APRIL 3/GOLD CLOSED UP $33.85 TO $2294.35//SILVER CLOSED UP $1.14 TO $26.94//PLATINUM CLOSED UP $13.20 TO $935.10 WHILE PALLADIUM CLOSED UP $20.15 UP T$1018.45//GOLD COMMENTARIES TODAY FROM SIMON WHITE, MIKE MAHARREY AND JAMES RICKARDS//ESTONIA CLAIMS THAT NATO COUNTRIES ALREADY HAVE BOOTS ON THE GROUND IN UKRAINE//ISRAEL VS HAMAS//ISRAEL VS HEZBOLLAH UPDATES//SWAMP STORIES FOR YOU TONIGHT/GREG HUNTER INTERVIEWING MARTIN ARMSTRONG//

The defense of $2300 gold is now upon us. Silver’s next line is $28.52. Then $34.76

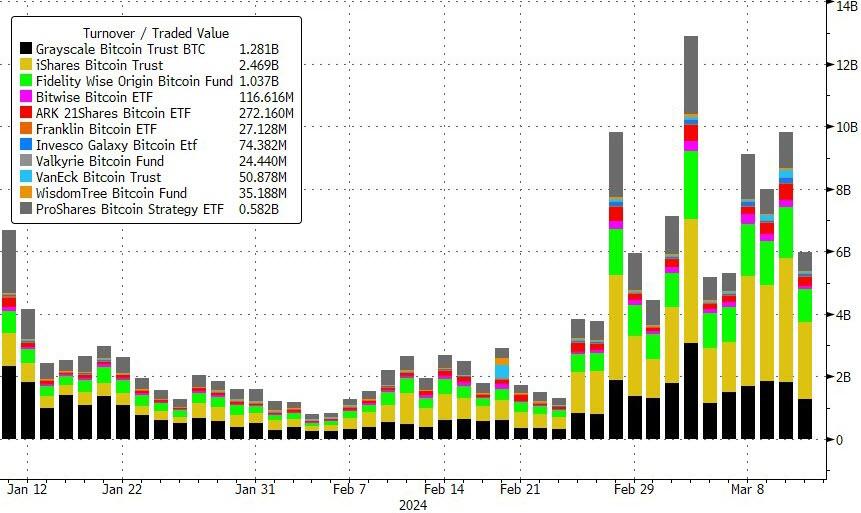

Bitcoin morning price:$66,109 DOWN 27 DOLLARS.

Bitcoin: afternoon price: $65,885 DOWN 1359 dollars

Platinum price closing UP $13.20 TO $935.10

Palladium price; UP $20.15 AT $1018.45

END

SHANGHAI GOLD PREMIUM 27 DOLLARS/COMEX GOLD

SHANGHAI GOLD……

…

SHANGHAI GOLD (USD) FUTURES – QUOTES

As of Monday, April 1, 2024, CME Group settlement data is no longer accessible through ftp.cmegroup.com and has a delayed publication time of 12:00 a.m. CT on all cmegroup.com web pages. Learn about alternate ways to access the data in our FAQ.

Last Updated 03 Apr 2024 07:34:45 AM CT.

Market data is delayed by at least 10 minutes.

MONTH

CHART

LAST

CHANGE

PRIOR SETTLE

OPEN

HIGH

LOW

VOLUME

UPDATED

APR 2024 SGUJ4

–

–

2293.0

–

–

–

0

21:30:01 CT 02 Apr 2024

MAY 2024 SGUK4

–

–

2292.9

–

–

–

0

21:30:01 CT 02 Apr 2024

JUN 2024 SGUM4

2329.7

+22.7 (+0.98%)

2307.0

2320.4

2332.2

2320.4

425

01:38:34 CT 03 Apr 2024

JUL 2024 SGUN4

–

–

–

–

–

–

0

–

AUG 2024 SGUQ4

–

–

2321.0

–

–

–

0

21:30:01 CT 02 Apr 2024

OCT 2024 SGUV4

2356.9

+25.9 (+1.11%)

2331.0

2354.4

2356.9

2354.4

98

01:00:36 CT 03 Apr 2024

DEC 2024 SGUZ4

–

–

2331.6

–

–

–

0

21:30:01 CT 02 Apr 2024

FEB 2025 SGUG5

–

–

2332.2

–

–

–

0

21:30:01 CT 02 Apr 2024

APR 2025 SGUJ5

–

–

–

–

–

–

0

I will now provide gold in Canadian dollars, British pounds and Euros

4: 15 PM ACCESS

*CANADIAN GOLD: $3109.34 UP $12.20- CDN dollars per oz( * NEW ALL TIME HIGH 3,109.34 CDN DOLLARS PER OZ//APRIL 3 2024)

*BRITISH GOLD: 1816.41 UP 1.06 pounds per oz// *(NEW ALL TIME HIGH//CLOSING///1816.41 BRITISH POUNDS/OZ) APRIL 3/2024

*EURO GOLD: 2120.82 UP 0.30 euros per oz //* (ALL TIME CLOSING HIGH: 2120.82 EUROS PER OZ//APRIL 3.2024)

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

118 H MACQUARIE FUT 20 132 C SG AMERICAS 7 190 H BMO CAPITAL 342 363 H WELLS FARGO SEC 11 435 H SCOTIA CAPITAL 154 555 C BNP PARIBAS SEC 3 624 H BOFA SECURITIES 3 657 C MORGAN STANLEY 127 661 C JP MORGAN 60 483 690 C ABN AMRO 3 732 C RBC CAP MARKETS 850 737 C ADVANTAGE 3 14

TOTAL: 1,040 1,040

JPMORGAN STOPPED (RECEIVED) 483/1040 CONTRACTS

FOR APRIL/2024

GOLD: NUMBER OF NOTICES FILED FOR APRIL/2024. CONTRACT: 1040 NOTICES FOR 104,000 OZ or 3.235 TONNES

total notices so far: 11,164 contracts for 1,116,400 Oz (34,724 tonnes)

FOR APRIL:

SILVER NOTICES: 11 NOTICE(S) FILED FOR 55,000 OZ/

total number of notices filed so far this month : 361 for 1,805,000 oz

XXXXXXXXXXXXXXXXXX

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD/

BOTH GLD AND SLV ARE FRAUDULENT VEHICLES//THEY ARE NOW RAIDING GLD AND SLV FOR PHYSICAL

THE CROOKS ARE STEALING GOLD AND SILVER FROM THE GLD/SLV AND REPLACING THE PHYSICAL WITH PAPER DOLLARS.

WITH GOLD UP $33.85

INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD/ :

NO CHANGES IN GOLD INVENTORY AT THE GLD:

/ /INVENTORY RESTS AT 829.00 TONNES

INVENTORY RESTS AT 829.00 TONNES

SLV//

WITH NO SILVER AROUND AND SILVER UP $1.14 AT THE SLV//

HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.835 MILLION OZ OF SILVER INTO THE SLV

// INVENTORY RISES TO 433.641 MILLION OZ/

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV.

CLOSING INVENTORY: 433.641 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A MEGA MEGA HUMONGOUS SIZED 5070 CONTRACTS TO 166,823 AND CLOSER TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THIS HUMONGOUS SIZED GAIN IN COMEX OI WAS ACCOMPLISHED WITH OUR STRONG GAIN IN PRICE OF $0.84 IN SILVER PRICING AT THE COMEX ON TUESDAY. WE HAD ZERO LONG LIQUIDATION AT THE COMEX SESSION WITH AGAIN PANICKING SHORT COVERING WITH THE PRICE GAIN. WE HAD A VERY STRONG 1084 T.A.S ISSUANCE AND THESE WILL BE USED FOR MANIPULATION LATER THIS MONTH/AS WELL AS TODAY. PLEASE NOTE THAT THE CROOKS NEED A HIGHER SILVER/GOLD T.A.S. TO CARRY ON THEIR CROOKED MANIPULATION ON A DAILY BASIS

CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON TUESDAY NIGHT: 1084 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS. IT THUS LOOKS LIKE THE FED (GOV’T) IS BEHIND ALL OF THESE TRADES.

WE HAVE NOW SET ANOTHER RECORD LOW AT 114,102 CONTRACTS ///JULY 3.2023// OUR BANKERS WITH THE HELP OF SPECULATORS AND HIGH FREQUENCY TRADERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.84), AND WERE UNSUCCESSFUL IN KNOCKING ANY SILVER LONGS AS WE HAD A MEGA HUMONGOUS SIZED GAIN OF 6650 CONTRACTS ON OUR TWO EXCHANGES WITH THE HUGE GAIN IN PRICE OF 85 CENTS.

