MARCH 15 B/THE IDES OF MARCH//GOLD CLOSED DOWN $5.20 TO $2158.00/SILVER CLOSED UP 32 CENTS TO $25.18/PLATINUM CLOSED UP $7.70 TO $940.60 WHILE PALLADIUM CLOSED UP $13.05 TO $1082.65//JAPAN ANNOUNCES THE END OF NEGATIVE RATES AS THEY WILL BEGIN TO RAISE ITS KEY I.R.//ISRAEL VS HAMAS: ISRAEL GREENLIGHTS THAT IT WILL SHUN BIDEN AND ENTER RAFAH//ISRAEL VS HEZBOLLAH/WEST BANK NEWS//HOUTHIS NEWS//

Bitcoin: afternoon price: $69,874 DOWN 120 dollars

Platinum price closing UP $7.70 AT $940.60

Palladium price; UP 13.05 AT $1082.65

END

SHANGHAI GOLD PREMIUM 40 DOLLARS/COMEX GOLD

SHANGHAI GOLD………

SHANGHAI GOLD (USD) FUTURES – QUOTES

Beginning Monday, April 1, 2024, CME Group settlement data will no longer be accessible through ftp.cmegroup.com and will have a delayed publication time of 12:00 a.m. CT on all cmegroup.com web pages. Learn about alternate ways to access the data in our FAQ.

GOLD: NUMBER OF NOTICES FILED FOR MAR/2024. CONTRACT: 16 NOTICES FOR 1600 OZ or 0.0493 TONNES

total notices so far: 5172 contracts for 517,200 Oz (16.087 tonnes)

FOR MARCH:

SILVER NOTICES: 3 NOTICE(S) FILED FOR 15,000 OZ/

total number of notices filed so far this month : 5114 for 25,570,000 oz

XXXXXXXXXXXXXXXXXX

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

BOTH GLD AND SLV ARE FRAUDULENT VEHICLES//THEY ARE NOW RAIDING GLD AND SLV FOR PHYSICAL

GLD

THE CROOKS ARE STEALING GOLD AND SILVER FROM THE GLD/SLV AND REPLACING THE PHYSICAL WITH PAPER DOLLARS.

WITH GOLD DOWN $5.20

INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD/ :

NO CHANGES IN GOLD INVENTORY AT THE GLD:

//INVENTORY RESTS AT 816.86 TONNES

INVENTORY RESTS AT 816.86 TONNES

SLV//

WITH NO SILVER AROUND AND SILVER UP 32 CENTS AT THE SLV//

HUGE CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 1.006 MILLION OZ FROM THE SLV.: INVENTORY REMAINS AT 417.866 MILLION OZ/

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV.

CLOSING INVENTORY: 417.866 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A HUMONGOUS SIZED 1109 CONTRACTS TO 148,533 AND CLOSER TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THIS HUGE SIZED GAIN IN COMEX OI WAS ACCOMPLISHED DESPITE OUR LOSS IN PRICE OF $0.09 IN SILVER PRICING AT THE COMEX ON THURSDAY. WE HAD ZERO LONG LIQUIDATION AT THE COMEX SESSION WITH AGAIN MAJOR SHORT COVERING DESPITE THE PRICE LOSS. WE HAD A STRONG 522 T.A.S ISSUANCE AND THESE WILL BE USED FOR MANIPULATION LATER THIS MONTH/AS WELL AS TODAY. PLEASE NOTE THAT THE CROOKS NEED A HIGHER SILVER/GOLD T.A.S. TO CARRY ON THEIR CROOKED MANIPULATION ON A DAILY BASIS

CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON THURSDAY NIGHT: 522 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS. IT THUS LOOKS LIKE THE FED (GOV’T) IS BEHIND ALL OF THESE TRADES.

WE HAVE NOW SET ANOTHER RECORD LOW AT 114,102 CONTRACTS ///JULY 3.2023// OUR BANKERS WITH THE HELP OF SPECULATORS AND HIGH FREQUENCY TRADERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.09),BUT WERE UNSUCCESSFUL IN KNOCKING ANY SILVER LONGS AS WE HAD A MEGA HUMONGOUS SIZED GAIN OF 3234 CONTRACTS ON OUR TWO EXCHANGES DESPITE THE LOSS IN PRICE OF 9 CENTS.

WE MUST HAVE HAD:

A GIGANTIC SIZED 2125 ISSUANCE OF EXCHANGE FOR PHYSICALS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 22.270 MILLION OZ (FIRST DAY NOTICE) FOLLOWED BY TODAY,S 0.060 MILLION OZ E.F.P JUMP TO LONDON //NEW TOTALS DECREASES TO : 26.920 MILLION OZ

//NEW STANDING FOR SILVER IS THUS 26.920 MILLION OZ

WE HAD:

/ HUMONGOUS SIZED COMEX OI GAIN/ GIGANTIC SIZED EFP ISSUANCE/ VI) STRONG SIZED NUMBER OF T.A.S. CONTRACT ISSUANCE 522 CONTRACTS)/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL -REMOVED A HUGE 669 CONTRACTS //

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS FEB. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF MARCH

TOTAL CONTRACTS for 11 days, total 18,720 contracts: OR 93.600 MILLION OZ (1701 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 93.600 MILLION OZ

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH 2022: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 118.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 85.745 MILLION OZ (SMALLER THAN LAST MONTH)

AUGUST: 171.43 MILLION OZ (THIS MONTH IS GOING TO BE HUGE //2ND HIGHEST ON RECORD

SEPT: 72.705 MILLION OZ (SMALLER THIS MONTH)

OCT: 97.455 MILLION OZ

NOV. 50.050 MILLION OZ

DEC. 66.140 MILLION OZ//

TOTAL 2023: 1,104.10 MILLION OZ/

JAN ’24 : 78.655 MILLION OZ//

FEB /2024 : 66.135 MILLION OZ./FINAL

MARCH: 93.600 MILLION OZ//WILL BE MUCH LARGER THIS MONTH//MAYBE CLOSE TO A RECORD ISSUANCE

RESULT: WE HAD A HUGE SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 1109 CONTRACTS DESPITE OUR SMALL LOSSIN PRICE OF SILVER PRICING AT THE COMEX//THURSDAY.,. THE CME NOTIFIED US THAT WE HAD A GIGANTIC EFP ISSUANCE CONTRACTS: 2125 ISSUED FOR MAY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS. WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR MARCH. OF 23.385 MILLION OZ ON FIRST DAY NOTICE FOLLOWED BY TODAY’S SMALL 0.060 MILLION OZ E.F.P/ JUMP TO LONDON

//NEW TOTAL STANDING RISES TO 26.920 MILLION OZ

WE HAVE A HUMONGOUS GAIN OF 3234 OI CONTRACTS ON THE TWO EXCHANGES DESPITE THE LOSS IN PRICE. THE TOTAL OF TAS INITIATED CONTRACTS TODAY: A STRONG SIZED 522 CONTRACTS//HUGE FRONT END OF THE TAS CONTRACTS WERE LIQUIDATED DURING THE THURSDAY COMEX SESSION/// WITH MAJOR SHORT COVERING FROM OUR SPEC SHORTS

THE NEW TAS ISSUANCE THURSDAY NIGHT (522) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE//PROBABLY TODAY., .

WE HAD 3 NOTICE(S) FILED TODAY FOR 0.0150 MILLION OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A SMALL SIZED 1083 CONTRACTS TO 539,571 AND FURTHER FROM THE RECORD (SET JAN 24/2020) AT 799,733 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110, BUT WE ARE NOW CLOSER TO OUR ALL TIME LOW OF 390,000 CONTRACTS.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED 313 CONTRACTS

WE HAD A SMALL SIZED DECREASE IN COMEX OI (1083 CONTRACTS) WITH OUR $12.20 LOSS IN PRICE//THURSDAY. THE BANKERS WERE FORCED TO SUPPLY THE NECESSARY SHORT PAPER TO CONTAIN GOLD’S RISE.WE ALSO HAD A RATHER LARGE INITIAL STANDING IN GOLD TONNAGE FOR MARCH. AT 10.270 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’’S HUGE QUEUE JUMP OF 50,000 OZ.

NEW TOTAL Of INITIAL GOLD STANDING RISES TO: 18.364 TONNES // ALL OF THIS HAPPENED WITH OUR $12.20 LOSS IN PRICE WITH RESPECT TO THURSDAY’S TRADING. WE HAD A FAIR SIZED GAIN OF 1313 OI CONTRACTS (4.083) PAPER TONNES) ON OUR TWO EXCHANGES.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 3751CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 539,571

IN ESSENCE WE HAVE A FAIR SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 1313 CONTRACTS WITH 1083 CONTRACTS DECREASED AT THE COMEX// AND A FAIR SIZED 2396 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 1313 CONTRACTS.. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): STRONG BUT SMALLER THAN BEFORE SIZED 3002 CONTRACTS,

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD STRONG SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (2396 CONTRACTS) ACCOMPANYING THE SMALL SIZED LOSS IN COMEX OI (1083) //TOTAL GAIN FOR OUR THE TWO EXCHANGES: 1626 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR FORMER FORMAT OF BANKERS GOING LONG AND SPECULATORS GOING SHORT ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR MARCH. AT 7.502 TONNES FOLLOWED BY TODAY’S STRONG QUEUE JUMP OF 1.555 TONNES/NEW STANDING ADVANCES TO 18.364 TONNES.

/ 3) ZERO LONG LIQUIDATION // 4) SMALL SIZED COMEX OPEN INTEREST LOSS/ 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER///6: STRONG T.A.S. ISSUANCE: 3002CONTRACTS//SOME SHORT COVERING AGAIN

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023-2024 INCLUDING TODAY

MARCH

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF MARCH. :

TOTAL EFP CONTRACTS ISSUED: 59,681 CONTRACTS OR 5,968,100OZ OR 185,63 TONNES IN 11TRADING DAY(S) AND THUS AVERAGING: 5948 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 11TRADING DAY(S) IN TONNES 185.63 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2022, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 185.63/3550 x 100% TONNES 5.23% OF GLOBAL ANNUAL PRODUCTION

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH/2022: 409.30 TONNES //FINAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 151.69 TONNES (WEAKER THAN LAST MONTH)

AUGUST: 195.28 TONNES (A STRONGER MONTH)//FINAL

SEPT: 254.709 TONNES (WILL BE LARGER THAN LAST MONTH AND A STRONG MONTH)

OCT. 248.09 TONNES. LIKE SILVER, THIS MONTH IS GOING TO BE A STRONG E.F.P. ISSUANCE.

NOV. 239.16 TONNES//WILL BE STRONG THIS MONTH,

DEC. 213.704 TONNES. A STRONG MONTH//

TOTAL FOR YEAR 2023: 2,569.57 TONNES VS 2578 TONNES LAST YEAR

JAN ’24: 291.76 TONNES (WILL BE MUCH GREATER THAN LAST MONTH.//3RD HIGHEST EVER RECORDED EXCHANGE FOR PHYSICAL)

FEB’24: 201.947 TONNES

MARCH 2024: 185.63 TONNES//THIS IS GOING TO BE ONE HUMDINGER OF AN E,F,P. ISSUANCE.

