MARCH 21//GOLD CLOSED UP $24.80 TO $2182.90//SILVER CLOSED DOWN $0.08 TO $24.91//PLATINUM CLOSED UP $12.15 TO $910.50 WHILE PALLADIUM CLOSED UP $15.05 TO $1010.85//IMPORTANT COMMENTARIES TODAY FROM TOM LUONGO AND AMBROSE EVANS PRITCHARD//SWITZERLAND LOWERS ITS INTEREST RATE//ISRAEL VS HAMAS/ISRAEL VS HEZBOLLAH/WEST BANK UPDATES/HOUTHIS UPDATES/COVID UPDATES/DR PAUL ALEXANDER/SLAY NEWS ETC//USA ECONOMIC NEWS AND DATA//VICTOR DAVIS HANSON//SWAMP STORIES FOR YOU TONIGHT//

Bitcoin: afternoon price: $64,793 DOWN 5081 dollars

Platinum price closing UP $12.15 TO $910.50

Palladium price; UP $15.05 AT $1010.86

END

SHANGHAI GOLD PREMIUM 30 DOLLARS/COMEX GOLD

SHANGHAI GOLD………

SHANGHAI GOLD (USD) FUTURES – QUOTES

Beginning Monday, April 1, 2024, CME Group settlement data will no longer be accessible through ftp.cmegroup.com and will have a delayed publication time of 12:00 a.m. CT on all cmegroup.com web pages. Learn about alternate ways to access the data in our FAQ.

GOLD: NUMBER OF NOTICES FILED FOR MAR/2024. CONTRACT: 6 NOTICES FOR 600 OZ or 0.01866 TONNES

total notices so far: 5269 contracts for 526,900 Oz (16.388 tonnes)

FOR MARCH:

SILVER NOTICES: 75 NOTICE(S) FILED FOR 375,000 OZ/

total number of notices filed so far this month : 5402 for 27,010,000 oz

XXXXXXXXXXXXXXXXXX

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD/

BOTH GLD AND SLV ARE FRAUDULENT VEHICLES//THEY ARE NOW RAIDING GLD AND SLV FOR PHYSICAL

THE CROOKS ARE STEALING GOLD AND SILVER FROM THE GLD/SLV AND REPLACING THE PHYSICAL WITH PAPER DOLLARS.

WITH GOLD UP $24.80

INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD/ :

HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A PAPER DEPOSIT OF 1.15 TONNES OF GOLD INTO THE GLD// /INVENTORY RESTS AT 838..50 TONNES

INVENTORY RESTS AT 838.50 TONNES

SLV//

WITH NO SILVER AROUND AND SILVER DOWN 8 CENTS AT THE SLV//

HUGE CHANGES IN SILVER INVENTORY AT THE SLV A HUGE WITHDRAWAL OF 2.606 MILLION OZ OUT OF THE SLV.:

// INVENTORY FALLS TO 423.720 MILLION OZ/

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV.

CLOSING INVENTORY: 423.720 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY AN ULTRA- HUGE SIZED 3516 CONTRACTS TO 156,670 AND CLOSER TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THIS HUGE SIZED GAIN IN COMEX OI WAS ACCOMPLISHED DESPITE OUR LOSS IN PRICE OF $0.05 IN SILVER PRICING AT THE COMEX ON WEDNESDAY. WE HAD ZERO LONG LIQUIDATION AT THE COMEX SESSION WITH AGAIN MAJOR SHORT COVERING DESPITE THE PRICE LOSS. WE HAD A SMALL 288 T.A.S ISSUANCE AND THESE WILL BE USED FOR MANIPULATION LATER THIS MONTH/AS WELL AS TODAY. PLEASE NOTE THAT THE CROOKS NEED A HIGHER SILVER/GOLD T.A.S. TO CARRY ON THEIR CROOKED MANIPULATION ON A DAILY BASIS

CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON WEDNESDAY NIGHT: 288 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS. IT THUS LOOKS LIKE THE FED (GOV’T) IS BEHIND ALL OF THESE TRADES.

WE HAVE NOW SET ANOTHER RECORD LOW AT 114,102 CONTRACTS ///JULY 3.2023// OUR BANKERS WITH THE HELP OF SPECULATORS AND HIGH FREQUENCY TRADERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.05),BUT WERE UNSUCCESSFUL IN KNOCKING ANY SILVER LONGS AS WE HAD A MEGA HUGE SIZED GAIN OF 4,597 CONTRACTS ON OUR TWO EXCHANGES DESPITE THE LOSS IN PRICE OF 5 CENTS.

WE MUST HAVE HAD:

A STRONG SIZED 525 ISSUANCE OF EXCHANGE FOR PHYSICALS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 22.270 MILLION OZ (FIRST DAY NOTICE) FOLLOWED BY TODAY,S 375,000 OZ QUEUE JUMP

/NEW TOTALS INCREASES TO : 27.375 MILLION OZ

//NEW STANDING FOR SILVER IS THUS 27.375 MILLION OZ

WE HAD:

/ HUMONGOUS SIZED COMEX OI GAIN/ STRONG SIZED EFP ISSUANCE/ VI) FAIR SIZED NUMBER OF T.A.S. CONTRACT ISSUANCE 288 CONTRACTS)/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL -REMOVED 556 CONTRACTS //

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS FEB. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF MARCH

TOTAL CONTRACTS for 15 days, total 22,606 contracts: OR 113.030 MILLION OZ (1507 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 113.03 MILLION OZ

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH 2022: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 118.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 85.745 MILLION OZ (SMALLER THAN LAST MONTH)

AUGUST: 171.43 MILLION OZ (THIS MONTH IS GOING TO BE HUGE //2ND HIGHEST ON RECORD

SEPT: 72.705 MILLION OZ (SMALLER THIS MONTH)

OCT: 97.455 MILLION OZ

NOV. 50.050 MILLION OZ

DEC. 66.140 MILLION OZ//

TOTAL 2023: 1,104.10 MILLION OZ/

JAN ’24 : 78.655 MILLION OZ//

FEB /2024 : 66.135 MILLION OZ./FINAL

MARCH: 113.03 MILLION OZ//WILL BE MUCH LARGER THIS MONTH//MAYBE CLOSE TO A RECORD ISSUANCE

RESULT: WE HAD A MEGA HUGE SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 3516 CONTRACTS DESPITE OUR LOSSIN PRICE OF SILVER PRICING AT THE COMEX//WEDNESDAY.,. THE CME NOTIFIED US THAT WE HAD A STRONG EFP ISSUANCE CONTRACTS: 525 ISSUED FOR MAY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS. WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR MARCH. OF 23.385 MILLION OZ ON FIRST DAY NOTICE FOLLOWED BY TODAY’S STRONG 375,000 OZ QUEUE JUMP

//NEW TOTAL STANDING RISES TO 27.375 MILLION OZ

WE HAVE A HUMONGOUS GAIN OF 4041 OI CONTRACTS ON THE TWO EXCHANGES DESPITE THE LOSS IN PRICE. THE TOTAL OF TAS INITIATED CONTRACTS TODAY: A SMALL SIZED 288 CONTRACTS//HUGE FRONT END OF THE TAS CONTRACTS WERE LIQUIDATED DURING THE WEDNESDAY COMEX SESSION/// WITH MAJOR SHORT COVERING FROM OUR SPEC SHORTS

THE NEW TAS ISSUANCE WEDNESDAY NIGHT (288) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE//PROBABLY TODAY., .

WE HAD 75 NOTICE(S) FILED TODAY FOR 375,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A FAIR SIZED 2567 CONTRACTS TO 537,614 AND CLOSER TO THE RECORD (SET JAN 24/2020) AT 799,733 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110, BUT WE ARE NOW CLOSER TO OUR ALL TIME LOW OF 390,000 CONTRACTS.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED 1321 CONTRACTS

WE HAD A FAIR SIZED INCREASE IN COMEX OI (2567 CONTRACTS) WITH OUR $1.45 GAIN IN PRICE//WEDNESDAY. THE BANKERS WERE FORCED TO SUPPLY THE NECESSARY SHORT PAPER TO CONTAIN GOLD’S RISE.WE ALSO HAD A RATHER LARGE INITIAL STANDING IN GOLD TONNAGE FOR MARCH. AT 10.270 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’’S QUEUE JUMP OF 400 OZ.

NEW TOTAL Of INITIAL GOLD STANDING RISES TO: 18.668 TONNES // ALL OF THIS HAPPENED WITH OUR $1.45 GAIN IN PRICE WITH RESPECT TO WEDNESDAY’S TRADING. WE HAD A STRONG SIZED GAIN OF 75454 OI CONTRACTS (23.49) PAPER TONNES) ON OUR TWO EXCHANGES.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A VERY STRONG SIZED 4987CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 538,945

IN ESSENCE WE HAVE A STRONG SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 7554 CONTRACTS WITH 2567 CONTRACTS INCREASED AT THE COMEX// AND A STRONG SIZED 4987 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 7554 CONTRACTS.. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): A FAIR SIZED 2131 CONTRACTS,

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A STRONG SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (4987 CONTRACTS) ACCOMPANYING THE FAIR SIZED GAIN IN COMEX OI (2567) //TOTAL GAIN FOR OUR THE TWO EXCHANGES: 7554 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR FORMER FORMAT OF BANKERS GOING LONG AND SPECULATORS GOING SHORT ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR MARCH. AT 7.502 TONNES FOLLOWED BY TODAY’S QUEUE JUMP OF 0.01244 TONNES/NEW STANDING ADVANCES TO 18.668 TONNES.

