FEB 13/BLOG FOR TUESDAY//GOLD CLOSED DOWN $20.15 TO $1994.75/SILVER WAS DOWN 60 CENTS TO $22.10//PLATINUM WAS DOWN $18.65 TO $874.45 WHILE PALLADIUM WAS DOWN $29.45 TO $866.90//RAID TODAY ORCHESTRATED BY OUR BANKING CROOKS AS THE FED IS TRYING TO BUY BACK ITS 117 TONNES OF GOLD BORROWED FROM THE BIS//CPI REPORT HOT AND VERY INFLATIONARY//ISRAEL VS HAMAS//ISRAEL VS HEZBOLLAH//HOUTHIS HITS AN IRANIAN SHIP//COVID UPDATES//VACCINE INJURIES//DR PAUL ALEXANDER//SLAY NEWS ETC/EVOL NEWS//NEWS ADDICTS//CRE’s AND REGIONAL BANKS READY TO IMPLODE ON HIGHER RATES//SWAMP STORIES ALONG WITH THE BIDEN MESS //KING NEWS REPORTS//

this week is China’s golden week so physical demand will be slow. It will dramatically pick up starting this Friday.

Bitcoin morning price:, 49,951 UP 179 DOLLARS

Bitcoin: afternoon price: $49,212 DOWN 560 dollars

Platinum price closing $874.45 DOWN $18.65

Palladium price; $861.90 DOWN $29.45

END

SHANGHAI GOLD PREMIUM 58 DOLLARS/COMEX GOLD

SHANGHAI GOLD (USD) FUTURES – QUOTES

Beginning Monday, April 1, 2024, CME Group settlement data will no longer be accessible through ftp.cmegroup.com and will have a delayed publication time of 12:00 a.m. CT on all cmegroup.com web pages. Learn about alternate ways to access the data in our FAQ.

363 H WELLS FARGO SEC 7 657 C MORGAN STANLEY 1 661 C JP MORGAN 17 737 C ADVANTAGE 3 880 H CITIGROUP 10 905 C ADM 2

TOTAL: 20 20 MONTH TO DATE: 16,527

JPMorgan stopped 0/20 contracts.

FOR FEB.:

GOLD: NUMBER OF NOTICES FILED FOR FEB/2024. CONTRACT: 20 NOTICES FOR 2000 OZ or 0.0622 TNNES

total notices so far: 16,527 contracts for 1,652,700 Oz (51.390 tonnes)

FOR FEBRUARY:

SILVER NOTICES 0 NOTICE(S) FILED FOR nil OZ/

total number of notices filed so far this month : 1066 for 5,330,000 oz

XXXXXXXXXXXXXXXXXX

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

BOTH GLD AND SLV ARE FRAUDULENT VEHICLES//THEY ARE NOW RAIDING GLD AND SLV FOR PHYSICAL

GLD

WITH GOLD DOWN $20.15//CROOKS

INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD/ : NO CHANGES IN GOLD INVENTORY AT THE GLD:

INVENTORY RESTS AT 841.92 TONNES

SLV//

WITH NO SILVER AROUND AND SILVER DOWN 60 CENTS AT THE SLV//

SMALL CHANGES IN SILVER INVENTORY AT THE SLV AGAIN: A WITHDRAWAL OF 0.504 MILLION OZ OUT OF THE SLV

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV.

CLOSING INVENTORY: 437.615 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A SMALL SIZED 240 CONTRACTS TO 146,762 AND FURTHER FROM THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THIS FAIR SIZED GAIN IN COMEX OI WAS ACCOMPLISHED DESPITE OUR GAIN OF $0.14 IN SILVER PRICING AT THE COMEX ON MONDAY. WE HAD ZERO LONG LIQUIDATION AT THE COMEX SESSION AND LITTLE SHORT COVERING AS THE OPEN INTEREST FELL SLIGHTLY. WE HAD A MEGA HUMONGOUS 3707 T.A.S ISSUANCE AND THESE WILL BE USED FOR MANIPULATION LATER THIS MONTH/AS WELL AS TODAY. PLEASE NOTE THAT THE CROOKS NEED A HIGHER SILVER T.A.S. TO CARRY ON THEIR CROOKED MANIPULATION.

CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON MONDAY NIGHT: 3707 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS. IT THUS LOOKS LIKE THE FED (GOV’T) IS BEHIND ALL OF THESE TRADES.

WE HAVE NOW SET ANOTHER RECORD LOW AT 114,102 CONTRACTS ///JULY 3.2023// OUR BANKERS WITH THE HELP OF SPECULATORS AND HIGH FREQUENCY TRADERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.14), AND WERE SUCCESSFUL IN KNOCKING SOME MINOR SILVER LONGS AS WE HAD A TINY SIZED GAIN OF 10 CONTRACTS ON OUR TWO EXCHANGES.

WE MUST HAVE HAD:

A FAIR SIZED 250 ISSUANCE OF EXCHANGE FOR PHYSICALS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 3.535 MILLION OZ (FIRST DAY NOTICE) ACCOMPANYING A STRANGE 89 CONTRACT ISSUANCE FOR EX. FOR RISK FOR 445,000 OZ ON FIRST DAY NOTICE/ FOLLOWED BY TODAY’S SMALL 25,000 OZ E.F.P. JUMP TO LONDON//NEW TOTAL; 6.97 MILLION OZ

//NEW STANDING FOR SILVER IS THUS 6.97 MILLION OZ

/ SMALL SIZED COMEX OI LOSS/FAIR SIZED EFP ISSUANCE/ VI) HUMONGOUS SIZED NUMBER OF T.A.S. CONTRACT ISSUANCE 3707 CONTRACTS)/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL -REMOVED A HUGE 530 CONTRACTS //

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS FEB. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF FEB

TOTAL CONTRACTS for 9 days, total 4410 contracts: OR 22.050 MILLION OZ (490 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 20.050 MILLION OZ

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH 2022: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 118.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 85.745 MILLION OZ (SMALLER THAN LAST MONTH)

AUGUST: 171.43 MILLION OZ (THIS MONTH IS GOING TO BE HUGE //2ND HIGHEST ON RECORD

SEPT: 72.705 MILLION OZ (SMALLER THIS MONTH)

OCT: 97.455 MILLION OZ

NOV. 50.050 MILLION OZ

DEC. 66.140 MILLION OZ//

TOTAL 2023: 1,104.10 MILLION OZ/

JAN ’24 : 78.655 MILLION OZ//

FEB /2024 : 22.0500 MILLION OZ.

RESULT: WE HAD A SMALL SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 240CONTRACTS DESPITE OUR GAININ PRICE OF SILVER PRICING AT THE COMEX//MONDAY.,. THE CME NOTIFIED US THAT WE HAD A FAIR EFP ISSUANCE CONTRACTS: 250 ISSUED FOR MARCH AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS. WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR FEB. OF 3.535 MILLION OZ ACCOMPANIED BY FIRST DAY NOTICE OF 445,000 OZ EX. FOR RISK FOLLOWED BY TODAY’S 25,000 OZ E.F.P. JUMP TO LONDON //NEW TOTAL 6.97 MILLION OZ

NEW STANDING 6.97 MILLION OZ /// WE HAVE A STRONG GAIN OF 540 OI CONTRACTS ON THE TWO EXCHANGES WITH THE GAIN IN PRICE. THE TOTAL OF TAS INITIATED CONTRACTS TODAY: A HUMONGOUS SIZED 3707 CONTRACTS//HUGE FRONT END OF THE TAS CONTRACTS WERE LIQUIDATED DURING THE MONDAY COMEX SESSION/// WITH SOME SHORT COVERING FROM OUR SPEC SHORTS (OPEN INTEREST FELL) . THE NEW TAS ISSUANCE MONDAY NIGHT (3707) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE//PROBABLY TODAY., .

WE HAD 0 NOTICE(S) FILED TODAY FOR nil OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A SMALL SIZED 309 CONTRACTS TO 417,298 AND FURTHER FROM THE RECORD (SET JAN 24/2020) AT 799,733 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: – REMOVED 85 CONTRACTS

WE HAD A SMALL SIZED DECREASE IN COMEX OI ( 224 CONTRACTS) WITH OUR $4.80 LOSS IN PRICE//MONDAY. WE ALSO HAD A RATHER LARGE INITIAL STANDING IN GOLD TONNAGE FOR FEB. AT 49.773 TONNES ON FIRST DAY NOTICE ACCOMPANIED BY FIRST DAY NOTICE : 55,400 OZ EX. FOR RISK //THUS INITIAL STANDING FOR FEB: 51.494 TONNES FOLLOWED BY TODAY’S 800 OZ QUEUE JUMP //NEW TOTAL OF GOLD STANDING: 54.273 TONNES // ALL OF THIS HAPPENED WITH OUR $4,80 LOSS IN PRICE WITH RESPECT TO MONDAY’S TRADING. WE HAD A FAIR SIZED GAIN OF 1947 OI CONTRACTS (6.055) PAPER TONNES) ON OUR TWO EXCHANGES.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 2256CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 417,298

IN ESSENCE WE HAVE A FAIR SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 1947 CONTRACTS WITH 309 CONTRACTS DECREASED AT THE COMEX// AND A FAIR SIZED 2256 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 1947 CONTRACTS.. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): A STRONG SIZED 2249 CONTRACTS.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (2256CONTRACTS) ACCOMPANYING THE SMALL SIZED LOSS IN COMEX OI (309) //TOTAL GAIN FOR OUR THE TWO EXCHANGES: 1947 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR FORMER FORMAT OF BANKERS GOING LONG AND SPECULATORS GOING SHORT ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR FEB. AT 49.773 TONNES PLUS FIRST DAY NOTICE OF 1.723 TONNE OZ EX. FOR RISK FOLLOWED BY TODAY’S 9000 OZ QUEUE JUMP //NEW STANDING 54.548 TONNES. / 3) ZERO LONG LIQUIDATION // 4) SMALL SIZED COMEX OPEN INTEREST LOSS/ 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER///6: GOOD T.A.S. ISSUANCE: 2249CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023-2024 INCLUDING TODAY

FEB.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF FEB. :

TOTAL EFP CONTRACTS ISSUED: 30,739 CONTRACTS OR 3,073,900OZ OR 95.611 TONNES IN 9TRADING DAY(S) AND THUS AVERAGING: 3560 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 9TRADING DAY(S) IN TONNES 95.611 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2022, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 95.611/3550 x 100% TONNES 2.69% OF GLOBAL ANNUAL PRODUCTION

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH/2022: 409.30 TONNES //FINAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 151.69 TONNES (WEAKER THAN LAST MONTH)

AUGUST: 195.28 TONNES (A STRONGER MONTH)//FINAL

SEPT: 254.709 TONNES (WILL BE LARGER THAN LAST MONTH AND A STRONG MONTH)

OCT. 248.09 TONNES. LIKE SILVER, THIS MONTH IS GOING TO BE A STRONG E.F.P. ISSUANCE.

NOV. 239.16 TONNES//WILL BE STRONG THIS MONTH,

DEC. 213.704 TONNES. A STRONG MONTH//

TOTAL FOR YEAR 2023: 2,569.57 TONNES VS 2578 TONNES LAST YEAR

JAN ’24: 291.76 TONNES (WILL BE MUCH GREATER THAN LAST MONTH.//3RD HIGHEST EVER RECORDED EX FOR PHYSICAL)

FEB’24: 95.611 TONNES (SHOULD BE A WEAKER ISSUANCE MONTH)

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF FEB. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (FEB), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER FELL BY A SMALL SIZED 240CONTRACTS OI TO 146,762 AND FURTHER FROM THE COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 250 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MARCH 250 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 250 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 240 CONTRACTS AND ADD TO THE 250 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A STRONG GAIN OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 540CONTRACTS

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTAL 0.05 MILLION OZ

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS//

TUESDAY MORNING/MONDAY NIGHT

SHANGHAI CLOSED XXX //Hang Seng CLOSED XXX /The Nikkei CLOSED UP 1066.55 PTS OR 2.89% //Australia’s all ordinaries CLOSED DOWN 0.16% /Chinese yuan (ONSHORE) closed XXXX

//OFFSHORE CHINESE YUAN CLOSED DOWN TO 7.2151 /Oil UP TO 76.88 dollars per barrel for WTI and BRENT DOWN AT 82..48/ Stocks in Europe OPENED ALL RED// ONSHORE YUAN TRADING XXXX LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING XXXXX AGAINST US DOLLAR/OFFSHORE WEAKER

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A SMALL SIZED 309 CONTRACTS TO 417,298 WITH OUR LOSS IN PRICE OF $4.80 WITH RESPECT TO MONDAY TRADING.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE ACTIVE DELIVERY MONTH OF FEB..… THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 2256 EFP CONTRACTS WERE ISSUED: : APRIL 2256 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 2256CONTRACTS

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A FAIR SIZED TOTAL OF 1947 CONTRACTS IN THAT 2224 LONGS WERE TRANSFERRED AS EXCHANGE FOR PHYSICALS TO LONDON AND WE HAD A SMALL SIZED LOSS OF 309 COMEX CONTRACTS..AND THIS GAIN ON OUR TWO EXCHANGES HAPPENED DESPITE OUR LOSS IN PRICE OF $4.80 MONDAY COMEX. AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS DURING MID MONTH IN THE DELIVERY CYCLE), THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR FRIDAY NIGHT WAS A GOOD SIZED 3600 CONTRACTS. THROUGHOUT THE PAST SEVERAL WEEKS, THE BANKERS SOLD OFF THE LONG SIDE OF THE SPREAD WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR/T.A.S. SPREAD WHICH WILL BE LIQUIDATED IN DAYS HENCE//.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: FEB (54.548 TONNES) ( ACTIVE MONTH)

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 24 MONTHS OF 2021-2023:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707TONNES

TOTAL 2023 YEAR : 436.546 TONNES

JAN ’24. 22.706 TONNES

FEB. ’24: 54.548 TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

THE SPECS/HFT WERE SUCCESSFUL IN LOWERING GOLD’S PRICE( IT LOST $4.80 //// BUT WERE UNSUCCESSFUL IN KNOCKING ANY SPECULATOR LONGS AS WE HAD A FAIR SIZED GAIN OF1947 TOTAL CONTRACTS ON OUR TWO EXCHANGES. WE HAD A STRONG T.A.S. LIQUIDATION ON THE FRONT END OF MONDAY’S TRADING . THE T.A.S. ISSUED ON MONDAY NIGHT, WILL BE “PUT INTO THE BANK” TO BE USED AT A LATER DATE AT THE COLLUSIVE CHOOSING OF OUR BANKERS. WE ALSO EXPERIENCED NERVOUS SPECULATOR SHORT COVERING AS LONGS NOTIFIED THE CME THAT THEY WERE TAKING DELIVERY ON THEIR JUST PURCHASED GOLD CONTRACTS.

