GOLD PRICE CLOSED UP $23.90 TO $2260.90

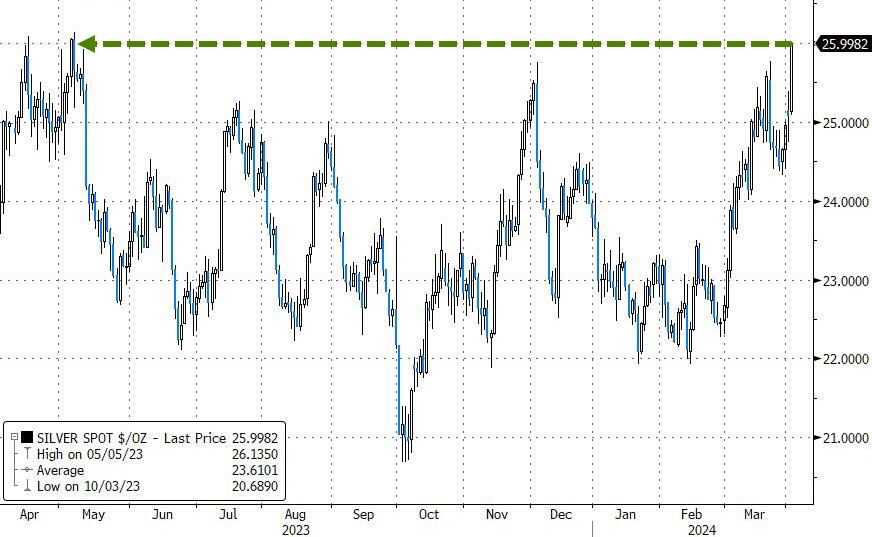

SILVER PRICE UP 84 cents TO $25.80

Gold ACCESS CLOSED $2283.60

Silver ACCESS CLOSED: $26.17

Bitcoin morning price:$66,605 DOWN 4027 DOLLARS.

Bitcoin: afternoon price: $69,632 DOWN 1135 dollars

Platinum price closing UP $20.30 TO $921.90

Palladium price; UP $1.30 AT $998.30

END

SHANGHAI GOLD PREMIUM 21 DOLLARS/COMEX GOLD

SHANGHAI GOLD……

…

SHANGHAI GOLD (USD) FUTURES – QUOTES

VENUE:

- GLOBEX

Beginning Monday, April 1, 2024, CME Group settlement data will no longer be accessible through ftp.cmegroup.com and will have a delayed publication time of 12:00 a.m. CT on all cmegroup.com web pages. Learn about alternate ways to access the data in our FAQ.

AUTO-REFRESH IS OFF

Last Updated 02 Apr 2024 06:30:03 AM CT.

Market data is delayed by at least 10 minutes.

I will now provide gold in Canadian dollars, British pounds and Euros

4: 15 PM ACCESS

*CANADIAN GOLD: $3097..21 UP $44.20- CDN dollars per oz( * NEW ALL TIME HIGH 3097.21CDN DOLLARS PER OZ//APRIL 2 2024)

*BRITISH GOLD: 1815.54 UP 23.20 pounds per oz// *(NEW ALL TIME HIGH//CLOSING///23.20 BRITISH POUNDS/OZ) APRIL 2/2024

*EURO GOLD: 2120.54 UP 26.12 euros per oz //* (ALL TIME CLOSING HIGH: 21.02.54 EUROS PER OZ//APRIL 2.2024)

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

EXCHANGE: COMEX

EXCHANGE: COMEX

CONTRACT: APRIL 2024 COMEX 100 GOLD FUTURES

SETTLEMENT: 2,236.500000000 USD

INTENT DATE: 04/01/2024 DELIVERY DATE: 04/03/2024

FIRM ORG FIRM NAME ISSUED STOPPED

072 C GOLDMAN 90

118 H MACQUARIE FUT 6

132 C SG AMERICAS 2

167 C MAREX 1

190 H BMO CAPITAL 80

435 H SCOTIA CAPITAL 38

624 H BOFA SECURITIES 1

661 C JP MORGAN 97 122

690 C ABN AMRO 2

726 C CUNNINGHAM COM 1

737 C ADVANTAGE 30 3

800 C MAREX SPEC 1

905 C ADM 30

TOTAL: 252 252

MONTH TO DATE: 10,124

JPMORGAN STOPPED (RECEIVED) 122/252 CONTRACTS

FOR APRIL/2024

GOLD: NUMBER OF NOTICES FILED FOR APRIL/2024. CONTRACT: 252 NOTICES FOR 25,200 OZ or 0.7838 TONNES

total notices so far: 10,124 contracts for 1,012,400 Oz (31.489 tonnes)

FOR APRIL:

SILVER NOTICES: 11 NOTICE(S) FILED FOR 55,000 OZ/

total number of notices filed so far this month : 50 for 1,750,000 oz

XXXXXXXXXXXXXXXXXX

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD/

BOTH GLD AND SLV ARE FRAUDULENT VEHICLES//THEY ARE NOW RAIDING GLD AND SLV FOR PHYSICAL

THE CROOKS ARE STEALING GOLD AND SILVER FROM THE GLD/SLV AND REPLACING THE PHYSICAL WITH PAPER DOLLARS.

WITH GOLD UP $23.90

INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD/ :

HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.15 TONNES

/ /INVENTORY RESTS AT 829.00 TONNES

INVENTORY RESTS AT 829.00 TONNES

SLV//

WITH NO SILVER AROUND AND SILVER UP 84 CENTS AT THE SLV//

HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 6.721 MILLION OZ OF SILVER INTO THE SLV

// INVENTORY RISES TO 430.806 MILLION OZ/

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV.

CLOSING INVENTORY: 430.806 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A HUMONGOUS SIZED 1658 CONTRACTS TO 161,753 AND CLOSER TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THIS SMALL SIZED GAIN IN COMEX OI WAS ACCOMPLISHED WITH OUR STRONG GAIN IN PRICE OF $0.14 IN SILVER PRICING AT THE COMEX ON MONDAY. WE HAD ZERO LONG LIQUIDATION AT THE COMEX SESSION WITH AGAIN MAJOR SHORT COVERING WITH THE PRICE GAIN. WE HAD A STRONG 797 T.A.S ISSUANCE AND THESE WILL BE USED FOR MANIPULATION LATER THIS MONTH/AS WELL AS TODAY. PLEASE NOTE THAT THE CROOKS NEED A HIGHER SILVER/GOLD T.A.S. TO CARRY ON THEIR CROOKED MANIPULATION ON A DAILY BASIS

CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON MONDAY NIGHT: 797 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS. IT THUS LOOKS LIKE THE FED (GOV’T) IS BEHIND ALL OF THESE TRADES.

WE HAVE NOW SET ANOTHER RECORD LOW AT 114,102 CONTRACTS ///JULY 3.2023// OUR BANKERS WITH THE HELP OF SPECULATORS AND HIGH FREQUENCY TRADERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.14), AND WERE UNSUCCESSFUL IN KNOCKING ANY SILVER LONGS AS WE HAD A HUGE SIZED GAIN OF 2220 CONTRACTS ON OUR TWO EXCHANGES WITH THE STRONG GAIN IN PRICE OF 20 CENTS.

WE MUST HAVE HAD:

A STRONG SIZED 562 ISSUANCE OF EXCHANGE FOR PHYSICALS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 2.465 MILLION OZ (FIRST DAY NOTICE) FOLLOWED BY TODAY’S 75,000 OZ QUEUE JUMP//NEW STANDING 2.6050 MILLION OZ//

//NEW STANDING FOR SILVER IS THUS 2.6060 MILLION OZ

WE HAD:

/ HUGE SIZED COMEX OI GAIN/ STRONG SIZED EFP ISSUANCE/ VI) STRONG SIZED NUMBER OF T.A.S. CONTRACT ISSUANCE 797 CONTRACTS)/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL -REMOVED 564 CONTRACTS //

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS FEB. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF APRIL

TOTAL CONTRACTS for 2 days, total 2359 contracts: OR 11.785 MILLION OZ (11795 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 11.785 MILLION OZ

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH 2022: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 118.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 85.745 MILLION OZ (SMALLER THAN LAST MONTH)

AUGUST: 171.43 MILLION OZ (THIS MONTH IS GOING TO BE HUGE //2ND HIGHEST ON RECORD

SEPT: 72.705 MILLION OZ (SMALLER THIS MONTH)

OCT: 97.455 MILLION OZ

NOV. 50.050 MILLION OZ

DEC. 66.140 MILLION OZ//

TOTAL 2023: 1,104.10 MILLION OZ/

JAN ’24 : 78.655 MILLION OZ//

FEB /2024 : 66.135 MILLION OZ./FINAL

MARCH: 143.750 MILLION OZ// 4TH HIGHEST ON RECORD.

APRIL: 11.785 MILLION OZ

RESULT: WE HAD A HUGE SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 1658 CONTRACTS WITH OUR GAIN IN PRICE OF SILVER PRICING AT THE COMEX//MONDAY.,. THE CME NOTIFIED US THAT WE HAD A STRONG EFP ISSUANCE CONTRACTS: 562 ISSUED FOR MAY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS. WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR APRIL. OF 2.465 MILLION OZ ON FIRST DAY NOTICE FOLLOWED BY TODAYS’ 75,000 OZ QUEUE JUMP

//NEW TOTAL STANDING RISES TO 2.6050 MILLION OZ

WE HAVE A HUGE GAIN OF 2220 OI CONTRACTS ON THE TWO EXCHANGES WITH THE GAIN IN PRICE. THE TOTAL OF TAS INITIATED CONTRACTS TODAY: A STRONG SIZED 797 CONTRACTS//SOME FRONT END OF THE TAS CONTRACTS WERE LIQUIDATED DURING THE MONDDAY COMEX SESSION/// WITH MAJOR SHORT COVERING FROM OUR SPEC SHORTS

THE NEW TAS ISSUANCE THURSDAY NIGHT (797) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE//PROBABLY TODAY., .

