GOLD PRICE CLOSED UP $17.80 TO $2038.80

SILVER PRICE UP $.18 TO $22.95

Gold ACCESS CLOSED 2036.00

Silver ACCESS CLOSED: 22.93

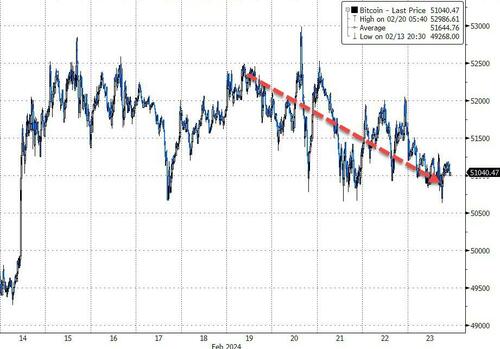

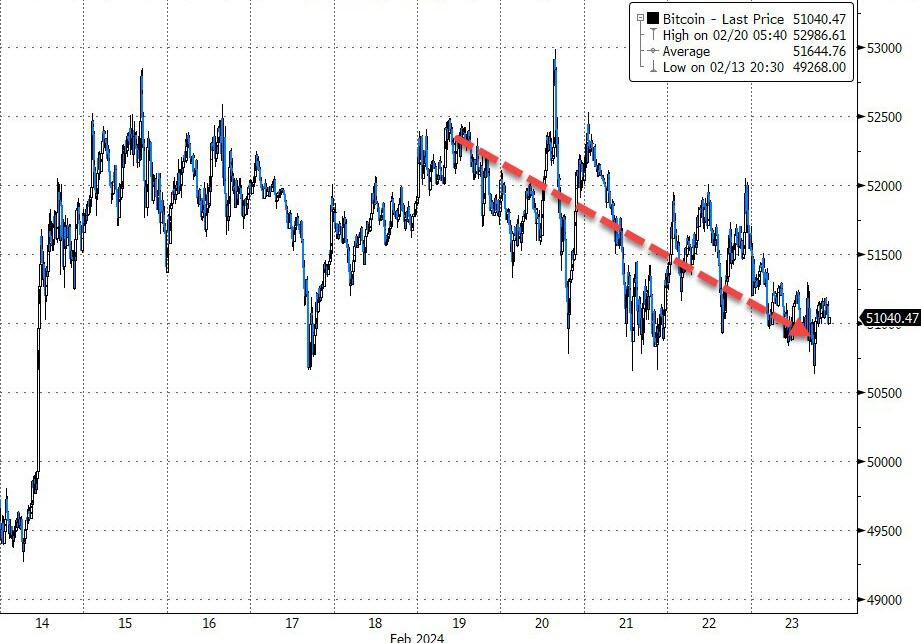

Bitcoin morning price:, 50,956 DOWN 952 DOLLARS.

Bitcoin: afternoon price: $51,012 DOWN 896 dollars

Platinum price closing $905.05 UP $2.20

Palladium price; $969.45 UP $14.95

END

SHANGHAI GOLD PREMIUM 43 DOLLARS/COMEX GOLD

SHANGHAI GOLD (USD) FUTURES – QUOTES

SHANGHAI GOLD (USD) FUTURES – QUOTES

Beginning Monday, April 1, 2024, CME Group settlement data will no longer be accessible through ftp.cmegroup.com and will have a delayed publication time of 12:00 a.m. CT on all cmegroup.com web pages. Learn about alternate ways to access the data in our FAQ.

Last Updated 23 Feb 2024 03:22:40 PM CT.

Market data is delayed by at least 10 minutes.

I will now provide gold in Canadian dollars, British pounds and Euros

4: 15 PM ACCESS

*CANADIAN GOLD: $2,749.11 UP 19.28 CDN dollars per oz( * NEW ALL TIME HIGH 2,795.90 CDN DOLLARS PER OZ//DEC 1 2023)

*BRITISH GOLD: 1607.05 UP 8.05 pounds per oz// *(NEW ALL TIME HIGH//CLOSING///1655.17 BRITISH POUNDS/OZ) OCT 2/2023

*EURO GOLD: 1881.34 UP 11.08 euros per oz //* (ALL TIME CLOSING HIGH: 1903.75 EUROS PER OZ//DEC 1.2023)

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

EXCHANGE: COMEX

EXCHANGE: COMEX

CONTRACT: FEBRUARY 2024 COMEX 100 GOLD FUTURES

SETTLEMENT: 2,019.700000000 USD

INTENT DATE: 02/22/2024 DELIVERY DATE: 02/26/2024

FIRM ORG FIRM NAME ISSUED STOPPED

323 C HSBC 265

363 H WELLS FARGO SEC 300

435 H SCOTIA CAPITAL 572

657 C MORGAN STANLEY 61

661 C JP MORGAN 598

686 H STONEX FINANCIA 71

905 C ADM 1

TOTAL: 934 934

JPMorgan stopped 598/934 contracts.

FOR FEB/2024

GOLD: NUMBER OF NOTICES FILED FOR FEB/2024. CONTRACT: 934 NOTICES FOR 93,400 OZ or 2.905 TONNES

total notices so far: 19,896 contracts for 1,989,600 Oz (61.885 tonnes)

FOR FEBRUARY:

SILVER NOTICES NOTICE(S) FILED FOR NIL OZ/

total number of notices filed so far this month : 1294 for 6,420,000 oz

XXXXXXXXXXXXXXXXXX

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

BOTH GLD AND SLV ARE FRAUDULENT VEHICLES//THEY ARE NOW RAIDING GLD AND SLV FOR PHYSICAL

GLD

WITH GOLD UP 17.80//

INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD/ : HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A MASSIVE WITHDRAWAL OF 2.01 TONNES OF GOLD FROM THE GLD//MAKES NO SENSE

INVENTORY RESTS AT 827.81 TONNES

SLV//

WITH NO SILVER AROUND AND SILVER UP 18 CENTS AT THE SLV//

HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A HUGE WITHDRAWAL OF 1.098 MILLION OZ FROM THE SLV/.

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV.

CLOSING INVENTORY: 431.668 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A GOOD SIZED 489 CONTRACTS TO 145,906 AND FURTHER FROM THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THIS HUGE SIZED LOSS IN COMEX OI WAS ACCOMPLISHED WITH OUR FALL OF $0.10 IN SILVER PRICING AT THE COMEX ON THURSDAY. WE HAD ZERO LONG LIQUIDATION AT THE COMEX SESSION WITH SOME SHORT COVERING AS THE PRICE OF SILVER FELL BY A SMALL AMOUNT. WE HAD A HUGE 872 T.A.S ISSUANCE AND THESE WILL BE USED FOR MANIPULATION LATER THIS MONTH/AS WELL AS TODAY. PLEASE NOTE THAT THE CROOKS NEED A HIGHER SILVER T.A.S. TO CARRY ON THEIR CROOKED MANIPULATION ON A DAILY BASIS

CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON THURSDAY NIGHT: 872 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS. IT THUS LOOKS LIKE THE FED (GOV’T) IS BEHIND ALL OF THESE TRADES.

WE HAVE NOW SET ANOTHER RECORD LOW AT 114,102 CONTRACTS ///JULY 3.2023// OUR BANKERS WITH THE HELP OF SPECULATORS AND HIGH FREQUENCY TRADERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.10), BUT WERE UNSUCCESSFUL IN KNOCKING ANY SILVER LONGS AS WE HAD A HUGE SIZED GAIN OF 1153 CONTRACTS ON OUR TWO EXCHANGES BUT WITH A MUCH LOWER PRICE.

WE MUST HAVE HAD:

A HUMONGOUS SIZED 1440 ISSUANCE OF EXCHANGE FOR PHYSICALS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 3.535 MILLION OZ (FIRST DAY NOTICE) ACCOMPANYING A STRANGE 89 CONTRACT ISSUANCE FOR EX. FOR RISK FOR 445,000 OZ ON FIRST DAY NOTICE/ FOLLOWED BY TODAY’S 0 OZ QUEUE JUMP TO LONDON //NEW TOTAL LOWERS TO ; 6.975 MILLION OZ

//NEW STANDING FOR SILVER IS THUS 6.975 MILLION OZ

/ GOOD SIZED COMEX OI LOSS/HUMONGOUS SIZED EFP ISSUANCE/ VI) STRONG SIZED NUMBER OF T.A.S. CONTRACT ISSUANCE 872 CONTRACTS)/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL -REMOVED A HUGE 202 CONTRACTS //

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS FEB. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF FEB

TOTAL CONTRACTS for 16 days, total 9,802 contracts: OR 49.010 MILLION OZ (612 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 49.010 MILLION OZ

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH 2022: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 118.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 85.745 MILLION OZ (SMALLER THAN LAST MONTH)

AUGUST: 171.43 MILLION OZ (THIS MONTH IS GOING TO BE HUGE //2ND HIGHEST ON RECORD

SEPT: 72.705 MILLION OZ (SMALLER THIS MONTH)

OCT: 97.455 MILLION OZ

NOV. 50.050 MILLION OZ

DEC. 66.140 MILLION OZ//

TOTAL 2023: 1,104.10 MILLION OZ/

JAN ’24 : 78.655 MILLION OZ//

FEB /2024 : 41.81 MILLION OZ.

