GOLD PRICE CLOSED UP $8.60 TO $2012.30

SILVER PRICE UP $.53 TO $23.43

Gold ACCESS CLOSED 2013.00

Silver ACCESS CLOSED: 23.41

this week was China’s golden week. The crooks like to raid during this week. They tried and failed

Bitcoin morning price:, 52,290 UP 487 DOLLARS

Bitcoin: afternoon price: $51,803 UP 6 dollars

Platinum price closing $906.95 UP $14.55

Palladium price; $951.20 UP $11.20

END

SHANGHAI GOLD PREMIUM 73 DOLLARS/COMEX GOLD

SHANGHAI GOLD (USD) FUTURES – QUOTES

Beginning Monday, April 1, 2024, CME Group settlement data will no longer be accessible through ftp.cmegroup.com and will have a delayed publication time of 12:00 a.m. CT on all cmegroup.com web pages. Learn about alternate ways to access the data in our FAQ.

Last Updated 16 Feb 2024 02:40:22 PM CT.

Market data is delayed by at least 10 minutes.

I will now provide gold in Canadian dollars, British pounds and Euros

4: 15 PM ACCESS

*CANADIAN GOLD: $2,715.15 UP 15.90 CDN dollars per oz( * NEW ALL TIME HIGH 2,795.90 CDN DOLLARS PER OZ//DEC 1 2023)

*BRITISH GOLD: 1597.15 UP 7.00 pounds per oz// *(NEW ALL TIME HIGH//CLOSING///1655.17 BRITISH POUNDS/OZ) OCT 2/2023

*EURO GOLD: 1867.70 UP 7.20 euros per oz //* (ALL TIME CLOSING HIGH: 1903.75 EUROS PER OZ//DEC 1.2023)

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

EXCHANGE: COMEX

EXCHANGE: COMEX

CONTRACT: FEBRUARY 2024 COMEX 100 GOLD FUTURES

SETTLEMENT: 2,002.100000000 USD

INTENT DATE: 02/15/2024 DELIVERY DATE: 02/20/2024

FIRM ORG FIRM NAME ISSUED STOPPED

363 H WELLS FARGO SEC 45

435 H SCOTIA CAPITAL 116

657 C MORGAN STANLEY 10

661 C JP MORGAN 77

737 C ADVANTAGE 48 1

880 H CITIGROUP 21

991 H CME 120

TOTAL: 219 219

MONTH TO DATE: 18,617

JPMorgan stopped 77/219 contracts.

FOR FEB.:

GOLD: NUMBER OF NOTICES FILED FOR FEB/2024. CONTRACT: 219 NOTICES FOR 21,900 OZ or 0,6811 TNNES

total notices so far: 18,617 contracts for 1,861,700 Oz (57.906 tonnes)

FOR FEBRUARY:

SILVER NOTICES 0 NOTICE(S) FILED FOR nil OZ/

total number of notices filed so far this month : 1066 for 5,330,000 oz

XXXXXXXXXXXXXXXXXX

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

BOTH GLD AND SLV ARE FRAUDULENT VEHICLES//THEY ARE NOW RAIDING GLD AND SLV FOR PHYSICAL

GLD

WITH GOLD UP $8.60//

INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD/ : HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A HUGE WITHDRAWAL OF 1.73 TONNES

INVENTORY RESTS AT 837.393 TONNES

SLV//

WITH NO SILVER AROUND AND SILVER UP 53 CENTS AT THE SLV//

HUGE CHANGES IN SILVER INVENTORY AT THE SLV A DEPOSIT OF 1.235 MILLION OZ INTO THE SLV/

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV.

CLOSING INVENTORY: 438.393 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A GIGANTIC SIZED 1106 CONTRACTS TO 150,643 AND FURTHER FROM THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THIS FAIR SIZED LOSS IN COMEX OI WAS ACCOMPLISHED DESPITE OUR GAIN OF $0.56 IN SILVER PRICING AT THE COMEX ON THURSDAY. WE HAD ZERO LONG LIQUIDATION AT THE COMEX SESSION BUT CONSIDERABLE SHORT COVERING AS THE PRICE OF SILVER ROSE APPRECIABLY//NO OTHER PLAUSIBLE EXPLANATION. WE HAD A HUMONGOUS 667 T.A.S ISSUANCE AND THESE WILL BE USED FOR MANIPULATION LATER THIS MONTH/AS WELL AS TODAY. PLEASE NOTE THAT THE CROOKS NEED A HIGHER SILVER T.A.S. TO CARRY ON THEIR CROOKED MANIPULATION.

CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON THURSDAY NIGHT: 667 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS. IT THUS LOOKS LIKE THE FED (GOV’T) IS BEHIND ALL OF THESE TRADES.

WE HAVE NOW SET ANOTHER RECORD LOW AT 114,102 CONTRACTS ///JULY 3.2023// OUR BANKERS WITH THE HELP OF SPECULATORS AND HIGH FREQUENCY TRADERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.56), AND WERE UNSUCCESSFUL IN KNOCKING ANY SILVER LONGS AS WE HAD A GIGANTIC SIZED LOSS OF 981 CONTRACTS ON OUR TWO EXCHANGES BUT WITH A MUCH HIGHER PRICE. THE SHORTS EXITED THEIR SHORTFALL AS FAST AS THEY COULD.

WE MUST HAVE HAD:

A VERY SMALL SIZED 125 ISSUANCE OF EXCHANGE FOR PHYSICALS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 3.535 MILLION OZ (FIRST DAY NOTICE) ACCOMPANYING A STRANGE 89 CONTRACT ISSUANCE FOR EX. FOR RISK FOR 445,000 OZ ON FIRST DAY NOTICE/ FOLLOWED BY TODAY’S 0 OZ QUEUE JUMP //NEW TOTAL REMAINS THE SAME AT ; 6.98 MILLION OZ

//NEW STANDING FOR SILVER IS THUS 6.98 MILLION OZ

/ HUGE SIZED COMEX OI LOSS/SMALL SIZED EFP ISSUANCE/ VI) HUMONGOUS SIZED NUMBER OF T.A.S. CONTRACT ISSUANCE 667 CONTRACTS)/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL -REMOVED 761 CONTRACTS //

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS FEB. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF FEB

TOTAL CONTRACTS for 12 days, total 6125 contracts: OR 30.625 MILLION OZ (510 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 30.625 MILLION OZ

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH 2022: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 118.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 85.745 MILLION OZ (SMALLER THAN LAST MONTH)

AUGUST: 171.43 MILLION OZ (THIS MONTH IS GOING TO BE HUGE //2ND HIGHEST ON RECORD

SEPT: 72.705 MILLION OZ (SMALLER THIS MONTH)

OCT: 97.455 MILLION OZ

NOV. 50.050 MILLION OZ

DEC. 66.140 MILLION OZ//

TOTAL 2023: 1,104.10 MILLION OZ/

JAN ’24 : 78.655 MILLION OZ//

FEB /2024 : 30.625 MILLION OZ.

RESULT: WE HAD A HUGE SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 1106 CONTRACTS DESPITE OUR GAIN IN PRICE OF SILVER PRICING AT THE COMEX//THURSDAY.,. THE CME NOTIFIED US THAT WE HAD A SMALL EFP ISSUANCE CONTRACTS: 125 ISSUED FOR MARCH AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS. WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR FEB. OF 3.535 MILLION OZ ACCOMPANIED BY FIRST DAY NOTICE OF 445,000 OZ EX. FOR RISK FOLLOWED BY TODAY’S 0 OZ QUEUE JUMP //NEW TOTAL REMAINS THE SAME AT 6.98 MILLION OZ

NEW STANDING 6.98 MILLION OZ /// WE HAVE A HUGE LOSS OF 981 OI CONTRACTS ON THE TWO EXCHANGES DESPITE THE GAIN IN PRICE. THE TOTAL OF TAS INITIATED CONTRACTS TODAY: A HUMONGOUS SIZED 667 CONTRACTS//HUGE FRONT END OF THE TAS CONTRACTS WERE LIQUIDATED DURING THE THURSDAY COMEX SESSION/// WITH MAJOR SHORT COVERING FROM OUR SPEC SHORTS (DRAMATIC PRICE OF SILVER RISE) . THE NEW TAS ISSUANCE THURSDAY NIGHT (667) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE//PROBABLY TODAY., .

WE HAD 0 NOTICE(S) FILED TODAY FOR nil OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A STRONG SIZED 6716 CONTRACTS TO 412,454 AND FURTHER FROM THE RECORD (SET JAN 24/2020) AT 799,733 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110, BUT CLOSER TO OUR ALL TIME LOW OF 390,000 CONTRACTS.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: – REMOVED 50 CONTRACTS

WE HAD A STRONG SIZED DECREASE IN COMEX OI ( 6716 CONTRACTS) DESPITE OUR $11.70 GAIN IN PRICE//THURSDAY. WE ALSO HAD A RATHER LARGE INITIAL STANDING IN GOLD TONNAGE FOR FEB. AT 49.773 TONNES ON FIRST DAY NOTICE ACCOMPANIED BY FIRST DAY NOTICE : 55,400 OZ EX. FOR RISK //THUS INITIAL STANDING FOR FEB: 51.494 TONNES FOLLOWED BY TODAY’S 200 OZ E.F.P. JUMP //NEW TOTAL OF GOLD STANDING LOWERS TO: 60.087 TONNES // ALL OF THIS HAPPENED DESPITE OUR $11.70 GAIN IN PRICE WITH RESPECT TO THURSDAY’S TRADING. WE HAD A GOOD SIZED LOSS OF 4179 OI CONTRACTS (12.998) PAPER TONNES) ON OUR TWO EXCHANGES.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 2539 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 412,454