WE HAD 11 NOTICE(S) FILED TODAY FOR 55,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A STRONG SIZED 8630 CONTRACTS TO 507,408 AND CLOSER TO THE RECORD (SET JAN 24/2020) AT 799,733 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110, BUT WE ARE NOW CLOSER TO OUR ALL TIME LOW OF 390,000 CONTRACTS.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED 268 CONTRACTS

WE HAD A STRONG SIZED DECREASE IN COMEX OI (8362 CONTRACTS) DESPITE OUR $18.70 GAIN IN PRICE//MONDAY. THE BANKERS WERE FORCED TO SUPPLY THE NECESSARY SHORT PAPER TO CONTAIN GOLD’S RISE.WE ALSO HAD A RATHER LARGE INITIAL STANDING IN GOLD TONNAGE FOR APRIL. AT 44.8615 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’’S EFP. JUMP TO LONDON OF 1900 OZ.(0.0590 TONNES)

NEW TOTAL Of INITIAL GOLD STANDING 42.043 TONNES FOLLOWED BY TODAY’S 1900 OZ E.F.P JUMP//NEW STANDING 41.9844 TONNES// ALL OF THIS HAPPENED WITH OUR $18.70 GAIN IN PRICE WITH RESPECT TO MONDAY’S TRADING. WE HAD A STRONG SIZED LOSS OF 6088 OI CONTRACTS (18.94 PAPER TONNES) ON OUR TWO EXCHANGES.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 2542 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 498,778

IN ESSENCE WE HAVE A STRONG SIZED DECREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 6088 CONTRACTS WITH 8630 CONTRACTS DECREASED AT THE COMEX// AND A FAIR SIZED 2542 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI LOSS ON THE TWO EXCHANGES OF 6088 CONTRACTS.. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): A FAIR SIZED 1275 CONTRACTS,

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (2542 CONTRACTS) ACCOMPANYING THE STRONG SIZED LOSS IN COMEX OI (8630) //TOTAL LOSS FOR OUR THE TWO EXCHANGES: 5820 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR FORMER FORMAT OF BANKERS GOING LONG AND SPECULATORS GOING SHORT ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR APRIL. AT 44.8615 TONNES FOLLOWED BY TODAY’S 0.059 TONNES EFP JUMP TO LONDON//NEW STANDING 41.9844 TONNES.

/ 3) ZERO LONG LIQUIDATION WITH THE HUGE JUMP IN PRICE.(ALL OI LOSS DUE TO T.A.S. LIQUIDATION)

// 4) STRONG SIZED COMEX OPEN INTEREST LOSS/ 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER///6: FAIR T.A.S. ISSUANCE: 1275 CONTRACTS/SHORT COVERING FOR SURE.

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023-2024 INCLUDING TODAY

MARCH

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF APRIL. :

TOTAL EFP CONTRACTS ISSUED: 7664 CONTRACTS OR 766,400 OZ OR 23.838 TONNES IN 2 TRADING DAY(S) AND THUS AVERAGING: 3832 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 2 TRADING DAY(S) IN TONNES 23.838 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2022, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 23.838/3550 x 100% TONNES 0.67% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2023

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH/2022: 409.30 TONNES //FINAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 151.69 TONNES (WEAKER THAN LAST MONTH)

AUGUST: 195.28 TONNES (A STRONGER MONTH)//FINAL

SEPT: 254.709 TONNES (WILL BE LARGER THAN LAST MONTH AND A STRONG MONTH)

OCT. 248.09 TONNES. LIKE SILVER, THIS MONTH IS GOING TO BE A STRONG E.F.P. ISSUANCE.

NOV. 239.16 TONNES//WILL BE STRONG THIS MONTH,

DEC. 213.704 TONNES. A STRONG MONTH//

TOTAL FOR YEAR 2023: 2,569.57 TONNES VS 2578 TONNES LAST YEAR

JAN ’24: 291.76 TONNES (WILL BE MUCH GREATER THAN LAST MONTH.//3RD HIGHEST EVER RECORDED EXCHANGE FOR PHYSICAL)

FEB’24: 201.947 TONNES

MARCH 2024: 352.21 TONNES//2ND HIGHEST EVER RECORDED EFP ISSUANCE.

APRIL: 23.838 TONNES

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF FEB. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (APRIL), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER ROSE BY A GIGANTIC SIZED 1658 CONTRACTS OI TO 162.317 AND CLOSER TO THE COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 6 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 562 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAY 1795 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 562 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 1658 CONTRACTS AND ADD TO THE 562 E.FP. ISSUED

WE OBTAIN A HUMONGOUS SIZED GAIN OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 2220 CONTRACTS

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTAL 11.100 MILLION OZ

OCCURRED WITH OUR $.14 GAIN IN PRICE …..

END

OUTLINE FOR TODAY’S COMMENTARY

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

b, ) Gold/silver trading overnight Europe,//GOLD COMMENTARIES

(Peter Schiff)

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS//

TUESDAY MORNING/MONDAY NIGHT

SHANGHAI CLOSED DOWN 2.42 PTS OR 0.08% //Hang Seng CLOSED UP 390.10 OR 2.36%

/ Nikkei CLOSED UP 35.82 PTS OR 0.09% //Australia’s all ordinaries CLOSED DOWN .10%

/Chinese yuan (ONSHORE) closed DOWN 7.2359 //OFFSHORE CHINESE YUAN CLOSED DOWN TO 7.2627 /Oil UP TO 85.22 dollars per barrel for WTI and BRENT DOWN AT 88.80/ Stocks in Europe OPENED MOSTLY ALL MIXED// ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE YUAN WEAKER

A)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

9. USA

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A STRONG 8630 CONTRACTS TO 498,778 DESPITE OUR STRONG GAIN IN PRICE OF $18.70 WITH RESPECT TO MONDAY TRADING. WE HAD ZERO SPREADER LIQUIDATION BUT MAJOR T.A.S. LIQUIDATION

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE NON ACTIVE DELIVERY MONTH OF APRIL..… THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 2542 EFP CONTRACTS WERE ISSUED: : JUNE 2542 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 2542 CONTRACTS

ON A NET BASIS IN OPEN INTEREST WE LOST THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A STRONG SIZED TOTAL OF 6088 CONTRACTS IN THAT 2542 LONGS WERE TRANSFERRED AS EXCHANGE FOR PHYSICALS TO LONDON AND WE HAD A STRONG SIZED LOSS OF 8630 COMEX CONTRACTS..AND THIS STRONG LOSS ON OUR TWO EXCHANGES HAPPENED DESPITE OUR HUGE GAIN IN PRICE OF $18.70 MONDAY COMEX. AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS DURING MID MONTH IN THE DELIVERY CYCLE), THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR MONDAY NIGHT WAS A FAIR SIZED 1275 CONTRACTS. WE HAD 0 EX FOR RISK ISSUANCE

THROUGHOUT THE PAST SEVERAL WEEKS, THE BANKERS CONTINUE TO SELL OFF THE LONG SIDE OF THE SPREAD WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR/T.A.S. SPREAD WHICH WILL BE LIQUIDATED IN DAYS HENCE//. IT SEEMS THAT OUR CROOKS ARE HAVING A HARD TIME TRYING TO CONTROL THE PRICE OF GOLD AND THUS THE NEED FOR RECORD T.A.S. ISSUANCE.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: APRIL (41.9844 TONNES) ( ACTIVE MONTH)

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 24 MONTHS OF 2021-2023:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

NOV: 18.7122 TONNES + 16.2505 EX. FOR RISK = 34.9627 TONNES

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276 TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 41.9844 TONNES

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT ROSE $18.70 //// AND WERE UNSUCCESSFUL IN KNOCKING ANY SPECULATOR LONGS AS WE HAD A STRONG SIZED LOSS OF 6088 TOTAL CONTRACTS ON OUR TWO EXCHANGES DESPITE OUR HIGHER PRICE 0F $18.70. THE ENTIRE LOSS IN OI WAS DUE TO T.A.S. LIQUIDATION.

WE HAD A VERY STRONG T.A.S. LIQUIDATION ON THE FRONT END OF MONDAY’S TRADING ALONG. THE T.A.S. ISSUED ON MONDAY NIGHT, WILL BE “PUT INTO THE BANK” TO BE USED AT A LATER DATE AT THE COLLUSIVE CHOOSING OF OUR BANKERS. THE HIGH T.A.S. ISSUANCE IS MEANT TO CONTROL THE PRICE OF GOLD

WE HAVE LOST A TOTAL OI OF 18.102 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR APRIL. (44.8615 TONNES) ON FIRST DAY NOTICE FOLLOWED BY TODAY’S E.F.P. JUMP TO LONDON OF 1900 OZ (0.05909 TONNES)//NEW STANDING; 41.9844

NEW STANDING: 41.988 TONNES

ALL OF THIS WAS ACCOMPLISHED DESPITE OUR GAIN IN PRICE TO THE TUNE OF $18.70

WE HAD REMOVED 268 CONTRACTS TO THE COMEX TRADES TO OPEN INTEREST (CROOKS)

NET LOSS ON THE TWO EXCHANGES 6088 CONTRACTS OR 608,800 OZ (18.94 TONNES)

estimated volume today 232,503 //fair

final gold volumes/yesterday 230,124 fair

//speculators have left the gold arena

APRIL 2/ INITIAL APRIL GOLD

/ /// THE APRIL 2024 GOLD CONTRACT

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | nil oz . |

| Deposit to the Dealer Inventory in oz | nil oz |

| Deposits to the Customer Inventory, in oz | nil oz |

| No of oz served (contracts) today | 252 notice(s) 25,200 OZ 0.7838 TONNES |

| No of oz to be served (notices) | 3374 contracts 337400 oz 10.494 TONNES |

| Total monthly oz gold served (contracts) so far this month | 10,124 notices 1012400 oz 31.489 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | x |

0 dealer deposits:

total dealer deposits: nil oz

total customer withdrawals: 0

i

total customer withdrawal: nil oz

we had 0

total deposit 0 oz

Adjustments: 1

i) dealer to customer

i) out of ASAHI 86,599.825 oz

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR APRIL.

