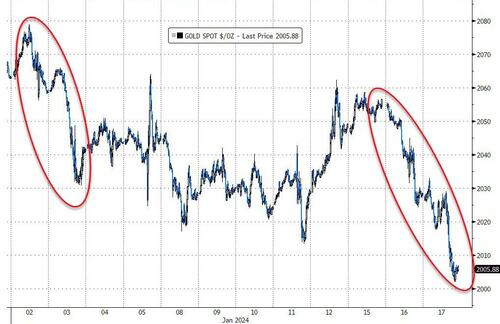

GOLD PRICE CLOSED: DOWN $23.25 TO $2004.00

SILVER PRICE CLOSED: DOWN 38 cents AT $22.57

Access prices: closes 4: 15 PM

Gold ACCESS CLOSED 2005.60

Silver ACCESS CLOSED: 22.56

Bitcoin morning price:, 42,662 DOWN 665 DOLLARS

Bitcoin: afternoon price: $42,710 DOWN 617 dollars

Platinum price closing $887.60 DOWN $12.50

Palladium price; $920.95 DOWN $21.50

END

SHANGHAI GOLD (USD) FUTURES – QUOTES

VENUE:

- GLOBEX

Beginning Monday, April 1, 2024, CME Group settlement data will no longer be accessible through ftp.cmegroup.com and will have a delayed publication time of 12:00 a.m. CT on all cmegroup.com web pages. Learn about alternate ways to access the data in our FAQ.

AUTO-REFRESH IS OFF

Last Updated 17 Jan 2024 12:41:45 PM CT.

Market data is delayed by at least 10 minutes.

PREMIUM SHANGHAI OVER NY: $50.35

Due to the huge rise in the dollar, we must look at gold and silver in currencies other than the dollar to understand where we are heading

I will now provide gold in Canadian dollars, British pounds and Euros

4: 15 PM ACCESS

*CANADIAN GOLD: $2,709.74 DOWN 27.10 CDN dollars per oz( * NEW ALL TIME HIGH 2,795.90 CDN DOLLARS PER OZ//DEC 1 272023)

*BRITISH GOLD: 1581.17 DOWN 23.60 pounds per oz// *(NEW ALL TIME HIGH//CLOSING///1655.17 BRITISH POUNDS/OZ) OCT 2/2023

*EURO GOLD: 1842,96 DOWN 21.28 euros per oz //* (ALL TIME CLOSING HIGH: 1903.75 EUROS PER OZ//DEC 1.2023)

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

EXCHANGE: COMEX

EXCHANGE: COMEX

CONTRACT: JANUARY 2024 COMEX 100 GOLD FUTURES

SETTLEMENT: 2,026.000000000 USD

INTENT DATE: 01/16/2024 DELIVERY DATE: 01/18/2024

FIRM ORG FIRM NAME ISSUED STOPPED

190 H BMO CAPITAL 2

363 H WELLS FARGO SEC 16

435 H SCOTIA CAPITAL 2

661 C JP MORGAN 20 5

737 C ADVANTAGE 7 2

TOTAL: 27 27

MONTH TO DATE: 3,478

JPMorgan stopped 5/27 contracts.

FOR JAN.:

GOLD: NUMBER OF NOTICES FILED FOR JAN/2024. CONTRACT: 27 NOTICES FOR 2700 OZ or 0.0839 TONNES

total notices so far: 3478 contracts for 347800 oz (10.818 tonnes)

FOR JANUARY:

SILVER NOTICES 0 NOTICE(S) FILED FOR nil OZ/

total number of notices filed so far this month : 765 for 3,825,000 oz

XXXXXXXXXXXXXXXXXX

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

BOTH GLD AND SLV ARE FRAUDULENT VEHICLES

GLD

WITH GOLD DOWN $23.25

INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD/ : /HUGE CHANGES AT THE GLD: A DEPOSIT OF .779 TONNES OF GOLD INTO THE GLD/

INVENTORY RESTS AT 864.40 TONNES

SLV//

WITH NO SILVER AROUND AND SILVER DOWN 38 CENTS AT THE SLV//

HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A LWITHDRAWAL OF 549,000 OZ FROM THE SLV.

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV.

CLOSING INVENTORY: 432.951 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A GOOD SIZED 312 CONTRACTS TO 131,956 AND FURTHER FROM THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THIS TINY SIZED LOSS IN COMEX OI WAS ACCOMPLISHED WITH OUR LOSS OF $0.08 IN SILVER PRICING AT THE COMEX ON TUESDAY. WE HAD SMALL LONG LIQUIDATION, AND FEW SPEC SHORT COVERING. WE HAD CONSIDERABLE T.A.S. LIQUIDATION AT THE COMEX SESSION. WE HAD A GOOD 465 T.A.S ISSUANCE AND THESE WILL BE USED FOR MANIPULATION LATER THIS MONTH/AS WELL AS TODAY.

CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON TUESDAY NIGHT: 465 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS. IT THUS LOOKS LIKE THE FED (GOV’T) IS BEHIND ALL OF THESE TRADES.

WE HAVE NOW SET ANOTHER RECORD LOW AT 114,102 CONTRACTS ///JULY 3.2023// OUR BANKERS WITH THE HELP OF SPECULATORS AND HIGH FREQUENCY TRADERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.08), BUT WERE UNSUCCESSFUL IN KNOCKING ANY SILVER LONGS AS WE HAD A GOOD 390 CONTRACT GAIN ON OUR TWO EXCHANGES..

WE MUST HAVE HAD:

A GOOD SIZED 407 ISSUANCE OF EXCHANGE FOR PHYSICALS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 6.650 MILLION OZ (FIRST DAY NOTICE) FOLLOWED BY TODAY’S NIL OZ QUEUE. JUMP NEW TOTALS 6.460 MILLION OZ//

//NEW STANDING FOR SILVER IS THUS 6.460 MILLION OZ

//TINY SIZED COMEX OI LOSS/GOOD SIZED EFP ISSUANCE/ VI) GOOD SIZED NUMBER OF T.A.S. CONTRACT ISSUANCE 465 CONTRACTS)/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL -REMOVED 295 CONTRACTS //

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS JAN ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF JAN

TOTAL CONTRACTS for 11 days, total 8572 contracts: OR 42.860 MILLION OZ (779 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 42.860 MILLION OZ

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH 2022: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 118.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 85.745 MILLION OZ (SMALLER THAN LAST MONTH)

AUGUST: 171.43 MILLION OZ (THIS MONTH IS GOING TO BE HUGE //2ND HIGHEST ON RECORD

SEPT: 72.705 MILLION OZ (SMALLER THIS MONTH)

OCT: 97.455 MILLION OZ

NOV. 50.050 MILLION OZ

DEC. 66.140 MILLION OZ//

TOTAL 2023: 1,104.10 MILLION OZ/

JAN ’24 : 42.860 MILLION OZ//WILL BE A VERY STRONG MONTH FOR ISSUANCE

RESULT: WE HAD A TINY SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 312 CONTRACTS WITH OUR LOSS IN PRICE OF SILVER PRICING AT THE COMEX//TUESDAY.,. THE CME NOTIFIED US THAT WE HAD A GOOD EFP ISSUANCE CONTRACTS: 407 ISSUED FOR FEB AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS. WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR JAN. OF 6.665 MILLION OZ FOLLOWED BY TODAY’S NIL OZ QUEUE JUMP //NEW TOTAL 5.460 MILLION OZ TO WHICH WE ADD EX. FOR RISK ISSUANCE/PRIOR FOR 1.0 MILLION OZ //NEW TOTALS; 6.460 MILLION OZ/

NEW STANDING 6.460 million OZ /// WE HAVE A SMALL SIZED GAIN OF 95 OI CONTRACTS ON THE TWO EXCHANGES DESPITE THE LOSS IN PRICE. THE TOTAL OF TAS INITIATED CONTRACTS TODAY: A GOOD SIZED 465 CONTRACTS//HUGE FRONT END OF THE TAS CONTRACTS WERE LIQUIDATED DURING THE TUESDAY COMEX SESSION/RAID// WITH CONSIDERABLE SHORT COVERINGS FROM OUR SPEC SHORTS. THE NEW TAS ISSUANCE TUESDAY NIGHT (465) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE//PROBABLY TODAY., .

