GOLD PRICE CLOSED UP $40.50 TO $2086.40

SILVER PRICE UP $.49 TO $23.17

Gold ACCESS CLOSED 2083.70

Silver ACCESS CLOSED: 23.13

Bitcoin morning price:$62,152 UP 998 DOLLARS.

Bitcoin: afternoon price: $62,543 UP 1388 dollars

Platinum price closing UP $4.20 AT $886.35

Palladium price; UP $11.05 AT $955.15

END

SHANGHAI GOLD PREMIUM 32 DOLLARS/COMEX GOLD

SHANGHAI GOLD (USD) FUTURES – QUOTES

Beginning Monday, April 1, 2024, CME Group settlement data will no longer be accessible through ftp.cmegroup.com and will have a delayed publication time of 12:00 a.m. CT on all cmegroup.com web pages. Learn about alternate ways to access the data in our FAQ.

Last Updated 01 Mar 2024 09:26:45 AM CT.

Market data is delayed by at least 10 minutes.

SHANGHAI GOLD (USD) FUTURES – QUOTES

I will now provide gold in Canadian dollars, British pounds and Euros

4: 15 PM ACCESS

*CANADIAN GOLD: $2,824.92 UP $49.17 CDN dollars per oz( * NEW ALL TIME HIGH 2,824.92CDN DOLLARS PER OZ//MARCH 1 2023)

*BRITISH GOLD: 1646,16 UP 27.26 pounds per oz// *(NEW ALL TIME HIGH//CLOSING///1655.17 BRITISH POUNDS/OZ) OCT 2/2023

*EURO GOLD: 1923,03 UP 31.19 euros per oz //* (ALL TIME CLOSING HIGH: 1923.03 EUROS PER OZ//MARCH 1.2023)

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

EXCHANGE: COMEX

ACCESS MARKET:

EXCHANGE: COMEX

CONTRACT: MARCH 2024 COMEX 100 GOLD FUTURES

SETTLEMENT: 2,045.700000000 USD

INTENT DATE: 02/29/2024 DELIVERY DATE: 03/04/2024

FIRM ORG FIRM NAME ISSUED STOPPED

092 C DEUTSCHE BANK 1

190 H BMO CAPITAL 10

323 C HSBC 4

363 H WELLS FARGO SEC 9

435 H SCOTIA CAPITAL 3

661 C JP MORGAN 9

690 C ABN AMRO 7

737 C ADVANTAGE 31 2

TOTAL: 38 38

JPMorgan stopped 9/38 contracts.

FOR FEB/2024

GOLD: NUMBER OF NOTICES FILED FOR MAR/2024. CONTRACT: 38 NOTICES FOR 3800 OZ or 0.1182 TONNES

total notices so far: 1185 contracts for 118500 Oz (3.685 tonnes)

FOR MARCH:

SILVER NOTICES: 89 NOTICE(S) FILED FOR 445,000 OZ/

total number of notices filed so far this month : 2947 for 14,735,000 oz

XXXXXXXXXXXXXXXXXX

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

BOTH GLD AND SLV ARE FRAUDULENT VEHICLES//THEY ARE NOW RAIDING GLD AND SLV FOR PHYSICAL

GLD

WITH GOLD UP $40.50//

INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD/ : NO CHANGES IN GOLD INVENTORY AT THE GLD:

INVENTORY RESTS AT 822.91 TONNES

SLV//

WITH NO SILVER AROUND AND SILVER UP 49 CENTS AT THE SLV//

NO CHANGES IN SILVER INVENTORY AT THE SLV:

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV.

CLOSING INVENTORY: 430.982 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A HUMONGOUS SIZED 3659 CONTRACTS TO 142,561 AND FURTHER FROM THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THIS HUGE SIZED LOSS IN COMEX OI WAS ACCOMPLISHED DESPITE OUR RISE IN PRICE OF $0.25 IN SILVER PRICING AT THE COMEX ON THURSDAY. WE HAD ZERO LONG LIQUIDATION AT THE COMEX SESSION WITH AGAIN SOME SHORT COVERING DESPITE THE PRICE OF SILVER RISING BY A CONSIDERABLE AMOUNT. WE HAD A STRONG 666 T.A.S ISSUANCE AND THESE WILL BE USED FOR MANIPULATION LATER THIS MONTH/AS WELL AS TODAY. PLEASE NOTE THAT THE CROOKS NEED A HIGHER SILVER T.A.S. TO CARRY ON THEIR CROOKED MANIPULATION ON A DAILY BASIS

CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON THURSDAY NIGHT: 666 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS. IT THUS LOOKS LIKE THE FED (GOV’T) IS BEHIND ALL OF THESE TRADES.

WE HAVE NOW SET ANOTHER RECORD LOW AT 114,102 CONTRACTS ///JULY 3.2023// OUR BANKERS WITH THE HELP OF SPECULATORS AND HIGH FREQUENCY TRADERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.25),AND WERE UNSUCCESSFUL IN KNOCKING ANY SILVER LONGS AS DESPITE WE HAD A MEGA HUMONGOUS SIZED LOSS OF 3454 CONTRACTS ON OUR TWO EXCHANGES, IT OCCURRED WITH A MUCH HIGHER PRICE.

WE MUST HAVE HAD:

A SMALL SIZED 200 ISSUANCE OF EXCHANGE FOR PHYSICALS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 22.270 MILLION OZ (FIRST DAY NOTICE) FOLLOWED BY TODAY,S 480,000 OZ E.F.P. JUMP TO LONDON//NEW TOTALS : 21.790 MILLLION OZ

//NEW STANDING FOR SILVER IS THUS 21.790 MILLION OZ

/ HUGE SIZED COMEX OI LOSS/STRONG SIZED EFP ISSUANCE/ VI) HUGE SIZED NUMBER OF T.A.S. CONTRACT ISSUANCE 666 CONTRACTS)/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL -REMOVED A HUGE 497 CONTRACTS //

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS FEB. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF FEB

TOTAL CONTRACTS for 1 days, total 200 contracts: OR 1.00 MILLION OZ (200 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 1.0 MILLION OZ

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH 2022: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 118.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 85.745 MILLION OZ (SMALLER THAN LAST MONTH)

AUGUST: 171.43 MILLION OZ (THIS MONTH IS GOING TO BE HUGE //2ND HIGHEST ON RECORD

SEPT: 72.705 MILLION OZ (SMALLER THIS MONTH)

OCT: 97.455 MILLION OZ

NOV. 50.050 MILLION OZ

DEC. 66.140 MILLION OZ//

TOTAL 2023: 1,104.10 MILLION OZ/

JAN ’24 : 78.655 MILLION OZ//

FEB /2024 : 66.135 MILLION OZ./FINAL

MARCH: 1.0 MILLION OZ//

RESULT: WE HAD A HUGE SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 3654 CONTRACTS DESPITE OUR GAIN IN PRICE OF SILVER PRICING AT THE COMEX//THURSDAY.,. THE CME NOTIFIED US THAT WE HAD A SMALL EFP ISSUANCE CONTRACTS: 200 ISSUED FOR MAY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS. WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR MARCH. OF 22.270 MILLION OZ ON FIRST DAY NOTICE FOLLOWED BY TODAY’S 480,000 OZ E.F.P. JUMP TO LONDON/

//NEW TOTAL STANDING LOWERS TO 21.790 MILLION OZ

WE HAVE A MEGA HUMONGOUS LOSS OF 3454 OI CONTRACTS ON THE TWO EXCHANGES DESPITE THE STRONG GAIN IN PRICE. THE TOTAL OF TAS INITIATED CONTRACTS TODAY: A STRONG SIZED 666 CONTRACTS//HUGE FRONT END OF THE TAS CONTRACTS WERE LIQUIDATED DURING THE THURSDAY COMEX SESSION/// WITH MAJOR SHORT COVERING FROM OUR SPEC SHORTS ( WITH PRICE OF SILVER RISING) . THE NEW TAS ISSUANCE THURSDAY NIGHT (666) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE//PROBABLY TODAY., .

WE HAD 89 NOTICE(S) FILED TODAY FOR .445 MILLION OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A HUGE SIZED 12,393 CONTRACTS TO 424,082 AND CLOSER TO THE RECORD (SET JAN 24/2020) AT 799,733 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110, BUT WE ARE NOW CLOSER TO OUR ALL TIME LOW OF 390,000 CONTRACTS.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: removed 134 CONTRACTS

WE HAD A HUGE SIZED INCREASE IN COMEX OI ( 12,527 CONTRACTS) WITH OUR $12.60 GAIN IN PRICE//THURSDAY. WE ALSO HAD A RATHER LARGE INITIAL STANDING IN GOLD TONNAGE FOR MARCH. AT 10.270 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’;S SMALL 200 OZ QUEUE JUMP

NEW TOTAL Of INITIAL GOLD STANDING TO: 10.363 TONNES // ALL OF THIS HAPPENED WITH OUR $12.60 GAIN IN PRICE WITH RESPECT TO THURSDAY’S TRADING. WE HAD A HUMONGOUS SIZED GAIN OF 16,903 OI CONTRACTS (52.57) PAPER TONNES) ON OUR TWO EXCHANGES.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 4510 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 424,082

IN ESSENCE WE HAVE A HUMONGOUS SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 16,903 CONTRACTS WITH 12,393 CONTRACTS INCREASED AT THE COMEX// AND A STRONG SIZED 4510 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 16,903 CONTRACTS.. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): GOOD SIZED 3158 CONTRACTS.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD STRONG SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (4510 CONTRACTS) ACCOMPANYING THE HUGE SIZED GAIN IN COMEX OI (12,393) //TOTAL GAIN FOR OUR THE TWO EXCHANGES: 16,903 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR FORMER FORMAT OF BANKERS GOING LONG AND SPECULATORS GOING SHORT ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR MARCH. AT 10.270 TONNES

/ 3) ZERO LONG LIQUIDATION // 4) HUGE SIZED COMEX OPEN INTEREST GAIN/ 5) STRONG ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER///6: STRONG T.A.S. ISSUANCE: 3158 CONTRACTS//CONSIDERABLE SHORT COVERING AGAIN

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023-2024 INCLUDING TODAY

MARCH

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF MARCH. :

TOTAL EFP CONTRACTS ISSUED: 4510 CONTRACTS OR 451,000 OZ OR 14.027 TONNES IN 1 TRADING DAY(S) AND THUS AVERAGING: 4510 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 1 TRADING DAY(S) IN TONNES 14.027 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2022, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 14.027/3550 x 100% TONNES 0.399% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2023

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH/2022: 409.30 TONNES //FINAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 151.69 TONNES (WEAKER THAN LAST MONTH)

AUGUST: 195.28 TONNES (A STRONGER MONTH)//FINAL

SEPT: 254.709 TONNES (WILL BE LARGER THAN LAST MONTH AND A STRONG MONTH)

OCT. 248.09 TONNES. LIKE SILVER, THIS MONTH IS GOING TO BE A STRONG E.F.P. ISSUANCE.