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF FEB. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (APRIL), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER ROSE BY A HUGE SIZED 1083 CONTRACTS OI TO 148,533 AND CLOSER TO THE COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 6 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 2125 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAY 2125 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 1100 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 1109 CONTRACTS AND ADD TO THE 2125 E.FP. ISSUED

WE OBTAIN A MEGA HUMONGOUS SIZED GAIN OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 3234CONTRACTS

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTAL 16.170 MILLION OZ

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS//

FRIDAY MORNING/THURSDAY NIGHT

SHANGHAI CLOSED UP 16.40 PTS OR 0.54% //Hang Seng CLOSED DOWN 240,77 PTS OR 1.42% / Nikkei CLOSED DOWN 99.74 PTS OR 0.26%//Australia’s all ordinaries CLOSED DOWN 0.63% /Chinese yuan (ONSHORE) closed DOWN 7.1960 //OFFSHORE CHINESE YUAN CLOSED DOWN TO 7.2037 /Oil UP TO 80.64 dollars per barrel for WTI and BRENT UP AT 84,76/ Stocks in Europe OPENED ALL GREEN// ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE YUAN WEAKER

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY SMALL 1083 CONTRACTS TO 539,571 WITH OUR LOSS IN PRICE OF $12.20 WITH RESPECT TO THURSDAY TRADING. MOST LIKELY IT WAS THE BANKERS SUPPLYING THE NECESSARY PAPER WITH OUR SHORT PLAYERS EXITING AS FAST AS THEIR FEET COULD CARRY THEM. THE SHORTS HAVE BEEN KILLED LATELY, AS THEY HAVE BEEN LED BY THE NOSE BY OUR BANKER-HIGH FREQUENCY TRADERS.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE NON ACTIVE DELIVERY MONTH OF MARCH..… THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 2396 EFP CONTRACTS WERE ISSUED: : APRIL 2396 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 2396CONTRACTS

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A FAIR SIZED TOTAL OF 1,313 CONTRACTS IN THAT 2396 LONGS WERE TRANSFERRED AS EXCHANGE FOR PHYSICALS TO LONDON AND WE HAD A SMALL LOSS OF 1083 COMEX CONTRACTS..AND THIS LOSS ON OUR TWO EXCHANGES HAPPENED DESPITE OUR FALL IN PRICE OF $12.20 THURSDAY COMEX. AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS DURING MID MONTH IN THE DELIVERY CYCLE), THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR THURSDAY NIGHT WAS A MUCH SMALLER SIZED 3002 CONTRACTS,

THROUGHOUT THE PAST SEVERAL WEEKS, THE BANKERS CONTINUE TO SELL OFF THE LONG SIDE OF THE SPREAD WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR/T.A.S. SPREAD WHICH WILL BE LIQUIDATED IN DAYS HENCE//. IT SEEMS THAT OUR CROOKS ARE HAVING A HARD TIME TRYING TO CONTROL THE PRICE OF GOLD AND THUS THE NEED FOR RECORD T.A.S. ISSUANCE.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: MARCH (18.340 TONNES) ( NON ACTIVE MONTH)

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 24 MONTHS OF 2021-2023:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276 TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.340 TONNES

THE SPECS/HFT WERE SUCCESSFUL IN LOWERING GOLD’S PRICE( IT LOST $12.20 //// BUT WERE UNSUCCESSFUL IN KNOCKING ANY SPECULATOR LONGS AS WE HAD A FAIR SIZED GAIN OF1313 TOTAL CONTRACTS ON OUR TWO EXCHANGES DESPITE OUR LOWER PRICE.

WE HAD A STRONG T.A.S. LIQUIDATION ON THE FRONT END OF THURSDAY’S TRADING . THE T.A.S. ISSUED ON THURSDAY NIGHT, WILL BE “PUT INTO THE BANK” TO BE USED AT A LATER DATE AT THE COLLUSIVE CHOOSING OF OUR BANKERS. THE HIGH T.A.S. ISSUANCE IS MEANT TO CONTROL THE PRICE OF GOLD (AS WELL AS INITIATE A RAID).

WE HAVE GAINED A TOTAL OI OF 4.083 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR MARCH. (10.3576 TONNES) ON FIRST DAY NOTICE FOLLOWED BY TODAY’S 50,000 OZ QUEUE JUMP//NEW STANDING INCREASES TO 18.340 TONNES

ALL OF THIS WAS ACCOMPLISHED DESPITE OUR LOSS IN PRICE TO THE TUNE OF $12.20

WE HAD -REMOVED 313 CONTRACTS TO THE COMEX TRADES TO OPEN INTEREST (CROOKS)

NET GAIN ON THE TWO EXCHANGES 1313 CONTRACTS OR 131300 OZ OR 4.083 TONNES. estimated volume today 331,590 strong

the latter 3: 39 kilobars 102 kilobars Manfra 165 kilobars

.

Deposit to the Dealer Inventory in oz

nil oz

Deposits to the Customer Inventory, in oz

15,598.513 oz HSBC

No of oz served (contracts) today

16 notice(s) 1600 OZ 0.0487 TONNES

No of oz to be served (notices)

732 contracts 73,200 oz 2.276 TONNES

Total monthly oz gold served (contracts) so far this month

5172 notices 517200 oz 16.087 TONNES

Total accumulative withdrawals of gold from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of gold from the Customer inventory this month

x

0 dealer deposits:

total dealer deposits: nil oz

total customer withdrawals: 3

14,075.635oz HSBC JPMorgan; Loomis Manfra

the latter 3: 39 kilobars 102 kilobars Manfra 165 kilobars

total customer withdrawal: nil oz

we had 1 customer deposit

i) Into HSBC 15,598.513 oz

total deposit 15,598.513 oz

Adjustments: 0

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR MAR.

For the front month of MARCH we have an oi of 748 contracts having GAINED 477 contracts. We had 23 contracts filed upon on Thursday, so we gained a HUGE 500 contracts or an additional 50,000 oz of gold(1.555 tonnes) will stand at the comex in this non active delivery month of March

APRIL LOST 12,848 CONTRACTS FALLING TO 249,256.

MAY EARNED 65 CONTRACTS TO STAND AT 711

JUNE INCREASED ITS OI BY 10,676 CONTRACTS UP TO 231,255 CONTRACTS.

We had 16 contracts filed for today representing 1600 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 10 notices were issued from their client or customer account. The total of all issuance by all participants equate to 16 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 16 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for the MARCH. /2024. contract month, we take the total number of notices filed so far for the month (5172 x 100 oz ), to which we add the difference between the open interest for the front month of MARCH. (748 CONTRACTS) minus the number of notices served upon today 16 x 100 oz per contract equals 590,400 OZ OR 18.364 TONNES

thus the INITIAL standings for gold for the MARCH. contract month: No of notices filed so far (5172) x 100 oz + (748) {OI for the front month} minus the number of notices served upon today (16) x 100 oz which equals 590,400 oz (18.364 TONNES)

TOTAL COMEX GOLD STANDING FOR MARCH: 18/364 TONNES WHICH IS HUGE FOR A NON ACTIVE DELIVERY MONTH IN THE CALENDAR.

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD: 17,875,735.178 OZ

TOTAL REGISTERED GOLD 7,736,608.131 (240.64 tonnes).

TOTAL OF ALL ELIGIBLE GOLD: 10,139,727.077 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 6,403443 oz (REG GOLD- PLEDGED GOLD) 199.17 tonnes/dropping like a stone

END

SILVER/COMEX

MARCH 15 THE IDES OF MARCH/INITIAL

//2024// THE MARCH 2024 SILVER CONTRACT//INITIAL

Silver

Ounces

Withdrawals from Dealers Inventory

NIL oz

Withdrawals from Customer Inventory

1193,911.700 oz ASAHI Delaware

.

Deposits to the Dealer Inventory

nil OZ

Deposits to the Customer Inventory

68,458.411 oz CNT Delaware

No of oz served today (contracts)

3 CONTRACT(S) (15,000 OZ)

No of oz to be served (notices)

270 contracts (1.350 MILLION oz)

Total monthly oz silver served (contracts)

5114 Contracts (25.570 MILLION oz)

Total accumulative withdrawal of silver from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of silver from the Customer inventory this month

i) 0 dealer deposit

total dealer deposit:nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: 0 oz

We had 2 deposits customer account:

i) Into CNT: 67,490.811 oz

ii) Into Delaware: 967.00 ozz

total customer deposits 68,458.411 oz

JPMorgan has a total silver weight: 129.806 million oz/285.358 million or 45.61%

adjustment: 0

Comex withdrawals: 2

i) Out of ASAHI 1193,911.700 oz

ii) Out of Delaware 1022.400 oz

total withdrawal: 1193,911.700 oz

TOTAL REGISTERED SILVER: 48.213MILLION OZ//.TOTAL REG + ELIGIBLE. 285,358million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR DECEMBER:

silver open interest data:

FRONT MONTH OF MARCH /2023 OI: 273 CONTRACTS HAVING LOST 12 CONTRACT(S).

WE HAD 0 NOTICES FILED ON THURSDAY SO LOST 12 CONTRACTS OR AN ADDITIONAL 60,000 OZ WILL NOT STAND AT THE COMEX AS THESE GUYS COULD NOT WAIT FOR DELIVERY OVER HERE SO THEY FERRIED OVER TO LONDON TO TAKE DELIVERY OVER ON THAT SIDE OF THE POND.

APRIL SAW A GAIN OF 3 CONTRACTS TO STAND AT 822

MAY SAW A GAIN OF 337 CONTRACTS UP TO 115,848.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 3 for 15,000 oz

Comex volumes// est. volume today 76,973 good

Comex volume: confirmed yesterday 55,216 fair

To calculate the number of silver ounces that will stand for delivery in MARCH. we take the total number of notices filed for the month so far at 5114 x 5,000 oz = 25,570,000 oz

to which we add the difference between the open interest for the front month of MARCH. (273) and the number of notices served upon today 3 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the MARCH/2024 contract month: 5114 (notices served so far) x 5000 oz + OI for the front month of MARCH. (273) – number of notices served upon today (3 )x 500 oz of silver standing for the MARCH contract month equates to 26.920 MILLION OZ.

New total standing: 26.920 million oz.

There are 48.213 million oz of registered silver.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS//

BOTH GLD AND SLV ARE MASSIVE FRAUDS!