WE HAD 0 NOTICE(S) FILED TODAY FOR nil OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A STRONG SIZED 8405 CONTRACTS TO 489,334 AND CLOSER TO THE RECORD (SET JAN 24/2020) AT 799,733 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: – removed 590 CONTRACTS

WE HAD A STRONG SIZED DECREASE IN COMEX OI ( 8.405 CONTRACTS) WITH OUR $27.75 LOSS IN PRICE//TUESDAY. WE ALSO HAD A RATHER STRONG INITIAL STANDING IN GOLD TONNAGE FOR JAN. AT 8.214 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S 3900 OZ QUEUE JUMP//NEW STANDING: 11.698 TONNES // ALL OF THIS HAPPENED WITH OUR $27.75 LOSS IN PRICE WITH RESPECT TO TUESDAY’S TRADING. WE HAD A FAIR SIZED LOSS OF 4344 OI CONTRACTS (13.51) PAPER TONNES) ON OUR TWO EXCHANGES.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 4061 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 489,334

IN ESSENCE WE HAVE A FAIR SIZED DECREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 4061 CONTRACTS WITH 8405 CONTRACTS DECREASED AT THE COMEX// AND A STRONG SIZED 4016 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI LOSS ON THE TWO EXCHANGES OF 4061 CONTRACTS.. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): A STRONG SIZED 2,765 CONTRACTS. ( THIS ENDS THE CONSECUTIVE HUGE T.A.S. ISSUANCE AT 5)

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A STRONG SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (4061 CONTRACTS) ACCOMPANYING THE STRONG SIZED LOSS IN COMEX OI (8405) //TOTAL LOSS FOR OUR THE TWO EXCHANGES: 4,061 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR FORMER FORMAT OF BANKERS GOING LONG AND SPECULATORS GOING SHORT ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR JAN AT 8.214 TONNES FOLLOWED BY TODAY’S 3900 OZ QUEUE JUMP//NEW STANDING 11.698 TONNES. / 3) SOME LONG LIQUIDATION AND HUGE TAS LIQUIDATION WITH MAJOR SHORT COVERINGS// 4) STRONG SIZED COMEX OPEN INTEREST LOSS/ 5) STRONG ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER///6: STRONG T.A.S. ISSUANCE: 2265 CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023-2024 INCLUDING TODAY

JAN.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF JAN. :

TOTAL EFP CONTRACTS ISSUED: 38,501 CONTRACTS OR 3,850,100 OZ OR 119.75 TONNES IN 11 TRADING DAY(S) AND THUS AVERAGING: 3500 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 11 TRADING DAY(S) IN TONNES 119.75 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2022, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 119.75/3550 x 100% TONNES 3.38% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2023

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH/2022: 409.30 TONNES //FINAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 151.69 TONNES (WEAKER THAN LAST MONTH)

AUGUST: 195.28 TONNES (A STRONGER MONTH)//FINAL

SEPT: 254.709 TONNES (WILL BE LARGER THAN LAST MONTH AND A STRONG MONTH)

OCT. 248.09 TONNES. LIKE SILVER, THIS MONTH IS GOING TO BE A STRONG E.F.P. ISSUANCE.

NOV. 239.16 TONNES//WILL BE STRONG THIS MONTH,

DEC. 213.704 TONNES. A STRONG MONTH//

TOTAL FOR YEAR 2023: 2,569.57 TONNES VS 2578 TONNES LAST YEAR

JAN ’24: 119.75 TONNES (WILL EQUAL LAST MONTH’S ISSUANCE OR A LITTLE GREATER)

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF FEB. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (FEB), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER FELL BY A GOOD SIZED 312 CONTRACTS OI TO 131,956 AND FURTHER FROM THE COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 407 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MARCH 407 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 407 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 17 CONTRACTS AND ADD TO THE 407 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A SMALL SIZED GAIN OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 95 CONTRACTS

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTAL 0.475 MILLION OZ

OCCURRED DESPITE OUR $.08 LOSS IN PRICE …..

END

OUTLINE FOR TODAY’S COMMENTARY

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

b, ) Gold/silver trading overnight Europe,//GOLD COMMENTARIES

(Peter Schiff)

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS//

TUESDAY MORNING/MONDAY NIGHT

SHANGHAI CLOSED UP 7.70 PTS OR 0.27% //Hang Seng CLOSED DOWN 350.41 PTS OR 2.16% /The Nikkei CLOSED DOWN 282.61 OR 0.79% //Australia’s all ordinaries CLOSED DOWN 1.07% /Chinese yuan (ONSHORE) closed DOWN AT 7.1895 /OFFSHORE CHINESE YUAN CLOSED DOWN TO 7.2137 /Oil DOWN TO 73.08 dollars per barrel for WTI and BRENT UP AT 7.24/ Stocks in Europe OPENED ALL RED// ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER

A)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

9. USA

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A STRONG SIZED 8.405 CONTRACTS TO 489,334 WITH OUR LOSS IN PRICE OF $27.75 WITH RESPECT TO TUESDAY TRADING. WE MUST HAVE SOME LONG SPEC LIQUIDATIONS IN THE COMEX SESSION WITH SOME SPEC SHORT COVERINGS AT THE LOWER PRICES.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE NON ACTIVE DELIVERY MONTH OF JAN..… THE CME REPORTS THAT THE BANKERS ISSUED A STRONG SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 4016 EFP CONTRACTS WERE ISSUED: : FEB 4016 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 4016 CONTRACTS

ON A NET BASIS IN OPEN INTEREST WE LOST THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A FAIR SIZED TOTAL OF 4,344 CONTRACTS IN THAT 4016 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A STRONG SIZED 8405 LOST COMEX CONTRACTS..AND THIS FAIR LOSS ON OUR TWO EXCHANGES HAPPENED WITH OUR LOSS IN PRICE OF $27.75 TUESDAY COMEX. AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS DURING MID MONTH IN THE DELIVERY CYCLE), THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR TUESDAY NIGHT WAS A STRONG SIZED 2,765 CONTRACTS. THROUGHOUT THE PAST SEVERAL WEEKS, THE BANKERS SOLD OFF THE LONG SIDE OF THE SPREAD WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR/T.A.S. SPREAD WHICH WILL BE LIQUIDATED IN DAYS HENCE//.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: JAN (11.698 TONNES) ( NON ACTIVE MONTH)

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

NOV: 18.7122 TONNES + 16.2505 EX. FOR RISK = 34.9627 TONNES

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707TONNES

TOTAL 2023 YEAR : 436.546 TONNES

JAN ’24. 11.5769 TONNES

THE SPECS/HFT WERE SUCCESSFUL IN LOWERING GOLD’S PRICE( IT LOST $27.75) //// AND WERE SUCCESSFUL IN KNOCKING SOME SPECULATOR LONGS AS WE HAD A FAIR SIZED LOSS OF 4344 TOTAL CONTRACTS ON OUR TWO EXCHANGES. WE HAD A STRONG T.A.S. LIQUIDATION ON THE FRONT END OF TUESDAY’S TRADING . THE T.A.S. ISSUED ON TUESDAY NIGHT, WILL BE “PUT INTO THE BANK” TO BE USED AT A LATER DATE AT THE COLLUSIVE CHOOSING OF OUR BANKERS. WE ALSO EXPERIENCED CONSIDERABLE SPECULATOR SHORT COVERING

WE HAVE LOST A TOTAL OI OF 13.51 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR JAN. (8,214 TONNES) ON FIRST DAY NOTICE FOLLOWED BY TODAY’S 3900 OZ QUEUE JUMP (0.1213 TONNES): NEW TOTAL STANDING 11.698 TONNES/ ALL OF THIS WAS ACCOMPLISHED WITH OUR LOSS IN PRICE TO THE TUNE OF $27.75

WE HAD – REMOVED 590 CONTRACTS TO THE COMEX TRADES TO OPEN INTEREST (CROOKS)

NET LOSS ON THE TWO EXCHANGES 4344 CONTRACTS OR 434400 OZ OR 13.51 TONNES.

Estimated gold volume today:// 271,971 good //t.a.s. induced.

final gold volumes/yesterday 317,185 strong t.a.s. induced

//speculators have left the gold arena

JAN 17 INITIAL

/ /// THE JAN 2024 GOLD CONTRACT

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 3215.100 OZ brinks 100 kilobars . |

| Deposit to the Dealer Inventory in oz | 70,432.349 oz ASAHI |

| Deposits to the Customer Inventory, in oz | nil oz |

| No of oz served (contracts) today | 27 notice(s) 2700 OZ 0.0839 TONNES |

| No of oz to be served (notices) | 283 contracts 28300 oz 0.880 TONNES |

| Total monthly oz gold served (contracts) so far this month | 3478 notices 347800 oz 10.816 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | x |

2 dealer deposits:

i) Into ASAHI 64,427.674 oz

ii)Into ASAHI enhanced: 6404.675 oz

total dealer deposits: 70,432.349 oz

total customer withdrawals: 1

i)Brinks: 3215,100 oz

(100 kilobars)

total withdrawals 3215.100 oz

we had 0 customer deposits

total deposits NIL oz

Adjustments; 0

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR JAN.

For the front month of JANUARY we have an oi of 310 contracts having LOST 139 contracts. We had 178 notices served on Tuesday, so we gained 39 contracts or an additional 3900 oz will stand for delivery at the comex

FEB LOST ONLY 13,597 CONTRACTS FALLING TO 228,389

March GAINED 188 contracts to stand at 523.

APRIL GAINED 4615 CONTRACTS RISING TO 195,292.

We had 27 contracts filed for today representing 2700 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 20 notices were issued from their client or customer account. The total of all issuance by all participants equate to 27 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 5 notice(s) was (were) stopped ( received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the JAN. /2023. contract month, we take the total number of notices filed so far for the month (3478 x 100 oz ), to which we add the difference between the open interest for the front month of JAN. (310 CONTRACTS) minus the number of notices served upon today 27 x 100 oz per contract equals 376,100 OZ OR 11.698 TONNES

thus the INITIAL standings for gold for the JAN. contract month: No of notices filed so far (3478) x 100 oz + (310) {OI for the front month} minus the number of notices served upon today (27) x 100 oz) which equals 376,100 oz standing OR 11.687 TONNES

TOTAL COMEX GOLD STANDING FOR JAN: 11.698 TONNES WHICH IS GREAT FOR AN INACTIVE DELIVERY MONTH IN THE CALENDAR.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 1,474,682.951 45.86 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD: 20,092,349.294 OZ

TOTAL REGISTERED GOLD 9,237,397.739 (287,32 tonnes).