RESULT: WE HAD A GOOD SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 489 CONTRACTS WITH OUR LOSS IN PRICE OF SILVER PRICING AT THE COMEX//THURSDAY.,. THE CME NOTIFIED US THAT WE HAD A HUGE EFP ISSUANCE CONTRACTS: 1440 ISSUED FOR MARCH AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS. WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR FEB. OF 3.535 MILLION OZ ACCOMPANIED BY FIRST DAY NOTICE OF 445,000 OZ EX. FOR RISK FOLLOWED BY TODAY’S 0 OZ QUEUE JUMP //NEW TOTAL REMAINS AT 6.975 MILLION OZ

NEW STANDING 6.975 MILLION OZ /// WE HAVE A HUGE GAIN OF 2942 OI CONTRACTS ON THE TWO EXCHANGES DESPITE THE LOSS IN PRICE. THE TOTAL OF TAS INITIATED CONTRACTS TODAY: A VERY STRONG SIZED 1440 CONTRACTS//HUGE FRONT END OF THE TAS CONTRACTS WERE LIQUIDATED DURING THE THURSDAY COMEX SESSION/// WITH SOME SHORT COVERING FROM OUR SPEC SHORTS ( PRICE OF SILVER FELL) . THE NEW TAS ISSUANCE THURSDAY NIGHT (872) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE//PROBABLY TODAY., .

WE HAD 0 NOTICE(S) FILED TODAY FOR 0 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A SMALL SIZED 874 CONTRACTS TO 408,043 AND CLOSER TO THE RECORD (SET JAN 24/2020) AT 799,733 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110, BUT WE ARE NOW CLOSER TO OUR ALL TIME LOW OF 390,000 CONTRACTS.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: – REMOVED 29 CONTRACTS

WE HAD A SMALL SIZED INCREASE IN COMEX OI ( 874 CONTRACTS) DESPITE OUR $2.10 LOSS IN PRICE//THURSDAY. WE ALSO HAD A RATHER LARGE INITIAL STANDING IN GOLD TONNAGE FOR FEB. AT 49.773 TONNES ON FIRST DAY NOTICE ACCOMPANIED BY FIRST DAY NOTICE : 55,400 OZ EX. FOR RISK //THUS INITIAL STANDING FOR FEB: 51.494 TONNES FOLLOWED BY TODAY’S 1900 OZ QUEUE JUMP //NEW TOTAL OF GOLD STANDING ADVANCES TO: 64.248 TONNES // ALL OF THIS HAPPENED DESPITE OUR $2.10 LOSS IN PRICE WITH RESPECT TO THURSDAY’S TRADING. WE HAD A FAIR SIZED GAIN OF 2933 OI CONTRACTS (9.122) PAPER TONNES) ON OUR TWO EXCHANGES.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 2059 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 408043

IN ESSENCE WE HAVE A FAIR SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 2933 CONTRACTS WITH 883 CONTRACTS INCREASED AT THE COMEX// AND A FAIR SIZED 2059 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 2933 CONTRACTS.. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): A SMALL SIZED 410 CONTRACTS.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (2059 CONTRACTS) ACCOMPANYING THE SMALL SIZED GAIN IN COMEX OI (874) //TOTAL GAIN FOR OUR THE TWO EXCHANGES: 2933 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR FORMER FORMAT OF BANKERS GOING LONG AND SPECULATORS GOING SHORT ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR FEB. AT 49.773 TONNES PLUS FIRST DAY NOTICE OF 1.723 TONNE OZ EX. FOR RISK FOLLOWED BY TODAY’S 1900 OZ QUEUE JUMP //NEW STANDING ADVANCES TO 64.248 TONNES. / 3) ZERO LONG LIQUIDATION // 4) SMALL SIZED COMEX OPEN INTEREST GAIN/ 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER///6: SMALL T.A.S. ISSUANCE: 410 CONTRACTS//SOME SHORT COVERING AGAIN

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023-2024 INCLUDING TODAY

FEB.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF FEB. :

TOTAL EFP CONTRACTS ISSUED: 51,513 CONTRACTS OR 5,151,300 OZ OR 160.22 TONNES IN 16 TRADING DAY(S) AND THUS AVERAGING: 3296 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 16 TRADING DAY(S) IN TONNES 160.22 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2022, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 160.22/3550 x 100% TONNES 4.50% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2023

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH/2022: 409.30 TONNES //FINAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 151.69 TONNES (WEAKER THAN LAST MONTH)

AUGUST: 195.28 TONNES (A STRONGER MONTH)//FINAL

SEPT: 254.709 TONNES (WILL BE LARGER THAN LAST MONTH AND A STRONG MONTH)

OCT. 248.09 TONNES. LIKE SILVER, THIS MONTH IS GOING TO BE A STRONG E.F.P. ISSUANCE.

NOV. 239.16 TONNES//WILL BE STRONG THIS MONTH,

DEC. 213.704 TONNES. A STRONG MONTH//

TOTAL FOR YEAR 2023: 2,569.57 TONNES VS 2578 TONNES LAST YEAR

JAN ’24: 291.76 TONNES (WILL BE MUCH GREATER THAN LAST MONTH.//3RD HIGHEST EVER RECORDED EX FOR PHYSICAL)

FEB’24: 160.22 TONNES (SHOULD BE A WEAKER ISSUANCE MONTH)

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF FEB. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (FEB), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER FELL BY A FAIR SIZED 489 CONTRACTS OI TO 145,906 AND FURTHER FROM THE COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 6 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 872 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MARCH 1440 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 1440 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 489 CONTRACTS AND ADD TO THE 1440 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A HUGE GAIN OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 951 CONTRACTS

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTAL 4.755 MILLION OZ

OCCURRED DESPITE OUR $.10 LOSS IN PRICE …..

END

OUTLINE FOR TODAY’S COMMENTARY

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

b, ) Gold/silver trading overnight Europe,//GOLD COMMENTARIES

(Peter Schiff)

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS//

FRIDAY MORNING/THURSDAY NIGHT

SHANGHAI CLOSED UP 16.52 PTS OR 0.56% //Hang Seng CLOSED DOWN 17.09 PTS OR 0.10% / Nikkei CLOSED FOR HOLIDAY

//Australia’s all ordinaries CLOSED UP 0.43% /Chinese yuan (ONSHORE) closed DOWN 7.1970

//OFFSHORE CHINESE YUAN CLOSED DOWN TO 7.2058 /Oil DOWN TO 77.44 dollars per barrel for WTI and BRENT DOWN AT 82.45/ Stocks in Europe OPENED MOSTLY ALL GREEN// ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE YUAN WEAKER

A)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

9. USA

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A SMALL SIZED 874 CONTRACTS TO 408,043 DESPITE OUR LOSS IN PRICE OF $2.10 WITH RESPECT TO THURSDAY TRADING. WE ARE GETTING AWFULLY CLOSE TO OUR LOW OI OF 390,000 CONTRACTS

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE ACTIVE DELIVERY MONTH OF FEB..… THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 2059 EFP CONTRACTS WERE ISSUED: : APRIL 2059 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 2059 CONTRACTS

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A FAIR SIZED TOTAL OF 2942 CONTRACTS IN THAT 2059 LONGS WERE TRANSFERRED AS EXCHANGE FOR PHYSICALS TO LONDON AND WE HAD A SMALL SIZED GAIN OF 874 COMEX CONTRACTS..AND THIS GAIN ON OUR TWO EXCHANGES HAPPENED DESPITE OUR LOSS IN PRICE OF $2.10 THURSDAY COMEX. AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS DURING MID MONTH IN THE DELIVERY CYCLE), THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR THURSDAY NIGHT WAS A SMALL SIZED 410 CONTRACTS. THROUGHOUT THE PAST SEVERAL WEEKS, THE BANKERS SOLD OFF THE LONG SIDE OF THE SPREAD WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR/T.A.S. SPREAD WHICH WILL BE LIQUIDATED IN DAYS HENCE//.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: FEB (64.248 TONNES) ( ACTIVE MONTH)

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 24 MONTHS OF 2021-2023:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

NOV: 18.7122 TONNES + 16.2505 EX. FOR RISK = 34.9627 TONNES

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707TONNES

TOTAL 2023 YEAR : 436.546 TONNES

JAN ’24. 22.706 TONNES

FEB. ’24: 64.248 TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

THE SPECS/HFT WERE SUCCESSFUL IN LOWERING GOLD’S PRICE( IT LOST $2.10 //// BUT WERE UNSUCCESSFUL IN KNOCKING ANY SPECULATOR LONGS AS WE HAD A FAIR SIZED GAIN OF 2933 TOTAL CONTRACTS ON OUR TWO EXCHANGES DESPITE THE LOWER PRICE. WE HAD TO HAVE HAD ANOTHER EPISODE OF STRONG SHORT COVERING. WE HAD A SMALL T.A.S. LIQUIDATION ON THE FRONT END OF THURSDAY’S TRADING . THE T.A.S. ISSUED ON THURSDAY NIGHT, WILL BE “PUT INTO THE BANK” TO BE USED AT A LATER DATE AT THE COLLUSIVE CHOOSING OF OUR BANKERS.