IN ESSENCE WE HAVE A GOOD SIZED DECREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 4179 CONTRACTS WITH 6716 CONTRACTS DECREASED AT THE COMEX// AND A FAIR SIZED 2,539 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI LOSS ON THE TWO EXCHANGES OF 4127 CONTRACTS.. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): A STRONG SIZED 3485 CONTRACTS.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (2539 CONTRACTS) ACCOMPANYING THE STRONG SIZED LOSS IN COMEX OI (6716) //TOTAL LOSS FOR OUR THE TWO EXCHANGES: 4127 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR FORMER FORMAT OF BANKERS GOING LONG AND SPECULATORS GOING SHORT ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR FEB. AT 49.773 TONNES PLUS FIRST DAY NOTICE OF 1.723 TONNE OZ EX. FOR RISK FOLLOWED BY TODAY’S 200 OZ E.F.P. JUMP TO LONDON //NEW STANDING LOWERS TO 60.087 TONNES. / 3) ZERO LONG LIQUIDATION // 4) STRONG SIZED COMEX OPEN INTEREST LOSS/ 5) STRONG ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER///6: GOOD T.A.S. ISSUANCE: 3485 CONTRACTS//MAJOR SHORT COVERING

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023-2024 INCLUDING TODAY

FEB.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF FEB. :

TOTAL EFP CONTRACTS ISSUED: 42,283 CONTRACTS OR 4,228,300 OZ OR 131.52 TONNES IN 12 TRADING DAY(S) AND THUS AVERAGING: 3523 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 12 TRADING DAY(S) IN TONNES 131.52 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2022, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 131.52/3550 x 100% TONNES 3.69% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2023

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH/2022: 409.30 TONNES //FINAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 151.69 TONNES (WEAKER THAN LAST MONTH)

AUGUST: 195.28 TONNES (A STRONGER MONTH)//FINAL

SEPT: 254.709 TONNES (WILL BE LARGER THAN LAST MONTH AND A STRONG MONTH)

OCT. 248.09 TONNES. LIKE SILVER, THIS MONTH IS GOING TO BE A STRONG E.F.P. ISSUANCE.

NOV. 239.16 TONNES//WILL BE STRONG THIS MONTH,

DEC. 213.704 TONNES. A STRONG MONTH//

TOTAL FOR YEAR 2023: 2,569.57 TONNES VS 2578 TONNES LAST YEAR

JAN ’24: 291.76 TONNES (WILL BE MUCH GREATER THAN LAST MONTH.//3RD HIGHEST EVER RECORDED EX FOR PHYSICAL)

FEB’24: 131.52 TONNES (SHOULD BE A WEAKER ISSUANCE MONTH)

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF FEB. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (FEB), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER FELL BY A HUMONGOUS SIZED 1106 CONTRACTS OI TO 150,643 AND FURTHER FROM THE COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 6 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 125 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MARCH 125 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 125 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 345 CONTRACTS AND ADD TO THE 125 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A SMALL LOSS OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 981 CONTRACTS

THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES TOTAL 4.905 MILLION OZ

OCCURRED DESPITE OUR $.56 GAIN IN PRICE …..

END

OUTLINE FOR TODAY’S COMMENTARY

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

b, ) Gold/silver trading overnight Europe,//GOLD COMMENTARIES

(Peter Schiff)

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

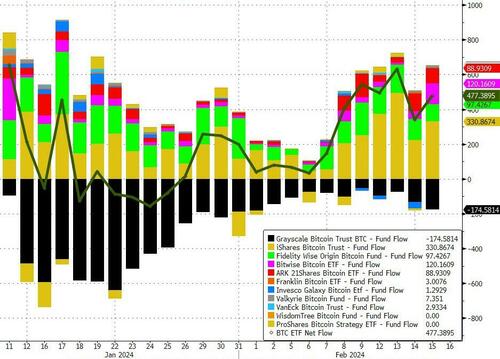

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS//

FRIDAY MORNING/THURSDAY NIGHT

SHANGHAI CLOSED XXX //Hang Seng CLOSED UP 329.30 PTS OR .86% /The Nikkei CLOSED UP 329,30 PTS OR 0.86% //Australia’s all ordinaries CLOSED UP 0.69% /Chinese yuan (ONSHORE) closed XXXX

//OFFSHORE CHINESE YUAN CLOSED UP TO 7.2187 /Oil UP TO 77.52 dollars per barrel for WTI and BRENT DOWN AT 82.09/ Stocks in Europe OPENED ALL GREEN// ONSHORE YUAN TRADING XXXX LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING XXXXX AGAINST US DOLLAR/OFFSHORE STRONGER

A)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

9. USA

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A STRONG SIZED 6716 CONTRACTS TO 412,506 DESPITE OUR GAIN IN PRICE OF $11.70 WITH RESPECT TO THURSDAY TRADING. WE ARE GETTING AWFULLY CLOSE TO OUR LOW OI OF 390,000 CONTRACTS

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE ACTIVE DELIVERY MONTH OF FEB..… THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 2539 EFP CONTRACTS WERE ISSUED: : APRIL 2539 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 2539 CONTRACTS

ON A NET BASIS IN OPEN INTEREST WE LOST THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A GOOD SIZED TOTAL OF 4179 CONTRACTS IN THAT 2539 LONGS WERE TRANSFERRED AS EXCHANGE FOR PHYSICALS TO LONDON AND WE HAD A STRONG SIZED LOSS OF 6716 COMEX CONTRACTS..AND THIS LOSS ON OUR TWO EXCHANGES HAPPENED DESPITE OUR GAIN IN PRICE OF $11.70 THURSDAY COMEX. AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS DURING MID MONTH IN THE DELIVERY CYCLE), THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR THURSDAY NIGHT WAS A GOOD SIZED 3485 CONTRACTS. THROUGHOUT THE PAST SEVERAL WEEKS, THE BANKERS SOLD OFF THE LONG SIDE OF THE SPREAD WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR/T.A.S. SPREAD WHICH WILL BE LIQUIDATED IN DAYS HENCE//.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: FEB (60.087 TONNES) ( ACTIVE MONTH)

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 24 MONTHS OF 2021-2023:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

NOV: 18.7122 TONNES + 16.2505 EX. FOR RISK = 34.9627 TONNES

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707TONNES

TOTAL 2023 YEAR : 436.546 TONNES

JAN ’24. 22.706 TONNES

FEB. ’24: 60.087 TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT GAINED $11.70 //// AND WERE UNSUCCESSFUL IN KNOCKING ANY SPECULATOR LONGS AS WE HAD A GOOD SIZED LOSS OF 4,179 TOTAL CONTRACTS ON OUR TWO EXCHANGES WITH THE MUCH HIGHER PRICE. WE HAD TO HAVE HAD A STRONG SHORT COVERING.WE HAD A STRONG T.A.S. LIQUIDATION ON THE FRONT END OF THURSDAY’S TRADING . THE T.A.S. ISSUED ON THURSDAY NIGHT, WILL BE “PUT INTO THE BANK” TO BE USED AT A LATER DATE AT THE COLLUSIVE CHOOSING OF OUR BANKERS.

WE HAVE GAINED A TOTAL OI OF 12.998 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR FEB. (49.773 TONNES) ON FIRST DAY NOTICE ALONG WITH AN EXCHANGE FOR RISK FOR 1.7235 TONNES. THIS WAS FOLLOWED WITH TODAY’S 200 OZ E.F.P. JUMP TO LONDON (0.00622 TONNES//NEW TOTAL STANDING 60.087: ALL OF THIS WAS ACCOMPLISHED WITH OUR GAIN IN PRICE TO THE TUNE OF $11.70

WE HAD -REMOVED 50 CONTRACTS TO THE COMEX TRADES TO OPEN INTEREST (CROOKS)

NET LOSS ON THE TWO EXCHANGES 4179 CONTRACTS OR 412,700 OZ OR 12.836 TONNES.

estimated volume today 157,166 poor

final gold volumes/yesterday 216,131 fair

//speculators have left the gold arena

FEB 16 INITIAL FEB GOLD

/ /// THE FEB 2024 GOLD CONTRACT

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 9547.46 oz HSBC Int Delaware incl. 17 KILOBARS . |

| Deposit to the Dealer Inventory in oz | nil oz |

| Deposits to the Customer Inventory, in oz | nil |

| No of oz served (contracts) today | 219 notice(s) 21,900 OZ 0.6811 TONNES |

| No of oz to be served (notices) | 147 contracts 14,700 oz /0.4572 TONNES |

| Total monthly oz gold served (contracts) so far this month | 18,617 notices 1861700 oz 57.906 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | x |

0 dealer deposits:

total dealer deposits: nil oz

total customer withdrawals: 1

i) Out of HSBC 546.56 of 17 kilobars

2. Out of Int. Delaware: 900.900 oz

total withdrawal: 9547.46 oz

we had 0 customer deposits

Adjustments: 1 dealer to customer

a) Out of HSBC: 494,700..489 (15.38 tonnes)

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR FEB.

For the front month of FEBRUARY we have an oi of 366 contracts having LOST 1640 contracts. We had 1638 notices filed on Thursday, so we lost 2 contracts or an additional 200 oz will not stand for delivery at the comex as these guys were ferried over to London to take delivery over there via EFP’s.

We also had 554 notices filed under exchange for risk on first day notice for a total of 55,400 oz or 1.723 tonnes to which must be added to the delivery cycle.

Thus initial standing for gold for February is 50.136 tonnes + 1.723 tonnes = 51.859 tonnes. This was followed with today’s EFP jump of 200 o//New standing 58.363 tonnes + 1.723 tonnes = 60.086 TONNES

March gained 128 contracts to stand at 2778

APRIL lost 5469 CONTRACTS FALLING TO 326,146.

We had 219 contracts filed for today representing 21,900 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 219 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 77 notice(s) was (were) stopped ( (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for the FEB. /2024. contract month, we take the total number of notices filed so far for the month (18,617 x 100 oz ), to which we add the difference between the open interest for the front month of FEB. (366 CONTRACTS) minus the number of notices served upon today 219 x 100 oz per contract equals 1,876,400 OZ OR 58.363 TONNES + 1.723 Ex for Risk/prior = 60.087 tonnes

thus the INITIAL standings for gold for the FEB. contract month: No of notices filed so far (18,617) x 100 oz + (366) {OI for the front month} minus the number of notices served upon today (219) x 100 oz which equals 1,876,400 oz (58.37 TONNES) + 54,400 oz (1.723 TONNES) ex. for risk/prior// NEW total standing OR 60.087 TONNES

TOTAL COMEX GOLD STANDING FOR FEB: 60.093 TONNES WHICH IS GREAT FOR AN ACTIVE DELIVERY MONTH IN THE CALENDAR.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 1,401,068.091 43.579 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD: 18,460,807.209 OZ

TOTAL REGISTERED GOLD 8,134,531.537 (253.00 tonnes).