/ 3) ZERO LONG LIQUIDATION // 4) FAIR SIZED COMEX OPEN INTEREST LOSS/ 5) VERY STRONG ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER///6: FAIR T.A.S. ISSUANCE: 2131CONTRACTS//SOME SHORT COVERING AGAIN

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023-2024 INCLUDING TODAY

MARCH

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF MARCH. :

TOTAL EFP CONTRACTS ISSUED: 77,598 CONTRACTS OR 7,759,800OZ OR 241,36 TONNES IN 15TRADING DAY(S) AND THUS AVERAGING: 5186 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 15TRADING DAY(S) IN TONNES 241.36 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2022, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 241.36/3550 x 100% TONNES 6.78% OF GLOBAL ANNUAL PRODUCTION

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH/2022: 409.30 TONNES //FINAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 151.69 TONNES (WEAKER THAN LAST MONTH)

AUGUST: 195.28 TONNES (A STRONGER MONTH)//FINAL

SEPT: 254.709 TONNES (WILL BE LARGER THAN LAST MONTH AND A STRONG MONTH)

OCT. 248.09 TONNES. LIKE SILVER, THIS MONTH IS GOING TO BE A STRONG E.F.P. ISSUANCE.

NOV. 239.16 TONNES//WILL BE STRONG THIS MONTH,

DEC. 213.704 TONNES. A STRONG MONTH//

TOTAL FOR YEAR 2023: 2,569.57 TONNES VS 2578 TONNES LAST YEAR

JAN ’24: 291.76 TONNES (WILL BE MUCH GREATER THAN LAST MONTH.//3RD HIGHEST EVER RECORDED EXCHANGE FOR PHYSICAL)

FEB’24: 201.947 TONNES

MARCH 2024: 241.36 TONNES//THIS IS GOING TO BE ONE HUMDINGER OF AN E,F,P. ISSUANCE.

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF FEB. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (APRIL), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER ROSE BY A MEGA HUGE SIZED 3516 CONTRACTS OI TO 156,670 AND CLOSER TO THE COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 6 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 525 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAY 525 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 525 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 3516 CONTRACTS AND ADD TO THE 1580 E.FP. ISSUED

WE OBTAIN A ULTRA HUMONGOUS SIZED GAIN OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 4041CONTRACTS

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTAL 20.205 MILLION OZ

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS//

THURSDAY MORNING/WEDNESDAY NIGHT

SHANGHAI CLOSED DOWN 2.57 PTS OR 0.08% //Hang Seng CLOSED UP 320.03 PTS OR 1.93% / Nikkei CLOSED UP 812.06 PTS OR 2.03% //Australia’s all ordinaries CLOSED UP 1.13% /Chinese yuan (ONSHORE) closed DOWN 7.1990 //OFFSHORE CHINESE YUAN CLOSED DOWN TO 7.2138 /Oil DOWN TO 80.99 dollars per barrel for WTI and BRENT UP AT 85.66/ Stocks in Europe OPENED MOSTLY ALL GREEN// ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE YUAN WEAKER

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A FAIR 2567 CONTRACTS TO 537,614 DESPITE OUR SMALL LOSS IN PRICE OF $4.10 WITH RESPECT TO THURSDAY TRADING.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE NON ACTIVE DELIVERY MONTH OF MARCH..… THE CME REPORTS THAT THE BANKERS ISSUED A VERY STRONG SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 4987 EFP CONTRACTS WERE ISSUED: : APRIL 4987 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 4987CONTRACTS

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A STRONG SIZED TOTAL OF 7554 CONTRACTS IN THAT 4987 LONGS WERE TRANSFERRED AS EXCHANGE FOR PHYSICALS TO LONDON AND WE HAD A GOOD SIZED GAIN OF 2567 COMEX CONTRACTS..AND THIS GAIN ON OUR TWO EXCHANGES HAPPENED WITH OUR SMALL RISE IN PRICE OF $1.45 WEDNESDAY COMEX. AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS DURING MID MONTH IN THE DELIVERY CYCLE), THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR WEDNESDAY NIGHT WAS A FAIR SIZED 2131 CONTRACTS,

THROUGHOUT THE PAST SEVERAL WEEKS, THE BANKERS CONTINUE TO SELL OFF THE LONG SIDE OF THE SPREAD WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR/T.A.S. SPREAD WHICH WILL BE LIQUIDATED IN DAYS HENCE//. IT SEEMS THAT OUR CROOKS ARE HAVING A HARD TIME TRYING TO CONTROL THE PRICE OF GOLD AND THUS THE NEED FOR RECORD T.A.S. ISSUANCE.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: MARCH (18.681 TONNES) ( NON ACTIVE MONTH)

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 24 MONTHS OF 2021-2023:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276 TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.681 TONNES

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT ROSE $1.45 //// AND WERE UNSUCCESSFUL IN KNOCKING ANY SPECULATOR LONGS AS WE HAD A STRONG SIZED GAIN OF8885 TOTAL CONTRACTS ON OUR TWO EXCHANGES WITH OUR SLIGHTLY HIGHER PRICE.

WE HAD A FAIR T.A.S. LIQUIDATION ON THE FRONT END OF WEDNESDAY’S TRADING . THE T.A.S. ISSUED ON WEDNESDAY NIGHT, WILL BE “PUT INTO THE BANK” TO BE USED AT A LATER DATE AT THE COLLUSIVE CHOOSING OF OUR BANKERS. THE HIGH T.A.S. ISSUANCE IS MEANT TO CONTROL THE PRICE OF GOLD (AS WELL AS INITIATE A RAID).

WE HAVE GAINED A TOTAL OI OF 23.49 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR MARCH. (10.3576 TONNES) ON FIRST DAY NOTICE FOLLOWED BY TODAY’S 400 OZ QUEUE JUMP//NEW STANDING INCREASES TO 18.681 TONNES

ALL OF THIS WAS ACCOMPLISHED DESPITE OUR GAIN IN PRICE TO THE TUNE OF $1.45

WE HAD REMOVED 1321 CONTRACTS TO THE COMEX TRADES TO OPEN INTEREST (CROOKS)

NET GAIN ON THE TWO EXCHANGES 7554 CONTRACTS OR 755,400 OZ OR 23.49 TONNES. estimated volume today 495,803 criminals//real heroes providing massive paper

Total monthly oz gold served (contracts) so far this month

5269 notices 526,900 oz 16.388 TONNES

Total accumulative withdrawals of gold from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of gold from the Customer inventory this month

x

0 dealer deposits:

total dealer deposits: nil oz

total customer withdrawals: 0

total customer withdrawal: NIL oz

we had 0 customer deposit

total deposit nil oz

Adjustments: 0

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR MAR.

For the front month of MARCH we have an oi of 743 contracts having GAINED 4 contracts. We had 0 contracts filed upon on Wednesday, so we gained 4 contracts or an additional 400 oz of gold(0.01244 tonnes) will stand at the comex in this non active delivery month of March.

APRIL LOST 10,378 CONTRACTS FALLING TO 190,009.

MAY EARNED 95 CONTRACTS TO STAND AT 985

JUNE INCREASED ITS OI BY 11,631 CONTRACTS UP TO 284,437 CONTRACTS.

We had 6 contracts filed for today representing 600 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 6 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 6 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for the MARCH. /2024. contract month, we take the total number of notices filed so far for the month (5269 x 100 oz ), to which we add the difference between the open interest for the front month of MARCH. (743 CONTRACTS) minus the number of notices served upon today 6 x 100 oz per contract equals 600,200 OZ OR 18.668 TONNES

thus the INITIAL standings for gold for the MARCH. contract month: No of notices filed so far (5269) x 100 oz + (754) {OI for the front month} minus the number of notices served upon today (6) x 100 oz which equals 600,600 oz (18.681 TONNES)

TOTAL COMEX GOLD STANDING FOR MARCH: 18.681 TONNES WHICH IS HUGE FOR A NON ACTIVE DELIVERY MONTH IN THE CALENDAR.

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD: 17,733,522.260 OZ

TOTAL REGISTERED GOLD 7,736,801.037 (240.64 tonnes).

TOTAL OF ALL ELIGIBLE GOLD: 9,996,721.223 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 6,403,443 oz (REG GOLD- PLEDGED GOLD) 199.17 tonnes/dropping like a stone

END

SILVER/COMEX

MARCH 21

INITIAL

//2024// THE MARCH 2024 SILVER CONTRACT//INITIAL

Silver

Ounces

Withdrawals from Dealers Inventory

NIL oz

Withdrawals from Customer Inventory

605,510.430 oz asahi

.