WE HAVE GAINED A TOTAL OI OF 9.122 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR FEB. (49.773 TONNES) ON FIRST DAY NOTICE ALONG WITH AN EXCHANGE FOR RISK FOR 1.7235 TONNES. THIS WAS FOLLOWED WITH TODAY’S 1900 OZ QUEUE JUMP (0.0590 TONNES//NEW TOTAL STANDING 64.248: ALL OF THIS WAS ACCOMPLISHED WITH OUR LOSS IN PRICE TO THE TUNE OF $2.10

WE HAD -REMOVED 9 CONTRACTS TO THE COMEX TRADES TO OPEN INTEREST (CROOKS)

NET GAIN ON THE TWO EXCHANGES 2933 CONTRACTS OR 293,300 OZ OR 9.122 TONNES.

estimated volume today 201,533 poor

final gold volumes/yesterday 158,218 poor

//speculators have left the gold arena

FEB 23 INITIAL FEB GOLD

/ /// THE FEB 2024 GOLD CONTRACT

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 57,068.020 oz Brinks 1.775 tonnes (1775 kilobars) . |

| Deposit to the Dealer Inventory in oz | nil oz |

| Deposits to the Customer Inventory, in oz | 55,780.318 oz HSBC 1.73 tonnes |

| No of oz served (contracts) today | 934 notice(s) 93400 OZ 2/905 TONNES |

| No of oz to be served (notices) | 206 contracts 20600 oz 0.6407 TONNES |

| Total monthly oz gold served (contracts) so far this month | 19,896 notices 1,989,600 oz 61.885 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | x |

0 dealer deposits:

total dealer deposits: nil oz

total customer withdrawals: 1

i) Out of Brinks: 57,068.6200 oz 1775 kilobars

1.775 tonnes and equal to 1775 kilobars

total withdrawal: 57,068.62 oz

we had 1 customer deposit

i) Into HSBC 55,780.918 oz

Adjustments: 5 all dealer to customer//comex in stress

i) Asahi: 52,336.951 oz

ii) HSBC 1900.23 oz

iii) JPMorgan: 782.561 oz

v) Malca: 20,772.637 oz

iv) Manfra: 1676.939 ooz

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR FEB.

For the front month of FEBRUARY we have an oi of 1140 contracts having GAINED 10 contracts. We had 9 notices filed on Thursday, so we GAINED 19 contracts or an additional 1900 oz (0.0590 tonnes) will stand for delivery at the comex.

We also had 554 notices filed under exchange for risk on first day notice for a total of 55,400 oz or 1.723 tonnes to which must be added to the delivery cycle.

Thus initial standing for gold for February is 50.136 tonnes + 1.723 tonnes = 51.859 tonnes. This was followed with today’s QUEUE jump of 1900 oz//New standing 62.525 tonnes + 1.723 tonnes = 64.248 TONNES

March GAINED 794 contracts to stand at 3223

APRIL lost 234 CONTRACTS FALLING TO 317,407.

We had 934 contracts filed for today representing 93,400 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 934 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 698 notice(s) was (were) stopped ( (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for the FEB. /2024. contract month, we take the total number of notices filed so far for the month (19,896 x 100 oz ), to which we add the difference between the open interest for the front month of FEB. (1140 CONTRACTS) minus the number of notices served upon today 934 x 100 oz per contract equals 2,008,300 OZ OR 62.466 TONNES + 1.723 Ex for Risk/prior = 64.180 tonnes

thus the INITIAL standings for gold for the FEB. contract month: No of notices filed so far (19,896) x 100 oz + (1140) {OI for the front month} minus the number of notices served upon today (934) x 100 oz which equals 2,010,200 oz (62.525 TONNES) + 54,400 oz (1.723 TONNES) ex. for risk/prior// NEW total standing OR 64.248 TONNES

TOTAL COMEX GOLD STANDING FOR FEB: 64.248 TONNES WHICH IS GREAT FOR AN ACTIVE DELIVERY MONTH IN THE CALENDAR.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 1,354,385.502 42.127 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD: 18,237,040.238 OZ

TOTAL REGISTERED GOLD 8,056,296 (250.58 tonnes).

TOTAL OF ALL ELIGIBLE GOLD: 10,179,456.780 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 6,702411 oz (REG GOLD- PLEDGED GOLD) 209.47 tonnes

END

SILVER/COMEX

FEB 23/INITIAL

//2024// THE FEB 2024 SILVER CONTRACT//INITIAL

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 348,550.110 oz Brinks . |

| Deposits to the Dealer Inventory | nil OZ |

| Deposits to the Customer Inventory | 1,140,787.950 oz CNT HSBC |

| No of oz served today (contracts) | 0 CONTRACT(S) (NIL OZ) |

| No of oz to be served (notices) | 12 contracts (60,000 oz) |

| Total monthly oz silver served (contracts) | 1294 Contracts (6,470,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

i) 0 dealer deposit

total dealer deposit: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: 0 oz

We had 2 deposits customer account:

i) Into CNT 599.753.4600 oz

ii) Inro HSBC: 541,034.490 oz

total customer deposits 1,140,787.950 oz

JPMorgan has a total silver weight: 129.806 million oz/280.972 million or 46.26%

adjustment: 1 customer to dealer

i) Asahi: 1,779,257.600 oz

Comex withdrawals: 1

i) Out of Brinks 348,550.110 oz

total withdrawal: 348,550.110 oz oz

TOTAL REGISTERED SILVER: 46.715 MILLION OZ//.TOTAL REG + ELIGIBLE. 280.972 million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR DECEMBER:

silver open interest data:

FRONT MONTH OF FEB. /2023 OI: 12 CONTRACTS HAVING LOST 109 CONTRACT(S). WE HAD 109 NOTICES FILED ON THURSDAY SO WE LOST 0 CONTRACT OR AN ADDITIONAL NIL OZ OF SILVER CONTRACTS WILL STAND FOR DELIVERY AT THE COMEX

MARCH LOST 9110 CONTRACTS TO 40,735

APRIL SAW A GAIN OF 51 CONTRACTS TO STAND AT 169

MAY SAW A GAIN OF 8466 CONTRACTS UP TO 84,570.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 0 for NIL oz

Comex volumes// est. volume today 69,747 good

Comex volume: confirmed yesterday 77,858 good//

To calculate the number of silver ounces that will stand for delivery in FEB. we take the total number of notices filed for the month so far at 1294 x 5,000 oz = 6,470,000 oz

to which we add the difference between the open interest for the front month of FEB. (12) and the number of notices served upon today 0 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the FEB/2024 contract month: 1294 (notices served so far) x 5000 oz + OI for the front month of FEB. (12) – number of notices served upon today (0 )x 500 oz of silver standing for the FEB contract month equates to 6.530 MILLION OZ. + .445 MILLION OZ EX. FOR RISK PRIOR//NEW TOTAL 6.975 MILLION OZ

New total standing: 6.975 million oz.

There are 46.715 million oz of registered silver.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS//

BOTH GLD AND SLV ARE MASSIVE FRAUDS!

FEB23/WITH GOLD UP $17.80 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.01 TONNES OF GOLD FROM THE GLD.//INVENTORY RESTS AT 827.81 TONNES

FEB22/WITH GOLD DOWN $2.15 TODAY NO CHANGES IN GOLD INVENTORY AT THE GLD://INVENTORY RESTS AT 829.82 TONNES

FEB21/WITH GOLD DOWN $5.30 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 7.59 TONNES OF GOLD OUT OF THE GLD///INVENTORY RESTS AT 29.82 TONNES

FEB20/WITH GOLD UP $16.15 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 0.58 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 837.89 TONNES

FEB16/WITH GOLD UP $8,60 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.73 TONNES OF GOLD FROM THE GLD///INVENTORY RESTS AT 837.31 TONNES

FEB15/WITH GOLD UP $11.70 TODAY NO CHANGES IN GOLD INVENTORY AT THE GLD:/INVENTORY RESTS AT 841.92 TONNES

FEB14/WITH GOLD DOWN $2.75 TODAY NO CHANGES IN GOLD INVENTORY AT THE GLD:/INVENTORY RESTS AT 841.92 TONNES

FEB13/WITH GOLD DOWN $20.15 TODAY NO CHANGES IN GOLD INVENTORY AT THE GLD:/INVENTORY RESTS AT 841.92 TONNES

FEB12/WITH GOLD DOWN $4.80 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A STRONG WITHDRAWAL OF 1.74 TONNES OF GOLD FROM THE GLD. / //://INVENTORY RESTS AT 841.92 TONNES

FEB9/WITH GOLD DOWN $8.60 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A STRONG DEPOSIT OF 1.44 TONNES OF GOLD FROM THE GLD. / //://INVENTORY RESTS AT 843.66 TONNES

FEB8/WITH GOLD DOWN $2.70 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A MASSIVE WITHDRAWAL OF 5.47 TONNES OF GOLD FROM THE GLD. / //://INVENTORY RESTS AT 842.22 TONNES:

FEB7/WITH GOLD UP $0.40 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A MASSIVE WITHDRAWAL OF 4.04 TONNES OF GOLD FROM THE GLD. / //://INVENTORY RESTS AT 847.69 TONNES:

FEB6/WITH GOLD UP $8.50 TODAY NO CHANGES IN GOLD INVENTORY AT THE GLD:/ / //://INVENTORY RESTS AT 851.73 TONNES:

FEB5/WITH GOLD DOWN $9.85 TODAY SMALL CHANGES IN GOLD INVENTORY AT THE GLD:A DEPOSIT OF .58 TONNES OF GOLD INTO THE GLD// / //://INVENTORY RESTS AT 851.73 TONNES:

FEB 2/WITH GOLD DOWN $17.95 TODAY SMALL CHANGES IN GOLD INVENTORY AT THE GLD:A WITHDRAWAL OF .58 TONNES OF GOLD FROM THE GLD// / //://INVENTORY RESTS AT 851.15 TONNES:

FEB 1/WITH GOLD UP $5.00 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD:A WITHDRAWAL OF 1.73 TONNES OF GOLD FROM THE GLD// / //://INVENTORY RESTS AT 851.15 TONNES:

JAN 31/WITH GOLD UP $16.40 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD:A WITHDRAWAL OF 2.01 TONNES OF GOLD FROM THE GLD// / //://INVENTORY RESTS AT 852.88 TONNES:

JAN 30/WITH GOLD UP $6.50 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD:A WITHDRAWAL OF 1.16 TONNES OF GOLD FROM THE GLD// / //://INVENTORY RESTS AT 854.89 TONNES:

TOTAL IN LAST 18 DAYS WITHDRAWAL OF 14.12 TONNES

JAN 29/WITH GOLD UP $8.70 TODAYHUGE CHANGES IN GOLD INVENTORY AT THE GLD:A WITHDRAWAL OF 2.88 TONNES OF GOLD FROM THE GLD// / //://INVENTORY RESTS AT 856.05 TONNES

JAN 26/WITH GOLD DOWN $0.10 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD: / //://INVENTORY RESTS AT 858.93 TONNES

JAN 25/WITH GOLD UP $2.50 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD: / //://INVENTORY RESTS AT 858.93 TONNES

JAN 24/WITH GOLD DOWN $9.75 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD: / //://INVENTORY RESTS AT 858.93 TONNES

JAN 23/WITH GOLD UP $3.95 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.02 TONNES OF GOLD FROM THE GLD/ //://INVENTORY RESTS AT 858.93 TONNES

JAN 22/WITH GOLD DOWN $6.00 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.15 TONNES OF GOLD FROM THE GLD/ //://INVENTORY RESTS AT 860.95 TONNES

JAN 19/WITH GOLD UP $8.15 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD //://INVENTORY RESTS AT 862.10 TONNES

JAN 18/WITH GOLD UP $14.85 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 2.30 TONNES OF GOLD FROM THE GLD//://INVENTORY RESTS AT 862.10 TONNES

JAN 17/WITH GOLD DOWN $23.25 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF .549 TONNES OF GOLD INTO THE GLD.;//://INVENTORY RESTS AT 864.40 TONNES

JAN 12/WITH GOLD UP $31.65 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD; A MASSIVE WITHDRAWAL OF 4.61 TONNES OF GOLD FROM THE GLD//://INVENTORY RESTS AT 864.99 TONNES

GLD INVENTORY: 827.81 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

FEB 23/WITH SILVER UP 18 CENTS TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.098 MILLION OZ FROM THE SLV//// : SLV INVENTORY RESTS AT 431.668 MILLION OZ

FEB 22/WITH SILVER DOWN 10 CENTS TODAY NO CHANGES IN SILVER INVENTORY AT THE SLV

// : SLV INVENTORY RESTS AT 432.766 MILLION OZ

FEB 21/WITH SILVER DOWN 28 CENTS TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 2.348 MILLION OZ OF SILVER FROM THE SLV// : SLV INVENTORY RESTS AT 432.766 MILLION OZ

FEB 20/WITH SILVER DOWN 33 CENTS TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 3.385 MILLION OZ OF SILVER FROM THE SLV// : SLV INVENTORY RESTS AT 435.008 MILLION OZ

FEB 16/WITH SILVER UP 53 CENTS TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV A DEPOSIT OF 1.235 MILLION OZ OF SILVER FROM THE SLV// : SLV INVENTORY RESTS AT 438.393 MILLION OZ

FEB 15/WITH SILVER UP 56 CENTS TODAY NO CHANGES IN SILVER INVENTORY AT THE SLV : SLV INVENTORY RESTS AT 437.615 MILLION OZ

FEB 14/WITH SILVER UP 24 CENTS TODAY NO CHANGES IN SILVER INVENTORY AT THE SLV : SLV INVENTORY RESTS AT 437.615 MILLION OZ

FEB 13/WITH SILVER DOWN 60 CENTS TODAY SMALL CHANGES IN SILVER INVENTORY AT THE SLV A SMALL WITHDRAWAL OF 0.504 MILLION OZ OZ OUT OF THE SLV: SLV INVENTORY RESTS AT 437.615 MILLION OZ

FEB 12/WITH SILVER UP 14 CENTS TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV A HUGE WITHDRAWAL OF 1.921 MILLION OZ OZ OUT OF THE SLV: SLV INVENTORY RESTS AT 438.119 MILLION OZ

FEB 9/WITH SILVER DOWN 4 CENTS TODAY SMALL CHANGES IN SILVER INVENTORY AT THE SLV A SMALL DEPOSIT OF 600,000 OZ INTO THE SLV: SLV INVENTORY RESTS AT 440.040 MILLION OZ

FEB 8/WITH SILVER UP 29 CENTS TODAY NO CHANGES IN SILVER INVENTORY AT THE SLV: SLV INVENTORY RESTS AT 439.994 MILLION OZ

FEB 7/WITH SILVER DOWN 18 CENTS TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A MASSIVE DEPOSIT OF 4.04 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 439.994 MILLION OZ//LAST 9 DAYS: 10.7598 MILLION OZ WITHDRAWAL

FEB 6/WITH SILVER UP 11 CENTS TODAY NO CHANGES IN SILVER INVENTORY AT THE SLV: /INVENTORY RESTS AT 435.144 MILLION OZ//LAST 9 DAYS: 10.7598 MILLION OZ WITHDRAWAL

FEB 5/WITH SILVER DOWN 32 CENTS TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.345 MILLION OZ FROM THE SLV(FAIRY TALES) // /INVENTORY RESTS AT 435.144 MILLION OZ//LAST 8 DAYS: 10.7598 MILLION OZ WITHDRAWAL

FEB 2/WITH SILVER DOWN 50 CENTS TODAY SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 0.58 MILLION OZ INTO THE SLV(FAIRY TALES) // /INVENTORY RESTS AT 438.489 MILLION OZ//LAST 7 DAYS: 14.105 MILLION OZ WITHDRAWAL

FEB 1/WITH SILVER UP 7 CENTS TODAY MEGA CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.19 MILLION OZ INTO THE SLV(FAIRY TALES) // /INVENTORY RESTS AT 438.947 MILLION OZ//LAST 6 DAYS: 10.3018 MILLION OZ WITHDRAWAL

JAN 31/WITH SILVER DOWN 8 CENTS TODAY MEGA CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.7438 MILLION OZ INTO THE SLV(FAIRY TALES) // /INVENTORY RESTS AT 440.137 MILLION OZ//LAST 5 DAYS: 9.1118 MILLION OZ WITHDRAWAL

JAN 30/WITH SILVER DOWN 5 CENTS TODAY MEGA CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.876 MILLION OZ INTO THE SLV(FAIRY TALES) // /INVENTORY RESTS AT 442.699 MILLION OZ//LAST 4 DAYS: 7.368 MILLION OZ WITHDRAWAL

JAN 29/WITH SILVER UP $.37 TODAY MEGA CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.105 MILLION OZ INTO THE SLV(FAIRY TALES) // /INVENTORY RESTS AT 444.575 MILLION OZ

JAN 26/WITH SILVER DOWN $0.03 TODAY MEGA CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.556 MILLION OZ INTO THE SLV(FAIRY TALES) // /INVENTORY RESTS AT 446.680 MILLION OZ

JAN 25/WITH SILVER UP $0.03 TODAY MEGA CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.831 MILLION OZ INTO THE SLV(FAIRY TALES) // /

INVENTORY RESTS AT 448.236 MILLION OZ

JAN 24/WITH SILVER UP $0.44 TODAY MEGA CHANGES IN SILVER INVENTORY AT THE SLV: ANOTHER DEPOSIT OF 1.375 MILLION OZ INTO THE SLV(FAIRY TALES) // //INVENTORY RESTS AT 450.067 MILLION OZ

JAN 23/WITH SILVER UP $0.21 TODAY MEGA CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 16.201 MILLION OZ INTO THE SLV(FAIRY TALES) // //INVENTORY RESTS AT 448.694 MILLION OZ

JAN 22/WITH SILVER DOWN $0.45 TODAY NO CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 458,000 OZ OUT OF THE SLV // //INVENTORY RESTS AT 432.493 MILLION OZ

