FEB 21/BLOG FOR WEDNESDAY: work in progess will complete later tonight//GOLD CLOSED DOWN $5.30 TO $2023.15//SILVER WAS DOWN ANOTHER 28 CENTS TO $23.10//PLATINUM WAS DOWN $22.35 TO $885.20 WHILE PALLADIUMW AS DOWN $30.85 TO $934.50//CHINA STOPS FUNDS FORM SELLING STOCKS AT THE OPENING AND CLOSING//ISRAEL VS HAMAS//ISRAEL VS HEZBOLLAH//WEST BANK UPDATES/HOUTHIS VS USA AND UK UPDATES//COVID UPDATES/VACCINE INJURIES/DR PAUL ALEXANDER/SLAY NEWS ETC//REPORT ON THE ILLEGAL 10 MILLION USA MIGRANTS//MISH SHEDLOCK ON USA INTEREST RATE PROBLEMS//SWAMP NEWS//

323 C HSBC 92 624 H BOFA SECURITIES 237 661 C JP MORGAN 199 686 H STONEX FINANCIA 24 737 C ADVANTAGE 78

TOTAL: 315 315 MONTH TO DATE: 18,95

JPMorgan stopped 199/315 contracts.

FOR FEB.:

GOLD: NUMBER OF NOTICES FILED FOR FEB/2024. CONTRACT: 315 NOTICES FOR 31,500 OZ or 0.9797 TNNES

total notices so far: 18,953 contracts for 1,895,300 Oz (58/952 tonnes)

FOR FEBRUARY:

SILVER NOTICES 0 NOTICE(S) FILED FOR nil OZ/

total number of notices filed so far this month : 1185 for 5,925,000 oz

XXXXXXXXXXXXXXXXXX

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

BOTH GLD AND SLV ARE FRAUDULENT VEHICLES//THEY ARE NOW RAIDING GLD AND SLV FOR PHYSICAL

GLD

WITH GOLD DOWN $5.30//CRIME OF THE CENTURY!!

INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD/ : HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 7.59 TONNES OF GOLD INTO THE GLD/.

INVENTORY RESTS AT 829.82 TONNES

SLV//

WITH NO SILVER AROUND AND SILVER DOWN 28 CENTS AT THE SLV//

HUGE CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 2.348 MILLION OZ INTO THE SLV/

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV.

CLOSING INVENTORY: 432.766 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A MEGA GIGANTIC SIZED 6636 CONTRACTS TO 146,584 AND FURTHER FORM THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THIS HUGE SIZED LOSS IN COMEX OI WAS ACCOMPLISHED WITH OUR STRONG FALL OF $0.33 IN SILVER PRICING AT THE COMEX ON TUESDAY. WE HAD SOME LONG LIQUIDATION AT THE COMEX SESSION WITH ZERO SHORT COVERING AS THE PRICE OF SILVER FELL APPRECIABLY. WE HAD A STRONG 774 T.A.S ISSUANCE AND THESE WILL BE USED FOR MANIPULATION LATER THIS MONTH/AS WELL AS TODAY. PLEASE NOTE THAT THE CROOKS NEED A HIGHER SILVER T.A.S. TO CARRY ON THEIR CROOKED MANIPULATION.

CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON TUESDAY NIGHT: 774 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS. IT THUS LOOKS LIKE THE FED (GOV’T) IS BEHIND ALL OF THESE TRADES.

WE HAVE NOW SET ANOTHER RECORD LOW AT 114,102 CONTRACTS ///JULY 3.2023// OUR BANKERS WITH THE HELP OF SPECULATORS AND HIGH FREQUENCY TRADERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.33), AND WERE UNSUCCESSFUL IN KNOCKING SOME SILVER LONGS AS WE HAD A GIGANTIC SIZED LOSS OF 5,886 CONTRACTS ON OUR TWO EXCHANGES BUT WITH A MUCH LOWER PRICE.

WE MUST HAVE HAD:

A HUGE SIZED 750 ISSUANCE OF EXCHANGE FOR PHYSICALS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 3.535 MILLION OZ (FIRST DAY NOTICE) ACCOMPANYING A STRANGE 89 CONTRACT ISSUANCE FOR EX. FOR RISK FOR 445,000 OZ ON FIRST DAY NOTICE/ FOLLOWED BY TODAY’S 0 OZ QUEUE JUMP //NEW TOTAL REMAINS THE SAME AT ; 6.98 MILLION OZ

//NEW STANDING FOR SILVER IS THUS 6.98 MILLION OZ

/ HUGE SIZED COMEX OI LOSS/HUGE SIZED EFP ISSUANCE/ VI) STRONG SIZED NUMBER OF T.A.S. CONTRACT ISSUANCE 774 CONTRACTS)/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL -REMOVED A HUGE 555 CONTRACTS //

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS FEB. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF FEB

TOTAL CONTRACTS for 14 days, total 7957 contracts: OR 39.785 MILLION OZ (568 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 39.785 MILLION OZ

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH 2022: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 118.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 85.745 MILLION OZ (SMALLER THAN LAST MONTH)

AUGUST: 171.43 MILLION OZ (THIS MONTH IS GOING TO BE HUGE //2ND HIGHEST ON RECORD

SEPT: 72.705 MILLION OZ (SMALLER THIS MONTH)

OCT: 97.455 MILLION OZ

NOV. 50.050 MILLION OZ

DEC. 66.140 MILLION OZ//

TOTAL 2023: 1,104.10 MILLION OZ/

JAN ’24 : 78.655 MILLION OZ//

FEB /2024 :39.785 MILLION OZ.

RESULT: WE HAD A MEGA GIGANTIC SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 6636CONTRACTS WITH OUR LOSSIN PRICE OF SILVER PRICING AT THE COMEX//TUESDAY.,. THE CME NOTIFIED US THAT WE HAD A HUGE EFP ISSUANCE CONTRACTS: 774 ISSUED FOR MARCH AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS. WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR FEB. OF 3.535 MILLION OZ ACCOMPANIED BY FIRST DAY NOTICE OF 445,000 OZ EX. FOR RISK FOLLOWED BY TODAY’S 0 OZ QUEUE JUMP //NEW TOTAL REMAINS THE SAME AT 6.98 MILLION OZ

NEW STANDING 6.98 MILLION OZ /// WE HAVE A MEGA GIGANTIC LOSS OF 5886 OI CONTRACTS ON THE TWO EXCHANGES WITH THE LOSS IN PRICE. THE TOTAL OF TAS INITIATED CONTRACTS TODAY: A VERY STRONG SIZED 750 CONTRACTS//HUGE FRONT END OF THE TAS CONTRACTS WERE LIQUIDATED DURING THE TUESDAY COMEX SESSION/// WITH MAJOR SHORT COVERING FROM OUR SPEC SHORTS (DRAMATIC PRICE OF SILVER RISE) . THE NEW TAS ISSUANCE TUESDAY NIGHT (1390) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE//PROBABLY TODAY., .

WE HAD 0 NOTICE(S) FILED TODAY FOR nil OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A TINY SIZED 64 CONTRACTS TO 407,063 AND CLOSER TO THE RECORD (SET JAN 24/2020) AT 799,733 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110, BUT CLOSER TO OUR ALL TIME LOW OF 390,000 CONTRACTS.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: – REMOVED 299 CONTRACTS

WE HAD A TINY SIZED INCREASE IN COMEX OI ( 64 CONTRACTS) DESPITE OUR $16.15 GAIN IN PRICE//TUESDAY. WE ALSO HAD A RATHER LARGE INITIAL STANDING IN GOLD TONNAGE FOR FEB. AT 49.773 TONNES ON FIRST DAY NOTICE ACCOMPANIED BY FIRST DAY NOTICE : 55,400 OZ EX. FOR RISK //THUS INITIAL STANDING FOR FEB: 51.494 TONNES FOLLOWED BY TODAY’S 130,700 OZ QUEUE JUMP //NEW TOTAL OF GOLD STANDING ADVANCES TO: 64.180 TONNES // ALL OF THIS HAPPENED DESPITE OUR $16.15 GAIN IN PRICE WITH RESPECT TO TUESDAY’S TRADING. WE HAD A GOOD SIZED GAIN OF 4084 OI CONTRACTS (12.784) PAPER TONNES) ON OUR TWO EXCHANGES.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A GOOD SIZED 4030CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 407,063

IN ESSENCE WE HAVE A GOOD SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 4084 CONTRACTS WITH 64 CONTRACTS INCREASED AT THE COMEX// AND A GOOD SIZED 4030 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 4084 CONTRACTS.. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): A FAIR SIZED 1390 CONTRACTS.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD GOOD SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (4030 CONTRACTS) ACCOMPANYING THE TINY SIZED GAIN IN COMEX OI (64) //TOTAL GAIN FOR OUR THE TWO EXCHANGES: 4084 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR FORMER FORMAT OF BANKERS GOING LONG AND SPECULATORS GOING SHORT ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR FEB. AT 49.773 TONNES PLUS FIRST DAY NOTICE OF 1.723 TONNE OZ EX. FOR RISK FOLLOWED BY TODAY’S 130,700 OZ QUEUE JUMP //NEW STANDING ADVANCES TO 64.180 TONNES. / 3) ZERO LONG LIQUIDATION // 4) TINY SIZED COMEX OPEN INTEREST LOSS/ 5) GOOD ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER///6: FAIR T.A.S. ISSUANCE: 1398CONTRACTS//MAJOR SHORT COVERING AGAIN

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023-2024 INCLUDING TODAY

FEB.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF FEB. :

TOTAL EFP CONTRACTS ISSUED: 48,054 CONTRACTS OR 4,805,400OZ OR 149.47 TONNES IN 14TRADING DAY(S) AND THUS AVERAGING: 3467 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 14TRADING DAY(S) IN TONNES 149.47 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2022, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 149.47/3550 x 100% TONNES 4.22% OF GLOBAL ANNUAL PRODUCTION

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH/2022: 409.30 TONNES //FINAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 151.69 TONNES (WEAKER THAN LAST MONTH)

AUGUST: 195.28 TONNES (A STRONGER MONTH)//FINAL

SEPT: 254.709 TONNES (WILL BE LARGER THAN LAST MONTH AND A STRONG MONTH)

OCT. 248.09 TONNES. LIKE SILVER, THIS MONTH IS GOING TO BE A STRONG E.F.P. ISSUANCE.

