WILL COMPLETE EARLY EVENING

H

GOLD PRICE CLOSED UP $12.60 TO $2045.90

SILVER PRICE UP $.25 TO $22.68

Gold ACCESS CLOSED 2044.15

Silver ACCESS CLOSED: 22.70

Bitcoin morning price:$62,430 UP 2550 DOLLARS.

Bitcoin: afternoon price: $61,150 DOWN 818 dollars

Platinum price closing FLAT AT $882.15

Palladium price; UP $15.85 AT $944.40

END

SHANGHAI GOLD PREMIUM 50 DOLLARS/COMEX GOLD

SHANGHAI GOLD (USD) FUTURES – QUOTES

Beginning Monday, April 1, 2024, CME Group settlement data will no longer be accessible through ftp.cmegroup.com and will have a delayed publication time of 12:00 a.m. CT on all cmegroup.com web pages. Learn about alternate ways to access the data in our FAQ.

Last Updated 29 Feb 2024 09:17:05 AM CT.

Market data is delayed by at least 10 minutes.

I will now provide gold in Canadian dollars, British pounds and Euros

4: 15 PM ACCESS

*CANADIAN GOLD: $2,775.75 UP $14.00 CDN dollars per oz( * NEW ALL TIME HIGH 2,795.90 CDN DOLLARS PER OZ//DEC 1 2023)

*BRITISH GOLD: 1619.45 UP 12.58 pounds per oz// *(NEW ALL TIME HIGH//CLOSING///1655.17 BRITISH POUNDS/OZ) OCT 2/2023

*EURO GOLD: 1891.91 UP 14.73 euros per oz //* (ALL TIME CLOSING HIGH: 1903.75 EUROS PER OZ//DEC 1.2023)

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

EXCHANGE: COMEX

ACCESS MARKET:

EXCHANGE: COMEX

CONTRACT: MARCH 2024 COMEX 100 GOLD FUTURES

SETTLEMENT: 2,033.000000000 USD

INTENT DATE: 02/28/2024 DELIVERY DATE: 03/01/2024

FIRM ORG FIRM NAME ISSUED STOPPED

092 C DEUTSCHE BANK 34

190 H BMO CAPITAL 293

323 C HSBC 640 248

363 H WELLS FARGO SEC 149

365 H MAREX CAPITAL M 1

435 H SCOTIA CAPITAL 379

657 C MORGAN STANLEY 5

661 C JP MORGAN 120 372

686 C STONEX FINANCIA 3

690 C ABN AMRO 7

737 C ADVANTAGE 35

905 C ADM 8

TOTAL: 1,147 1,147

MONTH TO DATE: 1,147

JPMorgan stopped 372/1147 contracts.

FOR FEB/2024

GOLD: NUMBER OF NOTICES FILED FOR MAR/2024. CONTRACT: 1147 NOTICES FOR 114,700 OZ or 3.5676 TONNES

total notices so far: 1147 contracts for 114700 Oz (3.5676 tonnes)

FOR MARCH:

SILVER NOTICES 2858 NOTICE(S) FILED FOR 14,290,000 OZ/

total number of notices filed so far this month : 2858 for 14,290,000 oz

XXXXXXXXXXXXXXXXXX

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

BOTH GLD AND SLV ARE FRAUDULENT VEHICLES//THEY ARE NOW RAIDING GLD AND SLV FOR PHYSICAL

GLD

WITH GOLD UP $12.85//

INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD/ : HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.03 TONNES OF GOLD FROM THE GLD.

INVENTORY RESTS AT 822.91 TONNES

SLV//

WITH NO SILVER AROUND AND SILVER UP 25 CENTS AT THE SLV//

HUGE CHANGES IN SILVER INVENTORY AT THE SLV: HUGE WITHDRAWAL OF 2.104 MILLION OZ OUT OF THE SLV/.

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV.

CLOSING INVENTORY: 430.982 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A HUMONGOUS SIZED 2153 CONTRACTS TO 146.515 AND CLOSER TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THIS HUGE SIZED LOSS IN COMEX OI WAS ACCOMPLISHED DESPITE OUR FALL IN PRICE OF $0.07 IN SILVER PRICING AT THE COMEX ON WEDNESDAY. WE HAD ZERO LONG LIQUIDATION AT THE COMEX SESSION WITH AGAIN SOME SHORT COVERING DESPITE THE PRICE OF SILVER FALLNG BY A SMALL AMOUNT. WE HAD A STRONG 709 T.A.S ISSUANCE AND THESE WILL BE USED FOR MANIPULATION LATER THIS MONTH/AS WELL AS TODAY. PLEASE NOTE THAT THE CROOKS NEED A HIGHER SILVER T.A.S. TO CARRY ON THEIR CROOKED MANIPULATION ON A DAILY BASIS

CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON WEDNESDAY NIGHT: 709 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS. IT THUS LOOKS LIKE THE FED (GOV’T) IS BEHIND ALL OF THESE TRADES.

WE HAVE NOW SET ANOTHER RECORD LOW AT 114,102 CONTRACTS ///JULY 3.2023// OUR BANKERS WITH THE HELP OF SPECULATORS AND HIGH FREQUENCY TRADERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.07), BUT WERE UNSUCCESSFUL IN KNOCKING ANY SILVER LONGS AS WE HAD A TMEGA HUMONGOUS SIZED GAIN OF 2065 CONTRACTS ON OUR TWO EXCHANGES DESPITE A LOWER PRICE.

WE MUST HAVE HAD:

A STRONG SIZED 600 ISSUANCE OF EXCHANGE FOR PHYSICALS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 22.270 MILLION OZ (FIRST DAY NOTICE)

//NEW STANDING FOR SILVER IS THUS 22.270 MILLION OZ

/ HUGE SIZED COMEX OI GAIN/STRONG SIZED EFP ISSUANCE/ VI) STRONG SIZED NUMBER OF T.A.S. CONTRACT ISSUANCE 709 CONTRACTS)/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL -REMOVED A HUGE XXX CONTRACTS //

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS FEB. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF FEB

TOTAL CONTRACTS for 20 days, total 13,227 contracts: OR 66.135 MILLION OZ (661 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 63,135 MILLION OZ

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH 2022: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 118.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 85.745 MILLION OZ (SMALLER THAN LAST MONTH)

AUGUST: 171.43 MILLION OZ (THIS MONTH IS GOING TO BE HUGE //2ND HIGHEST ON RECORD

SEPT: 72.705 MILLION OZ (SMALLER THIS MONTH)

OCT: 97.455 MILLION OZ

NOV. 50.050 MILLION OZ

DEC. 66.140 MILLION OZ//

TOTAL 2023: 1,104.10 MILLION OZ/

JAN ’24 : 78.655 MILLION OZ//

FEB /2024 : 66.135 MILLION OZ./FINAL

MARCH:

RESULT: WE HAD A HUGE SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 2153 CONTRACTS DESPITE OUR LOSS IN PRICE OF SILVER PRICING AT THE COMEX//WEDNESDAY.,. THE CME NOTIFIED US THAT WE HAD A STRONG EFP ISSUANCE CONTRACTS: 600 ISSUED FOR MAY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS. WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR MARCH. OF 22.270 MILLION OZ ON FIRST DAY NOTICE.

//NEW TOTAL REMAINS AT 22.270 MILLION OZ

WE HAVE A MEGA HUMONGOUS GAIN OF 2753 OI CONTRACTS ON THE TWO EXCHANGES DESPITE THE LOSS IN PRICE. THE TOTAL OF TAS INITIATED CONTRACTS TODAY: A STRONG SIZED 709 CONTRACTS//HUGE FRONT END OF THE TAS CONTRACTS WERE LIQUIDATED DURING THE WEDNESDAY COMEX SESSION/// WITH SOME SHORT COVERING FROM OUR SPEC SHORTS ( WITH PRICE OF SILVER FALLING) . THE NEW TAS ISSUANCE WEDNESDAY NIGHT (709) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE//PROBABLY TODAY., .

WE HAD 2858 NOTICE(S) FILED TODAY FOR 14.290 MILLION OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A SMALL SIZED 494 CONTRACTS TO 411,289 AND CLOSER TO THE RECORD (SET JAN 24/2020) AT 799,733 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110, BUT WE ARE NOW CLOSER TO OUR ALL TIME LOW OF 390,000 CONTRACTS.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: removed 36 CONTRACTS

WE HAD A SMALL SIZED INCREASE IN COMEX OI ( 494 CONTRACTS) WITH OUR $1.00 LOSS IN PRICE//WEDNESDAY. WE ALSO HAD A RATHER LARGE INITIAL STANDING IN GOLD TONNAGE FOR MARCH. AT 10.270 TONNES ON FIRST DAY NOTICE

NEW TOTAL Of INITIAL GOLD STANDING TO: 10.270 TONNES // ALL OF THIS HAPPENED DESPITE OUR $1.00 LOSS IN PRICE WITH RESPECT TO WEDNESDAY’S TRADING. WE HAD A FAIR SIZED GAIN OF 2025 OI CONTRACTS (10.125) PAPER TONNES) ON OUR TWO EXCHANGES.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 1495 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 411,689

IN ESSENCE WE HAVE A FAIR SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 1989 CONTRACTS WITH 494 CONTRACTS INCREASED AT THE COMEX// AND A FAIR SIZED 1495 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 1989 CONTRACTS.. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): GOOD SIZED 3410 CONTRACTS.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (1495 CONTRACTS) ACCOMPANYING THE SMALL SIZED GAIN IN COMEX OI (494) //TOTAL GAIN FOR OUR THE TWO EXCHANGES: 1989 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR FORMER FORMAT OF BANKERS GOING LONG AND SPECULATORS GOING SHORT ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR MARCH. AT 10.270 TONNES

/ 3) ZERO LONG LIQUIDATION // 4) SMALL SIZED COMEX OPEN INTEREST GAIN/ 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER///6: STRONG T.A.S. ISSUANCE: 3410 CONTRACTS//CONSIDERABLE SHORT COVERING AGAIN

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023-2024 INCLUDING TODAY

FEB.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF FEB. :

TOTAL EFP CONTRACTS ISSUED: 64,926 CONTRACTS OR 6,492,600 OZ OR 201.947 TONNES IN 20 TRADING DAY(S) AND THUS AVERAGING: 3254 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 20 TRADING DAY(S) IN TONNES 201.947 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2022, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 201.947/3550 x 100% TONNES 5.69% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2023

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH/2022: 409.30 TONNES //FINAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 151.69 TONNES (WEAKER THAN LAST MONTH)

AUGUST: 195.28 TONNES (A STRONGER MONTH)//FINAL

SEPT: 254.709 TONNES (WILL BE LARGER THAN LAST MONTH AND A STRONG MONTH)

OCT. 248.09 TONNES. LIKE SILVER, THIS MONTH IS GOING TO BE A STRONG E.F.P. ISSUANCE.

NOV. 239.16 TONNES//WILL BE STRONG THIS MONTH,

DEC. 213.704 TONNES. A STRONG MONTH//

TOTAL FOR YEAR 2023: 2,569.57 TONNES VS 2578 TONNES LAST YEAR

JAN ’24: 291.76 TONNES (WILL BE MUCH GREATER THAN LAST MONTH.//3RD HIGHEST EVER RECORDED EX FOR PHYSICAL)

FEB’24: 201.947 TONNES (SHOULD BE A WEAKER ISSUANCE MONTH)

MARCH 2024:

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF FEB. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (FEB), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER ROSE BY A HUGE SIZED 2153 CONTRACTS OI TO 146,666 AND CLOSER TO THE COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 6 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 600 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAY 600 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 600 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 2153 CONTRACTS AND ADD TO THE 600 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A HUMONGOUS SIZED GAIN OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 2753 CONTRACTS

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTAL 13.765 MILLION OZ

OCCURRED WDESPITE OUR $.07 LOSS IN PRICE …..

END

OUTLINE FOR TODAY’S COMMENTARY

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

b, ) Gold/silver trading overnight Europe,//GOLD COMMENTARIES

(Peter Schiff)

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

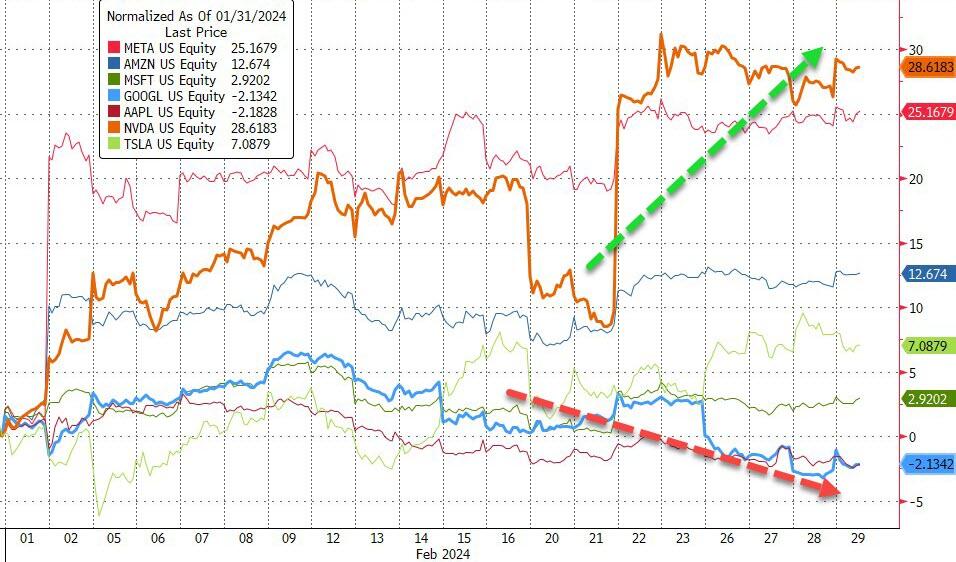

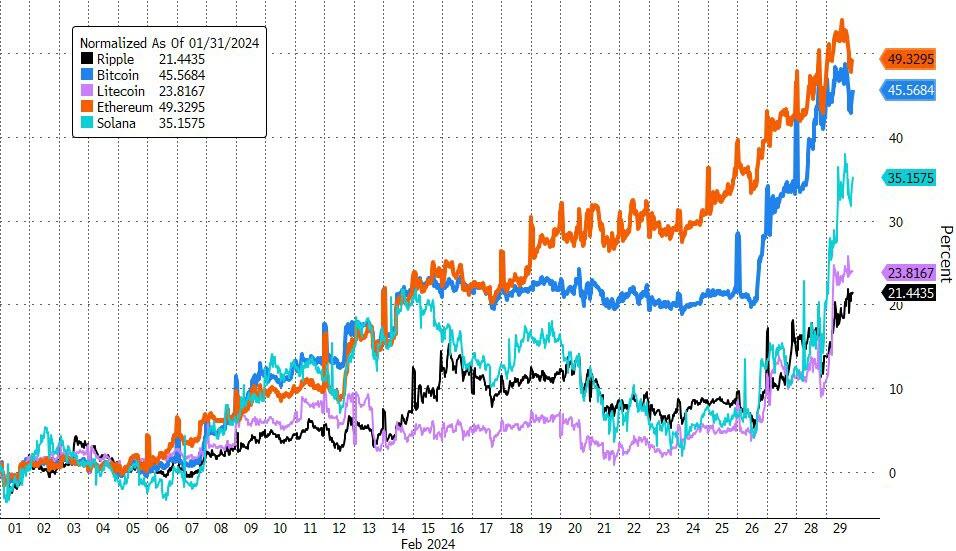

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS//

THURSDAY MORNING/WEDNESDAY NIGHT

SHANGHAI CLOSED UP 57.32 PTS OR 1.94% //Hang Seng CLOSED DOWN 25.41 PTS OR 0.15% / Nikkei CLOSED DOWN 41.84 PTS OR .11%//Australia’s all ordinaries CLOSED UP 0.54% /Chinese yuan (ONSHORE) closed UP 7.1950 //OFFSHORE CHINESE YUAN CLOSED TO 7.2108 /Oil UP TO 78.47 dollars per barrel for WTI and BRENT UP AT 82.06/ Stocks in Europe OPENED MOSTLY ALL MIXED// ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE YUAN STRONGER

