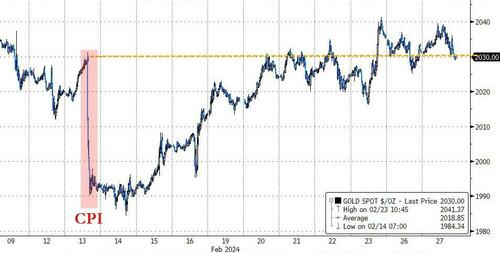

GOLD PRICE CLOSED UP $4.40 TO $2034.30

SILVER PRICE UP $.03 TO $22.51

Gold ACCESS CLOSED 2030.50

Silver ACCESS CLOSED: 22.45

Bitcoin morning price:, 57,067 UP 2552 DOLLARS.

Bitcoin: afternoon price: $56,629 up 2104 dollars

Platinum price closing UP $15.20 AT $894.25

Palladium price; DOWN $8.55 AT $947.00

END

SHANGHAI GOLD PREMIUM 33 DOLLARS/COMEX GOLD

SHANGHAI GOLD (USD) FUTURES – QUOTES

Beginning Monday, April 1, 2024, CME Group settlement data will no longer be accessible through ftp.cmegroup.com and will have a delayed publication time of 12:00 a.m. CT on all cmegroup.com web pages. Learn about alternate ways to access the data in our FAQ.

AUTO-REFRESH IS OFF

Last Updated 27 Feb 2024 09:13:33 AM CT.

Market data is delayed by at least 10 minutes.

I will now provide gold in Canadian dollars, British pounds and Euros

4: 15 PM ACCESS

*CANADIAN GOLD: $2,746.52 UP $2.50 CDN dollars per oz( * NEW ALL TIME HIGH 2,795.90 CDN DOLLARS PER OZ//DEC 1 2023)

*BRITISH GOLD: 1600.21 DOWN 1.75 pounds per oz// *(NEW ALL TIME HIGH//CLOSING///1655.17 BRITISH POUNDS/OZ) OCT 2/2023

*EURO GOLD: 1871.65 DOWN 0.39 euros per oz //* (ALL TIME CLOSING HIGH: 1903.75 EUROS PER OZ//DEC 1.2023)

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

EXCHANGE: COMEX

EXCHANGE: COMEX

CONTRACT: FEBRUARY 2024 COMEX 100 GOLD FUTURES

SETTLEMENT: 2,028.500000000 USD

INTENT DATE: 02/26/2024 DELIVERY DATE: 02/28/2024

FIRM ORG FIRM NAME ISSUED STOPPED

323 C HSBC 7

363 H WELLS FARGO SEC 50

661 C JP MORGAN 41

686 H STONEX FINANCIA 2

TOTAL: 50 50

MONTH TO DATE: 19,958

JPMorgan stopped 41/50 contracts.

FOR FEB/2024

GOLD: NUMBER OF NOTICES FILED FOR FEB/2024. CONTRACT: 50 NOTICES FOR 5000 OZ or 0.1555 TONNES

total notices so far: 19,958 contracts for 1,995,800 Oz (62 tonnes)

FOR FEBRUARY:

SILVER NOTICES 4 NOTICE(S) FILED FOR 20,000 OZ/

total number of notices filed so far this month : 1308 for 6,540,000 oz

XXXXXXXXXXXXXXXXXX

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

BOTH GLD AND SLV ARE FRAUDULENT VEHICLES//THEY ARE NOW RAIDING GLD AND SLV FOR PHYSICAL

GLD

WITH GOLD UP $4.40//

INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD/ : HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .87 TONNES OF GOLD FROM THE GLD

INVENTORY RESTS AT 826.94 TONNES

SLV//

WITH NO SILVER AROUND AND SILVER UP 3 CENTS AT THE SLV//

HUGE CHANGES IN SILVER INVENTORY AT THE SLV: ANOTHER WITHDRAWAL OF .640 MILLION OZ FROM THE SLV/.

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV.

CLOSING INVENTORY: 427.963 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A SMALL SIZED 122 CONTRACTS TO 145,766 AND FURTHER FROM THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THIS TINY SIZED GAIN IN COMEX OI WAS ACCOMPLISHED DESPITE OUR FALL IN PRICE OF $0.44 IN SILVER PRICING AT THE COMEX ON MONDAY. WE HAD ZERO LONG LIQUIDATION AT THE COMEX SESSION WITH AGAIN SOME SHORT COVERING DESPITE THE PRICE OF SILVER FALLING BY A CONSIDERABLE AMOUNT. WE HAD A HUGE 954 T.A.S ISSUANCE AND THESE WILL BE USED FOR MANIPULATION LATER THIS MONTH/AS WELL AS TODAY. PLEASE NOTE THAT THE CROOKS NEED A HIGHER SILVER T.A.S. TO CARRY ON THEIR CROOKED MANIPULATION ON A DAILY BASIS

CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON MONDAY NIGHT: 954 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS. IT THUS LOOKS LIKE THE FED (GOV’T) IS BEHIND ALL OF THESE TRADES.

WE HAVE NOW SET ANOTHER RECORD LOW AT 114,102 CONTRACTS ///JULY 3.2023// OUR BANKERS WITH THE HELP OF SPECULATORS AND HIGH FREQUENCY TRADERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.44), BUT WERE UNSUCCESSFUL IN KNOCKING ANY SILVER LONGS AS WE HAD A HUGE SIZED GAIN OF 1375 CONTRACTS ON OUR TWO EXCHANGES DESPITE A MUCH LOWER PRICE.

WE MUST HAVE HAD:

A FAIR SIZED 385 ISSUANCE OF EXCHANGE FOR PHYSICALS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 3.535 MILLION OZ (FIRST DAY NOTICE) ACCOMPANYING A STRANGE 89 CONTRACT ISSUANCE FOR EX. FOR RISK FOR 445,000 OZ ON FIRST DAY NOTICE/ FOLLOWED BY TODAY’S 30,000 OZ E.F.P. JUMP TO LONDON //NEW TOTAL LOWERS TO ; 6.985 MILLION OZ

//NEW STANDING FOR SILVER IS THUS 6.985 MILLION OZ

/ SMALL SIZED COMEX OI LOSS/FAIR SIZED EFP ISSUANCE/ VI) HUGE SIZED NUMBER OF T.A.S. CONTRACT ISSUANCE 954 CONTRACTS)/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL -REMOVED A HUGE 1112 CONTRACTS //

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS FEB. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF FEB

TOTAL CONTRACTS for 18 days, total 11,177 contracts: OR 55.885 MILLION OZ (620 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 55.885 MILLION OZ

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH 2022: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 118.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 85.745 MILLION OZ (SMALLER THAN LAST MONTH)

AUGUST: 171.43 MILLION OZ (THIS MONTH IS GOING TO BE HUGE //2ND HIGHEST ON RECORD

SEPT: 72.705 MILLION OZ (SMALLER THIS MONTH)

OCT: 97.455 MILLION OZ

NOV. 50.050 MILLION OZ

DEC. 66.140 MILLION OZ//

TOTAL 2023: 1,104.10 MILLION OZ/

JAN ’24 : 78.655 MILLION OZ//

FEB /2024 : 55.885 MILLION OZ.

RESULT: WE HAD A SMALL SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 122 CONTRACTS DESPITE OUR LOSS IN PRICE OF SILVER PRICING AT THE COMEX//MONDAY.,. THE CME NOTIFIED US THAT WE HAD A FAIR EFP ISSUANCE CONTRACTS: 385 ISSUED FOR MAY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS. WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR FEB. OF 3.535 MILLION OZ ACCOMPANIED BY FIRST DAY NOTICE OF 445,000 OZ EX. FOR RISK FOLLOWED BY TODAY’S 30,000 OZ E.F.P. JUMP TO LONDON //NEW TOTAL FALLS TO 6.985 MILLION OZ

NEW STANDING 6.985 MILLION OZ /// WE HAVE A HUGE GAIN OF 1375 OI CONTRACTS ON THE TWO EXCHANGES DESPITE THE LOSS IN PRICE. THE TOTAL OF TAS INITIATED CONTRACTS TODAY: A HUMONGOUS SIZED 954 CONTRACTS//HUGE FRONT END OF THE TAS CONTRACTS WERE LIQUIDATED DURING THE MONDAY COMEX SESSION/// WITH MAJOR SHORT COVERING FROM OUR SPEC SHORTS ( DESPITE PRICE OF SILVER FELL) . THE NEW TAS ISSUANCE MONDAY NIGHT (954) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE//PROBABLY TODAY., .

WE HAD 4 NOTICE(S) FILED TODAY FOR 20,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A GOOD SIZED 3400 CONTRACTS TO 410,324 AND FURTHER FORM THE RECORD (SET JAN 24/2020) AT 799,733 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110, BUT WE ARE NOW CLOSER TO OUR ALL TIME LOW OF 390,000 CONTRACTS.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: – REMOVED XXX CONTRACTS

WE HAD A GOOD SIZED DECREASE IN COMEX OI ( 3400 CONTRACTS) WITH OUR $8.90 LOSS IN PRICE//MONDAY. WE ALSO HAD A RATHER LARGE INITIAL STANDING IN GOLD TONNAGE FOR FEB. AT 49.773 TONNES ON FIRST DAY NOTICE ACCOMPANIED BY FIRST DAY NOTICE : 55,400 OZ EX. FOR RISK //THUS INITIAL STANDING FOR FEB: 51.494 TONNES FOLLOWED BY TODAY’S 4,500 OZ QUEUE JUMP //NEW TOTAL OF GOLD STANDING ADVANCES TO: 64.398 TONNES // ALL OF THIS HAPPENED DESPITE OUR $8.90 LOSS IN PRICE WITH RESPECT TO MONDAY’S TRADING. WE HAD A SMALL SIZED LOSS OF 651 OI CONTRACTS (2.024) PAPER TONNES) ON OUR TWO EXCHANGES.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 2794 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 410,324

IN ESSENCE WE HAVE A SMALL SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 651 CONTRACTS WITH 3400 CONTRACTS DECREASED AT THE COMEX// AND A FAIR SIZED 2749 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 651 CONTRACTS.. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): FAIR SIZED 1635 CONTRACTS.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (2749 CONTRACTS) ACCOMPANYING THE FAIR SIZED LOSS IN COMEX OI (3400) //TOTAL GAIN FOR OUR THE TWO EXCHANGES: 651 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR FORMER FORMAT OF BANKERS GOING LONG AND SPECULATORS GOING SHORT ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR FEB. AT 49.773 TONNES PLUS FIRST DAY NOTICE OF 1.723 TONNE OZ EX. FOR RISK FOLLOWED BY TODAY’S 4500 OZ QUEUE JUMP //NEW STANDING ADVANCES TO 64.398 TONNES. / 3) ZERO LONG LIQUIDATION // 4) FAIR SIZED COMEX OPEN INTEREST L;OSS/ 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER///6: FAIR T.A.S. ISSUANCE: 1654 CONTRACTS//CONSIDERABLE SHORT COVERING AGAIN

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023-2024 INCLUDING TODAY

FEB.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF FEB. :

TOTAL EFP CONTRACTS ISSUED: 60,426 CONTRACTS OR 6,042,600 OZ OR 187.75. TONNES IN 18 TRADING DAY(S) AND THUS AVERAGING: 3357 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 18 TRADING DAY(S) IN TONNES 179.39 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2022, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 187.75/3550 x 100% TONNES 5.25% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2023

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH/2022: 409.30 TONNES //FINAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 151.69 TONNES (WEAKER THAN LAST MONTH)

AUGUST: 195.28 TONNES (A STRONGER MONTH)//FINAL

SEPT: 254.709 TONNES (WILL BE LARGER THAN LAST MONTH AND A STRONG MONTH)

OCT. 248.09 TONNES. LIKE SILVER, THIS MONTH IS GOING TO BE A STRONG E.F.P. ISSUANCE.

