GOLD PRICE CLOSED: DOWN $0.10 TO $2017.60

SILVER PRICE CLOSED: DOWN 3 cents AT $22.79

Access prices: closes 4: 15 PM

Gold ACCESS CLOSED 2018.85

Silver ACCESS CLOSED: 22.81

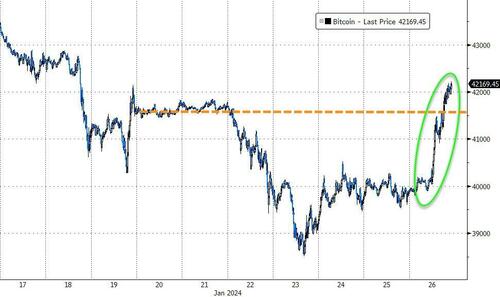

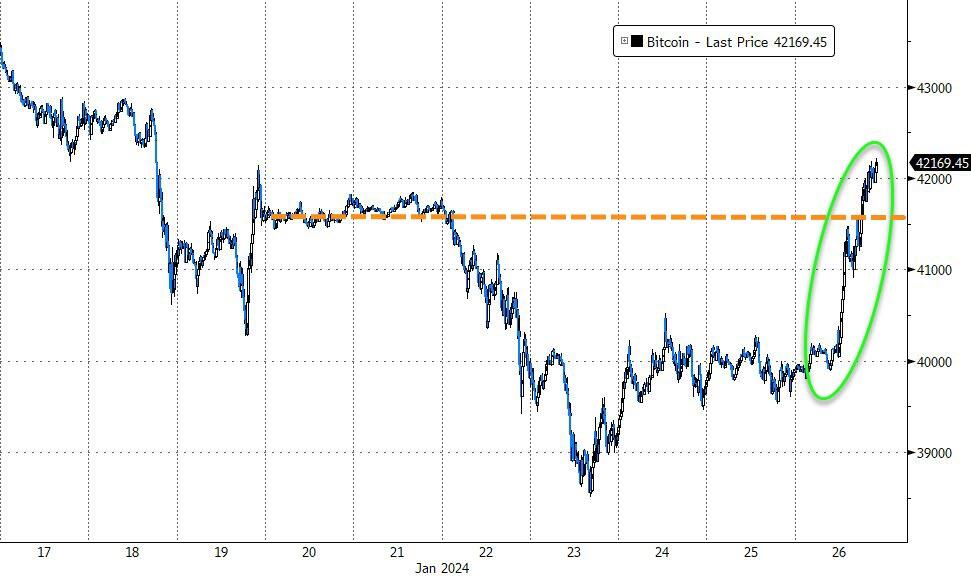

Bitcoin morning price:, 41,408 UP 1688 DOLLARS

Bitcoin: afternoon price: $41,957 up 2237 dollars

Platinum price closing $891.50 DOWN $16.25

Palladium price; $942.60 UDOWN $27.40

END

SHANGHAI GOLD (USD) FUTURES – QUOTE

SHANGHAI GOLD (USD) FUTURES – QUOTES

SHANGHAI OVER COMEX: PREMIUM OF $36.00

Beginning Monday, April 1, 2024, CME Group settlement data will no longer be accessible through ftp.cmegroup.com and will have a delayed publication time of 12:00 a.m. CT on all cmegroup.com web pages. Learn about alternate ways to access the data in our FAQ.

AUTO-REFRESH IS OFF

Last Updated 26 Jan 2024 11:27:37 AM CT.

Market data is delayed by at least 10 minutes.

Due to the huge rise in the dollar, we must look at gold and silver in currencies other than the dollar to understand where we are heading

I will now provide gold in Canadian dollars, British pounds and Euros

4: 15 PM ACCESS

*CANADIAN GOLD: $2,714.30 DOWN 6.95 CDN dollars per oz( * NEW ALL TIME HIGH 2,795.90 CDN DOLLARS PER OZ//DEC 1 272023)

*BRITISH GOLD: 1589,14 DOWN 1,00 pounds per oz// *(NEW ALL TIME HIGH//CLOSING///1655.17 BRITISH POUNDS/OZ) OCT 2/2023

*EURO GOLD: 1859.65DOWN 3.40 euros per oz //* (ALL TIME CLOSING HIGH: 1903.75 EUROS PER OZ//DEC 1.2023)

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

EXCHANGE: COMEX

EXCHANGE: COMEX

CONTRACT: JANUARY 2024 COMEX 100 GOLD FUTURES

SETTLEMENT: 2,016.900000000 USD

INTENT DATE: 01/25/2024 DELIVERY DATE: 01/29/2024

FIRM ORG FIRM NAME ISSUED STOPPED

190 H BMO CAPITAL 257

363 H WELLS FARGO SEC 29

435 H SCOTIA CAPITAL 74

624 H BOFA SECURITIES 199

737 C ADVANTAGE 12 11

880 H CITIGROUP 500

TOTAL: 541 541

MONTH TO DATE: 6,763

JPMorgan stopped 0/541 contracts.

FOR JAN.:

GOLD: NUMBER OF NOTICES FILED FOR JAN/2024. CONTRACT: 541 NOTICES FOR 54,100 OZ or 1.682 TONNES

total notices so far: 6763 contracts for 676,300 Oz (21.035 tonnes)

FOR JANUARY:

SILVER NOTICES 46 NOTICE(S) FILED FOR 230,000 OZ/

total number of notices filed so far this month : 1155 for 5,775,000 oz

XXXXXXXXXXXXXXXXXX

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

BOTH GLD AND SLV ARE FRAUDULENT VEHICLES

GLD

WITH GOLD DOWN $.10

INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD/ : NO CHANGES IN GOLD INVENTORY AT THE GLD//

INVENTORY RESTS AT 858.93 TONNES

SLV//

WITH NO SILVER AROUND AND SILVER DOWN $.03 CENTS AT THE SLV//

MEGA CHANGES IN SILVER INVENTORY AT THE SLV AGAIN: A WITHDRAWAL OF 1.556 MILLION OZ OF SILVER FROM THE SLV//

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV.

CLOSING INVENTORY: 446.680 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A FAIR SIZED 713 CONTRACTS TO 136,513 AND FURTHER FROM THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THIS HUGE SIZED LOSS IN COMEX OI WAS ACCOMPLISHED DESPITE OUR GAIN OF $0.03 IN SILVER PRICING AT THE COMEX ON THURSDAY. WE HAD A ZERO LONG LIQUIDATION AT THE COMEX SESSION BUT A CONSIDERABLE SHORT COVERING. WE HAD A HUGE 857 T.A.S ISSUANCE AND THESE WILL BE USED FOR MANIPULATION LATER THIS MONTH/AS WELL AS TODAY.

CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON THURSDAY NIGHT: 857 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS. IT THUS LOOKS LIKE THE FED (GOV’T) IS BEHIND ALL OF THESE TRADES.

WE HAVE NOW SET ANOTHER RECORD LOW AT 114,102 CONTRACTS ///JULY 3.2023// OUR BANKERS WITH THE HELP OF SPECULATORS AND HIGH FREQUENCY TRADERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.03), AND WERE UNSUCCESSFUL IN KNOCKING ANY SILVER LONGS AS WE HAD A TINY SIZED LOSS OF 13 CONTRACTS GAIN ON OUR TWO EXCHANGES ACCOMPANYING CONSIDERABLE SHORT COVERING

WE MUST HAVE HAD:

A VERY STRONG SIZED 700 ISSUANCE OF EXCHANGE FOR PHYSICALS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 6.650 MILLION OZ (FIRST DAY NOTICE) FOLLOWED BY TODAY’S 235,000 OZ QUEUE. JUMP NEW TOTALS 6.840 MILLION OZ//

//NEW STANDING FOR SILVER IS THUS 6.840 MILLION OZ

//FAIR SIZED COMEX OI LOSS/VERY STRONG SIZED EFP ISSUANCE/ VI) HUGE SIZED NUMBER OF T.A.S. CONTRACT ISSUANCE 857 CONTRACTS)/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL -REMOVED 317 CONTRACTS //

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS JAN ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF JAN

TOTAL CONTRACTS for 18 days, total 14,087 contracts: OR 70.435 MILLION OZ (782 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 70.435 MILLION OZ

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH 2022: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 118.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 85.745 MILLION OZ (SMALLER THAN LAST MONTH)

AUGUST: 171.43 MILLION OZ (THIS MONTH IS GOING TO BE HUGE //2ND HIGHEST ON RECORD

SEPT: 72.705 MILLION OZ (SMALLER THIS MONTH)

OCT: 97.455 MILLION OZ

NOV. 50.050 MILLION OZ

DEC. 66.140 MILLION OZ//

TOTAL 2023: 1,104.10 MILLION OZ/

JAN ’24 : 70.435 MILLION OZ//WILL BE A VERY STRONG MONTH FOR ISSUANCE

RESULT: WE HAD A STRONG SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 713 CONTRACTS DESPITE OUR GAIN IN PRICE OF SILVER PRICING AT THE COMEX//THURSDAY.,. THE CME NOTIFIED US THAT WE HAD A VERY STRONG EFP ISSUANCE CONTRACTS: 700 ISSUED FOR FEB AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS. WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR JAN. OF 6.665 MILLION OZ FOLLOWED BY TODAY’S 235,000 OZ QUEUE JUMP //NEW TOTAL 5.840 MILLION OZ TO WHICH WE ADD EX. FOR RISK ISSUANCE/PRIOR FOR 1.0 MILLION OZ //NEW TOTALS; 6.840 MILLION OZ/

NEW STANDING 6.840 million OZ /// WE HAVE A FAIR GAIN OF 304 OI CONTRACTS ON THE TWO EXCHANGES WITH THE GAIN IN PRICE. THE TOTAL OF TAS INITIATED CONTRACTS TODAY: A HUGE SIZED 857 CONTRACTS//SOME FRONT END OF THE TAS CONTRACTS WERE LIQUIDATED DURING THE THURSDAY COMEX SESSION/// WITH CONSIDERABLE SHORT COVERINGS FROM OUR SPEC SHORTS BUT AT HIGHER PRICES.. THE NEW TAS ISSUANCE THURSDAY NIGHT (857) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE//PROBABLY TODAY., .