MARCH 15 WITH GOLD DOWN $5.20 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD

//:INVENTORY REMAINS AT 816.86 TONNES

MARCH 14 WITH GOLD DOWN $12.20 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF 1.73 TONNES OF GOLD INTO THE GLD//:INVENTORY REMAINS AT 816.86 TONNES

MARCH 13 WITH GOLD UP $14.40 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD:INVENTORY REMAINS AT 815.13 TONNES

MARCH 12 WITH GOLD DOWN $21.15 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD:NOT AVAILABLE///LAST VALUE 815.13 TONNES

MARCH 11 WITH GOLD UP $3.20 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.44 TONNES OF GOLD OUT OF THE GLD AFTER 7 CONSECUTIVE GOLD PRICE RISES//INVENTORY RESTS AT 815.13 TONNES

MARCH 8 WITH GOLD UP $21.05 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 0.87 TONNES OF GOLD OUT OF THE GLD AFTER 7 CONSECUTIVE GOLD PRICE RISES//INVENTORY RESTS AT 816.57 TONNES

MARCH 7 WITH GOLD UP $7.20 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4,20 TONNES OF GOLD OUT OF THE GLD//INVENTORY RESTS AT 817.44 TONNES

MARCH 6 WITH GOLD UP $17.20 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.30 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 821.47 TONNES

MARCH 5 WITH GOLD UP $16.55 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.30 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 821.47 TONNES

MARCH 4 WITH GOLD UP $30.55 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF .86 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 823.77 TONNES

MARCH 1 WITH GOLD UP $40.40 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 822.91 TONNES

FEB29/WITH GOLD UP $12.60 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD//WITHDRAWAL OF 4.03 TONNES INVENTORY RESTS AT 822.91 TONNES

FEB28/WITH GOLD DOWN $1.00 TODAY NO CHANGES IN GOLD INVENTORY AT THE GLD INVENTORY RESTS AT 826.94 TONNES

FEB27/WITH GOLD UP $4.40 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF .87 TONNES OF GOLD FROM THE GLD:/INVENTORY RESTS AT 826.94 TONNES

FEB26/WITH GOLD DOWN $8.90 TODAY NO CHANGES IN GOLD INVENTORY AT THE GLD:/INVENTORY RESTS AT 827.81 TONNES

FEB23/WITH GOLD UP $17 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.01 TONNES OF GOLD FROM THE GLD.//INVENTORY RESTS AT 827.81 TONNES

FEB22/WITH GOLD DOWN $2.15 TODAY NO CHANGES IN GOLD INVENTORY AT THE GLD://INVENTORY RESTS AT 829.82 TONNES

FEB21/WITH GOLD DOWN $5.30 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 7.59 TONNES OF GOLD OUT OF THE GLD///INVENTORY RESTS AT 29.82 TONNES

FEB20/WITH GOLD UP $16.15 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 0.58 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 837.89 TONNES

FEB16/WITH GOLD UP $8,60 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.73 TONNES OF GOLD FROM THE GLD///INVENTORY RESTS AT 837.31 TONNES

FEB15/WITH GOLD UP $11.70 TODAY NO CHANGES IN GOLD INVENTORY AT THE GLD:/INVENTORY RESTS AT 841.92 TONNES

FEB14/WITH GOLD DOWN $2.75 TODAY NO CHANGES IN GOLD INVENTORY AT THE GLD:/INVENTORY RESTS AT 841.92 TONNES

FEB13/WITH GOLD DOWN $20.15 TODAY NO CHANGES IN GOLD INVENTORY AT THE GLD:/INVENTORY RESTS AT 841.92 TONNES

FEB12/WITH GOLD DOWN $4.80 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A STRONG WITHDRAWAL OF 1.74 TONNES OF GOLD FROM THE GLD. / //://INVENTORY RESTS AT 841.92 TONNES

FEB9/WITH GOLD DOWN $8.60 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A STRONG DEPOSIT OF 1.44 TONNES OF GOLD FROM THE GLD. / //://INVENTORY RESTS AT 843.66 TONNES

FEB8/WITH GOLD DOWN $2.70 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A MASSIVE WITHDRAWAL OF 5.47 TONNES OF GOLD FROM THE GLD. / //://INVENTORY RESTS AT 842.22 TONNES:

FEB7/WITH GOLD UP $0.40 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A MASSIVE WITHDRAWAL OF 4.04 TONNES OF GOLD FROM THE GLD. / //://INVENTORY RESTS AT 847.69 TONNES:

FEB6/WITH GOLD UP $8.50 TODAY NO CHANGES IN GOLD INVENTORY AT THE GLD:/ / //://INVENTORY RESTS AT 851.73 TONNES:

GLD INVENTORY: 816.86 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

MARCH 15/WITH SILVER DOWN 9 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 1.006 MILLION OZ FROM THE SLV: SLV INVENTORY RESTS AT 417.866 MILLION OZ

MARCH 14/WITH SILVER DOWN 9 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: SLV INVENTORY RESTS AT 418.872 MILLION OZ

MARCH 13/WITH SILVER UP 32 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: SLV INVENTORY RESTS AT 418.872 MILLION OZ…

MARCH 12/WITH SILVER DOWN 31 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A SMALL WITHDRAWAL OF 0.549 MILLION OZ OF SILVER INTO THE SLV//// : SLV INVENTORY RESTS AT 418.872 MILLION OZ…

MARCH 11/WITH SILVER UP 11 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A HUGE WITHDRAWAL OF 2.147 MILLION OZ OF SILVER FROM THE SLV//// : SLV INVENTORY RESTS AT 418.323 MILLION OZ…SUCH A MASSIVE FRAUD!

MARCH 8/WITH SILVER DOWN 5 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A HUGE WITHDRAWAL OF 4.299 MILLION OZ OF SILVER FROM THE SLV//// : SLV INVENTORY RESTS AT 420.519 MILLION OZ…SUCH A MASSIVE FRAUD!

MARCH 7/WITH SILVER UP 8 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A HUGE WITHDRAWAL OF 4.665 MILLION OZ OF SILVER FROM THE SLV//// : SLV INVENTORY RESTS AT 424.818 MILLION OZ…SUCH A MASSIVE FRAUD!

MARCH 6/WITH SILVER UP 52 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A HUGE WITHDRAWAL OF 2.378 MILLION OZ OF SILVER FROM THE SLV//// : SLV INVENTORY RESTS AT 427,105 MILLION OZ

MARCH 5/WITH SILVER DOWN 2 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A HUGE WITHDRAWAL OF 1.499 MILL;ION OZ OF SILVER FROM THE SLV//// : SLV INVENTORY RESTS AT 429.483 MILLION OZ

MARCH 4/WITH SILVER UP CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: // : SLV INVENTORY RESTS AT 430.982 MILLION OZ

MARCH 1/WITH SILVER UP 49 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: // : SLV INVENTORY RESTS AT 430.982 MILLION OZ

FEB 29/WITH SILVER UP 25 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.104 MILLION OZ OUT OF THE SLV//// : SLV INVENTORY RESTS AT 430/982 MILLION OZ

FEB 28/WITH SILVER DOWN 7 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 5.123 MILLION OZ INTO THE SLV//// : SLV INVENTORY RESTS AT 433.086 MILLION OZ

FEB 27/WITH SILVER UP 3 CENTS TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 0.64 MILLION OZ FROM THE SLV//// : SLV INVENTORY RESTS AT 427.943 MILLION OZ

FEB 26/WITH SILVER DOWN 44 CENTS TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.065 MILLION OZ FROM THE SLV//// : SLV INVENTORY RESTS AT 428.603 MILLION OZ

FEB 23/WITH SILVER DOWN 44 CENTS TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.065 MILLION OZ FROM THE SLV//// : SLV INVENTORY RESTS AT 428.603 MILLION OZ

FEB 22/WITH SILVER DOWN 10 CENTS TODAY NO CHANGES IN SILVER INVENTORY AT THE SLV

// : SLV INVENTORY RESTS AT 432.766 MILLION OZ

FEB 21/WITH SILVER DOWN 28 CENTS TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 2.348 MILLION OZ OF SILVER FROM THE SLV// : SLV INVENTORY RESTS AT 432.766 MILLION OZ

FEB 20/WITH SILVER DOWN 33 CENTS TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 3.385 MILLION OZ OF SILVER FROM THE SLV// : SLV INVENTORY RESTS AT 435.008 MILLION OZ

FEB 16/WITH SILVER UP 53 CENTS TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV A DEPOSIT OF 1.235 MILLION OZ OF SILVER FROM THE SLV// : SLV INVENTORY RESTS AT 438.393 MILLION OZ

FEB 15/WITH SILVER UP 56 CENTS TODAY NO CHANGES IN SILVER INVENTORY AT THE SLV : SLV INVENTORY RESTS AT 437.615 MILLION OZ

FEB 14/WITH SILVER UP 24 CENTS TODAY NO CHANGES IN SILVER INVENTORY AT THE SLV : SLV INVENTORY RESTS AT 437.615 MILLION OZ

FEB 13/WITH SILVER DOWN 60 CENTS TODAY SMALL CHANGES IN SILVER INVENTORY AT THE SLV A SMALL WITHDRAWAL OF 0.504 MILLION OZ OZ OUT OF THE SLV: SLV INVENTORY RESTS AT 437.615 MILLION OZ

FEB 12/WITH SILVER UP 14 CENTS TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV A HUGE WITHDRAWAL OF 1.921 MILLION OZ OZ OUT OF THE SLV: SLV INVENTORY RESTS AT 438.119 MILLION OZ

FEB 9/WITH SILVER DOWN 4 CENTS TODAY SMALL CHANGES IN SILVER INVENTORY AT THE SLV A SMALL DEPOSIT OF 600,000 OZ INTO THE SLV: SLV INVENTORY RESTS AT 440.040 MILLION OZ

FEB 8/WITH SILVER UP 29 CENTS TODAY NO CHANGES IN SILVER INVENTORY AT THE SLV: SLV INVENTORY RESTS AT 439.994 MILLION OZ

FEB 7/WITH SILVER DOWN 18 CENTS TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A MASSIVE DEPOSIT OF 4.04 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 439.994 MILLION OZ//LAST 9 DAYS: 10.7598 MILLION OZ WITHDRAWAL

CLOSING INVENTORY 417.866 MILLION OZ//

PHYSICAL GOLD/SILVER COMMENTARIES

1:Peter Schiff/Mike Maharrey

end

2.Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens/ SIMON WHITE..//

3. CHRIS POWELL//GATA

Brilliant! and Russia will surely listen:

AP

European Parliament says Russia should return Romania’s World War I gold

Submitted by admin on Thu, 2024-03-14 19:44 Section: Daily Dispatches

Now what about the Russian assets recently frozen in Europe?

* * *

From the Associated Press Thursday, March 14, 2024

BUCHAREST, Romania — Lawmakers in the European Parliament today adopted a non-binding resolution saying Russia should return to Romania gold and other valuable heritage items that were sent to Moscow during World War I for safekeeping, a Romanian lawmaker said.

During World War I, the kingdom of Romania sent by railroad 91.5 metric tons of gold coins and ingots to Moscow, along with jewels and cultural treasures such as works of art. In the war, Romania had sided with Russia, Britain, and France, against Germany and the Austro-Hungarian and Ottoman empires.