A)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

9. USA

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A SMALL SIZED 494 CONTRACTS TO 411,689 DESPITE OUR LOSS IN PRICE OF $1.00 WITH RESPECT TO WEDNESDAY TRADING. ACCORDING TO OUR EXPERT ANDREW MAGUIRE, THE LOW COMEX GOLD OI WAS DUE TO THE CRIMINAL BANKS LEAVING THE GOLD ARENA AND USING THEIR “SKILLS” ON THE NEW FUTURES OF BITCOIN. WITH CENTRAL BANK BUYING PHYSICAL GOLD IN RECORD NUMBERS, IT WOULD BE FUTILE TRYING TO SELL NAKED CALLS AGAINST GOLD AS CB’S WOULD JUST TURN AROUND AND TAKE DELIVERY.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE NON ACTIVE DELIVERY MONTH OF MARCH..… THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 1495 EFP CONTRACTS WERE ISSUED: : APRIL 1495 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 1495 CONTRACTS

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A FAIR SIZED TOTAL OF 1989 CONTRACTS IN THAT 1495 LONGS WERE TRANSFERRED AS EXCHANGE FOR PHYSICALS TO LONDON AND WE HAD A SMALL SIZED GAIN OF 494 COMEX CONTRACTS..AND THIS GAIN ON OUR TWO EXCHANGES HAPPENED DESPITE OUR LOSS IN PRICE OF $1.00 TUESDAY COMEX. AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS DURING MID MONTH IN THE DELIVERY CYCLE), THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR WEDNESDAY NIGHT WAS A GOOD SIZED 3410 CONTRACTS. THROUGHOUT THE PAST SEVERAL WEEKS, THE BANKERS SOLD OFF THE LONG SIDE OF THE SPREAD WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR/T.A.S. SPREAD WHICH WILL BE LIQUIDATED IN DAYS HENCE//.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: MARCH (10.3576 TONNES) ( ACTIVE MONTH)

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 24 MONTHS OF 2021-2023:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

NOV: 18.7122 TONNES + 16.2505 EX. FOR RISK = 34.9627 TONNES

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707TONNES

TOTAL 2023 YEAR : 436.546 TONNES

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276 TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 10.3576 TONNES

THE SPECS/HFT WERE SUCCESSFUL IN LOWERING GOLD’S PRICE( IT LOST $1.00 //// BUT WERE UNSUCCESSFUL IN KNOCKING ANY SPECULATOR LONGS AS WE HAD A FAIR SIZED GAIN OF 1989 TOTAL CONTRACTS ON OUR TWO EXCHANGES DESPITE OUR LOWER PRICE. WE HAD TO HAVE HAD ANOTHER HUGE EPISODE OF STRONG SHORT COVERING. WE HAD A GOOD T.A.S. LIQUIDATION ON THE FRONT END OF WEDNESDAY’S TRADING . THE T.A.S. ISSUED ON WEDNESDAY NIGHT, WILL BE “PUT INTO THE BANK” TO BE USED AT A LATER DATE AT THE COLLUSIVE CHOOSING OF OUR BANKERS.

WE HAVE GAINED A TOTAL OI OF 10.125 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR MARCH. (10.3576 TONNES) ON FIRST DAY NOTICE

ALL OF THIS WAS ACCOMPLISHED WITH OUR LOSS IN PRICE TO THE TUNE OF $1.00

WE HAD -REMOVED 36 CONTRACTS TO THE COMEX TRADES TO OPEN INTEREST (CROOKS)

NET GAIN ON THE TWO EXCHANGES 1989 CONTRACTS OR 198,900 OZ OR 6.189 TONNES.

estimated volume today 220,556 fair

final gold volumes/yesterday 144,899 poor

//speculators have left the gold arena

FEB 29 INITIAL FEB GOLD

/ /// THE MARCH 2024 GOLD CONTRACT

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 9530.261 oz ASAHI MALCA INCLUDES 116 kilobars . |

| Deposit to the Dealer Inventory in oz | nil oz |

| Deposits to the Customer Inventory, in oz | 89,315.478 oz Loomis |

| No of oz served (contracts) today | 1147 notice(s) 114,700 OZ 3.5676 TONNES |

| No of oz to be served (notices) | 2183 contracts 218,300 oz 6.79000. TONNES |

| Total monthly oz gold served (contracts) so far this month | 1147 notices 114700 oz 3.5676 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | x |

0 dealer deposits:

total dealer deposits: nil oz

total customer withdrawals: 2

i) Out of ASAHI: 5800.528 oz

ii) Out of Malca: 3729.679 oz (116 kilobars)

total withdrawal: 9530.761 oz

we had 0 customer deposit

total deposit nil

Adjustments:

0

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR FEB.

For the front month of MARCH we have an oi of 3330 contracts having GAINED 124 contracts.

Thus by definition, the initial amount of gold standing for this active delivery month of March is as follows:

3330 notices x 100 oz per notice = 333000 oz or 10.3376 tones

APRIL LOST 174 CONTRACTS RISING TO 316,359.

We had 1147 contracts filed for today representing 114,700 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 120 notices were issued from their client or customer account. The total of all issuance by all participants equate to 1147 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 372 notice(s) was (were) stopped ( (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for the MARCH. /2024. contract month, we take the total number of notices filed so far for the month (1147 x 100 oz ), to which we add the difference between the open interest for the front month of MARCH. (3330 CONTRACTS) minus the number of notices served upon today 1147 x 100 oz per contract equals 333,000 OZ OR 10.3576 TONNES

thus the INITIAL standings for gold for the MARCH. contract month: No of notices filed so far (1147) x 100 oz + (3330) {OI for the front month} minus the number of notices served upon today (1147) x 100 oz which equals 333,000 oz (10.3576 TONNES)

TOTAL COMEX GOLD STANDING FOR MARCH: 10.3576 TONNES WHICH IS HUGE FOR A NON ACTIVE DELIVERY MONTH IN THE CALENDAR.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 1,354,385.502 42.127 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD: 18,250,350.284 OZ

TOTAL REGISTERED GOLD 8,088,671.657 (251.59 tonnes).

TOTAL OF ALL ELIGIBLE GOLD: 10,161,678.647 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 6,734,286 oz (REG GOLD- PLEDGED GOLD) 209.464 tonnes/dropping like a stone

END

SILVER/COMEX

FEB 29/INITIAL

//2024// THE MARCH 2024 SILVER CONTRACT//INITIAL

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 1024.146 oz Delaware . |

| Deposits to the Dealer Inventory | nil OZ |

| Deposits to the Customer Inventory | 51,406.400 oz HSBC |

| No of oz served today (contracts) | 2858 CONTRACT(S) (14,290,000 OZ) |

| No of oz to be served (notices) | 1596 contracts (7.980 MILLION oz) |

| Total monthly oz silver served (contracts) | 2858 Contracts (14.290 MILLION oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

i) 0 dealer deposit

total dealer deposit: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: 0 oz

We had 1 deposits customer account:

i) Into HSBC 51,406.400 oz

total customer deposits 51,406.400 oz

JPMorgan has a total silver weight: 129.806 million oz/282.126 million or 46.26%

adjustment: customer to dealer/Delaware 9616.544 oz

dealer to customer CNT 1,964,870.620 oz

Comex withdrawals: 1

i)Delaware 1024.146 oz

total withdrawal: 1024.146 oz

TOTAL REGISTERED SILVER: 49.378 MILLION OZ//.TOTAL REG + ELIGIBLE. 282.075 million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR DECEMBER:

silver open interest data:

FRONT MONTH OF MARCH /2023 OI: 4454 CONTRACTS HAVING LOST 2100 CONTRACT(S).

THUS BY DEFINITION THE INITIAL AMOUNT OF SILVER STANDING IN THIS VERY ACTIVE DELIVERY MONTH OF MARCH IS AS FOLLOWS:

4454 NOTICES X 5000 OZ PER NOTICE = 22.270 MILLION OZ

APRIL SAW A GAIN OF 139 CONTRACTS TO STAND AT 912

MAY SAW A GAIN OF 559 CONTRACTS UP TO 117.,198.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 2858 for 14.290 MILLION oz

Comex volumes// est. volume today 53,275 poor

Comex volume: confirmed yesterday 56,181 poor

To calculate the number of silver ounces that will stand for delivery in MARCH. we take the total number of notices filed for the month so far at 2858 x 5,000 oz = 14,290,000 oz

to which we add the difference between the open interest for the front month of MARCH. (4454) and the number of notices served upon today 2858 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the MARCH/2024 contract month: 2858 (notices served so far) x 5000 oz + OI for the front month of MARCH. (4454) – number of notices served upon today (2858 )x 500 oz of silver standing for the MARCH contract month equates to 22.270 MILLION OZ.

New total standing: 22.270 million oz.

There are 49.378 million oz of registered silver.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS//

BOTH GLD AND SLV ARE MASSIVE FRAUDS!

FEB29/WITH GOLD UP $12.60 TODAY NO CHANGES IN GOLD INVENTORY AT THE GLD INVENTORY RESTS AT 826.94 TONNES

FEB28/WITH GOLD DOWN $1.00 TODAY NO CHANGES IN GOLD INVENTORY AT THE GLD INVENTORY RESTS AT 826.94 TONNES

FEB27/WITH GOLD UP $4.40 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF .87 TONNES OF GOLD FROM THE GLD:/INVENTORY RESTS AT 826.94 TONNES

FEB26/WITH GOLD DOWN $8.90 TODAY NO CHANGES IN GOLD INVENTORY AT THE GLD:/INVENTORY RESTS AT 827.81 TONNES

FEB23/WITH GOLD UP $17 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.01 TONNES OF GOLD FROM THE GLD.//INVENTORY RESTS AT 827.81 TONNES

FEB22/WITH GOLD DOWN $2.15 TODAY NO CHANGES IN GOLD INVENTORY AT THE GLD://INVENTORY RESTS AT 829.82 TONNES

FEB21/WITH GOLD DOWN $5.30 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 7.59 TONNES OF GOLD OUT OF THE GLD///INVENTORY RESTS AT 29.82 TONNES

FEB20/WITH GOLD UP $16.15 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 0.58 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 837.89 TONNES

FEB16/WITH GOLD UP $8,60 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.73 TONNES OF GOLD FROM THE GLD///INVENTORY RESTS AT 837.31 TONNES

FEB15/WITH GOLD UP $11.70 TODAY NO CHANGES IN GOLD INVENTORY AT THE GLD:/INVENTORY RESTS AT 841.92 TONNES

FEB14/WITH GOLD DOWN $2.75 TODAY NO CHANGES IN GOLD INVENTORY AT THE GLD:/INVENTORY RESTS AT 841.92 TONNES

FEB13/WITH GOLD DOWN $20.15 TODAY NO CHANGES IN GOLD INVENTORY AT THE GLD:/INVENTORY RESTS AT 841.92 TONNES

FEB12/WITH GOLD DOWN $4.80 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A STRONG WITHDRAWAL OF 1.74 TONNES OF GOLD FROM THE GLD. / //://INVENTORY RESTS AT 841.92 TONNES

FEB9/WITH GOLD DOWN $8.60 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A STRONG DEPOSIT OF 1.44 TONNES OF GOLD FROM THE GLD. / //://INVENTORY RESTS AT 843.66 TONNES

FEB8/WITH GOLD DOWN $2.70 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A MASSIVE WITHDRAWAL OF 5.47 TONNES OF GOLD FROM THE GLD. / //://INVENTORY RESTS AT 842.22 TONNES:

FEB7/WITH GOLD UP $0.40 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A MASSIVE WITHDRAWAL OF 4.04 TONNES OF GOLD FROM THE GLD. / //://INVENTORY RESTS AT 847.69 TONNES:

FEB6/WITH GOLD UP $8.50 TODAY NO CHANGES IN GOLD INVENTORY AT THE GLD:/ / //://INVENTORY RESTS AT 851.73 TONNES:

FEB5/WITH GOLD DOWN $9.85 TODAY SMALL CHANGES IN GOLD INVENTORY AT THE GLD:A DEPOSIT OF .58 TONNES OF GOLD INTO THE GLD// / //://INVENTORY RESTS AT 851.73 TONNES:

FEB 2/WITH GOLD DOWN $17.95 TODAY SMALL CHANGES IN GOLD INVENTORY AT THE GLD:A WITHDRAWAL OF .58 TONNES OF GOLD FROM THE GLD// / //://INVENTORY RESTS AT 851.15 TONNES:

FEB 1/WITH GOLD UP $5.00 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD:A WITHDRAWAL OF 1.73 TONNES OF GOLD FROM THE GLD// / //://INVENTORY RESTS AT 851.15 TONNES:

JAN 31/WITH GOLD UP $16.40 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD:A WITHDRAWAL OF 2.01 TONNES OF GOLD FROM THE GLD// / //://INVENTORY RESTS AT 852.88 TONNES:

JAN 30/WITH GOLD UP $6.50 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD:A WITHDRAWAL OF 1.16 TONNES OF GOLD FROM THE GLD// / //://INVENTORY RESTS AT 854.89 TONNES:

TOTAL IN LAST 18 DAYS WITHDRAWAL OF 14.12 TONNES

JAN 29/WITH GOLD UP $8.70 TODAYHUGE CHANGES IN GOLD INVENTORY AT THE GLD:A WITHDRAWAL OF 2.88 TONNES OF GOLD FROM THE GLD// / //://INVENTORY RESTS AT 856.05 TONNES

JAN 26/WITH GOLD DOWN $0.10 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD: / //://INVENTORY RESTS AT 858.93 TONNES

JAN 25/WITH GOLD UP $2.50 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD: / //://INVENTORY RESTS AT 858.93 TONNES

JAN 24/WITH GOLD DOWN $9.75 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD: / //://INVENTORY RESTS AT 858.93 TONNES

JAN 23/WITH GOLD UP $3.95 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.02 TONNES OF GOLD FROM THE GLD/ //://INVENTORY RESTS AT 858.93 TONNES

GLD INVENTORY: 826.04 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

FEB 29/WITH SILVER UP 25 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 5.123 MILLION OZ INTO THE SLV//// : SLV INVENTORY RESTS AT 433.086 MILLION OZ

FEB 28/WITH SILVER DOWN 7 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 5.123 MILLION OZ INTO THE SLV//// : SLV INVENTORY RESTS AT 433.086 MILLION OZ

FEB 27/WITH SILVER UP 3 CENTS TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 0.64 MILLION OZ FROM THE SLV//// : SLV INVENTORY RESTS AT 427.943 MILLION OZ

FEB 26/WITH SILVER DOWN 44 CENTS TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.065 MILLION OZ FROM THE SLV//// : SLV INVENTORY RESTS AT 428.603 MILLION OZ

FEB 23/WITH SILVER DOWN 44 CENTS TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.065 MILLION OZ FROM THE SLV//// : SLV INVENTORY RESTS AT 428.603 MILLION OZ

FEB 22/WITH SILVER DOWN 10 CENTS TODAY NO CHANGES IN SILVER INVENTORY AT THE SLV

// : SLV INVENTORY RESTS AT 432.766 MILLION OZ

FEB 21/WITH SILVER DOWN 28 CENTS TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 2.348 MILLION OZ OF SILVER FROM THE SLV// : SLV INVENTORY RESTS AT 432.766 MILLION OZ

FEB 20/WITH SILVER DOWN 33 CENTS TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 3.385 MILLION OZ OF SILVER FROM THE SLV// : SLV INVENTORY RESTS AT 435.008 MILLION OZ

FEB 16/WITH SILVER UP 53 CENTS TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV A DEPOSIT OF 1.235 MILLION OZ OF SILVER FROM THE SLV// : SLV INVENTORY RESTS AT 438.393 MILLION OZ

FEB 15/WITH SILVER UP 56 CENTS TODAY NO CHANGES IN SILVER INVENTORY AT THE SLV : SLV INVENTORY RESTS AT 437.615 MILLION OZ

FEB 14/WITH SILVER UP 24 CENTS TODAY NO CHANGES IN SILVER INVENTORY AT THE SLV : SLV INVENTORY RESTS AT 437.615 MILLION OZ

FEB 13/WITH SILVER DOWN 60 CENTS TODAY SMALL CHANGES IN SILVER INVENTORY AT THE SLV A SMALL WITHDRAWAL OF 0.504 MILLION OZ OZ OUT OF THE SLV: SLV INVENTORY RESTS AT 437.615 MILLION OZ

FEB 12/WITH SILVER UP 14 CENTS TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV A HUGE WITHDRAWAL OF 1.921 MILLION OZ OZ OUT OF THE SLV: SLV INVENTORY RESTS AT 438.119 MILLION OZ

FEB 9/WITH SILVER DOWN 4 CENTS TODAY SMALL CHANGES IN SILVER INVENTORY AT THE SLV A SMALL DEPOSIT OF 600,000 OZ INTO THE SLV: SLV INVENTORY RESTS AT 440.040 MILLION OZ

FEB 8/WITH SILVER UP 29 CENTS TODAY NO CHANGES IN SILVER INVENTORY AT THE SLV: SLV INVENTORY RESTS AT 439.994 MILLION OZ

FEB 7/WITH SILVER DOWN 18 CENTS TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A MASSIVE DEPOSIT OF 4.04 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 439.994 MILLION OZ//LAST 9 DAYS: 10.7598 MILLION OZ WITHDRAWAL

FEB 6/WITH SILVER UP 11 CENTS TODAY NO CHANGES IN SILVER INVENTORY AT THE SLV: /INVENTORY RESTS AT 435.144 MILLION OZ//LAST 9 DAYS: 10.7598 MILLION OZ WITHDRAWAL

FEB 5/WITH SILVER DOWN 32 CENTS TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.345 MILLION OZ FROM THE SLV(FAIRY TALES) // /INVENTORY RESTS AT 435.144 MILLION OZ//LAST 8 DAYS: 10.7598 MILLION OZ WITHDRAWAL

FEB 2/WITH SILVER DOWN 50 CENTS TODAY SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 0.58 MILLION OZ INTO THE SLV(FAIRY TALES) // /INVENTORY RESTS AT 438.489 MILLION OZ//LAST 7 DAYS: 14.105 MILLION OZ WITHDRAWAL

FEB 1/WITH SILVER UP 7 CENTS TODAY MEGA CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.19 MILLION OZ INTO THE SLV(FAIRY TALES) // /INVENTORY RESTS AT 438.947 MILLION OZ//LAST 6 DAYS: 10.3018 MILLION OZ WITHDRAWAL

JAN 31/WITH SILVER DOWN 8 CENTS TODAY MEGA CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.7438 MILLION OZ INTO THE SLV(FAIRY TALES) // /INVENTORY RESTS AT 440.137 MILLION OZ//LAST 5 DAYS: 9.1118 MILLION OZ WITHDRAWAL

JAN 30/WITH SILVER DOWN 5 CENTS TODAY MEGA CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.876 MILLION OZ INTO THE SLV(FAIRY TALES) // /INVENTORY RESTS AT 442.699 MILLION OZ//LAST 4 DAYS: 7.368 MILLION OZ WITHDRAWAL

JAN 29/WITH SILVER UP $.37 TODAY MEGA CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.105 MILLION OZ INTO THE SLV(FAIRY TALES) // /INVENTORY RESTS AT 444.575 MILLION OZ

JAN 26/WITH SILVER DOWN $0.03 TODAY MEGA CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.556 MILLION OZ INTO THE SLV(FAIRY TALES) // /INVENTORY RESTS AT 446.680 MILLION OZ

JAN 25/WITH SILVER UP $0.03 TODAY MEGA CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.831 MILLION OZ INTO THE SLV(FAIRY TALES) // /NVENTORY RESTS AT 448.236 MILLION OZ

JAN 24/WITH SILVER UP $0.44 TODAY MEGA CHANGES IN SILVER INVENTORY AT THE SLV: ANOTHER DEPOSIT OF 1.375 MILLION OZ INTO THE SLV(FAIRY TALES) // //INVENTORY RESTS AT 450.067 MILLION OZ

JAN 23/WITH SILVER UP $0.21 TODAY MEGA CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 16.201 MILLION OZ INTO THE SLV(FAIRY TALES) // //INVENTORY RESTS AT 448.694 MILLION OZ

JAN 22/WITH SILVER DOWN $0.45 TODAY NO CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 458,000 OZ OUT OF THE SLV // //INVENTORY RESTS AT 432.493 MILLION OZ

JAN 19/WITH SILVER DOWN $0.11 TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 458,000 OZ OUT OF THE SLV // //INVENTORY RESTS AT 432.493 MILLION OZ

JAN 18/WITH SILVER UP $0.13 TODAY NO CHANGES IN SILVER INVENTORY AT THE SLV: // //INVENTORY RESTS AT 432.951 MILLION OZ

JAN 17/WITH SILVER DOWN $0.38 TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 779,000 OZ FROM THE SLV.: // //INVENTORY RESTS AT 433.500 MILLION OZ

JAN 16/WITH SILVER DOWN $0.08 TODAY NO CHANGES IN SILVER INVENTORY AT THE SLV: // //INVENTORY RESTS AT 433.500 MILLION OZ

JAN 12/WITH SILVER UP $0.62 TODAY NO CHANGES IN SILVER INVENTORY AT THE SLV: // //INVENTORY RESTS AT 433.500 MILLION OZ

CLOSING INVENTORY 433.086 MILLION OZ//

PHYSICAL GOLD/SILVER COMMENTARIES

1:Peter Schiff/Mike Maharrey

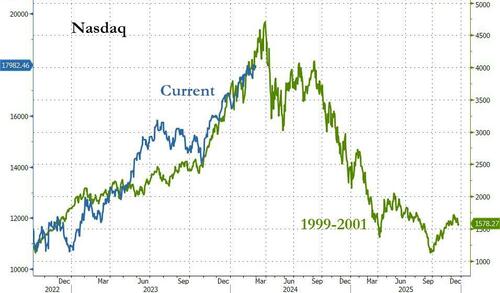

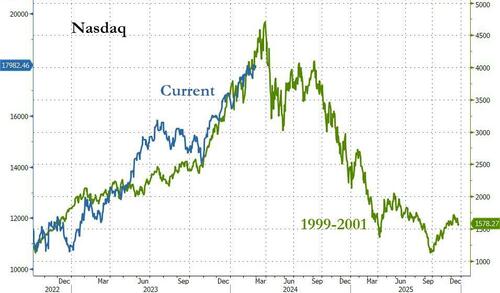

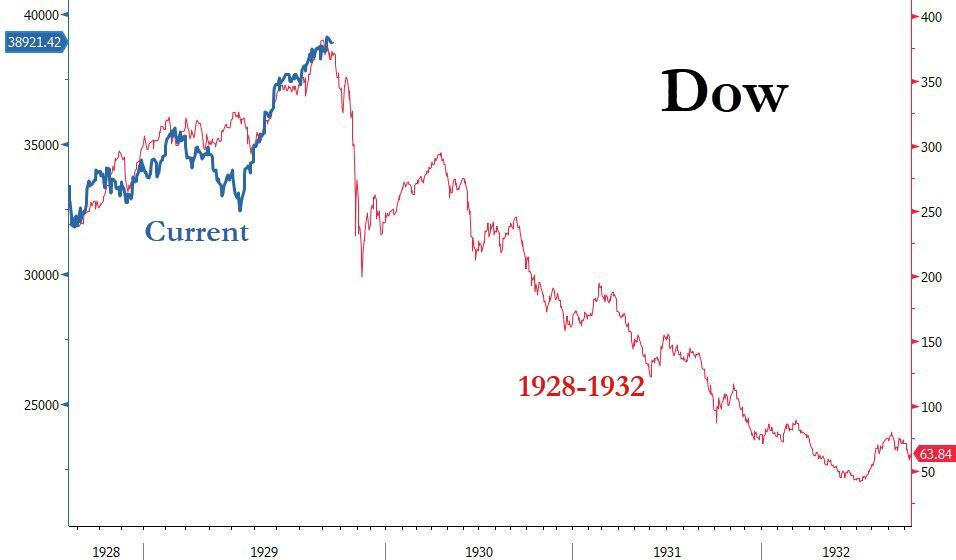

Peter Schiff: Booming Stock Market Mirrors Dot-Com Bubble

THURSDAY, FEB 29, 2024 – 11:00 AM

Via SchiffGold.com,

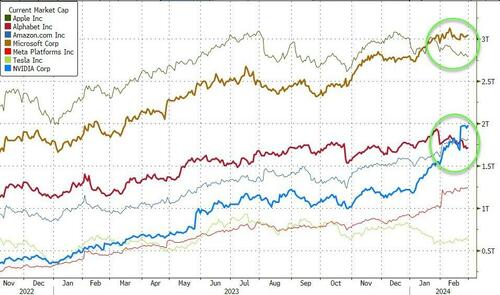

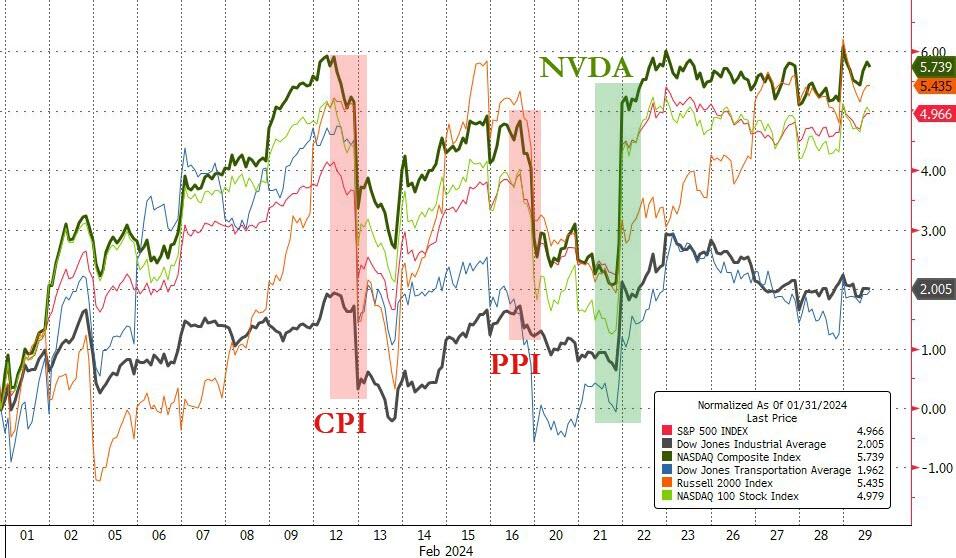

This week Peter covers the highlights of the last few weeks of volatile trading, paying special attention to Nvidia, Wall Street’s favorite AI stock, and Newmont Corporation, a heavy hitter in the gold mining industry.