WE HAD 46 NOTICE(S) FILED TODAY FOR 230,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A STRONG SIZED 5881 CONTRACTS TO 461,422 AND CLOSER TO THE RECORD (SET JAN 24/2020) AT 799,733 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: – REMOVED 98 CONTRACTS

WE HAD A STRONG SIZED DECREASE IN COMEX OI ( 5881 CONTRACTS) DESPITE OUR $2.50 GAIN IN PRICE//THURSDAY. WE ALSO HAD A RATHER LARGE INITIAL STANDING IN GOLD TONNAGE FOR JAN. AT 8.214 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S HUGE 54,200 OZ QUEUE JUMP//NEW STANDING: 21.073 TONNES // ALL OF THIS HAPPENED WITH OUR $2.50 GAIN IN PRICE WITH RESPECT TO THURSDAY’S TRADING. WE HAD A FAIR SIZED LOSS OF 1510 OI CONTRACTS (4.696) PAPER TONNES) ON OUR TWO EXCHANGES.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 4371 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 461,324

IN ESSENCE WE HAVE A FAIR SIZED DECREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 1510 CONTRACTS WITH 5,881 CONTRACTS DECREASED AT THE COMEX// AND A STRONG SIZED 4371 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI LOSS ON THE TWO EXCHANGES OF 1510 CONTRACTS.. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): A FAIR SIZED 2659 CONTRACTS.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A STRONG SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (4371 CONTRACTS) ACCOMPANYING THE STRONG SIZED LOSS IN COMEX OI (5881) //TOTAL LOSS FOR OUR THE TWO EXCHANGES: 1510 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR FORMER FORMAT OF BANKERS GOING LONG AND SPECULATORS GOING SHORT ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR JAN AT 8.214 TONNES FOLLOWED BY TODAY’S 54,200 OZ QUEUE JUMP//NEW STANDING 21.073 TONNES. / 3) ZERO LONG LIQUIDATION AND CONSIDERABLE TAS LIQUIDATION WITH CONSIDERABLE SHORT COVERINGS.// 4) FAIR SIZED COMEX OPEN INTEREST LOSS/ 5) STRONG ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER///6: FAIR T.A.S. ISSUANCE: 2659 CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023-2024 INCLUDING TODAY

JAN.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF JAN. :

TOTAL EFP CONTRACTS ISSUED: 80,039 CONTRACTS OR 8,003,900 OZ OR 248.95 TONNES IN 18 TRADING DAY(S) AND THUS AVERAGING: 4446 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 18 TRADING DAY(S) IN TONNES 248.95 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2022, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 248.95/3550 x 100% TONNES 7.01% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2023

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH/2022: 409.30 TONNES //FINAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 151.69 TONNES (WEAKER THAN LAST MONTH)

AUGUST: 195.28 TONNES (A STRONGER MONTH)//FINAL

SEPT: 254.709 TONNES (WILL BE LARGER THAN LAST MONTH AND A STRONG MONTH)

OCT. 248.09 TONNES. LIKE SILVER, THIS MONTH IS GOING TO BE A STRONG E.F.P. ISSUANCE.

NOV. 239.16 TONNES//WILL BE STRONG THIS MONTH,

DEC. 213.704 TONNES. A STRONG MONTH//

TOTAL FOR YEAR 2023: 2,569.57 TONNES VS 2578 TONNES LAST YEAR

JAN ’24: 248.95 TONNES (WILL BE MUCH GREATER THAN LAST MONTH.)

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF FEB. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (FEB), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER FELL BY A STRONG SIZED 713 CONTRACTS OI TO 136,513 AND FURTHER FROM THE COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 700 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MARCH 700 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 700 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 396 CONTRACTS AND ADD TO THE 700 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A TINY SIZED LOSS OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 13 CONTRACTS

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTAL 0.065 MILLION OZ

OCCURRED DESPITE OUR $.03 GAIN IN PRICE …..

END

OUTLINE FOR TODAY’S COMMENTARY

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

b, ) Gold/silver trading overnight Europe,//GOLD COMMENTARIES

(Peter Schiff)

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS//

FRIDAY MORNING/THURSDAY NIGHT

SHANGHAI CLOSED UP 4.11 PTS OR 0.14% //Hang Seng CLOSED DOWN 259.73 PTS OR 1.60% /The Nikkei CLOSED DOWN 485.40 OR 1.34% //Australia’s all ordinaries CLOSED UP 0.48% /Chinese yuan (ONSHORE) closed DOWN AT 7.1745 /OFFSHORE CHINESE YUAN CLOSED DOWN TO 7.1841 /Oil UP TO 76.60 dollars per barrel for WTI and BRENT DOWN AT 81.82/ Stocks in Europe OPENED ALL GREEN// ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER

A)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

9. USA

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A STRONG SIZED 5881 CONTRACTS TO 461,324 DESPITE OUR GAIN IN PRICE OF $2.50 WITH RESPECT TO THURSDAY TRADING. WE MUST HAVE HAD ZERO LONG SPEC LIQUIDATIONS IN THE COMEX SESSION WITH SOME SPEC SHORT COVERINGS AT THE HIGHER PRICES.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE NON ACTIVE DELIVERY MONTH OF JAN..… THE CME REPORTS THAT THE BANKERS ISSUED A STRONG SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 4371 EFP CONTRACTS WERE ISSUED: : FEB 4371 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 4371 CONTRACTS

ON A NET BASIS IN OPEN INTEREST WE LOST THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A FAIR SIZED TOTAL OF 1510 CONTRACTS IN THAT 4371 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A STRONG SIZED LOSS OF 5881 COMEX CONTRACTS..AND THIS FAIR SIZED LOSS ON OUR TWO EXCHANGES HAPPENED DESPITE OUR GAIN IN PRICE OF $2.50 THURSDAY COMEX. AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS DURING MID MONTH IN THE DELIVERY CYCLE), THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR THURSDAY NIGHT WAS A FAIR SIZED 2,659 CONTRACTS. THROUGHOUT THE PAST SEVERAL WEEKS, THE BANKERS SOLD OFF THE LONG SIDE OF THE SPREAD WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR/T.A.S. SPREAD WHICH WILL BE LIQUIDATED IN DAYS HENCE//.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: JAN (21.073 TONNES) ( NON ACTIVE MONTH)

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 24 MONTHS OF 2021-2023:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

NOV: 18.7122 TONNES + 16.2505 EX. FOR RISK = 34.9627 TONNES

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707TONNES

TOTAL 2023 YEAR : 436.546 TONNES

JAN ’24. 21.073 TONNES

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT GAINED $2.50 //// AND WERE UNSUCCESSFUL IN KNOCKING ANY SPECULATOR LONGS AS WE HAD A FAIR SIZED LOSS OF 1510 TOTAL CONTRACTS ON OUR TWO EXCHANGES. WE HAD A FAIR T.A.S. LIQUIDATION ON THE FRONT END OF THURSDAY’S TRADING . THE T.A.S. ISSUED ON THURSDAY NIGHT, WILL BE “PUT INTO THE BANK” TO BE USED AT A LATER DATE AT THE COLLUSIVE CHOOSING OF OUR BANKERS. WE ALSO EXPERIENCED CONSIDERABLE SPECULATOR SHORT COVERING AT HIGHER PRICES.

WE HAVE LOST A TOTAL OI OF 4.696 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR JAN. (8,214 TONNES) ON FIRST DAY NOTICE FOLLOWED BY TODAY’S 54,200 OZ QUEUE JUMP (1.685 TONNES): NEW TOTAL STANDING 19.387 TONNES/ ALL OF THIS WAS ACCOMPLISHED WITH OUR GAIN IN PRICE TO THE TUNE OF $2.50

WE HAD – REMOVED 98 CONTRACT TO THE COMEX TRADES TO OPEN INTEREST (CROOKS)

NET LOSS ON THE TWO EXCHANGES 1510 CONTRACTS OR 1,510,00 OZ OR 4.696 TONNES.

Estimated gold volume today:// 199,419 fair

final gold volumes/yesterday 298,583 very good

//speculators have left the gold arena

JAN 26 INITIAL

/ /// THE JAN 2024 GOLD CONTRACT

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 86,132.532 OZ brinks JPMorgan 2667 kilobars and 12 kilobars . |

| Deposit to the Dealer Inventory in oz | nil oz |

| Deposits to the Customer Inventory, in oz | 64,227,492 oz ASAHI |

| No of oz served (contracts) today | 541 notice(s) 54100 OZ 1.682 TONNES |

| No of oz to be served (notices) | 12 contracts 1200 oz 0.0373 TONNES |

| Total monthly oz gold served (contracts) so far this month | 6763 notices 676,300 oz 21.035 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | x |

0 dealer deposits:

total dealer deposits: nil oz

total customer withdrawals: 2

i)out of asahi: 1168.75 oz

ii) Out of Brinks 85,746.720 oz (2667 kilobars)

iii) Out of JPMorgan: 385.812 oz (12 kilobars

total withdrawals 86,132.532 oz (2679 tonnes)

we had 1 customer deposits

i)Into ASAHI: 64,227.492 oz

total deposits 64,227.492 oz

Adjustments; 1 dealer to customer

a) Malca: 64,337.157 oz (2001 kilobars)

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR JAN.

For the front month of JANUARY we have an oi of 553 contracts having GAINED 307 contracts. We had 235 notices served on THURSDAY, so we gained A WHOPPING 542 contracts or an additional 54200 oz will stand for delivery at the comex .

FEB LOST 34,569 CONTRACTS FALLING TO 89,681. WE HAVE 5 MORE READING DAYS BEFORE FIRST DAY NOTICE.

March LOST 28 contracts to stand at 876.

APRIL GAINED 27,908 CONTRACTS RISING TO 303,236.

We had 541 contracts filed for today representing 54,100 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 541 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped ( received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the JAN. /2024. contract month, we take the total number of notices filed so far for the month (6763 x 100 oz ), to which we add the difference between the open interest for the front month of JAN. (553 CONTRACTS) minus the number of notices served upon today 541 x 100 oz per contract equals 677,500 OZ OR 21.073 TONNES

thus the INITIAL standings for gold for the JAN. contract month: No of notices filed so far (6763) x 100 oz + (553) {OI for the front month} minus the number of notices served upon today (541) x 100 oz) which equals 677,500 oz standing OR 21.073 TONNES

TOTAL COMEX GOLD STANDING FOR JAN: 21.073 TONNES WHICH IS GREAT FOR AN INACTIVE DELIVERY MONTH IN THE CALENDAR.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 1,326,338.282 41.25 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD: 19,598,245.765 OZ

TOTAL REGISTERED GOLD 8,948,340.067 (278.33 tonnes).