Deposits to the Dealer Inventory

nil OZ

Deposits to the Customer Inventory

548,023.400 OZ asahi

No of oz served today (contracts)

75 CONTRACT(S) (375,000 OZ)

No of oz to be served (notices)

73 contracts (0.365 MILLION oz)

Total monthly oz silver served (contracts)

5402 Contracts (27,010,000 oz)

Total accumulative withdrawal of silver from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of silver from the Customer inventory this month

i) 0 dealer deposit

total dealer deposit :nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: 0 oz

We had 1 deposits customer account:

i) Into ASAHI 548,023.400 oz

total customer deposits 548,023.400 oz

JPMorgan has a total silver weight: 129.806 million oz/285.083 million or 45.61%

adjustment: 0/

Comex withdrawals: 1

i) Out of ASAHI: 605,510.430 oz

total withdrawal: 605,510.430 oz

TOTAL REGISTERED SILVER: 48.898MILLION OZ//.TOTAL REG + ELIGIBLE. 285.083million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR DECEMBER:

silver open interest data:

FRONT MONTH OF MARCH /2023 OI: 148 CONTRACTS HAVING GAINED 65 CONTRACT(S).

WE HAD 10 NOTICES FILED ON WEDNESDAY SO GAINED 75 CONTRACTS OR AN ADDITIONAL 375,000 OZ WILL STAND AT THE COMEX

APRIL SAW A GAIN OF 110 CONTRACTS TO STAND AT 965

MAY SAW A GAIN OF 2457 CONTRACTS UP TO 120,201.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 75 for 375,000 oz

Comex volumes// est. volume today 105,360 huge

Comex volume: confirmed yesterday 73,830 strong.

To calculate the number of silver ounces that will stand for delivery in MARCH. we take the total number of notices filed for the month so far at 5402 x 5,000 oz = 27,010,000 oz

to which we add the difference between the open interest for the front month of MARCH. (148) and the number of notices served upon today 75 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the MARCH/2024 contract month: 5402 (notices served so far) x 5000 oz + OI for the front month of MARCH. (148) – number of notices served upon today (75 )x 500 oz of silver standing for the MARCH contract month equates to 27.375 MILLION OZ.

New total standing: 27.375 million oz.

There are 48.898 million oz of registered silver.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS//

BOTH GLD AND SLV ARE MASSIVE FRAUDS!

MARCH 21 WITH GOLD UP $24.80 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD A STRONG PAPER DEPOSIT OF 1.15 TONNES OF GOLD INTO THE GLD/:INVENTORY RISES TO 838.50 TONNES

MARCH 20 WITH GOLD UP $1.45 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD A STRONG PAPER DEPOSIT OF 1.48 TONNES OF GOLD INTO THE GLD/:INVENTORY RISES TO 837.35 TONNES

MARCH 19 WITH GOLD DOWN $4.10 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD A STRONG PAPER DEPOSIT OF 1.48 TONNES OF GOLD INTO THE GLD/:INVENTORY RISES TO 833.32 TONNES

MARCH 15 WITH GOLD DOWN $5.20 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD/:INVENTORY REMAINS AT 816.86 TONNES

MARCH 14 WITH GOLD DOWN $12.20 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF 1.73 TONNES OF GOLD INTO THE GLD//:INVENTORY REMAINS AT 816.86 TONNES

MARCH 13 WITH GOLD UP $14.40 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD:INVENTORY REMAINS AT 815.13 TONNES

MARCH 12 WITH GOLD DOWN $21.15 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD:NOT AVAILABLE///LAST VALUE 815.13 TONNES

MARCH 11 WITH GOLD UP $3.20 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.44 TONNES OF GOLD OUT OF THE GLD AFTER 7 CONSECUTIVE GOLD PRICE RISES//INVENTORY RESTS AT 815.13 TONNES

MARCH 8 WITH GOLD UP $21.05 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 0.87 TONNES OF GOLD OUT OF THE GLD AFTER 7 CONSECUTIVE GOLD PRICE RISES//INVENTORY RESTS AT 816.57 TONNES

MARCH 7 WITH GOLD UP $7.20 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4,20 TONNES OF GOLD OUT OF THE GLD//INVENTORY RESTS AT 817.44 TONNES

MARCH 6 WITH GOLD UP $17.20 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.30 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 821.47 TONNES

MARCH 5 WITH GOLD UP $16.55 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.30 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 821.47 TONNES

MARCH 4 WITH GOLD UP $30.55 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF .86 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 823.77 TONNES

MARCH 1 WITH GOLD UP $40.40 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 822.91 TONNES

FEB29/WITH GOLD UP $12.60 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD//WITHDRAWAL OF 4.03 TONNES INVENTORY RESTS AT 822.91 TONNES

FEB28/WITH GOLD DOWN $1.00 TODAY NO CHANGES IN GOLD INVENTORY AT THE GLD INVENTORY RESTS AT 826.94 TONNES

FEB27/WITH GOLD UP $4.40 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF .87 TONNES OF GOLD FROM THE GLD:/INVENTORY RESTS AT 826.94 TONNES

FEB26/WITH GOLD DOWN $8.90 TODAY NO CHANGES IN GOLD INVENTORY AT THE GLD:/INVENTORY RESTS AT 827.81 TONNES

FEB23/WITH GOLD UP $17 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.01 TONNES OF GOLD FROM THE GLD.//INVENTORY RESTS AT 827.81 TONNES

FEB22/WITH GOLD DOWN $2.15 TODAY NO CHANGES IN GOLD INVENTORY AT THE GLD://INVENTORY RESTS AT 829.82 TONNES

FEB21/WITH GOLD DOWN $5.30 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 7.59 TONNES OF GOLD OUT OF THE GLD///INVENTORY RESTS AT 29.82 TONNES

FEB20/WITH GOLD UP $16.15 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 0.58 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 837.89 TONNES

FEB16/WITH GOLD UP $8,60 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.73 TONNES OF GOLD FROM THE GLD///INVENTORY RESTS AT 837.31 TONNES

FEB15/WITH GOLD UP $11.70 TODAY NO CHANGES IN GOLD INVENTORY AT THE GLD:/INVENTORY RESTS AT 841.92 TONNES

FEB14/WITH GOLD DOWN $2.75 TODAY NO CHANGES IN GOLD INVENTORY AT THE GLD:/INVENTORY RESTS AT 841.92 TONNES

FEB13/WITH GOLD DOWN $20.15 TODAY NO CHANGES IN GOLD INVENTORY AT THE GLD:/INVENTORY RESTS AT 841.92 TONNES

FEB12/WITH GOLD DOWN $4.80 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A STRONG WITHDRAWAL OF 1.74 TONNES OF GOLD FROM THE GLD. / //://INVENTORY RESTS AT 841.92 TONNES

FEB9/WITH GOLD DOWN $8.60 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A STRONG DEPOSIT OF 1.44 TONNES OF GOLD FROM THE GLD. / //://INVENTORY RESTS AT 843.66 TONNES

FEB8/WITH GOLD DOWN $2.70 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A MASSIVE WITHDRAWAL OF 5.47 TONNES OF GOLD FROM THE GLD. / //://INVENTORY RESTS AT 842.22 TONNES:

FEB7/WITH GOLD UP $0.40 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A MASSIVE WITHDRAWAL OF 4.04 TONNES OF GOLD FROM THE GLD. / //://INVENTORY RESTS AT 847.69 TONNES:

FEB6/WITH GOLD UP $8.50 TODAY NO CHANGES IN GOLD INVENTORY AT THE GLD:/ / //://INVENTORY RESTS AT 851.73 TONNES:

GLD INVENTORY: 833.32 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

MARCH 21/WITH SILVER DOWN 8 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A HUGE WITHDRAWAL OF 3.560 MILLION OZ INTO THE SLV: SLV INVENTORY RESTS AT 423.720 MILLION OZ

MARCH 20/WITH SILVER DOWN 5 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A HUGE DEPOSIT OF 11.792 MILLION OZ INTO THE SLV: SLV INVENTORY RESTS AT 427.280 MILLION OZ

MARCH 18/WITH SILVER DOWN 11 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A HUGE DEPOSIT OF 11.792 MILLION OZ INTO THE SLV: SLV INVENTORY RESTS AT 427.280 MILLION OZ

MARCH 15/WITH SILVER DOWN 9 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 1.006 MILLION OZ FROM THE SLV: SLV INVENTORY RESTS AT 417.866 MILLION OZ

MARCH 14/WITH SILVER DOWN 9 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: SLV INVENTORY RESTS AT 418.872 MILLION OZ

MARCH 13/WITH SILVER UP 32 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: SLV INVENTORY RESTS AT 418.872 MILLION OZ…

MARCH 12/WITH SILVER DOWN 31 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A SMALL WITHDRAWAL OF 0.549 MILLION OZ OF SILVER INTO THE SLV//// : SLV INVENTORY RESTS AT 418.872 MILLION OZ…

MARCH 11/WITH SILVER UP 11 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A HUGE WITHDRAWAL OF 2.147 MILLION OZ OF SILVER FROM THE SLV//// : SLV INVENTORY RESTS AT 418.323 MILLION OZ…SUCH A MASSIVE FRAUD!