Both companies’ shares experienced dramatic price action, with NVDA gaining $260 billion in market cap and pulling the market up after an excellent earnings report. Newmont, on the other hand, saw shares fall 7% after a disappointing last quarter.

Peter explains how monetary policy influences the profitability of mining:

“Part of the big problem for Newmont and all the other mining stocks is that it’s so much more expensive to mine gold now … Now why is that? Inflation. Inflation is taking a huge toll on the profits of these companies because the price of gold has not risen as much as the cost of mining it. And that is again why I keep saying gold mining stocks are the ironic victims of inflation.”

Nvidia and the tech sector’s recent surge is reminiscent of the market in the late 1990s, right before the Dot-com bubble popped:

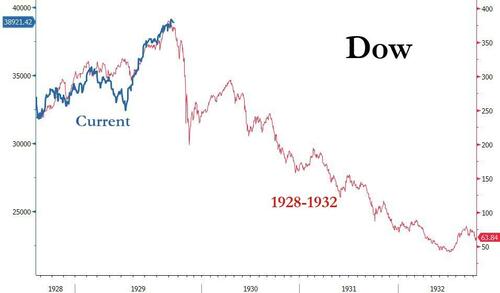

“What’s really significant about today’s situation is that you’ve got 1999-2000 all over again in the stock market, but it’s more like 2008 in terms of the disaster that’s waiting around the corner. We didn’t have a financial crisis in 2001. That didn’t happen until 2008.”

[ZH: Or 1930s…]

This doesn’t mean A.I. technology is doomed to fail. Rather, innovative companies like Nvidia are currently swept up in an overheating economy that will eventually give way to inflationary pressures:

“There’s no doubt that artificial intelligence will be helpful… The markets once again are way ahead of the reality of where all of this is going, and at the same time, they’re overlooking the tremendous economic problems and financial problems that are hiding in plain sight.“

[ZH: It’s different this time…]

Peter also discusses the FOMC minutes that were released this week, which showed Fed officials are still hesitant about cutting interest rates. Gold responded well to this news, as it did last week after higher-than-expected CPI figures were released:

“The gold market kinda shrugged it off, which really shows you the underlying strength in the market. There was a brief sell-off in stocks, but I think investors quickly realized that look, … we’re going to get these cuts… What the markets are focused on is that the hikes are over… We’ve got the wind at our back. The question is… how strong is that wind?”

Recent moves in the price of oil, mortgage rates, and treasury yields suggest these investors are overly optimistic:

“These market indicators are showing that inflation is coming back, that we’ve bottomed out, and we’re just moving higher. And the markets do not expect that this is possible… If they’re wrong, the stock market is going to collapse.”

Markets are expecting rates to fall this spring, but they need to rise:

“If the Fed doesn’t hike rates, it could be even worse— maybe not for the market, but for the dollar, for bonds, and even more bullish for gold… If the Fed doesn’t hike rates, then inflation is just going to run out of control. And in fact, even if the Fed doesn’t cut rates— if it leaves rates where they are— real rates are going down because inflation is going to go up!”

Advocates of rate hikes are wrong when they assert that recent rate hikes constitute “restrictive monetary policy:”

“This is not restrictive monetary policy. Again, less loose doesn’t qualify as tight… What is being restricted? Is the government being restricted? Is there any cutback in government spending? Is the government borrowing less because the Fed has increased the cost of borrowing money? No! The government is borrowing more! In fact, they’re borrowing more to pay the higher interest rates.”

Peter wraps up by discussing a hefty fine leveled against Donald Trump in a New York fraud case. In this case and others, a politicized legal system portends a riskier and increasingly unattractive business environment, both in New York and in the rest of the country:

“One of the reasons that a lot of international money has invested in America over the years is the confidence in our legal system, in the rule of law, in private property— that you can own property, assets, and business here, and you’re protected by the rule of law. It just can’t be arbitrarily taken from you, but what we’re now showing the world is that’s not the case!“

While Wall Street celebrates a record week, Peter’s insights are less optimistic. It is unlikely a handful of tech stocks can perpetually sustain an economy burdened by years of inflation and oppressive government debt. America is addicted to cheap credit, and this addiction will cripple the economy if left unchecked.

end

2.Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens/ CLAUDIO GLASS

END

3. CHRIS POWELL//GATA GOLD COMMENTARIES: daily Dispatches

The questions CFTC and Fed won’t answer expose gold price suppression policy

9:44p ET Wednesday, February 28, 2024

Dear Friend of GATA and Gold:

If mainstream financial news organizations ever work up the courage to report honestly about monetary gold, the commanding heights of the issue will have been mapped out for them by U.S. Rep. Alex X. Mooney, R-West Virginia.

After all, where can investigative journalism start better than with questions that already have been shown to be too politically sensitive for the highest government officials to answer, even when a member of Congress is asking?

Thanks to Mooney, in 2020 the U.S. Commodity Futures Trading Commission was shown refusing to answer whether it has jurisdiction over manipulative trading in the commodity futures markets when such trading is undertaken by or at the behest of the U.S. government:

END

E.J. Antoni and Peter St. Onge: Uniparty is only a few steps away from gutting the dollar

Submitted by admin on Wed, 2024-02-28 18:39 Section: Daily Dispatches

By E.J. Antoni and Peter St. Onge

The Heritage Foundation, Washington, D.C.

Tuesday, February 27, 2024

America’s political establishment has less respect for the U.S. dollar than our foreign adversaries.

That was made clear when Tucker Carlson recently interviewed the Russian strongman President Vladimir Putin, who clearly articulated how the uniparty in Washington is destroying America’s greatest strategic and economic asset—her currency.

Last year, led by the chairman and ranking member of the relevant House and Senate committees, a bipartisan and bicameral bill was introduced that would hand another $300 billion to the Ukraine, this time in the form of the confiscated U.S. dollars owned by the Russian central bank and the Russian people.

There are now renewed calls for this measure as both the budget battle at home and the war in the Ukraine drag on.

Not during the Vietnam or Korean wars or at any point during the height of the Cold War did America do this to the Soviet Union. U.S. statesmen understood then, as our adversaries do now, that the dollar’s reserve currency status is among our most important global assets, both economically and strategically.

… For the remainder of the analysis:

4. OTHER GOLD COMMENTARIES/PODCASTS/

END

5 a. IMPORTANT COMMENTARIES ON COMMODITIES /

END

5 B GLOBAL COMMODITY ISSUES/FOOD IN GENERAL//FREIGHT

END

6.CRYPTOCURRENCY//DIGITAL CURRENCY// COMMENTARIES/

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS THURSDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED UP 7.1950

OFFSHORE YUAN: UP TO 7.2108

SHANGHAI CLOSED UP 57.32 PPTS OR 1.94%

HANG SENG CLOSED DOWN 25.41 PTS OR 0.15%

2. Nikkei closed DOWN 41.84 PTS OR .11%

3. Europe stocks SO FAR: MOSTLY MIXED

USA dollar INDEX UP TO 103.92 EURO FALLS TO 1.0829 DOWN 8 BASIS PTS

3b Japan 10 YR bond yield: RISES TO. +.712 Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 149.96/JAPANESE YEN NOW FALLING AS WELL AS LONG TERM 10 YR. YIELDS RISING //EVENTUALLY THIS WILL BREAK THE JAPANESE CENTRAL BANK

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen UP CHINESE ONSHORE YUAN: UP/ OFFSHORE: UP

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and UP FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund UP TO +2.4995***/Italian 10 Yr bond yield UP to 3.939* /SPAIN 10 YR BOND YIELD UP TO 3.377…**

3i Greek 10 year bond yield UP TO 3.421

3j Gold at $2030.20 silver at: 22.36 1 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble UP 0 AND 25 /100 roubles/dollar; ROUBLE AT 90.89//

3m oil into the 78 dollar handle for WTI and 82 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 149.96// 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 0.712% STILL ON CENTRAL BANK (JAPAN) INTERVENTION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.8803 as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.9534 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.315 UP 4 BASIS PTS…

USA 30 YR BOND YIELD: 4.437 UP 3 BASIS PTS/

USA 2 YR BOND YIELD: 4.687 UP 4 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 31.23…(TURKEY SET TO BLOW UP FINANCIALLY)

GREAT BRITAIN/10 YEAR YIELD: UP 6 BASIS PTS AT 4.287

end

2.a Overnight: Newsquawk and Zero hedge

Futures Fall Ahead Of Key PCE Print

THURSDAY, FEB 29, 2024 – 08:14 AM

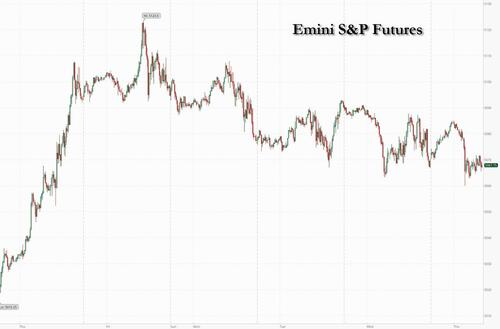

For the third day in a row, US equity futures dropped and bonds fell as investors braced for a print of the Federal Reserve’s favorite inflation metric, which will help identify the path forward for interest rates. As of 7:45am, futures contracts for the emini S&P 500 and the Nasdaq 100 both retreated by about 0.2%, off the worst levels of the session. European stocks fluctuated during another crowded day on the earnings calendar, while Asia closed modestly higher. MegaCaps are mixed with NVDA -1.3% and AAPL -0.7%, the largest movers pre-mkt. Bond yields are up 3-6bps as the yield curve bear flattens; the US Dollar is weaker while the yen holds most of the advance spurred by strongest signal yet from Bank of Japan that the end is near for its negative interest-rate policy. The commodity complex is also lower; oil is flat, while bitcoin continues to surge and was last seen around $63,000. Today’s macro data focus includes PCE/Core PCE, jobless claims, and regional activity indicators. While PCE has been de-risked due to the CPI print, there is still potential for volatility given positioning in the bond market. Month-end rebalancing is thought to provide additional pressure on stocks irrespective of PCE.

In premarket trading, cloud software giant Snowflake shares plunge 23% after the company gave a forecast for first-quarter product revenue that is weaker than expected. Analysts noted that the shares were pressured by a combination of CEO Frank Slootman stepping down and a conservative guide. Peers also decline, with MongoDB down 4.2%, and DataDog sliding 3.0%. Elsewhere, WW International, fka as Wight Watchers, shares crasjed 25% after the “health and wellness” company issued full-year revenue guidance that missed expectations. The company also said Oprah Winfrey has decided to not stand for re-election at its annual shareholders meeting in May, having served on the board since 2015. Here are some other notable premarket movers:

- C3.ai (AI US) shares jump 17.58% after the software firm’s third-quarter revenue beat estimates, showing that demand remains robust for its artificial intelligence-related products. Analysts highlighted strength in its subscription revenues, and demand from government clients.

- CRH (CRH US) shares gain 6.3% in New York premarket trading after the building-materials firm reported “excellent” full-year results, according to Davy, with UBS highlighting the firm’s strong growth prospects in 2024.

- Duolingo (DUOL US) shares soar 20% after full-year revenue guidance from the language-learning software company beat expectations, while fourth-quarter earnings per share also surpassed forecasts. A number of analysts lifted their price targets on the stock, noting robust growth in user numbers.

- HP Inc. (HPQ US) shares fall 3.4% after the computer hardware company reported first-quarter results that missed expectations on key metrics amid ongoing weakness in the market for personal computers.

- Macy’s (M US) shares dip 0.6% after the department store chain was downgraded to market perform from outperform at TD Cowen, which said the company’s restructuring plans will take some time to drive upside to guidance.

- Monster Beverage (MNST US) shares advance 5.6% after the energy-drink maker reported fourth-quarter gross margin that beat consensus estimates. Analysts saw the results as solid overall, highlighting the gross margin beat in the quarter, as well as the strong start to the first-quarter.

- Okta (OKTA US) shares rise 29% after the application software company reported fourth-quarter results that beat expectations. Analysts view the results as a relief in the wake of a recent breach.

- Paramount Global (PARA US) shares advance 3.9% after the media company reported results that were seen as mixed, although revenue in its direct-to-consumer (DTC) streaming business beat expectations.

- Salesforce (CRM US) shares fall 1.8% after the application software company gave a full-year revenue forecast that was weaker than expected, though analysts said it could be conservative. It also initiated a dividend of 40c/share and increased the share buyback authorization by $10b.