NOV. 239.16 TONNES//WILL BE STRONG THIS MONTH,

DEC. 213.704 TONNES. A STRONG MONTH//

TOTAL FOR YEAR 2023: 2,569.57 TONNES VS 2578 TONNES LAST YEAR

JAN ’24: 291.76 TONNES (WILL BE MUCH GREATER THAN LAST MONTH.//3RD HIGHEST EVER RECORDED EX FOR PHYSICAL)

FEB’24: 201.947 TONNES (SHOULD BE A WEAKER ISSUANCE MONTH)

MARCH 2024: 14.027 TONNES

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF FEB. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (FEB), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER FELL BY A HUGE SIZED 3654 CONTRACTS OI TO 143,358 AND CLOSER TO THE COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 6 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 200 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAY 600 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 200 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 3157 CONTRACTS AND ADD TO THE 200 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A HUMONGOUS SIZED LOSS OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 3454 CONTRACTS

THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES TOTAL 17.270 MILLION OZ

OCCURRED DESPITE OUR $.25 GAIN IN PRICE …..

END

OUTLINE FOR TODAY’S COMMENTARY

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

b, ) Gold/silver trading overnight Europe,//GOLD COMMENTARIES

(Peter Schiff)

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS//

FRIDAY MORNING/THURSDAY NIGHT

SHANGHAI CLOSED UP 11.85 PTS OR 0.39% //Hang Seng CLOSED UP 78.00 PTS OR 0.47% / Nikkei CLOSED UP 744.63 PTS OR 1.90%//Australia’s all ordinaries CLOSED UP 0.60% /Chinese yuan (ONSHORE) closed DOWN 7.1985 //OFFSHORE CHINESE YUAN CLOSED DOWN TO 7.2130 /Oil UP TO 79.53 dollars per barrel for WTI and BRENT UP AT 83.09/ Stocks in Europe OPENED ALL GREEN// ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE YUAN WEAKER

A)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

9. USA

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A HUGE SIZED 12,393 CONTRACTS TO 424,082 WITH OUR GAIN IN PRICE OF $12.60 WITH RESPECT TO THURSDAY TRADING. ACCORDING TO OUR EXPERT ANDREW MAGUIRE, THE LOW COMEX GOLD OI WE HAVE BEEN EXPERIENCING THESE PAST TWO MONTHS WAS DUE TO THE CRIMINAL BANKS LEAVING THE GOLD ARENA AND USING THEIR “SKILLS” ON THE NEW FUTURES OF BITCOIN. WITH CENTRAL BANK BUYING PHYSICAL GOLD IN RECORD NUMBERS, IT WOULD BE FUTILE TRYING TO SELL NAKED CALLS AGAINST GOLD AS CB’S WOULD JUST TURN AROUND AND TAKE DELIVERY. TODAY WE HAD NEWBIE SPECULATORS JOIN IN ON THE LONG SIDE OF GOLD.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE NON ACTIVE DELIVERY MONTH OF MARCH..… THE CME REPORTS THAT THE BANKERS ISSUED A STRONG SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 4510 EFP CONTRACTS WERE ISSUED: : APRIL 4510 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 4510 CONTRACTS

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A HUMONGOUS SIZED TOTAL OF 16,903 CONTRACTS IN THAT 4510 LONGS WERE TRANSFERRED AS EXCHANGE FOR PHYSICALS TO LONDON AND WE HAD A HUGE SIZED GAIN OF 12,393 COMEX CONTRACTS..AND THIS GAIN ON OUR TWO EXCHANGES HAPPENED WITH OUR GAIN IN PRICE OF $12.60 THURSDAY COMEX. AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS DURING MID MONTH IN THE DELIVERY CYCLE), THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR THURSDAY NIGHT WAS A GOOD SIZED 3158 CONTRACTS. THROUGHOUT THE PAST SEVERAL WEEKS, THE BANKERS SOLD OFF THE LONG SIDE OF THE SPREAD WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR/T.A.S. SPREAD WHICH WILL BE LIQUIDATED IN DAYS HENCE//.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: MARCH (10.363 TONNES) ( NON ACTIVE MONTH)

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 24 MONTHS OF 2021-2023:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

NOV: 18.7122 TONNES + 16.2505 EX. FOR RISK = 34.9627 TONNES

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707TONNES

TOTAL 2023 YEAR : 436.546 TONNES

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276 TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 10.363 TONNES

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT GAINED $12.60 //// AND WERE UNSUCCESSFUL IN KNOCKING ANY SPECULATOR LONGS AS WE HAD A HUMONGOUS SIZED GAIN OF 16,903 TOTAL CONTRACTS ON OUR TWO EXCHANGES WITH OUR HIGHER PRICE. WE HAD TO HAVE HAD ANOTHER HUGE EPISODE OF STRONG SHORT COVERING. WE HAD A GOOD T.A.S. LIQUIDATION ON THE FRONT END OF THURSDAY’S TRADING . THE T.A.S. ISSUED ON THURSDAY NIGHT, WILL BE “PUT INTO THE BANK” TO BE USED AT A LATER DATE AT THE COLLUSIVE CHOOSING OF OUR BANKERS.

WE HAVE GAINED A TOTAL OI OF 52.57 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR MARCH. (10.3576 TONNES) ON FIRST DAY NOTICE FOLLOWED BY TODAY’S SMALL 200 OZ QUEUE JUMP//NEW STANDING 10.363 TONNES

ALL OF THIS WAS ACCOMPLISHED WITH OUR GAIN IN PRICE TO THE TUNE OF $12.60

WE HAD -REMOVED 134 CONTRACTS TO THE COMEX TRADES TO OPEN INTEREST (CROOKS)

NET GAIN ON THE TWO EXCHANGES 16,903 CONTRACTS OR 1,690300 OZ OR 52.57 TONNES.

estimated volume today 354,337 huge

final gold volumes/yesterday 239,834 fair

//speculators have left the gold arena

MARCH 1/ INITIAL MARCH GOLD

/ /// THE MARCH 2024 GOLD CONTRACT

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 24,834.590 oz JPMORGAN LOOMIS MANFRA INCLUDES 102 kilobars//LOOMIS . |

| Deposit to the Dealer Inventory in oz | nil oz |

| Deposits to the Customer Inventory, in oz | 89,315.478 oz Loomis |

| No of oz served (contracts) today | 38 notice(s) 3800 OZ 0.1182 TONNES |

| No of oz to be served (notices) | 2147 contracts 214700 oz 6.678. TONNES |

| Total monthly oz gold served (contracts) so far this month | 1185 notices 118500 oz 3.685 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | x |

0 dealer deposits:

total dealer deposits: nil oz

total customer withdrawals: 3

i) Out of JPMorgan: 782.551 oz

ii) Out of Loomis: 3279.402 oz (102 kilobars)

iii) Out of Manfra 20,722.637 oz

total withdrawal: 24,834.570 oz

we had 0 customer deposit

total deposit nil

Adjustments:

0

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR FEB.

For the front month of MARCH we have an oi of 2185 contracts having LOST 1145 contracts. We had 1147 contracts filed upon yesterday, so we gained 2 contracts or an additional 200 oz of gold will stand at the comex in this non active delivery month of March.

APRIL GAINED 7844 CONTRACTS RISING TO 324,203.

MAY EARNED ITS FIRST 4 CONTRACTS TO STAND AT 4

JUNE INCREASED ITS OI BY 5374 CONTRACTS UP TO 50,641 CONTRACTS.

We had 38 contracts filed for today representing 3800 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 38 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 9 notice(s) was (were) stopped ( (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for the MARCH. /2024. contract month, we take the total number of notices filed so far for the month (1185 x 100 oz ), to which we add the difference between the open interest for the front month of MARCH. (2185 CONTRACTS) minus the number of notices served upon today 38 x 100 oz per contract equals 333,200 OZ OR 10.363 TONNES

thus the INITIAL standings for gold for the MARCH. contract month: No of notices filed so far (1185) x 100 oz + (2185) {OI for the front month} minus the number of notices served upon today (38) x 100 oz which equals 333,200 oz (10.363 TONNES)

TOTAL COMEX GOLD STANDING FOR MARCH: 10.363 TONNES WHICH IS HUGE FOR A NON ACTIVE DELIVERY MONTH IN THE CALENDAR.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 1,354,385.502 42.127 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD: 18,225,515.694 OZ

TOTAL REGISTERED GOLD 8,088,671.657 (251.59 tonnes).

TOTAL OF ALL ELIGIBLE GOLD: 10,136,844.077 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 6,734,286 oz (REG GOLD- PLEDGED GOLD) 209.464 tonnes/dropping like a stone

END

SILVER/COMEX

MARCH 1/INITIAL

//2024// THE MARCH 2024 SILVER CONTRACT//INITIAL

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 104,486.060 oz Brinks loomis . |

| Deposits to the Dealer Inventory | nil OZ |

| Deposits to the Customer Inventory | 108,420.460 oz CNT |

| No of oz served today (contracts) | 89 CONTRACT(S) (445,000 OZ) |

| No of oz to be served (notices) | 1411 contracts (7.055 MILLION oz) |

| Total monthly oz silver served (contracts) | 2947 Contracts (14.735 MILLION oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

i) 0 dealer deposit

total dealer deposit: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: 0 oz

We had 1 deposits customer account:

i) Into CNT 108,420.460 oz

total customer deposits 108,420.460 oz

JPMorgan has a total silver weight: 129.806 million oz/282.130 million or 46.26%

adjustment: 0

Comex withdrawals: i) CNT: 108,420.460 oz

total withdrawal: 108,402.406 oz

TOTAL REGISTERED SILVER: 51.293MILLION OZ//.TOTAL REG + ELIGIBLE. 282.130 million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR DECEMBER:

silver open interest data:

FRONT MONTH OF MARCH /2023 OI: 1500 CONTRACTS HAVING LOST 2954 CONTRACT(S).

WE HAD 2858 NOTICES FILED YESTERDAY SO STRANGELY WE LOST 96 CONTRACTS OR AN ADDITIONAL 480,000 OZ WILL NOT STAND AT THE COMEX AS THEY WERE IMMEDIATELY FERRIED OVER TO LONDON TRYING TO TAKE DELIVERY OVER THERE.

APRIL SAW A LOSS OF 77 CONTRACTS TO STAND AT 835

MAY SAW A LOSS OF 1108 CONTRACTS UP TO 116,090.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 89 for 0.445 MILLION oz

Comex volumes// est. volume today 68,047 poor

Comex volume: confirmed yesterday 59,402 poor

To calculate the number of silver ounces that will stand for delivery in MARCH. we take the total number of notices filed for the month so far at 2947 x 5,000 oz = 14,735,000 oz

to which we add the difference between the open interest for the front month of MARCH. (1500) and the number of notices served upon today 89 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the MARCH/2024 contract month: 2947 (notices served so far) x 5000 oz + OI for the front month of MARCH. (1500) – number of notices served upon today (89 )x 500 oz of silver standing for the MARCH contract month equates to 21.790 MILLION OZ.