For the front month of APRIL we have an oi of 3623 contracts having LOST 4658 contracts. We had 4636 contracts served on Monday, so we lost 19 contracts or an additional 1900 oz (0.0590 tonnes) will not stand at the comex as they were immediately EFP’d to London to take delivery over on that side of the pond on a T + 2 basis.

MAY LOST 18 CONTRACTS TO STAND AT 1596

JUNE DECREASED ITS OI BY 4,411 CONTRACTS DOWN TO 424,842 CONTRACTS.

We had 252 contracts filed for today representing 25,200 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 97 notices were issued from their client or customer account. The total of all issuance by all participants equate to 252 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 252 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for the APRIL. /2024. contract month, we take the total number of notices filed so far for the month (10,124 x 100 oz ), to which we add the difference between the open interest for the front month of APRIL. (3626 CONTRACTS) minus the number of notices served upon today 252 x 100 oz per contract equals 1,349,800 OZ OR 41.9844 TONNES.

thus the INITIAL standings for gold for the APRIL. contract month: No of notices filed so far (10,124) x 100 oz + (3626) {OI for the front month} minus the number of notices served upon today (252) x 100 oz which equals 1,349,800 oz (41.9844 TONNES)

TOTAL COMEX GOLD STANDING FOR APRIL: 41.9844 TONNES WHICH IS HUGE FOR A NON ACTIVE DELIVERY MONTH IN THE CALENDAR.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 1,615,085.921 50.23 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD: 17,779,096,149 OZ

TOTAL REGISTERED GOLD 7,550,370.137 (234.848 tonnes).

TOTAL OF ALL ELIGIBLE GOLD: 10,228,726.223 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 5,935,.285 oz (REG GOLD- PLEDGED GOLD) 184.612 tonnes/dropping like a stone

END

SILVER/COMEX

APRIL 2

INITIAL

//2024// THE APRIL 2024 SILVER CONTRACT//INITIAL

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 322,675.968 oz Brink CNT . |

| Deposits to the Dealer Inventory | nil OZ |

| Deposits to the Customer Inventory | 599,,692.200 OZ ASAHI |

| No of oz served today (contracts) | 11 CONTRACT(S) (55,000 OZ) |

| No of oz to be served (notices) | 171 contracts (855,000 oz) |

| Total monthly oz silver served (contracts) | 350 Contracts (1,750,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

i) 0 dealer deposit

total dealer deposit :nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: 0 oz

We had 1 deposits customer account:

i) Into

ASAHI 599,662.200 oz

total customer deposits 599,662.200 oz

JPMorgan has a total silver weight: 129.806 million oz/287.735 million or 45.18%

adjustment: 0

Comex withdrawals:

i) Into Brinks: 9022.260 oz

ii) CNT 313,708 oz

total withdrawal: 322,675..968 oz

TOTAL REGISTERED SILVER: 46.136MILLION OZ//.TOTAL REG + ELIGIBLE. 287.735million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR DECEMBER:

silver open interest data:

FRONT MONTH OF APRIL /2023 OI: 182 CONTRACTS HAVING LOST 0 CONTRACT(S).

WE HAD 15 CONTRACTS SERVED ON MONDAY, SO WE GAINED 15 CONTRACTS OR ADDITIONAL 75,000 OZ WILL STAND AT THE COMEX UNDERGOING A QUEUE JUMP.

MAY SAW A GAIN OF 196 CONTRACTS DOWN TO 117,708

JUNE WAS A GAIN OF 23 CONTRACTS RISING TO 31.

JULY SAW A GAIN OF 1436 CONTRACTS UP TO 26,051

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 15 for 75,000 oz

Comex volumes// est. volume today 70,542 VERY GOOD

Comex volume: confirmed yesterday 63,006 good.

To calculate the number of silver ounces that will stand for delivery in APRIL. we take the total number of notices filed for the month so far at 350 x 5,000 oz = 1,750,000 oz

to which we add the difference between the open interest for the front month of APRIL (182) and the number of notices served upon today 11 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the APRIL/2024 contract month: 350 (notices served so far) x 5000 oz + OI for the front month of APRIL. (182) – number of notices served upon today 11 )x 500 oz of silver standing for the APRIL contract month equates to 2.6050 MILLION OZ.

New total standing: 2.6050 million oz.

There are 46.136 million oz of registered silver.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS//

BOTH GLD AND SLV ARE MASSIVE FRAUDS!

APRIL 2 WITH GOLD UP $23.90 TODAY; HUG CHANGES IN GOLD INVENTORY AT THE GLD A WITH DRAWAL OF 1.15 TONNES OF GOLD FROM THE GLD.:// INVENTORY REMAINS AT 829.00 TONNES

APRIL 1 WITH GOLD UP $18.70 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD:// INVENTORY REMAINS AT 830.15 TONNES

MARCH 28 WITH GOLD UP $26.30 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD:// INVENTORY REMAINS AT 830.15 TONNES

MARCH 27 WITH GOLD UP $15.00 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 5.18 TONNES OF GOLD FROM THE GLD// INVENTORY FALLS TO 830.15 TONNES

MARCH 26 WITH GOLD UP $1.40 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD INVENTORY RISES TO 835.33 TONNES

MARCH 25 WITH GOLD UP $17.05 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD INVENTORY RISES TO 838.50 TONNES

MARCH 22 WITH GOLD DOWN $23.75 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD INVENTORY RISES TO 838.50 TONNES

MARCH 21 WITH GOLD UP $24.80 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD A STRONG PAPER DEPOSIT OF 1.15 TONNES OF GOLD INTO THE GLD/:INVENTORY RISES TO 838.50 TONNES

MARCH 20 WITH GOLD UP $1.45 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD A STRONG PAPER DEPOSIT OF 1.48 TONNES OF GOLD INTO THE GLD/:INVENTORY RISES TO 837.35 TONNES

MARCH 19 WITH GOLD DOWN $4.10 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD A STRONG PAPER DEPOSIT OF 1.48 TONNES OF GOLD INTO THE GLD/:INVENTORY RISES TO 833.32 TONNES

MARCH 15 WITH GOLD DOWN $5.20 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD/:INVENTORY REMAINS AT 816.86 TONNES

MARCH 14 WITH GOLD DOWN $12.20 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF 1.73 TONNES OF GOLD INTO THE GLD//:INVENTORY REMAINS AT 816.86 TONNES

MARCH 13 WITH GOLD UP $14.40 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD:INVENTORY REMAINS AT 815.13 TONNES

MARCH 12 WITH GOLD DOWN $21.15 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD:NOT AVAILABLE///LAST VALUE 815.13 TONNES

MARCH 11 WITH GOLD UP $3.20 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.44 TONNES OF GOLD OUT OF THE GLD AFTER 7 CONSECUTIVE GOLD PRICE RISES//INVENTORY RESTS AT 815.13 TONNES

MARCH 8 WITH GOLD UP $21.05 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 0.87 TONNES OF GOLD OUT OF THE GLD AFTER 7 CONSECUTIVE GOLD PRICE RISES//INVENTORY RESTS AT 816.57 TONNES

MARCH 7 WITH GOLD UP $7.20 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4,20 TONNES OF GOLD OUT OF THE GLD//INVENTORY RESTS AT 817.44 TONNES

MARCH 6 WITH GOLD UP $17.20 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.30 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 821.47 TONNES

MARCH 5 WITH GOLD UP $16.55 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.30 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 821.47 TONNES

MARCH 4 WITH GOLD UP $30.55 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF .86 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 823.77 TONNES

MARCH 1 WITH GOLD UP $40.40 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 822.91 TONNES

FEB29/WITH GOLD UP $12.60 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD//WITHDRAWAL OF 4.03 TONNES INVENTORY RESTS AT 822.91 TONNES

FEB28/WITH GOLD DOWN $1.00 TODAY NO CHANGES IN GOLD INVENTORY AT THE GLD INVENTORY RESTS AT 826.94 TONNES

FEB27/WITH GOLD UP $4.40 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF .87 TONNES OF GOLD FROM THE GLD:/INVENTORY RESTS AT 826.94 TONNES

FEB26/WITH GOLD DOWN $8.90 TODAY NO CHANGES IN GOLD INVENTORY AT THE GLD:/INVENTORY RESTS AT 827.81 TONNES

FEB23/WITH GOLD UP $17 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.01 TONNES OF GOLD FROM THE GLD.//INVENTORY RESTS AT 827.81 TONNES

FEB22/WITH GOLD DOWN $2.15 TODAY NO CHANGES IN GOLD INVENTORY AT THE GLD://INVENTORY RESTS AT 829.82 TONNES

FEB21/WITH GOLD DOWN $5.30 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 7.59 TONNES OF GOLD OUT OF THE GLD///INVENTORY RESTS AT 29.82 TONNES

FEB20/WITH GOLD UP $16.15 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 0.58 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 837.89 TONNES

FEB16/WITH GOLD UP $8,60 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.73 TONNES OF GOLD FROM THE GLD///INVENTORY RESTS AT 837.31 TONNES

FEB15/WITH GOLD UP $11.70 TODAY NO CHANGES IN GOLD INVENTORY AT THE GLD:/INVENTORY RESTS AT 841.92 TONNES

FEB14/WITH GOLD DOWN $2.75 TODAY NO CHANGES IN GOLD INVENTORY AT THE GLD:/INVENTORY RESTS AT 841.92 TONNES

FEB13/WITH GOLD DOWN $20.15 TODAY NO CHANGES IN GOLD INVENTORY AT THE GLD:/INVENTORY RESTS AT 841.92 TONNES

FEB12/WITH GOLD DOWN $4.80 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A STRONG WITHDRAWAL OF 1.74 TONNES OF GOLD FROM THE GLD. / //://INVENTORY RESTS AT 841.92 TONNES