WE HAVE GAINED A TOTAL OI OF 6.055 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR FEB. (49.773 TONNES) ON FIRST DAY NOTICE ALONG WITH AN EXCHANGE FOR RISK FOR 1.7235 TONNES. THIS WAS FOLLOWED WITH TODAY’S 9000 OZ QUEUE JUMP (.2799 TONNES//NEW TOTAL STANDING 54.548: ALL OF THIS WAS ACCOMPLISHED WITH OUR LOSS IN PRICE TO THE TUNE OF $4.80

WE HAD -REMOVED 85 CONTRACTS TO THE COMEX TRADES TO OPEN INTEREST (CROOKS)

NET GAIN ON THE TWO EXCHANGES 1947 CONTRACTS OR 194,700 OZ OR 6.055 TONNES. estimated volume today 206,675 fair

final gold volumes/yesterday 125,378 extremely poor

Total monthly oz gold served (contracts) so far this month

16,527 notices 1,652,700 oz 51.390 TONNES

Total accumulative withdrawals of gold from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of gold from the Customer inventory this month

x

0 dealer deposits:

total dealer deposits: nil oz

total customer withdrawals: 2

i) out of HSBC: 69,575.559 oz

ii) Out of JPMorgan 146,222.748 oz (4548 kilobars)

total withdrawals 215,798.307 oz 6.716 tonnes

we had 0 customer deposits

Adjustments: 1 dealer to customer

a) HSBC 77.64 oz

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR FEB.

For the front month of FEBRUARY we have an oi of 478 contracts having GAINED 65 contracts. We had 25 notices filed on Monday, so we gained 90 contracts or an additional 9000 oz will stand for delivery at the comex as they took delivery over on this side of the pond.

We also had 554 notices filed under exchange for risk on first day notice for a total of 55,400 oz or 1.723 tonnes to which must be added to the delivery cycle.

Thus initial standing for gold for February is 50.136 tonnes + 1.723 tonnes = 51.859 tonnes. This was followed with today’s queue jump of 9000 oz for .2799 tonnes//New standing 52.805 tonnes + 1.723 tonnes = 54.273 TONNES

March gained 89 contracts to stand at 2125

APRIL LOST 1874 CONTRACTS FALLING TO 335,681.

We had 20 contracts filed for today representing 2000 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 17 notices were issued from their client or customer account. The total of all issuance by all participants equate to 20 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped ( (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for the FEB. /2024. contract month, we take the total number of notices filed so far for the month (16,527 x 100 oz ), to which we add the difference between the open interest for the front month of FEB. (478 CONTRACTS) minus the number of notices served upon today 20 x 100 oz per contract equals 1,697,200 OZ OR 52.805 TONNES + 1.723 Ex for Risk/prior = 54.548 tonnes

thus the INITIAL standings for gold for the FEB. contract month: No of notices filed so far (16,527) x 100 oz + (478) {OI for the front month} minus the number of notices served upon today (20) x 100 oz which equals 1,697,200 oz (52.805 TONNES) + 54,400 oz (1.723 TONNES) ex. for risk/prior// NEW total standing OR 54.548 TONNES

TOTAL COMEX GOLD STANDING FOR FEB: 54.658 TONNES WHICH IS GREAT FOR AN ACTIVE DELIVERY MONTH IN THE CALENDAR.

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD: 18,470,836.934 OZ

TOTAL REGISTERED GOLD 8,641,770.916 (268.795 tonnes).

TOTAL OF ALL ELIGIBLE GOLD: 9,829,066.018 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 7,240,780 oz (REG GOLD- PLEDGED GOLD) 225.21 tonnes

END

SILVER/COMEX

FEB 13/INITIAL

//2024// THE FEB 2024 SILVER CONTRACT//INITIAL

Silver

Ounces

Withdrawals from Dealers Inventory

NIL oz

Withdrawals from Customer Inventory

1042.550 oz

Delaware

.

Deposits to the Dealer Inventory

nil OZ

Deposits to the Customer Inventory

1,681,392.588 oz ASAHI HSBC

No of oz served today (contracts)

0 CONTRACT(S) (nil OZ)

No of oz to be served (notices)

239 contracts (1,195,000 oz)

Total monthly oz silver served (contracts)

1066 Contracts (5,330,000 oz)

Total accumulative withdrawal of silver from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of silver from the Customer inventory this month

i) 0 dealer deposit

total dealer deposit: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: 0 oz

We had 2 deposits customer account:

i) Into ASAHI 586,291.200 oz

ii) Into HSBC 1095,101.388 oz

total customer deposits 1,681,392.588 oz

JPMorgan has a total silver weight: 129.806 million oz/276.209 million or 47.61%

adjustment: 0

Comex withdrawals: 1

i) Out of Delaware 1042.550 oz

total withdrawal: 1042.550 oz

TOTAL REGISTERED SILVER: 42.873 MILLION OZ//.TOTAL REG + ELIGIBLE. 276.259 million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR DECEMBER:

silver open interest data:

FRONT MONTH OF FEB. /2023 OI: 239 CONTRACTS HAVING LOST 5 CONTRACT(S). WE HAD 0 NOTICES FILED ON MONDAY SO WE LOST 5 CONTRACTS OR AN ADDITIONAL 25,000 OZ OF SILVER CONTRACTS WILL NOT STAND FOR DELIVERY AT THE COMEX AS THEY WERE FERRIED OVER TO LONDON FOR IMMEDIATE DELIVERY OVER THERE.

MARCH LOST 5841 CONTRACTS TO 78,718

APRIL SAW A GAIN OF 1 CONTRACT TO STAND AT 20

MAY SAW A GAIN OF 5017 CONTRACTS UP TO 49,649

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 0 for NIL oz

Comex volumes// est. volume today 108339 huge

Comex volume: confirmed yesterday 99,556 huge

To calculate the number of silver ounces that will stand for delivery in FEB. we take the total number of notices filed for the month so far at 1066 x 5,000 oz = 5,330,000 oz

to which we add the difference between the open interest for the front month of FEB. (239) and the number of notices served upon today 0 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the FEB/2024 contract month: 1066 (notices served so far) x 5000 oz + OI for the front month of FEB. (239) – number of notices served upon today (0 )x 500 oz of silver standing for the FEB contract month equates to 6.5250 MILLION OZ. + .445 MILLION OZ EX. FOR RISK PRIOR//NEW TOTAL 6.9700 MILLION OZ

New total standing: 6.9700 million oz.

There are 42.873 million oz of registered silver.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS//

BOTH GLD AND SLV ARE MASSIVE FRAUDS!

FEB13/WITH GOLD DOWN $20.15 TODAY NO CHANGES IN GOLD INVENTORY AT THE GLD:

/ //://INVENTORY RESTS AT 841.92 TONNES

FEB12/WITH GOLD DOWN $4.80 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A STRONG WITHDRAWAL OF 1.74 TONNES OF GOLD FROM THE GLD. / //://INVENTORY RESTS AT 841.92 TONNES

FEB9/WITH GOLD DOWN $8.60 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A STRONG DEPOSIT OF 1.44 TONNES OF GOLD FROM THE GLD. / //://INVENTORY RESTS AT 843.66 TONNES

FEB8/WITH GOLD DOWN $2.70 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A MASSIVE WITHDRAWAL OF 5.47 TONNES OF GOLD FROM THE GLD. / //://INVENTORY RESTS AT 842.22 TONNES:

FEB7/WITH GOLD UP $0.40 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A MASSIVE WITHDRAWAL OF 4.04 TONNES OF GOLD FROM THE GLD. / //://INVENTORY RESTS AT 847.69 TONNES:

FEB6/WITH GOLD UP $8.50 TODAY NO CHANGES IN GOLD INVENTORY AT THE GLD:/ / //://INVENTORY RESTS AT 851.73 TONNES:

FEB5/WITH GOLD DOWN $9.85 TODAY SMALL CHANGES IN GOLD INVENTORY AT THE GLD:A DEPOSIT OF .58 TONNES OF GOLD INTO THE GLD// / //://INVENTORY RESTS AT 851.73 TONNES:

FEB 2/WITH GOLD DOWN $17.95 TODAY SMALL CHANGES IN GOLD INVENTORY AT THE GLD:A WITHDRAWAL OF .58 TONNES OF GOLD FROM THE GLD// / //://INVENTORY RESTS AT 851.15 TONNES:

FEB 1/WITH GOLD UP $5.00 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD:A WITHDRAWAL OF 1.73 TONNES OF GOLD FROM THE GLD// / //://INVENTORY RESTS AT 851.15 TONNES:

JAN 31/WITH GOLD UP $16.40 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD:A WITHDRAWAL OF 2.01 TONNES OF GOLD FROM THE GLD// / //://INVENTORY RESTS AT 852.88 TONNES:

JAN 30/WITH GOLD UP $6.50 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD:A WITHDRAWAL OF 1.16 TONNES OF GOLD FROM THE GLD// / //://INVENTORY RESTS AT 854.89 TONNES:

TOTAL IN LAST 18 DAYS WITHDRAWAL OF 14.12 TONNES

JAN 29/WITH GOLD UP $8.70 TODAYHUGE CHANGES IN GOLD INVENTORY AT THE GLD:A WITHDRAWAL OF 2.88 TONNES OF GOLD FROM THE GLD// / //://INVENTORY RESTS AT 856.05 TONNES

JAN 26/WITH GOLD DOWN $0.10 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD: / //://INVENTORY RESTS AT 858.93 TONNES

JAN 25/WITH GOLD UP $2.50 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD: / //://INVENTORY RESTS AT 858.93 TONNES

JAN 24/WITH GOLD DOWN $9.75 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD: / //://INVENTORY RESTS AT 858.93 TONNES

JAN 23/WITH GOLD UP $3.95 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.02 TONNES OF GOLD FROM THE GLD/ //://INVENTORY RESTS AT 858.93 TONNES

JAN 22/WITH GOLD DOWN $6.00 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.15 TONNES OF GOLD FROM THE GLD/ //://INVENTORY RESTS AT 860.95 TONNES

JAN 19/WITH GOLD UP $8.15 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD //://INVENTORY RESTS AT 862.10 TONNES

JAN 18/WITH GOLD UP $14.85 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 2.30 TONNES OF GOLD FROM THE GLD//://INVENTORY RESTS AT 862.10 TONNES

JAN 17/WITH GOLD DOWN $23.25 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF .549 TONNES OF GOLD INTO THE GLD.;//://INVENTORY RESTS AT 864.40 TONNES

JAN 12/WITH GOLD UP $31.65 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD; A MASSIVE WITHDRAWAL OF 4.61 TONNES OF GOLD FROM THE GLD//://INVENTORY RESTS AT 864.99 TONNES

JAN 11/WITH GOLD DOWN $7.40 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD; A MASSIVE WITHDRAWAL OF 4.61 TONNES OF GOLD FROM THE GLD//://INVENTORY RESTS AT 864.99 TONNES

JAN 10/WITH GOLD DOWN $4.80 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD://INVENTORY RESTS AT 869.60 TONNES

JAN 9/WITH GOLD UP $0.95 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD://INVENTORY RESTS AT 869.60 TONNES

JAN 8/WITH GOLD DOWN $16.85 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD:A WITHDRAWAL OF 4.61 TONNES FROM THE GLD. INVENTORY RESTS AT 869.60 TONNES

JAN 5/WITH GOLD UP $0.80 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD:///. // INVENTORY RESTS AT 874.21 TONNES

JAN 4/WITH GOLD UP $7.60 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD:///. // INVENTORY RESTS AT 874.21 TONNES

JAN 3/WITH GOLD DOWN $29.40 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.90 TONNES OF GOLD INTO THE GLD///. // INVENTORY RESTS AT 874.21 TONNES