MARCH 8/WITH SILVER DOWN 5 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A HUGE WITHDRAWAL OF 4.299 MILLION OZ OF SILVER FROM THE SLV//// : SLV INVENTORY RESTS AT 420.519 MILLION OZ…SUCH A MASSIVE FRAUD!

MARCH 7/WITH SILVER UP 8 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A HUGE WITHDRAWAL OF 4.665 MILLION OZ OF SILVER FROM THE SLV//// : SLV INVENTORY RESTS AT 424.818 MILLION OZ…SUCH A MASSIVE FRAUD!

MARCH 6/WITH SILVER UP 52 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A HUGE WITHDRAWAL OF 2.378 MILLION OZ OF SILVER FROM THE SLV//// : SLV INVENTORY RESTS AT 427,105 MILLION OZ

MARCH 5/WITH SILVER DOWN 2 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A HUGE WITHDRAWAL OF 1.499 MILL;ION OZ OF SILVER FROM THE SLV//// : SLV INVENTORY RESTS AT 429.483 MILLION OZ

MARCH 4/WITH SILVER UP CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: // : SLV INVENTORY RESTS AT 430.982 MILLION OZ

MARCH 1/WITH SILVER UP 49 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: // : SLV INVENTORY RESTS AT 430.982 MILLION OZ

FEB 29/WITH SILVER UP 25 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.104 MILLION OZ OUT OF THE SLV//// : SLV INVENTORY RESTS AT 430/982 MILLION OZ

FEB 28/WITH SILVER DOWN 7 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 5.123 MILLION OZ INTO THE SLV//// : SLV INVENTORY RESTS AT 433.086 MILLION OZ

FEB 27/WITH SILVER UP 3 CENTS TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 0.64 MILLION OZ FROM THE SLV//// : SLV INVENTORY RESTS AT 427.943 MILLION OZ

FEB 26/WITH SILVER DOWN 44 CENTS TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.065 MILLION OZ FROM THE SLV//// : SLV INVENTORY RESTS AT 428.603 MILLION OZ

FEB 23/WITH SILVER DOWN 44 CENTS TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.065 MILLION OZ FROM THE SLV//// : SLV INVENTORY RESTS AT 428.603 MILLION OZ

FEB 22/WITH SILVER DOWN 10 CENTS TODAY NO CHANGES IN SILVER INVENTORY AT THE SLV

// : SLV INVENTORY RESTS AT 432.766 MILLION OZ

FEB 21/WITH SILVER DOWN 28 CENTS TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 2.348 MILLION OZ OF SILVER FROM THE SLV// : SLV INVENTORY RESTS AT 432.766 MILLION OZ

FEB 20/WITH SILVER DOWN 33 CENTS TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 3.385 MILLION OZ OF SILVER FROM THE SLV// : SLV INVENTORY RESTS AT 435.008 MILLION OZ

FEB 16/WITH SILVER UP 53 CENTS TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV A DEPOSIT OF 1.235 MILLION OZ OF SILVER FROM THE SLV// : SLV INVENTORY RESTS AT 438.393 MILLION OZ

FEB 15/WITH SILVER UP 56 CENTS TODAY NO CHANGES IN SILVER INVENTORY AT THE SLV : SLV INVENTORY RESTS AT 437.615 MILLION OZ

FEB 14/WITH SILVER UP 24 CENTS TODAY NO CHANGES IN SILVER INVENTORY AT THE SLV : SLV INVENTORY RESTS AT 437.615 MILLION OZ

FEB 13/WITH SILVER DOWN 60 CENTS TODAY SMALL CHANGES IN SILVER INVENTORY AT THE SLV A SMALL WITHDRAWAL OF 0.504 MILLION OZ OZ OUT OF THE SLV: SLV INVENTORY RESTS AT 437.615 MILLION OZ

FEB 12/WITH SILVER UP 14 CENTS TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV A HUGE WITHDRAWAL OF 1.921 MILLION OZ OZ OUT OF THE SLV: SLV INVENTORY RESTS AT 438.119 MILLION OZ

FEB 9/WITH SILVER DOWN 4 CENTS TODAY SMALL CHANGES IN SILVER INVENTORY AT THE SLV A SMALL DEPOSIT OF 600,000 OZ INTO THE SLV: SLV INVENTORY RESTS AT 440.040 MILLION OZ

FEB 8/WITH SILVER UP 29 CENTS TODAY NO CHANGES IN SILVER INVENTORY AT THE SLV: SLV INVENTORY RESTS AT 439.994 MILLION OZ

FEB 7/WITH SILVER DOWN 18 CENTS TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A MASSIVE DEPOSIT OF 4.04 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 439.994 MILLION OZ//LAST 9 DAYS: 10.7598 MILLION OZ WITHDRAWAL

CLOSING INVENTORY 423.720 MILLION OZ//

PHYSICAL GOLD/SILVER COMMENTARIES

1:Peter Schiff/Mike Maharrey

end

2.Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens/

3. CHRIS POWELL//GATA

This is a good read: How the Fed is preparing for a U turn on interest rates and what it means for us;

(Ambrose Evans Pritchard)

Ambrose Evans-Pritchard: Fed is preparing for a hand-brake U-turn on interest rates

Submitted by admin on Wed, 2024-03-20 10:46 Section: Daily Dispatches

By Ambrose Evans-Pritchard The Telegraph, London Tuesday, March 19, 2024

If you want an idea of how the current fiscal and asset bubble in the United States might end, pay close attention to Bernard Connolly, esteemed consigliere to hedge funds and central bankers across the world for the last quarter century.

It will not end in a soft landing — a “chimaera” — and will certainly not end in another leg of accelerating economic growth. Nor will it end in soggy stagflation.

The invidious choice facing the Federal Reserve, he warns, is either to allow a deep economic slump to unfold or slash rates to the bone before inflation has fallen back to target.

The latter course will send the dollar into free fall and destabilise the world’s dollarised financial system, an outcome already being sniffed out by the reawakening gold market.

Mr. Connolly is one of the very few prophets who foresaw both the Great Recession and the eurozone sovereign debt debacle, not just in vague terms — many did that — but with eerie precision and with a powerful intellectual argument for why they would happen and why they would prove so intractable.

His new magnum opus, “You Always Hurt the One You Love: Central Banks and the Murder of Capitalism,” is the story of the Faustian pact made by central bankers from the 1990s onwards, when they became addicted to bubbles and started stealing prosperity from the future.

His blistering critique over the decades has not stopped top officials at the Fed, the Bank of Japan, and the Bank of England from seeking his advice whenever trouble hits. After a long silence, he is again issuing warnings.

“There can be little doubt that there will be a U.S. recession unless the Fed loosens hard and soon. The labour market is weakening and ‘excess savings’ from the pandemic-era handouts are exhausted,” he said. …

Turks are piling into gold ad the dollar as inflation is ravaging the Turkish lira

(zerohedge)

Turks pile into the dollar, gold, and stocks as 67% inflation savages lira

Submitted by admin on Wed, 2024-03-20 17:52 Section: Daily Dispatches

By Scott McLean, Ipek Yezdani, and Anna Cooban CNN, Atlanta Wednesday, March 20, 2024

Down a dimly lit alleyway tucked just inside Istanbul’s Grand Bazaar, a few dozen men are packed together, shouting, waving, and frantically speaking on their phones, others nervously pacing.

This “standing market” — a low-rent version of a chaotic stock exchange floor — is where Istanbul’s traders come to deal in precious metals and currencies. These days it’s dollars and gold they’re after. Turkish lira, not so much

“Right now our money is almost worthless. Since people haven’t seen inflation fall, they don’t trust the Turkish lira anymore,” explained Adnan Kapukaya, a trader and market expert.

Inflation in Turkey remains sky-high — official figures show prices rose 67% last month compared with February 2023, though unofficial estimates suggest the real number is more than 100%. And this despite the Turkish central bank hiking interest rates to an eye-watering 45% in January — up from a low of 8.5% a year ago.

But even at that rate, savers are still losing money to inflation. So to shelter their savings, people are showing up in the gold markets of the Grand Bazaar with whatever they have — modest savings or, sometimes, a suitcase full of cash, says Omer Tozduman, a gold dealer. …

New book reveals history of U.S. dollar weaponization

Submitted by admin on Wed, 2024-03-20 18:02 Section: Daily Dispatches

By Neil Irwin Axios, Arlington, Virginia Wednesday, March 20, 2024

Some of the most important instruments of U.S. global power are deployed not by the warfighters at the Pentagon or the diplomats at the State Department, but by bureaucrats at 1500 Pennsylvania Ave. — the U.S. Treasury Department.

The big picture: A new book out this week brings to life the narrative of how Treasury officials have used the U.S. dollar as a tool of American foreign policy over the last three decades — along with the hazards that has created.