During World War I, the kingdom of Romania sent by railroad 91.5 metric tons of gold coins and ingots to Moscow, along with jewels and cultural treasures such as works of art. In the war, Romania had sided with Russia, Britain, and France, against Germany and the Austro-Hungarian and Ottoman empires.

The gold was confiscated after the Bolsheviks seized power in Russia in 1917. In later years efforts by Romania to recover the gold came to nothing. Some cultural items were returned by Soviet authorities in 1935 and 1956 — but not the gold. …

4. OTHER MAJOR GOLD COMMENTARIES/PODCASTS//LIVE FROM THE VAULT

end

end

5 a. IMPORTANT COMMENTARIES ON COMMODITIES/COPPER

Copper Soars, Iron Ore Tumbles As Goldman Says “Copper’s Time Is Now”

FRIDAY, MAR 15, 2024 – 02:25 PM

After languishing for the past two years in a tight range despite recurring speculation about declining global supply, copper has finally broken out, surging to the highest price in the past year, just shy of $9,000 a ton as supply cuts hit the market; At the same time the price of the world’s “other” most important mined commodity has diverged, as iron ore has tumbled amid growing demand headwinds out of China’s comatose housing sector where not even ghost cities are being built any more.

Copper surged almost 5% this week, ending a months-long spell of inertia, as investors focused on risks to supply at various global mines and smelters. As Bloomberg adds, traders also warmed to the idea that the worst of a global downturn is in the past, particularly for metals like copper that are increasingly used in electric vehicles and renewables.

Yet the commodity crash of recent years is hardly over, as signs of the headwinds in traditional industrial sectors are still all too obvious in the iron ore market, where futures fell below $100 a ton for the first time in seven months on Friday as investors bet that China’s years-long property crisis will run through 2024, keeping a lid on demand.

Indeed, while the mood surrounding copper has turned almost euphoric, sentiment on iron ore has soured since the conclusion of the latest National People’s Congress in Beijing, where the CCP set a 5% goal for economic growth, but offered few new measures that would boost infrastructure or other construction-intensive sectors.

As a result, the main steelmaking ingredient has shed more than 30% since early January as hopes of a meaningful revival in construction activity faded. Loss-making steel mills are buying less ore, and stockpiles are piling up at Chinese ports. The latest drop will embolden those who believe that the effects of President Xi Jinping’s property crackdown still have significant room to run, and that last year’s rally in iron ore may have been a false dawn.

Meanwhile, as Bloomberg notes, on Friday there were fresh signs that weakness in China’s industrial economy is hitting the copper market too, with stockpiles tracked by the Shanghai Futures Exchange surging to the highest level since the early days of the pandemic. The hope is that headwinds in traditional industrial areas will be offset by an ongoing surge in usage in electric vehicles and renewables.

And while industrial conditions in Europe and the US also look soft, there’s growing optimism about copper usage in India, where rising investment has helped fuel blowout growth rates of more than 8% — making it the fastest-growing major economy.

In any case, with the demand side of the equation still questionable, the main catalyst behind copper’s powerful rally is an unexpected tightening in global mine supplies, driven mainly by last year’s closure of a giant mine in Panama (discussed here), but there are also growing worries about output in Zambia, which is facing an El Niño-induced power crisis.

On Wednesday, copper prices jumped on huge volumes after smelters in China held a crisis meeting on how to cope with a sharp drop in processing fees following disruptions to supplies of mined ore. The group stopped short of coordinated production cuts, but pledged to re-arrange maintenance work, reduce runs and delay the startup of new projects. In the coming weeks investors will be watching Shanghai exchange inventories closely to gauge both the strength of demand and the extent of any capacity curtailments.

“The increase in SHFE stockpiles has been bigger than we’d anticipated, but we expect to see them coming down over the next few weeks,” Colin Hamilton, managing director for commodities research at BMO Capital Markets, said by phone. “If the pace of the inventory builds doesn’t start to slow, investors will start to question whether smelters are actually cutting and whether the impact of weak construction activity is starting to weigh more heavily on the market.”

* * *

Few have been as happy with the recent surge in copper prices as Goldman’s commodity team, where copper has long been a preferred trade (even if it may have cost the former team head Jeff Currie his job due to his unbridled enthusiasm for copper in the past two years which saw many hedge fund clients suffer major losses).

As Goldman’s Nicholas Snowdon writes in a note titled “Copper’s time is now” (available to pro subscribers in the usual place)…

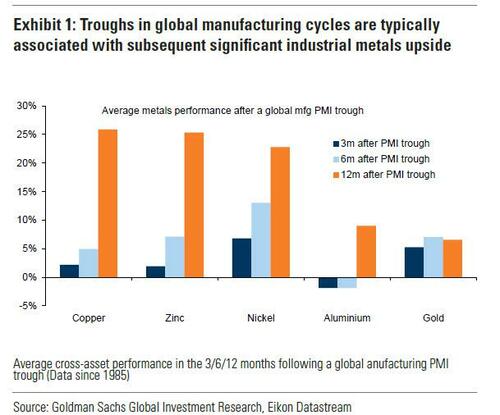

… there has been a “turn in the industrial cycle.” Specifically according to the Goldman analyst, after a prolonged downturn, “incremental evidence now points to a bottoming out in the industrial cycle, with the global manufacturing PMI in expansion for the first time since September 2022.” As a result, Goldman now expects copper to rise to $10,000/t by year-end and then $12,000/t by end of Q1-25.’

Here are the details:

Previous inflexions in global manufacturing cycles have been associated with subsequent sustained industrial metals upside, with copper and aluminium rising on average 25% and 9% over the next 12 months. Whilst seasonal surpluses have so far limited a tightening alignment at a micro level, we expect deficit inflexions to play out from quarter end, particularly for metals with severe supply binds. Supplemented by the influence of anticipated Fed easing ahead in a non-recessionary growth setting, another historically positive performance factor for metals, this should support further upside ahead with copper the headline act in this regard.

Goldman then turns to what it calls China’s “green policy put”:

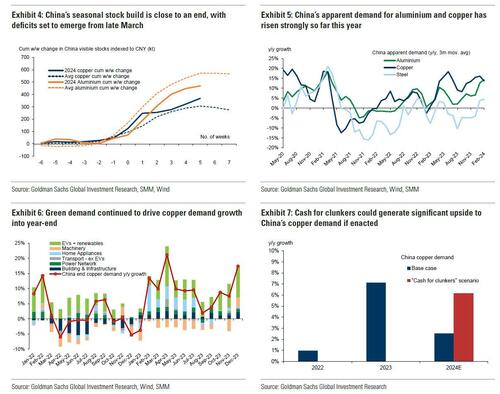

Much of the recent focus on the “Two Sessions” event centred on the lack of significant broad stimulus, and in particular the limited property support. In our view it would be wrong – just as in 2022 and 2023 – to assume that this will result in weak onshore metals demand. Beijing’s emphasis on rapid growth in the metals intensive green economy, as an offset to property declines, continues to act as a policy put for green metals demand. After last year’s strong trends, evidence year-to-date is again supportive with aluminium and copper apparent demand rising 17% and 12% y/y respectively. Moreover, the potential for a ‘cash for clunkers’ initiative could provide meaningful right tail risk to that healthy demand base case. Yet there are also clear metal losers in this divergent policy setting, with ongoing pressure on property related steel demand generating recent sharp iron ore downside.

Meanwhile, Snowdon believes that the driver behind Goldman’s long-running bullish view on copper – a global supply shock – continues:

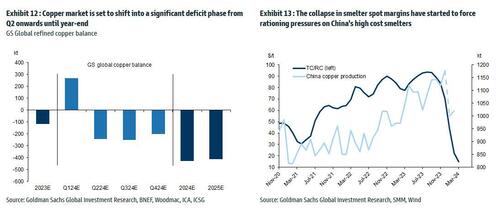

Copper’s supply shock progresses. The metal with most significant upside potential is copper, in our view. The supply shock which began with aggressive concentrate destocking and then sharp mine supply downgrades last year, has now advanced to an increasing bind on metal production, as reflected in this week’s China smelter supply rationing signal. With continued positive momentum in China’s copper demand, a healthy refined import trend should generate a substantial ex-China refined deficit this year. With LME stocks having halved from Q4 peak, China’s imminent seasonal demand inflection should accelerate a path into extreme tightness by H2. Structural supply underinvestment, best reflected in peak mine supply we expect next year, implies that demand destruction will need to be the persistent solver on scarcity, an effect requiring substantially higher pricing than current, in our view. In this context, we maintain our view that the copper price will surge into next year (GSe 2025 $15,000/t average), expecting copper to rise to $10,000/t by year-end and then $12,000/t by end of Q1-25’

Another reason why Goldman is doubling down on its bullish copper outlook: gold.

The sharp rally in gold price since the beginning of March has ended the period of consolidation that had been present since late December. Whilst the initial catalyst for the break higher came from a (gold) supportive turn in US data and real rates, the move has been significantly amplified by short term systematic buying, which suggests less sticky upside. In this context, we expect gold to consolidate for now, with our economists near term view on rates and the dollar suggesting limited near-term catalysts for further upside momentum. Yet, a substantive retracement lower will also likely be limited by resilience in physical buying channels. Nonetheless, in the midterm we continue to hold a constructive view on gold underpinned by persistent strength in EM demand as well as eventual Fed easing, which should crucially reactivate the largely for now dormant ETF buying channel. In this context, we increase our average gold price forecast for 2024 from $2,090/toz to $2,180/toz, targeting a move to $2,300/toz by year-end.