FEB9/WITH GOLD DOWN $8.60 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A STRONG DEPOSIT OF 1.44 TONNES OF GOLD FROM THE GLD. / //://INVENTORY RESTS AT 843.66 TONNES

FEB8/WITH GOLD DOWN $2.70 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A MASSIVE WITHDRAWAL OF 5.47 TONNES OF GOLD FROM THE GLD. / //://INVENTORY RESTS AT 842.22 TONNES:

FEB7/WITH GOLD UP $0.40 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A MASSIVE WITHDRAWAL OF 4.04 TONNES OF GOLD FROM THE GLD. / //://INVENTORY RESTS AT 847.69 TONNES:

FEB6/WITH GOLD UP $8.50 TODAY NO CHANGES IN GOLD INVENTORY AT THE GLD:/ / //://INVENTORY RESTS AT 851.73 TONNES:

GLD INVENTORY: 82900 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

APRIL 2/WITH SILVER UP 84 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 6.721 MILLION OZ INTO THE SLV// SLV INVENTORY RESTS AT 430.806 MILLION OZ

APRIL 1/WITH SILVER UP 14 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV// SLV INVENTORY RESTS AT 424.085 MILLION OZ

MARCH 28/WITH SILVER UP 20 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A DEPOSIT OF 1.005 MILLION OZ INTO THE SLV: SLV INVENTORY RESTS AT 424.085 MILLION OZ

MARCH 27/WITH SILVER UP 14 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A A DEPOSIT OF 1.691 MILLION OZ INTO THE SLV: SLV INVENTORY RESTS AT 423.079 MILLION OZ

MARCH 26/WITH SILVER DOWN 24 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV A A DEPOSIT OF 0.366 MILLION OZ INTO THE SLV: SLV INVENTORY RESTS AT 421.388 MILLION OZ

MARCH 25/WITH SILVER UP 8 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A HUGE WITHDRAWAL OF 3.887 MILLION OZ INTO THE SLV: SLV INVENTORY RESTS AT 421.022 MILLION OZ

MARCH 22/WITH SILVER DOWN 9 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A HUGE DEPOSIT OF 1.1899 MILLION OZ INTO THE SLV: SLV INVENTORY RESTS AT 424.909 MILLION OZ

MARCH 21/WITH SILVER DOWN 8 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A HUGE WITHDRAWAL OF 3.560 MILLION OZ INTO THE SLV: SLV INVENTORY RESTS AT 423.720 MILLION OZ

MARCH 20/WITH SILVER DOWN 5 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A HUGE DEPOSIT OF 11.792 MILLION OZ INTO THE SLV: SLV INVENTORY RESTS AT 427.280 MILLION OZ

MARCH 18/WITH SILVER DOWN 11 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A HUGE DEPOSIT OF 11.792 MILLION OZ INTO THE SLV: SLV INVENTORY RESTS AT 427.280 MILLION OZ

MARCH 15/WITH SILVER DOWN 9 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 1.006 MILLION OZ FROM THE SLV: SLV INVENTORY RESTS AT 417.866 MILLION OZ

MARCH 14/WITH SILVER DOWN 9 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: SLV INVENTORY RESTS AT 418.872 MILLION OZ

MARCH 13/WITH SILVER UP 32 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: SLV INVENTORY RESTS AT 418.872 MILLION OZ…

MARCH 12/WITH SILVER DOWN 31 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A SMALL WITHDRAWAL OF 0.549 MILLION OZ OF SILVER INTO THE SLV//// : SLV INVENTORY RESTS AT 418.872 MILLION OZ…

MARCH 11/WITH SILVER UP 11 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A HUGE WITHDRAWAL OF 2.147 MILLION OZ OF SILVER FROM THE SLV//// : SLV INVENTORY RESTS AT 418.323 MILLION OZ…SUCH A MASSIVE FRAUD!

MARCH 8/WITH SILVER DOWN 5 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A HUGE WITHDRAWAL OF 4.299 MILLION OZ OF SILVER FROM THE SLV//// : SLV INVENTORY RESTS AT 420.519 MILLION OZ…SUCH A MASSIVE FRAUD!

MARCH 7/WITH SILVER UP 8 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A HUGE WITHDRAWAL OF 4.665 MILLION OZ OF SILVER FROM THE SLV//// : SLV INVENTORY RESTS AT 424.818 MILLION OZ…SUCH A MASSIVE FRAUD!

MARCH 6/WITH SILVER UP 52 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A HUGE WITHDRAWAL OF 2.378 MILLION OZ OF SILVER FROM THE SLV//// : SLV INVENTORY RESTS AT 427,105 MILLION OZ

MARCH 5/WITH SILVER DOWN 2 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A HUGE WITHDRAWAL OF 1.499 MILL;ION OZ OF SILVER FROM THE SLV//// : SLV INVENTORY RESTS AT 429.483 MILLION OZ

MARCH 4/WITH SILVER UP CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: // : SLV INVENTORY RESTS AT 430.982 MILLION OZ

MARCH 1/WITH SILVER UP 49 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: // : SLV INVENTORY RESTS AT 430.982 MILLION OZ

FEB 29/WITH SILVER UP 25 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.104 MILLION OZ OUT OF THE SLV//// : SLV INVENTORY RESTS AT 430/982 MILLION OZ

FEB 28/WITH SILVER DOWN 7 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 5.123 MILLION OZ INTO THE SLV//// : SLV INVENTORY RESTS AT 433.086 MILLION OZ

FEB 27/WITH SILVER UP 3 CENTS TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 0.64 MILLION OZ FROM THE SLV//// : SLV INVENTORY RESTS AT 427.943 MILLION OZ

FEB 26/WITH SILVER DOWN 44 CENTS TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.065 MILLION OZ FROM THE SLV//// : SLV INVENTORY RESTS AT 428.603 MILLION OZ

FEB 23/WITH SILVER DOWN 44 CENTS TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.065 MILLION OZ FROM THE SLV//// : SLV INVENTORY RESTS AT 428.603 MILLION OZ

FEB 22/WITH SILVER DOWN 10 CENTS TODAY NO CHANGES IN SILVER INVENTORY AT THE SLV

// : SLV INVENTORY RESTS AT 432.766 MILLION OZ

FEB 21/WITH SILVER DOWN 28 CENTS TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 2.348 MILLION OZ OF SILVER FROM THE SLV// : SLV INVENTORY RESTS AT 432.766 MILLION OZ

FEB 20/WITH SILVER DOWN 33 CENTS TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 3.385 MILLION OZ OF SILVER FROM THE SLV// : SLV INVENTORY RESTS AT 435.008 MILLION OZ

FEB 16/WITH SILVER UP 53 CENTS TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV A DEPOSIT OF 1.235 MILLION OZ OF SILVER FROM THE SLV// : SLV INVENTORY RESTS AT 438.393 MILLION OZ

FEB 15/WITH SILVER UP 56 CENTS TODAY NO CHANGES IN SILVER INVENTORY AT THE SLV : SLV INVENTORY RESTS AT 437.615 MILLION OZ

FEB 14/WITH SILVER UP 24 CENTS TODAY NO CHANGES IN SILVER INVENTORY AT THE SLV : SLV INVENTORY RESTS AT 437.615 MILLION OZ

FEB 13/WITH SILVER DOWN 60 CENTS TODAY SMALL CHANGES IN SILVER INVENTORY AT THE SLV A SMALL WITHDRAWAL OF 0.504 MILLION OZ OZ OUT OF THE SLV: SLV INVENTORY RESTS AT 437.615 MILLION OZ

FEB 12/WITH SILVER UP 14 CENTS TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV A HUGE WITHDRAWAL OF 1.921 MILLION OZ OZ OUT OF THE SLV: SLV INVENTORY RESTS AT 438.119 MILLION OZ

FEB 9/WITH SILVER DOWN 4 CENTS TODAY SMALL CHANGES IN SILVER INVENTORY AT THE SLV A SMALL DEPOSIT OF 600,000 OZ INTO THE SLV: SLV INVENTORY RESTS AT 440.040 MILLION OZ

FEB 8/WITH SILVER UP 29 CENTS TODAY NO CHANGES IN SILVER INVENTORY AT THE SLV: SLV INVENTORY RESTS AT 439.994 MILLION OZ

FEB 7/WITH SILVER DOWN 18 CENTS TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A MASSIVE DEPOSIT OF 4.04 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 439.994 MILLION OZ//LAST 9 DAYS: 10.7598 MILLION OZ WITHDRAWAL

CLOSING INVENTORY 430.806 MILLION OZ//

PHYSICAL GOLD/SILVER COMMENTARIES

1:Peter Schiff/Mike Maharrey

2.Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens/

Jamie Dimon Huddles in Private with Biden Bigwigs as His Bank Faces More Crime Charges

By Pam Martens and Russ Martens: April 1, 2024

Remember that time in 2016 when Attorney General Loretta Lynch decided she would take a private meeting with Bill Clinton on her plane as it was parked on the tarmac in Phoenix – while his wife, Hillary Clinton, was under federal investigation for using an unsafe private email server at her New York home to receive classified government emails when she was Secretary of State?

What President Biden’s Vice President, Kamala Harris, and his Chief of Staff, Jeff Zients, did in mid-March was equally scandalous. Harris had a “one-on-one lunch at the White House” with Jamie Dimon, the Chairman and CEO of the most crime-riddled bank in the United States, JPMorgan Chase. Zients also separately met with Dimon. That reporting comes courtesy of reporters Joshua Franklin and James Politi of the Financial Times (paywall). It has not been disputed by the Biden administration.