NOV. 239.16 TONNES//WILL BE STRONG THIS MONTH,

DEC. 213.704 TONNES. A STRONG MONTH//

TOTAL FOR YEAR 2023: 2,569.57 TONNES VS 2578 TONNES LAST YEAR

JAN ’24: 291.76 TONNES (WILL BE MUCH GREATER THAN LAST MONTH.//3RD HIGHEST EVER RECORDED EX FOR PHYSICAL)

FEB’24: 187.75 TONNES (SHOULD BE A WEAKER ISSUANCE MONTH)

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF FEB. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (FEB), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER FELL BY A SMALL SIZED 122 CONTRACTS OI TO 145,766 AND CLOSER TO THE COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 6 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 385 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAY 385 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 385 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 990 CONTRACTS AND ADD TO THE 385 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A SMALL LOSS OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 263 CONTRACTS

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTAL 1.315 MILLION OZ

OCCURRED DESPITE OUR $.44 LOSS IN PRICE …..

END

OUTLINE FOR TODAY’S COMMENTARY

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

b, ) Gold/silver trading overnight Europe,//GOLD COMMENTARIES

(Peter Schiff)

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS//

TUESDAY MORNING/MONDAY NIGHT

SHANGHAI CLOSED UP 38.46 PTS OR 1.29% //Hang Seng CLOSED UP 156.06 PTS OR 0.94% / Nikkei CLOSED UP 5.83 PTS OR .17%//Australia’s all ordinaries CLOSED UP 0.18% /Chinese yuan (ONSHORE) closed DOWN 7.1979 //OFFSHORE CHINESE YUAN CLOSED DOWN TO 7.2108 /Oil UP TO 77.39 dollars per barrel for WTI and BRENT UP AT 82.25/ Stocks in Europe OPENED MOSTLY ALL GREEN EXCEPPT SPAIN// ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE YUAN WEAKER

A)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

9. USA

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A FAIR SIZED 3400 CONTRACTS TO 410,324 WITH OUR LOSS IN PRICE OF $8.90 WITH RESPECT TO MONDAY TRADING. ACCORDING TO OUR EXPERT ANDREW MAGUIRE, THE LOW COMEX GOLD OI WAS DUE TO THE CRIMINAL BANKS LEAVING THE GOLD ARENA AND USING THEIR “SKILLS” ON THE NEW FUTURES OF BITCOIN. WITH CENTRAL BANK BUYING PHYSICAL GOLD IN RECORD NUMBERS, IT WOULD BE FUTILE TRYING TO SELL NAKED CALLS AGAINST GOLD AS CB’S WOULD JUST TURN AROUND AND TAKE DELIVERY.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE ACTIVE DELIVERY MONTH OF FEB..… THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 2749 EFP CONTRACTS WERE ISSUED: : APRIL 2749 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 2749 CONTRACTS

ON A NET BASIS IN OPEN INTEREST WE LOST THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A FAIR SIZED TOTAL OF 651 CONTRACTS IN THAT 2749 LONGS WERE TRANSFERRED AS EXCHANGE FOR PHYSICALS TO LONDON AND WE HAD A FAIR SIZED LOSS OF 3400 COMEX CONTRACTS..AND THIS LOSS ON OUR TWO EXCHANGES HAPPENED WITH OUR FALL IN PRICE OF $8.90 MONDAY COMEX. AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS DURING MID MONTH IN THE DELIVERY CYCLE), THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR MONDAY NIGHT WAS A FAIR SIZED 1694 CONTRACTS. THROUGHOUT THE PAST SEVERAL WEEKS, THE BANKERS SOLD OFF THE LONG SIDE OF THE SPREAD WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR/T.A.S. SPREAD WHICH WILL BE LIQUIDATED IN DAYS HENCE//.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: FEB (64.398 TONNES) ( ACTIVE MONTH)

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 24 MONTHS OF 2021-2023:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

NOV: 18.7122 TONNES + 16.2505 EX. FOR RISK = 34.9627 TONNES

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707TONNES

TOTAL 2023 YEAR : 436.546 TONNES

JAN ’24. 22.706 TONNES

FEB. ’24: 64.398 TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

THE SPECS/HFT WERE SUCCESSFUL IN LOWERING GOLD’S PRICE( IT LOST $8.90 //// BUT WERE UNSUCCESSFUL IN KNOCKING ANY SPECULATOR LONGS AS WE HAD A FAIR SIZED LOSS OF 651 TOTAL CONTRACTS ON OUR TWO EXCHANGES WITH OUR LOWER PRICE. WE HAD TO HAVE HAD ANOTHER HUGE EPISODE OF STRONG SHORT COVERING. WE HAD A GOOD T.A.S. LIQUIDATION ON THE FRONT END OF MONDAY’S TRADING . THE T.A.S. ISSUED ON MONDAY NIGHT, WILL BE “PUT INTO THE BANK” TO BE USED AT A LATER DATE AT THE COLLUSIVE CHOOSING OF OUR BANKERS.

WE HAVE GAINED A TOTAL OI OF 8.470 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR FEB. (49.773 TONNES) ON FIRST DAY NOTICE ALONG WITH AN EXCHANGE FOR RISK FOR 1.7235 TONNES. THIS WAS FOLLOWED WITH TODAY’S 1900 OZ QUEUE JUMP (0.0590 TONNES//NEW TOTAL STANDING 64.248: ALL OF THIS WAS ACCOMPLISHED WITH OUR GAIN IN PRICE TO THE TUNE OF $17.80

WE HAD -REMOVED XX CONTRACTS TO THE COMEX TRADES TO OPEN INTEREST (CROOKS)

NET LOSS ON THE TWO EXCHANGES 651 CONTRACTS OR 65,100 OZ OR 2.024 TONNES.

estimated volume today 145,929 poor

final gold volumes/yesterday 137,311 poor

//speculators have left the gold arena

FEB 27 INITIAL FEB GOLD

/ /// THE FEB 2024 GOLD CONTRACT

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 68,935.068 oz Brinks 867 KILOBARS Manfra: 1167 kilobars . |

| Deposit to the Dealer Inventory in oz | nil oz |

| Deposits to the Customer Inventory, in oz | nil oz |

| No of oz served (contracts) today | 50 notice(s) 5000 OZ 0.1555 TONNES |

| No of oz to be served (notices) | 192 contracts 19,200 oz 0.59720 TONNES |

| Total monthly oz gold served (contracts) so far this month | 19,958 notices 1,995800 oz 62.077 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | x |

0 dealer deposits:

total dealer deposits: nil oz

total customer withdrawals: 2

i) Out of Brinks: 27,874.863 oz 867 kilobars

ii)

ii)Out of Manfra; 37,423.685 oz (1164 kilbars

total withdrawal: 68,935.068 oz 2.14 tonnes

we had 0 customer deposit

Adjustments: 2 all dealer to customer//comex in stress

i)Loomis: 12,538.890 oz

ii) Out of Manfra: 10,038.086 ooz

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR FEB.

For the front month of FEBRUARY we have an oi of 242 contracts having GAINED 33 contracts. We had 12 notices filed on Monday, so we GAINED 45 contracts or an additional 4500 oz (0.1399 tonnes) will stand for delivery at the comex.

We also had 554 notices filed under exchange for risk on first day notice for a total of 55,400 oz or 1.723 tonnes to which must be added to the delivery cycle.

Thus initial standing for gold for February is 50.136 tonnes + 1.723 tonnes = 51.859 tonnes. This was followed with today’s QUEUE jump of 4500 oz//New standing 62.675 tonnes + 1.723 tonnes = 64.358 TONNES

March LOST 92 contracts to stand at 3085

APRIL LOST 4600 CONTRACTS FALLING TO 316,780.

We had 12 contracts filed for today representing 1200 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 50 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 41 notice(s) was (were) stopped ( (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for the FEB. /2024. contract month, we take the total number of notices filed so far for the month (19,958 x 100 oz ), to which we add the difference between the open interest for the front month of FEB. (242 CONTRACTS) minus the number of notices served upon today 50 x 100 oz per contract equals 2,015,000 OZ OR 62.675 TONNES + 1.723 Ex for Risk/prior = 64.261 tonnes

thus the INITIAL standings for gold for the FEB. contract month: No of notices filed so far (19,958) x 100 oz + (xxx) {OI for the front month} minus the number of notices served upon today (50) x 100 oz which equals 2,015,000 oz (62.675 TONNES) + 54,400 oz (1.723 TONNES) ex. for risk/prior// NEW total standing OR 64.398 TONNES

TOTAL COMEX GOLD STANDING FOR FEB: 64.398 TONNES WHICH IS GREAT FOR AN ACTIVE DELIVERY MONTH IN THE CALENDAR.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 1,354,385.502 42.127 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD: 18,188,941.276 OZ

TOTAL REGISTERED GOLD 8,027,918.845 (249.70 tonnes).

TOTAL OF ALL ELIGIBLE GOLD: 10,092,087.363 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 6,673,533 oz (REG GOLD- PLEDGED GOLD) 207,57 tonnes/dropping like a stone

END

SILVER/COMEX

FEB 27/INITIAL

//2024// THE FEB 2024 SILVER CONTRACT//INITIAL

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | nil oz . |

| Deposits to the Dealer Inventory | nil OZ |

| Deposits to the Customer Inventory | nil |

| No of oz served today (contracts) | 4 CONTRACT(S) (20,000 OZ) |

| No of oz to be served (notices) | 0 contracts (NIL oz) |

| Total monthly oz silver served (contracts) | 1308 Contracts (6,550,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

i) 0 dealer deposit

i

total dealer deposit: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: 0 oz

We had 0 deposits customer account:

total customer deposits nil oz

JPMorgan has a total silver weight: 129.806 million oz/281.8199 million or 46.26%

adjustment: unusual: 33,423.000 oz removed from eligible ASAHI

nil

Comex withdrawals: 0

total withdrawal: 0 oz

TOTAL REGISTERED SILVER: 49.108 MILLION OZ//.TOTAL REG + ELIGIBLE. 281.817 million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR DECEMBER:

silver open interest data:

FRONT MONTH OF FEB. /2023 OI: 4 CONTRACTS HAVING LOST 16 CONTRACT(S). WE HAD 10 NOTICES FILED ON MONDAY SO WE LOST 6 CONTRACT OR AN ADDITIONAL 30,000 OZ OF SILVER CONTRACTS WILL NOT STAND FOR DELIVERY AT THE COMEX AS THEY WERE E.F.P’D DIRECTLY TO LONDON FOR IMMEDIATE DELIVERY.

MARCH LOST 11,853 CONTRACTS TO18,566. WE HAVE 2 MORE READING DAYS BEFORE FIRST DAY NOTICE.

APRIL SAW A GAIN OF 343 CONTRACTS TO STAND AT 577

MAY SAW A GAIN OF 11,680 CONTRACTS UP TO 104,691.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 10 for 50,000 oz

Comex volumes// est. volume today 83,877 excellent

Comex volume: confirmed yesterday 137,311 excellent//huge

To calculate the number of silver ounces that will stand for delivery in FEB. we take the total number of notices filed for the month so far at 1308 x 5,000 oz = 6,540,000 oz

to which we add the difference between the open interest for the front month of FEB. (4) and the number of notices served upon today 4 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the FEB/2024 contract month: 1308 (notices served so far) x 5000 oz + OI for the front month of FEB. (5) – number of notices served upon today (4 )x 500 oz of silver standing for the FEB contract month equates to 6.540 MILLION OZ. + .445 MILLION OZ EX. FOR RISK PRIOR//NEW TOTAL 6.985 MILLION OZ

New total standing: 6.985 million oz.

