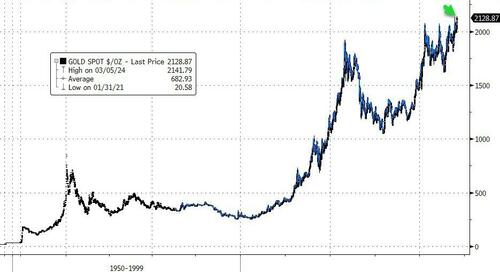

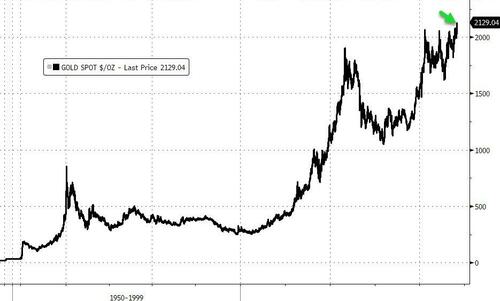

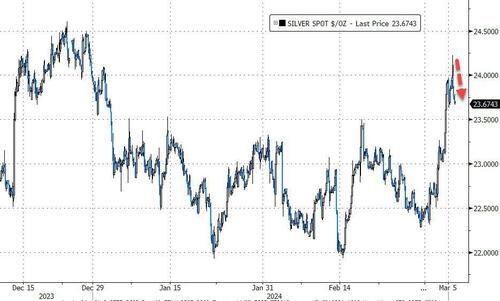

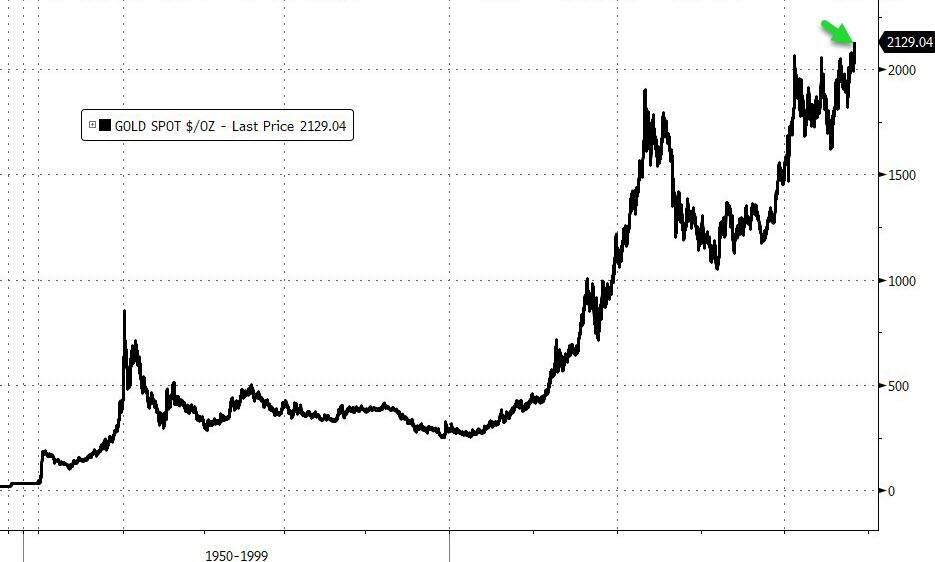

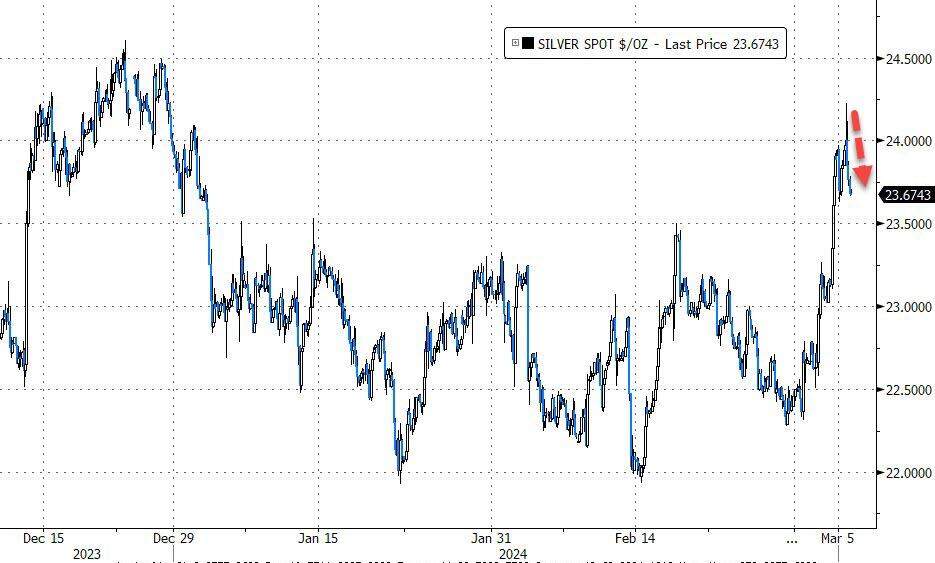

MARCH 5//GOLD CLOSED UP $16.55 TO $2133.50/SILVER WAS DOWN 2 CENTS TO $23.77/PLATINUM WAS DOWN $15.05 TO $885.20 WHILE PALLADIUM WAS UP $27.45 TO $951.70/CHINA’S APPLE SALES PLUNGE 24%//LEFTISTS KNOCK OUT ELECTRICAL GRID RESPONSIBLE FOR TESLA PRODUCTION IN GERMANY//ISRAEL VS HAMAS UPDATES//ISRAEL VS HEZBOLLAH UPDATES//WEST BANK UPDATES/HOUTHIS VS WEST//COVID UPDATES/VACCINE INJURIES//MARK CRISPIN MILLLER/SLAY NEWS ETC//USA SERVICE DATA SUGGESTS STAGLATION TO HAVE HIT IN FEBRUARY//OUR GOOD FRIEND JOE BIDEN SECRETLY FLEW IN 320,000 ILLEGAL IMMIGRANTS INTO THE USA WHICH MUST BE TREASONABLE//MORE SWAMP STORIES FOR YOU TONIGHT//

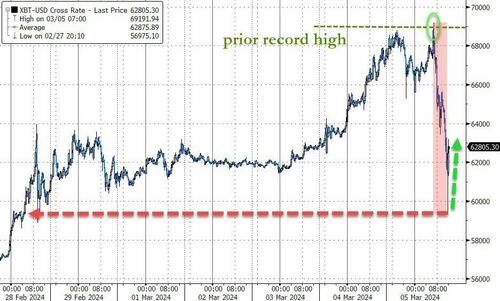

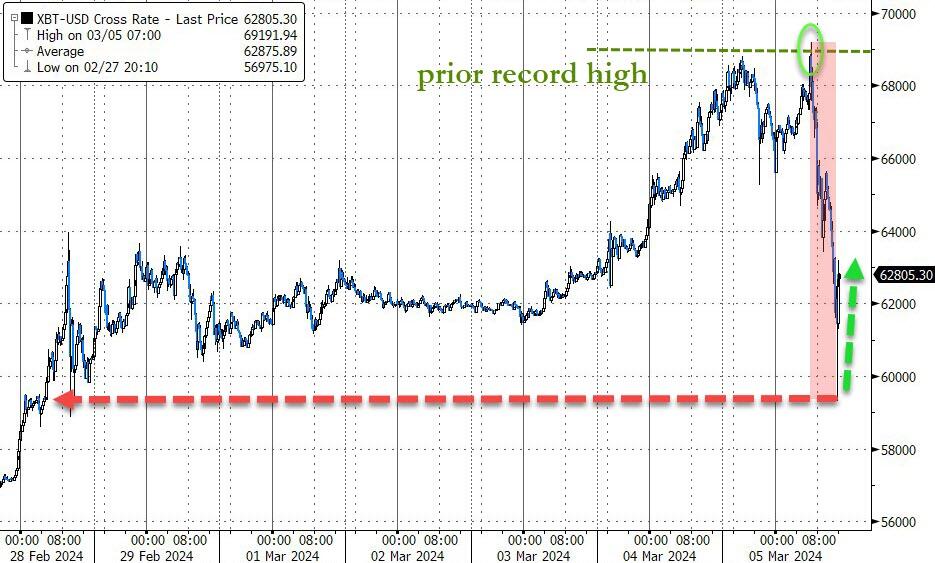

Bitcoin: afternoon price: $62,317 DOWN 5182 dollars

Platinum price closing UP $13.90 AT $900.25

Palladium price; DOWN $30.90 AT $924.25

END

SHANGHAI GOLD PREMIUM 4 DOLLARS/COMEX GOLD

SHANGHAI GOLD (USD) FUTURES – QUOTES

Beginning Monday, April 1, 2024, CME Group settlement data will no longer be accessible through ftp.cmegroup.com and will have a delayed publication time of 12:00 a.m. CT on all cmegroup.com web pages. Learn about alternate ways to access the data in our FAQ.

I will now provide gold in Canadian dollars, British pounds and Euros

4: 15 PM ACCESS

*CANADIAN GOLD: $2,894,00 UP $21.24 CDN dollars per oz( * NEW ALL TIME HIGH 2,894.00CDN DOLLARS PER OZ//MARCH 5 2024)

*BRITISH GOLD: 175,32 UP 9.00 pounds per oz// *(NEW ALL TIME HIGH//CLOSING///1675.32 BRITISH POUNDS/OZ) MARCH 5/2024

*EURO GOLD: 1960.50 UP 11.50 euros per oz //* (ALL TIME CLOSING HIGH: 1960.50 EUROS PER OZ//MARCH 4.2024)

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

A LITTLE HISTORY LESSON ON GOLD MANIPULATION AND THE FORMATION OF GATA:

I testified in the March 2010 hearing //we were also part of the BIS lawsuit filed in 2000.

GATA became incorporated in early 1999 to expose the manipulation and suppression of the gold/silver prices. We went all out do so, not only writing to the authorities, but going there and talking with them. We WENT THERE…*The following letter was sent to Chairman Saxton to prepare him for our meeting on April 27,1999:

The “bombshell” that GATA dropped at the CFTC Public Hearing on Precious Metals, March 25, 2010 was stunning. The video of Bill Murphy, Chairman of GATA, revealing a whistleblower source who has warned the CFTC Enforcement Division of market manipulation by JPMorganChase in advance of it happening and witnessed JPM traders bragging of their exploits can be viewed here (since obliterated).

092 C DEUTSCHE BANK 31 190 H BMO CAPITAL 526 323 C HSBC 114 363 H WELLS FARGO SEC 187 435 H SCOTIA CAPITAL 90 657 C MORGAN STANLEY 12 661 C JP MORGAN 50 69 686 C STONEX FINANCIA 3 690 C ABN AMRO 12 726 C CUNNINGHAM COM 1 737 C ADVANTAGE 58 905 C ADM 1

092 C DEUTSCHE BANK 34 190 H BMO CAPITAL 293 323 C HSBC 640 248 363 H WELLS FARGO SEC 149 365 H MAREX CAPITAL M 1 435 H SCOTIA CAPITAL 379 657 C MORGAN STANLEY 5 661 C JP MORGAN 120 372 686 C STONEX FINANCIA 3 690 C ABN AMRO 7 737 C ADVANTAGE 35 905 C ADM 8

TOTAL: 1,147 1,147 MONTH TO DATE: 1,147

ACCESS MARKET:

JPMorgan stopped 69/577 contracts.

FOR MARCH/2024

GOLD: NUMBER OF NOTICES FILED FOR MAR/2024. CONTRACT: 577 NOTICES FOR 57700 OZ or 1 TONNES

total notices so far: 1770 contracts for 177,000 Oz (5.505 tonnes)

FOR MARCH:

SILVER NOTICES: 936 NOTICE(S) FILED FOR 4,680,000 OZ/

total number of notices filed so far this month : 4170 for 20,850,000 oz

XXXXXXXXXXXXXXXXXX

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

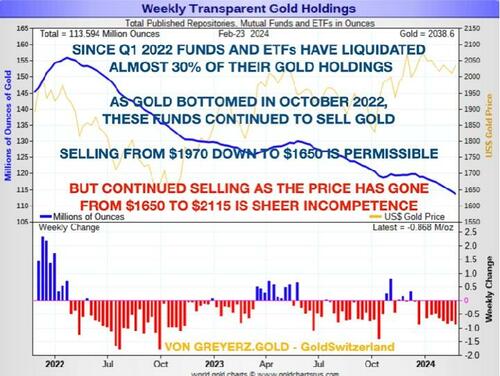

BOTH GLD AND SLV ARE FRAUDULENT VEHICLES//THEY ARE NOW RAIDING GLD AND SLV FOR PHYSICAL

GLD

WITH GOLD UP $16.55// the following makes lots of sense???

INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD/ : HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A HUGE WITHDRAWAL OF 2.3 TONNES OF GOLD OUT OF THE GLD

INVENTORY RESTS AT 823.77 TONNES

SLV//

WITH NO SILVER AROUND AND SILVER DOWN 2 CENTS AT THE SLV//

HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A MASSIVE WITHDRAWAL OF 1.499 MILLION OZ FROM THE SL

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV.

CLOSING INVENTORY: 429.483 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A SMALL SIZED 143 CONTRACTS TO 143,353 AND CLOSER TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THIS HUGE SIZED LOSS IN COMEX OI WAS ACCOMPLISHED WITH OUR RISE IN PRICE OF $0.80 IN SILVER PRICING AT THE COMEX ON MONDAY. WE HAD ZERO LONG LIQUIDATION AT THE COMEX SESSION WITH AGAIN MAJOR SHORT COVERING WITH THE HUGE PRICE RISE. WE HAD A HUGE 1267 T.A.S ISSUANCE AND THESE WILL BE USED FOR MANIPULATION LATER THIS MONTH/AS WELL AS TODAY. PLEASE NOTE THAT THE CROOKS NEED A HIGHER SILVER T.A.S. TO CARRY ON THEIR CROOKED MANIPULATION ON A DAILY BASIS

CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON MONDAY NIGHT: 1267 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS. IT THUS LOOKS LIKE THE FED (GOV’T) IS BEHIND ALL OF THESE TRADES.

WE HAVE NOW SET ANOTHER RECORD LOW AT 114,102 CONTRACTS ///JULY 3.2023// OUR BANKERS WITH THE HELP OF SPECULATORS AND HIGH FREQUENCY TRADERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.80),AND WERE UNSUCCESSFUL IN KNOCKING ANY SILVER LONGS AS WE HAD A HUMONGOUS SIZED GAIN OF 2007 CONTRACTS ON OUR TWO EXCHANGES, IT OCCURRED WITH A MUCH HIGHER PRICE OF 80 CENTS PER OZ OF SILVER.

WE MUST HAVE HAD:

A HUGE SIZED 1864 ISSUANCE OF EXCHANGE FOR PHYSICALS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 22.270 MILLION OZ (FIRST DAY NOTICE) FOLLOWED BY TODAY,S 4.180 MILLION OZ QUEUE JUMP //NEW TOTALS INCREASES TO : 23.385 MILLION OZ

//NEW STANDING FOR SILVER IS THUS 23.385 MILLION OZ

/ HUGE SIZED COMEX OI GAIN/GIGANTIC SIZED EFP ISSUANCE/ VI) HUGE SIZED NUMBER OF T.A.S. CONTRACT ISSUANCE 1267 CONTRACTS)/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL -REMOVED A HUGE 622 CONTRACTS //

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS FEB. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF FEB

TOTAL CONTRACTS for 3 days, total 3214 contracts: OR 16.070 MILLION OZ (1071 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 16.070 MILLION OZ

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH 2022: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 118.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 85.745 MILLION OZ (SMALLER THAN LAST MONTH)

AUGUST: 171.43 MILLION OZ (THIS MONTH IS GOING TO BE HUGE //2ND HIGHEST ON RECORD

SEPT: 72.705 MILLION OZ (SMALLER THIS MONTH)

OCT: 97.455 MILLION OZ

NOV. 50.050 MILLION OZ

DEC. 66.140 MILLION OZ//

TOTAL 2023: 1,104.10 MILLION OZ/

JAN ’24 : 78.655 MILLION OZ//

FEB /2024 :66.135 MILLION OZ./FINAL

MARCH: 6.75 MILLION OZ//

RESULT: WE HAD A SMALL SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 143CONTRACTS WITH OUR GAININ PRICE OF SILVER PRICING AT THE COMEX//MONDAY.,. THE CME NOTIFIED US THAT WE HAD A HUGE EFP ISSUANCE CONTRACTS: 1864 ISSUED FOR MAY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS. WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR MARCH. OF 23.385 MILLION OZ ON FIRST DAY NOTICE FOLLOWED BY TODAY’S HUGE 4,180 MILLION OZ QUEUE JUMP

//NEW TOTAL STANDING LOWERS TO 23.385 MILLION OZ

WE HAVE A HUMONGOUS GAIN OF 2007 OI CONTRACTS ON THE TWO EXCHANGES WITH THE STRONG GAIN IN PRICE. THE TOTAL OF TAS INITIATED CONTRACTS TODAY: A HUGE SIZED 1864 CONTRACTS//HUGE FRONT END OF THE TAS CONTRACTS WERE LIQUIDATED DURING THE MONDAY COMEX SESSION/// WITH MAJOR SHORT COVERING FROM OUR SPEC SHORTS ( WITH PRICE OF SILVER RISING) . THE NEW TAS ISSUANCE MONDAY NIGHT (1267) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE//PROBABLY TODAY., .

WE HAD 936 NOTICE(S) FILED TODAY FOR 4,680,000 MILLION OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A HUGE SIZED 13,310 CONTRACTS TO 467,693 AND CLOSER TO THE RECORD (SET JAN 24/2020) AT 799,733 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110, BUT WE ARE NOW CLOSER TO OUR ALL TIME LOW OF 390,000 CONTRACTS.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED 279 CONTRACTS

WE HAD A HUGE SIZED INCREASE IN COMEX OI ( 13,310 CONTRACTS) WITH OUR MEGA $30.55 GAIN IN PRICE//MONDAY. THE BANKERS WERE FORCED TO SUPPLY THE NECESSARY SHORT PAPER TO CONTAIN GOLD’S RISE.WE ALSO HAD A RATHER LARGE INITIAL STANDING IN GOLD TONNAGE FOR MARCH. AT 10.270 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’’S 1100 OZ QUEUE JUMP

NEW TOTAL Of INITIAL GOLD STANDING RISES TO: 7.502 TONNES // ALL OF THIS HAPPENED WITH OUR $30.55 GAIN IN PRICE WITH RESPECT TO MONDAY’S TRADING. WE HAD A HUMONGOUS SIZED GAIN OF 22,970 OI CONTRACTS (72.446) PAPER TONNES) ON OUR TWO EXCHANGES.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 9660CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 467,693

IN ESSENCE WE HAVE A HUMONGOUS SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 22,970 CONTRACTS WITH 13,310 CONTRACTS INCREASED AT THE COMEX// AND A STRONG SIZED 9660 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 22,970 CONTRACTS.. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): HUGE SIZED 6168 CONTRACTS.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD STRONG SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (9660 CONTRACTS) ACCOMPANYING THE HUGE SIZED GAIN IN COMEX OI (13,310) //TOTAL GAIN FOR OUR THE TWO EXCHANGES: 22,970 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR FORMER FORMAT OF BANKERS GOING LONG AND SPECULATORS GOING SHORT ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR MARCH. AT 7.502 TONNES

/ 3) ZERO LONG LIQUIDATION // 4) HUGE SIZED COMEX OPEN INTEREST GAIN/ 5) STRONG ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER///6: HUGE T.A.S. ISSUANCE: 6168CONTRACTS//HUGE SHORT COVERING AGAIN

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023-2024 INCLUDING TODAY

MARCH

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF MARCH. :

TOTAL EFP CONTRACTS ISSUED: 23,008 CONTRACTS OR 2,300,800OZ OR 71.564 TONNES IN 3TRADING DAY(S) AND THUS AVERAGING: 7669 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 3TRADING DAY(S) IN TONNES 71.564 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2022, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 71.564/3550 x 100% TONNES 2.02% OF GLOBAL ANNUAL PRODUCTION

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH/2022: 409.30 TONNES //FINAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 151.69 TONNES (WEAKER THAN LAST MONTH)

AUGUST: 195.28 TONNES (A STRONGER MONTH)//FINAL

SEPT: 254.709 TONNES (WILL BE LARGER THAN LAST MONTH AND A STRONG MONTH)

OCT. 248.09 TONNES. LIKE SILVER, THIS MONTH IS GOING TO BE A STRONG E.F.P. ISSUANCE.

NOV. 239.16 TONNES//WILL BE STRONG THIS MONTH,

DEC. 213.704 TONNES. A STRONG MONTH//

TOTAL FOR YEAR 2023: 2,569.57 TONNES VS 2578 TONNES LAST YEAR

JAN ’24: 291.76 TONNES (WILL BE MUCH GREATER THAN LAST MONTH.//3RD HIGHEST EVER RECORDED EX FOR PHYSICAL)

FEB’24: 201.947 TONNES

MARCH 2024: 71.564 TONNES

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF FEB. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (APRIL), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER ROSE BY A SMALL SIZED 143 CONTRACTS OI TO 143,975 AND CLOSER TO THE COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 6 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 1864 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAY 1864 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 1864 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 143 CONTRACTS AND ADD TO THE 1864 E.FP. ISSUED

WE OBTAIN A HUMONGOUS SIZED GAIN OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 2007CONTRACTS

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTAL 10.035 MILLION OZ

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS//

TUESDAY MORNING/MONDAY NIGHT

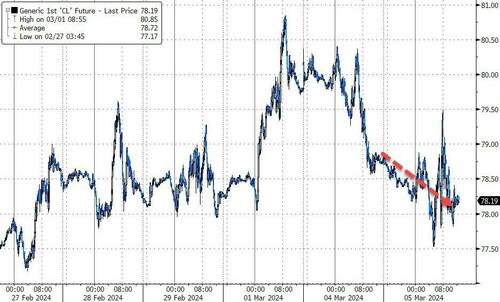

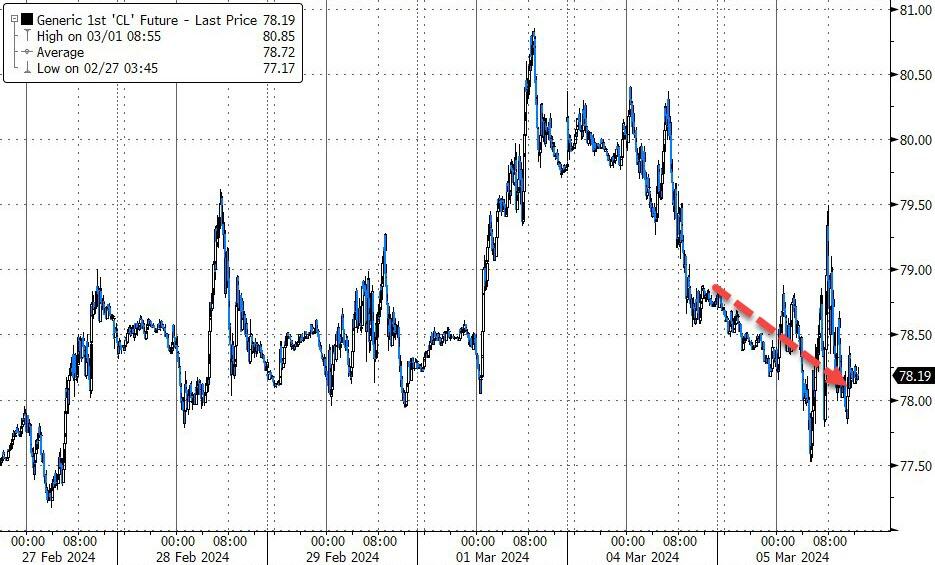

SHANGHAI CLOSED UP 8.49 PTS OR 0.28% //Hang Seng CLOSED DOWN 433.33 PTS OR 2.61% / Nikkei CLOSED DOWN 11.60 PTS OR 0.03%//Australia’s all ordinaries CLOSED DOWN 0.10% /Chinese yuan (ONSHORE) closed DOWN 7.1992 //OFFSHORE CHINESE YUAN CLOSED DOWN TO 7.2123 /Oil DOWN TO 78.14 dollars per barrel for WTI and BRENT UP AT 82.19/ Stocks in Europe OPENED ALL MOSTLY MIXED// ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE YUAN WEAKER

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A HUMONGOUS SIZED 13,310 CONTRACTS TO 467,693 WITH OUR GAIN IN PRICE OF $30.55 WITH RESPECT TO MONDAY TRADING. MOST LIKELY IT WAS THE BANKERS SUPPLYING THE NECESSARY PAPER WITH OUR SHORT PLAYERS EXITING AS FAST AS THEIR FEET COULD CARRY THEM. THE SHORTS HAVE BEEN KILLED SO IT IS UNLIKELY THAT ANY OF THEM WOULD DARE INTO THIS ARENA ESPECIALLY WITH CENTRAL BANKERS BUYING PHYSICAL GOLD ADDING TO THEIR OFFICIAL TOTALS.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE NON ACTIVE DELIVERY MONTH OF MARCH..… THE CME REPORTS THAT THE BANKERS ISSUED A STRONG SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 9660 EFP CONTRACTS WERE ISSUED: : APRIL 9660 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 9660CONTRACTS

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A MEGA HUMONGOUS SIZED TOTAL OF 22,970 CONTRACTS IN THAT 9660 LONGS WERE TRANSFERRED AS EXCHANGE FOR PHYSICALS TO LONDON AND WE HAD A HUGE SIZED GAIN OF 13,310 COMEX CONTRACTS..AND THIS GAIN ON OUR TWO EXCHANGES HAPPENED WITH OUR HUGE GAIN IN PRICE OF $30.55 MONDAY COMEX. AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS DURING MID MONTH IN THE DELIVERY CYCLE), THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR MONDAY NIGHT WAS A STRONG SIZED 6168 CONTRACTS. THROUGHOUT THE PAST SEVERAL WEEKS, THE BANKERS SOLD OFF THE LONG SIDE OF THE SPREAD WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR/T.A.S. SPREAD WHICH WILL BE LIQUIDATED IN DAYS HENCE//.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: MARCH (7.5023 TONNES) ( NON ACTIVE MONTH)

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 24 MONTHS OF 2021-2023:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276 TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 7.5023 TONNES

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT GAINED $30.55 //// AND WERE UNSUCCESSFUL IN KNOCKING ANY SPECULATOR LONGS AS WE HAD A HUMONGOUS SIZED GAIN OF22,970 TOTAL CONTRACTS ON OUR TWO EXCHANGES WITH OUR HIGHER PRICE. WE HAD TO HAVE HAD ANOTHER HUGE EPISODE OF STRONG SHORT COVERING. WE HAD A STRONG T.A.S. LIQUIDATION ON THE FRONT END OF MONDAY’S TRADING . THE T.A.S. ISSUED ON MONDAY NIGHT, WILL BE “PUT INTO THE BANK” TO BE USED AT A LATER DATE AT THE COLLUSIVE CHOOSING OF OUR BANKERS.