New total standing: 21.790 million oz.

There are 51.293 million oz of registered silver.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS//

BOTH GLD AND SLV ARE MASSIVE FRAUDS!

MARCH 1 WITH GOLD UP $40.40 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 822.91 TONNES

FEB29/WITH GOLD UP $12.60 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD//WITHDRAWAL OF 4.03 TONNES INVENTORY RESTS AT 822.91 TONNES

FEB28/WITH GOLD DOWN $1.00 TODAY NO CHANGES IN GOLD INVENTORY AT THE GLD INVENTORY RESTS AT 826.94 TONNES

FEB27/WITH GOLD UP $4.40 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF .87 TONNES OF GOLD FROM THE GLD:/INVENTORY RESTS AT 826.94 TONNES

FEB26/WITH GOLD DOWN $8.90 TODAY NO CHANGES IN GOLD INVENTORY AT THE GLD:/INVENTORY RESTS AT 827.81 TONNES

FEB23/WITH GOLD UP $17 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.01 TONNES OF GOLD FROM THE GLD.//INVENTORY RESTS AT 827.81 TONNES

FEB22/WITH GOLD DOWN $2.15 TODAY NO CHANGES IN GOLD INVENTORY AT THE GLD://INVENTORY RESTS AT 829.82 TONNES

FEB21/WITH GOLD DOWN $5.30 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 7.59 TONNES OF GOLD OUT OF THE GLD///INVENTORY RESTS AT 29.82 TONNES

FEB20/WITH GOLD UP $16.15 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 0.58 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 837.89 TONNES

FEB16/WITH GOLD UP $8,60 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.73 TONNES OF GOLD FROM THE GLD///INVENTORY RESTS AT 837.31 TONNES

FEB15/WITH GOLD UP $11.70 TODAY NO CHANGES IN GOLD INVENTORY AT THE GLD:/INVENTORY RESTS AT 841.92 TONNES

FEB14/WITH GOLD DOWN $2.75 TODAY NO CHANGES IN GOLD INVENTORY AT THE GLD:/INVENTORY RESTS AT 841.92 TONNES

FEB13/WITH GOLD DOWN $20.15 TODAY NO CHANGES IN GOLD INVENTORY AT THE GLD:/INVENTORY RESTS AT 841.92 TONNES

FEB12/WITH GOLD DOWN $4.80 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A STRONG WITHDRAWAL OF 1.74 TONNES OF GOLD FROM THE GLD. / //://INVENTORY RESTS AT 841.92 TONNES

FEB9/WITH GOLD DOWN $8.60 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A STRONG DEPOSIT OF 1.44 TONNES OF GOLD FROM THE GLD. / //://INVENTORY RESTS AT 843.66 TONNES

FEB8/WITH GOLD DOWN $2.70 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A MASSIVE WITHDRAWAL OF 5.47 TONNES OF GOLD FROM THE GLD. / //://INVENTORY RESTS AT 842.22 TONNES:

FEB7/WITH GOLD UP $0.40 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A MASSIVE WITHDRAWAL OF 4.04 TONNES OF GOLD FROM THE GLD. / //://INVENTORY RESTS AT 847.69 TONNES:

FEB6/WITH GOLD UP $8.50 TODAY NO CHANGES IN GOLD INVENTORY AT THE GLD:/ / //://INVENTORY RESTS AT 851.73 TONNES:

FEB5/WITH GOLD DOWN $9.85 TODAY SMALL CHANGES IN GOLD INVENTORY AT THE GLD:A DEPOSIT OF .58 TONNES OF GOLD INTO THE GLD// / //://INVENTORY RESTS AT 851.73 TONNES:

FEB 2/WITH GOLD DOWN $17.95 TODAY SMALL CHANGES IN GOLD INVENTORY AT THE GLD:A WITHDRAWAL OF .58 TONNES OF GOLD FROM THE GLD// / //://INVENTORY RESTS AT 851.15 TONNES:

FEB 1/WITH GOLD UP $5.00 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD:A WITHDRAWAL OF 1.73 TONNES OF GOLD FROM THE GLD// / //://INVENTORY RESTS AT 851.15 TONNES:

JAN 31/WITH GOLD UP $16.40 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD:A WITHDRAWAL OF 2.01 TONNES OF GOLD FROM THE GLD// / //://INVENTORY RESTS AT 852.88 TONNES:

JAN 30/WITH GOLD UP $6.50 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD:A WITHDRAWAL OF 1.16 TONNES OF GOLD FROM THE GLD// / //://INVENTORY RESTS AT 854.89 TONNES:

TOTAL IN LAST 18 DAYS WITHDRAWAL OF 14.12 TONNES

JAN 29/WITH GOLD UP $8.70 TODAYHUGE CHANGES IN GOLD INVENTORY AT THE GLD:A WITHDRAWAL OF 2.88 TONNES OF GOLD FROM THE GLD// / //://INVENTORY RESTS AT 856.05 TONNES

JAN 26/WITH GOLD DOWN $0.10 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD: / //://INVENTORY RESTS AT 858.93 TONNES

JAN 25/WITH GOLD UP $2.50 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD: / //://INVENTORY RESTS AT 858.93 TONNES

JAN 24/WITH GOLD DOWN $9.75 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD: / //://INVENTORY RESTS AT 858.93 TONNES

JAN 23/WITH GOLD UP $3.95 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.02 TONNES OF GOLD FROM THE GLD/ //://INVENTORY RESTS AT 858.93 TONNES

GLD INVENTORY: 822.91 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

MARCH 1/WITH SILVER UP 49 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: // : SLV INVENTORY RESTS AT 430.982 MILLION OZ

FEB 29/WITH SILVER UP 25 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.104 MILLION OZ OUT OF THE SLV//// : SLV INVENTORY RESTS AT 430/982 MILLION OZ

FEB 28/WITH SILVER DOWN 7 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 5.123 MILLION OZ INTO THE SLV//// : SLV INVENTORY RESTS AT 433.086 MILLION OZ

FEB 27/WITH SILVER UP 3 CENTS TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 0.64 MILLION OZ FROM THE SLV//// : SLV INVENTORY RESTS AT 427.943 MILLION OZ

FEB 26/WITH SILVER DOWN 44 CENTS TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.065 MILLION OZ FROM THE SLV//// : SLV INVENTORY RESTS AT 428.603 MILLION OZ

FEB 23/WITH SILVER DOWN 44 CENTS TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.065 MILLION OZ FROM THE SLV//// : SLV INVENTORY RESTS AT 428.603 MILLION OZ

FEB 22/WITH SILVER DOWN 10 CENTS TODAY NO CHANGES IN SILVER INVENTORY AT THE SLV

// : SLV INVENTORY RESTS AT 432.766 MILLION OZ

FEB 21/WITH SILVER DOWN 28 CENTS TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 2.348 MILLION OZ OF SILVER FROM THE SLV// : SLV INVENTORY RESTS AT 432.766 MILLION OZ

FEB 20/WITH SILVER DOWN 33 CENTS TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 3.385 MILLION OZ OF SILVER FROM THE SLV// : SLV INVENTORY RESTS AT 435.008 MILLION OZ

FEB 16/WITH SILVER UP 53 CENTS TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV A DEPOSIT OF 1.235 MILLION OZ OF SILVER FROM THE SLV// : SLV INVENTORY RESTS AT 438.393 MILLION OZ

FEB 15/WITH SILVER UP 56 CENTS TODAY NO CHANGES IN SILVER INVENTORY AT THE SLV : SLV INVENTORY RESTS AT 437.615 MILLION OZ

FEB 14/WITH SILVER UP 24 CENTS TODAY NO CHANGES IN SILVER INVENTORY AT THE SLV : SLV INVENTORY RESTS AT 437.615 MILLION OZ

FEB 13/WITH SILVER DOWN 60 CENTS TODAY SMALL CHANGES IN SILVER INVENTORY AT THE SLV A SMALL WITHDRAWAL OF 0.504 MILLION OZ OZ OUT OF THE SLV: SLV INVENTORY RESTS AT 437.615 MILLION OZ

FEB 12/WITH SILVER UP 14 CENTS TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV A HUGE WITHDRAWAL OF 1.921 MILLION OZ OZ OUT OF THE SLV: SLV INVENTORY RESTS AT 438.119 MILLION OZ

FEB 9/WITH SILVER DOWN 4 CENTS TODAY SMALL CHANGES IN SILVER INVENTORY AT THE SLV A SMALL DEPOSIT OF 600,000 OZ INTO THE SLV: SLV INVENTORY RESTS AT 440.040 MILLION OZ

FEB 8/WITH SILVER UP 29 CENTS TODAY NO CHANGES IN SILVER INVENTORY AT THE SLV: SLV INVENTORY RESTS AT 439.994 MILLION OZ

FEB 7/WITH SILVER DOWN 18 CENTS TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A MASSIVE DEPOSIT OF 4.04 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 439.994 MILLION OZ//LAST 9 DAYS: 10.7598 MILLION OZ WITHDRAWAL

FEB 6/WITH SILVER UP 11 CENTS TODAY NO CHANGES IN SILVER INVENTORY AT THE SLV: /INVENTORY RESTS AT 435.144 MILLION OZ//LAST 9 DAYS: 10.7598 MILLION OZ WITHDRAWAL

FEB 5/WITH SILVER DOWN 32 CENTS TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.345 MILLION OZ FROM THE SLV(FAIRY TALES) // /INVENTORY RESTS AT 435.144 MILLION OZ//LAST 8 DAYS: 10.7598 MILLION OZ WITHDRAWAL

FEB 2/WITH SILVER DOWN 50 CENTS TODAY SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 0.58 MILLION OZ INTO THE SLV(FAIRY TALES) // /INVENTORY RESTS AT 438.489 MILLION OZ//LAST 7 DAYS: 14.105 MILLION OZ WITHDRAWAL

FEB 1/WITH SILVER UP 7 CENTS TODAY MEGA CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.19 MILLION OZ INTO THE SLV(FAIRY TALES) // /INVENTORY RESTS AT 438.947 MILLION OZ//LAST 6 DAYS: 10.3018 MILLION OZ WITHDRAWAL

JAN 31/WITH SILVER DOWN 8 CENTS TODAY MEGA CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.7438 MILLION OZ INTO THE SLV(FAIRY TALES) // /INVENTORY RESTS AT 440.137 MILLION OZ//LAST 5 DAYS: 9.1118 MILLION OZ WITHDRAWAL

JAN 30/WITH SILVER DOWN 5 CENTS TODAY MEGA CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.876 MILLION OZ INTO THE SLV(FAIRY TALES) // /INVENTORY RESTS AT 442.699 MILLION OZ//LAST 4 DAYS: 7.368 MILLION OZ WITHDRAWAL

JAN 29/WITH SILVER UP $.37 TODAY MEGA CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.105 MILLION OZ INTO THE SLV(FAIRY TALES) // /INVENTORY RESTS AT 444.575 MILLION OZ