WE MUST HAVE HAD:

A HUMONGOUS SIZED 1580 CONTRACT ISSUANCE OF EXCHANGE FOR PHYSICALS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 2.465 MILLION OZ (FIRST DAY NOTICE) FOLLOWED BY TODAY’S 210,000 OZ QUEUE JUMP//NEW STANDING 2.8150 MILLION OZ//

//NEW STANDING FOR SILVER IS THUS 2.8150 MILLION OZ

WE HAD:

/ MEGA HUMONGOUS SIZED COMEX OI GAIN/ MEGA HUGE SIZED EFP ISSUANCE/ VI) HUGE SIZED NUMBER OF T.A.S. CONTRACT ISSUANCE 1084 CONTRACTS)/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL -REMOVED A WHOPPING 1767 CONTRACTS //

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS FEB. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF APRIL

TOTAL CONTRACTS for 3 days, total 3939 contracts: OR 15.515 MILLION OZ (1313 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 15.515 MILLION OZ

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH 2022: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 118.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 85.745 MILLION OZ (SMALLER THAN LAST MONTH)

AUGUST: 171.43 MILLION OZ (THIS MONTH IS GOING TO BE HUGE //2ND HIGHEST ON RECORD

SEPT: 72.705 MILLION OZ (SMALLER THIS MONTH)

OCT: 97.455 MILLION OZ

NOV. 50.050 MILLION OZ

DEC. 66.140 MILLION OZ//

TOTAL 2023: 1,104.10 MILLION OZ/

JAN ’24 : 78.655 MILLION OZ//

FEB /2024 : 66.135 MILLION OZ./FINAL

MARCH: 143.750 MILLION OZ// 4TH HIGHEST ON RECORD.

APRIL: 15.515 MILLION OZ

RESULT: WE HAD A MEGA HUMONGOUS SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 5070 CONTRACTS WITH OUR STRONG GAININ PRICE OF SILVER PRICING AT THE COMEX//TUESDAY.,. THE CME NOTIFIED US THAT WE HAD A HUMONGOUS EFP ISSUANCE CONTRACTS: 1580 ISSUED FOR MAY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS. WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR APRIL. OF 2.465 MILLION OZ ON FIRST DAY NOTICE FOLLOWED BY TODAYS’ 210,000 OZ QUEUE JUMP

//NEW TOTAL STANDING RISES TO 2.8150 MILLION OZ

WE HAVE A MEGA MEGA HUMONGOUS GAIN OF 6650 OI CONTRACTS ON THE TWO EXCHANGES WITH THE STRONG GAIN IN PRICE. THE TOTAL OF TAS INITIATED CONTRACTS TODAY: A HUGE SIZED 1084 CONTRACTS//SOME FRONT END OF THE TAS CONTRACTS WERE LIQUIDATED DURING THE TUESDAY COMEX SESSION/// WITH MAJOR SHORT COVERING FROM OUR SPEC SHORTS

THE NEW TAS ISSUANCE THURSDAY NIGHT (1084) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE//PROBABLY TODAY., .

WE HAD 11 NOTICE(S) FILED TODAY FOR 55,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A FAIR SIZED 1267 CONTRACTS TO 500,045 AND CLOSER TO THE RECORD (SET JAN 24/2020) AT 799,733 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110, BUT WE ARE NOW MUCH FURTHER FROM OUR ALL TIME LOW OF 390,000 CONTRACTS.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED 595 CONTRACTS

WE HAD A FAIR SIZED INCREASE IN COMEX OI (1862 CONTRACTS) WITH OUR $23.90 GAIN IN PRICE//TUESDAY. THE BANKERS WERE FORCED TO SUPPLY THE NECESSARY SHORT PAPER TO CONTAIN GOLD’S RISE.WE ALSO HAD A RATHER LARGE INITIAL STANDING IN GOLD TONNAGE FOR APRIL. AT 44.8615 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’’QUEUE. JUMP TO LONDON OF 14,100 OZ.(0.4386 TONNES)

NEW TOTAL Of INITIAL GOLD STANDING 42.043 TONNES FOLLOWED BY TODAY’S 14,100 OZ QUEUE JUMP//NEW STANDING 42.289 TONNES// ALL OF THIS HAPPENED WITH OUR $23.90 GAIN IN PRICE WITH RESPECT TO TUESDAY’S TRADING. WE HAD A STRONG SIZED GAIN OF 5834 OI CONTRACTS (19.87 PAPER TONNES) ON OUR TWO EXCHANGES.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 4527CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 500,045

IN ESSENCE WE HAVE A STRONG SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 5834 CONTRACTS WITH 1862 CONTRACTS INCREASED AT THE COMEX// AND A STRONG SIZED 4527 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 5834 CONTRACTS.. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): A STRONG SIZED 4527 CONTRACTS,

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A STRONG SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (4527 CONTRACTS) ACCOMPANYING THE FAIR SIZED GAIN IN COMEX OI (1267) //TOTAL GAIN FOR OUR THE TWO EXCHANGES: 5834 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR FORMER FORMAT OF BANKERS GOING LONG AND SPECULATORS GOING SHORT ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR APRIL. AT 44.8615 TONNES FOLLOWED BY TODAY’S 0.4386 TONNES QUEUE JUMP //NEW STANDING 42.289 TONNES.

/ 3) ZERO LONG LIQUIDATION WITH THE HUGE JUMP IN PRICE.

// 4) FAIR SIZED COMEX OPEN INTEREST GAIN/ 5) STRONG ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER///6: FAIR T.A.S. ISSUANCE: 2275CONTRACTS/ ATTEMPTED SHORT COVERING FOR SURE.

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023-2024 INCLUDING TODAY

MARCH

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF APRIL. :

TOTAL EFP CONTRACTS ISSUED: 12,201 CONTRACTS OR 1,220,100OZ OR 37.95 TONNES IN 3TRADING DAY(S) AND THUS AVERAGING: 3832 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 3TRADING DAY(S) IN TONNES 37.95 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2022, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 37.95/3550 x 100% TONNES 1.07% OF GLOBAL ANNUAL PRODUCTION

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH/2022: 409.30 TONNES //FINAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 151.69 TONNES (WEAKER THAN LAST MONTH)

AUGUST: 195.28 TONNES (A STRONGER MONTH)//FINAL

SEPT: 254.709 TONNES (WILL BE LARGER THAN LAST MONTH AND A STRONG MONTH)

OCT. 248.09 TONNES. LIKE SILVER, THIS MONTH IS GOING TO BE A STRONG E.F.P. ISSUANCE.

NOV. 239.16 TONNES//WILL BE STRONG THIS MONTH,

DEC. 213.704 TONNES. A STRONG MONTH//

TOTAL FOR YEAR 2023: 2,569.57 TONNES VS 2578 TONNES LAST YEAR

JAN ’24: 291.76 TONNES (WILL BE MUCH GREATER THAN LAST MONTH.//3RD HIGHEST EVER RECORDED EXCHANGE FOR PHYSICAL)

FEB’24: 201.947 TONNES

MARCH 2024: 352.21 TONNES//2ND HIGHEST EVER RECORDED EFP ISSUANCE.

APRIL: 37.95 TONNES

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF APRIL. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (APRIL), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER ROSE BY A MEGA GIGANTIC SIZED 5070 CONTRACTS OI TO 166,823 AND CLOSER TO THE COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 6 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 1580 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAY 1580 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 1580 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 6837 CONTRACTS AND ADD TO THE 1580 E.FP. ISSUED

WE OBTAIN A MEGA HUMONGOUS SIZED GAIN OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 6650CONTRACTS

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTAL 33.25 MILLION OZ

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS//

WEDNESDAY MORNING/TUESDAY NIGHT

SHANGHAI CLOSED DOWN 5.66 PTS OR 0.18% //Hang Seng CLOSED DOWN 206.42 OR 1.22%

/ Nikkei CLOSED DOWN 387.06 PTS OR 0.99% //Australia’s all ordinaries CLOSED DOWN 1.38%

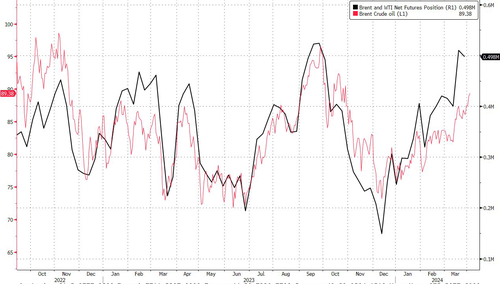

/Chinese yuan (ONSHORE) closed DOWN 7.2358 //OFFSHORE CHINESE YUAN CLOSED DOWN TO 7.2791 /Oil UP TO 85.91 dollars per barrel for WTI and BRENT DOWN AT 89.63/ Stocks in Europe OPENED MOSTLY ALL GREEN// ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE YUAN WEAKER

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A FAIR 1267 CONTRACTS TO 500,045 DESPITE OUR STRONG GAIN IN PRICE OF $23.90 WITH RESPECT TO TUESDAY TRADING. WE HAD ZERO SPREADER LIQUIDATION BUT STRONG T.A.S. LIQUIDATION

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE NON ACTIVE DELIVERY MONTH OF APRIL..… THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 4527 EFP CONTRACTS WERE ISSUED: : JUNE 4527 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 4527CONTRACTS