WE HAVE GAINED A TOTAL OI OF 71,446 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR MARCH. (10.3576 TONNES) ON FIRST DAY NOTICE FOLLOWED BY TODAY’S 7100 OZ QUEUE JUMP//NEW STANDING INCREASES TO 7.5023 TONNES

ALL OF THIS WAS ACCOMPLISHED WITH OUR HUGE GAIN IN PRICE TO THE TUNE OF $30.55

WE HAD -REMOVED 279 CONTRACTS TO THE COMEX TRADES TO OPEN INTEREST (CROOKS)

NET GAIN ON THE TWO EXCHANGES 22,970 CONTRACTS OR 2,297,000 OZ OR 71.446 TONNES. estimated volume today 277,477 fair to good

Total monthly oz gold served (contracts) so far this month

1770 notices 177,000 oz 5.505 TONNES

Total accumulative withdrawals of gold from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of gold from the Customer inventory this month

x

0 dealer deposits:

total dealer deposits: nil oz

total customer withdrawals: 1

i) Out of Malca: 11,574.360 oz

total withdrawal: 11,574.360 oz

we had 0 customer deposit

total deposit nil

Adjustments:2 dealer to customer;

i)JPMorgan 11,574.360 oz

ii) Manfra 675.171 oz

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR FEB.

For the front month of MARCH we have an oi of 1219 contracts having GAINED 63 contracts. We had 8 contracts filed upon on Monday, so we gained 71 contracts or an additional 7100 oz of gold(22.08 tonnes) will stand at the comex in this non active delivery month of March

APRIL LOST 3186 CONTRACTS FALLING TO 333,666.

MAY EARNED 49 CONTRACTS TO STAND AT 84

JUNE INCREASED ITS OI BY 15,180 CONTRACTS UP TO 82,818 CONTRACTS.

We had 577 contracts filed for today representing 57,700 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 50 notices were issued from their client or customer account. The total of all issuance by all participants equate to 577 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 69 notice(s) was (were) stopped ( (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for the MARCH. /2024. contract month, we take the total number of notices filed so far for the month (1770 x 100 oz ), to which we add the difference between the open interest for the front month of MARCH. (1219 CONTRACTS) minus the number of notices served upon today 577 x 100 oz per contract equals 234,200 OZ OR 7.2846 TONNES

thus the INITIAL standings for gold for the MARCH. contract month: No of notices filed so far (1770) x 100 oz + (1219) {OI for the front month} minus the number of notices served upon today (577) x 100 oz which equals 241,200 oz (7.5023 TONNES)

TOTAL COMEX GOLD STANDING FOR MARCH: 7.5023 TONNES WHICH IS HUGE FOR A NON ACTIVE DELIVERY MONTH IN THE CALENDAR.

To calculate the number of silver ounces that will stand for delivery in MARCH. we take the total number of notices filed for the month so far at 4170 x 5,000 oz = 20,858,000 oz

to which we add the difference between the open interest for the front month of MARCH. (1443) and the number of notices served upon today 936 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the MARCH/2024 contract month: 4170 (notices served so far) x 5000 oz + OI for the front month of MARCH. (1443) – number of notices served upon today (936 )x 500 oz of silver standing for the MARCH contract month equates to 23.385 MILLION OZ.

New total standing: 23.385 million oz.

There are 51.963 million oz of registered silver.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS//

BOTH GLD AND SLV ARE MASSIVE FRAUDS!

MARCH 5 WITH GOLD UP $16.55 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.30 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 821.47 TONNES

MARCH 4 WITH GOLD UP $30.55 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF .86 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 823.77 TONNES

MARCH 1 WITH GOLD UP $40.40 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 822.91 TONNES

FEB29/WITH GOLD UP $12.60 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD//WITHDRAWAL OF 4.03 TONNES INVENTORY RESTS AT 822.91 TONNES

FEB28/WITH GOLD DOWN $1.00 TODAY NO CHANGES IN GOLD INVENTORY AT THE GLD INVENTORY RESTS AT 826.94 TONNES

FEB27/WITH GOLD UP $4.40 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF .87 TONNES OF GOLD FROM THE GLD:/INVENTORY RESTS AT 826.94 TONNES

FEB26/WITH GOLD DOWN $8.90 TODAY NO CHANGES IN GOLD INVENTORY AT THE GLD:/INVENTORY RESTS AT 827.81 TONNES

FEB23/WITH GOLD UP $17 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.01 TONNES OF GOLD FROM THE GLD.//INVENTORY RESTS AT 827.81 TONNES

FEB22/WITH GOLD DOWN $2.15 TODAY NO CHANGES IN GOLD INVENTORY AT THE GLD://INVENTORY RESTS AT 829.82 TONNES

FEB21/WITH GOLD DOWN $5.30 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 7.59 TONNES OF GOLD OUT OF THE GLD///INVENTORY RESTS AT 29.82 TONNES

FEB20/WITH GOLD UP $16.15 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 0.58 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 837.89 TONNES

FEB16/WITH GOLD UP $8,60 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.73 TONNES OF GOLD FROM THE GLD///INVENTORY RESTS AT 837.31 TONNES

FEB15/WITH GOLD UP $11.70 TODAY NO CHANGES IN GOLD INVENTORY AT THE GLD:/INVENTORY RESTS AT 841.92 TONNES

FEB14/WITH GOLD DOWN $2.75 TODAY NO CHANGES IN GOLD INVENTORY AT THE GLD:/INVENTORY RESTS AT 841.92 TONNES

FEB13/WITH GOLD DOWN $20.15 TODAY NO CHANGES IN GOLD INVENTORY AT THE GLD:/INVENTORY RESTS AT 841.92 TONNES

FEB12/WITH GOLD DOWN $4.80 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A STRONG WITHDRAWAL OF 1.74 TONNES OF GOLD FROM THE GLD. / //://INVENTORY RESTS AT 841.92 TONNES

FEB9/WITH GOLD DOWN $8.60 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A STRONG DEPOSIT OF 1.44 TONNES OF GOLD FROM THE GLD. / //://INVENTORY RESTS AT 843.66 TONNES

FEB8/WITH GOLD DOWN $2.70 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A MASSIVE WITHDRAWAL OF 5.47 TONNES OF GOLD FROM THE GLD. / //://INVENTORY RESTS AT 842.22 TONNES:

FEB7/WITH GOLD UP $0.40 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A MASSIVE WITHDRAWAL OF 4.04 TONNES OF GOLD FROM THE GLD. / //://INVENTORY RESTS AT 847.69 TONNES:

FEB6/WITH GOLD UP $8.50 TODAY NO CHANGES IN GOLD INVENTORY AT THE GLD:/ / //://INVENTORY RESTS AT 851.73 TONNES:

FEB5/WITH GOLD DOWN $9.85 TODAY SMALL CHANGES IN GOLD INVENTORY AT THE GLD:A DEPOSIT OF .58 TONNES OF GOLD INTO THE GLD// / //://INVENTORY RESTS AT 851.73 TONNES:

FEB 2/WITH GOLD DOWN $17.95 TODAY SMALL CHANGES IN GOLD INVENTORY AT THE GLD:A WITHDRAWAL OF .58 TONNES OF GOLD FROM THE GLD// / //://INVENTORY RESTS AT 851.15 TONNES:

FEB 1/WITH GOLD UP $5.00 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD:A WITHDRAWAL OF 1.73 TONNES OF GOLD FROM THE GLD// / //://INVENTORY RESTS AT 851.15 TONNES:

JAN 31/WITH GOLD UP $16.40 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD:A WITHDRAWAL OF 2.01 TONNES OF GOLD FROM THE GLD// / //://INVENTORY RESTS AT 852.88 TONNES:

JAN 30/WITH GOLD UP $6.50 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD:A WITHDRAWAL OF 1.16 TONNES OF GOLD FROM THE GLD// / //://INVENTORY RESTS AT 854.89 TONNES:

TOTAL IN LAST 18 DAYS WITHDRAWAL OF 14.12 TONNES

JAN 29/WITH GOLD UP $8.70 TODAYHUGE CHANGES IN GOLD INVENTORY AT THE GLD:A WITHDRAWAL OF 2.88 TONNES OF GOLD FROM THE GLD// / //://INVENTORY RESTS AT 856.05 TONNES

JAN 26/WITH GOLD DOWN $0.10 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD: / //://INVENTORY RESTS AT 858.93 TONNES

JAN 25/WITH GOLD UP $2.50 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD: / //://INVENTORY RESTS AT 858.93 TONNES

JAN 24/WITH GOLD DOWN $9.75 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD: / //://INVENTORY RESTS AT 858.93 TONNES

JAN 23/WITH GOLD UP $3.95 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.02 TONNES OF GOLD FROM THE GLD/ //://INVENTORY RESTS AT 858.93 TONNES

GLD INVENTORY: 821.47 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

MARCH 5/WITH SILVER DOWN 2 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A HUGE WITHDRAWAL OF 1.499 MILION OZ OF SILLVER FROM THE SLV//// : SLV INVENTORY RESTS AT 429.483 MILLION OZ

MARCH 4/WITH SILVER UP CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: // : SLV INVENTORY RESTS AT 430.982 MILLION OZ

MARCH 1/WITH SILVER UP 49 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: // : SLV INVENTORY RESTS AT 430.982 MILLION OZ

FEB 29/WITH SILVER UP 25 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.104 MILLION OZ OUT OF THE SLV//// : SLV INVENTORY RESTS AT 430/982 MILLION OZ

FEB 28/WITH SILVER DOWN 7 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 5.123 MILLION OZ INTO THE SLV//// : SLV INVENTORY RESTS AT 433.086 MILLION OZ

FEB 27/WITH SILVER UP 3 CENTS TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 0.64 MILLION OZ FROM THE SLV//// : SLV INVENTORY RESTS AT 427.943 MILLION OZ

FEB 26/WITH SILVER DOWN 44 CENTS TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.065 MILLION OZ FROM THE SLV//// : SLV INVENTORY RESTS AT 428.603 MILLION OZ

FEB 23/WITH SILVER DOWN 44 CENTS TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.065 MILLION OZ FROM THE SLV//// : SLV INVENTORY RESTS AT 428.603 MILLION OZ

FEB 22/WITH SILVER DOWN 10 CENTS TODAY NO CHANGES IN SILVER INVENTORY AT THE SLV

// : SLV INVENTORY RESTS AT 432.766 MILLION OZ

FEB 21/WITH SILVER DOWN 28 CENTS TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 2.348 MILLION OZ OF SILVER FROM THE SLV// : SLV INVENTORY RESTS AT 432.766 MILLION OZ

FEB 20/WITH SILVER DOWN 33 CENTS TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 3.385 MILLION OZ OF SILVER FROM THE SLV// : SLV INVENTORY RESTS AT 435.008 MILLION OZ

FEB 16/WITH SILVER UP 53 CENTS TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV A DEPOSIT OF 1.235 MILLION OZ OF SILVER FROM THE SLV// : SLV INVENTORY RESTS AT 438.393 MILLION OZ