NOV. 239.16 TONNES//WILL BE STRONG THIS MONTH,

DEC. 213.704 TONNES. A STRONG MONTH//

TOTAL FOR YEAR 2023: 2,569.57 TONNES VS 2578 TONNES LAST YEAR

JAN ’24: 291.76 TONNES (WILL BE MUCH GREATER THAN LAST MONTH.//3RD HIGHEST EVER RECORDED EX FOR PHYSICAL)

FEB’24: 149.47 TONNES (SHOULD BE A WEAKER ISSUANCE MONTH)

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF FEB. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (FEB), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER FELL BY A MEGA HUMONGOUS SIZED 6636 CONTRACTS OI TO 146,584 AND FURTHER FROM THE COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 6 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 750 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MARCH 750 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 750 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 6636 CONTRACTS AND ADD TO THE 750 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A MEGA GIGANTIC LOSS OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 5886CONTRACTS

THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES TOTAL 29.430 MILLION OZ

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A TINY SIZED 64 CONTRACTS TO 407,063 DESPITE OUR HUGE GAIN IN PRICE OF $16.15 WITH RESPECT TO TUESDAY TRADING. WE ARE GETTING AWFULLY CLOSE TO OUR LOW OI OF 390,000 CONTRACTS

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE ACTIVE DELIVERY MONTH OF FEB..… THE CME REPORTS THAT THE BANKERS ISSUED A STRONG SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 4030 EFP CONTRACTS WERE ISSUED: : APRIL 4030 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 4030CONTRACTS

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A STRONG SIZED TOTAL OF 4084 CONTRACTS IN THAT 4030 LONGS WERE TRANSFERRED AS EXCHANGE FOR PHYSICALS TO LONDON AND WE HAD A TINY SIZED GAIN OF 64 COMEX CONTRACTS..AND THIS GAIN ON OUR TWO EXCHANGES HAPPENED WITH OUR GAIN IN PRICE OF $16.15 TUESDAY COMEX. AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS DURING MID MONTH IN THE DELIVERY CYCLE), THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR TUESDAY NIGHT WAS A FAIR SIZED 1390 CONTRACTS. THROUGHOUT THE PAST SEVERAL WEEKS, THE BANKERS SOLD OFF THE LONG SIDE OF THE SPREAD WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR/T.A.S. SPREAD WHICH WILL BE LIQUIDATED IN DAYS HENCE//.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: FEB (64.180 TONNES) ( ACTIVE MONTH)

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 24 MONTHS OF 2021-2023:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707TONNES

TOTAL 2023 YEAR : 436.546 TONNES

JAN ’24. 22.706 TONNES

FEB. ’24: 64.180 TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT GAINED $16.15 //// AND WERE UNSUCCESSFUL IN KNOCKING ANY SPECULATOR LONGS AS WE HAD A STRONG SIZED GAIN OF4084 TOTAL CONTRACTS ON OUR TWO EXCHANGES WITH THE MUCH HIGHER PRICE. WE HAD TO HAVE HAD A STRONG SHORT COVERING. WE HAD A STRONG T.A.S. LIQUIDATION ON THE FRONT END OF TUESDAY’S TRADING . THE T.A.S. ISSUED ON TUESDAY NIGHT, WILL BE “PUT INTO THE BANK” TO BE USED AT A LATER DATE AT THE COLLUSIVE CHOOSING OF OUR BANKERS.

WE HAVE GAINED A TOTAL OI OF 12.434 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR FEB. (49.773 TONNES) ON FIRST DAY NOTICE ALONG WITH AN EXCHANGE FOR RISK FOR 1.7235 TONNES. THIS WAS FOLLOWED WITH TODAY’S HUMONGOUS 130,700 OZ QUEUE JUMP (4.065 TONNES//NEW TOTAL STANDING 64.180: ALL OF THIS WAS ACCOMPLISHED WITH OUR GAIN IN PRICE TO THE TUNE OF $16.15

WE HAD -REMOVED 299 CONTRACTS TO THE COMEX TRADES TO OPEN INTEREST (CROOKS)

NET GAIN ON THE TWO EXCHANGES 4084 CONTRACTS OR 408,400 OZ OR 12.434 TONNES. estimated volume today 113,529 poor

Total monthly oz gold served (contracts) so far this month

18,953 notices 1,895,300 oz 58.952 TONNES

Total accumulative withdrawals of gold from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of gold from the Customer inventory this month

x

0 dealer deposits:

total dealer deposits: nil oz

total customer withdrawals: 1

i) Out of HSBC: 134,451.493 oz

4.182 tonnes and close to the 4.06 tonne queue jump today

total withdrawal: 134,451.493 oz

we had 0 customer deposit

Adjustments: 1 dealer to customer

a) Out of HSBC: 172.734oz

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR FEB.

For the front month of FEBRUARY we have an oi of 1442 contracts having GAINED 1286 contracts. We had 21 notices filed on Tuesday, so we GAINED 1307 contracts or an additional 130,700 oz (4.0653 tonnes) will stand for delivery at the comex.

We also had 554 notices filed under exchange for risk on first day notice for a total of 55,400 oz or 1.723 tonnes to which must be added to the delivery cycle.

Thus initial standing for gold for February is 50.136 tonnes + 1.723 tonnes = 51.859 tonnes. This was followed with today’s QUEUE jump of 130,700 oz//New standing 62.457 tonnes + 1.723 tonnes = 64.180 TONNES

March LOST 174 contracts to stand at 2498

APRIL lost 1125 CONTRACTS FALLING TO 317,823.

We had 315 contracts filed for today representing 31,500 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 315 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 99 notice(s) was (were) stopped ( (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for the FEB. /2024. contract month, we take the total number of notices filed so far for the month (18,953 x 100 oz ), to which we add the difference between the open interest for the front month of FEB. (1442 CONTRACTS) minus the number of notices served upon today 315 x 100 oz per contract equals 200,800 OZ OR 62.457 TONNES + 1.723 Ex for Risk/prior = 64.180 tonnes

thus the INITIAL standings for gold for the FEB. contract month: No of notices filed so far (18,953) x 100 oz + (1442) {OI for the front month} minus the number of notices served upon today (315) x 100 oz which equals 200,800 oz (62.457 TONNES) + 54,400 oz (1.723 TONNES) ex. for risk/prior// NEW total standing OR 64.180 TONNES

TOTAL COMEX GOLD STANDING FOR FEB: 64.180 TONNES WHICH IS GREAT FOR AN ACTIVE DELIVERY MONTH IN THE CALENDAR.

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD: 18,289,124.858 OZ

TOTAL REGISTERED GOLD 8,133,765.654 (252.99 tonnes).

TOTAL OF ALL ELIGIBLE GOLD: 10,155,359.204 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 6,733,463 oz (REG GOLD- PLEDGED GOLD) 209.43 tonnes

END

SILVER/COMEX

FEB 21/INITIAL

//2024// THE FEB 2024 SILVER CONTRACT//INITIAL

Silver

Ounces

Withdrawals from Dealers Inventory

NIL oz

Withdrawals from Customer Inventory

nil oz

.

Deposits to the Dealer Inventory

nil OZ

Deposits to the Customer Inventory

nil oz

No of oz served today (contracts)

0 CONTRACT(S) (5 OZ)

No of oz to be served (notices)

122 contracts (610,000 oz)

Total monthly oz silver served (contracts)

1185 Contracts (5,935,000 oz)

Total accumulative withdrawal of silver from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of silver from the Customer inventory this month

i) 0 dealer deposit

total dealer deposit: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: 0 oz

We had 0 deposits customer account:

total customer deposits nil oz

JPMorgan has a total silver weight: 129.806 million oz/280.137 million or 46.42%

adjustment: 0

Comex withdrawals: 0

i

total withdrawal: nil oz

TOTAL REGISTERED SILVER: 42.868 MILLION OZ//.TOTAL REG + ELIGIBLE. 280.137 million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR DECEMBER:

silver open interest data:

FRONT MONTH OF FEB. /2023 OI: 122 CONTRACTS HAVING LOST 119 CONTRACT(S). WE HAD 119 NOTICES FILED ON TUESDAY SO WE GAINED 0 CONTRACTS OR AN ADDITIONAL NIL OZ OF SILVER CONTRACTS WILL STAND FOR DELIVERY AT THE COMEX

MARCH LOST 10,277 CONTRACTS TO 57,012

APRIL SAW A GAIN OF 28 CONTRACTS TO STAND AT 88

MAY SAW A GAIN OF 3841 CONTRACTS UP TO 69,542.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 0 for NIL oz

Comex volumes// est. volume today 69,095 good

Comex volume: confirmed yesterday 126,004 mega huge//

To calculate the number of silver ounces that will stand for delivery in FEB. we take the total number of notices filed for the month so far at 1185 x 5,000 oz = 5,925,000 oz

to which we add the difference between the open interest for the front month of FEB. (122) and the number of notices served upon today 0 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the FEB/2024 contract month: 1185 (notices served so far) x 5000 oz + OI for the front month of FEB. (122) – number of notices served upon today (0 )x 500 oz of silver standing for the FEB contract month equates to 6.5350 MILLION OZ. + .445 MILLION OZ EX. FOR RISK PRIOR//NEW TOTAL 6.9800 MILLION OZ

New total standing: 6.9800 million oz.