JAN 2/WITH GOLD UP $1.50 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.44 TONNES OF GOLD INTO THE GLD///. // INVENTORY RESTS AT 879.11 TONNES

GLD INVENTORY: 841.92 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

FEB 13/WITH SILVER DOWN 60 CENTS TODAY SMALL CHANGES IN SILVER INVENTORY AT THE SLV A SMALL WITHDRAWAL OF 0.504 MILLION OZ OZ OUT OF THE SLV: SLV INVENTORY RESTS AT 437.615 MILLION OZ

FEB 12/WITH SILVER UP 14 CENTS TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV A HUGE WITHDRAWAL OF 1.921 MILLION OZ OZ OUT OF THE SLV: SLV INVENTORY RESTS AT 438.119 MILLION OZ

FEB 9/WITH SILVER DOWN 4 CENTS TODAY SMALL CHANGES IN SILVER INVENTORY AT THE SLV A SMALL DEPOSIT OF 600,000 OZ INTO THE SLV: SLV INVENTORY RESTS AT 440.040 MILLION OZ

FEB 8/WITH SILVER UP 29 CENTS TODAY NO CHANGES IN SILVER INVENTORY AT THE SLV: SLV INVENTORY RESTS AT 439.994 MILLION OZ

FEB 7/WITH SILVER DOWN 18 CENTS TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A MASSIVE DEPOSIT OF 4.04 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 439.994 MILLION OZ//LAST 9 DAYS: 10.7598 MILLION OZ WITHDRAWAL

FEB 6/WITH SILVER UP 11 CENTS TODAY NO CHANGES IN SILVER INVENTORY AT THE SLV: /INVENTORY RESTS AT 435.144 MILLION OZ//LAST 9 DAYS: 10.7598 MILLION OZ WITHDRAWAL

FEB 5/WITH SILVER DOWN 32 CENTS TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.345 MILLION OZ FROM THE SLV(FAIRY TALES) // /INVENTORY RESTS AT 435.144 MILLION OZ//LAST 8 DAYS: 10.7598 MILLION OZ WITHDRAWAL

FEB 2/WITH SILVER DOWN 50 CENTS TODAY SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 0.58 MILLION OZ INTO THE SLV(FAIRY TALES) // /INVENTORY RESTS AT 438.489 MILLION OZ//LAST 7 DAYS: 14.105 MILLION OZ WITHDRAWAL

FEB 1/WITH SILVER UP 7 CENTS TODAY MEGA CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.19 MILLION OZ INTO THE SLV(FAIRY TALES) // /INVENTORY RESTS AT 438.947 MILLION OZ//LAST 6 DAYS: 10.3018 MILLION OZ WITHDRAWAL

JAN 31/WITH SILVER DOWN 8 CENTS TODAY MEGA CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.7438 MILLION OZ INTO THE SLV(FAIRY TALES) // /INVENTORY RESTS AT 440.137 MILLION OZ//LAST 5 DAYS: 9.1118 MILLION OZ WITHDRAWAL

JAN 30/WITH SILVER DOWN 5 CENTS TODAY MEGA CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.876 MILLION OZ INTO THE SLV(FAIRY TALES) // /INVENTORY RESTS AT 442.699 MILLION OZ//LAST 4 DAYS: 7.368 MILLION OZ WITHDRAWAL

JAN 29/WITH SILVER UP $.37 TODAY MEGA CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.105 MILLION OZ INTO THE SLV(FAIRY TALES) // /INVENTORY RESTS AT 444.575 MILLION OZ

JAN 26/WITH SILVER DOWN $0.03 TODAY MEGA CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.556 MILLION OZ INTO THE SLV(FAIRY TALES) // /INVENTORY RESTS AT 446.680 MILLION OZ

JAN 25/WITH SILVER UP $0.03 TODAY MEGA CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.831 MILLION OZ INTO THE SLV(FAIRY TALES) // /

INVENTORY RESTS AT 448.236 MILLION OZ

JAN 24/WITH SILVER UP $0.44 TODAY MEGA CHANGES IN SILVER INVENTORY AT THE SLV: ANOTHER DEPOSIT OF 1.375 MILLION OZ INTO THE SLV(FAIRY TALES) // //INVENTORY RESTS AT 450.067 MILLION OZ

JAN 23/WITH SILVER UP $0.21 TODAY MEGA CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 16.201 MILLION OZ INTO THE SLV(FAIRY TALES) // //INVENTORY RESTS AT 448.694 MILLION OZ

JAN 22/WITH SILVER DOWN $0.45 TODAY NO CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 458,000 OZ OUT OF THE SLV // //INVENTORY RESTS AT 432.493 MILLION OZ

JAN 19/WITH SILVER DOWN $0.11 TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 458,000 OZ OUT OF THE SLV // //INVENTORY RESTS AT 432.493 MILLION OZ

JAN 18/WITH SILVER UP $0.13 TODAY NO CHANGES IN SILVER INVENTORY AT THE SLV: // //INVENTORY RESTS AT 432.951 MILLION OZ

JAN 17/WITH SILVER DOWN $0.38 TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 779,000 OZ FROM THE SLV.: // //INVENTORY RESTS AT 433.500 MILLION OZ

JAN 16/WITH SILVER DOWN $0.08 TODAY NO CHANGES IN SILVER INVENTORY AT THE SLV: // //INVENTORY RESTS AT 433.500 MILLION OZ

JAN 12/WITH SILVER UP $0.62 TODAY NO CHANGES IN SILVER INVENTORY AT THE SLV: // //INVENTORY RESTS AT 433.500 MILLION OZ

JAN 11/WITH SILVER DOWN 34 CENTS TODAY NO CHANGES IN SILVER INVENTORY AT THE SLV: // //INVENTORY RESTS AT 433.912 MILLION OZ

JAN 10/WITH SILVER DOWN 3 CENTS TODAY SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 450,000 OZ FROM THE SLV// //INVENTORY RESTS AT 433.912 MILLION OZ

JAN 9/WITH SILVER DOWN 20 CENTS TODAY NO CHANGES IN SILVER INVENTORY AT THE SLV //INVENTORY RESTS AT 434.370 MILLION OZ

JAN 8/WITH SILVER DOWN 8 CENTS TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 1,602,000 OZ INTO THE SLV//:././/////INVENTORY RESTS AT 434.370 MILLION OZ

JAN 5/WITH SILVER UP 20 CENTS TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV A DEPOSIT OF 916,000 OZ INTO THE SLV//:././/////INVENTORY RESTS AT 435.972 MILLION OZ

JAN 4/WITH SILVER UP 5 CENTS TODAY NO CHANGES IN SILVER INVENTORY AT THE SLV/:././/////INVENTORY RESTS AT 435.056 MILLION OZ

JAN 3/WITH SILVER DOWN 78 CENTS TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV/: A WITHDRAWALOF 2.294 MILLION OZ OZ FROM THE SLV././/////INVENTORY RESTS AT 435.056 MILLION OZ

JAN 2/WITH SILVER DOWN 9 CENTS TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV/: A WITHDRAWALOF 915,000 OZ FORM THE SLV././/////INVENTORY RESTS AT 437.35 MILLION OZ

CLOSING INVENTORY 437.616 MILLION OZ//

PHYSICAL GOLD/SILVER COMMENTARIES

1:Peter Schiff/Mike Maharrey

2) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens/JIM RICKARDS

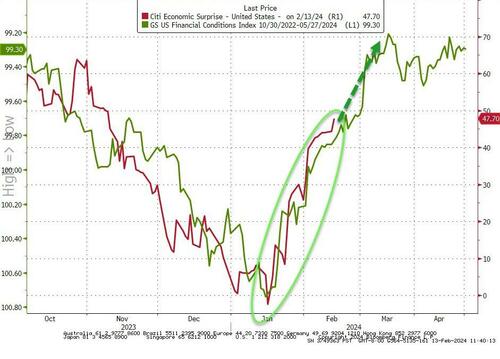

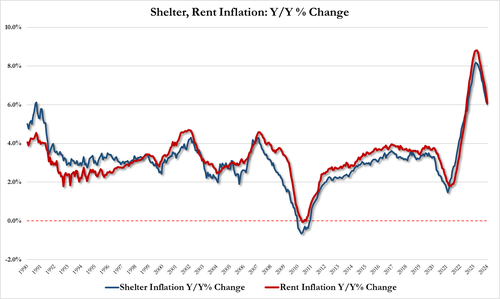

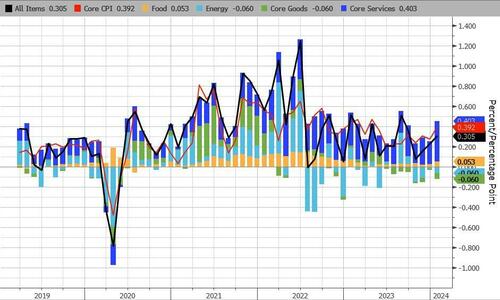

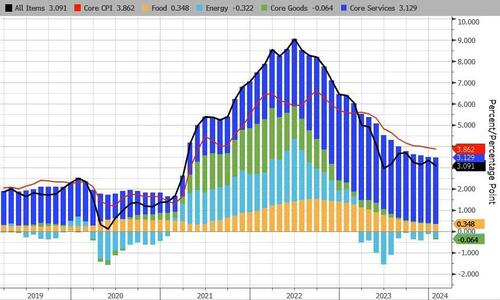

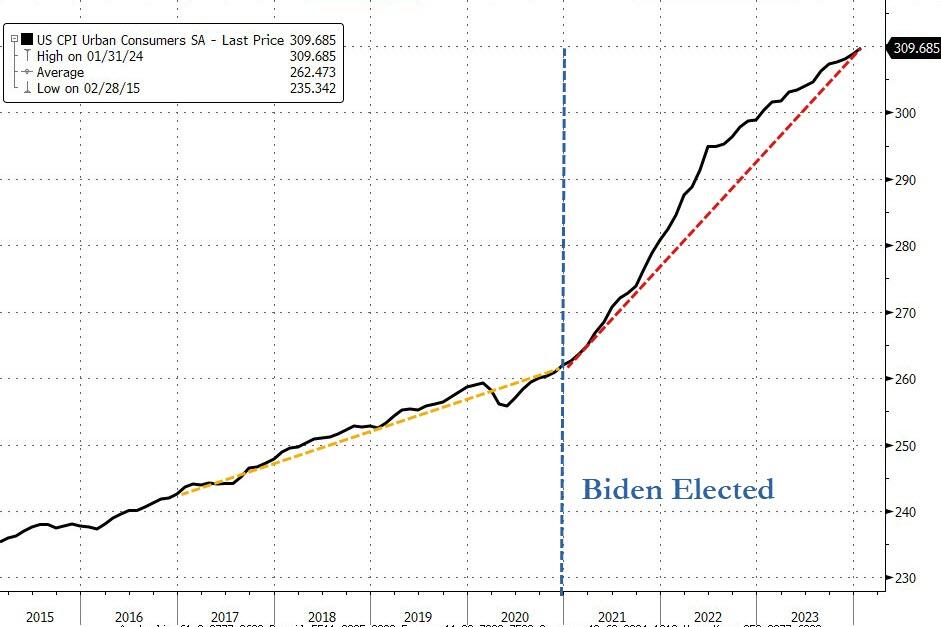

Despite the Wall Street happy talk about the Federal Reserve winning the battle against inflation, that battle has not been won.

