of the votes counted from the Iowa Caucus. Former President Donald Trump has easily won the first test of this election year with 51.1% of the vote so far, according to CNN. Florida Governor Ron DeSantis is in second place (21.2%) followed by a third-place finish for former South Carolina Governor Nikki Haley (19%). Also, Vivek Ramaswamy (7.7%), suspended his presidential campaign after a fourth-place finish. The polling averages in the state before the vote were Trump (53%), Haley (19%), and DeSantis (16%), so DeSantis has slightly outperformed.

The next stop is New Hampshire on Tuesday next we ek , where Haley is running in a strong second, with the current FiveThirtyEight polling average at Trump (43%), Haley (30%) and DeSantis (6%). Her campaign’s hope is they can win New Hampshire, and then also take the third contest in South Carolina on February 3 (where Haley was Governor from 2011-17).

Before the votes, yesterday was a lighter session for markets given the US holiday, but it was fairly negative where trading did take place, since European equities and bonds struggled after several ECB officials pushed back on the possibility of rate cuts. By the close, that meant the STOXX 600 was down -0.54%, whilst yields on 10yr bunds were also up +7.3bps to 2.23%. And that wasn’t just confined to Europe, as US futures markets were also pointing to bonds and equity losses there too. Overnight 2 and 10yr US yields are both +6bps higher and S&P and NASDAQ futures are -0.36% and -0.5% lower, respectively.

In terms of the comments, markets were partly reacting to an interview that had taken place on Saturday, with ECB chief economist Philip Lane. He warned that the “history of high inflation episodes tells us that if central banks try to normalise too quickly, before the problem is really conquered, then we get another inflation wave, and then another wave of interest rate hikes. That would be a far worse scenario.” So there was an open acknowledgement about the risks of easing prematurely, which is what happened in the 1970s and meant inflation became more entrenched as a result.

But it wasn’t just Lane who commented, as we also heard from some of the hawks on the ECB’s Governing Council, who similarly pushed back on the rate cut discussion. For instance, Bundesbank President Nagel said “I think it’s too early to talk about cuts”, and Austria’s Holzmann even said that “We should not bank on the rate cut at all for 2024.” Even Cyprus’ Herodotou, who’s been a more dovish voice, said that “Any discussion regarding the time and potency of the first rate cut, as well as the pace of further cuts thereafter, would be premature at the moment and would not constitute a data-dependent approach”. So there was a consistent message from various speakers on the hawk-dove spectrum that didn’t sound as though a Q1 rate cut was on the agenda.

All that meant investors grew more sceptical that the ECB would be cutting rates soon, and the likelihood of a cut by March fell to 29%, down from 43% on Friday. That was echoed more broadly as well, as the likelihood of a Fed cut by March fell from 83% on Friday to 74% by yesterday’s close, and the likelihood of a BoE cut by then was down from 35% to 31%. And in turn, that led to a sovereign bond sell-off across Europe, with yields on 10yr bunds (+4.8bps), OATs (+5.1bps) and BTPs (+7.3bps) all moving higher. 2yr bund and OATs were +6.1bps and +6.7bps higher respectively, so a slightly deeper inversion.

For equities it was much the same story, with the major indices across Europe all getting the week off to a rocky start. Indeed, for the STOXX 600 (-0.54%) it was the worst start to a week in over three months. That was echoed across the continent, with losses for the DAX (-0.49%), the CAC 40 (-0.72%) and the FTSE 100 (-0.39%). That came as the activity data we did get yesterday was fairly weak, with full-year German GDP growth for 2023 coming in at a contractionary -0.3%, in line with expectations. In fact, apart from the Covid pandemic year of 2020, that’s the weakest annual growth since 2009 as the economy faced the impact of the GFC. A technical recession was avoided though as Q3 was revised up a tenth to 0.0% with Q4 likely to be -0.3% when the flash is released on Jan 30th! It wasn’t all bad news, however, as European natural gas futures fell to their lowest level since August, with the front-month contract down to €29.92/MWh.

Asian equity markets are lower this morning with the Hang Seng (-1.92%) the biggest underperformer and with the Nikkei (-0.71%) also halting its record-breaking gains since the start of the year. Meanwhile, the KOSPI (-0.72%) is also losing ground while the CSI (-0.38%) and the Shanghai Composite (-0.62%) are also declining.