TOTAL OF ALL ELIGIBLE GOLD: 10,649,905.698 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 7,622,002 oz (REG GOLD- PLEDGED GOLD) 237,07 tonnes

END

SILVER/COMEX

JAN 26/INITIAL

//2024// THE JAN 2024 SILVER CONTRACT//INITIAL

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 1,292,317,139 oz ASAHI . |

| Deposits to the Dealer Inventory | nilOZ |

| Deposits to the Customer Inventory | 749,193.700 oz CNT Loomis |

| No of oz served today (contracts) | 46 CONTRACT(S) (230,000 OZ) |

| No of oz to be served (notices) | 13 contracts (65,000 oz) |

| Total monthly oz silver served (contracts) | 1155 Contracts (5,775,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

i) 0 dealer deposit

total dealer deposit: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: 0 oz

We had 2 deposits customer account:

i) Into Loomis: 598,265.410 oz

ii) Into CNT; 150,928.290 oz

total customer deposits 749,193.700 oz

JPMorgan has a total silver weight: 131.341 million oz/276,216 million or 47.46%

adjustment: 2

i) ASAHI: 593,456.226 oz removed

ii) Dealer to customer Brinks 360,674.820 oz

Comex withdrawals: 1

i) Out of ASAHI 1,202,317.130 oz

total withdrawal: 1,202,317.130 oz

TOTAL REGISTERED SILVER: 41.579 MILLION OZ//.TOTAL REG + ELIGIBLE. 276,216 million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR DECEMBER:

silver open interest data:

FRONT MONTH OF JAN. /2023 OI: 59 CONTRACTS HAVING LOST 180 CONTRACT(S). WE HAD 227 NOTICES SERVED ON THURSDAY, SO WE GAINED 47 CONTRACTS OR AN ADDITIONAL 235,000 OZ WILL STAND FOR DELIVERY AT THE COMEX

FEB GAINED 3 CONTRACTS TO STAND AT 716

MARCH LOST 1974 CONTRACTS TO 101,349

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 46 for 230,000 oz

Comex volumes// est. volume today 45,059 fair

Comex volume: confirmed yesterday 61,665 GOOD

To calculate the number of silver ounces that will stand for delivery in JAN. we take the total number of notices filed for the month so far at 1155 x 5,000 oz = 5,775,000 oz

to which we add the difference between the open interest for the front month of JAN. (59) and the number of notices served upon today 46 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the JAN/2024 contract month: 1155 (notices served so far) x 5000 oz + OI for the front month of JAN. (59) – number of notices served upon today (46 )x 500 oz of silver standing for the JAN contract month equates to 5.840 MILLION OZ. to which we add our exchange for RISK of 1.0 million oz//new total 6.804 million oz/

New total standing: 6.840 million oz.

There are 41.579 million oz of registered silver.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS//

BOTH GLD AND SLV ARE MASSIVE FRAUDS!

JAN 26/WITH GOLD DOWN $0.10 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD: / //://INVENTORY RESTS AT 858.93 TONNES

JAN 25/WITH GOLD UP $2.50 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD: / //://INVENTORY RESTS AT 858.93 TONNES

JAN 24/WITH GOLD DOWN $9.75 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD: / //://INVENTORY RESTS AT 858.93 TONNES

JAN 23/WITH GOLD UP $3.95 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.02 TONNES OF GOLD FROM THE GLD/ //://INVENTORY RESTS AT 858.93 TONNES

JAN 22/WITH GOLD DOWN $6.00 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.15 TONNES OF GOLD FROM THE GLD/ //://INVENTORY RESTS AT 860.95 TONNES

JAN 19/WITH GOLD UP $8.15 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD //://INVENTORY RESTS AT 862.10 TONNES

JAN 18/WITH GOLD UP $14.85 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 2.30 TONNES OF GOLD FROM THE GLD//://INVENTORY RESTS AT 862.10 TONNES

JAN 17/WITH GOLD DOWN $23.25 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF .549 TONNES OF GOLD INTO THE GLD.;//://INVENTORY RESTS AT 864.40 TONNES

JAN 12/WITH GOLD UP $31.65 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD; A MASSIVE WITHDRAWAL OF 4.61 TONNES OF GOLD FROM THE GLD//://INVENTORY RESTS AT 864.99 TONNES

JAN 11/WITH GOLD DOWN $7.40 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD; A MASSIVE WITHDRAWAL OF 4.61 TONNES OF GOLD FROM THE GLD//://INVENTORY RESTS AT 864.99 TONNES

JAN 10/WITH GOLD DOWN $4.80 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD://INVENTORY RESTS AT 869.60 TONNES

JAN 9/WITH GOLD UP $0.95 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD://INVENTORY RESTS AT 869.60 TONNES

JAN 8/WITH GOLD DOWN $16.85 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD:A WITHDRAWAL OF 4.61 TONNES FROM THE GLD. INVENTORY RESTS AT 869.60 TONNES

JAN 5/WITH GOLD UP $0.80 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD:///. // INVENTORY RESTS AT 874.21 TONNES

JAN 4/WITH GOLD UP $7.60 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD:///. // INVENTORY RESTS AT 874.21 TONNES

JAN 3/WITH GOLD DOWN $29.40 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.90 TONNES OF GOLD INTO THE GLD///. // INVENTORY RESTS AT 874.21 TONNES

JAN 2/WITH GOLD UP $1.50 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.44 TONNES OF GOLD INTO THE GLD///. // INVENTORY RESTS AT 879.11 TONNES

DEC 29/WITH GOLD DOWN $10.25 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.16 TONNES OF GOLD INTO THE GLD///. // INVENTORY RESTS AT 880.55 TONNES

DEC 28/WITH GOLD DOWN $8.35 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.45 TONNES OF GOLD INTO THE GLD///. // INVENTORY RESTS AT 881.71 TONNES

DEC 27/WITH GOLD UP $23.25 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.01 TONNES OF GOLD INTO THE GLD///. // INVENTORY RESTS AT 880.26 TONNES

DEC 26/WITH GOLD UP $1.25 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD:/. // INVENTORY RESTS AT 878.25 TONNES

DEC 22/WITH GOLD UP $17,85 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD:/. // INVENTORY RESTS AT 878.25 TONNES

DEC 21/WITH GOLD UP $5.10 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD:A DEPOSIT .58 TONNES OF 2.02 TONNES OF GOLD INTO THE GLD//. // INVENTORY RESTS AT 878.25 TONNES

DEC 20/WITH GOLD DOWN $3.60 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD:A WITHDRAWAL OF 2.02 TONNES OF GOLD FROM THE GLD//. // INVENTORY RESTS AT 877.67 TONNES

GLD INVENTORY: 858.93 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

JAN 26/WITH SILVER DOWN $0.03 TODAY MEGA CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.556 MILLION OZ INTO THE SLV(FAIRY TALES) // /INVENTORY RESTS AT 446.680 MILLION OZ

JAN 25/WITH SILVER UP $0.03 TODAY MEGA CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.831 MILLION OZ INTO THE SLV(FAIRY TALES) // /

INVENTORY RESTS AT 448.236 MILLION OZ

JAN 24/WITH SILVER UP $0.44 TODAY MEGA CHANGES IN SILVER INVENTORY AT THE SLV: ANOTHER DEPOSIT OF 1.375 MILLION OZ INTO THE SLV(FAIRY TALES) // //INVENTORY RESTS AT 450.067 MILLION OZ

JAN 23/WITH SILVER UP $0.21 TODAY MEGA CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 16.201 MILLION OZ INTO THE SLV(FAIRY TALES) // //INVENTORY RESTS AT 448.694 MILLION OZ

JAN 22/WITH SILVER DOWN $0.45 TODAY NO CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 458,000 OZ OUT OF THE SLV // //INVENTORY RESTS AT 432.493 MILLION OZ

JAN 19/WITH SILVER DOWN $0.11 TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 458,000 OZ OUT OF THE SLV // //INVENTORY RESTS AT 432.493 MILLION OZ

JAN 18/WITH SILVER UP $0.13 TODAY NO CHANGES IN SILVER INVENTORY AT THE SLV: // //INVENTORY RESTS AT 432.951 MILLION OZ

JAN 17/WITH SILVER DOWN $0.38 TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 779,000 OZ FROM THE SLV.: // //INVENTORY RESTS AT 433.500 MILLION OZ

JAN 16/WITH SILVER DOWN $0.08 TODAY NO CHANGES IN SILVER INVENTORY AT THE SLV: // //INVENTORY RESTS AT 433.500 MILLION OZ

JAN 12/WITH SILVER UP $0.62 TODAY NO CHANGES IN SILVER INVENTORY AT THE SLV: // //INVENTORY RESTS AT 433.500 MILLION OZ

JAN 11/WITH SILVER DOWN 34 CENTS TODAY NO CHANGES IN SILVER INVENTORY AT THE SLV: // //INVENTORY RESTS AT 433.912 MILLION OZ

JAN 10/WITH SILVER DOWN 3 CENTS TODAY SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 450,000 OZ FROM THE SLV// //INVENTORY RESTS AT 433.912 MILLION OZ

JAN 9/WITH SILVER DOWN 20 CENTS TODAY NO CHANGES IN SILVER INVENTORY AT THE SLV //INVENTORY RESTS AT 434.370 MILLION OZ

JAN 8/WITH SILVER DOWN 8 CENTS TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 1,602,000 OZ INTO THE SLV//:././/////INVENTORY RESTS AT 434.370 MILLION OZ

JAN 5/WITH SILVER UP 20 CENTS TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV A DEPOSIT OF 916,000 OZ INTO THE SLV//:././/////INVENTORY RESTS AT 435.972 MILLION OZ

JAN 4/WITH SILVER UP 5 CENTS TODAY NO CHANGES IN SILVER INVENTORY AT THE SLV/:././/////INVENTORY RESTS AT 435.056 MILLION OZ

JAN 3/WITH SILVER DOWN 78 CENTS TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV/: A WITHDRAWALOF 2.294 MILLION OZ OZ FROM THE SLV././/////INVENTORY RESTS AT 435.056 MILLION OZ

JAN 2/WITH SILVER DOWN 9 CENTS TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV/: A WITHDRAWALOF 915,000 OZ FORM THE SLV././/////INVENTORY RESTS AT 437.35 MILLION OZ

DEC 29/WITH SILVER DOWN 29 CENTS TODAY NO CHANGES IN SILVER INVENTORY AT THE SLV/: //////INVENTORY RESTS AT 438.265 MILLION OZ

DEC 28/WITH SILVER DOWN 25 CENTS TODAY NO CHANGES IN SILVER INVENTORY AT THE SLV/: //////INVENTORY RESTS AT 438.265 MILLION OZ

DEC 27/WITH SILVER UP 20 CENTS TODAY:HUGE CHANGES IN SILVER INVENTORY AT THE SLV/: A WITHDRAWAL OF 1.374 MILLION OZ FROM THE SLV//////INVENTORY RESTS AT 438.265 MILLION OZ