There are 42.868 million oz of registered silver.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS//

BOTH GLD AND SLV ARE MASSIVE FRAUDS!

FEB21/WITH GOLD DOWN $5.30 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A MASSIVE WITHDRAWAL OF 7.59 TONNES OF GOLD FROM THE GLD///INVENTORY RESTS AT 829/82 TONNES//HUGE CRIME

FEB20/WITH GOLD UP $16.15 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 0.58 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 837.89 TONNES

FEB16/WITH GOLD UP $8,60 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.73 TONNES OF GOLD FROM THE GLD///INVENTORY RESTS AT 837.31 TONNES

FEB15/WITH GOLD UP $11.70 TODAY NO CHANGES IN GOLD INVENTORY AT THE GLD:/INVENTORY RESTS AT 841.92 TONNES

FEB14/WITH GOLD DOWN $2.75 TODAY NO CHANGES IN GOLD INVENTORY AT THE GLD:/INVENTORY RESTS AT 841.92 TONNES

FEB13/WITH GOLD DOWN $20.15 TODAY NO CHANGES IN GOLD INVENTORY AT THE GLD:/INVENTORY RESTS AT 841.92 TONNES

FEB12/WITH GOLD DOWN $4.80 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A STRONG WITHDRAWAL OF 1.74 TONNES OF GOLD FROM THE GLD. / //://INVENTORY RESTS AT 841.92 TONNES

FEB9/WITH GOLD DOWN $8.60 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A STRONG DEPOSIT OF 1.44 TONNES OF GOLD FROM THE GLD. / //://INVENTORY RESTS AT 843.66 TONNES

FEB8/WITH GOLD DOWN $2.70 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A MASSIVE WITHDRAWAL OF 5.47 TONNES OF GOLD FROM THE GLD. / //://INVENTORY RESTS AT 842.22 TONNES:

FEB7/WITH GOLD UP $0.40 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A MASSIVE WITHDRAWAL OF 4.04 TONNES OF GOLD FROM THE GLD. / //://INVENTORY RESTS AT 847.69 TONNES:

FEB6/WITH GOLD UP $8.50 TODAY NO CHANGES IN GOLD INVENTORY AT THE GLD:/ / //://INVENTORY RESTS AT 851.73 TONNES:

FEB5/WITH GOLD DOWN $9.85 TODAY SMALL CHANGES IN GOLD INVENTORY AT THE GLD:A DEPOSIT OF .58 TONNES OF GOLD INTO THE GLD// / //://INVENTORY RESTS AT 851.73 TONNES:

FEB 2/WITH GOLD DOWN $17.95 TODAY SMALL CHANGES IN GOLD INVENTORY AT THE GLD:A WITHDRAWAL OF .58 TONNES OF GOLD FROM THE GLD// / //://INVENTORY RESTS AT 851.15 TONNES:

FEB 1/WITH GOLD UP $5.00 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD:A WITHDRAWAL OF 1.73 TONNES OF GOLD FROM THE GLD// / //://INVENTORY RESTS AT 851.15 TONNES:

JAN 31/WITH GOLD UP $16.40 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD:A WITHDRAWAL OF 2.01 TONNES OF GOLD FROM THE GLD// / //://INVENTORY RESTS AT 852.88 TONNES:

JAN 30/WITH GOLD UP $6.50 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD:A WITHDRAWAL OF 1.16 TONNES OF GOLD FROM THE GLD// / //://INVENTORY RESTS AT 854.89 TONNES:

TOTAL IN LAST 18 DAYS WITHDRAWAL OF 14.12 TONNES

JAN 29/WITH GOLD UP $8.70 TODAYHUGE CHANGES IN GOLD INVENTORY AT THE GLD:A WITHDRAWAL OF 2.88 TONNES OF GOLD FROM THE GLD// / //://INVENTORY RESTS AT 856.05 TONNES

JAN 26/WITH GOLD DOWN $0.10 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD: / //://INVENTORY RESTS AT 858.93 TONNES

JAN 25/WITH GOLD UP $2.50 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD: / //://INVENTORY RESTS AT 858.93 TONNES

JAN 24/WITH GOLD DOWN $9.75 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD: / //://INVENTORY RESTS AT 858.93 TONNES

JAN 23/WITH GOLD UP $3.95 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.02 TONNES OF GOLD FROM THE GLD/ //://INVENTORY RESTS AT 858.93 TONNES

JAN 22/WITH GOLD DOWN $6.00 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.15 TONNES OF GOLD FROM THE GLD/ //://INVENTORY RESTS AT 860.95 TONNES

JAN 19/WITH GOLD UP $8.15 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD //://INVENTORY RESTS AT 862.10 TONNES

JAN 18/WITH GOLD UP $14.85 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 2.30 TONNES OF GOLD FROM THE GLD//://INVENTORY RESTS AT 862.10 TONNES

JAN 17/WITH GOLD DOWN $23.25 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF .549 TONNES OF GOLD INTO THE GLD.;//://INVENTORY RESTS AT 864.40 TONNES

JAN 12/WITH GOLD UP $31.65 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD; A MASSIVE WITHDRAWAL OF 4.61 TONNES OF GOLD FROM THE GLD//://INVENTORY RESTS AT 864.99 TONNES

GLD INVENTORY: 829.82 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

FEB 21/WITH SILVER DOWN 28 CENTS TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 2/348 MILLION OZ OF SILVER FROM THE SLV// : SLV INVENTORY RESTS AT 432.766 MILLION OZ

FEB 20/WITH SILVER DOWN 33 CENTS TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 3.385 MILLION OZ OF SILVER FROM THE SLV// : SLV INVENTORY RESTS AT 435.008 MILLION OZ

FEB 16/WITH SILVER UP 53 CENTS TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV A DEPOSIT OF 1.235 MILLION OZ OF SILVER FROM THE SLV// : SLV INVENTORY RESTS AT 438.393 MILLION OZ

FEB 15/WITH SILVER UP 56 CENTS TODAY NO CHANGES IN SILVER INVENTORY AT THE SLV : SLV INVENTORY RESTS AT 437.615 MILLION OZ

FEB 14/WITH SILVER UP 24 CENTS TODAY NO CHANGES IN SILVER INVENTORY AT THE SLV : SLV INVENTORY RESTS AT 437.615 MILLION OZ

FEB 13/WITH SILVER DOWN 60 CENTS TODAY SMALL CHANGES IN SILVER INVENTORY AT THE SLV A SMALL WITHDRAWAL OF 0.504 MILLION OZ OZ OUT OF THE SLV: SLV INVENTORY RESTS AT 437.615 MILLION OZ

FEB 12/WITH SILVER UP 14 CENTS TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV A HUGE WITHDRAWAL OF 1.921 MILLION OZ OZ OUT OF THE SLV: SLV INVENTORY RESTS AT 438.119 MILLION OZ

FEB 9/WITH SILVER DOWN 4 CENTS TODAY SMALL CHANGES IN SILVER INVENTORY AT THE SLV A SMALL DEPOSIT OF 600,000 OZ INTO THE SLV: SLV INVENTORY RESTS AT 440.040 MILLION OZ

FEB 8/WITH SILVER UP 29 CENTS TODAY NO CHANGES IN SILVER INVENTORY AT THE SLV: SLV INVENTORY RESTS AT 439.994 MILLION OZ

FEB 7/WITH SILVER DOWN 18 CENTS TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A MASSIVE DEPOSIT OF 4.04 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 439.994 MILLION OZ//LAST 9 DAYS: 10.7598 MILLION OZ WITHDRAWAL

FEB 6/WITH SILVER UP 11 CENTS TODAY NO CHANGES IN SILVER INVENTORY AT THE SLV: /INVENTORY RESTS AT 435.144 MILLION OZ//LAST 9 DAYS: 10.7598 MILLION OZ WITHDRAWAL

FEB 5/WITH SILVER DOWN 32 CENTS TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.345 MILLION OZ FROM THE SLV(FAIRY TALES) // /INVENTORY RESTS AT 435.144 MILLION OZ//LAST 8 DAYS: 10.7598 MILLION OZ WITHDRAWAL

FEB 2/WITH SILVER DOWN 50 CENTS TODAY SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 0.58 MILLION OZ INTO THE SLV(FAIRY TALES) // /INVENTORY RESTS AT 438.489 MILLION OZ//LAST 7 DAYS: 14.105 MILLION OZ WITHDRAWAL

FEB 1/WITH SILVER UP 7 CENTS TODAY MEGA CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.19 MILLION OZ INTO THE SLV(FAIRY TALES) // /INVENTORY RESTS AT 438.947 MILLION OZ//LAST 6 DAYS: 10.3018 MILLION OZ WITHDRAWAL

JAN 31/WITH SILVER DOWN 8 CENTS TODAY MEGA CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.7438 MILLION OZ INTO THE SLV(FAIRY TALES) // /INVENTORY RESTS AT 440.137 MILLION OZ//LAST 5 DAYS: 9.1118 MILLION OZ WITHDRAWAL

JAN 30/WITH SILVER DOWN 5 CENTS TODAY MEGA CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.876 MILLION OZ INTO THE SLV(FAIRY TALES) // /INVENTORY RESTS AT 442.699 MILLION OZ//LAST 4 DAYS: 7.368 MILLION OZ WITHDRAWAL

JAN 29/WITH SILVER UP $.37 TODAY MEGA CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.105 MILLION OZ INTO THE SLV(FAIRY TALES) // /INVENTORY RESTS AT 444.575 MILLION OZ

JAN 26/WITH SILVER DOWN $0.03 TODAY MEGA CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.556 MILLION OZ INTO THE SLV(FAIRY TALES) // /INVENTORY RESTS AT 446.680 MILLION OZ

JAN 25/WITH SILVER UP $0.03 TODAY MEGA CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.831 MILLION OZ INTO THE SLV(FAIRY TALES) // /