JAN 26/WITH SILVER DOWN $0.03 TODAY MEGA CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.556 MILLION OZ INTO THE SLV(FAIRY TALES) // /INVENTORY RESTS AT 446.680 MILLION OZ

JAN 25/WITH SILVER UP $0.03 TODAY MEGA CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.831 MILLION OZ INTO THE SLV(FAIRY TALES) // /NVENTORY RESTS AT 448.236 MILLION OZ

JAN 24/WITH SILVER UP $0.44 TODAY MEGA CHANGES IN SILVER INVENTORY AT THE SLV: ANOTHER DEPOSIT OF 1.375 MILLION OZ INTO THE SLV(FAIRY TALES) // //INVENTORY RESTS AT 450.067 MILLION OZ

JAN 23/WITH SILVER UP $0.21 TODAY MEGA CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 16.201 MILLION OZ INTO THE SLV(FAIRY TALES) // //INVENTORY RESTS AT 448.694 MILLION OZ

JAN 22/WITH SILVER DOWN $0.45 TODAY NO CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 458,000 OZ OUT OF THE SLV // //INVENTORY RESTS AT 432.493 MILLION OZ

JAN 19/WITH SILVER DOWN $0.11 TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 458,000 OZ OUT OF THE SLV // //INVENTORY RESTS AT 432.493 MILLION OZ

JAN 18/WITH SILVER UP $0.13 TODAY NO CHANGES IN SILVER INVENTORY AT THE SLV: // //INVENTORY RESTS AT 432.951 MILLION OZ

JAN 17/WITH SILVER DOWN $0.38 TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 779,000 OZ FROM THE SLV.: // //INVENTORY RESTS AT 433.500 MILLION OZ

JAN 16/WITH SILVER DOWN $0.08 TODAY NO CHANGES IN SILVER INVENTORY AT THE SLV: // //INVENTORY RESTS AT 433.500 MILLION OZ

JAN 12/WITH SILVER UP $0.62 TODAY NO CHANGES IN SILVER INVENTORY AT THE SLV: // //INVENTORY RESTS AT 433.500 MILLION OZ

CLOSING INVENTORY 430.982 MILLION OZ//

PHYSICAL GOLD/SILVER COMMENTARIES

1:Peter Schiff/Mike Maharrey

Inflation’s Impact: The Penny’s Plunge Into Irrelevance

FRIDAY, MAR 01, 2024 – 06:30 AM

It’s no surprise to readers of this site that metals are often worth more than fiat currency. Gold, silver, and other precious metals are known for their value. But sometimes fiat currency can’t even compete with zinc.

The US penny, which is primarily made of zinc, costs roughly three cents to produce and is only worth one cent according to the federal government. This is the opposite of what has happened historically. Generally, governments produce currency that is worth far more than the cost of producing it. Imagine printing a one hundred dollar bill which costs far less than a hundred dollars in materials and printing costs. The profit from this is called seigniorage. With pennies, the US government is practicing reverse seigniorage.

This loss of money from producing pennies is one of the arguments for abolishing the US penny. There are other arguments against the penny such as the claim that it’s worth so little compared to the typical American wage that it makes no sense to denominate prices in pennies, would anyone argue that the United States needs a coin worth half a penny?

In fact, the United States used to have a half-cent coin which was abolished in 1857 for being worth too little. A half-cent in 1857 would be worth approximately 18 cents today. That of course is more valuable than not only the penny but the nickel and dime as well.

Of course, there are arguments in favor of retaining the penny. Perhaps the penny is worthwhile as it supports the zinc mining industry and its American employees. Perhaps we should be suspicious of moves by the government to phase out the penny as it might be the first step towards a cashless economy. Or perhaps ditching the penny would cause businesses to round prices up, hurting consumers.

Arguably more interesting than the debate about whether the penny should exist, is considering the political and cultural implications of abolishing the penny.

What would it say if the US government scrapped the penny now? What would it say if it followed the past practice of abolishing the half-cent coin and scrapped the nickel and the dime as well?

It would be an admission by the government that its monetary policies and the Federal Reserve have so devalued currency, that the majority of coins created by the federal government are worth so little they might as well not exist!

The rampant inflation since the start of the Biden inflation is so extreme that it’s impossible to ignore the toll it has inflicted on the American people. But many years when inflation is lower, it’s harder to notice. Coins are part of American culture from slot machines dishing out coins to elementary school students learning to add and subtract with pennies, nickels, and quarters.

When stores stop accepting coins, when banks stop stocking coin rolls, or when the federal government throws in the towel of pennies, will more Americans realize that the rest of fiat currency is following the same path of constant devaluation? People would only have to look through their spare change, their couches, and their pockets to get a visceral reminder of the reality of inflation.

end

2.Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens/ SIMON WHITE..

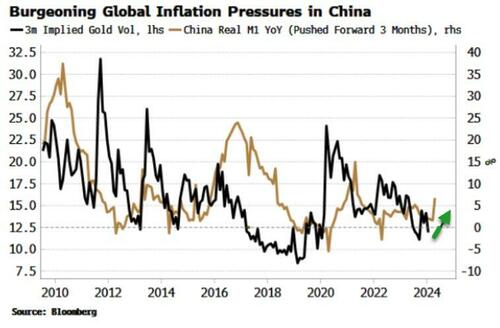

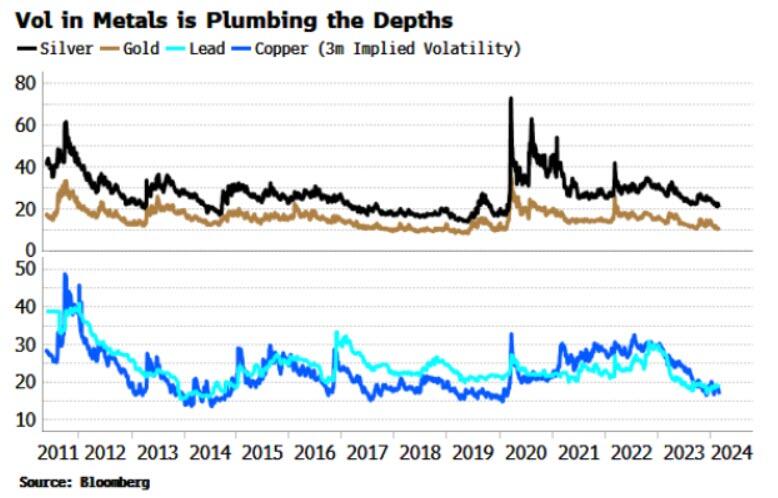

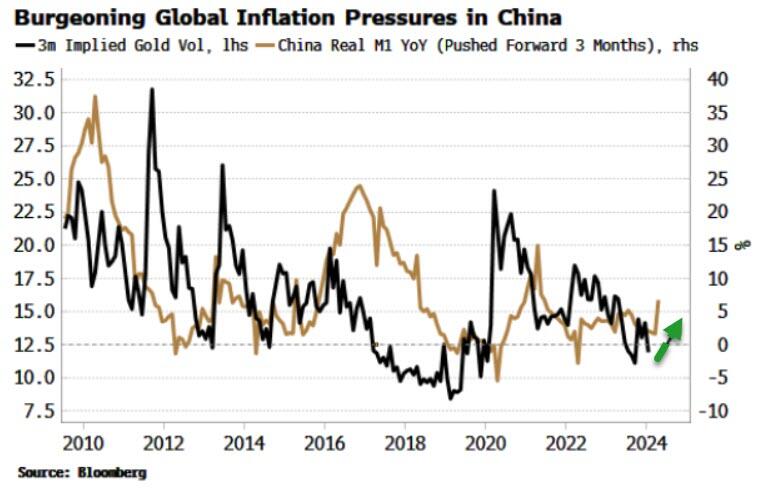

Low Volatility In Gold Is Calm Before Inflation Storm

FRIDAY, MAR 01, 2024 – 07:20 AM

Authored by Simon White, Bloomberg macro strategist,

Inflation is back on the radar this week after yesterday’s release of PCE in the US. It showed a modest fall from the prior month in the headline print (but under the surface the picture was more worrying), lending credence to the bigger picture signal of inflation pressures building again. Emblematic of how unpriced assets are for this likelihood, volatility in gold and silver and other metals is near decade lows.

Given how recently inflation was at generational highs, it is remarkable how complacent the market has become that the inflation problem is over. Normally after an inflation shock, there is a risk premium built into prices that persists for many years. It took a long time, and the brutal rate rises of Paul Volcker followed by the delphic utterances of Alan Greenspan, to finally convince the market to bring term premium back to the pre-Great Inflation levels of the 1960s.

Today, the fixing-swaps market foresees that CPI will return towards 2% CPI by the second half of this year. There is no risk premium for inflation built into yields, and money markets have a significant bias towards expecting lower not higher rates.

On top of that, commodity volatility is becalmed. Commodities and other real assets have historically performed well in in inflation regimes, with their volatility rising too. But implied vol in several commodities, especially metals and notably gold and silver, is preternaturally low.

This is not reflective of a market expecting a return of inflation, or indeed pricing much probability of it happening at all. No asset class, in fact, looks ready for an inflation redux.

One of the biggest drivers of US disinflation over the last two years has not been domestic monetary policy, but deflation in China. Yet, very slowly, leading indicators of activity and inflation are beginning to pick up in China as layers of fiscal and monetary stimulus start to bite.

A sign that China will soon be contributing positively to global and US price pressures again — and cause a repricing in markets — can be seen in the nascent rise in real narrow money (M1) growth, which has led gold volatility in recent years.

END

3. CHRIS POWELL//GATA GOLD COMMENTARIES: daily Dispatches

CHRIS POWELL…

The questions CFTC and Fed won’t answer expose gold price suppression policy

Submitted by admin on Wed, 2024-02-28 21:24 Section: Daily Dispatches

9:44p ET Wednesday, February 28, 2024

Dear Friend of GATA and Gold:

If mainstream financial news organizations ever work up the courage to report honestly about monetary gold, the commanding heights of the issue will have been mapped out for them by U.S. Rep. Alex X. Mooney, R-West Virginia.

After all, where can investigative journalism start better than with questions that already have been shown to be too politically sensitive for the highest government officials to answer, even when a member of Congress is asking?

Thanks to Mooney, in 2020 the U.S. Commodity Futures Trading Commission was shown refusing to answer whether it has jurisdiction over manipulative trading in the commodity futures markets when such trading is undertaken by or at the behest of the U.S. government:

https://www.gata.org/node/19917

And now, also thanks to Mooney, Federal Reserve Chairman Jerome Powell has been shown refusing to answer questions about the repatriation of gold vaulted by other nations at the Federal Reserve Bank of New York, repatriation being something that would signify foreign loss of faith in the Fed, the U.S. government, and the dollar.

In December Mooney wrote to Powell to ask:

“Has the Federal Reserve or the Federal Reserve Bank of New York repatriated any gold to foreign nations this year? If so, to which countries and how much?

And:

“How much gold is the Federal Reserve vaulting for foreign nations now and how does this compare to the amount vaulted at the end of 2022?”