THIS IS THE 3RD STRAIGHT DAY THAT THE SLV HAS ENGAGED IN WITHDRAWALS

DEC 26/WITH SILVER DOWN 14 CENTS TODAY:HUGE CHANGES IN SILVER INVENTORY AT THE SLV/: A WITHDRAWAL OF 1.465 MILLION OZ FROM THE SLV//////INVENTORY RESTS AT 439.639 MILLION OZ

DEC 22/WITH SILVER UP 0 CENTS TODAY:HUGE CHANGES IN SILVER INVENTORY AT THE SLV/: A WITHDRAWAL OF 2.289 MILLION OZ FROM THE SLV//////INVENTORY RESTS AT 441.104 MILLION OZ

DEC 21/WITH SILVER DOWN 2 CENTS TODAY:NO CHANGES IN SILVER INVENTORY AT THE SLV/: NO CHANGES IN SILVER INVENTORY AT THE SLV//////INVENTORY RESTS AT 443.393 MILLION OZ

DEC 20/WITH SILVER UP 28 CENTS TODAY:NO CHANGES IN SILVER INVENTORY AT THE SLV/: NO CHANGES IN SILVER INVENTORY AT THE SLV//////INVENTORY RESTS AT 443.393 MILLION OZ

CLOSING INVENTORY 446.680 MILLION OZ//

PHYSICAL GOLD/SILVER COMMENTARIES

1:Peter Schiff/Mike Maharrey

Bonds Away: Rate-Cuts & Junk-Debt In 2024

FRIDAY, JAN 26, 2024 – 01:40 PM

After a delicate dance of interest rate increases, Jerome Powell has declared victory on inflation and says to expect looser monetary policy this year. But with junk bond spreads not widening nearly as much as one would expect during an era of economic tightening, you’ve got to wonder if money is still actually looser than the Fed’s last round of hikes would lead you to believe.

As Marc Faber pointed out late last year:

“If money was tight, the spread between junk bonds and Treasuries would be much wider. It hasn’t widened much…So, I think the monetary policies are still inflationary at the present time.”

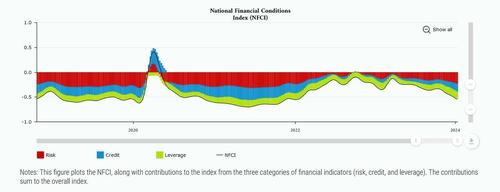

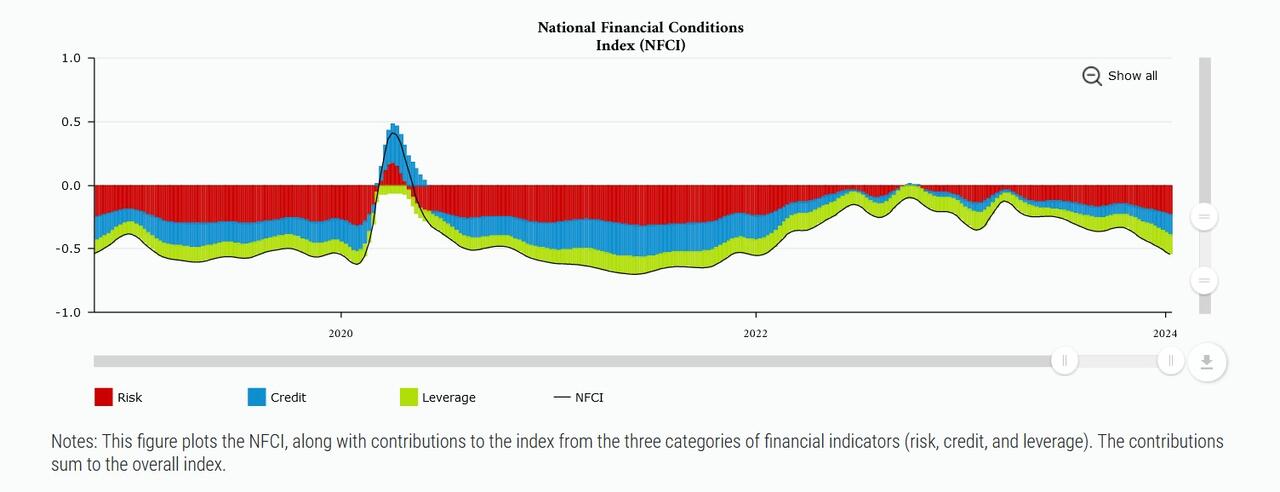

Indeed, the Chicago Fed’s current National Financial Conditions Index (NFCI) continues to confirm this, with numbers still in the negative range indicating relatively loose financial conditions as we start 2024:

And the Fed’s confidence in its mastery of an infinitely complex economy is, as usual, misplaced. But investors are responding to the rate cut news with a refreshed interest in junk debt as spreads remain relatively narrow. Reuters reported earlier this month:

“Junk bond spreads, or the premium investors charge over U.S. Treasuries for taking on the risk, have on average tightened 38 basis points since September to 343 basis points…”

There has been an unusual disconnect between spreads and dollar prices, as described recently by Lord Abbett’s Riz Hussain:

“Treasury yields typically have rallied (on factors such as a flight to the safety of U.S. government debt, expectations of Fed easing, etc.)…We’ve had just the opposite this time around. Specifically, given the worries around persistent inflation that have not vexed investors for many decades to the same extent, the correlation of U.S. Treasury bond prices and risk assets has flipped to positive.”

Bullish bond traders are now starting to bet on lower US Treasury yields in response to expected rate cuts in 2024. For junk bonds issued by companies with low credit ratings, a lower cost of borrowing could lend a sigh of relief by increasing the relative attractiveness of their low-rated corporate debt.

The question is whether or not investors will respond by being even more willing to shoulder the higher risk of junk bonds in pursuit of higher returns, compressing yield spread, or if they will step back in recognition of broader economic weaknesses and become risk-averse despite a lower interest rate environment.

Widening fiscal deficits, new rounds of money printing to finance a rapidly expanding Middle East war, and accelerating global de-dollarization are only a few of the dangerous economic trends shaping up for 2024.

A lower cost of borrowing often provides relief for companies that have been squeezed by higher interest rates, but if a collapsing dollar causes increased costs and a debt that’s harder to service, it could also contribute to a wave of defaults. This is particularly true for companies in more inflation-sensitive industries.

But higher inflation doesn’t necessarily mean more corporate defaults, especially as the use of leverage decreases. The question is whether or not other risks have sufficiently destabilized the broader system to cause an unraveling. Riz Hussain at Lord Abbett doesn’t think so:

“…we believe at least part of the resilience we have seen in high yield credit this year can be attributable to supportive fundamental factors that surface in a higher inflation and nominal growth environment.”

Hussain expects that resilience to continue, but also doesn’t expect inflation to worsen significantly in 2024 — a forecast I’m not nearly as confident about. If inflation starts to heat up enough that the Fed reverses course on cutting rates, companies with low credit ratings could see lowered demand for their debt. This seems unlikely, however, as the Fed has little choice but to start cutting rates now despite it being too little, too late to prevent a “hard landing” for the fragile economy.

But if inflation starts looking really bad, maybe the Fed will just look for rosier ways to present it. When the sum perception of economic well-being becomes so dependent on Central Bank data and FOMC announcements, there’s a natural incentive to make that data look as positive as possible. Gina Bolvin of Bolvin Wealth Management said as much in a recent CNBC article about declining Treasury yields, all without much hint of concern for the implications:

“I’ve never really seen a market, in a very long time, that hinges so much on economic data coming out…The market just clings to every single piece…And it keeps cheering it along.”

The trouble is, no matter what the Fed says or how accurate the data it presents is, economic reality always has a way of rearing its head as the chickens of monetary policy inevitably come home to roost. If we encounter a full-blown recession combined with runaway inflation, junk bonds could be some of the hardest-hit assets.

END

2) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

MATHEW PIEPENBURG

The US Is Living on Borrowed Time

Matthew Piepenburg

January 26, 2024

In late December, I published a final report on the themes of 2023 while looking ahead at their implications for the year to come.

I repeated my claim that debt markets and debt levels made the future of Fed policies, currency moves, rate markets and gold’s endgame fairly clear to see.

Of course, as facts change, opinions change as well.

But the facts are only worsening, which means my opinions in late 2023 are only growing stronger as we conclude the first month of 2024.

Then as now, the debt-soaked US is tilting ever more toward policies which will weaken its currency, wound its middleclass and reward its false idols (and false markets) with even greater desperation.

In particular, some recent facts below are emerging which further support my otherwise sad conviction that the American economy (not to be confused with its Fed-supported stock exchanges) is literally living on borrowed time.

The Latest Bits of Crazy from the CBO

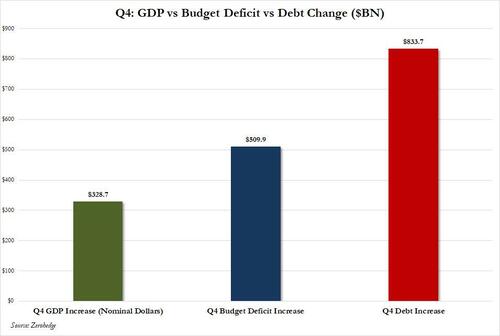

Almost a year ago to date, I was shaking my head and rubbing my eyes as the Congressional Budget Office (CBO) announced a staggering $422B Federal budget deficit for Q1 2023.

Now that’s a lot of borrowing in a short amount of time…

For some strange reason, this bothered me in early 2023, as I was still under this odd impression that debt, and hence deficits, actually mattered.