Dems nervous that so much money is going to cryptos and thus hurting the dollar

(zerohedge)

Desperate Dems Demand SEC Block All Future Crypto ETFs, Pressure Brokers Due To “Enormous Risks”

FRIDAY, MAR 15, 2024 – 08:06 AM

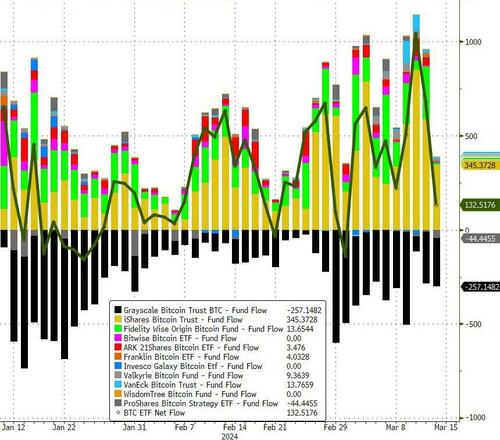

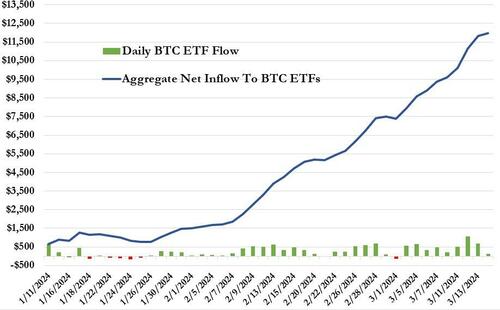

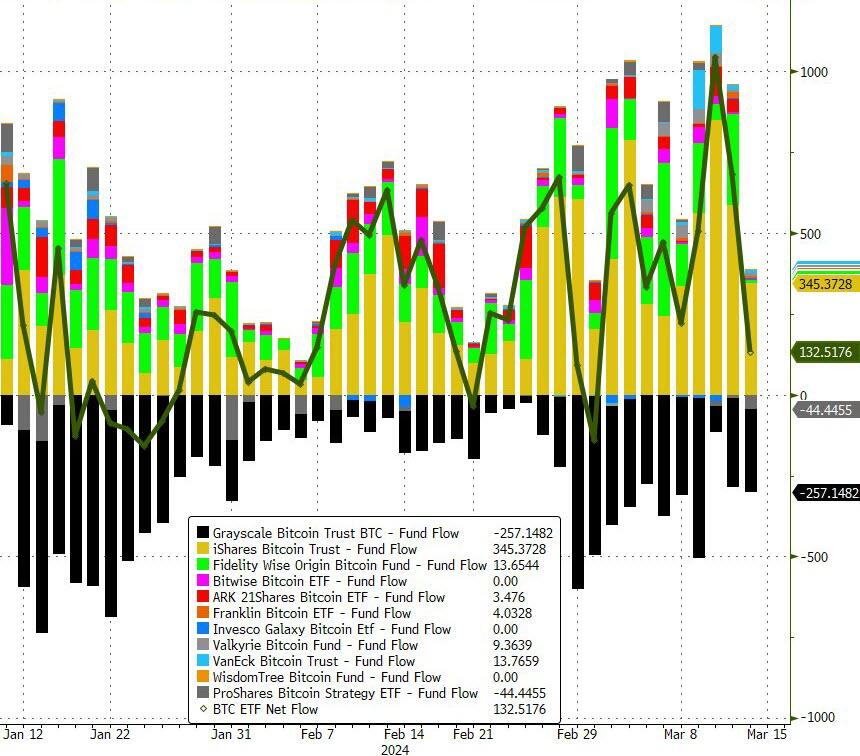

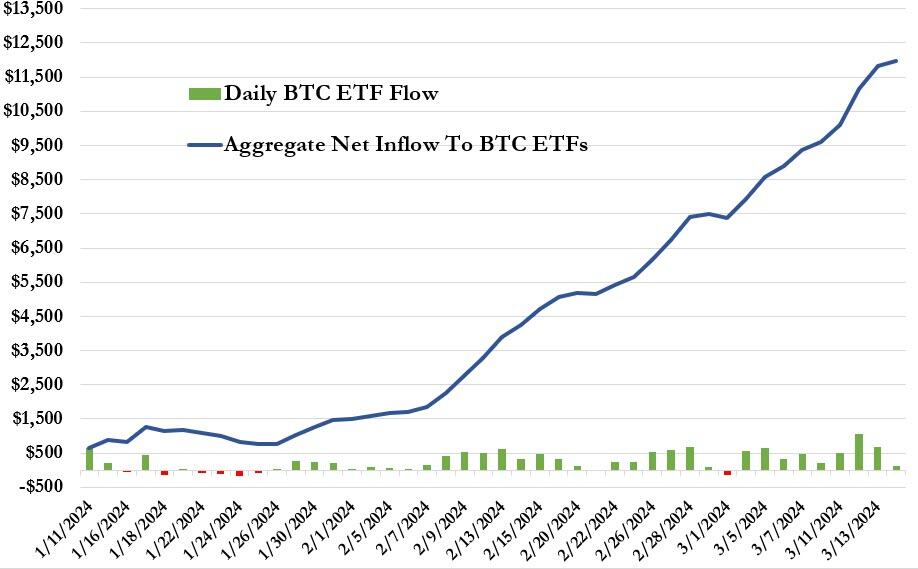

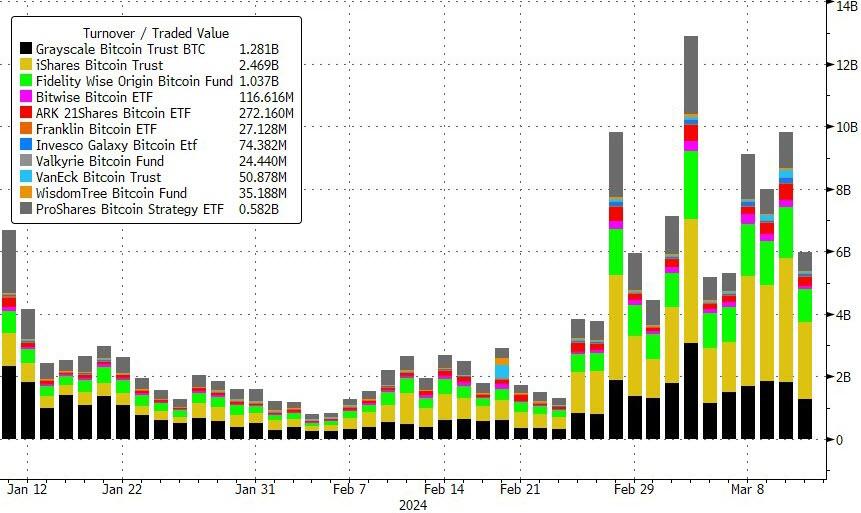

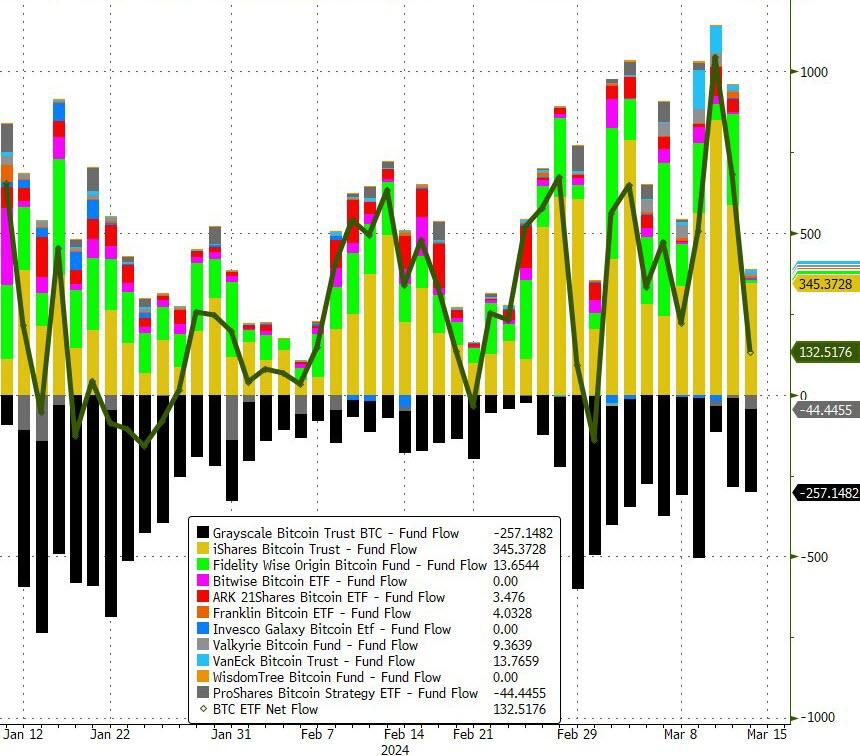

For the 9th straight day (and 15th of the last 16), Bitcoin ETFs saw net inflows yesterday…

Source: Bloomberg

…lifting the total net inflow of assets to $12BN in 44 trading days…

Source: Bloomberg

The unprecedented success of these new investment vehicles in democratizing access to an alternative currency (away from the manipulative money-printing largesse of bigger and bigger government) is apparently pissing Democrats off.

And so, having seen Senator Warren fail in her constant pressure efforts to stop SEC Chair Gary Gensler approving Bitcoiin ETFs, two Democrat Senators are urging the SEC to block any further crypto exchange-traded products (ETPs) to protect retail investors from risks associated with poor broker disclosure and thin liquidity in major cryptocurrencies.

As CoinDesk reports, Sen. Jack Reed (D-R.I.) and Sen. Laphonza Butler (D-CA) write that a FINRA survey disclosed that 70% of brokers’ communications with retail investors violated fair disclosure rules.

“Brokers’ communications falsely equated cryptocurrency with cash; in others, they provided misleading explanations of cryptocurrency’s risks,” they wrote.

“These alarming deficiencies raise significant concerns that brokers and advisers may now provide incomplete and deceptive information about bitcoin ETPs to retail investors.”

The Senators also argue that by naming bitcoin exchange-traded funds as such, the name “obfuscates important characteristics about these investments.”

“Retail investors should be made aware of how these ETPs differ from more common funds which they may have experience,” they said in the letter, writing that bitcoin is not subject to the same protections under the Investment Company Act of 1940 that ETFs which hold shares of various companies would have.

The two lawmakers also say that bitcoin (BTC) – which they call the most established and scrutinized cryptocurrency – is displaying weakness, and other cryptos are far more susceptible to misconduct.

“We do not believe that other cryptocurrencies show the trading volumes or integrity to support associated ETPs,” they wrote.

“Retail investors would face enormous risks from ETPs…whose prices are especially susceptible to pump-and-dump or other fraudulent schemes.”

WTF are you talking about! BTC ETF volumes have been enormous…

END

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGSFRIDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED DOWN 7.1960

OFFSHORE YUAN: DOWN TO 7.2037

SHANGHAI CLOSED UP 16.40 PPTS OR 0.54%

HANG SENG CLOSED DOWN 240.77 PTS OR 1.42%

2. Nikkei closed DOWN 99.76 PTS OR 0.26%

3. Europe stocks SO FAR: ALL GREEN

USA dollar INDEX DOWN TO 102.97 EURO RISES TO 1.0891 UP 9 BASIS PTS

3b Japan 10 YR bond yield: RISES TO. +.772 Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 147.70/JAPANESE YEN NOW FALLING AS WELL AS LONG TERM 10 YR. YIELDS RISING //EVENTUALLY THIS WILL BREAK THE JAPANESE CENTRAL BANK

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen DOWN CHINESE ONSHORE YUAN: DOWN/ OFFSHORE: DOWN

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and UP FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund YIELD UP TO +2.4335***/Italian 10 Yr bond yield UP to 3.664* /SPAIN 10 YR BOND YIELD UP TO 3.223…**

3i Greek 10 year bond yield UP TO 3.264

3j Gold at $2160.00 silver at: 25.16 1 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble DOWN 0 AND 50 /100 roubles/dollar; ROUBLE AT 92.23//

3m oil into the 80 dollar handle for WTI and 84 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 147.70// 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 0.772% STILL ON CENTRAL BANK (JAPAN) INTERVENTION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.8820 as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.9608 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.283 DOWN 2 BASIS PTS…

USA 30 YR BOND YIELD: 4.409 DOWN 3 BASIS PTS/

USA 2 YR BOND YIELD: 4.694 UP 1 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 32.22…(TURKEY SET TO BLOW UP FINANCIALLY)

GREAT BRITAIN/10 YEAR YIELD: UP 10 BASIS PTS AT 4.142

end

2.a Overnight: Newsquawk and Zero hedge

Futures Gain As Ides Of March “Quad Witching” Looms

FRIDAY, MAR 15, 2024 – 08:32 AM

S&P futures are modestly in the green, paying no attention to today’s historical “Ides of March” cautionary date as we continue higher ahead of today’s quad witching day, and after the latest hot PPI data which weakened the case for imminent Federal Reserve rate cuts. As of 8:15am, S&P futures were up 0.1%, while Nasdaq futures gained 0.2% with Goldman’s Michael Nocerino writing that the market bid this morning follows a heavier tape yesterday with PPI coming in stronger than expected (boosting PCE est for next week + pushing market pricing of rate cuts in June to 54% from 68%).

