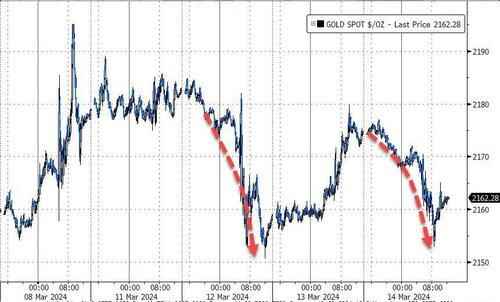

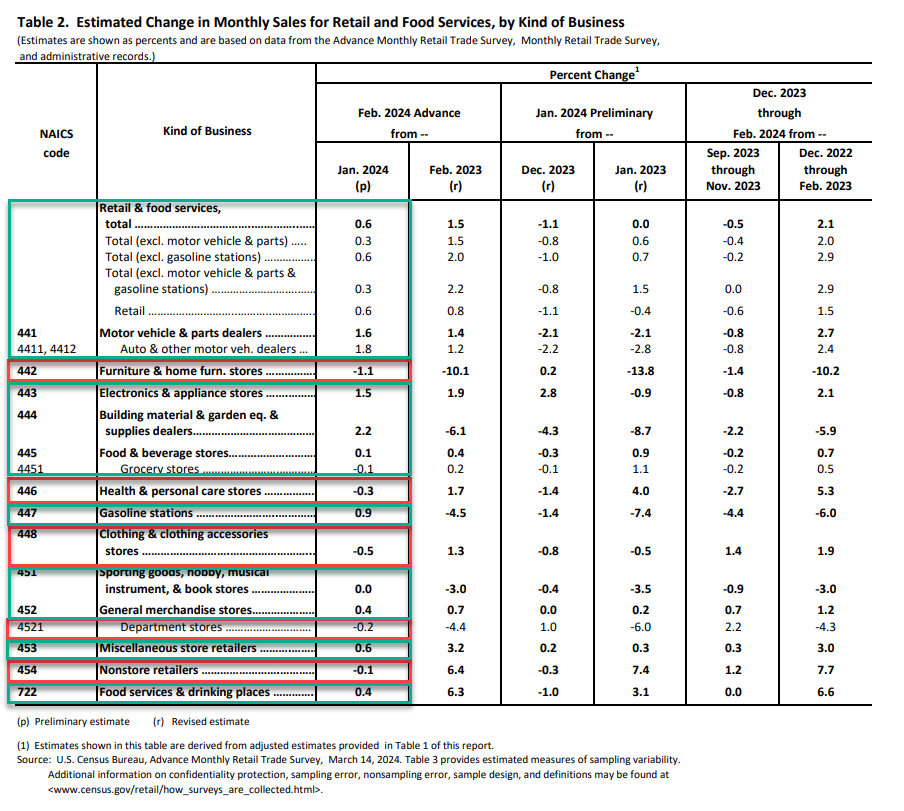

GOLD PRICE CLOSED DOWN $12.20 TO $2163,20

SILVER PRICE DOWN 9 cents TO $24.86

Gold ACCESS CLOSED 2163.30

Silver ACCESS CLOSED: 24,85

Bitcoin morning price:$72,800 DOWN 287 DOLLARS.

Bitcoin: afternoon price: $69,994 DOWN 3093 dollars

Platinum price closing DOWN $9.75 AT $932.90

Palladium price; UP 4.10 AT $1069.60

END

SHANGHAI GOLD PREMIUM 30 DOLLARS/COMEX GOLD

SHANGHAI GOLD………

SHANGHAI GOLD (USD) FUTURES – QUOTES

Beginning Monday, April 1, 2024, CME Group settlement data will no longer be accessible through ftp.cmegroup.com and will have a delayed publication time of 12:00 a.m. CT on all cmegroup.com web pages. Learn about alternate ways to access the data in our FAQ.

Last Updated 14 Mar 2024 03:17:59 PM CT.

Market data is delayed by at least 10 minutes.

I will now provide gold in Canadian dollars, British pounds and Euros

4: 15 PM ACCESS

*CANADIAN GOLD: $2,927.40 UP $0.40 CDN dollars per oz( * NEW ALL TIME HIGH 2,941.47CDN DOLLARS PER OZ//MARCH 11 2024)

*BRITISH GOLD: 1696.39 DOWN 1.00 pounds per oz// *(NEW ALL TIME HIGH//CLOSING///1703.22 BRITISH POUNDS/OZ) MARCH 11/2024

*EURO GOLD: 1987.39 UP 4.10 euros per oz //* (ALL TIME CLOSING HIGH: 1997.12 EUROS PER OZ//MARCH 11.2024)

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

EXCHANGE: COMEX

EXCHANGE: COMEX

CONTRACT: MARCH 2024 COMEX 100 GOLD FUTURES

SETTLEMENT: 2,175.400000000 USD

INTENT DATE: 03/13/2024 DELIVERY DATE: 03/15/2024

FIRM ORG FIRM NAME ISSUED STOPPED

363 H WELLS FARGO SEC 6

661 C JP MORGAN 22

737 C ADVANTAGE 6 1

905 C ADM 11

TOTAL: 23 23

MONTH TO DATE: 5,156

JPMorgan stopped 22/23 contracts.

FOR MARCH/2024

GOLD: NUMBER OF NOTICES FILED FOR MAR/2024. CONTRACT: 23 NOTICES FOR 2300 OZ or 0.0715 TONNES

total notices so far: 5156 contracts for 515,600 Oz (16.037 tonnes)

FOR MARCH:

SILVER NOTICES: 0 NOTICE(S) FILED FOR nil OZ/

total number of notices filed so far this month : 5111 for 25,555,000 oz

XXXXXXXXXXXXXXXXXX

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

BOTH GLD AND SLV ARE FRAUDULENT VEHICLES//THEY ARE NOW RAIDING GLD AND SLV FOR PHYSICAL

GLD

THE CROOKS ARE STEALING GOLD AND SILVER FROM THE GLD/SLV AND REPLACING THE PHYSICAL WITH PAPER DOLLARS.

WITH GOLD DOWN $12.20

INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD/ :

HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.73 TONNES OF GOLD INTO THE GLD..//INVENTORY RESTS AT 816.86 TONNES

INVENTORY RESTS AT 816.86 TONNES

SLV//

WITH NO SILVER AROUND AND SILVER DOWN 9 CENTS AT THE SLV//

NO CHANGES IN SILVER INVENTORY AT THE SLV: INVENTORY REMAINS AT 418.872 MILLION OZ/

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV.

CLOSING INVENTORY: 418.872 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A MEGA HUMONGOUS SIZED 2890 CONTRACTS TO 147,424 AND CLOSER TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THIS HUGE SIZED GAIN IN COMEX OI WAS ACCOMPLISHED WITH OUR HUGE GAIN IN PRICE OF $0.78 IN SILVER PRICING AT THE COMEX ON WEDNESDAY. WE HAD ZERO LONG LIQUIDATION AT THE COMEX SESSION WITH AGAIN MAJOR SHORT COVERING WITH THE STRONG PRICE GAIN. WE HAD A HUGE 1196 T.A.S ISSUANCE AND THESE WILL BE USED FOR MANIPULATION LATER THIS MONTH/AS WELL AS TODAY. PLEASE NOTE THAT THE CROOKS NEED A HIGHER SILVER/GOLD T.A.S. TO CARRY ON THEIR CROOKED MANIPULATION ON A DAILY BASIS

CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON WEDNESDAY NIGHT: 1196 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS. IT THUS LOOKS LIKE THE FED (GOV’T) IS BEHIND ALL OF THESE TRADES.

WE HAVE NOW SET ANOTHER RECORD LOW AT 114,102 CONTRACTS ///JULY 3.2023// OUR BANKERS WITH THE HELP OF SPECULATORS AND HIGH FREQUENCY TRADERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.78),BUT WERE UNSUCCESSFUL IN KNOCKING ANY SILVER LONGS AS WE HAD A MEGA HUMONGOUS SIZED GAIN OF 5725 CONTRACTS ON OUR TWO EXCHANGES WITH THE STRONG GAIN IN PRICE OF 78 CENTS.

WE MUST HAVE HAD:

A GIGANTIC SIZED 2835 ISSUANCE OF EXCHANGE FOR PHYSICALS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 22.270 MILLION OZ (FIRST DAY NOTICE) FOLLOWED BY TODAY,S 0.085 MILLION OZ QUEUE JUMP //NEW TOTALS INCREASES TO : 26.980 MILLION OZ

//NEW STANDING FOR SILVER IS THUS 26.980 MILLION OZ

WE HAD:

/ HUMONGOUS SIZED COMEX OI GAIN/ GIGANTIC SIZED EFP ISSUANCE/ VI) HUGE SIZED NUMBER OF T.A.S. CONTRACT ISSUANCE 1196 CONTRACTS)/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL -REMOVED A HUGE 669 CONTRACTS //

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS FEB. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF MARCH

TOTAL CONTRACTS for 10 days, total 16,545 contracts: OR 82.725 MILLION OZ (1655 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 82.725725 MILLION OZ

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH 2022: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 118.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 85.745 MILLION OZ (SMALLER THAN LAST MONTH)

AUGUST: 171.43 MILLION OZ (THIS MONTH IS GOING TO BE HUGE //2ND HIGHEST ON RECORD

SEPT: 72.705 MILLION OZ (SMALLER THIS MONTH)

OCT: 97.455 MILLION OZ

NOV. 50.050 MILLION OZ

DEC. 66.140 MILLION OZ//

TOTAL 2023: 1,104.10 MILLION OZ/

JAN ’24 : 78.655 MILLION OZ//

FEB /2024 : 66.135 MILLION OZ./FINAL

MARCH: 82.725 MILLION OZ//WILL BE MUCH LARGER THIS MONTH//MAYBE CLOSE TO A RECORD ISSUANCE

RESULT: WE HAD A HUGE SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 2835 CONTRACTS WITH OUR HUGE GAIN IN PRICE OF SILVER PRICING AT THE COMEX//WEDNESDAY.,. THE CME NOTIFIED US THAT WE HAD A GIGANTIC EFP ISSUANCE CONTRACTS: 2855 ISSUED FOR MAY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS. WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR MARCH. OF 23.385 MILLION OZ ON FIRST DAY NOTICE FOLLOWED BY TODAY’S SMALL 0.085 MILLION OZ QUEUE JUMP

//NEW TOTAL STANDING RISES TO 26.980 MILLION OZ

WE HAVE A HUMONGOUS GAIN OF 5735 OI CONTRACTS ON THE TWO EXCHANGES WITH THE HUGE GAIN IN PRICE. THE TOTAL OF TAS INITIATED CONTRACTS TODAY: A HUGE SIZED 1196 CONTRACTS//HUGE FRONT END OF THE TAS CONTRACTS WERE LIQUIDATED DURING THE WEDNESDAY COMEX SESSION/// WITH MAJOR SHORT COVERING FROM OUR SPEC SHORTS

THE NEW TAS ISSUANCE WEDNESDAY NIGHT (1196) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE//PROBABLY TODAY., .

