MARCH 19/GOLD CLOSED DOWN $4.10 TO $2156.65//SILVER CLOSED DOWN 11 CENTS TO $24.96/PLATINUM CLOSED DOWN $21.50 TO $920.55 WHILE PALLADIUM CLOSED DOWN $39.45 TO $995.80//GOLD COMMENTARIES TONIGHT FROM PETER SCHIFF AND DR. DANIEL LACALLE//JAPAN FINALLY ENDS NEGATIVE INTEREST RATES BY RAISING RATES AND YET THE YEN FALLS INSTEAD OF RISING///ISRAEL VS HAMAS UPDATES//UKRAINE VS RUSSIA UPDATES/COVID UPDATES//VACCINE INJURY UPDATES/DR PAUL ALEXANDER/SLAY NEWS ETC//BRAZIL’S BOLSONARO ARRESTED FOR FAKING HIS VACCINE CARD AS HE REFUSED TO TAKE THE KILLAR COVID SHOT//SWAMP STORIES FOR YOU TONIGHT//

Bitcoin: afternoon price: $64,793 DOWN 5081 dollars

Platinum price closing DOWN $20.05 AT $920.55

Palladium price; DOWN 47.40 AT $1035.25

END

SHANGHAI GOLD PREMIUM 45 DOLLARS/COMEX GOLD

SHANGHAI GOLD………

SHANGHAI GOLD (USD) FUTURES – QUOTES

Beginning Monday, April 1, 2024, CME Group settlement data will no longer be accessible through ftp.cmegroup.com and will have a delayed publication time of 12:00 a.m. CT on all cmegroup.com web pages. Learn about alternate ways to access the data in our FAQ.

435 H SCOTIA CAPITAL 1 657 H MORGAN STANLEY 2 661 C JP MORGAN 12 730 C PTG DIVISION SG 10 737 C ADVANTAGE 1

TOTAL: 13 13 MONTH TO DATE: 5,263

JPMORGAN STOPPED (RECEIVED) 12/13 CONTRACTS

FOR MARCH/2024

GOLD: NUMBER OF NOTICES FILED FOR MAR/2024. CONTRACT: 13 NOTICES FOR 6500 OZ or 0.0464 TONNES

total notices so far: 5263 contracts for 526,300 Oz (16.370 tonnes)

FOR MARCH:

SILVER NOTICES: 195 NOTICE(S) FILED FOR 975,000 OZ/

total number of notices filed so far this month : 5317 for 26,585,000 oz

XXXXXXXXXXXXXXXXXX

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD/

BOTH GLD AND SLV ARE FRAUDULENT VEHICLES//THEY ARE NOW RAIDING GLD AND SLV FOR PHYSICAL

THE CROOKS ARE STEALING GOLD AND SILVER FROM THE GLD/SLV AND REPLACING THE PHYSICAL WITH PAPER DOLLARS.

WITH GOLD DOWN $4.10

INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD/ :

WOW!! HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A STRONG PAPER DEPOSIT OF 1.48 TONNES OF GOLD INTO THE GLD// /INVENTORY RESTS AT 833.32 TONNES

INVENTORY RESTS AT 833.32 TONNES

SLV// WHAT ON EARTH IS GOING ON>?????

WITH NO SILVER AROUND AND SILVER DOWN 11 CENTS AT THE SLV//

HUGE CHANGES IN SILVER INVENTORY AT THE SLV A MASSIVE DEPOSIT OF 11.782 MILLION OZ INTO THE SLV.: AND THE REGULATORS ARE LOOKING THE OTHER WAY/// INVENTORY “RISES” AT 427.280 MILLION OZ/

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV.

CLOSING INVENTORY: 427.280 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A HUGE SIZED 892 CONTRACTS TO 151,389 AND CLOSER TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THIS HUGE SIZED GAIN IN COMEX OI WAS ACCOMPLISHED DESPITE OUR LOSS IN PRICE OF $0.11 IN SILVER PRICING AT THE COMEX ON MONDAY. WE HAD ZERO LONG LIQUIDATION AT THE COMEX SESSION WITH AGAIN MAJOR SHORT COVERING DESPITE THE PRICE LOSS. WE HAD A FAIR 383 T.A.S ISSUANCE AND THESE WILL BE USED FOR MANIPULATION LATER THIS MONTH/AS WELL AS TODAY. PLEASE NOTE THAT THE CROOKS NEED A HIGHER SILVER/GOLD T.A.S. TO CARRY ON THEIR CROOKED MANIPULATION ON A DAILY BASIS

CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON MONDAY NIGHT: 383 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS. IT THUS LOOKS LIKE THE FED (GOV’T) IS BEHIND ALL OF THESE TRADES.

WE HAVE NOW SET ANOTHER RECORD LOW AT 114,102 CONTRACTS ///JULY 3.2023// OUR BANKERS WITH THE HELP OF SPECULATORS AND HIGH FREQUENCY TRADERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.11),BUT WERE UNSUCCESSFUL IN KNOCKING ANY SILVER LONGS AS WE HAD A HUGE SIZED GAIN OF 1042 CONTRACTS ON OUR TWO EXCHANGES DESPITE THE LOSS IN PRICE OF 11 CENTS.

WE MUST HAVE HAD:

A SMALL SIZED 150 ISSUANCE OF EXCHANGE FOR PHYSICALS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 22.270 MILLION OZ (FIRST DAY NOTICE) FOLLOWED BY TODAY,S 10,000 OZ E.F.P. JUMP TO LONDON //NEW TOTALS DECREASES TO : 26.990 MILLION OZ

//NEW STANDING FOR SILVER IS THUS 26.990 MILLION OZ

WE HAD:

/ HUMONGOUS SIZED COMEX OI GAIN/ SMALL SIZED EFP ISSUANCE/ VI) FAIR SIZED NUMBER OF T.A.S. CONTRACT ISSUANCE 383 CONTRACTS)/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL -REMOVED A HUGE XX CONTRACTS //

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS FEB. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF MARCH

TOTAL CONTRACTS for 13 days, total 20,501 contracts: OR 102.505 MILLION OZ (1577 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 102.505 MILLION OZ

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH 2022: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 118.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 85.745 MILLION OZ (SMALLER THAN LAST MONTH)

AUGUST: 171.43 MILLION OZ (THIS MONTH IS GOING TO BE HUGE //2ND HIGHEST ON RECORD

SEPT: 72.705 MILLION OZ (SMALLER THIS MONTH)

OCT: 97.455 MILLION OZ

NOV. 50.050 MILLION OZ

DEC. 66.140 MILLION OZ//

TOTAL 2023: 1,104.10 MILLION OZ/

JAN ’24 : 78.655 MILLION OZ//

FEB /2024 : 66.135 MILLION OZ./FINAL

MARCH: 102.505 MILLION OZ//WILL BE MUCH LARGER THIS MONTH//MAYBE CLOSE TO A RECORD ISSUANCE

RESULT: WE HAD A HUGE SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 892 CONTRACTS DESPITE OUR LOSSIN PRICE OF SILVER PRICING AT THE COMEX//MONDAY.,. THE CME NOTIFIED US THAT WE HAD A FAIR EFP ISSUANCE CONTRACTS: 150 ISSUED FOR MAY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS. WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR MARCH. OF 23.385 MILLION OZ ON FIRST DAY NOTICE FOLLOWED BY TODAY’S SMALL 0.01 MILLION OZ E.F.P./ JUMP TO LONDON

//NEW TOTAL STANDING RISES TO 26.9900 MILLION OZ

WE HAVE A HUMONGOUS GAIN OF 1456 OI CONTRACTS ON THE TWO EXCHANGES DESPITE THE LOSS IN PRICE. THE TOTAL OF TAS INITIATED CONTRACTS TODAY: A SMALL SIZED 383 CONTRACTS//HUGE FRONT END OF THE TAS CONTRACTS WERE LIQUIDATED DURING THE MONDAY COMEX SESSION/// WITH MAJOR SHORT COVERING FROM OUR SPEC SHORTS

THE NEW TAS ISSUANCE MONDAY NIGHT (383) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE//PROBABLY TODAY., .

WE HAD 195 NOTICE(S) FILED TODAY FOR 995,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A GOOD SIZED 4146 CONTRACTS TO 539,420 AND CLOSER TO THE RECORD (SET JAN 24/2020) AT 799,733 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110, BUT WE ARE NOW CLOSER TO OUR ALL TIME LOW OF 390,000 CONTRACTS.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED 496 CONTRACTS

WE HAD A GOOD SIZED INCREASE IN COMEX OI (4146 CONTRACTS) WITH OUR $2,75 GAIN IN PRICE//MONDAY. THE BANKERS WERE FORCED TO SUPPLY THE NECESSARY SHORT PAPER TO CONTAIN GOLD’S RISE.WE ALSO HAD A RATHER LARGE INITIAL STANDING IN GOLD TONNAGE FOR MARCH. AT 10.270 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’’S QUEUE JUMP OF 600 OZ.

NEW TOTAL Of INITIAL GOLD STANDING RISES TO: 18.656 TONNES // ALL OF THIS HAPPENED WITH OUR $2.75 GAIN IN PRICE WITH RESPECT TO MONDAY’S TRADING. WE HAD A STRONG SIZED GAIN OF 6162 OI CONTRACTS (19.166) PAPER TONNES) ON OUR TWO EXCHANGES.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 4355CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 539,420

IN ESSENCE WE HAVE A STRONG SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 6162 CONTRACTS WITH 4146 CONTRACTS DECREASED AT THE COMEX// AND A FAIR SIZED 2016 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 6162 CONTRACTS.. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): STRONG SIZED 4335 CONTRACTS,

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD STRONG SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (2016 CONTRACTS) ACCOMPANYING THE STRONG SIZED GAIN IN COMEX OI (4146) //TOTAL GAIN FOR OUR THE TWO EXCHANGES: 6162 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR FORMER FORMAT OF BANKERS GOING LONG AND SPECULATORS GOING SHORT ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR MARCH. AT 7.502 TONNES FOLLOWED BY TODAY’S QUEUE JUMP OF 0.01867 TONNES/NEW STANDING ADVANCES TO 18.656 TONNES.

/ 3) ZERO LONG LIQUIDATION // 4) GOOD SIZED COMEX OPEN INTEREST GAIN/ 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER///6: STRONG T.A.S. ISSUANCE: 4335CONTRACTS//SOME SHORT COVERING AGAIN

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023-2024 INCLUDING TODAY

MARCH

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF MARCH. :

TOTAL EFP CONTRACTS ISSUED: 63,955 CONTRACTS OR 6,395,500OZ OR 198.93 TONNES IN 13TRADING DAY(S) AND THUS AVERAGING: 5161 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 13TRADING DAY(S) IN TONNES 198..93 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2022, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 198.93/3550 x 100% TONNES 5.50% OF GLOBAL ANNUAL PRODUCTION

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH/2022: 409.30 TONNES //FINAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 151.69 TONNES (WEAKER THAN LAST MONTH)

AUGUST: 195.28 TONNES (A STRONGER MONTH)//FINAL

SEPT: 254.709 TONNES (WILL BE LARGER THAN LAST MONTH AND A STRONG MONTH)

OCT. 248.09 TONNES. LIKE SILVER, THIS MONTH IS GOING TO BE A STRONG E.F.P. ISSUANCE.

NOV. 239.16 TONNES//WILL BE STRONG THIS MONTH,

DEC. 213.704 TONNES. A STRONG MONTH//

TOTAL FOR YEAR 2023: 2,569.57 TONNES VS 2578 TONNES LAST YEAR

JAN ’24: 291.76 TONNES (WILL BE MUCH GREATER THAN LAST MONTH.//3RD HIGHEST EVER RECORDED EXCHANGE FOR PHYSICAL)

FEB’24: 201.947 TONNES

MARCH 2024: 198.93 TONNES//THIS IS GOING TO BE ONE HUMDINGER OF AN E,F,P. ISSUANCE.