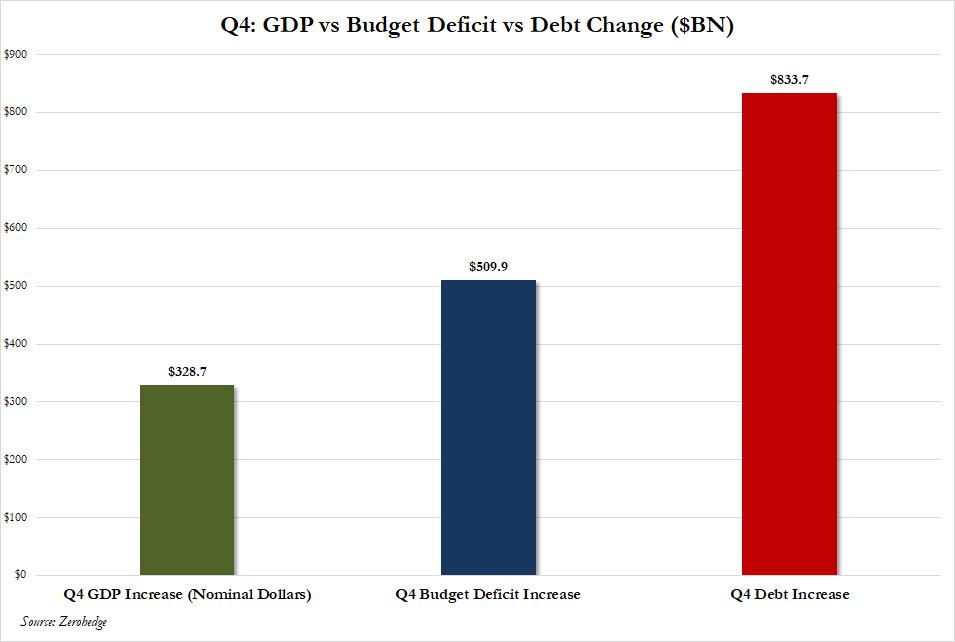

Fast forward to January 2024, and that same CBO has just announced a $509B Federal budget deficit for Q1 2024.

Folks, that adds up to annual deficit run rate of $2.2T.

Please: Re-read that last line again.

Do the Math: DC is Getting Even Dumber

In this 12-month interim, fiscal revenues did increase by about 8%, but outlays (i.e., expenses) for that same period rose by 12%, which is just a mathematical way of saying that either: 1) Uncle Sam is out of his mind in debt; or 2) that I am out of my mind in common sense.

But it seems I’m not the alone in saying out loud what no one DC can say to themselves, namely: The US is now in an open and obvious debt spiral.

Uncle Sam’s embarrassing bar tab of debt is now racing at a rate that far exceeds his GDP, pushing the deficit to GDP ratio toward 8% and higher–ratios we’ve never seen except during the GFC of 2008 and the “COVID” (i.e., hidden bond) crisis of 2020.

From Debt Spiral to Super QE

If recent memory serves me correctly, in both of those embarrassing years (and ratios), what followed was QE to the moon and the ongoing fantasy that every debt problem can be solved with trillions of fiat dollars mouse-clicked out of thin air.

And this time around will likely be no different, as I and others like Luke Gromen have been warning week after week, and month after month.

Such warnings, which NO ONE can time, are not merely bearish “opinions” and don’t require a crystal ball or sensational guessing.

They just require a calculator and a basic understanding of history.

Simple Math

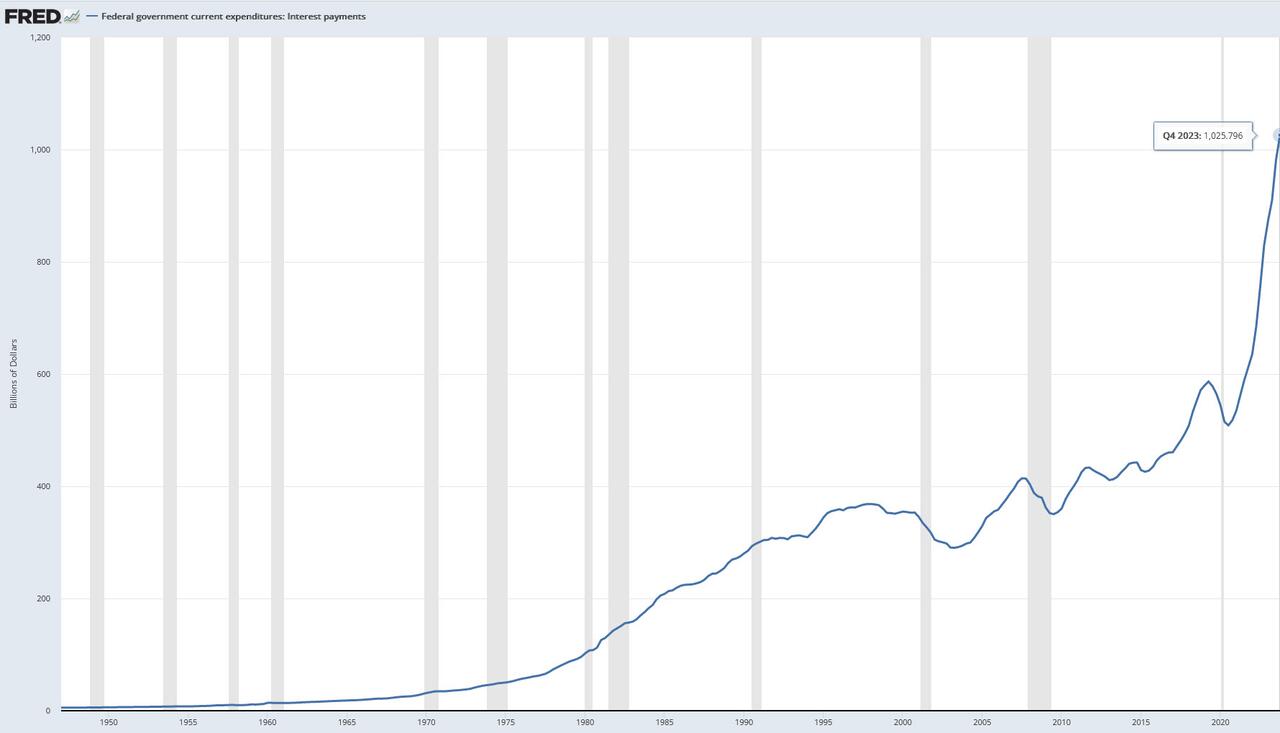

As to basic math, one can have their own opinions but not their own facts, and the facts (i.e., math) tell us that the current cost of servicing the aforementioned debt is 16% of Federal tax receipts.

Again: Please re-read that last line. It matters, because, well…debt destroys nations.

Nor am I alone in this sober understanding.

As the former head of European block trading at Goldman Sachs, Alex Harfouche, just warned, these sickening debt ratios mean the US economy’s ability to shoulder such debt is both “horrible” and “crippling.”

Which means we all know (or should know) what’s coming next.

The Patterns of the Foolish

As in 2008 and 2020, we can now see a pattern playing out in 2024, namely an inevitable shift from rate hikes and pauses toward rate cuts and the inevitable shift from QT to QE.

Why inevitable?

Because stupidity combined with a Will to Power that would make Nietzsche blush are the profile traits of nearly all math-ignorant but ego-savvy policy makers seeking re-election or a Nobel Prize in Economics (fiction?).

That is, and especially in an election year, policy makers will not cut spending but increase it in a desperate bid to bribe the gullible masses into a Pavlovian voting pattern based on generations of political over-promising and grotesque under-delivering.

This political inability to cut entitlement spending makes a US debt spiral (and hence QE to the moon) as foreseeable as the NY Yankees beating my high-school baseball team.

DC Cutting Rates Rather than Spending

Furthermore, since the DC children running our country into the ground won’t cut spending, the only thing they can (and will) cut is interest rates.

Why?

Because cutting rates not only takes pressure off Uncle Sam’s IOUs (USTs), but also eases the pain of those complicit S&P zombies staring down the barrel of over $740B in debt rollovers in 2024.

Main Street Screwed Again

Remember: The Fed serves TBTF banks and exchanges, not citizens and their realities.

Interest rate cuts + QE = a further debased USD and rising inflation (with a deflationary recession in the middle).

And this means the voters on Main Street are about to feel the darker side of DC’s real mandate: Covering their own A$$’es while keeping Wall Street on a respirator.

Meanwhile, the masses feel pain, but can’t quite see from where it’s coming, as the media, MMT hucksters and political Ken and Barbies keep telling them that deficits don’t matter.

Deficits Don’t Matter?

EEven worse, there are those sitting in private wealth management suites smugly reminding their clients that Japan is in much worse debt (see below) than Uncle Sam, and if Japan can muddle through, certainly the US has nothing to fear.

But as I recently reminded the attendees at the Vancouver Resource Investment Conference, Japan does not have twin deficits, a negative 65% Net International Investment Position nor an externally financed bond market.

In short: Japan aint America. But even if it were, it’s nothing of which to boast…

Whistling Past the Debt Graveyard with More Spending

Like Luke Gromen, I am of the sober and math-based view that unless the US cuts entitlement and defense spending by 40% (unthinkable in an election year and a world of beating [US?] war drums almost everywhere), such austerity is about as likely as an honest man in Congress…

Failing such needed cuts and sound budget honesty, policy makers will merely whistle past another year of multi-trillion deficit levels and pass the bill on to current and future generations while inflating their way out of debt with more of the debased money in your pockets.

As I’ve written before, this is no surprise. In fact, it was the plan all along, despite Powell’s efforts to pretend otherwise.

Keep It Simple: Powell Will Pivot

Debtors, including Uncle Sam, need inflation and need a debased currency.

They need negative real rates whereby inflation outpaces the yield on 10Y bonds.

Powell, of course, tried pushing real rates to a positive 2% to allegedly “fight inflation,” but, and as in 2018-19, the net result was that he simply broke nearly everything but the USD in the process.

In fact, Powell was merely raising rates and thinning the Fed balance sheet so that he’d have something (anything) to cut (rates) and fatten (balance sheet) when the recession that his higher-for-longer policies ushered in (and then denied) became too impossible to ignore.

Or stated more bluntly: His recent QT was a planned precursor to more QE, and his recent rate hikes were a planned precursor to more rate cuts.

Keep It Simple: A Future of Debased Currency

Thus, and long before hitting “target 2%,” Powell will once again throw in the towel in 2024 on rate hikes for the simple reason that Uncle Sam can’t afford them.

Or stated (and repeated) more simply, his “war on inflation,” waged in the last 2 years, will ultimately (and ironically) end in even greater inflation.

Ahhh the ironies. Or better yet: “The horror, the horror…”

History confirms this pattern in one debt-failed nation after the next.

In fact, and without exception, currencies are always sacrificed to save a broken regime. And folks, our regime is objectively broke(n).

Thus, for those who know the math (above), and the history of yesterday, preparing for tomorrow is simple.

Projected rate cuts (and the scent of more synthetic liquidity) can and (already have) sent inflated risk assets higher as the inherent purchasing power of the currency gets weaker.

Keep It Simple: Natural Gold vs. An Un-Natural Dollar

This simply means gold, though never marching in a straight line, will reach higher highs and lower lows for no other reason than paper currencies like the USD will get more debased.

And this is all because the issuance of unloved sovereign USTs will become greater and greater, as the opening data from the CBO in Q1 now makes factually clear.