WE HAD 0 NOTICE(S) FILED TODAY FOR 0.000 MILLION OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A HUMONGOUS SIZED 24,348 CONTRACTS TO 540,654 AND CLOSER TO THE RECORD (SET JAN 24/2020) AT 799,733 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110, BUT WE ARE NOW CLOSER TO OUR ALL TIME LOW OF 390,000 CONTRACTS.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED 358 CONTRACTS

WE HAD A HUMONGOUS SIZED INCREASE IN COMEX OI ( 24,597 CONTRACTS) WITH OUR $14.40 GAIN IN PRICE//WEDNESDAY. THE BANKERS WERE FORCED TO SUPPLY THE NECESSARY SHORT PAPER TO CONTAIN GOLD’S RISE.WE ALSO HAD A RATHER LARGE INITIAL STANDING IN GOLD TONNAGE FOR MARCH. AT 10.270 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’’S QUEUE JUMP OF 1400 OZ.

NEW TOTAL Of INITIAL GOLD STANDING RISES TO: 16.762 TONNES // ALL OF THIS HAPPENED WITH OUR $14.40 GAIN IN PRICE WITH RESPECT TO WEDNESDAY’S TRADING. WE HAD A HUMONGOUS SIZED GAIN OF 28,706 OI CONTRACTS (89.28) PAPER TONNES) ON OUR TWO EXCHANGES.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 3751 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 540.654

IN ESSENCE WE HAVE A HUMONGOUS SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 28,348 CONTRACTS WITH 24,597 CONTRACTS INCREASED AT THE COMEX// AND A STRONG SIZED 3751 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 28,348 CONTRACTS.. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): MEGA MEGA HUMONGOUS SIZED 37,807 CONTRACTS,

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD STRONG SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (3751 CONTRACTS) ACCOMPANYING THE HUMONGOUS SIZED GAIN IN COMEX OI (24,955) //TOTAL GAIN FOR OUR THE TWO EXCHANGES: 28,348 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR FORMER FORMAT OF BANKERS GOING LONG AND SPECULATORS GOING SHORT ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR MARCH. AT 7.502 TONNES FOLLOWED BY TODAY’S STRONG QUEUE JUMP OF 0.0435 TONNES/NEW STANDING ADVANCES TO 16.871 TONNES.

/ 3) ZERO LONG LIQUIDATION // 4) HUMONGOUS SIZED COMEX OPEN INTEREST LOSS/ 5) STRONG ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER///6: MEGA HUMONGOUS T.A.S. ISSUANCE: 37,807 CONTRACTS//SOME SHORT COVERING AGAIN

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023-2024 INCLUDING TODAY

MARCH

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF MARCH. :

TOTAL EFP CONTRACTS ISSUED: 57,285 CONTRACTS OR 5,728,500 OZ OR 178.18 TONNES IN 10 TRADING DAY(S) AND THUS AVERAGING: 5948 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 10 TRADING DAY(S) IN TONNES 178.18 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2022, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 178.18/3550 x 100% TONNES 5.01% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2023

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH/2022: 409.30 TONNES //FINAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 151.69 TONNES (WEAKER THAN LAST MONTH)

AUGUST: 195.28 TONNES (A STRONGER MONTH)//FINAL

SEPT: 254.709 TONNES (WILL BE LARGER THAN LAST MONTH AND A STRONG MONTH)

OCT. 248.09 TONNES. LIKE SILVER, THIS MONTH IS GOING TO BE A STRONG E.F.P. ISSUANCE.

NOV. 239.16 TONNES//WILL BE STRONG THIS MONTH,

DEC. 213.704 TONNES. A STRONG MONTH//

TOTAL FOR YEAR 2023: 2,569.57 TONNES VS 2578 TONNES LAST YEAR

JAN ’24: 291.76 TONNES (WILL BE MUCH GREATER THAN LAST MONTH.//3RD HIGHEST EVER RECORDED EXCHANGE FOR PHYSICAL)

FEB’24: 201.947 TONNES

MARCH 2024: 178.18 TONNES//THIS IS GOING TO BE ONE HUMDINGER OF AN E,F,P. ISSUANCE.

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF FEB. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (APRIL), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER ROSE BY A HUGE SIZED 2890 CONTRACTS OI TO 147,424 AND CLOSER TO THE COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 6 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 2835 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAY 2835 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 1100 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 2890 CONTRACTS AND ADD TO THE 2835 E.FP. ISSUED

WE OBTAIN A MEGA HUMONGOUS SIZED GAIN OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 5725 CONTRACTS

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTAL 28.625 MILLION OZ

OCCURRED DESPITE OUR HUGE $.78 GAIN IN PRICE …..

END

OUTLINE FOR TODAY’S COMMENTARY

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

b, ) Gold/silver trading overnight Europe,//GOLD COMMENTARIES

(Peter Schiff)

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS//

THURSDAY MORNING/WEDNESDAY NIGHT

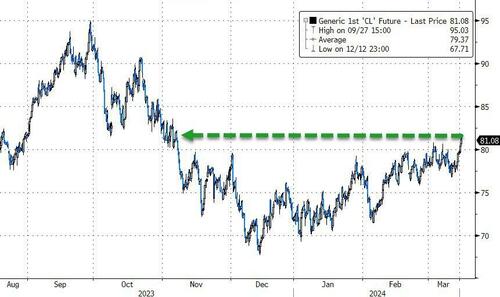

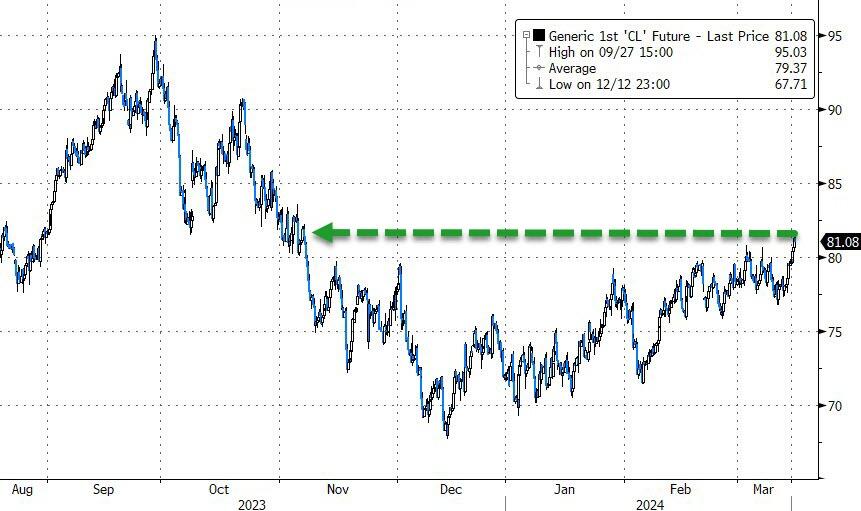

SHANGHAI CLOSED DOWN 5.60 PTS OR 0.18% //Hang Seng CLOSED DOWN 120.45 PTS OR 0.71% / Nikkei CLOSED UP 1121.41 PTS OR 0.29%//Australia’s all ordinaries CLOSED DOWN 0.19% /Chinese yuan (ONSHORE) closed UP 7.1894 //OFFSHORE CHINESE YUAN CLOSED UP TO 7.1943 /Oil UP TO 80.37 dollars per barrel for WTI and BRENT UP AT 84,55/ Stocks in Europe OPENED ALL GREEN// ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE YUAN STRONGER

A)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

9. USA

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY MEGA HUMONGOUS 24,597 CONTRACTS TO 540.654 WITH OUR GAIN IN PRICE OF $14.40 WITH RESPECT TO WEDNESDAY TRADING. MOST LIKELY IT WAS THE BANKERS SUPPLYING THE NECESSARY PAPER WITH OUR SHORT PLAYERS EXITING AS FAST AS THEIR FEET COULD CARRY THEM. THE SHORTS HAVE BEEN KILLED LATELY, AS THEY HAVE BEEN LED BY THE NOSE BY OUR BANKER-HIGH FREQUENCY TRADERS.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE NON ACTIVE DELIVERY MONTH OF MARCH..… THE CME REPORTS THAT THE BANKERS ISSUED A STRONG SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 3751 EFP CONTRACTS WERE ISSUED: : APRIL 3751 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 3751 CONTRACTS

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A HUMONGOUS SIZED TOTAL OF 28,348 CONTRACTS IN THAT 3751 LONGS WERE TRANSFERRED AS EXCHANGE FOR PHYSICALS TO LONDON AND WE HAD A HUMONGOUS SIZED GAIN OF 24,597 COMEX CONTRACTS..AND THIS GAIN ON OUR TWO EXCHANGES HAPPENED WITH OUR RISE IN PRICE OF $14.40 WEDNESDAY COMEX. AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS DURING MID MONTH IN THE DELIVERY CYCLE), THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR WEDNESDAY NIGHT WAS A MEGA MEGA HUMONGOUS SIZED 37,807 CONTRACTS,

THROUGHOUT THE PAST SEVERAL WEEKS, THE BANKERS CONTINUE TO SELL OFF THE LONG SIDE OF THE SPREAD WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR/T.A.S. SPREAD WHICH WILL BE LIQUIDATED IN DAYS HENCE//. IT SEEMS THAT OUR CROOKS ARE HAVING A HARD TIME TRYING TO CONTROL THE PRICE OF GOLD AND THUS THE NEED FOR RECORD T.A.S. ISSUANCE.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: MARCH (16,871 TONNES) ( NON ACTIVE MONTH)

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 24 MONTHS OF 2021-2023:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

NOV: 18.7122 TONNES + 16.2505 EX. FOR RISK = 34.9627 TONNES

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276 TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 16.871 TONNES

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT GAINED $14.40 //// AND WERE UNSUCCESSFUL IN KNOCKING ANY SPECULATOR LONGS AS WE HAD A HUMONGOUS SIZED GAIN OF 28,348 TOTAL CONTRACTS ON OUR TWO EXCHANGES WITH OUR HIGHER PRICE.