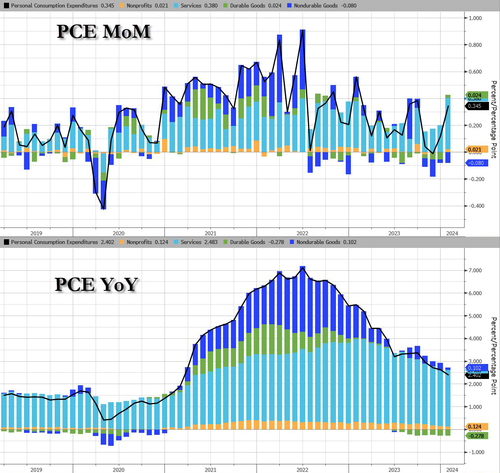

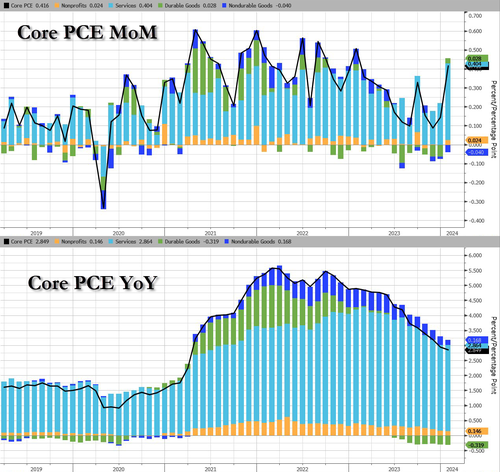

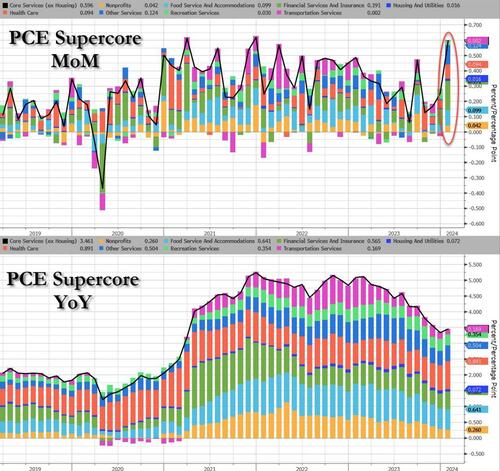

Thursday’s core PCE report, where the core print is expected to rise 0.4% MoM and 2.8% YoY, will likely validate recent commentary from Fed officials showing no rush to ease monetary policy and underscore the twists and turns on the route to the central bank’s 2% inflation target. A higher-than-anticipated reading could undermine expectations for three quarter-point rate cuts by year-end.

“The market always needs to focus on something, and with earnings out of the way and the rates outlook priced in, inflation is the next catalyst,” said Beata Manthey, equity strategist at Citigroup Inc. “It’ll depend on how bad or good the print is today, but when we look at the fundamentals, earnings have shown they’re delivering.”

Stocks are rounding off a strong February, with the S&P 500 and the Nasdaq 100 up more than 4% after excitement around artificial intelligence drove a tech-powered, record-breaking run on Wall Street. MSCI’s global equity index is rising for a fourth month, its longest winning streak since 2021.

For Ulrich Urbahn, head of multi-asset strategy and research at Berenberg, trading on the final day of February is likely to be influenced more by month-end rebalancing than by data, as inflation trends have already been priced into markets following this month’s consumer and producer price reports.

“The focus on PCE ‘because that’s what the Fed cares about’ is valid,” Urbahn said. “But it’s mostly already baked in the cake. Markets will be more affected by some rebalancing flows as equities have hugely outperformed bonds this year.”

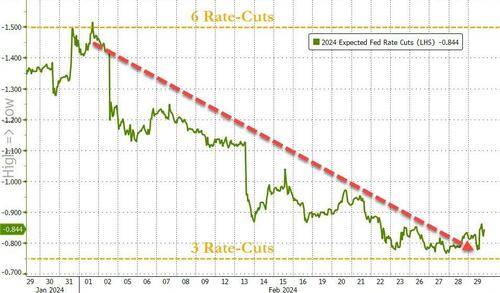

New York Fed President John Williams said Wednesday the central bank has “a ways to go,” in its battle against inflation and Atlanta Fed chief Raphael Bostic urged patience in regard to policy tweaks. Meanwhile, traders are currently pricing around 80 basis points of easing by year-end — almost in line with what officials in December indicated as the likeliest outcome. That would equate to three cuts in 2024 — as the Fed moves have historically been increments of 25 basis points. To put things in perspective, swaps were projecting almost 150 basis points of cuts this year at the start of February.

“Fedspeak and economic data so far this week suggest that central bankers remain data-dependent, which raises volatility around key economic data releases, and that inflation seems to be re-accelerating in the short term, which may make it harder to reach the 2% inflation goal,” Kathleen Brooks, research director at XTB, wrote in a note.

European stocks fluctuated during another crowded day on the earnings calendar as traders reduced bets on how fast and far the European Central Bank will lower interest rates this year after a flurry of inflation readings from the region. Moncler SpA rallied after the Italian luxury company beat profit expectations. Air France-KLM slumped after a fourth-quarter loss. The Stoxx 600 added 0.1% with construction, media and retail shares the best performers. Here are the most notable movers:

- Haleon rises as much as 9%, the most since Dec. 2022, after delivering results that were better than feared, following the weak numbers posted by rival Reckitt yesterday

- Universal Music Group gains as much as 6.5%, the most since July, after the Amsterdam-listed music and entertainment group impressed with its fourth-quarter earnings

- Moncler shares rise as much as 6.3%, to the highest since June, after the Italian luxury company reported results that beat estimates

- Eiffage gains as much as 5.4%, the most since March 2022, as Morgan Stanley flags the infrastructure company’s strong cash generation and in-line earnings performance

- AMS-Osram shares plunge 45% after a major customer — believed by analysts to be Apple — canceled the Swiss chipmaker’s key project around microLED

- Howden Joinery rises as much as 8.5%, the most since Dec. 2020, after 2023 results broadly met estimates

- Drax climbs as much as 8.6% after the UK renewable energy company’s results, which analysts say look solid. Morgan Stanley highlights Drax’s long-term guidance and positive impact

- Argenx falls as much as 4.5% after it reported full-year results that analysts said weren’t surprising

- Beiersdorf shares fall as much as 6.1%, their steepest drop since May 2022, after the Nivea maker reported results that RBC described as “disappointing”

- Technip Energies shares reverse an earlier gain to slip as much as 3.6%, after the France-based engineering and technology company posted a 2023 Ebit beat but issued guidance that missed

In FX, the dollar steadied, while the yen was the best-performing G-10 currency, rising 0.4% versus the greenback, the most in more than a week, after Bank of Japan Board Member Hajime Takata sent one of the strongest signals yet that the end is near for its negative interest rate policy.

In rates, Treasury yields rose, with the more policy sensitive two-year note up five basis points. 10-year TSY yields last traded around 4.31% near session high, outperforming gilts by around 3bp in the sector; the UK curve cheaper on the day by as much as 7bp in 5-year sector. Yields in Europe climbed after mixed readings on price pressures from France and Spain, with German inflation coming in on the softer side of expectations (CPI printed 0.4% MoM, vs exp. 0.5%, and 2.5% YoY, vs exp 2.6%). Traders reduced bets on how fast and far the European Central Bank will lower interest rates this year after a flurry of inflation readings from the region – Bloomberg Economics still expect euro-area headline inflation to slow on Friday. Short-end bonds are leading a selloff in European government debt. German two-year yields rise 7bps to 2.99%. IG dollar issuance slate empty so far; seven names priced $14.4b Wednesday, taking weekly volume past $50b; issuers paid about 6bps in new-issue concessions on order books said to be 3.8x oversubscribed. Robust calendar could materialize Thursday if inflation readings are benign. US January personal income and spending data at 8:30am New York time include PCE inflation gauge with potential to alter corresponding outlook for Fed.

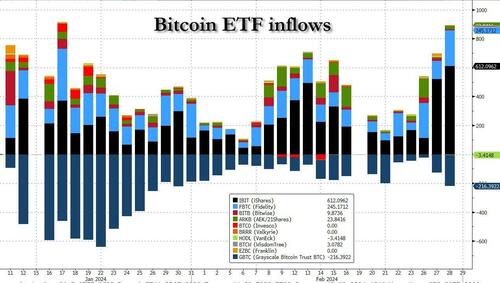

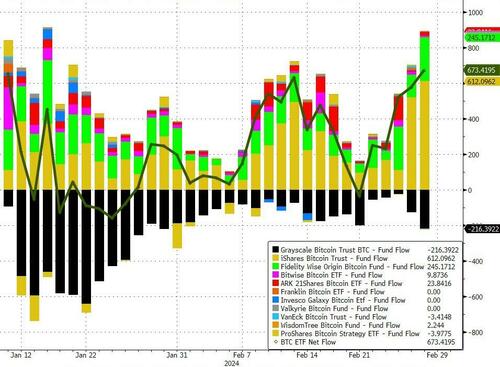

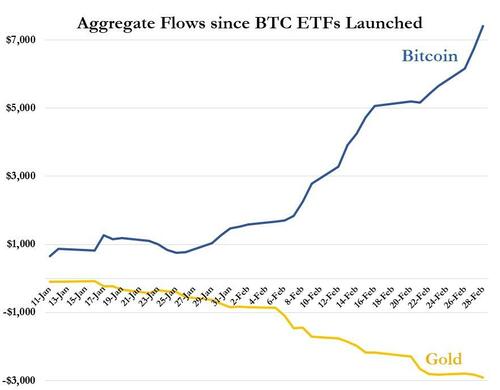

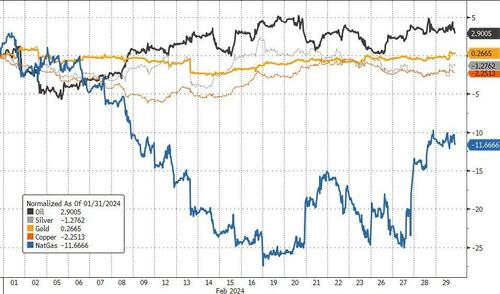

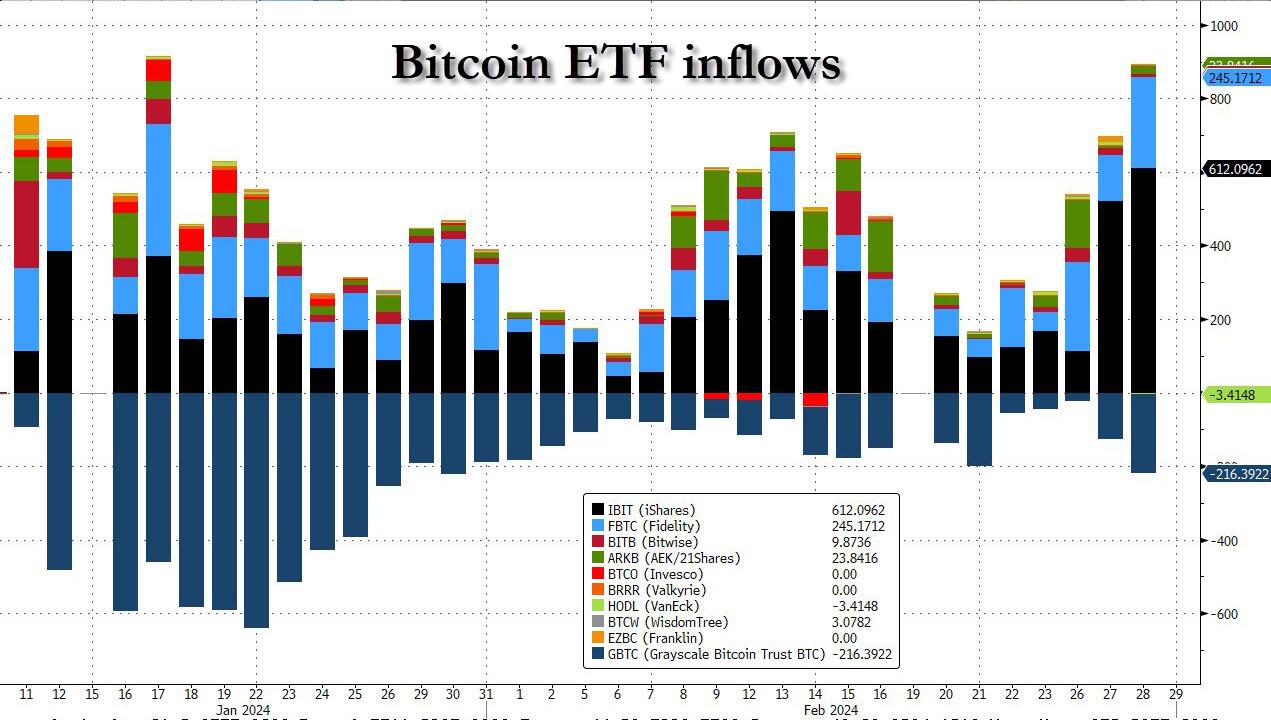

In commodities, oil prices are little changed, with WTI trading near $78.50. Spot gold falls 0.2%. Bitcoin jumps ~3% and is above $62,000.