ON A NET BASIS IN OPEN INTEREST WE LOST THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A STRONG SIZED TOTAL OF 5834 CONTRACTS IN THAT 4537 LONGS WERE TRANSFERRED AS EXCHANGE FOR PHYSICALS TO LONDON AND WE HAD A FAIR SIZED GAIN OF 1267 COMEX CONTRACTS..AND THIS STRONG GAIN ON OUR TWO EXCHANGES HAPPENED DESPITE OUR HUGE GAIN IN PRICE OF $23.90 TUESDAY COMEX. AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS DURING MID MONTH IN THE DELIVERY CYCLE), THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR TUESDAY NIGHT WAS A FAIR SIZED 2275 CONTRACTS. WE HAD 0 EX FOR RISK ISSUANCE

THROUGHOUT THE PAST SEVERAL WEEKS, THE BANKERS CONTINUE TO SELL OFF THE LONG SIDE OF THE SPREAD WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR/T.A.S. SPREAD WHICH WILL BE LIQUIDATED IN DAYS HENCE//. IT SEEMS THAT OUR CROOKS ARE HAVING A HARD TIME TRYING TO CONTROL THE PRICE OF GOLD AND THUS THE NEED FOR RECORD T.A.S. ISSUANCE.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: APRIL (42.289 TONNES) ( ACTIVE MONTH)

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 24 MONTHS OF 2021-2023:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 42.289 TONNES

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT ROSE $23.90 //// AND WERE UNSUCCESSFUL IN KNOCKING ANY SPECULATOR LONGS AS WE HAD A STRONG SIZED GAIN OF6389 TOTAL CONTRACTS ON OUR TWO EXCHANGES DESPITE OUR HUGE PRICE GAIN 0F $23.90.

WE HAD A STRONG T.A.S. LIQUIDATION ON THE FRONT END OF TUESDAY’S TRADING ALONG. THE T.A.S. ISSUED ON TUESDAY NIGHT, WILL BE “PUT INTO THE BANK” TO BE USED AT A LATER DATE AT THE COLLUSIVE CHOOSING OF OUR BANKERS. THE HIGH T.A.S. ISSUANCE IS MEANT TO CONTROL THE PRICE OF GOLD

WE HAVE GAINED A TOTAL OI OF 19.87 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR APRIL. (44.8615 TONNES) ON FIRST DAY NOTICE FOLLOWED BY TODAY’S QUEUE JUMP OF 14,100 OZ (0.4386 TONNES)//NEW STANDING; 42.289

NEW STANDING: 42.289 TONNES

ALL OF THIS WAS ACCOMPLISHED DESPITE OUR GAIN IN PRICE TO THE TUNE OF $23.90

WE HAD REMOVED 595 CONTRACTS TO THE COMEX TRADES TO OPEN INTEREST (CROOKS)

NET LOSS ON THE TWO EXCHANGES 5834 CONTRACTS OR 583,400 OZ (18L146 TONNES)

Total monthly oz gold served (contracts) so far this month

11,124 notices 1,112,400 oz 34.724 TONNES

Total accumulative withdrawals of gold from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of gold from the Customer inventory this month

x

0 dealer deposits:

total dealer deposits: nil oz

total customer withdrawals: 1

i) Out of JPMorgan: 482.262 oz

(15 kilobars)

total customer withdrawal: 482.262oz

we had total deposit 0 oz

Adjustments: 1

i) dealer to customer

i) out of JPMorgan 9645,300 oz (300 kilobars)

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR APRIL.

For the front month of APRIL we have an oi of 3512 contracts having LOST 111 contracts. We had 252 contracts served on Tuesday, so we gained 141 contracts or an additional 14100 oz (0.4386 tonnes) will stand at the comex

MAY GAINED 153 CONTRACTS TO STAND AT 1749

JUNE INCREASED ITS OI BY 5 CONTRACTS UP TO 424,847 CONTRACTS.

We had 1040 contracts filed for today representing 104,000 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 60 notices were issued from their client or customer account. The total of all issuance by all participants equate to 1040 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 483 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for the APRIL. /2024. contract month, we take the total number of notices filed so far for the month (11,164 x 100 oz ), to which we add the difference between the open interest for the front month of APRIL. (3512 CONTRACTS) minus the number of notices served upon today 1040 x 100 oz per contract equals 1,359,600 OZ OR 42.289 TONNES.

thus the INITIAL standings for gold for the APRIL. contract month: No of notices filed so far (11,164) x 100 oz + (3512) {OI for the front month} minus the number of notices served upon today (1040) x 100 oz which equals 1,359,600 oz (42.289 TONNES)

TOTAL COMEX GOLD STANDING FOR APRIL: 42.289 TONNES WHICH IS HUGE FOR A NON ACTIVE DELIVERY MONTH IN THE CALENDAR.

To calculate the number of silver ounces that will stand for delivery in APRIL. we take the total number of notices filed for the month so far at 361 x 5,000 oz = 1,805,000 oz

to which we add the difference between the open interest for the front month of APRIL (XXX) and the number of notices served upon today 11 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the APRIL/2024 contract month: 361 (notices served so far) x 5000 oz + OI for the front month of APRIL. (XXX) – number of notices served upon today 11 )x 500 oz of silver standing for the APRIL contract month equates to 2.8150 MILLION OZ.

New total standing: 2.8150 million oz.

There are 46.136 million oz of registered silver.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS//

BOTH GLD AND SLV ARE MASSIVE FRAUDS!

APRIL 3 WITH GOLD UP $33.85 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD // INVENTORY REMAINS AT 829.00 TONNES

APRIL 2 WITH GOLD UP $23.90 TODAY; HUG CHANGES IN GOLD INVENTORY AT THE GLD A WITH DRAWAL OF 1.15 TONNES OF GOLD FROM THE GLD.:// INVENTORY REMAINS AT 829.00 TONNES

APRIL 1 WITH GOLD UP $18.70 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD:// INVENTORY REMAINS AT 830.15 TONNES

MARCH 28 WITH GOLD UP $26.30 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD:// INVENTORY REMAINS AT 830.15 TONNES

MARCH 27 WITH GOLD UP $15.00 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 5.18 TONNES OF GOLD FROM THE GLD// INVENTORY FALLS TO 830.15 TONNES

MARCH 26 WITH GOLD UP $1.40 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD INVENTORY RISES TO 835.33 TONNES

MARCH 25 WITH GOLD UP $17.05 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD INVENTORY RISES TO 838.50 TONNES

MARCH 22 WITH GOLD DOWN $23.75 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD INVENTORY RISES TO 838.50 TONNES

MARCH 21 WITH GOLD UP $24.80 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD A STRONG PAPER DEPOSIT OF 1.15 TONNES OF GOLD INTO THE GLD/:INVENTORY RISES TO 838.50 TONNES

MARCH 20 WITH GOLD UP $1.45 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD A STRONG PAPER DEPOSIT OF 1.48 TONNES OF GOLD INTO THE GLD/:INVENTORY RISES TO 837.35 TONNES

MARCH 19 WITH GOLD DOWN $4.10 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD A STRONG PAPER DEPOSIT OF 1.48 TONNES OF GOLD INTO THE GLD/:INVENTORY RISES TO 833.32 TONNES

MARCH 15 WITH GOLD DOWN $5.20 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD/:INVENTORY REMAINS AT 816.86 TONNES

MARCH 14 WITH GOLD DOWN $12.20 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF 1.73 TONNES OF GOLD INTO THE GLD//:INVENTORY REMAINS AT 816.86 TONNES

MARCH 13 WITH GOLD UP $14.40 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD:INVENTORY REMAINS AT 815.13 TONNES

MARCH 12 WITH GOLD DOWN $21.15 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD:NOT AVAILABLE///LAST VALUE 815.13 TONNES

MARCH 11 WITH GOLD UP $3.20 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.44 TONNES OF GOLD OUT OF THE GLD AFTER 7 CONSECUTIVE GOLD PRICE RISES//INVENTORY RESTS AT 815.13 TONNES

MARCH 8 WITH GOLD UP $21.05 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 0.87 TONNES OF GOLD OUT OF THE GLD AFTER 7 CONSECUTIVE GOLD PRICE RISES//INVENTORY RESTS AT 816.57 TONNES

MARCH 7 WITH GOLD UP $7.20 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4,20 TONNES OF GOLD OUT OF THE GLD//INVENTORY RESTS AT 817.44 TONNES

MARCH 6 WITH GOLD UP $17.20 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.30 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 821.47 TONNES

MARCH 5 WITH GOLD UP $16.55 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.30 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 821.47 TONNES

MARCH 4 WITH GOLD UP $30.55 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF .86 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 823.77 TONNES

MARCH 1 WITH GOLD UP $40.40 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 822.91 TONNES

FEB29/WITH GOLD UP $12.60 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD//WITHDRAWAL OF 4.03 TONNES INVENTORY RESTS AT 822.91 TONNES

FEB28/WITH GOLD DOWN $1.00 TODAY NO CHANGES IN GOLD INVENTORY AT THE GLD INVENTORY RESTS AT 826.94 TONNES

FEB27/WITH GOLD UP $4.40 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF .87 TONNES OF GOLD FROM THE GLD:/INVENTORY RESTS AT 826.94 TONNES