INVENTORY RESTS AT 448.236 MILLION OZ

JAN 24/WITH SILVER UP $0.44 TODAY MEGA CHANGES IN SILVER INVENTORY AT THE SLV: ANOTHER DEPOSIT OF 1.375 MILLION OZ INTO THE SLV(FAIRY TALES) // //INVENTORY RESTS AT 450.067 MILLION OZ

JAN 23/WITH SILVER UP $0.21 TODAY MEGA CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 16.201 MILLION OZ INTO THE SLV(FAIRY TALES) // //INVENTORY RESTS AT 448.694 MILLION OZ

JAN 22/WITH SILVER DOWN $0.45 TODAY NO CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 458,000 OZ OUT OF THE SLV // //INVENTORY RESTS AT 432.493 MILLION OZ

JAN 19/WITH SILVER DOWN $0.11 TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 458,000 OZ OUT OF THE SLV // //INVENTORY RESTS AT 432.493 MILLION OZ

JAN 18/WITH SILVER UP $0.13 TODAY NO CHANGES IN SILVER INVENTORY AT THE SLV: // //INVENTORY RESTS AT 432.951 MILLION OZ

JAN 17/WITH SILVER DOWN $0.38 TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 779,000 OZ FROM THE SLV.: // //INVENTORY RESTS AT 433.500 MILLION OZ

JAN 16/WITH SILVER DOWN $0.08 TODAY NO CHANGES IN SILVER INVENTORY AT THE SLV: // //INVENTORY RESTS AT 433.500 MILLION OZ

JAN 12/WITH SILVER UP $0.62 TODAY NO CHANGES IN SILVER INVENTORY AT THE SLV: // //INVENTORY RESTS AT 433.500 MILLION OZ

CLOSING INVENTORY 432.766 MILLION OZ//

PHYSICAL GOLD/SILVER COMMENTARIES

1:Peter Schiff/Mike Maharrey

end

2.Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

END

END

3. CHRIS POWELL//GATA GOLD COMMENTARIES: daily Dispatches

Bad property debt exceeds reserves at largest U.S. banks

Submitted by admin on Tue, 2024-02-20 10:10 Section: Daily Dispatches

By Stephen Gandel Financial Times, London Tuesday, February 20, 2024

Bad commercial real estate loans have overtaken loss reserves at the biggest U.S. banks after a sharp increase in late payments linked to offices, shopping centers, and other properties.

The average reserves at JPMorgan Chase, Bank of America, Wells Fargo, Citigroup, Goldman Sachs, and Morgan Stanley have fallen from $1.60 to 90 cents for every dollar of commercial real estate debt on which a borrower is at least 30 days late, according to filings to the Federal Deposit Insurance Corp.

The sharp deterioration took place in the last year after delinquent commercial property debt for the six big banks nearly tripled to $9.3 billion. …

Submitted by admin on Mon, 2024-02-19 19:55 Section: Daily Dispatches

By Joseph N. DiStefano Philadelphia Inquirer Monday, February 19, 2024

Robert Leroy Higgins’ Delaware gold and silver storage businesses ran out of operating funds in 2012, but, according to a federal grand jury, the West Chester precious-metals dealer was able to attract new clients and stay in business for 10 more years by stealing coins and bullion that a thousand customers had entrusted to the vaults at his Wilmington warehouse

Higgins is due in Delaware’s federal court Thursday for arraignment on criminal fraud and tax charges first leveled in 2022 and amended three times, the last filed Feb. 15 after attorneys for Higgins and the U.S. attorney for Delaware failed to settle the case without a trial.

If convicted on all charges, Higgins faces up to 45 years in prison. He remains free on condition that he not leave the area, said his lawyer, Jeremy Gonzalez Ibrahim of Chadds Ford.

Higgins, 68, a longtime coin, bullion, and currency dealer, owned First State Depository, one of several Delaware businesses that hold precious metals for companies and individual investors. …

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGSWEDNESDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED UP 7.1912

OFFSHORE YUAN: UP TO 7.1976

SHANGHAI CLOSED UP 28.22 PPTS OR 0.97%

HANG SENG CLOSED UP 255.59 PTS OR 1.57%

2. Nikkei closed DOWN 101.45 OR 0.26%

3. Europe stocks SO FAR: MOSTLY ALL GREEN

USA dollar INDEX DOWN TO 103.97 EURO FALLS TO 1.0808 DOWN 1 BASIS PTS

3b Japan 10 YR bond yield: FALLS TO. +.715 Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 150.09/JAPANESE YEN NOW RISING AS WELL AS LONG TERM 10 YR. YIELDS RISING //EVENTUALLY THIS WILL BREAK THE JAPANESE CENTRAL BANK

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen UP CHINESE ONSHORE YUAN: UP/ OFFSHORE: UP

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

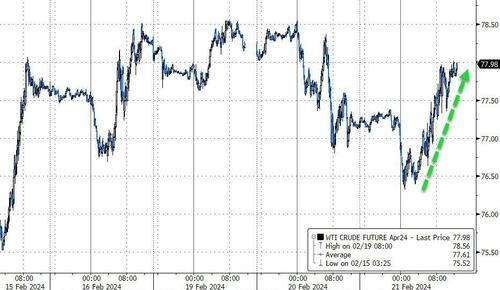

3g Oil DOWN for WTI and DOWN FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund UP TO +2.3910***/Italian 10 Yr bond yield UP to 3.872* /SPAIN 10 YR BOND YIELD UP TO 3.299…**

3i Greek 10 year bond yield UP TO 3.338

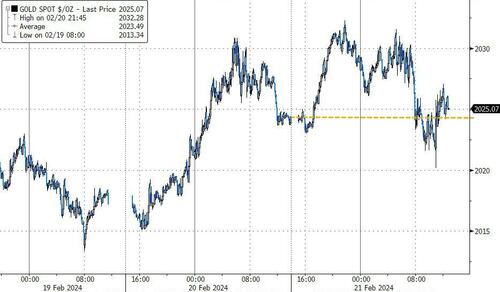

3j Gold at $2028.60 silver at: 23.02 1 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble DOWN 0 AND 6 /100 roubles/dollar; ROUBLE AT 92.40//

3m oil into the 77 dollar handle for WTI and 82 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 149.96// 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 0.715% STILL ON CENTRAL BANK (JAPAN) INTERVENTION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.8798 as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.9510 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.263 DOWN 1 BASIS PTS…

USA 30 YR BOND YIELD: 4.443 DOWN 1 BASIS PTS/

USA 2 YR BOND YIELD: 4.589 DOWN 2 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 31.01…(TURKEY SET TO BLOW UP FINANCIALLY)

GREAT BRITAIN/10 YEAR YIELD: UP 6 BASIS PTS AT 4.143

end

2.a Overnight: Newsquawk and Zero hedge

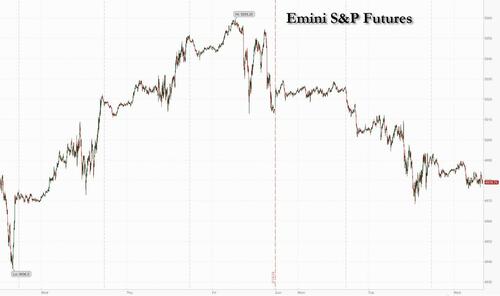

Futures Slide Ahead Of Earnings By “The Most Important Stock On Planet Earth”

WEDNESDAY, FEB 21, 2024 – 08:23 AM

US futures extended their slide, bucking a strong Asian session with European stocks mixed, ahead of what Goldman trader Scott Rubner called “the most important stock on planet earth” –that would be Nvidia for anyone who has been living in a cave the past year – reports after the close facing sky-high expectations, and where another Goldman trader, Peter Callahan, said that the tactical debate is whether this print will be a local top or a ‘break-out’ moment for the stock and for the AI trade (from where he sits, this “feels like consensus is learning more towards the former“). And with options implying the stock may move about 11% in either direction, i.e., a whopping $200BN in market cap may be gained or lost for a company that recently surpassed GOOGL and AMZN in market cap, it’s not surprising why the market is on edge. With that preamble out of the way, S&P 500 futures dropped 0.2% as of 7:40am and Nasdaq contracts lost about 0.5%, suggesting Wall Street may be in for a third day of declines. Bond yields are lower, the 10Y dropping 2bps, with steepening across most of the curve; the USD is flat and commodities are weaker. The macro data focus is on Fed Minutes this afternoon; while possible to see a dovish surprise regarding QT this most likely comes at the March 20 Fed meeting where we may see a reduction in the pace of QT.

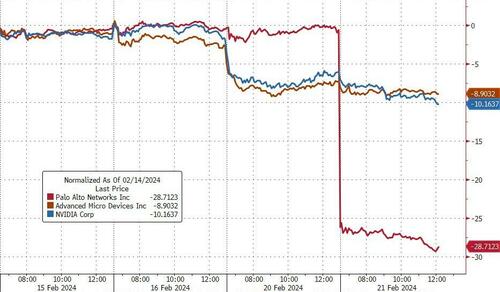

In premarket trading, Palo Alto Networks plunged more than 20% after the cybersecurity firm cut its forecasts for both revenue and billing and warned of “spending fatigue” among its customers; Piper Sandler downgraded its rating on the stock. Amazon.com rose 1.2% after replacing Walgreens Boots Alliance Inc. in the Dow Jones Industrial Average. Walgreens fell 2.8%. Here are some other notable premarket movers:

Community Health Systems falls 18% after the hospital owner and operator released a 2024 adjusted Ebitda guidance that was below the average analyst estimate.

International Flavors & Fragrances shares fall 8.6% after providing a disappointing sales outlook. The company, which provides ingredients, flavors and scents for industries including food and beverage, also cut the dividend.

Intuitive Machines shares jump 22% after giving an update on its lunar lander, Odysseus. The company, seeking to land a US spacecraft on the moon this week, closed higher by 50% during the regular session on Tuesday, for a third straight gain.