FEB 15/WITH SILVER UP 56 CENTS TODAY NO CHANGES IN SILVER INVENTORY AT THE SLV : SLV INVENTORY RESTS AT 437.615 MILLION OZ

FEB 14/WITH SILVER UP 24 CENTS TODAY NO CHANGES IN SILVER INVENTORY AT THE SLV : SLV INVENTORY RESTS AT 437.615 MILLION OZ

FEB 13/WITH SILVER DOWN 60 CENTS TODAY SMALL CHANGES IN SILVER INVENTORY AT THE SLV A SMALL WITHDRAWAL OF 0.504 MILLION OZ OZ OUT OF THE SLV: SLV INVENTORY RESTS AT 437.615 MILLION OZ

FEB 12/WITH SILVER UP 14 CENTS TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV A HUGE WITHDRAWAL OF 1.921 MILLION OZ OZ OUT OF THE SLV: SLV INVENTORY RESTS AT 438.119 MILLION OZ

FEB 9/WITH SILVER DOWN 4 CENTS TODAY SMALL CHANGES IN SILVER INVENTORY AT THE SLV A SMALL DEPOSIT OF 600,000 OZ INTO THE SLV: SLV INVENTORY RESTS AT 440.040 MILLION OZ

FEB 8/WITH SILVER UP 29 CENTS TODAY NO CHANGES IN SILVER INVENTORY AT THE SLV: SLV INVENTORY RESTS AT 439.994 MILLION OZ

FEB 7/WITH SILVER DOWN 18 CENTS TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A MASSIVE DEPOSIT OF 4.04 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 439.994 MILLION OZ//LAST 9 DAYS: 10.7598 MILLION OZ WITHDRAWAL

FEB 6/WITH SILVER UP 11 CENTS TODAY NO CHANGES IN SILVER INVENTORY AT THE SLV: /INVENTORY RESTS AT 435.144 MILLION OZ//LAST 9 DAYS: 10.7598 MILLION OZ WITHDRAWAL

FEB 5/WITH SILVER DOWN 32 CENTS TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.345 MILLION OZ FROM THE SLV(FAIRY TALES) // /INVENTORY RESTS AT 435.144 MILLION OZ//LAST 8 DAYS: 10.7598 MILLION OZ WITHDRAWAL

FEB 2/WITH SILVER DOWN 50 CENTS TODAY SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 0.58 MILLION OZ INTO THE SLV(FAIRY TALES) // /INVENTORY RESTS AT 438.489 MILLION OZ//LAST 7 DAYS: 14.105 MILLION OZ WITHDRAWAL

FEB 1/WITH SILVER UP 7 CENTS TODAY MEGA CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.19 MILLION OZ INTO THE SLV(FAIRY TALES) // /INVENTORY RESTS AT 438.947 MILLION OZ//LAST 6 DAYS: 10.3018 MILLION OZ WITHDRAWAL

JAN 31/WITH SILVER DOWN 8 CENTS TODAY MEGA CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.7438 MILLION OZ INTO THE SLV(FAIRY TALES) // /INVENTORY RESTS AT 440.137 MILLION OZ//LAST 5 DAYS: 9.1118 MILLION OZ WITHDRAWAL

JAN 30/WITH SILVER DOWN 5 CENTS TODAY MEGA CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.876 MILLION OZ INTO THE SLV(FAIRY TALES) // /INVENTORY RESTS AT 442.699 MILLION OZ//LAST 4 DAYS: 7.368 MILLION OZ WITHDRAWAL

JAN 29/WITH SILVER UP $.37 TODAY MEGA CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.105 MILLION OZ INTO THE SLV(FAIRY TALES) // /INVENTORY RESTS AT 444.575 MILLION OZ

JAN 26/WITH SILVER DOWN $0.03 TODAY MEGA CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.556 MILLION OZ INTO THE SLV(FAIRY TALES) // /INVENTORY RESTS AT 446.680 MILLION OZ

JAN 25/WITH SILVER UP $0.03 TODAY MEGA CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.831 MILLION OZ INTO THE SLV(FAIRY TALES) // /NVENTORY RESTS AT 448.236 MILLION OZ

JAN 24/WITH SILVER UP $0.44 TODAY MEGA CHANGES IN SILVER INVENTORY AT THE SLV: ANOTHER DEPOSIT OF 1.375 MILLION OZ INTO THE SLV(FAIRY TALES) // //INVENTORY RESTS AT 450.067 MILLION OZ

JAN 23/WITH SILVER UP $0.21 TODAY MEGA CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 16.201 MILLION OZ INTO THE SLV(FAIRY TALES) // //INVENTORY RESTS AT 448.694 MILLION OZ

JAN 22/WITH SILVER DOWN $0.45 TODAY NO CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 458,000 OZ OUT OF THE SLV // //INVENTORY RESTS AT 432.493 MILLION OZ

JAN 19/WITH SILVER DOWN $0.11 TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 458,000 OZ OUT OF THE SLV // //INVENTORY RESTS AT 432.493 MILLION OZ

JAN 18/WITH SILVER UP $0.13 TODAY NO CHANGES IN SILVER INVENTORY AT THE SLV: // //INVENTORY RESTS AT 432.951 MILLION OZ

JAN 17/WITH SILVER DOWN $0.38 TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 779,000 OZ FROM THE SLV.: // //INVENTORY RESTS AT 433.500 MILLION OZ

JAN 16/WITH SILVER DOWN $0.08 TODAY NO CHANGES IN SILVER INVENTORY AT THE SLV: // //INVENTORY RESTS AT 433.500 MILLION OZ

JAN 12/WITH SILVER UP $0.62 TODAY NO CHANGES IN SILVER INVENTORY AT THE SLV: // //INVENTORY RESTS AT 433.500 MILLION OZ

CLOSING INVENTORY 429.483 MILLION OZ//

PHYSICAL GOLD/SILVER COMMENTARIES

1:Peter Schiff/Mike Maharrey

Peter Schiff: Bitcoin Lives And Dies By ETFs

TUESDAY, MAR 05, 2024 – 06:30 AM

Via SchiffGold.com,

On this year’s Leap Day, Peter analyzed another round of inflation data and the economic factors at play in the quickly approaching 2024 general election. Bitcoin also surged back above $60,000 after the SEC approved bitcoin ETFs. Inflation came in worse than expected for personal consumption, and gold finished the week at nearly $2090/oz.

Peter thinks Bitcoin’s revival this week is the last gasp of breath before the asset blows up completely:

“These ETFs are really the tail that is wagging the Bitcoin dog. I think it’s all now about the ETFs, and of course, Bitcoin lives by the ETFs, it’s going to die by the ETFs and [it’s] probably not going to be a very long life.”

Investors eagerly buying into these ETFs may have a tough time moving back into gold if the yellow metal continues to climb in price:

“It’s going to be like a…roach motel. The money checks in. It doesn’t check out. It goes to money heaven because it’s one thing to put money into a Bitcoin ETF. It’s going to be a whole other thing to get it back out.”

With new home sales and durable goods orders declining faster than expected, Peter explains the bizarre state of the housing market:

“[Housing] prices are still up, even though the interest rates are up. It’s an unprecedented situation that makes housing extremely unaffordable and means that more people are stuck renting, no matter how high the rent goes.”

All of these factors weigh on voters’ minds at the ballot box, and so far, Biden has received most of the blame:

“This also confirms what I’m saying, and what the voters are saying: the economy is lousy. The reason that Biden is not getting credit is because he’s getting the blame. …Whether it’s Biden’s fault or not, the voters know the economy is lousy. They can’t afford to eat, and they’re working two or three jobs. And they’re blaming Biden, and they’re hoping that maybe things will be different under Trump.”

“Donald Trump is a better bet to win than Biden. So the markets say that Trump has a better chance of becoming the next president than Biden. But the betting markets also say that it’s more likely that a Democrat wins the White House than a Republican. So what are the markets betting? The markets are actually betting that Biden doesn’t run and that somebody else takes his place. Because the only way Trump is going to lose is if he’s not running against Biden.”

The only promising figures released this week were on personal income and spending, although Peter argues they’re hardly worth celebrating:

“Now normally, hey, that’s good news, right? People are earning more money. But they didn’t really earn more money. They received more money from government transfers. The big source of that 1 percent gain was government transfer payments. Mainly social security. … So some people on social security got a bigger check.”

Because this income was created by the government, it’ll likely make inflation worse:

“I don’t think that people on social security are going to save that money for long. They’re going to spend it. It’s just taking them a little longer to get to the store. So this is not good news. … This new spending power came into existence, not through effort and work, which would be productive and help to increase the supply of goods. It’s just people collecting money that the government created out of thin air. So it’s inflation.”

With gold stocks down this week and gold holding steady above $2000, now is a great time to buy the dip in gold stocks before the economy gets even worse:

“So we’ve got weak economic data, strong inflation data. We’ve got a bubble in the stock market. We’ve got a bubble in crypto. We’ve got a great opportunity to fade that trade, to bet against that bubble. All bubbles ultimately pop. It’s just a question of when and what’s the pin.”

The coming months will be crucial for the economy. As inflation continues to hang on and important indicators keep falling, precious metals stand out as a great defense against a weakening dollar and asset bubbles in the broader economy.

end

2.Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens/ SIMON WHITE..//ALASDAIR MACLEOD…

END

3. CHRIS POWELL//GATA GOLD COMMENTARIES: daily Dispatches

Ted Butler: The CFTC’s (non)response

Submitted by admin on Mon, 2024-03-04 19:45 Section: Daily Dispatches

By Ted Butler SilverSeek.com Monday, March 4, 2024

The long-awaited response from the U.S. Commodity Futures Trading Commission to my congressman’s office about my concerns about the possible double-counting of publicly reported silver inventories, originally sent to the agency in mid-November, was received by me Friday morning, March 1.

To refresh you with the issue, I asked the CFTC (along with the Securities and Exchange Commission) to make clear whether the 103 million ounces reported in the I-Shares Silver Trust (SLV) and being held in New York by JPMorgan on behalf of the trust were also being reported in the JPMorgan Comex warehouse or whether these were two separate silver inventories. …

The long-awaited response from the CFTC to my congressman’s office about my concerns of the possible double-counting of publicly reported silver inventories, originally sent to the agency in mid-November was received by me Friday morning, March 1. To refresh you with the issue, I asked the CFTC (along with the S.E.C.) to make clear whether the 103 million oz reported in the I-Shares Silver Trust, SLV, and being held in New York by JPMorgan on behalf of the trust, was also being reported in the JPMorgan COMEX warehouse or whether these were two separate silver inventories. Here’s an article I made public at the time, which included my original letter, as well as some commentary.

The S.E.C. responded within two weeks, but avoided answering whether the silver inventories in question were being double-counted. The CFTC has taken more than three and half months to respond and also has avoided answering what was a very simple question on my part, after telling my congressman’s office on several occasions that it was “working on” a response. As is my custom, here is the agency’s response in its entirety for you to review, before I share my thoughts.

The CFTC’s response included a literal word-salad of unrelated information describing the functioning of the agency not all related to my question and designed to put as many words in the response to make it sound like much deep thought went into the response. It did declare that the agency had no direct control of the reporting of silver inventories, but in declaring that, avoided its responsibility to deal with the dissemination of false market data that could mislead market participants. There have been numerous actions taken by the agency in the past related to false data and price signals being disseminated in other markets, so the implication that the sending of false price signals related to the misreporting of recorded silver inventories is disingenuous, at best.

Besides, I am sick and tired of those (particularly bureaucrats) who’s standard knee-jerk response to any question is an automatic “it’s not my job”. WTF? If it is not the federal commodities regulator’s job to answer a direct and simple question about the potential sending of information creating false price signals – then who the heck’s job is it?

Let’s face it, if the silver inventories in question are being double-counted, as now appears obvious as a result of this response, that amounts to the sending of false price signals, period. There is not the slightest hint in the daily publishing of these two silver inventories, one covering the holdings in SLV and under the control of BlackRock, and the other reported by the CME Group, that the two inventories may be one and the same and, in effect, are being double-counted to the vast majority of market observers (including by me in my weekly reviews). Seeking clarity on the matter was why I asked the CFTC in the first place and now its response virtually guarantees the two inventories are double-counted.

Then there is the tantalizing boiler plate language (apparently added as an afterthought, as evidenced by the different type or font settings on each page) which promises that if this were to amount to the sending of false price signals, then the agency is more than capable to deal with it – except, of course, it can’t disclose that. Having heard this line from the CFTC in the past, you’ll forgive me if I don’t take the agency at its word. What I do know is this – the CFTC took the better part of three and a half months to offer a non-response, all the while that the silver price suppression remained firmly in place. It’s hard not to conclude that the agency is up to its eyeballs in prolonging a manipulation that has existed for 40 years.