There are 49.108 million oz of registered silver.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS//

BOTH GLD AND SLV ARE MASSIVE FRAUDS!

FEB27/WITH GOLD UP $4.40 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF .87 TONNES OF GOLD FROM THE GLD:/INVENTORY RESTS AT 826.94 TONNES

FEB26/WITH GOLD DOWN $8.90 TODAY NO CHANGES IN GOLD INVENTORY AT THE GLD:/INVENTORY RESTS AT 827.81 TONNES

FEB23/WITH GOLD UP $17 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.01 TONNES OF GOLD FROM THE GLD.//INVENTORY RESTS AT 827.81 TONNES

FEB22/WITH GOLD DOWN $2.15 TODAY NO CHANGES IN GOLD INVENTORY AT THE GLD://INVENTORY RESTS AT 829.82 TONNES

FEB21/WITH GOLD DOWN $5.30 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 7.59 TONNES OF GOLD OUT OF THE GLD///INVENTORY RESTS AT 29.82 TONNES

FEB20/WITH GOLD UP $16.15 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 0.58 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 837.89 TONNES

FEB16/WITH GOLD UP $8,60 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.73 TONNES OF GOLD FROM THE GLD///INVENTORY RESTS AT 837.31 TONNES

FEB15/WITH GOLD UP $11.70 TODAY NO CHANGES IN GOLD INVENTORY AT THE GLD:/INVENTORY RESTS AT 841.92 TONNES

FEB14/WITH GOLD DOWN $2.75 TODAY NO CHANGES IN GOLD INVENTORY AT THE GLD:/INVENTORY RESTS AT 841.92 TONNES

FEB13/WITH GOLD DOWN $20.15 TODAY NO CHANGES IN GOLD INVENTORY AT THE GLD:/INVENTORY RESTS AT 841.92 TONNES

FEB12/WITH GOLD DOWN $4.80 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A STRONG WITHDRAWAL OF 1.74 TONNES OF GOLD FROM THE GLD. / //://INVENTORY RESTS AT 841.92 TONNES

FEB9/WITH GOLD DOWN $8.60 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A STRONG DEPOSIT OF 1.44 TONNES OF GOLD FROM THE GLD. / //://INVENTORY RESTS AT 843.66 TONNES

FEB8/WITH GOLD DOWN $2.70 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A MASSIVE WITHDRAWAL OF 5.47 TONNES OF GOLD FROM THE GLD. / //://INVENTORY RESTS AT 842.22 TONNES:

FEB7/WITH GOLD UP $0.40 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A MASSIVE WITHDRAWAL OF 4.04 TONNES OF GOLD FROM THE GLD. / //://INVENTORY RESTS AT 847.69 TONNES:

FEB6/WITH GOLD UP $8.50 TODAY NO CHANGES IN GOLD INVENTORY AT THE GLD:/ / //://INVENTORY RESTS AT 851.73 TONNES:

FEB5/WITH GOLD DOWN $9.85 TODAY SMALL CHANGES IN GOLD INVENTORY AT THE GLD:A DEPOSIT OF .58 TONNES OF GOLD INTO THE GLD// / //://INVENTORY RESTS AT 851.73 TONNES:

FEB 2/WITH GOLD DOWN $17.95 TODAY SMALL CHANGES IN GOLD INVENTORY AT THE GLD:A WITHDRAWAL OF .58 TONNES OF GOLD FROM THE GLD// / //://INVENTORY RESTS AT 851.15 TONNES:

FEB 1/WITH GOLD UP $5.00 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD:A WITHDRAWAL OF 1.73 TONNES OF GOLD FROM THE GLD// / //://INVENTORY RESTS AT 851.15 TONNES:

JAN 31/WITH GOLD UP $16.40 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD:A WITHDRAWAL OF 2.01 TONNES OF GOLD FROM THE GLD// / //://INVENTORY RESTS AT 852.88 TONNES:

JAN 30/WITH GOLD UP $6.50 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD:A WITHDRAWAL OF 1.16 TONNES OF GOLD FROM THE GLD// / //://INVENTORY RESTS AT 854.89 TONNES:

TOTAL IN LAST 18 DAYS WITHDRAWAL OF 14.12 TONNES

JAN 29/WITH GOLD UP $8.70 TODAYHUGE CHANGES IN GOLD INVENTORY AT THE GLD:A WITHDRAWAL OF 2.88 TONNES OF GOLD FROM THE GLD// / //://INVENTORY RESTS AT 856.05 TONNES

JAN 26/WITH GOLD DOWN $0.10 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD: / //://INVENTORY RESTS AT 858.93 TONNES

JAN 25/WITH GOLD UP $2.50 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD: / //://INVENTORY RESTS AT 858.93 TONNES

JAN 24/WITH GOLD DOWN $9.75 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD: / //://INVENTORY RESTS AT 858.93 TONNES

JAN 23/WITH GOLD UP $3.95 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.02 TONNES OF GOLD FROM THE GLD/ //://INVENTORY RESTS AT 858.93 TONNES

JAN 22/WITH GOLD DOWN $6.00 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.15 TONNES OF GOLD FROM THE GLD/ //://INVENTORY RESTS AT 860.95 TONNES

JAN 19/WITH GOLD UP $8.15 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD //://INVENTORY RESTS AT 862.10 TONNES

JAN 18/WITH GOLD UP $14.85 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 2.30 TONNES OF GOLD FROM THE GLD//://INVENTORY RESTS AT 862.10 TONNES

JAN 17/WITH GOLD DOWN $23.25 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF .549 TONNES OF GOLD INTO THE GLD.;//://INVENTORY RESTS AT 864.40 TONNES

JAN 12/WITH GOLD UP $31.65 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD; A MASSIVE WITHDRAWAL OF 4.61 TONNES OF GOLD FROM THE GLD//://INVENTORY RESTS AT 864.99 TONNES

GLD INVENTORY: 826.04 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

FEB 27/WITH SILVER UP 3 CENTS TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 0.64 MILLION OZ FROM THE SLV//// : SLV INVENTORY RESTS AT 427.943 MILLION OZ

FEB 26/WITH SILVER DOWN 44 CENTS TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.065 MILLION OZ FROM THE SLV//// : SLV INVENTORY RESTS AT 428.603 MILLION OZ

FEB 23/WITH SILVER DOWN 44 CENTS TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.065 MILLION OZ FROM THE SLV//// : SLV INVENTORY RESTS AT 428.603 MILLION OZ

FEB 22/WITH SILVER DOWN 10 CENTS TODAY NO CHANGES IN SILVER INVENTORY AT THE SLV

// : SLV INVENTORY RESTS AT 432.766 MILLION OZ

FEB 21/WITH SILVER DOWN 28 CENTS TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 2.348 MILLION OZ OF SILVER FROM THE SLV// : SLV INVENTORY RESTS AT 432.766 MILLION OZ

FEB 20/WITH SILVER DOWN 33 CENTS TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 3.385 MILLION OZ OF SILVER FROM THE SLV// : SLV INVENTORY RESTS AT 435.008 MILLION OZ

FEB 16/WITH SILVER UP 53 CENTS TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV A DEPOSIT OF 1.235 MILLION OZ OF SILVER FROM THE SLV// : SLV INVENTORY RESTS AT 438.393 MILLION OZ

FEB 15/WITH SILVER UP 56 CENTS TODAY NO CHANGES IN SILVER INVENTORY AT THE SLV : SLV INVENTORY RESTS AT 437.615 MILLION OZ

FEB 14/WITH SILVER UP 24 CENTS TODAY NO CHANGES IN SILVER INVENTORY AT THE SLV : SLV INVENTORY RESTS AT 437.615 MILLION OZ

FEB 13/WITH SILVER DOWN 60 CENTS TODAY SMALL CHANGES IN SILVER INVENTORY AT THE SLV A SMALL WITHDRAWAL OF 0.504 MILLION OZ OZ OUT OF THE SLV: SLV INVENTORY RESTS AT 437.615 MILLION OZ

FEB 12/WITH SILVER UP 14 CENTS TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV A HUGE WITHDRAWAL OF 1.921 MILLION OZ OZ OUT OF THE SLV: SLV INVENTORY RESTS AT 438.119 MILLION OZ

FEB 9/WITH SILVER DOWN 4 CENTS TODAY SMALL CHANGES IN SILVER INVENTORY AT THE SLV A SMALL DEPOSIT OF 600,000 OZ INTO THE SLV: SLV INVENTORY RESTS AT 440.040 MILLION OZ

FEB 8/WITH SILVER UP 29 CENTS TODAY NO CHANGES IN SILVER INVENTORY AT THE SLV: SLV INVENTORY RESTS AT 439.994 MILLION OZ

FEB 7/WITH SILVER DOWN 18 CENTS TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A MASSIVE DEPOSIT OF 4.04 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 439.994 MILLION OZ//LAST 9 DAYS: 10.7598 MILLION OZ WITHDRAWAL

FEB 6/WITH SILVER UP 11 CENTS TODAY NO CHANGES IN SILVER INVENTORY AT THE SLV: /INVENTORY RESTS AT 435.144 MILLION OZ//LAST 9 DAYS: 10.7598 MILLION OZ WITHDRAWAL

FEB 5/WITH SILVER DOWN 32 CENTS TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.345 MILLION OZ FROM THE SLV(FAIRY TALES) // /INVENTORY RESTS AT 435.144 MILLION OZ//LAST 8 DAYS: 10.7598 MILLION OZ WITHDRAWAL

FEB 2/WITH SILVER DOWN 50 CENTS TODAY SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 0.58 MILLION OZ INTO THE SLV(FAIRY TALES) // /INVENTORY RESTS AT 438.489 MILLION OZ//LAST 7 DAYS: 14.105 MILLION OZ WITHDRAWAL

FEB 1/WITH SILVER UP 7 CENTS TODAY MEGA CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.19 MILLION OZ INTO THE SLV(FAIRY TALES) // /INVENTORY RESTS AT 438.947 MILLION OZ//LAST 6 DAYS: 10.3018 MILLION OZ WITHDRAWAL

JAN 31/WITH SILVER DOWN 8 CENTS TODAY MEGA CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.7438 MILLION OZ INTO THE SLV(FAIRY TALES) // /INVENTORY RESTS AT 440.137 MILLION OZ//LAST 5 DAYS: 9.1118 MILLION OZ WITHDRAWAL

JAN 30/WITH SILVER DOWN 5 CENTS TODAY MEGA CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.876 MILLION OZ INTO THE SLV(FAIRY TALES) // /INVENTORY RESTS AT 442.699 MILLION OZ//LAST 4 DAYS: 7.368 MILLION OZ WITHDRAWAL

JAN 29/WITH SILVER UP $.37 TODAY MEGA CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.105 MILLION OZ INTO THE SLV(FAIRY TALES) // /INVENTORY RESTS AT 444.575 MILLION OZ

JAN 26/WITH SILVER DOWN $0.03 TODAY MEGA CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.556 MILLION OZ INTO THE SLV(FAIRY TALES) // /INVENTORY RESTS AT 446.680 MILLION OZ

JAN 25/WITH SILVER UP $0.03 TODAY MEGA CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.831 MILLION OZ INTO THE SLV(FAIRY TALES) // /NVENTORY RESTS AT 448.236 MILLION OZ

JAN 24/WITH SILVER UP $0.44 TODAY MEGA CHANGES IN SILVER INVENTORY AT THE SLV: ANOTHER DEPOSIT OF 1.375 MILLION OZ INTO THE SLV(FAIRY TALES) // //INVENTORY RESTS AT 450.067 MILLION OZ

JAN 23/WITH SILVER UP $0.21 TODAY MEGA CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 16.201 MILLION OZ INTO THE SLV(FAIRY TALES) // //INVENTORY RESTS AT 448.694 MILLION OZ

JAN 22/WITH SILVER DOWN $0.45 TODAY NO CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 458,000 OZ OUT OF THE SLV // //INVENTORY RESTS AT 432.493 MILLION OZ

JAN 19/WITH SILVER DOWN $0.11 TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 458,000 OZ OUT OF THE SLV // //INVENTORY RESTS AT 432.493 MILLION OZ

JAN 18/WITH SILVER UP $0.13 TODAY NO CHANGES IN SILVER INVENTORY AT THE SLV: // //INVENTORY RESTS AT 432.951 MILLION OZ

JAN 17/WITH SILVER DOWN $0.38 TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 779,000 OZ FROM THE SLV.: // //INVENTORY RESTS AT 433.500 MILLION OZ

JAN 16/WITH SILVER DOWN $0.08 TODAY NO CHANGES IN SILVER INVENTORY AT THE SLV: // //INVENTORY RESTS AT 433.500 MILLION OZ

JAN 12/WITH SILVER UP $0.62 TODAY NO CHANGES IN SILVER INVENTORY AT THE SLV: // //INVENTORY RESTS AT 433.500 MILLION OZ

CLOSING INVENTORY 428.603 MILLION OZ//

PHYSICAL GOLD/SILVER COMMENTARIES

1:Peter Schiff/Mike Maharrey

end

2.Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens/ CLAUDIO GLASS

CLAUDIO GLASS..