JAN 19/WITH SILVER DOWN $0.11 TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 458,000 OZ OUT OF THE SLV // //INVENTORY RESTS AT 432.493 MILLION OZ

JAN 18/WITH SILVER UP $0.13 TODAY NO CHANGES IN SILVER INVENTORY AT THE SLV: // //INVENTORY RESTS AT 432.951 MILLION OZ

JAN 17/WITH SILVER DOWN $0.38 TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 779,000 OZ FROM THE SLV.: // //INVENTORY RESTS AT 433.500 MILLION OZ

JAN 16/WITH SILVER DOWN $0.08 TODAY NO CHANGES IN SILVER INVENTORY AT THE SLV: // //INVENTORY RESTS AT 433.500 MILLION OZ

JAN 12/WITH SILVER UP $0.62 TODAY NO CHANGES IN SILVER INVENTORY AT THE SLV: // //INVENTORY RESTS AT 433.500 MILLION OZ

CLOSING INVENTORY 431.668 MILLION OZ//

PHYSICAL GOLD/SILVER COMMENTARIES

1:Peter Schiff/Mike Maharrey

end

2.Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

END

END

3. CHRIS POWELL//GATA GOLD COMMENTARIES: daily Dispatches

Ted Butler: Locked and loaded

Submitted by admin on Thu, 2024-02-22 21:54 Section: Daily Dispatches

By Ted Butler

SilverSeek.com

Thursday, February 22, 2024

We have now reached the point in silver (and gold) where it is difficult for me to see how prices don’t quickly explode.

Everything I look at, from a physical supply/demand perspective to the paper positioning set up on the Comex, tells me we are at the point where only an upward price surge makes any sense.

.

Yes, I am well aware of the thoroughly corrupt behavior of the collusive commercials on the Comex and how their manipulative success over the past 40 years makes it nearly impossible to pinpoint in advance the exact moment such a long-term scam and fraud will come to an end.

But recent developments scream out to me that the manipulation’s end is at hand. …

… For the remainder of the analysis:

https://silverseek.com/article/locked-and-loaded

*

Locked and Loaded

February 22, 2024

Ted Butler

We have now reached the point in silver (and gold) where it is difficult for me to see how prices don’t quickly explode. Everything I look at, from a physical supply/demand perspective to the paper positioning set up on the COMEX, tells me we are at the point where only an upward price surge makes any sense. Yes, I am well-aware of the thoroughly corrupt behavior of the collusive commercials on the COMEX and how their manipulative success over the past 40 years makes it nearly impossible to pinpoint in advance the exact moment such a long-term scam and fraud will come to an end – but recent developments scream out to me that the manipulation’s end is at hand.

First, I would like to distinguish between silver and gold. While I have rarely seen gold in as bullish a physical supply/demand and COMEX positioning set up as it is now and fully expect it to momentarily surge higher, gold is a very different market from silver. For one thing, the amount of gold in the world and the gold market in general is vastly larger than in silver – almost to the point of making a legitimate comparison of the two metals unrealistic. In dollar terms, the amount of gold in the world is some hundred times larger than the amount of silver, and I’m not aware of any other comparison between any two items similarly mismatched in size being attempted to be measured. It would be like trying to compare the GDP of the US, close to $25 trillion, with the GDP of Portugal or New Zealand, each of which is around $250 billion. I fully understand the long history that invites the gold/silver comparison; it’s just that the actual circumstances of each metal have changed over the decades and last century.

While I do admit that gold’s actual supply/demand fundamentals are tighter than I’ve seen previously, that’s a far cry from being in a deepening physical shortage brought about by industrial consumption overwhelming current physical supply, as is the case in silver. Simply put, gold is not an industrial commodity, while silver is. Only an industrial or consumable commodity can find itself in a genuine physical shortage. Plus, since there is a hundred times more gold in the world than silver in dollar terms, common sense would suggest in any serious upsurge in price, the smaller item (silver) would likely surge much more in percentage terms and that’s what past price surges in the two metals have indicated. Bottom line, I’m expecting gold to surge by hundreds of dollars per ounce, while I expect silver to surge by (many) tens of dollars per ounce.

One thing that does definitely unite gold and silver is that both are primary investment assets, in fact, gold is a pure investment asset. Silver, of course, is both an investment asset plus an industrial commodity – the only true commodity with such a dual demand profile. The fact that it has been silver’s industrial demand that has created the current physical shortage doesn’t mean silver’s investment demand won’t kick in. It means that when silver’s investment demand does kick in, it is bound to have an outsized impact on price – for the simple reason that silver’s industrial demand has already depleted much of the metal that investment demand would seek to buy. Plus, it’s a well-known fact that collective investment demand grows on higher, not lower prices. This can be readily observed in the extreme collective investment demand in a few high-tech stocks (the magnificent 7), and the historic concentration these stocks represent in overall stock ownership.

Further illustrating silver’s highly unusual dual demand profile is that several readers had sent me copies of a recent article on Zerohedge concerning the historic run up in cocoa prices being due to a deepening physical shortage between consumption and supply, which seemed to mirror the current circumstances in silver. Before I try to explain the difference between cocoa and silver, I must disclose a previous personal experience with cocoa more than 40 years ago, before I picked up the silver “bug”. Back in the day, I had arranged (as a commodity broker) to accept physical delivery of a large quantity of cocoa (more than 100 contracts, as I recall) on behalf of a client, as part of a “cash and carry” spread transaction, where the actual deliveries would be re-delivered the following delivery month. I did insure with the delivery department, many times, that there would be no problems in re-delivering the cocoa accepted for delivery and received such assurances and financing commitments. Then, a few days before re-delivery was to take place, I received a call from the re-delivery clerk that the client’s cocoa had worms and couldn’t be re-delivered. The whole thing became a mess, legal and otherwise and as a result, no pun intended, whenever the subject of cocoa comes up, it leaves me with a bad taste.

And I also recall, separately, a famous passage in a book by George Goodman (writing under the pseudonym Adam Smith), where he described a similar bad personal experience with cocoa to the point as whenever the word even came up, he had to go lie down someplace quiet, until the thought of cocoa went away. My memories aren’t quite so harsh and while I don’t doubt that the developing physical shortage in cocoa is, indeed, driving prices higher, I would take the opportunity to point out that cocoa, unlike silver, has little true intrinsic investment demand. No doubt there is speculation in cocoa futures contracts and other derivatives, but cocoa is not about to become a primary and everyday investment asset – as silver already is such an investment asset. True, investment demand for silver has yet to kick in forcefully, but at some yet to be determined higher price, it appears unavoidable that silver investment demand will become the dominant price force.

Another of the differences between silver and gold is that I’m not aware of any behind-the-scenes potential regulatory controversies in gold, where I know some to exist in silver, not the least of which is the question of possible double-counting in recorded silver bullion inventories. Yes, I do believe gold bullion inventories have been shifting from West to East (same as in silver), but I am unaware of any allegations of double-counting in gold inventories. We are now past the 14-week mark since I wrote to the CFTC and S.E.C. on the matter of possible double-counting in the silver inventories held in SLV and in the COMEX warehouses. The S.E.C. responded in two weeks (to my congressman), although it avoided any acknowledgement as to whether there was double-counting or not. But the CFTC has avoided any response. In a follow up with my congressman’s office yesterday, I was told that they did hear from the CFTC and that the agency was “working on a response”. Hello – working on? The question is as simple as it gets – the recorded silver inventories in question are separate or there is double-counting, so there is nothing to “work on”.

And considering the sharp selloff that started in silver in the wee hours Sunday evening into Monday’s Presidential Day holiday, which has continued through today, there can be little doubt that the selloff was just another case of collusive commercial price rigging on the COMEX to induce managed money selling – in order to enable the commercials to buy. As such it does two things, improve the COMEX positioning market structure from what it was on Friday and also increase the ugly perception that the CFTC is delaying any comment on the question of inventory double-counting until the crooked commercials have positioned themselves as favorably as possible. Somewhat perversely, the CFTC openly siding with the commercials on this recent price-rigging to the downside only enhances my thoughts that we are locked and loaded for the upside, with any additional managed money selling only adding more rocket fuel for the coming price blast higher.

As can be inferred from the even greater price carnage in the shares of the silver miners, we are at the point where lower silver prices are blatantly in the beyond overkill category. With every sign of a deepening physical shortage more obvious daily, the continued suppressed silver prices are now threatening to destroy much needed future supplies. Even for me, who has complained about a COMEX-induced silver price suppression for nearly four decades, witnessing the current circumstances of future silver mining supplies being severely undermined is other-worldly. In such circumstances, it is inconceivable to me that the primary federal commodities regular would sit by and allow the “ seed corn” (future silver mine supplies) to be destroyed or prevented from coming into existence in a scam and fraud as obvious as what is occurring on the COMEX. Yet, here we are. It has become so stunningly obvious that silver prices are artificially depressed by the COMEX manipulation that far from any expected reaction from the federal agency primarily tasked with preventing such an overt price manipulation, instead we find the agency fumbling and stumbling in attempting to answer a simple question about inventory double-counting.