Mooney’s letter to Powell is posted here:

Powell replied to Mooney last week without even acknowledging the congressman’s questions:

“Thank you for your letter of December 14, 2023, regarding the gold market. The Federal Reserve Bank of New York provides gold custody on behalf of certain official-sector account holders, which include the U.S. government, foreign governments, other central banks, and official international organizations. The Federal Reserve Bank of New York does not own any of the gold it holds as custodian, and no other part of the Federal Reserve System owns gold.”

The Fed chairman’s reply to Mooney is here:

In not even acknowledging Mooney’s questions, Powell was arrogant and insolent, especially insofar as the Federal Reserve in previous years has disclosed the tonnage of custodial gold vaulted at the New York Fed and the number of countries vaulting gold there. Indeed, even now the New York Fed’s internet site claims that it is vaulting 6,331 tonnes of gold for foreign nations:

https://www.newyorkfed.org/aboutthefed/goldvault.html

Is that data no longer accurate? The Fed chairman’s refusal to acknowledge the congressman’s questions suggests as much.

But Powell’s refusal to acknowledge Mooney’s questions also demonstrated absolute confidence that his arrogance and insolence would never be noted and challenged by mainstream financial news organizations, which seem to understand the Fed’s position that gold price suppression is crucial to maintenance of the dollar as the world reserve currency, that it is the foremost weapon of U.S. imperialism and economic exploitation of the rest of the world, and thus is “the elephant in the room” — something that must never be discussed.

In turn the cowardice or collaboration of mainstream financial news organizations, their refusal to press critical questions to central banks, is central banking’s greatest advantage — an advantage greater even than central banking’s power to create and allocate infinite money.

Mooney’s latest exposure of the Federal Reserve’s unaccountability has been added to GATA’s extensive file of documentation of gold price suppression policy —

https://www.gata.org/taxonomy/term/21

— whose history is summarized (if at length) here:

https://www.gata.org/node/20925

If you know any financial journalists with integrity and courage, please forward this dispatch to them as an invitation to start trying to do their job of speaking truth to power instead of being afraid of power.

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

* * *

4. OTHER GOLD COMMENTARIES/PODCASTS/LIVE FROM THE VAULT: LYNETTE ZANG NO 162

https://kinesis.money/live-from-the-vault/sound-money-outside-system/

Episode 162

Posted 1st March 2024

Sound money outside of the system Feat. Lynette Zang

In this week’s episode of Live from the Vault, Andrew Maguire is joined for the first time by renowned US-based banker, stockbroker, and economist Lynette Zang to talk about the growing sound money movement and ways to preserve wealth.

Lynette takes listeners through an American perspective on the failing dollar and recent developments in certain states, before offering a message of hope: people are waking up to the manipulation of the mainstream media.

END

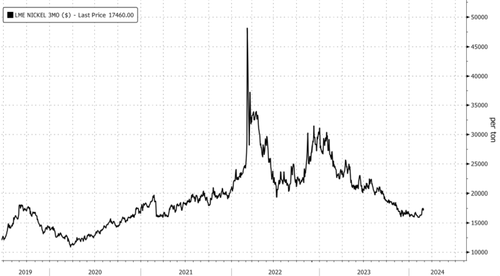

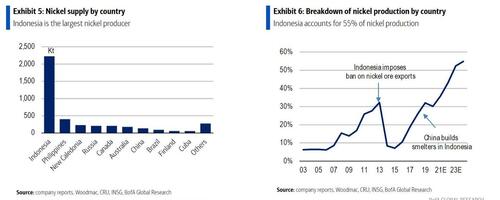

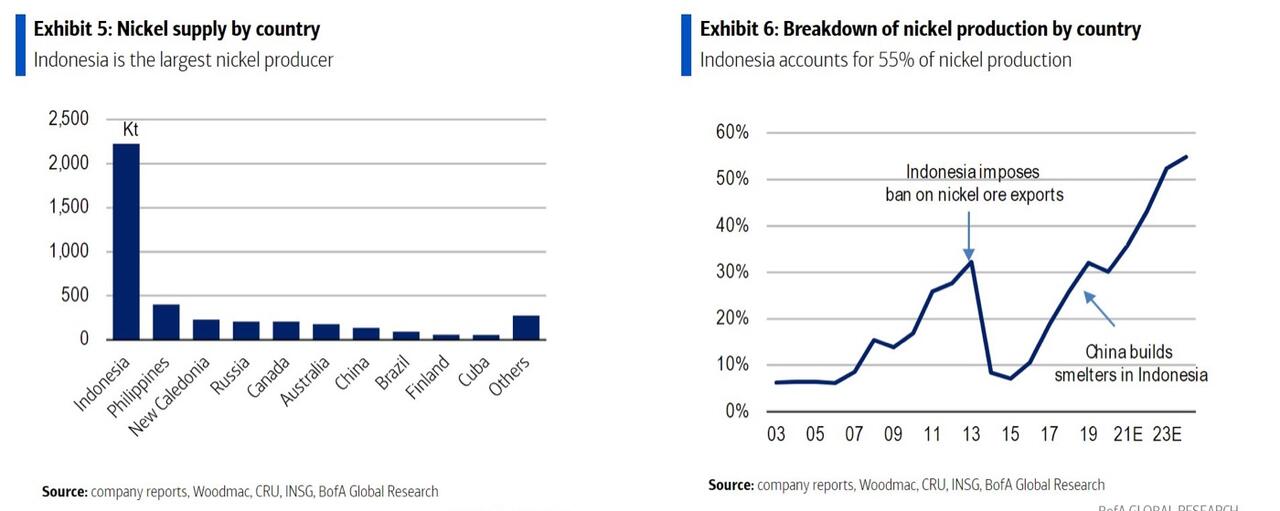

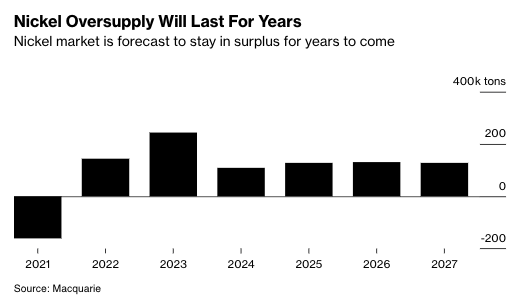

5 a. IMPORTANT COMMENTARIES ON COMMODITIES /NICKEL

Seismic Shift: Indonesia Floods Market With Cheap Nickel, Sparking Wave Of Unprofitable Mines

THURSDAY, FEB 29, 2024 – 07:25 PM

The global nickel industry is experiencing a seismic shift as Indonesia emerges as a major low-cost supplier, contributing to a collapse in prices of the metal used in everything from making stainless steel to high-grade batteries.

Nickel is trading at just above $17,400 a ton, according to the London Metal Exchange, down from $48,800 a ton in early 2022.

Miners are writing down their businesses and closing mines due to a massive drop in income. At least six projects were closed in Australia last year as Indonesia flooded the world with cheap nickel. Bloomberg notes the supply of cheap nickel could mean upwards of at least half the world’s mines could become unprofitable.

Christel Bories, the head of Eramet, told the Financial Times that Indonesia has the world’s largest nickel reserves and could soon account for 75% of all high-grade nickel production by the end of the decade.

“It has really made a big part of the old traditional players structurally non-competitive for the future,” Bories said, adding, “This is part of the industry will either disappear or be subsidized by governments.”

She continued: “The uncompetitive mines elsewhere will close. I’m not sure there will be so many governments deciding to subsidize big production with a lot of money just to compete with Indonesia production.”

Bories’ gloomy prediction for the oversupplied nickel markets is similar to other mining CEOs, like BHP chief executive Mike Henry, who recently warned that its flagship nickel business in Australia could close in the next few months. He said help from the government “may not be enough” to save the company’s nickel operation in the western part of the country.

Two weeks ago, BHP wrote down the entire value of its Western Australian nickel mining operation. The firm reported a shocking 86% year-on-year plunge in net income for the second half of 2023.

Bloomberg pointed out that Indonesia’s move to flood the world with cheap nickel will keep markets oversupplied through the decade’s end.

“There is a serious structural challenge as a result of Indonesian nickel,” said Duncan Wanblad, chief executive officer of Anglo American Plc. The miner was forced to take a $500 million writedown on its nickel business last week.

Wanblad added: “They don’t seem to be letting up anytime soon.”

The imploding nickel market is great news for electric vehicle companies, who were once battered by skyrocketing battery material costs during Covid.

END

COCOA

Cocoa Panic? World’s Largest Chocolatier Plans 19% Workforce Cut As Prices Hit Record Highs

FRIDAY, MAR 01, 2024 – 04:15 AM

The world’s largest maker of bulk chocolate is planning to cut about 19% of its workforce, totaling 2,500 jobs, as part of a cost-reduction strategy in response to a worsening cocoa shortage in West Africa, which has driven prices to record highs.

“It’s about reducing complexity and eliminating duplication and inefficient structures,” Swiss chocolate maker Barry Callebaut CEO Peter Feld said in an interview with German newspaper Handelsblatt on Monday.

Feld continued: “It’s about reducing complexity and eliminating duplication and inefficient structures.”

Handelsblatt said the job cuts will be implemented across Barry Callebaut’s operations worldwide over the coming 18 months.

The move signifies Barry Callebaut is likely preparing for future demand woes as cocoa output in top grower Ivory Coast collapses, sending prices in London to record highs.

According to trader Ecom Agroindustrial Corp., Ivory Coast’s cocoa output is expected to plunge by as much as 20% this growing season.

In a report viewed by Bloomberg, Ecom Agroindustrial forecasts 1.75 million tons of cocoa from the region in the season that ends in September. Based on International Cocoa Organization data, that would be the lowest total in eight years.

Cocoa’s price surge has been absolutely stunning to spectate over the last 15 months. Futures have soared to record highs, overtaking the highs last seen in 1977. Citigroup has warned prices could hit as high as $10,000 a ton.

And the chocolate maker US Hershey Company warned in recent weeks: “Historic cocoa prices are expected to limit earnings growth this year.”

It’s only a matter of time before consumers are battered by candy inflation. Who will Biden’s PR team blame for soaring candy prices?