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF FEB. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (APRIL), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER ROSE BY A HUGE SIZED 892 CONTRACTS OI TO 151,803 AND CLOSER TO THE COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 6 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 150 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAY 150 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 150 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 892 CONTRACTS AND ADD TO THE 150 E.FP. ISSUED

WE OBTAIN A HUMONGOUS SIZED GAIN OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 1042CONTRACTS

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTAL 5.210 MILLION OZ

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

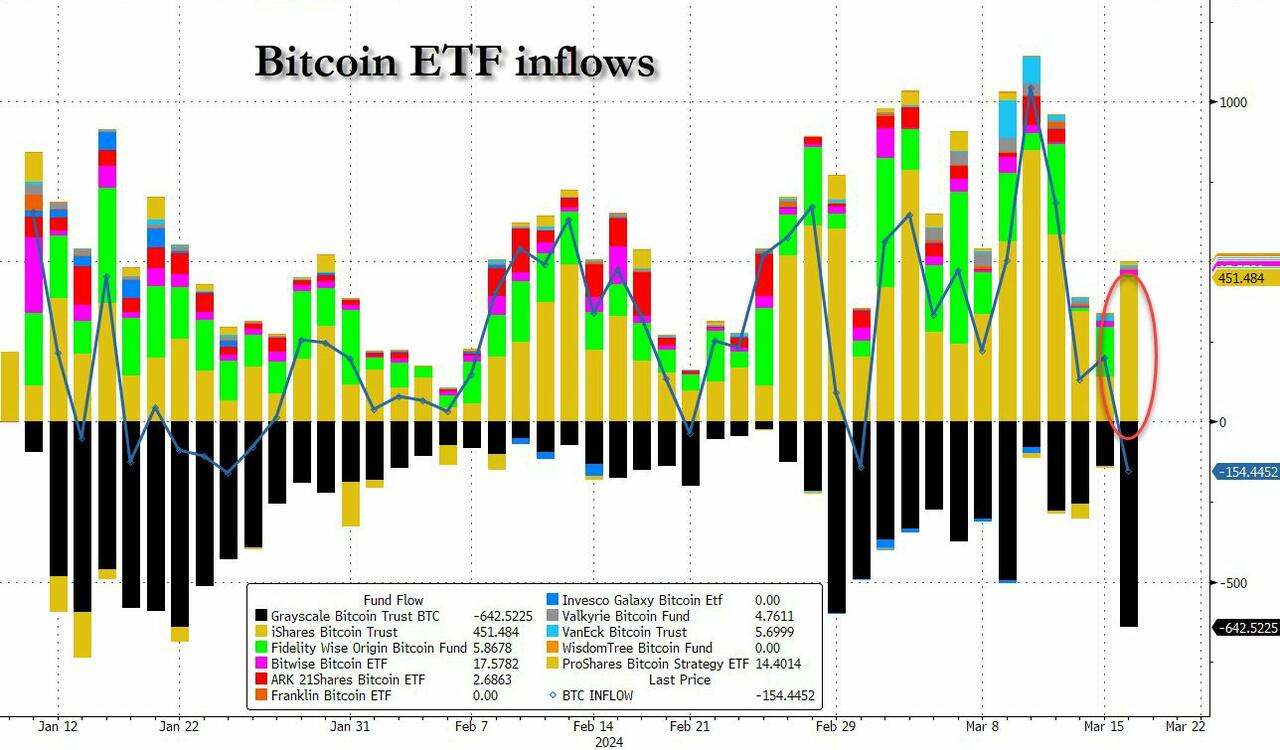

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS//

TUESDAY MORNING/MONDAY NIGHT

SHANGHAI CLOSED DOWN 22.17 PTS OR 0.72% //Hang Seng CLOSED DOWN 207.64 PTS OR 1.24% / Nikkei CLOSED UP 263.16 PTS OR 0.06%//Australia’s all ordinaries CLOSED UP 0.44% /Chinese yuan (ONSHORE) closed DOWN 7.1992 //OFFSHORE CHINESE YUAN CLOSED DOWN TO 7.2108 /Oil UP TO 82.82 dollars per barrel for WTI and BRENT UP AT 86,83/ Stocks in Europe OPENED MOSTLY ALL GREEN// ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE YUAN WEAKER

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A GOOD 4146 CONTRACTS TO 539,420 WITH OUR GAIN IN PRICE OF $2.75 WITH RESPECT TO MONDAY TRADING. MOST LIKELY IT WAS THE BANKERS SUPPLYING THE NECESSARY PAPER WITH OUR SHORT PLAYERS EXITING AS FAST AS THEIR FEET COULD CARRY THEM. THE SHORTS HAVE BEEN KILLED LATELY, AS THEY HAVE BEEN LED BY THE NOSE BY OUR BANKER-HIGH FREQUENCY TRADERS.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE NON ACTIVE DELIVERY MONTH OF MARCH..… THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 2016 EFP CONTRACTS WERE ISSUED: : APRIL 2016 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 2016CONTRACTS

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A STRONG SIZED TOTAL OF 6162 CONTRACTS IN THAT 2016 LONGS WERE TRANSFERRED AS EXCHANGE FOR PHYSICALS TO LONDON AND WE HAD A GOOD SIZED GAIN OF 4146 COMEX CONTRACTS..AND THIS GAIN ON OUR TWO EXCHANGES HAPPENED WITH OUR RISE IN PRICE OF $2.75 MONDAY COMEX. AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS DURING MID MONTH IN THE DELIVERY CYCLE), THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR MONDAY NIGHT WAS A MUCH LARGER SIZED 4335 CONTRACTS,

THROUGHOUT THE PAST SEVERAL WEEKS, THE BANKERS CONTINUE TO SELL OFF THE LONG SIDE OF THE SPREAD WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR/T.A.S. SPREAD WHICH WILL BE LIQUIDATED IN DAYS HENCE//. IT SEEMS THAT OUR CROOKS ARE HAVING A HARD TIME TRYING TO CONTROL THE PRICE OF GOLD AND THUS THE NEED FOR RECORD T.A.S. ISSUANCE.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: MARCH (18.656 TONNES) ( NON ACTIVE MONTH)

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 24 MONTHS OF 2021-2023:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276 TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.656 TONNES

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT ROSE $2.75 //// AND WERE UNSUCCESSFUL IN KNOCKING ANY SPECULATOR LONGS AS WE HAD A STRONG SIZED GAIN OF6162 TOTAL CONTRACTS ON OUR TWO EXCHANGES WITH OUR SLIGHTLY HIGHER PRICE.

WE HAD A STRONG T.A.S. LIQUIDATION ON THE FRONT END OF MONDAY’S TRADING . THE T.A.S. ISSUED ON MONDAY NIGHT, WILL BE “PUT INTO THE BANK” TO BE USED AT A LATER DATE AT THE COLLUSIVE CHOOSING OF OUR BANKERS. THE HIGH T.A.S. ISSUANCE IS MEANT TO CONTROL THE PRICE OF GOLD (AS WELL AS INITIATE A RAID).

WE HAVE GAINED A TOTAL OI OF 19.166 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR MARCH. (10.3576 TONNES) ON FIRST DAY NOTICE FOLLOWED BY TODAY’S 600 OZ QUEUE JUMP//NEW STANDING INCREASES TO 18.656 TONNES

ALL OF THIS WAS ACCOMPLISHED DESPITE OUR GAIN IN PRICE TO THE TUNE OF $2.75

WE HAD -REMOVED 496 CONTRACTS TO THE COMEX TRADES TO OPEN INTEREST (CROOKS)

NET GAIN ON THE TWO EXCHANGES 6162 CONTRACTS OR 616,200 OZ OR 19.166 TONNES. estimated volume today 203,790 fair

Total monthly oz gold served (contracts) so far this month

5263 notices 526,300 oz 16.370 TONNES

Total accumulative withdrawals of gold from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of gold from the Customer inventory this month

x

0 dealer deposits:

total dealer deposits: nil oz

total customer withdrawals: 1

i) Out of Brinks: 39,352.824 oz

total customer withdrawal: 39,352.824 oz

we had 1 customer deposit

i) Into Brinks: 128.604 oz

total deposit 128.604 oz

Adjustments: 1

i) Brinks customer to dealer: 192.906 oz

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR MAR.

For the front month of MARCH we have an oi of 276 contracts having LOST 70 contracts. We had 78 contracts filed upon on Monday, so we gained 8 contracts or an additional 800 oz of gold(0.01867 tonnes) will stand at the comex in this non active delivery month of March.

APRIL LOST 13.914 CONTRACTS FALLING TO 222,136.

MAY EARNED 50 CONTRACTS TO STAND AT 835

JUNE INCREASED ITS OI BY 17,357 CONTRACTS UP TO 256,659 CONTRACTS.

We had 13 contracts filed for today representing 6500 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 13 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 12 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for the MARCH. /2024. contract month, we take the total number of notices filed so far for the month (5263 x 100 oz ), to which we add the difference between the open interest for the front month of MARCH. (748 CONTRACTS) minus the number of notices served upon today 13 x 100 oz per contract equals 599,800 OZ OR 18.656 TONNES

thus the INITIAL standings for gold for the MARCH. contract month: No of notices filed so far (5263) x 100 oz + (748) {OI for the front month} minus the number of notices served upon today (13) x 100 oz which equals 599,800 oz (18.6560 TONNES)

TOTAL COMEX GOLD STANDING FOR MARCH: 18.656 TONNES WHICH IS HUGE FOR A NON ACTIVE DELIVERY MONTH IN THE CALENDAR.

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD: 17,779,096.47 OZ

TOTAL REGISTERED GOLD 7,736,801.037 (240.64 tonnes).

TOTAL OF ALL ELIGIBLE GOLD: 10,081,712.559 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 6,403,443 oz (REG GOLD- PLEDGED GOLD) 199.17 tonnes/dropping like a stone

END

SILVER/COMEX

MARCH 19

INITIAL

//2024// THE MARCH 2024 SILVER CONTRACT//INITIAL

Silver

Ounces

Withdrawals from Dealers Inventory

NIL oz

Withdrawals from Customer Inventory

1136,766.769 oz ASAHI Delaware CNT

.

Deposits to the Dealer Inventory

nil OZ

Deposits to the Customer Inventory

1,815,967.272 oz CNT

HSBC Manfra

No of oz served today (contracts)

195 CONTRACT(S) (995,000 OZ)

No of oz to be served (notices)

81 contracts (0.405 MILLION oz)

Total monthly oz silver served (contracts)

5317 Contracts (26.585 MILLION oz)

Total accumulative withdrawal of silver from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of silver from the Customer inventory this month

i) 0 dealer deposit

total dealer deposit :nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: 0 oz

We had 0 deposits customer account:

total customer deposits nil oz

JPMorgan has a total silver weight: 129.806 million oz/285.110 million or 45.26%

adjustment: 1/customer to dealer: 25,766.855 oz

Comex withdrawals: 3

i) Out of ASAHI 1129,786.930 oz

ii) Out of Delaware 974.80 oz

iii) Out of CNT: 6005.039 oz

total withdrawal: 1136,766.769 oz

TOTAL REGISTERED SILVER: 48.888MILLION OZ//.TOTAL REG + ELIGIBLE. 285,110million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR DECEMBER:

silver open interest data:

FRONT MONTH OF MARCH /2023 OI: 276 CONTRACTS HAVING LOST 10 CONTRACT(S).

WE HAD 8 NOTICES FILED ON MONDAY SO LOST 2 CONTRACTS OR AN ADDITIONAL 10,000 OZ WILL NOT STAND AT THE COMEXAS THEY WERE E.F.P.’D TO LONDON

APRIL SAW A LOSS OF 5 CONTRACTS TO STAND AT 803

MAY SAW A GAIN OF 406 CONTRACTS UP TO 117,162.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 195 for 995,000 oz

Comex volumes// est. volume today 50,751 fair

Comex volume: confirmed yesterday 52,300 fair.

To calculate the number of silver ounces that will stand for delivery in MARCH. we take the total number of notices filed for the month so far at 5317 x 5,000 oz = 26,585,000 oz

to which we add the difference between the open interest for the front month of MARCH. (276) and the number of notices served upon today 195 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the MARCH/2024 contract month: 5317 (notices served so far) x 5000 oz + OI for the front month of MARCH. (276) – number of notices served upon today (195 )x 500 oz of silver standing for the MARCH contract month equates to 26.990 MILLION OZ.

New total standing: 26.990 million oz.

There are 48.239 million oz of registered silver.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS//

BOTH GLD AND SLV ARE MASSIVE FRAUDS!