Dimon’s private meetings in Washington come as the bank (that has already admitted to a string of five criminal felony charges) is currently facing a serious investigation for “billions” of improperly conducted trades by its federally-insured bank. Two of its federal regulators, the Office of the Comptroller of the Currency and the Federal Reserve, settled those charges in March for a combined $348 million. Both regulators provided extremely sketchy details as to the precise nature of the trading misconduct. JPMorgan Chase revealed in an SEC filing in February that it remains under investigation in the same matter by a third regulator “but there is no assurance that such discussions will result in a resolution,” the bank wrote in the filing.

It would certainly not be the first time that Dimon attempted to throw his weight around in Washington to get his bank out of trouble. During Congressional hearings in 2012, when Dimon was called to testify about his bank allowing its traders to use deposits from its federally-insured bank to gamble in derivatives in London and lose what eventually tallied up to $6.2 billion (the infamous “London Whale” scandal), Dimon had the temerity to wear presidential cuff links to show off a gift from the White House.

Then there was Dimon’s meeting with Attorney General Eric Holder during the Obama administration when JPMorgan Chase was being investigated for widespread mortgage fraud. For what the bank got away with in that matter, see Matt Taibbi’s report revealing that the Justice Department sandbagged their key witness, a former lawyer/ whistleblower inside JPMorgan Chase, who called it “the biggest financial cover-up in history.”

According to the recent Financial Times report, Vice President Harris did not list the luncheon on her official daily calendar, suggesting she knew it was inappropriate. The FT reporters also reveal the following:

“Dimon, one of the most influential voices on Wall Street, also separately met White House chief of staff Jeff Zients while he was in Washington, as well as federal regulators and members of Congress. It could not be learnt what was discussed at the meetings. The White House and JPMorgan, the largest US bank by assets, declined to comment.”

The only reason that Dimon is still called “one of the most influential voices on Wall Street” is because sycophants in mainstream media still call him that. Engaged Americans, like former Labor Secretary and Public Policy Professor Robert Reich, call Dimon an “oligarch” who has “hijacked the system.” Trial attorneys Helen Davis Chaitman and Lance Gotthoffer released a book, JPMadoff: The Unholy Alliance Between America’s Biggest Bank and America’s Biggest Crook, in which they provided this take on Dimon:

“In Chapter 4, we compared JPMC [JPMorgan Chase] to the Gambino crime family to demonstrate the many areas in which these two organizations had the same goals and strategies. In fact, the most significant difference between JPMC and the Gambino Crime Family is the way the government treats them. While Congress made it a national priority to eradicate organized crime, there is an appalling lack of appetite in Washington to decriminalize Wall Street. Congress and the executive branch of the government seem determined to protect Wall Street criminals, which simply assures their proliferation…

“If Jamie Dimon is running a criminal institution, he should be prosecuted for it. And law enforcement has the perfect tool for such a prosecution: the Racketeer Influenced and Corrupt Organizations ACT (RICO).”

In 2014, the non-profit watchdog, Better Markets, filed a federal lawsuit against the U.S. Department of Justice and the man who sat at its helm, Attorney General Eric Holder. The lawsuit challenged what had emerged out of that cozy meeting between Holder and Dimon – a $13 billion out-of-court settlement over the bank’s sale of toxic mortgages.

Better Markets wrote on its website that this was at the time “The largest settlement in U.S. history from a single entity by more than 300%” and that it “granted JP Morgan blanket civil immunity for years of alleged, but undisclosed, pervasive, egregious and knowing fraudulent and illegal conduct that contributed to the 2008 financial crash and the worst economy since the Great Depression.”

Among the allegations in the Better Markets’ press release, these three stood out:

“The Attorney General and other senior DOJ political appointees negotiated directly and entirely in secret with the CEO of JP Morgan Chase [Jamie Dimon], someone who was considered a possible Treasury Secretary just a few years ago.

“The cellphone of DOJ’s third highest ranking official rang with the ‘familiar’ phone number of JP Morgan Chase’s CEO [Jamie Dimon], who called to offer billions of dollars to stop DOJ from holding a press conference and filing a lawsuit in just a few hours. The call worked, and the press conference and lawsuit were both called off.

“DOJ gave complete civil immunity to JP Morgan Chase for defrauding thousands in exchange for $13 billion, via a contract that was negotiated and finalized in secret without any review or approval by a federal court.”

Attorneys for the Justice Department asked the federal court to dismiss the Better Markets lawsuit on the basis that Better Markets lacked standing to file the lawsuit. The U.S. District Court for the District of Columbia did just that in a longwinded decision that effectively stripped Americans of their ability to fight back against the increasingly corrupt nexus between Washington and Wall Street.

If you agree with Wall Street On Parade that the current banking structure in the U.S. represents a threat to national security and economic stability, please contact your U.S. Senators today via the U.S. Capitol switchboard by dialing (202) 224-3121. Tell your Senators to hold immediate hearings on the urgent need to restore the Glass-Steagall Act to separate Wall Street’s trading casinos from federally-insured commercial banks.

END

MATHEW PIEPENBURG

The Implications Of Fatal Debt? Expect More Lies

MONDAY, APR 01, 2024 – 07:00 PM

Authored by Matthew Piepenburg via VonGreyerz/gold,

If you want to understand the direction of debt, rates, the USD, inflation, risk asset markets, gold and the US endgame, it might be better not to listen to the experts.

In fact, Johny Cash is a far better source…

Five Feet High & Rising

In a classic 1959 tune by Johny Cash, the singer asks: “How high’s the water mama?”

This question is then answered by a riff which chants, “she said it’s two feet high and risin.’”

And with each subsequent refrain, the water level goes to three feet, four feet and then five feet, “high and risin’.”

In short: An obvious flood.

And when it comes to debt in the land of the world reserve currency, Johny Cash may have something to teach Jerome Powell and the other DC children drowning the US (and its debt-soaked Dollar) into a slow but steady debt flood.

Boring?

I’ve often said that good journalism, like honest economics, is boring.

One has to understand “hard” indicators like bond yields (which move inversely to bond price) and the high-school level basics of supply and demand forces.

But as I’ve also said countless times, and will say countless times more: The bond market is THE thing, because bonds are all about DEBT.

If you understand bonds, and in particular, the Fed’s hidden (real) mandate to save Uncle Sam’s sovereign IOU’s from sinking in price, then you will be able to easily foresee (rather than date predict) the future of risk assets, gold, BTC, the USD and yes, inflation.

The complex truly is that simple.

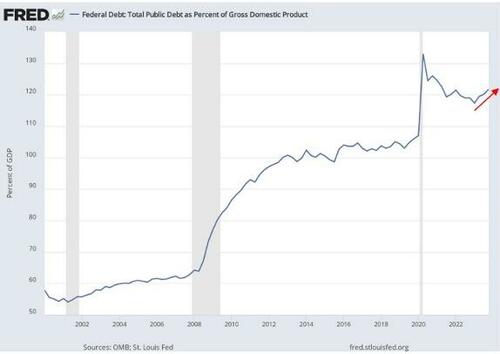

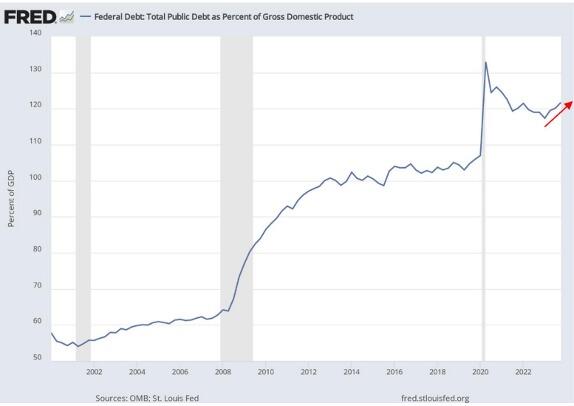

How High’s the Debt Mama? 120% and Risin’

And if you turn to Johny Cash and ask “How high’s the debt level mama?” well… the blunt answer informs just about everything you need to know.

So, let’s keep it simple.

Simple, Not Boring

Debt is WHERE it all begins, and it tells you exactly HOW the American song ends.

And just how high is the water (debt) mama?

Ten years ago, US public debt was $17T “and risin’.”

Today it’s $34.5T “and risin’.”

America’s debt to GDP is 120%, its deficit to GDP is around 6%, and every 100 days we add another $1T in borrowing to our shameless bar tab of debt addiction masquerading as capitalism.

Even our own Congressional Budget Office will confess that unless we issue more debt (and print more debased money to monetize it), our Medicare and social security piggy bank will be empty by 2030.

Meanwhile, the USA is staring down the barrel of $212T in unfunded liabilities yet only $190T in assets.

In other words, and based on objective math, America literally has the balance sheet of a banana republic.

No Crisis?

Apologists (i.e., truth and math-challenged politicos), however, will tell you there is no crisis, even as the water levels rise past our closed eyes.

The clever ones will remind us that America’s USD comprises 85% of FX transactions, the vast bulk (80%) of international trade settlements, and is in constant “milk-shake” demand from the Eurodollar, derivative and SWIFT payment systems.

In other words, the Dollar is gonna be just fine.

Hmmm…

Facts vs. “Just Fine”

As warned from day-1 of the myopic (and suicidal) sanctions against Putin in which the US weaponized the world reserve currency, those days of a “just fine” USD simply ended.

Not all at once, but slow and steady, like a flood’s water line…

In just 2 years, we’ve seen undeniable signs of de-dollarization from the BRICS+ nations and an extraordinarily telling shift in the petrodollar dynamics (20% of 2023 global oil sold outside the USD), which would have been otherwise unimaginable in the pre-sanction era.

But, if you remain convinced that America and its reserve currency have magical immunity from the de-dollarization’s slow drip greenback demise, let’s get back to the oh-so boring but oh-so honest cries of the US Treasury market.

Why?

Again. Because the bond market is everything.

As important, the bond market has everything to do with debt, and current US debt is drowning the nation and diluting the USD, one slow trillion at a time.