TOTAL OF ALL ELIGIBLE GOLD: 10,326,275.672 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 6,733,463 oz (REG GOLD- PLEDGED GOLD) 209.43 tonnes

END

SILVER/COMEX

FEB 16/INITIAL

//2024// THE FEB 2024 SILVER CONTRACT//INITIAL

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 600,198.830oz CNT . |

| Deposits to the Dealer Inventory | nil OZ |

| Deposits to the Customer Inventory | 579,727.69 oz hsbc manfra |

| No of oz served today (contracts) | 0 CONTRACT(S) (nil OZ) |

| No of oz to be served (notices) | 241 contracts (1,205,000 oz) |

| Total monthly oz silver served (contracts) | 1066 Contracts (5,330,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

i) 0 dealer deposit

total dealer deposit: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: 0 oz

We had 2 deposits customer account:

i) Into HSBC: 1070.598 oz

ii) Into Manfra 578,687.100 oz

total customer deposits 579,727.69 oz

JPMorgan has a total silver weight: 129.806 million oz/278.193 million or 46.76%

adjustment: 0

Comex withdrawals: 1

Out of CNT 600,198.88 oz

total withdrawal: 600,198.88 oz

TOTAL REGISTERED SILVER: 42.868 MILLION OZ//.TOTAL REG + ELIGIBLE. 278.193 million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR DECEMBER:

silver open interest data:

FRONT MONTH OF FEB. /2023 OI: 241 CONTRACTS HAVING GAINED 0 CONTRACT(S). WE HAD 0 NOTICES FILED ON WEDNESDAY SO WE GAINED 0 CONTRACTS OR AN ADDITIONAL NIL OZ OF SILVER CONTRACTS WILL STAND FOR DELIVERY AT THE COMEX

MARCH LOST 5179 CONTRACTS TO 68,172

APRIL SAW A GAIN OF 7 CONTRACT TO STAND AT 54

MAY SAW A GAIN OF 3741 CONTRACTS UP TO 62,838

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 0 for NIL oz

Comex volumes// est. volume today 84,289 huge

Comex volume: confirmed yesterday 115,203 huge//

To calculate the number of silver ounces that will stand for delivery in FEB. we take the total number of notices filed for the month so far at 1066 x 5,000 oz = 5,330,000 oz

to which we add the difference between the open interest for the front month of FEB. (241) and the number of notices served upon today 0 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the FEB/2024 contract month: 1066 (notices served so far) x 5000 oz + OI for the front month of FEB. (241) – number of notices served upon today (0 )x 500 oz of silver standing for the FEB contract month equates to 6.5350 MILLION OZ. + .445 MILLION OZ EX. FOR RISK PRIOR//NEW TOTAL 6.9700 MILLION OZ

New total standing: 6.9800 million oz.

There are 42.868 million oz of registered silver.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS//

BOTH GLD AND SLV ARE MASSIVE FRAUDS!

FEB16/WITH GOLD UP $8,60 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.73 TONNES OF GOLD FROM THE GLD///INVENTORY RESTS AT 837.31 TONNES

FEB15/WITH GOLD UP $11.70 TODAY NO CHANGES IN GOLD INVENTORY AT THE GLD:/INVENTORY RESTS AT 841.92 TONNES

FEB14/WITH GOLD DOWN $2.75 TODAY NO CHANGES IN GOLD INVENTORY AT THE GLD:/INVENTORY RESTS AT 841.92 TONNES

FEB13/WITH GOLD DOWN $20.15 TODAY NO CHANGES IN GOLD INVENTORY AT THE GLD:/INVENTORY RESTS AT 841.92 TONNES

FEB12/WITH GOLD DOWN $4.80 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A STRONG WITHDRAWAL OF 1.74 TONNES OF GOLD FROM THE GLD. / //://INVENTORY RESTS AT 841.92 TONNES

FEB9/WITH GOLD DOWN $8.60 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A STRONG DEPOSIT OF 1.44 TONNES OF GOLD FROM THE GLD. / //://INVENTORY RESTS AT 843.66 TONNES

FEB8/WITH GOLD DOWN $2.70 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A MASSIVE WITHDRAWAL OF 5.47 TONNES OF GOLD FROM THE GLD. / //://INVENTORY RESTS AT 842.22 TONNES:

FEB7/WITH GOLD UP $0.40 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A MASSIVE WITHDRAWAL OF 4.04 TONNES OF GOLD FROM THE GLD. / //://INVENTORY RESTS AT 847.69 TONNES:

FEB6/WITH GOLD UP $8.50 TODAY NO CHANGES IN GOLD INVENTORY AT THE GLD:/ / //://INVENTORY RESTS AT 851.73 TONNES:

FEB5/WITH GOLD DOWN $9.85 TODAY SMALL CHANGES IN GOLD INVENTORY AT THE GLD:A DEPOSIT OF .58 TONNES OF GOLD INTO THE GLD// / //://INVENTORY RESTS AT 851.73 TONNES:

FEB 2/WITH GOLD DOWN $17.95 TODAY SMALL CHANGES IN GOLD INVENTORY AT THE GLD:A WITHDRAWAL OF .58 TONNES OF GOLD FROM THE GLD// / //://INVENTORY RESTS AT 851.15 TONNES:

FEB 1/WITH GOLD UP $5.00 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD:A WITHDRAWAL OF 1.73 TONNES OF GOLD FROM THE GLD// / //://INVENTORY RESTS AT 851.15 TONNES:

JAN 31/WITH GOLD UP $16.40 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD:A WITHDRAWAL OF 2.01 TONNES OF GOLD FROM THE GLD// / //://INVENTORY RESTS AT 852.88 TONNES:

JAN 30/WITH GOLD UP $6.50 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD:A WITHDRAWAL OF 1.16 TONNES OF GOLD FROM THE GLD// / //://INVENTORY RESTS AT 854.89 TONNES:

TOTAL IN LAST 18 DAYS WITHDRAWAL OF 14.12 TONNES

JAN 29/WITH GOLD UP $8.70 TODAYHUGE CHANGES IN GOLD INVENTORY AT THE GLD:A WITHDRAWAL OF 2.88 TONNES OF GOLD FROM THE GLD// / //://INVENTORY RESTS AT 856.05 TONNES

JAN 26/WITH GOLD DOWN $0.10 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD: / //://INVENTORY RESTS AT 858.93 TONNES

JAN 25/WITH GOLD UP $2.50 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD: / //://INVENTORY RESTS AT 858.93 TONNES

JAN 24/WITH GOLD DOWN $9.75 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD: / //://INVENTORY RESTS AT 858.93 TONNES

JAN 23/WITH GOLD UP $3.95 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.02 TONNES OF GOLD FROM THE GLD/ //://INVENTORY RESTS AT 858.93 TONNES

JAN 22/WITH GOLD DOWN $6.00 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.15 TONNES OF GOLD FROM THE GLD/ //://INVENTORY RESTS AT 860.95 TONNES

JAN 19/WITH GOLD UP $8.15 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD //://INVENTORY RESTS AT 862.10 TONNES

JAN 18/WITH GOLD UP $14.85 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 2.30 TONNES OF GOLD FROM THE GLD//://INVENTORY RESTS AT 862.10 TONNES

JAN 17/WITH GOLD DOWN $23.25 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF .549 TONNES OF GOLD INTO THE GLD.;//://INVENTORY RESTS AT 864.40 TONNES

JAN 12/WITH GOLD UP $31.65 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD; A MASSIVE WITHDRAWAL OF 4.61 TONNES OF GOLD FROM THE GLD//://INVENTORY RESTS AT 864.99 TONNES

GLD INVENTORY: 841.92 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

FEB 16/WITH SILVER UP 53 CENTS TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV A DEPOSIT OF 1.235 MILLION OZ OF SILVER FROM THE SLV// : SLV INVENTORY RESTS AT 438.393 MILLION OZ

FEB 15/WITH SILVER UP 56 CENTS TODAY NO CHANGES IN SILVER INVENTORY AT THE SLV : SLV INVENTORY RESTS AT 437.615 MILLION OZ

FEB 14/WITH SILVER UP 24 CENTS TODAY NO CHANGES IN SILVER INVENTORY AT THE SLV : SLV INVENTORY RESTS AT 437.615 MILLION OZ

FEB 13/WITH SILVER DOWN 60 CENTS TODAY SMALL CHANGES IN SILVER INVENTORY AT THE SLV A SMALL WITHDRAWAL OF 0.504 MILLION OZ OZ OUT OF THE SLV: SLV INVENTORY RESTS AT 437.615 MILLION OZ

FEB 12/WITH SILVER UP 14 CENTS TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV A HUGE WITHDRAWAL OF 1.921 MILLION OZ OZ OUT OF THE SLV: SLV INVENTORY RESTS AT 438.119 MILLION OZ

FEB 9/WITH SILVER DOWN 4 CENTS TODAY SMALL CHANGES IN SILVER INVENTORY AT THE SLV A SMALL DEPOSIT OF 600,000 OZ INTO THE SLV: SLV INVENTORY RESTS AT 440.040 MILLION OZ

FEB 8/WITH SILVER UP 29 CENTS TODAY NO CHANGES IN SILVER INVENTORY AT THE SLV: SLV INVENTORY RESTS AT 439.994 MILLION OZ

FEB 7/WITH SILVER DOWN 18 CENTS TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A MASSIVE DEPOSIT OF 4.04 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 439.994 MILLION OZ//LAST 9 DAYS: 10.7598 MILLION OZ WITHDRAWAL

FEB 6/WITH SILVER UP 11 CENTS TODAY NO CHANGES IN SILVER INVENTORY AT THE SLV: /INVENTORY RESTS AT 435.144 MILLION OZ//LAST 9 DAYS: 10.7598 MILLION OZ WITHDRAWAL