Manchester United shares slip 2.5% after Jim Ratcliffe completed the acquisition of 25% of Class A shares and 25% of Class B shares for $33 per share.

Matterport shares drop 13% after giving first-quarter subscription and revenue guidance that came in below the average analyst estimate. Fourth-quarter revenue also missed expectations.

SolarEdge plunges 16% as the solar equipment maker’s first-quarter revenue forecast missed Wall Street estimates. Fourth-quarter results disappointed as well.

Teladoc Health shares slide 22% after the healthcare services company reported fourth-quarter revenue that was weaker than expected. Additionally, the company gave first-quarter forecast below consensus expectations.

Wendy’s shares decline 1.3% after the fast-food chain was downgraded to neutral from overweight at JPMorgan, which sees the stock remaining rangebound.

RingCentral falls 4% after the provider of cloud-based communications services gave an outlook that analysts said wasn’t strong enough to be compelling.

Wix.com shares rise 5.9% as the web platform company’s fourth-quarter revenue edged past the average estimate of analysts, who noted revenue growth momentum and expectations for margin expansion in the coming years.

Going back to today’s main highlight, Nvidia, the stock fell 1.7% in pre-market trading after sliding 4.4% yesterday. “It feels like these earnings today are a barometer of where we are in the global cycle,” said Justin Onuekwusi, chief investment officer at St James’s Place. “Concentration in the stock market has got to levels where one company’s earnings can have a big macro effect. It’s gone beyond being just a portfolio construction issue; it’s a macro challenge which you can’t get away from.”

Meanwhile, Europe’s stock benchmark retreated from near a record high amid disappointing earnings from some of the region’s biggest companies. The Stoxx Europe 600 gauge edged lower 0.1% for a second day, still about four points from its January 2022 peak. Banks were among the leading decliners as HSBC Holdings Plc tumbled more than 7% after reporting an 80% plunge in fourth-quarter profit. Weak earnings from commodities trader Glencore Plc and Rio Tinto Plc, the world’s biggest iron ore miner, weighed on the basic resources sub-index, which slumped to a four-month low. On the positive side, Carrefour SA gained after the French grocer announced a share buy-back, even as quarterly sales disappointed. Here are all the notable European movers:

Fresenius SE shares rise as much as 4.7% after the German health-care company reported 4Q Ebit before special items for beat estimates and provided reassuring 2024 guidance

NKT gains as much as 8.8%, to a record high, after the Copenhagen-listed power cable manufacturer’s 4Q report and guidance both impressed with solid numbers, Carnegie says

Aedifica rises as much as 3.7% after releasing results described as “excellent” by KBC analysts. A highlight was the Belgian healthcare property operator’s occupancy rates

Conduit rises as much as 6.2%, the most in about 13 months, after the reinsurer delivers results which Peel Hunt says are strong, and highlight the maturity of the business

Inditex advances to a fresh record, with Oddo BHF increasing its price target for the Spanish retailer ahead of 4Q earnings that the broker expects will show strong sales growth

EFG International shares climb as much as 4.2%, to the highest level since 2015, after the Swiss private bank posted solid results according to Vontobel

HSBC slides as much as 7.6% in London after the bank reported profit that was hit by charges and offered guidance for the year that analysts said was unclear, with Jefferies calling them “messy”

Glencore shares slump 6.4% after the mining giant posted results showing lower thermal coal prices, which will likely lead to consensus downgrades, according to RBC says

JDE Peet’s shares drop as much as 6.7%, hitting the lowest level on record, after the Dutch coffee company reported full-year adjusted Ebit that missed estimates

BAE Systems retreats as much as 3.6% on Wednesday, paring a rally which has fueled the defense and aerospace systems manufacturer to a record high

Fresenius Medical Care falls as much as 5.5%, adding to Tuesday’s 4.5% drop, following earnings and guidance that failed to turn analysts more bullish on the German dialysis provider

Nel shares fall as much as 4.2% and to 2019 lows after SEB cut the Norwegian supplier of hydrogen technology’s price target, citing low visibility and forecasts for an Ebitda loss

Positive economic surprises had buoyed European stocks even as traders trimmed bets on interest rate cuts by the European Central Bank. Volatility measures are at historical lows, suggesting some complacency has crept into a market still facing potential headwinds, including rising bond yields, according to Bloomberg Intelligence.

“European stocks could consolidate recent gains in the near term as investor sentiment looks overheated,” BI strategists Laurent Douillet and Tim Craighead wrote in a report. “Rising government bond yields haven’t curbed enthusiasm so far, as highly leveraged companies slightly outperform, and remain a key 2024 risk for equities.”

Earlier in the session, Asian stocks erased an early loss and edged higher as China rallied after authorities rolled out more measures to restore investor confidence, offsetting broader weakness ahead of Nvidia’s earnings. The MSCI Asia Pacific Index rose 0.1% after falling as much as 0.5% earlier, driven by gains in Chinese tech giants including Tencent and Alibaba. Miners dragged on the gauge as iron ore extended declines amid concerns about demand outlook in China, while chip-related stocks declined in Taiwan, South Korea and Japan. Chinese benchmarks jumped, with a gauge of offshore-listed shares surging more than 3% in Hong Kong, as the nation’s two bourses vowed to tighten supervision of quantitative trading after imposing a freeze on a major fund’s accounts. Bloomberg also reported that China has banned major institutional investors from reducing equity holdings at the open and close of each trading day, part of the government’s most forceful attempt yet to prop up the nation’s $8.6 trillion stock market. Banks meanwhile ramped up funding help for the troubled property sector.

Hang Seng and Shanghai Comp. shrugged off early weakness with outperformance in Hong Kong driven by strength in property and tech, while the mainland also recovered its initial losses and more following recent stability efforts by Chinese authorities.

ASX 200 was dragged lower by consumer stocks and miners in another busy day of earnings.

Nikkei 225 continued its gradual pullback from near-record levels but remained above the 38,000 level.

Indian stocks snapped a six-day rally, dragged by a selloff in information technology companies and as investors likely booked profits. The S&P BSE Sensex Index fell 0.6% to 72,623.09 in Mumbai, while the NSE Nifty 50 Index declined by a similar measure. Both gauges posted their biggest single-day slump since Feb. 12.

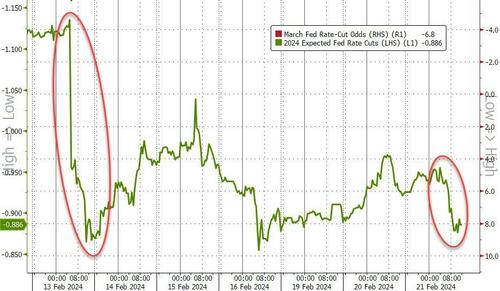

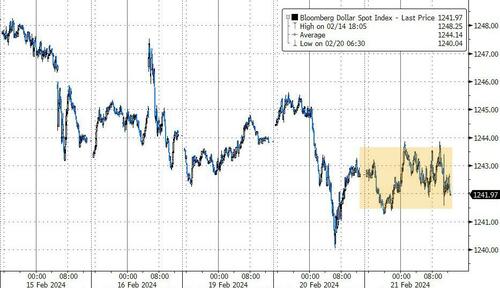

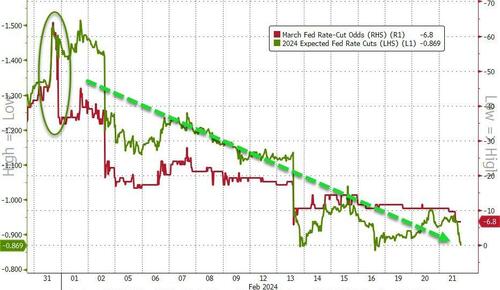

In FX, the Bloomberg Dollar Spot Index is little changed after posting a small drop for two straight days; one-year risk reversals in the Bloomberg Dollar Spot Index closed yesterday at the least bullish level in eight months. Markets are close to fully discounting a 25bps cut in June, and see a 33% chance of a cut in May.

USD/JPY consolidated around 150 while EUR/USD fell back below 1.08 after hitting 1.0839 on Tuesday, its highest since Feb.

GBP/USD fell 0.1% to 1.2606, in line with recent range

AUD/USD rose on buying from leveraged accounts in view of solid gains in Chinese stock indexes, according to Asia-based FX traders

In rates, Treasuries are slightly richer across the curve with gains led by front-end, where 2-year yields are lower by ~2bp vs Tuesday’s close. Treasury 10-year yields around 4.26%, richer by around 1.5bp on the day, outperforming bunds and gilts by 2bp and 3bp in the sector. Front-end-led gains in Treasuries steepen 2s10s, 5s30s curves by 0.5bp and 0.7bp, with both spreads off session wides. Bunds lag as the market digests German 10-year auction, while gilts give back a portion of Tuesday’s aggressive rally. US session includes 20-year bond auction, January FOMC minutes and Nvidia Corp. results, scheduled to be reported after the close. Corporate new-issue calendar is said to be under consideration for a large offering. Treasury auctions resume with $16b 20-year bond sale at 1pm; the WI level around 4.535% is above auction stops since November and ~11bp cheaper than January’s, which tailed by 0.8bp.

In commodities, aluminum surged on speculation that a fresh wave of US sanctions against Russia may target the metal, potentially disrupting supplies. Iron ore futures hit the lowest since October after a volatile session in which prices flipped between gains and losses. Oil edged lower with WTI falling 0.7% to trade near $76.50. Spot gold rises 0.2%.

In crypto, Bitcoin (-1.3%) fell back below USD 52k, and Ethereum (-2.2%) dips back under 3k after briefly breaking out above.