“A House Of Cards, Supported & Backed By Blind Faith…”

TUESDAY, FEB 27, 2024 – 07:20 AM

Submitted by Claudio Grass,

Private property rights under siege

People invest in gold for many different reasons. Many do so out of concern over economic, monetary or political uncertainty. Others seek a hedge against inflation, a way to protect and preserve the real purchasing power of their savings. There are also those who simply seek some peace of mind, a dependable insurance, so that no matter what the future holds and no matter how bad the “worst case scenario” turns out to be, they would still have a solid “Plan B”.

All these are valid, sound and sensible reasons to invest in gold; at least for long-term investors, for those who truly understand the true value and the core purpose of physical precious metals.

Yet ultimately, all these concerns share a common denominator. They all emanate from the same, very well founded and clearly troubling realization that our entire sociopolitical, economic and monetary system is merely a mirage – it is a house of cards, supported and backed by nothing but blind faith. It is also designed to favor and reward recklessness, opportunism, improvidence and sheer greed and to punish and penalize prudence, restraint, patience and personal responsibility.

This entire system, as complex and intricate as it might seem, is actually built on a very simple premise: It all relies upon the individual’s willingness to trade a promise of compliance, obedience and submission to a higher authority in exchange for security, order, protection and stability.

For those of us who have attained a meaningful understanding of history, of economics and of geopolitics, it will likely be clear that anyone tempted by this bargain is not only cowardly and dishonorable, but exceptionally foolish too. As Benjamin Franklin famously and concisely put it: “Those who would give up essential liberty to purchase a little temporary safety, deserve neither liberty nor safety.”

Still, in realistic, pragmatic, and purely cynical terms, such as those that underpin every modern, advanced, “enlightened” democracy, there remains a reasonable expectation of fairness. The citizens’ rights and (especially) their obligations are plainly laid out, but the State’s duties and limitations are also clearly defined. After all, that’s what Constitutions are for, on paper at least.

In modern democracies, those in government are supposed to be the servants of the people, not their masters. All state institutions, ministries and public offices are supposed to function as mere tools and conveniences for the average citizen, not as their whips or their shackles. In theory, both the government and the governed have distinct roles to play and there are clear, thoroughly negotiated and mutually accepted rules they must adhere to. In practice, however, this is rarely, if ever, the case. Much more often than not what actually happens deviates wildly from what was originally expected or agreed upon.

This is because those in positions of power tend to abuse said power unilaterally, surreptitiously and arbitrarily, and they bend, or even totally change, the rules in their favor. This inevitably leads to system that is fundamentally and inherently unjust, one which operates under the assumption that there are “rules for thee, not for me” and which functions under the tacit understanding that “we are all equal, but some of us are more equal than others”.

For any individual citizen, the “law of the land” is clearly laid out. It is strict and unyielding (e.g. there is no negotiation to be had or any “wiggle room” over the taxes they are compelled to pay, or over the permissions, licenses or official documents they have to obtain just in order to be able to work and earn a living, to travel or to relocate, to sell a property they own or to buy a new one, to build a business wherever and with whomever they deem fit, or even to freely speak their minds and voice their opinions and criticisms). For the governed, there is no choice but to abide by the rules, no matter how absurd or feckless they may be – if they dare oppose or defy them, swift and severe consequences will surely follow.

They could be heavily fined, they could have their bank accounts frozen, or their savings and their assets seized – as we saw over the last couple of years. Any and all of these punitive measures could leave them irreparably and irredeemably financially ruined.

Or perhaps they could be stripped of their basic civil rights, like the right to privacy, to free expression and self-determination. Maybe they could become targets for ideological zealots and all kinds of deranged lunatics on- and offline. They could be “cancelled”, they could lose their jobs, they could be banished from their social circles, shunned by their loved ones and ostracized from “polite society”. And if they were to persist and maintain their objections and if their reasons for doing so were dangerously well-founded and alarmingly compelling, they could even be physically detained and incarcerated.

Faced with such formidable opposition, that has access to and control over immense, diverse and powerful resources and that has the capability and willingness to deploy every offensive tool and weapon in its arsenal, clearly, it is easier, safer and patently more prudent for any individual citizen to simply comply, to conform and to just follow the rules. There is thus a clear guarantee that they’ll keep their side of that original deal and to deliver the compliance and obedience they promised; by force if not by will.

When it comes to the State, however, and all its ministries, branches and institutions, a very different set of rules seems to apply – a much more lenient, flexible and liberal one.

For example, the core pledge of security, protection and stability has yet to be fulfilled: no government has ever delivered on any of these promises socially, economically, geopolitically, or monetarily for any meaningful period of time. No matter how consistently and how faithfully the people keep their end of the deal, those in power always seem to have a ready excuse as to why they failed to honor their own and a confident assurance that they definitely, absolutely and unquestionably will, if you reelect them of course.

It is such an obvious and long-standing pattern. And this is why it is very hard to understand why and how any mature and rational citizen would place their trust in the next aspiring leader who embraces the very same ideas and values as everyone before them but still insists they will deliver different results. It is even harder to understand how anyone in their right mind could believe the oft-repeated commitment that politicians and State officials never tire of regurgitating: the promise to maintain order and to defend the rule of law.

How can any reasonable, cultivated, enlightened and decent person ever allow a fox to guard a henhouse? There are numerous historical and recent examples that clearly demonstrate the deep disregard that governments have toward their own laws and towards the rights of their own citizens. Those who have studied history know exactly how often and how easily those in power openly disregard and flout their own rules. Throughout history, governments have been known to renege on their promises. It might be justified by “special circumstances”, by invoking “emergency powers”, or in the name “national security”, but the result is what we’ve repeatedly witnessed over the last decades, all the violations of fundamental, constitutional, human and civil rights, of international law and of common decency.

In the last three years alone we saw too many disgraceful and truly flagitious examples: From infringing upon the individual citizen’s privacy, their financial sovereignty and individual liberties to brazenly violating their private property rights, their freedom of speech, their freedom of movement and their freedom of assembly.

Clearly, the rules don’t apply to those who make them.

Bearing in mind this bigger picture and keeping this wider context in mind, is it really surprising that the State (along with all its dependents, its agents and its cronies) routinely and consistently deceives, cheats, and exploits the very citizens it is theoretically bound to serve, defend, and protect?

For example, I recently came across a very interesting story from the US that perfectly illustrates how far governments have strayed from their constitutionally defined functions, powers and limitations. Specifically, one would expect law enforcement agencies and the individuals they employ to abide by and to adhere to the letter and the sprit of the Law, to respect the citizen they are supposedly serving, as well as their private property and their fundamental human and civil rights.

And yet, as the Los Angeles Times recently reported, the FBI egregiously violated said rights, when it opened and “inventoried” the contents of hundreds of safe deposit boxes in Beverly Hills during a raid in March 2021. Federal agents reportedly spent days shifting through personal belongings stored in nearly 1,400 safe deposit boxes, while they also seized assets from people who had not been charged with any crimes. They confiscated gold coins, family heirlooms, as well as piles of cash, which the total value of the seized assets exceeding $86 million. This entire operation bluntly violated the limitations of the warrant that authorized this raid, which clearly stated that it did not “authorize a criminal search or seizure of the safety deposit boxes.”

At the end of last year, a a federal appellate court ruled that “the agency’s cataloging of the contents of the privately rented boxes, without individual criminal warrants for each, violated the box holders’ 4th Amendment rights against unreasonable searches and seizures.” Court records also showed that the FBI had developed a plan to permanently confiscate everything in the boxes worth more than $5,000, as part of a wholesale forfeiture, based on an assumption that those assets were somehow tied to unknown crimes – even though there was no evidence provided to support this assumption.

No warrant was issued and no legal case was filed against the owners of said assets – they weren’t even notified of this “raid”; they only found out about this blatant violation after it was completed. Their basic constitutional rights, the very ones that every American citizen profoundly values and holds so dear, were just brazenly and flagrantly violated: their private property rights, their right against unreasonable searches and seizures, and their Sixt Amendment rights, especially their right to be informed of the nature and cause of the accusations against them and to face their accusers, their right to a speedy and public trial by an impartial jury and their right to counsel for their defense.

This case is far from unique, nor is it exclusive to the US. In Europe too, the long and multitudinous arms of the State also routinely and casually violate fundamental property, privacy and basic civil rights of innocent individual citizens. After all, what more can one expect from a system that is run by career apparatchiks and pencil pushers and principally controlled by unelected, unqualified, unremarkable, and thoroughly unaccomplished aspiring despots?

To be sure, this is not to say that Switzerland is some kind of perfect utopia, or that it is somehow magically and completely immune to the corruption and the threats of the State. To the contrary, I am the first to recognize the dangers that our small alpine nation faces and to sound the alarm against the steps it has taken in the wrong direction in recent years. For many years, I have, still do, and will continue to ardently oppose, vociferously criticize, fervently object to and fiercely rail against all these incremental (but potentially pivotal) changes that seek to erase the identity, the culture, the mentality and the character of the Swiss.

Nevertheless, as vocal and as persistent and as relentless as I have been and always will be, I never have and never will be genuinely worried about the future of this country. As I mentioned before, Switzerland is far from perfect, but it does still have one fundamental, distinctive, extraordinary and (in practical terms, truly unique) advantage: Direct democracy. This offers an ironclad protection against State overreach, or even any attempts to this end, and against any violation of private property rights.

Of course, the idea of direct democracy alone is no panacea. It only makes sense on a small scale and only among like-minded, enlightened and freedom-loving individuals. It must also be understood, embraced and practically implemented as a means to decentralization, as a manifestation of the principles of subsidiarity and as a tangible demonstration and as incontrovertible proof of the axiomatic, rudimental and foundational idea that every human being is born free. Their skills, their talents, their ideas, their efforts, their beliefs and their goals are theirs and theirs alone and they have the right to pursue, to express and to fulfill them in any way and to any extent they see fit – the only limitation is the age-old adage “my freedom stops where yours begins”.

This simple, yet very rarely practiced, sentiment lies at the heart of the Swiss identity and it represents the foundation of our small, but extraordinary, nation. This deeply engrained reverence for our own individual liberty and the equally unshakable respect for that of our neighbor is part of the Swiss DNA. It is what made this country what it is today and what guarantees it will endure and continue to thrive and be defined by its own will.