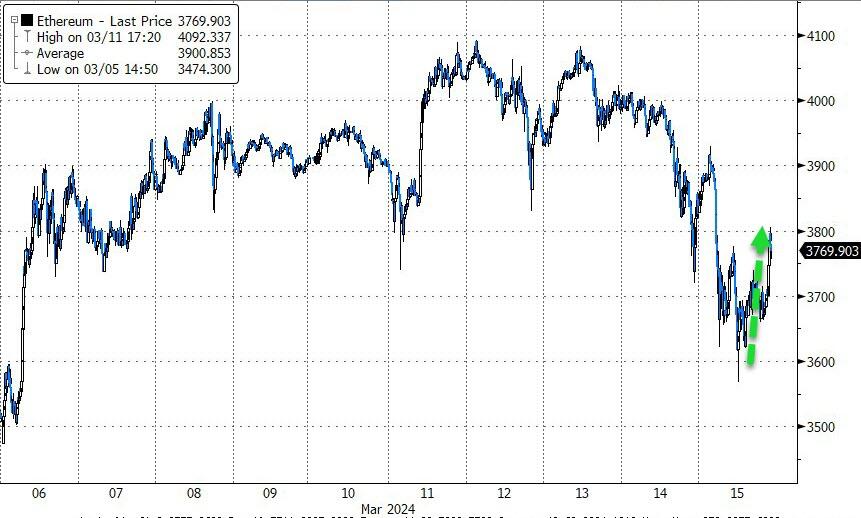

Europe’s Estoxx 50 gained 0.5% in London session with outperformance in banks, healthcare energy, telecom but weakness from the luxury sector (Brunello Cuccinelli earnings) and tech underperforming; earlier Asia was mixed/mostly lower. Elsewhere, 10Y yields are unchanged around 4.29%, WTI futures are lower by 0.5%, unwinding some of this week’s aggressive rally. The dollar is flat while the yen dropped even after Japan’s largest union group announced stronger-than-expected annual wage deals, keeping the prospect of policy tightening from the BOJ next week on the table. USDJPY rises 0.3% to ~148.70 as a clueless Mrs Watanabe remains firmly in control. Bitcoin tumbled overnight after hitting a new record high above $73,000 just hours earlier. Headlines fairly quiet, with a lot of market attention pulled forward to next week’s NVDA AI developer conference, a potential hike from the BoJ, and Wednesday’s FOMC meeting.

Doubts about whether policymakers can take their foot off the monetary brake are creeping into otherwise bullish markets that have taken stock indexes to fresh highs. European stocks are on track for their eighth consecutive week of gains — the longest winning streak since 2018 — lifted by conviction that euro-area interest rates will start to fall in the coming months. Equities could face additional volatility with Friday’s multiple options expiry, known as a triple witching. Markets are now especially vulnerable to any setback, either in optimistic economic outlooks or bets on monetary easing, according to Guy Miller, chief market strategist at Zurich Insurance Company Ltd.

“I think we’re getting to a more challenging period in markets because we’ve had all of the good news,” Miller said. “There isn’t much risk premium priced into risk assets and therefore if any of the following happen, namely if we don’t have a soft landing or no landing or if we don’t have a rate cut this year, that’s going to becomes a problem for the market.”

European stocks edge higher, with the Stoxx 600 up 0.2% and on track for their eighth consecutive week of gains — the longest winning streak since 2018 — lifted by conviction that euro-area interest rates will start to fall in the coming months. Telecom and auto shares are the best performers while among individual movers, Swisscom gains as the operator says it agrees to buy Vodafone Italia for €8 billion. Here are some of the biggest movers on Friday:

HelloFresh shares advance as much as 8.5%, recovering slightly from a slump triggered by its shock warning last week, after the meal-kit maker reported detailed full-year earnings which analysts said contained no surprises. While free cash flow was better than consensus analyst forecasts, the report showed a 7% y/y decline in active customers, suggesting the German firm is still struggling to attract customers for its core meal-kit business in both the US and other international markets.

IAG shares climb as much as 4.7% after a double upgrade to outperform at BNP Paribas Exane, which says the airline group has addressed all the issues in the broker’s bear case. Wizz Air has its rating cut as it continues to deal with capacity constraints after Pratt & Whitney engine issues grounded some of its fleet.

Hypoport rises as much as 6.7%, heading for its highest close since August 2022, as BNP Paribas Exane says the German financial services platform is reaching an inflection point and upgrades its rating to outperform.

Galp rises as much as 6.9% after the Portuguese oil company said after the close of trading on Thursday that it successfully drilled the Mopane-2X well in the PEL83 block in Namibia and found “a significant column with light oil in reservoirs of high quality.”

Brunello Cucinelli shares drop as much as 9.1% in Milan trading, the biggest decrease since March 2022, after the Italian luxury company reported net income for the full year that missed analyst expectations, due to higher tax charges.

Vonovia drops as much as 8.2% following its full-year results, which although overall in-line are seen as a “mixed bag” by Baader Helvea. The German real estate firm’s dividend proposal is ahead of expectations, but analysts are divided over the revised dividend policy going forward.

Shares of European chipmakers trade lower on Friday after Bloomberg News reported that the Chinese government has asked electric-vehicle makers to sharply increase their purchases from local auto chipmakers

Ahold slips as much as 1.6% after ING cuts the stock to hold from buy on expectation of “continued downward pressure” in the retailer’s US operations due to the macroeconomic environment and issues at its Stop&Shop brand.

EuroAPI falls as much as 31% to the lowest on record since the French drug-ingredients group was spun off from Sanofi in 2022. The firm suspended its outlook, with Oddo saying there is “no visibility” at this stage.

Intertek drops as much as 3.1%, a third day of declines since closing on Tuesday at highest since May 2022. Shore Capital cuts its rating on the testing and inspection company to sell from hold, saying valuation is rich.

Earlier in the session, Asian stocks declined, with Chinese and Korean stocks leading a broad regional selloff, after the latest US data was seen as discouraging the Federal Reserve from cutting interest rates. The MSCI Asia Pacific Index fell as much as 0.9%, taking its loss this week to 1.7%. That’s after seven straight weekly gains, which marked the longest winning run since December 2020. The technology sector was the biggest drag on the regional benchmark on Friday, led by TSMC as analysts warned the stock’s rally had gone too far, too fast.

A measure of Chinese shares listed in Hong Kong slid more than 2% to be Asia’s worst performer as the nation’s central bank drained cash from the financial system with a medium-term liquidity tool for the first time since November 2022. Still, the gauge is up about 15% from this year’s low in January thanks to the government’s measures to bolster the economy and markets.

“This is a healthy correction,” said Kerry Goh, chief investment officer at Kamet Capital Partners Pte. “I don’t think China is short on liquidity, but confidence to spend or invest. The draining of liquidity is probably one off to balance the amount of cash sitting in the system.”

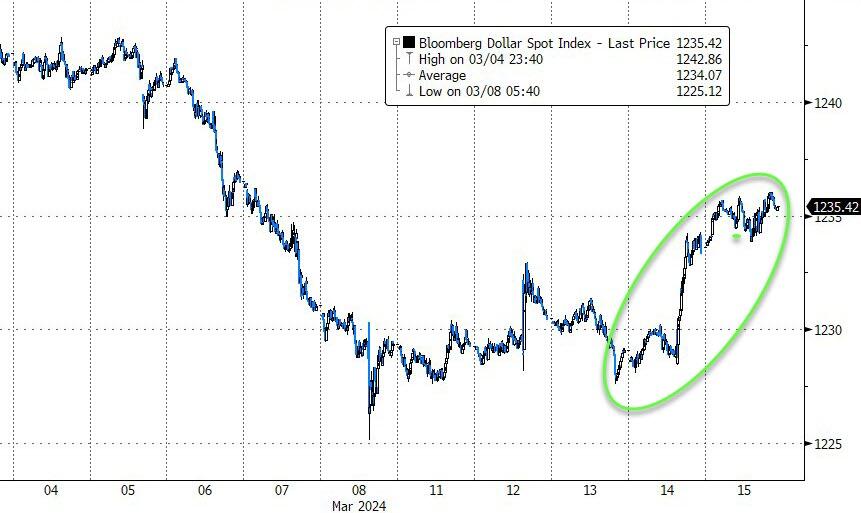

In FX, the dollar extended gains for a second day, on course for the first weekly advance in four; G-10 currency traded mixed with Swiss franc and euro leading gains while commodity currencies underperformed. the yen is lower even after Japan’s largest union group announced stronger-than-expected annual wage deals, keeping the prospect of some form of policy tightening from the BOJ next week on the table. USD/JPY rises 0.3% to ~148.70. The kiwi is still the weakest of the G-10 currencies, falling 0.6% versus the greenback after some downbeat remarks from the finance minister.

In rates, treasuries traded in a narrow range with yields slightly cheaper across the curve and gains led by the long-end, unwinding a portion of Thursday’s aggressive selloff. US yields richer by up to 2bp across the long-end of the curve with both 2s10s and 5s30s spreads flatter by around 1bp on the day; 10-year yields around 4.28% remain near top of Thursday’s session range and outperforming bunds and gilts both by 2bp in the sector. Bunds lag, after French inflation is revised higher and money markets trim pricing for potential ECB easing for a fourth day. The US session is set to focus on data, which includes industrial production and University of Michigan sentiment.

In commodities, oil prices decline, with WTI falling 0.6% to trade near $80.80 but near a four-month high after the IEA forecast a supply deficit through 2024, changing its earlier projection of a surplus, on the premise OPEC+ maintains production cuts. Copper, typically seen as a bellwether of the global economy, surged to $9,000 a ton, as bets that a pick-up in global manufacturing activity will push up demand for industrial commodities. Spot gold rises 0.4%. Bitcoin drops ~4%.

Bitcoin tumbled as much as 6% off its price, falling to as low as $65.5K, before paring the move back to around $68K.