US economic data calendar includes only MBA mortgage applications, which declined 10.6% as interest rates rose. Federal Reserve members scheduled to speak include Bostic (8am), Barkin (9:10am) and Collins (5:30pm). FOMC minutes from Jan. 30-31 meeting are due to be released at 2pm

Market Snapshot

S&P 500 futures down 0.2% to 4,979.75

STOXX Europe 600 down 0.2% to 490.85

MXAP little changed at 171.21

MXAPJ little changed at 523.44

Nikkei down 0.3% to 38,262.16

Topix down 0.2% to 2,627.30

Hang Seng Index up 1.6% to 16,503.10

Shanghai Composite up 1.0% to 2,950.96

Sensex down 0.7% to 72,582.18

Australia S&P/ASX 200 down 0.7% to 7,608.36

Kospi down 0.2% to 2,653.31

German 10Y yield little changed at 2.40%

Euro down 0.1% to $1.0796

Brent Futures down 0.6% to $81.83/bbl

Gold spot up 0.2% to $2,027.48

U.S. Dollar Index little changed at 104.17

Top Overnight News

Beijing is overhauling how China’s fast-growing quant trading industry is regulated after one of the sector’s largest operators was hit with a trading ban this week for dumping shares. Stock exchanges in Shanghai and Shenzhen announced late on Tuesday that all market activity by computer-driven quant funds, which rely on complex automated trading strategies, would be closely scrutinized under a new monitoring scheme jointly run by both bourses and the China Securities Regulatory Commission. FT

HSBC slid as its profit plunged 80% after taking unexpected charges on holdings in a Chinese bank. CEO Noel Quinn said it has de-risked its US commercial real-estate exposure and that China’s moves to prop up its property sector will lead to a more lasting recovery. The bank announced a $2 billion buyback. BBG

Honda and Mazda agree to union wage demands, the latest sign that compensation is rising enough for the BOJ to begin tightening policy. BBG

Japan’s exports for Jan come in a bit ahead of plan at +11.9% (vs. the Street +9.5%), although the Reuters Tankan survey revealed a deterioration in sentiment while the Japanese gov’t reduced its economic assessment for the first time in 3 months. RTRS

Boaz Weinstein is building up positions across UK investment trusts that now account for about a quarter of his $5.4 billion bet on closed-end funds trading near historic discounts. His targets include funds managed by JPMorgan, BlackRock, Schroders and Baillie Gifford. BBG

As Russia’s war in Ukraine enters a third year, President Vladimir Putin’s forces have shifted to the offensive and captured the eastern city of Avdiivka after months of fighting. In a conflict where momentum has ebbed and flowed, the mood is now noticeably darker in Kyiv. BBG

Private equity firms are increasingly raising money to buy individual companies on a deal-by-deal basis, as they struggle with a downturn in the market and investors look for ways to cut management fees. A record $31bn was deployed by “deal-by-deal” investors last year, according to data provided by private equity advisory firm Triago, defying a broader dealmaking and fundraising slump in the industry. FT

Donald Trump entered the 2024 election year with about 200,000 fewer donors than in the previous presidential campaign four years ago, raising questions about his fundraising machine just as legal bills eat into his war chest. FT

Bank reserve balances remain ample, suggesting liquidity levels remain ample despite the drop in reverse repo balances (which means the Fed may not need to slow the pace of QT). BBG

A more detailed look at global markets courtesy of Newsquawk

APAC stocks traded mixed with headwinds following the tech-led declines stateside ahead of Nvidia earnings and FOMC Minutes. ASX 200 was dragged lower by consumer stocks and miners in another busy day of earnings. Nikkei 225 continued its gradual pullback from near-record levels but remained above the 38,000 level. Hang Seng and Shanghai Comp. shrugged off early weakness with outperformance in Hong Kong driven by strength in property and tech, while the mainland also recovered its initial losses and more following recent stability efforts by Chinese authorities.

Top Asian News

China’s housing authority said a total of CNY 123.6bln of development loans have been approved and that CNY 29.4bln have been issued under China’s “whitelist” mechanism which was launched on January 26th and is aimed at injecting liquidity to the property sector.

Chinese Foreign Minister Wang met with his French counterpart and said China is ready to strengthen strategic communication with France and forge more consensus, strengthen solidarity and cooperation, as well respond more effectively to global challenges. Wang also stated the two sides had in-depth communication on issues related to peace and security, while they agreed that multi-polarisation is indispensable for peace and stability, and will continue to strengthen strategic coordination. Furthermore, Wang said in a meeting with French President Macron that he hopes France will continue to play a constructive role in the healthy and stable development of Sino-European relations, while China hopes France will also create a fair and just business environment for Chinese enterprises there and provide positive and stable long-term expectations.

China state asset regulator says state-owned firms should take steps to develop and promote artificial intelligence and should speed up in building smart computer centres.

China’s draft legislation of private economy promotion has commenced, according to state media.

Japanese government cuts its view on the economy for the first time since November 2023.

China is said to be tightening its grip on stocks with net sale ban at the open and close, according to Bloomberg sources. Major institutional investors have been banned form reducing equity holdings at the open and close of each session. Firms affected by the ban are not able to offload more shares than they buy during the first and last 30 minutes of the trading day. The order was delivered from China’s securities watchdog to major asset managers and proprietary trading desks of brokerages, sources said. The CSRC (with newly appointed Chairman Qing) also created a task force to monitor short-selling.

European bourses, Stoxx600 (-0.1%) are mixed with a slight positive bias, following on from a similar APAC handover. FTSE 100 (-0.8%) underperforms, hampered by significant losses in index heavyweights. European sectors are on a mixed footing; Autos outperform with broad-based gains within the sector. Basic Resources is at the foot of the pile, weighed on by Glencore (-5.5%) and Rio Tinto (-2.1%) following poorly received earnings. Banks are also lower, after softer HSBC (-7.1%) results. US Equity Futures (ES -0.2%, NQ -0.4%, RTY -0.2%), are modestly in the red, continuing the losses seen in the prior session. Nvidia (-1.7%) is softer in the pre-market, ahead of earnings. In terms of pre-market movers; Amazon (+1.0%) and Uber (+0.6%) are firmer, after S&P Dow Jones Indices said they are set to join the DJIA and DJTA respectively.

Top European News

UK Chancellor Hunt will have GBP 23bln of headroom for pre-election tax reductions in next month’s budget, according to the Resolution Foundation, via Bloomberg.

Earnings

BAE Systems (BA/ LN) – FY (GBP): Sales 25.2bln (exp. 24.6bln), adj. EBIT 26.82bln (exp. 27.1bln), Board has recommended a final dividend of 18.5p. Q4: EPS 63.2p (prev. 55.5p Y/Y), Adj. EBIT 2.68bln (prev. 2.48bln Y/Y). Order backlog 69.8bln (prev. 58.9bln Y/Y). Guides initial FY24 adj. EPS +6-8%, Revenue +10-12%, adj. EBIT +11-13%. Shares -3.5% in European trade

Glencore (GLEN LN) – FY23 (USD): Revenue 217.83bln (exp. 216.02bln). adj. EBTIDA 17.10bln (exp. 17.35bln). Net Debt 4.92bln (exp. 4.43bln). Adj. Marketing EBIT 3.5bln (exp. 3.67bln); Recommends to shareholders a USD 0.13/shr base cash distribution. “Although the current macroeconomic environment remains challenging, global economic growth is forecast to bottom out in 2024.” “Supply constraints and energy transition demand prevented large inventory increases in most commodities during this cyclical trough, leaving markets well-positioned for a strong recovery as demand conditions improve.” “This is particularly the case for copper, where the closure of a major mine and various cuts to production guidance through the second half of 2023 have highlighted the persistent supply challenges facing the industry. These are likely to keep the market tight throughout 2024 against previous expectations of oversupply.” Shares -5.5% in European trade

HSBC (5 HK / HSBA LN) – FY23 (USD): Revenue 66.06bln (exp. 66.69bln). Pretax profit 30.35bln (exp. 34.12bln). Announces up to USD 2bln in share buybacks and a fourth interim dividend of USD 0.31/shr. Co. says the outlook for loan growth remains cautious for H1. OTHER METRICS: CET1 ratio 14.8% (exp. 14.5%). NIM 1.66% (prev. 1.42% Y/Y). Cost efficiency ratio 48.5% (prev. 64.6% Y/Y). OUTLOOK: Sees ROTE in the mid-teens for 2024. Expect banking NII Of At Least USD 41bln For 2024. The dividend payout ratio target remains at 50% for 2024, excluding material notable items and related impacts. Shares -7.1% in European trade

Rio Tinto (RIO AT / RIO LN) – FY23 (USD): Adj. EPS 7.25 (exp. 7.27). Underlying Profit 11.8bln (exp. 11.7bln). Revenue 54.04bln (exp. 53.94bln). Net Income 10.6bln (exp. 11.15bln). Underlying EBITDA 23.90bln (exp. 23.85bln). Co. said cost pressures and weaker market demand lowered underlying EBITDA by USD 1.0bln. Shares -2.1% in European trade

Carrefour (CA FP) – FY23 (EUR): Adj. Net 1.3bln (prev. 1.2bln Y/Y), Sales 94.13bln (prev. 90.81bln Y/Y). Raises dividend by 55% to 0.87/shr and launches new 700mln share buyback programme. CFO says the retailer plans to keep cutting prices this year in France to be more competitive; the Red Sea crisis has caused delays of one-to-two weeks on products coming from Asia to Europe and increased transport costs. Shares +4.6% in European trade

FX

Dollar is mixed vs its peers following yesterday’s session of losses which sent the DXY down to a low of 103.79 but stopped shy of testing the 200DMA at 103.68.

EUR is back on a 1.07 handle after pulling back from yesterday’s 1.0839 peak and back below its 100DMA at 1.0806. Yesterday’s low sits at 1.0761 with not much in the way of notable EZ newsflow to guide price action thus far.

JPY is relatively steady vs. the USD as the pair continues to pivot around the 150 mark and remains within yesterday’s 149.68-150.44 range.