END

END

3. CHRIS POWELL//GATA GOLD COMMENTARIES: daily Dispatches

4. OTHER GOLD COMMENTARIES/PODCASTS/

END

5 a. IMPORTANT COMMENTARIES ON COMMODITIES /

END

5 B GLOBAL COMMODITY ISSUES/FOOD IN GENERAL//FREIGHT

END

6.CRYPTOCURRENCY//DIGITAL CURRENCY// COMMENTARIES/

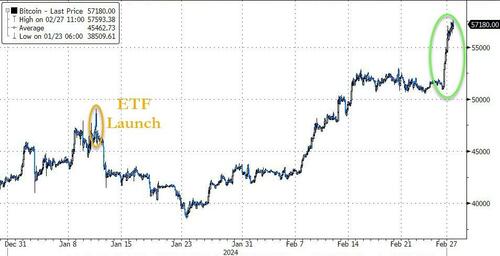

This has the Biden team worried as Bitcoin tops $57,000 as this is perceived to be a threat to the dollar

(zerohedge)

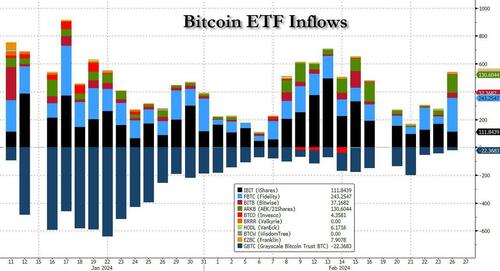

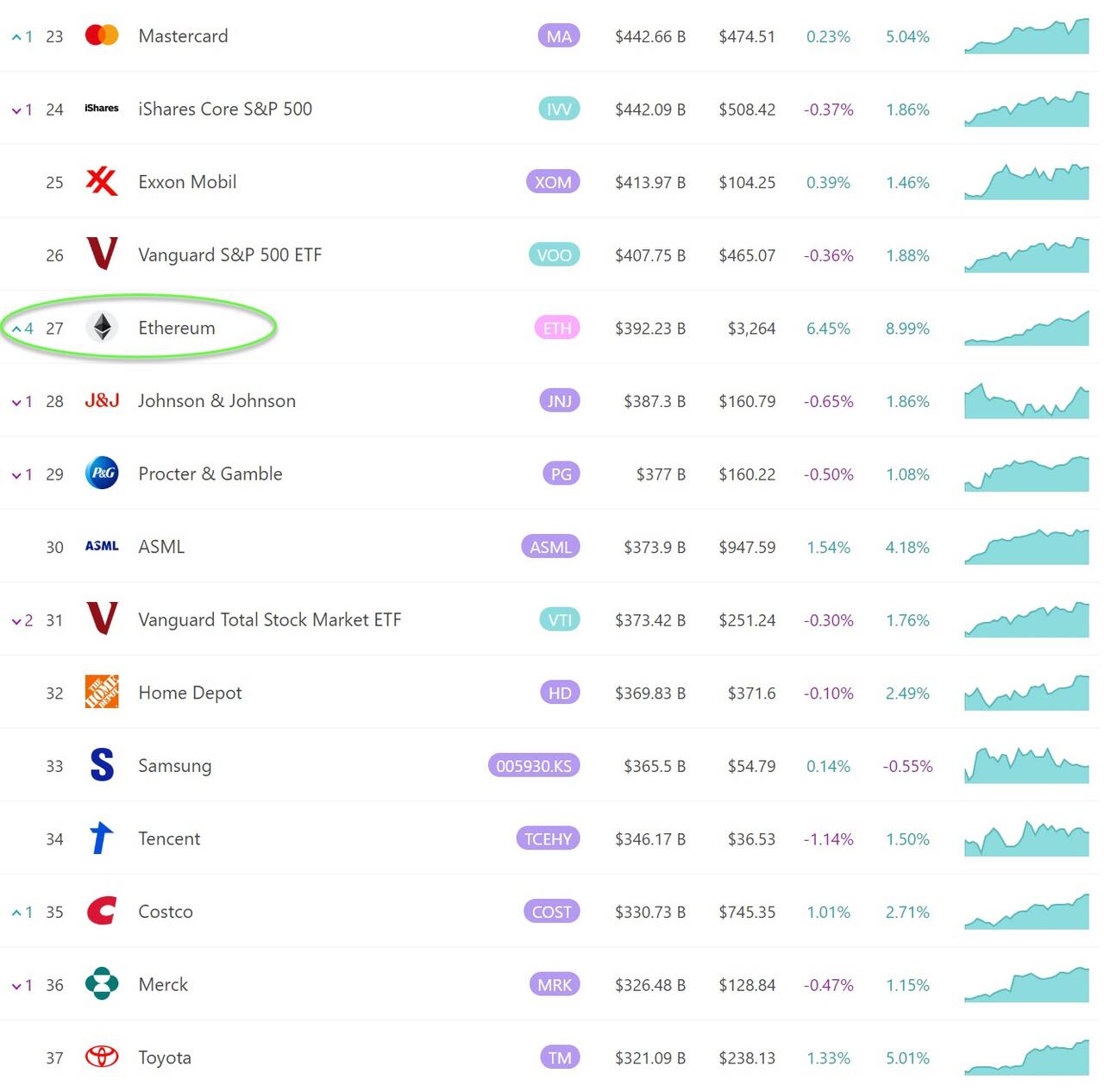

Bitcoin Tops $57,000 As ETF Inflows Soar, Ethereum Bigger Than ASML & Samsung

TUESDAY, FEB 27, 2024 – 09:40 AM

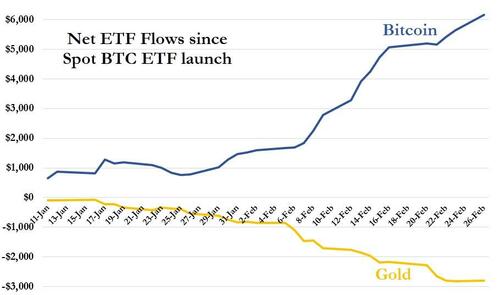

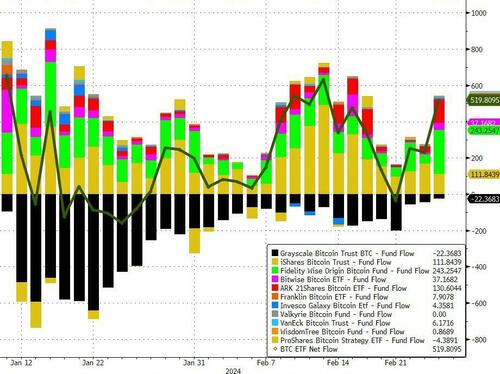

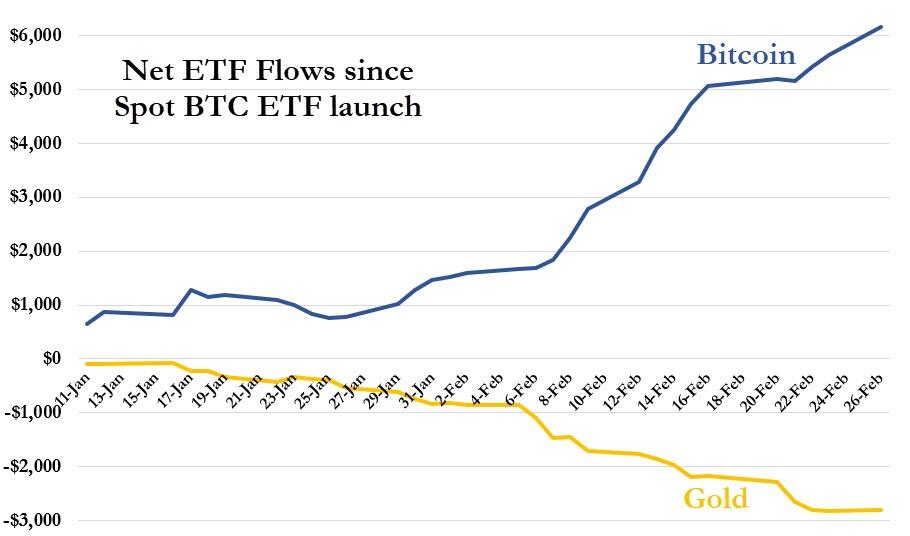

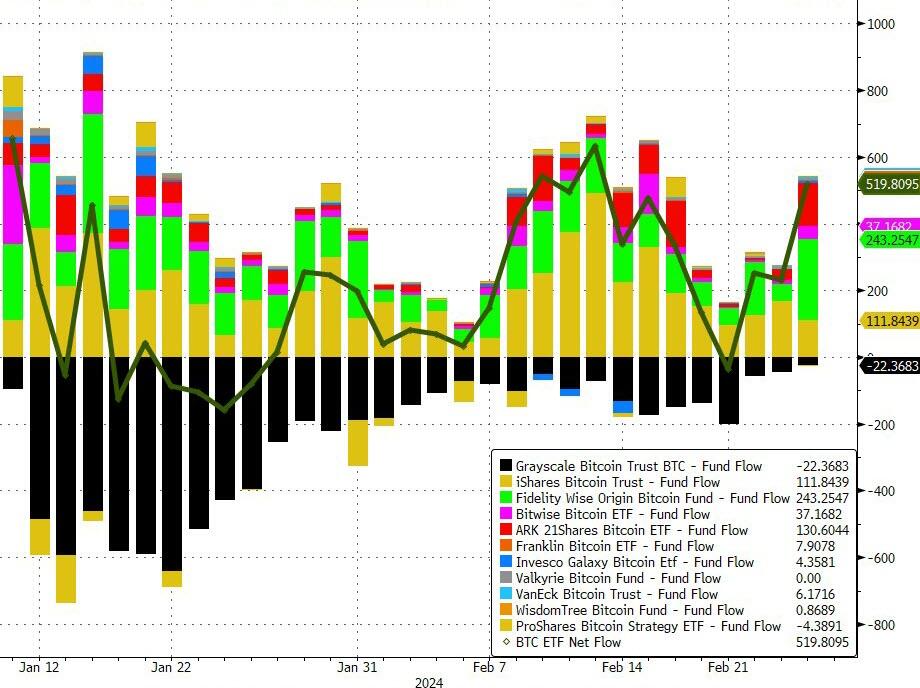

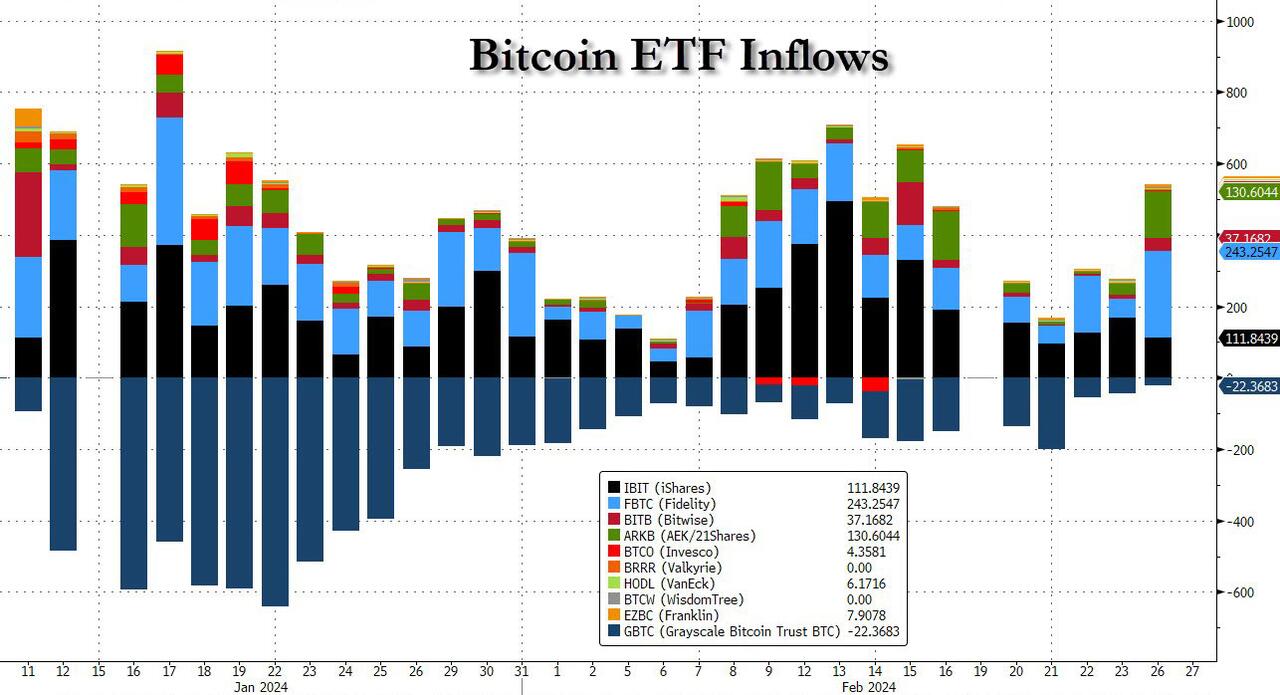

Since the launch of spot bitcoin ETFs – much to the chagrin of Gensler, Warren et al. – over $6BN of net inflows have been invested into the various vehicles (while Gold ETFs have seen almost $3BN of net outflows)…