FEB26/WITH GOLD DOWN $8.90 TODAY NO CHANGES IN GOLD INVENTORY AT THE GLD:/INVENTORY RESTS AT 827.81 TONNES

FEB23/WITH GOLD UP $17 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.01 TONNES OF GOLD FROM THE GLD.//INVENTORY RESTS AT 827.81 TONNES

FEB22/WITH GOLD DOWN $2.15 TODAY NO CHANGES IN GOLD INVENTORY AT THE GLD://INVENTORY RESTS AT 829.82 TONNES

FEB21/WITH GOLD DOWN $5.30 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 7.59 TONNES OF GOLD OUT OF THE GLD///INVENTORY RESTS AT 29.82 TONNES

FEB20/WITH GOLD UP $16.15 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 0.58 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 837.89 TONNES

FEB16/WITH GOLD UP $8,60 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.73 TONNES OF GOLD FROM THE GLD///INVENTORY RESTS AT 837.31 TONNES

FEB15/WITH GOLD UP $11.70 TODAY NO CHANGES IN GOLD INVENTORY AT THE GLD:/INVENTORY RESTS AT 841.92 TONNES

FEB14/WITH GOLD DOWN $2.75 TODAY NO CHANGES IN GOLD INVENTORY AT THE GLD:/INVENTORY RESTS AT 841.92 TONNES

FEB13/WITH GOLD DOWN $20.15 TODAY NO CHANGES IN GOLD INVENTORY AT THE GLD:/INVENTORY RESTS AT 841.92 TONNES

FEB12/WITH GOLD DOWN $4.80 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A STRONG WITHDRAWAL OF 1.74 TONNES OF GOLD FROM THE GLD. / //://INVENTORY RESTS AT 841.92 TONNES

FEB9/WITH GOLD DOWN $8.60 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A STRONG DEPOSIT OF 1.44 TONNES OF GOLD FROM THE GLD. / //://INVENTORY RESTS AT 843.66 TONNES

FEB8/WITH GOLD DOWN $2.70 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A MASSIVE WITHDRAWAL OF 5.47 TONNES OF GOLD FROM THE GLD. / //://INVENTORY RESTS AT 842.22 TONNES:

FEB7/WITH GOLD UP $0.40 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A MASSIVE WITHDRAWAL OF 4.04 TONNES OF GOLD FROM THE GLD. / //://INVENTORY RESTS AT 847.69 TONNES:

FEB6/WITH GOLD UP $8.50 TODAY NO CHANGES IN GOLD INVENTORY AT THE GLD:/ / //://INVENTORY RESTS AT 851.73 TONNES:

GLD INVENTORY: 829.00 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

APRIL 3/WITH SILVER UP $1.14 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.835 MILLION OZ INTO THE SLV// SLV INVENTORY RESTS AT 433.641 MILLION OZ

APRIL 2/WITH SILVER UP 84 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 6.721 MILLION OZ INTO THE SLV// SLV INVENTORY RESTS AT 430.806 MILLION OZ

APRIL 1/WITH SILVER UP 14 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV// SLV INVENTORY RESTS AT 424.085 MILLION OZ

MARCH 28/WITH SILVER UP 20 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A DEPOSIT OF 1.005 MILLION OZ INTO THE SLV: SLV INVENTORY RESTS AT 424.085 MILLION OZ

MARCH 27/WITH SILVER UP 14 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A A DEPOSIT OF 1.691 MILLION OZ INTO THE SLV: SLV INVENTORY RESTS AT 423.079 MILLION OZ

MARCH 26/WITH SILVER DOWN 24 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV A A DEPOSIT OF 0.366 MILLION OZ INTO THE SLV: SLV INVENTORY RESTS AT 421.388 MILLION OZ

MARCH 25/WITH SILVER UP 8 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A HUGE WITHDRAWAL OF 3.887 MILLION OZ INTO THE SLV: SLV INVENTORY RESTS AT 421.022 MILLION OZ

MARCH 22/WITH SILVER DOWN 9 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A HUGE DEPOSIT OF 1.1899 MILLION OZ INTO THE SLV: SLV INVENTORY RESTS AT 424.909 MILLION OZ

MARCH 21/WITH SILVER DOWN 8 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A HUGE WITHDRAWAL OF 3.560 MILLION OZ INTO THE SLV: SLV INVENTORY RESTS AT 423.720 MILLION OZ

MARCH 20/WITH SILVER DOWN 5 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A HUGE DEPOSIT OF 11.792 MILLION OZ INTO THE SLV: SLV INVENTORY RESTS AT 427.280 MILLION OZ

MARCH 18/WITH SILVER DOWN 11 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A HUGE DEPOSIT OF 11.792 MILLION OZ INTO THE SLV: SLV INVENTORY RESTS AT 427.280 MILLION OZ

MARCH 15/WITH SILVER DOWN 9 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 1.006 MILLION OZ FROM THE SLV: SLV INVENTORY RESTS AT 417.866 MILLION OZ

MARCH 14/WITH SILVER DOWN 9 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: SLV INVENTORY RESTS AT 418.872 MILLION OZ

MARCH 13/WITH SILVER UP 32 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: SLV INVENTORY RESTS AT 418.872 MILLION OZ…

MARCH 12/WITH SILVER DOWN 31 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A SMALL WITHDRAWAL OF 0.549 MILLION OZ OF SILVER INTO THE SLV//// : SLV INVENTORY RESTS AT 418.872 MILLION OZ…

MARCH 11/WITH SILVER UP 11 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A HUGE WITHDRAWAL OF 2.147 MILLION OZ OF SILVER FROM THE SLV//// : SLV INVENTORY RESTS AT 418.323 MILLION OZ…SUCH A MASSIVE FRAUD!

MARCH 8/WITH SILVER DOWN 5 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A HUGE WITHDRAWAL OF 4.299 MILLION OZ OF SILVER FROM THE SLV//// : SLV INVENTORY RESTS AT 420.519 MILLION OZ…SUCH A MASSIVE FRAUD!

MARCH 7/WITH SILVER UP 8 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A HUGE WITHDRAWAL OF 4.665 MILLION OZ OF SILVER FROM THE SLV//// : SLV INVENTORY RESTS AT 424.818 MILLION OZ…SUCH A MASSIVE FRAUD!

MARCH 6/WITH SILVER UP 52 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A HUGE WITHDRAWAL OF 2.378 MILLION OZ OF SILVER FROM THE SLV//// : SLV INVENTORY RESTS AT 427,105 MILLION OZ

MARCH 5/WITH SILVER DOWN 2 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A HUGE WITHDRAWAL OF 1.499 MILL;ION OZ OF SILVER FROM THE SLV//// : SLV INVENTORY RESTS AT 429.483 MILLION OZ

MARCH 4/WITH SILVER UP CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: // : SLV INVENTORY RESTS AT 430.982 MILLION OZ

MARCH 1/WITH SILVER UP 49 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: // : SLV INVENTORY RESTS AT 430.982 MILLION OZ

FEB 29/WITH SILVER UP 25 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.104 MILLION OZ OUT OF THE SLV//// : SLV INVENTORY RESTS AT 430/982 MILLION OZ

FEB 28/WITH SILVER DOWN 7 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 5.123 MILLION OZ INTO THE SLV//// : SLV INVENTORY RESTS AT 433.086 MILLION OZ

FEB 27/WITH SILVER UP 3 CENTS TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 0.64 MILLION OZ FROM THE SLV//// : SLV INVENTORY RESTS AT 427.943 MILLION OZ

FEB 26/WITH SILVER DOWN 44 CENTS TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.065 MILLION OZ FROM THE SLV//// : SLV INVENTORY RESTS AT 428.603 MILLION OZ

FEB 23/WITH SILVER DOWN 44 CENTS TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.065 MILLION OZ FROM THE SLV//// : SLV INVENTORY RESTS AT 428.603 MILLION OZ

FEB 22/WITH SILVER DOWN 10 CENTS TODAY NO CHANGES IN SILVER INVENTORY AT THE SLV

// : SLV INVENTORY RESTS AT 432.766 MILLION OZ

FEB 21/WITH SILVER DOWN 28 CENTS TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 2.348 MILLION OZ OF SILVER FROM THE SLV// : SLV INVENTORY RESTS AT 432.766 MILLION OZ

FEB 20/WITH SILVER DOWN 33 CENTS TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 3.385 MILLION OZ OF SILVER FROM THE SLV// : SLV INVENTORY RESTS AT 435.008 MILLION OZ

FEB 16/WITH SILVER UP 53 CENTS TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV A DEPOSIT OF 1.235 MILLION OZ OF SILVER FROM THE SLV// : SLV INVENTORY RESTS AT 438.393 MILLION OZ

FEB 15/WITH SILVER UP 56 CENTS TODAY NO CHANGES IN SILVER INVENTORY AT THE SLV : SLV INVENTORY RESTS AT 437.615 MILLION OZ

FEB 14/WITH SILVER UP 24 CENTS TODAY NO CHANGES IN SILVER INVENTORY AT THE SLV : SLV INVENTORY RESTS AT 437.615 MILLION OZ