WE HAD A STRONG T.A.S. LIQUIDATION ON THE FRONT END OF WEDNESDAY’S TRADING . THE T.A.S. ISSUED ON WEDNESDAY NIGHT, WILL BE “PUT INTO THE BANK” TO BE USED AT A LATER DATE AT THE COLLUSIVE CHOOSING OF OUR BANKERS. THE HIGH T.A.S. ISSUANCE IS MEANT TO CONTROL THE PRICE OF GOLD (AS WELL AS INITIATE A RAID).

WE HAVE GAINED A TOTAL OI OF 88.174 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR MARCH. (10.3576 TONNES) ON FIRST DAY NOTICE FOLLOWED BY TODAY’S 1400 OZ QUEUE JUMP//NEW STANDING INCREASES TO 16.871 TONNES

ALL OF THIS WAS ACCOMPLISHED WITH OUR GAIN IN PRICE TO THE TUNE OF $14.40

WE HAD -REMOVED 669 CONTRACTS TO THE COMEX TRADES TO OPEN INTEREST (CROOKS)

NET GAIN ON THE TWO EXCHANGES 28,348 CONTRACTS OR 2,834,800 OZ OR 88.174 TONNES.

estimated volume today 331,590 strong

final gold volumes/yesterday 334,172 strong

//speculators have left the gold arena

MARCH 14/ INITIAL MARCH GOLD

/ /// THE MARCH 2024 GOLD CONTRACT

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | nil oz . |

| Deposit to the Dealer Inventory in oz | nil oz |

| Deposits to the Customer Inventory, in oz | NIL oz |

| No of oz served (contracts) today | 23 notice(s) 2300 OZ 0.0715 TONNES |

| No of oz to be served (notices) | 268 contracts 26800 oz 0.8336 TONNES |

| Total monthly oz gold served (contracts) so far this month | 5156 notices 515,600 oz 16.037 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | x |

0 dealer deposits:

total dealer deposits: nil oz

total customer withdrawals: 0

total customer withdrawal: nil oz

we had 0 customer deposit

total deposit NIL oz

Adjustments: 0

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR MAR.

For the front month of MARCH we have an oi of 291 contracts having LOST 496 contracts. We had 510 contracts filed upon on Wednesday, so we gained a 14 contracts or an additional 1400 oz of gold(0435 tonnes) will stand at the comex in this non active delivery month of March

APRIL LOST 5783 CONTRACTS FALLING TO 262,104.

MAY EARNED 26 CONTRACTS TO STAND AT 646

JUNE INCREASED ITS OI BY 28,289 CONTRACTS UP TO 220,579 CONTRACTS.

We had 23 contracts filed for today representing 2,300 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 23 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 22 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for the MARCH. /2024. contract month, we take the total number of notices filed so far for the month (5156 x 100 oz ), to which we add the difference between the open interest for the front month of MARCH. (291 CONTRACTS) minus the number of notices served upon today 23 x 100 oz per contract equals 542,400 OZ OR 16.871 TONNES

thus the INITIAL standings for gold for the MARCH. contract month: No of notices filed so far (5156) x 100 oz + (291) {OI for the front month} minus the number of notices served upon today (23) x 100 oz which equals 542,400 oz (16.871 TONNES)

TOTAL COMEX GOLD STANDING FOR MARCH: 16.871 TONNES WHICH IS HUGE FOR A NON ACTIVE DELIVERY MONTH IN THE CALENDAR.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 1,333,165.842 41,40 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD: 17,887,532.221 OZ

TOTAL REGISTERED GOLD 7,782,182.341 (242,05 tonnes).

TOTAL OF ALL ELIGIBLE GOLD: 10,092.069.959 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 6,449,017 oz (REG GOLD- PLEDGED GOLD) 200.59 tonnes/dropping like a stone

END

SILVER/COMEX

MARCH 14/INITIAL

//2024// THE MARCH 2024 SILVER CONTRACT//INITIAL

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 597,171.800 oz ASAHI . |

| Deposits to the Dealer Inventory | nil OZ |

| Deposits to the Customer Inventory | 594,486.200 oz ASAHI |

| No of oz served today (contracts) | 0 CONTRACT(S) (nil OZ) |

| No of oz to be served (notices) | 285 contracts (1.425 MILLION oz) |

| Total monthly oz silver served (contracts) | 5111 Contracts (25.555 MILLION oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

i) 0 dealer deposit

total dealer deposit:nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: 0 oz

We had 1 deposits customer account:

i) Into ASAHI: 594,486.2 oz

total customer deposits 594,486. 2 oz

JPMorgan has a total silver weight: 129.806 million oz/286.483 million or 45.30%

adjustment: 0

Comex withdrawals: 1

i) Out of ASAHI 597,171.800 oz

total withdrawal: 597,171.800 oz

TOTAL REGISTERED SILVER: 48.213MILLION OZ//.TOTAL REG + ELIGIBLE. 286.483million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR DECEMBER:

silver open interest data:

FRONT MONTH OF MARCH /2023 OI: 285 CONTRACTS HAVING LOST 14 CONTRACT(S).

WE HAD 31 NOTICES FILED ON WEDNESDAY SO GAINED 17 CONTRACTS OR AN ADDITIONAL 85,000 OZ WILL STAND AT THE COMEX

APRIL SAW A GAIN OF 106 CONTRACTS TO STAND AT 819

MAY SAW A GAIN OF 2157 CONTRACTS UP TO 115,511.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 0 for 0.00 MILLION oz

Comex volumes// est. volume today 76,973 good

Comex volume: confirmed yesterday 55,216 fair

To calculate the number of silver ounces that will stand for delivery in MARCH. we take the total number of notices filed for the month so far at 5111 x 5,000 oz = 25,555,000 oz

to which we add the difference between the open interest for the front month of MARCH. (285) and the number of notices served upon today 0 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the MARCH/2024 contract month: 5111 (notices served so far) x 5000 oz + OI for the front month of MARCH. (285) – number of notices served upon today (0 )x 500 oz of silver standing for the MARCH contract month equates to 26.980 MILLION OZ.

New total standing: 26.980 million oz.

There are 48.213 million oz of registered silver.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS//

BOTH GLD AND SLV ARE MASSIVE FRAUDS!

MARCH 14 WITH GOLD DOWN $12.20 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF 1.73 TONNES OF GOLD INTO THE GLD//:INVENTORY REMAINS AT 816.86 TONNES

MARCH 13 WITH GOLD UP $14.40 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD:INVENTORY REMAINS AT 815.13 TONNES

MARCH 12 WITH GOLD DOWN $21.15 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD:NOT AVAILABLE///LAST VALUE 815.13 TONNES

MARCH 11 WITH GOLD UP $3.20 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.44 TONNES OF GOLD OUT OF THE GLD AFTER 7 CONSECUTIVE GOLD PRICE RISES//INVENTORY RESTS AT 815.13 TONNES

MARCH 8 WITH GOLD UP $21.05 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 0.87 TONNES OF GOLD OUT OF THE GLD AFTER 7 CONSECUTIVE GOLD PRICE RISES//INVENTORY RESTS AT 816.57 TONNES

MARCH 7 WITH GOLD UP $7.20 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4,20 TONNES OF GOLD OUT OF THE GLD//INVENTORY RESTS AT 817.44 TONNES

MARCH 6 WITH GOLD UP $17.20 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.30 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 821.47 TONNES

MARCH 5 WITH GOLD UP $16.55 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.30 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 821.47 TONNES

MARCH 4 WITH GOLD UP $30.55 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF .86 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 823.77 TONNES

MARCH 1 WITH GOLD UP $40.40 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 822.91 TONNES

FEB29/WITH GOLD UP $12.60 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD//WITHDRAWAL OF 4.03 TONNES INVENTORY RESTS AT 822.91 TONNES

FEB28/WITH GOLD DOWN $1.00 TODAY NO CHANGES IN GOLD INVENTORY AT THE GLD INVENTORY RESTS AT 826.94 TONNES

FEB27/WITH GOLD UP $4.40 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF .87 TONNES OF GOLD FROM THE GLD:/INVENTORY RESTS AT 826.94 TONNES

FEB26/WITH GOLD DOWN $8.90 TODAY NO CHANGES IN GOLD INVENTORY AT THE GLD:/INVENTORY RESTS AT 827.81 TONNES

FEB23/WITH GOLD UP $17 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.01 TONNES OF GOLD FROM THE GLD.//INVENTORY RESTS AT 827.81 TONNES

FEB22/WITH GOLD DOWN $2.15 TODAY NO CHANGES IN GOLD INVENTORY AT THE GLD://INVENTORY RESTS AT 829.82 TONNES

FEB21/WITH GOLD DOWN $5.30 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 7.59 TONNES OF GOLD OUT OF THE GLD///INVENTORY RESTS AT 29.82 TONNES

FEB20/WITH GOLD UP $16.15 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 0.58 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 837.89 TONNES

FEB16/WITH GOLD UP $8,60 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.73 TONNES OF GOLD FROM THE GLD///INVENTORY RESTS AT 837.31 TONNES

FEB15/WITH GOLD UP $11.70 TODAY NO CHANGES IN GOLD INVENTORY AT THE GLD:/INVENTORY RESTS AT 841.92 TONNES

FEB14/WITH GOLD DOWN $2.75 TODAY NO CHANGES IN GOLD INVENTORY AT THE GLD:/INVENTORY RESTS AT 841.92 TONNES

FEB13/WITH GOLD DOWN $20.15 TODAY NO CHANGES IN GOLD INVENTORY AT THE GLD:/INVENTORY RESTS AT 841.92 TONNES

FEB12/WITH GOLD DOWN $4.80 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A STRONG WITHDRAWAL OF 1.74 TONNES OF GOLD FROM THE GLD. / //://INVENTORY RESTS AT 841.92 TONNES

FEB9/WITH GOLD DOWN $8.60 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A STRONG DEPOSIT OF 1.44 TONNES OF GOLD FROM THE GLD. / //://INVENTORY RESTS AT 843.66 TONNES

FEB8/WITH GOLD DOWN $2.70 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A MASSIVE WITHDRAWAL OF 5.47 TONNES OF GOLD FROM THE GLD. / //://INVENTORY RESTS AT 842.22 TONNES:

FEB7/WITH GOLD UP $0.40 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A MASSIVE WITHDRAWAL OF 4.04 TONNES OF GOLD FROM THE GLD. / //://INVENTORY RESTS AT 847.69 TONNES:

FEB6/WITH GOLD UP $8.50 TODAY NO CHANGES IN GOLD INVENTORY AT THE GLD:/ / //://INVENTORY RESTS AT 851.73 TONNES:

GLD INVENTORY: 816.86 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

MARCH 14/WITH SILVER DOWN 9 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: SLV INVENTORY RESTS AT 418.872 MILLION OZ

MARCH 13/WITH SILVER UP 78 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: SLV INVENTORY RESTS AT 418.872 MILLION OZ…

MARCH 12/WITH SILVER DOWN 31 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A SMALL WITHDRAWAL OF 0.549 MILLION OZ OF SILVER INTO THE SLV//// : SLV INVENTORY RESTS AT 418.872 MILLION OZ…

MARCH 11/WITH SILVER UP 11 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A HUGE WITHDRAWAL OF 2.147 MILLION OZ OF SILVER FROM THE SLV//// : SLV INVENTORY RESTS AT 418.323 MILLION OZ…SUCH A MASSIVE FRAUD!