Antipodeans are both firmer vs. the USD but NZD more so. NZD/USD has mounted yesterday’s peak and the 50DMA at 0.6181 with focus now on a potential test of 0.62. AUD/USD currently below yesterday’s best of 0.6579 and the 200DMA at 0.6563.

PBoC set USD/CNY mid-point at 7.1030 vs exp. 7.1877 (prev. 7.1068).

Fixed Income

USTs are essentially unchanged after Tuesday’s light session into the 20yr supply. An outing which hasn’t spurred any overt concession just yet, but this could well emerge into the US session. The yield curve is slightly steeper, whilst the benchmark itself is comfortably within Tuesday’s 109-19 to 110-05 bounds.

Bunds started the session on bearish/defensive footing, printing a trough at 132.89; initially unreactive to a strong German outing, but modest upside has emerged since.

Gilt price action is in-fitting with the above ahead of BoE speak from Dhingra; incremental upside to a strong 2028 outing.

Germany sells EUR 3.712bln vs exp. EUR 4.5bln 2.20% 2034 Bund: b/c 2.1x (prev. 1.77x), average yield 2.38% (prev. 2.23%) and retention 17.53% (prev. 19.78%)

Commodities

Crude is lower with fresh catalysts light, though focus still remains on the Middle East and China; Brent futures hover off lows and holds around USD 82/bbl.

Precious metals see upward biases despite the modest gains seen in the Dollar, but as market sentiment is tilting lower and geopolitics largely show signs of expanding; XAU met resistance at its 50 DMA (2,031.04/oz today).

Mostly firmer trade across base metals. 3M LME copper rose back above the 8,500/t mark and LME aluminium soared over 3% in early trade

Geopolitics: Middle East

China’s envoy to the UN said the objection to a ceasefire in Gaza equals a license to kill and is nothing different from giving the green light to a continued slaughter following the US veto of the Security Council draft resolution on a ceasefire in Gaza, while China expressed its strong disappointment at and dissatisfaction with the US veto, according to Reuters.

US Central Command said Houthis fired two anti-ship ballistic missiles at a Greek-flagged and US-owned bulk carrier bound for Yemen’s Port of Aden, while one of the missiles detonated near the ship and caused minor damage

UKMTO received a report of heightened uncrewed aerial system activity 40NM west of Yemen’s Hodeidah.

“Israeli sources: progress in hostage talks, Israeli delegation will head to Cairo”, according to Sky News Arabia

Geopolitics: Other

Ukrainian military intelligence chief Budanov said Russia will struggle to keep up the fight and Russians don’t have the strength to achieve the goal of seizing two eastern regions this year, according to WSJ.

Taiwan’s Defence Ministry denied increasing military deployments on Taiwan’s offshore islands and said there is nothing unusual regarding the military situation around Taiwan, but stated that it is making preparations with the coast guard for possible new scenarios near offshore islands, according to Reuters.

US Event Calendar

07:00: Feb. MBA Mortgage Applications, prior -2.3%

14:00: Jan. FOMC Meeting Minutes

Central Bank speakers

08:00: Fed’s Bostic Gives Welcoming Remarks

09:10: Fed’s Barkin Speaks on SiriusXM

14:00: Jan. FOMC Meeting Minutes

17:30: Fed’s Collins Participates in Fireside Chat

DB’s Jim Reid concludes the overnight wrap

One of the proudest moment of my career arrived in the last 24 hours as after 29 years of having a Bloomberg terminal, I found out that I breached their monthly download limit for the first time and was locked out. Before I apply for a pay rise based on my increased productivity, I can only think it’s because of the colossal spreadsheets that were involved in the making of the Mag-7 chartbook where Galina in my team and I worked out the profitability of every listed stock in every G20 country and amalgamated them to compare with the Mag-7. A quick call to their help desk and my account was thankfully restored.

Between publishing the above chart book 9 days ago and now, Nvidia has gone from being the 5th largest company in the US to initially the 4th and then the 3rd largest but yesterday it slipped back to the 5th again as it fell -4.35% ahead of a very important earnings release today. This was the worst daily performance since last October. However implied options suggest that that the post results move is priced to be 10.5% in either direction so stand by for potential fireworks across markets in either direction. After having said that they’ll probably end up being flat in after-hours trading by tomorrow’s EMR!

This move contributed to the S&P 500 (-0.60%) losing ground with the Mag-7 (-1.46%) and the Nasdaq (-0.92%) underperforming. Small caps also lost significant ground, with the Russell 2000 (-1.41%) moving back into the red year-to-date. To be fair, most sectors within the S&P 500 posted pretty modest declines, and the equal-weighted S&P 500 saw a moderate -0.31% decline with 197 advancers. That included a strong performance for Walmart (+3.23%), which was the fifth best performer in the index after their earnings beat estimates. And over in Europe, it was much the same story, with technology stocks helping to drag the broader indices lower, as the STOXX Technology Index fell -1.93%, even though the STOXX 600 (-0.10%) only experienced a marginal decline. Moreover in France, the CAC 40 (+0.34%) hit a new all-time high.

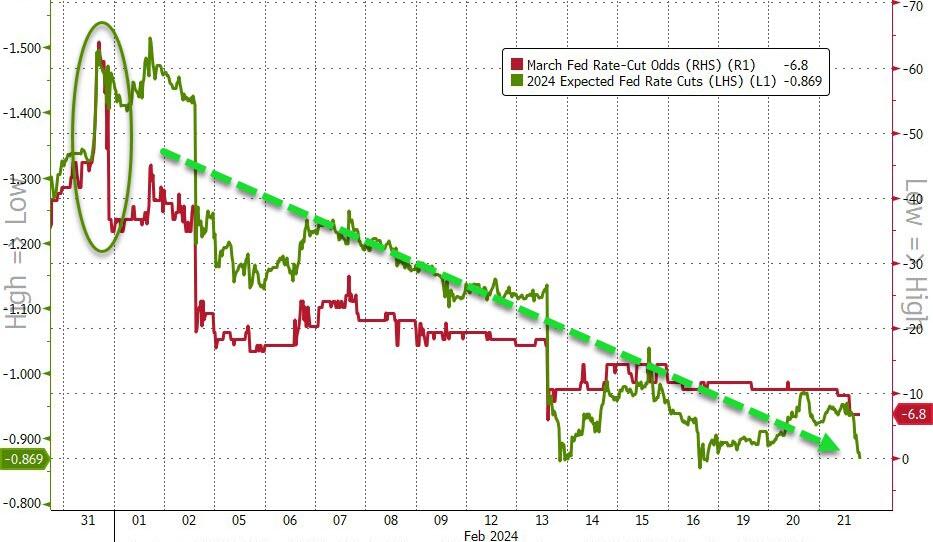

In the meantime, sovereign bonds got support from more dovish news over the last 24 hours, as the Canadian CPI print for January surprised on the downside. That was welcome news for investors, as recent prints from the US and Sweden had seen upside surprises, which added to fears that the path back to target was likely to prove a bumpy one. So with Canadian headline inflation down to +2.9% (vs. +3.3% expected), and core inflation also falling, that led to growing expectations that the Bank of Canada would soon be able to cut rates. Indeed, the chance of a rate cut by June surged from 58% on Monday to 84% by the close yesterday, and yields on 10yr Canadian government bonds fell -7.1bps.

That backdrop helped support a global sovereign bond rally. There were modest declines in Treasury yields, with the 10yr down -0.5bps to 4.28%, and 2yr down -3.0bps. The bond rally was slightly stronger in Europe, where yields on 10yr bunds (-3.8bps), OATs (-3.6bps) and BTPs (-4.2bps) all fell back. And it was UK gilts (-6.9bps) that saw one of the biggest moves after comments from BoE Governor Bailey. He said that they “ don’t need obviously inflation to come back to target before we cut interest rates. I must be very clear on that, that’s not necessary ”. In addition, Bailey also said he was “comfortable with a profile that has cuts in it”, suggesting that the next move was likely to be a rate cut. In turn, investors became more confident in the likelihood of a cut by June, with the chance up to 66% by the close from 52% the day before.

Otherwise on the inflation side, there was better news from the latest commodity declines, with Brent oil prices (-1.46% to $82.34) falling back from their 3-month high the previous day. At the same time, there was a notable decline in iron ore futures (-2.01%), which hit a 3-month low amidst ongoing concern about demand from China. The Bloomberg commodity index declined by -0.44%, although it stayed half a percent above its 2-year lows seen last week.

Chinese stocks are bucking the global trend this morning as actions to boost sentiment are winning out for now. The Hang Seng (+2.40%) is off its highs but with the CSI (+2.30%) and the Shanghai Composite (+2.13%) catching up after the lunch break.

Other Asian markets are lower with the Nikkei (-0.24%), KOSPI (-0.32%) and the S&P/ASX 200 (-0.66%) trading lower alongside S&P 500 (-0.13%) and NASDAQ 100 (-0.27%) futures. 2yr and 10yr US treasuries are -2.3bps and -0.6bps lower respectively.

Early morning data showed that Japan’s exports rose for the second consecutive month advancing +11.9% y/y in January (v/s +9.5% expected and against a +9.7% downwardly revised increase in December) on higher demand for cars and semiconductor-manufacturing equipment. Imports fell -9.6% y/y, versus Bloomberg’s estimate for an -8.7% decrease. As such the trade deficit of -1.758 trillion yen was slightly smaller than the -1.855 trillion yen expected.

There wasn’t too much data yesterday, although the US Conference Board’s Leading Index fell for a 22nd consecutive month in January, with a -0.4% decline (vs. -0.3% expected).

To the day ahead now, and an important highlight will be Nvidia’s earnings after the US close. Otherwise from central banks, we’ll get the FOMC’s minutes from the January meeting, and hear from the Fed’s Bostic and the BoE’s Dhingra. Data releases include Euro Area consumer confidence for February.