“Paper Soldiers: How the Weaponization of the Dollar Changed the World Order,” by Bloomberg senior reporter Saleha Mohsin, arrives as cracks in that order are starting to appear.

The aggressive use of economic countermeasures against Russia in retaliation for its invasion of Ukraine — an effort steered out of Treasury — has caused blowback as other nations with tense U.S. relationships seek alternatives to the dollar-based global financial system. …

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGSTHURSDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED DOWN 7.1990

OFFSHORE YUAN: DOWN TO 7.2138

SHANGHAI CLOSED DOWN 2.57 PPTS OR 0.08%

HANG SENG CLOSED UP 320.03 PTS OR 1.93%

2. Nikkei closed UP 812.06 OR 2.03%

3. Europe stocks SO FAR: MOSTLY ALL GREEN

USA dollar INDEX UP TO 103.14 EURO FALLS TO 1.0916 DOWN 22 BASIS PTS

3b Japan 10 YR bond yield: RISES TO. +.732 Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 151.03/JAPANESE YEN NOW FALLING AS WELL AS LONG TERM 10 YR. YIELDS RISING //EVENTUALLY THIS WILL BREAK THE JAPANESE CENTRAL BANK

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen DOWN CHINESE ONSHORE YUAN: DOWN/ OFFSHORE: DOWN

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil DOWN for WTI and DOWN FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund YIELD DOWN TO +2.3935***/Italian 10 Yr bond yield DOWN to 3.655* /SPAIN 10 YR BOND YIELD DOWN TO 3.1980…**

3i Greek 10 year bond yield DOWN TO 3.257

3j Gold at $2207.00 silver at: 25.45 1 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble UP 0 AND 67 /100 roubles/dollar; ROUBLE AT 91.57//

3m oil into the 80 dollar handle for WTI and 85 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 151.03// 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 0.735% STILL ON CENTRAL BANK (JAPAN) INTERVENTION

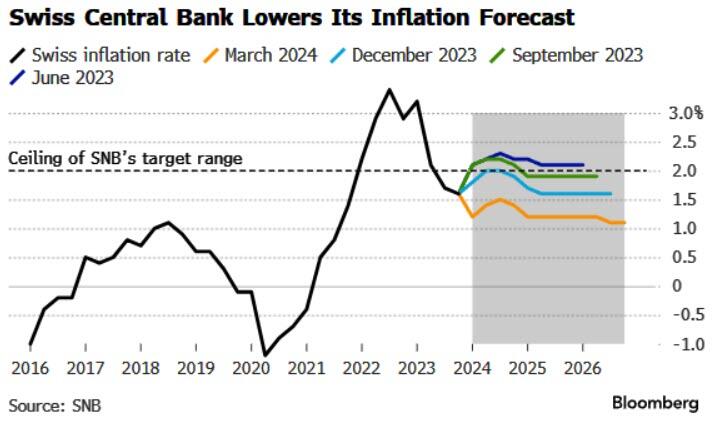

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.8924 as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.9741 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.228 DOWN 4 BASIS PTS…

USA 30 YR BOND YIELD: 4.421 DOWN 3 BASIS PTS/

USA 2 YR BOND YIELD: 4.566 DOWN 4 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 32.13…(TURKEY SET TO BLOW UP FINANCIALLY)

GREAT BRITAIN/10 YEAR YIELD: DOWN 7 BASIS PTS AT 3.997

end

2.a Overnight: Newsquawk and Zero hedge

Futures, Global Stocks Soar After Dovish Powell Greenlights Meltup

THURSDAY, MAR 21, 2024 – 08:16 AM

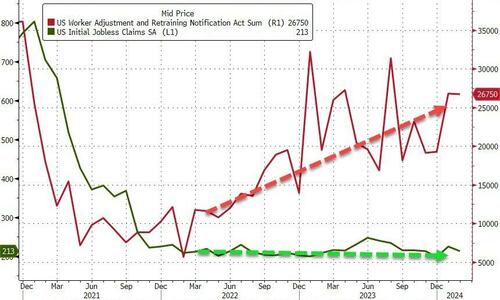

Futures and global stocks are soaring and building on Wednesday’s powerful gains after the Fed signaled expectations for three rate cuts this year and said inflation eased substantially while Powell greenlit the next big pre-election leg to the rally with dovish press conference comments that suggested the Fed has all but raised its inflation target to 3%. Both Tech and Small-caps are outperforming; while all of the Mag 7 are higher pre-mkt ex-AAPL which was hit on some negative regulatory headlines (AAPL shares have been a funding short for the group). As of 8:00am, S&P futures were 0.4% higher, trading just above 5,300 while Nasdaq futures up 0.8%, both in record territory. 10Y Treasury yields are lower, trading around 4.22% are the curve bull flattens while the USD trades higher after a shock rate cut by the SNB sent the swiss franc plunging. Today’s macro data focus includes flash PMIs, leading index, existing home sales, and jobless data. Powell flagged that a weakening labor market is cue for when to cut rates but did not indicate which data release is the most impactful but in the 5 years leading into COVID, weekly claims averaged 244k and today consensus is 213k.

In premarket trading, Micron shares surged 18%, lifting peers with it, after the maker of computer memory chips gave a 3Q forecast that was much stronger than expected. Chip equipment makers also gain after Micron said it plans to boost capital spending in fiscal 2025: Western Digital (WDC US) +6.7%, Seagate Technology (STX US) +1.2%; chip equipment makers Applied Materials (AMAT US) +3.4%, Lam Research (LRCX US) +3.1%. Here are some other notable premarket movers:

Astera Labs shares rise 5.6%, set to extend Wednesday’s 72% gain. The semiconductor connectivity company’s initial public offering topped expectations to raise $713 million, adding momentum to AI-related stocks and a listings rebound.

Broadcom shares gain 2.7% as analysts were positive about the chipmaker’s opportunities following its AI event. Cowen raised its rating to outperform from market perform.

Guess shares advance 12% after the clothing company reported 4Q adjusted earnings per share and sales above consensus estimates.

Li Auto ADRs fall 6.8% after the Chinese EV maker reduced its 1Q vehicle deliveries target, citing lower-than-expected order intake. CEO Li Xiang said the firm’s operating strategy for its newly launched Mega model was “mis-paced.”

Stock optimism was reignited after Federal Reserve policymakers kept their outlook for three cuts this year, despite a recent rebound in price pressures. While Chair Jerome Powell continued to highlight that officials would like to see more evidence prices are coming down, he also said it will be appropriate to start easing “at some point this year.” As part of the dovish hurricane response, treasuries advanced, lowering the 10-year yield by four basis points, while the dollar posted small moves. Brent crude traded around $86 a barrel and Bitcoin held at about $67,000. Gold rallied above $2,200 an ounce for the first time and a gauge of emerging-market stocks climbed the most since December.

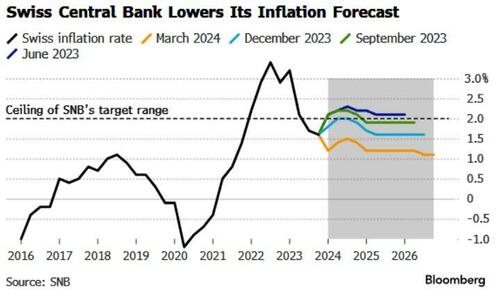

While the Fed decision surprised some – especially the bears – there were more central bank shockers overnight, notably Taiwan which unexpected hiked 25bps to 2.00% and from the SNB which shockingly cut rates, sending the Swiss franc tumbling. The franc fell more than 1% against the dollar after the SNB lowered its key rate by 25 basis points in a move only a small minority of economists anticipated.

The decision to cut by Swiss policymakers was the first such reduction for one of the world’s 10 most-traded currencies since the pandemic abated.

“This signals to the world that we have turned a corner,” said Philipp Hildebrand, vice chairman at BlackRock and former Chairman of the SNB. “Central banks are easing and the question is where does all this settle in the long term.”