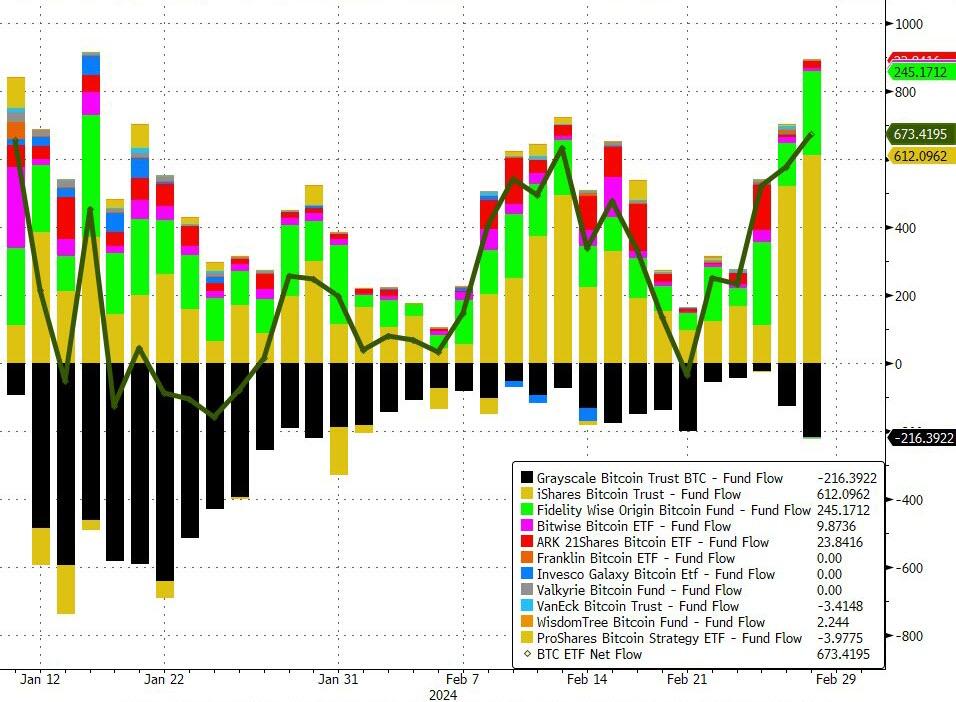

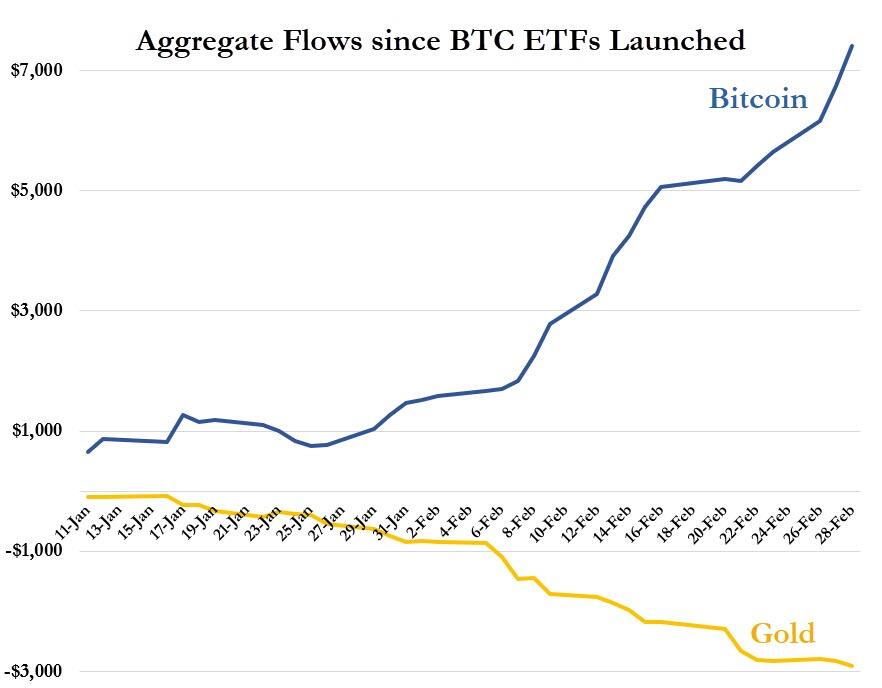

Bitcoin continues to march higher and back above the $62k level, after it was revealed that yesterday’s record volume surge across the ETF sector led to a record net inflows as demand for crypto just won’t slow. Meanwhile, Ether continues to outperform, printing a peak incrementally above USD 3.5k. Elsewhere, Coinbase said all services on Coinbase.com have been restored; after some users reported a zero balance on their accounts.

Looking to the day ahead now, the US economic data calendar includes weekly jobless claims (8:30am), February MNI Chicago PMI (9:45am, three minutes earlier to subscribers), January pending home sales (10am) and February Kansas City Fed manufacturing activity (11am). Fed speakers scheduled include Bostic (10:50am), Goolsbee (11am), Mester (1:15pm, 3:30pm) and Williams (8:10pm). Elsewhere, there’s the February flash CPI inflation prints from Germany and France, along with German unemployment for February, UK mortgage approvals for January, and Canada’s Q4 GDP. From central banks, we’ll hear from the Fed’s Bostic, Goolsbee, Mester and Williams.

Market Snapshot

- S&P 500 futures down 0.3% to 5,065.00

- STOXX Europe 600 little changed at 495.04

- MXAP up 0.4% to 172.73

- MXAPJ up 0.2% to 524.61

- Nikkei down 0.1% to 39,166.19

- Topix little changed at 2,675.73

- Hang Seng Index down 0.2% to 16,511.44

- Shanghai Composite up 1.9% to 3,015.17

- Sensex little changed at 72,263.43

- Australia S&P/ASX 200 up 0.5% to 7,698.70

- Kospi down 0.4% to 2,642.36

- German 10Y yield little changed at 2.49%

- Euro little changed at $1.0847

- Brent Futures down 0.4% to $83.32/bbl

- Gold spot up 0.0% to $2,035.55

- U.S. Dollar Index down 0.16% to 103.81

Top Overnight News

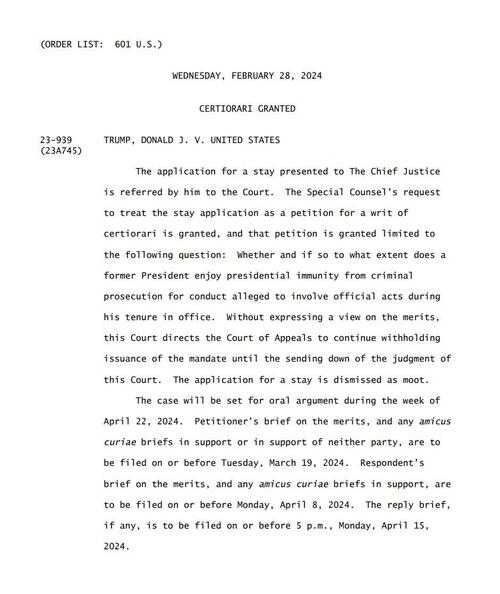

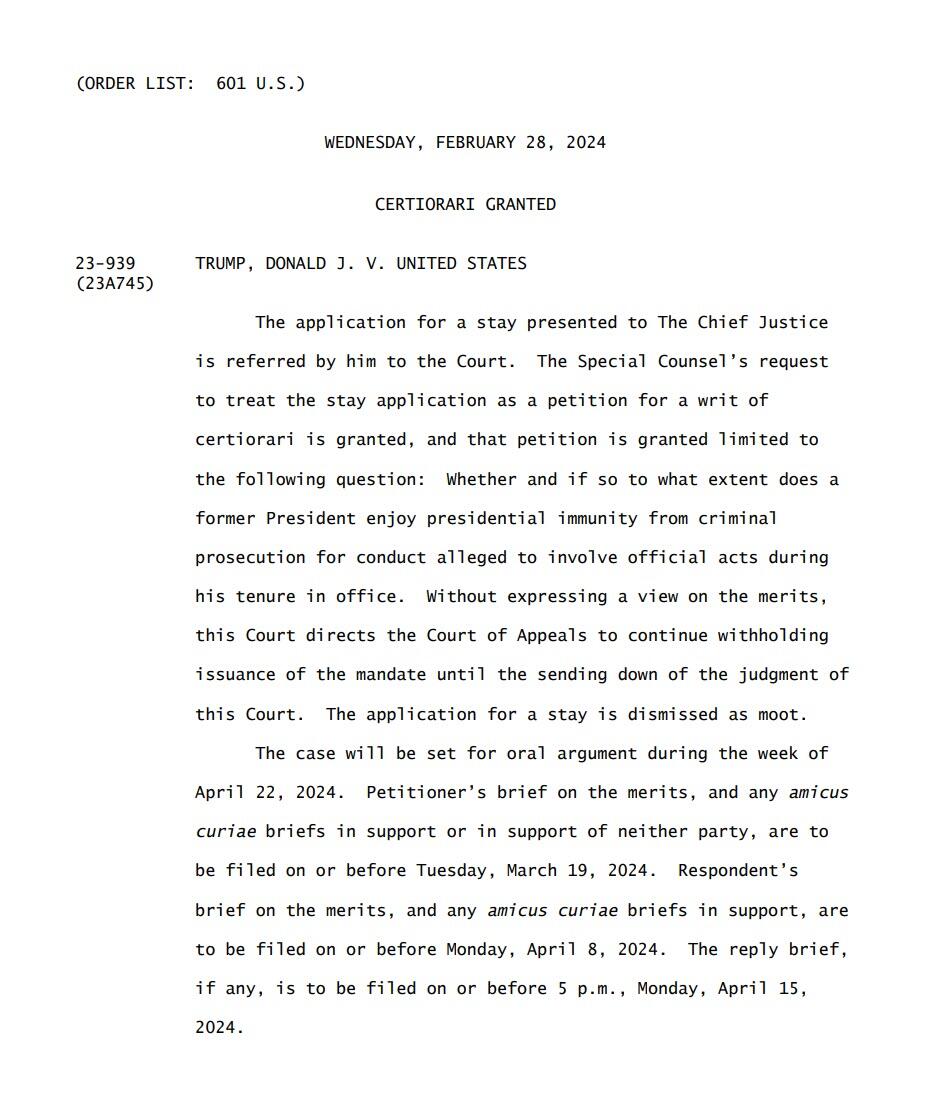

- The Supreme Court’s decision to take up Donald Trump’s bid for immunity from criminal prosecution raises the prospect that a trial to hold him accountable for trying to overturn the 2020 election could face a lengthy delay — potentially until after the November election

- An Illinois judge barred Trump from appearing on the Republican presidential primary ballot, marking the third state to impose such a ban on the former president for his role in the insurrection at the US Capitol on Jan 6.

- Ben Bernanke’s global savings glut is drying up. Long-term interest rates worldwide may be heading higher as a result.

- China banned a top-performing quant fund from the stock-index futures market and vowed tighter oversight of high-speed trading, expanding a crackdown on computer-driven investment strategies that some have blamed for exacerbating market turmoil

- Wall Street traders bracing for key inflation data waded through mixed economic figures and remarks from Federal Reserve speakers for clues on the interest-rate outlook.

Earnings

- Covestro (1COV GY) – Q4 (EUR): adj. EBITDA 132mln (exp. 99mln), Revenue 3.35bln (exp. 3.44bln). Decides not to pay a dividend. Expects economic conditions to remain challenging in 2024. Guides Q1 EBITDA 180-280mln (exp. 204mln). Guides initial FY24 EBITDA 1-1.6bln (exp. 1.36bln), Revenue 14-15bln (exp. 14.7bln). Shares +1.8% in European trade

- IAG (IAG LN) – FY (EUR): Revenue 29.5bln (exp. 29.4bln), adj. Net 2.66bln (exp. 2.29bln), adj. Operating 3.5bln (exp. 3.5bln). 92% booked for Q1 and 62% for H1. Positive outlook for 2024, expect to generate significant cashflow throughout the year. Shares +1.2% in European trade

- MTU Aero (MTX GY) – FY23 (EUR): Adj. Revenue 6.3bln (prev. forecast 6.1-6.3bln), Adj. EBIT 818mln (prev. forecast 800mln), Adj. Net Income 594mln (exp. 600mln). Outlook: FY Revenue 7.3-7.5bln, Adj. EBIT margin 12%. Shares -0.5% in European trade

- Snowflake (SNOW) – Q4 2024 (USD): Adj. EPS 0.35 (exp. 0.18), Revenue 774.7mln (exp. 760.4mln); Q1 product revenue view 745-750mln (exp. 769.5mln), FY25 product revenue view 3.25bln (exp. 3.46bln). (Newswires) Shares -22.8% in pre-market trade

- Salesforce (CRM) – Shares slipped by 1.6% in afterhours trade as it provided light guidance for the FY. Q4 adj. EPS 2.29 (exp. 2.26), Q4 revenue USD 9.29bln (exp. 9.22bln). Increases share repurchase authorisation by USD 10bln. Initiated a common stock dividend of USD 0.40/shr. Sees Q1 adj. EPS between USD 2.37-2.39 (exp. 2.20), and Q1 revenue between USD 9.12bln-9.19bln (exp. 9.19bln); sees FY25 revenue between USD 37.7bln-38.0bln (exp. 38.6bln). Shares -1.8% in pre-market trade

A more detailed look at global markets courtesy of Newsquawk

APAC stocks were choppy at month-end after the lacklustre handover from the US ahead of PCE price data. ASX 200 eventually shrugged off the initial indecision and briefly climbed above 7,700 to eke a fresh record high. Nikkei 225 briefly dipped below the 39,000 level amid a firmer currency and hawkish comments from BoJ’s Takata, although the index gradually recovered all of its losses in late trade. Hang Seng and Shanghai Comp. were positive with outperformance in the latter which momentarily reclaimed the 3,000 level amid lower yields and after the PBoC voiced support for Shanghai’s high-level opening up financially, while it was also reported that China is to crack down on illegal activity to maintain market order. Conversely, the gains in Hong Kong were limited with earnings on the radar.

Top Asian News

- US limits the sales of Americans’ data to China and other rivals with President Biden signing an executive order restricting the ability of data brokers to sell sensitive information abroad, according to WSJ.

- BoJ Board Member Takata said Japan’s economy is at an inflexion point of changing the ‘norm’ that people think wages and prices are not rising, while he added achievement of the price target is coming into sight despite the uncertainty of the economic outlook. Takata also said need to consider taking a flexible response including exit from monetary stimulus and that momentum is rising in this spring’s wage talks with many companies offering higher-than-2023 wage hikes. BoJ Board Member Takata later stated that he would call for a gear shift in policy and not go backwards but added he has not made up his mind yet on a monetary policy decision when asked about whether to end negative interest rates in March or April, while he is not thinking of raising interest rates one after another and said gradual steps will be needed amid mixed circumstances surrounding small firms.

- RBNZ Governor Orr said as aggregate demand has slowed, it has been harder to pass on cost increases and he is confident the current level of the OCR is restricting demand, while the inflation outlook is very balanced. Orr said the economy has developed as they expected and the latest data confirmed inflation is slowing, while he added the easing of interest rates won’t happen anytime soon.

European bourses, Stoxx600 (+0.1%) are mixed and trade has remained rangebound throughout the session; the DAX 40 (+0.4%) outperforms, and continues to trade towards/at ATHs. European sectors are mixed; Construction & Materials takes the top spot, lifted by gains in CRH (+7.3%) post-earnings. Tech is found at the bottom of the pile, with many of the chip names continuing to underperform. US Equity Futures (ES -0.3%, NQ -0.3%, RTY +0.1%) are mostly lower, with trade continuing the downbeat price action seen in the prior session. In terms of individual movers, Salesforce (-1.9%) slipped on its results, which although reported strong metrics, its FY25 guidance missed analyst expectations.

Top European News

- ECB’s Vasle said the ECB is looking at a rate-cutting phase if there are no big surprises and the timing of cuts depends on inflation.