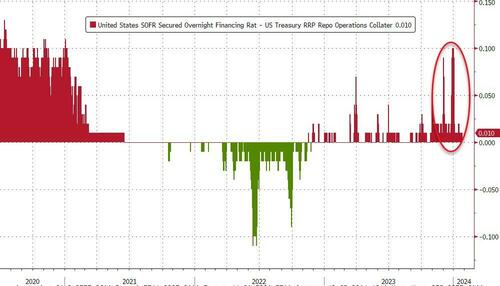

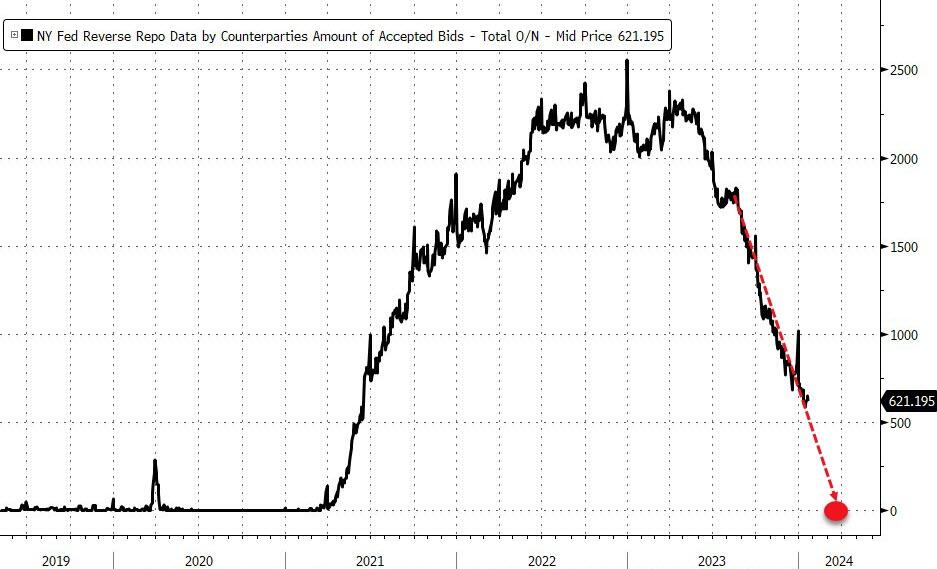

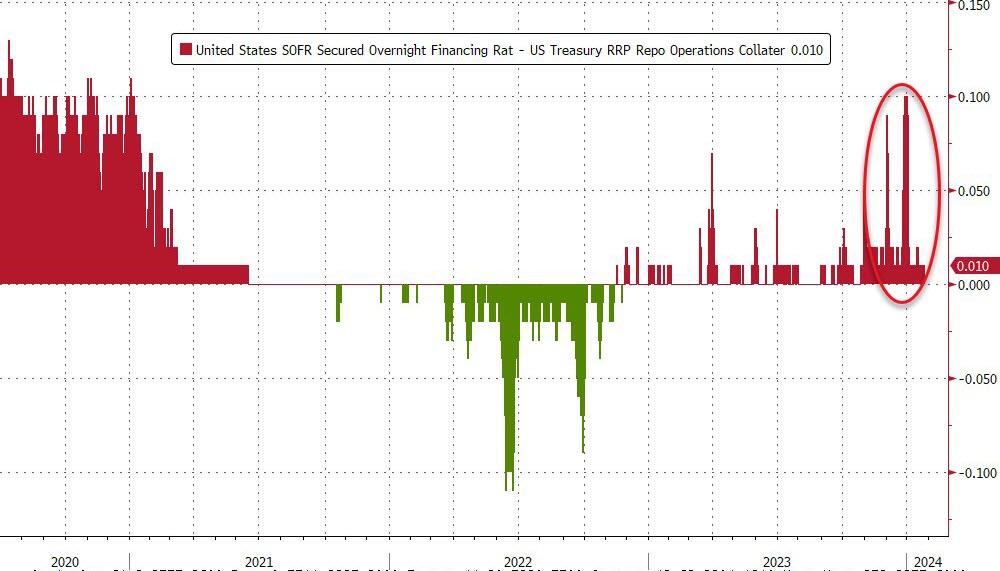

Soon the Fed will run out of tricks within Treasury General Account (Yellen’s game) and the Reverse Repo Markets to generate fake liquidity for those over-supplied and under-demanded USTs.

And this means Powell will once again crank out the money printers at the Eccles Building to “buy” those IOUs.

Fortunately, Powell has no machine in DC to produce physical gold, which means this natural precious metal of unlimited duration yet finite supply will rise, while USTs, an unnatural asset of finite duration yet infinite supply, will continue to sink./p>

It’s just that simple.

END

3. CHRIS POWELL//GATA GOLD COMMENTARIES:

END

end

4. OTHER GOLD/SILVER //COMMENTARIES//PODCASTS// live from the vault//Andrew Maguire

Russia & China’s dedollarisation tactics exposed

In this week’s episode of Live from the Vault, An

END

5 a. IMPORTANT COMMENTARIES ON COMMODITIES /

END

5 B GLOBAL COMMODITY ISSUES/FOOD IN GENERAL//FREIGHT

END

6.CRYPTOCURRENCY//DIGITAL CURRENCY// COMMENTARIES/

end

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS FRIDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED DOWN 7.1745

OFFSHORE YUAN: UP TO 7.1841

SHANGHAI CLOSED UP 4.11 PTS OR 0.14%

HANG SENG CLOSED DOWN 259.73 PTS OR 1.60%

2. Nikkei closed DOWN 485.40 PTS OR 1.34%

3. Europe stocks SO FAR: ALL GREEN

USA dollar INDEX UP TO 103.09 EURO RISES TO 1.0871 UP 25 BASIS PTS

3b Japan 10 YR bond yield:FALLS TO. +.702 Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 147.70/JAPANESE YEN NOW RISING AS WELL AS LONG TERM 10 YR. YIELDS RISING //EVENTUALLY THIS WILL BREAK THE JAPANESE CENTRAL BANK

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen UP CHINESE ONSHORE YUAN: DOWN// OFFSHORE: DOWN

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and UP FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund DOWN TO +2.2980***/Italian 10 Yr bond yield DOWN to 3.797** /SPAIN 10 YR BOND YIELD DOWN TO 3.184…**

3i Greek 10 year bond yield DOWN TO 3.2666

3j Gold at $2020.95 silver at: 22.88 1 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble DOWN 0 AND 74 /100 roubles/dollar; ROUBLE AT 89.63//

3m oil into the 76 dollar handle for WTI and 82 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 147,70// 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 0.702% STILL ON CENTRAL BANK (JAPAN) INTERVENTION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.8635 as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.9387 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.124 DOWN 1 BASIS PTS…

USA 30 YR BOND YIELD: 4.372 DOWN 1 BASIS PTS/

USA 2 YR BOND YIELD: 4.312 DOWN 0 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 30.31…(TURKEY SET TO BLOW UP FINANCIALLY)

GREAT BRITAIN/10 YEAR YIELD: DOWN 4 BASIS PTS AT 4.0225

end

2.a Overnight: Newsquawk and Zero hedge

Daily All Time High In Peril As Futures Dip After Intel Tumbles

FRIDAY, JAN 26, 2024 – 08:23 AM

After hitting a record high for 5 consecutive days, the daily tech-led meltup is in peril after Intel reported solid earnings but disappointed consensus with weak guidance, sending the stock tumbling 11%, and putting pressure on the Nasdaq which is down 0.2% as disappointing guidance from KLA also hit semiconductor stocks; AMD and Nvidia also retreated. S&P futures are also lower on the day, if well above session lows, while Europe is higher 1% to a 2 year-high led by luxury stocks after LVMH gave reassuring results. Asian stocks closed lower, snapping a six-day win streak, as tech shares stumbled and the China rally halted amid some skepticism over the impact of market rescue measures. 10Y yields inched modestly higher, rising 2bps to 4.12% after earlier falling below 4.10%. The US dollar dropped, also reversing an earlier move in the opposite direction. Oil dipped after surging on Thursday and bitcoin recovered recent losses, trading above $41000.

In premarket trading, Intel tumbled after providing a disappointing forecast, renewing doubts about a long-promised turnaround at the once-dominant chipmaker. Intel’s first-quarter projection for both sales and profit came in well short of Wall Street estimates, with analysts calling into question its ability to compete with competitors capitalizing on the AI boost. The results suggest Intel is struggling to defend its position in data center chips as demand weakens and it continues to lag behind chipmaking peers like Nvidia. Intel’s shares fell more than 12% in premarket trading, and if the decline in early trading holds, the company will be set for its biggest fall since October 2021. European semi-conductor stocks dropped after the update and after disappointing results from KLA. Here are some other notable premarket movers:

- Archer-Daniels-Midland shares fall 2.4% after UBS cut its recommendation on the food processing and commodities trading corporation’s stock to neutral from buy, citing lower growth and margins.

- KLA Corporation shares fall 7.5% after the semiconductor equipment maker provided guidance for third-quarter adjusted earnings per share and revenue that fell short of estimates at the midpoint.

- Snap shares rise 2.6% after Deutsche Bank upgrades its rating on the social media company to buy in a sector note on the online advertising outlook for the fourth quarter.

- T-Mobile shares decline 3.2% after the telecommunications company reported fourth-quarter earnings per share that missed estimates. Despite the praise for a strong quarter, analysts noted that share buybacks did not meet their expectations and that churn was greater than anticipated.

- Visa shares fall 3.2%, with analysts saying that while the payments firm’s fiscal first-quarter was robust, there may be some disappointment that volumes in January could be affected by adverse weather. They also cite guidance for higher opex as a potential concern, especially after the shares closed at a record on Thursday.

Despite Friday’s setback for the Nasdaq, optimism is running high on equities. Investors channeled $17.6 billion into global equity funds in the week through Jan. 24, BofA strategists said while US equity funds took in $5.3 billion. Gains are being fed by strong earnings and conviction the Federal Reserve and European Central Bank are gearing up to cut rates.

Vincent Juvyns, global market strategist at JPMorgan Asset Management, noted funds that started the year with big cash positions have been under pressure to buy stocks.

“Markets are now comfortable with the idea of a soft landing,” Juvyns said. “Central banks have confirmed that interest rate cuts would come rather later than was first expected, but that message has now been digested by the market.”

The view of a soft landing for the US economy was confirmed by Thursday’s gross domestic product data. Investors will get another key reading of US pricing pressures later Friday, with the release of the core personal consumption expenditures index, the Fed’s preferred gauge of underlying inflation.

“There was something for everyone in yesterday’s data. The soft landing scenario looks good for earnings, but it also looks like the Fed is succeeding in bringing inflation down, which has benefits for bonds too,” said Sarah Hewin, head of Europe and Americas research at Standard Chartered Bank.