FEB 5/WITH SILVER DOWN 32 CENTS TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.345 MILLION OZ FROM THE SLV(FAIRY TALES) // /INVENTORY RESTS AT 435.144 MILLION OZ//LAST 8 DAYS: 10.7598 MILLION OZ WITHDRAWAL

FEB 2/WITH SILVER DOWN 50 CENTS TODAY SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 0.58 MILLION OZ INTO THE SLV(FAIRY TALES) // /INVENTORY RESTS AT 438.489 MILLION OZ//LAST 7 DAYS: 14.105 MILLION OZ WITHDRAWAL

FEB 1/WITH SILVER UP 7 CENTS TODAY MEGA CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.19 MILLION OZ INTO THE SLV(FAIRY TALES) // /INVENTORY RESTS AT 438.947 MILLION OZ//LAST 6 DAYS: 10.3018 MILLION OZ WITHDRAWAL

JAN 31/WITH SILVER DOWN 8 CENTS TODAY MEGA CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.7438 MILLION OZ INTO THE SLV(FAIRY TALES) // /INVENTORY RESTS AT 440.137 MILLION OZ//LAST 5 DAYS: 9.1118 MILLION OZ WITHDRAWAL

JAN 30/WITH SILVER DOWN 5 CENTS TODAY MEGA CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.876 MILLION OZ INTO THE SLV(FAIRY TALES) // /INVENTORY RESTS AT 442.699 MILLION OZ//LAST 4 DAYS: 7.368 MILLION OZ WITHDRAWAL

JAN 29/WITH SILVER UP $.37 TODAY MEGA CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.105 MILLION OZ INTO THE SLV(FAIRY TALES) // /INVENTORY RESTS AT 444.575 MILLION OZ

JAN 26/WITH SILVER DOWN $0.03 TODAY MEGA CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.556 MILLION OZ INTO THE SLV(FAIRY TALES) // /INVENTORY RESTS AT 446.680 MILLION OZ

JAN 25/WITH SILVER UP $0.03 TODAY MEGA CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.831 MILLION OZ INTO THE SLV(FAIRY TALES) // /

INVENTORY RESTS AT 448.236 MILLION OZ

JAN 24/WITH SILVER UP $0.44 TODAY MEGA CHANGES IN SILVER INVENTORY AT THE SLV: ANOTHER DEPOSIT OF 1.375 MILLION OZ INTO THE SLV(FAIRY TALES) // //INVENTORY RESTS AT 450.067 MILLION OZ

JAN 23/WITH SILVER UP $0.21 TODAY MEGA CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 16.201 MILLION OZ INTO THE SLV(FAIRY TALES) // //INVENTORY RESTS AT 448.694 MILLION OZ

JAN 22/WITH SILVER DOWN $0.45 TODAY NO CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 458,000 OZ OUT OF THE SLV // //INVENTORY RESTS AT 432.493 MILLION OZ

JAN 19/WITH SILVER DOWN $0.11 TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 458,000 OZ OUT OF THE SLV // //INVENTORY RESTS AT 432.493 MILLION OZ

JAN 18/WITH SILVER UP $0.13 TODAY NO CHANGES IN SILVER INVENTORY AT THE SLV: // //INVENTORY RESTS AT 432.951 MILLION OZ

JAN 17/WITH SILVER DOWN $0.38 TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 779,000 OZ FROM THE SLV.: // //INVENTORY RESTS AT 433.500 MILLION OZ

JAN 16/WITH SILVER DOWN $0.08 TODAY NO CHANGES IN SILVER INVENTORY AT THE SLV: // //INVENTORY RESTS AT 433.500 MILLION OZ

JAN 12/WITH SILVER UP $0.62 TODAY NO CHANGES IN SILVER INVENTORY AT THE SLV: // //INVENTORY RESTS AT 433.500 MILLION OZ

CLOSING INVENTORY 438.393 MILLION OZ//

PHYSICAL GOLD/SILVER COMMENTARIES

1:Peter Schiff/Mike Maharrey

The Gold/Silver Ratio Says Silver’s Still Cheap

FRIDAY, FEB 16, 2024 – 07:20 AM

The silver price has dipped since December, from almost $26 per ounce to around $22 today. We reported on silver being a relative bargain at the time, and with lower spot prices and an even higher gold/silver ratio today, gold’s monetary sibling is looking like an even more attractive buy than it was late last year.

The gold/silver ratio refers to how many ounces of silver would buy a single ounce of gold, and at one point, the number was fixed by law. A lot has changed since then, with gold no longer backing the US dollar, and a whole array of precious metals-linked financial products like futures and ETFs adding to the complexity of the market.

Without a legally imposed gold/silver ratio or dollar peg, the number is now free to fluctuate and can be a valuable tool when considering if it’s a good time to buy. Gold has been on a tear lately, hovering not far from its all-time high last December when it topped at over $2,100 per ounce. The price of silver often follows suit.

A high gold/silver ratio signals that silver is being potentially undervalued, and in December the number was 81-1, far above the modern average between 40-1 to 60-1. Since then, it has ratcheted up another 5-10 points, currently above 1-90.

The last time the ratio was higher than it is now was in August 2022, when it hovered around 95 ounces of silver for one ounce of gold. From then until April the following year, the price of silver worked its way up from around $20 an ounce up to a high of $25 before retracing again. It will be interesting to see if the ratio touches these levels again (or beyond) — and if we see a similar bull market for silver in the next 6-8 months. The following chart shows the gold/silver ratio since April 2022:

In the context of bargain-price silver, the best bet is still using it as a companion to gold as a long-term inflation hedge rather than cashing out on short or medium-term trades. Even perfectly-timed buys and sells are subject to capital gains taxes and other mark-up. If you zoom out, industrial demand for silver is expected to skyrocket in the next decade, and history has proven that silver will always be a better form of money than fiat.

The long-term fundamentals are as solid as ever, while the high gold/silver ratio is a bullish sign for silver on a shorter time scale especially when the Fed finally decides to cut rates later in the year. As noted in The Silver Institute’s January report:

“…the Fed is expected to signal further and accelerated easing next year. The impact of falling real yields and pressure on the U.S. dollar should also favor fresh silver and gold investment.”

So, with the Fed expected to fire up its money printers again soon, cutting rates and funding expanding global conflicts with new debt, silver traders would be better off accumulating bullion to beat inflation over the long-term instead of gunning for short-term taxable returns by trading in and out of a rapidly-depreciating currency.

2) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens/JIM RICKARDS

END

3. CHRIS POWELL//GATA GOLD COMMENTARIES: daily Dispatches

4. OTHER GOLD COMMENTARIES/PODCASTS

AGNICO EAGLE RESULTS//EARNINGS OF 57 CENTS USA AND BETTER BY 8 CENTS ACCORDING TO ANALYSTS. MOST IMPORTANT RESERVES INCREASED BY 10.5% TO 53.8 MILLION OZ

NO DOUBT, THE BEST MINING COMPANY IN THE WORLD.

THEY REFUSE TO HELP US BUT THEY ARE THE BEST AT WHAT THEY DO:

AGNICO EAGLE REPORTS FOURTH QUARTER AND FULL YEAR 2023 RESULTS – RECORD QUARTERLY AND ANNUAL GOLD PRODUCTION AND FREE CASH FLOW; RECORD MINERAL RESERVES INCREASED 10.5%; UPDATED THREE-YEAR GUIDANCE

February 15, 2024

Download this Press ReleasePDF Format (opens in new window)

(All amounts expressed in U.S. dollars unless otherwise noted)

Stock Symbol: AEM (NYSE and TSX)

TORONTO, Feb. 15, 2024 /CNW/ – Agnico Eagle Mines Limited (NYSE:AEM) (TSX:AEM) (“Agnico Eagle” or the “Company”) today reported financial and operating results for the fourth quarter and full year of 2023, as well as future operating guidance.

“We had a very strong close to 2023, with our fourth quarter results driving a record year in terms of safety, operating and financial performance. We achieved the top end of our gold production guidance range and the mid-point of our cost guidance ranges despite inflationary pressures throughout the year,” said Ammar Al-Joundi, Agnico Eagle’s President and Chief Executive Officer. “We are extremely pleased with the results that our teams have accomplished with their hard work this year and we have much to look forward to. We are reporting record mineral reserves and a stable production profile at industry leading costs, anchored by the two largest gold operations in Canada, the Detour Lake mine and the Canadian Malartic complex. We continue to advance studies on optimizing our Abitibi platform and we expect to provide additional updates in the first half of 2024. Our track record of executing and delivering results demonstrates the strength of our business and we are well positioned to create long-term value and generate strong returns,” added Mr. Al-Joundi.