5 B GLOBAL COMMODITY ISSUES/FOOD IN GENERAL//FREIGHT

END

6.CRYPTOCURRENCY//DIGITAL CURRENCY// COMMENTARIES/

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS FRIDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED DOWN 7.1985

OFFSHORE YUAN: UP TO 7.2130

SHANGHAI CLOSED UP 11.85 PPTS OR 0.39%

HANG SENG CLOSED UP 78.00 PTS OR 1.47%

2. Nikkei closed UP 744.63 PTS OR 1.90%

3. Europe stocks SO FAR: ALL GREEN

USA dollar INDEX UP TO 103.98 EURO RISES TO 1.0824 UP 18 BASIS PTS

3b Japan 10 YR bond yield: FALLS TO. +.710 Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 150.45/JAPANESE YEN NOW FALLING AS WELL AS LONG TERM 10 YR. YIELDS RISING //EVENTUALLY THIS WILL BREAK THE JAPANESE CENTRAL BANK

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen DOWN CHINESE ONSHORE YUAN: DOWN/ OFFSHORE: DOWN

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and UP FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund DOWN TO +2.4395***/Italian 10 Yr bond yield DOWN to 3.899* /SPAIN 10 YR BOND YIELD DOWN TO 3.332…**

3i Greek 10 year bond yield DOWN TO 3.382

3j Gold at $2053.20 silver at: 22.70 1 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble DOWN 0 AND 25 /100 roubles/dollar; ROUBLE AT 91.29//

3m oil into the 79 dollar handle for WTI and 83 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 150.44// 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 0.710% STILL ON CENTRAL BANK (JAPAN) INTERVENTION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.8831 as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.9581 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

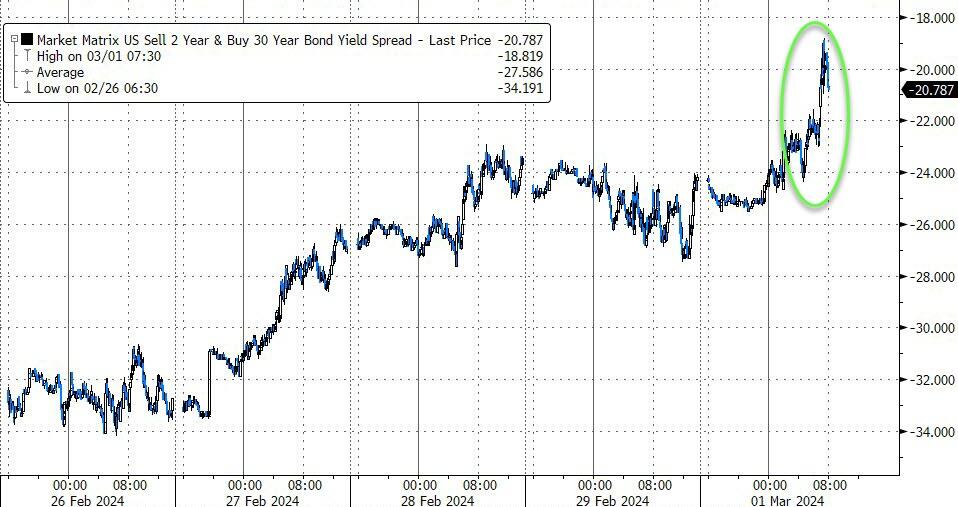

USA 10 YR BOND YIELD: 4.239 DOWN 1 BASIS PTS…

USA 30 YR BOND YIELD: 4.369 DOWN 0 BASIS PTS/

USA 2 YR BOND YIELD: 4.600 DOWN 5 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 31.34…(TURKEY SET TO BLOW UP FINANCIALLY)

GREAT BRITAIN/10 YEAR YIELD: DOWN 10 BASIS PTS AT 4.186

end

2.a Overnight: Newsquawk and Zero hedge

Futures Flat As Rally Fades, CRE Stress Returns

FRIDAY, MAR 01, 2024 – 08:30 AM

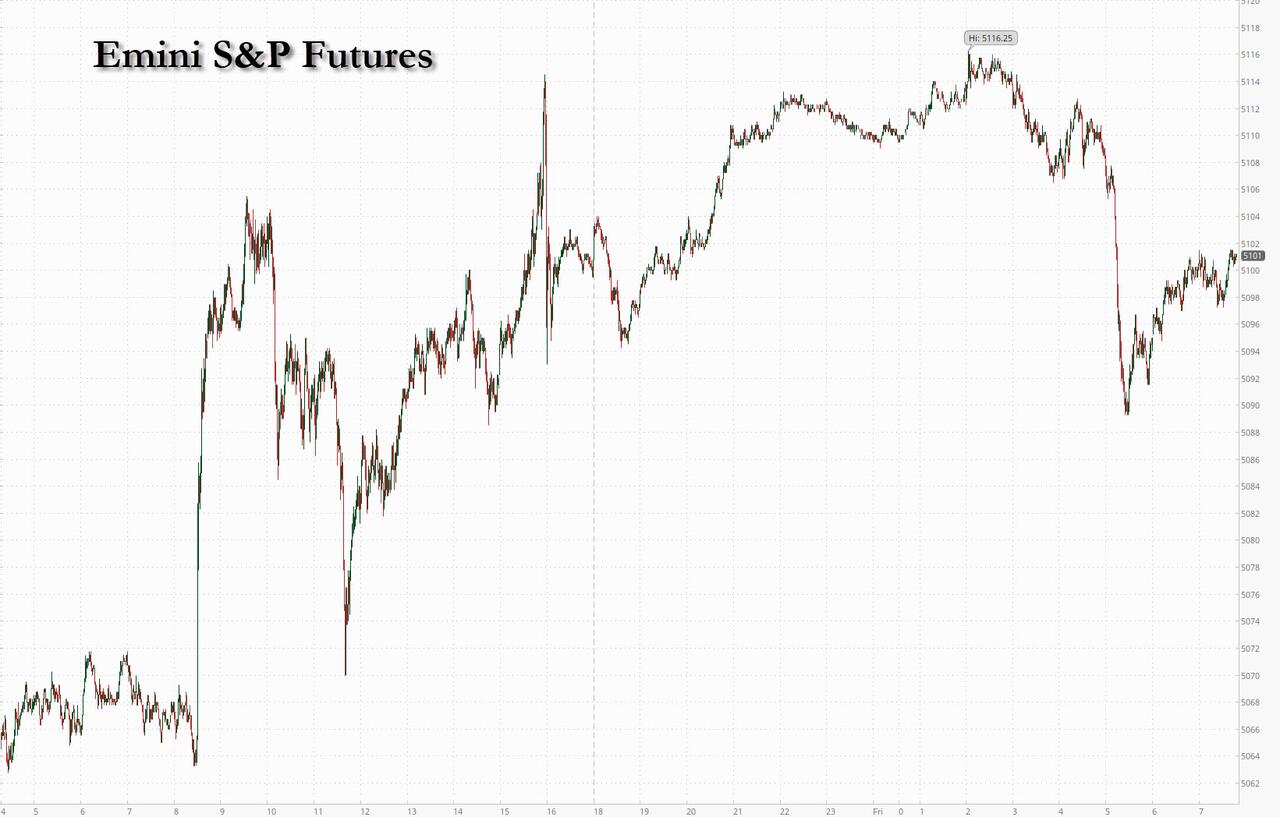

US stock futures briefly fell to a session low – then quickly recovered – as Apple slumped in premarket trading after Goldman removed the company from its conviction buy list (but retained a buy rating). As of 8:00am, S&P and Nasdaq futures traded flat and European stocks retreated from their highs as the relief rally which sent US stocks to an all time high on Thursday encouraged by an in-line reading on core PCE faded, while New York Community Bancorp plunged more than 30% in Friday’s premarket after identifying “material weaknesses” in how it tracks loan risks. Europe’s Stoxx 600 gained 0.5%, reversing an earlier dip, after Euro area inflation printed hotter than expected. Treasury yields are lower, the dollar is flat, and bitcoin is higher and back over $62,000. Today, focus will be the ISM-Mfg report at 10am ET (exp. 49.5 survey vs. 49.1 prior). Keep an eye on ISM-Mfg Prices Paid: consensus sees prices to grow again: 53.2 vs. 52.9

In premarket trading, NYCB tumbled as much as 30% after the troubled commercial real estate lender said it discovered “material weaknesses” in how it tracks loan risks, wrote down the value of companies acquired years ago and replaced its CEO to grapple with the turmoil. Dell Technologies soared 21% after its results beat expectations, boosted by the buzz around artificial intelligence. Apple fell 0.6% as Goldman removed the stock from its conviction list, while keeping a buy rating. It also removed Merck and Vertex Pharmaceuticals from its conviction list, replacing them with Amgen, Monday.com and Vulcan Materials. Here are some other notable movers:

- Caret Holdings shares jump 10% after the insurance technology company was upgraded to buy from hold at Jefferies and the broker raised its price target to a Street high.

- Eli Lilly gains 1.6% after BofA Global Research raised its price target on the weight-loss drugmaker to a Street-high of $1,000 on continued upside for its diabetes and obesity programs.

- Everbridge jumps 25% after the software firm said Thoma Bravo agreed to boost its acquisition price for the company by $6.40 per share to $35.00 per share, after it received a higher bid during the “go-shop” period.

- Ginkgo Bioworks shares slide 14%, after the synthetic biology firm’s forecast for the year disappointed, with Cowen saying that its guidance and quarter were “underwhelming” and noting that the company attributed the revenue decline to the biosecurity unit’s transition, and the lumpy impact of equity milestones that did not recur in 2023.

- HP Enterprise falls 5.6% after the computer hardware and storage company narrowed its adjusted earnings per share forecast for the full year. The firm cited cooling demand for networking products and a lack of availability of graphics processor units required to deliver high-powered servers.

- Humacyte falls 24%, after the biotech company offered shares to raise about $40 million at a 31% discount.

- New York Community Bancorp falls 21% after the company said it identified material weaknesses in its internal controls related to internal loan reviews. NYCB also replaced its CEO, saying that Executive Chairman Alessandro DiNello will take on the role.

- Senseonics shares drop 8.9% after the medical technology company reported fourth-quarter results. While the company beat expectations, Raymond James flagged the slower-than-expected adoption of Eversense.

- SoundHound AI falls 22%, with the voice AI software company retreating in the wake of its fourth-quarter results, as well as a massive rally in the stock price. Analysts are mixed on the report, and Cantor notes concerns about valuation.

- Sweetgreen jumps 20% after the salad chain’s first-quarter revenue forecast came ahead of expectations. Additionally, the company reported fourth-quarter same-store sales that were better than consensus. William Blair called the print a “sweet end” to the year.

Equity sentiment turned more cautious following Thursday’s core PCE data – t he Fed’s preferred inflation measure – which rose in January at the fastest pace in nearly a year, but matched economist forecasts. Traders were also comforted by jobless claims data that indicated labor-market softening. “The data came as a relief for those who were prepared for the worst,” said Ipek Ozkardeskaya, senior analyst at Swissquote Bank.

On the monetary policy front, euro-zone inflation eased less than anticipated in February — supporting European Central Bank officials who don’t want to rush into lowering rates. Meanwhile, Thursday’s US PCE report appeared not to dent the broader disinflationary trend underpinning rate-cut forecasts.

Federal Reserve Bank of San Francisco President Mary Daly said central bank officials are ready to lower interest rates as needed, but emphasized there’s no urgent need to cut given the strength of the economy. Her Atlanta counterpart Raphael Bostic said the central bank could begin cutting this summer. “For markets keenly focused on when the Fed will transition toward easing rates, this report will help restore confidence that it isn’t ‘if’ the Fed will begin to cut rates in 2024, but ‘when,’” said Quincy Krosby at LPL Financial.