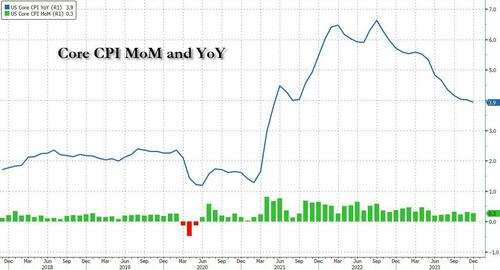

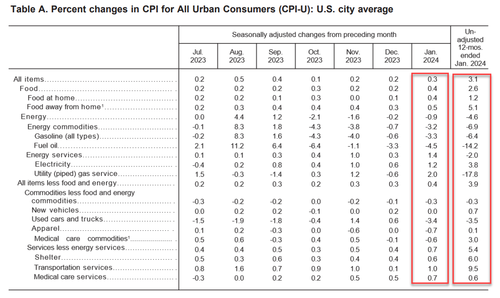

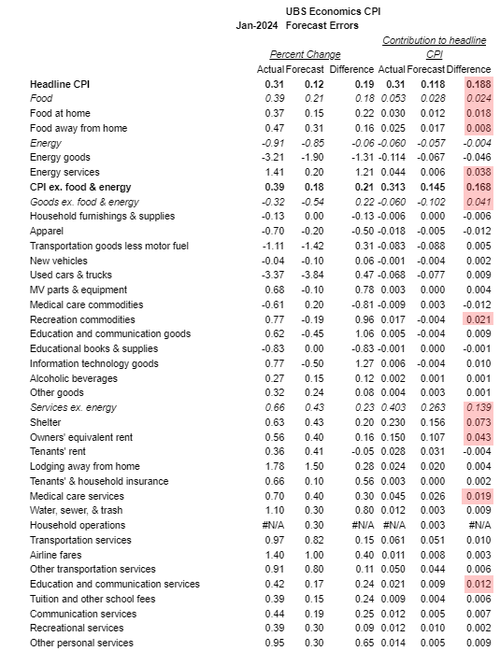

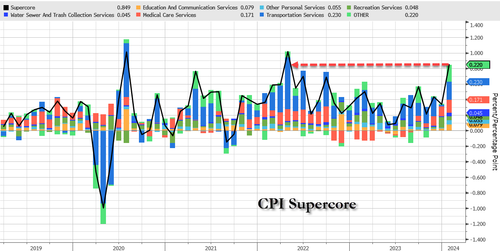

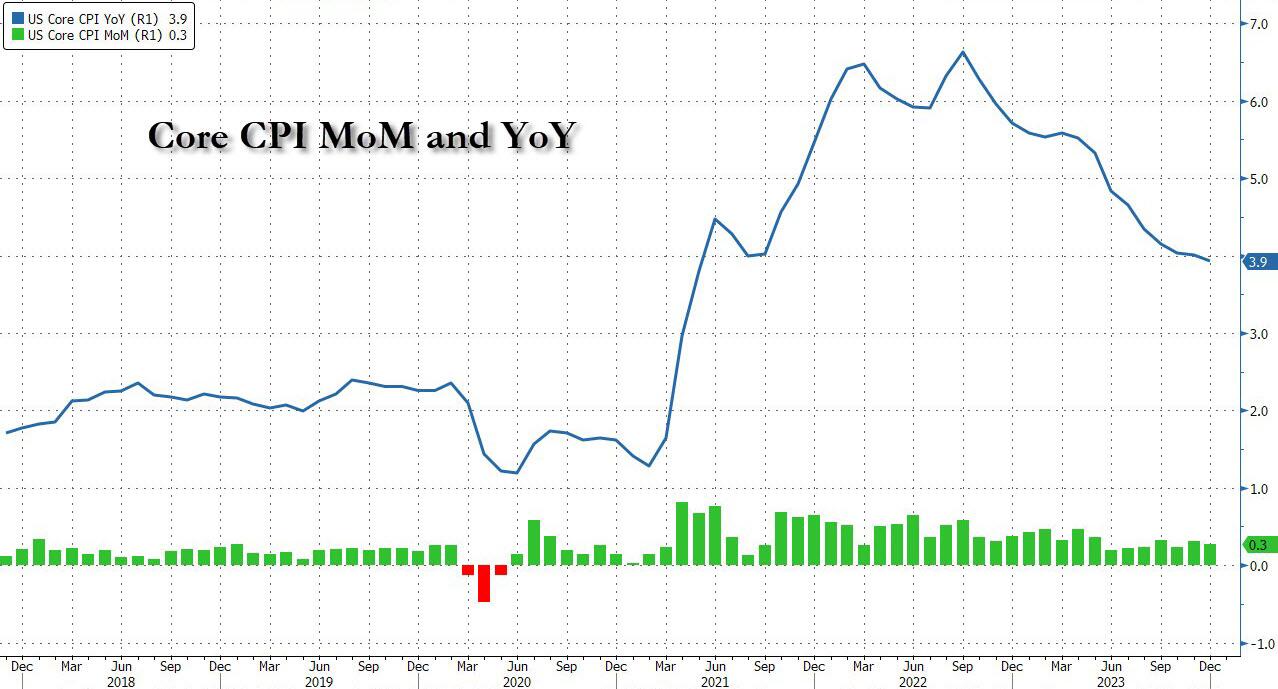

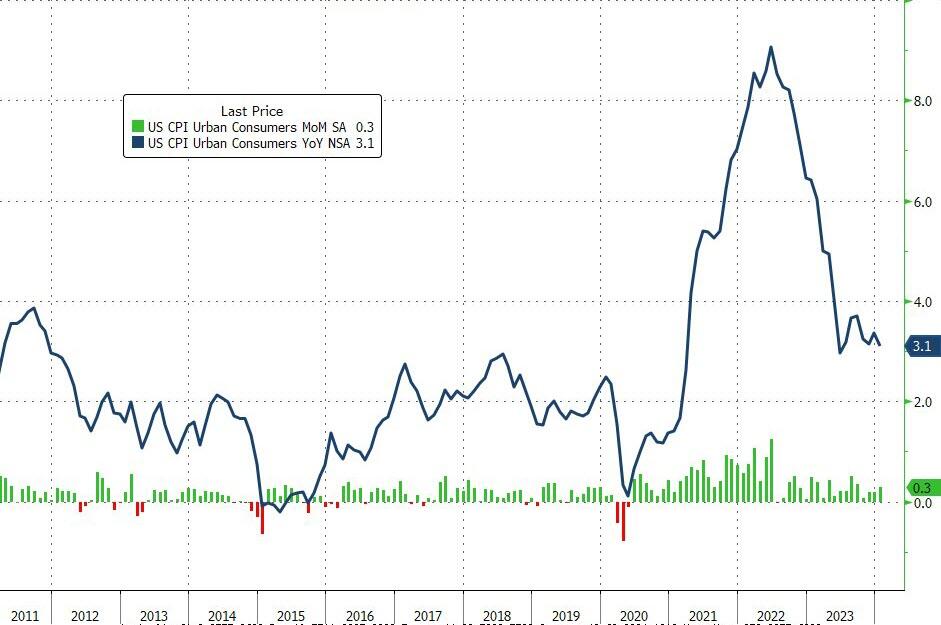

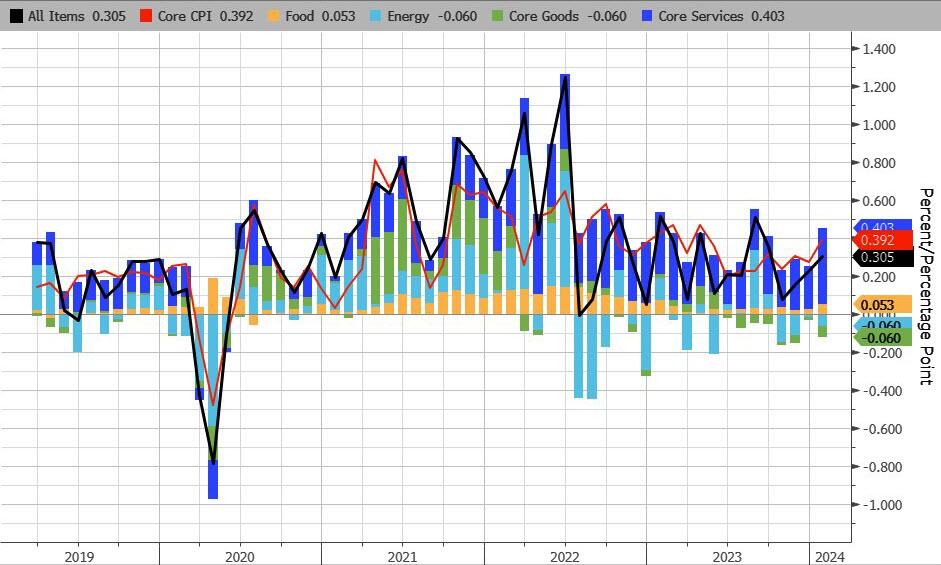

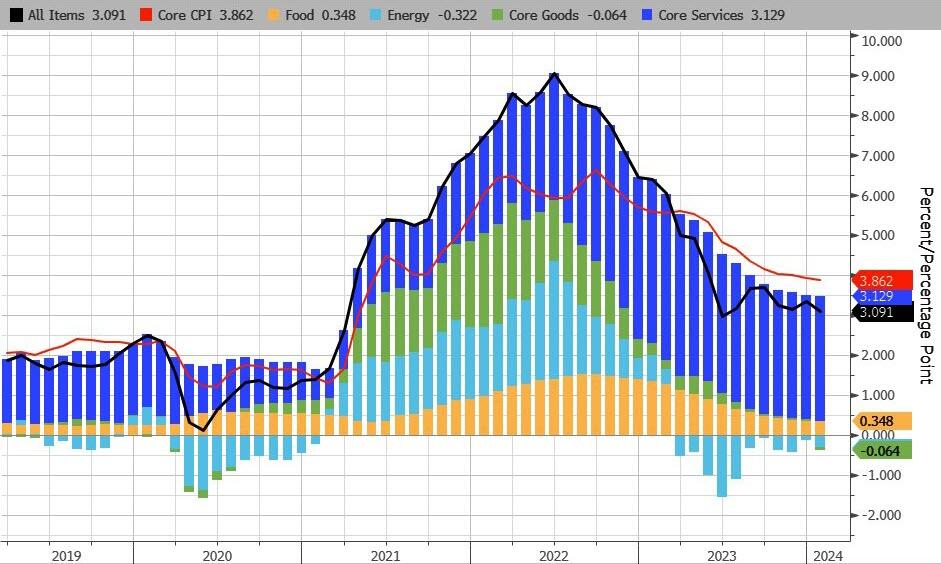

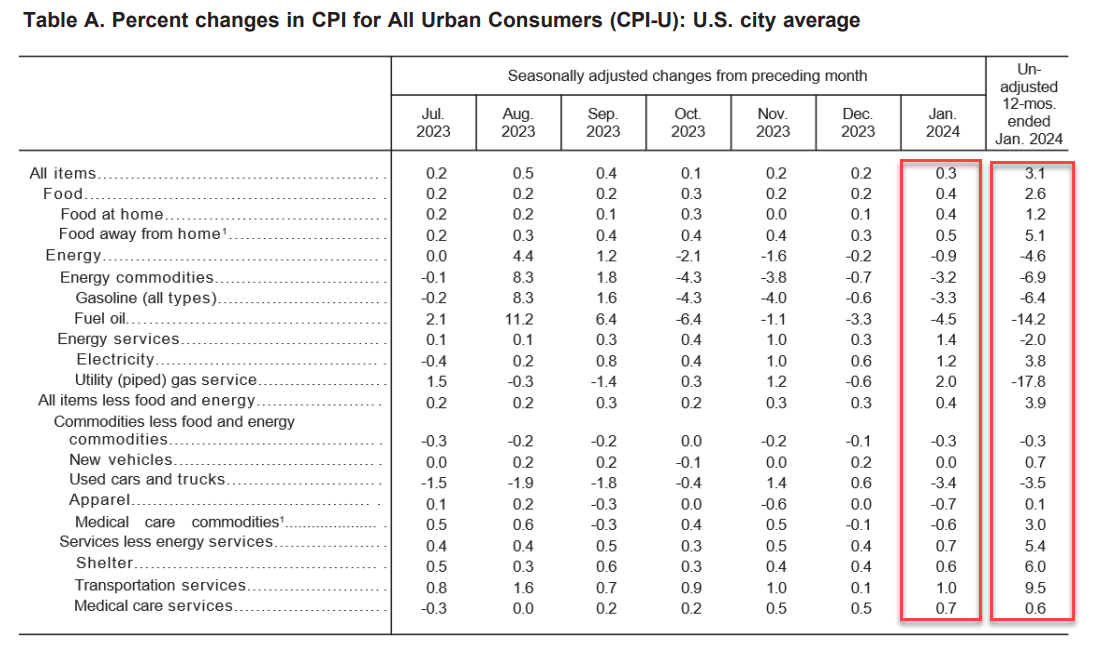

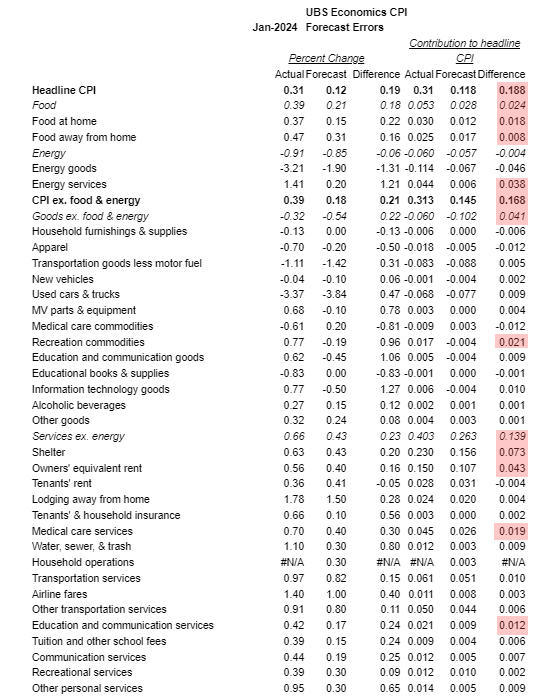

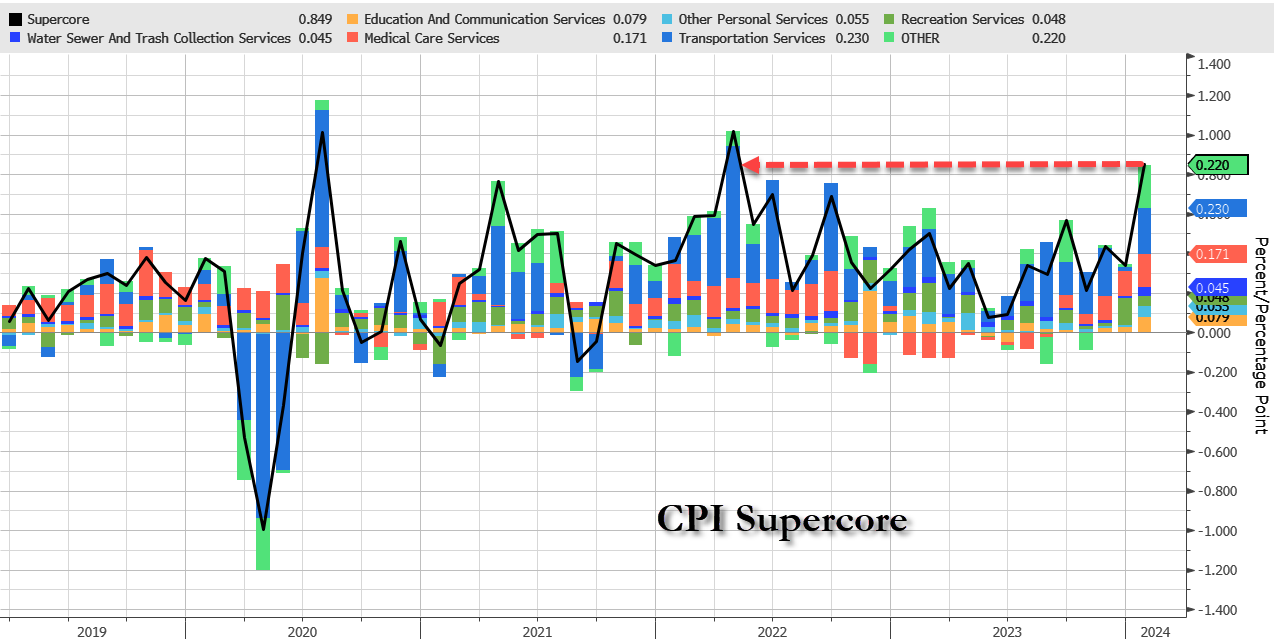

Headline CPI (the kind Americans actually pay) was 3.1% in January – lower than December but notably above expectations. However, ‘core’ and ‘supercore’ were more problematic – up 3.9% YoY (flat from December) and up 4.4% YoY (highest since May 2023) respectively.