A number of weeks back, I did raise the ugly possibility that the CFTC was delaying its response to my question, in order to give the crooked and collusive COMEX commercials the time to arrange their affairs as best as possible before it would respond. Considering the week’s results in the silver and gold COT reports, as well as the uneventful passage of the key first delivery days this week, I’d be lying if I said those ugly thoughts of mine had departed.

What to do? Unfortunately, I can’t act in the CFTC’s place, because if I could, then this silver price manipulation would have ended long ago. So that leaves me with trying to work around the agency. Specifically, I have continued to complain to the Department of Justice, as recently as again on Friday. My allegations not only involve the sending of false price signals (now confirmed) by JPMorgan for silver inventories under its direct control (and in direct violation of JPM’s recently-expired deferred criminal prosecution agreement), but also my more recent allegation against JPM for the uneconomic and manipulative dumping of physical silver via SLV. I can’t decide which is worse – the continued sending of false price signals by JPMorgan or its dumping of physical silver.

I do know that both are clearly against commodity law and must come to an immediate halt. As things turned out, I believe the CFTC may have done us all a big favor (quite unintentionally) in its long-delay in responding to the inventory double-counting question, by elevating the matter to a higher level than if it had responded much sooner. This extreme delay allowed me to peruse the data in the interim in SLV, which uncovered my allegation of dumping. I guess what I’m saying is that this response from the CFTC clearly confirms my allegation of double-counting, and thereby elevates my additional complaint about dumping. I’d ask the CFTC about the dumping of physical silver by JPM in the SLV, but Lord knows how long it would take for it to offer a non-response, so I’ll stick to the Justice Department on this matter.

Further, I can’t help but believe that the fairest and most effective manner of dealing with JPMorgan’s continued serious violations in the silver and gold markets is to simply disallow this crooked bank from dealing in these markets. In no uncertain terms, the world would be a better place if JPMorgan and silver and gold were mutually exclusive.

All Empires die without fail, so do all Fiat currencies. But gold has been shining for 5000 years and as I explain in this article, Gold is likely to outshine virtually all assets in the next 5-10 years.

In early 2002 we made major investments in physical gold for our investors and ourselves. At the time gold was around $300. Our primary objective was wealth preservation. The Nasdaq had already crashed 67% but before the bottom was reached, it lost another 50%. The total loss was 80% with many companies going bankrupt.

In 2006, just over 4 years later, the Great Financial Crisis started. In 2008, the financial system was minutes from imploding. Banks like JP Morgan, Morgan Stanley and many others were bankrupt – BANCA ROTTA – (see my article First Gradually then Suddenly, The Everything Collapse)

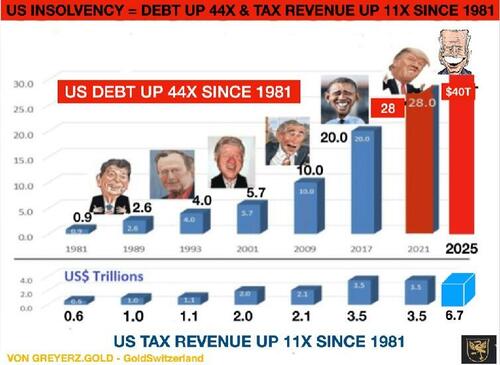

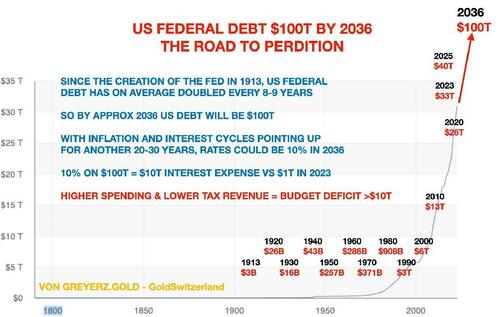

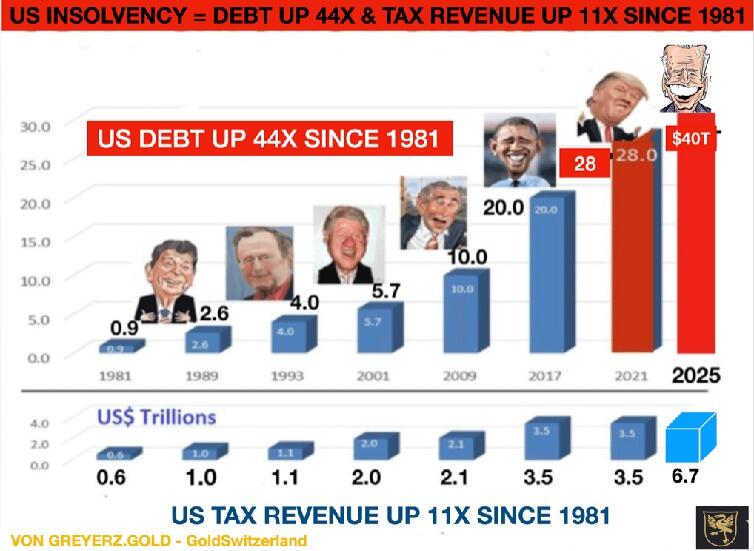

Virtually unlimited money printing postponed the collapse and since 2008 US total debt has almost doubled to $100 trillion.

Gold backing of a currency doesn’t always solve a debt problem but it certainly makes it more difficult for the government to cook the books which they do without fail.

BONFIRE OF THE US BUDGET BOOKS

So tricky Dick (Nixon) couldn’t make ends meet in the late 1960s – early 70s partly due to the Vietnam war.

Thus in 1971 Nixon, by closing the Gold window, started the most spectacular bonfire of the US government budget books. How wonderful, no more accountability, no more shackles and no more gold deliveries to de Gaulle in France who was clever to ask for gold instead of dollars in debt settlement from the US.

So from August 1971, the US embarked on a money printing and credit expansion bonanza never seen before in history.

Total US debt went from $2 trillion in 1971 to $200 trillion today – up 100X!

Since most major currencies were linked to the dollar under the Bretton Woods system, the closing of the gold window started a global free for all with the printing press (including bank credit) replacing REAL MONEY i.e. GOLD.

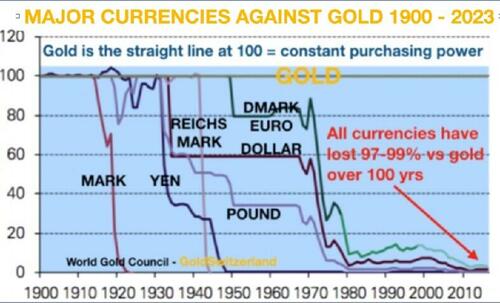

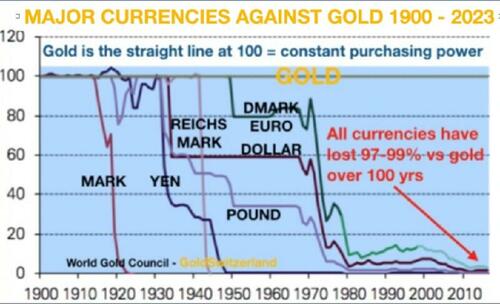

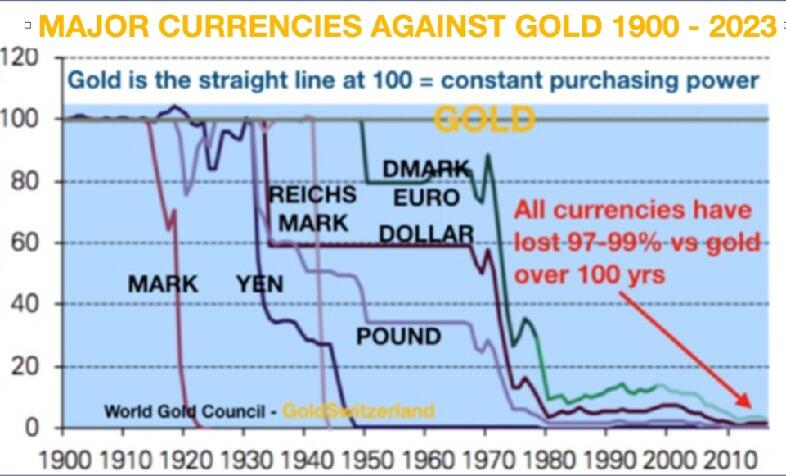

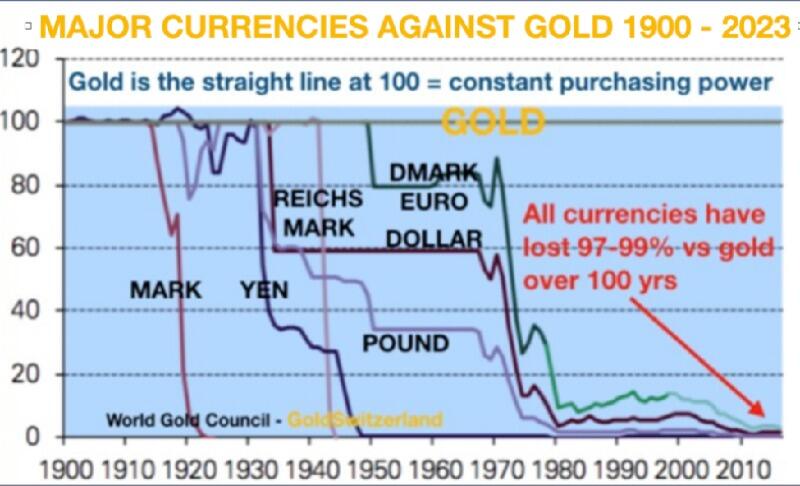

The consequences of this “temporary” move by Nixon is that all Fiat or paper money has declined by 97-99% since 1971.

The price of assets have obviously inflated correspondingly. In 1971 total US financial assets were $2 trillion. Today they are $130 trillion, up 65X.

And if we include off balance sheet assets including the shadow banking system and derivatives, we are looking at assets (which will become liabilities) in excess of $2 quadrillion.

Luke Gromen in his Tree Rings report puts forward two options for the world economy which can be summarised as follows:

1. Dedollarisation continues, the Petrodollar dies and gold gradually replaces the dollar as a global commodity trading currency especially in the commodity rich BRICS countries. This would allow commodity prices to stay low as gold rises and drives a virtuous circle of global trade.

If the above option sounds too good to be true especially bearing in mind the bankrupt status of the global financial system, Luke puts forward a much less pleasant outcome.

And in my view, Luke’s alternative outcome is sadly more likely, namely:

2. “China, the US Treasury market, and the global economy implode spectacularly, sending the world into a new Great Depression, political instability, and possibly WW3…in which case, gold probably rises spectacularly all the same, as bonds and then equities scramble for one of the only assets with no counterparty risk – gold. (BTC is another.)”

Yes, Bitcoin couldgo to $1 million as I have often said but it could also go to Zero if it is banned. Too binary for me and not a good wealth preservation risk in any case.

As Gromen says, there is a virtuous case and there is a vicious case for the world economy.

But above both cases shines GOLD!

So why hold the worthless paper money or bubble assets when you can protect yourself with Gold!

FOR THE CBO BAD TIMES DON’T EXIST

The US Central Budget Office – CBO – has recently made a 10 year forecast.

Obviously, the CBO assumes no depression or even a little recession in the next 10 years!

Isn’t it wonderful to be a government employee and have a mandate to only forecast GOOD NEWS!

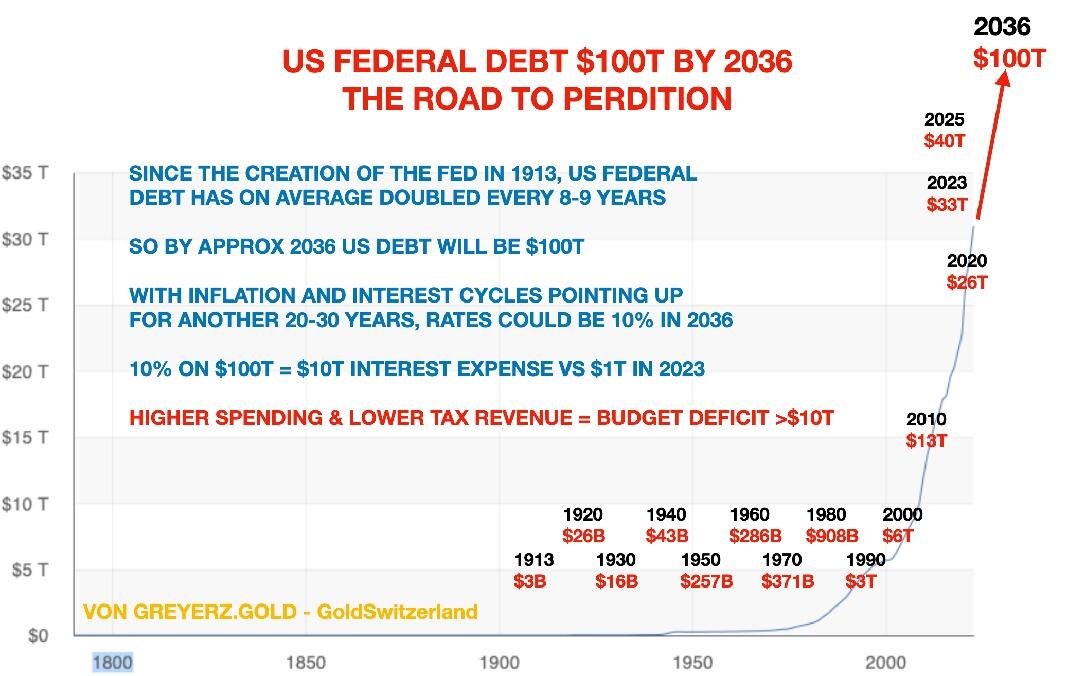

And although the CBO forecasts a debt increase of $21 trillion by 2034 to a total of $55 trillion, they expect inflation to stay around 2%!