MARCH 8/WITH SILVER DOWN 5 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A HUGE WITHDRAWAL OF 4.299 MILLION OZ OF SILVER FROM THE SLV//// : SLV INVENTORY RESTS AT 420.519 MILLION OZ…SUCH A MASSIVE FRAUD!

MARCH 7/WITH SILVER UP 8 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A HUGE WITHDRAWAL OF 4.665 MILLION OZ OF SILVER FROM THE SLV//// : SLV INVENTORY RESTS AT 424.818 MILLION OZ…SUCH A MASSIVE FRAUD!

MARCH 6/WITH SILVER UP 52 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A HUGE WITHDRAWAL OF 2.378 MILLION OZ OF SILVER FROM THE SLV//// : SLV INVENTORY RESTS AT 427,105 MILLION OZ

MARCH 5/WITH SILVER DOWN 2 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A HUGE WITHDRAWAL OF 1.499 MILL;ION OZ OF SILVER FROM THE SLV//// : SLV INVENTORY RESTS AT 429.483 MILLION OZ

MARCH 4/WITH SILVER UP CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: // : SLV INVENTORY RESTS AT 430.982 MILLION OZ

MARCH 1/WITH SILVER UP 49 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: // : SLV INVENTORY RESTS AT 430.982 MILLION OZ

FEB 29/WITH SILVER UP 25 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.104 MILLION OZ OUT OF THE SLV//// : SLV INVENTORY RESTS AT 430/982 MILLION OZ

FEB 28/WITH SILVER DOWN 7 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 5.123 MILLION OZ INTO THE SLV//// : SLV INVENTORY RESTS AT 433.086 MILLION OZ

FEB 27/WITH SILVER UP 3 CENTS TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 0.64 MILLION OZ FROM THE SLV//// : SLV INVENTORY RESTS AT 427.943 MILLION OZ

FEB 26/WITH SILVER DOWN 44 CENTS TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.065 MILLION OZ FROM THE SLV//// : SLV INVENTORY RESTS AT 428.603 MILLION OZ

FEB 23/WITH SILVER DOWN 44 CENTS TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.065 MILLION OZ FROM THE SLV//// : SLV INVENTORY RESTS AT 428.603 MILLION OZ

FEB 22/WITH SILVER DOWN 10 CENTS TODAY NO CHANGES IN SILVER INVENTORY AT THE SLV

// : SLV INVENTORY RESTS AT 432.766 MILLION OZ

FEB 21/WITH SILVER DOWN 28 CENTS TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 2.348 MILLION OZ OF SILVER FROM THE SLV// : SLV INVENTORY RESTS AT 432.766 MILLION OZ

FEB 20/WITH SILVER DOWN 33 CENTS TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 3.385 MILLION OZ OF SILVER FROM THE SLV// : SLV INVENTORY RESTS AT 435.008 MILLION OZ

FEB 16/WITH SILVER UP 53 CENTS TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV A DEPOSIT OF 1.235 MILLION OZ OF SILVER FROM THE SLV// : SLV INVENTORY RESTS AT 438.393 MILLION OZ

FEB 15/WITH SILVER UP 56 CENTS TODAY NO CHANGES IN SILVER INVENTORY AT THE SLV : SLV INVENTORY RESTS AT 437.615 MILLION OZ

FEB 14/WITH SILVER UP 24 CENTS TODAY NO CHANGES IN SILVER INVENTORY AT THE SLV : SLV INVENTORY RESTS AT 437.615 MILLION OZ

FEB 13/WITH SILVER DOWN 60 CENTS TODAY SMALL CHANGES IN SILVER INVENTORY AT THE SLV A SMALL WITHDRAWAL OF 0.504 MILLION OZ OZ OUT OF THE SLV: SLV INVENTORY RESTS AT 437.615 MILLION OZ

FEB 12/WITH SILVER UP 14 CENTS TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV A HUGE WITHDRAWAL OF 1.921 MILLION OZ OZ OUT OF THE SLV: SLV INVENTORY RESTS AT 438.119 MILLION OZ

FEB 9/WITH SILVER DOWN 4 CENTS TODAY SMALL CHANGES IN SILVER INVENTORY AT THE SLV A SMALL DEPOSIT OF 600,000 OZ INTO THE SLV: SLV INVENTORY RESTS AT 440.040 MILLION OZ

FEB 8/WITH SILVER UP 29 CENTS TODAY NO CHANGES IN SILVER INVENTORY AT THE SLV: SLV INVENTORY RESTS AT 439.994 MILLION OZ

FEB 7/WITH SILVER DOWN 18 CENTS TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A MASSIVE DEPOSIT OF 4.04 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 439.994 MILLION OZ//LAST 9 DAYS: 10.7598 MILLION OZ WITHDRAWAL

CLOSING INVENTORY 418.872 MILLION OZ//

PHYSICAL GOLD/SILVER COMMENTARIES

1:Peter Schiff/Mike Maharrey

end

2.Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens/ SIMON WHITE..//

Wall Street Mega Banks Have Drawn a Law-Free Zone Around Themselves – The Media Is Complicit

By Pam Martens:

March 13, 2024

From revoking the American people’s right to a jury trial in matters involving Wall Street; to brazenly thumbing their nose at anti-trust law; to trading the stock of their own bank in the darkness of their own dark pools; to forming their own stock exchange; to committing serial felonies without being criminally prosecuted or having their bank charters revoked – Wall Street mega banks have drawn a law-free zone around themselves and are more dangerous today than they have ever been in U.S. history.The most dangerous eras for the American people versus Wall Street mega banks have been the late 1920s and 1930s; 2007 to 2010; and today. We know that today is the most dangerous era because we read 12,000 pages produced by the Senate Banking Committee of the early 1930s on the Wall Street corruption in the late 20s and 30s; we read every government report produced on the causes of the crash of 2008 and its aftermath, as well as every important book on the subject; and we have personally chronicled at Wall Street On Parade the unprecedented corruption of the Wall Street mega banks since 2008.One key factor stands out in our mind as to why today’s Wall Street mega bank era is so much more corrupt and dangerous than earlier times: the failure of mainstream media to do its job.For the past decade, mainstream media has failed to adequately report to the American people the activities of the Wall Street mega banks and the insidious role of the Federal Reserve in being their secret bailout kingpin. Consider what happened with the Fed’s so-called repo loan bailouts in the last quarter of 2019.On September 17, 2019 the overnight repo loan rate spiked from an average of about 2 percent to 10 percent – signaling that one or more important Wall Street firms were in trouble. The repo loan market is an overnight loan market where banks, brokerage firms, mutual funds and others make predominantly one-day loans to each other against safe collateral, typically Treasury securities. Repo stands for “repurchase agreement.” When firms back away from lending to each other, someone is in trouble and spreading fear of the kind of contagion that occurred in 2008.Because the repo market dried up, the Fed effectively became the repo loan market on September 17, 2019. It exponentially grew the amount of emergency repo loans it was making over the following months. And, instead of just making the customary overnight loans, the Fed also added loans lasting for weeks, up to 42-day loans in some cases. The dollar amounts of the Fed’s repo loans grew to staggering levels. On October 24, 2019, we reported the following:“The New York Fed will now be lavishing up to $120 billion a day in cheap overnight loans to Wall Street securities trading firms, a daily increase of $45 billion from its previously announced $75 billion a day. In addition, it is increasing its 14-day term loans to Wall Street, a program which also came out of the blue in September, to $45 billion. Those term loans since September have been occurring twice a week, meaning another $90 billion a week will be offered, bringing the total weekly offering to an astounding $690 billion. It should be noted that if the same Wall Street firms are getting these loans continuously rolled over, they are effectively permanent loans. (That’s exactly what happened during the 2007-2010 Wall Street collapse: some teetering Wall Street casinos received, individually, $2 trillion in cumulative loans that were rolled over for two and one-half years – without the authorization or even awareness of Congress or the American people. One bank, Citigroup, received over $2.5 trillion in Fed loans, much of them at an interest rate below 1 percent, at a time when it was insolvent and couldn’t have obtained loans in the open market at even high double-digit interest rates.)”The names of the banks receiving the repo loans in 2019 remained secret from the American people for two years. When the stunning data was finally released by the Fed, it received a total news blackout by mainstream media. We have never seen anything that unprecedented in our 40 years of working on Wall Street or covering Wall Street on this website. The names of the banks in desperate need of cash in the fourth quarter of 2019 included some of the biggest and most iconic names on Wall Street.The Fed’s cumulative repo loans for the fourth quarter of 2019 on a term-adjusted basis came to $19.87 trillion, based on the data the Fed released two years later. Just six trading units of the Wall Street mega banks received 62 percent of the $19.87 trillion: Nomura ($3.7 trillion), JPMorgan ($2.59 trillion), Goldman Sachs ($1.67 trillion), Barclays ($1.48 trillion), Citigroup ($1.43 trillion), and Deutsche Bank ($1.39 trillion).Consider this news blackout involving the biggest names on Wall Street to what occurred after the Fed bailouts of 2007 to 2010.In response to the financial crisis of 2008, the Fed stepped in with an alphabet soup of emergency lending programs, as well as cranking out discount window loans. While the Fed released general details of what the programs were created to do, it did not release the names of the Wall Street mega banks and their trading units that were doing the bulk of the borrowing, or the sums borrowed by each institution.A tenacious investigative reporter at Bloomberg News, Mark Pittman, filed a Freedom of Information Act (FOIA) request with the Fed for the names of the banks, the amounts borrowed and the terms. Under the law, the Fed had to respond in 20 business days. The Fed stalled Pittman for six months, leading to the parent of Bloomberg News, Bloomberg LP, filing a lawsuit against the Fed in November 2008. Bloomberg won that suit. The Fed then appealed to the Second Circuit Appellate Court in 2009, attempting to continue to keep the details secret from the American people.What is particularly noteworthy about that appellate case is that the very same media outlets that drew a dark curtain around the Fed’s revelations of the names of the banks taking its massive repo loans of 2019 filed an Amicus Curiae (Friend of the Court) brief in Bloomberg’s appellate case in 2009. Those news outlets included Dow Jones & Company, Inc. (owner of the Wall Street Journal and MarketWatch), Reuters, Associated Press, and the New York Times.The Amicus writers told the appellate court this: “The public interest in disclosure in this case could hardly be greater. The [Federal Reserve] Board has lent out more than $2 trillion under the lending programs documented in the Remaining Term Reports. Despite this massive outlay, the public knows little about who has received these funds or the terms of their loans…While the Board releases aggregate data…it refuses to reveal any transaction-level data identifying where money has gone. Without this information, it is impossible to monitor the Board’s actions, and FOIA’s core purpose is defeated.”Let this sink in for a few moments. In 2019, just 11 years after the worst financial crisis since the Great Depression, the same mega banks on Wall Street are running amok again and back at the trough demanding trillions of dollars in cheap loans from the Fed – despite no apparent financial crisis in the general economy – and mainstream media does not go to court to demand the information and then, uniformly, blacks out the details to the American people when the data is finally reported by the Fed.The Fed lost on the Bloomberg case at the Second Circuit Appellate Court. The Fed was too embarrassed to take the case to the U.S. Supreme Court, because President Obama’s acting Solicitor General, Neal Katyal, planned to file a brief contrary to the Fed’s position, so a group called The Clearing House Association LLC, made up of some of the very same mega banks that were being bailed out by the Fed, filed their own appeal with the Supreme Court. The Supreme Court declined to hear the case in March of 2011, leaving the decision of the Second Circuit Appellate Court in place and making way for the release of the data.The Dodd-Frank financial reform legislation of 2010 had forced the Fed to release the transaction details of its seven emergency lending facilities in December of 2010. When the Supreme Court declined to hear the court case, the discount window transactions were released in March 2011. When the various data was released, it was widely covered by mainstream media.On March 21, 2011, Bloomberg News Editor in Chief Matthew Winkler released this statement:“At some point long before the credit markets seized up in 2007, financial markets collapsed and the economy plunged into the worst recession since the 1930s, the Federal Reserve forgot that it is the central bank for the people of the United States and not a private academy where decisions of great importance may be withheld from public scrutiny. As only Congress has the constitutional power to coin money, Congress delegates that power to the Fed and the Fed must be accountable to Congress, especially in disclosing what it does with the people’s money.”