Early morning data showed that Japanese input prices were unchanged last month from a year earlier, marking its weakest reading in almost three years as the yen’s recent gains (now largely unwound) helped cap import costs. The expectation were for -0.3% though. They increased +0.3% m/m in December as against an upwardly revised gain of +0.3% in November and expectations for 0.0%.

To the day ahead now, and data releases include UK labour market data, Germany’s ZEW survey for January, Canada’s CPI for December, and the US Empire State manufacturing survey for January. From central banks, we’ll hear from BoE Governor Bailey, Fed Governor Waller and the ECB’s Villeroy. Lastly, earnings releases include Goldman Sachs and Morgan Stanley.

2 B) NOW NEWSQUAWK (EUROPE/REPORT)

Negative risk tone with equities lower and Dollar bid, Crude remains firm; Fed’s Waller due – Newsquawk US Market Open

TUESDAY, JAN 16, 2024 – 06:13 AM

- European bourses are weaker following a negative handover from APAC trade, with US futures also pressured amid yield upside & into earnings

- Dollar is firmer and Antipodeans are lower amid the risk-averse mood; GBP weighed by Dollar strength and softer UK wage metrics

- Bonds mixed, with Treasuries pressured as markets react to hawkish ECB speak; Gilts eventually firm post dovish data

- Crude continues to gain despite Dollar strength amid escalating geopolitical tensions & Chinese stimulus/reports; Base metals initially pressured though bounced such reporting

- Former US President Trump won the Iowa Republican Caucus with over 51% of the vote, Ramaswamy dropped out

- Looking ahead, US NY Fed & Canadian CPI, BoE’s Bailey & Fed’s Waller, Earnings from Goldman Sachs, PNC Financial Services, Morgan Stanley & Charles Schwab.

More Newsquawk in 3 steps:

1. Subscribe to the free premarket movers reports

2. Listen to this report in the market open podcast (available on Apple and Spotify)

3. Trial Newsquawk’s premium real-time audio news squawk box for 7 days

EUROPEAN TRADE

EQUITIES

- European equities, Stoxx 600 (-0.5%), are trading on the back-foot having sunk at the open, following a negative handover from APAC trade overnight, in the absence of a lead from Wall Street.

- European sectors have a strong negative tilt; Media is marginally firmer after a broker upgrade at Publicis (+1.2%). Banks are lower following a slew of downgrades at JPM and a cut in EPS estimates for Commerzbank (-4.5%).

- US equity futures are lower across the board, in tandem with European counterparts, though with losses slightly more pronounced; the Russell 2000 (-0.9%) underperforms. Earnings from Goldman Sachs and Morgan Stanley due, among others, in the pre-market.

- Click here and here for the sessions European pre-market equity newsflow, including earnings.

- Click here for more details.

FX

- Dollar is firmer alongside the risk averse mood and as US yields rise after cash closure for MLK day; DXY took out 103.00 and surpassed the post-NFP high of 103.10, with the 200DMA at 103.41 now in sight. Fed’s Waller at 16:00GMT/11:00EST will be in focus for the Dollar.

- EUR/USD has lost its 1.09 status amid the strength in the USD, less hawkish ECB speak and softer consumer inflation expectations. Today’s trough at 1.0881 with yesterday’s low at 1.0876 just below.

- Cable is swept up by Dollar buying, with lower UK wage data also not helping the Pound. On release, Cable sank lower before then entirely paring the move.

- Antipodeans are the G10 underperformers, in tandem with the cautious risk tone; support at 0.66 for the AUD/USD has broken in recent trade.

- USD/CNH bid and continuing to lift; focus on earlier sources around potential special bond stimulus and thereafter Premier Li on GDP, ahead of Wednesday’s figures.

- PBoC set USD/CNY mid-point at 7.1134 vs exp. 7.1783 (prev. 7.1084).

- Click here for more details.

- Click here for the Option Expires for the NY Cut.

FIXED INCOME

- Treasuries pressured to a 112-05 trough, yields bear-flattening as cash reacts to Monday’s ECB speak.