MARCH 18 WITH GOLD DOWN $4.10 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD A STRONG PAPER DEPOSIT OF 1.48 TONNES OF GOLD INTO THE GLD/:INVENTORY RISES TO 833.32 TONNES

MARCH 15 WITH GOLD DOWN $5.20 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD/:INVENTORY REMAINS AT 816.86 TONNES

MARCH 14 WITH GOLD DOWN $12.20 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF 1.73 TONNES OF GOLD INTO THE GLD//:INVENTORY REMAINS AT 816.86 TONNES

MARCH 13 WITH GOLD UP $14.40 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD:INVENTORY REMAINS AT 815.13 TONNES

MARCH 12 WITH GOLD DOWN $21.15 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD:NOT AVAILABLE///LAST VALUE 815.13 TONNES

MARCH 11 WITH GOLD UP $3.20 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.44 TONNES OF GOLD OUT OF THE GLD AFTER 7 CONSECUTIVE GOLD PRICE RISES//INVENTORY RESTS AT 815.13 TONNES

MARCH 8 WITH GOLD UP $21.05 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 0.87 TONNES OF GOLD OUT OF THE GLD AFTER 7 CONSECUTIVE GOLD PRICE RISES//INVENTORY RESTS AT 816.57 TONNES

MARCH 7 WITH GOLD UP $7.20 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4,20 TONNES OF GOLD OUT OF THE GLD//INVENTORY RESTS AT 817.44 TONNES

MARCH 6 WITH GOLD UP $17.20 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.30 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 821.47 TONNES

MARCH 5 WITH GOLD UP $16.55 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.30 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 821.47 TONNES

MARCH 4 WITH GOLD UP $30.55 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF .86 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 823.77 TONNES

MARCH 1 WITH GOLD UP $40.40 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 822.91 TONNES

FEB29/WITH GOLD UP $12.60 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD//WITHDRAWAL OF 4.03 TONNES INVENTORY RESTS AT 822.91 TONNES

FEB28/WITH GOLD DOWN $1.00 TODAY NO CHANGES IN GOLD INVENTORY AT THE GLD INVENTORY RESTS AT 826.94 TONNES

FEB27/WITH GOLD UP $4.40 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF .87 TONNES OF GOLD FROM THE GLD:/INVENTORY RESTS AT 826.94 TONNES

FEB26/WITH GOLD DOWN $8.90 TODAY NO CHANGES IN GOLD INVENTORY AT THE GLD:/INVENTORY RESTS AT 827.81 TONNES

FEB23/WITH GOLD UP $17 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.01 TONNES OF GOLD FROM THE GLD.//INVENTORY RESTS AT 827.81 TONNES

FEB22/WITH GOLD DOWN $2.15 TODAY NO CHANGES IN GOLD INVENTORY AT THE GLD://INVENTORY RESTS AT 829.82 TONNES

FEB21/WITH GOLD DOWN $5.30 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 7.59 TONNES OF GOLD OUT OF THE GLD///INVENTORY RESTS AT 29.82 TONNES

FEB20/WITH GOLD UP $16.15 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 0.58 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 837.89 TONNES

FEB16/WITH GOLD UP $8,60 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.73 TONNES OF GOLD FROM THE GLD///INVENTORY RESTS AT 837.31 TONNES

FEB15/WITH GOLD UP $11.70 TODAY NO CHANGES IN GOLD INVENTORY AT THE GLD:/INVENTORY RESTS AT 841.92 TONNES

FEB14/WITH GOLD DOWN $2.75 TODAY NO CHANGES IN GOLD INVENTORY AT THE GLD:/INVENTORY RESTS AT 841.92 TONNES

FEB13/WITH GOLD DOWN $20.15 TODAY NO CHANGES IN GOLD INVENTORY AT THE GLD:/INVENTORY RESTS AT 841.92 TONNES

FEB12/WITH GOLD DOWN $4.80 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A STRONG WITHDRAWAL OF 1.74 TONNES OF GOLD FROM THE GLD. / //://INVENTORY RESTS AT 841.92 TONNES

FEB9/WITH GOLD DOWN $8.60 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A STRONG DEPOSIT OF 1.44 TONNES OF GOLD FROM THE GLD. / //://INVENTORY RESTS AT 843.66 TONNES

FEB8/WITH GOLD DOWN $2.70 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A MASSIVE WITHDRAWAL OF 5.47 TONNES OF GOLD FROM THE GLD. / //://INVENTORY RESTS AT 842.22 TONNES:

FEB7/WITH GOLD UP $0.40 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A MASSIVE WITHDRAWAL OF 4.04 TONNES OF GOLD FROM THE GLD. / //://INVENTORY RESTS AT 847.69 TONNES:

FEB6/WITH GOLD UP $8.50 TODAY NO CHANGES IN GOLD INVENTORY AT THE GLD:/ / //://INVENTORY RESTS AT 851.73 TONNES:

GLD INVENTORY: 833.32 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

MARCH 18/WITH SILVER DOWN 11 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A HUGE DEPOSIT OF 11.792 MILLION OZ INTO THE SLV: SLV INVENTORY RESTS AT 427.280 MILLION OZ

MARCH 15/WITH SILVER DOWN 9 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 1.006 MILLION OZ FROM THE SLV: SLV INVENTORY RESTS AT 417.866 MILLION OZ

MARCH 14/WITH SILVER DOWN 9 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: SLV INVENTORY RESTS AT 418.872 MILLION OZ

MARCH 13/WITH SILVER UP 32 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: SLV INVENTORY RESTS AT 418.872 MILLION OZ…

MARCH 12/WITH SILVER DOWN 31 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A SMALL WITHDRAWAL OF 0.549 MILLION OZ OF SILVER INTO THE SLV//// : SLV INVENTORY RESTS AT 418.872 MILLION OZ…

MARCH 11/WITH SILVER UP 11 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A HUGE WITHDRAWAL OF 2.147 MILLION OZ OF SILVER FROM THE SLV//// : SLV INVENTORY RESTS AT 418.323 MILLION OZ…SUCH A MASSIVE FRAUD!

MARCH 8/WITH SILVER DOWN 5 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A HUGE WITHDRAWAL OF 4.299 MILLION OZ OF SILVER FROM THE SLV//// : SLV INVENTORY RESTS AT 420.519 MILLION OZ…SUCH A MASSIVE FRAUD!

MARCH 7/WITH SILVER UP 8 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A HUGE WITHDRAWAL OF 4.665 MILLION OZ OF SILVER FROM THE SLV//// : SLV INVENTORY RESTS AT 424.818 MILLION OZ…SUCH A MASSIVE FRAUD!

MARCH 6/WITH SILVER UP 52 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A HUGE WITHDRAWAL OF 2.378 MILLION OZ OF SILVER FROM THE SLV//// : SLV INVENTORY RESTS AT 427,105 MILLION OZ

MARCH 5/WITH SILVER DOWN 2 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A HUGE WITHDRAWAL OF 1.499 MILL;ION OZ OF SILVER FROM THE SLV//// : SLV INVENTORY RESTS AT 429.483 MILLION OZ

MARCH 4/WITH SILVER UP CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: // : SLV INVENTORY RESTS AT 430.982 MILLION OZ

MARCH 1/WITH SILVER UP 49 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: // : SLV INVENTORY RESTS AT 430.982 MILLION OZ

FEB 29/WITH SILVER UP 25 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.104 MILLION OZ OUT OF THE SLV//// : SLV INVENTORY RESTS AT 430/982 MILLION OZ

FEB 28/WITH SILVER DOWN 7 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 5.123 MILLION OZ INTO THE SLV//// : SLV INVENTORY RESTS AT 433.086 MILLION OZ

FEB 27/WITH SILVER UP 3 CENTS TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 0.64 MILLION OZ FROM THE SLV//// : SLV INVENTORY RESTS AT 427.943 MILLION OZ

FEB 26/WITH SILVER DOWN 44 CENTS TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.065 MILLION OZ FROM THE SLV//// : SLV INVENTORY RESTS AT 428.603 MILLION OZ

FEB 23/WITH SILVER DOWN 44 CENTS TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.065 MILLION OZ FROM THE SLV//// : SLV INVENTORY RESTS AT 428.603 MILLION OZ

FEB 22/WITH SILVER DOWN 10 CENTS TODAY NO CHANGES IN SILVER INVENTORY AT THE SLV

// : SLV INVENTORY RESTS AT 432.766 MILLION OZ

FEB 21/WITH SILVER DOWN 28 CENTS TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 2.348 MILLION OZ OF SILVER FROM THE SLV// : SLV INVENTORY RESTS AT 432.766 MILLION OZ

FEB 20/WITH SILVER DOWN 33 CENTS TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 3.385 MILLION OZ OF SILVER FROM THE SLV// : SLV INVENTORY RESTS AT 435.008 MILLION OZ

FEB 16/WITH SILVER UP 53 CENTS TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV A DEPOSIT OF 1.235 MILLION OZ OF SILVER FROM THE SLV// : SLV INVENTORY RESTS AT 438.393 MILLION OZ

FEB 15/WITH SILVER UP 56 CENTS TODAY NO CHANGES IN SILVER INVENTORY AT THE SLV : SLV INVENTORY RESTS AT 437.615 MILLION OZ

FEB 14/WITH SILVER UP 24 CENTS TODAY NO CHANGES IN SILVER INVENTORY AT THE SLV : SLV INVENTORY RESTS AT 437.615 MILLION OZ

FEB 13/WITH SILVER DOWN 60 CENTS TODAY SMALL CHANGES IN SILVER INVENTORY AT THE SLV A SMALL WITHDRAWAL OF 0.504 MILLION OZ OZ OUT OF THE SLV: SLV INVENTORY RESTS AT 437.615 MILLION OZ

FEB 12/WITH SILVER UP 14 CENTS TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV A HUGE WITHDRAWAL OF 1.921 MILLION OZ OZ OUT OF THE SLV: SLV INVENTORY RESTS AT 438.119 MILLION OZ

FEB 9/WITH SILVER DOWN 4 CENTS TODAY SMALL CHANGES IN SILVER INVENTORY AT THE SLV A SMALL DEPOSIT OF 600,000 OZ INTO THE SLV: SLV INVENTORY RESTS AT 440.040 MILLION OZ

FEB 8/WITH SILVER UP 29 CENTS TODAY NO CHANGES IN SILVER INVENTORY AT THE SLV: SLV INVENTORY RESTS AT 439.994 MILLION OZ

FEB 7/WITH SILVER DOWN 18 CENTS TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A MASSIVE DEPOSIT OF 4.04 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 439.994 MILLION OZ//LAST 9 DAYS: 10.7598 MILLION OZ WITHDRAWAL

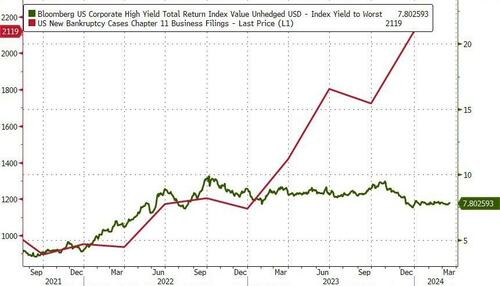

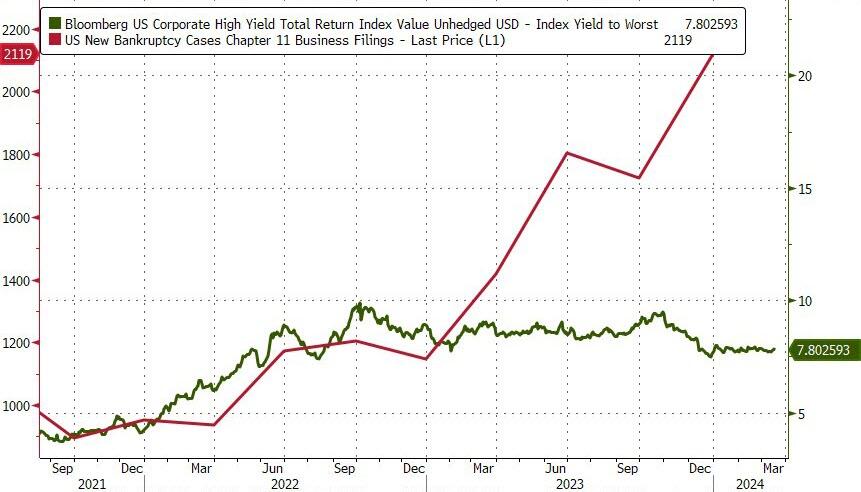

Consumers aren’t the only ones defaulting on their debts: Corporate bond defaults were up massively in 2023, especially for high-risk junk debt, and the trend is continuing this year at a pace not seen since the 2008 global financial crisis. Unsurprisingly, companies selling low-rated junk debt are being hit the worst.

Last year, according to S&P Global Ratings, corporate bond defaults increased by a disconcerting 80%. High interest rates coupled with high inflation have made it a struggle for companies to make good on their commitments even as waves of new bond buyers continue to arrive, eager to lock in higher yields before rates go down. Demand remains strong for junk bonds and hybrid debt, but for companies with poor liquidity, poor to negative cash flow, and/or an outsized existing debt burden, the result is a compelling setup for even more defaults in 2024.

For now, with rate cuts on the horizon, interest remains strong in junk bond debt even as effective yields have fallen from their 2023 highs, and yield spreads remain relatively low:

Junk Bond Effective Yields vs Ch.11 Bankruptcy Filings, Summer 2022 to Now

Meanwhile, debts that were financed in a low-interest rate environment are due to mature in the next few years, to the tune of over $1.8 trillion by 2028 according to the Fed. When those payments come due, more companies will fall to the default wave. And if the junk bond market goes off of a cliff, it could pop the broader $13.7 trillion corporate bond bubble and take the rest of the economy with it.

Even Bank of America is calling the overheated bond market “bubbly.” With no sign of a short-term slowdown in bond sales, the pressure on premiums is expected to keep increasing for high-risk debt as borrowers rush to fill the demand for high-yield offerings before the Fed cuts rates.

However, as quoted in Bloomberg, Band of America strategists said:

“The unusually supportive technicals currently are unlikely to be sustainable in the longer term.”

Last month, Moody’s changed their rating methodology to align with Fitch and S&P’s rules, making hybrid debt more attractive to overstretched companies in sectors like media, tech, and others. The rule change lets companies take on more hybrid debt to raise money without taking as much of a potential hit to their creditworthiness. As far as the next wave of defaults goes, Moody’s itself reported earlier this year that about 16% of speculative-grade companies are at high risk of defaulting on their obligations, including healthcare companies and airlines:

“Names added to the list last quarter include radio platform iHeart Communications and Spirit Airlines (SAVE.N), whose proposed merger with peer JetBlue (JBLU.O), was blocked on Tuesday…At the same time, as defaults have risen, the ratio of Moody’s downgrades to upgrades among speculative-grade companies grew to 1.8x in the fourth quarter of 2023, up from 1.3x in the previous quarter.”