The core PCE deflator — the Fed’s preferred inflation measure — likely grew at a subdued pace in December, according to Bloomberg Economics. “The personal income and outlays data may be a “Goldilocks” report — showing robust consumption and income even with inflation more than half way to the Fed’s target”

Europeans stocks are set to rise for a third day, while bonds in the region add to their post-ECB rally. The Stoxx 600 is up 1%, hitting the highest level in two years as luxury stocks rally after LVMH gave a reassuring set of results, bucking weakness in US equity futures and Asian markets. LVMH shares jumped 9.1%, the most since March 2022, adding just shy of €29 billion ($31.5 billion) of extra market value. LVMH’s fourth-quarter sales were boosted by high-end shoppers splashing out on its Dior fashions, Louis Vuitton handbags and Moët & Chandon Champagne. The strong performance follows a similarly upbeat report from Cartier owner Richemont, suggesting the strongest brands are weathering the broader slowdown in the luxury sector. The results come as LVMH’s French billionaire owner Bernard Arnault plans to appoint two of his sons to the board of the luxury conglomerate, underscoring the family’s firm grip on the company. Here are the other notable premarket movers:

- Shares in Sartorius surge as much as 12%, the most since March 2021, after the German laboratory equipment supplier reported a book-to-bill ratio in the fourth quarter that impressed analysts. The outlook for the year is also positive, according to those covering the stock.

- Shares in Remy gain as much as 17% after the cognac maker reported third-quarter results. Both Morgan Stanley and Jefferies see the results providing some relief, while Citi says the absence of new negatives on the FY25 outlook should enable investors to start looking forward.

- Shares in Salvatore Ferragamo rise as much as 5.9%, reversing earlier declines, as analysts said results from the Italian luxury accessories maker were slightly above expectations, though noted that this was driven by the firm’s lower quality wholesale channel. Overall, luxury stocks got a boost from a resilient set of results from LVMH.

- Shares in Lonza soar as much as 15%, their steepest gain ever, after the Swiss maker of drug ingredients named former Unilever CFO Jean-Marc Huet as its new chairman, and posted a confirmed outlook for 2024-2028, which analysts said was welcome.

- Shares in JCDecaux rise as much as 8.9% after the outdoor advertising firm reported stronger-than-expected organic sales growth during the fourth quarter. Growth was driven by digital revenue during the year-end period and a recovery of transport activities, the company said.

- Shares in Merck KGaA advance as much as 6.8%, the most since July 2022. Results from ASML, TSMC, Lonza, and Sartorius provide a reassuring readacross for the German pharmaceutical company, according to Citi.

- Shares in Europe Chip Stocks fall across the board after once-dominant chipmaker Intel gave a first-quarter forecast that was much weaker than expected.

- Shares in Volvo slide as much as 5.8%, before paring the decline, after the Swedish truckmaker missed expectations on quarterly order intake. Guidance for a slower 2024 also weighs on sentiment.

- Shares in Bayer fall as much as 2.9% after being downgraded to underperform from neutral at Bank of America. The broker advises caution on the German conglomerate due to continued overhang from litigation, a cut dividend and an “unclear path” to deleverage.

Earlier in the session, Chinese and Hong Kong shares dropped after the biggest three-day rally since 2022, shrugging off fresh stimulus signals from Beijing. However, Bank of America highlighted a record $12.1 billion of inflow into Chinese equity funds, a possible sign investors are tiptoeing back into the beaten-up market. The MSCI Asia Pacific Index fell as much as 0.5%, with Toyota, Alibaba and Tencent among the biggest drags on the benchmark. Chip and PC stocks fell after a disappointing outlook from Intel. Still, the regional benchmark was poised for a weekly advance of 1.5%, its best so far this year. Chinese equities retreated after notching their biggest three-day advance since 2022 on bets that the latest efforts from Beijing will support the economy and backstop markets. Investors are now trying to gauge how long those gains might be sustained.

In FX, the Bloomberg Dollar Spot Index falls 0.2% and is flat for the week while the Swiss franc tops the G-10 FX pile, rising 0.4% versus the greenback. Treasury 10-year yields dropped two basis points to 4.10%, extending Thursday’s six-basis-point decline. “While additional short-term USD gains are possible as the market reprices Fed expectations, most of the technical backdrops favor using such rallies as a selling opportunity,” George Davis, chief technical strategist at RBC Capital Markets, writes in a note

In rates, treasuries are mixed with the yield curve flatter as US trading day begins, unwinding a portion of Thursday’s sharp steepening in 2s10s and 5s30s spreads ahead of a key inflation reading for December. US long-end yields are flat; 10-year yields around 4.12% with bunds outperforming and gilts lagging slightly. Front-end underperformance flattens 2s10s by ~2bp, 5s30s by ~1bp on the day. Dollar issuance slate empty so far; five names priced $4.65b Thursday. German bunds extended a rally that was sparked on Thursday, when President Christine Lagarde’s gave a muted affirmation that the ECB may begin lowering interest rates from around mid-2024. Bunds rose despite a generally hawkish tone from ECB policymakers – Governing Council member Boris Vujcic argued they did not turn dovish on Thursday; the German front-end extends outperformance since Wednesday’s ECB meeting.

In commodities, oil prices decline, with WTI falling 1% to trade near $76.55. Spot gold rises 0.1%.

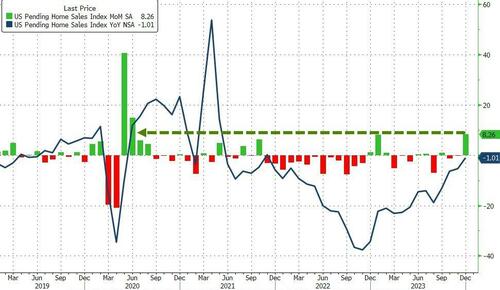

To the day ahead now, and data releases from the US include the PCE inflation data for December, along with personal income and personal spending, and pending home sales. Meanwhile in the Euro Area, we’ll get the M3 money supply for December. From central banks, we’ll hear from the ECB’s Panetta, Kazaks and Vujcic. Finally, earnings releases include American Express.

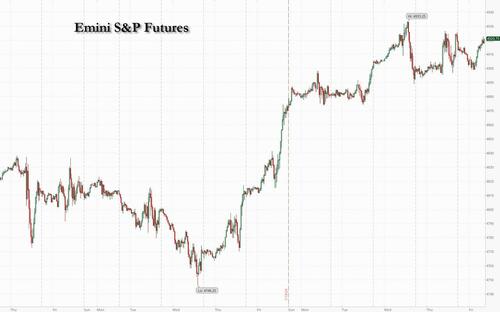

Market Snapshot

- S&P 500 futures down 0.3% to 4,907.75

- MXAP down 0.8% to 165.16

- STOXX Europe 600 up 0.7% to 482.02

- German 10Y yield down 2.5 bps at 2.26%

- Euro little changed at $1.0843

- MXAPJ down 0.4% to 506.20

- Nikkei down 1.3% to 35,751.07

- Topix down 1.4% to 2,497.65

- Hang Seng Index down 1.6% to 15,952.23

- Shanghai Composite up 0.1% to 2,910.22

- Sensex down 0.5% to 70,700.67

- Australia S&P/ASX 200 up 0.5% to 7,555.36

- Kospi up 0.3% to 2,478.56

- Brent Futures down 0.7% to $81.85/bbl

- Gold spot down 0.0% to $2,020.06

- US Dollar Index little changed at 103.50

Top Overnight News

- European stocks rose on Friday, bucking weakness in US equity futures and in Asian markets, as an update from the world’s largest luxury retailer showed that spending among the wealthiest consumers remains resilient.

- China’s central bank unveiled broad plans to guide money into sectors of national importance to boost the faltering economy this year, after making an unusual reserve requirement ratio announcement.

- Vladimir Putin is testing the waters on whether the US is ready to engage in talks for ending Russia’s war in Ukraine.

- European Central Bank Governing Council member Gediminas Simkus said that while he’s less optimistic than markets on the prospect of an April reduction in interest rates, he’s open-minded and will look at the data that arrives in the meantime.

A more detailed look at global markets courtesy of Newsquawk

Asia=Pac stocks failed to sustain the broad positive momentum from Wall St with the region mostly lower in quietened conditions amid a lack of fresh drivers and as markets in Australia and India were closed for holiday. Nikkei 225 was pressured and retreated beneath the 36,000 level despite softer-than-expected Tokyo inflation data which showed the slowest pace of core inflation in Japan’s capital area since March 2022. Hang Seng and Shanghai Comp were choppy as the effects of recent Chinese support measures waned.

Top Asian News

- Chinese Commerce Minister said China’s trade faces a more complex and severe external situation, while the rise of trade protectionism, intensification of geopolitical conflicts and the risk of spillover has increased significantly, according to Reuters.

- BoJ Minutes from the December 18th-19th meeting stated that members agreed they must patiently maintain easy policy and must confirm a positive wage-inflation cycle to consider ending negative rates and YCC. Furthermore, a few members said the decision on whether a positive wage-inflation cycle is in place must be made comprehensively and not by looking at particular data, while a few members said they don’t see the risk of the BoJ being behind the curve and can wait for developments in the spring annual wage talks.Members also agreed they must continue deepening the debate on exit timing and the appropriate pace of hiking rates after the end of negative rates.

European bourses are in the green, Stoxx600 (+0.6%); with the CAC 40 (+1.7%) outperforming alongside significant strength in the Luxury sector, post-LVMH earnings coupled with Barclays upgrading the sector to Overweight. European sectors hold a strong positive tilt; Consumer Products & Services sits highest after strong LVMH earnings, with Food Beverage and Tobacco also propped up post-Remy Cointreau results. Tech lags after weaker Intel guidance. US equity futures are on a mixed footing, with the NQ (-0.5%) significantly underperforming as Tech drags the index lower post-Intel earnings after-hours; Co. shares are seen lower by 11% in the pre-market after guiding Q1 revenue to be significantly lower than expectations.

Top European News

- ECB Survey of Professional Forecasters: 2024 inflation seen at 2.4% vs. prev. view of 2.7%. 2025 2.0% vs. prev. view of 2.1%. GDP: 2024 0.6% vs. prev. view of 0.9%. 2025 1.3% vs. prev. view of 1.5%. Core inflation: 2024 2.6% vs. prev. view of 2.9%.

- ECB Bulletin: Contacts painted a largely unchanged picture of activity stagnating or contracting slightly in the fourth quarter of 2023, with little or no pick-up expected in the first quarter of 2024. Wage growth is expected to ease somewhat this year.