The Stoxx 600 traded up 0.4% after hitting a record earlier in the session. Mining and real estate stocks lead gains, while the health care sector lags. Equities in Europe paired some of their gains after euro-area manufacturing data missed estimates. S&P Global’s purchasing managers’ index showed sustained weakness in Germany and France — the bloc’s top two economies — even as overall private-sector activity for the euro-area rose to a nine-month high in March. Here are some of the most notable premarket movers:

Chip equipment stocks lead a rally in European tech stocks after the US Fed maintained its outlook for interest-rate cuts, and US firm Micron signaled it will increase capex next year

Glencore rises as much as 4% as it eyes a stake in Indonesian miner Harita Nickel, a sign of growing interest in the country’s fast-expanding nickel sector

Argenx gains as much as 12% after a rival for the biotech firm said a phase 3 Luminesce study of Enspryng as an investigational treatment for generalized myasthenia gravis failed

Remy Cointreau rises as much as 6.1% after Deutsche Bank lifts its recommendation on the stock to buy from hold, with inventory levels seen materially ahead of current market value

3i Group shares gain as much as 4.4%, reaching record highs, after its Action unit reported 21% like-for-like sales growth vs. a year earlier, which analysts note shows continued strength

Energean rises as much as 6.1% as the company reiterated its guidance for this year. Analysts say markets are pleased that operations in Israel have so far not been disrupted

Esso surged as much as 23%, its biggest intraday gain since April 2022, after the French unit of Exxon Mobil announced a €12-a-share special dividend as part of its full-year report

Pernod Ricard rises as much as 2.9% as Deutsche Bank upgrades to hold from sell, saying the cognac maker is now “broadly fairly valued,” also seeing a fairly evenly balanced risk profile

M&G gains as much as 4.2% as the pension fund and asset manager sees better-than-expected institutional flows and operating profit for the full year period

Next gains as much as 5.9% after full-year results beat estimates and 2025 guidance was maintained. Analysts described the earnings as “pleasing”

Douglas falls as much against its IPO price as the German perfume retailer began trading in Frankfurt, trading at €23.8 as of 11am, down from the IPO price of €26.

Nemetschek falls as much as 5.4% after refining its 2024 guidance first proposed in March last year. Analysts deemed Ebitda margin and revenue growth targets cautious

Earlier in the session, the MSCI Asia Pacific Index advanced as much as 2.2%, the most since Nov. 15, with Taiwan Semiconductor, Toyota and Samsung among the biggest contributors to the move. The bullish session echoes US gains after Fed policymakers kept their outlook for three cuts in 2024 and moved toward slowing the pace of reducing their bond holdings, suggesting they aren’t alarmed by a recent rebound in price pressures. Sentiment on Chinese tech stocks got a lift after Tencent Holdings Ltd. announced plans to more than double its stock buyback program and boosted dividends. The region’s semiconductor shares gained after Micron Technology Inc. gave a surprisingly strong revenue forecast for the current quarter, buoyed by demand for memory chips used in artificial intelligence applications.

“With the FOMC event risk out and market pricing roughly in line with dot plots, we think focus of Asian equity investors should return to earlier themes of AI momentum,” Chetan Seth, a strategist at Nomura Holdings Inc., wrote in a note. “We still expect a US soft landing.”

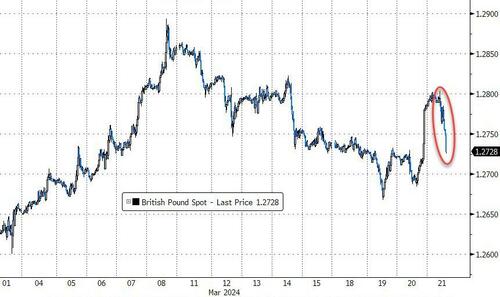

In FX,the Swiss franc sits at the bottom of the G-10 FX pile, falling 0.7% against the dollar after the Swiss National Bank surprised with a 25bps interest rate cut. The Norges Bank stood pat, as expected, prompting an uptick in the krone. The pound is little changed as investors now turn their attention to the Bank of England decision at noon UK time.

In rates, treasuries extended Wednesday’s post-Fed rally, supported by gains in UK front-end as traders fully price in 75bps of easing by Bank of England easing this year for first time since March 12. Treasury yields richer by 3bp to 5bp across the curve with gains led by belly, steepening 5s30s spread by around 1.5bp and adding to Wednesday’s sharp steepening move as additional easing was priced back into the front-end; 10-year trades around 4.23% with bunds lagging by 1bp in the sector, gilts trading broadly in line. European bonds are firmly in the green, with rate markets drawing additional support from SNB’s surprise cut. US session includes several economic indicators and 10Y TIPS auction.

In commodities, oil prices decline, with WTI falling 0.3% to trade near $81. Spot gold rises 1%.

Bitcoin climbed back to best levels at USD 68k, before paring back to around the USD 66k level.

Looking at today’s calendar, economic data calendar includes 4Q current account balance, March Philadelphia Fed business outlook and weekly jobless claims (8:30am), March preliminary S&P Global manufacturing and services PMIs (9:45am), February leading index and existing home sales (10am). Fed members scheduled to speak include Barr at 12pmTo contact the reporter on this story:

Market Snapshot

S&P 500 futures up 0.5% to 5,311.25

STOXX Europe 600 up 0.8% to 509.14

MXAP up 2.0% to 178.40

MXAPJ up 1.9% to 540.84

Nikkei up 2.0% to 40,815.66

Topix up 1.6% to 2,796.21

Hang Seng Index up 1.9% to 16,863.10

Shanghai Composite little changed at 3,077.11

Sensex up 0.7% to 72,624.50

Australia S&P/ASX 200 up 1.1% to 7,781.97

Kospi up 2.4% to 2,754.86

German 10Y yield little changed at 2.41%

Euro down 0.2% to $1.0901

Brent Futures up 0.5% to $86.36/bbl

Gold spot up 0.7% to $2,202.16

US Dollar Index up 0.19% to 103.58

Top Overnight News

Taiwan’s central bank unexpectedly raises rates from 1.875% to 2% (the consensus was looking for rates to be unchanged). WSJ

China’s PBOC signals an openness to additional bank reserve requirement ratio (RRR) cuts, but sounds reluctant about lowering interest rates until the Fed begins easing. BBG

BOJ Governor Kazuo Ueda said the central bank scrapped its massive easing program this week partly to avoid the need for aggressive action later, a comment that may help market players judge his next moves. BBG

SNB unexpectedly lowers its policy rate from 1.75% to 1.5% (the Street was looking for rates to stay unchanged) as the central bank highlights progress in the battle against inflation. RTRS

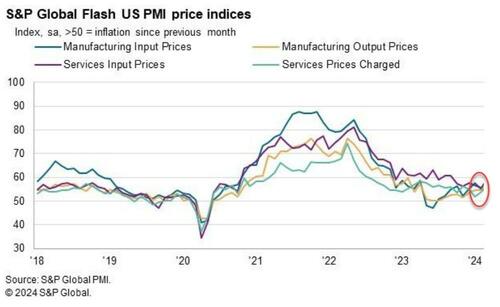

Eurozone flash PMIs are mixed, with a soft manufacturing figure (45.7, down from 46.5 in Feb and below the Street’s 47 forecast) and a decent services number (51.1, up from 50.2 in Feb and above the Street’s 50.5 forecast). BBG

AMZN is focusing its attention on combating Shein and Temu as the firm views both as larger competitive threats than Walmart and Target. WSJ

Korean Air Lines passed Boeing over to order 33 Airbus SE A350 wide-body jets in a $14 billion deal. And Japan Airlines said it’ll buy 11 Airbus A321neos — alongside some Boeings — breaking the US planemaker’s hold as its sole single-aisle supplier. BBG

The DOJ will sue Apple in federal court as soon as today for alleged antitrust violations, people familiar said, escalating the crackdown on Big Tech by regulators in the US and abroad. Apple is accused of blocking rivals from accessing hardware and software features of its iPhones. Shares slipped premarket. BBG

MU +17% pre mkt after reporting strong EPS upside in FQ2/Feb at 42c (the Street was looking for a 24c loss), w/the beat driven by better sales ($5.82B vs. the Street $5.35B), higher gross margins (20% vs. the Street 13/5%), and superior operating margins (pos. 3.5% vs. the Street’s neg. 4.4% forecast). The FQ3 guide was very. Mgmt said supply/demand conditions are improving thanks to a “confluence of factors”, including strong AI server demand, a healthier demand backdrop in most other end markets (it sees PCs growing in the low-single digits this year, w/AI PCs becoming a larger factor in 2025, while smartphones grow in the low/mid-single digits), and supply reductions across the industry. RTRS

Central Banks

SNB cut its Policy Rate by 25bps to 1.50% (exp. 1.75%); FX language reiterated “willing to be active in the foreign exchange market as necessary”, Ready to intervene in FX; Loosening permitted by inflation progress.

SNB Chairman Jordan says that rates were able to be lowered as the fight against inflation has been effective. Says we give no forward guidance on future interest rates and will see where we are in 3 months time. Says we remain willing to sue balance to be active on forex market and could be sales of purchases; situation in ME is tricky; neither sales of forex are in focus at the moment

Norges Bank maintains its Key Policy Rate at 4.50% as expected; reiterates guidance that “policy rate will likely need to be maintained at the current level for some time ahead”.