The Fed hopes that its interest rate cuts will decrease the burden on indebted companies, but it will come at the cost of adding fuel to inflationary pressures that the higher-interest rate environment has failed to contain. Besides, a decrease in interest rates won’t be enough for many low-rated companies to successfully refinance their obligations or take on additional debt. If investors keep flocking to them in search of higher yield compared to Treasurys, that only makes a frothy market even frothier.

Either way, when the entire economy is addicted to an artificially low interest rate environment, the Fed constantly backs itself into a corner and turns to its only real policy tool: printing money. Feverish bond-buying inspired, in part, by artificially-induced interest rate changes is just one of the endless ways that the Fed’s meddling creates a zombie economy. This banker-run fantasyland acts not upon the laws of nature or the principles of sound economics, but the hubris-fueled whims of central bankers who eagerly play the roles of both pseudo-wizard and pseudo-scientist at the dire expense of the governed.

end

2.Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens/ SIMON WHITE..//

3. CHRIS POWELL//GATA

Wisconsin is near to ending taxes on gold and silver bullion

Submitted by admin on Mon, 2024-03-18 19:41 Section: Daily Dispatches

By JP Cortez Money Metals Exchange, Eagle, Idaho Friday, March 15, 2024

The Wisconsin Senate has voted in favor of Assembly Bill 29 to end the state sales tax on purchases of gold and silver.

Joining the state Assembly, which overwhelmingly voted to approve this law last week, senators voted 23-9 in favor of this pro-sound money legislation. The bill will now be transmitted to Gov. Tony Evers for his signature.

Assembly Bill 29, primarily sponsored by Rep. Shae Sortwell, also passed out of the state Assembly by a bipartisan vote of 86-12. This popular bill is co-sponsored by almost two dozen other legislators and enjoys wide support — and would align Wisconsin with the policies of 43 other U.S. states.

AB 29 would exempt “precious metals bullion,” defined as coins, bars, rounds, and sheets that contain at least 35% gold, silver, copper, platinum, or palladium.

Imposing taxes on the exchange of Federal Reserve notes for monetary metals (i.e., gold and silver) has become an unusual and outmoded practice in the United States. Only seven states still engage in it. …

Submitted by admin on Mon, 2024-03-18 18:46 Section: Daily Dispatches

Sugar-Coated Gold Nanoparticles Can Quickly Eliminate Bacterial Infections, No Antibiotics Required

From the National Institutes of Health Bethesda, Maryland via Phys.org, Douglas, Isle of Man, United Kingdom Wednesday, March 13, 2024

Researchers at the University of Pennsylvania, Stanford University, and the New Jersey Institute of Technology have developed sugar-coated gold nanoparticles that they used both to image and destroy biofilms, the slimy scaffolding that bacteria can develop on our teeth or wounded skin if left unattended.

In a study published in the Journal of Clinical Investigation, the authors demonstrated the diagnostic and therapeutic potential of the nanoparticles on the teeth and wounded skin of rats and mice, eliminating the biofilms in as little as one minute and outperforming common antimicrobials.

“With this platform, you can bust biofilms without surgically debriding infections, which can be necessary when using antibiotics,” Luisa Russell, a program director in the Division of Discovery Science & Technology at the National Institute of Biomedical Imaging and Bioengineering, said in a media statement. “Plus, this method could treat patients if they are allergic to antibiotics or are infected by strains that are resistant to medication. The fact that this method is antibiotic-free is a huge strength.” …

Submitted by admin on Mon, 2024-03-18 16:20 Section: Daily Dispatches

By Brien Lundin Gold Newsletter / Golden Opportunities, Metairie, Louisiana Monday, March 18, 2024

The big story in gold is silver.

Every secular bull market in gold has seen silver outperform its glittering cousin. That means two things:

1) Silver’s outperformance is a confirmation that a gold bull market has truly begun, and. …

2) It’s a great way to play gold during such a bull market.

So if you believe that the macroeconomic environment is bullish for gold, then you need to own silver as well to boost the performance of your precious metals portfolio.

As I’ve always put it, if you like gold, you should love silver.

Of course, this begs the question of what silver is telling us now…

If you’ve been perusing gold-oriented commentators on social media and in newsletters, you’ve noticed a general consensus view that silver hasn’t been doing its job during the remarkable gold rally this month.

But if you look at the data, nothing could be further from the truth. …

The manufacturing and consumer confidence weaknesses of the United States are deeply concerning, particularly considering that all those allegedly infallible Keynesian policies are being applied intensely.

Considering the insanity of deficit spending driven by entitlement programs, the decline in the headline University of Michigan consumer sentiment index in March—from 76.9 to 76.5—is even worse than expected. Let us remember that this index was at 101 in 2019 and has not recovered the brief bounce shown by the reopening effect in March 2021. Consumer confidence is still incredibly low, and a decline in the expectations index fully explains the most recent decline. Persistent inflation, high gas prices, and declining real wages may explain the poor expectations of the average citizen. Furthermore, this poor consumer confidence reading comes after poor control group retail sales last month.

No, this is not a strong economy. The consumer confidence index, labor participation, and unemployment-to-population ratios, as well as real wage growth, remain significantly below the pre-pandemic level, and this after $6.3 trillion in new public debt that will likely reach $8 trillion by the end of 2024.

The manufacturing weakness of the United States is also a problem because this should be a period of high growth, considering the opportunities generated all over the world. Industrial output bounced 0.8 percent in February, but the January figure was revised to a larger 1.1 percent slump. If we factor in the decline in the Empire State survey, to -20.9 in March, it looks like the manufacturing decline will persist.

The shape of the U.S. economy also reflects the impossibility of the soft-landing narrative. Inflation remains well above target, and bond yields are reflecting the reality of persistent inflation. Furthermore, money supply growth stopped declining months ago.

If the money supply rises and government spending continues to rise, the Federal Reserve will be unable to cut interest rates, and the impoverishment of citizens by a loss of purchasing power will continue.

This is the result of an insane fiscal policy that increases spending and taxes. Weak growth, manufacturing decline, and worsening consumer confidence.

Demand-side policies and Keynesian experiments are leaving a once-strong economy on the same path as the eurozone: stagflation. A warning sign should be the fact that the increase in public debt completely justifies the gross domestic product recovery.

This is the problem of extraordinary monetary and fiscal experiments. Governments embrace massive spending and debt monetization under the premise that they will implement control policies if the warning signs appear, but when they do, they never stop spending. Economists close to the government said that the administration would reconsider and adjust its budget if inflation rose, and alarm bells rang. Now we have heard all the alarm bells, and the administration continues as if nothing happened. The Inflation Reduction Act became the Inflation Perpetuation Act; the rise in government borrowing is now evident in the 10- and 30-year curve; and the private sector is in an obvious contraction.

Trusting governments to moderate spending after an expenditure binge is simply an extremely dangerous bet that always ends with worse conditions for citizens. Once they start, they cannot stop, and the inevitable end is higher taxes, weaker growth, lower real wages, and a decline in the purchasing power of the dollar. All the figures in the U.S. economy scream “buy gold” because the government will always prefer to destroy the currency than to moderate the budget deficit and government size in the economy.

end

end

5 a. IMPORTANT COMMENTARIES ON COMMODITIES

.

5 B GLOBAL COMMODITY ISSUES/FOOD IN GENERAL//FREIGHT

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGSTUESDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED DOWN 7.1992

OFFSHORE YUAN: DOWN TO 7.2108

SHANGHAI CLOSED DOWN 22.17 PPTS OR 0.72%

HANG SENG CLOSED DOWN 207.64 PTS OR 1.24%

2. Nikkei closed UP 263.16 PTS OR 0.66%

3. Europe stocks SO FAR: MOSTLY ALL GREEN

USA dollar INDEX UP TO 103.56 EURO FALLS TO 1.0848 UP 23 BASIS PTS

3b Japan 10 YR bond yield: FALLS TO. +.720 Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 150.42/JAPANESE YEN NOW FALLING AS WELL AS LONG TERM 10 YR. YIELDS RISING //EVENTUALLY THIS WILL BREAK THE JAPANESE CENTRAL BANK

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen DOWN CHINESE ONSHORE YUAN: DOWN/ OFFSHORE: DOWN

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and UP FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund YIELD DOWN TO +2.4535***/Italian 10 Yr bond yield UP to 3.694* /SPAIN 10 YR BOND YIELD UP TO 3.247…**

3i Greek 10 year bond yield UP TO 3.301

3j Gold at $2155.75 silver at: 24.93 1 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble DOWN 0 AND 60 /100 roubles/dollar; ROUBLE AT 92.51//

3m oil into the 82 dollar handle for WTI and 86 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 150.42// 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 0.720% STILL ON CENTRAL BANK (JAPAN) INTERVENTION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.8876 as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.9623 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.332 DOWN 2 BASIS PTS…

USA 30 YR BOND YIELD: 4.453 DOWN 1 BASIS PTS/

USA 2 YR BOND YIELD: 4.717 DOWN 2 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 32.34…(TURKEY SET TO BLOW UP FINANCIALLY)

GREAT BRITAIN/10 YEAR YIELD: DOWN 3 BASIS PTS AT 4.098

end

2.a Overnight: Newsquawk and Zero hedge

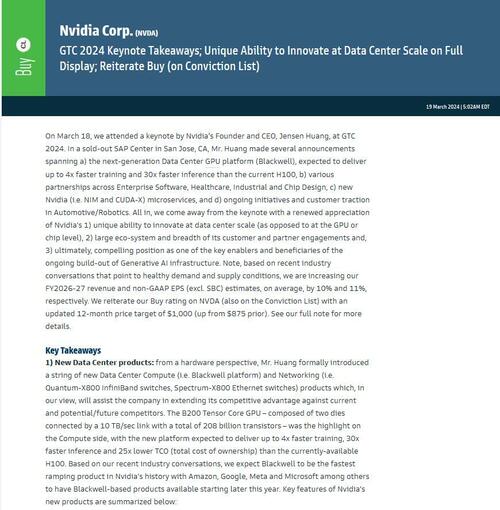

US Futures Slide As Nvidia Keynote Disappoints And FOMC Decision Looms

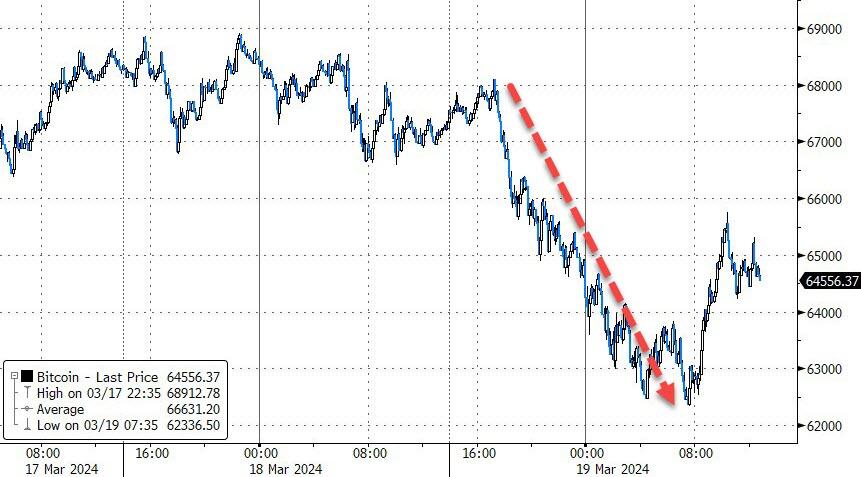

TUESDAY, MAR 19, 2024 – 08:28 AM

One day after we asked if Jensen Huang’s keynote speech at the NVDA GTC presentation would be a “sell the news”event, the answer is yes, because this morning US stock futures have slumped, after the AI chip giant’s CEO disappointed markets by not revealing anything that the market wasn’t already expecting. As a result, as of 7:50am, S&P futures were trading at session lows, down 0.5%, with Nasdaq futures sliding 0.6% and bitcoin dumping after an overnight fat-finger sent the crypto briefly to $8,900. And now that the BOJ has finally exited negative rates after a decade of with all eyes on the Federal Reserve’s policy meeting for clues on the rates outlook. Bizarrelly, the BOJ’s historic rate hike has sent the yen sliding and thus, the dollar higher with 10Y yields unchanged around 4.32%. Commodities are flat with metals outperforming and Brent crude trading near a five month high of $87. Today’s macro data focus will be on housing data with an update on TIC flows.