To be sure, if I were expecting the CFTC to ever ride to the rescue in any way in ending the COMEX silver manipulation, except in an unintended way, I would need my head examined. This regulator has demonstrated in no uncertain terms it has no interest in interpreting commodity law as it should be interpreted. On the other hand, by allowing the price suppression to last as long as it has, the CFTC has, effectively, done just that, namely, brought about the very circumstances from which silver prices must explode. There is no more powerful an economic equation than the law of supply and demand and under that law, no greater price force than a physical shortage in any commodity. This is now apparent in cocoa and soon will also be apparent in silver, with the price reaction in silver greatly amplified with the inevitable investment demand, currently missing. I can say that as an American citizen and taxpayer, as much as I now view the CFTC as being nearly-powerless in counteracting the coming price force of the physical silver shortage, I am also dis-heartened and ashamed by the decades of malfeasance by the agency – despite me trying to warn it about silver on countless occasions. But, in a very real sense, this is all water under the bridge and the arrival of the physical silver shortage changes everything – as it signals the start of brand-new era, one in which, quite literally, no one has ever experienced.

As far as what to expect in Friday’s new Commitments of Traders (COT) report, all I can say is what a difference a day makes. Had you asked me on Friday of my expectations for the new report, my answer would have been around trying to quantify the amount of deterioration (managed money buying and commercial selling) had taken place in silver, based upon the quite sharp price rally into week’s end. Since then, however, the pronounced price weakness into yesterday’s cutoff for the reporting week would appear to have offset much of the prior deterioration through Friday. At this point, I am not sure at all what the new report will reveal. I do know, of course, that the prior weeks’ reports were quite bullish in both silver and gold, so I’m fairly sure all of the increasingly bullish market structures in both silver and gold couldn’t have become close to being undone, regardless of what Friday’s report indicates.

My “locked and loaded” evaluation of the current state of the market in silver and gold is made with the full knowledge of potential further price weakness, such as seen today, although I am encouraged by the quite-low trading volumes, which I believe suggest a drying up of managed money selling. Just to be as clear as possible, it’s not particularly important – apart from what it does emotionally and financially on a short-term basis – how many additional low volume price slices the commercial crooks can pull off in the very short-term. What matters most is the nature of the coming silver price explosion, which promises to be monumental in terms of both price force as well as how quickly it unfolds. Try as I might, I just can’t envision the termination of the 40-year-old COMEX silver price manipulation occurring under any ordinary two steps up, one step back price scenario. Forty years of artificial price suppression simply cannot be resolved with what would be considered “normal” price action. The end of such a long-term price manipulation must be commensurate with the longevity and severity of the body and nature of the manipulation.

Ted Butler

February 22, 2024 (originally sent to subscribers on Feb 21, 2024)

* *

The Worst Time for Yet Another Grotesque Stock Bubble

Egon von Greyerz

February 22, 2024

In this critically important Gold Matters discussion, VON GREYERZ principals, Egon von Greyerz and Matthew Piepenburg, place the enormous risks of the current U.S. equity bubble within the much-needed context of unprecedented global economic factors.

Egon opens the discussion with a brief review of the unprecedented string-cite of global geopolitical, social, economic and debt risks. From a preventable and escalating land war in the Ukraine to conflicts in Gaza and the broader Arab world to nose-bleed global debt levels in the backdrop of now undeniable social tensions and de-dollarization, the need to be realistic rather than just “negative” is of common-sense importance. As we head into a year already marked by such massive fissures, any attempt to gloss over these facts with an S&P making record highs would be missing the forest for the trees. In fact, the current U.S. bubble is far more of a dangerous rather than safe indicator when placed into needed context.

Toward this end, Matt speaks to something all-too familiar, having managed a hedge fund as well as a family office during prior asset bubbles. Matt gives particular attention to the overt risk indicators of the current S&P bubble, which teeters on the twin edge of unprecedented concentration and over-valuation metrics.

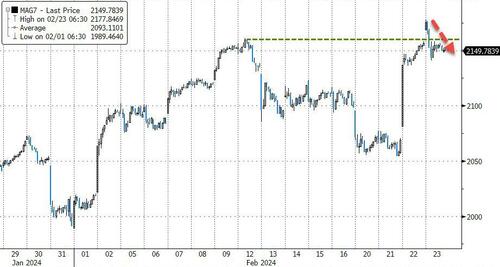

Matt’s perspective is not theoretical, but hands-on, as he explains how the current asset bubble, like the dot.com bubble of 2000, is in fact driven by the same fundamentals. He compares the Magnificent 7 to equally profitable and “good” names like the Microsoft, Cisco and Qualcomm of 1999-2000, noting that such otherwise profitable companies rising on margin growth eventually experience inevitable contraction in net income once price, volume and cost advantages trend negatively. No one, of course, can time such shifts, but “this time is NOT different,” as all such bubbles end the same: They pop.

What makes the current bubble (AI mania) so much more dangerous, however, is that it is led by 5-7 names, and when they mean-revert, as all over-valued companies do, there’s nothing left to prop the S&P. In short, when these names fall, everything falls with it, and this time around, the entire global economy is already on its knees. This is bad.

Egon closes the conversation with his own, and equally hands-on, perspective of investing through asset cycles and bubbles, offering needed insights on the risks, as well as lessons, of prior manias. Naturally, the conversation turns to real money and real assets, namely the far less “maniacal” gold. As the foregoing risks continue their exponential growth, gold rewards the far-sighted investor in obvious ways not otherwise understood by speculators. Matt, though not averse to the speculative mind-set, warns of the seductive appeal of chasing (and buying tops) and makes an equally straightforward case for gold in a world losing perspective.

end

4. OTHER GOLD COMMENTARIES/PODCASTS//ANDREW MAGUIRE LIVE FROM THE VAULT; NO 161

Episode 161

Posted 23rd February 2024

40 Million ounces of COMEX gold vaporised!

In this week’s episode of Live from the Vault, Andrew Maguire tackles a burning question from a US-based bullion dealer: is it possible that the Federal Reserve could try and confiscate your hard-earned gold savings?

The precious metals expert provides an update on the effects of Bitcoin ETFs on the gold price and comments on the strong geopolitically-driven demand for precious metals. Finally, Andrew shares some very good news for Silver Stackers.

https://kinesis.money/live-from-the-vault/40m-ounces-gold-vaporised/

END

5 a. IMPORTANT COMMENTARIES ON COMMODITIES /

END

5 B GLOBAL COMMODITY ISSUES/FOOD IN GENERAL//FREIGHT

END

6.CRYPTOCURRENCY//DIGITAL CURRENCY// COMMENTARIES/

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS FRIDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED DOWN 7.1970

OFFSHORE YUAN: DOWN TO 7.2058

SHANGHAI CLOSED UP 16.52 PPTS OR 0.56%

HANG SENG CLOSED DOWN 17.09 PTS OR 0.10%

2. Nikkei closed

3. Europe stocks SO FAR: MOSTLY ALL GREEN

USA dollar INDEX DOWN TO 103.71 EURO RISES TO 1.0838 UP 13 BASIS PTS

3b Japan 10 YR bond yield: FALLS TO. +.711 Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 150.48/JAPANESE YEN NOW RISING AS WELL AS LONG TERM 10 YR. YIELDS RISING //EVENTUALLY THIS WILL BREAK THE JAPANESE CENTRAL BANK

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen DOWN CHINESE ONSHORE YUAN: DOWN/ OFFSHORE: DOWN

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil DOWN for WTI and DOWN FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund DOWN TO +2.410***/Italian 10 Yr bond yield DOWN to 3.868* /SPAIN 10 YR BOND YIELD DOWN TO 3.322…**

3i Greek 10 year bond yield DOWN TO 3.343

3j Gold at $2027.55 silver at: 22.76 1 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble UP 0 AND 0 /100 roubles/dollar; ROUBLE AT 92.85//

3m oil into the 77 dollar handle for WTI and 82 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 150.48// 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 0.711% STILL ON CENTRAL BANK (JAPAN) INTERVENTION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.8783 as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.9521 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.313 DOWN 1 BASIS PTS…

USA 30 YR BOND YIELD: 4.460 UP 0 BASIS PTS/

USA 2 YR BOND YIELD: 4.711 UP 0 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 31.09…(TURKEY SET TO BLOW UP FINANCIALLY)

GREAT BRITAIN/10 YEAR YIELD: DOWN 1 BASIS PTS AT 4.1350

end

2.a Overnight: Newsquawk and Zero hedge

Futures Flat After Nvidia Sparks Biggest Rally In Over A Year

FRIDAY, FEB 23, 2024 – 08:34 AM

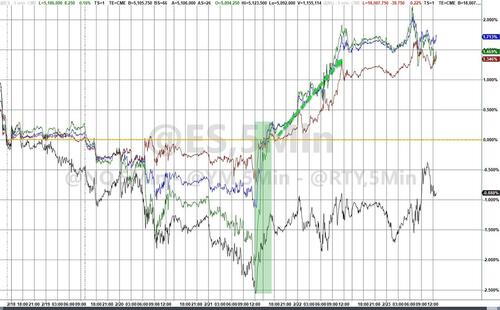

US equity futures were poised for a muted end to the week after Thursday’s blowout rally which sent the S&P over 2.1% higher, its biggest one-day gain since Jan 2023, after Nvidia’s blowout earnings rekindled global euphoria about artificial intelligence (even as Google demonstrated just how racist and useless it actually is) and pushed the S&P to its highest close on record, while also sending European and Japanese markets to all time highs. At 8:00am, S&P 500 futures were unchanged while Nasdaq 100 contracts slipped 0.2% – even as NVDA rose above $800 to sport a $2 trillion market cap – after soaring 3% yesterday. Treasury yields dropped with the 10Y sliding 3bps to 4.30% and the dollar extending its losses, as oil and bitcoin also reversed recent gains. The US economic data calendar is empty for the session, while no Federal Reserve members are scheduled to speak

In premarket trading, Nvidia rose 2.1% extending Thursday’s 16% jump, and set to surpass a $2 trillion market cap when it opens. Block was quoted 13% higher as the payments technology company’s results and outlook beat estimates. Intuitive Machines was set for a 45% surge after the startup’s spacecraft landed on the Moon. By contrast, Booking Holdings gave a disappointing forecast and reported headwinds from the war in Israel, sending its shares down 8.5%. Here are some other notable permarket movers:

- Applied Optoelectronics sinks 37% after the maker of fiber-optic networking products posted a surprise drop in revenue in the fourth quarter.