Fourth quarter and full year 2023 highlights:

- Record quarterly gold production – Payable gold production1 in the fourth quarter of 2023 was 903,208 ounces at production costs per ounce of $861, total cash costs per ounce2 of $888 and all-in sustaining costs (“AISC”) per ounce3 of $1,227. Gold production in the fourth quarter of 2023 was led by strong production at the Detour Lake mine, the LaRonde complex and the Macassa mine, offsetting lower production at the Fosterville mine

- Record quarterly cash provided by operating activities and free cash flow – The Company reported a quarterly net loss of $381.0 million or $0.77 per share and adjusted net income4 of $282.3 million or $0.57 per share for the fourth quarter of 2023. Included in the quarterly net loss are impairment charges totaling $667 million (net of tax) or $1.35 per share relating to the Macassa and Pinos Altos mines. Cash provided by operating activities was $1.47 per share ($1.57 per share before working capital adjustments5) and free cash flow5 was $0.61 per share ($0.71 per share before working capital adjustments5)

- Record annual safety performance, annual gold production and free cash flow driven by solid operational performance – Payable gold production in 2023 was 3,439,654 ounces at production costs per ounce of $853, total cash costs per ounce of $865 and AISC per ounce of $1,179. Production for 2023 was at the very top end of the Company’s 2023 guidance range of 3.24 million ounces to 3.44 million ounces. Total cash costs per ounce were at the midpoint of the Company’s 2023 guidance and AISC per ounce were in the range of the Company’s 2023 guidance. Free cash flow for the full year 2023 was $947.4 million ($1,093.8 million before changes in non-cash components of working capital)

- Record gold mineral reserves driven by declaration of initial mineral reserves at East Gouldie – Year-end 2023 gold mineral reserves increased by 10.5% to 53.8 million ounces of gold (1,287 million tonnes grading 1.30 grams per tonne (“g/t”) gold). The year-over-year increase in mineral reserves is largely due to the declaration of initial mineral reserves at East Gouldie, the acquisition of the remaining 50% interest in the Canadian Malartic complex and net mineral reserve additions at Macassa. At year-end 2023, measured and indicated mineral resources were 44.0 million ounces (1,189 million tonnes grading 1.15 g/t gold) and inferred mineral resources were 33.1 million ounces (411 million tonnes grading 2.50 g/t gold), including initial underground inferred mineral resources at Detour Lake. For further details, see the Company’s exploration news release dated February 15, 2024

- Stable three-year production outlook – Payable gold production is forecast to be approximately 3.35 to 3.55 million ounces in 2024 and approximately 3.40 to 3.60 million ounces in 2025 (unchanged from prior three-year guidance issued on February 16, 2023 (“Previous Guidance”)). Payable gold production is forecast to remain stable in 2026 at an expected range of approximately 3.40 to 3.60 million ounces

- Unit costs reflect easing rate of inflation – Total cash costs per ounce and AISC per ounce in 2024 are forecast to be $875 to $925 and $1,200 to $1,250, respectively. The midpoints of these ranges each represent an approximate 4% increase when compared to the full year 2023 total cash costs per ounce of $865 and AISC per ounce of $1,179. The expected cost increases in 2024 are mostly related to labour, spare parts and maintenance

- Capital expenditures forecast to be approximately $1.65 billion in 2024 – Capital expenditures in 2024 (excluding capitalized exploration) are expected to increase relative to Previous Guidance of $1.40 to 1.60 billion. The expected increase in 2024 is mostly attributable to 100% ownership of Canadian Malartic for the full year, inflation and additional capital expenditures at Detour Lake

- Strategic optimization initiatives improve Canadian production base, with further clarity on the medium term potential to be provided through 2024 – Key developments in 2023 included the declaration of commercial production at Canadian Malartic’s Odyssey South deposit, a 12% increase in mill throughput at Detour Lake year-over-year and development of the Near Surface (“NSUR”) and Amalgamated Kirkland (“AK”) deposits at Macassa. The Company expects to provide updates on additional opportunities that are being evaluated in the Abitibi region in the first half of 2024

- Odyssey mine at the Canadian Malartic complex – The planned mining rate of 3,500 tonnes per day (“tpd”) at Odyssey South was reached earlier than anticipated and sustained through the fourth quarter of 2023. Ramp development has also exceeded target, reaching a depth of 715 metres as at December 31, 2023. The Company is evaluating the potential to accelerate initial production from East Gouldie to 2026 from 2027. Surface construction is progressing as planned, with approximately 65% completed at year-end, and shaft sinking activities continued to ramp up through the quarter. Infill and expansion drilling in 2023 resulted in the declaration of an initial mineral reserve in the central portion of the East Gouldie deposit of 5.17 million ounces of gold (47.0 million tonnes grading 3.42 g/t gold) and the extension of the East Gouldie mineral resource laterally by 870 metres

- Detour Lake – The mill delivered a strong performance in the fourth quarter of 2023, operating at a throughput rate of 71,826 tpd (equivalent to an annualized rate of approximately 26.2 million tonnes per annum (“Mtpa”). With sustained improvements year-over-year, the Company now expects the mill to reach a throughput rate of approximately 76,700 tpd (equivalent to an annualized rate of approximately 28 Mtpa) late in the second half of 2024, previously expected in 2025. At year-end 2023, the Company reported an initial underground inferred mineral resource below and to the west of the existing pit, totaling 1.56 million ounces of gold (21.8 million tonnes grading 2.23 g/t gold) and continues to evaluate the potential for underground mining. Exploration in 2024 is expected to continue to test the west plunge extension of the main deposit. An exploration ramp is also being considered to facilitate drilling that would increase confidence in the continuity of the inferred mineral resource and, potentially, to collect a bulk sample. The Company expects to provide an update on mill optimization efforts, the Detour underground project and ongoing exploration results in the first half of 2024

- Abitibi region of Quebec and Ontario – Macassa’s NSUR and AK deposits have now been incorporated in the Company’s production guidance. At Upper Beaver, the Company is conducting a trade-off analysis comparing transporting and processing ore at the LaRonde mill to a standalone central mill for Upper Beaver and satellite deposits. An exploration ramp and shaft are being considered at Upper Beaver in order to upgrade and further explore the deeper portions of the deposit. At Wasamac, the Company is assessing hauling alternatives and the optimal mining rate for transporting and processing ore at the Canadian Malartic mill. The Company expects to complete internal technical evaluations for Upper Beaver and Wasamac in the first half of 2024

- Amaruq mine at the Meadowbank complex – The Company extended Amaruq’s mine life to 2028 (previous mine life was to 2026), adding approximately 500,000 ounces of gold to the expected mining profile, as a result of continuous improvement and cost optimization efforts, positive infill drilling and positive reconciliation to the geological model

- Hope Bay – At the Madrid deposit, the target area in the gap between the Suluk and Patch 7 zones delivered strong drill results in the quarter, including 16.3 g/t gold over 28.6 metres at 385 metres depth and 12.7 g/t gold over 4.6 metres at 677 metres depth. Results confirm the potential to expand gold mineralization in the Madrid deposit at depth and along strike to the south. Based on recent exploration success, the Company is evaluating a larger potential production scenario for Hope Bay. The Company expects to report results from this internal technical evaluation in 2025

- A quarterly dividend of $0.40 per share has been declared

END

live from the vault; 160

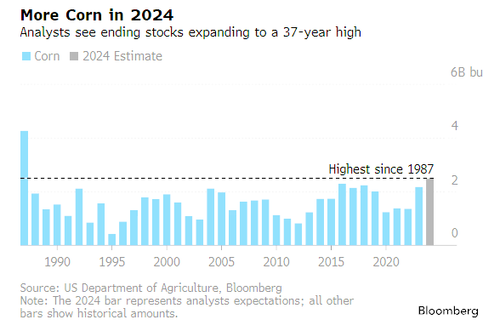

5 a. IMPORTANT COMMENTARIES ON COMMODITIES /CORN

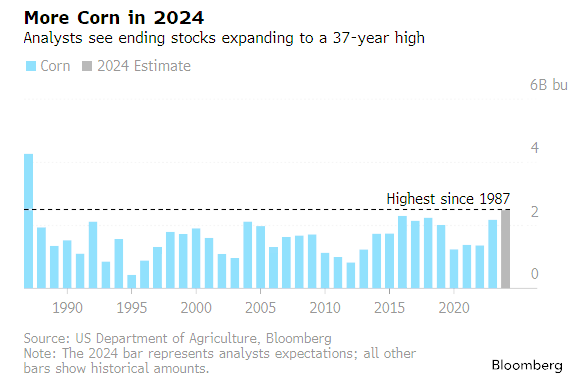

Corn Drops To 3-Year Low As Supplies Expected To Surge To 1987 Levels

FRIDAY, FEB 16, 2024 – 05:45 AM

Corn futures hit a three-year low as traders waited for the US Department of Agriculture’s annual outlook forum on Thursday. The USDA’s initial outlook for the coming season could show higher domestic crop supplies and elevated spring plantings.

According to Bloomberg, USDA’s annual outlook forum is expected to project the largest domestic stockpile since 1987.

Traders have already been pricing in a dismal outlook, with money managers holding the largest bearish bet in almost five years. Corn for March delivery has nearly roundtripped all Covid gains.

A survey of Bloomberg analysts expected the upcoming 2024-25 season will reach upwards of 2.493 billion bushels. This will exert continued downward pressure on US farmers and force them to decrease spring plantings of corn in favor of planting more soybeans.

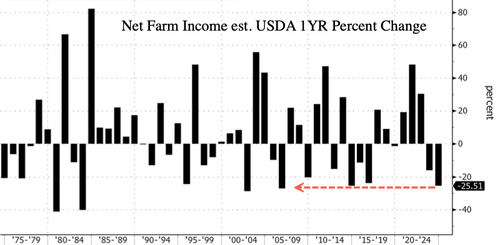

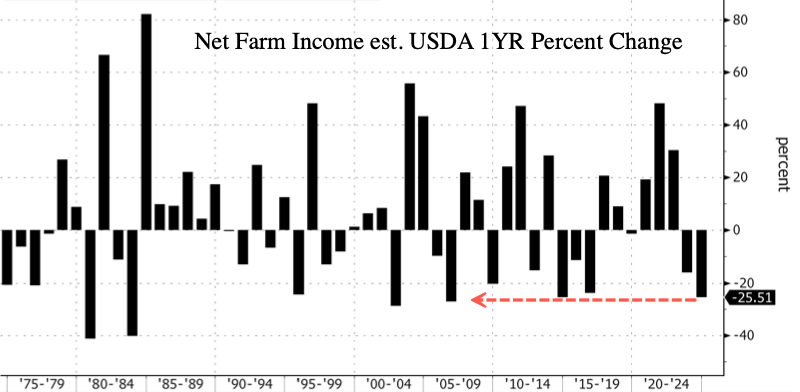

Meanwhile, in a separate USDA report, new forecasts show US farmers are poised for another year of financial misery, facing the most significant decline in incomes in almost two decades as grain prices slide and US dominance in ag exports wanes.

USDA forecasts net farm income, a broad measure of profits, to plunge $39.8 billion, or 25.5%, to $116.1 billion in 2024. This follows a forecasted decrease of $29.7 billion, or 16%, from 2022 to $155.9 billion in 2023.

If the estimate holds, farmers face the largest income drop since 2006 and back-to-back years of financial pain.

“With this expected decline, net farm income in 2024 would be 1.7 percent below its 20-year average (2003–22) of $118.2 billion and 40.9 percent below the record high in 2022 in inflation-adjusted dollars,” USDA wrote in the report.