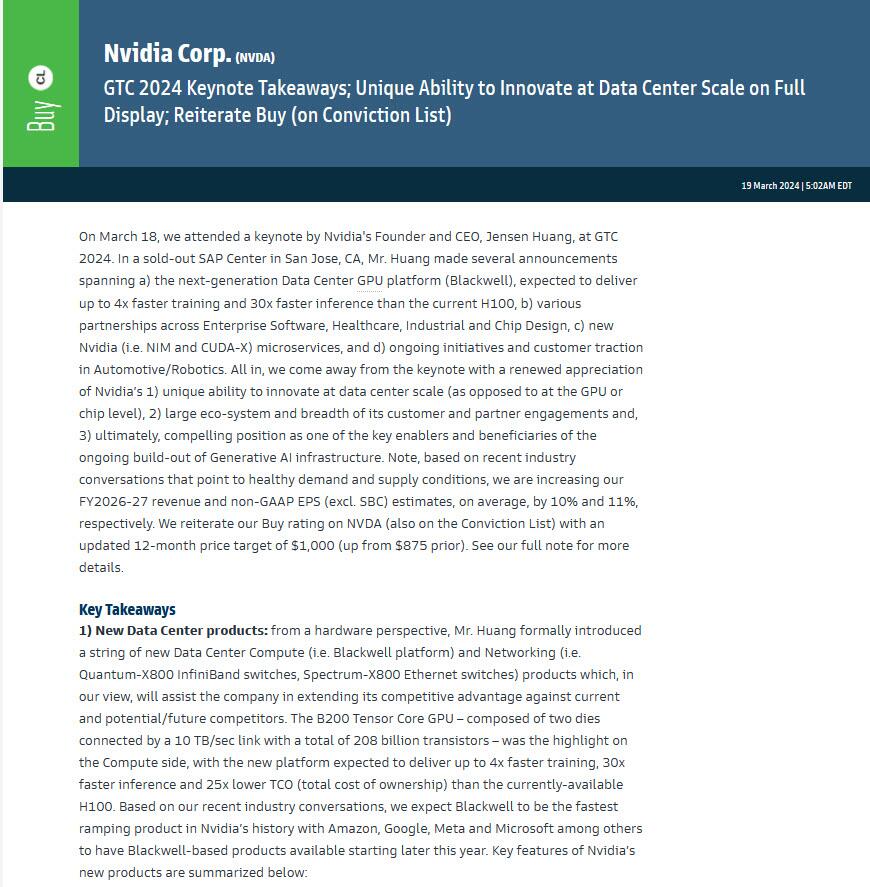

In premarket trading, NVDA stock was down and Mag7 names were mixed with semis lower, despite a price target increase by Goldman which now expects NVDA to trade at $1000 in 12 months, up from $875 (full note available to pro subs).

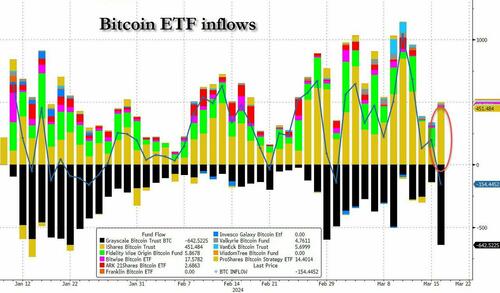

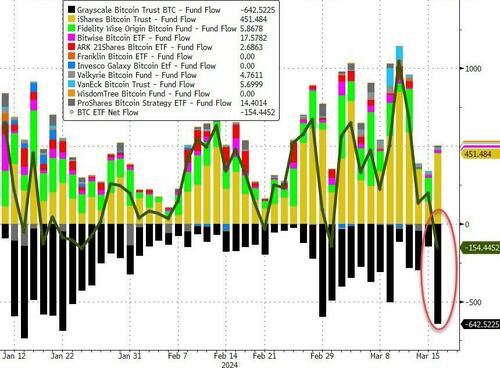

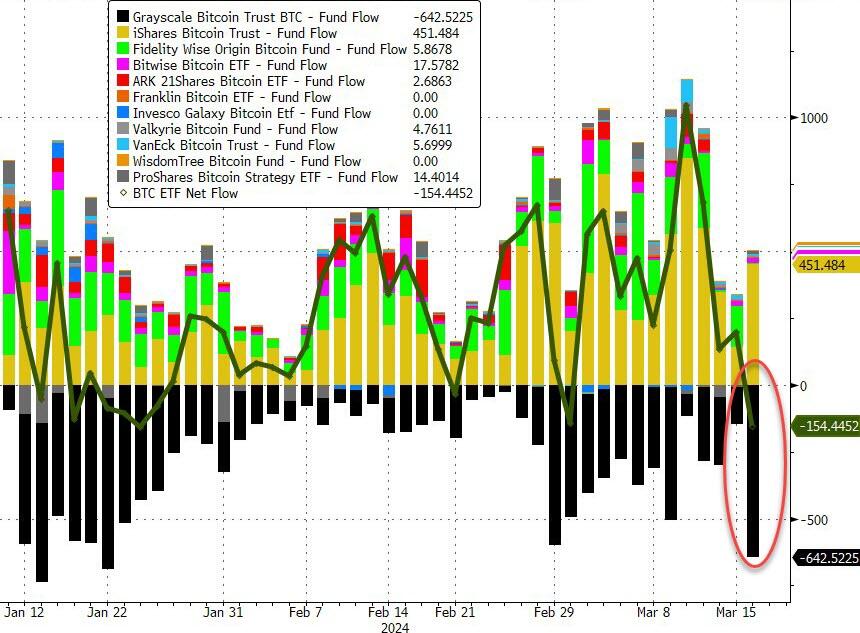

Elsewhere, cryptocurrency-linked stocks dropped as Bitcoin extended a retreat following a record daily outflow from the doomed GBTC ETN which may have precipitated yesterday’s crypto rout, offset however by another BTFD burst in the Blackrock IBIT ETF. Among the bigger movers, Coinbase Global -5%, Riot Platforms (RIOT) -5%, Marathon Digital (MARA) -7%,

Here are some other notable premarket movers:

Beyond Meat falls 5% after the plant-based protein company filed a $250 million mixed securities shelf registration.

Caleres slips about 2% after the retailer reported a decline in Famous Footwear comparable sales and issued weaker-than-expected first-quarter guidance.

Crinetics Pharmaceuticals rises 14% after saying its once-daily oral paltusotine achieved the primary and all secondary endpoints in the Phase 3 PATHFNDR-2 study in acromegaly patients.

Fusion Pharma (FUSN) soars 100% after AstraZeneca agreed to buy the biotech company for as much as $2.4 billion.

National CineMedia (NCMI) jumps 24% after the company announced a $100 million share buyback and reported fourth-quarter earnings per share that beat consensus estimates.

Nvidia (NVDA) slips 1% as analysts noted that its much-anticipated AI event had no major surprise announcements.

StoneCo (STNE) drops 9% after the digital payments firm announced its co-founder André Street would leave his position as chairman. The company also reported fourth-quarter payment volume that came below consensus expectations.

Finally, one month after we asked when Supermicro would sell stock to take advantage of its ridiculous stock price…

… we got the answer this morning when Super Micro Computer announced an offering to sell 2 million shares of common stock, sending the stock tumbling 8%.

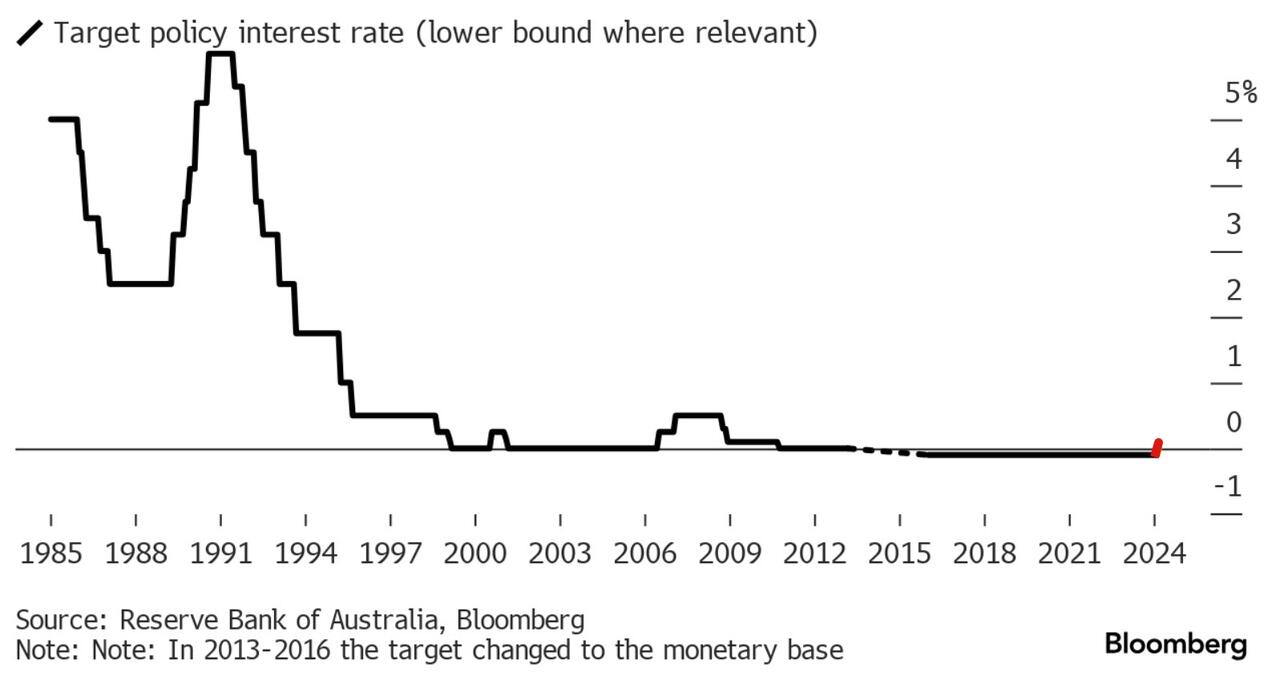

Turning to the main overnight event, the yen paradoxically tumbled after the Bank of Japan brought an end to the world’s last negative interest-rate policy and emphasized that financial conditions will remain easy. The BOJ’s first hike in 17 years had been widely expected and Governor Kazuo Ueda struck a neutral tone at a news conference, saying there’s still a chance its inflation goal will not be hit. While the central bank scrapped its yield curve control program, it also pledged to keep buying long-term government debt.

“It’s a very, very dovish hike, as dovish hike as they come,” said Frederic Neumann, HSBC’s chief Asia economist, said on Bloomberg Television. Japanese bonds gained and the Topix closed at the highest since 1990 because the yen dropped 0.9% versus the dollar to 150.43, usually the opposite of what happens after a rate hike, and effectively dooms the BOJ to panic hiking as the plunging yen means Japan’s inflation troubles will only get worse.

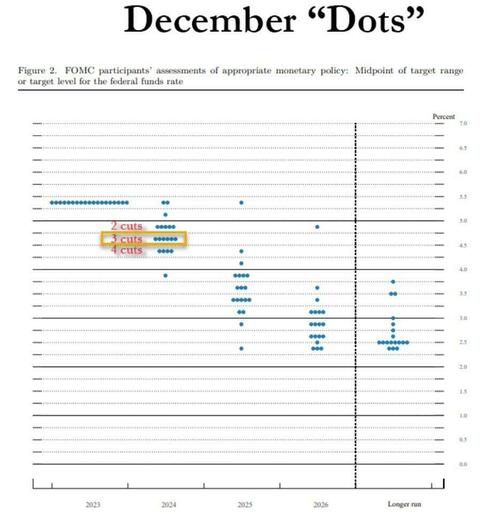

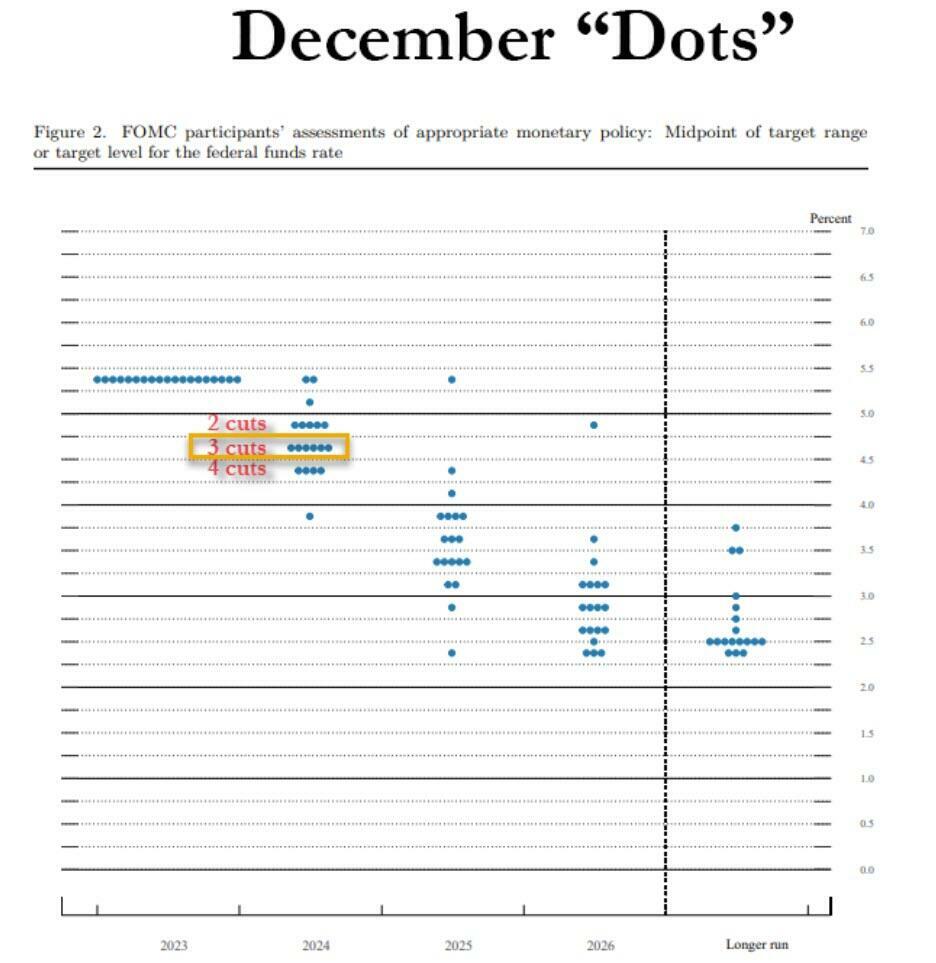

In a busy week for central bank decisions, attention now shifts to the Federal Reserve’s meeting on Wednesday, where investors will be focused on the US central bank’s projections — the dot plot — to gauge how many rate cuts policymakers are expecting to deliver this year.