TOTAL OF ALL ELIGIBLE GOLD: 10,854,951.555 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 7,762,715 oz (REG GOLD- PLEDGED GOLD) 241.45 tonnes

END

SILVER/COMEX

JAN 17/INITIAL

//2024// THE JAN 2023 SILVER CONTRACT//INITIAL

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 610,887.500 oz JPMorgan . |

| Deposits to the Dealer Inventory | nil OZ |

| Deposits to the Customer Inventory | 609,697.347 oz CNT Brinks Delaware |

| No of oz served today (contracts) | 0 CONTRACT(S) (nil OZ) |

| No of oz to be served (notices) | 327 contracts (1,635,000 oz) |

| Total monthly oz silver served (contracts) | 765 Contracts (3,825,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

i) 0 dealer deposit

total dealer deposit: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: 0 oz

We had 3 deposits customer account:

i) Into CNT 29,240.750 oz

ii) Into Brinks 579,434.750 oz

iii) Into Delaware: 1021.847 oz

total customer deposits 609,697.347 oz

JPMorgan has a total silver weight: 131.923 million oz/280.976 million or 46.97%

adjustment 547,251.222 oz adjusted from dealer to customer//vault ASAHI

Comex withdrawals: 1

i) Out of JPMorgan: 610,847.500 oz

total deposit: 610,847.500 oz

TOTAL REGISTERED SILVER: 42.263 MILLION OZ//.TOTAL REG + ELIGIBLE. 280.976 million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR DECEMBER:

silver open interest data:

FRONT MONTH OF JAN. /2023 OI: 327 CONTRACTS HAVING LOST 4 CONTRACT(S). WE HAD 4 NOTICES SERVED ON tuesDAY, SO WE GAINED 0 CONTRACTS OR AN ADDITIONAL nil OZ WILL STAND FOR DELIVERY AT THE COMEX

FEB GAINED 11 CONTRACTS TO STAND AT 181

MARCH LOST 598 CONTRACTS TO 101,956

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 4 for 20,000 oz

Comex volumes// est. volume today 51,054//fair

Comex volume: confirmed yesterday 65,011 good//t.a.s. induced

To calculate the number of silver ounces that will stand for delivery in JAN. we take the total number of notices filed for the month so far at 765 x 5,000 oz = 3,825,000 oz

to which we add the difference between the open interest for the front month of JAN. (327) and the number of notices served upon today 0 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the DEC/2023 contract month: 765 (notices served so far) x 5000 oz + OI for the front month of JAN. (327) – number of notices served upon today (0 )x 500 oz of silver standing for the JAN contract month equates to 5.460 MILLION OZ. to which we add our exchange for RISK of 1.0 million oz//new total 6.460 million oz/

New total standing: 6.460 million oz.

There are 42,263 million oz of registered silver.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS//

BOTH GLD AND SLV ARE MASSIVE FRAUDS!

JAN 16/WITH GOLD DOWN $ZZZ TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD;//://INVENTORY RESTS AT 864.99 TONNES

JAN 17/WITH GOLD DOWN $23.25 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF .549 TONNES OF GOLD INTO THE GLD;//://INVENTORY RESTS AT 864.40 TONNES

JAN 12/WITH GOLD UP $31.65 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD; A MASSIVE WITHDRAWAL OF 4.61 TONNES OF GOLD FROM THE GLD//://INVENTORY RESTS AT 864.99 TONNES

JAN 11/WITH GOLD DOWN $7.40 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD; A MASSIVE WITHDRAWAL OF 4.61 TONNES OF GOLD FROM THE GLD//://INVENTORY RESTS AT 864.99 TONNES

JAN 10/WITH GOLD DOWN $4.80 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD://INVENTORY RESTS AT 869.60 TONNES

JAN 9/WITH GOLD UP $0.95 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD://INVENTORY RESTS AT 869.60 TONNES

JAN 8/WITH GOLD DOWN $16.85 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD:A WITHDRAWAL OF 4.61 TONNES FROM THE GLD. INVENTORY RESTS AT 869.60 TONNES

JAN 5/WITH GOLD UP $0.80 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD:///. // INVENTORY RESTS AT 874.21 TONNES

JAN 4/WITH GOLD UP $7.60 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD:///. // INVENTORY RESTS AT 874.21 TONNES

JAN 3/WITH GOLD DOWN $29.40 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.90 TONNES OF GOLD INTO THE GLD///. // INVENTORY RESTS AT 874.21 TONNES

JAN 2/WITH GOLD UP $1.50 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.44 TONNES OF GOLD INTO THE GLD///. // INVENTORY RESTS AT 879.11 TONNES

DEC 29/WITH GOLD DOWN $10.25 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.16 TONNES OF GOLD INTO THE GLD///. // INVENTORY RESTS AT 880.55 TONNES

DEC 28/WITH GOLD DOWN $8.35 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.45 TONNES OF GOLD INTO THE GLD///. // INVENTORY RESTS AT 881.71 TONNES

DEC 27/WITH GOLD UP $23.25 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.01 TONNES OF GOLD INTO THE GLD///. // INVENTORY RESTS AT 880.26 TONNES

DEC 26/WITH GOLD UP $1.25 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD:/. // INVENTORY RESTS AT 878.25 TONNES

DEC 22/WITH GOLD UP $17,85 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD:/. // INVENTORY RESTS AT 878.25 TONNES

DEC 21/WITH GOLD UP $5.10 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD:A DEPOSIT .58 TONNES OF 2.02 TONNES OF GOLD INTO THE GLD//. // INVENTORY RESTS AT 878.25 TONNES

DEC 20/WITH GOLD DOWN $3.60 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD:A WITHDRAWAL OF 2.02 TONNES OF GOLD FROM THE GLD//. // INVENTORY RESTS AT 877.67 TONNES

DEC19/WITH GOLD UP $12.15 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD:. // INVENTORY RESTS AT 879.69 TONNES

DEC18/WITH GOLD UP $5.50 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD:. /A DEPOSIT OF 173 TONNES INTO THE GLD// INVENTORY RESTS AT 879.69 TONNES

DEC14/WITH GOLD UP $47.35 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD:. /A DEPOSIT OF 2.42 TONNES FROM THE GLD// INVENTORY RESTS AT 877.96 TONNES

DEC13/WITH GOLD UP $3.90 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD:. /A WITHDRAWAL OF 2.89 TONNES FROM THE GLD// INVENTORY RESTS AT 875,65 TONNES

DEC12/WITH GOLD DOWN $0.60 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD:. /A WITHDRAWAL OF 2.01 TONNES FROM THE GLD// INVENTORY RESTS AT 878.54 TONNES

GLD INVENTORY: 864.40 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

JAN 17/WITH SILVER DOWN $0.38 TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 779,000 OZ FROM THE SLV/// //INVENTORY RESTS AT 432.951 MILLION OZ

JAN 16/WITH SILVER DOWN $0.08 TODAY NO CHANGES IN SILVER INVENTORY AT THE SLV: // //INVENTORY RESTS AT 433.500 MILLION OZ

JAN 12/WITH SILVER UP $0.62 TODAY NO CHANGES IN SILVER INVENTORY AT THE SLV: // //INVENTORY RESTS AT 433.500 MILLION OZ

JAN 11/WITH SILVER DOWN 34 CENTS TODAY NO CHANGES IN SILVER INVENTORY AT THE SLV: // //INVENTORY RESTS AT 433.912 MILLION OZ

JAN 10/WITH SILVER DOWN 3 CENTS TODAY SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 450,000 OZ FROM THE SLV// //INVENTORY RESTS AT 433.912 MILLION OZ

JAN 9/WITH SILVER DOWN 20 CENTS TODAY NO CHANGES IN SILVER INVENTORY AT THE SLV //INVENTORY RESTS AT 434.370 MILLION OZ

JAN 8/WITH SILVER DOWN 8 CENTS TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 1,602,000 OZ INTO THE SLV//:././/////INVENTORY RESTS AT 434.370 MILLION OZ

JAN 5/WITH SILVER UP 20 CENTS TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV A DEPOSIT OF 916,000 OZ INTO THE SLV//:././/////INVENTORY RESTS AT 435.972 MILLION OZ

JAN 4/WITH SILVER UP 5 CENTS TODAY NO CHANGES IN SILVER INVENTORY AT THE SLV/:././/////INVENTORY RESTS AT 435.056 MILLION OZ

JAN 3/WITH SILVER DOWN 78 CENTS TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV/: A WITHDRAWALOF 2.294 MILLION OZ OZ FROM THE SLV././/////INVENTORY RESTS AT 435.056 MILLION OZ

JAN 2/WITH SILVER DOWN 9 CENTS TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV/: A WITHDRAWALOF 915,000 OZ FORM THE SLV././/////INVENTORY RESTS AT 437.35 MILLION OZ

DEC 29/WITH SILVER DOWN 29 CENTS TODAY NO CHANGES IN SILVER INVENTORY AT THE SLV/: //////INVENTORY RESTS AT 438.265 MILLION OZ

DEC 28/WITH SILVER DOWN 25 CENTS TODAY NO CHANGES IN SILVER INVENTORY AT THE SLV/: //////INVENTORY RESTS AT 438.265 MILLION OZ

DEC 27/WITH SILVER UP 20 CENTS TODAY:HUGE CHANGES IN SILVER INVENTORY AT THE SLV/: A WITHDRAWAL OF 1.374 MILLION OZ FROM THE SLV//////INVENTORY RESTS AT 438.265 MILLION OZ