In other words, inflation is not gone and may even be on the rise with higher oil prices lately due to geopolitical concerns. The Fed will not raise rates, but they will not be quick to cut them given continued inflation.

Inflation has a way of sneaking up on investors in small increments and can do a lot of damage before investors see it for what it is. Sure, 3.4% inflation is a lot better than 9% inflation.

But a 3.4% inflation rate cuts the value of a dollar in half in 21 years and half again in another 21 years. That’s a 75% dollar devaluation in just 42 years or the course of a typical career from age 23 to age 65.

(By the way, I’ll be live tomorrow at 7:00 p.m. ET as part of the Zero Hedge debate series on the future of the U.S. dollar. If you want to check it out, go here to learn how.)

That’s one of the main reasons I recommend gold. Gold is priced in dollars. Inflation means the dollar is worth less in terms of purchasing power. That means it takes more dollars to buy gold, so the dollar price of gold goes up.

What you may lose in the rest of your portfolio in terms of dollar purchasing power is made up in part or all from the profits you make on the higher dollar price of gold. Owning gold will protect you from the ravages of inflation. You’ll have your inflation protection in place 24/7 and won’t be caught off-guard.

Get Diversified!

Geopolitical conflicts and political turmoil often result in unforeseen consequences. These consequences can include supply chain disruptions, economic sanctions, asset seizures and freezes, bond defaults, bank failures and inflation. Oil prices can spike if key waterways are closed, or a vessel is sunk.

Economic sanctions and financial warfare can cause recession or a banking crisis almost overnight. Assets such as stocks, bonds, real estate and alternative investments can be adversely affected by such changes without warning.

Gold tends to be insulated from such shocks because there is no issuer, no creditor and no country involved. It’s just gold. That means you can hold it safely and wait out the turmoil without adverse effects.

Gold prices do not correlate closely to stock prices. Gold and stocks are driven by separate factors. That makes gold a good diversification asset for portfolios that are heavily in stocks. When a portfolio is highly diversified, it can produce higher expected returns without adding risk.

The difficult part is finding asset classes that really are diversified. Buying 50 different stocks is not diversification since you only have one asset class — stocks — and the behavior of various shares will be highly correlated in times of stress. Gold is genuinely diversified from stocks and will improve portfolio returns.

Golden Tailwinds

Gold prices have been trending higher lately with some volatility along the way. Gold hit an interim bottom of $1,831 per ounce on Oct. 5, 2023, and then rallied to $2,089 per ounce on Dec. 1, close to an all-time high.

Gold retreated slightly and then hit another high of $2,093 on Dec. 27. The rally from Oct. 5 to Dec. 27 was a 14% gain in just under three months. That’s an excellent performance.

Today, gold is around $2,033 per ounce, still close to the recent highs. These trends toward higher prices have been driven by lower interest rates; continued inflation; geopolitical concerns about the Middle East; and continued buying by central banks, especially Russia and China.

All those trends will continue. One of the principal drivers of the gold price rally is the steep decline in interest rates in recent months. The interest rate (expressed as a yield-to-maturity) on the 10-year U.S. Treasury note plunged from around 5.0% to 4.0% in a matter of weeks at the end of 2023.

Don’t mistake a 1.0% move for something small. That’s an earthquake in bond markets, especially in such a short period of time (47 days). A 1.0% move in that short a period of time has only happened in the Treasury market six times in the past 30 years.

Rates have backed up slightly in the past month, but that’s to be expected. Nothing moves in a straight line. The decline in rates will resume in the months ahead as the U.S. economy moves into disinflation and recession. That will give a boost to the dollar price of gold since notes and gold compete for investor allocations. Lower interest rates generally make gold relatively more attractive since gold has no yield.

Meanwhile, Russia and China and other central banks have been adding to their gold reserves consistently since 2008. Total gold reserves have increased from about 600 metric tonnes to 3,000 metric tonnes in Russia, and over 2,000 metric tonnes in China (although there is good reason to believe that China’s gold reserves are much higher, perhaps double the official figures or more).

That increase in gold holdings will continue and probably accelerate as the U.S. threatens to seize Russian reserves in the form of Treasury securities and as progress is made on the new BRICS gold-linked currency.

The 10% Rule

Every investor should have an allocation to gold in her portfolio. It’s an excellent diversification and can be a powerful asset to have in the face of natural disaster, infrastructure collapse or social unrest.

I recommend a 10% allocation of investable assets to gold. In calculating investable assets, you should exclude home equity and the value of any private business. Don’t gamble with your house and livelihood.

Whatever is left (stocks, bonds, real estate, alternatives) are your investible assets. Allocate 10% of that amount to gold. That allocation is high enough that you’ll make significant profits (and protect against losses in the rest of your portfolio) if gold soars, but small enough that your overall portfolio won’t be hurt badly if gold goes down.

A 10% allocation is the sweet spot for both profits and downside protection. The bottom line is gold is like an anchor for the rest of a diversified portfolio. It is physical so it is not easily frozen by government fiat.

It offers diversification because it does not correlate to other asset performance (except Treasury notes on occasion). It is the best hedge against inflation.

Gold should not dominate any portfolio, but it should be part of every portfolio.

END

3. CHRIS POWELL//GATA GOLD COMMENTARIES: daily Dispatches

Zimbabwe considers using gold to back its currency

Submitted by admin on Mon, 2024-02-12 09:50 Section: Daily Dispatches

By Ray Ndlovu Bloomberg News Monday, February 12, 2024

Zimbabwe may back its currency with gold in an effort to end exchange-rate instability, Finance Minister Mthuli Ncube said.

“To manage growth of liquidity, we may link the exchange rate to a hard asset such as gold,” Ncube said in an online press briefing held today to announce a conference of African ministers that Zimbabwe will host at the end of this month.

Zimbabwean President Emmerson Mnangagwa last week signaled the authorities are considering a revamp of the world’s worst-performing currency. He said the Treasury and monetary authorities are working on a “structured currency.” …

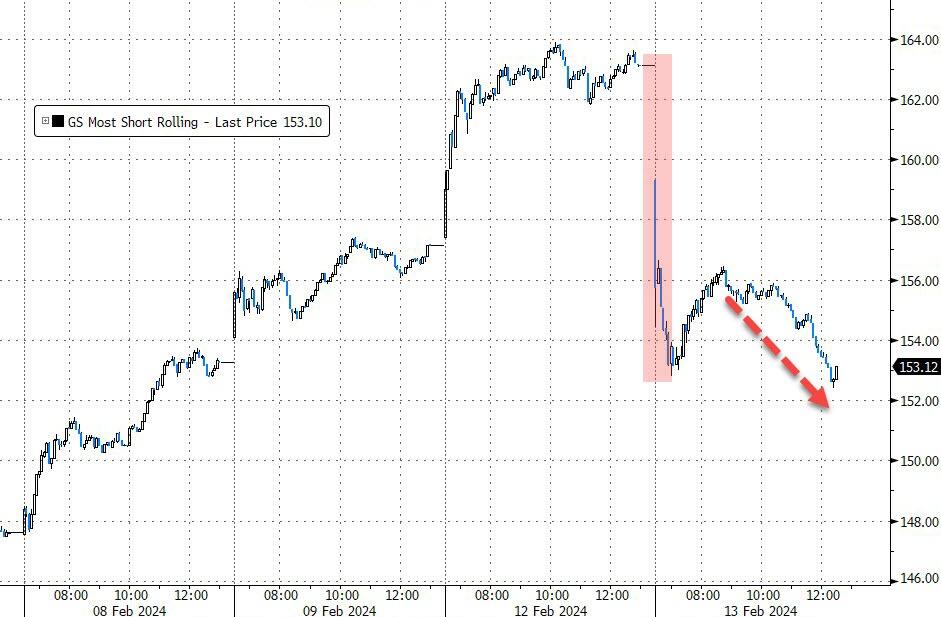

Because SLV and GLD are suppose to be physical in nature, the shorting of these vehicles is preposterous.

(ed Steer)

Ed Steer: The short position in SLV drops 25%

Submitted by admin on Mon, 2024-02-12 17:43 Section: Daily Dispatches

5:41p ET Monday, February 12, 2024

Dear Friend of GATA and Gold (and Silver):

The weekend edition of Ed Steer’s Gold and Silver Digest, published by GATA board member Ed Steer, is headlined “The Short Position in SLV Drops 25%” and it’s posted in the clear at GoldSeek’s companion site, SilverSeek, here:

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGSTUESDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED

OFFSHORE YUAN: DOWN TO 7.2151

SHANGHAI CLOSED

HANG SENG CLOSED

2. Nikkei closed

3. Europe stocks SO FAR: ALL RED

USA dollar INDEX UP TO 103.96 EURO FALLS TO 1.0782 DOWN 9 BASIS PTS

3b Japan 10 YR bond yield: FALLS TO. +.721 Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 149.34/JAPANESE YEN NOW RISING AS WELL AS LONG TERM 10 YR. YIELDS RISING //EVENTUALLY THIS WILL BREAK THE JAPANESE CENTRAL BANK

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen UP CHINESE ONSHORE YUAN: XXX// OFFSHORE: DOWN

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and UP FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund UP TO +2.3440***/Italian 10 Yr bond yield DOWN to 3.877* /SPAIN 10 YR BOND YIELD DOWN TO 3.292…**

3i Greek 10 year bond yield DOWN TO 3.343

3j Gold at $2028.75 silver at: 22.86 1 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble UP 0 AND 7 /100 roubles/dollar; ROUBLE AT 91.24//

3m oil into the 76 dollar handle for WTI and 82 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 149.34// 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 0.721% STILL ON CENTRAL BANK (JAPAN) INTERVENTION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.8774 as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.9482 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