“We are now thinking perhaps we get slightly higher dots — could we see fewer cuts being priced in?” said Andrea DiCenso, co-portfolio manager at Loomis Sayles, in an interview with Bloomberg TV. “We are seeing less than potentially three cuts priced into the market.”

European stocks are little changed following three straight days of declines. Energy and auto shares are outperforming and countering losses in utilities and consumer products. Investor confidence in Germany’s economic outlook jumped to the highest in more than two years, driven by expectations that the European Central Bank is ready to cut interest rates in the coming months. ECB President Christine Lagarde is due to speak Wednesday. Here are the most notable European movers:

Unilever gains as much as 6% in London on news it plans to separate its ice cream business, including brands such as Ben & Jerry’s, as the UK consumer-goods conglomerate streamlines its business.

Hannover Rueck rises as much as 4.2% as RBC boosts its price target on the German insurer to a Street-high on scope for continued “best-in-class” return of equity.

Hemnet gains as much as 6.8% after Jefferies double-upgraded the property platform in a note that analysed the impact of Costar’s entry into the European market.

Close Brothers jumps as much as 17%, the most since 2009, after the British merchant banking group presented 1H results which beat estimates. Shares are still down about 52% year to date.

HelloFresh falls as much as 5.4% as Barclays downgraded the stock to equal-weight, citing a lack of stabilization in new customer additions in the company’s meal-kit business.

Richemont and Swatch fell as data showed Swiss watch exports fell in February due to underlying deceleration in the US, China and Hong Kong.

Atos shares drop as much as 25%, hitting a record low, after the debt-laden French IT firm said talks to sell its BDS unit to Airbus have ended.

Moncler falls as much as 3.4% after an offering of up to 3.23 million shares by Carlo Rivetti’s Grinta priced at €67 apiece, representing a 3.2% discount to the last close.

Fraport falls as much as 6.9% after the airport operator’s guidance for 2024 Ebitda and free cash flow left analysts wanting more, with Morgan Stanley saying guidance is “light.”

Lottomatica falls as much as 6% after Gamma Intermediate completed a placing of 20 million shares in the gambling operator at €10.90 apiece, representing a 7.5% discount to the last close.

Earlier in the session, Asian stocks traded mixed as markets digested the first of this week’s central bank announcements.

Hang Seng and Shanghai Comp. lagged with the Hong Kong benchmark dragged lower by weakness in tech stocks as the EU mulls joining the US in reviewing risks of Chinese legacy chips and is flagging potential risks to national security and supply chains.

Nikkei 225 was underpinned after a widely telegraphed and dovish exit from NIRP, YCC and ETF/J-REIT buying which a Nikkei source report had flagged, while the central bank also announced its monthly bond purchase intentions and said it will make nimble responses with JGB purchases and could increase the amount of JGB buying or conduct fixed-rate operations in the event of a rapid rise in yields.

ASX 200 finished with mild gains after a lack of hawkish surprises at the RBA policy announcement in which it kept rates unchanged and reiterated that the Board remains resolute in its determination, while there was also a slight tweak in its language as guidance around further tightening was softened.

In FX, the Bloomberg Dollar Spot Index rose 0.4% with Wednesday’s Fed decision now firmly in focus as the yen tumbles despite the BOJ’s first rate hike in nearly two decades. USD/JPY rises as high as 150.60 after BOJ’s decision. AUD/USD falls under mid 0.65-0.66 as traders price in greater probability of a RBA rate cut this year following its policy decision. NZD/USD falls to hold under 0.61. The New Zealand dollar is sold by leveraged funds after comments from the NZ Treasury saying the economy is in a “severe economic slowdown,” according to Asia-based FX traders, who say the Aussie is also weighed by the news. EUR/USD remains under 1.09 while GBP/USD drifts down toward 1.27. The Bloomberg Dollar Spot Index falls for the fourth day

In rates, treasuries climb, with US 10-year yields falling 1bps to 4.31%. US rates had little reaction to Bank of Japan’s first interest-rate hike since 2007, which was anticipated, remaining near year-to-date highs ahead of 20-year bond auction at 1pm New York time. Front-end yields are lower by ~2bp, steepening curve spreads by around 1bp vs Monday’s closing levels; 10-year at around 4.31% is ~1bp richer on the day with gilts outperforming by 4bp in the sector. Bunds and gilts are also in the green with UK yields down 3bp-4bp. Treasury auctions resume with $13b 20-year bond reopening at 1pm; WI yield at around 4.562% is above auction stops since November and ~3bp cheaper than February’s result.

In commodities, oil prices decline, with WTI falling 0.3% to trade near $82.50. Spot gold falls 0.3%.

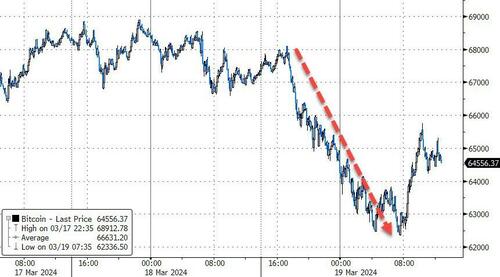

Bitcoin drops ~6% to near $63,000.