- ECB will continue to put a ‘floor’ underneath market interest rates in the years ahead, though banks will have a greater role in determining how much liquidity they want, via Reuters citing sources.

- UK appoints Clare Lombardelli as the the next BoE Deputy Governor for monetary policy; replaces Broadbent who leaves at the end of June.

- ECB’s Holzmann says a serious discussion at the ECB on rate reductions is unlikely before June, via Politico [published Feb. 28th]

FX

- DXY is a touch softer as a by-product of JPY strength. DXY has ventured to a low of 103.75, stopping shy of the 200DMA at 103.69 and yesterday’s low at 103.60. The fate for the index today will almost certainly be determined by US PCE metrics.

- EUR marginally gains vs. the USD amid a slew of EZ data with (on balance) firmer regional CPIs taking focus ahead of tomorrow’s EZ-wide metrics. EUR/USD mounted yesterday’s best at 1.0840.

- JPY is the standout outperformer across the majors following “hawkish” BoJ comments overnight. This has given JPY some reprieve with USD/JPY pulling back to a low of 149.62 (matches 21DMA) from a high of 150.69. A hot core PCE release could reverse the pair’s fortunes and bring attention back to the YTD peak at 150.88.

- Differing fortunes for the antipodes with AUD/USD back on a 0.65 handle after bottoming out yesterday at 0.6488 post-USD strength. NZD/USD remains above yesterday’s 0.6082 trough but is unable to reclaim 0.61 status.

- PBoC set USD/CNY mid-point at 7.1036 vs exp. 7.1938 (prev. 7.1075).

Fixed Income

- The bearish narrative continues for Bunds; French CPI sparked some initial downside, though further hotter-than-expected releases from Spain and Germany (state), firmly guided the hawkish direction. Bunds have been drifting lower and are now at a fresh YTD low at 131.62, with the 10yr yield above 2.5%.

- USTs are driven by EGBs so far but also potentially positioning into the US January PCE data, which will be gauged to see if it conforms to the hotter narrative of other January pricing metrics; currently holds just above 110-00.

- Gilt price action conformed with EGBs into the latest BoE mortgage data with no reaction to the numbers despite lending and approvals printing below/above their respective forecast ranges. EGB-driven action has similarly pushed Gilts to a fresh YTD low at 96.83.

Commodities

- Crude benchmarks are under modest pressure but are comparably contained when judged against Wednesday’s whipsaw price action; currently holds around the USD 82/bbl mark.

- Spot gold is incrementally softer initially benefitting from a weaker Dollar, though now off best levels; USD 2032/oz 50-DMA remains untested with the current low at USD 2034/oz.

- Base metals are bid and deriving support from USD downside, the overall European risk tone and strength in China.

Geopolitics

- Japan’s top currency diplomat Kanda said using frozen Russian assets for Ukraine must be based on international law and he thinks EU’s proposal is along those lines, while he added that Japan strongly condemned Russia’s invasion of Ukraine at the G20 and that the G7 discussed ways to make use of frozen Russian assets for Ukraine reconstruction.

- Russian President Putin says “don’t they understand there is danger of nuclear conflict?”; on talk of NATO troops in Ukraine, says consequences for the intruders will be more tragic and we have weapon which is able to hit targets on their territory.

- Ukraine sees a risk of Russia breaking through its defences by the summer unless allies increase supplies of ammunition, according to Bloomberg sources