THIS IS THE 3RD STRAIGHT DAY THAT THE SLV HAS ENGAGED IN WITHDRAWALS

DEC 26/WITH SILVER DOWN 14 CENTS TODAY:HUGE CHANGES IN SILVER INVENTORY AT THE SLV/: A WITHDRAWAL OF 1.465 MILLION OZ FROM THE SLV//////INVENTORY RESTS AT 439.639 MILLION OZ

DEC 22/WITH SILVER UP 0 CENTS TODAY:HUGE CHANGES IN SILVER INVENTORY AT THE SLV/: A WITHDRAWAL OF 2.289 MILLION OZ FROM THE SLV//////INVENTORY RESTS AT 441.104 MILLION OZ

DEC 21/WITH SILVER DOWN 2 CENTS TODAY:NO CHANGES IN SILVER INVENTORY AT THE SLV/: NO CHANGES IN SILVER INVENTORY AT THE SLV//////INVENTORY RESTS AT 443.393 MILLION OZ

DEC 20/WITH SILVER UP 28 CENTS TODAY:NO CHANGES IN SILVER INVENTORY AT THE SLV/: NO CHANGES IN SILVER INVENTORY AT THE SLV//////INVENTORY RESTS AT 443.393 MILLION OZ

DEC 19/WITH SILVER UP 27 CENTS TODAY:BIG CHANGES IN SILVER INVENTORY AT THE SLV/: A MASSIVE DEPOSIT OF 2.747 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 443.393 MILLION OZ

DEC 18/WITH SILVER DOWN 9 CENTS TODAY:BIG CHANGES IN SILVER INVENTORY AT THE SLV/: A WITHDRAWAL OF 0.794 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 440.646 MILLION OZ

DEC 14/WITH SILVER DOWN 8 CENTS TODAY:BIG CHANGES IN SILVER INVENTORY AT THE SLV/: A MASSIVE WITHDRAWAL OF 3.00000 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 441.470 MILLION OZ

DEC 13/WITH SILVER DOWN 8 CENTS TODAY:BIG CHANGES IN SILVER INVENTORY AT THE SLV/: A DEPOSIT OF 10.326 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 444.470 MILLION OZ

DEC 12/WITH SILVER DOWN 5 CENTS TODAY:BIG CHANGES IN SILVER INVENTORY AT THE SLV/: A WITHDRAWAL OF 594,000 OZ FROM THE SLV////INVENTORY RESTS AT 434.144 MILLION OZ

CLOSING INVENTORY 433.500 MILLION OZ//

PHYSICAL GOLD/SILVER COMMENTARIES

1:Peter Schiff/Mike Maharrey

END

2,c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens, John Rubino

Mathew Piepenburg…

END

3. CHRIS POWELL//GATA GOLD COMMENTARIES:

END

3. CHRIS POWELL//GATA GOLD COMMENTARIES:

I guess this is to be expected at the Moscow exchange: Chinese yuan surpasses the dollar in the most traded currency in 2023

(Reuters/GATA)

China’s yuan ousts dollar to become most-traded currency in Moscow in 2023

Submitted by admin on Tue, 2024-01-16 21:50Section: Daily Dispatches

By Elena Fabrichnaya and Alexander Marrow

Reuters

Tuesday, January 16, 2024

MOSCOW — The Moscow Exchange trading volume in Chinese yuan surpassed that of the U.S. dollar in 2023, the Kommersant daily reported today, as Moscow pursues a de-dollarisation strategy in the face of Western sanctions on its financial system.

Moscow is becoming increasingly dependent on Beijing and the “no limits” partnership between the two countries, having increased energy supplies to China and stepped up purchases of Chinese goods from cars to smartphones as European and U.S. brands left the Russian market over Russia’s actions in Ukraine.

Yuan trading accounted for almost 42% of all foreign currency traded on Moscow Exchange with the volume in 2023 more than tripling year on year to 34.15 trillion roubles ($391.5 billion), Kommersant reported, citing Moscow Exchange data.

The dollar’s share stood at 39.5%, with a volume of 32.49 trillion roubles, down from 49.90 trillion roubles in 2022 and a more than 63% share. Yuan trading accounted for a 13% share in 2022. …

… For the remainder of the report:

END

4. OTHER GOLD/SILVER //COMMENTARIES//PODCASTS

END

4. OTHER GOLD/SILVER //COMMENTARIES//PODCASTS

end

5 a. IMPORTANT COMMENTARIES ON COMMODITIES /URANIUM

Uranium prices eclipse 100 dollars per lb.

(Paraskova/OilPrice.com)

Uranium Energy Restarts Wyoming Production Amid Soaring Prices

WEDNESDAY, JAN 17, 2024 – 06:30 AM

By Tsvetana Paraskova of OilPrice.com

U.S.-based Uranium Energy Corp said on Tuesday it would restart uranium production at its fully permitted site in Wyoming as the resurgence in nuclear power has led to a new bull market in uranium.

Uranium Energy will resume 100% unhedged uranium production at its fully permitted, and past producing, Christensen Ranch In-Situ Recovery (ISR) operations in Wyoming. The recovered uranium will be processed at the fully operational Irigaray Central Processing Plant with a current licensed capacity of 2.5 million pounds U3O8 per year, the company said.

The first uranium production is expected in August 2024 and will be funded with existing cash on the company’s balance sheet. As Uranium Energy’s strategy has been to remain 100% unhedged, produced uranium will be sold at prevailing spot market prices which was $106 per pound U3O8 as of January 15, 2024 as reported by UxC.

“Uranium market fundamentals are the best the industry has witnessed, and various supply shocks have accelerated the bull market with recent prices eclipsing the $100 per pound level,” Uranium Energy president and CEO Amir Adnani said.

Combined with South Texas Hub and Spoke ISR Platform, Uranium Energy controls the largest S-K 1300 compliant ISR resource base in the United States with over 75,000,000 lbs of measured and indicated resources and 25,000,000 lbs of inferred resources.

At the end of 2023, TerraPower and Uranium announced a memorandum of understanding with objectives of reestablishing domestic supply chains of uranium fuel.

The renewed focus on nuclear energy in many developed economies has created a bull market for uranium in recent months.

Early in January, spot prices for uranium concentrate used in nuclear power generation hit a new 16-year high, climbing to $92.45 per pound.

Uranium prices have further room to rise after Kazatomprom—the largest uranium miner in the world—said last week that sulfuric acid shortages and construction delays at newly discovered deposits could lead to the company missing production targets—challenges that could remain into next year.

5 B GLOBAL COMMODITY ISSUES/FOOD IN GENERAL//FREIGHT

END

6.CRYPTOCURRENCY//DIGITAL CURRENCY// COMMENTARIES/

end

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS WEDNESDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED DOWN AT 7.1955

OFFSHORE YUAN: DOWN TO 7.2191

SHANGHAI CLOSED DOWN 60.37 PTS OR 2.09%

HANG SENG CLOSED DOWN 589.02 PTS OR 3.71%

2. Nikkei closed DOWN 164.43 PTS OR 0.40%

3. Europe stocks SO FAR: ALL RED

USA dollar INDEX UP TO 103.19 EURO FALLS TO 1.0872 DOWN 7 BASIS PTS

3b Japan 10 YR bond yield:RISES TO. +.600 Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 147.67/JAPANESE YEN NOW RISING AS WELL AS LONG TERM 10 YR. YIELDS RISING //EVENTUALLY THIS WILL BREAK THE JAPANESE CENTRAL BANK

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen DOWN CHINESE ONSHORE YUAN: DOWN// OFFSHORE: DOWN

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil DOWN for WTI and DOWN FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund UP TO +2.2509***/Italian 10 Yr bond yield UP to 3.857** /SPAIN 10 YR BOND YIELD UP TO 3.205…**

3i Greek 10 year bond yield UP TO 3.325

3j Gold at $2026.45 silver at: 22.80 1 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble DOWN 0 AND 24 /100 roubles/dollar; ROUBLE AT 88.35//

3m oil into the 71 dollar handle for WTI and 76 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 147,67// 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 0.600% STILL ON CENTRAL BANK (JAPAN) INTERVENTION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.8645 as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.9399 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.074 UP 1 BASIS PTS…

USA 30 YR BOND YIELD: 4.295 DOWN 1 BASIS PTS/

USA 2 YR BOND YIELD: 4.285 UP 6 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 30.14…(TURKEY SET TO BLOW UP FINANCIALLY)

GREAT BRITAIN/10 YEAR YIELD: UP 15 BASIS PTS AT 3.9512

end

2.a Overnight: Newsquawk and Zero hedge.

Futures, Global Markets Slide As Central Banks Push Back Against Market Hopes For Early Rate Cuts

WEDNESDAY, JAN 17, 2024 – 08:20 AM

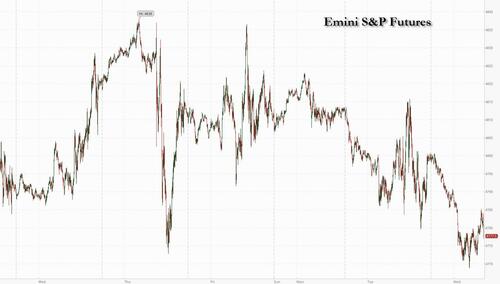

US equity futures and global markets extended their decline on Wednesday after central bankers continued their push-back against market bets for interest rate cuts, deepening a global selloff across stocks and bonds. At 8:00am ET, S&P futures fall 0.4% and Nasdaq contracts ease about 0.5% suggesting another weak day ahead for US equities after ECB President Christine Lagarde and Governing Council member Klaas Knot warned on Wednesday that aggressive bets on interest-rate cuts aren’t helping policymakers in the battle against lingering price pressures, echoing hawkish comments from the Fed’s Waller on Tuesday who urged caution on the pace of easing. The VIX rose to 14.60, the highest leve since mid-November. The Bloomberg Dollar Spot Index extended its rally to a fourth day while the 2Y Treasury yields climbed six basis points to 4.29% and 10-year yields rose 2bps to 4.08%. Oil dropped again with Brent sliding to $77 as gold also eases to near $2,025.