FEB 13/WITH SILVER DOWN 60 CENTS TODAY SMALL CHANGES IN SILVER INVENTORY AT THE SLV A SMALL WITHDRAWAL OF 0.504 MILLION OZ OZ OUT OF THE SLV: SLV INVENTORY RESTS AT 437.615 MILLION OZ

FEB 12/WITH SILVER UP 14 CENTS TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV A HUGE WITHDRAWAL OF 1.921 MILLION OZ OZ OUT OF THE SLV: SLV INVENTORY RESTS AT 438.119 MILLION OZ

FEB 9/WITH SILVER DOWN 4 CENTS TODAY SMALL CHANGES IN SILVER INVENTORY AT THE SLV A SMALL DEPOSIT OF 600,000 OZ INTO THE SLV: SLV INVENTORY RESTS AT 440.040 MILLION OZ

FEB 8/WITH SILVER UP 29 CENTS TODAY NO CHANGES IN SILVER INVENTORY AT THE SLV: SLV INVENTORY RESTS AT 439.994 MILLION OZ

FEB 7/WITH SILVER DOWN 18 CENTS TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A MASSIVE DEPOSIT OF 4.04 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 439.994 MILLION OZ//LAST 9 DAYS: 10.7598 MILLION OZ WITHDRAWAL

CLOSING INVENTORY 433.641 MILLION OZ//

PHYSICAL GOLD/SILVER COMMENTARIES

1:Peter Schiff/Mike Maharrey

Here’s a Dirty Little Secret: Federal Reserve Monetary Policy Is Still Loose

April 03, 2024

Everybody wants to know when the Federal Reserve is going to declare victory over price inflation and begin loosening monetary policy.

The real question is – when are they going to make monetary policy tight again?

Because despite all the worry about high interest rates, monetary policy remains relatively loose.

Sure, hiking rates by 500 basis points is significant, especially in an economy loaded up with debt. And rolling a little over $1.4 trillion off a central bank balance sheet is nothing to sneeze at.

But given the amount of inflation the Federal Reserve created over the last decade-plus, the Fed’s war against inflation amounts to shooting paper wads at a Panzer division.

The Fed Knows Monetary Policy Isn’t Tight

The Fed people know monetary policy isn’t particularly tight. They have their own index that tells them so.

As of March 22, the NFCI stood at –0.56. The negative number tells us that monetary policy conditions are loose from a historical perspective.

As the Chicago Fed explains,

“Positive values of the NFCI have been historically associated with tighter-than-average financial conditions, while negative values have been historically associated with looser-than-average financial conditions.”

So, despite its efforts and a lot of jawboning, the Fed still hasn’t pushed monetary policy over the edge too tight. That means this has been a pretty lame inflation fight.

Balance sheet reduction tells the same story.

Yes, the Fed has managed to shrink the balance sheet by almost $1.5 trillion. That sounds impressive until you remember that the Fed added nearly $5 trillion during the pandemic. That was on top of the massive $4 trillion blowup of the balance sheet during the Great Recession that the Fed could never run off as promised.

In effect, the balance sheet runoff is a little like taking a bucket of water out of my pool.

In fact, the balance sheet reduction plan was pretty tepid to begin with.

Based on the central bank’s balance sheet reduction plan announced in March 2022, it would take 7.8 years for the Fed to shrink its balance sheet back to pre-pandemic levels. That doesn’t even begin to touch the trillions added to the balance sheet in the decade after the 2008 financial crisis.

The Gorilla in the Fed’s Meeting Room

I’m not the only one who has noticed this inconvenient truth.

Bloomberg macro strategist Simon White called loose monetary policy the gorilla in the room.

“A famous experiment asks volunteers to watch a video of a basketball game and count the passes. Halfway through, a gorilla strolls through the action. Almost no one spots it, so focused they are on the game. As we count the dots and parse the language at this week’s Fed meeting, it’s easy to miss the fact that policy overall remains very loose despite over 500 bps of rate hikes. The gorilla has gone by largely unnoticed.”

White points out that despite the Fed hiking rates higher and faster than it has since 2000, the effective Fed rate has actually dropped – by more than it has in 30 years!

Let that sink in for a moment. Financial conditions are looser today than they were when the Fed started this so-called inflation fight.

And yet the markets are desperate for rate cuts. They want their easy money liquor back even though their glasses remain half full. The bartenders at the Fed will almost certainly deliver.

As White put it, “The Fed may end up spiking the punch bowl with more booze when the party is already quite tipsy.”

But hasn’t the Fed beaten inflation?

Well, no.

Yes, CPI fell from its high of 9.1 percent in the summer of 2022. But even taking CPI at face value, price inflation remains sticky.

Inflation is worse than the government data suggest. The government revised the CPI formula in the 1990s so that it understates the actual rise in prices. Based on the formula used in the 1970s, CPI is closer to double the official numbers. So, if the BLS was using the old formula, CPI peaked closer to 18 percent. And using an honest formula, it would probably be worse than that.

To beat down price inflation, interest rates need to rise above CPI. Based on a more honest CPI formula, the Fed never got close.

This may explain why cyclical price inflation remains elevated.

The San Francisco Fed splits core PCE (The Fed’s favorite price inflation measure) into two components – cyclical and acyclical. As White explains, the components making up cyclical price inflation are more sensitive to Federal Reserve interest rate policy.

“While acyclical inflation has fallen all the way back to its pre-pandemic average, cyclical PCE remains at its 40-year highs. The Wizard of the Fed has been pulling the rate-hiking levers, but they have done little to directly quell inflation.”

Borrowing costs also reveal Fed monetary policy remains loose. As part of its revision campaign, the BLS removed mortgage costs from the CPI in 1983. It stripped out car repayments in 1998.

Larry Summers and other economists from Harvard and the International Monetary Fund reconstructed the CPI to include these borrowing costs for a paper published in February 2024. According to their calculations, inflation not only peaked higher than it did in the 1970s, but it continues to run around 8 percent – far above the headline 3.2 percent CPI reported in February.

White sums it up this way:

“Gorillas playing basketball is a very odd thing; the Fed cutting rates before the last quarter of this year would be even odder. Before then, though, markets are likely to try to re-impose some sobriety by reducing or eliminating the number of rate cuts priced in.”

The Fed Hasn’t Done Enough to Win the Inflation Fight

White reveals an ugly truth – the Fed hasn’t done enough to win this inflation fight and any declaration of victory is actually a surrender.

Looking at how Federal Reserve Chairman Paul Volker handled the 1970s and 80s inflation is informative.

Volker went on the warpath in 1980 and raised rates to 20 percent. At the time, CPI was in the 14 percent range. CPI didn’t return to 2 percent until 1986. At that point, the average Fed funds rate was 14.35 percent. Even with that, the CPI spiked back up for several years in the late 80s and early 90s.

You’ll notice that Volker drove rates significantly above the CPI. But Powell is no Volker. You can claim that the Fed drove rates modestly above CPI, but as we’ve seen, it’s all smoke and mirrors.

Monetary policy is still loose.

The problem is raising rates was still enough to pop bubbles and break things. Easy money is the mother’s milk of this debt-riddled economy. And while Fed policy isn’t tight, it is tighter – too tight for the level of debt.

It’s only a matter of time before the crisis manifests.

On the one hand, it can choose to stick to its guns, keep rates higher for longer, and bring down inflation. But that will almost certainly drag the economy into a crisis.

On the other hand, it can pick inflation and maybe rescue the economy.

And the reality is we may get both the rock and the hard place – stagflation.

This week Peter returned from vacation, and he was just in time for a surge in the price of gold. He discusses the factors contributing to gold’s record prices, the similarities between today and the 1970s, and data pointing to future inflation in America.

Peter starts this episode by noting how gold’s recent rise hasn’t received much coverage from the mainstream financial press:

“$30 on a Sunday night— that’s very rare to see that kind of move. But what’s even more rare is that there was no news. It’s not like something happened. Nobody dropped the bomb anywhere, right? It just went up. And that was on top of the near $40 rise that gold had on Friday before the holiday weekend. … Very rare to have that kind of move. But also very rare was the complete lack of attention that the gold rally has been getting.”

The media’s silence on gold serves larger financial interests in America that benefit from a weak economy and dollar:

“Another reason that CNBC and other financial analysts don’t want to talk about gold is because of the message that gold is sending. … Gold is not just some commodity. It is a commodity, but it’s a special commodity. … Gold is special because of the monetary properties and the monetary role that gold plays. If anything can be said to be the canary in the coal mine, it’s gold.

…

What is gold telling people, if they’re smart enough to listen? What gold is screaming is that what the Fed is contemplating is a mistake, that cutting interest rates whenever these cuts begin is the wrong policy.”

Even widely respected Fed Chairman Alan Greenspan has acknowledged the signaling power of gold’s price, but Jerome Powell and the current Fed are ignoring the signs of a weak economy:

“The Fed says they’re data dependent. Well, why are they ignoring all of this data that says everything they’re saying about inflation is BS? Powell keeps saying, ‘yes, we’re confident we think inflation is going to go back down to 2%.’ Why? Why should it do that? What gives him this confidence? Just because he’s raised interest rates up to 5.25%? Big deal! That’s not a high rate of interest, especially when you have a big inflation problem.”