3. CHRIS POWELL//

end

4. OTHER MAJOR GOLD COMMENTARIES/PODCASTS//LIVE FROM THE VAULT

end

end

5 a. IMPORTANT COMMENTARIES ON COMMODITIES /EGGS

Time For A Backyard Chicken Coop? Supermarket Egg Prices Soaring Once-Again

WEDNESDAY, MAR 13, 2024 – 06:00 PM

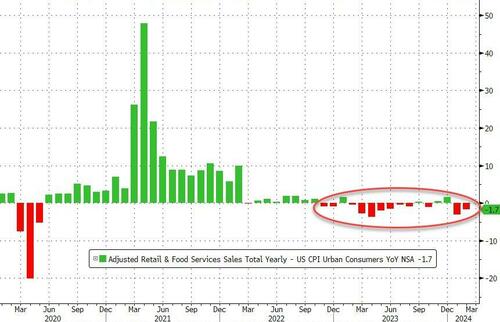

As of Wednesday, there are just 18 days left until Easter celebrations begin. For those who have recently visited the supermarket, egg prices are trending in the wrong direction, although well off the highs recorded in December 2022.

Data from the United States Department of Agriculture shows that Grade A egg prices per dozen jumped 40% from $2.13 to $3 between November and February.

Customer review and consumer news platform “ConsumerAffairs” reports that egg prices have “zoomed higher by a significant percentage in certain parts of the country,” indicating the largest surges have been at supermarkets in Minneapolis and Buffalo/Rochester, adding “Orlando’s egg prices went up as well.”

ConsumerAffairs noted that the price surges were mainly seen in “large central metro areas, but in non-core rural areas, there was a fairly noticeable decrease.”

“You can try and pin this on grocer greed, but that’s a wasted accusation. The higher prices of eggs in the US are actually due to several factors. There has been a significant reduction in the supply of eggs as a result of the avian influenza outbreak, which has resulted in the euthanasia of millions of chickens and ducks,” ConsumerAffairs said.

What intrigues us is the price gap in egg prices that ConsumerAffairs finds in cities versus rural areas. This means anyone who lives in big cities and wants to escape the inflation horror show under Bidenomics should at least consider rural communities where food can be sourced locally and sometimes a lot cheaper.

It probably wouldn’t hurt to homeschool the kids while living out in rural America.

Alternatively, starting a farm and taking control of one’s food supply is a powerful step towards independence from the overreaching state and mega-corporations.

For those who can’t move because the Federal Reserve has paralyzed the housing market with high-interest rates, consider a backyard garden and chicken coop.

5 B GLOBAL COMMODITY ISSUES/FOOD IN GENERAL//FREIGHT

END

6.CRYPTOCURRENCY//DIGITAL CURRENCY// COMMENTARIES/

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS THURSDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED UP 7.1894

OFFSHORE YUAN: UP TO 7.1943

SHANGHAI CLOSED DOWN 5.60 PPTS OR 0.13%

HANG SENG CLOSED DOWN 120.45 PTS OR 0.71%

2. Nikkei closed UP 111.41 PTS OR 0.29%

3. Europe stocks SO FAR: ALL GREEN

USA dollar INDEX UP TO 102.45 EURO FALLS TO 1.0943 DOWN 10 BASIS PTS

3b Japan 10 YR bond yield: RISES TO. +.768 Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 147.67/JAPANESE YEN NOW FALLING AS WELL AS LONG TERM 10 YR. YIELDS RISING //EVENTUALLY THIS WILL BREAK THE JAPANESE CENTRAL BANK

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen DOWN CHINESE ONSHORE YUAN: UP/ OFFSHORE: UP

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and UP FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund YIELD UP TO +2.3625***/Italian 10 Yr bond yield UP to 3.595* /SPAIN 10 YR BOND YIELD UP TO 3.136…**

3i Greek 10 year bond yield UP TO 3.141

3j Gold at $2168.35 silver at: 25.00 1 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble UP 0 AND 3 /100 roubles/dollar; ROUBLE AT 91.46//

3m oil into the 80 dollar handle for WTI and 84 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 147.67// 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 0.768% STILL ON CENTRAL BANK (JAPAN) INTERVENTION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.8794 as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.9623 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.189 UP 1 BASIS PTS…

USA 30 YR BOND YIELD: 4.343 DOWN 1 BASIS PTS/

USA 2 YR BOND YIELD: 4.626 UP 1 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 32.13…(TURKEY SET TO BLOW UP FINANCIALLY)

GREAT BRITAIN/10 YEAR YIELD: UP 1 BASIS PTS AT 4.040

end

2.a Overnight: Newsquawk and Zero hedge

Futures Rise To New Record High Ahead Of Data Deluge

THURSDAY, MAR 14, 2024 – 08:19 AM

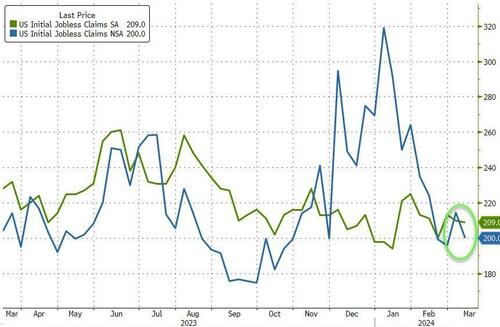

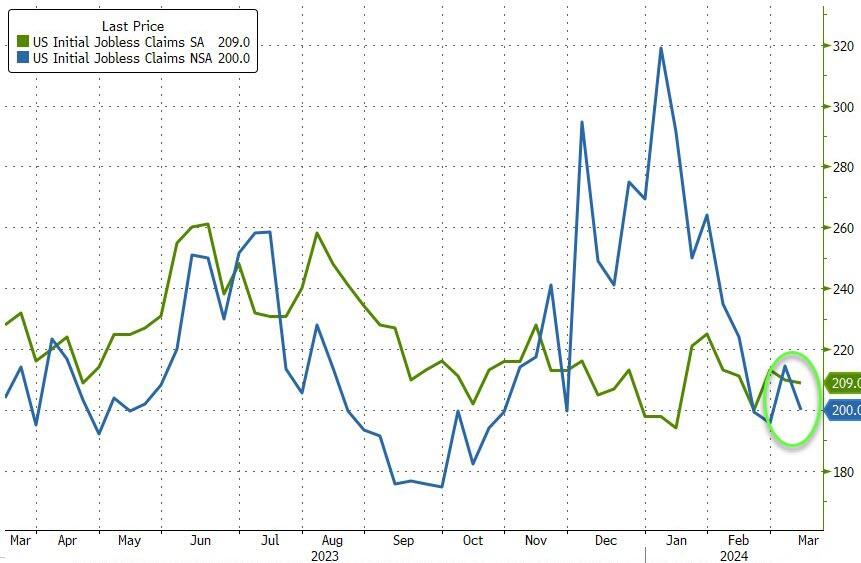

Another day, another all time high on deck. US equity futures are higher ahead of today’s PPI / Retail sales data, which we expect to be a big miss to expectations based on real-time card spending data. As of 8:00am, S&P futures were 0.3% higher trading around 5,250 while Nasdaq futures gained 0.4%, led by tech with the Mag7 stocks higher premarket (ex-NVDA, TSLA) as semis outperform pre-market. Europe trades mainly higher led by France while Asia is mixed on light overnight news. The yield curve is seeing some bear steepening with 10Y yield unchanged at 4.19%; keep an eye on the backend of the curve as we approach next week’s BOJ. The USD is stronger and commodities are mixed: energy is leading as WTI crude futures rise higher by almost 1% on the day after IEA projected a supply deficit for the rest of 2024. Today’s macro data focus includes Retail Sales (consensus +0.4%, last -0.4%), PPI (cons +0.2%, last +0.5% core PPI m/m) and Jobless Claims (exp. 218k, last 217k).

In premarket trading, Netflix and Meta Platforms rose with analysts flagging potential benefits to social-media and streaming companies from legislation targeting TikTok. Dollar General jumped after an upbeat forecast. Here are some other notable premarket movers:

- Citigroup shares rise 1.9% as Goldman Sachs raised the recommendation on the lender to buy from neutral. The broker sees “a realistic path” to higher returns and “compelling valuation support.”