Meanwhile, fresh concerns about China’s economy added another headwind for equities. US-listed Chinese stocks fell in premarket trading as disappointing economic data and a lack of major stimulus deter investors, with the exchange-traded KraneShares CSI China Internet Fund, which holds over 30 US- and Hong Kong-listed Chinese tech firms, trading more than 3% lower. Here are some other notable premarket movers:

- Allakos drops 10% and appears set to extend Tuesday’s 60% plunge after the drug developer was downgraded to hold at Jefferies following two mid-stage trials that failed to meet their main goals.

- Donald Trump-tied stocks fall and appear set to give back some of Tuesday’s double-digit gains after the former president scored a big win at the Iowa caucuses. Digital World (DWAC) -8%, Phunware (PHUN) -60%

- Fisker (FSR) drops 3% after TD Cowen downgrades to market perform, saying the electric-vehicle maker’s growing pains are continuing to accumulate.

- Interactive Brokers (IBKR) falls 4% after the firm reported fourth-quarter total net interest income that missed estimates.

- Mattel (MAT) falls 3% after Morgan Stanley downgrades the toymaker to equal-weight, citing a tougher category outlook in 2024 and limited growth drivers.

- Morgan Stanley (MS) slips 1% after being downgraded to neutral at JPMorgan, which said the bank is now fairly valued, with limited near-term catalysts to propel shares higher.

- Plexus (PLXS) falls 1.7% after the company reported preliminary first-quarter revenue that missed the average analyst estimate.

- Polaris (PII) gains 1% as Morgan Stanley upgrades its rating to overweight, saying the risk/reward for shares in the maker of off-road vehicles is “too attractive to ignore.”

- Spirit Airlines (SAVE) declines 15% after a federal judge blocked JetBlue’s $3.8 billion acquisition of the budget airline.

Following the recent hawkish comments from central bankers, swaps market pricing for a Fed rate cut in March has dropped to around 65% from 80% on Friday, while money markets pushed back bets on the timing of the ECB’s first quarter-point cut to June, from April.

“Inflation was never going to be a straight line down, as we have seen in the US and Europe,” said Luke Hickmore, investment director at abrdn. “Rates will fall this year but market expectations around when and how much are going to be very volatile.”

Still more evidence that the battle against inflation isn’t over came from the UK, where price increases accelerated unexpectedly for the first time in 10-months, prompting traders to scale back their expectations for rate cuts from the Bank of England this year. Gilts tumbled and the pound gained as traders aggressively trimmed expectations for monetary-policy easing this year.

Basic resources and luxury-goods stocks were among the biggest decliners in Europe amid worries about slackening demand in China, a key market. The Stoxx Europe 600 index slumped more than 1%. All industry sectors were in the red, with real estate and retailers among the hardest hit. German two-year yields rose five basis points to 2.65%. Here are the biggest European movers Wednesday:

- IMI rises as much as 3.9% and is the top gainer in the Stoxx Europe 600 index in early trade after being upgraded to buy from neutral by Goldman Sachs, which sees scope for the engineering firm’s shares to outperform over the next year

- Telecom Italia shares rise as much as 3% in Milan trading, the most in two weeks, as the Italian government cleared the sale of the company’s landline network to KKR & Co. after a review process for an asset deemed to be of strategic interest to the state

- IAG was raised to buy from neutral at Goldman Sachs, with analysts expecting the British Airways parent to see earnings growth this year and sustain higher margins. Shares rise as much as 0.9%

- Basic-Fit shares rises as much as 3.5% after the health and fitness club operator received a double upgrade to buy from underperform from Jefferies, which says its valuation has fallen too low

- BP shares fall as much as 1.5%, , to its lowest intraday level since Oct. after the oil giant said interim Chief Executive Officer Murray Auchincloss will take up the role permanently

- Antofagasta declined as much as 4.9%, the most since July, after costs increased in the fourth quarter. Peers with copper exposure also edged lower

- Pearson shares fall as much as 2.5%, retreating further from recent 13-month highs, after the education publishing firm said adjusted operating profit for 2023 will slightly undershoot forecasts due to pound-dollar exchange-rate fluctuations

- 888 drops as much as 15%, the most since September, after the online gambling group reported lower 4Q revenue. Though analysts across the board cut their Ebitda forecasts for 2023 and 2024

- Meyer Burger shares slump as much as 46%, the most ever, after the Swiss solar panel maker announced it could shift focus to the US, shut one of its European production sites, and possibly raise more equity

Earlier in the session, Asian equities suffered broad losses for a second day with Hong Kong leading the selloff after Chinese economic data failed to moderate bearish momentum. Hang Seng Tech index slumped almost 4% and H shares plunged 3%. Shanghai Composite drops 0.6%, ChiNext dropped 1.2%, and the CSI 300 mainland Chinese benchmark also fell 2.2%. The losses came after official figures showed while China reached its 2023 economic goal, the country’s housing slump has worsened and domestic demand remained listless. South Korean stocks are also sharply lower, while Japanese shares extend 2024 outperformance by staying narrowly in the green thanks to the renewed implosion of the yen.

The Bloomberg Dollar Spot Index steadied around a one-month high while the yen extended its recent tumble, sending the USDJPY hovering around 147.6. Traders awaited the release of the central bank’s beige book and US retail sales, after the Fed’s Waller warned rates are unlikely to come down as quickly as they have done in the past

- GBP/USD rose as much as 0.5% to 1.2694 leading G-10 gains against the dollar; UK inflation unexpectedly picked up in December as CPI rose 4% from a year earlier

- EUR/USD pared losses to trade around 1.0880 after dropping 0.2% to 1.0856, the lowest level since Dec. 13; ECB President Christine Lagarde told Bloomberg it’s likely interest rates will be cut in the summer in a push back to current market pricing

- AUD/USD fell 0.7% to 0.6535 as the Australian dollar led G-10 losses on disappointing Chinese economic data; China’s 4Q GDP rose 5.2% from a year ago, compared with a 5.3% estimate, home prices fell the most in almost nine years

- The loonie is set to drop for a fifth day as growing fears of inflation following UK data undermines investor sentiment, sending bonds and stocks lower.

In rates, the treasuries curve was aggressively flatter on the day, with front-end underperforming following a wider bear flattening move in gilts after data showed UK inflation picked up unexpectedly for the first time in 10 months. The 10Y TSY yield rose to session highs of 4.08%, reversing earlier losses; long-end Treasury yields were slightly richer on the day while front-end of the curve is cheaper by around 6bp vs Tuesday close; curve subsequently shifts flatter, following move in gilts with US 2s10s, 5s30s spreads tighter by 6bp and 4.5bp, remains near lows into early US session. On outright basis, UK 2-year yields remain cheaper by around 14bp on the day into early US session, which includes retail sales and a 20-year bond auction. US economic data includes January NY services business activity, December retail sales, import/export prices (8:30am), industrial production (9:15am), November business inventories and January NAHB housing market index (10am). Federal Reserve members scheduled to speak include Barr, Bowman (9am) and Williams (3pm); Fed release Beige book at 2pm

In commodities, oil fell again as a broad risk-off tone across markets coupled with a stronger US dollar offset concerns over Middle East tensions, including continued attacks on ships in the Red Sea by Iran-backed Houthi rebels. WTI crude futures paused around $71.80 while Brent traded down to $77. In other news, BP Plc appointed Murray Auchincloss as its permanent chief executive officer, four months after the shock resignation of his predecessor.

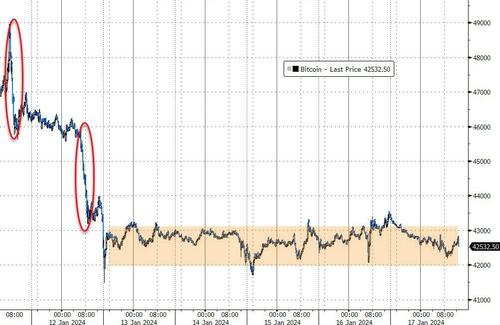

Elsewhere, gold was steady after a Tuesday decline of more than 1% to trade around $2,028 per ounce and Bitcoin dropped below $43,000 while Ether is also lower, sliding 2%. A new rule requiring US businesses to report cryptocurrency transactions over USD 10k has been postponed until the IRS issues new regulations on digital asset reporting, according to Cointelegraph.

Looking the day ahead now, and data releases include UK CPI for December, US retail sales, industrial production and capacity utilisation for December, along with the NAHB’s housing market index for January. From central banks, we’ll hear from ECB President Lagarde, the ECB’s Cipollone, Vasle, Simkus, Villeroy, Vujcic, Knot and Nagel, as well as the Fed’s Barr, Bowman and Williams. The Fed will also be releasing their Beige Book.