Meanwhile, Bank of Americas’s Michael Hartnett said Chinese stock funds saw the largest weekly outflow since October, as the government seeks to stem a decline in the equity market. About $1.6 billion was pulled from Chinese funds in the week through Feb. 28, Hartnett wrote citing EPFR Global data. Beijing is attempting to restore market confidence after years of decline and slowing growth following the pandemic. As the turmoil deepened in recent months, the authorities have stepped up measures to help bolster sentiment, including restricting short selling and cracking down on high-speed trading.

European stocks advanced 0.5%, reversed earlier weakness after Eurozone CPI came in hotter than expected; banks and automobile shares leading gains, while construction and media stocks are the biggest laggards. Here are the biggest European movers:

- Daimler Truck shares rise as much as 15% to a record after the German truck maker posted fourth quarter results that were described “strong” by analysts, thanks to North American orders and the Mercedes-Benz trucks division

- IMCD shares rise as much as 10%, the biggest jump since August 2021, after the Dutch chemicals distributor reported margins that were better than analysts had expected

- Grifols shares jumped as much as 22%, rebounding from a 35% record decline on Thursday, after the Spanish plasma company said a key deal is coming closer to completion

- ITV shares jump as much as 16%, marking their biggest gain since April 2020, after the broadcaster sold its stake in streaming service BritBox and announced the net proceeds will be returned to shareholders through a buyback

- Bekaert gains as much as 9.1%, hitting the highest level since May 2017, with analysts planning to increase their 2024 estimates following the Belgian steel wire company’s results and outlook

- Corbion gains as much as 7.2% after the Dutch ingredients maker proposed a 9% dividend hike on the back of positive free cash flow momentum. Degroof Petercam analyst Fernand De Boer anticipates this could be followed by share buybacks

- Rightmove shares fall as much as 5.3%, the worst performance in the Stoxx 600 Real Estate Index on Friday, after the properly listings portal reported results that were in line with expectations

- IMI shares fall as much as 3.2%, extending losses into a fifth consecutive session, after the engineering firm’s EPS guidance for this year came in slightly below expectations, according to Liberum

- Acerinox declined 7.8% in early trading in Madrid, most since July 2022, after the Spanish stainless steel producer missed estimates and gave a weaker first-quarter outlook that Morgan Stanley says suggests high-single-digit downgrades to consensus Ebitda for 2024

- AMS-Osram’s shares extend drop after Thursday’s plunge of almost 40%, declining another 8.3% after Stifel cut the recommendation on the Swiss chipmaker to hold from buy

Earlier in the session, Asian stocks rose with Japan’s Nikkei 225 climbing 1.9% to its strongest-ever close near the 40,000 mark. Asian equities kickstarted March with gains after registering their best February performance in nine years, buoyed by a climb in Japan and China. The MSCI Asia Pacific Index rose as much as 0.5% , with technology and consumer discretionary stocks among the main advancers. Shares climbed on the mainland and Hong Kong ahead of next week’s crucial National People’s Congress meeting, where traders are awaiting more policy support from Beijing. Chinese authorities will likely display “a sense of urgency to show that there is no acceleration in this deflationary environment,” Xavier Baraton, global CIO at HSBC Global Asset Management in France, told Bloomberg television. “Valuations are extremely attractive, which means limited downside for us.”

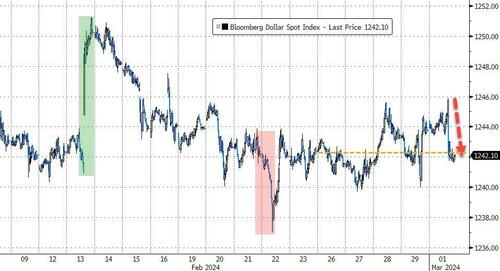

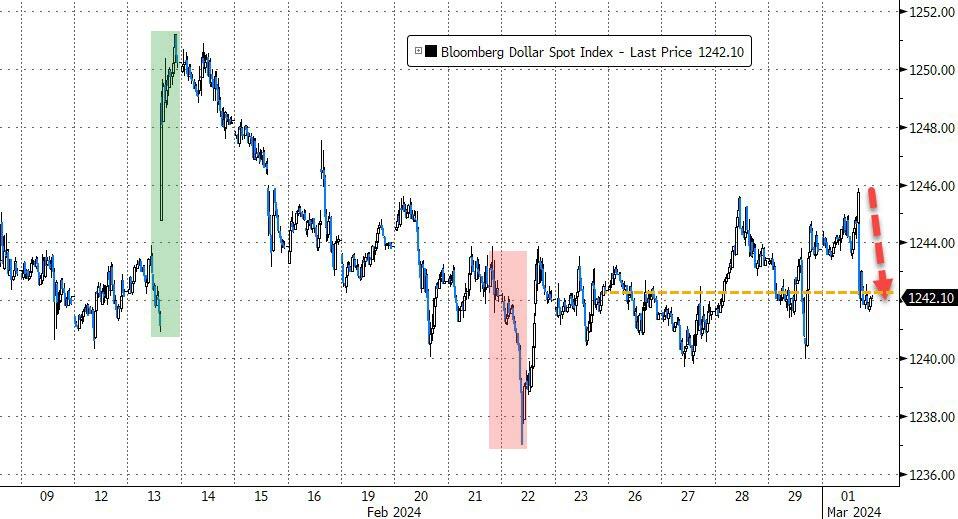

In FX, the Bloomberg Dollar Spot Index rose 0.1%. The yen was the weakest of the G-10 currencies, falling 0.3% versus the greenback after Bank of Japan Governor Ueda told reporters the price target is not already in sight, reversing hawkish comments from one of his co-workers just the day before as the BOJ confirms it has no idea what it will do next. His comment tempered speculation the bank’s first rate hike since 2007 could come as early as March.

In rates, treasuries rose while European government bonds pared an earlier decline as US equity futures fall. US 10-year yields drop 4bps to 4.22% while European bonds recovered despite euro-area inflation slowing less than expected in February.

In commodities, oil was on track for a modest weekly gain as market gauges continued to show signs of strength, with OPEC+ set to decide early this month whether to extend supply cuts into the next quarter. WTI rose 1.1% to trade near $79.10. Spot gold rose 0.5%.

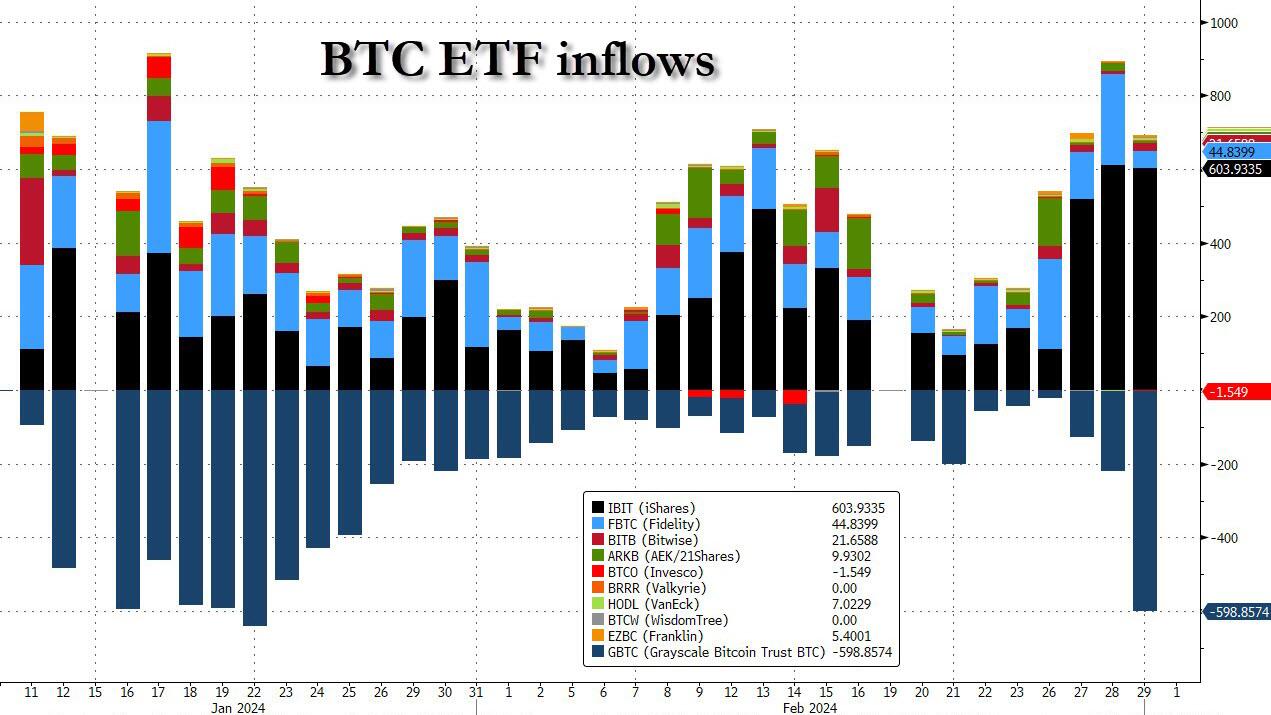

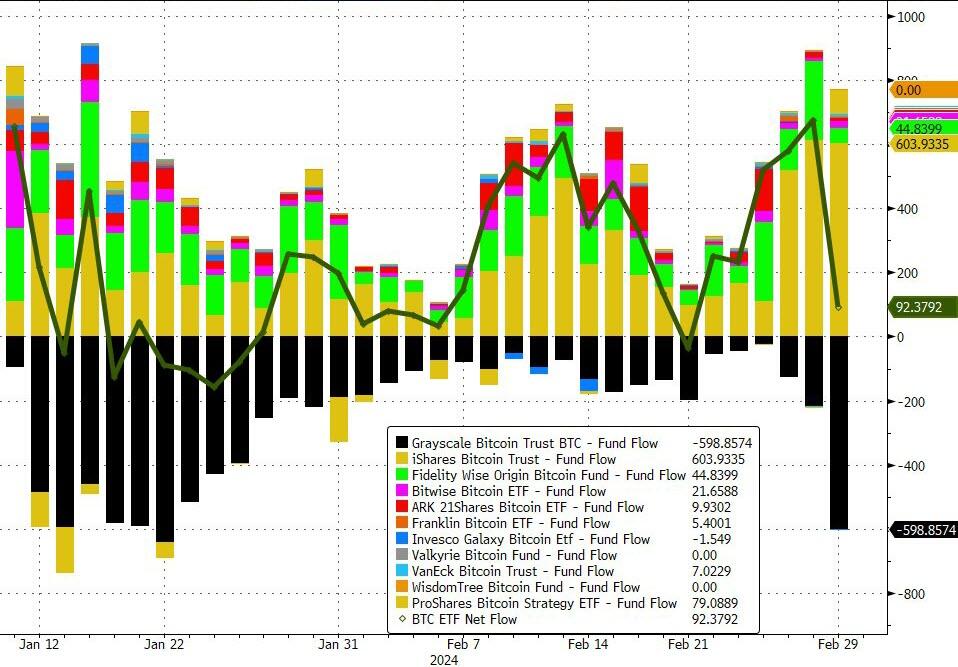

Bitcoin gained for a seventh day, trading above $62,000 as demand from exchange-traded funds continues. BlackRock Inc.’s iShares Bitcoin Trust netted a $604 million inflow on Thursday following a record $612 million on Wednesday.