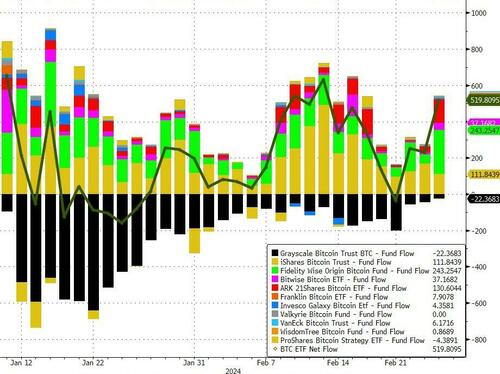

The last few days have also seen outflows from the legacy GBTC slow to a trickle with yesterday’s net inflow over $500 million…

Source: Bloomberg

Volumes have been relatively stable but we do note that volumes are switching from fund to fund. Last week we saw a surge in volumes in HODL and as Bloomberg’s ETF guru, Eric Balchunas (@EricBalchunas) points out, this week has seen a rising interesting in IBIT:

“Another thing about $IBIT volume that’s notable is the amt of pre-market activity..

check this out, it’s already seen $80m traded… only 5 ETFs have seen more activity ahead of mkt open. Unprecedented for 2mo-old ETF.

$BITO in 9th place makes me think lot of arb volume going on.”

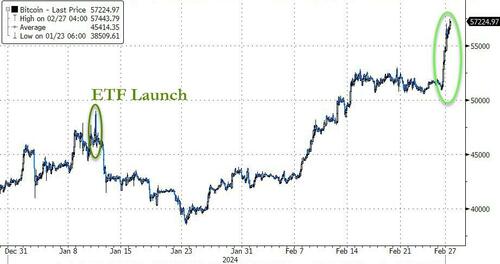

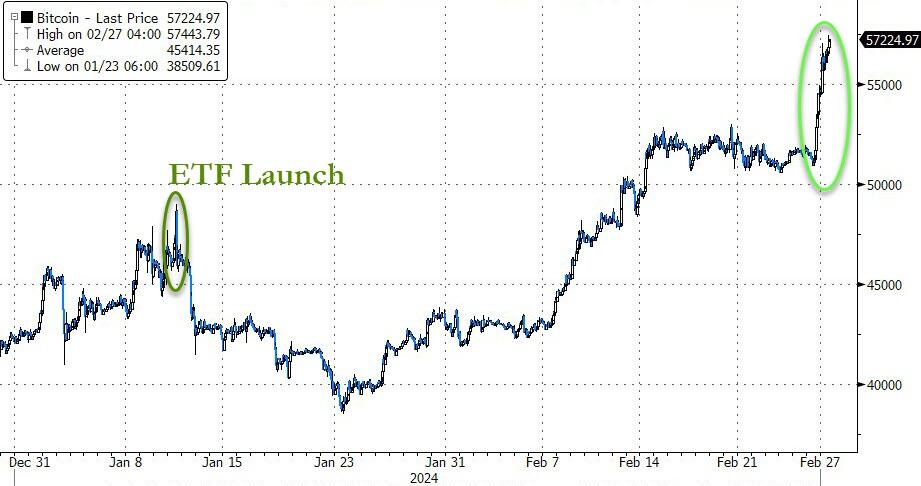

This has all helped push bitcoin back above $57,000 for the first time since Nov 2021…

Source: Bloomberg

In fact, as CoinTelegraph reports, Bitcoin short sellers are nursing millions in losses after Bitcoin rocketed upward by nearly 11% to briefly notch a new yearly high of $57,000.

According to data from crypto data platform CoinGlass, over $161 million in BTC shorts were liquidated in the last 24 hours. Traders looking to gain short exposure to Ethereum didn’t fare much better, with liquidations reaching almost $44 million within the same timeframe. More than $268 million in short positions were liquidated as Bitcoin briefly touched $57,000.

More than $270 million in short positions were liquidated in total as the market spiked upward.

In a statement to Cointelegraph, Swyftx lead analyst Pav Hundal described the crypto market as being “on fire right now.”

“We’re at average per-person trade volumes in retail that we last witnessed at the top of the last bull run in November 2021, plus institutional buying pressure is immense,” he said.

“Exchange Traded Funds alone are cannibalizing close to a quarter of the Bitcoin that is currently being produced by the network,” Hundal added.

Tyler Winklevoss, co-founder of United States-based crypto exchange Gemini, offered succinctly, “We’re so back!” while outspoken BTC bull Dan Held said today’s price action marked “the beginning of the Bitcoin bull run.”

Welcome to the beginning of the Bitcoin bull run.

Be prepared for many sleepless nights 😂— Dan Held (@danheld) February 27, 2024

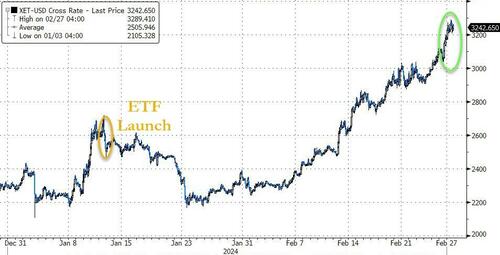

And ethereum up near $3300 for the first time since April 2022…

Source: Bloomberg

Options traders appeared to be anticipating some upward movement in ETH…

Top traded ETH options (via the block) pic.twitter.com/XpsaguZsoJ— zerohedge (@zerohedge) February 23, 2024

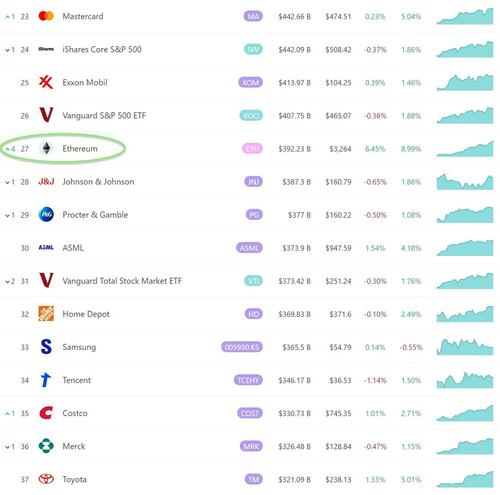

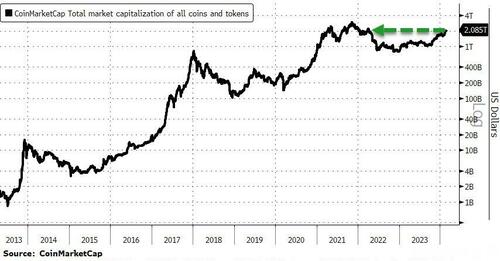

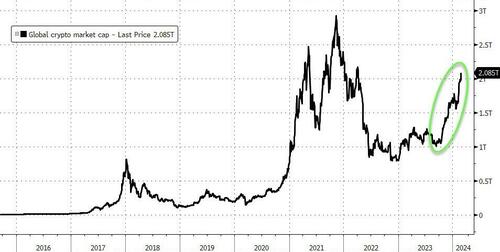

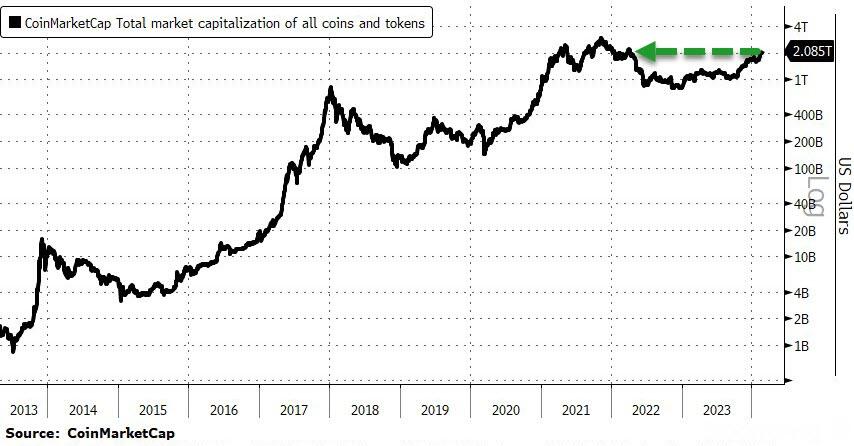

This surge in price has pushed bitcoin above $1.1 trillion in market cap (bigger than Berkshire Hathaway and almopst as large as Meta) and ethereum

And overall, the combined value of the cryptocurrency market has jumped to around $2 trillion for the first time in almost two years on the back of the ETF-fueled rally in Bitcoin.

Source: Bloomberg

“Bullish momentum in crypto is unfolding despite an uptick in rates,” Fundstrat Global Advisors Head of Digital-Asset Strategy Sean Farrell wrote in a note.

“We do not expect a major pullback from Bitcoin given its breakout and positive intermediate-term momentum,” Katie Stockton, founder of Fairlead Strategies, wrote in a note.