Norges Bank Governor Bache says the rate path indicates a cut is most likely in September, second rate cut indicated by end of Q1’25

Taiwan hikes its benchmark interest rate to 2.0% from 1.875%

A more detailed look at global markets courtesy of Newsquawk

APAC stocks were mostly underpinned after the fresh record levels on Wall St post-dovish FOMC where the Fed maintained the projection for 3 rate cuts in 2024 and Powell downplayed recent hot inflation data. ASX 200 strengthened with sentiment also helped by a stellar jobs report and a fall in unemployment, while gold miners outperformed after the precious metal rose above USD 2,200/oz to a new all-time high. Nikkei 225 rallied from the open to unprecedented levels north of 40,800 despite recent hawkish source reports. Hang Seng and Shanghai Comp. were mixed in which the Hong Kong benchmark rallied to just shy of the 17,000 level amid strength in the property sector and as the Fed projection for three rate cuts keeps similar action on the table for the HKMA. Conversely, the mainland lagged as the PBoC injected the least amount of funds in its open market operations since August last year despite the PBoC’s Deputy Governor reaffirming that China’s monetary policy has ample room and there is still room for cutting RRR

Top Asian News

HKMA maintained its base rate unchanged at 5.75%, as expected. HKMA said financial and monetary markets in Hong Kong continue to operate in a smooth and orderly manner, while it added that the HKD exchange rate remains stable and Hong Kong dollar interbank rates might remain high for some time.

PBoC Deputy Governor Changneng Xuan said they will promote effective investment and help resolve excess capacity, while he added that China’s monetary policy has ample room and there is still room for cutting RRR. PBoC Deputy said he expects China’s nominal economic growth to be around 8% in 2024 and will maintain appropriate growth in credit and total social financing, while they will guide banks to lower deposit rates and lower financing costs, support consumption and investment, as well as promote a rebound in prices.

China’s Vice Finance Minister said fiscal policy will provide the necessary support for achieving the 2024 growth target and China’s government debt is at an appropriate level, while he said China has continued to reduce the overall level of tariffs, which has now been reduced to 7.3% and is relatively low in the world, according to Reuters and Global Times.

China state planner vice chair said they will speed up approval for investment projects and that total bond funds for government investment will exceed CNY 6tln, while they will step up support for private investment and encourage private firms to participate in infrastructure investment projects, according to Reuters.

BoJ Governor Ueda said the BoJ is expected to maintain an accommodative monetary policy for the time being and accommodative monetary policy is likely to underpin the economy, while he added that cost-push pressure on inflation is dissipating but service prices continue to rise moderately and the preliminary wage negotiation outcome tends to be revised down but even so, they thought the final outcome would be a fairly strong number. BoJ Governor Ueda said as they end massive stimulus, they will likely gradually shrink the balance sheet and at some point reduce JGB purchases but at present, they have no clear idea regarding the timing of reducing JGB buying and scaling back the size of the balance sheet. Furthermore, he said they are not immediately thinking of selling BoJ’s ETF holdings and will take plenty of time examining how to reduce ETF holdings.

BoJ is reportedly seen weighing the next rate hike in July or October as the Yen weakens, according to Nikkei. A source noted that additional hikes are of course on the table and that an early hike leaves room for the BoJ to consider rolling out another increase before the end of the year, while the timeline would keep the BoJ coming off like they are rushing to hike rates. Furthermore, it was stated that a growing number see a July rate boost as another possibility if a weak yen raises the price of imports and accelerates inflation, forcing the BoJ to step in. It was earlier reported that the Yen’s decline appears to be raising little alarm at the BoJ for now which was to be expected given that Governor Ueda is maintaining an accommodative stance on policy, according to a source at the BoJ cited by Nikkei. However, it was noted that some at Japan’s Finance Ministry are wary of rapid fluctuations in the currency market driven by speculative trades.

Fitch expects BoJ to raise policy rate to 0.25% by 2025.

CNOOC (600938 CH) FY (CNY) IFRS Net 123.84bln (exp. 130.33bln); In 2024, will insist on increasing oil and gas reserves and production; ongoing recovery trajectory in China will support demand for oil and gas

European equities, Stoxx600 (+0.4%) are entirely in the green, with sentiment lifted following a post-FOMC equity rally in the US & APAC. Following the release of poor French PMIs and bleak German commentary, equities have edged off best levels. European sectors are firmer; Tech takes the top spot, with optimism permeating within the sector after strong Micron results and Basic Resources benefits from broader strength in base metal prices. US equity futures (ES +0.4%, NQ +0.7%, RTY +0.6%) are stronger, in a continuation of the prior day’s post-FOMC rally; Micron (+16% pre-market) is soaring after beating on EPS/Revenue and lifting guidance.

Top European News

EU New car registrations (Feb): +10.1% (prev. 12.1%); battery electric market share 12% (prev. 10.9%). EU27 New Car Registrations by Manufacturer (Y/Y). Volkswagen (VOW3 GY) +8.7%; Stellantis (STLAM IM/STLAP FP) +11.2%; Renault (RNO FP) +5.9%; BMW (BMW GY) +7.0%; Mercedes Benz Group (MBG GY) -2.1%; Volvo Cars (VOLCAR SS) +33.9%. (acea)

Portugal’s President named centre-right democratic alliance leader Luis Montenegro as the new PM, according to Reuters.

FX

USD is attempting to claw back post-FOMC losses with some help via EZ-PMI releases. DXY still has some way to go to close the gap to yesterday’s best at 104.14. High print for today at 103.66 coincides with the 200DMA.

EUR has been dragged lower by EZ PMIs which were indicative of the composite figure approaching neutral territory; EUR/USD on a 1.09 handle after slipping to a low of 1.0888.

GBP is a touch softer vs. the USD but near post-FOMC highs which saw Cable peak at 1.2803. UK PMIs saw services and composite miss but the manufacturing print edge closer to neutral. Focus ahead is firmly on the BoE.

JPY pausing for breath vs. the USD after vaulting to a high of 151.81 yesterday, which saw the pair stop shy of the 2023 high at 151.91 and 2022 peak at 151.94.

AUD the best performer across the majors following encouraging jobs metrics. AUD/USD as high as 0.6634 but unable to breach last week’s best at 0.6638. NZD marginally higher vs. USD despite the surprise contraction in Q4 GDP data.

CHF is the clear laggard across the majors as the SNB surprises with a 25bps rate cut and reiterates a willingness to intervene in the FX market. EUR/CHF as been as high as 0.9782 to its highest level since July last year; 0.9842 was the high that year.

An unchanged announcement from the Norges Bank but one which sparked NOK strength given the repo path has not formalised a Q4-2024 rate cut as some were hoping for. As such, EUR/NOK slipped from 11.5300 to 11.4857. However, a modest dovish move was seen on Governor Bache indicating the first cut is “likely” in September.

PBoC set USD/CNY mid-point at 7.0942 vs exp. 7.1792 (prev. 7.0968).

Fixed Income

Choppy price action for Bunds owing to varied PMIs from France and Germany. The former sparked a dovish reaction with Bunds lifting from 131.90 to 132.72, whilst the German metrics sent Bunds back down to 131.85, though downside was shortlived given the Manuf. miss and SNB rate cut.

USTs are underpinned by the dovish fixed narrative which is dictating EGBs/Gilts into the BoE post-SNB/PMIs. Action which has taken USTs to a 110-24+ high, eclipsing the post-FOMC 110-22 peak.

Gilt price action is in-fitting with EGBs and as such approached their own PMIs with gains of around 30 ticks on the session. A release which saw two-way action with Gilts initially slipping to 99.24 (strong Manuf.) before rebounding to 99.46 (Comp. & Serv. miss); BoE up next.

France sells EUR 12.498bln vs exp. EUR 11-12.5bln 2.50% 2027, 2.75% 2029, and 1.50% 2031 OAT

Commodities

Crude was initially firmer after the Fed-induced Dollar decline coupled with broader risk appetite, and geopolitics. However, the complex then trimmed gains after PMIs for France and Germany painted a bleak economic recovery picture; Brent is now lower on the session and just shy of USD 86/bbl.

Precious metals extend on post-Powell gains despite an attempted recovery in the Dollar, with spot gold topping USD 2,200/oz to fresh ATHs in APAC trade while spot silver gained status above USD 25.50/oz.

Base metals are higher across the board in the after-math of the FOMC which boosted broader market sentiment.

Geopolitics

US military said coalition forces destroyed an unmanned aerial vehicle fired by Yemen’s Houthis in the Red Sea and destroyed an unmanned surface vessel on March 20th, according to Reuters.

Australia and Britain signed a defence pact which includes a status of forces agreement and makes it easier for the respective forces to operate together in each other’s countries, while the agreement also formalises the established practice of consulting on issues that affect our sovereignty and regional security.

“Al-Arabiya sources: Pressure on Israel to postpone the Rafah operation for at least 45 days”, according to Al Arabiya; “The mediators and America rejected a preliminary Israeli proposal on the military operation in Rafah”

US Event Calendar

08:30: March Initial Jobless Claims, est. 213,000, prior 209,000

March Continuing Claims, est. 1.82m, prior 1.81m

08:30: 4Q Current Account Balance, est. -$209b, prior -$200.3b

08:30: March Philadelphia Fed Business Outl, est. -2.5, prior 5.2

09:45: March S&P Global US Manufacturing PM, est. 51.8, prior 52.2

March S&P Global US Services PMI, est. 52.0, prior 52.3

March S&P Global US Composite PMI, est. 52.2, prior 52.5

10:00: Feb. Existing Home Sales MoM, est. -1.3%, prior 3.1%

10:00: Feb. Leading Index, est. -0.1%, prior -0.4%

DB’s Jim Reid concludes the overnight wrap

Considering that US inflation has surprised notably on the upside this year, last night saw a remarkably relaxed Fed as Chair Powell indicated that January’s higher inflation could have been seasonal, and that February’s print had already seen improvements. The dots continued to show three cuts for 2024 and alongside a dovish-leaning press conference, this drove equities higher and yields lower, especially at the front end.