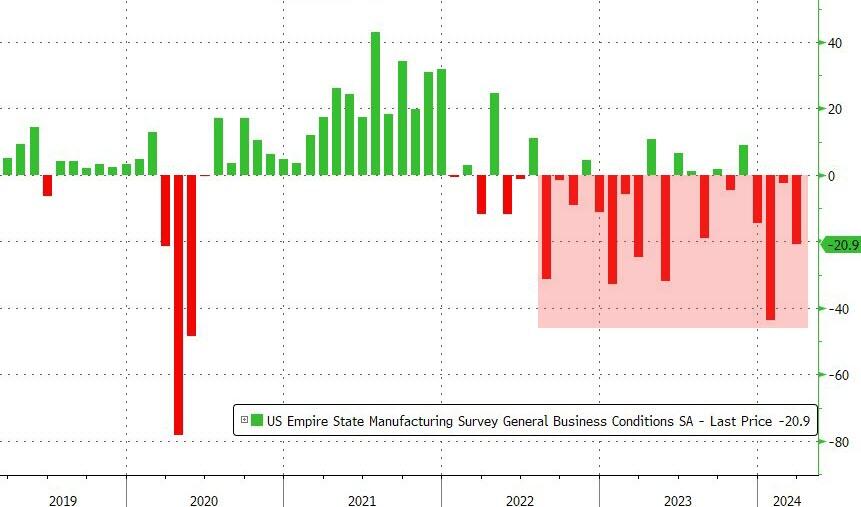

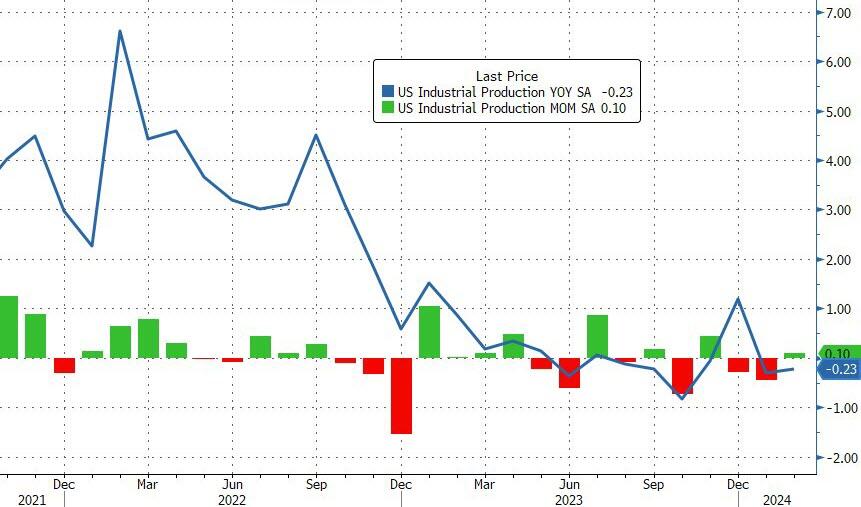

Looking at today’s calendar, the US data calendar includes March Empire manufacturing, February import/export prices (8:30am), industrial production, capacity utilization (9:15am) and March University of Michigan sentiment (10am). There are no scheduled Fed speakers due before the March 20 policy decision; we’ll hear from the ECB’s Panetta, Vujcic and Lane.

Market Snapshot

S&P 500 futures little changed at 5,152.75

MXAP down 1.0% to 174.65

MXAPJ down 1.5% to 533.00

Nikkei down 0.3% to 38,707.64

Topix up 0.3% to 2,670.80

Hang Seng Index down 1.4% to 16,720.89

Shanghai Composite up 0.5% to 3,054.64

Sensex down 0.5% to 72,710.31

Australia S&P/ASX 200 down 0.6% to 7,670.28

Kospi down 1.9% to 2,666.84

STOXX Europe 600 little changed at 506.03

German 10Y yield little changed at 2.45%

Euro little changed at $1.0886

Brent Futures down 0.4% to $85.05/bbl

Gold spot up 0.2% to $2,166.23

US Dollar Index little changed at 103.43

Top Overnight News

China left its 1-year MLF (Medium-Term Lending Facility) rate unchanged (as expected) and withdrew liquidity from the banking system as the gov’t prioritizes currency stability over stimulus. RTRS

China’s home prices continued to fall in February, underscoring the challenge for authorities as they step up efforts to salvage the beleaguered market. BBG

The Chinese government has quietly asked electric-vehicle makers from BYD Co. to Geely Automobile Holdings Ltd. to sharply increase their purchases from local auto chipmakers, part of a campaign to reduce reliance on Western imports and boost China’s domestic semiconductor industry. BBG

Japan’s unions reveal more evidence of robust wage hikes in the latest round of negotiations, providing further impetus for a BOJ rate increase next week. RTRS

OpenAI is in talks to raise money from Abu Dhabi for the firm’s new AI chip venture it hopes will reduce its reliance on Nvidia semiconductors. FT

Electricity demand in the US has been flat for nearly 20 years but is suddenly starting to surge on back of an explosion in data centers, a resurgence in domestic manufacturing, and the advent of electric vehicles. NYT

Vodafone sells its Italian business to Swisscom for an enterprise value of EU8B, and the company is updating its capital return framework, w/the dividend cut to 4.5p per share (from 9c) while the buyback is increased. RTRS

The US plans to award more than $6 billion to Samsung to expand beyond a project in Texas, people familiar said. Federal funding for the chipmaker would come alongside significant additional investment by the company. BBG

President Javier Milei’s sweeping executive decree was rejected by the Argentine Senate and now goes to the lower house of Congress, where a simple majority can scrap it. This is the first presidential edict in recent memory to be repealed by the senate. BBG

The focus on artificial intelligence (AI) has re-intensified in 2024. Initial ebullience about AI in 2023 drove a massive increase in public and investor focus on AI, as measured by search volumes and news stories. These measures plateaued in 2H 2023, albeit at a high level, but have surged again in 2024. Similarly, the share of S&P 500 companies mentioning AI on earnings calls dipped slightly from 35% in 2Q 2023 to 31% in 3Q 2023. However, the share increased to 37% in 4Q 2023, led by Info Tech and Comm Services. GIR

Earnings and company news

Adobe Inc (ADBE) – Q1 2024 (USD): Adj. EPS 4.48 (exp. 4.38), Revenue 5.18bln (exp. 5.14bln), announces new USD 25bln share repurchase program. Co. drove record Q1 revenue demonstrating strong momentum across Creative Cloud, Document Cloud and Experience Cloud. The chair and CEO said they have done an incredible job harnessing the power of generative AI to deliver ground-breaking innovation across our product portfolio. Co noted Q1 results and record RPO reflect strong customer adoption of their innovative products and services. Sees Q2 Adj. EPS USD 4.35-4.40 (exp. 4.39). Sees Q2 rev. 5.25bln-5.30bln (exp. 5.30bln). (Newswires) Shares -10.9% after-hours.

Apple (AAPL) – Buys AI startup DarwinAI as part of race to add features; has added dozens of DarwinAI staff to its AI division, according to Bloomberg. (Bloomberg)

A more detailed look at global markets courtesy of Newsquawk

APAC stocks declined amid data-related headwinds from the US including hot PPI and weak Retail Sales. ASX 200 was dragged lower by underperformance in mining-related industries after iron ore resumed its slide. Nikkei 225 retreated amid cautiousness ahead of the RENGO wage announcement and its potential ramifications on BoJ policy as reports had suggested strong wage hikes could be the deciding factor on whether the BoJ hikes at next week’s crucial meeting. Hang Seng and Shanghai Comp. were negative with heavy losses in tech and property sectors in Hong Kong where the Hang Seng Mainland Properties Index fell more than 3% after a steeper decline in Chinese New Home Prices, while the mainland was only marginally pressured after the PBoC kept its 1-year MLF rate unchanged and opted to not fully roll over the maturing amount.

Top Asian News

PBoC announced a CNY 387bln 1-year Medium-term Lending Facility operation vs. CNY 500bln maturing with the rate kept unchanged at 2.50%, as expected.

China is said to tighten IPO listing requirements according to the regulator cited by Bloomberg.

China is reportedly urging EV makers to purchase local chips as the clash with the US escalates, via Bloomberg.

Chinese FX Regulator says foreign investors increased their holdings of domestic bonds by a net of USD 1.1bln in Feb; foreign holdings of Chinese onshore bonds remain at relatively high levels in Feb and foreigners net increase onshore stocks. Major economies expected to shift monetary policy stance in 2024, external liquidity tensions to ease and conducive to China’s FX market stability.

S&P Global Cuts outlook on China’s Vanke BBB+ Credit Rating to Negative from Stable

European bourses, Stoxx600 (+0.2%) began the session around the unchanged mark, before sentiment improved and edging into the green. European sectors are mixed; Telcoms takes the top spot, propped up by Vodafone (+4.5%) and Swisscom (+2.5%), whilst Real Estate is hampered by post-earnings losses in Vonovia (-6.1%). US equity futures (ES +0.1%, NQ +0.1%, RTY +0.3%) are modestly firmer with price action mimicking that seen in Europe; Adobe (-11.6% pre-market) is weaker after providing soft guidance.

Top European News

ECB’s Rehn reiterates data dependence, says inflation is set to enable easing to occur near the summer. On rates “… Therefore, there are no obvious reasons why adjustment measures could not be taken from the point of view of economic policy”. Subsequnt comments: Says at last week’s meeting of the ECB council we started a discussion about reducing the restrictive dimension of monetary policy and about when it is appropriate to begin lowering rates. If inflation continues to fall and according to our estimate, sustainably downwards towards the target. We can already slowly start easing our foot off the brake pedal monpol.

UK PM Sunak ruled out an early election on May 2nd and noted his working assumption is that the election would be held in H2.

The Bank of England/Ipsos Inflation Attitudes Survey: 1yr inflation expectation slips to 3% from 3.3%. Median expectations of the rate of inflation over the coming year were 3%, down from 3.3% in November 2023. Asked about expected inflation in the twelve months after that, respondents gave a median answer of 2.8%, unchanged from 2.8% in November 2023. Asked about expectations of inflation in the longer term, say in five years’ time, respondents gave a median answer of 3.1%, down from 3.2% in November 2023. When asked about the future path of interest rates, 36% of respondents expected rates to rise over the next 12 months, down from 44% in November 2023.

German Economy Ministry says no tangible recovery yet in sight, according to a report.

FX

Contained trade for DXY and within 103.37-48 parameters, holding onto yesterday’s PPI and IJC-induced gains. Upside sees the 50 and 100DMA at 103.53 and 200DMA at 103.65. To the downside, little in the way of support until 103.

EUR/USD is unable to reclaim 1.09 with 1.0889 the high watermark for the session in quiet newsflow. If 1.09 is reclaimed, the 10DMA sits just above at 1.0905. Downside sees 1.0867 from 7th March.

Steady trade for GBP vs. USD as UK-specifics remain light ahead of a CPI, PMI, retail sales data and the BoE announcement next week. The range for Cable stands at 1.2731-1.2756.