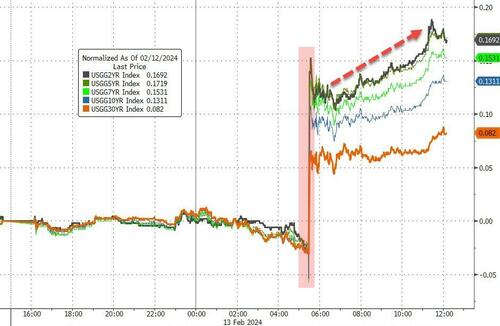

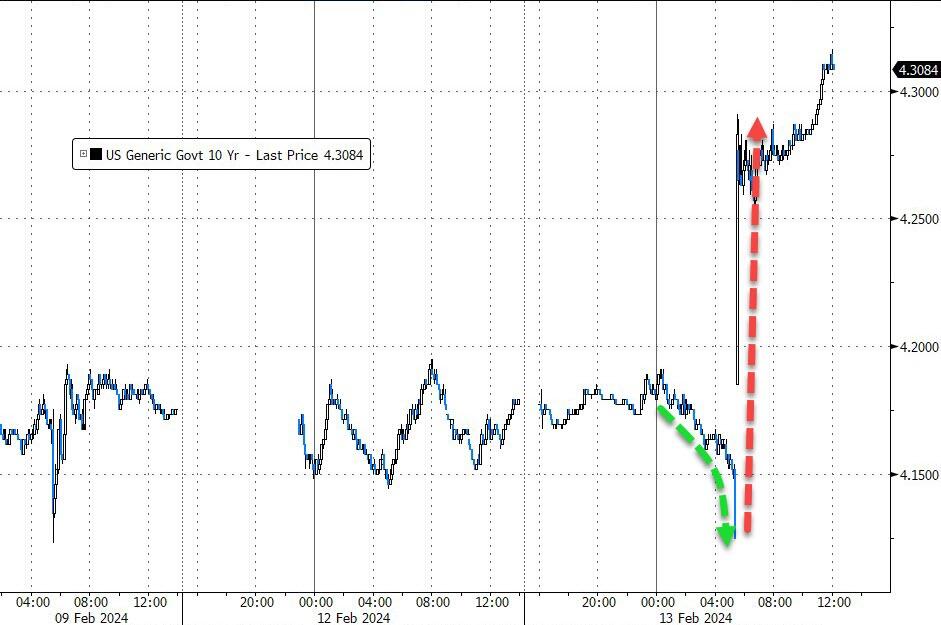

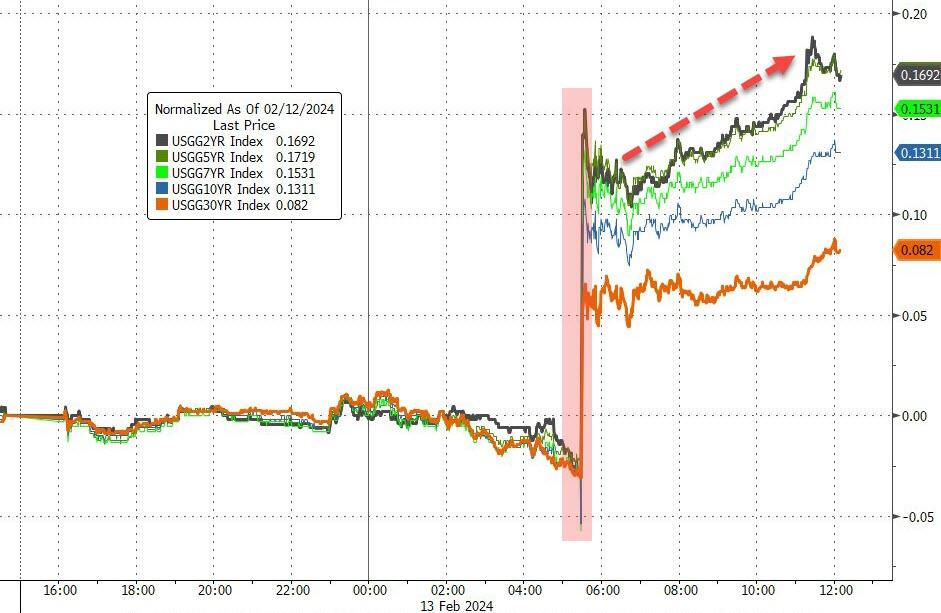

USA 10 YR BOND YIELD: 4.166 DOWN 1 BASIS PTS…

USA 30 YR BOND YIELD: 4.365 DOWN 0 BASIS PTS/

USA 2 YR BOND YIELD: 4.468 DOWN 0 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 30.73…(TURKEY SET TO BLOW UP FINANCIALLY)

GREAT BRITAIN/10 YEAR YIELD: UP 3 BASIS PTS AT 4.1095

end

2.a Overnight: Newsquawk and Zero hedge

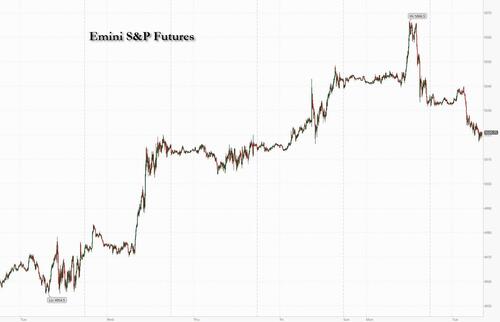

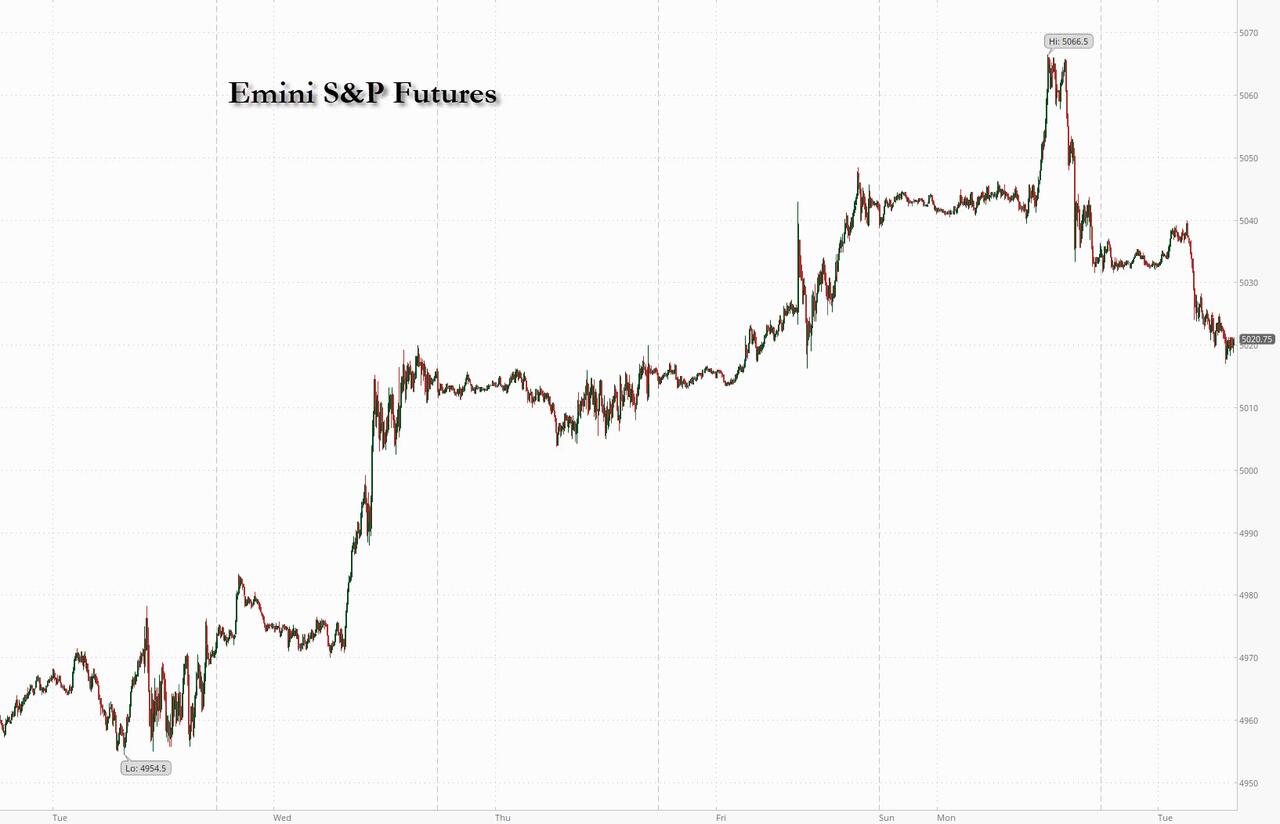

Futures Slump, Tech Giants Drop Ahead Of CPI Report

TUESDAY, FEB 13, 2024 – 08:14 AM

US equity futures and European bourses slumped before the release of closely watched CPI data that could set the stage for the timing of the Federal Reserve move to interest-rate cuts. Contracts on the Nasdaq 100 slid 0.6% while those on the S&P 500 fell 0.4%, extending Monday’s decline in the main US stock gauge from a high of near 5,050. Nvidia dropped 1% in premarket trading with all Mag 7 stocks down. Bond yields are down 3bps, the dollar fell and bitcoin traded around $50,000, the highest in over two years. Commodities are higher pre-mkt led by both Energy and Metals. CPI is the key macro focus for today but we also receive Small Business Optimism; full CPI preview and scenario analysis is below.

In premarket trading, all Mag7 names were lower pre-mkt as it is becoming increasingly clear that someone has been gaming a gamma squeeze (most likely SoftBank in names like Arm Holdings).

Arista Networks shares fell 7.1% after the cloud networking company’s first-quarter results and outlook were seen by some as underwhelming, given AI-related expectations.

Beamr Imaging rose 16%, on track to extend gains after rallying more than 370% on Monday after the video optimization technology and solutions company announced that it teamed up with Nvidia on a joint research.

Cadence Design System shares fell 6.7% on Tuesday, after the application software company gave a first-quarter forecast that was weaker than expected.

G1 Therapeutics shares slumped 38% after the biopharmaceutical company announced plans to continue its phase 3 trial of Trilaciclib in metastatic triple negative breast cancer after analysis from an independent data monitoring committee.

JetBlue shares jumped 14% after activist investor Carl Icahn disclosed a 9.91% stake in the airline and said he had held talks with management about the possibility of representation on the board.

Lattice Semiconductor fell 7.8% after the chipmaker’s fourth-quarter revenue as well as 1Q forecast fell short of average estimates.

Teradata shares slid 14% after the infrastructure-software company issued guidance for full-year adjusted earnings per share that missed estimates. TD Cowen said this was a setback in Teradata’s cloud migration momentum.

TripAdvisor shares climbed 12% after announcing the formation of a special committee to evaluate any proposals that may be brought forward for a potential deal, following Liberty TripAdvisor’s board authorizing talks on a possible acquisition of the travel-services platform.

ZoomInfo Technologies shares soared 21% after the infrastructure software company reported fourth-quarter revenue that beat consensus estimates. Analysts said the results were solid overall, particularly due to the low expectations going into the report.

2U fell 24% after the online educational services company flagged “substantial doubt” about its ability to continue as a going concern, citing debt as a concern. Its 2024 revenue forecasts also missed estimates. Morgan Stanley halves its share price target on the stock.

Investors are taking a breather from the torrid meltup after optimism about corporate earnings – driven by what Bloomberg calls a combination of resilient US growth and expected interest-rate cuts – helped push the market to extremely overbought territory. The latest BofA Fund Managers Survey found that allocation to US equities has risen, with exposure to the tech industry at the highest since August 2020.

Today’s inflation report (which we previewed in depth here), which is expected to show the first reading below 3% on year-over-year headline inflation since March 2021, may not be enough to justify a more rapid shift to monetary easing. Employment (as much as that number is not completely made up), manufacturing and economic growth in the US have surprised on the upside, proving resilient to the fastest rate increases in a generation.

“Despite expecting CPI to print below 3% later, we still think the market is over-exuberant when it comes to when that first cut comes in,” Grace Peters, head of global investment strategy at JPMorgan Private Bank, said in an interview with Bloomberg TV.

Policy makers, meanwhile, are driving home the message that rate-cut bets have become overblown. Federal Reserve Bank of Richmond President Thomas Barkin Monday warned US businesses accustomed to raising prices in recent years may continue to fan inflation. The market is overlooking the risk of rate increases following the easing cycle, strategists at Citigroup Inc. warned Monday.

Derivatives markets point to the first fully-priced quarter-point rate cut in June, with three more to follow in 2024, taking the Fed Funds Rate lower by 1 percentage point by December, according to data compiled by Bloomberg.

European stocks and US futures are on the back foot as investors look ahead to the release of US consumer price data. The Stoxx 600 fell 0.3% led lower by technology names which fell from Monday’s highest close since December 2000, as chip stocks pulled back after wafer maker Siltronic gave full-year guidance that was much weaker than expected; healthcare and auto stocks advanced. ASML lost over 7% at the open before recovering, with some traders blaming a “fat finger.” Here are the key European movers:

Michelin shares rise as much as 4.1% as analysts welcomed the French tire-maker’s results and a buyback announcement, though several noted the company’s cautious guidance.

Neste shares gain as much as 1.6% after Redburn raises rating to neutral from sell, saying the Finland-based refiner’s disappointing 2024 margin guidance has put a floor under expectations.

Lundbeck shares rise as much as 3.5% after the Danish pharmaceutical group was upgraded to buy at Deutsche Bank, which says it’s at a “good entry point” following recent weakness.

TUI shares rise as much as 8.2% in Frankfurt after the tour operator surprised markets by posting a 1Q underlying Ebit for the first time, bolstering confidence in full-year guidance.

ThyssenKrupp Nucera shares gain as much as 5.1% after the German firm’s orders beat estimates. Deutsche Bank said the release showed a good start to the year.

Believe shares gain as much as 19% after investment firms in partnership with its founder Denis Ladegaillerie offered to take the French record label private Monday at €15 per share.

Tokmanni shares gain as much as 6.1% after raising its revenue target and announcing it targets a store network of 360+ Tokmanni, Dollarstore and Bigdollar stores in Nordics by end 2025.

Basilea shares gain as much as 15%, the most since August, after the Swiss pharmaceutical company boosted its guidance for 2024, offsettinga revenue miss.

ASML shares fall as much as 7.1% early on Tuesday before quickly trimming the decline, with several traders citing an erroneous trade known as a ‘fat finger.’

Genmab shares drop as much as 4.4% after Carnegie decreased its price target on the Danish biotechnology company, scheduled to report full-year earnings on Wednesday.

Kemira shares fall as much as 5.3% after a share sale by holder Solidium priced at €16 apiece, representing a roughly 5.9% discount to the last close.

Siltronic shares falls as much as 10% after the wafer maker gave full-year guidance that was much weaker than expected, driven by elevated inventories at chipmaker clients. Peers drop.