Sound sensational?

Pounding A Fact-Based Fist

For years, I have pounded my fist reminding readers and viewers that debt destroys nations and currencies. Every time, and without exception.

And for years I have pounded my fist saying the Powell’s “war on inflation” was a ruse, as every debt-soaked nation needs to debase its currency to inflate away debt.

And from day-1 of Powell’s claim (lie) that inflation was “transitory,” I’ve been calling his bluff.

For years, I’ve argued that the Fed would simply lie about inflation (i.e., grossly under-report it) in order to make it appear statistically lower than what we actually knew/felt it to be.

Even Larry Summers, who is the classic arsonist (from his repeal of Glass-Steagall to deregulating the derivatives markets) now playing at fireman, has publicly stated that the actual US CPI scale, using pre-1983 housing methods, peaked last year at 18%, not the official 3.7% range…

If we then tack on a US debt/GDP ratio that is 30% higher today than in 2009, we mathematically see that despite Powell’s repressive “higher-for-longer” rate polices, we’ve made zero dent in our debt—instead, we’ve increased it.

In other words, our war against inflation is a loss; and our debts have increased.

And in the last couple of years, I’ve been pounding my fist that Powell would pivot from rising rates, to pausing rate cuts to eventually cutting rates followed in turn by outright money printing (or rather mouse-clicking Dollars) to “pay” Uncle Sam’s debt at the expense of our currency via what Luke Gromen calls “super QE.”

And all modesty aside, I think I/we have been right…

Right or Wrong?

Already, and as of last week, Powell has openly projected rate cuts in 2024, and they are likely to come by or near September.

We’ll see.

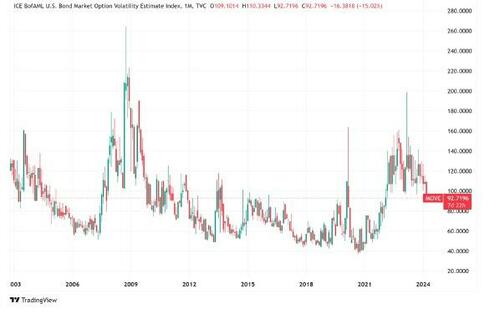

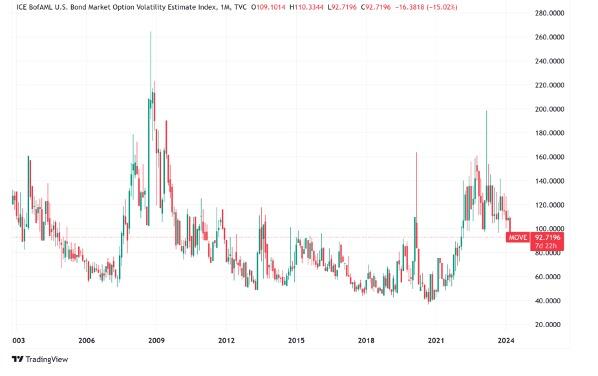

For now, just the promise (words) of rate cuts have been enough to send Pavlovian (Fed-dependent) markets to all-time-highs despite a real economy already under water.

And the subsequent decline in the Market Option Volatility Estimate (“MOVE” Index) was a neon-flashing sign that the market is getting ready for a new flood of dollar-diluting liquidity…

Where’s the QE, Matt?

But what about my forewarned QE?

What about that ultimate moment when Powell admits full defeat in his so-called “war” on inflation (while quietly seeking inflation) and openly does what many off us (nod again to Luke Gromen et al) already know he will do, that is: Debase the currency to “save” a rigged-to-fail (i.e., debt-based) USA?

Clearly, it seems, I/we have been wrong about that QE, no?

Well…Not so fast.

Coming Through the Back Door

In fact, Powell, along with his former Fed colleague-turned-mind-numbing Treasury Secretary, Janet Yellen, have been doing un-noticed back-door QE at staggering levels too complex (or obvious) for the mental midgets in our so-called main stream media to even notice.

Shocker? Hardly…

Facts Are Stubborn Things

The fact is that five times in the last four years, DC has been doing QE by just another name (what I call “backdoor QE”) to avoid the embarrassment of direct QE.

Notwithstanding the “not-QE” (which really was QE) in 2019 when the Fed bailed out a cash-dry repo market (which, by design, no one understood), the DC magicians have been doing trillions worth of QE-like liquidity measures without having to call it, well QE…

That is, the Fed and Treasury Dept. have been pulling liquidity out of the drying Treasury General Account, the now retired “BTFP” measures, and the intentionally confusing reverse repo markets.

More recently (and equally as well intentionally confusing to the masses), the Fed is quietly on the verge of allowing the Fed banks to use unlimited leverage to buy unlimited amounts of USTs off the Fed’s balance sheet via the removal of what the fancy lads call “Supplementary Reserve Ratios.”

This latest trick, by the way, is just off-balance sheet QE, and yet another symptom of the big banks becoming branch offices of the Fed, as our already centralized America becomes even more grotesquely, well…centralized, which is a classic symptom of a desperate and debt-soaked regime.

But just in case none of the foregoing tricks of backdoor QE have convinced you of what basically amounts to just QE, we can get our clearest signals from—you guessed it: THE BOND MARKET.

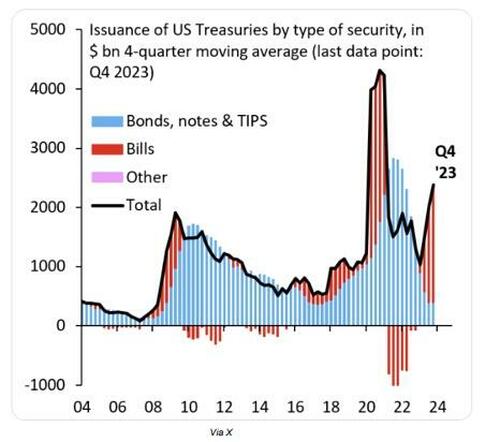

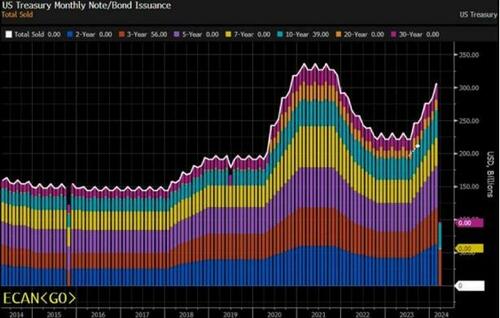

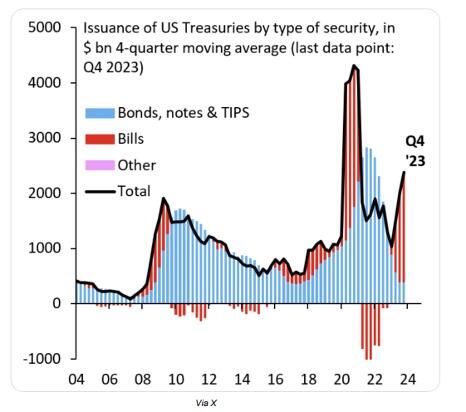

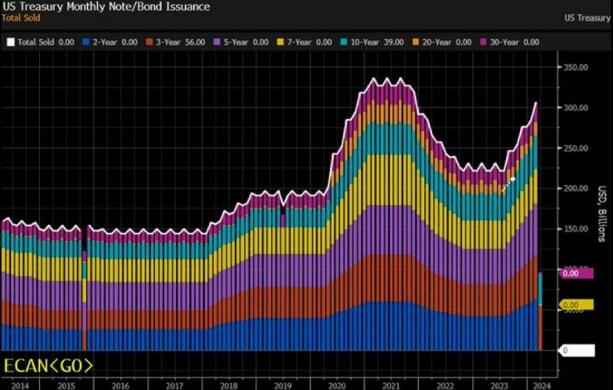

That is, one of the most obvious examples of “backdoor QE” is the Treasury Department’s open yet ignored trick of issuing most of its recent debt from the short duration end of the yield curve.

What The T-Bills Are Saying

By issuing more short-term IOUs in the form of T-Bills, this takes the supply-push inflation pressure off the openly unloved 10Y USTs, whose price declines (and subsequent as well as fatally unpayable yield/rate spikes) not only crushed regional banks, but Uncle Sam’s wallet as well.

OK. Yield curves and duration implications may sound, well… boring, but stick with me because this really, really matters.

The extreme levels of T-Bill issuance (as opposed to 10Y IOUs) has immense implications and is a flashing neon sign that the US is not heading into an economic crisis, but is in fact, ALREADY in a crisis.

Today, T-Bill issuance is at a two-decade high, and comprises greater than 85% of all US Treasury issuance.

This short-end issuance is far more like QE, i.e. simple money printing—which, we remind you, is highly inflationary/reflationary.

Hard to believe? See for yourself:

The last time we saw such QE-like desperation from the T-Bill side of the yield curve was during the Great Financial Crisis and the COVID crisis.

No Crisis? Huh?

But according to our so-called “leaders,” we are not at all in a crisis today. As they keep reminding us, we are at “full employment” (eh-hmmm) and nominal GDP is growing at 6%.

Then again, nominal GDP “growing” on the back of over $23T in UST issuance (bonds, notes and bills) is simply debt-driven “growth,” and debt-driven growth is not growth, it’s just debt.

In short, and as Luke Gromen concluded far better than I: “You know the debt crisis is real when the US resorts to short-term debt issuance.”

Summing Up

Whenever one is dealing with truth-challenged profiles like the Fed, Treasury Dept or White House, it is far better/simpler to watch what they do rather than what they say, as the difference is approximately 180 degrees…

All of the evidence above (from debt levels, de-dollarization trends, petrodollar shifts, backdoor QE measures and T-Bill over-issuance) screams of an open and obvious debt crisis which ALWAYS indicates a consequent currency crisis.

Always.