JPY is pressured despite a strong outcome to the RENGO wage tally. Possibly a buy-the-rumour sell-the-fact move given that the data was expected to be on the hawkish side. Currently holds towards the upper end of a 148.83-04 range.

Antipodeans are both softer vs. the USD but NZD more so amid cross-related buying in AUD/NZD. Antipodean-specific newsflow remains light ahead of the RBA next week.

Fixed Income

USTs are rangebound and remain around 110-06 following the hawkish PPI/IJC move yesterday, with support at 110-01+ from 14th Feb; focus turns to US Import Prices & UoM Inflation Expectations.

Bund price action is steady and relatively rangebound within a 131.31-99 range; ECB’s Lane to give remarks at 14:30 GMT / 10:30 ET.

Gilts are once again the incremental underperformer, but only modestly so and holding above the 98.00 mark and by extension last week’s 97.91 trough.

Fixed Income

Crude initially traded sideways, taking a breather following yesterday’s rally, before succumbing to some weakness into the European morning around the time details of the Hamas ceasefire proposal emerged; profit-taking may also be a factor. Brent Apr now holds below USD 85/bbl.

Firm trade in precious metals despite the stronger Dollar but against the backdrop of the global risk aversion experienced yesterday (and into APAC) coupled with the ongoing geopolitical tensions in Russia/Ukraine and the Middle East; XAU resides within yesterday’s USD 2.152-77.04/oz.

Base metals are higher across the board this morning as momentum picked up with Shanghai copper reaching near-three-year highs and 3M LME touched a 10-month peak.

Commerzbank lifts silver year-end price forecast to USD 29/oz.

JP Morgan believes that Russia can maintain oil exports at its current levels through June, even as it cuts crude production by 0.5mln BPD. Drop in Russian exports could spur price pressures of an additional USD 5/bbl to the forecast of USD 88-90/bbl by May and the mid-80/bbl region in H2-2024.

German Chemical Industry Association (VCI): 2023 production -7.9% Y/Y, Producer Prices -0.4% Y/Y; Revenue -12.2% Y/Y

Japan wage negotiations and upcoming rate hike

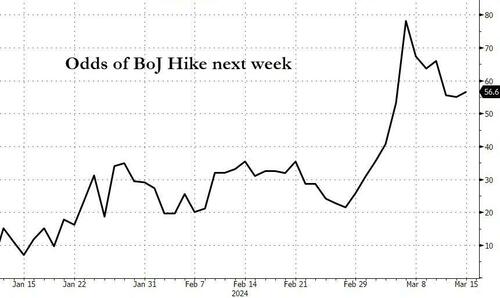

Japanese Finance Minister Suzuki said they are seeing a strong pay hike move in wage talks and the government is to mobilise all policy steps available to continue the wave of wage hikes, while he added that Japan is no longer in deflation.

A Reuters poll showed 35% of economists expect the BoJ to end negative rates in March and 62% expect April, while 31% of economists expect the BoJ to end YCC in March and 62% expect April.

Japanese Unions said to have won over 5% average (exp. 4.1%, demand 5.85%) in wage hike talks, according to Kyodo News

Japan RENGO 1st Wage Tally: 5.28% (exp. 4.1%; 2023 final figure 3.6%). Base Pay to rise 3.70% (Initial 2.33% in 2023). Japan’s FY24 pay increases is the largest in over three decades.

BoJ is reportedly making final arrangements to end negative interest rates at next week’s meeting, according to JiJi.

RENGO says part-timers wage hikes reached 6% for 2024.

Head of Japan’s biggest trade union confederation RENGO says rising inequality, inflation and labour crunch among factors behind big wage hikes.

Japanese government and BoJ are to keep the joint statement including the 2% price target, according to JiJi.

Geopolitics

At least 11 Palestinians were killed and 100 injured in Israeli forces targeting people waiting for humanitarian aid in Gaza, according to the Gaza health ministry cited by Reuters.

Australia’s Foreign Minister said Australia is to resume funding for UNRWA which is the UN’s main Palestinian relief agency.

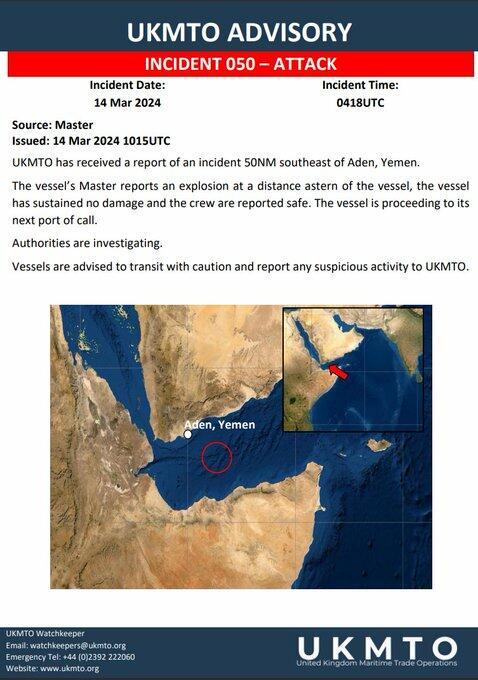

US military said Houthis fired two anti-ship ballistic missiles from Yemen towards the Gulf of Aden and two towards the Red Sea although there were no injuries or damage reported to US or coalition ships, while the US military said it destroyed nine anti-ship missiles and two drones in Houthi-controlled areas of Yemen, according to Reuters.

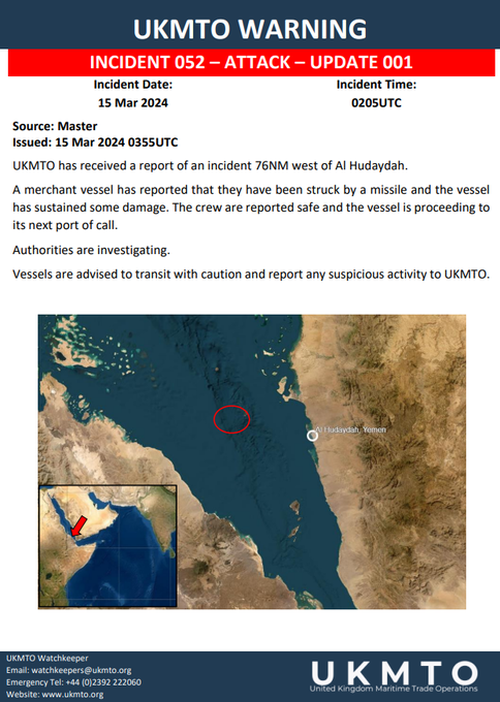

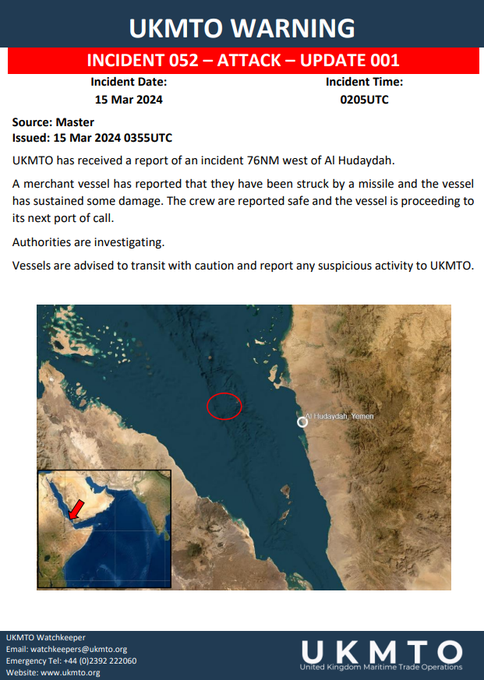

UKMTO received a report of an incident 76NM west of Yemen’s Hodeida and announced a merchant vessel was struck by a missile and sustained some damage, although the crew were reported safe and the vessel is proceeding to its next port of call.

Hamas ceasefire proposal to mediators includes first stage of releasing Israeli women, children, elderly, and ill in exchange for 700-1000 Palestinian prisoners, according to the proposal seen by Reuters

Ambrey says a tanker was subject to a missile strike on the starboard side circa. 88NM north-west of Hodeidah, Yemen; damage report, no crew injuries.

Russia’s Kremlin, on French President Macron’s latest statement on Ukraine, says France is already involved in the war and has signaled it’s ready for deeper involvement

US Event Calendar

08:30: Feb. Import Price Index MoM, est. 0.3%, prior 0.8%

Feb. Import Price Index YoY, est. -0.8%, prior -1.3%

Feb. Import Price Index ex Petroleu, est. -0.2%, prior 0.6%

Feb. Export Price Index YoY, est. -2.4%, prior -2.4%

Feb. Manufacturing (SIC) Production, est. 0.3%, prior -0.5%

09:15: Feb. Capacity Utilization, est. 78.5%, prior 78.5%

10:00: March U. of Mich. 5-10 Yr Inflation, est. 2.9%, prior 2.9%

March U. of Mich. 1 Yr Inflation, est. 3.1%, prior 3.0%

March U. of Mich. Expectations, est. 75.1, prior 75.2

March U. of Mich. Current Conditions, est. 79.7, prior 79.4

DB’s Jim Reid concludes the overnight wrap

The last 24 hours have seen a dramatic bond sell-off, with 10yr Treasury yields (+10.0bps) up to 4.29% as concerns mounted about stubborn inflation. The main driver was a strong US PPI report, which showed that producer prices were rising faster than expected in February. But alongside that, oil prices closed at their highest level since November, which added to fears that inflation was still gathering momentum. And on top of that, there was growing anticipation that the Bank of Japan would end their negative interest rate policy at next week’s meeting, which added to the upward pressure on global yields.

For markets, the big question is what this means for rate cuts. Up to now, futures had been focused on June as the most likely timing for the Fed’s first cut. But this week’s releases have led to growing doubts about that. For example, futures are now pricing in roughly a one-in-three likelihood that the Fed won’t cut at all by June. And for 2024 as a whole, just 76bps of cuts are priced in by the December meeting, which is the fewest so far this year. That’s a big turnaround from the start of the year, when 158bps of cuts were expected by December, and the first cut was fully priced in by March. So we’re seeing yet another hawkish repricing, which echoes several other points over the last couple of years when markets have priced in a dovish pivot before progressively dialling that back. Indeed, this pattern of pricing a dovish pivot has happened at least 7 times now in this cycle (we counted them before here), and on the previous 6 it was followed by even more hawkish outcomes.

That sets the stage for a very important week of central bank meetings ahead, with decisions from both the Bank of Japan and the Federal Reserve next week. Notably at the Bank of Japan, there’s been growing anticipation that they’re about to end their negative interest rate policy, and investors are pricing in a 61% likelihood of a shift. That’s what DB’s economist is expecting in his own preview (link here), but we should get some important information today, as we’ll get the outcome of wage negotiations from Rengo, the country’s largest union group. Meanwhile at the Fed, the big question next week is what they’ll signal in their new dot plot, and whether the median dot still points towards three cuts for 2024, as happened in December.