Any student of history can recognize the political parallels between the inflation of the 1970s and now:

“We had the Vietnam War, which was expensive. We had the war on poverty, which was also expensive. Interestingly, we’ve lost both of those wars. … Poverty won, but we spent a lot of money on both of those wars. Then we also had the space race. … So the government was running these big deficits. … Where did the government get all the money to pay for all this stuff? Well, it borrowed it, right? They ran deficits, and they printed a lot of money. And so naturally, the consequence was inflation, rising prices.”

Peter sees a weakening dollar as the main recent driver behind gold’s price. If the dollar depreciates against other foreign currencies, gold could take off:

“I still believe that soon we’re going to see the dollar crack against other fiat currencies. And when that happens, you’re going to see a much more spectacular rise in the price of gold. If you think about what’s already happened, we’ve seen this big jump in gold prices without a weak dollar relative to other fiat currencies. Imagine how much stronger gold would be if the dollar were also falling in relation to the euro or the Australian dollar, Canadian dollar, emerging market currencies, the yen.”

Apparently foreign central banks can see what Powell can’t, and they’re stockpiling gold because of it:

“Foreign central banks realize that we don’t care [about inflation]. They’re holding all these dollars, and they see that we’re about to create more of them. We’re going to cut rates in the face of mounting evidence that they’re ignoring that inflation is going to be moving in the opposite direction. They claim that they want it down at 2%. All the evidence shows that it’s headed higher and their response is ‘we’re going to cut rates.’ And so foreign central banks want to get out.“

With its price at record highs and foreign central banks clamoring for the yellow metal, gold is strengthening as a hedge against terrible monetary policy. If Peter is right about future price action, now is the perfect time for investors to add to their precious metal holdings.

END

2.Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens/

Remember that time in 2016 when Attorney General Loretta Lynch decided she would take a private meeting with Bill Clinton on her plane as it was parked on the tarmac in Phoenix – while his wife, Hillary Clinton, was under federal investigation for using an unsafe private email server at her New York home to receive classified government emails when she was Secretary of State?

What President Biden’s Vice President, Kamala Harris, and his Chief of Staff, Jeff Zients, did in mid-March was equally scandalous. Harris had a “one-on-one lunch at the White House” with Jamie Dimon, the Chairman and CEO of the most crime-riddled bank in the United States, JPMorgan Chase. Zients also separately met with Dimon. That reporting comes courtesy of reporters Joshua Franklin and James Politi of the Financial Times (paywall). It has not been disputed by the Biden administration.

Dimon’s private meetings in Washington come as the bank (that has already admitted to a string of five criminal felony charges) is currently facing a serious investigation for “billions” of improperly conducted trades by its federally-insured bank. Two of its federal regulators, the Office of the Comptroller of the Currency and the Federal Reserve, settled those charges in March for a combined $348 million. Both regulators provided extremely sketchy details as to the precise nature of the trading misconduct. JPMorgan Chase revealed in an SEC filing in February that it remains under investigation in the same matter by a third regulator “but there is no assurance that such discussions will result in a resolution,” the bank wrote in the filing.

It would certainly not be the first time that Dimon attempted to throw his weight around in Washington to get his bank out of trouble. During Congressional hearings in 2012, when Dimon was called to testify about his bank allowing its traders to use deposits from its federally-insured bank to gamble in derivatives in London and lose what eventually tallied up to $6.2 billion (the infamous “London Whale” scandal), Dimon had the temerity to wear presidential cuff links to show off a gift from the White House.

Then there was Dimon’s meeting with Attorney General Eric Holder during the Obama administration when JPMorgan Chase was being investigated for widespread mortgage fraud. For what the bank got away with in that matter, see Matt Taibbi’s report revealing that the Justice Department sandbagged their key witness, a former lawyer/ whistleblower inside JPMorgan Chase, who called it “the biggest financial cover-up in history.”

According to the recent Financial Times report, Vice President Harris did not list the luncheon on her official daily calendar, suggesting she knew it was inappropriate. The FT reporters also reveal the following:

“Dimon, one of the most influential voices on Wall Street, also separately met White House chief of staff Jeff Zients while he was in Washington, as well as federal regulators and members of Congress. It could not be learnt what was discussed at the meetings. The White House and JPMorgan, the largest US bank by assets, declined to comment.”

“In Chapter 4, we compared JPMC [JPMorgan Chase] to the Gambino crime family to demonstrate the many areas in which these two organizations had the same goals and strategies. In fact, the most significant difference between JPMC and the Gambino Crime Family is the way the government treats them. While Congress made it a national priority to eradicate organized crime, there is an appalling lack of appetite in Washington to decriminalize Wall Street. Congress and the executive branch of the government seem determined to protect Wall Street criminals, which simply assures their proliferation…

“If Jamie Dimon is running a criminal institution, he should be prosecuted for it. And law enforcement has the perfect tool for such a prosecution: the Racketeer Influenced and Corrupt Organizations ACT (RICO).”

In 2014, the non-profit watchdog, Better Markets, filed a federal lawsuit against the U.S. Department of Justice and the man who sat at its helm, Attorney General Eric Holder. The lawsuit challenged what had emerged out of that cozy meeting between Holder and Dimon – a $13 billion out-of-court settlement over the bank’s sale of toxic mortgages.

Better Markets wrote on its website that this was at the time “The largest settlement in U.S. history from a single entity by more than 300%” and that it “granted JP Morgan blanket civil immunity for years of alleged, but undisclosed, pervasive, egregious and knowing fraudulent and illegal conduct that contributed to the 2008 financial crash and the worst economy since the Great Depression.”

“The Attorney General and other senior DOJ political appointees negotiated directly and entirely in secret with the CEO of JP Morgan Chase [Jamie Dimon], someone who was considered a possible Treasury Secretary just a few years ago.

“The cellphone of DOJ’s third highest ranking official rang with the ‘familiar’ phone number of JP Morgan Chase’s CEO [Jamie Dimon], who called to offer billions of dollars to stop DOJ from holding a press conference and filing a lawsuit in just a few hours. The call worked, and the press conference and lawsuit were both called off.

“DOJ gave complete civil immunity to JP Morgan Chase for defrauding thousands in exchange for $13 billion, via a contract that was negotiated and finalized in secret without any review or approval by a federal court.”

Attorneys for the Justice Department asked the federal court to dismiss the Better Markets lawsuit on the basis that Better Markets lacked standing to file the lawsuit. The U.S. District Court for the District of Columbia did just that in a longwinded decision that effectively stripped Americans of their ability to fight back against the increasingly corrupt nexus between Washington and Wall Street.

If you agree with Wall Street On Parade that the current banking structure in the U.S. represents a threat to national security and economic stability, please contact your U.S. Senators today via the U.S. Capitol switchboard by dialing (202) 224-3121. Tell your Senators to hold immediate hearings on the urgent need to restore the Glass-Steagall Act to separate Wall Street’s trading casinos from federally-insured commercial banks.

END

JAMES RICKARDS…

Rickards is correct: Russia has no interest in invading European countries

A lot of people seem to have forgotten about the war in Ukraine. That’s a mistake.

Russia is slowly but steadily defeating Ukraine, which is becoming increasingly obvious to everyone except the most anti-Russian diehards.

That’s leading to desperation in elite Western circles determined to stop Russia one way or the other. In their minds, they simply can’t let Putin win. They think that if Putin wins in Ukraine, he’ll next move on to the Baltic states, Poland and elsewhere.

You know the West is getting desperate based on recent threats by France’s Emmanuel Macron to send troops to Ukraine.

The vice president of the Russia Duma, Pyotr Tolstoy (descendant of the great Russian writer Leo Tolstoy), warned that French troops would be priority targets for Russian forces if they entered Ukraine.

Even though France would send troops independent of NATO, that puts us on a very dangerous path that ultimately leads to direct conflict between NATO and Russia. And that path ends in nuclear war ultimately.

Tolstoy added that it would take “just two minutes to nuke Paris.” It’s not hard to envision how quickly things could escalate if France decided to send troops to Ukraine.

More Escalation

Meanwhile, NATO is preparing to send F-16s to Ukraine. Airfields in Ukraine are highly vulnerable to Russian attack, especially since Ukraine’s air defenses are heavily depleted at this point and the Russian air force is becoming increasingly active in Ukraine.

But if NATO allows the F-16s to be based on its own airbases, Putin has warned that these airfields would become a “legitimate target” if strikes against Russian forces were launched from them.

By the way, Russia has hypersonic missiles that NATO has no practical ability to shoot down, so these attacks would likely be successful. Of course, NATO would have to retaliate in kind. You can imagine where all this could lead.

We’re already well along the escalation ladder. And the higher you go, the more face you stand to lose if you back down. I warned about that from the outset of the war.

But the entire notion that Russia poses some existential threat to NATO or Europe is absurd.

Putin Has Nothing to Gain and Everything to Lose

First off, the theory that Putin will invade other countries if he wins in Ukraine is nonsense. The Russian army lacks the men and materiel to occupy Ukraine while simultaneously invading other countries.