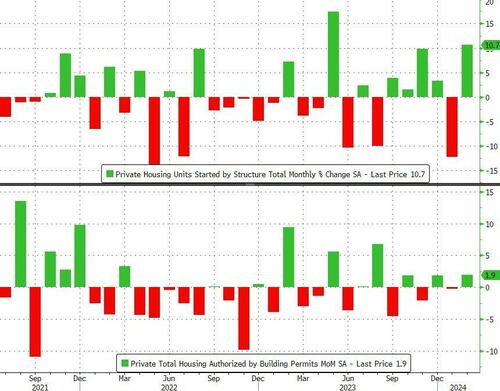

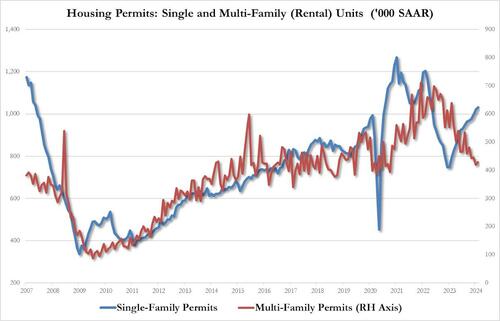

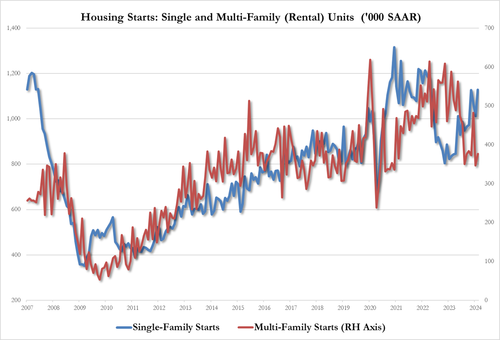

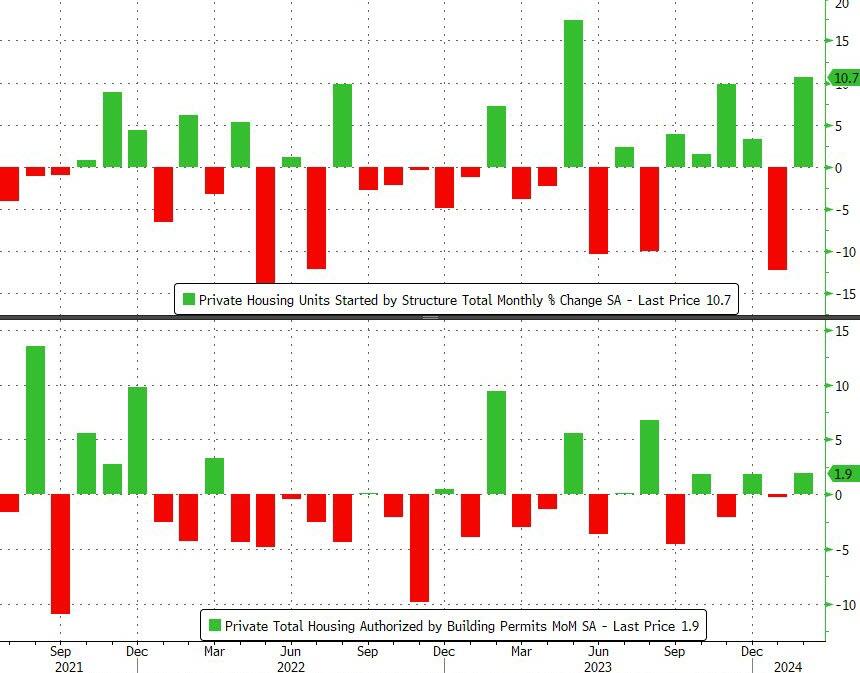

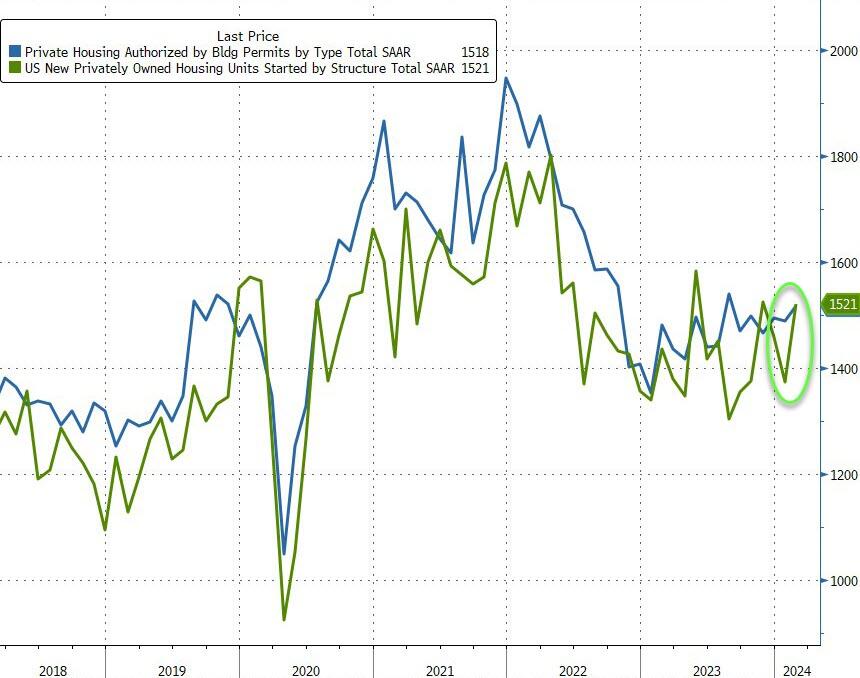

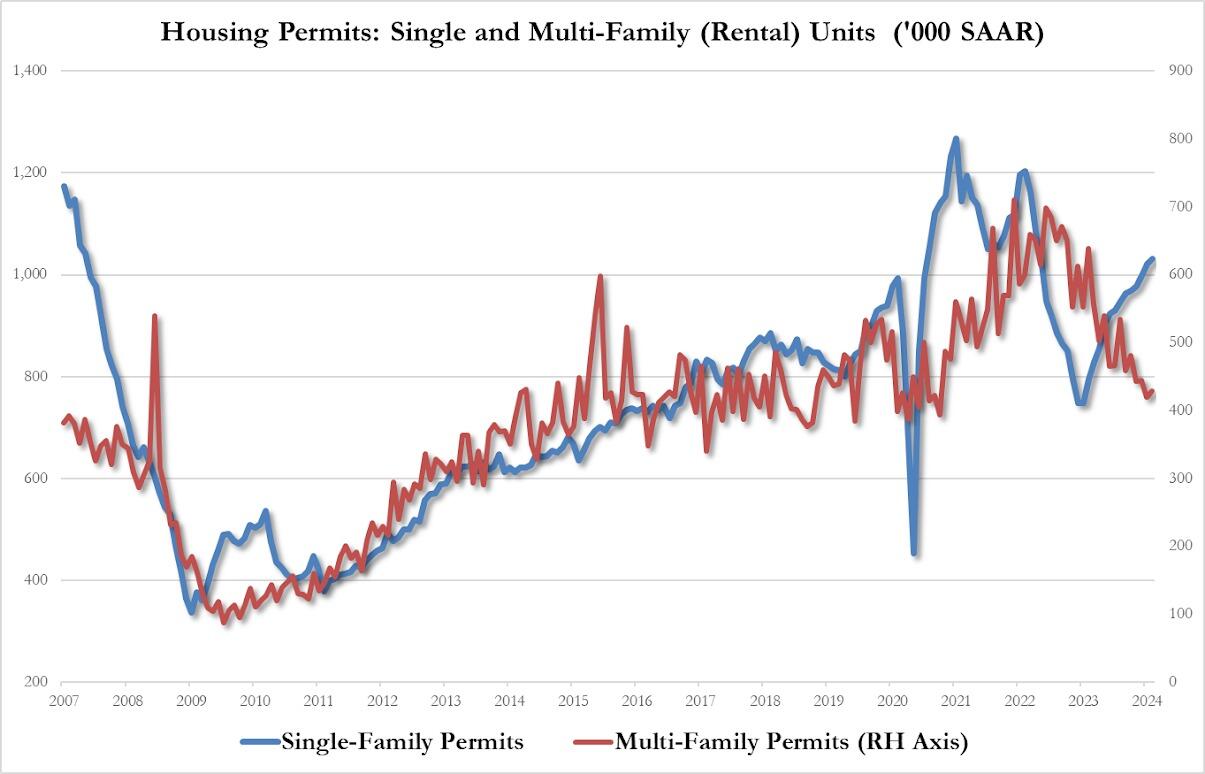

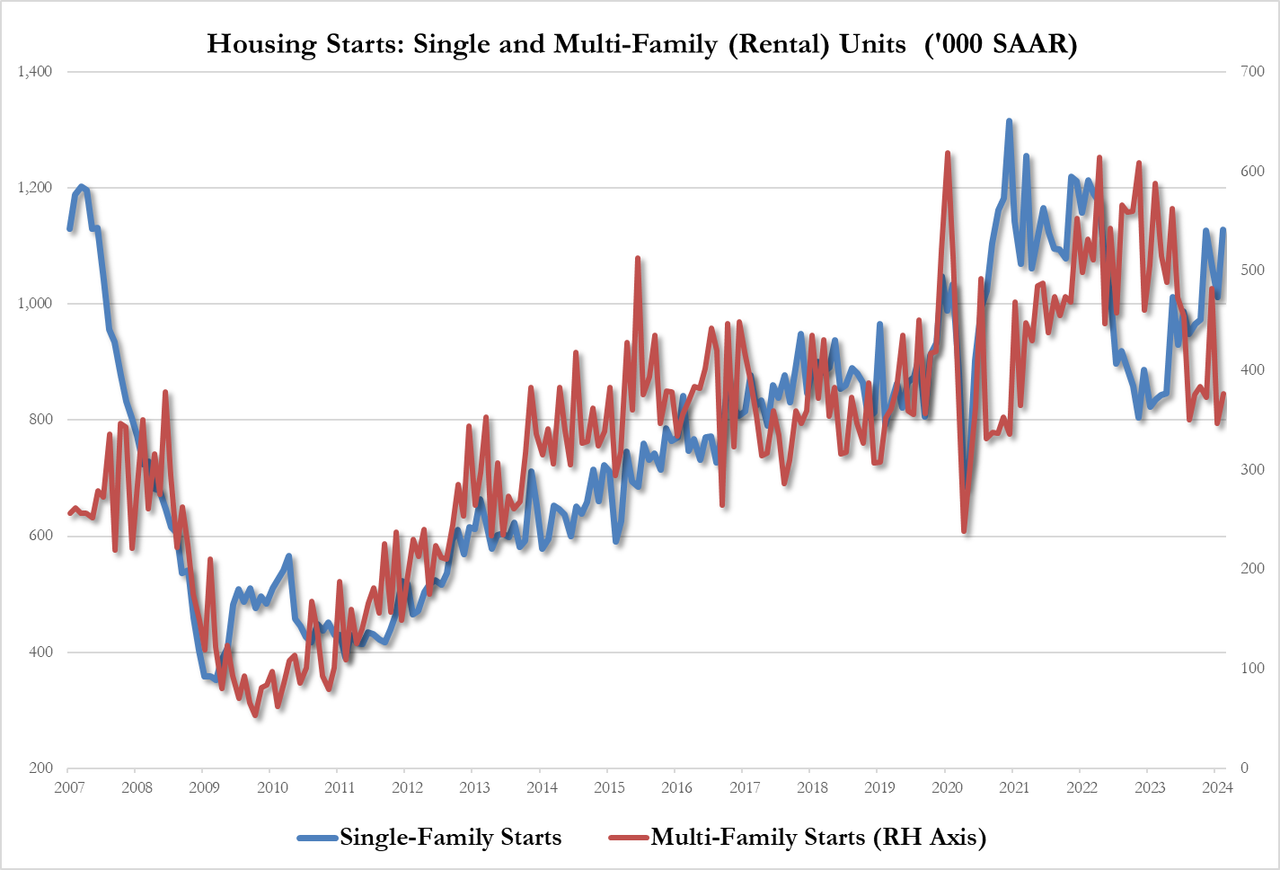

Looking at today’s economic data calendar we get February housing starts/building permits (8:30am) and January TIC flows (4pm). There are no Fed speakers scheduled before March 20 policy decision

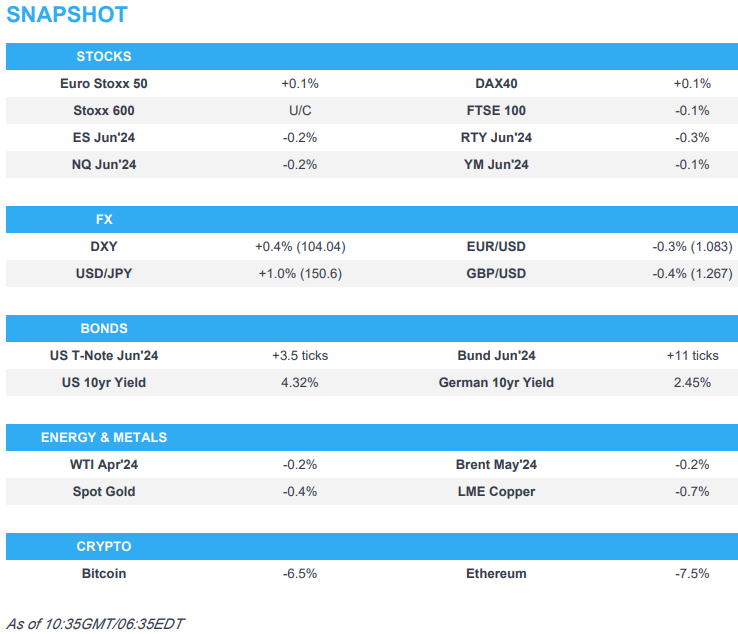

Market Snapshot

S&P 500 futures down 0.5% to 5,189

STOXX Europe 600 little changed at 503.87

MXAP down 0.5% to 175.29

MXAPJ down 1.0% to 529.89

Nikkei up 0.7% to 40,003.60

Topix up 1.1% to 2,750.97

Hang Seng Index down 1.2% to 16,529.48

Shanghai Composite down 0.7% to 3,062.76

Sensex down 1.0% to 72,004.06

Australia S&P/ASX 200 up 0.4% to 7,703.23

Kospi down 1.1% to 2,656.17

German 10Y yield little changed at 2.45%

Euro down 0.2% to $1.0846

Brent Futures down 0.2% to $86.68/bbl

Gold spot down 0.5% to $2,150.05

US Dollar Index up 0.35% to 103.94

Top Overnight News

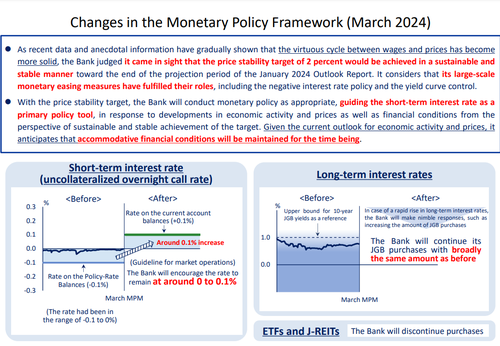

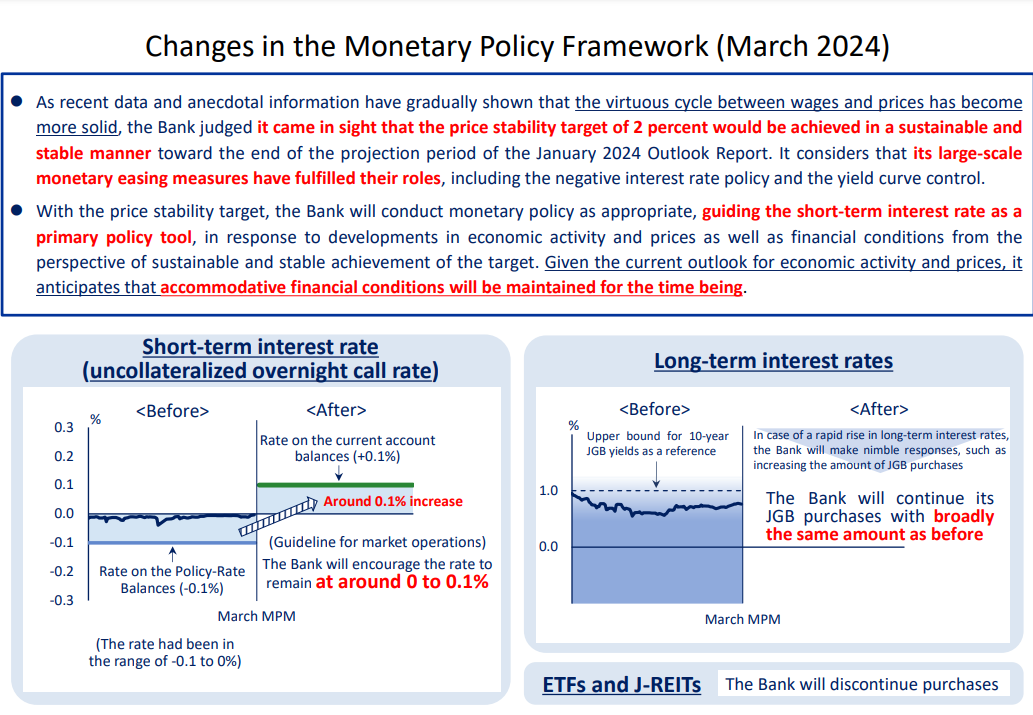

Japan’s BOJ hiked rates (as was widely expected) from -0.1% to 0-0.1%, although the accompanying language had a dovish tone, with the central bank ensuring that accommodative policy would be maintained for the time being. The YCC (yield curve control) policy was formally ended, although the BOJ said it would still purchase about the same amount of government bonds each month. The BOJ will discontinue buying equity ETFs and REITs. FT

Chinese factories are flooding global markets with cars, appliances, computer chips and electronics, setting the stage for a fresh round of trade tensions with the United States and Europe, economists said. WaPo

The ECB will be in position to discuss an interest rate cut in June, Vice President Luis de Guindos said on Tuesday, joining a long list of policymakers putting the June 6 meeting on the table for a potential start of policy easing. RTRS

European luxury stocks see some pressure following soft Swiss watch export numbers (Swiss watch exports fell 3.8% Y/Y in Feb vs. +3.2% in Jan). BBG

Indian oil refiners are on track to take the most American crude in almost a year after tighter enforcement of US sanctions crimped trade with Russia and forced processors to look elsewhere for supply. BBG

The EU is preparing to levy tariffs on grain imports from Russia and Belarus to placate farmers and some member states, the first restriction on food products since Moscow’s full-scale invasion of Ukraine. FT

Saudi Aramco’s CEO warned that the global drive to phase out oil and gas is a dangerous fantasy that’s bound to fail as there aren’t any credible alternatives to fossil fuels. CNBC

MSFT schedules an AI event for Mon May 20 (right before the Build conf. May 21-23) at which it will discuss the firm’s AI vision across hardware and software. The Verge

NVDA unveiled its (much-anticipated) new Blackwell platform, the successor product to Hopper. Blackwell contains 6 new technologies and will enable AI training and real-time LLM inference for models scaling up to 10 trillion parameters. Among the many organizations expected to adopt Blackwell are Amazon Web Services, Dell Technologies, Google, Meta, Microsoft, OpenAI, Oracle, Tesla xAI. RTRS

BOJ

BoJ changed its monetary policy framework in which it ended negative interest rate policy and abandoned YCC, while it will guide the overnight call rate in the range of 0%-0.1% and apply 0.1% interest to all excess reserves parked at the central bank. BoJ also announced to end ETF and J-REIT purchases, as well as gradually reduce the amount of purchases of commercial paper and corporate bonds whereby it will discontinue purchases of CP and corporate bonds in about one year. However, it stated that it will continue roughly the current amount of JGB buying and it expects to maintain an accommodative monetary environment for the time being. Furthermore, the BoJ announced its planned bond purchases and stated that in case of a rapid rise in long-term rates, it will make nimble responses with JGB purchases and could increase the amount of JGB purchases or conduct fixed-rate purchase operations of JGBs, while it will provide loans under Fund Provisioning Measure to stimulate bank lending with an interest rate of 0.1% and a 1-year duration.