And as I have said for years, including a public discussion with Brent Johnson, the US can’t afford a strong USD because its debt levels require a weaker, inflated USD, regardless of its “relative”/DXY “strength.”

The string cite of evidence above (and beyond just rate cuts) is simply a cleverly veiled way of the Fed and Treasury telling us they want (need) a much weaker USD to save their necks at the expense of the dollar in your portfolio, checking account or wallet.

Gold, of course, is sniffing this out.

So are the stock markets and BTC.

So are the global central banks, who are stacking gold and dumping USTs at record levels.

The COMEX and London exchanges are also sniffing this out, as physical gold and silver is going from churn motions to actual physical delivery at record levels.

Meanwhile, even the BIS has made gold a Tier-1 asset.

Just saying…

The empirical (rather than “sensational”) evidence of an unloved UST and distrusted (debased and weaponized) USD is there for all who have eyes to see and ears to hear.

Gold has hit all-time-highs (and will go much, much higher) simply because the USD is going much, much lower.

But, of course, no one in DC will say the quiet part out loud.

3. CHRIS POWELL//GATA

4. OTHER MAJOR GOLD COMMENTARIES/PODCASTS/

5 a. IMPORTANT COMMENTARIES ON COMMODITIES/

5 B GLOBAL COMMODITY ISSUES/FOOD IN GENERAL//FREIGHT

END

6.CRYPTOCURRENCY//DIGITAL CURRENCY// COMMENTARIES/

END

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS TUESDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED DOWN 7.2359

OFFSHORE YUAN: DOWN TO 7.2627

SHANGHAI CLOSED DOWN 2.42 PPTS OR 0.08%

HANG SENG CLOSED U 390.10 OR 2.36%

2. Nikkei closed UP 35.82 OR 0.09%

3. Europe stocks SO FAR: MOSTLY ALL MIXED

USA dollar INDEX UP TO 104.69 EURO RISES TO 1.0745 UP 8 BASIS PTS

3b Japan 10 YR bond yield: RISES TO. +.742 Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 151.68/JAPANESE YEN NOW FALLING AS WELL AS LONG TERM 10 YR. YIELDS RISING //EVENTUALLY THIS WILL BREAK THE JAPANESE CENTRAL BANK

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen DOWN CHINESE ONSHORE YUAN: DOWN/ OFFSHORE: DOWN

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and UP FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund YIELD UP TO +2.4020***/Italian 10 Yr bond yield UP to 3.732* /SPAIN 10 YR BOND YIELD UP TO 3.247…**

3i Greek 10 year bond yield UP TO 3.349

3j Gold at $2257.05 silver at: 25.44 1 am est) SILVER NEXT RESISTANCE LEVEL AT $26.40

3k USA vs Russian rouble;// Russian rouble DOWN 0 AND 33 /100 roubles/dollar; ROUBLE AT 92.48//

3m oil into the 85 dollar handle for WTI and 87 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 151.68// 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 0.742% STILL ON CENTRAL BANK (JAPAN) INTERVENTION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.9084 as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.9761 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

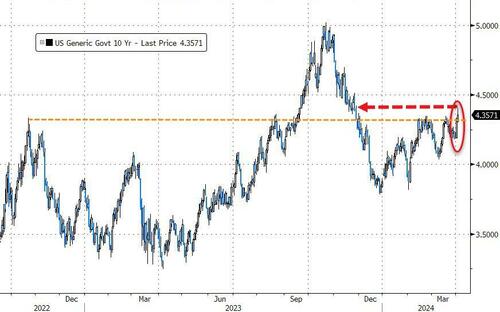

USA 10 YR BOND YIELD: 4.367 UP 4 BASIS PTS…

USA 30 YR BOND YIELD: 4.494 UP 3 BASIS PTS/

USA 2 YR BOND YIELD: 4.720 UP 0 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 32.25…(TURKEY SET TO BLOW UP FINANCIALLY)

GREAT BRITAIN/10 YEAR YIELD: UP 22 BASIS PTS AT 4.101

end

2.a Overnight: Newsquawk and Zero hedge,

Futures Slide As Yields Jump And Oil Surges

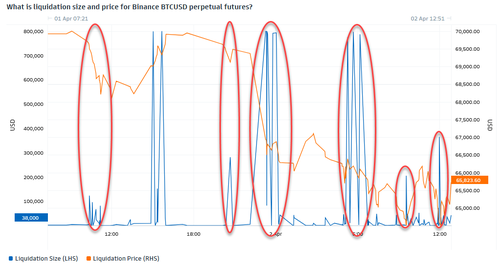

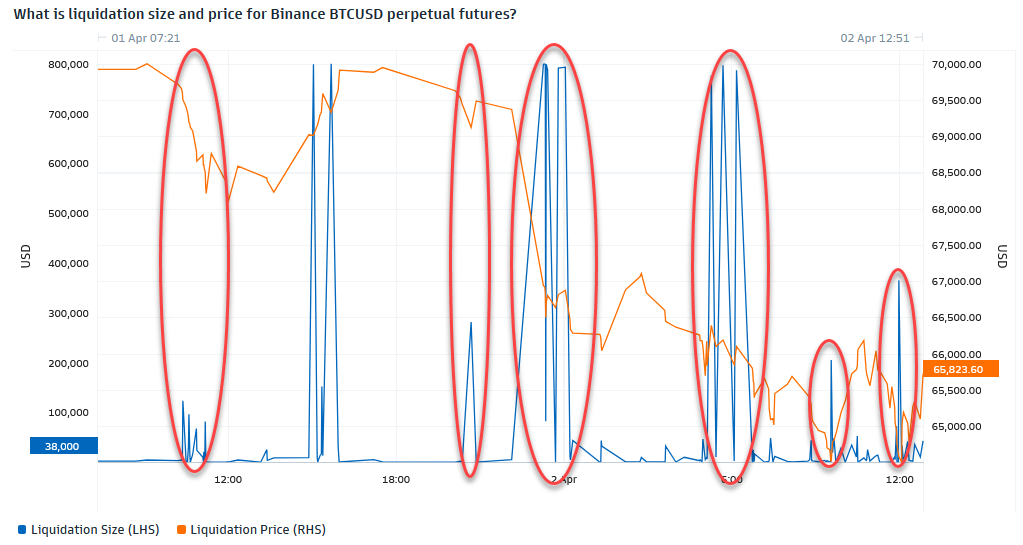

US equity futures are sliding as bond yields spike to 4.36%, the highest level since November, and the price of Brent crude rises to a new five-month high above $89 driven mostly by supply/demand dynamics but a geopolitical fear premium over the brewing Israel-Iran conflict begins to build, and as fears that the Fed may not cut rates in June start to percolate. The rest of the commodities complex is also pushing higher with strength in metals notable as Ags come from sale and gold jumps right back to all time highs despite the recent strength in the dollar. As of 7:50am, S&P and Nasdaq futures drop 0.4%, as health insurance stocks tumbled after regulators didn’t boost payments for private Medicare plans like the industry had come to expect; Mag7 names are mixed with Semis up small despite NVDA sliding. In Europe, most markets are mostly higher after reopening after the Easter holiday with only Spain in the red: energy, AI, and semis the best performing segments with additional support from banks, as regional curves bear steepen. The risk-on tone in APAC where HK showed significant outperformance. The yield curve is steeper, and the Bloomberg dollar index dropped. Bitcoin slumped after several sharp sell orders hit futures during Asian trading. Today’s macro data focus is on JOLTS and 3x Fedspeakers.

In premarket trading, crypto-related stocks fell with Coinbase Global down 2.5%, as pressure continued to build on Bitcoin, which shed 5% to trade below $67,000, having fallen about 10% from its mid-March peaks. US health insurance stocks were the other big premarket losers, after regulators didn’t boost payments for private Medicare plans like the industry had come to expect. Humana heavily exposed to Medicare, fell 9.2%, while UnitedHealth Group Inc. dropped 4.3%. Here are some other notable premarket movers:

- Clorox shares dip 1% after the cleaning and consumer products company was downgraded to neutral from buy at Citigroup, which said their call for a quick recovery following the cyberattack last year has “largely played out.”

- PVH shares slump 23% after the Calvin Klein owner forecast current fiscal year sales to decline more than consensus had expected. Analysts noted that the clothing company’s fourth-quarter results beat expectations, but expressed disappointment over the first-quarter and full-year outlook.

- Trump Media fell 3.8%, putting the stock on course to extend declines for a third consecutive session, after the firm disclosed a more than $58 million loss in 2023. The shares tumbled 21% on Monday.

All eyes were on interest rates as 10-year treasury yields rose about three basis points, adding to a 10 basis-point jump on Monday, when data showed an unexpected expansion in US manufacturing for the first time since September 2022. The impact was felt worldwide, with British 10-year yields climbing as much as 12 basis points, and German borrowing costs up almost 10 basis points.

As a result of rising oil price inflation, traders now reckon that the Fed will deliver fewer than three rate cuts this year, a view that could be bolstered if data at the end of this week show the US economy continued to add jobs at a healthy clip in March. They also see a good chance the central bank will push back the timing of its first rate cut, with odds of a June cut briefly falling below 50% on Monday.

Fed Chair Powell, who is due to speak again on Wednesday, said Friday that officials are awaiting more evidence prices are contained, adding that it wouldn’t be appropriate to lower rates until officials are sure inflation is in check. “The Fed is a difficult spot right now because if it eases too soon it could reignite the economy and inflation comes back, but if it doesn’t ease quickly enough, you get a bigger-than-expected economic slowdown,” said Andrew Pease, global head of investment strategy at Russell Investments Ltd. “At the margin, the data noise could convince the Fed to wait beyond June.”

Expectations of higher-for-longer Fed rates kept the dollar close to six-week highs against a basket of Group-of-Ten peers. The yen also stayed in focus, as the Japanese currency slipped further toward the 152-per-dollar level that many traders believe could force authorities’ hand toward intervention.