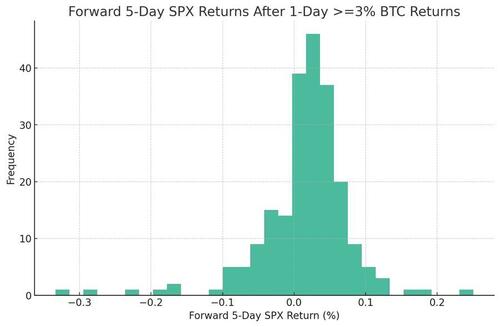

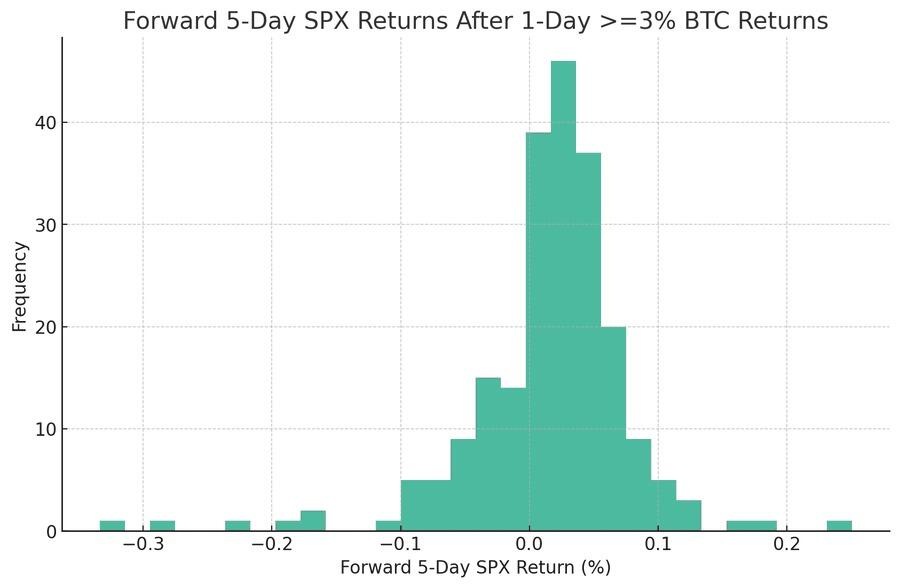

Finally, SpotGamma made an interesting observation. Big BTC days appears to be correlated to positive equity returns. Here are the forward 5 day SPX returns after times where prior 1 day BTC returns are +3%…

As Bloomberg reports, the massive inflows into Bitcoin ETFs have prompted some industry watchers to warn of a looming supply squeeze as miners fail to generate enough coins to keep up with demand. Some 80% if Bitcoin’s supply hasn’t changed hands in the past six months, potentially exacerbating the squeeze and adding to the upward price pressure, according to Julius Baer digital-assets analyst Manuel Villegas.

After the token’s so-called halving in April — where the block reward for miners will shrink to 3.125 Bitcoin from 6.25 Bitcoin — overall supply will fall further and the shortage “would reach aggravated levels,” Villegas said in a note on Tuesday.

“All in all, we see a very sound fundamental backdrop for Bitcoin and believe that prices are well supported around current levels with further upside potential,” Villegas wrote.

Bitcoin has outperformed all traditional asset classes this year.

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS TUESDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED DOWN 7.1979

OFFSHORE YUAN: DOWN TO 7.2108

SHANGHAI CLOSED UP 38.46 PPTS OR 1.29%

HANG SENG CLOSED UP 156.06 PTS OR 0.94%

2. Nikkei closed UP 5.83 PTS OR .17%

3. Europe stocks SO FAR: MOSTLY ALL GREEN EXCEPT SPAIN

USA dollar INDEX DOWN TO 103.59 EURO RISES TO 1.0861 DOWN 16 BASIS PTS

3b Japan 10 YR bond yield: RISES TO. +.687 Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 150.17/JAPANESE YEN NOW FALLING AS WELL AS LONG TERM 10 YR. YIELDS RISING //EVENTUALLY THIS WILL BREAK THE JAPANESE CENTRAL BANK

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UPP /JAPANESE Yen UPP CHINESE ONSHORE YUAN: DOWN/ OFFSHORE: DOWN

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and UP FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund UP TO +2.4260***/Italian 10 Yr bond yield UP to 3.881* /SPAIN 10 YR BOND YIELD UP TO 3.315…**

3i Greek 10 year bond yield UP TO 3.361

3j Gold at $2037.10 silver at: 22.62 1 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble UP 0 AND 21 /100 roubles/dollar; ROUBLE AT 92.18//

3m oil into the 77 dollar handle for WTI and 82 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 150.17// 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 0.687% STILL ON CENTRAL BANK (JAPAN) INTERVENTION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.8786 as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.9543 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

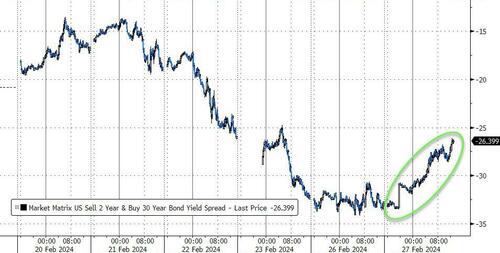

USA 10 YR BOND YIELD: 4.265 DOWN 3 BASIS PTS…

USA 30 YR BOND YIELD: 4.385 DOWN 3 BASIS PTS/

USA 2 YR BOND YIELD: 4.679 DOWN 4 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 31.15…(TURKEY SET TO BLOW UP FINANCIALLY)

GREAT BRITAIN/10 YEAR YIELD: UP 4 BASIS PTS AT 4.1800

end

2.a Overnight: Newsquawk and Zero hedge

Futures Flat Ahead Of Flood Of Economic Data

TUESDAY, FEB 27, 2024 – 08:19 AM

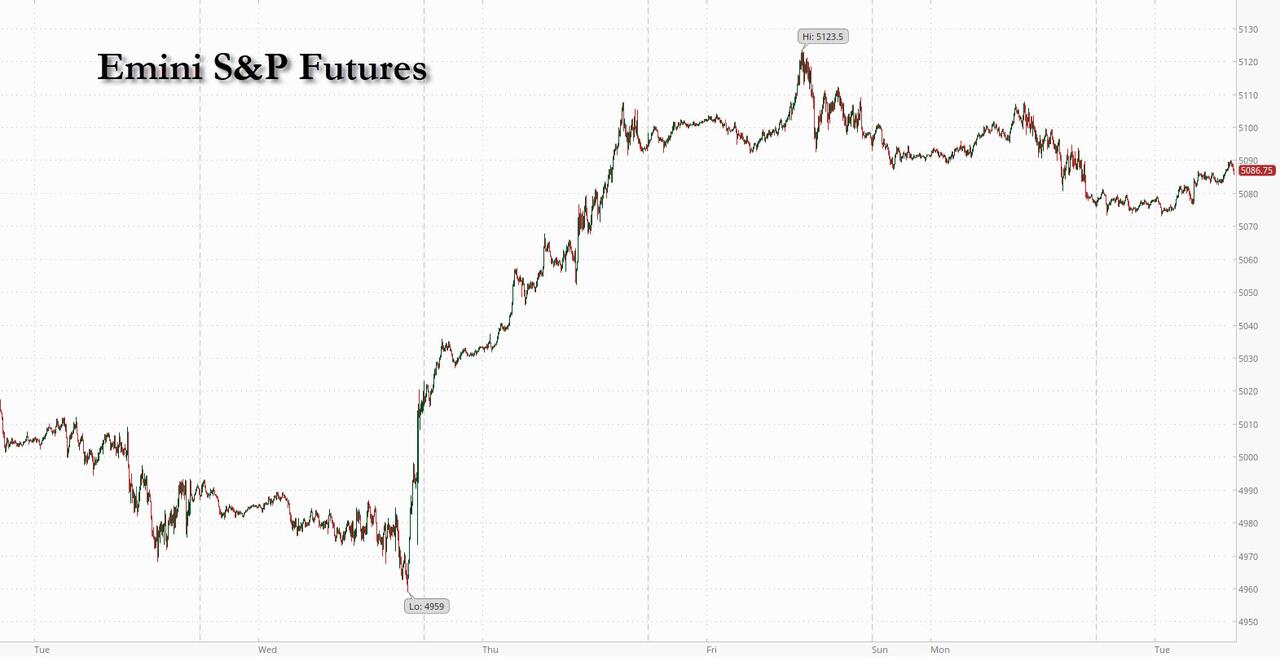

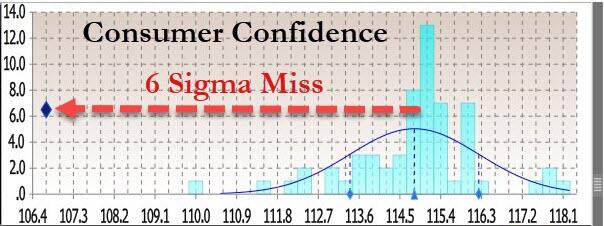

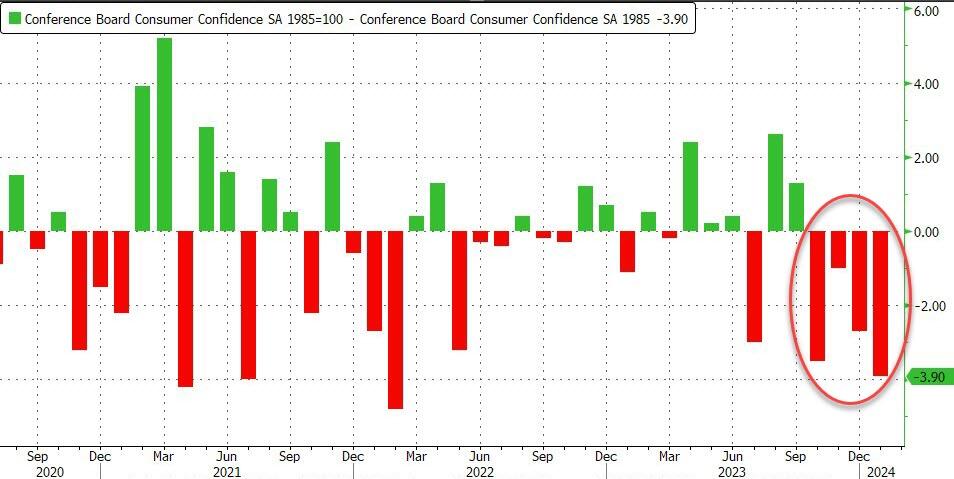

US equity futures pointed to modest gains, led by tech stocks – following Monday’s 38bps drop which was the worst Monday since early December and the second worst Monday since last June – as investors looked ahead to economic data and commentary from Federal Reserve speakers in coming days for clues on the outlook for interest rates. As of 8:00am ET, S&P 500 futures rose 0.1% while Nasdaq 100 contracts added 0.3%. Europe’s Stoxx 600 index was also flat, hovering near its all-time high. Two-year notes led gains as Treasuries rose, retracing some of Monday’s drop. The dollar slipped, oil dipped and bitcoin soared above $57,000. It’s a busy day for economic data, which includes January durable goods orders (8:30am), Case-Shiller home prices (9am), consumer confidence, Richmond Fed and Dallas Fed.

In premarket trading, cryptocurrency-linked stocks rise after Bitcoin’s price reached the $57,000 level for the first time since late 2021 (Cleanspark (CLSK) +16%, Coinbase (COIN) +6, Marathon Digital (MARA) +12%). Hess shares dropped premarket after Chevron said its $53BN acquisition of Hess faces potential disruption as rivals ExxonMobil and CNOOC claim pre-emptive rights over Chevron’s stake in a crucial Guyana oil project (the largest oil discovery in a decade). Discussions are ongoing, but failure to resolve this could jeopardise the Hess takeover, Chevron said.

Macy’s shares were volatile after it said it plans to close 150 unproductive locations as the department-store chain seeks to fight off a pair of activist firms seeking to buy the company. Zoom shares jumped 13% in US premarket trading after the video-conferencing software company’s guidance for adjusted earnings per share was stronger than expected. Additionally, Zoom also said its board approved a buyback program. Here are some other notable premarket movers:

- Aaron’s slumps 25% after providing disappointing 2024 forecasts.

- Altice USA gains 4% after Bloomberg reported that Charter Communications is exploring a takeover of the cable provider.

- Cava rises 7% after the restaurant chain posted fourth-quarter sales that beat expectations as diners splurged on premium dishes.

- Hims & Hers Health (HIMS) soars 18% after the telehealth group’s forecast for first-quarter revenue topped the average analyst estimate.

- Workday shares fell 7.2% in US premarket trading after the human resources software company issued full-year subscription revenue forecast that was weaker than expected at the midpoint. The company also reported fourth-quarter results that analysts said showed less upside than usual.

- Unity Software shares slid 17% in US premarket trading after the video-game software development company’s forecast for revenue fell short of expectations amid a portfolio review that includes exiting some businesses.