- Block Inc. rallies 16% after the payments technology company raised its forecast for adjusted Ebitda for 2024.

- Booking Holdings slips 8.1% after giving a disappointing forecast for travel reservations and gross bookings, with the war in Israel and currency fluctuations weighing on results.

- Carvana soars 30% after the used-car retailer topped Wall Street’s profit expectations in the final months of 2023 and said it expects improved earnings this quarter.

- Fluence Energy advances 7.6% as JPMorgan raises its recommendation on the energy-storage company to overweight, saying Thursday’s selloff triggered by a short report was overdone.

- Maravai LifeSciences climbs 30% after its revenue outlook for the year topped the average analyst estimate.

- MercadoLibre falls 6.7% after recording earnings per share for the fourth quarter that fell short of Wall Street’s estimates for the e-commerce company.

With S&P futures trading around 5,100 Investors are taking a breather after two rampy weeks as they weigh optimism about corporate earnings and US economic resilience against elevated valuations and hawkish signals from the Federal Reserve.

“We continue to remain of the view that the secular bull market remains firmly intact,” said strategist Mathieu Racheter at Julius Baer. “While the risk of a short-term market pullback has increased, as several sentiment and positioning indicators have shot up above the historical normal levels again, we would use any weakness as opportunity to increase the exposure to equities.”

“The speed of the tech rally has left investors wondering whether to take profits,” said Mark Haefele, chief investment officer at UBS Global Wealth Management. “While we see merit in re-balancing portfolios, we believe that retaining strategic exposure to US large-cap technology is important, and the rise in tech stocks could go further still.”

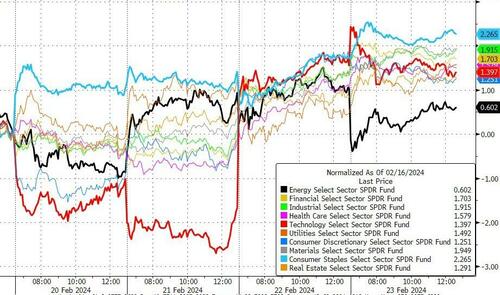

The Stoxx Europe 600 index rose 0.1% and was headed for a fifth weekly gain, amid mixed earnings after also closing at a record on Thursday. The automotive and chemicals sectors the biggest outperformers, the latter on German chemicals giant BASF’s latest results. The telecommunications subindex is the worst performer after Deutsche Telekom reported disappointing earnings. UK-based lender Standard Chartered Plc climbed more than 8% after unveiling a profit beat and share buyback. German insurer Allianz SE declined after non-life insurance earnings missed analysts’ expectations. Deutsche Telekom AG, Europe’s largest telecommunications operator, slipped after a miss in non-US earnings.Here are the most notable European movers:

- Standard Chartered rises as much as 8.4% following the bank’s fourth-quarter adjusted pretax profit beat, with analysts highlighting lower loan losses as well as a $1 billion buyback

- BASF climbs as much as 4.0% after announcing deepened cost cuts and releasing results that pointed to a future rebound in earnings, with som analysts reckoning the weakness in volumes has bottomed out

- Italian banking stocks climb in Milan trading on renewed speculation of possible consolidation in the industry, after newspaper Il Foglio reported that unnamed investment banks are studying the sector

- Magyar Telekom jumps as much as 4.4% to highest since 2009 after Hungary’s largest telecommunications company issued strong guidance especially for Ebitda AL, a key metric in the sector, Erste says

- Mercedes-Benz shares rise as much as 2.3%, building on Thursday’s gains, after Barclays upgraded the German carmaker to overweight in light of the “compelling” increase in shareholder returns

- Deutsche Lufthansa shares fall as much as 4.8%, the biggest intraday drop since December, after the group reshuffled its executive board, with the exit of its CFO seen as a negative

- Allianz falls as much as 3.8%, the most since May, as underlying weaknesses in the German insurance group’s fourth-quarter result overshadowed a profit jump and higher dividends

- Hensoldt falls as much as 8.7% after releasing results that failed to inspire enthusiasm. Oddo analysts say the company’s unchanged guidance could have disappointed investors

- Deutsche Telekom shares fall as much as 2.6% after the telecom operator reported Ebitda slightly below estimates, a result of lower rental sales registered in the group headquarters segment, according to analysts

- Trainline shares fall as much as 2.7% after the train ticketing platform was downgraded to neutral by UBS, citing a lack of near-term catalysts, even as the long-term prospects for the firm look solid

The Bloomberg Dollar Spot Index extended declines into a fifth day, on course for the first weekly drop in 2024. Almost all developed-nation peers advanced on Friday, with the exception of Norwegian krone, which is the most volatile G-10 currency this week and under-performs peers. The Australian and New Zealand dollars briefly gave up gains following Waller’s comments before bouncing back after China reported slower declines in home prices in January. Fed Governor Christopher Waller said January’s jump in consumer prices warrants caution in deciding when to start cutting interest rates. That’s after Fed Vice Chair Philip Jefferson and Governor Lisa Cook made clear they want more evidence that inflation is headed back to their 2% target before lowering borrowing costs.

Earlier in the session, Asian stocks were on track for a fifth straight week of gains as investors took heart from Beijing’s recent market rescue efforts, which have spurred a strong rebound in Chinese shares. The MSCI Asia Pacific Index was set for a 1.3% increase this week and headed for its longest winning streak in a year. Trading on Friday was largely range bound as Japan was shut for a holiday after surpassing a historical high reached more than three decades ago. The upbeat sentiment in Asia comes as Chinese authorities took further steps to restore investor confidence, including restrictions on equity net sales, stock purchases by state funds and a clampdown on quant trading. Chinese stocks as a result posted their longest run of gains since July 2020 in the mainland, while a measure in Hong Kong edged closer to erasing losses this year.

In rates, treasuries are slightly cheaper across the curve with losses led by the front and belly, adding to recent flattening pressure seen on 2s10s and 5s30s spreads. Treasuries are cheaper by up to 2bp across the 2-year out to the 7-year sector with 2s10s, 5s30s spreads flatter by 0.3bp and 1.2bp on the day; 10-year yields drop by 2bps to 4.305%, with bunds and gilts slightly outperforming in the sector. Friday’s US session is set to be quiet for scheduled events, with the focus on potential deal hedging by corporates and supply pressure ahead of Monday’s Treasury auction. According to Bloomberg, the dollar issuance slate is empty and follows Thursday’s five-deal $19.7b calendar led by AbbVie pricing $15b across seven tranches. Issuers paid less than 1 basis point in new issue concessions, with deals nearly five times oversubscribed on average. Monday’s session is expected to be active, which could warrant some deal-related hedging flows for Friday’s session. Solventum is a candidate for either Friday or Monday, contemplating a deal in the context of $7bn with proceeds earmarked to fund a payment to 3M. Monday also sees a US double auction of 2- and 5-year notes for combined $127b

In commodities, oil prices decline, with WTI falling 1.3% to trade near $77.60. Spot gold falls 0.3%.

Looking to the day ahead, we have UK February GfK consumer confidence, Germany Q4 private consumption, government spending and capital investment, and the February ifo survey, as well as the ECB’s Consumer Expectations Survey. The US economic data calendar is empty for the session; we also hear from the Fed’s Waller, the ECB’s Schnabel, and the BoE’s Greene.