As I have stated in many articles, the US Federal debt has doubled every 8 years on average since Reagan became President in 1981!

I see no reason to deviate from that long term trend although there can be short term deviations. So based on that simple but historically accurate extrapolation, I could forecast the increase from $10 trillion to $20 trillion debt in 2009 when Obama took over from Bush Jr.

Extrapolating this trend, the US Federal Debt will reach $100 trillion in 2036.

With debts and deficits increasing exponentially, it is not unlikely that as inflation catches fire again, $100 trillion Federal Debt will be reached earlier than 2036.

Just think about a big number of bank failures, which is guaranteed, plus major defaults in the $2+ quadrillion derivative market. Against such dire background, it would be surprising if US debt doesn’t go far beyond $100 trillion by the mid 2030s!

STOCK MARKET BUBBLE & LEADERSHIP SWAPS

Investors and many analysts are still bullish about the stock market. As we know, markets will move higher until all investors, especially retail, are sucked in and until most of the shorts have liquidated their positions.

It has been a remarkable bull market based on unlimited debt creation. Nobody worries about the fact that 7 stocks are creating this mania. These stocks are well known to most investors: Alphabet (Google), Amazon, Apple, Meta (Facebook), Microsoft, Nvidia and Tesla.

These Magnificent 7 have a total market cap of $13 trillion. That is the same as the combined GDP of Germany, Japan, India and the UK! Only the US and China are bigger.

When 7 companies are greater than 4 of the biggest industrial economies in the world, it is time to fire the management of these countries and maybe do a swap.

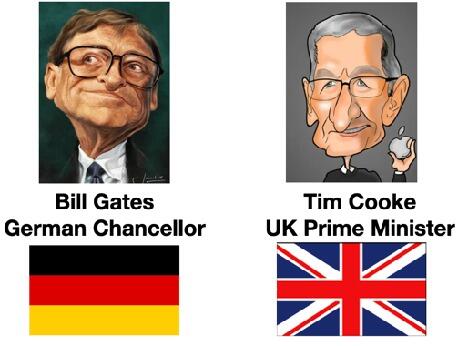

GATES, COOKE, MUSK TAKING OVER GERMANY, UK & FRANCE

What about Germany’s Chancellor Scholz running Amazon. Or Rishi Sunak in the UK being in charge of Microsoft? How long would it take them to destroy these companies? Not many years in my view. They would quickly double the benefits for workers and increase debts to unsustainable levels.

But Germany and the UK would most certainly benefit from Bill Gates of Microsoft taking on Germany and Tim Cooke of Apple running the UK. They would of course need dictatorial powers in order to take the draconian measures required. Only then could they slash inefficiencies, halve benefits and reduce taxes by at least 50%.

If the entrepreneurs just got a very small percentage of the improvement in the countries’ finances as remuneration, they would make much more money than they are currently.

Even more fascinating would be to see Elon Musk as French President. He would fire at least 80% of state employees and by doing that he might even get the militant French unions on his side and get the country back on its feet.

An interesting thought experiment that of course will never happen.

WHY IS EVERYONE WAITING FOR NEW GOLD HIGHS IN ORDER TO BUY???

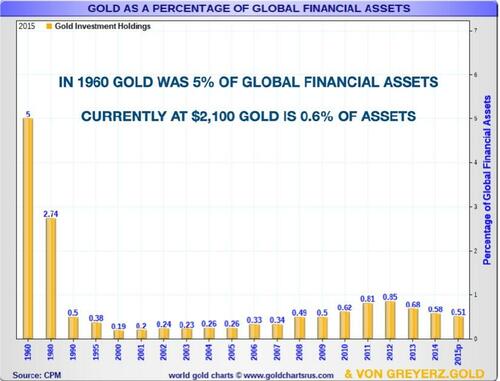

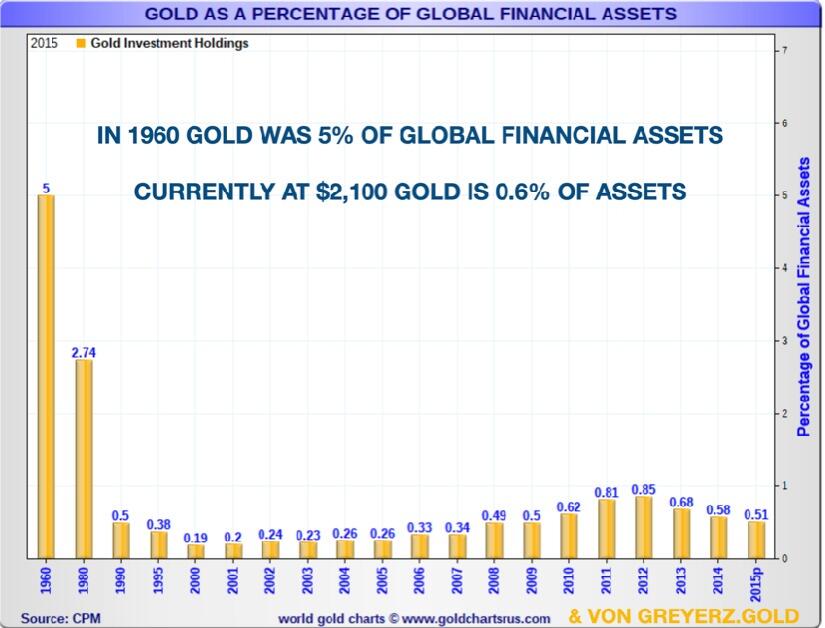

For almost 25 years I have been standing on a soapbox to inform investors of the importance of wealth preservation.

Still only just over 0.5% of global financial assets have been invested in gold. In 1960 it was 5% in gold and in 1980 when gold peaked at $850, it was 2.7%.

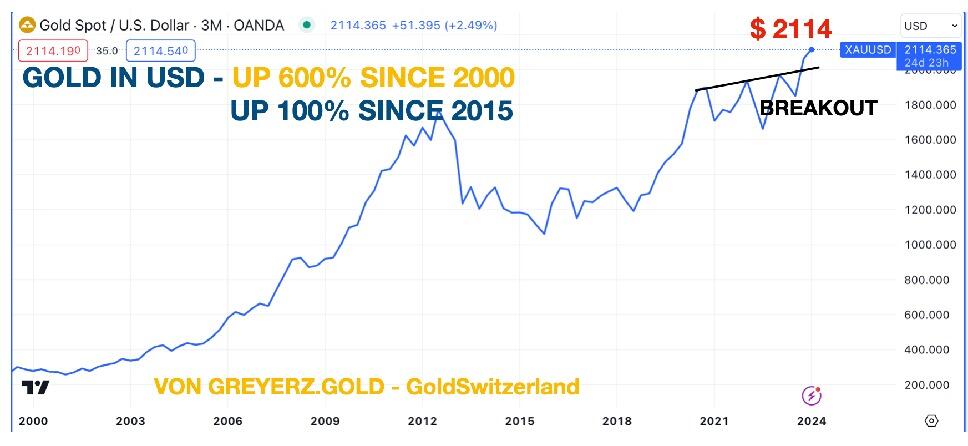

For a quarter of a century, gold has gone up 7- 8X in most Western currencies and exponentially more in weak currencies like the Argentine Pesos or Venezuelan Bolivar.

In spite of gold outperforming most asset classes in this century, it remains at less than 1% of Global Financial Assets – GFA. Currently at $2,100 gold is at 0.6% of GFA.

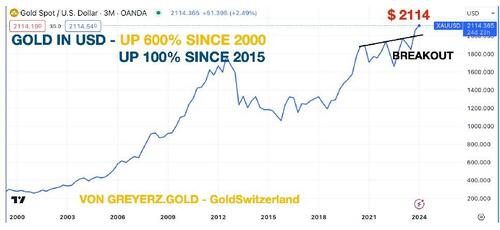

WE HAVE LIFTOFF!

So gold has now broken out and very few investors are participating.

This stealth move that gold has made has left virtually every investor behind as this table shows:

The clever buyers are of course the BRICS central banks. Almost all of their purchases are off market so in the short term it has only a marginal effect on the gold price.

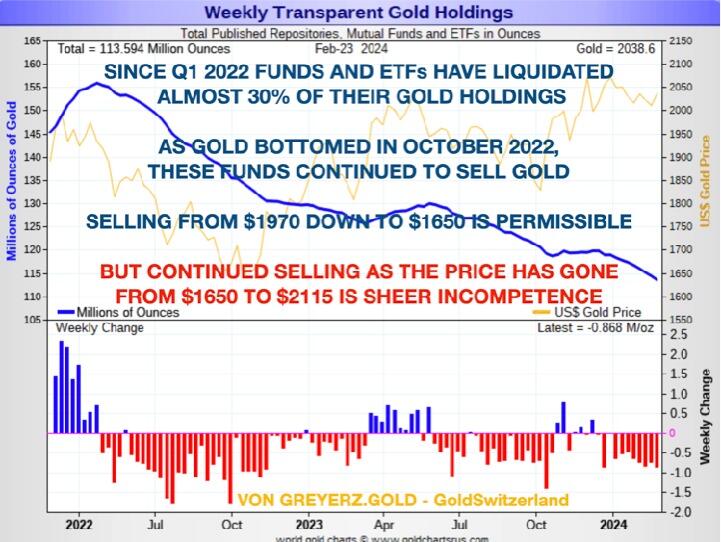

But now the squeeze has started as my good friend Alasdair Macleod explains so well on King World News. The Comex was never meant for physical deliveries but only for cash settlements. But now buyers are standing for physical delivery. We have also seen last month major exports of gold from the US to Switzerland. These are either Comex 400 ounce bars or US government bars sold/leased and sent to the Swiss refiners and broken down to 1 kg bars for onwards export to the BRICS. These bars will never return again even if they are only leased and not sold.

The above process will one day bring panic to the gold market as there will be nowhere near enough physical gold for all the paper claims.

So for any gold investors who don’t hold physical gold in a safe jurisdiction (NOT USA), I suggest that they quickly move their gold to a private vault where they have personal access, preferably in Switzerland or Singapore.

So NO FRACTIONAL GOLD OWNERSHIP, NO GOLD ETFs or FUNDS and NO GOLD IN BANKS!

At least not if you want to be sure to get hold of your gold as the gold squeeze starts.

GOLD IS ON THE CUSP OF A MAJOR MOVE

Having just broken out, gold is now on its way to much, much higher levels.

As I keep on saying, forecasting the gold price is a mug’s game.

What is the purpose of predicting a price level when the unit you measure gold in (USD, EUR, GBP etc) is continually debasing and worth less every month.

All investors need to know is that every single currency in history has without fail gone to ZERO as Voltaire said already in 1727.

Since the early 1700s, over 500 currencies have become extinct, most of them due to hyperinflation.

Only since 1971 all major currencies have lost 97-99% of their purchasing power measured in gold. In the next 5-10 years they will lose the remaining 1-3% which of course is 100% from here.

But gold will not only continue to maintain purchasing power, it will do substantially better. This is due to the coming collapse of all bubble assets – Stocks, Bonds, Property etc. The world will not be able to avoid the Everything Collapse or First Gradually then Suddenly – The Everything Collapse as I wrote about in two articles in 2023.

YES, GOLD IS ON THE CUSP OF A MAJOR MOVE AS:

Wars continue to ravage the world.

Inflation rises strongly due to ever increasing debts and deficits.

Currency continues their journey to ZERO.

The world flees from stocks, bonds, and the US dollar.

The BRICS countries continue to buy ever bigger amounts of gold.

Central Banks buy major amounts of gold as currency reserves instead of US dollars.

Investors rush into gold at any price to preserve their wealth.