BoJ PRESS CONFERENCE: Governor Ueda says BoJ has confirmed the virtuous cycle of wages and prices; Accommodative financial conditions will be maintained for the time being. Click here for full commentary.

Japanese Finance Minister Suzuki says the government’s view of the economy is the same as that of the BoJ; closely monitoring the economy and financial markets, including FX after the BoJ decision.

Japan’s Business Lobby Keidanren Chief says the appropriate decision was taken at the appropriate time, when asked on the BoJ announcement; does not think USD/JPY at 150 reflects Japan’s economic fundamentals; Yen should be firmer considering fundamentals.

Japan PM Kishida believes it is appropriate that accommodative monetary environment is maintained; did not discuss current issues with BoJ’s Ueda

A more detailed analysis of markets from Newsquawk

APAC stocks traded mixed as markets digested the first of this week’s central bank announcements. ASX 200 finished with mild gains after a lack of hawkish surprises at the RBA policy announcement in which it kept rates unchanged and reiterated that the Board remains resolute in its determination, while there was also a slight tweak in its language as guidance around further tightening was softened. Nikkei 225 was underpinned after a widely telegraphed and dovish exit from NIRP, YCC and ETF/J-REIT buying which a Nikkei source report had flagged, while the central bank also announced its monthly bond purchase intentions and said it will make nimble responses with JGB purchases and could increase the amount of JGB buying or conduct fixed-rate operations in the event of a rapid rise in yields. Hang Seng and Shanghai Comp. lagged with the Hong Kong benchmark dragged lower by weakness in tech stocks as the EU mulls joining the US in reviewing risks of Chinese legacy chips and is flagging potential risks to national security and supply chains.

Top Asian News

RBA kept its Cash Rate Target unchanged at 4.35%, as expected, while it reiterated that the Board remains resolute in its determination to return inflation to the target and inflation continues to moderate but remains high. RBA stated the board is not ruling anything in or out on interest rates (prev. a further increase in interest rates cannot be ruled out) and data is consistent with continuing excess demand in the economy and strong domestic cost pressures, both for labour and non-labour inputs. Furthermore, it noted that higher interest rates are working to establish a more sustainable balance between aggregate demand and supply in the economy and the board expects that it will be some time yet before inflation is sustainably in the target range.

RBA Governor Bullock said they are making progress in the fight against inflation but reiterated inflation remains high and noted recent data suggests they are on the right track and they are keeping a keen eye on employment numbers. Bullock stated that risks to the outlook are finely balanced and war isn’t won yet on inflation, while she noted the change of statement language is in response to data.

Chinese Foreign Minister Wang Yi said during a visit to New Zealand that China is ready to work with New Zealand to implement an upgraded version of the China-New Zealand FTA and the two sides should launch negotiations on a negative list of service trade as soon as possible to push bilateral cooperation to a new level. Furthermore, he stated that China-New Zealand relations maintain a leading position among China’s relations with developed countries, while it was also reported that New Zealand PM Luxon intends to visit China in the coming months following this week’s meetings with China’s Foreign Minister.

China State Council issues action plan to make greater efforts to attract and utilise foreign investments; plan is to expand market access and raise the level of liberalisation of foreign investment

Tencent Music Entertainment Group (TME) Q4 2023 (USD): EPS 0.12 (exp. 0.14), Revenue 0.97bln (exp. 0.93bln).

European bourses, Stoxx600 (+0.1%) began the session on a mixed footing though have caught a slight bid in recent trade, and reside near session highs; the AEX (+0.4%) outperforms, lifted by gains in Unilever (+4.5%). European sectors are mixed; Energy takes the top spot, with Crude just off recent highs whilst Consumer Products and Services is hampered by broader weakness in Luxury names, after weak Chinese price action overnight. US equity futures (ES -0.1%, NQ -0.1%, RTY -0.3%) are modestly lower, with mild underperformance in the RTY as it continues the prior day’s weakness.

Top European News

ECB’s Centeno said cutting rates may help prevent a recession.

ECB’s de Guindos says “looking at recent inflation developments, we can see a very clear disinflationary process. This is reflected in both headline and core inflation readings; will have more information in June”.

ECB’s De Cos says in June we could start cutting rates but it is conditional on data

SNB: Identifies a need for action with capital regulations. Regarding AT1 instruments, the aim should be to strengthen their contribution through a timely suspension of buybacks/interest payments alongside a conversion into CET1 capital earlier

FX

DXY is boosted by the post-BoJ softness in the JPY. DXY has reached a high of 104.06, bringing into play the March peak of 104.29 into view.

EUR is swept up by the broadly firmer USD as the pair pulls back from a 1.0906 peak yesterday. If the descent continues, support comes via the 200DMA at 1.0838. EUR downside came to a halt on firm German ZEW metrics.

GBP is softer vs. the USD. Cable is resting on its 50DMA at 1.2683 with UK-specifics lacking ahead of CPI metrics tomorrow and the BoE on Thursday.

JPY is the laggard across the majors despite the BoJ ending NIRP. The move was widely expected and despite Ueda opening the door to further hikes, markets expect any hiking campaign by the Bank to be a shallow one. USD/JPY up to 150.69 at best.

Antipodeans are both faring poorly vs. the USD. AUD eyeing a test of 0.65 to the downside where a large option expiry lies and bids are expected; the RBA kept its Cash Rate Target unchanged at 4.35%.

PBoC set USD/CNY mid-point at 7.0985 vs exp. 7.2056 (prev. 7.0943).

Fixed Income

Bunds are firmer after being incrementally softer on Monday. Newsflow has been dominated by the BoJ but read-across to EGBs is ultimately limited; EGBs saw modest upside following the better-than-expected German ZEW figures, with Bunds printing highs at 131.89.

USTs are following EGBs and holds around the 110-00 mark. 20yr supply takes attention ahead of the FOMC on Wednesday.

Gilt price action is in-fitting with EGBs; Gilts caught a bid following the UK auction and in tandem with a lift in EGBs post-ZEW, currently at 98.90.

The BoJ’s exit from NIRP & YCC saw an initial dip in JGBs and sent the accompanying 10yr yield back to its earlier session high of 0.77%. Thereafter, JGB price action was volatile before settling around 145.60. A pullback which occurred as some of the dovish elements were digested.

EU opens books to sell EUR-denominated Feb 2050 green NGEU bonds; guidance +82bps to mid-swap; to sell EUR 6bln.

Order for the new Italian 10yr I/L BTP are in excess of EUR 35bln, according to leads; spread a +23bps over the maturing May 2023 BTP.

UK sells GBP 2bln 4.75% 2043 Gilt: b/c 3.41x (prev. 3.62x), average yield 4.467% (prev. 4.391%), tail 0.4bps (prev. 0.2bps)

Commodities

Subdued trade across the crude complex this morning, with prices taking a breather after yesterday’s rise; Brent meanders around USD 86.75/bbl after printing a high above USD 87/bbl yesterday.

Mild downward bias across precious metals amid a firmer Dollar with little reaction to the BoJ overnight as traders gear up for the FOMC and then the BoE; XAU hovers just above USD 2,150/oz.

Base metals are softer across the board amid the stronger Dollar and following weak Chinese trade overnight.

UBS sees Brent likely trading between USD 80-90/bbl range this year, with end-June forecast of USD 86/bbl; extension of voluntary OPEC+ cuts for another three months will likely keep oil market underpinned in Q2 2024.

Geopolitics: Middle East

Israeli PM Netanyahu said he spoke with Biden about achieving goals in the Gaza war while providing needed humanitarian aid, while it was also reported that President Biden reiterated ‘deep concerns’ about Israel conducting ground operations in Rafah during the call with Israeli PM Netanyahu.

Israeli officials said PM Netanyahu narrowed the mandate of the negotiating delegation and set red lines for what they can accept, according to Axios.

US military said it destroyed seven anti-ship missiles and three unmanned aerial vehicles in Houthi-controlled areas of Yemen, while Houthi media reported six US-British raids near Hodeidah, Yemen, according to Al Arabiya.

Syrian army ground defences confronted targets in the sky of Damascus and state media reported that Israeli airstrikes were targeting the countryside of Syria’s Damascus.

“Israeli official to the broadcaster: The talks in Doha were positive and we expect difficult, complex and long negotiations”, according to Sky News Arabia.

US Event Calendar

08:30: Feb. Building Permits MoM, est. 0.5%, prior -1.5%, revised -0.3%

08:30: Feb. Housing Starts MoM, est. 8.2%, prior -14.8%

08:30: Feb. Building Permits, est. 1.5m, prior 1.47m, revised 1.49m

08:30: Feb. Housing Starts, est. 1.44m, prior 1.33m

16:00: Jan. Total Net TIC Flows, prior $139.8b

16:00: Jan. Net Foreign Security Purchases, prior $160.2b

DB’s Jim Reid concludes the overnight wrap

I’ve been back from Asia for three days now but I continue to fall asleep in front of the telly every night, get prodded by my wife on the sofa, and then wake up bright awake 90 minutes before my alarm in the morning. Today was one of those days that it was useful as I got to see the first BoJ hike in 17 years live this morning. So far their policy moves are pretty much as leaked over the last few days so there are no real surprises. They lifted rates from -0.1% to a range of 0-0.1%. They also scrapped YCC and ended ETF and REIT purchases but these programs had been pretty dormant of late. They are continuing JGB purchases at the same rate for now but, according to our Japanese economist Kentaro Koyama, the fund supplied through the Loan Support Program (similar to the TLTRO, with a current balance of JPY81 trillion yen) will decrease going forward given the conditions for the program have become stricter. As a result, the monetary base and the BoJ’s balance sheet will decline going forward.

Forward guidance is a bit dovish, according to Kentaro. In the statement, the bank says that it anticipates that accommodative financial conditions will be maintained for the time being given the current outlook for economic activity and prices. In our view, this does not exclude policy rate hikes in the near future and could change depending on the economic and inflation outlook. So all paths are open. We will see what the press conference brings.

Against this well flagged move, the Japanese yen (-0.78%) is weakening, trading above 150 again for the first time in two weeks while 10yr JGB yields (-2.6bps) have moved lower to 0.74%. So for now, it’s buy the rumour and sell the fact. The house view is that the market is underestimating where terminal rates might end up in Japan but that it will be a steady process discovering that.

Separately, the Reserve Bank of Australia (RBA) kept the benchmark rate at 4.35%, a 12-year high for the third meeting in a row, aligning with broad market expectations. In its post-meeting statement, the RBA indicated that it can’t rule out the possibility that interest rates will need to be raised further while acknowledging that inflation is moderating, consistent with its latest forecasts but remains too high and that the “economic outlook remains uncertain”. In response, the Aussie dollar (-0.50%) is losing ground, trading at a two-week low of 0.6527 versus the dollar with the policy-sensitive 3yr government bond yield dropping -5.3bps to 3.69% as I check my screens.

In terms of wider Asia moves, the Nikkei (+0.36%) is reversing initial losses as the Yen falls, with the S&P/ASX 200 (+0.36%) also edging higher while the KOSPI (-1.15%), the Hang Seng (-1.06%), the CSI (-0.31%) and the Shanghai Composite (-0.17%) are lower. S&P 500 (-0.13%) and Nasdaq (-0.27%) futures are lower with 10yr UST yields ticking down -1bps to 4.31%.

Ahead of the BoJ decision, US markets put in a strong performance yesterday, with the S&P 500 (+0.63%) bouncing back from two small weekly declines. That was driven by the Magnificent 7 (+2.00%), particularly after the news came through that Apple (+0.64%) was in talks to use Google’s Gemini for new iPhone features, meaning that Alphabet (+4.60%) saw its best daily performance in over three months. But even outside of big tech, risk appetite remained mostly firm among investors, as the equal-weighted S&P 500 (+0.28%) also rose, whilst US HY spreads closed at their tightest level in over two years. The small cap Russell 2000 was a notable underperformer, down -0.72%.