Market Snapshot

- S&P 500 futures down 0.5% to 4,776.25

- STOXX Europe 600 down 1.2% to 467.23

- MXAP down 1.7% to 162.13

- MXAPJ down 2.2% to 491.66

- Nikkei down 0.4% to 35,477.75

- Topix down 0.3% to 2,496.38

- Hang Seng Index down 3.7% to 15,276.90

- Shanghai Composite down 2.1% to 2,833.62

- Sensex down 2.2% to 71,506.16

- Australia S&P/ASX 200 down 0.3% to 7,393.08

- Kospi down 2.5% to 2,435.90

- German 10Y yield little changed at 2.28%

- Euro little changed at $1.0869

- Brent Futures down 1.9% to $76.84/bbl

- Gold spot down 0.4% to $2,021.15

- U.S. Dollar Index little changed at 103.44

Top Overnight News

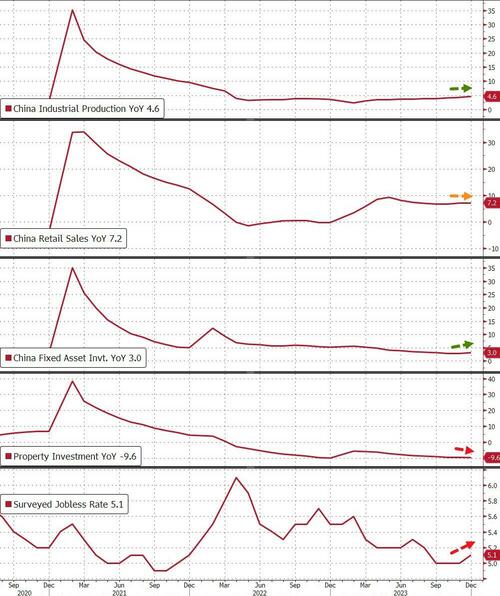

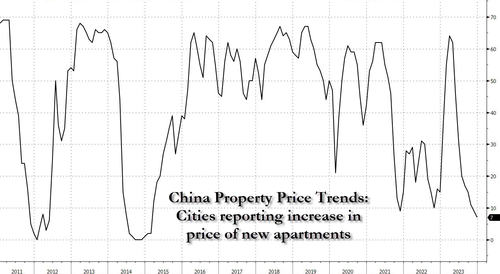

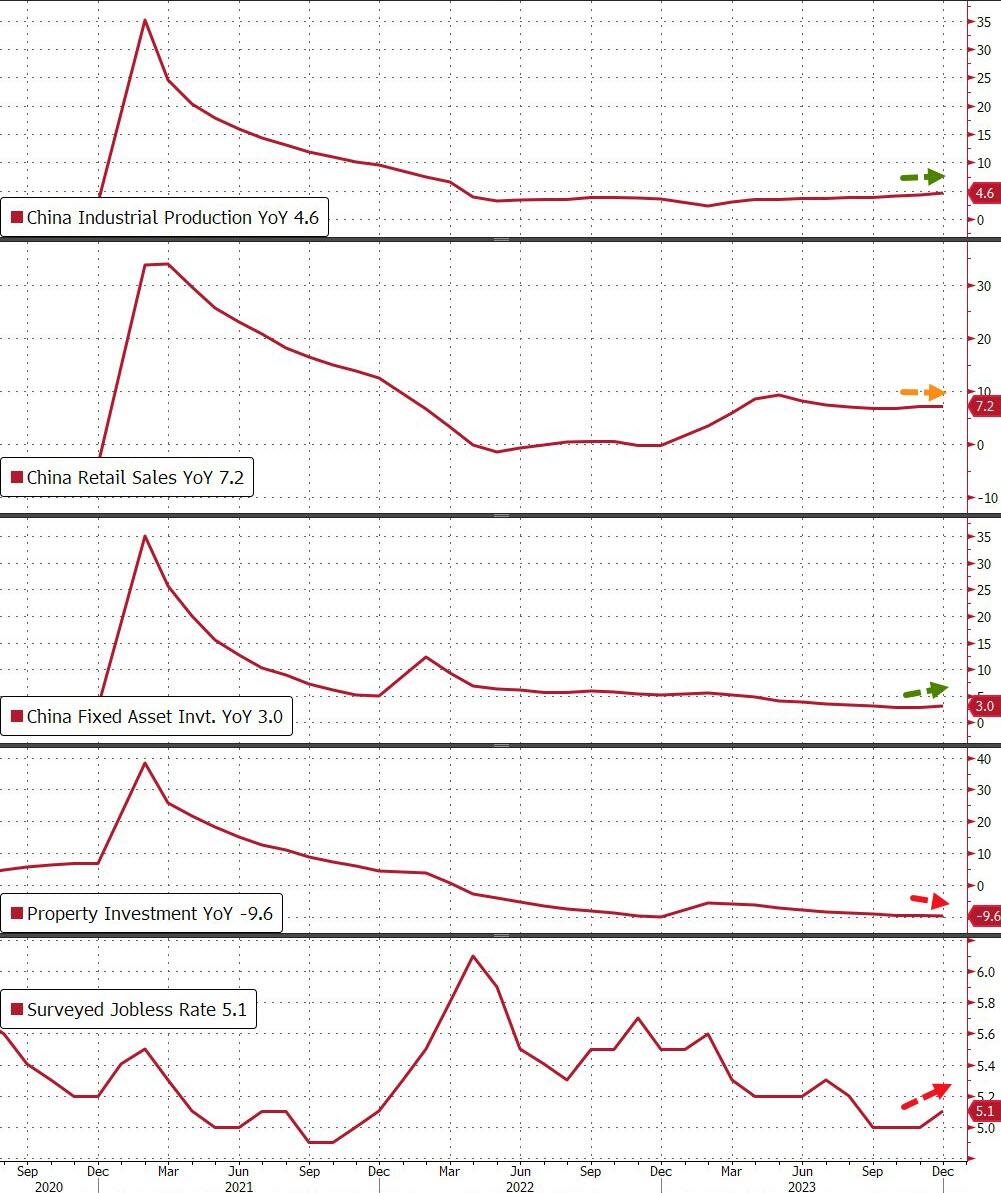

- China’s Q4 GDP numbers were largely inline with expectations (which isn’t a surprise since Premier Li preannounced GDP at Davos Tues morning) and industrial production for Dec was a bit better than anticipated (+6.8% vs. the Street +6.6%), but the GDP deflator shows the country still grappling with deflation while retail sales fell short in Dec (+7.4% vs. the Street +8%), the population decline accelerated, and property investment stayed weak. FT

- Aramco’s CEO said global oil markets can cope with Red Sea disruptions in the short-term, but prolonged attacks could create a problem. RTRS

- The ECB is “likely” to cut rates by or in the summer, Christine Lagarde said in response to a question on whether there’s majority support among officials for such a move. Policy makers are “on the right path” in curbing inflation, she said, adding that overoptimistic rate-cut bets in the market don’t help. BBG

- UK CPI runs hotter than anticipated, with headline +4% in Dec (up from +3.9% in Nov and firmer than the Street’s +3.8% forecast) and core +5.1% (flat vs. Nov and firmer than the Street’s +4.9% forecast). FT

- Qatar brokered a deal to permit medications to reach Israeli hostages in exchange for additional aid and medicine for Palestinian civilians. NYT

- The US is stepping up efforts to broker a diplomatic solution to the intensifying hostilities between Israel and Lebanon’s Hizbollah, as fears grow in Washington that the window is narrowing to avert a full-blown war erupting on the shared border. FT

- Biden has invited Congressional leaders to the White House for a meeting on Wed to discuss Ukraine aid and other fiscal matters (this will be the first face-to-face discussion between Biden and the congressional leadership in months). NYT

- Iran isn’t yet restocking Houthi rebels with weapons by sea after US and UK air strikes last week, Western officials said, signaling cautious optimism that the military action was successful in disrupting arms supplies. BBG

- JPMorgan plans to add to its headcount this year, President Daniel Pinto said. The bank sees opportunities in investment banking, international retail and US wealth management. BBG

A more detailed look at global markets courtesy of Newsquawk

APAC stocks were mostly pressured after the recent upside in yields and tapering of Fed rate cut expectations, while participants also digested mixed Chinese economic releases including GDP and activity data. ASX 200 declined as losses in the commodity-related sectors overshadowed the gains in defensives and tech. Nikkei 225 was initially boosted at the open on the back of a weaker currency and briefly climbed back above 36,000 but then pulled back from fresh three-decade highs and wiped out all of its gains as it succumbed to the risk-off mood. Hang Seng and Shanghai Comp retreated amid the mixed data releases from China and with Hong Kong significantly underperforming amid hefty losses in tech and property, with the latter pressured by the decline in Chinese home prices.

Top Asian News

- China’s stats bureau head said the economy faces a complex external environment and insufficient demand in 2024, as well as noted that low consumer prices reflect insufficient effective demand and expects a modest consumer price rise in 2024. NBS head stated China’s economy is at a crucial stage of recovery and its property market is showing some positive changes, while he added there is still relatively big room for China’s property sector to develop and there is still room to unveil more policy steps to support growth.

- China has drafted guideline on formatting standards for AI sector; details light

- China’s BYD (1211 HK) to stop making pouch-type batteries for its hybrid EVs on concerns they may leak; plans to completely stop using pouch cells by 2025, via Reuters citing sources.

- Former BoJ official Maeda says that the BoJ could end NIRP in April, but will likely move slowly in any additional normalisation steps, via Reuters.