In terms of the details, the statement was little changed as the FOMC continued to see that “ it will likely be appropriate to begin dialing back policy restraint at some point this yea r” while wanting to gain “greater confidence that inflation is moving sustainably toward 2%”.

The dot plot showed the median 2024 dot unchanged at three cuts this year. This came even as 2024’s economic projections were revised higher, with real GDP growth revised up from 1.4% to 2.1%, core PCE inflation up two-tenths to 2.6%, and unemployment a tenth lower to 4.0%. Our US economists note that this forecast implies core PCE averaging 19bps a month for the rest of the year – only a little above the 2% target run rate. So a pretty Goldilocks take for now even if this was accompanied by 25bp upward revisions to the 2025-26 median dots, and a larger share of FOMC members seeing inflation risks as tilted to the upside.

Powell’s press conference also erred on the dovish side, with his comments notably suggesting that the upside inflation data for January and February did not alter the Fed’s baseline, with the inflation story “essentially the same”. He also mentioned a couple of times that unexpected labor market weakening could warrant a policy response (though the FOMC did not see this currently), while expressing no concern about the ongoing easing in financial conditions.

When asked about rate cut timing, Powell made no effort to rule out the possibility of a May move, saying the FOMC “didn’t make any decisions about future meetings”. Our US economists continue to expect the first rate cut to come in June with 100bps of cuts in total this year, but with risks skewed to a more hawkish outcome. See their full reaction here.

On the balance sheet side, Powell indicated that a decision on slowing the pace of QT would come “fairly soon”. He emphasized that slowing QT did not equate to stopping it, noting that moving to a slower run-off pace could actually allow for a greater reduction in the balance sheet over time by reducing the risk of liquidity problems emerging.

Following the FOMC, futures dialled up the probability of a June cut to 84% from 66% the previous day, with 84bps of cuts now priced by year-end (+10.7bps on the day). This backdrop saw a bull steepening of the Treasury curve, as 2yr yields fell by -8.1bps while 10yr yields were down -2.0bps on the day to 4.27% (and closing near their pre-FOMC levels). This came as higher breakevens offset most of a -5.9bps decline in 10yr real yields. The 2s10s slope reached its steepest level in over month at -33.2bps. And overnight, there’s been a further decline in yields, with those on 10yr Treasuries down another -0.8bps.

Equities basked in a risk-on mood following the Fed, with the S&P 500 (+0.89%), NASDAQ (+1.25%) and Dow Jones (+1.03%) all reaching new records. Small-caps led the gains, with the Russell 2000 up +1.92%, whilst the VIX index of volatility fell to its lowest since early February (-0.78pts to 13.04).

That rally has continued in Asia overnight, with strong advances for the Nikkei (+1.97%), the Hang Seng (+1.80%) and the KOSPI (+2.18%). Moreover, US equity futures are pointing to further gains, with those on the S&P 500 up +0.40%. That comes amidst some strong data releases, as we’ve started to get the March flash PMI releases from around the world. For instance in Japan, the composite PMI rose to 52.3 in March, which is the highest it’s been since August. Likewise in Australia, the composite PMI was up to 52.4, the highest since April. And Australia also had some strong employment data for February as well, with employment up by +116.5k (vs. +40.0k expected). However, even as markets have been positive for the most part, there have been losses for Chinese equities, with the CSI 300 (-0.11%) and the Shanghai Comp (-0.14%) both seeing modest declines.

In FX, the Japanese yen (+0.32%) has strengthened against the dollar, trading at 150.90 this morning after the Nikkei newspaper reported that investors were speculating about another hike in July or October. Before the news broke out, the Japanese yen was trading at 151.91, within a whisker of its post-1990 low.

Before the Fed, European markets had struggled to gain much traction yesterday, with the STOXX 600 unchanged (-0.00%) by the close. That came as ECB President Lagarde stuck to her previous message on monetary policy, saying that “when it comes to the data that is relevant for our policy decisions, we will know a bit more by April and a lot more by June.” That’s meant investors continue to see the June meeting as the most likely for an initial rate cut, and sovereign bonds were also fairly subdued in response. So there was only a modest decline in yields across most of the continent, with those 10yr bunds (-1.8bps) and OATs (-1.1bps) falling slightly.

The main exception to that pattern was in the UK, where 10yr gilts fell by a larger -4.6bps after the latest CPI release surprised on the downside. That showed headline CPI falling to +3.4% in February (vs. +3.5% expected), which is the lowest since September 2021. Moreover, core CPI fell to a two-year low of +4.5% (vs. +4.6% expected). In turn, that led investors to dial up the chance of rate cuts this year, and the chance of a cut by the June meeting moved up from 52% on Tuesday to 58% by the close yesterday.

That inflation release comes ahead of the Bank of England’s latest policy decision today, where they’re widely expected to keep rates on hold as well. So the focus will instead be on any signals about the timing of future rate cuts, along with the vote split. In his preview (link here), our UK economist Sanjay Raja sees the risks skewed towards a dovish surprise, but thinks that the MPC will stick to its February guidance that Bank Rate is restrictive and “will need to remain restrictive for sufficiently long to return inflation to the 2% target”.

Lastly, there was some marginally brighter data from the Euro Area, as the European Commission’s preliminary consumer confidence indicator rose to -14.9 in March (vs. -15.0 expected). That was the highest reading since February 2022, just before Russia’s invasion of Ukraine began.

To the day ahead now, and the main data highlight will be the flash PMIs for March. Alongside that, we’ll get the US weekly initial jobless claims, the Conference Board’s leading index for February, existing home sales for February, the Philadelphia Fed’s business outlook for March, and the Q4 current account balance. From central banks, there’s a policy decision from the Bank of England, and we’ll hear from Fed Vice Chair for Supervision Barr. Today’s earnings releases include Nike and FedEx. And in the political sphere, a summit of EU leaders is taking place in Brussels.

2 B) NOW NEWSQUAWK (EUROPE/REPORT)

Equities climb higher, AUD bid post-jobs data & Bonds benefit from EZ PMIs; US IJC due – Newsquawk US Market Open

THURSDAY, MAR 21, 2024 – 06:56 AM

Equities firmer in a continuation of the post-Fed rally; European bourses off best after EZ PMIs

Dollar stronger, AUD bid post-jobs data and CHF lower after SNB cut rates by 25bps

Bonds higher taking impetus from the poor French PMI and dire accompanying German commentary

Crude pares initial gains, base metals benefit from risk sentiment

Looking ahead, US IJC, Fed’s Barr, Supply from the US, Earnings from FedEx, Nike

2. Listen to this report in the market open podcast (available on Apple and Spotify)

3. Trial Newsquawk’s premium real-time audio news squawk box for 7 days

EUROPEAN TRADE

EQUITIES

European equities, Stoxx600 (+0.4%) are entirely in the green, with sentiment lifted following a post-FOMC equity rally in the US & APAC. Following the release of poor French PMIs and bleak German commentary, equities have edged off best levels.

European sectors are firmer; Tech takes the top spot, with optimism permeating within the sector after strong Micron results and Basic Resources benefits from broader strength in base metal prices.

US equity futures (ES +0.4%, NQ +0.7%, RTY +0.6%) are stronger, in a continuation of the prior day’s post-FOMC rally; Micron (+16% pre-market) is soaring after beating on EPS/Revenue and lifting guidance.

Click here and here for the sessions European pre-market equity newsflow, including earnings.

USD is attempting to claw back post-FOMC losses with some help via EZ-PMI releases. DXY still has some way to go to close the gap to yesterday’s best at 104.14. High print for today at 103.66 coincides with the 200DMA.

EUR has been dragged lower by EZ PMIs which were indicative of the composite figure approaching neutral territory; EUR/USD on a 1.09 handle after slipping to a low of 1.0888.

GBP is a touch softer vs. the USD but near post-FOMC highs which saw Cable peak at 1.2803. UK PMIs saw services and composite miss but the manufacturing print edge closer to neutral. Focus ahead is firmly on the BoE.

JPY pausing for breath vs. the USD after vaulting to a high of 151.81 yesterday, which saw the pair stop shy of the 2023 high at 151.91 and 2022 peak at 151.94.

AUD the best performer across the majors following encouraging jobs metrics. AUD/USD as high as 0.6634 but unable to breach last week’s best at 0.6638. NZD marginally higher vs. USD despite the surprise contraction in Q4 GDP data.

CHF is the clear laggard across the majors as the SNB surprises with a 25bps rate cut and reiterates a willingness to intervene in the FX market. EUR/CHF as been as high as 0.9782 to its highest level since July last year; 0.9842 was the high that year.