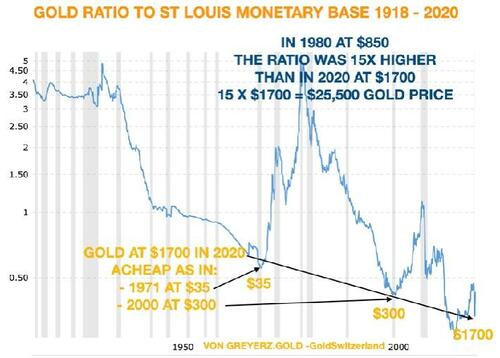

GOLD AS CHEAP AS IN 1971 OR 2000

The chart below indicates that gold in early 2020 at $1700 was as cheap as in 1971at $35 and in 2000 at $1700 in relation to money supply.

At this point we do not have an updated chart but it is our estimate that the monetary base has probably kept pace with the gold price meaning that the level in 2024 is similar to 2020.

So let me repeat my mantra:

Please jump on the Gold Wagon while there is still time to preserve your wealth.

The coming surge in gold demand cannot be met by more gold because more than the current 3000 tonnes of gold per annum cannot be mined.

END

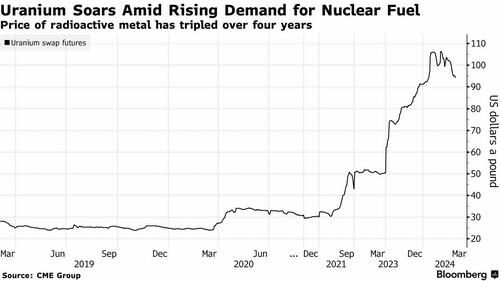

5 a. IMPORTANT COMMENTARIES ON COMMODITIES /URANIUM

The Nuclear Boom Is Here: Uranium Projects Jump Back On Line As Price Soars

MONDAY, MAR 04, 2024 – 08:00 PM

It’s been a long time coming, but the bulls are finally back in uranium. And with them comes the restart of multiple uranium projects that have been taken offline in the years while the commodity slouched in price.

We have long stated here on Zero Hedge that nuclear power is an obvious win/win: it’s clean, it’s safe, it provides robust power and, most importantly to our liberal friends, it has minimal emissions. So why isn’t it more prominent?

In the wake of the 2011 Fukushima nuclear disaster, uranium mining in the United States, particularly in Wyoming, Texas, Arizona, and Utah, experienced a significant downturn.

This decline wasn’t helped by uranium prices plummeting and nations such as Germany and Japan moving away from nuclear energy. However, as global efforts to reduce emissions renew interest in nuclear power, and as leading uranium producers face challenges in meeting demand, prices for the metal have risen sharply, a new Bloomberg report says.

This resurgence in prices is offering previously unprofitable American uranium mines an opportunity to re-enter the market and address the supply shortfall.

According to the report, as the Prospectors & Developers Association of Canada’s annual meeting takes place in Toronto, attracting thousands from the mining industry, uranium will be a key focus.

With participants including major uranium firms like Denison Mines Corp., Fission Uranium Corp., and IsoEnergy Ltd., the event highlights the growing importance of uranium in the context of climate change and nuclear power.

The International Atomic Energy Agency predicts a significant rise in uranium demand, foreseeing a need for over 100,000 metric tons annually by 2040, necessitating a near doubling of current mining and processing efforts.

Scott Melbye, executive vice president of Texas-based Uranium Energy Corp. said: “We’re in an old-fashioned, plain-and-simple supply squeeze. Demand is increasing again, with new reactors coming online.”

John Ciampagli, Chief Executive Officer of Sprott Asset Management added: “The industry is clearly trying to respond with smaller mines reopening, but when you have a mine that hasn’t operated for that long, it’s obviously not very substantive.”

Cameco has resumed operations at MacArthur River and Key Lake, the world’s largest high-grade uranium mine and mill in Saskatchewan, Canada, after halting from 2018 to 2021 due to poor market conditions.

The reopening of U.S. mines signifies a comeback for an industry that nearly vanished five years ago, with production plummeting to 174,000 pounds in 2019 from a peak of 44 million pounds in 1980. This decline was accompanied by increased reliance on uranium imports from nations such as Canada, Australia, Kazakhstan, and Russia.

Amid geopolitical tensions, particularly sanctions on Russia after its 2022 invasion of Ukraine affecting uranium shipments from Kazakhstan, the U.S. is motivated by both supply security and political reasons to boost its uranium production. The Uranium Producers of America suggests the U.S. will need to open 8 to 10 major new mines within the next decade to meet demand.

5 B GLOBAL COMMODITY ISSUES/FOOD IN GENERAL//FREIGHT

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGSTUESDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED DOWN 7.1992

OFFSHORE YUAN: UP TO 7.2123

SHANGHAI CLOSED UP 8,49 PPTS OR 0.28%

HANG SENG CLOSED DOWN 433.33 PTS OR 2.61%

2. Nikkei closed DOWN 11.60 PTS OR 0.03%

3. Europe stocks SO FAR: ALL MOSTLY MIXED

USA dollar INDEX UP TO 103.86 EURO FALLS TO 1.0848 DOWN 6 BASIS PTS

3b Japan 10 YR bond yield: FALLS TO. +.702 Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 150.41/JAPANESE YEN NOW FALLING AS WELL AS LONG TERM 10 YR. YIELDS RISING //EVENTUALLY THIS WILL BREAK THE JAPANESE CENTRAL BANK

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen UP CHINESE ONSHORE YUAN: DOWN/ OFFSHORE: DOWN

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil DOWN for WTI and DOWN FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund DOWN TO +2.3655***/Italian 10 Yr bond yield DOWN to 3.737* /SPAIN 10 YR BOND YIELD DOWN TO 3.211…**

3i Greek 10 year bond yield DOWN TO 3.302

3j Gold at $2123.50 silver at: 23.92 1 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble UP 0 AND 45 /100 roubles/dollar; ROUBLE AT 90.79//

3m oil into the 78 dollar handle for WTI and 82 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 150.41// 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 0.702% STILL ON CENTRAL BANK (JAPAN) INTERVENTION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.8864 as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.9614 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.188 DOWN 3 BASIS PTS…

USA 30 YR BOND YIELD: 4.327 DOWN 3 BASIS PTS/

USA 2 YR BOND YIELD: 4.581 DOWN 2 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 31.65…(TURKEY SET TO BLOW UP FINANCIALLY)

GREAT BRITAIN/10 YEAR YIELD: DOWN 4 BASIS PTS AT 4.092

end

2.a Overnight: Newsquawk and Zero hedge

Futures Fall As Apple China Sales Tumble, China Congress Forecast Disappoints

TUESDAY, MAR 05, 2024 – 08:18 AM

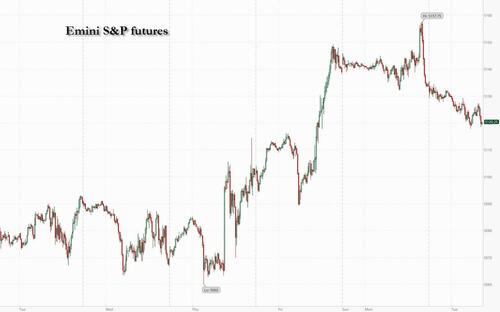

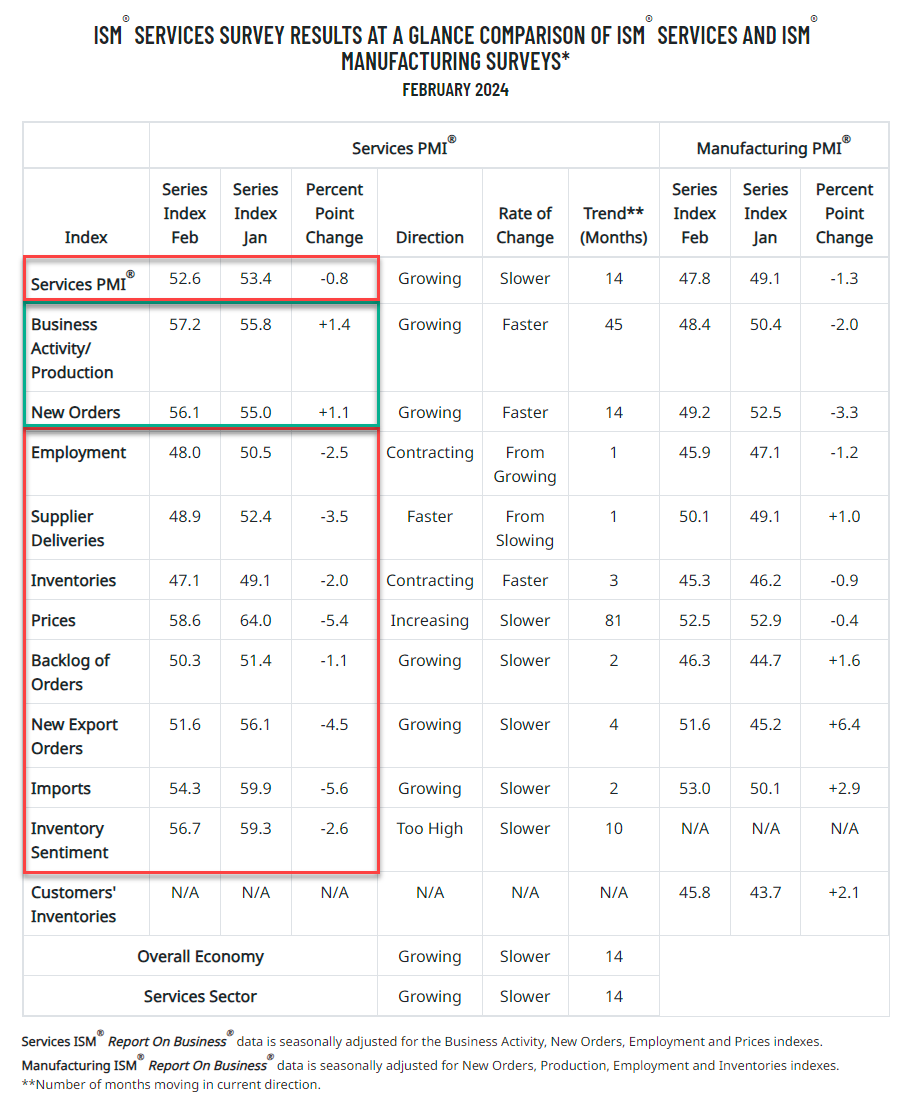

And just like that the momentum-driven buying frenzy is over: S&P 500 futures are down 0.3%, and Nasdaq 100 futures slide 0.6%, jeopardizing the ridiculous stock market rally which is up 16 of the pat 18 weeks, as Apple shares tumbled more than 2% in premarket trading after reporting 24% drop in iPhone sales in China over first six weeks of year. Large-cap technology companies were also pressured by the selling in Apple, while sentiment was also dented by the lukewarm response to China’s new growth target which for the 2nd year in a row was “around 5%”; finally the mood turned more dour after hawkish comments on Monday by Atlanta Fed president Bostic who said he sees a Q3 cut and then a pause and then one more for the year. Bond yields are down 2bps across the curve, taking the 10Y to 4.18% while the USD is flat and bitcoin continues to trade just shy of its all time high of $68,888.99. Commodities are mixed with Ags/Energy lower and metals higher, while gold is also making a new ATH. Today’s macro data focus will be on ISM-Srvcs and Durable/Cap Goods, plus we get some Consumer-sector earnings including Target.

In premarket trading, Apple fell more than 2%, set to extend losses for a fifth consecutive session as Counterpoint Research says iPhone sales in China declined by 24% over the first six weeks of this year. The divergence between AAPL and the Nasdaq is getting rather glaring.

Also in premarket trading, AMD slipped more than 2.5%, after Bloomberg reported it has hit a US government roadblock in its plan to sell an artificial intelligence chip tailored for China. Tesla fell 2.2%, set to extend losses after dropping 7.2% on Monday following disappointing China vehicle shipment figures. Additionally, Tesla halted production at its factory near Berlin and sent workers home after a fire – which appears to have been the result of industrial sabotage – at a high-voltage pylon caused power failures throughout the region. Here are the other notable premarket movers:

AeroVironment (AVAV US) rose 19% after the defense contractor reported adjusted earnings per share that beat the average analyst estimate.

Gitlab (GTLB US) shares sink 24% after the application software company gave a full-year forecast that is weaker than expected. Analysts noted that the tepid outlook overshadowed otherwise strong 4Q results.