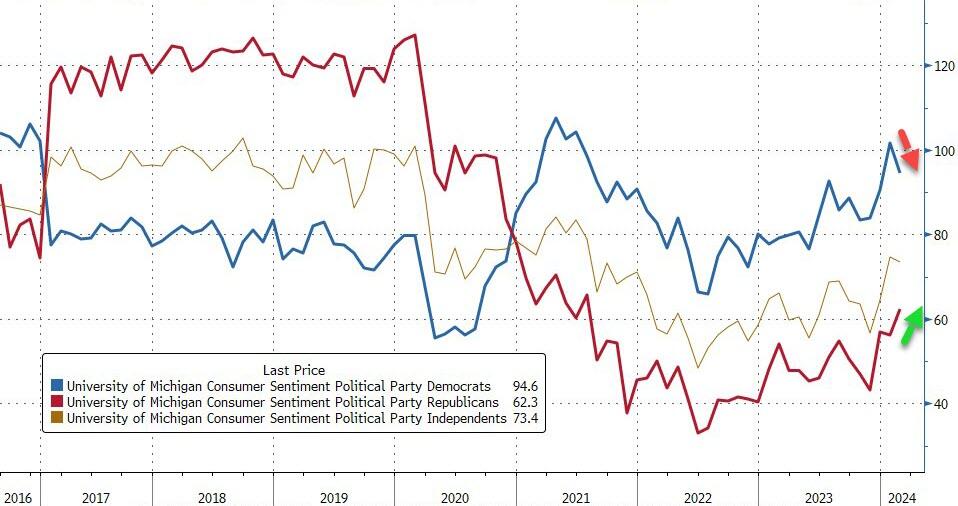

Today’s US economic data calendar includes February final S&P manufacturing PMI (9:45am), January construction spending, February final University of Michigan sentiment, February ISM manufacturing (10am) and February Kansas City Fed services activity (11am). Fed speakers scheduled include Barkin (8:30am), Goolsbee (10am, 4pm), Waller, Logan (10:15am), Bostic (12:15pm), Daly (1:30pm) and Kugler (3:20pm).

Market Snapshot

- S&P 500 futures up 0.1% to 5,109.25

- STOXX Europe 600 up 0.5% to 496.98

- MXAP up 0.5% to 173.76

- MXAPJ up 0.3% to 526.58

- Nikkei up 1.9% to 39,910.82

- Topix up 1.3% to 2,709.42

- Hang Seng Index up 0.5% to 16,589.44

- Shanghai Composite up 0.4% to 3,027.02

- Sensex up 1.7% to 73,768.05

- Australia S&P/ASX 200 up 0.6% to 7,745.61

- Kospi down 0.4% to 2,642.36

- German 10Y yield little changed at 2.45%

- Euro little changed at $1.0812

- Brent Futures up 0.9% to $82.63/bbl

- Gold spot up 0.0% to $2,045.04

- US Dollar Index little changed at 104.14

Top Overnight News

- Stocks advanced Friday after a reassuring reading on US inflation calmed traders’ worst fears on the outlook for interest rates and spurred fresh record highs on Wall Street.

- Pacific Investment Management Co. is warning that US fiscal profligacy threatens to drag the Treasury market back to 1980s, a time when bond vigilantes demanded far higher compensation to own longer-dated bonds.

- Federal Reserve Bank of New York President John Williams said he doesn’t see a need for officials to tighten policy further and reiterated that he expects the central bank to cut rates later this year.

- Swiss National Bank President Thomas Jordan will step down in September after more than a decade on the job, according to a statement on Friday.

- Returns on carry trades using the world’s biggest currencies. This often profitable but potentially risky strategy involves borrowing the lowest-yielding currencies in the Group-of-10 economies and using the funds to bet on the highest-yielding ones.

- Bank of Japan Governor Kazuo Ueda is keeping his options open for the timing of a widely expected interest rate hike, a position that may fuel further market volatility as investors and economists speculate over a March or April move

Earnings

- Dell Technologies Inc (DELL) – Q4 2023 (USD): Adj. EPS 2.20 (exp. 1.73), Revenue 22.32bln (exp. 22.16bln). Shares +22.4% in pre-market trade.

- Saint Gobain (SGO FP) – FY23 (EUR): Recurring 6.39bln (prev. 6.48bln Y/Y), EBITDA 7bln (exp. 6.9bln, prev. 7.12bln Y/Y), Revenue 47.9bln (exp. 47.8bln, prev. 51.2bln Y/Y). Expects to complete previously announced 5yr 2bln buyback in 2024. Guides initial FY24 Op. margin “double digit”. Shares -4.2% in European trade

- Daimler Truck (DTG GY) – Q4 (EUR): Adj. EBIT 1.56bln (exp. 1.36bln), Revenue 15bln (exp. 14.85bln). Raises dividend to 1.9/shr (prev 1.30/shr). Guides initial FY24 Revenue 55-75bln. (Newswires) Shares +12.8% in European trade

A more detailed look at global markets courtesy of Newsquawk

APAC stocks traded with positive bias amid tailwinds from the US following an absence of any hawkish surprises in the PCE data, while participants also reflected on the latest Chinese PMI figures. ASX 200 printed fresh record highs and entered bull market territory after gaining over 20% from its 2022 low. Nikkei 225 extended on its best levels and advanced closer to the 40,000 level amid a weaker currency and after BoJ Governor Ueda said Japan’s economy is not yet in a situation where sustained achievement of 2% inflation can be foreseen, which is in contrast with the prior day’s hawkish rhetoric from board member Takata. Hang Seng and Shanghai Comp. lagged behind their regional peers although the Hong Kong benchmark clawed back initial losses with the help of tech strength, while the mainland was indecisive after the PBoC drained liquidity and as participants digested Chinese PMI data which was mostly encouraging although Official Manufacturing PMI remained in contraction territory for the 5th consecutive month.

Top Asian News

- China’s Commerce Ministry said China’s trade faces a complex, severe, and uncertain external environment, while it will help companies explore the market and expand imports to ensure domestic demand, according to Reuters.

- BoJ Governor Ueda said inflation is easing at a quick pace and wage negotiations will offer a tailwind, while he added that Japan’s economy will continue a gradual recovery and the economy is not yet in a situation where sustained achievement of 2% inflation can be foreseen. Ueda also commented that in judging whether a sustained achievement of the 2% inflation target can be foreseen, this year’s annual wage negotiation outcome is key.

- RBNZ Governor Orr said the economy is evolving as anticipated and inflation expectations have declined, while inflation is still too high but is declining and policy needs to stay restrictive for some time. Orr also said he expects to begin normalising policy next year and economic growth to begin picking up this year.

- RBNZ Deputy Governor Hawkesby said restrictive policy is needed to ensure inflation expectations anchor at 2% and policy is going to stay restrictive for some time yet, while they don’t have a lot of room to manoeuvre when it comes to future inflation shocks. Hawkesby said they are on the right path with inflation and have to hold their course, as well as noted they are not in a mindset to cut rates now and will be cutting sometime down the track.

- Fitch cuts China new home sales forecast, sees wider effects from a slower recovery. Cuts forecast for the Chinese hosing market to a 5-10% decline in 2024 new home sales

European bourses, Stoxx600 (+0.1%) began the session firmly in the green, though did succumb to some early morning pressure ahead of EZ inflation. Thereafter, European equities took another leg lower, with sentiment subdued following the hotter-than-expected print. However, the move came alongside marked uptick in EGBs, with the move seen across assets and has a risk-feel to it; though, it does appear to have been driven by the ‘relief’ in EGBs post-HICP which while hotter-than-expected continues the cooling narrative. European sectors hold a positive tilt; Autos is firmer, being propped up by post-earning gains in Daimler Truck (+12.8%). Energy has been lifted by recent strength in the crude complex; BP (+1.2%)/Shell (+1%). To the downside, Saint-Gobain weighs on Construction & Materials, after poor results. US Equity Futures (ES -0.2%, NQ -0.2%, RTY -0.4%) are entirely in the red. The RTY underperforms, largely hampered by regional banking fears after NYCB (-24% pre-market) announced it had identified weaknesses in internal controls.

Top European news

- Portuguese Finance Minister Medina called for the ECB to start lowering borrowing costs and warned that maintaining them at their current level is a “high risk”, while he noted various European countries are experiencing a strong slowdown with some already in stagnation and recession, according to Bloomberg.

- SNB Chairman Thomas Jordan to step down at end of September 2024.

- UK Chancellor Hunt has ruled out stamp duty cuts in the March budget, according to i news; due to a belief this would fuel inflation

FX

- Contained trade for the DXY and within a 104.04-21 range, respecting yesterday’s 103.65-104.20 parameters. Upcoming data/speaker slate could provide impetus and bring the weekly high of 104.24 into view.

- EUR/USD is ultimately around flat after the hotter-than-expected inflation metrics but respecting yesterday’s 1.0795-1.0856 range. Interim resistance provided by the 100DMA at 1.0824.

- JPY is the underperformer across the majors following dovishly-perceived comments from Ueda. USD/JPY is up to 150.68 at best with all eyes on the YTD peak at 150.88.

- Antipodeans are marginally firmer vs. the USD in uneventful trade with AUD continuing to pivot around the 0.65 mark after making a base for the week yesterday at 0.6486. NZD/USD unable to crack 0.61 after printing a YTD trough yesterday at 0.6077.

- PBoC set USD/CNY mid-point at 7.1059 vs exp. 7.2011 (prev. 7.1036).

Fixed Income

- USTs began the session with a bearish bias, attempting to pare back some of the PCE-induced gains. However, after the EZ CPI (which sparked a fleeting hawkish reaction), the bond complex caught a bid, taking treasuries to fresh session highs; currently around 6 ticks firmer with the curve steeper into US ISM & Fed speak.

- Bunds also began the session on a softer footing. Following the hotter-than-expected CPI there was a fleeting downward move to a test of 132.00 however this was shortlived with Bunds now bouncing and briefly surpassing the 132.54 overnight high. Perhaps driven by the view that while HICP was hotter than expected, it is still cooling overall and does not change the pre-existing narrative of a June move.

- Gilt price action is in-fitting with EGBs, and unreactive to its own PMI (the HCOB commentary brought attention to ongoing inflationary pressures); Gilts following suit, briefly moved into the green as EGBs bounced but have settled near unchanged.

Commodities

- Crude is firmer after a relatively contained start to the session. The complex caught a bid in the European morning, just after the release of EZ Manufacturing PMIs which were revised up but remain bleak overall; Brent holds just shy of USD 83/bbl.