What could reverse sliding grain prices? More Black Sea destabilization…

END

5 B GLOBAL COMMODITY ISSUES/FOOD IN GENERAL//FREIGHT

END

6.CRYPTOCURRENCY//DIGITAL CURRENCY// COMMENTARIES/

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS FRIDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED

OFFSHORE YUAN: UP TO 7.2187

SHANGHAI CLOSED

HANG SENG CLOSED UP 395.33 PTS OR 2.48%

2. Nikkei closed UP 329..30 OR 0.86%

3. Europe stocks SO FAR: ALL GREEN

USA dollar INDEX UP TO 104.22 EURO RISES TO 1.0771 DOWN 2 BASIS PTS

3b Japan 10 YR bond yield: RISES TO. +.720 Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 150.22/JAPANESE YEN NOW RISING AS WELL AS LONG TERM 10 YR. YIELDS RISING //EVENTUALLY THIS WILL BREAK THE JAPANESE CENTRAL BANK

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen UP CHINESE ONSHORE YUAN: XXX// OFFSHORE: UP

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and UP FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund UP TO +2.3975***/Italian 10 Yr bond yield UP to 3.87340* /SPAIN 10 YR BOND YIELD UP TO 3.292…**

3i Greek 10 year bond yield UP TO 3.353

3j Gold at $2006.40 silver at: 22.97 1 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble DOWN 0 AND 58 /100 roubles/dollar; ROUBLE AT 92.75//

3m oil into the 77 dollar handle for WTI and 82 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 150.22// 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 0.720% STILL ON CENTRAL BANK (JAPAN) INTERVENTION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.8868 as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.9489 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.274 UP 4 BASIS PTS…

USA 30 YR BOND YIELD: 4.436 UP 2 BASIS PTS/

USA 2 YR BOND YIELD: 4.608 UP 5 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 30.83…(TURKEY SET TO BLOW UP FINANCIALLY)

GREAT BRITAIN/10 YEAR YIELD: UP 8 BASIS PTS AT 4.1385

end

2.a Overnight: Newsquawk and Zero hedge

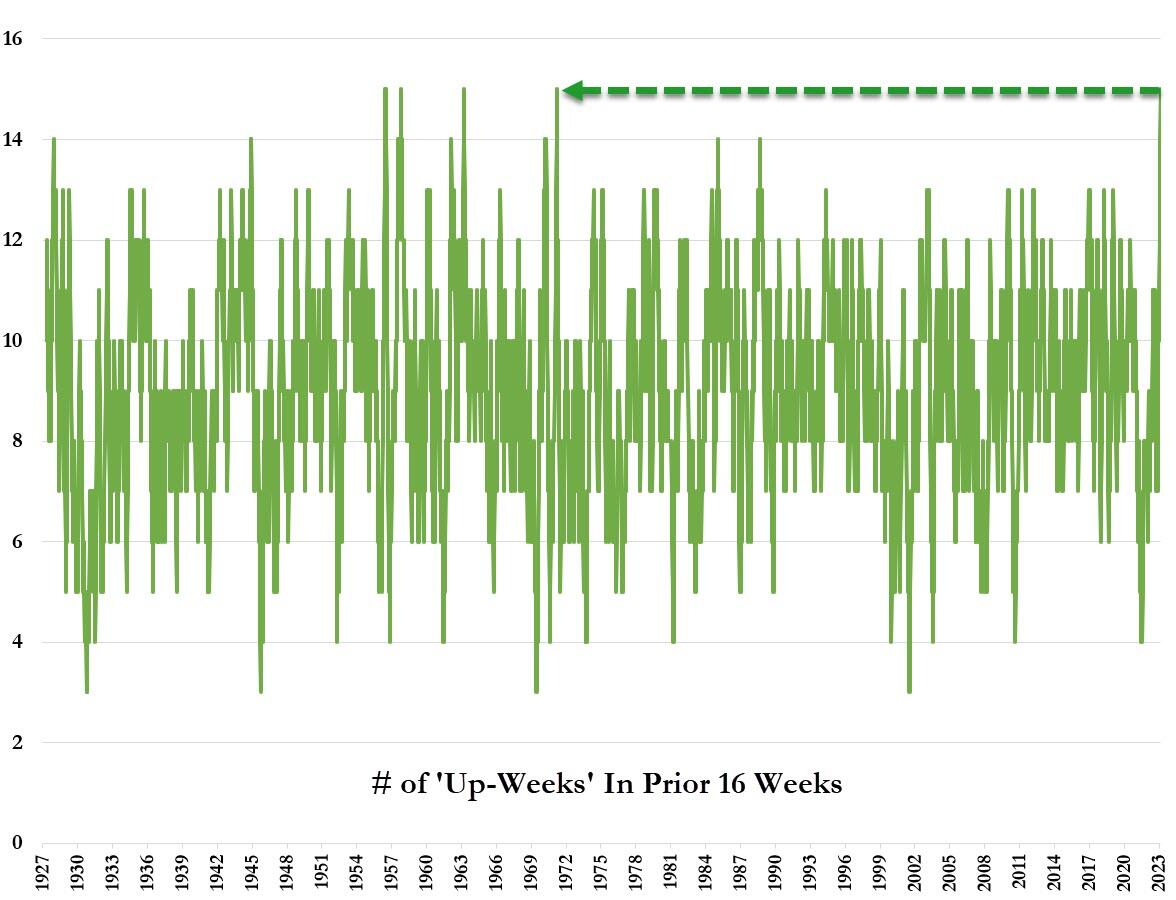

Stocks Set To Make It A Record 15 Weeks Higher Out Of 16 As Tech Surge Goes On

FRIDAY, FEB 16, 2024 – 08:13 AM

After stocks successfully recovered from a mid-week rout following the much hotter than expected CPI print, resulting in a burst of BTFD and flurry of 0DTE buying, on the last day of the week, S&P 500 futures were up 0.2% – amid bigger gains in European stocks …

… and were on pace to dodge a weekly red candle in the process setting up a record 15th weekly gain of the past 16, as the market no longer drop. Ever. Meanwhile, the euphoria was even more ridiculous over in tech world where Nasdaq futures accelerated their silly meltup, rising 0.5%, propelled by Applied Materials rising ~13% in premarket trading while the current generation’s Gamestop, Supermicro, was up another 6% premarket, sending its RSI to a record 98.

Treasuries declined, sending the 10Y yield up 3bps to 4.27% after Atlanta Fed President Raphael Bostic said there’s no rush to cut rates with the US labor market and economy still strong.

In premarket trading, Applied Materials, the largest US maker of chipmaking machinery, jumped 13% in premarket trading after giving a bullish revenue forecast that signalled some of the largest semiconductor companies are increasing their investments in new production. The update pushed up shares in European peers including Aixtron SE and ASML Holding NV. Here are some other notable premarket movers:

- Bloom Energy falls 19% after the company’s 2024 revenue guidance missed the average analyst estimate.

- Coinbase gains 15% after the cryptocurrency exchange reported revenue and earnings per share for the fourth quarter that beat.

- DoorDash drops 7% after the company’s guidance for full-year marketplace gross order value trailed the average analyst estimate at the midpoint.

- DraftKings slips 5% after company’s 4Q adjusted Ebitda missed estimates, with Morgan Stanley flagging headwinds from “unfavorable sports outcomes.”

- Dropbox drops 13% after the file management software company reported fourth-quarter results that are seen as weak.

- Roku falls 16% after first-quarter forecasts from the streaming-video platform company failed to impress.

- SunPower tumbles 11% after the struggling rooftop solar installer announced $155 million in new financing from its majority investors — a development that will ease a cash crunch but also dilute the shares.

- Toast rises 9% after the restaurant software company gave a full-year forecast for adjusted Ebitda that was stronger than expected.

- Trade Desk gains 18% after the advertising technology company gave a first-quarter forecast that is much stronger than expected.

- TreeHouse Foods falls 11% after the company issued net sales projections for year that trailed the average analyst estimates.

- Yelp drops 9% after guiding for lower-than-expected adjusted Ebitda for 2024.

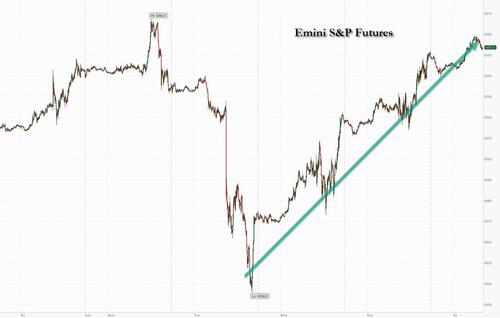

The S&P 500 climbed to its latest record high Thursday, erasing all this week’s losses, as a drop in US retail sales tempered investor worries about overheated consumer demand. Data on US producer prices later will draw higher-than-usual scrutiny after a hot consumer price index earlier this week roiled financial markets, with traders resetting their bets on Fed rate-cuts in 2024.

Meanwhile the latest bubble euphoria just won’t stop, as US equity funds registered inflows of $11 billion in the week through Feb. 14, the most in seven weeks, according to Bank of America. On the downside, breadth of the S&P 500 is currently the weakest since 2009 as the top five stocks in the index have fueled 75% of its gain so far this year, according to the Bank of America report.

“Q4 earnings have helped equities to cope with rates volatility,” said Emmanuel Cau, a strategist at Barclays Plc, in a note to clients. “Sticky US inflation keeps Goldilocks in check, but post the latest hawkish repricing, rates expectations have converged more toward the Fed forecasts.”

European stocks rise for a third day meanwhile, tracking a broadly positive session in Asia. Mining stocks led the advance in Europe that took Europe’s Stoxx 600 index to its fourth consecutive week of gains. Glencore Plc and Anglo American Plc both rose more than 3% amid optimism of a rebound in Chinese demand for metals. European commercial real estate stocks also gained after major US peer CBRE Group reported strong fourth-quarter earnings and suggested the worst was over for the downtrodden market for office leasing. Shares of CBRE, the world’s largest commercial real estate stock, jumped to the highest level in almost two years. Here are the most notable movers in Europe:

- European chip-tool makers’ shares advance after their largest US peer, Applied Materials, gave a bullish revenue forecast for the current period, signaling that some of the biggest semiconductor companies are increasing their investments in new production.