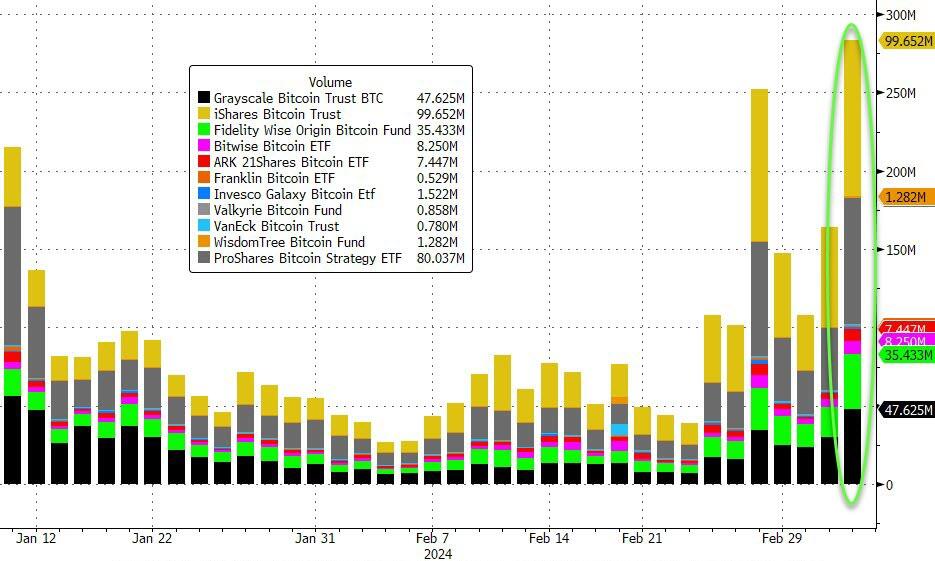

MicroStrategy (MSTR US) leads cryptocurrency-linked stocks lower in premarket trading on Tuesday as Bitcoin’s blinding rally takes a breather. The largest corporate holder of Bitcoin also proposed to sell $600 million in convertible senior notes to buy more of the largest cryptocurrency.

Paymentus (PAY US) shares climbed 16% after the provider of cloud-based bill payment technology issued stronger-than-expected adjusted Ebitda forecasts for the current quarter and full year. The company’s fourth-quarter revenue and adjusted Ebitda also topped the average analyst estimates.

Stitch Fix (SFIX US) shares slumped 14% after the online personal styling service cut its full-year net revenue from continued operations guidance, which missed analyst estimates. Additionally, the company reported a heavier-than-expected loss per share from continuing operations for the second quarter.

Investors are also jittery ahead of Congressional testimony from Fed Chair Jerome Powell on Wednesday and Thursday. That will be followed on Friday by monthly payrolls data. Powell is expected to double down on the message that the Fed will be patient in cutting rates. That’s especially so after Atlanta Fed President Raphael Bostic said Monday he expects the first cut — which he has penciled in for the third quarter — to be followed by a pause. A string of strong economic data has already forced markets to push back the first rate cut to at least mid-year and trim the number of reductions this year to three.

“If Bostic wants one cut then a pause, you can’t help but wonder if the Fed is wavering on three cuts,” said Societe Generale strategist Kenneth Broux. “The data is doing the talking and it’s really not screaming for the Fed to cut rates. We have taken out three Fed cuts in the past two months, so now the question is: do we need to take out more?”

In Europe, the Stoxx 600 index slipped 0.2%, with automotive and mining shares the hardest hit as China’s latest market-support measures, announced Tuesday, failed to reassure investors. Among individual stocks, defense firm Thales SA jumped after forecast-beating results and Spirent Communications Plc soared after Viavi Solutions Inc. agreed to buy the electronic solutions provider.

Earlier in the session, Chinese equities were mixed and yuan little changed after China’s National People’s Congress delivered a slew of announcements on growth and inflation targets, as well as steps to shore up the economy and fiscal goals for 2024 which were very much as expected if somewhat on the disappointing side. The CSI 300 index close 0.7% and Shanghai Composite also eked out modest small gain, while Hong Kong tech shares pull Hang Seng 2.2% lower. Japanese equities grind higher; South Korean stocks were modestly weaker

“Overall, I would say it probably disappoints more based on announcements thus far,” said Xin-Yao Ng, an investment director at abrdn. “Investors still will like more forceful fiscal measures to boost the economy.”

In FX, the Bloomberg Dollar Spot Index is flat while the Aussie is the worst performer among the G-10’s, falling 0.3% versus the greenback. The yen modestly advanced after Tokyo price growth rising above the Bank of Japan’s target in February

In rates, treasury yields slipped after rising across the curve on Monday, when buyers shied away from US three-and six-month bill auctions amid uncertainty over Powell. Treasuries are richer by 2bp-3bp across the curve with 10-year around 4.185%, trailing gilts, which lead gains in European rates, by around 3.5bp in the sector. Curve spreads little changed. Core European rates likewise better on the day after French industrial production data were weaker than expected. IG credit issuance slate includes Israel multi-tranche $benchmark, continuing the YTD corporate borrowing binge. IG dollar issuance slate also includes EIB $4b 3Y and EBRD $1b 10Y; 14 issuers priced $21.5b across 29 tranches Monday, taking YTD volume past $400 billion. At least 1-2 borrowers stood down and intend to look again Tuesday

In commodities, oil prices are little changed, with WTI trading near $78.70. Spot gold rises 0.5%

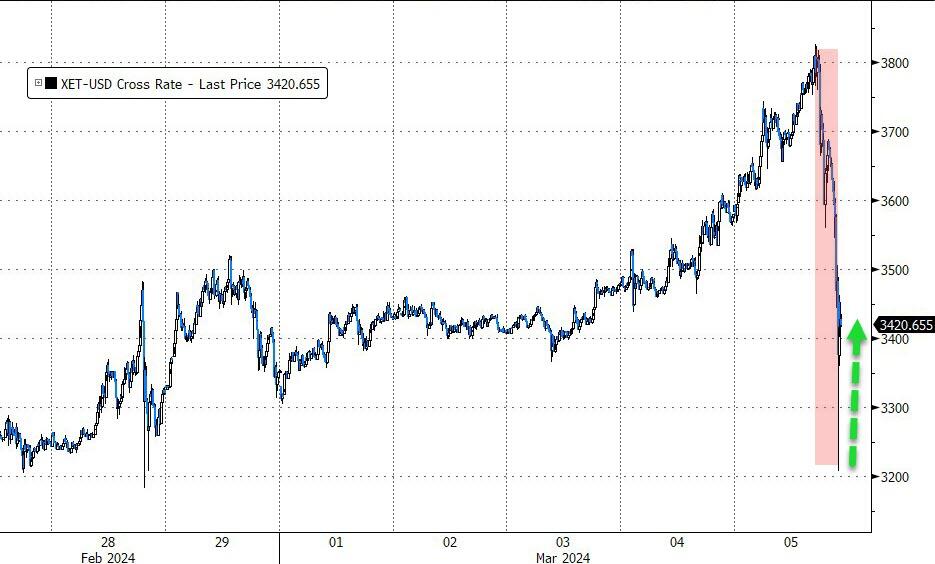

Bitcoin takes a breather and holds just beneath its record high of $69k, while Ethereum (+3.6%) continues to advance higher.

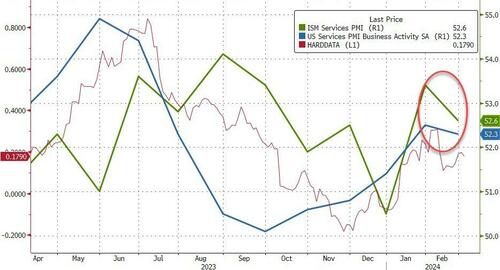

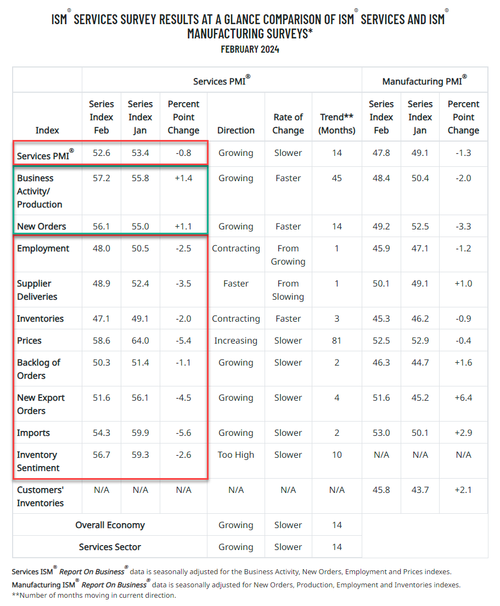

Looking at the US economic calendar, data today includes February S&P Global services PMI (9:45am), January factory orders and February ISM services index (10am). Fed speakers scheduled include Barr at 12pm and 2:15pm. Today’s earnings releases include Target. And in US politics, it’s Super Tuesday, with lots of primaries taking place for both Republicans and Democrats

Market Snapshot

S&P 500 futures down 0.3% to 5,124.25

STOXX Europe 600 down 0.2% to 496.40

MXAP down 0.4% to 173.99

MXAPJ down 0.9% to 525.75

Nikkei little changed at 40,097.63

Topix up 0.5% to 2,719.93

Hang Seng Index down 2.6% to 16,162.64

Shanghai Composite up 0.3% to 3,047.79

Sensex down 0.2% to 73,750.62

Australia S&P/ASX 200 down 0.1% to 7,724.20

Kospi down 0.9% to 2,649.40

German 10Y yield little changed at 2.37%

Brent Futures little changed at $82.81/bbl

Gold spot up 0.5% to $2,124.82

U.S. Dollar Index little changed at 103.85

Euro little changed at $1.0855

Top Overnight News

China’s 2024 economic objectives/targets were largely inline with expectations (no new incremental stimulus measures), including growth of “around 5%” and a fiscal deficit of ~3% (the country will issue CNY1T in special ultralong gov’t bonds, which aren’t counted in the deficit). WSJ

China drops “peaceful reunification” language with regards to Taiwan as it pledges to boost defense spending by 7.2% this year. RTRS

Apple Inc.’s iPhone sales in China fell by a surprising 24% over the first six weeks of this year, according to independent research that may stoke fears about worsening demand for the marquee but aging device. BBG

Japan’s Tokyo CPI came in at +2.6% Y/Y on the headline (up from +1.8% in Jan, and firmer than the consensus forecast of +2.5%) while core (ex-food/energy) cooled to +3.1% (down from +3.3% in Jan and inline with the Street). BBG

Gaza ceasefire talks end in Cairo without a breakthrough as pressure builds for a deal before the start of Ramadan on 3/10. RTRS

Hawkish policymakers at the European Central Bank have been emboldened to resist calls for an imminent cut to interest rates at their meeting this week after inflation proved stickier than expected in February. FT

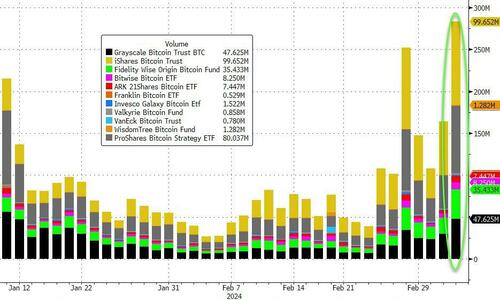

Bitcoin ETFs are seeing assets rise at a record pace – total inflows have been nearly $50B since the approvals arrived on Jan 11 (BlackRock’s product became the fastest new ETF in history to hit $10B). WSJ

TGT +6% pre market after reporting strong FQ4/Jan EPS upside, w/a ~60% Y/Y spike to 2.98 (vs. the Street’s 2.40 forecast). The EPS beat was driven primarily by margins while comps were inline (comps fell 4.4% vs. the Street -4.5%, with brick-and-mortar down 5.4% and digital down 0.7%). RTRS

AMD fell after its plan to sell an AI chip tailored for the Chinese market hit a roadblock. US officials found the low-performance chip was still too powerful and AMD must obtain a license to sell it, people familiar said. BBG

A more detailed look at global markets courtesy of Newsquawk

APAC stocks traded mixed as the region digested China’s Work Report and Caixin Services PMI data. ASX 200 closed slightly lower as strength in mining and health care was offset by losses in the consumer sectors. Nikkei 225 initially retreated beneath the 40,000 level after the latest Tokyo CPI data showed an acceleration in price growth, but then gradually recovered its losses and returned to positive territory. Hang Seng and Shanghai Comp. were mixed with notable underperformance in the Hong Kong benchmark amid weakness in tech and health care, while the miss on Chinese Caixin Services PMI also provides a headwind for risk appetite. Conversely, the mainland just about remained afloat after the announcement of the government Work Report with the GDP growth target maintained at around 5%, as expected, although Premier Li noted the foundation of China’s economic recovery is not solid yet and domestic demand is not strong.

Top Asian News

China unveiled the government work report with the 2024 GDP growth target set at around 5%, as expected, but noted achieving this year’s economic growth target will not be easy, while it will continue to implement proactive fiscal policy and prudent monetary policy, as well as noted that China should intensify cross-cyclical and counter-cyclical adjustments through macro policies. China will launch a year-long program to stimulate consumption and roll out a “worry-free consumption” initiative to improve the consumption environment and will make concerted efforts to defuse local government debt risks. Furthermore, China will take tough measures against illegal financial activities and will move faster to foster a new development model for real estate.