- Hello Group the parent firm of Chinese dating apps Momo and Tantan, trades 16% lower after reporting a drop in paying users for both apps.

- Fisker shares plunge 38% after the Wall Street Journal reported the electric-vehicle startup has hired advisers to assist with a possible bankruptcy filing.

- Robinhood shares rise 12% after the online brokerage platform reported positive operating data in February including rising assets under custody and surging trading volume.

- SentinelOne shares drop 11% after the security software company gave a full-year revenue forecast that was weaker than expected at the midpoint of the range.

- Turtle Beach shares soar 27% after the sound technology company reported its fourth-quarter results and said it would buy PDP at an enterprise value of $118 million.

- UiPath shares rise 7.0% after the automation software company reported fourth-quarter results that beat expectations.

- Under Armour shares are down 7.2% after the company announced the return of Kevin Plank as chief executive officer, replacing Stephanie Linnartz, who was in the role for just over a year. Jefferies said the surprise change in leadership suggests uncertainty on the strategic direction of the sportswear maker.

- Weibo ADRs climb 5.5% after the Chinese social media company declared its second special cash dividend of $200m in a year, offsetting adjusted earnings and active users that missed analyst expectations.

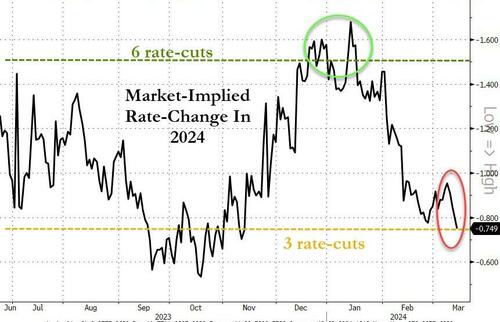

While traders have been trimming bets on deep and imminent rate cuts, that hasn’t dampened enthusiasm for stocks, with the S&P 500 setting new records in its longest stretch since 2018 without a decline of at least 2%, according to Bloomberg data. Today’s PPI data will be the final inflation report before next week’s Fed policy meeting. Officials are expected to hold interest rates steady for a fifth straight meeting, but the question is when they’ll start lowering borrowing costs.

“We’ve just upgraded our price target on the S&P 500, European stocks and Japanese equities because underlying data continues to be pretty resilient,” said Grace Peters, head of global investment strategy at JPMorgan Private Bank, who sees the US benchmark reaching 5,600 in a bull-case scenario. “The most realistic bull case is that corporate profits are stronger than expected.”

In politics, Donald Trump floated hedge fund titan John Paulson as possible Treasury secretary if he wins the November presidential election, and has held a series of meetings with other potential cabinet picks. Treasury Secretary Janet Yellen said it’s “unlikely” that market interest rates will return to levels that prevailed before the Covid-19 pandemic.

ECB Governing Council member Yannis Stournaras recommended two interest-rate cuts before the August summer break, and another two by the end of the year. Money markets maintained wagers on the scope for rate cuts this year, with the first quarter-point move seen by June, followed by two more and a 70% chance of a fourth. Bunds trimmed a small decline and the euro was steady.

Sentiment remained fragile in Chinese markets despite officials pledging central government funds to encourage consumers and businesses to replace old equipment and goods. Shares linked to Asian copper miners advanced after the metal jumped to an 11-month high on likely capacity cuts at Chinese smelters.

European stocks rose for a third day as Stoxx 600 touches a fresh record even as tech firms extend their decline for a second session. The mood points to a sector rotation in the background as retail, real estate and consumer products lead this month’s Stoxx 600 gains. Here are some of the biggest movers on Thursday:

- Encavis gains as much as 28% and trades slightly below the value of KKR’s recommended cash offer for the renewable-energy producer. Analysts see a high likelihood of deal completion, even as the offer price is below their respective PTs.

- Trainline shares jump as much as 12%, reaching the highest intraday since September 2022, after the train-ticketing platform reported full-year net ticket sales that topped estimates. Morgan Stanley highlighted the company’s performance in the UK, which was a main driver of the beat to net ticket sales.

- K+S shares rise as much as 9% after the German agricultural chemicals firm posted results which Citi called “encouraging” and guidance that showed scope for further earnings growth. Analysts pointed to the cash flow outlook as bringing some relief.

- NEL shares rise as much as 5.9% after the Norwegian hydrogen technology firm received $84 million of funding from the State of Michigan and the US Department of Energy, which RBC said confirms the company as a key green hydrogen player.

- IG Group rises as much as 4.9% after the UK trading platform reported third-quarter earnings which RBC said were better-than-expected and showed resilient trading revenues, client numbers and cash balances.

- RWE gains as much as 3.7% after the German utility reiterated its guidance, which Morgan Stanley said will trigger renewed interest in the stock. The company also expects to raise its dividend for the current fiscal year.

- OSB Group shares slump as much as 30%, the biggest drop since July, as the British banking group’s weaker-than-expected guidance for net interest margin overshadowed a full-year results beat.

- Basic-Fit drops as much as 16% as the health and fitness club operator’s growth plans disappoint.

- Lanxess shares fall as much as 11% after the German specialty chemicals firm’s 2023 sales and margins fell short of estimates, while its first-quarter adjusted Ebitda outlook also undershot consensus.

Earlier in the session, Asian stocks edged lower, with the regional gauge on track for its first weekly drop in two months, weighed down by losses in Chinese technology shares and Australian banks. The MSCI Asia Pacific Index fell as much as 0.2% amid choppy trading. Financial names including Westpac Banking and ANZ were among the biggest drags on the index after Macquarie downgraded the Australian lenders. Copper miners were a bright spot in the region after the metal jumped to an 11-month high. BHP was the top positive contributor to the Asian gauge as Citigroup raised the stock to buy.

Equities in mainland China and Hong Kong ended lower, with the Hang Seng Tech Index falling more than 1% despite officials pledging central government funds to encourage consumers and businesses to replace old equipment and goods. Shares linked to Asian copper miners advanced after the metal jumped to an 11-month high on likely capacity cuts at Chinese smelters. The US House of Representatives passed a bill to ban TikTok in the country unless its Chinese owner sells the video-sharing app.

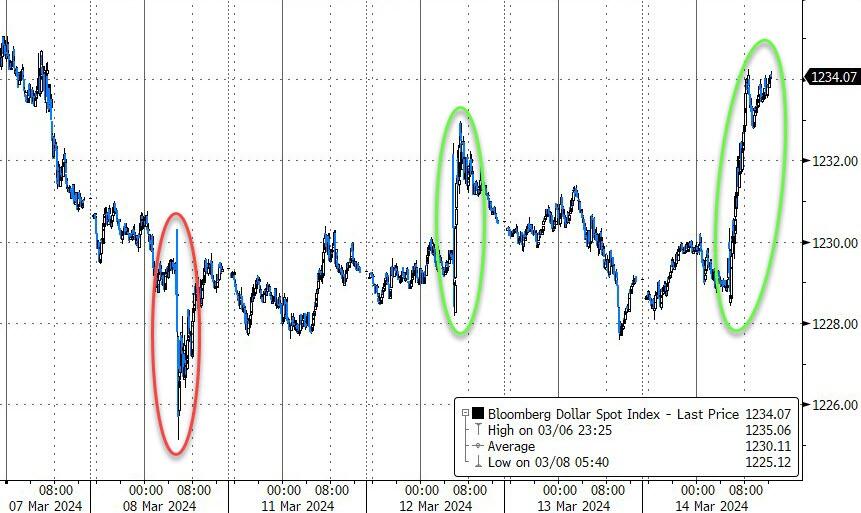

In FX, bloomberg dollar spot index gained 0.1% to erase Wednesday’s decline. The yen reversed an initial gain as Treasury yields turned higher and ahead of Rengo wage outcomes on Friday, which may affect the Bank of Japan’s policy decision. SEK and CHF are the weakest performers in G-10 FX, NZD and GBP outperform.

In rates, treasuries were narrowly mixed after yields edged to new weekly highs ahead of economic data slate including PPI and retail sales. US yields slightly richer from front-end out to belly of the curve and slightly cheaper across long-end, steepening 2s10s by almost 1bp on the day; 10-year yields around 4.19% with gilts outperforming by 1.2bp in the sector. Gilts outperform slightly, and core European rates drew support from comments by ECB’s Yannis Stournaras, who recommended two interest-rate cuts before the summer break in August. S&P 500 futures advance toward last week’s all-time high and WTI crude oil futures top $80/bbl; peripheral spreads tighten to Germany with 10y BTP/Bund narrowing 2.9bps to 119.8bps amid dovish remarks from ECB speakers. German, gilt and Treasury 10-year yields are steady as traders await US producer-price data, which comes after a sticky consumer reading earlier this week.

In commodities, crude oil added to the biggest gain in about five weeks after the International Energy Agency said global oil markets face a supply deficit throughout 2024 as OPEC+ looks set to continue output cuts. Iron ore extended its decline toward $100 a ton, with few signs of a turnaround in Chinese steel demand. Gold edged lower. Spot gold falls roughly $5 to trade near $2,170/oz.

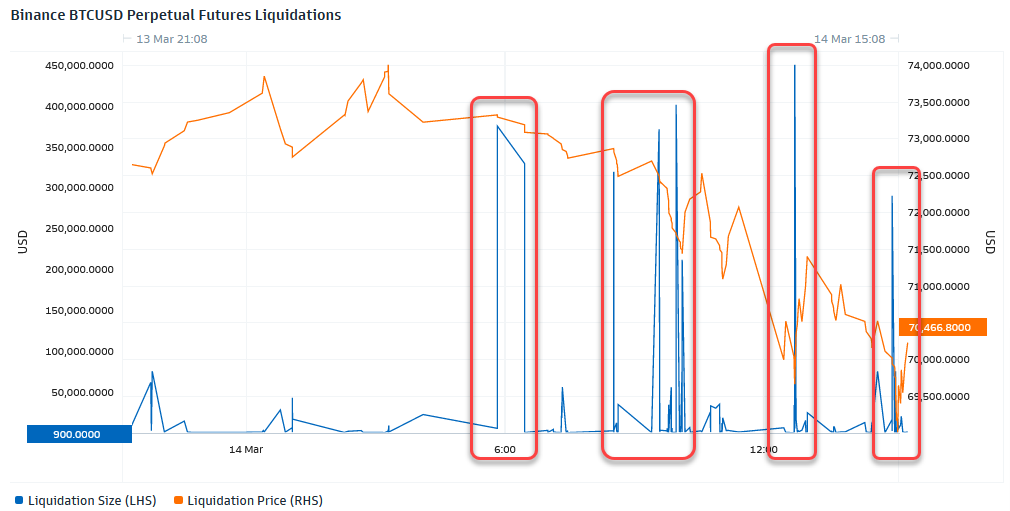

Bitcoin took a breather after soaring to highs yesterday, and currently holds just shy of USD 73.5k.