US Event Calendar

- 08:30: Feb. Initial Jobless Claims, est. 210,000, prior 201,000

- Feb. Continuing Claims, est. 1.87m, prior 1.86m

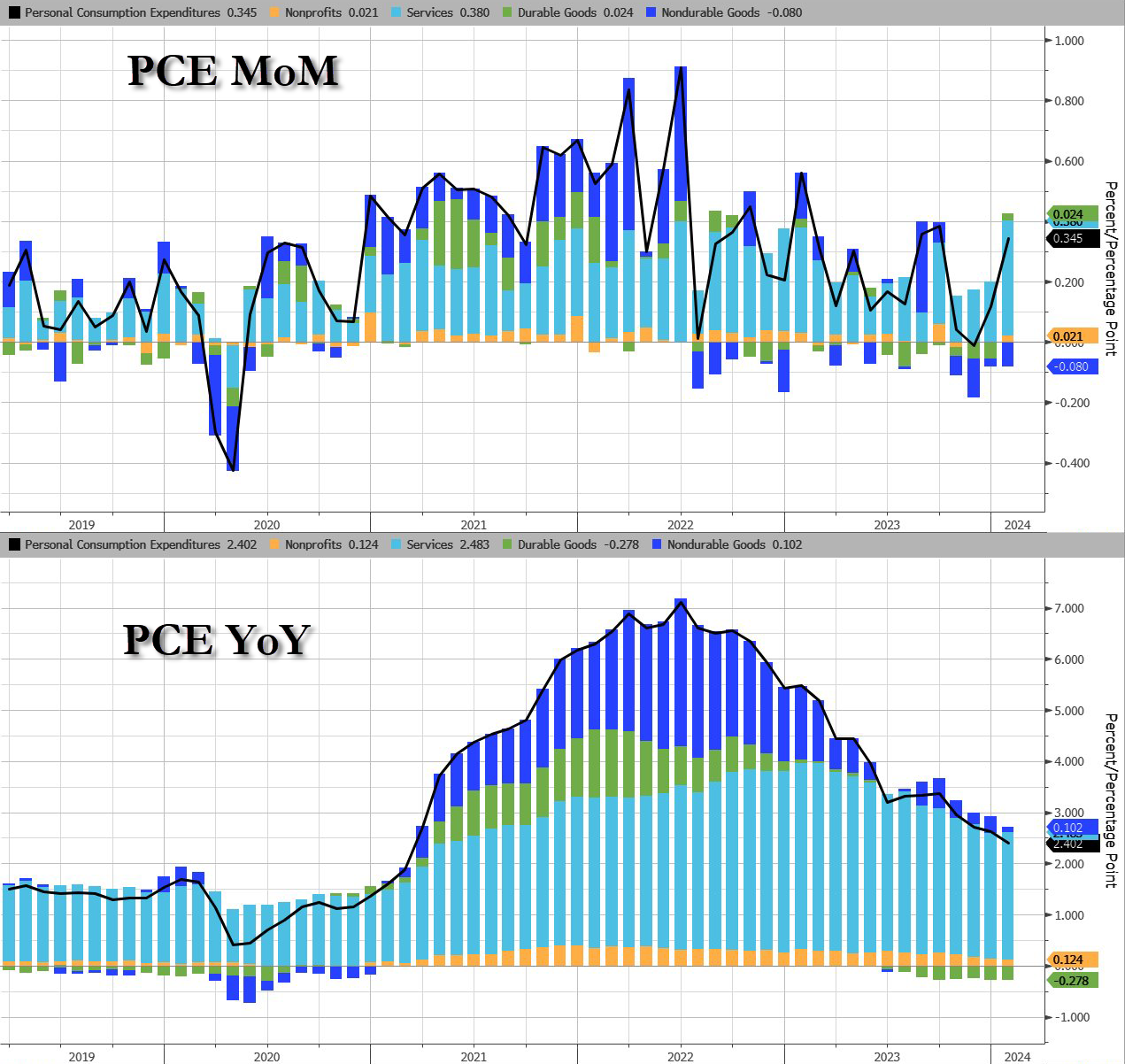

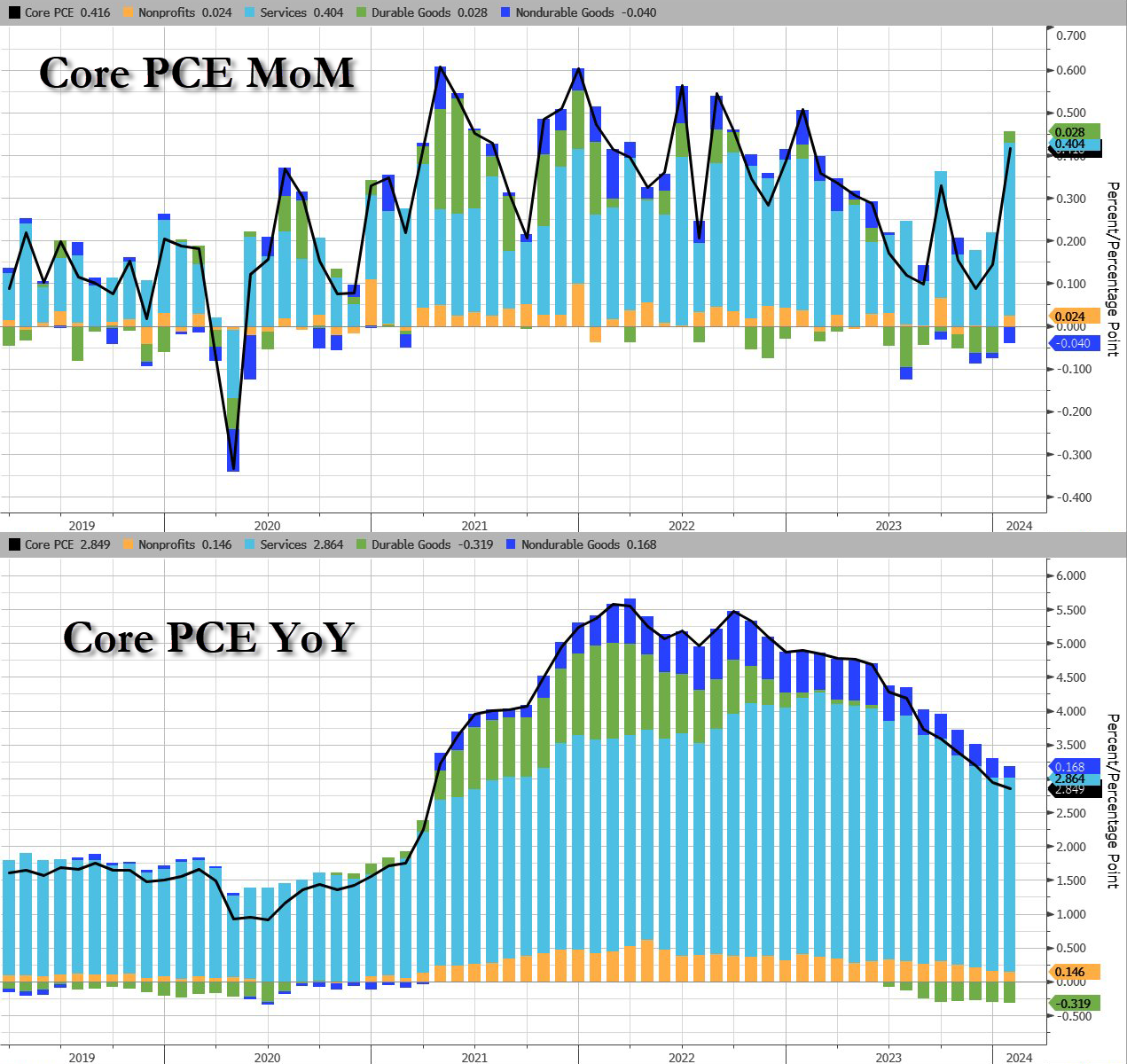

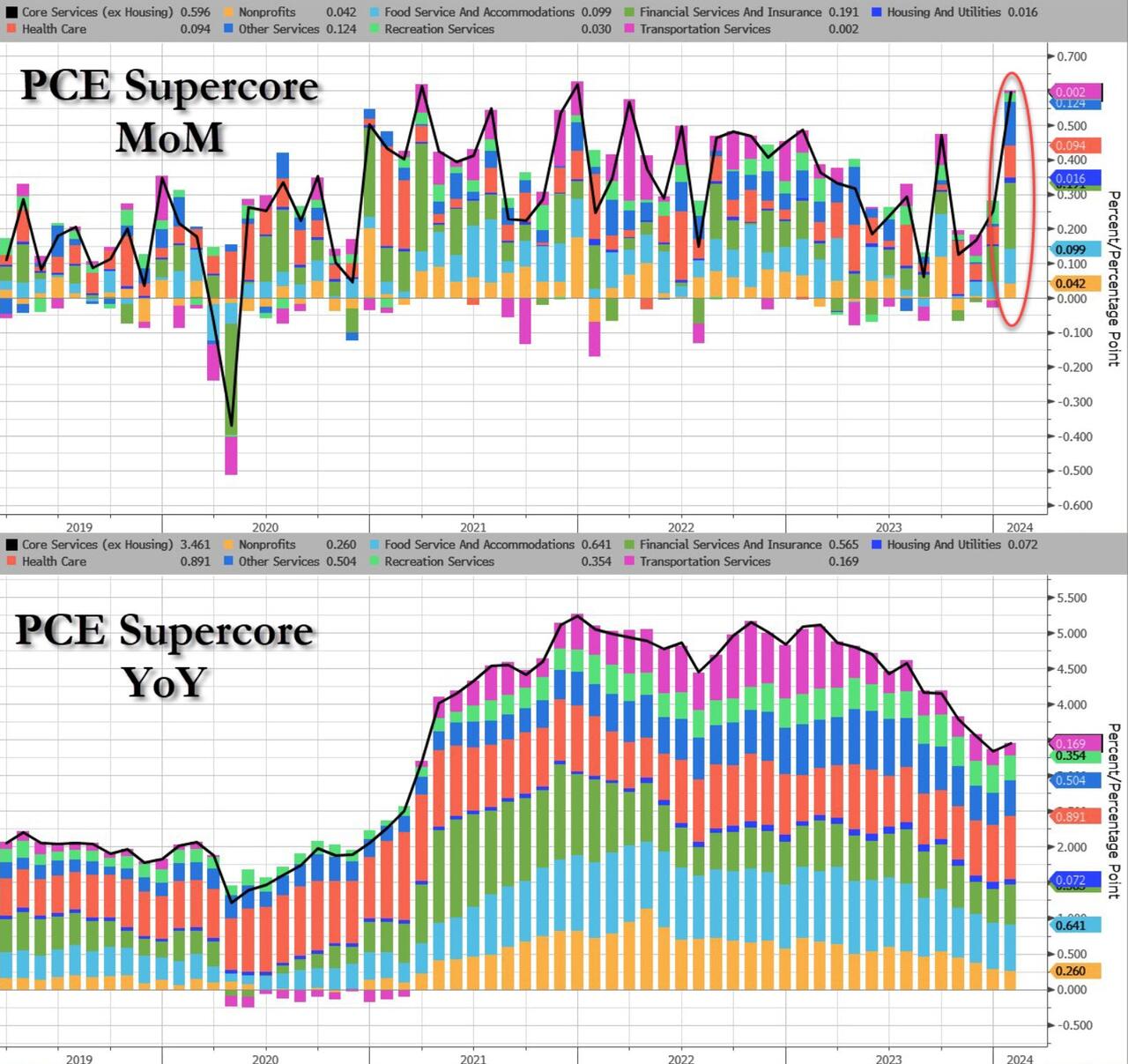

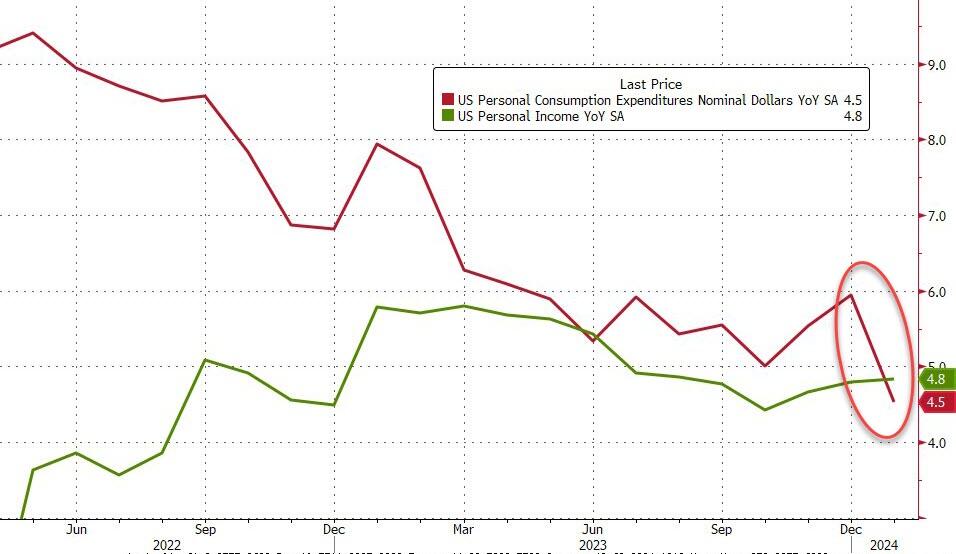

- 08:30: Jan. Personal Income, est. 0.4%, prior 0.3%

- Jan. Personal Spending, est. 0.2%, prior 0.7%

- Jan. Real Personal Spending, est. -0.1%, prior 0.5%

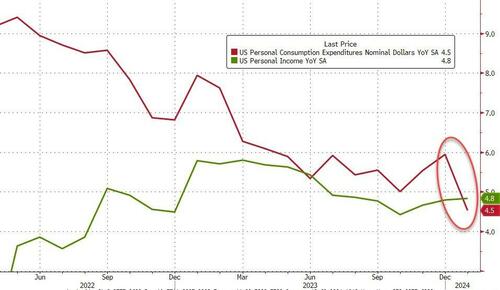

- 08:30: Jan. PCE Deflator MoM, est. 0.3%, prior 0.2%

- Jan. PCE Core Deflator YoY, est. 2.8%, prior 2.9%

- Jan. PCE Core Deflator MoM, est. 0.4%, prior 0.2%

- Jan. PCE Deflator YoY, est. 2.4%, prior 2.6%

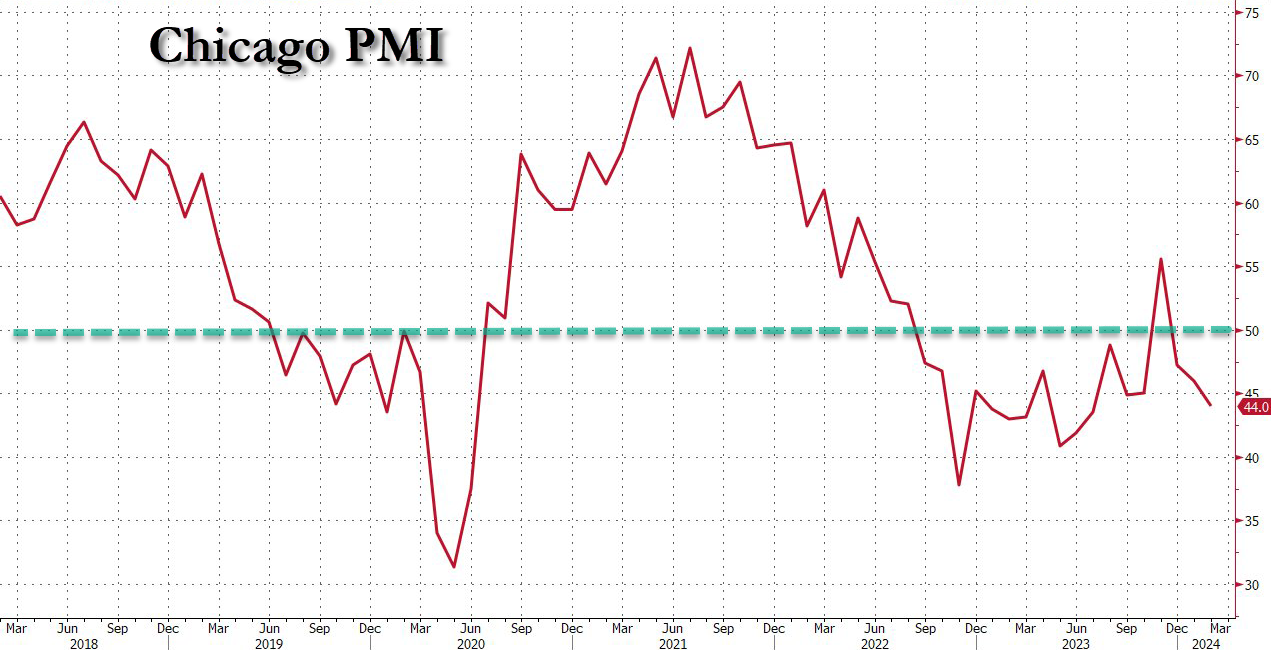

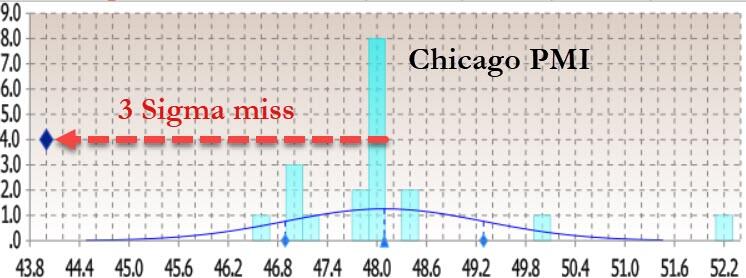

- 09:45: Feb. MNI Chicago PMI, est. 48.0, prior 46.0

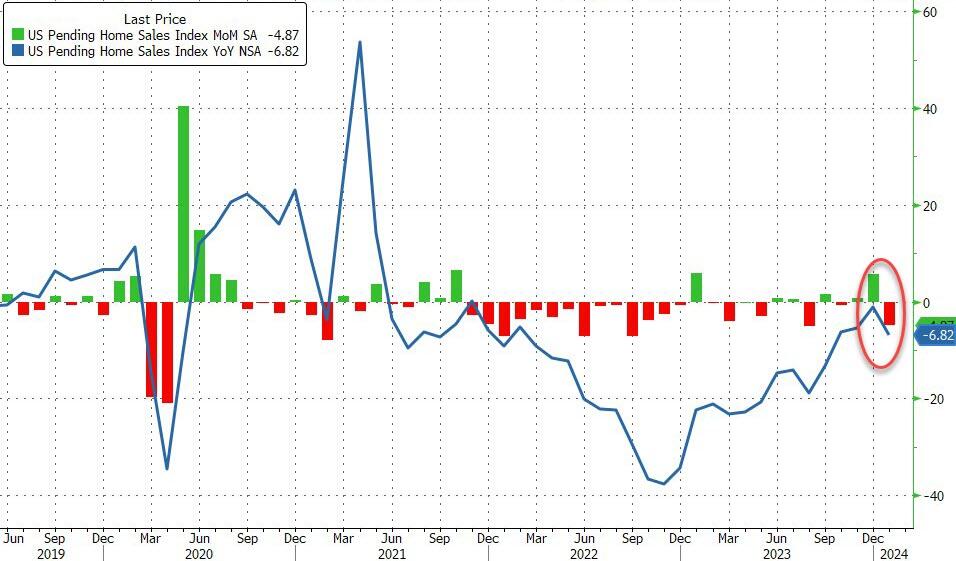

- 10:00: Jan. Pending Home Sales (MoM), est. 1.5%, prior 8.3%

- Jan. Pending Home Sales YoY, est. -4.4%, prior -1.0%

- 11:00: Feb. Kansas City Fed Manf. Activity, est. -2, prior -9

Central Bank Speakers

- 10:50: Fed’s Bostic Participates in Fireside Chat

- 11:00: Fed’s Goolsbee Gives Remarks on Monetary Policy

- 13:15: Fed’s Mester Speaks on Financial Stability and Regulation

- 15:30: Fed’s Mester Speaks to Yahoo Finance

- 20:10: Fed’s Williams Participates in Moderated Discussion

DB’s Jim Reid concludes the overnight wrap

Happy February 29. I’m hearing lots about how this day happens every four years, but strictly speaking that’s not true. The rule is it’s a leap year if it’s divisible by 4, unless it’s divisible by 100, but not if it’s also divisible by 400. Make sense? So 1700, 1800 and 1900 weren’t leap years, 2000 was a leap year, but 2100 won’t be one. In other words, you get one every 97/400 years rather than 1/4, as the earth’s rotation around the sun is actually a bit less than 365.25 days. This might seem trivial (and you may be right), but the previous Julian calendar hadn’t adjusted for this and had a leap day every four years, hence the shift to the modern Gregorian calendar from the 16th century onwards. But when countries made the adjustment, it meant the date shifted forward. So in Britain, the recorded date went from 2 September 1752 one day to 14 September 1752 on the next, skipping over the 11 calendar days in the middle.

If we missed the next 11 days right now, we’d skip over an awful lot, including the next US jobs report, an array of US primary elections on Super Tuesday, the ECB’s policy decision, Fed Chair Powell’s congressional testimonies, and the UK budget. But today, the main focus will be on the PCE inflation data from the US, which is the measure of inflation that the Fed officially targets, and is therefore closely watched in markets. Readers will remember that a couple of weeks ago, the CPI and PPI inflation reports both surprised on the upside, and the components that feed into the core PCE reading are pointing to a strong print for January. As a result, o ur US economists are expecting core PCE to come in at +0.36% for the month, which if realised would be the strongest monthly print since another +0.36% reading in February last year. So that’s one to look out for as investors seek to gauge the timing of potential rate cuts from the Fed.

Ahead of that, markets in Asia have put in a mixed performance overnight. Chinese equities have advanced, including the CSI 300 (+1.11%) and the Shanghai Comp (+1.00%), and the Shanghai Comp is currently on track to record its best monthly performance since November 2022. But other indices have been more negative, and the Hang Seng is down -0.02%, the Nikkei is down -0.02%, and the KOSPI (-0.49%) has posted larger declines. Futures have also been subdued, with those on the S&P 500 up just +0.05% after yesterday’s decline.

In Japan, sentiment wasn’t helped by the latest industrial production data, which showed a decline of -7.5% in January (vs. -6.8% expected), which is the biggest monthly decline since May 2020. Nevertheless, investors have continued to grow in confidence that the end of the negative interest rate policy could be near, following comments from the BoJ’s Hajime Takata, who said that “my view is that the price target is finally coming into sight”. That’s helped the Japanese Yen to strengthen +0.44% against the US Dollar overnight, whilst 2yr government bond yields are up +2.3bps to 0.18%, which is their highest level since 2011. Moreover, overnight index swaps are now pricing in a 33% chance of a move away from negative interest rates at the next meeting in April, up from 21% the previous day.

Ahead of that yesterday, markets were mostly in a holding pattern, with the S&P 500 (-0.17%) still experiencing little movement since Nvidia’s earnings last week. The latest decline means the index is still on track for a weekly loss, and there were larger falls for the NASDAQ (-0.55%) and the Magnificent 7 (-0.58%). Meanwhile in Europe, the story was also one of losses yesterday, with the STOXX 600 down -0.35%. That said, the DAX (+0.25%) continued to outperform, posting a 6th consecutive advance and closing at a fresh all-time high.

Over on the rates side, the moves were also modest in scope yesterday, though yields did extend moderate declines during the US session. This came even as central bank speakers continued to echo the recent consensus on policy, suggesting that rate cuts are likely to happen over the coming months, but not yet. For instance, Boston Fed President Collins said that it “will likely become appropriate to begin easing policy later this year”, but also that “I want to see more evidence of a sustained trajectory to price stability”. Separately, New York Fed President Williams said that they still had “a ways to go on the journey to sustained 2% inflation”. Meanwhile at the ECB, we heard from Slovakia’s Kazimir, who said in a Reuters interview that for a rate cut, “June would be my preferred date, April would surprise me and March is a no go”. Lithuania’s Simkus made similar comments, saying that “June is really the month to consider the rate cut”. And later in the evening, Germany’s Nagel said that “we can’t make any mistakes in the final stretch of the journey”, suggesting it would be “fatal” if rates were eased too early only for inflation to rebound.

That backdrop saw expectations for rate cuts tick up a little yesterday. For the Fed, investors still expect that June is the most likely meeting for a cut, with futures pricing in a 77% chance of a cut by June (up from 73% the day before). In turn, that helped yields on 2yr Treasuries fell -5.6bps, while 10yr yields were down -3.9bps to 4.265%. Over in Europe the bond rally was more marginal, with yields on 10yr bunds (-0.6bps), OATs (-1.2bps) and BTPs (-1.8bps) all seeing modest declines.