This isn’t the Soviet Union with its massive tank armies poised to roll over Western Europe. And Soviet communism is long dead, so there’s no ideological basis for Russia to invade Europe. These days Russia is a conservative, Orthodox Christian nation.

But more importantly, Putin has absolutely no incentive to invade any of these nations, which are NATO members. What do they have that he wants?

All it would do is trigger Article 5 of the NATO Charter, which stipulates that an attack on one member is an attack on all, inviting a massive NATO response. At that point, you’re on the fast track to nuclear war.

Putin is fully aware of that.

Fearmongers like to point to what Putin once said in a speech:

“Whoever doesn’t miss the Soviet Union doesn’t have a heart.”

They take that as proof that he wants to recreate the Soviet Union. But they conveniently omit what he said next:

“Whoever wants it back doesn’t have a brain.”

Whatever you think of Putin, he definitely has a brain. He has no intention to restore the Soviet Union.

It’s Not Just About Intentions

But like any great power, Russia has interests, and Ukraine has always been a vital strategic interest to Russia.

And Russia is not going to tolerate Ukraine joining a NATO alliance that’s hostile to Russia. Critics say Ukraine is a free and independent nation that can join NATO if it wants. Russia has no say in the matter, even though Ukraine borders Russia.

Well, I guess they never heard of the Monroe Doctrine. The U.S. basically declared the entire Western hemisphere its own domain. But a great power like Russia can’t have a say in its own backyard?

Critics also say that the idea of NATO invading Russia is ridiculous. That’s just Russian paranoia. And that’s true, NATO isn’t going to actually invade Russia. But it’s not just intentions that count in the world of geopolitics. It’s also capabilities.

As Bismarck once noted: “What matters in politics is capabilities, not intentions. Intentions change, capabilities remain.”

Given Russia’s long history of being invaded, it’s not hard to imagine why it might seem a bit paranoid of exterior threats.

If you look at a map, parts of Ukraine are actually east of Moscow.

Source: The Economist

Will the U.S. Keep the War Going?

Of course, Ukraine can’t continue fighting without U.S. assistance. The Biden White House wants $60 billion of new money to give to Ukraine to fight the war. This is on top of several hundred billion already provided.

This was proposed last summer but has stalled in the Senate and House of Representatives ever since. The House passed a separate bill to aid Israel last fall, but the Senate refused to take it up because they want to tie that aid to money for Ukraine.

The Senate passed a bill that would provide aid for Ukraine, Israel and Taiwan in one package combined with some money for phony border security.

That bill was so unpopular it could not even make it out of the Senate. Then the House insisted on passing regular appropriations before considering Ukraine.

That process was completed on March 23, but now Congress is on a two-week Easter recess so nothing further will happen until mid-April. No one has even answered the most important question, which is what would Ukraine do with the money.

They can’t buy badly needed 155mm artillery shells because the Western arsenals are bare and factories are not geared to make more than a handful. It will take years to expand that manufacturing capacity.

You can walk into a store with a wallet full of $100 bills, but if the shelves are empty, it doesn’t do you any good. The products simply aren’t there.

Meanwhile, wonder weapons from the West such as tanks, cruise missiles, armored personnel carriers, HIMARS precision-guided artillery and anti-missile batteries have all been destroyed, disabled or shot down by Russia.

The war in Ukraine hasn’t been good advertising for Western weapons.

Fallout

To repeat what I said earlier, Ukraine is losing the war badly. Russia is advancing on the southern and eastern fronts in Ukraine.

Still, the pressure on House Speaker Mike Johnson to do something remains. The Republican warmongers in the Senate like Lindsey Graham and Joni Ernst won’t let up. Many Republicans in the House such as Chip Roy and Marjorie Taylor Greene are opposed to Johnson on this.

Incredibly, Johnson may respond to the pressure with a solution worse than an outright appropriation. He may get behind efforts to steal $300 billion in Russian central bank assets held in the form of U.S. Treasury securities.

That would destroy confidence in the U.S. dollar, U.S. Treasury securities and the U.S. rule of law. Russia would quickly recover the loss by seizing $300 billion or more of Western assets still in Russia. No one in Congress seems to understand any of this.

If they follow through, the economic fallout would be bad enough. But if this war doesn’t stop soon, we could ultimately be looking at nuclear fallout.

END

Inflation-Risk Latecomers Pile Into Silver

WEDNESDAY, APR 03, 2024 – 10:50 AM

Authored by Simon White, Bloomberg macro strategist,

As gold makes new highs, speculators’ net longs in silver are jumping higher.

Inflation and global growth risks – as well as demand from China – are helping to drive gold to new all-time highs. For those late to the trade, silver is serving as the next best thing.

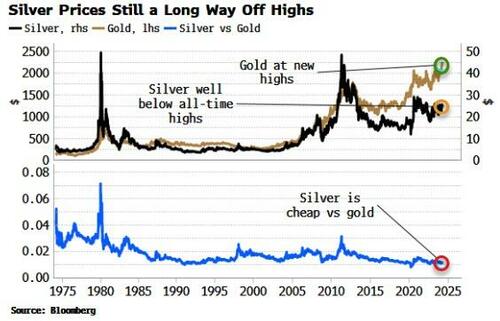

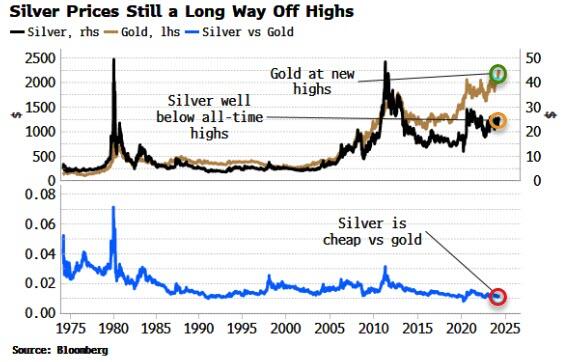

Silver remains well off the highs it reached in 1980 (the Hunt brothers’ infamous corner) and in 2011, and it is very cheap in comparison to gold.

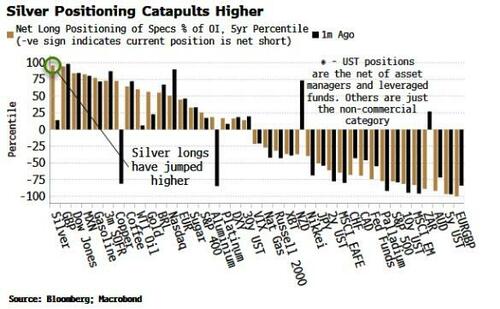

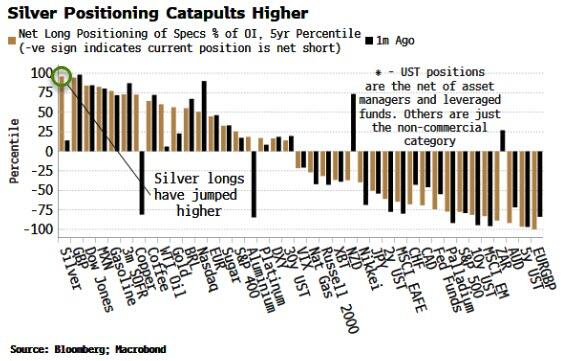

That probably explains the surge higher in speculator net longs in silver, according to the Commitment of Traders data.

Silver positioning, from being nearly flat a month ago, is now near five-year highs, and longer on a percentile basis than any other major bond, equity or commodity future.

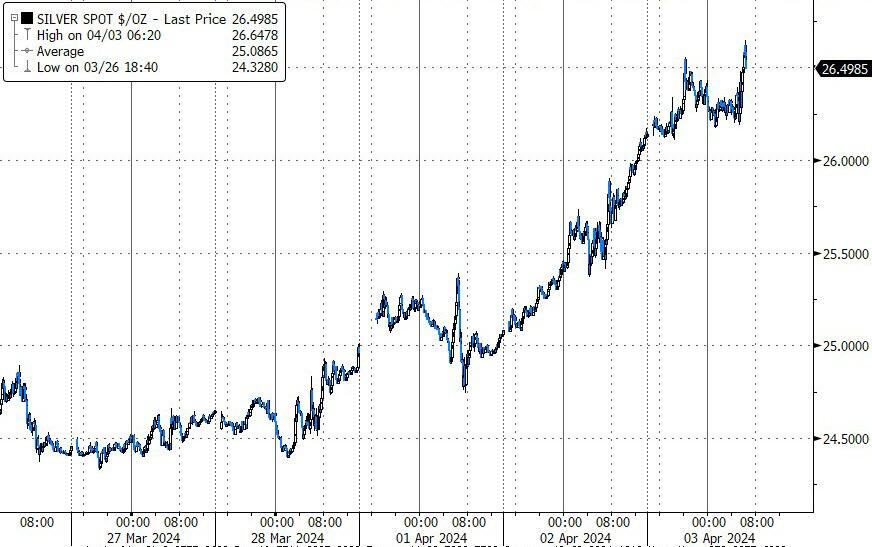

Silver is notoriously volatile, and if speculators are correct in their view, the gains could be rapid and large.