The US economic data calendar includes February retail sales and PPI and weekly jobless claims (8:30am) and January business inventories (10am). No scheduled Fed speakers due before March 20 policy decision. From central banks, we’ll hear from ECB Vice President de Guindos, along with the ECB’s de Cos, Schnabel, Knot and Stournaras.

Market Snapshot

- S&P 500 futures up 0.3% to 5,184.75

- STOXX Europe 600 up 0.2% to 508.44

- MXAP up 0.2% to 176.55

- MXAPJ little changed at 540.98

- Nikkei up 0.3% to 38,807.38

- Topix up 0.5% to 2,661.59

- Hang Seng Index down 0.7% to 16,961.66

- Shanghai Composite down 0.2% to 3,038.23

- Sensex up 0.3% to 73,006.82

- Australia S&P/ASX 200 down 0.2% to 7,713.63

- Kospi up 0.9% to 2,718.76

- German 10Y yield little changed at 2.38%

- Euro little changed at $1.0941

- Brent Futures up 0.2% to $84.19/bbl

- Gold spot down 0.2% to $2,169.72

- US Dollar Index little changed at 102.85

Top Overnight News

- US Treasury Secretary Janet Yellen said it’s “unlikely” that market interest rates will return to levels that prevailed before the Covid-19 pandemic triggered a wave of inflation and higher yields. BBG

- BOJ Governor Kazuo Ueda will likely take his time normalizing ultra-loose monetary policy after ending negative interest rates, former central bank executive Hideo Hayakawa said on Thursday. RTRS

- Japan’s largest industrial union said on Thursday the average pay rise offered by 231 firms for both full-time and part-time employees was the biggest since 2013, amid signs wage hikes were broadening. RTRS

- Chinese wheat importers have cancelled or postponed about one million metric tons of Australian wheat cargoes, trade sources with direct knowledge of the deals said, as growing world stockpiles drag down prices. RTRS

- The crude market faces a supply deficit throughout 2024 — instead of the surplus previously expected — as OPEC+ looks set to continue output cuts in the second half, the IEA said. The agency bolstered forecasts for global demand growth by 9% to 1.3 million barrels a day, on a stronger US outlook. BBG

- The ECB must lower borrowing costs twice before its August summer break and two more times before the end of the year, without being swayed by the US Federal Reserve, according to Governing Council member Yannis Stournaras. BBG

- The US has held secret talks with Iran this year in a bid to convince Tehran to use its influence over Yemen’s Houthi movement to end attacks on ships in the Red Sea, according to US and Iranian officials. FT

- Tuesday’s CPI report shouldn’t fundamentally alter expectations that the Fed will cut rates around three times this year because it isn’t likely to justify a meaningful revision in officials’ forecasts for inflation as measured by that index, said Eric Rosengren, who headed the Boston Fed from 2007 to 2021. WSJ

- Donald Trump has talked about hedge fund titan John Paulson as Treasury secretary if he wins the November presidential election, and has held a series of meetings with potential cabinet picks. Other potential names in the mix for the top Treasury post, should Trump defeat incumbent President Joe Biden, include former US trade representative Robert Lighthizer, Susquehanna International Group LLP founder Jeff Yass and Key Square Group LP founder Scott Bessent. BBG

- Microsoft (MSFT) and Oracle (ORCL) expand partnership to satisfy global demand for oracle database Azure.

MicroStrategy Incorporated (MSTR) – The crypto investor announced its intention to offer USD 500mln of convertible senior notes due 2031, with an additional option for purchasers to buy up to USD 75mln more. MSTR intended to use the proceeds to purchase additional bitcoin and for general corporate purposes. Shares +4.5 pre-market trade - Under Armour (UAA) – Kevin Plank will assume the roles of President and CEO from April 1st, succeeding Stephanie Linnartz. Mohamed El-Erian will become the non-executive Chair of the Board. Plank, founder of Under Armour, transitions from the Executive Chair role, while Linnartz will remain to advise until April 30th. Shares -4.5% in pre-market trade

A more detailed look at global markets courtesy of Newsquawk

APAC stocks were mixed after the indecisive performance stateside amid light catalysts and tech weakness, with participants lacking conviction ahead of next week’s central bank bonanza. ASX 200 was subdued as losses in financials and tech overshadowed the gains in the commodity-related sectors. Nikkei 225 traded indecisively after a slew of BoJ-related source reports suggesting a policy shift next week. Hang Seng and Shanghai Comp. were somewhat varied with the Hong Kong benchmark pressured amid tech-related headwinds after the US House approved the bill which threatens to ban TikTok, while the mainland was indecisive with downside initially cushioned after China issued plans to promote trading in consumer goods and equipment upgrades.

Top Asian news

- BoJ will discuss whether to end its negative interest rate policy as pay hikes by major companies bring the central bank’s 2% price stability target within reach. Furthermore, with more BoJ policymakers embracing the idea, the decision is seen coming down to the results of Japan’s annual wage negotiations, to be published by top labour confederation Rengo on Friday, according to Nikkei.

- Japanese Federation of Textile, Chemical, Commerce, Food and General Services Workers’ Unions which is the largest industrial union and known as UA Zensen stated that the average pay increase offered by 231 firms reached the biggest on record since 2013 compared with the same period last year.

- Taiwan Central Bank Governor said they are concerned potential electricity price hikes will result in a chain reaction effect on inflation expectations and they will be very prudent about discussions on interest rates this time, while he added that they will not likely cut interest rates before June, according to Reuters.

- Foxconn (2317 TT) sees 2024 revenue to increase significantly Y/Y; sees Q1 revenue to slightly decline Y/Y, sees Q1 revenue for smart consumer electronics to slightly decline Y/Y. Q4 net profit TWD 53.14bln (exp. 43.5bln; prev. 43.1bln Q/Q). Sees Q1 revenue for cloud and networking products to be flat Y/Y. Sees Q1 revenue for computing products to be flat Y/Y. Says major growth momentum this year will be AI servers, expects the servers business to grow strongly this year; sees very strong demand in AI from clients. AI server growth in 2023-25 could be stronger than the market average, potentially above 30% or higher annually. Semiconductor revenue will surpass TWD 100bln this year.

- China’s Commerce Ministry on the review into Australian wine tariffs says the final ruling will be made in accordance with the investigation procedures.

- Chinese State Planner has issued a draft rules to support high-quality firms to take on medium and long-term foreign debt.

European bourses are mostly in the green, with sentiment lifted after dovish remarks from ECB’s Stournaras. The SMI (-0.3%) underperforms, hampered by post-earnings weakness in Swiss Life (-5.7%). European sectors are mixed, with Basic Resources found at the foot of the pile, hampered by broader weakness in base metals, whilst Energy benefits from firmer crude prices. US equity futures (ES +0.2%, NQ +0.5%, RTY +0.2) are trading on a firmer footing, with slight outperformance in the NQ, attempting to pare back some of its losses from the prior session.

Top European news

- ECB’s Stournaras says they have to cut rates twice prior to the summer break, via Bloomberg; four cuts in 2024 seems reasonable. Need to begin cutting soon; policy must not become too restrictive. Dismisses the idea that the ECB cannot cut before the Fed. Don’t exaggerate the risk of a wage-price-spiral. Structural portfolio will include government bonds. Remarks which sparked a modest uptick in EGBs.

- ECB Chief Economist Lane says the ECB has a bit more confidence that they are heading towards the inflation goal, more data will help gain more confidence, via CNBC; Better not to analyse whether it is April or June when it comes to lowering rates

- Norges Bank Regional Network Report Q1 2024 : Expects overall activity to remain virtually unchanged in the first half of 2024. Prospects have been revised up somewhat since the previous survey.Employment plans for 2024 Q1 have been revised up slightly since the previous survey. Contacts expect annual wage growth of 4.9% in 2024, which is an upward revision from the 4.5% estimate in November.

FX

- DXY is broadly flat vs. peers ahead of a slew of Tier 1 US data, with the index contained within yesterday’s 102.66-103.02 range. Strong data could see DXY reclaim 103 and approach the weekly high at 103.17. A soft release could see the index approach the post-NFP low at 102.35.

- EUR is steady vs. the USD and contained within yesterday’s 1.0920-1.0963 range. ECB’s Stournaras sparked modest pressure for the Single-Currency, though the move quickly faded.

- JPY is a touch softer vs. the USD but ultimately contained within yesterday’s 147.23-148.05 range. Markets are on tenterhooks ahead of tomorrow’s Rengo announcement which will likely shape expectations for next week’s BoJ decision.

- AUD/USD is flat vs. the USD in what has been a week of contained price action, and currently sits within yesterday’s 0.6599-0.6635 range. NZD is trivially firmer vs. USD after edging above yesterday’s peak at 0.6170.

- SEK is weaker vs. peers given soft inflation metrics which has seen odds of a May cut creep higher. EUR/SEK made a new high for the week at 11.218 but still some way off March highs.

Fixed Income

- Once again, USTs are marginally in the red within the European morning. Specifics since the 30yr auction (strong) have been light and USTs are now back to pre-auction levels of 110-30; data and 20yr announcement due.

- Gilts are the relative laggard as they continue to pare from the outperformance seen on Tuesday’s labour data, with few fresh drivers able to change the narrative. Gilts hold towards the lower end of a 99.01-98.80 range.

- Bunds are in the red but off the 132.42 trough after remarks from ECB’s Stournaras who said that two cuts are needed before the summer break and four for 2024 is reasonable. Commentary which has helped to lift Bunds to a 132.66 high. Comments from ECB’s Lane failed to spark any price action in Bunds.

Commodities

- Crude is firmer with gains facilitated by Russian facility outages, bullish US energy inventory data and several geological updates. Brent May rose from support at USD 83.98/bbl and currently holds just shy of USD 84.75/bbl.

- A subdued morning thus far for precious metals and with overall trade rangebound, awaiting impetus from US Tier 1 data. XAU trades within a tight range between USD 2,167.47-2,177.05/oz.

- Base metals are mostly subdued as a function of the Dollar and quiet macro updates. Copper holds onto a bulk of the prior day’s gains (following reports that major Chinese copper smelters agreed to curb output) whilst iron ore overnight continued trundling lower amid ongoing Chinese demand woes.