- European luxury stocks climb in early trading, boosted by a resurgence in Chinese travel over the Lunar New Year holiday.

- Sika shares gain as much as 3.9% after the Swiss building materials group presented new guidance which reassured analysts amid weak macroeconomic trends.

- NatWest shares turn higher in volatile trading Friday, rising after an initial drop following earnings. The bank downgraded its return on tangible equity target due to an expected peak in yields, but RBC says it may be trying to get bad news out of the way early.

- Metso shares rise as much as 8.5%, hitting highest in almost five months, after the Finnish machinery producer said activity in Aggregates is expected to improve. Analysts see the results as positive overall, with scope for some small consensus upgrades.

- Norwegian Air shares jump as much as 12%, to the highest price since May 2021, after giving a higher-than-expected forecast for 2024 Ebit. Pareto Securities notes that the airline’s 2024 pre-sale bookings are strong.

- Dowlais Group shares rise as much as 5.7% after Barclays initiated coverage at overweight, saying the engineering specialist “ticks all the right boxes” when it comes to what investors are looking for in 2024.

- Eni shares drop as much as 1.9% following fourth-quarter results that met expectations, with RBC saying some investors may find it disappointing that one-off income in its gas business made up for weakness elsewhere.

- Nibe shares fall as much as 8.7%, the most since August, after the Swedish heat-pump maker’s 2024 outlook disappointed as weakening demand for its low-energy heating impact its order intake.

- Umicore shares fall as much as 5.8% to their lowest intraday in eight years. The Belgian specialty chemicals firm reported second-half results Citi called “soft,” with metal prices and lower cathode volumes weighing on earnings.

- Temenos shares fall as much as 9.5% in Zurich, hitting the lowest level since Thursday’s publication of a report by activist short-seller Hindenburg Research.

- XP Power shares tumble as much as 41% after warning that the outlook for 2024 will fall “significantly” short of market expectations amid a slowdown in the semiconductor manufacturing equipment industry.

Earlier in the session, Asian stocks gained as Japanese equities steamed closer to their first record high in 34 years and Hong Kong stocks extended their rally to a third day. The MSCI Asia Pacific Index climbed as much as 1%, headed for its highest close since April 2022. Japan’s Toyota, Recruit Holdings and Mitsubishi UFJ Financial contributed most to the advance. The regional gauge is on course for a fourth-straight week of gains, its longest win streak in over a year. Key measures were higher in nearly every market except Taiwan.

- Hang Seng climbed back above the 16,000 level with notable gains in biopharmaceuticals and property with the latter underpinned after a court dismissed liquidation petitions against Chinese developer Logan Group.

- Nikkei 225 rallied and briefly approached within 100 points of its record high before reversing some of the gains.

- ASX 200 was led higher by the mining sector but with the upside capped as large insurers faltered post-earnings.

- Indian stocks capped off the week rising for a fourth straight day, led by a rally in automobile and healthcare stocks. The S&P BSE Sensex rose 0.5% to 72,426.64 in Mumbai, while the NSE Nifty 50 Index advanced 0.6% to 22,040.70. Most regional equity benchmarks advanced on the day, led by gains in Hong Kong and Japan.

In FX, the pound is down 0.1% having briefly gained after UK retail sales topped estimates. The yen is the weakest of the G-10 currencies, falling 0.2% versus the greenback.

In rates, treasuries were slightly cheaper across the curve, holding losses from Asia session after Fed Atlanta President Raphael Bostic said there’s no rush to cut rates with the US labor market and economy still strong. “My expectation is that the rate of inflation will continue to decline, but more slowly than the pace implied by where the markets signal monetary policy should be,” Bostic said in a speech Thursday in New York. He said policy decisions would be taken “without oppressive urgency.”

As a result, TSY yields are cheaper by 2bp-3bp across the curve with 5s30s spread flatter by around 1bp as belly and front-end underperform; 10-year yields around 4.26%, slightly outperforming bunds and gilts in the sector. According to Bloomberg, dollar issuance slate empty so far; Intel and British American Tobacco headlined a six-deal, $6.8b calendar Thursday, bringing this week’s volume to $37b. Early expectations for next week are in the $45b to $50b range, with some acquisition-related offerings possible

In commodities, oil prices decline, with WTI down 0.9% near $77.35 though near the highest close in three months as the risk-on mood in wider markets and signs OPEC+ members are complying with supply cuts overshadowed a gloomy demand outlook from the IEA. Spot gold is flat around $2,006/oz.

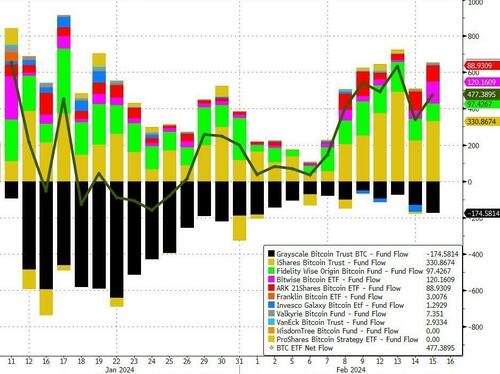

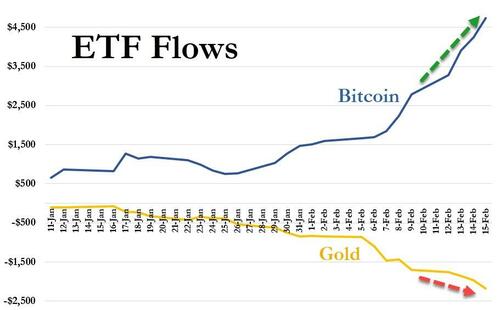

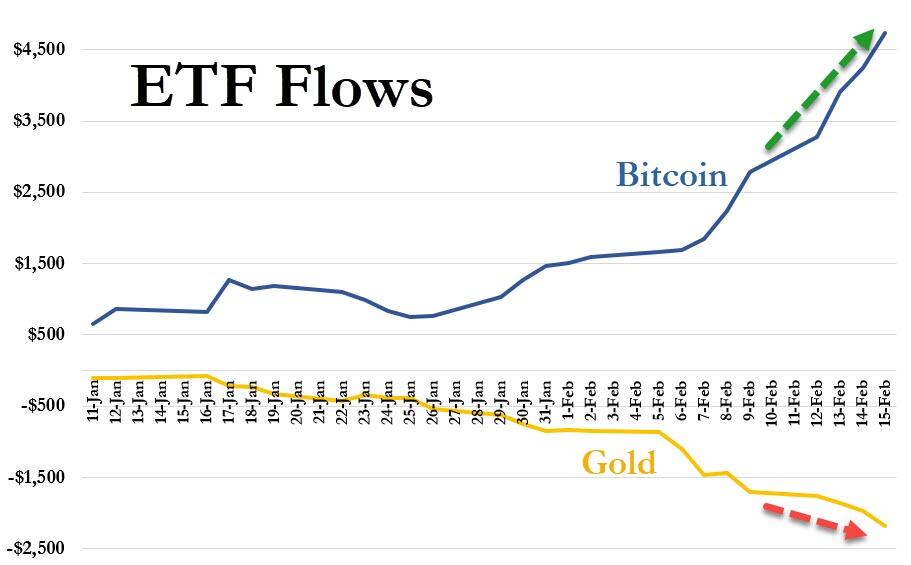

Bitcoin is firmer on the session, though still holds just shy of the USD 52k mark, as bitcoin ETF inflows just won’t stop.

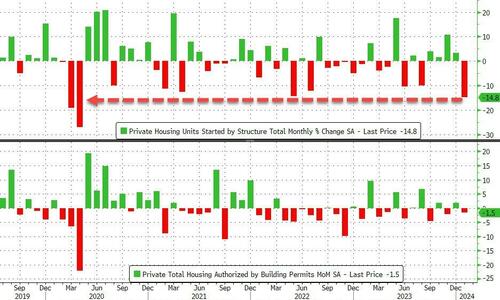

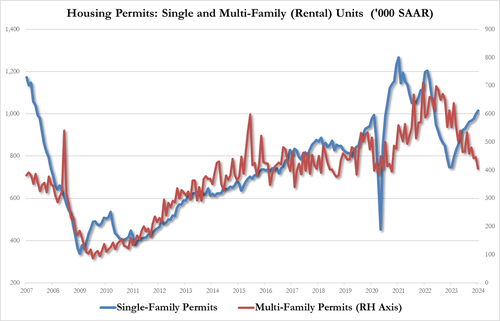

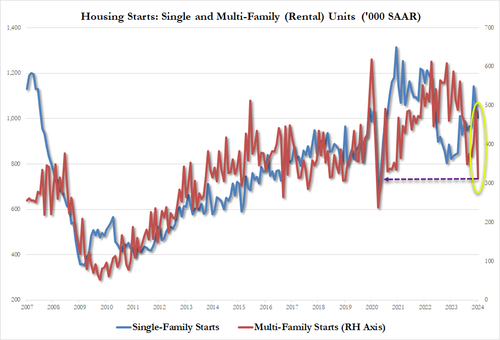

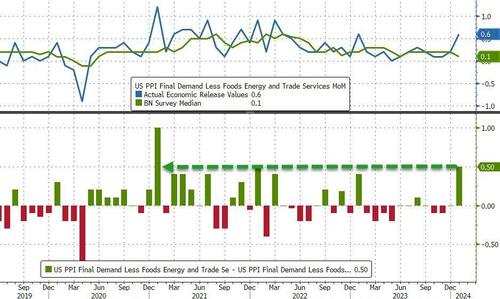

Turning to the day ahead, the US economic data calendar includes January PPI data, January housing starts/building permits, February New York Fed services business activity (8:30am) and February preliminary University of Michigan consumer sentiment (10am). Scheduled Fed speakers include Barkin (8am), Barr (9:10am) and Daly (12:10pm). Elsewhere we have the UK January retail sales and the Canadian International securities transactions.