Market Snapshot

- S&P 500 futures little changed at 5,092.75

- STOXX Europe 600 little changed at 495.25

- MXAP little changed at 172.84

- MXAPJ little changed at 528.43

- Nikkei up 2.2% to 39,098.68

- Topix up 1.3% to 2,660.71

- Hang Seng Index down 0.1% to 16,725.86

- Shanghai Composite up 0.6% to 3,004.88

- Sensex little changed at 73,119.16

- Australia S&P/ASX 200 up 0.4% to 7,643.59

- Kospi up 0.1% to 2,667.70

- German 10Y yield little changed at 2.48%

- Euro little changed at $1.0820

- Brent Futures down 1.2% to $82.67/bbl

- Gold spot down 0.3% to $2,018.05

- US Dollar Index little changed at 104.02

Top Overnight News

- China’s housing crisis is getting worse, w/Dec new home prices in 70 major cities falling 1.24% Y/Y in Jan (vs. -0.89% in Dec) while secondhand prices sank even more. WSJ

- Constrained on all sides, China’s central bank is aiming to squeeze more value out of its policy actions by catching markets unaware with surprise easing aimed at putting a floor under the struggling economy. A record cut to a key lending rate earlier this week announced by the People’s Bank of China was just the latest unexpected move since Governor Pan Gongsheng took office last summer. At a press briefing last month, he shocked with an outsized cut to banks’ reserve requirement ratio. BBG

- A bill in the U.S. Congress targeting Chinese biotech companies may end up being more “narrowly tailored”, the U.S. lawmaker who proposed it said on Friday, adding that he was cautiously optimistic something could be passed this year. RTRS

- The US and China are discussing new debt plans to prevent a wave of EM sovereign defaults, in potentially their biggest joint economic cooperation in years, people familiar said. Any plan — which may include extending loan periods before defaults — may require buy-in from private creditors. BBG

- ECB Governing Council member Robert Holzmann said he doesn’t see reductions in interest rates coming before the US — suggesting he reckons any move by policymakers in Frankfurt may still be some way off. BBG

- Fed officials (Waller, Jefferson, Cook) signal rate cuts will arrive eventually (and likely this year), but additional disinflationary evidence will be required first. BBG

- Prime Minister Benjamin Netanyahu has finally unveiled Israel’s plans for Gaza after hostilities end in the enclave, submitting to his war cabinet a formal proposal that directly contradicts the objectives of the US. FT

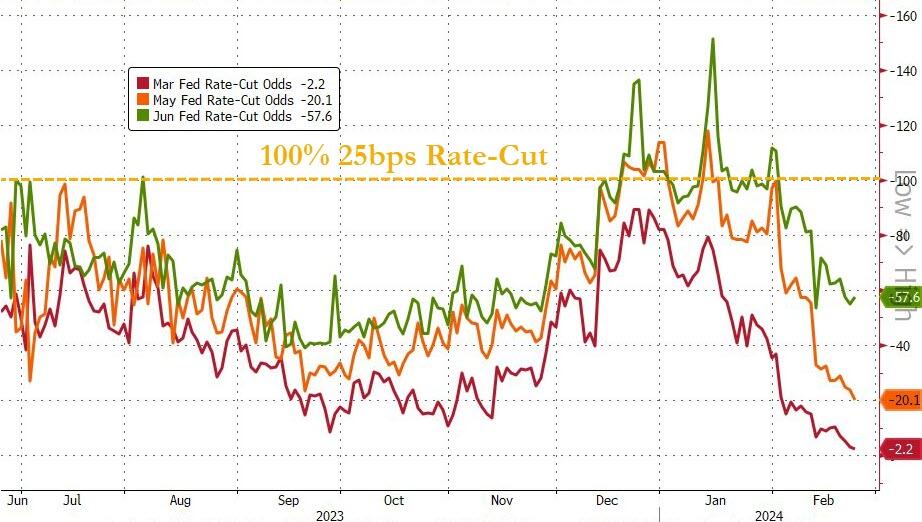

- Comments this week from Fed officials and the minutes to the January FOMC meeting suggest that the first rate cut is unlikely to come as early as our previous forecast of the May meeting. We have therefore dropped our forecast of a May cut and now expect 4 cuts total in 2024 (vs. 5 previously) in June, July, September, and December, followed by 4 more cuts in 2025 (vs. 3 cuts previously), to the same terminal rate of 3.25-3.5%. GIR

- Intuitive Machines leapt premarket after becoming the first private firm to land a robotic spacecraft intact on the moon. NASA paid almost $118 million for the mission that ended a string of failures. BBG

- Mutual fund cash allocations are nearing record lows. Mutual fund PMs can express directional views on the forward path of equities through the share of their assets they choose to hold in cash. Mutual funds continued to deploy cash reserves into the equity market in 4Q23, cutting their allocation to cash from 1.9% to 1.7% of assets. Fund cash allocations now stand just 20 bp above their all-time low of 1.5% reached in December 2021. GIR

Earnings

- Standard Chartered (2888 HK / STAN LN) – FY23 (USD): adj. Pretax 5.7bln (exp. 5.89bln, prev. 4.76bln Y/Y), adj. Op Revenue 17.4bln (exp. 18.6bln, prev. 16.3bln Y/Y). Announces USD 1bln share repurchase. Guides initial FY24-26 op. income growth at the top of the range +5-7%. Underlying profit before tax rose 27% Y/Y to 5.7bln, NII rose 23% Y/Y to 9.6bln, Q4 adj. pretax 1.08bln (exp. 989.6mln), Co. announces USD 1bln buyback. (Newswires) Index Weightings: FTSE 100 (0.8%). Shares +8.1% in European trade

- Allianz (ALV GY) – Q4 (EUR): Adj. EPS 6.00 (exp. 5.69, prev. 4.99 Y/Y), Op. 3.77bln Y/Y (prev. 3.96bln Y/Y). Guides initial FY24 Op. 13.8-15.8bln. Proposes to increase FY dividend to EUR 13.80 (exp. 12.08, prev. 11.40), announces buyback programme of up to EUR 1bln, to be conducted between March 2024 and year-end. Regular dividend payout ratio increased to 60% (prev. 50%). This new dividend policy shall already apply to the dividend for fiscal year 2023 (Newswires) Index Weightings: DAX (7.9% – third largest), Euro Stoxx 50 (3.0%), Stoxx 600 (1.0%) Shares -3.2% in European trade

- BASF (BAS GY) – Q4 (EUR): Revenue 15.9bln (exp. 16.2bln). Adj. EBIT 292mln (exp. 398mln). Sees 2024 operating profit between EUR 13.8-15.8bln (exp. 15.48bln). Guides FY24 EBITDA 8-8.6bln, FCF 0.1-0.6bln. Proposes dividend of EUR 3.40/shr for FY23. Targeting cost-saving plans of up to EUR 1bln by the end of 2026. (Newswires) Index Weightings: DAX 40 (3.6%), Euro Stoxx 50 (1.4%), Stoxx 600 (0.4%) Shares +0.5% in European trade

- Deutsche Telekom (DTE GY) – Q4 (EUR): Adj. Net 1.83bln (exp. 1.63bln), Adj. EBITDA 10.06bln (exp. 10.1bln), Revenue 29.4bln (exp. 28.5bln). Guides initial FY24 EPS > 1.75 (exp. 1.84), Adj. EBITDA 42.9bln. (Newswires) Index Weightings: DAX 40 (6.2%), Euro Stoxx 50 (2.3%), Stoxx 600 (0.8%) Shares -2.7% in European trade

A more detailed look at global markets courtesy of Newsquawk

APAC stocks mostly benefitted amid tailwinds from the tech-led surge in the US on the NVIDIA wave as its shares surged over 16% and its market cap increased by a record USD 277bln. ASX 200 finished higher with gains led by outperformance in tech, consumer stocks and financials. KOSPI kept afloat with South Korea to execute a record KRW 398tln budget in H1 to prop up domestic demand. Hang Seng and Shanghai Comp. were mixed with the tech sector facing headwinds from ongoing trade-related frictions, while the mainland was indecisive as participants digested the PBoC’s liquidity injection, CSRC’s denial of regulatory measures, and the latest Home Price data which showed a steeper Y/Y fall in property prices.

Top Asian News

- US and China are in talks over innovative emerging market debt plans to prevent a surge in defaults.

- China has reportedly turned to private firms to hack an array of foreign governments and organisations, while files indicate China infiltrated the cyberinfrastructure and collected data of government departments in Malaysia, Thailand and Mongolia, according to FT citing a large data leak from Shanghai Anxun Information Technology.

- China’s Embassy in the UK commented regarding UK sanctions on Chinese companies in which it stated that sanctions against relevant companies are ‘unilateral actions that have no basis in international law’ and it is firmly opposed to them, while it would like to inform the British side that any act that undermines China’s interests will be resolutely countered by the Chinese side, according to Reuters.

- US export curbs on China won’t extend to legacy chips which generally refers to 28-nanometer and older-generation semiconductors, according to US official cited by Nikkei.

- US lawmakers urged Volkswagen (VOW3 GY) to halt operations in Xinjiang after vehicles with Chinese components were held at US customs.

- Chinese commercial banks sold a net USD 9.8bln of FX in Jan (vs net sale of USD 4.3bln in Dec), according to FX regulator.

- China’s CSRC vows to crack down on market manipulation and insider trading, will step up onsite inspection of listing candidates.

- Fitch on China says it believes rate cuts will deliver only a minor boost to economic activity.

- Chinese Cabinet meeting says they are to study measures to attract and utilise foreign investment on a larger scale; to study measures to prevent and resolve local debt risks