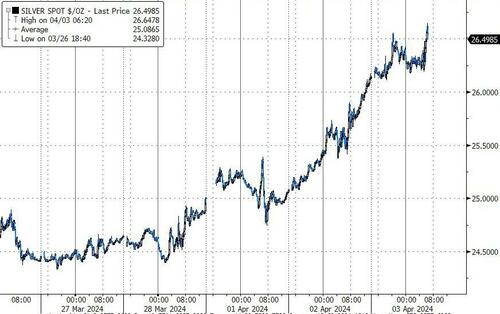

It’s up today over 9% in the last few days, topping its recent high of ~$26.

In these days of rampant inflation, it’s imperative that we return to the gold standard – and the real thing too.

By this I mean the classical gold standard, not the so-called “gold exchange” standard, and with no fractional reserve banking, just as the great Murray Rothbard wanted. In what follows, I’ll discuss some of the economic issues below, but it’s important to realize that it’s a moral issue as well.

I spoke about the difference between the classical gold standard and the fake gold standard. This might seem a technical issue, but it’s one of vital importance. Joe Salerno, the leading contemporary Austrian School authority on monetary economics and Academic Vice President of the Mises Institute, explains:

“The historical embodiment of monetary freedom is the gold standard. The era of its greatest flourishing was not coincidentally the 19th century, the century in which classical liberal ideology reigned, a century of unprecedented material progress and peaceful relations between nations. Unfortunately, the monetary freedom represented by the gold standard, along with many other freedoms of the classical liberal era, was brought to a calamitous end by World War I.

Also, and not so coincidentally, this was the “War to Make the World Safe for Mass Democracy,” a political system which we have all learned by now is the great enemy of freedom in all its social and economic manifestations.

Now, it is true that the gold standard did not disappear overnight, but limped along in weakened form into the early 1930s. But this was not the pre-1914 classical gold standard, in which the actions of private citizens operating on free markets ultimately controlled the supply and value of money and governments had very little influence.

Under this monetary system, if people in one nation demanded more money to carry out more transactions or because they were more uncertain of the future, they would export more goods and financial assets to the rest of the world, while importing less. As a result, additional gold would flow in through a surplus in the balance of payments increasing the nation’s money supply.

Sometimes, private banks tried to inflate the money supply by issuing additional bank notes and deposits, called “fiduciary media,” promising to pay gold but unbacked by gold reserves. They lent these notes and deposits to either businesses or the government. However, as soon as the borrowers spent these additional fractional-reserve notes and deposits, domestic incomes and prices would begin to rise.

As a result, foreigners would reduce their purchases of the nation’s exports, and domestic residents would increase their spending on the relatively cheap foreign imports. Gold would flow out of the coffers of the nation’s banks to finance the resulting trade deficit, as the excess paper notes and checks were returned to their issuers for redemption in gold.

To check this outflow of gold reserves, which made their depositors very nervous, the banks would contract the supply of fiduciary media bringing about a monetary deflation and an ensuing depression.

Temporarily chastened by the experience, banks would refrain from again expanding credit for a while. If the Treasury tried to issue convertible notes only partially backed by gold, as it occasionally did, it too would face these consequences and be forced to restrain its note issue within narrow bounds.

Thus, governments and commercial banks under the gold standard did not have much influence over the money supply in the long run. The only sizable inflations that occurred during the 19th century did so during wartime when almost all belligerent nations would “go off the gold standard.” They did so in order to conceal the staggering costs of war from their citizens by printing money rather than raising taxes to pay for it.

For example, Great Britain experienced a substantial inflation at the beginning of the 19th century during the period of the Napoleonic Wars, when it had suspended the convertibility of the British pound into gold. Likewise, the United States and the Confederate States of America both suffered a devastating hyperinflation during the War for Southern Independence, because both sides issued inconvertible Treasury notes to finance budget deficits. It is because politicians and their privileged banks were unable to tamper with and inflate a gold money that prices in the United States and in Great Britain at the close of the 19th century were roughly the same as they were at the beginning of the century.

Within weeks of the outbreak of World War I, all belligerent nations departed from the gold standard. Needless to say by the war’s end the paper fiat currencies of all these nations were in the throes of inflations of varying degrees of severity, with the German hyperinflation that culminated in 1923 being the worst. To put their currencies back in order and to restore the public’s confidence in them, one country after another reinstituted the gold standard during the 1920s.

Unfortunately, the new gold standard of the 1920s was fundamentally different from the classical gold standard. For one thing, under this latter version, gold coin was not used in daily transactions. In Great Britain, for example, the Bank of England would only redeem pounds in large and expensive bars of gold bullion. But gold bullion was mainly useful for financing international trade transactions.

Other countries such as Germany and the smaller countries of Central and Eastern Europe used gold-convertible foreign currencies such as the US dollar or the pound sterling as reserves for their own domestic currencies. This was called the gold-exchange standard.

While the US dollar was technically redeemable in honest-to-goodness gold coin, banks no longer held reserves in gold coin but in Federal Reserve notes. All gold reserves were centralized, by law, in the hands of the Fed and banks were encouraged to use Fed notes to cash checks and pay for checking and savings deposit withdrawals. This meant that very little gold coin circulated among the public in the 1920s, and residents of all nations came increasingly to view the paper IOUs of their central banks as the ultimate embodiment of the dollar, franc, pound, etc.

This state of affairs gave governments and their central banks much greater leeway for manipulating their national money supplies. The Bank of England, for example, could expand the amount of paper claims to gold pounds through the banking system without fearing a run on its gold reserves for two reasons.

Foreign countries on the gold exchange standard would be willing to pile up the paper pounds that flowed out of Great Britain through its balance of payments deficit and not demand immediate conversion into gold. In fact by issuing their own currency to tourists and exporters in exchange for the increasing quantities of inflated paper pounds, foreign central banks were in effect inflating their own money supplies in lock-step with the Bank of England. This drove up prices in their own countries to the inflated level attained by British prices and put an end to the British deficits.

In effect, this system enabled countries such as Great Britain and the United States to export monetary inflation abroad and to run “a deficit without tears” — that is, a balance-of-payments deficit that does not involve a loss of gold.

But even if gold reserves were to drain out of the vaults of the Bank of England or the Fed to foreign nations, British and US citizens would be disinclined, either by law or by custom, to put further pressure on their respective central banks to stop inflating by threatening bank runs to rid themselves of their depreciating notes and retrieve their rightful property left with the banks for safekeeping.

Unfortunately, contemporary economists and economic historians do not grasp the fundamental difference between the hard-money classical gold standard of the 19th century and the inflationary phony gold standard of the 1920s.” See here.

Many people think that even if 100% reserve banking is desirable as an ideal, it would never work in practice. How could banks stay in business if they couldn’t lend their checking deposits? Doesn’t the supply of money need to expand as the economy grows? Murray Rothbard demolishes these objections with characteristic force:

“Certain standard objections have been raised against 100 percent banking and against 100 percent gold currency in particular. One generally accepted argument against any form of 100 percent banking I find particularly and strikingly curious: that under 100 percent reserves, banks would not be able to continue profitably in business. I see no reason why banks should not be able to charge their customers for their services, as do all other useful businesses. This argument points to the supposedly enormous benefits of banking; if these benefits were really so powerful, then surely the consumers would be willing to pay a service charge for them, just as they pay for traveler’s checks now. If they were not willing to pay the costs of the banking business as they pay the costs of all other industries useful to them, then that would demonstrate the advantages of banking to have been highly overrated. At any rate, there is no reason why banking should not take its chance in the free market with every other industry.

The major objection against 100 percent gold is that this would allegedly leave the economy with an inadequate money supply. Some economists advocate a secular increase of the supply of money in accordance with some criterion: population growth, growth of volume of trade, and the like; others wish the money supply to be adjusted to provide a stable and fixed price level. In both cases, of course, the adjusting and manipulating could only be done by government. These economists have not fully absorbed the great monetary lesson of classical economics: that the supply of money essentially does not matter. Money performs its function by being a medium of exchange; any change in its supply, therefore, will simply adjust itself in the purchasing power of the money unit, that is, in the amount of other goods that money will be able to buy. An increase in the supply of money means merely that more units of money are doing the social work of exchange and therefore that the purchasing power of each unit will decline. Because of this adjustment, money, in contrast to all other useful commodities employed in production or consumption, does not confer a social benefit when its supply increases. The only reason that increased gold mining is useful, in fact, is that the large supply of gold will satisfy more of the non–monetary uses of the gold commodity.

There is therefore never any need for a larger supply of money (aside from the non-monetary uses of gold or silver). An increased supply of money can only benefit one set of people at the expense of another set, and, as we have seen, that is precisely what happens when government or the banks inflate the money supply. And that is precisely what my proposed reform is designed to eliminate. There can, incidentally, never be an actual monetary “shortage,” since the very fact that the market has established and continues to use gold or silver as a monetary commodity shows that enough of it exists to be useful as a medium of exchange.