Market Snapshot

- S&P 500 futures up 0.2% to 5,056.25

- STOXX Europe 600 up 0.6% to 491.35

- MXAP up 1.0% to 170.90

- MXAPJ up 1.0% to 522.12

- Nikkei up 0.9% to 38,487.24

- Topix up 1.3% to 2,624.73

- Hang Seng Index up 2.5% to 16,339.96

- Shanghai Composite up 1.3% to 2,865.90

- Sensex up 0.6% to 72,466.63

- Australia S&P/ASX 200 up 0.7% to 7,658.32

- Kospi up 1.3% to 2,648.76

- German 10Y yield little changed at 2.38%

- Euro little changed at $1.0771

- Brent Futures down 0.8% to $82.21/bbl

- Brent Futures down 0.8% to $82.23/bbl

- Gold spot up 0.1% to $2,006.25

- U.S. Dollar Index little changed at 104.32

Top Overnight News

- The BOJ is on track to end negative interest rates in coming months despite the economy’s fall into recession, say sources familiar with its thinking, though weak domestic demand means they may seek more clues on wages growth before acting. RTRS

- China’s gov’t could dramatically expand its real estate footprint, buying up distressed projects and/or building more subsidized housing as Xi looks to put more of the industry under state control. WSJ

- A resurgence in travel over China’s Lunar New Year holiday is offering some signs of a consumer spending pickup in the world’s second-largest economy as it struggles with low confidence and deflation. More than 61 million rail trips were made in the first six days of the national new year holiday, according to official reports. That was the highest in data compiled by Bloomberg News in the last five years, and it marked a 61% increase over the same vacation period in 2023. BBG

- The ECB should avoid waiting too long to cut rates as it will still have flexibility over the pace and degree of policy loosening after its first move, Governing Council member Francois Villeroy de Galhau said. BBG

- Federal Reserve Bank of Atlanta President Raphael Bostic said there’s no rush to cut interest rates with the US labor market and economy still strong, and cautioned it’s not yet clear that inflation is heading sustainably to the central bank’s 2% target. BBG

- The space-based weapon U.S. intelligence believes Russia may be developing is more likely a nuclear-powered device to blind, jam or fry the electronics inside satellites than an explosive nuclear warhead to shoot them down, analysts said on Thursday. The intelligence came to light on Wednesday after Representative Mike Turner, Republican chair of the U.S. House of Representatives intelligence committee, issued an unusual statement warning of a “serious national security threat.” RTRS

- Egyptian authorities, fearful that an Israeli military push further into southern Gaza will set off a flood of refugees, are building an 8-square-mile walled enclosure in the Sinai Desert near the border, according to Egyptian officials and security analysts. WSJ

- The US House will not pass another temporary spending bill to avert a partial government shutdown when the latest deadline expires on March 1, the chamber’s No. 3 leader said Thursday. BBG

- FBI informant at the center of the House GOP bribery allegations against Biden gets indicted over making false statements (the indictment claims the false statements were made due to the individual’s opposition to Biden’s candidacy). The Hill

Earnings

- Applied Materials (AMAT) – Q1 2024 (USD): Adj. EPS 2.13 (exp. 1.91), Revenue 6.71bln (exp. 6.48bln). Sees Q2 Adj. EPS USD 1.79-2.15 (exp. 1.80). Sees Q2 rev. USD 6.5bln (exp. 5.92bln). CEO says there is a reacceleration in capital investment by cloud companies; memory investment levels are normalising; fab utilisation is increasing across all device types. The DRAM market is strengthening. Sees leading-edge foundry logic being stronger Y/Y in 2024 even though some important projects are delayed. Expect NAND revenues to be up Y/Y but NAND to remain less than 10% of total wafer fab equipment spending. CFO says expect the equipment market to grow as fast or faster than semiconductors over time. (Newswires) Shares +12.7% in pre-market trade

- Coinbase Global Inc (COIN) – Q4 2023 (USD): EPS 1.04 (exp. -0.01), Revenue 953.8mln (exp. 826.3mln). Q1 subscription and services revenue view USD 410-480mln (exp. 367.3mln). (Newswires) Shares +10.7% in pre-market trade

- DoorDash Inc (DASH) – Q4 2023 (USD): EPS -0.39 (exp. -0.16), Revenue 2.3bln (exp. 2.24bln). FY gross order value view 74-78bln (exp. 76.54bln). FY adj. EBITDA 1.5-1.9bln (exp. 1.62bln). Q1 EBITDA view 320-380mln (exp. 360.3mln). Q1 Marketplace gross order value 18.5-18.9bln (exp. 18.57bln). (DoorDash IR) Shares -7.5% in pre-market trade

- DraftKings Inc (DKNG) – Q4 2023 (USD): EPS -0.10 (exp. 0.08), Net income -44.6mln (exp. profit 39.7mln), Revenue 1.23bln (exp. 1.24bln). Monthly Unique Payers 3.5mln (exp. 3.44mln). Average revenue per monthly unique payer 116 (exp. 119.79). FY24 revenue view 4.65-4.9bln (prev. 4.5-4.8bln). FY24 adj. EBITDA view 410-510mln (prev. 350-450mln). DraftKings to acquire Jackpocket for USD 750mln. (DraftKings IR) Shares -3.5% in pre-market trade

- Eni (ENI IM) – Q4 (EUR): adj. PBT 3.16bln (exp. 3.39bln), adj. Net 1.6bln (exp. 1.71bln), adj. EBIT 3.76bln (prev. 4.98bln). FY24 outlook will be provided at the 14th March capital markets day. Shares -1.7% in European trade

A more detailed look at global markets courtesy of Newsquawk

APAC stocks sustained the positive momentum from Wall St where yields softened after the US data deluge. ASX 200 was led higher by the mining sector but with the upside capped as large insurers faltered post-earnings. Nikkei 225 rallied and briefly approached within 100 points of its record high before reversing some of the gains. Hang Seng climbed back above the 16,000 level with notable gains in biopharmaceuticals and property with the latter underpinned after a court dismissed liquidation petitions against Chinese developer Logan Group.

Top Asian News

- BoJ Governor Ueda said when a sustained and stable achievement of the price target comes into sight, they will examine whether to maintain various easing measures including the negative interest rate. Ueda also noted the specific means of rolling back stimulus will depend on economic conditions at the time and based on the current economic and price outlook, monetary conditions will likely remain accommodative even after ending negative rates.

- Japanese Finance Minister Suzuki said a weak yen has merits and demerits, while he is concerned about the negative aspects of a weak yen and reiterated that rapid FX moves are undesirable and is closely watching FX moves with a sense of urgency.

- RBNZ Governor Orr refrained from talking about the rate outlook and said they have more work to do to get inflation expectations anchored to 2%. Governor Orr said a flexible approach to inflation targeting with a medium-term focus remains appropriate and bringing levels of core inflation back in line with the bank’s 1-3% target is an important part of bringing inflation back to the 2% midpoint, while he also noted the removal of the maximum sustainable employment objective does not mean any big changes to RBNZ’s monetary policy strategy.

European bourses, Stoxx600 (+0.6%) began the session entirely in the green and continued to grind higher throughout the morning. The AEX (+1.0%) is the European outperformer, lifted by strength in semi-conductor names after US-listed Applied Materials (+13.2%) reported strong earnings after-hours; BE Semiconductor (+3.2%), ASM (+3.2%), ASML (+1.3%). European sectors hold a positive tilt, with Basic Resources leading, boosted by higher underlying base metal prices. Tech benefits in a read-across from Applied Materials results. Telecoms lags, hampered by losses in Vodafone (-1.0%). US Equity Futures (ES +0.2%, NQ +0.5%, RTY +0.1%) are mixed, with clear outperformance in the NQ, with optimism permeating within the index after Applied Materials (+13.2%) reported strong results.

Top European News

- UK opposition Labour Party won the by-elections in Wellingborough and Kingswood which were both previously held by the Tories, according to The Times.

- ECB’s Villeroy said the principle of a rate cut this year seems to be a given and there is still a question of a precise calendar for a rate cut, while he added there are several reasons as to why the ECB should not wait for too long before making the first rate cut, according to an interview with L’Echo cited by Reuters.

- ECB’s Schnabel says monetary policy needs to remain restrictive until can be confident that inflation will sustainably return to our medium-term target. Must be cautious not to adjust the policy stance prematurely. Productivity growth is a key determinant of medium-term inflation and real interest rates, which means it directly affects the conduct of monetary policy. Persistently low, and recently even negative, productivity growth exacerbates the effects that the current strong growth in nominal wages has on unit labour costs for firms. This increases the risk that firms may pass higher wage costs on to consumers, which could delay inflation returning to our 2% target. New estimates show that an increase in trend productivity growth by one percentage point can increase r-star by 0.6 percentage points; a higher r-star would reduce the need to embark on unconventional policy measures that often come with larger side effects.

- Russian Federation Central Bank Key Rate (Feb) 16.0% vs. Exp. 16.0% (Prev. 16.0%); sees its average key rate at 13.5-15.5% in 2024 (prev. forecast 12.5-14.5%;

FX

- Contained trade for DXY and within a tight 104.26-44 range, respecting yesterday’s 104.18-71 range. Upside sees the WTD peak at 104.97, as the index awaits impetus from US PPI.

- EUR/USD is contained within yesterday’s 1.0724-84 range as ECB speak does little to sway price action. Any USD selling could prompt a test of 1.08 but Monday’s move above the level was unconvincing.

- Following UK Retail Sales Cable initially spiked higher to 1.2605 before gains were trimmed as some desks questioned seasonality issues with the data and with the BoE focussed on wages/inflation. Downside targets include 200DMA at 1.2654.

- JPY is the laggard across the majors with some noting BoJ Governor Ueda remaining dovish overnight. So far USD/JPY has printed a peak of 150.36 and is yet to threaten yesterday’s top of 150.58.

Fixed Income

- Gilts gapped lower by just under 30 ticks to 97.67 at the open and then waned further to 97.56, following strong Jan. Retail Sales which speak to the signs of an upturn flagged by Bailey pre-GDP.

- Bunds have been driven lower by UK Retail Sales with newsflow limited; as such Bunds have not meaningfully moved from their 133.08 session trough.