Earlier in the session, Asian stocks advanced, boosted by a rally in semiconductor and technology stocks that lifted markets like Korea and Japan. The MSCI Asia Pacific Index rose as much as 0.8%, with Tokyo Electron, Toyota Motor and Tokio Marine contributing the most. Japanese stocks surged the most in a month after trading resumed following Monday’s holiday, driven by gains in chipmakers, exporters and ARM-rigging Softbank. Stocks in China, Vietnam, Taiwan and Hong Kong remained closed on account of Lunar New Year holidays. A Bloomberg gauge of semiconductor stocks in Asia was on pace for its highest close in nearly two years, propelled by Tokyo Electron’s strong earnings forecast and a rally in Nvidia shares overnight. The gains also helped Korea, which was on verge of erasing its year-to-date losses. Australia’s ASX 200 was choppy as gains in mining, utilities and financials were offset by weakness in healthcare, telecoms and tech, while data showed an improvement in Westpac Consumer Sentiment but NAB Business Confidence and Conditions were mixed.

In FX, the Bloomberg Dollar Spot Index is also little changed. Gilts are in the red after UK wage growth slowed less than expected in the fourth quarter. The data also pushed the pound to the top of the G-10 FX pile – cable is up 0.3%.

In rates, treasuries were slightly richer across the curve amid outperformance by bunds during European morning. US 10-year at 4.165% trails bunds in the sector by 0.5bp. US intermediate to long-end yields richer by as much as 1.5bp; front-end lags, flattening 2s10s spread by less than 1bp toward middle of Monday’s range. Gilts lag by 2.5bps, with 10-year yields reaching highest level since Dec. 5 after UK December earnings data. Ahead of US CPI data, Fed-dated swaps price in around 3bp of easing for the March policy meeting and 16bp for May; further out, around 112bp of cuts are priced in for the year. Dollar issuance slate includes EBRD 4Y FRN; seven companies combined to price $11.3b on Monday as issuers paid about 6bps in new-issue concessions, driven by order books that were just under three times covered. US economic data calendar includes only January CPI at 8:30am.

In commodities, oil prices advanced again, with WTI rising 1.2%, to trade near $77.80 while Brent briefly topped $83. Spot gold adds 0.3%.

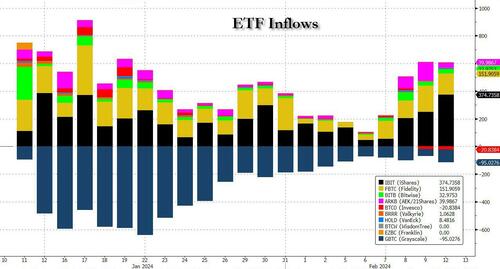

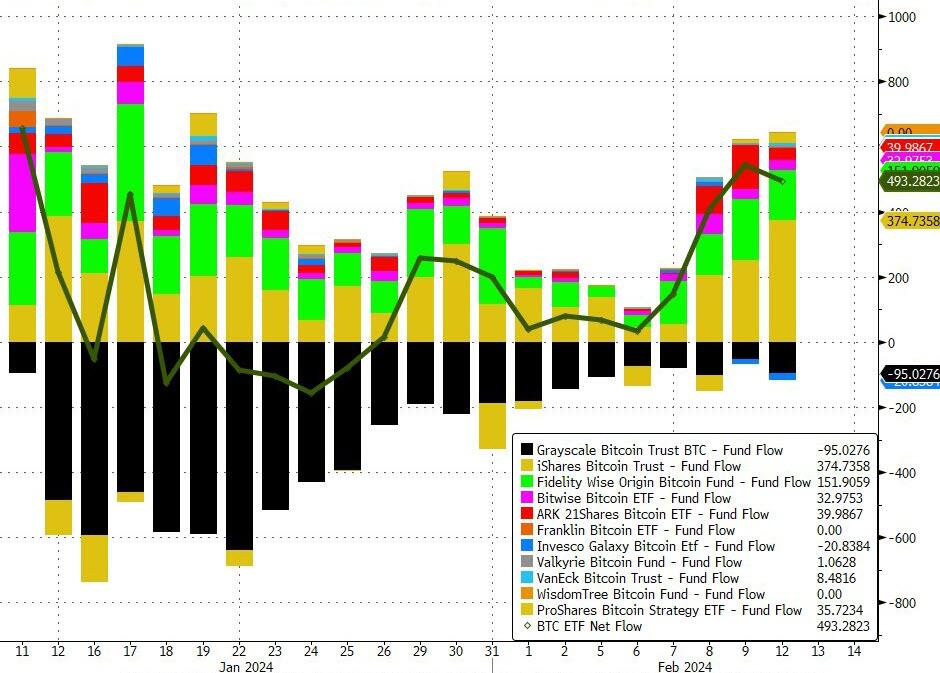

Bitcoin continues to hold above the USD 50k mark and Ethereum (+1.2%) plays catch-up. The aggressive flood of retail flows into bitcoin ETFs continues.

Looking to the day ahead now, data releases include the US January CPI, NFIB small business optimism, UK January jobless claims, December average weekly earnings, Germany and Eurozone February Zew survey, Germany December current account balance and the French Q4 ilo unemployment rate. Finally, we will have earnings releases from Coca-Cola, Shopify, Airbnb, Zoetis, Marriott, Biogen, and Restaurant Brands.

Market Snapshot

S&P 500 futures down 0.3% to 5,024.00

STOXX Europe 600 down 0.3% to 486.03

MXAP up 0.9% to 168.66

MXAPJ up 0.1% to 512.04

Nikkei up 2.9% to 37,963.97

Topix up 2.1% to 2,612.03

Hang Seng Index down 0.8% to 15,746.58

Shanghai Composite up 1.3% to 2,865.90

Sensex up 0.7% to 71,545.85

Australia S&P/ASX 200 down 0.1% to 7,603.58

Kospi up 1.1% to 2,649.64

German 10Y yield little changed at 2.35%

Euro down 0.1% to $1.0761

Brent Futures up 0.8% to $82.65/bbl

Brent Futures up 0.8% to $82.66/bbl

Gold spot up 0.3% to $2,026.07

U.S. Dollar Index little changed at 104.24

Top Overnight News

MSCI Inc. is cutting dozens of Chinese companies from its global benchmarks following a market rout that’s erased trillions of dollars in value from the nation’s stocks. BBG

Japanese Prime Minister Fumio Kishida is intensifying efforts to meet North Korea’s Kim Jong Un, as he pushes for a diplomatic breakthrough with the dictator in a bid to save his faltering premiership. FT

Russia intends to double the number of its troops stationed along its border with the Baltic states and Finland as it prepares for a potential military conflict with Nato within the next decade, according to Estonia’s foreign intelligence service. FT

UK wage growth in Dec cools by less than expected vs. Nov, with core +6.2% Y/Y (down from +6.7% in Nov, but higher than the consensus forecast of +6%). WSJ

Swiss CPI for Jan tumbles by much more than anticipated, coming in at +1.3% Y/Y headline (vs. the Street +1.7% and vs. +1.7% in Dec) and +1.2% core (vs. the Street +1.6% and vs. +1.5% in Dec). BBG

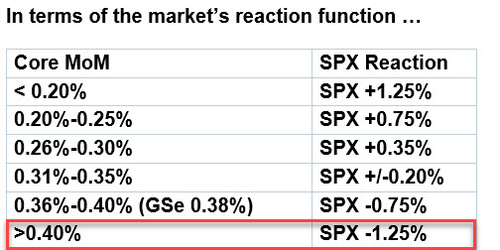

CPI GIR estimates a 0.38% increase in January core MoM CPI (vs consensus +.3% and last +.3%). Our forecast reflects a temporary boost from above-normal start-of-year price increases, including for prescription drugs, car insurance, tobacco, and medical services. US equities rally should continue on anything sub 30bps here….north of 40bps will hit stocks…everything else in-between will be noisy which is likely where we land. GS GBM

Nearly 20% of outstanding debt on US commercial and multifamily real estate — $929 billion — will mature this year, requiring refinancing or property sales. The volume of loans coming due swelled 40% from an earlier estimate by the Mortgage Bankers Association of $659 billion, a surge attributed to loan extensions and other delays rather than new transactions. BBG

The Senate passed a $95 billion national security package to aid Israel, Ukraine and other U.S. allies early Tuesday morning after a monthslong debate that has deeply divided congressional Republicans. The bill passed 70 to 29, after 22 Republicans joined Democrats in approving the aid. WaPo

Asset managers from BlackRock to Grayscale have launched an online advertising blitz for their bitcoin exchange traded funds, taking advantage of a change to Google’s marketing rules on promoting cryptocurrency instruments. Google’s new marketing rules allow ads touting “cryptocurrency coin trusts” to appear alongside search results for queries such as “bitcoin ETF”. They took effect on January 29, weeks after 10 asset managers launched bitcoin ETFs on January 11. FT

2024 YTD buyback authorizations are on pace for the second largest on record, with $166B authorizations with a tilt towards large cap tech. If you remove CVX, $75B authorization from 2023, authorizations would be +26% y/y. (166b v 132b), a new record

A more detailed look at global markets courtesy of Newsquawk

APAC stocks traded mixed albeit with a positive bias as several markets reopened from the extended weekend. ASX 200 was choppy as gains in mining, utilities and financials were offset by weakness in healthcare, telecoms and tech, while data showed an improvement in Westpac Consumer Sentiment but NAB Business Confidence and Conditions were mixed. Nikkei 225 outperformed and extended on its highest levels since February 1990 as the earnings deluge resumed.

Top Asian News

RBA’s Head of Economic Analysis Kohler said inflation is coming down but is still too high and it will take some time for inflation to get back within the 2%-3% target range and based on their central forecast, inflation is expected to return to the target range in 2025 and to the midpoint in 2026. Furthermore, Kohler said services price inflation remains high and broadly based, while she also noted that high inflation, higher tax payments and higher interest rates have significantly reduced household incomes.

Brussels is now reportedly preparing to sanction four Chinese entities which it believes are helping the Kremlin buy European dual-use goods, according to a draft of the proposal cited by Politico

European bourses, Stoxx600 (-0.3%), initially opened on a mixed footing before dipping into the red as sentiment waned throughout the early hours. The Eurostoxx50 (-0.7%) is dragged down by Tech names Infineon (-2.3%), SAP (-2.3%) and ASML (-3.8%), after Siltronic (-8.1%) issued a profit warning. European sectors are generally lower, though the overall breadth of the market is fairly narrow (ex-Tech). Tech is the clear laggard, after Siltronic announced poor guidance. Healthcare marginally outperforms after GSK (+1.1%) received a broker upgrade at Citi. US Equity Futures (ES -0.3%, NQ -0.6%, RTY -0.4%) are softer across the board, with price action generally following that seen in European trade. The docket for today sees US CPI where expectations are for the headline to cool to 0.2% (prev. revised 0.3%).

Top European News

BoE reportedly plans to stress test insurers on exposure to reinsurance firms, according to FT.

Riksbank’s Jansson says hard to believe that rates could be cut at each meeting when the time comes for rate cuts to be lowered. There is not a zero chance that the first rate cut could come after this summer. Can not exclude that we could cut rates before Fed and ECB.

FX

USD firmer vs. most peers but gains tentative as US CPI looms large. DXY incrementally took out yesterday’s best of 104.27 with the next upside target the 8th Feb high at 104.43.

EUR is contained within Monday’s 1.0756-1.0805 range with that session’s venture above 1.08 unconvincing. However, a soft US CPI print could change that and prompt a test of the 200DMA at 1.0829.

GBP is the best performer vs. the USD and EUR/GBP is at its lowest level since August post-jobs data. Cable shot to a high of 1.2655, matching yesterday’s best but stopped ahead of its 21DMA at 1.2665.

Antipodeans are both softer vs. the USD but to varying degrees with NZD more so, following soft inflation expectation survey data. NZD/USD has now pared all of Friday’s upside. AUD remains rangebound since printing a YTD low last week with AUD/USD chopping and changing around the 0.65 mark.

CHF is the worst performer across the majors following soft Swiss CPI metrics which have boosted the odds of a March SNB cut to over 50% from 28%. EUR/CHF advanced to a high of 0.9493 (highest since Dec 18th) with all eyes on a potential test of 0.95.

Fixed Income

Bunds were initially bearish as the complex reacted to hawkish UK wage data, resulting in the 133.28 session trough. This move has now entirely pared and back towards session highs of 133.65, after an additional boost on a well-received German outing.

USTs moved in tandem with Bunds post-UK data, but magnitudes more limited as we await US CPI where downward inflation trends are expected to be evident once again, headline & core seen easing further.

Gilts opened lower by 20 ticks from Monday’s 97.68 close and thereafter slipped incrementally further to a 97.42 trough as the benchmark reacted to the earlier UK data. However, the move has since pared with Gilts now back towards the mentioned close as focus turns to upcoming events today before UK inflation & GDP later in the week.

Germany sells EUR 3.292bln vs exp. EUR 4.0bln 2.10% 2029 Bobl: b/c 2.30x, average yield 2.30%, and retention 17.68%.

UK sells GBP 1.5bln 0.75% 2033 I/L: b/c 2.97x (prev. 2.68x) and real yield 0.634% (prev. 0.724%).