2 B) NOW NEWSQUAWK (EUROPE/REPORT)

US futures are lower ahead of NVDA earnings, NZD bid & Crude softer; FOMC Minutes due – Newsquawk US Market Open

WEDNESDAY, FEB 21, 2024 – 06:00 AM

European bourses are generally firmer, though the FTSE 100 lags after significant underperformance in Glencore & HSBC; US futures lower pre-Nvidia

Dollar is incrementally firmer, Antipodeans bid in tandem with strong Chinese equity trade overnight

Bonds are mixed but edging higher in recent trade post-supply; attention on US 20yr supply later today

Crude is softer and Gold is modestly firmer with specifics light

Looking ahead, EZ Consumer Confidence, NZ Trade, Australian PMI, FOMC Minutes, Comments from Fed’s Bostic, Bowman & BoE’s Dhingra, Supply from the US, Earnings from NVIDIA, Analog Devices & Synopsys

2. Listen to this report in the market open podcast (available on Apple and Spotify)

3. Trial Newsquawk’s premium real-time audio news squawk box for 7 days

EUROPEAN TRADE

EQUITIES

European bourses, Stoxx600 (-0.1%) are mixed with a slight positive bias, following on from a similar APAC handover. FTSE 100 (-0.8%) underperforms, hampered by significant losses in index heavyweights.

European sectors are on a mixed footing; Autos outperform with broad-based gains within the sector. Basic Resources is at the foot of the pile, weighed on by Glencore (-5.5%) and Rio Tinto (-2.1%) following poorly received earnings. Banks are also lower, after softer HSBC (-7.1%) results.

US Equity Futures (ES -0.2%, NQ -0.4%, RTY -0.2%), are modestly in the red, continuing the losses seen in the prior session. Nvidia (-1.7%) is softer in the pre-market, ahead of earnings.

In terms of pre-market movers; Amazon (+1.0%) and Uber (+0.6%) are firmer, after S&P Dow Jones Indices said they are set to join the DJIA and DJTA respectively.

Click here and here for the sessions European pre-market equity newsflow, including earnings from Rio Tinto, Glencore, HSBC, BAE Systems and more.

Dollar is mixed vs its peers following yesterday’s session of losses which sent the DXY down to a low of 103.79 but stopped shy of testing the 200DMA at 103.68.

EUR is back on a 1.07 handle after pulling back from yesterday’s 1.0839 peak and back below its 100DMA at 1.0806. Yesterday’s low sits at 1.0761 with not much in the way of notable EZ newsflow to guide price action thus far.

JPY is relatively steady vs. the USD as the pair continues to pivot around the 150 mark and remains within yesterday’s 149.68-150.44 range.

Antipodeans are both firmer vs. the USD but NZD more so. NZD/USD has mounted yesterday’s peak and the 50DMA at 0.6181 with focus now on a potential test of 0.62. AUD/USD currently below yesterday’s best of 0.6579 and the 200DMA at 0.6563.

PBoC set USD/CNY mid-point at 7.1030 vs exp. 7.1877 (prev. 7.1068).

USTs are essentially unchanged after Tuesday’s light session into the 20yr supply. An outing which hasn’t spurred any overt concession just yet, but this could well emerge into the US session. The yield curve is slightly steeper, whilst the benchmark itself is comfortably within Tuesday’s 109-19 to 110-05 bounds.

Bunds started the session on bearish/defensive footing, printing a trough at 132.89; initially unreactive to a strong German outing, but modest upside has emerged since.

Gilt price action is in-fitting with the above ahead of BoE speak from Dhingra; incremental upside to a strong 2028 outing.

Crude is lower with fresh catalysts light, though focus still remains on the Middle East and China; Brent futures hover off lows and holds around USD 82/bbl.

Precious metals see upward biases despite the modest gains seen in the Dollar, but as market sentiment is tilting lower and geopolitics largely show signs of expanding; XAU met resistance at its 50 DMA (2,031.04/oz today).

Mostly firmer trade across base metals. 3M LME copper rose back above the 8,500/t mark and LME aluminium soared over 3% in early trade

UK Chancellor Hunt will have GBP 23bln of headroom for pre-election tax reductions in next month’s budget, according to the Resolution Foundation, via Bloomberg.

DATA RECAP

UK PSNB Ex Banks GBP (Jan) -16.691B GB vs. Exp. -18.7B GB (Prev. 7.77B GB, Rev. 7.375B GB); PSNB, GBP (Jan) -17.615B GB (Prev. 6.846B GB, Rev. 6.451B GB)

South African Core Inflation YY (Jan) 4.7% vs. Exp. 4.5% (Prev. 4.5%); Core Inflation MM (Jan) 0.3% vs. Exp. 0.2% (Prev. 0.2%)

South African CPI YY (Jan) 5.3% vs. Exp. 5.4% (Prev. 5.1%); CPI MM (Jan) 0.1% vs. Exp. 0.1%

EARNINGS

BAE Systems (BA/ LN) – FY (GBP): Sales 25.2bln (exp. 24.6bln), adj. EBIT 26.82bln (exp. 27.1bln), Board has recommended a final dividend of 18.5p. Q4: EPS 63.2p (prev. 55.5p Y/Y), Adj. EBIT 2.68bln (prev. 2.48bln Y/Y). Order backlog 69.8bln (prev. 58.9bln Y/Y). Guides initial FY24 adj. EPS +6-8%, Revenue +10-12%, adj. EBIT +11-13%. Shares -3.5% in European trade

Glencore (GLEN LN) – FY23 (USD): Revenue 217.83bln (exp. 216.02bln). adj. EBTIDA 17.10bln (exp. 17.35bln). Net Debt 4.92bln (exp. 4.43bln). Adj. Marketing EBIT 3.5bln (exp. 3.67bln); Recommends to shareholders a USD 0.13/shr base cash distribution. “Although the current macroeconomic environment remains challenging, global economic growth is forecast to bottom out in 2024.” “Supply constraints and energy transition demand prevented large inventory increases in most commodities during this cyclical trough, leaving markets well-positioned for a strong recovery as demand conditions improve.” “This is particularly the case for copper, where the closure of a major mine and various cuts to production guidance through the second half of 2023 have highlighted the persistent supply challenges facing the industry. These are likely to keep the market tight throughout 2024 against previous expectations of oversupply.” Shares -5.5% in European trade

HSBC (5 HK / HSBA LN) – FY23 (USD): Revenue 66.06bln (exp. 66.69bln). Pretax profit 30.35bln (exp. 34.12bln). Announces up to USD 2bln in share buybacks and a fourth interim dividend of USD 0.31/shr. Co. says the outlook for loan growth remains cautious for H1. OTHER METRICS: CET1 ratio 14.8% (exp. 14.5%). NIM 1.66% (prev. 1.42% Y/Y). Cost efficiency ratio 48.5% (prev. 64.6% Y/Y). OUTLOOK: Sees ROTE in the mid-teens for 2024. Expect banking NII Of At Least USD 41bln For 2024. The dividend payout ratio target remains at 50% for 2024, excluding material notable items and related impacts. Shares -7.1% in European trade

Rio Tinto (RIO AT / RIO LN) – FY23 (USD): Adj. EPS 7.25 (exp. 7.27). Underlying Profit 11.8bln (exp. 11.7bln). Revenue 54.04bln (exp. 53.94bln). Net Income 10.6bln (exp. 11.15bln). Underlying EBITDA 23.90bln (exp. 23.85bln). Co. said cost pressures and weaker market demand lowered underlying EBITDA by USD 1.0bln. Shares -2.1% in European trade

Carrefour (CA FP) – FY23 (EUR): Adj. Net 1.3bln (prev. 1.2bln Y/Y), Sales 94.13bln (prev. 90.81bln Y/Y). Raises dividend by 55% to 0.87/shr and launches new 700mln share buyback programme. CFO says the retailer plans to keep cutting prices this year in France to be more competitive; the Red Sea crisis has caused delays of one-to-two weeks on products coming from Asia to Europe and increased transport costs. Shares +4.6% in European trade

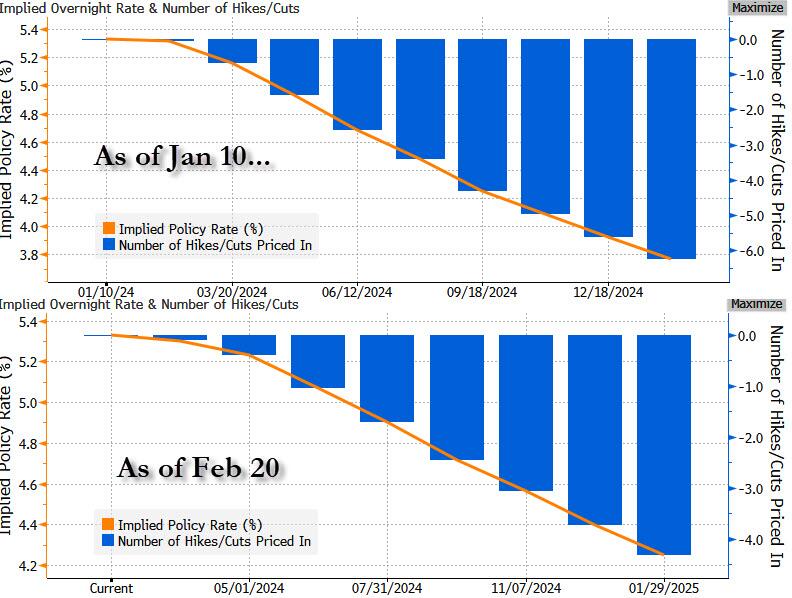

NOTABLE US HEADLINES

US House Republicans are reportedly expecting a government shutdown behind closed doors, according to Axios.

UBS Global Wealth Management now sees the Fed cutting rates from June (vs prev. view of May)

GEOPOLITICS

MIDDLE EAST