European bourses are lower, with over 90% of the Stoxx600 (-1.1%) in the red, amid a negative risk tone following mixed Chinese data overnight, initial hawkish-tone and hotter-than-expected UK CPI; the FTSE 100 (-1.7%) lags, dragged down by miners. European sectors are entirely in the red; Real Estate suffers from the higher yield environment, Basic Resources and Energy are dragged lower by broader weakness in the commodity markets. US equity futures are trading on the backfoot, in tandem with losses seen in the European session. The RTY (-1.3%) significantly underperforms, continuing to extend on yesterday’s hefty losses. ES/NQ (-0.4%), into Retail Sales, Fed speak and a handful of earnings. Headline US Specifics: JPM will increase headcount this year; IBKR down after results; TSLA reduces Model Y prices in Germany.

Top European News

- Tesla Cuts Model Y Prices in Europe: Investor’s Business Daily

- Bank of Italy’s Panetta Sees Growth Under 1% in 2024: Radiocor

- Oil in Retreat as Risk-Off Mood Swamps Impact of Mideast Crisis

- Basic-Fit Climbs on Double Upgrade To Buy From Jefferies

- Frankfurt Airport Cancels Flights Amid Icy Winter Weather

FX

- USD continues to gain as Waller tempers the pace of rate cut expectations. DXY has advanced to a high of 103.58 with not much resistance until 104.

- EUR is one of the better performers vs. the USD today amid hawkish ECB speak. That said, EUR/USD saw a hefty decline from yesterday’s 1.0951 high. Further downside could bring its 200DMA at 1.0845 into play.

- The Pound is the only G10 currency firmer vs. USD amid hawkish inflation metrics; Cable hit a high just shy of the 1.27 mark but remains some way off yesterday’s best of 1.2729.

- Antipodeans both remain battered by risk environment with AUD lagging on account of Chinese sell-off overnight; AUD/USD next target is a Dec 7th low at 0.6525 with NZD/USD selling putting a test of 0.61 on the cards.

- PBoC set USD/CNY mid-point at 7.1168 vs exp. 7.1986 (prev. 7.1134).

Fixed Income

- USTs are contained, but with a modest bearish-bias given a hotter than expected UK CPI print and additional hawkish commentary from ECB speakers. Yields continue to bear-flatten a touch as participants digest Waller before Retail Sales and thereafter Bowman, Barr & Williams

- Bunds started the session on the backfoot and felt additional pressure on UK CPI which saw the 134.37 trough print (matches 8/12 low); since, benchmarks have found some reprieve though still remain in negative territory.

- Gilts are the clear laggard after an unexpected rise in UK CPI for December, which led benchmarks to fall to a 98.82 trough; levels to the downside include 98.29, Dec 12th low.

Commodities

- Crude is at lows, Brent (-2.1%), amid a concoction of bearish factors including the firmer Dollar, soured risk tone, hotter-than-expected UK CPI data, and the mixed Chinese GDP data overnight; Brent Mar is back under USD 77.00/bbl and markets await OPEC MOMR at 12:45GMT/07:45EST.

- Gold is subdued amid the firmer Dollar, but losses in the yellow metal are cushioned, potentially amid haven flows coupled with technical support; XAU resides around USD 2,025/oz.

- Base metals are softer across the board, in-fitting with the broader market mood, and in the aftermath of the mixed Chinese GDP data overnight.

- China is to cut gasoline price by CNY 50/t starting Jan 18th, according to the NDRC

- Saudi Aramco CEO says Red Sea attacks are manageable in the short-term, may create tanker shortage and weigh on market if it lasts longer

- Pemex reports that it is carrying out work activity which could result in flaring at the Deer Park, Texas facility (340k BPD)

- Exxon’s (XOM) 250k BPD Joliet Illinois refinery reports flaring, according to Reuters

- Antofagasta (ANTO LN) reports FY23 copper production at 661kt (vs guided 640-670kt)

ECB Speak

- ECB President Lagarde (Neutral) says inflation is not where the ECB wants it to be; confident the ECB will get inflation to the 2% target; Will stay restrictive for as long as necessary. Too optimistic markets do not help the ECB in its inflation fight. Cannot should victory until inflation is sustainably at 2%. Watching wages, profit margins, energy and supply chains. Second-round effects would be a cause for concern. ECB has reached peak rates, short of a major shock.

- ECB President Lagarde (Neutral) says it is likely that the ECB will cut rates by the summer, according to Bloomberg.

- ECB’s Knot (Hawk) says markets are getting ahead of themselves on rate cuts; a lot must go well to hit the 2% inflation in 2025; rate path priced by markets can be self-defeating, via CNBC; “rate hike in the first half is rather unlikely”.

- ECB’s Vasle (Neutral) says his rate expectations are significantly different to the market; says it is absolutely premature to expect rate cuts at the start of Q2.

- ECB’s Panetta (Dove) says disinflation is happening, and is strong and will continue; says risks are emerging for raw material costs; adds that monetary conditions should adjust; awaiting data first to confirm the disinflation outlook.

- ECB’s Villeroy (Neutral) says the job of monetary policy is not finished yet; premature to say when the ECB will reduce rates this year

Geopolitics

- Maersk CEO sees Red Sea disruptions “lasting a few months at least”

- US President Biden’s administration is expected to announce plans to designate Yemen’s Houthi rebel group as a global terrorist organisation, according to an official cited by CBS News.

- US National Security Council spokesperson said the US welcomed the announcement by Qatar that an agreement was reached to have medicine delivered to hostages in Gaza, according to Reuters.

- Iran’s Defense Minister said the country is engaged in talks with Russia over concluding an MoU on respect for national sovereignty, territorial integrity and regional interests, according to journalist Aslani.

- China’s Taiwan Affairs Office said Taiwan’s election result cannot stop the trend towards reunification and China is willing to create the widest space for peaceful reunification, while it added that Taiwan has never been a country and China will never leave any space for Taiwan independence, according to Reuters.

US Event Calendar

- 07:00: Jan. MBA Mortgage Applications 10.4%, prior 9.9%

- 08:30: Jan. New York Fed Services Business, prior -14.6

- 08:30: Dec. Import Price Index MoM, est. -0.5%, prior -0.4%

- 08:30: Dec. Import Price Index YoY, est. -2.0%, prior -1.4%

- 08:30: Dec. Export Price Index YoY, est. -0.7%, prior -5.2%

- 08:30: Dec. Export Price Index MoM, est. -0.6%, prior -0.9%

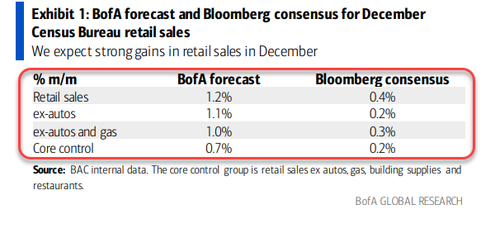

- 08:30: Dec. Retail Sales Advance MoM, est. 0.4%, prior 0.3%

- 08:30: Dec. Retail Sales Ex Auto MoM, est. 0.2%, prior 0.2%

- 08:30: Dec. Retail Sales Control Group, est. 0.2%, prior 0.4%

- 08:30: Dec. Retail Sales Ex Auto and Gas, est. 0.3%, prior 0.6%

- 09:15: Dec. Industrial Production MoM, est. -0.1%, prior 0.2%

- 09:15: Dec. Capacity Utilization, est. 78.7%, prior 78.8%

- 10:00: Nov. Business Inventories, est. -0.1%, prior -0.1%

- 10:00: Jan. NAHB Housing Market Index, est. 39, prior 37

- 14:00: Federal Reserve Releases Beige Book

Central Bank Speakers

- 09:00: Fed’s Barr Speaks at Conference on Cyber Risk

- 09:00: Fed’s Bowman Speaks About Future of Bank Capital Reform

- 14:00: Federal Reserve Releases Beige Book

- 15:00: Fed’s Williams Speaks at NY Fed Event

DB’s Jim Reid concludes the overnight wrap

After all the comparisons with the 1970s over the last few years, Henry pointed out yesterday that actually the late-1960s are becoming an increasingly good parallel. That was another period of low unemployment, rising deficits, and growing geopolitical risks. But it also saw inflation rebound, as the Fed cut rates just as fiscal spending rose because of the Vietnam War. Although markets are encouraging and hoping for significant rate cuts this year, today’s policymakers are cautious about a repeat. Interestingly since the ECB’s Lane spoke over the weekend, the central bank speak has certainly turned a little more cautious about endorsing the amount of cuts currently priced in by markets. Our view is that the pricing is very aggressive versus history absent a recession so for it to be correct you have to believe in the immaculate soft landing scenario or a recession. We will see. Back to Henry’s note and overall the late 1960s shows that with tight labour markets, fiscal stimulus and geopolitical shocks, that’s the sort of environment where inflation can return if policy errors are made. See the report here.

On this theme, markets have struggled over the last 24 hours, with bonds and equities selling off after Fed Governor Waller pushed back on market expectations for rapid rate cuts. His November 28th speech was a big part of the rates and risk repricing towards the end of the year but this time his comments were more balanced but perhaps that was as much due to how far markets have come in terms of Fed pricing. What was dovish back then may look more hawkish now.

Yesterday’s speech had several important lines, but when it came to the market reaction, the key point was that he saw “no reason to move as quickly or cut as rapidly as in the past”. So that was an explicit pushback on market pricing, which had been expecting 165bps of rate cuts in 2024 before the speech, and it meant that 10yr Treasury yields (+11.8bps) saw their largest daily increase in over two months (albeit with some catch-up needed after the holiday), ending the day at 4.06%. Other assets also saw significant moves, with the Dollar Index (+0.93%) seeing its biggest daily increase since last March, whilst the S&P 500 shed -0.37%. China risk is slumping overnight as we’ll see below. Today’s highlights are US retail sales, UK CPI as we go to print, and lots of ECB speakers.