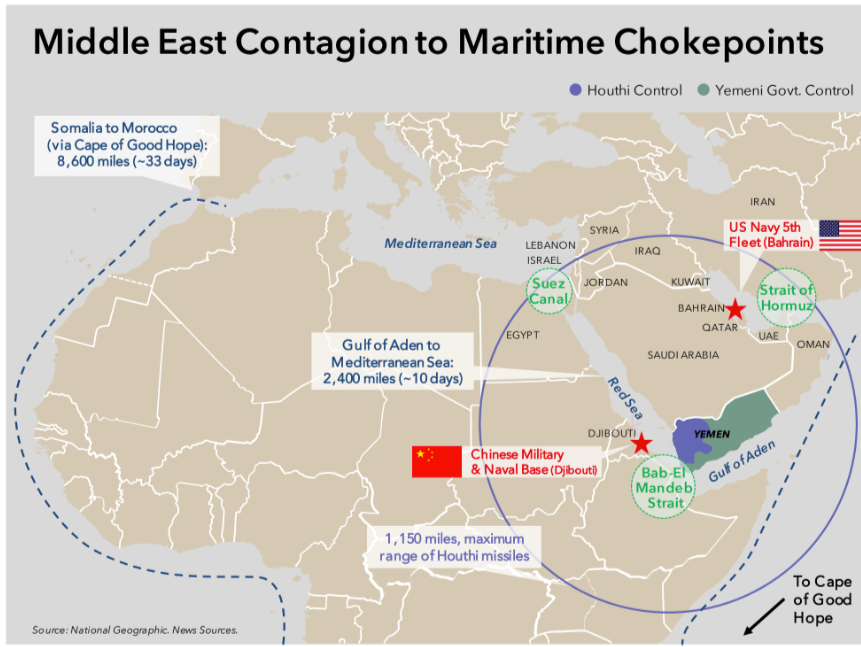

- Maersk (MAERSKB DC) MECL vessels will now also be avoiding the Red Sea region

ECB speak

- ECB’s Kazaks says the ECB is data, not date, dependent, via Bloomberg TV; sees some softening in the labour market. Technical recession is a possibility.

- ECB’s Muller says it is still too soon to talk about rate cuts. Too little confidence now that inflation has been defeated.

- ECB’s Vujcic says there was no dovish tilt at the January ECB meeting; we are data dependent not date dependent, via Bloomberg. We need patience and must have sufficient data; need reassurance that inflation is headed for 2%.

- ECB’s Simkus says does not expect a rate cut in March. The further into 2024, the more likely a rate cut becomes; expectations increases exponentially not linearly.

Earnings

- Intel Corp (INTC) – Q4 2023 (USD): EPS 0.63 (exp. 0.45), Revenue 15.4bln (exp. 15.16bln). Q1 adj. EPS view 0.13 (exp. 0.34).Q1 adj. revenue view 12.2-13.2bln (exp. 14.25bln). REVENUE BREAKDOWN: Client Computing 8.84bln (exp. 8.42bln). Datacenter & AI 4bln (exp. 4.08bln). Network & Edge 1.47bln (exp. 1.55bln). Mobileye 637mln (exp. 627.2mln). Intel Foundry Services 291mln (exp. 342.5mln). KEY METRICS: Adj. operating income 2.58bln (exp. 2.1bln). Adj. operating margin 16.7% (exp. 13.9%). Adj. gross margin 48.8% (exp. 46.5%). R&D expenses 3.99bln (exp. 3.9bln). COMMENTARY: On track to meet the goal of five nodes in four years. (Newswires) Shares -11.3% pre-market

- T-Mobile US Inc (TMUS) – Q4 2023 (USD): EPS 1.67 (exp. 1.90), Revenue 20.48bln (exp. 19.64bln). (Newswires) Shares -2.8% pre-market

- Visa Inc (V) – Q1 2024 (USD): Adj. EPS 2.41 (exp. 2.34), Revenue 8.6bln (exp. 8.54bln). Guides Q2 net revenue growth to upper mid-to-high single-digit (exp. +8.67%). Q2 EPS growth high teens (exp. +12.15%). KEY METRICS: Payments volume at constant currency +8% (exp +8.03%). Cross-border volumes at constant currency +16% (exp. +14.9%). Total Visa processed transactions 57.5bln (exp. 57.77bln). Shares -3.1% pre-market

- LVMH (MC FP) – FY 2023 (EUR): Revenue 86.153bln (exp. 85.626bln); FCF 8.104bln, -20%; Net Income 15.174bln, +8%; Is confident in continued growth in 2024. Q4 RESULTS: Revenue 23.95bln (exp. 23.72bln). Organic revenue +10% (exp. +8.17%). Fashion & Leather Goods organic sales +9% (exp. +9.14%). Wines & Spirits organic sales +4% (exp. -7.47%). Perfumes & Cosmetics organic sales +10% (exp. +9.41%). Watches & Jewelry organic sales +3% (exp. +2.93%). Selective Retailing organic sales +21% (exp. +14%). FY23 OPERATING INCOME: Recurring 22.80B (exp. 22.46bln). Fashion & Leather Goods 16.84bln (exp. 16.9bln). Wines & Spirits 2.11bln (exp. 1.85bln). Perfume & Cosmetics 713mln (exp. 769mln). Watches & Jewelry 2.16bln (exp. 2.02bln). Selective Retailing 1.39bln (exp. 1.51bln). FY23 REVENUE BREAKDOWN: Revenue 86.15bln (exp. 85.88bln). Fashion & Leather Goods 42.17bln (exp. 42.47bln). Wines & Spirits 6.60bln (exp. 6.46bln). Perfume & Cosmetics 8.27bln (exp. 8.3bln). Watches & Jewelry 10.90bln (exp. 10.97bln). Selective Retailing 17.89bln (exp. 17.61bln). Dividend per share 13 (exp. 13.59). Net income 15.17bln (exp. 15.67bln). CEO Arnault does not intend to leave in the near or medium term. CFO says sales trends with Chinese clientele remained good; doesn’t expect Chinese groups to return soon to Europe but managing to make ‘significant’ business with wealthy Chinese in Europe. CEO says Co. is definitely not considering an asset spin-off, it would be a mistake. Co. not planning additional price hikes this year. (LVMH) Co. holds a 6.5% weighting in the Eurostoxx50; 12% in the CAC40; fifth largest in the Stoxx600 Shares +11.5% in European trade

- Remy Cointreau (RCO FP) – Q3 (EUR): Revenue 319.9mln (exp. 320.7mln), Notes major destocking in China ahead of Chinese New Year. Cooperating with the Chinese authorities in anti-dumping investigation. Cuts FY23/24 Organic Revenue guidance to “lower end” -20% to -15% (prev. guidance -20% to -15%). Cognac +31.4% Y/Y, Liqueurs +1.5%, Partner Brands -7.3% Y/Y, Group Brands -22.9% Y/Y. (Newswires) Shares +15.2% in European trade

- Sartorius (SRT GY) – FY23 (EUR): Net 339mln (exp. 655mln Y/Y), EBITDA 963mln (exp. 961mln), Revenue 3.4bln (exp. 3.42bln), Orden intake 3.07bln, -21.5% Y/Y. Guides FY24 Revenue in the “mid to high single digit % range”. Expects profitable growth in 2024. (Newswires) Shares +8.4% in European trade

FX

- DXY is around flat, though initially picked up in the European morning to 103.73 before fading the move in quiet trade as markets await US PCE data; currently holds below the 103.50 mark.

- EUR is largely moving at the whim of the USD and as ECB speakers push back on talk of rate cuts; still some way off yesterday’s high of 1.0901.

- USD/JPY has continued to tick higher but the next move will likely come via Fed vs. BoJ divergence/convergence plays with PCE due later today and FOMC next week; currently holds around flat at 147.70.

- NZD suffering vs. the USD to a greater extent than AUD which is possibly being buoyed by sentiment around China post-RRR cut. AUD/NZD looking to test 1.08 to the upside as NZD/USD slips below 0.61.

- PBoC set USD/CNY mid-point at 7.1074 vs exp. 7.1733 (prev. 7.1044).

Fixed Income

- USTs are holding in the green, but only modestly so, with focus entirely on US PCE for December; USTs marginally bull-flattening into this.

- Bunds are contained around the top-end of Thursday’s parameters, contracts printed an incremental WTD high of 135.02 this morning, before gradually waning.

- Gilt action has been in-fitting with EGBs, though did not print a fresh WTD peak on the open with the 98.78 current high markedly shy of Monday’s 99.45 best, resistance thereafter limited until 100.00.

Coommodities

- Crude benchmarks are pulling back marginally, with specifics light and the complex thus far largely unaffected by USD action; Brent futures are back below USD 82.00/bbl.

- Spot gold is unchanged, in a narrow USD 2018.34-2024.22/oz bound with specifics light and the yellow metal thus far also unaffected by the USD; XAU holding just shy of USD 2025/oz; base metals are a touch softer echoing the tone of US equity futures with overall specifics light.

- US is pausing the pending decisions of new LNG export projects in order to review economic and environmental impacts; Pause comes with exceptions for unanticipated and immediate national security emergencies.

Geopolitics: Middle East

- Israeli war council discussed a possible exchange deal with Hamas, according to Sky News Arabia.

- Hamas said if the ICJ issues a ruling for a ceasefire, Hamas will abide by it if Israel reciprocates, while Hamas will release all Israeli hostages in Gaza if Israel releases all Palestinian prisoners.

- American weapons arrived in Israel including dozens of F-35 and F-15 fighters and Apache helicopters, according to Al Jazeera.

- US National Security Adviser Sullivan is to meet with Chinese Foreign Minister Wang Yi for talks on Houthi attacks in the Red Sea, according to WSJ. It was later reported that the White House confirmed National Security Adviser Sullivan will travel to Bangkok this week to meet with Thailand’s PM and will also meet with Chinese Foreign Minister Wang, according to Reuters.

- Chinese officials asked their Iranian counterparts to help rein in attacks on ships in the Red Sea by the Iran-backed Houthis, or risk harming business relations with Beijing, according to Iranian sources and a diplomat familiar with the matter cited by Reuters.

- US and Iraq are to shift to bilateral military relations and US officials will stay in Iraq to defeat Islamic State, according to Bloomberg.

- US President Biden last week pressed Israeli Prime Minister Benjamin Netanyahu to scale down the Israeli military operation in Gaza, two U.S. officials told Axios.

Geopolitics: Other

- Kremlin denies Bloomberg reports that Putin is “putting our feelers” to the the US over terms for ending the Ukraine war.