- IEA OMR: Raises 2024 oil demand growth forecast by 110k BPD to 1.3mln BPD; says if OPEC+ voluntary cuts remain in place through 2024, market is seen in a slight deficit rather than a surplus. While 2024 growth has been revised up by 110 kb/d from last month’s Report, the pace of expansion is on track to slow from 2.3 mb/d in 2023 to 1.3 mb/d, as demand growth returns to its historical trend while efficiency gains and EVs reduce use. World oil production is projected to fall by 870 kb/d in 1Q24 vs 4Q23 due to heavy weather-related shut-ins and new curbs from the OPEC+ bloc. Refining margins improved through mid-February before receding, with the US Midcontinent and Gulf Coast as well as Europe leading the gains. In this Report, we are now holding OPEC+ voluntary cuts in place through 2024 – unwinding them only when such a move is confirmed by the producer alliance (see OPEC+ cuts extended). On that basis, our balance for the year shifts from a surplus to a slight deficit, but oil tanks may get some relief as the massive volumes of oil on water reach their final destination.

Geopolitics: Middle East

- US Secretary of State Blinken held a video call with officials from Cyprus, Britain, UAE, Qatar, EU and the UN to discuss getting a new maritime corridor for delivering humanitarian aid into Gaza up and running, according to Reuters.

- US is expected to impose new sanctions on two illegal outposts in the occupied West Bank that were used as a base for attacks by extremist Israeli settlers against Palestinian civilians, according to three US officials cited by Axios.

- US CENTCOM said Iranian-backed Houthis fired one anti-ship ballistic missile in the Gulf of Aden although the missile did not impact any vessels and there was no damage reported, while its forces successfully engaged and destroyed four unmanned aerial systems and one surface-to-air missile in Houthi-controlled areas of Yemen.

Geopolitics: Other

- Taiwan and China authorities both dispatched teams to join a rescue mission after a Chinese fishing boat capsized near Taiwan-controlled Kinmen Islands on Thursday morning, according to Taiwanese press.

- Philippines President Marcos and US Secretary of State Blinken to meet on March 19th to discuss cooperation and security matters, while Marcos vowed to defend maritime rights in the face of a ‘more active attempt by China to annex some territories’.

- North Korean leader Kim guided a military demonstration involving a tank unit on Wednesday, according to KCNA.

US Event Calendar

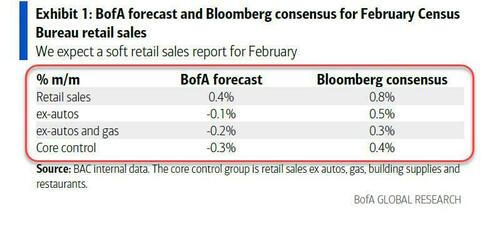

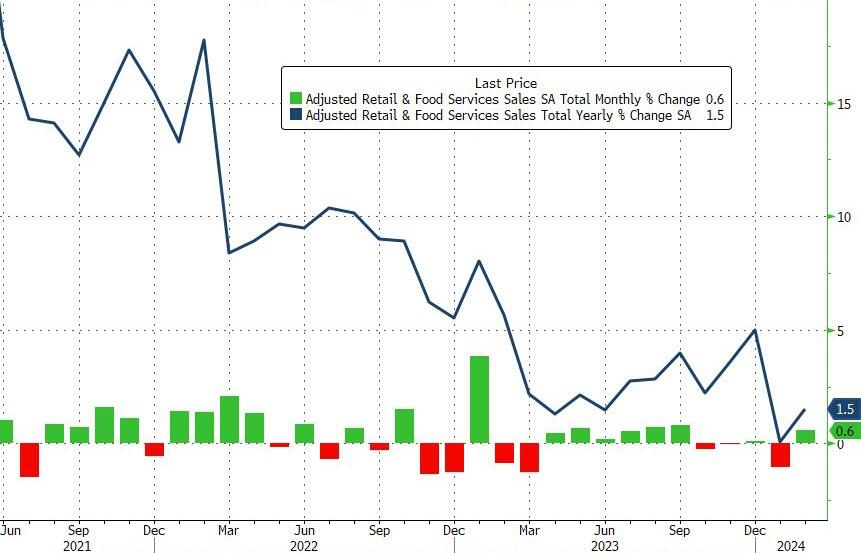

- 08:30: Feb. Retail Sales Ex Auto and Gas, est. 0.3%, prior -0.5%

- Feb. Retail Sales Control Group, est. 0.4%, prior -0.4%

- Feb. Retail Sales Ex Auto MoM, est. 0.5%, prior -0.6%

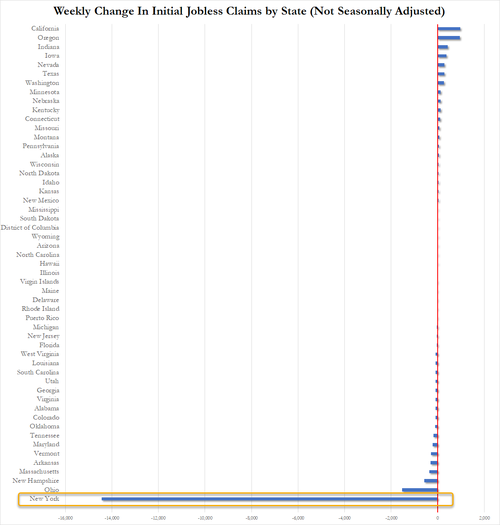

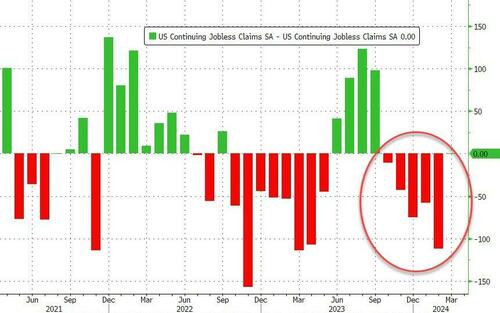

- 08:30: March Initial Claims, est. 218K, prior 217K

- March Continuing Claims, est. 1.91m, prior 1.91m

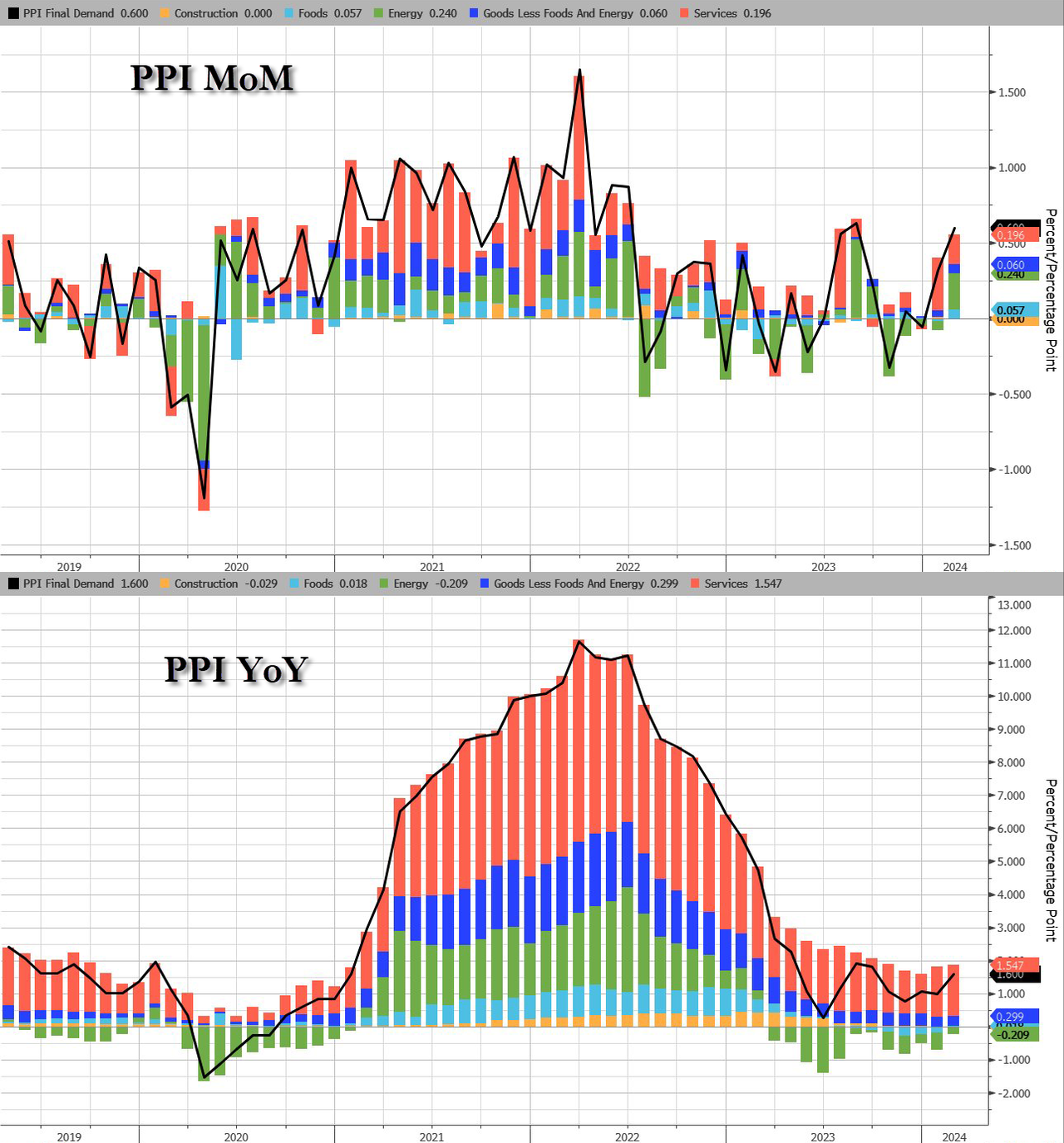

- 08:30: Feb. PPI Final Demand MoM, est. 0..3%, prior 0.3%

- Feb. PPI Final Demand YoY, est. 1.2%, prior 0.9%

- Feb. PPI Ex Food and Energy YoY, est. 1.9%, prior 2.0%

- Feb. PPI Ex Food and Energy MoM, est. 0.2%, prior 0.5%

- 10:00: Jan. Business Inventories, est. 0.2%, prior 0.4%

DB’s Jim Reid concludes the overnight wrap

Markets struggled to keep up their momentum yesterday, with the S&P 500 (-0.19%) falling back from its all-time high, whilst yields on 10yr Treasuries (+3.9bps) moved up for a third day running. That came amidst growing concern about how stretched the rally was becoming, with the S&P 500 having risen by more than +25% in less than 100 trading days. Moreover, there’s still quite a bit of focus on inflation, and the US CPI release this week has led to some scepticism about whether the Fed will be able to cut rates by June after all.