In terms of the rest of Waller’s speech, it did look towards rate cuts in 2024, saying that if “inflation doesn’t rebound and stay elevated, I believe the FOMC will be able to lower the target range for the federal funds rate this year.” But his view was that cuts should proceed “methodically and carefully”, and that he’d also be focusing on the CPI revisions scheduled for February 9. Readers may recall that last year, the revisions showed that inflation was declining slower than previously thought, so that’ll be a crucial update affecting the timing of any potential rate cuts.

However, even with Waller’s speech, it was striking that investors remained pretty confident that the Fed will be cutting rates by March, and fairly rapidly over 2024 as a whole. This echoes what we saw after the CPI last week, when the upside surprise didn’t seem to affect investor conviction much about future rate cuts. In fact by the close, the pricing for a cut by March was only down slightly to 69%, having been at 74% the previous day. Likewise for 2024 as a whole, the amount of cuts priced in by the December meeting came down from 165bps intraday just before the speech, to 157bps by the end, so still a rapid pace by historical standards. That means there’s still a tension between what Fed officials are saying and market pricing, since Waller was openly discussing a pace of cuts that were slower than previous cycles. Moreover, officials only have until Friday before the blackout period starts ahead of the next meeting, so after that the next scheduled remarks won’t be until Chair Powell’s press conference on January 31.

As noted at the top, this hawkish backdrop meant that US Treasuries struggled, with the 2yr yield up +7.7bps to 4.22%, whilst the 10yr yield was up +11.8bps to 4.06%. And in Canada, there was an even larger move for the 10yr yield (+13.8bps) after their latest inflation print for December showed that core CPI was proving stickier than anticipated. Looking at the measures followed by the Bank of Canada, the trim core rate was up to +3.7% (vs. +3.4% expected), and the median core rate remained at +3.6% (vs. +3.3% expected). And in turn, that saw investors push back the timing of future rate cuts, and the likelihood of a cut by March came down from 35% to 23%.

Over in Europe, we had several pieces of ECB commentary, with pushback against near-term pricing of cuts again evident. Among the hawks, Germany’s Nagel repeated his comments that market discussion of rate cuts had come too soon, while Lithuania’s Simkus said he was “far less optimistic” than markets on rate cuts. France’s Villeroy suggested it was premature to speak of when in 2024 rate cuts are likely to come. Pricing of a March cut inched lower again from 29% to 25% yesterday (it was 43% on Friday). In bonds, the 2yr bund yield (+0.2bps) was little changed after the sizeable sell-off on Monday, but the 10yr yield rose by +2.5bps to 2.26%, its highest since December 11. We have another busy day of ECB speakers ahead today so watch out for them in what has been a more hawkish week to date.

For equities, it was also a fairly negative session, with the S&P 500 (-0.37%) declining as US markets returned after Monday’s holiday. In addition, the decline was broader than the headline loss suggested, as the index was dragged up by the outperformance of the Magnificent 7, which were flat on the day. The latter was supported by a +3.06% gain for chipmaker Nvidia. Within the S&P 500, energy (-2.40%) and materials (-1.19%) stocks led the declines. Otherwise, the small-cap Russell 2000 (-1.21%) fell for a 3rd consecutive session, reaching its lowest level in over a month. And there were also declines in Europe, where the STOXX 600 (-0.24%) lost ground for a second day running.

In Asia the Hang Seng (-2.81%) is sharply lower led by real estate and consumer non-cyclical stocks. The KOSPI (-2.43%) is not far behind. Mainland Chinese stocks are also trading in the red with the CSI (-0.73%) and the Shanghai Composite (-0.64%) down. S&P 500 (-0.19%) and NASDAQ 100 (-0.27%) futures are also slipping.

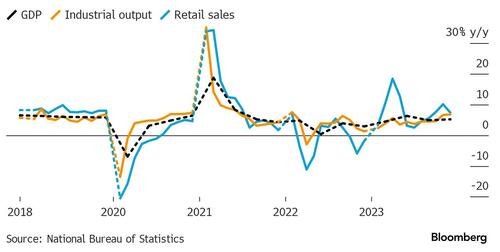

Coming back to China, the economy expanded by +5.2% in 2023, hitting the government’s official target after the previous year’s miss but the outlook for 2024 remains uncertain as the world’s second-biggest economy is still contending with the ongoing property crisis, deflationary pressures and sluggish consumer and business confidence. On a quarterly basis, the economy grew +1.0% (+1.1% expected) in Q4, slowing from a revised +1.5% pace in the previous quarter. The fact that the deflator fell -1.5% in the quarter is also gaining a lot of attention as deflation continues.

Retail sales advanced +7.4% y/y in December (v/s +8.0% expected), slowing from a +10.1% increase in November. At the same time, production rose by +6.8% y/y in December, slightly higher than the previous month’s +6.6%, and meeting market forecasts. Housing data was also soft overnight.

Elsewhere yesterday, UK gilts outperformed (with the 10yr yield flat at 3.80%) after data showed wage growth was running slower than expected. For instance, averageweekly earnings were up by +6.5% over the three months to November compared with the previous year, beneath the +6.8% reading expected. We also found out that the number of payrolled employees was down by -24k in December (vs. -13k expected). Shortly after we go to press this morning, we’ll get the CPI release for December as well, so keep an eye out for that in terms of the timing of any potential rate cut.

Lastly, there were also a few other data releases out yesterday. In the US, the Empire State manufacturing survey fell to -43.7 in January (vs. -5.0 expected), which is the lowest since the first Covid wave in spring 2020, and otherwise the lowest since the start of the series in 2001. We also had the ECB’s latest Consumer Expectations Survey for November, which showed 1yr inflation expectations were down to 3.2%, and 3yr expectations were down to 2.2%. In both cases, that was the lowest reading since February 2022. That said, our European economists’ own dbDIG survey, which is one month ahead (for December), suggests that inflation expectations may be stabilising at still slightly elevated levels.

To the day ahead now, and data releases include UK CPI for December, US retail sales, industrial production and capacity utilisation for December, along with the NAHB’s housing market index for January. From central banks, we’ll hear from ECB President Lagarde, the ECB’s Cipollone, Vasle, Simkus, Villeroy, Vujcic, Knot and Nagel, as well as the Fed’s Barr, Bowman and Williams. The Fed will also be releasing their Beige Book.

2 B) NOW NEWSQUAWK (EUROPE/REPORT)

Negative sentiment continues with equities and crude lower, Dollar firmer and GBP bid post-CPI; US Retail Sales due – Newsquawk US Market Open

WEDNESDAY, JAN 17, 2024 – 06:12 AM

- European bourses and US futures are entirely in the red owing to a soured risk tone and mixed Chinese data overnight

- Dollar is firmer, Pound is bid following hotter-than-expected UK CPI and Antipodeans lag

- Bonds weaker amid hawkish central bank speak and hot UK CPI; Fed speak & Retail Sales due

- Crude sinks due to a firmer Dollar & mixed Chinese data; XAU is weaker though losses are cushioned amid haven flows, base metals entirely in the red

- Looking ahead, US MBA, Import Prices, Retail Sales, Industrial Production, Japanese Machinery Orders, Fed Beige Book, Comments from ECB’s Knot & Lagarde, Fed’s Williams, Barr & Bowman, Supply from the US, Earnings from, US Bancorp & Citizen Financial Group.

More Newsquawk in 3 steps:

1. Subscribe to the free premarket movers reports

2. Listen to this report in the market open podcast (available on Apple and Spotify)

3. Trial Newsquawk’s premium real-time audio news squawk box for 7 days

EUROPEAN TRADE

EQUITIES

- European bourses are lower, with over 90% of the Stoxx600 (-1.1%) in the red, amid a negative risk tone following mixed Chinese data overnight, initial hawkish-tone and hotter-than-expected UK CPI; the FTSE 100 (-1.7%) lags, dragged down by miners.

- European sectors are entirely in the red; Real Estate suffers from the higher yield environment, Basic Resources and Energy are dragged lower by broader weakness in the commodity markets.

- US equity futures are trading on the backfoot, in tandem with losses seen in the European session. The RTY (-1.3%) significantly underperforms, continuing to extend on yesterday’s hefty losses. ES/NQ (-0.4%), into Retail Sales, Fed speak and a handful of earnings.

- Headline US Specifics: JPM will increase headcount this year; IBKR down after results; TSLA reduces Model Y prices in Germany.

- Click here and here for the sessions European pre-market equity newsflow, including earnings.

- Click here for more details.

FX

- USD continues to gain as Waller tempers the pace of rate cut expectations. DXY has advanced to a high of 103.58 with not much resistance until 104.

- EUR is one of the better performers vs. the USD today amid hawkish ECB speak. That said, EUR/USD saw a hefty decline from yesterday’s 1.0951 high. Further downside could bring its 200DMA at 1.0845 into play.

- The Pound is the only G10 currency firmer vs. USD amid hawkish inflation metrics; Cable hit a high just shy of the 1.27 mark but remains some way off yesterday’s best of 1.2729.

- Antipodeans both remain battered by risk environment with AUD lagging on account of Chinese sell-off overnight; AUD/USD next target is a Dec 7th low at 0.6525 with NZD/USD selling putting a test of 0.61 on the cards.