Italy sells EUR 8.5bln vs exp. EUR 7-8.5bln 2.95% 2027, 3.70% 2030, 4.00% 2030, and 4.45% 2043 BTP.

Commodities

Crude complex trades with gains after settling relatively flat yesterday, although off Monday’s intraday troughs amid heightened geopolitics and Saudi jawboning. Trade is within a tight range as markets look ahead to the OPEC Monthly Oil Report followed by US CPI. Upside in crude prices coincided with commentary from the OPEC Sec Gen with Brent near peaks of USD 82.50/bbl.

Precious metals hold an underlying bid despite the somewhat resilient pre-CPI Dollar and steady USTs, potentially propped up by the ongoing geopolitical developments which are showing no signs of cooling; XAU found support at USD 2,016.67/oz as it eyes its 21 DMA (USD 2,027.66/oz) to the upside.

Base metals are modestly firmer despite the resilient Dollar and subdued risk tone, with no obvious catalyst to explain broader base metals’ price action, whilst Chinese markets remain on holiday.

Morgan Stanley raises oil demand growth forecast to 1.5mln BPD (prev. 1.3mln BPD) and reduces non-OPEC growth forecast to 1.5mln BPD (prev. 1.7mln BPD); bringing the two in-line.

IEA sees 2024 global oil demand growth between 1.2-1.3mln BPD (vs 1.24mln BPD in Jan OMR), according to IEA Executive Director Birol cited by BBG TV. IEA expects more comfortable oil markets and moderate prices this year. Oil supply growth will more than satisfy demand this year. OPEC+ is largely showing good discipline with cuts. Warns against moves that push oil prices up.

OPEC Secretary General Al Ghais stands by long-term demand outlook; says Saudi decision to postpone capacity expansion should not be misconstrued as a view demand is falling; voluntary cuts show OPEC+ flexibility. Sees strong global economy this year with positive implications. Market is in a good state and rather stable.

EIA said US oil output from top shale-producing regions in March is due to climb to its highest since December 2023.

American Petroleum Institute sues the Biden administration over offshore drilling curbs, according to FT

Geopolitics: Middle East

Israeli warplanes reportedly bombed areas in northern Rafah, according to Al Arabiya via social media platform X.

The heads of the CIA and Israel’s Mossad spy agency are expected to hold talks with senior Egyptian and Qatari officials on Tuesday in a bid to revive negotiations on a deal to stop the war and release hostages, according to FT sources.

France’s proposal for a truce on the Lebanon-Israeli border was delivered to Lebanon by France which called for fighters including Hezbollah elite forces to withdraw 10km away from the Israel border and aims to enforce a potential ceasefire when the conditions are right, while the proposal also called for the resumption of talks to demarcate the border. Hezbollah official Fadlallah said the group won’t discuss the matter relating to south Lebanon before the Israeli offensive in Gaza stops and that Israel is not in a position to impose conditions.

Russia’s Kremlin said they invited Palestinian President Abbas and hope that he will visit Russia, according to RIA.

US military said Houthi militants fired two missiles from Yemen towards the ship Star Iris in the Bab Al-Mandeb, while the ship reported being seaworthy with minor damage and no injuries to the crew, according to Reuters.

“Israeli newspaper Haaretz: Some progress has been made in detainee deal negotiations in recent days”, according to Sky News Arabia

Iranian Revolutionary Guards says “if the enemy hits our ships, we will hit the same number or more”, according to Sky News Arabia citing Tasnim

Geopolitics: Other

White House said the US sees no indication there are about to be hostilities at the Venezuela-Guyana border.

Japanese PM Kishida is seeking a summit with North Korean leader Kim, according to FT.

US Event Calendar

06:00: Jan. SMALL BUSINESS OPTIMISM 89.9, est. 92.3, prior 91.9

08:30: Jan. CPI MoM, est. 0.2%, prior 0.3%, revised 0.2%

Jan. CPI Ex Food and Energy MoM, est. 0.3%, prior 0.3%

Jan. CPI YoY, est. 2.9%, prior 3.4%

Jan. CPI Ex Food and Energy YoY, est. 3.7%, prior 3.9%

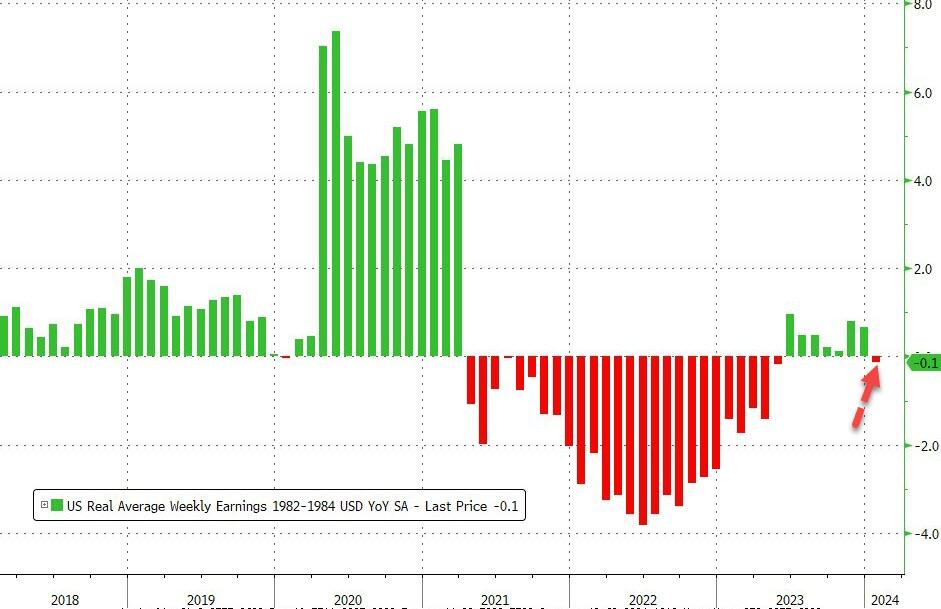

Jan. Real Avg Hourly Earning YoY, prior 0.8%, revised 1.0%

DB’s Jim Reid concludes the overnight wrap

Welcome to inflation Tuesday as US CPI today will be a very important staging post for any Fed cuts this year. Before we preview this, this morning I’ve just published a new chart book with my colleague Galina Pozdnyakova for macro generalists on the Magnificent Seven. This group has become so big that they are effectively countries and not just companies now in scale. They have already impacted global risk sentiment in recent years and especially in recent months and no market participant can ignore them in whatever asset they look at. Their size has left the S&P 500 at its most concentrated since the 1929 bubble but in the pack we show how these companies are already as profitable as the entire stock market in many countries. We show a number of long term charts that explain how they arrived at this level of dominance and also highlight what happened to all the top 5 S&P 500 stocks over the last 60 years. It was a fun and fascinating pack to put together so hopefully you’ll find it useful in framing the discussion of their future. You can see it here.

Yesterday was one of the rarer sessions where the Magnificent Seven (-0.83%) clearly underperformed, with the pullback in tech sentiment leading the S&P 500 to a marginal decline (-0.09%). But it was also a day when a more prevalent theme this year of differentiation within the mega caps was evident. The reversal was led by a -2.81% decline for Tesla, which is now the second worst performer in the S&P 500 so far in 2024 (-24.3%). By contrast, Nvidia, which eked out a new all-time high yesterday (+0.16%), has been the best performing S&P 500 stock year-to-date, having already risen by +45.9%, adding $561bn in market cap. Just to hammer home the message from the chart book that you can’t ignore these stocks, this six-week gain for Nvidia is larger than the entire market cap of the largest company in Europe (Novo Nordisk at $540bn). Indeed, Nvidia briefly surpassed Amazon to be the 4th largest fully listed company in the world yesterday, rising more than 3% earlier in the session as chipmaker sentiment benefited from dramatic gains for ARM Holdings (+29.3% yesterday and +93.4% over the past three sessions) after its results last week. SoftBank is +6.3% higher overnight given its large stake in the chipmaker.

Elsewhere, small-caps out-performed, with a +1.75% gain for the Russell 2000 yesterday moving the index back into the black year-to-date (+0.90%). Banks also gained, with the S&P 500 banks group (+1.06%) seeing its strongest day since the New York Community Bancorp results two weeks ago, while the KBW index of regional banks was up +1.83%. This easing of banking sector concerns came even as NYCB itself ended the day near flat despite trading up by more than +12% early on. On this, Luke Templeman and Galina Pozdnyakova (she was busy yesterday) published their latest private capital monitor (link here) with a special look at the CRE market. In short private investors don’t seem to be too concerned. Over in Europe equities saw a solid rally, with the STOXX 600 +0.54%, DAX (+0.65%) and CAC (+0.55%) all higher – a similar gain to the equal-weighted version of the S&P 500 (+0.63%).

Supporting the risk on mood outside of tech was the NY Fed inflation expectation report, which showed that 3-year inflation expectations fell to 2.35% (from 2.62%), its lowest level since 2013. 1-year inflation expectations were largely unchanged at 3.00% (previously 3.01%). With today’s US CPI report, given that seasonally adjusted gas prices were down almost 2.5% in January from December, our US economists expect headline CPI to come in at +0.15% (vs. +0.23% previously, consensus +0.2%), with core more elevated at +0.27% (vs. +0.28% previously, consensus +0.3%). This would see core YoY CPI falling two-tenths to 3.7%, and headline down by four-tenths to 2.9%, both in line with consensus. Chair Powell shifted his attention in the January Fed press conference from the three- and six-month annualised rates to year-on-year rates so we expect the market to refocus on these numbers. See our economists preview here.

Talking of the Fed, the speakers yesterday continued to caution regarding Fed cuts, albeit largely reiterating their recent comments. A known hawk, Fed Governor Bowman stated it is still “too soon to project when, how much the Fed will cut rates”, as “many risks remain for the Fed’s inflation fight”. Richmond Fed President Barkin noted that while the Fed was closing in on its inflation target, it was not there yet as there was “a real risk that there will be continued inflationary pressure”.

Against this backdrop, market expectations of Fed rate cuts saw little change, with a slightly less than one in five chance priced in that the Fed cuts by 25bps at the March meeting and an unchanged 112bps of cuts priced by December. Treasury yields were flat on the day, with the 10yr up +0.4bps while 2yr yields fell -0.6bps.

On the other hand, in Europe, the ECB’s Wunsch commented that there was “no big risk in waiting or not for data” in terms of deciding when to cut, as markets have already priced in future rate cuts which provide some easing for financial conditions even before a cutting cycle begins. Expanding, he suggested there was not a “huge difference” whether to start rates cuts earlier and proceed gradually or “wait a bit more and then go faster”. Market expectations of ECB rate cuts saw a moderate rise, with chances of a cut by April up to 60% from a three-month low of 52% on Friday. And the amount of cuts expected by the December meeting rose by +6.2bps on the day to 120bps. 10yr bund yields fell -2.0bps, with a stronger rally in OATs (-2.9bps) and BTPs (-5.7bps).

Talking of Europe and in light of the weekend NATO comments on the US election campaign trail, our German economists yesterday put out a note on potential catalysts for a fiscal regime change in Germany (including uncertainty around NATO post the US election) and then present three potential scenarios for the 2025 budget. See it here.

Asian equity markets are higher but with many still on holiday. As I check my screens, the Nikkei (+2.57%) is sharply higher sustaining its previous gains and making fresh 34-year highs with the KOSPI (+1.01%) also starting the day on a positive note. Chinese markets will remain closed for the week but the Hang Seng will resume trading tomorrow. S&P 500 (-0.17%) and NASDAQ 100 (-0.20%) futures are ticking lower. Treasury yields are flat.

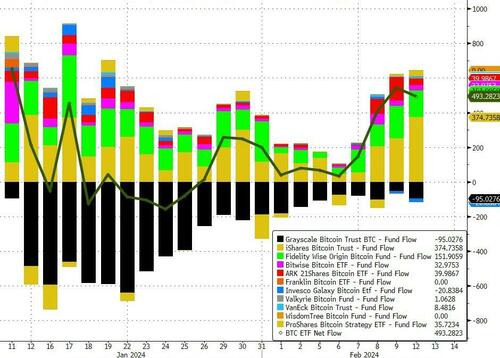

In other notable market moves yesterday, Bitcoin (+3.23%) broke through the $50,000 level for the first time since December 2021, supported by the recent spot Bitcoin ETF by the SEC (more on that here), though it retreated to a touch below this level at the close and as I type.

To the day ahead now, data releases include the US January CPI, NFIB small business optimism, UK January jobless claims, December average weekly earnings, Germany and Eurozone February Zew survey, Germany December current account balance and the French Q4 ilo unemployment rate. Finally, we will have earnings releases from Coca-Cola, Shopify, Airbnb, Zoetis, Marriott, Biogen, and Restaurant Brands.

2 B) NOW NEWSQUAWK (EUROPE/REPORT)

Equities softer as US CPI looms, GBP bid post-jobs data & CHF lags after cooler CPI, Crude firmer – Newsquawk US Market Open

TUESDAY, FEB 13, 2024 – 06:06 AM

European equities are softer across the board, with Tech lagging following poor Siltronic guidance, weighing on heavyweight ASML (-2.7%)

US equity futures mirror price action in Europe, though the NQ slightly underperforms.