Markets are also keeping a close eye on geopolitical developments, as an Israeli airstrike on Iran’s embassy in Syria sent gold prices surging to a record high. Oil rallied above $85 as the attack added a risk premium to an already tight market.

European stocks rose but erased much of their earlier gains, with energy and mining stocks keading gains among sectors as US crude futures hit $85 a barrel for the first time since October, while real estate and media stocks laggedThe Stoxx 600 adds 0.1%, but well of earlier highs, while the FTSE 100 earlier topped 8,000 for the first time since February 2023. Here are the most notable European movers:

- Europe’s energy sub-index rises as much as 2.2% as oil advanced to a five-month high, buoyed by heightened geopolitical risks in the Middle East and tighter supply from Mexico.

- The basic resources sector gains as much as 2.3% as the price of aluminium, copper, nickel and iron ore all rise.

- Henkel shares gain as much as 2.4% to the highest in almost a year as Barclays (equal weight) raises its price target on the German industrial product manufacturer.

- Rheinmetall gains as much as 2.6% after getting an order to supply components for 22 self-propelled howitzers PzH2000 from KNDS Germany worth around €135 million.

- Delivery Hero shares rise as much as 7% in Frankfurt following local reports that its South Korean arm Woowa Brothers recorded a 65% increase in operating profit in 2023.

- Aker Carbon Capture shares surge as much as 49% after the company was awarded a contract from Norway’s Statkraft to capture 220,000 tonnes of carbon dioxide each year at the Heimdal waste-to-energy plant.

- Krones shares rise as much as 6% to a record high after Berenberg upgrades, saying the bottling machine manufacturer’s shares now represent an attractive buying opportunity.

- Ionos shares jump as much as 11% to the highest since its 2023 IPO following a DPA report that the cloud provider won a contract with Germany’s Federal Administration worth up to €410 million.

- Jungheinrich shares climb as much as 4.9% after Barclays gave the German machinery manufacturer a price target boost, citing constructive 2024 guidance and an attractive valuation.

- SSAB shares slide as much as 4.9% after the Sweden steelmaker unveiled plans to invest up to €4.5 billion on a new plant in Lulea that will help clean up one of the world’s dirtiest industries.

- Munters shares drop as much as 7.1% after Berenberg downgrades the Swedish industrial climate firm to hold from buy, saying the stock looks “somewhat inflated” following a strong run.

- S4 Capital shares fall as much as 8.2% after Citi said the advertising and marketing specialist’s near-term outlook is cloudy following disappointing guidance for 2024.

Earlier in the session, Asian stocks gained rebounding after Monday’s slump, with technology stocks climbing and Hong Kong posting strong gains as the market reopened following holidays.The MSCI Asia Pacific Index climbed as much as 0.6%, with chipmakers TSMC and Samsung among the biggest contributors. Hong Kong benchmarks gained more than 2%, leading the region higher, while mainland China stocks drifted lower after a three-day gain on improving economic data. Japanese stocks were mixed. Key gauges advanced in Taiwan, Singapore, South Korea and the Philippines.

- Hang Seng and Shanghai Comp. were mixed in which the Hong Kong benchmark outperformed as it played catch up on return from the Easter holiday closures, while the mainland was indecisive after a tepid PBoC liquidity operation

- Nikkei 225 was choppy and failed to sustain a brief foray back above the 40,000 status.

- Australia’s ASX 200 initially printed a fresh record high but then pared its gains as strength in the commodity-related industries was offset by losses in the consumer-related sectors, while RBA Minutes did little to spur price action.

“China is one of the most under-owned equity markets globally, so there is definitely some catch-up,” Stephanie Leung, chief investment officer at StashAway, told Bloomberg TV. “Leading indicators are telling us that China has already seen its worst in terms of cyclical downturn,” she said.

In FX, the Bloomberg Dollar Spot Index erased earlier gains, while Treasury yields extended yesterday’s sharp selloff and European bonds fell, catching up with Monday’s drop in USTs

- EUR/USD drops 0.2% to 1.0725, its lowest since Feb. 15; Bavaria March CPI slowed to 2.3% annually from 2.6% prior

- USD/CHF rallies 0.5% to 0.9086, a five-month high; Switzerland’s manufacturing PMI to 45.2 (estimate 45.0) in March from 44 in February

- Demand for USD/JPY during and after the Tokyo fix saw it climb to 151.80; investors are considering whether the macro backdrop is now strong enough for spot to breach 152 and possibly force the hand of Japanese authorities, according to Asia-based FX traders

- GBP/USD reverses losses, rises 0.1% to 1.2561; UK house prices fell for the first time in three months, suggesting the market may be stagnating due to high mortgage rates and strained affordability

In emerging markets, the Turkish lira surged against the dollar after President Recep Tayyip Erdogan indicated his economic team will be allowed to stay the course with orthodox monetary policies, despite a rout for the ruling party in local elections over the weekend.

In rates, treasuries extended Monday’s aggressive selloff, sending 10-year yields to four-month highs over 4.36%. Yields are near cheapest levels of the day in early US session amid latest rise in oil futures, up nearly 2% at highest level since October. Yields are cheaper by 2bp-6bp across the curve with front-end outperformance steepening 2s10s spread by 4bp; 10-year yields around 4.36% are more than 5bp higher on the day, while core European government bonds drop, echoing the sharp decline in Treasuries on Monday. Bunds did pare losses after German state CPI numbers suggested a slightly lower-than-forecast national reading. German 10-year yields rise 7bps to 2.37%. WTI crude oil futures over $85/bbl are a source of upward pressure on Treasury yields, along with technical factors as 10-year tests 4.35%. Fed-dated OIS rates are little changed, pricing in around 14bp of rate cuts for June meeting; further out, around 63bp of cuts remain priced in for December FOMC.

Pressure continues to build on Bitcoin, which shed 5% to trade below $67,000, having fallen about 10% from its mid-March peaks. Crypto-related stocks fell in US premarket trading, with Coinbase Global down 2.5%.

In commodities, crude futures pierced $85 for the first time since October, the latest milestone in a market that has rallied against a backdrop of OPEC+ cuts, strong demand and heightened geopolitical risk. WTI added as much as 1.8% in New York, while the global Brent benchmark neared $89 a barrel, after Iran vowed revenge on Israel after blaming it for a deadly air strike on its embassy in Syria — a rare direct confrontation in the adversaries’ escalating proxy conflict over the war in Gaza. Israel “will be punished. We will make them regret their crime,” Iran’s Supreme Leader, Ayatollah Ali Khamenei, said on Tuesday, according to the state-run Islamic Republic News Agency. Spot gold rises 0.5% to a new record high.

Looking at today’s calendar, the US economic data slate includes February JOLTS job openings and factory orders (10am) along with four scheduled Fed speakers: Bowman (10:10am), Williams (12pm), Mester (12:05pm) and Daly (1:30pm)

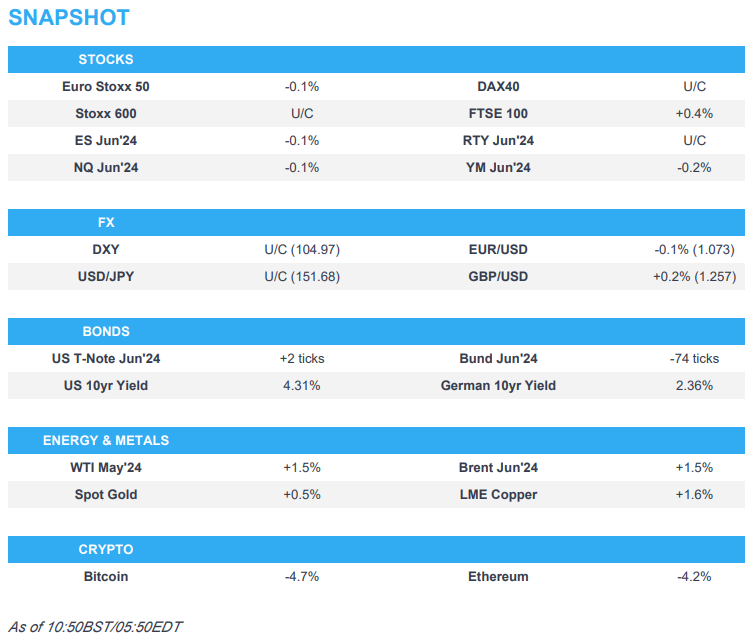

Market Snapshot

- S&P 500 futures little changed at 5,294.25

- STOXX Europe 600 up 0.4% to 514.50

- MXAP up 0.5% to 176.49

- MXAPJ up 0.7% to 541.07

- Nikkei little changed at 39,838.91

- Topix down 0.2% to 2,714.45

- Hang Seng Index up 2.4% to 16,931.52

- Shanghai Composite little changed at 3,074.96

- Sensex down 0.3% to 73,782.30

- Australia S&P/ASX 200 down 0.1% to 7,887.87

- Kospi up 0.2% to 2,753.16

- German 10Y yield little changed at 2.34%

- Euro down 0.1% to $1.0731

- Brent Futures up 1.3% to $88.55/bbl

- Brent Futures up 1.3% to $88.55/bbl

- Gold spot up 0.5% to $2,261.71

- US Dollar Index little changed at 105.01

Top Overnight News

- WTI hit $85 for the first time since October as Iran vowed revenge for what it says was an Israeli airstrike on its embassy in Syria, and amid tighter supply from Mexico. Adding to momentum, OPEC+ may decide tomorrow to continue with output curbs, while both Brent and WTI’s prompt spread jumped. BBG

- Australia’s central bank signaled a further shift toward a neutral stance as minutes of its March meeting showed the board didn’t consider the case to raise interest rates for the first time since May 2022. BBG

- Several Chinese developers’ shares have been suspended from trading in Hong Kong starting Tuesday due to their failure to meet the deadline for publishing last year’s annual results, another sign of the turmoil in the country’s real-estate sector. WSJ