- Lowe’s said its sales will fall further this year as consumers continue to hold off from sprucing up their homes amid higher mortgage rates and a drop in new construction projects.

- Janux Therapeutics jumps 106% after the company reported updated clinical data.

- PubMatic rises 27% after the advertising technology company’s fourth-quarter earnings beat expectations, with analysts highlighting a boost from new products.

- TransMedics gains 21% after the transplant therapy biotechnology company reported fourth-quarter revenue that beat the average analyst estimate.

Readings on the US economy are in sharp focus this week, with the Fed’s favored inflation gauge due on Thursday grabbing the most attention. Markets have already dialed back expectations for early and rapid Fed easing after hotter-than-expected data on jobs and price gains, pushing out bets on a first cut to June or July.

“We have always been in the camp that the Fed is unlikely to move as quickly as the market was pricing and data for the first couple of months will only confirm that the first cut will be pushed into the third quarter,” said Matt Stucky, chief portfolio manager for equities at Northwestern Mutual Wealth Management Co.

In response to some arguments that stocks are in another tech bubble, Citigroup strategists said they don’t regard the US equity market as being in a bubble like that of 1999-2000, and suggested the rally could spread to other sectors. Valuation multiples for stocks are well below 2000 levels and, while cash flow expectations around tech companies have increased, forecasts for other industry groups aren’t stretched. That supports the case for broader equity gains.

“We argue that ‘bubble’ is the wrong term to describe the current market setup,” the Citigroup team led by Scott Chronert wrote. “Rather, the recent rally puts pressure on fundamentals to deliver.”

Elsewhere, Bitcoin climbed, rising briefly beyond $57,000 for the first time since late 2021, supported by investor demand through exchange-traded funds as well as further purchases by MicroStrategy Inc.

European stocks were little changed, with mining and autos & parts shares leading gains, while personal care and media stocks are the biggest laggards; drinkmakers’ stocks rose as earnings from Aperol-maker Davide Campari-Milano exceed analyst forecasts. The moves followed sharp drops over the past year for beverage manufacturers amid worries about destocking and consumers turning to cheaper alternatives. Campari gained as much as 7.5% while Remy Cointreau (+2.2%), Pernod Ricard (+1.8%), Diageo (+1.6%) also rise. Here are the biggest movers Tuesday:

- Bouygues rises as much as 5.3% after the French conglomerate reported full-year results, with Morgan Stanley saying that a beat on free cash flow was the main highlight

- GTT shares gain as much as 9%, to touch their highest since August 2022, after the French engineering company’s guidance for 2024 Ebitda beat analysts’ consensus at the mid-point, according to data tracked by Bloomberg

- Flutter shares gain as much as 5.7% in London as Barclays upgrades the stock to overweight from equal-weight, seeing earnings growth over several years as the gambling operator’s US market share strengthens

- Abrdn rose as much as 7.8% after the UK asset manager reported adjusted operating profit above estimates, with analysts also drawing attention to stable net interest margins

- SIG Group shares rise as much as 3.6%, the most since February 2023, after the Swiss carton-packaging maker’s cashflow turned positive thanks a strong 4Q, according to Vontobel

- Puma shares advance as much as 3.9% after the sportswear brand reported full-year results. The company also said it sees weaker demand for sneakers and sports gear persisting through the first half of the year before picking up amid major sporting events

- Eurofins Scientific shares fall as much as 12%, the most in a year. Morgan Stanley said cashflow was disappointing from the laboratory testing services company, citing the cost of higher start-up losses and more restructuring

- Straumann shares decline as much as 7.1% after the Swiss dental equipment company reported operating profit was much weaker due to restructuring and impairment

- Croda shares fall as much as 3.6% after the British specialty chemicals firm reported FY23 results. Citi analysts say though the figures mark the end of a difficult year

- Rovi declines as much as 9% after the Spanish pharmaceutical company said it expects revenue to decrease by a mid-single-digit percentage in 2024. It’s the steepest drop since May last year

Earlier in the session, Asian stocks declined in the absence of fresh catalysts to drive the regional benchmark’s longest stretch of weekly gains in more than a year, with shares in Japan and Hong Kong reversing earlier advances. The MSCI Asia Pacific Index fell 0.2%, reversing a rise of as much as 0.3%, with losses in technology stocks weighing on the index. Japan’s benchmarks, reversed an early advance, while stocks also fell in Korea, Taiwan and Singapore. Mainland and Hong Kong-listed Chinese shares declined, extending Monday’s slide, as attention shifts to next week’s NPC meet. Hong Kong’s benchmark dropped ahead of the budget announcement on Wednesday.

- Hang Seng and Shanghai Comp. were mixed with the mainland mildly positive after the PBoC injected liquidity and with China said to consider approving additional REITs to support consumption.

- ASX 200 was choppy as strength in the consumer sector was partially offset by weakness in miners.

- Nikkei 225 printed fresh record highs before reversing the advances as participants digested the latest CPI data.

Japan’s two-year yield climbed to the highest since 2011 after stronger-than-expected inflation data boosted bets the central bank will end its negative-interest-rate policy in coming months. Traders increased the probability of Bank of Japan exiting its negative rate policy by April to about 82%, up from 78% on Monday, according to swaps data compiled by Bloomberg. The yen strengthened against the dollar.

The inflation report “is adding to speculation that the BOJ will end negative-rate policy as early as March and is serving as a selling catalyst for bonds,” said Kazuya Fujiwara, a fixed-income strategist at Mitsubishi UFJ Morgan Stanley Securities Co. in Tokyo. The data underscores persistent inflationary pressures, he said.

In FX, the Bloomberg Dollar Spot Index drops as much as 0.2% before paring losses to 0.1% while the yen stood atop the G-10 FX leader board, rising 0.3% versus the greenback after Japanese CPI topped estimates and pushed two-year JGB yields to the highest since 2011. The greenback also lagged the Australian dollar, though outperformed others incuding Sweden’s krona.

In rates, treasuries held small gains across the curve after being led higher by bunds and gilts after data showed inflation in UK stores slowed to the lowest level since March 2022. 10-year US TSY yields were around 4.26%, about ~2bps lower on the day, with bunds and gilts outperforming by 0.5bp and 2bp in the sector; gilts, richer by 3bp-4bp on the day, lead gains in core European rates as BOE rate cuts are more aggressively priced. Supply remains the main theme, with $42 billion 7-year note auction at 1pm and another heavy slate of new corporate bonds anticipated after $27 billion was priced Monday. The week’s coupon issuance concludes with today’s 7-year note auction, and follows small tails for 2- and 5-year notes Monday; the WI 7-year yield near 4.30% is about 19bp cheaper than January’s, which tailed by 0.3bp. The dollar IG credit issuance slate includes a handful of deals already; 18 names priced $27b across 37 tranches Monday on order books that were three times oversubscribed according to Bloomberg, spreads compressed nearly 25bps across execution and attrition rates climbed. Another busy session is is expected Tuesday, before critical inflation data later this week.

In commodities, oil steadied after Monday’s gains as pockets of strength in physical markets supported wider sentiment; WTI trade near $77.60 while Brent was at $82.40. Iron ore gained after Monday’s hefty loss, as market watchers looked for signs China’s approaching construction season will bolster demand after costs of the raw material dropped. Spot gold is up 0.2%.

Bitcoin surged more than 4%, hitting a fresh two-year high and rose above $57,000, extending on the sharp gains seen on Monday, with the latest ETF inflows confirming that retail interest continues to surge.

Looking at today’s calendar, US economic data includes January durably goods orders (8:30am), 4Q house price purchase index, December FHFA house price index and S&P CoreLogic Case-Shiller home prices (9am), February Richmond Fed manufacturing index, consumer confidence, and Richmond Fed business conditions (10am) and Dallas Fed services activity (10:30am). Fed speakers scheduled include Barr at 9:05am.

Market Snapshot

- S&P 500 futures up 0.1% to 5,085.50

- STOXX Europe 600 little changed at 495.81

- MXAP up 0.3% to 173.34

- MXAPJ up 0.2% to 527.76

- Nikkei little changed at 39,239.52

- Topix up 0.2% to 2,678.46

- Hang Seng Index up 0.9% to 16,790.80

- Shanghai Composite up 1.3% to 3,015.48

- Sensex up 0.5% to 73,141.23

- Australia S&P/ASX 200 up 0.1% to 7,663.01

- Kospi down 0.8% to 2,625.05

- German 10Y yield little changed at 2.43%

- Euro little changed at $1.0854

- Brent Futures little changed at $82.57/bbl

- Gold spot up 0.2% to $2,035.73

- U.S. Dollar Index down 0.12% to 103.71

Top overnight news

- Japan’s Jan CPI overshoots the Street, with headline coming in at +2.2% (vs. the Street +1.9% and vs. +2.6% in Dec) while core rises 3.5% (vs. the Street +3.3% and vs. +3.7% in Dec). BBG

- Chinese regulators are taking measures to keep the renminbi’s dollar exchange rate stable as Beijing seeks to bolster confidence in the country’s currency and economy ahead of a key leadership summit. FT

- China’s state-backed funds have poured more than 410 billion yuan ($57 billion) into onshore shares this year in a bid to prop up the market. Further purchases are expected. BBG

- Samsonite is weighing its options following interest from suitors including buyout firms, people familiar said. Some PE firms are considering acquiring the company and relisting it in another market — such as the US — at a higher valuation. Shares jumped in Hong Kong. BBG

- President Emmanuel Macron of France on Monday said “nothing should be ruled out” after he was asked about the possibility of sending Western troops to Ukraine in support of the embattled nation’s war against Russia. NYT

- Iran reduced its stockpile of near-weapons-grade nuclear material even as it continued expanding its overall nuclear program, the United Nations’ atomic watchdog said Monday, marking a surprise step that could ease tensions with Washington. WSJ

- President Biden said Monday that fighting in Gaza could stop as early as this coming weekend, the most detailed timeline to date from the White House on a cease-fire between Hamas and Israel in Gaza. WSJ

- Federal Reserve Bank of Kansas City President Jeffrey R. Schmid said the US central bank should be patient in cutting interest rates with inflation above its 2% target and the job market still strong. In his first major speech since taking the job six months ago, Schmid also said he’s in no hurry to stop the ongoing reduction of the Fed’s balance sheet. BBG

- Sixth Street wants to go big on beaten down real estate to capitalize as banks grapple with stress in their portfolios. “We don’t think this is systemic risk, but there are obviously large exposures, particularly in some of the small and regional-sized banks,” CEO Alan Waxman said. BBG

Earnings

- Hess (HES), Chevron (CVX) – Chevron’s USD 53bln acquisition of Hess faces potential disruption as rivals ExxonMobil (XOM) and CNOOC (883 HK) claim pre-emptive rights over Chevron’s stake in a crucial Guyana oil project (the largest oil discovery in a decade). Discussions are ongoing, but failure to resolve this could jeopardise the Hess takeover, Chevron said. (Newswires) HES -2.9%, CVX -0.6% in pre-market trade

- Puma (PUM GY) – Q4 (EUR): Revenue 1.98bln (exp. 2.094bln). EBIT 94.4mln (exp. 100mln). Net 0.8mln (exp. 28mln). Adverse currencies lead to a negative impact on sales of more than EUR 400mln. Asia/Pacific sales increased by 2.8% Y/Y, supported by strong growth in Greater China and India. The rest of Asia was softer, impacted by consumer sentiment and warm weather conditions. Sales in the Americas region decreased by 2.4% Y/Y due to the devaluation of the Argentine peso. 2024 EBIT guidance 620-700mln (exp. 663mln). “Going into 2024, we see that the market environment remains challenging.” (Puma) +0.5% in European trade